UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-3334

CALVERT SOCIAL INVESTMENT FUND

(Exact name of registrant as specified in charter)

4550 Montgomery Avenue

Suite 1000N

Bethesda, Maryland 20814

(Address of Principal Executive Offices)

William M. Tartikoff, Esq.

4550 Montgomery Avenue

Suite 1000N

Bethesda, Maryland 20814

(Name and Address of Agent for Service)

Registrant's telephone number, including area code: (301) 951-4800

Date of fiscal year end: September 30

Date of reporting period: Twelve months ended September 30, 2010

Choose Planet-friendly E-delivery!

Sign up now for on-line statements, prospectuses, and fund reports. In less than five minutes you can help reduce paper mail and lower fund costs.

Just go to www.calvert.com, click on My Account, and select the documents you would like to receive via e-mail.

If you’re new to account access, you’ll be prompted to set up a personal identification number for your account. Once you’re in, click on the E-delivery sign-up at the bottom of the Account Portfolio page and follow the quick, easy steps.

TABLE

OF CONTENTS

4 Founding Chairman’s Letter

8 President’s Letter

11 Money Market Portfolio Management Discussion

14 Balanced Portfolio Management Discussion

19 Bond Portfolio Management Discussion

24 Equity Portfolio Management Discussion

29 Enhanced Equity Portfolio Management Discussion

34 Shareholder Expense Example

39 Report of Independent Registered Public Accounting Firm

40 Statements of Net Assets

75 Notes to Statements of Net Assets

80 Statements of Operations

82 Statements of Changes in Net Assets

91 Notes to Financial Statements

107 Financial Highlights

127 Explanation of Financial Tables

129 Proxy Voting and Availability of Quarterly Portfolio Holdings

130 Trustee and Officer Information Table

Dear Shareholder,

As this fiscal year comes to a close, the country is still a bit shell-shocked from the effects of the Great Recession. The high unemployment rate of 9.6% as of September shows little sign of improvement. Housing prices have not recovered and millions of homes are in foreclosure. People are angry about Wall Street’s greed and the lack of concern shown for investors. Neither those who invested in the banks nor the banks themselves overall have made much money in recent years. In spite of this, the bank executives continue to take home billions in salaries and bonuses.

The good news in this story is the changing attitudes of many in the younger generation who are beginning to think in terms of taking charge through self reliance, social business, making an impact, and other world views your fund has long supported. Indeed, the most popular club now at Harvard Business School is the Social Enterprise Club.

In My View

Some suggest we are in a process of deleveraging our debts that will take several years to complete. It’s true that the negative U.S. savings rate we saw before the financial crisis is now a healthy positive number. But the higher savings rate has come at the cost of lower overall demand, which is keeping the economy in the doldrums. Economists have not yet figured out how to send a memo about this imbalance to the financial economy while keeping the real economy on track.

The Obama administration’s economists, whom I do admire, haven’t been able to articulate a vision to inspire the country forward. In fact, for the first time in American history, the next generation does not expect to live as well as their parents. We need programs that will provide America the productivity for the future and take care of the many retirees.

We also need to change our immigration policies and encourage more talented entrepreneurs to come here. And frankly, we need to make it simple for the new rich throughout the world to buy second homes, spend money, and educate their children in the universities here. We have borrowed so much money from abroad to buy goods from abroad that letting people spend those earnings in our great country would be a pretty good deal for the United States.

Since Congress can’t seem to agree on anything, the Federal Reserve is using its few remaining bullets to flood the country with money through what they call “Quantitative Easing Program #2” (QE2)--in short, printing money and buying up certain types of bonds to drive down long-term rates and “encourage” people to take more risk with their money. But monetary policy can only do so much, and forcing people onto a risk curve by not paying them for holding onto their money is a dubious policy that may end with much disappointment. Due to this QE2 policy, bond prices have risen and interest rates have fallen. Many now think, as I do, that it may be better for long-term investors to keep a good portion of their assets in stocks, particularly in U.S. companies that have substantial earnings from abroad, and take advantage of the recovery of stock markets around the world over the next few years.

We need more bold approaches and out-of-the-box ideas to get the economy moving again. As I write this, I am at an Opportunity Collaboration conference in Mexico, which is focused on serving the poor around the world. Perhaps we should be making major social impact investments to relieve poverty through training and infrastructure--like clean water--to enfranchise billions into the world economy. We need to have a vision for a global economy. And we need to build up the much larger emerging world so that it can buy the higher-value U.S. products and services that create sustainable jobs.

In the meantime, Calvert continues to work hard to ensure that you have a say in charting new paths to a more prosperous future. Below are a few ways we have done so over the past 12 months.

Shareholder Resolutions

For the 2010 proxy season, Calvert filed a record 45 resolutions—including 30 as the lead filer. Resolution issues focused on climate change, board and employee diversity, executive compensation, sustainability reporting, and political contributions. Thus far, we have negotiated 31 successful withdrawals after the companies have agreed to address our objectives.

The resolutions featured two new issues this year—climate change adaptation and board chair independence. The first asked Dover Corporation to report on how it plans to assess and manage the impact of climate change on its business. Management agreed, so the resolution was successfully withdrawn.

On the second new issue, we recommended that Chesapeake Energy and Eaton Corporation separate the Board of Directors Chair and CEO positions to strengthen the Board’s oversight of company management and accountability to shareholders (which is emerging as a corporate governance best practice). Both resolutions were successfully withdrawn after management agreed to appoint a Lead Independent Director.

Community Investments

Many of our Funds participate in Calvert’s High Social Impact Investing program, which is administered through the Calvert Social Investment Foundation. This community investment program may allocate a small percentage of Fund assets at below-market interest rates to investments that provide economic opportunity for struggling populations.1

The Foundation recently launched its Green Strategies to Fight Poverty™ investment initiative, which allows investors to target their Community Investment Note investments to organizations and projects that both fight poverty and protect the environment. Finally, although we were sad to see her go, we’re excited that Calvert Foundation President Shari Berenbach was asked to join the Obama administration and lead microfinance initiatives for USAID.

Special Equities

A modest but important portion of certain funds is allocated to small private companies that are developing products or services that address important sustainability or environmental issues. CSIF Equity Portfolio has invested in Marrone Bio Innovations, which uses bio-based systems to control pests and weeds and recently received emergency-use approval from the EPA to sell its new invasive mussel control system in certain areas of the western U.S. The company also submitted a second organic herbicide product--for use on both organic and industrial farms--for approval to the EPA.

Calvert Large Cap Growth Fund invested in the Berkeley Renewable Energy Asia Fund, which brings renewable energy to areas of the world without access to a central power grid. Led by a management team with a long history in the industry, Berkeley mitigates the construction risk by helping communities build the plants and then sell them to a service provider once they’re up and running.2

Finally, I just want to say that so many people at these conferences I attend have said thank you for the work Calvert’s been doing in this area for such a long time. While I am happy to hear their appreciation, the thanks truly go to you--because your participation in the Fund has made this pioneering work possible.

Wayne Silby

Founding Chair

October 2010

1 As of September 30, 2010, Calvert Social Investment Foundation Community Investment Notes represented the following percentages of Fund net assets: Calvert Social Investment Fund (CSIF) Balanced Portfolio 0.94%, CSIF Bond Portfolio 0.34%, CSIF Equity Portfolio 0.52%, Calvert Capital Accumulation Fund 1.29%, Calvert World Values International Equity Fund 1.19%, Calvert New Vision Small Cap Fund 0.78%, and Calvert Large Cap Growth Fund 0.56%. The Calvert Social Investment Foundation is a 501(c)(3) nonprofit organization. The Foundation’s Community Investment Note Program is not a mutual fund and should not be confused with any Calvert Group-sponsored investment product.

2 As of September 30, 2010, Marrone Bio Innovations represented 0.05% of CSIF Equity Portfolio; Berkeley Renewable Energy Asia Fund represented 0.002% of Calvert Large Cap Growth Fund. All holdings are subject to change without notice.

As of September 30, 2010, the following companies represented the following percentages of Fund net assets: Dover Corporation represented 0.15% of Calvert Social Index Fund. Chesapeake Energy represented 0.22% of CSIF Balanced Portfolio, 0.79% of CSIF Bond Portfolio, and 0.22% of Calvert Social Index Fund. Eaton Corporation represented 0.52% of CSIF Enhanced Equity Portfolio and 0.20% of Calvert Social Index Fund. All holdings are subject to change without notice.

Dear Shareholders:

Over the 12-month reporting period, the U.S. financial markets and economy continued to recover, in fits and starts, from the “Great Recession.” As economic data vacillated between good and bad news on employment, housing trends, business strength, and consumer confidence, market volatility and investor sentiment also see-sawed.

During the winter, investors became less risk averse, pouring money into higher-yielding areas of the bond market as well as stocks, which reached 18-month highs in March. Later in the spring, however, investor sentiment took an abrupt turn as confidence in the global economic recovery waned and fears of a double-dip recession grew. Following a dismal August for the stock market, September saw a surge in stock prices lifted by strong corporate earnings reports and renewed investor interest in bargain-priced stocks. In the bond market, Treasury yields moved lower over the 12-month reporting period and corporate bonds generally performed well.

Economic Recovery Slow But on Track

Looking ahead, the pace of economic recovery has clearly slowed, causing Federal Reserve (Fed) Chairman Ben Bernanke to say that the Fed stands ready to use all of the tools at its disposal to reinvigorate the U.S. economy. In our view, while the country faces sobering challenges related to the unemployment rate, high levels of government debt, and the stumbling housing market, we also see encouraging signs of economic recovery. Overall, companies have strong balance sheets and cash positions, have reported stronger-than-expected corporate earnings, and are investing in their businesses. Consumers are generally “deleveraging” by saving more and paying down their debt. Financial reform is under way in the U.S. that may help reassure investors and stabilize the markets. Globally, central banks around the world are continuing to pursue extremely accommodative monetary policies to encourage economic recovery.

In this transitional environment, we believe that both the equity and fixed-income markets are likely to continue to be somewhat volatile. In our view, investment strategies that include sustainability criteria may be better positioned to weather these uncertainties and provide long-term value.

Markets Challenged, But Gain Ground

Despite the volatility over the course of the 12-month reporting period, domestic and international stocks had moved solidly ahead by the end of the period. U.S. stock indexes reported 12-month gains across all styles, strategies, and capitalization ranges. The large-cap Russell 1000 Index and the Standard & Poor’s 500 Index returned 10.75% and 10.16%, respectively. Mid-cap stocks were the top-performing category, with the Russell Midcap Index up 17.54%, while the small-cap Russell 2000 Index rose 13.35%. In terms of style, growth stocks moderately outpaced value stocks. On the international front, the MSCI EAFE Investable Market Index (IMI), a benchmark for international stocks, edged up 4.23%, and the MSCI Emerging Markets IMI was up 21.97%.

In the fixed-income markets, the Barclays Capital U.S. Credit Index, a market barometer for investment-grade bonds, was up 11.67%. In line with the Fed’s federal funds rate target of 0% to 0.25%, money market returns remained very low.

The Gulf of Mexico Oil Spill and the Extractives Industry

In the wake of the April 20 oil spill in the Gulf of Mexico, Americans have continued to grapple with the devastation caused by the spill and its long-term environmental, societal, and economic implications. Calvert shares the concern and the frustration felt by the millions of people affected by this tragedy.

Following the spill, Calvert met with BP officials, urging BP not only to clean up the current spill, but also to implement stronger safety and process management standards for its contractors. We are also evaluating how our advocacy objectives with deepwater oil-drilling companies may help prevent such disasters in the future.

In terms of extraction methodologies, Calvert has long recognized that as readily accessible supplies of oil and gas dry up, companies may be forced to seek mineral resources in countries with poor governance, weak rule of law, and high levels of corruption. Accordingly, over the past two years, we have been a leading advocate for transparency requirements for extractive industries. In July, the U.S. Congress passed legislation requiring companies to disclose payments that they make to the U.S. or foreign governments for the purpose of commercial development of oil, natural gas, or minerals. We believe this legislation is a milestone toward helping advance environmental sustainability in this industry.

In our view, the oil spill also underlines the urgency for expanded investment—with greater federal incentives—in alternative energy sources.

Financial Reform Under Way

Looking ahead, long-awaited financial reform is under way with Congressional passage of the largest financial reform bill since the Great Depression. The Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act) is designed to address inadequate regulation of Wall Street firms and the type of unrestrained environment that contributed to the credit crisis of 2008 and the ensuing global market meltdown. The Dodd-Frank Act seeks to establish strong consumer protections, shield taxpayers from future corporate bailouts, shine a light on the “shadow markets” and derivatives trading, and expand the role of shareholders in corporate governance. While these goals are laudable, the impact of the Dodd-Frank Act on the financial industry—and ultimately its ability to prevent another financial crisis—must stand the test of time.

As the Obama administration and Congress work to implement key financial reforms, we believe that over time these efforts may work to redress some systemic imbalances in the financial system and provide additional stability to the economy and markets.

Review Your Portfolio Allocations

In our view, the financial markets are likely to be in transition for some time as the government tackles financial reform, the global economy continues to recover, and political elections in the U.S. impact a variety of government policies. Now may be an opportune time to review your overall investment strategy and portfolio allocations with your financial advisor. Check to ensure that your target mix of U.S. and international stocks, bonds, and cash is well-diversified and appropriate given your investment goals, stage of life, and attitude toward risk.

For up-to-date economic and market commentary from Calvert professionals, along with information on current Calvert sustainability initiatives, please visit our website,

www.calvert.com.

As always, we appreciate your investing with Calvert.

Sincerely,

Barbara J. Krumsiek

President and CEO

Calvert Group, Ltd.

October 2010

CSIF Money Market Portfolio

September 30, 2010

Investment Performance

(Total Return)

| 6 Months | 12 Months |

| ended | ended |

| 9/30/10 | 9/30/10 |

Class A | 0.005% | 0.01% |

Lipper Money Market Funds Average | 0.02% | 0.03% |

Average Annual Total Returns |

|

One year | 0.01% |

Five year | 2.51% |

Ten year | 2.16% |

7-Day Simple/Effective Yield |

|

|

|

7-day simple yield | 0.01% |

7-day effective yield | 0.01% |

| % of Total |

Investment Allocation | Investments |

Variable Rate | 80% |

Demand Notes |

|

U.S. Government Agencies and Instrumentalities | 14.7% |

Commercial Paper | 3.1% |

U.S. Treasury | 2.1% |

Loans and Deposit Receipts Guaranteed by U.S. Government Agencies | 0.1% |

Total | 100% |

Total return assumes reinvestment of dividends. The performance data shown represents past performance and does not guarantee future results. Investment return will fluctuate so that current performance may be lower or higher than the performance data quoted. An investment in the Fund/portfolio is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Although the Fund/Portfolio seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in the Fund/Portfolio. Visit www.calvert.com for current performance data.

Portfolio

Management

Discussion

Thomas A. Dailey of Calvert Asset Management Company

Investment Performance

For the 12-month period ended September 30, 2010, CSIF Money Market Portfolio returned 0.005%. Its benchmark, the Lipper Money Market Funds Average, returned 0.03% over the same period. The reporting period featured extremely low short-term interest rates.

Investment Climate

The 12-month period that ended September 30, 2010 was another eventful chapter in the history of the U.S. economy and financial markets. The period can be divided, roughly, into three parts. The first, from fall 2009 through winter 2010, featured solid economic growth driven by federal stimulus funding and corporate inventory replenishment. During this time, interest rates increased, with the yield on 10-year Treasury notes reaching 4% early in April.1 The Federal Reserve (Fed) began to passively withdraw monetary stimulus and prepared to more actively draw off excess reserves later in the year.

In the spring, the brewing European sovereign debt crisis boiled over and investors’ risk aversion returned. The European Union and European Central Bank struggled to establish control, which eventually affected U.S. markets. Yields on liquid, low-risk instruments like Treasuries declined, while the prices of stocks and riskier bonds fell. In addition, there was evidence that the U.S. recovery had stumbled. Indeed, economic growth, which had reached a 5% annualized rate during the last quarter of 2009,2 slowed to 1.7% annualized for the April through June period. The pace of private sector job creation also slowed, and the Fed shelved its plan to withdraw monetary stimulus.

In the summer, European leaders firmly took control of the debt crisis. Investors’ risk appetite revived and markets recovered globally. Savers sought to escape money-market yields, which were near zero percent, and investors sought higher-yielding opportunities. The U.S. economic outlook, however, remained uncertain. During the last three months of the reporting period, the Fed made it clear that low interest rates would persist. In addition, the Fed revived its Treasury purchase program during August. Bonds continued to rally, providing strong returns in the July through September quarter.

As of early October, estimates of economic growth from the Wall Street Journal survey of economic forecasters indicated that the economy grew 3.2% over the entire reporting period. This is in line with the long-term average growth rate for the United States, but is only about one-half the pace experienced during the recovery stages of past deep recessions. We believe that the recovery phase will probably end in the first quarter of 2011, when GDP growth will likely match or eclipse its 2007 high.

The core inflation rate dropped steadily during the first half of the reporting period before settling at 0.9%. It has remained at that level for the past several months.3 The dollar declined broadly, except against the euro, as investors expected the U.S. government and central bank to continue to pursue weak-dollar policies to support exports.

Portfolio Strategy

Since the Fed kept the federal funds rate at historic lows during the period, we continued to invest primarily in variable-rate demand notes and U.S. Treasury and agency securities. This strategy allowed us to provide liquidity and preserve principal without sacrificing credit quality or increasing interest-rate risk.

Outlook

Looking ahead, we think that the process of economic recovery, repair, and restructuring after the severe financial crisis of 2008 and 2009 will continue. However, deleveraging in the private sector will probably continue to act as a drag on economic growth, limiting the strength of the recovery. We expect the Fed to continue with its expansionary monetary policy to support the anemic economic recovery. On the other hand, in the current political environment, we don’t foresee the passage of any large new fiscal stimulus packages unless the economy falls into another recession.

Since the Fed has continued to use the fed funds rate to keep short-term interest rates pegged to the floor, money-market yields remain paltry. Regardless, taxable and tax-exempt money-market assets remain substantial at roughly $2.8 trillion. When the fed funds rate eventually begins to rise, the rates on variable-rate demand notes will immediately rise in response, quickly passing the income benefits on to our investors.

October 2010

1 Source for interest rate data: Federal Reserve

2 Bureau of Economic Analysis

3 Bureau of Labor Statistics

CSIF Balanced

portfolio

September 30, 2010

Investment Performance

(total return at NAV*)

| 6 Months | 12 Months |

| ended | ended |

| 9/30/10 | 9/30/10 |

Class A | 1.11% | 9.12% |

Class B | 0.63% | 8.02% |

Class C | 0.71% | 8.17% |

Class I | 1.42% | 9.72% |

Russell 1000 Index** | -1.21% | 10.75% |

Balanced Composite Benchmark | 2.50% | 11.12% |

Lipper Mixed-Asset Target Allocation Growth Funds Average | 1.20% | 9.34% |

Ten Largest Stock Holdings

| % of Net Assets |

EMC Corp. | 1.7% |

Nike, Inc., Class B | 1.7% |

Express Scripts, Inc. | 1.7% |

Microsoft Corp. | 1.5% |

Aflac, Inc. | 1.5% |

Cummins, Inc. | 1.5% |

AT&T, Inc. | 1.5% |

Colgate-Palmolive Co. | 1.5% |

FMC Technologies, Inc. | 1.5% |

Qualcomm, Inc. | 1.4% |

Total | 15.5% |

*Investment performance/return at NAV does not reflect the deduction of the Fund’s maximum 4.75% front-end sales charge or any deferred sales charge.

**In December 2009 the Fund changed its broad-based benchmark to the Russell 1000 Index from the Calvert Balanced Composite Benchmark Blend (the “Balanced Composite Benchmark”), 60% of which is comprised of the Russell 1000 Index and 40% of which is comprised of the Barclays Capital U.S. Credit Index, in order to adopt an index that is not blended. The Fund also continues to show the Balanced Composite Benchmark because it is more consistent with the Fund’s portfolio construction process and represents a more accurate reflection of the Fund’s anticipated risk and return patterns.

Portfolio Management Discussion

Natalie A. Trunow,

Senior Vice President, Chief Investment Officer - Equities of Calvert Asset Management Company

Performance

CSIF Balanced Portfolio Class A shares (at NAV) returned 9.12% for the 12-month period ended September 30, 2010, underperforming its benchmark, the Russell 1000 Index, which posted a return of 10.75%. The Portfolio’s stock and bond allocations both contributed to the underperformance.

In the Portfolio Strategy discussion below, we provide an analysis of the performance of the Portfolio relative to a secondary benchmark, which is more representative of the stock and bond allocation of this Portfolio.

Investment Climate

After a year of uncertainty about global economic recovery, stock markets worldwide ended the reporting period in positive territory. Overall, markets have largely built on the rally that started in early March 2009 as investors fluctuated between optimism and uncertainty about the sustainability of an economic recovery, including fears of a double-dip recession. However, we saw sharp sell-offs in the second quarter of 2010 after dramatic downgrades in the sovereign creditworthiness of Greece, Spain, and Dubai rattled global financial markets and escalated the economic uncertainty. But European leaders gained control of the debt crisis during the summer--reviving investors’ risk appetite and helping markets recover globally.

In the U.S., economic news throughout the period suggested a slow and sometimes uneven recovery was underway. GDP growth in the fourth quarter of 2009 turned positive for the first time since the second quarter of 2008, largely due to government stimulus efforts. However, economic recovery in the second half of 2010 has been slower than most original forecasts, with early estimates of 2.4% for the second quarter of 2010 lowered to 1.7%.

The housing market improved for a time but fell again after the first-time homebuyer credit expired, so depressed home prices continued to weigh on consumers’ shaky confidence. Since consumer spending makes up 75% of the economy, recovery will remain slow until consumers become more comfortable.

Savers sought to escape money-market yields near zero percent, and investors sought higher-yielding opportunities. During the last quarter of the period, the Fed made it clear that low interest rates would continue and also restored its U.S. Treasuries purchase program. Bonds continued to rally and provide strong returns through period end.

Early October estimates from the Wall Street Journal survey of economic forecasters indicated the economy grew 3.2% over the entire reporting period. While this is in line with the long-term average growth rate for the U.S., it is only about one-half the pace during the recovery stages of past deep recessions. We believe the recovery phase will probably end in the first quarter of 2011, when GDP growth will likely match or eclipse its 2007 high.

Portfolio Strategy

Calvert generally maintains a weighting of 60% stocks and 40% bonds in the Portfolio. With the high level of market volatility over the past year, the actual weighting has fluctuated as stock and bond returns varied. Calvert tracked the Portfolio’s stock and bond exposure throughout the period to make sure this weighting did not fluctuate excessively. Still, the sudden market shifts created a slight drag on performance during the reporting period.

Equities

The Portfolio’s stock allocation underperformed for the period primarily due to poor stock selection in the Financials and Consumer Discretionary sectors. In the Consumer Discretionary sector, Kohl’s and McGraw-Hill were among the biggest contributors to this underperformance. In Financials , investments in Goldman Sachs, Northern Trust, and Principal Financial underperformed.1

However, stock selection in the Energy and Industrials sectors benefited the Portfolio. In Energy, Smith International rose after being acquired. EOG Resources and FMC Technologies produced strong returns as well. In the Industrials sector, heavy equipment manufacturers Cummins and Deere each gained more than 60%.

Fixed Income

While the gains from our yield-curve and credit-quality strategies helped the performance of the fixed-income portion of the Portfolio, these gains were more than offset by a relatively short duration.

At the beginning of the period, we positioned the bond portion of the Portfolio for a flattening yield curve, which helped as the yield differential between two- and 10-year U.S. Treasuries compressed from 2.36 percentage points to 2.09 percentage points over the past year.

Since we also anticipated a rising interest rate environment, we allocated 6.95% of the Portfolio’s fixed-income allocation to high-yield bonds, which are not in the benchmark index. Again, this proved to be favorable as high-yield securities, as measured by the Barclays Capital U.S. Corporate High Yield Index, returned 18.44% versus 11.67% for the broad investment-grade benchmark index.

However, these gains were not enough to overcome the disadvantage of the Portfolio’s short duration relative to the benchmark. (Duration is a measure of a portfolio’s sensitivity to changes in interest rates. The longer the duration, the greater the change in price relative to interest rate movements.) The Portfolio uses Treasury futures to hedge its interest rate position. As two- and 10-year Treasury yields fell, bond prices rose. While this helped the Portfolio’s absolute returns, it helped the benchmark, with its longer relative duration, more.

Outlook

Looking ahead, we believe the process of economic recovery, repair, and restructuring will continue. However, it’s likely that deleveraging in the private sector will continue to act as a drag on economic growth and limit the strength of the recovery. But while we anticipate a somewhat more challenged earnings environment later this year, we believe that corporate sector strength is likely to persist and continue to support the overall economic recovery.

We also believe that, given relative valuations and capital flows, the sharp outperformance of bonds versus equities over the past several months is bound to reverse, with equities likely outperforming bonds over the next six to 18 months. Overall, our outlook continues to call for a slow, gradual pace to the economic recovery and a generally positive environment for the markets, barring any major geopolitical calamities.

October 2010

1All returns shown for individual holdings reflect that part of the reporting period the holdings were held.

As of September 30, 2010, the following companies represented the following percentages of Portfolio net assets: Kohl’s 0%, McGraw-Hill 1.29%, Goldman Sachs 2.35%, Northern Trust 0%, Principal Financial 0%, Smith International 0%, EOG Resources 0%, FMC Technologies 3.06%, Cummins 3.55%, and Deere 1.20%. All holdings are subject to change without notice.

CSIF Balanced

portfolio

September 30, 2010

Average Annual Total Returns

Class A Shares | (with max. load) |

One year | 4.01% |

Five year | 0.06% |

Ten year | 0.17% |

|

|

Class B Shares | (with max. load) |

One year | 3.15% |

Five year | -0.16% |

Ten year | -0.35% |

|

|

Class C Shares | (with max. load) |

One year | 7.30% |

Five year | 0.12% |

Ten year | -0.30% |

|

|

Class I Shares* |

|

One year | 9.72% |

Five year | 1.56% |

Ten year | 1.10% |

|

|

|

|

Asset Allocation | % of Total Investments |

Equity Investments | 63% |

Bonds | 37% |

| 100% |

* Note Regarding Class I Shares Total Returns: There were times during the reporting period when there were no shareholders in Class I. For purposes of reporting Average Annual Total Return, Class A performance at NAV (i.e. does not reflect deduction of the Class A front-end sales charge) is used during these periods in which there were no shareholders in Class I. For purposes of this Average Annual Total Return, the Class A performance at NAV was used during the period June 30, 2003 through December 27, 2004.

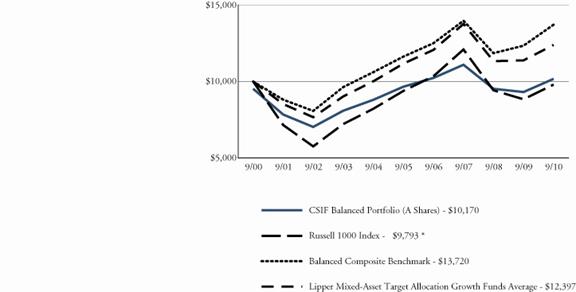

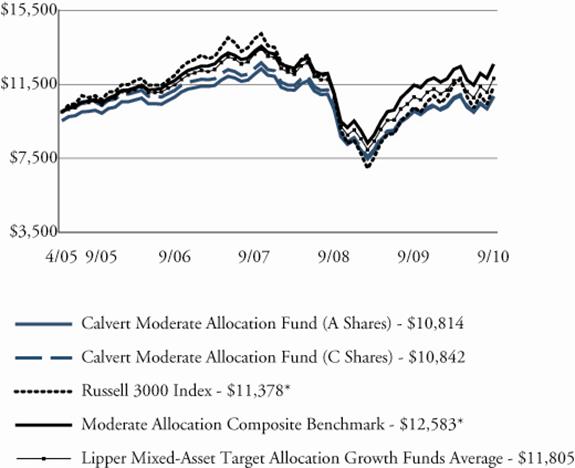

Growth of $10,000

The graph below shows the value of a hypothetical $10,000 investment in the fund over the past 10 fiscal year periods or since inception (for funds without 10-year records). The results shown are for Class A shares and reflect the deduction of the maximum front-end Class A sales charge of 4.75% and assume the reinvestment of dividends. The result is compared with benchmarks that include a broad based market index and a Lipper peer group average. Market indexes are unmanaged and their results do not reflect the effect of expenses or sales charges. The Lipper average reflects the deduction of the category’s average front-end sales charge. The value of an investment in a different share class would be different.

In December 2009 the Fund changed its broad-based benchmark to the Russell 1000 Index from the Calvert Balanced Composite Benchmark Blend (the “Balanced Composite Benchmark”), 60% of which is comprised of the Russell 1000 Index and 40% of which is comprised of the Barclays Capital U.S. Credit Index, in order to adopt an index that is not blended. The Fund also continues to show the Balanced Composite Benchmark because it is more consistent with the Fund’s portfolio construction process and represents a more accurate reflection of the Fund’s anticipated risk and return patterns.

All performance data shown, including the graph above and the adjacent table, represents past performance, does not guarantee future results, assumes reinvestment of dividends and distributions and does not reflect the deduction of taxes that a shareholder would pay on the Fund’s/Portfolio’s distributions or the redemption of the Fund/Portfolio shares. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted; for current performance data visit www.calvert.com. The gross expense ratio from the current prospectus for Class A shares is 1.31%. This number may differ from the expense ratio shown elsewhere in this report because it is based on a different tim e period and, if applicable, does not include fee or expense waivers. Performance data quoted already reflects the deduction of the Fund’s/Portfolio’s operating expenses.

CSIF Bond Portfolio

September 30, 2010

Investment Performance

(total return at NAV*)

| 6 Months | 12 Months |

| ended | ended |

| 9/30/10 | 9/30/10 |

Class A | 5.10% | 8.54% |

Class B | 4.58% | 7.47% |

Class C | 4.71% | 7.73% |

Class I | 5.48% | 9.26% |

Class Y | 5.24% | 8.83% |

Barclays Capital U.S. Credit Index | 8.07% | 11.67% |

Lipper A-Rated Corporate Debt Funds Average | 6.18% | 9.93% |

SEC Yields

| 30 days ended | |

| 9/30/10 | 9/30/09 |

Class A | 2.02% | 2.44% |

Class B | 1.06% | 1.58% |

Class C | 1.32% | 1.76% |

Class I | 2.71% | 3.15% |

Class Y | 2.32% | 2.76% |

* Investment performance/return at NAV does not reflect the deduction of the Fund’s maximum 3.75% front-end sales charge or any deferred sales charge.

Portfolio Management Discussion

Gregory Habeeb

Senior Vice President and Senior Portfolio Manager of Calvert Asset Management Company

Performance

For the 12-month reporting period ended September 30, 2010, CSIF Bond Portfolio Class (A shares at NAV) returned 8.54%, underperforming its benchmark, the Barclays Capital U.S. Credit Index (the “Index”), which returned 11.67% for the same period. The Fund’s relatively short duration was the primary reason for its underperformance.

Investment Climate

The 12-month period that ended September 30, 2010 was another eventful chapter in the history of the U.S. economy and financial markets. The period can be divided, roughly, into three parts. The first, from fall 2009 through winter 2010, featured solid economic growth driven by federal stimulus funding and corporate inventory replenishment. During this time, interest rates increased, with the yield on 10- year Treasury notes reaching 4% early in April.1 The Federal Reserve (Fed) began to passively withdraw monetary stimulus and prepared to more actively draw off excess reserves later in the year.

In the spring, the brewing European sovereign debt crisis boiled over and investors’ risk aversion returned. The European Union and European Central Bank struggled to establish control, which eventually affected U.S. markets. Yields on liquid, low-risk instruments like Treasuries declined, while the prices of stocks and riskier bonds fell. In addition, there was evidence that the U.S. recovery had stumbled. Indeed, economic growth, which had reached a 5% annualized rate during the last quarter of 2009,2 slowed to 1.7% annualized for the April through June period. The pace of private sector job creation also slowed, and the Fed shelved its plan to withdraw monetary stimulus.

In the summer, European leaders firmly took control of the debt crisis. Investors’ risk appetite revived and markets recovered globally. Savers sought to escape money-market yields, which were near zero percent, and investors sought higher-yielding opportunities. The U.S. economic outlook, however, remained uncertain. During the last three months of the reporting period, the Fed made it clear that low interest rates would persist. In addition, the Fed revived its Treasury purchase program during August. Bonds continued to rally, providing strong returns in the July through September quarter.

As of early October, estimates of economic growth from the Wall Street Journal survey of economic forecasters indicated that the economy grew 3.2% over the entire reporting period. This is in line with the long-term average growth rate for the United States, but is only about one-half the pace experienced during the recovery stages of past deep recessions. We believe that the recovery phase will probably end in the first quarter of 2011, when GDP growth will likely match or eclipse its 2007 high.

The core inflation rate dropped steadily during the first half of the reporting period before settling at 0.9%. It has remained at that level for the past several months.3 The dollar declined broadly, except against the euro, as investors expected the U.S. government and central bank to continue to pursue weak-dollar policies to support exports.

Portfolio Strategy

At the beginning of the reporting period, we expected the yield difference between long- and short-maturity Treasury securities to narrow. Consequently, we positioned the Portfolio for a flattening yield curve. As we thought, over the full reporting period the yield differential between two- and 10-year Treasuries compressed from 2.36 percentage points to 2.09 percentage points.

We also anticipated a rising interest rate environment in which returns on corporate and high-yield securities would continue to outpace Treasury returns. Accordingly, at the beginning of the reporting period, 6.95% of the Portfolio’s assets were allocated to high-yield bonds, which are not included in the benchmark index. High-yield securities, as measured by the Barclays Capital U.S. Corporate High Yield Index, returned 18.44% during the period, while the broad investment-grade benchmark index returned 11.67%.

Both our yield-curve and credit-quality strategies helped relative returns during the reporting period. However, these gains were more than offset by the Portfolio’s short duration relative to the benchmark. Duration is a measure of a portfolio’s sensitivity to changes in interest rates. The longer the duration, the greater the change in price relative to interest rate movements. The Portfolio uses Treasury futures to hedge its interest rate position. Over the 12-month reporting period, two- and 10-year Treasury yields fell by 52 and 80 basis points,4 respectively. Typically, when bond yields decline, bond prices increase. Consequently, the fund experienced a smaller increase in value than the benchmark because it had a shorter duration.

Outlook

Looking ahead, we think that the process of economic recovery, repair, and restructuring will persist. However, deleveraging in the private sector probably will continue to act as a drag on economic growth, limiting the strength of the recovery. We expect the Fed to continue to pursue expansionary monetary policy to support economic recovery. On the other hand, in the current political environment, we don’t foresee the passage of any large new fiscal stimulus packages unless the economy falls into another recession.

October 2010

1 Source for interest rate data: Federal Reserve

2 Bureau of Economic Analysis

3 Bureau of Labor Statistics

4 A basis point is 0.01 percentage points.

CSIF Bond Portfolio

September 30, 2010

| % of Total |

Economic Sectors | Investments |

Asset Backed Securities | 3.9% |

Communications | 1.9% |

Consumer, Cyclical | 1.1% |

Consumer, Non-cyclical | 2.0% |

Energy | 5.1% |

Financials | 35.5% |

Government | 41.8% |

Industrials | 2.7% |

Mortgage Securities | 4.8% |

Technology | 0.9% |

Utilities | 0.3% |

Total | 100% |

CSIF Bond Portfolio

September 30, 2010

Average Annual Total Returns

Class A Shares | (with max. load) |

One year | 4.42% |

Five year | 4.09% |

Ten year | 5.80% |

|

|

Class B Shares | (with max. load) |

One year | 3.40% |

Five year | 3.87% |

Ten year | 5.19% |

|

|

Class C Shares | (with max. load) |

One year | 6.67% |

Five year | 4.06% |

Ten year | 5.27% |

|

|

Class I Shares |

|

One year | 9.19% |

Five year | 5.52% |

Ten year | 6.83% |

|

|

Class Y Shares* |

|

One year | 8.76% |

Five year | 4.98% |

Ten year | 6.25% |

* Calvert Social Investment Fund Bond Portfolio first offered Class Y shares on October 31, 2008. Performance prior to that date reflects the performance of Class A shares at net asset value (NAV). Actual Class Y share performance would have been different.

Growth of $10,000

The graph below shows the value of a hypothetical $10,000 investment in the fund over the past 10 fiscal year periods or since inception (for funds without 10-year records). The results shown are for Class A shares and reflect the deduction of the maximum front-end sales Class A charge of 3.75% and assume the reinvestment of dividends. The result is compared with benchmarks that include a broad based market index and a Lipper peer group average. Market indexes are unmanaged and their results do not reflect the effect of expenses or sales charges. The Lipper average reflects the deduction of the category’s average front-end sales charge. The value of an investment in a different share class would be different.

All performance data shown, including the graph above and the adjacent table, represents past performance, does not guarantee future results, assumes reinvestment of dividends and distributions and does not reflect the deduction of taxes that a shareholder would pay on the Fund’s/Portfolio’s distributions or the redemption of the Fund/Portfolio shares. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted; for current performance data visit www.calvert.com. The gross expense ratio from the current prospectus for Class A shares is 1.15%. This number may differ from the expense ratio shown elsewhere in this report because it is based on a different tim e period and, if applicable, does not include fee or expense waivers. Performance data quoted already reflects the deduction of the Fund’s/Portfolio’s operating expenses.

CSIF Equity Portfolio

September 30, 2010

Investment Performance

(total return at NAV*)

| 6 Months | 12 Months |

| ended | ended |

| 9/30/10 | 9/30/10 |

Class A | 0.93% | 11.44% |

Class B | 0.46% | 10.40% |

Class C | 0.54% | 10.57% |

Class I | 1.20% | 12.04% |

Class Y | 1.05% | 11.73% |

S&P 500 Index | -1.42% | 10.16% |

Lipper Large-Cap Growth Funds Avg. | -1.18% | 10.19% |

Ten Largest Stock Holdings

| % of Net Assets |

NetFlix, Inc. | 4.6% |

Apple, Inc. | 4.4% |

QUALCOMM, Inc. | 4.2% |

Novartis AG (ADR) | 3.6% |

Hewlett-Packard Co. | 3.6% |

CVS Caremark Corp. | 3.5% |

Target Corp. | 3.0% |

Google, Inc. | 2.7% |

Gilead Sciences, Inc. | 2.7% |

Cisco Systems, Inc. | 2.7% |

Total | 35.0% |

*Investment performance/return at NAV does not reflect the deduction of the Fund’s maximum 4.75% front-end sales charge or any deferred sales charge.

Portfolio Management Discussion

Richard England

of Atlanta Capital Management Company

Performance

For the 12 months ended September 30, 2010, CSIF Equity Portfolio Class A shares (at NAV) returned 11.44%, compared with a return of 10.16% for the Standard and Poor’s (S&P) 500 Index. Strong stock selection in the Consumer Discretionary and Industrial sectors was primarily responsible for the outperformance.

Investment Climate

According to the government, the most recent recession ended in the summer of 2009. While that may be technically true, you’d have a hard time convincing most Americans. Unemployment remains high, housing is still in a funk, and much of the domestic economy simply feels stuck in the mud, so consumers are understandably in a sour mood. This has been turning the political environment on its head and keeping consumer spending uneven.

With the economy slowly bumping along, the stock market has struggled to turn the surge that began in March 2009 into a sustainable advance. We saw mostly improving economic conditions, and progress was sufficient to keep stocks generally moving higher. All that changed by April of this year. Between new fears about sovereign debt in Europe, some softer economic data in the U.S., and the thoroughly depressing oil spill in the Gulf of Mexico, investors grew skeptical about the recovery’s durability and reduced their risk exposures. As a result, stocks slid sharply into early summer.

It’s been a roller coaster since then, as stocks have risen or fallen the same 10%-12% three times. We closed out this reporting period near the high end of that range. Not only are investors lacking confidence that the U.S. economy can sustain even the tepid recovery to date, they’re also not confident that foreign economies can make up for our weakness. Finally, confidence is rapidly decreasing that politicians and policymakers care about, understand, or are capable of responding to the challenges that businesses and consumers are facing. Markets hate uncertainty and, unfortunately, we’ve got a lot of it right now.

The market’s pronounced volatility over the past year makes it tough to draw meaningful conclusions about sector performance. Among the few things that do make sense, Financials brought up the rear with a 3% decline. We think these stocks are generally quite cheap, but they need stronger conviction about a recovery to do well. It’s also understandable that Energy and Health Care lagged the market. Energy is dependent on the perception of strong global growth and the spill in the Gulf has set back the sector’s fundamentals. Health Care fundamentals are slipping a bit, partly due to the early impact of health care reform.

Some less intuitive results include Consumer Discretionary and Telecommunications stocks fighting for the top spot. Consumer Discretionary includes more than retailers, but is nonetheless tied to consumers being willing to part with their dollars. On the other hand, Telecommunications is a classic defensive sector that usually only does well when the stock market is sinking. Finally, Industrials were also strong--reflecting better growth in developing markets and, more importantly, sector-wide operational improvements that resulted in much greater earnings and cash flow than during the last recession.

Portfolio Strategy

Repositioning the Portfolio in late 2008 for the recovery we anticipated in 2009 proved crucial to our outperformance over the reporting period, despite the economic recovery lagging expectations. The changes we have made over the last 12 months have been more subtle. Individual stock decisions were the primary source of our positive relative performance, but sector-level shifts have been a net plus too.

In fact, more than 25% of our holdings—16 stocks in all—rose by more than double the market average. Netflix led the pack by a wide margin, rising 251%.1 The company has vanquished nearly all of its DVD rental competition and has been staking out an equally dominant position in Internet movie delivery—the rental method of the future. Other large gainers included Deere, Apple, and Priceline, although the latter was more about Internet hotel reservations in Europe than the “name your price” model seen in U.S. television ads.

Unfortunately, a few of our stock picks didn’t fare as well--most notably, retailer GameStop. Price-cutting last holiday season caused the company’s profits to fall well short of expectations. Believing the problems may persist, we sold the stock in January. Gilead Sciences, the leading maker of biotech drugs for HIV treatment, declined as budget pressures in various government entities modestly reduced reimbursements. While the impact on profits has been small, the market is concerned about how robustly the company can continue to grow.

As for sector positioning, an increased weighting in Consumer Discretionary and reduced weighting in Health Care helped performance. An increased weighting in Financials has not yet paid off. However, we continue to believe Financials stocks are significantly undervalued and expect this position to help performance in the year ahead.

Outlook

The stock market seems to be at a crossroads. We believe it is a mistake for investors to reduce their stock exposure in the face of all this economic uncertainty, and that stocks are quite attractive. In fact, we believe there’s compelling evidence to suggest an above-average decade may be ahead for equities. In broad terms, the best time to invest is when few are willing--and following what seems fashionable or obvious has historically been a losing strategy for the long term.

Our base case is that the U.S. economy will avoid a double dip recession in the short term. We believe the recovery will continue to gather momentum, though we aren’t forecasting robust growth. Corporate America should continue to post solid earnings and cash flow. Balance sheets are already quite strong and cash will likely be channeled into increased share repurchases, dividends, and mergers and acquisitions. All of this supports higher stock prices.

While it’s always tough to forecast near-term movements in stock prices, we believe a gradual economic recovery and solid earnings growth should allow respectable gains over the coming 12 months. We continue to search for companies with the best combinations of strong earnings growth and reasonable valuation. Overall, we think the more muted economic environment in the near- to intermediate-term should favor the type of high-quality growth-oriented stocks that make up the Portfolio.

October 2010

1All returns shown for individual holdings reflect that part of the reporting period the holdings were held.

As of September 30, 2010, the following companies represented the following percentages of Fund net assets: Netflix 4.58%, Deere 0.83%, Apple 4.40%, Priceline 1.57%, GameStop 0%, and Gilead Sciences 2.69%. All holdings are subject to change without notice.

Equity Portfolio Statistics

September 30, 2010

| % of Total |

Economic Sectors | Investments |

Consumer Discretionary | 16.1% |

Consumer Staples | 9.0% |

Energy | 7.1% |

Financials | 13.4% |

Government | 2.9% |

Health Care | 14.6% |

Industrials | 9.8% |

Information Technology | 24.1% |

Limited Partnership Interest | 0.1% |

Materials | 2.3% |

Venture Capital | 0.6% |

Total | 100% |

CSIF Equity Portfolio

September 30, 2010

Average Annual Total Returns

Class A Shares | (with max. load) |

One year | 6.15% |

Five year | 1.43% |

Ten year | 2.20% |

|

|

Class B Shares | (with max. load) |

One year | 5.40% |

Five year | 1.34% |

Ten year | 1.79% |

|

|

Class C Shares | (with max. load) |

One year | 9.57% |

Five year | 1.63% |

Ten year | 1.88% |

|

|

Class I Shares |

|

One year | 12.04% |

Five year | 2.98% |

Ten year | 3.24% |

|

|

Class Y Shares* |

|

One year | 11.73% |

Five year | 2.54% |

Ten year | 2.76% |

*Calvert Social Investment Fund Equity Portfolio first offered Class Y shares on October 31, 2008. Performance prior to that date reflects the performance of Class A shares at net asset value (NAV). Actual Class Y share performance would have been different.

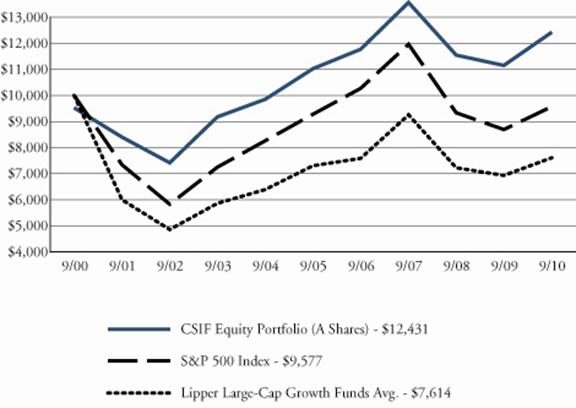

Growth of $10,000

The graph below shows the value of a hypothetical $10,000 investment in the fund over the past 10 fiscal year periods or since inception (for funds without 10-year records). The results shown are for Class A shares and reflect the deduction of the maximum front-end sales Class A charge of 4.75% and assume the reinvestment of dividends. The result is compared with benchmarks that include a broad based market index and a Lipper peer group average. Market indexes are unmanaged and their results do not reflect the effect of expenses or sales charges. The Lipper average reflects the deduction of the category’s average front-end sales charge. The value of an investment in a different share class would be different.

All performance data shown, including the graph above and the adjacent table, represents past performance, does not guarantee future results, assumes reinvestment of dividends and distributions and does not reflect the deduction of taxes that a shareholder would pay on the Fund’s/Portfolio’s distributions or the redemption of the Fund/Portfolio shares. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted; for current performance data visit www.calvert.com. The gross expense ratio from the current prospectus for Class A shares is 1.28%. This number may differ from the expense ratio shown elsewhere in this report because it is based on a different tim e period and, if applicable, does not include fee or expense waivers. Performance data quoted already reflects the deduction of the Fund’s/Portfolio’s operating expenses.

CSIF Enhanced Equity

Portfolio

September 30, 2010

Investment Performance

(total return at NAV*)

| 6 Months | 12 Months |

| ended | ended |

| 9/30/10 | 9/30/10 |

Class A | -1.89% | 11.10% |

Class B | -2.44% | 9.79% |

Class C | -2.27% | 10.18% |

Class I | -1.61% | 11.77% |

Russell 1000 Index | -1.21% | 10.75% |

Lipper Large-Cap Core Funds Average | -2.62% | 7.93% |

Ten Largest Stock Holdings

| % of Net Assets |

Apple, Inc. | 4.5% |

AT&T, Inc. | 3.7% |

Johnson & Johnson | 3.7% |

Microsoft Corp. | 3.6% |

JPMorgan Chase & Co. | 3.3% |

Bank of America Corp. | 3.1% |

Intel Corp. | 2.7% |

Home Depot, Inc. | 2.6% |

DIRECTV | 2.5% |

Costco Wholesale Corp. | 2.5% |

Total | 32.2% |

*Investment performance/return at NAV does not reflect the deduction of the Fund’s maximum 4.75% front-end sales charge or any deferred sales charge.

Portfolio Management Discussion

Natalie A. Trunow,

Senior Vice President, Chief Investment Officer - Equities of Calvert Asset Management Company

Performance

CSIF Enhanced Equity Portfolio Class A shares (at NAV) returned 11.10% for the 12-month period ended September 30, 2010, outperforming the 10.75% return of the Russell 1000 Index. The Fund’s outperformance was driven primarily by strong stock selection, although sector allocation also helped returns.

Investment Climate

After a year of uncertainty about global economic recovery, markets worldwide ended the reporting period in positive territory. In the U.S., the Standard & Poor’s 500 and Russell 1000 Indices returned 10.16% and 10.75%, respectively. Abroad, the Morgan Stanley Capital International Europe, Australasia, Far East Index (MSCI EAFE) rose 3.71% and the MSCI Emerging Markets Index gained 4.23%.

In general, growth stocks outperformed value stocks, as the Russell 1000 Growth Index outperformed the Russell 1000 Value Index with a return of 12.65% versus 8.90%. Mid-cap stocks were the best-performing domestic asset class for the year with a return of 17.54%, besting both large-cap stocks and the small-cap stocks of the Russell 2000 Index, which returned 13.35%.1

Overall, markets have largely built on the rally that started in early March 2009 as investors fluctuated between optimism and uncertainty about the sustainability of an economic recovery, including fears of a double-dip recession. However, we saw some market disruption, particularly sharp sell-offs in the second quarter of 2010, as the uncertainty escalated, causing the re-pricing of risk in both equity and fixed-income assets.

Dramatic downgrades in the sovereign creditworthiness of Greece, Spain, and Dubai rattled global financial markets in the spring of 2010--leading many to question the overall strength of the euro-zone’s economic recovery. In response, several European Union countries implemented austerity programs to slash their budget deficits and slow economic growth, and a new set of rules to toughen European banks’ capital and liquidity requirements was introduced.

China had some success with its attempt to engineer a soft landing for its overheated economy, which should improve global growth prospects--especially since it is now the world’s second-largest economy, eclipsing Japan in the second quarter of 2010, according to gross domestic product (GDP) data.

In the U.S., economic news throughout the period suggested a slow and sometimes uneven recovery was underway. GDP growth in the fourth quarter of 2009 turned positive for the first time since the second quarter of 2008, largely due to government stimulus efforts designed to increase consumer spending and inventory rebuilding. However, economic recovery in the second half of 2010 has been slower than most original forecasts, with early estimates of 2.4% for the second quarter of 2010 lowered to 1.7%.

Several conflicting trends have contributed to this slowdown. On the positive side, corporations have reported higher-than-expected earnings this year. Corporate sector strength also continues to boost company balance sheets and cash flow, fueling strong merger and acquisition (M&A) activity. Unfortunately, while M&A activity benefits many of the businesses involved and their stock prices, the net outcome is usually a reduction in the workforce, which exacerbates the already high unemployment rate.

The housing market improved for a time as home prices stabilized and purchases increased, but fell again after the first-time homebuyer credit expired. Depressed home prices and shrinking home equity, not to mention the uncertainties in the foreclosure process, weighed on consumers’ shaky confidence. Since consumer spending makes up 75% of the economy, recovery will remain slow until consumers become more comfortable. In the meantime, consumers continued to take on less debt, spend less, and save more.

Budget deficit levels are at unprecedented highs and remain a risk area. Despite the positive inflation numbers, the Federal Reserve (Fed) has maintained its commitment to keep interest rates low and away from deflationary territory.

Portfolio Strategy

For the reporting period, strong stock selection was the main driver of the Portfolio’s outperformance, particularly in the Energy, Utilities, and Industrials sectors. Stock selection was also positive in the Consumer Staples, Health Care, Telecommunications, and Materials sectors.

On an individual stock basis, Apple, Estee Lauder, and Lubrizol were the top contributors to relative performance over this period. Calvert’s environmental, social, and governance (ESG) criteria also added value, with the exclusion of ExxonMobil adding 0.57 percentage points to the Portfolio’s active return.

On the other hand, stock selection in the Financials, Information Technology, and Consumer Discretionary sectors hampered relative performance. Top stock detractors included JPMorgan Chase, Microsoft, EnCana, and Intel.

Given that our investment process is designed to emphasize stock selection, we do not expect sector selection to play a large role in performance. However, an overweight to Consumer Discretionary and an underweight to Energy slightly increased the Portfolio’s return for the period.

Outlook

We believe that, given relative valuations and capital flows, the sharp outperformance of bonds versus equities over the past several months is bound to reverse, with equities likely outperforming bonds over the next six to 18 months. In September, equity markets looked more attractive relative to bonds than they have since 1993 (except for the market bottom in March of 2009), with 10-year Treasuries yielding 2.51% versus the Dow Jones Industrial Average’s dividend yield of 2.6%, and an attractive forward price/earnings multiple of 12.2.

The economy has slowed, but sustained economic recovery continues. As we have said in the past, we don’t believe negative GDP growth is likely, which would constitute a double-dip recession. While we anticipate a somewhat more challenged earnings environment later this year, we believe that corporate sector strength is likely to persist and continue to support the overall economic recovery. Overall, our outlook continues to call for a slow, gradual pace to the economic recovery and a generally positive environment for stock picking, barring any major geopolitical calamities.

October 2010

1 Mid-cap stocks are represented by the Russell Mid Cap Index. Large cap stocks are represented by the Russell 1000 Index, which returned 10.75%

As of September 30, 2010, the following companies represented the following percentages of Fund net assets: Apple 4.51%, Estee Lauder 0%, Lubrizol, ExxonMobil 0%, JPMorgan Chase 3.31%, Microsoft 3.62%, EnCana 1.76%, and Intel 2.70%. All holdings are subject to change without notice.

CSIF Enhanced Equity Portfolio

September 30, 2010

| % of Total |

Economic Sectors | Investments |

Consumer Discretionary | 13.9% |

Consumer Staples | 7.5% |

Energy | 7.3% |

Financials | 15.0% |

Health Care | 14.8% |

Industrials | 13.9% |

Information Technology | 17.9% |

Materials | 1.0% |

Telecommunication Services | 4.2% |

Utilities | 4.5% |

Total | 100% |

Enhanced Equity

Portfolio Statistics

September 30, 2010

Average Annual Total Returns

Class A Shares | (with max. load) |

One year | 5.82% |

Five year | -2.07% |

Ten year | -1.54% |

|

|

Class B Shares | (with max. load) |

One year | 4.79% |

Five year | -2.38% |

Ten year | -2.12% |

|

|

Class C Shares | (with max. load) |

One year | 9.18% |

Five year | -1.97% |

Ten year | -2.00% |

|

|

Class I Shares* |

|

One year | 11.77% |

Five year | -0.65% |

Ten year | -0.72% |

* Note Regarding Class I Shares Total Returns: There were times during the reporting period when there were no shareholders in Class I. For purposes of reporting Average Annual Total Return, Class A performance at NAV (i.e. does not reflect deduction of the Class A front-end sales charge) is used during these periods in which there were no shareholders in Class I. For purposes of this Average Annual Total Return, the Class A performance at NAV was used during the period January 18, 2002 through April 29, 2005.

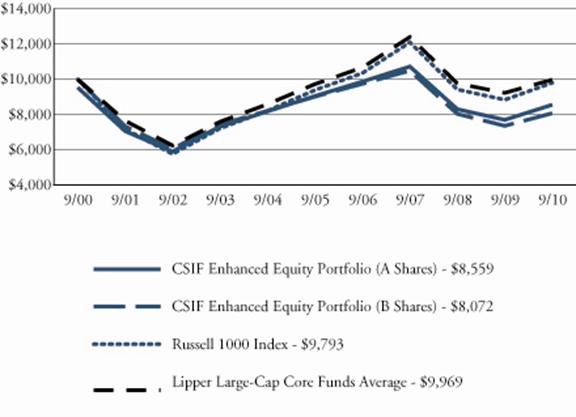

Growth of $10,000

The graph below shows the value of a hypothetical $10,000 investment in the fund over the past 10 fiscal year periods or since inception (for funds without 10-year records). The results shown are for Classes A and B shares and reflect the deduction of Class A’s the maximum front-end sales charge of 4.75% and assume the reinvestment of dividends. The result is compared with benchmarks that include a broad based market index and a Lipper peer group average. Market indexes are unmanaged and their results do not reflect the effect of expenses or sales charges. The Lipper average reflects the deduction of the category’s average front-end sales charge. The value of an investment in a different share class would be different.

All performance data shown, including the graph above and the adjacent table, represents past performance, does not guarantee future results, assumes reinvestment of dividends and distributions and does not reflect the deduction of taxes that a shareholder would pay on the Fund’s/Portfolio’s distributions or the redemption of the Fund/Portfolio shares. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted; for current performance data visit www.calvert.com. The gross expense ratio from the current prospectus for Class A shares is 1.54%. This number may differ from the expense ratio shown elsewhere in this report because it is based on a different tim e period and, if applicable, does not include fee or expense waivers. Performance data quoted already reflects the deduction of the Fund’s/Portfolio’s operating expenses.

Shareholder Expense Example

As a shareholder of the Portfolio, you incur two types of costs: (1) transaction costs, including sales charges and redemption fees; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Portfolio expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Portfolio and to compare these costs with the ongoing costs of investing in other mutual funds.

This Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (April 1, 2010 to September 30, 2010).

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

The Money Market Portfolio charges a monthly low balance account fee of $3 to those shareholders whose account balance is less than $2,000. The Enhanced Equity Portfolio charges an annual low balance account fee of $15 to those shareholders whose regular account balance is less than $5,000.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Portfolio’s actual expense ratios and an assumed rate of return of 5% per year before expenses, which is not the Portfolio’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Portfolio and other funds. To do so, compare the 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) or redemption fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning | Ending Account | Expenses Paid |

| Account Value | Value | During Period* |

CSIF Money Market | 4/1/10 | 9/30/10 | 4/1/10 - 9/30/10 |

Actual | $1,000.00 | $1,000.05 | $2.36 |

Hypothetical | $1,000.00 | $1,022.71 | $2.38 |

(5% return per |

|

|

|

year before expenses) |

|

|

|

*Expenses for Money Market are equal to the annualized expense ratio of .47%, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period).

| Beginning | Ending Account | Expenses Paid |

| Account Value | Value | During Period* |

CSIF Balanced | 4/1/10 | 9/30/10 | 4/1/10 - 9/30/10 |

Class A |

|

|

|

Actual | $1,000.00 | $1,011.10 | $6.14 |

Hypothetical | $1,000.00 | $1,018.96 | $6.16 |

(5% return per |

|

|

|

year before expenses) |

|

|

|

Class B |

|

|

|

Actual | $1,000.00 | $1,006.30 | $11.34 |

Hypothetical | $1,000.00 | $1,013.76 | $11.38 |

(5% return per |

|

|

|

year before expenses) |

|

|

|

Class C |

|

|

|

Actual | $1,000.00 | $1,007.10 | $10.58 |

Hypothetical | $1,000.00 | $1,014.52 | $10.62 |

(5% return per |

|

|

|

year before expenses) |

|

|

|

Class I |

|

|

|

Actual | $1,000.00 | $1,014.20 | $3.64 |

Hypothetical | $1,000.00 | $1,021.46 | $3.65 |

(5% return per |

|

|

|

year before expenses) |

|

|

|

*Expenses for Balanced are equal to the annualized expense ratios of 1.22%, 2.26%, 2.10% and .72% for Class A, Class B, Class C and Class I, respectively, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period).

| Beginning | Ending Account | Expenses Paid |

| Account Value | Value | During Period* |

CSIF Bond | 4/1/10 | 9/30/10 | 4/1/10 - 9/30/10 |

Class A |

|

|

|

Actual | $1,000.00 | $1,051.00 | $5.80 |

Hypothetical | $1,000.00 | $1,019.42 | $5.71 |

(5% return per |

|

|

|

year before expenses) |

|

|

|

Class B |

|

|

|

Actual | $1,000.00 | $1,045.80 | $11.15 |

Hypothetical | $1,000.00 | $1,014.17 | $10.97 |

(5% return per |

|

|

|

year before expenses) |

|

|

|

Class C |

|

|

|

Actual | $1,000.00 | $1,047.10 | $9.82 |

Hypothetical | $1,000.00 | $1,015.47 | $9.67 |

(5% return per |

|

|

|

year before expenses) |

|

|

|

Class I |

|

|

|

Actual | $1,000.00 | $1,054.80 | $2.65 |

Hypothetical | $1,000.00 | $1,022.49 | $2.60 |

(5% return per |

|

|

|

year before expenses) |

|

|

|

Class Y |

|

|

|

Actual | $1,000.00 | $1,052.40 | $4.73 |

Hypothetical | $1,000.00 | $1,020.46 | $4.66 |

(5% return per |

|

|

|

year before expenses) |

|

|

|

*Expenses for Bond are equal to the annualized expense ratios of 1.13%, 2.17%, 1.91%, .51% and .92% for Class A, Class B, Class C, Class I and Class Y, respectively, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period).

| Beginning | Ending Account | Expenses Paid |

| Account Value | Value | During Period* |

CSIF Equity | 4/1/10 | 9/30/10 | 4/1/10 - 9/30/10 |

Class A |

|

|

|

Actual | $1,000.00 | $1,009.30 | $6.13 |

Hypothetical | $1,000.00 | $1,018.97 | $6.16 |

(5% return per |

|

|

|

year before expenses) |

|

|

|

Class B |

|

|

|

Actual | $1,000.00 | $1,004.60 | $10.63 |

Hypothetical | $1,000.00 | $1,014.47 | $10.68 |

(5% return per |

|

|

|

year before expenses) |

|

|

|

Class C |

|

|

|

Actual | $1,000.00 | $1,005.40 | $10.04 |

Hypothetical | $1,000.00 | $1,015.06 | $10.09 |

(5% return per |

|

|

|

year before expenses) |

|

|

|

Class I |

|

|

|

Actual | $1,000.00 | $1,012.00 | $3.39 |

Hypothetical | $1,000.00 | $1,021.70 | $3.41 |

(5% return per |

|

|

|

year before expenses) |

|

|

|

Class Y |

|

|

|

Actual | $1,000.00 | $1,010.50 | $4.84 |

Hypothetical | $1,000.00 | $1,020.26 | $4.86 |

(5% return per |

|

|

|

year before expenses) |

|

|

|

*Expenses for Equity are equal to the annualized expense ratios of 1.22%, 2.11%, 2.00%, .67%, and .96% for Class A, Class B, Class C, Class I and Class Y, respectively, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period).

| Beginning | Ending Account | Expenses Paid |

| Account Value | Value | During Period* |

CSIF Enhanced Equity | 4/1/10 | 9/30/10 | 4/1/10 - 9/30/10 |

Class A |

|

|

|

Actual | $1,000.00 | $981.10 | $6.81 |

Hypothetical | $1,000.00 | $1,018.19 | $6.94 |

(5% return per |

|

|

|

year before expenses) |

|

|

|

Class B |

|

|

|

Actual | $1,000.00 | $975.60 | $13.18 |

Hypothetical | $1,000.00 | $1,011.72 | $13.42 |

(5% return per |

|

|

|

year before expenses) |

|

|

|

Class C |

|

|

|

Actual | $1,000.00 | $977.30 | $11.49 |

Hypothetical | $1,000.00 | $1,013.45 | $11.70 |

(5% return per |

|

|

|

year before expenses) |

|

|

|

Class I |

|

|

|

Actual | $1,000.00 | $983.90 | $4.03 |

Hypothetical | $1,000.00 | $1,021.01 | $4.10 |

(5% return per |

|

|

|

year before expenses) |

|

|

|

*Expenses for Enhanced Equity are equal to the annualized expense ratios of 1.37%, 2.66%, 2.32% and .81% for Class A, Class B, Class C, and Class I respectively, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period).

report of independent registered public accounting firm

The Board of Trustees and Shareholders of Calvert Social Investment Fund:

We have audited the accompanying statements of net assets of the Calvert Money Market, Balanced, Bond, Equity, and Enhanced Equity Portfolios (collectively the Portfolios), each a series of the Calvert Social Investment Fund, as of September 30, 2010, and the related statements of operations for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years in the five-year period then ended. These financial statements and financial highlights are the responsibility of the Portfolios’ management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.