UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-173

DODGE & COX FUNDS

(Exact name of registrant as specified in charter)

| | |

555 California Street, 40th Floor San Francisco, CA 94104 |

|

| (Address of principal executive offices) (Zip code) |

Thomas M. Mistele, Esq.

555 California Street, 40th Floor

San Francisco, CA 94104

(Name and address of agent for service)

Registrant’s telephone number, including area code: 415-981-1710

Date of fiscal year end: December 31, 2004

Date of reporting period: from July 1, 2004 through December 31, 2004

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss. 3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

The following are the December 31, 2004 annual reports for the Dodge & Cox Funds, a Delaware statutory trust, consisting of four series: Dodge & Cox Stock Fund, Dodge & Cox International Stock Fund, Dodge & Cox Balanced Fund and Dodge & Cox Income Fund. The reports of each series were transmitted to their respective shareholders on March 1, 2005.

Stock Fund

(Closed to New Investors)

Established 1965

40th Annual Report

December 31, 2004

2004

Stock Fund

www.dodgeandcox.com

For Fund literature, transactions and account

information, please visit the Funds’ web site.

or write or call:

Dodge & Cox Funds

c/o Boston Financial Data Services

P.O. Box 8422

Boston, Massachusetts 02266-8422

(800) 621-3979

Investment Manager

Dodge & Cox

555 California Street, 40th Floor

San Francisco, California 94104

(415) 981-1710

This report is submitted for the general information of the shareholders of the Fund. The report is not authorized for distribution to prospective investors in the Fund unless it is accompanied by a current prospectus.

This report reflects our views, opinions and portfolio holdings as of December 31, 2004, the end of the reporting period. Any such views are subject to change at any time based upon market or other conditions and Dodge & Cox disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Dodge & Cox Fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Dodge & Cox Fund.

12/04 SF AR  Printed on recycled paper

Printed on recycled paper

To Our Shareholders

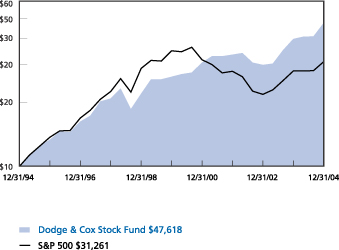

In last year’s Stock Fund Annual Report we wrote, “At the risk of looking like a stopped clock, we want to reiterate our caution about future equity returns.” Fortunately, we also wrote, “Forecasting the market on a short-term basis has a large error rate,” as returns in the equity markets exceeded our expectations. For the year ended December 31, 2004, the Fund returned 19.2%, compared to 10.9% for the S&P 500 Index (S&P 500). Returns for longer periods are listed on the following page.

Please note that the five-year return comparisons are measured from the top of the stock market bubble—a period in which the Fund benefited from avoiding most of the declining high-priced “growth” companies, while the ten-year return comparisons include 1995 through 1999—years when the Fund lagged the returns of the S&P 500 as those same growth companies ascended.

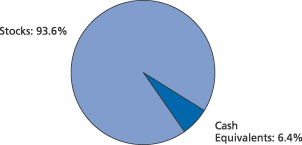

At year-end, the Fund had net assets of $43.3 billion and a cash position of 6.4%. The share price of the Fund rose from $113.78 at the end of 2003 to $130.22 on December 31, 2004. In addition, during the year, the Fund distributed income of $1.53 per share, a short-term capital gain of $1.21 per share and long-term capital gains of $2.44 per share.

2004 Performance Review

A surprisingly strong rally in the fourth quarter (the Stock Fund returned 12.6% compared to 9.2% for the S&P 500) boosted the full year results. During 2004, every sector in the Fund contributed positively to results. The Fund’s holdings in the Information Technology (e.g., Computer Sciences up 27%, Motorola up 38% and NCR Corp. up 78%) and Financial (e.g., Capital One up 38% and Loews up 44%) sectors were particularly strong contributors. Additional notable performers in 2004 included AT&T Wireless (up 87% until its sale to Cingular), Amerada Hess (up 57%), and FedEx (up 46%). Not all holdings fared as well, as 16 stocks ended the year with lower prices, including Pfizer (down 22%), Alcoa (down 16%), Hewlett-Packard (down 7%) and Delphi (down 9%). For each of the Fund’s holdings, we continuously reassess our long-term outlook for the company and then compare that outlook to its current stock price. While the Fund’s investment in each of these companies detracted from returns, we remain optimistic about their opportunities for capital appreciation in the years ahead.

Strategy

The Fund’s portfolio is built one security at a time, based on our fundamental research effort, a three-to-five year time horizon and a strong price discipline. Because we are sensitive to how much we pay for each company’s future earnings and cash flow, the valuation characteristics (such as price-to-earnings ratio or “P/E”) of the Stock Fund are typically lower than the market’s, and Dodge & Cox has become known as a “value” manager. We think it is less useful to distinguish between growth and value management styles, and more important to understand the potential outcomes for each company and determine a reasonable value based on those long-term fundamentals.

The firm’s 19 analysts work alongside the eight members of the Investment Policy Committee to provide continuous analysis and management of the Fund. We often find investment opportunity when valuations decline as a result of bad news affecting near-term earnings, but where we believe the long-term earnings opportunity remains largely intact. For example, over the last year, as investors became more skeptical about the positive long-term trends in Health Care, an area traditionally associated with growth investing, we have found more companies at attractive valuations, such as GlaxoSmithKline and Cardinal Health. In fact, for the first time in many years the Fund now has a higher weighting in Health Care stocks (13.6%) than the S&P 500 (12.8%).

Diversification

Diversification is a hallmark of the Dodge & Cox investment philosophy, and is driven by our individual security selection approach. As a result, the Stock Fund is economically diversified, yet looks different than the S&P 500. Most obviously, the Fund is more concentrated than the market, currently investing in 89 companies versus the 500 in the S&P 500. While 71 of these companies were also found in the S&P 500 at year end, they represented over 80% of the value of the Fund, but only 20% of the value of the S&P 500. Furthermore, our search for investment value has led us to invest in companies based outside the U.S., an area that is only marginally represented in the S&P 500. At year-end, 14.5% of the Stock Fund was invested in 16 foreign-domiciled companies whose stocks trade in the U.S. (primarily as American Depository Receipts or “ADRs”). The Fund can invest up to 20% of its assets in U.S. dollar-denominated foreign securities. The Fund’s cash position is another investment class not represented in the S&P 500. Given these differences, we would expect the Fund’s returns to continue to vary from those of the S&P 500.

Opportunities in Media Stocks

Valuations have been declining in recent years in the Media sector (an area also associated with growth investing), and we have increased the Fund’s weighting to 8.7% in five companies (News Corp., Time Warner, Comcast, Liberty Media and Interpublic Group). We believe these companies offer a blend of attractive fundamental business operations and exposure to ongoing consumer technology adoption. For example, both Comcast and Time Warner currently derive significant revenue from subscription-based services (e.g., cable and broadband data) with recurring, utility-like cash flow. Both companies are also poised to launch advanced Voice-Over-Internet Protocol (VOIP) telephone services in 2005.

| | |

| 1 / Dodge & Cox Stock Fund | | |

Another example is News Corp., which the Fund has held continuously for over seven years. We believe News Corp. remains well positioned for profitable growth potential in entertainment “content” (e.g., cable networks and 20th Century Fox film studio), satellite television subscriptions (e.g., partial ownership in DirecTV), as well as a rebound in advertising spending around the world. While approximately 85% of News Corp.’s consolidated earnings come from its U.S. business franchises, it also owns significant foreign assets, such as several British newspapers and the satellite television providers STAR in Asia and BSkyB in the U.K. (36% stake). We believe that the complexity in valuing News Corp.’s diverse global assets has created an investment opportunity. At the same time, CEO Rupert Murdoch and his management team are working hard to simplify the company and build long-term shareholder value.

Importantly, we believe that each of the Fund’s media investments currently trades at a reasonable valuation compared to long-term growth prospects. Also, please note that we discuss these holdings to illustrate our investment approach, not because we think they are more attractive than the Fund’s other holdings.

Outlook

Looking out over a three-to-five year period, we continue to believe that returns from the broad equity market will be modest and could be punctuated by some unpleasant negative contractions. While we are optimistic about the continued expansion of the global economy in the years ahead, P/E multiples are above average and profit margins are historically high. If interest rates and/or inflation rise, there is a risk that P/E multiples could contract. But as we noted earlier, forecasting is difficult, and rather than overly concerning ourselves with anticipating the direction of the broad market, we focus our energy attempting to understand the long-term risks and opportunities of each company in the Fund relative to its current price.

On the occasion of the Fund’s 40th anniversary we would like to thank you for the continued confidence you have placed in our firm as a shareholder of the Stock Fund. As always, we welcome your comments and questions.

For the Board of Trustees,

| | |

| |

|

| |

| Harry R. Hagey, Chairman | | John A. Gunn, President |

February 18, 2005

Ten Years of Investment Performance

through December 31, 2004 (in thousands)

Average annual total return for periods ended December 31, 2004

| | | | | | | | | | | | |

| | | 1 Year | | | 5 Years | | | 10 Years | | | 20 Years | |

| Dodge & Cox Stock Fund | | 19.16 | % | | 12.40 | % | | 16.89 | % | | 16.14 | % |

| S&P 500 | | 10.86 | | | (2.29 | ) | | 12.07 | | | 13.22 | |

Past performance does not guarantee future results. Investment return and share price will fluctuate with market conditions, and investors may have a gain or loss when shares are sold. Mutual fund performance changes over time and currently may be significantly lower than stated above. Performance is updated and published monthly. Visit the Fund’s web site at www.dodgeandcox.com or call 800-621-3979 for current performance figures.

The Fund’s total returns include the reinvestment of dividend and capital gain distributions, but have not been adjusted for any income taxes payable by shareholders on these distributions. The Standard & Poor’s 500 (S&P 500) is a broad-based unmanaged measure of common stocks. Index returns include dividends and/or interest income and, unlike Fund returns, do not reflect fees or expenses.

Standard & Poor’s, Standard & Poor’s 500, and S&P 500® are trademarks of The McGraw-Hill Companies, Inc.

| | |

| | | Dodge & Cox Stock Fund / 2 |

Fund Expenses

As a shareholder of the Fund, you incur ongoing costs, which include costs for portfolio management, administrative services, and shareholder reports (like this one), among others. Operating expenses, which are deducted from a Fund’s gross income, directly reduce the investment return of the Fund. The following examples are intended to help you understand the ongoing costs (in dollars) of investing in the Fund and to compare these costs with those of other mutual funds. The examples are based on an investment of $1,000 made at the beginning of the period shown and held for the entire period.

The table below illustrates the Fund’s costs in two ways:

Actual Fund Expenses

This section helps you to estimate the actual expenses that you paid over the period. The “Ending Account Value” shown is derived from the Fund’s actual return, and the third column shows the dollar amount that would have been paid by an investor who started with $1,000 in the Fund. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period. To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for the Fund under the heading “Expenses Paid During Period.”

Hypothetical Example for Comparison

This section is intended to help you compare the Fund’s costs with those of other mutual Funds. It assumes that the Fund had a yearly return of 5% before expenses, but that the expense ratio is unchanged. In this case—because the return used is not the Fund’s actual return—the results do not apply to your investment. The example is useful in making comparisons because the Securities and Exchange Commission requires all mutual funds to calculate expenses based on a 5% return. You can assess the Fund’s costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

| | | | | | |

Six Months Ended

December 31, 2004 | | Beginning

Account Value 7/1/2004 | | Ending

Account Value 12/31/2004 | | Expenses Paid

During Period* |

| Based on Actual Fund Return | | $1,000.00 | | $1,123.50 | | $2.80 |

| Based on Hypothetical 5% Yearly Return | | 1,000.00 | | 1,022.37 | | 2.66 |

| * | | These calculations are based on expenses incurred in the most recent fiscal half-year. The Fund’s annualized six-month expense ratio for that period is 0.52%. The dollar amounts shown as “Expenses Paid” are equal to the annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year, then divided by 366. |

The expenses shown in the table are meant to highlight and help you compare ongoing costs only and do not reflect any transactional costs, account maintenance fees or charges by processing organizations. While other mutual funds may charge such fees, please note that the Fund does not charge any transaction fee (e.g., redemption fee), account maintenance fee (e.g., small account fee), nor does it charge a “sales load.”

| | |

| 3 / Dodge & Cox Stock Fund | | |

Fund Information | December 31, 2004 |

General Information

| | |

Net Asset Value Per Share | | $130.22 |

Total Net Assets (millions) | | $43,266 |

2004 Expense Ratio | | 0.53% |

2004 Portfolio Turnover | | 11% |

30-Day SEC Yield1 | | 1.29% |

Fund Inception Date | | 1965 |

Investment Manager: Dodge & Cox, San Francisco. Managed by the Investment Policy Committee, whose eight members’ average tenure at Dodge & Cox is 23 years.

Asset Allocation

| | | | |

| Stock Characteristics | | Fund | | S&P 500 |

Number of Stocks | | 90 | | 500 |

Median Market Capitalization (billions) | | $15 | | $11 |

Weighted-Average Market Cap. (billions) | | $39 | | $92 |

Price-to-Earnings Ratio2 | | 16x | | 17x |

Price-to-Book Value Ratio | | 2.1x | | 3.0x |

Foreign Stocks3 (% of Fund) | | 14.5% | | 0.0% |

| | |

| Ten Largest Holdings | | % of Fund |

Comcast Class A | | 3.2 |

Hewlett-Packard | | 3.0 |

HCA, Inc. | | 2.4 |

Cardinal Health | | 2.4 |

News Corp. Class A | | 2.4 |

Time Warner | | 2.4 |

AT&T | | 2.3 |

Sony ADR (Japan) | | 2.2 |

Union Pacific | | 2.2 |

McDonald’s | | 2.1 |

| | | | | | |

| Sector Diversification | | Fund | | | S&P 500 | |

Consumer Discretionary | | 20.4 | % | | 11.5 | % |

Financials | | 17.5 | | | 20.9 | |

Health Care | | 13.6 | | | 12.8 | |

Information Technology | | 11.5 | | | 16.1 | |

Energy | | 8.5 | | | 7.2 | |

Materials | | 8.2 | | | 3.2 | |

Industrials | | 6.5 | | | 11.5 | |

Utilities | | 2.9 | | | 3.0 | |

Telecommunication Services | | 2.8 | | | 3.3 | |

Consumer Staples | | 1.7 | | | 10.5 | |

| 1 | | SEC Yield is an annualization of the Fund’s total net investment income per share for the 30-day period ended on the last day of the month. |

| 2 | | The Fund’s price-to-earnings (P/E) ratio is calculated using Dodge & Cox’s estimated forward earnings and excludes extraordinary items. The S&P 500’s P/E ratio is calculated by Standard & Poor’s and uses an aggregated estimate of forward earnings. |

| 3 | | All U.S. dollar-denominated. |

| | |

| | | Dodge & Cox Stock Fund / 4 |

Portfolio of Investments | December 31, 2004 |

| | | | | |

| COMMON STOCKS: 93.6% |

| | |

| | | SHARES | | MARKET VALUE |

| CONSUMER DISCRETIONARY: 20.4% | | | |

| MEDIA: 8.7% | | | | | |

Comcast Corp. Class A(a) | | 41,114,330 | | $ | 1,368,284,902 |

News Corp. Class A | | 54,679,238 | | | 1,020,314,581 |

Time Warner, Inc.(a) | | 52,462,900 | | | 1,019,878,776 |

Liberty Media Corp. Series A(a) | | 33,502,700 | | | 367,859,646 |

Interpublic Group of Companies, Inc.(a) | | 337,800 | | | 4,526,520 |

| | | | |

|

|

| | | | | | 3,780,864,425 |

| CONSUMER DURABLES & APPAREL: 5.2% | | | |

Sony Corp. ADR(b) (Japan) | | 24,527,700 | | | 955,599,192 |

Matsushita Electric Industrial Co., Ltd. ADR(b) (Japan) | | 34,434,200 | | | 552,668,910 |

Whirlpool Corp.(c) | | 4,388,050 | | | 303,696,941 |

Eastman Kodak Co. | | 7,629,089 | | | 246,038,120 |

VF Corp. | | 3,467,900 | | | 192,052,302 |

| | | | |

|

|

| | | | | | 2,250,055,465 |

| HOTELS, RESTAURANTS & LEISURE: 2.4% | | | |

McDonald’s Corp. | | 28,880,400 | | | 925,905,624 |

InterContinental Hotels Group PLC ADR(b) (United Kingdom) | | 8,855,548 | | | 111,757,018 |

| | | | |

|

|

| | | | | | 1,037,662,642 |

| RETAILING: 2.0% | | | | | |

May Department Stores Co.(c) | | 17,894,400 | | | 526,095,360 |

Gap, Inc. | | 8,972,500 | | | 189,499,200 |

Dillard’s, Inc. Class A(c) | | 5,177,500 | | | 139,119,425 |

| | | | |

|

|

| | | | | | 854,713,985 |

| AUTOMOBILES & COMPONENTS: 1.2% | | | |

Delphi Corp.(c) | | 36,051,632 | | | 325,185,721 |

Honda Motor Co. Ltd. ADR(b) (Japan) | | 7,670,400 | | | 199,890,624 |

| | | | |

|

|

| | | | | | 525,076,345 |

| TRADING COMPANIES & DISTRIBUTORS: 0.9% | | | |

Genuine Parts Co.(c) | | 8,953,800 | | | 394,504,428 |

| | | | |

|

|

| | | | | | 8,842,877,290 |

| FINANCIALS: 17.5% | | | | | |

| INSURANCE: 6.4% | | | | | |

St. Paul Travelers Companies, Inc. | | 19,206,550 | | | 711,986,809 |

Loews Corp. | | 7,518,900 | | | 528,578,670 |

Chubb Corp. | | 5,738,750 | | | 441,309,875 |

Safeco Corp. | | 5,058,600 | | | 264,261,264 |

Torchmark Corp. | | 4,525,800 | | | 258,604,212 |

Genworth Financial, Inc. Class A | | 8,869,300 | | | 239,471,100 |

UnumProvident Corp. | | 11,748,800 | | | 210,773,472 |

MBIA, Inc. | | 1,567,000 | | | 99,159,760 |

| | | | |

|

|

| | | | | | 2,754,145,162 |

| DIVERSIFIED FINANCIALS: 4.8% | | | |

Capital One Financial Corp. | | 10,676,000 | | | 899,025,960 |

JPMorgan Chase & Co. | | 18,460,328 | | | 720,137,395 |

CIT Group, Inc. | | 9,570,100 | | | 438,501,982 |

| | | | |

|

|

| | | | | | 2,057,665,337 |

| | | | | |

| | |

| | | SHARES | | MARKET VALUE |

| BANKS: 3.9% | | | | | |

Wachovia Corp. | | 14,950,300 | | $ | 786,385,780 |

Golden West Financial Corp. | | 8,898,600 | | | 546,552,012 |

Wells Fargo & Co. | | 6,046,600 | | | 375,796,190 |

| | | | |

|

|

| | | | | | 1,708,733,982 |

| REAL ESTATE: 2.4% | | | | | |

Equity Office Properties Trust(c) | | 22,260,300 | | | 648,219,936 |

Equity Residential Properties Trust | | 11,143,500 | | | 403,171,830 |

| | | | |

|

|

| | | | | | 1,051,391,766 |

| | | | |

|

|

| | | | | | 7,571,936,247 |

| HEALTH CARE: 13.6% | | | | | |

| HEALTH CARE EQUIPMENT & SERVICES: 7.1% | | | |

HCA, Inc.(c) | | 26,418,400 | | | 1,055,679,264 |

Cardinal Health, Inc. | | 17,893,150 | | | 1,040,486,673 |

Wellpoint, Inc.(a) | | 4,245,950 | | | 488,284,250 |

Becton, Dickinson & Co. | | 4,222,350 | | | 239,829,480 |

Thermo Electron Corp(a) | | 7,433,400 | | | 224,414,346 |

| | | | |

|

|

| | | | | | 3,048,694,013 |

| PHARMACEUTICALS & BIOTECHNOLOGY: 6.5% | | | |

Schering-Plough Corp. | | 41,890,500 | | | 874,673,640 |

Pfizer, Inc. | | 25,517,925 | | | 686,177,003 |

GlaxoSmithKline PLC ADR(b)

(United Kingdom) | | 12,998,900 | | | 616,017,871 |

Wyeth | | 10,268,800 | | | 437,348,192 |

Bristol-Myers Squibb Co. | | 8,105,050 | | | 207,651,381 |

| | | | |

|

|

| | | | | | 2,821,868,087 |

| | | | |

|

|

| | | | | | 5,870,562,100 |

| INFORMATION TECHNOLOGY: 11.5% | | | |

| TECHNOLOGY HARDWARE & EQUIPMENT: 7.3% | | | |

Hewlett-Packard Co. | | 61,127,163 | | | 1,281,836,608 |

Xerox Corp.(a) | | 45,764,500 | | | 778,454,145 |

NCR Corp.(a) | | 3,711,900 | | | 256,974,837 |

Motorola, Inc. | | 14,685,900 | | | 252,597,480 |

Storage Technology Corp.(a,c) | | 7,511,200 | | | 237,429,032 |

Avaya, Inc.(a) | | 12,229,400 | | | 210,345,680 |

Freescale Semiconductor, Inc. Class A | | 5,482,700 | | | 97,701,714 |

Freescale Semiconductor, Inc. Class B | | 1,621,547 | | | 29,771,603 |

| | | | |

|

|

| | | | | | 3,145,111,099 |

| SOFTWARE & SERVICES: 4.2% | | | | | |

Electronic Data Systems Corp.(c) | | 33,204,400 | | | 767,021,640 |

Computer Sciences Corp.(a,c) | | 12,893,600 | | | 726,812,232 |

BMC Software, Inc.(a,c) | | 11,787,600 | | | 219,249,360 |

Compuware Corp.(a,c) | | 19,357,100 | | | 125,240,437 |

| | | | |

|

|

| | | | | | 1,838,323,669 |

| | | | |

|

|

| | | | | | 4,983,434,768 |

| | |

| 5 / Dodge & Cox Stock Fund | | See accompanying Notes to Financial Statements |

Portfolio of Investments | December 31, 2004 |

| | | | | |

| COMMON STOCKS (continued) | | | | |

| | |

| | | SHARES | | MARKET VALUE |

| ENERGY: 8.5% | | | | | |

ChevronTexaco Corp. | | 13,960,128 | | $ | 733,046,321 |

Shell Transport & Trading Co. PLC ADR(b) (United Kingdom) | | 12,111,400 | | | 622,525,960 |

Unocal Corp. | | 11,456,400 | | | 495,374,736 |

ConocoPhillips | | 5,643,400 | | | 490,016,422 |

Baker Hughes, Inc. | | 9,717,750 | | | 414,656,393 |

Occidental Petroleum Corp. | | 6,254,500 | | | 365,012,620 |

Amerada Hess Corp. | | 4,346,700 | | | 358,081,146 |

Schlumberger Ltd.(b) (Netherlands Antilles) | | 2,901,700 | | | 194,268,815 |

| | | | |

|

|

| | | | | | 3,672,982,413 |

| MATERIALS: 8.2% | | | | | |

| CHEMICALS: 6.2% | | | | | |

Dow Chemical Co. | | 17,593,114 | | | 871,035,074 |

Akzo Nobel N.V. ADR(b),(c) (Netherlands) | | 18,186,723 | | | 772,753,859 |

Rohm and Haas Co. | | 6,784,500 | | | 300,078,437 |

Syngenta A.G. ADR(b) (Switzerland) | | 12,651,800 | | | 270,115,930 |

NOVA Chemicals Corp.(b,c) (Canada) | | 4,752,570 | | | 224,796,561 |

Engelhard Corp.(c) | | 6,266,100 | | | 192,181,287 |

Lubrizol Corp. | | 929,100 | | | 34,246,626 |

Bayer A.G. ADR(b) (Germany) | | 116,900 | | | 3,972,262 |

| | | | |

|

|

| | | | | | 2,669,180,036 |

| METALS AND MINING: 1.5% | | | | | |

Rio Tinto PLC ADR(b) (United Kingdom) | | 4,630,831 | | | 552,041,363 |

Alcoa, Inc. | | 3,671,983 | | | 115,373,706 |

| | | | |

|

|

| | | | | | 667,415,069 |

| PAPER AND FOREST PRODUCTS: 0.5% | | | | | |

International Paper Co. | | 5,239,300 | | | 220,050,600 |

| | | | |

|

|

| | | | | | 3,556,645,705 |

| INDUSTRIALS: 6.5% | | | | | |

| TRANSPORTATION: 3.5% | | | | | |

Union Pacific Corp.(c) | | 13,860,950 | | | 932,148,887 |

Fedex Corp. | | 5,699,900 | | | 561,383,151 |

| | | | |

|

|

| | | | | | 1,493,532,038 |

| CAPITAL GOODS: 1.7% | | | | | |

Masco Corp. | | 9,510,900 | | | 347,433,177 |

Fluor Corp.(c) | | 4,375,550 | | | 238,511,231 |

Volvo A.B. ADR(b) (Sweden) | | 3,360,200 | | | 133,231,930 |

| | | | |

|

|

| | | | | | 719,176,338 |

| COMMERCIAL SERVICES & SUPPLIES: 1.1% | | | |

Pitney Bowes, Inc. | | 6,157,150 | | | 284,952,902 |

R.R. Donnelley & Sons Co. | | 5,259,000 | | | 185,590,110 |

| | | | |

|

|

| | | | | | 470,543,012 |

| ELECTRONIC EQUIPMENT & INSTRUMENTS: 0.2% |

American Power Conversion Corp. | | 4,862,281 | | | 104,052,813 |

| | | | |

|

|

| | | | | | 2,787,304,201 |

| | | | | |

| | |

| | | SHARES | | MARKET VALUE |

| UTILITIES: 2.9% | | | | | |

Duke Energy Corp. | | 26,869,200 | | $ | 680,596,836 |

American Electric Power Co., Inc. | | 7,630,910 | | | 262,045,449 |

FirstEnergy Corp. | | 4,486,500 | | | 177,261,615 |

Scottish Power PLC ADR(b)

(United Kingdom) | | 4,586,800 | | | 142,924,688 |

| | | | |

|

|

| | | | | | 1,262,828,588 |

| TELECOMMUNICATION SERVICES: 2.8% | | | |

AT&T Corp.(c) | | 52,008,200 | | | 991,276,292 |

Vodafone Group PLC ADR(b)

(United Kingdom) | | 8,073,000 | | | 221,038,740 |

| | | | |

|

|

| | | | | | 1,212,315,032 |

| CONSUMER STAPLES: 1.7% | | | | | |

| FOOD, BEVERAGE AND TOBACCO: 1.7% | | | |

Unilever N.V.(b) (Netherlands) | | 11,244,000 | | | 750,087,240 |

| | | | |

|

|

| | | | | | 750,087,240 |

| | | | |

|

|

Total Common Stocks (Cost $30,615,421,151) | | | 40,510,973,584 |

| | | | |

|

|

| | | | | | |

|

| SHORT-TERM INVESTMENTS: 6.5% |

| | |

| | | PAR VALUE | | MARKET VALUE |

SSgA Prime Money Market Fund | | $ | 216,771,900 | | $ | 216,771,900 |

State Street Repurchase Agreement, 1.40%, 1/3/05, maturity value $582,327,930 (collateralized by U.S. Treasury Securities, value $593,953,293, 1.935%–8.125%, 6/30/05–5/15/21) | | | 582,260,000 | | | 582,260,000 |

U.S. Treasury Bills | | | | | | |

1/6/2005 | | | 150,000,000 | | | 149,957,604 |

1/20/2005 | | | 300,000,000 | | | 299,724,500 |

1/27/2005 | | | 300,000,000 | | | 299,601,514 |

2/3/2005 | | | 300,000,000 | | | 299,477,500 |

2/10/2005 | | | 300,000,000 | | | 299,323,333 |

2/17/2005 | | | 100,000,000 | | | 99,739,111 |

4/28/2005 | | | 250,000,000 | | | 248,318,125 |

5/19/2005 | | | 300,000,000 | | | 297,395,248 |

| | | | | |

|

|

Total Short-Term Investments

(Cost $2,792,568,835) | | | | | | 2,792,568,835 |

| | | | | |

|

|

| | | | | | | |

| | | | | | | | |

TOTAL INVESTMENTS

(Cost $33,407,989,986) | | 100.1 | % | | | 43,303,542,419 | |

OTHER ASSETS LESS LIABILITIES | | (0.1 | ) | | | (37,199,023 | ) |

| | |

|

| |

|

|

|

TOTAL NET ASSETS | | 100.0 | % | | $ | 43,266,343,396 | |

| | |

|

| |

|

|

|

| (b) | | Securities denominated in U.S. Dollars |

| (c) | | Affiliated issuer. See Note 4 of Notes to Financial Statements. |

| | |

| See accompanying Notes to Financial Statements | | Dodge & Cox Stock Fund / 6 |

Statement of Assets and Liabilities

| | | |

|

| December 31, 2004 |

| Assets: | | | |

Investments (identified cost $33,407,989,986) | | | |

Unaffiliated issuers, at market value | | $ | 34,483,620,526 |

Affiliated issuers, at market value | | | 8,819,921,893 |

| | |

|

|

| | | | 43,303,542,419 |

Cash | | | 49,935,875 |

Receivable for investments sold | | | 38,264,461 |

Receivable for Fund shares sold | | | 13,432,527 |

Dividends and interest receivable | | | 53,587,911 |

Prepaid expenses and other assets | | | 261,256 |

| | |

|

|

| | | | 43,459,024,449 |

| | |

|

|

| Liabilities: | | | |

Payable for investments purchased | | | 159,634,515 |

Payable for Fund shares redeemed | | | 12,604,685 |

Management fees payable | | | 18,086,199 |

Accounts payable | | | 2,355,654 |

| | |

|

|

| | | | 192,681,053 |

| | |

|

|

| Net Assets | | $ | 43,266,343,396 |

| | |

|

|

| Net Assets Consist of: | | | |

Paid in capital | | $ | 33,102,729,732 |

Accumulated undistributed

net investment income | | | 8,922,900 |

Accumulated undistributed net

realized gain on investments | | | 259,138,331 |

Net unrealized appreciation on investments | | | 9,895,552,433 |

| | |

|

|

| | | $ | 43,266,343,396 |

| | |

|

|

Fund shares outstanding (par value

$0.01 each, unlimited shares authorized) | | | 332,246,229 |

Net asset value per share | | | $130.22 |

| |

| Statement of Operations | | | |

|

Year Ended

December 31, 2004 |

| Investment Income: | | | |

Dividends (net of foreign taxes of $8,887,593) | | | |

Unaffiliated issuers | | $ | 424,818,661 |

Affiliated issuers | | | 210,795,271 |

Interest | | | 29,505,499 |

| | |

|

|

| | | | 665,119,431 |

| | |

|

|

| Expenses: | | | |

Management fees | | | 179,639,203 |

Custodian and fund accounting fees | | | 608,621 |

Transfer agent fees | | | 6,400,426 |

Professional services | | | 85,592 |

Shareholder reports | | | 1,460,658 |

Registration fees | | | 1,723,533 |

Trustees’ fees | | | 82,000 |

Miscellaneous | | | 267,081 |

| | |

|

|

| | | | 190,267,114 |

| | |

|

|

| Net Investment Income | | | 474,852,317 |

| | |

|

|

| Realized and Unrealized Gain on Investments: | | | |

Net realized gain from: | | | |

Investments in unaffiliated issuers | | | 1,290,734,715 |

Investments in affiliated issuers | | | 127,031,462 |

Net change unrealized appreciation | | | 4,726,648,936 |

| | |

|

|

Net realized and unrealized gain | | | 6,144,415,113 |

| | |

|

|

| Net Increase in Net Assets from Operations | | $ | 6,619,267,430 |

| | |

|

|

Statement of Changes in Net Assets

| | | | | | | | |

| | |

| | | Year Ended

December 31, 2004 | | | Year Ended

December 31, 2003 | |

| Operations: | | | | | | | | |

Net investment income | | $ | 474,852,317 | | | $ | 339,700,192 | |

Net realized gain | | | 1,417,766,177 | | | | 330,946,926 | |

Net change in unrealized appreciation | | | 4,726,648,936 | | | | 5,488,029,040 | |

| | |

|

|

| |

|

|

|

Net increase in net assets from operations | | | 6,619,267,430 | | | | 6,158,676,158 | |

| | |

|

|

| |

|

|

|

| | |

Distributions to

Shareholders from: | | | | | | | | |

Net investment income | | | (469,055,741 | ) | | | (340,525,138 | ) |

Net realized gain | | | (1,173,587,700 | ) | | | (214,176,406 | ) |

| | |

|

|

| |

|

|

|

Total distributions | | | (1,642,643,441 | ) | | | (554,701,544 | ) |

| | |

|

|

| |

|

|

|

| | |

| Fund Share Transactions: | | | | | | | | |

Amounts received from

sale of shares | | | 11,863,567,462 | | | | 12,166,924,022 | |

Net asset value of shares issued in reinvestment of distributions | | | 1,513,787,692 | | | | 505,674,193 | |

Amounts paid for

shares redeemed | | | (4,524,858,539 | ) | | | (2,875,628,981 | ) |

| | |

|

|

| |

|

|

|

Net increase from Fund

share transactions | | | 8,852,496,615 | | | | 9,796,969,234 | |

| | |

|

|

| |

|

|

|

Total increase in net assets | | | 13,829,120,604 | | | | 15,400,943,848 | |

| | |

| Net Assets: | | | | | | | | |

Beginning of year | | | 29,437,222,792 | | | | 14,036,278,944 | |

| | |

|

|

| |

|

|

|

End of year (including undistributed net investment income of $8,922,900 and

$3,126,324, respectively) | | $ | 43,266,343,396 | | | $ | 29,437,222,792 | |

| | |

|

|

| |

|

|

|

| | |

Shares sold | | | 99,334,591 | | | | 124,244,324 | |

Shares issued in

reinvestment of distributions | | | 11,920,322 | | | | 4,855,626 | |

Shares redeemed | | | (37,725,900 | ) | | | (29,796,487 | ) |

| | |

|

|

| |

|

|

|

Net increase in

shares outstanding | | | 73,529,013 | | | | 99,303,463 | |

| | |

|

|

| |

|

|

|

| | |

| 7 / Dodge & Cox Stock Fund | | See accompanying Notes to Financial Statements |

Notes to Financial Statements

Note 1 — Organization and Significant Accounting Policies

Dodge & Cox Stock Fund (the “Fund”) is one of the funds constituting the Dodge & Cox Funds (the “Trust”). The Trust is organized as a Delaware statutory trust and is registered under the Investment Company Act of 1940, as amended, as a diversified, open-end management investment company. The Fund commenced operations on January 4, 1965, and seeks long-term growth of principal and income. Risk considerations and investment strategies of the Fund are discussed in the Fund’s Prospectus. The Fund is closed to new investors.

The Fund consistently follows accounting policies which are in conformity with accounting principles generally accepted in the United States of America. In preparing these financial statements, management is required to make estimates and assumptions that affect reported amounts and disclosures. Actual results could differ from those estimates. Significant accounting policies are as follows:

Security valuation. The Fund’s net assets are valued as of the close of trading on the New York Stock Exchange (the “NYSE”), generally 4:00 p.m. Eastern Time, each day that the NYSE is open for business. Stocks are valued at market, using as a price the official quoted close price or the last sale of the day at the close of the NYSE or, if not available, at the mean between the exchange listed bid and ask prices for the day. A security which is listed or traded on more than one exchange is valued at the quotation on the exchange determined to be the primary market for such security. Security values are not discounted based on the size of the Fund’s position. Securities for which market quotations are not readily available are valued at fair value as determined in good faith by or at the direction of the Board of Trustees. Short-term securities are valued at amortized cost which approximates current value. All securities held by the Fund are denominated in U.S. dollars.

Security transactions and related investment income. Security transactions are recorded by the Fund as of the date the trades are executed with brokers. Realized gains and losses on securities sold are determined on the basis of identified cost. Dividend income and corporate action transactions are recorded on the ex-dividend date, except for certain dividends or corporate actions from foreign securities where the ex-dividend date may have passed, which are recorded as soon as the Fund is informed of the ex-dividend date. Withholding taxes on foreign dividends have been provided for in accordance with the Fund’s understanding of the applicable country’s tax rules and rates. Non-cash dividends included in dividend income, if any, are recorded at the fair market value of the securities received. Distributions received in excess of income are recorded as a reduction of cost of investments and/or realized gain. The Fund may estimate the character of distributions received from Real Estate Investment Trusts (“REITs”). Interest income is recorded on the accrual basis.

Expenses. Expenses are recorded on the accrual basis. Most expenses of the Trust can be directly attributed to a specific fund. Expenses which cannot be directly attributed are apportioned among all of the funds in the Trust.

Repurchase agreements. The Fund may enter into repurchase agreements secured by U.S. government securities which involve the purchase of securities from a counterparty with a simultaneous commitment to resell the securities at an agreed-upon date and price. It is the Fund’s policy that its custodian take possession of the underlying collateral securities, the fair value of which exceeds the principal amount of the repurchase transaction, including accrued interest, at all times. In the event of default by the counterparty, the Fund has the contractual right to liquidate the securities and to apply the proceeds in satisfaction of the obligation.

Income taxes and distributions to shareholders. No provision for federal income taxes has been included in the accompanying financial statements since the Fund intends to distribute all of its taxable income and continue to comply with requirements for regulated investment companies. Distributions to shareholders of income and capital gains are reflected in the net asset value per share computation on the ex-dividend date. Income and capital gain distributions are determined in accordance with income tax regulations, which may differ from accounting principles generally accepted in the United States of America. Temporary differences between financial statement and tax treatments may occur when certain items of income, expense, gain or loss are recognized in different periods for financial statement

| | |

| | | Dodge & Cox Stock Fund / 8 |

Notes to Financial Statements (continued)

and tax purposes. Differences in classification may also arise due to the treatment of short-term realized gains as ordinary income for tax purposes. Permanent differences are reclassified among capital accounts in the financial statements to reflect their tax character. These adjustments have no impact on net assets or results of operations.

Note 2 — Related Party Transactions

Management fees. Under a written agreement, the Fund pays an annual management fee of 0.50% of the Fund’s average daily net asset value to Dodge & Cox, investment manager of the Fund. The agreement further provides that Dodge & Cox shall waive its fee to the extent that such fee plus all other ordinary operating expenses of the Fund exceed 0.75% of the average daily net assets for the year.

Trustees’ fees. All officers and three of the trustees of the Trust are officers and employees of Dodge & Cox. Those trustees who are not affiliated with Dodge & Cox receive from the Trust an annual fee plus an attendance fee for each Board or Committee meeting attended. Payments to trustees are shared equally among each fund in the Trust. The Trust does not pay any other remuneration to its officers or trustees.

Indemnifications. Under the Trust’s organizational documents, its officers and trustees are indemnified against certain liabilities arising out of the performance of their duties to the Trust. In addition, in the normal course of business the Trust enters into contracts that provide general indemnifications to other parties. The Trust’s maximum exposure under these arrangements is unknown as this would involve future claims that may be made against the Trust that have not yet occurred.

Note 3 — Distributions Paid, Distributable Earnings and Investment Transactions

Distributions paid during the years ended December 31, 2004 and 2003 were characterized as follows for federal tax purposes:

| | | | |

| | | 2004

| | 2003

|

Ordinary income | | $862,230,499 | | $440,163,145 |

| | | ($2.74 per share) | | ($2.01 per share) |

Long-term capital gain | | $780,412,942 | | $114,538,399 |

| | | ($2.44 per share) | | ($0.45 per share) |

At December 31, 2004, the tax basis components of accumulated undistributed income and net realized gain include $59,231,655 of ordinary income and $208,829,576 of long-term capital gain. In 2004, the Fund recognized net capital gain of $82,601,070 from the delivery of appreciated securities in an in-kind redemption transaction. For federal income tax purposes, this gain is not recognized as taxable income to the Fund and therefore will not be distributed to shareholders. At December 31, 2004, the cost of investments for federal income tax purposes was equal to the cost for financial reporting purposes. Net unrealized appreciation aggregated $9,895,552,433, of which $10,062,614,207 represented appreciated securities and $167,061,774 represented depreciated securities.

For the year ended December 31, 2004, purchases and sales of securities, other than short-term securities and U.S. government securities, aggregated $11,475,134,108 and $3,839,712,362, respectively.

| | |

| 9 / Dodge & Cox Stock Fund | | |

Notes to Financial Statements (continued)

Note 4 — Investments in Affiliates

Each of the companies listed below is considered to be an affiliate of the Fund because the Fund owned at least 5% of the company’s voting securities during the year ended December 31, 2004. Transactions during the period in securities of affiliated companies were as follows:

| | | | | | | | | | | | | | | |

| | | Shares at

Beginning

of Period | | Additions | | Reductions | | | Shares at

End of

Period | | Dividend

Income 2 | | Market Value of

Investment in

Affiliates at

December 31,

2004 |

AT&T Corp. | | 41,562,080 | | 10,654,720 | | (208,600 | ) | | 52,008,200 | | $ | 49,128,951 | | $ | 991,276,292 |

Akzo Nobel N.V. ADR (Netherlands) | | 13,562,223 | | 4,697,400 | | (72,900 | ) | | 18,186,723 | | | 19,561,783 | | | 772,753,859 |

Amerada Hess Corp. | | 5,639,100 | | 5,000 | | (1,297,400 | ) | | 4,346,700 | | | 6,005,130 | | | —1 |

BMC Software, Inc. | | 2,518,500 | | 9,316,400 | | (47,300 | ) | | 11,787,600 | | | —4 | | | 219,249,360 |

CIT Group, Inc. | | 11,320,000 | | 16,000 | | (1,765,900 | ) | | 9,570,100 | | | 5,823,675 | | | —1 |

Computer Sciences Corp. | | 7,718,300 | | 5,227,000 | | (51,700 | ) | | 12,893,600 | | | —4 | | | 726,812,232 |

Compuware Corp. | | 19,401,100 | | 33,600 | | (77,600 | ) | | 19,357,100 | | | —4 | | | 125,240,437 |

Delphi Corp. | | 30,557,032 | | 5,639,200 | | (144,600 | ) | | 36,051,632 | | | 9,891,534 | | | 325,185,721 |

Dillard's Inc. Class A | | 5,190,700 | | 7,600 | | (20,800 | ) | | 5,177,500 | | | 831,112 | | | 139,119,425 |

Electronic Data Systems Corp. | | 24,105,200 | | 9,232,400 | | (133,200 | ) | | 33,204,400 | | | 12,631,350 | | | 767,021,640 |

Engelhard Corp. | | 5,682,700 | | 608,400 | | (25,000 | ) | | 6,266,100 | | | 2,590,291 | | | 192,181,287 |

Equity Office Properties Trust | | 18,569,200 | | 3,780,000 | | (88,900 | ) | | 22,260,300 | | | 31,292,2483 | | | 648,219,936 |

Fluor Corp. | | 4,386,550 | | 6,500 | | (17,500 | ) | | 4,375,550 | | | 2,808,912 | | | 238,511,231 |

Genuine Parts Co. | | 8,976,800 | | 12,900 | | (35,900 | ) | | 8,953,800 | | | 10,777,770 | | | 394,504,428 |

HCA, Inc. | | 15,210,800 | | 11,313,600 | | (106,000 | ) | | 26,418,400 | | | 9,306,895 | | | 1,055,679,264 |

May Department Stores Co. | | 16,320,900 | | 1,645,300 | | (71,800 | ) | | 17,894,400 | | | 17,023,864 | | | 526,095,360 |

NCR Corp. | | 5,819,800 | | 5,200 | | (2,113,100 | ) | | 3,711,900 | | | —4 | | | —1 |

Nova Chemicals Corp. (Canada) | | 5,756,770 | | 7,600 | | (1,011,800 | ) | | 4,752,570 | | | 1,474,691 | | | 224,796,561 |

Storage Technology Corp. | | 6,000,100 | | 2,406,200 | | (895,100 | ) | | 7,511,200 | | | —4 | | | 237,429,032 |

Union Pacific Corp. | | 5,744,050 | | 8,172,500 | | (55,600 | ) | | 13,860,950 | | | 14,127,540 | | | 932,148,887 |

Unocal Corp. | | 13,155,700 | | 880,600 | | (2,579,900 | ) | | 11,456,400 | | | 10,866,780 | | | —1 |

Whirlpool Corp. | | 3,291,350 | | 1,114,300 | | (17,600 | ) | | 4,388,050 | | | 6,652,745 | | | 303,696,941 |

Xerox Corp. | | 41,985,600 | | 3,962,500 | | (183,600 | ) | | 45,764,500 | | | —4 | | | —1 |

| | | | | | | | | | | |

|

| |

|

|

| | | | | | | | | | | | $ | 210,795,271 | | $ | 8,819,921,893 |

| | | | | | | | | | | |

|

| |

|

|

| 1 | | Company was not an affiliate at the end of the period |

| 2 | | Net of foreign taxes, if any |

| 3 | | In addition to dividend income, also paid capital gain distributions of $5,754,837 |

| | |

| | | Dodge & Cox Stock Fund / 10 |

Financial Highlights

| | | | | | | | | | | | | | | |

| SELECTED DATA AND RATIOS (for a share outstanding throughout each year) | | | Year Ended December 31, | |

| | | 2004 | | | 2003 | | | 2002 | | | 2001 | | | 2000 | |

Net asset value, beginning of year | | $113.78 | | | $ 88.05 | | | $100.51 | | | $ 96.67 | | | $100.52 | |

| | | | | |

Income from investment operations: | | | | | | | | | | | | | | | |

Net investment income | | 1.54 | | | 1.60 | | | 1.53 | | | 1.72 | | | 2.06 | |

Net realized and unrealized gain (loss) | | 20.08 | | | 26.59 | | | (12.06 | ) | | 7.05 | | | 13.28 | |

| | |

|

| |

|

| |

|

| |

|

| |

|

|

Total from investment operations | | 21.62 | | | 28.19 | | | (10.53 | ) | | 8.77 | | | 15.34 | |

| | |

|

| |

|

| |

|

| |

|

| |

|

|

Distributions to shareholders from: | | | | | | | | | | | | | | | |

Net investment income | | (1.53 | ) | | (1.62 | ) | | (1.51 | ) | | (1.73 | ) | | (2.09 | ) |

Net realized gain | | (3.65 | ) | | (0.84 | ) | | (0.42 | ) | | (3.20 | ) | | (17.10 | ) |

| | |

|

| |

|

| |

|

| |

|

| |

|

|

Total distributions | | (5.18 | ) | | (2.46 | ) | | (1.93 | ) | | (4.93 | ) | | (19.19 | ) |

| | |

|

| |

|

| |

|

| |

|

| |

|

|

Net asset value, end of year | | $130.22 | | | $113.78 | | | $ 88.05 | | | $100.51 | | | $ 96.67 | |

| | |

|

| |

|

| |

|

| |

|

| |

|

|

Total return | | 19.16 | % | | 32.35 | % | | (10.52 | )% | | 9.33 | % | | 16.30 | % |

Ratios/supplemental data: | | | | | | | | | | | | | | | |

Net assets, end of year (millions) | | $43,266 | | | $29,437 | | | $14,036 | | | $9,396 | | | $5,728 | |

Ratio of expenses to average net assets | | 0.53 | % | | 0.54 | % | | 0.54 | % | | 0.54 | % | | 0.54 | % |

Ratio of net investment income to average net assets | | 1.32 | % | | 1.72 | % | | 1.74 | % | | 1.80 | % | | 2.13 | % |

Portfolio turnover rate | | 11 | % | | 8 | % | | 13 | % | | 10 | % | | 32 | % |

| | |

| 11 / Dodge & Cox Stock Fund | | |

Report of Independent Registered Public Accounting Firm

To the Trustees of Dodge & Cox Funds and Shareholders of Dodge & Cox Stock Fund

In our opinion, the accompanying statement of assets and liabilities, including the portfolio of investments, and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of the Dodge & Cox Stock Fund (the “Fund”, one of the series constituting Dodge & Cox Funds) at December 31, 2004, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management; our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities at December 31, 2004 by correspondence with the custodian and brokers, provide a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

San Francisco, California

February 18, 2005

| | |

| | | Dodge & Cox Stock Fund / 12 |

Special 2004 Tax Information (unaudited)

The following information is provided pursuant to provisions of the Internal Revenue Code:

The Fund designates $600,784,411 of its distributions paid to shareholders in 2004 as qualified dividends (treated for federal income tax purposes in the hands of shareholders as taxable at a maximum rate of 15%).

For shareholders that are corporations, the Fund designates 52% of its ordinary dividends (including short-term gains) paid to shareholders in 2004 as dividends from domestic corporations eligible for the corporate dividends received deduction, provided that the shareholder otherwise satisfies applicable requirements to claim that deduction.

Fund’s Holdings

The Funds provide a complete list of their holdings four times in each fiscal year, at the quarter-ends. The lists appear in the Funds’ First Quarter, Semi-Annual, Third Quarter and Annual Reports to shareholders. The Funds file the lists with the Securities and Exchange Commission (SEC) on Form N-CSR (second and fourth quarters) and Form N-Q (first and third quarters). Shareholders may view the Funds’ Forms N-CSR and N-Q on the SEC’s website at www.sec.gov. Forms N-CSR and N-Q may also be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information regarding the operations of the Public Reference Room may be obtained by 1-202-942-8090 (direct) or 1-800/SEC-0330 (general SEC number). A complete list of the Funds’ quarter-end holdings are also available at www.dodgeandcox.com on or about 15 days following each quarter end.

Proxy Voting

For a free copy of the Fund’s proxy voting policies and procedures, please call (800) 621-3979, visit www.dodgeandcox.com or the Securities and Exchange Commission’s web site at www.sec.gov. Information regarding how Dodge & Cox, on behalf of the Fund, voted proxies relating to the Fund’s portfolio securities for the most recent twelve-month period ending June 30 is available at www.dodgeandcox.com or the SEC’s web site at www.sec.gov.

| | |

| 13 / Dodge & Cox Stock Fund | | |

THIS PAGE INTENTIONALLY LEFT BLANK

| | |

| | | Dodge & Cox Stock Fund / 14 |

Dodge & Cox Funds—Executive Officer & Trustee Information (unaudited)

| | | | | | |

Name (Age) and

Address* | | Position with Trust

(Year of Election

or Appointment) | | Principal Occupation During Past 5 Years | | Other Directorships Held by Trustees |

| Interested Trustees & Officers |

Harry R. Hagey (63) | | Chairman and Trustee (Trustee since 1975) | | Chairman, Chief Executive Officer and Director of Dodge & Cox, Portfolio Manager and member of Investment Policy Committee (IPC) | | — |

John A. Gunn (61) | | President and Trustee

(Trustee since 1985) | | President, Chief Investment Officer and Director of Dodge & Cox, Portfolio Manager, and member of IPC, Fixed Income Strategy Committee (FISC) and International Investment Policy Committee (IIPC) | | — |

Dana M. Emery (43) | | Vice President and Trustee (Trustee since 1993) | | Senior Vice President and Director of Dodge & Cox, Manager of the Fixed Income Department, Portfolio Manager, and member of IPC and FISC | | — |

A. Horton Shapiro (65) | | Executive Vice President (Officer since 1985) | | Senior Vice President and Director of Dodge & Cox and Portfolio Manager | | — |

| Katherine Herrick Drake (50) | | Vice President (Officer since 1993) | | Vice President of Dodge & Cox and Portfolio Manager | | — |

Kenneth E. Olivier (52) | | Vice President

(Officer since 1992) | | Executive Vice President (since 2002) and Director of Dodge & Cox, Portfolio Manager and member of IPC | | — |

| Diana S. Strandberg (45) | | Vice President

(Officer since 2001) | | Vice President of Dodge & Cox, Portfolio Manager and member of the IIPC | | |

John M. Loll (38) | | Treasurer and Assistant Secretary (Officer since 2000) | | Vice President and Treasurer of Dodge & Cox | | — |

| Thomas M. Mistele (51) | | Secretary and Assistant Treasurer (Officer since 2000) | | Chief Operating Officer (since 2004), Secretary and General Counsel of Dodge & Cox | | — |

| Marcia P. Venegas (36) | | Chief Compliance Officer

(Officer since 2004) | | Chief Compliance Officer of the Trust (since 2004), Compliance Officer of Dodge & Cox (2003-2004); Compliance and Business Risk Manager of Deutsche Asset Management, Australia Limited (1999-2001) | | — |

| Independent Trustees |

William F. Ausfahl (64) | | Trustee (Since 2002) | | CFO, The Clorox Co. (1982-1997); Director, The Clorox Co. (1984-1997) | | — |

L. Dale Crandall (63) | | Trustee (Since 1999) | | President, Kaiser Foundation Health Plan, Inc. and Kaiser Foundation Hospitals (2000-2002); Senior Vice President–Finance and Administration & CFO, Kaiser Foundation Health Plan, Inc. and Kaiser Foundation Hospitals (1998-2000) | | Director, Union BanCal Corporation (bank holding company) and Union Bank of California (commercial bank) (2001-Present); Director, Covad Communications Group (broadband communications services) (2002-Present); Director, Ansell Limited (medical equipment and supplies) (2002-Present); Director, BEA Systems, Inc. (software and programming) (2003-Present); Director, Coventry Health Care, Inc. (managed healthcare) (2004-Present) |

Thomas A. Larsen (55) | | Trustee (Since 2002) | | Director in Howard, Rice, Nemerovski, Canady, Falk & Rabkin (law firm) | | — |

Will C. Wood (65) | | Trustee (Since 1992) | | Principal, Kentwood Associates, Financial Advisers | | Director, Banco Latinoamericano de Exportaciones S.A. (Latin American Foreign Trade Bank) (1999-Present); Director, Dover Investment Corp. (real estate development) (1992-Present) |

| * | | The address for each Officer and Trustee is 555 California Street, 40th Floor, San Francisco, California 94104. Each Officer and Trustee oversees all four series in the Dodge & Cox Funds complex and serves for an indefinite term. |

Additional information about the Trust’s Trustees is available in the Trust’s Statement of Additional Information (SAI). You can get a free copy of the SAI by contacting Dodge & Cox Funds at (800) 621-3979.

International

Stock Fund

Established 2001

4th Annual Report

December 31, 2004

2004

International Stock Fund

www.dodgeandcox.com

For Fund literature, transactions and account

information, please visit the Funds’ web site.

or write or call:

Dodge & Cox Funds

c/o Boston Financial Data Services

P.O. Box 8422

Boston, Massachusetts 02266-8422

(800) 621-3979

Investment Manager

Dodge & Cox

555 California Street, 40th Floor

San Francisco, California 94104

(415) 981-1710

This report is submitted for the general information of the shareholders of the Fund. The report is not authorized for distribution to prospective investors in the Fund unless it is accompanied by a current prospectus.

This report reflects our views, opinions and portfolio holdings as of December 31, 2004, the end of the reporting period. Any such views are subject to change at any time based upon market or other conditions and Dodge & Cox disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Dodge & Cox Fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Dodge & Cox Fund.

12/04 ISF AR  Printed on recycled paper

Printed on recycled paper

To Our Shareholders

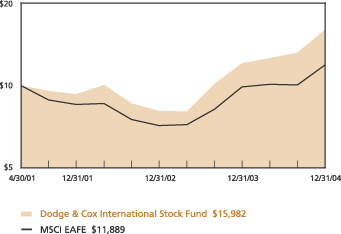

The Dodge & Cox International Stock Fund had a total return of 32.5% for the year ended 2004, compared to a total return of 20.2% for the Morgan Stanley Capital International Europe, Australasia, Far East Index (MSCI EAFE) benchmark. Since inception on May 1, 2001, the Fund had an annualized total return of 13.6% compared to 4.9% for the MSCI EAFE.

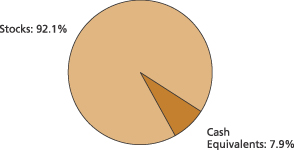

At year-end, the Fund had net assets of $4.2 billion and a cash position of 7.9%. The share price of the Fund rose from $23.48 at the end of 2003 to $30.64 on December 31, 2004. In addition, during the year, the Fund distributed income per share of $0.24 per share, short-term capital gain of $0.12 per share and long-term capital gain of $0.10 per share.

Performance Review

The International Stock Fund performed well on an absolute basis and relative to the MSCI EAFE. The following are performance perspectives:

| • | | Investments in the United Kingdom, Europe, and Japan each contributed over 3% of outperformance relative to the MSCI EAFE. |

| • | | Investments in the Materials, Energy, and Consumer Discretionary sectors each contributed over 2% of outperformance relative to the MSCI EAFE benchmark. |

| • | | Investments in a number of strong performers including Stolt Offshore (up 164%), Standard Bank (up 106%), Yara (up 79%), Nova (up 76%), Makita (up 78%) and Kidde (up 72%). |

Although no one sector of the Fund negatively impacted performance, two individual holdings were particularly weak. Converium Holdings, a Swiss re-insurance company, lost 19% of its value since the Fund’s initial purchase. Seiko Epson, a Japanese manufacturer of color inkjet printers, lost 4% of its value in 2004.

While we are pleased with the performance over the past few years, extrapolating future returns from the recent past is neither prudent nor realistic. When the Fund began on May 1, 2001, the initial net asset value (NAV) was $20.00. On March 12, 2003, after a severe market downturn, the NAV reached a low of $13.34. While we do not expect such severe price movements in the future, they cannot be ruled out. We urge fellow shareholders to invest with an eye on the long term.

Common Threads Through All Our Funds

As the Fund has grown and the number of shareholders has increased dramatically, we would like to take this opportunity to review how Dodge & Cox’s investment philosophy is implemented in the International Stock Fund.

As is the case with all of the Dodge & Cox Funds, we analyze the International Stock Fund’s investments using a three-to-five year investment horizon and adhere to a strict price discipline. Through a research-intensive process, we search for companies whose current stock valuations do not reflect our outlook for their long-term earnings and cash flow prospects. With this bottom-up approach, we construct an economically and geographically diversified portfolio of international stocks.

The Emerging Consumer

The developing world is playing a larger role both as an engine of global growth and as a catalyst for change at many companies. The developing world now represents approximately 85% of the world’s population, yet only 20% of its gross production.

We believe this disparity between population and production could be reduced over time as many companies are now increasing their productive capacity in the developing world (e.g., Honda’s motorcycle plants in India and Nestle’s expansion of operations in China). This growth in capacity should lead to more and higher wage earners, and consequently, more consumption. The expanding class of consumers should, in turn, necessitate additional investments in capacity—a beneficial cycle of economic growth.

We expect few companies—regardless of whether they are based inside or outside of the developing world—to be immune from at least one of the following collateral effects of global development:

| • | | New market demand: Energy and materials companies, like Royal Dutch Shell, BHP Billiton and Rio Tinto, have benefited greatly as growth in the developing world has boosted demand and pricing for their commodities. |

| • | | New investment opportunities: Companies such as Unilever, Nestle, Standard Chartered, Honda and Suzuki are focused on strengthening their footholds in these growing markets. |

| • | | New competition forces change: The threat of competition from companies in these new economies has forced companies based in the developed world, such as Bayer, Matsushita and Sony, to restructure their operations and move more aggressively than before. Companies are also being forced to place a greater emphasis on financial transparency and shareholder returns in order to attract capital from the global investor. |

Foreign Currency and Stock Selection

There are numerous experts predicting a continued decline in the U.S. dollar given our nation’s large trade and fiscal deficits. All else being equal, when the dollar declines, foreign securities increase in value in dollar terms. While it may be the case that the dollar continues to decline, currency movements can be highly volatile and unpredictable in the short-term, as evidenced in 2004.

| | |

| 1 / Dodge & Cox International Stock Fund | | |

In the fourth quarter last year, a declining U.S. dollar contributed meaningfully to the total return of the Fund and the market as measured by the MSCI EAFE. Currency impacts (defined as the differential between local currency returns and U.S. dollar returns) were over half of the market’s 15.3% return. However, currency impacts actually hurt returns for the nine months ended September 30, with the MSCI EAFE up 5.5% in local currency, but only 4.3% in U.S. dollar terms.

Since 1970, when the MSCI EAFE was created, through the end of 2004, earnings growth and dividend yield has provided most of the market’s total return. Accordingly, we evaluate currency movements in the context of how they might impact an individual company’s long-term earnings and cash flow prospects.

Currency movements can have a different effect on a company, depending on its geographical mix of revenues and costs. For example, Honda, the Japanese automaker, has a large revenue base in the U.S., but a significant cost base in Japan. Consequently, a declining dollar hurts Honda’s margins, as U.S. dollar revenues are translated into fewer Yen, while Yen-based costs remain unchanged. Honda is responding to this challenge by increasing its overseas production capabilities to better match its revenues with its costs. Honda also hedges its currency exposure on an opportunistic basis. In contrast, a company such as Aderans, a Japanese wig-maker, has most of its revenues and costs in Japan; thus, a weak dollar has little impact on its profitability.

In Closing

Looking forward, we do not expect the high returns of the past two years for the Fund and the MSCI EAFE to be repeated. That said, the world’s equity markets do not always move in sync and over half of the world’s leading companies are domiciled outside of the U.S., so investing internationally adds diversification to one’s portfolio. We encourage our shareholders to look beyond short-term price swings, and take a long-term view toward international investing.

Thank you for the continued confidence you have placed in our firm as a shareholder of the International Stock Fund. As always, we welcome your comments and questions.

Sincerely,

| | |

| |  |

Harry R. Hagey

Chairman February 18, 2005 | | Diana S. Strandberg Vice President |

Investment Performance

Total return for periods ended December 31, 2004

Average Annual Total return for periods ending December 31, 2004

| | | | | | | | | |

| | | 1 Year | | | 3 Years | | | Since

Inception

(5/1/01) | |

| Dodge & Cox International Stock Fund* | | 32.46 | % | | 19.81 | % | | 13.63 | % |

| MSCI EAFE | | 20.24 | | | 11.89 | | | 4.91 | |

Past performance does not guarantee future results. Investment return and share price will fluctuate with market conditions, and investors may have a gain or loss when shares are sold. Mutual fund performance changes over time and currently may be significantly lower than stated above. Performance is updated and published monthly. Visit the Fund’s web site at www.dodgeandcox.com or call 800-621-3979 for current performance figures.

* | | Through April 30, 2005, Dodge & Cox has contractually agreed to reimburse the Fund for all ordinary expenses to the extent necessary to maintain total Fund operating expenses at 0.90%. Expense reimbursements were paid since the Fund’s inception through June 30, 2003, but have not been required after this point as assets in the Fund increased and the Fund’s ratio of expenses to average net assets fell below 0.90%. Without reimbursement, returns for the Fund for periods beginning before June 30, 2003 would have been lower. |

The Morgan Stanley Capital International Europe, Australasia, Far East Index (MSCI EAFE) is a widely recognized benchmark of the world’s stock markets, excluding the United States. The Fund’s total returns include the reinvestment of dividend and capital gain distributions, but have not been adjusted for any income taxes payable on these distributions. Index returns include dividends and, unlike Fund returns, do not reflect fees or expenses.

Morgan Stanley®, Morgan Stanley Capital International, and EAFE® are trademarks of Morgan Stanley.

Risks of International Investing: Foreign investing, especially in developing countries,

has special risks such as currency and market volatility and political and social instability.

These and other risk considerations are

discussed in the Fund’s prospectus.

| | |

| | | Dodge & Cox International Stock Fund / 2 |

Fund Expenses

As a shareholder of the Fund, you incur ongoing costs, which include costs for portfolio management, administrative services, and shareholder reports (like this one), among others. Operating expenses, which are deducted from a Fund’s gross income, directly reduce the investment return of the Fund. The following examples are intended to help you understand the ongoing costs (in dollars) of investing in the Fund and to compare these costs with those of other mutual funds. The examples are based on an investment of $1,000 made at the beginning of the period shown and held for the entire period.

The table below illustrates the Fund’s costs in two ways:

Actual Fund Expenses

This section helps you to estimate the actual expenses that you paid over the period. The “Ending Account Value” shown is derived from the Fund’s actual return, and the third column shows the dollar amount that would have been paid by an investor who started with $1,000 in the Fund. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period. To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for the Fund under the heading “Expenses Paid During Period.”

Hypothetical Example for Comparison

This section is intended to help you compare the Fund’s costs with those of other mutual Funds. It assumes that the Fund had a yearly return of 5% before expenses, but that the expense ratio is unchanged. In this case—because the return used is not the Fund’s actual return—the results do not apply to your investment. The example is useful in making comparisons because the Securities and Exchange Commission requires all mutual funds to calculate expenses based on a 5% return. You can assess the Fund’s costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

| | | | | | | | | |

Six Months Ended

December 31, 2004 | | Beginning

Account Value 7/1/2004 | | Ending

Account Value 12/31/2004 | | Expenses Paid

During Period* |

| Based on Actual Fund Return | | $1,000.00 | | $1,203.70 | | $4.19 |

| Based on Hypothetical 5% Yearly Return | | 1,000.00 | | 1,021.20 | | 3.84 |

| * | | These calculations are based on expenses incurred in the most recent fiscal half-year. The Fund’s annualized six-month expense ratio for that period is 0.76%. The dollar amounts shown as “Expenses Paid” are equal to the annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year, then divided by 366. |

The expenses shown in the table are meant to highlight and help you compare ongoing costs only and do not reflect any transactional costs, account maintenance fees or charges by processing organizations. While other mutual funds may charge such fees, please note that the Fund does not charge any transaction fee (e.g., redemption fee), account maintenance fee (e.g., small account fee), nor does it charge a “sales load.”

| | |

| 3 / Dodge & Cox International Stock Fund | | |

Fund Information | December 31, 2004 |

General Information

| | |

Net Asset Value Per Share | | $30.64 |

Total Net Assets (millions) | | $4,203 |

2004 Expense Ratio | | 0.77% |

2004 Turnover Ratio | | 6% |

30-Day SEC Yield1 | | 1.43% |

Fund Inception Date | | May 1, 2001 |

Investment Manager: Dodge & Cox, San Francisco. Managed by the International Investment Policy Committee, whose seven members’ average tenure at Dodge & Cox is 16 years.

Asset Allocation

| | | | |

| Portfolio Characteristics | | Fund | | MSCI

EAFE |

Number of Stocks | | 67 | | 1,070 |

Median Market Capitalization (billions) | | $11 | | $3 |

Weighted-Average Market Capitalization (billions) | | $40 | | $45 |

Price-to-Earnings Ratio2 | | 14x | | 16x |

Price-to-Book Value Ratio | | 1.8x | | 2.1x |

| | | | | |

| | |

Ten Largest Holdings | | % of Fund |

GlaxoSmithKline PLC ADR (United Kingdom) | | 3.0 |

Sony ADR (Japan) | | 2.9 |

Electrolux A.B. (Sweden) | | 2.8 |

Royal Dutch Petroleum (Netherlands) | | 2.7 |

KT Corp. ADR (South Korea) | | 2.4 |

Lafarge S.A. (France) | | 2.2 |

Banco Santander Central Hispano (Spain) | | 2.2 |

Uniao de Bancos Brasileiros GDR (Brazil) | | 2.2 |

Petroleo Brasileiro S.A. ADR (Brazil) | | 2.2 |

Royal Bank of Scotland Group PLC (United Kingdom) | | 2.1 |

| | | | | | |

| Region Diversification | | Fund | | | MSCI

EAFE | |

Europe (excluding United Kingdom) | | 39.4 | % | | 45.3 | % |

Japan | | 16.2 | | | 21.9 | |

United Kingdom | | 13.1 | | | 25.0 | |

Pacific (excluding Japan) | | 8.8 | | | 7.8 | |

Latin America | | 8.7 | | | 0.0 | |

United States3 | | 2.1 | | | 0.0 | |

Africa | | 1.9 | | | 0.0 | |

Middle East | | 1.1 | | | 0.0 | |

Canada | | 0.8 | | | 0.0 | |

| | | | | | |

| Sector Diversification | | Fund | | | MSCI

EAFE | |

Financials | | 18.1 | % | | 27.6 | % |

Materials | | 17.2 | | | 7.3 | |

Consumer Discretionary | | 14.6 | | | 12.3 | |

Energy | | 10.4 | | | 8.1 | |

Consumer Staples | | 7.4 | | | 8.1 | |

Health Care | | 6.5 | | | 8.0 | |

Information Technology | | 6.0 | | | 6.3 | |

Telecommunication Services | | 4.5 | | | 7.6 | |

Industrials | | 4.4 | | | 9.5 | |

Utilities | | 3.0 | | | 5.2 | |

| 1 | | SEC Yield is an annualization of the Fund’s total net investment income per share for the 30-day period ended on the last day of the month. |

| 2 | | The Fund’s price-to-earnings (P/E) ratio is calculated using fiscal year-end earnings and excludes extraordinary items. |

| 3 | | In the fourth quarter of 2004 News Corp. reincorporated as a Delaware corporation (formerly New South Wales, Australia) headquartered in New York, NY (formerly Sydney, Australia). |

Dodge & Cox International Stock Fund / 4

Portfolio of Investments | December 31, 2004 |

COMMON STOCKS: 85.2%

| | | | | |

| | | SHARES | | MARKET VALUE |

| MATERIALS: 17.2% | | | | | |

| CHEMICALS: 11.5% | | | |

BASF A.G. (Germany) | | 1,043,400 | | $ | 75,105,936 |

Akzo Nobel N.V. (Netherlands) | | 1,591,100 | | | 67,810,660 |

Bayer A.G. (Germany) | | 1,917,000 | | | 64,933,098 |

Kemira Oyj (Finland) | | 4,434,800 | | | 61,194,911 |

Yara International A.S.A.(a) (Norway) | | 3,991,310 | | | 52,463,138 |

Makhteshim-Agan Industries, Ltd. (Israel) | | 8,244,284 | | | 44,313,026 |

NOVA Chemicals Corp. (Canada) | | 751,200 | | | 35,519,360 |

Givaudan (Switzerland) | | 43,100 | | | 28,347,295 |

Imperial Chemical Industries PLC (United Kingdom) | | 4,778,000 | | | 22,092,657 |

Syngenta A.G. ADR(b) (Switzerland) | | 1,005,500 | | | 21,467,425 |

Kemira GrowHow Oyj (Finland) | | 1,511,393 | | | 11,556,687 |

| | | | |

|

|

| | | | | | 484,804,193 |

| CONSTRUCTION MATERIALS: 3.0% | | | |

Lafarge S.A. (France) | | 973,422 | | | 93,865,731 |

Rinker Group Ltd. (Australia) | | 3,850,000 | | | 32,084,463 |

| | | | |

|

|

| | | | | | 125,950,194 |

| METALS AND MINING: 2.7% | | | |

BHP Billiton Ltd. (Australia) | | 5,260,078 | | | 63,139,622 |

Rio Tinto PLC (United Kingdom) | | 1,684,400 | | | 49,541,842 |

| | | | |

|

|

| | | | | | 112,681,464 |

| | | | |

|

|

| | | | | | 723,435,851 |

| FINANCIALS: 15.9% | | | |

| BANKS: 13.1% | | | |

Banco Santander Central Hispano (Spain) | | 7,620,000 | | | 94,487,271 |

Royal Bank of Scotland Group PLC (United Kingdom) | | 2,640,972 | | | 88,773,360 |

Standard Bank Group Limited (South Africa) | | 6,746,234 | | | 78,597,365 |

Kookmin Bank ADR(a),(b) (South Korea) | | 1,906,000 | | | 74,486,480 |

Shinsei Bank, Ltd. (Japan) | | 7,865,000 | | | 53,629,366 |

Mitsubishi Tokyo Financial Group, Inc. ADR(b) (Japan) | | 4,956,800 | | | 50,658,496 |

Danske Bank (Denmark) | | 1,445,300 | | | 44,253,838 |

DBS Group Holdings Ltd. (Singapore) | | 4,142,000 | | | 40,854,132 |

Standard Chartered PLC (United Kingdom) | | 1,405,000 | | | 26,107,225 |

| | | | |

|

|

| | | | | | 551,847,533 |

| DIVERSIFIED FINANCIALS: 1.9% | | | |

Credit Suisse Group (Switzerland) | | 1,570,000 | | | 65,899,192 |

Euler & Hermes (France) | | 210,100 | | | 14,467,103 |

| | | | |

|

|

| | | | | | 80,366,295 |

| INSURANCE: 0.9% | | | |

Converium Holdings AG (Switzerland) | | 4,233,328 | | | 37,731,190 |

| | | | |

|

|

| | | | | | 669,945,018 |

| | | | | |

| | | SHARES | | MARKET VALUE |

| CONSUMER DISCRETIONARY: 14.6% | | | |

| CONSUMER DURABLES & APPAREL: 9.0% | | | |

Sony Corp. ADR(b) (Japan) | | 3,146,500 | | $ | 122,587,640 |

Electrolux A.B. (Sweden) | | 5,067,700 | | | 116,011,085 |

Matsushita Electric Industrial Co., Ltd. ADR(b) (Japan) | | 3,431,700 | | | 55,078,785 |

Consorcio Ara S.A.(a,d) (Mexico) | | 18,217,700 | | | 54,769,178 |

Makita Corp. (Japan) | | 883,000 | | | 15,457,783 |