| UNITED STATES |

| SECURITIES AND EXCHANGE COMMISSION |

| Washington, D.C. 20549 |

| FORM N-CSR |

| CERTIFIED SHAREHOLDER REPORT |

| OF |

| REGISTERED MANAGEMENT INVESTMENT COMPANIES |

| Investment Company Act File Number: 811-03599 |

| Name of Registrant: The Royce Fund |

| Address of Registrant: 745 Fifth Avenue |

| New York, NY 10151 |

| Name and address of agent for service: | John E. Denneen, Esquire | |

| 745 Fifth Avenue | ||

| New York, NY 10151 |

| Registrant’s telephone number, including area code: (212) 508-4500 |

| Date of fiscal year end: December 31 |

| Date of reporting period: January 1, 2016 - December 31, 2016 | **Explanatory Note**

The Registrant is filing this amendment to its Form N-CSR for the period ended December 31, 2016, originally filed with the Securities and Exchange Commission on March 3, 2017 (Accession Number 0000949377-17-000056), in order to correct the information appearing in the chart of “Top Contributors to Performance and Top Detractors from Performance” in the Managers’ Discussion of Fund Performance for Royce International Premier Fund contained in the 2016 Annual Review and Report to the Registrant’s Shareholders. Other than such change, no other information or disclosures contained in Item 1 of the Registrant’s Form N-CSR for the period ended December 31, 2016, originally filed with the Securities and Exchange Commission on March 3, 2017 (Accession Number 0000949377-17-000056), is being amended or modified by this Form N-CSR/A.

|

Item 1. Reports to Shareholders.

|

| DECEMBER 31, 2016 | ||

| 2016 Annual | ||

| Review and Report to Shareholders | ||

| Royce Dividend Value Fund | |||

| Royce Global Financial Services Fund | |||

| Royce Heritage Fund | |||

| Royce International Micro-Cap Fund | |||

| Royce International Premier Fund | |||

| Royce International Small-Cap Fund | |||

| Royce Low-Priced Stock Fund | |||

| Royce Micro-Cap Fund | |||

| Royce Micro-Cap Opportunity Fund | |||

| Royce Opportunity Fund | |||

| Royce Pennsylvania Mutual Fund | |||

| Royce Premier Fund | |||

| Royce Small-Cap Leaders Fund | |||

| Royce Small-Cap Value Fund | |||

| Royce Smaller-Companies Growth Fund | |||

| Royce Special Equity Fund | |||

| Royce Special Equity Multi-Cap Fund | |||

| Royce Total Return Fund | |||

| roycefunds.com |  | ||

| Table of Contents | |||

| Annual Review | |||

| Letter to Our Shareholders | 2 | ||

| Performance and Expenses | 6 | ||

| The Royce Funds and Rolling Returns | 7 | ||

| Annual Report to Shareholders | |||

| Managers’ Discussions of Fund Performance | |||

Royce Dividend Value Fund | 8 | ||

Royce Global Financial Services Fund | 10 | ||

Royce Heritage Fund | 12 | ||

Royce International Micro-Cap Fund | 14 | ||

Royce International Premier Fund | 16 | ||

Royce International Small-Cap Fund | 18 | ||

Royce Low-Priced Stock Fund | 20 | ||

Royce Micro-Cap Fund | 22 | ||

Royce Micro-Cap Opportunity Fund | 24 | ||

Royce Opportunity Fund | 26 | ||

Royce Pennsylvania Mutual Fund | 28 | ||

Royce Premier Fund | 30 | ||

Royce Small-Cap Leaders Fund | 32 | ||

Royce Small-Cap Value Fund | 34 | ||

Royce Smaller-Companies Growth Fund | 36 | ||

Royce Special Equity Fund | 38 | ||

Royce Special Equity Multi-Cap Fund | 40 | ||

Royce Total Return Fund | 42 | ||

| Schedules of Investments and Financial Statements | 44 | ||

| Notes to Financial Statements | 112 | ||

| Report of Independent Registered Public Accounting Firm | 129 | �� | |

| Understanding Your Fund’s Expenses | 130 | ||

| Trustees and Officers | 133 | ||

| Notes to Performance and Other Important Information | 134 |

| This page is not part of the 2016 Annual Report to Shareholders | 1 |

Letter to Our Shareholders

A MOST WONDERFUL YEAR FOR SMALL-CAPS,

VALUE, AND CYCLICALS

| By any measure, 2016 was a terrific year for small-cap stocks, one that featured a double-digit positive return for the Russell 2000 Index, which advanced 21.3%, and a solid advantage over their large-cap counterparts. It was an even better year for small-cap value stocks and a highly rewarding one for cyclical sectors. These last two factors were critical in boosting results for certain active management approaches within the asset class, including a number of our own. Arguably even more important was what these developments may be telling us about the subsequent direction of small-cap equity returns. We flesh out the details later in this letter, but these three reversals—positive results for small-caps, leadership for value over growth, and outperformance for cyclicals—should be key in setting the tone for the direction of small-caps going forward. They coalesced around the central, normalizing force of rising interest rates. |

The major impact of these reversals was both highly welcome and long overdue. We saw 2015—a year in which large-cap beat small-cap, the Russell 2000 had a negative return, and market leadership was extremely narrow—as a hinge year. It marked the transition out of the period that began in 2011, when an unprecedented amount of monetary intervention into the global economy had the unintended effect of stoking an intense appetite |

| for yield and safety at one extreme of the U.S. equity markets and a hunger for high risk at the other. The bottom of a commodity super cycle, with the attendant slowdowns in the world’s largest developing markets, only exacerbated the challenges then faced by value stocks and active management approaches. |

As has usually been the case historically, the longer market trends last, the more regularly they are mistaken for permanent realignments. In this most recent instance, the consensus lined up around the perpetuation of near-zero rates, growth stock dominance, and the futility of active management. Whether in good times or bad for our own approaches, however, we have always stayed mindful of the fact that trends do not last forever—they persist, then, more often than not, they reverse. This investment truism should serve as a corrective for those who would take the example of a highly anomalous period for the markets and economy to validate an implacable bias against active management. |

| THE POWER OF RATES AND THE IMPACT OF THE PARADIGM SHIFT |

| Even as small-cap specialists, we recognize that few forces act as powerfully on the value of investments as interest rates. The effects can be as obvious as they are subtle. We think three conditions matter most: the level of rates, the spread between short- and long-term rates, and the disparity in borrowing rates between better-run companies and |

| 2 | This page is not part of the 2016 Annual Report to Shareholders |

LETTER TO OUR SHAREHOLDERS

| worse ones. Capitalism tends to best foster economic growth when short rates hover a bit above inflation; when long rates are high enough to encourage lenders but not so high as to discourage borrowers; and when there is a premium for fiscal prudence and a commensurate penalty for profligate debtors. During the era of zero (or near-zero) rates—roughly 2011-2015—these historically “normal” conditions were largely absent. Yet we believe they began to manifest themselves again in 2016, marking a paradigm shift to a period of higher rates and a consequent reassessment of the relative values of financial assets. More normalized rates have historically been better for stocks than bonds. More important for our purposes, they have also supported small-caps over large, value over growth stocks, and cyclicals over defensive areas. In many ways, 2016’s results exemplified exactly this shift—and we think it is just the beginning of what could be a steady, though not linear, multi-year run. |

| With 2016’s stellar results fresh in the mind, it may be difficult to recall just how poorly the year started and how fatalistic the expectations were for equities. Small-cap stocks plunged from the first peal of 2016’s opening bell. The downdraft exacerbated a trend that had begun the previous summer following the small-cap peak on June 23, 2015. By the time it was all over with the small-cap bottom on February 11, 2016, the Russell 2000 had fallen 25.7%. The last leg of the downdraft included many of the signs of a classic bottoming-out process—panic selling in a number of sectors (most notably within the biopharma complex), small-caps losing more than large-caps, and more resilience from value stocks-to us, the most significant development in the down phase. As unpleasant as any bear market is, we noted that the leadership shift, because it was nearly concomitant with the rate hike, was likely to last. |

| Moreover, these signs also gave us some assurance that this was a historically conventional decline, making us confident that the small-cap market was undergoing its own important and familiar shift. The depths plumbed by this bear market were comparable to previous downturns—and that encouraged our belief that the worst was over just before the Russell 2000 rebounded sharply from its February low through the end of the year. These small-cap bear and bull markets received so little comment beyond our own and that |

| By any measure, 2016 was a terrific year for small-cap stocks, one that featured a double-digit positive return for the Russell 2000 Index, which advanced 21.3%, and a solid advantage over their large-cap counterparts. It was an even better year for small-cap value stocks and a highly rewarding one for cyclical sectors. |

| of fellow small-cap specialists that we refer to them as “stealth” markets. They also reinforced our contention that this small-cap rally has room to run. Despite its strong showing in 2016, the Russell 2000 finished the year only 7.2% above its June 2015 peak. For additional context, it is worth noting that small-cap upswings usually extend well beyond the 47.4% advance the small-cap index made from its February bottom through the end of 2016. There have been 12 declines of 15% or more for the Russell 2000 since its 1979 inception. The median return for the subsequent recovery period was 98.8%. So both history and the currently hospitable economic environment suggest to us that there may well be plenty of life left in the small-cap rally. |

| VALUE’S TURN? |

| The recent extended run of small-cap growth leadership makes it worth recalling that it is actually small-cap value stocks that own the pronounced long-term historical edge in relative performance. Of course, it makes sense that many investors were not conscious of this history at the beginning of the year. Prior to resuming leadership, the Russell 2000 Value Index trailed the Russell 2000 Growth Index in six out of seven years between 2009 and 2015. Based on their long-term performance and leadership history, this was an inordinately lengthy span. Is it now value’s turn, then? We think so. Prolonged periods of leadership for small-cap growth have historically been followed by long tenures at the helm for value. Multi-year trends typically do not have brief reversals before reappearing. Based on this pattern, we think the current leadership status of small-cap value is likely to last. Further, value stocks have historically outpaced growth issues when the economy is expanding—growth companies generally being most highly valued when growth is scarce in the economy. Rising interest rates have also historically provided a relative headwind for |

| This page is not part of the 2016 Annual Report to Shareholders | 3 |

LETTER TO OUR SHAREHOLDERS

| We firmly believe that we are back on the road to a more historically normal market environment. We expect a multi-year run for the current environment of increased return dispersion, declining correlation, and a steepening yield curve. |

| growth stocks because their valuations typically have a long-duration bond aspect to them that is highly sensitive to changes in rates. |

| We saw the post-election rally and the sudden shift in investor perspective that came with it as more symptom than cause of an overall improved environment for both the economy and stocks. After all, some had forecast the pickup in GDP growth prior to any votes being cast just as many investors realized that the era of “lower forever” interest rates had reached its conclusion before the Fed officially announced the hike in December. There were also encouraging pickups in employment and incremental growth in wages. Along with the added certainty that comes after nearly every election, especially a contentious one, all of this stoked bullishness. So while the election was undoubtedly an accelerant, it seemed to us that many investors—and management teams—simply needed the experience of a tangible event before they felt comfortable enough to embrace the good news that had been accumulating prior to November. |

| The aftermath of the election has set the stage for changes that could benefit small-cap companies, beginning with a lower corporate tax rate. With the bulk of their money coming from domestic sources, many small-cap businesses would receive a disproportionate benefit from any rate reduction. Also encouraging are the prospects for repatriation. It was not surprising, then, that the post-election period also witnessed a dramatic rotation away from safety—bonds and defensive stocks most notably. Investors are bullish on the potential for accelerated economic growth and the policy shift from monetary to fiscal—chiefly in the form of tax cuts and projected spending increases on infrastructure and defense. The critical question going forward is, how much of this has already been priced in? |

| TURN THE PAGE |

| All of this has convinced us that we have turned the page on that 2011-2015 period in which financial markets behaved in such odd and unprecedented ways. We firmly believe that we are back on the road to a more historically normal market environment. We expect a multi-year run for the current environment of increased return dispersion, declining correlation, and a steepening yield curve, such as we saw in 2016, and think this will also lead to more historically normal relative return patterns for equity asset classes. |

| Only time will tell, of course. However, we do not think a significant correction-that is, a decline of 15% or more—is in the offing. We see no signs of a recession or financial crisis. Still, a downdraft of anywhere from 8-10% would not be at all unexpected, and arguably healthy, given the strength of small-cap’s 2016 run. When one does occur, we are prepared to act opportunistically by trying to turn any volatility to our investors’ long-term advantage. In any event, we see ongoing leadership not only for small-cap value but for many cyclical sectors as well. Cyclicals lagged for so long that, as with value stocks (with which there is substantial overlap), we were anticipating a shift, which is precisely what we are seeing in the current cycle. Financials are benefiting from the steepening yield curve, which should help to lift bank profits, while the potential for accelerated economic growth is boosting Industrials |

| If we are correct in our argument that a multi-year period of value leadership is just beginning, then we also expect it to be a strong period for thoughtful and disciplined small-cap active management. |

| Equity Indexes as of December 31, 2016 (%) | |||||||||||

| 1-YR | 3-YR | 5-YR | 10-YR | ||||||||

| Russell 2000 | 21.31 | 6.74 | 14.46 | 7.07 | |||||||

| Russell 2000 Value | 31.74 | 8.31 | 15.07 | 6.26 | |||||||

| Russell 2000 Growth | 11.32 | 5.05 | 13.74 | 7.76 | |||||||

| S&P 500 | 11.96 | 8.87 | 14.66 | 6.95 | |||||||

| Russell 1000 | 12.05 | 8.59 | 14.69 | 7.08 | |||||||

| Nasdaq Composite | 7.50 | 8.83 | 15.62 | 8.34 | |||||||

| Russell Midcap | 13.80 | 7.92 | 14.72 | 7.86 | |||||||

| Russell Microcap | 20.37 | 5.77 | 15.59 | 5.47 | |||||||

| Russell Global ex-U.S. Small Cap | 5.04 | 0.57 | 7.22 | 2.65 | |||||||

| Russell Global ex-U.S. Large Cap | 4.30 | -1.51 | 5.35 | 1.24 | |||||||

| For details on The Royce Funds’ performance in the period, please turn to the Managers’ Discussions that begin on page 8. |

| 4 | This page is not part of the 2016 Annual Report to Shareholders |

LETTER TO OUR SHAREHOLDERS

| and many Materials stocks. The latter are also benefiting from rebounding commodity prices that ignited energy stocks as well. In addition, the U.S. consumer continues to spend. We see all of these as potentially ongoing trends. And although the global outlook is admittedly less certain, any rebound in worldwide industrial activity would be an additional, and significant, positive. |

| A NEW DAY FOR ACTIVE MANAGEMENT |

| Ongoing leadership for value and the related strength of cyclicals could produce distinct advantages for small-cap active management. As rates continue to rise and access to capital begins to contract more consistently, the number of bankruptcies should escalate, restoring the healthy, Darwinian force that generally ensures survival for the best-run, most prudently managed enterprises while putting others at potentially greater risk. It creates challenges for more debt-dependent, long-duration growth while offering potential benefits for companies that are conservatively capitalized. If we are correct in our argument that a multi-year period of value leadership is just |

| beginning, then we also expect it to be a strong period for thoughtful and disciplined small-cap active management. |

| To be sure, this was the case in 2016. Twelve of our 13 domestic small-cap portfolios advanced 16% or more in the calendar year; seven increased at least 23% (and bested their benchmark in the process). These performances were largely rooted in our dogged commitment to disciplined approaches to small-cap stock investing. They support the confidence we have going forward, which is also bolstered by the fact that our analysis of the dynamics in our asset class was sound. We felt validated not only by the high returns for several portfolios but also that performance took place against the backdrop of a gradually growing economy. Historically, value-led periods have been good for many Royce Funds, and we remain committed to the effort of delivering strong results for our investors in the years to come. |

| You have our great thanks and deep appreciation for the commitment you have shown to us and our approaches over the years. |

| Sincerely, |

|  |  | ||

| Charles M. Royce | Christopher D. Clark | Francis D. Gannon | ||

| Chairman, | Chief Executive Officer and | Co-Chief Investment Officer, | ||

| Royce & Associates, LP | Co-Chief Investment Officer, | Royce & Associates, LP | ||

| Royce & Associates, LP | ||||

| January 31, 2017 |

| This page is not part of the 2016 Annual Report to Shareholders | 5 |

Performance and Expenses

| Performance and Expenses | AVERAGE ANNUAL TOTAL RETURNS (%) | ANNUAL OPERATING EXPENSES (%) | |||||||||||||||||

| 1-YR | 5-YR | 10-YR | 15-YR | 20-YR | 40-YR/SINCE INCEPTION | INCEPTION DATE | GROSS | NET | |||||||||||

| Royce Dividend Value Fund | 16.36 | 10.42 | 6.76 | N/A | N/A | 8.46 | 5/3/04 | 1.39 | 1.39 | ||||||||||

| Royce Global Financial Services Fund | 12.93 | 13.80 | 5.02 | N/A | N/A | 7.72 | 12/31/03 | 1.85 | 1.69 | ||||||||||

| Royce Heritage Fund | 17.84 | 9.41 | 5.91 | 8.04 | 11.72 | 12.35 | 12/27/95 | 1.37 | 1.37 | ||||||||||

| Royce International Micro-Cap Fund | 6.33 | 6.79 | N/A | N/A | N/A | 1.45 | 12/31/10 | 3.11 | 1.64 | ||||||||||

| Royce International Premier Fund | -1.06 | 9.03 | N/A | N/A | N/A | 4.24 | 12/31/10 | 2.35 | 1.44 | ||||||||||

| Royce International Small-Cap Fund | -1.72 | 3.80 | N/A | N/A | N/A | 3.14 | 6/30/08 | 1.92 | 1.45 | ||||||||||

| Royce Low-Priced Stock Fund | 16.09 | 3.46 | 2.97 | 5.99 | 9.27 | 10.08 | 12/15/93 | 1.50 | 1.50 | ||||||||||

| Royce Micro-Cap Fund | 19.74 | 5.45 | 3.91 | 7.74 | 9.40 | 11.05 | 12/31/91 | 1.50 | 1.50 | ||||||||||

| Royce Micro-Cap Opportunity Fund | 23.85 | 14.09 | N/A | N/A | N/A | 12.26 | 8/31/10 | 1.39 | 1.25 | ||||||||||

| Royce Opportunity Fund | 29.86 | 14.46 | 7.03 | 9.93 | 12.07 | 12.28 | 11/19/96 | 1.17 | 1.17 | ||||||||||

| Royce Pennsylvania Mutual Fund | 26.47 | 11.50 | 6.45 | 9.10 | 10.33 | 13.19 | N/A | 0.93 | 0.93 | ||||||||||

| Royce Premier Fund | 23.00 | 9.36 | 7.76 | 10.09 | 10.71 | 11.49 | 12/31/91 | 1.13 | 1.13 | ||||||||||

| Royce Small-Cap Leaders Fund | 25.51 | 9.17 | 6.62 | N/A | N/A | 9.70 | 6/30/03 | 1.54 | 1.49 | ||||||||||

| Royce Small-Cap Value Fund | 21.06 | 8.44 | 5.54 | 8.97 | N/A | 9.87 | 6/14/01 | 1.48 | 1.48 | ||||||||||

| Royce Smaller-Companies Growth Fund | 9.37 | 11.25 | 4.68 | 10.03 | N/A | 11.04 | 6/14/01 | 1.48 | 1.48 | ||||||||||

| Royce Special Equity Fund | 32.21 | 11.82 | 8.50 | 10.18 | N/A | 9.54 | 5/1/98 | 1.15 | 1.15 | ||||||||||

| Royce Special Equity Multi-Cap Fund | 13.69 | 10.29 | N/A | N/A | N/A | 9.77 | 12/31/10 | 1.29 | 1.24 | ||||||||||

| Royce Total Return Fund | 25.86 | 12.45 | 6.86 | 8.95 | 9.83 | 10.93 | 12/15/93 | 1.22 | 1.22 | ||||||||||

| INDEX | |||||||||||||||||||

| Russell 2000 Index | 21.31 | 14.46 | 7.07 | 8.49 | 8.25 | N/A | N/A | N/A | N/A | ||||||||||

| Russell Microcap Index | 20.37 | 15.59 | 5.47 | 8.16 | N/A | N/A | N/A | N/A | N/A | ||||||||||

| Russell 1000 Index | 12.05 | 14.69 | 7.08 | 7.00 | 7.86 | N/A | N/A | N/A | N/A | ||||||||||

| Russell Global ex-U.S. Small Cap Index | 5.04 | 7.22 | 2.65 | 9.53 | 5.95 | N/A | N/A | N/A | N/A | ||||||||||

Important Performance, Expense, and Risk Information

All performance information in this Review and Report reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Investment and Service Class shares redeemed within 30 days of purchase may be subject to a 1% redemption fee payable to the Fund (2% for Royce International Micro-Cap, International Premier, and International Small-Cap Funds). Redemption fees are not reflected in the performance shown above; if they were, performance would be lower. Current performance may be higher or lower than performance quoted. Current month-end performance may be obtained at www.roycefunds.com. All performance and expense information reflects results of the Funds’ oldest share Class (Investment Class or Service Class, as the case may be). Price and total return information is based on net asset values calculated for shareholder transactions. Gross annual operating expenses reflect the Fund’s gross total annual operating expenses and include management fees, any 12b-1 distribution and service fees, other expenses, and any applicable acquired fund fees and expenses. Net annual operating expenses reflect contractual fee waivers and/or reimbursements. All expense information is reported as of the Fund’s most current prospectus. Royce & Associates has contractually agreed to waive fees and/or reimburse operating expenses, excluding brokerage commissions, taxes, interest litigation expenses, acquired fund fees and expenses, and other expenses not borne in the ordinary course of business, to the extent necessary to maintain net operating expenses at or below: 1.49% for Royce Global Financial Services and Small-Cap Leaders Funds; 1.64% for Royce International Micro-Cap Fund; 1.44% for Royce International Premier and International Small-Cap Funds; 1.24% for Royce Micro-Cap Opportunity and Special Equity Multi-Cap Funds through April 30, 2017; at or below: 1.99% for Royce International Micro-Cap and International Premier Funds through April 30, 2026. Acquired fund fees and expenses reflect the estimated amount of fees and expenses incurred indirectly by the Fund through its investments in mutual funds, hedge funds, private equity funds, and other investment companies.

Service Class shares bear an annual distribution expense that is not borne by the Funds’ Investment Class. If such distribution expenses had been reflected for Funds showing Investment Class performance, returns would have been lower. Investments in securities of micro-cap, small-cap, and/or mid-cap companies may involve considerably more risk than investments in securities of larger-cap companies. (Please see “Primary Risks for Fund Investors” in the prospectus.) Certain Funds invest a significant portion of their respective assets in foreign companies that may be subject to different risks than investments in securities of U.S. companies, including adverse political, social, economic, or other developments that are unique to a particular country or region. (Please see “Investing in Foreign Securities” in the prospectus.) Therefore, the prices of securities of foreign companies in particular countries or regions may, at times, move in a different direction than those of securities of U.S. companies. (Please see “Primary Risk of Fund Investors” in the prospectus.) Certain Funds generally invest a significant portion of their assets in a limited number of stocks, which may involve considerably more risk than a more broadly diversified portfolio because a decline in the value of any of these stocks would cause their overall value to decline to a greater degree. A broadly diversified portfolio, however, does not ensure a profit or guarantee against loss. This Review and Report must be preceded or accompanied by a prospectus. Please read the prospectus carefully before investing or sending money. Russell Investment Group is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group. The Russell 2000 Index is an unmanaged, capitalization-weighted index of domestic small-cap stocks. It measures the performance of the 2,000 smallest publicly traded U.S. companies in the Russell 3000 Index. The Russell Microcap Index includes 1,000 of the smallest securities in the small-cap Russell 2000 Index along with the next smallest eligible securities as determined by Russell. The Russell 1000 is an unmanaged, capitalization-weighted index of domestic large-cap stocks. It measures the performance of the 1,000 largest publicly traded U.S. companies in the Russell 3,000 Index. The Russell Global ex-U.S. Small Cap Index is an index of global small-cap stocks, excluding the United States. The performance of an index does not represent exactly any particular investment as you cannot invest directly in an index. Distributor: Royce Fund Services, Inc.

| 6 | This page is not part of the 2016 Annual Report to Shareholders |

The Royce Funds and Rolling Returns

We believe strongly in the idea that a long-term perspective is crucial for determining the success of an investment approach. Flourishing in an up market is wonderful, but surviving a bear market by losing less (or not at all) is equally desirable. In any case, the true tests of a portfolio’s mettle are results over bull and bear periods. This is why we prefer to examine results that include up and down market phases–primarily by looking at rolling return periods.

| When evaluating fund performance, it is common practice to review results for the most recent year (often the calendar year) along with its related longer-term trailing periods. However, a calendar-year return is not necessarily any more or less important to consider than any other 12-month period (or related trailing period) during a manager’s tenure. It is also true that few investors buy mutual funds on New Year’s Eve and then sell exactly five or 10 years later. Of course, the reality is that trailing returns ending last month or last quarter are the most commonly available and easily comparable results, so these otherwise arbitrary periods often drive investor decisions and flows. |

| Keeping in mind that investors will buy and sell at any time throughout any given year, we think it makes sense to examine performance over a larger series of dates. We believe rolling returns offer a more effective measure because they provide a more accurate and in-depth picture of a portfolio’s performance. Rather than “point-in-time” results anchored by the end of the month or quarter, |

| rolling returns account for the fact that investors typically do not invest at the beginning of the current five- or 10-year period but instead are in fact investing over many periods. |

| So instead of assuming that an investment was made on January 1, rolling returns calculate all of the periods starting not only in January, but also in February, March, April, etc. For example, a monthly five-year rolling return accounts for all of the five-year returns beginning at a given inception date and advancing one month sequentially. This method allows an investor to evaluate the consistency of a fund’s performance over time—including the ups and downs of market cycles, which are an important test of a manager’s skill. |

| We believe that rolling returns provide a particularly robust analytical tool for evaluating manager performance, especially during volatile periods when simply shifting the performance date range one or two months in either direction can paint a very different picture. |

| Royce Funds1 vs. The Benchmark2 |

| Monthly Rolling Average Annual Return Periods and Relative Results Since Fund Inception or Most Recent 20 Years through December 31, 2016 |

| Average Annual 10-Year Rolling Return | Average Annual 5-Year Rolling Return | ||||||||||||||||||||||||||

| FUND | PERIODS BEATING THE INDEX | FUND AVG (%)3 | INDEX AVG (%)3 | PERIODS BEATING THE INDEX | FUND AVG (%)3 | INDEX AVG (%)3 | |||||||||||||||||||||

| U.S. EQUITY | |||||||||||||||||||||||||||

| Dividend Value | 28/32 | 88% | 8.0 | 7.4 | 57/92 | 62% | 8.8 | 7.9 | |||||||||||||||||||

| Heritage | 105/121 | 87% | 10.0 | 6.9 | 145/181 | 80% | 10.7 | 7.6 | |||||||||||||||||||

| Low-Priced Stock | 72/121 | 60% | 8.9 | 6.9 | 125/181 | 69% | 9.3 | 7.6 | |||||||||||||||||||

| Micro-Cap | 60/79 | 76% | 8.3 | 6.2 | 92/139 | 66% | 8.7 | 7.7 | |||||||||||||||||||

| Opportunity | 103/121 | 85% | 10.1 | 6.9 | 138/181 | 76% | 11.6 | 7.6 | |||||||||||||||||||

| Pennsylvania Mutual | 97/121 | 80% | 9.3 | 6.9 | 133/181 | 73% | 10.1 | 7.6 | |||||||||||||||||||

| Premier | 120/121 | 99% | 10.8 | 6.9 | 137/181 | 76% | 11.0 | 7.6 | |||||||||||||||||||

| Small-Cap Leaders | 25/43 | 58% | 8.3 | 7.8 | 61/103 | 59% | 7.9 | 7.3 | |||||||||||||||||||

| Small-Cap Value | 44/67 | 66% | 9.4 | 7.9 | 76/127 | 60% | 9.8 | 8.5 | |||||||||||||||||||

| Smaller-Companies Growth | 37/67 | 55% | 8.8 | 7.9 | 54/127 | 43% | 9.7 | 8.5 | |||||||||||||||||||

| Special Equity | 90/104 | 87% | 9.4 | 6.7 | 106/164 | 65% | 10.7 | 8.1 | |||||||||||||||||||

| Total Return | 78/121 | 64% | 8.4 | 6.9 | 121/181 | 67% | 9.4 | 7.6 | |||||||||||||||||||

| GLOBAL/INTERNATIONAL EQUITY | |||||||||||||||||||||||||||

| Global Financial Services | 19/37 | 51% | 7.3 | 7.6 | 29/97 | 30% | 6.7 | 7.3 | |||||||||||||||||||

| 1 Included are all Royce Funds with at least 12 years of history. |

| 2 The Russell 2000 Index is the benchmark for most funds. Royce Micro-Cap Fund is compared to the Russell Microcap Index from the inception of that index. |

| 3 Average return shown is the average of all month-end trailing five- and 10-year total returns. |

| Past performance is no guarantee of future results. For more information on performance please see page 6. |

| This page is not part of the 2016 Annual Report to Shareholders | 7 |

| MANAGERS’ DISCUSSION |

| Royce Dividend Value Fund (RDV) |

|

| Chuck Royce Jay Kaplan, CFA |

| FUND PERFORMANCE |

| Royce Dividend Value Fund advanced 16.4% in 2016, trailing its small-cap benchmark, the Russell 2000 Index, which gained 21.3% for the same period. Three factors had an outsized effect on calendar-year underperformance: At the end of 2016 a significant percentage of the Fund’s assets were invested in mid-cap stocks, which meaningfully underperformed their small-cap peers (the Russell Midcap Index rose 13.8% in 2016); 23.4% of the Fund’s net assets were invested in international stocks, which significantly trailed their domestic counterparts; and the Fund had a high weighting in capital markets companies, a number of which were non-U.S., and the group as a whole underperformed relative to the Russell 2000. However, we were pleased to see value recapture leadership from growth in 2016 and cyclicals beat defensives. Based on history and reversion to the mean, we believe that these two developments should have staying power, in particular because the previous five years (2011-2015) were so odd, with unprecedented levels of monetary policy intervention and little, if any, in the way of fiscal stimulus. Finally, we were intrigued by the number of holdings that entered 2017 with what we thought were very attractive valuations. |

| During the first half of 2016, Dividend Value increased 4.4% compared to 2.2% for the small-cap index. During the third quarter the Fund lost some ground, gaining 4.4% versus 9.0% for the benchmark. The Fund also lagged for the fourth quarter, up 6.7% versus 8.8% for the Russell 2000. The Fund’s average annual total return since inception was 8.5%. |

| WHAT WORKED...AND WHAT DIDN’T |

| Nine of the Fund’s 11 equity sectors showed net gains for 2016. Industrials and Financials led by a sizable margin, followed by a solid contribution from Materials. Telecommunication Services detracted most, albeit modestly, while Health Care saw a very small loss. At the industry level, machinery (Industrials), metals & mining (Materials), capital markets (Financials), and banks (Financials) were the leaders. The biggest detractors among the portfolio’s industry groups were diversified telecommunication services (a low weighting in one of the Fund’s smallest sectors, Telecommunication Services), technology hardware, storage & peripherals (Information Technology), and marine (Industrials). |

| The portfolio’s top contributor at the position level was Worthington Industries, a metals manufacturing company that earlier in the year was able to improve margins and keep earnings positive in spite of some sales declines. Its stock was then galvanized by post-election optimism for significant infrastructure spending before pulling back a bit toward the end of the year. We reduced our position in November. Top-10 holding and long-time Royce favorite Reliance Steel & Aluminum distributes metals. Its shares rose through much of the year and gained a similar boost following the election. Not long after Parker Hannifin announced plans to buy the company in December, we began to sell our shares of CLARCOR, which makes replacement filters for trucks and construction equipment. Detracting most on the position level was SEI Investments, an asset manager that also provides technology solutions. We have long liked its core businesses and were happy to hold a good-sized position at the end of 2016 owing to our confidence in its long-term prospects and its previous record of success. London-based Inmarsat has a global business providing satellite broadband services on land, at sea, and in the air. Sales declines were driven by the recession in the commercial shipping industry along with ongoing weakness in international trade. However, the firm also saw better-than-expected growth in its government and aviation businesses before the end of the year, which aided our decision to hold our shares. In spite of its stock price volatility through much of the year, we held on to top-10 position Diebold Nixdorf, which makes software-based self-service delivery and security systems. The company announced an expensive acquisition that, while making the combined company the world’s largest maker of automated teller machines, also sported a price tag which worried other investors. Relative to the Russell 2000, the calendar year’s largest detractor was Financials where, in addition to the previously mentioned overweight and stock selection missteps in capital markets, our underweight in banks created a significant lag. Stock selection in Industrials was also a factor in underperformance. Helping relative results most was our appreciably lower exposure to Health Care—the only sector in the Russell 2000 to show a net loss in 2016. |

| Top Contributors to Performance | |||

| For 2016 (%)1 | |||

| Worthington Industries | 1.02 | ||

| Reliance Steel & Aluminum | 0.90 | ||

| CLARCOR | 0.86 | ||

| Quaker Chemical | 0.66 | ||

| TD Ameritrade Holding Corporation | 0.62 | ||

| 1 Includes dividends | |||

| Top Detractors from Performance | |||

| For 2016 (%)2 | |||

| SEI Investments | -0.47 | ||

| Inmarsat | -0.35 | ||

| Diebold Nixdorf | -0.24 | ||

| Westwood Holdings Group | -0.21 | ||

| MTS Systems | -0.21 | ||

| 2 Net of dividends | |||

| CURRENT POSITIONING AND OUTLOOK |

| We firmly believe that we have turned the page on the anomalous 2011-2015 period, in which extraordinary monetary accommodations caused financial markets to behave in odd and unprecedented ways. In our view, we are on the road back to a more historically normal market environment. We think this bodes well for small-cap stocks. In our view cyclicals look well-positioned for ongoing leadership. In addition to our usual cyclical tilt, we are looking in some defensive areas such as healthcare. It is very much on a stock-by-stock basis, with a focus on individual companies that combine attractive valuations with strong fundamentals. |

| 8 | The Royce Funds 2016 Annual Report to Shareholders |

| PERFORMANCE AND PORTFOLIO REVIEW | TICKER SYMBOLS RYDVX RDVIX RDIIX RDVCX |

| Performance and Expenses Average Annual Total Return (%) Through 12/31/16 | ||||||||||||

| JUL-DEC 20161 | 1-YR | 3-YR | 5-YR | 10-YR | SINCE INCEPTION (05/03/04) | |||||||

| RDV | 11.47 | 16.36 | 2.40 | 10.42 | 6.76 | 8.46 | ||||||

| Annual Operating Expenses: 1.39% | ||||||||||||

| 1 Not Annualized | ||||||||||||

| Relative Risk Adjusted Returns: Monthly Rolling Sharpe Ratios Since Inception Through 12/31/16 On a monthly rolling risk-adjusted basis, the Fund outperformed the Russell 2000 in 100% of all 10-year periods and 71% of all 5-year periods. | ||||||||||||

| PERIODS BEATING THE INDEX | FUND AVG (%)1 | INDEX AVG (%)1 | ||||||||||||

| 10-year | 32/32 | 100% | 0.47 | 0.40 | ||||||||||

| 5-year | 65/92 | 71% | 0.53 | 0.46 | ||||||||||

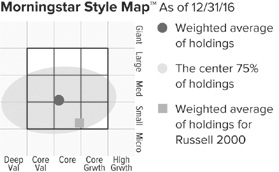

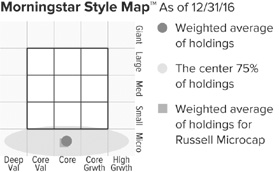

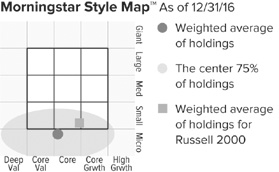

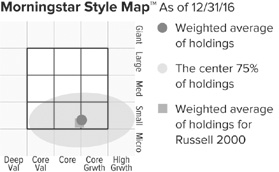

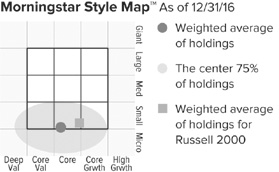

The Morningstar Style Map is the Morningstar Style Box™ with the center 75% of fund holdings plotted as the Morningstar Ownership Zone™. The Morningstar Style Box is designed to reveal a fund’s investment strategy. The Morningstar Ownership Zone provides detail about a portfolio’s investment style by showing the range of stock sizes and styles. The Ownership Zone is derived by plotting each stock in the portfolio within the proprietary Morningstar Style Box. Over time, the shape and location of a fund's ownership zone may vary. See page 134 for additional information. |

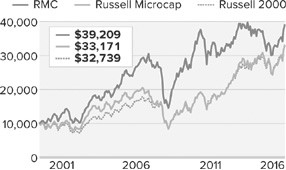

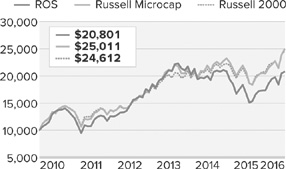

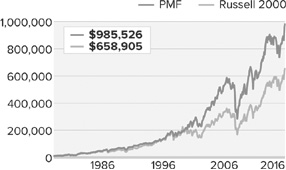

Value of $10,000

| Top 10 Positions | |||

| % of Net Assets | |||

| FLIR Systems | 2.5 | ||

| KKR & Co. L.P. | 2.0 | ||

| Reliance Steel & Aluminum | 2.0 | ||

| First Republic Bank | 1.9 | ||

| Diebold Nixdorf | 1.9 | ||

| Western Union | 1.8 | ||

| Expeditors International of Washington | 1.8 | ||

| ManpowerGroup | 1.7 | ||

| Donaldson Company | 1.7 | ||

| Quaker Chemical | 1.6 | ||

| Portfolio Sector Breakdown | |||

| % of Net Assets | |||

| Financials | 29.4 | ||

| Industrials | 24.7 | ||

| Materials | 11.6 | ||

| Consumer Discretionary | 10.2 | ||

| Information Technology | 7.7 | ||

| Health Care | 3.5 | ||

| Consumer Staples | 2.5 | ||

| Energy | 2.4 | ||

| Telecommunication Services | 1.7 | ||

| Utilities | 1.4 | ||

| Real Estate | 0.2 | ||

| Miscellaneous | 3.2 | ||

| Corporate Bond | 0.2 | ||

| Cash and Cash Equivalents | 1.3 | ||

| Calendar Year Total Returns (%) | |||

| YEAR | RDV | ||

| 2016 | 16.4 | ||

| 2015 | -5.7 | ||

| 2014 | -2.1 | ||

| 2013 | 30.7 | ||

| 2012 | 16.9 | ||

| 2011 | -4.5 | ||

| 2010 | 30.1 | ||

| 2009 | 37.7 | ||

| 2008 | -31.5 | ||

| 2007 | -0.0 | ||

| 2006 | 19.9 | ||

| 2005 | 7.3 | ||

| Upside/Downside Capture Ratios | |||

| Periods Ended 12/31/16 (%) | |||

| UPSIDE | DOWNSIDE | |||

| 10-Year | 85 | 81 | ||

| From 6/30/04 (Start of Fund’s First Full Quarter) | 86 | 76 | ||

| Portfolio Diagnostics | |||

| Fund Net Assets | $217 million | ||

| Number of Holdings | 137 | ||

| Turnover Rate | 21% | ||

| Average Market Capitalization1 | $3,414 million | ||

| Weighted Average P/E Ratio2,3 | 21.0x | ||

| Weighted Average P/B Ratio2 | 2.5x | ||

| Active Share4 | 97% | ||

| U.S. Investments (% of Net Assets) | 75.3% | ||

| Non-U.S. Investments (% of Net Assets) | 23.4% | ||

| 1 | Geometric Average. This weighted calculation uses each portfolio holding’s market cap in a way designed to not skew the effect of very large or small holdings; instead, it aims to better identify the portfolio’s center, which Royce believes offers a more accurate measure of average market cap than a simple mean or median. |

| 2 | Harmonic Average. This weighted calculation evaluates a portfolio as if it were a single stock and measures it overall. It compares the total market value of the portfolio to the portfolio’s share in the earnings or book value, as the case may be, of its underlying stocks. |

| 3 | The Fund’s P/E ratio calculation excludes companies with zero or negative earnings (5% of portfolio holdings as of 12/31/16). |

| 4 | Active Share is the sum of the absolute values of the different weightings of each holding in the Fund versus each holding in the benchmark, divided by two. |

| Important Performance and Expense Information |

All performance information in this Report reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Shares redeemed within 30 days of purchase may be subject to a 1% redemption fee payable to the Fund, which is not reflected in the performance shown above; if it were, performance would be lower. Current month-end performance may be higher or lower than performance quoted and may be obtained at www.roycefunds.com. All performance and risk information reflects results of the Service Class (its oldest class). Certain immaterial adjustments were made to the net assets of Royce Dividend Value Fund at 6/30/15 for financial reporting purposes, and as a result the net asset values for shareholder transactions on that date and the calendar year Total Returns (%) based on those net asset values differ from the adjusted net asset values and calendar year total returns reported in the Financial Highlights. Operating expenses reflect the Fund’s gross total annual operating expenses for the Service Class as of the Fund’s most current prospectus and include management fees, 12b-1 distribution and service fees, other expenses, and acquired fund fees and expenses. Acquired fund fees and expenses reflect the estimated amount of the fees and expenses incurred indirectly by the Fund through its investments in mutual funds, hedge funds, private equity funds, and other investment companies. Regarding the “Top Contributors” and “Top Detractors” tables shown above, the sum of all contributors to, and all detractors from, performance for all securities in the portfolio would approximate the Fund’s year-to-date performance for 2016. The Sharpe Ratio is calculated for a specified period by dividing a fund’s annualized excess returns by its annualized standard deviation. The higher the Sharpe ratio, the better the fund’s historical risk-adjusted performance. Upside Capture Ratio measures a manager’s performance in up markets relative to the Fund’s benchmark. It is calculated by measuring the Fund’s performance in quarters when the benchmark went up and dividing it by the benchmark’s return in those quarters. Downside Capture Ratio measures a manager’s performance in down markets relative to the Fund’s benchmark (Russell 2000). It is calculated by measuring the Fund’s performance in quarters when the benchmark goes down and dividing it by the benchmark’s return in those quarters. |

| The Royce Funds 2016 Annual Report to Shareholders | 9 |

| MANAGERS’ DISCUSSION |

| Royce Global Financial Services (RFS) |

|

| Chuck Royce Chris Flynn |

| FUND PERFORMANCE |

| Royce Global Financial Services Fund gained 12.9% in 2016. Although this result was significantly higher than its long-term returns, it still lagged both its small-cap benchmark, the Russell 2000 Index, and the financial services component of the Russell 2500 Index, which advanced 21.3% and 22.6%, respectively, for the same period. Two related factors contributed to calendar-year underperformance: First was the portfolio’s significantly larger weighting in capital markets companies. This category lagged several other industries in the Financials sector (the second-best performer in the small-cap index) within the Russell 2000. The second factor was the presence of many non-U.S. stocks in this group, which collectively underperformed their domestic counterparts in 2016. |

| For the first half of 2016, the Fund increased 0.5% compared to a gain of 2.2% for the Russell 2000 and 5.0% for the financial services companies in the Russell 2500. Global Financial’s results showed marked improvement on an absolute basis in the second half, though it could not keep pace with the two indexes. In the second half of 2016, the Fund rose 12.4% versus respective gains of 18.7% and 16.8% for the Russell 2000 and the financial services component of the Russell 2500, thanks largely to the beneficial effect the steepening yield curve had on banks and thrifts & mortgage finance companies. |

| WHAT WORKED... AND WHAT DIDN’T |

| We have long seen the capital markets industry as home to many niche companies with talented management, differentiated business models, and attractive financial profiles, which are among the key attributes that we seek. While we remain confident in their long-term prospects, many capital markets holdings did not advance as much as others in the sector. Nonetheless, the overall effect for the group on 2016’s performance was positive. Banks were also a significant contributor to calendar-year results. The Fund’s top three contributors were also top-10 holdings at the end of the year. Ares Management is a global alternative asset manager specializing in credit, private equity and real estate investing. Strong fund performance, improved fee-related earnings, and a bright outlook for future growth seemed to draw investors to its shares in 2016. MBIA provides financial guarantee insurance and other forms of credit protection. The firm has a meaningful exposure to Puerto Rican bonds, which has weighed down its stock price in recent years. Promising signs of a successful resolution to the Puerto Rican debt crisis contributed to a sharp fourth-quarter rally for MBIA’s stock. Popular is a bank holding company that provides commercial banking services through branches in the U.S., Puerto Rico, the British Virgin Islands, and the Dominican Republic. Its shares advanced more or less steadily throughout the year as investors saw more evidence of a turnaround in its U.S. business, as well as progress in Puerto Rico in addressing lingering issues that would enable the bank to capitalize on its leading position in that market. |

| As for positions that detracted, four of the top five positions came from the capital markets industry. Value Partners Group is a Hong Kong-based asset manager that emphasizes value approaches similar to some of our own. Subpar short-term performance, net outflows, and a CEO resignation all contributed to investors’ concerns. Because we remain confident in its long-term prospects, particularly in China, as well as in its Chairman, who has assumed CEO responsibilities, we were comfortable holding our stake at the end of 2016. Och-Ziff Capital Management Group is an institutional alternative asset manager that offers multi-strategy, credit, equity, and real estate funds. Its stock declined as the company worked through poor short-term investment performance in key funds and an ongoing Department of Justice investigation into certain international fundraising activities. Although the firm settled in September, its assets under management continued to decline, which influenced our decision to sell our shares in December. Stifel Financial provides wealth management, investment banking, and related financial services. Global volatility hit the advisory fee end of its business particularly hard at the end of 2015 and early in 2016, leading us to sell our position in February. |

| Top Contributors to Performance | |||

| For 2016 (%)1 | |||

| Ares Management L.P. | 1.16 | ||

| MBIA | 1.14 | ||

| Popular | 1.03 | ||

| BM&FBOVESPA | 0.97 | ||

| Franco-Nevada Corporation | 0.90 | ||

| 1 Includes dividends | |||

| Top Detractors from Performance | |||

| For 2016 (%)2 | |||

| Value Partners Group | -0.55 | ||

| Och-Ziff Capital Management Group LLC Cl. A | -0.55 | ||

| Stifel Financial | -0.38 | ||

| Jupiter Fund Management | -0.32 | ||

| Clarkson | -0.31 | ||

| 2 Net of dividends | |||

| CURRENT POSITIONING AND OUTLOOK |

| Using our proprietary industry classification model, the Fund’s three largest industry weighting were in banks, which we expect to continue benefitting from a steepening yield curve and perhaps increased loan demand, specialist vendors, where we often find niche businesses with what we see as sustainable competitive advantages, and alternative asset managers, with a current preference for private credit managers, where we see strong asset growth and undervaluation due to the complexity of the business models. We firmly believe that we have turned the page on the anomalous 2011-2015 period, in which extraordinary monetary accommodations caused financial markets to behave in odd and unprecedented ways. In our view, we are on the road back to a more historically normal market environment. We think this bodes well for small-cap stocks in general, and many of our preferred types of financial companies specifically. In addition, we think an accelerating U.S. economy and increased business confidence can help many capital markets businesses both in and outside the U.S. |

| 10 | The Royce Funds 2016 Annual Report to Shareholders |

| PERFORMANCE AND PORTFOLIO REVIEW | TICKER SYMBOLS RYFSX RGFIX |

| Performance and Expenses | ||||||||||||||

| Average Annual Total Return (%) Through 12/31/16 | ||||||||||||||

| JUL-DEC 20161 | 1-YR | 3-YR | 5-YR | 10-YR | SINCE INCEPTION (12/31/03) | |||||||||

| RFS | 12.36 | 12.93 | 3.64 | 13.80 | 5.02 | 7.72 | ||||||||

| Annual Gross Operating Expenses: 1.85% Annual Net Operating Expenses: 1.69% | ||||||||||||||

| 1 Not Annualized | ||||||||||||||

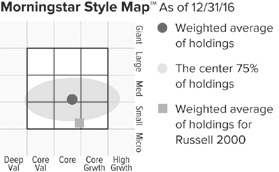

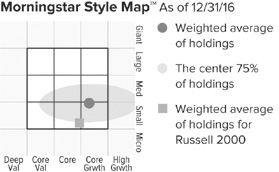

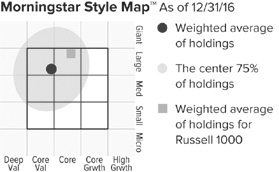

The Morningstar Style Map is the Morningstar Style Box™ with the center 75% of fund holdings plotted as the Morningstar Ownership Zone™. The Morningstar Style Box is designed to reveal a fund’s investment strategy. The Morningstar Ownership Zone provides detail about a portfolio’s investment style by showing the range of stock sizes and styles. The Ownership Zone is derived by plotting each stock in the portfolio within the proprietary Morningstar Style Box. Over time, the shape and location of a fund's ownership zone may vary. See page 134 for additional information. |

Value of $10,000

| Top 10 Positions | ||

| % of Net Assets | ||

| FirstService Corporation | 2.9 | |

| E-L Financial | 2.6 | |

| Popular | 2.5 | |

| First Citizens BancShares Cl. A | 2.5 | |

| Ares Management L.P. | 2.3 | |

| MBIA | 2.0 | |

| BOK Financial | 2.0 | |

| Ashmore Group | 2.0 | |

| SEI Investments | 2.0 | |

| First Republic Bank | 1.9 | |

| Portfolio Industry Breakdown | ||

| % of Net Assets (Subject to Change) | ||

| Capital Markets | 49.5 | |

| Banks | 14.7 | |

| Insurance | 6.2 | |

| Real Estate Management & Development | 4.8 | |

| IT Services | 3.6 | |

| Software | 2.4 | |

| Professional Services | 2.0 | |

| Investment Companies | 1.8 | |

| Metals & Mining | 1.8 | |

| Thrifts & Mortgage Finance | 1.5 | |

| Marine | 1.2 | |

| Trading Companies & Distributors | 1.0 | |

| Diversified Financial Services | 0.5 | |

| Hotels, Restaurants & Leisure | 0.2 | |

| Internet Software & Services | 0.0 | |

| Miscellaneous | 4.5 | |

| Cash and Cash Equivalents | 4.3 | |

| Upside/Downside Capture Ratios | ||||

| Periods Ended 12/31/16 (%) | ||||

| UPSIDE | DOWNSIDE | |||

| 10-Year | 83 | 90 | ||

| Fund’s First Full Quarter (12/31/03) | 85 | 81 | ||

| Calendar Year Total Returns (%) | ||

| YEAR | RFS | |

| 2016 | 12.9 | |

| 2015 | -4.7 | |

| 2014 | 3.5 | |

| 2013 | 42.0 | |

| 2012 | 20.7 | |

| 2011 | -11.3 | |

| 2010 | 18.5 | |

| 2009 | 32.1 | |

| 2008 | -35.4 | |

| 2007 | -4.7 | |

| 2006 | 24.8 | |

| 2005 | 12.2 | |

| 2004 | 15.1 | |

| Portfolio Country Breakdown1,2 | ||

| % of Net Assets | ||

| United States | 53.6 | |

| Canada | 13.7 | |

| United Kingdom | 9.7 | |

| Singapore | 3.1 | |

| Switzerland | 2.3 | |

| South Africa | 1.9 | |

| Hong Kong | 1.5 | |

| 1 | Represents countries that are 1.5% or more of net assets. |

| 2 | Securities are categorized by the country of their headquarters. |

| Portfolio Diagnostics | ||

| Fund Net Assets | $50 million | |

| Number of Holdings | 96 | |

| Turnover Rate | 37% | |

| Average Market Capitalization1 | $2,006 million | |

| Weighted Average P/E Ratio2,3 | 20.2x | |

| Weighted Average P/B Ratio2 | 2.0x | |

| Active Share4 | 99% | |

| 1 | Geometric Average. This weighted calculation uses each portfolio holding’s market cap in a way designed to not skew the effect of very large or small holdings; instead, it aims to better identify the portfolio’s center, which Royce believes offers a more accurate measure of average market cap than a simple mean or median. |

| 2 | Harmonic Average. This weighted calculation evaluates a portfolio as if it were a single stock and measures it overall. It compares the total market value of the portfolio to the portfolio’s share in the earnings or book value, as the case may be, of its underlying stocks. |

| 3 | The Fund’s P/E ratio calculation excludes companies with zero or negative earnings (11% of portfolio holdings as of 12/31/16). |

| 4 | Active Share is the sum of the absolute values of the different weightings of each holding in the Fund versus each holding in the benchmark, divided by two. |

| Important Performance and Expense Information All performance information in this Report reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Shares redeemed within 30 days of purchase may be subject to a 1% redemption fee payable to the Fund, which is not reflected in the performance shown above; if it were, performance would be lower. Current month-end performance may be higher or lower than performance quoted and may be obtained at www.roycefunds.com. Gross operating expenses reflect the Fund’s gross total annual operating expenses for the Service Class and include management fees, 12b-1 distribution and service fees, other expenses and acquired fund fees and expenses. Net operating expenses reflect contractual fee waivers and/or expense reimbursements. All expense information is reported as of the Fund’s most current prospectus. Royce & Associates has contractually agreed to waive fees and/or reimburse expenses to the extent necessary to maintain the Fund’s net annual operating expenses, (excluding brokerage commissions, taxes, interest, litigation expenses, acquired fund fees and expenses, and other expenses not borne in the ordinary course of business), at or below 1.49% through April 30, 2017. Acquired fund fees and expenses reflect the estimated amount of the fees and expenses incurred indirectly by the Fund through its investments in mutual funds, hedge funds, private equity funds, and other investment companies. Regarding the “Top Contributors” and “Top Detractors” tables shown above, the sum of all contributors to, and all detractors from, performance for all securities in the portfolio would approximate the Fund’s year-to-date performance for 2016. Upside Capture Ratio measures a manager’s performance in up markets relative to the Fund’s benchmark. It is calculated by measuring the Fund’s performance in quarters when the benchmark went up and dividing it by the benchmark’s return in those quarters. Downside Capture Ratio measures a manager’s performance in down markets relative to the Fund’s benchmark (Russell 2000). It is calculated by measuring the Fund’s performance in quarters when the benchmark goes down and dividing it by the benchmark’s return in those quarters. |

| The Royce Funds 2016 Annual Report to Shareholders | 11 |

| MANAGER’S DISCUSSION | ||

| Royce Heritage Fund (RHF) |

|

| Steven McBoyle, CPA, CA |

| FUND PERFORMANCE Royce Heritage Fund increased 17.8% versus a gain of 21.3% for its small-cap benchmark, the Russell 2000 Index, for the same period. Despite trailing the small-cap index, we were pleased with the Fund’s absolute performance. The portfolio’s weighted average market cap has moved up over the last few years—it stood at $4.3 billion at year-end, $3.6 billion at the end of 2015, and $2.9 billion at the end of 2014—embracing more fully its ability to invest in both small- and mid-cap stocks that meet our exacting criteria for high quality and attractive valuation. In this light, it is worth noting that the smid-cap Russell 2500 Index gained 17.6% in 2016 and also trailed the small-cap index. In addition, the market saw three reversals that we think bode well for the Fund and active management: Small-caps had positive returns, value recaptured leadership from growth, and cyclical stocks beat their defensive counterparts. During the first half of 2016, Heritage advanced 5.3%, ahead of the 2.2% increase for the Russell 2000. The second half of the year was more rewarding on an absolute basis though less so on a relative scale. The Fund advanced 11.9% in the second half of 2016 compared to 18.7% for the benchmark. Turning to longer-term spans, Heritage outperformed the small-cap index for the 20-year and since inception (12/27/95) periods ended December 31, 2016. The Fund’s average annual total return since inception was 12.3%. |

| WHAT WORKED... AND WHAT DIDN’T |

| Of the Fund’s 10 equity sectors, seven finished the year with net contributions. Its two largest, Industrials and Consumer Discretionary, also made the biggest positive impact on performance. Of the three sectors that detracted—Real Estate, Health Care, and Energy—only the first had a meaningful negative impact, and the portfolio was significantly underweighted in each throughout 2016. At the industry level, auto components (Consumer Discretionary) had by far the greatest positive effect on returns, led by top-15 holding and significant contributor LCI Industries, while chemicals (Materials) also made a notable positive impact. The effect of detracting industries was more modest, led by real estate management & development (Real Estate) and capital markets (Financials). The first industry was home to three of the Fund’s five top detracting positions. |

| The top contributor at the position level was recreational vehicle (RV) maker Thor Industries, the largest manufacturer in its industry and one of three stocks in the top five from the Consumer Discretionary sector. Thor benefited from numerous advantageous developments during the year, including its acquisition of Jayco, which bolstered Thor’s leading market position in low-end towable RVs, its fastest-growing sector. Robust growth in orders from both retail and dealer sources, the growing popularity of RVs, and favorable consumer financing all helped its shares to accelerate. Minerals Technologies produces performance-enhancing minerals, as well as mineral-based and synthetic mineral products. Its stock appreciated through much of the year before spiking after the election. We think the company has done an excellent job improving underperforming operations and maintaining margins in key divisions where organic growth has been modest due to macroeconomic factors. It also continues executing a material penetration opportunity in China of precipitated calcium carbonate (PCC) in paper production, an opportunity that remains large and has been gaining traction generating ample free cash flow. |

| Of those positions that detracted, we sold our shares of Signet Jewelers in June before reinitiating a position in November. The company, which operates the Jared, Kay, and Zales chains, was hurt earlier in the year by financing concerns that were followed by allegations of precious stone-swapping by its employees. Jones Lang LaSalle, which provides real estate brokerage and property management services, continues to execute well. However, a deceleration in commercial real estate transaction volumes and a material reset in capital markets fee streams caused an adjustment to certain fundamentals. We reduced our position during the year. |

| Relative to the Russell 2000, the Fund was hurt most by its underweight in banks and poor stock selection in capital markets, both of which led Financials to lag considerably. Stock selection challenges also had a meaningful impact in the aforementioned real estate management & development group. In addition, the Fund’s large cash position affected relative results. Conversely, stock selection was a relative strength in Consumer Discretionary, thanks in large part to LCI Industries and Standard Motor Products. We also benefited from having limited exposure to Health Care, which was the only Russell 2000 sector to decline in 2016. |

| Top Contributors to Performance For 2016 (%)1 | |||

| Thor Industries | 1.69 | ||

| Minerals Technologies | 1.43 | ||

| LCI Industries | 1.30 | ||

| Copart | 1.17 | ||

| Standard Motor Products | 1.04 | ||

| 1 Includes dividends | |||

| Top Detractors from Performance For 2016 (%)2 | |||

| Signet Jewelers | -0.67 | ||

| Jones Lang LaSalle | -0.47 | ||

| Kennedy Wilson Europe Real Estate | -0.43 | ||

| Anixter International | -0.35 | ||

| Kennedy-Wilson Holdings | -0.29 | ||

| 2 Net of dividends | |||

| CURRENT POSITIONING AND OUTLOOK |

| The politically driven fourth quarter of 2016 notwithstanding, we continue to anticipate lower returns, higher volatility, and lower correlation levels. Evidence is building that a normalization in the markets is taking place, which should make them far more discriminating. For these reasons, we believe our bottom-up, quality-oriented process has the potential to do well. During 2016 we continued to reduce the number of names in the portfolio while raising cash, particularly in the fourth quarter, by selling holdings that had exceeded their reward targets. Portfolio positioning has otherwise remained largely intact. |

| 12 | The Royce Funds 2016 Annual Report to Shareholders |

| PERFORMANCE AND PORTFOLIO REVIEW | TICKER SYMBOLS RGFAX RHFHX RYGCX RHFRX |

| Performance and Expenses | ||||||||||||||||

| Average Annual Total Return (%) Through 12/31/16 | ||||||||||||||||

| JUL-DEC 20161 | 1-YR | 3-YR | 5-YR | 10-YR | 15-YR | 20-YR | SINCE INCEPTION (12/27/95) | |||||||||

| RHF | 11.91 | 17.84 | 2.88 | 9.41 | 5.91 | 8.04 | 11.72 | 12.35 | ||||||||

| Annual Operating Expenses: 1.37% | ||||||||||||||||

| 1 Not Annualized | ||||||||||||||||

Relative Returns: Monthly Rolling Average Annual Return Periods

| On a monthly rolling basis, the Fund outperformed the Russell 2000 in 87% of all 10-year periods; 80% of all 5-year periods; and 62% of all 1-year periods. |

| PERIODS BEATING THE INDEX | FUND AVG (%)1 | INDEX AVG (%)1 | ||||||||||||

| 10-year | 105/121 | 87% | 10.0 | 6.9 | ||||||||||

| 5-year | 145/181 | 80% | 10.7 | 7.6 | ||||||||||

| 1-year | 142/229 | 62% | 13.3 | 9.2 | ||||||||||

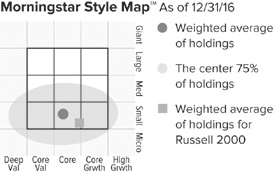

The Morningstar Style Map is the Morningstar Style Box™ with the center 75% of fund holdings plotted as the Morningstar Ownership Zone™. The Morningstar Style Box is designed to reveal a fund’s investment strategy. The Morningstar Ownership Zone provides detail about a portfolio’s investment style by showing the range of stock sizes and styles. The Ownership Zone is derived by plotting each stock in the portfolio within the proprietary Morningstar Style Box. Over time, the shape and location of a fund's ownership zone may vary. See page 134 for additional information. |

Invested on 12/27/95 as of 12/31/16 ($)

| Top 10 Positions | ||

| % of Net Assets | ||

| Alleghany Corporation | 3.0 | |

| Thor Industries | 2.8 | |

| Copart | 2.8 | |

| Westlake Chemical | 2.6 | |

| Standard Motor Products | 2.5 | |

| LKQ Corporation | 2.4 | |

| Gentex Corporation | 2.2 | |

| ManpowerGroup | 2.1 | |

| Hubbell Cl. B | 2.1 | |

| Kirby Corporation | 1.9 | |

| Portfolio Sector Breakdown | ||

| % of Net Assets | ||

| Consumer Discretionary | 25.4 | |

| Industrials | 21.6 | |

| Materials | 9.5 | |

| Financials | 7.2 | |

| Information Technology | 6.3 | |

| Real Estate | 4.7 | |

| Utilities | 1.8 | |

| Health Care | 1.1 | |

| Consumer Staples | 0.3 | |

| Miscellaneous | 2.1 | |

| Cash and Cash Equivalents | 20.0 | |

| Calendar Year Total Returns (%) | ||

| YEAR | RHF | |

| 2016 | 17.8 | |

| 2015 | -6.5 | |

| 2014 | -1.1 | |

| 2013 | 26.0 | |

| 2012 | 14.3 | |

| 2011 | -9.3 | |

| 2010 | 27.5 | |

| 2009 | 51.8 | |

| 2008 | -36.2 | |

| 2007 | 1.2 | |

| 2006 | 22.6 | |

| 2005 | 8.7 | |

| 2004 | 20.4 | |

| 2003 | 38.1 | |

| 2002 | -18.9 | |

| Upside/Downside Capture Ratios | ||||||||||||||

| Periods Ended 12/31/16 (%) | ||||||||||||||

| UPSIDE | DOWNSIDE | |||||||||||||

| 10-Year | 90 | 93 | ||||||||||||

| From 12/31/95 (Start of Fund’s First Full Quarter) | 108 | 87 | ||||||||||||

| Portfolio Diagnostics | ||

| Fund Net Assets | $226 million | |

| Number of Holdings | 77 | |

| Turnover Rate | 67% | |

| Average Market Capitalization1 | $4,311 million | |

| Weighted Average P/E Ratio2,3 | 20.2x | |

| Weighted Average P/B Ratio2 | 2.6x | |

| Active Share4 | 98% | |

| U.S. Investments (% of Net Assets) | 73.7% | |

| Non-U.S. Investments (% of Net Assets) | 6.3% | |

| 1 | Geometric Average. This weighted calculation uses each portfolio holding’s market cap in a way designed to not skew the effect of very large or small holdings; instead, it aims to better identify the portfolio’s center, which Royce believes offers a more accurate measure of average market cap than a simple mean or median. |

| 2 | Harmonic Average. This weighted calculation evaluates a portfolio as if it were a single stock and measures it overall. It compares the total market value of the portfolio to the portfolio’s share in the earnings or book value, as the case may be, of its underlying stocks. |

| 3 | The Fund’s P/E ratio calculation excludes companies with zero or negative earnings (2% of portfolio holdings as of 12/31/16). |

| 4 | Active Share is the sum of the absolute values of the different weightings of each holding in the Fund versus each holding in the benchmark, divided by two. |

| Important Performance and Expense Information |

All performance information in this Report reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Shares redeemed within 30 days of purchase may be subject to a 1% redemption fee payable to the Fund, which is not reflected in the performance shown above; if it were, performance would be lower. Current month-end performance may be higher or lower than performance quoted and may be obtained at www.roycefunds.com. All performance and risk information reflects results of the Service Class (its oldest class). Price and total return information is based on net asset values calculated for shareholder transactions. Operating expenses reflect the Fund’s total annual operating expenses for the Service Class as of the Fund’s most current prospectus and include management fees, 12b-1 distribution and service fees, other expenses, and acquired fund fees and expenses. Acquired fund fees and expenses reflect the estimated amount of the fees and expenses incurred indirectly by the Fund through its investments in mutual funds, hedge funds, private equity funds, and other investment companies. Regarding the “Top Contributors” and “Top Detractors” tables shown above, the sum of all contributors to, and all detractors from, performance for all securities in the portfolio would approximate the Fund’s year-to-date performance for 2016. Upside Capture Ratio measures a manager’s performance in up markets relative to the Fund’s benchmark. It is calculated by measuring the Fund’s performance in quarters when the benchmark went up and dividing it by the benchmark’s return in those quarters. Downside Capture Ratio measures a manager’s performance in down markets relative to the Fund’s benchmark (Russell 2000). It is calculated by measuring the Fund’s performance in quarters when the benchmark goes down and dividing it by the benchmark’s return in those quarters. |

| The Royce Funds 2016 Annual Report to Shareholders | 13 |

| MANAGERS’ DISCUSSION | ||

| Royce International Micro-Cap Fund (RMI) |

|

| Jim Harvey, CFA Dilip Badlani, CFA |

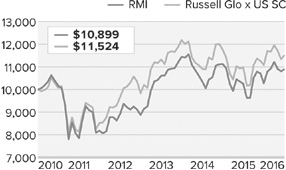

| FUND PERFORMANCE Royce International Micro-Cap Fund advanced 6.3% in 2016, outperforming its benchmark, the Russell Global ex-U.S. Small Cap Index, which was up 5.0% for the same period. We were pleased that this solid performance came in the context of sector results that were choppier than those of domestic micro-caps, with the benchmark’s two cyclical, commodity-based sectors, Energy and Materials, doing best, followed by strong results for defensive Utilities. This stood in sharp contrast to the U.S. small- and micro-cap markets, in which cyclical leadership was more pronounced. During the first half of the calendar year, the Fund gained 0.2% versus 1.0% for its benchmark. The second half was more of a tale of two quarters. The third quarter saw International Micro-Cap advance 9.2% versus 7.9% for the benchmark as many stocks rebounded following the Brexit vote. During the fourth quarter, however, most international small- and micro-caps declined. The Fund fell 2.8% compared to a decline of 3.6% for the Russell Global ex-U.S. Small Cap. A lot of this was due to currency effects as the growing strength of the U.S. dollar affected holdings based in the U.K., where the British pound declined significantly in 2016. |

| WHAT WORKED... AND WHAT DIDN’T |

| Five of the portfolio’s nine equity sectors made contributions to 2016 performance, led by Information Technology and Consumer Discretionary. Detractors made a far lower impact and were led by Energy (the best-performing sector in the benchmark) and Consumer Staples. The leading industries by contribution were media (Consumer Discretionary), semiconductors & semiconductor equipment (Information Technology), and metals & mining (Materials). As with sectors, detracting industries had much less of an effect on results, with oil, gas & consumable fuels (Energy), commercial services & supplies, and building products (both from Industrials) the leaders. |

| The Fund’s top contributor at the position level was Brazil’s T4F Entretenimento. The company operates at multiple levels of the entertainment industry, including venue operation, ticketing, food & beverage, merchandise sales, and corporate sponsorships. T4F participated in a strong rally that saw Brazilian small-caps rise approximately 60% in 2016. After a few difficult years in which profitability suffered from heightened competition, T4F increased its profits for the second consecutive year. We reduced our stake as its shares climbed. Manappuram Finance, one of India’s leading Non-Bank Financial Companies (NBFC), has been enjoying robust market conditions for its specialized lending focus which offers loans against gold collateral. A stable gold market coupled with healthy demand helped Manappuram to continue its mid-double-digit growth rate. We sold the last of our shares in October. Imdex is an Australian company with a global business providing drilling fluids and leading downhole instrumentation to the mining, water well, and civil engineering industries. A summer earnings announcement showed stable profitability and offered a more favorable outlook boosted by the company shedding an unprofitable business segment. The combination helped to send shares soaring between June and year-end. |

| Turning to detractors, Banca Sistema is an Italian bank specializing in financing and managing trade receivables owed by the Italian Public Administrations. Despite its unique business model and attractive growth profile, it was initially caught up in the widespread downdraft for Italian banks, considered one of the more vulnerable areas of European finance in the aftermath of Brexit. However, the company continued to execute effectively and delivered strong earnings growth. We think that it is well positioned to take advantage of the large opportunity set in front of it. We also held shares of Ardmore Shipping, which owns and operates shipping tankers, primarily for chemicals. With shipping index volumes bouncing along all-time lows during the first half of the year, its stock was not spared. However, the fact that it was trading at about half its book value or lower through most of the second half made it worth holding as we await a recovery for its industry. Zealand Pharma is a Danish biotechnology company whose share price decline was mostly driven by the sell-off in its industry. Seeing what we thought was better value elsewhere, we sold the last of our shares in May. |

| Companies headquartered in Canada and Australia had the largest positive impact on performance while those based in the U.K. and Italy detracted most. Relative to its benchmark, the Fund had significant stock selection advantages in Consumer Discretionary, especially in the media industry, and Information Technology. Conversely poor stock picks in oil, gas & consumable fuels hurt relative performance, as did our substantial underweight in the Materials sector. |

| Top Contributors to Performance For 2016 (%)1 | |||

| T4F Entretenimento | 1.00 | ||

| Manappuram Finance | 0.89 | ||

| Imdex | 0.59 | ||

| Morneau Shepell | 0.56 | ||

| I.T | 0.46 | ||

| 1 Includes dividends | |||

| Top Detractors from Performance For 2016 (%)2 | |||

| Banca Sistema | -0.65 | ||

| Ardmore Shipping | -0.46 | ||

| Zealand Pharma | -0.45 | ||

| GCA | -0.37 | ||

| Pendragon | -0.34 | ||

| 2 Net of dividends | |||

| CURRENT POSITIONING AND OUTLOOK |

| We continue to find attractive opportunities in international micro-cap companies as valuations in many parts of the world remain compelling to us. With three times as many small- and micro-cap companies headquartered outside the U.S., we continue to see ample opportunity to uncover well-run, underfollowed micro-cap companies trading at attractive valuations. Of our four largest sectors at year-end—three were overweighted versus the benchmark, Information Technology, Industrials, and Consumer Discretionary. |

| 14 | The Royce Funds 2016 Annual Report to Shareholders |

| PERFORMANCE AND PORTFOLIO REVIEW | TICKER SYMBOL ROIMX |

| Performance and Expenses | ||||||||||||

| Average Annual Total Return (%) Through 12/31/16 | ||||||||||||

| JUL-DEC 20161 | 1-YR | 3-YR | 5-YR | SINCE INCEPTION (12/31/10) | ||||||||

| RMI | 6.11 | 6.33 | 0.92 | 6.79 | 1.45 | |||||||

| Annual Gross Operating Expenses: 3.11% Annual Net Operating Expenses: 1.64% | ||||||||||||

| 1 Not Annualized | ||||||||||||