UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-173

DODGE & COX FUNDS

(Exact name of registrant as specified in charter)

555 California Street, 40th Floor

San Francisco, CA 94104

(Address of principal executive offices) (Zip code)

Thomas M. Mistele, Esq.

555 California Street, 40th Floor

San Francisco, CA 94104

(Name and address of agent for service)

Registrant’s telephone number, including area code: 415-981-1710

Date of fiscal year end: DECEMBER 31, 2017

Date of reporting period: JUNE 30, 2017

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss. 3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

The following are the June 30, 2017 semi-annual reports for the Dodge & Cox Funds, a Delaware statutory trust, consisting of six series: Dodge & Cox Stock Fund, Dodge & Cox Global Stock Fund, Dodge & Cox International Stock Fund, Dodge & Cox Balanced Fund, Dodge & Cox Income Fund and Dodge & Cox Global Bond Fund. The reports of each series were transmitted to their respective shareholders on August 15, 2017.

DODGE & COX FUNDS®

Semi-Annual Report

June 30, 2017

Stock Fund

ESTABLISHED 1965

TICKER: DODGX

06/17 SF SAR  Printed on recycled paper

Printed on recycled paper

TO OUR SHAREHOLDERS

The Dodge & Cox Stock Fund had a total return of 6.8% for the six months ended June 30, 2017, compared to a return of 9.3% for the S&P 500 Index.

MARKET COMMENTARY

U.S. equity markets continued to climb during the first half of 2017: the S&P 500 reached an all-time high in mid-June and ended the period up 9%, marking its strongest first half since 2013. Information Technology was the best-performing sector of the S&P 500, and Energy was the worst-performing sector amid lower oil prices. Solid corporate earnings growth, combined with expectations of an improving economy, boosted U.S. equity returns and propelled valuations further above longer-term averages.

We see signs of continuing steady economic growth, increasing corporate earnings, and rising interest rates, all of which would benefit the Fund. Economic data released during the first half has been generally strong, confirming that the U.S. economy remains solid. The Trump administration’s objectives for tax cuts and increased infrastructure spending could further stimulate growth. Meanwhile, the Federal Reserve (Fed) has signaled that additional rate hikes are forthcoming, indicating the Fed has confidence in the economy. These factors, combined with accelerating global GDP growth, a recovery in energy and commodity prices, and corporate cost reductions could drive corporate earnings higher and support current market valuations.

INVESTMENT STRATEGY

At Dodge & Cox, we approach each investment from the perspective of being a long-term part owner of a business and make gradual changes based on a three- to five-year investment horizon. The Fund has historically had low portfolio turnover; 2017 has been no exception with turnover of only 4% in the first half. As a result of individual stock selection, the Fund holds 63 companies across nine sectors; areas of emphasis are Financials, Health Care, and Information Technology.(a)

During the volatility of 2016, we highlighted how the Fund’s financial services holdings were trading at inexpensive valuations despite their asset growth, improved credit quality, cost reductions, and capital return prospects. Since then, however, share prices have risen and we have trimmed a number of the Fund’s Financials holdings, including Bank of America and Bank of New York Mellon.(b) Nevertheless, we remain enthusiastic about the Fund’s position in Financials (27.7% compared to 14.5% for the S&P 500) and specific holdings, which continue to have attractive fundamentals as well as attributes that could lead to higher share prices. Increased profitability and strong capital generation allow banks to return capital to shareholders via share buybacks and dividends, making them a compelling alternative to other dividend-paying stocks, in our view. The Trump administration may create potential tailwinds for the banking system through tax reform and regulatory relief. Moreover, the Fed raised short-term rates twice in the first half of the year and signaled expectations for one additional hike in 2017, which should increase the federal

funds rate to 1.5%. If interest rates increase further, the Financials sector stands to benefit from improved earnings and higher net interest margins.

While we have trimmed Financials and certain other holdings amid higher U.S. equity market valuations, we continue to find areas of value offering long-term investment opportunities. For example, we recently added to several Health Care holdings, including AstraZeneca, and Energy companies in the Fund.

AstraZeneca

AstraZeneca, which is based in the United Kingdom, is a global pharmaceutical company with strengths in treatments for cancer, respiratory illnesses, cardiovascular problems, and infectious diseases. In the second half of 2016, the share price was under pressure due to concerns about recent and upcoming patent expirations for several of its major drugs. Despite this headwind, we added to the Fund’s holding in early 2017 after reaffirming our investment thesis.

The company’s long-term growth outlook is favorable given its robust new drug pipeline, particularly in oncology (cancer treatment). AstraZeneca has an attractive position in the revolutionary field of cancer immunotherapy, which harnesses the disease-fighting capabilities of the body’s immune system to attack cancerous tumors. We have conducted extensive due diligence, which included industry conferences and management meetings, and we continue to believe the immuno-oncology (IO) field holds great promise. Since the IO market is in its very early stages, sponsors and the scientific community are investing heavily into understanding which tumors can be targeted with IO and which patients will be most responsive to IO treatments (i.e., biomarkers). We think the field will evolve rapidly over the next five to ten years as physicians develop a better understanding of how these drugs work, creating a massive revenue and profit opportunity. With a 4.3% dividend yield, the current valuation is reasonable at 17 times forward earnings and does not appear to reflect potential success from the immunotherapy drug pipeline. AstraZeneca represented 1.9% of the Fund on June 30.

Energy

Oil prices dropped 16% over the past six months, weighing heavily on the outlook for profitability and growth in the Energy sector. While the short-term direction of oil prices is difficult to forecast, we believe the long-term fundamentals of supply and demand point to higher prices. The current demand for oil, which is about 98 million barrels a day, continues to grow about one percent per year, driven by growing transportation demand in the developing world. Oil fields deplete as the resource is extracted, reducing the global production base about two to three percent per year, so continuing investment is required to meet current demand and to prepare for future demand growth. We anticipate that 15 to 20 million barrels per day of additional production will be needed over the next five years to meet demand if these trends continue. However, upstream capital investment has declined to a 10-year low, fewer new projects are being approved, and North American

PAGE 2 § DODGE & COX STOCK FUND

unconventional resources (including shale) are unlikely to grow enough to bridge this eventual gap.

The Fund remains modestly overweight the Energy sector (7.4% compared to 6.0% for the S&P 500). Amid depressed valuations for energy companies, we recently added to selected holdings, including Anadarko Petroleum (discussed below) and Schlumberger (the world’s leading provider of oil services for drilling, production, and processing), among other holdings.

Anadarko Petroleum

Anadarko Petroleum (a 1.3% position) is an independent oil and gas exploration and production (E&P) company, one of three held in the Fund. The company’s stock price has been negatively impacted in 2017 by a gas leak that caused a fatal explosion. While tragic, this incident did not materially impact our long-term investment outlook for the company. Recent meetings with company management affirmed our belief that Anadarko remains an attractive investment over our three- to five-year investment horizon.

As a leading global explorer with strong operational capabilities, Anadarko has a record of success in generating high returns on capital over energy price cycles. In the coming years, we believe the key differentiators for E&Ps will be a company’s asset quality and its ability to develop those assets, particularly large-scale unconventional resources. Anadarko is well positioned to manage these challenges. For example, in the DJ Basin in Colorado, Anadarko systematically developed all of the needed infrastructure to execute its plan, which allowed the company to achieve growth targets at competitive costs; Anadarko is now applying the same approach of systematic field and infrastructure development to the Permian Basin.

The company’s conservative management team has an excellent track record of disciplined capital allocation. In addition, Anadarko continues to invest substantially in exploration, which it sees as the means to create upside opportunity for the company. This focus on exploration differentiates Anadarko from its peers and will likely create value across business cycles. After considering the company’s risks, opportunities, and valuation, we added to Anadarko during the first half of 2017.

IN CLOSING

Since U.S. equity valuations are now near recent highs, we have adopted a tempered outlook for broader U.S. equity market returns. However, as an active manager with a value-oriented approach, we remain optimistic about the long-term prospects for the portfolio to preserve and enhance purchasing power. On June 30, the Fund’s equity holdings collectively traded at 15.4 times forward earnings, a discount to the S&P 500, which traded at 18.6 times forward earnings.

We believe the rewards of active management are most likely to accrue to those investors who have the discipline to maintain a long-term investment horizon. Thank you for your continued confidence in our firm. As always, we welcome your comments and questions.

For the Board of Trustees,

| | |

| |  |

Charles F. Pohl, Chairman | | Dana M. Emery, President |

July 31, 2017

| (a) | | Unless otherwise specified, all weightings and characteristics are as of June 30, 2017. |

| (b) | | The use of specific examples does not imply that they are more or less attractive investments than the portfolio’s other holdings. |

DODGE & COX STOCK FUND §PAGE 3

YEAR-TO-DATE PERFORMANCE REVIEW

The Fund underperformed the S&P 500 by 2.5 percentage points year to date.

Key Detractors from Relative Results

| | § | | The Fund’s average overweight position (29% versus 14%) and holdings in the Financials sector (up 4% compared to up 7% for the S&P 500 sector) hurt relative performance. Goldman Sachs (down 7%) and Capital One Financial (down 4%) lagged. | |

| | § | | Poor returns from the Fund’s holdings in the Energy sector (down 21% compared to down 13% for the S&P 500 sector), combined with a slightly higher average weighting (8% versus 7%), detracted from results. Anadarko Petroleum (down 35%), Apache (down 24%), and Schlumberger (down 21%) were especially weak. | |

| | § | | Outstanding performance from several large internet and technology stocks not held by the Fund (e.g., Facebook, Amazon, Apple, Netflix) boosted S&P 500 returns and hurt the Fund’s relative results. The negative impact was particularly significant in the Information Technology sector (up 12% compared to up 17% for S&P 500 sector), which was the strongest area of the market. | |

Key Contributors to Relative Results

| | § | | The Fund’s average overweight position (19% versus 14%) and holdings in the Health Care sector (up 17% compared to up 16% for the S&P 500 sector) enhanced performance. Alnylam Pharmaceuticals (up 113%), AstraZeneca (up 29%), Cigna (up 26%), and Sanofi (up 21%) were particularly strong. | |

| | § | | Returns from holdings in the Telecommunication Services sector (down 3% compared to down 11% for the S&P 500 sector) helped relative results. | |

| | § | | Charter Communications (up 17%) also contributed. | |

KEY CHARACTERISTICS OF DODGE & COX

Independent Organization

Dodge & Cox is one of the largest privately owned investment managers in the world. We remain committed to independence, with a goal of providing the highest quality investment management service to our existing clients.

Over 85 Years of Investment Experience

Dodge & Cox was founded in 1930. We have a stable and well-qualified team of investment professionals, most of whom have spent their entire careers at Dodge & Cox.

Experienced Investment Team

The U.S. Equity Investment Committee, which is the decision-making body for the Stock Fund, is an eight-member committee with an average tenure at Dodge & Cox of 24 years.

One Business with a Single Research Office

Dodge & Cox manages equity (domestic, international, and global), fixed income (domestic and global), and balanced investments, operating from one office in San Francisco.

Consistent Investment Approach

Our team decision-making process involves thorough, bottom-up fundamental analysis of each investment.

Long-Term Focus and Low Expenses

We invest with a three- to five-year investment horizon, which has historically resulted in low turnover relative to our peers. We manage Funds that maintain low expense ratios.

Risks: The Fund is subject to market risk, meaning holdings in the Fund may decline in value for extended periods due to the financial prospects of individual companies, or due to general market and economic conditions. Please read the prospectus and summary prospectus for specific details regarding the Fund’s risk profile.

PAGE 4 § DODGE & COX STOCK FUND

GROWTH OF $10,000 OVER 10 YEARS

FOR AN INVESTMENT MADE ON JUNE 30, 2007

AVERAGE ANNUAL TOTAL RETURN

FOR PERIODS ENDED JUNE 30, 2017

| | | | | | | | | | | | | | | | |

| | | 1 Year | | | 5 Years | | | 10 Years | | | 20 Years | |

Dodge & Cox Stock Fund | | | 28.62 | % | | | 16.36 | % | | | 5.89 | % | | | 9.45 | % |

S&P 500 Index | | | 17.90 | | | | 14.63 | | | | 7.18 | | | | 7.15 | |

Returns represent past performance and do not guarantee future results. Investment return and share price will fluctuate with market conditions, and investors may have a gain or loss when shares are sold. Fund performance changes over time and currently may be significantly lower than stated. Performance is updated and published monthly. Visit the Fund’s website at dodgeandcox.com or call 800-621-3979 for current performance figures.

The Fund’s total returns include the reinvestment of dividend and capital gain distributions, but have not been adjusted for any income taxes payable by shareholders on these distributions or on Fund share redemptions. Index returns include dividends but, unlike Fund returns, do not reflect fees or expenses. The S&P 500 Index is a market capitalization-weighted index of 500 large-capitalization stocks commonly used to represent the U.S. equity market.

S&P 500® is a trademark of S&P Global Inc.

FUND EXPENSE EXAMPLE

As a Fund shareholder, you incur ongoing Fund costs, including management fees and other Fund expenses. All mutual funds have ongoing costs, sometimes referred to as operating expenses. The following example shows ongoing costs of investing in the Fund and can help you understand these costs and compare them with those of other mutual funds. The example assumes a $1,000 investment held for the six months indicated.

ACTUAL EXPENSES

The first line of the table below provides information about actual account values and expenses based on the Fund’s actual returns. You may use the information in this line, together with your account balance, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

HYPOTHETICAL EXAMPLE FOR COMPARISON WITH OTHER MUTUAL FUNDS

Information on the second line of the table can help you compare ongoing costs of investing in the Fund with those of other mutual funds. This information may not be used to estimate the actual ending account balance or expenses you paid during the period. The hypothetical “Ending Account Value” is based on the actual expense ratio of the Fund and an assumed 5% annual rate of return before expenses (not the Fund’s actual return). The amount under the heading “Expenses Paid During Period” shows the hypothetical expenses your account would have incurred under this scenario. You can compare this figure with the 5% hypothetical examples that appear in shareholder reports of other mutual funds.

| | | | | | | | | | | | |

Six Months Ended

June 30, 2017 | | Beginning Account Value

1/1/2017 | | | Ending Account Value

6/30/2017 | | | Expenses Paid

During Period* | |

Based on Actual Fund Return | | $ | 1,000.00 | | | $ | 1,068.10 | | | $ | 2.69 | |

Based on Hypothetical 5% Yearly Return | | | 1,000.00 | | | | 1,022.20 | | | | 2.63 | |

| * | | Expenses are equal to the Fund’s annualized expense ratio of 0.52%, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period). |

The expenses shown in the table highlight ongoing costs only and do not reflect any transactional fees or account maintenance fees. Though other mutual funds may charge such fees, please note that the Fund does not charge transaction fees (e.g., redemption fees, sales loads) or universal account maintenance fees (e.g., small account fees).

DODGE & COX STOCK FUND §PAGE 5

| | | | |

| FUND INFORMATION (unaudited) | | | June 30, 2017 | |

| | | | |

| GENERAL INFORMATION | | | |

Net Asset Value Per Share | | | $192.69 | |

Total Net Assets (billions) | | | $66.1 | |

Expense Ratio | | | 0.52% | |

Portfolio Turnover Rate (1/1/17 to 6/30/17, unannualized) | | | 4% | |

30-Day SEC Yield(a) | | | 1.13% | |

Number of Companies | | | 63 | |

Fund Inception | | | 1965 | |

No sales charges or distribution fees | | | | |

Investment Manager: Dodge & Cox, San Francisco. Managed by the U.S. Equity Investment Committee, whose eight members’ average tenure at Dodge & Cox is 24 years.

| | | | | | | | |

| PORTFOLIO CHARACTERISTICS | | Fund | | | S&P 500 | |

Median Market Capitalization (billions) | | | $41 | | | | $21 | |

Weighted Average Market Capitalization (billions) | | | $125 | | | | $169 | |

Price-to-Earnings Ratio(b) | | | 15.4x | | | | 18.6x | |

Foreign Securities not in the S&P 500(c) | | | 10.0% | | | | 0.0% | |

| | | | |

| TEN LARGEST HOLDINGS (%)(d) | | Fund | |

Charles Schwab Corp. | | | 3.8 | |

Bank of America Corp. | | | 3.8 | |

Wells Fargo & Co. | | | 3.6 | |

Capital One Financial Corp. | | | 3.4 | |

Charter Communications, Inc. | | | 3.0 | |

Novartis AG (Switzerland) | | | 3.0 | |

Sanofi (France) | | | 3.0 | |

Time Warner, Inc. | | | 2.9 | |

Goldman Sachs Group, Inc. | | | 2.8 | |

Alphabet, Inc. | | | 2.8 | |

| | | | | | | | |

| SECTOR DIVERSIFICATION (%) | | Fund | | | S&P 500 | |

Financials | | | 27.7 | | | | 14.5 | |

Health Care | | | 19.7 | | | | 14.5 | |

Information Technology | | | 17.7 | | | | 22.3 | |

Consumer Discretionary | | | 15.6 | | | | 12.3 | |

Energy | | | 7.4 | | | | 6.0 | |

Industrials | | | 5.0 | | | | 10.3 | |

Telecommunication Services | | | 1.8 | | | | 2.1 | |

Consumer Staples | | | 1.5 | | | | 9.1 | |

Materials | | | 1.0 | | | | 2.8 | |

Utilities | | | 0.0 | | | | 3.2 | |

Real Estate | | | 0.0 | | | | 2.9 | |

| (a) | SEC Yield is an annualization of the Fund’s net investment income for the trailing 30-day period. Dividends paid by the Fund may be higher or lower than implied by the SEC Yield. |

| (b) | Price-to-earnings (P/E) ratios are calculated using 12-month forward earnings estimates from third-party sources. |

| (c) | Foreign securities are U.S. dollar denominated. |

| (d) | The Fund’s portfolio holdings are subject to change without notice. The mention of specific securities is not a recommendation to buy, sell, or hold any particular security and is not indicative of Dodge & Cox’s current or future trading activity. |

| (e) | Net Cash & Other includes cash, short-term investments, derivatives, receivables, and payables. |

PAGE 6 § DODGE & COX STOCK FUND

| | | | |

| PORTFOLIO OF INVESTMENTS (unaudited) | | | June 30, 2017 | |

| | | | | | | | |

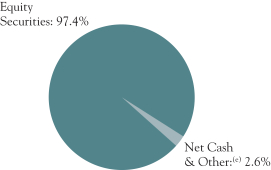

| COMMON STOCKS: 97.4% | | | | | | |

| | |

| | | SHARES | | | VALUE | |

| CONSUMER DISCRETIONARY: 15.6% | |

AUTOMOBILES & COMPONENTS: 0.5% | |

Harley-Davidson, Inc. | | | 5,610,647 | | | $ | 303,087,151 | |

|

CONSUMER DURABLES & APPAREL: 0.6% | |

Coach, Inc. | | | 8,813,900 | | | | 417,250,026 | |

| | |

MEDIA: 11.7% | | | | | | | | |

Charter Communications, Inc., Class A(a) | | | 5,934,486 | | | | 1,999,031,609 | |

Comcast Corp., Class A | | | 44,997,594 | | | | 1,751,306,358 | |

DISH Network Corp., Class A(a) | | | 9,727,476 | | | | 610,496,394 | |

News Corp., Class A | | | 6,892,103 | | | | 94,421,811 | |

Time Warner, Inc. | | | 18,778,332 | | | | 1,885,532,316 | |

Twenty-First Century Fox, Inc., Class A | | | 41,334,626 | | | | 1,171,423,301 | |

Twenty-First Century Fox, Inc., Class B | | | 9,350,000 | | | | 260,584,500 | |

| | | | | | | | |

| | | | | | | 7,772,796,289 | |

RETAILING: 2.8% | | | | | | | | |

Liberty Interactive Corp. QVC Group, Series A(a) | | | 15,980,376 | | | | 392,158,427 | |

Target Corp. | | | 11,761,054 | | | | 614,985,514 | |

The Priceline Group, Inc.(a) | | | 453,400 | | | | 848,093,768 | |

| | | | | | | | |

| | | | | | | 1,855,237,709 | |

| | | | | | | | |

| | | | | | | 10,348,371,175 | |

| CONSUMER STAPLES: 1.5% | |

FOOD & STAPLES RETAILING: 1.5% | |

Wal-Mart Stores, Inc. | | | 12,988,050 | | | | 982,935,624 | |

| | |

| ENERGY: 7.4% | | | | | | | | |

Anadarko Petroleum Corp. | | | 19,695,521 | | | | 892,994,922 | |

Apache Corp. | | | 18,045,994 | | | | 864,944,492 | |

Baker Hughes, Inc. | | | 15,371,113 | | | | 837,879,370 | |

Concho Resources, Inc.(a) | | | 3,615,000 | | | | 439,330,950 | |

National Oilwell Varco, Inc. | | | 18,798,000 | | | | 619,206,120 | |

Schlumberger, Ltd. (Curacao/United States) | | | 17,549,245 | | | | 1,155,442,291 | |

Weatherford International PLC(a) (Ireland) | | | 28,007,400 | | | | 108,388,638 | |

| | | | | | | | |

| | | | | | | 4,918,186,783 | |

| FINANCIALS: 27.7% | | | | | | | | |

BANKS: 10.6% | | | | | | | | |

Bank of America Corp. | | | 102,436,500 | | | | 2,485,109,490 | |

BB&T Corp. | | | 13,100,144 | | | | 594,877,539 | |

JPMorgan Chase & Co. | | | 16,797,800 | | | | 1,535,318,920 | |

Wells Fargo & Co. | | | 43,253,341 | | | | 2,396,667,625 | |

| | | | | | | | |

| | | | | | | 7,011,973,574 | |

DIVERSIFIED FINANCIALS: 14.3% | |

American Express Co. | | | 16,997,300 | | | | 1,431,852,552 | |

Bank of New York Mellon Corp. | | | 27,003,324 | | | | 1,377,709,590 | |

Capital One Financial Corp.(b) | | | 27,087,711 | | | | 2,237,986,683 | |

Charles Schwab Corp. | | | 58,867,600 | | | | 2,528,952,096 | |

Goldman Sachs Group, Inc. | | | 8,488,700 | | | | 1,883,642,530 | |

| | | | | | | | |

| | | | | | | 9,460,143,451 | |

INSURANCE: 2.8% | | | | | | | | |

AEGON NV (Netherlands) | | | 71,584,960 | | | | 365,799,146 | |

MetLife, Inc. | | | 26,532,700 | | | | 1,457,706,538 | |

| | | | | | | | |

| | | | | | | 1,823,505,684 | |

| | | | | | | | |

| | | | | | | 18,295,622,709 | |

| HEALTH CARE: 19.7% | | | | | | | | |

HEALTH CARE EQUIPMENT & SERVICES: 7.1% | |

Cigna Corp. | | | 8,293,217 | | | | 1,388,201,593 | |

Danaher Corp. | | | 3,437,600 | | | | 290,099,064 | |

Express Scripts Holding Co.(a) | | | 21,234,871 | | | | 1,355,634,165 | |

Medtronic PLC (Ireland) | | | 6,510,900 | | | | 577,842,375 | |

UnitedHealth Group, Inc. | | | 5,830,760 | | | | 1,081,139,519 | |

| | | | | | | | |

| | | | | | | 4,692,916,716 | |

| | | | | | | | |

| | |

| | | SHARES | | | VALUE | |

PHARMACEUTICALS, BIOTECHNOLOGY & LIFE SCIENCES: 12.6% | |

Alnylam Pharmaceuticals, Inc.(a)(b) | | | 5,500,735 | | | $ | 438,738,624 | |

AstraZeneca PLC ADR (United Kingdom) | | | 37,517,873 | | | | 1,278,984,291 | |

Bristol-Myers Squibb Co. | | | 17,941,339 | | | | 999,691,409 | |

Eli Lilly and Co. | | | 3,191,832 | | | | 262,687,774 | |

Merck & Co., Inc. | | | 7,767,900 | | | | 497,844,711 | |

Novartis AG ADR (Switzerland) | | | 23,673,500 | | | | 1,976,027,045 | |

Roche Holding AG ADR (Switzerland) | | | 27,975,399 | | | | 889,617,688 | |

Sanofi ADR (France) | | | 41,035,028 | | | | 1,965,988,191 | |

| | | | | | | | |

| | | | | | | 8,309,579,733 | |

| | | | | | | | |

| | | | | | | 13,002,496,449 | |

| INDUSTRIALS: 5.0% | |

CAPITAL GOODS: 1.4% | |

Johnson Controls International PLC (Ireland) | | | 20,810,986 | | | | 902,364,353 | |

|

TRANSPORTATION: 3.6% | |

FedEx Corp. | | | 6,897,099 | | | | 1,498,946,525 | |

Union Pacific Corp. | | | 8,070,000 | | | | 878,903,700 | |

| | | | | | | | |

| | | | | | | 2,377,850,225 | |

| | | | | | | | |

| | | | | | | 3,280,214,578 | |

| INFORMATION TECHNOLOGY: 17.7% | |

SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT: 0.8% | |

Maxim Integrated Products, Inc. | | | 12,064,675 | | | | 541,703,908 | |

|

SOFTWARE & SERVICES: 8.0% | |

Alphabet, Inc., Class A(a) | | | 148,100 | | | | 137,685,608 | |

Alphabet, Inc., Class C(a) | | | 1,920,253 | | | | 1,744,991,509 | |

Dell Technologies, Inc., Class V(a) | | | 4,022,510 | | | | 245,815,586 | |

DXC Technology Co. | | | 8,221,227 | | | | 630,732,535 | |

Microsoft Corp. | | | 24,747,300 | | | | 1,705,831,389 | |

Synopsys, Inc.(a) | | | 4,051,969 | | | | 295,510,099 | |

VMware, Inc.(a) | | | 5,955,511 | | | | 520,690,327 | |

| | | | | | | | |

| | | | | | | 5,281,257,053 | |

TECHNOLOGY, HARDWARE & EQUIPMENT: 8.9% | |

Cisco Systems, Inc. | | | 39,252,711 | | | | 1,228,609,854 | |

Corning, Inc. | | | 9,831,700 | | | | 295,442,585 | |

Hewlett Packard Enterprise Co.(b) | | | 103,083,316 | | | | 1,710,152,212 | |

HP Inc. | | | 71,435,195 | | | | 1,248,687,209 | |

Juniper Networks, Inc. | | | 11,497,165 | | | | 320,540,960 | |

NetApp, Inc.(b) | | | 7,652,331 | | | | 306,475,857 | |

TE Connectivity, Ltd. (Switzerland) | | | 9,976,475 | | | | 784,949,053 | |

| | | | | | | | |

| | | | | | | 5,894,857,730 | |

| | | | | | | | |

| | | | | | | 11,717,818,691 | |

| MATERIALS: 1.0% | | | | | | | | |

Celanese Corp., Series A(b) | | | 7,158,398 | | | | 679,618,306 | |

|

| TELECOMMUNICATION SERVICES: 1.8% | |

Sprint Corp.(a) | | | 104,462,856 | | | | 857,640,048 | |

Zayo Group Holdings, Inc.(a) | | | 9,750,000 | | | | 301,275,000 | |

| | | | | | | | |

| | | | | | | 1,158,915,048 | |

| | | | | | | | |

TOTAL COMMON STOCKS

(Cost $41,702,810,991) | | | | | | $ | 64,384,179,363 | |

| | |

| See accompanying Notes to Financial Statements | | DODGE & COX STOCK FUND §PAGE 7 |

| | | | |

| PORTFOLIO OF INVESTMENTS (unaudited) | | | June 30, 2017 | |

| | | | | | | | |

| SHORT-TERM INVESTMENTS: 2.5% | |

| | |

| | | PAR VALUE | | | VALUE | |

MONEY MARKET FUND: 0.1% | | | | | |

State Street Institutional Treasury Plus Money Market Fund | | $ | 66,033,346 | | | $ | 66,033,346 | |

|

REPURCHASE AGREEMENT: 2.4% | |

Fixed Income Clearing Corporation(c) 0.60%, dated 6/30/17, due 7/3/17, maturity value $1,594,166,704 | | | 1,594,087,000 | | | | 1,594,087,000 | |

| | | | | | | | |

TOTAL SHORT-TERM INVESTMENTS

(Cost $1,660,120,346) | | | $ | 1,660,120,346 | |

| | | | | | | | |

TOTAL INVESTMENTS

(Cost $43,362,931,337) | | | 99.9 | % | | $ | 66,044,299,709 | |

OTHER ASSETS LESS LIABILITIES | | | 0.1 | % | | | 91,371,703 | |

| | | | | | | | |

| NET ASSETS | | | 100.0 | % | | $ | 66,135,671,412 | |

| | | | | | | | |

| (b) | See Note 9 regarding holdings of 5% voting securities |

| (c) | Repurchase agreement is collateralized by U.S. Treasury Notes 1.50%-2.125%, 11/15/21-4/30/23. Total collateral value is $1,625,974,305. |

In determining a company’s country designation, the Fund generally references the country of incorporation. In cases where the Fund considers the country of incorporation to be a “jurisdiction of convenience” chosen primarily for tax purposes or in other limited circumstances, the Fund uses the country designation of an appropriate broad-based market index. In those cases, two countries are listed — the country of incorporation and the country designated by an appropriate index, respectively.

ADR: American Depositary Receipt

FUTURES CONTRACTS

| | | | | | | | | | | | | | | | |

| Description | | Number of

Contracts | | | Expiration

Date | | | Notional Amount | | | Unrealized

Appreciation/

(Depreciation) | |

E-mini S&P 500 Index—Long Position | | | 11,647 | | | | Sep 2017 | | | $ | 1,409,811,115 | | | $ | (5,420,299 | ) |

| | |

| PAGE 8 § DODGE & COX STOCK FUND | | See accompanying Notes to Financial Statements |

| | | | |

STATEMENT OF ASSETS AND LIABILITIES (unaudited) | |

| |

| | | June 30, 2017 | |

ASSETS: | | | | |

Investments, at value | | | | |

Unaffiliated issuers (cost $40,404,334,088) | | $ | 60,977,803,884 | |

Affiliated issuers (cost $2,958,597,249) | | | 5,066,495,825 | |

| | | | |

| | | 66,044,299,709 | |

Cash held at broker | | | 48,916,242 | |

Receivable for investments sold | | | 70,023,062 | |

Receivable from broker for variation margin | | | 2,853,515 | |

Receivable for Fund shares sold | | | 43,814,725 | |

Dividends and interest receivable | | | 64,596,846 | |

Prepaid expenses and other assets | | | 104,705 | |

| | | | |

| | | 66,274,608,804 | |

| | | | |

LIABILITIES: | | | | |

Payable for investments purchased | | | 68,085,773 | |

Payable for Fund shares redeemed | | | 42,911,344 | |

Management fees payable | | | 27,040,675 | |

Accrued expenses | | | 899,600 | |

| | | | |

| | | 138,937,392 | |

| | | | |

NET ASSETS | | $ | 66,135,671,412 | |

| | | | |

NET ASSETS CONSIST OF: | | | | |

Paid in capital | | $ | 42,521,487,606 | |

Undistributed net investment income | | | 7,997,157 | |

Undistributed net realized gain | | | 930,238,576 | |

Net unrealized appreciation | | | 22,675,948,073 | |

| | | | |

| | $ | 66,135,671,412 | |

| | | | |

Fund shares outstanding (par value $0.01 each, unlimited shares authorized) | | | 343,224,956 | |

Net asset value per share | | $ | 192.69 | |

|

STATEMENT OF OPERATIONS (unaudited) | |

| |

| | | Six Months Ended

June 30, 2017 | |

INVESTMENT INCOME: | | | | |

Dividends (net of foreign taxes of $25,431,443) | | | | |

Unaffiliated issuers | | $ | 572,988,155 | |

Affiliated issuers | | | 45,348,714 | |

Interest | | | 2,701,324 | |

| | | | |

| | | 621,038,193 | |

| | | | |

EXPENSES: | | | | |

Management fees | | | 160,897,971 | |

Custody and fund accounting fees | | | 402,452 | |

Transfer agent fees | | | 1,710,999 | |

Professional services | | | 81,993 | |

Shareholder reports | | | 612,474 | |

Registration fees | | | 195,797 | |

Trustees’ fees | | | 130,000 | |

ADR depository services fees | | | 4,024,180 | |

Miscellaneous | | | 557,979 | |

| | | | |

| | | 168,613,845 | |

| | | | |

NET INVESTMENT INCOME | | | 452,424,348 | |

| | | | |

REALIZED AND UNREALIZED GAIN (LOSS): | | | | |

Net realized gain (loss) | | | | |

Investments in unaffiliated issuers | | | 771,966,460 | |

Investments in affiliated issuers | | | 74,364,617 | |

Futures contracts | | | 114,867,062 | |

Net change in unrealized appreciation/depreciation | | | | |

Investments | | | 2,795,332,975 | |

Futures contracts | | | 9,320,155 | |

| | | | |

Net realized and unrealized gain | | | 3,765,851,269 | |

| | | | |

NET CHANGE IN NET ASSETS FROM OPERATIONS | | $ | 4,218,275,617 | |

| | | | |

| | | | | | | | |

STATEMENT OF CHANGES IN NET ASSETS (unaudited) | |

| | |

| | | Six Months Ended

June 30, 2017 | | | Year Ended

December 31, 2016 | |

OPERATIONS: | | | | | | | | |

Net investment income | | $ | 452,424,348 | | | $ | 1,011,975,095 | |

Net realized gain | | | 961,198,139 | | |

| 2,967,136,896

|

|

Net change in unrealized appreciation/depreciation | | | 2,804,653,130 | | | | 7,026,623,876 | |

| | | | | | | | |

| | | 4,218,275,617 | | |

| 11,005,735,867

|

|

| | | | | | | | |

| | |

DISTRIBUTIONS TO SHAREHOLDERS FROM: | | | | | | | | |

Net investment income | | | (451,809,266 | ) | | | (1,006,582,969 | ) |

Net realized gain | | | (926,622,294 | ) | | | (2,967,981,956 | ) |

| | | | | | | | |

Total distributions | | | (1,378,431,560 | ) | | | (3,974,564,925 | ) |

| | | | | | | | |

| | |

FUND SHARE TRANSACTIONS: | | | | | | | | |

Proceeds from sale of shares | | | 5,321,067,392 | | | | 7,078,053,220 | |

Reinvestment of distributions | | | 1,306,390,530 | | | | 3,757,250,793 | |

Cost of shares redeemed | | | (4,932,106,426 | ) | | | (11,111,123,603 | ) |

| | | | | | | | |

Net change from Fund share transactions | | | 1,695,351,496 | | | | (275,819,590 | ) |

| | | | | | | | |

Total change in net assets | | | 4,535,195,553 | | | | 6,755,351,352 | |

| | |

NET ASSETS: | | | | | | | | |

Beginning of period | | | 61,600,475,859 | | | | 54,845,124,507 | |

| | | | | | | | |

End of period (including undistributed net investment income of $7,997,157 and $7,382,075, respectively) | | $ | 66,135,671,412 | | | $ | 61,600,475,859 | |

| | | | | | | | |

| | |

SHARE INFORMATION: | | | | | | | | |

Shares sold | | | 27,885,017 | | | | 42,458,419 | |

Distributions reinvested | | | 6,903,842 | | | | 21,705,948 | |

Shares redeemed | | | (25,811,424 | ) | | | (66,866,904 | ) |

| | | | | | | | |

Net change in shares outstanding | | | 8,977,434 | | | | (2,702,537 | ) |

| | | | | | | | |

| | |

| See accompanying Notes to Financial Statements | | DODGE & COX STOCK FUND §PAGE 9 |

NOTES TO FINANCIAL STATEMENTS (unaudited)

NOTE 1—ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES

Dodge & Cox Stock Fund (the “Fund”) is one of the series constituting the Dodge & Cox Funds (the “Trust” or the “Funds”). The Trust is organized as a Delaware statutory trust and is registered under the Investment Company Act of 1940, as amended, as an open-end management investment company. The Fund commenced operations on January 4, 1965, and seeks long-term growth of principal and income. Risk considerations and investment strategies of the Fund are discussed in the Fund’s Prospectus.

The financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America, which require the use of estimates and assumptions by management. Actual results may differ from those estimates. Significant accounting policies are as follows:

Security valuation The Fund’s net assets are normally valued as of the scheduled close of trading on the New York Stock Exchange (NYSE), generally 4:00 p.m. Eastern Time, each day that the NYSE is open for business.

Portfolio holdings for which market quotes are readily available are valued at market value. Listed securities for example, are generally valued using the official quoted close price or the last sale on the exchange that is determined to be the primary market for the security. Exchange-traded derivatives are generally valued at the settlement price determined by the relevant exchange. Short-term securities less than 60 days to maturity may be valued at amortized cost if amortized cost approximates current value. Mutual funds are valued at their respective net asset values. Security values are not discounted based on the size of the Fund’s position and may differ from the value a Fund receives upon sale of the securities. All securities held by the Fund are denominated in U.S. dollars.

If market quotations are not readily available or if normal valuation procedures produce valuations that are deemed unreliable or inappropriate under the circumstances existing at the time, the investment will be valued at fair value as determined in good faith by or under the direction of the Fund’s Board of Trustees. The Board of Trustees has appointed Dodge & Cox, the Fund’s investment manager, to make fair value determinations in accordance with the Dodge & Cox Funds Valuation Policies (“Valuation Policies”), subject to Board oversight. Dodge & Cox has established a Pricing Committee that is comprised of representatives from Treasury, Legal, Compliance, and Operations. The Pricing Committee is responsible for implementing the Valuation Policies, including determining the fair value of securities and other investments when necessary. The Pricing Committee considers relevant indications of value that are reasonably available to it in determining the fair value assigned to a particular security, such as the value of similar financial instruments, trading volumes, contractual restrictions on disposition, related corporate actions, and changes in economic conditions. In doing so, the Pricing Committee employs various

methods for calibrating fair valuation approaches, including a regular review of key inputs and assumptions, back-testing, and review of any related market activity.

Valuing securities through a fair value determination involves greater reliance on judgment than valuation of securities based on readily available market quotations. In some instances, lack of information and uncertainty as to the significance of information may lead to a conclusion that a prior valuation is the best indication of a security’s value. When fair value pricing is employed, the prices of securities used by the Fund to calculate its NAV may differ from quoted or published prices for the same securities.

Security transactions, investment income, expenses, and distributions Security transactions are recorded on the trade date. Realized gains and losses on securities sold are determined on the basis of identified cost.

Dividend income and corporate action transactions are recorded on the ex-dividend date, or when the Fund first learns of the dividend/corporate action if the ex-dividend date has passed. Withholding taxes on foreign dividends have been provided for in accordance with the Fund’s understanding of the applicable country’s tax rules and rates. Non-cash dividends included in dividend income, if any, are recorded at the fair market value of the securities received. Dividends characterized as return of capital for U.S. tax purposes are recorded as a reduction of cost of investments and/or realized gain. Interest income is recorded on the accrual basis.

Expenses are recorded on the accrual basis. Some expenses of the Trust can be directly attributed to a specific series. Expenses which cannot be directly attributed are allocated among the Funds in the Trust using methodologies determined by the nature of the expense.

Distributions to shareholders are recorded on the ex-dividend date.

Repurchase agreements Repurchase agreements are transactions under which a Fund purchases a security from a dealer counterparty and agrees to resell the security to that counterparty on a specified future date at the same price, plus a specified interest rate. The Fund’s repurchase agreements are secured by U.S. government or agency securities. It is the Fund’s policy that its custodian take possession of the underlying collateral securities, the fair value of which exceeds the principal amount of the repurchase transaction, including accrued interest, at all times. In the event of default by the counterparty, the Fund has the contractual right to liquidate the collateral securities and to apply the proceeds in satisfaction of the obligation.

Foreign taxes The Fund may be subject to foreign taxes which may be imposed by certain countries in which the Fund invests. The Fund endeavors to record foreign taxes based on applicable foreign tax law. Withholding taxes are incurred on certain foreign dividends and are accrued at the time the associated dividend is recorded. The Fund files withholding tax reclaims in certain jurisdictions to recover a portion of amounts previously withheld. The Fund records a reclaim receivable based on, among other things, a jurisdiction’s

PAGE 10 § DODGE & COX STOCK FUND

NOTES TO FINANCIAL STATEMENTS (unaudited)

legal obligation to pay reclaims as well as payment history and market convention. In consideration of recent decisions rendered by European courts, the Fund has filed for additional reclaims related to prior years. A corresponding receivable is established when both the amount is known and significant contingencies or uncertainties regarding collectability are removed. These amounts, if any, are reported in “dividends and interest receivable” on the Statement of Assets and Liabilities.

Futures Contracts Futures contracts involve an obligation to purchase or sell (depending on whether the Fund has entered a long or short futures contract, respectively) an asset at a future date, at a price set at the time of the contract. Upon entering into a futures contract, the Fund is required to deposit an amount of cash or liquid assets (referred to as initial margin) in a segregated account with the clearing broker. Subsequent payments (referred to as variation margin) to and from the clearing broker are made on a daily basis based on changes in the market value of futures contracts. Futures contracts are traded publicly and their market value changes daily. Changes in the market value of open futures contracts are recorded as unrealized appreciation or depreciation in the Statement of Operations. Realized gains and losses on futures contracts are recorded in the Statement of Operations at the closing or expiration of the contracts. Cash deposited with a broker as initial margin is recorded on the Statement of Assets and Liabilities. A receivable and/or payable to brokers for daily variation margin is also recorded on the Statement of Assets and Liabilities.

Investments in futures contracts may include certain risks, which may be different from, and potentially greater than, those of the underlying securities. To the extent the Fund uses futures, it is exposed to additional volatility and potential losses resulting from leverage.

The Fund has maintained long S&P 500 futures contracts to provide equity exposure that approximates the Fund’s “net cash and other” position, which includes cash, short-term investments, receivables, and payables. During the six months ended June 30, 2017, these S&P 500 futures contracts had notional values ranging from 1% to 3% of net assets.

Indemnification Under the Trust’s organizational documents, its officers and trustees are indemnified against certain liabilities arising out of the performance of their duties to the Trust. In addition, in the normal course of business the Trust enters into contracts that provide general indemnities to other parties. The Trust’s maximum exposure under these arrangements is unknown as this would involve future claims that may be made against the Trust that have not yet occurred.

NOTE 2—VALUATION MEASUREMENTS

Various inputs are used in determining the value of the Fund’s investments. These inputs are summarized in the three broad levels listed below.

| § | | Level 1: Quoted prices in active markets for identical securities |

| § | | Level 2: Other significant observable inputs (including quoted prices for similar securities, market indices, interest rates, credit risk, forward exchange rates, etc.) |

| § | | Level 3: Significant unobservable inputs (including Fund management’s assumptions in determining the fair value of investments) |

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

The following is a summary of the inputs used to value the Fund’s holdings at June 30, 2017:

| | | | | | | | |

| Classification(a) | | LEVEL 1

(Quoted Prices) | | | LEVEL 2

(Other Significant

Observable Inputs) | |

Securities | | | | | | | | |

Common Stocks(b) | | $ | 64,384,179,363 | | | $ | — | |

Short-term Investments | | | | | | | | |

Money Market Fund | | | 66,033,346 | | | | — | |

Repurchase Agreement | | | — | | | | 1,594,087,000 | |

| | | | | | | | |

Total Securities | | $ | 64,450,212,709 | | | $ | 1,594,087,000 | |

| | | | | | | | |

Other Financial Instruments | | | | | | | | |

Futures Contracts | | | | | | | | |

Depreciation | | $ | (5,420,299 | ) | | $ | — | |

| | | | | | | | | |

| (a) | There were no transfers between Level 1 and Level 2 during the six months ended June 30, 2017. There were no Level 3 securities at June 30, 2017 and December 31, 2016, and there were no transfers to Level 3 during the period. |

| (b) | All common stocks held in the Fund are Level 1 securities. For a detailed break-out of common stocks by major industry classification, please refer to the Portfolio of Investments. |

NOTE 3—RELATED PARTY TRANSACTIONS

Management fees Under a written agreement approved by a unanimous vote of the Board of Trustees, the Fund pays an annual management fee of 0.50% of the Fund’s average daily net assets to Dodge & Cox, investment manager of the Fund. The agreement further provides that Dodge & Cox shall waive its fee to the extent that such fee plus all other ordinary operating expenses of the Fund exceed 0.75% of the average daily net assets for the year.

Fund officers and trustees All officers and two of the trustees of the Trust are officers or employees of Dodge & Cox. The Trust pays a fee only to those trustees who are not affiliated with Dodge & Cox.

NOTE 4—INCOME TAX INFORMATION AND DISTRIBUTIONS TO SHAREHOLDERS

A provision for federal income taxes is not required since the Fund intends to continue to qualify as a regulated investment company under Subchapter M of the Internal Revenue Code and distribute all of its taxable income to shareholders. Distributions are determined in accordance with income tax regulations, and such amounts may differ from net investment income and realized gains for financial reporting purposes. Financial reporting records are adjusted for permanent book to tax differences at year end to reflect tax character.

DODGE & COX STOCK FUND §PAGE 11

NOTES TO FINANCIAL STATEMENTS (unaudited)

Book to tax differences are primarily due to differing treatments of wash sales, net short-term realized gain (loss), certain dividends, and futures contracts. At June 30, 2017, the cost of investments for federal income tax purposes was $43,408,498,879.

Distributions during the periods noted below were characterized as follows for federal income tax purposes:

| | | | | | | | |

| | | Six Months Ended June 30, 2017 | | | Year Ended

December 31, 2016 | |

Ordinary income | | $ | 499,423,605 | | | $ | 1,056,249,886 | |

| | | ($1.471 per share | ) | | ($ | 3.183 per share | ) |

Long-term capital gain | | $ | 879,007,955 | | | $ | 2,918,315,039 | |

| | | ($2.603 per share | ) | | ($ | 8.899 per share | ) |

At June 30, 2017, the tax basis components of distributable earnings were as follows:

| | | | |

Unrealized appreciation | | $ | 24,274,482,776 | |

Unrealized depreciation | | | (1,638,681,946 | ) |

| | | | |

Net unrealized appreciation | | | 22,635,800,830 | |

Undistributed ordinary income | | | 92,385,160 | |

Undistributed long-term capital gain | | | 885,997,816 | |

| | | | | |

Fund management has reviewed the tax positions for open periods (three years and four years, respectively, from filing the Fund’s Federal and State tax returns) as applicable to the Fund, and has determined that no provision for income tax is required in the Fund’s financial statements.

NOTE 5—LOAN FACILITIES

Pursuant to an exemptive order issued by the Securities and Exchange Commission (SEC), the Fund may participate in an interfund lending facility (Facility). The Facility allows the Fund to borrow money from or loan money to the Funds. Loans under the Facility are made for temporary or emergency purposes, such as to fund shareholder redemption requests. Interest on borrowings is the average of the current repurchase agreement rate and the bank loan rate. There was no activity in the Facility during the period.

All Funds in the Trust participate in a $500 million committed credit facility (Line of Credit) with State Street Bank and Trust Company, to be utilized for temporary or emergency purposes to fund shareholder redemptions or for other short-term liquidity purposes. The maximum amount available to the Fund is $250 million. Each Fund pays an annual commitment fee on its pro-rata portion of the Line of Credit. For the six months ended June 30, 2017, the Fund’s commitment fee amounted to $213,688 and is reflected as a Miscellaneous Expense in the Statement of Operations. Interest on borrowings is charged at the prevailing rate. There were no borrowings on the Line of Credit during the period.

NOTE 6—PURCHASES AND SALES OF INVESTMENTS

For the six months ended June 30, 2017, purchases and sales of securities, other than short-term securities, aggregated $3,495,289,450 and $2,538,000,360, respectively.

NOTE 7—NEW ACCOUNTING GUIDANCE

In October 2016, the SEC issued a new rule, Investment Company Reporting Modernization, which, among other provisions, amends Regulation S-X to require standardized, enhanced disclosures, particularly related to derivatives, in investment company financial statements. Compliance with the guidance is required for financial statements for fiscal periods ending on or after August 1, 2017. Management is currently assessing the impact of this rule to the Fund’s financial statements and other filings and does not expect any impact to the Fund’s net assets or results of operations.

NOTE 8—SUBSEQUENT EVENTS

Fund management has determined that no material events or transactions occurred subsequent to June 30, 2017, and through the date of the Fund’s financial statements issuance, which require additional disclosure in the Fund’s financial statements.

PAGE 12 § DODGE & COX STOCK FUND

NOTES TO FINANCIAL STATEMENTS (unaudited)

NOTE 9—HOLDINGS OF 5% VOTING SECURITIES

Each of the companies listed below was considered to be an affiliate of the Fund because the Fund owned 5% or more of the company’s voting securities during all or part of the six months ended June 30, 2017. Purchase and sale transactions and dividend income earned during the period on these securities were as follows:

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Shares at

Beginning of Period | | | Additions | | | Reductions | | | Shares at

End of Period | | | Dividend

Income(a) | | | Value at

End of Period | |

Alnylam Pharmaceuticals, Inc. | | | 5,430,735 | | | | 70,000 | | | | — | | | | 5,500,735 | | | $ | — | (b) | | $ | 438,738,624 | |

Capital One Financial Corp. | | | 27,167,711 | | | | — | | | | (80,000 | ) | | | 27,087,711 | | | | 21,702,169 | | | | 2,237,986,683 | |

Celanese Corp., Series A | | | 7,779,698 | | | | — | | | | (621,300 | ) | | | 7,158,398 | | | | 6,379,352 | | | | 679,618,306 | |

Hewlett Packard Enterprise Co. | | | 93,402,495 | | | | 9,680,821 | | | | — | | | | 103,083,316 | | | | 12,888,578 | | | | 1,710,152,212 | |

NetApp, Inc. | | | 14,368,331 | | | | — | | | | (6,716,000 | ) | | | 7,652,331 | | | | 4,378,615 | | | | — | (c) |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | $ | 45,348,714 | | | $ | 5,066,495,825 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| (a) | Net of foreign taxes, if any |

| (c) | Company was not an affiliate at period end |

FINANCIAL HIGHLIGHTS (unaudited)

| | | | | | | | | | | | | | | | | | | | | | | | |

SELECTED DATA AND RATIOS (for a share outstanding throughout each period) | | Six Months Ended June 30, | | | Year Ended December 31, | |

| | | 2017 | | | 2016 | | | 2015 | | | 2014 | | | 2013 | | | 2012 | |

| | | | | | | | |

Net asset value, beginning of period | | | $184.30 | | | | $162.77 | | | | $180.94 | | | | $168.87 | | | | $121.90 | | | | $101.64 | |

Income from investment operations: | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | 1.33 | | | | 3.05 | | | | 2.42 | | | | 2.83 | | | | 2.11 | | | | 1.98 | |

Net realized and unrealized gain (loss) | | | 11.13 | | | | 30.56 | | | | (10.55 | ) | | | 14.60 | | | | 46.97 | | | | 20.26 | |

| | | | | | | | |

Total from investment operations | | | 12.46 | | | | 33.61 | | | | (8.13 | ) | | | 17.43 | | | | 49.08 | | | | 22.24 | |

| | | | | | | | |

Distributions to shareholders from: | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | (1.33 | ) | | | (3.03 | ) | | | (2.46 | ) | | | (2.80 | ) | | | (2.11 | ) | | | (1.98 | ) |

Net realized gain | | | (2.74 | ) | | | (9.05 | ) | | | (7.58 | ) | | | (2.56 | ) | | | — | | | | — | |

| | | | | | | | |

Total distributions | | | (4.07 | ) | | | (12.08 | ) | | | (10.04 | ) | | | (5.36 | ) | | | (2.11 | ) | | | (1.98 | ) |

| | | | | | | | |

Net asset value, end of period | | | $192.69 | | | | $184.30 | | | | $162.77 | | | | $180.94 | | | | $168.87 | | | | $121.90 | |

| | | | | | | | |

Total return | | | 6.81 | % | | | 21.27 | % | | | (4.47 | )% | | | 10.43 | % | | | 40.55 | % | | | 22.01 | % |

Ratios/supplemental data: | | | | | | | | | | | | | | | | | | | | | | | | |

Net assets, end of period (millions) | | | $66,136 | | | | $61,600 | | | | $54,845 | | | | $60,260 | | | | $54,848 | | | | $39,841 | |

Ratios of expenses to average net assets | | | 0.52 | %(a) | | | 0.52 | % | | | 0.52 | % | | | 0.52 | % | | | 0.52 | % | | | 0.52 | % |

Ratios of net investment income to average net assets | | | 1.41 | %(a) | | | 1.83 | % | | | 1.36 | % | | | 1.62 | % | | | 1.45 | % | | | 1.72 | % |

Portfolio turnover rate | | | 4 | % | | | 16 | % | | | 15 | % | | | 17 | % | | | 15 | % | | | 11 | % |

See accompanying Notes to Financial Statements

DODGE & COX STOCK FUND §PAGE 13

FUND HOLDINGS

The Fund provides a complete list of its holdings four times each fiscal year, as of the end of each quarter. The Fund files the lists with the Securities and Exchange Commission (SEC) on Form N-CSR (second and fourth quarters) and Form N-Q (first and third quarters). Shareholders may view the Fund’s Forms N-CSR and N-Q on the SEC’s website at sec.gov. Forms N-CSR and N-Q may also be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information regarding the operations of the Public Reference Room may be obtained by calling 202-551-8090 (direct) or 800-732-0330 (general SEC number). A list of the Fund’s quarter-end holdings is also available at dodgeandcox.com on or about 15 days following each quarter end and remains available on the website until the list is updated in the subsequent quarter.

PROXY VOTING

For a free copy of the Fund’s proxy voting policies and procedures, please call 800-621-3979, visit the Fund’s website at dodgeandcox.com, or visit the SEC’s website at sec.gov. Information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ending June 30 is also available at dodgeandcox.com or at sec.gov.

HOUSEHOLD MAILINGS

The Fund routinely mails shareholder reports and summary prospectuses to shareholders and, on occasion, proxy statements. In order to reduce the volume of mail, when possible, only one copy of these documents will be sent to shareholders who are part of the same family and share the same residential address.

If you have a direct account with the Funds and you do not want the mailing of shareholder reports and summary prospectuses combined with other members in your household, contact the Funds at 800-621-3979. Your request will be implemented within 30 days.

PAGE 14 § DODGE & COX STOCK FUND

TRUSTEES AND EXECUTIVE OFFICERS

Charles F. Pohl, Chairman and Trustee

Chairman, Dodge & Cox

Dana M. Emery, President and Trustee

Chief Executive Officer and President, Dodge & Cox

Thomas A. Larsen, Independent Trustee

Senior Counsel, Arnold & Porter Kaye Scholer LLP

Ann Mather, Independent Trustee

Former Executive Vice President, Chief Financial Officer, and Company Secretary, Pixar Animation Studios

Robert B. Morris III, Independent Trustee

Former Partner and Managing Director - Global Investment Research, Goldman Sachs; former Advisory Director, The Presidio Group

Gary Roughead, Independent Trustee

Robert and Marion Oster Distinguished Fellow, Hoover Institution, and former U.S. Navy Chief of Naval Operations

Mark E. Smith, Independent Trustee

Former Executive Vice President and Managing Director - Fixed Income, Loomis Sayles & Company, L.P.

John B. Taylor, Independent Trustee

Professor of Economics, Stanford University; Senior Fellow, Hoover Institution; and former Under Secretary for International Affairs, United States Treasury

Diana S. Strandberg, Senior Vice President

Senior Vice President and Director of International Equity, Dodge & Cox

David H. Longhurst, Treasurer

Vice President and Assistant Treasurer, Dodge & Cox

Thomas M. Mistele, Secretary

Executive Vice President, Secretary, and Senior Counsel, Dodge & Cox

Katherine M. Primas, Chief Compliance Officer

Vice President and Chief Compliance Officer, Dodge & Cox

Roberta R.W. Kameda, Assistant Secretary

Vice President and General Counsel, Dodge & Cox

William W. Strickland, Assistant Secretary and Assistant Treasurer

Vice President and Chief Operating Officer, Dodge & Cox

Additional information about the Trust’s Trustees and Officers is available in the Trust’s Statement of Additional Information (SAI). You can get a free copy of the SAI by visiting the Funds’ website at dodgeandcox.com or calling 800-621-3979.

DODGE & COX STOCK FUND §PAGE 15

dodgeandcox.com

For Fund literature, transactions, and account

information, please visit the Funds’ website.

or write or call:

DODGE & COX FUNDS

c/o Boston Financial Data Services

P.O. Box 8422

Boston, Massachusetts 02266-8422

(800) 621-3979

INVESTMENT MANAGER

Dodge & Cox

555 California Street, 40th Floor

San Francisco, California 94104

(415) 981-1710

This report is submitted for the general information of the shareholders of the Fund. The report is not authorized for distribution to prospective investors in the Fund unless it is accompanied by a current prospectus.

This report reflects our views, opinions, and portfolio holdings as of June 30, 2017, the end of the reporting period. Any such views are subject to change at any time based upon market or other conditions and Dodge & Cox disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Dodge & Cox Fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Dodge & Cox Fund.

DODGE & COX FUNDS®

Semi-Annual Report

June 30, 2017

Global Stock Fund

ESTABLISHED 2008

TICKER: DODWX

6/17 GSF SAR Printed on recycled paper

TO OUR SHAREHOLDERS

The Dodge & Cox Global Stock Fund had a total return of 10.9% for the six months ended June 30, 2017, compared to a return of 10.7% for the MSCI World Index.

MARKET COMMENTARY

Global equity markets had the strongest first half in years with 26 of the world’s top 30 stock markets rising. Every sector save Energy posted gains in both the MSCI World, the benchmark for developed markets including the United States, and the MSCI Emerging Markets Index. Within this context, emerging markets outperformed their peers in developed markets, rising 18% in U.S. dollars compared to 11% for the MSCI World. This served the Fund well because it has substantial exposure to the developing world: 17% of its net assets are invested in companies domiciled in emerging market countries.(a)

U.S. equity markets also continued to climb during the first half of 2017: the S&P 500 reached an all-time high in mid-June and ended the period up 9%, marking its strongest first half since 2013. Information Technology was the best-performing sector of the S&P 500, and Energy was the worst-performing sector amid lower oil prices. Solid corporate earnings growth, combined with expectations of an improving economy, boosted U.S. equity returns and propelled valuations further above longer-term averages.

Though international equity markets outperformed the United States through the first half of 2017, international equities have underperformed U.S. equities on a three-, five-, and ten-year basis. Robust U.S. earnings growth, a strong U.S. dollar, and price-to-earnings multiple expansion are the key reasons for this performance differential. Today, international equity valuations are less expensive than U.S. valuations. Overall, global equity valuations remain reasonable: as of June 30, the MSCI World traded at 16.5 times forward earnings, close to its 20-year average.

INVESTMENT STRATEGY

As a value-oriented manager, we weigh valuation and fundamentals in assessing long-term investment opportunity. In some cases, a company’s valuation may overly discount concerns regarding earnings and cash flow prospects. In other cases, the valuation may not give proper credit to a robust fundamental outlook. Examples include Anadarko Petroleum, Medtronic, and the Fund’s four Chinese internet holdings, which are discussed below.(b) Their valuations are reasonable yet do not reflect each company’s long-term growth potential and strong market position.

Energy

Oil prices dropped 16% over the past six months, weighing heavily on the outlook for profitability and growth in the Energy sector. While the short-term direction of oil prices is difficult to forecast, we believe the long-term fundamentals of supply and demand point to higher prices. The current demand for oil, which is about 98 million barrels a day, continues to grow about one percent per year, driven by growing transportation demand in the developing world. Oil fields deplete as the resource is extracted, reducing the

global production base about two to three percent per year, so continuing investment is required to meet current demand and to prepare for future demand growth. We anticipate that 15 to 20 million barrels per day of additional production will be needed over the next five years to meet demand if these trends continue. However, upstream capital investment has declined to a 10-year low, fewer new projects are being approved, and North American unconventional resources (including shale) are unlikely to grow enough to bridge this eventual gap.

Amid depressed valuations for energy companies, we recently added to selected holdings, including Suncor Energy (a Canadian company with best-in-class management that has a large, low-cost, and long-lived resource basin in the Canadian oil sands) and Anadarko Petroleum, among other holdings.

Anadarko Petroleum

Anadarko Petroleum (a 1.1% position) is an independent oil and gas exploration and production (E&P) company, one of two held in the Fund. The company’s stock price has been negatively impacted in 2017 by a gas leak that caused a fatal explosion. While tragic, this incident did not materially impact our long-term investment outlook for the company. Recent meetings with company management affirmed our belief that Anadarko remains an attractive investment over our three- to five-year investment horizon.

As a leading global explorer with strong operational capabilities, Anadarko has a record of success in generating high returns on capital over energy price cycles. In the coming years, we believe the key differentiators for E&Ps will be a company’s asset quality and its ability to develop those assets, particularly large-scale unconventional resources. Anadarko is well positioned to manage these challenges. For example, in the DJ Basin in Colorado, Anadarko systematically developed all of the needed infrastructure to execute its plan, which allowed the company to achieve growth targets at competitive costs; Anadarko is now applying the same approach of systematic field and infrastructure development to the Permian Basin.

The company’s conservative management team has an excellent track record of disciplined capital allocation. In addition, Anadarko continues to invest substantially in exploration, which it sees as the means to create upside opportunity for the company. This focus on exploration differentiates Anadarko from its peers and will likely create value across business cycles. After considering the company’s risks, opportunities, and valuation, we added to Anadarko during the first half of 2017.

Health Care

We continue to find attractive investment opportunities within the Health Care sector. For example, we recently added to Bristol-Myers Squibb (a U.S. biopharmaceutical company) and Novartis (a Swiss-domiciled global pharmaceutical company), and also initiated a position in Medtronic, which is discussed below.

PAGE 2 § DODGE & COX GLOBAL STOCK FUND

Medtronic

Based in Ireland, Medtronic is a global leader in medical technology that serves physicians, hospitals, and patients in approximately 160 countries worldwide. The company has a highly diversified product portfolio and dominant market positions across its four business segments of cardiac and vascular, minimally invasive therapies, restorative therapies, and diabetes. Medtronic benefits from stable demand drivers, including an aging population, rising disease incidence, increased emerging market penetration, and technological advances. As one of the largest investors in research and development (R&D) in the Health Care Equipment sub-industry, Medtronic is committed to defending current businesses and driving growth through innovation.

We view Medtronic’s management as an asset—they plan to give shareholders roughly 100% of free cash flow generated this year and 50% thereafter and also are exploring unique models that incorporate services and outcomes (e.g., catheterization laboratory management, diabetes clinics). While company profit margins are high, we believe they are sustainable and could even improve due to new product launches and synergies associated with Medtronic’s acquisition of Covidien, a global leader in surgical instruments. We started a position in Medtronic early in 2017 because we believe its valuation, at 18 times forward earnings, is reasonable given the company’s asset quality and long-term growth opportunities. On June 30, Medtronic was a 1.0% position in the Fund.

Chinese Internet Holdings

On a bottom-up basis, we have invested in four Chinese internet companies—58.com, Tencent (through Naspers), JD.com, and Baidu—comprising 5.3% of the Fund compared to 0% in the MSCI World and 1.1% in the MSCI All Country World Index. Each is a market leader, run by an owner-operator with significant wealth invested in the company. Thus, we think there is alignment with the interests of long-term owners like ourselves. These companies are reasonably valued in light of their excellent growth prospects. We believe the market for internet services in China is particularly attractive due to high economic growth, increasing internet penetration, and the potential to leapfrog traditional technologies (e.g., online versus brick-and-mortar retail, mobile versus landline, digital versus print advertising).

We recently started a position in 58.com, China’s dominant online classifieds marketplace. The company has leading positions in a number of attractive online domains (e.g., job listings, yellow pages), significant margin expansion potential, growth opportunities from new initiatives, and a focused owner/operator management team.

The Fund owns Tencent, a leading provider of internet value-added services in China, through Naspers, one of the largest holdings in the Fund. Naspers’ 34% ownership stake in Tencent is worth more than Naspers’ market cap. The core of Tencent’s value proposition is its enormous, extremely sticky, and highly engaged user base (e.g., 861 million active instant messenger accounts, 938 million WeChat mobile app users). More than 50% of all mobile internet user time in China is spent on Tencent’s apps.

Tencent has dominant positions in online and mobile gaming, social networking, and digital content distribution and is achieving growing importance in online advertising, payments, and cloud computing. The company operates in a strong ecosystem built on e-commerce, online-to-offline, and other verticals. Tencent has an innovative, product-driven, and commercially oriented culture, led by an owner-operator founder and a management team with an exceptional execution track record.

JD.com is the largest online retailer and the second largest e-commerce platform in China, known for the authenticity of its products and the quality of its service. The company benefits from attractive growth within the business-to-consumer segment of China’s e-commerce market and is gaining share from its competitors. We believe that online retail in China not only has the potential to grow much faster than in the United States but could also become a much larger portion of total retail sales. China’s strong economic growth and transition from an industrial-led to a consumer-led economy point to higher retail growth prospects. The fact that brick-and-mortar retail is less developed in China raises the possibility that consumers in China may jump straight to online retail.

Baidu—the dominant search engine in China, with over 70% search traffic and over 80% revenue share—has a profitable business model that allows the company to invest in R&D to retain its leading edge. Since search is typically a “winner-take-all” market, Baidu enjoys significant barriers to entry.

While these four companies share many characteristics, we note that their stock price movements reflect their individual company risks and opportunities more than a single industry risk exposure.

IN CLOSING

Global equity valuations remain reasonable, and we continue to see numerous investment opportunities in both developed and emerging markets. However, we have adopted a tempered outlook for future returns given recent strong performance. As an active manager with a value-oriented approach, we remain optimistic about the long-term prospects for the Fund’s holdings.

We want to express gratitude to the Fund’s shareholders for taking the long view and having confidence in Dodge & Cox. Our strategy requires patience and persistence, and we thank you for yours. As always, we welcome your comments and questions.

For the Board of Trustees,

| | |

| | |

Charles F. Pohl, Chairman | | Dana M. Emery, President |

July 31, 2017

| (a) | | Unless otherwise specified, all weightings and characteristics are as of June 30, 2017. |

| (b) | | The use of specific examples does not imply that they are more or less attractive investments than the portfolio’s other holdings. |

DODGE & COX GLOBAL STOCK FUND §PAGE 3

YEAR-TO-DATE PERFORMANCE REVIEW

The Fund outperformed the MSCI World by 0.3 percentage points year to date.

Key Contributors to Relative Results

| | § | | The Fund’s holdings in the Consumer Discretionary sector (up 17% compared to up 11% for the MSCI World sector) contributed significantly to results. JD.com (up 54%) and Naspers (up 32%) were strong performers. | |

| | § | | Relative returns in the Health Care sector (up 19% compared to up 16% for the MSCI World sector), combined with a higher average weighting (18% versus 12%), aided performance. Alnylam Pharmaceuticals (up 113%) and Sanofi (up 20%) were notable contributors. | |

| | § | | Strong returns from the Fund’s holdings in emerging markets (up 23%) had a positive impact, including Samsung Electronics (up 38%), ICICI Bank (up 32%), and some already listed above. | |

| | § | | Additional contributors included Millicom International Cellular (up 43%), UniCredit (up 30%), and Standard Chartered (up 23%). | |

Key Detractors from Relative Results

| | § | | The Fund’s holdings in the Energy sector (down 22% compared to down 10% for the MSCI World sector) had a negative impact. Anadarko Petroleum (down 35%) and Apache (down 24%) were notable detractors. | |

| | § | | Relative returns from holdings in the Information Technology sector (up 14% compared to up 18% for the MSCI World sector) also detracted from results. Hewlett Packard Enterprise (down 4%) lagged. | |

| | § | | Additional detractors included Express Scripts (down 7%), Goldman Sachs (down 7%), and Barclays (down 4%). | |

KEY CHARACTERISTICS OF DODGE & COX

Independent Organization

Dodge & Cox is one of the largest privately owned investment managers in the world. We remain committed to independence, with a goal of providing the highest quality investment management service to our existing clients.

Over 85 Years of Investment Experience

Dodge & Cox was founded in 1930. We have a stable and well-qualified team of investment professionals, most of whom have spent their entire careers at Dodge & Cox.

Experienced Investment Team

The Global Equity Investment Committee, which is the decision-making body for the Global Stock Fund, is an eight-member committee with an average tenure at Dodge & Cox of 22 years.

One Business with a Single Research Office

Dodge & Cox manages equity (domestic, international, and global), fixed income (domestic and global), and balanced investments, operating from one office in San Francisco.

Consistent Investment Approach

Our team decision-making process involves thorough, bottom-up fundamental analysis of each investment.

Long-Term Focus and Low Expenses

We invest with a three- to five-year investment horizon, which has historically resulted in low turnover relative to our peers. We manage Funds that maintain low expense ratios.

Risks: The Fund is subject to market risk, meaning holdings in the Fund may decline in value for extended periods due to the financial prospects of individual companies, or due to general market and economic conditions. Investing in non-U.S. securities may entail risk due to foreign economic and political developments; this risk may be increased when investing in emerging markets. The Fund is also subject to currency risk. Please read the prospectus and summary prospectus for specific details regarding the Fund’s risk profile.

PAGE 4 § DODGE & COX GLOBAL STOCK FUND

GROWTH OF $10,000 SINCE INCEPTION

FOR AN INVESTMENT MADE ON MAY 1, 2008

AVERAGE ANNUAL TOTAL RETURN

FOR PERIODS ENDED JUNE 30, 2017

| | | | | | | | | | | | | | | | |

| | | 1 Year | | | 3 Years | | | 5 Years | | | Since

Inception

(5/1/08) | |

Dodge & Cox Global Stock Fund | | | 30.50 | % | | | 5.52 | % | | | 14.13 | % | | | 5.70 | % |