UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-02958

T. Rowe Price International Funds, Inc.

(Exact name of registrant as specified in charter)

100 East Pratt Street, Baltimore, MD 21202

(Address of principal executive offices)

David Oestreicher

100 East Pratt Street, Baltimore, MD 21202

(Name and address of agent for service)

Registrant’s telephone number, including area code: (410) 345-2000

Date of fiscal year end: December 31

Date of reporting period: December 31, 2024

Item 1. Reports to Shareholders

(a) Report pursuant to Rule 30e-1

Annual Shareholder Report

December 31, 2024

This annual shareholder report contains important information about Dynamic Credit Fund (the "fund") for the period of January 1, 2024 to December 31, 2024. You can find the fund’s prospectus, financial information on Form N‑CSR (which includes required tax information for dividends), holdings, proxy voting information, and other information atwww.troweprice.com/prospectus. You can also request this information without charge by contacting T. Rowe Price at 1‑800‑638‑5660 or info@troweprice.com or contacting your intermediary.

What were the fund costs for the last year? (based on a hypothetical $10,000 investment)

| | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| Dynamic Credit Fund - Investor Class | $65 | 0.63% |

|---|

What drove fund performance during the past 12 months?

The global investment-grade fixed income market declined over the trailing 12-month period amid rising bond yields, despite many central banks easing monetary policies, and weakening global currencies relative to the U.S. dollar.

Despite sovereign yield volatility, the fund’s credit holdings, especially among high yield, emerging markets, securitized, and bank loans, helped drive positive performance. With central banks looking to unwind restrictive monetary policy, credit sectors largely benefited from increased risk appetite and demand for attractive yields.

The fund utilizes short credit positions to reflect an investment view where our global research team has low conviction, and this sleeve of the fund weighed on performance amid a generally healthy environment for credit assets.

The fund employs a flexible, cross-sector approach to source high-conviction security selection from our global multi-sector research platform while aiming to deliver attractive returns and targeting lower beta to high yield and equities. Over the period, the fund took a mostly defensive stance in terms of credit risk and duration, but we moderated that position somewhat after the uncertainty surrounding the U.S. presidential election cleared.

The fund held material exposure to derivatives, including currency, interest rate, and credit derivatives, which we use to manage positioning more nimbly across the fund’s wide investment universe. Credit derivatives had a negative impact on performance, but other derivative exposure modestly aided returns for the period.

How has the fund performed?

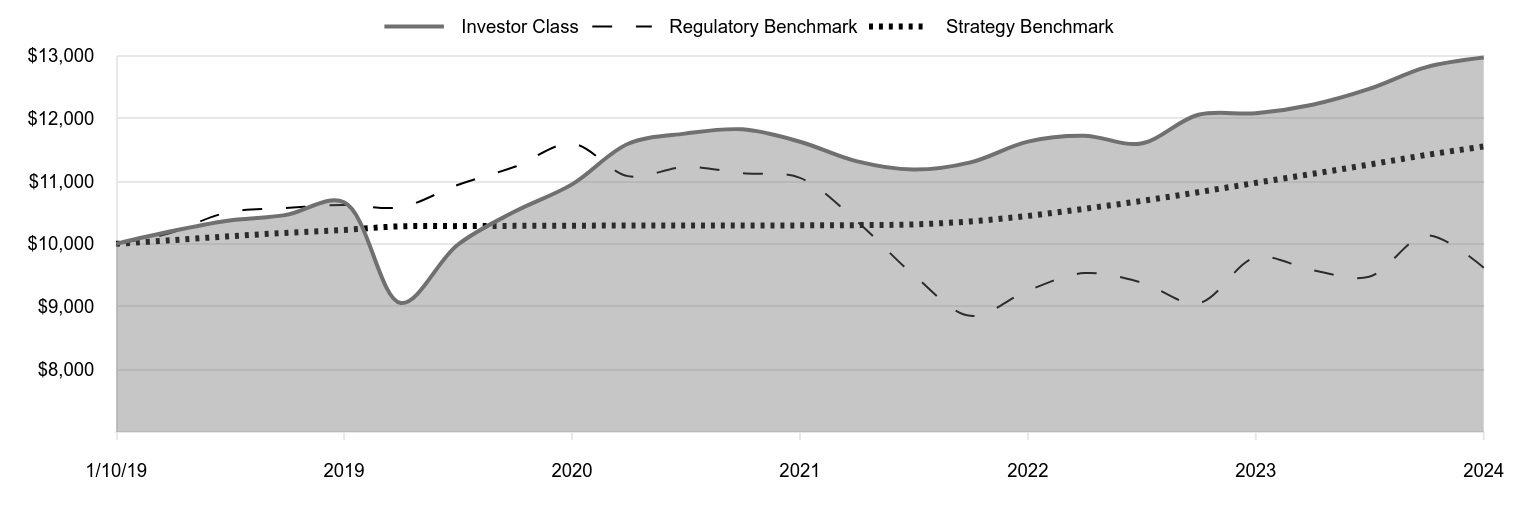

Cumulative Returns of a Hypothetical $10,000 Investment as of December 31, 2024

| Investor Class | Regulatory Benchmark | Strategy Benchmark |

|---|

| 1/10/19 | 10,000 | 10,000 | 10,000 |

|---|

| 3/31/19 | 10,188 | 10,160 | 10,054 |

|---|

| 6/30/19 | 10,365 | 10,495 | 10,118 |

|---|

| 9/30/19 | 10,458 | 10,570 | 10,175 |

|---|

| 12/31/19 | 10,664 | 10,621 | 10,222 |

|---|

| 3/31/20 | 9,057 | 10,586 | 10,280 |

|---|

| 6/30/20 | 9,982 | 10,938 | 10,283 |

|---|

| 9/30/20 | 10,516 | 11,229 | 10,287 |

|---|

| 12/31/20 | 10,949 | 11,598 | 10,290 |

|---|

| 3/31/21 | 11,596 | 11,080 | 10,292 |

|---|

| 6/30/21 | 11,758 | 11,226 | 10,292 |

|---|

| 9/30/21 | 11,826 | 11,127 | 10,294 |

|---|

| 12/31/21 | 11,629 | 11,052 | 10,295 |

|---|

| 3/31/22 | 11,320 | 10,371 | 10,299 |

|---|

| 6/30/22 | 11,186 | 9,514 | 10,310 |

|---|

| 9/30/22 | 11,300 | 8,853 | 10,358 |

|---|

| 12/31/22 | 11,631 | 9,256 | 10,446 |

|---|

| 3/31/23 | 11,724 | 9,534 | 10,559 |

|---|

| 6/30/23 | 11,600 | 9,388 | 10,683 |

|---|

| 9/30/23 | 12,058 | 9,052 | 10,824 |

|---|

| 12/31/23 | 12,083 | 9,785 | 10,973 |

|---|

| 3/31/24 | 12,219 | 9,581 | 11,116 |

|---|

| 6/30/24 | 12,470 | 9,475 | 11,264 |

|---|

| 9/30/24 | 12,818 | 10,137 | 11,418 |

|---|

| 12/31/24 | 12,971 | 9,620 | 11,553 |

|---|

202501-4140694, 202502-4108400

Average Annual Total Returns

| | 1 Year | 5 Years | Since Inception 1/10/19 |

|---|

| Dynamic Credit Fund (Investor Class) | 7.34% | 3.99% | 4.45% |

|---|

| Bloomberg Global Aggregate Bond Index (Regulatory Benchmark) | -1.69 | -1.96 | -0.65 |

|---|

| ICE BofA US 3-Month Treasury Bill Index (Strategy Benchmark) | 5.28 | 2.48 | 2.45 |

|---|

The preceding line graph shows the value of a hypothetical $10,000 investment in the fund over the past 10 fiscal year periods or since inception (for funds lacking 10-year records). The fund’s performance information included in the line graph and table above is compared with a regulatory required index that represents an overall securities market (Regulatory Benchmark). In addition, the line graph and table may also include one or more indexes that more closely aligns to the fund's investment strategy (Strategy Benchmark(s)). Due to new SEC Rules on shareholder reporting the fund adopted a new broad-based securities market index, referred to as the Regulatory Benchmark. Market index returns do not include expenses, which are deducted from fund returns. The fund's total return figures reflect the reinvestment of dividends and capital gains, if any.Neither the fund’s returns nor the index returns reflect the deduction of taxes that a shareholder would pay on fund distributions or redemptions of fund shares.The fund’s past performance is not a good predictor of the fund’s future performance.Updated performance information can be found at www.troweprice.com.

What are some fund statistics?

- Total Net Assets (000s)$1,015,889

- Number of Portfolio Holdings272

- Investment Advisory Fees Paid (000s)$(160)

- Portfolio Turnover Rate178.6%

What did the fund invest in?

Security Allocation (as a % of Net Assets)

| Corporate Bonds | 39.2% |

| Bank Loans | 14.2 |

| Government Bonds | 13.0 |

| Asset-Backed Securities | 11.6 |

| U.S. Treasury Obligations | 7.6 |

| Municipal Securities | 2.9 |

| Non-U.S. Government Mortgage-Backed Securities | 2.5 |

| Securities Lending Collateral | 2.1 |

| Short-Term and Other | 6.9 |

Top Ten Holdings (as a % of Net Assets)

| U.S. Treasury Bills | 7.5% |

| Brazil Notas do Tesouro Nacional | 4.4 |

| Republic of Colombia | 2.9 |

| Republic of Sri Lanka | 2.2 |

| Cloud Software Group | 2.2 |

| Transocean | 2.0 |

| Asurion | 2.0 |

| DISH DBS | 1.9 |

| Puerto Rico Commonwealth | 1.8 |

| DISH Network | 1.7 |

If you invest directly with T. Rowe Price, you can elect to receive future shareholder reports or other important documents through electronic delivery by enrolling at www.troweprice.com/paperless. If you invest through a financial intermediary such as an investment advisor, a bank, retirement plan sponsor or a brokerage firm, please contact that organization and ask if it can provide electronic delivery.

Bloomberg and ICE do not accept any liability for any errors or omissions in the indexes or data, and hereby expressly disclaim all warranties of originality, accuracy, completeness, timeliness, merchantability and fitness for a particular purpose. No party may rely on any indexes or data contained in this communication. Visit www.troweprice.com/en/us/market-data-disclosures for additional legal notices & disclaimers.

Dynamic Credit Fund

Investor Class (RPIDX)

T. Rowe Price Investment Services, Inc.

100 East Pratt Street

Baltimore, MD 21202

Annual Shareholder Report

December 31, 2024

This annual shareholder report contains important information about Dynamic Credit Fund (the "fund") for the period of January 1, 2024 to December 31, 2024. You can find the fund’s prospectus, financial information on Form N‑CSR (which includes required tax information for dividends), holdings, proxy voting information, and other information atwww.troweprice.com/prospectus. You can also request this information without charge by contacting T. Rowe Price at 1‑800‑638‑5660 or info@troweprice.com or contacting your intermediary.

What were the fund costs for the last year? (based on a hypothetical $10,000 investment)

| | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| Dynamic Credit Fund - I Class | $58 | 0.56% |

|---|

What drove fund performance during the past 12 months?

The global investment-grade fixed income market declined over the trailing 12-month period amid rising bond yields, despite many central banks easing monetary policies, and weakening global currencies relative to the U.S. dollar.

Despite sovereign yield volatility, the fund’s credit holdings, especially among high yield, emerging markets, securitized, and bank loans, helped drive positive performance. With central banks looking to unwind restrictive monetary policy, credit sectors largely benefited from increased risk appetite and demand for attractive yields.

The fund utilizes short credit positions to reflect an investment view where our global research team has low conviction, and this sleeve of the fund weighed on performance amid a generally healthy environment for credit assets.

The fund employs a flexible, cross-sector approach to source high-conviction security selection from our global multi-sector research platform while aiming to deliver attractive returns and targeting lower beta to high yield and equities. Over the period, the fund took a mostly defensive stance in terms of credit risk and duration, but we moderated that position somewhat after the uncertainty surrounding the U.S. presidential election cleared.

The fund held material exposure to derivatives, including currency, interest rate, and credit derivatives, which we use to manage positioning more nimbly across the fund’s wide investment universe. Credit derivatives had a negative impact on performance, but other derivative exposure modestly aided returns for the period.

How has the fund performed?

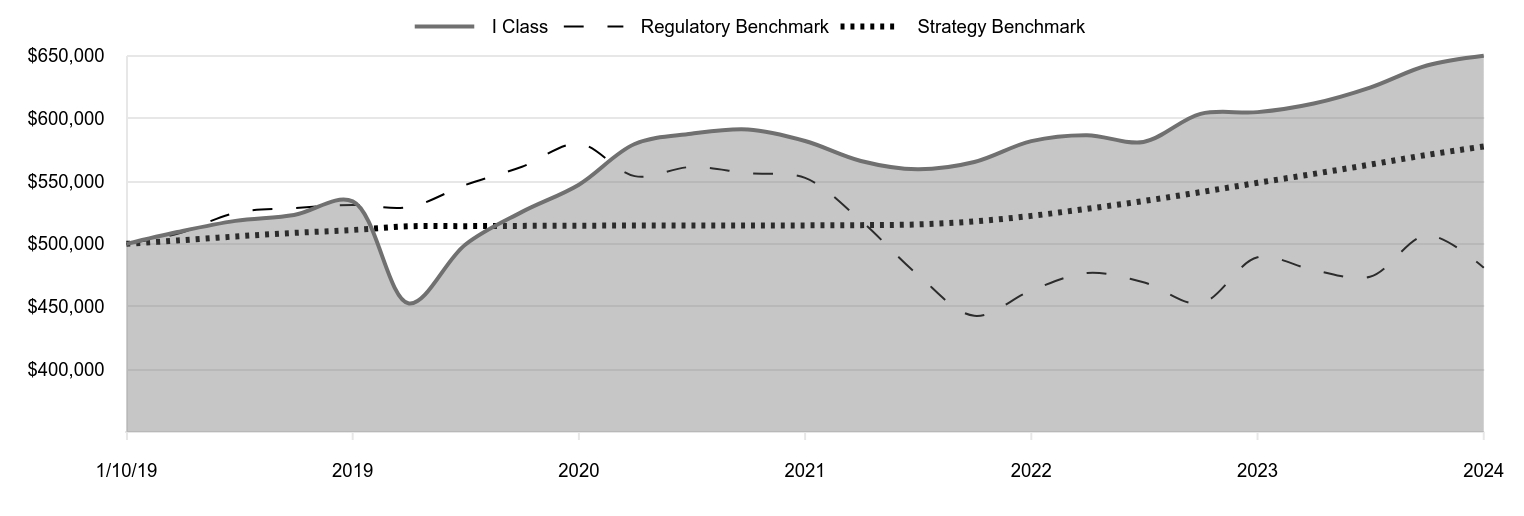

Cumulative Returns of a Hypothetical $500,000 Investment as of December 31, 2024

| I Class | Regulatory Benchmark | Strategy Benchmark |

|---|

| 1/10/19 | 500,000 | 500,000 | 500,000 |

|---|

| 3/31/19 | 509,449 | 507,997 | 502,680 |

|---|

| 6/30/19 | 518,344 | 524,733 | 505,892 |

|---|

| 9/30/19 | 522,972 | 528,485 | 508,736 |

|---|

| 12/31/19 | 533,855 | 531,049 | 511,079 |

|---|

| 3/31/20 | 452,496 | 529,313 | 514,015 |

|---|

| 6/30/20 | 499,329 | 546,889 | 514,130 |

|---|

| 9/30/20 | 525,508 | 561,444 | 514,332 |

|---|

| 12/31/20 | 547,206 | 579,885 | 514,488 |

|---|

| 3/31/21 | 579,608 | 554,018 | 514,617 |

|---|

| 6/30/21 | 587,758 | 561,290 | 514,617 |

|---|

| 9/30/21 | 591,217 | 556,331 | 514,691 |

|---|

| 12/31/21 | 582,026 | 552,590 | 514,741 |

|---|

| 3/31/22 | 566,113 | 518,545 | 514,943 |

|---|

| 6/30/22 | 559,508 | 475,703 | 515,482 |

|---|

| 9/30/22 | 565,302 | 442,669 | 517,902 |

|---|

| 12/31/22 | 581,953 | 462,803 | 522,309 |

|---|

| 3/31/23 | 586,691 | 476,718 | 527,954 |

|---|

| 6/30/23 | 581,275 | 469,425 | 534,161 |

|---|

| 9/30/23 | 603,655 | 452,590 | 541,218 |

|---|

| 12/31/23 | 605,039 | 489,252 | 548,662 |

|---|

| 3/31/24 | 611,923 | 479,061 | 555,788 |

|---|

| 6/30/24 | 624,597 | 473,770 | 563,180 |

|---|

| 9/30/24 | 642,177 | 506,853 | 570,916 |

|---|

| 12/31/24 | 649,954 | 480,988 | 577,642 |

|---|

202501-4140694, 202502-4108400

Average Annual Total Returns

| | 1 Year | 5 Years | Since Inception 1/10/19 |

|---|

| Dynamic Credit Fund (I Class) | 7.42% | 4.01% | 4.49% |

|---|

| Bloomberg Global Aggregate Bond Index (Regulatory Benchmark) | -1.69 | -1.96 | -0.65 |

|---|

| ICE BofA US 3-Month Treasury Bill Index (Strategy Benchmark) | 5.28 | 2.48 | 2.45 |

|---|

The preceding line graph shows the value of a hypothetical $500,000 investment in the fund over the past 10 fiscal year periods or since inception (for funds lacking 10-year records). The fund’s performance information included in the line graph and table above is compared with a regulatory required index that represents an overall securities market (Regulatory Benchmark). In addition, the line graph and table may also include one or more indexes that more closely aligns to the fund's investment strategy (Strategy Benchmark(s)). Due to new SEC Rules on shareholder reporting the fund adopted a new broad-based securities market index, referred to as the Regulatory Benchmark. Market index returns do not include expenses, which are deducted from fund returns. The fund's total return figures reflect the reinvestment of dividends and capital gains, if any.Neither the fund’s returns nor the index returns reflect the deduction of taxes that a shareholder would pay on fund distributions or redemptions of fund shares.The fund’s past performance is not a good predictor of the fund’s future performance.Updated performance information can be found at www.troweprice.com.

What are some fund statistics?

- Total Net Assets (000s)$1,015,889

- Number of Portfolio Holdings272

- Investment Advisory Fees Paid (000s)$(160)

- Portfolio Turnover Rate178.6%

What did the fund invest in?

Security Allocation (as a % of Net Assets)

| Corporate Bonds | 39.2% |

| Bank Loans | 14.2 |

| Government Bonds | 13.0 |

| Asset-Backed Securities | 11.6 |

| U.S. Treasury Obligations | 7.6 |

| Municipal Securities | 2.9 |

| Non-U.S. Government Mortgage-Backed Securities | 2.5 |

| Securities Lending Collateral | 2.1 |

| Short-Term and Other | 6.9 |

Top Ten Holdings (as a % of Net Assets)

| U.S. Treasury Bills | 7.5% |

| Brazil Notas do Tesouro Nacional | 4.4 |

| Republic of Colombia | 2.9 |

| Republic of Sri Lanka | 2.2 |

| Cloud Software Group | 2.2 |

| Transocean | 2.0 |

| Asurion | 2.0 |

| DISH DBS | 1.9 |

| Puerto Rico Commonwealth | 1.8 |

| DISH Network | 1.7 |

If you invest directly with T. Rowe Price, you can elect to receive future shareholder reports or other important documents through electronic delivery by enrolling at www.troweprice.com/paperless. If you invest through a financial intermediary such as an investment advisor, a bank, retirement plan sponsor or a brokerage firm, please contact that organization and ask if it can provide electronic delivery.

Bloomberg and ICE do not accept any liability for any errors or omissions in the indexes or data, and hereby expressly disclaim all warranties of originality, accuracy, completeness, timeliness, merchantability and fitness for a particular purpose. No party may rely on any indexes or data contained in this communication. Visit www.troweprice.com/en/us/market-data-disclosures for additional legal notices & disclaimers.

Dynamic Credit Fund

I Class (RPELX)

T. Rowe Price Investment Services, Inc.

100 East Pratt Street

Baltimore, MD 21202

Annual Shareholder Report

December 31, 2024

This annual shareholder report contains important information about Dynamic Credit Fund (the "fund") for the period of January 1, 2024 to December 31, 2024. You can find the fund’s prospectus, financial information on Form N‑CSR (which includes required tax information for dividends), holdings, proxy voting information, and other information atwww.troweprice.com/prospectus. You can also request this information without charge by contacting T. Rowe Price at 1‑800‑638‑5660 or info@troweprice.com or contacting your intermediary.

What were the fund costs for the last year? (based on a hypothetical $10,000 investment)

| | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| Dynamic Credit Fund - Z Class | $0 | 0.00% |

|---|

What drove fund performance during the past 12 months?

The global investment-grade fixed income market declined over the trailing 12-month period amid rising bond yields, despite many central banks easing monetary policies, and weakening global currencies relative to the U.S. dollar.

Despite sovereign yield volatility, the fund’s credit holdings, especially among high yield, emerging markets, securitized, and bank loans, helped drive positive performance. With central banks looking to unwind restrictive monetary policy, credit sectors largely benefited from increased risk appetite and demand for attractive yields.

The fund utilizes short credit positions to reflect an investment view where our global research team has low conviction, and this sleeve of the fund weighed on performance amid a generally healthy environment for credit assets.

The fund employs a flexible, cross-sector approach to source high-conviction security selection from our global multi-sector research platform while aiming to deliver attractive returns and targeting lower beta to high yield and equities. Over the period, the fund took a mostly defensive stance in terms of credit risk and duration, but we moderated that position somewhat after the uncertainty surrounding the U.S. presidential election cleared.

The fund held material exposure to derivatives, including currency, interest rate, and credit derivatives, which we use to manage positioning more nimbly across the fund’s wide investment universe. Credit derivatives had a negative impact on performance, but other derivative exposure modestly aided returns for the period.

How has the fund performed?

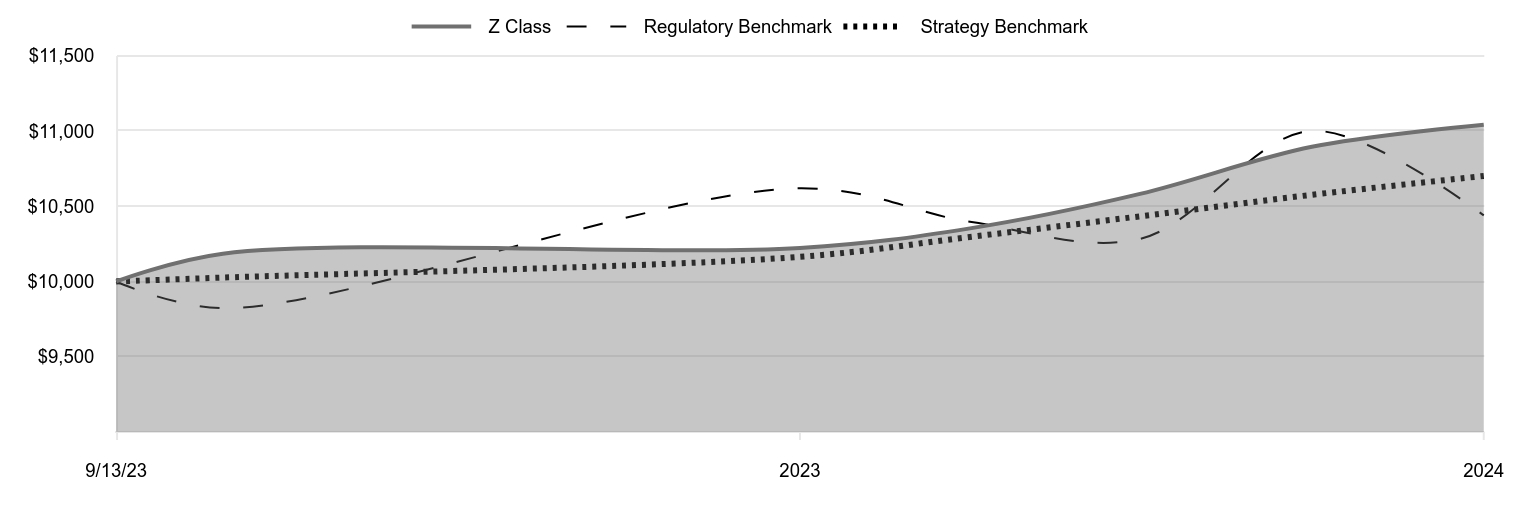

Cumulative Returns of a Hypothetical $10,000 Investment as of December 31, 2024

| Z Class | Regulatory Benchmark | Strategy Benchmark |

|---|

| 9/13/23 | 10,000 | 10,000 | 10,000 |

|---|

| 9/30/23 | 10,185 | 9,823 | 10,026 |

|---|

| 12/31/23 | 10,223 | 10,619 | 10,164 |

|---|

| 3/31/24 | 10,353 | 10,397 | 10,296 |

|---|

| 6/30/24 | 10,582 | 10,283 | 10,433 |

|---|

| 9/30/24 | 10,895 | 11,001 | 10,576 |

|---|

| 12/31/24 | 11,042 | 10,439 | 10,701 |

|---|

202501-4140694, 202502-4108400

Average Annual Total Returns

| | 1 Year | Since Inception 9/13/23 |

|---|

| Dynamic Credit Fund (Z Class) | 8.02% | 7.94% |

|---|

| Bloomberg Global Aggregate Bond Index (Regulatory Benchmark) | -1.69 | 3.37 |

|---|

| ICE BofA US 3-Month Treasury Bill Index (Strategy Benchmark) | 5.28 | 5.36 |

|---|

The preceding line graph shows the value of a hypothetical $10,000 investment in the fund over the past 10 fiscal year periods or since inception (for funds lacking 10-year records). The fund’s performance information included in the line graph and table above is compared with a regulatory required index that represents an overall securities market (Regulatory Benchmark). In addition, the line graph and table may also include one or more indexes that more closely aligns to the fund's investment strategy (Strategy Benchmark(s)). Due to new SEC Rules on shareholder reporting the fund adopted a new broad-based securities market index, referred to as the Regulatory Benchmark. Market index returns do not include expenses, which are deducted from fund returns. The fund's total return figures reflect the reinvestment of dividends and capital gains, if any.Neither the fund’s returns nor the index returns reflect the deduction of taxes that a shareholder would pay on fund distributions or redemptions of fund shares.The fund’s past performance is not a good predictor of the fund’s future performance.Updated performance information can be found at www.troweprice.com.

What are some fund statistics?

- Total Net Assets (000s)$1,015,889

- Number of Portfolio Holdings272

- Investment Advisory Fees Paid (000s)$(160)

- Portfolio Turnover Rate178.6%

What did the fund invest in?

Security Allocation (as a % of Net Assets)

| Corporate Bonds | 39.2% |

| Bank Loans | 14.2 |

| Government Bonds | 13.0 |

| Asset-Backed Securities | 11.6 |

| U.S. Treasury Obligations | 7.6 |

| Municipal Securities | 2.9 |

| Non-U.S. Government Mortgage-Backed Securities | 2.5 |

| Securities Lending Collateral | 2.1 |

| Short-Term and Other | 6.9 |

Top Ten Holdings (as a % of Net Assets)

| U.S. Treasury Bills | 7.5% |

| Brazil Notas do Tesouro Nacional | 4.4 |

| Republic of Colombia | 2.9 |

| Republic of Sri Lanka | 2.2 |

| Cloud Software Group | 2.2 |

| Transocean | 2.0 |

| Asurion | 2.0 |

| DISH DBS | 1.9 |

| Puerto Rico Commonwealth | 1.8 |

| DISH Network | 1.7 |

If you invest directly with T. Rowe Price, you can elect to receive future shareholder reports or other important documents through electronic delivery by enrolling at www.troweprice.com/paperless. If you invest through a financial intermediary such as an investment advisor, a bank, retirement plan sponsor or a brokerage firm, please contact that organization and ask if it can provide electronic delivery.

Bloomberg and ICE do not accept any liability for any errors or omissions in the indexes or data, and hereby expressly disclaim all warranties of originality, accuracy, completeness, timeliness, merchantability and fitness for a particular purpose. No party may rely on any indexes or data contained in this communication. Visit www.troweprice.com/en/us/market-data-disclosures for additional legal notices & disclaimers.

Dynamic Credit Fund

Z Class (TRCDX)

T. Rowe Price Investment Services, Inc.

100 East Pratt Street

Baltimore, MD 21202

Item 1. (b) Notice pursuant to Rule 30e-3.

Not applicable.

Item 2. Code of Ethics.

The registrant has adopted a code of ethics, as defined in Item 2 of Form N-CSR, applicable to its principal executive officer, principal financial officer, principal accounting officer or controller, or persons performing similar functions. A copy of this code of ethics is filed as an exhibit to this Form N-CSR. No substantive amendments were approved or waivers were granted to this code of ethics during the period covered by this report.

Item 3. Audit Committee Financial Expert.

The registrant’s Board of Directors has determined that Mr. Paul F. McBride qualifies as an audit committee financial expert, as defined in Item 3 of Form N-CSR. Mr. McBride is considered independent for purposes of Item 3 of Form N-CSR.

Item 4. Principal Accountant Fees and Services.

(a) – (d) Aggregate fees billed for the last two fiscal years for professional services rendered to, or on behalf of, the registrant by the registrant’s principal accountant were as follows:

| | | | | | | | | | |

| | | 2024 | | | 2023 | | | |

| | | | | | | |

Audit Fees | | | $46,029 | | | | $46,733 | |

Audit-Related Fees | | | - | | | | - | |

Tax Fees | | | - | | | | - | |

All Other Fees | | | - | | | | - | | | |

Audit fees include amounts related to the audit of the registrant’s annual financial statements and services normally provided by the accountant in connection with statutory and regulatory filings. Audit-related fees include amounts reasonably related to the performance of the audit of the registrant’s financial statements and specifically include the issuance of a report on internal controls and, if applicable, agreed-upon procedures related to fund acquisitions. Tax fees include amounts related to services for tax compliance, tax planning, and tax advice. The nature of these services specifically includes the review of distribution calculations and the preparation of Federal, state, and excise tax returns. All other fees include the registrant’s pro-rata share of amounts for agreed-upon procedures in conjunction with service contract approvals by the registrant’s Board of Directors/Trustees.

(e)(1) The registrant’s audit committee has adopted a policy whereby audit and non-audit services performed by the registrant’s principal accountant for the registrant, its investment adviser, and any entity controlling, controlled by, or under common control with the investment adviser that provides ongoing services to the registrant require pre-approval in advance at regularly scheduled audit committee meetings. If such a service is required between regularly scheduled audit committee meetings, pre-approval may be authorized by one audit committee member with ratification at the next scheduled audit committee meeting. Waiver of pre-approval for audit or non-audit services requiring fees of a de minimis amount is not permitted.

(2) No services included in (b) – (d) above were approved pursuant to paragraph (c)(7)(i)(C) of Rule 2-01 of Regulation S-X.

(f) Less than 50 percent of the hours expended on the principal accountant’s engagement to audit the registrant’s financial statements for the most recent fiscal year were attributed to work performed by persons other than the principal accountant’s full-time, permanent employees.

(g) The aggregate fees billed for the most recent fiscal year and the preceding fiscal year by the registrant’s principal accountant for non-audit services rendered to the registrant, its investment adviser, and any entity controlling, controlled by, or under common control with the investment adviser that provides ongoing services to the registrant were $1,262,000 and $1,524,000, respectively.

(h) All non-audit services rendered in (g) above were pre-approved by the registrant’s audit committee. Accordingly, these services were considered by the registrant’s audit committee in maintaining the principal accountant’s independence.

(i) Not applicable.

(j) Not applicable.

Item 5. Audit Committee of Listed Registrants.

Not applicable.

Item 6. Investments.

(a) Not applicable. The complete schedule of investments is included in Item 7 of this Form N-CSR.

(b) Not applicable.

Item 7. Financial Statements and Financial Highlights for Open-End Management Investment Companies.

(a – b) Report pursuant to Regulation S-X.

Financial

Highlights

Portfolio

of

Investments

Financial

Statements

and

Notes

Additional

Fund

Information

Financial

Statements

and

Other

Information

For

more

insights

from

T.

Rowe

Price

investment

professionals,

go

to

troweprice.com

.

T.

ROWE

PRICE

RPIDX

Dynamic

Credit

Fund

RPELX

Dynamic

Credit

Fund–

.

I Class

TRCDX

Dynamic

Credit

Fund–

.

Z Class

T.

ROWE

PRICE

Dynamic

Credit

Fund

For

a

share

outstanding

throughout

each

period

The

accompanying

notes

are

an

integral

part

of

these

financial

statements.

Investor

Class

..

Year

..

..

Ended

.

12/31/24

12/31/23

12/31/22

12/31/21

12/31/20

NET

ASSET

VALUE

Beginning

of

period

$

8.84

$

9.02

$

9.83

$

9.75

$

10.20

Investment

activities

Net

investment

income

(1)(2)

0.68

0.55

0.41

0.37

0.48

Net

realized

and

unrealized

gain/loss

(0.05)

(0.21)

(0.42)

0.24

(0.23)

Total

from

investment

activities

0.63

0.34

(0.01)

0.61

0.25

Distributions

Net

investment

income

(0.61)

(0.52)

(0.35)

(0.34)

(0.38)

Net

realized

gain

—

—

(0.45)

(0.19)

(0.32)

Total

distributions

(0.61)

(0.52)

(0.80)

(0.53)

(0.70)

NET

ASSET

VALUE

End

of

period

$

8.86

$

8.84

$

9.02

$

9.83

$

9.75

Ratios/Supplemental

Data

Total

return

(2)(3)

7.34%

3.89%

0.02%

6.21%

2.67%

Ratios

to

average

net

assets:

(2)

Gross

expenses

before

waivers/payments

by

Price

Associates

0.84%

1.31%

1.53%

1.30%

1.38%

Net

expenses

after

waivers/

payments

by

Price

Associates

0.63%

0.64%

0.63%

0.65%

0.64%

Net

investment

income

7.64%

6.14%

4.40%

3.61%

4.97%

Portfolio

turnover

rate

178.6%

146.5%

217.6%

252.1%

301.7%

Net

assets,

end

of

period

(in

thousands)

$24,593

$18,157

$29,716

$38,760

$26,423

0%

0%

0%

0%

0%

(1)

Per

share

amounts

calculated

using

average

shares

outstanding

method.

(2)

Includes

the

impact

of

expense-related

arrangements

with

Price

Associates.

(3)

Total

return

reflects

the

rate

that

an

investor

would

have

earned

on

an

investment

in

the

fund

during

each

period,

assuming

reinvestment

of

all

distributions,

and

payment

of

no

redemption

or

account

fees,

if

applicable.

T.

ROWE

PRICE

Dynamic

Credit

Fund

For

a

share

outstanding

throughout

each

period

The

accompanying

notes

are

an

integral

part

of

these

financial

statements.

I

Class

..

Year

..

..

Ended

.

12/31/24

12/31/23

12/31/22

12/31/21

12/31/20

NET

ASSET

VALUE

Beginning

of

period

$

8.83

$

9.01

$

9.83

$

9.74

$

10.21

Investment

activities

Net

investment

income

(1)(2)

0.68

0.57

0.42

0.36

0.48

Net

realized

and

unrealized

gain/loss

(0.05)

(0.22)

(0.43)

0.26

(0.25)

Total

from

investment

activities

0.63

0.35

(0.01)

0.62

0.23

Distributions

Net

investment

income

(0.61)

(0.53)

(0.36)

(0.34)

(0.38)

Net

realized

gain

—

—

(0.45)

(0.19)

(0.32)

Total

distributions

(0.61)

(0.53)

(0.81)

(0.53)

(0.70)

NET

ASSET

VALUE

End

of

period

$

8.85

$

8.83

$

9.01

$

9.83

$

9.74

Ratios/Supplemental

Data

Total

return

(2)(3)

7.42%

3.97%

(0.01)%

6.36%

2.50%

Ratios

to

average

net

assets:

(2)

Gross

expenses

before

waivers/payments

by

Price

Associates

0.58%

0.94%

1.48%

1.06%

1.30%

Net

expenses

after

waivers/payments

by

Price

Associates

0.56%

0.56%

0.56%

0.60%

0.61%

Net

investment

income

7.72%

6.43%

4.48%

3.51%

5.01%

Portfolio

turnover

rate

178.6%

146.5%

217.6%

252.1%

301.7%

Net

assets,

end

of

period

(in

thousands)

$32,409

$29,384

$5,646

$1,943

$24,169

0%

0%

0%

0%

0%

(1)

Per

share

amounts

calculated

using

average

shares

outstanding

method.

(2)

Includes

the

impact

of

expense-related

arrangements

with

Price

Associates.

(3)

Total

return

reflects

the

rate

that

an

investor

would

have

earned

on

an

investment

in

the

fund

during

each

period,

assuming

reinvestment

of

all

distributions,

and

payment

of

no

redemption

or

account

fees,

if

applicable.

T.

ROWE

PRICE

Dynamic

Credit

Fund

For

a

share

outstanding

throughout

each

period

The

accompanying

notes

are

an

integral

part

of

these

financial

statements.

Z

Class

(1)

.

.

Year

Ended

12/31/24

9/13/23

(1)

Through

12/31/23

NET

ASSET

VALUE

Beginning

of

period

$

8.83

$

8.82

Investment

activities

Net

investment

income

(2)(3)

0.73

0.19

Net

realized

and

unrealized

gain/loss

(0.05)

0.01

(4)

Total

from

investment

activities

0.68

0.20

Distributions

Net

investment

income

(0.66)

(0.19)

NET

ASSET

VALUE

End

of

period

$

8.85

$

8.83

Ratios/Supplemental

Data

Total

return

(3)(5)

8.02%

2.22%

Ratios

to

average

net

assets:

(3)

Gross

expenses

before

waivers/payments

by

Price

Associates

0.55%

0.55%

(6)

Net

expenses

after

waivers/payments

by

Price

Associates

0.00%

0.00%

(6)

Net

investment

income

8.27%

7.19%

(6)

Portfolio

turnover

rate

178.6%

146.5%

Net

assets,

end

of

period

(in

millions)

$959

$861

0%

0%

(1)

Inception

date

(2)

Per

share

amounts

calculated

using

average

shares

outstanding

method.

(3)

Includes

the

impact

of

expense-related

arrangements

with

Price

Associates.

(4)

The

amount

presented

is

inconsistent

with

the

fund's

aggregate

gains

and

losses

because

of

the

timing

of

sales

and

redemptions

of

fund

shares

in

relation

to

fluctuating

market

values

for

the

investment

portfolio.

(5)

Total

return

reflects

the

rate

that

an

investor

would

have

earned

on

an

investment

in

the

fund

during

each

period,

assuming

reinvestment

of

all

distributions,

and

payment

of

no

redemption

or

account

fees,

if

applicable.

Total

return

is

not

annualized

for

periods

less

than

one

year.

(6)

Annualized

T.

ROWE

PRICE

Dynamic

Credit

Fund

December

31,

2024

Par/Shares

$

Value

(

Cost

and

value

in

$000s)

‡

ANGOLA 1.3%

Government

Bonds 1.3%

Republic

of

Angola,

8.75%,

4/14/32

(USD)

14,725,000

13,041

Total

Angola

(Cost

$13,006)

13,041

AUSTRIA 0.9%

Corporate

Bonds 0.9%

Benteler

International,

10.50%,

5/15/28

(USD) (1)

9,075,000

9,524

Total

Austria

(Cost

$9,567)

9,524

BRAZIL 6.7%

Corporate

Bonds 2.4%

Banco

do

Estado

do

Rio

Grande

do

Sul,

VR,

5.375%,

1/28/31

(USD) (2)

665,000

656

CSN

Resources,

5.875%,

4/8/32

(USD)

12,050,000

9,736

Raizen

Fuels

Finance,

6.95%,

3/5/54

(USD) (1)(3)

5,490,000

5,419

Samarco

Mineracao,

9.00%,

6/30/31,

(9.00%

PIK)

(USD) (4)

8,296,092

8,119

23,930

Government

Bonds 4.3%

Brazil

Notas

do

Tesouro

Nacional,

Series

NTNF,

10.00%,

1/1/29

324,720,000

44,192

44,192

Total

Brazil

(Cost

$72,153)

68,122

CANADA 0.9%

Asset-Backed

Securities 0.4%

Cologix

Canadian

Issuer,

Series

2022-1CAN,

Class

A2,

4.94%,

1/25/52 (1)

6,000,000

4,045

4,045

Corporate

Bonds 0.5%

TER

Finance

Jersey,

Series

21,

Zero

Coupon,

1/2/25

(USD) (1)(5)

4,900,000

4,899

4,899

Total

Canada

(Cost

$9,205)

8,944

T.

ROWE

PRICE

Dynamic

Credit

Fund

Par/Shares

$

Value

(Cost

and

value

in

$000s)

CHILE 0.6%

Corporate

Bonds 0.6%

AES

Andes,

VR,

8.15%,

6/10/55

(USD) (1)(2)

6,040,000

6,121

Total

Chile

(Cost

$6,040)

6,121

CHINA 0.0%

Corporate

Bonds 0.0%

Kaisa

Group

Holdings,

11.95%,

10/22/22

(USD) (6)(7)

985,000

62

Total

China

(Cost

$275)

62

COLOMBIA 4.5%

Corporate

Bonds 1.6%

Bancolombia,

VR,

8.625%,

12/24/34

(USD) (2)(3)

7,410,000

7,765

Ecopetrol,

8.375%,

1/19/36

(USD)

8,370,000

8,079

15,844

Government

Bonds 2.9%

Republic

of

Colombia,

3.25%,

4/22/32

(USD)

26,490,000

20,364

Republic

of

Colombia,

4.125%,

5/15/51

(USD)

15,730,000

9,043

29,407

Private

Investment

Company 0.0%

Bona

Fide

Investments

Feeder

LLC,

Acquisition

Date:

6/7/23,

Cost $16

(USD) (6)(8)

†

21

Bona

Fide

Investments

Holdings

III,

Acquisition

Date:

6/14/24,

Cost $10

(USD) (6)(8)

†

10

31

Total

Colombia

(Cost

$46,290)

45,282

EL

SALVADOR 1.3%

Government

Bonds 1.3%

Republic

of

El

Salvador,

0.25%,

4/17/30

(USD) (1)

3,580,000

73

Republic

of

El

Salvador,

9.25%,

4/17/30

(USD) (1)

12,695,000

13,472

Total

El

Salvador

(Cost

$12,638)

13,545

T.

ROWE

PRICE

Dynamic

Credit

Fund

Par/Shares

$

Value

(Cost

and

value

in

$000s)

FRANCE 1.0%

Corporate

Bonds 1.0%

Altice

France

Holding,

10.50%,

5/15/27

(USD) (1)

14,003,000

3,956

Societe

Generale,

VR,

8.125%

(USD) (1)(2)(9)

6,030,000

5,909

Total

France

(Cost

$15,480)

9,865

GERMANY 1.4%

Corporate

Bonds 1.4%

Deutsche

Bank,

Series

2020,

VR,

6.00%

(USD) (2)(9)

14,800,000

14,504

Total

Germany

(Cost

$14,555)

14,504

GHANA 0.9%

Corporate

Bonds 0.9%

Kosmos

Energy,

8.75%,

10/1/31

(USD) (1)(3)

9,150,000

8,629

Total

Ghana

(Cost

$9,150)

8,629

ITALY 1.4%

Corporate

Bonds 1.4%

Golden

Goose,

FRN,

3M

EURIBOR

+

4.875%,

7.898%,

5/14/27

13,939,000

14,614

Total

Italy

(Cost

$14,786)

14,614

JERSEY 1.0%

Corporate

Bonds 1.0%

Africell

Holding,

10.50%,

10/23/29

(USD) (1)

10,065,000

9,889

Total

Jersey

(Cost

$10,065)

9,889

LUXEMBOURG 0.4%

Corporate

Bonds 0.4%

Altice

Financing,

9.625%,

7/15/27

(USD) (1)

3,916,000

3,603

Total

Luxembourg

(Cost

$3,885)

3,603

MAURITIUS 0.6%

Corporate

Bonds 0.6%

Axian

Telecom,

7.375%,

2/16/27

(USD) (1)

200,000

201

T.

ROWE

PRICE

Dynamic

Credit

Fund

Par/Shares

$

Value

(Cost

and

value

in

$000s)

Axian

Telecom,

7.375%,

2/16/27

(USD)

5,500,000

5,515

Total

Mauritius

(Cost

$5,307)

5,716

MEXICO 6.0%

Bank

Loans 1.4% (10)

Mercury

Data

Center

Bidco,

FRN,

3M

TSFR

+

4.75%,

9.222%,

9/5/29

(USD) (5)

15,000,000

14,925

14,925

Corporate

Bonds 4.6%

BBVA

Bancomer,

VR,

8.125%,

1/8/39

(USD) (1)(2)

13,695,000

13,981

Comision

Federal

de

Electricidad,

5.70%,

1/24/30

(USD) (1)

15,540,000

14,930

Metalsa,

3.75%,

5/4/31

(USD) (1)(3)

7,135,000

5,739

Petroleos

Mexicanos,

5.50%,

6/27/44

(USD)

5,805,000

3,616

Petroleos

Mexicanos,

6.70%,

2/16/32

(USD)

700,000

610

Petroleos

Mexicanos,

10.00%,

2/7/33

(USD) (3)

7,304,000

7,590

46,466

Total

Mexico

(Cost

$61,389)

61,391

MONTENEGRO 1.0%

Government

Bonds 1.0%

Republic

of

Montenegro,

7.25%,

3/12/31

(USD) (1)

9,640,000

9,905

Total

Montenegro

(Cost

$9,861)

9,905

SRI

LANKA 2.2%

Government

Bonds 2.2%

Republic

of

Sri

Lanka,

4.00%,

4/15/28

(USD) (1)

4,332,478

4,068

Republic

of

Sri

Lanka,

STEP,

3.10%,

1/15/30

(USD) (1)

3,457,316

2,869

Republic

of

Sri

Lanka,

STEP,

3.35%,

3/15/33

(USD) (1)

6,781,466

5,163

Republic

of

Sri

Lanka,

STEP,

3.60%,

6/15/35

(USD) (1)

4,579,050

3,320

Republic

of

Sri

Lanka,

STEP,

3.60%,

5/15/36

(USD) (1)

3,177,968

2,423

Republic

of

Sri

Lanka,

STEP,

3.60%,

2/15/38

(USD) (1)

6,358,605

4,873

Total

Sri

Lanka

(Cost

$21,794)

22,716

SURINAME 0.0%

Government

Bonds 0.0%

Republic

of

Suriname,

7.95%,

7/15/33,

(4.95%

Cash

and

3.00%

PIK)

(USD) (1)(4)

275,533

248

T.

ROWE

PRICE

Dynamic

Credit

Fund

Par/Shares

$

Value

(Cost

and

value

in

$000s)

Republic

of

Suriname,

VR,

9.00%,

12/31/50

(USD) (1)

130,000

130

Total

Suriname

(Cost

$273)

378

UNITED

KINGDOM 2.4%

Bank

Loans 1.4% (10)

CD&R

Firefly

Bidco,

FRN,

3M

EURIBOR

+

3.75%,

6.802%,

4/29/29

(EUR)

6,420,000

6,679

CD&R

Firefly

Bidco,

FRN,

GBP

SONIA

+

5.75%,

10.70%,

6/21/28

4,670,000

5,832

ZPG,

FRN,

GBP

SONIA

+

5.50%,

10.20%,

7/31/28

1,250,000

1,567

14,078

Convertible

Bonds 0.1%

Immunocore

Holdings,

2.50%,

2/1/30

(USD) (1)

553,000

464

464

Corporate

Bonds 0.9%

Vmed

O2

U.K.

Financing

I,

7.75%,

4/15/32

(USD) (1)

9,555,000

9,544

9,544

Total

United

Kingdom

(Cost

$24,402)

24,086

UNITED

STATES 52.3%

Asset-Backed

Securities 11.2%

Auxilior

Term

Funding,

Series

2023-1A,

Class

E,

10.97%,

12/15/32 (1)

6,770,000

6,946

Bayview

Opportunity

Master

Fund

VII,

Series

2024-CAR1,

Class

E,

FRN,

SOFR30A

+

3.60%,

8.169%,

12/26/31 (1)

2,267,005

2,296

Blackbird

Capital

Aircraft

Lease

Securitization,

Series

2016-

1A,

Class

A,

STEP,

6.50%,

12/16/41 (1)

165,180

165

Blue

Owl

Asset

Leasing

Trust,

Series

2024-1A,

Class

D,

8.00%,

12/15/31 (1)

5,011,000

4,995

Carvana

Auto

Receivables

Trust,

Series

2024-N2,

Class

E,

8.16%,

6/10/31 (1)

7,300,000

7,321

Driven

Brands

Funding,

Series

2019-2A,

Class

A2,

3.981%,

10/20/49 (1)

4,157,925

4,058

Elara

HGV

Timeshare

Issuer,

Series

2019-A,

Class

C,

3.45%,

1/25/34 (1)

28,648

28

Elara

HGV

Timeshare

Issuer,

Series

2023-A,

Class

D,

10.10%,

2/25/38 (1)

132,389

136

FOCUS

Brands

Funding,

Series

2023-2,

Class

A2,

8.241%,

10/30/53 (1)

8,840,700

9,314

Frontier

Issuer,

Series

2023-1,

Class

C,

11.50%,

8/20/53 (1)

10,865,765

11,588

T.

ROWE

PRICE

Dynamic

Credit

Fund

Par/Shares

$

Value

(Cost

and

value

in

$000s)

Frontier

Issuer,

Series

2024-1,

Class

C,

11.16%,

6/20/54 (1)

1,098,880

1,228

Goto

Foods

Funding,

Series

2017-1A,

Class

A2II,

5.093%,

4/30/47 (1)

2,090,500

2,060

Hardee's

Funding,

Series

2020-1A,

Class

A2,

3.981%,

12/20/50 (1)

1,597,969

1,502

Hardee's

Funding,

Series

2021-1A,

Class

A2,

2.865%,

6/20/51 (1)

1,215,900

1,089

Hardee's

Funding,

Series

2024-1A,

Class

A2,

7.253%,

3/20/54 (1)

9,835,675

10,046

Hilton

Grand

Vacations

Trust,

Series

2024-1B,

Class

D,

8.85%,

9/15/39 (1)

2,065,823

2,105

Huntington

Bank

Auto

Credit-Linked

Notes,

Series

2024-1,

Class

C,

FRN,

SOFR30A

+

3.15%,

7.755%,

5/20/32 (1)

2,107,618

2,129

Jersey

Mike's

Funding,

Series

2019-1A,

Class

A2,

4.433%,

2/15/50 (1)

230,260

227

Jersey

Mike's

Funding,

Series

2021-1A,

Class

A2I,

2.891%,

2/15/52 (1)

49,750

48

MVW,

Series

2023-2A,

Class

D,

9.33%,

11/20/40 (1)

4,378,213

4,472

Octane

Receivables

Trust,

Series

2023-1A,

Class

E,

9.25%,

8/20/30 (1)

255,000

267

Post

Road

Equipment

Finance,

Series

2024-1A,

Class

E,

8.50%,

12/15/31 (1)

3,338,000

3,302

Santander

Bank

Auto

Credit-Linked

Notes,

Series

2023-A,

Class

E,

10.068%,

6/15/33 (1)

80,479

82

Santander

Bank

Auto

Credit-Linked

Notes,

Series

2023-B,

Class

E,

8.408%,

12/15/33 (1)

4,705,278

4,812

SCF

Equipment

Leasing,

Series

2022-1A,

Class

F,

6.00%,

7/20/32 (1)

5,650,000

5,483

SCF

Equipment

Leasing,

Series

2024-1A,

Class

E,

9.00%,

12/20/34 (1)

3,300,000

3,338

SEB

Funding,

Series

2024-1A,

Class

A2,

7.386%,

4/30/54 (1)

14,435,000

14,761

Sierra

Timeshare

Receivables

Funding,

Series

2021-1A,

Class

D,

3.17%,

11/20/37 (1)

832,668

806

Sierra

Timeshare

Receivables

Funding,

Series

2023-3A,

Class

D,

9.44%,

9/20/40 (1)

3,101,487

3,201

Sierra

Timeshare

Receivables

Funding,

Series

2024-1A,

Class

D,

8.02%,

1/20/43 (1)

1,456,929

1,472

Stonepeak

ABS,

Series

2021-1A,

Class

B,

3.821%,

2/28/33 (1)

148,520

140

TPIC

SPV

I,

Series

2024-1A,

Class

A,

Acquisition

Date:

12/10/24,

Cost $4,300,

7.131%,

11/30/44 (8)

4,300,000

4,300

113,717

T.

ROWE

PRICE

Dynamic

Credit

Fund

Par/Shares

$

Value

(Cost

and

value

in

$000s)

Bank

Loans 11.4% (10)

Asurion,

FRN,

1M

TSFR

+

4.25%,

8.707%,

8/19/28

19,584,831

19,585

Asurion,

FRN,

1M

TSFR

+

5.25%,

9.721%,

1/31/28

185,904

181

Chromalloy,

FRN,

3M

TSFR

+

3.75%,

8.06%,

3/27/31

13,920,050

13,922

Cloud

Software

Group,

FRN,

1M

TSFR

+

3.75%,

8.079%,

3/21/31

7,465,000

7,481

Cloud

Software

Group,

FRN,

3M

TSFR

+

3.50%,

7.829%,

3/30/29

4,207,995

4,217

CMG

Media,

FRN,

1M

TSFR

+

3.50%,

7.929%,

6/18/29

9,763,746

8,724

CSC

Holdings,

FRN,

1M

TSFR

+

2.50%,

7.173%,

4/15/27

5,725,000

5,273

CSC

Holdings,

FRN,

1M

TSFR

+

4.50%,

8.806%,

1/18/28

9,785,202

9,579

Ellucian

Holdings,

FRN,

1M

TSFR

+

3.00%,

7.357%,

10/9/29

5,233,194

5,263

Ellucian

Holdings,

FRN,

1M

TSFR

+

4.75%,

9.107%,

11/14/32

4,925,000

5,007

Icon

Parent,

FRN,

1M

TSFR

+

3.00%,

7.516%,

11/13/31

8,815,000

8,840

LTI

Holdings,

FRN,

1M

TSFR

+

4.75%,

9.107%,

7/29/29

6,962,550

6,966

Radiate

Holdco,

FRN,

1M

TSFR

+

3.25%,

7.721%,

9/25/26

17,068,343

14,884

RFS

OPCO,

FRN,

1M

TSFR

+

4.75%,

9.079%,

4/4/31 (5)

6,264,300

6,202

116,124

Common

Stocks 0.0%

Altera

Infrastructure,

Acquisition

Date:

1/19/23,

Cost $13 (5)

(6)(8)

639

18

18

Convertible

Bonds 0.8%

Wolfspeed,

1.875%,

12/1/29

19,595,000

8,083

8,083

Convertible

Preferred

Stocks 1.5%

Ares

Management,

Series

B,

6.75%,

10/1/27

111,744

6,151

Boeing,

6.00%,

10/15/27

74,353

4,527

Kobold

Metals,

Series

C-2,

Acquisition

Date:

9/20/24,

Cost $4,009 (5)(6)(8)

51,015

4,334

15,012

Corporate

Bonds 21.0%

Alliant

Holdings

Intermediate,

6.50%,

10/1/31 (1)

9,895,000

9,747

American

Airlines,

5.75%,

4/20/29 (1)

4,618,182

4,572

AP

Grange

Holdings,

Acquisition

Date:

6/12/24,

Cost $8,925,

6.50%,

3/20/45 (5)(8)

8,925,000

8,925

At

Home

Group,

4.875%,

7/15/28 (1)

210,000

84

T.

ROWE

PRICE

Dynamic

Credit

Fund

Par/Shares

$

Value

(Cost

and

value

in

$000s)

Blackstone

Mortgage

Trust,

7.75%,

12/1/29 (1)

5,230,000

5,367

Centene,

3.00%,

10/15/30

2,458,000

2,114

Centene,

4.625%,

12/15/29

2,462,000

2,314

CHS,

10.875%,

1/15/32 (1)

5,655,000

5,818

Cloud

Software

Group,

8.25%,

6/30/32 (1)

2,939,000

3,031

Cloud

Software

Group,

9.00%,

9/30/29 (1)

7,175,000

7,274

Comstock

Resources,

6.75%,

3/1/29 (1)

8,796,000

8,554

Crescent

Energy

Finance,

7.375%,

1/15/33 (1)

5,925,000

5,762

CVS

Health,

VR,

6.75%,

12/10/54 (2)

2,305,000

2,247

DISH

DBS,

5.25%,

12/1/26 (1)

15,035,000

13,644

DISH

DBS,

5.75%,

12/1/28 (1)

606,000

518

DISH

DBS,

7.75%,

7/1/26

6,145,000

5,146

DISH

Network,

11.75%,

11/15/27 (1)

16,700,000

17,639

Icahn

Enterprises,

9.00%,

6/15/30

12,450,000

11,905

LCPR

Senior

Secured

Financing,

6.75%,

10/15/27 (1)

10,355,000

9,332

MPT

Operating

Partnership,

2.50%,

3/24/26

(GBP) (3)

12,665,000

14,013

Navient,

11.50%,

3/15/31

13,445,000

14,991

Neptune

Bidco

U.S.,

9.29%,

4/15/29 (1)

17,130,000

15,888

NGL

Energy

Operating,

8.125%,

2/15/29 (1)

3,348,000

3,381

OneMain

Finance,

7.125%,

11/15/31

11,030,000

11,237

Transocean,

8.75%,

2/15/30 (1)

19,575,500

20,163

Venture

Global

LNG,

VR,

9.00% (1)(2)(9)

9,775,000

10,203

213,869

Municipal

Securities 2.9%

Colorado

HFA,

Covenant

Living

Community,

Series

B,

4.48%,

12/1/40

235,000

189

Michigan

Tobacco

Settlement

Fin.

Auth.,

Series

B,

Zero

Coupon,

6/1/46

25,000

3

Port

of

Beaumont

Navigation

Dist.,

Jefferson

Gulf

Coast,

Series

B,

10.00%,

7/1/26 (1)

10,720,000

10,954

Puerto

Rico

Commonwealth,

GO,

VR,

11/1/43 (11)

29,468,352

18,049

Puerto

Rico

Electric

Power

Auth.,

Build

America,

5.95%,

7/1/30 (6)(12)

40,000

22

Puerto

Rico

Electric

Power

Auth.,

Build

America,

6.05%,

7/1/32 (6)(12)

150,000

81

Tobacco

Settlement

Fin.,

Series

A-1,

6.706%,

6/1/46

250,000

209

Tobacco

Settlement

Fin.

Auth.,

Series

B,

4.875%,

6/1/49

90,000

85

Tobacco

Settlement

Fin.

Auth.,

Series

B,

Zero

Coupon,

6/1/47

460,000

43

29,635

T.

ROWE

PRICE

Dynamic

Credit

Fund

Par/Shares

$

Value

(Cost

and

value

in

$000s)

Non-U.S.

Government

Mortgage-Backed

Securities 2.5%

Alen

Mortgage

Trust,

Series

2021-ACEN,

Class

A,

ARM,

1M

TSFR

+

1.264%,

5.662%,

4/15/34 (1)

2,120,000

1,966

Bayview

Financing

Trust,

Series

2024-2F,

Class

A,

CMO,

ARM,

Acquisition

Date:

8/29/24,

Cost $5,031,

8.10%,

9/25/29 (5)(8)

5,030,628

5,031

BBCMS

Mortgage

Trust,

Series

2019-BWAY,

Class

E,

ARM,

1M

TSFR

+

2.964%,

7.361%,

11/15/34 (1)

120,000

1

BBCMS

Trust,

Series

2015-SRCH,

Class

D,

ARM,

4.957%,

8/10/35 (1)

2,131,000

1,909

BSREP

Commercial

Mortgage

Trust,

Series

2021-DC,

Class

C,

ARM,

1M

TSFR

+

1.664%,

6.062%,

8/15/38 (1)

1,170,417

925

BX

Trust,

Series

2021-VIEW,

Class

F,

ARM,

1M

TSFR

+

4.044%,

8.441%,

6/15/36 (1)

145,000

136

CAFL,

Series

2021-RTL1,

Class

A1,

CMO,

STEP,

2.239%,

3/28/29 (1)

49,373

49

CAMB

Commercial

Mortgage

Trust,

Series

2019-LIFE,

Class

E,

ARM,

1M

TSFR

+

2.447%,

6.845%,

12/15/37 (1)

2,912,500

2,913

Cantor

Commercial

Real

Estate

Lending,

Series

2019-CF1,

Class

65C,

ARM,

4.123%,

5/15/52 (1)

115,000

39

Cantor

Commercial

Real

Estate

Lending,

Series

2019-CF1,

Class

65D,

ARM,

4.66%,

5/15/52 (1)

70,000

19

Finance

of

America

HECM

Buyout,

Series

2024-HB1,

Class

M5,

ARM,

6.00%,

10/1/34 (1)

8,725,000

6,287

LSTAR

Commercial

Mortgage

Trust,

Series

2017-5,

Class

D,

ARM,

4.667%,

3/10/50 (1)

220,000

176

Oceanview

Mortgage

Loan

Trust,

Series

2020-1,

Class

A3,

CMO,

ARM,

3.285%,

5/28/50 (1)

115,000

97

ONE

Mortgage

Trust,

Series

2021-PARK,

Class

D,

ARM,

1M

TSFR

+

1.614%,

6.011%,

3/15/36 (1)

711,000

679

TX

Trust,

Series

2024-HOU,

Class

D,

ARM,

1M

TSFR

+

3.239%,

7.636%,

6/15/39 (1)

2,805,000

2,803

Verus

Securitization

Trust,

Series

2021-2,

Class

M1,

CMO,

ARM,

2.187%,

2/25/66 (1)

150,000

114

Verus

Securitization

Trust,

Series

2021-5,

Class

M1,

CMO,

ARM,

2.331%,

9/25/66 (1)

3,270,000

2,259

25,403

U.S.

Government

&

Agency

Mortgage-Backed

Securities 1.0%

Federal

National

Mortgage

Assn.,

CMO,

IO

2.00%,

5/25/51

-

4/25/52

45,712,511

5,977

Government

National

Mortgage

Assn.,

CMO,

IO

2.00%,

11/20/50

-

12/20/50

4,347,185

533

T.

ROWE

PRICE

Dynamic

Credit

Fund

Par/Shares

$

Value

(Cost

and

value

in

$000s)

2.50%,

8/20/49

-

11/20/51

24,435,152

3,437

9,947

Total

United

States

(Cost

$528,636)

531,808

SHORT-TERM

INVESTMENTS 12.0%

Money

Market

Funds 4.4%

T.

Rowe

Price

Government

Reserve

Fund,

4.53% (13)(14)

45,008,624

45,009

45,009

U.S.

Treasury

Obligations 7.6%

U.S.

Treasury

Bills,

4.399%,

2/27/25 (15)

76,775,000

76,270

76,270

Total

Short-Term

Investments

(Cost

$121,254)

121,279

SECURITIES

LENDING

COLLATERAL 2.1%

INVESTMENTS

IN

A

POOLED

ACCOUNT

THROUGH

SECURITIES

LENDING

PROGRAM

WITH

JPMORGAN

CHASE

BANK 1.4%

Money

Market

Funds 1.4%

T.

Rowe

Price

Government

Reserve

Fund,

4.53% (13)(14)

14,254,626

14,255

Total

Investments

in

a

Pooled

Account

through

Securities

Lending

Program

with

JPMorgan

Chase

Bank

14,255

INVESTMENTS

IN

A

POOLED

ACCOUNT

THROUGH

SECURITIES

LENDING

PROGRAM

WITH

STATE

STREET

BANK

AND

TRUST

COMPANY 0.7%

Money

Market

Funds 0.7%

T.

Rowe

Price

Government

Reserve

Fund,

4.53% (13)(14)

7,438,238

7,438

Total

Investments

in

a

Pooled

Account

through

Securities

Lending

Program

with

State

Street

Bank

and

Trust

Company

7,438

Total

Securities

Lending

Collateral

(Cost

$21,693)

21,693

T.

ROWE

PRICE

Dynamic

Credit

Fund

(Amounts

in

000s,

except

for

contracts)

OPTIONS

PURCHASED 0.3%

OTC

Options

Purchased

0.3%

Counterparty

Description

Contracts

Notional

Amount

$

Value

Barclays

Bank

Credit

Default

Swap,

Protection

Bought

(Relevant

Credit:

Markit

CDX.

NA.HY-S43,

5

Year

Index,

12/20/29),

Pay

5.00%

Quarterly,

Receive

upon

credit

default,

4/16/25

@

1.05%* (6)

2

126,900

923

Morgan

Stanley

10

Year

Interest

Rate

Swap,

7/1/35

Pay

Fixed

4.55%

Annually,

Receive

Variable

4.49%

(SOFR)

Annually,

6/27/25

@

4.55%* (6)

1

119,735

1,096

Morgan

Stanley

Credit

Default

Swap,

Protection

Sold

(Relevant

Credit:

Markit

iTraxx

Europe-S42,

5

Year

Index,

12/20/29),

Receive

1.00%

Quarterly,

Pay

upon

credit

default,

3/19/25

@

0.50%*

(EUR) (6)

2

406,900

128

T.

ROWE

PRICE

Dynamic

Credit

Fund

(Amounts

in

000s,

except

for

contracts)

Counterparty

Description

Contracts

Notional

Amount

$

Value

Morgan

Stanley

Credit

Default

Swap,

Protection

Sold

(Relevant

Credit:

Markit

iTraxx

Europe-S42,

5

Year

Index,

12/20/29),

Receive

1.00%

Quarterly,

Pay

upon

credit

default,

3/19/25

@

0.53%*

(EUR) (6)

1

203,450

126

Morgan

Stanley

iShares

Russell

2000

ETF,

Call,

3/21/25

@

$250.00 (6)

233

5,148

30

Morgan

Stanley

S&P

500

Index,

Put,

4/17/25

@

$5,950.00 (6)

33

19,409

576

Morgan

Stanley

S&P

500

Index,

Put,

12/19/25

@

$5,700.00 (6)

23

13,528

529

Morgan

Stanley

Technology

Select

Sector

SPDR

Fund,

Call,

3/21/25

@

$230.00 (6)

66

1,535

80

Wells

Fargo

Energy

Select

Sector

SPDR

Fund,

Call,

3/21/25

@

$91.00 (6)

182

1,559

29

Wells

Fargo

SPDR

S&P

Regional

Banking

ETF,

Call,

3/21/25

@

$68.00 (6)

520

3,138

52

Total

Options

Purchased

(Cost

$4,300)

3,569

Total

Investments

in

Securities

101.2%

of

Net

Assets

(Cost

$1,036,004)

$

1,028,286

T.

ROWE

PRICE

Dynamic

Credit

Fund

‡

Country

classifications

are

generally

based

on

MSCI

categories

or

another

unaffiliated

third

party

data

provider;

Par/Shares

and

Notional

Amount

are

denominated

in

the

currency

of

the

country

presented

unless

otherwise

noted.

†

Investment

fund

is

not

unitized.

*

Exercise

Spread

(1)

Security

was

purchased

pursuant

to

Rule

144A

under

the

Securities

Act

of

1933

and

may

be

resold

in

transactions

exempt

from

registration

only

to

qualified

institutional

buyers.

Total

value

of

such

securities

at

period-end

amounts

to

$435,117

and

represents

42.8%

of

net

assets.

(2)

Security

is

a

fix-to-float

security,

which

carries

a

fixed

coupon

until

a

certain

date,

upon

which

it

switches

to

a

floating

rate.

Reference

rate

and

spread

are

provided

if

the

rate

is

currently

floating.

(3)

See

Note

4

.

All

or

a

portion

of

this

security

is

on

loan

at

December

31,

2024.

(4)

Security

has

the

ability

to

pay

in-kind

or

pay

in

cash.

When

applicable,

separate

rates

of

such

payments

are

disclosed.

(5)

See

Note

2.

Level

3

in

fair

value

hierarchy.

(6)

Non-income

producing

(7)

Security

is

in

default

or

has

failed

to

make

a

scheduled

interest

and/or

principal

payment.

(8)

Security

cannot

be

offered

for

public

resale

without

first

being

registered

under

the

Securities

Act

of

1933

and

related

rules

("restricted

security").

Acquisition

date

represents

the

day

on

which

an

enforceable

right

to

acquire

such

security

is

obtained

and

is

presented

along

with

related

cost

in

the

security

description.

The

fund

may

have

registration

rights

for

certain

restricted

securities.

Any

costs

related

to

such

registration

are

generally

borne

by

the

issuer.

The

aggregate

value

of

restricted

securities

(excluding

144A

holdings)

at

period

end

amounts

to

$22,639

and

represents

2.2%

of

net

assets.

(9)

Perpetual

security

with

no

stated

maturity

date.

(10)

Bank

loan

positions

may

involve

multiple

underlying

tranches.

In

those

instances,

the

position

presented

reflects

the

aggregate

of

those

respective

underlying

tranches

and

the

rate

presented

reflects

the

weighted

average

rate

of

the

settled

positions.

(11)

Contingent

value

instrument

that

only

pays

out

if

a

portion

of

the

territory's

Sales

and

Use

Tax

outperforms

the

projections

in

the

Oversight

Board’s

Certified

Fiscal

Plan.

(12)

Issuer

is

currently

in

a

bankruptcy

reorganization

proceeding;

the

amount

and

timing

of

future

distributions

is

uncertain.

(13)

Seven-day

yield

(14)

Affiliated

Companies

(15)

At

December

31,

2024,

all

or

a

portion

of

this

security

is

pledged

as

collateral

and/or

margin

deposit

to

cover

future

funding

obligations.

T.

ROWE

PRICE

Dynamic

Credit

Fund

1M

TSFR

One

month

term

SOFR

(Secured

overnight

financing

rate)

3M

EURIBOR

Three

month

EURIBOR

(Euro

interbank

offered

rate)

3M

TSFR

Three

month

term

SOFR

(Secured

overnight

financing

rate)

ARM

Adjustable

Rate

Mortgage

(ARM);

rate

shown

is

effective

rate

at

period-end.

The

rates

for

certain

ARMs

are

not

based

on

a

published

reference

rate

and

spread

but

may

be

determined

using

a

formula

based

on

the

rates

of

the

underlying

loans.

AUD

Australian

Dollar

BRL

Brazilian

Real

CAD

Canadian

Dollar

CHF

Swiss

Franc

CMO

Collateralized

Mortgage

Obligation

CORRA

Canadian

Overnight

Repo

Rate

Average

CPI

Consumer

Price

Index

ETF

Exchange-Traded

Fund

EUR

Euro

FRN

Floating

Rate

Note

GBP

British

Pound

GO

General

Obligation

HFA

Health

Facility

Authority

IO

Interest-only

security

for

which

the

fund

receives

interest

on

notional

principal

JPY

Japanese

Yen

NOK

Norwegian

Krone

NZD

New

Zealand

Dollar

OTC

Over-the-counter

PIK

Payment-in-kind

SEK

Swedish

Krona

SOFR

Secured

overnight

financing

rate

SOFR30A

30-day

Average

SOFR

(Secured

overnight

financing

rate)

SONIA

Sterling

Overnight

Index

Average

STEP

Stepped

coupon

bond

for

which

the

coupon

rate

of

interest

adjusts

on

specified

date(s);

rate

shown

is

effective

rate

at

period-end.

USD

U.S.

Dollar

VR

Variable

Rate;

rate

shown

is

effective

rate

at

period-end.

The

rates

for

certain

variable

rate

securities

are

not

based

on

a

published

reference

rate

and

spread

but

are

determined

by

the

issuer

or

agent

and

based

on

current

market

conditions.

T.

ROWE

PRICE

Dynamic

Credit

Fund

(Amounts

in

000s)

SWAPS

(1.1)%

Description

Notional

Amount

$

Value

Upfront

Payments/

$

(Receipts)

Unrealized

$

Gain/(Loss)

BILATERAL

SWAPS

(0.3)%

Credit

Default

Swaps,