UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-173

DODGE & COX FUNDS

(Exact name of registrant as specified in charter)

555 California Street, 40th Floor

San Francisco, CA 94104

(Address of principal executive offices) (Zip code)

Thomas M. Mistele, Esq.

555 California Street, 40th Floor

San Francisco, CA 94104

(Name and address of agent for service)

Registrant’s telephone number, including area code: 415-981-1710

Date of fiscal year end: DECEMBER 31, 2014

Date of reporting period: JUNE 30, 2014

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss. 3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

The following are the June 30, 2014 semi-annual reports for the Dodge & Cox Funds, a Delaware statutory trust, consisting of six series: Dodge & Cox Stock Fund, Dodge & Cox Global Stock Fund, Dodge & Cox International Stock Fund, Dodge & Cox Balanced Fund, Dodge & Cox Income Fund and Dodge & Cox Global Bond Fund. The reports of each series were transmitted to their respective shareholders on August 18, 2014.

| | | | |

| | | |  |

www.dodgeandcox.com

For Fund literature, transactions, and account

information, please visit the Funds’ website.

or write or call:

DODGE & COX FUNDS

c/o Boston Financial Data Services

P.O. Box 8422

Boston, Massachusetts 02266-8422

(800) 621-3979

INVESTMENT MANAGER

Dodge & Cox

555 California Street, 40th Floor

San Francisco, California 94104

(415) 981-1710

This report is submitted for the general information of the shareholders of the Fund. The report is not authorized for distribution to prospective investors in the Fund unless it is accompanied by a current prospectus.

This report reflects our views, opinions, and portfolio holdings as of June 30, 2014, the end of the reporting period. Any such views are subject to change at any time based upon market or other conditions and Dodge & Cox disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Dodge & Cox Fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Dodge & Cox Fund.

6/14 SF SAR  Printed on recycled paper

Printed on recycled paper

Semi-Annual Report

June 30, 2014

Stock Fund

ESTABLISHED 1965

TICKER: DODGX

TO OUR SHAREHOLDERS

The Dodge & Cox Stock Fund had a total return of 7.0% for the six months ended June 30, 2014, compared to a return of 7.1% for the S&P 500 Index. On June 30, the Fund had net assets of $58.4 billion with a cash position of 0.8%.

MARKET COMMENTARY

After exceptionally strong returns in 2013, U.S. equity markets continued to rise during the first half of 2014: the quarter ended June 30 marked the S&P 500’s sixth consecutive quarter of gains. While every sector of the S&P 500 generated positive returns for the six-month period, Utilities and Energy were the strongest. Following a slow start to the year, growth in U.S. economic activity rebounded and assuaged concerns that the economy was losing momentum. The labor market and household spending showed further signs of improvement, and businesses invested more in fixed assets. However, the housing recovery remained slow and turmoil in the Middle East modestly increased oil prices.

Corporate balance sheets and cash flows are robust; we continue to be optimistic about the long-term prospects for corporate earnings growth. In our opinion, U.S. equity market valuations remain reasonable: the S&P 500 traded at 16 times forward estimated earnings, which is close to its 10-year average, with a 2.0% dividend yield.(a)

INVESTMENT STRATEGY:

FINDING OPPORTUNITIES IN MEDIA

We build the portfolio one security at a time, exercise a strict price discipline, and evaluate potential investments based on our three- to five-year investment horizon. Any sector over- or underweights are a result of our fundamental, bottom-up research process, which we have employed for decades.

To determine whether a company’s share price presents a compelling investment opportunity, we weigh the company’s valuation against its fundamentals (e.g., competitive positioning, financial strength, long-term growth prospects, management quality, and corporate governance). The Fund’s overweight position in the Media industry (10.9% compared to 3.6% for the S&P

500 industry) illustrates our investment process. Through individual security analysis, we have identified Media companies that we believe have durable business franchises, long-term growth prospects, and reasonable valuations. The Fund’s Media holdings fall into two broad categories: content and distribution.

Content-oriented holdings in the Fund include Time Warner, Twenty-First Century Fox, News Corp., and Time.(b) Such companies have growth opportunities in digital media, interactive content, and cable networks, however they must compensate for slow secular growth in mature media (newspapers and publishing) and loss of advertising market share to internet and other media outlets. The Fund’s distribution holdings (Comcast, Time Warner Cable, and DISH Network) stand to benefit from rising broadband penetration, stable financial conditions, and reasonable valuations, although they face an increasingly competitive video distribution environment. Time Warner, Comcast, and Time Warner Cable are highlighted in detail below.

Content: Time Warner

Time Warner, a strategically well-positioned media conglomerate, was a 2.7% position in the Fund on June 30. We believe its valuation of 16 times forward earnings is reasonable in relation to its earnings and free cash flow growth prospects. Some investors have questioned whether cable networks will be able to continue to push through price increases, but we believe this risk is modest. Time Warner’s television-related businesses are estimated to account for more than 90% of its cash flow, and the majority of the company’s businesses (e.g., cable networks, television licensing) are characterized by multi-year contracts with guaranteed annual revenue increases. In addition, the continued viewership migration from broadcast networks to cable networks is driving ad revenue, and the company’s film and television studios are increasing revenue by licensing content to newer digital distribution services.

We believe Time Warner’s management is one of the most disciplined capital allocators in the Media industry and is focused on maximizing returns for long-term shareholders. As evidence, they have repurchased over

PAGE 1 § DODGE & COX STOCK FUND

30% of the company’s shares since 2006 and have avoided large-scale mergers and acquisitions (M&A). Furthermore, since we initiated the Fund’s position in 2003, management has spun off businesses methodically to increase shareholder value. All of these spinoffs are still held in the Fund and have augmented returns: Time Warner Cable (up 559% since its March 2009 spin off), AOL (up 96% since its December 2009 spin off, including a $5.15 per share special dividend), and Time (up 4% since its early June 2014 spinoff). We continue to believe these businesses have attractive long-term growth opportunities; in total, Time Warner, Time Warner Cable, AOL, and Time accounted for 5.7% of the Fund on June 30.

Distribution: Comcast and Time Warner Cable

In response to evolving consumer habits, media companies are altering their long-term strategies and the industry is consolidating. Two of the Fund’s Media holdings have entered into a merger agreement: in February 2014, Comcast (the largest cable operator in the United States) agreed to acquire Time Warner Cable (the second largest) for $45 billion in stock at the time of the announcement.

What is Comcast’s rationale for the deal? Combining the companies presents significant opportunities for cost reductions, operating synergies, and enhanced revenue growth. Comcast and Time Warner Cable currently do not compete directly in any markets. If the merger is completed, Comcast will gain access to the premier New York and Los Angeles markets, and thereby have a national presence. The proposed new entity would be the dominant provider of pay-TV and wireline broadband services in the United States (reaching ~70% of U.S. households).

We believe the proposed deal could build long-term shareholder value, depending upon merger concessions. Comcast’s management team is astute and has a proven M&A track record. While they have already made deal concessions, substantial regulatory hurdles lie ahead: both the Federal Communications Commission and the Department of Justice need to approve the merger. On a standalone basis, Comcast and Time Warner Cable remain reasonably valued and were held in the Fund on June 30 with 3.1% and 2.3% positions, respectively.

IN CLOSING

We remain enthusiastic about the long-term prospects for the Fund’s holdings. In addition to Media, the Fund remains overweight in the Financials, Health Care, and Information Technology sectors, as well as the Energy Equipment & Services industry. The most significant underweight positions in the Fund are in Utilities, Consumer Staples, and Industrials. The Fund’s holdings collectively trade at a discount (14 times forward earnings) to the S&P 500 and have earnings growth and cash flow potential.

As evidenced by the Fund’s low portfolio turnover, we continue to invest with a long-term horizon. Acknowledging that stock prices can be volatile over the short term, we encourage shareholders to also remain focused on the long term.

Thank you for your continued confidence in our firm. As always, we welcome your comments and questions.

For the Board of Trustees,

| | |

| |  |

Charles F. Pohl, Chairman | | Dana M. Emery, President |

July 29, 2014

| (a) | | Unless otherwise specified, all weightings and characteristics are as of June 30, 2014. |

| (b) | | The use of specific examples does not imply that they are more attractive investments than the Fund’s other holdings. |

DODGE & COX STOCK FUND §PAGE 2

YEAR-TO-DATE PERFORMANCE REVIEW

The Fund paced the S&P 500 year to date.

Key Detractors from Relative Results

| | § | | The Fund’s underweight position in the Utilities sector (no holdings compared to 3% for the S&P 500 sector), the strongest sector of the market (up 19%), hurt results. | |

| | § | | The Fund’s holdings in the Industrials sector (flat compared to up 4% for the S&P 500 sector) hindered performance. ADT Corp. (down 13%) was especially weak. | |

| | § | | Returns from holdings in the Information Technology sector (up 8% compared to up 9% for the S&P 500 sector) modestly detracted from results. NetApp (down 11%), eBay (down 9%), and Symantec (down 1%) lagged. | |

| | § | | Selected additional detractors included Coach (down 38%) and Goldman Sachs (down 5%). | |

Key Contributors to Relative Results

| | § | | The Fund’s holdings in the Energy sector (up 25% compared to up 13% for the S&P 500 sector) contributed significantly to results. Oil Services holdings, Weatherford International (up 48%), Baker Hughes (up 35%), and Schlumberger (up 32%) were particularly strong. | |

| | § | | The Fund’s holdings in the Materials sector (up 17% compared to up 8% for the S&P 500 sector) helped returns. Dow Chemical (up 18%) and Celanese (up 17%) performed well. | |

| | § | | Selected additional contributors included Forest Laboratories (up 52% to date of sale), Hewlett-Packard (up 22%), and Wells Fargo (up 17%). | |

KEY CHARACTERISTICS OF DODGE & COX

Independent Organization

Dodge & Cox is one of the largest privately owned investment managers in the world. We remain committed to independence, with a goal of providing the highest quality investment management service to our existing clients.

Over 80 Years of Investment Experience

Dodge & Cox was founded in 1930. We have a stable and well-qualified team of investment professionals, most of whom have spent their entire careers at Dodge & Cox.

Experienced Investment Team

The Investment Policy Committee, which is the decision-making body for the Stock Fund, is a nine-member committee with an average tenure at Dodge & Cox of 26 years.

One Business with a Single Research Office

Dodge & Cox manages equity (domestic, international, and global), fixed income (domestic and global), and balanced investments, operating from one office in San Francisco.

Consistent Investment Approach

Our team decision-making process involves thorough, bottom-up fundamental analysis of each investment.

Long-Term Focus and Low Expenses

We invest with a three- to five-year investment horizon, which has historically resulted in low turnover relative to our peers. We manage Funds that maintain low expense ratios.

Risks: The Fund is subject to stock market risk, meaning stocks in the Fund may decline in value for extended periods due to the financial prospects of individual companies, or due to general market and economic conditions. Please read the prospectus and summary prospectus for specific details regarding the Fund’s risk profile.

PAGE 3 § DODGE & COX STOCK FUND

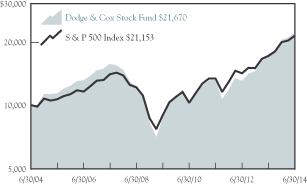

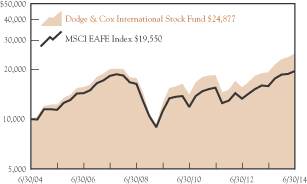

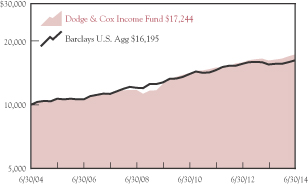

GROWTH OF $10,000 OVER 10 YEARS

FOR AN INVESTMENT MADE ON JUNE 30, 2004

AVERAGE ANNUAL TOTAL RETURN

FOR PERIODS ENDED JUNE 30, 2014

| | | | | | | | | | | | | | | | |

| | | 1 Year | | | 5 Years | | | 10 Years | | | 20 Years | |

Dodge & Cox Stock Fund | | | 27.95 | % | | | 20.14 | % | | | 8.05 | % | | | 12.01 | % |

S&P 500 | | | 24.62 | | | | 18.84 | | | | 7.78 | | | | 9.79 | |

Returns represent past performance and do not guarantee future results. Investment return and share price will fluctuate with market conditions, and investors may have a gain or loss when shares are sold. Fund performance changes over time and currently may be significantly lower than stated. Performance is updated and published monthly. Visit the Fund’s website at www.dodgeandcox.com or call 800-621-3979 for current performance figures.

The Fund’s total returns include the reinvestment of dividend and capital gain distributions, but have not been adjusted for any income taxes payable by shareholders on these distributions or on Fund share redemptions. Index returns include dividends but, unlike Fund returns, do not reflect fees or expenses. The S&P 500 Index is a market capitalization-weighted index of 500 large-capitalization stocks commonly used to represent the U.S. equity market.

S&P 500® is a trademark of McGraw Hill Financial.

FUND EXPENSE EXAMPLE

As a Fund shareholder, you incur ongoing Fund costs, including management fees and other Fund expenses. All mutual funds have ongoing costs, sometimes referred to as operating expenses. The following example shows ongoing costs of investing in the Fund and can help you understand these costs and compare them with those of other mutual funds. The example assumes a $1,000 investment held for the six months indicated.

ACTUAL EXPENSES

The first line of the table below provides information about actual account values and expenses based on the Fund’s actual returns. You may use the information in this line, together with your account balance, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

HYPOTHETICAL EXAMPLE FOR COMPARISON WITH OTHER MUTUAL FUNDS

Information on the second line of the table can help you compare ongoing costs of investing in the Fund with those of other mutual funds. This information may not be used to estimate the actual ending account balance or expenses you paid during the period. The hypothetical “Ending Account Value” is based on the actual expense ratio of the Fund and an assumed 5% annual rate of return before expenses (not the Fund’s actual return). The amount under the heading “Expense Paid During the Period” shows the hypothetical expenses your account would have incurred under this scenario. You can compare this figure with the 5% hypothetical examples that appear in shareholder reports of other mutual funds.

| | | | | | | | | | | | |

Six Months Ended

June 30, 2014 | | Beginning Account Value

1/1/2014 | | | Ending Account Value

6/30/2014 | | | Expenses Paid

During Period* | |

Based on Actual Fund Return | | $ | 1,000.00 | | | $ | 1,070.20 | | | $ | 2.70 | |

Based on Hypothetical 5% Yearly Return | | | 1,000.00 | | | | 1,022.18 | | | | 2.64 | |

| * | | Expenses are equal to the Fund’s annualized expense ratio of 0.53%, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period). |

The expenses shown in the table highlight ongoing costs only and do not reflect any transactional fees or account maintenance fees. Though other mutual funds may charge such fees, please note that the Fund does not charge transaction fees (e.g., redemption fees, sales loads) or universal account maintenance fees (e.g., small account fees).

DODGE & COX STOCK FUND §PAGE 4

| | | | |

| FUND INFORMATION | | | June 30, 2014 | |

| | | | |

| GENERAL INFORMATION | | | |

Net Asset Value Per Share | | | $178.73 | |

Total Net Assets (billions) | | | $58.4 | |

2013 Expense Ratio (per 5/1/14 Prospectus) | | | 0.52% | |

Expense Ratio (1/1/14 to 6/30/14, annualized) | | | 0.53% | |

Portfolio Turnover Rate

(1/1/14 to 6/30/14, unannualized) | | | 7% | |

30-Day SEC Yield(a) | | | 1.27% | |

Fund Inception | | | 1965 | |

| No sales charges or distribution fees | | | | |

Investment Manager: Dodge & Cox, San Francisco. Managed by the Investment Policy Committee, whose nine members’ average tenure at Dodge & Cox is 26 years.

| | | | | | | | |

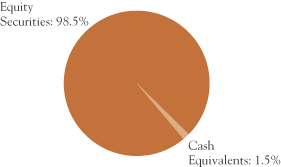

PORTFOLIO CHARACTERISTICS | | Fund | | | S&P 500 | |

Number of Equity Securities | | | 71 | | | | 501 | |

Median Market Capitalization (billions) | | | $36 | | | | $18 | |

Weighted Average Market Capitalization (billions) | | | $114 | | | | $125 | |

Price-to-Earnings Ratio(b) | | | 14.2x | | | | 15.6x | |

Foreign Securities not in the S&P 500(c) | | | 15.5% | | | | 0.0% | |

| | | | |

| TEN LARGEST HOLDINGS(d) | | Fund | |

Hewlett-Packard Co. | | | 4.1 | % |

Capital One Financial Corp. | | | 4.0 | |

Wells Fargo & Co. | | | 4.0 | |

Microsoft Corp. | | | 3.6 | |

Novartis AG (Switzerland) | | | 3.4 | |

Comcast Corp. | | | 3.1 | |

Schlumberger, Ltd. | | | 2.7 | |

Time Warner, Inc. | | | 2.7 | |

Bank of New York Mellon Corp. | | | 2.6 | |

Charles Schwab Corp. | | | 2.5 | |

| | | | | | | | |

| SECTOR DIVERSIFICATION | | Fund | | | S&P 500 | |

Financials | | | 23.1 | % | | | 16.1 | % |

Information Technology | | | 22.7 | | | | 18.8 | |

Health Care | | | 18.6 | | | | 13.3 | |

Consumer Discretionary | | | 14.3 | | | | 12.0 | |

Energy | | | 9.5 | | | | 10.9 | |

Industrials | | | 6.3 | | | | 10.5 | |

Consumer Staples | | | 2.5 | | | | 9.5 | |

Materials | | | 1.9 | | | | 3.4 | |

Telecommunication Services | | | 0.3 | | | | 2.4 | |

Utilities | | | 0.0 | | | | 3.1 | |

| (a) | SEC Yield is an annualization of the Fund’s total net investment income per share for the 30-day period ended on the last day of the month. |

| (b) | Price-to-earnings (P/E) ratios are calculated using 12-month forward earnings estimates from third-party sources. |

| (c) | Foreign stocks are U.S. dollar denominated. |

| (d) | The Fund’s portfolio holdings are subject to change without notice. The mention of specific securities is not a recommendation to buy, sell, or hold any particular security and is not indicative of Dodge & Cox’s current or future trading activity. |

PAGE 5 § DODGE & COX STOCK FUND

| | | | |

| PORTFOLIO OF INVESTMENTS (unaudited) | | | June 30, 2014 | |

| | | | | | | | |

| COMMON STOCKS: 99.2% | |

| | |

| | | SHARES | | | VALUE | |

| CONSUMER DISCRETIONARY: 14.3% | |

CONSUMER DURABLES & APPAREL: 1.3% | | | | | |

Coach, Inc. | | | 10,424,200 | | | $ | 356,403,398 | |

NVR, Inc.(a) | | | 79,700 | | | | 91,702,820 | |

Panasonic Corp. ADR(b) (Japan) | | | 23,861,597 | | | | 290,634,251 | |

| | | | | | | | |

| | | | 738,740,469 | |

MEDIA: 10.9% | |

Comcast Corp., Class A | | | 33,212,397 | | | | 1,782,841,471 | |

DISH Network Corp., Class A(a) | | | 6,587,549 | | | | 428,717,689 | |

News Corp., Class A(a) | | | 6,392,306 | | | | 114,677,969 | |

Time Warner Cable, Inc. | | | 9,284,910 | | | | 1,367,667,243 | |

Time Warner, Inc. | | | 22,430,732 | | | | 1,575,758,923 | |

Time, Inc.(a) | | | 4,803,841 | | | | 116,349,029 | |

Twenty-First Century Fox, Inc. | | | 28,508,826 | | | | 1,002,085,234 | |

| | | | | | | | |

| | | | 6,388,097,558 | |

RETAILING: 2.1% | |

CarMax, Inc.(a) | | | 4,874,350 | | | | 253,514,944 | |

Liberty Interactive, Series A(a) | | | 13,743,075 | | | | 403,496,682 | |

Target Corp. | | | 10,050,000 | | | | 582,397,500 | |

| | | | | | | | |

| | | | 1,239,409,126 | |

| | | | | | | | |

| | | | 8,366,247,153 | |

| CONSUMER STAPLES: 2.5% | |

FOOD & STAPLES RETAILING: 2.1% | |

Wal-Mart Stores, Inc. | | | 16,465,150 | | | | 1,236,038,811 | |

|

FOOD, BEVERAGE & TOBACCO: 0.4% | |

Unilever PLC ADR(b) (United Kingdom) | | | 5,305,500 | | | | 240,392,205 | |

| | | | | | | | |

| | | | 1,476,431,016 | |

| ENERGY: 9.5% | |

Apache Corp. | | | 10,564,428 | | | | 1,062,992,745 | |

Baker Hughes, Inc. | | | 10,223,850 | | | | 761,165,633 | |

Chevron Corp. | | | 6,559,980 | | | | 856,405,389 | |

National Oilwell Varco, Inc. | | | 8,450,000 | | | | 695,857,500 | |

Schlumberger, Ltd.(b) (Curacao/United States) | | | 13,606,645 | | | | 1,604,903,778 | |

Weatherford International PLC(a),(b) (Ireland) | | | 24,728,700 | | | | 568,760,100 | |

| | | | | | | | |

| | | | 5,550,085,145 | |

| FINANCIALS: 23.1% | |

BANKS: 9.4% | |

Bank of America Corp. | | | 84,078,900 | | | | 1,292,292,693 | |

BB&T Corp. | | | 10,362,144 | | | | 408,579,338 | |

HSBC Holdings PLC ADR(b) (United Kingdom) | | | 6,344,029 | | | | 322,276,673 | |

JPMorgan Chase & Co. | | | 13,040,900 | | | | 751,416,658 | |

SunTrust Banks, Inc. | | | 10,356,933 | | | | 414,898,736 | |

Wells Fargo & Co. | | | 44,216,341 | | | | 2,324,010,883 | |

| | | | | | | | |

| | | | 5,513,474,981 | |

| | | | | | | | |

| | |

| | | SHARES | | | VALUE | |

DIVERSIFIED FINANCIALS: 11.8% | |

Bank of New York Mellon Corp. | | | 40,793,824 | | | $ | 1,528,952,523 | |

Capital One Financial Corp.(c) | | | 28,462,711 | | | | 2,351,019,929 | |

Charles Schwab Corp. | | | 54,467,600 | | | | 1,466,812,468 | |

Goldman Sachs Group, Inc. | | | 7,490,600 | | | | 1,254,226,064 | |

McGraw Hill Financial, Inc. | | | 3,783,025 | | | | 314,104,566 | |

| | | | | | | | |

| | | | 6,915,115,550 | |

INSURANCE: 1.9% | |

AEGON NV(b) (Netherlands) | | | 66,305,587 | | | | 581,499,998 | |

MetLife, Inc. | | | 9,297,600 | | | | 516,574,656 | |

| | | | | | | | |

| | | | 1,098,074,654 | |

| | | | | | | | |

| | | | 13,526,665,185 | |

| HEALTH CARE: 18.6% | |

HEALTH CARE EQUIPMENT & SERVICES: 4.5% | |

Boston Scientific Corp.(a) | | | 26,998,600 | | | | 344,772,122 | |

Cigna Corp. | | | 3,907,184 | | | | 359,343,713 | |

Express Scripts Holding Co.(a) | | | 10,800,000 | | | | 748,764,000 | |

Medtronic, Inc. | | | 5,226,000 | | | | 333,209,760 | |

UnitedHealth Group, Inc. | | | 9,869,400 | | | | 806,823,450 | |

| | | | | | | | |

| | | | 2,592,913,045 | |

PHARMACEUTICALS, BIOTECHNOLOGY & LIFE SCIENCES: 14.1% | |

GlaxoSmithKline PLC ADR(b) (United Kingdom) | | | 24,435,300 | | | | 1,306,799,844 | |

Merck & Co., Inc. | | | 21,731,700 | | | | 1,257,178,845 | |

Novartis AG ADR(b) (Switzerland) | | | 21,936,900 | | | | 1,985,947,557 | |

Pfizer, Inc. | | | 30,081,264 | | | | 892,811,915 | |

Roche Holding AG ADR(b) (Switzerland) | | | 36,142,200 | | | | 1,348,104,060 | |

Sanofi ADR(b) (France) | | | 27,370,329 | | | | 1,455,280,393 | |

| | | | | | | | |

| | | | 8,246,122,614 | |

| | | | | | | | |

| | | | 10,839,035,659 | |

| INDUSTRIALS: 6.3% | |

CAPITAL GOODS: 2.4% | |

General Electric Co. | | | 41,023,675 | | | | 1,078,102,179 | |

Koninklijke Philips NV(b) (Netherlands) | | | 8,167,675 | | | | 259,405,358 | |

NOW, Inc.(a) | | | 2,112,500 | | | | 76,493,625 | |

| | | | | | | | |

| | | | 1,414,001,162 | |

COMMERCIAL & PROFESSIONAL SERVICES: 1.6% | |

ADT Corp.(c) | | | 11,942,537 | | | | 417,272,243 | |

Tyco International, Ltd.(b) (Switzerland) | | | 10,772,075 | | | | 491,206,620 | |

| | | | | | | | |

| | | | 908,478,863 | |

TRANSPORTATION: 2.3% | |

FedEx Corp. | | | 8,966,799 | | | | 1,357,394,032 | |

| | | | | | | | |

| | | | 3,679,874,057 | |

| | |

| See accompanying Notes to Financial Statements | | DODGE & COX STOCK FUND §PAGE 6 |

| | | | |

| PORTFOLIO OF INVESTMENTS (unaudited) | | | June 30, 2014 | |

| | | | | | | | |

| COMMON STOCKS (continued) | |

| | |

| | | SHARES | | | VALUE | |

| INFORMATION TECHNOLOGY: 22.7% | |

SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT: 0.7% | |

Maxim Integrated Products, Inc. | | | 12,859,440 | | | $ | 434,777,666 | |

|

SOFTWARE & SERVICES: 11.6% | |

Adobe Systems, Inc.(a) | | | 4,201,641 | | | | 304,030,743 | |

AOL, Inc.(a),(c) | | | 7,381,954 | | | | 293,727,950 | |

Cadence Design Systems, Inc.(a) | | | 11,467,600 | | | | 200,568,324 | |

Computer Sciences Corp. | | | 1,254,294 | | | | 79,271,381 | |

eBay, Inc.(a) | | | 14,346,609 | | | | 718,191,246 | |

Google, Inc., Class A(a) | | | 768,100 | | | | 449,085,027 | |

Google, Inc., Class C(a) | | | 1,538,100 | | | | 884,838,168 | |

Microsoft Corp. | | | 50,892,700 | | | | 2,122,225,590 | |

Symantec Corp.(c) | | | 51,653,700 | | | | 1,182,869,730 | |

Synopsys, Inc.(a),(c) | | | 14,022,569 | | | | 544,356,128 | |

| | | | | | | | |

| | | | 6,779,164,287 | |

TECHNOLOGY, HARDWARE & EQUIPMENT: 10.4% | |

Corning, Inc. | | | 34,626,400 | | | | 760,049,480 | |

EMC Corp. | | | 24,200,000 | | | | 637,428,000 | |

Hewlett-Packard Co. | | | 71,835,395 | | | | 2,419,416,104 | |

NetApp, Inc.(c) | | | 18,626,700 | | | | 680,247,084 | |

Nokia Corp. ADR(b) (Finland) | | | 96,379,400 | | | | 728,628,264 | |

TE Connectivity, Ltd.(b) (Switzerland) | | | 13,313,875 | | | | 823,330,030 | |

| | | | | | | | |

| | | | 6,049,098,962 | |

| | | | | | | | |

| | | | 13,263,040,915 | |

| MATERIALS: 1.9% | |

Celanese Corp., Series A(c) | | | 9,317,071 | | | | 598,901,324 | |

Dow Chemical Co. | | | 5,945,389 | | | | 305,949,718 | |

Vulcan Materials Co. | | | 2,881,115 | | | | 183,671,081 | |

| | | | | | | | |

| | | | 1,088,522,123 | |

| TELECOMMUNICATION SERVICES: 0.3% | |

Sprint Corp.(a) | | | 21,932,896 | | | | 187,087,603 | |

| | | | | | | | |

| |

TOTAL COMMON STOCKS

(Cost $39,317,938,638) | | | $ | 57,976,988,856 | |

| | | | | | | | |

| SHORT-TERM INVESTMENTS: 0.7% | |

| | |

| | | PAR VALUE | | | VALUE | |

MONEY MARKET FUND: 0.2% | |

SSgA U.S. Treasury Money

Market Fund | | $ | 116,890,314 | | | $ | 116,890,314 | |

|

REPURCHASE AGREEMENT: 0.5% | |

Fixed Income Clearing Corporation(d) 0.00%, dated 6/30/14, due 7/1/14, maturity value $288,622,592 | | | 288,622,592 | | | | 288,622,592 | |

| | | | | | | | |

TOTAL SHORT-TERM INVESTMENTS

(Cost $405,512,906) | | | $ | 405,512,906 | |

| | | | | | | | |

TOTAL INVESTMENTS

(Cost $39,723,451,544) | | | 99.9 | % | | $ | 58,382,501,762 | |

OTHER ASSETS LESS LIABILITIES | | | 0.1 | % | | | 66,340,406 | |

| | | | | | | | |

| NET ASSETS | | | 100.0 | % | | $ | 58,448,842,168 | |

| | | | | | | | |

| (b) | Security denominated in U.S. dollars |

| (c) | See Note 8 regarding holdings of 5% voting securities |

| (d) | Repurchase agreement is collateralized by U.S. Treasury Note 1.000%-1.625%, 2/28/19-6/30/19. Total collateral value is $294,398,525. |

In determining a company’s country designation, the Fund generally references the country of incorporation. In cases where the Fund considers the country of incorporation to be a “jurisdiction of convenience” chosen primarily for tax purposes, the Fund uses the country designation of an appropriate broad-based market index. In that circumstance, two countries are listed - the country of incorporation and the country designated by an appropriate index, respectively.

ADR: American Depositary Receipt

| | |

| PAGE 7 § DODGE & COX STOCK FUND | | See accompanying Notes to Financial Statements |

| | | | |

STATEMENT OF ASSETS AND LIABILITIES (unaudited) | |

| |

| | | June 30, 2014 | |

ASSETS: | | | | |

Investments, at value | | | | |

Unaffiliated issuers (cost $36,751,818,131) | | $ | 54,665,127,303 | |

Affiliated issuers (cost $2,971,633,413) | | | 3,717,374,459 | |

| | | | |

| | | 58,382,501,762 | |

Receivable for investments sold | | | 9,928,556 | |

Receivable for Fund shares sold | | | 47,427,870 | |

Dividends and interest receivable | | | 110,882,197 | |

Prepaid expenses and other assets | | | 180,125 | |

| | | | |

| | | 58,550,920,510 | |

| | | | |

LIABILITIES: | | | | |

Payable for investments purchased | | | 3,927,203 | |

Payable for Fund shares redeemed | | | 72,907,057 | |

Management fees payable | | | 23,694,003 | |

Accrued expenses | | | 1,550,079 | |

| | | | |

| | | 102,078,342 | |

| | | | |

NET ASSETS | | $ | 58,448,842,168 | |

| | | | |

NET ASSETS CONSIST OF: | | | | |

Paid in capital | | $ | 38,863,549,070 | |

Undistributed net investment income | | | 8,987,731 | |

Undistributed net realized gain | | | 917,255,149 | |

Net unrealized appreciation | | | 18,659,050,218 | |

| | | | |

| | $ | 58,448,842,168 | |

| | | | |

Fund shares outstanding (par value $0.01 each, unlimited shares authorized) | | | 327,028,293 | |

Net asset value per share | | $ | 178.73 | |

|

STATEMENT OF OPERATIONS

(unaudited) | |

| | | Six Months Ended June 30, 2014 | |

INVESTMENT INCOME: | | | | |

Dividends (net of foreign taxes of $29,669,786) | | | | |

Unaffiliated issuers | | $ | 720,049,981 | |

Affiliated issuers | | | 46,091,423 | |

Interest | | | 438 | |

| | | | |

| | | 766,141,842 | |

| | | | |

EXPENSES: | | | | |

Management fees | | | 136,832,396 | |

Custody and fund accounting fees | | | 628,370 | |

Transfer agent fees | | | 1,851,234 | |

Professional services | | | 97,017 | |

Shareholder reports | | | 2,799,840 | |

Registration fees | | | 217,508 | |

Trustees’ fees | | | 139,442 | |

Miscellaneous | | | 1,636,035 | |

| | | | |

| | | 144,201,842 | |

| | | | |

NET INVESTMENT INCOME | | | 621,940,000 | |

| | | | |

REALIZED AND UNREALIZED GAIN: | | | | |

Net realized gain | | | | |

Unaffiliated issuers | | | 1,331,302,852 | |

Affiliated issuers | | | 42,608,262 | |

Net change in unrealized appreciation/depreciation | | | 1,824,811,068 | |

| | | | |

Net realized and unrealized gain | | | 3,198,722,182 | |

| | | | |

NET INCREASE IN NET ASSETS FROM OPERATIONS | | $ | 3,820,662,182 | |

| | | | |

| | | | | | | | |

STATEMENT OF CHANGES IN NET ASSETS (unaudited) | |

| | |

| | | Six Months Ended June 30, 2014 | | | Year Ended

December 31, 2013 | |

OPERATIONS: | | | | | | | | |

Net investment income | | $ | 621,940,000 | | | $ | 691,471,816 | |

Net realized gain | | | 1,373,911,114 | | | | 2,942,196,702 | |

Net change in unrealized appreciation/depreciation | | | 1,824,811,068 | | | | 12,466,351,142 | |

| | | | | | | | |

| | | 3,820,662,182 | | | | 16,100,019,660 | |

| | | | | | | | |

| | |

DISTRIBUTIONS TO SHAREHOLDERS FROM: | | | | | | | | |

Net investment income | | | (620,954,392 | ) | | | (688,649,453 | ) |

Net realized gain | | | – | | | | — | |

| | | | | | | | |

Total distributions | | | (620,954,392 | ) | | | (688,649,453 | ) |

| | | | | | | | |

| | |

FUND SHARE TRANSACTIONS: | | | | | | | | |

Proceeds from sale of shares | | | 4,486,274,743 | | | | 7,505,695,700 | |

Reinvestment of distributions | | | 569,757,965 | | | | 638,450,488 | |

Cost of shares redeemed | | | (4,654,413,862 | ) | | | (8,549,348,435 | ) |

| | | | | | | | |

Net increase/(decrease) from Fund share transactions | | | 401,618,846 | | | | (405,202,247 | ) |

| | | | | | | | |

Total increase in net assets | | | 3,601,326,636 | | | | 15,006,167,960 | |

| | |

NET ASSETS: | | | | | | | | |

Beginning of period | | | 54,847,515,532 | | | | 39,841,347,572 | |

| | | | | | | | |

End of period (including undistributed net investment income of $8,987,731 and $8,002,123, respectively) | | $ | 58,448,842,168 | | | $ | 54,847,515,532 | |

| | | | | | | | |

| | |

SHARE INFORMATION: | | | | | | | | |

Shares sold | | | 26,367,125 | | | | 52,247,087 | |

Distributions reinvested | | | 3,294,318 | | | | 4,391,872 | |

Shares redeemed | | | (27,426,639 | ) | | | (58,685,059 | ) |

| | | | | | | | |

Net increase/(decrease) in shares outstanding | | | 2,234,804 | | | | (2,046,100 | ) |

| | | | | | | | |

| | |

| See accompanying Notes to Financial Statements | | DODGE & COX STOCK FUND §PAGE 8 |

NOTES TO FINANCIAL STATEMENTS (unaudited)

NOTE 1—ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES

Dodge & Cox Stock Fund (the “Fund”) is one of the series constituting the Dodge & Cox Funds (the “Trust” or the “Funds”). The Trust is organized as a Delaware statutory trust and is registered under the Investment Company Act of 1940, as amended, as an open-end management investment company. The Fund commenced operations on January 4, 1965, and seeks long-term growth of principal and income. Risk considerations and investment strategies of the Fund are discussed in the Fund’s Prospectus.

The financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America, which require the use of estimates and assumptions by management. Actual results may differ from those estimates. Significant accounting policies are as follows:

Security valuation The Fund’s net assets are valued as of the close of trading on the New York Stock Exchange (NYSE), generally 4:00 p.m. Eastern Time, each day that the NYSE is open for business. Portfolio securities and other financial instruments for which market quotes are readily available are valued at market value. Listed securities are generally valued using the official quoted close price or the last sale on the exchange that is determined to be the primary market for the security. Security values are not discounted based on the size of the Fund’s position. Securities for which market quotations are not readily available are valued at fair value as determined in good faith by or under the direction of the Board of Trustees. Short-term securities less than 60 days to maturity may be valued at amortized cost if amortized cost approximates current value. All securities held by the Fund are denominated in U.S. dollars.

The Board of Trustees has delegated authority to Dodge & Cox, the Fund’s investment manager, to make fair value determinations in accordance with the Dodge & Cox Funds Valuation Policies (“Valuation Policies”), subject to Board oversight. Dodge & Cox has established a Pricing Committee that is comprised of representatives from Treasury, Legal, Compliance, and Operations. The Pricing Committee is responsible for implementing the Valuation Policies, including determining the fair value of

securities when market quotations or market-based valuations are not readily available or are deemed unreliable. The Pricing Committee considers relevant indications of value that are reasonably available to it in determining the fair value assigned to a particular security, such as the value of similar financial instruments, trading volumes, contractual restrictions on disposition, related corporate actions, and changes in economic conditions.

Valuing securities at fair value involves greater reliance on judgment than valuation of securities based on readily available market quotations. In some instances, lack of information and uncertainty as to the significance of information may lead to a conclusion that a prior valuation is the best indication of a security’s present value. When fair value pricing is employed, the prices of securities used by the Fund to calculate its net asset value may differ from quoted or published prices for the same securities.

Security transactions, investment income, expenses, and distributions Security transactions are recorded on the trade date. Realized gains and losses on securities sold are determined on the basis of identified cost.

Dividend income and corporate action transactions are recorded on the ex-dividend date, or when the Fund first learns of the dividend/corporate action if the ex-dividend date has passed. Withholding taxes on foreign dividends have been provided for in accordance with the Fund’s understanding of the applicable country’s tax rules and rates. Non-cash dividends included in dividend income, if any, are recorded at the fair market value of the securities received. Dividends characterized as return of capital for U.S. tax purposes are recorded as a reduction of cost of investments and/or realized gain. Interest income is recorded on the accrual basis.

Expenses are recorded on the accrual basis. Most expenses of the Trust can be directly attributed to a specific series. Expenses which cannot be directly attributed are allocated among the Funds in the Trust based on relative net assets or other expense methodologies determined by the nature of the expense.

Distributions to shareholders are recorded on the ex-dividend date.

PAGE 9 § DODGE & COX STOCK FUND

NOTES TO FINANCIAL STATEMENTS (unaudited)

Repurchase agreements The Fund enters into repurchase agreements, secured by U.S. government or agency securities, which involve the purchase of securities from a counterparty with a simultaneous commitment to resell the securities at an agreed-upon date and price. It is the Fund’s policy that its custodian take possession of the underlying collateral securities, the fair value of which exceeds the principal amount of the repurchase transaction, including accrued interest, at all times. In the event of default by the counterparty, the Fund has the contractual right to liquidate the collateral securities and to apply the proceeds in satisfaction of the obligation.

Indemnification Under the Trust’s organizational documents, its officers and trustees are indemnified against certain liabilities arising out of the performance of their duties to the Trust. In addition, in the normal course of business the Trust enters into contracts that provide general indemnities to other parties. The Trust’s maximum exposure under these arrangements is unknown as this would involve future claims that may be made against the Trust that have not yet occurred.

NOTE 2—VALUATION MEASUREMENTS

Various inputs are used in determining the value of the Fund’s investments. These inputs are summarized in the three broad levels listed below.

| § | | Level 1: Quoted prices in active markets for identical securities |

| § | | Level 2: Other significant observable inputs (including quoted prices for similar securities, market indices, interest rates, credit risk, etc.) |

| § | | Level 3: Significant unobservable inputs (including Fund management’s assumptions in determining the fair value of investments) |

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

The following is a summary of the inputs used to value the Fund’s holdings at June 30, 2014:

| | | | | | | | |

| Security Classification(a) | | LEVEL 1

(Quoted Prices) | | | LEVEL 2

(Other Significant

Observable Inputs) | |

Common Stocks(b) | | $ | 57,976,988,856 | | | $ | — | |

Short-term Investments | | | | | | | | |

Money Market Fund | | | 116,890,314 | | | | — | |

Repurchase Agreement | | | — | | | | 288,622,592 | |

| | | | | | | | |

Total | | $ | 58,093,879,170 | | | $ | 288,622,592 | |

| | | | | | | | |

| | | | | | | | | |

| (a) | There were no transfers between Level 1 and Level 2 during the six months ended June 30, 2014. There were no Level 3 securities at June 30, 2014 and December 31, 2013, and there were no transfers to Level 3 during the period. |

| (b) | All common stocks held in the Fund are Level 1 securities. For a detailed break-out of common stocks by major industry classification, please refer to the Portfolio of Investments. |

NOTE 3—RELATED PARTY TRANSACTIONS

Management fees Under a written agreement approved by a unanimous vote of the Board of Trustees, the Fund pays an annual management fee of 0.50% of the Fund’s average daily net assets to Dodge & Cox, investment manager of the Fund. The agreement further provides that Dodge & Cox shall waive its fee to the extent that such fee plus all other ordinary operating expenses of the Fund exceed 0.75% of the average daily net assets for the year.

Fund officers and trustees All officers and two of the trustees of the Trust are officers or employees of Dodge & Cox. The Trust pays a fee only to those trustees who are not affiliated with Dodge & Cox.

NOTE 4—INCOME TAX INFORMATION AND DISTRIBUTIONS TO SHAREHOLDERS

A provision for federal income taxes is not required since the Fund intends to continue to qualify as a regulated investment company under Subchapter M of the Internal Revenue Code and distribute all of its taxable income to shareholders. Distributions are determined in accordance with income tax regulations, and such amounts may differ from net investment income and realized gains for financial reporting purposes. Financial reporting records are adjusted for permanent book/tax differences at year end to reflect tax character.

DODGE & COX STOCK FUND §PAGE 10

NOTES TO FINANCIAL STATEMENTS (unaudited)

Book/tax differences are primarily due to differing treatments of wash sales, in-kind redemptions, and net short-term realized gain (loss). During the period, the Fund recognized net realized gains of $286,884,947 from the delivery of appreciated securities in an in-kind redemption transaction. For federal income tax purposes, this gain is not recognized as taxable income to the Fund and therefore will not be distributed to shareholders. At June 30, 2014, the cost of investments for federal income tax purposes was $39,739,481,281.

Distributions during the periods noted below were characterized as follows for federal income tax purposes:

| | | | | | |

| | | Six Months Ended June 30, 2014 | | Year Ended

December 31, 2013 | |

Ordinary income | | $620,954,392 | | | $688,649,453 | |

| | ($1.920 per share) | | | ($2.105 per share) | |

| | |

Long-term capital gain | | — | | | — | |

At June 30, 2014, the tax basis components of distributable earnings were as follows:

| | | | |

Unrealized appreciation | | $ | 19,412,897,623 | |

Unrealized depreciation | | | (769,877,142 | ) |

| | | | |

Net unrealized appreciation | | | 18,643,020,481 | |

Undistributed ordinary income | | | 8,987,731 | |

Accumulated capital gain(a) | | | 1,087,026,166 | |

Capital loss carryforward(b) | | | (440,626,227 | ) |

| (a) | Represents capital gain realized for tax purposes during the period January 1, 2014 to June 30, 2014. |

| (b) | Represents accumulated capital loss as of December 31, 2013, which may be carried forward to offset future capital gains. During 2013, the Fund utilized $2,791,744,593 of the capital loss carryforward. If not utilized, the remaining capital loss carryforward will expire in 2017. |

Under the Regulated Investment Company Modernization Act of 2010, capital losses incurred by the Fund after January 1, 2011, are not subject to expiration. In addition, such losses must be utilized prior to the losses incurred in the years preceding enactment.

Fund management has reviewed the tax positions for open periods (three years and four years, respectively, from filing the Fund’s Federal and State tax returns) as applicable to the Fund, and has determined that no provision for income tax is required in the Fund’s financial statements.

NOTE 5—LOAN FACILITIES

Pursuant to an exemptive order issued by the Securities and Exchange Commission (SEC), the Fund may participate in an interfund lending facility (Facility). The Facility allows the Fund to borrow money from or loan money to the Funds. Loans under the Facility are made for temporary or emergency purposes, such as to fund shareholder redemption requests. Interest on borrowings is the average of the current repurchase agreement rate and the bank loan rate. There was no activity in the Facility during the period.

All Funds in the Trust participate in a $500 million committed credit facility (Line of Credit) with State Street Bank and Trust Company, to be utilized for temporary or emergency purposes to fund shareholder redemptions or for other short-term liquidity purposes. The maximum amount available to the Fund is $250 million. Each Fund pays an annual commitment fee on its pro-rata portion of the Line of Credit. The Fund’s commitment fee for the six months ended June 30, 2014, amounted to $80,585 and is reflected as a Miscellaneous Expense in the Statement of Operations. Interest on borrowings is charged at the prevailing rate. There were no borrowings on the Line of Credit during the period.

NOTE 6—PURCHASES AND SALES OF INVESTMENTS

For the six months ended June 30, 2014, purchases and sales of securities, other than short-term securities, aggregated $5,697,747,715 and $4,862,413,754, respectively.

NOTE 7—SUBSEQUENT EVENTS

Fund management has determined that no material events or transactions occurred subsequent to June 30, 2014, and through the date of the Fund’s financial statements issuance, which require additional disclosure in the Fund’s financial statements.

PAGE 11 § DODGE & COX STOCK FUND

NOTES TO FINANCIAL STATEMENTS (unaudited)

NOTE 8—HOLDINGS OF 5% VOTING SECURITIES

Each of the companies listed below was considered to be an affiliate of the Fund because the Fund owned 5% or more of the company’s voting securities during all or part of the six months ended June 30, 2014. Purchase and sale transactions and dividend income earned during the period on these securities were as follows:

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Shares at

Beginning of Period | | | Additions | | | Reductions | | | Shares at

End of Period | | | Dividend

Income(a) | | | Value at

End of Period | |

ADT Corp. | | | 12,073,537 | | | | — | | | | (131,000 | ) | | | 11,942,537 | | | | 4,777,015 | | | | 417,272,243 | |

AOL, Inc. | | | 5,997,054 | | | | 1,550,000 | | | | (165,100 | ) | | | 7,381,954 | | | | — | (b) | | | 293,727,950 | |

Capital One Financial Corp. | | | 28,876,111 | | | | — | | | | (413,400 | ) | | | 28,462,711 | | | | 17,077,627 | | | | — | (c) |

Celanese Corp., Series A | | | 9,419,271 | | | | — | | | | (102,200 | ) | | | 9,317,071 | | | | 4,006,341 | | | | 598,901,324 | |

NetApp, Inc. | | | 14,635,500 | | | | 4,150,000 | | | | (158,800 | ) | | | 18,626,700 | | | | 4,809,330 | | | | 680,247,084 | |

Symantec Corp. | | | 50,304,000 | | | | 1,900,000 | | | | (550,300 | ) | | | 51,653,700 | | | | 15,421,110 | | | | 1,182,869,730 | |

Synopsys, Inc. | | | 13,596,636 | | | | 579,733 | | | | (153,800 | ) | | | 14,022,569 | | | | — | (b) | | | 544,356,128 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | $ | 46,091,423 | | | $ | 3,717,374,459 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| (a) | Net of foreign taxes, if any |

| (c) | Company was not an affiliate at period end |

FINANCIAL HIGHLIGHTS

| | | | | | | | | | | | | | | | | | | | | | | | |

SELECTED DATA AND RATIOS (for a share outstanding throughout each period) | | Six Months

Ended June 30, | | | Year Ended December 31, | |

| | | 2014 (a) | | | 2013 | | | 2012 | | | 2011 | | | 2010 | | | 2009 | |

| | | | | | | | |

Net asset value, beginning of period | | | $168.87 | | | | $121.90 | | | | $101.64 | | | | $107.76 | | | | $96.14 | | | | $74.37 | |

Income from investment operations: | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | 1.92 | | | | 2.11 | | | | 1.98 | | | | 1.76 | | | | 1.23 | | | | 1.15 | |

Net realized and unrealized gain (loss) | | | 9.86 | | | | 46.97 | | | | 20.26 | | | | (6.13 | ) | | | 11.62 | | | | 21.82 | |

| | | | | | | | |

Total from investment operations | | | 11.78 | | | | 49.08 | | | | 22.24 | | | | (4.37 | ) | | | 12.85 | | | | 22.97 | |

| | | | | | | | |

Distributions to shareholders from: | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | (1.92 | ) | | | (2.11 | ) | | | (1.98 | ) | | | (1.75 | ) | | | (1.23 | ) | | | (1.20 | ) |

Net realized gain | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | |

| | | | | | | | |

Total distributions | | | (1.92 | ) | | | (2.11 | ) | | | (1.98 | ) | | | (1.75 | ) | | | (1.23 | ) | | | (1.20 | ) |

| | | | | | | | |

Net asset value, end of period | | | $178.73 | | | | $168.87 | | | | $121.90 | | | | $101.64 | | | | $107.76 | | | | $96.14 | |

| | | | | | | | |

Total return | | | 7.02 | % | | | 40.55 | % | | | 22.01 | % | | | (4.08 | )% | | | 13.48 | % | | | 31.27 | % |

Ratios/supplemental data: | | | | | | | | | | | | | | | | | | | | | | | | |

Net assets, end of period (millions) | | | $58,449 | | | | $54,848 | | | | $39,841 | | | | $36,562 | | | | $43,038 | | | | $39,991 | |

Ratio of expenses to average net assets | | | 0.53 | %(b) | | | 0.52 | % | | | 0.52 | % | | | 0.52 | % | | | 0.52 | % | | | 0.52 | % |

Ratio of net investment income to average net assets | | | 2.27 | %(b) | | | 1.45 | % | | | 1.72 | % | | | 1.62 | % | | | 1.25 | % | | | 1.42 | % |

Portfolio turnover rate | | | 7 | % | | | 15 | % | | | 11 | % | | | 16 | % | | | 12 | % | | | 18 | % |

See accompanying Notes to Financial Statements

DODGE & COX STOCK FUND §PAGE 12

SHAREHOLDER MEETING RESULTS (unaudited)

A special meeting of shareholders was held on April 23, 2014. At the meeting, proposals to elect Trustees to the Board of Trustees and to amend the Fund’s fundamental investment restrictions listed below were approved. The following is a report of the total votes cast by the Trust’s and the Fund’s shareholders.

| | | | | | | | | | | | | | |

| PROPOSAL | | | | AFFIRMATIVE | | | WITHHOLD | | | TOTAL | |

1 Elect Trustees to the Board of Trustees: | | | | | | | | | | | | | | |

| | | | |

| | Dana M. Emery | | | 2,724,363,325 | | | | 37,845,024 | | | | 2,762,208,349 | |

| | | | |

| | Charles F. Pohl | | | 2,724,265,808 | | | | 37,942,541 | | | | 2,762,208,349 | |

| | | | |

| | Thomas A. Larsen | | | 2,723,251,516 | | | | 38,956,833 | | | | 2,762,208,349 | |

| | | | |

| | Ann Mather | | | 2,696,172,728 | | | | 66,035,621 | | | | 2,762,208,349 | |

| | | | |

| | Robert B. Morris III | | | 2,722,376,906 | | | | 39,831,443 | | | | 2,762,208,349 | |

| | | | |

| | Gary Roughead | | | 2,721,551,032 | | | | 40,657,317 | | | | 2,762,208,349 | |

| | | | |

| | Mark E. Smith | | | 2,723,441,491 | | | | 38,766,858 | | | | 2,762,208,349 | |

| | | | |

| | John B. Taylor | | | 2,722,862,534 | | | | 39,345,815 | | | | 2,762,208,349 | |

| | | | | | | | | | | | | | | | | | | | |

| PROPOSAL | | AFFIRMATIVE | | | AGAINST | | | ABSTAIN | | | BROKER NON-VOTE | | | TOTAL | |

2 To remove the Fund’s fundamental investment restriction with respect to investing in any company for the purpose of exercising control or management. | | | 146,007,769 | | | | 9,131,886 | | | | 2,924,469 | | | | 22,526,075 | | | | 180,590,199 | |

| | | | | |

3 To remove the Fund’s fundamental investment restriction with respect to purchasing securities on margin and short selling. | | | 139,236,165 | | | | 15,825,412 | | | | 3,002,547 | | | | 22,526,075 | | | | 180,590,199 | |

| | | | | |

4 To remove the Fund’s fundamental investment restriction with respect to investments in securities that are illiquid and replace it with a uniform non-fundamental policy for all Funds. | | | 145,009,433 | | | | 9,880,686 | | | | 3,174,005 | | | | 22,526,075 | | | | 180,590,199 | |

| | | | | |

6 To amend the Fund’s fundamental investment restriction with respect to underwriting securities of other issuers. | | | 144,849,576 | | | | 9,943,566 | | | | 3,270,981 | | | | 22,526,075 | | | | 180,590,199 | |

PAGE 13 § DODGE & COX STOCK FUND

FUND HOLDINGS

The Fund provides a complete list of its holdings four times each fiscal year, as of the end of each quarter. The Fund files the lists with the Securities and Exchange Commission (SEC) on Form N-CSR (second and fourth quarters) and Form N-Q (first and third quarters). Shareholders may view the Fund’s Forms N-CSR and N-Q on the SEC’s website at www.sec.gov. Forms N-CSR and N-Q may also be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information regarding the operations of the Public Reference Room may be obtained by calling 202-942-8090 (direct) or 800-732-0330 (general SEC number). A list of the Fund’s quarter-end holdings is also available at www.dodgeandcox.com on or about 15 days following each quarter end and remains available on the website until the list is updated in the subsequent quarter.

PROXY VOTING

For a free copy of the Fund’s proxy voting policies and procedures, please call 800-621-3979, visit the Fund’s website at www.dodgeandcox.com, or visit the SEC’s website at www.sec.gov. Information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ending June 30 is also available at www.dodgeandcox.com or at www.sec.gov.

HOUSEHOLD MAILINGS

The Fund routinely mails shareholder reports and summary prospectuses to shareholders and, on occasion, proxy statements. In order to reduce the volume of mail, when possible, only one copy of these documents will be sent to shareholders who are part of the same family and share the same residential address.

If you have a direct account with the Funds and you do not want the mailing of shareholder reports and summary prospectuses combined with other members in your household, contact the Funds at 800-621-3979. Your request will be implemented within 30 days.

DODGE & COX STOCK FUND §PAGE 14

TRUSTEES AND EXECUTIVE OFFICERS

Charles F. Pohl, Chairman and Trustee

Chairman and Chief Investment Officer, Dodge & Cox

Dana M. Emery, President and Trustee

Chief Executive Officer, President, and Director of Fixed Income, Dodge & Cox

Thomas A. Larsen, Independent Trustee

Senior Counsel, Arnold & Porter LLP

Ann Mather, Independent Trustee

Former Executive Vice President, Chief Financial Officer, and Company Secretary of Pixar Studios

Robert B. Morris III, Independent Trustee

Former Partner and Managing Director of Global Research at Goldman Sachs & Co.

Gary Roughead, Independent Trustee

Annenberg Distinguished Visiting Fellow, Hoover Institution

Mark E. Smith, Independent Trustee

Former Executive Vice President, Managing Director - Fixed Income at Loomis Sayles & Company, L.P.

John B. Taylor, Independent Trustee

Professor of Economics, Stanford University; Senior Fellow, Hoover Institute and former Under Secretary for International Affairs, United States Treasury

John A. Gunn, Senior Vice President

Former Chairman and Chief Executive Officer, Dodge & Cox

Diana S. Strandberg, Senior Vice President

Senior Vice President and Director of International Equity, Dodge & Cox

David H. Longhurst, Treasurer

Vice President and Assistant Treasurer, Dodge & Cox

Thomas M. Mistele, Secretary

Chief Operating Officer, Secretary, and Senior Counsel, Dodge & Cox

Katherine M. Primas, Chief Compliance Officer

Chief Compliance Officer, Dodge & Cox

Additional information about the Trust’s Trustees and Officers is available in the Trust’s Statement of Additional Information (SAI). You can get a free copy of the SAI by visiting the Funds’ website at www.dodgeandcox.com or calling 800-621-3979.

PAGE 15 § DODGE & COX STOCK FUND

| | | | |

| | | | |

www.dodgeandcox.com

For Fund literature, transactions, and account information, please visit the Funds’ website.

or write or call:

DODGE & COX FUNDS

c/o Boston Financial Data Services

P.O. Box 8422

Boston, Massachusetts 02266-8422

(800) 621-3979

INVESTMENT MANAGER

Dodge & Cox

555 California Street, 40th Floor

San Francisco, California 94104

(415) 981-1710

This report is submitted for the general information of the shareholders of the Fund. The report is not authorized for distribution to prospective investors in the Fund unless it is accompanied by a current prospectus.

This report reflects our views, opinions, and portfolio holdings as of June 30, 2014, the end of the reporting period. Any such views are subject to change at any time based upon market or other conditions and Dodge & Cox disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Dodge & Cox Fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Dodge & Cox Fund.

6/14 GSF SAR Printed on recycled paper

Semi-Annual Report

June 30, 2014

Global Stock

Fund

ESTABLISHED 2008

TICKER: DODWX

TO OUR SHAREHOLDERS

The Dodge & Cox Global Stock Fund had a total return of 8.7% for the six months ending June 30, 2014, compared to a return of 6.2% for the MSCI World Index. On June 30, the Fund had net assets of $5.4 billion with a cash position of 2.2%.

MARKET COMMENTARY

For the first half of 2014, global equity markets were strong: most developed and emerging markets appreciated in both U.S.-dollar and local currency terms. Every sector of the MSCI World generated positive returns. U.S. equity markets (up 7%) continued to rise: the quarter ended June 30 marked the S&P 500’s sixth consecutive quarter of gains. Following a slow start to the year, growth in U.S. economic activity rebounded and assuaged concerns that the economy was losing momentum. Europe (up 5% in local currency) showed encouraging signs of economic improvement in early 2014. However, manufacturing activity later slowed and economic sentiment fell amid concerns that turmoil in Iraq and an escalation of the Ukraine/Russia crisis could significantly increase oil prices and impact Eurozone growth. Japan (down 3% in local currency) was the worst performing region of the market as investors continued to weigh the efficacy of its structural reform proposals.

Emerging markets were volatile: after performing poorly in the first quarter, they rebounded and finished the six-month period up 5% in local currency. Turkey (up 19%), Indonesia (up 19%), and India (up 18%) were the region’s best performing countries; Russia (down 3%) and China (down 1%) lagged.

The U.S. dollar’s depreciation against the Japanese yen, British pound, and emerging market currencies was a tailwind to performance. While the U.S. dollar’s appreciation against the euro was a headwind, the Fund’s partial hedge of the euro reduced the negative currency impact.

INVESTMENT STRATEGY:

FINDING OPPORTUNITIES IN CONNECTIVITY

To construct the portfolio, we employ a consistent and disciplined investment approach that focuses on intensive bottom-up research, a three- to five-year investment horizon, and a strict price discipline. We seek to identify

well-established companies that have long-term earnings and cash flow prospects that are not reflected in the current valuation. While we primarily focus on company-specific factors, we also consider external factors (e.g., industry trends, impact of regulatory policies, legal backdrop) as a component of our research process. These factors are all evaluated in relation to the company’s current valuation, which helps us understand how much optimism or concern is reflected in the stock price.

Investment themes emerge from our bottom-up research. One such theme is connectivity: consumers want instant access to content and the ability to bring their digital world with them wherever they go. Companies are responding to that demand while also creating more ways for individuals to connect with each other. Around the world, cheaper, faster computing technology and improving communications networks are significantly changing the competitive landscape and fueling global consumption of media, internet, and telecommunication services. Over the long term, we believe these tectonic shifts create the potential for high growth for companies that are positioned to capitalize on the opportunities.

Due to faster economic growth, we believe media and internet consumption in emerging markets will continue to outpace that of the developed world. In developing markets, while the absolute number of internet users is large, the percentage of the total population that is using the internet remains low, which creates an attractive long-term growth opportunity. Increased demand for content and communications equipment should also impact future trends in mobile data, wireline broadband penetration, and online video consumption.

The Fund is invested in an array of reasonably valued holdings that are poised to take advantage of these global growth opportunities. Examples include media and internet companies (e.g., Naspers, Comcast, and Time Warner Cable(a)), telecom services providers (e.g., China Mobile), and network equipment providers (e.g., Ericsson), each of which is described in detail below. On June 30, 17.4% of the Fund was invested in companies driven by “connectivity,” compared to 7.5% for the MSCI World.(b)

PAGE 1 § DODGE & COX GLOBAL STOCK FUND

Naspers

Naspers, a South Africa-based media company, was one of the Fund’s largest holdings at 2.1% on June 30. The company is well positioned to benefit from changes in technology and consumer behavior through its three core businesses: satellite pay-TV distribution in Africa; internet businesses in emerging markets such as China, Russia, India, and Poland; and print media in South Africa and Brazil.

Over the past decade, Naspers’ management team has developed a track record of creating value through shrewd investments and partnerships in communication services, e-commerce, online games, and social media. For example, Naspers acquired a stake in Tencent for $32 million in 2001, which is now worth $48 billion. Tencent—the largest internet company in China (over 800 million users)—operates leading online gaming, social networking, communications, and internet portal businesses on both desktop and mobile platforms, and stands to benefit from growth in Chinese internet usage. Naspers’ internet investments also include minority stakes in Mail.Ru (Russia’s leading communications and social networking company), Flipkart (e-commerce in India), and Avito (internet classified sites in Russia), among others. While Tencent enjoys a high valuation, Naspers trades at a discount to the sum of its parts and is reasonably valued in our opinion.

Every company has risks, and Naspers is no exception. Naspers’ businesses are operationally complex and span dozens of countries, some of which are located in politically and economically unstable parts of the world. The competitive landscapes, local laws, and regulatory restrictions in these markets can change rapidly. So far, we believe Naspers’ strategy and operational control have enabled them to navigate these issues successfully and implement best practices across their portfolio of investments.

Comcast and Time Warner Cable

In the United States, the Fund has several holdings that stand to benefit from increased broadband penetration. U.S. media companies also are altering their long-term strategies, and the industry is consolidating. Two of the Fund’s Media holdings have entered into a merger agreement: in February 2014, Comcast (the largest cable

operator in the United States) agreed to acquire Time Warner Cable (the second largest) for $45 billion in stock at the time of the announcement.

What is Comcast’s rationale for the deal? Combining the companies presents significant opportunities for cost reductions, operating synergies, and enhanced revenue growth. Comcast and Time Warner Cable currently do not compete directly in any markets. If the merger is completed, Comcast will gain access to the premier New York and Los Angeles markets, and thereby have a national presence. The proposed new entity would be the dominant provider of pay-TV and wireline broadband services in the United States (reaching ~70% of U.S. households).

We believe the proposed deal could build long-term shareholder value, depending upon merger concessions. Comcast’s management team is astute and has a proven merger and acquisition track record. While they have already made deal concessions, substantial regulatory hurdles lie ahead: both the Federal Communications Commission and the Department of Justice need to approve the merger. On a standalone basis, Comcast and Time Warner Cable remain reasonably valued and were held in the Fund on June 30 with 1.2% and 2.0% positions, respectively.

China Mobile

During the second quarter of 2014, we initiated a position in China Mobile (the largest mobile telecommunications operator in China with over 60% market share and over 70% revenue share); on June 30, the holding represented 1.0% of the Fund. After following the company for years, we were presented with an opportunity to purchase China Mobile in the Fund at a historically low valuation (three times forward enterprise value to EBITDA(c)).

While the company faces intense competition, margin pressure, and regulatory uncertainty, we believe its scale, significant growth opportunities, and valuation outweigh these concerns. In the Chinese wireless telecom market, China Mobile is a leader in network size, service quality, brand recognition, and balance sheet strength. The company is poised to benefit from industry trends, which include increasing disposable income, urbanization, proliferation of low-cost smartphones, and online video consumption. Furthermore, Chinese telecommunication

DODGE & COX GLOBAL STOCK FUND §PAGE 2

services companies are currently shielded from foreign competition in their home market.

Ericsson

Over the past decade, global broadband penetration and time spent online have increased dramatically, and we believe this trend will continue. One Fund holding that stands to benefit from such demand growth is Ericsson, a 0.7% position on June 30. Ericsson has a strong presence in mobile broadband—one of the main growth drivers of connectivity. Based in Sweden, the company has developed mobile and fixed-line communication networks across the globe.

Competition is fierce and technological disruption is always a risk. However, Ericsson is well positioned to benefit from the ongoing rollout and higher utilization of next generation technology based on their share of new orders, large installed base, substantial research and development spending, and managed services operation. Ericsson has a large proportion of recurring revenue that provides some stability to earnings. Moreover, the company has a strong balance sheet, high cash flow, proactive management team with a track record of cutting costs, and reasonable valuation at 1.2 times sales.

IN CLOSING

We continue to be optimistic about the long-term opportunity for global equities as valuations remain reasonable relative to long-term averages: the MSCI World traded at 15.1 times forward earnings with a 2.4% dividend yield at quarter end. Corporate balance sheets and cash flows continue to be robust. The Fund is invested in companies that we believe have favorable long-term growth opportunities over our three- to five-year investment horizon. Acknowledging that markets can be volatile over the short term, we encourage shareholders to remain focused on the long term.

Thank you for your continued confidence in our firm. As always, we welcome your comments and questions.

For the Board of Trustees,

| | |

| |

|

Charles F. Pohl, Chairman | | Dana M. Emery, President |

July 29, 2014

| (a) | The use of specific examples does not imply that they are more attractive investments than the Fund’s other holdings. |

| (b) | Unless otherwise specified, all weightings and characteristics are as of June 30, 2014. We define “connectivity” to include Telecommunication Services, Cable & Satellite, Internet Software & Services, and Communications Equipment (including Nokia and Blackberry). |

| (c) | EBITDA: Earnings before interest, taxes, depreciation, and amortization. |

PAGE 3 § DODGE & COX GLOBAL STOCK FUND

YEAR-TO-DATE PERFORMANCE REVIEW

The Fund outperformed the MSCI World by 2.5 percentage points year to date.

Key Contributors to Relative Results

| | § | | The Fund’s holdings in the Financials sector (up 9% compared to up 4% for the MSCI World sector), especially in emerging markets, had a positive impact. Yapi Kredi (up 44% since date of purchase), ICICI Bank (up 35%), and Kasikornbank (up 33%) were particularly strong. | |

| | § | | The Fund’s holdings in the Energy sector (up 29% compared to up 14% for the MSCI World sector) contributed to results. Weatherford International (up 48%) and Schlumberger (up 32%) were notable contributors. | |

| | § | | Selected additional contributors included Telecom Italia (up 30%), Nidec (up 26%), and Hewlett-Packard (up 22%). | |

Key Detractors from Relative Results

| | § | | Relative returns in the Health Care sector (up 7% compared to up 11% for the MSCI World sector) had a negative impact. | |

| | § | | The Fund’s underweight position in the Utilities sector (no holdings versus average 3% for the MSCI World sector), the strongest sector of the market (up 16%), detracted from results. | |

| | § | | Selected additional detractors included Coach (down 38%), America Movil (down 11%), AEGON (down 6%), and Millicom International Cellular (down 6%). | |

KEY CHARACTERISTICS OF DODGE & COX

Independent Organization

Dodge & Cox is one of the largest privately owned investment managers in the world. We remain committed to independence, with a goal of providing the highest quality investment management service to our existing clients.

Over 80 Years of Investment Experience

Dodge & Cox was founded in 1930. We have a stable and well-qualified team of investment professionals, most of whom have spent their entire careers at Dodge & Cox.

Experienced Investment Team

The Global Stock Investment Policy Committee, which is the decision-making body for the Global Stock Fund, is a seven-member committee with an average tenure at Dodge & Cox of 18 years.

One Business with a Single Research Office

Dodge & Cox manages equity (domestic, international, and global), fixed income (domestic and global), and balanced investments, operating from one office in San Francisco.

Consistent Investment Approach

Our team decision-making process involves thorough, bottom-up fundamental analysis of each investment.

Long-Term Focus and Low Expenses

We invest with a three- to five-year investment horizon, which has historically resulted in low turnover relative to our peers. We manage Funds that maintain low expense ratios.

Risks: The Fund is subject to stock market risk, meaning stocks in the Fund may decline in value for extended periods due to the financial prospects of individual companies, or due to general market and economic conditions. Investing in non-U.S. securities may entail risk due to foreign economic and political developments; this risk may be increased when investing in emerging markets. The Fund is also subject to currency risk. Please read the prospectus and summary prospectus for specific details regarding the Fund’s risk profile.

DODGE & COX GLOBAL STOCK FUND §PAGE 4

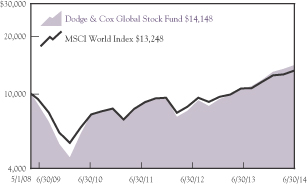

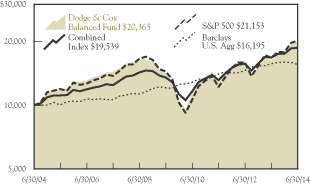

GROWTH OF $10,000 SINCE INCEPTION

FOR AN INVESTMENT MADE ON MAY 1, 2008

AVERAGE ANNUAL TOTAL RETURN

FOR PERIODS ENDED JUNE 30, 2014

| | | | | | | | | | | | | | | | |

| | | 1 Year | | | 3 Years | | | 5 Years | | | Since

Inception

(5/1/08) | |

Dodge & Cox Global Stock Fund | | | 29.76 | % | | | 14.38 | % | | | 18.31 | % | | | 5.79 | % |

MSCI World Index | | | 24.05 | | | | 11.81 | | | | 14.99 | | | | 4.66 | |

Returns represent past performance and do not guarantee future results. Investment return and share price will fluctuate with market conditions, and investors may have a gain or loss when shares are sold. Fund performance changes over time and currently may be significantly lower than stated. Performance is updated and published monthly. Visit the Fund’s website at www.dodgeandcox.com or call 800-621-3979 for current performance figures.

The Fund’s total returns include the reinvestment of dividend and capital gain distributions, but have not been adjusted for any income taxes payable by shareholders on these distributions or on Fund share redemptions. Index returns include dividends but, unlike Fund returns, do not reflect fees or expenses. The MSCI World Index is a broad-based, unmanaged equity market index aggregated from 23 developed market country indices, including the United States. MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed, or produced by MSCI.

MSCI World is a service mark of MSCI Barra.

FUND EXPENSE EXAMPLE

As a Fund shareholder, you incur ongoing Fund costs, including management fees and other Fund expenses. All mutual funds have ongoing costs, sometimes referred to as operating expenses. The following example shows ongoing costs of investing in the Fund and can help you understand these costs and compare them with those of other mutual funds. The example assumes a $1,000 investment held for the six months indicated.

ACTUAL EXPENSES

The first line of the table below provides information about actual account values and expenses based on the Fund’s actual returns. You may use the information in this line, together with your account balance, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

HYPOTHETICAL EXAMPLE FOR COMPARISON WITH OTHER MUTUAL FUNDS