UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-00558

THE HARTFORD MUTUAL FUNDS II, INC.

(Exact name of registrant as specified in charter)

P. O. Box 2999, Hartford, Connecticut 06104-2999

(Address of Principal Executive Offices)

Edward P. Macdonald, Esquire

Life Law Unit

The Hartford Financial Services Group, Inc.

200 Hopmeadow Street

Simsbury, Connecticut 06089

(Name and Address of Agent for Service)

Registrant’s telephone number, including area code: (860) 843-9934

Date of fiscal year end: October 31, 2011

Date of reporting period: November 1, 2010 – October 31, 2011

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

THE HARTFORD MUTUAL FUNDS 2011 Annual Report The Hartford Growth Fund |

A MESSAGE FROM THE PRESIDENT

Dear Fellow Shareholders:

I want to take this opportunity to say thank you for investing in The Hartford Mutual Funds.

This has been a tumultuous year. In the beginning of 2011, we witnessed tension-fueled political uprisings in the already-volatile Middle East and North Africa region. We also watched as Japan dealt with a series of crises including a massive earthquake and subsequent tsunami. Yet, U.S. economic conditions continued to improve, with gains in consumer confidence and retail sales. During the first half of 2011, domestic, international, and world indices (as measured by the S&P 500, MSCI EAFE and MSCI World) were all up more than 5% through June, 30 2011.

The economic recovery, however, lost momentum in the second half of 2011. The employment and housing markets both remain extremely challenged. Investors continue to be concerned about the implications of the European sovereign debt crisis, as well as our own high levels of domestic debt. Fears that the European sovereign debt crisis could continue to drag down the global economy have weighed heavily on stocks.

Ongoing apprehension regarding the U.S. debt ceiling during the summer, and the resulting downgrade of the U.S. sovereign credit rating by Standard & Poor’s, also contributed to weaker investor confidence.

There are, however, some reasons to remain confident. Corporations have record levels of cash on their balance sheets—corporate cash has doubled in the past 10 years. In addition, U.S. gross domestic product expanded at a 2.5 percent annual rate in the third quarter according to the Commerce Department, as consumers and businesses set aside fears about the recovery and stepped up spending. Corporate earnings have also remained positive, with a majority of companies beating expectations each quarter this year. This momentum will hopefully continue through the fourth quarter and into next year.

As we approach the end of 2011, in light of the continued market volatility, now would be a good time to schedule a meeting with your financial advisor to examine your current investment strategy and determine whether you are on the right track.

| | • Does your fixed-income portfolio complement your equity portfolio? |

| | • Are you receiving diversified sources of income? |

| | • Is your portfolio still in line with your risk tolerance and investment time horizon? |

Talk to your advisor to see what changes you should make to address these concerns and opportunities. Thank you again for investing with The Hartford Mutual Funds.

James Davey

President

The Hartford Mutual Funds

The Hartford Growth Fund

| Fund Performance (Unaudited) | 2 |

| Manager Discussion (Unaudited) | 3 |

| Financial Statements | |

| 5 |

| 7 |

| 8 |

| 9 |

| 10 |

| 11 |

| 24 |

| 26 |

| 27 |

| 29 |

| 29 |

| 30 |

| 31 |

| 32 |

The views expressed in the Fund’s Manager Discussion under ‘‘Why did the Fund perform this way?’’ and ‘‘What is the outlook?’’ are views of the Fund’s sub-adviser and portfolio management team through the end of the period and are subject to change based on market and other conditions.

The Hartford Growth Fund inception 06/08/1949 |

(sub-advised by Wellington Management Company, LLP) |

| |

Investment objective – Seeks long-term capital appreciation. |

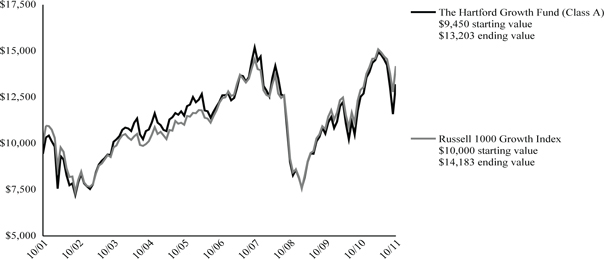

Performance Overview(1) 10/31/01 - 10/31/11

The chart above shows the growth of a $10,000 investment in Class A which includes a sales charge. Growth results in classes other than Class A will vary from what is seen above due to differences in the expenses charged to those share classes.

Average Annual Total Returns (as of 10/31/11) |

| | 1 Year | 5 Year | 10 Year |

| Growth A# | 5.39% | 1.50% | 3.40% |

| Growth A## | -0.41% | 0.36% | 2.82% |

| Growth B# | 4.51% | 0.81% | NA* |

| Growth B## | -0.49% | 0.47% | NA* |

| Growth C# | 4.66% | 0.78% | 2.68% |

| Growth C## | 3.66% | 0.78% | 2.68% |

| Growth I# | 5.70% | 1.86% | 3.83% |

| Growth R3# | 5.12% | 1.25% | 3.52% |

| Growth R4# | 5.42% | 1.56% | 3.68% |

| Growth R5# | 5.75% | 1.76% | 3.78% |

| Growth Y# | 5.88% | 1.97% | 3.89% |

| Russell 1000 Growth Index | 9.92% | 3.04% | 3.56% |

| * | Since inception returns are not applicable for Class B because after 8 years Class B converts to Class A. |

PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS.

The initial investment in Classes A shares reflects the maximum sales charge and Classes B and C reflect a contingent deferred sales charge.

Total returns presented above were calculated using the Fund's net asset value available to shareholders for sale or redemption of Fund shares on October 31, 2011, which excludes investment transactions as of this date.

Effective 9/30/09, Class B shares of The Hartford Mutual Funds were closed to new investments.

Class A, B, C and Y shares commenced operations on 2/19/02. Class A and C share performance prior to that date reflects Class L and N share performance and operating expenses less Class A or C share sales charges, respectively. (Class L and N shares are no longer offered.) Class Y share performance prior to 2/19/02 reflects Class L share performance and operating expenses, adjusted to reflect that Class Y has no sales charges. Class I shares commenced operations on 8/31/06. Performance prior to that date is that of the Fund's Class A shares (excluding sales charges), which had different operating expenses.Class R3, R4 and R5 shares commenced operations on 12/22/06. Class R3, R4 and R5 share performance between 2/19/02 and 12/22/06 reflects Class Y share performance and operating expenses. Class R3, R4 and R5 share performance prior to 2/19/02 reflects Class L share performance and operating expenses, adjusted to reflect the fact that Class R3, R4 and R5 have no sales charges.

Russell 1000 Growth Index is an unmanaged index which measures the performance of those Russell 1000 Index companies with higher price-to-book ratios and higher forecasted growth values. (The Russell 1000 Index is an unmanaged index that measures the performance of the 1,000 largest companies in the Russell 3000 Index, which measures the performance of the 3,000 largest U.S. companies based on total market capitalization.)

You cannot invest directly in an index.

The chart represents a hypothetical investment in the Fund. Performance data represents past performance and current performance could be higher or lower.

The value of shares will fluctuate so that, when redeemed, shares may be worth more or less than their original cost. The chart and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Performance information may reflect historical or current expense waivers/reimbursements from the investment adviser, without which performance would have been lower. For information on current expense waivers/reimbursements, please see the prospectus.

| The Hartford Growth Fund |

| Manager Discussion (Unaudited) |

| October 31, 2011 |

| Portfolio Manager |

| Andrew J. Shilling, CFA |

| Senior Vice President |

| |

How did the Fund perform?

The Class A shares of The Hartford Growth Fund returned 5.39%, before sales charges, for the twelve-month period ended October 31, 2011, underperforming its benchmark, the Russell 1000 Growth Index, which returned 9.92% for the same period. The Fund also underperformed the 6.76% return of the average fund in the Lipper Large-Cap Growth Funds peer group, a group of funds with investment strategies similar to those of the Fund.

Why did the Fund perform this way?

U.S. equities moved higher in the period despite a high degree of volatility caused by unrest in North Africa and the Middle East, as well as the devastating earthquake and tsunami in Japan. Fears of a global economic slowdown, due to the Japanese earthquake and concerns about heightened geopolitical risks, were not enough to offset strong corporate earnings, generally solid economic data, and a continued accommodative Federal Reserve policy. In the latter half of the period, positive returns from strong corporate earnings and generally solid economic data were offset by European sovereign debt concerns and a deteriorating outlook for economic growth. October, the final month of the period, produced a sharp so-called relief rally, as evidence began to surface that Europe’s leaders would take steps to address the continent’s financial crises.

Nine of the ten sectors in the Russell 1000 Growth Index had positive returns for the period. Utilities (+18%), Energy (+18%), and Consumer Discretionary (+14%) performed the best, while Telecommunication Services (-2%) and Materials (+3%) lagged on a relative basis. Growth stocks (+10%) outperformed Value stocks (+6%), as measured by the Russell 1000 Growth and Russell 1000 Value Indices, respectively.

Security selection in Information Technology, Financials, and Health Care detracted from the portfolio’s relative returns (i.e. performance of the Fund as measured against the benchmark). This was partially offset by strong security selection in Consumer Staples and Consumer Discretionary. Sector allocation, which is a residual of bottom-up (i.e. stock by stock fundamental research) stock selection, aided relative performance. Positive effects from an overweight (i.e. the Fund’s sector position was greater than the benchmark position) to Consumer Discretionary essentially neutralized the negative effects of the Fund’s underweight (i.e. the Fund’s sector position was less than the benchmark position)exposure to Energy.

Top detractors from relative performance during the period were Acme Packet (Information Technology), Juniper Networks (Information Technology), and IBM (Information Technology). Shares of Acme Packet, a leading provider of session border control solutions, which enable the delivery of VoIP (voice over internet protocol) and data communications across network borders, declined sharply during the period. We have had a positive view based on the firm's leading position in a fast growing market, but the current slower carrier spending environment has proved a headwind. Shares of Juniper Networks, a leading provider of routing and security solutions, lagged due to estimates coming down on the back of sluggish Japan demand and multiple product transitions. Not holding the strongly performing IBM during the period hindered the portfolio’s results. Cisco Systems (Information Technology) and Netflix (Consumer Discretionary) were also top detractors from absolute returns.

Green Mountain Coffee Roasters (Consumer Staples), Polo Ralph Lauren (Consumer Discretionary), and Hewlett-Packard (Information Technology) were the top contributors to relative performance during the period. Shares of Green Mountain Coffee Roasters nearly doubled during the period. For much of the period, core results topped expectations and management had raised guidance amid strong sales growth of the firm's Keurig single serving products. Shares of Polo Ralph Lauren, a producer of apparel, accessories, fragrances, and home furnishings, rose during the period. We sold our position to fund other attractive opportunities; the stock has been a solid performer and was beginning to approach our price target. The Fund benefited by not holding Hewlett-Packard, which struggled during the period. Additionally, Apple (Information Technology) and Altera (Information Technology) were among the top contributors to absolute performance.

What is the outlook?

In this environment we continue to focus our efforts on stock-by-stock fundamental research, picking one stock at a time based upon our view of the attractiveness of each company’s fundamentals and valuation. As a result of this bottom up stock selection, at the end of the period our largest overweight positions versus the benchmark were Information Technology and Consumer Discretionary. At the end of the period, we had underweight exposure to the defensive Consumer Staples and Health Care sectors as we were finding limited opportunities for growth in those areas. We were also modestly underweight Industrials at the period’s end.

| The Hartford Growth Fund |

Manager Discussion (Unaudited) – (continued) |

| October 31, 2011 |

At the end of the period, greater-than-benchmark exposure to Information Technology favored Technology Hardware. We believe our holdings were leveraged to several strong product cycles and emerging product categories. We increased our overweight exposure to Consumer Discretionary during the period. We favored companies with strong fundamentals, which should also benefit from an economic recovery. We trimmed our exposure to Financials and had a slight underweight position in the sector at the end of the period. We believe this group may face some headwinds in the near term due to continued weakness in the U.S. housing market and ongoing regulatory concerns.

| Diversification by Industry | |

| as of October 31, 2011 | |

| | | |

| Automobiles & Components (Consumer Discretionary) | | | 3.3 | % |

| Capital Goods (Industrials) | | | 8.9 | |

| Consumer Durables & Apparel (Consumer Discretionary) | | | 3.7 | |

| Consumer Services (Consumer Discretionary) | | | 3.0 | |

| Diversified Financials (Financials) | | | 3.5 | |

| Energy (Energy) | | | 9.4 | |

| Food, Beverage & Tobacco (Consumer Staples) | | | 2.7 | |

| Health Care Equipment & Services (Health Care) | | | 3.4 | |

| Materials (Materials) | | | 4.4 | |

| Media (Consumer Discretionary) | | | 3.8 | |

| Pharmaceuticals, Biotechnology & Life Sciences (Health Care) | | | 1.7 | |

| Retailing (Consumer Discretionary) | | | 4.9 | |

| Semiconductors & Semiconductor Equipment (Information Technology) | | | 8.7 | |

| Software & Services (Information Technology) | | | 17.8 | |

| Technology Hardware & Equipment (Information Technology) | | | 17.2 | |

| Transportation (Industrials) | | | 1.2 | |

| Short-Term Investments | | | 2.0 | |

| Other Assets and Liabilities | | | 0.4 | |

| Total | | | 100.0 | % |

|

| Schedule of Investments |

October 31, 2011 |

| Shares or Principal Amount | Market Value ╪ | |

COMMON STOCKS - 97.6% | |

| | | Automobiles & Components - 3.3% | |

| | 268 | | Harley-Davidson, Inc. | | $ | 10,441 | |

| | 418 | | Johnson Controls, Inc. | | | 13,779 | |

| | | | | | | 24,220 | |

| | | | Capital Goods - 8.9% | |

| | 184 | | AMETEK, Inc. | | | 7,271 | |

| | 109 | | Boeing Co. | | | 7,196 | |

| | 51 | | Caterpillar, Inc. | | | 4,813 | |

| | 125 | | Cummins, Inc. | | | 12,417 | |

| | 161 | | Eaton Corp. | | | 7,201 | |

| | 139 | | Illinois Tool Works, Inc. | | | 6,771 | |

| | 112 | | Joy Global, Inc. | | | 9,735 | |

| | 161 | | PACCAR, Inc. | | | 6,967 | |

| | 15 | | Precision Castparts Corp. | | | 2,503 | |

| | | | | | | 64,874 | |

| | | | Consumer Durables & Apparel - 3.7% | |

| | 190 | | Coach, Inc. | | | 12,377 | |

| | 86 | | Fossil, Inc. ● | | | 8,929 | |

| | 10 | | Lululemon Athletica, Inc. ● | | | 560 | |

| | 31 | | Ralph Lauren Corp. | | | 4,843 | |

| | | | | | | 26,709 | |

| | | | Consumer Services - 3.0% | |

| | 173 | | Las Vegas Sands Corp. ● | | | 8,101 | |

| | 575 | | MGM Resorts International ● | | | 6,626 | |

| | 170 | | Starbucks Corp. | | | 7,198 | |

| | | | | | | 21,925 | |

| | | | Diversified Financials - 3.5% | |

| | 84 | | American Express Co. | | | 4,252 | |

| | 208 | | Ameriprise Financial, Inc. | | | 9,707 | |

| | 72 | | BlackRock, Inc. | | | 11,427 | |

| | | | | | | 25,386 | |

| | | | Energy - 9.4% | |

| | 155 | | Anadarko Petroleum Corp. | | | 12,131 | |

| | 186 | | Consol Energy, Inc. | | | 7,942 | |

| | 181 | | ENSCO International plc | | | 9,008 | |

| | 109 | | EOG Resources, Inc. | | | 9,721 | |

| | 174 | | National Oilwell Varco, Inc. | | | 12,428 | |

| | 39 | | Occidental Petroleum Corp. | | | 3,641 | |

| | 182 | | Schlumberger Ltd. | | | 13,402 | |

| | | | | | | 68,273 | |

| | | | Food, Beverage & Tobacco - 2.7% | |

| | 298 | | Green Mountain Coffee Roasters, Inc. ● | | | 19,358 | |

| | | | | | | | |

| | | | Health Care Equipment & Services - 3.4% | |

| | 129 | | Covidien International plc | | | 6,049 | |

| | 111 | | Edwards Lifesciences Corp. ● | | | 8,392 | |

| | 373 | | Hologic, Inc. ● | | | 6,007 | |

| | 90 | | UnitedHealth Group, Inc. | | | 4,313 | |

| | | | | | | 24,761 | |

| | | | Materials - 4.4% | |

| | 114 | | Freeport-McMoRan Copper & Gold, Inc. | | | 4,578 | |

| | 170 | | Monsanto Co. | | | 12,362 | |

| | 116 | | Mosaic Co. | | | 6,820 | |

| | 71 | | Rio Tinto plc ADR | | | 3,864 | |

| | 53 | | Walter Energy, Inc. | | | 4,000 | |

| | | | | | | 31,624 | |

| | | | Media - 3.8% | |

| | 780 | | News Corp. Class A | | | 13,659 | |

| | 2,898 | | Sirius XM Radio, Inc. w/ Rights ● | | | 5,188 | |

| | 248 | | Walt Disney Co. | | | 8,652 | |

| | | | | | | 27,499 | |

| | | Pharmaceuticals, Biotechnology & Life Sciences - 1.7% | |

| | 340 | | Agilent Technologies, Inc. ● | | | 12,601 | |

| | | | | | | | |

| | | | Retailing - 4.9% | |

| | 158 | | Abercrombie & Fitch Co. Class A | | | 11,731 | |

| | 45 | | Amazon.com, Inc. ● | | | 9,700 | |

| | 13 | | Netflix, Inc. ● | | | 1,107 | |

| | 25 | | Priceline.com, Inc. ● | | | 12,855 | |

| | | | | | | 35,393 | |

| | | | Semiconductors & Semiconductor Equipment - 8.7% | |

| | 722 | | Altera Corp. | | | 27,380 | |

| | 308 | | Analog Devices, Inc. | | | 11,278 | |

| | 349 | | Broadcom Corp. Class A | | | 12,610 | |

| | 263 | | Skyworks Solutions, Inc. ● | | | 5,212 | |

| | 222 | | Texas Instruments, Inc. | | | 6,808 | |

| | | | | | | 63,288 | |

| | | | Software & Services - 17.8% | |

| | 120 | | Alliance Data Systems Corp. ● | | | 12,323 | |

| | 188 | | BMC Software, Inc. ● | | | 6,542 | |

| | 259 | | Citrix Systems, Inc. ● | | | 18,848 | |

| | 114 | | Cognizant Technology Solutions Corp. ● | | | 8,264 | |

| | 824 | | eBay, Inc. ● | | | 26,224 | |

| | 7 | | Google, Inc. ● | | | 3,923 | |

| | 808 | | Oracle Corp. | | | 26,479 | |

| | 138 | | Rovi Corp. ● | | | 6,838 | |

| | 28 | | Salesforce.com, Inc. ● | | | 3,697 | |

| | 199 | | Tibco Software, Inc. ● | | | 5,757 | |

| | 188 | | VeriSign, Inc. | | | 6,033 | |

| | 43 | | VMware, Inc. ● | | | 4,196 | |

| | | | | | | 129,124 | |

| | | | Technology Hardware & Equipment - 17.2% | |

| | 185 | | Acme Packet, Inc. ● | | | 6,706 | |

| | 125 | | Apple, Inc. ● | | | 50,427 | |

| | 818 | | EMC Corp. ● | | | 20,057 | |

| | 77 | | F5 Networks, Inc. ● | | | 8,038 | |

| | 511 | | Juniper Networks, Inc. ● | | | 12,511 | |

| | 293 | | NetApp, Inc. ● | | | 12,002 | |

| | 295 | | Qualcomm, Inc. | | | 15,236 | |

| | | | | | | 124,977 | |

| | | | Transportation - 1.2% | |

| | 45 | | C.H. Robinson Worldwide, Inc. | | | 3,137 | |

| | 136 | | J.B. Hunt Transport Services, Inc. | | | 5,733 | |

| | | | | | | 8,870 | |

| | | | Total common stocks | | | | |

| | | | (cost $590,938) | | $ | 708,882 | |

| | | | | | | | |

| | | | Total long-term investments | | | | |

| | | | (cost $590,938) | | $ | 708,882 | |

| | | | | | | | |

SHORT-TERM INVESTMENTS - 2.0% | |

| Repurchase Agreements - 2.0% | |

| | | | Bank of America Merrill Lynch TriParty Joint Repurchase Agreement (maturing on 11/01/2011 in the amount of $868, collateralized by FHLMC 4.50%, 2040, FNMA 5.00, 2041, value of $885) | | | | |

| $ | 868 | | 0.11%, 10/31/2011 | | $ | 868 | |

The accompanying notes are an integral part of these financial statements

| The Hartford Growth Fund |

| Schedule of Investments – (continued) |

October 31, 2011 |

Shares or Principal Amount | | | | | Market Value ╪ | |

SHORT-TERM INVESTMENTS - 2.0% - (continued) | | | | | | |

| Repurchase Agreements - 2.0% - (continued) | | | | | | |

| | | Barclays Capital TriParty Joint Repurchase Agreement (maturing on 11/01/2011 in the amount of $8,287, collateralized by FNMA 5.50%, 2041, GNMA 4.00%, 2040, U.S. Treasury Bond 8.13%, 2021, U.S. Treasury Note 2.50% - 3.63%, 2015 - 2020, value of $8,453) | | | | | | |

| $ | 8,287 | | 0.11%, 10/31/2011 | | | | | $ | 8,287 | |

| | | | Deutsche Bank Securities TriParty Joint Repurchase Agreement (maturing on 11/01/2011 in the amount of $1,172, collateralized by GNMA 4.00% - 5.00%, 2040, value of $1,195) | | | | | | | |

| | 1,172 | | 0.11%, 10/31/2011 | | | | | | 1,172 | |

| | | | UBS Securities, Inc. Joint Repurchase Agreement (maturing on 11/01/2011 in the amount of $-, collateralized by U.S. Treasury Note 1.88%, 2014, value of $-) | | | | | | | |

| | – | | 0.11%, 10/31/2011 | | | | | | – | |

| | | | UBS Securities, Inc. TriParty Joint Repurchase Agreement (maturing on 11/01/2011 in the amount of $4,035, collateralized by GNMA 3.50% - 4.50%, 2041, value of $4,116) | | | | | | | |

| | 4,035 | | 0.11%, 10/31/2011 | | | | | | 4,035 | |

| | | | | | | | | | 14,362 | |

| | | | Total short-term investments | | | | | | | |

| | | | (cost $14,362) | | | | | $ | 14,362 | |

| | | | | | | | | | | |

| | | | Total investments | | | | | | | |

| | | | (cost $605,300) ▲ | | | 99.6 | % | | $ | 723,244 | |

| | | | Other assets and liabilities | | | 0.4 | % | | | 2,662 | |

| | | | Total net assets | | | 100.0 | % | | $ | 725,906 | |

| Note: | Percentage of investments as shown is the ratio of the total market value to total net assets. Market value of long-term investments in foreign securities represents 1.9% of total net assets at October 31, 2011. |

Prices of foreign equities that are principally traded on certain foreign markets may be adjusted daily pursuant to a fair value pricing service approved by the Board of Directors in order to reflect an adjustment for factors occurring after the close of certain foreign markets but before the close of the New York Stock Exchange.

| ▲ | At October 31, 2011, the cost of securities for federal income tax purposes was $608,161 and the aggregate gross unrealized appreciation and depreciation based on that cost were: |

| Unrealized Appreciation | | $ | 146,946 | |

| Unrealized Depreciation | | | (31,863 | ) |

| Net Unrealized Appreciation | | $ | 115,083 | |

| ╪ | See Significant Accounting Policies of accompanying Notes to Financial Statements regarding valuation of securities. |

The accompanying notes are an integral part of these financial statements

|

| Investment Valuation Hierarchy Level Summary |

| October 31, 2011 |

| (000’s Omitted) |

| | | | | | | | | | | | | |

| Assets: | | | | | | | | | | | | |

| Common Stocks ‡ | | $ | 708,882 | | | $ | 708,882 | | | $ | – | | | $ | – | |

| Short-Term Investments | | | 14,362 | | | | – | | | | 14,362 | | | | – | |

| Total | | $ | 723,244 | | | $ | 708,882 | | | $ | 14,362 | | | $ | – | |

| ♦ | For the year ended October 31, 2011, there were no significant transfers between Level 1 and Level 2. |

| ‡ | The Fund has all or primarily all of the equity securities categorized in a particular level. Refer to the Schedule of Investments for further industry breakout. |

The accompanying notes are an integral part of these financial statements

|

| Statement of Assets and Liabilities |

| October 31, 2011 |

| (000’s Omitted) |

| Assets: | | | |

| Investments in securities, at market value (cost $605,300) | | $ | 723,244 | |

| Cash | | | 10 | |

| Receivables: | | | | |

| Investment securities sold | | | 3,326 | |

| Fund shares sold | | | 1,132 | |

| Dividends and interest | | | 186 | |

| Other assets | | | 79 | |

| Total assets | | | 727,977 | |

| Liabilities: | | | | |

| Payables: | | | | |

| Investment securities purchased | | | 750 | |

| Fund shares redeemed | | | 1,024 | |

| Investment management fees | | | 103 | |

| Administrative fees | | | — | |

| Distribution fees | | | 30 | |

| Accrued expenses | | | 164 | |

| Total liabilities | | | 2,071 | |

| Net assets | | $ | 725,906 | |

| Summary of Net Assets: | | | | |

| Capital stock and paid-in-capital | | $ | 694,314 | |

| Accumulated undistributed net investment income | | | — | |

| Accumulated net realized loss on investments and foreign currency transactions | | | (86,351 | ) |

| Unrealized appreciation of investments and the translation of assets and liabilities denominated in foreign currency | | | 117,943 | |

| Net assets | | $ | 725,906 | |

| | | | | |

| Shares authorized | | | 27,000,000 | |

| Par value | | $ | 0.0001 | |

Class A: Net asset value per share/Maximum offering price per share | | | $17.01/$18.00 | |

| Shares outstanding | | | 23,792 | |

| Net assets | | $ | 404,630 | |

Class B: Net asset value per share | | $ | 14.14 | |

| Shares outstanding | | | 949 | |

| Net assets | | $ | 13,411 | |

Class C: Net asset value per share | | $ | 14.16 | |

| Shares outstanding | | | 2,781 | |

| Net assets | | $ | 39,365 | |

Class I: Net asset value per share | | $ | 17.26 | |

| Shares outstanding | | | 8,079 | |

| Net assets | | $ | 139,421 | |

Class R3: Net asset value per share | | $ | 17.26 | |

| Shares outstanding | | | 17 | |

| Net assets | | $ | 298 | |

Class R4: Net asset value per share | | $ | 17.51 | |

| Shares outstanding | | | 224 | |

| Net assets | | $ | 3,918 | |

Class R5: Net asset value per share | | $ | 17.65 | |

| Shares outstanding | | | 39 | |

| Net assets | | $ | 689 | |

Class Y: Net asset value per share | | $ | 17.82 | |

| Shares outstanding | | | 6,970 | |

| Net assets | | $ | 124,174 | |

The accompanying notes are an integral part of these financial statements

|

| Statement of Operations |

| For the Year Ended October 31, 2011 |

| (000’s Omitted) |

| Investment Income: | | | |

| Dividends | | $ | 7,252 | |

| Interest | | | 8 | |

| Less: Foreign tax withheld | | | (38 | ) |

| Total investment income | | | 7,222 | |

| | | | | |

| Expenses: | | | | |

| Investment management fees | | | 5,419 | |

| Administrative services fees | | | 7 | |

| Transfer agent fees | | | 1,317 | |

| Distribution fees | | | | |

| Class A | | | 744 | |

| Class B | | | 168 | |

| Class C | | | 439 | |

| | | 389 | |

| Class R3 | | | 2 | |

| Class R4 | | | 10 | |

| Custodian fees | | | 6 | |

| Accounting services fees | | | 89 | |

| Registration and filing fees | | | 142 | |

| Board of Directors' fees | | | 15 | |

| Audit fees | | | 12 | |

| Other expenses | | | 133 | |

| Total expenses (before waivers and fees paid indirectly) | | | 8,892 | |

| Expense waivers | | | (35 | ) |

| Transfer agent fee waivers | | | (22 | ) |

| Commission recapture | | | (16 | ) |

| Total waivers and fees paid indirectly | | | (73 | ) |

| Total expenses, net | | | 8,819 | |

| Net Investment Loss | | | (1,597 | ) |

| Net Realized Gain on Investments and Foreign Currency Transactions: | | | | |

| Net realized gain on investments in securities | | | 51,401 | |

| Net realized gain on foreign currency contracts | | | — | |

| Net realized gain on other foreign currency transactions | | | 16 | |

| Net Realized Gain on Investments and Foreign Currency Transactions | | | 51,417 | |

| Net Changes in Unrealized Depreciation of Investments and Foreign Currency Transactions: | | | | |

| Net unrealized depreciation of investments | | | (12,876 | ) |

| Net unrealized depreciation on translation of other assets and liabilities in foreign currencies | | | (14 | ) |

| Net Changes in Unrealized Depreciation of Investments and Foreign Currency Transactions | | | (12,890 | ) |

| Net Gain on Investments and Foreign Currency Transactions | | | 38,527 | |

| Net Increase in Net Assets Resulting from Operations | | $ | 36,930 | |

* Class L merged into Class A on August 5, 2011. Please refer to the Notes to Financial Statements for further details.

The accompanying notes are an integral part of these financial statements

|

| Statement of Changes in Net Assets |

| |

| (000’s Omitted) |

| | | For the Year Ended October 31, 2011 | | | For the Year Ended October 31, 2010 | |

| Operations: | | | | | | |

| Net investment loss | | $ | (1,597 | ) | | $ | (1,425 | ) |

| Net realized gain on investments and foreign currency transactions | | | 51,417 | | | | 49,390 | |

| Net unrealized appreciation (depreciation) of investments and foreign currency transactions | | | (12,890 | ) | | | 68,730 | |

| Net Increase In Net Assets Resulting From Operations | | | 36,930 | | | | 116,695 | |

| Distributions to Shareholders: | | | | | | | | |

| From net investment income | | | | | | | | |

| Class I | | | — | | | | (239 | ) |

| Class L* | | | — | | | | (500 | ) |

| Class R3 | | | — | | | | — | |

| Class R4 | | | — | | | | (5 | ) |

| Class R5 | | | — | | | | — | |

| Class Y | | | — | | | | (509 | ) |

| Total distributions | | | — | | | | (1,253 | ) |

| Capital Share Transactions: | | | | | | | | |

| Class A | | | 105,155 | | | | (39,203 | ) |

| Class B | | | (5,074 | ) | | | (4,827 | ) |

| Class C | | | (6,415 | ) | | | (8,332 | ) |

| Class I | | | 79,116 | | | | (4,679 | ) |

| Class L* | | | (184,338 | ) | | | (20,296 | ) |

| Class R3 | | | 61 | | | | 36 | |

| Class R4 | | | 230 | | | | 449 | |

| Class R5 | | | 540 | | | | 26 | |

| Class Y | | | 18,053 | | | | (16,861 | ) |

| Net increase (decrease) from capital share transactions | | | 7,328 | | | | (93,687 | ) |

| Net Increase In Net Assets | | | 44,258 | | | | 21,755 | |

| Net Assets: | | | | | | | | |

| Beginning of period | | | 681,648 | | | | 659,893 | |

| End of period | | $ | 725,906 | | | $ | 681,648 | |

| Accumulated undistributed (distribution in excess of) net investment income (loss) | | $ | — | | | $ | — | |

| * | Class L merged into Class A on August 5, 2011. Please refer to the Notes to Financial Statements for further details. |

The accompanying notes are an integral part of these financial statements

|

| Notes to Financial Statements |

| October 31, 2011 |

| (000’s Omitted) |

The Hartford Mutual Funds II, Inc. (“Company”) is an open-end management investment company comprised of five portfolios. Financial statements for The Hartford Growth Fund (the “Fund”), a series of the Company, are included in this report.

The Company is organized under the laws of the State of Maryland and is registered with the Securities and Exchange Commission (“SEC”) under the Investment Company Act of 1940, as amended (“1940 Act”). The Fund is a diversified open-end management investment company.

Class A shares are sold with a front-end sales charge of up to 5.50%. Class B shares were sold with a contingent deferred sales charge which is assessed on the lesser of the per share net asset value (“NAV”) of the shares at the time of redemption or the original purchase price, and declines from up to 5.00% to zero depending on the period of time the shares are held (see note below regarding the closing of Class B shares). Class C shares are sold with a contingent deferred sales charge of up to 1.00% on shares redeemed within twelve months of purchase. Class I shares are sold without sales charges to certain eligible investors primarily through advisory fee-based wrap programs. Class R3, R4 and R5 shares, which are offered to employer-sponsored retirement plans, and Class Y shares, which are sold to certain eligible institutional investors, are sold without a sales charge. All classes of shares have identical voting, redemption, dividend, liquidation and other rights and the same terms and conditions, with the exceptions that each class may have different expenses, which may affect performance, and that Class B shares automatically convert to Class A shares after 8 years.

No new or additional investments are allowed in Class B shares of The Hartford Mutual Funds (including investments through any systematic investment plan). Existing shareholders of Class B shares may continue to hold their Class B shares, exchange their Class B shares for Class B shares of another Hartford Mutual Fund (as permitted by existing exchange privileges), or redeem their Class B shares as described in the Fund’s prospectus. Reinstatement privileges with respect to Class B shares will continue under the current policy. For investors electing to reinvest capital gains and dividends, any such capital gains or dividends on Class B shares will continue to be reinvested in Class B shares of the Fund. All Class B share attributes, including the 12b-1 fee, contingent deferred sales charge schedule, and conversion to Class A shares, remain unchanged.

| 2. | Significant Accounting Policies: |

The following is a summary of significant accounting policies of the Fund in the preparation of its financial statements, which are in accordance with the United States Generally Accepted Accounting Principles (“U.S. GAAP”). The preparation of financial statements in accordance with U.S. GAAP may require management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

| | a) | Determination of Net Asset Value – The NAV of each class of the Fund's shares is determined as of the close of regular trading (normally 4:00 p.m. Eastern Time) (the “NYSE Close”) on each day that the New York Stock Exchange (the “Exchange”) is open (“Valuation Date”). Information that becomes known to the Fund after the NAV has been calculated on a particular day will not generally be used to retroactively adjust the NAV determined earlier that day. |

| | b) | Investment Valuation and Fair Value Measurements – For purposes of calculating the NAV, portfolio securities and other assets held by the Fund's portfolio for which market quotes are readily available are valued at market value. Market value is generally determined on the basis of last reported sales prices or official close price. If no sales are reported, market value is based on quotes obtained from a quotation reporting system, established market makers, or independent pricing services. If market prices are not readily available or are deemed unreliable, the Fund will use the fair value of |

| The Hartford Growth Fund |

Notes to Financial Statements – (continued) |

| October 31, 2011 |

| (000’s Omitted) |

| | the security as determined in good faith under policies and procedures established by and under the supervision of the Company’s Board of Directors. Market quotes are considered not readily available where there is an absence of current or reliable market-based data (e.g., trade information or broker quotes), including where events occur after the close of the relevant market, but prior to the NYSE Close that materially affect the values of the Fund’s portfolio securities or assets. In addition, market quotes are considered not readily available when, due to extraordinary circumstances, the exchanges or markets on which the securities trade do not open for trading for the entire day and no other market prices are available. In addition, prices of foreign equities that are principally traded on certain foreign markets are adjusted daily pursuant to a fair value pricing service approved by the Board of Directors in order to reflect an adjustment for the factors occurring after the close of certain foreign markets but before the NYSE Close. Securities that are primarily traded on foreign markets may trade on days that are not business days of the Fund. The value of the foreign securities in which the Fund invests may change on days when a shareholder will not be able to purchase or redeem shares of the Fund. Fair value pricing is subjective in nature and the use of fair value pricing by the Fund may cause the NAV of its shares to differ significantly from the NAV that would have been calculated using market prices at the close of the exchange on which a portfolio security is primarily traded. There can be no assurance that the Fund could obtain the fair market value assigned to a security if the Fund were to sell the security at approximately the time at which the Fund determines its NAV. |

Investments valued in currencies other than U.S. dollars are converted to U.S. dollars using exchange rates obtained from independent pricing services for calculation of the NAV. As a result, the NAV of the Fund’s shares may be affected by changes in the value of currencies in relation to the U.S. dollar. The value of securities traded in markets outside the United States or denominated in currencies other than the U.S. dollar may be affected significantly on a day that the NYSE is closed and the market value may change on days when an investor is not able to purchase, redeem or exchange shares of the Fund.

Foreign currency contracts represent agreements to exchange currencies on specific future dates at predetermined rates. Foreign currency contracts are valued using foreign currency exchange rates and forward rates as provided by an independent pricing service on the Valuation Date.

Financial instruments for which prices are not available from an independent pricing service may be valued using market quotations obtained from one or more dealers that make markets in the respective financial instrument in accordance with procedures established by the Company’s Board of Directors.

U.S. GAAP defines fair value as the price that the Fund would receive to sell an asset or pay to transfer a liability in an orderly transaction between market participants. The U.S. GAAP fair value measurement standards require disclosure of a fair value hierarchy for each major category of assets and liabilities. Various inputs are used in determining the fair value of the Fund’s investments. These inputs are summarized into three broad hierarchy levels. This hierarchy is based on whether the valuation inputs are observable or unobservable. These levels are:

| | · | Level 1 – Quoted prices in active markets for identical securities. Level 1 may include exchange traded instruments, such as domestic equities, some foreign equities, options, futures, mutual funds, exchange traded funds, rights and warrants. |

| | · | Level 2 – Observable inputs other than Level 1 prices, such as quoted prices for similar securities; quoted prices in markets that are not active; or other inputs that are observable or can be corroborated by observable market data. Level 2 may include debt securities that are traded less frequently than exchange traded instruments and which are valued using third party pricing services; foreign equities, that are principally traded on certain foreign markets and are adjusted daily pursuant to a fair value pricing service in order to reflect an adjustment for the factors occurring after the close of certain foreign markets but before the NYSE Close; and short-term securities, which are valued at amortized cost. |

| | · | Level 3 – Significant unobservable inputs that are supported by limited or no market activity. Level 3 may include financial instruments whose values are determined using broker quotes or require significant management judgment or estimation. These unobservable valuation inputs may include estimates for current |

| | yields, maturity/duration, prepayment speed, and broker quotes for comparable securities along with other assumptions relating to credit quality, collateral value, complexity of the security structure, general market conditions and liquidity. This category may include securities where trading has been halted or there are certain restrictions on trading. While these securities are priced using unobservable inputs, the valuation of these securities reflects the best available data and management believes the prices are a reasonable representation of exit price. |

Valuation levels are not necessarily indicative of the risk associated with investing in such securities. Individual securities within any of the above mentioned asset classes may be assigned a different hierarchical level than those presented above, as individual circumstances dictate.

During the year ended October 31, 2011, the Fund held no Level 3 securities; therefore, no reconciliation of Level 3 securities is presented.

For additional information, refer to the Investment Valuation Hierarchy Level Summary which follows the Schedule of Investments.

For purposes of reporting transfers between different hierarchy levels, both transfers in and out of each level, as applicable, are shown as if they occurred at the beginning of the period.

| | c) | Security Transactions and Investment Income – Security transactions are recorded as of the trade date (the date the order to buy or sell is executed) for financial reporting purposes. Securities purchased or sold on a when-issued or delayed-delivery basis may be settled a month or more after the trade date. Realized gains and losses are determined on the basis of identified cost. |

Dividend income is accrued as of the ex-dividend date, except certain dividends from foreign securities where the ex-dividend date may have passed are recorded as soon as the Fund is informed of the dividend. Interest income, including amortization of premium and accretion of discounts, is accrued on a daily basis.

| �� | d) | Foreign Currency Transactions – Assets and liabilities denominated in currencies other than U.S. dollars are translated into U.S. dollars at the exchange rates in effect on the valuation date. Purchases and sales of investment securities, income, and expenses are translated into U.S. dollars at the exchange rates on the dates of such transactions. |

The Fund does not isolate that portion of portfolio security valuation resulting from fluctuations in the foreign currency exchange rates from the fluctuations arising from changes in the market prices of securities held. Exchange rate fluctuations are included with the net realized and unrealized gain or loss on investments in the accompanying financial statements.

Net realized foreign exchange gains or losses arise from sales of foreign currencies and the difference between asset and liability amounts initially stated in foreign currencies and the U.S. dollar value of the amounts actually received or paid. Net unrealized foreign exchange gains or losses arise from changes in the value of other assets and liabilities at the end of the reporting period, resulting from changes in the exchange rates.

| | e) | Joint Trading Account – The Fund may invest cash balances into a joint trading account that may be invested in one or more repurchase agreements. |

| | f) | Fund Share Valuation and Dividend Distributions to Shareholders – Orders for the Fund’s shares are executed in accordance with the investment instructions of the shareholders. The NAV of the Fund’s shares is determined as of the close of business on each business day of the Exchange. The NAV is determined separately for each class of shares of the Fund by dividing the Fund’s net assets attributable to that class by the number of shares of the class outstanding. |

| The Hartford Growth Fund |

| Notes to Financial Statements – (continued) |

| October 31, 2011 |

| (000’s Omitted) |

| | Each class of shares offered by the Fund has equal rights as to assets and voting privileges (except that shareholders of a class have exclusive voting rights regarding any matter relating solely to that class of shares). Income and non-class specific expenses are allocated daily to each class on the basis of the relative net assets of the class. Realized and unrealized capital gains and losses are allocated daily based on the relative net assets of each class of shares of the Fund. |

Orders for the purchase of the Fund’s shares received prior to the close of the Exchange on any day the Exchange is open for business are priced at the NAV determined as of the close of the Exchange. Orders received after the close of the Exchange, or on a day on which the Exchange and/or the Fund is not open for business, are priced at the next determined NAV.

Dividends are declared pursuant to a policy adopted by the Company’s Board of Directors based upon the investment performance of the Fund. The policy of the Fund is to pay dividends from net investment income and realized capital gains, if any, at least once a year.

Distributions from net investment income, net realized capital gains and capital are determined in accordance with federal income tax regulations, which may differ from U.S. GAAP with respect to character and timing. These differences may include but are not limited to losses deferred due to wash sale adjustments, foreign currency gains and losses, adjustments related to Passive Foreign Investment Companies (“PFICs”), Real Estate Investment Trusts (“REITs”), Regulated Investment Companies (“RICs”), certain derivatives and partnerships. Permanent book and federal income tax basis differences relating to shareholder distributions will result in reclassifications to certain of the Fund’s capital accounts (see Federal Income Taxes: Reclassification of Capital Accounts note).

| 3. | Securities and Other Investments: |

| | a) | Repurchase Agreements – A repurchase agreement is an agreement by which a counterparty agrees to sell a security and agrees to repurchase the security sold at a mutually agreed upon time and price. At the time the Fund enters into a repurchase agreement, the value of the underlying collateral security(ies), including accrued interest, will be equal to or exceed the value of the repurchase agreement. Repurchase agreements expose the Fund to counterparty risk. To minimize counterparty risk, the securities that serve to collateralize the repurchase agreement are held by the Fund's custodian in book entry or physical form in the custodial account of the Fund or in a third party custodial account. Repurchase agreements are valued at cost plus accrued interest. The Fund, as shown on the Schedule of Investments, had outstanding repurchase agreements as of October 31, 2011. |

| | b) | Securities Purchased on a When-Issued or Delayed-Delivery Basis – Delivery and payment for securities that have been purchased by the Fund on a forward commitment, or when-issued or delayed-delivery basis, take place beyond the customary settlement period. A fund may dispose of or renegotiate a delayed-delivery transaction after it is entered into, and may sell delayed-delivery securities before they are delivered, which may result in a realized gain or loss. During this period, such securities are subject to market fluctuations, and the Fund identifies securities segregated in its records with value at least equal to the amount of the commitment. As of October 31, 2011, the Fund had no outstanding when-issued or delayed delivery securities. |

| 4. | Financial Derivative Instruments: |

The following disclosures contain information on how and why the Fund uses derivative instruments, the credit-risk-related contingent features in certain derivative instruments, and how derivative instruments affect the Fund’s financial position and results of operations. The location and fair value amounts of these instruments on the Statement of Assets and Liabilities and the realized gains and losses and changes in unrealized gains and losses on the Statement of Operations, each categorized by type of derivative contract, are included in the following Additional Derivative Instrument Information footnote. The derivative instruments outstanding as of period-end are disclosed in the notes to

the Schedule of Investments and the amounts of realized gains and losses and changes in unrealized gains and losses on derivative instruments during the period are disclosed in the Statement of Operations.

| | a) | Foreign Currency Contracts – The Fund may enter into foreign currency contracts that obligate the Fund to purchase or sell currencies at specified future dates. Foreign currency contracts are used to hedge the currency exposure associated with some or all of the Fund's securities and/or as part of an investment strategy. Foreign currency contracts are marked to market daily and the change in value is recorded by the Fund as an unrealized gain or loss. The Fund will record a realized gain or loss when the foreign currency contract is settled. |

Foreign currency contracts involve elements of market risk in excess of the amounts reflected in the Statement of Assets and Liabilities. In addition, risks may arise upon entering into these contracts from the potential inability of the counterparties to meet the terms of the contracts and from unanticipated movements in the value of the foreign currencies relative to the U.S. dollar. The Fund had no outstanding foreign currency contracts as of October 31, 2011.

| | b) | Additional Derivative Instrument Information: |

The volume of derivative activity was minimal during the year ended October 31, 2011.

| The Effect of Derivative Instruments on the Statement of Operations for the year ended October 31, 2011: | |

| | | | |

| | | Risk Exposure Category | |

| | | | | | | | | | | | | | | | | | | | | | |

| Realized Gain (Loss) on Derivatives Recognized as a Result of Operations: | | | | | | | | | | |

| Net realized gain on foreign currency contracts | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | — | |

| Total | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | — | |

| | a) | Counterparty Risk – The Fund may be exposed to counterparty risk, or the risk that an institution or other entity with which the Fund has unsettled or open transactions will default. |

| | b) | Market Risks – If the Fund invests directly in foreign currencies or in securities that trade in, and receive revenues in, foreign currencies, or in derivatives that provide exposure to foreign currencies, it will be subject to the risk that those currencies will decline in value relative to the base currency of the Fund, or, in the case of hedging positions, that the Fund’s base currency will decline in value relative to the currency being hedged. Currency rates in foreign countries may fluctuate significantly over short periods of time for a number of reasons, including changes in interest rates, intervention (or the failure to intervene) by U.S. or foreign governments, central banks or supranational entities, such as the International Monetary Fund, or by the imposition of currency controls or other political developments in the United States or abroad. As a result, the Fund’s investments in foreign currency denominated securities may reduce the returns of the Fund. The market values of equity securities, such as common stocks and preferred stocks, or equity related investments, such as futures and options, may decline due to general market conditions which are not specifically related to a particular company, such as real or perceived adverse economic conditions, changes in the general outlook for corporate earnings, changes in interest or currency rates or adverse investor sentiment generally. The market value of equity securities may also decline due to factors which affect a particular industry or industries, such as labor shortages or increased production costs and competitive conditions within an industry. Equity securities and equity related investments generally have greater market price volatility than fixed income securities. |

| The Hartford Growth Fund |

| Notes to Financial Statements – (continued) |

| October 31, 2011 |

| (000’s Omitted) |

| | a) | Federal Income Taxes – For federal income tax purposes, the Fund intends to continue to qualify as a RIC under Subchapter M of the Internal Revenue Code (“IRC”) by distributing substantially all of its taxable net investment income and net realized capital gains to its shareholders and otherwise complying with the requirements of RICs. The Fund has distributed substantially all of its income and capital gains in prior years, if applicable, and intends to distribute substantially all of its income and capital gains during the calendar year ending December 31, 2011. Accordingly, no provision for federal income or excise taxes has been made in the accompanying financial statements. Distributions from short-term capital gains are treated as ordinary income distributions for federal income tax purposes. |

| | b) | Net Investment Income (Loss), Net Realized Gains (Losses) – Net investment income (loss) and net realized gains (losses) may differ for financial statement and tax purposes primarily because of losses deferred due to wash sale adjustments, foreign currency gains and losses, adjustments related to PFICs, REITs, RICs, certain derivatives and partnerships. The character of distributions made during the year from net investment income or net realized gains may differ from their ultimate characterization for federal income tax purposes. Also, due to the timing of dividend distributions, the fiscal year in which amounts are distributed may differ from the year that the income or realized gains (losses) were recorded by the Fund. |

| | c) | Distributions and Components of Distributable Earnings – The tax character of distributions paid by the Fund for the periods indicated is as follows (as adjusted for dividends payable): |

| | | For the Year Ended October 31, 2011 | | | For the Year Ended October 31, 2010 | |

| Ordinary Income | | $ | — | | | $ | 1,253 | |

As of October 31, 2011, the Fund’s components of distributable earnings (deficit) on a tax basis were as follows:

| | | Amount | |

| Accumulated Capital Losses * | | $ | (83,489 | ) |

| Unrealized Appreciation † | | | 115,081 | |

| Total Accumulated Earnings | | $ | 31,592 | |

| | * | The Fund has capital loss carryforwards that are identified in the Capital Loss Carryforward note that follows. |

| | † | The differences between book-basis and tax-basis unrealized appreciation (depreciation) may be attributable to the losses deferred due to wash sale adjustments, foreign currency gains and losses, adjustments related to PFICs, REITs, RICs, certain derivatives and partnerships. |

| | d) | Reclassification of Capital Accounts – The Fund may record reclassifications in its capital accounts. These reclassifications have no impact on the total net assets of the Fund. The reclassifications are a result of permanent differences between U.S. GAAP and tax accounting for such items as foreign currency, PFICs, expiration or utilization of capital loss carryforwards or net operating losses. Adjustments are made to reflect the impact these items have on current and future distributions to shareholders. Therefore, the source of the Fund’s distributions may be shown in the accompanying Statement of Changes in Net Assets as from accumulated undistributed net investment income, from accumulated net realized gains on investments or from capital depending on the type of book and tax differences that exist. For the year ended October 31, 2011, the Fund recorded reclassifications to increase (decrease) the accounts listed below: |

| | | Amount | |

| Accumulated Undistributed Net Investment Income | | $ | 1,597 | |

| Accumulated Net Realized Gain (Loss) on Investments and Foreign Currency Transactions | | | 65 | |

| Capital Stock and Paid-In-Capital | | | (1,662 | ) |

| | | | | |

| | e) | Capital Loss Carryforward – At October 31, 2011 (tax-year-end), the Fund had capital loss carryforwards for U.S. federal income tax purposes of approximately: |

Year of Expiration | | Amount | |

| 2017 | | $ | 83,489 | |

| Total | | $ | 83,489 | |

| | | | | |

| As of October 31, 2011, the Fund utilized $47,565 of prior year capital loss carryforwards. | |

| | f) | Accounting for Uncertainty in Income Taxes – The Fund has adopted financial reporting rules that require the Fund to analyze all open tax years, as defined by the statute of limitations, for all major jurisdictions. Generally, tax authorities can examine all tax returns filed for the last three years. The Fund does not have an examination in progress. |

The Fund has reviewed all open tax years and major jurisdictions and concluded that these financial reporting rules had no effect on the Fund’s financial position or results of operations. There is no tax liability resulting from unrecognized tax benefits relating to uncertain income tax positions taken or expected to be taken on the tax return for the fiscal year ended October 31, 2011. The Fund is also not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will significantly change in the next twelve months.

| | a) | Investment Management Agreement – Hartford Investment Financial Services, LLC (“HIFSCO”), a wholly-owned indirect subsidiary of The Hartford Financial Services Group, Inc. (“The Hartford”), serves as investment manager to the Fund pursuant to an Investment Management Agreement with the Company. As investment manager, HIFSCO has overall investment supervisory responsibility for the Fund. In addition, HIFSCO provides administrative personnel, services, equipment, facilities and office space for proper operation of the Fund. HIFSCO has contracted with Wellington Management Company, LLP (“Wellington Management”) under a sub-advisory agreement for the provision of day-to-day investment management services to the Fund in accordance with the Fund’s investment objective and policies. The Fund pays a fee to HIFSCO, a portion of which may be used to compensate Wellington Management. |

The schedule below reflects the rates of compensation paid to HIFSCO for investment management services rendered as of October 31, 2011; the rates are accrued daily and paid monthly:

| Average Daily Net Assets | | Annual Fee | |

| On first $250 million | | | 0.8000 | % |

| On next $4.75 billion | | | 0.7000 | % |

| On next $5 billion | | | 0.6975 | % |

| Over $10 billion | | | 0.6950 | % |

| | b) | Accounting Services Agreement – Pursuant to the Fund Accounting Agreement between Hartford Life Insurance Company (“HLIC”) and the Company, on behalf of the Fund, HLIC provides accounting services to the Fund and receives monthly compensation based on the Fund’s average net assets at the rates set forth below. The Fund’s accounting services fees are accrued daily and paid monthly. |

| Average Daily Net Assets | | Annual Fee | |

| On first $5 billion | | | 0.012 | % |

| Over $5 billion | | | 0.010 | % |

| The Hartford Growth Fund |

| Notes to Financial Statements – (continued) |

| October 31, 2011 |

| (000’s Omitted) |

| | c) | Operating Expenses – Allocable expenses incurred by the Company are allocated to each Fund and allocated to classes within the Fund in proportion to the average daily net assets of the Fund and each class, except where allocation of certain expenses is more fairly made directly to the Fund or to specific classes within a Fund. As of October 31, 2011, HIFSCO contractually limited the total operating expenses of this Fund, exclusive of taxes, interest expense, brokerage commissions, acquired fund fees and expenses and extraordinary expenses as follows: |

| Class A | | | Class B | | | Class C | | | Class I | | | Class R3 | | | Class R4 | | | Class R5 | | | Class Y | |

| | 1.25 | % | | | 2.00 | % | | | 2.00 | % | | | 1.00 | % | | | 1.50 | % | | | 1.20 | % | | | 0.90 | % | | | 0.85 | % |

From November 1, 2010 through February 28, 2011, HIFSCO contractually limited the total operating expenses of this Fund, exclusive of taxes, interest expense, brokerage commissions, acquired fund fees and expenses and extraordinary expenses as follows:

| Class A | | | Class B | | | Class C | | | Class I | | | Class R3 | | | Class R4 | | | Class R5 | | | Class Y | |

| | 1.30 | % | | | 2.05 | % | | | 2.05 | % | | | 1.05 | % | | | 1.50 | % | | | 1.20 | % | | | 0.90 | % | | | 0.85 | % |

| | d) | Fees Paid Indirectly – The Fund has entered into agreements with State Street Global Markets, LLC and Russell Implementation Services Inc. to partially recapture non-discounted trade commissions. Such rebates are used to pay a portion of the Fund’s expenses. In addition, the Fund’s custodian bank, State Street Bank and Trust Co., has also agreed to reduce its fees when the Fund maintains cash on deposit in a non-interest-bearing custody account. For the year ended October 31, 2011, these amounts are included in the Statement of Operations. |

The ratio of expenses to average net assets in the accompanying financial highlights excludes the reduction in expenses related to fees paid indirectly. The annualized expense ratio for the period listed below including the fees paid indirectly is as follows:

| | | Year Ended October 31, 2011 | |

| Class A Shares | | | 1.25 | % |

| Class B Shares | | | 2.04 | |

| Class C Shares | | | 1.95 | |

| Class I Shares | | | 0.95 | |

| Class R3 Shares | | | 1.50 | |

| Class R4 Shares | | | 1.19 | |

| Class R5 Shares | | | 0.90 | |

| Class Y Shares | | | 0.79 | |

| | e) | Distribution and Service Plan for Class A, B, C, R3 and R4 Shares – HIFSCO is the principal underwriter and distributor of the Fund. HIFSCO is engaged in distribution activities, which include marketing and distribution of shares through broker-dealers, financing distribution costs and maintaining financial books and records. For the year ended October 31, 2011, HIFSCO received front-end load sales charges of $456 and contingent deferred sales charges of $17 from the Fund. |

The Fund has adopted a Distribution and Service Plan in accordance with Rule 12b-1 of the 1940 Act to compensate the distributor (HIFSCO) for activities intended to result in the sale and distribution of Class A, B, C, R3 and R4 shares and for providing services for shareholders. During its May 3, 2011 meeting, the Board of Directors approved an amendment to the Fund’s Class A Plan to, effective August 1, 2011, lower the amount of Rule 12b-1 distribution fees that may be charged in respect of Class A shares of the Fund from an annual rate of 0.35% of the Fund’s average daily net assets attributable to Class A shares to 0.25%. The Board of Directors has authorized Rule 12b-1 payments of up to 0.25% of the Fund’s average daily net assets attributable to Class A shares. As a result, the amendment to the Class A Plan did not affect the fees charged under the plan. Some or all of the fee may be used for shareholder servicing expenses with the remainder used for distribution expenses. Some or the entire Rule 12b-1 fee for Class B shares may be remitted to

broker-dealers for distribution and/or shareholder account services. Under the Class B Plan, the Fund pays the distributor 1.00% of the average daily net assets of Class B shares that are outstanding for 8 years or less, 0.25% of which is a fee for services provided to existing shareholders with the remainder used for distribution expenses. After eight years, Class B shares convert to Class A shares. Upon conversion to Class A shares, the Class A plan described above will apply to those shares. Under the Class C Plan, the Fund pays the distributor 1.00% of the average daily net assets of Class C shares outstanding, 0.25% of which is intended as a fee for services provided to existing shareholders with the remainder used for distribution expenses. For Class C shares, some or the entire fee may be remitted to broker-dealers for distribution and/or shareholder account services. Class R3 shares have a distribution fee of 0.50% and Class R4 shares have a distribution fee of 0.25%. For Class R3 and R4 shares, some or the entire fee may be remitted to broker dealers for distribution and/or shareholder account services. The Fund’s 12b-1 fees are accrued daily and paid monthly.

For the year ended October 31, 2011, total sales commissions paid to affiliated brokers/dealers of The Hartford for distributing the Fund's shares were $50. These commissions are in turn paid to sales representatives of the broker/dealers.

| | f) | Other Related Party Transactions – Certain officers of the Fund are directors and/or officers of HIFSCO and/or The Hartford or its subsidiaries. For the year ended October 31, 2011, a portion of the Fund’s chief compliance officer’s compensation was paid by all of the investment companies in the Hartford fund complex. The portion allocated to the Fund was in the amount of $1. Hartford Administrative Services Company (“HASCO”), an indirect wholly-owned subsidiary of The Hartford, provides transfer agent services to the Fund. HASCO has contractually agreed to reimburse any portion of the transfer agency fees over 0.30% of average daily net assets per fiscal year for each class. HASCO was compensated on a per account basis, which varies by share class, for providing such services. The amount to HASCO and any related contractual reimbursement amounts, if applicable, can be found in the Statement of Operations. These fees are accrued daily and paid monthly. |

Administrative services fees are paid to HASCO for third-party recordkeeping services that are payable as a percentage of net assets in the amount of 0.20%, 0.15% and 0.10% for Classes R3, R4 and R5 shares, respectively. The total administrative services fees are shown on the Statement of Operations. These fees are accrued daily and paid monthly.

| | g) | Payment from Affiliate – On November 8, 2006, the SEC issued an order setting forth the terms of a settlement reached with three subsidiaries of The Hartford that resolved the SEC’s Division of Enforcement’s investigation of aspects of The Hartford’s variable annuity and mutual fund operations related to directed brokerage and revenue sharing. The Hartford settled this matter without admitting or denying the findings of the SEC. |

The total return in the accompanying financial highlights includes a payment from affiliate. Had the payment from affiliate been excluded, the impact and total return for the periods listed below would have been as follows:

| | | Impact from Payment from Affiliate for SEC Settlement for the Year Ended October 31, 2007 | | | Total Return Excluding Payment from Affiliate for the Year Ended October 31, 2007 | |

| Class A | | | 0.01 | % | | | 23.90 | % |

| Class B | | | 0.01 | | | | 23.00 | |

| Class C | | | 0.01 | | | | 23.08 | |

| Class I | | | 0.01 | | | | 24.35 | |

| Class L | | | 0.01 | | | | 24.20 | |

| Class Y | | | 0.01 | | | | 24.50 | |

| The Hartford Growth Fund |

| Notes to Financial Statements – (continued) |

| October 31, 2011 |

| (000’s Omitted) |

As of October 31, 2011, affiliates of The Hartford had ownership of shares in the Fund as follows:

| | | Shares | |

| Class R4 | | | 6 | |

| Class R5 | | | 7 | |

| 9. | Investment Transactions: |

For the year ended October 31, 2011, the Fund's aggregate purchases and sales of investment securities (excluding short-term investments) were as follows:

| | | Amount | |

| Cost of Purchases Excluding U.S. Government Obligations | | $ | 344,809 | |

| Sales Proceeds Excluding U.S. Government Obligations | | | 353,536 | |

| 10. | Capital Share Transactions: |

The following information is for the year ended October 31, 2011, and the year ended October 31, 2010:

| | | For the Year Ended October 31, 2011 | | | For the Year Ended October 31, 2010 | |

| | | | | | Shares Issued for Reinvested Dividends | | | | | | | | | Net Increase (Decrease) of Shares | | | | | | Shares Issued for Reinvested Dividends | | | | | | | | | Net Increase (Decrease) of Shares | |

| Class A | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Shares | | | 2,922 | | | | — | | | | (6,522 | ) | | | 10,830 | | | | 7,230 | | | | 2,081 | | | | — | | | | (4,737 | ) | | | — | | | | (2,656 | ) |

| Amount | | $ | 52,714 | | | $ | — | | | $ | (115,672 | ) | | $ | 168,113 | | | $ | 105,155 | | | $ | 30,559 | | | $ | — | | | $ | (69,762 | ) | | $ | — | | | $ | (39,203 | ) |

| Class B | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Shares | | | 52 | | | | — | | | | (399 | ) | | | — | | | | (347 | ) | | | 15 | | | | — | | | | (405 | ) | | | — | | | | (390 | ) |

| Amount | | $ | 761 | | | $ | — | | | $ | (5,835 | ) | | $ | — | | | $ | (5,074 | ) | | $ | 188 | | | $ | — | | | $ | (5,015 | ) | | $ | — | | | $ | (4,827 | ) |

| Class C | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Shares | | | 285 | | | | — | | | | (721 | ) | | | — | | | | (436 | ) | | | 284 | | | | — | | | | (961 | ) | | | — | | | | (677 | ) |

| Amount | | $ | 4,183 | | | $ | — | | | $ | (10,598 | ) | | $ | — | | | $ | (6,415 | ) | | $ | 3,522 | | | $ | — | | | $ | (11,854 | ) | | $ | — | | | $ | (8,332 | ) |

| Class I | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Shares | | | 5,804 | | | | — | | | | (1,371 | ) | | | — | | | | 4,433 | | | | 1,726 | | | | 15 | | | | (2,059 | ) | | | — | | | | (318 | ) |

| Amount | | $ | 103,384 | | | $ | — | | | $ | (24,268 | ) | | $ | — | | | $ | 79,116 | | | $ | 25,815 | | | $ | 221 | | | $ | (30,715 | ) | | $ | — | | | $ | (4,679 | ) |

| Class L | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Shares | | | 172 | | | | — | | | | (1,051 | ) | | | (10,593 | ) | | | (11,472 | ) | | | 182 | | | | 32 | | | | (1,568 | ) | | | — | | | | (1,354 | ) |

| Amount | | $ | 3,138 | | | $ | — | | | $ | (19,363 | ) | | $ | (168,113 | ) | | $ | (184,338 | ) | | $ | 2,760 | | | $ | 480 | | | $ | (23,536 | ) | | $ | — | | | $ | (20,296 | ) |

| Class R3 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Shares | | | 9 | | | | — | | | | (6 | ) | | | — | | | | 3 | | | | 5 | | | | — | | | | (3 | ) | | | — | | | | 2 | |

| Amount | | $ | 164 | | | $ | — | | | $ | (103 | ) | | $ | — | | | $ | 61 | | | $ | 75 | | | $ | — | | | $ | (39 | ) | | $ | — | | | $ | 36 | |

| Class R4 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Shares | | | 47 | | | | — | | | | (34 | ) | | | — | | | | 13 | | | | 49 | | | | — | | | | (20 | ) | | | — | | | | 29 | |

| Amount | | $ | 857 | | | $ | — | | | $ | (627 | ) | | $ | — | | | $ | 230 | | | $ | 751 | | | $ | 5 | | | $ | (307 | ) | | $ | — | | | $ | 449 | |

| Class R5 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Shares | | | 32 | | | | — | | | | (1 | ) | | | — | | | | 31 | | | | 9 | | | | — | | | | (7 | ) | | | — | | | | 2 | |

| Amount | | $ | 555 | | | $ | — | | | $ | (15 | ) | | $ | — | | | $ | 540 | | | $ | 137 | | | $ | 1 | | | $ | (112 | ) | | $ | — | | | $ | 26 | |

| Class Y | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Shares | | | 1,580 | | | | — | | | | (589 | ) | | | — | | | | 991 | | | | 501 | | | | 33 | | | | (1,622 | ) | | | — | | | | (1,088 | ) |

| Amount | | $ | 28,941 | | | $ | — | | | $ | (10,888 | ) | | $ | — | | | $ | 18,053 | | | $ | 7,596 | | | $ | 508 | | | $ | (24,965 | ) | | $ | — | | | $ | (16,861 | ) |

| Total | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Shares | | | 10,903 | | | | — | | | | (10,694 | ) | | | 237 | | | | 446 | | | | 4,852 | | | | 80 | | | | (11,382 | ) | | | — | | | | (6,450 | ) |

| Amount | | $ | 194,697 | | | $ | — | | | $ | (187,369 | ) | | $ | — | | | $ | 7,328 | | | $ | 71,403 | | | $ | 1,215 | | | $ | (166,305 | ) | | $ | — | | | $ | (93,687 | ) |

The following reflects the conversion of Class B shares into Class A shares (reflected as Class A shares sold) for the year ended October 31, 2011, and the year ended October 31, 2010:

| | | Shares | | | Dollars | |

| For the Year Ended October 31, 2011 | | | 88 | | | $ | 1,544 | |

| For the Year Ended October 31, 2010 | | | 67 | | | $ | 1,005 | |

The Fund is one of several Hartford funds that participate in a $500 million committed revolving line of credit facility. The facility is to be used for temporary or emergency purposes. Under the arrangement, the funds are required to own securities having a market value in excess of 300% of the total bank borrowings. The interest rate on borrowings varies depending on the nature of the loan. The facility also requires a fee to be paid based on the amount of the commitment. This commitment fee is allocated to all of the funds participating in the line of credit based on the average net assets of the funds. During the year ended October 31, 2011, the Fund did not have any borrowings under this facility.

At its May 3, 2011, meeting, the Board of Directors of The Hartford Mutual Funds II, Inc. approved the reclassification of Class L shares into Class A shares of the Fund.

Effective with the close of business on August 5, 2011, Class L was merged into Class A. The merger was accomplished by a tax-free exchange as detailed below:

| | | Class A | | | Class L | |

| Shares exchanged | | | N/A | | | | 10,593 | |

| Shares issued - to Class L shareholders | | | 10,830 | | | | N/A | |

| Net assets immediately before merger | | $ | 229,124 | | | $ | 179,517 | |

| Net assets immediately after merger | | $ | 408,641 | | | | N/A | |

| 13. | Industry Classifications: |

Other than the industry classifications “Other Investment Pools and Funds” and “Exchange Traded Funds,” equity industry classifications used in this report are the Global Industry Classification Standard, which was developed by and is the exclusive property and service mark of MSCI, Inc. and Standard & Poor’s.

| 14. | Pending Legal Proceedings: |

On February 25, 2011, Jennifer L. Kasilag, Louis Mellinger, Judith M. Menendez, Jacqueline M. Robinson, and Linda A. Russell filed a derivative lawsuit against HIFSCO on behalf of six funds: The Hartford Global Health Fund (now known as The Hartford Healthcare Fund), The Hartford Conservative Allocation Fund, The Hartford Growth Opportunities Fund, The Hartford Inflation Plus Fund, The Hartford Advisers Fund and The Hartford Money Market Fund. The lawsuit, which was filed in the United States District Court for the District of New Jersey, seeks recovery under Section 36(b) of the 1940 Act for the alleged overpayment of investment management and 12b-1 distribution fees to HIFSCO. The plaintiffs seek recovery of the alleged overpayments or, alternatively, rescission of the contracts and restitution of all fees paid, together with lost earnings. On November 14, 2011, the plaintiffs filed an amended complaint, which dropped The Hartford Money Market Fund and added The Hartford Capital Appreciation Fund as a plaintiff. The Hartford intends to vigorously defend the action.

| The Hartford Growth Fund |

| Notes to Financial Statements – (continued) |

| October 31, 2011 |

| (000’s Omitted) |