UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

| Investment Company Act file number: 811-02968-99 | ||

| Name of Registrant: Vanguard Trustees’ Equity Fund | ||

| Address of Registrant: | ||

| P.O. Box 2600 | ||

| Valley Forge, PA 19482 | ||

| Name and address of agent for service: | ||

| Heidi Stam, Esquire | ||

| P.O. Box 876 | ||

| Valley Forge, PA 19482 | ||

| Registrant’s telephone number, including area code: (610) 669-1000 | ||

| Date of fiscal year end: October 31 | ||

| Date of reporting period: November 1, 2013 – October 31, 2014 | ||

| Item 1: Reports to Shareholders | ||

Annual Report | October 31, 2014

Vanguard International Value Fund

The mission continues

On May 1, 1975, Vanguard began operations, a fledgling company based on the simple but revolutionary idea that a mutual fund company should be managed solely in the interest of its investors.

Four decades later, that revolutionary spirit continues to animate the enterprise. Vanguard remains on a mission to give investors the best chance of investment success.

As we mark our 40th anniversary, we thank you for entrusting your assets to Vanguard and giving us the opportunity to help you reach your financial goals in the decades to come.

| Contents | |

| Your Fund’s Total Returns. | 1 |

| Chairman’s Letter. | 2 |

| Advisors’ Report. | 9 |

| Fund Profile. | 14 |

| Performance Summary. | 16 |

| Financial Statements. | 18 |

| Your Fund’s After-Tax Returns. | 33 |

| About Your Fund’s Expenses. | 34 |

| Glossary. | 36 |

Please note: The opinions expressed in this report are just that—informed opinions. They should not be considered promises or advice. Also, please keep in mind that the information and opinions cover the period through the date on the front of this report. Of course, the risks of investing in your fund are spelled out in the prospectus.

See the Glossary for definitions of investment terms used in this report.

About the cover: Since our founding, Vanguard has drawn inspiration from the enterprise and valor demonstrated by British naval hero Horatio Nelson and his command at the Battle of the Nile in 1798. The photograph displays a replica of a merchant ship from the same era as Nelson’s flagship, the HMS Vanguard.

Your Fund’s Total Returns

| Fiscal Year Ended October 31, 2014 | |

| Total | |

| Returns | |

| Vanguard International Value Fund | 1.20% |

| MSCI All Country World Index ex USA | 0.06 |

| International Funds Average | 0.04 |

| International Funds Average: Derived from data provided by Lipper, a Thomson Reuters Company. | |

| Your Fund’s Performance at a Glance | ||||

| October 31, 2013, Through October 31, 2014 | ||||

| Distributions Per Share | ||||

| Starting | Ending | |||

| Share | Share | Income | Capital | |

| Price | Price | Dividends | Gains | |

| Vanguard International Value Fund | $37.12 | $36.87 | $0.697 | $0.000 |

1

Chairman’s Letter

Dear Shareholder,

International stock markets significantly trailed the broad U.S. stock market for the fiscal year ended October 31, 2014. Mounting concerns about the global economy, especially the threat of deflation in Europe and a slowdown in China and other emerging markets, contributed to the weakness.

Vanguard International Value Fund returned 1.20% for the fiscal year. Although modest, the fund’s result exceeded that of its benchmark, the MSCI All Country World Index ex USA, and the average return of its peers.

The advisors’ holdings in Europe and the Pacific region contributed most to the outperformance; their choices in emerging markets weakened results.

During the fiscal year, the U.S. dollar strengthened against most major currencies, including the euro and the Japanese yen. The stronger dollar weighed on the returns of U.S.-based investors. (For more on currency effects and international diversification, see the text box on page 6.)

If you hold the International Value Fund in a taxable account, you may wish to review the discussion of after-tax returns later in this report.

2

Their smooth ride turned jagged, but U.S. stocks ended higher

The global stock market’s occasional zigs and zags during the year were punctuated by a roller-coaster ride in October that left international markets several steps behind the U.S. stock market for the 12 months ended October 31. Emerging markets advanced modestly, while the developed European and Pacific markets finished in negative territory.

In contrast, the broad U.S. stock market returned about 16% for the 12 months. Impressive corporate earnings and various global stimulus measures generally supported stocks against a bleaker backdrop that included tensions in the Middle East and Ukraine and other international economic concerns. After falling in the first two weeks of October, several major U.S. indexes rebounded to finish at record highs. Reflecting confidence in the U.S. economy, the Federal Reserve announced October 29 that it was ending its stimulative bond-buying program as anticipated.

U.S. bonds posted positive returns as already low yields declined

The broad U.S. taxable bond market returned 4.14%. Bond prices, which backtracked at times over the summer, climbed in October as investors sought sanctuary from stock market volatility.

Overall, bond returns have been strong despite many analysts’ expectations that already low yields wouldn’t decline further. Prices rose and yields fell even as the Fed

| Market Barometer | |||

| Average Annual Total Returns | |||

| Periods Ended October 31, 2014 | |||

| One | Three | Five | |

| Year | Years | Years | |

| Stocks | |||

| Russell 1000 Index (Large-caps) | 16.78% | 19.90% | 16.98% |

| Russell 2000 Index (Small-caps) | 8.06 | 18.18 | 17.39 |

| Russell 3000 Index (Broad U.S. market) | 16.07 | 19.77 | 17.01 |

| FTSE All-World ex US Index (International) | 0.45 | 8.07 | 6.38 |

| Bonds | |||

| Barclays U.S. Aggregate Bond Index (Broad taxable market) | 4.14% | 2.73% | 4.22% |

| Barclays Municipal Bond Index (Broad tax-exempt market) | 7.82 | 4.93 | 5.26 |

| Citigroup Three-Month U.S. Treasury Bill Index | 0.04 | 0.04 | 0.06 |

| CPI | |||

| Consumer Price Index | 1.66% | 1.60% | 1.89% |

3

began steadily reducing its bond purchases in January. (Bond prices and yields move in opposite directions.) The yield of the 10-year U.S. Treasury note ended October at 2.31%, down from 2.54% a year earlier.

Municipal bonds returned 7.82%, with tax-exempt issues in high demand even at a time of reduced supply.

International bond markets (as measured by the Barclays Global Aggregate Index ex USD) slid in September and October en route to a –2.53% return for the 12 months.

The Fed’s target for short-term interest rates remained at 0%–0.25%, restraining returns for money market funds and savings accounts.

Selections in Europe and Japan lifted the fund above its index

The International Value Fund’s three advisors scour developed and emerging markets outside the United States in search of stocks that, while perhaps temporarily out of favor, have the potential for a resurgence.

| Expense Ratios | ||

| Your Fund Compared With Its Peer Group | ||

| Peer Group | ||

| Fund | Average | |

| International Value Fund | 0.43% | 1.36% |

| The fund expense ratio shown is from the prospectus dated February 26, 2014, and represents estimated costs for the current fiscal year. For the fiscal year ended October 31, 2014, the fund’s expense ratio was 0.44%. The peer-group expense ratio is derived from data provided by Lipper, a Thomson Reuters Company, and captures information through year-end 2013. | ||

Peer group: International Funds.

4

The most recent period was, as I mentioned earlier, a challenging time for international stocks. But the team managing the International Value Fund was able to coax positive relative results from it, in part by avoiding some of the worst performers.

After a robust start to the fiscal year, many markets in Europe—including France, Germany, Italy, and Spain—lost ground in its second half as clouds appeared on the economic horizon in the form of lower growth prospects and looming deflation. Still, the International Value Fund’s European portfolio, which constituted about half its assets, eked out a positive result. Limited exposure to France, which had a negative return, and an overweight allocation to Denmark, one of the few European countries to register double-digit gains, enhanced performance. The advisors’ selections in Spain also helped.

In the Pacific region, which made up about a third of the fund’s assets, the fund advanced modestly, while its benchmark counterpart finished just slightly positive.

Japan, the largest country holding in the region and the fund, stood out. The advisors have sought out more opportunities there in recent years, resulting in the fund’s notably larger exposure to Japanese stocks than the benchmark’s. Prime Minister Shinzo Abe’s efforts to spur growth has led to economic improvements, and the Bank of Japan’s surprise announcement in late

| Total Returns | |

| Ten Years Ended October 31, 2014 | |

| Average | |

| Annual Return | |

| International Value Fund | 6.85% |

| Spliced International Index | 5.14 |

| International Funds Average | 5.64 |

| For a benchmark description, see the Glossary. International Funds Average: Derived from data provided by Lipper, a Thomson Reuters Company. The figures shown represent past performance, which is not a guarantee of future results. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at vanguard.com/performance.) Note, too, that both investment returns and principal value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost. | |

5

October that it would expand its stimulus efforts was considered a positive sign. The advisors’ superior selection among Japanese information technology and telecommunication services stocks boosted results.

The fund’s emerging-market portfolio detracted from performance, returning about –4% compared with about 1% for its benchmark counterpart.

| Currency fluctuation is one reason U.S. and international stocks diverge |

| Diversification is a proven way to reduce volatility and manage risk. That’s why it can make |

| sense for investors to allocate a portion of their stock portfolios to international equities |

| (20% of the equity allocation can be a good starting point). International stocks, which make |

| up about half of the world’s stock market capitalization, perform somewhat differently than |

| stocks in the U.S. market. One of the many reasons for this is currency fluctuation. Currency |

| movements historically have not been correlated to stock price movements, meaning they |

| tend not to move together. |

| International stocks have underperformed U.S. stocks recently for U.S.-based investors, |

| in part because many foreign currencies have weakened against the U.S. dollar. But that |

| divergence actually highlights the diversification benefit of owning both U.S. and international |

| stocks. As you can see from the accompanying chart, at other times, international stocks have |

| outshone their U.S. counterparts. (For more insight, see Global Equities: Balancing Home Bias |

| and Diversification, available at vanguard.com/research.) |

| Trailing 12-month return differential between U.S. and non-U.S. stocks |

| Notes: U.S. equities are represented by the MSCI USA Index; international equities are represented by the MSCI All Country World Index ex USA. Data are from October 31, 1994, through October 31, 2014. Sources: Vanguard, Thomson Reuters Datastream, and MSCI. |

6

During the fiscal year, China’s decelerating economic growth and reduced appetite for commodities and other imports weighed on emerging-market stocks. Subpar selection among Chinese material stocks and light exposure to Chinese financial companies hurt the fund’s performance. Russian holdings were another source of weakness. Russian energy stocks have been under pressure from lower oil prices as well as the international sanctions put in place amid the conflict in Ukraine.

Among industries, six of the International Value Fund’s ten sectors notched gains for the fiscal year. Industrials, materials, and health care, were key outperformers. Consumer staples, energy, and financials were among the largest detractors.

For more information on the fund’s investment strategies and positioning, please see the Advisors’ Report that follows this letter.

Over ten years, the fund did well versus both its index and its peers

For the decade ended October 31, 2014, the International Value Fund posted an average annual return of 6.85%, more than a percentage point better than the average return of its benchmark index and peer group.

International Value’s long-term performance exceeded the benchmark’s in all but one of the last ten years. This is the second year that the fund has been managed by its current three advisors. Each brings to the table a slightly different approach, providing a diversification benefit to investors.

As we reflect upon the past decade, and indeed the fiscal year, it’s important to consider the benefits of global diversification. The past year vividly illustrated how global stock markets don’t always move in lockstep. A portfolio that includes both U.S. and international stocks and other asset classes can provide some cushion for investors to weather the inevitable variations in global market performance.

When market volatility heats up, the best response is to keep cool

After several years of strength, stocks hit a rough patch toward the close of the fiscal year, as I noted earlier. For the first half of October, global stock markets (as measured by the FTSE Global All Cap Index) returned –5.56%. Even though stocks rebounded in the second half of the month, many investors undoubtedly were left feeling unsettled.

What’s my best advice to anxious shareholders? Remain calm and remember that volatility is a normal part of stock market investing. The value of keeping a cool head is highlighted in a Vanguard research paper that looked at how investors behaved during the financial crisis, when global stocks declined about 58% and U.S. stocks about 55%.

7

The 2010 paper, Resilience in Volatile Markets: 401(k) Participant Behavior, September 2007–December 2009, examined the behavior of participants in Vanguard-administered retirement plans. During that time, about three-quarters of participants made no changes to their accounts, and only 3% gave up on stocks completely.

As stocks recovered, this discipline yielded big benefits. From the end of 2008 to the end of 2013, the average Vanguard 401(k) portfolio nearly doubled in value, largely because of the surge in stock prices.

I’m pleased that, over time, our clients have demonstrated an impressive ability to remain focused on their long-term goals.

They stayed the course through the 1987 correction, the dot-com boom of the 1990s, and the more recent financial crisis, and they continue to do so today.

As always, thank you for investing with Vanguard.

Sincerely,

F. William McNabb III

Chairman and Chief Executive Officer

November 14, 2014

8

Advisors’ Report

For the 12 months ended October 31, 2014, Vanguard International Value Fund returned 1.20%. Your fund is managed by three independent advisors, a strategy that enhances the fund’s diversification by providing exposure to distinct yet complementary investment approaches. It is not uncommon for different advisors to have different views about individual securities or the broader investment environment.

The table below presents the advisors, the percentage and amount of fund assets that each manages, and brief descriptions of their investment strategies. Each advisor has also prepared a discussion of the investment environment during the fiscal year and of how the portfolio’s positioning reflects this assessment. These reports were prepared on November 19, 2014.

| Vanguard International Value Fund Investment Advisors | ||||

| Fund Assets Managed | ||||

| Investment Advisor | % | $ Million | Investment Strategy | |

| Lazard Asset Management LLC | 39 | 3,243 | The advisor uses a research-driven, bottom-up, | |

| relative-value approach in selecting stocks. The goal is | ||||

| to identify individual stocks that offer an appropriate | ||||

| trade-off between low relative valuation and high | ||||

| financial productivity. | ||||

| Edinburgh Partners Limited | 35 | 2,871 | The advisor employs a concentrated, low-turnover, | |

| value-oriented investment approach that results in a | ||||

| portfolio of companies with good long-term prospects | ||||

| and below-market price/earnings ratios. In-depth | ||||

| fundamental research on industries and companies is | ||||

| central to this investment process. | ||||

| ARGA Investment Management, | 24 | 1,989 | The advisor believes that investors overreact to | |

| LP | short-term developments, leading to opportunities to | |||

| generate gains from investing in “good businesses at | ||||

| great prices.” Its valuation-focused process uses a | ||||

| dividend discount model to select stocks that trade at a | ||||

| discount to intrinsic value based on the company’s | ||||

| long-term earnings power and dividend-paying | ||||

| capability. | ||||

| Cash Investments | 2 | 168 | These short-term reserves are invested by Vanguard in | |

| equity index products to simulate investments in | ||||

| stocks. Each advisor may also maintain a modest cash | ||||

| position. | ||||

9

Lazard Asset Management LLC

Portfolio Managers:

Michael G. Fry, Managing Director

Michael A. Bennett, CPA,

Managing Director

International markets moderately rose during the period and continued to be driven by macroeconomic factors at a time when corporate earnings generally met expectations. Geopolitical factors, such as the Russia-Ukraine border disputes and unrest in the Middle East, contributed to volatility in both the equity and fixed income markets. In local currencies, international equity market indexes finished higher, but U.S.-based investors missed out on a lot of those gains because of the strong U.S. dollar. Its strength was partly due to the difference between expected U.S. and non-U.S. growth rates and to the diverging monetary policies of the Federal Reserve and other central banks. All major currencies except the British pound saw steep declines versus the U.S. dollar.

The materials and energy sectors were among the worst performers; they were primarily affected by falling commodity prices, notably oil, which was down more than 15%. Health care was the best performer as the pharmaceutical industry consolidated further.

Within health care, heavy exposure and stock selection helped the portfolio’s returns compared with those of the benchmark index. The sector experienced strong gains, and the portfolio benefited from its pharmaceutical holdings such as Denmark’s Novo Nordisk, Switzerland’s Novartis, and Germany’s Bayer.

In the consumer discretionary sector, stock selection helped drive the portfolio’s relative returns. British-based Signet Jewelers performed well amid strong results and the market’s favorable reaction to its Zales acquisition.

Stock selection and exposure to emerging markets also added to relative returns. The fund benefited from positions in Brazilian private-education provider Estácio and in Taiwan Semiconductor, which makes microprocessors.

In contrast, selection in financials and telecommunications services detracted from relative returns as shares of Russia’s Sberbank and Mobile TeleSystems declined amid the levying of sanctions on Russia over its conflict with Ukraine.

Limited exposure to the poorly performing energy sector partly offset negative selection. Our stake in Norway’s Petroleum Geo-Services declined amid falling oil prices, weak demand, and excess capacity, and we recently sold it.

10

Edinburgh Partners Limited

Portfolio Manager:

Sandy Nairn, Director and CEO

The world economy continues to grow at what is perceived as a relatively sedate and possibly disappointing pace. Economists’ expectations are beginning to gradually adjust to a future in which 3% global growth is as much as can be expected. This has not yet fully translated to equity markets. As a consequence, we are seeing profits matching expectations but accompanied by a cautionary note on future progression.

This leaves markets in a real quandary. Inflation is not a problem in the short term Monetary policy remains relaxed, although it is beginning to tighten, but valuations are on the full side in many markets. Various geopolitical flare-ups are triggering equity market disruptions that are then followed by recovery. In our view, the likely result of all this is that equity returns will stay positive but subdued for some time.

Reflecting this uncertainty, the unwinding of the premium paid for companies with predictable earnings streams has further to go; thus, the portfolio’s exposure to such companies remains relatively limited. The portfolio maintains a relatively cyclical orientation, though we think this has probably peaked, as evidenced by our sale of shipping company AP Moller–Maersk, which reached our price targets.

Since the calendar year began, Japanese holdings in general have lagged other global equity markets. Concerns over a sales tax increase have played a role, as have questions about the extent to which the government would follow through on its reflation policy. We remain relatively sanguine about both matters. The sales tax increase is necessary to raise revenue, but the counterpart is the package of reflationary measures and reforms. Our view is that Prime Minister Shinzo Abe and his key officials are well aware of this and that the policy will be pursued to its conclusion.

We have made some changes to the portfolio’s holdings that simply reflect the appreciation of the affected stocks and their consequent valuation—hence our sale of Fujitsu, Fujikura, and Seven & I. We also sold Tokyo Electron, which is being taken over by Applied Materials (officially, the transaction is a merger). It is a sign of the changes taking place in Japan that a leading technology company is being acquired by a foreign one with the full blessing of Japan’s government. That there remains value in Japan is evidenced by the fact that we have found other opportunities to replace the holdings we sold. We bought Toshiba in part for the potential of its NAND flash memory business. Sumitomo Mitsui Trust Holdings is benefiting from domestic reflation, and East Japan Railway has huge prime real estate assets that are being redeveloped.

11

The portfolio has also added exposure to pharmaceuticals. Our analysis suggested that the market was not rewarding greater efficiency in research and development and in drug discovery. Accordingly, toward the end of 2013, we invested in AstraZeneca, followed by Novartis and Roche. Pfizer’s putative bid for AstraZeneca was largely portrayed in the media as tax-driven, but although tax considerations were undoubtedly a factor, the principal business motivation was access to AstraZeneca’s drug pipeline.

Valuations remain reasonably full, but not to the point at which we can predict sharp and prolonged declines. Periodic setbacks will most likely produce positive but lower-than-historic returns. The value we see in pockets globally does not yet push us to keep the portfolio highly cautious. Nevertheless, we believe the cyclical exposure has now peaked, and we anticipate a gradual reduction as valuation gaps diminish. As for emerging markets, our view is the same as in our last report: They are still in transition, and although some value has begun to surface, it remains patchy, and an increase in exposure would probably depend on appropriate price falls.

ARGA Investment Management, LP

Portfolio Managers:

A. Rama Krishna, CFA, Founder and

Chief Investment Officer

Steven Morrow, CFA, Director of Research

International equity markets, while volatile, ended the fiscal year almost unchanged. Strong performance in the first half reflected growing confidence in the global economy amid further signs of European economic stabilization. The positive returns were mostly erased in the second half by signs of Europe’s slowdown and re-escalating tensions in Ukraine. Wide performance differences between regions, sectors, and individual stocks have created a new set of valuation opportunities.

The current portfolio’s positioning and changes over the past year reflect ARGA’s long-term orientation and valuation-driven investment discipline. Our practice of owning the most attractively valued businesses led us to shift exposures across many regions and sectors.

We took advantage of the strong European stock performance early in the year to trim or sell holdings for which valuations had become less compelling than other opportunities. This sharply

12

reduced the portfolio’s European exposure. We used the proceeds largely to buy Japanese equities, whose valuations had grown attractive because of fears about an impending sales tax increase and the lack of additional stimulus from Japan’s central bank.

Japanese equities now appear more attractively valued versus other developed markets than they have in the past 25 years. Ironically, this undervaluation comes at a time when both the Japanese government and pension organizations are urging Japanese corporations to boost returns through improved governance. We identified a large number of attractively valued Japanese automotive and other companies with diverse domestic and overseas exposures. In addition, the poor performance of emerging markets over the past few years has led us to uncover many undervalued emerging-market companies.

Although the recent decline in oil prices is likely to dampen near-term profitability and growth for oil and oil-services companies, the supply/demand imbalance that has driven prices lower has also created a significant valuation opportunity. Based on our analysis of the energy industry’s cost structure and long-term economics, we recently increased our exposure to selected oil-related companies that show long-term ability to generate cash.

We consider the current portfolio well-positioned to benefit from the attractive valuations available across a diverse range of businesses and regions.

13

International Value Fund

Fund Profile

As of October 31, 2014

| Portfolio Characteristics | ||

| MSCI AC | ||

| World Index | ||

| Fund | ex USA | |

| Number of Stocks | 163 | 1,819 |

| Median Market Cap | $42.5B | $33.5B |

| Price/Earnings Ratio | 18.3x | 16.9x |

| Price/Book Ratio | 1.6x | 1.7x |

| Return on Equity | 13.3% | 14.9% |

| Earnings Growth | ||

| Rate | 14.6% | 11.7% |

| Dividend Yield | 2.4% | 2.9% |

| Turnover Rate | 37% | — |

| Ticker Symbol | VTRIX | — |

| Expense Ratio1 | 0.43% | — |

| Short-Term Reserves | 2.5% | — |

| Sector Diversification (% of equity exposure) | ||

| MSCI AC | ||

| World Index | ||

| Fund | ex USA | |

| Consumer Discretionary | 15.5% | 10.7% |

| Consumer Staples | 9.1 | 9.9 |

| Energy | 8.3 | 8.5 |

| Financials | 22.5 | 27.5 |

| Health Care | 11.1 | 8.6 |

| Industrials | 12.9 | 10.8 |

| Information Technology | 8.8 | 7.0 |

| Materials | 4.0 | 7.8 |

| Telecommunication Services | 6.4 | 5.5 |

| Utilities | 1.4 | 3.7 |

| Volatility Measures | |

| MSCI AC | |

| World Index | |

| ex USA | |

| R-Squared | 0.96 |

| Beta | 1.00 |

| These measures show the degree and timing of the fund’s fluctuations compared with the indexes over 36 months. | |

| Ten Largest Holdings (% of total net assets) | ||

| Novartis AG | Pharmaceuticals | 2.5% |

| KDDI Corp. | Wireless | |

| Telecommunication | ||

| Services | 2.5 | |

| Sumitomo Mitsui | ||

| Financial Group Inc. | Diversified Banks | 2.3 |

| Samsung Electronics Co. | Technology | |

| Ltd. | Hardware, Storage & | |

| Peripherals | 1.8 | |

| Japan Tobacco Inc. | Tobacco | 1.8 |

| BNP Paribas SA | Diversified Banks | 1.6 |

| Royal Dutch Shell plc | Integrated Oil & Gas | 1.5 |

| Royal Bank of Scotland | ||

| Group plc | Diversified Banks | 1.4 |

| SAP SE | Application Software | 1.3 |

| Omron Corp. | Electronic | |

| Components | 1.3 | |

| Top Ten | 18.0% | |

| The holdings listed exclude any temporary cash investments and equity index products. | ||

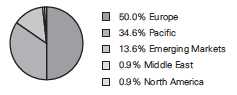

Allocation by Region (% of equity exposure)

1 The expense ratio shown is from the prospectus dated February 26, 2014, and represents estimated costs for the current fiscal year. For the fiscal year ended October 31, 2014, the expense ratio was 0.44%.

14

International Value Fund

| Market Diversification (% of equity exposure) | ||

| MSCI AC | ||

| World | ||

| Index | ||

| Fund | ex USA | |

| Europe | ||

| United Kingdom | 18.2% | 14.8% |

| Germany | 8.0 | 6.2 |

| Switzerland | 6.4 | 6.5 |

| France | 5.0 | 6.8 |

| Italy | 2.8 | 1.7 |

| Netherlands | 2.2 | 1.9 |

| Sweden | 2.1 | 2.1 |

| Denmark | 1.7 | 1.1 |

| Belgium | 1.1 | 0.9 |

| Other | 2.5 | 4.1 |

| Subtotal | 50.0% | 46.1% |

| Pacific | ||

| Japan | 25.3% | 14.8% |

| South Korea | 3.3 | 3.2 |

| Hong Kong | 3.1 | 2.2 |

| Singapore | 1.5 | 1.1 |

| Australia | 1.4 | 5.7 |

| Other | 0.0 | 0.1 |

| Subtotal | 34.6% | 27.1% |

| Emerging Markets | ||

| Brazil | 2.9% | 2.3% |

| Russia | 2.1 | 1.0 |

| China | 2.0 | 4.4 |

| Thailand | 1.4 | 0.5 |

| Turkey | 1.3 | 0.4 |

| South Africa | 1.2 | 1.7 |

| Taiwan | 1.2 | 2.7 |

| Other | 1.5 | 5.9 |

| Subtotal | 13.6% | 18.9% |

| North America | 0.9% | 7.5% |

| Middle East | 0.9% | 0.4% |

15

International Value Fund

Performance Summary

All of the returns in this report represent past performance, which is not a guarantee of future results that may be achieved by the fund. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at vanguard.com/performance.) Note, too, that both investment returns and principal value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost. The returns shown do not reflect taxes that a shareholder would pay on fund distributions or on the sale of fund shares.

Cumulative Performance: October 31, 2004, Through October 31, 2014

Initial Investment of $10,000

| Average Annual Total Returns | |||||

| Periods Ended October 31, 2014 | |||||

| Final Value | |||||

| One | Five | Ten | of a $10,000 | ||

| Year | Years | Years | Investment | ||

| International Value Fund* | 1.20% | 6.79% | 6.85% | $19,400 | |

| ••••••• | Spliced International Index | 0.06 | 5.19 | 5.14 | 16,511 |

| – – – – | International Funds Average | 0.04 | 6.72 | 5.64 | 17,309 |

| MSCI All Country World Index ex | |||||

| USA | 0.06 | 6.09 | 6.59 | 18,927 | |

| For a benchmark description, see the Glossary. International Funds Average: Derived from data provided by Lipper, a Thomson Reuters Company. | |||||

See Financial Highlights for dividend and capital gains information.

16

International Value Fund

Fiscal-Year Total Returns (%): October 31, 2004, Through October 31, 2014

| Average Annual Total Returns: Periods Ended September 30, 2014 | ||||

| This table presents returns through the latest calendar quarter—rather than through the end of the fiscal period. | ||||

| Securities and Exchange Commission rules require that we provide this information. | ||||

| Inception | One | Five | Ten | |

| Date | Year | Years | Years | |

| International Value Fund | 5/16/1983 | 5.84% | 6.26% | 7.11% |

17

International Value Fund

Financial Statements

Statement of Net Assets

As of October 31, 2014

The fund reports a complete list of its holdings in regulatory filings four times in each fiscal year, at the quarter-ends. For the second and fourth fiscal quarters, the lists appear in the fund’s semiannual and annual reports to shareholders. For the first and third fiscal quarters, the fund files the lists with the Securities and Exchange Commission on Form N-Q. Shareholders can look up the fund’s Forms N-Q on the SEC’s website at sec.gov. Forms N-Q may also be reviewed and copied at the SEC’s Public Reference Room (see the back cover of this report for further information).

| Market | ||

| Value | ||

| Shares | ($000) | |

| Common Stocks (95.2%)1 | ||

| Australia (1.1%) | ||

| QBE Insurance Group Ltd. | 4,815,103 | 49,009 |

| BHP Billiton Ltd. | 1,440,637 | 43,000 |

| 92,009 | ||

| Belgium (1.0%) | ||

| Anheuser-Busch InBev NV | 772,743 | 85,639 |

| Brazil (2.8%) | ||

| BB Seguridade | ||

| Participacoes SA | 3,647,100 | 48,655 |

| Estacio Participacoes SA | 3,874,400 | 44,851 |

| AMBEV SA | 5,021,100 | 33,242 |

| Cielo SA | 1,980,304 | 32,494 |

| Cia de Saneamento | ||

| Basico do Estado | ||

| de Sao Paulo | 4,040,600 | 31,623 |

| Petroleo Brasileiro | ||

| SA ADR | 2,525,900 | 30,892 |

| * PDG Realty SA | ||

| Empreendimentos | ||

| e Participacoes | 21,893,800 | 10,781 |

| 232,538 | ||

| China (1.9%) | ||

| China Shenhua | ||

| Energy Co. Ltd. | 28,281,500 | 79,635 |

| * Baidu Inc. ADR | 193,960 | 46,312 |

| Industrial & Commercial | ||

| Bank of China Ltd. | 17,298,000 | 11,433 |

| China Construction | ||

| Bank Corp. | 15,052,000 | 11,208 |

| China Machinery | ||

| Engineering Corp. | 19,693,000 | 11,168 |

| 159,756 | ||

| Denmark (1.7%) | ||

| Novo Nordisk A/S Class B | 1,243,346 | 56,193 |

| TDC A/S | 6,398,383 | 48,844 |

| Carlsberg A/S Class B | 263,397 | 23,196 |

| DSV A/S | 318,300 | 9,525 |

| 137,758 | ||

| Market | |||

| Value | |||

| Shares | ($000) | ||

| Finland (0.6%) | |||

| Sampo Oyj Class A | 987,587 | 47,313 | |

| France (4.6%) | |||

| BNP Paribas SA | 2,035,558 | 128,362 | |

| Sanofi | 553,493 | 51,269 | |

| ArcelorMittal | 3,202,278 | 41,978 | |

| Valeo SA | 365,718 | 41,106 | |

| Schneider Electric SE | 481,214 | 38,095 | |

| Airbus Group NV | 553,442 | 33,133 | |

| Total SA | 425,956 | 25,419 | |

| GDF Suez | 869,200 | 21,100 | |

| 380,462 | |||

| Germany (7.5%) | |||

| SAP SE | 1,601,063 | 108,856 | |

| Fresenius Medical Care | |||

| AG & Co. KGaA | 1,431,632 | 105,021 | |

| Bayer AG | 589,060 | 83,786 | |

| United Internet AG | 1,538,554 | 60,189 | |

| Volkswagen AG | |||

| Preference Shares | 270,846 | 57,760 | |

| Siemens AG | 313,845 | 35,379 | |

| * | METRO AG | 1,034,972 | 32,996 |

| adidas AG | 392,859 | 28,604 | |

| Bayerische Motoren | |||

| Werke AG | 246,571 | 26,381 | |

| BASF SE | 275,761 | 24,290 | |

| RWE AG | 640,802 | 22,687 | |

| Allianz SE | 129,292 | 20,538 | |

| HeidelbergCement AG | 251,877 | 17,155 | |

| 623,642 | |||

| Greece (0.3%) | |||

| * | Piraeus Bank SA | 17,051,197 | 24,824 |

| Hong Kong (3.0%) | |||

| Swire Pacific Ltd. | |||

| Class A | 7,817,850 | 102,549 | |

| Hutchison Whampoa Ltd. | 5,838,000 | 74,018 | |

| Li & Fung Ltd. | 43,624,000 | 53,429 | |

18

International Value Fund

| Market | ||

| Value | ||

| Shares | ($000) | |

| Esprit Holdings Ltd. | 8,372,934 | 10,581 |

| * Global Brands Group | ||

| Holding Ltd. | 43,624,000 | 9,677 |

| 250,254 | ||

| India (0.4%) | ||

| Infosys Ltd. ADR | 453,734 | 30,337 |

| Indonesia (0.5%) | ||

| Telekomunikasi Indonesia | ||

| Persero Tbk PT ADR | 1,001,969 | 45,439 |

| Ireland (0.5%) | ||

| * Ryanair Holdings plc ADR | 676,805 | 37,590 |

| Israel (0.9%) | ||

| Teva Pharmaceutical | ||

| Industries Ltd. ADR | 1,344,935 | 75,949 |

| Italy (2.6%) | ||

| Eni SPA | 3,987,407 | 84,922 |

| Intesa Sanpaolo SPA | ||

| (Registered) | 23,369,772 | 68,605 |

| Atlantia SPA | 1,496,635 | 35,233 |

| Mediolanum SPA | 4,361,357 | 29,366 |

| 218,126 | ||

| Japan (24.2%) | ||

| KDDI Corp. | 3,218,900 | 207,372 |

| Sumitomo Mitsui | ||

| Financial Group Inc. | 4,656,400 | 189,284 |

| Japan Tobacco Inc. | 4,263,700 | 147,724 |

| Omron Corp. | 2,189,200 | 106,197 |

| Panasonic Corp. | 7,365,300 | 88,845 |

| Sumitomo Mitsui Trust | ||

| Holdings Inc. | 21,056,000 | 86,820 |

| Toyota Motor Corp. | 1,254,900 | 75,490 |

| SoftBank Corp. | 1,018,600 | 75,477 |

| East Japan Railway Co. | 941,200 | 74,434 |

| Bridgestone Corp. | 2,169,400 | 72,501 |

| Mitsubishi Corp. | 3,537,200 | 70,522 |

| Sumitomo Electric | ||

| Industries Ltd. | 4,439,000 | 61,028 |

| Toshiba Corp. | 13,536,000 | 60,462 |

| Seven & I Holdings | ||

| Co. Ltd. | 1,528,683 | 60,362 |

| Dai Nippon Printing | ||

| Co. Ltd. | 5,866,000 | 58,472 |

| Honda Motor Co. Ltd. | 1,837,700 | 58,470 |

| Daiwa House Industry | ||

| Co. Ltd. | 2,974,000 | 57,314 |

| Nissan Motor Co. Ltd. | 5,593,300 | 51,770 |

| ^ Yamada Denki Co. Ltd. | 15,804,600 | 50,780 |

| Daikin Industries Ltd. | 805,300 | 50,703 |

| Makita Corp. | 850,500 | 49,828 |

| Daihatsu Motor Co. Ltd. | 3,545,200 | 49,480 |

| Market | |||

| Value | |||

| Shares | ($000) | ||

| Isuzu Motors Ltd. | 2,663,500 | 35,645 | |

| Ryohin Keikaku Co. Ltd. | 230,700 | 31,369 | |

| Komatsu Ltd. | 1,272,100 | 30,567 | |

| Yamato Kogyo Co. Ltd. | 873,400 | 29,329 | |

| ^ | Dena Co. Ltd. | 1,634,200 | 21,181 |

| Miraca Holdings Inc. | 452,600 | 19,190 | |

| Lintec Corp. | 569,400 | 12,070 | |

| Nexon Co. Ltd. | 1,187,500 | 10,482 | |

| Nintendo Co. Ltd. | 82,000 | 8,920 | |

| 2,002,088 | |||

| Netherlands (2.1%) | |||

| Heineken NV | 876,630 | 65,497 | |

| Unilever NV | 1,428,277 | 55,454 | |

| * | NXP Semiconductor NV | 378,900 | 26,053 |

| Akzo Nobel NV | 256,503 | 17,075 | |

| Wolters Kluwer NV | 373,533 | 9,978 | |

| 174,057 | |||

| Norway (0.2%) | |||

| ^ | TGS Nopec Geophysical | ||

| Co. ASA | 602,893 | 14,111 | |

| Philippines (0.5%) | |||

| Alliance Global | |||

| Group Inc. | 73,103,700 | 41,839 | |

| Russia (2.1%) | |||

| Gazprom OAO ADR | 12,977,363 | 86,129 | |

| Mobile Telesystems | |||

| OJSC ADR | 1,751,347 | 25,044 | |

| Sberbank of Russia ADR | 2,316,079 | 17,617 | |

| Sberbank of Russia | 9,657,936 | 17,122 | |

| * | Lenta Ltd. GDR | 1,498,074 | 14,586 |

| * | X5 Retail Group NV GDR | 573,992 | 10,493 |

| 170,991 | |||

| Singapore (1.4%) | |||

| DBS Group Holdings Ltd. | 4,684,000 | 67,687 | |

| Genting Singapore plc | 58,872,000 | 50,436 | |

| 118,123 | |||

| South Africa (1.2%) | |||

| Mediclinic | |||

| International Ltd. | 4,541,733 | 40,583 | |

| Nampak Ltd. | 7,406,690 | 30,209 | |

| Mr Price Group Ltd. | 1,372,195 | 28,404 | |

| 99,196 | |||

| South Korea (3.2%) | |||

| Samsung Electronics | |||

| Co. Ltd. | 129,673 | 150,221 | |

| E-Mart Co. Ltd. | 253,606 | 47,110 | |

| Hyundai Mobis Co. Ltd. | 103,434 | 24,656 | |

| Hyundai Home Shopping | |||

| Network Corp. | 141,604 | 17,989 | |

| Hana Financial Group Inc. | 470,830 | 16,262 | |

| SK Innovation Co. Ltd. | 142,413 | 11,624 | |

| 267,862 | |||

19

International Value Fund

| Market | |||

| Value | |||

| Shares | ($000) | ||

| Spain (0.8%) | |||

| * | Banco Santander SA | 3,242,356 | 28,607 |

| Red Electrica Corp. SA | 326,060 | 28,500 | |

| Banco Bilbao Vizcaya | |||

| Argentaria SA | 848,311 | 9,485 | |

| 66,592 | |||

| Sweden (2.0%) | |||

| Swedbank AB Class A | 2,370,898 | 62,705 | |

| Assa Abloy AB Class B | 1,023,890 | 54,452 | |

| Getinge AB | 1,726,835 | 40,046 | |

| ^ | Oriflame Cosmetics SA | 466,439 | 8,126 |

| 165,329 | |||

| Switzerland (6.3%) | |||

| Novartis AG | 2,253,198 | 208,971 | |

| Roche Holding AG | 234,346 | 69,216 | |

| ABB Ltd. | 2,756,144 | 60,440 | |

| Credit Suisse Group AG | 1,835,579 | 48,894 | |

| Julius Baer Group Ltd. | 924,976 | 40,526 | |

| Cie Financiere | |||

| Richemont SA | 386,381 | 32,555 | |

| Holcim Ltd. | 354,333 | 25,125 | |

| Swatch Group AG (Bearer) | 49,612 | 23,521 | |

| GAM Holding AG | 577,710 | 9,860 | |

| 519,108 | |||

| Taiwan (1.2%) | |||

| Taiwan Semiconductor | |||

| Manufacturing Co. Ltd. | 22,565,704 | 97,403 | |

| Wistron Corp. | 109,047 | 115 | |

| 97,518 | |||

| Thailand (1.4%) | |||

| Bangkok Bank PCL | 13,166,800 | 80,495 | |

| Kasikornbank PCL | |||

| (Foreign) | 4,325,600 | 31,716 | |

| 112,211 | |||

| Turkey (1.3%) | |||

| * | Turkcell Iletisim | ||

| Hizmetleri AS | 6,895,597 | 40,015 | |

| Turkiye Halk Bankasi AS | 5,980,422 | 39,943 | |

| KOC Holding AS | 4,687,628 | 23,892 | |

| 103,850 | |||

| United Kingdom (17.0%) | |||

| Royal Dutch Shell plc | |||

| Class A | 3,489,928 | 125,092 | |

| * | Royal Bank of Scotland | ||

| Group plc | 18,165,550 | 112,919 | |

| AstraZeneca plc | 1,227,908 | 89,404 | |

| Prudential plc | 3,741,533 | 86,463 | |

| BG Group plc | 4,827,873 | 80,460 | |

| Carnival plc | 1,779,082 | 70,941 | |

| British American | |||

| Tobacco plc | 1,212,581 | 68,872 | |

| Vodafone Group plc | 19,784,694 | 65,742 | |

| Market | |||

| Value | |||

| Shares | ($000) | ||

| * | Lloyds Banking | ||

| Group plc | 51,893,211 | 64,124 | |

| HSBC Holdings plc | 5,877,471 | 60,167 | |

| Barclays plc | 14,725,337 | 56,445 | |

| Serco Group plc | 10,282,143 | 49,022 | |

| BP plc ADR | 1,082,625 | 47,051 | |

| Signet Jewelers Ltd. | 385,653 | 46,407 | |

| Informa plc | 5,760,883 | 44,389 | |

| Rexam plc | 5,714,247 | 43,548 | |

| Rolls-Royce Holdings plc | 3,033,401 | 40,984 | |

| Shire plc | 601,050 | 40,013 | |

| * | RSA Insurance Group plc | 5,082,207 | 39,328 |

| Wolseley plc | 706,258 | 37,530 | |

| Ashtead Group plc | 2,216,327 | 37,114 | |

| Unilever plc | 771,289 | 31,038 | |

| Associated British | |||

| Foods plc | 698,960 | 30,845 | |

| Anglo American plc | |||

| London Shares | 1,044,803 | 22,042 | |

| ^ | Petrofac Ltd. | 1,008,993 | 17,143 |

| Ladbrokes plc | 398,959 | 755 | |

| Inchcape plc | 21,654 | 241 | |

| 1,408,079 | |||

| United States (0.9%) | |||

| Carnival Corp. | 558,500 | 22,424 | |

| *,^ | Ultra Petroleum Corp. | 1,045,105 | 23,828 |

| * | Weatherford | ||

| International plc | 1,786,000 | 29,326 | |

| 75,578 | |||

| Total Common Stocks | |||

| (Cost $7,349,255) | 7,878,168 | ||

| Temporary Cash Investments (5.6%)1 | |||

| Money Market Fund (5.4%) | |||

| 2,3 | Vanguard Market | ||

| Liquidity Fund, | |||

| 0.114% | 446,376,565 | 446,377 | |

| Face | |||

| Amount | |||

| ($000) | |||

| U.S. Government and Agency Obligations (0.2%) | |||

| 4 | Federal Home Loan Bank | ||

| Discount Notes, | |||

| 0.073%, 11/26/14 | 1,000 | 1,000 | |

| 4,5 | Federal Home Loan Bank | ||

| Discount Notes, | |||

| 0.074%, 12/3/14 | 2,000 | 2,000 | |

| 4,6 | Federal Home Loan Bank | ||

| Discount Notes, | |||

| 0.074%, 12/5/14 | 200 | 200 | |

| 4,5,6 Federal Home Loan Bank | |||

| Discount Notes, | |||

| 0.033%, 12/19/14 | 8,800 | 8,799 | |

20

International Value Fund

| Face | Market | ||

| Amount | Value | ||

| ($000) | ($000) | ||

| 4,5,6 Federal Home Loan Bank | |||

| Discount Notes, | |||

| 0.100%, 2/4/15 | 2,000 | 1,999 | |

| 6,7 | Freddie Mac Discount | ||

| Notes, 0.070%, 12/8/14 | 1,000 | 1,000 | |

| 5,7 | Freddie Mac Discount | ||

| Notes, 0.100%, 12/29/14 | 500 | 500 | |

| 6,7 | Freddie Mac Discount | ||

| Notes, 0.075%, 2/3/15 | 1,000 | 1,000 | |

| 16,498 | |||

| Total Temporary Cash Investments | |||

| (Cost $462,875) | 462,875 | ||

| Total Investments (100.8%) | |||

| (Cost $7,812,130) | 8,341,043 | ||

| Other Assets and Liabilities (-0.8%) | |||

| Other Assets | 106,748 | ||

| Liabilities3 | (176,302) | ||

| (69,554) | |||

| Net Assets (100%) | |||

| Applicable to 224,367,590 outstanding | |||

| $.001 par value shares of beneficial | |||

| interest (unlimited authorization) | 8,271,489 | ||

| Net Asset Value Per Share | $36.87 | ||

| At October 31, 2014, net assets consisted of: | |

| Amount | |

| ($000) | |

| Paid-in Capital | 7,699,483 |

| Undistributed Net Investment Income | 184,413 |

| Accumulated Net Realized Losses | (135,169) |

| Unrealized Appreciation (Depreciation) | |

| Investment Securities | 528,913 |

| Futures Contracts | 394 |

| Forward Currency Contracts | (5,295) |

| Foreign Currencies | (1,250) |

| Net Assets | 8,271,489 |

See Note A in Notes to Financial Statements.

* Non-income-producing security.

^ Includes partial security positions on loan to broker-dealers. The total value of securities on loan is $81,581,000.

1 The fund invests a portion of its cash reserves in equity markets through the use of index futures contracts. After giving effect to futures investments, the fund’s effective common stock and temporary cash investment positions represent 97.3% and 3.5%, respectively, of net assets.

2 Affiliated money market fund available only to Vanguard funds and certain trusts and accounts managed by Vanguard. Rate shown is the 7-day yield.

3 Includes $86,848,000 of collateral received for securities on loan.

4 The issuer operates under a congressional charter; its securities are generally neither guaranteed by the U.S. Treasury nor backed by the full faith and credit of the U.S. government.

5 Securities with a value of $3,275,000 have been segregated as collateral for open forward currency contracts.

6 Securities with a value of $9,039,000 have been segregated as initial margin for open futures contracts.

7 The issuer was placed under federal conservatorship in September 2008; since that time, its daily operations have been managed by the Federal Housing Finance Agency and it receives capital from the U.S. Treasury, as needed to maintain a positive net worth, in exchange for senior preferred stock.

ADR—American Depositary Receipt.

GDR—Global Depositary Receipt.

See accompanying Notes, which are an integral part of the Financial Statements.

21

International Value Fund

Statement of Operations

| Year Ended | |

| October 31, 2014 | |

| ($000) | |

| Investment Income | |

| Income | |

| Dividends1 | 249,916 |

| Interest2 | 467 |

| Securities Lending | 4,916 |

| Total Income | 255,299 |

| Expenses | |

| Investment Advisory Fees—Note B | |

| Basic Fee | 13,889 |

| Performance Adjustment | 2,219 |

| The Vanguard Group—Note C | |

| Management and Administrative | 17,836 |

| Marketing and Distribution | 1,382 |

| Custodian Fees | 1,383 |

| Auditing Fees | 43 |

| Shareholders’ Reports | 63 |

| Trustees’ Fees and Expenses | 17 |

| Total Expenses | 36,832 |

| Net Investment Income | 218,467 |

| Realized Net Gain (Loss) | |

| Investment Securities Sold | 548,783 |

| Futures Contracts | 15,866 |

| Foreign Currencies and Forward Currency Contracts | (7,387) |

| Realized Net Gain (Loss) | 557,262 |

| Change in Unrealized Appreciation (Depreciation) | |

| Investment Securities | (664,351) |

| Futures Contracts | (7,297) |

| Foreign Currencies and Forward Currency Contracts | (7,691) |

| Change in Unrealized Appreciation (Depreciation) | (679,339) |

| Net Increase (Decrease) in Net Assets Resulting from Operations | 96,390 |

| 1 Dividends are net of foreign withholding taxes of $9,968,000. 2 Interest income from an affiliated company of the fund was $456,000. | |

See accompanying Notes, which are an integral part of the Financial Statements.

22

International Value Fund

Statement of Changes in Net Assets

| Year Ended October 31, | ||

| 2014 | 2013 | |

| ($000) | ($000) | |

| Increase (Decrease) in Net Assets | ||

| Operations | ||

| Net Investment Income | 218,467 | 161,014 |

| Realized Net Gain (Loss) | 557,262 | 735,899 |

| Change in Unrealized Appreciation (Depreciation) | (679,339) | 879,769 |

| Net Increase (Decrease) in Net Assets Resulting from Operations | 96,390 | 1,776,682 |

| Distributions | ||

| Net Investment Income | (151,178) | (174,874) |

| Realized Capital Gain | — | — |

| Total Distributions | (151,178) | (174,874) |

| Capital Share Transactions | ||

| Issued | 957,145 | 855,250 |

| Issued in Lieu of Cash Distributions | 144,177 | 166,322 |

| Redeemed | (802,689) | (1,060,870) |

| Net Increase (Decrease) from Capital Share Transactions | 298,633 | (39,298) |

| Total Increase (Decrease) | 243,845 | 1,562,510 |

| Net Assets | ||

| Beginning of Period | 8,027,644 | 6,465,134 |

| End of Period1 | 8,271,489 | 8,027,644 |

| 1 Net Assets—End of Period includes undistributed (overdistributed) net investment income of $184,413,000 and $119,548,000. | ||

See accompanying Notes, which are an integral part of the Financial Statements.

23

International Value Fund

Financial Highlights

| For a Share Outstanding | Year Ended October 31, | ||||

| Throughout Each Period | 2014 | 2013 | 2012 | 2011 | 2010 |

| Net Asset Value, Beginning of Period | $37.12 | $29.78 | $28.98 | $31.92 | $29.95 |

| Investment Operations | |||||

| Net Investment Income | . 9771 | .757 | .804 | .843 | .698 |

| Net Realized and Unrealized Gain (Loss) | |||||

| on Investments | (.530) | 7.402 | . 838 | (3.103) | 2.007 |

| Total from Investment Operations | .447 | 8.159 | 1.642 | (2.260) | 2.705 |

| Distributions | |||||

| Dividends from Net Investment Income | (.697) | (.819) | (.842) | (.680) | (.735) |

| Distributions from Realized Capital Gains | — | — | — | — | — |

| Total Distributions | (.697) | (.819) | (.842) | (.680) | (.735) |

| Net Asset Value, End of Period | $36.87 | $37.12 | $29.78 | $28.98 | $31.92 |

| Total Return2 | 1.20% | 27.94% | 6.00% | -7.27% | 9.12% |

| Ratios/Supplemental Data | |||||

| Net Assets, End of Period (Millions) | $8,271 | $8,028 | $6,465 | $6,553 | $7,532 |

| Ratio of Total Expenses to Average Net Assets3 | 0.44% | 0.43% | 0.40% | 0.39% | 0.39% |

| Ratio of Net Investment Income to | |||||

| Average Net Assets | 2.64%1 | 2.24% | 2.77% | 2.59% | 2.41% |

| Portfolio Turnover Rate | 37% | 52% | 53% | 39% | 51% |

| 1 Net investment income per share and the ratio of net investment income to average net assets include $.175 and 0.47%, respectively, resulting from income received from Vodafone Group plc in the form of cash and shares in Verizon Communications Inc. in February 2014. 2 Total returns do not include transaction or account service fees that may have applied in the periods shown. Fund prospectuses provide information about any applicable transaction and account service fees. 3 Includes performance-based investment advisory fee increases (decreases) of 0.03%, 0.01%, (0.03%), (0.05%), and (0.04%). | |||||

See accompanying Notes, which are an integral part of the Financial Statements.

24

International Value Fund

Notes to Financial Statements

Vanguard International Value Fund is registered under the Investment Company Act of 1940 as an open-end investment company, or mutual fund. The fund invests in securities of foreign issuers, which may subject it to investment risks not normally associated with investing in securities of United States corporations.

A. The following significant accounting policies conform to generally accepted accounting principles for U.S. investment companies. The fund consistently follows such policies in preparing its financial statements.

1. Security Valuation: Securities are valued as of the close of trading on the New York Stock Exchange (generally 4 p.m., Eastern time) on the valuation date. Equity securities are valued at the latest quoted sales prices or official closing prices taken from the primary market in which each security trades; such securities not traded on the valuation date are valued at the mean of the latest quoted bid and asked prices. Securities for which market quotations are not readily available, or whose values have been affected by events occurring before the fund’s pricing time but after the close of the securities’ primary markets, are valued at their fair values calculated according to procedures adopted by the board of trustees. These procedures include obtaining quotations from an independent pricing service, monitoring news to identify significant market- or security-specific events, and evaluating changes in the values of foreign market proxies (for example, ADRs, futures contracts, or exchange-traded funds), between the time the foreign markets close and the fund’s pricing time. When fair-value pricing is employed, the prices of securities used by a fund to calculate its net asset value may differ from quoted or published prices for the same securities. Investments in Vanguard Market Liquidity Fund are valued at that fund’s net asset value. Temporary cash investments acquired over 60 days to maturity are valued using the latest bid prices or using valuations based on a matrix system (which considers such factors as security prices, yields, maturities, and ratings), both as furnished by independent pricing services. Other temporary cash investments are valued at amortized cost, which approximates market value.

2. Foreign Currency: Securities and other assets and liabilities denominated in foreign currencies are translated into U.S. dollars using exchange rates obtained from an independent third party as of the fund’s pricing time on the valuation date. Realized gains (losses) and unrealized appreciation (depreciation) on investment securities include the effects of changes in exchange rates since the securities were purchased, combined with the effects of changes in security prices. Fluctuations in the value of other assets and liabilities resulting from changes in exchange rates are recorded as unrealized foreign currency gains (losses) until the assets or liabilities are settled in cash, at which time they are recorded as realized foreign currency gains (losses).

3. Futures and Forward Currency Contracts: The fund uses index futures contracts to a limited extent, with the objective of maintaining full exposure to the stock market while maintaining liquidity. The fund may purchase or sell futures contracts to achieve a desired level of investment, whether to accommodate portfolio turnover or cash flows from capital share transactions. The primary risks associated with the use of futures contracts are imperfect correlation between changes in market values of stocks held by the fund and the prices of futures contracts, and the possibility of an illiquid market. Counterparty risk involving futures is mitigated because a regulated clearinghouse is the counterparty instead of the clearing broker. To further mitigate counterparty risk, the fund trades futures contracts on an exchange, monitors the financial strength of its clearing brokers and clearinghouse, and has entered into clearing agreements with its clearing brokers. The clearinghouse imposes initial margin requirements to secure the fund’s performance and requires daily settlement of variation margin representing changes in the market value of each contract.

25

International Value Fund

The fund enters into forward currency contracts to provide the appropriate currency exposure related to any open futures contracts or to protect the value of securities and related receivables and payables against changes in foreign exchange rates. The fund’s risks in using these contracts include movement in the values of the foreign currencies relative to the U.S. dollar and the ability of the counterparties to fulfill their obligations under the contracts. The fund mitigates its counterparty risk by entering into forward currency contracts only with a diverse group of prequalified counterparties, monitoring their financial strength, entering into master netting arrangements with its counterparties, and requiring its counterparties to transfer collateral as security for their performance. The master netting arrangements provide that, in the event of a counterparty’s default (including bankruptcy), the fund may terminate the forward currency contracts, determine the net amount owed by either party in accordance with its master netting arrangements, and sell or retain any collateral held up to the net amount owed to the fund under the master netting arrangements. The forward currency contracts contain provisions whereby a counterparty may terminate open contracts if the fund’s net assets decline below a certain level, triggering a payment by the fund if the fund is in a net liability position at the time of the termination. The payment amount would be reduced by any collateral the fund has pledged. Any assets pledged as collateral for open contracts are noted in the Statement of Net Assets. The value of collateral received or pledged is compared daily to the value of the forward currency contracts exposure with each counterparty, and any difference, if in excess of a specified minimum transfer amount, is adjusted and settled within two business days.

Futures contracts are valued at their quoted daily settlement prices. Forward currency contracts are valued at their quoted daily prices obtained from an independent third party, adjusted for currency risk based on the expiration date of each contract. The aggregate settlement values and notional amounts of the contracts are not recorded in the Statement of Net Assets. Fluctuations in the value of the contracts are recorded in the Statement of Net Assets as an asset (liability) and in the Statement of Operations as unrealized appreciation (depreciation) until the contracts are closed, when they are recorded as realized gains (losses) on futures or forward currency contracts.

During the year ended October 31, 2014, the fund’s average investments in long and short futures contracts represented 2% and 0% of net assets, respectively, based on the average of aggregate settlement values at each quarter-end during the period. The fund’s average investment in forward currency contracts represented 2% of net assets, based on the average of notional amounts at each quarter-end during the period.

4. Federal Income Taxes: The fund intends to continue to qualify as a regulated investment company and distribute all of its taxable income. Management has analyzed the fund’s tax positions taken for all open federal income tax years (October 31, 2011–2014), and has concluded that no provision for federal income tax is required in the fund’s financial statements.

5. Distributions: Distributions to shareholders are recorded on the ex-dividend date.

6. Securities Lending: To earn additional income, the fund lends its securities to qualified institutional borrowers. Security loans are required to be secured at all times by collateral in an amount at least equal to the market value of securities loaned. Daily market fluctuations could cause the value of loaned securities to be more or less than the value of the collateral received. When this occurs, the collateral is adjusted and settled on the next business day. The fund further mitigates its counterparty risk by entering into securities lending transactions only with a diverse group of prequalified counterparties, monitoring their financial strength, and entering into master securities lending

26

International Value Fund

agreements with its counterparties. The master securities lending agreements provide that, in the event of a counterparty’s default (including bankruptcy), the fund may terminate any loans with that borrower, determine the net amount owed, and sell or retain the collateral up to the net amount owed to the fund; however, such actions may be subject to legal proceedings. While collateral mitigates counterparty risk, in the absence of a default the fund may experience delays and costs in recovering the securities loaned. The fund invests cash collateral received in Vanguard Market Liquidity Fund, and records a liability in the Statement of Net Assets for the return of the collateral, during the period the securities are on loan. Securities lending income represents fees charged to borrowers plus income earned on invested cash collateral, less expenses associated with the loan.

7. Credit Facility: The fund and certain other funds managed by The Vanguard Group participate in a $2.89 billion committed credit facility provided by a syndicate of lenders pursuant to a credit agreement that may be renewed annually; each fund is individually liable for its borrowings, if any, under the credit facility. Borrowings may be utilized for temporary and emergency purposes, and are subject to the fund’s regulatory and contractual borrowing restrictions. The participating funds are charged administrative fees and an annual commitment fee of 0.06% of the undrawn amount of the facility; these fees are allocated to the funds based on a method approved by the fund’s board of trustees and included in Management and Administrative expenses on the fund’s Statement of Operations. Any borrowings under this facility bear interest at a rate equal to the higher of the federal funds rate or LIBOR reference rate plus an agreed-upon spread.

The fund had no borrowings outstanding at October 31, 2014, or at any time during the period then ended.

8. Other: Dividend income is recorded on the ex-dividend date. Interest income includes income distributions received from Vanguard Market Liquidity Fund and is accrued daily. Premiums and discounts on debt securities purchased are amortized and accreted, respectively, to interest income over the lives of the respective securities. Security transactions are accounted for on the date securities are bought or sold. Costs used to determine realized gains (losses) on the sale of investment securities are those of the specific securities sold.

B. Lazard Asset Management LLC, Edinburgh Partners Limited, and ARGA Investment Management, LP, each provide investment advisory services to a portion of the fund for a fee calculated at an annual percentage rate of average net assets managed by the advisor. The basic fee of Lazard Asset Management LLC is subject to quarterly adjustments based on performance for the preceding five years relative to the MSCI All Country World Index ex USA. The basic fee of Edinburgh Partners Limited is subject to quarterly adjustments based on performance for the preceding three years relative to the MSCI All Country World Index ex USA. The basic fee of ARGA Investment Management, LP, is subject to quarterly adjustments based on performance since October 31, 2012, relative to the MSCI All Country World Index ex USA.

The Vanguard Group manages the cash reserves of the fund on an at-cost basis.

For the year ended October 31, 2014, the aggregate investment advisory fee represented an effective annual basic rate of 0.17% of the fund’s average net assets, before an increase of $2,219,000 (0.03%) based on performance.

27

International Value Fund

C. The Vanguard Group furnishes at cost corporate management, administrative, marketing, and distribution services. The costs of such services are allocated to the fund based on methods approved by the board of trustees. The fund has committed to invest up to 0.40% of its net assets in Vanguard. At October 31, 2014, the fund had contributed capital of $825,000 to Vanguard (included in Other Assets), representing 0.01% of the fund’s net assets and 0.33% of Vanguard’s capitalization. The fund’s trustees and officers are also directors and officers of Vanguard.

D. Various inputs may be used to determine the value of the fund’s investments. These inputs are summarized in three broad levels for financial statement purposes. The inputs or methodologies used to value securities are not necessarily an indication of the risk associated with investing in those securities.

Level 1—Quoted prices in active markets for identical securities.

Level 2—Other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.).

Level 3—Significant unobservable inputs (including the fund’s own assumptions used to determine the fair value of investments).

The following table summarizes the market value of the fund’s investments as of October 31, 2014, based on the inputs used to value them:

| Level 1 | Level 2 | Level 3 | |

| Investments | ($000) | ($000) | ($000) |

| Common Stocks | 414,192 | 7,463,976 | — |

| Temporary Cash Investments | 446,377 | 16,498 | — |

| Futures Contracts—Assets1 | 3,896 | — | — |

| Forward Currency Contracts—Assets | — | 345 | — |

| Forward Currency Contracts—Liabilities | — | (5,640) | — |

| Total | 864,465 | 7,475,179 | — |

| 1 Represents variation margin on the last day of the reporting period. | |||

Securities in certain countries may transfer between Level 1 and Level 2 because of differences in stock market closure times that may result from transitions between standard and daylight saving time in those countries and the United States. Based on values on the date of transfer, securities valued at $159,042,000 based on Level 1 inputs were transferred from Level 2 during the fiscal year. Additionally, based on values on the date of transfer, securities valued at $189,263,000 based on Level 2 inputs were transferred from Level 1 during the fiscal year.

28

International Value Fund

E. At October 31, 2014, the fair values of derivatives were reflected in the Statement of Net Assets as follows:

| Foreign | |||

| Equity | Exchange | ||

| Contracts | Contracts | Total | |

| Statement of Net Assets Caption | ($000) | ($000) | ($000) |

| Other Assets | 3,896 | 345 | 4,241 |

| Liabilities | — | (5,640) | (5,640) |

Realized net gain (loss) and the change in unrealized appreciation (depreciation) on derivatives for the year ended October 31, 2014, were:

| Foreign | |||

| Equity | Exchange | ||

| Contracts | Contracts | Total | |

| Realized Net Gain (Loss) on Derivatives | ($000) | ($000) | ($000) |

| Futures Contracts | 15,866 | — | 15,866 |

| Forward Currency Contracts | — | (4,963) | (4,963) |

| Realized Net Gain (Loss) on Derivatives | 15,866 | (4,963) | 10,903 |

| Change in Unrealized Appreciation (Depreciation) on Derivatives | |||

| Futures Contracts | (7,297) | — | (7,297) |

| Forward Currency Contracts | — | (6,445) | (6,445) |

| Change in Unrealized Appreciation (Depreciation) on Derivatives | (7,297) | (6,445) | (13,742) |

At October 31, 2014, the aggregate settlement value of open futures contracts and the related unrealized appreciation (depreciation) were:

| ($000) | ||||

| Aggregate | ||||

| Number of | Settlement | Unrealized | ||

| Long (Short) | Value | Appreciation | ||

| Futures Contracts | Expiration | Contracts | Long (Short) | (Depreciation) |

| FTSE 100 Index | December 2014 | 514 | 53,497 | (1,141) |

| Dow Jones EURO STOXX 50 Index | December 2014 | 1,367 | 53,112 | (965) |

| Topix Index | December 2014 | 345 | 41,146 | 1,896 |

| S&P ASX 200 Index | December 2014 | 188 | 22,796 | 604 |

| 394 |

Unrealized appreciation (depreciation) on open FTSE 100 Index and Dow Jones EURO STOXX

50 Index futures contracts is required to be treated as realized gain (loss) for tax purposes.

29

International Value Fund

At October 31, 2014, the fund had open forward currency contracts to receive and deliver currencies as follows. Unrealized appreciation (depreciation) on open forward currency contracts is treated as realized gain (loss) for tax purposes.

| Unrealized | ||||||

| Contract | Appreciation | |||||

| Settlement | Contract Amount (000) | (Depreciation) | ||||

| Counterparty | Date | Receive | Deliver | ($000) | ||

| BNP Paribas | 12/24/14 | EUR | 45,978 | USD | 59,649 | (2,011) |

| UBS AG | 12/24/14 | GBP | 24,557 | USD | 40,029 | (761) |

| BNP Paribas | 12/16/14 | JPY | 3,637,637 | USD | 34,088 | (1,686) |

| Bank of America NA | 12/23/14 | AUD | 26,384 | USD | 23,673 | (543) |

| Goldman Sachs International | 12/24/14 | EUR | 8,584 | USD | 10,958 | (196) |

| Deutsche Bank AG | 12/24/14 | GBP | 6,302 | USD | 10,085 | (8) |

| Deutsche Bank AG | 12/16/14 | JPY | 814,640 | USD | 7,691 | (435) |

| BNP Paribas | 12/24/14 | GBP | 4,009 | USD | 6,396 | 14 |

| BNP Paribas | 12/24/14 | EUR | 4,456 | USD | 5,579 | 7 |

| Goldman Sachs International | 12/23/14 | AUD | 4,345 | USD | 3,747 | 63 |

| Deutsche Bank AG | 12/23/14 | AUD | 3,870 | USD | 3,365 | 28 |

| Morgan Stanley Capital Services LLC | 12/24/14 | USD | 19,032 | EUR | 15,006 | 220 |

| UBS AG | 12/23/14 | USD | 8,172 | AUD | 9,306 | 13 |

| (5,295) | ||||||

| AUD—Australian dollar. | ||||||

| EUR—Euro. | ||||||

| GBP—British pound. | ||||||

| JPY—Japanese yen. | ||||||

| USD—U.S. dollar. | ||||||

F. Distributions are determined on a tax basis and may differ from net investment income and realized capital gains for financial reporting purposes. Differences may be permanent or temporary. Permanent differences are reclassified among capital accounts in the financial statements to reflect their tax character. Temporary differences arise when certain items of income, expense, gain, or loss are recognized in different periods for financial statement and tax purposes. These differences will reverse at some time in the future. Differences in classification may also result from the treatment of short-term gains as ordinary income for tax purposes.

During the year ended October 31, 2014, the fund realized net foreign currency losses of $2,424,000, which decreased distributable net income for tax purposes; accordingly, such losses have been reclassified from accumulated net realized losses to undistributed net investment income.

For tax purposes, at October 31, 2014, the fund had $205,751,000 of ordinary income available for distribution. The fund used capital loss carryforwards of $547,619,000 to offset taxable capital gains realized during the year ended October 31, 2014. At October 31, 2014, the fund had available capital losses totaling $140,621,000 to offset future net capital gains through October 31, 2017.

30

International Value Fund

At October 31, 2014, the cost of investment securities for tax purposes was $7,818,739,000. Net unrealized appreciation of investment securities for tax purposes was $522,304,000, consisting of unrealized gains of $1,078,413,000 on securities that had risen in value since their purchase and $556,109,000 in unrealized losses on securities that had fallen in value since their purchase.

G. During the year ended October 31, 2014, the fund purchased $3,254,188,000 of investment securities and sold $2,929,173,000 of investment securities, other than temporary cash investments.

H. Capital shares issued and redeemed were:

| Year Ended October 31, | ||

| 2014 | 2013 | |

| Shares | Shares | |

| (000) | (000) | |

| Issued | 25,713 | 26,152 |

| Issued in Lieu of Cash Distributions | 3,902 | 5,360 |

| Redeemed | (21,491) | (32,360) |

| Net Increase (Decrease) in Shares Outstanding | 8,124 | (848) |

I. Management has determined that no material events or transactions occurred subsequent to October 31, 2014, that would require recognition or disclosure in these financial statements.

31

Report of Independent Registered

Public Accounting Firm

To the Board of Trustees of Vanguard Trustees’ Equity Fund and the Shareholders of Vanguard International Value Fund:

In our opinion, the accompanying statement of net assets and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of Vanguard International Value Fund (constituting a separate portfolio of Vanguard Trustees’ Equity Fund, hereafter referred to as the “Fund”) at October 31, 2014, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities at October 31, 2014 by correspondence with the custodian and brokers, by agreement to the underlying ownership records of the transfer agent and the application of alternative auditing procedures where securities purchased had not been received, provide a reasonable basis for our opinion.

/s/PricewaterhouseCoopers LLP

Philadelphia, Pennsylvania

December 11, 2014

| Special 2014 tax information (unaudited) for Vanguard International Value Fund |

| This information for the fiscal year ended October 31, 2014, is included pursuant to provisions of the Internal Revenue Code. |

| The fund distributed $117,586,000 of qualified dividend income to shareholders during the fiscal year. |

| The fund designates to shareholders foreign source income of $204,996,000 and foreign taxes paid of $9,266,000. Shareholders will receive more detailed information with their Form 1099-DIV in January 2015 to determine the calendar-year amounts to be included on their 2014 tax returns. |

32

Your Fund’s After-Tax Returns

This table presents returns for your fund both before and after taxes. The after-tax returns are shown in two ways: (1) assuming that an investor owned the fund during the entire period and paid taxes on the fund’s distributions, and (2) assuming that an investor paid taxes on the fund’s distributions and sold all shares at the end of each period.

Calculations are based on the highest individual federal income tax and capital gains tax rates in effect at the times of the distributions and the hypothetical sales. State and local taxes were not considered. After-tax returns reflect any qualified dividend income, using actual prior-year figures and estimates for 2014. (In the example, returns after the sale of fund shares may be higher than those assuming no sale. This occurs when the sale would have produced a capital loss. The calculation assumes that the investor received a tax deduction for the loss.)

Please note that your actual after-tax returns will depend on your tax situation and may differ from those shown. Also note that if you own the fund in a tax-deferred account, such as an individual retirement account or a 401(k) plan, this information does not apply to you. Such accounts are not subject to current taxes.

Finally, keep in mind that a fund’s performance—whether before or after taxes—does not guarantee future results.

| Average Annual Total Returns: International Value Fund | |||