UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-03651

Touchstone Strategic Trust-March Funds

(Exact name of registrant as specified in charter)

303 Broadway, Suite 1100

Cincinnati, Ohio 45202-4203

(Address of principal executive offices) (Zip code)

Jill T. McGruder

303 Broadway, Suite 1100

Cincinnati, Ohio 45202-4203

(Name and address of agent for service)

Registrant's telephone number, including area code:800-638-8194

Date of fiscal year end:March 31

Date of reporting period:March 31, 2020

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The Report to Shareholders is attached herewith.

March 31, 2020

Annual Report

Touchstone Strategic Trust

Touchstone Flexible Income Fund

Touchstone Focused Fund

Touchstone Global ESG Equity Fund (formerly known as Touchstone Sustainability and Impact Equity Fund)

Touchstone Growth Opportunities Fund

Touchstone Mid Cap Growth Fund

Touchstone Sands Capital Emerging Markets Growth Fund

IMPORTANT NOTE: Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Touchstone Funds’ annual and semi-annual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the shareholder reports from Touchstone Funds or from your financial intermediary, such as a broker-dealer or bank. Instead, annual and semi-annual shareholder reports will be available on the Touchstone Funds’ website (TouchstoneInvestments.com/Resources), and you will be notified by mail each time a report is posted and provided with a website link to access the report.

You may elect to receive all future annual and semi-annual shareholder reports in paper, free of charge. If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. To elect to receive paper copies of shareholder reports through the mail or otherwise change your delivery method, contact your financial intermediary or, if you hold your shares directly through Touchstone Funds, visit TouchstoneInvestments.com/Resources/Edelivery or call Touchstone Funds toll-free at 1.800.543.0407. Your election to receive shareholder reports in paper will apply to all Touchstone Funds that you hold through the financial intermediary, or directly with Touchstone.

Table of Contents

This report identifies the Funds' investments on March 31, 2020. These holdings are subject to change. Not all investments in each Fund performed the same, nor is there any guarantee that these investments will perform as well in the future. Market forecasts provided in this report may not occur.

Letter from the President

Dear Shareholder:

We are pleased to provide you with the Touchstone Strategic Trust Annual Report. Inside is key financial information, as well as manager commentaries for the Funds, for the 12 months ended March 31, 2020.

Trade-related rhetoric between the U.S. and China drove market volatility through the first nine months of the fiscal period. By the end of year, the U.S.-China trade discussions took a more constructive tone, culminating in an announcement of a “phase one” agreement in early 2020 to reduce some tariff levels. Aside from this conflict, the U.S. economy continued its steady pace, driven by strong employment data and solid consumer spending. Outside the U.S., economic growth in developed markets such as the U.K., European Union and Japan continued at a slow pace, while each of their central banks continued to maintain low-to-zero overnight rates. Outside of the U.S. and developed markets, emerging markets continued to show overall weakness, driven by the U.S.-China trade slowdown and lower-than-expected Indian economic growth. This already fragile, low-growth environment was upended in the first quarter of 2020 as COVID-19 swept the globe, bringing with it containment measures resulting in massive shutdowns of economic activity. In addition to the spread of the COVID-19 virus, geopolitical tensions between Russia and Saudi Arabia flooded the market with oil, pushing prices to lows unseen in nearly 20 years.

Equities recorded a significant decline in the first quarter of 2020, which drove the trailing 12-month return into negative territory, regardless of style and market capitalization. Atypical for such declines, U.S. growth stocks continued their dominance over value stocks as has been the case through most of the post-Credit Crisis bull market. Strong relative results from Information Technology (IT) and Healthcare stocks helped drive the growth style outperformance while Energy and Financials lagged. Large cap stocks declined less than mid and small cap stocks, bolstered by relatively stronger balance sheets and more stable profit outlooks.

Non-U.S. developed equity markets trailed U.S. markets over the past 12 months. Japan performed relatively well due to slow growth in COVID-19 cases and aggressive stimulus measures, while Europe was hit harder. Similar to the U.S., IT and Healthcare stocks were among the top relative contributors, while Energy and Financials lagged. In emerging markets, equities exhibited the same pattern as the U.S. and developed markets with IT leading the way and China being a surprising bright spot as signs of virus impact started to abate.

Within fixed income, U.S. Treasury prices benefited and yields compressed to cycle lows from U.S. Federal Reserve Board (Fed) actions and a flight to safety during the rapid selloff of risk assets in the first quarter of 2020. Meanwhile, credit-sensitive sectors saw the strong results of the first three quarters of the period nearly or completely erased as concerns over potential for rising defaults and technical selling pressures mounted. Spreads across investment grade credit, high yield credit, bank loans and collateralized loan obligations reached levels unseen since the 2008 Credit Crisis. The Fed acted during the volatility to provide liquidity and support market functioning, helping ease the volatility and negative sentiment that appeared in March 2020.

Periods such as these especially remind us of the essential role performed by the steady hands of financial professionals, the importance of trust in your investment strategy and the risks that accompany trying to time the market. Furthermore, we believe that environments that are more volatile create opportunities for active managers over the long-term. We greatly value your continued support. Thank you for including Touchstone as part of your investment plan.

Sincerely,

Jill T. McGruder

President

Touchstone Strategic Trust

Management's Discussion of Fund Performance (Unaudited)

Touchstone Flexible Income Fund

Sub-Advised by Bramshill Investments, LLC

Investment Philosophy

The Touchstone Flexible Income Fund seeks total return through a combination of income and capital appreciation by investing primarily in income producing securities. The Fund’s sub-advisor, Bramshill Investments, LLC, implements a tactical fixed-income strategy, actively managing the portfolio by rotating among asset classes and tactically hedging during various interest rate and market environments. The sub-advisor seeks to identify relative value across asset classes and capture opportunities primarily within the corporate, U.S. Treasury, municipal and preferred security markets. The Fund focuses on liquid securities with transparent pricing and actively-traded capital structures.

Fund Performance

The Touchstone Flexible Income Fund (Class A Shares) underperformed its benchmark, the Bloomberg Barclays U.S. Aggregate Bond Index, for the 12-month period ended March 31, 2020. The Fund’s total return was -3.33 percent (calculated excluding the maximum sales charge) while the total return of the benchmark was 8.93 percent.

Market Environment

The historic bull-run was full steam ahead for most of 2019, finishing out the decade producing some of the largest calendar year returns in recent memory across asset classes. In a banner year for risk assets, U.S. Treasuries still managed to produce solid gains. This was due to falling interest rates as uncertainty around trade negotiations with China rattled the U.S. Treasury market causing the yield curve to invert for most of the year. Later in the period the curve twisted back to a steeper shape as tensions eventually cooled and both sides resolved the dispute. Tariffs, concern over global growth, inflation consistently below the U.S. Federal Reserve Board’s (Fed) 2.0 percent target and modest but resilient U.S. growth, roughly 1.5 to 2.0 percent, kept a cap on interest rates providing an accommodative environment in terms of easy financial conditions.

Growth in the U.S. continued to show resilience with the economy expanding at near trend pace at about 1.5 to 2.0 percent. As stimulus from fiscal effects and tax cuts faded, the single most influential factor for maintaining the expansion at that pace continued to be the strength of labor markets and the consumer. The unemployment rate declined throughout the year ending at 3.5 percent, the lowest since the late 1960s. Negotiations between China and the U.S. were tumultuous with hostile rhetoric and tit-for-tat tariff retaliations causing markets to swing into volatile extremes. Markets remained on edge, uncertain of the policy that would eventually be set and the impact that it would have on business confidence/investment and ultimately the consumer. It wasn’t until the end of the fourth quarter of 2019 when developments came to light of a potential deal set to be the first of many and take place in multiple phases. Tensions cooled and PresidentTrump announced that the U.S. and China would sign a Phase OneTrade Agreement, which meant the pullback of additional December 15th tariffs on Chinese goods and implicit agreement to halt any future actions. It was the first sign of conciliation that could bring both sides to the table thus steadying nerves and restoring business confidence, and providing a boost to capital spending. Outside the U.S., most notably in Europe, countries experienced further declines in economic growth.

Going into calendar year 2020, stocks made new all-time highs, driven by an economy operating at full employment, absent inflationary pressures, an accommodative Fed, and waning concerns over trade negotiations. However, markets turned sharply lower in February when it became apparent that COVID-19 had arrived in the U.S. and containment was no longer possible. The rise of the virus impaired the economic backdrop for global growth and precipitated the sharpest and fastest decline ever for the economy and the stock market. Deleveraging and forced liquidations of stocks and bonds resulted in extreme volatility as investors sought the safety of cash above all else. Oil demand dried up, credit spreads showed signs of stress and massive stimulus measures were implemented across the world.

Portfolio Review

The Fund’s exposure to lower rated investment grade corporate bonds and preferred equities drove underperformance relative to the benchmark. The aforementioned COVID-19 pandemic sell-off in the final weeks of the 12-month period saw corporate bonds, investment grade and non-investment grade, decline and credit spreads widen to levels not seen since the Great Financial Crisis of 2008. Preferred equities were no exception, declining dramatically in mid-March before rebounding at the close of the 12-month period. In addition to the Fund’s credit exposure, the portfolio’s shorter duration relative to the benchmark also detracted from performance during much of the 12-month period. As the Fed cut rates beginning in mid-2019 despite a strong U.S. economy, longer-term U.S. Treasuries rallied as the yield curve shifted downward across all maturities.

From an asset sector perspective, the Fund modestly re-allocated within the preferred equity exposure. The Fund began the 12-month period with predominate exposure to preferred equity securities that are originally issued with a fixed coupon that transitions to a floating rate at a pre-determined rate in the near-term (usually three to five years following issuance). By favoring these so-called

Management's Discussion of Fund Performance (Unaudited) (Continued)

fixed-to-float preferred securities, the Fund was able to maintain a more defensive duration posture, shorter compared to the benchmark. Following the strong capital market returns experienced during calendar year 2019, we took profits in some preferred positions that had reached rich valuation levels. As calendar year 2020 began, the COVID-19 sell-off hit, overall rate levels shifted downward and credit spreads widened dramatically. As a result, we are finding valuation opportunities in fixed coupon preferreds, incrementally adding to the portfolio’s duration. Despite the modest changes to the Fund’s preferred exposure, the portfolio remains in high quality, larger issuers thus maintaining a high degree of liquidity.

The Fund’s bond holdings maintained a large allocation to short maturity, high quality investment grade structured securities such as Asset-Backed, Commercial and Residential Mortgage-Backed Securities. Our structured bond team was able to identify good relative valuation, highly-rated investment opportunities as corporate credit spreads remained at narrow levels for much of the 12-month period. As the market sell-off took place at the end of the period, we identified more corporate bond investment opportunities but did not make large, material re-allocations. A large allocation to cash and short-term U.S. Treasury securities for the 12-month period was a slight drag on performance, until the significant market sell-off in March 2020. With the sell-off and investors buying safe assets such as cash and U.S. Treasury securities across the yield curve, this allocation helped to off-set declines from the previously-mentioned credit exposures in the portfolio.

Outlook

We will deploy some of the Fund’s cash and U.S. Treasury exposure in the near-term as certain higher quality assets such as investment grade corporate bonds increase the yield on the portfolio. However, we also see a particular opportunity in lower tier investment grade debt, often crossover rated or BBB- to BB-rated within the capital structures of investment grade issuers. Our view is “post-corona” and following the current quarantines we believe there will be a longer “U” shaped type of recovery, while we must also be conscious of a potentially risky “L” shape recovery. We envision the corporate credit portion of the Fund to be positioned well, holding bonds of businesses which we believe will participate near-term in a recovery. We think these subordinated investments are trading at attractive prices and yields and are generally the preferred, or junior subordinated tranches of credits which have historically demonstrated solid liquidity. Following the Fed’s investment grade corporate bond buying program, these firms also have access to capital at the senior parts of their capital structures and solid balance sheets. We view these names as higher quality securities, relative to generic non-investment grade corporate bonds that are under duress due to the current risk-off environment, and therefore an opportunity.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Flexible Income Fund - Class A* and the Bloomberg Barclays U.S. Aggregate Bond Index

| * | The chart above represents performance of Class A shares only, which will vary from the performance of Class C shares, Class Y shares and Institutional Class shares based on the differences in sales loads and fees paid by shareholders in the different classes. The inception date of Institutional Class shares was September 10, 2012. Institutional Class shares performance information was calculated using the historical performance of Class Y shares for the periods prior to September 10, 2012. The returns have been restated for sales loads and fees applicable to Institutional Class shares. |

| ** | The average annual total returns shown above are adjusted for maximum sales loads and fees, if applicable. The maximum offering price per share of Class A shares is equal to the net asset value (“NAV”) per share plus a sales load equal to 2.04% of the NAV (or 2.00% of the offering price). Class C shares are subject to a contingent deferred sales charge (“CDSC”) of 1.00%. The CDSC will be assessed on an amount equal to the lesser of (1) the NAV at the time of purchase of the shares being redeemed or (2) the NAV of such shares being redeemed, if redeemed within a one-year period from the date of purchase. Class Y shares and Institutional Class shares are not subject to sales charges. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Note to Chart

Bloomberg Barclays U.S. Aggregate Bond Index is an unmanaged index comprised of U.S. investment grade, fixed rate bond market securities, including government, government agency, corporate and mortgage-backed securities between one and ten years.

Management's Discussion of Fund Performance (Unaudited)

Touchstone Focused Fund

Sub-Advised by Fort Washington Investment Advisors, Inc.

Investment Philosophy

The Touchstone Focused Fund seeks to provide investors with capital appreciation. The Fund seeks to invest in companies of all capitalizations that are trading below what is believed to be the estimate of their intrinsic value and have a sustainable competitive advantage or a high barrier to entry in place. The barrier(s) to entry can be created through a cost advantage, economies of scale, high customer loyalty or a government barrier (e.g. license or subsidy). Fort Washington believes that the strongest barrier to entry is the combination of economies of scale and high customer loyalty.

Fund Performance

The Touchstone Focused Fund (Class A Shares) underperformed its primary benchmark, the Russell 3000® Index, and its secondary benchmark, the S&P 500® Index, for the 12-month period ended March 31, 2020, although all posted negative returns. The Fund’s total return, was -9.14 percent (calculated excluding the maximum sales charge) while the total return of the Russell 3000® Index was -9.13 percent and the total return of the S&P 500® Index was -6.98 percent.

Market Environment

In the final three quarters of 2019, U.S. equities recorded a fairly steady climb higher primarily due to accommodative monetary policy from the U.S. Federal Reserve Board (Fed) and optimism late in the year around the phase one trade agreement between the U.S. and China. In the first quarter of 2020, U.S. equity markets pulled back significantly due to concerns over the global spread of the coronavirus and the oil price war between Russia and Saudi Arabia. Over the 12-month period ending March 31, 2020, the Energy sector was, by far, the worst performing sector in the primary benchmark. The Information Technology sector was the only sector with a positive return.

Portfolio Review

Within the Fund, the sectors where holdings outperformed relative to the primary benchmark were Consumer Discretionary, Health Care, Financials, and InformationTechnology. Sectors that lagged relative to the primary benchmark included Materials, Real Estate, Consumer Staples, Energy, and Communication Services. Industrials performed roughly in line with the primary benchmark. Stock selection was additive to relative performance led by stock picks within the Consumer Discretionary, Health Care, Financials and Information Technology sectors. Conversely, sector allocation decisions detracted primarily due to underweighting Information Technology and overweighting Financials.

The three stocks that contributed the most to performance were Microsoft Corp. (Information Technology sector), Amazon.com Inc. (Consumer Discretionary sector), and Bristol-Myers Squibb Co. (Health Care sector). Microsoft outperformed due to favorable performance in its legacy franchises and better than expected results in its cloud business. Amazon.com rose due to acceleration of growth in Prime and Amazon Web Services both before and through the outbreak of COVID-19. Bristol-Myers Squibb outperformed primarily due to positive developments in its non-small cell lung cancer business and favorable pipeline activity in recently acquired Celgene Corp.

Among the stocks that detracted from performance were Simon Property Group Inc. (Real Estate sector), Carnival Corp. (Consumer Discretionary sector), and Jones Lang LaSalle Inc. (Real Estate sector). Simon Property Group underperformed primarily due to a continuation of weak trends for mall-based retail tenants. Carnival underperformed primarily due to demand concerns amid the coronavirus outbreak. The Fund exited the position during the period. Jones Lang LaSalle underperformed as sentiment weakened amid concerns over the pandemic’s impact on commercial real estate.

From a market cap perspective, the Fund ended the period with no weight in smaller-cap stocks (companies with a market cap below $2 billion). The primary benchmark weight for this segment was 4.3 percent. The Fund remained underweight to mid-cap businesses which now comprise 10.3 percent of assets, compared to a primary benchmark weight of 11.8 percent. Last, the Fund continued to maintain an overweight to larger-cap businesses (companies with a market cap above $10 billion). The Fund’s weight to that segment is currently 89.6 percent which is higher than the primary benchmark weight of 83.9 percent. This allocation decision was positive to performance during the period as large-cap stocks outperformed small-cap stocks.

Investments made in international companies which comprised approximately 6.2 percent of assets at the end of the period outperformed the primary benchmark.

During the period, the Fund added UnitedHealth Group Inc. (Health Care sector), Netflix Inc. (Consumer Discretionary sector), Hubbell Inc. (Industrials sector), DuPont de Nemours Inc. (Materials sector),Trip.com Group Ltd. (Consumer Discretionary sector), Americold Realty Trust (Real Estate sector), Texas Instruments Inc. (Information Technology sector), Philip Morris International

Management's Discussion of Fund Performance (Unaudited) (Continued)

Inc. (Consumer Staples sector), Workday Inc. (InformationTechnology sector), first sold then bought back Starbucks Corp. (Consumer Discretionary sector), and Parker Hannifin Corp. (Industrials sector) to the portfolio. The Fund exited Dunkin Brands Group Inc. (Consumer Discretionary sector), Booking Holding Inc. (Consumer Discretionary sector), Simon Property Group Inc. (Real Estate sector), Biogen Inc. (Health Care sector), Halliburton Co. (Energy sector), Unilever NV (Consumer Staples sector), and Carnival Corp. (Consumer Discretionary sector).

As the period came to a close, the Fund had an overweight to the Communication Services, Financials, and Consumer Discretionary sectors and an underweight to the Consumer Staples, Health Care, Materials, and Energy sectors. The weight to the Real Estate, Industrials, and Information Technology sectors was roughly in line with the primary benchmark. The Fund held no positions in the Utilities sector.

Outlook

We believe the markets are approaching the near future with looming questions about the ongoing impact of the global pandemic and oil price war. Our current thinking about COVID-19 is characterized by several important themes. First is the precedent set by many past health contagions. While this novel virus certainly poses unique challenges, we believe the key is that the markets have recovered from every prior outbreak after temporary setbacks. While the hit to global economies has and will continue to be severe, we believe that the markets will bottom before the economy. In past health related downturns, the market has tended to look through near-term economic impact around the time travel restrictions are lifted and the new case ramp peaks. Also, U.S. economic fundamentals were solid and many global economies were showing signs of positive inflection before the turmoil. We believe the solid backdrop heading into the downturn combined with unprecedented government action suggest we may avoid worst case outcomes on the path to recovery. We have been keeping an eye on vaccines and, especially in the near term, treatments for COVID-19 patients. While we don’t expect any individual drug to be a miracle cure, we do anticipate steady progress, with new options being added and doctors learning which regimens are likely to work best for each patient. As of now, it is our working assumption that the economic impact of this virus will be contained to quarters as opposed to years.

With this framework in mind, our investment team has kept top down portfolio positioning relatively consistent through the outbreak while taking bottom-up opportunities amidst volatility. We have deployed or re-deployed capital at a measured pace. We have not implemented a defensive posture for overall portfolio construction as we believe the impact on most Fund holdings will be temporary rather than structural. We have been reducing position sizes in businesses that we view as more expensive, those that could have potential balance sheet issues, or those that are less likely to free up capital for more attractive business models. In our opinion, current events have demonstrated the importance of owning a portfolio of businesses that are supported by barriers to entry with strong balance sheets. History is littered with unexpected events that cause downturns in the markets. Our process seeks to consistently own high excess return on capital businesses that are mispriced.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Focused Fund - Class A*, the Russell 3000® Index and the S&P 500® Index

| * | The chart above represents performance of Class A shares only, which will vary from the performance of Class C shares, Class Y shares and Institutional Class shares based on the differences in sales loads and fees paid by shareholders in the different classes. The inception date of Class C shares was April 12, 2012. Class C shares performance information was calculated using the historical performance of Class Y shares for the periods prior to April 12, 2012. The returns have been restated for sales loads and fees applicable to Class C shares. |

| ** | The average annual total returns shown above are adjusted for maximum sales loads and fees, if applicable. The maximum offering price per share of Class A shares is equal to the net asset value (“NAV”) per share plus a sales load equal to 5.26% of the NAV (or 5.00% of the offering price). Class C shares are subject to a contingent deferred sales charge (“CDSC”) of 1.00%. The CDSC will be assessed on an amount equal to the lesser of (1) the NAV at the time of purchase of the shares being redeemed or (2) the NAV of such shares being redeemed, if redeemed within a one-year period from the date of purchase. Class Y shares and Institutional Class shares are not subject to sales charges. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Notes to Chart

Russell 3000®Index measures the performance of the 3,000 largest U.S. companies based on total market capitalization, which represents approximately 98% of the investable U.S. equity market.

S&P 500® Index is a group of 500 widely held stocks and is commonly regarded to be representative of the large capitalization stock universe.

The Frank Russell Company (FRC) is the source and owner of the Russell 3000® Index data contained or reflected in this material and all trademarks and copyrights related thereto. The material may contain confidential information and unauthorized use, disclosure, copying, dissemination or redistribution is strictly prohibited. This is a Touchstone Investments presentation of the data, and FRC is not responsible for the formatting or configuration of this material or for any inaccuracy in the presentation thereof.

Management's Discussion of Fund Performance (Unaudited)

Touchstone Global ESG Equity Fund*

Sub-Advised by Rockefeller & Co., LLC

Investment Philosophy

The Touchstone Global ESG Equity Fund (formerly known as Touchstone Sustainability and Impact Equity Fund) seeks long-term growth of capital. The Fund primarily invests in equity securities of U.S. and non-U.S. companies and generally focuses on larger, more established companies. The Fund selects investments based on an evaluation of a company’s sustainability and impact practices which considers environmental, social and governance (ESG) impacts and risks of a company, how well the company manages these impacts and risks and ascertains the company’s willingness and ability to take a leadership position in implementing best practices.

Fund Performance

The Touchstone Global ESG Equity Fund (Class A Shares) underperformed its benchmark, the MSCI All Country World Index, for the 12-month period ended March 31, 2020. The Fund’s total return was -13.61 percent (calculated excluding the maximum sales charge), while the total return of the benchmark was -11.26 percent.

Market Environment

The 12-month period ending March 31, 2020 started with a uniformly dovish tone from central banks in response to concerns of a global economic slowdown. The market in 2019 performed well on the back of a rebound from the selloff in late 2018 and accommodative monetary policies but was primarily driven by multiples expansion as opposed to earnings growth. We also experienced a significant bifurcation in the markets as stocks characterized as growth and bond proxies outperformed, while cyclical value stocks were overlooked by the market.

Moving to 2020, global equities, as represented by the MSCI All Country World Index, entered a bear market with a negative 21 percent total return during the first quarter of 2020. The Index hit its all-time peak on February 12, 2020, and then lost as much as one-third of its value during the depth of the sell-off. The global equity sell-offs were triggered by the COVID-19 pandemic, which first led to more than a month of lockdown across China, and then spread worldwide causing an unprecedented collapse in economic activity as governments sought to contain the outbreak through varying degrees of lockdowns. Financials markets were also roiled by a price war between Saudi Arabia and Russia over crude oil, which was already suffering from weak demand. The unprecedented nature of the COVID-19 crisis drove the U.S. Federal Reserve Board (Fed) to aggressively inject liquidity into financial markets, with asset purchases expanded to include investment grade corporate and municipal bonds. Congress also passed three rounds of stimulus adding up to more than $2 trillion of financial aid to individuals, municipalities and various industries. Similarly, policymakers around the globe also rolled out aggressive monetary and fiscal stimulus. The aggressive policy responses helped to arrest the market decline and led to a market rebound toward the end of the quarter.

Portfolio Review

The Fund’s sector allocation and stock selection detracted from relative performance during the period. An underweight in Information Technology and an overweight in Financials and Industrials were the largest detractors. European financials were a particularly large detractor, as Swedbank AB (Financials sector) was negatively impacted by anti-money laundering (AML) lapses in its Estonian operations. An underweight position in Apple Inc. (Information Technology sector), a large benchmark holding, was also a detractor from relative performance.

Communication Services was the largest contributing sector, with KDDI Corp. in Japan being the largest contributor within the sector. This was in part due to the significant market sell off in the first quarter of 2020. Most companies within the Communication Services sector were relative outperformers as their businesses are usually less cyclical.

The Fund made several changes during the 12-month period, including several in the first quarter of 2020 to adjust to the evolving macro environment. Specifically, the Fund took advantage of the market sell-offs to initiate new positions in several industry leaders, including Apple Inc., while also adding businesses with less economic cyclicality including GlaxoSmithKline PLC (Health Care sector), and Verizon Communications Inc. (Communication Services sector).

Apple appears to be well-positioned with its strong balance sheet and loyal customer base. The recent market downturn has afforded us the opportunity to purchase the shares at an attractive valuation especially considering the 5G handset cycle. We do not believe demand for its handsets will be impacted long-term despite the current challenging environment. We believe disruptions to the supply chain should be worked out and the new products will launch as planned. The company has significantly improved the environmental sustainability of its products. It provides a complete life cycle assessment of its products, and increasingly seeks opportunity in safer materials, while also procuring 100 percent of its energy from renewable sources. GlaxoSmithKline’s pharmaceutical and consumer healthcare businesses are also defensive in the current market environment. We also believe there are low expectations on its pipeline, coupled with a reasonable valuation for a non-cyclical business. Additionally, GlaxoSmithKline has ranked first on

Management's Discussion of Fund Performance (Unaudited) (Continued)

the Global Access to Medicines Index for the past seven years for its work in low and middle income countries on vaccine distribution and HIV/AIDS among other health issues. In early February, we initiated Fund positions in a number of stocks with less economic cyclicality as we believed with the market continuing to run higher in January, it was not taking into account the risk of a pandemic or economic slowdown. These new positions included Verizon, a telecommunications company, which we believed offered attractive risk-adjusted shareholder returns. The dividend yield of just under 5 percent is funded with just over half of free cash flow. We believe wireless service revenue should stabilize after turning positive in 2018 as the effects of unlimited pricing plans and embedded device subsidies have worked through the base, while competitive threats also appear to have settled. Verizon performs in-line or slightly above U.S. peers across a number of ESG material issues, particularly when it comes to employee satisfaction, diversity & inclusion, and corporate governance issues.

To fund these purchases, we exited several Fund positions that we believed would be materially impacted by the COVID-19 pandemic, in addition to stocks in industries that will potentially be structurally challenged for the foreseeable future. We reduced Fund exposure to the Financials sector by exiting several banks, including ING Groep NV. We believed an extended period of extremely low interest rates will likely pressure the company for a while. We also exited Royal Caribbean Cruises Ltd. and Southwest Airlines Co. (both Consumer Discretionary sector). While these have been long-term holdings in the Fund supported by our belief that aging demographics and changes in consumer preferences would manifest themselves in heightened demand for air travel and cruising, we believed both companies would be materially impacted by the COVID-19 pandemic.

Outlook

There is a tug of war between two major forces: the biggest public health and economic crisis in decades, and the most aggressive monetary and fiscal stimulus in modern history. The former led to a bear market selloff in a little over four weeks, and the latter has generated some optimism that led to a rebound in late March. We believe the initial shock-and-awe of both forces have been absorbed, and investors’ attention will shift to fundamentals and the post-lockdown. We believe most companies will be given a pass for the weak results in the first half of the year, and investors will instead focus on balance sheet strength and the recovery potential to separate the strong from the weak.

As for the market, the panic phase of selling is likely over. However, we believe the road to recovery will take time as the world adjusts to a “new normality” until effective vaccines become available in sufficient quantity. While we have shifted the Fund slightly away from more economically cyclical stocks to those less economically cyclical, we are optimistic about the opportunity given Fund’s positioning of investing in companies where we believe there is lower risk of structural impairment and an opportunity to come out of the pandemic stronger.

* Formerly known as Touchstone Sustainability and Impact Equity Fund.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the Touchstone Global ESG Equity Fund

- Class A* and the MSCI All Country World Index

| | * | The chart above represents performance of Class A shares only, which will vary from the performance of Class C shares, Class Y shares and Institutional Class shares based on the differences in sales loads and fees paid by shareholders in the different classes. The inception date of Institutional Class shares was May 4, 2015. Institutional Class shares performance information was calculated using the historical performance of Class A shares for periods prior to May 4, 2015. The returns have been restated for sales loads and fees applicable to Institutional Class shares. |

| | | |

| ** | The average annual total returns shown above are adjusted for maximum sales loads and fees, if applicable. The maximum offering price per share of Class A shares is equal to the net asset value (“NAV”) per share plus a sales load equal to 5.26% of the NAV (or 5.00% of the offering price). Class C shares are subject to a contingent deferred sales charge (“CDSC”) of 1.00%. The CDSC will be assessed on an amount equal to the lesser of (1) the NAV at the time of purchase of the shares being redeemed or (2) the NAV of such shares being redeemed, if redeemed within a one-year period from the date of purchase. Class Y shares and Institutional Class shares are not subject to sales charges. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Notes to Chart

MSCI All Country World Index measures the equity market performance of developed and emerging markets.

MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used to create indices or financial products. This report is not approved or produced by MSCI.

Management's Discussion of Fund Performance (Unaudited)

Touchstone Growth Opportunities Fund

Sub-Advised by Westfield Capital Management Company, L.P.

Investment Philosophy

The Touchstone Growth Opportunities Fund seeks long-term growth of capital by primarily investing in stocks of U.S. companies with large, medium and small market capitalizations. The Fund’s portfolio managers place focus on companies they believe to have demonstrated records of achievement with excellent prospects for earnings growth over a 1- to 3-year period. Westfield looks for companies that it believes are reasonably priced with high forecasted earnings potential.

Fund Performance

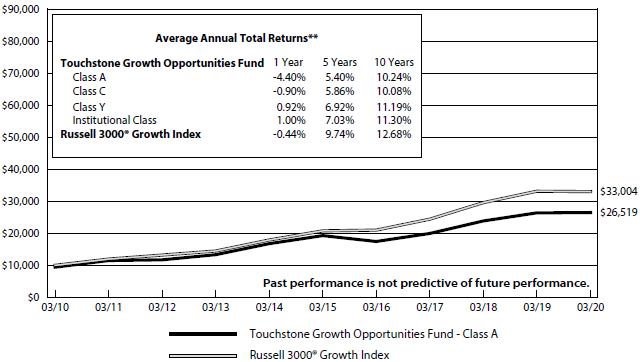

The Touchstone Growth Opportunities Fund (Class A Shares) outperformed its benchmark, the Russell 3000®Growth Index, for the 12-month period ended March 31, 2020. The Fund’s total return was 0.63 percent (calculated excluding the maximum sales charge), while the total return of the benchmark was -0.44 percent.

Market Environment

Throughout 2019, U.S. equity markets steadily advanced, closing out their best year since 2013 despite ongoing skepticism of the market’s strength. An accommodative U.S Federal Reserve Board (Fed) and easing trade tensions combined with continued U.S. consumer strength and low unemployment to fuel the market advance throughout the year. 2020 began with stocks making new all-time highs, driven by an economy operating at full employment, absent inflationary pressures, an accommodative Fed, and waning concerns over trade negotiations. However, markets turned sharply lower in February when it became apparent that COVID-19 had arrived in the U.S. and containment was no longer possible. The rise of the virus impaired the economic backdrop for global growth and precipitated the sharpest and fastest decline ever for the economy and the stock market. Deleveraging and forced liquidations of stocks and bonds resulted in extreme volatility as investors sought the safety of cash above all else. Oil demand dried up, credit spreads showed signs of stress, and massive stimulus measures were implemented across the world.

Within the benchmark, only the Information Technology sector generated positive returns. The Energy, Materials and Industrials sectors all declined more than ten percent.

Portfolio Review

The Fund’s relative outperformance was driven primarily by stock selection within the Health Care sector, which was broad based across industries. We continued to find opportunities within the Health Care sector that offer exciting, innovation-driven growth. We remained constructive on the group, broadly, and believe that there are attractive opportunities across a variety of sub-sectors including health care tools and equipment, medical technology, and therapeutics. The Medicines Company, a late-stage drug developer focused on cholesterol management therapies for cardiovascular disease and long-term high conviction holding of the Fund, was a key driver for both the sector and the Fund during the period. The stock climbed after the late November announcement that Novartis International AV was acquiring the company at a premium. The Fund also benefited from exposure to Vertex Pharmaceuticals Incorporated. Vertex increased following the announcement of an early approval for its triple combo therapy for the treatment of Cystic Fibrosis (“CF”), expanding its addressable market to nearly 90 percent of the existing CF population with little to no competition. We continue to believe that Vertex is one of the cleanest growth stories in large-cap biotechnology, and that its dominance in the CF space is only just getting reflected in its value. The Fund also benefited from exposure to health insurance services company Humana Inc., which was added to the Fund during the first quarter of 2020. Humana has been largely insulated from the global macroeconomic and employment disruptions caused by COVID-19, with much of its business tied to the sale of Medicare and state-based Medicaid services. We believe that Humana represents an opportunity to gain exposure to the growth in managed care and is well positioned in Medicare Advantage plans, which may be critical throughout the 2020 election.

The Consumer Discretionary sector also contributed to Fund performance. Stock selection drove the majority of the relative strength in the sector; however, the Fund’s underweight positioning also benefited relative results, in particular, the strategic avoidance of many traditional retailers and many travel/restaurant names. Throughout 2019, we maintained a generally cautious outlook toward the group, consistent with our long-held views that lack of pricing power, over capacity, and challenges competing with ecommerce juggernauts created a challenging environment for many industry players. More recently, the COVID-19 pandemic has brought substantial additional pressure to the group. Significant restrictions on consumer’s physical freedom, including “stay at home” orders impacting much of the country, have resulted in unprecedented store closures across most discretionary retail categories. The travel and leisure industry has been devastated with a nearly absolute shutdown of business travel, group meetings and inbound air traffic. Lastly, widespread layoffs and stock market wealth destruction has created an uncertain outlook for big ticket spending over the near to intermediate term. In regard to specific stock drivers, the Fund’s position in Amazon.com, Inc. added to relative performance during the period. We remain positive on Amazon.com as it continued to gain market share, generated impressive free cash flow

Management's Discussion of Fund Performance (Unaudited) (Continued)

and improved margins. Additionally, Amazon.com potentially benefits from the rapid transition to work-from-home operations and a shift in consumer traffic to predominantly online.

The Energy sector was the primary detractor from relative results during the period. An unprecedented combination of supply and demand issues led to a dramatic decline in energy commodities and stocks within the sector in the first quarter of 2020. The effects of COVID-19, the most disruptive event ever for Energy companies, has the potential for global demand to be down nearly 25 percent in the second quarter 2020. Contributing to the negative results in the sector is the ongoing conflict between Russia and Saudi Arabia, introducing additional long-term concerns to industry supply discipline. Given the macro uncertainty facing the sector, we decided to exit the Fund’s investments in the group, Marathon Petroleum Corporation and Pioneer Natural Resources Company, in March. We will continue to monitor the space and look to opportunistically reinvest in idiosyncratic growth stories that can benefit from future changes in supply or demand.

The Financials sector also detracted during the period. More recently, the sector faced headwinds due to rapidly falling interest rates, exacerbated in part by deleveraging and illiquidity, and additional signs of credit market stress. While there were some bright spots in the Fund during the period, like S&P Global, Inc., weakness in banks resulted in relative underperformance. Citigroup Inc. was the biggest source of relative weakness in the industry and sector. The stock traded down in the second half of the first quarter 2020 over general concerns on rates and credit as well as its exposure to international markets relative to peers - including 21 percent of total revenues derived from Asia. Despite the near-term weakness, we maintain conviction in the business as we believe the stock’s valuation is compelling even after fairly draconian new assumptions for low rates and higher credit costs. We believe valuation will rebound once investors have a better sense of the duration of the downturn.

Exposure to the Information Technology sector was the largest absolute change in Fund positioning during the period. In this environment, we believe that high quality businesses supported by strong cash flows and healthy revenue streams have the potential to better weather the storm. Additionally, we believe many technology companies may benefit from the rapid transition to work-from-home operations and a shift in consumer traffic to predominantly online. With that said, we continue to be selective in the space, focusing our attention on companies driving organic sales growth through innovate products and strong pipelines. It is important to remember that we take a bottom-up, fundamental approach when identifying securities for inclusion within the Fund and sector exposures are the result of our fundamental conviction in individual companies.

Outlook

While headlines continue to show spikes in reported infections, and another move lower is certainly possible, we do believe that the brunt of the risk repricing has already occurred. We could also point to signs that are typically evident during a “bottoming” process like panic selling, forced liquidations, and deleveraging by quantitative strategies but acknowledge we are in unchartered territory. Our view, and hope, is that the policies enacted in the U.S. will help the economy bridge the gap from now until workers can safely return to their jobs. When that happens, our expectation remains for recovery in economic activity, albeit at a measured pace until a viable therapeutic agent and, ultimately, a vaccine is mass produced. We remain committed to a balanced approach within the Fund and have exposure to both defensive stocks which provide a ballast during turbulent times, as well as those more economically sensitive names that we believe will benefit most when activity resumes to pre-crisis levels.

As a fundamental, bottom-up manager, macro-economic forecasts do not drive our stock selection process but do help to shape our investment themes. We continue to find exciting opportunities in areas that offer secular growth and innovation. In regard to specific sectors, we believe Health Care and Information Technology represent some of the top sectors of the market. In this environment, we believe that high quality businesses supported by strong cash flows and healthy revenue streams should be better able to weather the storm. Additionally, we believe that the Health Care and Information Technology sectors are both beneficiaries of some of the impacts from COVID-19.

Following the market sell-off, we are now beginning to see variations in price action which suggest that price discovery is once again taking place after a period where forced liquidations drove much of the market. Additionally, we have tried to be opportunistic during these dislocations, adding to high conviction holdings and swapping positions for stocks with what we believe are better risk-return profiles. We like the way the Fund is positioned. As a bottom-up, fundamental manager, we continue to focus on company fundamentals and look to buy stocks of quality U.S. companies at attractive valuations with strong growth prospects over time.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the Touchstone Growth Opportunities

Fund - Class A* and the Russell 3000® Growth Index

| | * | The chart above represents performance of Class A shares only, which will vary from the performance of Class C shares, Class Y shares and Institutional Class shares based on the differences in sales loads and fees paid by shareholders in the different classes. |

| | | |

| ** | The average annual total returns shown above are adjusted for maximum sales loads and fees, if applicable. The maximum offering price per share of Class A shares is equal to the net asset value (“NAV”) per share plus a sales load equal to 5.26% of the NAV (or 5.00% of the offering price). Class C shares are subject to a contingent deferred sales charge (“CDSC”) of 1.00%. The CDSC will be assessed on an amount equal to the lesser of (1) the NAV at the time of purchase of the shares being redeemed or (2) the NAV of such shares being redeemed, if redeemed within a one-year period from the date of purchase. Class Y shares and Institutional Class shares are not subject to sales charges. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Notes to Chart

Russell 3000® Growth Index measures the performance of those Russell 3000® companies with higher price-to-book ratios and higher forecasted growth values.

The Frank Russell Company (FRC) is the source and owner of the Index data contained or reflected in this material and all trademarks and copyrights related thereto. The material may contain confidential information and unauthorized use, disclosure, copying, dissemination or redistribution is strictly prohibited. This is a Touchstone Investments presentation of the data, and FRC is not responsible for the formatting or configuration of this material or for any inaccuracy in the presentation thereof.

Management's Discussion of Fund Performance (Unaudited)

Touchstone Mid Cap Growth Fund

Sub-Advised by Westfield Capital Management Company, L.P.

Investment Philosophy

The Touchstone Mid Cap Growth Fund seeks to increase the value of Fund shares by primarily investing in stocks of mid-cap U.S. companies. The Fund’s portfolio managers place focus on companies that they believe to have a demonstrated record of achievement with excellent prospects for earnings growth over a 1-to-3-year period. Westfield looks for companies that it believes are reasonably priced with high forecasted earnings potential.

Fund Performance

The Touchstone Mid Cap Growth Fund (Class A Shares) outperformed its benchmark, the Russell Midcap®Growth Index, for the 12-month period ended March 31, 2020, although both posted negative returns. The Fund’s total return was -8.78 percent (calculated excluding the maximum sales charge), while the total return of the benchmark was -9.45 percent.

Market Environment

Throughout 2019, U.S. equity markets steadily advanced, closing out their best year since 2013 despite ongoing skepticism of the market’s strength. An accommodative U.S Federal Reserve Board (Fed) and easing trade tensions combined with continued U.S. consumer strength and low unemployment to fuel the market advance throughout the year. 2020 began with stocks making new all-time highs, driven by an economy operating at full employment, absent inflationary pressures, an accommodative Fed, and waning concerns over trade negotiations. However, markets turned sharply lower in February when it became apparent that COVID-19 had arrived in the U.S. and containment was no longer possible. The rise of the virus impaired the economic backdrop for global growth and precipitated the sharpest and fastest decline ever for the economy and the stock market. Deleveraging and forced liquidations of stocks and bonds resulted in extreme volatility as investors sought the safety of cash above all else. Oil demand dried up, credit spreads showed signs of stress, and massive stimulus measures were implemented across the world.

Within the benchmark, only the Real Estate and Consumer Staples sectors generated positive returns. The Energy, Consumer Discretionary, Communication Services, Materials and Industrials sectors all declined more than ten percent.

Portfolio Review

Strong stock selection within the Health Care, Industrials, Financials, and Real Estate sectors contributed to the Fund’s relative results. Health Care posted the top relative and absolute results during the twelve months. Stock selection drove the majority of the relative strength in the Health Care sector; however, the Fund’s overweight positioning was also beneficial to relative results. We continued to find opportunities within the Health Care sector that offer exciting, innovation-driven growth. We remain constructive on the group broadly, and believe that there are attractive opportunities across a variety of sub-sectors including health care tools and equipment, medical technology, and therapeutics. The Medicines Company, a late-stage drug developer focused on cholesterol management therapies for cardiovascular disease and long-term high conviction holding of the Fund, was the key driver for both the sector and the Fund during the period. The stock was up after the late November announcement that Novartis International AG was acquiring the company at a premium. The Fund also benefited from exposure to DexCom, Inc., a leader in continuous glucose monitoring (CGM). We believe DexCom has further distanced itself from competitors with advancements in technology allowing its sensor to work with newer insulin pumps. We continue to see a strong growth runway for the company, positioning itself to capitalize on a growing total addressable market in the sensor space.

The Industrials sector was also a source of both relative and absolute strength for the Fund, driven by strong stock selection. This sector has been particularly impacted by slowing business activity and recession fears brought about by trade worries, slowing global growth and more recently COVID-19. Despite macroeconomic concerns, we believe exciting growth opportunities remain in the group, especially within certain segments such as domestic manufacturing, transportation, and machinery. Given the more recent change in economic backdrop, we have reduced exposure to the more cyclically sensitive Industrials stocks and added to more defensive investments. One notable investment within the sector is Teledyne Technologies, Inc., an aerospace & defense company which provides electronic and communication products for wireless and satellite systems. Management continued to execute at a high level and the long-term secular growth story remains intact in our view.

The Information Technology sector was the primary detractor from relative results during the period. Technology stocks outperformed the broader market during the period, led by strength within the semiconductors & semiconductor equipment and software industries. Within semiconductors, the performance shortfall stemmed from businesses the Fund didn’t own, while the Fund’s investments within the industry added to relative results. Despite relative strength from many holdings within software, returns for the group were held back by relative weakness within a few businesses. We believe companies in this sector are playing an increasingly important role across many different segments of the economy, some by driving forward the digital transformations of modern businesses while others provide key enabling technologies for future growth areas such as autonomous driving, artificial intelligence, and the

Management's Discussion of Fund Performance (Unaudited) (Continued)

internet of things. Many companies are also benefiting from the rapid transition to work-from-home operations and a shift in consumer traffic to predominantly online. We continue to seek out companies with advantaged exposure to some key growth areas whether it’s through a unique product pipeline, a large addressable market, or an advantaged competitive position. Palo Alto Networks, Inc., a provider of network security solutions, detracted from results after reporting disappointing product revenues for three consecutive quarters. The stock was sold in March as the risk of further downside remained due to an insufficient reset of investor expectations, in our opinion.

The Energy sector was also a source of relative weakness. An unprecedented combination of supply and demand issues led to a dramatic decline in energy commodities and stocks within the sector in the first quarter of 2020. The effects of COVID-19, the most disruptive event ever for Energy companies, has the potential for global demand to be down nearly 25 percent in the second quarter 2020. Contributing to the negative results in the sector was the ongoing conflict between Russia and Saudi Arabia, introducing additional long-term concerns to industry supply discipline. Given the macro uncertainty facing the sector, we decided to exit Fund investments in the group, Marathon Petroleum Corporation and Pioneer Natural Resources Company. We continue to monitor the space and look to opportunistically reinvest in idiosyncratic growth stories that can benefit from future changes in supply or demand.

Outlook

While headlines continue to show spikes in reported infections, and another move lower is certainly possible, we do believe that the brunt of the risk repricing has already occurred. We could also point to signs that are typically evident during a “bottoming” process like panic selling, forced liquidations, and deleveraging by quantitative strategies but acknowledge we are in unchartered territory. Our view, and hope, is that the policies enacted in the U.S. will help the economy bridge the gap from now until workers can safely return to their jobs. When that happens, our expectation remains for recovery in economic activity, albeit at a measured pace until a viable therapeutic agent and, ultimately, a vaccine is mass produced. We remain committed to a balanced approach within the Fund and have exposure to both defensive stocks which provide a ballast during turbulent times, as well as those more economically sensitive names that we believe will benefit most when activity resumes to pre-crisis levels.

As a fundamental, bottom-up manager, macro-economic forecasts do not drive our stock selection process but do help to shape our investment themes. We continue to find exciting opportunities in areas that offer secular growth and innovation. In regard to specific sectors, we believe Health Care and Information Technology represent some of the top sectors of the market. In this environment, we believe that high quality businesses supported by strong cash flows and healthy revenue streams should be better able to weather the storm. Additionally, we believe that the Health Care and Information Technology sectors are both beneficiaries of some of the impacts from COVID-19.

Following the market sell-off, we are now beginning to see variations in price action which suggest that price discovery is once again taking place after a period where forced liquidations drove much of the market. Additionally, we have tried to be opportunistic during these dislocations, adding to high-conviction holdings and swapping positions for stocks with what we believe are better risk-return profiles. We like the way the Fund is positioned. As a bottom-up, fundamental manager, we continue to focus on company fundamentals and look to buy stocks of quality U.S. companies at attractive valuations with strong growth prospects over time.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the Touchstone Mid Cap Growth Fund - Class

A* and the Russell Midcap® Growth Index

| | * | The chart above represents performance of Class A shares only, which will vary from the performance of Class C shares, Class Y shares, Class R6 shares and Institutional Class shares based on the differences in sales loads and fees paid by shareholders in the different classes. The inception date of Class R6 shares and Institutional Class shares was February 10, 2020 and April 1, 2011, respectively. Institutional Class shares performance information was calculated using the historical performance of Class A shares for periods prior to April 1, 2011. Class R6 shares performance information was calculated using the historical performance of Institutional Class shares for periods prior to February 10, 2020. The returns have been restated for fees applicable to Class R6 and Institutional Class shares. |

| | | |

| ** | The average annual total returns shown above are adjusted for maximum sales loads and fees, if applicable. The maximum offering price per share of Class A shares is equal to the net asset value (“NAV”) per share plus a sales load equal to 5.26% of the NAV (or 5.00% of the offering price). Class C shares are subject to a contingent deferred sales charge (“CDSC”) of 1.00%. The CDSC will be assessed on an amount equal to the lesser of (1) the NAV at the time of purchase of the shares being redeemed or (2) the NAV of such shares being redeemed, if redeemed within a one-year period from the date of purchase. Class Y shares, Class R6 shares, and Institutional Class shares are not subject to sales charges. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Notes to Chart

Russell Midcap®Growth Index measures the performance of those Russell Midcap® companies with higher price-to-book ratios and higher forecasted growth values.

The Frank Russell Company (FRC) is the source and owner of the Index data contained or reflected in this material and all trademarks and copyrights related thereto. The material may contain confidential information and unauthorized use, disclosure, copying, dissemination or redistribution is strictly prohibited. This is a Touchstone Investments presentation of the data, and FRC is not responsible for the formatting or configuration of this material or for any inaccuracy in the presentation thereof.

Management's Discussion of Fund Performance (Unaudited)

Touchstone Sands Capital Emerging Markets Growth Fund

Sub-Advised by Sands Capital Management, LLC

Investment Philosophy

The Touchstone Sands Capital Emerging Markets Growth Fund seeks long-term capital appreciation. The Fund invests in equity and equity-related securities issued by companies located in Emerging or Frontier Market countries. The Fund’s sub-advisor, Sands Capital Management LLC, uses a “bottom-up” approach to investment selection, as opposed to sector or regional allocations, that focuses on a company’s long-term business fundamentals. Sands Capital seeks companies that have: sustainable above-average earnings growth; a leadership position in a promising business space; significant competitive advantages such as profitability, superior quality or distribution relative to competitors or strong brand and consumer loyalty; a clear mission in an understandable business model; financial strength; and a rational valuation in relation to competitors, the market and business prospects.

Fund Performance

The Touchstone Sands Capital Emerging Markets Growth Fund (Class A Shares) outperformed its benchmark, the MSCI Emerging Markets Index, for the 12-month period ended March 31, 2020, although both posted negative returns. The Fund’s total return was -13.19 percent (calculated excluding the maximum sales charge), while the total return of the benchmark was -17.69 percent.

Market Environment

Following a volatile six months, easing U.S./China trade tensions in the fourth quarter of 2019 resulted in a “risk on” environment for equities globally. This proved short lived, however, as the global coronavirus outbreak sank stocks around the world.

Only one constituent country—Taiwan—eked out a positive return for the period, with all other countries, except for China, falling by double digits. Seventeen constituents experienced drops of more than 30 percent, led by Argentina, which was down over 50 percent. India, Brazil, South Korea, and China were the largest detractors to emerging markets equity returns.

Information Technology was the only sector to produce a positive return, and was one of the top contributors, along with Health Care. The Financials and Energy sectors were the top benchmark detractors.

Portfolio Review

The Fund outperformed the benchmark during the 12-month period largely due to positive allocation and currency effects. Singapore and China were the largest relative contributors from a country perspective, and India was the primary country detractor, largely attributable to Financials and travel-related businesses. From a sector perspective, Communication Services and Consumer Discretionary were the top contributors, while Information Technology and Industrials were the top detractors.

The top five relative individual contributors to investment results were Sea Ltd., Alibaba Group Holding Ltd., Hansoh Pharmaceutical Group Co. Ltd., Anta Sports Products Ltd., and New Oriental Education & Technology Group Inc.

Sea Ltd.: The stock was bolstered by strong results from Sea’s core gaming and ecommerce businesses. Sea was relatively unaffected by the social distancing measures spurred by the coronavirus outbreak given the digital nature of its operations, and the additional free time for users to play games and shop online.

Hansoh Pharmaceutical: The stock rose during the period in response to positive clinical and business results. The Fund sold the business in the third quarter of 2019 due to valuation concerns.

Anta Sports Products: The stock rose as the company executed on its “multibrand, omnichannel, full coverage” strategy. While not immune to the coronavirus outbreak, our long-term thesis remains intact, and our recent consumer surveys strengthened our conviction in the Chinese sportswear industry and Anta’s brand strength.

The top five relative detractors were Trip.com Group Ltd., Bajaj Finance Ltd., Bandhan Bank Ltd., HDFC Bank Ltd., and MakeMyTrip Ltd.

Trip.com: The COVID-19 outbreak meaningfully affected Trip’s business, as all domestic and overseas travel was effectively halted. Despite the near-term headwind, we believe that travel will resume once the outbreak subsides, and we believe that the secular trend of bookings moving online will remain intact.

Bandhan Bank: The stock has been pressured by several factors, including political tensions, promoter stock ownership concerns, and general stress in the Indian financial sector. Despite these external pressures, we continue to favorably view Bandhan’s position as India’s largest microfinance lender by market share.

Management's Discussion of Fund Performance (Unaudited) (Continued)

HDFC Bank: The Indian financials sector has faced several quarters of lingering issues, but most recently, the Reserve Bank of India’s rescue of failing Yes Bank caused panic, threatening a bank run on other private lenders. This, coupled with the coronavirus outbreak, affected all of the Fund’s Indian financials businesses, despite their continued fundamental strength.

During the period, the Fund purchased Bandhan Bank, Hansoh Pharmaceutical, Globant SA, Localiza Rent-a-Car SA, PagSeguro Digital Ltd., Prosus NV,Titan Co. Ltd., and Vincom Retail JSC.The Fund sold Adani Ports, Eicher Motors Ltd., Hansoh Pharmaceutical, IndusInd Bank Ltd., ITC Ltd., Larsen & Toubro Ltd., Medy-Tox Inc., Maruti Suzuki India Ltd., Naspers Ltd., Sands China Ltd., and Zee Entertainment Enterprises Ltd.

The regional and sector exposures are largely a byproduct of the Fund’s bottom-up investment process. While general positioning remained directionally unchanged, below are some highlights from the past year:

| • | The Fund’s allocation to Emerging Asia fell in absolute and relative terms. However, this remains the Fund’s largest regional overweight. The reduction was largely due to exits, which included six Indian businesses. |

| • | Emerging Asia’s decrease was balanced in part by an absolute increase to Asia/Pacific ex-Japan. The Fund purchased no new businesses in this region, but raised the weights in existing holdings due to stronger conviction. Despite the increased weight, the region remains the Fund’s largest underweight. |

| • | The Fund’s allocation to Latin America also increased in absolute terms, resulting in an overweight to the region. Holdings in the region increased over the period from three to six. |

| • | From a sector perspective, the Fund’s largest overweights remained Consumer Discretionary, Communication Services, and Health Care, while the largest underweights remained Information Technology, Financials, and Energy. |

Outlook

We continue to monitor the effects of the global coronavirus outbreak on portfolio businesses and the broader economy. We believe that businesses that can survive and thrive are those that continue to invest in their people, processes, product/services, and brands. These businesses’ earnings will likely be higher over a five-year period, resulting in opportunities for active investors in leading, innovative growth businesses.

We believe powerful secular trends will continue beyond the outbreak, and these shifts will change how people bank, communicate, and shop. In some cases, the outbreak may even cause these trends to accelerate. Many of the businesses in the Fund’s portfolio have the potential to benefit from one or more of the following secular trends: 1) Rise of Internet Penetration; 2) Formalization of Retail; 3) Hard & Soft Infrastructure; and 4) Financial Penetration.

Rising internet connectivity and mobile device penetration are spurring broad-based economic activity in emerging markets. Commercial opportunities—including ecommerce, online travel, and ride sharing—are being enabled by new cloud, logistics, and enterprise solutions. The internet is changing how people consume information, leading to opportunities for advertisers and digital media providers. Potential portfolio beneficiaries include Alibaba Group Holding Ltd., MercadoLibre Inc., Sea Ltd., and Tencent Holdings Ltd.

The shift from fragmented industries to consolidated operators offers powerful opportunities in many emerging economies. Informal “mom and pop” vendors lack the product selection, quality, and shopping experience offered by formal competitors. Formal retailers with compelling brands and/or store formats have the opportunity to take share and consolidate the market, particularly as consumer incomes rise and demand increases for better quality and greater selection. Potential portfolio beneficiaries include Anta Sports Products Ltd., Asian Paints Ltd., CP All PLC, and Jubilant Foodworks Ltd.

Substantial infrastructure investment and development are required to enhance productivity and stimulate demand. We see several countries beginning to enact pro-growth policies that should help sustain future domestic growth. Opportunities exist in both hard infrastructure—such as new roads and airports, and in soft infrastructure, which includes education and health care. Potential portfolio beneficiaries include Apollo Hospitals Enterprise Ltd., Grupo Aeroportuario del Sureste, New Oriental Education & Technology Group Inc. and Wuxi Biologics Cayman Inc.

Approximately a third of the world’s adult population remains unbanked, and nearly all of them live in emerging markets. New technologies are enabling access to basic financial products and services. Businesses serving the needs of the growing middle class should benefit from increasing demand for consumer financing. Potential portfolio beneficiaries include AIA Group Ltd., Bajaj Finance Ltd., Bank Central Asia, and HDFC Bank Ltd.

Not all emerging markets are created equal. The opportunity set consists of companies from over 25 countries, each with distinct growth prospects, central bank policy, demographics, and economic composition/exposures.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Selectivity matters, and we continue to believe that our criteria-driven approach enables us to navigate the complexities and nuances within emerging markets. Ultimately, we believe that stock prices follow earnings growth, and we seek to invest in those businesses capable of driving above-average growth across market cycles.

We don’t know what the next quarter or year will bring. However, we remain comfortable with accepting short-term volatility for long-term value-creation potential, and are confident that the businesses we own will continue to deliver above-average earnings growth over our investment horizon.

Comparison of the Change in Value of a $10,000 Investment in the Touchstone Sands Capital Emerging

Markets Growth Fund - Class A* and the MSCI Emerging Markets Index

* The chart above represents performance of Class A shares only, which will vary from the performance of Class C shares, Class Y shares and Institutional Class shares based on the differences in sales loads and fees paid by shareholders in the different classes. The inception date of Class A shares, Class C shares, Class Y shares and Institutional Class shares was November 16, 2018, November 16, 2018, May 9, 2014 and May 9, 2014, respectively. Class A shares and Class C shares performance information was calculated using the historical performance of Class Y shares for periods prior to November 16, 2018. The returns have been restated for sales loads and fees applicable to Class A and Class C shares. The returns of the index listed above are based on the inception date of the Fund.

| ** | The average annual total returns shown above are adjusted for maximum sales loads and fees, if applicable. The maximum offering price per share of Class A shares is equal to the net asset value (“NAV”) per share plus a sales load equal to 5.26% of the NAV (or 5.00% of the offering price). Class C shares are subject to a contingent deferred sales charge (“CDSC”) of 1.00%. The CDSC will be assessed on an amount equal to the lesser of (1) the NAV at the time of purchase of the shares being redeemed or (2) the NAV of such shares being redeemed, if redeemed within a one-year period from the date of purchase. Class Y shares and Institutional Class shares are not subject to sales charges. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Notes to Chart

MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.