UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-173

(Exact name of registrant as specified in charter)

|

555 California Street, 40th Floor San Francisco, CA 94104 |

(Address of principal executive offices) (Zip code)

|

Thomas M. Mistele, Esq. 555 California Street, 40th Floor San Francisco, CA 94104 |

(Name and address of agent for service)

Registrant’s telephone number, including area code: 415-981-1710

Date of fiscal year end: DECEMBER 31, 2012

Date of reporting period: JUNE 30, 2012

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss. 3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

The following are the June 30, 2012 semi-annual reports for the Dodge & Cox Funds, a Delaware statutory trust, consisting of five series: Dodge & Cox Stock Fund, Dodge & Cox Global Stock Fund, Dodge & Cox International Stock Fund, Dodge & Cox Balanced Fund and Dodge & Cox Income Fund. The reports of each series were transmitted to their respective shareholders on August 13, 2012.

| | | | |

| | | |  |

www.dodgeandcox.com

For Fund literature, transactions, and account

information, please visit the Funds’ website.

or write or call:

DODGE & COX FUNDS

c/o Boston Financial Data Services

P.O. Box 8422

Boston, Massachusetts 02266-8422

(800) 621-3979

INVESTMENT MANAGER

Dodge & Cox

555 California Street, 40th Floor

San Francisco, California 94104

(415) 981-1710

This report is submitted for the general information of the shareholders of the Fund. The report is not authorized for distribution to prospective investors in the Fund unless it is accompanied by a current prospectus.

This report reflects our views, opinions, and portfolio holdings as of June 30, 2012, the end of the reporting period. Any such views are subject to change at any time based upon market or other conditions and Dodge & Cox disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Dodge & Cox Fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Dodge & Cox Fund.

6/12 SF SAR  Printed on recycled paper

Printed on recycled paper

Semi-Annual Report

June 30, 2012

Stock Fund

ESTABLISHED 1965

TICKER: DODGX

TO OUR SHAREHOLDERS

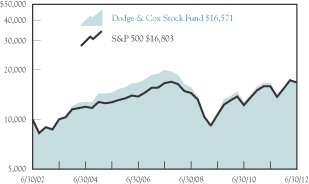

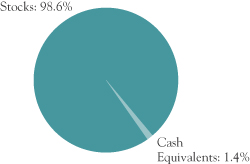

The Dodge & Cox Stock Fund had a total return of 9.8% for the six months ended June 30, 2012, compared to 9.5% for the S&P 500 Index. On June 30, the Fund had net assets of $38.2 billion with a cash position of 1.4%.

MARKET COMMENTARY

After a strong first quarter in which the S&P 500 rose 12.6%, the market fell 2.8% during the second quarter and ended the first half of 2012 up 9.5%. Market returns during the second quarter of the year were characterized by an increase in volatility, as macroeconomic concerns continued to weigh heavily on investors. Although first quarter estimated GDP growth was revised down to 1.9%, the modest U.S. economic recovery continued. Reported unemployment declined to 8.2%, inflation and interest rates remained low, consumer credit expanded, home prices rose, and residential real estate began to show signs of recovery. Since March 2009, corporate earnings have grown faster than stock prices, which we believe has created compelling valuations for stocks. On June 30, the S&P 500 was trading at 13 times forward(a) earnings.

Eurozone economic concerns have contributed to investor anxiety around the world. The growth previously seen in some emerging markets—such as China, India, and Brazil—has slowed. The decline in oil prices has negatively impacted the health of those emerging markets dependent on oil revenues, such as Russia, although it benefits the U.S. consumer. Political turmoil in the Middle East also continues to feed uncertainty. Closer to home, fear-based investing has caused a “flight” to perceived safety, driving the yields on U.S. Treasuries to all-time lows.

INVESTMENT STRATEGY

Despite the current turmoil, we are confident in our longstanding approach to investing, which emphasizes bottom-up stock selection with a focus on intensive fundamental analysis. Over time, we have built sizeable positions in established franchises at attractive valuations. We continue to have confidence in the long-term outlook for the Fund. Here is an assessment of four of the Fund’s largest holdings, two of which have helped the Fund’s six-month results, and two of which have hurt.(b)

Strong Performers: Wells Fargo and Comcast

Wells Fargo (4.4% of the Fund on June 30) and Comcast (4.3%) helped the Fund’s relative results in the first half of the year. Although investors’ fears did negatively impact many financial services firms with capital market operations, well-run banks such as Wells Fargo have proved more resilient. Wells Fargo, the second largest U.S. bank by deposits, ended the first half of the year up 23%. The company has strong consumer and small business banking franchises, is gaining market share, and remains attractively valued relative to its peers.

Comcast rose 36% in the first half of the year. The Fund has held Comcast since 2002, and we continue to be optimistic about its prospects. It is the largest pay-television and residential broadband service provider in the United States and operates a strong portfolio of cable networks. In addition, Comcast has growth potential from its broadband internet business and from expanding its services to business customers. Over the past four years, Comcast has generated consistent free cash flow growth; on June 30, it traded at an enterprise value of 6.6 times estimated 2013 EBITDA.(c)

Weak Performers: Hewlett-Packard and Novartis

Hewlett-Packard (3.4% of the Fund on June 30) and Novartis (2.4%) both hurt relative results in the first half of the year. Hewlett-Packard, down 21% year to date, has been one of the Fund’s largest holdings for the past several years. The company has struggled recently with management changes, acquisition integrations, and disappointing earnings. Despite these concerns, we have confidence in the company’s prospects due to its collection of durable business franchises (such as printers and servers), attractive valuation (trading at 0.3 times sales and 4.7 times forward earnings on June 30), CEO Meg Whitman and her management team, and scale advantages from its position as one of the largest technology companies in the world.

Novartis, a Swiss pharmaceutical manufacturer whose return was 2% year to date, has seen its stock price impacted by Eurozone concerns over the past several years. We note, though, that less than half of its revenues

PAGE 1 § DODGE & COX STOCK FUND

are from Europe, and the valuation appears compelling (trading at 2.3 times sales and 9.6 times forward earnings on June 30). In addition, Novartis has growth potential from an encouraging pipeline of new compounds and other medical products, such as eye care.

Our investment decisions for the Fund are not based on recent share price performance alone. Importantly, we also consider the current valuation and our assessment of the long-term fundamental outlook for each holding. Our investment process and team remain unchanged. Our 24 equity analysts have been with the firm for an average of 12 years, and the nine members of the Investment Policy Committee managing the Fund have an average tenure with Dodge & Cox of 27 years. We believe that the Fund’s portfolio of 75 stocks is well positioned in areas of long-term growth, such as technology, media, and health care.

IN CLOSING

Uncertainty associated with the Eurozone debt crisis has been a lingering concern for companies in Europe and the United Kingdom in general and banks in particular (representing 16.6% and 1.2%, respectively, of the Fund on June 30). The Fund had no holdings domiciled in the peripheral countries (Portugal, Ireland, Italy, Greece, and Spain), and all of the Fund’s European holdings are multinational firms that derive significant revenues outside of Europe.

Despite slowing economic conditions worldwide and mixed recent economic data in the United States, we remain optimistic about the long-term prospects for equities. Valuations have been pushed to low levels, reflecting investors’ low expectations and risk aversion. Earnings growth has remained positive, and consumer activity has improved. We believe that the combination of low valuations and optimism about future growth creates opportunities for patient, long-term investors.

Thank you for your continued confidence in our firm. As always, we welcome your comments and questions.

For the Board of Trustees,

| | |

| |  |

Kenneth E. Olivier, Chairman and President | | Charles F. Pohl, Senior Vice President |

July 26, 2012

| (a) | Forward estimates are from third-party sources. |

| (b) | We use these examples to illustrate our investment process, not to imply that we think they are more attractive than the Fund’s other holdings. |

| (c) | EBITDA is earnings before interest, taxes, depreciation, and amortization. Enterprise value is a measure of a company’s firm value and is generally calculated as the sum of a company’s market capitalization and debt minus its cash. |

DODGE & COX STOCK FUND §PAGE 2

YEAR-TO-DATE PERFORMANCE REVIEW

The Fund outperformed the S&P 500 by 0.3 percentage points year to date.

Key Contributors to Relative Results

| | § | | Returns from holdings in the Financials sector (up 21% versus up 14% for the S&P 500 sector) and a higher average weighting (20% versus 14%) contributed. Bank of America (up 48%), Capital One (up 30%), and Wells Fargo (up 23%) were strong performers. | |

| | § | | Returns in the Consumer Discretionary sector (up 18% versus up 13% for the S&P 500 sector), in combination with a higher average weighting (16% versus 11%), had a positive impact. Comcast (up 36%), Time Warner Cable (up 31%), and News Corp. (up 25%) were strong performers. | |

| | § | | Industrials sector holdings (up 13% versus up 7% for the S&P 500 sector) helped results. General Electric was up 18%. | |

| | § | | Additional contributors included tech firms eBay (up 39%) and Microsoft (up 19%), as well as Sprint (up 39%). | |

Key Detractors from Relative Results

| | § | | Weak relative returns in the Information Technology sector (up 4% versus up 13% for the S&P 500 sector) hurt results. Nokia (down 55%) and Hewlett-Packard (down 21%) were significant detractors. | |

| | § | | Weak relative returns in Health Care (up 8% versus up 11% for the S&P 500 sector), combined with a higher average weighting (20% versus 12%), detracted. | |

| | § | | Additional detractors included Celanese (down 22%), Sony (down 21%), and Baker Hughes (down 15%). | |

KEY CHARACTERISTICS OF DODGE & COX

Independent Organization

Dodge & Cox is one of the largest privately owned investment managers in the world. We remain committed to independence, with a goal of providing the highest quality investment management service to our existing clients.

80 Years of Investment Experience

Dodge & Cox was founded in 1930. We have a stable and well-qualified team of investment professionals, most of whom have spent their entire careers at Dodge & Cox.

Experienced Investment Team

The Investment Policy Committee, which is the decision-making body for the Stock Fund, is a nine-member committee with an average tenure at Dodge & Cox of 27 years.

One Business with a Single Research Office

Dodge & Cox manages domestic, international, and global equity, fixed income, and balanced investments, operating from one office in San Francisco.

Consistent Investment Approach

Our team decision-making process involves thorough, bottom-up fundamental analysis of each investment.

Long-Term Focus and Low Expenses

We invest with a three- to five-year investment horizon, which has historically resulted in low turnover relative to our peers. We manage Funds that maintain low expense ratios.

PAGE 3 § DODGE & COX STOCK FUND

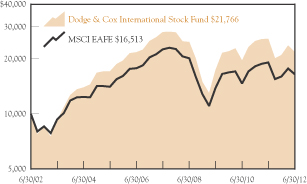

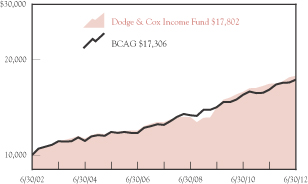

GROWTH OF $10,000 OVER 10 YEARS

FOR AN INVESTMENT MADE ON JUNE 30, 2002

AVERAGE ANNUAL TOTAL RETURN

FOR PERIODS ENDED JUNE 30, 2012

| | | | | | | | | | | | | | | | |

| | | 1 Year | | | 5 Years | | | 10 Years | | | 20 Years | |

Dodge & Cox Stock Fund | | | -.91 | % | | | -3.64 | % | | | 5.18 | % | | | 10.51 | % |

S&P 500 | | | 5.44 | | | | .22 | | | | 5.33 | | | | 8.34 | |

Returns represent past performance and do not guarantee future results. Investment return and share price will fluctuate with market conditions, and investors may have

a gain or loss when shares are sold. Fund performance changes over time and currently may be significantly lower than stated. Performance is updated and published monthly. Visit the Fund’s website at www.dodgeandcox.com or call 1-800-621-3979 for current performance figures.

The Fund’s total returns include the reinvestment of dividend and capital gain distributions, but have not been adjusted for any income taxes payable by shareholders on these distributions or on Fund share redemptions. Index returns include dividends but, unlike Fund returns, do not reflect fees or expenses. The S&P 500 Index is a market capitalization-weighted index of 500 large-capitalization stocks commonly used to represent the U.S. equity market.

S&P 500® is a trademark of The McGraw-Hill Companies, Inc.

Risks: The Fund is subject to stock market risk, meaning stocks in the Fund may decline in value for extended periods due to the financial prospects of individual companies, or due to general market and economic conditions. Please read the prospectus and summary prospectus for specific details regarding the Fund’s risk profile.

FUND EXPENSE EXAMPLE

As a Fund shareholder, you incur ongoing Fund costs, including management fees and other Fund expenses. All mutual funds have ongoing costs, sometimes referred to as operating expenses. The following example shows ongoing costs of investing in the Fund and can help you understand these costs and compare them with those of other mutual funds. The example assumes a $1,000 investment held for the six months indicated.

ACTUAL EXPENSES

The first line of the table below provides information about actual account values and expenses based on the Fund’s actual returns. You may use the information in this line, together with your account balance, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

HYPOTHETICAL EXAMPLE FOR COMPARISON WITH OTHER MUTUAL FUNDS

Information on the second line of the table can help you compare ongoing costs of investing in the Fund with those of other mutual funds. This information may not be used to estimate the actual ending account balance or expenses you paid during the period. The hypothetical “Ending Account Value” is based on the actual expense ratio of the Fund and an assumed 5% annual rate of return before expenses (not the Fund’s actual return). The amount under the heading “Expense Paid During the Period” shows the hypothetical expenses your account would have incurred under this scenario. You can compare this figure with the 5% hypothetical examples that appear in shareholder reports of other mutual funds.

| | | | | | | | | | | | |

Six Months Ended

June 30, 2012 | | Beginning Account Value

1/1/2012 | | | Ending Account Value

6/30/2012 | | | Expenses Paid

During Period* | |

Based on Actual Fund Return | | $ | 1,000.00 | | | $ | 1,098.20 | | | $ | 2.74 | |

Based on Hypothetical 5% Yearly Return | | | 1,000.00 | | | | 1,022.25 | | | | 2.64 | |

| * | Expenses are equal to the Fund’s annualized expense ratio of 0.52%, multiplied by the average account value over the period, multiplied by 182/366 (to reflect the one-half year period). |

The expenses shown in the table highlight ongoing costs only and do not reflect any transactional fees or account maintenance fees. Though other mutual funds may charge such fees, please note that the Fund does not charge transaction fees (e.g., redemption fees, sales loads) or universal account maintenance fees (e.g., small account fees).

DODGE & COX STOCK FUND §PAGE 4

| | | | |

| FUND INFORMATION | | | June 30, 2012 | |

| | | | |

| GENERAL INFORMATION | | | |

Net Asset Value Per Share | | | $110.47 | |

Total Net Assets (billions) | | | $38.2 | |

Expense Ratio | | | 0.52% | |

Portfolio Turnover Rate (1/1/12 to 6/30/12, unannualized) | | | 6% | |

30-Day SEC Yield(a) | | | 1.58% | |

Fund Inception | | | 1965 | |

No sales charges or distribution fees | | | | |

Investment Manager: Dodge & Cox, San Francisco. Managed by the Investment Policy Committee, whose nine members’ average tenure at Dodge & Cox is 27 years.

| | | | | | | | |

| PORTFOLIO CHARACTERISTICS | | Fund | | | S&P 500 | |

Number of Stocks | | | 75 | | | | 500 | |

Median Market Capitalization (billions) | | | $20 | | | | $12 | |

Weighted Average Market

Capitalization (billions) | | | $77 | | | | $111 | |

Price-to-Earnings Ratio(b) | | | 10.4x | | | | 12.9x | |

Foreign Stocks not in the S&P 500(c) | | | 16.0 | % | | | 0.0 | % |

| | | | |

| TEN LARGEST HOLDINGS (%)(d) | | Fund | |

Wells Fargo & Co. | | | 4.4 | |

Capital One Financial Corp. | | | 4.3 | |

Comcast Corp. | | | 4.3 | |

Merck & Co., Inc. | | | 3.6 | |

Hewlett-Packard Co. | | | 3.4 | |

General Electric Co. | | | 3.3 | |

Time Warner, Inc. | | | 3.0 | |

Sanofi (France) | | | 2.8 | |

Microsoft Corp. | | | 2.8 | |

GlaxoSmithKline PLC (United Kingdom) | | | 2.7 | |

| | | | | | | | |

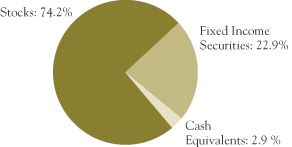

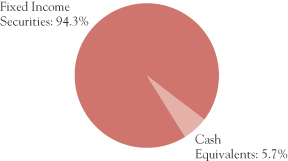

| SECTOR DIVERSIFICATION (%) | | Fund | | | S&P 500 | |

Information Technology | | | 20.3 | | | | 19.7 | |

Financials | | | 20.2 | | | | 14.4 | |

Health Care | | | 19.3 | | | | 12.0 | |

Consumer Discretionary | | | 16.0 | | | | 11.1 | |

Industrials | | | 7.3 | | | | 10.5 | |

Energy | | | 7.1 | | | | 10.8 | |

Materials | | | 3.4 | | | | 3.3 | |

Telecommunication Services | | | 2.7 | | | | 3.2 | |

Consumer Staples | | | 2.3 | | | | 11.3 | |

Utilities | | | 0.0 | | | | 3.7 | |

| (a) | SEC Yield is an annualization of the Fund’s total net investment income per share for the 30-day period ended on the last day of the month. |

| (b) | Price-to-earnings (P/E) ratios are calculated using 12-month forward earnings estimates from third-party sources. |

| (c) | Foreign stocks are U.S. dollar-denominated. |

| (d) | The Fund’s portfolio holdings are subject to change without notice. The mention of specific securities is not a recommendation to buy, sell, or hold any particular security and is not indicative of Dodge & Cox’s current or future trading activity. |

PAGE 5 § DODGE & COX STOCK FUND

| | | | |

| PORTFOLLO OF INVESTMENTS (unaudited) | | | June 30, 2012 | |

| | | | | | | | |

| COMMON STOCKS: 98.6% | |

| | |

| | | SHARES | | | VALUE | |

| CONSUMER DISCRETIONARY: 16.0% | |

CONSUMER DURABLES & APPAREL: 1.1% | |

NVR, Inc.(a) | | | 89,600 | | | $ | 76,160,000 | |

Panasonic Corp. ADR(b) (Japan) | | | 18,018,774 | | | | 145,952,069 | |

Sony Corp. ADR(b) (Japan) | | | 15,219,950 | | | | 216,732,088 | |

| | | | | | | | |

| | | | 438,844,157 | |

MEDIA: 12.7% | | | | | |

Comcast Corp., Class A | | | 50,955,197 | | | | 1,629,037,648 | |

DISH Network Corp., Class A(a) | | | 7,431,553 | | | | 212,170,838 | |

Liberty Global, Inc., Series A(a) | | | 750,010 | | | | 37,222,996 | |

Liberty Global, Inc., Series C(a) | | | 978,853 | | | | 46,740,231 | |

McGraw-Hill Companies, Inc. | | | 4,300,400 | | | | 193,518,000 | |

News Corp., Class A | | | 40,063,426 | | | | 893,013,766 | |

Time Warner Cable, Inc. | | | 8,634,010 | | | | 708,852,221 | |

Time Warner, Inc. | | | 29,871,732 | | | | 1,150,061,682 | |

| | | | | | | | |

| | | | | | | 4,870,617,382 | |

RETAILING: 2.2% | | | | | | | | |

CarMax, Inc.(a) | | | 3,911,700 | | | | 101,469,498 | |

Home Depot, Inc. | | | 3,518,970 | | | | 186,470,220 | |

J. C. Penney Co., Inc.(a) | | | 9,663,740 | | | | 225,261,780 | |

Liberty Interactive, Series A(a) | | | 17,570,075 | | | | 312,571,634 | |

| | | | | | | | |

| | | | 825,773,132 | |

| | | | | | | | |

| | | | 6,135,234,671 | |

| CONSUMER STAPLES: 2.3% | |

FOOD & STAPLES RETAILING: 1.7% | |

Wal-Mart Stores, Inc. | | | 9,060,050 | | | | 631,666,686 | |

FOOD, BEVERAGE & TOBACCO: 0.6% | |

Unilever PLC ADR(b)

(United Kingdom) | | | 7,019,700 | | | | 236,774,481 | |

| | | | | | | | |

| | | | 868,441,167 | |

| ENERGY: 7.1% | |

Baker Hughes, Inc. | | | 14,436,750 | | | | 593,350,425 | |

Chevron Corp. | | | 3,756,580 | | | | 396,319,190 | |

Occidental Petroleum Corp. | | | 9,548,100 | | | | 818,940,537 | |

Schlumberger, Ltd.(b)

(Curacao/United States) | | | 13,808,645 | | | | 896,319,147 | |

| | | | | | | | |

| | | | 2,704,929,299 | |

| FINANCIALS: 20.2% | |

BANKS: 6.7% | |

BB&T Corp. | | | 12,368,344 | | | | 381,563,412 | |

HSBC Holdings PLC ADR(b)

(United Kingdom) | | | 5,391,129 | | | | 237,910,523 | |

SunTrust Banks, Inc. | | | 11,208,733 | | | | 271,587,601 | |

Wells Fargo & Co. | | | 50,013,141 | | | | 1,672,439,435 | |

| | | | | | | | |

| | | | 2,563,500,971 | |

DIVERSIFIED FINANCIALS: 12.4% | |

Bank of America Corp. | | | 77,271,000 | | | | 632,076,780 | |

Bank of New York Mellon Corp. | | | 35,171,124 | | | | 772,006,172 | |

Capital One Financial Corp.(c) | | | 30,052,911 | | | | 1,642,692,115 | |

Charles Schwab Corp. | | | 49,011,900 | | | | 633,723,867 | |

| | | | | | | | |

| | |

| | |

| | | SHARES | | | VALUE | |

Credit Suisse Group AG ADR(b) (Switzerland) | | | 12,788,200 | | | $ | 234,407,706 | |

Goldman Sachs Group, Inc. | | | 7,149,700 | | | | 685,370,242 | |

JPMorgan Chase & Co. | | | 2,700,000 | | | | 96,471,000 | |

Legg Mason, Inc. | | | 1,918,252 | | | | 50,584,305 | |

| | | | | | | | |

| | | | 4,747,332,187 | |

INSURANCE: 1.1% | | | | | | | | |

AEGON NV(b) (Netherlands) | | | 63,541,231 | | | | 293,560,487 | |

Genworth Financial, Inc.,

Class A(a) | | | 22,207,857 | | | | 125,696,471 | |

| | | | | | | | |

| | | | 419,256,958 | |

| | | | | | | | |

| | | | 7,730,090,116 | |

| HEALTH CARE: 19.3% | |

HEALTH CARE EQUIPMENT & SERVICES: 1.5% | |

Boston Scientific Corp.(a) | | | 59,704,900 | | | | 338,526,783 | |

Medtronic, Inc. | | | 6,156,200 | | | | 238,429,626 | |

| | | | | | | | |

| | | | 576,956,409 | |

PHARMACEUTICALS, BIOTECHNOLOGY & LIFE SCIENCES: 17.8% | |

Amgen, Inc. | | | 9,162,100 | | | | 669,199,784 | |

GlaxoSmithKline PLC ADR(b)

(United Kingdom) | | | 22,342,100 | | | | 1,018,129,497 | |

Merck & Co., Inc. | | | 32,598,500 | | | | 1,360,987,375 | |

Novartis AG ADR(b) (Switzerland) | | | 16,363,300 | | | | 914,708,470 | |

Pfizer, Inc. | | | 43,362,464 | | | | 997,336,672 | |

Roche Holding AG ADR(b)

(Switzerland) | | | 17,472,800 | | | | 755,174,416 | |

Sanofi ADR(b) (France) | | | 28,428,929 | | | | 1,074,044,938 | |

| | | | | | | | |

| | | | 6,789,581,152 | |

| | | | | | | | |

| | | | 7,366,537,561 | |

| INDUSTRIALS: 7.3% | |

CAPITAL GOODS: 4.7% | |

General Electric Co. | | | 60,822,175 | | | | 1,267,534,127 | |

Koninklijke Philips Electronics NV(b) (Netherlands) | | | 14,295,021 | | | | 281,183,063 | |

Tyco International, Ltd.(b)

(Switzerland) | | | 5,237,675 | | | | 276,811,124 | |

| | | | | | | | |

| | | | 1,825,528,314 | |

COMMERICAL & PROFESSIONAL SERVICES: 0.1% | |

Pitney Bowes, Inc. | | | 1,306,230 | | | | 19,554,263 | |

| | | | | | | | |

TRANSPORTATION: 2.5% | | | | | | | | |

FedEx Corp. | | | 10,547,399 | | | | 966,247,222 | |

| | | | | | | | |

| | | | 2,811,329,799 | |

| INFORMATION TECHNOLOGY: 20.3% | |

SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT: 0.8% | |

Maxim Integrated Products, Inc.(c) | | | 11,687,800 | | | | 299,675,192 | |

| | |

| See accompanying Notes to Financial Statements | | DODGE & COX STOCK FUND §PAGE 6 |

| | | | |

| PORTFOLLO OF INVESTMENTS (unaudited) | | | June 30, 2012 | |

| | | | | | | | |

| COMMON STOCKS (continued) | |

| | |

| | | SHARES | | | VALUE | |

SOFTWARE & SERVICES: 10.7% | |

Adobe Systems, Inc.(a) | | | 10,676,800 | | | $ | 345,608,016 | |

Amdocs, Ltd.(a),(b)

(Guernsey/United States) | | | 3,984,980 | | | | 118,433,606 | |

AOL, Inc.(a),(c) | | | 8,403,254 | | | | 235,963,372 | |

BMC Software, Inc.(a),(c) | | | 7,515,140 | | | | 320,746,175 | |

Cadence Design Systems, Inc.(a),(c) | | | 13,903,900 | | | | 152,803,861 | |

Computer Sciences Corp.(c) | | | 9,119,362 | | | | 226,342,565 | |

Compuware Corp.(a),(c) | | | 14,771,012 | | | | 137,222,701 | |

eBay, Inc.(a) | | | 14,793,100 | | | | 621,458,131 | |

Microsoft Corp. | | | 34,364,800 | | | | 1,051,219,232 | |

Symantec Corp.(a) | | | 33,964,600 | | | | 496,222,806 | |

Synopsys, Inc.(a),(c) | | | 13,287,669 | | | | 391,056,099 | |

| | | | | | | | |

| | | | 4,097,076,564 | |

TECHNOLOGY, HARDWARE & EQUIPMENT: 8.8% | |

Corning, Inc. | | | 14,200,000 | | | | 183,606,000 | |

Dell, Inc.(a) | | | 14,300,000 | | | | 179,036,000 | |

Hewlett-Packard Co. | | | 64,466,895 | | | | 1,296,429,259 | |

Molex, Inc. | | | 2,500,400 | | | | 59,859,576 | |

Molex, Inc., Class A | | | 9,060,630 | | | | 183,296,545 | |

NetApp, Inc.(a) | | | 12,050,000 | | | | 383,431,000 | |

Nokia Corp. ADR(b) (Finland) | | | 53,286,400 | | | | 110,302,848 | |

TE Connectivity, Ltd.(b)

(Switzerland) | | | 14,064,675 | | | | 448,803,779 | |

Xerox Corp. | | | 66,746,682 | | | | 525,296,387 | |

| | | | | | | | |

| | | | 3,370,061,394 | |

| | | | | | | | |

| | | | 7,766,813,150 | |

| MATERIALS: 3.4% | |

Celanese Corp., Series A(c) | | | 7,882,503 | | | | 272,892,254 | |

Cemex SAB de CV ADR(a),(b)

(Mexico) | | | 22,960,171 | | | | 154,521,951 | |

Domtar Corp. | | | 682,349 | | | | 52,342,992 | |

Dow Chemical Co. | | | 17,561,145 | | | | 553,176,067 | |

Vulcan Materials Co.(c) | | | 6,358,925 | | | | 252,512,912 | |

| | | | | | | | |

| | | | 1,285,446,176 | |

| TELECOMMUNICATION SERVICES: 2.7% | |

Sprint Nextel Corp.(a),(c) | | | 171,357,839 | | | | 558,626,555 | |

Vodafone Group PLC ADR(b)

(United Kingdom) | | | 16,266,600 | | | | 458,392,788 | |

| | | | | | | | |

| | | | 1,017,019,343 | |

| | | | | | | | |

TOTAL COMMON STOCKS

(Cost $35,971,249,164) | | | $ | 37,685,841,282 | |

| | | | | | | | |

| SHORT-TERM INVESTMENTS: 0.7% | |

| | |

| | | PAR VALUE | | | VALUE | |

MONEY MARKET FUND: 0.1% | |

SSgA U.S. Treasury Money Market Fund | | $ | 37,147,154 | | | $ | 37,147,154 | |

REPURCHASE AGREEMENT: 0.6% | |

Fixed Income Clearing Corporation(d) 0.11%, 7/2/12, maturity value $248,981,282 | | | 248,979,000 | | | | 248,979,000 | |

| | | | | | | | |

TOTAL SHORT-TERM INVESTMENTS

(Cost $286,126,154) | | | $ | 286,126,154 | |

| | | | | | | | |

TOTAL INVESTMENTS

(Cost $36,257,375,318) | | | 99.3 | % | | $ | 37,971,967,436 | |

OTHER ASSETS LESS LIABILITIES | | | 0.7 | % | | | 260,861,707 | |

| | | | | | | | |

| NET ASSETS | | | 100.0 | % | | $ | 38,232,829,143 | |

| | | | | | | | |

| (b) | Security denominated in U.S. dollars |

| (c) | See Note 8 regarding holdings of 5% voting securities |

| (d) | Repurchase agreement is collateralized by Federal Home Loan Bank 3.75%, 9/9/16; Freddie Mac 2.50%, 5/27/16 and U.S. Treasury Note 3.125%, 10/31/16. Total collateral value is 253,963,418. |

In determining a company’s country designation, the Fund generally references the country of incorporation. In cases where the Fund considers the country of incorporation to be a “jurisdiction of convenience” chosen primarily for tax purposes, the Fund uses the country designation of an appropriate broad-based market index. In that circumstance, two countries are listed - the country of incorporation and the country designated by an appropriate index, respectively.

ADR: American Depositary Receipt

| | |

| PAGE 7 § DODGE & COX STOCK FUND | | See accompanying Notes to Financial Statements |

| | | | |

STATEMENT OF ASSETS AND LIABILITIES

(unaudited) | |

| |

| | | June 30, 2012 | |

ASSETS: | | | | |

Investments, at value | | | | |

Unaffiliated issuers (cost $31,949,216,638) | | $ | 34,354,367,914 | |

Affiliated issuers (cost $4,308,158,680) | | | 3,617,599,522 | |

| | | | |

| | | 37,971,967,436 | |

Receivable for investments sold | | | 362,299,483 | |

Receivable for Fund shares sold | | | 63,992,670 | |

Dividends and interest receivable | | | 98,879,043 | |

Prepaid expenses and other assets | | | 86,994 | |

| | | | |

| | | 38,497,225,626 | |

| | | | |

LIABILITIES: | | | | |

Payable for investments purchased | | | 194,873,735 | |

Payable for Fund shares redeemed | | | 53,058,730 | |

Management fees payable | | | 15,137,278 | |

Accrued expenses | | | 1,326,740 | |

| | | | |

| | | 264,396,483 | |

| | | | |

NET ASSETS | | $ | 38,232,829,143 | |

| | | | |

NET ASSETS CONSIST OF: | | | | |

Paid in capital | | $ | 40,761,090,244 | |

Undistributed net investment income | | | 20,259,572 | |

Accumulated net realized loss | | | (4,263,112,791 | ) |

Net unrealized appreciation | | | 1,714,592,118 | |

| | | | |

| | $ | 38,232,829,143 | |

| | | | |

Fund shares outstanding (par value $0.01 each, unlimited shares authorized) | | | 346,100,522 | |

Net asset value per share | | | $110.47 | |

|

STATEMENT OF OPERATIONS

(unaudited) | |

| | | Six Months Ended

June 30, 2012 | |

INVESTMENT INCOME: | | | | |

Dividends (net of foreign taxes of $20,638,230) | | | | |

Unaffiliated issuers | | $ | 500,652,869 | |

Affiliated issuers | | | 13,648,105 | |

Interest | | | 53,621 | |

| | | | |

| | | 514,354,595 | |

| | | | |

EXPENSES: | | | | |

Management fees | | | 96,464,544 | |

Custody and fund accounting fees | | | 560,096 | |

Transfer agent fees | | | 1,875,552 | |

Professional services | | | 63,568 | |

Shareholder reports | | | 535,196 | |

Registration fees | | | 239,227 | |

Trustees’ fees | | | 98,800 | |

Miscellaneous | | | 1,420,610 | |

| | | | |

| | | 101,257,593 | |

| | | | |

NET INVESTMENT INCOME | | | 413,097,002 | |

| | | | |

REALIZED AND UNREALIZED

GAIN ON INVESTMENTS: | | | | |

Net realized gain | | | | |

Unaffiliated issuers | | | 1,536,250,146 | |

Affiliated issuers | | | 127,932,356 | |

Net change in unrealized appreciation/depreciation | | | 1,454,171,394 | |

| | | | |

Net realized and unrealized gain | | | 3,118,353,896 | |

| | | | |

NET INCREASE IN NET ASSETS FROM OPERATIONS | | $ | 3,531,450,898 | |

| | | | |

| | | | | | | | |

STATEMENT OF CHANGES IN NET ASSETS | |

| | |

| | | Six Months Ended June 30, 2012

(unaudited) | | | Year Ended

December 31, 2011 | |

OPERATIONS: | | | | | | | | |

Net investment income | | $ | 413,097,002 | | | $ | 664,516,079 | |

Net realized gain | | | 1,664,182,502 | | | | 512,064,516 | |

Net change in unrealized appreciation/depreciation | | | 1,454,171,394 | | | | (2,850,476,884 | ) |

| | | | | | | | |

| | | 3,531,450,898 | | | | (1,673,896,289 | ) |

| | | | | | | | |

| | |

DISTRIBUTIONS TO SHAREHOLDERS FROM: | | | | | | | | |

Net investment income | | | (399,366,815 | ) | | | (664,086,748 | ) |

Net realized gain | | | — | | | | — | |

| | | | | | | | |

Total distributions | | | (399,366,815 | ) | | | (664,086,748 | ) |

| | | | | | | | |

| | |

FUND SHARE TRANSACTIONS: | | | | | | | | |

Proceeds from sale of shares | | | 3,095,339,062 | | | | 5,006,315,221 | |

Reinvestment of distributions | | | 371,957,607 | | | | 625,800,158 | |

Cost of shares redeemed | | | (4,928,928,813 | ) | | | (9,769,356,748 | ) |

| | | | | | | | |

Net decrease from Fund share transactions | | | (1,461,632,144 | ) | | | (4,137,241,369 | ) |

| | | | | | | | |

Total increase (decrease) in net assets | | | 1,670,451,939 | | | | (6,475,224,406 | ) |

| | |

NET ASSETS: | | | | | | | | |

Beginning of period | | | 36,562,377,204 | | | | 43,037,601,610 | |

| | | | | | | | |

End of period (including undistributed net investment income of $20,259,572 and $6,529,385, respectively) | | $ | 38,232,829,143 | | | $ | 36,562,377,204 | |

| | | | | | | | |

| | |

SHARE INFORMATION: | | | | | | | | |

Shares sold | |

| 28,016,982

|

| | | 46,452,278 | |

Distributions reinvested | | | 3,372,602 | | | | 5,991,930 | |

Shares redeemed | | | (45,016,964 | ) | | | (92,083,372 | ) |

| | | | | | | | |

Net decrease in shares outstanding | | | (13,627,380 | ) | | | (39,639,164 | ) |

| | | | | | | | |

| | |

| See accompanying Notes to Financial Statements | | DODGE & COX STOCK FUND §PAGE 8 |

NOTES TO FINANCIAL STATEMENTS (unaudited)

NOTE 1—ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES

Dodge & Cox Stock Fund (the “Fund”) is one of the series constituting the Dodge & Cox Funds (the “Trust” or the “Funds”). The Trust is organized as a Delaware statutory trust and is registered under the Investment Company Act of 1940, as amended, as a diversified, open-end management investment company. The Fund commenced operations on January 4, 1965, and seeks long-term growth of principal and income. Risk considerations and investment strategies of the Fund are discussed in the Fund’s Prospectus.

The financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America, which require the use of estimates and assumptions by management. Actual results may differ from those estimates. Significant accounting policies are as follows:

Security valuation The Fund’s net assets are valued as of the close of trading on the New York Stock Exchange (NYSE), generally 4:00 p.m. Eastern Time, each day that the NYSE is open for business. Listed securities are valued at market, using the official quoted close price or the last sale of the day at the close of the NYSE or, if not available, at the mean between the exchange listed bid and ask prices. A security that is listed or traded on more than one exchange is valued at the quotation on the exchange determined to be the primary market for such security. Security values are not discounted based on the size of the Fund’s position. Securities for which market quotations are not readily available are valued at fair value as determined in good faith by or under the direction of the Board of Trustees. Short-term securities are valued at amortized cost, which approximates current value. All securities held by the Fund are denominated in U.S. dollars.

Security transactions, investment income, expenses, and distributions Security transactions are recorded on the trade date. Realized gains and losses on securities sold are determined on the basis of identified cost.

Dividend income and corporate action transactions are recorded on the ex-dividend date, or when the Fund first learns of the dividend/corporate action if the ex-dividend date has passed. Withholding taxes on foreign dividends have been provided for in accordance with the

Fund’s understanding of the applicable country’s tax rules and rates. Non-cash dividends included in dividend income, if any, are recorded at the fair market value of the securities received. Dividends characterized as return of capital are recorded as a reduction of cost of investments and/or realized gain. Interest income is recorded on the accrual basis.

Expenses are recorded on the accrual basis. Most expenses of the Trust can be directly attributed to a specific series. Expenses which cannot be directly attributed are allocated among the Funds in the Trust based on relative net assets or other expense methodologies determined by the nature of the expense.

Distributions to shareholders are recorded on the ex-dividend date.

Repurchase agreements The Fund enters into repurchase agreements, secured by U.S. government or agency securities, which involve the purchase of securities from a counterparty with a simultaneous commitment to resell the securities at an agreed-upon date and price. It is the Fund’s policy that its custodian take possession of the underlying collateral securities, the fair value of which exceeds the principal amount of the repurchase transaction, including accrued interest, at all times. In the event of default by the counterparty, the Fund has the contractual right to liquidate the collateral securities and to apply the proceeds in satisfaction of the obligation.

Indemnification Under the Trust’s organizational documents, its officers and trustees are indemnified against certain liabilities arising out of the performance of their duties to the Trust. In addition, in the normal course of business the Trust enters into contracts that provide general indemnities to other parties. The Trust’s maximum exposure under these arrangements is unknown as this would involve future claims that may be made against the Trust that have not yet occurred.

NOTE 2—VALUATION MEASUREMENTS

Various inputs are used in determining the value of the Fund’s investments. These inputs are summarized in the three broad levels listed below.

| § | | Level 1: Quoted prices in active markets for identical securities |

PAGE 9 § DODGE & COX STOCK FUND

NOTES TO FINANCIAL STATEMENTS (unaudited)

| § | | Level 2: Other significant observable inputs (including quoted prices for similar securities, market indices, interest rates, credit risk, etc.) |

| § | | Level 3: Significant unobservable inputs (including Fund management’s assumptions in determining the fair value of investments) |

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

The following is a summary of the inputs used to value the Fund’s holdings as of June 30, 2012:

| | | | | | | | |

| Security Classification(a) | | LEVEL 1

(Quoted Prices) | | | LEVEL 2

(Other Significant

Observable Inputs) | |

Common Stocks(b) | | $ | 37,685,841,282 | | | $ | — | |

Money Market Fund | | | 37,147,154 | | | | — | |

Repurchase Agreement | | | — | | | | 248,979,000 | |

| | | | | | | | |

Total | | $ | 37,722,988,436 | | | $ | 248,979,000 | |

| | | | | | | | |

| | | | | | | | | |

| (a) | There were no transfers between Level 1 and Level 2 during the six months ended June 30, 2012. There were no Level 3 securities at June 30, 2012, and December 31, 2011, and there were no transfers to Level 3 during the period. |

| (b) | All common stocks held in the Fund are Level 1 securities. For a detailed break-out of common stocks by major industry classification, please refer to the Portfolio of Investments. |

NOTE 3—RELATED PARTY TRANSACTIONS

Management fees Under a written agreement approved by a unanimous vote of the Board of Trustees, the Fund pays an annual management fee of 0.50% of the Fund’s average daily net assets to Dodge & Cox, investment manager of the Fund. The agreement further provides that Dodge & Cox shall waive its fee to the extent that such fee plus all other ordinary operating expenses of the Fund exceed 0.75% of the average daily net assets for the year.

Fund officers and trustees All officers and three of the trustees of the Trust are officers or employees of Dodge & Cox. The Trust pays a fee only to those trustees who are not affiliated with Dodge & Cox.

NOTE 4—INCOME TAX INFORMATION

A provision for federal income taxes is not required since the Fund intends to continue to qualify as a regulated investment company under Subchapter M of the Internal Revenue Code and distribute all of its taxable income to

shareholders. Distributions are determined in accordance with income tax regulations, and such amounts may differ from net investment income and realized gains for financial reporting purposes. Financial reporting records are adjusted for permanent book/tax differences at year end to reflect tax character.

Book/tax differences are primarily due to differing treatments of wash sales, in-kind redemptions, and net short-term realized gain (loss). During the period, the Fund recognized net realized gains of $59,680,161 from the delivery of appreciated securities in an in-kind redemption transaction. For federal income tax purposes, this gain is not recognized as taxable income to the Fund and therefore will not be distributed to shareholders. At June 30, 2012, the cost of investments for federal income tax purposes was $36,330,937,034.

Distributions during the six months ended June 30, 2012, and for the year ended December 31, 2011, were characterized as follows for federal income tax purposes:

| | | | | | | | |

| | | Six Months Ended

June 30, 2012 | | | Year Ended December 31, 2011 | |

Ordinary income | | | $399,366,815 | | | | $664,086,748 | |

| | | ($1.14 per share) | | | | ($1.754 per share) | |

| | |

Long-term capital gain | | | — | | | | — | |

At June 30, 2012, the tax basis components of distributable earnings were as follows:

| | | | |

Unrealized appreciation | | $ | 6,500,197,260 | |

Unrealized depreciation | | | (4,859,166,858 | ) |

| | | | |

Net unrealized appreciation | | | 1,641,030,402 | |

Undistributed ordinary income | | | 20,259,572 | |

Accumulated capital gain(a) | | | 1,604,502,340 | |

Capital loss carryforward(b) | | | (5,853,733,576 | ) |

| (a) | Represents capital gain realized for tax purposes during the period January 1, 2012 to June 30, 2012. |

| (b) | Represents accumulated capital loss as of December 31, 2011, which may be carried forward to offset future capital gains. During 2011, the Fund utilized $443,284,672 of the carryforward. If not utilized, the remaining capital loss carryforward will expire in 2017. |

Under the Regulated Investment Company Modernization Act of 2010, capital losses incurred by the Fund after January 1, 2011, will not be subject to expiration.

DODGE & COX STOCK FUND §PAGE 10

NOTES TO FINANCIAL STATEMENTS (unaudited)

In addition, such losses must be utilized prior to the losses incurred in the years preceding enactment. (The Fund had net capital gains in 2011.)

Fund management has reviewed the tax positions for open periods (three years and four years, respectively, from filing the Fund’s Federal and State tax returns) as applicable to the Fund, and has determined that no provision for income tax is required in the Fund’s financial statements.

NOTE 5—LOAN FACILITIES

Pursuant to an exemptive order issued by the Securities and Exchange Commission (SEC), the Fund may participate in an interfund lending facility (Facility). The Facility allows the Fund to borrow money from or loan money to the Funds. Loans under the Facility are made for temporary or emergency purposes, such as to fund shareholder redemption requests. Interest on borrowings is the average of the current repurchase agreement rate and the bank loan rate. There was no activity in the Facility during the period.

All Funds in the Trust participate in a $500 million committed credit facility (Line of Credit) with

State Street Bank and Trust Company, to be utilized for temporary or emergency purposes to fund shareholder redemptions or for other short-term liquidity purposes. The maximum amount available to the Fund is $250 million. Each Fund pays an annual commitment fee on its pro-rata portion of the Line of Credit. The Fund’s commitment fee for the six months ended June 30, 2012, amounted to $87,014 and is reflected as a Miscellaneous Expense in the Statement of Operations. Interest on borrowings is charged at the prevailing rate. There were no borrowings on the Line of Credit during the period.

NOTE 6—PURCHASES AND SALES OF INVESTMENTS

For the six months ended June 30, 2012, purchases and sales of securities, other than short-term securities, aggregated $2,240,733,602 and $4,046,146,749, respectively.

NOTE 7—SUBSEQUENT EVENTS

Fund management has determined that no material events or transactions occurred subsequent to June 30, 2012, and through the date of the Fund’s financial statements issuance, which require additional disclosure in the Fund’s financial statements.

NOTE 8—HOLDINGS OF 5% VOTING SECURITIES

Each of the companies listed below was considered to be an affiliate of the Fund because the Fund owned 5% or more of the company’s voting securities during all or part of the six months ended June 30, 2012. Purchase and sale transactions and dividend income earned during the period on these securities were as follows:

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Shares at

Beginning of Period | | | Additions | | | Reductions | | | Shares at

End of Period | | | Dividend

Income(a) | | | Value at

End of Period | |

AOL, Inc. | | | 8,439,054 | | | | — | | | | (35,800 | ) | | | 8,403,254 | | | | — | (b) | | | 235,963,372 | |

BMC Software, Inc. | | | 8,250,140 | | | | — | | | | (735,000 | ) | | | 7,515,140 | | | | — | (b) | | | — | (c) |

Cadence Design Systems, Inc. | | | 19,448,500 | | | | — | | | | (5,544,600 | ) | | | 13,903,900 | | | | — | (b) | | | 152,803,861 | |

Capital One Financial Corp. | | | 30,180,911 | | | | — | | | | (128,000 | ) | | | 30,052,911 | | | | 3,005,291 | | | | 1,642,692,115 | |

Celanese Corp., Series A | | | 4,602,003 | | | | 3,300,000 | | | | (19,500 | ) | | | 7,882,503 | | | | 657,762 | | | | 272,892,254 | |

Computer Sciences Corp. | | | 8,996,552 | | | | 122,810 | | | | — | | | | 9,119,362 | | | | 3,647,745 | | | | 226,342,565 | |

Compuware Corp. | | | 15,838,112 | | | | — | | | | (1,067,100 | ) | | | 14,771,012 | | | | — | (b) | | | 137,222,701 | |

Maxim Integrated Products, Inc. | | | 17,296,400 | | | | — | | | | (5,608,600 | ) | | | 11,687,800 | | | | 6,194,628 | | | | — | (c) |

Sprint Nextel Corp. | | | 135,934,139 | | | | 36,000,000 | | | | (576,300 | ) | | | 171,357,839 | | | | — | (b) | | | 558,626,555 | |

Synopsys, Inc. | | | 13,695,769 | | | | — | | | | (408,100 | ) | | | 13,287,669 | | | | — | (b) | | | 391,056,099 | |

Vulcan Materials Co. | | | 7,942,625 | | | | — | | | | (1,583,700 | ) | | | 6,358,925 | | | | 142,679 | | | | — | (c) |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | $ | 13,648,105 | | | $ | 3,617,599,522 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| (a) | Net of foreign taxes, if any |

| (c) | Company was not an affiliate at period end |

PAGE 11 § DODGE & COX STOCK FUND

FINANCIAL HIGHLIGHTS

| | | | | | | | | | | | | | | | | | | | | | | | |

SELECTED DATA AND RATIOS (for a share outstanding throughout each period) | | Six Months

Ended June 30, | | | Year Ended December 31, | |

| | | 2012(a) | | | 2011 | | | 2010 | | | 2009 | | | 2008 | | | 2007 | |

| | | | | | | | |

Net asset value, beginning of period | | | $101.64 | | | | $107.76 | | | | $96.14 | | | | $74.37 | | | | $138.26 | | | | $153.46 | |

Income from investment operations: | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | 1.18 | | | | 1.76 | | | | 1.23 | | | | 1.15 | | | | 1.91 | | | | 2.30 | |

Net realized and unrealized gain (loss) | | | 8.79 | | | | (6.13 | ) | | | 11.62 | | | | 21.82 | | | | (59.83 | ) | | | (1.90 | ) |

| | | | | | | | |

Total from investment operations | | | 9.97 | | | | (4.37 | ) | | | 12.85 | | | | 22.97 | | | | (57.92 | ) | | | 0.40 | |

| | | | | | | | |

Distributions to shareholders from: | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | (1.14 | ) | | | (1.75 | ) | | | (1.23 | ) | | | (1.20 | ) | | | (1.84 | ) | | | (2.34 | ) |

Net realized gain | | | — | | | | — | | | | — | | | | — | | | | (4.13 | ) | | | (13.26 | ) |

| | | | | | | | |

Total distributions | | | (1.14 | ) | | | (1.75 | ) | | | (1.23 | ) | | | (1.20 | ) | | | (5.97 | ) | | | (15.60 | ) |

| | | | | | | | |

Net asset value, end of period | | | $110.47 | | | | $101.64 | | | | $107.76 | | | | $96.14 | | | | $74.37 | | | | $138.26 | |

| | | | | | | | |

Total return | | | 9.82 | % | | | (4.08 | )% | | | 13.48 | % | | | 31.27 | % | | | (43.31 | )% | | | 0.14 | % |

Ratios/supplemental data: | | | | | | | | | | | | | | | | | | | | | | | | |

Net assets, end of period (millions) | | | $38,233 | | | | $36,562 | | | | $43,038 | | | | $39,991 | | | | $32,721 | | | | $63,291 | |

Ratio of expenses to average net assets | | | 0.52 | %(b) | | | 0.52 | % | | | 0.52 | % | | | 0.52 | % | | | 0.52 | % | | | 0.52 | % |

Ratio of net investment income to average net assets | | | 2.14 | %(b) | | | 1.62 | % | | | 1.25 | % | | | 1.42 | % | | | 1.75 | % | | | 1.44 | % |

Portfolio turnover rate | | | 6 | % | | | 16 | % | | | 12 | % | | | 18 | % | | | 31 | % | | | 27 | % |

See accompanying Notes to Financial Statements

DODGE & COX STOCK FUND §PAGE 12

FUND HOLDINGS

The Fund provides a complete list of its holdings four times each fiscal year, as of the end of each quarter. The Fund files the lists with the Securities and Exchange Commission (SEC) on Form N-CSR (second and fourth quarters) and Form N-Q (first and third quarters). Shareholders may view the Fund’s Forms N-CSR and N-Q on the SEC’s website at www.sec.gov. Forms N-CSR and N-Q may also be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information regarding the operations of the Public Reference Room may be obtained by calling 202-942-8090 (direct) or 800-732-0330 (general SEC number). A list of the Fund’s quarter-end holdings is also available at www.dodgeandcox.com on or about 15 days following each quarter end and remains available on the website until the list is updated in the subsequent quarter.

PROXY VOTING

For a free copy of the Fund’s proxy voting policies and procedures, please call 800-621-3979, visit the Fund’s website at www.dodgeandcox.com, or visit the SEC’s website at www.sec.gov. Information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ending June 30 is also available at www.dodgeandcox.com or at www.sec.gov.

HOUSEHOLD MAILINGS

The Fund routinely mails shareholder reports and summary prospectuses to shareholders and, on occasion, proxy statements. In order to reduce the volume of mail, when possible, only one copy of these documents will be sent to shareholders who are part of the same family and share the same residential address.

If you have a direct account with the Funds and you do not want the mailing of shareholder reports and summary prospectuses combined with other members in your household, contact the Funds at 800-621-3979. Your request will be implemented within 30 days.

PAGE 13 § DODGE & COX STOCK FUND

THIS PAGE INTENTIONALLY LEFT BLANK

DODGE & COX STOCK FUND §PAGE 14

TRUSTEES AND EXECUTIVE OFFICERS

Kenneth E. Olivier, Chairman, President, and Trustee

Chairman and Chief Executive Officer, Dodge & Cox

Dana M. Emery, Senior Vice President and Trustee

Co-President and Director of Fixed Income, Dodge & Cox

John A. Gunn, Trustee

Chairman Emeritus, Dodge & Cox

L. Dale Crandall, Independent Trustee

Former President, Kaiser Foundation Health Plan and Hospitals

Thomas A. Larsen, Independent Trustee

Director, Howard, Rice, Nemerovski, Canady, Falk & Rabkin

Ann Mather, Independent Trustee

Former Executive Vice President, Chief Financial Officer, and Company Secretary of Pixar Studios

Robert B. Morris III, Independent Trustee

Former Partner and Managing Director of Global Research at Goldman Sachs & Co.

John B. Taylor, Independent Trustee

Professor of Economics, Stanford University; Senior Fellow, Hoover Institute and former Under Secretary for International Affairs, United States Treasury

Charles F. Pohl, Senior Vice President

Co-President and Chief Investment Officer, Dodge & Cox

Diana S. Strandberg, Senior Vice President

Senior Vice President and Director of International Equity, Dodge & Cox

David H. Longhurst, Treasurer

Vice President and Assistant Treasurer, Dodge & Cox

Thomas M. Mistele, Secretary

Chief Operating Officer, Secretary, and Senior Counsel, Dodge & Cox

Katherine M. Primas, Chief Compliance Officer

Chief Compliance Officer, Dodge & Cox

Additional information about the Trust’s Trustees and Officers is available in the Trust’s Statement of Additional Information (SAI). You can get a free copy of the SAI by visiting the Funds’ website at www.dodgeandcox.com or calling 1-800-621-3979.

PAGE 15 § DODGE & COX STOCK FUND

| | | | |

| | | | |

www.dodgeandcox.com

For Fund literature, transactions, and account information, please visit the Funds’ website.

or write or call:

DODGE & COX FUNDS

c/o Boston Financial Data Services

P.O. Box 8422

Boston, Massachusetts 02266-8422

(800) 621-3979

INVESTMENT MANAGER

Dodge & Cox

555 California Street, 40th Floor

San Francisco, California 94104

(415) 981-1710

This report is submitted for the general information of the shareholders of the Fund. The report is not authorized for distribution to prospective investors in the Fund unless it is accompanied by a current prospectus.

This report reflects our views, opinions, and portfolio holdings as of June 30, 2012, the end of the reporting period. Any such views are subject to change at any time based upon market or other conditions and Dodge & Cox disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Dodge & Cox Fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Dodge & Cox Fund.

6/12 GSF SAR Printed on recycled paper

Semi-Annual Report

June 30, 2012

Global Stock

Fund

ESTABLISHED 2008

TICKER: DODWX

TO OUR SHAREHOLDERS

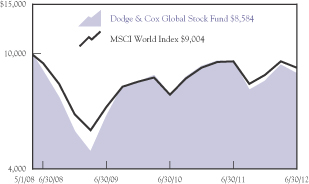

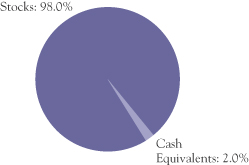

The Dodge & Cox Global Stock Fund had a total return of 6.4% for the six months ended June 30, 2012, compared to 5.9% for the MSCI World Index. On June 30, the Fund had net assets of $2.1 billion with a cash position of 2.0%.

MARKET COMMENTARY

After a strong first quarter in which the MSCI World rose 11.6%, the market fell 5.1% during the second quarter and ended the first half of 2012 up 5.9%. In the first quarter, investor optimism increased as companies reported healthy earnings, concerns about Eurozone banks were alleviated with the liquidity provided by the European Central Bank, and job growth in the United States was robust. In the second quarter, questions about the fate of the euro and potential impact of austerity measures on European economies resurfaced. Manufacturing activity in China and employment growth in the United States also showed signs of slowing down.

Equity valuations have declined to low levels: the MSCI World traded at 14 times trailing earnings on June 30. Low valuations have historically been associated with attractive subsequent long-term returns. As a result, we continue to believe that now is a compelling time to invest in equities.

INVESTMENT STRATEGY

Our longstanding approach to investing remains unchanged. We practice bottom-up stock selection based on intensive fundamental analysis. Investment decisions for the Fund are based on current valuation relative to our assessment of the long-term fundamental outlook for each holding. Market turmoil creates opportunities to invest in established franchises at attractive valuations. We have assembled a diversified portfolio of such investments. We remain confident in the long-term outlook for the Fund. Our assessment of two leading contributors to, and two leading detractors from, the Fund’s six-month performance follows.(a)

Strong Performers: Wells Fargo and Comcast

Wells Fargo (2.8% of the Fund on June 30) and Comcast (1.6%) helped the Fund’s results in the first half of the

year. Wells Fargo, the second largest U.S. bank by deposits, ended the first half of the year up 23%. The company has a long record of growth and strong risk management. It has leading consumer and small business banking franchises, is gaining market share, and yet remains attractively valued relative to its peers.

Comcast rose 36% in the first half of the year. Comcast has been a holding since the Fund’s inception in 2008, and we continue to be optimistic about its prospects. It is the largest pay-television and residential broadband service provider in the United States and operates a strong portfolio of cable networks. In addition, Comcast has growth potential from its broadband internet business and from expanding its services to business customers. Over the past four years, Comcast has generated consistent free cash flow growth; on June 30, it traded at an enterprise value of 6.6 times estimated(b) 2013 EBITDA.(c)

Weak Performers: Hewlett-Packard and Credit Suisse

Hewlett-Packard (2.6% of the Fund on June 30) and Credit Suisse (1.5%) both hurt results in the first half of the year. Hewlett-Packard, down 21% year to date, has been one of the Fund’s largest holdings for the past several years. The company has struggled recently with management changes, acquisition integrations, and disappointing earnings. Despite these concerns, we have confidence in the company’s prospects due to its collection of durable business franchises (such as printers and servers), its attractive valuation (trading at 0.3 times sales and 4.7 times forward earnings on June 30), and scale advantages from its position as one of the largest technology companies in the world.

PAGE 1 § DODGE & COX GLOBAL STOCK FUND

Credit Suisse, a leading global private and investment bank, was down 20% in the first half of the year due to disappointing results in its investment banking division and concerns over a relatively weak capital position. In July, the company initiated a series of actions to increase its capitalization levels. Credit Suisse is well positioned to benefit from growth in private banking and capital markets around the world, while it is relatively insulated from the challenges of the Eurozone banking system.

IN CLOSING

Global equity markets are trading at compelling valuations, reflecting concerns about the course of the world economy. And yet, we note that most companies are better capitalized today than five years ago, with stronger cash flows and lower cost structures. Thus, they have greater ability to withstand an uncertain environment and take actions to build long-term value. Markets could continue to be volatile over the short term, but we are enthusiastic about the long-term prospects for equities in general, and especially for the holdings in the Fund.

Thank you for your continued confidence in our firm. As always, we welcome your comments and questions.

For the Board of Trustees,

| | |

| | |

Kenneth E. Olivier, Chairman and President | | Charles F. Pohl Senior Vice President |

July 26, 2012

| (a) | | We use these examples to illustrate our investment process, not to imply that we think they are more attractive than the Fund’s other holdings. |

| (b) | | Forward estimates are from third-party sources. |

| (c) | | EBITDA is earnings before interest, taxes, depreciation, and amortization. Enterprise value is a measure of a company’s firm value and is generally calculated as the sum of a company’s market capitalization and debt minus its cash. |

DODGE & COX GLOBAL STOCK FUND §PAGE 2

YEAR-TO-DATE PERFORMANCE REVIEW

The Fund outperformed the MSCI World by 0.5 percentage points year to date.

Key Contributors to Relative Results

| | § | | Strong returns in the Financials sector (up 14% versus up 9% for the MSCI World sector), combined with a higher average weighting (25% versus 18%), had a positive impact. Bank of America (up 48%), Capital One (up 30%), and Wells Fargo (up 23%) were strong performers. | |

| | § | | Returns in the Materials sector (up 8% versus down 2% for the MSCI World sector) contributed to relative performance. | |

| | § | | The Energy sector was the weakest sector of the market. Therefore, the Fund’s lower average weighting (6% versus 11% for the MSCI World sector) contributed to relative results. | |

| | § | | Additional contributors included AOL (up 86%), Comcast (up 36%), and Microsoft (up 19%). | |

Key Detractors from Relative Results

| | § | | Weak returns from holdings in the Information Technology sector (down 2% versus up 10% for the MSCI World sector) hurt results. Nokia (down 56%) and Hewlett-Packard (down 21%) were notable detractors. | |

| | § | | Weak relative returns in the Consumer Discretionary sector (up 5% versus up 11% for the MSCI World sector) also hindered performance. Yamaha Motor (down 25%) was a weak performer. | |

| | § | | Additional detractors included Unicredit (down 31%), Celanese (down 22%), and Credit Suisse (down 20%). | |

KEY CHARACTERISTICS OF DODGE & COX

Independent Organization

Dodge & Cox is one of the largest privately owned investment managers in the world. We remain committed to independence, with a goal of providing the highest quality investment management service to our existing clients.

80 Years of Investment Experience

Dodge & Cox was founded in 1930. We have a stable and well-qualified team of investment professionals, most of whom have spent their entire careers at Dodge & Cox.

Experienced Investment Team

The Global Investment Policy Committee, which is the decision-making body for the Global Stock Fund, is a seven-member committee with an average tenure at Dodge & Cox of 21 years.

One Business with a Single Research Office

Dodge & Cox manages domestic, international, and global equity, fixed income, and balanced investments, operating from one office in San Francisco.

Consistent Investment Approach

Our team decision-making process involves thorough, bottom-up fundamental analysis of each investment.

Long-Term Focus and Low Expenses

We invest with a three- to five-year investment horizon, which has historically resulted in low turnover relative to our peers. We manage Funds that maintain low expense ratios.

PAGE 3 § DODGE & COX GLOBAL STOCK FUND

GROWTH OF $10,000 SINCE INCEPTION

FOR AN INVESTMENT MADE ON MAY 1, 2008

AVERAGE ANNUAL TOTAL RETURN

FOR PERIODS ENDED JUNE 30, 2012

| | | | | | | | | | | | |

| | | 1 Year | | | 3 Years | | | Since

Inception

(5/01/08) | |

Dodge & Cox Global Stock Fund | | | -9.21 | % | | | 12.04 | % | | | -3.60 | % |

MSCI World Index | | | -4.99 | | | | 10.98 | | | | -2.49 | |

Returns represent past performance and do not guarantee future results. Investment return and share price will fluctuate with market conditions, and investors may have a gain or loss when shares are sold. Fund performance changes over time and currently may be significantly

lower than stated. Performance is updated and published monthly. Visit the Fund’s website at www.dodgeandcox.com or call 1-800-621-3979 for current performance figures.

The Fund’s total returns include the reinvestment of dividend and capital gain distributions, but have not been adjusted for any income taxes payable by shareholders on these distributions or on Fund share redemptions. Index returns include dividends but, unlike Fund returns, do not reflect fees or expenses. The MSCI World Index is a broad-based, unmanaged equity market index aggregated from 24 developed market country indices, including the United States. MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed, or produced by MSCI.

MSCI World is a service mark of MSCI Barra.

Risks: The Fund is subject to stock market risk, meaning stocks in the Fund may decline in value for extended periods due to the financial prospects of individual companies, or due to general market and economic conditions. Investing in non-U.S. securities may entail risk due to foreign economic and political developments; this risk may be increased when investing in emerging markets. Please read the prospectus and summary prospectus for specific details regarding the Fund’s risk profile.

FUND EXPENSE EXAMPLE

As a Fund shareholder, you incur ongoing Fund costs, including management fees and other Fund expenses. All mutual funds have ongoing costs, sometimes referred to as operating expenses. The following example shows ongoing costs of investing in the Fund and can help you understand these costs and compare them with those of other mutual funds. The example assumes a $1,000 investment held for the six months indicated.

ACTUAL EXPENSES

The first line of the table below provides information about actual account values and expenses based on the Fund’s actual returns. You may use the information in this line, together with your account balance, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

HYPOTHETICAL EXAMPLE FOR COMPARISON WITH OTHER MUTUAL FUNDS

Information on the second line of the table can help you compare ongoing costs of investing in the Fund with those of other mutual funds. This information may not be used to estimate the actual ending account balance or expenses you paid during the period. The hypothetical “Ending Account Value” is based on the actual expense ratio of the Fund and an assumed 5% annual rate of return before expenses (not the Fund’s actual return). The amount under the heading “Expense Paid During the Period” shows the hypothetical expenses your account would have incurred under this scenario. You can compare this figure with the 5% hypothetical examples that appear in shareholder reports of other mutual funds.

| | | | | | | | | | | | |

Six Months Ended June 30, 2012 | | Beginning Account Value

1/1/2012 | | | Ending Account Value

6/30/2012 | | | Expenses Paid During Period* | |

Based on Actual Fund Return | | $ | 1,000.00 | | | $ | 1,063.80 | | | $ | 3.37 | |

Based on Hypothetical 5% Yearly Return | | | 1,000.00 | | | | 1,021.60 | | | | 3.30 | |

| * | Expenses are equal to the Fund’s annualized expense ratio of 0.66%, multiplied by the average account value over the period, multiplied by 182/366 (to reflect the one-half year period). |

The expenses shown in the table highlight ongoing costs only and do not reflect any transactional fees or account maintenance fees. Though other mutual funds may charge such fees, please note that the Fund does not charge transaction fees (e.g., redemption fees, sales loads) or universal account maintenance fees (e.g., small account fees).

DODGE & COX GLOBAL STOCK FUND §PAGE 4

| | | | |

| FUND INFORMATION | | | June 30, 2012 | |

| | | | |

| GENERAL INFORMATION | | | |

Net Asset Value Per Share | | | $8.17 | |

Total Net Assets (billions) | | | $2.1 | |

Expense Ratio | | | 0.66% | |

Portfolio Turnover Rate (1/1/12 to 6/30/12, unannualized) | | | 6% | |

30-Day SEC Yield(a) | | | 2.01% | |

Fund Inception | | | 2008 | |

No sales charges or distribution fees | | | | |

Investment Manager: Dodge & Cox, San Francisco. Managed by the Global Investment Policy Committee, whose seven members’ average tenure at Dodge & Cox is 21 years.

| | | | | | | | |

| PORTFOLIO CHARACTERISTICS | | Fund | | | MSCI

World | |

Number of Stocks | | | 97 | | | | 1,626 | |

Median Market Capitalization (billions) | | | $21 | | | | $8 | |

Weighted Average Market

Capitalization (billions) | | | $66 | | | | $77 | |

Price-to-Earnings Ratio(b) | | | 10.0x | | | | 11.1x | |

Countries Represented | | | 22 | | | | 24 | |

Emerging Markets (Brazil, China, India, Indonesia, Mexico, South Africa, South Korea, Turkey) | | | 12.2% | | | | 0.0% | |

| | | | |

| TEN LARGEST HOLDINGS (%)(c) | | Fund | |

Sanofi (France) | | | 2.9 | |

Roche Holding AG (Switzerland) | | | 2.8 | |

Wells Fargo & Co. (United States) | | | 2.8 | |

Merck & Co., Inc. (United States) | | | 2.7 | |

Hewlett-Packard Co. (United States) | | | 2.6 | |

Microsoft Corp. (United States) | | | 2.5 | |

General Electric Co. (United States) | | | 2.2 | |

Naspers, Ltd. (South Africa) | | | 2.1 | |

GlaxoSmithKline PLC (United Kingdom) | | | 1.9 | |

Capital One Financial Corp. (United States) | | | 1.9 | |

| | | | | | | | |

| REGION DIVERSIFICATION (%)(d) | | Fund | | | MSCI

World | |

United States | | | 44.2 | | | | 54.3 | |

Europe (excluding United Kingdom) | | | 27.5 | | | | 16.6 | |

United Kingdom | | | 9.0 | | | | 9.5 | |

Japan | | | 5.5 | | | | 8.9 | |

Latin America | | | 4.9 | | | | 0.0 | |

Africa/Middle East | | | 3.5 | | | | 0.2 | |

Pacific (excluding Japan) | | | 3.4 | | | | 5.6 | |

Canada | | | 0.0 | | | | 4.9 | |

| | | | | | | | |

| SECTOR DIVERSIFICATION (%) | | Fund | | | MSCI

World | |

Financials | | | 23.9 | | | | 18.6 | |

Health Care | | | 16.6 | | | | 10.7 | |

Information Technology | | | 13.7 | | | | 12.6 | |

Consumer Discretionary | | | 12.1 | | | | 10.8 | |

Industrials | | | 8.2 | | | | 10.9 | |

Telecommunication Services | | | 8.0 | | | | 4.2 | |

Energy | | | 5.9 | | | | 10.6 | |

Materials | | | 5.7 | | | | 6.8 | |

Consumer Staples | | | 3.9 | | | | 11.0 | |

Utilities | | | 0.0 | | | | 3.8 | |

| (a) | | SEC Yield is an annualization of the Fund’s total net investment income per share for the 30-day period ended on the last day of the month. |

| (b) | | Price-to-earnings (P/E) ratios are calculated using 12-month forward earnings estimates from third-party sources. |

| (c) | | The Fund’s portfolio holdings are subject to change without notice. The mention of specific securities is not a recommendation to buy, sell, or hold any particular security and is not indicative of Dodge & Cox’s current or future trading activity. |

| (d) | | The Fund may classify a company in a different category than the MSCI World. The Fund generally classifies a company based on its country of incorporation, but may designate a different country in certain circumstances. |

PAGE 5 § DODGE & COX GLOBAL STOCK FUND

| | | | |

| PORTFOLIO OF INVESTMENTS (unaudited) | | | June 30, 2012 | |

| | | | | | | | |

| COMMON STOCKS: 96.6% | |

| | |

| | | SHARES | | | VALUE | |

| CONSUMER DISCRETIONARY: 12.1% | |

AUTOMOBILES & COMPONENTS: 1.8% | | | | | |

Bayerische Motoren Werke AG (Germany) | | | 102,400 | | | $ | 7,419,689 | |

Mahindra & Mahindra, Ltd. (India) | | | 655,100 | | | | 8,303,529 | |

Yamaha Motor Co., Ltd. (Japan) | | | 2,283,700 | | | | 21,787,262 | |

| | | | | | | | |

| | | | | | | 37,510,480 | |

CONSUMER DURABLES & APPAREL: 1.7% | | | | | |

LG Electronics, Inc. (South Korea) | | | 127,700 | | | | 6,889,125 | |

Li Ning Co., Ltd.(a) (Cayman Islands/China) | | | 10,911,300 | | | | 6,145,922 | |

Panasonic Corp. (Japan) | | | 1,814,400 | | | | 14,757,571 | |

Sony Corp. (Japan) | | | 429,600 | | | | 6,113,470 | |

| | | | | | | | |

| | | | | | | 33,906,088 | |

MEDIA: 7.3% | | | | | |

Comcast Corp., Class A (United States) | | | 1,050,600 | | | | 33,587,682 | |

DISH Network Corp., Class A(a) (United States) | | | 256,300 | | | | 7,317,365 | |

Grupo Televisa SAB ADR (Mexico) | | | 934,100 | | | | 20,064,468 | |

Naspers, Ltd. (South Africa) | | | 821,600 | | | | 43,936,190 | |

Television Broadcasts, Ltd. (Hong Kong) | | | 2,523,100 | | | | 17,598,460 | |

Time Warner Cable, Inc. (United States) | | | 153,171 | | | | 12,575,339 | |

Time Warner, Inc. (United States) | | | 412,466 | | | | 15,879,941 | |

| | | | | | | | |

| | | | | | | 150,959,445 | |

RETAILING: 1.3% | | | | | |

J. C. Penney Co., Inc.(a) (United States) | | | 718,800 | | | | 16,755,228 | |

Liberty Interactive, Series A(a) (United States) | | | 592,357 | | | | 10,538,031 | |

| | | | | | | | |

| | | | | | | 27,293,259 | |

| | | | | | | | |

| | | | | | | 249,669,272 | |

| CONSUMER STAPLES: 3.9% | | | | | |

FOOD & STAPLES RETAILING: 1.2% | | | | | |

Wal-Mart Stores, Inc. (United States) | | | 370,000 | | | | 25,796,400 | |

| |

FOOD, BEVERAGE & TOBACCO: 2.7% | | | | | |

Anadolu Efes Biracilik ve Malt Sanayii AS (Turkey) | | | 1,602,600 | | | | 20,551,864 | |

Diageo PLC ADR (United Kingdom) | | | 132,800 | | | | 13,687,696 | |

Unilever PLC (United Kingdom) | | | 616,700 | | | | 20,726,775 | |

| | | | | | | | |

| | | | | | | 54,966,335 | |

| | | | | | | | |

| | | | | | | 80,762,735 | |

| ENERGY: 4.5% | | | | | | | | |

Baker Hughes, Inc. (United States) | | | 542,687 | | | | 22,304,436 | |

Occidental Petroleum Corp. (United States) | | | 234,525 | | | | 20,115,209 | |

| | | | | | | | |

| | |

| | |

| | | SHARES | | | VALUE | |

Royal Dutch Shell PLC ADR (United Kingdom) | | | 300,374 | | | $ | 20,254,219 | |

Schlumberger, Ltd. (Curacao/United States) | | | 467,900 | | | | 30,371,389 | |

| | | | | | | | |

| | | | | | | 93,045,253 | |

| FINANCIALS: 23.9% | | | | | | | | |

BANKS: 8.7% | | | | | |

Banco Santander SA (Spain) | | | 2,235,024 | | | | 14,927,247 | |

Barclays PLC (United Kingdom) | | | 11,003,400 | | | | 28,166,421 | |

BB&T Corp. (United States) | | | 534,200 | | | | 16,480,070 | |

HSBC Holdings PLC (United Kingdom) | | | 2,568,162 | | | | 22,644,630 | |

ICICI Bank, Ltd. (India) | | | 56,664 | | | | 911,283 | |

Mitsubishi UFJ Financial Group, Inc. (Japan) | | | 1,525,000 | | | | 7,298,332 | |

Standard Chartered PLC (United Kingdom) | | | 514,722 | | | | 11,221,373 | |

SunTrust Banks, Inc. (United States) | | | 413,795 | | | | 10,026,253 | |

UniCredit SPA(a) (Italy) | | | 2,984,199 | | | | 11,307,903 | |

Wells Fargo & Co. (United States) | | | 1,717,773 | | | | 57,442,329 | |

| | | | | | | | |

| | | | | | | 180,425,841 | |

DIVERSIFIED FINANCIALS: 10.2% | | | | | |

Bank of America Corp. (United States) | | | 3,345,500 | | | | 27,366,190 | |

Bank of New York Mellon Corp. (United States) | | | 1,748,700 | | | | 38,383,965 | |

Capital One Financial Corp. (United States) | | | 731,900 | | | | 40,005,654 | |

Charles Schwab Corp. (United States) | | | 2,466,200 | | | | 31,887,966 | |

Credit Suisse Group AG (Switzerland) | | | 1,674,516 | | | | 30,591,360 | |

Goldman Sachs Group, Inc. (United States) | | | 304,200 | | | | 29,160,612 | |

Haci Omer Sabanci Holding AS (Turkey) | | | 3,344,188 | | | | 14,106,536 | |

| | | | | | | | |

| | | | | | | 211,502,283 | |