Alcan Investor Workshop

Toronto, October 3, 2006

Dick Evans

President and CEO

© 2 0 06 A L C A N I N C.Slide 2

Statements made in the course of this presentation which describe

the Company's or management’s objectives, projections, estimates,

expectations or predictions may be "forward-looking statements"

within the meaning of securities laws. All statements that address the

Company's expectations or projections about the future including

statements about the Company's growth, cost reduction goals,

operations reorganization plans, expenditures and financial results

are forward-looking statements. nature, forward-looking statements involve risk and uncertainty and

actual actions or results could differ materially. Reference should be

made to the most recent Form 10-Q or 10-K for a summary of

factors that could cause such differences. In addition, certain

non-GAAP measures are used which are reconciled to the

comparable GAAP measures herein or on the Company’s website at

www.alcan.com in the “Investors” section.

expectations or predictions may be "forward-looking statements"

within the meaning of securities laws. All statements that address the

Company's expectations or projections about the future including

statements about the Company's growth, cost reduction goals,

operations reorganization plans, expenditures and financial results

are forward-looking statements. nature, forward-looking statements involve risk and uncertainty and

actual actions or results could differ materially. Reference should be

made to the most recent Form 10-Q or 10-K for a summary of

factors that could cause such differences. In addition, certain

non-GAAP measures are used which are reconciled to the

comparable GAAP measures herein or on the Company’s website at

www.alcan.com in the “Investors” section.

Forward Looking Statements

© 2 0 06 A L C A N I N C.Slide 3

A premier global investment, partner of choice, and provider

of materials and technology-based solutions committed to

the success of our shareholders, customers, employees and

the communities in which we operate.

the success of our shareholders, customers, employees and

the communities in which we operate.

n

Long-term TSR in top quartile of S&P materials index

n

Leading positions in attractive sectors

n

Superior reputation among diverse global stakeholders

Clear Vision

© 2 0 06 A L C A N I N C.Slide 4

n

Modern, Low Cost Assets

n

Leading Market Positions and Strong Customer Relationships

n

Integrated Management System (AIMS)

n

Advanced Technology

n

Recognized Leader in Sustainability

Many strengths to build on

Advantaged Platform

© 2 0 06 A L C A N I N C.Slide 5

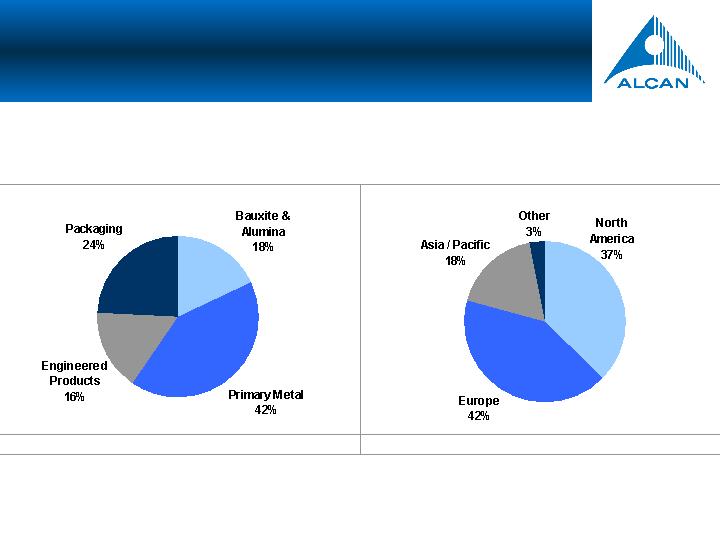

Assets by Business

Upstream: 60% Downstream: 40%

Assets by Geography

Global Presence

As at June 30, 2006

Effective Diversification

© 2 0 06 A L C A N I N C.Slide 6

Proven Management System

CI

EHS

First

VBM

People

Ø

VBM guiding methodology

Ø

Steadily improving EHS

performance

Ø

Accelerating CI benefits

Ø

New people component

AIMS

© 2 0 06 A L C A N I N C.Slide 7

Build Selectively on Core Strengths

Ø

secure long-term alumina position

Ø

accelerate development of primary pipeline

Ø

fully leverage AP technology

Ø

develop adjacent growth opportunities

- products/markets

- geography

Ø

explore potential new platforms

Focused Strategy

© 2 0 06 A L C A N I N C.Slide 8

Maintain Discipline

Ø

ROCE through the cycle

- Capital Allocation

- Portfolio Optimization

- Cost Control

Ø

Emphasis on cash

Focused Strategy

© 2 0 06 A L C A N I N C.Slide 9

n

Bauxite & AluminaGove, Alumar, Guinea, Ghana

n

Primary MetalSohar, Kitimat, Coega, Iceland

n

Engineered ProductsAerospace, Composites, Adjacencies

n

PackagingDeveloping economies

High-growth market segments

Attractive Growth Options

© 2 0 06 A L C A N I N C.Slide 10

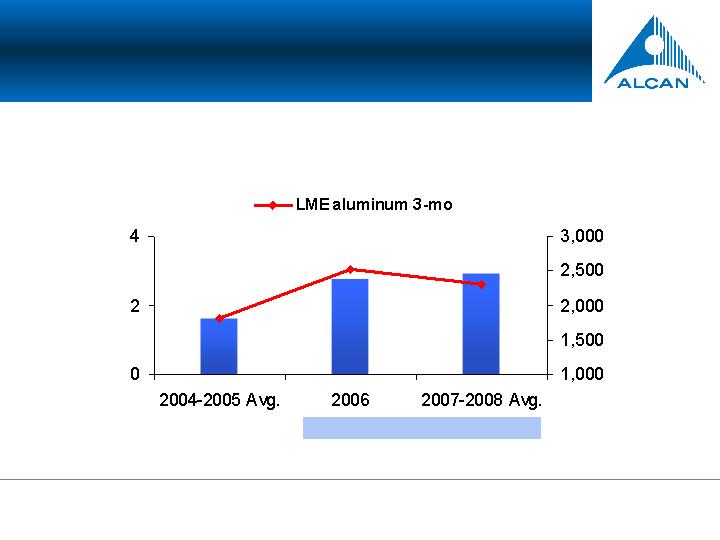

* Assumes currency and metal at forward rates as of September 2006

Annual Cash Flow from Operations ($M)

$/t

$B

2006-08 outlook based on forward rates*

Financial Strength

© 2 0 06 A L C A N I N C.Slide 11

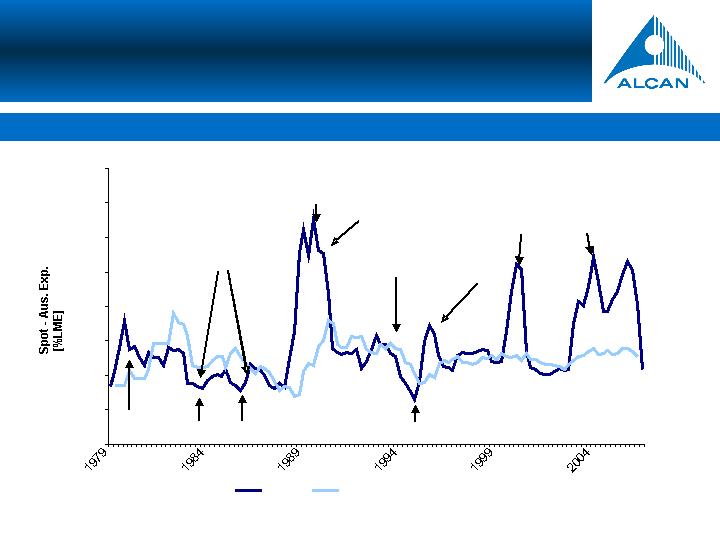

Spot and Australian export prices

Spot

Aus. Export Price

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

San Ciprian

Aughinish

Worsley

Alumina

oversupply

High metal

prices

Hurricane

Eastern block

sell-down

Hurricane

Gramercy

explosion

Structural

tightness

(China)

Alunorte

Source: CRU

Alumina Price Evolution

© 2 0 06 A L C A N I N C.Slide 12

n

China Impact?

Ø

Smelter re-starts being absorbed

Ø

Annual demand growth still exceeding supply growth

Ø

Primary metal exports down 10% YTD

n

Physical Demand Remains Strong

Ø

Global market outlook for 2007 near balance

Sound Aluminum Fundamentals

© 2 0 06 A L C A N I N C.Slide 13