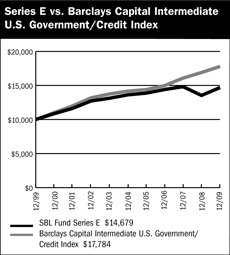

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| | |

Investment Company Act file number | | 811-02753 |

SBL FUND

| | | | |

| (Exact name of registrant as specified in charter) |

| | |

| ONE SECURITY BENEFIT PLACE, TOPEKA, KANSAS | | 66636-0001 |

| (Address of principal executive offices) | | (Zip code) |

RICHARD M. GOLDMAN, PRESIDENT

SBL FUND

ONE SECURITY BENEFIT PLACE

TOPEKA, KANSAS 66636-0001

|

| (Name and address of agent for service) |

Registrant’s telephone number, including area code: (785) 438-3000

Date of fiscal year end: December 31

Date of reporting period: December 31, 2009

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. §3507.

| Item 1. | Reports to Stockholders. |

SBL Fund

December 31, 2009

Annual Report

Table of Contents

1

Information About Your Series Expenses

December 31, 2009 (unaudited)

Calculating your ongoing Series expenses

As a shareholder of the Series, you incur ongoing costs, including management fees and other series expenses. Performance figures and expense ratios do not reflect fees and expenses associated with an investment in variable insurance products. Shares of a Series of SBL Fund are available only through the purchase of such products. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Series and to compare these costs with ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period, July 1, 2009 through December 31, 2009.

Actual Expenses

The first table provides information about actual account values and actual expenses. You may use the information in this table, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the table under the heading entitled “Expenses Paid During the Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second table provides information about hypothetical account values and hypothetical expenses based on the Series actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Series actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Series and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other mutual funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any fees and expenses associated with an investment in variable insurance products. Therefore, the second table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these fees and expenses associated with an investment in variable insurance products were included, your costs would have been higher.

| | | | | | | | | | | | | | | |

| | | Expense

Ratio1 | | | Fund Return | | | Beginning

Account

Value

7/1/2009 | | Ending

Account Value

12/31/2009 | | Expenses

Paid

During

Period2 |

Table 1. Based on actual Series return3 | | | | | | | | | | | | | | | |

Series A (Equity Series) | | 0.91 | % | | 22.82 | % | | $ | 1,000.00 | | $ | 1,228.17 | | $ | 5.11 |

Series B (Large Cap Value Series) | | 0.80 | % | | 21.58 | % | | | 1,000.00 | | | 1,215.77 | | | 4.47 |

Series C (Money Market Series) | | 0.68 | % | | (0.29 | )% | | | 1,000.00 | | | 997.06 | | | 3.42 |

Series D (Global Series) | | 1.26 | % | | 16.73 | % | | | 1,000.00 | | | 1,167.33 | | | 6.88 |

Series E (U.S. Intermediate Bond Series) | | 0.76 | % | | 3.82 | % | | | 1,000.00 | | | 1,038.17 | | | 3.90 |

Series H (Enhanced Index Series) | | 0.76 | % | | 22.95 | % | | | 1,000.00 | | | 1,229.49 | | | 4.27 |

Series J (Mid Cap Growth Series) | | 0.91 | % | | 20.64 | % | | | 1,000.00 | | | 1,206.38 | | | 5.06 |

Series N (Managed Asset Allocation Series) | | 1.67 | % | | 16.36 | % | | | 1,000.00 | | | 1,163.65 | | | 9.11 |

Series O (All Cap Value Series) | | 0.85 | % | | 22.61 | % | | | 1,000.00 | | | 1,226.14 | | | 4.77 |

Series P (High Yield Series) | | 0.92 | % | | 23.67 | % | | | 1,000.00 | | | 1,236.67 | | | 5.19 |

Series Q (Small Cap Value Series) | | 1.12 | % | | 25.57 | % | | | 1,000.00 | | | 1,255.69 | | | 6.37 |

Series V (Mid Cap Value Series) | | 0.91 | % | | 23.37 | % | | | 1,000.00 | | | 1,233.65 | | | 5.12 |

Series X (Small Cap Growth Series) | | 1.07 | % | | 26.26 | % | | | 1,000.00 | | | 1,262.61 | | | 6.10 |

Series Y (Select 25 Series) | | 0.98 | % | | 23.80 | % | | | 1,000.00 | | | 1,238.03 | | | 5.53 |

Series Z (Alpha Opportunity Series) | | 1.65 | % | | 25.49 | % | | | 1,000.00 | | | 1,254.92 | | | 9.38 |

| | | | | |

Table 2. Based on hypothetical 5% return (before expenses) | | | | | | | | | | | | | | | |

Series A (Equity Series) | | 0.91 | % | | 5.00 | % | | $ | 1,000.00 | | $ | 1,020.62 | | $ | 4.63 |

Series B (Large Cap Value Series) | | 0.80 | % | | 5.00 | % | | | 1,000.00 | | | 1,021.17 | | | 4.08 |

Series C (Money Market Series) | | 0.68 | % | | 5.00 | % | | | 1,000.00 | | | 1,021.78 | | | 3.47 |

Series D (Global Series) | | 1.26 | % | | 5.00 | % | | | 1,000.00 | | | 1,018.85 | | | 6.41 |

Series E (U.S. Intermediate Bond Series) | | 0.76 | % | | 5.00 | % | | | 1,000.00 | | | 1,021.37 | | | 3.87 |

Series H (Enhanced Index Series) | | 0.76 | % | | 5.00 | % | | | 1,000.00 | | | 1,021.37 | | | 3.87 |

Series J (Mid Cap Growth Series) | | 0.91 | % | | 5.00 | % | | | 1,000.00 | | | 1,020.62 | | | 4.63 |

Series N (Managed Asset Allocation Series) | | 1.67 | % | | 5.00 | % | | | 1,000.00 | | | 1,016.79 | | | 8.49 |

Series O (All Cap Value Series) | | 0.85 | % | | 5.00 | % | | | 1,000.00 | | | 1,020.92 | | | 4.33 |

Series P (High Yield Series) | | 0.92 | % | | 5.00 | % | | | 1,000.00 | | | 1,020.57 | | | 4.69 |

Series Q (Small Cap Value Series) | | 1.12 | % | | 5.00 | % | | | 1,000.00 | | | 1,019.56 | | | 5.70 |

Series V (Mid Cap Value Series) | | 0.91 | % | | 5.00 | % | | | 1,000.00 | | | 1,020.62 | | | 4.63 |

Series X (Small Cap Growth Series) | | 1.07 | % | | 5.00 | % | | | 1,000.00 | | | 1,019.81 | | | 5.45 |

Series Y (Select 25 Series) | | 0.98 | % | | 5.00 | % | | | 1,000.00 | | | 1,020.27 | | | 4.99 |

Series Z (Alpha Opportunity Series) | | 1.65 | % | | 5.00 | % | | | 1,000.00 | | | 1,016.89 | | | 8.39 |

| 2 | Expenses are equal to the Series annualized expense ratio, net of any applicable fee waivers, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). |

| 3 | Actual cumulative return at net asset value for the period July 1, 2009 to December 31, 2009. |

2

Managers’ Commentary

February 15, 2010

| | | | |

| | Advised by: | |  |

To Our Shareholders:

Series A of the SBL Fund – Equity Series returned 29.84% during the year, outperforming the benchmark S&P 500 Index’s return of 26.46% and the Series’ peer group median return of 27.77%.

The Series’ strategy uses a blended approach, investing in growth and value stocks. Growth oriented stocks are securities of established companies that typically have a record of consistent earnings growth greater than the overall market. Value oriented stocks are securities of companies that are believed to be trading well below their intrinsic value.

Our strategy is to buy companies that are trading at a significant discount to their intrinsic value. Our investment approach is a defined and disciplined process of three clear philosophical tenants that drive our investment decisions: a valuation focus, a long-term perspective and an opportunistic approach.

This investment process is fundamentally driven and quantitatively aided. We use proprietary screens to identify potential companies for investment and then perform rigorous fundamental analysis to identify the best ideas. Through this fundamental research, we determine an estimate of intrinsic value and thus a valuation target for each idea. We construct the portfolios based on the level of conviction generated by this bottom-up analysis and the upside/downside profile associated with each company.

Health Care and Industrials Top Performers

While the health care sector was an underweighted position, portfolio holdings nearly doubled that of the S&P 500 Index, 39% to 20%. Schering-Plough Corporation and Hospira, Inc. led the sector for the portfolio with gains of 67% and 90%, respectively, due to the larger weight based on our conviction. Other health care holdings that were of benefit to the strategy were Amgen, Inc., Pfizer, Inc., and Medco Health Solutions, Inc.

Superior stock selection boosted performance in the industrials sector as the portfolio holdings increased 35% compared to a 21% gain for the Index. Underweighting General Electric Company, which produced a negative return for the year, helped portfolio performance. Adding to returns for the strategy were Union Pacific Corporation Parker Hannifin Corporation and Goodrich Corporation.

Financials and Consumer Discretionary Disappoint

The largest detractor for the Series was the financials sector due to stock selection, gaining just 7% against the 13% return posted by the benchmark. The sector was a close weight to the Index. Capital One Financial Corporation declined 68% in the portfolio while MetLife, Inc. lost 61%.

Stock selection in the consumer discretionary sector also hurt strategy performance. Gains for the portfolio were 20%, which was well below the 42% increase for the benchmark. Best Buy Company, Inc. and Coach, Inc. were the biggest losers for the strategy. If held during the entire period, Coach, Inc. would have generated a gain of 77%. Instead, the position lost 32% while held in the portfolio. Darden Restaurants, Inc. and Lowe’s Companies, Inc. were other holdings in the sector that hurt overall performance.

Market Outlook

Our bottom-up approach looks at market uncertainty in the context of the potential long-term impact on individual companies. It is in times as these when our core philosophy and disciplined process becomes paramount. We continue to use a rigorous fundamental research process to identify strong companies from a risk perspective. Our focus is on identifying companies with the ability to be substantially better over the next three to five years or have the potential to maintain their return on capital at current levels in a difficult economic environment. We are confident in our ability to find these companies.

We believe that investing is a long-term pursuit that requires patience and a consistent approach. We recognize there are many investment fund alternatives available today and thank you for the confidence you place in us.

Sincerely,

Mark A. Mitchell, Portfolio Manager

Mark P. Bronzo, Portfolio Manager

3

| | |

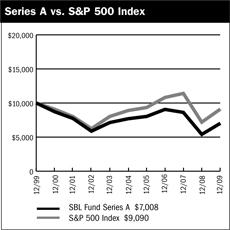

| Performance Summary | | Series A (Equity Series) |

December 31, 2009 | | (unaudited) |

PERFORMANCE

$10,000 Over 10 Years

The chart above assumes a hypothetical $10,000 investment in Series A (Equity Series) on December 31, 1999 and reflects the fees and expenses of Series A. The S&P 500 Index is a capitalization-weighted index composed of 500 selected common stocks that represent the broad domestic economy and is a widely recognized unmanaged index of market performance.

Average Annual Returns

| | | | | | | | | |

Periods Ended 12-31-091 | | 1 Year | | | 5 Years | | | 10 Years | |

Series A | | 29.84 | % | | (1.86 | )% | | (3.49 | )% |

| 1 | Performance figures do not reflect fees and expenses associated with an investment in variable insurance products offered by Security Benefit Life Insurance Company. If returns had taken into account these fees and expenses, performance would have been lower. Shares of a Series of SBL Fund are available only through the purchase of such products. |

The performance data quoted above represents past performance. Past performance is not predictive of future performance. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

Portfolio Composition by Sector

| | | |

Consumer Discretionary | | 11.39 | % |

Consumer Staples | | 7.22 | |

Energy | | 11.72 | |

Financials | | 11.12 | |

Health Care | | 11.45 | |

Industrials | | 17.95 | |

Information Technology | | 20.93 | |

Materials | | 4.11 | |

Telecommunication Services | | 0.58 | |

Utilities | | 2.14 | |

Cash & Other Assets, Less Liabilities | | 1.39 | |

Total Net Assets | | 100.00 | % |

| | | |

The accompanying notes are an integral part of the financial statements

4

| | |

| Schedule of Investments | | Series A |

December 31, 2009 | | (Equity Series) |

| | | | | |

| | | Shares | | Value |

COMMON STOCKS—98.6% | | | | | |

Advertising—1.7% | | | | | |

Omnicom Group, Inc. | | 81,000 | | $ | 3,171,150 |

| | | | | |

Aerospace & Defense—5.1% | | | | | |

Boeing Company | | 57,600 | | | 3,117,888 |

Goodrich Corporation | | 51,260 | | | 3,293,454 |

Precision Castparts Corporation | | 1,333 | | | 147,097 |

United Technologies Corporation | | 39,400 | | | 2,734,754 |

| | | | | |

| | | | | 9,293,193 |

| | | | | |

Air Freight & Logistics—1.4% | | | | | |

FedEx Corporation | | 31,500 | | | 2,628,675 |

| | | | | |

Apparel Retail—1.6% | | | | | |

TJX Companies, Inc. | | 82,000 | | | 2,997,100 |

| | | | | |

Application Software—0.5% | | | | | |

Synopsys, Inc.* | | 41,800 | | | 931,304 |

| | | | | |

Asset Management & Custody Banks—0.7% | | | | | |

Bank of New York Mellon Corporation | | 46,900 | | | 1,311,793 |

| | | | | |

Biotechnology—1.7% | | | | | |

Amgen, Inc.* | | 56,700 | | | 3,207,519 |

| | | | | |

Building Products—1.2% | | | | | |

USG Corporation* | | 163,200 | | | 2,292,960 |

| | | | | |

Coal & Consumable Fuels—1.6% | | | | | |

Peabody Energy Corporation | | 64,260 | | | 2,905,195 |

| | | | | |

Communications Equipment—3.4% | | | | | |

Cisco Systems, Inc.* | | 127,700 | | | 3,057,138 |

Qualcomm, Inc. | | 66,265 | | | 3,065,419 |

| | | | | |

| | | | | 6,122,557 |

| | | | | |

Computer Hardware—3.8% | | | | | |

Apple, Inc.* | | 20,720 | | | 4,369,018 |

Hewlett-Packard Company | | 47,900 | | | 2,467,329 |

| | | | | |

| | | | | 6,836,347 |

| | | | | |

Computer Storage & Peripherals—2.1% | | | | | |

EMC Corporation* | | 226,760 | | | 3,961,497 |

| | | | | |

Construction Materials—0.2% | | | | | |

Vulcan Materials Company | | 7,900 | | | 416,093 |

| | | | | |

Consumer Finance—0.1% | | | | | |

First Marblehead Corporation* | | 103,452 | | | 220,353 |

| | | | | |

Data Processing & Outsourced Services—2.3% | | | | | |

Western Union Company | | 231,100 | | | 4,356,235 |

| | | | | |

Department Stores—2.4% | | | | | |

JC Penney Company, Inc. | | 61,400 | | | 1,633,854 |

Kohl’s Corporation* | | 50,950 | | | 2,747,734 |

| | | | | |

| | | | | 4,381,588 |

| | | | | |

Diversified Banks—2.0% | | | | | |

U.S. Bancorp | | 85,875 | | | 1,933,047 |

Wells Fargo & Company | | 66,564 | | | 1,796,562 |

| | | | | |

| | | | | 3,729,609 |

| | | | | |

Diversified Chemicals—0.8% | | | | | |

Dow Chemical Company | | 52,500 | | | 1,450,575 |

| | | | | |

Diversified Metals & Mining—1.5% | | | | | |

Freeport-McMoRan Copper & Gold, Inc. (CI.B) | | 35,500 | | | 2,850,295 |

| | | | | |

Drug Retail—1.0% | | | | | |

CVS Caremark Corporation | | 58,000 | | | 1,868,180 |

| | | | | |

Electric Utilities—1.6% | | | | | |

Edison International | | 86,300 | | | 3,001,514 |

| | | | | |

Electrical Components & Equipment—3.3% | | | | | |

Cooper Industries plc | | 72,780 | | | 3,103,338 |

Emerson Electric Company | | 70,690 | | | 3,011,394 |

| | | | | |

| | | | | 6,114,732 |

| | | | | |

Electronic Manufacturing Services—1.1% | | | | | |

Tyco Electronics, Ltd. | | 85,200 | | | 2,091,660 |

| | | | | |

Fertilizers & Agricultural Chemicals—1.6% | | | | | |

Potash Corporation of Saskatchewan, Inc. | | 26,905 | | | 2,919,193 |

| | | | | |

Health Care Equipment—4.1% | | | | | |

Covidien plc | | 105,670 | | | 5,060,536 |

Hospira, Inc.* | | 48,400 | | | 2,468,400 |

| | | | | |

| | | | | 7,528,936 |

| | | | | |

Health Care Services—0.9% | | | | | |

Medco Health Solutions, Inc.* | | 27,300 | | | 1,744,743 |

| | | | | |

Home Improvement Retail—1.5% | | | | | |

Lowe’s Companies, Inc. | | 117,500 | | | 2,748,325 |

| | | | | |

Hotels, Resorts & Cruise Lines—1.5% | | | | | |

Carnival Corporation* | | 89,900 | | | 2,848,931 |

| | | | | |

Household Products—1.7% | | | | | |

Colgate-Palmolive Company | | 38,050 | | | 3,125,808 |

| | | | | |

Hypermarkets & Super Centers—2.8% | | | | | |

Costco Wholesale Corporation | | 45,100 | | | 2,668,567 |

Wal-Mart Stores, Inc. | | 47,800 | | | 2,554,910 |

| | | | | |

| | | | | 5,223,477 |

| | | | | |

Independent Power Producers & Energy Traders—0.5% | | | | | |

NRG Energy, Inc.* | | 41,600 | | | 982,176 |

| | | | | |

Industrial Conglomerates—3.2% | | | | | |

3M Company | | 39,000 | | | 3,224,130 |

McDermott International, Inc.* | | 117,000 | | | 2,809,170 |

| | | | | |

| | | | | 6,033,300 |

| | | | | |

The accompanying notes are an integral part of the financial statements

5

| | |

| Schedule of Investments | | Series A |

December 31, 2009 | | (Equity Series) |

| | | | | |

| | | Shares | | Value |

COMMON STOCKS—98.6% (continued) | | | | | |

Industrial Machinery—1.0% | | | | | |

Parker Hannifin Corporation | | 33,603 | | $ | 1,810,530 |

| | | | | |

Insurance Brokers—0.9% | | | | | |

AON Corporation | | 45,700 | | | 1,752,138 |

| | | | | |

Integrated Oil & Gas—5.0% | | | | | |

Chevron Corporation | | 31,700 | | | 2,440,583 |

ConocoPhillips | | 15,200 | | | 776,264 |

Exxon Mobil Corporation | | 48,400 | | | 3,300,396 |

Occidental Petroleum Corporation | | 36,000 | | | 2,928,600 |

| | | | | |

| | | | | 9,445,843 |

| | | | | |

Integrated Telecommunication Services—0.6% | | | | | |

Windstream Corporation | | 98,200 | | | 1,079,218 |

| | | | | |

Internet Software & Services—2.5% | | | | | |

AOL, Inc.* | | 5,945 | | | 138,400 |

Google, Inc.* | | 7,235 | | | 4,485,555 |

| | | | | |

| | | | | 4,623,955 |

| | | | | |

Investment Banking & Brokerage—1.6% | | | | | |

Morgan Stanley | | 100,500 | | | 2,974,800 |

| | | | | |

IT Consulting & Other Services—1.6% | | | | | |

Cognizant Technology Solutions Corporation* | | 67,440 | | | 3,055,032 |

| | | | | |

Managed Health Care—0.8% | | | | | |

Aetna, Inc. | | 49,600 | | | 1,572,320 |

| | | | | |

Movies & Entertainment—1.0% | | | | | |

Time Warner, Inc. | | 65,400 | | | 1,905,756 |

| | | | | |

Oil & Gas Drilling—1.9% | | | | | |

Transocean, Ltd.* | | 41,840 | | | 3,464,352 |

| | | | | |

Oil & Gas Equipment & Services—1.2% | | | | | |

Halliburton Company | | 74,200 | | | 2,232,678 |

| | | | | |

Oil & Gas Exploration & Production—0.9% | | | | | |

Chesapeake Energy Corporation | | 64,200 | | | 1,661,496 |

| | | | | |

Oil & Gas Storage & Transportation—1.1% | | | | | |

Williams Companies, Inc. | | 99,500 | | | 2,097,460 |

| | | | | |

Other Diversified Financial Services—2.4% | | | | | |

JPMorgan Chase & Company | | 104,106 | | | 4,338,096 |

| | | | | |

Pharmaceuticals—3.9% | | | | | |

Merck & Company, Inc. | | 17,358 | | | 634,261 |

Pfizer, Inc. | | 169,900 | | | 3,090,481 |

Teva Pharmaceutical Industries, Ltd. ADR | | 62,490 | | | 3,510,689 |

| | | | | |

| | | | | 7,235,431 |

| | | | | |

Property & Casualty Insurance—2.2% | | | | | |

Berkshire Hathaway, Inc.* | | 42 | | | 4,166,400 |

| | | | | |

Railroads—1.3% | | | | | |

Union Pacific Corporation | | 37,200 | | | 2,377,080 |

| | | | | |

Regional Banks—1.2% | | | | | |

BB&T Corporation | | 33,700 | | | 854,969 |

Fifth Third Bancorp | | 41,000 | | | 399,750 |

Regions Financial Corporation | | 178,000 | | | 941,620 |

| | | | | |

| | | | | 2,196,339 |

| | | | | |

Research & Consulting Services—1.5% | | | | | |

Equifax, Inc. | | 91,900 | | | 2,838,791 |

| | | | | |

Semiconductor Equipment—1.6% | | | | | |

Lam Research Corporation* | | 75,750 | | | 2,970,158 |

| | | | | |

Semiconductors—2.1% | | | | | |

Intel Corporation | | 195,050 | | | 3,979,020 |

| | | | | |

Soft Drinks—2.1% | | | | | |

PepsiCo, Inc. | | 63,810 | | | 3,879,648 |

| | | | | |

Tobacco—1.3% | | | | | |

Altria Group, Inc. | | 50,500 | | | 991,315 |

Philip Morris International, Inc. | | 30,500 | | | 1,469,795 |

| | | | | |

| | | | | 2,461,110 |

| | | | | |

TOTAL COMMON STOCKS (cost $172,811,350) | | | | $ | 183,412,664 |

| | | | | |

Total Investments—98.6%1 (cost $172,811,350) | | | | $ | 183,412,664 |

Cash & Other Assets, Less Liabilities—1.4% | | | | | 2,594,781 |

| | | | | |

Total Net Assets—100.0% | | | | $ | 186,007,445 |

| | | | | |

For federal income tax purposes the identified cost of investments owned at December 31, 2009 was $173,165,753.

| * | Non-income producing security |

| 1 | Unless otherwise indicated, the values of the securities of the Portfolio are determined based on Level 1 inputs. |

The accompanying notes are an integral part of the financial statements

6

Statement of Assets and Liabilities

December 31, 2009

| | | | |

Assets: | | | | |

Investments, at value* | | $ | 183,412,664 | |

Cash | | | 2,932,270 | |

Receivables: | | | | |

Fund shares sold | | | 391,256 | |

Securities sold | | | 296,724 | |

Dividends | | | 243,233 | |

Prepaid expenses | | | 3,665 | |

| | | | |

Total assets | | | 187,279,812 | |

| | | | |

| |

Liabilities: | | | | |

| |

Payable for: | | | | |

Fund shares redeemed | | | 395,157 | |

Securities purchased | | | 643,830 | |

Management fees | | | 118,522 | |

Administration fees | | | 15,133 | |

Transfer agent/maintenance fees | | | 2,083 | |

Custodian fees | | | 1,176 | |

Directors’ fees | | | 5,478 | |

Professional fees | | | 33,350 | |

Other fees | | | 57,638 | |

| | | | |

Total liabilities | | | 1,272,367 | |

| | | | |

Net assets | | $ | 186,007,445 | |

| | | | |

| |

Net assets consist of: | | | | |

Paid in capital | | $ | 230,763,789 | |

Undistributed net investment income | | | 1,140,095 | |

Accumulated net realized loss on sale of investments | | | (56,497,753 | ) |

Net unrealized appreciation in value of investments | | | 10,601,314 | |

| | | | |

Net assets | | $ | 186,007,445 | |

| | | | |

| |

Capital shares authorized | | | unlimited | |

Capital shares outstanding | | | 9,314,012 | |

Net asset value per share (net assets divided by shares outstanding) | | $ | 19.97 | |

| | | | |

| |

* Investments, at cost | | $ | 172,811,350 | |

Statement of Operations

For Year Ended December 31, 2009

| | | | |

Investment Income: | | | | |

Dividends | | $ | 2,678,032 | |

Interest | | | 4,423 | |

| | | | |

Total investment income | | | 2,682,455 | |

| | | | |

| |

Expenses: | | | | |

Management fees | | | 1,253,402 | |

Administration fees | | | 159,095 | |

Transfer agent/maintenance fees | | | 25,315 | |

Custodian fees | | | 7,740 | |

Directors’ fees | | | 15,695 | |

Professional fees | | | 41,123 | |

Reports to shareholders | | | 28,002 | |

Other | | | 11,988 | |

| | | | |

Total expenses | | | 1,542,360 | |

| | | | |

Net investment income | | | 1,140,095 | |

| | | | |

| |

Net Realized and Unrealized Gain (Loss): | | | | |

Net realized gain (loss) during the year on: | | | | |

Investments | | | (27,019,679 | ) |

Options written | | | 7,098 | |

| | | | |

Net realized loss | | | (27,012,581 | ) |

| | | | |

Net unrealized appreciation (depreciation) during the year on: | | | | |

Investments | | | 69,815,569 | |

| | | | |

Net unrealized appreciation | | | 69,815,569 | |

| | | | |

Net realized and unrealized gain | | | 42,802,988 | |

| | | | |

Net increase in net assets resulting from operations | | $ | 43,943,083 | |

| | | | |

The accompanying notes are an integral part of the financial statements

7

| | |

| | Series A |

| Statement of Changes in Net Assets | | (Equity Series) |

| | | | | | | | |

| | | Year Ended

December 31, 2009 | | | Year Ended

December 31, 2008 | |

Increase (decrease) in net assets from operations: | | | | | | | | |

Net investment income | | $ | 1,140,095 | | | $ | 1,665,710 | |

Net realized loss during the year on investments | | | (27,012,581 | ) | | | (21,709,270 | ) |

Net unrealized appreciation (depreciation) during the year on investments | | | 69,815,569 | | | | (85,457,350 | ) |

| | | | | | | | |

Net increase (decrease) in net assets resulting from operations | | | 43,943,083 | | | | (105,500,910 | ) |

| | | | | | | | |

| | |

Capital share transactions: | | | | | | | | |

Proceeds from sale of shares | | | 17,506,604 | | | | 24,426,853 | |

Cost of shares redeemed | | | (40,551,126 | ) | | | (82,812,481 | ) |

| | | | | | | | |

Net decrease from capital share transactions | | | (23,044,522 | ) | | | (58,385,628 | ) |

| | | | | | | | |

Net increase (decrease) in net assets | | | 20,898,561 | | | | (163,886,538 | ) |

| | | | | | | | |

| | |

Net assets: | | | | | | | | |

Beginning of year | | | 165,108,884 | | | | 328,995,422 | |

| | | | | | | | |

End of year | | $ | 186,007,445 | | | $ | 165,108,884 | |

| | | | | | | | |

Undistributed net investment income at end of year | | $ | 1,140,095 | | | $ | 1,665,710 | |

| | | | | | | | |

| | |

Capital share activity: | | | | | | | | |

Shares sold | | | 1,102,467 | | | | 1,174,494 | |

Shares redeemed | | | (2,524,592 | ) | | | (3,831,105 | ) |

| | | | | | | | |

Total capital share activity | | | (1,422,125 | ) | | | (2,656,611 | ) |

| | | | | | | | |

The accompanying notes are an integral part of the financial statements

8

| | |

| Financial Highlights | | Series A |

Selected data for each share of capital stock outstanding throughout each year | | (Equity Series) |

| | | | | | | | | | | | | | | | | | | | |

| | | 2009 | | | 2008 | | | 2007 | | | 2006 | | | Year Ended

December 31,

2005 | |

Per Share Data | | | | | | | | | | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 15.38 | | | $ | 24.57 | | | $ | 25.83 | | | $ | 22.88 | | | $ | 21.93 | |

| | | | | | | | | | | | | | | | | | | | |

Income (loss) from investment operations: | | | | | | | | | | | | | | | | | | | | |

Net investment incomea | | | 0.11 | | | | 0.14 | | | | 0.14 | | | | 0.11 | | | | 0.16 | |

Net gain (loss) on securities (realized and unrealized) | | | 4.48 | | | | (9.33 | ) | | | (1.40 | ) | | | 2.84 | | | | 0.79 | |

| | | | | | | | | | | | | | | | | | | | |

Total from investment operations | | | 4.59 | | | | (9.19 | ) | | | (1.26 | ) | | | 2.95 | | | | 0.95 | |

| | | | | | | | | | | | | | | | | | | | |

Net asset value, end of period | | $ | 19.97 | | | $ | 15.38 | | | $ | 24.57 | | | $ | 25.83 | | | $ | 22.88 | |

| | | | | | | | | | | | | | | | | | | | |

Total Returnb | | | 29.84 | % | | | (37.40 | )% | | | (4.88 | )% | | | 12.89 | % | | | 4.33 | % |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Ratios/Supplemental Data | | | | | | | | | | | | | | | | | | | | |

Net assets, end of period (in thousands) | | $ | 186,007 | | | $ | 165,109 | | | $ | 328,995 | | | $ | 441,788 | | | $ | 466,931 | |

| | | | | | | | | | | | | | | | | | | | |

Ratios to average net assets: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | 0.68 | % | | | 0.66 | % | | | 0.52 | % | | | 0.33 | % | | | 0.55 | % |

Total expensesc | | | 0.92 | % | | | 0.90 | % | | | 0.89 | % | | | 0.90 | % | | | 0.89 | % |

Net expensesd | | | 0.92 | % | | | 0.90 | % | | | 0.89 | % | | | 0.90 | % | | | 0.89 | % |

Net expenses prior to custodian earnings credits and net of expense waivers | | | 0.92 | % | | | 0.90 | % | | | 0.89 | % | | | 0.90 | % | | | 0.89 | % |

| | | | | | | | | | | | | | | | | | | | |

Portfolio turnover rate | | | 78 | % | | | 142 | %e | | | 14 | % | | | 26 | % | | | 37 | % |

| a | Net investment income (loss) was computed using average shares outstanding throughout the period. |

| b | Total return does not take into account any of the expenses associated with an investment in variable insurance products offered by Security Benefit Life Insurance Company. If total return had taken into account these expenses, performance would have been lower. Shares of a series of SBL Fund are available only through the purchase of such products. |

| c | Total expense information reflects the expense ratios absent expense reductions by the Investment Manager and custodian earnings credits, as applicable. |

| d | Net expense information reflects the expense ratios after voluntary expense waivers, reimbursements and custodian earnings credits, as applicable. |

| e | Significant variation in the portfolio turnover rate is due to Investment Manager’s appointment of new portfolio manager for the Series. |

The accompanying notes are an integral part of the financial statements

9

This page left blank intentionally.

10

Manager’s Commentary

February 15, 2010

| | | | |

| | Advised by: | | |

To Our Shareholders:

Series B of the SBL Fund – Large Cap Value Series returned 26.50% during the year, leading the benchmark Russell 1000 Value Index’s return of 19.69%. The Series outperformed its peer group median return of 24.28%.

Our strategy is to buy companies that are trading at a significant discount to their intrinsic value. Our investment approach is a defined and disciplined process with three clear philosophical tenets that drive our investment decisions: a valuation focus, a long-term perspective and an opportunistic approach.

Our investment process is fundamentally driven and quantitatively aided. We use proprietary screens to identify potential companies for investment and then perform rigorous fundamental analysis to identify the best ideas. Through this fundamental research, we determine an estimate of intrinsic value and thus a valuation target for each idea. We construct the portfolios based on the level of conviction generated by this bottom-up analysis and the upside/downside profile associated with each company. For Series B, we apply this philosophy to a broad range of value names.

Health Care and Industrials Top Performers

The Series’ health care sector led the portfolio due to superior security selection. While a slightly underweight position, holdings in the strategy increased 67% compared to a 23% return for the benchmark. Schering-Plough Corporation added the largest relative return to the sector while returns for Hospira, Inc. were 90%. Another contributor for the portfolio in the sector was Medco Health Solutions, Inc.

The Series has a significant overweight position in the industrials sector at 22%, more than double the 9% weight of the benchmark. Holdings in the sector for the portfolio outdistanced that of the Index 40% to 15%, respectively. Leaders for the portfolio were USG Corporation and Union Pacific Corporation, which increased 75% and 37%, respectively. Other contributing performers in the sector were General Electric Company and FedEx Corporation.

Financials and Consumer Discretionary Disappoint

The largest detractor from the portfolio was the financials sector due to underperforming stock selection. Capital One Financial Corporation dropped 71% during the period causing it to the be largest drag on performance for the sector. While JPMorgan Chase & Company gained 34% during the year, it was a significant underweight against the benchmark allowing the Index to increase its relative return. Finally, AON Corporation was a drag on portfolio performance due to its large relative overweight in a security that had negative returns.

The strategy’s consumer discretionary sector was an even weight position but held the portfolio back due to security selection. While the sector in the portfolio gained 27%, it was well short of the 47% return for the benchmark. Portfolio securities in the sector that detracted from performance were Lowe’s Companies, Inc., CBS Corporation (Cl B), and News Corporation (Cl A). Had the portfolio held CBS Corporation and News Corporation during the entire year, it would have realized the Index’s gains of 77% and 53%, respectively, rather than the actual 7% and 3% returns.

Market Outlook

Our bottom-up approach looks at market uncertainty in the context of the potential long-term impact on individual companies. Often times, volatility provides opportunity. We are maintaining flexibility in the portfolios to take advantage of these opportunities as they arise. Our focus is on identifying companies with the ability to be substantially better over the next three to five years or have the potential to maintain their return on capital at current levels in a difficult economic environment. We are confident in our ability to find these companies.

We believe that investing is a long-term pursuit that requires patience and a consistent approach. We recognize there are many investment fund alternatives available today and thank you for your business and the confidence you place in us.

Sincerely,

Mark A. Mitchell, Portfolio Manager

11

| | |

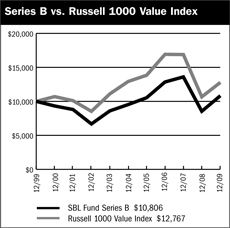

| | Series B |

| Performance Summary | | (Large Cap Value Series) |

December 31, 2009 | | (unaudited) |

PERFORMANCE

$10,000 Over 10 Years

The chart above assumes a hypothetical $10,000 investment in Series B (Large Cap Value Series) on December 31, 1999 and reflects the fees and expenses of Series B. The Russell 1000 Value Index is an unmanaged index representing the performance of those Russell 1000 Index companies with lower price-to-book ratios and lower forecasted growth values.

Average Annual Returns

| | | | | | | | | |

Periods Ended 12-31-091 | | 1 Year | | | 5 Years | | | 10 Years | |

Series B | | 26.50 | % | | 2.54 | % | | 0.78 | % |

| 1 | Performance figures do not reflect fees and expenses associated with an investment in variable insurance products offered by Security Benefit Life Insurance Company. If returns had taken into account these fees and expenses, performance would have been lower. Shares of a Series of SBL Fund are available only through the purchase of such products. |

The performance data quoted above represents past performance. Past performance is not predictive of future performance. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

Portfolio Composition by Sector

| | | |

Consumer Discretionary | | 7.22 | % |

Consumer Staples | | 10.17 | |

Energy | | 13.68 | |

Financials | | 16.68 | |

Health Care | | 8.96 | |

Industrials | | 20.07 | |

Information Technology | | 11.13 | |

Materials | | 2.22 | |

Telecommunication Services | | 1.30 | |

Utilities | | 4.62 | |

Exchange Traded Funds | | 1.01 | |

Commercial Paper | | 1.25 | |

Cash & Other Assets, Less Liabilities | | 1.69 | |

Total Net Assets | | 100.00 | % |

| | | |

The accompanying notes are an integral part of the financial statements

12

| | |

| Schedule of Investments | | Series B |

December 31, 2009 | | (Large Cap Value Series) |

| | | | | |

| | | Shares | | Value |

COMMON STOCKS—97.1% | | | | | |

Aerospace & Defense—3.1% | | | | | |

Precision Castparts Corporation | | 4,180 | | $ | 461,263 |

United Technologies Corporation | | 117,300 | | | 8,141,793 |

| | | | | |

| | | | | 8,603,056 |

| | | | | |

Air Freight & Logistics—3.0% | | | | | |

FedEx Corporation | | 101,643 | | | 8,482,108 |

| | | | | |

Application Software—1.1% | | | �� | | |

Synopsys, Inc.* | | 134,800 | | | 3,003,344 |

| | | | | |

Asset Management & Custody Banks—1.5% | | | | | |

Bank of New York Mellon Corporation | | 151,400 | | | 4,234,658 |

| | | | | |

Building Products—2.6% | | | | | |

USG Corporation* | | 528,000 | | | 7,418,400 |

| | | | | |

Computer Hardware—2.5% | | | | | |

Hewlett-Packard Company | | 137,300 | | | 7,072,323 |

| | | | | |

Construction Materials—0.5% | | | | | |

Vulcan Materials Company | | 25,400 | | | 1,337,818 |

| | | | | |

Consumer Finance—0.2% | | | | | |

First Marblehead Corporation* | | 317,112 | | | 675,449 |

| | | | | |

Data Processing & Outsourced Services—4.9% | | | | | |

Western Union Company | | 737,500 | | | 13,901,875 |

| | | | | |

Department Stores—1.9% | | | | | |

JC Penney Company, Inc. | | 198,800 | | | 5,290,068 |

| | | | | |

Diversified Banks—4.6% | | | | | |

U.S. Bancorp | | 277,806 | | | 6,253,413 |

Wells Fargo & Company | | 242,405 | | | 6,542,511 |

| | | | | |

| | | | | 12,795,924 |

| | | | | |

Diversified Chemicals—1.7% | | | | | |

Dow Chemical Company | | 176,400 | | | 4,873,932 |

| | | | | |

Drug Retail—2.1% | | | | | |

CVS Caremark Corporation | | 186,200 | | | 5,997,502 |

| | | | | |

Electric Utilities—3.5% | | | | | |

Edison International | | 282,400 | | | 9,821,872 |

| | | | | |

Electronic Manufacturing Services—2.4% | | | | | |

Tyco Electronics, Ltd. | | 273,950 | | | 6,725,473 |

| | | | | |

Exchange Traded Funds—1.0% | | | | | |

iShares Russell 1000 Value Index Fund | | 49,500 | | | 2,840,805 |

| | | | | |

Health Care Equipment—4.5% | | | | | |

Covidien plc | | 101,650 | | | 4,868,019 |

Hospira, Inc.* | | 148,000 | | | 7,547,999 |

| | | | | |

| | | | | 12,416,018 |

| | | | | |

Health Care Services—2.0% | | | | | |

Medco Health Solutions, Inc.* | | 88,200 | | | 5,636,862 |

| | | | | |

Home Improvement Retail—2.8% | | | | | |

Lowe’s Companies, Inc. | | 343,500 | | | 8,034,465 |

| | | | | |

Hypermarkets & Super Centers—5.7% | | | | | |

Costco Wholesale Corporation | | 126,400 | | | 7,479,088 |

Wal-Mart Stores, Inc. | | 154,500 | | | 8,258,025 |

| | | | | |

| | | | | 15,737,113 |

| | | | | |

Independent Power Producers & Energy Traders—1.1% | | | | | |

NRG Energy, Inc.* | | 133,500 | | | 3,151,935 |

| | | | | |

Industrial Conglomerates—3.3% | | | | | |

McDermott International, Inc.* | | 379,900 | | | 9,121,399 |

| | | | | |

Industrial Machinery—2.1% | | | | | |

Parker Hannifin Corporation | | 109,810 | | | 5,916,563 |

| | | | | |

Insurance Brokers—2.0% | | | | | |

AON Corporation | | 147,900 | | | 5,670,486 |

| | | | | |

Integrated Oil & Gas—7.1% | | | | | |

Chevron Corporation | | 98,600 | | | 7,591,214 |

ConocoPhillips | | 41,200 | | | 2,104,084 |

Exxon Mobil Corporation | | 151,700 | | | 10,344,423 |

| | | | | |

| | | | | 20,039,721 |

| | | | | |

Integrated Telecommunication Services—1.3% | | | | | |

Windstream Corporation | | 331,932 | | | 3,647,933 |

| | | | | |

Internet Software & Services—0.2% | | | | | |

AOL, Inc.* | | 21,593 | | | 502,685 |

| | | | | |

Managed Health Care—1.8% | | | | | |

Aetna, Inc. | | 158,000 | | | 5,008,600 |

| | | | | |

Movies & Entertainment—2.5% | | | | | |

Time Warner, Inc. | | 237,533 | | | 6,921,712 |

| | | | | |

Oil & Gas Equipment & Services—2.6% | | | | | |

Halliburton Company | | 244,000 | | | 7,341,960 |

| | | | | |

Oil & Gas Exploration & Production—1.7% | | | | | |

Chesapeake Energy Corporation | | 179,200 | | | 4,637,696 |

| | | | | |

Oil & Gas Storage & Transportation—2.3% | | | | | |

Williams Companies, Inc. | | 300,700 | | | 6,338,756 |

| | | | | |

Other Diversified Financial Services—1.0% | | | | | |

JPMorgan Chase & Company | | 69,469 | | | 2,894,773 |

| | | | | |

The accompanying notes are an integral part of the financial statements

13

| | |

| Schedule of Investments | | Series B |

| December 31, 2009 | | (Large Cap Value Series) |

| | | | | | |

| | | Shares | | Value |

COMMON STOCKS—97.1% (continued) | | | | | | |

Pharmaceuticals—0.7% | | | | | | |

Merck & Company, Inc. | | | 56,170 | | $ | 2,052,452 |

| | | | | | |

Property & Casualty Insurance—4.9% | | | | | | |

Berkshire Hathaway, Inc.* | | | 135 | | | 13,392,000 |

| | | | | | |

Railroads—2.7% | | | | | | |

Union Pacific Corporation | | | 120,000 | | | 7,668,000 |

| | | | | | |

Regional Banks—2.5% | | | | | | |

BB&T Corporation | | | 109,200 | | | 2,770,404 |

Fifth Third Bancorp | | | 133,000 | | | 1,296,750 |

Regions Financial Corporation | | | 575,500 | | | 3,044,395 |

| | | | | | |

| | | | | | 7,111,549 |

| | | | | | |

Research & Consulting Services—3.3% | | | | | | |

Equifax, Inc. | | | 295,500 | | | 9,127,994 |

| | | | | | |

Tobacco—2.4% | | | | | | |

Altria Group, Inc. | | | 108,000 | | | 2,120,040 |

Philip Morris International, Inc. | | | 97,100 | | | 4,679,249 |

| | | | | | |

| | | | | | 6,799,289 |

| | | | | | |

TOTAL COMMON STOCKS (cost $262,147,025) | | | | | $ | 272,244,568 |

| | | | | | |

| | |

| | | Principal

Amount | | Value |

COMMERCIAL PAPER—1.2% | | | | | | |

Automotive—1.2% | | | | | | |

Toyota Motor Credit Corporation | | | | | | |

0.03%, 01/04/20101 | | $ | 3,500,000 | | $ | 3,499,991 |

| | | | | | |

TOTAL COMMERCIAL PAPER (cost $3,499,991) | | | | | $ | 3,499,991 |

| | | | | | |

Total Investments—98.3%2 (cost $265,647,016) | | | | | $ | 275,744,559 |

Cash & Other Assets, Less Liabilities—1.7% | | | | | | 4,728,827 |

| | | | | | |

Total Net Assets—100.0% | | | | | $ | 280,473,386 |

| | | | | | |

For federal income tax purposes the identified cost of investments owned at December 31, 2009 was $265,859,070.

| plc | Public Limited Company |

| * | Non-income producing security |

| 1 | Value determined based on Level 2 inputs. |

| 2 | Unless otherwise indicated, the values of the securities of the Portfolio are determined based on Level 1 inputs. |

The accompanying notes are an integral part of the financial statements

14

Series B

(Large Cap Value Series)

Statement of Assets and Liabilities

December 31, 2009

| | | | |

Assets: | | | | |

Investments, at value* | | $ | 275,744,559 | |

Cash | | | 5,589,947 | |

Receivables: | | | | |

Fund shares sold | | | 204,743 | |

Securities sold | | | 959,225 | |

Dividends | | | 457,031 | |

Prepaid expenses | | | 5,473 | |

| | | | |

Total assets | | | 282,960,978 | |

| | | | |

Liabilities: | | | | |

| |

Payable for: | | | | |

Fund shares redeemed | | | 133,054 | |

Securities purchased | | | 2,074,253 | |

Management fees | | | 155,170 | |

Administration fees | | | 22,768 | |

Transfer agent/maintenance fees | | | 2,083 | |

Custodian fees | | | 556 | |

Directors’ fees | | | 4,182 | |

Professional fees | | | 43,600 | |

Other fees | | | 51,926 | |

| | | | |

Total liabilities | | | 2,487,592 | |

| | | | |

Net assets | | $ | 280,473,386 | |

| | | | |

Net assets consist of: | | | | |

Paid in capital | | $ | 441,314,284 | |

Undistributed net investment income | | | 2,616,829 | |

Accumulated net realized loss on sale of investments | | | (173,555,270 | ) |

Net unrealized appreciation in value of investments | | | 10,097,543 | |

| | | | |

Net assets | | $ | 280,473,386 | |

| | | | |

| |

Capital shares authorized | | | unlimited | |

Capital shares outstanding | | | 12,635,575 | |

Net asset value per share (net assets divided by shares outstanding) | | $ | 22.20 | |

| | | | |

| |

* Investments, at cost | | $ | 265,647,016 | |

|

Statement of Operations For Year Ended December 31, 2009 | |

Investment Income: | | | | |

Dividends | | $ | 4,664,091 | |

Interest | | | 11,183 | |

| | | | |

Total investment income | | | 4,675,274 | |

| | | | |

| |

Expenses: | | | | |

Management fees | | | 1,647,391 | |

Administration fees | | | 241,019 | |

Transfer agent/maintenance fees | | | 25,352 | |

Custodian fees | | | 10,111 | |

Directors’ fees | | | 23,688 | |

Professional fees | | | 48,545 | |

Reports to shareholders | | | 44,240 | |

Other | | | 18,099 | |

| | | | |

Total expenses | | | 2,058,445 | |

| | | | |

Net investment income | | | 2,616,829 | |

| | | | |

| |

Net Realized and Unrealized Gain (Loss): | | | | |

Net realized gain (loss) during the year on: | | | | |

Investments | | | (21,745,604 | ) |

Options written | | | 22,775 | |

| | | | |

Net realized loss | | | (21,722,829 | ) |

| | | | |

| |

Net unrealized appreciation (depreciation) during the year on: | | | | |

Investments | | | 77,753,258 | |

| | | | |

Net unrealized appreciation | | | 77,753,258 | |

| | | | |

Net realized and unrealized gain | | | 56,030,429 | |

| | | | |

Net increase in net assets resulting from operations | | $ | 58,647,258 | |

| | | | |

The accompanying notes are an integral part of the financial statements

15

| | |

| Series B |

| Statement of Changes in Net Assets | | (Large Cap Value Series) |

| | | | | | | | |

| | | Year Ended

December 31, 2009 | | | Year Ended

December 31, 2008 | |

Increase (decrease) in net assets from operations: | | | | | | | | |

Net investment income | | $ | 2,616,829 | | | $ | 4,509,471 | |

Net realized loss during the year on investments | | | (21,722,829 | ) | | | (35,097,727 | ) |

Net unrealized appreciation (depreciation) during the year on investments | | | 77,753,258 | | | | (128,705,287 | ) |

| | | | | | | | |

Net increase (decrease) in net assets resulting from operations | | | 58,647,258 | | | | (159,293,543 | ) |

| | | | | | | | |

| | |

Capital share transactions: | | | | | | | | |

Proceeds from sale of shares | | | 40,712,808 | | | | 97,567,905 | |

Cost of shares redeemed | | | (69,858,540 | ) | | | (167,274,870 | ) |

| | | | | | | | |

Net decrease from capital share transactions | | | (29,145,732 | ) | | | (69,706,965 | ) |

| | | | | | | | |

Net increase (decrease) in net assets | | | 29,501,526 | | | | (229,000,508 | ) |

| | | | | | | | |

| | |

Net assets: | | | | | | | | |

Beginning of year | | | 250,971,860 | | | | 479,972,368 | |

| | | | | | | | |

End of year | | $ | 280,473,386 | | | $ | 250,971,860 | |

| | | | | | | | |

| | |

Undistributed net investment income at end of year | | $ | 2,616,829 | | | $ | 4,509,471 | |

| | | | | | | | |

| | |

Capital share activity: | | | | | | | | |

Shares sold | | | 2,258,834 | | | | 3,899,132 | |

Shares redeemed | | | (3,921,822 | ) | | | (6,778,642 | ) |

| | | | | | | | |

Total capital share activity | | | (1,662,988 | ) | | | (2,879,510 | ) |

| | | | | | | | |

The accompanying notes are an integral part of the financial statements

16

| | |

| Financial Highlights | | Series B |

Selected data for each share of capital stock outstanding throughout each year | | (Large Cap Value Series) |

| | | | | | | | | | | | | | | | | | | | |

| | | 2009 | | | 2008 | | | 2007 | | | 2006 | | | Year Ended

December 31,

2005a | |

Per Share Data | | | | | | | | | | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 17.55 | | | $ | 27.94 | | | $ | 26.40 | | | $ | 21.64 | | | $ | 19.58 | |

| | | | | | | | | | | | | | | | | | | | |

Income (loss) from investment operations: | | | | | | | | | | | | | | | | | | | | |

Net investment incomeb | | | 0.19 | | | | 0.29 | | | | 0.25 | | | | 0.20 | | | | 0.24 | |

Net gain (loss) on securities (realized and unrealized) | | | 4.46 | | | | (10.68 | ) | | | 1.29 | | | | 4.56 | | | | 1.82 | |

| | | | | | | | | | | | | | | | | | | | |

Total from investment operations | | | 4.65 | | | | (10.39 | ) | | | 1.54 | | | | 4.76 | | | | 2.06 | |

| | | | | | | | | | | | | | | | | | | | |

Net asset value, end of period | | $ | 22.20 | | | $ | 17.55 | | | $ | 27.94 | | | $ | 26.40 | | | $ | 21.64 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Total Returnc | | | 26.50 | % | | | (37.19 | )% | | | 5.83 | % | | | 22.00 | % | | | 10.52 | % |

| | | | | | | | | | | | | | | | | | | | |

Ratios/Supplemental Data | | | | | | | | | | | | | | | | | | | | |

Net assets, end of period (in thousands) | | $ | 280,473 | | | $ | 250,972 | | | $ | 479,972 | | | $ | 480,683 | | | $ | 410,692 | |

| | | | | | | | | | | | | | | | | | | | |

Ratios to average net assets: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | 1.03 | % | | | 1.21 | % | | | 0.90 | % | | | 0.80 | % | | | 0.98 | % |

Total expensesd | | | 0.81 | % | | | 0.80 | % | | | 0.79 | % | | | 0.79 | % | | | 0.84 | % |

Net expensese | | | 0.81 | % | | | 0.80 | % | | | 0.79 | % | | | 0.79 | % | | | 0.84 | % |

Net expenses prior to custodian earnings credits and net of expense waivers | | | 0.81 | % | | | 0.80 | % | | | 0.79 | % | | | 0.79 | % | | | 0.84 | % |

| | | | | | | | | | | | | | | | | | | | |

Portfolio turnover rate | | | 16 | % | | | 32 | % | | | 29 | % | | | 20 | % | | | 99 | % |

| a | Security Global Investors (SGI), formerly Security Management Company, LLC, became the advisor of Series B effective June 30, 2005. Prior to June 30, 2005, SGI paid Dreyfus Corporation for sub-advisory services. |

| b | Net investment income (loss) was computed using average shares outstanding throughout the period. |

| c | Total return does not take into account any of the expenses associated with an investment in variable insurance products offered by Security Benefit Life Insurance Company. If total return had taken into account these expenses, performance would have been lower. Shares of a series of SBL Fund are available only through the purchase of such products. |

| d | Total expense information reflects the expense ratios absent expense reductions by the Investment Manager and custodian earnings credits, as applicable. |

| e | Net expense information reflects the expense ratios after voluntary expense waivers, reimbursements and custodian earnings credits, as applicable. |

The accompanying notes are an integral part of the financial statements

17

This page left blank intentionally.

18

Manager’s Commentary

February 15, 2010

| | | | |

| | Advised by: | | |

To Our Shareholders:

Series C of the SBL Fund – Money Market Series returned -0.37% for the year ended December 31, 2009, less than the benchmark I-Money Net Retail Tier 1 of 0.18% and the 0.13% performance of its peer group for the same period.

The Federal Reserve Board continues to hold rates near 0%, making it a challenge to maintain a positive yield. The Fed has signaled that it will continue to keep rates low in the near future.

Composition of Portfolio Assets

At December 31, 2009, the average maturity of the holdings in the Series was 84 days.

The Series’ assets were concentrated in commercial paper and U.S. government sponsored agency bonds and notes. At year-end, approximately 52% of the Series consisted of commercial paper and 48% in U.S. government/ agency obligations, less liabilities.

Market Review

A Federal Funds rate near 0% continued to be challenging for money market portfolios, as there was very little yield available. Bond markets were choppy in the first half of 2009 while the last half of the year was better due to less headline volatility. Unlike some peer competitors, the Series did not experience any security defaults that required firm backing.

While earnings were stronger and the economy improved in the third and fourth quarters, it remained necessary to manage the portfolio in a conservative manner since the economy was unable to gain a strong foothold. Adding to uncertainty were newly proposed SEC regulations regarding average weighted maturity, floating NAVs, liquidity constraints, and additional reporting requirements.

The Money Market Series does not invest in SIVs, or Structured Investment Vehicles securities. The manager remained focused on liquidity and credit quality, and the sub-prime mortgage securities never passed these tests. While a small portion of the portfolio was invested in asset-backed commercial paper, which posed no risk to the portfolio, we chose to take the conservative approach and keep exposure to this type of investment low.

Market Outlook

The upcoming year should prove to be another challenging year with respect to yields as the Federal Reserve has stated its intention to keep rates low for the foreseeable future. Our philosophy in managing the Money Market Series is to take a conservative approach that doesn’t add risk to the portfolio by reaching for marginal gains in yield. With the yield environment likely to remain as is for the time being, we will continue to manage the Series’ conservatively with expectations of low returns. As always, we will continue to monitor the economic and market conditions when deciding portfolio strategies and will adjust the asset mix and maturity structure in the portfolio accordingly.

Thank you for your investment in the Money Market Series.

We appreciate the confidence that you have placed in us and continue to focus on achieving the Series’ investment goals.

Sincerely,

Christina Fletcher, Portfolio Manager

19

| | |

| Performance Summary | | Series C (Money Market Series) |

| December 31, 2009 | | (unaudited) |

PERFORMANCE

Portfolio Composition by Quality Ratings

| | | |

Tier 1 Investments | | 99.43 | % |

Cash & Other Assets, Less Liabilities | | 0.57 | |

Total Net Assets | | 100.00 | % |

| | | |

Average Annual Returns

| | | | | | | | | |

Periods Ended 12-31-091 | | 1 Year | | | 5 Years | | | 10 Years | |

Series C | | (0.37 | )% | | 2.70 | % | | 2.56 | % |

| 1 | Performance figures do not reflect fees and expenses associated with an investment in variable insurance products offered by Security Benefit Life Insurance Company. If returns had taken into account these fees and expenses, performance would have been lower. Shares of a Series of SBL Fund are available only through the purchase of such products. |

The performance data quoted above represents past performance. Past performance is not predictive of future performance. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

The accompanying notes are an integral part of the financial statements

20

| | |

| Schedule of Investments | | Series C |

| December 31, 2009 | | (Money Market Series) |

| | | | | | |

| | | Principal

Amount | | Value |

ASSET BACKED SECURITIES—0.3% | | | | | | |

Other Non-Agency—0.3% | | | | | | |

Small Business Administration Pools | | | | | | |

#503308, 0.75%, 20101,2,3 | | $ | 64,007 | | $ | 64,007 |

#503343, 0.88%, 20101,2,3 | | | 123,168 | | | 123,168 |

#503347, 0.88%, 20101,2,3 | | | 72,840 | | | 72,839 |

#502353, 1.00%, 20101,2,3 | | | 31,163 | | | 31,163 |

#503295, 0.75%, 20101,2,3 | | | 67,972 | | | 67,189 |

#503303, 0.75%, 20101,2,3 | | | 123,627 | | | 122,204 |

| | | | | | |

| | | | | $ | 480,570 |

| | | | | | |

TOTAL ASSET BACKED SECURITIES (cost $482,896) | | | | | $ | 480,570 |

| | | | | | |

| | |

| | | Principal

Amount | | Value |

U.S. GOVERNMENT SPONSORED AGENCY BONDS & NOTES—51.4% | | | | | | |

Federal Farm Credit Bank | | | | | | |

0.17%, 5/26/20101,2 | | $ | 2,000,000 | | $ | 1,999,988 |

0.50%, 6/1/20101 | | | 2,000,000 | | | 2,002,938 |

0.22%, 7/9/20101 | | | 2,000,000 | | | 1,997,934 |

0.20%, 8/3/20101 | | | 3,120,000 | | | 3,115,610 |

0.40%, 10/1/20101 | | | 3,000,000 | | | 2,996,451 |

0.45%, 10/21/20101 | | | 2,000,000 | | | 1,998,098 |

0.39%, 12/1/20101 | | | 2,500,000 | | | 2,495,658 |

0.38%, 12/1/20101 | | | 3,000,000 | | | 2,994,519 |

Federal Home Loan Mortgage Corporation | | | | | | |

0.57%, 1/8/20101,2 | | | 1,000,000 | | | 1,000,035 |

0.13%, 1/27/20101 | | | 2,300,000 | | | 2,299,970 |

0.03%, 2/22/20101 | | | 2,200,000 | | | 2,199,905 |

0.17%, 3/16/20101 | | | 2,000,000 | | | 1,999,802 |

0.17%, 5/4/20101 | | | 2,000,000 | | | 1,999,200 |

0.15%, 5/24/20101 | | | 2,389,000 | | | 2,387,884 |

Federal Home Loan Bank | | | | | | |

0.17%, 1/8/20101,2 | | | 1,000,000 | | | 1,000,002 |

0.50%, 8/24/20101,4 | | | 1,500,000 | | | 1,500,062 |

0.51%, 10/28/20101 | | | 3,035,000 | | | 3,033,491 |

0.55%, 11/3/20101 | | | 2,000,000 | | | 1,999,638 |

0.40%, 12/27/20101 | | | 2,000,000 | | | 1,996,228 |

0.45%, 12/29/20101 | | | 2,000,000 | | | 1,996,964 |

0.41%, 12/29/20101 | | | 2,000,000 | | | 1,996,178 |

0.45%, 12/30/20101 | | | 2,000,000 | | | 1,996,950 |

0.16%, 1/14/20111,2 | | | 2,000,000 | | | 1,998,946 |

Federal National Mortgage Association | | | | | | |

0.20%, 1/22/20101 | | | 2,000,000 | | | 1,999,980 |

0.21%, 2/8/20101,2 | | | 3,000,000 | | | 3,000,651 |

0.17%, 2/24/20101 | | | 1,300,000 | | | 1,299,945 |

0.05%, 4/1/20101 | | | 1,154,000 | | | 1,153,721 |

0.18%, 5/12/20101 | | | 2,000,000 | | | 1,999,146 |

0.18%, 5/26/20101 | | | 1,528,000 | | | 1,527,277 |

0.17%, 7/13/20101,2 | | | 1,800,000 | | | 1,799,809 |

0.20%, 8/2/20101 | | | 2,000,000 | | | 1,997,200 |

0.30%, 9/13/20101 | | | 2,000,000 | | | 1,996,500 |

0.31%, 10/1/20101 | | | 1,100,000 | | | 1,097,608 |

0.34%, 11/1/20101 | | | 3,500,000 | | | 3,490,344 |

0.38%, 12/1/20101 | | | 3,600,000 | | | 3,587,753 |

0.40%, 12/2/20101 | | | 4,900,000 | | | 4,883,280 |

| | | | | | |

TOTAL U.S. GOVERNMENT SPONSORED AGENCY BONDS & NOTES (cost $78,862,983) | | | | | $ | 78,839,665 |

| | | | | | |

| | |

| | | Principal

Amount | | Value |

COMMERCIAL PAPER—47.7% | | | | | | |

Automotive—8.9% | | | | | | |

American Honda Finance | | | | | | |

0.20%, 01/05/20101 | | $ | 2,000,000 | | $ | 1,999,955 |

0.17%, 01/13/20101 | | | 2,600,000 | | | 2,599,854 |

0.15%, 01/26/20101 | | | 2,000,000 | | | 1,999,792 |

0.15%, 01/27/20101 | | | 1,000,000 | | | 999,892 |

Toyota Motor Credit Corporation | | | | | | |

0.04%, 01/06/20101 | | | 1,500,000 | | | 1,499,969 |

0.15%, 01/14/20101 | | | 2,500,000 | | | 2,499,865 |

0.15%, 01/15/20101 | | | 2,000,000 | | | 1,999,891 |

| | | | | | |

| | | | | | 13,599,218 |

| | | | | | |

Banking—3.7% | | | | | | |

JP Morgan Chase & Company | | | | | | |

0.14%, 01/19/20101 | | | 2,000,000 | | | 1,999,860 |

JP Morgan Chase Funding | | | | | | |

018% 01/19/20101,5 | | | 2,500,000 | | | 2,499,776 |

0.17%, 01/26/20101,5 | | | 1,200,000 | | | 1,199,843 |

| | | | | | |

| | | | | | 5,699,479 |

| | | | | | |

Brokerage—3.1% | | | | | | |

Goldman Sachs Group, Inc. | | | | | | |

0.15%, 01/21/20101 | | | 2,000,000 | | | 1,999,801 |

0.11%, 01/22/20101 | | | 1,500,000 | | | 1,499,904 |

0.11%, 01/25/20101 | | | 1,300,000 | | | 1,299,905 |

| | | | | | |

| | | | | | 4,799,610 |

| | | | | | |

Electric—6.6% | | | | | | |

FPL Group Capital, Inc. | | | | | | |

0.14%, 01/11/20101,5 | | | 1,700,000 | | | 1,699,934 |

0.15%, 01/13/20101,5 | | | 1,200,000 | | | 1,199,940 |

0.12%, 01/15/20101,5 | | | 1,200,000 | | | 1,199,944 |

0.15%, 01/20/20101,5 | | | 3,500,000 | | | 3,499,715 |

Southern Company Funding Corporation | | | | | | |

0.12%, 01/12/20101,5 | | | 2,500,000 | | | 2,499,908 |

| | | | | | |

| | | | | | 10,099,441 |

| | | | | | |

Food & Beverage—8.1% | | | | | | |

Cargill, Inc. | | | | | | |

0.13%, 01/05/20101,5 | | | 2,000,000 | | | 1,999,971 |

0.13%, 01/12/20101,5 | | | 1,800,000 | | | 1,799,929 |

0.15%, 02/01/20101,5 | | | 2,000,000 | | | 1,999,742 |

0.13%, 02/08/20101,5 | | | 1,500,000 | | | 1,499,794 |

Coca-Cola Company | | | | | | |

0.11%, 01/13/20101 | | | 1,100,000 | | | 1,099,960 |

0.10%, 01/28/20101 | | | 2,000,000 | | | 1,999,850 |

0.13%, 02/03/20101 | | | 2,000,000 | | | 1,999,739 |

| | | | | | |

| | | | | | 12,398,985 |

| | | | | | |

Life Insurance—2.9% | | | | | | |

General Reinsurance Corporation | | | | | | |

0.12%, 01/21/20101 | | | 3,000,000 | | | 2,999,795 |

Swiss Re Treasury U.S. Corporation | | | | | | |

0.19%, 01/29/20101,5 | | | 1,400,000 | | | 1,399,793 |

| | | | | | |

| | | | | | 4,399,588 |

| | | | | | |

Non U.S. Banking—3.3% | | | | | | |

BNP Paribas Finance, Inc. | | | | | | |

0.16%, 01/14/20101 | | | 2,000,000 | | | 1,999,884 |

| | | | |

0.18%, 01/26/20101 | | 1,600,000 | | 1,599,800 |

0.12%, 01/29/20101 | | 1,500,000 | | 1,499,860 |

| | | | |

| | | | 5,099,544 |

| | | | |

Pharmaceuticals—11.1% | | | | |

Abbott Laboratories | | | | |

0.10%, 01/11/20101,5 | | 2,000,000 | | 1,999,944 |

The accompanying notes are an integral part of the financial statements

21

| | |

| Schedule of Investments | | Series C |

| December 31, 2009 | | (Money Market Series) |

| | | | | | |

| | | Principal

Amount | | Value |

COMMERCIAL PAPER—47.7% (continued) | | | | | | |

Pharmaceuticals—11.1% (continued) | | | | | | |

Abbott Laboratories, Inc. | | | | | | |

0.10%, 02/08/20101,5 | | $ | 1,985,000 | | $ | 1,984,790 |

GlaxoSmithKline Finance plc | | | | | | |

0.11%, 01/06/20101,5 | | | 2,500,000 | | | 2,499,962 |

0.11%, 01/20/20101,5 | | | 2,000,000 | | | 1,999,884 |

0.12%, 01/27/20101,5 | | | 1,800,000 | | | 1,799,844 |

Johnson & Johnson, Inc. | | | | | | |

0.16%, 04/19/20101,5 | | | 2,000,000 | | | 1,998,898 |

0.15%, 04/20/20101,5 | | | 2,200,000 | | | 2,198,770 |

0.20%, 05/25/20101,5 | | | 2,500,000 | | | 2,497,563 |

| | | | | | |

| | | | | | 16,979,655 |

| | | | | | |

TOTAL COMMERCIAL PAPER (cost $73,076,385) | | | | | $ | 73,075,520 |

| | | | | | |

Total Investments—99.4%6 (cost $152,422,264) | | | | | $ | 152,395,755 |

Cash & Other Assets, Less Liabilities—0.6% | | | | | | 865,881 |

| | | | | | |

Total Net Assets—100.0% | | | | | $ | 153,261,636 |

| | | | | | |

For federal income tax purposes the identified cost of investments owned at December 31, 2009 was $152,422,264.

| plc | Public Limited Company |

| 1 | Value determined based on Level 2 inputs. |

| 2 | Variable rate security. Rate indicated is rate effective at December 31, 2009. |

| 3 | Maturity date indicated is next interest reset date. |

| 4 | Security is a step up/step down bond. The coupon increases or decreases at regular intervals until the bond reaches full maturity. |

| 5 | Security is a 144A or Section 4(2) security. The total market value of 144A or Section 4(2) securities is $39,477,944 (cost $39,478,768), or 25.8% of total net assets. |

| 6 | Unless otherwise indicated, the values of the securities of the Portfolio are determined based on Level 1. |

The accompanying notes are an integral part of the financial statements

22

Series C

(Money Market Series)

Statement of Assets and Liabilities

December 31, 2009

| | | | |

Assets: | | | | |

Investments, at value* | | $ | 152,395,755 | |

Cash | | | 849,412 | |

Receivables: | | | | |

Fund shares sold | | | 438,914 | |

Securities sold | | | 3,983 | |

Interest | | | 19,539 | |

Prepaid expenses | | | 3,540 | |

| | | | |

Total assets | | | 153,711,143 | |

| | | | |

Liabilities: | | | | |

| |

Payable for: | | | | |

Fund shares redeemed | | | 324,292 | |

Management fees | | | 65,323 | |

Administration fees | | | 15,711 | |

Transfer agent/maintenance fees | | | 2,083 | |

Custodian fees | | | 438 | |

Directors’ fees | | | 2,285 | |

Professional fees | | | 15,375 | |

Other fees | | | 24,000 | |

| | | | |

Total liabilities | | | 449,507 | |

| | | | |

Net assets | | $ | 153,261,636 | |

| | | | |

Net assets consist of: | | | | |

Paid in capital | | $ | 153,288,145 | |

Net unrealized depreciation in value of investments | | | (26,509 | ) |

| | | | |

Net assets | | $ | 153,261,636 | |

| | | | |

| |

Capital shares authorized | | | unlimited | |

Capital shares outstanding | | | 11,298,797 | |

Net asset value per share (net assets divided by shares outstanding) | | $ | 13.56 | |

| | | | |

| |

* Investments, at cost | | $ | 152,422,264 | |

|

Statement of Operations For Year Ended December 31, 2009 | |

Investment Income: | | | | |

Interest | | | 923,773 | |

| | | | |

Total investment income | | | 923,773 | |

| | | | |

| |

Expenses: | | | | |

Management fees | | | 1,043,540 | |

Administration fees | | | 213,547 | |

Transfer agent/maintenance fees | | | 25,381 | |

Custodian fees | | | 18,350 | |

Directors’ fees | | | 21,611 | |

Professional fees | | | 24,398 | |

Reports to shareholders | | | 46,298 | |

Other | | | 10,618 | |

| | | | |

Total expenses | | | 1,403,743 | |

| | | | |

Net investment loss | | | (479,970 | ) |

| | | | |

| |

Net Unrealized Gain (Loss): | | | | |

Net unrealized appreciation (depreciation) during the year on: | | | | |

Investments | | | (209,951 | ) |

| | | | |

Net decrease in net assets resulting from operations | | $ | (689,921 | ) |

| | | | |

The accompanying notes are an integral part of the financial statements

23

| | |

| | Series C |

| Statement of Changes in Net Assets | | (Money Market Series) |

| | | | | | | | |

| | | Year Ended

December 31, 2009 | | | Year Ended

December 31, 2008 | |

Increase (decrease) in net assets from operations: | | | | | | | | |

Net investment income (loss) | | $ | (479,970 | ) | | $ | 4,249,459 | |

Net unrealized appreciation (depreciation) during the year on investments | | | (209,951 | ) | | | 190,920 | |

| | | | | | | | |

Net increase (decrease) in net assets resulting from operations | | | (689,921 | ) | | | 4,440,379 | |

| | | | | | | | |

| | |

Capital share transactions: | | | | | | | | |

Proceeds from sale of shares | | | 191,606,637 | | | | 533,443,332 | |

Cost of shares redeemed | | | (305,973,233 | ) | | | (438,227,047 | ) |

| | | | | | | | |

Net increase (decrease) from capital share transactions | | | (114,366,596 | ) | | | 95,216,285 | |

| | | | | | | | |

Net increase (decrease) in net assets | | | (115,056,517 | ) | | | 99,656,664 | |

| | | | | | | | |

| | |

Net assets: | | | | | | | | |

Beginning of year | | | 268,318,153 | | | | 168,661,489 | |

| | | | | | | | |

End of year | | $ | 153,261,636 | | | $ | 268,318,153 | |

| | | | | | | | |

Undistributed net investment income at end of year | | $ | — | | | $ | 4,249,459 | |

| | | | | | | | |

| | |

Capital share activity: | | | | | | | | |

Shares sold | | | 14,085,993 | | | | 39,510,948 | |

Shares redeemed | | | (22,496,450 | ) | | | (32,452,086 | ) |

| | | | | | | | |

Total capital share activity | | | (8,410,457 | ) | | | 7,058,862 | |

| | | | | | | | |

The accompanying notes are an integral part of the financial statements

24

| | | |

| Financial Highlights | | Series C | |

Selected data for each share of capital stock outstanding throughout each year | | (Money Market Series | ) |

| | | | | | | | | | | | | | | | | | | | |

| | | 2009 | | | 2008 | | | 2007 | | | 2006 | | | Year Ended

December 31,

2005 | |

Per Share Data | | | | | | | | | | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 13.61 | | | $ | 13.33 | | | $ | 12.73 | | | $ | 12.19 | | | $ | 11.87 | |

| | | | | | | | | | | | | | | | | | | | |

Income (loss) from investment operations: | | | | | | | | | | | | | | | | | | | | |

Net investment income (loss)a | | | (0.03 | ) | | | 0.26 | | | | 0.60 | | | | 0.45 | | | | 0.33 | |

Net gain (loss) on securities (realized and unrealized) | | | (0.02 | ) | | | 0.02 | | | | — | | | | 0.09 | | | | (0.01 | ) |

| | | | | | | | | | | | | | | | | | | | |

Total from investment operations | | | (0.05 | ) | | | 0.28 | | | | 0.60 | | | | 0.54 | | | | 0.32 | |

| | | | | | | | | | | | | | | | | | | | |

Net asset value, end of period | | $ | 13.56 | | | $ | 13.61 | | | $ | 13.33 | | | $ | 12.73 | | | $ | 12.19 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Total Returnb | | | (0.37 | )% | | | 2.10 | % | | | 4.71 | % | | | 4.43 | % | | | 2.70 | % |

| | | | | | | | | | | | | | | | | | | | |

Ratios/Supplemental Data | | | | | | | | | | | | | | | | | | | | |

Net assets, end of period (in thousands) | | $ | 153,262 | | | $ | 268,318 | | | $ | 168,661 | | | $ | 99,044 | | | $ | 71,655 | |

| | | | | | | | | | | | | | | | | | | | |

Ratios to average net assets: | | | | | | | | | | | | | | | | | | | | |

Net investment income (loss) | | | (0.23 | )% | | | 1.94 | % | | | 4.59 | % | | | 4.43 | % | | | 2.63 | % |

Total expensesc | | | 0.67 | % | | | 0.65 | % | | | 0.66 | % | | | 0.68 | % | | | 0.69 | % |

Net expensesd | | | 0.67 | % | | | 0.65 | % | | | 0.66 | % | | | 0.68 | % | | | 0.69 | % |

Net expenses prior to custodian earnings credits and net of expense waivers | | | 0.67 | % | | | 0.65 | % | | | 0.66 | % | | | 0.68 | % | | | 0.69 | % |

| a | Net investment income (loss) was computed using average shares outstanding throughout the period. |

| b | Total return does not take into account any of the expenses associated with an investment in variable insurance products offered by Security Benefit Life Insurance Company. If total return had taken into account these expenses, performance would have been lower. Shares of a series of SBL Fund are available only through the purchase of such products. |

| c | Total expense information reflects the expense ratios absent expense reductions by the Investment Manager and custodian earnings credits, as applicable. |

| d | Net expense information reflects the expense ratios after voluntary expense waivers, reimbursements and custodian earnings credits, as applicable. |

The accompanying notes are an integral part of the financial statements

25

This page left blank intentionally.

26

Managers’ Commentary

February 15, 2010

| | | | |

| | Advised by: | | |

To Our Shareholders

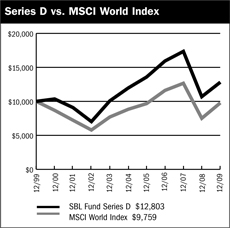

Series D of the SBL Fund – Global Series returned 19.73%, underperforming the benchmark, Morgan Stanley Capital International, Inc. (MSCI) World Index return of 29.99% and the peer group median return of 33.23%.

The SGI global team believes that excess return opportunities exist in global stock markets and that those opportunities are best identified and captured at the security level. Investing globally offers the greatest exposure to excess return opportunities while enhancing the ability to diversify risk. Successfully identifying and exploiting these opportunities requires thorough fundamental research. Superior stock selection continues to be the trademark for the team’s performance as selection effect accounts for nearly all the return of the portfolio.

The investment team employs a bottom-up approach to the global equity universe to identify and invest in the best opportunities around the world. The team melds sophisticated screening techniques, input from management meetings, and insights into global/regional trends to identify investment opportunities from around the world. Relative valuation and relative business momentum is a specific focus of the screening criteria. The team’s fundamental research is original and uses primary sources to substantiate forecasts and investment theses.

Energy and Information Technology Top Performers

The Global Series held an underweight position in energy during the year however, the sector was the best performing sector in the portfolio due to stock selection that generated 46% returns. A significant weight in Oil Search, Ltd. generated a return of 72%. Avoiding Exxon Mobil Corporation benefited performance as the stock dropped 13% during the period. Other gainers in the sector for the strategy included CNOOC, Ltd. and Transocean, Ltd.

As an even weight, the portfolio benefited from superior stock selection in the information technology sector, gaining 64% over the year. Check Point Software Technologies, Ltd., a significant holding during the period, gained 55% while Gree, Inc. soared 108%. Other sector holdings that contributed to performance include Google, Inc. (Cl A) and Tandberg ASA.

Consumer Staples, Consumer Discretionary, and Industrials Disappoint