UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-3334

CALVERT SOCIAL INVESTMENT FUND

(Exact name of registrant as specified in charter)

4550 Montgomery Avenue

Suite 1000N

Bethesda, Maryland 20814

(Address of Principal Executive Offices)

William M. Tartikoff, Esq.

4550 Montgomery Avenue

Suite 1000N

Bethesda, Maryland 20814

(Name and Address of Agent for Service)

Registrant's telephone number, including area code: (301) 951-4800

Date of fiscal year end: September 30

Date of reporting period: Twelve months ended September 30, 2011

<PAGE>

Item 1. Report to Stockholders. (Calvert Money Market Portfolio, Calvert Equity Portfolio and Calvert Enhanced Equity Portfolio only)

INFORMATION REGARDING CALVERT OPERATING COMPANY

NAME CHANGES

Effective on April 30, 2011, the following Calvert operating companies changed their names as indicated:

| Old Name | New Name | Company Description |

| Calvert Group, Ltd. | Calvert Investments, Inc. | Corporate parent of each |

| operating company listed | ||

| below | ||

| Calvert Asset Management | Calvert Investment | Investment advisor to the |

| Company, Inc. | Management, Inc. | Calvert Funds |

| Calvert Distributors, Inc. | Calvert Investment Distributors, | Principal underwriter |

| Inc. | and distributor for the | |

| Calvert Funds | ||

| Calvert Administrative | Calvert Investment | Administrative services |

| Services Company | Administrative Services, Inc. | provider for the Calvert |

| Funds | ||

| Calvert Shareholder | Calvert Investment Services, | Shareholder servicing |

| Services, Inc. | Inc. | provider for the Calvert |

| Funds | ||

Choose Planet-friendly E-delivery!

Sign up now for on-line statements, prospectuses, and fund reports. In less than five minutes you can help reduce paper mail and lower fund costs.

Just go to www.calvert.com. If you already have an online account at Calvert, click on My Account, and select the documents you would like to receive via e-mail.

If you’re new to online account access, click on Login/Register to open an online account. Once you’re in, click on the E-delivery sign-up at the bottom of the Account Portfolio page and follow the quick, easy steps. Note: if your shares are not held directly at Calvert but through a brokerage firm, you must contact your broker for electronic delivery options available through their firm.

TABLE

OFCONTENTS

4 Founding Chairman’s Letter

7 President’s Letter

10 SRI Update

12 Calvert Money Market Portfolio Management Discussion

15 Calvert Equity Portfolio Management Discussion

20 Calvert Enhanced Equity Portfolio Management Discussion

25 Shareholder Expense Example

28 Report of Independent Registered Public Accounting Firm

29 Statements of Net Assets

40 Notes to Statements of Net Assets

43 Statements of Operations

44 Statements of Changes in Net Assets

49 Notes to Financial Statements

63 Financial Highlights

74 Explanation of Financial Tables

76 Proxy Voting and Availability of Quarterly Portfolio Holdings

78 Trustee and Officer Information Table

Dear Investor,

Financial markets have been very volatile over the past year. While your Calvert Portfolios have provided modest positive returns, investors overall are understandably nervous.

All investments entail a higher degree of uncertainty right now as markets are highly correlated and continue to suffer from the “risk on, risk off” syndrome—where investors seek risk everywhere when they’re feeling better about the economy and shun it completely when fears renew. The good news is so much money sits on the sidelines at the moment that any improvement in sentiment can quickly rally the markets.

While markets are typically driven by the financial economy, today they’re much more concerned with the political economy. America’s loss of its Standard & Poor’s AAA credit rating had more to do with political gridlock in Washington than inherent financial problems. European politicians seem to be delaying the necessary bazooka-like changes to resolve ongoing sovereign debt issues, although the financial markets no longer believe they have much road left for “kicking the can.” China is undergoing its scheduled leadership change, which often impedes needed progressive reforms and encourages the hardlin-ers.

In My Opinion

In these times, we need our leaders to articulate a strong vision. Instead, our leaders seem to have a vision of political compromises, which leaves everyone confused as to the underlying plan. The Tea Party and Occupy Wall Street are sparking important conversations about values in this increasingly globalized world. The question is: are the participants just estranged from the system or did the system become estranged from them?

One in four Americans does not graduate high school in four years. One percent of the population has more than 40% of the financial wealth. Wall Street is no longer about the responsible allocation of capital, but about personal bonuses—the largest of which are derived from playing zero-sum games. A few bad apples cause a proliferation of regulations that are burdensome to business and increase consumer costs. Given all this, it’s easy to see how the system may have contributed to the public’s growing alienation.

Meanwhile, the list of issues our government needs to address keeps growing, such as climate change, military spending, the housing crisis, entitlement reform, energy policy, and immigration reform. I can’t remember a time when our financial economy has been so dependent on political resolve. On one level, it’s good the public has awakened around our more intractable issues. But globalization is a reality and the unskilled jobs are not coming back.

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 4

Sustainable and Responsible Investing in Turbulent Times

As stewards of your money in these turbulent times, Calvert continues to engage with companies about taking the high road with environmental, social, and governance factors.

Shareholder Advocacy

Calvert filed 38 resolutions in the 2011 proxy season with 28 successfully withdrawn after companies agreed to the terms of the resolution. Topics included climate change risks and principles, sustainability reporting, board diversity, disclosure of political contributions, and majority voting procedures.

As the impact of climate change becomes increasingly evident, the consequences on vulnerable, impoverished communities around the world cannot be ignored. We believe businesses can contribute to—and benefit from—their own preparation efforts. To that end, Calvert has joined with leading companies to launch the Partnership for Resilience and Environmental Preparedness (PREP), which promotes business practices that help companies and communities gear up for climate change. PREP also advocates for climate adaptation and resilience-building public policies to mitigate the risk of climate variability.

In October, Calvert will co-host UNEP FI, a United Nations initiative to bring investors and companies together on more detailed initiatives and best practices, such as energy efficiency in buildings. Barbara Krumsiek, Calvert’s CEO, is providing leadership among the more than 300 attendees and serves as co-chair.

Special Equities

A small part of your fund’s investment goes into small new companies that are not yet public but aim to be financially rewarding and have strong social impact that addresses real human needs.1 One recent investment was PresenceLearning, a firm that provides live, online speech therapy to students via web-based video conference technology. A national shortage of speech therapists prevents many students with severe communication disorders from receiving therapy. Now, the company’s distributed network technology enables specialists to serve more students in a more cost-efficient manner.

Another recent investment was DBL Equity Fund. DBL is a women-led firm that stands for “double bottom line” and invests in companies seeking to deliver venture capital returns while working with their companies to create social, environmental, and economic improvement in their region.

Community Investments

Many of our Funds participate in Calvert’s High Social Impact Investing program, which is administered through the Calvert Foundation.2 This community investment program may allocate a small percentage of Fund assets at below-market interest rates to investments that provide economic opportunity for struggling populations.

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 5

Local banks were unwilling to help South African company Bio2Watt, which converts manure into energy, but Foundation partner E + Co supported the company with funding as well as technology assistance. Today, Bio2Watt can generate enough power round-the-clock for 1,000 homes. It is also decentralizing the power supply, alleviating landfill burdens and water pollution, and generating jobs for locals.

St. John’s Bread & Life in Brooklyn, New York was able to expand to serving 450,000 meals a year thanks to funding from Foundation borrower Low Income Investment Fund. St. John’s also provides nutrition counseling, health and hygiene products, workforce development, literacy training, psychiatric services, and substance abuse counseling to its clients. Client Naishaune Spencer said, “I ran with the wrong crowd and ended up homeless, jobless, and in a whole lot of trouble. With the help of St. Johns, I was able to go back to school, get a great job, have a steady income and, most significantly, get my first apartment.” You can read more about the Foundation’s activities at its website.

We thank you again for your investment, which has enabled Calvert to be a leader in the area of corporate responsibility and the growing impact investing movement through the innovative programs named above. The values expressed by our work and your investments create positive models for governments in these times of global political crisis.

D. Wayne Silby

Founding Chair

1 As of September 30, 2011, PresenceLearning and DBL Equity Fund represented 0.01% and 0.02% of Calvert Equity Portfolio. All holdings are subject to change without notice.

2 As of September 30, 2011, Calvert Social Investment Foundation (“Calvert Foundation” or “Foundation”) Community Investment Notes represented 0.50% of the net assets of Calvert Equity Portfolio. The Calvert Foundation is a 501(c)(3) nonprofit organization. The Foundation’s Community Investment Note Program is not a mutual fund and should not be confused with any Calvert Investments-sponsored investment product.

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 6

Dear Shareholders:

After a strong finish to 2010 and start of the new year, the U.S. economy lost its footing in the summer of 2011. Hope for a second-half rebound gave way to concerns we were heading into another recession as consumer insecurity, a weak job market, the looming sovereign debt crisis in Europe, and uncertainty about the direction of U.S. and European policy weighed on economic growth and turned markets into a roller coaster.

The final months of the reporting period were particularly difficult for equities amid significant market volatility in the financial markets. After U.S. government debt lost its Standard & Poor’s triple A rating for the first time in history, already anxious investors flocked to the relative safety of cash and Treasuries, despite very low short-term yields. In the end, third-quarter market turmoil more than erased stock market gains made through the first six months of 2011. In fact, the -13.87% third-quarter return for the Standard & Poor’s 500 Index was the biggest quarterly drop for that index since the financial meltdown in the fourth quarter of 2008.

The 2008-2009 Financial Crisis -- Where Are We Now?

There have been many media comparisons to the third quarter of 2008 recently, so I think it’s worth noting some key differences. Despite third-quarter events, equity markets are still generally ahead of where they were in the depths of the financial crisis, as the S&P 500 Index and Russell Mid-Cap Index returned an annualized 1.23% and 3.96% for the three-year period ended September 30, 2011. Also, unlike 2008, the stock market seems to be rebounding quickly, having regained much of the lost ground in the first two weeks of October.

While still high, the unemployment rate has decreased a full percentage point from its recession peak. And in a direct month-to-month comparison, the United States added 103,000 jobs in September 2011 (58,000 if you exclude the return of striking Verizon workers) versus losing 434,000 jobs in September 2008.1 In housing, builder confidence in the current market for new single-family homes as measured by the National Association of Home Builders/Wells Fargo Housing Market Index (HMI) rose four points to 18 for October 2011--a sign that pockets of recovery in housing may be starting to emerge across the country. The HMI index is also four points higher than it was in October 2008.

Energy prices have fallen, too--after soaring to $150 a barrel, crude oil hovered around $80 a barrel at the end of September 2011. While prices at the pump did not decrease proportionately, they are lower, which is good for consumers’ wallets and oil-dependent industries. In fact, reports show retail sales have notched up in recent weeks--a sign that consumers are starting to spend a bit more freely now. And although household debt still exceeds consumers’ after-tax income, it fell 12% between its record high in September 2007 and June of this year.2

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 7

The bottom line is that economic recovery may continue to be more two-steps-forward-one-step-back rather than the straight line progress we’d all prefer, but the recovery is happening. In the meantime, the expertise of your Calvert fund managers will help guide your investments through the ups and downs that may lie ahead.

Board Diversity and Company Competitiveness

As always, we filed several shareholder resolutions this year asking companies to consider diverse candidates during their board selection. Most were successfully withdrawn after the companies agreed to add specific considerations of race, gender and ethnicity to their selection process. However, Urban Outfitters was one of two companies that opposed the resolution that we filed.

Unlike its five biggest apparel-industry competitors, Urban Outfitters doesn’t have any women or minorities on its board. This is particularly disconcerting since 53% of its North American net retail store sales in fiscal 2011 came from its Anthropologie and Free People stores for women. Of course, the Urban Outfitters flagship store heavily caters to women too. Smart companies understand the importance of having management that reflects their target audiences and Urban Outfitters is certainly missing the mark.

We pressed on and 22% of shareholders voted in favor of the resolution. The battle received a good deal of attention in the press, although it remains to be seen if the company will heed the call of its shareholders.

Your Financial Advisor Is Always Available

It’s easy to be a long-term investor when markets are strong. The challenge is to remain one when markets are going through a protracted period of uncertainty. While it may take longer than we’d like, markets have always recovered in the past and I am confident they will do so again. These cycles are simply the nature of the market.

In times like these, it’s best to stay the course, maintaining a well-diversified mix of U.S. and international stocks, bonds, and cash appropriate for your goals and risk tolerance. However, if you think your financial needs or risk tolerance have changed, your financial advisor is always available to discuss your concerns.

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 8

We also invite you to visit our website, www.calvert.com, for fund information, portfolio updates, and commentary from Calvert professionals. As always, we thank you for entrusting your investments to Calvert.

Barbara J. Krumsiek

President and CEO

Calvert Investments, Inc.

October 2011

1 Bureau of Labor Statistics

2 Center for American Progress, Economic Snapshot for September 2011

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 9

As always, Calvert continues to work hard to ensure you have a say in the responsible management of environmental, social, and governance (ESG) factors for the companies in which we invest. While some highlights from the reporting period were noted in the Founding Chairman’s letter, more are detailed below.

Majority Vote in Director Elections

Shareholders’ role in electing a board of directors is a fundamental part of ensuring accountability. Unfortunately, many companies weaken this role by conducting elections under a plurality rather than a majority standard—which essentially means a director nominee can be elected with only his or her own affirmative vote.

Calvert filed four shareholder proposals calling for companies to adopt majority voting this year. Those at Plains Exploration and Production, Global Payments, and Agco were withdrawn after the companies agreed to the requested changes. Hansen Natural responded with minor improvements to their election process. But we felt they were insufficient, so we kept the resolution on the ballot and 48% of shareholders voted in favor of it.

Update on Board Diversity

Persuading companies to make their boards more representative of their customers, employees and other target audiences continues to be an important initiative. In August, Calvert Senior Sustainability Analyst Aditi Mohapatra published an article in Forbes magazine, “Are There Really Boards With No Women?” The article highlighted the fact that women still hold only 18% of corporate board posts at S&P 100 companies, despite a growing body of evidence proving the business case for diverse boards.

Also, five resolutions seeking a proactive commitment to include women and minorities as part of every board director search were filed this year. Three were successfully withdrawn before the annual meeting. The remaining two—at Urban Outfitters and American Financial Group—received strong support with 22% and 27% of shareholder votes.

First U.S. Automaker Added to Calvert Social Index

Another notable event was Ford Motor becoming the first U.S. automaker to qualify for Calvert Signature Funds and be added to the Calvert Social Index. Ford has emerged in recent years as the fuel efficiency leader among the big three U.S. auto manufacturers. A review of Ford’s key industry impacts, as well as our engagement with the company over the past four years, ensured that it met our environment, social, and governance (ESG) criteria for investment.

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 10

While we remain concerned about the overall impact of automobile companies on issues such as greenhouse emissions, we believe Ford and the foreign automakers Calvert invests in are taking meaningful steps to reduce the negative environmental impacts of their products. Of course, we will continue to seek improvement on key issues by working with senior management of all these companies.

As of September 30, 2011, the following companies represented the following percentages of net assets: Global Payments 0%, Agco 0%, Hansen Natural 0%, Urban Outfitters 0%, American Financial Group 2.18% of Calvert Enhanced Equity Portfolio, and Ford 0%. All holdings are subject to change with out notice.

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 11

| CALVERT MONEY MARKET PORTFOLIO September 30, 2011 Investment performance (total return) | |||||

| 6 months | 12 months | ||||

| ended | ended | ||||

| 9/30/11 | 9/30/11 | ||||

| Class O | 0.005 | % | 0.01 | % | |

| Lipper Money Market Funds Average | 0.01 | % | 0.02 | % | |

| Performance For the 12-month period ended September 30, 2011, Calvert Money Market Portfolio returned 0.01% compared to 0.02% for its benchmark, the Lipper Money Market Funds Average. | |||||

| Average Annual Total Returns | |||||

| One year | 0.01 | % | |||

| Five year | 1.72 | % | |||

| Ten year | 1.70 | % | |||

| 7-day Simple/Effective Yield | |||||

| Investment Climate | 7-day simple yield | 0.01 | % | ||

| The 12-month period that ended September 30, 2011 was marked by unexpected turns and financial market volatility. U.S. economic growth slowed to an estimated 1.5% annual rate during the reporting period,1 while the inflation rate rose. The core consumer price index (CPI) annual rate was 2.0% by August 2011.2 | |||||

| 7-day effective yield | 0.01 | % | |||

| Investment Allocation | % of Total Investments | ||||

| Variable Rate | 85.7 | % | |||

| Demand Notes | |||||

| U.S. Government Agencies and Instrumentalities | 8.8 | % | |||

| Municipal Obligations | 3.0 | % | |||

| Total return assumes reinvestment of represents past performance and does not guarantee future results. Investment return will fluctuate so that current performance may be lower or higher than the performance data quoted. An investment in the Portfolio is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Although the Portfolio seeks to preserve the value of your invest- ment at $1.00 per share, it is possible to lose money by investing in the Portfolio. Visit www.calvert.com for current performance data. | U.S. Treasury | 2.2 | % | ||

| Time Deposit | 0.2 | % | |||

| Loans and Deposit Receipts | |||||

| Guaranteed by U.S. | |||||

| Government Agencies | 0.1 | % | |||

| Total | 100 | % | |||

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 12

After completing its second round of quantitative easing (known as QE2), the Federal Reserve (Fed) was expected to move to the sidelines. However, it proceeded to introduce two additional easing measures. In August, shortly after QE2 ended, the Fed announced that it would extend the promise of near-zero short-term interest rates perhaps until mid-2013. Then, in September, the Fed introduced “operation twist,” a program to sell $400 billion of shorter-maturity Treasuries and buy longer-maturity Treasuries with the proceeds.

After a period of calm, the euro-area debt crisis surged to the forefront of investors’ concerns once again in mid-2011. Widespread unease about the effects of sovereign debt on European banks flowed over into non-European markets. This made for a rough trading summer, as stocks and bonds with credit risk fell. The U.S. Congress’s mid-year flirt with voluntary default on U.S. government debt heightened investors’ anxiety. Policy tightening by central banks in emerging countries, where stronger growth has pushed inflation higher, also contributed to concerns about global growth.

In this uncertain environment, major U.S. bond market sector indices delivered positive returns for the reporting period.3 Interest rates generally moved lower over the reporting period. The three-month Treasury bill yield fell to 0.02% from 0.16%. The benchmark 10-year Treasury note yield declined 0.61 percentage points to finish the reporting period at 1.92%. The average yield for Moody’s Baa-rated corporate bonds was 5.22% at the end of September 2011, down 0.36 percentage points. Finally, the average rate on a 30-year conventional mortgage fell 0.31 percentage points to 4.01%.4

Portfolio Strategy

Since money-market rates remained at historically low levels, we maintained our strategy of investing in high-grade, conservative securities. The Portfolio’s primary investments include liquid variable-rate demand notes and U.S. government securities, including agencies and Treasuries. We believe the strategy helps us provide liquidity and preserve principal, while remaining true to the Fund’s sustainable investment criteria.

Our Fund, like all money-market funds, is subject to the stringent guidelines of Rule 2a-7, which was established under the Investment Company Act of 1940 and influences the credit quality, maturity, and liquidity of investments in money-market funds. Recent changes to the rule have created even stronger guidelines designed to further enhance credit, liquidity, and transparency. Calvert’s internal diversification guidelines are designed to limit risk even further.

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 13

Outlook

We expect the rest of 2011 to unfold with financial markets fitfully trying to understand and adjust to the ongoing debt struggles of the major western nations and Japan. Policymakers’ decisions will continue to have great potential to move global financial markets. Government footprints in credit markets will remain large. The U.S. gross domestic product growth rate is likely to remain modest and choppy as the country continues to recover from the severe financial crisis of 2007 through 2009. History suggests that recovery from a severe financial crisis that was rooted in excessive debt will take several more years at least. It also indicates that rates of economic growth and consumer price inflation will tend to run below pre-crisis averages. This does not, however, preclude stretches of stronger growth, something markets have heavily discounted.

Within this bigger picture, we expect the issues that have driven markets in 2011 to remain intact. First, the potential for very slow U.S. economic growth remains high, and there is a higher risk of recession amid tightening U.S. fiscal policy and little additional capacity for strong monetary stimulus. Second, it is likely that we will experience ongoing financial market volatility stemming from the euro-area debt crisis. Finally, tighter monetary policies in emerging countries may constrain global growth. As investors’ perceptions of these factors change, markets will react, at times sharply. We expect to experience generally heightened levels of financial market volatility. There is potential for acute bouts of great volatility.

The Fed has taken the highly unusual stance of forecasting its intention to keep the federal funds rate low until mid-2013. Therefore, we foresee continuing with our current strategy of conservative investing with the objective of preserving principal. We believe this is what many investors are seeking, as approximately $2.6 trillion was invested in taxable and tax-exempt money-market funds as of September 2011.

October 2011

1 Calculated based on data from the Commerce Department and the Wall Street Journal Survey of Economic Forecasters.

2 Bureau of Labor Statistics

3 Barclays Capital

4 Source for all interest rates: Federal Reserve H.15 report

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 14

PORTFOLIO MANAGEMENT DISCUSSION

Richard England

of Atlanta Capital Management Company

Investment Performance

For the 12 months ended September 30, 2011, Calvert Equity Portfolio’s Class A shares (at NAV) returned 1.07% compared with a return of 1.14% for the Standard and Poor’s (S&P) 500 Index.

Investment Climate

Here we go again. As I write this letter in early October, the markets struggle to find their footing and gloom about the global economy seems to grow almost every day. The relative calm of fall 2010 seems long ago. Renewal of the so-called Bush tax cuts provided a rare moment of bipartisanship and helped the economy and market gather a bit of steam. But that was about as good as it got.

The push for political freedom in the Middle East and North Africa, higher oil prices, disasters in Japan, and the resurfacing sovereign debt crisis in Europe affected companies and economies around the globe as softening data painted a picture of an economy sliding backward.

| CALVERT EQUITY |

| PORTFOLIO |

| September 30, 2011 |

| Investment performance | ||||

| (total return at NAV*) | ||||

| 6 months | 12 months | |||

| ended | ended | |||

| 9/30/11 | 9/30/11 | |||

| Class A | -14.01 | % | 1.07 | % |

| Class B | -14.38 | % | 0.21 | % |

| Class C | -14.30 | % | 0.34 | % |

| Class I | -13.76 | % | 1.62 | % |

| Class Y | -13.86 | % | 1.43 | % |

| S&P 500 Index | -13.78 | % | 1.14 | % |

| Lipper Large-Cap | ||||

| Growth Funds | ||||

| Average | -14.59 | % | 0.27 | % |

| Ten Largest Stock Holdings | % of Net Assets | |

| Allergan, Inc. | 4.9 | % |

| Apple, Inc. | 4.8 | % |

| QUALCOMM, Inc. | 4.3 | % |

| Cameron International Corp. | 3.2 | % |

| T. Rowe Price Group, Inc. | 3.2 | % |

| Gilead Sciences, Inc. | 2.9 | % |

| Cognizant Technology | ||

| Solutions Corp. | 2.6 | % |

| Novartis AG (ADR) | 2.5 | % |

| CVS Caremark Corp. | 2.5 | % |

| International Business | ||

| Machines Corp. | 2.5 | % |

| Total | 33.4 | % |

*Investment performance/return at NAV does not reflect the deduction of the Fund’s maximum 4.75% front-end sales charge or any deferred sales charge.

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 15

The final straw for investors was the game of chicken Republicans and Democrats played over the debt ceiling and subsequent downgrade of U.S. sovereign debt by Standard and Poor’s. If we have to worry about whether the United States can pay its debts, how can anything be counted on? Uncertainty reigns so the markets remain extremely volatile.

More recently, a toxic brew of fear, uncertainty and politics combined to drive stocks even lower. The market can adjust to what it understands, but investors eventually throw up their hands and head for the exits when the ability to reasonably forecast is absent. That’s exactly what we got.

The extreme market volatility since early June dominated sector returns for the year. While the S&P 500 Index as a whole rose about 1%, the spread between the best and worst sectors was very wide. Financials was by far the worst, falling over 16%, although Materials and Industrials declined moderately as well. On the other hand, the ultra-safe Utilities sector rose nearly 12% and Consumer Staples did almost as well, rising nearly 10%. Everything else was fairly tightly clustered around a 4% to 6% increase.

Portfolio Strategy

Throughout the period, we remained positioned to benefit from continued growth in the global economy. We realize growth is hardly robust, but in many cases our stocks are outgrowing their peers and industries or creating new markets. The nicks and dings to economic growth through the spring and early summer were largely shrugged off by our holdings. However, that changed in mid-August.

Since the U.S. debt downgrade and resulting big sell-off, the market has risen or fallen almost 10% eight different times. That’s a historic amount of volatility and reflects ris-

CALVERT EQUITY PORTFOLIO

September 30, 2011

Average Annual Total Returns

| Class A Shares | (with max. load) | |

| One year | -3.72 | % |

| Five year | 0.33 | % |

| Ten year | 3.60 | % |

| Class B Shares | (with max. load) | |

| One year | -4.79 | % |

| Five year | 0.22 | % |

| Ten year | 3.21 | % |

| Class C Shares | (with max. load) | |

| One year | -0.66 | % |

| Five year | 0.53 | % |

| Ten year | 3.30 | % |

| Class I Shares | ||

| One year | 1.62 | % |

| Five year | 1.87 | % |

| Ten year | 4.68 | % |

| Class Y Shares* | ||

| One year | 1.43 | % |

| Five year | 1.50 | % |

| Ten year | 4.21 | % |

*Calvert Equity Portfolio first offered Class Y shares on October 31, 2008. Performance prior to that date reflects the performance of Class A shares at net asset value (NAV). Actual Class Y share performance would have been different.

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 16

Growth of $10,000

The graph below shows the value of a hypothetical $10,000 investment in the fund over the past 10 fiscal year periods. The results shown are for Class A shares and reflect the deduction of the maximum front-end sales Class A charge of 4.75% and assume the reinvestment of dividends. The result is compared with benchmarks that include a broad based market index and a Lipper peer group average. Market indexes are unmanaged and their results do not reflect the effect of expenses or sales charges. The Lipper average reflects the deduction of the category’s average front-end sales charge. The value of an investment in a different share class would be different.

All performance data shown, including the graph above and the adjacent table, represents past performance, does not guarantee future results, assumes reinvestment of dividends and distributions and does not reflect the deduction of taxes that a shareholder would pay on the Portfolio’s distributions or the redemption of the Portfolio shares. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted; for current performance data visit www.calvert.com. The gross expense ratio from the current prospectus for Class A shares is 1.23%. This number may differ from the expense ratio shown elsewhere in this report because it is based on a different time period and, if applicable, does not include fee or expense waivers. Performance data quoted already reflects the deduction of the Portfolio’s operating expenses.

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 17

ing uncertainty and pessimism and increasing acceptance that another recession is inevitable. The results have been both a rush for the exits and a push into very defensive sectors where investors stayed invested. Our growth-oriented holdings did not fare as well during this churning.

Positive performance primarily came from stocks that fared better than their peers. The leading performer was Green Mountain Coffee Roasters, as deals to deliver Dunkin’ Donuts and Starbucks products with Green Mountain’s Keurig single-serve brewing system bolstered the company’s growth. Chipotle Mexican Grill, Amazon.com and Allergan also made very significant contributions.

We had poor performers too, as Suncor and several other Energy companies fell sharply in the last quarter due to deteriorating expectations for global growth. In that environment, big, slow-growing, integrated producers we don’t own (like ExxonMobil) outperformed.

Peculiarly, some of our worst performers were banks. We have been favorably disposed to them based on extremely low valuations, improving credit performance, and growing returns of capital to shareholders. While our expectations for the fundamentals have largely been met, the stocks have still performed poorly due to mounting fears of a renewed recession. However, many of the banks we didn’t own fared even worse.

CALVERT EQUITY PORTFOLIO STATISTICS

September 30, 2011

| % of Total | ||

| Economic Sectors | Investments | |

| Consumer Discretionary | 14.1 | % |

| Consumer Staples | 8.8 | % |

| Energy | 8.4 | % |

| Financials | 13.8 | % |

| Health Care | 14.0 | % |

| Industrials | 8.9 | % |

| Information Technology | 26.4 | % |

| Limited Partnership Interest | 0.3 | % |

| Materials | 2.2 | % |

| Time Deposit | 2.6 | % |

| Venture Capital | 0.5 | % |

| Total | 100 | % |

I’d be remiss if I didn’t comment on Netflix, a large Portfolio holding, which stubbed its toe badly in mid-September. The dramatic decline cost us significant performance, although its previous strong performance still led to a positive return for the period. That doesn’t make me feel much better, but it’s worth noting. I have issues with the company’s moves and as I write these words, I’m on a plane to meet with the CEO and CFO and get some key questions answered. It’s hard not to believe in the company’s long-term

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 18

positioning, but we’ll see.

Outlook

It’s hard not to be pessimistic. Unemployment seems intractable. Housing is still in the doldrums. Both political parties are in campaign mode, not solutions mode. Europe seems very complicated, opaque, and difficult to handicap. Emerging markets today are slowing and may slow too much to provide a dependable source of global growth. The average American and European increasingly feels like the system, be it political or economic, doesn’t work any more.

From an intermediate- to longer-term perspective, the best time to purchase any asset is when it feels most uncomfortable. I’m not really sure what three months from now looks like; the three-year view is a lot clearer. After all, it doesn’t make much sense to me that investors would buy a 10-year U.S. Treasury note with a certain 1.9% yield instead of the S&P 500 Index, which has a near-certain yield of 2.0% and gives you a call option on appreciation of the underlying stocks over the coming 10 years. But that’s the math of extreme fear and uncertainty.

More practically, we do not expect a new recession. The U.S. economy is muddling through, and as long as Europe does not implode, we expect that to continue. It will be harder for Europe to avoid recession, but we believe stock markets around the world already discount a renewed recession. If it does not arrive, the stock market right now is very cheap.

It’s tough out there right now. The silver lining in the current stock market cloud is that it creates opportunities to position the Portfolio for the rebound to come—whenever it comes. The companies we own are well-positioned to prosper in the years ahead. When the fear recedes, their advantages will again be recognized.

October 2011

The following companies represented the following percentages of net assets as of September 30, 2011: Green Mountain Coffee Roasters 2.35%, Chipotle 1.71%, Suncor 2.44%, Amazon 1.50%, Allergan 4.85%, ExxonMobil 0%, and Netflix 0.92%. Holdings are subject to change without notice.

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 19

PORTFOLIO MANAGEMENT DISCUSSION

Natalie A.

Trunow,

Senior Vice President, Chief Investment Officer - Equities of Calvert Investment Management, Inc.

Investment Performance

Calvert Enhanced Equity Portfolio Class A shares (at NAV) returned 1.43% for the 12-month period ended September 30, 2011, outperforming the 0.91% return of the Russell 1000 Index. The Fund’s outperformance was driven primarily by strong stock selection, although sector allocation also helped returns.

Investment Climate

A strong performance by equity markets in the fourth quarter of 2010 and modest gains in the first half of 2011 were largely erased by stocks’ dismal performance in the third quarter of 2011. Despite healthy earnings from U.S. companies, macroeconomic troubles became the focus of attention and weighed on investor sentiment.

Over the past four quarters, the Standard & Poor’s 500 and Russell 1000 Indices returned 1.14% and 0.91%, respectively. International stocks fared considerably worse with the MSCI EAFE IMI and MSCI Emerging Markets IMI Indices returning

CALVERT ENHANCED EQUITY PORTFOLIO

September 30, 2011

Investment Performance

(total return at NAV*)

| 6 months | 12 months | |||

| ended | ended | |||

| 9/30/11 | 9/30/11 | |||

| Class A | -11.50 | % | 1.43 | % |

| Class B | -12.17 | % | 0.00 | % |

| Class C | -11.93 | % | 0.51 | % |

| Class I | -11.32 | % | 2.02 | % |

| Russell 1000 Index | -14.58 | % | 0.91 | % |

| Lipper Large-Cap | ||||

| Core Funds | ||||

| Average | -15.16 | % | -1.51 | % |

| Ten Largest Stock Holdings | % of Net Assets | |

| Apple, Inc. | 5.6 | % |

| International Business | ||

| Machines Corp. | 4.6 | % |

| Microsoft Corp. | 4.2 | % |

| Johnson & Johnson | 4.1 | % |

| AT&T, Inc. | 3.4 | % |

| Bristol-Myers Squibb Co. | 3.4 | % |

| Kimberly-Clark Corp. | 3.2 | % |

| ACE Ltd. | 2.9 | % |

| Prudential Financial, Inc. | 2.9 | % |

| Time Warner Cable, Inc. | 2.7 | % |

| Total | 37.0 | % |

*Investment performance/return at NAV does not reflect the deduction of the Fund’s maximum 4.75% front-end sales charge or any deferred sales charge.

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 20

-8.51% and -16.46%. Small caps under-

| ||||

| CALVERT ENHANCED | ||||

| EQUITY PORTFOLIO | ||||

| September 30, 2011 | ||||

| % of Total | ||||

| Economic Sectors | Investments | |||

| Consumer Discretionary | 10.5 | % | ||

| Consumer Staples | 12.1 | % | ||

| Energy | 8.5 | % | ||

| Financials | 13.7 | % | ||

| Health Care | 12.8 | % | ||

| Industrials | 9.8 | % | ||

| Information Technology | 19.6 | % | ||

| Materials | 3.3 | % | ||

| Telecommunication Services | 3.4 | % | ||

| Utilities | 6.3 | % | ||

| Total | 100 | % | ||

In general, most U.S. companies, led by those in the Technology and Health Care sectors, continued to show financial strength, and to rely on their healthy balance sheets and impressive cash reserves for mergers and acquisitions.

The eurozone crisis continued to unfold, weighed down by struggling peripheral economies. Although leaders attempted to assure investors that the proposed long-term solutions to the debt crisis were viable, the fear of contagion intensified. Germany and France braced for a Greek default by taking steps to insulate their financial institutions from large losses. While we don’t see a high probability of a Greek default driving the U.S. into recession, the possibility still seemed to drive market sentiment.

European bank stocks continued to be among those most adversely impacted by the eurozone debt crisis, driven by longer-term funding stress, as well as by U.S. money market funds’ further reductions in their exposure to these banks.

The S&P downgrade of U.S. government debt on August 5 was another blow to investor confidence, contributing to a global equity market sell-off and pushing U.S. Treasury yields down as risk aversion in the markets increased. The resulting equity market volatility was also fed by concerns about the political stalemate in Washington, the European sovereign debt issues, and a significant slowdown in U.S. economic growth—or, more ominously, the possibility of a double-dip recession in the United States.

After the completion of QE2 in June, the Federal Reserve (Fed) supplemented its accommodative policy with the well-timed September 21 announcement of “operation twist,” a plan to sell $400 billion in short-term Treasuries while purchasing the same amount of longer-term Treasuries. This could boost investment and refinancing in the U.S. by

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 21

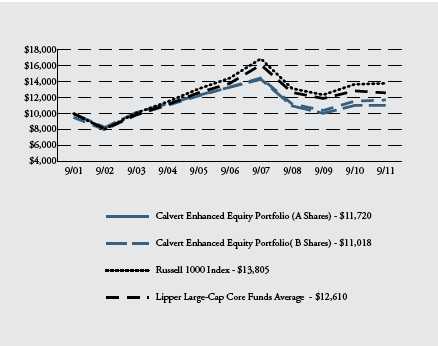

Growth of $10,000

The graph below shows the value of a hypothetical $10,000 investment in the fund over the past 10 fiscal year periods. The results shown are for Classes A and B shares and reflect the deduction of Class A’s the maximum front-end sales charge of 4.75% and assume the reinvestment of dividends. The result is compared with benchmarks that include a broad based market index and a Lipper peer group average. Market indexes are unmanaged and their results do not reflect the effect of expenses or sales charges. The Lipper average reflects the deduction of the category’s average front-end sales charge. The value of an investment in a different share class would be different.

All performance data shown, including the graph above and the adjacent table, represents past performance, does not guarantee future results, assumes reinvestment of dividends and distributions and does not reflect the deduction of taxes that a shareholder would pay on the Portfolio’s distributions or the redemption of the Portfolio shares. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted; for current performance data visit www.calvert.com. The gross expense ratio from the current prospectus for Class A shares is 1.48%. This number may differ from the expense ratio shown elsewhere in this report because it is based on a different time period and, if applicable, does not include fee or expense waivers. Performance data quoted already reflects the deduction of the Portfolio’s operating expenses.

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 22

reducing long-term interest rates. The Fed also promised to keep interest rates low for the next two years. However, the announcement was accompanied by alarming statements about U.S. economic weakness, which further unsettled markets.

In fact, worries about anemic global economic growth intensified over the last 12 months, with U.S. gross domestic product (GDP) growth numbers revised down for the first half of the year to less than a 1% average annual growth rate, according to the Bureau of Economic Analysis.

The most recent release of employment figures by the Bureau of Labor Statistics showed that the unemployment rate remained at 9.1% in August. Jobs data is likely to be a lagging indicator of economic activity in this economic cycle and may not improve until other economic indicators are more firmly in positive territory.

Although the secular upward trend in commodity prices may persist in the long term, decreasing commodity prices are a positive for global economic growth in the near term. A continued price break should reduce risks to top-line inflation, lift the drag on economic growth, and provide additional stability to the Fed’s actions.

In China, the threat of inflation still looms and may make it difficult for that country and other emerging markets to implement more accommodative monetary policy in the near term. However, recent industrial production numbers in China were positive and although manufacturing data was slightly contractionary, it was not at hard landing levels.

CALVERT ENHANCED EQUITY PORTFOLIO STATISTICS

September 30, 2011

Average Annual Total Returns

| Class A Shares | (with max. load) | |

| One year | -3.40 | % |

| Five year | -3.48 | % |

| Ten year | 1.60 | % |

| Class B Shares | (with max. load) | |

| One year | -5.00 | % |

| Five year | -3.90 | % |

| Ten year | 0.97 | % |

| Class C Shares | (with max. load) | |

| One year | -0.56 | % |

| Five year | -3.41 | % |

| Ten year | 1.13 | % |

| Class I Shares* | ||

| One year | 2.02 | % |

| Five year | -2.01 | % |

| Ten year | 2.43 | % |

* Note Regarding Class I Shares Total Returns: There were times during the reporting period when there were no shareholders in Class I. For purposes of reporting Average Annual Total Return, Class A performance at NAV (i.e. does not reflect deduction of the Class A front-end sales charge) is used during these periods in which there were no shareholders in Class I. For purposes of this Average Annual Total Return, the Class A performance at NAV was used during the period January 18, 2002 through April 29, 2005.

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 23

Portfolio Strategy

For the reporting period, strong stock selection, particularly in the Information Technology and Financials sectors, was the main driver of the Portfolio’s outperformance of the Russell 1000 Index.

On an individual stock basis, NiSource, W. W. Grainger, Dell, Apple, and Bristol-Myers Squibb were the top contributors to relative performance over this period. Stock selection was negative only in the Energy sector. Detractors in Energy included EnCana and SEACOR Holdings. Other top stock detractors included Avery Dennison, JPMorgan Chase, and VISA.

Calvert’s environmental, social, and governance (ESG) criteria modestly detracted over the last 12 months, primarily in the Energy sector. However, ESG criteria in the Financials sector generated a modest performance boost.

Given that our investment process is designed to emphasize stock selection, we do not expect sector selection to play a large role in performance. However, an overweight to Utilities increased the Portfolio’s return for the period.

Outlook

While we may see further volatility in the equity markets, those who step in to buy the dips in a time of uncertainty could have the potential for greater returns. Combined with generally positive U.S. economic data and attractive equity valuations--the 12-month forward price/earnings ratio for the S&P 500 Index was 10.61 after market close on September 30--as well as signs that China’s growth momentum has not stalled, we continue to believe the market can see a healthy recovery in the next few months. We remain cautiously optimistic on U.S. economic growth, albeit less so on European and global growth.

We also believe the U.S. earnings season that started on October is likely to provide positive earnings surprises and serve as a positive catalyst for the U.S. and possibly global equity markets, especially given current valuation levels, which may present some of the best buying opportunities in the equity markets.

October 2011

The following companies represented the following percentages of Portfolio net assets as of September 30, 2011: NiSource 2.43%, W. W. Grainger 2.61%, Dell 0.87%, Apple 5.61%, Bristol-Myers Squibb 3.41%, EnCana 1.93%, SEACOR 1.97%, Avery Dennison 0%, JPMorgan Chase 2.26% and VISA 0.84%. Holdings are subject to change without notice.

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 24

SHAREHOLDER EXPENSE EXAMPLE

As a shareholder of the Portfolio, you incur two types of costs: (1) transaction costs, including sales charges and redemption fees; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Portfolio expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Portfolio and to compare these costs with the ongoing costs of investing in other mutual funds.

This Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (April 1, 2011 to September 30, 2011).

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

The Money Market Portfolio charges a monthly low balance account fee of $3 to those shareholders whose account balance is less than $2,000. The Enhanced Equity Portfolio charges an annual low balance account fee of $15 to those shareholders whose regular account balance is less than $5,000.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Portfolio’s actual expense ratios and an assumed rate of return of 5% per year before expenses, which is not the Portfolio’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Portfolio and other funds. To do so, compare the 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) or redemption fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 25

| BEGINNING | ENDING | EXPENSES PAID | |

| ACCOUNT VALUE | ACCOUNT VALUE | DURING PERIOD* | |

| MONEY MARKET | 4/1/11 | 9/30/11 | 4/1/11 - 9/30/11 |

| Actual | $1,000.00 | $1,000.05 | $1.19 |

| Hypothetical | $1,000.00 | $1,023.88 | $1.20 |

| (5% return per | |||

| year before expenses) |

*Expenses for Money Market are equal to the annualized expense ratio of .24%, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period).

| BEGINNING | ENDING | EXPENSES PAID | |

| ACCOUNT VALUE | ACCOUNT VALUE | DURING PERIOD* | |

| EQUITY | 4/1/11 | 9/30/11 | 4/1/11 - 9/30/11 |

| CLASS A | |||

| Actual | $1,000.00 | $859.90 | $5.61 |

| Hypothetical | $1,000.00 | $1,019.03 | $6.09 |

| (5% return per | |||

| year before expenses) | |||

| CLASS B | |||

| Actual | $1,000.00 | $856.20 | $9.62 |

| Hypothetical | $1,000.00 | $1,014.70 | $10.44 |

| (5% return per | |||

| year before expenses) | |||

| CLASS C | |||

| Actual | $1,000.00 | $857.00 | $9.02 |

| Hypothetical | $1,000.00 | $1,015.36 | $9.79 |

| (5% return per | |||

| year before expenses) | |||

| CLASS I | |||

| Actual | $1,000.00 | $862.40 | $3.09 |

| Hypothetical | $1,000.00 | $1,021.75 | $3.36 |

| (5% return per | |||

| year before expenses) | |||

| CLASS Y | |||

| Actual | $1,000.00 | $861.40 | $3.83 |

| Hypothetical | $1,000.00 | $1,020.95 | $4.16 |

| (5% return per | |||

| year before expenses) |

*Expenses for Equity are equal to the annualized expense ratios of 1.20%, 2.07%, 1.94%, .66%, and .82% for Class A, Class B, Class C, Class I and Class Y, respectively, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period).

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 26

| BEGINNING | ENDING | EXPENSES PAID | |

| ACCOUNT VALUE | ACCOUNT VALUE | DURING PERIOD* | |

| ENHANCED EQUITY | 4/1/11 | 9/30/11 | 4/1/11 - 9/30/11 |

| CLASS A | |||

| Actual | $1,000.00 | $885.00 | $6.26 |

| Hypothetical | $1,000.00 | $1,018.42 | $6.71 |

| (5% return per | |||

| year before expenses) | |||

| CLASS B | |||

| Actual | $1,000.00 | $878.30 | $12.65 |

| Hypothetical | $1,000.00 | $1,011.60 | $13.54 |

| (5% return per | |||

| year before expenses) | |||

| CLASS C | |||

| Actual | $1,000.00 | $880.70 | $10.42 |

| Hypothetical | $1,000.00 | $1,013.99 | $11.15 |

| (5% return per | |||

| year before expenses) | |||

| CLASS I | |||

| Actual | $1,000.00 | $886.80 | $3.69 |

| Hypothetical | $1,000.00 | $1,021.15 | $3.95 |

| (5% return per | |||

| year before expenses) | |||

*Expenses for Enhanced Equity are equal to the annualized expense ratios of 1.33%, 2.69%, 2.21% and .78% for Class A, Class B, Class C, and Class I respectively, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period).

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 27

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

The Board of Trustees and Shareholders of Calvert Social Investment Fund: We have audited the accompanying statements of net assets of the Calvert Money Market, Equity, and Enhanced Equity Portfolios (collectively the Portfolios), each a series of the Calvert Social Investment Fund, as of September 30, 2011, and the related statements of operations for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years or periods in the five-year period then ended. These financial statements and financial highlights are the responsibility of the Portfolios’ management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of September 30, 2011, by correspondence with the custodians, and brokers or other appropriate auditing procedures. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of the Calvert Money Market, Equity, and Enhanced Equity Portfolios as of September 30, 2011, the results of their operations for the year then ended, the changes in their net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years or periods in the five-year period then ended, in conformity with U.S. generally accepted accounting principles.

Philadelphia, Pennsylvania

November 28, 2011

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 28

| MONEY MARKET PORTFOLIO | ||||

| STATEMENT OF NET ASSETS | ||||

| September 30, 2011 | ||||

| DEPOSITORY RECEIPTS FOR U.S. GOVERNMENT | PRINCIPAL | |||

| GUARANTEED LOANS - 0.0% | AMOUNT | VALUE | ||

| Colson Services Corporation Loan Sets: | ||||

| 2.125%, 5/29/12 (c)(h)(r) | $ | 28,992 | $ | 28,991 |

| 2.00%, 8/10/12 (c)(h)(r) | 23,460 | 23,474 | ||

| Total Depository Receipts For U.S. Government | ||||

| Guaranteed Loans (Cost $52,465) | 52,465 | |||

| VARIABLE RATE DEMAND NOTES - 81.7% | ||||

| 2880 Stevens Creek LLC, 0.45%, 11/1/33, LOC: Bank of the West (r) 3,220,000 | 3,220,000 | |||

| Akron Hardware Consultants, Inc., 0.45%, 11/1/22, | ||||

| LOC: FirstMerit Bank, C/LOC: FHLB (r) | 1,433,000 | 1,433,000 | ||

| Bayfront Regional Development Corp., 0.19%, 11/1/27, | ||||

| LOC: PNC Bank (r) | 5,500,000 | 5,500,000 | ||

| Bochasanwais Shree Akshar Purushottam Swaminarayan Sanstha, | ||||

| Inc., 0.25%, 6/1/22, LOC: Comerica Bank (r) | 1,875,000 | 1,875,000 | ||

| Butler County Alabama IDA Revenue, 0.90%, 3/1/12, | ||||

| LOC: Whitney National Bank, C/LOC: FHLB (r) | 220,000 | 220,000 | ||

| California Statewide Communities Development Authority MFH Revenue: | ||||

| 0.28%, 11/1/31, LOC: U.S. Bank (r) | 1,300,000 | 1,300,000 | ||

| 0.18%, 3/15/34, CEI: Fannie Mae (r) | 2,250,000 | 2,250,000 | ||

| CIDC-Hudson House LLC New York Revenue, 0.65%, 12/1/34, | ||||

| LOC: Hudson River Bank & Trust, C/LOC: FHLB (r) | 385,000 | 385,000 | ||

| Colorado State HFA Revenue, 0.13%, 10/15/16, CEI: Fannie Mae (r) | 500,000 | 500,000 | ||

| District of Columbia HFA MFH Revenue, 0.14%, 11/1/38, | ||||

| CEI: Freddie Mac (r) | 200,000 | 200,000 | ||

| Florida State Housing Finance Corp. MFH Revenue: | ||||

| Series B, 0.27%, 10/15/32, CEI: Fannie Mae (r) | 2,400,000 | 2,400,000 | ||

| Series J-1, 0.16%, 10/15/32, CEI: Fannie Mae (r) | 900,000 | 900,000 | ||

| Series J-2, 0.27%, 10/15/32, CEI: Fannie Mae (r) | 1,430,000 | 1,430,000 | ||

| Series N-2, 0.28%, 11/1/32, CEI: Freddie Mac (r) | 350,000 | 350,000 | ||

| Hawaii State Department of Budget & Finance Revenue, 0.25%, | ||||

| 12/1/21, LOC: Union Bank (r) | 3,200,000 | 3,200,000 | ||

| HBPWH Building Co., 0.27%, 11/1/22, | ||||

| LOC: Wells Fargo Bank (r) | 750,000 | 750,000 | ||

| HHH Investment Co., 0.28%, 7/1/29, LOC: Bank of the West (r) | 2,030,000 | 2,030,000 | ||

| Hills City Iowa Health Facilities Revenue, 0.16%, 8/1/35, | ||||

| LOC: U.S. Bank (r) | 5,090,000 | 5,090,000 | ||

| Illinois State Toll Highway Authority Revenue, 0.11%, 7/1/30, | ||||

| LOC: Northern Trust Co. (r) | 5,900,000 | 5,900,000 | ||

| Kaneville Road Joint Venture, Inc., 0.27%, 11/1/32, | ||||

| LOC: First American Bank, C/LOC: FHLB (r) | 6,475,000 | 6,475,000 | ||

| Kansas State Development Finance Authority MFH Revenue, | ||||

| 0.16%, 7/1/30, CEI: Freddie Mac (r) | 400,000 | 400,000 | ||

| Legacy Park LLC, 0.36%, 1/1/58, LOC: Fifth Third Bank (r) | 2,500,000 | 2,500,000 | ||

| Los Angeles California MFH Revenue, 0.32%, 12/15/34, | ||||

| CEI: Fannie Mae (r) | 1,375,000 | 1,375,000 | ||

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 29

| PRINCIPAL | ||||

| VARIABLE RATE DEMAND NOTES - CONT’D | AMOUNT | VALUE | ||

| Milpitas California MFH Revenue, 0.16%, 8/15/33, | ||||

| CEI: Fannie Mae (r) | $ | 2,200,000 | $ | 2,200,000 |

| Missouri State Health & Educational Facilities Authority Revenue: | ||||

| 0.22%, 11/1/32, LOC: Bank of America (r) | 4,400,000 | 4,400,000 | ||

| 0.17%, 12/1/35, LOC: Commerce Bank (r) | 4,500,000 | 4,500,000 | ||

| Montgomery New York Industrial Development Board Pollution | ||||

| Control Revenue, 0.38%, 5/1/25, LOC: FHLB (r) | 2,670,000 | 2,670,000 | ||

| Ness Family Partners LP, 0.40%, 9/1/34, LOC: Bank of the West (r) | 390,000 | 390,000 | ||

| Nevada State Housing Division Revenue, 0.15%, 4/15/39, | ||||

| CEI: Fannie Mae (r) | 4,400,000 | 4,400,000 | ||

| New York City Housing Development Corp. MFH Mortgage | ||||

| Revenue, 0.16%, 5/15/39, CEI: Fannie Mae (r) | 1,235,000 | 1,235,000 | ||

| New York City Housing Development Corp. MFH Rent Revenue: | ||||

| 0.17%, 11/15/31, CEI: Fannie Mae (r) | 1,450,000 | 1,450,000 | ||

| 0.17%, 6/15/34, CEI: Fannie Mae (r) | 1,300,000 | 1,300,000 | ||

| 0.17%, 11/15/35, CEI: Fannie Mae (r) | 1,495,000 | 1,495,000 | ||

| 0.17%, 12/1/35, CEI: Freddie Mac (r) | 5,130,000 | 5,130,000 | ||

| New York City Housing Development Corp. MFH Revenue: | ||||

| 0.18%, 11/15/37, CEI: Fannie Mae (r) | 1,200,000 | 1,200,000 | ||

| 0.16%, 11/1/38, CEI: Freddie Mac (r) | 4,000,000 | 4,000,000 | ||

| New York City IDA Revenue, 0.22%, 2/1/35, | ||||

| LOC: M&T Trust Co. (r) | 1,670,000 | 1,670,000 | ||

| New York State MMC Corp. Revenue, 0.65%, 11/1/35, | ||||

| LOC: JPMorgan Chase Bank (r) | 3,395,000 | 3,395,000 | ||

| Osprey Property Co., LLC, 0.22%, 6/1/27, LOC: Wells Fargo Bank (r) . 3,800,000 | 3,800,000 | |||

| Peoploungers, Inc., 0.40%, 4/2/18, LOC: Bank of New Albany, | ||||

| C/LOC: FHLB (r) | 1,880,000 | 1,880,000 | ||

| Portage Indiana Industrial Pollution Control Revenue, 0.36%, | ||||

| 5/1/18, LOC: Bank of Tokyo-Mitsubishi UFJ (r) | 5,150,000 | 5,150,000 | ||

| Rathbone LLC, 0.28%, 1/1/38, LOC: Comerica Bank (r) | 2,600,000 | 2,600,000 | ||

| Shawnee Kansas Private Activity Revenue, 0.60%, 12/1/12, | ||||

| LOC: JPMorgan Chase Bank (r) | 1,575,000 | 1,575,000 | ||

| Spencer County Indiana Industrial Pollution Control Revenue, | ||||

| 0.36%, 11/1/18, LOC: Mizuho Corp. Bank Ltd. (r) | 3,680,000 | 3,680,000 | ||

| St. Joseph County Indiana Economic Development Revenue, | ||||

| 1.73%, 6/1/27, LOC: FHLB (r) | 235,000 | 235,000 | ||

| Utah State Housing Corp. MFH Revenue, 0.21%, 4/1/42, | ||||

| CEI: Freddie Mac (r) | 225,000 | 225,000 | ||

| Utah State Housing Corp. Single Family Revenue, 0.18%, | ||||

| 7/1/36, CEI: Fannie Mae & Freddie Mac (r) | 2,220,000 | 2,220,000 | ||

| Virginia Commonwealth University Health System Revenue, 0.12%, | ||||

| 7/1/37, LOC: Branch Bank & Trust (r) | 2,000,000 | 2,000,000 | ||

| Washington State MFH Finance Commission Revenue: | ||||

| 0.23%, 6/15/32, CEI: Fannie Mae (r) | 665,000 | 665,000 | ||

| 0.23%, 7/15/32, CEI: Fannie Mae (r) | 605,000 | 605,000 | ||

| 0.18%, 7/15/34, CEI: Fannie Mae (r) | 1,365,000 | 1,365,000 | ||

| 0.22%, 5/1/37, CEI: Freddie Mac (r) | 1,350,000 | 1,350,000 | ||

| Total Variable Rate Demand Notes (Cost $116,468,000) | 116,468,000 | |||

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 30

| PRINCIPAL | |||||

| MUNICIPAL OBLIGATIONS - 2.9% | AMOUNT | VALUE | |||

| Oregon State GO Bonds, 2.00%, 6/29/12 | $ | 2,000,000 | $ | 2,026,423 | |

| Wisconsin GO Bonds, 5.25%, 5/1/17 (prerefunded 5/01/12 @ 100) | 2,000,000 | 2,056,936 | |||

| Total Municipal Obligations (Cost $4,083,359) | 4,083,359 | ||||

| U.S. GOVERNMENT AGENCIES AND INSTRUMENTALITIES - 8.4% | |||||

| Fannie Mae Discount Notes, 6/18/12 | 3,000,000 | 2,996,303 | |||

| Federal Home Loan Bank: | |||||

| 0.30%, 9/10/12 | 2,000,000 | 2,000,000 | |||

| 0.375%, 10/3/12 | 2,000,000 | 2,000,000 | |||

| Federal Home Loan Bank Discount Notes: | |||||

| 10/25/11 | 3,000,000 | 2,999,600 | |||

| 8/3/12 | 2,000,000 | 1,996,077 | |||

| Total U.S. Government Agencies And Instrumentalities | |||||

| (Cost $11,991,980) | 11,991,980 | ||||

| U.S. TREASURY - 2.1% | |||||

| United States Treasury Notes, 0.375%, 8/31/12 | 3,000,000 | 3,006,289 | |||

| Total U.S. Treasury (Cost $3,006,289) | 3,006,289 | ||||

| TIME DEPOSIT - 0.1% | |||||

| State Street Time Deposit, 0.113%, 10/3/11 | 211,952 | 211,952 | |||

| Total Time Deposit (Cost $211,952) | 211,952 | ||||

| TOTAL INVESTMENTS (Cost $135,814,045) - 95.2% | 135,814,045 | ||||

| Other assets and liabilities, net - 4.8% | 6,780,910 | ||||

| NET ASSETS - 100% | $ | 142,594,955 | |||

| NET ASSETS CONSIST OF: | |||||

| Paid-in capital applicable to the following shares of beneficial interest | |||||

| unlimited number of no par value shares authorized, | |||||

| 142,664,064 shares outstanding | $ | 142,598,057 | |||

| Undistributed net investment income | 5,973 | ||||

| Accumulated net realized gain (loss) on investments | (9,075 | ) | |||

| NET ASSETS | $ | 142,594,955 | |||

| NET ASSET VALUE PER SHARE | $ | 1.00 | |||

See notes to statements of net assets and notes to financial statements.

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 31

| EQUITY PORTFOLIO | |||

| STATEMENT OF NET ASSETS | |||

| September 30, 2011 | |||

| EQUITY SECURITIES - 95.5% | SHARES | VALUE | |

| Air Freight & Logistics - 3.6% | |||

| C.H. Robinson Worldwide, Inc | 646,333 | $ | 44,254,421 |

| Expeditors International of Washington, Inc. | 766,897 | 31,097,673 | |

| 75,352,094 | |||

| Auto Components - 0.7% | |||

| Johnson Controls, Inc | 513,967 | 13,553,310 | |

| Beverages - 1.8% | |||

| PepsiCo, Inc | 588,549 | 36,431,183 | |

| Biotechnology - 2.9% | |||

| Gilead Sciences, Inc.* | 1,528,258 | 59,296,410 | |

| Capital Markets - 3.9% | |||

| Charles Schwab Corp | 1,230,706 | 13,870,057 | |

| T. Rowe Price Group, Inc | 1,381,233 | 65,981,500 | |

| 79,851,557 | |||

| Chemicals - 2.2% | |||

| Ecolab, Inc. | 926,715 | 45,307,096 | |

| Commercial Banks - 3.4% | |||

| SunTrust Banks, Inc. | 2,013,848 | 36,148,572 | |

| Wells Fargo & Co | 1,422,627 | 34,313,763 | |

| 70,462,335 | |||

| Communications Equipment - 5.5% | |||

| Acme Packet, Inc.* | 616,702 | 26,265,338 | |

| QUALCOMM, Inc. | 1,817,290 | 88,374,813 | |

| 114,640,151 | |||

| Computers & Peripherals - 4.7% | |||

| Apple, Inc.* | 257,872 | 98,295,649 | |

| Consumer Finance - 2.2% | |||

| American Express Co. | 1,007,539 | 45,238,501 | |

| Diversified Financial Services - 3.2% | |||

| IntercontinentalExchange, Inc.* | 320,310 | 37,879,861 | |

| JPMorgan Chase & Co. | 946,206 | 28,499,725 | |

| 66,379,586 | |||

| Electrical Equipment - 1.6% | |||

| Cooper Industries plc | 719,971 | 33,205,063 | |

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 32

| EQUITY SECURITIES - CONT’D | SHARES | VALUE | |

| Energy Equipment & Services - 4.5% | |||

| Cameron International Corp.* | 1,596,608 | $ | 66,323,096 |

| Noble Corp.* | 891,209 | 26,156,984 | |

| 92,480,080 | |||

| Food & Staples Retailing - 3.9% | |||

| Costco Wholesale Corp | 339,747 | 27,900,024 | |

| CVS Caremark Corp. | 1,558,899 | 52,347,828 | |

| 80,247,852 | |||

| Food Products - 2.4% | |||

| Green Mountain Coffee Roasters, Inc.* | 524,454 | 48,742,755 | |

| Health Care Equipment & Supplies - 3.6% | |||

| Edwards Lifesciences Corp.* | 344,900 | 24,584,472 | |

| Intuitive Surgical, Inc.* | 63,500 | 23,131,780 | |

| St. Jude Medical, Inc. | 724,963 | 26,236,411 | |

| 73,952,663 | |||

| Hotels, Restaurants & Leisure - 5.2% | |||

| Chipotle Mexican Grill, Inc.* | 116,776 | 35,377,289 | |

| Darden Restaurants, Inc | 650,702 | 27,817,511 | |

| Starbucks Corp. | 1,170,212 | 43,637,205 | |

| 106,832,005 | |||

| Household Products - 0.8% | |||

| Procter & Gamble Co. (t) | 250,094 | 15,800,939 | |

| Industrial Conglomerates - 3.5% | |||

| 3M Co. | 490,609 | 35,220,820 | |

| Danaher Corp. | 898,916 | 37,700,537 | |

| 72,921,357 | |||

| Insurance - 0.5% | |||

| Aflac, Inc. | 292,856 | 10,235,317 | |

| Internet & Catalog Retail - 4.4% | |||

| Amazon.com, Inc.* | 143,484 | 31,025,545 | |

| Netflix, Inc.* | 168,280 | 19,042,565 | |

| priceline.com, Inc.* | 91,116 | 40,952,997 | |

| 91,021,107 | |||

| Internet Software & Services - 3.3% | |||

| Google, Inc.* | 83,580 | 42,991,880 | |

| MercadoLibre, Inc. | 472,260 | 25,383,975 | |

| 68,375,855 | |||

| IT Services - 5.1% | |||

| Cognizant Technology Solutions Corp.* | 870,568 | 54,584,614 | |

| International Business Machines Corp. | 289,948 | 50,749,598 | |

| 105,334,212 | |||

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 33

| EQUITY SECURITIES - CONT’D | SHARES | VALUE | |

| Multiline Retail - 2.0% | |||

| Kohl’s Corp. | 853,934 | $ | 41,928,159 |

| Oil, Gas & Consumable Fuels - 3.8% | |||

| QEP Resources, Inc. | 1,042,531 | 28,221,314 | |

| Suncor Energy, Inc. | 1,983,156 | 50,451,489 | |

| 78,672,803 | |||

| Pharmaceuticals - 7.4% | |||

| Allergan, Inc | 1,218,146 | 100,350,867 | |

| Novartis AG (ADR) | 938,927 | 52,363,959 | |

| 152,714,826 | |||

| Software - 7.4% | |||

| Informatica Corp.* | 447,670 | 18,332,087 | |

| Intuit, Inc.* | 762,340 | 36,165,410 | |

| Microsoft Corp. | 937,082 | 23,323,971 | |

| Salesforce.com, Inc.* | 392,380 | 44,841,186 | |

| VMware, Inc.* | 384,550 | 30,910,129 | |

| 153,572,783 | |||

| Specialty Retail - 1.7% | |||

| CarMax, Inc.* | 1,513,463 | 36,096,093 | |

| Venture Capital - 0.3% | |||

| 20/20 Gene Systems, Inc.: | |||

| Common Stock (b)(i)* | 43,397 | 48,822 | |

| Warrants (strike price $.01/share, expires 8/27/13) (b)(i)* | 30,000 | 33,450 | |

| Better Energy Systems, Inc.: | |||

| Series B, Preferred (b)(i)* | 992,555 | 266,997 | |

| Series B, Preferred Warrants (strike price $0.75/share, | |||

| expires 8/3/13) (b)(i)* | 133,333 | - | |

| Chesapeake PERL, Inc., Series A-2, Preferred (b)(i)* | 240,000 | 2,400 | |

| Cylex, Inc.: | |||

| Common Stock (b)(i)* | 285,706 | - | |

| Series B, Preferred (b)(i)* | 1,134,830 | - | |

| Series C-1, Preferred (b)(i)* | 2,542,915 | 679,299 | |

| Digital Directions International, Inc. (a)(b)(i)* | 354,389 | 531,585 | |

| Envisionier Medical Technologies, Inc., Warrants (strike price | |||

| $.50/share, expires 8/6/20) (b)(i)* | 50,000 | - | |

| Global Resource Options, Inc.: | |||

| Series A, Preferred (a)(b)(i)* | 750,000 | 155,357 | |

| Series B, Preferred (a)(b)(i)* | 244,371 | 155,357 | |

| Series C, Preferred (a)(b)(i)* | 297,823 | 207,143 | |

| Series D, Preferred (a)(b)(i)* | 228,138 | 1,424,533 | |

| Marrone Bio Innovations, Inc.: | |||

| Series A, Preferred (b)(i)* | 240,761 | 407,853 | |

| Series B, Preferred (b)(i)* | 181,244 | 307,030 | |

| Series C, Preferred (b)(i)* | 295,157 | 500,000 | |

| Napo Pharmaceuticals, Inc.: | |||

| Common Stock (b)(i)* | 294,196 | 588,392 | |

| Common Warrants (strike price $0.55/share, expires 9/15/14) (b)(i)* 54,061 | 78,388 | ||

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 34

| EQUITY SECURITIES - CONT’D | SHARES | VALUE | ||

| NeoDiagnostix, Inc.: | ||||

| Series AE, Preferred Contingent Deferred Distribution (b)(i)* | 300,000 | $ | 61,373 | |

| Series AE, Preferred Warrants Contingent Deferred | ||||

| Distribution (b)(i)* | 600,000 | - | ||

| Series B, Preferred Contingent Deferred Distribution (b)(i)* | 179,723 | 235,485 | ||

| New Day Farms, Inc., Series B, Preferred (a)(b)(i)* | 4,547,804 | 72,037 | ||

| Orteq Bioengineering Ltd., Series A, Preferred (b)(i)* | 74,910 | 760,707 | ||

| PresenceLearning, Inc., Series A, Preferred (b)(i)* | 600,000 | 300,000 | ||

| Sword Diagnostics, Series B, Preferred (b)(i)* | 640,697 | - | ||

| Village Laundry Services, Inc. (b)(i)* | 9,444 | 30,599 | ||

| 6,846,807 | ||||

| Total Equity Securities (Cost $1,918,166,420) | 1,973,788,548 | |||

| VENTURE CAPITAL LIMITED | ADJUSTED | |||

| PARTNERSHIP INTEREST - 0.3% | BASIS | |||

| Blackstone Cleantech Venture Partners (b)(i)* | $ | 335,646 | 258,996 | |

| China Environment Fund 2004 (b)(i)* | - | 500,193 | ||

| China Environment Fund III (b)(i)* | 923,658 | 1,076,165 | ||

| Core Innovations Capital I (b)(i)* | 153,721 | 96,310 | ||

| DBL Equity Fund - BAEF II (b)(i)* | 424,621 | 411,417 | ||

| Ignia Fund I (b)(i)* | 523,833 | 398,705 | ||

| Impact Ventures II (b)(i)* | 544,757 | 689,090 | ||

| LeapFrog Financial Inclusion Fund (b)(i)* | 304,813 | 259,517 | ||

| New Markets Venture Partners II (b)(i)* | 250,000 | 270,963 | ||

| Renewable Energy Asia Fund (b)(i)* | 512,648 | 382,383 | ||

| SEAF India International Growth Fund (b)(i)* | 394,032 | 403,585 | ||

| Sustainable Jobs Fund II (b)(i)* | 608,991 | 900,391 | ||

| New Markets Education Partners, (a)(b)(i)* | 175,000 | 175,000 | ||

| Total Venture Capital Limited Partnership | ||||

| Interest (Cost $5,151,719) | 5,822,715 | |||

| PRINCIPAL | ||||

| HIGH SOCIAL IMPACT INVESTMENTS - 0.5% | AMOUNT | |||

| Calvert Social Investment Foundation Notes, 0.94%, 7/1/12 (b)(i)(r) | 10,833,877 | 10,439,524 | ||

| Total High Social Impact Investments (Cost $10,833,877) | 10,439,524 | |||

| VENTURE CAPITAL DEBT OBLIGATIOINS - 0.2% | ||||

| Envisionier Medical Technologies, Inc.: | ||||

| Note I, 7.00%, 12/31/11 (b)(i)(xx)* | 200,000 | 100,000 | ||

| Note II, 7.00%, 12/31/11 (b)(i)(xx)* | 100,000 | 50,000 | ||

| New Day Farms Participation Interest Note, 9.00%, 9/1/12 (a)(b)(i) | 6,225 | 6,225 | ||

| Quantum Intech, Inc., 11.50%, 9/10/15 (b)(i) | 101,870 | 101,870 | ||

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 35

| PRINCIPAL | |||||||

| VENTURE CAPITAL DEBT OBLIGATIONS - CONT’D | AMOUNT | VALUE | |||||

| SEAF Global SME Facility: | |||||||

| 9.00%, 12/16/14 (b)(i) | $ | 1,500,000 | $ | 1,500,000 | |||

| 9.00%, 4/20/15 (b)(i) | 1,000,000 | 1,000,000 | |||||

| 9.00%, 11/5/15 (b)(i) | 1,000,000 | 655,849 | |||||

| 9.00%, 3/31/16 (b)(i) | 450,000 | 450,000 | |||||

| 9.00%, 6/14/16 (b)(i) | 400,000 | 400,000 | |||||

| 9.00%, 7/12/16 (b)(i) | 650,000 | 650,000 | |||||

| Sword Diagnostics Series C Convertible Bridge Note, 10.00%, | |||||||

| 7/31/12 (b)(i)(zz)* | 25,000 | 18,750 | |||||

| Sword Diagnostics Series C Convertible Bridge Note II, 10.00%, | |||||||

| 7/31/12 (b)(i)(zz)* | 100,000 | 75,000 | |||||

| Total Venture Capital Debt Obligations (Cost $5,533,095) | 5,007,694 | ||||||

| TIME DEPOSIT - 2.6% | |||||||

| State Street Time Deposit, 0.113%, 10/3/11 | 54,371,685 | 54,371,685 | |||||

| Total Time Deposit (Cost $54,371,685) | 54,371,685 | ||||||

| TOTAL INVESTMENTS (Cost $1,994,056,796) - 99.1% | 2,049,430,166 | ||||||

| Other assets and liabilities, net - 0.9% | 18,601,735 | ||||||

| NET ASSETS - 100% | $ | 2,068,031,901 | |||||

| NET ASSETS CONSIST OF: | |||||||

| Paid-in capital applicable to the following shares of beneficial interest, | |||||||

| unlimited number of no par value shares authorized: | |||||||

| Class A: 39,419,494 shares outstanding | $ | 1,231,343,356 | |||||

| Class B: 1,262,505 shares outstanding | 24,102,692 | ||||||