UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-02968-99

Name of Registrant: Vanguard Trustees’ Equity Fund

Address of Registrant:

P.O. Box 2600

Valley Forge, PA 19482

Name and address of agent for service:

Heidi Stam, Esquire

P.O. Box 876

Valley Forge, PA 19482

Registrant’s telephone number, including area code: (610) 669-1000

Date of fiscal year end: October 31

Date of reporting period: November 1, 2014 – October 31, 2015

Item 1: Reports to Shareholders

Annual Report | October 31, 2015

Vanguard International Value Fund

Vanguard’s Principles for Investing Success

We want to give you the best chance of investment success. These principles, grounded in Vanguard’s research and experience, can put you on the right path.

Goals. Create clear, appropriate investment goals.

Balance. Develop a suitable asset allocation using broadly diversified funds. Cost. Minimize cost.

Discipline. Maintain perspective and long-term discipline.

A single theme unites these principles: Focus on the things you can control.

We believe there is no wiser course for any investor.

| Contents | |

| Your Fund’s Total Returns. | 1 |

| Chairman’s Letter. | 2 |

| Advisors’ Report. | 8 |

| Fund Profile. | 14 |

| Performance Summary. | 16 |

| Financial Statements. | 18 |

| Your Fund’s After-Tax Returns. | 33 |

| About Your Fund’s Expenses. | 34 |

| Glossary. | 36 |

Please note: The opinions expressed in this report are just that—informed opinions. They should not be considered promises or advice. Also, please keep in mind that the information and opinions cover the period through the date on the front of this report. Of course, the risks of investing in your fund are spelled out in the prospectus.

See the Glossary for definitions of investment terms used in this report.

About the cover: Pictured is a sailing block on the Brilliant, a 1932 schooner docked in Mystic, Connecticut. A type of pulley, the sailing block helps coordinate the setting of the sails. At Vanguard, the intricate coordination of technology and people allows us to help millions of clients around the world reach their financial goals.

| Your Fund’s Total Returns | ||||

| Fiscal Year Ended October 31, 2015 | ||||

| Total | ||||

| Returns | ||||

| Vanguard International Value Fund | -7.43% | |||

| MSCI All Country World Index ex USA | -4.68 | |||

| International Funds Average | -1.46 | |||

| International Funds Average: Derived from data provided by Lipper, a Thomson Reuters Company. | ||||

| Your Fund’s Performance at a Glance | ||||

| October 31, 2014, Through October 31, 2015 | ||||

| Distributions Per Share | ||||

| Starting | Ending | |||

| Share | Share | Income | Capital | |

| Price | Price | Dividends | Gains | |

| Vanguard International Value Fund | $36.87 | $33.22 | $0.946 | $0.000 |

1

Chairman’s Letter

Dear Shareholder,

International stock markets posted a modest gain in the first half of the fiscal year ended October 31, 2015, but it was more than offset by a second-half slide. Persistent worries about global growth, including deflation signals in Europe and a slowdown in China and other emerging markets, contributed to the decline. For U.S. dollar-based investors, the already weak returns of many international markets were further eroded by the dollar’s strength against many foreign currencies.

Vanguard International Value Fund returned –7.43% for the 12 months. The fund’s result was lower than that of its benchmark, the MSCI All Country World Index ex USA, and the average return of its peers. Relative to its index, the fund’s shortfall reflected a combination of underperforming investment selections and fairvalue pricing adjustments. These adjustments, which are required by the Securities and Exchange Commission, address pricing discrepancies that may arise because of timezone differences among global stock markets.

If you hold the International Value Fund in a taxable account, you may wish to review the discussion of aftertax returns later in this report.

U.S. stock market fluctuated on its way to modest returns

The broad U.S. stock market returned more than 4% for the fiscal year ended October 31. Stocks generally climbed during the first nine months before

2

dropping sharply in August and September. Fears surfaced in late summer that slower economic growth in China would spread across the globe.

In October, however, stocks rallied as the Federal Reserve maintained its historically low shortterm interest rates. Central banks in Europe and Asia also signaled or implemented additional stimulus measures to counter sluggish growth and low inflation. Corporate earnings, although generally lower than in the past couple of years, mostly exceeded expectations.

The strength of the U.S. dollar against foreign currencies contributed to a return of about –4% for international stocks. Returns for the developed markets of the Pacific region and Europe were essentially flat. Stocks tumbled in emerging markets, where concerns about China seemed to weigh most heavily.

The search for a safe haven gave bonds a bit of a boost

The broad U.S. taxable bond market, which returned 1.96% over the fiscal year, benefited from investors’ desire for safehaven assets during periods of stock market volatility. The yield of the 10year Treasury note ended October at 2.17%, down from 2.31% a year earlier. (Bond prices and yields move in opposite directions.)

International bond markets (as measured by the Barclays Global Aggregate Index ex USD) returned –6.74%, held back by

| Market Barometer | |||

| Average Annual Total Returns | |||

| Periods Ended October 31, 2015 | |||

| One | Three | Five | |

| Year | Years | Years | |

| Stocks | |||

| Russell 1000 Index (Large-caps) | 4.86% | 16.28% | 14.32% |

| Russell 2000 Index (Small-caps) | 0.34 | 13.90 | 12.06 |

| Russell 3000 Index (Broad U.S. market) | 4.49 | 16.09 | 14.14 |

| FTSE All-World ex US Index (International) | -3.83 | 5.20 | 2.99 |

| Bonds | |||

| Barclays U.S. Aggregate Bond Index (Broad taxable market) | 1.96% | 1.65% | 3.03% |

| Barclays Municipal Bond Index (Broad tax-exempt market) | 2.87 | 2.91 | 4.28 |

| Citigroup Three-Month U.S. Treasury Bill Index | 0.02 | 0.02 | 0.04 |

| CPI | |||

| Consumer Price Index | 0.17% | 0.93% | 1.69% |

3

the dollar’s strength against many foreign currencies. Without this currency effect, international bond returns were positive.

Returns for money market funds and savings accounts continued to be constrained by the Fed’s 0%–0.25% target for shortterm interest rates.

A strong U.S. dollar hurt returns; emerging markets also lagged

The dampening effect of the stronger U.S. dollar was evident in Vanguard International Value Fund’s returns. When measured in local currencies, the fund’s holdings in most developed European and Pacific markets registered gains for the fiscal year. But returns for both regions were negative for U.S. dollarbased investors after foreign currency translation effects. Of course, whenever the tide turns and foreign currencies strengthen, U.S. investor returns will benefit.

Monetary exchange rates reflect differences in interest rates and other factors across countries, and the fiscal year brought several significant developments in these areas. Notably, the European Central Bank embarked on a stimulative bondbuying program that led to negative rates on some European sovereign bonds and a weaker euro. This program, along with a generally improving economic outlook, was welcomed by many European stock markets.

However, in Europe’s largest markets—the United Kingdom, Germany, and France—the fund’s stocks lagged,

| Expense Ratios | ||

| Your Fund Compared With Its Peer Group | ||

| Peer Group | ||

| Fund | Average | |

| International Value Fund | 0.44% | 1.39% |

The fund expense ratio shown is from the prospectus dated February 25, 2015, and represents estimated costs for the current fiscal year. For the fiscal year ended October 31, 2015, the fund’s expense ratio was 0.46%. The peer-group expense ratio is derived from data provided by Lipper, a Thomson Reuters Company, and captures information through year-end 2014.

Peer group: International Funds.

4

contributing to its underperformance. (The fund’s sliver of holdings in beleaguered Greece, which dominated headlines for many months, had only a small negative impact.)

The more upbeat tone in Europe was counterbalanced by the less sanguine outlook for growth in China. This had a domino effect on emerging markets whose economies depend on exporting commodities to China and elsewhere. As a group, emerging markets declined in double digits in both local currencies and dollars. The fund’s holdings included some small pockets of strength, but losses in China and Brazil weighed on relative performance.

The advisors’ selections in developed Pacific nations managed to break even in U.S. dollar terms. Their decision to overweight Japan, the fund’s largest market in this category on average, was beneficial, even though the fund’s Japanese holdings lagged those in the benchmark.

The benchmark’s Australian listings lost more than 20% for U.S. investors, but the advisors significantly underweighted Australia, providing a net positive against the index. The same was true in Canada, which, like Australia, has suffered from the fall in commodity prices.

| Total Returns | |

| Ten Years Ended October 31, 2015 | |

| Average | |

| Annual Return | |

| International Value Fund | 4.17% |

| Spliced International Index | 2.91 |

| International Funds Average | 3.77 |

For a benchmark description, see the Glossary.

International Funds Average: Derived from data provided by Lipper, a Thomson Reuters Company.

The figures shown represent past performance, which is not a guarantee of future results. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at vanguard.com/performance.) Note, too, that both investment returns and principal value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost.

5

Among industry sectors, energy was among the worst performers in both your fund and its index amid the steep drop in oil prices. Materials and industrials also had significant losses, and two larger sectors, financials and information technology, finished in the red as well.

In terms of relative performance, the fund benefited from an underweight allocation to materials but suffered from poor stock picks in the industrial and consumer discretionary sectors.

For more information on the fund’s investment strategies and positioning, please see the Advisors’ Report that follows this letter.

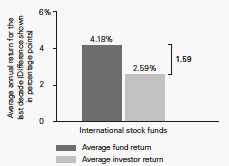

Staying the course can help you stay closer to your fund’s return

When stock markets are highly volatile, as in recent months, it’s tempting to run for cover. But the price of panic can be high.

A rough measure of what can be lost from attempts to time the market is the difference between the returns produced by a fund and the returns earned by the fund’s investors.

The results shown in the Performance Summary later in this report are your fund’s time-weighted returns—the average annual returns investors would have earned if they had invested a lump sum in the fund at the start of the period and reinvested any distributions they received. Their actual returns, however, depend on whether they subsequently bought or sold any shares. There’s often a gap between this dollar-weighted return for investors and the fund’s timeweighted return, as shown in the figure to the right.

Many sensible investment behaviors can contribute to the difference in returns, but industry cash flow data suggest that one important factor is the generally counter

productive effort to buy and sell at the “right” time. Keeping your emotions in check can help narrow the gap.

Fund returns vs. investor returns

Notes: Data are for the decade ended September 30, 2015. The average fund return and average investor return are from Morningstar, based on U.S.-domiciled international equity funds that have reported ten-year returns. The average fund return is the average of the international stock funds’ time-weighted returns. The average investor return assumes that the growth of a fund’s total net assets for a given period is driven by market returns and investor cash ‚ow. To calculate investor return, a fund’s change in assets for the period is discounted by the return of the fund to isolate how much of the asset growth was driven by cash ‚ow. A model similar to an internal rate-of-return calculation is then used to calculate a constant growth rate that links the beginning total net assets and periodic cash ‚ows to the ending total net assets.

Sources: Vanguard and Morningstar, Inc.

6

Over ten years, the fund continues to outperform its index and peers

For the decade ended October 31, 2015, the International Value Fund recorded an average annual return of 4.17%. This result was more than a percentage point better than the average return of the benchmark index and fourtenths of a percentage point ahead of peer funds.

In fact, International Value’s annual return has exceeded that of its benchmark in all but two of the last ten fiscal years, thanks to the skill and experience of its advisors. The tenyear average annual return is low by historical standards.

But it’s worth remembering that the U.S. Dollar Index has risen more than 8% during the decade, which has dampened results for U.S. investors. Because currency fluctuations are unpredictable, this negative effect could reverse at any time and provide a performance boost. We remain convinced that investing in both U.S. and international stocks is a smart strategy to manage risk and gain exposure to global opportunities.

A dose of discipline is crucial when markets become volatile

The developments over the past few months remind us that nobody can control the markets or reliably predict where they’ll go in the short term. However, investors can control how they react to unstable and turbulent markets.

During periods of market adversity, it’s more important than ever to keep sight of one of Vanguard’s key principles: Maintain perspective and longterm discipline. Whether you’re investing for yourself or on behalf of clients, your success is affected greatly by how you respond—or don’t respond—during turbulent markets. (You can read

Vanguard’s Principles for Investing Success at vanguard.com/research.)

As I’ve written in the past, the best course for longterm investors is generally to ignore daily market moves and not make decisions based on emotion. This is also a good time to evaluate your portfolio and make sure your asset allocation is aligned with your time horizon, goals, and risk tolerance.

The markets are unpredictable and often confounding. Keeping your longterm plans clearly in focus can help you weather these periodic storms.

As always, thank you for investing with Vanguard.

Sincerely,

F. William McNabb III

Chairman and Chief Executive Officer

November 17, 2015

7

Advisors’ Report

For the 12 months ended October 31, 2015, Vanguard International Value Fund returned –7.43%. Your fund is managed by three independent advisors, a strategy that enhances the fund’s diversification by providing exposure to distinct yet complementary investment approaches. It is not uncommon for different advisors to have different views about individual securities or the broader investment environment.

The table below presents the advisors, the percentage and amount of fund assets that each manages, and brief descriptions of their investment strategies. Each advisor has also prepared a discussion of the investment environment during the fiscal period and of how the portfolio’s positioning reflects this assessment. These reports were prepared on November 16, 2015.

Vanguard International Value Fund Investment Advisors

| Fund Assets Managed | |||

| Investment Advisor | % | $ Million | Investment Strategy |

| Lazard Asset Management LLC | 40 | 3,141 | The advisor uses a research-driven, bottom-up, |

| relative-value approach in selecting stocks. The goal is | |||

| to identify individual stocks that offer an appropriate | |||

| trade-off between low relative valuation and high | |||

| financial productivity. | |||

| Edinburgh Partners Limited | 34 | 2,727 | The advisor employs a concentrated, low-turnover, |

| value-oriented investment approach that results in a | |||

| portfolio of companies with good long-term prospects | |||

| and below-market price/earnings ratios. In-depth | |||

| fundamental research on industries and companies is | |||

| central to this investment process. | |||

| ARGA Investment Management, | 24 | 1,911 | The advisor believes that investors overreact to |

| LP | short-term developments, leading to opportunities to | ||

| generate gains from investing in “good businesses at | |||

| great prices.” Its valuation-focused process uses a | |||

| dividend discount model to select stocks that trade at a | |||

| discount to intrinsic value based on the company’s | |||

| long-term earnings power and dividend-paying | |||

| capability. | |||

| Cash Investments | 2 | 153 | These short-term reserves are invested by Vanguard in |

| equity index products to simulate investments in | |||

| stocks. Each advisor may also maintain a modest cash | |||

| position. | |||

8

Lazard Asset Management LLC

Portfolio Managers:

Michael G. Fry, Managing Director

Michael A. Bennett, CPA, Managing Director

During the period, international equities rose in local terms but declined in U.S. dollar terms because of weakness in many currencies. Emerging markets lagged developed markets; equities in Brazil and Greece were both among the worst performers globally. In Brazil, the central bank raised interest rates to combat high inflation, and a corruption probe reached almost all corners of the government.

China announced an approximate 3% devaluation of its currency, leading to an acceleration in capital outflows and fears of further currency declines. Continued weak Chinese economic data spurred growth concerns, which spilled over to some developed stock markets left vulnerable by strong multiyear performance and associated high valuations.

Japanese equities were among the best performers; the country’s economy expanded faster than expected, and corporate governance improved at a number of companies. British equities also gained after the surprise victory of the incumbent—and traditionally businessfriendly—Conservative Party. The euro zone is doing relatively well, with betterthanexpected economic data. Recent comments from European Central Bank President Draghi suggest further quantitative easing.

Sectors most exposed to oil and China, such as energy and materials, performed worst, while defensive sectors such as consumer staples and health care generally stayed positive.

Our stock selection in and low allocation to the sagging energy sector were beneficial to relative returns. Shares of U.K.based BG Group held up well after competitor Royal Dutch Shell announced a bid for the company.

High exposure to and stock selection in the health care sector also helped relative returns. Shares of Danish pharmaceutical company Novo Nordisk increased on news that the company might be able to introduce Tresiba, a longacting insulin treatment for diabetes, in the United States as early as next year. And British company Shire rebounded strongly after initially overreacting to news that competitor AbbVie would abandon a proposed merger.

In industrials, the continued European economic recovery and lower oil prices boosted both domestic and international travel, which benefited Ireland’s discount airline Ryanair and Spanish airport operator Aena. Aena had its IPO early in 2015; we sold the stock as it approached fair valuation after performing strongly.

9

In contrast, stock selection in telecommunication services detracted from relative returns. Shares of Japanese conglomerate SoftBank fell on concerns about slowing growth at its Chinese ecommerce holding Alibaba, although the stock recovered somewhat in October as Alibaba reported encouraging results. Holdings in Turkish mobile phone operator Turkcell also hurt returns, exacerbated by a weak Turkish lira and political uncertainty despite strong company fundamentals.

In consumer discretionary, shares of Brazilian private education company Estacio declined in January after the government made an unexpected negative change to its studentloan program. British education materials provider Pearson Education also lost ground after weakerthanexpected revenues. And we sold our holdings in Macau casino operator Sands China when they fell amid China’s continuing corruption crackdown, which has taken a toll on the country’s conspicuous consumption.

The portfolio suffered from stock selection in emerging markets. Companies in Brazil such as BB Seguridade and Sabesp were hurt by the drop in Brazil’s currency, the real. South African holding Nampak declined on disappointing results and the threat of increasing competition. In Greece, shares of Piraeus Bank suffered from the uncertainty of the country leaving the euro. We sold our position before capital controls closed the banking system for three weeks.

During the fiscal year, interesting stockspecific opportunities led to changes in our exposures. In financials, our underweight to the benchmark narrowed. We purchased shares in U.K. firms Aon and London Stock Exchange, Credit Suisse, Belgian bank KBC, and South African group Sanlam. And we exited our positions in French banker BNP Paribas, Piraeus Bank, and Sberbank in Russia.

In consumer discretionary, we sold our holdings in BMW and Swatch. But purchases including U.K. food services provider Compass, Pearson Education, and Sony increased our slightly belowindex sector weighting to an overweight position.

A slight overweight to information technology increased with the additions of Israel’s Check Point Software Technologies, HCL Technologies from India, and U.K. firm Worldpay. We sold our holdings in Dutch firm NXP Semiconductors when they quickly approached fair valuation, as well as our shares in Brazilian payment system company Cielo.

Our exposure to consumer staples declined as we sold our positions in Denmark’s Carlsberg and Russian retailer Lenta. In industrials, we bought shares in German technology firm GEA, France’s Vinci construction group, U.K. engineering business The Weir Group, and heating and plumbing distributor Wolseley UK. Our overweight to the sector narrowed, however, when we sold out of Airbus,

10

Italian infrastructure company Atlantia, Japanese equipment manufacturer Komatsu, and RollsRoyce.

From a regional perspective, we increased our holdings in the United Kingdom and Canada, adding to our U.K. overweight and reducing our underweight to Canada. Our exposures to Japan and emerging markets declined.

Global growth is slowing as China continues to adjust its economic model, emerging markets become less liquid, and the commodity and energy booms unwind. Broadly, consumers look better positioned in developed markets, and the United States and Japan are showing signs of labor tightness. Many technology and health care segments remain strong. Corporations are generally healthy, but profit forecasts and, in some cases, margins are under pressure in a number of areas, and credit is showing some early signs of deterioration.

Share prices today appear dependent on both some level of economic recovery and a continuation of the current very low interest rates. This is dangerous, as the combination appears unlikely to occur over the medium term.

Our team is keeping its focus on stock selection, seeking to find those with sustainably high or improving returns trading at attractive valuations. We remain confident that the portfolio’s strong track record will continue in a variety of market conditions.

Edinburgh Partners Limited

Portfolio Manager:

Sandy Nairn, Director and CEO

Market levels have not changed dramatically since last year, and the global economy is expanding at a subdued pace. Recent concerns over China notwithstanding, we expect this to continue. Equities are not cheap globally and are potentially vulnerable to setbacks related to economic growth. However, we remain able to find new investment areas for the portfolio.

The investment world is still agonizing about energy stocks and whether oil price weakness is a supply or demandside issue. We are firmly of the view that the root cause is supply, and that this is not permanent. Oil company stocks that were priced for crude oil selling at $90 to $100 or more per barrel have retreated to reflect crude prices in the mid$70s. At this level, more oil stocks are worthy of consideration. If crude prices stay below $70 and stocks respond accordingly, we would expect our portfolio exposure to rise significantly.

Thus far, we have focused on undervalued companies such as BG Group and BP, whose assets would be attractive to their peers in an environment of cost reduction. We expect to maintain this strategy, but we could add to the major oil companies if further disappointments occur.

The prolonged decline in emerging markets has begun to reveal some value. If this continues, we would anticipate adding more investments.

11

We are still finding some of the best value in Japan. Even in U.S. dollar terms, Japanese corporate earnings growth over the past three years has been more than double that of the United States. Our Japanese exposure is unlikely to rise but may well remain at elevated levels.

As aggregate valuations rose over the past three to five years, the equity world became heavily momentum driven. This has been a difficult environment for valuationdriven investors, but the past few months suggest that conditions may be beginning to unwind to their benefit.

One promising case is that of Nokia, which we recently added to the portfolio. After the sale of its handset and mapping businesses and forthcoming merger with Alcatel, Nokia will become the secondlargest global wireless equipment company. The top three players in that market will account for 80% to 90% of sales.

Against a backdrop of moderate sales growth, an industry that faced extreme price competition ten years ago could experience more price stability and a return to sensible profit margins. We believe this will transform Nokia’s longterm profit potential and eventually be reflected in the share price.

These are some of the areas of opportunity we have identified for the portfolio. Our investment disciplines occasionally may deem it appropriate to sell a stock that has reached its target before we have found a replacement. That would entail a rise in liquidity until appropriate opportunities arose.

ARGA Investment Management, LP

Portfolio Managers:

A. Rama Krishna, CFA, Founder and Chief Investment Officer

Steven Morrow, CFA, Director of Research

International equity markets rose in the first half of the fiscal year, then reversed direction to finish lower. Positive drivers earlier in the period, such as quantitative easing by the European Central Bank, later gave way to concerns about prospective U.S. rate hikes and slowing global growth.

Our portion of the portfolio focuses on the long term, seeking to maximize returns over time by investing in companies that trade at discounts to their intrinsic value. Temporary factors such as macroeconomic, regulatory, industry, or companyspecific stress often allow us to purchase strong companies at deeply discounted valuations and then profit when those valuations recover. Two current examples demonstrate this approach.

The oil price slump has created many compelling valuations and opportunities among energy companies. Industry returns on invested capital in 2015 have plunged to low singledigit levels seen only a few times in the past 100 years. Naturally, share prices also have dropped dramatically. Instead of shunning these as many others have, we took advantage of the lower valuations to increase our energy exposure.

Our analysis shows that during past periods of low returns, energy companies cut overhead, consolidated, and otherwise

12

significantly reduced costs. This drove improved return on invested capital even before oil prices eventually recovered. Our industry analysis does project higher oil prices eventually. But even if they remain at current levels for some time, signs that the industry is now focused on reducing costs support our projected upturn in returns as early as next year. We believe stock prices will follow.

To fund our expanded exposure to energy, we exited Japanese automotive, financial services, and other positions whose valuations had become less attractive as their share prices rose.

Opportunities in emerging markets also shifted during the year as fears of a U.S. rate hike, a slowdown in China, and

political issues in Brazil pressured valuations. Despite the nearterm pressures, longterm growth rates should remain higher in emerging markets than in developed markets. We took advantage of this volatility to purchase undervalued emergingmarket companies with strong franchises. As several of our Chinese and Indian holdings recovered, we sold at higher prices to purchase attractively valued companies in Korea and elsewhere.

Many longerterm opportunities dragged on recent performance. Although such holdings caused shortterm pain, we expect these businesses’ solid earnings power to deliver strong future returns and recover their valuation over time.

13

International Value Fund

Fund Profile

As of October 31, 2015

| Portfolio Characteristics | ||

| MSCI AC | ||

| World Index | ||

| Fund | ex USA | |

| Number of Stocks | 158 | 1,831 |

| Median Market Cap | $31.8B | $30.5B |

| Price/Earnings Ratio | 18.5x | 17.3x |

| Price/Book Ratio | 1.5x | 1.7x |

| Return on Equity | 13.6% | 15.2% |

| Earnings Growth | ||

| Rate | 12.8% | 11.0% |

| Dividend Yield | 2.7% | 3.0% |

| Turnover Rate | 36% | — |

| Ticker Symbol | VTRIX | — |

| Expense Ratio1 | 0.44% | — |

| Short-Term Reserves | 1.9% | — |

Sector Diversification (% of equity exposure)

| MSCI AC | ||

| World Index | ||

| Fund | ex USA | |

| Consumer Discretionary | 15.5% | 12.1% |

| Consumer Staples | 8.9 | 10.8 |

| Energy | 8.7 | 6.5 |

| Financials | 23.4 | 27.1 |

| Health Care | 10.0 | 9.3 |

| Industrials | 11.9 | 11.3 |

| Information Technology | 9.9 | 7.4 |

| Materials | 3.5 | 6.8 |

| Telecommunication Services | 6.0 | 5.2 |

| Utilities | 2.2 | 3.5 |

| Volatility Measures | |

| MSCI AC | |

| World Index | |

| ex USA | |

| R-Squared | 0.96 |

| Beta | 1.05 |

These measures show the degree and timing of the fund’s fluctuations compared with the indexes over 36 months.

Ten Largest Holdings (% of total net assets)

| Novartis AG | Pharmaceuticals | 2.6% |

| Sumitomo Mitsui | ||

| Financial Group Inc. | Diversified Banks | 1.8 |

| BP plc | Integrated Oil & Gas | 1.7 |

| Samsung Electronics Co. Technology | ||

| Ltd. | Hardware, Storage & | |

| Peripherals | 1.7 | |

| Bayer AG | Pharmaceuticals | 1.6 |

| KDDI Corp. | Wireless | |

| Telecommunication | ||

| Services | 1.6 | |

| Japan Tobacco Inc. | Tobacco | 1.6 |

| Royal Dutch Shell plc | Integrated Oil & Gas | 1.6 |

| BHP Billiton | Diversified Metals & | |

| Mining | 1.4 | |

| Unilever | Personal Products | 1.4 |

| Top Ten | 17.0% | |

The holdings listed exclude any temporary cash investments and equity index products.

Allocation by Region (% of equity exposure)

1 The expense ratio shown is from the prospectus dated February 25, 2015, and represents estimated costs for the current fiscal year. For the fiscal year ended October 31, 2015, the expense ratio was 0.46%.

14

International Value Fund

Market Diversification (% of equity exposure)

| MSCI AC | ||

| World | ||

| Index | ||

| Fund | ex USA | |

| Europe | ||

| United Kingdom | 24.4% | 14.8% |

| Germany | 8.3 | 6.7 |

| Switzerland | 6.6 | 6.9 |

| France | 4.3 | 7.4 |

| Sweden | 1.6 | 2.1 |

| Belgium | 1.6 | 1.0 |

| Netherlands | 1.4 | 2.1 |

| Finland | 1.3 | 0.6 |

| Spain | 1.3 | 2.5 |

| Other | 2.9 | 4.0 |

| Subtotal | 53.7% | 48.1% |

| Pacific | ||

| Japan | 22.3% | 16.9% |

| South Korea | 4.5 | 3.3 |

| Hong Kong | 2.3 | 2.2 |

| Singapore | 1.2 | 0.9 |

| Other | 0.7 | 4.8 |

| Subtotal | 31.0% | 28.1% |

| Emerging Markets | ||

| China | 1.5% | 4.9% |

| Brazil | 1.5 | 1.2 |

| Russia | 1.5 | 0.8 |

| Turkey | 1.5 | 0.3 |

| South Africa | 1.4 | 1.6 |

| Taiwan | 1.3 | 2.5 |

| Thailand | 1.1 | 0.5 |

| Other | 1.5 | 5.3 |

| Subtotal | 11.3% | 17.1% |

| North America | ||

| United States | 2.8% | 0.0% |

| Other | 0.2 | 6.2 |

| Subtotal | 3.0% | 6.2% |

| Middle East | ||

| Israel | 1.0% | 0.5% |

15

International Value Fund

Performance Summary

All of the returns in this report represent past performance, which is not a guarantee of future results that may be achieved by the fund. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at vanguard.com/performance.) Note, too, that both investment returns and principal value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost. The returns shown do not reflect taxes that a shareholder would pay on fund distributions or on the sale of fund shares.

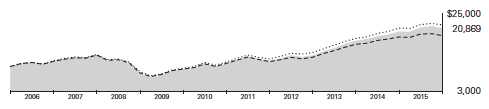

Cumulative Performance: October 31, 2005, Through October 31, 2015

Initial Investment of $10,000

See Financial Highlights for dividend and capital gains information.

16

International Value Fund

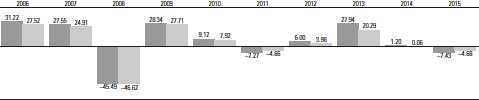

Fiscal-Year Total Returns (%): October 31, 2005, Through October 31, 2015

International Value Fund

Spliced International Index

For a benchmark description, see the Glossary.

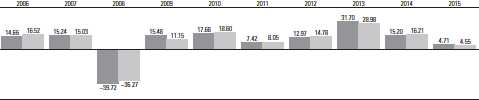

Average Annual Total Returns: Periods Ended September 30, 2015

This table presents returns through the latest calendar quarter—rather than through the end of the fiscal period.

Securities and Exchange Commission rules require that we provide this information.

| Inception | One | Five | Ten | |

| Date | Year | Years | Years | |

| International Value Fund | 5/16/1983 | -13.87% | 2.64% | 3.05% |

17

International Value Fund

Financial Statements

Statement of Net Assets

As of October 31, 2015

The fund reports a complete list of its holdings in regulatory filings four times in each fiscal year, at the quarter-ends. For the second and fourth fiscal quarters, the lists appear in the fund’s semiannual and annual reports to shareholders. For the first and third fiscal quarters, the fund files the lists with the Securities and Exchange Commission on Form N-Q. Shareholders can look up the fund’s Forms N-Q on the SEC’s website at sec.gov. Forms N-Q may also be reviewed and copied at the SEC’s Public Reference Room (see the back cover of this report for further information).

| Market | ||

| Value• | ||

| Shares | ($000) | |

| Common Stocks (96.8%)1 | ||

| Australia (0.6%) | ||

| BHP Billiton Ltd. | 2,539,890 | 41,723 |

| * South32 Ltd. | 1,913,298 | 1,970 |

| 43,693 | ||

| Belgium (1.5%) | ||

| Anheuser-Busch InBev SA | 785,457 | 93,677 |

| KBC Groep NV | 423,300 | 25,726 |

| 119,403 | ||

| Brazil (1.5%) | ||

| BB Seguridade | ||

| Participacoes SA | 5,790,000 | 39,936 |

| Ambev SA | 5,103,700 | 25,263 |

| Cia de Saneamento Basico | ||

| do Estado de Sao Paulo | 4,107,100 | 17,828 |

| * | Petroleo Brasileiro |

| SA ADR | 4,349,900 | 17,356 |

| Estacio Participacoes SA | 3,938,100 | 15,787 |

| 116,170 | ||

| Canada (0.2%) | ||

| Encana Corp. | 1,836,000 | 13,971 |

| China (1.5%) | ||

| * Baidu Inc. ADR | 297,160 | 55,708 |

| Lenovo Group Ltd. | 38,000,000 | 35,248 |

| China Shenhua | ||

| Energy Co. Ltd. | 15,797,500 | 26,688 |

| 117,644 | ||

| Denmark (0.6%) | ||

| Novo Nordisk A/S Class B | 899,603 | 47,655 |

| Finland (1.2%) | ||

| Sampo Oyj Class A | 1,003,836 | 48,974 |

| Nokia Oyj | 6,514,348 | 48,342 |

| 97,316 | ||

| France (3.9%) | ||

| BNP Paribas SA | 1,219,150 | 73,947 |

| TOTAL SA | 1,189,868 | 57,660 |

| Valeo SA | 281,586 | 43,480 |

| Market | |||

| Value• | |||

| Shares | ($000) | ||

| ^ | Vinci SA | 556,801 | 37,529 |

| Vivendi SA | 1,272,900 | 30,631 | |

| ^ | Vallourec SA | 2,668,158 | 29,593 |

| ArcelorMittal | 3,798,769 | 21,115 | |

| ^ | Engie SA | 965,914 | 16,919 |

| 310,874 | |||

| Germany (7.9%) | |||

| Bayer AG | 980,319 | 130,853 | |

| SAP SE | 868,619 | 68,671 | |

| United Internet AG | 1,299,269 | 67,497 | |

| E.ON SE | 6,285,881 | 66,335 | |

| * | Commerzbank AG | 5,521,923 | 60,790 |

| adidas AG | 617,196 | 55,326 | |

| Fresenius Medical Care | |||

| AG & Co. KGaA | 554,914 | 49,990 | |

| Siemens AG | 366,019 | 36,811 | |

| Continental AG | 114,453 | 27,517 | |

| METRO AG | 858,568 | 26,461 | |

| RWE AG | 1,672,495 | 23,276 | |

| GEA Group AG | 389,400 | 15,589 | |

| 629,116 | |||

| Greece (0.9%) | |||

| CK Hutchison | |||

| Holdings Ltd. | 5,040,692 | 68,860 | |

| Hong Kong (2.3%) | |||

| Swire Pacific Ltd. Class A | 6,451,850 | 74,524 | |

| Galaxy Entertainment | |||

| Group Ltd. | 18,827,000 | 64,064 | |

| Li & Fung Ltd. | 38,162,000 | 30,807 | |

| ^ | Esprit Holdings Ltd. | 9,909,234 | 11,101 |

| * | Global Brands Group | ||

| Holding Ltd. | 8,514,000 | 1,757 | |

| 182,253 | |||

| India (0.6%) | |||

| HCL Technologies Ltd. | 3,600,945 | 47,990 | |

| Indonesia (0.5%) | |||

| Telekomunikasi Indonesia | |||

| Persero Tbk PT ADR | 1,018,469 | 40,494 | |

18

| International Value Fund | |||

| Market | |||

| Value• | |||

| Shares | ($000) | ||

| Ireland (0.4%) | |||

| * | Ryanair Holdings plc ADR | 388,657 | 30,389 |

| Israel (0.9%) | |||

| Teva Pharmaceutical | |||

| Industries Ltd. ADR | 838,345 | 49,621 | |

| * | Check Point Software | ||

| Technologies Ltd. | 301,445 | 25,605 | |

| 75,226 | |||

| Italy (0.3%) | |||

| Mediolanum SPA | 3,034,942 | 24,683 | |

| Japan (21.5%) | |||

| Sumitomo Mitsui | |||

| Financial Group Inc. | 3,670,200 | 145,915 | |

| KDDI Corp. | 5,326,300 | 128,661 | |

| Japan Tobacco Inc. | 3,691,400 | 127,527 | |

| Sumitomo Mitsui Trust | |||

| Holdings Inc. | 26,024,000 | 99,588 | |

| East Japan Railway Co. | 941,200 | 89,344 | |

| Panasonic Corp. | 7,365,300 | 86,431 | |

| Daiwa House | |||

| Industry Co. Ltd. | 3,022,900 | 78,928 | |

| Nippon Telegraph | |||

| & Telephone Corp. | 2,141,800 | 78,654 | |

| Toyota Motor Corp. | 1,254,900 | 76,838 | |

| Nomura Holdings Inc. | 12,169,400 | 76,242 | |

| Omron Corp. | 2,189,200 | 72,211 | |

| Daihatsu Motor Co. Ltd. | 5,405,600 | 65,934 | |

| Mitsubishi Corp. | 3,537,200 | 64,078 | |

| Sumitomo Electric | |||

| Industries Ltd. | 4,439,000 | 60,390 | |

| SoftBank Group Corp. | 1,035,400 | 57,631 | |

| JGC Corp. | 3,533,000 | 55,796 | |

| Honda Motor Co. Ltd. | 1,657,800 | 55,039 | |

| Makita Corp. | 864,500 | 47,146 | |

| Seven & i Holdings | |||

| Co. Ltd. | 974,883 | 44,053 | |

| * | Toshiba Corp. | 13,536,000 | 38,071 |

| Sony Corp. | 1,265,800 | 35,899 | |

| Daikin Industries Ltd. | 538,900 | 34,502 | |

| Ryohin Keikaku Co. Ltd. | 144,200 | 28,900 | |

| ^ | DeNA Co. Ltd. | 1,521,100 | 24,387 |

| Yamato Kogyo Co. Ltd. | 873,400 | 23,217 | |

| Takashimaya Co. Ltd. | 1,057,000 | 9,416 | |

| 1,704,798 | |||

| Netherlands (1.3%) | |||

| ^ | Unilever NV | 1,239,351 | 55,863 |

| Wolters Kluwer NV | 1,245,958 | 42,084 | |

| Akzo Nobel NV | 128,418 | 9,074 | |

| 107,021 | |||

| Norway (0.6%) | |||

| ^ | Telenor ASA | 1,740,400 | 32,758 |

| ^ | TGS Nopec | ||

| Geophysical Co. ASA | 814,121 | 16,131 | |

| 48,889 | |||

| Market | |||

| Value• | |||

| Shares | ($000) | ||

| Other (0.4%) | |||

| 2 | Vanguard FTSE All-World | ||

| ex-US ETF | 718,406 | 32,673 | |

| Philippines (0.4%) | |||

| Alliance Global Group Inc. | 74,306,500 | 28,855 | |

| Russia (1.5%) | |||

| Gazprom PAO ADR | |||

| (London Shares) | 9,420,057 | 39,694 | |

| Sberbank PAO ADR | 3,610,156 | 22,060 | |

| * | X5 Retail Group NV GDR | 998,538 | 20,657 |

| * | Lukoil PJSC ADR | 466,261 | 16,925 |

| Mobile TeleSystems | |||

| PJSC ADR | 1,780,147 | 12,514 | |

| Gazprom PAO ADR | 740,167 | 3,119 | |

| 114,969 | |||

| Singapore (1.2%) | |||

| DBS Group Holdings Ltd. | 4,684,000 | 57,673 | |

| Genting Singapore plc | 58,872,000 | 34,206 | |

| 91,879 | |||

| South Africa (1.4%) | |||

| Mediclinic | |||

| International Ltd. | 4,616,458 | 40,524 | |

| Sanlam Ltd. | 7,570,592 | 34,130 | |

| * | Mr Price Group Ltd. | 1,394,772 | 21,386 |

| Nampak Ltd. | 9,955,805 | 16,123 | |

| 112,163 | |||

| South Korea (4.4%) | |||

| Samsung | |||

| Electronics Co. Ltd. | 112,662 | 134,958 | |

| E-MART Inc. | 292,935 | 54,488 | |

| SK Hynix Inc. | 1,863,063 | 49,771 | |

| Hyundai Mobis Co. Ltd. | 221,706 | 46,625 | |

| Hana Financial Group Inc. | 1,149,411 | 27,902 | |

| Shinhan Financial | |||

| Group Co. Ltd. | 561,096 | 21,356 | |

| Hyundai Home Shopping | |||

| Network Corp. | 141,604 | 15,092 | |

| 350,192 | |||

| Spain (1.2%) | |||

| Banco Santander SA | 8,762,845 | 49,071 | |

| Red Electrica Corp. SA | 481,950 | 42,471 | |

| 91,542 | |||

| Sweden (1.6%) | |||

| * | Assa Abloy AB Class B | 3,122,208 | 61,921 |

| Swedbank AB Class A | 2,409,906 | 55,285 | |

| * | Oriflame Holding AG | 466,439 | 6,461 |

| 123,667 | |||

| Switzerland (6.5%) | |||

| Novartis AG | 2,275,542 | 206,314 | |

| Credit Suisse Group AG | 2,666,311 | 66,396 | |

| Roche Holding AG | 234,346 | 63,475 | |

| ABB Ltd. | 2,756,144 | 51,912 | |

| LafargeHolcim Ltd. | 718,331 | 40,399 | |

19

| International Value Fund | |||

| Market | |||

| Value• | |||

| Shares | ($000) | ||

| Actelion Ltd. | 285,863 | 39,650 | |

| Cie Financiere | |||

| Richemont SA | 392,738 | 33,592 | |

| GAM Holding AG | 577,710 | 10,560 | |

| 512,298 | |||

| Taiwan (1.2%) | |||

| Taiwan Semiconductor | |||

| Manufacturing Co. Ltd. | 22,936,704 | 96,944 | |

| Thailand (1.0%) | |||

| Bangkok Bank PCL | 13,166,800 | 61,872 | |

| Kasikornbank PCL | |||

| (Foreign) | 4,396,800 | 21,272 | |

| 83,144 | |||

| Turkey (1.4%) | |||

| Turkcell Iletisim | |||

| Hizmetleri AS | 10,534,007 | 41,899 | |

| KOC Holding AS | 7,895,022 | 35,732 | |

| Turkiye Halk Bankasi AS | 9,458,809 | 35,503 | |

| 113,134 | |||

| United Kingdom (23.7%) | |||

| BG Group plc | 6,458,104 | 101,727 | |

| Carnival plc | 1,779,082 | 98,908 | |

| Prudential plc | 3,803,092 | 88,769 | |

| British American | |||

| Tobacco plc | 1,386,832 | 82,317 | |

| HSBC Holdings plc | 10,219,327 | 79,822 | |

| Royal Dutch Shell plc | |||

| Class A | 3,029,201 | 79,215 | |

| AstraZeneca plc | 1,227,908 | 78,378 | |

| BHP Billiton plc | 4,556,281 | 72,870 | |

| BP plc ADR | 2,011,040 | 71,794 | |

| * | Royal Bank of Scotland | ||

| Group plc | 14,611,000 | 71,414 | |

| Vodafone Group plc | 19,784,694 | 65,223 | |

| BP plc | 10,714,058 | 63,596 | |

| Shire plc | 792,832 | 60,036 | |

| Lloyds Banking Group plc | 52,747,008 | 59,851 | |

| RSA Insurance Group plc | 8,877,405 | 57,517 | |

| Unilever plc | 1,195,755 | 53,103 | |

| * | Tesco plc | 18,407,953 | 51,864 |

| Compass Group plc | 2,869,750 | 49,435 | |

| Wolseley plc | 828,278 | 48,611 | |

| Royal Dutch Shell plc | |||

| Class B | 1,813,137 | 47,360 | |

| ^ | Standard Chartered plc | 4,136,439 | 45,909 |

| * | Serco Group plc | 29,728,498 | 42,896 |

| Barclays plc | 11,476,200 | 40,844 | |

| Informa plc | 4,601,133 | 40,199 | |

| Rexam plc | 4,739,551 | 39,412 | |

| Associated British | |||

| Foods plc | 710,460 | 37,782 | |

| Rolls-Royce Holdings plc | 3,524,316 | 37,286 | |

| Ashtead Group plc | 2,252,792 | 34,663 | |

| London Stock Exchange | |||

| Group plc | 872,500 | 34,132 | |

| Market | |||

| Value• | |||

| Shares | ($000) | ||

| *,3 | Worldpay Group plc | 7,901,800 | 33,987 |

| Signet Jewelers Ltd. | 202,410 | 30,557 | |

| RELX plc | 1,442,500 | 25,785 | |

| Weir Group plc | 1,314,800 | 21,596 | |

| Petrofac Ltd. | 1,590,239 | 20,588 | |

| Pearson plc | 1,195,214 | 15,827 | |

| 1,883,273 | |||

| United States (2.7%) | |||

| Aon plc | 468,455 | 43,711 | |

| * | Michael Kors Holdings Ltd. | 957,100 | 36,982 |

| RenaissanceRe | |||

| Holdings Ltd. | 363,400 | 39,840 | |

| *,^ | Ultra Petroleum Corp. | 3,707,440 | 20,317 |

| * | Weatherford | ||

| International plc | 7,254,800 | 74,289 | |

| 215,139 | |||

| Total Common Stocks | |||

| (Cost $8,014,246) | 7,676,317 | ||

| Temporary Cash Investments (5.1%)1 | |||

| Money Market Fund (4.9%) | |||

| 4,5 | Vanguard Market Liquidity | ||

| Fund, 0.207% | 384,885,000 | 384,885 | |

| Face | |||

| Amount | |||

| ($000) | |||

| U.S. Government and Agency Obligations (0.2%) | |||

| 6 | Federal Home Loan | ||

| Bank Discount Notes, | |||

| 0.105%, 11/2/15 | 2,000 | 2,000 | |

| 6,7 | Federal Home Loan | ||

| Bank Discount Notes, | |||

| 0.180%, 11/4/15 | 2,000 | 2,000 | |

| 6,7 | Federal Home Loan | ||

| Bank Discount Notes, | |||

| 0.182%, 11/25/15 | 5,000 | 5,000 | |

| 6,7,8 Federal Home Loan | |||

| Bank Discount Notes, | |||

| 0.192%, 11/27/15 | 3,500 | 3,500 | |

| 6,8 | Federal Home Loan | ||

| Bank Discount Notes, | |||

| 0.200%, 11/30/15 | 3,300 | 3,300 | |

| 6 | Federal Home Loan | ||

| Bank Discount Notes, | |||

| 0.197%, 12/4/15 | 1,100 | 1,100 | |

| 6 | Federal Home Loan | ||

| Bank Discount Notes, | |||

| 0.235%, 3/23/16 | 1,000 | 999 | |

| 17,899 | |||

| Total Temporary Cash Investments | |||

| (Cost $402,783) | 402,784 | ||

| Total Investments (101.9%) | |||

| (Cost $8,417,029) | 8,079,101 | ||

20

| International Value Fund | |

| Amount | |

| ($000) | |

| Other Assets and Liabilities (-1.9%) | |

| Other Assets | |

| Investment in Vanguard | 684 |

| Receivables for Investment Securities Sold 48,127 | |

| Receivables for Accrued Income | 23,284 |

| Receivables for Capital Shares Issued | 4,862 |

| Other Assets | 5,268 |

| Total Other Assets | 82,225 |

| Liabilities | |

| Payables for Investment | |

| Securities Purchased | (52,656) |

| Collateral for Securities on Loan | (149,895) |

| Payables to Investment Advisor | (4,147) |

| Payables for Capital Shares | |

| Redeemed | (1,885) |

| Payables to Vanguard | (17,088) |

| Other Liabilities | (4,059) |

| Total Liabilities | (229,730) |

| Net Assets (100%) | |

| Applicable to 238,781,192 outstanding | |

| $.001 par value shares of beneficial | |

| interest (unlimited authorization) | 7,931,596 |

| Net Asset Value Per Share | $33.22 |

| At October 31, 2015, net assets consisted of: | |

| Amount | |

| ($000) | |

| Paid-in Capital | 8,188,953 |

| Undistributed Net Investment Income | 123,930 |

| Accumulated Net Realized Losses | (48,802) |

| Unrealized Appreciation (Depreciation) | |

| Investment Securities | (337,928) |

| Futures Contracts | 7,406 |

| Forward Currency Contracts | (1,415) |

| Foreign Currencies | (548) |

| Net Assets | 7,931,596 |

- See Note A in Notes to Financial Statements.

- Non-income-producing security.

- Includes partial security positions on loan to broker-dealers. The total value of securities on loan is $103,654,000.

- The fund invests a portion of its cash reserves in equity markets through the use of index futures contracts. After giving effect to futures investments, the fund’s effective common stock and temporary cash investment positions represent 98.3% and 3.6%, respectively, of net assets.

- Considered an affiliated company of the fund as the issuer is another member of The Vanguard Group.

- Security exempt from registration under Rule 144A of the Securities Act of 1933. Such securities may be sold in transactions exempt from registration, normally to qualified institutional buyers. At October 31, 2015, the value of this security represented 0.4% of net assets.

- Affiliated money market fund available only to Vanguard funds and certain trusts and accounts managed by Vanguard. Rate shown is the 7-day yield.

- Includes $149,895,000 of collateral received for securities on loan.

- The issuer operates under a congressional charter; its securities are generally neither guaranteed by the U.S. Treasury nor backed by the full faith and credit of the U.S. government.

- Securities with a value of $10,100,000 have been segregated as initial margin for open futures contracts.

- Securities with a value of $3,319,000 have been segregated as collateral for open forward currency contracts. ADR—American Depositary Receipt.

GDR—Global Depositary Receipt.

See accompanying Notes, which are an integral part of the Financial Statements.

21

| International Value Fund | |

| Statement of Operations | |

| Year Ended | |

| October 31, 2015 | |

| ($000) | |

| Investment Income | |

| Income | |

| Dividends1 | 192,593 |

| Interest2 | 600 |

| Securities Lending | 4,029 |

| Total Income | 197,222 |

| Expenses | |

| Investment Advisory Fees—Note B | |

| Basic Fee | 13,777 |

| Performance Adjustment | 3,277 |

| The Vanguard Group—Note C | |

| Management and Administrative | 17,806 |

| Marketing and Distribution | 1,322 |

| Custodian Fees | 1,194 |

| Auditing Fees | 44 |

| Shareholders’ Reports | 102 |

| Trustees’ Fees and Expenses | 16 |

| Total Expenses | 37,538 |

| Net Investment Income | 159,684 |

| Realized Net Gain (Loss) | |

| Investment Securities Sold | 95,610 |

| Futures Contracts | 13,209 |

| Foreign Currencies and Forward Currency Contracts | (28,695) |

| Realized Net Gain (Loss) | 80,124 |

| Change in Unrealized Appreciation (Depreciation) | |

| Investment Securities | (866,841) |

| Futures Contracts | 7,012 |

| Foreign Currencies and Forward Currency Contracts | 4,582 |

| Change in Unrealized Appreciation (Depreciation) | (855,247) |

| Net Increase (Decrease) in Net Assets Resulting from Operations | (615,439) |

| 1 Dividends are net of foreign withholding taxes of $11,327,000. | |

| 2 Interest income from an affiliated company of the fund was $576,000. | |

See accompanying Notes, which are an integral part of the Financial Statements.

22

| International Value Fund | ||

| Statement of Changes in Net Assets | ||

| Year Ended October 31, | ||

| 2015 | 2014 | |

| ($000) | ($000) | |

| Increase (Decrease) in Net Assets | ||

| Operations | ||

| Net Investment Income | 159,684 | 218,467 |

| Realized Net Gain (Loss) | 80,124 | 557,262 |

| Change in Unrealized Appreciation (Depreciation) | (855,247) | (679,339) |

| Net Increase (Decrease) in Net Assets Resulting from Operations | (615,439) | 96,390 |

| Distributions | ||

| Net Investment Income | (213,924) | (151,178) |

| Realized Capital Gain | — | — |

| Total Distributions | (213,924) | (151,178) |

| Capital Share Transactions | ||

| Issued | 1,241,161 | 957,145 |

| Issued in Lieu of Cash Distributions | 201,817 | 144,177 |

| Redeemed | (953,508) | (802,689) |

| Net Increase (Decrease) from Capital Share Transactions | 489,470 | 298,633 |

| Total Increase (Decrease) | (339,893) | 243,845 |

| Net Assets | ||

| Beginning of Period | 8,271,489 | 8,027,644 |

| End of Period1 | 7,931,596 | 8,271,489 |

1 Net Assets—End of Period includes undistributed (overdistributed) net investment income of $123,930,000 and $184,413,000.

See accompanying Notes, which are an integral part of the Financial Statements.

23

| International Value Fund | |||||

| Financial Highlights | |||||

| For a Share Outstanding | Year Ended October 31, | ||||

| Throughout Each Period | 2015 | 2014 | 2013 | 2012 | 2011 |

| Net Asset Value, Beginning of Period | $36.87 | $37.12 | $29.78 | $28.98 | $31.92 |

| Investment Operations | |||||

| Net Investment Income | . 669 | . 9771 | .757 | .804 | .843 |

| Net Realized and Unrealized Gain (Loss) | |||||

| on Investments | (3.373) | (. 530) | 7.402 | .838 | (3.103) |

| Total from Investment Operations | (2.704) | .447 | 8.159 | 1.642 | (2.260) |

| Distributions | |||||

| Dividends from Net Investment Income | (.946) | (.697) | (.819) | (.842) | (. 680) |

| Distributions from Realized Capital Gains | — | — | — | — | — |

| Total Distributions | (.946) | (.697) | (.819) | (.842) | (. 680) |

| Net Asset Value, End of Period | $33.22 | $36.87 | $37.12 | $29.78 | $28.98 |

| Total Return2 | -7.43% | 1.20% | 27.94% | 6.00% | -7.27% |

| Ratios/Supplemental Data | |||||

| Net Assets, End of Period (Millions) | $7,932 | $8,271 | $8,028 | $6,465 | $6,553 |

| Ratio of Total Expenses to | |||||

| Average Net Assets3 | 0.46% | 0.44% | 0.43% | 0.40% | 0.39% |

| Ratio of Net Investment Income to | |||||

| Average Net Assets | 1.95% | 2.64%1 | 2.24% | 2.77% | 2.59% |

| Portfolio Turnover Rate | 36% | 37% | 52% | 53% | 39% |

1 Net investment income per share and the ratio of net investment income to average net assets include $.175 and 0.47%, respectively, resulting from income received from Vodafone Group plc in the form of cash and shares in Verizon Communications Inc. in February 2014.

2 Total returns do not include transaction or account service fees that may have applied in the periods shown. Fund prospectuses provide information about any applicable transaction and account service fees.

3 Includes performance-based investment advisory fee increases (decreases) of 0.04%, 0.03%, 0.01%, (0.03%), and (0.05%).

See accompanying Notes, which are an integral part of the Financial Statements.

24

International Value Fund

Notes to Financial Statements

Vanguard International Value Fund is registered under the Investment Company Act of 1940 as an open-end investment company, or mutual fund. The fund invests in securities of foreign issuers, which may subject it to investment risks not normally associated with investing in securities of U.S. corporations.

A. The following significant accounting policies conform to generally accepted accounting principles for U.S. investment companies. The fund consistently follows such policies in preparing its financial statements.

1. Security Valuation: Securities are valued as of the close of trading on the New York Stock Exchange (generally 4 p.m., Eastern time) on the valuation date. Equity securities are valued at the latest quoted sales prices or official closing prices taken from the primary market in which each security trades; such securities not traded on the valuation date are valued at the mean of the latest quoted bid and asked prices. Securities for which market quotations are not readily available, or whose values have been affected by events occurring before the fund’s pricing time but after the close of the securities’ primary markets, are valued at their fair values calculated according to procedures adopted by the board of trustees. These procedures include obtaining quotations from an independent pricing service, monitoring news to identify significant market- or security-specific events, and evaluating changes in the values of foreign market proxies (for example, ADRs, futures contracts, or exchange-traded funds), between the time the foreign markets close and the fund’s pricing time. When fair-value pricing is employed, the prices of securities used by a fund to calculate its net asset value may differ from quoted or published prices for the same securities. Investments in Vanguard Market Liquidity Fund are valued at that fund’s net asset value. Temporary cash investments acquired over 60 days to maturity are valued using the latest bid prices or using valuations based on a matrix system (which considers such factors as security prices, yields, maturities, and ratings), both as furnished by independent pricing services. Other temporary cash investments are valued at amortized cost, which approximates market value.

2. Foreign Currency: Securities and other assets and liabilities denominated in foreign currencies are translated into U.S. dollars using exchange rates obtained from an independent third party as of the fund’s pricing time on the valuation date. Realized gains (losses) and unrealized appreciation (depreciation) on investment securities include the effects of changes in exchange rates since the securities were purchased, combined with the effects of changes in security prices. Fluctuations in the value of other assets and liabilities resulting from changes in exchange rates are recorded as unrealized foreign currency gains (losses) until the assets or liabilities are settled in cash, at which time they are recorded as realized foreign currency gains (losses).

3. Futures and Forward Currency Contracts: The fund uses index futures contracts to a limited extent, with the objective of maintaining full exposure to the stock market while maintaining liquidity. The fund may purchase or sell futures contracts to achieve a desired level of investment, whether to accommodate portfolio turnover or cash flows from capital share transactions. The primary risks associated with the use of futures contracts are imperfect correlation between changes in market values of stocks held by the fund and the prices of futures contracts, and the possibility of an illiquid market. Counterparty risk involving futures is mitigated because a regulated clearinghouse is the counterparty instead of the clearing broker. To further mitigate counterparty risk, the fund trades

25

International Value Fund

futures contracts on an exchange, monitors the financial strength of its clearing brokers and clearing-house, and has entered into clearing agreements with its clearing brokers. The clearinghouse imposes initial margin requirements to secure the fund’s performance and requires daily settlement of variation margin representing changes in the market value of each contract.

The fund enters into forward currency contracts to provide the appropriate currency exposure related to any open futures contracts or to protect the value of securities and related receivables and payables against changes in foreign exchange rates. The fund’s risks in using these contracts include movement in the values of the foreign currencies relative to the U.S. dollar and the ability of the counterparties to fulfill their obligations under the contracts. The fund mitigates its counterparty risk by entering into forward currency contracts only with a diverse group of prequalified counterparties, monitoring their financial strength, entering into master netting arrangements with its counterparties, and requiring its counterparties to transfer collateral as security for their performance. The master netting arrangements provide that, in the event of a counterparty’s default (including bankruptcy), the fund may terminate the forward currency contracts, determine the net amount owed by either party in accordance with its master netting arrangements, and sell or retain any collateral held up to the net amount owed to the fund under the master netting arrangements. The forward currency contracts contain provisions whereby a counterparty may terminate open contracts if the fund’s net assets decline below a certain level, triggering a payment by the fund if the fund is in a net liability position at the time of the termination. The payment amount would be reduced by any collateral the fund has pledged. Any assets pledged as collateral for open contracts are noted in the Statement of Net Assets. The value of collateral received or pledged is compared daily to the value of the forward currency contracts exposure with each counterparty, and any difference, if in excess of a specified minimum transfer amount, is adjusted and settled within two business days.

Futures contracts are valued at their quoted daily settlement prices. Forward currency contracts are valued at their quoted daily prices obtained from an independent third party, adjusted for currency risk based on the expiration date of each contract. The aggregate settlement values and notional amounts of the contracts are not recorded in the Statement of Net Assets. Fluctuations in the value of the contracts are recorded in the Statement of Net Assets as an asset (liability) and in the Statement of Operations as unrealized appreciation (depreciation) until the contracts are closed, when they are recorded as realized gains (losses) on futures or forward currency contracts.

During the year ended October 31, 2015, the fund’s average investments in long and short futures contracts represented 2% and 0% of net assets, respectively, based on the average of aggregate settlement values at each quarter-end during the period. The fund’s average investment in forward currency contracts represented 3% of net assets, based on the average of notional amounts at each quarter-end during the period.

4. Federal Income Taxes: The fund intends to continue to qualify as a regulated investment company and distribute all of its taxable income. Management has analyzed the fund’s tax positions taken for all open federal income tax years (October 31, 2012–2015), and has concluded that no provision for federal income tax is required in the fund’s financial statements.

5. Distributions: Distributions to shareholders are recorded on the ex-dividend date.

26

International Value Fund

6. Securities Lending: To earn additional income, the fund lends its securities to qualified institutional borrowers. Security loans are required to be secured at all times by collateral in an amount at least equal to the market value of securities loaned. Daily market fluctuations could cause the value of loaned securities to be more or less than the value of the collateral received. When this occurs, the collateral is adjusted and settled on the next business day. The fund further mitigates its counter-party risk by entering into securities lending transactions only with a diverse group of prequalified counterparties, monitoring their financial strength, and entering into master securities lending agreements with its counterparties. The master securities lending agreements provide that, in the event of a counterparty’s default (including bankruptcy), the fund may terminate any loans with that borrower, determine the net amount owed, and sell or retain the collateral up to the net amount owed to the fund; however, such actions may be subject to legal proceedings. While collateral mitigates counterparty risk, in the absence of a default the fund may experience delays and costs in recovering the securities loaned. The fund invests cash collateral received in Vanguard Market Liquidity Fund, and records a liability in the Statement of Net Assets for the return of the collateral, during the period the securities are on loan. Securities lending income represents fees charged to borrowers plus income earned on invested cash collateral, less expenses associated with the loan.

7. Credit Facility: The fund and certain other funds managed by The Vanguard Group (“Vanguard”) participate in a $3 billion committed credit facility provided by a syndicate of lenders pursuant to a credit agreement that may be renewed annually; each fund is individually liable for its borrowings, if any, under the credit facility. Borrowings may be utilized for temporary and emergency purposes, and are subject to the fund’s regulatory and contractual borrowing restrictions. The participating funds are charged administrative fees and an annual commitment fee of 0.06% of the undrawn amount of the facility; these fees are allocated to the funds based on a method approved by the fund’s board of trustees and included in Management and Administrative expenses on the fund’s Statement of Operations. Any borrowings under this facility bear interest at a rate equal to the higher of the federal funds rate or LIBOR reference rate plus an agreed-upon spread.

The fund had no borrowings outstanding at October 31, 2015, or at any time during the period then ended.

8. Other: Dividend income is recorded on the ex-dividend date. Interest income includes income distributions received from Vanguard Market Liquidity Fund and is accrued daily. Premiums and discounts on debt securities purchased are amortized and accreted, respectively, to interest income over the lives of the respective securities. Security transactions are accounted for on the date securities are bought or sold. Costs used to determine realized gains (losses) on the sale of investment securities are those of the specific securities sold.

Withholding taxes on foreign dividends and capital gains have been provided for in accordance with the fund’s understanding of the applicable countries’ tax rules and rates. In consideration of recent decisions rendered by European courts, the fund has filed additional tax reclaims for previously withheld taxes on dividends earned in certain European Union countries. These filings are subject to various administrative and judicial proceedings within these countries. Such tax reclaims received during the year are included in dividend income. No other amounts for additional tax reclaims are reflected in the financial statements due to the uncertainty as to the ultimate resolution of proceedings, the likelihood of receipt of these reclaims, and the potential timing of payment.

27

International Value Fund

B. The investment advisory firms Lazard Asset Management LLC, Edinburgh Partners Limited, and ARGA Investment Management, LP, each provide investment advisory services to a portion of the fund for a fee calculated at an annual percentage rate of average net assets managed by the advisor. The basic fee of Lazard Asset Management LLC is subject to quarterly adjustments based on performance relative to the MSCI All Country World Index ex USA for the preceding five years. The basic fee of Edinburgh Partners Limited is subject to quarterly adjustments based on performance relative to the MSCI All Country World Index ex USA for the preceding three years. The basic fee of ARGA Investment Management, LP, is subject to quarterly adjustments based on performance relative to the MSCI All Country World Index ex USA since October 31, 2012.

Vanguard manages the cash reserves of the fund as described below.

For the year ended October 31, 2015, the aggregate investment advisory fee represented an effective annual basic rate of 0.17% of the fund’s average net assets, before an increase of $3,277,000 (0.04%) based on performance.

C. In accordance with the terms of a Funds’ Service Agreement (the “FSA”) between Vanguard and the fund, Vanguard furnishes to the fund corporate management, administrative, marketing, distribution and cash management services at Vanguard’s cost of operations (as defined by the FSA). These costs of operations are allocated to the fund based on methods and guidelines approved by the board of trustees. Vanguard does not require reimbursement in the current period for certain costs of operations (such as deferred compensation/benefits and risk/insurance costs); the fund’s liability for these costs of operations is included in Payables to Vanguard on the Statement of Net Assets.

Upon the request of Vanguard, the fund may invest up to 0.40% of its net assets as capital in Vanguard. At October 31, 2015, the fund had contributed to Vanguard capital in the amount of $684,000, representing 0.01% of the fund’s net assets and 0.27% of Vanguard’s capitalization. The fund’s trustees and officers are also directors and employees, respectively, of Vanguard.

D. Various inputs may be used to determine the value of the fund’s investments. These inputs are summarized in three broad levels for financial statement purposes. The inputs or methodologies used to value securities are not necessarily an indication of the risk associated with investing in those securities.

Level 1—Quoted prices in active markets for identical securities.

Level 2—Other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.).

Level 3—Significant unobservable inputs (including the fund’s own assumptions used to determine the fair value of investments).

28

International Value Fund

The following table summarizes the market value of the fund’s investments as of October 31, 2015, based on the inputs used to value them:

| Level 1 | Level 2 | Level 3 | |

| Investments | ($000) | ($000) | ($000) |

| Common Stocks | 582,191 | 7,094,126 | — |

| Temporary Cash Investments | 384,885 | 17,899 | — |

| Futures Contracts—Assets1 | 243 | — | — |

| Futures Contracts—Liabilities1 | (174) | — | — |

| Forward Currency Contracts—Assets | — | 1,560 | — |

| Forward Currency Contracts—Liabilities | — | (2,975) | — |

| Total | 967,145 | 7,110,610 | — |

| 1 Represents variation margin on the last day of the reporting period. |

Securities in certain countries may transfer between Level 1 and Level 2 because of differences in stock market closure times that may result from transitions between standard and daylight saving time in those countries and the United States. Based on values on the date of transfer, securities valued at $127,588,000 based on Level 1 inputs were transferred from Level 2 during the fiscal year. Additionally, based on values on the date of transfer, securities valued at $103,106,000 based on Level 2 inputs were transferred from Level 1 during the fiscal year.

E. At October 31, 2015, the fair values of derivatives were reflected in the Statement of Net Assets as follows:

| Foreign | |||

| Equity | Exchange | ||

| Contracts | Contracts | Total | |

| Statement of Net Assets Caption | ($000) | ($000) | ($000) |

| Other Assets | 243 | 1,560 | 1,803 |

| Other Liabilities | (174) | (2,975) | (3,149) |

Realized net gain (loss) and the change in unrealized appreciation (depreciation) on derivatives for the

| year ended October 31, 2015, were: | |||

| Foreign | |||

| Equity | Exchange | ||

| Contracts | Contracts | Total | |

| Realized Net Gain (Loss) on Derivatives | ($000) | ($000) | ($000) |

| Futures Contracts | 13,209 | — | 13,209 |

| Forward Currency Contracts | — | (22,390) | (22,390) |

| Realized Net Gain (Loss) on Derivatives | 13,209 | (22,390) | (9,181) |

| Change in Unrealized Appreciation (Depreciation) on Derivatives | |||

| Futures Contracts | 7,012 | — | 7,012 |

| Forward Currency Contracts | — | 3,880 | 3,880 |

| Change in Unrealized Appreciation (Depreciation) on Derivatives | 7,012 | 3,880 | 10,892 |

29

International Value Fund

At October 31, 2015, the aggregate settlement value of open futures contracts and the related unrealized appreciation (depreciation) were:

| ($000) | ||||

| Aggregate | ||||

| Number of | Settlement | Unrealized | ||

| Long (Short) | Value | Appreciation | ||

| Futures Contracts | Expiration | Contracts | Long (Short) | (Depreciation) |

| Dow Jones EURO STOXX 50 Index | December 2015 | 1,485 | 55,823 | 3,400 |

| Topix Index | December 2015 | 226 | 29,188 | 2,415 |

| FTSE 100 Index | December 2015 | 251 | 24,499 | 1,104 |

| S&P ASX 200 Index | December 2015 | 126 | 11,768 | 487 |

| 7,406 |

Unrealized appreciation (depreciation) on open Dow Jones EURO STOXX 50 Index and FTSE 100 Index futures contracts is required to be treated as realized gain (loss) for tax purposes.

At October 31, 2015, the fund had open forward currency contracts to receive and deliver currencies as follows. Unrealized appreciation (depreciation) on open forward currency contracts is treated as realized gain (loss) for tax purposes.

| Unrealized | ||||||

| Contract | Appreciation | |||||

| Contract Amount (000) | ||||||

| Settlement | (Depreciation) | |||||

| Counterparty | Date | Receive | Deliver | ($000) | ||

| BNP Paribas | 12/23/15 | EUR | 79,668 | USD | 90,047 | (2,356) |

| Bank of America N.A. | 12/15/15 | JPY | 5,281,784 | USD | 44,168 | (363) |

| BNP Paribas | 12/23/15 | GBP | 26,205 | USD | 40,294 | 96 |

| BNP Paribas | 12/22/15 | AUD | 27,052 | USD | 19,166 | 73 |

| UBS AG | 12/23/15 | USD | 22,929 | EUR | 20,266 | 622 |

| Citibank, N.A. | 12/23/15 | USD | 13,456 | EUR | 11,817 | 449 |

| Bank of America N.A. | 12/15/15 | USD | 11,327 | JPY | 1,343,730 | 183 |

| Morgan Stanley Capital | 12/23/15 | USD | 11,319 | GBP | 7,440 | (148) |

| BNP Paribas | 12/15/15 | USD | 6,289 | JPY | 753,244 | 42 |

| Citibank, N.A. | 12/23/15 | USD | 6,060 | GBP | 3,945 | (20) |

| UBS AG | 12/22/15 | USD | 5,106 | AUD | 7,303 | (88) |

| Morgan Stanley Capital | 12/22/15 | USD | 3,069 | AUD | 4,183 | 95 |

| (1,415) | ||||||

| AUD—Australian dollar. | ||||||

| EUR—Euro. | ||||||

| GBP—British pound. | ||||||

| JPY—Japanese yen. | ||||||

| USD—U.S. dollar. | ||||||

30

International Value Fund

F. Distributions are determined on a tax basis and may differ from net investment income and realized capital gains for financial reporting purposes. Differences may be permanent or temporary. Permanent differences are reclassified among capital accounts in the financial statements to reflect their tax character. Temporary differences arise when certain items of income, expense, gain, or loss are recognized in different periods for financial statement and tax purposes. These differences will reverse at some time in the future. Differences in classification may also result from the treatment of short-term gains as ordinary income for tax purposes.

During the year ended October 31, 2015, the fund realized net foreign currency losses of $6,305,000, which decreased distributable net income for tax purposes; accordingly, such losses have been reclassified from accumulated net realized losses to undistributed net investment income. Certain of the fund’s investments are in securities considered to be passive foreign investment companies, for which any unrealized appreciation and/or realized gains are required to be included in distributable net income for tax purposes. During the year ended October 31, 2015, the fund realized gains on the sale of passive foreign investment companies of $62,000, which have been included in current and prior periods’ taxable income; accordingly, such gains have been reclassified from accumulated net realized losses to undistributed net investment income. Passive foreign investment companies held at October 31, 2015, had unrealized appreciation of $5,940,000 of which $4,756,000 has been distributed and is reflected in the balance of undistributed net investment income.

For tax purposes, at October 31, 2015, the fund had $141,854,000 of ordinary income available for distribution. The fund used capital loss carryforwards of $90,504,000 to offset taxable capital gains realized during the year ended October 31, 2015. At October 31, 2015, the fund had available capital losses totaling $50,118,000 to offset future net capital gains through October 31, 2017.