Alcan Investor Workshop

Toronto, October 3, 2006

Cynthia Carroll

President and CEO - Alcan Primary Metal

© 2 0 06 A L C A N I N C.Slide 2

Forward Looking Statements

Statements made in the course of this presentation which describe the

Company's or management’s objectives, projections, estimates,

expectations or predictions may be "forward-looking statements" within the

meaning of securities laws. All statements that address the Company's

expectations or projections about the future including statements about the

Company's growth, cost reduction goals, operations reorganization plans,

expenditures and financial results are forward-looking statements. Company cautions that, by their nature, forward-looking statements involve

risk and uncertainty and actual actions or results could differ materially.

Reference should be made to the most recent Form 10-Q for a summary of

factors that could cause such differences. In addition, certain non-GAAP

measures are used which are reconciled to the comparable GAAP

measures herein or on the Company’s website at www.alcan.com in the

“Investors” section.

expectations or predictions may be "forward-looking statements" within the

meaning of securities laws. All statements that address the Company's

expectations or projections about the future including statements about the

Company's growth, cost reduction goals, operations reorganization plans,

expenditures and financial results are forward-looking statements. Company cautions that, by their nature, forward-looking statements involve

risk and uncertainty and actual actions or results could differ materially.

Reference should be made to the most recent Form 10-Q for a summary of

factors that could cause such differences. In addition, certain non-GAAP

measures are used which are reconciled to the comparable GAAP

measures herein or on the Company’s website at www.alcan.com in the

“Investors” section.

© 2 0 06 A L C A N I N C.Slide 3

Agenda

n

Business Context

n

Operational Excellence

n

Technology Leadership

n

Profitable Growth Opportunities

n

Summary

© 2 0 06 A L C A N I N C.Slide 4

n

One of the two largest

aluminum producers in

the world with total

primary metal capacity of

3.5 Mt (10% of world)

the world with total

primary metal capacity of

3.5 Mt (10% of world)

n

21 smelters on 5

continents

n

12 power facilities with

total owned capacity of

4,370 Mw

4,370 Mw

n

World leading market

position in smelting

technology

technology

Key Facts

North America

Smelting: 1.9 Mt

Power: 3,583 Mw

Australia

Smelting: 0.3

Mt

Power: na

Europe

Smelting: 1.2

Mt

Power: 529 Mw

Africa:

Smelting: 0.05

Mt

Power: na

Asia:

Smelting: 0.1 Mt

Power: 261 Mw

Primary Metal Operations

© 2 0 06 A L C A N I N C.Slide 5

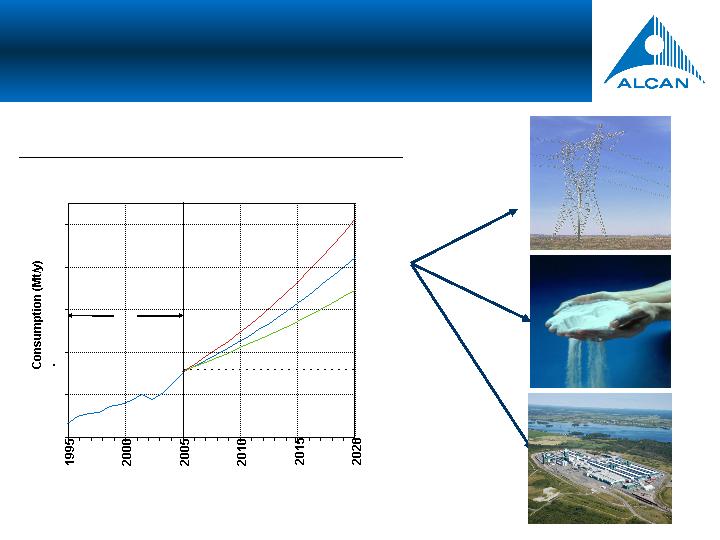

Energy: 43,000

MW

Alumina: ~50 Mt

15

25

35

45

55

65

4.5%

+34 MT

+18 MT

+25 MT

3% CAGR

4% CAGR

5% CAGR

31.85

Primary Aluminum Consumption, 1995 - 2020

Capital ≈ $100

Billion

Primary Aluminum Consumption and

Production Constraints

© 2 0 06 A L C A N I N C.Slide 6

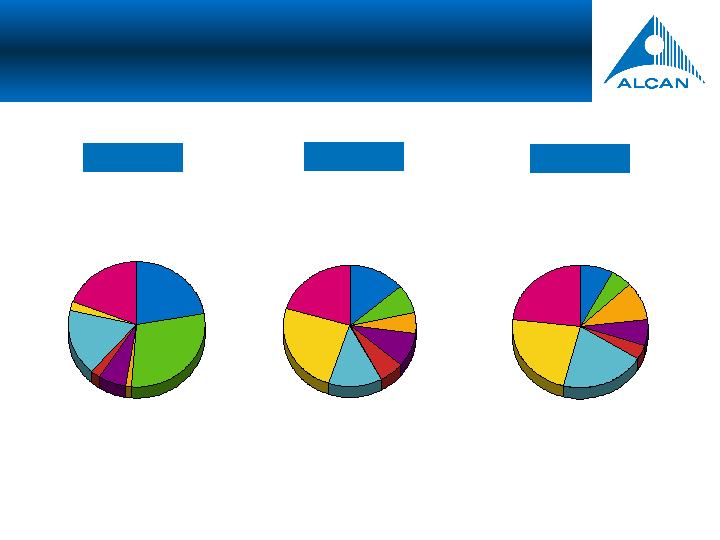

2020

(57.5 Mt)

Europe

8%

Other

23%

Middle East

10%

China

23%

Australia

4%

Canada

7%

USA

5%

exUSSR

20%

2005

(31.9 Mt)

Europe

14%

Middle East

6%

Canada

9%

Other

20%

Australia

6%

exUSSR

13%

USA

8%

China

24%

1980

(16.1 Mt)

Europe

22%

Other

19%

Middle East

1%

China

2%

Australia

2%

Canada

7%

USA

30%

exUSSR

17%

Shift In Aluminum Production Centers:

1980 – 2005 – 2020

© 2 0 06 A L C A N I N C.Slide 7

Strategic Direction

APMG is becoming the global leader in the

primary aluminum industry and the supplier of

choice through:

choice through:

<

World class, low-cost operational excellence

<

Market leading position with cutting-edge AP

technology package and engineering

solutions

solutions

<

World-class EHS performance

<

Sustainable value-creating solutions

© 2 0 06 A L C A N I N C.Slide 8

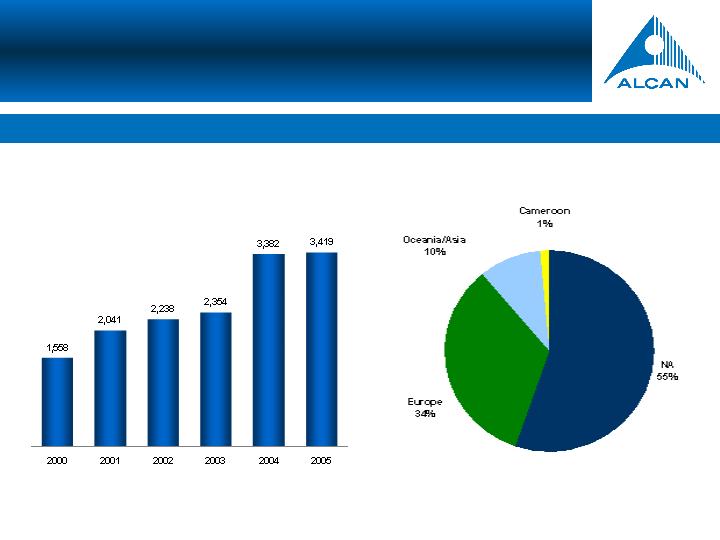

Alcan’s production has significantly increased and diversified geographically

Hot Metal Production (000kt)

APMG Geographic Smelting Capacity

A Leader in Aluminum Production

© 2 0 06 A L C A N I N C.Slide 9

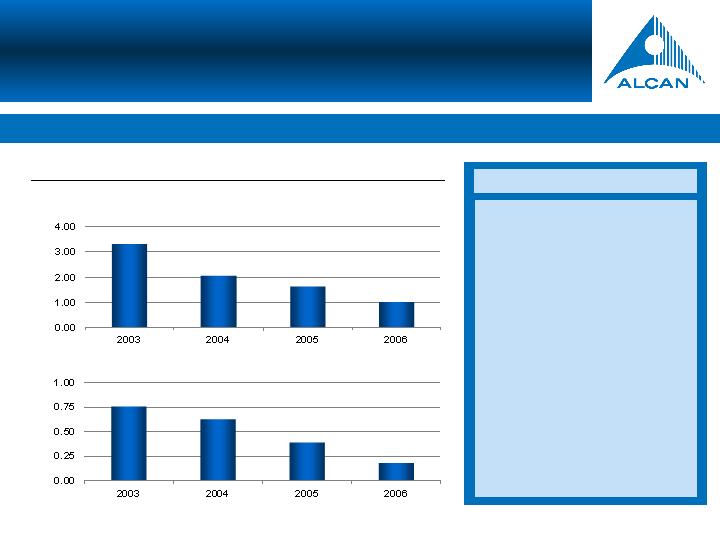

Recordable and Lost Time Injury / Illness Case Rate

n

Since 2003, 70%

improvement in recordable

and LTII case rate

and LTII case rate

n

All sites have been

certified OHSAS 18000

and ISO 14001.

and ISO 14001.

n

Implementation of EHS

FIRST.

n

Initiatives on pedestrian

safety and hazardous

energy control reduced

the severity of APMG

injuries.

energy control reduced

the severity of APMG

injuries.

Key Facts

Safety results improving continuously

Recordable Case Rate

LTII Case Rate

EHS Performance - Safety

© 2 0 06 A L C A N I N C.Slide 10

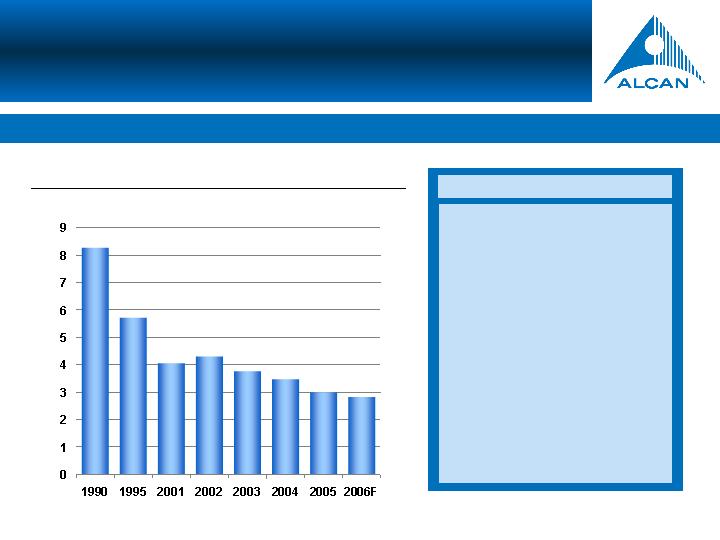

Direct Total GHG Emissions

tCO2e/t Al

n

Since 1990, GHG emissions

rates have been reduced by

more than 50%

more than 50%

n

Significant efforts are being

applied in operations and

R&D to further reduce

emissions

R&D to further reduce

emissions

Key Facts

Successfully addressing GHG emissions while increasing production

EHS Performance - Environment

© 2 0 06 A L C A N I N C.Slide 11

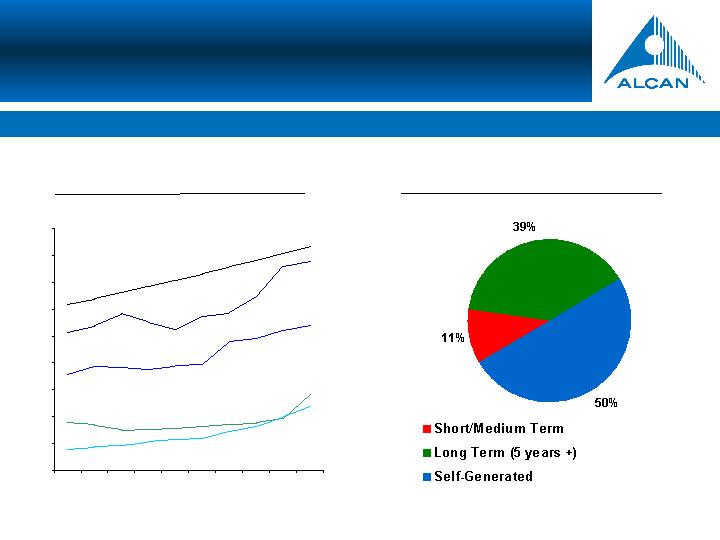

APMG Production Exposure to

Power Contract

Projected Market Power Price

Evolution

Close to 90% of APMG production is based on self-generated power and long term

contracts

10

15

20

25

30

35

40

45

50

55

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

China

Europe

excl. Iceland

USA

Middle East

Canada

$/MWh -

nominal

Competitive Position

© 2 0 06 A L C A N I N C.Slide 12

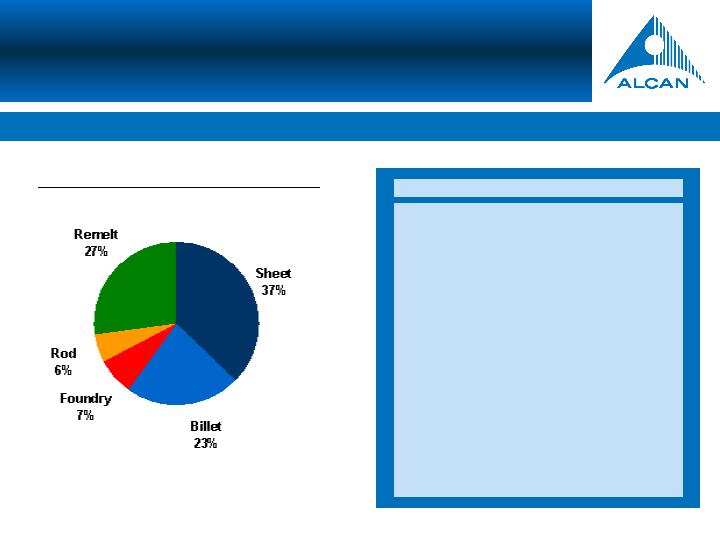

In 2006, APMG will reach new sales record for total VAP sales

n

World’s largest third party supplier

of Value Added Products (VAP)

n

In 2006, we expect record sales in

4 of 5 our product lines.

n

Total 2006 VAP sales will exceed

previous record sales

n

Industry player with the best overall

market knowledge.

Key Facts

Product Mix

Value-Added Products

© 2 0 06 A L C A N I N C.Slide 13

Achievement

Moving simultaneously on all value drivers, through our current asset optimization initiatives

and technological solutions, creates a sustainable business for the future

Energy Consumption

(kWh/kg)

Manpower Productivity

(MT/Empl/Year)

Incremental Aluminum Production (kt)

Alcan Leadership on Cost Drivers

© 2 0 06 A L C A N I N C.Slide 14

Cumulative Annual BGP Realized ($M)

<

CI projects

§

More than 800 projects since

2004 with US$ 88 million

BGP realized and another

US$ 51 million in execution

BGP realized and another

US$ 51 million in execution

<

Very good deployment

progress; By end 2007 all

young high potential employees

would have been trained as BB

young high potential employees

would have been trained as BB

<

Average annual BGP from a BB

project is around US$ 0.4 million

Key Facts

sectors

CI deployment delivering substantial value across all Primary Metal Group

Continuous Improvement System

© 2 0 06 A L C A N I N C.Slide 15

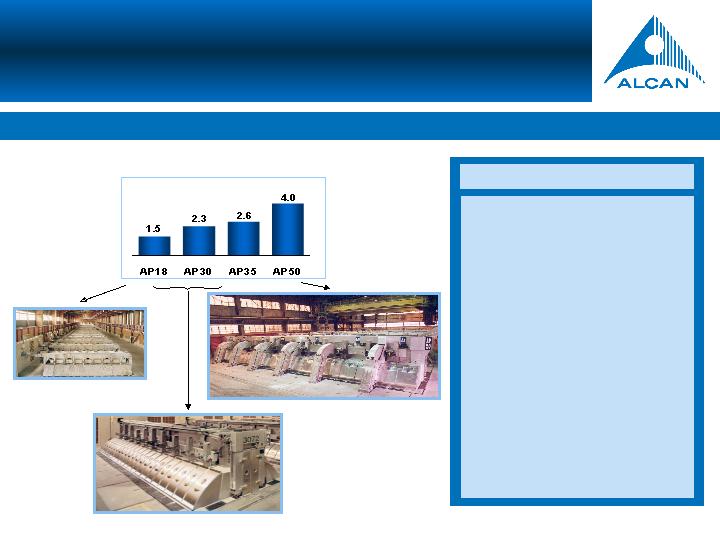

Cell Technology Leadership

AP Technology Global Presence

AP-18 (3,492 pots)

AP-30 (3,859 pots)

Australia:

§

Boyne

§

Tomago

Canada:

§

Alma

§

Lauralco

§

Alouette

§

Baie-Comeau

§

Becancour

Norway:

Karmoy

Bahrain:

Alba

Argentina:

Aluar

Mozambique:

Mozal

South Africa:

Hillside

UK:

Lochaber

Slovenija:

Talum

India:

Nalco

France:

§

Dunkerque

§

St-Jean

With a track record of ~6,000kt of production, Alcan’s AP technology leads the global

market

with proven leadership in all aspect of operating cost drivers

© 2 0 06 A L C A N I N C.Slide 16

Alcan’s global leading edge smelting technology package is an unparalleled competitive

advantage

Market Leadership

Cell Length=9 m

AP18

Cell Length=18 m

AP50

Cell Length=14 m

AP30

Daily Production (t)

Key Facts

n

Most sustainable,

comprehensive and

proven smelting

technology, engineering

and services package

proven smelting

technology, engineering

and services package

n

Leadership in full

economic cost

n

Substantially higher

returns on Alcan

sponsored projects

sponsored projects

n

Increased focus on

potential breakthroughs

related to AP30 and

AP50 platforms

related to AP30 and

AP50 platforms

Alcan’s Smelting Technology:

An Unsurpassed Offer

© 2 0 06 A L C A N I N C.Slide 17

Assessment

Development

Execution

A,B,C,D,E,F,G,H,I,J

Sohar

Kitimat, Coega, ISAL

Growth Through Strategic Initiatives

© 2 0 06 A L C A N I N C.Slide 18

Expansion /

Retrofit

Greenfield

Kitimat Modernization (Canada)

n

State of the art facility (400 kt)

n

Self generated Energy

ISAL Brownfield (Iceland)

n

Europe’s largest smelter (460 kt)

n

Mainly geothermal power

Coega Greenfield (South Africa)

n

720 kt to be built consequently

n

Long-term energy contract (25 years)

Sohar Greenfield (Oman)

n

Phase I under construction (350 kt)

n

Dedicated power supply

n

Potential phase II (350 kt)

Alouette Brownfield (Canada)

n

America’s largest smelter (554 kt)

n

Completed on budget and ahead of

schedule

Growth Through Strategic Initiatives

Using AP Smelting Technology

All projects are in the 1st Quartile of the industry curve

© 2 0 06 A L C A N I N C.Slide 19

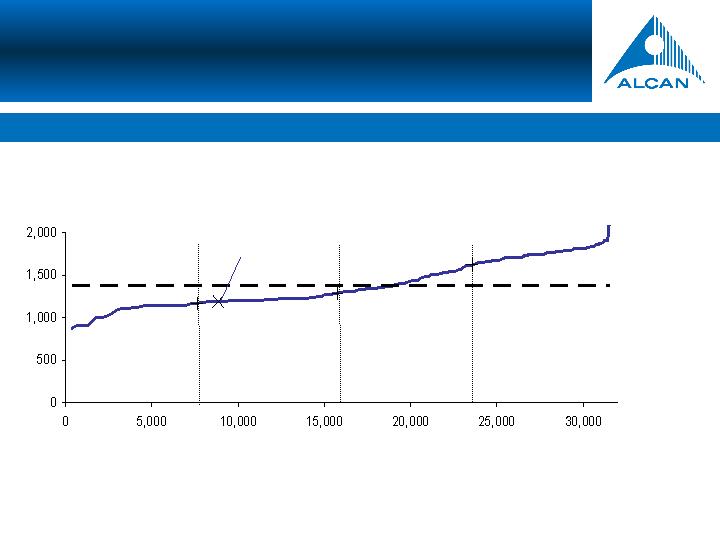

Target: 55% of production in first quartile

Unique energy position and

efficient, low cost facilities

Source: CRU

1) Position in 2004

World Ranking Site Corporate Operating Costs - 2005

(US$/t)

Cumulative Production (Kt)

Industry Average

$1,375/t

($1,240/t)1

Alcan 1st

Quartile

48%

Alcan 2nd

Quartile

24%

Alcan 3rd

Quartile

28%

Alcan 4th

Quartile

0%

Alcan

(44%)1

(22%)1

(21%)1

(13%)1

© 2 0 06 A L C A N I N C.Slide 20

n

Significant self-generated energy assets and long-term,

competitively-priced energy contracts

n

World-class, low-cost smelting operations with further AOS potential

n

Diversified operational position from geographic and customer

standpoint

n

Market leading position with AP technology combined with proven

engineering expertise providing:

§

Access to attractive new smelter projects

§

Incremental profit from sales of technology licenses, equipment,

and services

n

Access to diverse pipeline of new project opportunities due to

superior market intelligence, ‘preferred company’ status, and regional

know-how

know-how

Sources of Advantage

© 2 0 06 A L C A N I N C.Slide 21