UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-03599

Name of Registrant: The Royce Fund

Address of Registrant: 745 Fifth Avenue

New York, NY 10151

| Name and address of agent for service: | John E. Denneen, Esquire 745 Fifth Avenue New York, NY 10151 |

Registrant’s telephone number, including area code: (212) 508-4500

Date of fiscal year end: December 31

Date of reporting period: January 1, 2019 - December 31, 2019

1

Item 1. Reports to Shareholders.

The Royce Funds 2019 Annual

Review and Report to Shareholders

December 31, 2019

Royce Dividend Value Fund

Royce Global Financial Services Fund

Royce International Premier Fund

Royce Micro-Cap Fund

Royce Opportunity Fund

Royce Pennsylvania Mutual Fund

Royce Premier Fund

Royce Small-Cap Value Fund

Royce Smaller-Companies Growth Fund

Royce Special Equity Fund

Royce Total Return Fund

Beginning on January 1, 2021, as permitted by regulations adopted by the U.S. Securities and Exchange Commission, paper copies of the Funds’ shareholder reports like this one will no longer be sent by mail, unless you specifically request paper copies of the reports from the Funds or from your financial intermediary (such as a broker-dealer or bank). Instead, the reports will be made available on the Funds’ website (www.royceinvest.com), and you will be notified by mail each time a report is posted and provided with a website link to access the report. If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Funds electronically anytime by contacting your financial intermediary or, if you are a direct investor with the Funds, by calling 1-800-841-1180. Beginning on January 1, 2019, you may elect to receive all future reports in paper free of charge. If you invest through a financial intermediary, you can contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. If you invest directly with the Funds, you can call 1-800-841-1180 to let the Funds know you wish to continue receiving paper copies of your shareholder reports. Your election to receive reports in paper will apply to all Funds held in your account if you invest through your financial intermediary or all Funds held with our fund complex if you invest directly with the Funds.

Table of Contents

This page is not part of theThe Royce Funds 2019 Annual Report to Shareholders | 1

A BIG YEAR FOR STOCKS

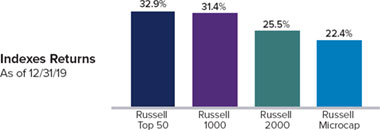

Aperiod of pauses, pivots, and rallies, 2019 ended as a highly rewarding year for equities. The major domestic and international indexes posted healthy double-digit returns, most in the range of 20-35%. The small-cap Russell 2000 Index gained 25.5% while the Russell Top 50 Mega Cap Index advanced 32.9%, the large-cap Russell 1000 Index was up 31.4%, and the Russell Microcap Index increased 22.4%—generally, bigger was better in 2019. Still, the 25.5% gain for the Russell 2000 placed it in the index’s top 27% of calendar-year showings since its 1978 inception. The advance was also impressively broad, with 70% of the stocks in the small-cap index posting positive returns, 61% advancing at least 10%, and 49% posting a calendar-year gain of 20% or more. Additionally, 10 of 11 Russell 2000 sectors were positive for the year (Energy was the sole detractor).

Although many investors think that some event, or series of events, must be present to propel share prices, there are times when the absence of negative developments is more than enough to push stocks consistently upward. This was the case in 2019, when both a

recession and a more hawkish Fed failed to materialize, which was all it took to kick-start the recovery that succeeded the dramatic downturn that saw out 2018. The Fed’s course was especially interesting. Arguably out of touch with the anxieties bred by slipping oil prices and an inverted yield curve in December 2018, the Fed raised rates and announced that 2019 would likely see at least two more hikes—all of this based on the central bank’s cautiously optimistic outlook on the U.S. economy. Once the market’s plunge showed that investors did not share this view, the Fed paused, saying it would hold the line on rates. The central bank then pivoted in July 2019, reversing course by lowering rates—which it proceeded to do again in September and October. These cuts fueled a healthy fourth quarter and helped stocks to end the year on a decidedly upbeat note.

WHAT WILL FOLLOW MEGA-CAP MANIA?

Performance in 2019 was mostly in line with previous snapbacks off precipitous declines—biotech, software, and other growth stocks were among those that did best, along with non-dividend payers and companies with high debt. The somewhat peculiar exception to the pattern was large-cap outperformance. In high-octane markets such as what we saw in 2019, small-cap stocks have typically contended with few, if any, competitors for leadership. This pattern was undone by the ongoing leadership of mega-cap stocks—including the now familiar “FAANG” group of Facebook, Apple, Amazon, Netflix, and Google—which have led the market by a substantial margin over the last 18 months. For example, from 6/30/18-12/31/19, the Russell

2 | This page is not part of theThe Royce Funds2019 Annual Report to Shareholders

LETTER TO OUR SHAREHOLDERS

Top 50 Index advanced 26.1% cumulatively compared with a paltry 3.7% gain for small-caps—and a decline of 3.9% for micro-caps.

If the dominance of mega-caps were to unwind, or even pause, we see the potential for a subsequent rotation to small-caps. We think one point effectively illustrates the size of the potential opportunity: over the last 20 years, the 50 biggest stocks in the Russell 3000 Index have averaged a combined total market cap of about four times the total market cap of the Russell 2000. At the end of 2019, however, that ratio was more than six times, which is higher than it was even at the height of the Internet bubble in 2000. We’re certainly not expecting mega-caps to collapse any time soon, which would be anomalous behavior in what we think will be an advancing market. But we do think a performance pause at their current high valuations could occur, allowing small- and micro-cap stocks to catch up.

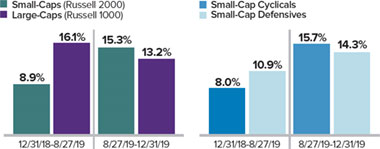

We may have seen the first seeds of such a leadership reversal in the last four months of 2019, which from our perspective provided the year’s most compelling developments. Beginning on August 27th, several reversals inverted previous market leadership patterns, each of which held through the end of 2019: small-caps outpaced large-caps, cyclicals outperformed defensives, small-cap value beat small-cap growth, and micro-caps led domestic equity performance. What was of particular interest to us about these reversals was their simultaneity. Leadership rotation is common, but the changes typically emerge over longer stretches of time before they take root.

August’s Reversals Held

Late August Saw Key Market Shifts That Held Through The End Of 2019

Equally important, we would also argue that valuations—both relative and absolute—must be kept in mind when looking at returns. In spite of the performance boosts that came with the late August reversals, relative valuations for small-cap versus large-cap, small-cap cyclicals versus small-cap defensives, and small-cap value versus small-cap growth still looked attractive to us. At the end of 2019, each remained near the 20-year lows they hit in late August.

Small-Cap’s Relative Valuation Is Below Its Long-Term Average

Russell 2000 vs. Russell 1000 Median LTM EV/EBIT¹ (ex. Negative EBIT Companies) from 12/31/01 to 12/31/19

1Earnings before interest and taxes. Source: FactSet

As the chart above shows, small-cap stocks have lagged large-caps for so long that they were relatively cheaper at the end of 2019 than at any other time since 2001 based on our favorite valuation metric, EV/EBIT, (enterprise value over earnings before interest and taxes).

BEWARE OF THE CALENDAR

When thinking about the prospects for small-cap performance, we think it’s important to avoid a common pitfall that we all stumble into occasionally—the tendency to put more emphasis on year-end results than on other month-end periods. From the vantage point of the calendar year, small-cap performance certainly looks good. But if we look at the two-year annualized return for the Russell 2000, we see a markedly lower gain of 5.7%. Moreover, three- and five-year annualized returns for the Russell 2000 were below their respective monthly rolling averages since inception (12/31/78) at the end of 2019.

Recent 3- and 5-Year Returns Lower Than History

Russell 2000 Average Annual Total Returns vs. Long-Term Rolling Monthly Averages as of 12/31/19

Finally, the Russell 2000 finished 2019 2.2% off its most recent peak—and all-time high—reached on 8/31/18. What do these observations of historical performance suggest? Taken together, we think they suggest that, despite 2019’s strong calendar-year return, caution or pessimism about future small-cap returns and opportunities may be misplaced.

This page is not part of theThe Royce Funds2019 Annual Report to Shareholders | 3

LETTER TO OUR SHAREHOLDERS

THE CASE FOR SMALL-CAP CYCLICALS

To be sure, we believe that small-cap stocks are more than capable of a strong run in 2020—and certainly resumed market leadership could be part of the equation. Even after a terrific 2019, many small-caps are still carrying what we would call a recession discount from the deep downturn at the end of 2018. Small-cap cyclicals continued to trade at a significant valuation discount to defensives at the end of 2019—based on EV/EBIT. In fact, the spread was wider than it was in October 2008, when a recession was exacerbated by the Great Financial Crisis.

These historically low relative valuations offer support for our view that late August’s performance reversals can be sustained in 2020. This confidence has led us to be active buyers in areas as diverse as energy services; healthcare devices, diagnostics, and testing; paper & packaging; semiconductors & semiconductor equipment; chemicals; and consumer finance.

Small-Cap Cyclicals Are Relatively Cheaper Than in 2008

Russell 2000 Relative Median EV/EBIT (Ex Negative EBIT) From 12/31/99 to 12/31/19

Small-caps have also historically outpaced large-caps when the economy is growing and have lagged when it’s contracting. They have beaten large-caps, for example, in 70% of all trailing monthly rolling one-year periods—74 out of 106—when the ISM PMI rose over the last 20 years.1 This dynamic holds true for cyclicals versus defensives as well. So if the most recent slowdown is behind us, and the global economy is gradually improving (which appears to be the case), then renewed expansion supports a continuation of August’s reversals.

THE GLOBAL SMALL-CAP SCENE

Our confidence for small-cap extends beyond our borders. Japan has shown intermittent but promising signs of renewed growth, as had

1The ISM PMI rose in 106 of 229 periods.

China prior to the outbreak of the coronavirus. Europe, particularly Germany, has been caught in the middle of the U.S.-China trade and tariff disputes given its more export-driven economies. It was also slowed by the protracted uncertainty over Brexit. Yet December showed marginal improvements through much of Europe, including upticks in business confidence and retail sales, which indicate that the global economy has bottomed—it grew by about 2% in 2019. If it were to begin rebounding towards the 20-year average annual nominal GDP rate of around 5%—a not unreasonable expectation, we think—then that should create tailwinds to sustain small-cap cyclicals.

Also worth noting is that the cumulative two-year return for non-U.S. small-caps, as measured by the MSCI ACWI ex USA Small Cap Index, was essentially flat, up just 0.1%. Over this same period, however, earnings have been growing at a healthy clip, suggesting that returns can narrow this gap. We think that the combination of attractive valuations for cyclicals, a strengthening global economy, and the flat two-year return imply that the next few years are likely to be at least as good for international small-caps as the last few—and quite possibly better.

Of course, our greatest source of confidence is not macroeconomic analysis or the examination of long-term performance patterns (though they certainly help)—it comes from our own research into companies and industries as well as the numerous conversations we have with small-cap management teams. Much to our satisfaction, most of the management teams we’ve been meeting with report that they are hiring or holding steady and seeing little if any contraction in their orders or demand.

GOOD-BYE TO ALL THAT?

2019 closes out one of the most interesting—and challenging—decades that we have seen in more than 45 years of managing small-cap portfolios. It was a decade in which financial assets performed far better than the economy did—mostly due to frequent central bank interventions that suppressed rates and kept the capital markets flush with liquidity. We also saw developments that we would never have thought possible, such as negative interest rates. In addition, years of highly accommodative monetary policy had the unintended consequence of creating few, if any, penalties for companies that borrowed extensively.

4 | This page is not part of theThe Royce Funds2019 Annual Report to Shareholders

LETTER TO OUR SHAREHOLDERS

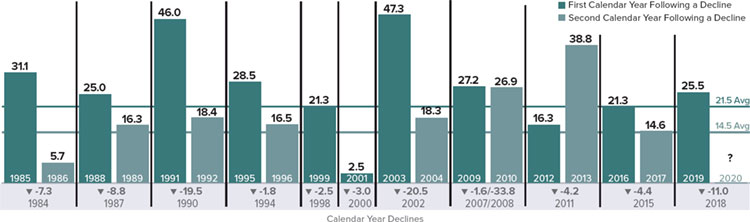

Does the Small-Cap Recovery Have Room to Run?

Russell 2000 Declines and Two Subsequent Calendar Year’s Performance from 12/31/78 through 12/31/19 (%)

Past performance is no guarantee of future results.

We anticipate that each of these unusual developments should unwind to some extent over the next decade. This makes us highly confident about the prospects for select small-caps, particularly in cyclical areas, that haven’t fully participated in the decade that just passed. However, the persistence of these peculiar developments has thrown up numerous road blocks on the road back to normalization. (Indeed, one thing that has not changed over the last 10 years is the humbling nature of the prediction business.)

The question is whether or not the last decade-plus (stretching back to the 2007 market peaks and the Great Financial Crisis of 2008) of slow growth, historically low rates, and regular central bank interventions represents a “New Normal.” While our initial contention was that it did not, we now suspect that we will arrive at a blend of the old and the new. As Mark Twain is said to have quipped, “History doesn’t repeat itself, but it often rhymes.” Perhaps, then, this will result in a series of lows—low rates, low inflation, and low (by which we mean slow) economic growth—which will translate into lower U.S. equity returns than what we have seen over the last decade, along with more frequent bouts of volatility and wider variations in stock returns. While this menu may seem unpalatable, periods with more modest performance have historically been very favorable for disciplined active management approaches.

FAVORABLE CONDITIONS FOR SMALL-CAPS

The current backdrop looks quite promising to us for solid to strong small-cap performance overall thanks to the four favorable factors that we cited in July’s “Letter to Our Shareholders”—low inflation, modest valuations, moderate growth, and ample access to capital. Together, they suggest that small-cap returns can go higher, especially the many small-cap cyclical areas that we typically like best. A few historical factors are also worth noting. Over the past 30 years, 76% of all monthly rolling one-year returns for the Russell 2000 have been positive—with an average return of 11.5%. So investors who are bearish on small-cap stocks are betting against the odds. To get a firmer sense of what 2020 may hold, we went back to the inception of the Russell 2000 and looked at the 11 calendar years when small-caps declined, as in 2018, and examined what happened in the second subsequent year. In nine of those 11 years the small-cap index advanced by an average of 14.5%. (2000 and 2002 were the exceptions.)

And two consecutive years of double-digit increases are fairly common for small-caps. Periods in which a healthy second year followed a strong one occurred in the following two-year spans: 1988-89, 1991-92, 1995-96, 2003-04, 2009-10, 2012-13, and 2016-17. With the favorable conditions we’ve outlined above in mind, we suspect that the current small-cap rally can continue, with the potential to add 2019-20 to this list.

| Sincerely, | ||

|  |  |

| Charles M. Royce | Christopher D. Clark | Francis D. Gannon |

| Chairman, | Chief Executive Officer, and | Co-Chief Investment Officer, |

| Royce Investment Partners | Co-Chief Investment Officer, | Royce Investment Partners |

| Royce Investment Partners | ||

| January 31, 2020 |

This page is not part of theThe Royce Funds 2019 Annual Report to Shareholders | 5

Performance and Expenses

| ANNUAL OPERATING EXPENSES (%) | ||||||||||

| 45-YR/SINCE | INCEPTION | |||||||||

| 1-YR | 3-YR | 5-YR | 10-YR | 15-YR | 20-YR | INCEPTION | DATE | GROSS | NET | |

| Royce Dividend Value Fund | 29.78 | 9.76 | 7.73 | 10.43 | 8.22 | N/A | 8.71 | 5/3/04 | 1.43 | 1.34 |

| Royce Global Financial Services Fund | 24.17 | 9.60 | 7.22 | 10.20 | 7.62 | N/A | 8.07 | 12/31/03 | 1.77 | 1.58 |

| Royce International Premier Fund | 34.22 | 17.86 | 13.49 | N/A | N/A | N/A | 8.59 | 12/31/10 | 1.59 | 1.44 |

| Royce Micro-Cap Fund | 21.16 | 5.17 | 3.84 | 5.66 | 5.79 | 8.51 | 10.40 | 12/31/91 | 1.25 | 1.24 |

| Royce Opportunity Fund | 28.21 | 7.74 | 7.02 | 11.09 | 7.77 | 10.43 | 11.68 | 11/19/96 | 1.20 | 1.20 |

| Royce Pennsylvania Mutual Fund | 26.56 | 9.95 | 8.28 | 10.52 | 8.08 | 10.12 | 15.37 | N/A | 0.92 | 0.92 |

| Royce Premier Fund | 34.13 | 14.15 | 10.52 | 11.30 | 9.69 | 11.01 | 11.77 | 12/31/91 | 1.17 | 1.17 |

| Royce Small-Cap Value Fund | 18.21 | 4.92 | 4.35 | 7.20 | 6.87 | N/A | 9.06 | 6/14/01 | 1.53 | 1.49 |

| Royce Smaller-Companies Growth Fund | 23.67 | 9.36 | 7.03 | 9.16 | 7.08 | N/A | 10.77 | 6/14/01 | 1.52 | 1.49 |

| Royce Special Equity Fund | 12.63 | 3.07 | 4.88 | 8.65 | 7.09 | 10.32 | 8.62 | 5/1/98 | 1.18 | 1.18 |

| Royce Total Return Fund | 23.45 | 7.09 | 7.49 | 10.36 | 7.49 | 9.45 | 10.48 | 12/15/93 | 1.20 | 1.20 |

| INDEX | ||||||||||

| Russell 2000 | 25.52 | 8.59 | 8.23 | 11.83 | 7.92 | 7.59 | N/A | N/A | N/A | N/A |

| Russell Microcap | 22.43 | 6.39 | 6.57 | 11.26 | 6.16 | N/A | N/A | N/A | N/A | N/A |

| Russell 2000 Value | 22.39 | 4.77 | 6.99 | 10.56 | 6.92 | 9.41 | N/A | N/A | N/A | N/A |

| Russell 2500 | 27.77 | 10.33 | 8.93 | 12.58 | 8.79 | 8.68 | N/A | N/A | N/A | N/A |

| MSCI ACWI ex USA Small Cap | 22.42 | 9.65 | 7.04 | 6.92 | 6.92 | 6.71 | N/A | N/A | N/A | N/A |

Important Performance, Expense, and Risk Information

All performance information in thisReview and Report reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Investment and Service Class shares redeemed within 30 days of purchase may be subject to a 1% redemption fee payable to the Fund (2% for Royce International Premier Fund). Redemption fees are not reflected in the performance shown above; if they were, performance would be lower. Current performance may be higher or lower than performance quoted. Current month-end performance may be obtained at www.royceinvest.com. All performance and expense information reflects results of the Funds’ oldest share Class (Investment Class or Service Class, as the case may be). Price and total return information is based on net asset values calculated for shareholder transactions. Certain immaterial adjustments were made to the net assets of Royce International Premier Fund at 12/31/19 for financial reporting purposes, and as a result the calendar year total returns based on those net asset values differ from the adjusted net values and calendar year total returns reported in the Financial Highlights. Gross annual operating expenses reflect the Fund’s gross total annual operating expenses and include management fees, any 12b-1 distribution and service fees, other expenses, and any applicable acquired fund fees and expenses. Net annual operating expenses reflect contractual fee waivers and/or expense reimbursements. All expense information is reported as of the Fund’s most current prospectus. Royce & Associates has contractually agreed to waive fees and/or reimburse operating expenses, excluding brokerage commissions, taxes, interest, litigation expenses, acquired fund fees and expenses, and other expenses not borne in the ordinary course of business, to the extent necessary to maintain net operating expenses at or below: 1.24% for Royce Micro-Cap Fund; 1.34% for Royce Dividend Value Fund; 1.44% for Royce International Premier Fund; 1.49% for Royce Global Financial Services, Small-Cap Value, and Smaller-Companies Growth Funds through April 30, 2020. Acquired fund fees and expenses reflect the estimated amount of the fees and expenses incurred indirectly by the Fund through its investments in mutual funds, hedge funds, private equity funds, and other investment companies.

Service Class shares bear an annual distribution expense that is not borne by the Funds’ Investment Class. If such distribution expenses had been reflected for Funds showing Investment Class performance, returns would have been lower. Investments in securities of micro-cap, small-cap, and/or mid-cap companies may involve considerably more risk than investments in securities of larger-cap companies. (Please see “Primary Risks for Fund Investors” in the prospectus.) Certain Funds invest a significant portion of their respective assets in foreign companies that may be subject to different risks than investments in securities of U.S. companies, including adverse political, social, economic, or other developments that are unique to a particular country or region. (Please see “Investing in Foreign Securities” in the prospectus.) Therefore, the prices of securities of foreign companies in particular countries or regions may, at times, move in a different direction than those of securities of U.S. companies. (Please see “Primary Risk of Fund Investors” in the prospectus.) Certain Funds generally invest a significant portion of their assets in a limited number of stocks, which may involve considerably more risk than a more broadly diversified portfolio because a decline in the value of any of these stocks would cause their overall value to decline to a greater degree. A broadly diversified portfolio, however, does not ensure a profit or guarantee against loss. This Review and Report must be preceded or accompanied by a prospectus. Please read the prospectus carefully before investing or sending money. Source: MSCI. MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indexes or any securities or financial products. This report is not approved, endorsed, reviewed or produced by MSCI. None of the MSCI data is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Russell Investment Group is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group. The Russell 2000 Index is an unmanaged, capitalization-weighted index of domestic small-cap stocks. It measures the performance of the 2,000 smallest publicly traded U.S. companies in the Russell 3000 Index. The Russell Microcap Index includes 1,000 of the smallest securities in the small-cap Russell 2000 Index along with the next smallest eligible securities as determined by Russell. The Russell 2000 Value Index consists of the respective value stocks within the Russell 2000 as determined by Russell Investments. The Russell 2500 is an unmanaged, capitalization-weighted index of the 2,500 smallest publicly traded U.S. companies in the Russell 3000 index. The MSCI ACWI ex USA Small Cap Index is an unmanaged, capitalization-weighted index of global small-cap stocks, excluding the United States. The performance of an index does not represent exactly any particular investment as you cannot invest directly in an index. Distributor: Royce Fund Services, LLC.

6 | This page is not part of theThe Royce Funds 2019 Annual Report to Shareholders

The Royce Funds and Relative Risk-Adjusted Rolling Returns

We have always believed that a long-term perspective is crucial for determining the success of an investment approach.

Flourishing in an up market is wonderful, but surviving a bear market by losing less (or not at all) is equally desirable, making results over bull and bear periods the true tests of a portfolio’s mettle. This is why we prefer to examine results that include up and down market phases—primarily by looking at rolling return periods.

Our rationale for using long-term rolling periods is based on the fact that investors buy and sell at many times throughout any given year. In our view, examining performance over a larger series of dates using rolling returns provides a more comprehensive picture of performance, providing a more in-depth measure than calendar-based annualized periods. This allows an investor to evaluate the consistency of performance over time—including the ups and downs of market cycles.

Closely related to this preference for rolling period analysis is the idea that the success of an investment approach should also be evaluated based on the return it generates compared with the amount of risk taken. We aim to achieve strong, long-term absolute and relative returns on both a traditional and risk-adjusted basis. We use Sharpe ratios, a widely used measure of return per unit of risk that measures the volatility of returns to gauge how our major domestic strategies with more than 20 years of history have fared versus their benchmark, the Russell 2000 Index. We calculate the Sharpe Ratio for each relevant Fund and the index for each rolling five- and 10-year period over the past 20 years and then show both the average Sharpe ratio for these periods as well as each Fund’s batting average—that is, the number and percentage of times the Fund beat the index over the total number of periods—as a measure of that Fund’s success.

We are very pleased that on a monthly rolling risk-adjusted basis, our four largest Funds had higher average Sharpe Ratios than the Russell 2000 for the majority of both the 10- and 5-year periods for the 20 years ended 12/31/19.

Royce Funds Relative Risk Adjusted Returns: Monthly Rolling Sharpe Ratios

5- and 10-Year Monthly Rolling Sharpe Ratios–20 Years through 12/31/19

Included are all Royce Funds benchmarked against the Russell 2000 with at least 20 years of history.

TheSharpe Ratiois calculated for a specified period by dividing the fund or index’s average excess returns by its annualized standard deviation. The higher the Sharpe Ratio, the better the fund or index’s historical risk-adjusted performance.

Standard deviationis a statistical measure within which a fund or index’s total returns have varied over time. The greater the standard deviation, the greater a fund or index’s volatility. The performance of an index does not represent exactly any particular investment, as you cannot invest directly in an index.

Past performance is no guarantee of future results. For more information on performance please see page 6.

This page is not part of theThe Royce Funds2019 Annual Report to Shareholders | 7

| MANAGERS’ DISCUSSION (UNAUDITED) |

| Royce Dividend Value Fund (RDV) |

| Chuck Royce Jay Kaplan, CFA |

| FUND PERFORMANCE |

Royce Dividend Value Fund came back strong in 2019, advancing 29.8% and outpacing its small- and smid-cap benchmarks, the Russell 2000 and Russell 2500 Indexes, which rose 25.5% and 27.8%, respectively, for the same period.The Fund also beat the Russell 2000 for the three-, 15-year, and since inception (5/3/04) periods ended 12/31/19. The portfolio’s performance was notable in that small-cap dividend payers lagged their non-dividend-paying peers in 2019. |

| WHAT WORKED… AND WHAT DIDN’T |

Nine of the 10 equity sectors in which the Fund held investments had a positive impact on 2019’s performance. Two areas dominated, as Financials and Industrials—the portfolio’s two largest sectors—made respective contributions that more than doubled the positive impact of Information Technology, the third-largest contributor. Consumer Staples detracted very modestly while the smallest contributions came from Real Estate and Consumer Discretionary. At the industry level, capital markets (Financials) made by far the biggest positive impact, followed by notable contributions from metals & mining (Materials) and machinery (Industrials). Detractors at this level had a far more modest effect and were led by food & staples retailing (Consumer Staples), chemicals (Materials), and textiles, apparel & luxury goods (Consumer Discretionary).

The Fund’s top contributing position was global investment firm Carlyle Group, whose shares reaped the rewards of sustained earnings growth. This was the result of successful deals—both acquisitions and sales—as well as more than doubling its fee-related earnings from the prior-year period in the second quarter and boosting its total assets under management to a record-high $223 billion in July 2019. The firm also pays a steady dividend. KBR, another consistent dividend payer, offers differentiated engineering and related services and technologies. The company operates in three synergistic segments: Government Solutions, Technology Solutions, and Energy Solutions. Its shares benefited from KBR exceeding earnings estimates for four consecutive quarters as of October 2019. This growth was driven by robust book-to-bill rates and notable strength in its Energy Solutions division. Each company was a top-10 holding at year-end.

The top detractor at the position level was Value Partners Group, an asset management business that focuses mainly on investors in China and other parts of the Asia-Pacific region. We were initially drawn to its success managing assets with a risk-conscious, value orientation and dominant position in a fast-growing region. We chose to sell our stake in Dividend Value’s portfolio in August, however, after the company reported double-digit second-quarter declines in its revenues and operating income from the previous year. We maintained our position in the Fund’s next largest detractor, American Eagle Outfitters, which designs, markets, and sells its own brand of casual clothing, targeting younger consumers with affordable, high-quality merchandise. Few areas have been hit harder by the expansion of e-commerce than brick-and-mortar clothing retailers. While this has created challenges for American Eagle’s business, we think its stock’s decline was more attributable to the misguided perception that retail is dying—as opposed to changing. We therefore placed greater weight on the company’s efforts to navigate the seismic shifts faced by its industry. Additionally, a new denim cycle began in 2019 and the firm’s subbrand, Aerie, is growing rapidly.

Outperformance relative to the Russell 2000 was driven entirely by stock selection—sector allocation was negative in the calendar year. The biggest advantages on a sector level came from stock selection in Financials (where our larger exposure detracted slightly) and Industrials, where our overweight also proved additive. Savvy stock picks also gave us an advantage in Energy that more than compensated for the negative effect of our sector overweight. Among the Fund’s industries, the aforementioned capital markets group was especially strong on a relative basis. Conversely, stock selection detracted from relative performance in Consumer Discretionary, as did our lower exposure to Health Care, particularly in biotechnology, where conservatively capitalized dividend payers are thin on the ground. The portfolio’s cash position also detracted from results versus the small-cap index.

| Top Contributors to Performance | Top Detractors from Performance | |||||

| For 2019 (%)1 | For 2019 (%)2 | |||||

| Carlyle Group | 1.81 | Value Partners Group | -0.30 | |||

| KBR | 1.79 | American Eagle Outfitters | -0.21 | |||

| KKR & Co. Cl. A | 1.48 | Designer Brands Cl. A | -0.21 | |||

| HEICO Corporation Cl. A | 1.46 | Alliance Resource Partners L.P. | -0.18 | |||

| Reliance Steel & Aluminum | 1.44 | FamilyMart | -0.15 | |||

| 1 Includes dividends | 2 Net of dividends | |||||

| CURRENT POSITIONING AND OUTLOOK |

The backdrop looks quite favorable to us for solid to strong small-cap performance overall. We have previously cited four favorable factors in the current market environment—low inflation, modest valuations, moderate growth, and ample access to capital, which all remain in force and which suggest that small-cap returns can go higher. We see a global economy that’s showing signs of renewed life (the coronavirus outbreak not withstanding), an ISM Manufacturing Index that’s been incrementally rising (despite December’s setback), and, most important, valuations that range from reasonable to attractive among the many small-cap cyclical areas that we typically like best. During the second half of 2019, we increased investments in professional services firms that appear well positioned to benefit from a growing economy and added a turnaround investment in a consumer rental business that’s been benefiting from cost containment, increased traffic trends, and improved cash flows while reducing its debt load. |

| 8 | The Royce Funds 2019 Annual Report to Shareholders |

|

| PERFORMANCE AND PORTFOLIO REVIEW (UNAUDITED) | TICKER SYMBOLS RYDVX RDVIX RDIIX RDVCX |

Performance and Expenses

Average Annual Total Return (%) Through 12/31/19

| JUL-DEC 20191 | 1-YR | 3-YR | 5-YR | 10-YR | 15-YR | SINCE INCEPTION (5/3/04) | |

| RDV | 7.52 | 29.78 | 9.76 | 7.73 | 10.43 | 8.22 | 8.71 |

| Annual Gross Operating Expenses: 1.43% Annual Net Operating Expenses: 1.34% | |||||||

1Not annualized

Relative Risk Adjusted Returns: Monthly Rolling Sharpe Ratios

Since Inception Through 12/31/19

On a monthly rolling risk-adjusted basis, the Fund outperformed the Russell 2000 in 88% of all 10-year periods and 52% of all 5-year periods.

| PERIODS BEATING THE INDEX | FUND AVG (%)1 | INDEX AVG (%)1 | |||||

| 10-year | 60/68 | 88% | 0.55 | 0.51 | |||

| 5-year | 66/128 | 52% | 0.56 | 0.54 | |||

1 Average of monthly rolling Sharpe Ratios over the specified periods.

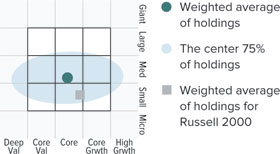

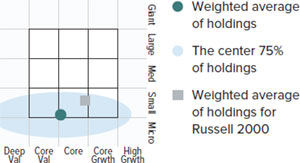

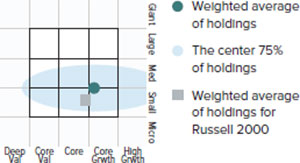

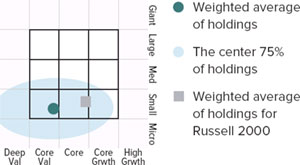

Morningstar Style Map™As of 12/31/19

TheMorningstar Style Map is theMorningstar Style Box™ with the center 75% of fund holdings plotted as theMorningstar Ownership Zone™. The Morningstar Style Box is designed to reveal a fund’s investment strategy. The Morningstar Ownership Zone provides detail about a portfolio’s investment style by showing the range of stock sizes and styles. The Ownership Zone is derived by plotting each stock in the portfolio within the proprietary Morningstar Style Box. Over time, the shape and location of a fund’s ownership zone may vary. See page 89 for additional information.

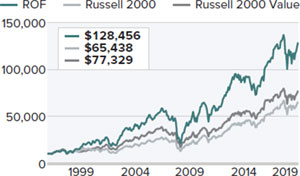

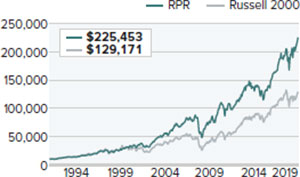

Value of $10,000

Invested on 5/3/04 as of 12/31/19 ($)

Top 10 Positions

% of Net Assets

| HEICO Corporation Cl. A | 3.3 |

| KKR & Co. Cl. A | 3.3 |

| FLIR Systems | 3.3 |

| KBR | 3.1 |

| Carlyle Group | 2.7 |

| Reliance Steel & Aluminum | 2.6 |

| Franco-Nevada | 2.6 |

| Quaker Chemical | 2.6 |

| AptarGroup | 2.5 |

| SEI Investments | 2.4 |

Portfolio Sector Breakdown

% of Net Assets

| Financials | 29.6 |

| Industrials | 24.6 |

| Materials | 14.1 |

| Information Technology | 9.5 |

| Consumer Discretionary | 8.2 |

| Energy | 5.7 |

| Health Care | 2.1 |

| Utilities | 1.8 |

| Consumer Staples | 0.5 |

| Real Estate | 0.5 |

| Cash and Cash Equivalents | 3.4 |

Calendar Year Total Returns (%)

| YEAR | RDV |

| 2019 | 29.8 |

| 2018 | -16.2 |

| 2017 | 21.7 |

| 2016 | 16.4 |

| 2015 | -5.7 |

| 2014 | -2.1 |

| 2013 | 30.7 |

| 2012 | 16.9 |

| 2011 | -4.5 |

| 2010 | 30.1 |

| 2009 | 37.7 |

| 2008 | -31.5 |

| 2007 | -0.0 |

| 2006 | 19.9 |

| 2005 | 7.3 |

Upside/Downside Capture Ratios

Periods Ended 12/31/19 (%)

| UPSIDE | DOWNSIDE | |

| 10-Year | 86 | 84 |

| From 6/30/04 (Start of Fund’s First Full Quarter) | 89 | 78 |

Portfolio Diagnostics

| Fund Net Assets | $104 million |

| Number of Holdings | 79 |

| Turnover Rate | 8% |

| Average Market Capitalization1 | $4,704 million |

| Weighted Average P/E Ratio2,3 | 18.6x |

| Weighted Average P/B Ratio2 | 2.6x |

| Active Share4 | 97% |

| U.S. Investments (% of Net Assets) | 67.3% |

| Non-U.S. Investments (% of Net Assets) | 29.3% |

| 1 | Geometric Average. This weighted calculation uses each portfolio holding’s market cap in a way designed to not skew the effect of very large or small holdings; instead, it aims to better identify the portfolio’s center, which Royce believes offers a more accurate measure of average market cap than a simple mean or median. |

| 2 | Harmonic Average.This weighted calculation evaluates a portfolio as if it were a single stock and measures it overall. It compares the total market value of the portfolio to the portfolio’s share in the earnings or book value, as the case may be, of its underlying stocks. |

| 3 | The Fund’s P/E ratio calculation excludes companies with zero or negative earnings (3% of portfolio holdings as of 12/31/19). |

| 4 | Active Shareis the sum of the absolute values of the different weightings of each holding in the Fund versus each holding in the benchmark, divided by two. |

Important Performance and Expense Information

All performance information in thisReport reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Shares redeemed within 30 days of purchase may be subject to a 1% redemption fee payable to the Fund, which is not reflected in the performance shown above; if it were, performance would be lower. Current month-end performance may be higher or lower than performance quoted and may be obtained at www.royceinvest.com. All performance and risk information reflects results of the Service Class (its oldest class). Certain immaterial adjustments were made to the net assets of Royce Dividend Value Fund at 6/30/15 for financial reporting purposes, and as a result the net asset values for shareholder transactions on that date and the calendar year Total Returns (%) based on those net asset values differ from the adjusted net asset values and calendar year total returns reported in the Financial Highlights. Gross operating expenses reflect the Fund’s total gross annual operating expenses for the Service Class and include management fees, 12b-1 distribution and service fees, and other expenses. Net operating expenses reflect contractual fee waivers and/or expense reimbursements. All expense information is reported as of the Fund’s most current prospectus. Royce & Associates has contractually agreed, without right of termination, to waive fees and/or reimburse expenses to the extent necessary to maintain the Service Class’s net annual operating expenses (excluding brokerage commissions, taxes, interest, litigation expenses, acquired fund fees and expenses, and other expenses not borne in the ordinary course of business) at or below 1.34% through April 30, 2020. Regarding the “Top Contributors” and “Top Detractors” tables shown above, the sum of all contributors to, and all detractors from, performance for all securities in the portfolio would approximate the Fund’s year-to-date performance for 2019. The Sharpe Ratio is calculated for a specified period by dividing a fund’s annualized excess returns by its annualized standard deviation. The higher the Sharpe ratio, the better the fund’s historical risk-adjusted performance. Upside Capture Ratio measures a manager’s performance in up markets relative to the Fund’s benchmark. It is calculated by measuring the Fund’s performance in quarters when the benchmark went up and dividing it by the benchmark’s return in those quarters. Downside Capture Ratio measures a manager’s performance in down markets relative to the Fund’s benchmark (Russell 2000). It is calculated by measuring the Fund’s performance in quarters when the benchmark goes down and dividing it by the benchmark’s return in those quarters.

The Royce Funds 2019 Annual Report to Shareholders | 9

| MANAGERS’ DISCUSSION (UNAUDITED) |

| Royce Global Financial Services Fund (RFS) |

| Chuck Royce Chris Flynn |

| FUND PERFORMANCE |

Royce Global Financial Services Fund posted a strong absolute return in 2019, up 24.2% and bouncing back from 2018’s decline.This compares to an increase of 25.5% for the domestic small-cap Russell 2000 Index and an increase of 27.2% for the Financial Services stocks in the domestic smid-cap Russell 2500 Index in 2019. We think the Fund’s calendar-year result was more impressive when seen in the context of a year in which international stocks generally lagged those in the U.S., and financials mostly lagged the overall market. Although the Fund only modestly lagged the 2019 gain for the Russell 2000, an arguably more relevant comparison is that the portfolio bested the financial stocks within the MSCI ACWI Small Cap Index, a global small-cap index that advanced 20.3% in 2019. |

| WHAT WORKED... AND WHAT DIDN’T |

The Fund’s gains were notably broad based in 2019, as 77% of our holdings advanced. Moreover, stocks in 72%—that is, 13 out of 18—of the countries where the Fund had holdings rose. In contrast with the broad market’s experience, the Fund’s international holdings slightly outpaced its U.S. stocks. (Currency translations added a minor contribution in 2019 as well.) The countries that made the most significant contribution on a country basis were the U.S., Canada, and the United Kingdom, while holdings headquartered in India, France, and South Africa detracted most, albeit on a comparably more modest scale.

Ares Management was the top-contributing position in 2019. The firm is an asset manager that focuses on tradable credit, direct lending, private equity, and real estate. Ares’s stock more than doubled during the year as investors became more optimistic about the company’s ability to sustain mid-teens, high margin earnings growth for an extended period. The company also converted to C-corp. status, which broadened ownership, supporting an increase in its valuation. MarketAxess Holdings operates an electronic, multi-dealer trading platform for investment grade and high-yield corporate and emerging market bonds. The company seems very well positioned to benefit from the continued electronification of corporate bond trading. While we are optimistic about continued growth and potential margin expansion, we also found its stock’s valuation a bit high, which led us to trim our position in the second half.

Virtu Financial detracted most at the position level. Virtu is a New York City based financial company that uses its technology to act as a market maker and liquidity provider to the global financial markets. Its business endured a slump through most of the year as the company typically does best in highly volatile markets—which were mostly absent in 2019—and/or when global trading volumes are heavy. Believing that higher volatility is more likely, we held our position. Benefitfocus is a cloud-based software provider of benefits solutions to employers and brokers. The company continued to disappoint investors with organic growth that fell below expectations. We retained our shares because the company provides the worthwhile value of helping its customers manage escalating benefits costs efficiently, and we are hopeful of seeing better execution in the coming year.

| Top Contributors to Performance | Top Detractors from Performance | |||||

| For 2019 (%)1 | For 2019 (%)2 | |||||

| Ares Management Cl. A | 2.11 | Virtu Financial Cl. A | -1.18 | |||

| MarketAxess Holdings | 2.05 | Benefitfocus | -0.67 | |||

| Carlyle Group Inc | 1.54 | Edelweiss Financial Services | -0.49 | |||

| Franco-Nevada | 1.53 | Rothschild & Co | -0.48 | |||

| Ashmore Group | 1.25 | JSE | -0.32 | |||

| 1 Includes dividends | 2Net of dividends | |||||

| CURRENT POSITIONING AND OUTLOOK |

We significantly narrowed the Fund’s holdings in 2019, moving from 84 to 68 positions, as we focused more intensively on business models where we have the greatest conviction. This net reduction in holdings came despite adding six new positions that we have identified as attractive opportunities, including the recently publicly listed Tel Aviv Stock Exchange, which in our view has a well-protected franchise with solid growth prospects. The year-end portfolio reflected some additional repositioning. We reduced our weightings in more traditional financial industries such as insurance and banks while we increased our exposure to capital markets. Our perspective is that the combination of ongoing low interest rates and a flattish yield curve is a persistent headwind to the business models of many banks and insurance companies. In contrast, we are more optimistic about selected areas within capital markets, including traditional non-U.S. exchanges—we currently own nine—alternative transaction platforms, specialist traditional asset managers, and alternative asset managers. |

While we are not in the business of making macroeconomic forecasts, we do believe that the odds favor a rebound in global growth from 2019’s more subdued levels. If that scenario develops, it is helpful to note that many of the Fund’s holdings, like many financial stocks, have a pro-cyclical bias in that their profits tend to grow faster when economies are rebounding. Beyond this potential cyclical boost, we believe that many of our holdings are equally well positioned to capitalize on more durable secular trends, including the persistent need of investors for attractive income and the opportunities to use technology in order to provide lower cost alternatives, to automate processes, and/or to deliver analytical insights. |

| 10 | The Royce Funds 2019 Annual Report to Shareholders |

|

| PERFORMANCE AND PORTFOLIO REVIEW (UNAUDITED) | TICKER SYMBOLS RYFSX RGFIX |

Performance and Expenses

Average Annual Total Return (%) Through 12/31/19

| JUL-DEC 20191 | 1-YR | 3-YR | 5-YR | 10-YR | 15-YR | SINCE INCEPTION (12/31/03) | |

| RFS | 6.80 | 24.17 | 9.60 | 7.22 | 10.20 | 7.62 | 8.07 |

| Annual Gross Operating Expenses: 1.77% Annual Net Operating Expenses: 1.58% | |||||||

1Not annualized

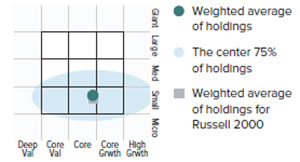

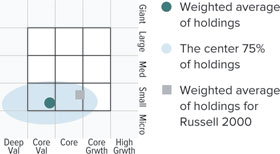

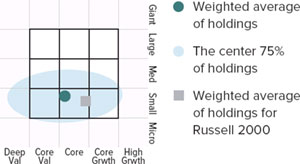

Morningstar Style Map™As of 12/31/19

TheMorningstar Style Mapis theMorningstar Style BoxTM with the center 75% of fund holdings plotted as theMorningstar Ownership ZoneTM. The Morningstar Style Box is designed to reveal a fund’s investment strategy. The Morningstar Ownership Zone provides detail about a portfolio’s investment style by showing the range of stock sizes and styles. The Ownership Zone is derived by plotting each stock in the portfolio within the proprietary Morningstar Style Box. Over time, the shape and location of a fund’s ownership zone may vary. See page 89 for additional information.

Value of $10,000

Invested on 12/31/03 as of 12/31/19 ($)

| Top 10 Positions | ||

| % of Net Assets | ||

| Franco-Nevada | 3.7 | |

| Popular | 3.7 | |

| MarketAxess Holdings | 3.4 | |

| Ares Management Cl. A | 3.4 | |

| FirstService Corporation | 3.2 | |

| E-L Financial | 3.1 | |

| Sprott | 3.1 | |

| Ashmore Group | 2.9 | |

| First Citizens BancShares Cl. A | 2.6 | |

| Altus Group | 2.5 | |

| ||

| Portfolio Industry Breakdown | ||

| % of Net Assets (Subject to Change) | ||

| Capital Markets | 53.3 | |

| Banks | 17.1 | |

| Real Estate Management & Development | 8.0 | |

| Insurance | 3.8 | |

| Metals & Mining | 3.7 | |

| Software | 3.2 | |

| Trading Companies & Distributors | 2.5 | |

| IT Services | 2.0 | |

| Professional Services | 1.3 | |

| Closed-End Funds | 1.0 | |

| Thrifts & Mortgage Finance | 0.8 | |

| Diversified Financial Services | 0.7 | |

| Consumer Finance | 0.5 | |

| Hotels, Restaurants & Leisure | 0.2 | |

| Cash and Cash Equivalents | 1.9 | |

| Upside/Downside Capture Ratios | ||||

| Periods Ended 12/31/19 (%) | ||||

| UPSIDE | DOWNSIDE | |||

| 10-Year | 85 | 84 | ||

| Fund’s First Full Quarter (12/31/03) | 85 | 78 | ||

| Calendar Year Total Returns (%) | ||

| YEAR | RFS | |

| 2019 | 24.2 | |

| 2018 | -13.4 | |

| 2017 | 22.5 | |

| 2016 | 12.9 | |

| 2015 | -4.7 | |

| 2014 | 3.5 | |

| 2013 | 42.0 | |

| 2012 | 20.7 | |

| 2011 | -11.3 | |

| 2010 | 18.5 | |

| 2009 | 32.1 | |

| 2008 | -35.4 | |

| 2007 | -4.7 | |

| 2006 | 24.8 | |

| 2005 | 12.2 | |

| Portfolio Country Breakdown1,2 | ||

| % of Net Assets | ||

| United States | 53.2 | |

| Canada | 21.6 | |

| United Kingdom | 6.7 | |

| India | 2.2 | |

| France | 2.2 | |

| Israel | 2.1 | |

| Brazil | 1.8 | |

| South Africa | 1.7 | |

| ¹ Represents countries that are 1.5% or more of net assets. | ||

| ² Securities are categorized by the country of their headquarters. | ||

| Portfolio Diagnostics | ||

| Fund Net Assets | $37 million | |

| Number of Holdings | 68 | |

| Turnover Rate | 5% | |

| Average Market Capitalization1 | $2,469 million | |

| Weighted Average P/E Ratio2,3 | 17.3x | |

| Weighted Average P/B Ratio2 | 1.9x | |

| Active Share4 | 99% | |

| 1 | Geometric Average. This weighted calculation uses each portfolio holding’s market cap in a way designed to not skew the effect of very large or small holdings; instead, it aims to better identify the portfolio’s center, which Royce believes offers a more accurate measure of average market cap than a simple mean or median. |

| 2 | Harmonic Average.This weighted calculation evaluates a portfolio as if it were a single stock and measures it overall. It compares the total market value of the portfolio to the portfolio’s share in the earnings or book value, as the case may be, of its underlying stocks. |

| 3 | The Fund’s P/E ratio calculation excludes companies with zero or negative earnings (11% of portfolio holdings as of 12/31/19). |

| 4 | Active Shareis the sum of the absolute values of the different weightings of each holding in the Fund versus each holding in the benchmark, divided by two. |

Important Performance and Expense Information

All performance information in thisReport reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Shares redeemed within 30 days of purchase may be subject to a 1% redemption fee payable to the Fund, which is not reflected in the performance shown above; if it were, performance would be lower. Current month-end performance may be higher or lower than performance quoted and may be obtained at www.royceinvest.com. Gross operating expenses reflect the Fund’s gross total annual operating expenses for the Service Class and include management fees, 12b-1 distribution and service fees, other expenses and acquired fund fees and expenses. Net operating expenses reflect contractual fee waivers and/or expense reimbursements. All expense information is reported as of the Fund’s most current prospectus. Royce & Associates has contractually agreed to waive fees and/or reimburse expenses to the extent necessary to maintain the Fund’s net annual operating expenses, (excluding brokerage commissions, taxes, interest, litigation expenses, acquired fund fees and expenses, and other expenses not borne in the ordinary course of business), at or below 1.49% through April 30, 2020. Acquired fund fees and expenses reflect the estimated amount of the fees and expenses incurred indirectly by the Fund through its investments in mutual funds, hedge funds, private equity funds, and other investment companies. Regarding the “Top Contributors” and “Top Detractors” tables shown above, the sum of all contributors to, and all detractors from, performance for all securities in the portfolio would approximate the Fund’s year-to-date performance for 2019. Upside Capture Ratio measures a manager’s performance in up markets relative to the Fund’s benchmark. It is calculated by measuring the Fund’s performance in quarters when the benchmark went up and dividing it by the benchmark’s return in those quarters. Downside Capture Ratio measures a manager’s performance in down markets relative to the Fund’s benchmark (Russell 2000). It is calculated by measuring the Fund’s performance in quarters when the benchmark goes down and dividing it by the benchmark’s return in those quarters.

The Royce Funds2019 Annual Report to Shareholders | 11

| MANAGER’S DISCUSSION (UNAUDITED) |

| Royce International Premier Fund (RIP) |

| Mark Rayner, CA |

| FUND PERFORMANCE |

The Fund gained an impressive 34.2% in 2019, once again outpacing the MSCI ACWI ex USA Small Cap Index, which was up 22.4% for the same period.This strong calendar-year result helped the portfolio to solidify its long-term relative edge as the Fund beat its benchmark for the three-, five-year, and since inception (12/31/10) periods ended 12/31/19. |

| WHAT WORKED... AND WHAT DIDN’T |

All nine of the equity sectors in which the portfolio had investments in 2019 made a positive contribution to performance. Industrials— the Fund’s largest sector weighting—made by far the biggest positive contribution, followed by a strong showing for Information Technology. The smallest contributions came from Communication Services, Consumer Discretionary, and Energy—three sectors to which the Fund had little exposure in 2019. The top-contributing industries in 2019 were professional services (Industrials) and software (Information Technology), followed by health care equipment & supplies (Health Care). Construction & engineering (Industrials) was the only industry that detracted—and it did so modestly—while the smallest contributions came from interactive media & services (Communication Services) and containers & packaging (Materials).

The Fund’s top contributor at the position level was Brazil’s TOTVS, which provides enterprise resource planning and supply chain management software solutions. TOTVS capped a strong 2019 with robust revenue growth, effective cost management that created greater operational efficiency, and adjusted EBITDA margin expansion, driven by its core software business. The cost of its new initiatives also did not significantly impact the firm’s profits. Finally, TOTVS acquired SUPPLIER, a credit card company with a virtual private label B2B solution.

Amadeus Fire, which focuses on finance professionals in Germany, was the next biggest contributor. We initially purchased it as a replacement for another company with a similar ‘employee leasing’ model that we like. These models work especially well in countries with strict labor laws and tight labor markets. The client receives increased workforce flexibility and access to skilled personnel for which it is willing to pay a premium. Amadeus bears the employment risk, which it can dissipate through economies of scale. Earnings grew and its margins expanded through most of 2019. In addition, Amadeus announced the takeover of Comcave in late December. This is a 25% EBITDA margin business that retrains white-collar professionals who are leaving their existing employment or are in-between jobs. Within Amadeus, it will also act as a funnel for recruitment into Amadeus’s core employee leasing business. The market aggressively re-rated Amadeus’s stock following the acquisition.

We sold our stake in each of the Fund’s two biggest detractors for 2019. Consort Medical is a U.K.-based Contract Development & Manufacturing Organization that makes high-volume, disposable drug delivery devices primarily for respiratory treatments. Full-year results announced in June showed revenues and operating profits both down, but in line with the reduced expectations. The company also reported mixed news on the development of a relatively narrow, though expanding, portfolio of commercialized and in-development projects. Adding to its challenges was an explosion in its Northumberland facility in July, though we began to reduce our position in June. SH Kelkar & Company is a family-run fragrance producer based in India whose ongoing declines in earnings and revenues led us to sell the last of our shares in April.

Relative outperformance for the calendar year was due primarily to stock selection, though sector allocation was also positive versus the benchmark. The strongest sector by far on a relative basis was Industrials, driven overwhelmingly by superior stock picking. The portfolio also benefited from its significantly larger weighting in Information Technology. Conversely, our lack of exposure to Utilities was a modest disadvantage while the portfolio’s cash holdings created an additional drag on relative performance.

| Top Contributors to Performance | Top Detractors from Performance | |||||

| For 2019 (%)1 | For 2019 (%)2 | |||||

| TOTVS | 2.09 | Consort Medical | -0.34 | |||

| Amadeus Fire | 1.29 | SH Kelkar & Company | -0.17 | |||

| Altus Group | 1.28 | AIA Engineering | -0.11 | |||

| Restore | 1.24 | Burkhalter Holding | -0.04 | |||

| XP Power | 1.21 | Cyient | -0.03 | |||

| 1 Includes dividends | 2Net of dividends | |||||

| CURRENT POSITIONING AND OUTLOOK |

Over the last few years, we’ve been cautious and somewhat underweight when contrasted with the potential to invest in U.K. companies based on the strong fundamental opportunity set. As the political risks have diminished in the aftermath of the elections, however, we’ve been reevaluating the opportunities for many U.K. companies both in and out of our database of high-quality international small-caps. The portfolio’s exposure to the U.K. increased in 2019—it finished the year as our second-largest country weighting. Our strategy typically places a materially lower emphasis on short- to medium-term macroeconomic news or forecasts and rarely if ever positions itself to take account of such data. During 2019, we made our investment decisions based on this core philosophy and remain constructive with regard to the long-term opportunities for high-quality international small-caps. We are encouraged by incremental but solid improvements in the global economy, which should help to diffuse recession risk. Moreover, central banks throughout the developed world remain accommodative, keeping rates low and/or providing ample liquidity. Each of these developments should remain supportive for equities in 2020. |

| 12 | The Royce Funds 2019 Annual Report to Shareholders |

|

| PERFORMANCE AND PORTFOLIO REVIEW (UNAUDITED) | TICKER SYMBOLS RYIPX RIPNX RINPX RIPIX |

Performance and Expenses

Average Annual Total Return (%) Through 12/31/19

| JUL-DEC 20191 | 1-YR | 3-YR | 5-YR | SINCE INCEPTION (12/31/10) | |

| RIP | 10.58 | 34.22 | 17.86 | 13.49 | 8.59 |

| Annual Gross Operating Expenses: 1.59% Annual Net Operating Expenses: 1.44% | |||||

1Not annualized

Relative Returns: Monthly Rolling Average Annual Return Periods

Since Inception Through 12/31/19

On a monthly rolling basis, the Fund outperformed the MSCI ACWI x USA SC in 100% of all 5-year periods; 85% of all 3-year periods; and 71% of all 1-year periods.

| PERIODS BEATING THE INDEX | FUND AVG (%)1 | INDEX AVG (%)1 | |||||

| 5-year | 49/49 | 100% | 8.7 | 6.0 | |||

| 3-year | 62/73 | 85% | 9.4 | 6.8 | |||

| 1-year | 69/97 | 71% | 8.9 | 5.8 | |||

1 Average of monthly rolling average annual total returns over the specified periods.

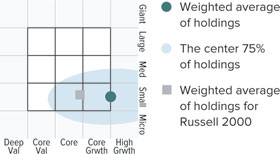

Morningstar Style Map™As of 12/31/19

TheMorningstar Style Mapis theMorningstar Style BoxTM with the center 75% of fund holdings plotted as theMorningstar Ownership ZoneTM. The Morningstar Style Box is designed to reveal a fund’s investment strategy. The Morningstar Ownership Zone provides detail about a portfolio’s investment style by showing the range of stock sizes and styles. The Ownership Zone is derived by plotting each stock in the portfolio within the proprietary Morningstar Style Box. Over time, the shape and location of a fund’s ownership zone may vary. See page 89 for additional information.

Value of $10,000

Invested on 12/31/10 as of 12/31/19 ($)

| Top 10 Positions | ||

| % of Net Assets | ||

| IMCD | 2.8 | |

| Victrex | 2.8 | |

| Intertrust | 2.7 | |

| Loomis Cl. B | 2.6 | |

| Daifuku | 2.6 | |

| Croda International | 2.5 | |

| TKC Corporation | 2.4 | |

| Spirax-Sarco Engineering | 2.3 | |

| Amadeus Fire | 2.2 | |

| XP Power | 2.2 | |

| Portfolio Sector Breakdown | ||

| % of Net Assets | ||

| Industrials | 42.8 | |

| Information Technology | 19.4 | |

| Health Care | 9.0 | |

| Materials | 7.0 | |

| Financials | 5.9 | |

| Energy | 2.0 | |

| Consumer Discretionary | 1.7 | |

| Real Estate | 1.5 | |

| Communication Services | 1.2 | |

| Preferred Stock | 1.9 | |

| Cash and Cash Equivalents | 7.6 | |

| Upside/Downside Capture Ratios | ||||

| Periods Ended 12/31/19 (%) | ||||

| UPSIDE | DOWNSIDE | |||

| Fund’s First Full Quarter (12/31/10) | 110 | 80 | ||

| Calendar Year Total Returns (%) | ||

| YEAR | RIP | |

| 2019 | 34.2 | |

| 2018 | -12.8 | |

| 2017 | 39.8 | |

| 2016 | -1.1 | |

| 2015 | 16.2 | |

| 2014 | -8.2 | |

| 2013 | 18.3 | |

| 2012 | 23.4 | |

| 2011 | -16.8 | |

| Portfolio Country Breakdown1,2 | ||

| % of Net Assets | ||

| Japan | 17.7 | |

| United Kingdom | 13.6 | |

| Switzerland | 11.6 | |

| Sweden | 9.3 | |

| Australia | 8.4 | |

| Germany | 7.2 | |

| Netherlands | 5.5 | |

| Brazil | 3.0 | |

| ¹ Represents countries that are 3% or more of net assets. | ||

| ² Securities are categorized by the country of their headquarters. | ||

| Portfolio Diagnostics | ||

| Fund Net Assets | $809 million | |

| Number of Holdings | 54 | |

| Turnover Rate | 40% | |

| Average Market Capitalization1 | $2,133 million | |

| Weighted Average P/E Ratio2,3 | 26.3x | |

| Weighted Average P/B Ratio2 | 3.9x | |

| Active Share4 | 98% | |

| 1 | Geometric Average. This weighted calculation uses each portfolio holding’s market cap in a way designed to not skew the effect of very large or small holdings; instead, it aims to better identify the portfolio’s center, which Royce believes offers a more accurate measure of average market cap than a simple mean or median. |

| 2 | Harmonic Average.This weighted calculation evaluates a portfolio as if it were a single stock and measures it overall. It compares the total market value of the portfolio to the portfolio’s share in the earnings or book value, as the case may be, of its underlying stocks. |

| 3 | The Fund’s P/E ratio calculation excludes companies with zero or negative earnings (1% of portfolio holdings as of 12/31/19). |

| 4 | Active Shareis the sum of the absolute values of the different weightings of each holding in the Fund versus each holding in the benchmark, divided by two. |

Important Performance and Expense Information

All performance information in thisReport reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Shares redeemed within 30 days of purchase may be subject to a 2% redemption fee payable to the Fund, which is not reflected in the performance shown above; if it were, performance would be lower. Current month-end performance may be higher or lower than performance quoted and may be obtained at www.royceinvest.com. All performance and risk information reflects results of the Service Class (its oldest class). Price and total return information is based on net asset values for shareholder transactions. Certain immaterial adjustments were made to the net assets of Royce International Premier Fund at 12/31/19 for financial reporting purposes, and as a result the calendar year total returns based on those net asset values differ from the adjusted net asset values and calendar year total returns reported in the Financial Highlights. Gross operating expenses reflect total gross annual operating expenses for the Service Class and include management fees, 12b-1 distribution and service fees, and other expenses. Net operating expenses reflect contractual fee waivers and/or expense reimbursements. All expense information is reported as of the Fund’s most current prospectus. Royce & Associates has contractually agreed to waive its fees and/or reimburse operating expenses to the extent necessary to maintain the Fund’s net annual operating expenses, (excluding brokerage commissions, taxes, interest, litigation expenses, acquired fund fees and expenses, and other expenses not borne in the ordinary course of business), at or below 1.44% through April 30, 2020. Regarding the “Top Contributors” and “Top Detractors” tables shown above, the sum of all contributors to, and all detractors from, performance for all securities in the portfolio would approximate the Fund’s year-to-date performance for 2019. Upside Capture Ratio measures a manager’s performance in up markets relative to the Fund’s benchmark. It is calculated by measuring the Fund’s performance in quarters when the benchmark went up and dividing it by the benchmark’s return in those quarters. Downside Capture Ratio measures a manager’s performance in down markets relative to the Fund’s benchmark (MSCI ACWI x USA SC). It is calculated by measuring the Fund’s performance in quarters when the benchmark goes down and dividing it by the benchmark’s return in those quarters.

The Royce Funds 2019 Annual Report to Shareholders | 13

| MANAGERS’ DISCUSSION (UNAUDITED) |

| Royce Micro-Cap Fund (RMC) |

| Jim Stoeffel Brendan Hartman |

| FUND PERFORMANCE |

Royce Micro-Cap Fund delivered a strong absolute return of 21.2% for 2019, though the Fund lagged the Russell Microcap and the Russell 2000 Indexes, which returned 22.4% and 25.5%, respectively, for the same period. |

| WHAT WORKED... AND WHAT DIDN’T |

Six of the Fund’s 10 equity sectors finished 2019 in the black. Information Technology made the most sizable positive contribution by far, followed by Industrials and Health Care. Consumer Discretionary, Energy, and Communication Services detracted from performance, but they did so on a modest scale. At the industry level, semiconductors & semiconductor equipment (Information Technology) generated the biggest impact on performance, more than tripling the impact of the portfolio’s next best contributor, machinery (Industrials). Conversely, energy equipment & services (Energy) was the worst performing industry, followed by leisure products (Consumer Discretionary).

Biotechnology company Axsome Therapeutics was the top-contributing position in 2019. The company saw positive clinical results across its product portfolio, which includes developing therapies for central nervous system disorders. AXS-05, Axsome’s lead molecule, has been performing well in clinical trials that are expected to be finished quickly because two of its ingredients were previously approved by the Food and Drug Administration. Ultra Clean Holdings develops and supplies critical subsystems for the semiconductor capital equipment and flat panel display industries. Not only did the stock benefit from the recent semiconductor industry upturn, but performance was also boosted by management’s decision to diversify its service offerings and customer base. Zealand Pharma focuses on developing peptide-based therapeutics for metabolic and gastrointestinal diseases. The Copenhagen-based company’s two latest stage products targeting short bowel system and hypoglycemia in diabetics had positive results during the year. Zealand Pharma also completed its first ever acquisition, buying Encycle Therapeutics in October.

Conversely, Red Lion Hotels was hurt in its efforts to transition from company-owned hotels to a franchise model. Selling its company-owned units took longer than anticipated, and Red Lion experienced greater-than-expected attrition in its newly acquired franchisees—factors that led us to sell our position. Correvio Pharma develops and discovers cardiovascular drugs for the treatment of atrial arrhythmia, congestive heart failure, and bacterial skin infections. The company’s atrial fibrillation drug, which is used extensively in Europe, failed to gain approval from an FDA Advisory Panel. This led us to exit the position. Branded fitness and apparel product maker Nautilus also detracted from performance. Two consecutive failed product launches resulted in a decision to remove the CEO. While we liked several of the strategic decisions the company made over the past several years, we sold our position based on our lack of confidence in management’s ability to effectively judge the rapidly changing fitness markets. We also expected it to take at least a year to rebuild its product pipeline.

The Fund’s narrow relative underperformance versus the Russell Micro-cap was a result of sector allocation—stock selection was additive to relative results in 2019. Consumer Discretionary hampered relative performance mostly due to poor stock picks—our overexposure detracted very modestly. The sector was home to three of the top five relative detracting positions: Red Lion Hotels, Nautilus, and Kirkland’s. Ineffective stock picks in Energy also hindered results. Our lower exposure to biotechnology (Health Care)—the strongest contributor to the micro-cap index’s returns—hurt results most at the industry level. Conversely, Information Technology was the strongest contributor to performance, as the sector’s relative contribution made more than six times the impact of the next best contributor, Industrials. Savvy stock selection drove outperformance in both sectors. Two of the top five relative performing positions came from Information Technology—Ultra Clean Holdings and Adesto Technologies. At the industry level, semiconductors & semiconductor equipment (Information Technology) aided performance versus the benchmark most, followed by construction & engineering (Industrials).

| Top Contributors to Performance | Top Detractors from Performance | |||||

| For 2019 (%)1 | For 2019 (%)2 | |||||

| Axsome Therapeutics | 2.07 | Red Lion Hotels | -0.65 | |||

| Ultra Clean Holdings | 1.30 | Correvio Pharma | -0.53 | |||

| Zealand Pharma | 1.28 | Nautilus | -0.50 | |||

| NeoGenomics | 0.98 | Kirkland’s | -0.45 | |||

| Zealand Pharma | 0.77 | ORBCOMM | -0.43 | |||

| 1Includes dividends | 2Net of dividends | |||||

| CURRENT POSITIONING AND OUTLOOK |

While issues surrounding trade have finally begun to stabilize, we find ourselves in the midst of what promises to be an eventful U.S. election cycle, with outcomes that could have major implications for investors. Despite this uncertainty, we remain generally constructive of the U.S. economy, particularly because the current Fed tightening cycle appears to have ended. Along with a possible truce in the trade wars, we believe the favorable backdrop should support underlying growth for our overweighted sectors, such as Information Technology and Industrials. Valuations look relatively attractive to us in many corners of the micro-cap world, even as recent returns show that the performance gap between micro-caps and large-caps is gradually beginning to narrow. We took advantage of these opportunities for much of the second half of 2019 as micro-cap stocks were selling at their steepest discount to large-caps since 2001. We don’t know if this recent upward move will last, but after a long period of underperformance for micro-caps, we anticipate some degree of mean reversion. |

| 14 | The Royce Funds 2019 Annual Report to Shareholders |

|

| PERFORMANCE AND PORTFOLIO REVIEW (UNAUDITED) | TICKER SYMBOLS RYOTX RMCFX RYMCX | |

| Performance and Expenses | |||||||||||||||||

| Average Annual Total Return (%) Through 12/31/19 | |||||||||||||||||

| JUL-DEC 20191 | 1-YR | 3-YR | 5-YR | 10-YR | 15-YR | 20-YR | 25-YR | SINCE INCEPTION (12/31/91) | |||||||||

| RCM | 9.56 | 21.16 | 5.17 | 3.84 | 5.66 | 5.79 | 8.51 | 9.49 | 10.40 | ||||||||

| Annual Gross Operating Expenses: 1.25% Annual Net Operating Expenses: 1.24% | |||||||||||||||||

| 1 Not annualized | |||||||||||||||||

Morningstar Style Map™As of 12/31/19

TheMorningstar Style Map is theMorningstar Style Box™ with the center 75% of fund holdings plotted as theMorningstar Ownership Zone™. The Morningstar Style Box is designed to reveal a fund’s investment strategy. The Morningstar Ownership Zone provides detail about a portfolio’s investment style by showing the range of stock sizes and styles. The Ownership Zone is derived by plotting each stock in the portfolio within the proprietary Morningstar Style Box. Over time, the shape and location of a fund’s ownership zone may vary. See page 89 for additional information.

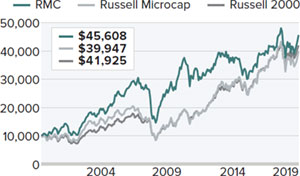

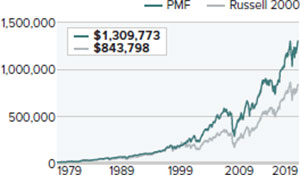

Value of $10,000

Invested on 6/30/00 (Russell Microcap Index Inception) as of 12/31/19 ($)

| Top 10 Positions | ||

| % of Net Assets | ||

| Ultra Clean Holdings | 1.4 | |

| Photronics | 1.4 | |

| Zealand Pharma | 1.4 | |

| Northwest Pipe | 1.3 | |

| Nova Measuring Instruments | 1.3 | |

| Axsome Therapeutics | 1.3 | |

| FormFactor | 1.2 | |

| QAD Cl. A | 1.2 | |

| OrthoPediatrics Corporation | 1.2 | |

| NeoGenomics | 1.1 | |

| Portfolio Sector Breakdown | ||

| % of Net Assets | ||

| Information Technology | 26.5 | |

| Industrials | 21.4 | |

| Financials | 13.2 | |

| Health Care | 11.7 | |

| Consumer Discretionary | 9.6 | |

| Materials | 3.2 | |

| Energy | 2.8 | |

| Real Estate | 2.1 | |

| Communication Services | 2.0 | |

| Consumer Staples | 0.2 | |

| Cash and Cash Equivalents | 7.3 | |

| Calendar Year Total Returns (%) | ||

| YEAR | RCM | |

| 2019 | 21.2 | |

| 2018 | -8.9 | |

| 2017 | 5.4 | |

| 2016 | 19.7 | |

| 2015 | -13.3 | |

| 2014 | -4.1 | |

| 2013 | 21.3 | |

| 2012 | 8.0 | |

| 2011 | -12.1 | |

| 2010 | 30.1 | |

| 2009 | 55.7 | |

| 2008 | -40.9 | |

| 2007 | 7.1 | |

| 2006 | 22.3 | |

| 2005 | 11.5 |

| Upside/Downside Capture Ratios | ||||

| Periods Ended 12/31/19 (%) | ||||

| UPSIDE | DOWNSIDE | |||

| 10-Year | 72 | 95 | ||

| From 6/30/00 (Russell Microcap Index Inception) | 90 | 81 | ||

Portfolio Diagnostics

| ||

| Fund Net Assets | $337 million | |

| Number of Holdings | 138 | |

| Turnover Rate | 21% | |

| Average Market Capitalization1 | $545 million | |

| Weighted Average P/B Ratio2 | 2.0x | |

| Active Share3 | 89% | |

| U.S. Investments (% of Net Assets) | 80.3% | |

| Non-U.S. Investments (% of Net Assets) | 12.4% | |

| 1 | Geometric Average. This weighted calculation uses each portfolio holding’s market cap in a way designed to not skew the effect of very large or small holdings; instead, it aims to better identify the portfolio’s center, which Royce believes offers a more accurate measure of average market cap than a simple mean or median. |

| 2 | Harmonic Average.This weighted calculation evaluates a portfolio as if it were a single stock and measures it overall. It compares the total market value of the portfolio to the portfolio’s share in the earnings or book value, as the case may be, of its underlying stocks. |

| 3 | Active Shareis the sum of the absolute values of the different weightings of each holding in the Fund versus each holding in the benchmark, divided by two. |