Jacynthe Côté

President – Bauxite and Alumina

Alcan Investor Workshop

Toronto, October 3, 2006

© 2 0 06 A L C A N I N C.Slide 2

Statements made in the course of this presentation which describe

the Company's or management’s objectives, projections, estimates,

expectations or predictions may be "forward-looking statements"

within the meaning of securities laws. All statements that address the

Company's expectations or projections about the future including

statements about the Company's growth, cost reduction goals,

operations reorganization plans, expenditures and financial results

are forward-looking statements. nature, forward-looking statements involve risk and uncertainty and

actual actions or results could differ materially. Reference should be

made to the most recent Form 10-Q and 10-K for a summary of

factors that could cause such differences. In addition, certain

non-GAAP measures are used which are reconciled to the

comparable GAAP measures herein or on the Company’s website at

www.alcan.com in the “Investors” section.

expectations or predictions may be "forward-looking statements"

within the meaning of securities laws. All statements that address the

Company's expectations or projections about the future including

statements about the Company's growth, cost reduction goals,

operations reorganization plans, expenditures and financial results

are forward-looking statements. nature, forward-looking statements involve risk and uncertainty and

actual actions or results could differ materially. Reference should be

made to the most recent Form 10-Q and 10-K for a summary of

factors that could cause such differences. In addition, certain

non-GAAP measures are used which are reconciled to the

comparable GAAP measures herein or on the Company’s website at

www.alcan.com in the “Investors” section.

Forward Looking Statements

© 2 0 06 A L C A N I N C.Slide 3

Discussion Topics

n

Group Performance

n

Update on Current Portfolio

n

Alumina Market / China

n

Additional Growth Opportunities

n

Summary

© 2 0 06 A L C A N I N C.Slide 4

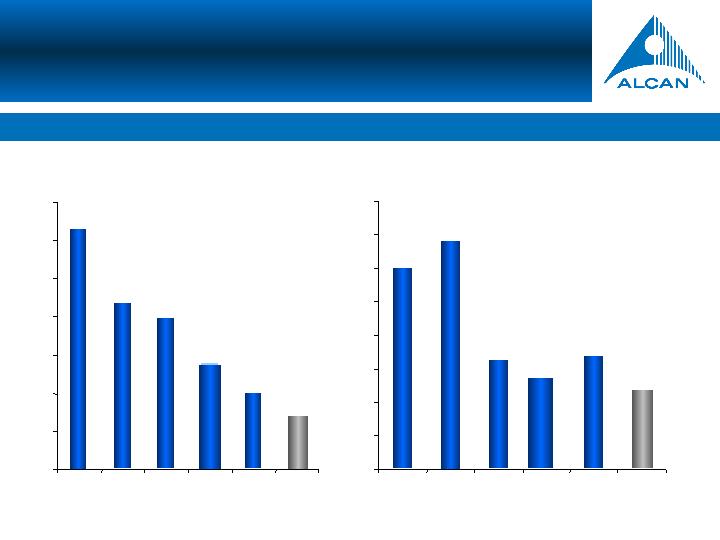

Recordable Case Rate

2.23

6.3

4.34

3.96

2.74

1.89

1.6

0

1

2

3

4

5

6

7

2001

2002

2003

2004

2005

2006

YTD

LTII Cases

1.2

1.36

0.65

0.54

0.65

0.48

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

2001

2002

2003

2004

2005

YTD

2006

Improving trend on environment, health and safety performance

EHS Performance

© 2 0 06 A L C A N I N C.Slide 5

Alumina Production & Revenues

Strong B&A production growth

LME

B&A SGA Production (Kt)

Gove expansion (Kt)

Alumar expansion (Kt)

Production

Production (Kt)

3,992

5,052

4,992

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2003

2004

2005

2006

2007

2008

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Revenues $M // LME

273

100

200

300

400

500

600

700

2003

2004

2005

2006

BGP $M

BGP, Revenues & LME

BGP H1

BGP H2

199

242

200

278

108

111

1,427

1,721

1,899

2,562

© 2 0 06 A L C A N I N C.Slide 6

Balance of Bauxite Portfolio (Kt) | Current | Post-Approved Expansions |

Internal Production | 16,500 | 19,900 |

Internal Demand | 13,500 | 17,300 |

Internal Balance | 3,000 | 2,600 |

Balance of Alumina Portfolio (Kt) | ||

Internal Production | 5,200 | 7,200 |

Internal Demand | 6,600 | 7,100 |

Internal Balance | (1,400) | 100 |

Alcan Bauxite and Alumina Balance

© 2 0 06 A L C A N I N C.Slide 7

Key Competitive Advantages

n

Low cost position

Ø

with completion of the Gove expansion, the gas to Gove project

and the Alumar expansion, B&A will have 50% of its production in

lowest cost quartile

lowest cost quartile

n

Technology/engineering capabilities

Ø

best commercially available technology

n

Preferred partner

Ø

sustainability consolidates our “license to operate” and supports

access to new resources

© 2 0 06 A L C A N I N C.Slide 8

Alcan’s technology is well-recognized

Process improvement

n

These 8 new grey tanks will

replace all 28 old tanks in the

centre of the picture while:

centre of the picture while:

•

Increasing production from

2m Mt to 3.8m Mt and

•

Freeing up space for

another possible expansion

and reducing capital cost

and reducing capital cost

Capex reduction

n

Low-cost country

sourcing of major

modules helped

reduce schedule

and exposure to

Australian market

conditions

modules helped

reduce schedule

and exposure to

Australian market

conditions

n

Breakthroughs are being realized in process improvement with impact on

capital costs, footprint and schedule

n

Alcan uses advanced exploration techniques with the contribution of satellite

imaging and 3D modelling, providing a new, sophisticated, low-cost

exploration approach

exploration approach

Technology and Innovation

© 2 0 06 A L C A N I N C.Slide 9

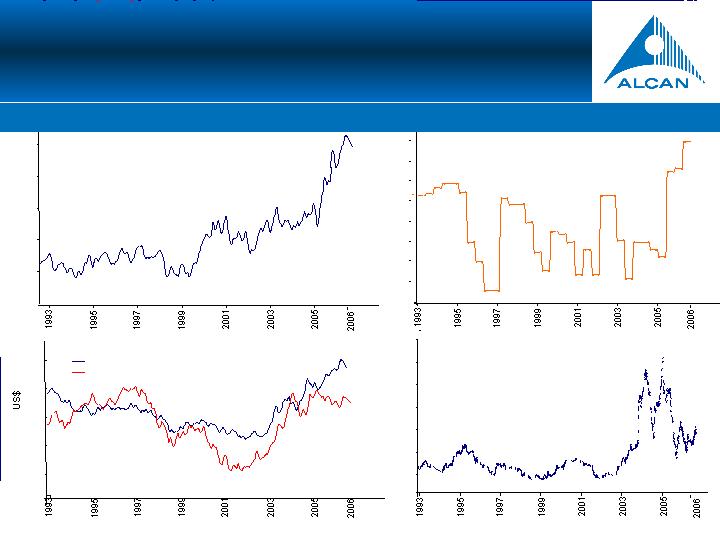

Raw Material Price & Currency

Volatility

Oil: SING 380 (US$/bbl)

CAGR Jan 98 - Aug 06: 19%

10

20

30

40

50

60

0.40

0.50

0.60

0.70

0.80

0.90

CAN$

AUS$

Caustic: ASP North America (US$/DMT)

CAGR Jan 00- Aug 06: 22%

0

50

100

150

200

250

300

350

400

450

Freight: BDI Index ($/day)

CAGR Jan 98 - Aug 06: 13%

1,000

2,000

3,000

4,000

5,000

6,000

7,000

1.00

1.00

1.00

1.00

The alumina industry has been affected by unprecedented price increases…

© 2 0 06 A L C A N I N C.Slide 10

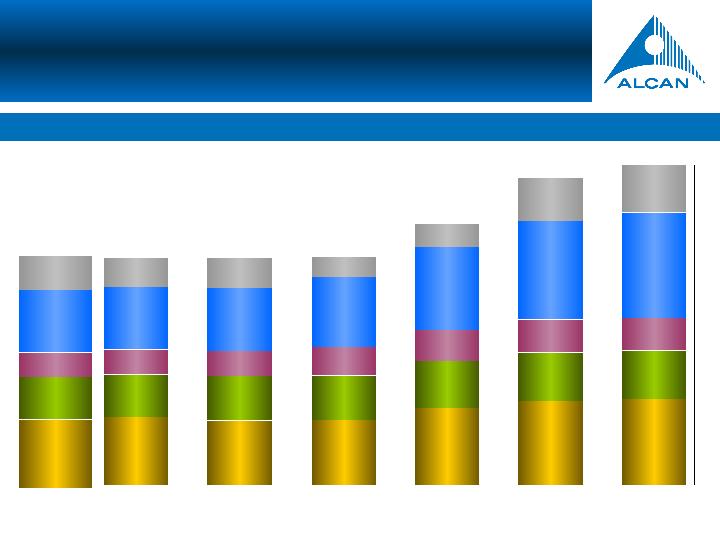

Alumina Industry Block Cost

2001-2006

… impacting substantially the industry cost curve

Source: CRU

40.63

38.45

38.98

46.02

50.31

51.31

25.50

26.72

26.81

28.03

28.91

28.94

14.77

15.12

16.73

18.78

19.60

19.63

37.35

37.36

41.96

49.71

58.82

63.30

17.7

18.1

12.1

13.6

25.8

28.3

2001

2002

2003

2004

2005

2006

136 $/t

136 $/t

137 $/t

156 $/t

183 $/t

191 $/t

Industry AVG

Cash Cost

$/t

Bauxite

Caustic

Energy

Labour

Maintenance

& Materials

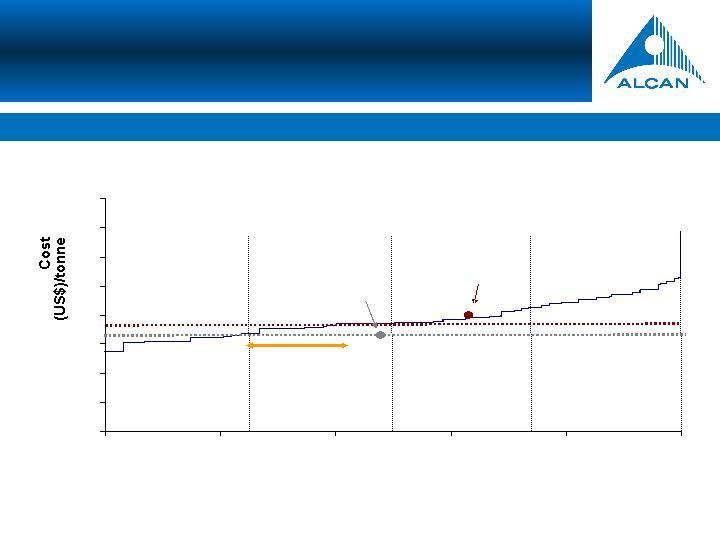

© 2 0 06 A L C A N I N C.Slide 11

World Ranking Site Operating Costs, 2005

Source: CRU & Alcan Internal.

Target 50% of production in 1st quartile by 2009

0

50

100

150

200

250

300

350

400

0

20

40

60

80

100

Cumulative

Production (%)

Industry Average ‘05: 184

$/t

Alcan ‘05: 191 $/t

Industry Average ‘04: 157

$/t

Alcan ‘04:

155 $/t

Alcan ‘05 1st

Quartile 33%

Alcan ‘05 2nd

Quartile 3%

Alcan ‘05 3rd

Quartile 37%

Alcan ‘05 4th

Quartile 27%

Improveme

nt range

nt range

Target 2010

50% ~ 60%

Target 2010

20% ~ 30%

Target 2010

0%

Target 2010

20%

Evolution of Competitive Position 2005

-2010

© 2 0 06 A L C A N I N C.Slide 12

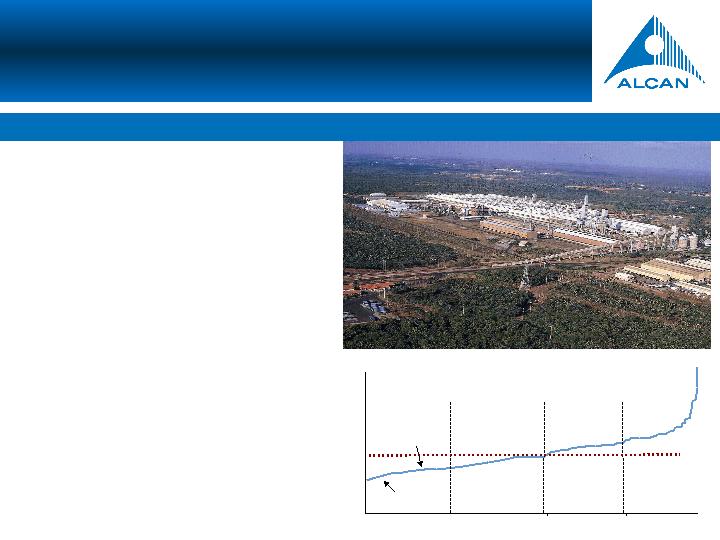

Gove Expansion

Project on schedule despite challenging industrial environment in Australia

n

Excellent EHS performance

n

Some 25-30% of the capital cost enhances current

operating efficiency and environmental performance

n

Assembly of modules in low-cost countries allowed

for:

•

Rapid construction schedule (27 months)

•

Partial mitigation of exposure to high-cost

environment in Australia

n

Unplanned hours for brownfield work became

obvious in July-August as we started commissioning

of some systems

of some systems

n

Expansion reduces cash cost by 30$/t

n

Gas conversion is also exposed to tight construction

environment in Australia and we are assessing other

options while maintaining support for PNG

options while maintaining support for PNG

© 2 0 06 A L C A N I N C.Slide 13

Gove Expansion

© 2 0 06 A L C A N I N C.Slide 14

n

Expansion of 2.1 Mt from existing

capacity of 1.4 Mt.

n

Alcan owns 10% with Alcoa and BHP

holding the remaining 90%

n

Construction underway (20% in overall

progress) with outstanding EHS

performance

performance

n

First production in Q3-2008 (expected

33-month construction)

Cumulative Production

Alumar current

Conversion Cost

Post-expansion

Conversion Cost

0

50

100

150

200

250

300

25%

50%

75%

Industry Conversion Costs, Forecast 2008

Source: CRU

$/t

Construction underway with excellent EHS performance

Alumar

© 2 0 06 A L C A N I N C.Slide 15

Cost Optimization

n

Gardanne

n

Continue concentration on value-added products

n

Closure of UPCA and migration of products to Gardanne

n

Vaudreuil

n

Productivity improvements and cost cutting measures being

implemented

•

Hydrate production increased by 11% in the last two

years

n

Increased outsourcing offering reduced labour cost and flexibility

to adjust to changing market conditions

© 2 0 06 A L C A N I N C.Slide 16

Sources : CRU, Metal Bulletin (MBR), Brook Hunt, Macquarie Bank, James F. King

Alcan

Moving from supply deficit to near-term surplus

Alumina World Market Balance Forecast

-2,000

-

2,000

4,000

6,000

8,000

10,000

-1,121

-1,104

-1,338

-1,361

-1,486

2005

447

1,483

2,999

2,626

1,178

2006

929

1,673

6,468

3,079

3,116

2007

1,285

2,015

4,452

5,337

2,221

2008

Macquarie Bank – July 06

CRU - Apr 06

MBR - Sept 06

Brook Hunt - Aug. 06

James F. King – Aug 06

Alumina World Balance

© 2 0 06 A L C A N I N C.Slide 17

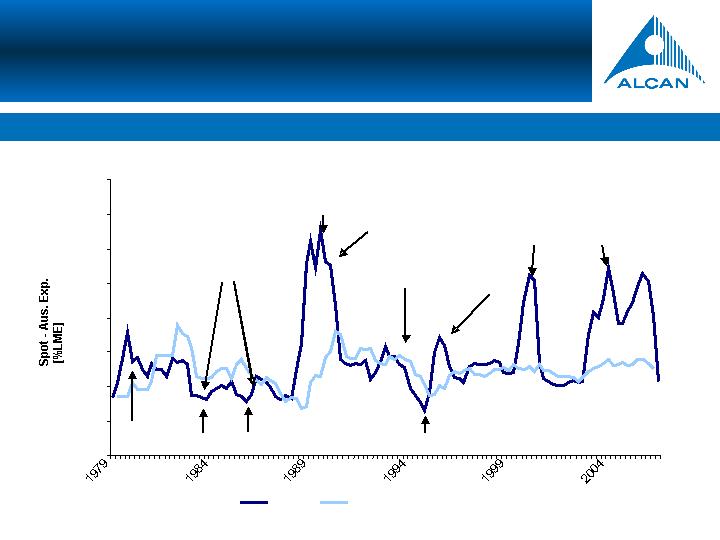

Market returns to surplus – immediate impact on spot prices

Spot and Australian Export Price Evolution

Spot

Aus. Export Price

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

San Ciprian

Aughinish

Worsley

Alumina

oversupply

High metal

prices

Hurricane

Eastern block

sell-down

Hurricane

Gramercy

explosion

Structural

tightness

(China)

Alunorte

Source: CRU

Historical Prices

© 2 0 06 A L C A N I N C.Slide 18

27

21

22

23

18

17

20

29

10

13

25

15

16

26

1

2

7

30

3

28

4

5

6

8

9

11

12

14

19

24

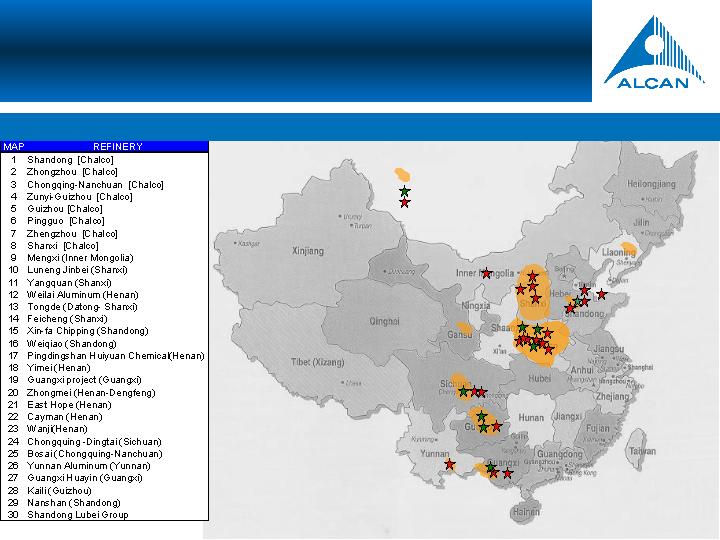

Non-Chalco

Chalco

Known Bauxite Reserves

Source : B&A Analysis, Brook Hunt

China could have up to 30 alumina refineries up and running by 2010

China Alumina Landscape

© 2 0 06 A L C A N I N C.Slide 19

China New Alumina Refineries

Cash costs

Domestic Prices

Min

Max

Min

Max

USD/t

Min

Max

Transport to

smelters

0

50

100

150

200

250

300

350

domestic

bauxite

imported

bauxite

tax+freight

premium

International

Spot Price

230$/t

© 2 0 06 A L C A N I N C.Slide 20

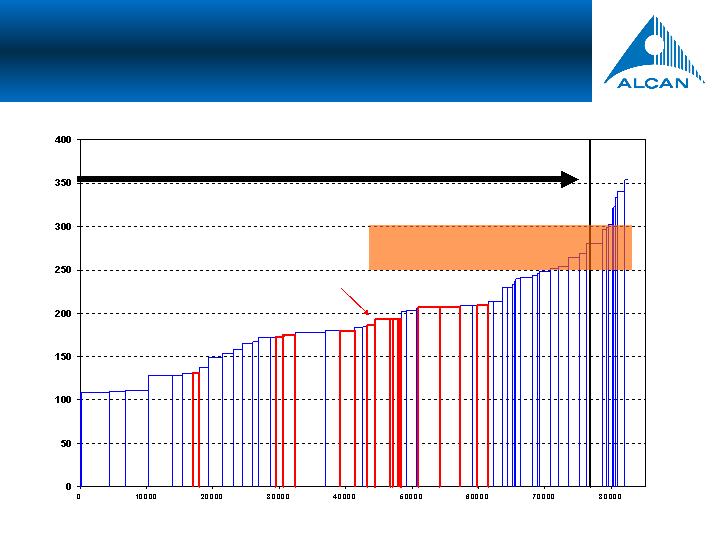

USD/t

2007 Alumina Cash Cost

Curve

tpy of production

Chinese capacity

Price zone

Alumina Demand

© 2 0 06 A L C A N I N C.Slide 21

Market Outlook

n

Alumina market expected in surplus for the next 2~3 years

n

China alone will represent more than 50% of the global growth in

supply and demand

n

Chinese alumina imports expected to decrease

n

Due to the poor quality of the Chinese bauxite and the use of

imported bauxite, the Chinese refineries are expected to be on the

3rd and 4th quartile of the industry cost curve

3rd and 4th quartile of the industry cost curve

n

Self-regulating price is expected to remain in the 250~300$/mt

range

© 2 0 06 A L C A N I N C.Slide 22

•

Potential development of a large-scale integrated aluminium

facility (bauxite mine + alumina refinery + aluminium smelter)

•

Large high-quality bauxite resources (in excess of 500 Mt)

Utkal

•

Greenfield project of 1.5 Mt in the province of Orissa, India

•

Alcan owns 45% with Hindalco holding the other 55%

•

Investment decision expected by H1-2007

Guinea

•

Greenfield project of 1.5Mt in Guinea

•

Alcan to own 40% with Alcoa holding another 40%

•

Basic Agreement with the Government of Guinea now effective

•

Expect to make a decision on DFS by the end of 2006

Cameroon

Project

Description and Benefits

Ghana

•

MoU signed for the analysis of a mine and an alumina refinery

project in joint venture with the State

•

Conceptual and pre-feasibility studies underway

Additional Growth Opportunities

Opportunities in lowest cost quartile

© 2 0 06 A L C A N I N C.Slide 23

Summary and Key Priorities

n

Leverage AIMS – operational excellence

n

Complete construction and start-up of Gove

n

Complete expansion of Alumar

n

Continue action on high-cost facilities

n

Leverage our sustainability & technology/engineering know-how to

pursue growth opportunities of large-scale assets in lowest cost

quartile

quartile

© 2 0 06 A L C A N I N C.Slide 24

APPENDIX

© 2 0 06 A L C A N I N C.Slide 25

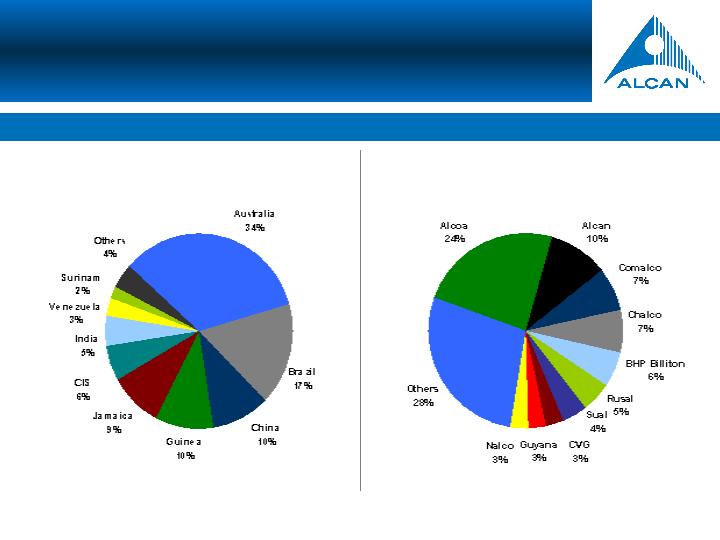

Source: James King, B&A analysis

Bauxite

10% of world bauxite production

Bauxite Production by Country

Bauxite Production by Company

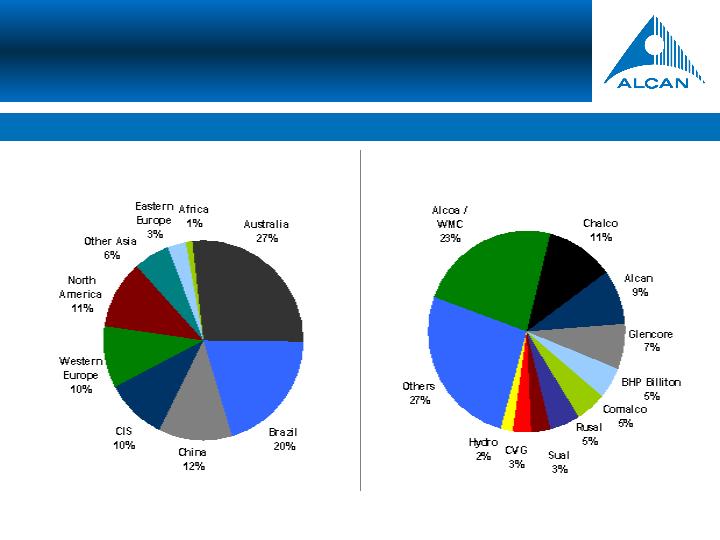

© 2 0 06 A L C A N I N C.Slide 26

Source: James King, B&A analysis

Alumina

Alumina Production by Region

Alumina Production by Company

9% of world alumina production

© 2 0 06 A L C A N I N C.Slide 27