UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| | |

Investment Company Act file number | | 811-02753 |

SBL FUND

|

| (Exact name of registrant as specified in charter) |

| | |

| ONE SECURITY BENEFIT PLACE, TOPEKA, KANSAS | | 66636-0001 |

| (Address of principal executive offices) | | (Zip code) |

MICHAEL G. ODLUM, PRESIDENT

SBL FUND

ONE SECURITY BENEFIT PLACE

TOPEKA, KANSAS 66636-0001

|

| (Name and address of agent for service) |

Registrant’s telephone number, including area code: (785) 438-3000

Date of fiscal year end: December 31

Date of reporting period: December 31, 2006

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. §3507.

| Item 1. | Reports to Stockholders. |

SBL Fund

December 31, 2006

Annual Report

Table of Contents

1

This page left blank intentionally.

2

| | |

| | Series A |

| Manager’s Commentary | | (Equity Series) |

| February 15, 2007 | | (unaudited) |

Advisor, Security Management Company, LLC

Mark A. Mitchell

Portfolio Manager

To Our Shareholders:

Series A of the SBL Fund - Equity Series returned 12.89% during the year, lagging the benchmark S&P 500 Index’s return of 15.79% and the Series’ peer group median return of 13.92%. Over the last few years, higher beta, smaller capitalization companies have helped drive equity markets higher. In such environments, we tend to under perform. We still believe the market is not yet recognizing the potential in several high quality large capitalization companies. Our performance has been disappointing and we feel not indicative of our potential. We are focused on improving your Series’ returns by upgrading the talent on our equity research team and strengthening our research process. We believe that our approach will deliver good performance over a long-term investment horizon.

Our investment philosophy is centered around three key tenants: First, good investments are purchased at less than their intrinsic value; second, a long-term approach and patience are critical to successful investing; and lastly, we concentrate our investments in companies that have the greatest return potential.

Our process is a bottom-up research driven investment process that attempts to identify companies that have a competitive advantage or have the ability to become more competitive in the future. We focus on owning these companies for three to five years or longer which we believe differentiates us from a majority of our peers and ultimately allows us to make better investment decisions. We buy these companies when their current price trades below their intrinsic value. We closely monitor each company’s progress. We will sell a company if the valuation no longer makes sense, we’ve made a mistake, our investment thesis is no longer valid, or we have a more attractive investment alternative. For this Series, we apply the approach to a broad range of both growth and value names.

Financial, Technology, and Industrial Stocks Top Performers

The Series’ financial holdings were up 35% compared to 19% for the Index. This was driven almost entirely by our position in First Marblehead Corporation, up over 150%. Ill-placed short-term concerns over the company’s competitive position offered a great buying opportunity for a leading student lender with a significant competitive advantage as a result of their loan under writing capability, superior economics, and additional value-added services.

The technology sector was up over 17% versus the comparable sector Index return of 9%. The largest contributor was Unisys Corporation, up 34%. The company benefited from improving its competitive position by lowering costs and improving business execution. Not owning Intel, down 17% and Yahoo, down 34%, helped the Series as well. While both are good companies, the valuations did not meet our criteria for an attractive risk/reward profile.

General Dynamics Corporation in the industrial sector was up 32%, with the company benefiting from strong results in its defense related segment and corporate aircraft segment.

Energy and Telecom Disappointing

Energy overall negatively impacted the Series. In the Series the sector was up just over 6% versus up 24% for the energy sector return within the Index. This was driven in part by Evergreen Energy, Inc., down over 42% (previously known as KFx), and Halliburton Company, up only 1%. Evergreen Energy was hurt by concerns over the viability of the initial production results of its proprietary clean coal technology. Halliburton was impacted more generally by the recent exodus from oil services related names as a result of a weakening energy commodity market.

The telecom sector in the benchmark was up over 36%, while our sector return was down 11%. Not owning AT&T, up 53%, and Bell South, up 80%, negatively impacted the Series. It appears the market is more confident in the newly-merged telecom players. We've avoided these names because we believe it’s very difficult to determine which, if any, company will be able to create a lasting competitive advantage that allows them to generate acceptable returns on the significant capital expenditures required to build out their services offerings. Our position in Sprint Nextel Corporation, down 10%, hurt the Series’ performance. Concerns over how the integration of Nextel was progressing and lack of improvement in its core legacy Sprint operations contributed to the weakness. We still believe in management’s ability to show steady improvement as demonstrated by the spinoff of its slower growing wireline business.

2007 Market Outlook

The current low return investment environment that exists outside of equities has continued to make available ample liquidity in the U.S. equity market. Falling energy prices have helped increase consumer confidence and provide support to corporate profit margins through lower raw material input prices. Additionally, businesses have very healthy balance sheets to help drive future growth initiatives.

3

| | |

| | | Series A |

| Manager’s Commentary | | (Equity Series) |

| February 15, 2007 | | (unaudited) |

As we noted in last year’s shareholder letter, we’ve been concerned about a slowdown in U.S. consumer spending for some time. This concern has yet to materialize, but we still think it will happen. Lower energy prices will help, however, higher interest rates and a housing market slowdown provide likely headwinds. The Federal Reserve is walking a fine line between managing inflation risks while supporting economic growth. We’re unsure, like most in the market, what the Fed’s next move is. This uncertainty will weigh on the markets until it’s resolved.

We believe that investing is a long-term pursuit that requires patience and a consistent approach. Dollar cost averaging is a sound way to build long-term value1. We recognize there are many investment fund alternatives available today and thank you for your business and the confidence you place in us.

|

| Sincerely, |

|

| |

| Mark A. Mitchell, Portfolio Manager |

1 | Dollar cost averaging does not assure profits or protect against loss in a declining market. |

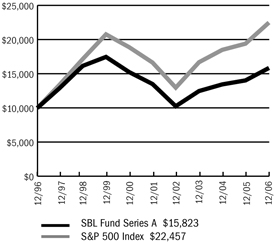

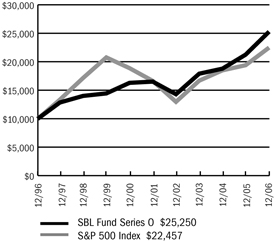

PERFORMANCE

Series A vs. S&P 500 Index

$10,000 Over 10 Years

The chart above assumes a hypothetical $10,000 investment in Series A (Equity Series) on December 31, 1996 and reflects the fees and expenses of Series A. The S&P 500 Index is a capitalization-weighted index composed of 500 selected common stocks that represent the broad domestic economy and is a widely recognized unmanaged index of market performance.

Average Annual Returns

| | | | | | | | | |

Periods Ended 12-31-061 | | 1 Year | | | 5 Years | | | 10 Years | |

Series A | | 12.89 | % | | 3.24 | % | | 4.70 | % |

1 | Performance figures do not reflect fees and expenses associated with an investment in variable insurance products offered by Security Benefit Life Insurance Company. If returns had taken into account these fees and expenses, performance would have been lower. Shares of a Series of SBL Fund are available only through the purchase of such products. |

The performance data quoted above represents past performance. Past performance is not predictive of future performance. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

Portfolio Composition by Sector

| | | |

Consumer Discretionary | | 11.51 | % |

Consumer Staples | | 8.58 | |

Energy | | 10.50 | |

Financials | | 20.43 | |

Health Care | | 17.08 | |

Industrials | | 16.40 | |

Information Technology | | 10.83 | |

Materials | | 0.88 | |

Telecommunication Services | | 2.11 | |

Asset Backed Commercial Paper | | 1.53 | |

Commercial Paper | | 0.29 | |

Repurchase Agreement | | 0.08 | |

Liabilities, less cash & other assets | | (0.22 | ) |

Total net assets | | 100.00 | % |

| | | |

See accompanying notes.

4

| | |

| | | Series A |

| Manager’s Commentary | | (Equity Series) |

| December 31, 2006 | | (unaudited) |

PERFORMANCE

Information About Your Series Expenses

Calculating your ongoing series expenses

Example

As a shareholder of the Series, you incur ongoing costs, including management fees and other series expenses. Performance figures and expense ratios do not reflect fees and expenses associated with an investment in variable insurance products. Shares of a Series of SBL Fund are available only through the purchase of such products. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Series and to compare these costs with ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period, July 1, 2006 - December 31, 2006.

Actual Expenses

The first line in the table provides information about actual account values and actual expenses. You may use the information in this table, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the table under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line in the table provides information about hypothetical account values and hypothetical expenses based on the Series actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Series actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Series and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other mutual funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any fees and expenses associated with an investment in variable insurance products. Therefore, the second line is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these fees and expenses associated with an investment in variable insurance products were included, your costs would have been higher.

Series Expenses

| | | | | | | | | |

| | | Beginning Account Value 07-01-06 | | Ending Account Value 12-31-061 | | Expenses Paid During Period2 |

| | | |

| | | |

Series A (Equity Series) | | | | | | | | | |

Actual | | $ | 1,000.00 | | $ | 1,107.60 | | $ | 4.83 |

Hypothetical | | | 1,000.00 | | | 1,020.62 | | | 4.63 |

1 | The actual ending account value is based on the actual total return of the Series for the period July 1, 2006 to December 31, 2006 after actual expenses and will differ from the hypothetical ending account value which is based on the Series expense ratio and a hypothetical annual return of 5% before expenses. The actual cumulative return at net asset value for the period July 1, 2006 to December 31, 2006 was 10.76%. |

2 | Expenses are equal to the Series annualized expense ratio of 0.91%, net of earnings credits, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). |

5

| | |

| Schedule of Investments | | Series A (Equity Series) |

| December 31, 2006 | | |

| | | | | | |

| | | Shares | | Value |

COMMON STOCK - 98.3% | | | | | | |

Aerospace & Defense - 4.0% | | | | | | |

General Dynamics Corporation | | | 184,100 | | $ | 13,687,835 |

L-3 Communications Holdings, Inc. | | | 46,000 | | | 3,761,880 |

| | | | | | |

| | | | | | 17,449,715 |

| | | | | | |

Air Freight & Logistics - 2.9% | | | | | | |

FedEx Corporation | | | 119,500 | | | 12,980,090 |

| | | | | | |

Biotechnology - 3.4% | | | | | | |

Amgen, Inc. * | | | 220,150 | | | 15,038,447 |

| | | | | | |

Broadcasting & Cable TV - 2.3% | | | | | | |

CBS Corporation (CI.B) | | | 152,950 | | | 4,768,981 |

Univision Communications, Inc. * | | | 155,500 | | | 5,507,810 |

| | | | | | |

| | | | | | 10,276,791 |

| | | | | | |

Coal & Consumable Fuels - 2.0% | | | | | | |

Evergreen Energy, Inc. * | | | 872,400 | | | 8,628,036 |

| | | | | | |

Communications Equipment - 1.6% | | | | | | |

ADC Telecommunications, Inc. * | | | 474,114 | | | 6,888,876 |

| | | | | | |

Construction & Engineering - 2.2% | | | | | | |

Shaw Group, Inc. * (1) | | | 292,200 | | | 9,788,700 |

| | | | | | |

Consumer Finance - 6.4% | | | | | | |

American Express Company | | | 222,700 | | | 13,511,209 |

First Marblehead Corporation | | | 267,900 | | | 14,640,735 |

| | | | | | |

| | | | | | 28,151,944 |

| | | | | | |

Data Processing & Outsourced Services - 3.1% | | | | | | |

First Data Corporation | | | 208,700 | | | 5,326,024 |

Western Union Company | | | 382,000 | | | 8,564,440 |

| | | | | | |

| | | | | | 13,890,464 |

| | | | | | |

Drug Retail - 2.9% | | | | | | |

CVS Corporation | | | 419,500 | | | 12,966,745 |

| | | | | | |

Health Care Equipment - 3.1% | | | | | | |

Hospira, Inc. * | | | 128,000 | | | 4,298,240 |

Zimmer Holdings, Inc. * | | | 121,300 | | | 9,507,494 |

| | | | | | |

| | | | | | 13,805,734 |

| | | | | | |

Health Care Services - 2.5% | | | | | | |

Medco Health Solutions, Inc. * | | | 206,200 | | | 11,019,328 |

| | | | | | |

Home Improvement Retail - 4.0% | | | | | | |

Home Depot, Inc. | | | 445,200 | | | 17,879,232 |

| | | | | | |

Hotels, Resorts & Cruise Lines - 2.6% | | | | | | |

Carnival Corporation | | | 237,500 | | | 11,649,375 |

| | | | | | |

Hypermarkets & Super Centers - 5.7% | | | | | | |

Costco Wholesale Corporation | | | 231,000 | | | 12,212,970 |

Wal-Mart Stores, Inc. | | | 275,800 | | | 12,736,444 |

| | | | | | |

| | | | | | 24,949,414 |

| | | | | | |

Industrial Conglomerates - 7.3% | | | | | | |

General Electric Company | | | 522,700 | | | 19,449,667 |

Tyco International, Ltd. | | | 419,600 | | | 12,755,840 |

| | | | | | |

| | | | | | 32,205,507 |

| | | | | | |

Industrial Gases - 0.9% | | | | | | |

Praxair, Inc. | | | 65,800 | | | 3,903,914 |

| | | | | | |

Integrated Oil & Gas - 6.5% | | | | | | |

Chevron Corporation | | | 134,000 | | | 9,853,020 |

Exxon Mobil Corporation | | | 246,900 | | | 18,919,947 |

| | | | | | |

| | | | | | 28,772,967 |

| | | | | | |

IT Consulting & Other Services - 2.7% | | | | | | |

Unisys Corporation * | | | 1,505,850 | | | 11,805,864 |

| | | | | | |

Managed Health Care - 5.1% | | | | | | |

UnitedHealth Group, Inc. | | | 172,000 | | | 9,241,560 |

WellPoint, Inc. * | | | 166,600 | | | 13,109,754 |

| | | | | | |

| | | | | | 22,351,314 |

| | | | | | |

Movies & Entertainment - 2.5% | | | | | | |

Time Warner, Inc. | | | 505,000 | | | 10,998,900 |

| | | | | | |

Multi-Line Insurance - 5.1% | | | | | | |

American International Group, Inc. | | | 315,800 | | | 22,630,228 |

| | | | | | |

Oil & Gas Drilling - 0.7% | | | | | | |

Transocean, Inc. * (1) | | | 40,200 | | | 3,251,778 |

| | | | | | |

Oil & Gas Equipment & Services - 1.3% | | | | | | |

BJ Services Company | | | 70,900 | | | 2,078,788 |

Halliburton Company | | | 117,700 | | | 3,654,585 |

| | | | | | |

| | | | | | 5,733,373 |

| | | | | | |

Other Diversified Financial Services - 5.3% | | | | | | |

Citigroup, Inc. | | | 278,600 | | | 15,518,020 |

JPMorgan Chase & Company | | | 165,900 | | | 8,012,970 |

| | | | | | |

| | | | | | 23,530,990 |

| | | | | | |

Pharmaceuticals - 3.0% | | | | | | |

Johnson & Johnson | | | 201,400 | | | 13,296,428 |

| | | | | | |

Property & Casually Insurance - 3.6% | | | | | | |

Berkshire Hathaway, Inc. * | | | 145 | | | 15,948,550 |

| | | | | | |

Systems Software -3.5% | | | | | | |

Microsoft Corporation | | | 510,200 | | | 15,234,572 |

| | | | | | |

Wireless Telecommunication Services - 2.1% | | | | | | |

Sprint Nextel Corporation | | | 492,800 | | | 9,308,992 |

| | | | | | |

TOTAL COMMON STOCK (Cost $350,874,900) | | | | | $ | 434,336,268 |

| | | | | | |

| | |

| | | Principal

Amount | | Value |

ASSET BACKED COMMERCIAL PAPER - 1.5% | | | | | | |

Financial Companies - Miscellaneous Receivables - 1.0% | | | | | | |

Fairway Finance Corporation | | | | | | |

5.35%, 1/5/2007 | | $ | 1,200,000 | | | 1,199,291 |

The accompanying notes are an integral part of the financial statements.

6

| | |

| Schedule of Investments | | Series A (Equity Series) |

| December 31, 2006 - continued | | |

| | | | | | | |

| | | Principal

Amount | | Value | |

ASSET BACKED COMMERCIAL PAPER (continued) | | | | | | | |

Financial Companies - Miscellaneous Receivables (continued) | | | | | | | |

Fairway Finance Corporation (continued) | | | | | | | |

5.35%, 1/9/2007 | | $ | 1,800,000 | | $ | 1,797,880 | |

Jupiter Securitization Corporation | | | | | | | |

5.35%, 1/8/2007 | | | 1,275,000 | | | 1,273,683 | |

| | | | | | | |

| | | | | | 4,270,854 | |

| | | | | | | |

Financial Companies - Trade Receivables - 0.5% | | | | | | | |

Old Line Funding LLC | | | 1,000,000 | | | 999,555 | |

5.26%, 1/4/2007 | | | | | | | |

Sheffield Receivables Corporation | | | 1,500,000 | | | 1,499,781 | |

5.265%, 1/2/2007 | | | | | | | |

| | | | | | | |

| | | | | | 2,499,336 | |

| | | | | | | |

TOTAL ASSET BACKED COMMERCIAL PAPER (Cost $6,770,190) | | | | | $ | 6,770,190 | |

| | | | | | | |

COMMERCIAL PAPER - 0.3% | | | | | | | |

Brokerage - 0.3% | | | | | | | |

ING (U.S.) Funding LLC | | | | | | | |

5.35%, 1/3/2007 | | | 1,300,000 | | | 1,299,614 | |

| | | | | | | |

TOTAL COMMERCIAL PAPER (Cost $1,299,614) | | | | | $ | 1,299,614 | |

| | | | | | | |

REPURCHASE AGREEMENT - 0.1% | | | | | | | |

United Missouri Bank, 4.85%, dated 12-29-06, matures 01-02-07; repurchase amount of $340,183 (Collateralized by FHLMC, 5.00%, 08-15-35 with a value of $346,821) | | $ | 340,000 | | $ | 340,000 | |

| | | | | | | |

TOTAL REPURCHASE AGREEMENT (Cost $340,000) | | | | | $ | 340,000 | |

| | | | | | | |

Total Investments (SBL A Fund) | | | | | $ | 442,746,072 | |

(Cost $359,284,704) - 100.2% | | | | | | | |

Liabilities in Excess of Other Assets - (0.2)% | | | | | | (957,992 | ) |

| | | | | | | |

TOTAL NET ASSETS - 100.0% | | | | | $ | 441,788,080 | |

| | | | | | | |

Footnotes

Percentages are stated as a percent of net assets.

For federal income tax purposes the identified cost of investments owned at 12/31/2006 was $359,423,041.

| * | - Non-income producing security |

| 1 | - Security is segregated as collateral for open written options contracts. |

See notes to financial statements.

The accompanying notes are an integral part of the financial statements.

7

Series A

(Equity Series)

Statement of Assets and Liabilities

December 31, 2006

| | | |

Assets: | | | |

Investments, at value1 | | $ | 442,746,072 |

Cash | | | 9 |

Receivables: | | | |

Fund shares sold | | | 70,395 |

Dividends | | | 334,570 |

Prepaid expenses | | | 9,800 |

| | | |

Total assets | | | 443,160,846 |

| | | |

Liabilities: | | | |

Payable for: | | | |

Fund shares redeemed | | | 780,398 |

Written options, at value (premiums received $121,596) | | | 178,500 |

Management fees | | | 280,197 |

Custodian fees | | | 8,088 |

Transfer agent/maintenance fees | | | 2,083 |

Administration fees | | | 35,581 |

Professional fees | | | 41,968 |

Directors’ fees | | | 10,000 |

Other | | | 35,951 |

| | | |

Total liabilities | | | 1,372,766 |

| | | |

Net Assets | | $ | 441,788,080 |

| | | |

Net assets consist of: | | | |

Paid in capital | | $ | 309,680,133 |

Undistributed net investment income | | | 1,466,765 |

Undistributed net realized gain on sale of investments and options written | | | 47,236,718 |

Net unrealized appreciation in value of investments and options written | | | 83,404,464 |

| | | |

Net assets | | $ | 441,788,080 |

| | | |

Capital shares authorized | | | unlimited |

Capital shares outstanding | | | 17,106,488 |

Net asset value per share (net assets divided by shares outstanding) | | $ | 25.83 |

| | | |

1Investments, at cost | | $ | 359,284,704 |

Statement of Operations

For the Year Ended December 31, 2006

| | | | |

Investment Income: | | | | |

Dividends | | $ | 5,216,765 | |

Interest | | | 237,743 | |

| | | | |

Total investment income | | | 5,454,508 | |

| | | | |

Expenses: | | | | |

Management fees | | | 3,321,940 | |

Administration fees | | | 421,083 | |

Transfer agent/maintenance fees | | | 25,229 | |

Custodian fees | | | 37,756 | |

Directors’ fees | | | 20,095 | |

Professional fees | | | 55,862 | |

Reports to shareholders | | | 84,267 | |

Other expenses | | | 21,517 | |

| | | | |

Total expenses | | | 3,987,749 | |

Less: Earnings credits applied | | | (6 | ) |

| | | | |

Net expenses | | | 3,987,743 | |

| | | | |

Net investment income | | | 1,466,765 | |

| | | | |

Net Realized and Unrealized Gain (Loss): | | | | |

Net realized gain during the year on: | | | | |

Investments | | | 45,524,152 | |

Options written | | | 1,712,566 | |

| | | | |

Net realized gain | | | 47,236,718 | |

| | | | |

Net unrealized appreciation (depreciation) during the year on: | | | | |

Investments | | | 4,576,552 | |

Options written | | | (131,470 | ) |

| | | | |

Net unrealized appreciation | | | 4,445,082 | |

| | | | |

Net realized and unrealized gain | | | 51,681,800 | |

| | | | |

Net increase in net assets resulting from operations | | $ | 53,148,565 | |

| | | | |

See accompanying notes.

8

| | |

| Statement of Changes in Net Assets | | Series A |

| | | (Equity Series) |

| | | | | | | | |

| | | Year Ended

December 31, 2006 | | | Year Ended

December 31, 2005 | |

Increase (decrease) in net assets from operations: | | | | | | | | |

Net investment income | | $ | 1,466,765 | | | $ | 2,686,549 | |

Net realized gain during the year on investments and options written | | | 47,236,718 | | | | 25,155,673 | |

Net unrealized appreciation (depreciation) during the year on investments and options written | | | 4,445,082 | | | | (9,007,148 | ) |

| | | | | | | | |

Net increase in net assets resulting from operations | | | 53,148,565 | | | | 18,835,074 | |

| | | | | | | | |

Capital share transactions: | | | | | | | | |

Proceeds from sale of shares | | | 37,464,659 | | | | 44,233,911 | |

Cost of shares redeemed | | | (115,755,780 | ) | | | (126,234,284 | ) |

| | | | | | | | |

Net decrease from capital share transactions | | | (78,291,121 | ) | | | (82,000,373 | ) |

| | | | | | | | |

Net decrease in net assets | | | (25,142,556 | ) | | | (63,165,299 | ) |

| | | | | | | | |

Net assets: | | | | | | | | |

Beginning of year | | | 466,930,636 | | | | 530,095,935 | |

| | | | | | | | |

End of year | | $ | 441,788,080 | | | $ | 466,930,636 | |

| | | | | | | | |

Undistributed net investment income at end of year | | $ | 1,466,765 | | | $ | 2,686,549 | |

| | | | | | | | |

Capital Share Activity: | | | | | | | | |

Shares sold | | | 1,582,979 | | | | 2,025,092 | |

Shares redeemed | | | (4,888,558 | ) | | | (5,789,676 | ) |

| | | | | | | | |

Total capital share activity | | | (3,305,579 | ) | | | (3,764,584 | ) |

| | | | | | | | |

See accompanying notes.

9

| | |

| Financial Highlights | | Series A |

| Selected data for each share of capital stock outstanding throughout each year | | (Equity Series) |

| | | | | | | | | | | | | | | | | | | | |

| | | 2006 | | | 2005 | | | 2004 | | | 2003 | | | Year Ended,

December 31,

2002 | |

Per Share Data | | | | | | | | | | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 22.88 | | | $ | 21.93 | | | $ | 20.37 | | | $ | 16.83 | | | $ | 22.36 | |

| | | | | | | | | | | | | | | | | | | | |

Income (loss) from investment operations: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | 0.11 | | | | 0.16 | | | | 0.18 | | | | 0.13 | | | | 0.10 | |

Net gain (loss) on securities (realized and unrealized) | | | 2.84 | | | | 0.79 | | | | 1.40 | | | | 3.53 | | | | (5.47 | ) |

| | | | | | | | | | | | | | | | | | | | |

Total from investment operations | | | 2.95 | | | | 0.95 | | | | 1.58 | | | | 3.66 | | | | (5.37 | ) |

| | | | | | | | | | | | | | | | | | | | |

Less distributions: | | | | | | | | | | | | | | | | | | | | |

Dividends from net investment income | | | — | | | | — | | | | (0.02 | ) | | | (0.12 | ) | | | (0.16 | ) |

| | | | | | | | | | | | | | | | | | | | |

Total distributions | | | — | | | | — | | | | (0.02 | ) | | | (0.12 | ) | | | (0.16 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net asset value, end of period | | $ | 25.83 | | | $ | 22.88 | | | $ | 21.93 | | | $ | 20.37 | | | $ | 16.83 | |

| | | | | | | | | | | | | | | | | | | | |

Total Returna | | | 12.89 | % | | | 4.33 | % | | | 7.77 | % | | | 21.74 | % | | | (24.10 | %) |

| | | | | | | | | | | | | | | | | | | | |

Ratios/Supplemental Data | | | | | | | | | | | | | | | | | | | | |

Net assets, end of period (in thousands) | | $ | 441,788 | | | $ | 466,931 | | | $ | 530,096 | | | $ | 559,290 | | | $ | 517,837 | |

| | | | | | | | | | | | | | | | | | | | |

Ratios to average net assets: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | 0.33 | % | | | 0.55 | % | | | 0.81 | % | | | 0.66 | % | | | 0.49 | % |

Total expensesb | | | 0.90 | % | | | 0.89 | % | | | 0.87 | % | | | 0.82 | % | | | 0.82 | % |

Net expensesc | | | 0.90 | % | | | 0.89 | % | | | 0.87 | % | | | 0.82 | % | | | 0.82 | % |

Expenses prior to custodian earnings credits and net of expense waivers | | | 0.90 | % | | | 0.89 | % | | | 0.87 | % | | | 0.82 | % | | | 0.82 | % |

| | | | | | | | | | | | | | | | | | | | |

Portfolio turnover rate | | | 26 | % | | | 37 | % | | | 27 | % | | | 53 | % | | | 25 | % |

a | Total return does not take into account any of the expenses associated with an investment in variable insurance products offered by Security Benefit Life Insurance Company. If total return had taken into account these expenses, performance would have been lower. Shares of a series of SBL Fund are available only through the purchase of such products. |

b | Total expense information reflects expense ratios absent fund expense reductions by the Investment Manager, and earnings credits, as applicable. |

c | Net expense information reflects the expense ratios after voluntary expense waivers, reimbursements and custodian earnings credits, as applicable. |

See accompanying notes.

10

| | |

| | Series B |

| Manager’s Commentary | | (Large Cap Value Series) |

| February 15, 2007 | | (unaudited) |

Advisor, Security Management Company, LLC

Mark Mitchell

Portfolio Manager

To Our Shareholders:

Series B of the SBL Fund - Large Cap Value series returned 22.00% during the year, lagging the benchmark Russell 1000 Value Index’s return of 22.25%, but out performing the Series’ peer group median return of 18.86%. Good stock selection was offset slightly by our sector weights in 2006. While being disappointed that our results were below the benchmark, we believe that our approach delivers performance over the long-term.

Our investment philosophy is centered around three key tenants: first, good investments are purchased at less than their intrinsic value; second, a long-term approach and patience are critical to successful investing; and lastly, we concentrate our investments in companies that have the greatest return potential.

Our process is a bottom-up research driven investment process that attempts to identify companies that have the ability to become more competitive in the future. We focus on owning these companies for three to five years or longer which we believe differentiates us from a majority of our peers and ultimately allows us to make better investment decisions. We buy these companies when their current price trades below their intrinsic value. We closely monitor each company’s progress. We will sell a company if the valuation no longer makes sense, we’ve made a mistake and our investment thesis is no longer valid, or we have a more attractive investment alternative. For this Series, we apply this philosophy to a broad range of value names.

Financials and Industrial Stocks Top Performers

The Series’ Financial holdings were up 37% compared to 20% for the Index. This was driven almost entirely by our position in First Marblehead Corporation, up over 150%. Ill-placed short-term concerns over the company’s competitive position offered a great buying opportunity for a leading student lender with a significant competitive advantage as a result of their loan underwriting capability, superior economics, and additional value-added services.

Holdings International, Inc., the industrial sector were up 28%. McDermott appreciated 71%, driven by strong demand for its energy infrastructure construction related services. Hughes Supply was up 27% as it agreed to be acquired by Home Depot, Inc. Hughes’ strong position in the professional contractor market fits well into Home Depot’s expansion plans in that segment.

Telecom and Energy Disappointing

The telecom sector in the benchmark was up over 39%, while our sector return was up just 1%. Not owning AT&T, up 53%, and Bell South, up 80%, negatively impacted the Series. It appears the market is more confident in the newly-merged telecom players. We’ve avoided these names because we believe it’s very difficult to determine which, if any, company will be able to create a lasting competitive advantage that allows them to generate acceptable returns on the significant capital expenditures required to build out their services offerings. Our position in Sprint Nextel Corporation, down 10%, hurt the Series’ performance. Concerns over how the integration of Nextel was progressing and lack of improvement in its core legacy Sprint operations contributed to the weakness. We still believe in management’s ability to show steady improvement as demonstrated by the spinoff of its slower growing wireline business.

Poor stock selection in the energy sector negatively impacted the Series as the sector underperformed the value index. Specifically, Halliburton Company, up just 1%, and an underweight position in Exxon Mobil Corporation, up 39%, had the largest negative impact. Halliburton was impacted more generally by the recent exodus from oil services related names as a result of a weakening energy commodity market. Exxon outperformed formed the diversified group of integrated oil companies we owned.

2007 Market Outlook

The current low return investment environment that exists outside of equities has continued to make available ample liquidity in the U.S. equity market. Falling energy prices have helped increase consumer confidence and provide support to corporate profit margins through lower raw material input prices. Additionally, businesses have very healthy balance sheets to help drive future growth initiatives.

As we noted in last year’s shareholder letter, we’ve been concerned about a slowdown in U.S. consumer spending for some time. This concern has yet to materialize, but we still think it will happen. Lower energy prices will help; however, higher interest rates and a housing market slowdown provide likely headwinds. The Federal Reserve is walking a fine line between managing inflation risks while supporting economic growth. We’re unsure, like most in the market, what the Fed’s next move is. This uncertainty will weigh on the markets until it’s resolved.

We believe that investing is a long-term pursuit that requires patience and a consistent approach. Dollar cost averaging is a sound way to build long-term value1. We recognize there are many investment fund alternatives available today and thank you for your business and the confidence you place in us.

|

| Sincerely, |

|

| |

| Mark A. Mitchell, Portfolio Manager |

1 | Dollar cost averaging does not assure profits or protect against loss in a declining market. |

11

| | |

| | Series B |

| Manager’s Commentary | | (Large Cap Value Series) |

| December 31, 2006 | | (unaudited) |

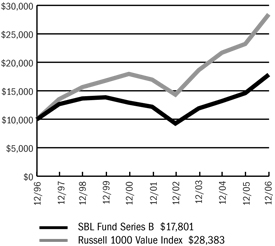

PERFORMANCE

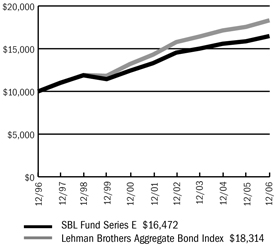

Series B vs. Russell 1000 Value Index

$10,000 Over 10 Years

The chart above assumes a hypothetical $10,000 investment in Series B (Large Cap Value Series) on December 31, 1996 and reflects the fees and expenses of Series B. The Russell 1000 Value Index is an unmanaged index representing the performance of those Russell 1000 Index companies with lower price-to-book ratios and lower forecasted growth values.

Average Annual Returns

| | | | | | | | | |

Periods Ended 12-31-061 | | 1 Year | | | 5 Years | | | 10 Years | |

Series B | | 22.00 | % | | 7.86 | % | | 5.94 | % |

1 | Performance figures do not reflect fees and expenses associated with an investment in variable insurance products offered by Security Benefit Life Insurance Company. If returns had taken into account these fees and expenses, performance would have been lower. Shares of a Series of SBL Fund are available only through the purchase of such products. |

The performance data quoted above represents past performance. Past performance is not predictive of future performance. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

Portfolio Composition by Sector

| | | |

Consumer Discretionary | | 11.09 | % |

Consumer Staples | | 9.67 | |

Energy | | 14.20 | |

Financials | | 16.89 | |

Health Care | | 6.65 | |

Industrials | | 16.84 | |

Information Technology | | 4.92 | |

Materials | | 5.86 | |

Telecommunication Services | | 3.57 | |

Utilities | | 1.86 | |

Exchange Traded Funds | | 5.93 | |

Asset Backed Commercial Paper | | 2.37 | |

Commercial Paper | | 0.48 | |

Repurchase Agreement | | 0.10 | |

Liabilities, less cash & other assets | | (0.43 | ) |

Total net assets | | 100.00 | % |

| | | |

See accompanying notes.

12

| | |

| | Series B |

| Manager’s Commentary | | (Large Cap Value Series) |

| December 31, 2006 | | (unaudited) |

PERFORMANCE

Information About Your Series Expenses

Calculating your ongoing series expenses

Example

As a shareholder of the Series, you incur ongoing costs, including management fees and other series expenses. Performance figures and expense ratios do not reflect fees and expenses associated with an investment in variable insurance products. Shares of a Series of SBL Fund are available only through the purchase of such products This example is intended to help you understand your ongoing costs (in dollars) of investing in the Series and to compare these costs with ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period, July 1, 2006 - December 31, 2006.

Actual Expenses

The first line in the table provides information about actual account values and actual expenses. You may use the information in this table, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the table under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line in the table provides information about hypothetical account values and hypothetical expenses based on the Series actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Series actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Series and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other mutual funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any fees and expenses associated with an investment in variable insurance products. Therefore, the second line is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these fees and expenses associated with an investment in variable insurance products were included, your costs would have been higher.

Series Expenses

| | | | | | | | | |

| | | Beginning

Account Value

07-01-06 | | Ending

Account Value

12-31-061 | | Expenses Paid

During

Period2 |

Series B (Large Cap Value Series) | | | | | | | | | |

Actual | | $ | 1,000.00 | | $ | 1,099.10 | | $ | 4.18 |

Hypothetical | | | 1,000.00 | | | 1,021.22 | | | 4.02 |

1 | The actual ending account value is based on the actual total return of the Series for the period July 1, 2006 to December 31, 2006 after actual expenses and will differ from the hypothetical ending account value which is based on the Series expense ratio and a hypothetical annual return of 5% before expenses. The actual cumulative return at net asset value for the period July 1, 2006 to December 31, 2006 was 9.91%. |

2 | Expenses are equal to the Series annualized expense ratio of 0.79%, net of earnings credits, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). |

13

| | |

| Schedule of Investments | | Series B (Large Cap Value Series) |

| December 31, 2006 | | |

| | | | | |

| | | Shares | | Value |

COMMON STOCK - 97.5% | | | | | |

Aerospace & Defense - 3.0% | | | | | |

United Technologies Corporation | | 228,400 | | $ | 14,279,568 |

| | | | | |

Agricultural Products - 1.9% | | | | | |

Archer-Daniels-Midland Company | | 281,400 | | | 8,993,544 |

| | | | | |

Aluminum - 0.7% | | | | | |

Alcoa, Inc. | | 119,600 | | | 3,589,196 |

| | | | | |

Broadcasting & Cable TV - 2.6% | | | | | |

CBS Corporation (CI.B) | | 402,100 | | | 12,537,478 |

| | | | | |

Computer Hardware - 2.8% | | | | | |

Hewlett-Packard Company | | 331,200 | | | 13,642,128 |

| | | | | |

Construction & Engineering - 2.9% | | | | | |

Shaw Group, Inc. * (1) | | 423,700 | | | 14,193,950 |

| | | | | |

Consumer Finance - 3.2% | | | | | |

First Marblehead Corporation | | 279,225 | | | 15,259,646 |

| | | | | |

Diversified Chemicals - 3.3% | | | | | |

Dow Chemical Company | | 176,400 | | | 7,045,416 |

E.I. Du Pont de Nemours & Company | | 178,600 | | | 8,699,606 |

| | | | | |

| | | | | 15,745,022 |

| | | | | |

Drug Retail - 3.1% | | | | | |

CVS Corporation | | 477,800 | | | 14,768,798 |

| | | | | |

Electric Utilities - 1.9% | | | | | |

Edison International | | 196,300 | | | 8,927,724 |

| | | | | |

Exchange Traded Funds - 5.9% | | | | | |

iShares Russell 1000 Value Index Fund | | 170,600 | | | 14,093,266 |

iShares S&P 500 Value Index Fund | | 187,600 | | | 14,424,564 |

| | | | | |

| | | | | 28,517,830 |

| | | | | |

Health Care Equipment - 1.0% | | | | | |

Hospira, Inc. * | | 139,000 | | | 4,667,620 |

| | | | | |

Health Care Services - 2.9% | | | | | |

Medco Health Solutions, Inc. * | | 258,200 | | | 13,798,208 |

| | | | | |

Home Improvement Retail - 2.0% | | | | | |

Home Depot, Inc. | | 242,000 | | | 9,718,720 |

| | | | | |

Hypermarkets & Super Centers - 2.8% | | | | | |

Costco Wholesale Corporation | | 254,200 | | | 13,439,554 |

| | | | | |

Industrial Conglomerates - 8.6% | | | | | |

General Electric Company | | 383,900 | | | 14,284,919 |

McDermott International, Inc. * | | 286,500 | | | 14,571,390 |

Tyco International, Ltd. | | 406,600 | | | 12,360,640 |

| | | | | |

| | | | | 41,216,949 |

| | | | | |

Integrated Oil & Gas - 9.7% | | | | | |

Chevron Corporation | | 151,000 | | | 11,103,030 |

ConocoPhillips | | 92,500 | | | 6,655,375 |

Exxon Mobil Corporation | | 204,600 | | | 15,678,498 |

Sasol, Ltd. ADR | | 360,500 | | | 13,302,450 |

| | | | | |

| | | | | 46,739,353 |

| | | | | |

Integrated Telecommunication Services - 1.0% | | | | | |

Windstream Corporation | | 331,932 | | | 4,720,073 |

| | | | | |

IT Consulting & Other Services - 2.1% | | | | | |

Unisys Corporation * | | 1,273,500 | | | 9,984,240 |

| | | | | |

Managed Health Care - 2.8% | | | | | |

WellPoint, Inc. * | | 171,500 | | | 13,495,335 |

| | | | | |

Movies & Entertainment - 6.5% | | | | | |

News Corporation | | 488,800 | | | 10,499,424 |

Time Warner, Inc. | | 712,600 | | | 15,520,428 |

Viacom, Inc. (CI.B) * | | 122,100 | | | 5,009,763 |

| | | | | |

| | | | | 31,029,615 |

| | | | | |

Multi-Line Insurance - 4.1% | | | | | |

American International Group, Inc. | | 272,600 | | | 19,534,516 |

| | | | | |

Oil & Gas Drilling - 0.7% | | | | | |

Transocean, Inc. * (1) | | 39,100 | | | 3,162,799 |

| | | | | |

Oil & Gas Equipment & Services - 1.5% | | | | | |

Halliburton Company | | 232,600 | | | 7,222,230 |

| | | | | |

Oil & Gas Storage & Transportation - 2.3% | | | | | |

Williams Companies, Inc. | | 426,800 | | | 11,148,016 |

| | | | | |

Other Diversified Financial Services - 5.3% | | | | | |

Citigroup, Inc. | | 266,300 | | | 14,832,910 |

JPMorgan Chase & Company | | 221,700 | | | 10,708,110 |

| | | | | |

| | | | | 25,541,020 |

| | | | | |

Packaged Foods & Meats - 0.3% | | | | | |

Tyson Foods, Inc. | | 83,700 | | | 1,376,865 |

| | | | | |

Property & Casually Insurance - 4.3% | | | | | |

Berkshire Hathaway, Inc. * | | 190 | | | 20,898,100 |

| | | | | |

Railroads - 2.3% | | | | | |

Union Pacific Corporation | | 122,800 | | | 11,300,056 |

| | | | | |

Specialty Chemicals - 1.8% | | | | | |

Rohm & Haas Company | | 172,200 | | | 8,802,864 |

| | | | | |

Tobacco - 1.6% | | | | | |

Altria Group, Inc. | | 91,800 | | | 7,878,276 |

| | | | | |

Wireless Telecommunication Services - 2.6% | | | | | |

Alltel Corporation | | 59,900 | | | 3,622,752 |

The accompanying notes are an integral part of the financial statements.

14

| | |

| Schedule of Investments | | Series B (Large Cap Value Series) |

| December 31, 2006 - continued | | |

| | | | | | | |

| | | Shares | | Value | |

COMMON STOCK (continued) | | | | | | | |

Wireless Telecommunication Services (continued) | | | | | | | |

Sprint Nextel Corporation | | | 466,600 | | $ | 8,814,074 | |

| | | | | | | |

| | | | | | 12,436,826 | |

| | | | | | | |

TOTAL COMMON STOCK (Cost $366,787,659) | | | | | $ | 468,566,119 | |

| | | | | | | |

| | |

| | | Principal

Amount | | Value | |

ASSET BACKED COMMERCIAL PAPER - 2.3% | | | | | | | |

Financial Companies - Diversified - 0.5% | | | | | | | |

Amsterdam Funding Corporation | | | | | | | |

5.28%, 1/4/2007 | | $ | 1,000,000 | | | 999,562 | |

5.28%, 1/10/2007 | | | 1,600,000 | | | 1,597,888 | |

| | | | | | | |

| | | | | | 2,597,450 | |

| | | | | | | |

Financial Companies - Miscellaneous Receivables - 0.9% | | | | | | | |

Fairway Finance Corporation | | | | | | | |

5.35%, 1/9/2007 | | | 1,608,000 | | | 1,606,088 | |

Falcon Asset Securitization Corporation | | | | | | | |

5.27%, 1/8/2007 | | | 1,300,000 | | | 1,298,668 | |

5.30%, 1/11/2007 | | | 1,500,000 | | | 1,497,791 | |

| | | | | | | |

| | | | | | 4,402,547 | |

| | | | | | | |

Financial Companies - Trade Receivables - 0.9% | | | | | | | |

Old Line Funding LLC | | | | | | | |

5.26%, 1/12/2007 | | | 1,400,000 | | | 1,397,750 | |

5.28%, 1/16/2007 | | | 1,500,000 | | | 1,496,700 | |

Sheffield Receivables Corporation | | | | | | | |

5.265%, 1/2/2007 | | | 1,500,000 | | | 1,499,781 | |

| | | | | | | |

| | | | | | 4,394,231 | |

| | | | | | | |

TOTAL ASSET BACKED COMMERCIAL PAPER (Cost $11,394,228) | | | | | $ | 11,394,228 | |

| | | | | | | |

COMMERCIAL PAPER - 0.5% | | | | | | | |

Brokerage - 0.5% | | | | | | | |

Credit Suisse First Boston USA | | | | | | | |

5.28%, 1/3/2007 | | | 1,300,000 | | | 1,299,619 | |

Goldman Sachs Group, Inc. | | | | | | | |

5.23%, 1/5/2007 | | | 1,000,000 | | | 999,419 | |

| | | | | | | |

| | | | | | 2,299,038 | |

| | | | | | | |

TOTAL COMMERCIAL PAPER (Cost $2,299,038) | | | | | $ | 2,299,038 | |

| | | | | | | |

REPURCHASE AGREEMENT - 0.1% | | | | | | | |

United Missouri Bank, 4. 85%, dated 12-29-06, matures 01-02-07; repurchase amount of $502,271 (Collateralized by FHLMC, 5.00%, 10-15-36 & FMNA, 5.00%, 06-01-18 with a combined value of $512,039) | | | 502,000 | | $ | 502,000 | |

| | | | | | | |

TOTAL REPURCHASE AGREEMENT (Cost $502,000) | | | | | $ | 502,000 | |

| | | | | | | |

Total Investments (SBL B Fund) (Cost $380,982,925) - 100.4% | | | | | $ | 482,761,385 | |

Liabilities in Excess of Other Assets - (0.4)% | | | | | | (2,077,978 | ) |

| | | | | | | |

TOTAL NET ASSETS - 100.0% | | | | | $ | 480,683,407 | |

| | | | | | | |

Footnotes

Percentages are stated as a percent of net assets.

For federal income tax purposes the identified cost of investments owned at 12/31/2006 was $381,029,891.

| * | - Non-income producing security |

| 1 | - Security is segregated as collateral for open written options contracts. |

Glossary:

ADR - American Depositary Receipt

See notes to financial statements.

The accompanying notes are an integral part of the financial statements.

15

Series B

(Large Cap Value Series)

Statement of Assets and Liabilities

December 31, 2006

| | | | |

Assets: | | | | |

Investments, at value1 | | $ | 482,761,385 | |

Cash | | | 471 | |

Receivables: | | | | |

Fund shares sold | | | 940,605 | |

Dividends | | | 584,404 | |

Prepaid expenses | | | 10,064 | |

| | | | |

Total assets | | | 484,296,929 | |

| | | | |

Liabilities: | | | | |

Payable for: | | | | |

Fund shares redeemed | | | 442,154 | |

Securities purchased | | | 2,665,073 | |

Written options, at value (premiums received $101,419) | | | 122,210 | |

Management fees | | | 262,073 | |

Directors’ fees | | | 10,000 | |

Custodian fees | | | 2,625 | |

Transfer agent/maintenance fees | | | 2,083 | |

Administration fees | | | 38,453 | |

Professional fees | | | 35,837 | |

Other | | | 33,014 | |

| | | | |

Total liabilities | | | 3,613,522 | |

| | | | |

Net Assets | | $ | 480,683,407 | |

| | | | |

Net assets consist of: | | | | |

Paid in capital | | $ | 602,529,743 | |

Undistributed net investment income | | | 3,504,848 | |

Accumulated net realized loss on sale of investments and options written | | | (227,108,853 | ) |

Net unrealized appreciation in value of investments and options written | | | 101,757,669 | |

| | | | |

Net assets | | $ | 480,683,407 | |

| | | | |

Capital shares authorized | | | unlimited | |

Capital shares outstanding | | | 18,206,160 | |

Net asset value per share (net assets divided by shares outstanding) | | $ | 26.40 | |

| | | | |

1Investments, at cost | | $ | 380,982,925 | |

Statement of Operations

For the Year Ended December 31, 2006

| | | | |

Investment Income: | | | | |

Dividends | | $ | 6,404,311 | |

Interest | | | 569,285 | |

| | | | |

Total investment income | | | 6,973,596 | |

| | | | |

Expenses: | | | | |

Management fees | | | 2,840,902 | |

Administration fees | | | 415,647 | |

Custodian fees | | | 22,097 | |

Transfer agent/maintenance fees | | | 25,234 | |

Directors’ fees | | | 20,120 | |

Professional fees | | | 45,859 | |

Reports to shareholders | | | 79,949 | |

Other expenses | | | 18,972 | |

| | | | |

Total expenses | | | 3,468,780 | |

Less: Earnings credits applied | | | (32 | ) |

| | | | |

Net expenses | | | 3,468,748 | |

| | | | |

Net investment income | | | 3,504,848 | |

| | | | |

Net Realized and Unrealized Gain (Loss): | | | | |

Net realized gain during the year on: | | | | |

Investments | | | 25,798,929 | |

Options written | | | 1,220,908 | |

| | | | |

Net realized gain | | | 27,019,837 | |

| | | | |

Net unrealized appreciation (depreciation) during the year on: | | | | |

Investments | | | 57,175,374 | |

Options written | | | (91,355 | ) |

| | | | |

Net unrealized appreciation | | | 57,084,019 | |

| | | | |

Net realized and unrealized gain | | | 84,103,856 | |

| | | | |

Net increase in net assets resulting from operations | | $ | 87,608,704 | |

| | | | |

See accompanying notes.

16

| | |

| | Series B |

| Statement of Changes in Net Assets | | (Large Cap Value Series) |

| | | | | | | | |

| | | Year Ended

December 31, 2006 | | | Year Ended

December 31, 2005 | |

Increase (decrease) in net assets from operations: | | | | | | | | |

Net investment income | | $ | 3,504,848 | | | $ | 3,971,506 | |

Net realized gain during the year on investments and options written | | | 27,019,837 | | | | 48,032,291 | |

Net unrealized appreciation (depreciation) during the year on investments and options written | | | 57,084,019 | | | | (11,665,891 | ) |

| | | | | | | | |

Net increase in net assets resulting from operations | | | 87,608,704 | | | | 40,337,906 | |

| | | | | | | | |

Capital share transactions: | | | | | | | | |

Proceeds from sale of shares | | | 88,964,012 | | | | 39,815,974 | |

Cost of shares redeemed | | | (106,581,077 | ) | | | (98,954,660 | ) |

| | | | | | | | |

Net decrease from capital share transactions | | | (17,617,065 | ) | | | (59,138,686 | ) |

| | | | | | | | |

Net increase (decrease) in net assets | | | 69,991,639 | | | | (18,800,780 | ) |

| | | | | | | | |

Net assets: | | | | | | | | |

Beginning of year | | | 410,691,768 | | | | 429,492,548 | |

| | | | | | | | |

End of year | | $ | 480,683,407 | | | $ | 410,691,768 | |

| | | | | | | | |

Undistributed net investment income at end of year | | $ | 3,504,848 | | | $ | 3,971,506 | |

| | | | | | | | |

Capital Share Activity: | | | | | | | | |

Shares sold | | | 3,705,999 | | | | 1,980,149 | |

Shares redeemed | | | (4,475,464 | ) | | | (4,944,509 | ) |

| | | | | | | | |

Total capital share activity | | | (769,465 | ) | | | (2,964,360 | ) |

| | | | | | | | |

See accompanying notes.

17

| | | |

| Financial Highlights | | Series B | |

| Selected data for each share of capital stock outstanding throughout each year | | (Large Cap Value Series | ) |

| | | | | | | | | | | | | | | | | | | | |

| | | 2006 | | | 2005d | | | 2004 | | | 2003 | | | Year Ended,

December 31,

2002 | |

Per Share Data | | | | | | | | | | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 21.64 | | | $ | 19.58 | | | $ | 17.68 | | | $ | 13.84 | | | $ | 18.59 | |

| | | | | | | | | | | | | | | | | | | | |

Income (loss) from investment operations: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | 0.20 | | | | 0.24 | | | | 0.21 | | | | 0.14 | | | | 0.13 | |

Net gain (loss) on securities (realized and unrealized) | | | 4.56 | | | | 1.82 | | | | 1.70 | | | | 3.84 | | | | (4.58 | ) |

| | | | | | | | | | | | | | | | | | | | |

Total from investment operations | | | 4.76 | | | | 2.06 | | | | 1.91 | | | | 3.98 | | | | (4.45 | ) |

| | | | | | | | | | | | | | | | | | | | |

Less distributions: | | | | | | | | | | | | | | | | | | | | |

Dividends from net investment income | | | — | | | | — | | | | (0.01 | ) | | | (0.14 | ) | | | (0.30 | ) |

| | | | | | | | | | | | | | | | | | | | |

Total distributions | | | — | | | | — | | | | (0.01 | ) | | | (0.14 | ) | | | (0.30 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net asset value, end of period | | $ | 26.40 | | | $ | 21.64 | | | $ | 19.58 | | | $ | 17.68 | | | $ | 13.84 | |

| | | | | | | | | | | | | | | | | | | | |

Total Returna | | | 22.00 | % | | | 10.52 | % | | | 10.82 | % | | | 28.81 | % | | | (24.14 | %) |

| | | | | | | | | | | | | | | | | | | | |

Ratios/Supplemental Data | | | | | | | | | | | | | | | | | | | | |

Net assets, end of period (in thousands) | | $ | 480,683 | | | $ | 410,692 | | | $ | 429,493 | | | $ | 434,575 | | | $ | 370,746 | |

| | | | | | | | | | | | | | | | | | | | |

Ratios to average net assets: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | 0.80 | % | | | 0.98 | % | | | 1.09 | % | | | 0.93 | % | | | 0.74 | % |

Total expensesb | | | 0.79 | % | | | 0.84 | % | | | 0.92 | % | | | 0.89 | % | | | 0.91 | % |

Net expensesc | | | 0.79 | % | | | 0.84 | % | | | 0.87 | % | | | 0.83 | % | | | 0.82 | % |

| | | | | | | | | | | | | | | | | | | | |

Portfolio turnover rate | | | 20 | % | | | 99 | % | | | 73 | % | | | 60 | % | | | 68 | % |

a | Total return does not take into account any of the expenses associated with an investment in variable insurance products offered by Security Benefit Life Insurance Company. If total return had taken into account these expenses, performance would have been lower. Shares of a series of SBL Fund are available only through the purchase of such products. |

b | Total expense information reflects expense ratios absent fund expense reductions by the Investment Manager, and earnings credits, as applicable. |

c | Net expense information reflects the expense ratios after voluntary expense waivers, reimbursements and custodian earnings credits, as applicable. |

d | SMC became the advisor of Series B effective June 30, 2005. Prior to June 30, 2005, SMC paid Dreyfus Corporation for sub-advisory services. |

See accompanying notes.

18

| | |

| | Series C |

| Manager’s Commentary | | (Money Market Series) |

| February 15, 2007 | | (unaudited) |

Advisor, Security Management Company, LLC

Christi Fletcher

Portfolio Manager

To Our Shareholders:

The first half of 2006 proved to be comparable to 2005. The Federal Reserve Board’s campaign to increase interest rates resulted in four rate increases during the Series’ fiscal year ending at 5.25%. The yield of the Series C of the SBL Fund—Money Market Series rose accordingly, returning 4.43% for the year ended December 31, 2006, which exceeded the benchmark I-Money Net Retail Tier 1 of 4.30% for the same period.

Aside from the increases in short-term interest rates, the continued threat of higher inflation and a flat yield curve the past year proved positive for credit issuers. Companies continued to display solid balance sheet fundamentals, strong cash flows and good profit growth. In addition, the trend continues as firms utilize the excess cash flows for increasing dividends or share repurchases (shareholder friendly), rather than bolstering credit quality.

Characteristics of Portfolio Assets

At December 31, 2006, the average maturity of Series C was 51 days, which was a couple of days longer than the benchmark. This strategy positioned the Series to take advantage of longer dated securities, as the threat of decreasing rates loomed.

The yield curve for money market instruments went from upward trending during the first half of 2006 to relatively flat in the second half. This made for interesting challenges for additional yield along the maturity spectrum and among various types of money market instruments. The majority of the Series assets lie in the corporate debt sector via commercial paper, floating rate securities and Yankee CD’s, due to the strong balance sheet fundamentals of credit and because it represented good value against other sectors. At year end, approximately 52% of the Series was made up of Commercial Paper, 30% in Floating Rate securities (which includes Corporate and U.S. Government-Backed), 7% in U.S. Government/Agency obligations, 7% in Yankee CD’s, 3% in funding agreements, and 1% Mortgage-related products.

Outlook for 2007

In 2006, the economy continued to grow but with strong head winds from the long anticipated correction in the housing market, the Federal Reserve rate increases that started to take effect, and commodity prices yet again hitting all time highs. Looking forward to 2007, the economy will continue to grow but at a slower pace versus recent years. We expect short-term rates to remain at 5.25% for most of 2007. We believe the approach the Federal Reserve will take is one of a wait-and-see attitude. We are not anticipating a cut in short-term rates but have not factored in an increase either, unless we see an increase in inflation. At this point, there is limited evidence of either situation unfolding during 2007.

With a stable U.S. economy predicted in 2007, as fundamentals in the corporate sector remain solid and companies continue to generate strong cash flows and earnings growth, the Series will continue to be invested heavily in the corporate debt sectors within the money market arena.

As always, we will continue to monitor the economic and market conditions when deciding portfolio strategies and will adjust the asset mix and maturity structure in the portfolio accordingly.

Thank you for your investment in Series C. We appreciate the confidence that you have placed in us and remain focused on achieving the Series’ investment goals.

|

| Sincerely, |

|

| |

Christina Fletcher Portfolio Manager |

19

| | | |

| | Series C | |

Manager’s Commentary | | (Money Market Series | ) |

December 31, 2006 | | (unaudited | ) |

PERFORMANCE

Portfolio Composition by Quality Ratings (Based on Standard and Poor’s Ratings)

| | | |

Tier 1 investments | | 106.78 | % |

Repurchase Agreement | | 0.24 | |

Liabilities, less cash & other assets | | (7.02 | ) |

Total net assets | | 100.00 | % |

| | | |

Average Annual Returns

| | | | | | | | | |

Periods Ended 12-31-061 | | 1 Year | | | 5 Years | | | 10 Years | |

Series C | | 4.43 | % | | 1.91 | % | | 3.41 | % |

1 | Performance figures do not reflect fees and expenses associated with an investment in variable insurance products offered by Security Benefit Life Insurance Company. If returns had taken into account these fees and expenses, performance would have been lower. Shares of a Series of SBL Fund are available only through the purchase of such products. |

The performance data quoted above represents past performance. Past performance is not predictive of future performance. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

See accompanying notes.

20

| | | |

| | Series C | |

Manager’s Commentary | | (Money Market Series | ) |

December 31, 2006 | | (unaudited | ) |

PERFORMANCE

Information About Your Series Expenses

Calculating your ongoing series expenses

Example

As a shareholder of the Series, you incur ongoing costs, including management fees and other series expenses. Performance figures and expense ratios do not reflect fees and expenses associated with an investment in variable insurance products. Shares of a Series of SBL Fund are available only through the purchase of such products. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Series and to compare these costs with ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period, July 1, 2006 - December 31, 2006.

Actual Expenses

The first line in the table provides information about actual account values and actual expenses. You may use the information in this table, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the table under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line in the table provides information about hypothetical account values and hypothetical expenses based on the Series actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Series actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Series and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other mutual funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any fees and expenses associated with an investment in variable insurance products. Therefore, the second line is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these fees and expenses associated with an investment in variable insurance products were included, your costs would have been higher.

Series Expenses

| | | | | | | | | |

| | | Beginning

Account Value

07-01-06 | | Ending

Account Value

12-31-061 | | Expenses Paid

During

Period2 |

Series C (Money Market Series) | | | | | | | | | |

Actual | | $ | 1,000.00 | | $ | 1,024.10 | | $ | 3.47 |

Hypothetical | | | 1,000.00 | | | 1,021.78 | | | 3.47 |

1 | The actual ending account value is based on the actual total return of the Series for the period July 1, 2006 to December 31, 2006 after actual expenses and will differ from the hypothetical ending account value which is based on the Series expense ratio and a hypothetical annual return of 5% before expenses. The actual cumulative return at net asset value for the period July 1, 2006 to December 31, 2006 was 2.41%. |

2 | Expenses are equal to the Series annualized expense ratio of 0.68%, net of earnings credits, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). |

21

| | | |

Schedule of Investments | | Series C | |

December 31, 2006 | | (Money Market Series | ) |

| | | | | | |

| | | Principal

Amount | | Value |

CERTIFICATE OF DEPOSIT - 8.1% | | | | | | |

Bank of Ireland | | | | | | |

5.32%, 2/08/2007 | | $ | 3,000,000 | | $ | 2,999,898 |

Barclay’s Bank pic NY | | | | | | |

5.31%, 4/02/2007 (1) | | | 3,000,000 | | | 3,000,000 |

BNP Paribas NY Branch | | | | | | |

5.33%, 3/16/2007 | | | 2,000,000 | | | 1,999,889 |

| | | | | | |

TOTAL CERTIFICATE OF DEPOSIT (Cost $8,000,000) | | | | | $ | 7,999,787 |

| | | | | | |

CORPORATE BOND - 30.8% | | | | | | |

Automotive - 6.1% | | | | | | |

American Honda Finance Corporation | | | | | | |

5.476%, 2/12/2007 (2)(3)(4)(5) | | $ | 1,550,000 | | | 1,550,970 |

Toyota Motor Credit Corporation | | | | | | |

5.21%, 1/02/2007 (2)(3) | | | 2,000,000 | | | 2,000,040 |

5.265%, 1/02/2007 (2)(3) | | | 2,500,000 | | | 2,501,173 |

| | | | | | |

| | | | | | 6,052,183 |

| | | | | | |

Brokerage - 12.5% | | | | | | |

Bear Stearns Companies, Inc. | | | | | | |

5.534%, 1/16/2007 (2)(3) | | | 1,300,000 | | | 1,300,083 |

Goldman Sachs Group, Inc. | | | | | | |

5.476%, 2/12/2007 (2)(3) | | | 1,100,000 | | | 1,100,495 |

5.50%, 1/02/2007 (2)(3) | | | 2,000,000 | | | 2,001,896 |

Lehman Brothers Holdings, Inc. | | | | | | |

5.35%, 1/02/2007 (2)(3) | | | 1,000,000 | | | 1,000,599 |

5.494%, 1/22/2007 (2)(3) | | | 2,000,000 | | | 2,001,306 |

Merrill Lynch & Company, Inc. | | | | | | |

5.30%, 1/03/2007 (2)(3) | | | 1,000,000 | | | 1,000,189 |

5.505%, 1/26/2007 (2)(3) | | | 2,385,000 | | | 2,385,267 |

Morgan Stanley | | | | | | |

5.50%, 2/15/2007 (2)(3) | | | 1,600,000 | | | 1,600,285 |

| | | | | | |

| | | | | | 12,390,120 |

| | | | | | |

Financial Companies - Captive - 7.7% | | | | | | |

Caterpillar Financial Services Corporate | | | | | | |

5.39%, 1/29/2007 (2)(3) | | | 2,000,000 | | | 2,000,918 |

General Electric Capital Corporation | | | | | | |

5.375%, 3/15/2007 | | | 1,000,000 | | | 1,000,117 |

HSBC Finance Corporation | | | | | | |

5.41%, 2/28/2007 (2)(3) | | | 3,000,000 | | | 3,000,519 |

5.525%, 2/09/2007 (2)(3) | | | 1,550,000 | | | 1,550,313 |

| | | | | | |

| | | | | | 7,551,867 |

| | | | | | |

Financial Companies - Noncaptive Consumer - 2.5% | | | | | | |

SLM Corporation | | | | | | |

5.50%, 1/25/2007 (2)(3) | | | 2,500,000 | | | 2,500,273 |

| | | | | | |

Non U.S. Banking - 2.0% | | | | | | |

Royal Bank of Scotland pic | | | | | | |

5.364%, 3/30/2007 (2)(3)(4) | | | 2,000,000 | | | 2,000,586 |

| | | | | | |

TOTAL CORPORATE BOND (Cost $30,491,715) | | | | | $ | 30,495,029 |

| | | | | | |

MISCELLANEOUS ASSET - 3.0% | | | | | | |

Life Insurance - 3.0% | | | | | | |

United of Omaha Life Insurance Company | | | | | | |

5.40%, 1/01/2007 (2) | | | 3,000,000 | | | 3,000,000 |

| | | | | | |

TOTAL MISCELLANEOUS ASSET (Cost $3,000,000) | | | | | $ | 3,000,000 |

| | | | | | |

MORTGAGE BACKED SECURITIES -1.5% | | | | | | |

Other Non-Agency - 1.5% | | | | | | |

Pass-Thru’s - 1.5% | | | | | | |

Small Business Administration Pools | | | | | | |

#503295, 5.75% - | | | | | | |

1/01/2007 (2)(3) | | | 131,048 | | | 131,769 |

#503303, 5.75% - | | | | | | |

1/01/2007 (2)(3) | | | 207,296 | | | 208,436 |

#503308, 5.75% - | | | | | | |

1/01/2007 (2)(3) | | | 148,783 | | | 148,783 |

#503459, 5.75% - | | | | | | |

1/01/2007 (2)(3) | | | 78,808 | | | 78,512 |

#503176, 5.87%- | | | | | | |

1/01/2007 (2)(3) | | | 25,335 | | | 25,462 |

#503343, 5.87% - | | | | | | |

1/01/2007 (2)(3) | | | 237,983 | | | 237,983 |

#503347, 5.87% - | | | | | | |

1/01/2007 (2)(3) | | | 416,797 | | | 416,797 |

#502353, 6.00% - | | | | | | |

1/01/2007 (2)(3) | | | 40,409 | | | 40,409 |

#502163,6.25% - | | | | | | |

1/01/2007 (2)(3) | | | 209,503 | | | 209,503 |

| | | | | | |

| | | | | | 1,497,654 |

| | | | | | |

TOTAL MORTGAGE BACKED SECURITIES (Cost $1,496,004) | | | | | $ | 1,497,654 |

| | | | | | |

U.S. GOVERNMENT SPONSORED AGENCY BONDS & NOTES - 7.6% | | | | | | |

Federal Home Loan Bank | | | | | | |

5.35% -11/21/2007 | | | 2,000,000 | | | 1,998,944 |

5.40% - 9/12/2007 | | | 2,000,000 | | | 1,999,638 |

5.50% -10/02/2007 | | | 2,000,000 | | | 2,000,000 |

Federal Home Loan Mortgage Corporate | | | | | | |

4.85% - 2/27/2007 | | | 1,500,000 | | | 1,499,386 |

| | | | | | |

TOTAL U.S. GOVERNMENT SPONSORED AGENCY BONDS & NOTES (Cost $7,499,862) | | | | | $ | 7,497,968 |

| | | | | | |

ASSET BACKED COMMERCIAL PAPER - 33.0% | | | | | | |

Financial Companies - Diversified - 8.3% | | | | | | |

Amstel Funding Corporation | | | | | | |

5.27%, 1/18/2007 | | | 1,900,000 | | | 1,895,272 |

Amsterdam Funding Corporation | | | | | | |

5.28%, 1/4/2007 | | | 1,500,000 | | | 1,499,340 |

5.25%, 1/5/2007 | | | 1,700,000 | | | 1,699,248 |

Govco, Inc. | | | | | | |

5.25%, 1/22/2007 | | | 2,000,000 | | | 1,994,064 |

5.23%, 3/7/2007 | | | 1,100,000 | | | 1,089,661 |

| | | | | | |

| | | | | | 8,177,585 |

| | | | | | |

The accompanying notes are an integral part of the financial statements.

22

| | |

Schedule of Investments | | Series C (Money Market Series) |

December 31, 2006 - continued | | |

| | | | | | | |

| | | Principal

Amount | | Value | |

ASSET BACKED COMMERCIAL PAPER (continued) | | | | | | | |

Financial Companies - Miscellaneous | | | | | | | |

Receivables - 8.8% | | | | | | | |

Fairway Finance Corporation | | | | | | | |

5.28%, 1/3/2007 | | $ | 1,500,000 | | $ | 1,499,557 | |

5.30%, 1/12/2007 | | | 1,500,000 | | | 1,497,584 | |

Falcon Asset Securitization Corporation | | | | | | | |

5.25%, 1/30/2007 | | | 1,500,000 | | | 1,493,656 | |

5.30%, 2/6/2007 | | | 1,000,000 | | | 994,700 | |

5.27%, 2/12/2007 | | | 1,300,000 | | | 1,292,007 | |

Jupiter Securitization Corporation | | | | | | | |

5.27%, 2/5/2007 | | | 2,000,000 | | | 1,989,753 | |

| | | | | | | |

| | | | | | 8,767,257 | |

| | | | | | | |

Financial Companies - Securities - 3.9% | | | | | | | |

Galaxy Funding, Inc. | | | | | | | |

5.275%, 1/10/2007 | | | 1,900,000 | | | 1,897,494 | |

5.255%, 1/29/2007 | | | 2,000,000 | | | 1,992,020 | |

| | | | | | | |

| | | | | | 3,889,514 | |

| | | | | | | |

Financial Companies - Trade & Term Receivables - 3.5% | | | | | | | |

Eureka Securitization | | | | | | | |

5.264%, 1/8/2007 | | | 700,000 | | | 699,375 | |

5.27%, 1/8/2007 | | | 1,500,000 | | | 1,498,463 | |

5.26%, 1/11/2007 | | | 1,300,000 | | | 1,298,258 | |

| | | | | | | |

| | | | | | 3,496,096 | |

| | | | | | | |

Financial Companies - Trade Receivables - 8.5% | | | | | | | |

Old Line Funding LLC | | | | | | | |

5.27%, 1/3/2007 | | | 1,400,000 | | | 1,399,590 | |

5.26%, 1/4/2007 | | | 1,300,000 | | | 1,299,430 | |

5.26%, 1/19/2007 | | | 1,400,000 | | | 1,396,318 | |

Sheffield Receivables Corporation | | | | | | | |

5.265%, 1/2/2007 | | | 2,000,000 | | | 1,999,708 | |

5.27%, 1/5/2007 | | | 1,300,000 | | | 1,299,239 | |

5.27%, 1/9/2007 | | | 1,000,000 | | | 998,829 | |

| | | | | | | |

| | | | | | 8,393,114 | |

| | | | | | | |

TOTAL ASSET BACKED COMMERCIAL PAPER (Cost $32,722,646) | | | | | $ | 32,723,566 | |

| | | | | | | |

COMMERCIAL PAPER - 22.8% | | | | | | | |

Banking - 1.1% | | | | | | | |

UBS Finance (DE) LLC | | | | | | | |

5.27%, 3/8/2007 (1) | | | 1,100,000 | | | 1,089,050 | |

| | | | | | | |

Brokerage - 6.0% | | | | | | | |

Goldman Sachs Group, Inc. | | | | | | | |

5.29%, 2/1/2007 | | | 1,100,000 | | | 1,094,989 | |

ING (US) Funding LLC | | | | | | | |

5.24%, 1/24/2007 | | | 1,600,000 | | | 1,594,858 | |

5.28%, 2/20/2007 | | | 1,000,000 | | | 992,667 | |

Morgan Stanley | | | | | | | |

5.20%, 5/21/2007 | | | 2,300,000 | | | 2,253,546 | |

| | | | | | | |

| | | | | | 5,936,060 | |

| | | | | | | |

Financial - Other - 4.0% | | | | | | | |

Bank of America | | | | | | | |

5.17%, 4/4/2007 | | | 3,000,000 | | | 2,959,750 | |

Countrywide Financial Corporation | | | | | | | |

5.42%, 1/2/2007 | | | 1,000,000 | | | 999,849 | |

| | | | | | | |

| | | | | | 3,959,599 | |

| | | | | | | |

Financial Companies - Trade & Term | | | | | | | |

Receivables - 2.3% | | | | | | | |

Countrywide Financial Corporation | | | | | | | |

5.27%, 2/2/2007 | | | 2,234,000 | | | 2,223,535 | |

| | | | | | | |

Non U.S. Banking - 9.4% | | | | | | | |

Danske Corporation | | | | | | | |

5.30%, 1/30/2007 | | | 1,100,000 | | | 1,095,304 | |

Societe Generale | | | | | | | |

5.23%, 3/5/2007 | | | 1,100,000 | | | 1,090,075 | |

5.26%, 3/12/2007 | | | 1,600,000 | | | 1,583,949 | |

5.22%, 3/29/2007 | | | 1,100,000 | | | 1,086,275 | |

Westpac Banking Corporation | | | | | | | |

5.26%, 1/3/2007 | | | 1,400,000 | | | 1,399,591 | |

5.30%, 2/5/2007 | | | 1,700,000 | | | 1,691,240 | |

5.27%, 2/16/2007 | | | 1,400,000 | | | 1,390,573 | |

| | | | | | | |

| | | | | | 9,337,007 | |

| | | | | | | |

TOTAL COMMERCIAL PAPER (Cost $22,544,877) | | | | | $ | 22,545,251 | |

| | | | | | | |

REPURCHASE AGREEMENT - 0.2% | | | | | | | |

United Missouri Bank, 4.85%, dated 12-29-06, matures 01-02-07; repurchase amount $236,127 (Collateralized by FHLMC, 5.00%, 08-15-35 with a value of $241,694) | | $ | 236,000 | | $ | 236,000 | |

| | | | | | | |

TOTAL REPURCHASE AGREEMENT (Cost $236,000) | | | | | $ | 236,000 | |

| | | | | | | |

Total Investments (SBL C Fund) (Cost $105,991,104) - 107.0% | | | | | $ | 105,995,255 | |

Liabilities in Excess of Other Assets - (7.0)% | | | | | | (6,950,983 | ) |

| | | | | | | |

TOTAL NET ASSETS - 100.0% | | | | | $ | 99,044,272 | |

| | | | | | | |

Footnotes

Percentages are stated as a percent of net assets.