UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-03015

Ohio National Fund, Inc.

(Exact name of registrant as specified in charter)

One Financial Way, Cincinnati, Ohio | 45242

| |

(Address of principal executive offices) |

(Zip code) |

CT Corporation 300 E. Lombard St. Suite 1400 Baltimore, MD 21202

(Name and address of agent for service)

Registrant’s telephone number, including area code: 513-794-6971

Date of fiscal year end: December 31

Date of reporting period: June 30, 2015

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

| Item 1. | Reports To Stockholders. |

OHIO NATIONAL FUND, INC.

| 1 | ||||

| 2 | ||||

| 3 | ||||

| 8 | ||||

| 10 | ||||

| 15 | ||||

| 21 | ||||

| 27 | ||||

| 31 | ||||

| 37 | ||||

| 40 | ||||

| 45 | ||||

| 49 | ||||

| 56 | ||||

| 60 | ||||

| 70 | ||||

| 74 | ||||

| 78 | ||||

| 81 | ||||

| 84 | ||||

| 91 | ||||

| 95 | ||||

| 98 | ||||

| 109 | ||||

| 112 | ||||

| 115 | ||||

| 121 | ||||

| 132 | ||||

| 157 | ||||

| 159 | ||||

Message |  |

Dear Investor:

Recently, I asked a colleague to describe the equity markets during the first half of the year, and this was the response I received, “flat, with brief spikes of volatility.”

After giving this some thought, I decided this statement is a fairly accurate description - or, at the very least, a reasonable response. Entertaining my curiosity to hear from others, I asked a few more investment professionals for their one-sentence description of the market. The first described the equity markets as “muted returns with volatility.” That sounded similar to the initial description and consistent with my view. The second reply is more interesting: “fairly valued with low volatility.” This colleague added that his assessment may be contrary to others’ opinions. His latter comment was certainly true, leading me to ponder which characterization of volatility is correct.

Muted equity markets

Determining whether equity market returns during the first half of the year were flat or muted is fairly simple. The two most well-known equity market indices, the S&P 500® Index and the Dow Jones Industrial Average, were up 1.2 percent and 0.03 percent respectively. These returns easily qualify as flat or muted. The MSCI All Country World Index, representing a more global view, was up 2.7 percent, which is also consistent with these descriptions.

Determining whether the equity markets are fairly valued is slightly more complicated, but not much. According to FactSet, the S&P 500® Index’s current price-to-earnings ratio is 16.6 times forward earnings. This is higher than both the five-year average of 13.9 and the 10-year average of 14.1, and just slightly above longer-term averages.

Based on these comparisons, I believe that equities are close to fair value.

More important, future expectations for additional returns based on an assumed current under-valuation are not likely. Equity returns have been flat this year, but fairly valued. Increased returns will now more likely be reliant on economic growth, which has not been very strong.

Assessing volatility

There is little question that equity markets have been muted. However, assessing volatility is more complicated. Perhaps that is one reason for the contradictory responses from my colleagues.

Let’s start by comparing 2015 year-to-date volatility with 2014: In 2014, average volatility as measured by the Chicago Board Options Exchange Volatility Index (VIX) was 14.2 percent. With a 15.1 percent average in 2015, volatility is higher, but not by much. Comparing the median volatility tells a similar story: 13.7 percent for 2014 and 14.2 percent for year-to-date 2015. It is worth noting that there was greater variability in volatility throughout 2014, with a higher peak and a lower trough than we’ve experienced so far in 2015. Even when factoring in variability, the difference in volatility between the two periods is small, and volatility remains relatively low.

The European markets paint a different picture. Volatility increased in Europe by 28 to 34 percent, depending on the index. This is not a surprise, considering that most of the triggering events that increased volatility occurred outside of the United States, with Greece being the most notable. My conclusion: assessing whether volatility increased or was just low depends on where you look.

| 1 |

The Ohio National Fund, Inc.

I’m pleased to report that most of the Ohio National Fund, Inc. Portfolios performed well during the first half of 2015. Eleven out of the 17 actively managed Portfolios either outperformed their benchmark, or ranked in the top half of their peer group. Some of our better performing Portfolios include the International Portfolio and the International Small-Mid Company Portfolio, both subadvised by Federated Global Investment Management Corp.; the Aggressive Growth Portfolio and the Small Cap Growth Portfolio, both subadvised by Janus Capital Management LLC; and all of the Portfolios subadvised by Suffolk Capital Management, LLC.

As always, it is important to stay diversified, because no one can accurately predict the future. Please consult your financial professional to make sure you are positioned appropriately. Thank you for entrusting your assets to the Ohio National Fund, Inc. We look forward to continuing to serve your investment needs.

Sincerely,

Christopher A. Carlson

President

Directors and Officers of Ohio National Fund, Inc.

John J. Palmer, Director

Madeleine W. Ludlow, Director

George M. Vredeveld, Director

John I. Von Lehman, Director

Geoffrey Keenan, Director

Christopher A. Carlson, President

Thomas A. Barefield, Vice President

R. Todd Brockman, Treasurer

Kimberly A. Plante, Secretary

Julie T. Thomas, Chief Compliance Officer

Catherine E. Gehr, Assistant Treasurer

Emily Bae, Assistant Secretary

The Statement of Additional Information of Ohio National Fund, Inc. (the “Fund”) includes additional information about the Fund’s Board of Directors (the “Board”) and is available at http://www.ohionationalfund.com or upon request, without charge, by calling 877-781-6392 (toll-free).

A description of the policies and procedures that the Fund uses in voting proxies relating to Fund securities, as well as information regarding how the Fund voted proxies during the most recent twelve-month period ended June 30, is available without charge, upon request, by calling 877-781-6392 (toll-free) and on the Securities and Exchange Commission (the “Commission”) website at http://www.sec.gov.

The Fund has filed its Schedules of Investments as of March 31 and September 30 with the Commission, as required, on Form N-Q. Form N-Q is required to be filed with the Commission for the first and third quarters of each fiscal year within sixty days after the end of each period and is available on the Commission website upon acceptance of each submission. The Fund’s Forms N-Q may be reviewed and copied at the Commission’s Public Reference Room in Washington, DC. Information about the Public Reference Room is available by calling 1-800-SEC-0330 (toll-free).

This report and the financial statements contained herein are submitted for the general information of the shareholders of the Fund. This report is not authorized for distribution to prospective investors in the Fund unless preceded or accompanied by an effective prospectus of Ohio National Fund, Inc. For a prospectus containing more complete information, including charges and expenses, please contact Ohio National Investments, Inc., One Financial Way, Cincinnati, OH 45242, telephone 877-781-6392 (toll-free).

| 2 |

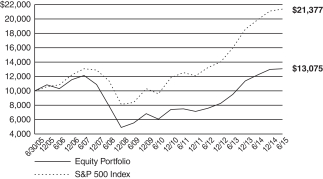

| Ohio National Fund, Inc. | Equity Portfolio |

Objective/Strategy

The Equity Portfolio seeks long-term growth of capital by investing at least 80% of its assets in equity securities.

Performance as of June 30, 2015

Average Annual Returns: | ||||

One year | 6.79% | |||

Five years | 16.51% | |||

Ten years | 2.72% |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. Total return figures include change in share price and reinvestment of dividends and capital gains. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information up to the most recent month end, call toll-free 1-877-781-6392.

The Portfolio is not open to direct retail investment. Beneficial interest in shares is obtained solely by purchase of variable life insurance policies and variable annuity contracts. Actual performance results for variable annuity and variable universal life contracts will be lower due to contract charges. Consult your contract for applicable charges.

Comments

For the six-month period ended June 30, 2015, the Equity Portfolio returned 0.75% versus 1.23% for the current benchmark, the S&P 500 Index.

Relative portfolio performance was driven by security selection effects and sector allocation, partially offset by positive interaction of sector allocation and security selection. An overweight position in Utilities generated the largest detraction due to sector allocation, as the sector underperformed the index. An underweight to Industrials contributed positively to allocation effects, as the sector also lagged the benchmark. Amazon.com, Inc., NXP Semiconductors NV, LyondellBasell Industries NV, UnitedHealth Group, Inc. and Broadcom Corp. were the largest contributors to performance, while the biggest detractors included Keurig Green Mountain, Inc., CONSOL Energy, Inc., Yahoo!, Inc., Calpine Corp. and Ralph Lauren Corp. (1)

The Nasdaq Composite separated from other major indices in the first half of the year, climbing 6.0% relative to the 1.2% advance for the S&P 500 Index and the stagnant performance of the Dow Jones Industrial Average. Growth stocks outperformed their value-oriented peers, with the Russell 1000 Growth Index returning 4.0% against a 0.6% loss in the Russell 1000 Value Index. Size has not aided performance thus far in 2015, with large caps trailing mid caps, which lag small caps. The Russell 1000, Russell Midcap and Russell 2000 indices returned 1.7%, 2.4% and 4.8% throughout the period, respectively. Within the S&P 500 Index, Utilities was the top detractor, down more than 10.0%, while Energy and Industrials fell 4.7% and 3.1%, respectively. On the upside, Health Care and Consumer Discretionary stood out, up 9.6% and 6.8%, respectively.

Major U.S. averages opened the year with mixed gains, as investors continued to focus on the Federal Reserve’s rate strategy amid mixed economic reports, suppressed crude prices and the climbing dollar, as well as another flurry of merger and acquisition announcements. Outside the U.S., continued Greek debt squabbles, European deflationary concerns and a market sell-off in China dominated the headlines. The U.S. dollar strengthened 9% against the euro over the period, and is now up nearly 20% against a broad basket of foreign currencies over the past twelve months. The 10-Year Treasury yield extended its slide to a low of 1.64% in

January before recovering to hit a June high of 2.48%; a level not seen since September of 2014. Oil prices fluctuated between $50 and $60 per barrel throughout the quarter, largely reacting to reports that capacity in Cushing, Oklahoma is running out for crude supplies, and the potential for Iranian supply to come back to the U.S. market.

U.S. gross domestic product expanded at an annualized rate of 2.2% in the fourth quarter of 2014, followed by a 0.2% contraction in the first quarter; both below consensus and well short of the 2014 third quarter’s 5.0% growth. Retail sales, excluding energy, declined three months in a row between December and February, with reports pointing to record-cold temperatures during the season as the culprit for the disappointment. Though personal spending and retail sales rebounded in the second quarter, consumer prices are flat relative to where the consumer price index closed the second quarter of 2014. On a positive note, U.S. employers added 1.23 million jobs in the first six months of the year, pushing down the unemployment rate to 5.3% from 5.6% at the end of year 2014. Consumer confidence also unexpectedly spiked to the highest level in 11 years.

The mixed bag of economic data once again spurred further target rate speculation, and minutes from the recent meetings indicate that officials are at odds over when to raise the target rate. Federal Reserve Chair Yellen commented that “if the economy continues to improve as I expect, I think it will be appropriate at some point this year to take the initial step to raise the federal funds rate target and begin the process of normalizing monetary policy.” Futures currently show the odds of a December hike at roughly 35%. However, the Federal Reserve Chair also commented that the timing of the initial rate increase is not what matters; rather it is the “entire path of rates.” Additionally, Yellen addressed the labor market, allowing that “wage increases are still running at a low level but there have been some tentative signs that wage growth is picking up.”

Roughly 70% of the S&P 500 Index’s constituents reported better-than-expected bottom-line results during both earnings seasons, while approximately 20% disappointed. However, many companies tempered guidance for 2015, citing significant foreign exchange headwinds. Meanwhile, low borrowing rates continued to foster merger & acquisition activity, as a slew of multibillion-dollar deals were announced recently, particularly in the health care sector. Notably, Royal Dutch Shell announced plans to purchase integrated gas company BG Group for a whopping seventy billion, Comcast walked away from its blockbuster deal with Time Warner Cable amid regulatory resistance and Blackstone Group LP and Wells Fargo & Co. joined to acquire a real estate portfolio from General Electric for roughly thirty billion dollars. In the Health Care sector, Netherlands-based Mylan began to fight against an unsolicited forty billion dollar bid from Teva amid its own attempt to acquire generic pharmaceutical manufacturer Perrigo Co. PLC for around thirty billion, and Aetna agreed to buy Humana. Elsewhere, H.J. Heinz and Kraft Foods Group signed a definitive merger agreement to form the Kraft Heinz Company, which will create the third-largest food and beverage company in North America. In other news, the Federal Reserve announced that its annual “stress test” of the thirty-one largest banks operating in the U.S. found that all the banks had sufficient capital to withstand a hypothetical economic shock. Nearly every bank’s capital return proposals passed the comprehensive capital analysis and review tests as well.

The World Bank lowered its 2015 growth expectations early in the year due to weakness in Japan and the Eurozone, though it pointed to the U.S. as one of the strongest economies. This tempered forecast was underscored by China’s 7.4% gross domestic product (“GDP”) expansion in 2014, its weakest pace in over 20 years.

| 3 | (continued) |

| Ohio National Fund, Inc. | Equity Portfolio (Continued) |

European GDP also expanded by only 0.3% in the fourth quarter thanks to German output buoying contractions and stagnation in other member countries. European Central Bank President Mario Draghi announced an expanded asset-purchase program through at least September 2016 to combat threats of deflation.

Elsewhere, after creditors approved a four-month loan extension in the first quarter, back-and-forth debt negotiations in Greece dominated the headlines in the final weeks of June. Greek Prime Minister Tsipras surprisingly called for a voter referendum that caused European officials to suspend financial support programs for Greece. Greek voters ultimately rejected the austerity measures demanded by creditors in return for additional aid, increasing the possibility that Greece could exit the euro.

Keurig Green Mountain, Inc. sold off recently after its management offered disappointing guidance and as the company’s KOLD brewing system demo saw mixed reviews. The weak guidance is a function of a rocky transition to Keurig 2.0, which is not compatible with unlicensed K-cups, and a mix shift in K-cup sales towards partnered brands like Starbucks. We expect the transition to Keurig 2.0 to improve as consumers begin to phase out unlicensed K-cups and embrace the improved model. Conversations with management have also confirmed that the negative sales impact from the mix shifting toward partnered portion pack sales is due to higher growth for the external brands, and is offset to a large extent by the higher margin on these partnered portion packs. Finally, we believe the stock embeds extreme pessimism for the KOLD system and does not reflect the potential for product improvements and cost reductions, both of which were part of the hot system’s evolution to current models. Our updated analysis points to an oversold stock with an attractive risk/reward profile. We are, therefore, maintaining our position in Keurig Green Mountain, Inc. (1)

CONSOL Energy Corp. has suffered as the fundamentals of the thermal coal industry have deteriorated due to a slew of headwinds. The global market is oversupplied, with new capacity coming online recently while demand is faltering. China, a major coal consumer, is pulling back on its massive infrastructure build out and U.S. power companies are shutting down coal plants and shifting towards gas. CONSOL Energy Corp., unlike many of its peers, boasts a decent balance sheet with little risk of breaking its debt covenants. The company is likely to survive this cycle and actually benefit from shuttering of supply. CONSOL Energy Corp. owns high-quality and low-cost coal assets, and management is improving its portfolio by spinning out and selling some of its coal businesses. The company also holds high-quality natural gas assets, which will provide substantial tailwinds should gas prices improve from these depressed levels. The market is still punishing the stock for its coal exposure, and we are effectively buying the gas business at a very attractive price. So, despite the challenged fundamentals of the industry, our analysis indicates an attractive price/value gap in CNX, and we are maintaining our position. (1)

Calpine Corp. detracted from returns, as the power generation industry has suffered from depressed prices stemming from weak demand. Supply and demand fundamentals will improve with time, but we expect the retirement of many coal-fired power generation plants in the meantime. Fortunately, the lack of any current fundamental tailwinds is allowing us to buy trough fundamentals at trough valuation levels. Calpine Corp. generates very strong free-cash-flow (FCF) streams, is valued at a double-digit FCF yield, and will benefit from any improvements in power pricing. We believe the stock’s valuation does not reflect an incredibly cheap option on potential power price volatility, especially in New England and Mid-Atlantic

power markets. We also see long-term power pricing potential from power demand increases in Texas power markets. Additionally, management’s capital allocation history is excellent. They consistently recognize the inherent value of the business, and have reduced share count well by nearly 25% over the past four years at prices well below fair value. (1)

Amazon.com, Inc. stock spiked after each earnings release over the past six months, bringing its year-to-date return at June 30 to roughly 40%. The company reported two straight quarters of earnings above Street estimates, with sales growing despite foreign exchange rate headwinds and margins improving. Additionally, management broke out the Amazon Web Services (“AWS”) business separately for the first time ever, surprising investors with 50% topline growth and a profitable bottom line. We expect this business to be a source of strong growth for Amazon.com, Inc. going forward. Finally, we remain encouraged with the new tone from management focusing on cost management and on transparency in operating reporting; moves that suggest we could see a much more shareholder-friendly management team going forward. We believe the company is poised to expand its operating margins into the double digits by leveraging its hefty fulfillment center investments and by growing its AWS business. (1)

NXP Semiconductors NV shares rallied after the company announced a deal to acquire Freescale Semiconductor to create the fourth-largest semiconductor company. NXP Semiconductors NV is using stock to fund the bulk of the deal, though the slim premium limits the shareholder value at risk, according to our analysis. The combined entity will enjoy a strong competitive positioning as the market-leading automotive semiconductor company and broad-based microcontroller unit (“MCU”) supplier, and should generate substantial cash synergy beyond the two hundred million to five hundred million dollar range that management projects. As such, we continue to hold the stock despite the recent rally. (1)

Broadcom Corp. was a top contributor this quarter after the stock spiked on a takeout offer by Avago Technologies. The stock also had a strong run in 2014 after announcing plans to exit its unprofitable cellular baseband business. We maintained our position going into 2015, as our analysis indicated that the company’s remaining wireless connectivity, infrastructure and broadband businesses were still undervalued. Following the bid by Avago Technologies, which put shares near our estimate of intrinsic value, we exited our position in Broadcom Corp. and allocated the capital elsewhere. (1)

Despite a broad industry shift towards passive investing, this cycle has featured dominant active stock pickers in the guise of the companies themselves. In many ways, companies have acted as managers of single-stock portfolios and, in aggregate, have aggressively bought back $1.7 trillion of their own stocks since 2009. As animal spirits have risen, boards have become increasingly comfortable with an uncertain future and have started to acquire other companies. The financial engineering logic behind these deals speaks for itself, given the ability to buy existing cash flow streams with cheap debt. Remarkably, roughly 2/3 of buying companies are seeing their stocks increase along with the selling companies.

Increasingly, deal activity is coming to dominate the returns in U.S. stocks, especially against the backdrop of flattish equity returns year-to-date. We have benefitted directly from deal activity, both as owners of acquiring companies, such as NXP Semiconductors NV and Expedia, and as owners of targeted companies, such as Perrigo Co. LLC and Broadcom Corp. In the case of the two targets, the offer price was very close to our assessment of business value, which

| 4 | (continued) |

| Ohio National Fund, Inc. | Equity Portfolio (Continued) |

suggests good valuation work on our part, and provided a welcome catalyst for price-and-value convergence. (1)

The challenge for long-term investors is that deals are now pushing prices towards fair value and beyond. Not surprisingly, at this point, we find many U.S. stocks broadly uninteresting, and yet we expect pro-cyclical deal activity to likely push prices well above business value for many stocks. Besides this rising valuation risk, we also expect that many deals will fail to meet current investor and boardroom expectations, and some of the popular current roll-up companies will inevitably blow up due to poorly executed integration and mismanaged complexity. As in all market cycles, as the perception of future uncertainty fades, valuation and risk rise, and our jobs as valuation managers gets tougher.

Fortunately, as active managers we have the luxury and the discipline not to buy most stocks, and we are still finding exploitable pockets of absolute value in financials, legacy tech and in the broad power generation sector.

Our financial stocks have recently performed well, as interest rates have moved up, and some of our holdings are closing in on fair value. However, the majority of our financial holdings are still just climbing out of the valuation basement of the housing crisis, persistently low interest rates and crushing regulatory costs. As a result, our core financial holdings, including Citigroup, Inc. and American International Group, Inc., are currently enjoying improving fundamentals and capital return profiles, which we think are still not fully reflected in their prices. (1)

The legacy technology names we own, such as Microsoft Corp. and Cisco Systems, Inc., continue to generate massive free-cash-flow streams, which are valued at narrowing, but still substantial, discounts from the overall market. The valuation discount of legacy tech reflects the ever-present risk of disruption, especially from the accelerating and dramatic transition to the cloud. Our goal is to find tech stocks that reflect the disruption risk of cloud, but have durable cash flow streams that will allow them to transition, and in some cases thrive, in a cloud-based world. (1)

The power generation, natural gas and coal sectors are all in various states of recession to depression. Power prices are depressed from weak demand, natural gas remains over-supplied, thanks to massive productivity gains from shale drilling, and the coal industry needs to cut supply by almost 40% to balance the market. Supply and demand fundamentals will improve with time, but we expect a rash of coal bankruptcies, further gas supply cuts and the retirement of many coal-fired power generation plants in the meantime. Fortunately, the lack of any current fundamental tailwinds and the time required to improve these fundamentals over the next several quarters is allowing us to buy trough fundamentals at trough valuation levels. In particular, AES Corp. and Calpine Corp. continue to generate very strong free-cash-flow streams, are valued at double-digit free cash flow yields, and will benefit from any improvements in power pricing. In the even-more-depressed gas and coal sector, CONSOL Energy, Inc. is one of the few well-capitalized coal and natural gas companies, with low-cost production assets in both segments. Fortunately, CONSOL Energy, Inc. saw the writing on the wall for coal during the China-induced coal boom of the last decade, and wisely diversified into gas. CONSOL Energy, Inc. is now proactively separating its coal and gas assets, and we think we are getting very cheap high-quality gas assets due to the coal overhang. (1)

Even with the continued convergence of price and value in most U.S. stocks, our focus on absolute value has allowed us to maintain what we believe is attractive potential risk-adjusted upside in the Portfolio.

We track this potential on a daily basis, and the current potential return profile of the Portfolio is similar to levels achieved during the deflationary-driven correction that occurred last October. While this upside potential is not at the home run levels we enjoyed a few years ago, we believe it is still absolutely attractive, and extremely attractive relative to most fixed-income alternatives.

In closing, we are in the judgment business, and our job is to execute an investment process that exploits expectation-driven gaps between price and underlying business value. Our judgment of these valuation opportunities is constantly evaluated by a probability-driven framework, which reinforces humility and constant learning. We could not execute this process without the long-term culture of ClearBridge that encourages investors to truly invest, and more importantly, the quality and long-term orientation of our shareholders.

| (1) | The Portfolio’s composition is subject to change. Holdings and weightings are as of June 30, 2015. |

Change in Value of $10,000 Investment

Hypothetical illustration based on past performance. Future performance will vary. The Portfolio’s returns reflect reinvested dividends. The Portfolio’s holdings may differ significantly from the securities in the index. The index is unmanaged and therefore does not reflect the cost of portfolio management and accounting.

The S&P 500 Index is a capitalization-weighted index designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The index presented herein includes the effects of reinvested dividends.

| 5 | (continued) |

| Ohio National Fund, Inc. | Equity Portfolio (Continued) |

Portfolio Composition as of June 30, 2015 (1)

| % of Net Assets | ||||

Common Stocks (3) | �� | 97.5 | ||

Master Limited Partnerships (3) | 1.5 | |||

Money Market Funds | 1.0 | |||

|

| |||

| 100.0 | ||||

|

|

Top 10 Portfolio Holdings as of June 30, 2015 (1) (2)

| % of Net Assets | ||||

1. Citigroup, Inc. | 4.3 | |||

2. Microsoft Corp. | 4.0 | |||

3. JPMorgan Chase & Co. | 3.2 | |||

4. Amazon.com, Inc. | 3.1 | |||

5. Wells Fargo & Co. | 3.0 | |||

6. Merck & Co., Inc. | 3.0 | |||

7. Cisco Systems, Inc. | 2.9 | |||

8. American International Group, Inc. | 2.9 | |||

9. UnitedHealth Group, Inc. | 2.7 | |||

10. Yahoo!, Inc. | 2.7 |

| (1) | Composition of Portfolio subject to change. |

| (2) | Short-term investments have been excluded from the list of Top 10 Portfolio Holdings. |

| (3) | Sectors (combined): |

| % of Net Assets | ||||

Financials | 24.0 | |||

Health Care | 16.7 | |||

Information Technology | 16.1 | |||

Consumer Discretionary | 13.1 | |||

Energy | 8.3 | |||

Industrials | 7.1 | |||

Materials | 5.2 | |||

Utilities | 4.9 | |||

Consumer Staples | 3.6 | |||

|

| |||

| 99.0 | ||||

|

|

| 6 |

| Ohio National Fund, Inc. | Equity Portfolio |

Schedule of Investments | June 30, 2015 (Unaudited) |

| Common Stocks – 97.5% | Shares | Value | ||||||||

CONSUMER DISCRETIONARY – 13.1% |

| |||||||||

McDonald’s Corp. (Hotels, Restaurants & Leisure) | 100,909 | $ | 9,593,419 | |||||||

PulteGroup, Inc. (Household Durables) | 689,697 | 13,897,395 | ||||||||

Amazon.com, Inc. (Internet & Catalog Retail) | (a) | 36,610 | 15,892,035 | |||||||

Expedia, Inc. (Internet & Catalog Retail) | 95,070 | 10,395,904 | ||||||||

Lowe’s Cos., Inc. (Specialty Retail) | 142,520 | 9,544,564 | ||||||||

Ralph Lauren Corp. (Textiles, Apparel & Luxury Goods) | 60,280 | 7,978,661 | ||||||||

|

| |||||||||

| 67,301,978 | ||||||||||

|

| |||||||||

CONSUMER STAPLES – 3.6% | ||||||||||

Keurig Green Mountain, Inc. (Food Products) | 139,330 | 10,676,858 | ||||||||

Colgate-Palmolive Co. (Household Products) | 121,360 | 7,938,158 | ||||||||

|

| |||||||||

| 18,615,016 | ||||||||||

|

| |||||||||

ENERGY – 8.3% | ||||||||||

Baker Hughes, Inc. (Energy Equip. & Svs.) | 116,430 | 7,183,731 | ||||||||

Apache Corp. (Oil, Gas & Consumable Fuels) | 186,210 | 10,731,282 | ||||||||

Chevron Corp. (Oil, Gas & Consumable Fuels) | 94,750 | 9,140,532 | ||||||||

CONSOL Energy, Inc. (Oil, Gas & Consumable Fuels) | 391,400 | 8,509,036 | ||||||||

Devon Energy Corp. (Oil, Gas & Consumable Fuels) | 118,830 | 7,069,197 | ||||||||

|

| |||||||||

| 42,633,778 | ||||||||||

|

| |||||||||

FINANCIALS – 22.5% | ||||||||||

Citigroup, Inc. (Banks) | 401,850 | 22,198,194 | ||||||||

Citizens Financial Group, Inc. (Banks) | 271,290 | 7,408,930 | ||||||||

JPMorgan Chase & Co. (Banks) | 244,190 | 16,546,314 | ||||||||

Wells Fargo & Co. (Banks) | 275,550 | 15,496,932 | ||||||||

E*TRADE Financial Corp. (Capital Markets) | (a) | 271,520 | 8,132,024 | |||||||

American Express Co. (Consumer Finance) | 59,410 | 4,617,345 | ||||||||

American International Group, Inc. (Insurance) | 239,160 | 14,784,871 | ||||||||

Genworth Financial, Inc. Class A (Insurance) | (a) | 994,830 | 7,530,863 | |||||||

Hartford Financial Services Group, Inc. / The (Insurance) | 211,270 | 8,782,494 | ||||||||

American Homes 4 Rent (Real Estate Investment Trusts) | 649,230 | 10,413,649 | ||||||||

|

| |||||||||

| 115,911,616 | ||||||||||

|

| |||||||||

HEALTH CARE – 16.7% | ||||||||||

Alexion Pharmaceuticals, Inc. (Biotechnology) | (a) | 48,541 | 8,774,757 | |||||||

Amgen, Inc. (Biotechnology) | 88,670 | 13,612,618 | ||||||||

Medtronic PLC (Health Care Equip. & Supplies) | 179,210 | 13,279,461 | ||||||||

Express Scripts Holding Co. (Health Care Providers & Svs.) | (a) | 130,650 | 11,620,011 | |||||||

UnitedHealth Group, Inc. (Health Care Providers & Svs.) | 115,194 | 14,053,668 | ||||||||

AbbVie, Inc. (Pharmaceuticals) | 138,776 | 9,324,359 | ||||||||

Merck & Co., Inc. (Pharmaceuticals) | 269,850 | 15,362,561 | ||||||||

|

| |||||||||

| 86,027,435 | ||||||||||

|

| |||||||||

| Common Stocks (Continued) | Shares | Value | ||||||||

INDUSTRIALS – 7.1% | ||||||||||

Boeing Co. / The (Aerospace & Defense) | 60,370 | $ | 8,374,526 | |||||||

United Continental Holdings, Inc. (Airlines) | (a) | 187,050 | 9,915,520 | |||||||

Rockwell Automation, Inc. (Electrical Equip.) | 77,070 | 9,606,005 | ||||||||

PACCAR, Inc. (Machinery) | 130,695 | 8,339,648 | ||||||||

|

| |||||||||

| 36,235,699 | ||||||||||

|

| |||||||||

INFORMATION TECHNOLOGY – 16.1% | ||||||||||

Cisco Systems, Inc. (Communications Equip.) | 550,530 | 15,117,554 | ||||||||

Yahoo!, Inc. (Internet Software & Svs.) | (a) | 354,920 | 13,944,807 | |||||||

NXP Semiconductors NV (Semiconductors & Equip.) | (a) | 94,497 | 9,279,605 | |||||||

Microsoft Corp. (Software) | 464,120 | 20,490,898 | ||||||||

Apple, Inc. (Tech. Hardware, Storage & Periph.) | 84,245 | 10,566,429 | ||||||||

EMC Corp. (Tech. Hardware, Storage & Periph.) | 509,530 | 13,446,497 | ||||||||

|

| |||||||||

| 82,845,790 | ||||||||||

|

| |||||||||

MATERIALS – 5.2% | ||||||||||

Albemarle Corp. (Chemicals) | 96,050 | 5,308,684 | ||||||||

LyondellBasell Industries NV Class A (Chemicals) | 116,410 | 12,050,763 | ||||||||

Steel Dynamics, Inc. (Metals & Mining) | 443,296 | 9,182,877 | ||||||||

|

| |||||||||

| 26,542,324 | ||||||||||

|

| |||||||||

UTILITIES – 4.9% | ||||||||||

AES Corp. (Ind. Power & Renewable Elec.) | 974,371 | 12,920,159 | ||||||||

Calpine Corp. (Ind. Power & Renewable Elec.) | (a) | 688,830 | 12,392,052 | |||||||

|

| |||||||||

| 25,312,211 | ||||||||||

|

| |||||||||

Total Common Stocks (Cost $460,359,443) | $ | 501,425,847 | ||||||||

|

| |||||||||

| Master Limited Partnerships – 1.5% | Shares | Value | ||||||||

FINANCIALS – 1.5% | ||||||||||

KKR & Co. LP (Capital Markets) | 344,830 | $ | 7,879,366 | |||||||

|

| |||||||||

Total Master Limited Partnerships (Cost $7,250,558) | $ | 7,879,366 | ||||||||

|

| |||||||||

| Money Market Funds – 2.1% | Shares | Value | ||||||||

Fidelity Institutional Money Market Funds | 10,822,000 | $ | 10,822,000 | |||||||

|

| |||||||||

Total Money Market Funds (Cost $10,822,000) | $ | 10,822,000 | ||||||||

|

| |||||||||

Total Investments – 101.1% (Cost $478,432,001) | (b) | $ | 520,127,213 | |||||||

Liabilities in Excess of Other Assets – (1.1)% | (5,557,319) | |||||||||

|

| |||||||||

Net Assets – 100.0% | $ | 514,569,894 | ||||||||

|

| |||||||||

Percentages are stated as a percent of net assets.

Footnotes:

| (a) | Non-income producing security. |

| (b) | Represents cost for financial reporting purposes, which may differ from cost basis for federal income tax purposes. See also Note 7 of the Notes to Financial Statements. |

The accompanying notes are an integral part of these financial statements.

| 7 |

| Ohio National Fund, Inc. | Money Market Portfolio |

Portfolio Composition as of June 30, 2015 (1)

| % of Net Assets | ||||

Commercial Paper (2) | 54.0 | |||

U.S. Government Agency Issues | 4.1 | |||

Money Market Funds and | 41.9 | |||

|

| |||

| 100.0 | ||||

|

|

Top 10 Portfolio Holdings as of June 30, 2015 (1) (2)

| % of Net Assets |

1. Prudential Funding LLC | 4.6 | |||

2. U.S. Bank | 4.6 | |||

3. Federated Prime Cash Obligations | 4.6 | |||

4. Fidelity Institutional Money Market | 4.6 | |||

5. First American Prime Obligations | 4.6 | |||

6. Wal-Mart Stores, Inc. | 4.6 | |||

7. Exxon Mobil Corp. | 4.6 | |||

8. Nestle Capital Corp. | 4.6 | |||

9. Johnson & Johnson | 4.6 | |||

10. Toyota Motor Credit Corp. | 4.6 |

| (1) | Composition of Portfolio subject to change. |

| (2) | Sectors: |

| % of Net Assets | ||||

Financials | 22.3 | |||

Consumer Staples | 9.1 | |||

Information Technology | 8.6 | |||

Energy | 5.3 | |||

Health Care | 4.6 | |||

Consumer Discretionary | 4.1 | |||

|

| |||

| 54.0 | ||||

|

|

| 8 |

| Ohio National Fund, Inc. | Money Market Portfolio |

Schedule of Investments | June 30, 2015 (Unaudited) |

| Commercial Paper – 54.0% | (b) Rate | Maturity | Face Amount | Amortized Cost | ||||||||||||

CONSUMER DISCRETIONARY – 4.1% | ||||||||||||||||

Walt Disney Co. / The (Media) | (a) | 0.070% | 07/01/2015 | $ | 8,000,000 | $ | 8,000,000 | |||||||||

|

| |||||||||||||||

CONSUMER STAPLES – 9.1% | ||||||||||||||||

Wal-Mart Stores, Inc. (Food & Staples Retailing) | (a) | 0.050% | 07/06/2015 | 9,000,000 | 8,999,938 | |||||||||||

Nestle Capital Corp. (Food Products) | (a) | 0.060% | 07/20/2015 | 9,000,000 | 8,999,715 | |||||||||||

|

| |||||||||||||||

| 17,999,653 | ||||||||||||||||

|

| |||||||||||||||

ENERGY – 5.3% | ||||||||||||||||

Chevron Corp. (Oil, Gas & Consumable Fuels) | (a) | 0.080% | 07/16/2015 | 1,500,000 | 1,499,950 | |||||||||||

Exxon Mobil Corp. (Oil, Gas & Consumable Fuels) | 0.080% | 07/06/2015 | 9,000,000 | 8,999,900 | ||||||||||||

|

| |||||||||||||||

| 10,499,850 | ||||||||||||||||

|

| |||||||||||||||

FINANCIALS – 22.3% | ||||||||||||||||

U.S. Bank (Commercial Banks) | 0.050% | 07/01/2015 | 9,000,000 | 9,000,000 | ||||||||||||

American Honda Finance Corp. (Consumer Finance) | 0.110% | 07/23/2015 | 9,000,000 | 8,999,395 | ||||||||||||

John Deere Capital Corp. (Consumer Finance) | (a) | 0.120% | 07/21/2015 | 8,000,000 | 7,999,466 | |||||||||||

Toyota Motor Credit Corp. (Consumer Finance) | 0.100% | 07/13/2015 | 9,000,000 | 8,999,700 | ||||||||||||

Prudential Funding LLC (Insurance) | 0.030% | 07/01/2015 | 9,000,000 | 9,000,000 | ||||||||||||

|

| |||||||||||||||

| 43,998,561 | ||||||||||||||||

|

| |||||||||||||||

HEALTH CARE – 4.6% | ||||||||||||||||

Johnson & Johnson (Pharmaceuticals) | (a) | 0.050% | 07/24/2015 | 9,000,000 | 8,999,713 | |||||||||||

|

| |||||||||||||||

INFORMATION TECHNOLOGY – 8.6% | ||||||||||||||||

International Business Machines Corp. (IT Services) | (a) | 0.090% | 07/27/2015 | 9,000,000 | 8,999,415 | |||||||||||

Microsoft Corp. (Software) | (a) | 0.070% | 07/22/2015 | 8,000,000 | 7,999,673 | |||||||||||

|

| |||||||||||||||

| 16,999,088 | ||||||||||||||||

|

| |||||||||||||||

Total Commercial Paper (Cost $106,496,865) | $ | 106,496,865 | ||||||||||||||

|

| |||||||||||||||

| U.S. Government Agency Issues – 4.1% | Rate | Maturity | Face Amount | Amortized Cost | ||||||||||||

Federal Home Loan Bank | 0.030% | 07/15/2015 | $ | 8,000,000 | $ | 7,999,907 | ||||||||||

|

| |||||||||||||||

Total U.S. Government Agency Issues (Cost $7,999,907) | $ | 7,999,907 | ||||||||||||||

|

| |||||||||||||||

| Money Market Funds – 13.7% | Shares | Value | ||||||||||||||

Federated Prime Cash Obligations Fund – Institutional Class | 0.070% | 07/01/2015 | 9,000,000 | $ | 9,000,000 | |||||||||||

Fidelity Institutional Money Market Funds Money Market Portfolio – Class I | 0.100% | 07/01/2015 | 9,000,000 | 9,000,000 | ||||||||||||

First American Prime Obligations Fund – Class Z | 0.030% | 07/01/2015 | 9,000,000 | 9,000,000 | ||||||||||||

|

| |||||||||||||||

Total Money Market Funds (Cost $27,000,000) | $ | 27,000,000 | ||||||||||||||

|

| |||||||||||||||

Total Investments – 71.8% (Cost $141,496,772) | (c) | $ | 141,496,772 | |||||||||||||

Other Assets in Excess of Liabilities – 28.2% | 55,694,038 | |||||||||||||||

|

| |||||||||||||||

Net Assets – 100.0% | $ | 197,190,810 | ||||||||||||||

|

| |||||||||||||||

Percentages are stated as a percent of net assets.

Footnotes:

| (a) | Security exempt from registration under Section 4 (2) of the Securities Act of 1933. These securities may be resold in transactions exempt from registration, normally to qualified buyers under Rule 144A. At June 30, 2015, the value of these securities totaled $61,497,870, or 31.2% of the Portfolio’s net assets. These securities were deemed liquid pursuant to procedures approved by the Board of Directors. |

| (b) | Rate presented is the effective yield at the time of purchase. |

| (c) | Represents cost for federal income tax and financial reporting purposes. See also Note 2 regarding the use of amortized cost for valuation of instruments in this Portfolio. |

The accompanying notes are an integral part of these financial statements.

| 9 |

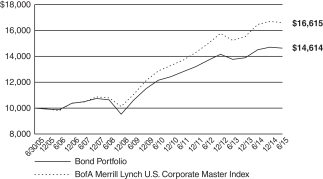

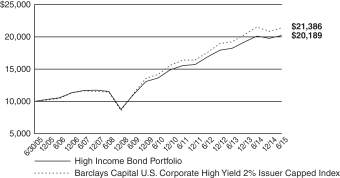

| Ohio National Fund, Inc. | Bond Portfolio |

Objective/Strategy

The Bond Portfolio seeks to obtain a high level of income and opportunity for capital appreciation consistent with the preservation of capital by investing primarily in intermediate-term and long-term fixed income securities.

Performance as of June 30, 2015

Average Annual Returns: | ||||

One year | 0.78% | |||

Five years | 3.79% | |||

Ten years | 3.87% |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. Total return figures include change in share price and reinvestment of dividends and capital gains. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information up to the most recent month end, call toll-free 1-877-781-6392.

The Portfolio is not open to direct retail investment. Beneficial interest in shares is obtained solely by purchase of variable life insurance policies and variable annuity contracts. Actual performance results for variable annuity and variable universal life contracts will be lower due to contract charges. Consult your contract for applicable charges.

Comments

For the six-month period ended June 30, 2015, the Bond Portfolio returned -0.58% versus -0.46% for the current benchmark, the BofA Merrill Lynch U.S. Corporate Master Index (the “Index”).

Both the Portfolio and the Index had small negative returns for the six-month period because U.S. Treasury yields increased across much of the yield curve, particularly on the long end, and credit spreads widened marginally. For the six-month period, the 10-year Treasury yield increased 18 basis points and the 30-year Treasury yield increased 37 basis points. Interest rates moved higher in anticipation of the Federal Reserve beginning to tighten credit later this year. As measured by the Index, credit spreads widened 4 basis points during the period. Credit spreads widened, primarily because of weakness in energy-related industries as a result of the collapse in oil prices last year and, to a lesser extent, from shareholder-friendly actions taken by companies that increased leverage marginally.

The Portfolio under-performed the Index by 12 basis points during the six-month period, primarily due to the Portfolio’s expenses. For the period, the Portfolio’s expense ratio was 32 basis points (not annualized). Other factors impacting relative performance include the Portfolio’s duration, its credit quality and the allocation to the energy sector. The Portfolio’s duration positioning benefited relative performance because the Portfolio’s duration was approximately 0.25 years short of the Index during a time period when Treasury yields rose. The Portfolio’s credit quality stratification also benefited relative performance. The Portfolio was under-weighted in A and AA rated securities, which under-performed, and was over-weighted in BBB rated securities which outperformed. The approximate 2% weighting in BB rated securities also added to relative performance. (1)

With the exception of one industry sector, differences in industry weighting between the Portfolio and the Index had little impact on relative performance. The Portfolio had a 4% under-weighting to the oil and gas sector at the start of the year, but after the energy sector performed so poorly early in the year, bonds in the oil and gas sector were purchased, bringing the allocation to this sector to a near 1% over-weighting by the end of the first-half. The increase in the

weighting to the oil and gas sector benefited relative performance because this sector performed very well late in the first-half of 2015. The approximate 10% under-weighting in the banking sector had little impact on relative performance because the banking sector performed about as well as the Index did overall. The Portfolio was over-weighted in the utilities sector by approximately 4% and this had a minor negative impact on relative performance because utilities under-performed. The approximate 4% under-weighting to the telecommunications sector also benefited relative performance because this sector underperformed. (1)

Because the U.S. economy continues its slow growth, and there were no significant leveraging events during the first half of 2015, the credit quality of the holdings in the Portfolio was maintained. That being said, the five bonds that performed the worst were Time Warner Cable, Inc., The Allstate Corp., Chesapeake Energy Corp., South Carolina Electric and Gas Co., and American International Group, Inc. All but one of these bonds have long maturities, and their bond prices were negatively impacted as interest rates rose during the period. In addition to having a long maturity, the price of the Time Warner Cable, Inc. bond was hurt when its merger with Comcast Corp. was called off and the company later agreed to a merger with Charter Communications, Inc. The price of the Chesapeake Energy Corp. security was negatively impacted by low oil prices. (1)

The five best performing bonds were The Williams Cos., Inc., Southwestern Energy Co., Targa Resources Partners LP, Kohl’s Corp., and LG&E and KU Energy LLC. The Williams Cos., Inc., bond performed very well on news that the holding company would be merged into its operating company. One energy-related name, Targa Resources Partners LP, was both bought and sold during the six-month period to take advantage of the opportunities available in the energy sector. (1)

We expect the U.S. economy to continue to grow through the end of the year. While concerns regarding China and Greece have made their way into the headlines, the risks to both regions should not impact the U.S. economy. The corporate profit picture looks positive but shareholder-friendly actions taken by companies will increase leverage and could pressure credit spreads. We can also expect rising interest rates as the year progresses because the Federal Reserve will likely begin to tighten the federal funds rate sometime in the second half of the year. For this reason, we expect to maintain the duration of the Portfolio short of the Index duration. Interest rates are so low now that the risk for fixed income investors is a rise in rates. Because the outlook for corporate profits continues to be good, we plan to continue to overweight what we consider to be solid BBB investment grade bonds. We also expect to add some BB high yield bonds to the Portfolio if credit spreads for these securities widen. We would rather take credit risk than interest rate risk given the low level of interest rates. (1)

| (1) | The Portfolio’s composition is subject to change. Holdings and weightings are as of June 30, 2015. |

| 10 | (continued) |

| Ohio National Fund, Inc. | Bond Portfolio (Continued) |

Change in Value of $10,000 Investment

Hypothetical illustration based on past performance. Future performance will vary. The Portfolio’s returns reflect reinvested dividends. The Portfolio’s holdings may differ significantly from the securities in the index. The index is unmanaged and therefore does not reflect the cost of portfolio management and accounting.

The BofA Merrill Lynch U.S. Corporate Master Index tracks the performance of all U.S. dollar-denominated, investment grade corporate public debt issued in the U.S. domestic bond market. Qualifying bonds must have an investment grade rating (based on an average of Moody’s, S&P, and Fitch). In addition, qualifying securities must have at least one year remaining term to maturity, a fixed coupon schedule, and a minimum amount outstanding of $250 million.

Portfolio Composition as of June 30, 2015 (1)

| % of Net Assets | ||||

Corporate Bonds (3) | 97.2 | |||

Asset-Backed Securities (3) | 0.6 | |||

Money Market Funds and | 2.2 | |||

|

| |||

| 100.0 | ||||

|

|

Top 10 Portfolio Holdings as of June 30, 2015 (1) (2)

| % of Net Assets |

1. Fifth Third Bancorp | 1.2 | |||

2. Union Electric Co. | 1.0 | |||

3. Janus Capital Group, Inc. | 1.0 | |||

4. Prudential Financial, Inc. | 1.0 | |||

5. Kansas City Power & Light Co. | 1.0 | |||

6. CSX Corp. | 1.0 | |||

7. Bunge NA Finance LP | 1.0 | |||

8. Comerica Bank | 1.0 | |||

9. Weatherford International Ltd. | 1.0 | |||

10. Hartford Financial Services | 1.0 |

| (1) | Composition of Portfolio subject to change. |

| (2) | Short-term investments have been excluded from the list of Top 10 Portfolio Holdings. |

| (3) | Sectors (combined): |

| % of Net Assets | ||||

Financials | 26.4 | |||

Energy | 16.8 | |||

Utilities | 12.0 | |||

Industrials | 10.6 | |||

Consumer Discretionary | 9.0 | |||

Health Care | 6.1 | |||

Information Technology | 5.7 | |||

Materials | 5.1 | |||

Consumer Staples | 4.1 | |||

Telecommunication Services | 2.0 | |||

|

| |||

| 97.8 | ||||

|

|

| 11 | (continued) |

| Ohio National Fund, Inc. | Bond Portfolio |

Schedule of Investments | June 30, 2015 (Unaudited) |

| Corporate Bonds – 97.2% | Rate | Maturity | Face Amount | Value | ||||||||||||

CONSUMER DISCRETIONARY – 9.0% |

| |||||||||||||||

Magna International, Inc. (Auto Components) | 3.625% | 06/15/2024 | $ | 1,000,000 | $ | 983,441 | ||||||||||

General Motors Co. (Automobiles) | 5.000% | 04/01/2035 | 900,000 | 883,669 | ||||||||||||

Darden Restaurants, Inc. (Hotels, Restaurants & Leisure) | 3.350% | 11/01/2022 | 206,000 | 193,130 | ||||||||||||

Newell Rubbermaid, Inc. (Household Durables) | 6.250% | 04/15/2018 | 500,000 | 553,919 | ||||||||||||

Mattel, Inc. (Leisure Products) | 2.350% | 05/06/2019 | 1,000,000 | 997,568 | ||||||||||||

Mattel, Inc. (Leisure Products) | 3.150% | 03/15/2023 | 625,000 | 604,379 | ||||||||||||

21st Century Fox America, Inc. (Media) | 4.500% | 02/15/2021 | 1,250,000 | 1,351,708 | ||||||||||||

Comcast Corp. (Media) | 4.250% | 01/15/2033 | 750,000 | 731,260 | ||||||||||||

Discovery Communications, LLC (Media) | 4.375% | 06/15/2021 | 1,000,000 | 1,050,889 | ||||||||||||

Discovery Communications, LLC (Media) | 3.300% | 05/15/2022 | 275,000 | 270,081 | ||||||||||||

Time Warner Cable, Inc. (Media) | 4.500% | 09/15/2042 | 425,000 | 348,240 | ||||||||||||

Time Warner, Inc. (Media) | 2.100% | 06/01/2019 | 1,400,000 | 1,389,786 | ||||||||||||

Viacom, Inc. (Media) | 4.850% | 12/15/2034 | 1,500,000 | 1,383,257 | ||||||||||||

Walt Disney Co. / The (Media) | 3.700% | 12/01/2042 | 925,000 | 846,322 | ||||||||||||

Kohl’s Corp. (Multiline Retail) | 4.000% | 11/01/2021 | 925,000 | 978,808 | ||||||||||||

AutoZone, Inc. (Specialty Retail) | 3.125% | 07/15/2023 | 925,000 | 895,838 | ||||||||||||

Bed Bath & Beyond, Inc. (Specialty Retail) | 5.165% | 08/01/2044 | 900,000 | 890,363 | ||||||||||||

|

| |||||||||||||||

| 14,352,658 | ||||||||||||||||

|

| |||||||||||||||

CONSUMER STAPLES – 4.1% |

| |||||||||||||||

Anheuser-Busch Cos., LLC (Beverages) | 5.500% | 01/15/2018 | 750,000 | 824,456 | ||||||||||||

Anheuser-Busch InBev Finance, Inc. (Beverages) | 4.000% | 01/17/2043 | 750,000 | 685,949 | ||||||||||||

CVS Health Corp. (Food & Staples Retailing) | 5.750% | 06/01/2017 | 301,000 | 325,243 | ||||||||||||

Kroger Co. / The (Food & Staples Retailing) | 2.950% | 11/01/2021 | 900,000 | 895,544 | ||||||||||||

Sysco Corp. (Food & Staples Retailing) | 4.350% | 10/02/2034 | 900,000 | 909,000 | ||||||||||||

Bunge NA Finance LP (Food Products) | 5.900% | 04/01/2017 | 1,500,000 | 1,602,162 | ||||||||||||

Philip Morris International, Inc. (Tobacco) | 4.125% | 05/17/2021 | 1,250,000 | 1,347,329 | ||||||||||||

|

| |||||||||||||||

| 6,589,683 | ||||||||||||||||

|

| |||||||||||||||

ENERGY – 16.8% | ||||||||||||||||

Ensco PLC (Energy Equip. & Svs.) | 5.200% | 03/15/2025 | 900,000 | 889,791 | ||||||||||||

Noble Holding International Ltd. (Energy Equip. & Svs.) | 4.000% | 03/16/2018 | 900,000 | 920,993 | ||||||||||||

Noble Holding International Ltd. (Energy Equip. & Svs.) | 5.950% | 04/01/2025 | 1,000,000 | 984,619 | ||||||||||||

Weatherford International Ltd. (Energy Equip. & Svs.) | 6.000% | 03/15/2018 | 1,500,000 | 1,596,049 | ||||||||||||

Anadarko Petroleum Corp. (Oil, Gas & Consumable Fuels) | 5.950% | 09/15/2016 | 1,000,000 | 1,054,080 | ||||||||||||

Buckeye Partners LP (Oil, Gas & Consumable Fuels) | 4.875% | 02/01/2021 | 1,000,000 | 1,041,702 | ||||||||||||

Chesapeake Energy Corp. (Oil, Gas & Consumable Fuels) | 4.875% | 04/15/2022 | 1,000,000 | 870,000 | ||||||||||||

Columbia Pipeline Group, Inc. (Oil, Gas & Consumable Fuels) | (a) | 4.500% | 06/01/2025 | 900,000 | 886,496 | |||||||||||

ConocoPhillips Co. (Oil, Gas & Consumable Fuels) | 3.350% | 05/15/2025 | 1,350,000 | 1,332,054 | ||||||||||||

Devon Energy Corp. (Oil, Gas & Consumable Fuels) | 3.250% | 05/15/2022 | 900,000 | 888,502 | ||||||||||||

Energy Transfer Partners LP (Oil, Gas & Consumable Fuels) | 4.750% | 01/15/2026 | 400,000 | 394,269 | ||||||||||||

Enterprise Products Operating LLC (Oil, Gas & Consumable Fuels) | 3.900% | 02/15/2024 | 1,000,000 | 1,002,810 | ||||||||||||

Kinder Morgan Energy Partners LP (Oil, Gas & Consumable Fuels) | 4.150% | 03/01/2022 | 1,000,000 | 1,000,510 | ||||||||||||

Kinder Morgan, Inc. (Oil, Gas & Consumable Fuels) | 5.300% | 12/01/2034 | 1,000,000 | 921,737 | ||||||||||||

Magellan Midstream Partners LP (Oil, Gas & Consumable Fuels) | 4.250% | 02/01/2021 | 1,000,000 | 1,062,923 | ||||||||||||

Marathon Oil Corp. (Oil, Gas & Consumable Fuels) | 3.850% | 06/01/2025 | 850,000 | 831,792 | ||||||||||||

Marathon Petroleum Corp. (Oil, Gas & Consumable Fuels) | 4.750% | 09/15/2044 | 1,000,000 | 909,481 | ||||||||||||

MarkWest Energy Partners LP / MarkWest Energy Finance Corp. (Oil, Gas & Consumable Fuels) | 4.875% | 12/01/2024 | 1,000,000 | 977,500 | ||||||||||||

Murphy Oil Corp. (Oil, Gas & Consumable Fuels) | 3.700% | 12/01/2022 | 1,400,000 | 1,279,509 | ||||||||||||

Occidental Petroleum Corp. (Oil, Gas & Consumable Fuels) | 3.125% | 02/15/2022 | 1,000,000 | 1,001,416 | ||||||||||||

Phillips 66 (Oil, Gas & Consumable Fuels) | 4.300% | 04/01/2022 | 1,300,000 | 1,363,059 | ||||||||||||

Plains All American Pipeline LP / PAA Finance Corp. (Oil, Gas & Consumable Fuels) | 2.850% | 01/31/2023 | 1,000,000 | 937,367 | ||||||||||||

Shell International Finance BV (Oil, Gas & Consumable Fuels) | 4.375% | 03/25/2020 | 1,250,000 | 1,367,314 | ||||||||||||

Southwestern Energy Co. (Oil, Gas & Consumable Fuels) | 4.050% | 01/23/2020 | 900,000 | 924,186 | ||||||||||||

TransCanada PipeLines Ltd. (Oil, Gas & Consumable Fuels) | 2.500% | 08/01/2022 | 1,425,000 | 1,350,129 | ||||||||||||

Williams Cos., Inc. / The (Oil, Gas & Consumable Fuels) | 5.750% | 06/24/2044 | 1,000,000 | 925,047 | ||||||||||||

|

| |||||||||||||||

| 26,713,335 | ||||||||||||||||

|

| |||||||||||||||

FINANCIALS – 26.4% |

| |||||||||||||||

Bank of America Corp. (Banks) | 5.650% | 05/01/2018 | 1,000,000 | 1,097,966 | ||||||||||||

Bank of America Corp. (Banks) | 4.200% | 08/26/2024 | 500,000 | 498,087 | ||||||||||||

Citigroup, Inc. (Banks) | 4.400% | 06/10/2025 | 900,000 | 895,296 | ||||||||||||

Comerica Bank (Banks) | 5.750% | 11/21/2016 | 1,500,000 | 1,598,994 | ||||||||||||

Fifth Third Bancorp (Banks) | 4.500% | 06/01/2018 | 1,750,000 | 1,852,685 | ||||||||||||

KeyCorp (Banks) | 5.100% | 03/24/2021 | 500,000 | 554,194 | ||||||||||||

PNC Bank NA (Banks) | 3.250% | 06/01/2025 | 850,000 | 828,821 | ||||||||||||

SunTrust Banks, Inc. (Banks) | 2.500% | 05/01/2019 | 1,400,000 | 1,406,898 | ||||||||||||

Wells Fargo & Co. (Banks) | 4.650% | 11/04/2044 | 1,000,000 | 954,987 | ||||||||||||

Goldman Sachs Group, Inc. / The (Capital Markets) | 3.750% | 05/22/2025 | 1,400,000 | 1,379,445 | ||||||||||||

Janus Capital Group, Inc. (Capital Markets) | (b) | 6.700% | 06/15/2017 | 1,500,000 | 1,632,186 | |||||||||||

| 12 | (continued) |

| Ohio National Fund, Inc. | Bond Portfolio (Continued) |

Schedule of Investments | June 30, 2015 (Unaudited) |

| Corporate Bonds (Continued) | Rate | Maturity | Face Amount | Value | ||||||||||||

FINANCIALS (continued) | ||||||||||||||||

Morgan Stanley (Capital Markets) | 3.750% | 02/25/2023 | $ | 1,250,000 | $ | 1,265,268 | ||||||||||

Morgan Stanley (Capital Markets) | 3.950% | 04/23/2027 | 1,000,000 | 941,241 | ||||||||||||

Northern Trust Corp. (Capital Markets) | 3.450% | 11/04/2020 | 1,000,000 | 1,057,036 | ||||||||||||

State Street Corp. (Capital Markets) | 4.375% | 03/07/2021 | 1,250,000 | 1,375,481 | ||||||||||||

Ally Financial, Inc. (Consumer Finance) | 5.125% | 09/30/2024 | 1,000,000 | 1,002,500 | ||||||||||||

Capital One Financial Corp. (Consumer Finance) | 2.450% | 04/24/2019 | 925,000 | 924,441 | ||||||||||||

Discover Financial Services (Consumer Finance) | 6.450% | 06/12/2017 | 750,000 | 814,441 | ||||||||||||

Synchrony Financial (Consumer Finance) | 4.250% | 08/15/2024 | 900,000 | 902,614 | ||||||||||||

General Electric Capital Corp. (Diversified Financial Svs.) | 5.625% | 05/01/2018 | 1,000,000 | 1,106,276 | ||||||||||||

Moody’s Corp. (Diversified Financial Svs.) | 5.250% | 07/15/2044 | 1,000,000 | 1,024,593 | ||||||||||||

Aflac, Inc. (Insurance) | 3.625% | 06/15/2023 | 1,425,000 | 1,438,184 | ||||||||||||

Allstate Corp. / The (Insurance) | 5.200% | 01/15/2042 | 500,000 | 526,195 | ||||||||||||

American International Group, Inc. (Insurance) | 3.875% | 01/15/2035 | 1,400,000 | 1,264,785 | ||||||||||||

Hartford Financial Services Group, Inc. / The (Insurance) | 5.375% | 03/15/2017 | 1,500,000 | 1,593,770 | ||||||||||||

Liberty Mutual Group, Inc. (Insurance) | (a) | 4.850% | 08/01/2044 | 1,500,000 | 1,444,116 | |||||||||||

Marsh & McLennan Cos., Inc. (Insurance) | 3.500% | 06/03/2024 | 1,400,000 | 1,393,564 | ||||||||||||

Metropolitan Life Global Funding I (Insurance) | (a) | 2.300% | 04/10/2019 | 1,500,000 | 1,508,269 | |||||||||||

New York Life Global Funding (Insurance) | (a) | 2.150% | 06/18/2019 | 1,000,000 | 1,001,832 | |||||||||||

Prudential Financial, Inc. (Insurance) | 6.100% | 06/15/2017 | 1,500,000 | 1,629,681 | ||||||||||||

Boston Properties LP (Real Estate Investment Trusts) | 3.125% | 09/01/2023 | 925,000 | 897,970 | ||||||||||||

Camden Property Trust (Real Estate Investment Trusts) | 4.250% | 01/15/2024 | 500,000 | 513,701 | ||||||||||||

Equity One, Inc. (Real Estate Investment Trusts) | 6.250% | 01/15/2017 | 1,250,000 | 1,332,269 | ||||||||||||

Federal Realty Investment Trust (Real Estate Investment Trusts) | 3.000% | 08/01/2022 | 1,425,000 | 1,402,180 | ||||||||||||

HCP, Inc. (Real Estate Investment Trusts) | 4.000% | 06/01/2025 | 1,500,000 | 1,466,262 | ||||||||||||

Simon Property Group LP (Real Estate Investment Trusts) | 3.750% | 02/01/2024 | 1,475,000 | 1,508,888 | ||||||||||||

|

| |||||||||||||||

| 42,035,116 | ||||||||||||||||

|

| |||||||||||||||

HEALTH CARE – 6.1% | ||||||||||||||||

Amgen, Inc. (Biotechnology) | 4.100% | 06/15/2021 | 1,000,000 | 1,064,141 | ||||||||||||

Baxalta, Inc. (Biotechnology) | (a) | 4.000% | 06/23/2025 | 1,400,000 | 1,390,844 | |||||||||||

Gilead Sciences, Inc. (Biotechnology) | 4.500% | 02/01/2045 | 900,000 | 893,127 | ||||||||||||

Becton Dickinson and Co. (Health Care Equip. & Supplies) | 5.000% | 05/15/2019 | 500,000 | 546,273 | ||||||||||||

AmerisourceBergen Corp. (Health Care Providers & Svs.) | 4.875% | 11/15/2019 | 500,000 | 550,907 | ||||||||||||

Express Scripts Holding Co. (Health Care Providers & Svs.) | 2.250% | 06/15/2019 | 1,400,000 | 1,387,644 | ||||||||||||

Laboratory Corp. of America Holdings (Health Care Providers & Svs.) | 3.750% | 08/23/2022 | 425,000 | 429,362 | ||||||||||||

Quest Diagnostics, Inc. (Health Care Providers & Svs.) | 2.700% | 04/01/2019 | 1,000,000 | 1,007,561 | ||||||||||||

AbbVie, Inc. (Pharmaceuticals) | 2.900% | 11/06/2022 | 1,425,000 | 1,378,575 | ||||||||||||

Merck Sharp & Dohme Corp. (Pharmaceuticals) | 5.000% | 06/30/2019 | 1,000,000 | 1,112,711 | ||||||||||||

|

| |||||||||||||||

| 9,761,145 | ||||||||||||||||

|

| |||||||||||||||

INDUSTRIALS – 10.0% | ||||||||||||||||

BAE Systems Holdings, Inc. (Aerospace & Defense) | (a) | 6.375% | 06/01/2019 | 750,000 | 854,739 | |||||||||||

Lockheed Martin Corp. (Aerospace & Defense) | 3.350% | 09/15/2021 | 1,000,000 | 1,028,106 | ||||||||||||

Lockheed Martin Corp. (Aerospace & Defense) | 3.600% | 03/01/2035 | 1,000,000 | 920,609 | ||||||||||||

Raytheon Co. (Aerospace & Defense) | 4.400% | 02/15/2020 | 1,250,000 | 1,367,560 | ||||||||||||

FedEx Corp. (Air Freight & Logistics) | 4.900% | 01/15/2034 | 1,425,000 | 1,473,055 | ||||||||||||

American Airlines Group, Inc. (Airlines) | (a) | 4.625% | 03/01/2020 | 1,000,000 | 967,500 | |||||||||||

Waste Management, Inc. (Commercial Svs. & Supplies) | 6.100% | 03/15/2018 | 500,000 | 557,927 | ||||||||||||

Deere & Co. (Machinery) | 4.375% | 10/16/2019 | 1,250,000 | 1,369,761 | ||||||||||||

Illinois Tool Works, Inc. (Machinery) | 3.375% | 09/15/2021 | 500,000 | 521,785 | ||||||||||||

Parker-Hannifin Corp. (Machinery) | 4.200% | 11/21/2034 | 1,400,000 | 1,391,340 | ||||||||||||

Burlington Northern Santa Fe, LLC (Road & Rail) | 4.550% | 09/01/2044 | 900,000 | 887,522 | ||||||||||||

CSX Corp. (Road & Rail) | 5.600% | 05/01/2017 | 1,500,000 | 1,616,664 | ||||||||||||

Norfolk Southern Corp. (Road & Rail) | 3.000% | 04/01/2022 | 600,000 | 596,167 | ||||||||||||

Union Pacific Corp. (Road & Rail) | 4.000% | 02/01/2021 | 1,250,000 | 1,348,208 | ||||||||||||

Union Pacific Corp. (Road & Rail) | 3.250% | 08/15/2025 | 1,000,000 | 988,005 | ||||||||||||

|

| |||||||||||||||

| 15,888,948 | ||||||||||||||||

|

| |||||||||||||||

INFORMATION TECHNOLOGY – 5.7% | ||||||||||||||||

Harris Corp. (Communications Equip.) | 2.700% | 04/27/2020 | 900,000 | 887,724 | ||||||||||||

QUALCOMM, Inc. (Communications Equip.) | 3.450% | 05/20/2025 | 1,000,000 | 972,959 | ||||||||||||

Denali Borrower LLC / Denali Finance Corp. (Computers & Peripherals) | (a) | 5.625% | 10/15/2020 | 900,000 | 946,125 | |||||||||||

Computer Sciences Corp. (IT Svs.) | 6.500% | 03/15/2018 | 1,000,000 | 1,104,148 | ||||||||||||

Intel Corp. (Semiconductors & Equip.) | 4.000% | 12/15/2032 | 1,500,000 | 1,433,273 | ||||||||||||

KLA-Tencor Corp. (Semiconductors & Equip.) | 3.375% | 11/01/2019 | 900,000 | 923,756 | ||||||||||||

Microsoft Corp. (Software) | 3.500% | 02/12/2035 | 400,000 | 364,499 | ||||||||||||

Oracle Corp. (Software) | 4.300% | 07/08/2034 | 1,500,000 | 1,474,769 | ||||||||||||

Apple, Inc. (Tech. Hardware, Storage & Periph.) | 2.500% | 02/09/2025 | 1,000,000 | 936,210 | ||||||||||||

|

| |||||||||||||||

| 9,043,463 | ||||||||||||||||

|

| |||||||||||||||

| 13 | (continued) |

| Ohio National Fund, Inc. | Bond Portfolio (Continued) |

Schedule of Investments | June 30, 2015 (Unaudited) |

| Corporate Bonds (Continued) | Rate | Maturity | Face Amount | Value | ||||||||||||

MATERIALS – 5.1% | ||||||||||||||||

Dow Chemical Co. / The (Chemicals) | 4.250% | 10/01/2034 | $ | 1,400,000 | $ | 1,311,128 | ||||||||||

Eastman Chemical Co. (Chemicals) | 3.600% | 08/15/2022 | 1,000,000 | 1,009,683 | ||||||||||||

FMC Corp. (Chemicals) | 3.950% | 02/01/2022 | 1,000,000 | 1,013,966 | ||||||||||||

Praxair, Inc. (Chemicals) | 2.650% | 02/05/2025 | 1,000,000 | 954,084 | ||||||||||||

Packaging Corp. of America (Containers & Packaging) | 4.500% | 11/01/2023 | 675,000 | 695,238 | ||||||||||||

Freeport-McMoRan, Inc. (Metals & Mining) | 3.550% | 03/01/2022 | 925,000 | 855,266 | ||||||||||||

Newmont Mining Corp. (Metals & Mining) | 3.500% | 03/15/2022 | 1,425,000 | 1,358,425 | ||||||||||||

Teck Resources Ltd. (Metals & Mining) | 3.750% | 02/01/2023 | 1,000,000 | 859,159 | ||||||||||||

|

| |||||||||||||||

| 8,056,949 | ||||||||||||||||

|

| |||||||||||||||

TELECOMMUNICATION SERVICES – 2.0% | ||||||||||||||||

AT&T, Inc. (Diversified Telecom. Svs.) | 3.400% | 05/15/2025 | 900,000 | 854,528 | ||||||||||||

Verizon Communications, Inc. (Diversified Telecom. Svs.) | 4.600% | 04/01/2021 | 1,250,000 | 1,341,921 | ||||||||||||

Verizon Communications, Inc. (Diversified Telecom. Svs.) | 3.850% | 11/01/2042 | 425,000 | 350,014 | ||||||||||||

Rogers Communications, Inc. (Wireless Telecom. Svs.) | 3.000% | 03/15/2023 | 700,000 | 671,505 | ||||||||||||

|

| |||||||||||||||

| 3,217,968 | ||||||||||||||||

|

| |||||||||||||||

UTILITIES – 12.0% | ||||||||||||||||

Appalachian Power Co. (Electric Utilities) | 4.600% | 03/30/2021 | 1,000,000 | 1,086,105 | ||||||||||||

Commonwealth Edison Co. (Electric Utilities) | 5.950% | 08/15/2016 | 1,500,000 | 1,581,858 | ||||||||||||

DTE Electric Co. (Electric Utilities) | 3.375% | 03/01/2025 | 1,000,000 | 1,010,833 | ||||||||||||

Duke Energy Florida, Inc. (Electric Utilities) | 4.550% | 04/01/2020 | 500,000 | 549,053 | ||||||||||||

ITC Holdings Corp. (Electric Utilities) | 3.650% | 06/15/2024 | 500,000 | 494,337 | ||||||||||||

Kansas City Power & Light Co. (Electric Utilities) | 5.850% | 06/15/2017 | 1,500,000 | 1,624,940 | ||||||||||||

South Carolina Electric & Gas Co. (Electric Utilities) | 4.350% | 02/01/2042 | 1,000,000 | 954,938 | ||||||||||||

Tenaska Georgia Partners LP (Electric Utilities) | 9.500% | 02/01/2030 | 439,987 | 547,328 | ||||||||||||

Union Electric Co. (Electric Utilities) | 6.400% | 06/15/2017 | 1,500,000 | 1,643,427 | ||||||||||||

Westar Energy, Inc. (Electric Utilities) | 4.125% | 03/01/2042 | 500,000 | 482,569 | ||||||||||||

Xcel Energy, Inc. (Electric Utilities) | 4.700% | 05/15/2020 | 1,000,000 | 1,089,847 | ||||||||||||

AGL Capital Corp. (Gas Utilities) | 5.250% | 08/15/2019 | 1,000,000 | 1,104,664 | ||||||||||||

Southwest Gas Corp. (Gas Utilities) | 3.875% | 04/01/2022 | 1,250,000 | 1,308,328 | ||||||||||||

Spectra Energy Capital LLC (Gas Utilities) | 3.300% | 03/15/2023 | 1,425,000 | 1,305,162 | ||||||||||||

Avista Corp. (Multi-Utilities) | 5.950% | 06/01/2018 | 1,000,000 | 1,120,865 | ||||||||||||

LG&E and KU Energy LLC (Multi-Utilities) | 4.375% | 10/01/2021 | 1,000,000 | 1,083,465 | ||||||||||||

Public Service Electric & Gas Co. (Multi-Utilities) | 3.950% | 05/01/2042 | 750,000 | 708,781 | ||||||||||||

American Water Capital Corp. (Water Utilities) | 4.300% | 12/01/2042 | 1,400,000 | 1,374,097 | ||||||||||||

|

| |||||||||||||||

| 19,070,597 | ||||||||||||||||

|

| |||||||||||||||

Total Corporate Bonds (Cost $152,543,352) | $ | 154,729,862 | ||||||||||||||

|

| |||||||||||||||

| Asset-Backed Securities – 0.6% | Rate | Maturity | Face Amount | Value | ||||||||||||

INDUSTRIALS – 0.6% | ||||||||||||||||

American Airlines 2015-1 Class B Pass Through Trust (Airlines) | 3.700% | 05/01/2023 | $ | 900,000 | $ | 882,000 | ||||||||||

|

| |||||||||||||||

Total Asset-Backed Securities (Cost $900,000) | $ | 882,000 | ||||||||||||||

|

| |||||||||||||||

| Money Market Funds – 0.7% | Shares | Value | ||||||||||||||

Fidelity Institutional Money Market Funds | 1,186,000 | $ | 1,186,000 | |||||||||||||

|

| |||||||||||||||

Total Money Market Funds (Cost $1,186,000) | $ | 1,186,000 | ||||||||||||||

|

| |||||||||||||||

Total Investments – 98.5% (Cost $154,629,352) | (c) | $ | 156,797,862 | |||||||||||||

Other Assets in Excess of Liabilities – 1.5% | 2,432,853 | |||||||||||||||

|

| |||||||||||||||

Net Assets – 100.0% | $ | 159,230,715 | ||||||||||||||

|

| |||||||||||||||

Percentages are stated as a percent of net assets.

Footnotes:

| (a) | Security exempt from registration under Regulation D of the Securities Act of 1933. These securities may be resold in transactions exempt from registration, normally to qualified buyers under Rule 144A. At June 30, 2015, the value of these securities totaled $8,999,921, or 5.7% of the Portfolio’s net assets. These securities were deemed liquid pursuant to procedures approved by the Board of Directors. |

| (b) | Represents bonds that are credit sensitive. The coupon rates for these bonds are subject to adjustment based on changes in national credit rating agency ratings. |

| (c) | Represents cost for financial reporting purposes, which may differ from cost basis for federal income tax purposes. See also Note 7 of the Notes to Financial Statements. |

The accompanying notes are an integral part of these financial statements.

| 14 |

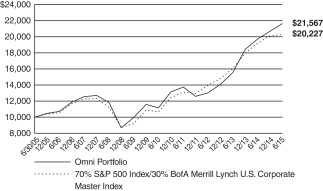

| Ohio National Fund, Inc. | Omni Portfolio |

Objective/Strategy

The Omni Portfolio seeks a high level of long-term total return consistent with preservation of capital by investing in stocks, bonds, and money market instruments.

Performance as of June 30, 2015

Average Annual Returns: | ||||

One year | 9.71% | |||

Five years | 14.12% | |||

Ten years | 7.99% |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. Total return figures include change in share price and reinvestment of dividends and capital gains. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information up to the most recent month end, call toll-free 1-877-781-6392.

The Portfolio is not open to direct retail investment. Beneficial interest in shares is obtained solely by purchase of variable life insurance policies and variable annuity contracts. Actual performance results for variable annuity and variable universal life contracts will be lower due to contract charges. Consult your contract for applicable charges.

Comments

For the six-month period ended June 30, 2015, the Omni Portfolio returned 4.55% versus 0.81% for the current benchmark, which is comprised of 70% S&P 500 Index and 30% BofA Merrill Lynch U.S. Corporate Master Index (the “Merrill Lynch Index”).

The 374 basis points of outperformance for the Portfolio versus the benchmark is the result of several factors, including outperformance by the equity portion of the Portfolio versus the S&P 500 Index, and outperformance of the bond portion of the Portfolio versus the Merrill Lynch Index. The asset allocation decision to overweight stocks and underweight bonds versus the blended benchmark also benefited relative performance because stocks outperformed bonds for the six-month period. (1)

The year began with many thinking macroeconomic fundamentals had firmed amidst global monetary easing. While the U.S. Federal Reserve ended its historic bond-buying stimulus program, the European Central Bank continued its own stimulus measures and the Japanese Central Bank continued efforts to create growth and inflation. But the end of the Federal Reserve’s quantitative easing introduced new controversy, as investors shifted to debating the timing of potential interest rate hikes. Economic data points that traditionally would have been seen as positive indicators began to raise fears that yields could move higher sooner than expected. Meanwhile, Greece reappeared in the headlines, as its position within the European Union became more uncertain. The Greek government finally agreed to more austerity and it appears that Greece will receive another bailout. Domestically, the turmoil in the North American energy sector continued to work its way through the system, with a lack of consensus about the length and depth of the downturn. These uncertainties were compounded by fear of the potential return of Iranian oil to global markets.

For the six-month period ended June 30, 2015, the equity portion of the Portfolio returned 6.51% versus 1.23% for the S&P 500 Index, for outperformance of 528 basis points. The Portfolio’s best performing stocks for the first half of 2015 were Intercept Pharmaceuticals, Inc., Pharmacyclics, Inc., Valeant Pharmaceuticals International, Inc., Humana, Inc. and Clovis Oncology, Inc. The Portfolio’s worst per-

forming stocks were Hewlett-Packard Co., PVH Corp., VeriFone Systems, Inc., Avago Technologies Ltd., and Intel Corp. The top contributors to stock performance were Clovis Oncology, Inc., Pharmacyclics, Inc., Intercept Pharmaceuticals, Inc., Valeant Pharmaceuticals International, Inc., and Mylan, Inc. The top detractors from stock performance were Hewlett-Packard Co., PVH Corp., Intel Corp., Yahoo!, Inc., and Avago Technologies Ltd. (1)

During the past six months, the equity portion of the Portfolio was overweighted in the Health Care sector, which added 748 basis points to performance, and was also overweighted in the Consumer Discretionary sector, which contributed 35 basis points to performance. The overweighted equity position in the Financials sector added 75 basis points to performance, while the overweighted equity position in the Information Technology sector detracted 97 basis points of performance. The underweighted position in the Industrials sector detracted 43 basis points, while the slight overweight in the Materials sector detracted 24 basis points of performance. (1)