Had the Group accounted for its goodwill and identifiable intangible assets that have indefinite lives under SFAS 142 for the year ending 31 December 2001, the impact on reported results would have been as follows:

The differences between UK GAAP as applied by Unilever and US GAAP on accounting for goodwill and intangible assets are set out in the tables and footnotes below.

Management have completed an impairment assessment during 2003 and have concluded that there was no impairment of goodwill or identifiable intangible assets with indefinite lives for the year ended 31 December 2003.

Back to Contents

Additional information for US investors

Unilever Group

Goodwill from joint ventures amounting to €4 million (2002: €211 million) primarily relates to the savoury and dressings segment. The goodwill from associates amounting to €122 million (2002: €154 million) primarily relates to the home care segment.

Intangible assets subject to amortisation

Finite-lived intangible assets principally comprise technologies and have a net book value of €445 million as at 31 December 2003 (2002: €567 million), net of accumulated amortisation of €86 million (2002: €72 million). Amortisation expense recorded in the period in respect of finite-lived intangible assets was €30 million (2002: €36 million). This expense is not expected to change materially over the next five years.

Intangible assets not subject to amortisation

Indefinite-lived intangible assets principally comprise trademarks and have a net book value of €6 355 million as at 31 December 2003 (2002: €7 161 million).

Capitalised software

Under UK GAAP as applied by Unilever, certain costs relating to the development and purchase of software for internal use are expensed when incurred. Under US GAAP, these costs are capitalised and subsequently amortised over the estimated useful life of the software in conformity with Statement of Financial Position 98-1, ’Accounting for the Cost of Computer Software Developed or Obtained for Internal Use’. During 2003 several IT projects met the criteria for capitalisation under US GAAP.

Restructuring costs

Under Unilever’s accounting policy, certain restructuring costs relating to employee terminations are recognised when a restructuring plan has been announced. Under US GAAP, liabilities related to exit costs are recognised when incurred. Employee termination costs are generally considered to be incurred when the company has a liability to the employee unless further service is required from the employee in which case costs are recognised as benefits are earned.

Costs related to excess lease costs are reduced by assumed sub-lease income for the periods impacted.

Interest

Unilever treats all interest costs as a charge to the profit and loss account in the current period. Under US GAAP, interest incurred during the construction periods of tangible fixed assets is capitalised and depreciated over the life of the assets.

Derivative financial instruments

Transition adjustment

Unilever applied the provisions of SFAS 133 ‘Accounting for Derivative Instruments and Hedging Activities’ in this divergence statement as from 1 January 2001. In accordance with the transition provisions of SFAS 133, an adjustment of €6 million (net of tax of €3 million) was recorded as the cumulative effect of a change in accounting principle to recognise the fair value of all the Group’s derivative financial instruments and hedge items under US GAAP. In addition, Unilever recorded a one-time unrealised loss of €85 million (net of tax of €37 million) to consolidated other comprehensive income under US GAAP. During the year ended 31 December 2003, a reclassification of derivative losses from other comprehensive income to net income of €31 million was recorded as a result of the underlying hedged transactions which impacted earnings.

Hedging policy

Unilever’s accounting policies in respect of derivative financial instruments are described in the accounting information and policies on page 75. In particular, under its accounting policies, Unilever applies hedge accounting to its portfolio of derivative financial instruments, meaning that changes in the value of forward foreign exchange contracts are recognised in the results in the same period as changes in the values of the assets and liabilities they are intended to hedge. Interest payments and receipts arising from interest rate derivatives such as swaps and forward rate agreements are matched to those arising from underlying debt and investment positions. Payments made or received in respect of the early termination of derivative instruments are spread over the original life of the instrument so long as the underlying exposure continues to exist.

Under US GAAP, Unilever has not designated any of its derivative instruments as qualifying hedge instruments under SFAS 133 and, accordingly, under US GAAP, all derivative financial instruments are valued at fair value, and changes in their fair value are reflected in earnings. All gains and losses arising on derivative financial instruments are recognised immediately; payments made or received in respect of the early termination of derivative instruments represent cash realisation of these gains and losses and therefore have no further impact on earnings.

Pensions

From 1 January 2003, Unilever has adopted UK Financial Reporting Standard (FRS) 17 as the basis for accounting for retirement benefits. Full details of this standard are given in note 17 on page 99.

Under FRS 17, the expected costs of providing retirement benefits are charged to the profit and loss account over the periods benefiting from the employees’ services. Variations from the expected cost are recognised as they occur in the statement of total recognised gains and losses. The assets and liabilities of pension plans are included in the Group balance sheet at fair value. Under US GAAP, pensions costs and liabilities are accounted for in accordance with the prescribed actuarial method and measurement principles of SFAS 87. The most significant difference is that variations from the expected costs are recognised in the profit and loss account over the expected service lives of the employees.

Under US GAAP, an additional minimum liability is recognised and a charge made to other comprehensive income when the accumulated benefit obligation exceeds the fair value of plan assets to the extent that this amount is not covered by the net liability recognised in the balance sheet.

With effect from 1 January 2002, and for the purposes of determining the expected return on plan assets for US purposes, Unilever changed the method of valuing its pension plan assets from a market-related value calculated by smoothing gains and losses over a five-year period to an actual fair value at the balance sheet date. Management believe that the actual fair value methodology provides a better representation of the financial position and results of Unilever’s pension plans.

134 | Unilever Annual Report & Accounts and Form 20-F 2003 |

Back to Contents

Additional information for US investors

Unilever Group

The impact of this change in methodology on reported results under US GAAP is given in the table below:

| | | | € million | |

| | | | 2001 | |

|

|

|

| |

| | | | Restated | |

| | | | | |

| Net income under US GAAP | | | 1 446 | |

| Change in basis of expected return on plan assets calculation | | | 86 | |

| | | |

| |

| Adjusted net income under US GAAP | | | 1 532 | |

|

|

|

| |

| | | | | |

| | Euro per € 0.51 | | Euro cents per 1.4p | |

| | 2001 | | 2001 | |

|

|

|

| |

| Adjusted net income per share | 1.51 | | 22.60 | |

| Adjusted diluted net income per share | 1.47 | | 21.99 | |

|

|

|

| |

As required under US APB 20 for a change in accounting policy, a cumulative effect adjustment has been calculated to record the impact of the change as if the fair value methodology had been the accounting policy from the initial adoption of SFAS 87 by Unilever. The cumulative effect adjustment net of tax was €522 million in 2002.

Investments

Unilever accounts for current investments, which are liquid funds temporarily invested, at their market value, which is consistent with UK GAAP.

Unilever accounts for changes in the market value of current investments as interest receivable in the profit and loss account for the year. Under US GAAP, such current asset investments are classified as ‘available for sale securities’ and changes in market values, which represent unrealised gains or losses, are excluded from earnings and taken to stockholders’ equity unless such losses are deemed to be other than temporary at which time they are recognised through the profit and loss account. Unrealised gains and losses arising from changes in the market values of securities available for sale are not material.

Unilever accounts for fixed investments other than in joint ventures and associates at cost less any amounts written off to reflect a permanent impairment. Under US GAAP such investments are held at fair value. The difference is not material.

Dividends

The proposed final ordinary dividends are provided for in the Unilever accounts in the financial year to which they relate. Under US GAAP such dividends are not provided for until they become irrevocable.

Deferred taxation

Following the adoption of the new pension accounting standard (FRS 17) with effect from 1 January 2003, Unilever has restated its deferred tax charge for the years ended 31 December 2001 and 2002 together with its deferred tax balances as at 31 December 2002. Corresponding changes are therefore needed to the deferred tax charges and balances in the Group accounts and in the reconciliation to US GAAP. In addition, deferred tax balances in respect of pensions are now reported as a separate component of the pensions balances and no longer aggregated with the rest of the deferred tax balances. A full description of FRS 17 is given in note 17 on page 99.

Under FRS 19, deferred tax is not recognised on fair value adjustments made to assets acquired; under US GAAP, deferred tax is recorded on all fair value adjustments. Also, FRS 19 changed the treatment of deferred tax on tax-deductible goodwill previously written off to reserves. Such goodwill is reinstated, net of amortisation, under US GAAP, and the tax effect of such restatement has been adjusted accordingly.

Classification differences between UK and US GAAP

Revenue recognition

Under US GAAP, certain sales incentive expenses which have been included in operating costs under Unilever’s accounting would be deducted from turnover. The decrease in turnover for the years to 31 December 2003, 2002 and 2001 is €1 238 million, €1 337 million and €1 279 million respectively. There is no impact on Unilever’s net profit.

Cash flow statement

Under US GAAP, various items would be reclassified within the consolidated cash flow statement. In particular, interest received, interest paid and taxation would be part of net cash flow from operating activities, and dividends paid would be included within net cash flow from financing. In addition, under US GAAP, cash and cash equivalents comprise cash balances and current investments with an original maturity at the date of investment of less than three months. Under Unilever’s presentation, cash includes only cash in hand or available on demand less bank overdrafts. Cash flows from movements in bank overdrafts would be classified as part of cash flows from financing activities under US GAAP. Cash flows from movements in bank overdrafts were €58 million for the year ended 31 December 2003 (2002: €(86) million; 2001: €(19) million). Movements in those current investments which are included under the heading of cash and cash equivalents under US GAAP form part of the movement entitled ‘Management of liquid resources’ in the cash flow statement. At 31 December 2003, the balance of such investments was €3 million (2002: €45 million).

Long leasehold interests in land

Under UK GAAP, Unilever treats the cost of acquiring a long leasehold interest in land as a fixed asset, and depreciates the cost of that asset over the lease term. Under US GAAP, the cost of long leasehold interests would be deferred within ‘Other assets’ and recognised on a straight-line basis over the lives of the leases as operating lease rentals. The balance of such assets were €58 million as at 31 December 2003 (2002: €63 million). In all other respects, there are no differences in accounting for these arrangements between UK and US GAAP.

UnileverAnnual Report & Accounts and Form 20-F 2003 | 135 |

Back to Contents

Additional information for US investors

Unilever Group

Equity in earnings related to investments in joint ventures and associated companies

Under US GAAP, equity in earnings related to investments in joint ventures and associated companies would be disclosed on a single line within the income statement. In particular, our share of the interest and taxation arising in respect of joint ventures and associated companies would be reported on this line, rather than as part of the total interest and taxation charge for the Group. US GAAP equity in earnings related to investments in joint ventures and associated companies were €(48) million for the year ended 31 December 2003 (2002: €(54) million; 2001: €(30) million).

Recently issued accounting pronouncements

In January 2003, the FASB issued Financial Interpretation No. 46 (FIN 46), ‘Consolidation of Variable Interest Entities’ and in December 2003 issued a revised interpretation FIN 46R. Under these interpretations, certain entities known as variable interest entities must be consolidated by the primary beneficiary of the entity. Certain measurement principles of these interpretations relating to new contracts entered into are effective for Unilever’s 2003 financial statements. We are still evaluating FIN 46R.

Documents on display in the United States

Unilever files and furnishes reports and information with the United States Securities and Exchange Commission (SEC), and such reports and information can be inspected and copied at the SEC’s public reference facilities in Washington DC, Chicago and New York. Certain of our reports and other information that we file or furnish to the SEC are also available to the public over the internet on the SEC’s website at www.sec.gov.

Corporate governance

Both NV and PLC are listed on The New York Stock Exchange and must therefore comply with such of the requirements of US legislation, such as The Sarbanes-Oxley Act of 2002, SEC regulations and the Listing Rules of The New York Stock Exchange as are applicable to foreign listed companies. In some cases the requirements are mandatory and in other cases the obligation is to ‘comply or explain’.

Unilever has complied with these requirements concerning corporate governance that were in force during 2003. Attention is drawn in particular to the Report of the Audit Committee on page 69. Actions taken to ensure compliance that are not specifically disclosed elsewhere or otherwise clear from reading this document include:

| • | the issue of a Code of Ethics for senior financial officers; |

| • | the issue of instructions restricting the employment of former employees of the audit firm; and |

| • | establishment of standards of professional conduct for US attorneys. |

In each of these cases, existing practices have been revised and/or documented in such a way as to conform to the new requirements.

The Code of Ethics applies to the senior executive, financial and accounting officers and comprises the standards prescribed by the SEC, and a copy has been posted on Unilever’s website at www.unilever.com/investorcentre/. The Code of Ethics comprises an extract of the relevant provisions of Unilever’s Code of Business Principles and the more detailed rules of conduct that implement it. The only amendment to these pre-existing provisions and rules that was made in preparing the Code of Ethics was made at the request of the Audit Committee and consisted of a strengthening of the explicit requirement to keep proper accounting records. No waiver from any provision of the Code of Ethics was granted to any of the persons falling within the scope of the SEC requirement in 2003.

Unilever has also taken into account the US requirements taking effect in 2004 and 2005 applicable to both foreign and US listed companies in preparing the changes in its corporate governance arrangements that will be effective from the NV and PLC Annual General Meetings on 12 May 2004. Further information will be placed on Unilever’s website www.unilever.com/investorcentre/ following those meetings, and will be reported in the Annual Report & Accounts and Form 20-F for 2004.

136 | Unilever Annual Report & Accounts and Form 20-F 2003 |

Back to Contents

Additional information for US investors

Unilever Group

Guarantor statements

On 2 October 2000, NV and Unilever Capital Corporation (UCC) filed a US $15 billion Shelf registration, which is unconditionally and fully guaranteed, jointly and severally, by NV, PLC and Unilever United States, Inc. (UNUS). Of the US $15 billion Shelf registration, US $4.25 billion of Notes were outstanding at 31 December 2003 (2002: US $5.75 billion) with coupons ranging from 5.90% to 7.125%. These Notes are to be repaid between 1 November 2005 and 15 November 2032.

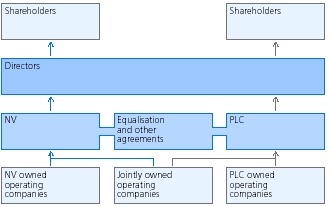

Provided below are the profit and loss accounts, cash flow statements and balance sheets of each of the companies discussed above, together with the profit and loss account, cash flow statement and balance sheet of non-guarantor subsidiaries. These have been prepared under the historical cost convention, and, aside from the basis of accounting for investments at net asset value (equity accounting), comply in all material respects with Netherlands law and with United Kingdom GAAP. Divergences from US GAAP are disclosed on pages 131 to 136. We have not provided reconciliations from the accounting principles used by Unilever to US GAAP for the columns relating to the guarantor entities, as such reconciliations would not materially affect an investor’s understanding of the nature of this guarantee. The financial information in respect of NV, PLC and UNUS has been prepared with all subsidiaries accounted for on an equity basis. The financial information in respect of the non-guarantor subsidiaries has been prepared on a consolidated basis.

Amounts for 2002 and 2001 have been restated following changes in our accounting policies for pensions and other post-employment benefits, for share-based payments and for the presentation of securities held as collateral. See note 14 on page 94, note 17 on page 99 and note 29 on page 116.

| | | | | | | | | | | | | | € million | |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Unilever | | | | | | Unilever | | | | | | |

| Capital | United |

| Corporation | Unilever N.V. | Unilever PLC | States Inc. | Non- |

| subsidiary | parent issuer/ | parent | subsidiary | guarantor | Unilever |

| issuer | guarantor | guarantor | guarantor | subsidiaries | Eliminations | Group |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Profit and loss account | | | | | | | | | | | | | | |

| for the year ended 31 December 2003 | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| Group turnover | – | | – | | – | | – | | 42 693 | | – | | 42 693 | |

| Operating costs | – | | 127 | | (26 | ) | (8 | ) | (37 303 | ) | – | | (37 210 | ) |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Group operating profit | – | | 127 | | (26 | ) | (8 | ) | 5 390 | | – | | 5 483 | |

| Share of operating profit of joint ventures | – | | – | | – | | – | | 46 | | – | | 46 | |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

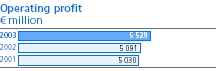

| Operating profit | – | | 127 | | (26 | ) | (8 | ) | 5 436 | | – | | 5 529 | |

| Share of operating profit of associates | – | | – | | – | | – | | 25 | | – | | 25 | |

| Dividends | – | | 1 235 | | 946 | | – | | (2 181 | ) | – | | – | |

| Other income from fixed investments | – | | – | | – | | – | | (3 | ) | – | | (3 | ) |

| Interest | (453 | ) | (84 | ) | (30 | ) | (3 | ) | (277 | ) | – | | (847 | ) |

| Other finance income/(cost) – pensions and similar | | | | | | | | | | | | | | |

| obligations | – | | (6 | ) | – | | (24 | ) | (136 | ) | – | | (166 | ) |

| Intercompany finance costs | 469 | | 533 | | (18 | ) | (51 | ) | (933 | ) | – | | – | |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Profit on ordinary activities before taxation | 16 | | 1 805 | | 872 | | (86 | ) | 1 931 | | – | | 4 538 | |

| Taxation | (6 | ) | (93 | ) | (53 | ) | 56 | | (1 431 | ) | – | | (1 527 | ) |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Profit on ordinary activities after taxation | 10 | | 1 712 | | 819 | | (30 | ) | 500 | | – | | 3 011 | |

| Minority interests | – | | – | | – | | – | | (249 | ) | – | | (249 | ) |

| Equity earnings of subsidiaries | – | | 1 050 | | 1 943 | | 86 | | – | | (3 079 | ) | – | |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Net profit | 10 | | 2 762 | | 2 762 | | 56 | | 251 | | (3 079 | ) | 2 762 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

| | | | | | | | | | | | | | |

UnileverAnnual Report & Accounts and Form 20-F 2003 | 137 |

Back to Contents

Additional information for US investors

Unilever Group

Guarantor statements continued

| | | | | | | | | | | | | | € million | |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| | Unilever | | | | | | Unilever | | | | | | | |

| Capital | United |

| Corporation | Unilever N.V. | Unilever PLC | States Inc. | Non- |

| subsidiary | parent issuer/ | parent | subsidiary | guarantor | Unilever |

| issuer | guarantor | guarantor | guarantor | subsidiaries | Eliminations | Group |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

| | | | | | | | | | | | | | | |

| Profit and loss account | | | | | | | | | | | | | | |

| for the year ended 31 December 2002 (restated) | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| Group turnover | – | | – | | – | | – | | 48 270 | | – | | 48 270 | |

| Operating costs | – | | 89 | | (53 | ) | (21 | ) | (43 278 | ) | – | | (43 263 | ) |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Group operating profit | – | | 89 | | (53 | ) | (21 | ) | 4 992 | | – | | 5 007 | |

| Share of operating profit of joint ventures | – | | – | | – | | – | | 84 | | – | | 84 | |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Operating profit | – | | 89 | | (53 | ) | (21 | ) | 5 076 | | – | | 5 091 | |

| Share of operating profit of associates | – | | – | | – | | – | | 34 | | – | | 34 | |

| Dividends | – | | 3 779 | | 1 011 | | – | | (4 790 | ) | – | | – | |

| Other income from fixed investments | – | | – | | – | | – | | (7 | ) | – | | (7 | ) |

| Interest | (395 | ) | (206 | ) | (83 | ) | (1 | ) | (488 | ) | – | | (1 173 | ) |

| Other finance income/(cost) – pensions and similar | | | | | | | | | | | | | | |

| obligations | – | | – | | – | | 28 | | 80 | | – | | 108 | |

| Intercompany finance costs | 403 | | 450 | | (3 | ) | (89 | ) | (761 | ) | – | | – | |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Profit on ordinary activities before taxation | 8 | | 4 112 | | 872 | | (83 | ) | (856 | ) | – | | 4 053 | |

| Taxation | (3 | ) | (41 | ) | (3 | ) | 31 | | (1 589 | ) | – | | (1 605 | ) |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Profit on ordinary activities after taxation | 5 | | 4 071 | | 869 | | (52 | ) | (2 445 | ) | – | | 2 448 | |

| Minority interests | – | | – | | – | | – | | (312 | ) | – | | (312 | ) |

| Equity earnings of subsidiaries | – | | (1 935 | ) | 1 267 | | 110 | | – | | 558 | | – | |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Net profit | 5 | | 2 136 | | 2 136 | | 58 | | (2 757 | ) | 558 | | 2 136 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

| | | | | | | | | | | | | | | |

| Profit and loss account | | | | | | | | | | | | | | |

| for the year ended 31 December 2001 (restated) | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| Group turnover | – | | – | | – | | – | | 51 514 | | – | | 51 514 | |

| Operating costs | – | | (27 | ) | 82 | | 14 | | (46 637 | ) | – | | (46 568 | ) |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Group operating profit | – | | (27 | ) | 82 | | 14 | | 4 877 | | – | | 4 946 | |

| Share of operating profit of joint ventures | – | | – | | – | | – | | 84 | | – | | 84 | |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Operating profit | – | | (27 | ) | 82 | | 14 | | 4 961 | | – | | 5 030 | |

| Dividends | – | | 2 202 | | 738 | | – | | (2 940 | ) | – | | – | |

| Other income from fixed investments | – | | – | | – | | – | | 12 | | – | | 12 | |

| Interest | (782 | ) | (444 | ) | (177 | ) | 2 | | (245 | ) | – | | (1 646 | ) |

| Other finance income/(cost) – pensions and similar | | | | | | | | | | | | | | |

| obligations | – | | – | | – | | 38 | | 4 | | – | | 42 | |

| Intercompany finance costs | 1 010 | | 423 | | 72 | | (424 | ) | (1 081 | ) | – | | – | |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Profit on ordinary activities before taxation | 228 | | 2 154 | | 715 | | (370 | ) | 711 | | – | | 3 438 | |

| Taxation | (84 | ) | (98 | ) | (24 | ) | 137 | | (1 450 | ) | – | | (1 519 | ) |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Profit on ordinary activities after taxation | 144 | | 2 056 | | 691 | | (233 | ) | (739 | ) | – | | 1 919 | |

| Minority interests | – | | – | | – | | – | | (239 | ) | – | | (239 | ) |

| Equity earnings of subsidiaries | – | | (376 | ) | 989 | | (345 | ) | – | | (268 | ) | – | |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Net profit | 144 | | 1 680 | | 1 680 | | (578 | ) | (978 | ) | (268 | ) | 1 680 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

| | |

138 | Unilever Annual Report & Accounts and Form 20-F 2003 |

Back to Contents

Additional information for US investors

Unilever Group

| Guarantor statements continued | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | € million | |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| | Unilever | | | | | | Unilever | | | | | | | |

| Capital | | | United | | | |

| Corporation | Unilever N.V. | Unilever PLC | States Inc. | Non- | | |

| subsidiary | parent issuer/ | parent | subsidiary | guarantor | | Unilever |

| issuer | guarantor | guarantor | guarantor | subsidiaries | Eliminations | Group |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Cash flow statement | | | | | | | | | | | | | | |

| for the year ended 31 December 2003 | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| Cash flow from group operating activities | 14 | | 56 | | (44 | ) | (18 | ) | 6 772 | | – | | 6 780 | |

| Dividends from joint ventures | – | | – | | – | | – | | 52 | | – | | 52 | |

| Returns on investments and servicing of finance | 4 | | 468 | | (49 | ) | (40 | ) | (1 563 | ) | – | | (1 180 | ) |

| Taxation | – | | (54 | ) | 51 | | (100 | ) | (1 320 | ) | – | | (1 423 | ) |

| Capital expenditure and financial investment | – | | (7 | ) | (74 | ) | (4 | ) | (939 | ) | – | | (1 024 | ) |

| Acquisitions and disposals | – | | – | | – | | – | | 622 | | – | | 622 | |

| Dividends paid on ordinary share capital | – | | (1 039) | | (703 | ) | – | | – | | 27 | | (1 715 | ) |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Cash flow before management of liquid resources | | | | | | | | | | | | | | |

| and financing | 18 | | (576 | ) | (819 | ) | (162 | ) | 3 624 | | 27 | | 2 112 | |

| Management of liquid resources | 8 | | 144 | | – | | – | | (193 | ) | – | | (41 | ) |

| Financing | (25 | ) | 217 | | 771 | | 162 | | (4 042 | ) | – | | (2 917 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Increase/(decrease) in cash in the period | 1 | | (215 | ) | (48 | ) | – | | (611 | ) | 27 | | (846 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

| | | | | | | | | | | | | | | |

| Cash flow statement | | | | | | | | | | | | | | |

| for the year ended 31 December 2002 (restated) | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| Cash flow from group operating activities | 34 | | 222 | | (52 | ) | (45 | ) | 7 724 | | – | | 7 883 | |

| Dividends from joint ventures | – | | – | | – | | – | | 83 | | – | | 83 | |

| Returns on investments and servicing of finance | 16 | | 155 | | (105 | ) | (50 | ) | (1 402 | ) | – | | (1 386 | ) |

| Taxation | – | | (6 | ) | 142 | | (335 | ) | (1 618 | ) | – | | (1 817 | ) |

| Capital expenditure and financial investment | – | | (554 | ) | (42 | ) | 16 | | (1 126 | ) | – | | (1 706 | ) |

| Acquisitions and disposals | – | | – | | – | | – | | 1 755 | | – | | 1 755 | |

| Dividends paid on ordinary share capital | – | | (910 | ) | (689 | ) | – | | – | | 19 | | (1 580 | ) |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Cash flow before management of liquid resources | | | | | | | | | | | | | | |

| and financing | 50 | | (1 093 | ) | (746 | ) | (414 | ) | 5 416 | | 19 | | 3 232 | |

| Management of liquid resources | 2 | | (126 | ) | – | | – | | (468 | ) | – | | (592 | ) |

| Financing | (53 | ) | 1 060 | | 578 | | 419 | | (5 082 | ) | – | | (3 078 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Increase/(decrease) in cash in the period | (1 | ) | (159 | ) | (168 | ) | 5 | | (134 | ) | 19 | | (438 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

| | | | | | | | | | | | | | | |

| Cash flow statement | | | | | | | | | | | | | | |

| for the year ended 31 December 2001 (restated) | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| Cash flow from group operating activities | 24 | | 2 | | 92 | | 66 | | 7 313 | | – | | 7 497 | |

| Dividends from joint ventures | – | | – | | – | | – | | 82 | | – | | 82 | |

| Returns on investments and servicing of finance | 202 | | 2 092 | | 900 | | (422 | ) | (4 659 | ) | – | | (1 887 | ) |

| Taxation | – | | (53 | ) | (154 | ) | (502 | ) | (1 496 | ) | – | | (2 205 | ) |

| Capital expenditure and financial investment | – | | (369 | ) | (32 | ) | 310 | | (1 267 | ) | – | | (1 358 | ) |

| Acquisitions and disposals | – | | – | | – | | – | | 3 477 | | – | | 3 477 | |

| Dividends paid on ordinary share capital | – | | (818 | ) | (614 | ) | – | | – | | 12 | | (1 420 | ) |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Cash flow before management of liquid resources | | | | | | | | | | | | | | |

| and financing | 226 | | 854 | | 192 | | (548 | ) | 3 450 | | 12 | | 4 186 | |

| Management of liquid resources | 50 | | 428 | | 400 | | – | | 228 | | – | | 1 106 | |

| Financing | (273 | ) | (1 496) | | (592 | ) | 551 | | (3 362) | | – | | (5 172 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Increase/(decrease) in cash in the period | 3 | | (214 | ) | – | | 3 | | 316 | | 12 | | 120 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

| | |

UnileverAnnual Report & Accounts and Form 20-F 2003 | 139 |

Back to Contents

Additional information for US investors

Unilever Group

| Guarantor statements continued | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | € million | |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| | Unilever | | | | | | Unilever | | | | | | | |

| Capital | | | United | | | |

| Corporation | Unilever N.V. | Unilever PLC | States Inc. | Non- | | |

| subsidiary | parent issuer/ | parent | subsidiary | guarantor | | Unilever |

| issuer | guarantor | guarantor | guarantor | subsidiaries | Eliminations | Group |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Balance sheet | | | | | | | | | | | | | | |

| as at 31 December 2003 | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| Goodwill and intangible assets | – | | – | | 34 | | – | | 17 679 | | – | | 17 713 | |

| Tangible fixed assets | – | | – | | – | | 3 | | 6 652 | | – | | 6 655 | |

| Fixed investments | – | | 381 | | – | | 12 384 | | (191 | ) | (12 375 | ) | 199 | |

| Net assets of subsidiaries (equity accounted) | – | | 8 819 | | 7 699 | | (4 250 | ) | (13 996 | ) | 1 728 | | – | |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Total fixed assets | – | | 9 200 | | 7 733 | | 8 137 | | 10 144 | | (10 647 | ) | 24 567 | |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| | | | | | | | | | | | | | | |

| Stocks | – | | – | | – | | – | | 4 175 | | – | | 4 175 | |

| Amounts due from group companies | 3 821 | | 19 619 | | 649 | | 1 049 | | (25 138 | ) | – | | – | |

| Debtors due within one year | – | | 215 | | 29 | | 154 | | 4 684 | | – | | 5 082 | |

| Debtors due after more than one year | 24 | | – | | 41 | | 2 | | 732 | | – | | 799 | |

| Cash and current investments | 1 | | 430 | | – | | – | | 2 914 | | – | | 3 345 | |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Total current assets | 3 846 | | 20 264 | | 719 | | 1 205 | | (12 633 | ) | – | | 13 401 | |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| | | | | | | | | | | | | | | |

| Borrowings | (269 | ) | (5 216 | ) | – | | (3 | ) | (1 946 | ) | – | | (7 434 | ) |

| Amounts due to group companies | – | | (13 587 | ) | (1 819 | ) | – | | 15 406 | | – | | – | |

| Trade and other creditors | (43 | ) | (962 | ) | (699 | ) | – | | (7 936 | ) | – | | (9 640 | ) |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Creditors due within one year | (312 | ) | (19 765 | ) | (2 518 | ) | (3 | ) | 5 524 | | – | | (17 074 | ) |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Total assets less current liabilities | 3 534 | | 9 699 | | 5 934 | | 9 339 | | 3 035 | | (10 647 | ) | 20 894 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

| | | | | | | | | | | | | | | |

| Borrowings | 3 352 | | 3 393 | | – | | – | | 1 721 | | – | | 8 466 | |

| Trade and other creditors | – | | 88 | | – | | 303 | | 273 | | – | | 664 | |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Creditors due after more than one year | 3 352 | | 3 481 | | – | | 303 | | 1 994 | | – | | 9 130 | |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| | | | | | | | | | | | | | | |

| Provisions for liabilities and charges | | | | | | | | | | | | | | |

| (excluding pensions and similar obligations) | – | | 156 | | 14 | | – | | 1 475 | | – | | 1 645 | |

| | | | | | | | | | | | | | | |

| Net liabilities for pensions and similar obligations | – | | 142 | | – | | 33 | | 3 584 | | – | | 3 759 | |

| | | | | | | | | | | | | | | |

| Minority interests | – | | – | | – | | – | | 440 | | – | | 440 | |

| | | | | | | | | | | | | | | |

| Capital and reserves attributable to: | | | | | | | | | | | | | | |

| PLC | – | | (952 | ) | – | | – | | – | | 952 | | – | |

| NV | – | | – | | 6 869 | | – | | – | | (6 869 | ) | – | |

| Called up share capital | – | | 421 | | 222 | | – | | (1 | ) | – | | 642 | |

| Share premium account | – | | 1 399 | | 133 | | – | | (2 | ) | – | | 1 530 | |

| Other reserves | – | | (1 783 | ) | (659 | ) | (464 | ) | (694 | ) | 1 158 | | (2 442 | ) |

| Profit retained | 182 | | 6 835 | | (645 | ) | 9 467 | | (3 761 | ) | (5 888 | ) | 6 190 | |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Total capital and reserves | 182 | | 5 920 | | 5 920 | | 9 003 | | (4 458 | ) | (10 647 | ) | 5 920 | |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| | | | | | | | | | | | | | | |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Total capital employed | 3 534 | | 9 699 | | 5 934 | | 9 339 | | 3 035 | | (10 647 | ) | 20 894 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

| | |

140 | Unilever Annual Report & Accounts and Form 20-F 2003 | |

Back to Contents

Additional information for US investors

Unilever Group

Guarantor statementscontinued

| | | | | | | | | | | | | | € million | |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| | Unilever | | | | | | Unilever | | | | | | | |

| Capital | | | United | | | |

| Corporation | Unilever N.V. | Unilever PLC | States Inc. | Non- | | |

| subsidiary | parent issuer/ | parent | subsidiary | guarantor | | Unilever |

| issuer | guarantor | guarantor | guarantor | subsidiaries | Eliminations | Group |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Balance sheet | | | | | | | | | | | | | | |

| as at 31 December 2002 (restated) | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| Goodwill and intangible assets | – | | – | | 5 | | – | | 20 269 | | – | | 20 274 | |

| Tangible fixed assets | – | | – | | – | | 5 | | 7 431 | | – | | 7 436 | |

| Fixed investments | – | | 576 | | – | | 10 296 | | 92 | | (10 285 | ) | 679 | |

| Net assets of subsidiaries (equity accounted) | – | | 8 182 | | 6 662 | | (9 223 | ) | (14 344 | ) | 8 723 | | – | |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Total fixed assets | – | | 8 758 | | 6 667 | | 1 078 | | 13 448 | | (1 562) | | 28 389 | |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| | | | | | | | | | | | | | | |

| Stocks | – | | – | | – | | – | | 4 500 | | – | | 4 500 | |

| Amounts due from group companies | 6 025 | | 20 303 | | 1 107 | | 3 996 | | (31 431 | ) | – | | – | |

| Debtors due within one year | – | | 299 | | 32 | | 331 | | 5 213 | | – | | 5 875 | |

| Debtors due after more than one year | 43 | | – | | 42 | | 14 | | 597 | | – | | 696 | |

| Cash and current investments | 9 | | 206 | | 51 | | – | | 2 638 | | – | | 2 904 | |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Total current assets | 6 077 | | 20 808 | | 1 232 | | 4 341 | | (18 483 | ) | – | | 13 975 | |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| | | | | | | | | | | | | | | |

| Borrowings | (1 780 | ) | (3 966 | ) | (1 407 | ) | (4 | ) | (1 780 | ) | – | | (8 937 | ) |

| Amounts due to group companies | – | | (14 121 | ) | (1 156 | ) | – | | 15 277 | | – | | – | |

| Trade and other creditors | (64 | ) | (1 248 | ) | (619 | ) | (125 | ) | (8 962 | ) | – | | (11 018 | ) |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Creditors due within one year | (1 844 | ) | (19 335 | ) | (3 182 | ) | (129 | ) | 4 535 | | – | | (19 955 | ) |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| | | | | | | | | | | | | | | |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Total assets less current liabilities | 4 233 | | 10 231 | | 4 717 | | 5 290 | | (500 | ) | (1 562 | ) | 22 409 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

| | | | | | | | | | | | | | | |

| Borrowings | 4 027 | | 5 257 | | – | | – | | 1 649 | | – | | 10 933 | |

| Trade and other creditors | – | | – | | – | | 76 | | 565 | | – | | 641 | |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Creditors due after more than one year | 4 027 | | 5 257 | | – | | 76 | | 2 214 | | – | | 11 574 | |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| | | | | | | | | | | | | | | |

| Provisions for liabilities and charges | | | | | | | | | | | | | | |

| (excluding pensions and similar obligations) | – | | 131 | | 15 | | – | | 1 432 | | – | | 1 578 | |

| | | | | | | | | | | | | | | |

| Net liabilities for pensions and similar obligations | – | | 141 | | – | | (52 | ) | 3 847 | | – | | 3 936 | |

| | | | | | | | | | | | | | | |

| Minority interests | – | | – | | – | | – | | 619 | | – | | 619 | |

| | | | | | | | | | | | | | | |

| Capital and reserves attributable to: | | | | | | | | | | | | | | |

| PLC | – | | (1 239 | ) | – | | – | | – | | 1 239 | | – | |

| NV | – | | – | | 5 937 | | – | | – | | (5 937 | ) | – | |

| Called up share capital | – | | 421 | | 222 | | – | | (1 | ) | – | | 642 | |

| Share premium account | – | | 1 399 | | 145 | | – | | (3 | ) | – | | 1 541 | |

| Other reserves | – | | (1 534 | ) | (610 | ) | (365 | ) | (624 | ) | 989 | | (2 144 | ) |

| Profit retained | 206 | | 5 655 | | (992 | ) | 5 631 | | (7 984 | ) | 2 147 | | 4 663 | |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Total capital and reserves | 206 | | 4 702 | | 4 702 | | 5 266 | | (8 612 | ) | (1 562 | ) | 4 702 | |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| | | | | | | | | | | | | | | |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Total capital employed | 4 233 | | 10 231 | | 4 717 | | 5 290 | | (500 | ) | (1 562 | ) | 22 409 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

| | |

UnileverAnnual Report & Accounts and Form 20-F 2003 | 141 |

Back to Contents

Principal group companies and fixed investments

Unilever Group as at 31 December 2003

The companies listed below and on pages 143 to 145 are those which, in the opinion of the Directors, principally affect the amount of profit and assets shown in the Unilever Group accounts. The Directors consider that those companies not listed are not significant in relation to Unilever as a whole.

Full information as required by Articles 379 and 414 of Book 2 of the Civil Code in the Netherlands has been filed by Unilever N.V. with the Commercial Registry in Rotterdam.

Particulars of PLC group companies and other significant holdings as required by the United Kingdom Companies Act 1985 will be annexed to the next Annual Return of Unilever PLC.

The main activities of the companies listed below are indicated according to the following key:

|

|

| Holding companies | H |

| Foods | F |

| Home & Personal Care | P |

| Other Operations | O |

|

|

Unless otherwise indicated, the companies are incorporated and principally operate in the countries under which they are shown.

The aggregate percentage of equity capital directly or indirectly held by NV or PLC is shown in the margin, except where it is 100%. All these percentages are rounded down to the nearest whole number.

Shares in the companies listed are usually held directly or indirectly by one of NV or PLC. A long-standing exception is in the United States where companies are jointly owned by NV (73%) and PLC (27%). As a result of the Bestfoods integration during 2002, the shares of certain Bestfoods and Unilever companies (or their merged successor) are held partly by Unilever United States, Inc. and, as a consequence, both NV and PLC have indirect shareholdings in them. The percentage of Unilever’s shareholdings held either directly or indirectly by NV and PLC are identified in the tables according to the following code:

|

|

| NV 100% | a |

| PLC 100% | b |

| NV 73%; PLC 27% | c |

| NV 89%; PLC 11% | d |

| NV 21%; PLC 79% | e |

|

| | | | | |

|

|

|

|

|

| Principal group companies | | | |

|

|

|

|

|

| % | Europe | Ownership | | Activity |

|

| | Austria | | | |

| | Österreichische Unilever Ges.m.b.H. | d | | FP |

|

| | Belgium | | | |

| 99 | Bestfoods Belgium B.V.B.A/S.P.R.L. | d | | F |

| | Unilever Belgium S.A./N.V. (Unibel) | d | | FP |

|

| | Bulgaria | | | |

| | Unilever Bulgaria E.O.O.D. | a | | FP |

|

| | Croatia | | | |

| | Unilever Croatia d.o.o. | a | | FP |

|

| | Czech Republic | | | |

| | Unilever CR spol. s.r.o. | a | | FP |

|

| | Denmark | | | |

| | Unilever Bestfoods A/S | d | | F |

| | Unilever Danmark A/S | a | | FP |

|

| | Estonia | | | |

| | Unilever Eesti OU | a | | FP |

|

| | Finland | | | |

| | Suomen Unilever Oy | a | | FP |

|

|

|

|

|

|

|

|

|

|

| % | Europecontinued | Ownership | | Activity |

|

| | France | | | |

| 99 | Amora Maille Société Industrielle S.A.S. | d | | F |

| 99 | Bestfoods France Société Industrielle S.A. | d | | F |

| 99 | Cogesal-Miko S.A.S. | d | | F |

| 99 | FRALIB Sourcing Unit S.A. | d | | F |

| 99 | Lever Fabergé France S.A. | d | | P |

| 99 | Unilever Bestfoods France S.A. | d | | F |

| 99 | Unilever France S.A.S. | d | | H |

|

| | Germany | | | |

| | Langnese-Iglo GmbH | d | | F |

| | Lever Fabergé Deutschland GmbH | d | | P |

| | Monda Beteiligungs GmbH | d | | F |

| | Monda IPR GmbH & Co. OHG(1) | d | | F |

| | Monda Vermögensverwaltungs | | | |

| | GmbH & Co. OHG(1) | d | | F |

| | Pfanni GmbH & Co. OHG Stavenhagen(1) | d | | F |

| | PW Vermietungs GmbH & Co. KG(1) | d | | F |

| | UBG Vermietungs GmbH & Co. OHG(1) | d | | H |

| | Unilever Bestfoods Deutschland GmbH | d | | F |

| | Unilever Beteiligungs GmbH | d | | H |

| | Unilever Deutschland GmbH | d | | H |

|

| | Greece | | | |

| 67 | ‘Elais’ Oleaginous Products A.E. | a | | F |

| | Unilever Hellas A.E.B.E. | a | | FP |

|

| | Hungary | | | |

| | Unilever Magyarország Kft | a | | FP |

|

| | Ireland | | | |

| | Lever Fabergé Ireland Ltd. | b | | P |

| | Unilever Bestfoods (Ireland) Limited | b | | F |

|

| | Italy | | | |

| | Lever Fabergé Italia Srl | d | | P |

| | Sagit Srl | d | | F |

| | Unilever Bestfoods Italia Srl | d | | F |

| | Unilever Italia SpA | d | | H |

|

| | Latvia | | | |

| | Unilever Baltic LLC | a | | FP |

|

| | Lithuania | | | |

| | Unilever Lietuva UAB | a | | FP |

|

| | The Netherlands | | | |

| | Iglo Mora Groep B.V. | a | | F |

| | Lever Fabergé Nederland B.V. | a | | P |

| | Mixhold B.V. | d | | H |

| | Unilever Bestfoods Nederland B.V. | d | | F |

| | Unilever N.V.(2) | | | H |

| | Unilever Nederland B.V. | a | | H |

|

| | Norway | | | |

| | Unilever Bestfoods AS | a | | F |

|

|

|

|

|

| | Poland | | | |

| 99 | Unilever Polska S.A. | d | | FP |

|

| | Portugal | | | |

| 74 | IgloOlá-Distribuição de Gelados e de | | | |

| | Ultracongelados Lda. | a | | F |

| 60 | LeverElida-Distribuição de Produtos de | | | |

| | Limpeza e Higiene Pessoal Lda. | a | | P |

| | Unilever Bestfoods Portugal-Produtos | | | |

| | Alimentares S.A. | d | | F |

|

|

|

|

|

| |

(1)

| Due to the inclusion of the partnerships in the consolidated group accounts of Unilever, para 264(b) of the German trade law grants an exemption from the duty to prepare individual statutory financial statements and management reports in accordance with the requirements for limited liability companies and to have these audited. |

(2)

| See ‘Basis of consolidation’ on page 73. |

| | |

142 | UnileverAnnual Report & Accounts and Form 20-F 2003 |

Back to Contents

Principal group companies and fixed investments

Unilever Group as at 31 December 2003

Principal group companiescontinued

|

|

|

|

|

| % | Europecontinued | Ownership | | Activity |

|

| | Romania | | | |

| 99 | Unilever South Central Europe S.R.L | a | | FP |

|

| | Russia | | | |

| | Unilever SNG | a | | FP |

|

| | Serbia | | | |

| | Unilever Belgrade | a | | FP |

|

| | Slovakia | | | |

| | Unilever Slovensko spol. s.r.o. | a | | FP |

|

| | Slovenia | | | |

| | Unilever Slovenia d.o.o. | a | | FP |

|

| | Spain | | | |

| | Unilever España S.A. | a | | HP |

| | Unilever Foods España S.A. | a | | F |

|

| | Sweden | | | |

| | GB Glace AB | a | | F |

| | Lever Fabergé AB | a | | P |

| | Unilever Bestfoods AB | a | | F |

|

| | Switzerland | | | |

| | Knorr-Nährmittel AG | d | | H |

| | Lever Fabergé GmbH | d | | P |

| | Meina Holding AG | d | | H |

| | Lusso Foods AG | d | | F |

| | Sunlight AG | a | | O |

| | Unilever Bestfoods Schweiz GmbH | d | | F |

| | Unilever Cosmetics International S.A. | a | | P |

| | Unilever (Schweiz) AG | a | | O |

| | Unilever Swiss Holdings AG | a | | H |

| | Unilever Raw Materials AG | a | | F |

|

| | Ukraine | | | |

| | Unilever Ukraine LLCM | a | | FP |

|

| | United Kingdom | | | |

| | Ben & Jerry’s Homemade Ltd. | e | | F |

| | Lever Fabergé Ltd. | b | | P |

| | Lipton Ltd. | b | | F |

| | Slim•Fast Foods Ltd. | b | | F |

| | Unilever Bestfoods UK Ltd. | e | | F |

| | Unilever Cosmetics International (UK) Ltd. | b | | P |

| | Unilever Ice Cream & Frozen Food Ltd. | e | | F |

| | Unilever PLC(2) | | | H |

| | Unilever UK Central Resources Ltd. | b | | O |

| | Unilever UK Holdings Ltd. | b | | H |

| | Unilever UK & CN Holdings Ltd. | e | | H |

|

| % | North America | Ownership | | Activity |

|

| | Canada | | | |

| | Unilever Canada Inc. | e | | FP |

|

| | United States of America | | | |

| | Ben & Jerry’s Homemade Inc. | c | | F |

| | Good Humor-Breyers Ice Cream(3) | c | | F |

| | Slim•Fast Foods Company(3) | c | | F |

| | Unilever Bestfoods(3) | c | | F |

| | Unilever Bestfoods Foodsolutions(3) | c | | F |

| | Unilever Capital Corporation | c | | O |

| | Unilever Cosmetics International(3) | c | | P |

| | Unilever Home & Personal Care(3) | c | | P |

| | Unilever Ice Cream(3) | c | | F |

| | Unilever United States, Inc. | c | | H |

|

|

|

|

|

| | |

| | |

| | |

| | |

(2)

| See ‘Basis of consolidation’ on page 73. |

(3)

| A division of Conopco, Inc., a subsidiary of Unilever United States, Inc. |

|

|

|

|

|

| % | Africa, Middle East and Turkey | Ownership | | Activity |

|

| | Algeria | | | |

| 60 | Unilever Algérie SPA | a | | P |

|

| | Côte d’Ivoire | | | |

| 90 | Unilever-Côte d’Ivoire | b | | FPO |

|

| | Democratic Republic of Congo | | | |

| 76 | Plantations et Huileries du Congo s.a.r.l. | a | | O |

|

| | Dubai | | | |

| | Unilever Gulf Free Zone Establishment | b | | FP |

|

| | Egypt | | | |

| 60 | Fine Food Products SAE | b | | F |

| 60 | Fine Tea Company SAE | b | | F |

| 60 | Lever Egypt SAE | b | | P |

|

| | Ethiopia | | | |

| 72 | Unilever Ethiopia Private Limited Company | b | | FP |

|

| | Ghana | | | |

| 67 | Unilever Ghana Ltd. | b | | FPO |

|

| | Israel | | | |

| 51 | Glidat Strauss Ltd. | b | | F |

| 59 | Unilever Bestfoods Israel Ltd. | c | | F |

| | Lever Israel Ltd. | b | | P |

|

| | Kenya | | | |

| 88 | Brooke Bond Kenya Ltd. | b | | O |

| | Unilever Kenya Ltd. | b | | FP |

|

| | Malawi | | | |

| | Lever Brothers (Malawi) Ltd. | b | | FP |

|

| | Morocco | | | |

| | Unilever Bestfoods Maghreb S.A. | a | | FP |

|

| | Nigeria | | | |

| 50 | Unilever Nigeria Plc | b | | FP |

|

| | Saudi Arabia | | | |

| 49 | Binzagr Lever Ltd.* | b | | FP |

| 49 | Lever Arabia Ltd.* | b | | P |

|

| | South Africa | | | |

| 59 | Unilever Bestfoods Robertsons (Pty) Limited | c | | F |

| | Lever Ponds (Pty) Ltd. | b | | FP |

|

| | Tanzania | | | |

| | Brooke Bond Tanzania Ltd. | b | | O |

|

| | Tunisia | | | |

| 99 | CODEPAR Tunisia | a | | P |

| 52 | Maghreb Alimentation S.A. | a | | F |

| 99 | Société de Produits Chimiques Détergents | a | | P |

|

| | Turkey | | | |

| 99 | Lever Elida Temizlik ve Kisisel Bakým Ürünleri | | | |

| | Sanayi ve Ticaret A.S. | a | | P |

| | Unilever Sanayi ve Ticaret Türk A.S. | a | | F |

| | Unilever Tüketim Ürünleri Satis Pazarlama | | | |

| | ve Ticaret A.S. | a | | FP |

|

| | Uganda | | | |

| | Unilever Uganda Ltd. | b | | FP |

|

| | Zambia | | | |

| | Unilever South East Africa Zambia Limited | b | | FP |

|

| | Zimbabwe | | | |

| | Unilever South East Africa (Pte) Ltd. | b | | FP |

|

|

|

|

|

| | |

| * | These companies are consolidated on the basis that Unilever exercises a dominant influence. |

UnileverAnnual Report & Accounts and Form 20-F 2003 | 143 |

Back to Contents

Principal group companies and fixed investments

Unilever Group as at 31 December 2003

Principal group companiescontinued

|

|

|

|

|

| % | Asia and Pacific | Ownership | | Activity |

|

| | Australia | | | |

| | Unilever Australia Ltd. | b | | FP |

|

| | Bangladesh | | | |

| 61 | Lever Brothers Bangladesh Ltd. | b | | FP |

|

| | Cambodia | | | |

| | Unilever (Cambodia) Limited | a | | FP |

|

| | China | | | |

| 80 | Bestfoods Guangzhou Foods Ltd. | c | | F |

| | Unilever (China) Ltd. | a | | H |

| 77 | Unilever Company Ltd. | a | | P |

| | Unilever Foods (China) Company Ltd. | a | | F |

| | Unilever Services (Shanghai) Limited | a | | P |

| | Wall’s (China) Company Ltd. | a | | F |

|

| | China S.A.R. | | | |

| 80 | Unilever Bestfoods Hong Kong Ltd. | d | | F |

| | Unilever Hong Kong Ltd. | c | | FP |

|

| | India | | | |

| 51 | Hindustan Lever Ltd. | b | | FPO |

|

| | Indonesia | | | |

| 85 | P.T. Unilever Indonesia Tbk | a | | FP |

|

| | Japan | | | |

| | Nippon Lever KK | a | | FP |

|

| | Malaysia | | | |

| | Unilever Bestfoods (Malaysia) Sdn. Bhd. | e | | F |

| 70 | Unilever (Malaysia) Holdings Sdn. Bhd. | e | | FP |

|

| | New Zealand | | | |

| | Unilever New Zealand Ltd. | b | | FP |

|

| | Pakistan | | | |

| 67 | Unilever Pakistan Ltd. | b | | FP |

|

| | Philippines | | | |

| 50 | California Manufacturing Company Inc. | d | | F |

| | Unilever Philippines, Inc. | d | | FP |

|

| | Singapore | | | |

| | Unilever Bestfoods Singapore Pte. Ltd. | e | | F |

| | Unilever Singapore Private Ltd. | e | | FP |

|

| | South Korea | | | |

| | Unilever Korea Chusik Hoesa | a | | FP |

|

| | Sri Lanka | | | |

| | Unilever Ceylon Ltd. | b | | FPO |

|

| | Taiwan | | | |

| 75 | Unilever Bestfoods (Taiwan) Ltd. | d | | F |

| | Unilever Taiwan Ltd. | d | | FP |

|

| | Thailand | | | |

| | Unilever Thai Holdings Ltd. | d | | FP |

| | Unilever Bestfoods (Thailand) Ltd. | d | | F |

| | Unilever Thai Trading Ltd. | d | | FP |

|

| | Vietnam | | | |

| 66 | Lever Vietnam JVC | a | | P |

| | Unilever Bestfoods and Elida P/S (Vietnam) Ltd | a | | FP |

|

|

|

|

|

|

|

|

|

|

| % | Latin America | Ownership | | Activity |

|

|

|

|

|

| | Argentina | | | |

| | Unilever Bestfoods de Argentina S.A. | d | | F |

| | Unilever de Argentina S.A. | d | | FP |

|

|

|

|

|

| | Bolivia | | | |

| | Unilever Andina Bolivia S.A. | a | | FP |

|

|

|

|

|

| | Brazil | | | |

| | Mavibel Brasil Ltda. | d | | H |

| | Unilever Brasil Ltda. | d | | FP |

| | Unilever Bestfoods Brasil Ltda. | d | | F |

|

|

|

|

|

| | Chile | | | |

| | Unilever Chile Ltda. | d | | FP |

|

|

|

|

|

| | Colombia | | | |

| | Disa Ltda. | d | | F |

| | Unilever Andina Colombia Ltda. | d | | FP |

| 60(4) | Varela S.A. | d | | P |

|

|

|

|

|

| | Costa Rica | | | |

| | Productos Agroindustriales del Caribe S.A. | c | | F |

| | Unilever de Centroamerica S.A. | a | | FP |

|

|

|

|

|

| | Dominican Republic | | | |

| | Knorr Alimentaria S.A. | a | | F |

| | Unilever Dominicana S.A. | a | | P |

|

|

|

|

|

| | Ecuador | | | |

| | Unilever Andina Ecuador S.A. | a | | FP |

|

|

|

|

|

| | El Salvador | | | |

| | Unilever de Centroamerica S.A. | a | | FP |

|

|

|

|

|

| | Guatemala | | | |

| | Unilever de Centroamerica S.A. | a | | FP |

|

|

|

|

|

| | Honduras | | | |

| | Unilever de Centroamerica S.A. | a | | FP |

|

|

|

|

|

| | Mexico | | | |

| | Circulo Esmeralda S.A. de C.V. | d | | F |

| | Corporativo Unilever de Mexico S.de R.L. de C.V. | d | | H |

| | Unilever de Mexico S.A. de C.V. | d | | FP |

|

|

|

|

|

| | Netherlands Antilles | | | |

| | Unilever Becumij N.V. | a | | O |

|

|

|

|

|

| | Nicaragua | | | |

| | Unilever de Centroamerica S.A. | a | | FP |

|

|

|

|

|

| | Panama | | | |

| | Unilever de Centroamerica S.A. | a | | FP |

|

|

|

|

|

| | Paraguay | | | |

| | Unilever de Paraguay S.A. | a | | FP |

|

|

|

|

|

| | Peru | | | |

| | Alimentos y Productos del Maíz S.A. | b | | F |

| 99 | Industrias Pacocha S.A. | a | | FP |

|

|

|

|

|

| | Trinidad & Tobago | | | |

| 50 | Lever Brothers West Indies Ltd. | b | | FP |

|

|

|

|

|

| | Uruguay | | | |

| | Unilever del Uruguay S.A. | c | | F |

| | Sudy Lever S.A. | a | | FP |

|

|

|

|

|

| | Venezuela | | | |

| | Unilever Andina Venezuela S.A. | a | | FP |

|

|

|

|

|

| | |

| (4) | The holders of the remaining shares have exercised a put option that, when completed, will increase the Unilever holding to 100%. |

| | |

144 | UnileverAnnual Report & Accounts and Form 20-F 2003 |

Back to Contents

Principal group companies and fixed investments

Unilever Group as at 31 December 2003

Principal fixed investments

Joint ventures |

|

| % | Europe | Ownership | Activity |

|

| | Portugal | | |

| 40 | FIMA/VG-Distribuição de Produtos | | |

| | Alimentares, Lda. | a | F |

|

| % | North America | | |

|

| | United States of America | | |

| 50 | The Pepsi/Lipton Partnership | c | F |

|

| | | | |

| | | | |

| Associated companies | | |

|

| % | Europe | Ownership | Activity |

|

| | United Kingdom | | |

| 33 | Langholm Capital Partners | b | O |

|

| % | North America | | |

|

| | United States of America | | |

| 33 | JohnsonDiversey Holdings Inc | a | P |

|

UnileverAnnual Report & Accounts and Form 20-F 2003 | 145 |

Back to Contents

Company accounts

Unilever N.V.

Balance sheet as at 31 December

| | € million | | € million | |

| | 2003 | | 2002 | |

|

|

|

| |

| | | | Restated | |

| Fixed assets | | | | |

| Fixed investments | 11 161 | | 11 416 | |

| | | | | |

| Current assets | | | | |

| Debtors | 19 834 | | 20 602 | |

| Cash at bank and in hand | 430 | | 206 | |

| |

|

|

| |

| Total current assets | 20 264 | | 20 808 | |

| Creditors due within one year | (19 765 | ) | (19 335 | ) |

| | | | | |

| Net current assets | 499 | | 1 473 | |

| |

|

|

| |

| Total assets less current liabilities | 11 660 | | 12 889 | |

|

|

|

| |

| Creditors due after more than one year | 3 481 | | 5 257 | |

| | | | | |

| Provisions for liabilities and charges (excluding pensions and similar obligations) | 156 | | 131 | |

| | | | | |

| Net pension liability for unfunded schemes | 142 | | 141 | |

| | | | | |

| Capital and reserves | 7 881 | | 7 360 | |

| Called up share capital: | | | | |

| Preferential share capital 21 | 130 | | 130 | |

| Ordinary share capital 21 | 291 | | 291 | |

| |

|

|

| |

| | 421 | | 421 | |

| Share premium account | 1 399 | | 1 399 | |

| Other reserves | (1 243 | ) | (1 041 | ) |

| Profit retained | 7 304 | | 6 581 | |

| |

|

|

| |

| Total capital employed | 11 660 | | 12 889 | |

|

|

|

| |

| | | | | |

| | | | | |

| Profit and loss accountfor the year ended 31 December | | | | |

| | € million | | € million | |

| | 2003 | | 2002 | |

|

|

|

| |

| Income from fixed investments after taxation | 1 235 | | 3 779 | |

| Other income and expenses | 477 | | 292 | |

| |

|

|

| |

| Profit for the year | 1 712 | | 4 071 | |

|

|

|

| |

Pages 73 to 125, 142 to 145 and 147 contain the notes to the NV company accounts. For the information required by Article 392 of Book 2 of the Civil Code in the Netherlands, refer to pages 72 and 148.

In accordance with Article 402 of Book 2 of the Civil Code in the Netherlands, the accounts of NV have been included in the consolidated accounts. The profit and loss account mentions only income from fixed investments after taxation as a separate item. The balance sheet includes the proposed profit appropriation.

As indicated on page 73, the company accounts of Unilever N.V. comply in all material respects with legislation in the Netherlands. As allowed by Article 362.1 of Book 2 of the Civil Code in the Netherlands, the company accounts are prepared in accordance with United Kingdom accounting standards.

Amounts for 2002 have been restated following changes in our accounting policies for pensions and other post-employment benefits and for the presentation of securities held as collateral.

The Board of Directors

2 March 2004

| | | |

| 146 | UnileverAnnual Report & Accounts and Form 20-F 2003 | |

Back to Contents

Notes to the company accounts

Unilever N.V.

| Fixed investments | | | | |

| | € million | | € million | |

| | 2003 | | 2002 | |

|

|

|

| |

| Shares in group companies | 11 008 | | 11 008 | |

| Book value of PLC shares held in | | | | |

| connection with share options | 381 | | 368 | |

| Less NV shares held by group companies | (228 | ) | (168 | ) |

| Other unlisted investments | – | | 208 | |

| |

|

|

| |

| | 11 161 | | 11 416 | |

| |

|

|

| |

| | | | | |

| Movements during the year: | | | | |

| 1 January | 11 416 | | | |

| Movement in PLC shares held in connection | | | | |

| with share options | 13 | | | |

| Movement in NV shares held by group companies | (60 | ) | | |

| Other unlisted investments | (208 | ) | | |

| Additions | – | | | |

| Decrease | – | | | |

| |

|

|

| |

| 31 December | 11 161 | | | |

|

|

|

| |

Shares in group companies are stated at cost in accordance with international accounting practice in various countries, in particular the United Kingdom. In accordance with Article 385.5 of the Civil Code in the Netherlands, Unilever N.V. shares held by Unilever N.V. subsidiaries are deducted from the carrying value of those subsidiaries.

| Debtors | | | | |

| | € million | | € million | |

| | 2003 | | 2002 | |

|

|

|

| |

| Loans to group companies | 17 088 | | 19 214 | |

| Other amounts owed by group companies | 2 531 | | 1 089 | |

| Amounts owed by undertakings in which | | | | |

| the company has a participating interest | – | | 1 | |

| Other | 215 | | 298 | |

| |

| |

| |

| | 19 834 | | 20 602 | |

| |

| |

| |

| Of which due after more than one year | 819 | | 882 | |

|

|

|

| |

| | | | | |

| Cash at bank and in hand | | | | |

| | € million | | € million | |

| | 2003 | | 2002 | |

|

|

|

| |

| This includes amounts for which repayment | | | | |

| notice is required of: | 43 | | 187 | |

|

|

|

| |

| | | | | |

| Creditors | | | | |

| | € million | | € million | |

| | 2003 | | 2002 | |

|

|

|

| |

| | | | Restated | |

| Due within one year: | | | | |

| Bank loans and overdrafts | 7 | | 4 | |

| Bonds and other loans | 5 209 | | 3 962 | |

| Loans from group companies | 311 | | 1 817 | |

| Other amounts owed to group companies | 13 276 | | 12 304 | |

| Taxation and social security | 76 | | 238 | |

| Accruals and deferred income | 232 | | 205 | |

| Dividends | 642 | | 643 | |

| Other | 12 | | 162 | |

| |

|

|

| |

| | 19 765 | | 19 335 | |

| |

|

|

| |

| Due after more than one year: | | | | |

| Accruals and deferred income | 88 | | – | |

| Bonds and other loans | 3 393 | | 5 257 | |

|

|

|

| |

During 2003 NV changed its accounting presentation for securities received and held as collateral in respect of derivative financial instruments. Until 2002 NV presented such collateral under cash on call and in hand and under bonds and other loans respectively. Because, in normal circumstances, NV has to return the securities in the same form as the original security received, and NV does not

retain the benefit of any dividends or interest on those securities, they are not presented as assets and liabilities of NV. As a result, both cash on call and in hand and bonds and other loans at 31 December 2002 have been reduced by €574 million.

In accordance with the UK Companies Act 1985 the Group presents the final dividend which is proposed after the balance sheet date as a creditor.

Provisions for liabilities and charges (excluding pensions and similar obligations)

| | € million | | € million | |

| | 2003 | | 2002 | |

|

|

|

| |

| Deferred taxation and other provisions | 156 | | 131 | |

| |

|

|

| |

| Of which due within one year | 68 | | 64 | |

|

|

|

| |

Ordinary share capital

Shares numbered 1 to 2 400 are held by a subsidiary of NV and a subsidiary of PLC, each holding 50%. Additionally, 22 163 785 €0.51 ordinary shares are held by NV and other group companies. Full details are given in note 29 on page 124.

Share premium account

The share premium shown in the balance sheet is not available for the issue of bonus shares or for repayment without incurring withholding tax payable by the company. This is despite the change in the Netherlands tax law, as a result of which dividends received from 2001 onwards by individual shareholders who are Netherlands residents are no longer taxed.

| Other reserves | | | | |

| | € million | | € million | |

| | 2003 | | 2002 | |

|

|

|

| |

| 1 January | (1 041) | | (783) | |

| Change in number of shares or certificates | | | | |

| held in connection with share options | (202) | | (258) | |

| |

|

|

| |

| 31 December | (1 243) | | (1 041) | |

|

|

|

| |

| | | | | |

| Profit retained | | | | |

| | € million | | € million | |

| | 2003 | | 2002 | |

|

|

|

| |

| Profit retained as reported in the Annual | | | | |

| Report & Accounts 2002 | | | 6 591 | |

| Accounting policy change – pensions | | | (10) | |

| |

|

|

| |

| Balance 31 December | 7 304 | | 6 581 | |

|

|

|

| |

Profit retained shown in the company accounts and the notes thereto is greater than the amount shown in the consolidated balance sheet, mainly because of certain inter-company transactions which are eliminated in the consolidated accounts.

Contingent liabilities

These are not expected to give rise to any material loss and include guarantees given for group and other companies, under which amounts outstanding at 31 December were:

| | € million | | € million | |

| | 2003 | | 2002 | |

|

|

|

| |

| Group companies | 6 278 | | 8 878 | |

| |

|

|

| |

| Of the above, guaranteed also by PLC | 4 946 | | 5 864 | |

|

|

|

| |

NV has issued joint and several liability undertakings, as defined in Article 403 of Book 2 of the Civil Code in the Netherlands, for almost all Dutch group companies. These written undertakings have been filed with the office of the Company Registry in whose area of jurisdiction the group company concerned has its registered office.

| | |

UnileverAnnual Report & Accounts and Form 20-F 2003 | 147 |

Back to Contents

Further statutory information

Unilever N.V.

The rules for profit appropriation in the Articles of Association

(summary of Article 41)

The profit for the year is applied firstly to the reserves required by law or by the Equalisation Agreement, secondly to cover losses of previous years, if any, and thirdly to the reserves deemed necessary by the Board of Directors. Dividends due to the holders of the Cumulative Preference Shares, including any arrears in such dividends, are then paid; if the profit is insufficient for this purpose, the amount available is distributed to them in proportion to the dividend percentages of their shares. Any profit remaining thereafter is at the disposal of the General Meeting. Distributions from this remaining profit are made to the holders of the ordinary shares pro rata to the nominal amounts of their holdings. The General Meeting can only decide to make distributions from reserves on the basis of a proposal by the Board and in compliance with the law and the Equalisation Agreement.

| | € million | | € million | |

| | 2003 | | 2002 | |

|

|

|

| |

| | | | Restated | |

| Proposed profit appropriation | | | | |

| Profit for the year | 1 712 | | 4 071 | |

| Preference dividends | (27 | ) | (42 | ) |

| |

|

|

| |

| Profit at disposal of the Annual General | | | | |

| Meeting of shareholders | 1 685 | | 4 029 | |

| Ordinary dividends | (962 | ) | (946 | ) |

| |

|

|

| |

| Profit for the year retained | 723 | | 3 083 | |

| Profit retained – 1 January | 6 581 | | 3 498 | |

| |

|

|

| |

| Profit retained – 31 December | 7 304 | | 6 581 | |

|

|

|

| |

Special controlling rights under the Articles of Association

See note 21 on page 110.

Auditors

A resolution will be proposed at the Annual General Meeting on 12 May 2004 for the re-appointment of PricewaterhouseCoopers Accountants N.V. as auditors of NV. The present appointment will end at the conclusion of the Annual General Meeting.

Corporate Centre

Unilever N.V.

Weena 455

PO Box 760

3000 DK Rotterdam

J A A van der Bijl

S G Williams

Joint Secretaries of Unilever N.V.

2 March 2004

| 148 | UnileverAnnual Report & Accounts and Form 20-F 2003 |

Back to Contents

Company accounts

Unilever PLC

| Balance sheet as at 31 December | | | | |

| | £ million | | £ million | |

| | 2003 | | 2002 | |

|

|

|

| |

| | | | Restated | |

| Fixed assets | | | | |

| Intangible assets | 24 | | 3 | |

| Fixed investments | 2 237 | | 2 237 | |

| | | | | |

| Current assets | | | | |

| Debtors | | | | |

| Debtors due within one year | 359 | | 787 | |