Neuberger Berman

Equity Funds

Investor Class Shares

Trust Class Shares

Advisor Class Shares

Institutional Class Shares

Dividend Growth Fund

Emerging Markets Equity Fund

Equity Income Fund

Focus Fund

Genesis Fund

Global Equity Fund

Global Real Estate Fund

Greater China Equity Fund

Guardian Fund

International Equity Fund

Class A Shares

Class C Shares

Class R3 Shares

Class R6 Shares

International Select Fund

International Small Cap Fund

Intrinsic Value Fund

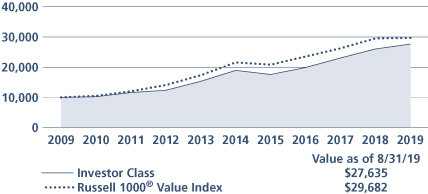

Large Cap Value Fund

Mid Cap Growth Fund

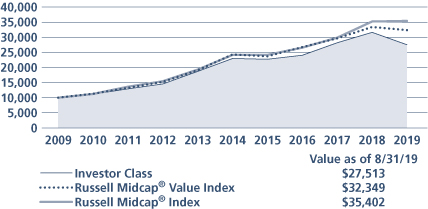

Mid Cap Intrinsic Value Fund

Multi-Cap Opportunities Fund

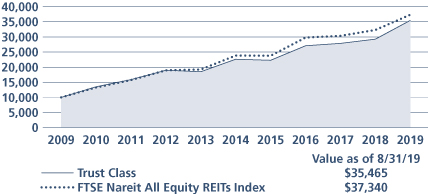

Real Estate Fund

Small Cap Growth Fund

Sustainable Equity Fund

Annual Report

August 31, 2019

Beginning on January 1, 2021, as permitted by regulations adopted by the U.S. Securities and Exchange Commission, paper copies of the Fund's annual and semi-annual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports. Instead, the reports will be made available on the Fund's website www.nb.com/fundliterature, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Fund electronically anytime by contacting your financial intermediary (such as a broker-dealer or bank) or, if you are a direct investor, by calling 800.877.9700 or by sending an e-mail request to fundinfo@nb.com.

Beginning on January 1, 2019, you may elect to receive all future reports in paper free of charge. If you invest through a financial intermediary, you can contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. If you invest directly with the Fund, you can call 800.877.9700 or send an email request to fundinfo@nb.com to inform the Fund that you wish to continue receiving paper copies of your shareholder reports. Your election to receive reports in paper will apply to all funds held in your account if you invest through your financial intermediary or all funds held with the fund complex if you invest directly with the Fund.

Contents

THE FUNDS

President's Letter | 1 | ||||||

PORTFOLIO COMMENTARY | |||||||

Dividend Growth Fund | 2 | ||||||

Emerging Markets Equity Fund | 5 | ||||||

Equity Income Fund | 9 | ||||||

Focus Fund | 13 | ||||||

Genesis Fund | 16 | ||||||

Global Equity Fund^ | 20 | ||||||

Global Real Estate Fund | 24 | ||||||

Greater China Equity Fund | 28 | ||||||

Guardian Fund | 32 | ||||||

International Equity Fund | 35 | ||||||

International Select Fund | 38 | ||||||

International Small Cap Fund | 41 | ||||||

Intrinsic Value Fund | 45 | ||||||

Large Cap Value Fund | 48 | ||||||

Mid Cap Growth Fund | 51 | ||||||

Mid Cap Intrinsic Value Fund | 54 | ||||||

Multi-Cap Opportunities Fund | 58 | ||||||

Real Estate Fund | 61 | ||||||

Small Cap Growth Fund | 64 | ||||||

Sustainable Equity Fund | 67 | ||||||

FUND EXPENSE INFORMATION | 77 | ||||||

LEGEND | 81 | ||||||

SCHEDULE OF INVESTMENTS | |||||||

Dividend Growth Fund | 82 | ||||||

Emerging Markets Equity Fund | 84 | ||||||

Positions by Industry | 87 | ||||||

Equity Income Fund | 90 | ||||||

Focus Fund | 95 | ||||||

Genesis Fund | 98 | ||||||

Global Equity Fund^ | 101 | ||||||

Positions by Industry | 103 | ||||||

Global Real Estate Fund | 105 | ||||||

Positions by Sector | 107 | ||||||

Greater China Equity Fund | 109 | ||||||

Guardian Fund | 111 | ||||||

International Equity Fund | 117 | ||||||

Positions by Industry | 119 | ||||||

International Select Fund | 121 | ||||||

Positions by Industry | 123 | ||||||

International Small Cap Fund | 125 | ||||||

Positions by Industry | 127 | ||||||

Intrinsic Value Fund | 129 | ||||||

Large Cap Value Fund | 132 | ||||||

Mid Cap Growth Fund | 135 | ||||||

Mid Cap Intrinsic Value Fund | 138 | ||||||

Multi-Cap Opportunities Fund | 140 | ||||||

Real Estate Fund | 142 | ||||||

Small Cap Growth Fund | 144 | ||||||

Sustainable Equity Fund | 146 | ||||||

FINANCIAL STATEMENTS | 149 | ||||||

FINANCIAL HIGHLIGHTS (ALL CLASSES)/PER SHARE DATA | |||||||

Dividend Growth Fund | 211 | ||||||

Emerging Markets Equity Fund | 213 | ||||||

Equity Income Fund | 215 | ||||||

Focus Fund | 215 | ||||||

Genesis Fund | 219 | ||||||

Global Equity Fund^ | 221 | ||||||

Global Real Estate Fund | 221 | ||||||

Greater China Equity Fund | 223 | ||||||

Guardian Fund | 225 | ||||||

International Equity Fund | 227 | ||||||

International Select Fund | 229 | ||||||

International Small Cap Fund | 233 | ||||||

Intrinsic Value Fund | 233 | ||||||

Large Cap Value Fund | 235 | ||||||

Mid Cap Growth Fund | 239 | ||||||

Mid Cap Intrinsic Value Fund | 241 | ||||||

Multi-Cap Opportunities Fund | 245 | ||||||

Real Estate Fund | 245 | ||||||

Small Cap Growth Fund | 249 | ||||||

Sustainable Equity Fund | 251 | ||||||

Reports of Independent Registered Public Accounting Firms | 260 | ||||||

Directory | 264 | ||||||

Trustees and Officers | 265 | ||||||

Proxy Voting Policies and Procedures | 276 | ||||||

Quarterly Portfolio Schedule | 276 | ||||||

Notice to Shareholders | 277 | ||||||

^ As previously announced, as of September 3, 2019, Neuberger Berman Global Equity Fund changed its name to Neuberger Berman Integrated Large Cap Fund, and changed its investment strategy, portfolio management team and fees and expenses.

The "Neuberger Berman" name and logo and "Neuberger Berman Investment Advisers LLC" name are registered service marks of Neuberger Berman Group LLC. The individual Fund names in this piece are either service marks or registered service marks of Neuberger Berman Investment Advisers LLC, an affiliate of Neuberger Berman BD LLC, distributor, member FINRA. ©2019 Neuberger Berman BD LLC, distributor. All rights reserved.

President's Letter

Dear Shareholder,

Equity markets shifted over the course of this fiscal period. In 2018, investors already distressed about indications of a global economic slowdown weighed the potential multiplier effects of the U.S./China trade war and delivered the first full calendar year loss for the S&P 500® Index since the financial crisis. In 2019, though these macroeconomic issues and other geopolitical tensions continued to create uncertainty and volatility, markets rallied, particularly in January and June, on apparent breaks in trade tensions and as the U.S. Federal Reserve Board (Fed) first hinted, and then lowered rates.

Current data suggests we are navigating a later-stage market cycle. While the U.S. economy remains healthy, there are signs of deceleration. Second quarter 2019 GDP growth slowed to 2.0%, down from 3.1% in first quarter and 2.9% for all of 2018. In August, the Institute for Supply Management reported slowing in manufacturing activity. August's job growth data slowed in manufacturing and declined in commodity-related sectors.

The trade war continues to weigh on both the U.S. and global economies—in the U.S., on farmers, consumers' finances and confidence, on steel, oil, and other economically sensitive commodities, on ports, trucking and railways, and on business decision-making. Outside the U.S., export-driven economies, including Germany and China, have shown signs of stress. Global interest rates are already low, giving the Fed and other central banks, including the European Central Bank, which in July committed to a "highly accommodative" stance, limited stimulus firepower should the economy stall.

At the same time, a feared decline in second quarter corporate earnings did not materialize. Earnings were flat-to-up, aligned with guidance for the rest of the year. This, along with an attentive Fed, suggests we may avoid the recession forecasted by the bond market via an inverted yield curve. Further, job growth in the service sector remained healthy in August, the unemployment rate was at a low 3.7%, and wages were increasing.

With the S&P 500 Index up 18.34% year-to-date through the end of August against earnings growth in the single digits, valuations and risk are high. From Brexit and tumult in Parliament, to protests in Hong Kong, to worsening relations between the U.S. and Iran, to North Korean missile tests, to the U.S. election cycle—there is plenty of fodder for disruption in a headline-driven, reactive market. At the same time, bond yields are low, supporting equities as an asset class.

With tested strategies intended to outperform over the longer term and an emphasis on fundamentals, our teams rely on independent research—as they weigh potential benefits against macro-level and company-specific risk factors, and as they work to buy and sell opportunistically. Until markets return to a more fundamentals-driven standard, our teams will continue using volatility in their efforts to strengthen and fine-tune portfolios for the longer term.

Thank you for your confidence in Neuberger Berman.

Sincerely,

JOSEPH V. AMATO

PRESIDENT AND CEO

NEUBERGER BERMAN EQUITY FUNDS

1

Dividend Growth Fund Commentary (Unaudited)

Neuberger Berman Dividend Growth Fund Institutional Class generated a –2.45% total return for the fiscal year ended August 31, 2019, underperforming its benchmark, the S&P 500® Index (the Index), which posted a 2.92% total return for the same period. (Performance for all share classes is provided in the table immediately following this letter.)

By late-July, the market set a new all-time high (as measured by the Index) as the economy's expansion officially became the longest in U.S. history, driven by "growth" stocks with limited or, in many cases, no dividend programs. However, in late July equities experienced headwinds as investors grappled with an uptick in volatility tied to fears surrounding waning global growth, and geopolitical headwinds.

The Fund seeks to provide gross current income in-line with its benchmark, while seeking capital appreciation driven by dividend per share growth. This approach seeks to identify companies with strong business models generating cash to grow their businesses while providing rising dividend distributions to shareholders. Overall, we look for companies with strong balance sheets, solid management teams, attractive free cash flow yields, and clear capital allocation strategies.

From a portfolio construction standpoint, the largest equity sectors on average during the fiscal year included Information Technology ~20%, Financials ~14%, and Health Care ~13%. This reporting period, the bulk of relative returns were generated from stock selection across Real Estate, Financials, and Utilities—while selection within Consumer Staples, Consumer Discretionary, and Energy weighed on results versus the Index.

While the broader commodity complex experienced downward pressure, negative stock selection across our Materials holdings were partially offset by outsized returns from Wheaton Precious Metals. This holding proved to be our top overall performer, and provided a revenue stream tied to high-quality gold, platinum, palladium, and copper mines. The business does not incur ongoing exploration costs faced by traditional mining companies. This position sharply advanced as global central banks purchased a record $15 billion of the precious metal in the first half of 2019. We believe this exposure could provide a hedge to potential inflationary pressures.

Our Energy names negatively impacted both absolute and relative performance. Within this space, Devon Energy fell among our laggards. This upstream business experienced selling pressure despite beating production expectations. While the recent environment has been challenging, we remain encouraged by improving well productivity from Delaware Basin and STACK plays (i.e., Anadarko Basin area of Oklahoma). From a capital allocation perspective, management continues to divest non-core assets while rewarding shareholders through stock buybacks and dividend increases, making this, we believe, an ideal position given our investment mandate.

The health of the U.S. economy seems mixed. The consumer remains in a strong position, with low unemployment and modestly growing wages. However, the industrial economy seems to be facing challenges, in part due to the U.S.-China tariff dispute. In our view, valuations across equities remain reasonable, and when evaluating investment candidates, we continue to identify pockets of value across stable businesses with clear capital allocation plans exhibiting dividend growth potential. We acknowledge potential weakness stemming from geopolitical tensions, and believe distortions from central banks continue to drive the hunt for yield amid aging global demographics. Today, we believe the Fund remains positioned to navigate cross-currents given our focus on what we believe to be high-quality cash-generative companies.

In closing, we thank you for investing in our Fund.

Sincerely,

DAVID A. KIEFER AND WILLIAM D. HUNTER

PORTFOLIO MANAGERS

Information about principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change without notice.

The opinions expressed are those of the Fund's portfolio manager(s). The opinions are as of the date of this report and are subject to change without notice.

2

Dividend Growth Fund (Unaudited)

TICKER SYMBOLS

Institutional Class | NDGIX | ||||||

Class A | NDGAX | ||||||

Class C | NDGCX | ||||||

Class R6 | NRDGX | ||||||

SECTOR ALLOCATION

(as a % of Total Investments*) | |||||||

Communication Services | 5.4 | % | |||||

Consumer Discretionary | 7.7 | ||||||

Consumer Staples | 9.4 | ||||||

Energy | 7.6 | ||||||

Financials | 15.5 | ||||||

Health Care | 12.6 | ||||||

Industrials | 4.2 | ||||||

Information Technology | 20.3 | ||||||

Materials | 3.8 | ||||||

Real Estate | 5.1 | ||||||

Utilities | 2.3 | ||||||

Short-Term Investments | 6.1 | ||||||

Total | 100.0 | % | |||||

* Derivatives (other than options purchased), if any, are excluded from this chart.

PERFORMANCE HIGHLIGHTS

| Average Annual Total Return Ended 08/31/2019 | |||||||||||||||

| Inception Date | 1 Year | Life of Fund | |||||||||||||

At NAV | |||||||||||||||

Institutional Class | 12/15/2015 | –2.45 | % | 9.87 | % | ||||||||||

Class A | 12/15/2015 | –2.75 | % | 9.50 | % | ||||||||||

Class C | 12/15/2015 | –3.55 | % | 8.64 | % | ||||||||||

Class R6 | 12/15/2015 | –2.33 | % | 9.95 | % | ||||||||||

With Sales Charge | |||||||||||||||

Class A | –8.35 | % | 7.76 | % | |||||||||||

Class C | –4.47 | % | 8.64 | % | |||||||||||

Index | |||||||||||||||

| S&P 500® Index1,15 | 2.92 | % | 12.75 | % | |||||||||||

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For performance data current to the most recent month-end, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Investment Advisers LLC ("Management") had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by Management) will decrease the class's returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

As stated in the Fund's most recent prospectus, the total annual operating expense ratios for fiscal year 2018 were 1.24%, 1.68%, 2.35% and 1.17% for Institutional Class, Class A, Class C and Class R6 shares, respectively (before expense reimbursements and/or fee waivers, if any, and after restatement for Class R6 shares). The expense ratios were 0.70%, 1.06%, 1.81% and 0.60% for Institutional Class, Class A, Class C and Class R6 shares, respectively, after expense reimbursements and/or fee waivers and/or restatement. The expense ratios for the annual period ended August 31, 2019 can be found in the Financial Highlights section of this report.

Returns shown with a sales charge reflect the deduction of the current maximum initial sales charge of 5.75% for Class A shares and the contingent deferred sales charge (CDSC) for Class C shares. The CDSC for Class C shares is 1.00%, which is reduced to 0% after 1 year. The performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses. Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

3

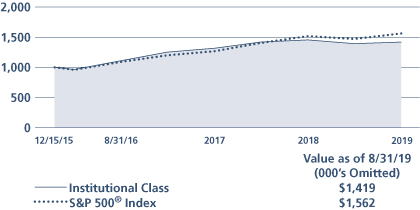

Dividend Growth Fund (Unaudited)

COMPARISON OF A $1,000,000 INVESTMENT

(000's omitted)

This graph shows the change in value of a hypothetical $1,000,000 investment in the Fund over the past 10 fiscal years, or since the Fund's inception if it has not operated for 10 years. The graph is based on the Institutional Class shares only; the performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

4

Emerging Markets Equity Fund Commentary (Unaudited)

Neuberger Berman Emerging Markets Equity Fund Institutional Class generated a total return of –1.56% for the fiscal year ended August 31, 2019, outperforming its benchmark, the MSCI Emerging Markets Index (Net) (the Index), which reported a total return of –4.36% for the same period. (Performance for all share classes is provided in the table immediately following this letter.)

Emerging markets (EM) equities trailed the U.S. (as measured by the S&P 500® Index) and developed international equities (as measured by the MSCI EAFE® Index) this fiscal year, closing with a loss. Sentiment suffered early in the period as trade tensions between the U.S. and China exacerbated concerns about a global economic slowdown. Oil prices and U.S. interest rates increased early on as well, adding to pressures. Calendar year-to-date, however, EM returns were positive, with rallies in January and June as dovish signals from global central banks and temporary breaks in trade tensions quieted some of the market's noise.

On a sector level within the Index, defensive areas, including Utilities and Consumer Staples, posted positive results. The sharpest losses occurred within Health Care—as various regulatory changes negatively impacted EM pharmaceuticals—and Materials. By country, Brazil, Russia and Turkey posted the strongest results in the Index while smaller markets, Pakistan and Argentina, along with global-trade driven Korea saw the largest declines.

The Fund's performance advantage resulted primarily from stock selection, with sector allocation a secondary benefit. Information Technology (IT), Consumer Staples and Financials holdings were standouts. By country, Brazilian, Taiwanese and Polish names outperformed relative to the Index.

Key individual contributors included Brazil's B3 and Energisa, and Ping An, a Chinese property and casualty insurer. B3, the Brazilian financial exchange provider, posted solid revenue growth figures, and benefited from positive sentiment about Brazilian equities. Electric power distributor Energisa rallied on solid earnings and profit figures. Ping An delivered better-than-expected earnings, aided by sustained new business value growth despite a drop in premiums, along with solid investment returns.

Stock selection in Communications Services, Materials and Industrials detracted the most from relative returns, and from a country perspective, headwinds included Chinese, South African and Indonesian holdings.

Detractors included Baidu, Sasol and Samsung. Baidu, the Chinese Internet search leader, sold off as trade tensions caused uncertainty about Chinese economic growth. This uncertainty weighed on advertising revenues while expenses continued to increase due to investments in newer initiatives. We exited the position. We also sold Sasol, the South African energy and chemicals firm, as cost overruns on a large project reduced our conviction in the firm's management team. Samsung, the Korean consumer electronics and chip manufacturer, fell along with the broader semiconductor sub-sector, on lower demand and pricing projections.

Looking ahead, we see continued U.S. trade tensions and weaker global growth data tempered by central bankers' shifts toward easing. While trade tensions have immediate negative impacts—with firms delaying investments and decisions—monetary policy measures may take longer to positively impact economies. As such, the team will continue closely monitoring both global and local domestic monetary, regulatory and fiscal policies.

Aggregate changes to the portfolio in recent months resulted from individual stock decisions. The team is currently emphasizing growing consumer-driven areas such as Consumer Staples and Communication Services. The portfolio also remains overweight IT versus the Index, with new additions offset by trims and sales. We maintain an underweight to cyclical areas such as Energy and Materials, and some subsectors within Consumer Discretionary.

We believe the current portfolio is well positioned to capture strong relative long-term returns driven by earnings trajectories, while remaining relatively insulated from the macroeconomic distractions that impacted short-term market movement this period.

5

Sincerely,

CONRAD SALDANHA

PORTFOLIO MANAGER

Information about principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change without notice.

The opinions expressed are those of the Fund's portfolio manager(s). The opinions are as of the date of this report and are subject to change without notice.

6

Emerging Markets Equity Fund (Unaudited)

TICKER SYMBOLS

Institutional Class | NEMIX | ||||||

Class A | NEMAX | ||||||

Class C | NEMCX | ||||||

Class R3 | NEMRX | ||||||

Class R6 | NREMX | ||||||

PERFORMANCE HIGHLIGHTS9

| Average Annual Total Return Ended 08/31/2019 | |||||||||||||||||||||||

| Inception Date | 1 Year | 5 Years | 10 Years | Life of Fund | |||||||||||||||||||

At NAV | |||||||||||||||||||||||

Institutional Class | 10/08/2008 | –1.56 | % | 1.76 | % | 4.42 | % | 7.63 | % | ||||||||||||||

Class A | 10/08/2008 | –1.77 | % | 1.50 | % | 4.17 | % | 7.37 | % | ||||||||||||||

Class C | 10/08/2008 | –2.50 | % | 0.74 | % | 3.39 | % | 6.57 | % | ||||||||||||||

| Class R310 | 06/21/2010 | –2.19 | % | 1.10 | % | 3.79 | % | 7.03 | % | ||||||||||||||

| Class R621 | 03/15/2013 | –1.45 | % | 1.83 | % | 4.48 | % | 7.68 | % | ||||||||||||||

With Sales Charge | |||||||||||||||||||||||

Class A | –7.44 | % | 0.30 | % | 3.55 | % | 6.79 | % | |||||||||||||||

Class C | –3.47 | % | 0.74 | % | 3.39 | % | 6.57 | % | |||||||||||||||

Index | |||||||||||||||||||||||

| MSCI Emerging Markets Index (Net)1,15 | –4.36 | % | 0.38 | % | 4.07 | % | 6.28 | % | |||||||||||||||

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For performance data current to the most recent month-end, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Investment Advisers LLC ("Management") had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by Management) will decrease the class's returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

As stated in the Fund's most recent prospectus, the total annual operating expense ratios for fiscal year 2018 were 1.29%, 1.66%, 2.38%, 1.92% and 1.17% for Institutional Class, Class A, Class C, Class R3 and Class R6 shares, respectively (before expense reimbursements and/or fee waivers, if any, and after restatement for Class R6 shares). The expense ratios were 1.26%, 1.51%, 2.26% and 1.16% for Institutional Class, Class A, Class C and Class R6 shares, respectively, after expense reimbursements and/or fee waivers and/or restatement. The expense ratios for the annual period ended August 31, 2019 can be found in the Financial Highlights section of this report.

Returns shown with a sales charge reflect the deduction of the current maximum initial sales charge of 5.75% for Class A shares and the contingent deferred sales charge (CDSC) for Class C shares. The CDSC for Class C shares is 1.00%, which is reduced to 0% after 1 year. The performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses. Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

7

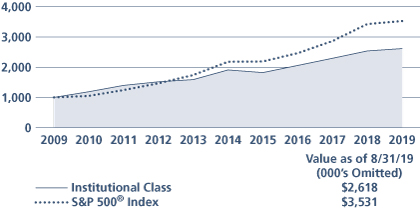

Emerging Markets Equity Fund (Unaudited)

COMPARISON OF A $1,000,000 INVESTMENT

(000's omitted)

This graph shows the change in value of a hypothetical $1,000,000 investment in the Fund over the past 10 fiscal years, or since the Fund's inception if it has not operated for 10 years. The graph is based on the Institutional Class shares only; the performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

8

Equity Income Fund Commentary (Unaudited)

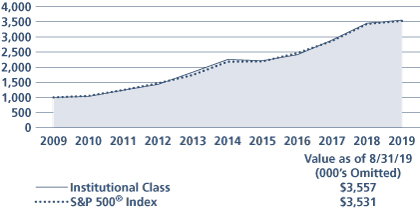

Neuberger Berman Equity Income Fund Institutional Class generated a 3.06% total return for the fiscal year ended August 31, 2019, outperforming its benchmark, the S&P 500® Index (the Index), which posted a 2.92% total return for the same period. (Performance for all share classes is provided in the table immediately following this letter.)

By late-July, the market set a new all-time high (as measured by the Index) as the economy's expansion officially became the longest in U.S. history, driven by "growth" stocks with limited or, in many cases, no dividend programs. However, in late July, equities experienced headwinds as investors grappled with an uptick in volatility tied to fears surrounding waning global growth, and geopolitical headwinds.

The Fund is an objective-based strategy, striving for a total return between stocks and bonds with limited volatility relative to the Index. This portfolio is diversified among dividend-paying stocks and convertible securities, selected through extensive analysis of cash flow prospects, which we believe have the ability to sustain and grow dividends.

From a portfolio construction standpoint, the largest equity sectors on average during the fiscal year included Utilities ~16%, Real Estate ~12%, and Financials ~10%. During the period, the Fund also maintained a 9% average allocation to convertible bonds, which we believe provides a differentiated approach to an equity income portfolio. Additionally, the Fund's ability to own securities issued under Rule 144A, where retail investors often have limited direct exposure, allows diversified exposure to the asset class.

The Fund generated the bulk of its absolute and relative returns versus the Index from its allocation to Utilities. Stock selection across our carefully selected electric/gas names generated gains driven by names tied to infrastructure modernization. This space benefitted from risk-aversion as investors favored defensive sectors amid turbulent market conditions. From a portfolio construction standpoint, Utilities often serve as a defensive ballast and therefore, NextEra Energy was our top performer. The common thread across our holdings is exposure to earnings per share and dividend growth above the sector average—fueled in part by renewable energy initiatives. The Fund also saw relative gains from its Real Estate and Industrials holdings.

On the commodity front, West Texas Intermediate oil prices experienced headwinds during the end of 2018, posting their worst calendar year decline since 2015, before recovering somewhat in 2019. Lower energy prices were driven by increased output coupled with fears of a global economic slowdown. In aggregate, our oil/gas holdings outperformed the broader Energy sector, however, Canada's Suncor Energy, weighed on our results. We believe our diversified holdings in the Energy and Materials sectors help to provide a potential hedge to inflationary pressures. Stock selection in Consumer Discretionary and Financials also detracted from relative returns.

Elsewhere, exposure to convertible bonds versus the Index was accretive to absolute results as this eclectic asset class dampened volatility. In retrospect, 2018 was a banner year for new issuance as U.S. companies sold over $30 billion of convertible securities. This was the fastest pace of new issuance in nearly a decade and the Fund capitalized on an uptick of quality issuance within this space. Historically, this asset class has been among the most conservative aspects of the Fund as we favor convertibles trading at a discount to par value with attractive conversion premiums.

The Fund's use of written options contributed positively to performance during the period.

The health of the U.S. economy seems mixed. The consumer remains in a strong position, with low unemployment and modestly growing wages. However, the industrial economy seems to be facing challenges, in part due to the U.S.-China tariff dispute. In our view, valuations across equities remain reasonable, and when evaluating investment candidates, we continue to identify pockets of value, across stable businesses with clear capital allocation plans exhibiting dividend growth potential. We acknowledge potential weakness stemming from geopolitical tensions, and believe distortions from central banks continue to drive the hunt for yield amid aging global demographics. Today, we believe the Fund remains positioned to navigate potential cross-currents given our focus on what we believe to be high-quality cash-generative companies.

In closing, we thank you for investing in our Fund.

9

Sincerely,

RICHARD LEVINE AND SANDY POMEROY

PORTFOLIO MANAGERS

Information about principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change without notice.

The opinions expressed are those of the Fund's portfolio manager(s). The opinions are as of the date of this report and are subject to change without notice.

10

Equity Income Fund (Unaudited)

TICKER SYMBOLS

Institutional Class | NBHIX | ||||||

Class A | NBHAX | ||||||

Class C | NBHCX | ||||||

Class R3 | NBHRX | ||||||

SECTOR ALLOCATION

(as a % of Total Investments*) | |||||||

Communication Services | 4.6 | % | |||||

Consumer Discretionary | 4.9 | ||||||

Consumer Staples | 5.3 | ||||||

Energy | 7.2 | ||||||

Financials | 9.4 | ||||||

Health Care | 7.9 | ||||||

Industrials | 7.0 | ||||||

Information Technology | 7.8 | ||||||

Materials | 3.3 | ||||||

Real Estate | 13.1 | ||||||

Utilities | 16.0 | ||||||

Convertible Bonds | 9.4 | ||||||

Short-Term Investments | 4.1 | ||||||

Total | 100.0 | % | |||||

* Derivatives (other than options purchased), if any, are excluded from this chart.

PERFORMANCE HIGHLIGHTS9

| Average Annual Total Return Ended 08/31/2019 | |||||||||||||||||||||||

| Inception Date* | 1 Year | 5 Years | 10 Years | Life of Fund | |||||||||||||||||||

At NAV | |||||||||||||||||||||||

| Institutional Class13 | 06/09/2008 | 3.06 | % | 6.51 | % | 10.10 | % | 7.56 | % | ||||||||||||||

| Class A13 | 06/09/2008 | 2.68 | % | 6.12 | % | 9.69 | % | 7.20 | % | ||||||||||||||

| Class C13 | 06/09/2008 | 1.91 | % | 5.34 | % | 8.89 | % | 6.52 | % | ||||||||||||||

| Class R313 | 06/21/2010 | 2.40 | % | 5.84 | % | 9.44 | % | 7.06 | % | ||||||||||||||

With Sales Charge | |||||||||||||||||||||||

| Class A13 | –3.21 | % | 4.87 | % | 9.05 | % | 6.71 | % | |||||||||||||||

| Class C13 | 0.95 | % | 5.34 | % | 8.89 | % | 6.52 | % | |||||||||||||||

Index | |||||||||||||||||||||||

| S&P 500® Index1,15 | 2.92 | % | 10.11 | % | 13.45 | % | 8.37 | % | |||||||||||||||

*The performance data for each class includes the performance of the Fund's oldest share class, Trust Class, from November 2, 2006 through June 9, 2008. The performance data for Class R3 also includes the performance of the Fund's Institutional Class from June 9, 2008 through June 21, 2010. See endnote 13 for information about the effects of the different fees paid by each class.

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For performance data current to the most recent month-end, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Investment Advisers LLC ("Management") had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by Management) will decrease the class's returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

As stated in the Fund's most recent prospectus, the total annual operating expense ratios for fiscal year 2018 were 0.69%, 1.05%, 1.80% and 1.33% for Institutional Class, Class A, Class C and Class R3 shares, respectively (before expense reimbursements and/or fee waivers, if any). The expense ratios for the annual period ended August 31, 2019 can be found in the Financial Highlights section of this report.

Returns shown with a sales charge reflect the deduction of the current maximum initial sales charge of 5.75% for Class A shares and the contingent deferred sales charge (CDSC) for Class C shares. The CDSC for Class C shares is 1.00%, which is reduced to 0% after 1 year. The performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses. Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

11

Equity Income Fund (Unaudited)

COMPARISON OF A $1,000,000 INVESTMENT13

(000's omitted)

This graph shows the change in value of a hypothetical $1,000,000 investment in the Fund over the past 10 fiscal years, or since the Fund's inception if it has not operated for 10 years. The graph is based on the Institutional Class shares only; the performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

12

Focus Fund Commentary (Unaudited)

Neuberger Berman Focus Fund Investor Class generated a –2.35% total return for the fiscal year ended August 31, 2019, underperforming its benchmark, the S&P 500® Index (the Index), which provided a 2.92% total return for the same period. (Performance for all share classes is provided in the table immediately following this letter.)

The overall U.S. stock market experienced periods of elevated volatility, but generated a modest gain during the reporting period. While the market posted positive returns over eight of the twelve months covered by this report, most of those gains were given back during several sharp downturns. These setbacks were triggered by a number of factors, including concerns over the escalating trade war between the U.S. and China, signs of moderating global growth and a host of geopolitical issues. Against this backdrop, the U.S. Federal Reserve Board (Fed) had a "dovish pivot" in January 2019, as it announced a pause from raising rates. Late in the reporting period, the yield curve inverted, which has typically foreshadowed more difficult economy conditions going forward. Then, as expected, the Fed lowered rates at its meeting in July 2019—the first cut since 2008.

Both stock selection and sector allocation detracted from relative performance versus the Index during the reporting period. In terms of stock selection, holdings in the Consumer Discretionary, Health Care and Energy sectors were the largest detractors from relative returns. In the Consumer Discretionary sector, the Fund's position in cruise ship company Carnival Corp. performed poorly. Within the Health Care sector, shares of pharmaceuticals company Pfizer, Inc. fell sharply. Within the Energy sector, several holdings in the Oil, Gas & Consumable Fuels industry performed poorly. In terms of sector allocation, underweights to Real Estate and Information Technology (IT), along with an overweight to Energy, were the largest detractors from relative performance.

On the upside, holdings in the Communication Services, IT and Materials sectors added the most relative value. In Communication Services, our position in entertainment company Activision Blizzard, Inc. was rewarded. Within IT, the Fund's position in Motorola Solutions, Inc., a data communications and telecommunications equipment provider, was the most beneficial for returns. Within the Materials sector, one of our holdings in the Chemicals industry rallied and aided the Fund's performance. From a sector allocation perspective, overweights to Communication Services and Industrials versus the Index were the only meaningful contributors to results.

The Fund's use of written options contributed positively to performance during the period.

Looking ahead, we remain cautious on the growth prospects for the U.S. economy given leading indicators that are slowing, uncertainties regarding the trade war between the U.S. and China and the inversion of the yield curve. While we do not believe a recession will occur in the short-term, we believe the pace of the U.S. economic expansion could further moderate in 2020. In our view, increased market volatility will continue as the year progresses. Against this backdrop, we anticipate an increase in price dislocations that could turn into attractive investment opportunities. We remain disciplined bottom-up managers, looking for opportunities to buy stocks that are trading below their fair value to generate results for the Fund's shareholders. We also believe that equities remain the most appropriate asset class over the long term given their potential to generate capital appreciation.

Sincerely,

TIMOTHY CREEDON AND DAVID LEVINE

PORTFOLIO MANAGERS

Information about principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change without notice.

The opinions expressed are those of the Fund's portfolio manager(s). The opinions are as of the date of this report and are subject to change without notice.

13

Focus Fund (Unaudited)

TICKER SYMBOLS

Investor Class | NBSSX | ||||||

Trust Class | NBFCX | ||||||

Advisor Class | NBFAX | ||||||

Institutional Class | NFALX | ||||||

Class A | NFAAX | ||||||

Class C | NFACX | ||||||

SECTOR ALLOCATION

(as a % of Total Investments*) | |||||||

Communication Services | 16.5 | % | |||||

Consumer Discretionary | 12.2 | ||||||

Consumer Staples | 6.1 | ||||||

Energy | 4.6 | ||||||

Financials | 15.4 | ||||||

Health Care | 13.4 | ||||||

Industrials | 6.5 | ||||||

Information Technology | 17.9 | ||||||

Materials | 2.7 | ||||||

Utilities | 3.5 | ||||||

Short-Term Investments | 1.2 | ||||||

Total | 100.0 | % | |||||

* Derivatives (other than options purchased), if any, are excluded from this chart.

PERFORMANCE HIGHLIGHTS8

| Average Annual Total Return Ended 08/31/2019 | |||||||||||||||||||||||

| Inception Date | 1 Year | 5 Years | 10 Years | Life of Fund | |||||||||||||||||||

At NAV | |||||||||||||||||||||||

Investor Class | 10/19/1955 | –2.35 | % | 6.69 | % | 10.92 | % | 10.32 | % | ||||||||||||||

| Trust Class3 | 08/30/1993 | –2.52 | % | 6.50 | % | 10.70 | % | 10.29 | % | ||||||||||||||

| Advisor Class4 | 09/03/1996 | –2.68 | % | 6.34 | % | 10.52 | % | 10.23 | % | ||||||||||||||

| Institutional Class5 | 06/21/2010 | –2.15 | % | 6.87 | % | 11.10 | % | 10.34 | % | ||||||||||||||

| Class A19 | 06/21/2010 | –2.51 | % | 6.48 | % | 10.73 | % | 10.29 | % | ||||||||||||||

| Class C19 | 06/21/2010 | –3.25 | % | 5.69 | % | 9.98 | % | 10.17 | % | ||||||||||||||

With Sales Charge | |||||||||||||||||||||||

| Class A19 | –8.12 | % | 5.23 | % | 10.08 | % | 10.19 | % | |||||||||||||||

| Class C19 | –4.14 | % | 5.69 | % | 9.98 | % | 10.17 | % | |||||||||||||||

Index | |||||||||||||||||||||||

| S&P 500® Index1,15 | 2.92 | % | 10.11 | % | 13.45 | % | 10.20 | % | |||||||||||||||

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For performance data current to the most recent month-end, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Investment Advisers LLC ("Management") had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by Management) will decrease the class's returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

As stated in the Fund's most recent prospectus, the total annual operating expense ratios for fiscal year 2018 were 0.92%, 1.10%, 1.26%, 0.76%, 1.13%, and 1.88% for Investor Class, Trust Class, Advisor Class, Institutional Class, Class A and Class C shares, respectively (before expense reimbursements and/or fee waivers, if any). The expense ratios were 0.76%, 1.12% and 1.87% for Institutional Class, Class A and Class C shares, respectively, after expense reimbursements and/or fee waivers. The total annual operating expense ratio for Institutional Class includes the class' repayment of expenses previously reimbursed and/or fees previously waived by Management. The expense ratios for the annual period ended August 31, 2019 can be found in the Financial Highlights section of this report.

Returns shown with a sales charge reflect the deduction of the current maximum initial sales charge of 5.75% for Class A shares and the contingent deferred sales charge (CDSC) for Class C shares. The CDSC for Class C shares is 1.00%, which is reduced to 0% after 1 year. The performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses. Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

14

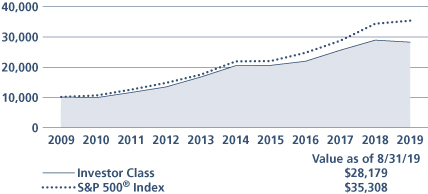

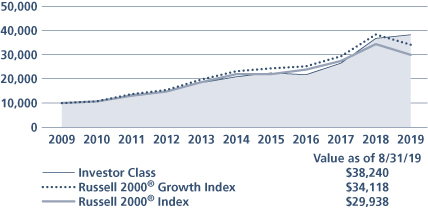

Focus Fund (Unaudited)

COMPARISON OF A $10,000 INVESTMENT

This graph shows the change in value of a hypothetical $10,000 investment in the Fund over the past 10 fiscal years, or since the Fund's inception if it has not operated for 10 years. The graph is based on the Investor Class shares only; the performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

15

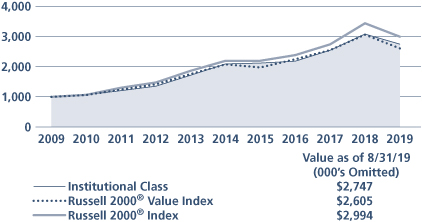

Genesis Fund Commentary (Unaudited)

Neuberger Berman Genesis Fund Investor Class generated a 0.53% total return for the fiscal year ended August 31, 2019, outperforming its benchmark, the Russell 2000® Index (the Index), which provided a –12.89% total return for the same period. (Performance for all share classes is provided in the table immediately following this letter.)

The overall U.S. stock market, as measured by the S&P 500® Index, experienced periods of elevated volatility, but generated a modest gain during the reporting period. While the market posted positive returns over eight of the twelve months covered by this report, most of those gains were given back during several sharp downturns. These setbacks were triggered by a number of factors, including concerns over the escalating trade war between the U.S. and China, signs of moderating global growth and a host of geopolitical issues. Against this backdrop, the U.S. Federal Reserve Board (Fed) had a "dovish pivot" in January 2019, as it announced a pause from raising rates. Then, as expected, the Fed lowered rates at its meeting in July 2019—the first cut since 2008. All told, the S&P 500 Index returned 2.92% during the reporting period. In contrast, small cap stocks, as measured by the Index, posted a negative return.

The Fund outperformed the Index during the reporting period. Stock selection contributed to relative results, whereas sector allocation modestly detracted from performance. We focus on investing in high quality companies, which we define as companies with the ability to generate significant free cash flow, above-average profitability supported by competitive barriers to entry, generally strong balance sheets, and less volatile/less economically sensitive businesses. Our style of investing was in favor during the period and acted as a tailwind to our absolute and relative performance. In terms of stock selection, holdings in the Health Care, Consumer Discretionary and Financials sectors were the most additive to results. In Health Care, several positions in the Heath Care Equipment & Supplies industry added the most value. In Consumer Discretionary, the Fund benefited from solid performance across several industries. In Financials, our Capital Markets holdings and Regional Bank positions outperformed. Among the various other sectors within the Index, none meaningfully detracted from relative stock selection results during the reporting period.

From a sector allocation perspective, the lack of exposure to bond proxies, namely real estate investment trusts (REITs) and Utilities, negatively impacted the Fund's returns. However, we do not typically own REITs as they do not meet our investment criteria and we felt there were better opportunities outside of Utilities. On the upside, an overweight to Information Technology, specifically Software, contributed to relative returns. Elsewhere, a lack of exposure to low quality biotechnology and pharmaceutical companies were additive for performance as they posted very poor results.

Evidence of moderating global economic growth continues to mount. Globally, long-term interest rates have responded by falling sharply. As a result, the Fed, as well as other central banks, have indicated a willingness to pursue more accommodative monetary policies, including possible rate cuts. Such actions could help prolong the economic expansion, but recessionary fears have risen as the U.S. yield curve has inverted. Meanwhile, the trade war between the U.S. and China remains an important wildcard. While both sides have political motivation for wanting an agreement, this is far from guaranteed and the chances for a resolution seem to change daily. Regardless of what happens in the near-term, it is our view that the relationship between the U.S. and China is likely to remain strained given significant differences in areas such as intellectual property.

While the nonstop news flow has led to elevated market volatility, we continue to see signs that lead us to believe that investors are increasingly favoring higher-quality businesses. Whether this will continue depends on a myriad of factors, including economic growth, trends for inflation/interest rates and investor sentiment. Despite aggressive central bank easing policies, there is evidence that capital markets are tightening to some degree. This is most prevalent in the private equity markets, where previously highly valued but money losing business models are rushing to go public to less than friendly public equity investors. Regardless, we believe that the key to outperformance over the long term will be driven by owning companies with superior business models that are defended by durable competitive moats and that enjoy attractive financial attributes, such as conservative balance sheets, high returns on capital, and above-market earnings and free cash flow growth. We seek to continually emphasize businesses with these characteristics for the Fund.

16

Sincerely,

JUDITH M. VALE, ROBERT W. D'ALELIO, BRETT S. REINER AND GREGORY G. SPIEGEL

PORTFOLIO CO-MANAGERS

Information about principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change without notice.

The opinions expressed are those of the Fund's portfolio manager(s). The opinions are as of the date of this report and are subject to change without notice.

17

Genesis Fund (Unaudited)

TICKER SYMBOLS

Investor Class | NBGNX | ||||||

Trust Class | NBGEX | ||||||

Advisor Class | NBGAX | ||||||

Institutional Class | NBGIX | ||||||

Class R6 | NRGSX | ||||||

SECTOR ALLOCATION

(as a % of Total Investments*) | |||||||

Communication Services | 2.7 | % | |||||

Consumer Discretionary | 11.1 | ||||||

Consumer Staples | 5.3 | ||||||

Energy | 2.1 | ||||||

Financials | 16.1 | ||||||

Health Care | 15.7 | ||||||

Industrials | 16.9 | ||||||

Information Technology | 23.1 | ||||||

Materials | 5.2 | ||||||

Real Estate | 1.0 | ||||||

Short-Term Investments | 0.8 | ||||||

Total | 100.0 | % | |||||

* Derivatives (other than options purchased), if any, are excluded from this chart.

PERFORMANCE HIGHLIGHTS

| Average Annual Total Return Ended 08/31/2019 | |||||||||||||||||||||||

| Inception Date | 1 Year | 5 Years | 10 Years | Life of Fund | |||||||||||||||||||

At NAV | |||||||||||||||||||||||

Investor Class | 09/27/1988 | 0.53 | % | 9.69 | % | 12.82 | % | 12.15 | % | ||||||||||||||

| Trust Class3 | 08/26/1993 | 0.43 | % | 9.60 | % | 12.73 | % | 12.12 | % | ||||||||||||||

| Advisor Class4 | 04/02/1997 | 0.18 | % | 9.31 | % | 12.43 | % | 11.90 | % | ||||||||||||||

| Institutional Class5 | 07/01/1999 | 0.69 | % | 9.88 | % | 13.02 | % | 12.30 | % | ||||||||||||||

| Class R622 | 03/15/2013 | 0.80 | % | 9.97 | % | 13.00 | % | 12.21 | % | ||||||||||||||

Index | |||||||||||||||||||||||

| Russell 2000® Index1,15 | –12.89 | % | 6.41 | % | 11.59 | % | 9.34 | % | |||||||||||||||

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For performance data current to the most recent month-end, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Investment Advisers LLC ("Management") had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by Management) will decrease the class's returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

As stated in the Fund's most recent prospectus, the total annual operating expense ratios for fiscal year 2018 were 1.02%, 1.10%, 1.35%, 0.85% and 0.75% for Investor Class, Trust Class, Advisor Class, Institutional Class and Class R6 shares, respectively (before expense reimbursements and/or fee waivers, if any, and after restatement for Class R6 shares). The expense ratios for the annual period ended August 31, 2019 can be found in the Financial Highlights section of this report.

18

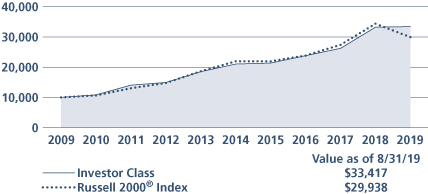

Genesis Fund (Unaudited)

COMPARISON OF A $10,000 INVESTMENT

This graph shows the change in value of a hypothetical $10,000 investment in the Fund over the past 10 fiscal years, or since the Fund's inception if it has not operated for 10 years. The graph is based on the Investor Class shares only; the performance of the Fund's share classes will differ primarily due to different class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

19

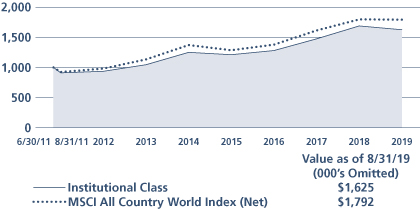

Global Equity Fund* Commentary (Unaudited)

Neuberger Berman Global Equity Fund Institutional Class generated a total return of –3.74% for the fiscal year ended August 31, 2019, trailing the –0.28% total return of its benchmark, the MSCI All Country World Index (Net) (the Index) for the same period. (Performance for all share classes is provided in the table immediately following this letter.)

As this reporting period began, signs of a global economic slowdown coupled with a damaging trade war between the world's largest economies weighed on investor sentiment and shook global markets. As the new year arrived, although these issues and others—including what path Brexit would take—persisted, sentiment improved on indications that central bankers were trending toward a more stimulative posture, and on periodic breaks in trade tensions. In the U.S., the S&P 500® Index outperformed developed international markets (as measured by the MSCI EAFE® Index) during this reporting period, and both the U.S. and developed international markets outperformed emerging markets (as measured by the MSCI Emerging Markets Index).

The Index saw a wide disparity in returns this period. The defensive and generally higher yielding Utilities, Real Estate and Consumer Staples sectors ended the fiscal year up by double digits. Energy posted a double-digit decline, with Materials and Financials also showing losses. By country, Argentina, Brazil and Russia led the Index, while Pakistan, Korea and Chile lagged.

The shortfall in relative performance versus the Index resulted primarily from stock selection within Energy, Communication Services and Consumer Discretionary holdings where global growth concerns weighed on several names. By country, underweights and stock selection in the U.S. and Germany, and stock selection in Hong Kong were a headwind to relative returns.

Individual detractors included Samsonite, Centene and EOG Resources. Samsonite, a Hong Kong-based luggage manufacturer, sold off on trade disputes between the U.S. and China, as tariffs caused retailers to defer orders, and on weakness in Europe. Centene, a U.S. managed care provider reported slower organic growth. EOG, an unconventional U.S. energy explorer, posted strong earnings but declined as oil prices fell.

Stock selection benefited relative performance within Materials and Industrials. An overweight to Information Technology (IT) versus the Index was also positive. On a country basis, holdings in Japan, an overweight to the Netherlands, and a zero weight to Korea were beneficial.

Key contributors included U.S. holdings, Estee Lauder and CDW, and Sonova, based in Switzerland. Beauty and skin care leader, Estee Lauder, reported robust growth in luxury skin care in Asia and Europe. CDW, a value-added reseller of IT solutions, announced solid earnings benefiting from sustained U.S. IT spending growth and market share gains. Hearing aid specialist Sonova continued to benefit from recent product launches, accelerating growth and profit margins.

Looking ahead, despite a historically wide valuation gap between value and growth stocks, we remain committed to our "Quality at a Reasonable Price" discipline, focusing on profitability and cash flows that may be under-recognized by the market. We seek to avoid deep value areas of the market where structural challenges may be a factor, and are wary of high-flying growth stocks where valuations seem disconnected from fundamentals.

Our focus remains on quality companies with strong balance sheets, continuing long-term growth opportunities, solid recurring revenues, and management teams that we believe can enhance shareholder value. We also favor multinationals, as geographically diversified revenues can help limit exposure to any single 'at-risk' country within the current macro environment.

We are comfortable paying a modest valuation premium for companies we believe offer superior characteristics, and believe that a diversified and risk-managed portfolio of such names will be well positioned for the medium to longer-term.

20

Sincerely,

BENJAMIN SEGAL AND ELIAS COHEN

PORTFOLIO MANAGERS

* As previously announced, as of September 3, 2019, Neuberger Berman Global Equity Fund changed its name to Neuberger Berman Integrated Large Cap Fund, and changed its investment strategy, portfolio management team and fees and expenses.

Information about principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change without notice.

The opinions expressed are those of the Fund's portfolio manager(s). The opinions are as of the date of this report and are subject to change without notice.

21

Global Equity Fund (Unaudited)

TICKER SYMBOLS

Institutional Class | NGQIX | ||||||

Class A | NGQAX | ||||||

Class C | NGQCX | ||||||

PERFORMANCE HIGHLIGHTS9

| Average Annual Total Return Ended 08/31/2019 | |||||||||||||||||||

| Inception Date | 1 Year | 5 Years | Life of Fund | ||||||||||||||||

At NAV | |||||||||||||||||||

Institutional Class | 06/30/2011 | –3.74 | % | 5.39 | % | 6.12 | % | ||||||||||||

Class A | 06/30/2011 | –4.19 | % | 5.04 | % | 5.75 | % | ||||||||||||

Class C | 06/30/2011 | –4.84 | % | 4.23 | % | 4.95 | % | ||||||||||||

With Sales Charge | |||||||||||||||||||

Class A | –9.71 | % | 3.80 | % | 4.98 | % | |||||||||||||

Class C | –5.74 | % | 4.23 | % | 4.95 | % | |||||||||||||

Index | |||||||||||||||||||

| MSCI All Country World Index (Net)1,15 | –0.28 | % | 5.51 | % | 7.40 | % | |||||||||||||

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For performance data current to the most recent month-end, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Investment Advisers LLC ("Management") had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by Management) will decrease the class's returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

As stated in the Fund's most recent prospectus, the estimated total annual operating expense ratios for fiscal year 2019 are 6.14%, 6.36% and 7.27% for Institutional Class, Class A and Class C shares, respectively (before expense reimbursements and/or fee waivers, if any, and after restatement). The estimated expense ratios for fiscal year 2019 are 0.41%, 0.77% and 1.52% for Institutional Class, Class A and Class C shares, respectively, after expense reimbursements and/or fee waivers and/or restatement. The expense ratios for the annual period ended August 31, 2019 can be found in the Financial Highlights section of this report.

Returns shown with a sales charge reflect the deduction of the current maximum initial sales charge of 5.75% for Class A shares and the contingent deferred sales charge (CDSC) for Class C shares. The CDSC for Class C shares is 1.00%, which is reduced to 0% after 1 year. The performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses. Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

22

Global Equity Fund (Unaudited)

COMPARISON OF A $1,000,000 INVESTMENT

(000's omitted)

This graph shows the change in value of a hypothetical $1,000,000 investment in the Fund over the past 10 fiscal years, or since the Fund's inception if it has not operated for 10 years. The graph is based on the Institutional Class shares only; the performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

23

Global Real Estate Fund Commentary (Unaudited)

The Neuberger Berman Global Real Estate Fund Institutional Class generated a 14.01% total return for the fiscal year ended August 31, 2019, outperforming its benchmark, the FTSE EPRA/Nareit Developed Index (Net) (the Index), which generated an 8.12% total return for the same period. (Performance for all share classes is provided in the table immediately following this letter.)

The global stock market (as measured by the MSCI All Country World Index (Net)) experienced periods of elevated volatility and generated a modest decline during the reporting period. While the market posted positive returns over several months covered by this report, those gains were given back during several sharp downturns. These setbacks were triggered by a number of factors, including concerns over the escalating trade war between the U.S. and China, signs of moderating global growth, the potential for a "hard Brexit" and political unrest in Hong Kong. Against this backdrop, the U.S. Federal Reserve Board (Fed) and a number of central banks announced that they would ease monetary policy in an attempt to stimulate growth. For example, the Fed lowered rates at its meeting in July 2019—the first cut since 2008. Comparatively, global real estate investment trusts (REITs) saw very strong results during the period.

The Fund outperformed the Index during the reporting period. Stock selection, overall, was the largest contributor to the Fund's relative results versus the Index. In particular, holdings in the Specialty, Residential and Diversified sectors were the most additive for returns. In terms of individual holdings, American Tower Corp., Equinix, Inc., Equity LifeStyle Properties, Inc., SBA Communications Corp. and Nippon Accommodations Fund, Inc. were the largest contributors to performance. The only sector detractors from relative results were the Fund's holdings in the Real Estate Holding & Development and Real Estate Services sectors. Several individual holdings were also negative for results, including Deutsche Wohnen SE, ADO Properties S.A., Gecina SA, Zayo Group Holdings, Inc. and Interxion Holding N.V—all of these positions were exited during the reporting period.

The Fund's positioning from a country perspective modestly detracted from results. In particular, versus the Index, an overweight in the UK, an underweight in Switzerland and an overweight in Spain were the largest detractors from relative performance. On the upside, underweights to Hong Kong and France, and an overweight to Belgium were the most additive for results. Meanwhile, while an underweight to the U.S. was a small headwind for relative performance, this was more than offset by very strong stock selection in the country.

Looking ahead, we anticipate continued, but modest economic growth for the U.S. for the rest of 2019. Many economic indicators point to good tenant demand for real estate. However, headwinds including slowing global growth, turmoil in Washington, and ongoing U.S.-China trade tension threaten to derail the long-lasting U.S. recovery. As the Fed tries to balance these factors it has signaled a more flexible stance for policy changes and rates. Resolution of some of these headwinds could be a catalyst for the capital markets. On balance, we believe solid real estate fundamentals, strong private market demand for real estate and a more dovish Fed will be supportive of the U.S. listed real estate market.

Overseas, in the UK and Europe equity markets are facing pressure from a number of areas, namely Brexit, political unrest in France, unstable Italian politics, trade disruption and slower growth. In order to position for these challenging times, we plan to continue to focus on businesses where we see a structural growth angle and a strong rental growth profile. Japan stands out to us as the more appealing opportunity within the Asia-Pacific region. The pricing of Japan's real estate, while looking pricey in historical terms, is reasonable relative to fundamentals. In Hong Kong, share prices have reflected the sharp housing price bounce in the first quarter of 2019. As such, they are no longer overly compelling, in our opinion, and a China slowdown will likely pose a material drag on demand. In addition, social discontent may give rise to slower housing sales. Singapore's residential market has significantly cooled in volume terms following government intervention in mid-2018 and stock valuation has returned to a reasonably attractive level. We believe the premium valuation of Australian REITs is well supported by bond yield declines this year.

24

Sincerely,

STEVE SHIGEKAWA, BRIAN C. JONES, GILLIAN TILTMAN AND ANTON KWANG

PORTFOLIO MANAGERS

Information about principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change without notice.

The opinions expressed are those of the Fund's portfolio manager(s). The opinions are as of the date of this report and are subject to change without notice.

25

Global Real Estate Fund (Unaudited)

TICKER SYMBOLS

Institutional Class | NGRIX | ||||||

Class A | NGRAX | ||||||

Class C | NGRCX | ||||||

PERFORMANCE HIGHLIGHTS9

| Average Annual Total Return Ended 08/31/2019 | |||||||||||||||

| Inception Date | 1 Year | Life of Fund | |||||||||||||

At NAV | |||||||||||||||

Institutional Class | 12/30/2014 | 14.01 | % | 6.87 | % | ||||||||||

Class A | 12/30/2014 | 13.65 | % | 6.48 | % | ||||||||||

Class C | 12/30/2014 | 12.75 | % | 5.70 | % | ||||||||||

With Sales Charge | |||||||||||||||

Class A | 7.13 | % | 5.14 | % | |||||||||||

Class C | 11.75 | % | 5.70 | % | |||||||||||

Index | |||||||||||||||

| FTSE EPRA/Nareit Developed Index (Net)1,15 | 8.12 | % | 4.79 | % | |||||||||||

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For performance data current to the most recent month-end, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Investment Advisers LLC ("Management") had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by Management) will decrease the class's returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

As stated in the Fund's most recent prospectus, the total annual operating expense ratios for fiscal year 2018 were 11.12%, 11.57% and 12.21% for Institutional Class, Class A and Class C shares, respectively (before expense reimbursements and/or fee waivers, if any). The expense ratios were 1.01%, 1.37% and 2.12% for Institutional Class, Class A and Class C shares, respectively, after expense reimbursements and/or fee waivers. The expense ratios for the annual period ended August 31, 2019 can be found in the Financial Highlights section of this report.

Returns shown with a sales charge reflect the deduction of the current maximum initial sales charge of 5.75% for Class A shares and the contingent deferred sales charge (CDSC) for Class C shares. The CDSC for Class C shares is 1.00%, which is reduced to 0% after 1 year. The performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses. Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

26

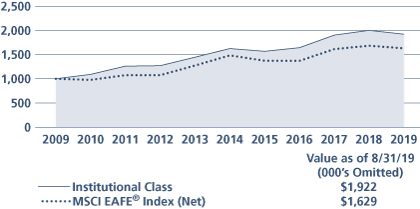

Global Real Estate Fund (Unaudited)

COMPARISON OF A $1,000,000 INVESTMENT

(000's omitted)

This graph shows the change in value of a hypothetical $1,000,000 investment in the Fund over the past 10 fiscal years, or since the Fund's inception if it has not operated for 10 years. The graph is based on the Institutional Class shares only; the performance of the Fund's share classes will differ primarily due to different sales charge structures and class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

27

Greater China Equity Fund Commentary (Unaudited)

Neuberger Berman Greater China Equity Fund Institutional Class generated a –1.03% total return for the fiscal year ended August 31, 2019, outperforming its benchmark, the MSCI China Index (Net) (the Index), which returned –5.25% over the same period. (Performance for all share classes is provided in the table immediately following this letter.)