UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-173

DODGE & COX FUNDS

(Exact name of registrant as specified in charter)

555 California Street, 40th Floor

San Francisco, CA 94104

(Address of principal executive offices) (Zip code)

Thomas M. Mistele, Esq.

555 California Street, 40th Floor

San Francisco, CA 94104

(Name and address of agent for service)

Registrant’s telephone number, including area code: 415-981-1710

Date of fiscal year end: DECEMBER 31, 2010

Date of reporting period: JUNE 30, 2010

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss. 3507.

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

The following are the June 30, 2010 semi-annual reports for the Dodge & Cox Funds, a Delaware statutory trust, consisting of five series: Dodge & Cox Stock Fund, Dodge & Cox Global Stock Fund, Dodge & Cox International Stock Fund, Dodge & Cox Balanced Fund and Dodge & Cox Income Fund. The reports of each series were transmitted to their respective shareholders on August 3, 2010.

| | | | |

| | | |  |

www.dodgeandcox.com

For Fund literature, transactions, and account

information, please visit the Funds’ web site.

or write or call:

DODGE & COX FUNDS

c/o Boston Financial Data Services

P.O. Box 8422

Boston, Massachusetts 02266-8422

(800) 621-3979

INVESTMENT MANAGER

Dodge & Cox

555 California Street, 40th Floor

San Francisco, California 94104

(415) 981-1710

This report is submitted for the general information of the shareholders of the Fund. The report is not authorized for distribution to prospective investors in the Fund unless it is accompanied by a current prospectus.

This report reflects our views, opinions, and portfolio holdings as of June 30, 2010, the end of the reporting period. Any such views are subject to change at any time based upon market or other conditions and Dodge & Cox disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Dodge & Cox Fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Dodge & Cox Fund.

06/10 SF SAR  Printed on recycled paper

Printed on recycled paper

Semi-Annual Report

June 30, 2010

Stock Fund

ESTABLISHED 1965

TICKER: DODGX

TO OUR SHAREHOLDERS

The Dodge & Cox Stock Fund had a total return of –13.7% for the second quarter of 2010, compared to –11.4% for the Standard & Poor’s 500 Index (S&P 500). For the six months ended June 30, 2010, the Fund had a total return of –7.9%, compared to –6.7% for the S&P 500. Please see the Fund’s longer-term performance results on page three. At quarter end, the Fund had net assets of $37.0 billion with a cash position of 1.5%. While the Fund and the S&P 500 are down over the past six months, they have increased 15.3% and 14.4%, respectively, over the past twelve months.

MARKET COMMENTARY

While the U.S. and global economies showed signs of continued improvement in the first half of 2010, the performance of the major financial markets reflected a lack of consensus regarding the prospects for economic growth. Gains in the broader indices during the first four months of 2010 were erased in May and June as optimism for a global economic recovery was replaced by pessimism over the health of several European economies and the damage created by the oil spill in the Gulf of Mexico, among other factors. The declining market during the second quarter also reflected concerns of a potential “double-dip” in the U.S. economy, as growth in consumer spending slowed and unemployment remained high at 9.5%. The Fund’s results followed a similar pattern, as its short-term performance is influenced by the movements of the broader market.

We believe a long-term perspective on investing is especially important during periods like the first half of 2010. Short-term concerns can often deflect attention from longer-term positive developments. After the events of 2008, it is not surprising that many are searching to identify the next “crisis.” In the United States, for example, high unemployment, rising health care costs, and weakness in real estate are real concerns. Past economic recoveries have struggled with similar issues, yet the economic rebound was sustained (the post-1982 and post-1991 recoveries are two examples). The current environment has significant positives: interest rates are at record lows, inflation remains subdued, home prices are stabilizing, and household net worth is rising. While some

economic indicators may lag, the economic recovery can continue.

Despite what we believe is a very promising outlook for equities, the aforementioned challenges faced by certain members of the European Monetary Union and the ecological and economic damage from the Gulf oil spill are getting much attention and are contributing to unduly pessimistic expectations for investors. While these issues are significant, they do not dampen our enthusiasm for the prospects of the global economy. Although these issues have had an impact on the companies we invest in on your behalf in the Fund, they have not changed our belief that the future could be rewarding for patient long-term investors.

INVESTMENT STRATEGY

European Challenges and the Global Economy

The difficulties faced by Greece, Italy, Spain, Portugal, and Ireland have led to concerns about all of Europe, and the sustainability of economic recovery around the world. The Fund has investments in a number of large European-based multinational companies whose shares have declined more in U.S. dollar terms than in their local currencies. This factor accounted for more than one percentage point of the Fund’s total decline for this six-month period. Although most of these holdings have meaningful operations in Europe, none of them has large exposure to the countries facing the most difficulties, and all derive a substantial portion of their revenues from other regions of the world. We are cognizant of the impact that persistent weakness in Europe could have on the operations of these companies; however, we believe valuations for the Fund’s holdings generally incorporate other investors’ low expectations for future earnings, and do not reflect the companies’ attractive long-term fundamentals.

A good example is Vodafone, the United Kingdom–based global communications company with operations in more than 30 countries.1 While Vodafone has significant exposure to Europe, it also has valuable assets in other regions, including the United States and emerging markets. Vodafone is currently selling at less than nine times estimated 2010 earnings and has a 6% dividend

PAGE 1 § DODGE & COX STOCK FUND

yield, compared to 14 times estimated earnings and a 2% dividend yield for the S&P 500. We believe that Vodafone’s valuation discounts the current concerns about Europe, and does not reflect its strong and growing presence in other regions.

The Outlook for Energy

We believe that demand for oil and gas (the primary sources of energy, along with coal) will continue to rise due to growth in the developing world. The Fund’s largest exposure within the Energy sector is in the oil services industry. Our expectation is that demand for oil services will increase as exploration and production continue to move into more complex, technically challenging areas, such as deepwater and shale resource development. In particular, we believe that Schlumberger, the Fund’s largest Energy holding and the world’s leading oil services company, is uniquely positioned to benefit from these trends. The company’s management is focused on enhancing its already strong position in many segments of oil services. While the share price has increased from its low in early 2009 (along with the overall market), the valuation is well below its long-term average.

In spite of the environmental disaster in the Gulf of Mexico, our long-term outlook for the Energy sector is positive. The Deepwater Horizon oil spill has leaked large amounts of crude oil, despite the large-scale efforts of BP and others to contain the damage. BP, as majority owner and operator has received the most attention, and has accepted responsibility for the clean-up effort. The Fund did not own shares of BP or the other named responsible parties. Several Fund holdings (e.g., Baker Hughes and Schlumberger) have significant operations in the affected regions. As always, we are closely monitoring these holdings, but at this time do not believe the events have materially changed these companies’ long-term prospects.

INVESTMENT PHILOSOPHY

Dodge & Cox’s investment philosophy is based on evaluating the long-term opportunities and risks for each company, and comparing our outlook to that of other investors, as measured by the company’s valuation. However, our individual company analysis also takes into account the broader forces that dictate the external environment in which a company operates. Therefore, we evaluate macroeconomic and political factors as part of our assessment of the relative attractiveness of each investment. At the same time, we avoid basing our investment decisions solely on predictions regarding the short-term macroeconomic environment, such as predictions of interest rates, currency movements, and election outcomes.

IN CLOSING

Despite the many near-term uncertainties, we are optimistic that the U.S. and global economies are still in the early stages of a multi-year business recovery; in particular, growth conditions in the developing world look excellent. This optimism, combined with what we believe are attractive current valuations, leads us to the view that the long-term prospects for equity investing are favorable.

Thank you for your continued confidence in our firm. As always, we welcome your comments and questions.

For the Board of Trustees,

| | |

| |  |

John A. Gunn, Chairman | | Kenneth E. Olivier, President |

July 23, 2010

| 1 | | We use this example to illustrate our investment process, not to imply that we think it is more attractive than the Fund’s other holdings. |

| | | | | | |

| | DODGE & COX STOCK FUND § | | PAGE | | 2 |

SEMI-ANNUAL PERFORMANCE REVIEW

The Fund underperformed the S&P 500 by 1.3 percentage points for the six months ended June 30, 2010.

Key Detractors from Relative Results

| | § | | Weak returns from holdings in the Health Care sector (down 13% versus down 9% for the S&P 500 sector), combined with a higher average weighting (21% versus 12%), detracted from results. Boston Scientific (down 36%), Sanofi-Aventis (down 21%), and Pfizer (down 20%) were notably weak. | |

| | § | | Returns from holdings in the Consumer Staples sector (down 14% versus down 3% for the S&P 500 sector) hurt results. Walgreen was down 27%. | |

| | § | | Weak returns in the Industrials sector (down 6% versus down 1% for the S&P 500 sector) had a negative impact. FedEx was down 16%. | |

| | § | | Additional detractors included Hewlett-Packard (down 16%), Motorola (down 16%), Schlumberger (down 14%), and News Corp. (down 12%). | |

Key Contributors to Relative Results

| | § | | Relative returns from holdings in the Energy sector (down 8% versus down 12% for the S&P 500 sector) helped. Baker Hughes was up 3%. | |

| | § | | A much higher average weighting in the Consumer Discretionary sector (18% versus 10% for the S&P 500 sector) had a positive impact, as the area declined less than the market. Time Warner Cable (up 28%) and Comcast (up 4%) were strong performers. | |

| | § | | Returns from holdings in the Telecommunication Services sector (up 5% versus down 8% for the S&P 500 sector) contributed. Sprint Nextel was up 16%. | |

| | § | | Additional contributors included Hitachi (up 26% to date of sale), Ericsson (up 22%), SunTrust Banks (up 15%), and Capital One (up 5%). | |

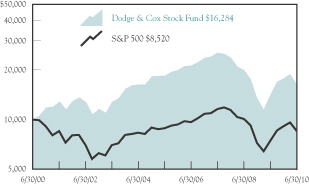

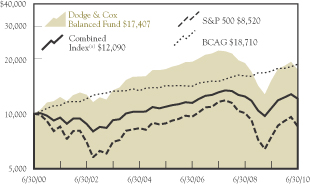

GROWTH OF $10,000 OVER 10 YEARS

FOR AN INVESTMENT MADE ON JUNE 30, 2000

AVERAGE ANNUAL TOTAL RETURN

FOR PERIODS ENDED JUNE 30, 2010

| | | | | | | | | | | | |

| | | 1 Year | | | 5 Years | | | 10 Years | | | 20 Years | |

Dodge & Cox Stock Fund | | 15.34 | % | | (2.44 | )% | | 5.00 | % | | 9.86 | % |

S&P 500 | | 14.42 | | | (0.79 | ) | | (1.59 | ) | | 7.67 | |

Returns represent past performance and do not guarantee future results. Investment return and share price will fluctuate with market conditions, and investors may have a gain or loss when shares are sold. Mutual fund performance changes over time and currently may be significantly lower than stated. Performance is updated and published monthly. Visit the Fund’s web site at www.dodgeandcox.com or call 1-800-621-3979 for current performance figures.

The Fund’s total returns include the reinvestment of dividend and capital gain distributions, but have not been adjusted for any income taxes payable by shareholders on these distributions or on Fund share redemptions. The Standard & Poor’s 500 (S&P 500) is a broad-based unmanaged measure of common stocks. Index returns include dividends and/or interest income but, unlike Fund returns, do not reflect fees or expenses.

Standard & Poor’s, Standard & Poor’s 500, and S&P 500® are trademarks of The McGraw-Hill Companies, Inc.

Risks: The Fund is subject to stock market risk, meaning stocks in the Fund may decline in value for extended periods due to the financial prospects of individual companies, or due to general market and economic conditions. Please read the prospectus for specific details regarding the Fund’s risk profile.

PAGE 3 § DODGE & COX STOCK FUND

FUND EXPENSE EXAMPLE

As a Fund shareholder, you incur ongoing Fund costs, including management fees and other Fund expenses. All mutual funds have ongoing costs, sometimes referred to as operating expenses. The following example shows ongoing costs of investing in the Fund and can help you understand these costs and compare them with those of other mutual funds. The example assumes a $1,000 investment held for the six months indicated.

ACTUAL EXPENSES

The first line of the table below provides information about actual account values and expenses based on the Fund’s actual returns. You may use the information in this line, together with your account balance, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

HYPOTHETICAL EXAMPLE FOR COMPARISON WITH OTHER MUTUAL FUNDS

Information on the second line of the table can help you compare ongoing costs of investing in the Fund with those of other mutual funds. This information may not be used to estimate the actual ending account balance or expenses you paid during the period. The hypothetical “Ending Account Value” is based on the actual expense ratio of the Fund and an assumed 5% annual rate of return before expenses (not the Fund’s actual return). The amount under the heading “Expense Paid During the Period” shows the hypothetical expenses your account would have incurred under this scenario. You can compare this figure with the 5% hypothetical examples that appear in shareholder reports of other mutual funds.

| | | | | | | | | |

Six Months Ended

June 30, 2010 | | Beginning Account Value

1/1/2010 | | Ending Account Value

6/30/2010 | | Expenses Paid

During Period* |

Based on Actual Fund Return | | $ | 1,000.00 | | $ | 920.90 | | $ | 2.51 |

Based on Hypothetical 5% Yearly Return | | | 1,000.00 | | | 1,022.18 | | | 2.64 |

| * | | Expenses are equal to the Fund’s annualized expense ratio of 0.52%, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period). |

The expenses shown in the table highlight ongoing costs only and do not reflect any transactional fees or account maintenance fees. While other mutual funds may charge such fees, please note that the Fund does not charge transaction fees (e.g., redemption fees, sales loads) or universal account maintenance fees (e.g., small account fees).

DODGE & COX STOCK FUND §PAGE 4

| | |

| FUND INFORMATION | | June 30, 2010 |

| | |

| GENERAL INFORMATION | | |

Net Asset Value Per Share | | $87.91 |

Total Net Assets (billions) | | $37.0 |

Expense Ratio | | 0.52% |

Portfolio Turnover Rate (1/1/10 to 6/30/10, unannualized) | | 7% |

30-Day SEC Yield(a) | | 1.32% |

Fund Inception | | 1965 |

No sales charges or distribution fees | | |

Investment Manager: Dodge & Cox, San Francisco. Managed by the Investment Policy Committee, whose nine members’ average tenure at Dodge & Cox is 24 years.

| | | | |

| PORTFOLIO CHARACTERISTICS | | Fund | | S&P 500 |

Number of Stocks | | 80 | | 500 |

Median Market Capitalization (billions) | | $17 | | $9 |

Weighted Average Market

Capitalization (billions) | | $55 | | $75 |

Price-to-Earnings Ratio(b) | | 10.8x | | 13.9x |

Foreign Stocks(c) | | 19.6% | | 0.0% |

| | | |

| TEN LARGEST HOLDINGS(d) | | Fund | |

Hewlett-Packard Co. | | 4.6 | % |

Comcast Corp. | | 3.6 | |

Capital One Financial Corp. | | 3.5 | |

Merck & Co., Inc. | | 3.4 | |

Schlumberger, Ltd. | | 3.4 | |

Novartis AG (Switzerland) | | 3.3 | |

Wells Fargo & Co. | | 3.3 | |

General Electric Co. | | 3.0 | |

Time Warner, Inc. | | 2.7 | |

GlaxoSmithKline PLC (United Kingdom) | | 2.6 | |

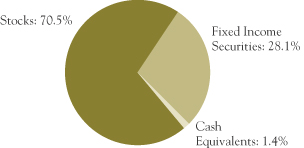

ASSET ALLOCATION

| | | | | | |

| SECTOR DIVERSIFICATION | | Fund | | | S&P 500 | |

Health Care | | 20.4 | % | | 12.1 | % |

Information Technology | | 20.2 | | | 18.7 | |

Consumer Discretionary | | 17.6 | | | 10.1 | |

Financials | | 16.0 | | | 16.3 | |

Energy | | 9.3 | | | 10.7 | |

Industrials | | 7.3 | | | 10.4 | |

Telecommunication Services | | 3.2 | | | 3.0 | |

Materials | | 2.4 | | | 3.4 | |

Consumer Staples | | 2.1 | | | 11.5 | |

Utilities | | 0.0 | | | 3.8 | |

| (a) | SEC yield is an annualization of the Fund’s total net investment income per share for the 30-day period ended on the last day of the month. |

| (b) | Price-to-earnings (P/E) ratios are calculated using 12-month forward earnings estimates. |

| (c) | Foreign stocks are U.S. dollar-denominated. |

| (d) | The Fund’s portfolio holdings are subject to change without notice. The mention of specific securities is not a recommendation or solicitation for any person to buy, sell, or hold any particular security. |

PAGE 5 § DODGE & COX STOCK FUND

| | |

| PORTFOLIO OF INVESTMENTS (unaudited) | | June 30, 2010 |

| | | | | |

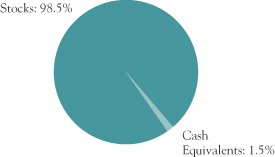

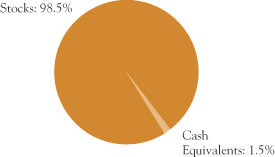

| COMMON STOCKS: 98.5% | | | | |

| | |

| | | SHARES | | VALUE |

| CONSUMER DISCRETIONARY: 17.6% |

CONSUMER DURABLES & APPAREL: 2.6% |

Panasonic Corp. ADR(b) (Japan) | | 33,933,474 | | $ | 425,186,429 |

Sony Corp. ADR(b) (Japan) | | 20,552,850 | | | 548,350,038 |

| | | | | |

| | | | | 973,536,467 |

MEDIA: 11.6% |

Comcast Corp., Class A | | 75,995,497 | | | 1,320,041,783 |

DIRECTV, Class A(a) | | 2,447,950 | | | 83,034,464 |

DISH Network Corp., Class A(a) | | 6,842,870 | | | 124,198,091 |

Interpublic Group of Companies, Inc.(a) | | 18,421,293 | | | 131,343,819 |

Liberty Global, Inc., Series A(a) | | 764,210 | | | 19,861,818 |

Liberty Global, Inc., Series C(a) | | 1,301,653 | | | 33,829,961 |

News Corp., Class A | | 76,353,526 | | | 913,188,171 |

Time Warner Cable, Inc. | | 12,785,610 | | | 665,874,569 |

Time Warner, Inc. | | 34,722,732 | | | 1,003,834,182 |

| | | | | |

| | | | | 4,295,206,858 |

RETAILING: 3.4% |

CarMax, Inc.(a) | | 9,007,200 | | | 179,243,280 |

Home Depot, Inc. | | 18,191,070 | | | 510,623,335 |

Liberty Interactive, Series A(a) | | 33,923,375 | | | 356,195,437 |

Macy’s, Inc. | | 10,590,092 | | | 189,562,647 |

| | | | | |

| | | | | 1,235,624,699 |

| | | | | |

| | | | | 6,504,368,024 |

| CONSUMER STAPLES: 2.1% |

FOOD & STAPLES RETAILING: 1.7% |

Wal-Mart Stores, Inc. | | 8,022,950 | | | 385,663,206 |

Walgreen Co. | | 8,807,075 | | | 235,148,903 |

| | | | | |

| | | | | 620,812,109 |

FOOD, BEVERAGE & TOBACCO: 0.4% |

Diageo PLC ADR(b) (United Kingdom) | | 2,500,000 | | | 156,850,000 |

| | | | | |

| | | | | 777,662,109 |

| ENERGY: 9.3% |

Baker Hughes, Inc. | | 13,136,850 | | | 546,098,854 |

Chevron Corp. | | 9,180,680 | | | 623,000,945 |

Occidental Petroleum Corp. | | 11,323,100 | | | 873,577,165 |

Royal Dutch Shell PLC ADR(b) (United Kingdom) | | 3,012,564 | | | 145,446,590 |

Schlumberger, Ltd. | | 22,522,312 | | | 1,246,384,746 |

| | | | | |

| | | | | 3,434,508,300 |

| FINANCIALS: 16.0% |

BANKS: 6.2% |

BB&T Corp. | | 12,462,844 | | | 327,897,426 |

HSBC Holdings PLC ADR(b) (United Kingdom) | | 6,129,229 | | | 279,431,550 |

SunTrust Banks, Inc. | | 10,669,405 | | | 248,597,136 |

U.S. Bancorp | | 8,800,000 | | | 196,680,000 |

Wells Fargo & Co. | | 47,862,841 | | | 1,225,288,730 |

| | | | | |

| | | | | 2,277,894,842 |

| | | | | |

| | |

| | | SHARES | | VALUE |

DIVERSIFIED FINANCIALS: 7.8% |

Bank of New York Mellon Corp. | | 24,856,624 | | $ | 613,710,047 |

Capital One Financial Corp.(c) | | 32,243,611 | | | 1,299,417,523 |

Charles Schwab Corp. | | 19,451,600 | | | 275,823,688 |

Credit Suisse Group AG ADR(b) (Switzerland) | | 2,167,900 | | | 81,144,497 |

Goldman Sachs Group, Inc. | | 1,480,000 | | | 194,279,600 |

Legg Mason, Inc. | | 5,656,700 | | | 158,557,301 |

SLM Corp.(a),(c) | | 26,185,882 | | | 272,071,314 |

| | | | | |

| | | | | 2,895,003,970 |

INSURANCE: 2.0% |

AEGON NV(a),(b) (Netherlands) | | 47,358,988 | | | 250,055,457 |

Genworth Financial, Inc., Class A(a) | | 5,987,660 | | | 78,258,716 |

Loews Corp. | | 3,608,000 | | | 120,182,480 |

The Travelers Companies, Inc. | | 5,981,750 | | | 294,601,187 |

| | | | | |

| | | | | 743,097,840 |

| | | | | |

| | | | | 5,915,996,652 |

| HEALTH CARE: 20.4% |

HEALTH CARE EQUIPMENT & SERVICES: 4.2% |

Boston Scientific Corp.(a) | | 69,969,500 | | | 405,823,100 |

CareFusion Corp.(a) | | 10,484,875 | | | 238,006,663 |

Covidien PLC(b) (Ireland) | | 5,463,291 | | | 219,515,032 |

Medtronic, Inc. | | 5,257,800 | | | 190,700,406 |

UnitedHealth Group, Inc. | | 490,505 | | | 13,930,342 |

WellPoint, Inc.(a) | | 9,611,854 | | | 470,308,016 |

| | | | | |

| | | | | 1,538,283,559 |

PHARMACEUTICALS, BIOTECHNOLOGY & LIFE SCIENCES: 16.2% |

Amgen, Inc.(a) | | 16,061,300 | | | 844,824,380 |

GlaxoSmithKline PLC ADR(b) (United Kingdom) | | 28,024,300 | | | 953,106,443 |

Merck & Co., Inc. | | 36,005,500 | | | 1,259,112,335 |

Novartis AG ADR(b) (Switzerland) | | 25,465,500 | | | 1,230,492,960 |

Pfizer, Inc. | | 60,512,864 | | | 862,913,441 |

Sanofi-Aventis ADR(b) (France) | | 28,568,600 | | | 858,772,116 |

| | | | | |

| | | | | 6,009,221,675 |

| | | | | |

| | | | | 7,547,505,234 |

| INDUSTRIALS: 7.3% |

CAPITAL GOODS: 4.6% |

Eaton Corp. | | 3,698,200 | | | 242,010,208 |

General Electric Co. | | 78,198,175 | | | 1,127,617,684 |

Tyco International, Ltd.(b) (Switzerland) | | 8,960,775 | | | 315,688,103 |

| | | | | |

| | | | | 1,685,315,995 |

COMMERCIAL & PROFESSIONAL SERVICES: 0.6% |

Dun & Bradstreet Corp. | | 35,340 | | | 2,372,021 |

Pitney Bowes, Inc. | | 10,286,950 | | | 225,901,422 |

| | | | | |

| | | | | 228,273,443 |

| | |

| See accompanying Notes to Financial Statements | | DODGE & COX STOCK FUND §PAGE 6 |

| | |

| PORTFOLIO OF INVESTMENTS (unaudited) | | June 30, 2010 |

| | | | | |

| COMMON STOCKS (continued) |

| | |

| | | SHARES | | VALUE |

TRANSPORTATION: 2.1% |

FedEx Corp. | | 11,133,599 | | $ | 780,576,626 |

| | | | | |

| | | | | 2,694,166,064 |

| INFORMATION TECHNOLOGY: 20.2% |

SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT: 1.0% |

Maxim Integrated Products, Inc.(c) | | 23,348,800 | | | 390,625,424 |

SOFTWARE & SERVICES: 7.5% |

AOL, Inc.(a),(c) | | 7,655,722 | | | 159,162,460 |

BMC Software, Inc.(a) | | 8,220,940 | | | 284,691,152 |

Cadence Design Systems, Inc.(a),(c) | | 23,282,600 | | | 134,806,254 |

Citrix Systems, Inc.(a),(c) | | 4,488,922 | | | 189,567,176 |

Computer Sciences Corp. | | 6,244,072 | | | 282,544,258 |

Compuware Corp.(a),(c) | | 22,088,112 | | | 176,263,134 |

EBay, Inc.(a) | | 27,473,300 | | | 538,751,413 |

Electronic Arts, Inc.(a),(c) | | 21,261,177 | | | 306,160,949 |

Symantec Corp.(a) | | 28,815,300 | | | 399,956,364 |

Synopsys, Inc.(a),(c) | | 14,402,369 | | | 300,577,441 |

| | | | | |

| | | | | 2,772,480,601 |

TECHNOLOGY, HARDWARE & EQUIPMENT: 11.7% |

Hewlett-Packard Co. | | 39,353,595 | | | 1,703,223,592 |

Molex, Inc. | | 2,547,600 | | | 46,468,224 |

Molex, Inc., Class A | | 8,724,330 | | | 134,790,899 |

Motorola, Inc.(a),(c) | | 131,758,711 | | | 859,066,796 |

Nokia Corp. ADR(b) (Finland) | | 34,112,300 | | | 278,015,245 |

Telefonaktiebolaget LM Ericsson ADR(b) (Sweden) | | 28,720,500 | | | 316,499,910 |

Tyco Electronics, Ltd.(b) (Switzerland) | | 16,789,775 | | | 426,124,489 |

Xerox Corp.(c) | | 68,842,082 | | | 553,490,339 |

| | | | | |

| | | | | 4,317,679,494 |

| | | | | |

| | | | | 7,480,785,519 |

| MATERIALS: 2.4% |

Cemex SAB de CV ADR(a),(b) (Mexico) | | 16,751,062 | | | 161,982,770 |

Domtar Corp. | | 1,470,959 | | | 72,297,635 |

Dow Chemical Co. | | 24,344,545 | | | 577,452,607 |

Vulcan Materials Co. | | 2,046,548 | | | 89,700,199 |

| | | | | |

| | | | | 901,433,211 |

| TELECOMMUNICATION SERVICES: 3.2% |

Sprint Nextel Corp.(a) | | 132,825,739 | | | 563,181,133 |

Vodafone Group PLC ADR(b) (United Kingdom) | | 29,000,400 | | | 599,438,268 |

| | | | | |

| | | | | 1,162,619,401 |

| | | | | |

TOTAL COMMON STOCKS

(Cost $40,807,658,482) | | | | $ | 36,419,044,514 |

| | | | | | | | |

| SHORT-TERM INVESTMENTS: 1.7% | |

| | |

| | | PAR VALUE | | | VALUE | |

MONEY MARKET FUND: 0.3% | |

SSgA Prime Money Market Fund | | $ | 112,377,027 | | | $ | 112,377,027 | |

REPURCHASE AGREEMENT: 1.4% | |

Fixed Income Clearing Corporation(d) 0.00%, 7/1/10, maturity value $524,082,000 | | | 524,082,000 | | | | 524,082,000 | |

| | | | | | | | |

TOTAL SHORT-TERM INVESTMENTS

(Cost $636,459,027) | | | $ | 636,459,027 | |

| | | | | | | | |

TOTAL INVESTMENTS

(Cost $41,444,117,509) | | | 100.2 | % | | $ | 37,055,503,541 | |

OTHER ASSETS LESS LIABILITIES | | | (0.2 | %) | | | (55,876,045 | ) |

| | | | | | | | |

| NET ASSETS | | | 100.0 | % | | $ | 36,999,627,496 | |

| | | | | | | | |

| (b) | Security denominated in U.S. dollars |

| (c) | See Note 8 regarding holdings of 5% voting securities |

| (d) | Repurchase agreement is collateralized by Fannie Mae 0.00%-6.25%, 2/1/11-4/26/11; and Freddie Mac 0.00%-4.75%, 1/18/11-2/24/11. Total collateral value is $534,568,225. |

ADR: American Depositary Receipt

| | |

| PAGE 7 § DODGE & COX STOCK FUND | | See accompanying Notes to Financial Statements |

| | | | |

STATEMENT OF ASSETS AND LIABILITIES (unaudited) | |

| |

| | | June 30, 2010 | |

ASSETS: | | | | |

Investments, at value | | | | |

Unaffiliated issuers (cost $35,689,360,519) | | $ | 33,157,352,246 | |

Affiliated issuers (cost $5,754,756,990) | | | 3,898,151,295 | |

| | | | |

| | | 37,055,503,541 | |

Receivable for investments sold | | | 1,690,877 | |

Receivable for Fund shares sold | | | 39,109,379 | |

Dividends and interest receivable | | | 91,930,537 | |

Prepaid expenses and other assets | | | 88,275 | |

| | | | |

| | | 37,188,322,609 | |

| | | | |

LIABILITIES: | | | | |

Payable for investments purchased | | | 112,508,530 | |

Payable for Fund shares redeemed | | | 57,918,818 | |

Management fees payable | | | 16,014,463 | |

Accrued expenses | | | 2,253,302 | |

| | | | |

| | | 188,695,113 | |

| | | | |

NET ASSETS | | $ | 36,999,627,496 | |

| | | | |

NET ASSETS CONSIST OF: | | | | |

Paid in capital | | $ | 48,254,684,644 | |

Undistributed net investment income | | | 21,579,651 | |

Accumulated net realized loss on investments | | | (6,888,022,831 | ) |

Net unrealized depreciation on investments | | | (4,388,613,968 | ) |

| | | | |

| | $ | 36,999,627,496 | |

| | | | |

Fund shares outstanding (par value $0.01 each, unlimited shares authorized) | | | 420,861,554 | |

Net asset value per share | | | $87.91 | |

|

STATEMENT OF OPERATIONS

(unaudited) | |

| |

| | | Six Months Ended

June 30, 2010 | |

INVESTMENT INCOME: | | | | |

Dividends (net of foreign taxes of $16,189,608) | | | | |

Unaffiliated issuers | | $ | 386,671,654 | |

Affiliated issuers | | | 18,400,458 | |

Interest | | | 145,961 | |

| | | | |

| | | 405,218,073 | |

| | | | |

EXPENSES: | | | | |

Management fees | | | 101,422,065 | |

Custody and fund accounting fees | | | 279,244 | |

Transfer agent fees | | | 2,818,681 | |

Professional services | | | 73,451 | |

Shareholder reports | | | 1,265,971 | |

Registration fees | | | 226,042 | |

Trustees’ fees | | | 77,000 | |

Miscellaneous | | | 808,489 | |

| | | | |

| | | 106,970,943 | |

| | | | |

NET INVESTMENT INCOME | | | 298,247,130 | |

| | | | |

REALIZED AND UNREALIZED GAIN/ (LOSS) ON INVESTMENTS: | | | | |

Net realized gain | | | | |

Unaffiliated issuers | | | 112,615,178 | |

Affiliated issuers | | | 81,998,461 | |

Net change in unrealized depreciation | | | (3,684,502,558 | ) |

| | | | |

Net realized and unrealized loss | | | (3,489,888,919 | ) |

| | | | |

NET DECREASE IN NET ASSETS FROM OPERATIONS | | $ | (3,191,641,789 | ) |

| | | | |

| | | | | | | | |

STATEMENT OF CHANGES IN NET ASSETS | |

| | | Six Months Ended

June 30, 2010

(unaudited) | | | Year Ended

December 31, 2009 | |

OPERATIONS: | | | | | | | | |

Net investment income | | $ | 298,247,130 | | | $ | 489,322,713 | |

Net realized gain/(loss) | | | 194,613,639 | | | | (6,582,700,408 | ) |

Net change in unrealized depreciation | | | (3,684,502,558 | ) | | | 15,810,026,274 | |

| | | | | | | | |

Net increase/(decrease) in net assets from operations | | | (3,191,641,789 | ) | | | 9,716,648,579 | |

| | | | | | | | |

|

DISTRIBUTIONS TO

SHAREHOLDERS FROM: | |

Net investment income | | | (284,461,328 | ) | | | (511,502,606 | ) |

Net realized gain | | | — | | | | — | |

| | | | | | | | |

Total distributions | | | (284,461,328 | ) | | | (511,502,606 | ) |

| | | | | | | | |

| | |

FUND SHARE TRANSACTIONS: | | | | | | | | |

Proceeds from sale of shares | | | 3,767,616,250 | | | | 6,004,678,797 | |

Reinvestment of distributions | | | 268,855,988 | | | | 483,257,450 | |

Cost of shares redeemed | | | (3,551,852,058 | ) | | | (8,423,170,138 | ) |

| | | | | | | | |

Net increase/(decrease) from Fund share transactions | | | 484,620,180 | | | | (1,935,233,891 | ) |

| | | | | | | | |

Total increase/(decrease) in net assets | | | (2,991,482,937 | ) | | | 7,269,912,082 | |

| | |

NET ASSETS: | | | | | | | | |

Beginning of period | | | 39,991,110,433 | | | | 32,721,198,351 | |

| | | | | | | | |

End of period (including undistributed net investment income of $21,579,651 and $7,793,849, respectively) | | $ | 36,999,627,496 | | | $ | 39,991,110,433 | |

| | | | | | | | |

| | |

SHARE INFORMATION: | | | | | | | | |

Shares sold | | | 38,592,150 | | | | 77,216,599 | |

Distributions reinvested | | | 2,783,077 | | | | 6,220,003 | |

Shares redeemed | | | (36,478,758 | ) | | | (107,436,792 | ) |

| | | | | | | | |

Net increase/(decrease) in shares outstanding | | | 4,896,469 | | | | (24,000,190 | ) |

| | | | | | | | |

| | |

| See accompanying Notes to Financial Statements | | DODGE & COX STOCK FUND §PAGE 8 |

NOTES TO FINANCIAL STATEMENTS (unaudited)

NOTE 1—ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES

Dodge & Cox Stock Fund (the “Fund”) is one of the series constituting the Dodge & Cox Funds (the “Trust” or the “Funds”). The Trust is organized as a Delaware statutory trust and is registered under the Investment Company Act of 1940, as amended, as a diversified, open-end management investment company. The Fund commenced operations on January 4, 1965, and seeks long-term growth of principal and income. Risk considerations and investment strategies of the Fund are discussed in the Fund’s Prospectus.

The financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America, which require the use of estimates and assumptions by management. Actual results may differ from those estimates. Significant accounting policies are as follows:

Security valuation The Fund’s net assets are valued as of the close of trading on the New York Stock Exchange (NYSE), generally 4:00 p.m. Eastern Time, each day that the NYSE is open for business. Stocks are valued at the official quoted close price or the last sale of the day at the close of the NYSE or, if not available, at the mean between the exchange listed bid and ask prices. A security that is listed or traded on more than one exchange is valued at the quotation on the exchange determined to be the primary market for such security. Security values are not discounted based on the size of the Fund’s position. Securities for which market quotations are not readily available are valued at fair value as determined in good faith by or at the direction of the Board of Trustees. Short-term securities are valued at amortized cost which approximates current value. All securities held by the Fund are denominated in U.S. dollars.

Security transactions, investment income, expenses, and distributions Security transactions are recorded on the trade date. Realized gains and losses on securities sold are determined on the basis of identified cost.

Dividend income and corporate action transactions are recorded on the ex-dividend date, except for certain dividends or corporate actions from foreign securities where the ex-dividend date may have passed, which are recorded

as soon as the Fund is informed of the ex-dividend date. Withholding taxes on foreign dividends have been provided for in accordance with the Fund’s understanding of the applicable country’s tax rules and rates. Non-cash dividends included in dividend income, if any, are recorded at the fair market value of the securities received. Distributions received in excess of income are recorded as a reduction of cost of investments and/or realized gain. Interest income is recorded on the accrual basis.

Expenses are recorded on the accrual basis. Most expenses of the Trust can be directly attributed to a specific series. Expenses which cannot be directly attributed are allocated among the Funds in the Trust.

Distributions to shareholders are recorded on the ex-dividend date.

Repurchase agreements The Fund may enter into repurchase agreements, secured by U.S. government or agency securities, which involve the purchase of securities from a counterparty with a simultaneous commitment to resell the securities at an agreed-upon date and price. It is the Fund’s policy that its custodian take possession of the underlying collateral securities, the fair value of which exceeds the principal amount of the repurchase transaction, including accrued interest, at all times. In the event of default by the counterparty, the Fund has the contractual right to liquidate the collateral securities and to apply the proceeds in satisfaction of the obligation.

NOTE 2—VALUATION MEASUREMENTS

Various inputs are used in determining the value of the Fund’s investments. These inputs are summarized in the three broad levels listed below.

| § | | Level 1: Quoted prices in active markets for identical securities |

| § | | Level 2: Other significant observable inputs (including quoted prices for similar securities, market indices, interest rates, credit risk, etc.) |

| § | | Level 3: Significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments) |

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

PAGE 9 § DODGE & COX STOCK FUND

NOTES TO FINANCIAL STATEMENTS (unaudited)

The following is a summary of the inputs used to value the Fund’s holdings as of June 30, 2010:

| | | | | | |

| Security Classification(a) | | LEVEL 1

(Quoted Prices) | | LEVEL 2

(Other Significant

Observable Inputs) |

Common Stocks(b) | | $ | 36,419,044,514 | | $ | — |

Money Market Fund | | | 112,377,027 | | | — |

Repurchase Agreement | | | — | | | 524,082,000 |

| | | | | | |

Total | | $ | 36,531,421,541 | | $ | 524,082,000 |

| | | | | | |

| | | | | | | |

| (a) | At June 30, 2010 the Fund held no securities that were considered to be “Level 3” securities (those valued using significant unobservable inputs). |

| (b) | All common stocks held in the Fund are Level 1 securities. For a detailed break-out of common stocks by major industry classification, please refer to the Portfolio of Investments. |

NOTE 3—RELATED PARTY TRANSACTIONS

Management fees Under a written agreement approved by a unanimous vote of the Board of Trustees, the Fund pays an annual management fee of 0.50% of the Fund’s average daily net assets to Dodge & Cox, investment manager of the Fund. The agreement further provides that Dodge & Cox shall waive its fee to the extent that such fee plus all other ordinary operating expenses of the Fund exceed 0.75% of the average daily net assets for the year.

Fund officers and trustees All officers and three of the trustees of the Trust are officers or employees of Dodge & Cox. The Trust pays a fee only to those trustees who are not affiliated with Dodge & Cox.

Indemnification Under the Trust’s organizational documents, its officers and trustees are indemnified against certain liabilities arising out of the performance of their duties to the Trust. In addition, in the normal course of business the Trust enters into contracts that provide general indemnities to other parties. The Trust’s maximum exposure under these arrangements is unknown as this would involve future claims that may be made against the Trust that have not yet occurred.

NOTE 4—INCOME TAX INFORMATION

A provision for federal income taxes is not required since the Fund intends to continue to qualify as a regulated investment company under Subchapter M of the Internal Revenue Code and distribute all of its taxable income to shareholders. Distributions are determined in accordance with income tax regulations, which may differ from net investment income and realized gains for financial

reporting purposes. Financial reporting records are adjusted for permanent book/tax differences to reflect tax character.

Book/tax differences are primarily due to differing treatments of wash sales and net short-term realized gain/(loss). At June 30, 2010, the cost of investments for federal income tax purposes was $41,506,965,516.

Distributions during the six months ended June 30, 2010 and for the year ended December 31, 2009 were characterized as follows for federal income tax purposes:

| | | | |

| | | Six Months Ended June 30, 2010 | | Year Ended December 31, 2009 |

Ordinary income | | $284,461,328 | | $511,502,606 |

| | ($0.680 per share) | | ($1.195 per share) |

| | |

Long-term capital gain | | — | | — |

At June 30, 2010, the tax basis components of distributable earnings were as follows:

| | | | |

Unrealized appreciation | | $ | 4,148,460,753 | |

Unrealized depreciation | | | (8,599,922,728 | ) |

| | | | |

Net unrealized depreciation | | | (4,451,461,975 | ) |

Undistributed ordinary income | | | 21,579,651 | |

Accumulated capital gain(a) | | | 68,202,577 | |

Capital Loss carryforward(b) | | | (6,893,377,401 | ) |

| (a) | Represents capital loss realized for tax purposes during the period from January 1, 2010 to June 30, 2010. |

| (b) | Represents accumulated capital loss as of December 31, 2009 which may be carried forward to offset future capital gains. If not utilized, the capital loss carryforward expires as follows: |

| | | |

Expiring in 2016 | | $ | 30,080,078 |

Expiring in 2017 | | | 6,863,297,323 |

| | | |

| | $ | 6,893,377,401 |

| | | |

Fund management has reviewed the tax positions for open periods (for Federal purposes, three years from the date of filing and for State purposes, four years from the date of filing) as applicable to the Fund, and has determined that no provision for income tax is required in the Fund’s financial statements.

DODGE & COX STOCK FUND §PAGE 10

NOTES TO FINANCIAL STATEMENTS (unaudited)

NOTE 5—LOAN FACILITIES

Pursuant to an exemptive order issued by the Securities and Exchange Commission (SEC), the Fund may participate in an interfund lending facility (Facility). The Facility allows the Fund to borrow money from or loan money to the Funds. Loans under the Facility are made for temporary or emergency purposes, such as to fund shareholder redemption requests. Interest on borrowings is the average of the current repurchase agreement rate and the bank loan rate. There was no activity in the Facility during the period.

The Fund also participates with the Funds in a $200 million committed credit facility (Line of Credit) with State Street Bank and Trust Company, to be utilized for temporary or emergency purposes to fund shareholder redemptions or for other short-term liquidity purposes. The Fund pays a commitment fee on its pro-rata portion of the line of credit, which amounted to $52,206 and is reflected as a Miscellaneous Expense in the Statement of Operations. Interest on borrowings is charged at the prevailing rate. There were no borrowings on the Line of Credit during the period.

NOTE 6—PURCHASES AND SALES OF INVESTMENTS

For the six months ended June 30, 2010, purchases and sales of securities, other than short-term securities, aggregated $3,244,784,281 and $2,596,154,950, respectively.

NOTE 7—SUBSEQUENT EVENTS

Fund management has determined that no material events or transactions occurred subsequent to June 30, 2010 and through the date of the Fund’s financial statements issuance, which require additional disclosure in the Fund’s financial statements.

NOTE 8—HOLDINGS OF 5% VOTING SECURITIES

Each of the companies listed below was considered to be an affiliate of the Fund because the Fund owned 5% or more of the company’s voting securities during all or part of the six-month period ended June 30, 2010. Purchase and sale transactions and dividend income earned during the period on these securities were as follows:

| | | | | | | | | | | | | | | | | |

| | | Shares at

Beginning of Period | | Additions | | Reductions | | | Shares at

End of Period | | Dividend

Income(a) | | | Value at

End of Period | |

AOL, Inc. | | 6,075,118 | | 1,580,604 | | — | | | 7,655,722 | | | — | (b) | | | 159,162,460 | |

Cadence Design Systems, Inc. | | 23,282,600 | | — | | — | | | 23,282,600 | | | — | (b) | | | 134,806,254 | |

Capital One Financial Corp. | | 31,943,611 | | 300,000 | | — | | | 32,243,611 | | | 3,209,361 | | | | 1,299,417,523 | |

Citrix Systems, Inc. | | 11,327,022 | | — | | (6,838,100 | ) | | 4,488,922 | | | — | (b) | | | — | (c) |

Compuware Corp. | | 22,088,112 | | — | | — | | | 22,088,112 | | | — | (b) | | | 176,263,134 | |

Electronic Arts, Inc. | | 11,161,177 | | 10,100,000 | | — | | | 21,261,177 | | | — | (b) | | | 306,160,949 | |

Maxim Integrated Products, Inc. | | 23,348,800 | | — | | — | | | 23,348,800 | | | 9,339,520 | | | | 390,625,424 | |

Motorola, Inc. | | 129,758,711 | | 2,000,000 | | — | | | 131,758,711 | | | — | (b) | | | 859,066,796 | |

SLM Corp. | | 26,185,882 | | — | | — | | | 26,185,882 | | | — | (b) | | | 272,071,314 | |

Synopsys, Inc. | | 10,122,369 | | 4,280,000 | | — | | | 14,402,369 | | | — | (b) | | | 300,577,441 | |

Xerox Corp. | | 67,997,300 | | 844,782 | | — | | | 68,842,082 | | | 5,851,577 | | | | — | (c) |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | $ | 18,400,458 | | | $ | 3,898,151,295 | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| (a) | Net of foreign taxes, if any |

| (c) | Company was not an affiliate at the end of the period |

PAGE 11 § DODGE & COX STOCK FUND

FINANCIAL HIGHLIGHTS

| | | | | | | | | | | | | | | | | | |

SELECTED DATA AND RATIOS (for a share outstanding throughout each period) | | Six Months

Ended June 30, | | | Year Ended December 31, | |

| | | 2010(a) | | | 2009 | | | 2008 | | | 2007 | | | 2006 | | | 2005 | |

| | | | | | |

Net asset value, beginning of period | | $96.14 | | | $74.37 | | | $138.26 | | | $153.46 | | | $137.22 | | | $130.22 | |

Income from investment operations: | | | | | | | | | | | | | | | | | | |

Net investment income | | 0.71 | | | 1.15 | | | 1.91 | | | 2.30 | | | 2.15 | | | 1.68 | |

Net realized and unrealized gain/(loss) | | (8.26 | ) | | 21.82 | | | (59.83 | ) | | (1.90 | ) | | 23.12 | | | 10.36 | |

| | | | | | |

Total from investment operations | | (7.55 | ) | | 22.97 | | | (57.92 | ) | | 0.40 | | | 25.27 | | | 12.04 | |

| | | | | | |

Distributions to shareholders from: | | | | | | | | | | | | | | | | | | |

Net investment income | | (0.68 | ) | | (1.20 | ) | | (1.84 | ) | | (2.34 | ) | | (2.12 | ) | | (1.70 | ) |

Net realized gain | | — | | | — | | | (4.13 | ) | | (13.26 | ) | | (6.91 | ) | | (3.34 | ) |

| | | | | | |

Total distributions | | (0.68 | ) | | (1.20 | ) | | (5.97 | ) | | (15.60 | ) | | (9.03 | ) | | (5.04 | ) |

| | | | | | |

Net asset value, end of period | | $87.91 | | | $96.14 | | | $74.37 | | | $138.26 | | | $153.46 | | | $137.22 | |

| | | | | | |

Total return | | (7.91 | )% | | 31.27 | % | | (43.31 | )% | | 0.14 | % | | 18.54 | % | | 9.36 | % |

Ratios/supplemental data: | | | | | | | | | | | | | | | | | | |

Net assets, end of period (millions) | | $37,000 | | | $39,991 | | | $32,721 | | | $63,291 | | | $66,185 | | | $52,184 | |

Ratio of expenses to average net assets | | 0.52 | %(b) | | 0.52 | % | | 0.52 | % | | 0.52 | % | | 0.52 | % | | 0.52 | % |

Ratio of net investment income to average net assets | | 1.47 | %(b) | | 1.42 | % | | 1.75 | % | | 1.44 | % | | 1.48 | % | | 1.29 | % |

Portfolio turnover rate | | 7 | % | | 18 | % | | 31 | % | | 27 | % | | 14 | % | | 12 | % |

See accompanying Notes to Financial Statements

DODGE & COX STOCK FUND §PAGE 12

FUND HOLDINGS

The Fund provides a complete list of its holdings four times each fiscal year, as of the end of each quarter. The lists appear in the Fund’s First Quarter, Semi-Annual, Third Quarter and Annual Reports to shareholders. The Fund files the lists with the Securities and Exchange Commission (SEC) on Form N-CSR (second and fourth quarters) and Form N-Q (first and third quarters). Shareholders may view the Fund’s Forms N-CSR and N-Q on the SEC’s website at www.sec.gov. Forms N-CSR and N-Q may also be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information regarding the operations of the Public Reference Room may be obtained by 1-202-942-8090 (direct) or 1-800-732-0330 (general SEC number). A complete list of the Fund’s quarter-end holdings is also available at www.dodgeandcox.com on or about 15 days following each quarter end and remains available on the web site until the list is updated in the subsequent quarter.

PROXY VOTING

For a free copy of the Fund’s proxy voting policies and procedures, please call 1-800-621-3979, visit the Fund’s web site at www.dodgeandcox.com or visit the SEC’s web site at www.sec.gov. Information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ending June 30 is also available at www.dodgeandcox.com or at www.sec.gov.

HOUSEHOLD MAILINGS

The Fund routinely mails shareholder reports and summary prospectuses to shareholders and, on occasion, proxy statements. In order to reduce the volume of mail, when possible, only one copy of these documents will be sent to shareholders who are part of the same family and share the same residential address.

If you have a direct account with the Funds and you do not want the mailing of shareholder reports and summary prospectuses combined with other members in your household, contact the Funds at 1-800-621-3979. Your request will be implemented within 30 days.

PAGE 13 § DODGE & COX STOCK FUND

THIS PAGE INTENTIONALLY LEFT BANK

DODGE & COXSTOCK FUND §PAGE 14

DODGE & COX FUNDS—EXECUTIVE OFFICER & TRUSTEE INFORMATION

| | | | | | |

Name (Age) and

Address* | | Position with Trust

(Year of Election or

Appointment) | | Principal Occupation During Past 5 Years | | Other Directorships Held by Trustees |

| INTERESTED TRUSTEES & OFFICERS |

John A. Gunn (66) | | Chairman and Trustee

(Trustee since 1985) | | Chairman (since 2007), Chief Executive Officer (2005-2010), and Director of Dodge & Cox, Portfolio Manager and member of Investment Policy Committee (IPC), Global Investment Policy Committee (GIPC) (since 2008), and International Investment Policy Committee (IIPC) | | — |

| Kenneth E. Olivier (58) | | President and Trustee

(Trustee since 2005) | | Chief Executive Officer (since 2010), President (since 2005), and Director of Dodge & Cox, Portfolio Manager, and member of IPC | | — |

| Dana M. Emery (48) | | Senior Vice President and Trustee (Trustee since 1993) | | Executive Vice President (since 2005) and Director of Dodge & Cox, Director of Fixed Income, Portfolio Manager, and member of Fixed Income Investment Policy Committee (FIIPC) | | — |

Charles F. Pohl (52) | | Senior Vice President (Officer since 2004) | | Senior Vice President and Director of Dodge & Cox, Chief Investment Officer (since 2007), Director of Credit Research, Portfolio Manager, Investment Analyst, and member of IPC, GIPC (since 2008), IIPC (since 2007), and FIIPC | | — |

| Diana S. Strandberg (50) | | Senior Vice President

(Officer since 2005) | | Vice President of Dodge & Cox, Director of International Equity (since 2009), Portfolio Manager, and member of IPC, GIPC (since 2008), and IIPC | | — |

| David H. Longhurst (53) | | Treasurer (Officer since 2006) | | Vice President (since 2008) and Assistant Treasurer of Dodge & Cox (since 2007); Fund Administrative and Accounting Senior Manager (2004-2007) | | — |

| Thomas M. Mistele (56) | | Secretary

(Officer since 2000) | | Chief Operating Officer, Director (since 2005), Secretary, and General Counsel of Dodge & Cox | | — |

| Katherine M. Primas (35) | | Chief Compliance Officer

(Officer since 2010) | | Chief Compliance Officer of Dodge & Cox (since 2008) and Associate Chief Compliance Officer of Dodge & Cox (2004-2008) | | — |

| INDEPENDENT TRUSTEES |

| William F. Ausfahl (70) | | Trustee (Since 2002) | | CFO, The Clorox Co. (1982-1997); Director, The Clorox Co. (1984-1997) | | — |

| L. Dale Crandall (68) | | Trustee (Since 1999) | | President, Kaiser Foundation Health Plan, Inc. and Kaiser Foundation Hospitals (2000-2002); Senior Vice President—Finance and Administration & CFO, Kaiser Foundation Health Plan, Inc. and Kaiser Foundation Hospitals (1998-2000) | | Director, Ansell Limited (medical equipment and supplies) (2002-present); Director, Coventry Health Care, Inc. (managed health care) (2004-present); Director, Metavante Technologies, Inc. (software) (2007 to 2009); Bridgeport Education, Inc. (education services) (2008 to present) |

| Thomas A. Larsen (60) | | Trustee (Since 2002) | | Director in Howard, Rice, Nemerovski, Canady, Falk & Rabkin (law firm) | | — |

John B. Taylor (63) | | Trustee (Since 2005) | | Professor of Economics, Stanford University; Senior Fellow, Hoover Institution; Under Secretary for International Affairs, United States Treasury (2001-2005) | | — |

Will C. Wood (70) | | Trustee (Since 1992) | | Principal, Kentwood Associates, Financial Advisers | | Director, Banco Latinoamericano de Exportaciones S.A. (Latin American foreign trade bank) (1999-Present) |

| * | | The address for each Officer and Trustee is 555 California Street, 40th Floor, San Francisco, California 94104. Each Officer and Trustee oversees all five series in the Dodge & Cox Funds complex and serves for an indefinite term. |

Additional information about the Trust’s Trustees and Officers is available in the Trust’s Statement of Additional Information (SAI). You can get a free copy of the SAI by visiting the Funds’ website at www.dodgeandcox.com or calling 1-800-621-3979.

PAGE 15 § DODGE & COX STOCK FUND

| | | | |

| | | | |

www.dodgeandcox.com

For Fund literature, transactions, and account information, please visit the Funds’ web site.

or write or call:

DODGE & COX FUNDS

c/o Boston Financial Data Services

P.O. Box 8422

Boston, Massachusetts 02266-8422

(800) 621-3979

INVESTMENT MANAGER

Dodge & Cox

555 California Street, 40th Floor

San Francisco, California 94104

(415) 981-1710

This report is submitted for the general information of the shareholders of the Fund. The report is not authorized for distribution to prospective investors in the Fund unless it is accompanied by a current prospectus.

This report reflects our views, opinions, and portfolio holdings as of June 30, 2010, the end of the reporting period. Any such views are subject to change at any time based upon market or other conditions and Dodge & Cox disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Dodge & Cox Fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Dodge & Cox Fund.

06/10 GSF SAR Printed on recycled paper

Semi-Annual Report

June 30, 2010

Global Stock

Fund

ESTABLISHED 2008

TICKER: DODWX

TO OUR SHAREHOLDERS

The Dodge & Cox Global Stock Fund had a total return of –14.2% for the second quarter of 2010, compared to –12.7% for the MSCI World Index. For the six months ended June 30, 2010, the Fund had a total return of –9.6%, compared to –9.8% for the MSCI World. Please see the Fund’s longer-term performance results on page three. At quarter end, the Fund had net assets of $1.2 billion with a cash position of 3.4%.

MARKET COMMENTARY AND INVESTMENT STRATEGY

While the U.S. and global economies showed signs of continued improvement in the first half of 2010, the performance of the major financial markets in the second quarter reflected uncertainty about future economic growth. Optimism for a global recovery was hampered by concerns of a potential “double-dip” U.S. recession, as growth in U.S. consumer spending slowed and unemployment remained elevated. In addition, substantial debt burdens caused uneasiness about the health of a number of European economies.

We believe that a long-term perspective on investing is important during periods of market volatility. While the aforementioned concerns about U.S. and European economic growth have had a negative impact on valuations of the Fund’s holdings, they have not changed our belief that the future could be rewarding for patient long-term investors. The Fund has invested primarily in global industry leaders that can overcome short-term adversity, and will, we believe, prosper when economic growth accelerates again. We have taken advantage of the low valuations available in the market—the MSCI World index is currently trading at 11.5 times forward earnings—and added to many of the Fund’s positions. Two examples of areas where we are finding opportunities are Financials and Pharmaceuticals.

Anxiety about the global economic recovery has had a particularly negative impact on the valuations of the companies in the Financials sector. For the first six months of 2010, the MSCI World Financials sector was down 12%. As we are optimistic about the long-term potential for the Funds’ holdings in the Financials sector, we have increased the sector allocation to 23% of the Fund from 20% at year end. One area of interest is the

capital markets industry, which includes broker-dealers, custodians, and asset managers. During the first half of 2010, we initiated a position in Charles Schwab,1 a leading U.S. retail brokerage firm with over $1.3 trillion in client assets. As a provider of retail brokerage, banking, custodian, and investment management services, Schwab generates profits from a variety of sources, including trading commissions, account management fees, and interest rate spreads on money market funds. Earnings are currently depressed due to muted trading activity and low interest rates, which have necessitated temporary fee waivers on Schwab’s money market funds. However, over the long term, the company’s strong franchise and superior service offering should allow it to grow assets under custody faster than its competitors, and its profitability should further benefit from economic growth and rising interest rates.

Another area of incremental investment for the Fund over the past six months has been the Pharmaceuticals industry, which now comprises 13.8% of the Fund. Sanofi-Aventis is a good example of what we find attractive in this group. A French multinational firm, it is one of the world’s largest pharmaceutical companies with a leading presence in the emerging markets. At seven times our estimate of forward earnings, its low valuation reflects concerns about the impending decline in earnings due to branded pharmaceuticals losing patent protection. However, more than half of Sanofi’s business is in areas that we expect to grow over the next three to five years, including vaccines, emerging markets, and animal health. Furthermore, while it is difficult to predict how successful any pharmaceutical company’s research and development efforts will be, we believe that Sanofi’s more than €4 billion per year R&D effort could produce new drugs with significant sales potential. In the meantime, the balance sheet and cash flows are healthy, management is cutting costs, and the 5% dividend yield is attractive.

INVESTMENT PHILOSOPHY

Dodge & Cox’s investment philosophy is based on evaluating the long-term opportunities and risks for each company, and comparing our outlook to that of other investors, as measured by the company’s valuation. Our

PAGE 1 § DODGE & COX GLOBAL STOCK FUND

individual company analysis also takes into account the broader forces that dictate the external environment in which a company operates. We evaluate macroeconomic and political factors as part of our assessment of the relative attractiveness of each investment. At the same time, we avoid basing our investment decisions solely on predictions regarding the short-term macroeconomic environment, such as predictions of interest rates, currency movements, and election outcomes.

IN CLOSING

Despite the many near-term uncertainties, we are optimistic that the U.S. and global economies are still in the early stages of a multi-year business recovery. In particular, growth conditions in the developing world appear excellent. This enthusiasm, combined with what we believe are attractive current valuations, leads us to believe that the long-term prospects for equity investing are favorable.

Thank you for your continued confidence in our firm. As always, we welcome your comments and questions.

For the Board of Trustees,

| | |

| |  |

John A. Gunn, Chairman | | Diana S. Strandberg, Senior Vice President |

July 23, 2010

| 1 | | We use these examples to illustrate our investment process, not to imply that we think they are more attractive than the Fund’s other holdings. |

SEMI-ANNUAL PERFORMANCE REVIEW

The Fund outperformed the MSCI World by 0.2 percentage points for the six months ended June 30, 2010.

Key Contributors to Relative Results

| | § | | Relative returns in the Financials sector (down 8% versus down 12% for the MSCI World sector) had a positive impact. SunTrust Banks (up 15%), Kasikornbank (up 15%), and Capital One (up 5%) were strong performers. | |

| | § | | Relative returns from holdings in the Energy sector (down 11% versus down 17% for the MSCI World sector) contributed. Fund holdings Baker Hughes (up 3%) and Ultrapar (up 2%) helped. | |

| | § | | Returns from holdings in the Consumer Discretionary sector (down 3% versus down 4% for the MSCI World sector), combined with a higher average weighting (14% versus 10%), also contributed. Time Warner Cable (up 28%) and Comcast (up 4%) were particularly strong. | |

| | § | | Additional contributors included Nintendo (up 28%), Mitsubishi Electric (up 8%), and Anadolu Efes (up 6%). | |

Key Detractors from Relative Results

| | § | | Weak returns from holdings in the Health Care sector (down 15% versus down 9% for the MSCI World sector) hurt results. Bayer (down 28%), Boston Scientific (down 36%), and GlaxoSmithKline (down 17%) were notable detractors. | |

| | § | | Relative returns in the Consumer Staples sector (down 8% versus down 4% for the MSCI World sector) had a negative effect. | |

| | § | | Weak returns from holdings in the Materials sector (down 17% versus down 14% for the MSCI World sector) also detracted from results. Norsk Hydro (down 41%) and Lafarge (down 33%) were weak. | |

| | § | | Additional detractors included Nokia (down 34%), Telefonica (down 31%), and Unicredit (down 29%). | |

DODGE & COX GLOBAL STOCK FUND §PAGE 2

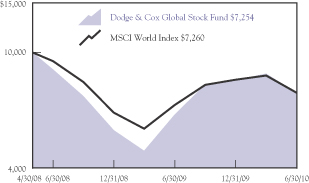

GROWTH OF $10,000 SINCE INCEPTION

FOR AN INVESTMENT MADE ON MAY 1, 2008

AVERAGE ANNUAL TOTAL RETURN

FOR PERIODS ENDED JUNE 30, 2010

| | | | | | |

| | | 1 Year | | | Since

Inception

(05/01/08) | |

Dodge & Cox Global Stock Fund | | 18.83 | % | | (13.78 | )% |

MSCI World Index | | 10.21 | | | (13.74 | ) |

Returns represent past performance and do not guarantee future results. Investment return and share price will fluctuate with market conditions, and investors may have a gain or loss when shares are sold. Mutual fund performance changes over time and currently may be significantly lower than stated. Performance is updated and published monthly. Visit the Fund’s web site at www.dodgeandcox.com or call 800-621-3979 for current performance figures.

The Fund’s total returns include the reinvestment of dividend and capital gain distributions, but have not been adjusted for any income taxes payable by shareholders on these distributions or on Fund share redemptions. The MSCI World is a widely recognized benchmark of the world’s stock markets, including the United States. Index returns include dividends and/or interest income but, unlike Fund returns, do not reflect fees or expenses.

MSCI World is a service mark of MSCI Barra.

Risks: The Fund is subject to stock market risk, meaning stocks in the Fund may decline in value for extended periods due to the financial prospects of individual companies, or due to general market and economic conditions. Investing in non-U.S. securities may entail risk due to foreign economic and political developments; this risk may be increased when investing in emerging markets. Please read the prospectus for specific details regarding the Fund’s risk profile.

PAGE 3 § DODGE & COX GLOBAL STOCK FUND

FUND EXPENSE EXAMPLE

As a Fund shareholder, you incur ongoing Fund costs, including management fees and other Fund expenses. All mutual funds have ongoing costs, sometimes referred to as operating expenses. The following example shows ongoing costs of investing in the Fund and can help you understand these costs and compare them with those of other mutual funds. The example assumes a $1,000 investment held for the six months indicated.

ACTUAL EXPENSES

The first line of the table below provides information about actual account values and expenses based on the Fund’s actual returns. You may use the information in this line, together with your account balance, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

HYPOTHETICAL EXAMPLE FOR COMPARISON WITH OTHER MUTUAL FUNDS

Information on the second line of the table can help you compare ongoing costs of investing in the Fund with those of other mutual funds. This information may not be used to estimate the actual ending account balance or expenses you paid during the period. The hypothetical “Ending Account Value” is based on the actual expense ratio of the Fund and an assumed 5% annual rate of return before expenses (not the Fund’s actual return). The amount under the heading “Expense Paid During the Period” shows the hypothetical expenses your account would have incurred under this scenario. You can compare this figure with the 5% hypothetical examples that appear in shareholder reports of other mutual funds.

| | | | | | | | | |

Six Months Ended June 30, 2010 | | Beginning Account Value

1/1/2010 | | Ending Account Value

6/30/2010 | | Expenses Paid During Period* |

Based on Actual Fund Return | | $ | 1,000.00 | | $ | 903.90 | | $ | 3.33 |

Based on Hypothetical 5% Yearly Return | | | 1,000.00 | | | 1,021.29 | | | 3.54 |

| * | | Expenses are equal to the Fund’s annualized six-month expense ratio of 0.71%, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period). |

The expenses shown in the table highlight ongoing costs only and do not reflect any transactional fees or account maintenance fees. While other mutual funds may charge such fees, please note that the Fund does not charge transaction fees (e.g., redemption fees, sales loads) or universal account maintenance fees (e.g., small account fees).

DODGE & COX GLOBAL STOCK FUND §PAGE 4

| | |

| FUND INFORMATION | | June 30, 2010 |

| | |

| GENERAL INFORMATION | | |

Net Asset Value Per Share | | $7.15 |

Total Net Assets (billions) | | $1.2 |

2009 Expense Ratio(a) | | 0.74% |

Expense Ratio (1/1/10 to 6/30/10, annualized) | | 0.71% |

Portfolio Turnover Rate (1/1/10 to 6/30/10, unannualized) | | 6% |

30-Day SEC Yield(b) | | 1.42% |

Fund Inception Date | | May 1, 2008 |

No sales charges or distribution fees | | |

Investment Manager: Dodge & Cox, San Francisco. Managed by the Global Investment Policy Committee, whose seven members’ average tenure at Dodge & Cox is 18 years.

| | | | |

| PORTFOLIO CHARACTERISTICS | | Fund | | MSCI

World |

Number of Stocks | | 98 | | 1,657 |

Median Market Capitalization (billions) | | $18 | | $6 |

Weighted Average Market

Capitalization (billions) | | $47 | | $55 |

Price-to-Earnings Ratio(c) | | 10.6x | | 11.5x |

Countries Represented | | 24 | | 24 |

Emerging Markets (Brazil, India, Indonesia, Mexico, Russia, South Africa, South Korea, Thailand, Turkey) | | 12.1% | | 0.0% |

| | | |

| TEN LARGEST HOLDINGS(d) | | Fund | |

Hewlett-Packard Co. (United States) | | 2.6 | % |

General Electric Co. (United States) | | 2.5 | |

Novartis AG (Switzerland) | | 2.4 | |

Vodafone Group PLC (United Kingdom) | | 2.4 | |

Merck & Co., Inc. (United States) | | 2.4 | |

Sanofi-Aventis (France) | | 2.3 | |

GlaxoSmithKline PLC (United Kingdom) | | 2.2 | |

Roche Holding AG (Switzerland) | | 2.2 | |

Bank of New York Mellon Corp. (United States) | | 2.0 | |

Capital One Financial Corp. (United States) | | 2.0 | |

ASSET ALLOCATION

| | | | | | |

| REGION DIVERSIFICATION | | Fund | | | MSCI

World | |

United States | | 39.3 | % | | 49.6 | % |

Europe (excluding United Kingdom) | | 32.7 | | | 19.2 | |

United Kingdom | | 9.7 | | | 9.5 | |

Japan | | 4.7 | | | 10.5 | |

Pacific (excluding Japan) | | 4.5 | | | 5.6 | |

Latin America | | 3.0 | | | 0.0 | |

Africa/Middle East | | 2.7 | | | 0.4 | |

Canada | | 0.0 | | | 5.2 | |

| | | | | | |

| SECTOR DIVERSIFICATION | | Fund | | | MSCI

World | |

Financials | | 23.1 | % | | 20.5 | % |

Health Care | | 17.0 | | | 10.2 | |

Consumer Discretionary | | 13.6 | | | 9.9 | |

Information Technology | | 13.0 | | | 11.9 | |

Industrials | | 8.8 | | | 11.0 | |

Materials | | 6.1 | | | 7.3 | |

Energy | | 6.1 | | | 10.0 | |

Telecommunication Services | | 5.7 | | | 4.3 | |

Consumer Staples | | 3.2 | | | 10.5 | |

Utilities | | 0.0 | | | 4.4 | |

| (a) | 2009 expense ratio per Fund prospectus, dated May 1, 2010. |

| (b) | SEC yield is an annualization of the Fund’s total net investment income per share for the 30-day period ended on the last day of the month. |

| (c) | Price-to-earnings (P/E) ratios are calculated using 12-month forward earnings estimates. |

| (d) | The Fund’s portfolio holdings are subject to change without notice. The mention of specific securities is not a recommendation or solicitation for any person to buy, sell, or hold any particular security. |

PAGE 5 § DODGE & COX GLOBAL STOCK FUND

| | |

| PORTFOLIO OF INVESTMENTS (unaudited) | | June 30, 2010 |

| | | | | |

| COMMON STOCKS 94.6% | | | | |

| | |

| | | SHARES | | VALUE |

| CONSUMER DISCRETIONARY: 12.7% |

AUTOMOBILES & COMPONENTS: 2.2% |

Bayerische Motoren Werke AG (Germany) | | 192,600 | | $ | 9,315,719 |

Yamaha Motor Co., Ltd.(a) (Japan) | | 1,252,400 | | | 16,530,556 |

| | | | | |

| | | | | 25,846,275 |

CONSUMER DURABLES & APPAREL: 2.3% |

LG Electronics, Inc. (South Korea) | | 121,800 | | | 9,301,111 |

Panasonic Corp. (Japan) | | 544,300 | | | 6,796,583 |

Sony Corp. (Japan) | | 398,000 | | | 10,594,034 |

| | | | | |

| | | | | 26,691,728 |

MEDIA: 6.2% |

Comcast Corp., Class A (United States) | | 1,055,200 | | | 18,328,824 |

Grupo Televisa SA ADR (Mexico) | | 253,800 | | | 4,418,658 |

Naspers, Ltd. (South Africa) | | 653,600 | | | 21,967,428 |

News Corp., Class A (United States) | | 337,445 | | | 4,035,842 |

Television Broadcasts, Ltd. (Hong Kong) | | 771,900 | | | 3,582,238 |

Time Warner Cable, Inc. (United States) | | 187,971 | | | 9,789,530 |

Time Warner, Inc. (United States) | | 350,266 | | | 10,126,190 |

| | | | | |

| | | | | 72,248,710 |

RETAILING: 2.0% |

Home Depot, Inc. (United States) | | 206,200 | | | 5,788,034 |

Liberty Interactive, Series A(a) (United States) | | 806,557 | | | 8,468,849 |

Macy’s, Inc. (United States) | | 496,500 | | | 8,887,350 |

| | | | | |

| | | | | 23,144,233 |

| | | | | |

| | | | | 147,930,946 |

| CONSUMER STAPLES: 3.2% |

FOOD & STAPLES RETAILING: 1.0% |

Walgreen Co. (United States) | | 445,500 | | | 11,894,850 |

FOOD, BEVERAGE & TOBACCO: 2.2% |

Anadolu Efes Biracilik ve Malt Sanayii AS (Turkey) | | 1,422,600 | | | 16,610,090 |

Diageo PLC ADR (United Kingdom) | | 144,000 | | | 9,034,560 |

| | | | | |

| | | | | 25,644,650 |

| | | | | |

| | | | | 37,539,500 |

| ENERGY: 5.0% |

Baker Hughes, Inc. (United States) | | 247,387 | | | 10,283,877 |

Chevron Corp. (United States) | | 74,800 | | | 5,075,928 |

OAO Lukoil ADR (Russia) | | 150,600 | | | 7,746,107 |

Occidental Petroleum Corp. (United States) | | 89,125 | | | 6,875,994 |

Royal Dutch Shell PLC ADR (United Kingdom) | | 111,400 | | | 5,594,508 |

Schlumberger, Ltd. (United States) | | 330,600 | | | 18,295,404 |

Total SA (France) | | 92,100 | | | 4,098,863 |

| | | | | |

| | | | | 57,970,681 |

| | | | | |

| | |

| | | SHARES | | VALUE |

| FINANCIALS: 23.1% |

BANKS: 10.3% |

Bangkok Bank PCL NVDR (Thailand) | | 1,505,300 | | $ | 5,762,681 |

Barclays PLC (United Kingdom) | | 4,281,600 | | | 16,974,500 |

BB&T Corp. (United States) | | 299,700 | | | 7,885,107 |

HSBC Holdings PLC (United Kingdom) | | 1,572,207 | | | 14,343,299 |

ICICI Bank, Ltd. ADR (India) | | 222,400 | | | 8,037,536 |

Kasikornbank PCL Foreign (Thailand) | | 2,830,600 | | | 8,220,983 |

Standard Bank Group, Ltd. (South Africa) | | 176,600 | | | 2,336,070 |

Standard Chartered PLC (United Kingdom) | | 549,999 | | | 13,351,734 |

SunTrust Banks, Inc. (United States) | | 333,795 | | | 7,777,423 |

Unicredit SPA (Italy) | | 7,682,333 | | | 17,052,490 |

Wells Fargo & Co. (United States) | | 703,273 | | | 18,003,789 |

| | | | | |

| | | | | 119,745,612 |

DIVERSIFIED FINANCIALS: 8.5% |

Bank of New York Mellon Corp. (United States) | | 963,500 | | | 23,788,815 |

Capital One Financial Corp. (United States) | | 579,700 | | | 23,361,910 |

Charles Schwab Corp. (United States) | | 816,200 | | | 11,573,716 |

Credit Suisse Group AG (Switzerland) | | 362,700 | | | 13,631,629 |

Goldman Sachs Group, Inc. (United States) | | 64,500 | | | 8,466,915 |

Haci Omer Sabanci Holding AS (Turkey) | | 2,038,588 | | | 8,156,603 |

Legg Mason, Inc. (United States) | | 345,000 | | | 9,670,350 |

| | | | | |

| | | | | 98,649,938 |

INSURANCE: 3.7% |

AEGON NV(a) (Netherlands) | | 3,514,974 | | | 18,829,871 |

Swiss Life Holding AG (Switzerland) | | 62,000 | | | 5,934,140 |

Swiss Reinsurance Co., Ltd. (Switzerland) | | 450,100 | | | 18,515,397 |

| | | | | |

| | | | | 43,279,408 |

REAL ESTATE: 0.6% |

Hang Lung Group, Ltd. (Hong Kong) | | 1,127,500 | | | 6,002,652 |

Hang Lung Properties, Ltd. (Hong Kong) | | 381,700 | | | 1,471,268 |

| | | | | |

| | | | | 7,473,920 |

| | | | | |

| | | | | 269,148,878 |

| HEALTH CARE: 17.0% |

HEALTH CARE EQUIPMENT & SERVICES: 2.2% |

Boston Scientific Corp.(a) (United States) | | 1,864,100 | | | 10,811,780 |

Covidien PLC (Ireland) | | 232,200 | | | 9,329,796 |

Medtronic, Inc. (United States) | | 155,700 | | | 5,647,239 |

| | | | | |

| | | | | 25,788,815 |

PHARMACEUTICALS, BIOTECHNOLOGY & LIFE SCIENCES: 14.8% |

Amgen, Inc.(a) (United States) | | 210,400 | | | 11,067,040 |

Bayer AG (Germany) | | 284,420 | | | 15,869,230 |

GlaxoSmithKline PLC ADR (United Kingdom) | | 750,900 | | | 25,538,109 |

| | |

| See accompanying Notes to Financial Statements | | DODGE & COX GLOBAL STOCK FUND §PAGE 6 |

| | |

| PORTFOLIO OF INVESTMENTS (unaudited) | | June 30, 2010 |

| | | | | |

| COMMON STOCKS: (continued) | | | | |

| | |

| | | SHARES | | VALUE |

Merck & Co., Inc. (United States) | | 792,200 | | $ | 27,703,234 |

Novartis AG ADR (Switzerland) | | 583,600 | | | 28,199,552 |

Pfizer, Inc. (United States) | | 816,100 | | | 11,637,586 |

Roche Holding AG (Switzerland) | | 184,400 | | | 25,322,474 |

Sanofi-Aventis (France) | | 443,700 | | | 26,756,388 |

| | | | | |

| | | | | 172,093,613 |

| | | | | |

| | | | | 197,882,428 |

| | | | | |

| INDUSTRIALS: 8.8% |

CAPITAL GOODS: 7.6% |

General Electric Co. (United States) | | 2,034,600 | | | 29,338,932 |

Koninklijke Philips Electronics NV (Netherlands) | | 296,965 | | | 8,851,744 |

Mitsubishi Electric Corp. (Japan) | | 1,802,700 | | | 14,041,068 |

Schneider Electric SA (France) | | 118,689 | | | 12,013,087 |