UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORMN-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number:811-00558

THE HARTFORD MUTUAL FUNDS II, INC.

(Exact name of registrant as specified in charter)

690 Lee Road, Wayne, Pennsylvania 19087

(Address of Principal Executive Offices) (Zip Code)

Thomas R. Phillips, Esquire

Hartford Funds Management Company, LLC

690 Lee Road

Wayne, Pennsylvania 19087

(Name and Address of Agent for Service)

Copy to:

John V. O’Hanlon, Esq.

Dechert LLP

One International Place, 40th Floor

100 Oliver Street

Boston, MA 02110-2605

Registrant’s telephone number, including area code: (610)386-4068

Date of fiscal year end: September 30

Date of reporting period: September 30, 2019

FormN-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule30e-1 under the Investment Company Act of 1940 (17 CFR270.30e-1). The Commission may use the information provided on FormN-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by FormN-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in FormN-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

Hartford Funds

Our benchmark is the investor*.

Hartford Multifactor Funds

Annual Report

September 30, 2019

Hartford Multifactor International Fund

Hartford Multifactor Large Cap Value Fund

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of each Fund’s shareholder reports like this one will no longer be sent by mail, unless you specifically request paper copies of the reports from the Fund or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on the Funds’ website (www.hartfordfunds.com). You will be notified by mail each time a report is posted and provided with a website link to access the report. You may at any time elect to receive paper copies of all shareholder reports free of charge by contacting your financial intermediary or, if you invest directly with a Fund, by calling 1-888-843-7824. Your election to receive reports in paper will apply to all Hartford Funds held in your account if you invest through your financial intermediary or directly with a Fund.

If you previously elected to receive shareholder reports and other communications electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications electronically anytime by contacting your financial intermediary.

A MESSAGE FROM THE PRESIDENT

Dear Fellow Shareholders:

Thank you for investing in Hartford Multifactor Mutual Funds. The following is the Funds’ Annual Report covering the fiscal period ended September 30, 2019.

Market Review

During the 12 months ended September 30, 2019, U.S. stocks, as measured by the S&P 500 Index (the “Index”),1 gained 4.25%.

Political uncertainty remained a core driver of increased market volatility throughout the period. Escalating trade tensions between the U.S. and China, continued debate over how the UK will handle its departure from the European Union, and the September announcement of an impeachment inquiry against President Trump all weighed on markets.

Against this backdrop, however, July 1, 2019 marked a significant milestone: The U.S. entered the longest period of economic expansion on record, according to The National Bureau of Economic Research. Strong consumer spending in the U.S. has continued to buoy the domestic economy, helped by an unemployment rate that stayed at or below 4% throughout the 12-month period ended September 30, 2019.

However, signs of a slowing global economy prompted central banks around the world to shift to more accommodating monetary policy. The U.S. Federal Reserve cut interest rates in July and September 2019, to 1.75-2%, while the European Central Bank, which already had established negative interest rates, further cut its rate to -0.5% as of September 18, 2019.

Politics, both at home and abroad, are likely to continue to play a key role in market movements this year. For this reason, we encourage you to maintain a strong relationship with your financial advisor, who can help guide you through shifting markets confidently. He or she can help you proactively build a portfolio that takes market uncertainty into account, along with your unique investment goals and risk tolerances. Your advisor can help you find a fit within our family of funds as you work toward those goals.

Thank you again for investing in Hartford Multifactor Mutual Funds. For the most up-to-date information on our funds, please take advantage of all the resources available at hartfordfunds.com.

James Davey

President

Hartford Funds

| 1 | S&P 500 Index is a market capitalization-weighted price index composed of 500 widely held common stocks. |

Hartford Multifactor Funds

| 2 | ||||

| 6 | ||||

| 7 | ||||

Financial Statements: | ||||

Schedules of Investments: | ||||

| 8 | ||||

| 14 | ||||

| 17 | ||||

| 18 | ||||

| 19 | ||||

| 20 | ||||

| 21 | ||||

| 22 | ||||

| 32 | ||||

| 33 | ||||

How to Obtain a Copy of each Fund’s Proxy Voting Policies and Voting Records (Unaudited) | 37 | |||

| 37 | ||||

Approval of Investment Management and InvestmentSub-Advisory Agreements (Unaudited) | 38 | |||

The views expressed in each Fund’s Manager Discussion contained in the Fund Overview section are views of that Fund’ssub-adviser and portfolio management team through the end of the period and are subject to change based on market and other conditions. Each Fund’s Manager Discussion is for informational purposes only and does not represent an offer, recommendation or solicitation to buy, hold or sell any security. The specific securities identified and described, if any, do not represent all of the securities purchased or sold and you should not assume that investments in the securities identified and discussed will be profitable.

| Hartford Multifactor International Fund |

September 30, 2019 (Unaudited)

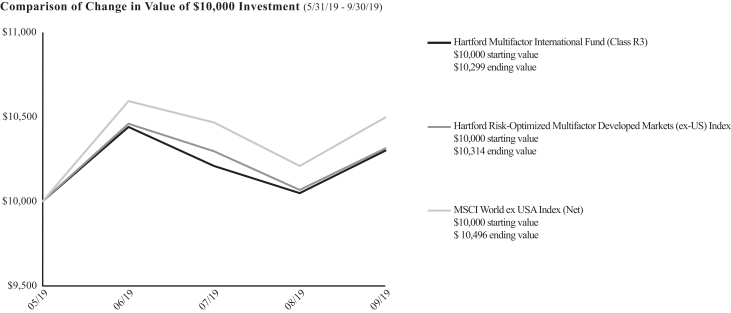

Inception 5/31/2019 (sub-advised by Mellon Investments Corporation) | Investment objective – The Fund seeks to provide investment results that, before fees and expenses, correspond to the total return performance of an index that tracks the performance of companies located in major developed markets of Europe, Canada and the Pacific Region. |

The chart above represents the hypothetical growth of a $10,000 investment in the Fund. The difference in returns between the Fund and the Index was primarily the result of the Fund’s operating expenses, including transaction costs, that are not reflected in the Index’s results.

Cumulative Total Returns

for the Period Ending 9/30/19

| Since Inception1 | ||||

Class R3 | 2.99% | |||

Class R4 | 3.02% | |||

Class R5 | 3.04% | |||

Class R6 | 3.05% | |||

Class Y | 3.04% | |||

Class F | 3.05% | |||

Hartford Risk-Optimized Multifactor Developed Markets (ex-US) Index | 3.14% | |||

MSCI World ex USA Index (Net) | 4.96% | |||

| 1 | Inception: 5/31/2019. Cumulative returns not annualized. |

PERFORMANCE DATA QUOTED REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE FUTURE RESULTS. The investment return and principal value of the investment will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. The chart and table do not reflect the deductions of taxes that a shareholder would pay on Fund distributions or the redemption or sale of Fund shares. Current performance may be lower or higher than the performance data quoted. To obtain performance data current to the most recentmonth-end, please visit our website hartfordfunds.com.

Total returns presented above were calculated using the Fund’s net asset value available to shareholders for sale or redemption of Fund shares on September 30, 2019, which may exclude investment transactions as of this date. All share class returns assume the reinvestment of all distributions at net asset value and the deduction of all fund expenses.

You cannot invest directly in an index.

See “Benchmark Glossary” for benchmark descriptions.

Performance information may reflect historical or current expense waivers/reimbursements without which performance would have been lower. For more information on current expense waivers/reimbursements, please see the prospectus.

Operating Expenses*

| Gross | Net | |||||||

Class R3 | 1.18% | 1.04% | ||||||

Class R4 | 0.88% | 0.74% | ||||||

Class R5 | 0.58% | 0.44% | ||||||

Class R6 | 0.46% | 0.34% | ||||||

Class Y | 0.57% | 0.44% | ||||||

Class F | 0.46% | 0.34% | ||||||

| * | Expenses as shown in the Fund’s most recent prospectus. Gross expenses do not reflect contractual expense reimbursement arrangements. Net expenses reflect such arrangements in instances when they reduce gross expenses. These arrangements remain in effect until May 31, 2020 unless the Fund’s Board of Directors approves an earlier termination. Actual expenses may be higher or lower. Please see accompanying Financial Highlights for expense ratios for the period ended September 30, 2019. |

| 2 |

|

| Hartford Multifactor International Fund |

Fund Overview – (continued)

September 30, 2019 (Unaudited)

Manager Discussion

Hartford Multifactor International Fund (“the Fund”) seeks to provide investment results that, before fees and expenses, correspond to the total return performance of Hartford Risk-Optimized Multifactor Developed Markets (ex-US) Index (LRODMX) (“the Index”), which tracks the performance of companies located in major developed markets of Europe, Canada, and the Pacific Region.

The Fund seeks to generate returns by investing in index constituents that are selected and weighted through a rules-based methodology that seeks to:

1) Deliberately Allocate Risks by providing exposure to the growth potential of international companies while explicitly seeking to reduce volatility and drawdown risk.

2) Improve Diversification by diversifying exposure across developed market economies and potentially reducing individual country, currency, and individual company risks.

3) Enhance Return Potential by selecting companies with a favorable combination of low valuation (50%), high momentum (30%), and high quality (20%) investment factors.

4) Maintain Consistency by reapplying the index methodology twice a year in March and September to maintain intended investment exposures.

Class F shares of the Fund returned 3.05% at net asset value (“NAV”) for the fiscal period ending September 30, 2019 compared to the Hartford Risk-Optimized Multifactor Developed Markets (ex-US) Index, which returned 3.14% for the same period. The difference in returns between the Fund and the Index was primarily the result of transaction costs and operating expenses that are not reflected in the Index’s results. Derivatives were not used in the Fund in a significant manner and did not affect the Fund’s performance during the period.

Important Risks

Investing involves risk, including the possible loss of principal. Security prices fluctuate in value depending on general market and economic conditions and the prospects of individual companies.• Foreign investments may be more volatile and less liquid than U.S. investments and are subject to the risk of currency fluctuations and adverse political and economic developments.• Investments focused in a sector, industry or group of industries may increase volatility and risk.•The Fund is not actively managed but rather attempts to track the performance of an index. The Fund’s returns may diverge from that of the index.

Composition by Sector(1)

as of September 30, 2019

| Sector | Percentage of Net Assets | |||

Equity Securities |

| |||

Communication Services | 7.0 | % | ||

Consumer Discretionary | 10.1 | |||

Consumer Staples | 9.3 | |||

Energy | 5.0 | |||

Financials | 21.2 | |||

Health Care | 11.8 | |||

Industrials | 13.4 | |||

Information Technology | 5.8 | |||

Materials | 5.2 | |||

Real Estate | 6.2 | |||

Utilities | 6.1 | |||

|

| |||

Total | 101.1 | % | ||

|

| |||

Short-Term Investments | 0.0 | * | ||

Other Assets & Liabilities | (1.1 | ) | ||

|

| |||

Total | 100.0 | % | ||

|

| |||

| * | Percentage rounds to zero. |

| (1) | A sector may be comprised of several industries. For Fund compliance purposes, the Fund may not use the same classification system. These sector classifications are used for financial reporting purposes. |

| 3 |

|

| Hartford Multifactor Large Cap Value Fund |

Fund Overview

September 30, 2019 (Unaudited)

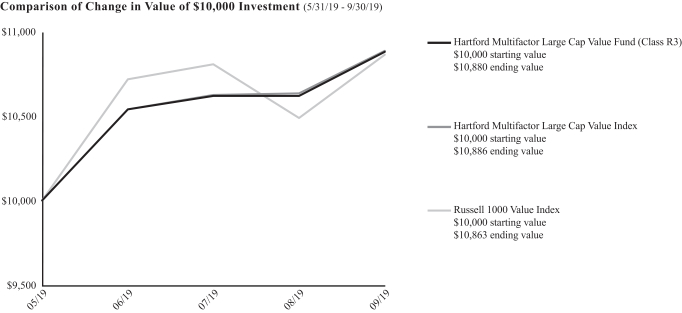

Inception 5/31/2019 (sub-advised by Mellon Investments Corporation) | Investment objective – The Fund seeks to provide investment results that, before fees and expenses, correspond to the total return performance of an index that tracks the performance of exchange traded value-oriented U.S. equity securities. |

The chart above represents the hypothetical growth of a $10,000 investment in the Fund. The difference in returns between the Fund and the Index was primarily the result of the Fund’s operating expenses, including transaction costs, that are not reflected in the Index’s results.

Cumulative Total Returns

for the Period Ending 9/30/19

| Since Inception1 | ||||

Class R3 | 8.80% | |||

Class R4 | 8.80% | |||

Class R5 | 8.80% | |||

Class R6 | 8.80% | |||

Class Y | 8.80% | |||

Class F | 8.80% | |||

Hartford Multifactor Large Cap Value Index | 8.86% | |||

Russell 1000 Value Index | 8.63% | |||

| 1 | Inception: 5/31/2019. Cumulative returns not annualized. |

PERFORMANCE DATA QUOTED REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE FUTURE RESULTS. The investment return and principal value of the investment will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. The chart and table do not reflect the deductions of taxes that a shareholder would pay on Fund distributions or the redemption or sale of Fund shares. Current performance may be lower or higher than the performance data quoted. To obtain performance data current to the most recentmonth-end, please visit our website hartfordfunds.com.

Total returns presented above were calculated using the Fund’s net asset value available to shareholders for sale or redemption of Fund shares on September 30, 2019, which may exclude investment transactions as of this date. All share class returns assume the reinvestment of all distributions at net asset value and the deduction of all fund expenses.

You cannot invest directly in an index.

See “Benchmark Glossary” for benchmark descriptions.

Performance information may reflect historical or current expense waivers/reimbursements without which performance would have been lower. For more information on current expense waivers/reimbursements, please see the prospectus.

Operating Expenses*

| Gross | Net | |||||||

Class R3 | 1.08% | 0.94% | ||||||

Class R4 | 0.78% | 0.64% | ||||||

Class R5 | 0.48% | 0.34% | ||||||

Class R6 | 0.36% | 0.24% | ||||||

Class Y | 0.47% | 0.34% | ||||||

Class F | 0.36% | 0.24% | ||||||

| * | Expenses as shown in the Fund’s most recent prospectus. Gross expenses do not reflect contractual expense reimbursement arrangements. Net expenses reflect such arrangements in instances when they reduce gross expenses. These arrangements remain in effect until May 31, 2020 unless the Fund’s Board of Directors approves an earlier termination. Actual expenses may be higher or lower. Please see accompanying Financial Highlights for expense ratios for the period ended September 30, 2019. |

| 4 |

|

| Hartford Multifactor Large Cap Value Fund |

Fund Overview – (continued)

September 30, 2019 (Unaudited)

Manager Discussion

Hartford Multifactor Large Cap Value Fund (“the Fund”) seeks to provide investment results that, before fees and expenses, correspond to the total return performance of Hartford Multifactor Large Cap Value Index (HMLCVX) (“the Index”), which tracks the performance of exchange traded value-oriented US equity securities.

The Fund seeks to generate returns by investing in index constituents that are selected and weighted through a rules-based methodology that seeks to:

1) Deliberately Allocate Risks by providing exposure to the growth potential of value-oriented US companies while explicitly seeking to reduce volatility and drawdown risk.

2) Improve Diversification by diversifying exposure across sectors and potentially reducing individual company risks.

3) Enhance Return Potential by selecting companies with a favorable combination of low valuation (50%), high momentum (30%), and high quality (20%) investment factors.

4) Maintain Consistency by reapplying the index methodology twice a year in March and September to maintain intended investment exposures.

Class F shares of the Fund returned 8.80% at net asset value (“NAV”) for the fiscal period ending September 30, 2019 compared to the Hartford Multifactor Large Cap Value Index, which returned 8.86% for the same period. The difference in returns between the Fund and the Index was primarily the result of transaction costs and operating expenses that are not reflected in the Index’s results. Derivatives were not used in the Fund in a significant manner and did not affect the Fund’s performance during the period.

Important Risks

Investing involves risk, including the possible loss of principal. Security prices fluctuate in value depending on general market and economic conditions and the prospects of individual companies.•Investments focused in a sector, industry or group of industries may increase volatility and risk.•The Fund is not actively managed but rather attempts to track the performance of an index. The Fund’s returns may diverge from that of the index.

Composition by Sector(1)

as of September 30, 2019

| Sector | Percentage of Net Assets | |||

Equity Securities |

| |||

Communication Services | 9.1 | % | ||

Consumer Discretionary | 7.1 | |||

Consumer Staples | 8.8 | |||

Energy | 6.6 | |||

Financials | 27.1 | |||

Health Care | 12.0 | |||

Industrials | 9.4 | |||

Information Technology | 7.7 | |||

Materials | 4.5 | |||

Real Estate | 4.1 | |||

Utilities | 7.2 | |||

|

| |||

Total | 103.6 | % | ||

|

| |||

Short-Term Investments | 0.1 | |||

Other Assets & Liabilities | (3.7 | ) | ||

|

| |||

Total | 100.0 | % | ||

|

| |||

| (1) | A sector may be comprised of several industries. For Fund compliance purposes, the Fund may not use the same classification system. These sector classifications are used for financial reporting purposes. |

| 5 |

|

| Hartford Multifactor Funds |

Hartford Risk-Optimized Multifactor Developed Markets(ex-US) Indexseeks to address risks and opportunities within developed market stocks located outside the United States by selecting equity securities exhibiting a favorable combination of factors, including value, momentum, and quality.

Hartford Multifactor Large Cap Value Index is designed to capture the performance potential of US equities by seeking the enhanced return potential of multiple risk factors while maintaining targeted ranges of exposures across size and sector dimensions.

MSCI World ex USA Index (Net)(reflects no deduction for fees, expenses or other taxes) is a free float-adjusted market capitalization index that is designed to capture large and mid cap representation across developed markets countries – excluding the United States.

Neither MSCI nor any other party involved in or related to compiling, computing or creating the MSCI data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling, computing or creating the data have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted without MSCI’s express written consent.

Russell 1000 Value Index(reflects no deduction for fees, expenses or taxes) is designed to measure the performance of those Russell 1000 Index companies with lowerprice-to-book ratios and lower forecasted growth values. The Russell 1000 Index is designed to measure the performance of the 1,000 largest companies in the Russell 3000 Index based on their market capitalization and current index membership.

| 6 |

|

| Hartford Multifactor Funds |

Your Fund’s Expenses

As a shareholder of a Fund, you incur two types of costs: (1) transaction costs and (2) ongoing costs, including investment management fees, distribution and/or service(12b-1) fees, if any, and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period of May 31, 2019 (commencement of operations) through September 30, 2019, except as indicated below. To the extent a Fund was subject to acquired fund fees and expenses during the period, acquired fund fees and expenses are not included in the annualized expense ratios below.

Actual Expenses

The first set of columns of the table below provides information about actual account values and actual expenses. You may use this information, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the line under the heading entitled “Expenses Paid During The Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second set of columns of the table below provides information about hypothetical account values and hypothetical expenses based on a Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in a Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the second set of columns of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would be higher. Expenses for a class of a Fund are equal to the class’s annualized expense ratio multiplied by average account value over the period, multiplied by 183/365 (to reflect theone-half year period).

| Actual Return | Hypothetical (5% return before expenses)* | |||||||||||||||||||||||||||

| Beginning Account Value May 31, 2019 | Ending Account Value September 30, 2019 | Expenses paid during the period May 31, 2019 through September 30, 2019(2) | Beginning Account Value April 1, 2019 | Ending Account Value September 30, 2019 | Expenses paid during the period April 1, 2019 through September 30, 2019 | Annualized expense ratio | ||||||||||||||||||||||

Hartford Multifactor International Fund(1) |

| |||||||||||||||||||||||||||

Class R3 | $ | 1,000.00 | $ | 1,029.90 | $ | 1.59 | $ | 1,000.00 | $ | 1,022.71 | $ | 2.38 | 0.47 | % | ||||||||||||||

Class R4 | $ | 1,000.00 | $ | 1,030.20 | $ | 1.39 | $ | 1,000.00 | $ | 1,023.01 | $ | 2.08 | 0.41 | % | ||||||||||||||

Class R5 | $ | 1,000.00 | $ | 1,030.40 | $ | 1.19 | $ | 1,000.00 | $ | 1,023.31 | $ | 1.78 | 0.35 | % | ||||||||||||||

Class R6 | $ | 1,000.00 | $ | 1,030.50 | $ | 1.15 | $ | 1,000.00 | $ | 1,023.36 | $ | 1.72 | 0.34 | % | ||||||||||||||

Class Y | $ | 1,000.00 | $ | 1,030.40 | $ | 1.19 | $ | 1,000.00 | $ | 1,023.31 | $ | 1.78 | 0.35 | % | ||||||||||||||

Class F | $ | 1,000.00 | $ | 1,030.50 | $ | 1.15 | $ | 1,000.00 | $ | 1,023.36 | $ | 1.72 | 0.34 | % | ||||||||||||||

Hartford Multifactor Large Cap Value Fund(1) |

| |||||||||||||||||||||||||||

Class R3 | $ | 1,000.00 | $ | 1,088.00 | $ | 1.29 | $ | 1,000.00 | $ | 1,023.21 | $ | 1.88 | 0.37 | % | ||||||||||||||

Class R4 | $ | 1,000.00 | $ | 1,088.00 | $ | 1.08 | $ | 1,000.00 | $ | 1,023.51 | $ | 1.57 | 0.31 | % | ||||||||||||||

Class R5 | $ | 1,000.00 | $ | 1,088.00 | $ | 0.87 | $ | 1,000.00 | $ | 1,023.82 | $ | 1.27 | 0.25 | % | ||||||||||||||

Class R6 | $ | 1,000.00 | $ | 1,088.00 | $ | 0.84 | $ | 1,000.00 | $ | 1,023.87 | $ | 1.22 | 0.24 | % | ||||||||||||||

Class Y | $ | 1,000.00 | $ | 1,088.00 | $ | 0.87 | $ | 1,000.00 | $ | 1,023.82 | $ | 1.27 | 0.25 | % | ||||||||||||||

Class F | $ | 1,000.00 | $ | 1,088.00 | $ | 0.84 | $ | 1,000.00 | $ | 1,023.87 | $ | 1.22 | 0.24 | % | ||||||||||||||

| * | Please note that while the Funds commenced operations on May 31, 2019, the hypothetical expenses paid during the period reflect projected activity for the full six month period for purposes of comparability. This projection assumes that annualized expense ratios were in effect during the period April 1, 2019 to September 30, 2019. |

| (1) | Commenced operations on May 31, 2019. |

| (2) | Expenses paid during the period May 31, 2019 through September 30, 2019. |

| 7 |

|

Schedule of Investments

September 30, 2019

| Shares or Principal Amount | Market Value† | |||||||

| COMMON STOCKS - 101.1% | ||||||||

| Australia - 8.5% | ||||||||

| 1,040 | AGL Energy Ltd. | $ | 13,455 | |||||

| 594 | Amcor plc | 5,717 | ||||||

| 272 | Ansell Ltd. | 5,035 | ||||||

| 639 | Aurizon Holdings Ltd. | 2,547 | ||||||

| 761 | AusNet Services | 932 | ||||||

| 336 | Australia & New Zealand Banking Group Ltd. | 6,455 | ||||||

| 1,082 | Bendigo & Adelaide Bank Ltd. | 8,395 | ||||||

| 484 | BHP Group Ltd. | 11,960 | ||||||

| 1,079 | Caltex Australia Ltd. | 19,172 | ||||||

| 539 | CIMIC Group Ltd. | 11,453 | ||||||

| 1,159 | Coca-Cola Amatil Ltd. | 8,340 | ||||||

| 55 | Cochlear Ltd. | 7,740 | ||||||

| 237 | Coles Group Ltd. | 2,464 | ||||||

| 152 | Commonwealth Bank of Australia | 8,292 | ||||||

| 48 | CSL Ltd. | 7,589 | ||||||

| 1,060 | Dexus REIT | 8,538 | ||||||

| 1,809 | GPT Group REIT | 7,523 | ||||||

| 388 | Insurance Australia Group Ltd. | 2,070 | ||||||

| 47 | Macquarie Group Ltd. | 4,166 | ||||||

| 3,628 | Mirvac Group REIT | 7,495 | ||||||

| 170 | National Australia Bank Ltd. | 3,409 | ||||||

| 1,623 | Orora Ltd. | 3,167 | ||||||

| 2,583 | Qantas Airways Ltd. | 10,977 | ||||||

| 69 | Ramsay Health Care Ltd. | 3,023 | ||||||

| 4,264 | Scentre Group REIT | 11,313 | ||||||

| 426 | Sonic Healthcare Ltd. | 8,078 | ||||||

| 849 | South32 Ltd. | 1,497 | ||||||

| 1,075 | Stockland REIT | 3,302 | ||||||

| 192 | Suncorp Group Ltd.* | 1,771 | ||||||

| 4,341 | Telstra Corp. Ltd. | 10,290 | ||||||

| 3,618 | Vicinity Centres REIT | 6,277 | ||||||

| 6,441 | Viva Energy Group Ltd.(1) | 8,487 | ||||||

| 49 | Washington H Soul Pattinson & Co., Ltd. | 696 | ||||||

| 854 | Wesfarmers Ltd. | 22,945 | ||||||

| 150 | Westpac Banking Corp. | 2,996 | ||||||

| 537 | Whitehaven Coal Ltd. | 1,129 | ||||||

| 588 | Woolworths Group Ltd. | 14,796 | ||||||

|

| |||||||

| 263,491 | ||||||||

|

| |||||||

| Austria - 0.3% | ||||||||

| 75 | BAWAG Group AG*(1) | 2,951 | ||||||

| 28 | Lenzing AG | 2,697 | ||||||

| 38 | Oesterreichische Post AG | 1,334 | ||||||

| 31 | OMV AG | 1,661 | ||||||

| 145 | UNIQA Insurance Group AG | 1,310 | ||||||

|

| |||||||

| 9,953 | ||||||||

|

| |||||||

| Belgium - 2.0% | ||||||||

| 15 | Ackermans & van Haaren N.V. | 2,278 | ||||||

| 222 | Ageas | 12,307 | ||||||

| 246 | Colruyt S.A. | 13,476 | ||||||

| 27 | Elia System Operator S.A. | 2,207 | ||||||

| 556 | Proximus SADP | 16,521 | ||||||

| 16 | Sofina S.A. | 3,553 | ||||||

| 119 | Telenet Group Holding N.V. | 5,616 | ||||||

| 80 | UCB S.A. | 5,804 | ||||||

|

| |||||||

| 61,762 | ||||||||

|

| |||||||

| Canada - 11.4% | ||||||||

| 193 | Air Canada* | 6,295 | ||||||

| 358 | Alimentation Couche-Tard, Inc. Class B | 10,971 | ||||||

| 75 | Atco Ltd. Class I | 2,744 | ||||||

| 270 | Bank of Montreal | 19,886 | ||||||

| 135 | Bank of Nova Scotia | 7,668 | ||||||

| 263 | BCE, Inc. | 12,721 | ||||||

| 202 | Canadian Apartment Properties REIT | 8,305 | ||||||

| Shares or Principal Amount | Market Value† | |||||||

| COMMON STOCKS - 101.1% - (continued) | ||||||||

| Canada - 11.4% - (continued) | ||||||||

| 29 | Canadian Imperial Bank of Commerce | $ | 2,393 | |||||

| 66 | Canadian Tire Corp. Ltd. Class A | 7,406 | ||||||

| 61 | Canadian Utilities Ltd. Class A | 1,798 | ||||||

| 271 | Capital Power Corp. | 6,276 | ||||||

| 235 | CGI, Inc.* | 18,582 | ||||||

| 4 | Constellation Software, Inc. | 3,995 | ||||||

| 83 | Emera, Inc. | 3,644 | ||||||

| 491 | Empire Co., Ltd. Class A | 13,294 | ||||||

| 5 | Fairfax Financial Holdings Ltd. | 2,204 | ||||||

| 42 | Fortis, Inc. | 1,776 | ||||||

| 162 | George Weston Ltd. | 13,629 | ||||||

| 661 | Great-West Lifeco, Inc. | 15,871 | ||||||

| 316 | Husky Energy, Inc. | 2,223 | ||||||

| 704 | Hydro One Ltd.(1) | 13,013 | ||||||

| 160 | iA Financial Corp., Inc. | 7,281 | ||||||

| 151 | Imperial Oil Ltd. | 3,932 | ||||||

| 65 | Intact Financial Corp. | 6,542 | ||||||

| 209 | Loblaw Cos., Ltd. | 11,904 | ||||||

| 31 | Magna International, Inc. | 1,652 | ||||||

| 468 | Manulife Financial Corp. | 8,584 | ||||||

| 183 | Metro, Inc. | 8,057 | ||||||

| 48 | National Bank of Canada | 2,388 | ||||||

| 13 | Onex Corp. | 806 | ||||||

| 37 | Open Text Corp. | 1,509 | ||||||

| 311 | Parkland Fuel Corp. | 9,974 | ||||||

| 442 | Power Corp. of Canada | 10,182 | ||||||

| 653 | Power Financial Corp. | 15,141 | ||||||

| 43 | Quebecor, Inc. Class B | 976 | ||||||

| 293 | RioCan Real Estate Investment Trust REIT | 5,834 | ||||||

| 240 | Rogers Communications, Inc. Class B | 11,690 | ||||||

| 232 | Royal Bank of Canada | 18,819 | ||||||

| 126 | Saputo, Inc. | 3,873 | ||||||

| 139 | Shaw Communications, Inc. Class B | 2,731 | ||||||

| 404 | Sun Life Financial, Inc. | 18,065 | ||||||

| 178 | Suncor Energy, Inc. | 5,615 | ||||||

| 279 | TELUS Corp. | 9,929 | ||||||

| 29 | Thomson Reuters Corp. | 1,940 | ||||||

| 68 | Toromont Industries Ltd. | 3,285 | ||||||

| 129 | Toronto-Dominion Bank | 7,522 | ||||||

|

| |||||||

| 352,925 | ||||||||

|

| |||||||

| China - 0.3% | ||||||||

| 1,000 | Kerry Logistics Network Ltd. | 1,599 | ||||||

| 8,700 | Yangzijiang Shipbuilding Holdings Ltd. | 6,049 | ||||||

|

| |||||||

| 7,648 | ||||||||

|

| |||||||

| Denmark - 1.9% | ||||||||

| 7 | Carlsberg A/S Class B | 1,035 | ||||||

| 48 | Coloplast A/S Class B | 5,775 | ||||||

| 26 | GN Store Nord A/S | 1,054 | ||||||

| 274 | H. Lundbeck A/S | 9,084 | ||||||

| 206 | ISS A/S | 5,093 | ||||||

| 355 | Novo Nordisk A/S Class B | 18,345 | ||||||

| 70 | Orsted A/S(1) | 6,507 | ||||||

| 18 | Pandora A/S | 722 | ||||||

| 17 | Rockwool International A/S Class B | 3,399 | ||||||

| 92 | Topdanmark A/S | 4,441 | ||||||

| 127 | Tryg A/S | 3,639 | ||||||

|

| |||||||

| 59,094 | ||||||||

|

| |||||||

| Finland - 0.8% | ||||||||

| 223 | DNA Oyj | 5,076 | ||||||

| 50 | Elisa Oyj | 2,578 | ||||||

| 45 | Kesko Oyj Class B | 2,842 | ||||||

| 48 | Kone Oyj Class B | 2,732 | ||||||

| 34 | Neste Oyj | 1,125 | ||||||

The accompanying notes are an integral part of these financial statements.

| 8 |

|

| Hartford Multifactor International Fund |

Schedule of Investments – (continued)

September 30, 2019

| Shares or Principal Amount | Market Value† | |||||||

| COMMON STOCKS - 101.1% - (continued) | ||||||||

| Finland - 0.8% - (continued) | ||||||||

| 64 | Orion Oyj Class B | $ | 2,385 | |||||

| 123 | Sampo Oyj Class A | 4,887 | ||||||

| 127 | Tieto Oyj | 3,253 | ||||||

| 38 | Valmet Oyj | 737 | ||||||

|

| |||||||

| 25,615 | ||||||||

|

| |||||||

| France - 6.1% | ||||||||

| 46 | Air Liquide S.A. | 6,547 | ||||||

| 179 | Alstom S.A. | 7,415 | ||||||

| 8 | Arkema S.A. | 746 | ||||||

| 132 | AXA S.A. | 3,370 | ||||||

| 55 | BioMerieux | 4,549 | ||||||

| 603 | Bouygues S.A. | 24,148 | ||||||

| 76 | Cie de Saint-Gobain | 2,979 | ||||||

| 135 | Cie Generale des Etablissements Michelin SCA | 15,031 | ||||||

| 408 | CNP Assurances | 7,884 | ||||||

| 21 | Covivio REIT | 2,223 | ||||||

| 6 | Eiffage S.A. | 622 | ||||||

| 29 | Eurazeo SE | 2,157 | ||||||

| 59 | Ipsen S.A. | 5,597 | ||||||

| 7 | Klepierre S.A. REIT | 238 | ||||||

| 173 | Korian S.A. | 7,112 | ||||||

| 11 | L’Oreal S.A. | 3,076 | ||||||

| 58 | Nexity S.A. | 2,761 | ||||||

| 595 | Orange S.A. | 9,313 | ||||||

| 135 | Peugeot S.A. | 3,369 | ||||||

| 75 | Rubis SCA | 4,356 | ||||||

| 146 | Sanofi | 13,524 | ||||||

| 20 | Sartorius Stedim Biotech | 2,797 | ||||||

| 10 | Schneider Electric SE | 874 | ||||||

| 374 | SCOR SE | 15,442 | ||||||

| 54 | Sodexo S.A. | 6,062 | ||||||

| 851 | Suez | 13,375 | ||||||

| 54 | Thales S.A. | 6,207 | ||||||

| 308 | TOTAL S.A. | 16,037 | ||||||

| 71 | Veolia Environnement S.A. | 1,799 | ||||||

|

| |||||||

| 189,610 | ||||||||

|

| |||||||

| Germany - 6.1% | ||||||||

| 130 | 1&1 Drillisch AG | 4,052 | ||||||

| 59 | Allianz SE | 13,734 | ||||||

| 373 | Alstria Office AG REIT | 6,399 | ||||||

| 1,629 | Aroundtown S.A. | 13,324 | ||||||

| 27 | BASF SE | 1,888 | ||||||

| 10 | Bayerische Motoren Werke AG | 704 | ||||||

| 16 | Carl Zeiss Meditec AG | 1,824 | ||||||

| 187 | Covestro AG(1) | 9,253 | ||||||

| 821 | Deutsche Telekom AG | 13,771 | ||||||

| 105 | DWS Group GmbH & Co. KGaA(1) | 3,100 | ||||||

| 201 | Evonik Industries AG | 4,962 | ||||||

| 77 | Hannover Rueck SE | 13,014 | ||||||

| 39 | HeidelbergCement AG | 2,818 | ||||||

| 27 | Hochtief AG | 3,077 | ||||||

| 86 | Knorr-Bremse AG | 8,084 | ||||||

| 35 | LEG Immobilien AG | 4,005 | ||||||

| 205 | Merck KGaA | 23,093 | ||||||

| 875 | Metro AG | 13,804 | ||||||

| 65 | Muenchener Rueckversicherungs-Gesellschaft AG in Muenchen | 16,789 | ||||||

| 21 | Rheinmetall AG | 2,656 | ||||||

| 433 | Siemens Healthineers AG(1) | 17,026 | ||||||

| 95 | Talanx AG* | 4,105 | ||||||

| 1,215 | Telefonica Deutschland Holding AG | 3,388 | ||||||

| 79 | Vonovia SE | 4,008 | ||||||

|

| |||||||

| 188,878 | ||||||||

|

| |||||||

| Shares or Principal Amount | Market Value† | |||||||

| COMMON STOCKS - 101.1% - (continued) | ||||||||

| Hong Kong - 4.3% | ||||||||

| 5,000 | Champion REIT | $ | 3,235 | |||||

| 2,200 | Chow Tai Fook Jewellery Group Ltd. | 1,816 | ||||||

| 500 | CK Hutchison Holdings Ltd. | 4,414 | ||||||

| 1,000 | CLP Holdings Ltd. | 10,511 | ||||||

| 600 | Dairy Farm International Holdings Ltd. | 3,782 | ||||||

| 300 | Hang Seng Bank Ltd. | 6,464 | ||||||

| 1,000 | Henderson Land Development Co., Ltd. | 4,658 | ||||||

| 5,000 | HK Electric Investments & HK Electric Investments Ltd. | 4,765 | ||||||

| 1,000 | Hong Kong & China Gas Co., Ltd. | 1,949 | ||||||

| 1,400 | Hongkong Land Holdings Ltd. | 7,871 | ||||||

| 1,000 | Hysan Development Co., Ltd. | 4,033 | ||||||

| 100 | Jardine Matheson Holdings Ltd. | 5,352 | ||||||

| 100 | Jardine Strategic Holdings Ltd. | 2,991 | ||||||

| 1,000 | Link REIT | 11,031 | ||||||

| 4,000 | New World Development Co., Ltd. | 5,195 | ||||||

| 2,000 | NWS Holdings Ltd. | 3,098 | ||||||

| 10,000 | PCCW Ltd. | 5,614 | ||||||

| 2,000 | Sino Land Co., Ltd. | 3,006 | ||||||

| 2,000 | SITC International Holdings Co., Ltd. | 2,060 | ||||||

| 1,000 | Swire Pacific Ltd. Class A | 9,307 | ||||||

| 1,000 | Swire Properties Ltd. | 3,138 | ||||||

| 500 | VTech Holdings Ltd. | 4,364 | ||||||

| 11,500 | WH Group Ltd.(1) | 10,299 | ||||||

| 1,000 | Wharf Real Estate Investment Co., Ltd. | 5,462 | ||||||

| 2,500 | Yue Yuen Industrial Holdings Ltd. | 6,830 | ||||||

|

| |||||||

| 131,245 | ||||||||

|

| |||||||

| Ireland - 0.7% | ||||||||

| 30 | CRH plc | 1,030 | ||||||

| 349 | Glanbia plc | 4,336 | ||||||

| 96 | ICON plc* | 14,145 | ||||||

| 25 | Kerry Group plc Class A | 2,924 | ||||||

|

| |||||||

| 22,435 | ||||||||

|

| |||||||

| Israel - 1.8% | ||||||||

| 103 | Bank Hapoalim BM* | 812 | ||||||

| 1,489 | Bank LeumiLe-Israel BM | 10,601 | ||||||

| 1,111 | Israel Chemicals Ltd. | 5,558 | ||||||

| 3,876 | Israel Discount Bank Ltd. Class A | 17,036 | ||||||

| 487 | Mizrahi Tefahot Bank Ltd. | 12,101 | ||||||

| 95 | Strauss Group Ltd. | 2,989 | ||||||

| 73 | Taro Pharmaceutical Industries Ltd. | 5,508 | ||||||

|

| |||||||

| 54,605 | ||||||||

|

| |||||||

| Italy - 2.9% | ||||||||

| 2,035 | A2A S.p.A. | 3,734 | ||||||

| 39 | ACEA S.p.A. | 779 | ||||||

| 426 | Assicurazioni Generali S.p.A. | 8,256 | ||||||

| 19 | DiaSorin S.p.A. | 2,210 | ||||||

| 1,036 | Enel S.p.A. | 7,738 | ||||||

| 995 | Eni S.p.A. | 15,208 | ||||||

| 1,608 | Italgas S.p.A. | 10,377 | ||||||

| 404 | Pirelli & C. S.p.A.(1) | 2,392 | ||||||

| 951 | Poste Italiane S.p.A.(1) | 10,810 | ||||||

| 168 | Recordati S.p.A. | 7,205 | ||||||

| 1,640 | Unipol Gruppo S.p.A. | 8,733 | ||||||

| 4,319 | UnipolSai Assicurazioni S.p.A. | 11,485 | ||||||

|

| |||||||

| 88,927 | ||||||||

|

| |||||||

| Japan - 21.7% | ||||||||

| 100 | ABC-Mart, Inc. | 6,357 | ||||||

| 100 | Aeon Co., Ltd. | 1,837 | ||||||

| 200 | Alfresa Holdings Corp. | 4,481 | ||||||

| 300 | ANA Holdings, Inc. | 10,107 | ||||||

| 300 | Aozora Bank Ltd. | 7,518 | ||||||

| 200 | Asahi Kasei Corp. | 1,984 | ||||||

The accompanying notes are an integral part of these financial statements.

| 9 |

|

| Hartford Multifactor International Fund |

Schedule of Investments – (continued)

September 30, 2019

| Shares or Principal Amount | Market Value† | |||||||

| COMMON STOCKS - 101.1% - (continued) | ||||||||

| Japan - 21.7% - (continued) | ||||||||

| 700 | Astellas Pharma, Inc. | $ | 10,013 | |||||

| 200 | Azbil Corp. | 5,371 | ||||||

| 200 | Bandai Namco Holdings, Inc. | 12,471 | ||||||

| 300 | Bic Camera, Inc. | 3,168 | ||||||

| 400 | Bridgestone Corp. | 15,566 | ||||||

| 400 | Brother Industries Ltd. | 7,289 | ||||||

| 200 | Canon Marketing Japan, Inc. | 4,264 | ||||||

| 400 | Canon, Inc. | 10,697 | ||||||

| 200 | Dai-ichi Life Holdings, Inc. | 3,041 | ||||||

| 1,800 | Daiwa Securities Group, Inc. | 8,055 | ||||||

| 400 | FUJIFILM Holdings Corp. | 17,620 | ||||||

| 100 | Fujitsu Ltd. | 8,037 | ||||||

| 400 | Hakuhodo DY Holdings, Inc. | 5,812 | ||||||

| 500 | Haseko Corp. | 5,848 | ||||||

| 200 | Heiwa Corp. | 4,125 | ||||||

| 100 | Hitachi High-Technologies Corp. | 5,813 | ||||||

| 200 | Hitachi Ltd. | 7,490 | ||||||

| 400 | Hitachi Metals Ltd. | 4,344 | ||||||

| 100 | Hitachi Transport System Ltd. | 2,929 | ||||||

| 400 | Honda Motor Co., Ltd. | 10,474 | ||||||

| 100 | Hoya Corp. | 8,190 | ||||||

| 400 | Iida Group Holdings Co., Ltd. | 6,531 | ||||||

| 600 | ITOCHU Corp. | 12,428 | ||||||

| 500 | Japan Airlines Co., Ltd. | 14,850 | ||||||

| 600 | Japan Post Holdings Co., Ltd. | 5,537 | ||||||

| 1,800 | JXTG Holdings, Inc. | 8,228 | ||||||

| 800 | K’s Holdings Corp. | 8,713 | ||||||

| 300 | Kajima Corp. | 3,952 | ||||||

| 100 | Kaken Pharmaceutical Co., Ltd. | 4,651 | ||||||

| 100 | Kansai Electric Power Co., Inc. | 1,120 | ||||||

| 300 | KDDI Corp. | 7,828 | ||||||

| 2,600 | Konica Minolta, Inc. | 18,191 | ||||||

| 300 | Kyushu Railway Co. | 9,576 | ||||||

| 100 | Lawson, Inc. | 5,121 | ||||||

| 200 | Marubeni Corp. | 1,334 | ||||||

| 700 | Mazda Motor Corp. | 6,274 | ||||||

| 1,900 | Mebuki Financial Group, Inc. | 4,699 | ||||||

| 400 | Medipal Holdings Corp. | 8,929 | ||||||

| 200 | Mitsubishi Chemical Holdings Corp. | 1,433 | ||||||

| 200 | Mitsubishi Corp. | 4,925 | ||||||

| 200 | Mitsubishi Electric Corp. | 2,668 | ||||||

| 300 | Mitsubishi Heavy Industries Ltd. | 11,792 | ||||||

| 100 | Mitsubishi Tanabe Pharma Corp. | 1,102 | ||||||

| 200 | NEC Corp. | 8,457 | ||||||

| 100 | NH Foods Ltd. | 4,026 | ||||||

| 300 | Nihon Kohden Corp. | 8,841 | ||||||

| 300 | Nikon Corp. | 3,764 | ||||||

| 200 | Nippo Corp. | 3,715 | ||||||

| 300 | Nippon Kayaku Co., Ltd. | 3,597 | ||||||

| 300 | Nippon Telegraph & Telephone Corp. | 14,353 | ||||||

| 500 | Nissan Motor Co., Ltd. | 3,122 | ||||||

| 200 | NTT Data Corp. | 2,596 | ||||||

| 400 | NTT DOCOMO, Inc. | 10,214 | ||||||

| 300 | Obayashi Corp. | 3,000 | ||||||

| 400 | ORIX Corp. | 5,984 | ||||||

| 400 | Osaka Gas Co., Ltd. | 7,683 | ||||||

| 100 | Otsuka Holdings Co., Ltd. | 3,756 | ||||||

| 700 | Panasonic Corp. | 5,705 | ||||||

| 200 | Resona Holdings, Inc. | 861 | ||||||

| 200 | Ricoh Co., Ltd. | 1,809 | ||||||

| 100 | Rohto Pharmaceutical Co., Ltd. | 2,745 | ||||||

| 200 | Sankyo Co., Ltd. | 6,882 | ||||||

| 200 | Sawai Pharmaceutical Co., Ltd. | 10,347 | ||||||

| 100 | Secom Co., Ltd. | 9,151 | ||||||

| 700 | Seiko Epson Corp. | 9,943 | ||||||

| Shares or Principal Amount | Market Value† | |||||||

| COMMON STOCKS - 101.1% - (continued) | ||||||||

| Japan - 21.7% - (continued) | ||||||||

| 100 | Sekisui Chemical Co., Ltd. | $ | 1,556 | |||||

| 700 | Sekisui House Ltd. | 13,812 | ||||||

| 200 | Seven & i Holdings Co., Ltd. | 7,665 | ||||||

| 300 | SG Holdings Co., Ltd. | 7,352 | ||||||

| 100 | Shimamura Co., Ltd. | 7,945 | ||||||

| 200 | Ship Healthcare Holdings, Inc. | 8,527 | ||||||

| 700 | Skylark Holdings Co., Ltd. | 12,745 | ||||||

| 300 | Softbank Corp. | 4,065 | ||||||

| 1,100 | Sojitz Corp. | 3,422 | ||||||

| 500 | Sony Financial Holdings, Inc. | 10,887 | ||||||

| 500 | Subaru Corp. | 14,140 | ||||||

| 200 | Sumitomo Dainippon Pharma Co., Ltd. | 3,309 | ||||||

| 600 | Sumitomo Electric Industries Ltd. | 7,657 | ||||||

| 500 | Sumitomo Forestry Co., Ltd. | 6,676 | ||||||

| 100 | Sumitomo Rubber Industries Ltd. | 1,191 | ||||||

| 200 | Suzuken Co., Ltd. | 10,766 | ||||||

| 100 | Taisei Corp. | 3,892 | ||||||

| 300 | Taiyo Nippon Sanso Corp. | 6,098 | ||||||

| 200 | Teijin Ltd. | 3,860 | ||||||

| 100 | Terumo Corp. | 3,236 | ||||||

| 300 | Tokio Marine Holdings, Inc. | 16,094 | ||||||

| 200 | Tokyo Electric Power Co. Holdings, Inc.* | 981 | ||||||

| 400 | Tokyo Gas Co., Ltd. | 10,117 | ||||||

| 300 | Toyota Boshoku Corp. | 4,219 | ||||||

| 100 | TS Tech Co., Ltd. | 3,059 | ||||||

| 200 | Tsumura & Co. | 5,374 | ||||||

| 200 | TV Asahi Holdings Corp. | 3,157 | ||||||

| 100 | West Japan Railway Co. | 8,461 | ||||||

| 600 | Yamada Denki Co., Ltd. | 2,907 | ||||||

| 200 | Yamazaki Baking Co., Ltd. | 3,577 | ||||||

| 100 | Zensho Holdings Co., Ltd. | 2,160 | ||||||

|

| |||||||

| 672,241 | ||||||||

|

| |||||||

| Luxembourg - 0.2% | ||||||||

| 251 | Grand City Properties S.A. | 5,647 | ||||||

| 750 | L’Occitane International S.A. | 1,492 | ||||||

|

| |||||||

| 7,139 | ||||||||

|

| |||||||

| Netherlands - 3.6% | ||||||||

| 493 | Aegon N.V.(2) | 2,047 | ||||||

| 447 | ASR Nederland N.V. | 16,494 | ||||||

| 132 | GrandVision N.V.(1) | 3,953 | ||||||

| 793 | Koninklijke Ahold Delhaize N.V. | 19,831 | ||||||

| 91 | Koninklijke DSM N.V. | 10,955 | ||||||

| 410 | NN Group N.V. | 14,530 | ||||||

| 342 | Randstad N.V. | 16,791 | ||||||

| 661 | Royal Dutch Shell plc Class A | 19,386 | ||||||

| 91 | Wolters Kluwer N.V. | 6,640 | ||||||

|

| |||||||

| 110,627 | ||||||||

|

| |||||||

| New Zealand - 0.5% | ||||||||

| 473 | Contact Energy Ltd. | 2,530 | ||||||

| 91 | EBOS Group Ltd. | 1,425 | ||||||

| 635 | Fisher & Paykel Healthcare Corp. Ltd. | 6,890 | ||||||

| 59 | Mainfreight Ltd. | 1,475 | ||||||

| 150 | Meridian Energy Ltd. | 488 | ||||||

| 1,013 | Spark New Zealand Ltd.* | 2,797 | ||||||

|

| |||||||

| 15,605 | ||||||||

|

| |||||||

| Norway - 1.4% | ||||||||

| 341 | Austevoll Seafood ASA | 3,238 | ||||||

| 628 | Equinor ASA | 11,896 | ||||||

| 321 | Leroy Seafood Group ASA | 1,953 | ||||||

| 238 | Marine Harvest ASA* | 5,497 | ||||||

| 890 | Orkla ASA | 8,098 | ||||||

| 20 | Salmar ASA | 878 | ||||||

| 210 | SpareBank 1SR-Bank ASA | 2,287 | ||||||

The accompanying notes are an integral part of these financial statements.

| 10 |

|

| Hartford Multifactor International Fund |

Schedule of Investments – (continued)

September 30, 2019

| Shares or Principal Amount | Market Value† | |||||||

| COMMON STOCKS - 101.1% - (continued) | ||||||||

| Norway - 1.4% - (continued) | ||||||||

| 509 | Telenor ASA | $ | 10,212 | |||||

|

| |||||||

| 44,059 | ||||||||

|

| |||||||

| Portugal - 0.5% | ||||||||

| 856 | Galp Energia SGPS S.A. | 12,874 | ||||||

| 614 | NOS SGPS S.A. | 3,352 | ||||||

|

| |||||||

| 16,226 | ||||||||

|

| |||||||

| Russia - 1.2% | ||||||||

| 3,582 | Evraz plc | 20,616 | ||||||

| 331 | Polymetal International plc | 4,649 | ||||||

| 519 | VEON Ltd. | 1,246 | ||||||

| 285 | X5 Retail Group N.V. GDR | 9,966 | ||||||

|

| |||||||

| 36,477 | ||||||||

|

| |||||||

| Singapore - 2.1% | ||||||||

| 6,700 | ComfortDelGro Corp. Ltd. | 11,641 | ||||||

| 400 | DBS Group Holdings Ltd. | 7,236 | ||||||

| 200 | Jardine Cycle & Carriage Ltd. | 4,344 | ||||||

| 1,400 | Mapletree Commercial Trust REIT | 2,321 | ||||||

| 3,100 | NetLink NBN Trust UNIT | 1,996 | ||||||

| 1,300 | Oversea-Chinese Banking Corp. Ltd. | 10,220 | ||||||

| 1,200 | SATS Ltd. | 4,208 | ||||||

| 1,400 | Singapore Airlines Ltd. | 9,260 | ||||||

| 1,100 | Singapore Technologies Engineering Ltd. | 3,057 | ||||||

| 900 | Singapore Telecommunications Ltd. | 2,027 | ||||||

| 700 | Venture Corp. Ltd. | 7,762 | ||||||

|

| |||||||

| 64,072 | ||||||||

|

| |||||||

| Spain - 2.5% | ||||||||

| 111 | Acciona S.A. | 11,747 | ||||||

| 148 | ACS Actividades de Construccion y Servicios S.A. | 5,913 | ||||||

| 103 | Ebro Foods S.A. | 2,059 | ||||||

| 218 | Enagas S.A. | 5,039 | ||||||

| 588 | Endesa S.A. | 15,468 | ||||||

| 1,001 | Gestamp Automocion S.A.(1) | 4,672 | ||||||

| 266 | Iberdrola S.A. | 2,765 | ||||||

| 103 | Inmobiliaria Colonial Socimi S.A. REIT | 1,243 | ||||||

| 1,579 | Mapfre S.A. | 4,253 | ||||||

| 496 | Merlin Properties Socimi S.A. REIT | 6,925 | ||||||

| 1,150 | Prosegur Cash S.A.(1) | 1,652 | ||||||

| 140 | Red Electrica Corp. S.A. | 2,836 | ||||||

| 311 | Repsol S.A. | 4,850 | ||||||

| 755 | Telefonica S.A. | 5,769 | ||||||

| 49 | Viscofan S.A. | 2,296 | ||||||

|

| |||||||

| 77,487 | ||||||||

|

| |||||||

| Sweden - 2.6% | ||||||||

| 74 | Atrium Ljungberg AB Class B | 1,635 | ||||||

| 345 | Axfood AB | 7,325 | ||||||

| 293 | BillerudKorsnas AB | 3,168 | ||||||

| 330 | Castellum AB | 7,065 | ||||||

| 81 | Electrolux AB Class B | 1,919 | ||||||

| 105 | Essity AB Class B | 3,064 | ||||||

| 212 | Fastighets AB Balder Class B* | 8,026 | ||||||

| 227 | Hennes & Mauritz AB Class B | 4,400 | ||||||

| 214 | ICA Gruppen AB | 9,883 | ||||||

| 138 | Loomis AB Class B | 4,846 | ||||||

| 611 | Securitas AB Class B | 9,356 | ||||||

| 38 | Skandinaviska Enskilda Banken AB Class A | 349 | ||||||

| 116 | Skanska AB Class B | 2,349 | ||||||

| 107 | Svenska Handelsbanken AB Class A | 1,001 | ||||||

| 796 | Swedbank AB Class A | 11,464 | ||||||

| 536 | Telia Co., AB | 2,398 | ||||||

| 33 | Volvo AB Class B | 463 | ||||||

| 89 | Wihlborgs Fastigheter AB | 1,446 | ||||||

|

| |||||||

| 80,157 | ||||||||

|

| |||||||

| Shares or Principal Amount | Market Value† | |||||||

| COMMON STOCKS - 101.1% - (continued) | ||||||||

| Switzerland - 6.2% | ||||||||

| 202 | Adecco Group AG | $ | 11,178 | |||||

| 131 | Baloise Holding AG | 23,472 | ||||||

| 4 | Banque Cantonale Vaudoise | 3,061 | ||||||

| 15 | Bucher Industries AG | 4,692 | ||||||

| 33 | Coca-Cola HBC AG* | 1,078 | ||||||

| 1 | Givaudan S.A. | 2,791 | ||||||

| 73 | Helvetia Holding AG | 10,075 | ||||||

| 76 | Julius Baer Group Ltd.* | 3,366 | ||||||

| 85 | Kuehne + Nagel International AG | 12,508 | ||||||

| 86 | Nestle S.A. | 9,327 | ||||||

| 119 | Novartis AG | 10,328 | ||||||

| 51 | PSP Swiss Property AG | 6,475 | ||||||

| 66 | Roche Holding AG | 19,217 | ||||||

| 2 | SGS S.A. | 4,958 | ||||||

| 20 | Sika AG | 2,926 | ||||||

| 25 | Sonova Holding AG | 5,817 | ||||||

| 47 | Swiss Life Holding AG | 22,471 | ||||||

| 113 | Swiss Re AG | 11,791 | ||||||

| 6 | Swisscom AG | 2,960 | ||||||

| 62 | Zurich Insurance Group AG | 23,746 | ||||||

|

| |||||||

| 192,237 | ||||||||

|

| |||||||

| United Kingdom - 11.4% | ||||||||

| 296 | 3i Group plc | 4,236 | ||||||

| 269 | Anglo American plc | 6,182 | ||||||

| 65 | Ashtead Group plc | 1,808 | ||||||

| 121 | AstraZeneca plc | 10,804 | ||||||

| 118 | Auto Trader Group plc(1) | 740 | ||||||

| 2,953 | Avast plc(1) | 14,107 | ||||||

| 552 | Barratt Developments plc | 4,394 | ||||||

| 254 | Bellway plc | 10,442 | ||||||

| 53 | Berkeley Group Holdings plc | 2,721 | ||||||

| 2,389 | BP plc | 15,124 | ||||||

| 583 | Britvic plc | 7,044 | ||||||

| 5,552 | BT Group plc | 12,178 | ||||||

| 32 | Burberry Group plc | 855 | ||||||

| 8,595 | Centrica plc | 7,794 | ||||||

| 162 | Close Brothers Group plc | 2,805 | ||||||

| 49 | Coca-Cola European Partners plc | 2,730 | ||||||

| 475 | Compass Group plc | 12,223 | ||||||

| 103 | Diageo plc | 4,208 | ||||||

| 3,722 | Direct Line Insurance Group plc | 13,732 | ||||||

| 375 | Electrocomponents plc | 2,965 | ||||||

| 133 | Ferguson plc* | 9,706 | ||||||

| 154 | Fiat Chrysler Automobiles N.V. | 1,994 | ||||||

| 499 | GlaxoSmithKline plc | 10,696 | ||||||

| 61 | Hiscox Ltd. | 1,245 | ||||||

| 976 | Howden Joinery Group plc | 6,717 | ||||||

| 811 | HSBC Holdings plc | 6,214 | ||||||

| 2,468 | Kingfisher plc | 6,272 | ||||||

| 6,175 | Legal & General Group plc | 18,848 | ||||||

| 252 | Marks & Spencer Group plc | 571 | ||||||

| 316 | Mondi plc | 6,051 | ||||||

| 683 | National Grid plc | 7,395 | ||||||

| 1,173 | Pearson plc | 10,637 | ||||||

| 126 | Pennon Group plc | 1,281 | ||||||

| 72 | Persimmon plc | 1,920 | ||||||

| 766 | Redrow plc | 5,817 | ||||||

| 475 | RELX plc | 11,281 | ||||||

| 894 | Rentokil Initial plc | 5,140 | ||||||

| 442 | Rio Tinto plc | 22,976 | ||||||

| 3,732 | Royal Mail plc | 9,690 | ||||||

| 720 | RSA Insurance Group plc | 4,724 | ||||||

| 525 | Sage Group plc | 4,461 | ||||||

| 892 | Smith & Nephew plc | 21,481 | ||||||

The accompanying notes are an integral part of these financial statements.

| 11 |

|

| Hartford Multifactor International Fund |

Schedule of Investments – (continued)

September 30, 2019

| Shares or Principal Amount | Market Value† | |||||||

| COMMON STOCKS - 101.1% - (continued) | ||||||||

| United Kingdom - 11.4% - (continued) | ||||||||

| 222 | Spectris plc | $ | 6,664 | |||||

| 130 | SSP Group plc | 990 | ||||||

| 854 | Tate & Lyle plc | 7,726 | ||||||

| 920 | Taylor Wimpey plc | 1,826 | ||||||

| 32 | Travis Perkins plc | 508 | ||||||

| 1,483 | Tritax Big Box plc REIT | 2,728 | ||||||

| 225 | Unilever plc | 13,523 | ||||||

| 241 | WH Smith plc | 5,889 | ||||||

|

| |||||||

| 352,063 | ||||||||

|

| |||||||

| United States - 0.1% | ||||||||

| 22 | Waste Connections, Inc. | 2,021 | ||||||

|

| |||||||

Total Common Stocks | $ | 3,126,599 | ||||||

|

| |||||||

| SHORT-TERM INVESTMENTS - 0.0% | ||||||||

| Other Investment Pools & Funds - 0.0% | ||||||||

| 1,013 | Fidelity Institutional Government Fund, Institutional Class, 1.92%(3) | $ | 1,013 | |||||

|

| |||||||

Total Short-Term Investments | $ | 1,013 | ||||||

|

| |||||||

Total Investments | �� | 101.1 | % | $ | 3,127,612 | |||||||

Other Assets and Liabilities | (1.1 | )% | (35,348 | ) | ||||||||

|

|

|

| |||||||||

Total Net Assets | 100.0 | % | $ | 3,092,264 | ||||||||

|

|

|

| |||||||||

| Note: | Percentage of investments as shown is the ratio of the total market value to total net assets. |

Prices of foreign equities that are principally traded on certain foreign markets will generally be adjusted daily pursuant to a fair value pricing service approved by the Board of Directors in order to reflect an adjustment for factors occurring after the close of certain foreign markets but before the close of the New York Stock Exchange. |

Equity industry classifications used in this report are the Global Industry Classification Standard, which was developed by and is the exclusive property and service mark of MSCI, Inc. and Standard & Poor’s. |

For Fund compliance purposes, the Fund may not use the same classification system. These classifications are used for financial reporting purposes. |

See “Glossary” for abbreviation descriptions. |

| * | Non-income producing. |

| (1) | Security was purchased pursuant to Rule 144A under the Securities Act of 1933 and may be sold in transactions that are exempt from registration (typically only to qualified institutional buyers) or in a public offering registered under the Securities Act of 1933. At September 30, 2019, the aggregate value of these securities was $108,962, representing 3.5% of net assets. |

| (2) | Represents entire or partial securities on loan. See Note 8 in the accompanying Notes to Financial Statements for securities lending information. |

| (3) | Current yield as of period end. |

| † | See Significant Accounting Policies of accompanying Notes to Financial Statements regarding valuation of investments. |

The accompanying notes are an integral part of these financial statements.

| 12 |

|

| Hartford Multifactor International Fund |

Schedule of Investments – (continued)

September 30, 2019

Fair Valuation Summary

The following is a summary of the fair valuations according to the inputs used as of September 30, 2019 in valuing the Fund’s investments.

Description | Total | Level 1 | Level 2 | Level 3(1) | ||||||||||||

Assets |

| |||||||||||||||

Common Stocks |

| |||||||||||||||

Australia | $ | 263,491 | $ | 1,771 | $ | 261,720 | $ | — | ||||||||

Austria | 9,953 | — | 9,953 | — | ||||||||||||

Belgium | 61,762 | 2,207 | 59,555 | — | ||||||||||||

Canada | 352,925 | 352,925 | — | — | ||||||||||||

China | 7,648 | — | 7,648 | — | ||||||||||||

Denmark | 59,094 | — | 59,094 | — | ||||||||||||

Finland | 25,615 | 5,831 | 19,784 | — | ||||||||||||

France | 189,610 | 6,062 | 183,548 | — | ||||||||||||

Germany | 188,878 | 17,871 | 171,007 | — | ||||||||||||

Hong Kong | 131,245 | 4,765 | 126,480 | — | ||||||||||||

Ireland | 22,435 | 21,405 | 1,030 | — | ||||||||||||

Israel | 54,605 | 5,508 | 49,097 | — | ||||||||||||

Italy | 88,927 | — | 88,927 | — | ||||||||||||

Japan | 672,241 | — | 672,241 | — | ||||||||||||

Luxembourg | 7,139 | — | 7,139 | — | ||||||||||||

Netherlands | 110,627 | — | 110,627 | — | ||||||||||||

New Zealand | 15,605 | — | 15,605 | — | ||||||||||||

Norway | 44,059 | — | 44,059 | — | ||||||||||||

Portugal | 16,226 | — | 16,226 | — | ||||||||||||

Russia | 36,477 | 1,246 | 35,231 | — | ||||||||||||

Singapore | 64,072 | 1,996 | 62,076 | — | ||||||||||||

Spain | 77,487 | — | 77,487 | — | ||||||||||||

Sweden | 80,157 | 1,635 | 78,522 | — | ||||||||||||

Switzerland | 192,237 | — | 192,237 | — | ||||||||||||

United Kingdom | 352,063 | 3,275 | 348,788 | — | ||||||||||||

United States | 2,021 | 2,021 | — | — | ||||||||||||

Short-Term Investments | 1,013 | 1,013 | — | — | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total | $ | 3,127,612 | $ | 429,531 | $ | 2,698,081 | $ | — | ||||||||

|

|

|

|

|

|

|

| |||||||||

| (1) | For the period ended September 30, 2019, there were no transfers in and out of Level 3. |

The accompanying notes are an integral part of these financial statements.

| 13 |

|

Schedule of Investments

September 30, 2019

| Shares or Principal Amount | Market Value† | |||||||

| COMMON STOCKS - 103.6% | ||||||||

| Automobiles & Components - 1.4% | ||||||||

| 782 | Ford Motor Co. | $ | 7,163 | |||||

| 206 | General Motors Co. | 7,721 | ||||||

|

| |||||||

| 14,884 | ||||||||

|

| |||||||

| Banks - 3.9% | ||||||||

| 76 | BB&T Corp. | 4,056 | ||||||

| 26 | Citigroup, Inc. | 1,796 | ||||||

| 142 | JP Morgan Chase & Co. | 16,712 | ||||||

| 41 | PNC Financial Services Group, Inc. | 5,747 | ||||||

| 123 | US Bancorp | 6,807 | ||||||

| 139 | Wells Fargo & Co. | 7,011 | ||||||

|

| |||||||

| 42,129 | ||||||||

|

| |||||||

| Capital Goods - 6.4% | ||||||||

| 76 | AGCO Corp. | 5,753 | ||||||

| 57 | Dover Corp. | 5,675 | ||||||

| 96 | Eaton Corp. plc | 7,982 | ||||||

| 61 | EMCOR Group, Inc. | 5,253 | ||||||

| 21 | General Dynamics Corp. | 3,837 | ||||||

| 63 | Ingersoll-Rand plc | 7,762 | ||||||

| 181 | Johnson Controls International plc | 7,944 | ||||||

| 83 | PACCAR, Inc. | 5,811 | ||||||

| 122 | Quanta Services, Inc. | 4,612 | ||||||

| 16 | Snap-on, Inc. | 2,505 | ||||||

| 54 | United Technologies Corp. | 7,372 | ||||||

| 11 | Wabco Holdings, Inc.* | 1,471 | ||||||

| 25 | Watsco, Inc. | 4,230 | ||||||

|

| |||||||

| 70,207 | ||||||||

|

| |||||||

| Commercial & Professional Services - 1.5% | ||||||||

| 83 | KAR Auction Services, Inc. | 2,038 | ||||||

| 22 | ManpowerGroup, Inc. | 1,853 | ||||||

| 59 | Republic Services, Inc. | 5,106 | ||||||

| 63 | Waste Management, Inc. | 7,245 | ||||||

|

| |||||||

| 16,242 | ||||||||

|

| |||||||

| Consumer Durables & Apparel - 0.6% | ||||||||

| 13 | Carter’s, Inc. | 1,186 | ||||||

| 154 | PulteGroup, Inc. | 5,629 | ||||||

|

| |||||||

| 6,815 | ||||||||

|

| |||||||

| Consumer Services - 2.4% | ||||||||

| 27 | Cracker Barrel Old Country Store, Inc. | 4,392 | ||||||

| 102 | McDonald’s Corp. | 21,900 | ||||||

|

| |||||||

| 26,292 | ||||||||

|

| |||||||

| Diversified Financials - 8.6% | ||||||||

| 311 | AGNC Investment Corp. REIT | 5,004 | ||||||

| 64 | American Express Co. | 7,570 | ||||||

| 548 | Annaly Capital Management, Inc. REIT | 4,822 | ||||||

| 126 | Berkshire Hathaway, Inc. Class B* | 26,211 | ||||||

| 16 | BlackRock, Inc. | 7,130 | ||||||

| 148 | Blackstone Mortgage Trust, Inc. Class A REIT | 5,306 | ||||||

| 269 | Chimera Investment Corp. REIT | 5,262 | ||||||

| 22 | CME Group, Inc. | 4,649 | ||||||

| 80 | Intercontinental Exchange, Inc. | 7,382 | ||||||

| 704 | MFA Financial, Inc. REIT | 5,181 | ||||||

| 42 | Nasdaq, Inc. | 4,173 | ||||||

| 223 | Starwood Property Trust, Inc. REIT | 5,401 | ||||||

| 167 | Synchrony Financial | 5,693 | ||||||

|

| |||||||

| 93,784 | ||||||||

|

| |||||||

| Energy - 6.6% | ||||||||

| 227 | Chevron Corp. | 26,922 | ||||||

| 367 | Exxon Mobil Corp. | 25,914 | ||||||

| 377 | Kinder Morgan, Inc. | 7,770 | ||||||

| 42 | ONEOK, Inc. | 3,095 | ||||||

| 76 | Phillips 66 | 7,782 | ||||||

|

| |||||||

| 71,483 | ||||||||

|

| |||||||

| Shares or Principal Amount | Market Value† | |||||||

| COMMON STOCKS - 103.6% - (continued) | ||||||||

| Food & Staples Retailing - 3.0% | ||||||||

| 101 | Sysco Corp. | $ | 8,020 | |||||

| 132 | US Foods Holding Corp.* | 5,425 | ||||||

| 165 | Walmart, Inc. | 19,582 | ||||||

|

| |||||||

| 33,027 | ||||||||

|

| |||||||

| Food, Beverage & Tobacco - 3.0% | ||||||||

| 19 | Altria Group, Inc. | 777 | ||||||

| 139 | Archer-Daniels-Midland Co. | 5,709 | ||||||

| 231 | Flowers Foods, Inc. | 5,343 | ||||||

| 109 | Hormel Foods Corp. | 4,766 | ||||||

| 36 | Ingredion, Inc. | 2,943 | ||||||

| 1 | JM Smucker Co. | 110 | ||||||

| 32 | Kellogg Co. | 2,059 | ||||||

| 100 | Mondelez International, Inc. Class A | 5,532 | ||||||

| 57 | Tyson Foods, Inc. Class A | 4,910 | ||||||

|

| |||||||

| 32,149 | ||||||||

|

| |||||||

| Health Care Equipment & Services - 7.2% | ||||||||

| 12 | Anthem, Inc. | 2,881 | ||||||

| 9 | Centene Corp.* | 389 | ||||||

| 79 | Cerner Corp. | 5,385 | ||||||

| 54 | Danaher Corp. | 7,799 | ||||||

| 10 | HCA Healthcare, Inc. | 1,204 | ||||||

| 87 | Henry Schein, Inc.* | 5,525 | ||||||

| 26 | Hill-Rom Holdings, Inc. | 2,736 | ||||||

| 22 | Humana, Inc. | 5,625 | ||||||

| 31 | Laboratory Corp. of America Holdings* | 5,208 | ||||||

| 249 | Medtronic plc | 27,046 | ||||||

| 6 | Molina Healthcare, Inc.* | 658 | ||||||

| 52 | Quest Diagnostics, Inc. | 5,566 | ||||||

| 39 | UnitedHealth Group, Inc. | 8,476 | ||||||

|

| |||||||

| 78,498 | ||||||||

|

| |||||||

| Household & Personal Products - 2.8% | ||||||||

| 53 | Kimberly-Clark Corp. | 7,529 | ||||||

| 187 | Procter & Gamble Co. | 23,259 | ||||||

|

| |||||||

| 30,788 | ||||||||

|

| |||||||

| Insurance - 14.6% | ||||||||

| 151 | Aflac, Inc. | 7,900 | ||||||

| 7 | Alleghany Corp.* | 5,584 | ||||||

| 74 | Allstate Corp. | 8,042 | ||||||

| 52 | American Financial Group, Inc. | 5,608 | ||||||

| 131 | Arch Capital Group Ltd.* | 5,499 | ||||||

| 58 | Arthur J Gallagher & Co. | 5,195 | ||||||

| 83 | Axis Capital Holdings Ltd. | 5,538 | ||||||

| 48 | Chubb Ltd. | 7,749 | ||||||

| 47 | Cincinnati Financial Corp. | 5,484 | ||||||

| 112 | CNA Financial Corp. | 5,516 | ||||||

| 22 | Everest Re Group Ltd. | 5,854 | ||||||

| 118 | Fidelity National Financial, Inc. | 5,240 | ||||||

| 9 | First American Financial Corp. | 531 | ||||||

| 59 | Globe Life, Inc. | 5,650 | ||||||

| 40 | Hanover Insurance Group, Inc. | 5,422 | ||||||

| 108 | Loews Corp. | 5,560 | ||||||

| 5 | Markel Corp.* | 5,910 | ||||||

| 55 | Marsh & McLennan Cos., Inc. | 5,503 | ||||||

| 173 | MetLife, Inc. | 8,159 | ||||||

| 223 | Old Republic International Corp. | 5,256 | ||||||

| 101 | Principal Financial Group, Inc. | 5,771 | ||||||

| 96 | Prudential Financial, Inc. | 8,635 | ||||||

| 35 | Reinsurance Group of America, Inc. | 5,596 | ||||||

| 28 | RenaissanceRe Holdings Ltd. | 5,417 | ||||||

| 51 | Travelers Cos., Inc. | 7,583 | ||||||

| 27 | Willis Towers Watson plc | 5,210 | ||||||

| 74 | WR Berkley Corp. | 5,345 | ||||||

|

| |||||||

| 158,757 | ||||||||

|

| |||||||

The accompanying notes are an integral part of these financial statements.

| 14 |

|

| Hartford Multifactor Large Cap Value Fund |

Schedule of Investments – (continued)

September 30, 2019

| Shares or Principal Amount | Market Value† | |||||||

| COMMON STOCKS - 103.6% - (continued) | ||||||||

| Materials - 4.5% | ||||||||

| 35 | AptarGroup, Inc. | $ | 4,146 | |||||

| 66 | Ball Corp. | 4,805 | ||||||

| 60 | Eastman Chemical Co. | 4,430 | ||||||

| 30 | Ecolab, Inc. | 5,941 | ||||||

| 28 | LyondellBasell Industries N.V. Class A | 2,505 | ||||||

| 11 | NewMarket Corp. | 5,193 | ||||||

| 30 | Packaging Corp. of America | 3,183 | ||||||

| 68 | PPG Industries, Inc. | 8,059 | ||||||

| 54 | Reliance Steel & Aluminum Co. | 5,382 | ||||||

| 95 | Sonoco Products Co. | 5,530 | ||||||

|

| |||||||

| 49,174 | ||||||||

|

| |||||||

| Media & Entertainment - 3.3% | ||||||||

| 2 | Cable One, Inc. | 2,509 | ||||||

| 129 | CBS Corp. Class B | 5,208 | ||||||

| 52 | Cinemark Holdings, Inc. | 2,009 | ||||||

| 293 | Comcast Corp. Class A | 13,208 | ||||||

| 267 | Interpublic Group of Cos., Inc. | 5,757 | ||||||

| 33 | Liberty Media Corp-Liberty SiriusXM* | 1,385 | ||||||

| 70 | Omnicom Group, Inc. | 5,481 | ||||||

|

| |||||||

| 35,557 | ||||||||

|

| |||||||

| Pharmaceuticals, Biotechnology & Life Sciences - 4.8% | ||||||||

| 50 | AbbVie, Inc. | 3,786 | ||||||

| 121 | Gilead Sciences, Inc. | 7,669 | ||||||

| 38 | IQVIA Holdings, Inc.* | 5,677 | ||||||

| 985 | Pfizer, Inc. | 35,391 | ||||||

|

| |||||||

| 52,523 | ||||||||

|

| |||||||

| Real Estate - 4.1% | ||||||||

| 81 | Apartment Investment & Management Co. Class A, REIT | 4,223 | ||||||

| 19 | Apple Hospitality, Inc. REIT | 315 | ||||||

| 13 | AvalonBay Communities, Inc. REIT | 2,799 | ||||||

| 23 | Camden Property Trust REIT | 2,553 | ||||||

| 153 | Equity Commonwealth REIT | 5,240 | ||||||

| 21 | Equity Residential REIT | 1,812 | ||||||

| 16 | Essex Property Trust, Inc. REIT | 5,226 | ||||||

| 131 | Gaming and Leisure Properties, Inc. REIT | 5,009 | ||||||

| 70 | HCP, Inc. REIT | 2,494 | ||||||

| 112 | Host Hotels & Resorts, Inc. REIT | 1,937 | ||||||

| 2 | Lamar Advertising Co., Class A, REIT | 164 | ||||||

| 38 | National Health Investors, Inc. REIT | 3,131 | ||||||

| 87 | National Retail Properties, Inc. REIT | 4,907 | ||||||

| 16 | Realty Income Corp. REIT | 1,227 | ||||||

| 21 | Service Properties Trust REIT | 542 | ||||||

| 19 | Simon Property Group, Inc. REIT | 2,957 | ||||||

|

| |||||||

| 44,536 | ||||||||

|

| |||||||

| Retailing - 2.7% | ||||||||

| 7 | AutoZone, Inc.* | 7,592 | ||||||

| 64 | Best Buy Co., Inc. | 4,415 | ||||||

| 14 | Expedia Group, Inc. | 1,882 | ||||||

| 58 | Genuine Parts Co. | 5,776 | ||||||

| 42 | Kohl’s Corp. | 2,086 | ||||||

| 10 | Macy’s, Inc. | 155 | ||||||

| 71 | Target Corp. | 7,591 | ||||||

|

| |||||||

| 29,497 | ||||||||

|

| |||||||

| Software & Services - 5.9% | ||||||||

| 81 | Amdocs Ltd. | 5,355 | ||||||

| 28 | Automatic Data Processing, Inc. | 4,520 | ||||||

| 7 | CACI International, Inc. Class A* | 1,619 | ||||||

| 55 | Fidelity National Information Services, Inc. | 7,302 | ||||||

| 156 | International Business Machines Corp. | 22,685 | ||||||

| 59 | j2 Global, Inc. | 5,358 | ||||||

| 25 | Leidos Holdings, Inc. | 2,147 | ||||||

| Shares or Principal Amount | Market Value† | |||||||

| COMMON STOCKS - 103.6% - (continued) | ||||||||

| Software & Services - 5.9% - (continued) | ||||||||

| 169 | Oracle Corp. | $ | 9,300 | |||||

| 240 | Western Union Co. | 5,561 | ||||||

|

| |||||||

| 63,847 | ||||||||

|

| |||||||

| Technology Hardware & Equipment - 1.8% | ||||||||

| 65 | Arrow Electronics, Inc.* | 4,848 | ||||||

| 183 | Hewlett Packard Enterprise Co. | 2,776 | ||||||

| 174 | HP, Inc. | 3,292 | ||||||

| 26 | Jabil, Inc. | 930 | ||||||

| 235 | Juniper Networks, Inc. | 5,816 | ||||||

| 9 | Seagate Technology plc | 484 | ||||||

| 16 | Tech Data Corp.* | 1,668 | ||||||

|

| |||||||

| 19,814 | ||||||||

|

| |||||||

| Telecommunication Services - 5.8% | ||||||||

| 702 | AT&T, Inc. | 26,564 | ||||||

| 98 | T-Mobile US, Inc.* | 7,719 | ||||||

| 486 | Verizon Communications, Inc. | 29,335 | ||||||

|

| |||||||

| 63,618 | ||||||||

|

| |||||||

| Transportation - 1.5% | ||||||||

| 9 | AMERCO | 3,510 | ||||||

| 93 | Delta Air Lines, Inc. | 5,357 | ||||||

| 5 | Kansas City Southern | 665 | ||||||

| 5 | Union Pacific Corp. | 810 | ||||||

| 63 | United Airlines Holdings, Inc.* | 5,570 | ||||||

|

| |||||||

| 15,912 | ||||||||

|

| |||||||

| Utilities - 7.2% | ||||||||

| 7 | Ameren Corp. | 560 | ||||||

| 67 | American Electric Power Co., Inc. | 6,277 | ||||||

| 28 | Atmos Energy Corp. | 3,189 | ||||||

| 164 | CenterPoint Energy, Inc. | 4,949 | ||||||

| 49 | CMS Energy Corp. | 3,134 | ||||||

| 81 | Consolidated Edison, Inc. | 7,652 | ||||||

| 18 | Dominion Energy, Inc. | 1,459 | ||||||

| 36 | DTE Energy Co. | 4,787 | ||||||

| 64 | Duke Energy Corp. | 6,135 | ||||||

| 27 | Entergy Corp. | 3,169 | ||||||

| 122 | Exelon Corp. | 5,894 | ||||||

| 93 | Hawaiian Electric Industries, Inc. | 4,242 | ||||||

| 33 | NextEra Energy, Inc. | 7,689 | ||||||

| 29 | Pinnacle West Capital Corp. | 2,815 | ||||||

| 44 | Public Service Enterprise Group, Inc. | 2,731 | ||||||

| 39 | Southern Co. | 2,409 | ||||||

| 73 | WEC Energy Group, Inc. | 6,942 | ||||||

| 60 | Xcel Energy, Inc. | 3,893 | ||||||

|

| |||||||

| 77,926 | ||||||||

|

| |||||||

Total Common Stocks | $ | 1,127,459 | ||||||

|

| |||||||

| SHORT-TERM INVESTMENTS - 0.1% | ||||||||

| Other Investment Pools & Funds - 0.1% | ||||||||

| 1,571 | Fidelity Institutional Government Fund, | $ | 1,571 | |||||

|

| |||||||

Total Short-Term Investments | $ | 1,571 | ||||||

|

| |||||||

Total Investments | 103.7 | % | $ | 1,129,030 | ||||||||

Other Assets and Liabilities | (3.7 | )% | (40,673 | ) | ||||||||

|

|

|

| |||||||||

Total Net Assets | 100.0 | % | $ | 1,088,357 | ||||||||

|

|

|

| |||||||||

The accompanying notes are an integral part of these financial statements.

| 15 |

|

| Hartford Multifactor Large Cap Value Fund |

Schedule of Investments – (continued)

September 30, 2019

| Note: | Percentage of investments as shown is the ratio of the total market value to total net assets. |

Equity industry classifications used in this report are the Global Industry Classification Standard, which was developed by and is the exclusive property and service mark of MSCI, Inc. and Standard & Poor’s. |

For Fund compliance purposes, the Fund may not use the same classification system. These classifications are used for financial reporting purposes. |

See “Glossary” for abbreviation descriptions. |

| * | Non-income producing. |

| (1) | Current yield as of period end. |

| † | See Significant Accounting Policies of accompanying Notes to Financial Statements regarding valuation of investments. |

Fair Valuation Summary

The following is a summary of the fair valuations according to the inputs used as of September 30, 2019 in valuing the Fund’s investments.

Description | Total | Level 1 | Level 2 | Level 3(1) | ||||||||||||

Assets |

| |||||||||||||||

Common Stocks |

| |||||||||||||||

Automobiles & Components | $ | 14,884 | $ | 14,884 | $ | — | $ | — | ||||||||

Banks | 42,129 | 42,129 | — | — | ||||||||||||

Capital Goods | 70,207 | 70,207 | — | — | ||||||||||||

Commercial & Professional Services | 16,242 | 16,242 | — | — | ||||||||||||

Consumer Durables & Apparel | 6,815 | 6,815 | — | — | ||||||||||||

Consumer Services | 26,292 | 26,292 | — | — | ||||||||||||

Diversified Financials | 93,784 | 93,784 | — | — | ||||||||||||

Energy | 71,483 | 71,483 | — | — | ||||||||||||

Food & Staples Retailing | 33,027 | 33,027 | — | — | ||||||||||||

Food, Beverage & Tobacco | 32,149 | 32,149 | — | — | ||||||||||||

Health Care Equipment & Services | 78,498 | 78,498 | — | — | ||||||||||||

Household & Personal Products | 30,788 | 30,788 | — | — | ||||||||||||

Insurance | 158,757 | 158,757 | — | — | ||||||||||||

Materials | 49,174 | 49,174 | — | — | ||||||||||||

Media & Entertainment | 35,557 | 35,557 | — | — | ||||||||||||

Pharmaceuticals, Biotechnology & Life Sciences | 52,523 | 52,523 | — | — | ||||||||||||

Real Estate | 44,536 | 44,536 | — | — | ||||||||||||

Retailing | 29,497 | 29,497 | — | — | ||||||||||||

Software & Services | 63,847 | 63,847 | — | — | ||||||||||||

Technology Hardware & Equipment | 19,814 | 19,814 | — | — | ||||||||||||

Telecommunication Services | 63,618 | 63,618 | — | — | ||||||||||||

Transportation | 15,912 | 15,912 | — | — | ||||||||||||

Utilities | 77,926 | 77,926 | — | — | ||||||||||||

Short-Term Investments | 1,571 | 1,571 | — | — | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total | $ | 1,129,030 | $ | 1,129,030 | $ | — | $ | — | ||||||||

|

|

|

|

|

|

|

| |||||||||

| (1) | For the period ended September 30, 2019, there were no transfers in and out of Level 3. |

The accompanying notes are an integral part of these financial statements.

| 16 |

|