| UNITED STATES |

| SECURITIES AND EXCHANGE COMMISSION |

| Washington, D.C. 20549 |

| FORM N-CSR |

| CERTIFIED SHAREHOLDER REPORT |

| OF |

| REGISTERED MANAGEMENT INVESTMENT COMPANIES |

| Investment Company Act file number: 811-03599 |

| Name of Registrant: The Royce Fund |

| Address of Registrant: 745 Fifth Avenue |

| New York, NY 10151 |

| Name and address of agent for service: | John E. Denneen, Esq. | |||

| 745 Fifth Avenue | ||||

| New York, NY 10151 |

| Registrant’s telephone number, including area code: (212) 508-4500 |

| Date of fiscal year end: December 31, 2012 |

| Date of reporting period: January 1, 2012 – June 30, 2012 |

Item 1. Reports to Shareholders.

|

SEMIANNUAL

REVIEW AND REPORT

TO SHAREHOLDERS

| CORE Royce Pennsylvania Mutual Fund Royce Heritage Fund CORE + DIVIDENDS Royce Total Return Fund Royce Dividend Value Fund FOCUSED Royce Premier Fund Royce Special Equity Fund Royce Value Fund Royce 100 Fund Royce Focus Value Fund Royce Partners Fund Royce Special Equity Multi-Cap Fund OPPORTUNISTIC THEMES Royce Low-Priced Stock Fund Royce Opportunity Fund Royce Value Plus Fund Royce Financial Services Fund MICRO-CAP Royce Micro-Cap Fund Royce Micro-Cap Discovery Fund MID-CAP Royce SMid-Cap Value Fund Royce Mid-Cap Fund | |||

www.roycefunds.com |  | ||

| Online Update |

| Visit www.roycefunds.com for Fund performance information, special messages and commentary from Co-CIOs Chuck Royce, Whitney George and other portfolio managers, news, literature and tools to help you better understand and compare our Funds. |

|

| eDelivery Saves! Sign Up Now. |

eDelivery saves paper, time and fund expenses.1 Sign up now to view statements, prospectuses, financial reports and tax forms online. |

| > www.roycefunds.com/edelivery |

1 Any direct Royce Funds IRA investor who chooses eDelivery of prospectuses, financial reports, and RWord will be exempt from the $15 annual IRA maintenance fee. (We will continue to also waive the fee for investors with more than $20,000 invested in Royce IRAs at the time the fee is charged, and for new transfer and rollover accounts in their first year.) |

| Stay Informed |

| Follow us on Twitter, watch us on YouTube, subscribe to our RSS feed and sign up for our monthly eWord newsletter to stay up to date on the latest from The Royce Funds. |

|

| Financial Professionals |

Login to our Financial Professional website to access up-to-date research, insights and whitepapers including: The Valuation Challenge: Inexpensive Quality Remains Plentiful in Small-Cap Quality is not only plentiful within the small-cap universe, but it is also attractively valued right now across the market cap spectrum. Cyclicality Is Our Friend: Market Downturns Can Build Better Future Returns The small-cap downturn in 2011 was no fun, but downturns are neither unusual nor unprecedented. More important, in our view they remain key components in building higher long-term returns. |

| > www.roycefunds.com/research-0612 |

Quarterly Advisor Materials Log into our Financial Professional site and manage your preferences to receive alerts about our: • Quarterly Review Book • Fund Impact and Attribution Reports • Longitudinal Studies • Fact Sheets |

| > www.roycefunds.com/advisors |

| This page is not part of the 2012 Semiannual Report to Shareholders |

| Table of Contents | |

| Semiannual Review | |

| Fund Guide | 2 |

| Performance and Expenses | 4 |

| Portfolio Characteristics | 5 |

| Market Cycle and Risk Adjusted Performance | 6 |

| Letter to Our Shareholders | 7 |

| Fund Focus | 14 |

| Postscript: Is the Business Cycle Dead? | Inside Back Cover |

| Semiannual Report to Shareholders | 15 |

| This page is not part of the 2012 Semiannual Report to Shareholders | 1 |

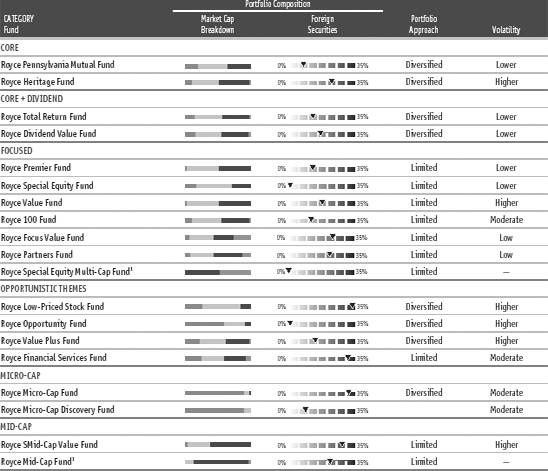

| Fund Guide |

| Understanding How We Think About Our Portfolios |

We are often asked, “If small companies are your primary area of focus, why are there so many Royce Funds?” To answer this question, we first point to the distinctive nature of the small-company universe. Small-cap is significantly larger than large-cap both in terms of names—with more than ten times the number of companies—and potential opportunities. |

The universe has evolved over the last 15 years into a recognized, professional asset class with a high level of institutional acceptance. Today, there are many small-cap and micro-cap indexes, as well as style indexes and sector groupings. This is why we believe the size and diversity of the universe make it ideally suited for multiple offerings. Small-cap and micro-cap securities also require their own particular approach. In addition, within each universe there are significant pockets of opportunity, such as dividend-paying companies, low-priced companies, high quality companies, etc., that go beyond classification by market cap. So while our portfolio managers share a common investment approach—one that emphasizes paying attention to risk and buying what each thinks are strong companies at attractively discounted prices—our portfolios also possess important distinctions that make each one unique.  Our Fund Guide is designed to help investors better understand both the different approaches and the common ground among our portfolios. Each Fund Category provides insight into how the respective portfolios are managed, while a closer look at our materials allows investors to see other important differences—capitalization range, volatility, other investment themes, portfolio diversification—within each category. We think that understanding these differences can be helpful in asset allocation decisions, especially when investors incorporate more than one Royce offering within their portfolios. |

| Investment Universe |

Our universe consists of three primary markets: micro-cap, small-cap and mid-cap companies. The Funds may also invest in foreign securities to varying degrees. |

U.S. Micro-Cap Market Caps up to $750 million1 • More than 3,380 companies • More than $540 billion in total capitalization This area offers many choices, but also features limited trading volumes and higher volatility. U.S. Small-Cap Market Caps between1 $750 million and $2.5 billion • More than 820 companies • More than $1.1 trillion in total capitalization This segment is more efficient, offering greater trading volumes and narrower bid/ask spreads. U.S. Mid-Cap Market Caps between1 $2.5 billion and $15 billion • More than 680 companies • More than $4.0 trillion in total capitalization Mid-cap companies generally possess more established businesses that attract greater institutional interest and thus enjoy greater liquidity. Foreign Securities2 This market consists of more than 15,360 companies in developed countries. Sources: 1 Compustat as of 6/30/12 2 Reuters as of 6/30/12 |

| 2 | This page is not part of the 2012 Semiannual Report to Shareholders |

| Multiple offerings tailored to specific investor needs. | ||

CORE | |

Royce Pennsylvania Mutual Fund | |

Royce Heritage Fund | |

| Generally invest across a wide spectrum of small companies using a diversified approach. We select stocks in these Funds using our core investment approach, which is based on attractive valuation, balance sheet quality and returns on invested capital. We developed this approach during the 1970s and ’80s in our flagship, Royce Pennsylvania Mutual Fund. These Funds may also incorporate ideas used in other portfolios, such as low-priced stocks, dividend-paying stocks, above-average growth companies and international securities. | |

CORE + DIVIDENDS | |

Royce Total Return Fund | |

Royce Dividend Value Fund | |

| Generally invest in a diversified portfolio of dividend-paying smaller companies using our core investment approach. We believe that an investment strategy that seeks both long-term growth and current income has the potential to generate above-average absolute returns over full market cycles with less volatility. These Funds may also invest a portion of the portfolio in preferred stocks and in fixed income securities, such as convertible bonds. | |

FOCUSED | |

Royce Premier Fund | |

Royce Special Equity Fund | |

Royce Value Fund | |

Royce 100 Fund | |

Royce Focus Value Fund | |

Royce Partners Fund | |

Royce Special Equity Multi-Cap Fund | |

| Generally employ a more limited portfolio approach—typically holding no more than 100 positions—and whose holdings possess what we believe are attractive valuations and higher-quality characteristics. These include strong balance sheets, above-average returns on invested capital and the ability to generate free cash flow. | |

OPPORTUNISTIC THEMES | |

Royce Low-Priced Stock Fund | |

Royce Opportunity Fund | |

Royce Value Plus Fund | |

Royce Financial Services Fund | |

| Generally invest in companies considered more opportunistic, with each emphasizing different themes, such as turnarounds, special situations, low-priced stocks and/or companies with high growth prospects. These portfolios are in general highly diversified and have the potential for higher returns, commensurate with each Fund’s higher level of risk. | |

MICRO-CAP | |

Royce Micro-Cap Fund | |

Royce Micro-Cap Discovery Fund | |

| Generally invest in micro-caps, those companies with market capitalizations up to $750 million, using our core investment approach. Due to the sector’s size and limited research coverage, there is more opportunity to find pricing inefficiencies. Therefore, we believe that the potential for higher returns, commensurate with a higher level of risk, is greater than for any other capitalization sector of the domestic equity marketplace. | |

MID-CAP | |

Royce SMid-Cap Value Fund | |

Royce Mid-Cap Fund | |

| Generally invest in mid-caps, those companies with market capitalizations from $2.5 billion to $15 billion, or smid-caps, those companies with market capitalizations from $750 million to $10 billion. While not restricted by number of holdings, we typically employ a more concentrated approach when investing in these companies, holding proportionately larger positions in a relatively limited number of stocks. | |

|

| Investments in securities of micro-cap, small-cap and/or mid-cap companies may involve considerably more risk than investments in securities of larger-cap companies. (Please see “Primary Risks for Fund Investors” in the prospectus.) Each Fund may invest a portion of its net assets in foreign securities, which may involve political, economic, currency, and other risks not encountered in U.S. investments. (Please see “Investing in Foreign Securities” in the prospectus.) |

| This page is not part of the 2012 Semiannual Report to Shareholders | 3 |

| Performance and Expenses | Through June 30, 2012 |

| Average Annual Total Returns | Gross Annual | Net Annual | ||||||||||||||||||||||||||||||

| CATEGORY | Since | Since | Operating | Operating | ||||||||||||||||||||||||||||

| Fund | Year-to-Date1 | 1-Year | 5-Year | 10-Year | Inception | Inception Date | Expenses | Expenses | ||||||||||||||||||||||||

| CORE | ||||||||||||||||||||||||||||||||

| Royce Pennsylvania Mutual Fund | 4.00 | % | -6.97 | % | 0.49 | % | 7.97 | % | n.a. | n.a. | 0.91 | % | 0.91 | % | ||||||||||||||||||

| Royce Heritage Fund | 2.38 | -11.57 | 1.53 | 8.51 | 13.01 | % | 12/27/95 | 1.50 | 1.50 | |||||||||||||||||||||||

| CORE + DIVIDENDS | ||||||||||||||||||||||||||||||||

| Royce Total Return Fund | 4.18 | -2.82 | 0.65 | 7.11 | 10.46 | 12/15/93 | 1.15 | 1.15 | ||||||||||||||||||||||||

| Royce Dividend Value Fund | 4.85 | -4.34 | 2.84 | n.a. | 7.37 | 5/3/04 | 1.50 | 1.50 | ||||||||||||||||||||||||

| FOCUSED | ||||||||||||||||||||||||||||||||

| Royce Premier Fund | 2.65 | -6.54 | 3.89 | 10.85 | 11.86 | 12/31/91 | 1.09 | 1.09 | ||||||||||||||||||||||||

| Royce Special Equity Fund | 5.99 | 2.87 | 4.27 | 8.07 | 8.85 | 5/1/98 | 1.15 | 1.15 | ||||||||||||||||||||||||

| Royce Value Fund | -1.65 | -14.23 | -0.20 | 11.08 | 9.90 | 6/14/01 | 1.45 | 1.45 | ||||||||||||||||||||||||

| Royce 100 Fund | 1.73 | -9.72 | 2.50 | n.a. | 9.65 | 6/30/03 | 1.47 | 1.47 | ||||||||||||||||||||||||

| Royce Focus Value Fund | 0.00 | -14.65 | n.a. | n.a. | 13.37 | 2/27/09 | 1.98 | 1.36 | ||||||||||||||||||||||||

| Royce Partners Fund | 7.33 | -9.19 | n.a. | n.a. | 8.65 | 4/27/09 | 4.28 | 1.38 | ||||||||||||||||||||||||

| Royce Special Equity Multi-Cap Fund | 6.67 | 6.17 | n.a. | n.a. | 9.38 | 12/31/10 | 1.97 | 1.39 | ||||||||||||||||||||||||

| OPPORTUNISTIC THEMES | ||||||||||||||||||||||||||||||||

| Royce Low-Priced Stock Fund | -1.05 | -18.17 | 0.33 | 7.39 | 11.59 | 12/15/93 | 1.58 | 1.51 | ||||||||||||||||||||||||

| Royce Opportunity Fund | 11.24 | -5.59 | -0.18 | 8.51 | 11.94 | 11/19/96 | 1.17 | 1.17 | ||||||||||||||||||||||||

| Royce Value Plus Fund | 5.92 | -8.41 | -2.73 | 10.30 | 11.00 | 6/14/01 | 1.45 | 1.45 | ||||||||||||||||||||||||

| Royce Financial Services Fund | 8.23 | -6.44 | -1.83 | n.a. | 4.81 | 12/31/03 | 1.89 | 1.54 | ||||||||||||||||||||||||

| MICRO-CAP | ||||||||||||||||||||||||||||||||

| Royce Micro-Cap Fund | 2.61 | -12.35 | 0.95 | 8.78 | 12.32 | 12/31/91 | 1.50 | 1.50 | ||||||||||||||||||||||||

| Royce Micro-Cap Discovery Fund | 0.00 | -4.78 | -2.62 | n.a. | 4.24 | 10/3/03 | 2.99 | 1.49 | ||||||||||||||||||||||||

| MID-CAP | ||||||||||||||||||||||||||||||||

| Royce SMid-Cap Value Fund | 2.67 | -13.37 | n.a. | n.a. | 0.90 | 9/28/07 | 1.95 | 1.35 | ||||||||||||||||||||||||

| Royce Mid-Cap Fund | -0.75 | -13.19 | n.a. | n.a. | 3.79 | 12/31/09 | 2.34 | 1.35 | ||||||||||||||||||||||||

| Russell 2000 Index | 8.53 | -2.08 | 0.54 | 7.00 | n.a. | n.a. | n.a. | n.a. | ||||||||||||||||||||||||

Royce Pennsylvania Mutual Fund’s average annual total return for the 35-year period ended 6/30/12 was 13.30%. |

Important Performance, Expense and Risk Information All performance information in this Review and Report reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions and does not reflect the deduction of taxes a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Shares redeemed within 180 days of purchase may be subject to a 1% redemption fee payable to the Fund. Redemption fees are not reflected in the performance shown above; if they were, performance would be lower. Current performance may be higher or lower than performance quoted. Current month-end performance may be obtained at www.roycefunds.com. All performance and expense information reflects results of the Fund’s oldest share Class (Investment Class or Service Class, as the case may be). Price and total return information is based on net asset values calculated for shareholder transactions. Certain immaterial adjustments were made to the net assets of Royce Heritage and Micro-Cap Funds at 12/30/11 and Royce Micro-Cap Discovery Fund at 6/29/12 for financial reporting purposes, and as a result the net asset values for shareholder transactions on those dates and the total returns based on those net asset values differ from the adjusted net asset values and total returns reported in the Financial Highlights. Gross annual operating expenses reflect the Fund’s gross total annual operating expenses and include management fees, any 12b-1 distribution and service fees, other expenses and any applicable acquired fund fees and expenses. Net annual operating expenses reflect contractual fee waivers and/or reimbursements. All expense information is reported as of the Fund’s most current prospectus. Royce & Associates has contractually agreed to waive fees and/or reimburse operating expenses, other than acquired fund fees and expenses, if any, to the extent necessary to maintain net operating expenses at or below: 1.35% for Royce Focus Value, Partners, SMid-Cap Value and Mid-Cap Funds; 1.49% for Royce Low-Priced Stock, Financial Services, and Micro-Cap Discovery Funds through April 30, 2013 and at or below 1.99% for Royce Partners, Micro-Cap Discovery and Mid-Cap Funds through April 30, 2022; and 1.39% for Royce Special Equity Multi-Cap Fund through April 30, 2014. Acquired fund fees and expenses reflect the estimated amount of fees and expenses incurred indirectly by the Fund through its investments in mutual funds, hedge funds, private equity funds and other investment companies. Shares of the Funds’ Service, Consultant, R and K Classes bear an annual distribution expense that is not borne by the Funds’ Investment Class. Investments in securities of micro-cap, small-cap and/or mid-cap companies may involve considerably more risk than investments in securities of larger-cap companies. (Please see “Primary Risks for Fund Investors” in the prospectus.) Please read the prospectus carefully before investing or sending money. Russell Investment Group is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group. The Russell 2000 Index is an unmanaged, capitalization-weighted index of domestic small-cap stocks. It measures the performance of the 2,000 smallest publicly traded U.S. companies in the Russell 3000 Index. Distributor: Royce Fund Services, Inc. |

| 4 | This page is not part of the 2012 Semiannual Report to Shareholders |

| Portfolio Characteristics | As of June 30, 2012 |

| |

Market Cap Breakdown Key:  Micro-Cap Micro-Cap  Small-Cap Small-Cap  Mid-Cap Mid-Cap  Large-Cap Large-Cap |

Investment Universe Micro-Cap: Market Caps up to $750 million Small-Cap: Market Caps between $750 million and $2.5 billion Mid-Cap: Market Caps between $2.5 billion and $15 billion Large-Cap: Market Caps greater than $15 billion Foreign Securities: Non-U.S. securities are those securities that do not trade on a U.S. exchange, trade outside the U.S. and/or are issued by companies that are domiciled outside the U.S. Portfolio Approach Diversified: A diversified portfolio at Royce is one that generally holds more than 100 securities and whose top positions generally do not exceed 2% of net assets. Limited: A limited portfolio at Royce is one that either (i) generally invests in no more than 100 companies, and whose top positions generally exceed 2% of net assets, or (ii) invests primarily in a single sector. Volatility Each Fund’s volatility is measured using Morningstar’s Risk Ratio, which measures variations in a fund’s monthly returns, with an emphasis on downside performance. Each Royce Fund’s overall Risk Ratio is a weighted combination of its three-, five- and 10-year scores, if applicable. Except as noted below, each Fund’s results reflect its score compared with all small-cap objective funds tracked by Morningstar with at least three years of history (367 funds as of 6/30/12). For Royce Financial Services Fund, all financial funds tracked by the Morningstar with at least three years of history (32 funds as of 6/30/12) are included. For Royce SMid-Cap Value Fund, all mid-cap stock funds with weighted average market caps between $750 million and $10 billion tracked by Morningstar with at least three years of history (403 funds as of 6/30/12) are included. We consider funds whose results rank in the top third of the category to have relatively low volatility; those in the middle third to have moderate volatility; and those in the bottom third to have high volatility. |

| This page is not part of the 2012 Semiannual Report to Shareholders | 5 |

| Market Cycle and Risk Adjusted Performance |

We believe strongly in the idea that a long-term investment perspective is crucial for determining the success of a particular investment approach. While flourishing in an up market is wonderful, surviving a bear market by losing less (or not at all) is at least as good. However, the true test of a portfolio’s mettle is performance over full market cycle periods, which include both an up and down market period. |

| Since the inception of the Russell 2000’s index on 12/31/78, there have been 10 full market cycles, with the most recent peaking on 4/29/11. Market cycles are defined as those that have retreated at least 15% from a previous market peak and have rebounded to establish a new peak above the previous one. Each market cycle contains a peak-to-trough and a trough-to-peak period. Interestingly, over the small-cap index’s 30+ year history, each style index—the Russell 2000 Value Index and the Russell 2000 Growth Index—outperformed in five of the 10 full market cycles. In fact, leadership has alternated between growth and value over the last six cycles. If history were to adhere to this pattern, value would lead in the current cycle that began on 4/29/11. |

| RISK/RETURN PROFILE 10-YEAR PERIOD ENDED JUNE 30, 2012 |

|

• | For the 10-year period ended 6/30/12, all 10 Royce Funds with 10 years of history outperformed the Russell 2000, and all did so with better risk-adjusted returns and Sharpe ratios. |

• | In addition, six of the 10 Royce Funds outperformed the Index with lower volatility. |

| All performance information above reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Current performance may be higher or lower than performance quoted. |

| SMALL-CAP MARKET CYCLE: RUSSELL 2000 INDEXES TOTAL RETURNS | |||||||||||||||

| |||||||||||||||

| ROYCE U.S. EQUITY FUNDS VS. RUSSELL 2000 INDEX: MARKET CYCLE RESULTS | |||||||||||||||

| Peak-to- Peak 3/9/00- 7/13/07 | Peak-to- Peak 7/13/07- 4/29/11 | Peak-to- Current 4/29/11- 6/30/12 | |||||||||||||

| Russell 2000 | 54.8 | % | 6.6 | % | -6.1 | % | |||||||||

| Russell 2000 Value | 189.4 | -1.4 | -5.6 | ||||||||||||

| Russell 2000 Growth | -14.8 | 14.3 | -6.6 | ||||||||||||

| CORE | |||||||||||||||

| Royce Pennsylvania Mutual | 207.1 | 11.6 | -10.7 | ||||||||||||

| Royce Heritage | 150.4 | 25.3 | -15.9 | ||||||||||||

| CORE + DIVIDENDS | |||||||||||||||

| Royce Total Return | 193.9 | 6.8 | -5.7 | ||||||||||||

| Royce Dividend Value | n.a. | 21.6 | -7.5 | ||||||||||||

| FOCUSED | |||||||||||||||

| Royce Premier | 198.1 | 29.9 | -9.8 | ||||||||||||

| Royce Special Equity | 227.4 | 20.8 | -1.1 | ||||||||||||

| Royce Value | n.a. | 17.4 | -18.6 | ||||||||||||

| Royce 100 | n.a. | 27.6 | -13.8 | ||||||||||||

| Royce Focus Value | n.a. | n.a. | -20.5 | ||||||||||||

| Royce Partners | n.a. | n.a. | -11.9 | ||||||||||||

| Royce Special Equity Multi Cap | n.a. | n.a. | -3.6 | ||||||||||||

| OPPORTUNISTIC THEMES | |||||||||||||||

| Royce Low-Priced Stock | 198.9 | 27.2 | -22.5 | ||||||||||||

| Royce Opportunity | 191.8 | 6.9 | -10.2 | ||||||||||||

| Royce Value Plus | n.a. | -3.0 | -13.1 | ||||||||||||

| Royce Financial Services | n.a. | 1.1 | -10.5 | ||||||||||||

| MICRO-CAP | |||||||||||||||

| Royce Micro-Cap | 197.4 | 24.9 | -17.9 | ||||||||||||

| Royce Micro-Cap Discovery | n.a. | -6.1 | -8.8 | ||||||||||||

| MID-CAP | |||||||||||||||

| Royce SMid-Cap Value | n.a. | n.a. | -16.4 | ||||||||||||

| Royce Mid-Cap | n.a. | n.a. | -17.9 | ||||||||||||

| 6 | This page is not part of the 2012 Semiannual Report to Shareholders |

| Letter to Our Shareholders | ||

| ||

“I Read the News Today, Oh Boy.” | ||

Another dismal summer has dawned with spring having brought a wave of worries back to the market for the third consecutive year. Karl Marx—as canny an observer of the global scene as he was a checkered prognosticator of its future—wrote in 1852 that all events in history occur twice: the first time as tragedy, the second as farce. Allowing for the accuracy of this observation, what are we then to make of this third round of wobbly recovery, sluggish markets, panic-stuffed headlines, and the by now reflexive anxiety about the potential horrors of European debt for the world economy? What lies beyond farce, other than lousy returns, high correlation, and growing numbers of investors disenchanted with equities? To this kind of question, too many investors have no answer, having lost not only their belief in the viability of investing in stocks, but also in the prospects for the global economy. Indeed, one unfortunate result of the contagion of uncertainty has been the erosion of confidence in the ability of equities to deliver returns that will beat inflation and build wealth over the long term. On May 7, a USA Today headline asked and answered, “Invest in stocks? Forget About It.” It was not quite as damning as the now infamous Business Week cover from August 1979 that proclaimed “The Death of Equities,” but the overall message was not much happier: “Wall Street’s long-running story about how stocks are the best way to build wealth seems tired, dated and less believable to many individual investors.” And the USA Today piece was published early in May, just before the current bear bit down most sharply. The implicit assumption that the best days for the stock market may be (way) behind it seems to us to be the distinguishing feature of this third round of poor results for most equities. Panic has given way to a shrug of resignation. This stance sees equity investing as a mug’s game, even if the alternatives—Treasuries, bonds, money markets, etc.—are not much more attractive or profitable. | Our collective experience tells us that this highly volatile, tightly correlated, range-bound market will be remembered as being as anomalous as it has been painful, one that tends to occur once or twice a century. It does not, in our view, change the fact that stocks remain the single best way of building wealth over the long run. | |

| This page is not part of the 2012 Semiannual Report to Shareholders | 7 |

Charles M. Royce, President We have often stressed the importance of capital preservation in asset management, arguing that not losing money is as critical as making it grow. Implicit in this belief is the idea that capital preservation is mostly synonymous with preserving purchasing power. However, we now find ourselves in a very non- traditional investment environment, an age marked by near-zero interest rates; regular, short-term bursts of volatility for equities; and relentless money printing on the part of the developed world’s central banks. While this has not altered our view of the significance of risk aversion, it has led us to ask if at this moment in history capital preservation and preservation of purchasing power should be defined differently. The answer approaches what we think is one of the most underappreciated risks to which investors are now subject: the potential for meaningful loss in the future purchasing power of investments. With so much attention being paid to preservation of capital, too little has been placed on what that capital, once returned, will actually be worth. Continued on page 10... | Letter to Our Shareholders Such a belief—as ultimately wrong-headed as we think it is—has the advantage that recent history, as far back as five years, is on its side. With a few exceptions, there is simply not much of a defense for equity investing as a whole since the respective index peaks in 2007. The explanation for why the market has been so troublesome and unprofitable seems simple: The world is still emerging from the most serious economic crisis since the Great Depression. Yet this account may be in equal parts true and unhelpful, at least to anyone who had been looking for a way to safely and effectively grow capital during the last few years, which helps to explain why panic and resignation are symptoms of the same fatalism that has gripped investors since the early days of the mortgage and banking crisis in 2008. We understand the pessimism and the unwillingness to take risks on the part of so many investors today. At the same time, we still see many of the same positive signs that have been inspiring our confidence about stocks and the economy as a whole since the spring of 2010. By taking the long view (a common perspective for us), we can offer, in addition to a Nostra Culpa for much recent fund performance, the benefit of nearly 40 years of small-cap value investing. Our collective experience tells us that this highly volatile, tightly correlated, range-bound market will be remembered as being as anomalous as it has been painful, one that tends to occur once or twice a century. It does not, in our view, change the fact that stocks remain the single best way of building wealth over the long run. We know that in the current environment these words may sound hollow or even self-serving. We are more than willing to assume that risk in the hope that investors will continue to look to equities (and to our portfolios) as effective and ultimately successful ways to invest in the years to come. “They’ve Been Going in and out of Style” The kind of dynamic rally that ushered out the first half of 2012 is always guaranteed to raise a smile, even if it could not completely erase earlier losses in the second quarter, losses that spoiled a promising upswing that lasted through most of the year’s opening quarter. Indeed, lack of direction has arguably been the most distinguishing characteristic of the recent market. Still, the major U.S. indexes finished the year-to-date period ended June 30, 2012 in decent condition, as did their overseas counterparts. Domestic small-caps brought up the rear. The Russell 2000 Index was up 8.5% in the first half, compared to respective gains of 9.4% and 9.5% for the large-cap Russell 1000 and S&P 500 Indexes and an electrifying 12.7% for the Nasdaq Composite. It was an interesting road for each index. The first quarter extended a rally that began following the October 2011 lows. Small-cap trailed, though its 12.4% gain was its best opening quarter since 2006. It was also not far behind its large-cap counterparts. The Russell 1000 rose 12.9%, and the S&P 500 gained 12.6%. The Nasdaq was especially impressive, notching an 18.7% increase for the quarter. We were among | ||

| 8 | This page is not part of the 2012 Semiannual Report to Shareholders |

| those hopeful souls who saw a nearly six-month bull run and thought that maybe the market was ready for some consistent recovery. Yet April and May were cruel months, the latter especially so, as the now-traditional spring downturn caused by concerns about European debt and the state of the American and Chinese economies spoiled the party and tamped down returns. (If not for the rally on the final trading day of June, that month would also have been less solidly in the black.) That rally was welcome—they always are—but second-quarter returns were still negative. The Nasdaq led on the downside, falling 5.1%, while the Russell 2000 slipped 3.5%. Large-caps held their value a bit better, with the Russell 1000 losing 3.1% and the S&P 500 declining 2.8%. So the first half concluded with a bang, but still left investors whimpering about the future. | Our expectation is for a less extreme, more historically normal phase, without so many of the stomach-churning drops followed by equally steep upticks that we saw last summer and fall and have seen so far in 2012. It is worth noting that a more historically normal range is one in which we think our funds can generate strong absolute and relative performance over the long run. | |

Looking at longer-term returns, this uncertainty has been well-earned. While three- and 10-year average annual total returns for the major indexes were solid-to-strong, one-, five-, and 12-year results for the periods ended June 30, 2012 were generally poor. The 12-year period—not a period that we, or anyone else, usually discusses—is instructive because it encompasses the Internet Bubble, the subsequent recovery, the recession that was followed by the financial crisis, and the market’s herky-jerky, volatile aftermath. So we think it is worth pointing out that for the 12-year period ended December 31, 2011, the average annual total return for the S&P 500 was its lowest since the end of World War II (beginning with the period from the end of 1945 through the end of 1957). Small-cap returns for that same period ended December 31, 2011 for the Russell 2000 and the CRSP 6-10, a small-cap proxy that dates back to the 1920s, were among the worst for both since the launch of the Russell 2000 on December 31, 1978 and since the end of 1945 for the CRSP 6-10. Recent performance for the two non-U.S. indexes that we track followed patterns similar to their domestic cousins, though with more muted results. This was not entirely surprising considering both Europe’s ongoing travails and worries about the pace of growth in China. Non-U.S. small-caps enjoyed an advantage over their large-cap siblings, with the Russell Global ex-U.S. Small Cap up 4.8% for the year-to-date period ended June 30, 2012 versus a 2.7% gain for the Russell Global ex-U.S. Large Cap Index. Both indexes enjoyed strong first-quarter results. The Russell Global ex-U.S. Small Cap Index rose 14.4%, and the Russell Global ex-U.S. Large Cap Index was up 11.5% in the first three months of 2012. Each index’s second quarter was far more difficult, as Europe’s troubles registered more dramatically outside the U.S. Small-cap lost a bit more in the downturn, with the Russell Global ex-U.S. Small Cap Index falling 8.5%, while the Russell Global ex-U.S. Large Cap Index was down 7.9%. |

| This page is not part of the 2012 Semiannual Report to Shareholders | 9 |

For more than three decades, an investment vehicle provided highly consistent returns with such low volatility that they were nearly devoid of risk—U.S. government bonds, specifically Treasury securities. They were the instruments that possessed that highly desired standard, “the risk-free rate of return.” The currently volatile investment climate has greatly expanded the appeal of this designation. Investors trying to cope with the economic uncertainty and asset-price volatility caused by the bursting credit bubble have grown increasingly sensitive to the possibilities of capital loss. Yet if history is any proxy—and we believe that it is—a healthy degree of skepticism should greet the notion that Treasuries remain risk free or provide an acceptable rate of return. If nothing else, the lens through which we see them needs to be adjusted to include the growing uncertainty of ultimate purchasing power (of real goods and services) of the currency in which they are denominated. This risk, one for which we have a healthy respect over the intermediate term, is the ominous combination of ongoing currency debasement and acceleration in inflationary pressures. These could erode the purchasing power of non- productive assets. Central banks around the world, with the U.S. Federal Reserve a primary contributor, have been pumping liquidity into the capital markets through a combination of historically low interest rates and quantitative easing or, more simply stated, money printing. Continued on page 12... | |||

| Letter to Our Shareholders | ||

U.S. mid-caps performed well on an absolute basis, though they were behind the domestic micro-cap, small-cap, and large-cap indexes in the first half. The Russell Midcap Index gained 8.0% through the end of June. Like the domestic indexes, they enjoyed a strong first quarter, up 12.9%, before slipping in the second quarter with a loss of 4.4%. Considering both the significant volatility and the unpopularity of stocks, the strength of micro-cap stocks was something of a surprise in the first half. Year-to-date through June 30, 2012, the Russell Microcap Index gained an impressive 13.0%. That the index accomplished this feat with stronger and steadier quarterly performances was equally notable: the Russell Microcap climbed 15.3% in the first quarter and fell only 2.0% in the bearish second. | ||

“The Act You’ve Known for all these Years...” If only our own portfolio had done as well. On an absolute basis, most of the Funds’ in this Semiannual Review and Report posted results that ranged from uninspiring to strong in the first half. With the exception of Royce Opportunity Fund, relative performance was a more significant issue. Normally, this does not trouble us. Long ago, we accepted that our disciplined approaches to stock selection would result in out-of-sync moments against our portfolios’ respective benchmarks. Our goal has always been strong absolute performance over long-term periods. If we met that standard, then relative results would most likely not be an issue, at least over long-term time spans. We have also been glad to accept the historical trade-off in which underperformance was more common for our Funds during short-term periods of 18 months or less, while outperformance was more typical over full market cycle and other long-term periods of three years or more. For too many time periods ended June 30, 2012, that history has become too exclusively long-term, even for us, with strong relative and absolute results coming only in periods of 10 years or longer. Three-year results were fine on an absolute basis in most cases, but trailed on a relative score, while the five-year returns were more mixed on a relative basis and underwhelming at best using the absolute standard that we prefer. This was particularly bad news for our newer portfolios, which lack history. With significant investments in all of our Funds, we share our investors’ frustrations with recent results. Those areas of the market in which we have seen both high quality and compelling valuations during the last three-to-five years—energy and mining companies, in particular—were among the worst performers in the first half, with net losses in some cases stretching back even further. Many of these stocks remain in our portfolios, as their attractive valuations and our ongoing high regard have combined to keep | ||

| 10 | This page is not part of the 2012 Semiannual Report to Shareholders |

| ||

1 Price and total return information is based on net asset values calculated for shareholder transactions. Certain immaterial adjustments were made to the net assets of Royce Heritage and Micro-Cap Funds at 12/30/11 and Royce Micro-Cap Discovery Fund at 6/29/12 for financial reporting purposes, and as a result the net asset values for shareholder transactions on those dates and the total returns based on those net asset values differ from the adjusted net asset values and total returns reported in the Financial Highlights. | ||

| Through all manner of markets—many of which were thought to establish a “New Normal”—we have never wavered in our convictions. We still believe that equities remain the best way—maybe the only way—to beat inflation and build wealth over the long term. |

| This page is not part of the 2012 Semiannual Report to Shareholders | 11 |

| Headline inflation numbers have remained subdued due to the continuing struggles in the labor market and stubbornly weak housing markets, but commodity inflation has been on the rise. With the recent uptick in U.S. leading economic indicators and encouraging signs of stability and improvement in the housing market, it would not take much to see a more broad-based uptick in inflation. So while U.S. government bonds are likely to continue to pay their meager coupons and return principal on schedule, the value of what is being returned to investors will be declining. For the first time in almost 30 years, we think that investors risk meaningful losses in that portion of their investment portfolio they deem to be the safest. Commodities offer one possible way to protect against the loss of purchasing power caused by currency debasement. Unsurprisingly, however, we prefer assets that are inherently productive and flexible and can adjust quickly to changing pricing environments. To us, investments in quality companies that possess embedded pricing power and high returns on their invested capital look to be some of the best investments to protect, and grow, purchasing power. We believe they need much broader representation in investors’ asset allocation. | |

| Letter to Our Shareholders |

|

Getting Better We do not know how much longer markets and economies will remain so uncertain. The fiscal turmoil that continues to haunt Europe has been hampering equity markets across the globe and contributing to the tight range of returns that have nonetheless demonstrated ample levels of volatility. The fragile recovery here in the U.S. has also played a role, as has the recent deceleration of the Chinese economy. These major macro events, which have been the dominant influence on investors’ behavior over the last three years, largely account for why stocks have struggled to create any direction for longer than a few months. Instead, markets have been mired in a pattern of short-term swings in which they have moved straight up or straight down, and for no longer than a few months at a time. One consequence of this closely correlated, range-bound cycle is that our Funds have not had the time to create the spread that we would usually seek to build through a full market cycle. However, we think that as Europe meets its challenges and as the U.S. begins to get its own fiscal house in order, which is not likely to happen until after the election, we will escape this range and move toward a more lasting upswing. Our expectation is for a less extreme, more historically normal phase, without so many of the stomach-churning drops followed by equally steep upticks that we saw last summer and fall and have seen so far in 2012. It is worth noting that a more historically normal range is one in which we think our Funds can generate strong absolute and relative performance over the long run. We would like to think that long-term history is on our side in this assessment. |

| 12 | This page is not part of the 2012 Semiannual Report to Shareholders |

Good Morning, Good Morning | |||||

Obviously, we would all like to reach a more hospitable market climate soon. As always, patience is critical. Indeed, the ability to be patient is probably the single most important quality that an investor who seeks strong long-term returns can possess. It is easy to talk about the importance of patience and discipline when markets are solid and portfolios are doing well. Yet at some point, these things will change, and both will be tested, as they have been in this market. It has been a very difficult time, but we believe it will pass. When it does, our disciplined approach will remain and, we believe, be effective. As we approach our 40th anniversary as a firm this coming November, we look back at what we have seen—the “Nifty Fifty” market of the ’70s, Black Friday in the ’80s, the first stirrings of the Internet boom in the ’90s, the horrific events of 9/11, our current era of uncertainty, and much, much more. Through all manner of markets—many of which were thought to establish a “New Normal”—we have never wavered in our convictions. We still believe that equities remain the best way—maybe the only way—to beat inflation and build wealth over the long term. (We also think that equities are capable of beating the fixed income markets over the next five years.) Our guess is that stocks can deliver returns in the mid- to upper-single digits, which we think would be respectable on an absolute basis and, equally important, higher than the rate of inflation. When things are working well, the underlying parts of an equity portfolio, the companies themselves, can act as compounding machines—compounding book value. We are confident that we can create portfolios that can grow commendably, especially in the more historically typical market climate that we believe we will eventually see. | |||||

Sincerely, | |||||

|  |  | |||

| Charles M. Royce | W. Whitney George | Jack E. Fockler, Jr. | |||

| President | Vice President | Vice President | |||

| July 31, 2012 | |||||

It is easy to talk about the importance of patience and discipline when markets are solid and portfolios are doing well. Yet at some point, these things will change, and both will be tested, as they have been in this market. It has been a very difficult time, but we believe it will pass. When it does, our disciplined approach will remain and, we believe, be effective. |

| This page is not part of the 2012 Semiannual Report to Shareholders | 13 |

| Fund Focus |

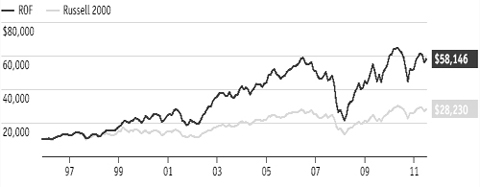

After enjoying a measure of success as a small-cap portfolio manager in the late ’70s and early ’80s, Buzz Zaino moved to a firm where his new employers were eager to learn more about how he had built his track record. What, they wanted to know, made his portfolio approach successful? The investigation into what had worked best in the past led to the development of the four investment themes he continues to use in Royce Opportunity Fund. Each theme focuses on a catalyst for potential growth in stocks that Buzz and assistant portfolio manager Bill Hench deem significantly discounted to their value as a business. The first theme that Buzz identified was Unrecognized Asset Values, which could be in the form of a valuable franchise, ample cash on the balance sheet, real estate, etc. These companies are generally selling below their probable liquidating value, franchise value, tangible book value or physical asset value relative to plant or liquid assets, an attractive discount to a bargain-conscious investor. Next are Turnarounds, situations that typically entail new management coming to a company and attempting to reverse the fortunes of a business that has fallen on hard times, whether the result of depressed operating margins, poor management or industry-specific factors. The third theme is Undervalued Growth, which covers companies that have been growing in industries that largely have not, so the stocks are often valued with the industry, not necessarily with the company’s own growth. Buzz and Bill look for companies that they believe can provide potential growth rates of at least 12%, possess strong balance sheets and whose stock prices reflect relatively low valuations. The fourth theme is Interrupted Earnings, a category they sometimes refer to as broken IPOs. Companies tend to go public when times are very good, but in the normal course of events, such a company is going to endure a bad quarter or a difficult year, which naturally disappoints shareholders who have grown used to the heady growth. In this area, Buzz and Bill look for companies that they think have the potential for either a 20% annual growth rate or a dominant market position, accompanied by a price-earnings multiple substantially lower than the business’s anticipated growth rate. The Fund’s singular opportunistic value approach has been tested over the last five years, which includes the recession, the previous small-cap peak on July 13, 2007, the financial crisis, and the pattern of high volatility and close correlation that have followed in its wake. The worst days of the bear market in late 2008 and early 2009 were the most challenging, because so many stocks were routinely testing new lows, and there was no way to catch the falling knife. Patience became their mantra during this time, as well as during the shorter bear phases in 2010, 2011, and the first half of 2012. Buzz and Bill believed that they were acquiring solid companies at very attractive prices, but also thought that it could take several years before many bore fruit; in the meantime, near-term performance might suffer. As can be seen in the performance table below, this has mostly been the case. The Fund’s opportunistic bent has served it particularly well during the recent rally, as well as over longer-term periods since Buzz assumed portfolio management duties in 1998. The Fund outperformed the Russell 2000 in 87% of all monthly rolling five-year return periods between July 31, 2002 and June 30, 2012. ROF’s average return for all 120 five-year periods was 10.6% versus 5.4% for the index. (See the table below and pages 6 and 40 for more information.) We think that Royce Opportunity Fund’s unique take on small-cap value investing makes it a viable choice for long-term investors with a reasonable tolerance for risk. |

| ROF vs the Russell 2000: Performance and Expense Information | Through June 30, 2012 | ||||||||||||||||||||

| Average Annual Total Returns | Net | ||||||||||||||||||||

| Since | Operating | ||||||||||||||||||||

One-Year | Three-Year | Five-Year | 10-Year | 15-Year | Inception | Expenses | |||||||||||||||

| Royce Opportunity Fund | -5.59 | % | 20.78 | % | -0.18 | % | 8.51 | % | 11.33 | % | 11.94% (11/19/96) | 1.17 | % | ||||||||

| Russell 2000 | -2.08 | 17.80 | 0.54 | 7.00 | 6.14 | 6.87 | n.a. | ||||||||||||||

| Important Performance, Expense and Risk Information All performance information is for the Fund’s Investment Class, reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Shares redeemed within 180 days of purchase may be subject to a 1% redemption fee, payable to the Fund, which is not reflected in the performance shown above; if it were, performance would be lower. Current performance may be higher or lower than performance quoted. Current month-end performance information may be obtained at www.roycefunds.com. Operating expenses reflect the Fund’s total annual operating expenses for the Investment Class as of the Fund’s most current prospectus and include management fees, other expenses and acquired fund fees and expenses. Acquired fund fees and expenses reflect the estimated amount of the fees and expenses incurred indirectly by the Fund through its investments in mutual funds, hedge funds, private equity funds and other investment companies. The Fund invests primarily in small-cap and micro-cap stocks, which may involve considerably more risk than investing in larger-cap stocks. (Please see “Primary Risks for Fund Investors” in the prospectus.) Russell Investment Group is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group. The Russell 2000 Index is an unmanaged, capitalization-weighted index of domestic small-cap stocks. It measures the performance of the 2,000 smallest publicly traded U.S. companies in the Russell 3000 Index. Distributor: Royce Fund Services, Inc. |

| 14 | This page is not part of the 2012 Semiannual Report to Shareholders |

| Table of Contents |

| Semiannual Report to Shareholders | ||||||||||

| Managers’ Discussions of Fund Performance | ||||||||||

| CORE | ||||||||||

| Royce Pennsylvania Mutual Fund | 16 | |||||||||

| Royce Heritage Fund | 18 | |||||||||

| CORE + DIVIDENDS | ||||||||||

| Royce Total Return Fund | 20 | |||||||||

| Royce Dividend Value Fund | 22 | |||||||||

| FOCUSED | ||||||||||

| Royce Premier Fund | 24 | |||||||||

| Royce Special Equity Fund | 26 | |||||||||

| Royce Value Fund | 28 | |||||||||

| Royce 100 Fund | 30 | |||||||||

| Royce Focus Value Fund | 32 | |||||||||

| Royce Partners Fund | 34 | |||||||||

| Royce Special Equity Multi-Cap Fund | 36 | |||||||||

| OPPORTUNISTIC THEMES | ||||||||||

| Royce Low-Priced Stock Fund | 38 | |||||||||

| Royce Opportunity Fund | 40 | |||||||||

| Royce Value Plus Fund | 42 | |||||||||

| Royce Financial Services Fund | 44 | |||||||||

| MICRO-CAP | ||||||||||

| Royce Micro-Cap Fund | 46 | |||||||||

| Royce Micro-Cap Discovery Fund | 48 | |||||||||

| MID-CAP | ||||||||||

| Royce SMid-Cap Value Fund | 50 | |||||||||

| Royce Mid-Cap Fund | 52 | |||||||||

| Schedules of Investments and Financial Statements | 54 | |||||||||

| Notes to Financial Statements | 133 | |||||||||

| Understanding Your Fund’s Expenses | 147 | |||||||||

| Trustees and Officers | 149 | |||||||||

| Notes to Performance and Other Important Information | 150 | |||||||||

| Board Approval of Investment Advisory Agreement | 151 | |||||||||

| The Royce Funds 2012 Semiannual Report to Shareholders | 15 |

| Royce Pennsylvania Mutual Fund |

| CORE | ||||||||||||

Core Funds generally invest across a wide spectrum of smaller companies using a diversified approach. | ||||||||||||

| ||||||||||||

| AVERAGE ANNUAL TOTAL RETURNS Through 6/30/12 | ||||||||||||

| Jan-June 20121 | 4.00 | % | ||||||||||

| One-Year | -6.97 | |||||||||||

| Three-Year | 15.84 | |||||||||||

| Five-Year | 0.49 | |||||||||||

| 10-Year | 7.97 | |||||||||||

| 15-Year | 9.32 | |||||||||||

| 20-Year | 10.27 | |||||||||||

| 25-Year | 10.05 | |||||||||||

| 30-Year | 12.82 | |||||||||||

| 35-Year | 13.30 | |||||||||||

| ANNUAL EXPENSE RATIO | ||||||||||||

| Operating Expenses | 0.91 | % | ||||||||||

| 1 Not annualized | ||||||||||||

| CALENDAR YEAR TOTAL RETURNS | ||||||||||||

| Year | PMF | Year | PMF | |||||||||

| 2011 | -4.2 | % | 2003 | 40.3 | % | |||||||

| 2010 | 23.9 | 2002 | -9.2 | |||||||||

| 2009 | 36.3 | 2001 | 18.4 | |||||||||

| 2008 | -34.8 | 2000 | 18.3 | |||||||||

| 2007 | 2.8 | 1999 | 6.0 | |||||||||

| 2006 | 14.8 | 1998 | 4.2 | |||||||||

| 2005 | 12.5 | 1997 | 25.0 | |||||||||

| 2004 | 20.2 | 1996 | 12.8 | |||||||||

| TOP 10 POSITIONS % of Net Assets | ||||||||||||

| Advisory Board (The) | 1.1 | % | ||||||||||

| Kennametal | 1.0 | |||||||||||

| Helmerich & Payne | 0.9 | |||||||||||

| IDEXX Laboratories | 0.8 | |||||||||||

| Nordson Corporation | 0.8 | |||||||||||

| Oil States International | 0.8 | |||||||||||

| Cirrus Logic | 0.8 | |||||||||||

| Federated Investors Cl. B | 0.7 | |||||||||||

| HEICO Corporation | 0.7 | |||||||||||

| Valmont Industries | 0.7 | |||||||||||

| PORTFOLIO SECTOR BREAKDOWN % of Net Assets | ||||||||||||

| Industrials | 25.5 | % | ||||||||||

| Information Technology | 20.9 | |||||||||||

| Consumer Discretionary | 15.3 | |||||||||||

| Financials | 11.3 | |||||||||||

| Materials | 8.0 | |||||||||||

| Health Care | 7.3 | |||||||||||

| Energy | 7.0 | |||||||||||

| Consumer Staples | 1.7 | |||||||||||

| Telecommunication Services | 0.1 | |||||||||||

| Miscellaneous | 1.0 | |||||||||||

| Bond | 0.0 | |||||||||||

| Cash and Cash Equivalents | 1.9 | |||||||||||

|

Manager’s Discussion The stock market’s choppy waters led to an underwhelming first-half result for our flagship, Royce Pennsylvania Mutual Fund (PMF). The Fund gained 4.0% for the year-to-date period ended June 30, 2012, compared to an 8.5% gain for its small-cap benchmark, the Russell 2000 Index, for the same period. The year began with a promising rally that lasted almost the entire first quarter, with small-caps reaching their year-to-date high on March 26, 2012. Correlation was again the order of the day, a fact reflected in a comparison of the Fund’s first-quarter return with that of its benchmark—PMF rose 12.1% in the year’s opening quarter versus a 12.4% gain for the Russell 2000. The first quarter’s positive results were an extension of the upswing that began following 2011’s small-cap low on October 3. Considering the volatility that has afflicted the equity markets over the last few years, this nearly six-month bull run was welcome not simply because of its steadily rising stock prices, but also because it ran in parallel with the recovery of the U.S. economy, giving hope to many that both the market and the economy were sailing more confidently forward. Such hopes were gradually dashed, however, as mildly negative returns for most stocks in April gave way to a far more bearish May that was followed by falling share prices into early June. |

Most disappointing about PMF’s second-quarter return was its difficulty in this more bearish and volatile period, in which it fell 7.2% versus a loss of 3.5% for the benchmark. (So much for correlation.) Needless to say, we expect to do relatively better when markets move downward (and have done so historically) and were disappointed that the Fund failed to hold its value, especially in the context of a market that has been so tightly correlated within a relatively narrow range for the past two years. We were pleased, however, that in the most recent peak-to-peak period from July 13, 2007 through April 29, 2011, PMF outpaced the Russell 2000, gaining 11.6% versus 6.6% for the small-cap benchmark. (Please see page 6 for more market cycle results.) The Fund also outperformed the Russell 2000 for the 10-, 15-, 20-, 25-, and 30-year periods ended June 30, 2012, and one challenge going forward is to restore the relative advantage the Fund previously enjoyed in more intermediate-term periods. PMF’s average annual total return for the 35-year period ended June 30, 2012 was 13.3%. As might be expected in a nondescript performance period, few names stood out very positively or negatively at the level of company, industry, or sector. Still, there were definite patterns and |

| GOOD IDEAS THAT WORKED Top Contributors to Performance Year-to-Date through 6/30/121 | ||

| Cirrus Logic | 0.35% | |

| Advisory Board (The) | 0.24 | |

| Federated Investors Cl. B | 0.23 | |

| Valmont Industries | 0.18 | |

| IDEXX Laboratories | 0.17 | |

| 1 Includes dividends | ||

Important Performance and Expense Information All performance information in this Report reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Shares redeemed within 180 days of purchase may be subject to a 1% redemption fee payable to the Fund, which is not reflected in the performance shown above; if it were, performance would be lower. Current month-end performance may be higher or lower than performance quoted and may be obtained at www.roycefunds.com. All performance and risk information reflects results of the Investment Class (its oldest class). Operating expenses reflect the Fund’s total annual operating expenses for the Investment Class as of the Fund’s most current prospectus and include management fees, other expenses and acquired fund fees and expenses. Acquired fund fees and expenses reflect the estimated amount of the fees and expenses incurred indirectly by the Fund through its investment in mutual funds, hedge funds, private equity funds and other investment companies. Shares of PMF’s Service, Consultant, R and K Classes bear an annual distribution expense that is not borne by the Investment Class. Regarding the two “Good Ideas” tables shown above, the sum of all contributors to, and all detractors from, performance for all securities in the portfolio would approximate the Fund’s year-to-date performance for 2012. |

16 | The Royce Funds 2012 Semiannual Report to Shareholders

Performance and Portfolio Review some noteworthy performances, although not necessarily for reasons that we liked. Four sectors made sizable net contributions to first-half results—Consumer Discretionary, Financials, Health Care, and Information Technology—while only the Energy sector, a problem area in the market as a whole, detracted. During the second quarter, three of the aforementioned net-gaining sectors suffered net losses, large ones in the case of the Information Technology and Consumer Discretionary sectors. In fact, only Health Care was able to extend its net gains through the end of the period; it was also the Fund’s only sector in the black from April through June. During that difficult second-quarter slide, Industrials and Energy were also significant detractors. Three of the Fund’s top net losers in the first half came from the Energy sector’s energy equipment & services industry. Each of these companies represents a traditional strategy for us in a volatile, commodity-based industry in which we focus more on conservatively capitalized service companies with strong business fundamentals rather than looking at firms more directly involved with energy production. Oil prices were highly volatile in the year’s first six months, spending most of the second quarter in a tailspin that also drove down share prices for many energy services companies. CARBO Ceramics is an old favorite that we first purchased in PMF’s portfolio in 1996 and have owned continuously since 2006. The company primarily manufactures resin-coated ceramic and sand proppants used in the hydraulic fracturing of natural gas and oil wells. Slumping natural gas prices crimped production, which led to a higher-than-desired inventory of proppants. We like its long-term prospects, especially with ample natural gas reserves still untapped here in the U.S. Another long-term holding, Helmerich & Payne, provides contract drilling for oil and gas wells in the Gulf of Mexico and South America and is one of the largest land drillers in the U.S. Moving from dry gas to wet gas plays caused some margin compression as prices in the latter area came down. However, we like its leading position in an industry that we think is likely to come back strong and, as we did with CARBO, added to our position in the first half. |

| In July, we modestly trimmed our stake in Cirrus Logic, a semiconductor maker that is the sole provider of audio codecs for Apple’s iPhones and iPads, among other products and customers. Its core business continues to show strength and promising new products are being developed, so we were content to hold a good-sized stake in the portfolio. A top gainer in 2011, The Advisory Board offers programs, services, and software focused on best practices research services while also providing management and advisory services. Strong execution and innovative technology appeared to boost the health of its stock price through the first half. |

GOOD IDEAS AT THE TIME | |

| CARBO Ceramics | -0.20% |

| Helmerich & Payne | -0.20 |

| Unit Corporation | -0.15 |

| Kennametal | -0.12 |

| GrafTech International | -0.12 |

| 1 Net of dividends | |

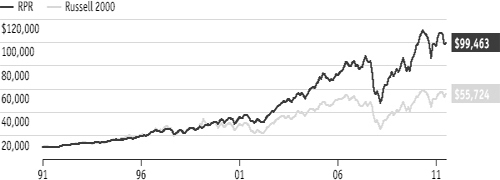

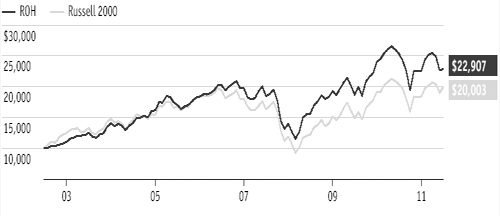

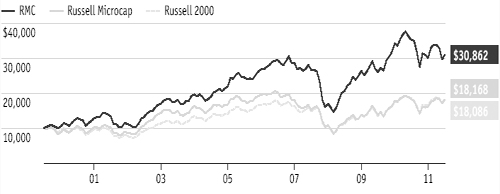

| ROYCE PENNSYLVANIA MUTUAL FUND VS. RUSSELL 2000 Value of $10,000 Invested on 6/30/82 | ||

| ||

Includes reinvestment of distributions. | ||

| PORTFOLIO DIAGNOSTICS | |||||

| Fund Net Assets | $5,844 million | ||||

| Number of Holdings | 506 | ||||

| Turnover Rate | 12% | ||||

| Average Market Capitalization1 | $1,518 million | ||||

| Weighted Average P/E Ratio2,3 | 14.7x | ||||

| Weighted Average P/B Ratio2 | 1.8x | ||||

| U.S. Investments (% of Net Assets) | 89.9% | ||||

| Non-U.S. Investments (% of Net Assets) | 8.2% | ||||

| Symbol | |||||

| Investment Class | PENNX | ||||

| Service Class | RYPFX | ||||

| Consultant Class | RYPCX | ||||

| Institutional Class | RPMIX | ||||

| R Class | RPMRX | ||||

| K Class | RPMKX | ||||

| 1 Geometric average | |||||

| 2 Harmonic average | |||||

3 The Fund’s P/E ratio calculation excludes companies with zero or negative earnings (6% of portfolio holdings as of 6/30/12). | |||||

| MORNINGSTAR STATISTICAL MEASURES1 | |||||

| PMF | Category Median | Best Quartile Breakpoint | |||

| Sharpe Ratio | 0.11 | 0.11 | 0.16 | ||

| Standard Deviation | 24.01 | 24.37 | 23.17 | ||

1 Five years ended 6/30/12. Category Median and Best Quartile Breakpoint based on 349 small-cap objective funds (oldest class only) with at least five years of history. | |||||

| RISK/RETURN COMPARISON Five-Year Period Ended 6/30/12 | |||||

| Average Annual Total Return | Standard Deviation | Return Efficiency1 | |||

| PMF | 0.49% | 24.01 | 0.02 | ||

| Russell 2000 | 0.54 | 24.90 | 0.02 | ||

1 Return Efficiency is the average annual total return divided by the annualized standard deviation over a designated time period. Please read the prospectus for a more complete discussion of risk. | |||||

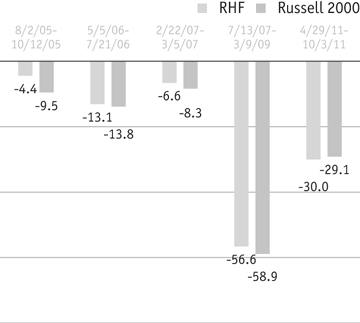

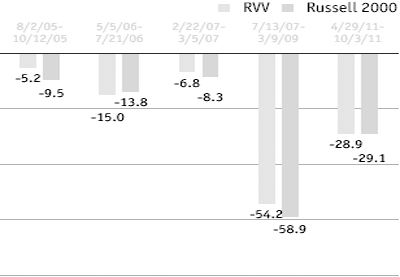

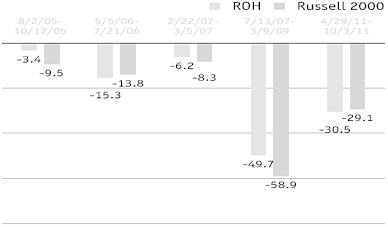

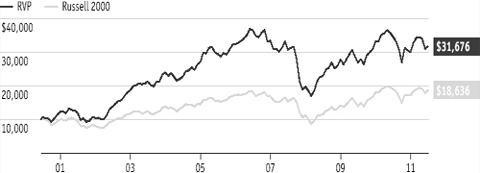

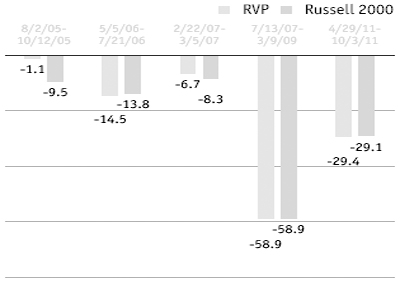

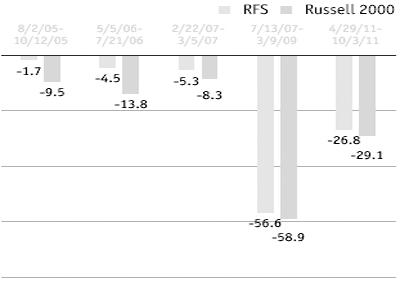

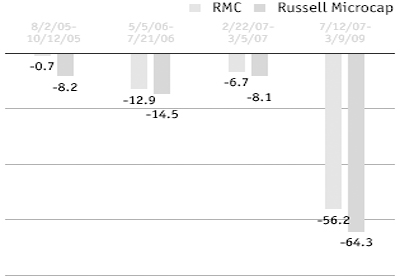

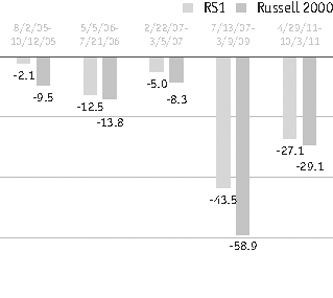

| DOWN MARKET PERFORMANCE COMPARISON All Down Periods of 7.5% or Greater Over the Last 7 Years, in Percentages(%) | |||||

| |||||

The Royce Funds 2012 Semiannual Report to Shareholders | 17

| Royce Heritage Fund |

| CORE | ||||||||||||

Core Funds generally invest across a wide spectrum of smaller companies using a diversified approach. | ||||||||||||

| ||||||||||||

| AVERAGE ANNUAL TOTAL RETURNS Through 6/30/12 | ||||||||||||

| Jan-June 20121 | 2.38 | % | ||||||||||

| One-Year | -11.57 | |||||||||||

| Three-Year | 14.69 | |||||||||||

| Five-Year | 1.53 | |||||||||||

| 10-Year | 8.51 | |||||||||||

| 15-Year | 11.81 | |||||||||||

| Since Inception (12/27/95) | 13.01 | |||||||||||

| ANNUAL EXPENSE RATIO | ||||||||||||

| Operating Expenses | 1.50 | % | ||||||||||

| 1 Not annualized | ||||||||||||

| CALENDAR YEAR TOTAL RETURNS | ||||||||||||

| Year | RHF | Year | RHF | |||||||||

| 2011 | -9.3 | % | 2003 | 38.1 | % | |||||||

| 2010 | 27.5 | 2002 | -18.9 | |||||||||

| 2009 | 51.8 | 2001 | 20.5 | |||||||||

| 2008 | -36.2 | 2000 | 11.7 | |||||||||

| 2007 | 1.2 | 1999 | 41.7 | |||||||||

| 2006 | 22.6 | 1998 | 19.5 | |||||||||

| 2005 | 8.7 | 1997 | 26.0 | |||||||||

| 2004 | 20.4 | 1996 | 25.6 | |||||||||

| TOP 10 POSITIONS % of Net Assets | ||||||||||||

| Alleghany Corporation | 1.9 | % | ||||||||||

| Verisk Analytics Cl. A | 1.7 | |||||||||||

| Advisory Board (The) | 1.5 | |||||||||||

| ANSYS | 1.4 | |||||||||||

| Landstar System | 1.4 | |||||||||||

| Mohawk Industries | 1.4 | |||||||||||

| Ashmore Group | 1.3 | |||||||||||

| Towers Watson & Company Cl. A | 1.3 | |||||||||||

| NVR | 1.3 | |||||||||||

| IPG Photonics | 1.2 | |||||||||||

| PORTFOLIO SECTOR BREAKDOWN % of Net Assets | ||||||||||||

| Industrials | 25.3 | % | ||||||||||

| Financials | 17.7 | |||||||||||

| Information Technology | 17.7 | |||||||||||

| Consumer Discretionary | 12.2 | |||||||||||

| Materials | 9.3 | |||||||||||

| Energy | 4.9 | |||||||||||

| Health Care | 4.0 | |||||||||||

| Consumer Staples | 1.4 | |||||||||||

| Utilities | 0.1 | |||||||||||

| Miscellaneous | 3.6 | |||||||||||

| Cash and Cash Equivalents | 3.8 | |||||||||||

|

Managers’ Discussion Royce Heritage Fund (RHF) gained 2.4% for the year-to-date period ended June 30, 2012, trailing the Russell 2000 Index, its small-cap benchmark, which rose 8.5% for the same period. Although the markets have been tightly correlated over the last couple of years, those attributes that we seek for portfolio holdings—strong balance sheets, established records of earnings, the ability to generate free cash flow, and high returns on invested capital—have not been in high demand. One consequence of this was that during three of the last four quarters RHF followed a similar pattern to its benchmark, while underperforming in both up and down markets, with the only exception being the bullish first quarter of 2012. The year began on a encouraging note, lengthening the rally that began following 2011’s small-cap market low on October 3. The Fund rose 12.9% in the first quarter of 2012, ahead of the 12.4% rise for the Russell 2000. The bull phase ended, or was at least derailed, on March 26, 2012, just before the end of the first quarter. This made for a markedly bearish second quarter, despite a furious rally on the last day of trading in June. For the third consecutive year, a market rally was rudely interrupted by fears of European defaults and questions about the pace of growth here in the U.S. and China. During the second quarter, RHF fell 9.3% (with most of its losses coming in a particularly brutal May) versus a loss of 3.5% for its small-cap benchmark. This displeased us not only because the Fund underperformed, but also because we take great pride in the portfolio’s historical track record during both down markets and down quarters. Unfortunately, the recent run of risk-on, risk-off behavior has prevented the market from establishing any consistent direction, which played a role in RHF’s second-quarter slide. Longer-term returns were better on a relative basis and were impressive on an absolute basis for the 10-year, and since inception (12/27/95) periods ended June 30, 2012. From the previous small-cap peak on July 13, 2007 through April 29, 2011, the Fund gained 25.3% versus 6.6% for the Russell 2000. From that same peak through June 30, 2012, RHF gained 5.3%, while its |

| GOOD IDEAS THAT WORKED Top Contributors to Performance Year-to-Date through 6/30/121 | |||||||||||

| Advisory Board (The) | 0.30% | ||||||||||

| IPG Photonics | 0.29 | ||||||||||

| Verisk Analytics Cl. A | 0.27 | ||||||||||

| Valmont Industries | 0.25 | ||||||||||

| Alleghany Corporation | 0.25 | ||||||||||

| 1 Includes dividends | |||||||||||

Important Performance and Expense Information All performance information in this Report reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Shares redeemed within 180 days of purchase may be subject to a 1% redemption fee payable to the Fund, which is not reflected in the performance shown above; if it were, performance would be lower. Current month-end performance may be higher or lower than performance quoted and may be obtained at www.roycefunds.com. All performance and risk information reflects results of the Service Class (its oldest class). Price and total return information is based on net asset values calculated for shareholder transactions. Certain immaterial adjustments were made to the net assets of Royce Heritage Fund at 12/30/11 for financial reporting purposes, and as a result the net asset values for shareholder transactions on that date and the total returns based on those net asset values differ from the adjusted net asset values and total returns reported in the Financial Highlights. Operating expenses reflect the Fund’s total annual operating expenses for the Service Class as of the Fund’s most current prospectus and include management fees, 12b-1 distribution and service fees, other expenses and acquired fund fees and expenses. Shares of RHF’s Consultant and R Classes bear an annual distribution expense that is higher than that of the Service Class. Acquired fund fees and expenses reflect the estimated amount of the fees and expenses incurred indirectly by the Fund through its investments in mutual funds, hedge funds, private equity funds and other investment companies. Regarding the two “Good Ideas” tables shown above, the sum of all contributors to, and all detractors from, performance for all securities in the portfolio would approximate the Fund’s year-to-date performance for 2012. | |||||||||||

18 | The Royce Funds 2012 Semiannual Report to Shareholders

Performance and Portfolio Review |

benchmark managed a slim gain of 0.04%. The Fund outperformed the small-cap index for the five-, 10-, 15-year, and since inception (12/27/95) periods ended June 30, 2012. RHF’s average annual total return since inception was 13.0%. Only two of the Fund’s nine equity sectors—Energy and Materials—finished the first half in the red, though net losses were relatively low. At the industry level, the energy equipment & services group detracted most significantly from both the Energy sector and the portfolio as a whole. A similar pattern could be seen in the Materials sector, but with two important differences—net losses for its top-detracting group, metals & mining, were lower and were also blunted by a small net gain from the chemicals group. In June, we parted ways with Lamprell, which repairs and refurbishes drilling rigs. The company faced problems with suppliers in its recent efforts to enter the rig construction business, but met with more serious issues when a profit warning announced in May came in the wake of insider selling that followed a series of investor meetings that were initially seen as unusually positive. It was no surprise when these events caused its share price to plummet. We had a more optimistic take on both Trican Well Service and Helmerich & Payne, two long-time Royce favorites that we first purchased in RHF in 2008 and 2007, respectively. We were first drawn to Trican Well Service by its growing business, talented management, and pristine balance sheet. The company provides specialized equipment and services for drilling, completion, and reworking oil and gas wells. Confident in its long-term prospects and believing that the market was punishing it disproportionately, we were pleased to hold a good-sized position at the end of the period. Helmerich & Payne—one of 2011’s top contributors—faced tougher times for its share price than in its business operations. The company is one of the largest land drillers in the U.S. and also provides contract drilling for oil and gas wells in the Gulf of Mexico and South America. While its business has slowed, the long-term outlook is positive, but impatient investors have shown little interest in the long run. Six sectors posted net gains, with Financials out in front, followed by Industrials, Consumer Discretionary, Information Technology, Health Care, and Consumer Staples. The Fund’s two top contributors were also top-ten positions at the end of June. Also a top gainer in 2011, The Advisory Board offers programs, services, and software focused on best practices research services while also providing management and advisory services. Strong execution and innovative technology appeared to boost the health of its stock price through the first half. IPG Photonics develops and manufactures fiber-optic lasers and other laser products. Its share price made its first-half high in February, a month in which we took gains before going on to begin adding to our stake in May at more attractive prices. |

| GOOD IDEAS AT THE TIME Top Detractors from Performance Year-to-Date through 6/30/121 | |

| Lamprell | -0.37% |

| Trican Well Service | -0.30 |

| Helmerich & Payne | -0.25 |

| Gardner Denver | -0.24 |

| Major Drilling Group International | -0.22 |

| 1 Net of dividends | |

| |||

Includes reinvestment of distributions. |

| PORTFOLIO DIAGNOSTICS | |||||

| Fund Net Assets | $265 million | ||||

| Number of Holdings | 233 | ||||

| Turnover Rate | 21% | ||||

| Average Market Capitalization1 | $2,303 million | ||||

| Weighted Average P/E Ratio2,3 | 14.9x | ||||

| Weighted Average P/B Ratio2 | 2.1x | ||||

| U.S. Investments (% of Net Assets) | 73.7% | ||||

| Non-U.S. Investments (% of Net Assets) | 22.5% | ||||

| Symbol | |||||

| Investment Class | RHFHX | ||||

| Service Class | RGFAX | ||||

| Consultant Class | RYGCX | ||||

| R Class | RHFRX | ||||

| K Class | RHFKX | ||||

| 1 Geometric average | |||||

| 2 Harmonic average | |||||

3 The Fund’s P/E ratio calculation excludes companies with zero or negative earnings (3% of portfolio holdings as of 6/30/12). | |||||

| MORNINGSTAR STATISTICAL MEASURES1 | |||||

| RHF | Category Median | Best Quartile Breakpoint | |||

| Sharpe Ratio | 0.16 | 0.11 | 0.16 | ||

| Standard Deviation | 26.21 | 24.37 | 23.17 | ||

1 Five years ended 6/30/12. Category Median and Best Quartile Breakpoint based on 349 small-cap objective funds (oldest class only) with at least five years of history. | |||||

| RISK/RETURN COMPARISON Five-Year Period Ended 6/30/12 | |||||

| Average Annual Total Return | Standard Deviation | Return Efficiency1 | |||

| RHF | 1.53% | 26.21 | 0.06 | ||

| Russell 2000 | 0.54 | 24.90 | 0.02 | ||

1 Return Efficiency is the average annual total return divided by the annualized standard deviation over a designated time period. Please read the prospectus for a more complete discussion of risk. | |||||

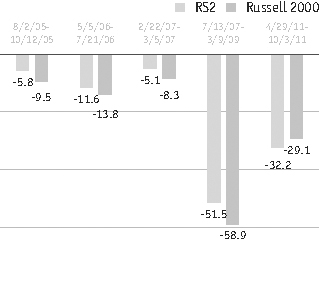

| DOWN MARKET PERFORMANCE COMPARISON All Down Periods of 7.5% or Greater Over the Last 7 Years, in Percentages(%) | |||||

| |||||

The Royce Funds 2012 Semiannual Report to Shareholders | 19

Royce Total Return Fund |

| CORE + DIVIDENDS | ||||||||||||

Core + Dividends Funds generally invest in dividend-paying smaller companies using a diversified approach. | ||||||||||||

| ||||||||||||

| AVERAGE ANNUAL TOTAL RETURNS Through 6/30/12 | ||||||||||||

| Jan-June 20121 | 4.18 | % | ||||||||||

| One-Year | -2.82 | |||||||||||

| Three-Year | 15.61 | |||||||||||

| Five-Year | 0.65 | |||||||||||

| 10-Year | 7.11 | |||||||||||

| 15-Year | 8.40 | |||||||||||

| Since Inception (12/15/93) | 10.46 | |||||||||||

| ANNUAL EXPENSE RATIO | ||||||||||||

| Operating Expenses | 1.15 | % | ||||||||||

| 1 Not annualized | ||||||||||||

| CALENDAR YEAR TOTAL RETURNS | ||||||||||||

| Year | RTR | Year | RTR | |||||||||

| 2011 | -1.7 | % | 2003 | 30.0 | % | |||||||

| 2010 | 23.5 | 2002 | -1.6 | |||||||||