UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-3334

CALVERT SOCIAL INVESTMENT FUND

(Exact name of registrant as specified in charter)

4550 Montgomery Avenue

Suite 1000N

Bethesda, Maryland 20814

(Address of Principal Executive Offices)

William M. Tartikoff, Esq.

4550 Montgomery Avenue

Suite 1000N

Bethesda, Maryland 20814

(Name and Address of Agent for Service)

Registrant's telephone number, including area code: (301) 951-4800

Date of fiscal year end: September 30

Date of reporting period: Twelve months ended September 30, 2013

Item 1. Report to Stockholders.

[Calvert Social Investment Fund Balanced, Bond, Equity and Large Cap Core Portfolios Annual Report]

[Calvert Asset Allocation Funds Annual Report]

Choose Planet-friendly E-delivery!

Sign up now for on-line statements, prospectuses, and fund reports. In less than five minutes you can help reduce paper mail and lower fund costs.

Just go to www.calvert.com. If you already have an online account at Calvert, click on My Account, and select the documents you would like to receive via e-mail.

If you’re new to online account access, click on Login/Register to open an online account. Once you’re in, click on the E-delivery sign-up at the bottom of the Account Portfolio page and follow the quick, easy steps. Note: if your shares are not held directly at Calvert but through a brokerage firm, you must contact your broker for electronic delivery options available through their firm.

Dear Calvert Shareholder,

In the past 12 months, financial equity markets have staged quite a rally. The S&P 500 Index is up more than 19%. A year ago, many troubling circumstances created some fears in the market (although this letter suggested investors should hang in there).

In My Opinion

Today, with the Federal Reserve flooding the country with quantitative easing money, there seems to be an acquiescence and belief that this pillow of easy money will keep the markets buoyant. Stock prices have increased due more to expansions of price-to-earnings multiples than higher earnings growth. While Wall Street consensus is for the equity markets to be up 7% in the second half of 2014, I am not so sure and admit to some uneasiness about this prediction. The Fed made the right moves, but easy money is not a cure-all for our long-term economic future.

The word at the Federal Reserve is that Janet Yellen, nominated to become the new Chairman, may keep short-term rates low into 2015. While we applaud the selection of a woman, I was also happy to learn she is married to a co-author of one of my favorite economic books, Animal Spirits, which is based on an old concept from economist John Maynard Keynes. Keynes suggested that, for all his theories, the psychology of the markets also played a mysterious but important role. And that is where I believe the mood of the country may be cause for concern.

As of this writing, the U.S. government has reopened and avoided default—but not without considerable consternation. I respect the intentions of the right wing, trying with unfortunate desperation, to bring the spending issue to the table. The Obama administration has not presented a long-term, credible plan to moderate the deficit spending.

Most Americans agree we need a mix of budget cuts and tax increases. I am in the camp that believes we should have a means test for Social Security. But with all the special interests, our political system can’t seem to do what to me is simply common sense on this vital issue. In my opinion, the divisiveness in Washington is contributing to a dour mood in the country. We are very fortunate to have a respite on energy security issues but also unfortunate that important discussions on climate change and carbon reduction seem to have waned.

Compounding this mood is not just the growing divide between rich and poor, but the fact we have a growing underclass for which we don’t have a plan. One-quarter of high school students don’t graduate.1 Twenty percent of families are on food stamps.2 More than four million people have exhausted regular federal unemployment benefits, increasing a sense of discouragement.3 Some suggest the American Dream is fading for too many. I believe some fixes, like the Affordable Care Act, go in the right direction.

4 www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT

But it’s uncertain whether this will reduce actual care costs, which are almost twice as high in the United States as in other developed nations.

While I have been an Obama supporter, I still don’t know what his vision is—although employees of his administration may well counter that their plans only allow what’s politically doable. To me, it seems obvious that we need to 1) focus on getting education to the underserved and 2) create a sensible immigration policy that brings needed and motivated talent into our country, however that’s defined and 3) adopt a tax on carbon to accelerate our transition to cleaner energy.

The rest of the world provides no anti-depressant to the global outlook. The Germans seem to have accepted their asymmetric role in Europe but that has only stabilized a despondent dynamic with other states. The Japanese are at least making efforts to moderate stagnation. China is having its quadrennial Congress in November, which will foretell if the new leadership is serious about much-needed reforms. Events in China could easily be the linchpin for the markets, as the various financial bubbles in that country could become a problem—decreasing their global consumption demands, causing stagnation in many emerging market countries, and affecting U.S. corporate earnings.

Even longer-term, the concern is that the U.S. is entering into decades of what some economists predict will be called The Great Stagnation. With declines in productivity indicators, research and development, and the working-age population,4 it’s hard to understand where the tax revenues will come from to support promised entitlements. U.S. politics and policymaking must act responsibly or social dislocation may be in our future.

Then again, perhaps these will be the times that remind us that true wealth is really in our relationships, our communities, and our spiritual practices. Maybe a more local focus, from the foods we eat to the ecological health of our immediate environment, will bring us sustenance and richness, similar to the romanticized agrarian times, and away from today’s getting and spending. Some reflection about how we can transform the “new normal” into the “real normal” may be a silver lining for the slower economic growth ahead.

Shareholder Engagement

Yet, animal spirits at Calvert remain high. Companies are becoming more responsive to our interactions in pushing for best-in-class standards, but not without the occasional arm-twisting. Over the past year, Calvert engaged with 139 companies and filed 22 shareholder proposals, which led to agreements with 14 companies on the issues of board diversity, sustainability reporting, and board oversight of sustainability, among others.

While these numbers tell our story, I was particularly moved by an informal interaction my assistant had with a retired big pharma executive at a recent Wharton awards dinner. He told her that Calvert’s inquiries were taken quite seriously at this global multinational corporation and provoked much internal discussion. He said having a shareholder ask these questions gives internal advocates more of a voice in policy-setting and implored her to keep up the good work!

This exchange was not only a strong validation for Calvert’s work—it shows the shareholder advocacy process is not necessarily as adversarial as some may believe. People inside the company are often already lobbying for the changes we propose. They simply don’t have

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 5

enough clout or know how to make them happen. But management has a much harder time ignoring a group of investors who own millions of dollars of the company’s stock.

350.Org Divestment Campaign On Fossil Fuels

Calvert closely watched the 350.org campaign urging college and university endowments, as well as other institutional investors, to divest from companies producing fossil fuels. We support the campaign’s broad objectives while making the case for a complementary strategy of active ownership and engagement, as we do on your behalf here at Calvert. After all, shareholders have a lot more leverage for getting management’s ear than outsiders. To illustrate that point, we highlighted specific fossil fuel companies that Calvert has successfully engaged on climate change, alternative energy, and revenue transparency in a web site statement on the matter last December.

In July, we also highlighted Calvert’s low and no-carbon portfolios, breaking down the percentage (between zero and three percent) of carbon exposure in your funds, as calculated by Carbon Tracker Top 200 and portfolio holding weight. Interestingly, some now argue that cleansing portfolios makes even more sense financially, as the carbon situation may become so severe that the oil industry may not be permitted to monetize “stranded assets” of petroleum.

Community Investments

Many of our Funds participate in Calvert’s High Social Impact Investing program, which is administered through the Calvert Foundation. This community investment program may allocate a small percentage of Fund assets at below-market interest rates to investments that provide economic opportunity for struggling populations.

As part of its WIN-WIN portfolio (Women Investing in Women), we recently invested $500,000 through the Foundation in Access to Capital for Entrepreneurs (ACE) to expand their lending to small businesses. ACE is a nonprofit community lender and a certified community development financial institution that provides loans to small businesses owned by low-income individuals, people of color and women who lack access to traditional forms of credit in Georgia.

Special Equities

A modest but important portion of certain funds is allocated to small private companies developing products or services that address important sustainability or environmental issues facing our society.

One recent investment was in Shangri-La Farms. This company in the Yunnan province of China trains minorities to be beekeepers, among other crafts. The honey is then nicely packaged for sale to upscale hotels and stores in Beijing. While this activity may never become large scale, we thought it was important to promote the concept of social enterprise investment in China, as an example to the Chinese, of this social impact investing.

Another investment, Revolution Foods, was held through the Westly Capital Partners Fund II, L.P. This company provides nutritious school meals for kids, educating them about real foods. Two of our companies providing bio-based products for pest management and agricultural plant health, Marrone Bio Innovations and Agraquest, also provided good returns to the fund this year as one was acquired and one conducted an IPO.

6 www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT

Your fund’s pioneering work in this area of social venture capital, now called “impact investing,” has been quite a contribution to this growing movement of the intersection between meaning and money, especially with the younger generation. Most of the business schools now have Impact Investing courses, and students no longer need to feel embarrassed asking about the social value of investments in class.

Your support of the Funds has made this difference happen. We thank you and continue to be rewarded with the challenges of our collective mission.

1. Alliance for Excellent Education, America’s Promise Alliance, Civic Enterprises, and Everyone Graduates Center at Johns Hopkins University, Building a Grad Nation: Progress and Challenge in Ending the High School Dropout Epidemic, February 2013 www.americaspromise.org/our-work/grad-nation/building-a-grad-nation.aspx

2. U.S. Department of Agriculture Monthly Supplemental Nutrition Assistance Program Report www.fns.usda.gov/pd/34SNAPmonthly.htm

3. Bureau of Labor Statistics Employment Situation Summary, September 2013, www.bls.gov/news.release/empsit.nr0.htm

4. Jonathan Laing, “Slowing to a Crawl,” Barron’s, October 28, 2013, http://online.barrons.com/article/SB50001424053111904897104579149772682783890.html

As of September 30, 2013, Calvert Social Investment Foundation (“Calvert Foundation” or “Foundation”) Community Investment Notes represented the following percentages of Fund net assets: Calvert Balanced Portfolio .72%, Calvert Equity Portfolio .39%, and Calvert Bond Portfolio .43%. The Calvert Foundation is a 501(c)(3) nonprofit organization. The Calvert Foundation is a 501(c)(3) nonprofit organization. The Foundation’s Community Investment Note Program is not a mutual fund and should not be confused with any Calvert Investments-sponsored investment product.

As of September 30, 2013, the following companies represented the following percentages of Portfolio net assets: Shangri-La Farms .007% of Calvert Equity Portfolio; Westly Capital Partners Fund II .01% of Calvert Equity Portfolio, Marrone Bio Innovations .14% of Calvert Equity Portfolio, and Agraquest .04% of Calvert Balanced Portfolio. Holdings are subject to change.

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 7

Dear Calvert Shareholder,

For the 12 months ended September 30, 2013, the global equity markets generally had a strong year, while bonds saw more mixed results. Large-cap stocks, as represented by the Russell 1000 Index, posted a healthy 20.9% return, while the smaller-cap Russell 2000 Index led with a 30.1% gain. This occurred despite political turmoil and market concerns worldwide about a forced shutdown of the U.S. government and the upcoming debt ceiling deadline.

Despite these advances, it was a challenging year for the financial markets overall. At various times, issues at home and abroad led to marked volatility in the performance of both stocks and bonds. Emerging-market performance was notably low, as fears of slowing growth in China and the Eurozone, along with continuing struggles in the Eurozone periphery, stalled regional investment. As a result, the formerly high-flying MSCI Emerging Markets Index gained only 1.3% for the period. The Barclays U.S. Credit Index, a barometer for the overall U.S. bond market, returned -1.9%.

Early in the Fall, Fed Chairman Ben Bernanke’s retirement was big news. The nomination of Vice Chair Janet Yellen as his replacement means the Fed will likely stay the course with current monetary policy. Yet, this is a historic moment for the United States, as Yellen, following Senate approval, will be the first woman to lead this critical agency.

Calvert Co-Founder Honored

I’m proud to congratulate Calvert co-founder Wayne Silby, who received the prestigious Joseph Wharton Award for Social Impact from The Alumni Club of New York, honoring his lifetime of achievement in impact investing and social entrepreneurship. Besides founding Calvert with John Guffey, Wayne is a co-founder of the Social Venture Network, Co-Chairman of the board of the Calvert Foundation, Chairman of Syntao Ltd., a CSR consultancy in Beijing, and active in other ventures in social impact and entrepreneurship.

Calvert Releases New Report on Diversity

In March, we published the latest edition of Examining the Cracks in the Glass Ceiling, which measures diversity practices of the companies that constitute the S&P 100 Index. As you know, Calvert believes companies with a diverse workforce are poised for greater success in today’s increasingly global marketplace and will enjoy greater long-term value—a view supported by a growing body of research from McKinsey, Credit Suisse, and others.

Companies in the report were rated on 10 indicators: EEO policy, internal diversity initiatives, external diversity initiatives, scope of diversity initiatives, family-friendly benefits, demographic disclosure of employees (EEO-1), highest-paid executives, board diversity,

8 www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT

director selection criteria, and overall corporate commitment. The highest-rated companies were Citigroup, Merck, The Coca-Cola Company, and J.P. Morgan Chase, all scoring at least 95 points or more out of 100. We hold these companies in a number of our Calvert portfolios.

While some progress has been achieved in corporate diversity practices since our last assessment in 2010, the S&P 100 companies are largely failing to translate progressive practices into increased promotion rates for women and minority employees. For example, women are now hired as often as men. However, more than half of the S&P 100 companies lack diversity among their highest-paid senior executive positions. And women still only represent 19% of board members among these large-cap companies. Much remains to be done, which is why we continue to work with a number of international, multi-stakeholder groups on these issues, as well as conduct advocacy work with individual companies.

Stay Informed in the Months Ahead

Maintaining a well-diversified mix of U.S. and international stocks, bonds, and cash—appropriate for your goals and risk tolerance—is one of the best ways to mitigate the effects of an uneven recovery in the economy and markets. Of course, we recommend consulting your financial advisor if you have questions or concerns about your investments.

We also invite you to visit our website, www.calvert.com, for fund information, portfolio updates, and commentary from Calvert professionals. As always, we thank you for investing with Calvert.

Sincerely,

The following companies represented the following percentages of Fund net assets: Citigroup 2.27% of Calvert Large Cap Value, 1.32% of Calvert Social Index; Merck 2.26% of Calvert Equity Income, 2.01% of Calvert Large Cap Value, and 1.25% of Calvert Social Index; Coca-Cola 1.29% of Calvert Social Index, 3.20% of Calvert Large Cap Core and 3.29% Calvert Equity Portfolio; J.P. Morgan Chase 2.54% of Calvert Equity Income, 1.74% of Calvert Social Index and 0.34% of Calvert Balanced Portfolio. Holdings are subject to change.

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 9

As always, Calvert continues to work hard to ensure you have a say in the responsible management of environmental, social, and governance (ESG) factors for the companies in which we invest. Below are highlights of our accomplishments during the reporting period.

Shareholder Advocacy

Over the past year, Calvert engaged with 139 companies via emails, letters, phone calls, and in-person meetings. We also filed 22 shareholder proposals during the 2013 proxy season, which led to agreements with 14 companies on the issues of board diversity and sustainability reporting, among others. We also presented at four annual meetings where the proposals came to a vote and received shareholder support that exceeded 40% at two companies.

One proposal was for diversified energy services company Cleco, which has significant assets in thermoelectricity, to report on its sustainability risks and opportunities, including an analysis of material water-related risks. The other at Pioneer Natural Resources focused on reporting the environmental and social challenges and opportunities associated with hydraulic fracturing.

Company Engagement

Research and an intensive dialogue across a range of corporate responsibility and sustainability issues led to McDonald’s and Walt Disney meeting our Signature® criteria1 for the first time. McDonald’s is improving its supply chain labor policies and practices, diversifying its menu options, and disclosing their nutritional content—although it continues to face challenges in both areas. Walt Disney now meets the criteria for workplace safety, while continuing to meet our criteria on supply chain labor and human rights practices.

We undertook more engagement with Coca-Cola and PepsiCo on labor and human rights, water, and sustainability issues. In fact, PepsiCo management credited our recommendations with influencing their decision to strengthen their human rights policy framework.

Climate Change And Energy

Calvert, the World Wildlife Fund (WWF) and Ceres published, “Power Forward: Why the World’s Largest Companies are Investing in Renewable Energy.” The report found that more than half of the largest U.S. corporations and more than two-thirds of the largest companies across the globe have set greenhouse gas (GHG) emissions reduction commitments and/or renewable energy commitments.

Calvert joined with other Investor Network on Climate Risk (INCR) members to speak at congressional staff briefings about recommendations for corporations in the report and

10 www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT

draft an investor letter to Congress supporting the production tax credit (PTC) for wind energy, which was due to expire at the end of 2012. The report, briefings and investor letter helped spur extension of the PTC to support the growth of renewable energy.

Burma

After the lifting of U.S. sanctions prohibiting new investment in Burma by American companies, the Calvert Social Funds Board approved revisions to Calvert’s long-standing policy language in September. Instead of urging U.S. companies to “cease operations” in Burma, the new language instead calls for Calvert to advocate for “responsible investment.”

Garment Industry Safety

Following the Rana Plaza tragedy earlier this year, where more than 1,100 Bangladesh garment factory workers were killed, Calvert assessed the state of significant country-level sourcing disclosure by retail companies, which is essential to assessing sourcing risks more effectively. After learning that only a handful of companies disclose this necessary data, we contacted 26 retail company CEOs requesting disclosure of sourcing information for those countries representing 5% or more of global order volume.

Human Rights Report

In March, Calvert, Interfaith Center on Corporate Responsibility and the Institute for Human Rights and Business launched “Investing the Rights Way: A Guide for Business and Human Rights” in both New York and London. The guide outlines how investors can apply the UN Guiding Principles on Business and Human Rights as a due diligence and risk assessment framework to assess companies in their portfolios.

Conflict Minerals

Calvert continued to be a leader among investors on “conflict minerals” through a multi-stakeholder group supporting disclosure requirements enacted as Section 1502 of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010. The disclosure would certify that certain minerals used in cell phones and other consumer electronic components (tin, titanium, tantalum and gold) are not illegally mined to fuel the continuing bloody conflict in the Democratic Republic of Congo (DRC).

After the SEC approved and released the final rule to implement the reporting requirements of Section 1502 in August 2012, the U.S. Chamber of Commerce filed a lawsuit against the Securities and Exchange Commission (SEC) to stop implementation. Calvert led the multi-stakeholder group’s effort to forge a common statement urging implementation of the law as outlined by the rule, regardless of the lawsuit. On July 23, the court upheld the “conflict minerals rule” in favor of the SEC and the statute requiring adoption of the rule—a major victory for Calvert and its allies.

Extractives Revenue Transparency

Widely credited for its leadership role among investors in supporting extractive revenue transparency as an imperative for investors interested in full disclosure of material information related to oil, gas and mining in certain countries, Calvert has remained actively engaged in the SEC rule-making process. The U.S. Chamber of Commerce and the American Petroleum Institute filed a lawsuit challenging the pro-disclosure rules, Calvert submitted a sworn statement about the problems investors would face if the rules were

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 11

delayed or revoked. We also sent letters to the SEC emphasizing the materiality of disclosures required by the rules and contributed research to Oxfam America’s January 2013 brief.

On July 2, the court “vacated” the SEC’s rule, declaring it inoperative until the SEC addresses certain key issues (the necessity for exemptions for certain countries and public reporting of the disclosures). Calvert subsequently drafted a letter to SEC Chairman Mary Jo White that acknowledged the value of the Commission’s rules to implement Section 1504 and urged her respond to the API vs. SEC decision by reinstating rules consistent with those issued in August 2012, which were endorsed by investors representing more than $5.6 trillion in assets under management.

1. Calvert’s Signature® criteria examine corporate performance across seven broad areas of concern: Governance and Ethics, Environment, Workplace, Product Safety and Impact, International Operations and Human Rights, Indigenous Peoples’ Rights, and Community Relations. For a company to be eligible for inclusion in a Calvert Signature portfolio, it must meet the criteria in all seven categories.

The following companies represented the following percentages of net assets: Cleco 0.02% of Calvert Social Index; Pioneer Natural Resources 0.23% of Calvert Social Index and 1.39% of Calvert Balanced Portfolio; McDonald’s 0.86% of Calvert Social Index and 2.35% of Calvert Equity Portfolio, Walt Disney 0.96% of Calvert Social Index and 2.25% of Calvert Equity Portfolio; Coca-Cola 1.29% of Calvert Social Index, 3.20% of Calvert Large Cap Core and 3.29% Calvert Equity Portfolio; PepsiCo 1.10% of Calvert Social Index, 1.20% of Calvert Equity Portfolio and 0.54% of Calvert Balanced Portfolio; Denbury Resources 0.06% of Calvert Social Index and 2.86% of Calvert Large Cap Core; and Suncor Energy 0.71%% of Calvert International Equity Portfolio. Holdings are subject to change.

12 www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT

Performance

For the 12-month period ended September 30, 2013, Calvert Balanced Portfolio Class A shares (at NAV) returned 11.60% versus 20.91% for its benchmark, the Russell 1000 Index.

The Portfolio’s relative underperformance versus the Russell 1000 Index was due to the Portfolio’s asset allocation strategy which is a mix of stocks and bonds. Stocks outperformed bonds substantially for the period. The Portfolio outperformed a blended return from the Balanced Composite Benchmark, a mix of market indices1 that more closely reflects the Portfolio’s asset allocation strategy, which returned 11.43% for the period.

The Portfolio benefited from Calvert’s tactical asset allocation decisions, the strong performance of the equity portion of the portfolio relative to its asset class benchmark, the Russell 1000 Index, as well as the outperformance of the fixed-income portfolio managed by CIM relative to its asset class benchmark, the Barclays U.S. Credit Index.

At the end of the third quarter, Calvert made a significant change to the management structure of Calvert Balanced Portfolio. On September 10, 2013, the Portfolio’s Board of Trustees voted to approve a new multi-manager structure for the equity portion of the Portfolio, consisting of Calvert Investment Management, Inc., (CIM) and Profit Investment Management, Inc. Calvert will continue to manage the allocation of assets among the two equity managers and the Portfolio’s fixed-income investments.

Investment Climate

Equity markets faced a brief pullback in late 2012, but recovered and posted strong gains over the last three quarters of the period. The third round of Quantitative Easing (QE), unleashed in mid-2012, provided an impetus for equity investors to look past numerous macro headwinds from fiscal cliff debates, sequester, slow growth in China and the Eurozone, and weak corporate earnings. The macro-economic picture in the U.S. continued to show improvement in the key economic sectors—housing and employment. For the year, the S&P 500, Russell 1000, Russell 2000, MSCI EAFE, and MSCI Emerging Markets Indices returned 19.34%, 20.91%, 30.06%, 24.92%, and 1.33%, respectively.

Value stocks outperformed growth stocks by 3.03%, as measured by the Russell 1000 Value and Growth Indices for the 12-month period. Within the Russell 1000 Index, Consumer Discretionary, Industrials, and Health Care were the top-performing sectors in the 12-month period, while Telecoms, Utilities, and Materials lagged.

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 13

| CALVERT BALANCED | ||

| PORTFOLIO | ||

| SEPTEMBER 30, 2013 | ||

| TEN LARGEST | % OF NET | |

| STOCK HOLDINGS | ASSETS | |

| Microsoft Corp. | 1.7 | % |

| Apple, Inc. | 1.6 | % |

| Wells Fargo & Co. | 1.4 | % |

| Google, Inc. | 1.4 | % |

| Express Scripts Holding Co. | 1.4 | % |

| Rockwell Automation, Inc. | 1.3 | % |

| EMC Corp. | 1.3 | % |

| Franklin Resources, Inc. | 1.3 | % |

| Capital One Financial Corp. | 1.3 | % |

| CIGNA Corp. | 1.2 | % |

| Total | 13.9 | % |

The U.S. fixed-income market was buffeted by the decisions of monetary and fiscal policymakers throughout the reporting period as the U.S. economy continued its slow recovery. Years of Fed quantitative-easing purchases reduced the pool of government bonds and drove investors to high-yield corporate bond yields, which reached a record low of 5.24% in May.2 Suggestions that the Fed would begin tapering QE3 in late spring drove intermediate and long-term interest rates higher, with the 10-year Treasury yield reaching 3% in early September. But the Fed’s subsequent decision to delay the taper caused yields to decline. In the end, the 10-year Treasury yield increased nearly a percentage point to 2.64% over the 12-month period.

| CALVERT BALANCED | ||||

| PORTFOLIO | ||||

| SEPTEMBER 30, 2013 | ||||

| INVESTMENT PERFORMANCE | ||||

| (TOTAL RETURN AT NAV*) | ||||

| 6 MONTHS | 12 MONTHS | |||

| ENDED | ENDED | |||

| 9/30/13 | 9/30/13 | |||

| Class A | 5.99 | % | 11.60 | % |

| Class B | 5.39 | % | 10.37 | % |

| Class C | 5.59 | % | 10.71 | % |

| Class I | 6.26 | % | 12.13 | % |

| Class Y** | 6.02 | % | 11.63 | % |

| Russell 1000 | ||||

| Index | 8.83 | % | 20.91 | % |

| Balanced | ||||

| Composite | ||||

| Benchmark*** | 4.15 | % | 11.43 | % |

| Lipper Mixed- | ||||

| Asset Target | ||||

| Alloc. Growth | ||||

| Funds Average | 5.37 | % | 13.64 | % |

* Investment performance/return at NAV does not reflect the deduction of the Fund’s maximum 4.75% front-end sales charge or any deferred sales charges.

** Calvert Balanced Portfolio first offered Class Y shares on April 30, 2013. Performance prior to that date reflects the performance of Class A shares at net asset value (NAV). Actual Class Y share performance would have been different.

*** Balanced Composite Benchmark 60% Russell 1000 Index and 40% Barclays U.S. Credit Index.

Corporate Earnings Are Weaker

Corporate earnings reports in late 2012 and throughout the first half of 2013 were largely weak on both the top- and bottom-line figures, with the sequester negatively impacting corporate results in the first half of 2013.

Sounding a cautious note, several bellwether companies that reported late in the summer of 2013, including names like Walmart and Cisco, issued reduced earnings forecasts cit-

14 www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT

ing everything from consumer weakness to fears of rising interest rates. We continue to believe that, going forward, the U.S. economic recovery can be sustained and able to support earnings growth for U.S. companies.

Improving Macroeconomic Picture in the U.S., Despite Continued Softness Abroad

Throughout the year, U.S. macro indicators continued to improve, albeit slowly. The unemployment rate ticked down to just above 7% and initial jobless claims hit post financial crisis lows in the third quarter of 2013. New job growth remains sluggish. However, consumers continue to remain upbeat and willing to spend on bigger ticket items, as reflected in improving vehicle and home sales. Sales of previously owned homes hit a three-year high in May of 2013 and housing prices continued to trend upward, despite the looming threat of rising interest rates.

During the first six months of the period, tax hikes and deep spending cuts (the “sequester”) created a drag on the U.S. economy, contributing to a poor growth rate of 0.6% annualized.3 The economy logged an estimated 2.3% growth pace4 for second half. For the entire 12 months, the U.S. economy likely grew in the neighborhood of 1.5%, less than half the 50-year average U.S. economic growth rate. The Federal Reserve’s (the Fed) inflation barometer ran at 1.2% annualized, well below the long-term comfort range of 2.0% to 2.25%.5

Federal Reserve: QE Taper and Transition Talk

During the summer, investor consensus largely settled around the view that the Federal Reserve (Fed) would begin tapering its QE program in September of 2013 by reducing both its Treasury and mortgage-backed security purchases. This view took hold despite weakness in both employment and inflation, the two areas highlighted by Fed Chairman Ben Bernanke as needing improvement before tapering would begin. Nevertheless, the “surprise” decision not to taper in September caught market participants off guard, sending equities up and sparking a retreat in bond yields.

As markets digested the lack of a QE taper – and largely gave back the equity gains won on the news – focus also returned to the transition of the Fed Chairman role. With Larry Summers removing himself from consideration, consensus coalesced around eventual nominee Vice Chair Janet Yellen, a selection largely signaling favor for continuing current monetary policy with little change.

With Political Stalemate in Washington It’s Déjà Vu All Over Again…

The debt ceiling drama of 2011 reared its head again in late September 2013. The government shutdown and debt ceiling impasse in Washington fueled uncertainty and created a negative feedback loop in the U.S. economy. Although labor conditions in the U.S. improved materially since the asset purchase program began, recent reductions in public sector employment were felt in the July and August employment reports.

The U.S. Congress failed to approve a budget to fund the government past September 30, which culminated in the shutdown of the federal government. Equity markets appeared largely unconcerned with the event in September despite the looming U.S. debt ceiling debate. Congress was not able to raise the debt ceiling until hours before the October 17th deadline identified by the Treasury Department. Although the markets welcomed the resolution, the turmoil took its toll. Estimates of fiscal drag from the

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 15

| CALVERT BALANCED | ||

| PORTFOLIO | ||

| SEPTEMBER 30, 2013 | ||

| % OF TOTAL | ||

| ASSET ALLOCATION | INVESTMENTS | |

| Equity Investments | 58 | % |

| Bonds | 42 | % |

| Total | 100 | % |

shutdown were in the billions while credit-rating firm Fitch put the nation’s credit rating on negative outlook as a result of the political stalemate and inability to take timely action on raising the debt ceiling.

Portfolio Strategy

Asset Allocation

The Portfolio benefited from a series of tactical asset allocation decisions executed during the period, particularly the decision to increase equity exposure at the end of 2012, which positioned the Portfolio to capture greater gains from the “relief rally” in the equity markets that took place in January following the last-minute fiscal cliff deal.

Equity

U.S. large-cap stocks posted impressive returns for the period and our portfolio managers’ stock selection further enhanced the Portfolio’s performance relative to the Russell 1000 Index—especially within the Energy, Consumer Staples, Industrials, and Materials sectors.

Highlights included Pioneer Natural Resources, which gained 80% after announcing an increase in production.6 The Portfolio also benefited from not holding ExxonMobil, which does not meet the Portfolio’s sustainability criteria and was down 3% for the period.

| CALVERT BALANCED | ||

| PORTFOLIO | ||

| SEPTEMBER 30, 2013 | ||

| AVERAGE ANNUAL TOTAL RETURNS | ||

| CLASS A SHARES | (WITH MAX. LOAD) | |

| One year | 6.28 | % |

| Five year | 6.50 | % |

| Ten year | 4.90 | % |

| CLASS B SHARES | (WITH MAX. LOAD) | |

| One year | 5.37 | % |

| Five year | 6.27 | % |

| Ten year | 4.34 | % |

| CLASS C SHARES | (WITH MAX. LOAD) | |

| One year | 9.74 | % |

| Five year | 6.62 | % |

| Ten year | 4.47 | % |

| CLASS I SHARES* | ||

| One year | 12.13 | % |

| Five year | 8.10 | % |

| Ten year | 5.87 | % |

| CLASS Y SHARES** | ||

| One year | 11.63 | % |

| Five year | 7.54 | % |

| Ten year | 5.41 | % |

* Note Regarding Class I Shares Total Returns: There were times during the reporting period when there were no shareholders in Class I. For purposes of reporting Average Annual Total Return, Class A performance at NAV (i.e. does not reflect deduction of the Class A front-end sales charge) is used during these periods in which there were no shareholders in Class I. For purposes of this Average Annual Total Return, the Class A performance at NAV was used during the period June 30, 2003 through December 27, 2004.

** Calvert Balanced Portfolio first offered Class Y shares on April 30, 2013. Performance prior to that date reflects the performance of Class A shares at net asset value (NAV). Actual Class Y share performance would have been different.

16 www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT

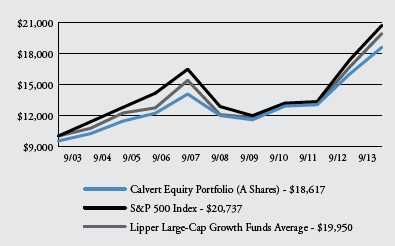

GROWTH OF $10,000

The graph below shows the value of a hypothetical $10,000 investment in the Fund over the past 10 fiscal year periods. The results shown are for Class A shares and reflect the deduction of the maximum front-end Class A sales charge of 4.75% and assume the reinvestment of dividends. The result is compared with benchmarks that include a broad based market index and a Lipper peer group average. Market indexes are unmanaged and their results do not reflect the effect of expenses or sales charges. The Lipper average reflects the deduction of the category’s average front-end sales charge. The value of an investment in a different share class would be different.

All performance data shown, including the graph above and the adjacent table, represents past performance, does not guarantee future results, assumes reinvestment of dividends and distributions and does not reflect the deduction of taxes that a shareholder would pay on the Fund’s distributions or the redemption of the Fund shares. All performance data reflects fee waivers and/or expense limitations, if any are in effect; in their absence performance would be lower. See Note B in Notes to Financial Statements. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted; for current performance data visit www.calvert.com. The gross expense ratio from the current prospectus for Class A shares is 1.24%. This number may differ from the expense ratio shown elsewhere in this report because it is based on a different time period and, if applicable, does not include fee or expense waivers. Performance data quoted already reflects the deduction of the Fund’s operating expenses.

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 17

In Consumer Staples, Walgreens gained 51%, after announcing an alliance with AmerisourceBergen and Alliance Booth to provide comprehensive distribution of branded and generic drugs.

Industrials company Rockwell Automation rose 57% for the period after increasing its dividend 11% in April and announcing a large contract with Daewoo shipbuilding in September. Ecolab, a holding in the Materials sector that helps food processors and health care companies maintain safe, clean facilities and processes, raised its 2013 earnings-per-share guidance leading to a 54% gain for the stock.

These positive contributions were partially offset by an overweight to the underperform-ing Information Technology sector and stock selection within the Financials sector. US Bancorp underperformed, returning just 2%, after settling a case with the U.S. government on foreclosures reviews and being named in a suit by the Commodity Futures Trading Commission over a customer’s misconduct.

Fixed Income

Amid a challenging fixed-income climate, bond holdings as a group were a drag on Portfolio returns. Broadly, a significant exposure to higher-quality corporate bonds restricted gains, although its shorter-than-benchmark duration7 was beneficial. The market environment was particularly volatile in the second half of the reporting period. The second quarter of 2013 saw a bond sell-off and lower-quality bonds struggling relative to Treasuries, causing credit spreads8 to widen.

This trend reversed in the third quarter and credit spreads compressed. Not only did corporate bonds outperform Treasuries, but lower-rated securities outperformed higher-rated bonds with high-yield bonds performing best. This trend hurt the Portfolio, which has a higher-quality tilt.

However, lagging performance from higher-quality positions was largely offset by the short relative duration. At the end of the reporting period, the Portfolio’s duration was 5.8 years compared with 6.6 years for the benchmark. With longer-term bond yields rising and prices falling during the period, a comparatively short duration helped protect against losses. The fixed income portion of the Portfolio uses Treasury futures to hedge its interest-rate and yield curve positions. This futures strategy did not materially impact the Portfolio’s performance.

The Portfolio’s positioning was been beneficial for the year as a whole. Its small, opportunistic allocation to out-of-benchmark, higher quality high-yield (non-investment grade) securities (currently 6.5% of assets9) has been a positive contributor.

And while an overweight to the intermediate part of the yield curve detracted from performance in 2013, a relatively short duration and decreased long-end interest-rate sensitivity contributed to positive performance. We intend to maintain these strategic positions for the foreseeable future, but will continue to rigorously review holdings and sector allocations as the markets change.

Outlook

As we have stated in the past, despite negative short-term investor sentiment, the long-term drivers of economic recovery continue to gain strength. Investors continue to look

18 www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT

beyond the headlines and focus on the improving macro-economic climate in the U.S. and, to some degree, overseas.

The path to recovery will not necessarily be smooth, however. The Fed is largely expected to taper QE as early as December and interest rates are expected to continue climbing. In such a scenario, higher-dividend stocks remain especially vulnerable. While growth stocks made an impressive recovery in the third quarter, value names may recover when the reality of Fed tapering and interest rate uptick returns to focus. But we expect the Fed will guide the markets not to expect a hike in the policy target rates until at least late in 2015.

However, longer-term factors such as historically low housing inventories and continued household formation will provide support for improving economic growth. Likewise, manufacturing is pulling out of its seasonal slump and the broader trend of consumer balance sheet repair is well underway.

As confidence sets in at both the consumer and corporate level, we continue to expect consumers to increase spending and companies to eventually expand capital expenditures and increase inventories. The sharp rise in interest rates that many feared would continue to 3% and beyond has tempered, and while consumers and companies alike must prepare for a rising-rate environment over the medium and longer term, a gradual shift up in borrowing costs may be a sign of an improving economy and not necessarily a near-term threat to growth.

Regarding fixed income, we expect the economy to continue its modest growth, with low inflation and an improving but soft labor recovery trend. Fiscal and monetary policy uncertainties, including the continued threat of another government shutdown and recurring debt ceiling debate, continue to be major headwinds for fixed-income securities in the near future.

We continue to think that interest rates, especially on the short-to-intermediate part of the yield curve, should remain well-anchored. We remain bullish on those sectors offering attractive yields relative to Treasury bonds, including investment-grade bonds, high-yield corporate bonds, and enhanced collateralized mortgage-backed securities (CMBS). We are maintaining a shorter relative duration for the fixed income portion of the Portfolio. Security selection and active management of duration and the yield curve should be key drivers of fixed income performance going forward.

Calvert Investment Management, Inc.

October 2013

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 19

1. Calvert Balanced Portfolio Composite Benchmark: 60% Russell 1000 Index and 40% Barclays U.S. Credit Index.

2. The effective yield of the Bank of America Merrill Lynch High Yield Master II.

3. GDP data source: Commerce Department.

4. Per actual Q2 2013 GDP data and the Q3 consensus from the September WSJ Survey of Professional Forecasters.

5. Source: Commerce Department. The September PCE data were not available at this writing.

6. Individual security returns reflect total returns for period held in portfolio.

7. Duration is a measure of a portfolio’s sensitivity to changes in interest rates. The longer the duration, the greater the change in price relative to interest rate movement.

8. Credit, or yield, spreads measure the difference in yield between a corporate bond and a Treasury security with a comparable maturity.

9. Includes non-rated securities deemed equivalent by the investment adviser.

As of September 30, 2013, the following holdings represented the following percentages of Portfolio net assets: Walmart 0%, Cisco 0%, Pioneer Natural Resources 1.39%, ExxonMobil 0%, Walgreens 1.26%, AmerisourceBergen 0%, Alliance Booth 0%, Rockwell Automation 1.32%, Daewoo 0%, Ecolab 1.33%, and US Bancorp .08%. Holdings are subject to change.

20 www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT

Performance

For the 12-month period ended September 30, 2013, Calvert Bond Portfolio (Class A shares at NAV) returned -2.27%. Its benchmark index, the Barclays U.S. Credit Index, returned -1.90% for the same period. The Portfolio’s underperformance was the result of several positions in higher-quality corporate bonds, as well as its overweight exposure to the intermediate part of the yield curve.

Market Review

The U.S. fixed-income market was buffeted by the decisions of monetary and fiscal policymakers throughout the reporting period, and the U.S. economy continued on its slow recovery trend. During the first six months, tax hikes and deep spending cuts (the “sequester”) created a drag on the U.S. economy, contributing to a poor growth rate of 0.6% annualized.1 In the second half, the economy logged an estimated 2.3% growth pace.2 For the entire 12 months, the U.S. economy likely grew in the neighborhood of 1.5%, less than half the 50-year average U.S. economic growth rate. The Federal Reserve’s (the Fed) inflation barometer ran at 1.2% annualized, well below the long-term comfort range of 2.0% to 2.25%.3 The unemployment rate posted a 0.5% decline, finishing the period at a relatively high 7.3%.4

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 21

| CALVERT BOND | ||

| PORTFOLIO | ||

| SEPTEMBER 30, 2013 | ||

| % OF TOTAL | ||

| ECONOMIC SECTORS | INVESTMENTS | |

| Corporate | 74.8 | % |

| Financial Institutions | 26.1 | % |

| Industrial | 46.0 | % |

| Utility | 2.7 | % |

| Government Related | 4.8 | % |

| Agency | 1.5 | % |

| Local Authority | 3.2 | % |

| Supranational | 0.1 | % |

| High Social Impact | ||

| Investments | 0.4 | % |

| Municipal | 2.0 | % |

| Education | 0.5 | % |

| Government Public Service | 0.1 | % |

| Health Care | 0.2 | % |

| Transportation | 0.5 | % |

| Utility | 0.7 | % |

| Securitized | 8.9 | % |

| Asset-Backed Securities | 2.7 | % |

| Commercial Mortgage- | ||

| Backed Securities | 5.2 | % |

| Covered | 1.0 | % |

| Short-Term Investments | 2.2 | % |

| Treasury | 6.9 | % |

| Total | 100 | % |

| CALVERT BOND | ||||

| PORTFOLIO | ||||

| SEPTEMBER 30, 2013 | ||||

| INVESTMENT PERFORMANCE | ||||

| (TOTAL RETURN AT NAV*) | ||||

| 6 MONTHS | 12 MONTHS | |||

| ENDED | ENDED | |||

| 9/30/13 | 9/30/13 | |||

| Class A | -2.88 | % | -2.27 | % |

| Class B | -3.37 | % | -3.28 | % |

| Class C | -3.30 | % | -3.01 | % |

| Class I | -2.60 | % | -1.69 | % |

| Class Y | -2.72 | % | -1.97 | % |

| Barclays U.S. | ||||

| Credit Index | -2.74 | % | -1.90 | % |

| Lipper A Rated | ||||

| Corporate Debt | ||||

| Funds Average | -2.66 | % | -1.79 | % |

| 30 DAYS ENDED | ||||

| SEC YIELD | 9/30/12 | 9/30/13 | ||

| Class A | 1.61 | % | 2.19 | % |

| Class B | 0.68 | % | 1.17 | % |

| Class C | 0.90 | % | 1.49 | % |

| Class I | 2.27 | % | 2.88 | % |

| Class Y | 1.97 | % | 2.59 | % |

* Investment performance/return at NAV does not reflect the deduction of the Fund’s maximum 3.75% front-end sales charge or any deferred sales charge.

There were several monetary policy decisions that moved the bond market. In September 2012, the Fed responded to slower growth, announcing bond purchases of $40 billion per month of mortgage-backed securities (called “QE3”). In December 2012, the Fed expanded QE3 by purchasing an additional $45 billion per month of Treasury securities. In late May, however, the Fed discussed a possible reduction in the $85 billion pace of bond purchasing.

As years of Fed quantitative-easing purchases reduced the pool of government bonds, private-sector investors were forced to search for higher-yielding bonds. This drove high-yield corporate bond yields to a record low of 5.24% in May.5 The Fed’s May and June suggestions that the pace of QE3 would be tapered, however, led to market expectation for less future demand for U.S. government bonds, which led to higher

22 www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORTintermediate and long term interest rates. The ten-year Treasury yield reached 3% in early September.

Soon thereafter, however, faced with greater uncertainty about fiscal policy and tighter financial conditions, the Fed chose to continue the $85 billion QE3 pace. This surprised global markets and yields came off their highs. At the end of the reporting period, markets braced for the first government shutdown in 17 years and a battle over raising the U.S. debt limit. Market and economic uncertainty was on the rise.

Over the reporting period, the benchmark 10-year Treasury yield increased 99 basis points6 to 2.64%. The broad bond-market Barclays U.S. Aggregate Index declined 1.7% for the 12-month period.

Portfolio Strategy

Throughout the reporting period, the Portfolio navigated a challenging fixed-income climate. Broadly, a significant exposure to higher-quality corporate bonds restricted the Portfolio’s gains for the period, although its shorter-than-benchmark duration7 was beneficial.

The market environment was particularly volatile in the second half of the reporting period. In the second quarter of 2013, there was a sell-off of bonds and lower-quality bonds struggled relative to Treasuries, causing credit spreads8 to widen. This trend reversed in the third quarter and credit spreads compressed. Not only did corporate bonds outperform Treasuries, but lower-rated securities outperformed higher-rated bonds, and high-yield bonds performed best. As a result, the Portfolio, which has a higher-quality tilt, was hurt by this trend.

However, the lagging performance from higher-quality positions was largely offset by the Portfolio’s short duration compared with the benchmark. At the end of the reporting period, the Portfolio’s duration was 5.8 years, as opposed to 6.6 years for the benchmark. With longer-term bond yields rising and prices falling during the period, a comparatively short duration was a helpful strategy for protecting against losses. The Portfolio also uses Treasury futures to hedge its interest-rate and yield curve positions. This futures strategy did not materially impact the Portfolio’s performance.

The Portfolio’s positioning has been beneficial for the year as a whole. Its small, opportunistic allocation to out-of-benchmark, higher-quality high-yield securities (currently 6.5% of assets9) has been a positive contributor. And while an overweight to the intermediate part of the yield curve has detracted from performance in 2013, a relatively short duration and reduced long-end interest-rate sensitivity has contributed to positive performance. We intend to maintain these strategic positions for the foreseeable future, but will continue to rigorously review holdings and sector allocations as the markets change.

Outlook

Looking ahead, we expect the economy to continue its modest growth, with low inflation and an improving but soft labor recovery trend. Fiscal and monetary policy uncertainties, including the continued threat of another government shutdown, the recurring debt ceiling debate, and the appointment of a new Fed chair, continue to be major headwinds in the near future.

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 23

Given our outlook for the economy and restrictive and uncertain fiscal policy, we expect the Fed will put a strong emphasis on improving economic data before deciding to taper and ultimately raise the Fed Funds rate. We expect the Fed will guide the markets not to expect a hike in the policy target rates until at least late in 2015.

In view of our not-so-bullish macroeconomic and policy outlook, we continue to think that interest rates, especially on the short-to-intermediate part of the yield curve, should remain well anchored. We remain bullish on those sectors offering attractive yields relative to Treasury bonds, including investment-grade and high-yield corporate bonds, as well as enhanced collateralized mortgage-backed securities (CMBS). We believe these “spread sectors” should outperform similar-maturity Treasury bonds over the next six to 12 months. We continue to maintain a shorter overall duration versus the Index. Security selection within these spread sectors, and active management of duration and the yield curve, should be key drivers of performance going forward.

Calvert Investment Management, Inc.

October 2013

| CALVERT BOND | ||

| PORTFOLIO | ||

| SEPTEMBER 30, 2013 | ||

| AVERAGE ANNUAL TOTAL RETURNS | ||

| CLASS A SHARES | (WITH MAX. LOAD) | |

| One year | -5.90 | % |

| Five year | 3.82 | % |

| Ten year | 4.02 | % |

| CLASS B SHARES | (WITH MAX. LOAD) | |

| One year | -7.15 | % |

| Five year | 3.54 | % |

| Ten year | 3.38 | % |

| CLASS C SHARES | (WITH MAX. LOAD) | |

| One year | -4.04 | % |

| Five year | 3.77 | % |

| Ten year | 3.56 | % |

| CLASS I SHARES | ||

| One year | -1.69 | % |

| Five year | 5.24 | % |

| Ten year | 5.03 | % |

| CLASS Y SHARES* | ||

| One year | -1.97 | % |

| Five year | 4.89 | % |

| Ten year | 4.55 | % |

* Calvert Bond Portfolio first offered Class Y shares on October 31, 2008. Performance prior to that date reflects the performance of Class A shares at net asset value (NAV). Actual Class Y share performance would have been different.

1. GDP data source: Commerce Department.

2. Per actual Q2 2013 GDP data and the Q3 consensus from the September WSJ Survey of Professional Forecasters.

3. Data source: Commerce Department. The September PCE data were not available at this writing.

4. Data source: BLS. Employment data for September were not available at this writing.

5. The effective yield of the Bank of America Merrill Lynch High Yield Master II.

6. A basis point is 0.01 percentage points.

7. Duration is a measure of a portfolio’s sensitivity to changes in interest rates. The longer the duration, the greater the change in price relative to interest rate movement.

8. Credit, or yield, spreads measure the difference in yield between a corporate bond and a Treasury security with a comparable maturity.

9. Includes non-rated securities deemed equivalent by the investment adviser.

24 www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT

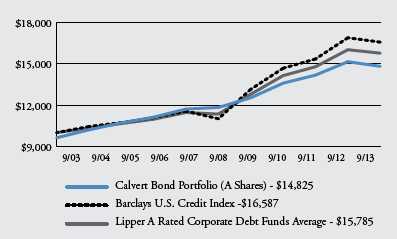

GROWTH OF $10,000

The graph below shows the value of a hypothetical $10,000 investment in the Fund over the past 10 fiscal year periods. The results shown are for Class A shares and reflect the deduction of the maximum front-end Class A sales charge of 3.75% and assume the reinvestment of dividends. The result is compared with benchmarks that include a broad based market index and a Lipper peer group average. Market indexes are unmanaged and their results do not reflect the effect of expenses or sales charges. The Lipper average reflects the deduction of the category’s average front-end sales charge. The value of an investment in a different share class would be different.

All performance data shown, including the graph above and the adjacent table, represents past performance, does not guarantee future results, assumes reinvestment of dividends and distributions and does not reflect the deduction of taxes that a shareholder would pay on the Fund’s distributions or the redemption of the Fund shares. All performance data reflects fee waivers and/or expense limitations, if any are in effect; in their absence performance would be lower. See Note B in Notes to Financial Statements. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted; for current performance data visit www.calvert.com. The gross expense ratio from the current prospectus for Class A shares is 1.16%. This number may differ from the expense ratio shown elsewhere in this report because it is based on a different time period and, if applicable, does not include fee or expense waivers. Performance data quoted already reflects the deduction of the Fund’s operating expenses.

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 25

Investment Performance

For the 12 months ended September 30, 2013, Calvert Equity Portfolio Class A shares (at NAV) returned 16.30%. This compares to a return of 19.34% for the S&P 500 Index. Our relative underperformance was entirely driven by our choice of holdings rather than decisions to overweight or underweight individual sectors.

Investment Climate

It’s been a reluctant market. We end this 12-month period just a few percentage points off of a mid-September all-time high and only 17% away from triple the low reached in March 2009 for the S&P 500 Index. That sounds like reason enough to be popping champagne corks and for wild-eyed bullishness to be rampant. However, you’d be hard-pressed to find an equity bull on Wall Street.

While sentiment is not outright bearish, cautiousness reigns, even among the more optimistic market prognosticators. But it’s not hard to explain the seemingly contradictory strong market returns and the major lack of enthusiasm.

The Federal Reserve’s efforts to keep interest rates very low and the resumption of money flows into equities have supported equity market appreciation these last few years and particularly over the past year. However, we believe the continuation of slow if steady improvement in the economy, and the fading of fears of some major economic event that pushes the global economy back into recession, deserve the majority of the credit.

It’s easy to dismiss economic progress as a driver of sentiment and stocks. After all, this has been a subpar recovery and even after four years of growth, many Americans believe the recession continues. While growth has been undeniably slow and uneven, jobs are being steadily created, consumers and business have de-levered, housing has turned the corner, and manufacturing is re-establishing itself here on U.S. soil. Europe has clearly stopped getting worse and many indicators show things beginning to get better. Europe’s progress will buoy our economy in the months ahead.

26 www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT

| CALVERT EQUITY | ||

| PORTFOLIO | ||

| SEPTEMBER 30, 2013 | ||

| % OF TOTAL | ||

| ECONOMIC SECTORS | INVESTMENTS | |

| Consumer Discretionary | 19.6 | % |

| Consumer Staples | 11.4 | % |

| Energy | 4.8 | % |

| Financials | 12.3 | % |

| Health Care | 14.2 | % |

| Industrials | 9.2 | % |

| Information Technology | 24.2 | % |

| Limited Partnership Interest | 0.3 | % |

| Materials | 2.7 | % |

| Short-Term Investments | 0.8 | % |

| Venture Capital | 0.5 | % |

| Total | 100 | % |

| CALVERT EQUITY | ||||

| PORTFOLIO | ||||

| SEPTEMBER 30, 2013 | ||||

| INVESTMENT PERFORMANCE | ||||

| (TOTAL RETURN AT NAV*) | ||||

| 6 MONTHS | 12 MONTHS | |||

| ENDED | ENDED | |||

| 9/30/13 | 9/30/13 | |||

| Class A | 6.84 | % | 16.30 | % |

| Class B | 6.37 | % | 15.29 | % |

| Class C | 6.48 | % | 15.51 | % |

| Class I | 7.16 | % | 16.95 | % |

| Class Y | 7.08 | % | 16.76 | % |

| S&P 500 Index | 8.31 | % | 19.34 | % |

| Lipper Large-Cap | ||||

| Growth Funds | ||||

| Average | 11.45 | % | 19.60 | % |

| TEN LARGEST | % OF NET | |

| STOCK HOLDINGS | ASSETS | |

| CVS Caremark Corp. | 4.1 | % |

| Google, Inc. | 3.9 | % |

| Apple, Inc. | 3.7 | % |

| QUALCOMM, Inc. | 3.7 | % |

| Microsoft Corp. | 3.3 | % |

| The Coca-Cola Co. | 3.3 | % |

| Cameron International Corp. | 2.9 | % |

| Costco Wholesale Corp. | 2.8 | % |

| Gilead Sciences, Inc. | 2.8 | % |

| Ecolab, Inc. | 2.6 | % |

| Total | 33.1 | % |

* Investment performance/return at NAV does not reflect the deduction of the Fund’s maximum 4.75% front-end sales charge or any deferred sales charges.

We believe another major stock-market driver has been a significant drop in the chances for a major event that plunges the global economy back into recession—so-called “tail risk.” While there’s always some very small chance of a shock, like a war, to hit markets, the last few years have felt like those events were lurking around every corner. The European debt crisis was the most obvious one, but U.S. debt defaults and a China bubble bursting took turns terrifying investors. Those fears kept the equity risk premium—the compensation required by investors to hold “risky” assets like stocks compared to “riskless” assets like bonds—historically high until last summer. The practical effect was the valuation of the U.S. market remained fairly low. As the probability of tail risk has faded, multiples have risen.

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 27

single digits. Secondly, although the economy and markets have powered through various Washington-induced crises, it’s hard for investors to get excited about buying stocks when the government won’t get out of the way.

The mostly onwards and upwards behavior of the market over the last 12 months belies the significant volatility. The market rotated leadership on multiple occasions, sometimes in violent fashion. Although the Index moved consistently higher, waves of optimism and pessimism about economic growth and earnings meant offensive and defensive sectors took turns leading. Looking at sector performance for the period doesn’t really tell you much. We can say this was a very difficult environment for active managers.

Portfolio Strategy

From the most recent low in the summer of 2012, the market moved higher as the European Central Bank stood by the euro and fears of a debt crisis receded. Our positioning benefited from being somewhat more levered to growth than safety. As the S&P 500 Index surged to new highs early in 2013, peculiarly led by defensive stocks, we grew a bit concerned the market was ahead of itself. After all, earnings growth was sharply slowing. Our efforts to get a bit more defensive came up short as growth, particularly cyclical growth like Information Technology, fell out of favor. Therefore, we lagged for much of the first and second quarter. At the margin, we added some growth exposure this past summer as our research indicated business was picking up. That helped us conclude the period on a stronger note.

| CALVERT EQUITY | ||

| PORTFOLIO | ||

| SEPTEMBER 30, 2013 | ||

| AVERAGE ANNUAL TOTAL RETURNS | ||

| CLASS A SHARES | (WITH MAX. LOAD) | |

| One year | 10.77 | % |

| Five year | 8.14 | % |

| Ten year | 6.41 | % |

| CLASS B SHARES | (WITH MAX. LOAD) | |

| One year | 10.29 | % |

| Five year | 8.08 | % |

| Ten year | 6.01 | % |

| CLASS C SHARES | (WITH MAX. LOAD) | |

| One year | 14.51 | % |

| Five year | 8.38 | % |

| Ten year | 6.12 | % |

| CLASS I SHARES | ||

| One year | 16.95 | % |

| Five year | 9.80 | % |

| Ten year | 7.52 | % |

| CLASS Y SHARES* | ||

| One year | 16.76 | % |

| Five year | 9.58 | % |

| Ten year | 7.12 | % |

* Calvert Equity Portfolio first offered Class Y shares on October 31, 2008. Performance prior to that date reflects the performance of Class A shares at net asset value (NAV). Actual Class Y share performance would have been different.

Whether we beat the index in any given period tends to depend more on which stocks we hold than picking the right sectors to overweight and that was true this past year. We held eight stocks that rose more than 50%, including notable winners such as Starbucks, Priceline, Lowe’s, Texas Instruments and Ecolab.1 When you look at both absolute return and weighting, these were all major contributors to relative performance, but none topped Gilead Sciences.

28 www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT

GROWTH OF $10,000

The graph below shows the value of a hypothetical $10,000 investment in the Fund over the past 10 fiscal year periods. The results shown are for Class A shares and reflect the deduction of the maximum front-end Class A sales charge of 4.75% and assume the reinvestment of dividends. The result is compared with benchmarks that include a broad based market index and a Lipper peer group average. Market indexes are unmanaged and their results do not reflect the effect of expenses or sales charges. The Lipper average reflects the deduction of the category’s average front-end sales charge. The value of an investment in a different share class would be different.

All performance data shown, including the graph above and the adjacent table, represents past performance, does not guarantee future results, assumes reinvestment of dividends and distributions and does not reflect the deduction of taxes that a shareholder would pay on the Fund’s distributions or the redemption of the Fund shares. All performance data reflects fee waivers and/or expense limitations, if any are in effect; in their absence performance would be lower. See Note B in Notes to Financial Statements. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted; for current performance data visit www.calvert.com. The gross expense ratio from the current prospectus for Class A shares is 1.22%. This number may differ from the expense ratio shown elsewhere in this report because it is based on a different time period and, if applicable, does not include fee or expense waivers. Performance data quoted already reflects the deduction of the Fund’s operating expenses.

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 29

Gilead has soared as they prepare to bring to market what appears to be a revolutionary treatment for Hepatitis C. This is an unsatisfied market as current treatments are only modestly effective with unpleasant side effects. Gilead will likely make great headway on both fronts and it looks like they will have no competition for one to two years. It remains a large position in the portfolio.

Since we lagged the benchmark for the year, clearly not everything went as we planned. By far, Edwards Lifesciences was the leading detractor. Edwards developed an artificial heart valve that can be delivered by catheter rather than open heart surgery—obviously a big advance for patients. However, the product launch has been fairly erratic with training and reimbursement confusion hampering sales. The stock fell sharply earlier this year after a sales disappointment proved to be too much for investors. We joined the selling, primarily because it looked like the lowered launch trajectory would now allow competitors to catch up.

Our large position in Apple also hurt performance, mostly in late 2012 and early 2013. We’ll admit to being surprised by how much earnings slipped as they transitioned to the recently released iPhone 5s and 5c. But it’s an inexpensive stock that we do not believe is broken and we’re happy they’ve begun to return some of their giant cash hoard to shareholders. The stock outperformed in the most recent quarter and we expect that to continue. Other stocks that hurt performance include Kohl’s, Suncor and QEP within Energy and C.H. Robinson within Industrials. We no longer hold any of them.

Outlook

The U.S. stock market seems to be in a holding pattern. Our expectations as well as the market’s hold that the economy and corporate earnings will accelerate in the final months of 2013 and push further ahead in 2014. The problem is that was the expectation three months ago, too, and evidence of either is not compelling so far. As a result, the market has gone more sideways than up in recent months.

The good news is that while the last three months have not provided current period evidence of acceleration, we can point to many developments that suggest that a pickup is around the corner. Housing momentum continues despite the recent back-up in mortgage rates. Factory order data is outright strong although production data does not yet reflect it.

Consumer and corporate balance sheets are in good shape and ready to spend and invest as confidence in the pick-up grows. Europe has turned the corner and will now add to global growth rather than subtract from it. Inventories are low and will have to be rebuilt as the acceleration gathers steam.

We wish we could say we see robust growth ahead. Unfortunately, we cannot. But we do believe the economy will continue to expand at a solid, if unspectacular pace. Corporate earnings growth should follow. We believe that will allow the stock market to push to new highs in the year ahead. There’s no reason to anticipate a downturn in the economy or the stock market for the foreseeable future, so only modest growth notwithstanding, we remain optimistic at a macro level.

Despite the handful of great performers in the portfolio this past year, it’s been a very tough market for the sort of high-quality, large-cap growth stocks that populate our

30 www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT

investment universe. We believe extremely low interest rates have had something to do with that. But that has left some very good values among stocks in our portfolio and within the universe. We will continue to work hard to find the best combinations of growth and attractive valuation and look forward to headwinds shifting to tailwinds in the years ahead as interest rates almost certainly will rise.

October 2013

1. Individual security returns reflect total returns for period held in portfolio.

As of September 30, 2013, the following companies represented the following percentages of Portfolio net assets: Starbucks 2.56%, Priceline 1.87%, Lowe’s 2.38%, Texas Instruments 1.37%, Ecolab 2.68%, Gilead Science 2.84%, Edwards Lifesciences 0%, Apple 3.78%, Kohl’s 0%, Suncor 0%, and C.H. Robinson 0%. Holdings are subject to change.

www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT 31

Investment Performance

Calvert Large Cap Core Portfolio Class A Shares (at NAV) returned 21.91% for the 12-month period through September 30, 2013, outperforming its benchmark, the Russell 1000 Index return of 20.91%. The Portfolio’s outperformance is attributable to a combination of sound stock selection and favorable industry and sector selection.

Investment Climate

Equity markets faced a brief pullback in late 2012, but recovered and posted strong gains in the last three quarters of the period. The third round of quantitative easing (QE), unleashed in mid-2012, provided an impetus for equity investors to look past numerous macro headwinds from fiscal cliff debates, sequester, slow growth in China and the Eurozone, and weak corporate earnings. The macro-economic picture in the U.S. continued to show improvement in the key economic drivers—housing and employment. For the year, the S&P 500, Russell 1000, Russell 2000, MSCI EAFE, and MSCI Emerging Markets Indices returned 19.34%, 20.91%, 30.06%, 24.92%, and 1.33%, respectively.

Value stocks outperformed growth stocks by 3.03%, as measured by the Russell 1000 Value and Russell 1000 Growth Indices for the 12-month period. Within the Russell 1000 Index, Consumer Discretionary, Industrials, and Health Care were the top-performing sectors, while Telecoms, Utilities, and Materials lagged.

Corporate Earnings Are Weaker

Corporate earnings reports in late 2012 and throughout the first half of 2013 were largely weak on both the top- and bottom-line figures, with the sequester negatively impacting corporate results in the first half of 2013.

Sounding a cautious note, several bellwether companies that reported late in the summer of 2013, including names like Walmart and Cisco, issued reduced earnings forecasts citing everything from consumer weakness to fears of rising interest rates. We continue to believe that, going forward, the U.S. economic recovery can be sustained and able to support earnings growth for U.S. companies.

Improving Macro-Economic Picture in the U.S., But Continued Softness Abroad

Throughout the year, U.S. macro indicators continued to improve, albeit slowly. The unemployment rate ticked down to just above 7% and initial jobless claims hit post-financial crisis lows in the third quarter of 2013. New job growth remains sluggish.

32 www.calvert.com CALVERT SOCIAL INVESTMENT FUND ANNUAL REPORT

| CALVERT LARGE CAP | ||

| CORE PORTFOLIO | ||

| SEPTEMBER 30, 2013 | ||

| % OF TOTAL | ||

| ECONOMIC SECTORS | INVESTMENTS | |

| Consumer Discretionary | 17.6 | % |

| Consumer Staples | 10.8 | % |

| Energy | 4.9 | % |

| Financials | 17.3 | % |

| Health Care | 12.3 | % |

| Industrials | 7.2 | % |

| Information Technology | 14.6 | % |

| Short-Term Investments | 10.0 | % |

| Telecommunication Services | 5.3 | % |

| Total | 100 | % |

| CALVERT LARGE CAP | ||||

| CORE PORTFOLIO | ||||

| SEPTEMBER 30, 2013 | ||||

| INVESTMENT PERFORMANCE | ||||

| (TOTAL RETURN AT NAV*) | ||||

| 6 MONTHS | 12 MONTHS | |||

| ENDED | ENDED | |||

| 9/30/13 | 9/30/13 | |||

| Class A | 7.40 | % | 21.91 | % |

| Class B | 6.59 | % | 20.11 | % |

| Class C | 6.95 | % | 20.84 | % |

| Class I | 7.65 | % | 22.47 | % |

| Class Y** | 7.45 | % | 21.97 | % |

| Russell 1000 | ||||

| Index | 8.83 | % | 20.91 | % |

| Lipper Large- | ||||

| Cap Core Funds | ||||

| Average | 8.43 | % | 19.68 | % |

| TEN LARGEST | % OF NET | |

| STOCK HOLDINGS | ASSETS | |

| Toyota Motor Corp. (ADR) | 4.2 | % |

| JPMorgan Chase & Co. | 4.1 | % |

| Wells Fargo & Co. | 3.9 | % |

| Time Warner, Inc. | 3.9 | % |

| Cisco Systems, Inc. | 3.8 | % |

| Amgen, Inc. | 3.8 | % |

| Goldman Sachs Group, Inc. | 3.7 | % |

| Symantec Corp. | 3.6 | % |

| CVS Caremark Corp. | 3.4 | % |

| Medtronic, Inc. | 3.3 | % |

| Total | 37.7 | % |

* Investment performance/return at NAV does not reflect the deduction of the Fund’s maximum 4.75% front-end sales charge or any deferred sales charges.

** Calvert Large Cap Core portfolio first offered Class Y shares on April 30, 2013. Performance prior to that date reflects the performance of Class A shares at net asset value (NAV). Actual Class Y share performance would have been different.