UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

CERTIFIED SHAREHOLDER REPORT

OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

| |

| Investment Company Act file number: 811-1027 |

| Name of Registrant: Vanguard World Funds |

| Address of Registrant: P.O. Box 2600 | |

| Valley Forge, PA 19482 |

| Name and address of agent for service: | Heidi Stam, Esquire |

| | P.O. Box 876 |

| | Valley Forge, PA 19482 |

| Registrant’s telephone number, including area code: (610) 669-1000 |

| Date of fiscal year end: August 31 | |

| Date of reporting period: September 1, 2008 – August 31, 2009 |

Item 1: Reports to Shareholders

| Vanguard U.S. Growth Fund |

| Annual Report |

| August 31, 2009 |

> Vanguard U.S. Growth Fund returned about –16% for the fiscal year ended

August 31, 2009.

> The fund’s disappointing return was nevertheless better than the return of its

benchmark index (about –17%) and the average return of competing funds

(about –18%).

> The fund’s result for the fiscal year encompassed two very different market

environments—a first half during which the fund returned about –39% and a

second half during which it returned about 37%.

| |

| Contents | |

| Your Fund’s Total Returns. | 1 |

| President’s Letter. | 2 |

| Advisors’ Report. | 7 |

| Results of Proxy Voting. | 10 |

| Fund Profile. | 11 |

| Performance Summary. | 13 |

| Financial Statements. | 15 |

| Your Fund’s After-Tax Returns. | 27 |

| About Your Fund’s Expenses. | 28 |

| Glossary. | 30 |

Please note: The opinions expressed in this report are just that—informed opinions. They should not be considered promises or advice.

Also, please keep in mind that the information and opinions cover the period through the date on the front of this report. Of course, the

risks of investing in your fund are spelled out in the prospectus.

See the Glossary for definitions of investment terms used in this report.

Cover photograph: Veronica Coia.

Your Fund’s Total Returns

| |

| Fiscal Year Ended August 31, 2009 | |

| | Total |

| | Returns |

| Vanguard U.S. Growth Fund | |

| Investor Shares | -16.29% |

| Admiral™ Shares | -16.15 |

| Russell 1000 Growth Index | -16.76 |

| Large-Cap Growth Funds Average | -17.84 |

| Large-Cap Growth Funds Average: Derived from data provided by Lipper Inc. | |

Admiral Shares are a lower-cost class of shares available to many longtime shareholders and to those with significant investments in the fund.

Your Fund’s Performance at a Glance

August 31, 2008, Through August 31, 2009

| | | | |

| | | | Distributions Per Share |

| | Starting | Ending | Income | Capital |

| | Share Price | Share Price | Dividends | Gains |

| Vanguard U.S. Growth Fund | | | | |

| Investor Shares | $17.89 | $14.83 | $0.116 | $0.000 |

| Admiral Shares | 46.37 | 38.41 | 0.376 | 0.000 |

1

President’s Letter

Dear Shareholder,

Vanguard U.S. Growth Fund returned about –16% for the fiscal year ended August 31, its second annual loss in a row. However, the results mask a dramatic turnaround in market sentiment and fund performance that began about midway through U.S. Growth’s fiscal year.

Investor confidence abruptly returned in March as turmoil in the credit markets began to subside and economic reports began to suggest that the economy was on the mend. The corporate bond market and the stock market rebounded, helping turn the second half of the fund’s fiscal year into a mirror image of the first.

U.S. Growth returned about 37% for the second half of the fiscal year, compared with a return of almost –39% for its opening six months. Because of the sometimes confounding mathematics of percentages, these more or less inverse returns netted to the 12-month loss of about –16%. U.S. Growth outdid its benchmark index and the average return of peer-group funds for the year as a whole. On a relative basis, at least, the fund’s performance marks a positive change from its struggles in recent years.

2

Stocks sank, then soared as credit and economy stabilized

The fiscal year began with the September collapse of a major investment bank and the government-engineered rescue of several giant financial institutions. Stocks sank as the ensuing crisis spread from Wall Street to Main Street and around the globe. Stricken by seized-up credit markets and a near-total lack of confidence, businesses and consumers put the brakes on economic growth.

Governments in the United States and abroad responded with unprecedented stimulus and other programs. Over the past six months, these efforts started to take hold. Credit-market conditions improved, and the outlook for the U.S.

economy brightened. From their early-March lows, stocks took off on an almost-unbroken winning streak.

Even so, the broad U.S. stock market ended the 12 months in negative territory, with a return of about –18%. International markets performed somewhat better, as major European economies emerged from recession; the MSCI All Country World Index ex USA returned about –14%.

Despite the robust second-half rally, it may be premature to sound the all-clear signal. As the fiscal year came to a close, home foreclosures and the unemployment rate were rising, and the federal government’s list of problem banks had climbed above 400—the most since June 1994. There is

| | | |

| Market Barometer | | | |

| |

| | Average Annual Total Returns |

| | Periods Ended August 31, 2009 |

| | One | Three | Five |

| | Year | Years | Years |

| Stocks | | | |

| Russell 1000 Index (Large-caps) | -18.39% | -5.61% | 0.94% |

| Russell 2000 Index (Small-caps) | -21.29 | -6.08 | 2.21 |

| Dow Jones U.S. Total Stock Market Index | -18.10 | -5.17 | 1.45 |

| MSCI All Country World Index ex USA (International) | -13.96 | -2.41 | 8.18 |

| |

| Bonds | | | |

| Barclays Capital U.S. Aggregate Bond Index (Broad | | | |

| taxable market) | 7.94% | 6.35% | 4.96% |

| Barclays Capital Municipal Bond Index | 5.67 | 4.14 | 4.15 |

| Citigroup Three-Month U.S. Treasury Bill Index | 0.51 | 2.77 | 2.98 |

| |

| CPI | | | |

| Consumer Price Index | -1.48% | 1.91% | 2.64% |

3

considerable historical evidence that recovery from a recession caused by a financial crisis tends to take longer than average.

Among bond investors, safety and yield traded places

The U.S. bond market also performed a U-turn during the year. Early on, as credit markets deteriorated, investors rushed to the relative safety and liquidity of U.S. Treasury securities, driving their prices up and yields down. Investors were so risk-averse that short-term Treasury yields briefly turned negative. November and December were among the ten best months ever for Treasury returns (adjusted for inflation). Corporate bonds, especially those of lower credit quality, struggled,

and their yield spreads above comparable Treasuries widened to near-historic levels during the first six months.

Several moves by the Treasury and the Federal Reserve Board—which slashed its target level for short-term interest rates to a range of 0%–0.25% in December—helped credit markets to attain some stability by the spring. In a dramatic reversal, investors regained their appetite for risk, favoring corporate bonds over Treasuries.

After all the ups and downs, Treasuries and high-yield corporate bonds produced similar 12-month returns of about 6%–7%. Overall, the broad U.S. taxable bond market returned about 8%. Tax-exempt municipal bonds, after a flat first half, returned more than 5% for the fiscal year.

Expense Ratios

Your Fund Compared With Its Peer Group

| | | |

| | | | Large-Cap |

| | Investor | Admiral | Growth Funds |

| | Shares | Shares | Average |

| U.S. Growth Fund | 0.50% | 0.31% | 1.34% |

The fund expense ratios shown are from the prospectus dated December 29, 2008, and represent estimated costs for the current fiscal year based on the fund’s net assets as of the prospectus date. For the fiscal year ended August 31, 2009, the expense ratios were 0.49% for the Investor Shares and 0.30% for the Admiral Shares. The peer-group expense ratio is derived from data provided by Lipper Inc. and captures information through year-end 2008.

4

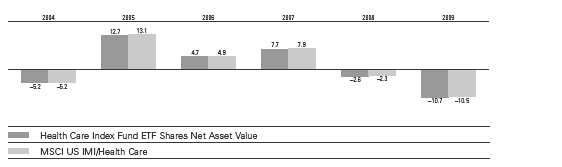

Health care and energy stocks drove the fund’s return

During the market’s free fall in the fiscal year’s first half, every sector in which the fund invested posted negative results. By contrast, each of these sectors contributed a solid positive return during the second half.

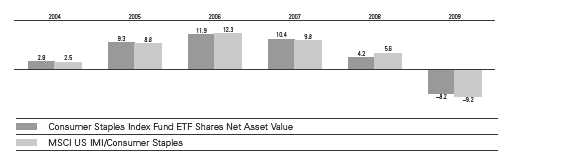

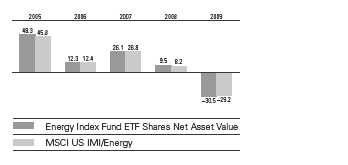

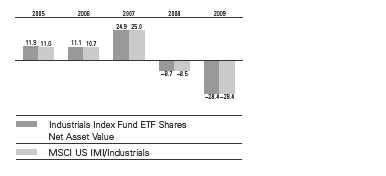

The fund’s holdings in health care and energy had the most significant impact on its full-year performance; they were responsible for about half of the fund’s negative return. The fund’s consumer staples and industrial stocks also took a large chunk from its fiscal-year result.

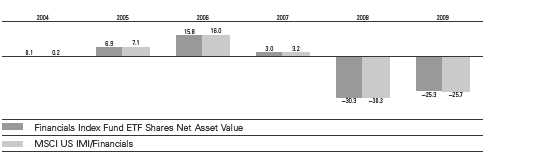

The negative impact of other sectors, such as financials and materials, was less severe, in part because of stocks

that swam against the general market tide, including those of bankers Goldman Sachs and JPMorgan Chase and copper-miner Freeport-McMoRan.

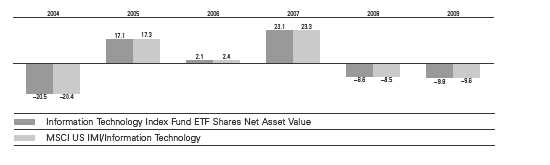

The fund’s substantial holdings in information technology stocks—which represented about a third of its assets at the end of the period—held up relatively well, as a powerful second-half rally offset most of the sector’s decline in the first half. Over the full 12 months, the fund’s tech stocks trimmed about 1 percentage point from its return.

The only sector holdings that made a positive contribution to the fiscal-year return were—despite the economic

| |

| Total Returns | |

| Ten Years Ended August 31, 2009 | |

| | Average |

| | Annual Return |

| U.S. Growth Fund Investor Shares | -6.30% |

| Russell 1000 Growth Index | -3.17 |

| Large-Cap Growth Funds Average | -3.34 |

| Large-Cap Growth Funds Average: Derived from data provided by Lipper Inc. | |

The figures shown represent past performance, which is not a guarantee of future results. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at www.vanguard.com/performance.) Note, too, that both investment returns and principal value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost.

5

slump—consumer discretionary stocks, which got a significant boost from Kohl’s, the department store chain.

Although it was difficult to find bright spots in the year’s disappointing results, the advisors’ stock selections helped the fund stay a few steps ahead of its comparative standards. Of course, we can’t forget that such “better” performance during market downturns is a relative concept.

A word on expenses

The fund’s expense ratio has risen over the past fiscal year. The explanation is twofold.

First, as the value of the fund assets has declined, the fund’s fixed expenses have accounted for a modestly higher percentage of fund assets. Second, the Vanguard funds’ contracts with external advisors typically include breakpoint pricing. As assets rise above a breakpoint threshold, advisory fees are paid at a lower rate. When assets fall, as they have during fiscal 2009, a smaller portion of assets is subject to the lower rate, causing the overall rate to increase.

A turn for the better after a tough stretch

U.S. Growth ended fiscal 2009 on a welcome note. The fund performed well compared with its benchmark index and peer funds during a very difficult time. The funds’ advisors—AllianceBernstein and William Blair & Company—deserve much credit for that performance.

Of course, a single year’s result is only a part of a long-term record. And, in truth, the fund’s performance in recent years has not consistently matched that of its

benchmark. Over the past decade, for example, the fund produced an average annual return of about –6%, compared with about –3% for its benchmark index.

Going forward, we have confidence in our advisors and their approach to large-cap growth investing, and we believe that the fund has the potential to produce competitive returns over the long term.

Keep in mind that the fund’s long-term results are likely to be composed of widely differing yearly returns, as you can see in the Performance Summary later in this report. That reflects a variety of factors, from changing economic circumstances to the changing fortunes of the fast-growing, dynamic companies in which the fund invests.

That is why we urge investors to maintain a portfolio that is balanced among stocks, bonds, and cash reserves and diversified within these asset classes—a portfolio that holds both growth and value stocks, for example. The exact mix of assets should be based on your unique objective, time horizon, and risk tolerance. U.S. Growth can serve as an element in such a diversified portfolio.

Thank you for entrusting your assets to Vanguard.

Sincerely,

F. William McNabb III

President and Chief Executive Officer

September 12, 2009

6

Advisors’ Report

For the 12 months ended August 31, 2009, Vanguard U.S. Growth Fund returned about –16%. Your fund is managed by two independent advisors, a strategy that enhances the fund’s diversification by providing exposure to distinct, yet complementary, investment approaches. It is not uncommon for different advisors to have different views about individual securities or the broader investment environment.

The table below presents the advisors, the percentage and amount of fund assets that each manages, and brief descriptions of their investment strategies. Each advisor has also prepared a discussion of the investment environment during the fiscal year and of how the portfolio’s

positioning reflects this assessment. These reports were prepared on September 10, 2009.

AllianceBernstein L.P.

Portfolio Managers:

James G. Reilly,

Executive Vice President

P. Scott Wallace, CFA,

Senior Vice President

After extending 2008’s sharp losses in January and February, U.S. equities rallied, with the S&P 500 gaining about 41% from March to August 2009 amid thawing credit markets, signs of economic recovery, and better-than-expected corporate profits.

| | | |

| Vanguard U.S. Growth Fund Investment Advisors | |

| |

| | Fund Assets Managed | |

| Investment Advisor | % | $ Million | Investment Strategy |

| AllianceBernstein L.P. | 68 | 2,565 | Uses a fundamentally based, research-driven approach |

| | | | to large-capitalization growth investing. The advisor |

| | | | seeks to build a diversified portfolio of successful, |

| | | | well-managed companies with sustainable competitive |

| | | | advantages and superior prospects for growth not fully |

| | | | reflected in relative valuation. |

| William Blair & Company, L.L.C. | 30 | 1,146 | Uses a fundamental investment approach in pursuit of |

| | | | superior long-term investment results from |

| | | | growth-oriented companies with leadership positions |

| | | | and strong market presence. |

| Cash Investments | 2 | 82 | These short-term reserves are invested by Vanguard in |

| | | | equity index products to simulate investment in stocks. |

| | | | Each advisor may also maintain a modest cash |

| | | | position. |

7

Still, the S&P 500 finished the 12 months ended August 31, 2009, down about 18%. The growth investment style outperformed value during the period, with the Russell 1000 Growth Index returning about –17% and the Russell 1000 Value Index returning about –20%. For the 12 months, the fund outperformed its Russell 1000 Growth benchmark.

In the portion of the portfolio that we manage, our stock selection and overweighting in health care helped overall returns, as investors gravitated toward sectors perceived as defensive during the market turmoil. Our financial holdings, led by Goldman Sachs and JPMorgan Chase, also outperformed, reflecting emerging indications of these companies’ ability to take advantage of weakened competition and gain share in capital-markets segments. Our technology holdings, hurt by concerns about cutbacks in global tech spending, were the largest source of underperformance.

The market’s recent strength has provided a clear indication that fears about end-of-the-world scenarios have been put to rest, although investors are now questioning the sustainability of a rebound because of weak consumer spending. But it wasn’t the consumer segment that drove the economy down in the latest recession, and consumer spending often doesn’t lead the way out, as a wait-and-see attitude among employers causes rehiring to lag recovery.

With fears of financial Armageddon behind them, investors are returning their focus to earnings. Recent earnings reports showed a spike in earnings surprises relative to disappointments, suggesting that analysts were caught off guard by the moderation in declines. Meanwhile, earnings for growth companies have held up better this year and look more promising for 2010. Growth stocks are now priced on parity with value stocks, a seemingly counterintuitive occurrence. We expect investors to become more discerning as an economic recovery takes shape, and to gravitate toward companies that provide greater confidence in earnings stability and expansion; that should, in our view, favor the growth style.

William Blair & Company, L.L.C.

Portfolio Manager:

John F. Jostrand, CFA, Principal

The last year was an extremely difficult period for U.S. equity investors. The portfolio’s benchmark, the Russell 1000 Growth Index, returned about –17%. The period began with severe declines as the global financial crisis deepened, and record levels of volatility and indiscriminate selling occurred. Losses continued into early 2009 as investors reacted negatively to deteriorating economic and equity market fundamentals. As risk aversion increased, investors flocked to defensive groups such as consumer staples, health care, and larger-cap stocks.

8

After March 9, U.S. equity markets recorded an impressive positive performance. Stocks rallied as investors anticipated an economic recovery based on improved global economic data resulting from aggressive fiscal and monetary policy, both here and abroad. In general, over the last six months, riskier assets surpassed more conservative ones, emerging markets outperformed developed markets, and smaller-capitalization stocks surpassed large-caps.

Early in the period, our portion of the portfolio held up relatively well owing to our quality growth focus, although stock selection and an underweighted position in consumer staples weighed on results. The consumer staples sector was a strong performer as investors sought safety, but our exposure to it was substantially less than that of the index because we believe there are better opportunities for earnings growth in other groups. Campbell Soup, our weakest holding in consumer staples, came under pressure because of product-price discounting concerns, and we eliminated it.

Conversely, the consumer discretionary sector was the greatest contributor to our portion of the portfolio because of strong stock selection and an overweighting in a relatively good performer: Johnson Controls rallied as the economy and outlook for the automotive industry looked less dire.

In our view, we are probably past the worst of the recessionary declines, and economic recovery has begun. Signs of stabilization and improvement in the U.S. and other economies continue to appear. Global stimulus programs will continue to help as more of their components take effect. Additionally, in the near term, we should see an uptick in production as restocking occurs after the rapid reduction in inventory between October and March. Overall, our outlook for U.S. economic growth remains at subdued levels.

Many stocks—especially small-caps and those of lower quality—reacted positively and quickly to early signs of a recovery, even though there had been only slight improvement from the lows. Moving into 2010, investors are likely to focus on a company’s ability to sustain its recent advance, as demonstrated by a revival in sales combined with expense control. In this environment, we believe our portfolio will continue to benefit from our quality growth philosophy and our research-intensive investment process, which will help us to identify industry-leading companies with competitive business models that have compelling and sustainable earnings growth profiles and strong financial positions.

9

Results of Proxy Voting

At a special meeting of shareholders on July 2, 2009, fund shareholders approved the following two proposals:

Proposal 1—Elect trustees for each fund.*

The individuals listed in the table below were elected as trustees for each fund. All trustees with the exception of Messrs. McNabb and Volanakis (both of whom already served as directors of The Vanguard Group, Inc.) served as trustees to the funds prior to the shareholder meeting.

| | | |

| | | | Percentage |

| Trustee | For | Withheld | For |

| John J. Brennan | 816,325,661 | 25,839,114 | 96.9% |

| Charles D. Ellis | 811,618,878 | 30,545,897 | 96.4% |

| Emerson U. Fullwood | 816,960,560 | 25,204,215 | 97.0% |

| Rajiv L. Gupta | 815,607,429 | 26,557,346 | 96.8% |

| Amy Gutmann | 818,039,387 | 24,125,388 | 97.1% |

| JoAnn Heffernan Heisen | 815,771,400 | 26,393,375 | 96.9% |

| F. William McNabb III | 817,559,701 | 24,605,074 | 97.1% |

| André F. Perold | 814,833,250 | 27,331,525 | 96.8% |

| Alfred M. Rankin, Jr. | 815,942,907 | 26,221,868 | 96.9% |

| Peter F. Volanakis | 817,780,699 | 24,384,076 | 97.1% |

| * Results are for all funds within the same trust. | | | |

Proposal 2—Update and standardize the funds’ fundamental policies regarding:

(a) Purchasing and selling real estate.

(b) Issuing senior securities.

(c) Borrowing money.

(d) Making loans.

(e) Purchasing and selling commodities.

(f) Concentrating investments in a particular industry or group of industries.

(g) Eliminating outdated fundamental investment policies not required by law.

The revised fundamental policies are clearly stated and simple, yet comprehensive, making oversight and compliance more efficient than under the former policies. The revised fundamental policies will allow the funds to respond more quickly to regulatory and market changes, while avoiding the costs and delays associated with successive shareholder meetings.

| | | | | |

| | | | | Broker | Percentage |

| Vanguard Fund | For | Abstain | Against | Non-Votes | For |

| U.S. Growth Fund | | | | | |

| 2a | 165,876,100 | 4,890,892 | 4,356,102 | 4,561,467 | 92.3% |

| 2b | 165,333,362 | 5,207,115 | 4,582,614 | 4,561,469 | 92.0% |

| 2c | 164,407,000 | 5,129,930 | 5,586,162 | 4,561,469 | 91.5% |

| 2d | 164,607,338 | 5,140,619 | 5,375,135 | 4,561,468 | 91.6% |

| 2e | 165,078,411 | 5,040,748 | 5,003,934 | 4,561,468 | 91.9% |

| 2f | 165,249,329 | 5,178,086 | 4,695,676 | 4,561,469 | 92.0% |

| 2g | 166,305,489 | 5,073,329 | 3,744,272 | 4,561,470 | 92.6% |

10

U.S. Growth Fund

Fund Profile

As of August 31, 2009

| | |

| Share-Class Characteristics | |

| | Investor | Admiral |

| | Shares | Shares |

| Ticker Symbol | VWUSX | VWUAX |

| Expense Ratio1 | 0.50% | 0.31% |

| 30-Day SEC Yield | 0.58% | 0.81% |

| | | |

| Portfolio Characteristics | | |

| | | Russell | DJ |

| | | 1000 | U.S. Total |

| | | Growth | Market |

| | Fund | Index | Index |

| Number of Stocks | 86 | 627 | 4,345 |

| Median Market Cap | $53.2B | $35.3B | $27.3B |

| Price/Earnings Ratio | 24.2x | 20.6x | 26.0x |

| Price/Book Ratio | 2.6x | 3.4x | 2.1x |

| Return on Equity | 29.5% | 23.6% | 19.2% |

| Earnings Growth Rate | 21.8% | 16.6% | 9.7% |

| Dividend Yield | 1.1% | 1.7% | 2.0% |

| Foreign Holdings | 8.0% | 0.0% | 0.0% |

| Turnover Rate | 101% | — | — |

| Short-Term Reserves | 0.7% | — | — |

| | |

| Volatility Measures | | |

| | | DJ |

| | U.S. Total |

| | Russell 1000 | Market |

| | Growth Index | Index |

| R-Squared | 0.97 | 0.93 |

| Beta | 0.95 | 0.91 |

| These measures show the degree and timing of the fund’s fluctuations compared with the indexes over 36 months. | |

| | |

| Ten Largest Holdings (% of total net assets) |

| Apple Inc. | Computer | |

| | Hardware | 6.0% |

| Google Inc. | Internet Software & | |

| | Services | 5.5 |

| The Goldman Sachs | Investment Banking | |

| Group, Inc. | & Brokerage | 4.2 |

| QUALCOMM Inc. | Communications | |

| | Equipment | 4.0 |

| Hewlett-Packard Co. | Computer | |

| | Hardware | 4.0 |

| JPMorgan Chase & Co. | Diversified Financial | |

| | Services | 3.9 |

| Schlumberger Ltd. | Oil & Gas | |

| | Equipment & | |

| | Services | 3.4 |

| Gilead Sciences, Inc. | Biotechnology | 3.4 |

| Intel Corp. | Semiconductors | 2.7 |

| Kohl's Corp. | Department Stores | 2.6 |

| Top Ten | | 39.7% |

| The holdings listed exclude any temporary cash investments and equity index products. |

Investment Focus

1 The expense ratios shown are from the prospectus dated December 29, 2008, and represent estimated costs for the current fiscal year based

on the fund’s net assets as of the prospectus date. For the fiscal year ended August 31, 2009, the expense ratios were 0.49% for the Investor

Shares and 0.30% for the Admiral Shares.

11

U.S. Growth Fund

Sector Diversification (% of equity exposure)

| | | Russell | DJ |

| | | 1000 | U.S. Total |

| | | Growth | Market |

| | Fund | Index | Index |

| Consumer | | | |

| Discretionary | 9.9% | 10.4% | 10.0% |

| Consumer Staples | 7.0 | 16.0 | 10.0 |

| Energy | 8.5 | 4.1 | 11.2 |

| Financials | 13.8 | 5.3 | 16.5 |

| Health Care | 14.2 | 16.8 | 13.2 |

| Industrials | 9.0 | 10.1 | 10.3 |

| Information | | | |

| Technology | 32.2 | 31.8 | 18.2 |

| Materials | 5.3 | 4.0 | 3.8 |

| Telecommunication | | | |

| Services | 0.0 | 0.5 | 2.9 |

| Utilities | 0.1 | 1.0 | 3.9 |

12

U.S. Growth Fund

Performance Summary

All of the returns in this report represent past performance, which is not a guarantee of future results that may be achieved by the fund. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at www.vanguard.com/performance.) Note, too, that both investment returns and principal value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost. The returns shown do not reflect taxes that a shareholder would pay on fund distributions or on the sale of fund shares.

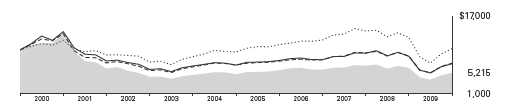

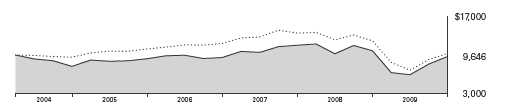

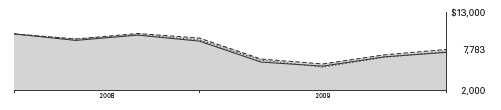

Cumulative Performance: August 31, 1999, Through August 31, 2009

Initial Investment of $10,000

| | | | | |

| | | | Average Annual Total Returns | |

| | | Periods Ended August 31, 2009 | |

| | | | | | Final Value |

| | | One | Five | Ten | of a $10,000 |

| | | Year | Years | Years | Investment |

| | U.S. Growth Fund Investor Shares | -16.29% | 1.11% | -6.30% | $5,215 |

| •••••••• | Dow Jones U.S. Total Stock Market | | | | |

| | Index | -18.10 | 1.45 | 0.26 | 10,259 |

| |

| |

| – – – – | Large-Cap Russell 1000 Growth Growth Funds Index Average | -17.84 -16.76 | 0.74 1.21 | -3.34 -3.17 | 7,119 7,249 |

Large-Cap Growth Funds Average: Derived from data provided by Lipper Inc.

| | | | |

| | | | Since | Final Value |

| | | | Inception | of a $100,000 |

| | One Year | Five Years | (8/13/2001) | Investment |

| U.S. Growth Fund Admiral Shares | -16.15% | 1.33% | -2.63% | $80,665 |

| Dow Jones U.S. Total Stock Market | | | | |

| Index | -18.10 | 1.45 | 1.15 | 109,681 |

| Russell 1000 Growth Index | -16.76 | 1.21 | -0.87 | 93,192 |

| Performance for the fund’s Admiral Shares and comparative standards is calculated since the Admiral Shares’ inception. | |

Vanguard fund total returns do not include the account service fee that may be applicable to certain accounts with balances below $10,000.

See Financial Highlights for dividend and capital gains information.

13

U.S. Growth Fund

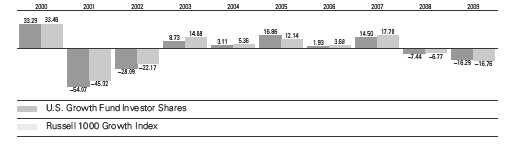

Fiscal-Year Total Returns (%): August 31, 1999, Through August 31, 2009

Average Annual Total Returns: Periods Ended June 30, 2009

This table presents average annual total returns through the latest calendar quarter—rather than through the end of

the fiscal period. Securities and Exchange Commission rules require that we provide this information.

| | | | |

| | Inception Date | One Year | Five Years | Ten Years |

| Investor Shares | 1/6/1959 | -23.81% | -2.46% | -7.46% |

| Admiral Shares | 8/13/2001 | -23.70 | -2.26 | -3.861 |

| 1 Return since inception. | | | | |

Vanguard fund total returns do not include the account service fee that may be applicable to certain accounts with balances below $10,000.

See Financial Highlights for dividend and capital gains information.

14

U.S. Growth Fund

Financial Statements

Statement of Net Assets

As of August 31, 2009

The fund provides a complete list of its holdings four times in each fiscal year, at the quarter-ends.

For the second and fourth fiscal quarters, the lists appear in the fund’s semiannual and annual reports to shareholders. For the first and third fiscal quarters, the fund files the lists with the Securities and

Exchange Commission on Form N-Q. Shareholders can look up the fund’s Forms N-Q on the SEC’s website at www.sec.gov. Forms N-Q may also be reviewed and copied at the SEC’s Public Reference Room (see the back cover of this report for further information).

| | | |

| | | | Market |

| | | | Value• |

| | | Shares | ($000) |

| Common Stocks (97.6%)1 | | |

| Consumer Discretionary (9.6%) | |

| * | Kohl’s Corp. | 1,897,191 | 97,876 |

| | Johnson Controls, Inc. | 1,662,400 | 41,178 |

| | Target Corp. | 871,600 | 40,965 |

| | McDonald’s Corp. | 688,790 | 38,737 |

| | Lowe’s Cos., Inc. | 1,752,600 | 37,681 |

| * | Discovery | | |

| | Communications Inc. | | |

| | Class A | 1,077,600 | 27,931 |

| * | O’Reilly Automotive, Inc. | 437,100 | 16,732 |

| | Omnicom Group Inc. | 372,630 | 13,534 |

| | Yum! Brands, Inc. | 393,600 | 13,481 |

| * | Amazon.com, Inc. | 160,600 | 13,039 |

| | The Walt Disney Co. | 446,800 | 11,635 |

| | Toyota Motor Corp. ADR | 134,500 | 11,458 |

| | | | 364,247 |

| Consumer Staples (6.8%) | | |

| | PepsiCo, Inc. | 1,334,600 | 75,632 |

| | Wal-Mart Stores, Inc. | 1,132,650 | 57,618 |

| | Costco Wholesale Corp. | 962,200 | 49,053 |

| | CVS Caremark Corp. | 810,840 | 30,422 |

| | Colgate-Palmolive Co. | 405,200 | 29,458 |

| | General Mills, Inc. | 174,800 | 10,441 |

| | Mead Johnson Nutrition Co. | 155,800 | 6,179 |

| | | | 258,803 |

| Energy (8.3%) | | |

| | Schlumberger Ltd. | 2,301,070 | 129,320 |

| | Occidental | | |

| | Petroleum Corp. | 737,900 | 53,941 |

| | Apache Corp. | 379,950 | 32,277 |

| * | Cameron | | |

| | International Corp. | 890,640 | 31,805 |

| | | |

| | | | Market |

| | | | Value• |

| | | Shares | ($000) |

| * | Suncor Energy, Inc. | | |

| | (New York Shares) | 586,000 | 17,955 |

| | Petroleo Brasileiro SA ADR | 376,800 | 14,936 |

| * | National Oilwell Varco Inc. | 366,100 | 13,308 |

| | EOG Resources, Inc. | 166,340 | 11,976 |

| | Petroleo Brasileiro SA | | |

| | Series A ADR | 236,200 | 7,842 |

| | | | 313,360 |

| Exchange-Traded Fund (0.0%) | | |

| ^,2 | Vanguard Growth ETF | 3,100 | 147 |

| |

| Financials (13.4%) | | |

| | The Goldman Sachs | | |

| | Group, Inc. | 952,537 | 157,607 |

| | JPMorgan Chase & Co. | 3,415,300 | 148,429 |

| | CME Group, Inc. | 196,455 | 57,176 |

| * | Credit Suisse Group | | |

| | AG ADR | 831,200 | 42,300 |

| | Invesco, Ltd. | 985,300 | 20,445 |

| | Franklin Resources, Inc. | 215,700 | 20,131 |

| | Bank of America Corp. | 984,300 | 17,314 |

| | Charles Schwab Corp. | 931,785 | 16,828 |

| | The Principal | | |

| | Financial Group, Inc. | 504,900 | 14,339 |

| | Janus Capital Group Inc. | 1,010,200 | 12,850 |

| | | | 507,419 |

| Health Care (13.9%) | | |

| * | Gilead Sciences, Inc. | 2,826,460 | 127,360 |

| | Teva Pharmaceutical | | |

| | Industries Ltd. | | |

| | Sponsored ADR | 1,465,060 | 75,451 |

| * | Celgene Corp. | 1,397,360 | 72,900 |

| | Baxter International, Inc. | 1,178,900 | 67,103 |

15

U.S. Growth Fund

| | | |

| | | | Market |

| | | | Value• |

| | | Shares | ($000) |

| | Alcon, Inc. | 516,140 | 66,825 |

| * | Medco Health | | |

| | Solutions, Inc. | 967,600 | 53,431 |

| * | Thermo Fisher | | |

| | Scientific, Inc. | 653,120 | 29,527 |

| | Allergan, Inc. | 332,435 | 18,590 |

| | UnitedHealth Group Inc. | 555,700 | 15,560 |

| | | | 526,747 |

| Industrials (8.7%) | | |

| | Danaher Corp. | 1,118,615 | 67,911 |

| | Illinois Tool Works, Inc. | 1,061,100 | 44,375 |

| | United Parcel Service, Inc. | 614,200 | 32,835 |

| * | Vestas Wind Systems A/S | 1,335,100 | 31,942 |

| | Union Pacific Corp. | 461,100 | 27,579 |

| | FedEx Corp. | 328,200 | 22,551 |

| | W.W. Grainger, Inc. | 215,300 | 18,832 |

| | J.B. Hunt Transport | | |

| | Services, Inc. | 632,210 | 17,721 |

| | Roper Industries Inc. | 367,690 | 17,421 |

| | Rockwell Automation, Inc. | 404,100 | 16,912 |

| | United Technologies Corp. | 267,300 | 15,867 |

| * | Quanta Services, Inc. | 574,600 | 12,710 |

| | Emerson Electric Co. | 144,270 | 5,319 |

| | | | 331,975 |

| Information Technology (31.7%) | |

| * | Apple Inc. | 1,346,306 | 226,462 |

| * | Google Inc. | 454,750 | 209,944 |

| | QUALCOMM Inc. | 3,236,995 | 150,261 |

| | Hewlett-Packard Co. | 3,338,000 | 149,843 |

| | Intel Corp. | 5,021,910 | 102,045 |

| | Microsoft Corp. | 2,585,595 | 63,735 |

| * | Cisco Systems, Inc. | 2,471,080 | 53,375 |

| * | EMC Corp. | 2,053,500 | 32,651 |

| | Visa Inc. | 443,000 | 31,497 |

| | Taiwan Semiconductor | | |

| | Manufacturing Co., | | |

| | Ltd. ADR | 2,558,939 | 27,381 |

| | Altera Corp. | 1,335,700 | 25,659 |

| * | Broadcom Corp. | 767,000 | 21,821 |

| * | Juniper Networks, Inc. | 831,000 | 19,171 |

| * | Cognizant Technology | | |

| | Solutions Corp. | 492,800 | 17,189 |

| | Amphenol Corp. Class A | 472,700 | 16,526 |

| * | McAfee Inc. | 394,400 | 15,689 |

| * | Activision Blizzard, Inc. | 1,320,800 | 15,335 |

| * | Adobe Systems, Inc. | 420,539 | 13,213 |

| * | Research In Motion Ltd. | 169,500 | 12,384 |

| | | | 1,204,181 |

| | |

| | | Market |

| | | Value• |

| | Shares | ($000) |

| Materials (5.2%) | | |

| Freeport-McMoRan | | |

| Copper & Gold, Inc. | | |

| Class B | 683,200 | 43,028 |

| Arcelor Mittal Class A | | |

| New York | | |

| Registered Shares | 1,051,500 | 37,465 |

| Praxair, Inc. | 411,640 | 31,540 |

| Rio Tinto PLC ADR | 167,000 | 25,912 |

| Air Products & | | |

| Chemicals, Inc. | 320,730 | 24,064 |

| Ecolab, Inc. | 420,320 | 17,775 |

| Monsanto Co. | 187,255 | 15,707 |

| | | 195,491 |

| Total Common Stocks | | |

| (Cost $3,676,708) | | 3,702,370 |

| Temporary Cash Investments (2.9%)1 | |

| Money Market Fund (2.4%) | | |

| 3,4 Vanguard Market | | |

| Liquidity Fund, | | |

| 0.277% | 90,274,855 | 90,275 |

| |

| | Face | |

| | Amount | |

| | ($000) | |

| U.S. Government and Agency Obligations (0.5%) |

| 5,6 Federal Home Loan | | |

| Bank, 0.275%, 2/19/10 | 18,000 | 17,978 |

| Total Temporary Cash Investments | |

| (Cost $108,251) | | 108,253 |

| Total Investments (100.5%) | | |

| (Cost $3,784,959) | | 3,810,623 |

| Other Assets and Liabilities (-0.5%) | |

| Other Assets | | 28,778 |

| Liabilities4 | | (46,018) |

| | | (17,240) |

| Net Assets (100%) | | 3,793,383 |

16

U.S. Growth Fund

| |

| At August 31, 2009, net assets consisted of: |

| | Amount |

| | ($000) |

| Paid-in Capital | 10,485,150 |

| Overdistributed Net Investment Income | (1,156) |

| Accumulated Net Realized Losses | (6,723,968) |

| Unrealized Appreciation (Depreciation) | |

| Investment Securities | 25,664 |

| Futures Contracts | 7,693 |

| Net Assets | 3,793,383 |

| |

| |

| Investor Shares—Net Assets | |

| Applicable to 199,343,891 outstanding | |

| $.001 par value shares of beneficial | |

| interest (unlimited authorization) | 2,955,597 |

| Net Asset Value Per Share— | |

| Investor Shares | $14.83 |

| |

| |

| Admiral Shares—Net Assets | |

| Applicable to 21,810,598 outstanding | |

| $.001 par value shares of beneficial | |

| interest (unlimited authorization) | 837,786 |

| Net Asset Value Per Share— | |

| Admiral Shares | $38.41 |

• See Note A in Notes to Financial Statements.

* Non-income-producing security.

^ Part of security position is on loan to broker-dealers. The total

value of securities on loan is $95,000.

1 The fund invests a portion of its cash reserves in equity markets

through the use of index futures contracts. After giving effect to

futures investments, the fund’s effective common stock and

temporary cash investment positions represent 99.8% and 0.7%,

respectively, of net assets.

2 Considered an affiliated company of the fund as the issuer is

another member of The Vanguard Group.

3 Affiliated money market fund available only to Vanguard funds

and certain trusts and accounts managed by Vanguard. Rate

shown is the 7-day yield.

4 Includes $98,000 of collateral received for securities on loan.

5 The issuer operates under a congressional charter; its securities

are not backed by the full faith and credit of the U.S.

government.

6 Securities with a value of $17,978,000 have been segregated as

initial margin for open futures contracts.

ADR—American Depositary Receipt.

See accompanying Notes, which are an integral part of the Financial Statements.

17

U.S. Growth Fund

Statement of Operations

| |

| | Year Ended |

| | August 31, 2009 |

| | ($000) |

| Investment Income | |

| Income | |

| Dividends1 | 41,434 |

| Interest1 | 2,154 |

| Security Lending | 295 |

| Total Income | 43,883 |

| Expenses | |

| Investment Advisory Fees—Note B&n bsp; | |

| Basic Fee | 5,688 |

| Performance Adjustment | (1,163) |

| The Vanguard Group—Note C | |

| Management and Administrative—Investor Shares | 8,366 |

| Management and Administrative—Admiral Shares | 1,046 |

| Marketing and Distribution—Investor Shares | 717 |

| Marketing and Distribution—Admiral Shares | 209 |

| Custodian Fees | 54 |

| Auditing Fees | 25 |

| Shareholders’ Reports and Proxies—Investor Shares | 310 |

| Shareholders’ Reports and Proxies—Admiral Shares | 32 |

| Trustees’ Fees and Expenses | 8 |

| Total Expenses | 15,292 |

| Expenses Paid Indirectly | (316) |

| Net Expenses | 14,976 |

| Net Investment Income | 28,907 |

| Realized Net Gain (Loss) | |

| Investment Securities Sold1 | (533,789) |

| Futures Contracts | (53,722) |

| Realized Net Gain (Loss) | (587,511) |

| Change in Unrealized Appreciation (Depreciation) | |

| Investment Securities | (240,494) |

| Futures Contracts | 14,406 |

| Change in Unrealized Appreciation (Depreciation) | (226,088) |

| Net Increase (Decrease) in Net Assets Resulting from Operations | (784,692) |

1 Dividend income, interest income, and realized net gain (loss) from affiliated companies of the fund were $2,000, $1,952,000, and

$0, respectively.

See accompanying Notes, which are an integral part of the Financial Statements.

18

U.S. Growth Fund

Statement of Changes in Net Assets

| | |

| | Year Ended August 31, |

| | 2009 | 2008 |

| | ($000) | ($000) |

| Increase (Decrease) in Net Assets | | |

| Operations | | |

| Net Investment Income | 28,907 | 27,319 |

| Realized Net Gain (Loss) | (587,511) | 138,171 |

| Change in Unrealized Appreciation (Depreciation) | (226,088) | (551,756) |

| Net Increase (Decrease) in Net Assets Resulting from Operations | (784,692) | (386,266) |

| Distributions | | |

| Net Investment Income | | |

| Investor Shares | (23,339) | (25,051) |

| Admiral Shares | (8,835) | (11,166) |

| Realized Capital Gain | | |

| Investor Shares | — | — |

| Admiral Shares | — | — |

| Total Distributions | (32,174) | (36,217) |

| Capital Share Transactions | | |

| Investor Shares | (65,408) | (351,798) |

| Admiral Shares | (77,153) | (106,170) |

| Net Increase (Decrease) from Capital Share Transactions | (142,561) | (457,968) |

| Total Increase (Decrease) | (959,427) | (880,451) |

| Net Assets | | |

| Beginning of Period | 4,752,810 | 5,633,261 |

| End of Period1 | 3,793,383 | 4,752,810 |

1 Net Assets—End of Period includes undistributed (overdistributed) net investment income of ($1,156,000) and $2,111,000.

See accompanying Notes, which are an integral part of the Financial Statements.

19

U.S. Growth Fund

Financial Highlights

| | | | | |

| Investor Shares | | | | | |

| |

| For a Share Outstanding | Year Ended August 31, |

| Throughout Each Period | 2009 | 2008 | 2007 | 2006 | 2005 |

| Net Asset Value, Beginning of Period | $17.89 | $19.44 | $17.06 | $16.77 | $14.39 |

| Investment Operations | | | | | |

| Net Investment Income | .105 | .089 | .113 | .059 | .040 |

| Net Realized and Unrealized Gain (Loss) | | | | | |

| on Investments | (3.049) | (1.523) | 2.354 | .266 | 2.385 |

| Total from Investment Operations | (2.944) | (1.434) | 2.467 | .325 | 2.425 |

| Distributions | | | | | |

| Dividends from Net Investment Income | (.116) | (.116) | (.087) | (.035) | (.045) |

| Distributions from Realized Capital Gains | — | — | — | — | — |

| Total Distributions | (.116) | (.116) | (.087) | (.035) | (.045) |

| Net Asset Value, End of Period | $14.83 | $17.89 | $19.44 | $17.06 | $16.77 |

| |

| Total Return1 | -16.29% | -7.44% | 14.50% | 1.93% | 16.86% |

| |

| Ratios/Supplemental Data | | | | | |

| Net Assets, End of Period (Millions) | $2,956 | $3,637 | $4,308 | $4,530 | $4,848 |

| Ratio of Total Expenses to | | | | | |

| Average Net Assets2 | 0.49% | 0.43% | 0.50% | 0.58% | 0.55% |

| Ratio of Net Investment Income to | | | | | |

| Average Net Assets | 0.79% | 0.47% | 0.60% | 0.34% | 0.30% |

| Portfolio Turnover Rate | 101% | 107% | 51% | 48% | 38% |

1 Total returns do not include the account service fee that may be applicable to certain accounts with balances below $10,000.

2 Includes performance-based investment advisory fee increases (decreases) of (0.03%), (0.03%), (0.01%), 0.02%, and (0.02%).

See accompanying Notes, which are an integral part of the Financial Statements.

20

U.S. Growth Fund

Financial Highlights

| | | | | |

| Admiral Shares | | | | | |

| |

| For a Share Outstanding | Year Ended August 31, |

| Throughout Each Period | 2009 | 2008 | 2007 | 2006 | 2005 |

| Net Asset Value, Beginning of Period | $46.37 | $50.42 | $44.24 | $43.47 | $37.29 |

| Investment Operations | | | | | |

| Net Investment Income | .335 | .325 | .416 | .271 | .226 |

| Net Realized and Unrealized Gain (Loss) | | | | | |

| on Investments | (7.919) | (3.950) | 6.107 | .677 | 6.163 |

| Total from Investment Operations | (7.584) | (3.625) | 6.523 | .948 | 6.389 |

| Distributions | | | | | |

| Dividends from Net Investment Income | (.376) | (.425) | (.343) | (.178) | (.209) |

| Distributions from Realized Capital Gains | — | — | — | — | — |

| Total Distributions | (.376) | (.425) | (.343) | (.178) | (.209) |

| Net Asset Value, End of Period | $38.41 | $46.37 | $50.42 | $44.24 | $43.47 |

| |

| Total Return | -16.15% | -7.28% | 14.80% | 2.16% | 17.16% |

| |

| Ratios/Supplemental Data | | | | | |

| Net Assets, End of Period (Millions) | $838 | $1,116 | $1,325 | $1,262 | $1,012 |

| Ratio of Total Expenses to | | | | | |

| Average Net Assets1 | 0.30% | 0.24% | 0.27% | 0.34% | 0.32% |

| Ratio of Net Investment Income to | | | | | |

| Average Net Assets | 0.98% | 0.66% | 0.83% | 0.58% | 0.53% |

| Portfolio Turnover Rate | 101% | 107% | 51% | 48% | 38% |

1 Includes performance-based investment advisory fee increases (decreases) of (0.03%), (0.03%), (0.01%), 0.02%, and (0.02%).

See accompanying Notes, which are an integral part of the Financial Statements.

U.S. Growth Fund

Notes to Financial Statements

Vanguard U.S. Growth Fund is registered under the Investment Company Act of 1940 as an open-end investment company, or mutual fund. The fund offers two classes of shares, Investor Shares and

Admiral Shares. Investor Shares are available to any investor who meets the fund’s minimum purchase requirements. Admiral Shares are designed for investors who meet certain administrative, service, tenure, and account-size criteria.

A. The following significant accounting policies conform to generally accepted accounting principles for

U.S. mutual funds. The fund consistently follows such policies in preparing its financial statements.

1. Security Valuation: Securities are valued as of the close of trading on the New York Stock Exchange (generally 4 p.m., Eastern time) on the valuation date. Equity securities are valued at the latest quoted sales prices or official closing prices taken from the primary market in which each security trades; such securities not traded on the valuation date are valued at the mean of the latest quoted bid and asked prices. Securities f or which market quotations are not readily available, or whose values have been materially affected by events occurring before the fund’s pricing time but after the close of the securities’ primary markets, are valued by methods deemed by the board of trustees to represent fair value. Investments in Vanguard Market Liquidity Fund are valued at that fund’s net asset value.

Temporary cash investments acquired over 60 days to maturity are valued using the latest bid prices or using valuations based on a matrix system (which considers such factors as security prices, yields, maturities, and ratings), both as furnished by independent pricing services. Other temporary cash investments are valued at amortized cost, which approximates market value.

2. Futures Contracts: The fund uses index futures contracts to a limited extent, with the objective of maintaining full exposure to the stock market while maintaining liquidity. Th e fund may purchase or sell futur es contracts to achieve a desired level of investment, whether to accommodate portfolio turnover or cash flows from capital share transactions. The primary risks associated with the use of futures contracts are imperfect correlation between changes in market values of stocks held by the fund and the prices of futures contracts, and the possibility of an illiquid market.

Futures contracts are valued at their quoted daily settlement prices. The aggregate principal amounts of the contracts are not recorded in the Statement of Net Assets. Fluctuations in the value of the contracts are recorded in the Statement of Net Assets as an asset (liability) and in the Statement of Operations as unrealized appreciation (depreciation) until the contracts are closed, when they are recorded as realized futures gains (losses).

3. Federal Income Taxes: The fund intends to continue to qualify as a regulated investment company and distribute all of its taxable income. Management has analyzed the fund’s tax positions taken for all open federal income tax years (August 31, 2006–2009), and has concluded that no provision for federal income tax is required in the fund’s financial statements.

4. Distributions: Distributions to shareholders are recorded on the ex-dividend date.

5. Security Lending: The fund may lend its securities to qualified institutional borrowers to earn additional income. Security loans are required to be secured at all times by collateral at least equal to the market value of securities loaned. The fund invests cash collateral received in Vanguard Market Liquidity Fund, and r ecords a liability for the return of the collateral, during the period the securities are on loan. Security lending income represents the income earned on investing cash collateral, less expenses associated with the loan.

22

U.S. Growth Fund

6. Other: Dividend income is recorded on the ex-dividend date. Interest income includes income distributions received from Vanguard Market Liquidity Fund and is accrued daily. Security transactions are accounted for on the date securities are bought or sold. Costs used to determine realized gains (losses) on the sale of investment securities are those of the specific securities sold.

Each class of shares has equal rights as to assets and earnings, except that each class separately bears certain class-specific expenses related to maintenance of shareholder accounts (included in Management and Administrative expenses), share holder reporting, and proxies. Marketing and distribution expenses are allocated to each class of s hares based on a method approved by the board of trustees. Income, other non-class-specific expenses, and gains and losses on investments are allocated to each class of shares based on its relative net assets.

B. AllianceBernstein L.P. and William Blair & Company, L.L.C., each provide investment advisory services to a portion of the fund for a fee calculated at an annual percentage rate of average net assets managed by the advisor. The basic fee for AllianceBernstein L.P. is subject to quarterly adjustments based on performance for the preceding three years relative to the Russell 1000 Growth Index. The basic fee for William Blair & Company, L.L.C., is subject to quarterly adjustments based on performance since June 1, 2004, relative to the Russell 1000 Growth Index.

The Vanguard Group manages the cash reserves of the fund on an at-cost basis.

For the year ended August 31, 2009, the aggregate investment advisory fee represented an effective annual basic rate of 0.17% of the fund’s average net assets, before a decrease of $1,163,000 (0.03%) based on performance.

C. The Vanguard Group furnishes at cost corporate management, administrative, marketing, and distribution services. The costs of such services are allocated to the fund under methods approved by the board of trustees. The fund has committed to provide up to 0.40% of its net assets in capital contributions to Vanguard. At August 31, 2009, the fund had contributed ca pital of $827,000 to Vanguard (included in Other Assets), representing 0.02% of the fund’s net assets and 0.33% of

Vanguard’s capitalization. The fund’s trustees and officers are also directors and officers of Vanguard.

D. The fund has asked its investment advisors to direct certain security trades, subject to obtaining the best price and execution, to brokers who have agreed to rebate to the fund part of the commissions generated. Such rebates are used solely to reduce the fund’s management and administrative expenses. For the year ended August 31, 2009, these arrangements reduced the fund’s expenses by $316,000 (an annual rate of 0.01% of average net assets).

E. Various inputs may be used to determine the value of the fund’s investments. These inputs are summarized in three broad levels for financial statement purposes. The inputs or methodologies used to value securities are not necessarily an indication of the risk associated with investing in those securities.

Level 1—Quoted prices in active markets for identical securities.

Level 2—Other significant observable inputs (including quo ted prices for similar securities, interest

rates, prepayment speeds, credit risk, etc.).

Level 3—Significant unobservable inputs (including the fund’s own assumptions used to determine

the fair value of investments).

23

U.S. Growth Fund

The following table summarizes the fund’s investments as of August 31, 2009, based on the inputs used to value them:

| | | |

| | Level 1 | Level 2 | Level 3 |

| Investments | ($000) | ($000) | ($000) |

| Common Stocks | 3,702,370 | — | — |

| Temporary Cash Investments | 90,275 | 17,978 | — |

| Futures Contracts—Assets1 | 24 | — | — |

| Futures Contracts—Liabilities1 | (819) | — | — |

| Total | 3,791,850 | 17,978 | — |

1 Represents variation margin on the last day of the reporting period.

F. At August 31, 2009, the aggregate settlement value of open futures contracts and the related unrealized appreciation (depreciation) were:

| | | | |

| | | | | ($000) |

| | | Number of | Aggregate | Unrealized |

| | | Long (Short) | Settlement | Appreciation |

| Futures Contracts | Expiration | Contracts | Value | (Depreciation) |

| S&P 500 Index | September 2009 | 177 | 45,122 | 4,436 |

| S&P Mid-Cap 400 Index | September 2009 | 100 | 32,700 | 3,287 |

| E-mini S&P 500 Index | September 2009 | 75 | 3,824 | (30) |

Unrealized appreciation (depreciation) on open futures contracts is required t o be treated as realized gain (loss) for tax purposes.

G. Distributions are determined on a tax basis and may differ from net investment income and realized capital gains for financial reporting purposes. Differences may be permanent or temporary. Permanent differences are reclassified among capital accounts in the financial statements to reflect their tax character. Temporary differences arise when certain items of income, expense, gain, or loss are recognized in different periods for financial statement and tax purposes; these differences will reverse at some time in the future. Differences in classification may also result from the treatment of shor t-term gains as ordinary income for tax purposes.

For tax purposes, at August 31, 2009, the fund had $14,725,000 of ordinary income available for distribution. The fund had available capital loss carryforwards totaling $6,398,578,000 to offset future net capital gains of $2,582,798,000 through August 31, 2010, $2,548,333,000 through August 31, 2011, $887,490,000 through August 31, 2012, $123,651,000 through August 31, 2013, and $256,306,000 through August 31, 2017. In addition, the fund realized losses of $316,709,000 during the period from November 1, 2008, through August 31, 2009, which are deferred and will be treated as realized for tax purposes in fiscal 2010.

At August 31, 2009, the cost of investment securities for tax purposes was $3,785,265,000. Net unrealized appreciation of investment securities for tax purposes was $25,358,000, consisting of unrealized gains of $266,479,000 on securities that had risen in value since their purchase and $241,121,000 in unrealized losses on securities that had fallen in value since their purchase.

24

U.S. Growth Fund

H. During the year ended August 31, 2009, the fund purchased $3,386,073,000 of investment securities and sold $3,454,896,000 of investment securities, other than temporary cash investments.

I. Capital share transactions for each class of shares were:

| | | | |

| | Year Ended August 31, |

| | 2009 | 2008 |

| | Amount | Shares | Amount | Shares |

| | ($000) | (000) | ($000) | (000) |

| Investor Shares | | | | |

| Issued | 397,147 | 30,584 | 488,406 | 26,158 |

| Issued in Lieu of Cash Distributions | 22,922 | 1,941 | 24,561 | 1,226 |

| Redeemed | (485,477) | (36,477) | (864,765) | (45,681) |

| Net Increase (Decrease)—Investor Shares | (65,408) | (3,952) | (351,798) | (18,297) |

| Admiral Shares | | | | |

| Issued | 135,668 | 4,030 | 207,633 | 4,245 |

| Issued in Lieu of Cash Distributions | 8,303 | 272 | 10,509 | 203 |

| Redeemed | (221,124) | (6,551) | (324,312) | (6,673) |

| Net Increase (Decrease)—Admiral Shares | (77,153) | (2,249) | (106,170) | (2,225) |

J. In preparing the financial statements as of August 31, 2009, management considered the impact of subsequent events occurring through October 15, 2009, for potential recognition or disclosure in these financial statements.

25

Report of Independent Registered

Public Accounting Firm

To the Trustees of Vanguard World Fund and the Shareholders of Vanguard U.S. Growth Fund:

In our opinion, the accompanying statement of net assets and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of Vanguard U.S. Growth Fund (the “Fund”) at August 31, 2009, the results of its operations for the year then e nded, the changes in its net assets for each of the two years in the period then ended and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America. Th ese financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management; our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform t he audit to obtain reasonable ass urance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities at August 31, 2009 by correspondence with the custodian and broker and by agreement to the underlying ownership records for Vanguard Market Liquidity Fund, provide a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

Philadelphia, Pennsylvania

October 15, 2009

Special 2009 tax information (unaudited) for Vanguard U.S. Growth Fund

This information for the fiscal year ended August 31, 2009, is included pursuant to provisions of the

Internal Revenue Code.

The fund distributed $32,174,000 of qualified dividend income to shareholders during the fiscal year.

For corporate shareholders, 100% of investment income (dividend income plus short-term gains, if any)

qualifies for the dividends-received deduction.

26

Your Fund’s After-Tax Returns

This table presents returns for your fund both before and after taxes. The after-tax returns are shown in two ways: (1) assuming that an investor owned the fund during the entire period and paid taxes on the fund’s distributions, and (2) assuming that an investor paid taxes on the fund’s distributions and sold all shares at the end of each period.

Calculations are based on the highest individual federal income tax and capital gains tax rates in effect at the times of the distributions and the hypothetical sales. State and local taxes were not considered. After-tax returns reflect any qualified dividend income, using actual prior-year figures and estimates for 2009. (In the example, returns after the sale of fund shares may be higher than those assuming no sale. This occurs when the sale would have produced a capital loss. The calculation assumes that the investor received a tax deduction for the loss.) The table shows returns for Investor Shares only; returns for other share classes will differ. Please note that your actual after-tax returns will depend on your tax situation and may differ from those shown. Also note that if you own the fund in a tax-deferred account, such as an individual retirement account or a 401(k) plan, this information does not apply to you. Such accounts are not subject to current taxes.

Finally, keep in mind that a fund’s performance—whether before or after taxes—does not guarantee future results.

| | | |

| Average Annual Total Returns: U.S. Growth Fund Investor Shares | | |

| Periods Ended August 31, 2009 | | | |

| | One | Five | Ten |

| | Year | Years | Years |

| Returns Before Taxes | -16.29% | 1.11% | -6.30% |

| Returns After Taxes on Distributions | -16.41 | 1.03 | -6.86 |

| Returns After Taxes on Distributions and Sale of Fund Shares | -10.48 | 0.94 | -4.97 |

Vanguard fund total returns do not include the account service fee that may be applicable to certain accounts with balances below $10,000.

27

About Your Fund’s Expenses

As a shareholder of the fund, you incur ongoing costs, which include costs for portfolio management, administrative services, and shareholder reports (like this one), among others. Operating expenses, which are deducted from a fund’s gross income, directly reduce the investment return of the fund.

A fund’s expenses are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The following examples are intended to help you understand the ongoing costs (in dollars) of investing in your fund and to compare these costs with those of other mutual funds. The examples are based on an investment of $1,000 made at the beginning of the period shown and held for the entire period.

The accompanying table illustrates your fund’s costs in two ways:

• Based on actual fund return. This section helps you to estimate the actual expenses that you paid over the period. The ”Ending Account Value“ shown is derived from the fund‘s actual return, and the third column shows the dollar amount that would have been paid by an investor who started with $1,000 in the fund. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period.

To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for your fund under the heading ”Expenses Paid During Period.“

• Based on hypothetical 5% yearly return. This section is intended to help you compare your fund‘s costs with those of other mutual funds. It assumes that the fund had a yearly return of 5% before expenses, but that the expense ratio is unchanged. In this case—because the return used is not the fund’s actual return—the results do not apply to your investment. The example is useful in making comparisons because the Securities and Exchange Commission requires all mutual funds to calculate expenses based on a 5% return. You can assess your fund’s costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

Note that the expenses shown in the table are meant to highlight and help you compare ongoing costs only and do not reflect transaction costs incurred by the fund for buying and selling securities. Further, the expenses do not include the account service fee described in the prospectus. If such a fee were applied to your account, your costs would be higher. Your fund does not charge transaction fees, such as purchase or redemption fees, nor does it carry a “sales load.” The calculations assume no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

You can find more information about the fund’s expenses, including annual expense ratios, in the Financial Statements section of this report. For additional information on operating expenses and other shareholder costs, please refer to your fund’s current prospectus.

28

| | | |

| Six Months Ended August 31, 2009 | | | |

| | Beginning | Ending | Expenses |

| | Account Value | Account Value | Paid During |

| U.S. Growth Fund | 2/28/2009 | 8/31/2009 | Period |

| Based on Actual Fund Return | | | |

| Investor Shares | $1,000.00 | $1,369.34 | $3.11 |

| Admiral Shares | 1,000.00 | 1,370.81 | 1.79 |

| |

| Based on Hypothetical 5% Yearly Return | | | |

| Investor Shares | $1,000.00 | $1,022.58 | $2.65 |

| Admiral Shares | 1,000.00 | 1,023.69 | 1.53 |

The calculations are based on expenses incurred in the most recent six-month period. The fund’s annualized six-month expense ratios for that period are 0.52% for the Investor Shares and 0.30% for the Admiral Shares. The dollar amounts shown as “Expenses Paid” are equal to the annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent six-month period, then divided by the number of days in the most recent 12-month period.

29

Glossary

30-Day SEC Yield. A fund’s 30-day SEC yield is derived using a formula specified by the U.S. Securities and Exchange Commission. Under the formula, data related to the fund’s security holdings in the previous 30 days are used to calculate the fund’s hypothetical net income for that period, which is then annualized and divided by the fund’s estimated average net assets over the calculation period. For the purposes of this calculation, a security’s income is based on its current market yield to maturity (in the case of bonds) or its projected dividend yield (for stocks). Because the SEC yield represents hypothetical annualized income, it will differ—at times significantly—from the fund’s actual experience. As a result, the fund’s income distributions may be higher or lower than implied by the SEC yield.

Beta. A measure of the magnitude of a fund’s past share-price fluctuations in relation to the ups and downs of a given market index. The index is assigned a beta of 1.00. Compared with a given index, a fund with a beta of 1.20 typically would have seen its share price rise or fall by 12% when the index rose or fell by 10%. For this report, beta is based on returns over the past 36 months for both the fund and the index. Note that a fund’s beta should be reviewed in conjunction with its R-squared (see definition). The lower the R-squared, the less correlation there is between the fund and the index, and the less reliable beta is as an indicator of volatility.

Dividend Yield. Dividend income earned by stocks, expressed as a percentage of the aggregate market value (or of net asset value, for a fund). The yield is determined by dividing the amount of the annual dividends by the aggregate value (or net asset value) at the end of the period. For a fund, the dividend yield is based solely on stock holdings and does not include any income produced by other investments.

Earnings Growth Rate. The average annual rate of growth in earnings over the past five years for the stocks now in a fund.

Equity Exposure. A measure that reflects a fund’s investments in stocks and stock futures. Any holdings in short-term reserves are excluded.

Expense Ratio. The percentage of a fund’s average net assets used to pay its annual administrative and advisory expenses. These expenses directly reduce returns to investors.

Foreign Holdings. The percentage of a fund represented by stocks or depositary receipts of companies based outside the United States.

Inception Date. The date on which the assets of a fund (or one of its share classes) are first invested in accordance with the fund’s investment objective. For funds with a subscription period, the inception date is the day after that period ends. Investment performance is measured from the inception date.

Median Market Cap. An indicator of the size of companies in which a fund invests; the midpoint of market capitalization (market price x shares outstanding) of a fund’s stocks, weighted by the proportion of the fund’s assets invested in each stock. Stocks representing half of the fund’s assets have market capitalizations above the median, and the rest are below it.

Price/Book Ratio. The share price of a stock divided by its net worth, or book value, per share. For a fund, the weighted average price/book ratio of the stocks it holds.

30

Price/Earnings Ratio. The ratio of a stock’s current price to its per-share earnings over the past year. For a fund, the weighted average P/E of the stocks it holds. P/E is an indicator of market expectations about corporate prospects; the higher the P/E, the greater the expectations for a company’s future growth.

R-Squared. A measure of how much of a fund’s past returns can be explained by the returns from the market in general, as measured by a given index. If a fund’s total returns were precisely synchronized with an index’s returns, its R-squared would be 1.00. If the fund’s returns bore no relationship to the index’s returns, its R-squared would be 0. For this report, R-squared is based on returns over the past 36 months for both the fund and the index.

Return on Equity. The annual average rate of return generated by a company during the past five years for each dollar of shareholder’s equity (net income divided by shareholder’s equity). For a fund, the weighted average return on equity for the companies whose stocks it holds.

Short-Term Reserves. The percentage of a fund invested in highly liquid, short-term securities that can be readily converted to cash.

Turnover Rate. An indication of the fund’s trading activity. Funds with high turnover rates incur higher transaction costs and may be more likely to distribute capital gains (which may be taxable to investors). The turnover rate excludes in-kind transactions, which have minimal impact on costs.

31

The People Who Govern Your Fund

The trustees of your mutual fund are there to see that the fund is operated and managed in your best interests since, as a shareholder, you are a part owner of the fund. Your fund’s trustees also serve on the board of directors of The Vanguard Group, Inc., which is owned by the Vanguard funds and provides services to them on an at-cost basis.

A majority of Vanguard’s board members are independent, meaning that they have no affiliation with Vanguard or the funds they oversee, apart from the sizable personal investments they have made as private individuals. The independent board members have distinguished backgrounds in business, academia, and public service. Each of the trustees and executive officers oversees 157 Vanguard funds.

The following table provides information for each trustee and executive officer of the fund. More information about the trustees is in the Statement of Additional Informatio n, which can be obtained, wit hout charge, by contacting Vanguard at 800-662-7447, or online at www.vanguard.com.

| |

| Interested Trustees | Emerson U. Fullwood |

| | Born 1948. Trustee Since January 2008. Principal |

| John J. Brennan1 | Occupation(s) During the Past Five Years: Retired |

| Born 1954. Trustee Since May 1987. Chairman of | Executive Chief Staff and Marketing Officer for North |

| the Board. Principal Occupation(s) During the Past | America and Corporate Vice President of Xerox |

| Five Years: Chairman of the Board and Director/Trustee | Corporation (photocopiers and printers); Director of |

| of The Vanguard Group, Inc., and of each of the | SPX Corporation (multi-industry manufacturing), the |

| investment companies served by The Vanguard Group; | United Way of Rochester, the Boy Scouts of America, |

| Chief Executive Officer and President of The Vanguard | Amerigroup Corporation (direct health and medical |

| Group and of each of the investment companies served | insurance carriers), and Monroe Community College |

| by The Vanguard Group (1996–2008); Chairman of | Foundation. |

| the Financial Accounting Foundation; Governor of | |

| the Financial Industry Regulatory Authority (FINRA); | Rajiv L. Gupta |

| Director of United Way of Southeastern Pennsylvania. | Born 1945. Trustee Since December 2001.2 Principal |

| | Occupation(s) During the Past Five Years: Retired |

| F. William McNabb III1 | Chairman and Chief Executive Officer of Rohm and |

| Born 1957. Trustee Since July 2009. Principal | Haas Co. (chemicals); President of Rohm and Haas Co. |

| Occupation(s) During the Past Five Years: Director of | (2006–2008); Board Member of American Chemistry |

| The Vanguard Group, Inc., since 2008; Chief Executive | Council; Director of Tyco International, Ltd. (diversified |

| Officer and President of The Vanguard Group and of | manufacturing and services) and Hewlett-Packard Co. |

| each of the investment companies served by The | (electronic computer manufacturing); Trustee of The |

| Vanguard Group since 2008; Director of Vanguard | Conference Board. |

| Marketing Corporation; Managing Director of The | |

| Vanguard Group (1995–2008). | Amy Gutmann |

| | Born 1949. Trustee Since June 2006. Principal |

| | Occupation(s) During the Past Five Years: President of |

| Independent Trustees | the University of Pennsylvania; Christopher H. Browne |

| | Distinguished Professor of Political Science in the School |

| Charles D. Ellis | of Arts and Sciences with Secondary Appointments |

| Born 1937. Trustee Since January 2001. Principal | at the Annenberg School for Communication and the |

| Occupation(s) During the Past Five Years: Applecore | Graduate School of Education of the University of |

| Partners (pro bono ventures in education); Senior | Pennsylvania; Director of Carnegie Corporation of |

| Advisor to Greenwich Associates (international business | New York, Schuylkill River Development Corporation, |

| strategy consulting); Successor Trustee of Yale University; | and Greater Philadelphia Chamber of Commerce; |

| Overseer of the Stern School of Business at New York | Trustee of the National Constitution Center. |

| University; Trustee of the Whitehead Institute for | |

| Biomedical Research. | |

| | |

| JoAnn Heffernan Heisen | Executive Officers | |

| Born 1950. Trustee Since July 1998. Principal | | |

| Occupation(s) During the Past Five Years: Retired | Thomas J. Higgins1 | |

| Corporate Vice President, Chief Global Diversity Officer, | Born 1957. Chief Financial Officer Since September |

| and Member of the Executive Committee of Johnson | 2008. Principal Occupation(s) During the Past Five |

| & Johnson (pharmaceuticals/consumer products); | Years: Principal of The Vanguard Group, Inc.; Chief |

| Vice President and Chief Information Officer of Johnson | Financial Officer of each of the investment companies |

| & Johnson (1997 –2005); Director of the University | served by The Vanguard Group since 2008; Treasurer |

| Medical Center at Princeton and Women’s Research | of each of the investment companies served by The |

| and Education Instit ute. | Vanguard Group (1998–2008). |

| |

| André F. Perold | Kathryn J. Hyatt1 | |

| Born 1952. Trustee Since December 2004. Principal | Born 1955. Treasurer Since November 2008. Principal |

| Occupation(s) During the Past Five Years: George Gund | Occupation(s) During the Past Five Years: Principal of |

| Professor of Finance and Banking, Harvard Business | The Vanguard Group, Inc.; Treasurer of each of the |

| School; Director and Chairman of UNX, Inc. (equities | investment companies served by The Vanguard |

| trading firm); Chair of the Investment Committee of | Group since 2008; Assistant Treasurer of each of the |

| HighVista Strategies LLC (private investment firm). | investment companies served by The Vanguard Group |

| | (1988–2008). | |

| Alfred M. Rankin, Jr. | | |

| Born 1941. Trustee Since January 1993. Principal | Heidi Stam1 | |

| Occupation(s) During the Past Five Years: Chairman, | Born 1956. Secretary Since July 2005. Principal |

| President, Chief Executive Officer, and Director of | Occupation(s) During the Past Five Years: Managing |

| NACCO Industries, Inc. (forklift trucks/housewares/ | Director of The Vanguard Group, Inc., since 2006; |

| lignite); Director of Goodrich Corporation (industrial | General Counsel of The Vanguard Group since 2005; |

| products/aircraft systems and services). | Secretary of The Vanguard Group and of each of the |

| | investment companies served by The Vanguard Group |

| Peter F. Volanakis | since 2005; Director and Senior Vice President of |

| Born 1955. Trustee Since July 2009. Principal | Vanguard Marketing Corporation since 2005; Principal |