| UNITED STATES |

| SECURITIES AND EXCHANGE COMMISSION |

| Washington, D.C. 20549 |

| |

| |

| FORM N-CSR |

| |

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT |

| INVESTMENT COMPANIES |

| |

| Investment Company Act file number 811-3721 |

| |

| DREYFUS INTERMEDIATE MUNICIPAL BOND FUND, INC. |

| (Exact name of Registrant as specified in charter) |

| |

| |

| c/o The Dreyfus Corporation |

| 200 Park Avenue |

| New York, New York 10166 |

| (Address of principal executive offices) (Zip code) |

| |

| Mark N. Jacobs, Esq. |

| 200 Park Avenue |

| New York, New York 10166 |

| (Name and address of agent for service) |

| |

| Registrant's telephone number, including area code: (212) 922-6000 |

| Date of fiscal year end: | | 5/31 |

| Date of reporting period: | | 5/31/05 |

| | | | | FORM N-CSR |

| Item 1. | | Reports to Stockholders. | | |

Save time. Save paper. View your next shareholder report online as soon as it’s available. Log into www.dreyfus.com and sign up for Dreyfus eCommunications. It’s simple and only takes a few minutes.

The views expressed in this report reflect those of the portfolio manager only through the end of the period covered and do not necessarily represent the views of Dreyfus or any other person in the Dreyfus organization. Any such views are subject to change at any time based upon market or other conditions and Dreyfus disclaims any responsibility to update such views.These views may not be relied on as investment advice and, because investment decisions for a Dreyfus fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Dreyfus fund.

Not FDIC-Insured • Not Bank-Guaranteed • May Lose Value

| | | Contents |

| |

| | | THE FUND |

| |

|

| 2 | | Letter from the Chairman |

| 3 | | Discussion of Fund Performance |

| 6 | | Fund Performance |

| 7 | | Understanding Your Fund’s Expenses |

| 7 | | Comparing Your Fund’s Expenses |

| | | With Those of Other Funds |

| 8 | | Statement of Investments |

| 22 | | Statement of Assets and Liabilities |

| 23 | | Statement of Operations |

| 24 | | Statement of Changes in Net Assets |

| 25 | | Financial Highlights |

| 26 | | Notes to Financial Statements |

| 32 | | Report of Independent Registered |

| | | Public Accounting Firm |

| 33 | | Important Tax Information |

| 34 | | Information About the Review and Approval |

| | | of the Fund’s Management Agreement |

| 38 | | Board Members Information |

| 40 | | Officers of the Fund |

| | | FOR MORE INFORMATION |

| |

|

| | | Back Cover |

The Fund

| Dreyfus Intermediate Municipal |

| Bond Fund, Inc. |

LETTER FROM THE CHAIRMAN

We are pleased to present this annual report for Dreyfus Intermediate Municipal Bond Fund, Inc., covering the 12-month period from June 1, 2004, through May 31, 2005. Inside, you’ll find valuable information about how the fund was managed during the reporting period, including a discussion with the fund’s portfolio manager, Monica S.Wieboldt.

Despite occasional bouts of heightened volatility, the reporting period produced generally good results for longer-term municipal bonds. Although the Federal Reserve Board began to raise short-term interest rates in June 2004, longer-term bonds remained remarkably resilient as investors responded to new signs of global economic weakness.These factors supported a market rally in April and May 2005, which more than offset earlier weakness among tax-exempt bonds, including those with intermediate-term maturities.

According to our economists, recent market turbulence probably is the result of a transition to a more mature phase of the economic cycle; one that typically is characterized by tighter monetary policy and slowing corporate profit growth. At times such as these, we believe it is especially important for investors to stay in touch with their financial advisors, as they can help you decide what adjustments, if any, you should make to your long-term investment strategy.

Thank you for your continued confidence and support.

DISCUSSION OF FUND PERFORMANCE

Monica S. Wieboldt, Senior Portfolio Manager

How did Dreyfus Intermediate Municipal Bond Fund, Inc.

perform relative to its benchmark?

|

For the 12-month period ended May 31, 2005, the fund achieved a total return of 5.59% .1 The Lehman Brothers 7-Year Municipal Bond Index (the “Index”), the fund’s benchmark, achieved a total return of 5.83% for the same period.2 In addition, the average total return for all funds reported in the Lipper Intermediate Municipal Debt Funds category was 4.83% .3

Although shorter-term bond prices generally declined during the reporting period amid steadily rising interest rates, longer-term securities gained value as inflationary pressures apparently remained in check. The fund produced a higher return than its Lipper category average, due in part to its relatively underweight positioning at the short-end of the yield curve, where volatility was particularly pronounced. However, the fund produced a slightly lower return than that of its benchmark — which is not subject to fund fees and expenses.

What is the fund’s investment approach?

The fund seeks the maximum amount of current income exempt from federal income tax as is consistent with the preservation of capital.To pursue this goal, the fund normally invests substantially all of its assets in municipal bonds that provide income exempt from federal personal income tax.

The fund invests at least 80% of its assets in municipal bonds rated A or higher, or the unrated equivalent as determined by Dreyfus. The fund may invest up to 20% of its assets in municipal bonds rated below A, including bonds rated below investment grade (“high yield” or “junk” bonds) or the unrated equivalent as determined by Dreyfus. The dollar-weighted average maturity of the fund’s portfolio ranges between three and 10 years.

| | DISCUSSION OF FUND PERFORMANCE (continued)

|

We may buy and sell bonds based on credit quality, market outlook and yield potential. In selecting municipal bonds for investment, we may assess the current interest-rate environment and the municipal bond’s potential volatility in different rate environments.We focus on bonds with the potential to offer attractive current income, typically looking for bonds that can provide consistently attractive current yields or that are trading at competitive market prices.A portion of the fund’s assets may be allocated to “discount” bonds, which are bonds that sell at a price below their face value, or to “premium” bonds, which are bonds that sell at a price above their face value.The fund’s allocation to either discount bonds or to premium bonds will change along with our changing views of the current interest-rate and market environment.We also may look to select bonds that are most likely to obtain attractive prices when sold.

What other factors influenced the fund’s performance?

When the reporting period began, the U.S. economy appeared to be gaining strength and inflationary pressures seemed to be rising as the labor market improved and energy prices surged. In late June 2004, these factors led the Federal Reserve Board (the “Fed”) to implement its first increase of short-term interest rates in approximately four years. Seven additional rate hikes followed, and the overnight federal funds rate rose to 3% by the end of the reporting period as the Fed attempted to bring interest rates to a level that neither stimulated nor restricted economic activity.

Although the Fed’s moves toward higher interest rates were steady and gradual throughout the reporting period, investor sentiment shifted relatively frequently, leading to heightened volatility among shorter-term fixed-income securities. In addition, intermediate-term bonds were adversely affected at times by the trading strategies of certain non-traditional market participants, such as hedge funds. However, longer-term bond prices remained relatively stable, as investors apparently believed that the pace of economic growth was not strong enough to fuel a reacceleration of inflation. In fact, signs of renewed

economic weakness late in the reporting period helped ease inflation concerns and sparked a sharp market rally, helping the fund post a solidly positive total return for the reporting period overall.

As short-term yields rose relative to longer-term yields, we attempted to protect the fund from volatility by reducing its exposure to securities at the shorter end of its maturity range.Instead,we tended to focus on securities in the intermediate-term range, generally the 10- to 15-year range, where returns proved to be relatively attractive.In addition,the fund benefited from strong performance among its holdings of corporate-backed bonds, such as securities backed by the states’ settlement of litigation with U.S. tobacco companies.These securities benefited from robust investor demand for high current income in a low interest-rate environment.

What is the fund’s current strategy?

In anticipation of further increases in interest rates, we have maintained the fund’s relatively light exposure to shorter-term securities. However, as yield differences between short- and long-term bonds continue to narrow, we will reevaluate the advantages of this position, and we may increase the fund’s holdings at the shorter end of its maturity range. In our view, these are prudent strategies as the economy moves to the next phase of the cycle.

| 1 | | Total return includes reinvestment of dividends and any capital gains paid. Past performance is no |

| | | guarantee of future results. Share price, yield and investment return fluctuate such that upon |

| | | redemption, fund shares may be worth more or less than their original cost. Income may be subject |

| | | to state and local taxes, and some income may be subject to the federal alternative minimum tax |

| | | (AMT) for certain investors. Capital gains, if any, are fully taxable. Return figure provided reflects |

| | | the absorption of fund expenses by The Dreyfus Corporation pursuant to an undertaking in effect |

| | | that may be modified, extended or terminated at any time. Had these expenses not been absorbed, |

| | | the fund’s return would have been lower. |

| 2 | | SOURCE: LIPPER INC. — Reflects reinvestment of dividends and, where applicable, capital |

| | | gain distributions.The Lehman Brothers 7-Year Municipal Bond Index is an unmanaged total |

| | | return performance benchmark for the investment-grade, geographically unrestricted 7-year tax- |

| | | exempt bond market, consisting of municipal bonds with maturities of 6-8 years. Index returns do |

| | | not reflect fees and expenses associated with operating a mutual fund. |

| 3 | | Source: Lipper Inc. |

| Average Annual Total Returns | | as of 5/31/05 | | | | | | |

| | | | | 1 Year | | 5 Years | | 10 Years |

| |

| |

| |

| |

|

| Fund | | | | 5.59% | | 5.25% | | 4.68% |

† Source: Lipper Inc.

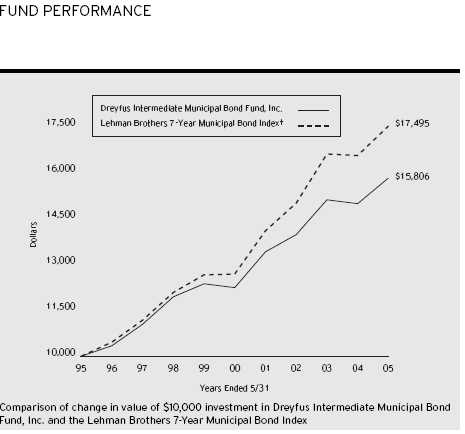

Past performance is not predictive of future performance.The fund’s performance shown in the graph and table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The above graph compares a $10,000 investment made in Dreyfus Intermediate Municipal Bond Fund, Inc. on 5/31/95 to a $10,000 investment made in the Lehman Brothers 7-Year Municipal Bond Index (the “Index”) on that date.All dividends and capital gain distributions are reinvested.

The fund invests primarily in municipal securities and maintains a portfolio with a weighted average maturity ranging between 3 and 10 years.The fund’s performance shown in the line graph above takes into account fees and expenses.The Index, unlike the fund, is an unmanaged total return performance benchmark for the investment-grade, geographically unrestricted 7-year tax-exempt bond market, consisting of municipal bonds with maturities of 6-8 years.The Index does not take into account charges, fees and other expenses.These factors can contribute to the Index potentially outperforming or underperforming the fund. Further information relating to fund performance, including expense reimbursements, if applicable, is contained in the Financial Highlights section of the prospectus and elsewhere in this report.

U N D E R S TA N D I N G YO U R F U N D ’ S E X P E N S E S ( U n a u d i t e d )

As a mutual fund investor, you pay ongoing expenses, such as management fees and other expenses. Using the information below, you can estimate how these expenses affect your investment and compare them with the expenses of other funds.You also may pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial adviser.

Review your fund’s expenses

The table below shows the expenses you would have paid on a $1,000 investment in Dreyfus Intermediate Municipal Bond Fund, Inc. from December 1, 2004 to May 31, 2005. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

| Expenses and Value of a $1,000 Investment |

| assuming actual returns for the six months ended May 31, 2005 |

|

| |

| Expenses paid per $1,000 † | | $ 3.68 |

| Ending value (after expenses) | | $1,022.50 |

COMPARING YOUR FUND’S EXPENSES

WITH THOSE OF OTHER FUNDS (Unaudited)

|

Using the SEC’s method to compare expenses

The Securities and Exchange Commission (SEC) has established guidelines to help investors assess fund expenses. Per these guidelines, the table below shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total cost) of investing in the fund with those of other funds.All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

| Expenses and Value of a $1,000 Investment |

| assuming a hypothetical 5% annualized return for the six months ended May 31, 2005 |

|

| |

| Expenses paid per $1,000 † | | $ 3.68 |

| Ending value (after expenses) | | $1,021.29 |

| |

| † Expenses are equal to the fund’s annualized expense ratio of .73%, multiplied by the average account value over the |

| period, multiplied by 182/365 (to reflect the one-half year period). |

| | STATEMENT OF INVESTMENTS

May 31, 2005

|

| | | Principal | | |

| Long-Term Municipal Investments—99.0% | | Amount ($) | | Value ($) |

| |

| |

|

| Alabama—1.8% | | | | |

| McIntosh Industrial Development Board, EIR | | | | |

| 4.65%, 6/1/2008 | | 1,450,000 | | 1,499,270 |

| Jefferson County, Limited Obligation School Warrants: | | |

| 5.50%, 1/1/2021 | | 7,500,000 | | 8,293,049 |

| 5.25%, 1/1/2023 | | 5,500,000 | | 5,928,834 |

| Alaska—5.1% | | | | |

| Alaska International Airports, Revenue: | | | | |

| 5.50%, 10/1/2011 (Insured; AMBAC) | | 2,560,000 | | 2,866,969 |

| 5.50%, 10/1/2012 (Insured; AMBAC) | | 1,620,000 | | 1,827,327 |

| Alaska Student Loan Corp., Student Loan Revenue: | | | | |

| 5.60%, 7/1/2011 (Insured; AMBAC) | | 4,700,000 | | 4,916,246 |

| 5.70%, 7/1/2013 (Insured; AMBAC) | | 5,990,000 | | 6,277,579 |

| 6%, 7/1/2016 (Insured; AMBAC) | | 6,380,000 | | 6,955,347 |

| Anchorage: | | | | |

| 5.875%, 12/1/2015 (Insured; FGIC) | | | | |

| (Prerefunded 12/1/2010) | | 2,365,000 a | | 2,691,323 |

| 5.875%, 12/1/2016 (Insured; FGIC) | | | | |

| (Prerefunded 12/1/2010) | | 1,500,000 a | | 1,706,970 |

| Electric Utility Revenue: | | | | |

| 6.50%, 12/1/2008 (Insured; MBIA) | | 2,755,000 | | 3,069,428 |

| 6.50%, 12/1/2009 (Insured; MBIA) | | 2,910,000 | | 3,314,985 |

| 5.875%, 2/1/2012 (Insured; FSA) | | | | |

| (Prerefunded 2/1/2010) | | 3,175,000 a | | 3,562,541 |

| Northern Tobacco Securitization Corp., | | | | |

| Tobacco Settlement Revenue: | | | | |

| 6%, 6/1/2013 | | 4,745,000 | | 5,050,720 |

| 6.20%, 6/1/2022 | | 2,250,000 | | 2,298,848 |

| Arizona—.3% | | | | |

| Glendale Municipal Property Corp., Excise Tax Revenue | | |

| 5%, 7/1/2017 (Insured; AMBAC) | | 2,160,000 | | 2,351,419 |

| Arkansas—.8% | | | | |

| Independence County, PCR | | | | |

| (Entergy Arkansas Inc., Project) 5%, 1/1/2021 | | 5,250,000 | | 5,352,375 |

| Springdale, Sales & Use Tax Revenue | | | | |

| 4%, 7/1/2016 (Insured; MBIA) | | 2,000,000 | | 2,044,180 |

| California—6.3% | | | | |

| ABAG Finance Authority for Nonprofit Corporations, | | | | |

| Revenue (San Diego Hospital Association) | | | | |

| 5.125%, 3/1/2018 | | 1,000,000 | | 1,053,080 |

| | | Principal | | | | |

| Long-Term Municipal Investments (continued) | | Amount ($) | | Value ($) |

| |

| |

|

| California (continued) | | | | | | |

| Alameda County Unified School District | | | | | | |

| Zero Coupon, 8/1/2018 (Insured; FSA) | | 3,785,000 | | | | 2,120,849 |

| California Economic Recovery | | | | | | |

| 5%, 7/1/2015 (Insured; MBIA) | | 5,000,000 | | | | 5,531,950 |

| California Educational Facilities Authority, Revenue | | | | | | |

| (Stanford University) 5.25%, 12/1/2013 | | 2,000,000 | | | | 2,283,520 |

| California Infrastructure & Economic Development, | | | | | | |

| Bank Revenue (Bay Area Toll Bridges—1st Lien) | | | | | | |

| 5.25%, 7/1/2017 (Insured; FSA) | | 3,300,000 | | | | 3,676,398 |

| California Public Works Board, LR | | | | | | |

| (Department of Mental Health—Coalinga) | | | | | | |

| 5.50%, 6/1/2018 | | 3,000,000 | | | | 3,367,440 |

| California Statewide Community Development Authority: | | | | | | |

| MFHR (Equity Residential) 5.20%, 6/15/2009 | | 3,000,000 | | | | 3,174,720 |

| Revenue (Huntington Memorial Hospital) | | | | | | |

| 5%, 7/1/2017 | | 2,895,000 | | | | 3,112,038 |

| Elsinore Valley Municipal Water District, COP | | | | | | |

| 5.375%, 7/1/2016 (Insured; FGIC) | | 3,295,000 | | | | 3,768,788 |

| Foothill/Eastern Transportation Corridor Agency, | | | | | | |

| Toll Road Revenue | | | | | | |

| 0% / 7%, 1/1/2008 | | 5,000,000 | | b | | 5,519,000 |

| Golden State Tobacco Securitization Corporation, | | | | | | |

| Tobacco Settlement Revenue: | | | | | | |

| 5.50%, 6/1/2018 | | 5,000,000 | | | | 5,231,500 |

| 5.75%, 6/1/2021 | | 6,950,000 | | | | 7,462,424 |

| 5.75%, 6/1/2023 | | 1,735,000 | | | | 1,853,674 |

| Los Angeles County Public Works Financing Authority, | | | | | | |

| Revenue (Regional Park & Open Space District): | | | | | | |

| 5%, 10/1/2019 (Prerefunded 10/1/2007) | | 3,635,000 | | a | | 3,853,027 |

| 5%, 10/1/2019 | | 1,915,000 | | | | 2,008,950 |

| Colorado—1.3% | | | | | | |

| Denver City & County, Airport Revenue | | | | | | |

| 5%, 11/15/2008 (Insured; XLCA) | | 5,000,000 | | | | 5,282,900 |

| El Paso County School District | | | | | | |

| (Number 11 Colorado Springs): | | | | | | |

| 6.25%, 12/1/2009 | | 1,000,000 | | | | 1,133,250 |

| 6.50%, 12/1/2010 | | 2,000,000 | | | | 2,337,140 |

| 6.50%, 12/1/2011 | | 2,040,000 | | | | 2,428,559 |

STATEMENT OF INVESTMENTS (continued)

|

| | | Principal | | |

| Long-Term Municipal Investments (continued) | | Amount ($) | | Value ($) |

| |

| |

|

| Connecticut—.7% | | | | |

| Connecticut: | | | | |

| Revenue (Mashantucket Western Pequot Tribe): | | | | |

| 6.50%, 9/1/2006 | | 2,475,000 c | | 2,585,905 |

| 6.50%, 9/1/2006 | | 2,525,000 c | | 2,607,669 |

| 5.60%, 9/1/2009 | | 1,000,000 c | | 1,066,760 |

| District of Columbia—.4% | | | | |

| District of Columbia 6%, 6/1/2012 (Insured; MBIA) | | 3,280,000 | | 3,794,665 |

| Florida—4.5% | | | | |

| Broward County, Airport System Revenue | | | | |

| (Convertible Lien) 5.25%, 10/1/2011 (Insured; AMBAC) | | 1,525,000 | | 1,619,550 |

| Capital Projects Finance Authority, Student Housing | | | | |

| Revenue (Capital Projects Loan Program) | | | | |

| 5.50%, 10/1/2015 (Insured; MBIA) | | 4,060,000 | | 4,434,576 |

| Collier County, Gas Tax Revenue | | | | |

| 5.25%, 6/1/2019 (Insured; AMBAC) | | 2,190,000 | | 2,418,417 |

| Hillsborough County Industrial Development Authority, | | | | |

| PCR (Tampa Electric Company Project) | | | | |

| 5.10%, 10/1/2013 | | 9,575,000 | | 10,106,700 |

| Miami-Dade County, Aviation Revenue | | | | |

| 5.25%, 10/1/2008 (Insured; FGIC) | | 3,000,000 | | 3,198,240 |

| Miami-Dade County School Board, COP | | | | |

| 5.25%, 10/1/2017 (Insured; FGIC) | | 5,000,000 | | 5,562,850 |

| Palm Beach County School Board, COP | | | | |

| 5.375%, 8/1/2014 (Insured; AMBAC) | | 4,000,000 | | 4,560,680 |

| Palm Beach County Solid Waste Authority, Revenue | | | | |

| 4%, 1/1/2011 (Insured; AMBAC) | | 5,000,000 | | 5,192,600 |

| Polk County, Utility System Revenue | | | | |

| 5.25%, 10/1/2018 (Insured; FGIC) | | 2,000,000 | | 2,218,940 |

| Georgia—1.4% | | | | |

| Athens Housing Authority, Student Housing LR | | | | |

| (Ugaref East Campus Housing): | | | | |

| 5.25%, 12/1/2015 (Insured; AMBAC) | | 2,560,000 | | 2,817,459 |

| 5.25%, 12/1/2016 (Insured; AMBAC) | | 2,700,000 | | 2,965,410 |

| Milledgeville-Baldwin County Development Authority, | | | | |

| Revenue (Georgia College & State | | | | |

| University Foundation): | | | | |

| 6%, 9/1/2010 | | 1,275,000 | | 1,394,582 |

| 5.25%, 9/1/2019 | | 1,710,000 | | 1,806,735 |

| Municipal Electric Authority (Combustion Turbine Project) | | | | |

| 5.25%, 11/1/2012 (Insured; MBIA) | | 2,735,000 | | 3,067,576 |

| |

| |

| 10 | | | | |

| | | Principal | | | | |

| Long-Term Municipal Investments (continued) | | Amount ($) | | Value ($) |

| |

| |

|

| Hawaii—1.5% | | | | | | |

| Hawaii Department of Budget & Finance, | | | | | | |

| Special Purpose Meeting Revenue | | | | | | |

| (Kapiolani Health Care System) | | | | | | |

| 6.40%, 7/1/2013 | | 8,775,000 | | | | 9,951,201 |

| Kuakini Health System, Special Purpose Revenue | | | | | | |

| 5.50%, 7/1/2012 | | 2,575,000 | | | | 2,740,830 |

| Illinois—2.3% | | | | | | |

| Chicago Housing Authority, Revenue (Capital Program): | | | | | | |

| 5%, 7/1/2009 | | 2,500,000 | | | | 2,654,675 |

| 5.25%, 7/1/2010 | | 2,420,000 | | | | 2,617,327 |

| Chicago O’Hare International Airport, Revenue | | | | | | |

| (Third Lien) 5.50%, 1/1/2015 (Insured; CIFG) | | 6,450,000 | | | | 7,274,181 |

| Illinois Health Facilities Authority, Revenue: | | | | | | |

| (Evangelical Hospital) 6.75%, 4/15/2007 | | 100,000 | | | | 104,668 |

| (Passavant Memorial Area Hospital Association) | | | | | | |

| 5.65%, 10/1/2016 | | 4,850,000 | | | | 5,241,250 |

| Metropolitan Pier & Exposition Authority, | | | | | | |

| Dedicated State Tax Revenue (McCormick Place) | | | | | | |

| 0/5.55%, 6/15/2021 (Insured; MBIA) | | 2,500,000 | | b | | 1,953,575 |

| Indiana—2.3% | | | | | | |

| Indiana Health Facility Financing Authority, | | | | | | |

| HR (Clarian Health Partners, Inc.): | | | | | | |

| 5.50%, 2/15/2010 | | 3,000,000 | | | | 3,155,640 |

| 5.50%, 2/15/2011 | | 5,000,000 | | | | 5,250,450 |

| Revenue (Ascension Health) Subordinated | | | | | | |

| Credit 5%, 5/1/2009 | | 2,500,000 | | | | 2,660,550 |

| Indianapolis Local Public Improvement Bond Bank | | | | | | |

| 6.50%, 1/1/2011 (Insured; FSA) | | 6,415,000 | | | | 7,473,283 |

| Westfield High School Building Corp., | | | | | | |

| First Mortgage Revenue | | | | | | |

| 5.25%, 7/5/2013 (Insured; AMBAC) | | 1,500,000 | | | | 1,593,795 |

| Kansas—1.2% | | | | | | |

| Wyandotte County—Kansas City Unified | | | | | | |

| Government, Utility System Revenue | | | | | | |

| 5.65%, 9/1/2018 (Insured; AMBAC) | | 9,130,000 | | | | 10,699,264 |

| Kentucky—.5% | | | | | | |

| Ashland, PCR (Ashland, Inc.) 5.70%, 11/1/2009 | | 4,000,000 | | | | 4,288,560 |

| Louisiana—1.0% | | | | | | |

| New Orleans 5.25%, 12/1/2019 (Insured; MBIA) | | 7,945,000 | | d | | 8,872,817 |

STATEMENT OF INVESTMENTS (continued)

|

| | | Principal | | |

| Long-Term Municipal Investments (continued) | | Amount ($) | | Value ($) |

| |

| |

|

| Massachusetts—5.0% | | | | |

| Boston Water & Sewer Commission, Revenue | | | | |

| 5%, 11/1/2020 | | 5,760,000 | | 6,271,776 |

| Massachusetts, Consolidated Loan | | | | |

| 5%, 12/1/2010 | | 3,000,000 | | 3,268,770 |

| Massachusetts Bay Transportation Authority, Sales Tax | | | | |

| Revenue 5.50%, 7/1/2017 | | 5,000,000 | | 5,809,400 |

| Massachusetts Municipal Wholesale Electric Co., | | | | |

| Power Supply System Revenue | | | | |

| (Project No. 6) 5.25%, 7/1/2015 (Insured; MBIA) | | 4,000,000 | | 4,406,640 |

| Massachusetts Water Resource Authority: | | | | |

| 5.25%, 8/1/2019 (Insured; MBIA) | | 8,420,000 | | 9,560,489 |

| 5%, 8/1/2022 (Insured; MBIA) | | 9,875,000 | | 10,823,395 |

| University of Massachusetts Building Authority, | | | | |

| Project Revenue 5.25%, 11/1/2019 (Insured; AMBAC) | | 3,500,000 | | 3,875,830 |

| Michigan—5.8% | | | | |

| Detroit Local Development Finance Authority | | | | |

| 5.20%, 5/1/2010 | | 5,745,000 | | 5,966,700 |

| Greater Detroit Resource Recovery Authority, Revenue: | | | | |

| 6.25%, Series A, 12/13/2008 (Insured; AMBAC) | | 11,000,000 | | 12,140,920 |

| 6.25%, Series B, 12/13/2008 (Insured; AMBAC) | | 7,755,000 | | 8,559,349 |

| Michigan Building Authority, Revenue | | | | |

| (State Police Communications System) | | | | |

| 5.25%, 10/1/2013 | | 1,945,000 | | 2,197,344 |

| Michigan Hospital Finance Authority, Revenue: | | | | |

| 7.603%, 11/15/2007 | | 5,750,000 c,e | | 6,324,310 |

| (Oakwood Obligation Group): | | | | |

| 5%, 11/1/2007 | | 3,000,000 | | 3,120,840 |

| 5.50%, 11/1/2011 | | 3,500,000 | | 3,856,160 |

| (Sparrow Obligation Group): | | | | |

| 5.25%, 11/15/2011 | | 2,500,000 | | 2,734,925 |

| 5.75%, 11/15/2016 | | 3,250,000 | | 3,585,140 |

| Michigan Municipal Bond Authority, Revenue | | | | |

| (Drinking Water Revolving Fund) | | | | |

| 5.25%, 10/1/2016 (Prerefunded 10/1/2009) | | 2,370,000 a | | 2,582,565 |

| Mississippi—.9% | | | | |

| Mississippi Development Bank, Special Obligation | | | | |

| (Adams County HR Project) | | | | |

| 5.75%, 7/1/2010 (Insured; FSA) | | 3,445,000 | | 3,582,456 |

| Mississippi Higher Education Assistance Corp. | | | | |

| Student Loan Revenue 5.30%, 9/1/2008 | | 2,390,000 | | 2,500,060 |

| |

| |

| |

| 12 | | | | |

| | | Principal | | |

| Long-Term Municipal Investments (continued) | | Amount ($) | | Value ($) |

| |

| |

|

| Mississippi (continued) | | | | |

| Walnut Grove Correctional Authority, COP | | | | |

| 5.50%, 11/1/2007 (Insured; AMBAC) | | 1,855,000 | | 1,967,394 |

| Missouri—1.8% | | | | |

| Joplin Industrial Development Authority, Revenue | | | | |

| (Catholic Health Initiatives): | | | | |

| 5.50%, 12/1/2009 | | 3,185,000 | | 3,378,170 |

| 5.625%, 12/1/2010 | | 3,340,000 | | 3,537,294 |

| Missouri Health & Educational | | | | |

| Facilities Authority, Revenue | | | | |

| (SSM Health Care) 5%, 6/1/2007 | | 2,940,000 | | 3,044,517 |

| Saint Louis, Airport Revenue | | | | |

| (Airport Development Program): | | | | |

| 5.50%, 7/1/2010 (Insured; MBIA) | | 3,000,000 | | 3,302,760 |

| 5.625%, 7/1/2015 (Insured; MBIA) | | 2,500,000 | | 2,783,675 |

| Nevada—1.2% | | | | |

| Director of the State of Nevada Department of Business | | | | |

| & Industry, SWDR (Republic Services, Inc. Project) | | | | |

| 5.625%, 6/2/2018 | | 5,000,000 | | 5,443,600 |

| Washoe County, Water Facility Revenue | | | | |

| (Sierra Pacific Power Company) 5%, 7/1/2009 | | 5,000,000 | | 5,101,200 |

| New Jersey—4.4% | | | | |

| Casino Reinvestment Development Authority, | | | | |

| Revenue 5.25%, 6/1/2019 (Insured; MBIA) | | 5,000,000 | | 5,517,500 |

| New Jersey Economic Development Authority: | | | | |

| Cigarette Tax Revenue 5.50%, 6/15/2016 | | 1,000,000 | | 1,111,260 |

| School Facilities Revenue (Construction 2001) | | | | |

| 5.25%, 6/15/2010 (Insured; AMBAC) | | 10,030,000 | | 11,022,870 |

| Waste Paper Recycling Revenue (Marcal Paper Mills Inc.) | | |

| 8.50%, 2/1/2010 (Insured; MBIA) | | 2,210,000 | | 2,150,838 |

| New Jersey Educational Facilities Authority, Revenue | | | | |

| (Rider University): | | | | |

| 5%, 7/1/2010 (Insured; Radian) | | 1,880,000 | | 2,010,679 |

| 5%, 7/1/2011 (Insured; Radian) | | 1,970,000 | | 2,121,079 |

| (Rowan University) 5.25%, 7/1/2016 (Insured; MBIA) | | 2,000,000 | | 2,244,620 |

| New Jersey Health Care Facilities | | | | |

| Financing Authority, Revenue | | | | |

| (South Jersey Hospital) 6%, 7/1/2012 | | 3,425,000 | | 3,866,277 |

| New Jersey Turnpike Authority, Revenue | | | | |

| 5.625%, 1/1/2015 (Insured MBIA) | | | | |

| (Prerefunded 1/1/2010) | | 3,910,000 a | | 4,343,697 |

STATEMENT OF INVESTMENTS (continued)

|

| | | Principal | | | | |

| Long-Term Municipal Investments (continued) | | Amount ($) | | Value ($) |

| |

| |

|

| New Jersey (continued) | | | | | | |

| Union County Utilities Authority, Solid Waste Revenue | | | | | | |

| (Ogden Martin) 5.50%, 6/1/2008 (Insured; AMBAC) | | 4,000,000 | | | | 4,262,120 |

| New Mexico—1.4% | | | | | | |

| Jicarilla, Apache Nation Revenue: | | | | | | |

| 5%, 9/1/2011 | | 1,500,000 | | | | 1,605,330 |

| 5%, 9/1/2013 | | 2,905,000 | | | | 3,116,745 |

| Las Cruces, Joint Utility Improvement Revenue | | | | | | |

| 5.50%, 7/1/2016 (Insured; MBIA) | | 7,000,000 | | | | 7,469,700 |

| New York—7.5% | | | | | | |

| New York City: | | | | | | |

| 6.25%, 8/1/2009 (Prerefunded 8/1/2006) | | 530,000 | | a | | 558,594 |

| 6.25%, 8/1/2009 | | 1,470,000 | | | | 1,544,985 |

| 5%, 8/1/2014 | | 5,000,000 | | | | 5,481,600 |

| 5%, 4/1/2020 | | 2,500,000 | | | | 2,675,225 |

| 5%, 4/1/2022 | | 5,110,000 | | | | 5,442,610 |

| New York State Dormitory Authority, Revenues: | | | | | | |

| (Department of Health) | | | | | | |

| 5.625%, 7/1/2011 (Prerefunded 7/1/2006) | | 3,240,000 | | a | | 3,399,602 |

| (Lenox Hill Hospital Obligation Group) | | | | | | |

| 5.50%, 7/1/2011 | | 1,000,000 | | | | 1,091,530 |

| New York State Local Government | | | | | | |

| Assistance Corporation: | | | | | | |

| 5.25%, 4/1/2016 | | 3,425,000 | | | | 3,860,866 |

| 5.25%, 4/1/2016 (Insured; FSA) | | 2,200,000 | | | | 2,488,332 |

| New York State Thruway Authority, Service Contract | | | | | | |

| Revenue (Local Highway & Bridge): | | | | | | |

| 6%, 4/1/2011 | | 2,040,000 | | | | 2,185,207 |

| 5.50%, 4/1/2012 | | 3,950,000 | | | | 4,446,673 |

| 5.50%, 4/1/2013 (Insured; XLCA) | | 5,000,000 | | | | 5,598,000 |

| New York State Urban Development Corp.: | | | | | | |

| Corporate Purpose 5.125%, 7/1/2019 | | 2,000,000 | | | | 2,170,680 |

| Correctional & Youth Facilities Service Contract | | | | | | |

| Revenue (Empire State Development Corp.): | | | | | | |

| 5%, 1/1/2009 | | 3,000,000 | | | | 3,168,360 |

| 5.25%, 1/1/2009 | | 8,575,000 | | | | 9,137,606 |

| Personal Income Tax 5.25%, 3/15/2011 | | 1,565,000 | | | | 1,723,237 |

| Tobacco Settlement Financing Corp., Revenue | | | | | | |

| 5.50%, 6/1/2018 | | 4,000,000 | | | | 4,465,280 |

| Triborough Bridge and Tunnel Authority, Revenue | | | | | | |

| 6.75%, 1/1/2009 | | 5,100,000 | | | | 5,531,919 |

| |

| |

| |

| 14 | | | | | | |

| | | Principal | | |

| Long-Term Municipal Investments (continued) | | Amount ($) | | Value ($) |

| |

| |

|

| North Carolina—3.7% | | | | |

| North Carolina Eastern Municipal Power Agency, | | | | |

| Power System Revenue: | | | | |

| 5.50%, 1/1/2012 | | 3,000,000 | | 3,293,580 |

| 5.125%, 1/1/2014 | | 3,000,000 | | 3,211,710 |

| 5%, 1/1/2021 | | 1,200,000 | | 1,353,768 |

| North Carolina Medical Care Commission, Revenue: | | | | |

| (FHA Insured Mortgage—Morehead Memorial Hospital) | | | | |

| 5%, 11/1/2020 (Insured; FSA) | | 5,000,000 d | | 5,405,850 |

| Retirement Facilities (Givens Estate Project): | | | | |

| 4.75%, 7/1/2010 | | 1,000,000 | | 1,015,750 |

| 5%, 7/1/2011 | | 500,000 | | 509,160 |

| 5.25%, 7/1/2012 | | 750,000 | | 770,033 |

| North Carolina Municipal Power Agency | | | | |

| Electric Revenue (Number 1 Catawba): | | | | |

| 5.25%, 1/1/2016 (Insured; FSA) | | 2,540,000 | | 2,796,413 |

| 5.25%, 1/1/2017 (Insured; FSA) | | 10,000,000 | | 10,961,000 |

| Raleigh Durham Airport Authority, Airport Revenue | | | | |

| 5.25%, 11/1/2012 (Insured; FGIC) | | 2,365,000 | | 2,614,058 |

| Ohio—1.3% | | | | |

| Cuyahoga County, Revenue | | | | |

| (Cleveland Clinic Health System): | | | | |

| 5.50%, 1/1/2014 | | 4,000,000 | | 4,456,080 |

| 6%, 1/1/2017 | | 5,000,000 | | 5,697,650 |

| Knox County, Hospital Facilities Revenue | | | | |

| (Knox Community Hospital Asset Guaranty) | | | | |

| 5%, 6/1/2012 (Insured; Radian) | | 1,500,000 | | 1,612,110 |

| Oklahoma—.6% | | | | |

| Oklahoma Development Finance Authority, LR | | | | |

| (Oklahoma State System Higher Education): | | | | |

| 4%, 6/1/2007 | | 1,020,000 | | 1,039,319 |

| 4%, 6/1/2008 | | 1,060,000 | | 1,087,952 |

| Washington County Medical Authority, Revenue | | | | |

| (Jane Phillips Medical Center) | | | | |

| 5.50%, 11/1/2010 (Insured; Connie Lee) | | 3,175,000 | | 3,309,779 |

| Oregon—1.1% | | | | |

| Gilliam County, SWDR | | | | |

| 4.15%, 5/1/2009 | | 3,400,000 | | 3,439,372 |

| Washington County Unified Sewer Agency, | | | | |

| Sewer Revenue 5.75%, 10/1/2012 (Insured; FGIC) | | 5,670,000 | | 6,550,041 |

STATEMENT OF INVESTMENTS (continued)

|

| | | Principal | | |

| Long-Term Municipal Investments (continued) | | Amount ($) | | Value ($) |

| |

| |

|

| Pennsylvania—8.3% | | | | |

| Allegheny County Industrial Development Authority, | | | | |

| PCR 4.05%, 9/1/2011 (Insured; AMBAC) | | 4,000,000 | | 4,157,240 |

| Carbon County Industrial Development Authority, RRR | | | | |

| (Panther Creek Partners Project) 6.65%, 5/1/2010 | | 8,925,000 | | 9,696,120 |

| Delaware County Industrial Development Authority | | | | |

| (Resource Recovery Facility) 6.10%, 7/1/2013 | | 12,000,000 | | 12,610,200 |

| Delaware River Joint Toll Bridge Commission, | | | | |

| Bridge Revenue 5.25%, 7/1/2013 | | 2,500,000 | | 2,790,725 |

| Delaware Valley Regional Finance Authority, | | | | |

| Local Government Revenue 5.75%, 7/1/2017 | | 6,830,000 | | 7,948,344 |

| Erie County Hospital Authority, Revenue | | | | |

| (Hamot Health Foundation) | | | | |

| 5.375%, 5/15/2010 (Insured; AMBAC) | | 2,340,000 | | 2,476,984 |

| Erie County Industrial Development Authority, | | | | |

| EIR (International Paper Company Project) | | | | |

| 5.25%, 9/1/2010 | | 2,100,000 | | 2,258,571 |

| Montgomery County Higher Education & Health | | | | |

| Authority, HR (Abington Memorial) | | | | |

| 6.10%, 6/1/2012 (Insured; AMBAC) | | 5,000,000 | | 5,790,200 |

| Montgomery County Industrial Development | | | | |

| Authority, Mortgage Revenue (Whitemarsh | | | | |

| Continuing Care) 6%, 2/1/2021 | | 5,000,000 | | 5,192,650 |

| Pennsylvania Higher Educational Facilities Authority, | | | | |

| Health Services Revenue (University of Pennsylvania) | | | | |

| 5.70%, 1/1/2011 (Prerefunded 1/1/2006) | | 3,250,000 a | | 3,334,598 |

| (UPMC Health System) 6.25%, 1/15/2015 | | 3,660,000 | | 4,156,442 |

| Rose Tree Media School District | | | | |

| 5.25%, 2/1/2018 (Insured; FSA) | | 5,900,000 | | 6,573,603 |

| Sayre Health Care Facilities Authority, Revenue | | | | |

| (Guthrie Health) 6%, 12/1/2012 | | 2,000,000 | | 2,236,580 |

| State Public School Building Authority, School | | | | |

| Lease Revenue (Colonial Intermediate | | | | |

| Unit) 5.25%, 5/15/2019 (Insured; FGIC) | | 2,175,000 | | 2,425,756 |

| Rhode Island—1.2% | | | | |

| Rhode Island Health and Educational Building Corp.: | | | | |

| Health Facilities Revenue (San Antoine) | | | | |

| 5.50%, 11/15/2009 | | 3,320,000 | | 3,510,502 |

| Hospital Financing Revenue | | | | |

| (Lifespan Obligation Group) | | | | |

| 5.75%, 5/15/2008 (Insured; MBIA) | | 5,560,000 | | 5,943,195 |

| Revenue (Roger Williams University) | | | | |

| 5%, 11/15/2021 (Insured; Radian) | | 1,360,000 | | 1,427,850 |

| |

| 16 | | | | |

| | | Principal | | |

| Long-Term Municipal Investments (continued) | | Amount ($) | | Value ($) |

| |

| |

|

| South Carolina—2.7% | | | | |

| Anderson County, IDR (Federal Paper Board) | | | | |

| 4.75%, 8/1/2010 | | 4,520,000 | | 4,674,132 |

| Berkeley County School District, Installment | | | | |

| Purchase Revenue (Securing Assets for Education) | | | | |

| 5.25%, 12/1/2021 | | 9,395,000 | | 10,017,982 |

| Charleston, COP (Public Facilities Corp.) | | | | |

| 5%, 9/1/2015 | | 2,145,000 | | 2,363,254 |

| Dorchester County School District No. 002, Installment | | | | |

| Purpose Revenue (Growth Remedy Opportunity | | | | |

| Tax Hike) 5.25%, 12/1/2021 | | 5,000,000 | | 5,383,450 |

| Hilton Head Island Public Facilities Corp., COP | | | | |

| 5%, 3/1/2013 (Insured; AMBAC) | | 1,065,000 | | 1,171,958 |

| South Dakota—.2% | | | | |

| Pennington County, PCR (Black Hills | | | | |

| Power Incorporated Project) | | | | |

| 4.80%, 10/1/2014 | | 2,050,000 | | 2,076,343 |

| Tennessee—1.5% | | | | |

| Chattanooga Health Educational & Housing Facility | | | | |

| Board, Revenue ( CDFI Phase I LLC Project) | | | | |

| 5%, 10/1/2015 | | 1,500,000 | | 1,561,980 |

| Johnson City Health and Educational Facility Board, HR | | | | |

| (Medical Center Hospital Improvement) | | | | |

| 5.125%, 7/1/2011 (Insured; MBIA) | | 6,720,000 | | 7,205,453 |

| Tennessee Housing Development Agency | | | | |

| (Homeownership Program): | | | | |

| 5.20%, 7/1/2010 | | 1,815,000 | | 1,921,468 |

| 5.30% 7/1/2011 | | 2,140,000 | | 2,264,141 |

| Texas—8.4% | | | | |

| Bexar County, Revenue (Venue) | | | | |

| 5.75%, 8/15/2013 (Insured; MBIA) | | 5,000,000 | | 5,564,050 |

| Cypress—Fairbanks Independent School District | | | | |

| (Schoolhouse) 6.75%, 2/15/2012 | | | | |

| (Prerefunded 2/15/2010) | | 1,700,000 a | | 1,969,637 |

| Dallas—Fort Worth International Airport, Revenue | | | | |

| Facility Improvement Corporation | | | | |

| (Bombardier Inc.) 6.15%, 1/1/2016 | | 4,000,000 | | 4,033,080 |

| Gulf Coast Waste Disposal Authority: | | | | |

| Revenue (Bayport Area System) | | | | |

| 5%, 10/1/2014 (Insured; AMBAC) | | 2,065,000 | | 2,270,860 |

| SWDR (Quaker Oats Co. Project) | | | | |

| 5.70%, 5/1/2006 | | 3,210,000 | | 3,275,548 |

STATEMENT OF INVESTMENTS (continued)

|

| | | Principal | | |

| Long-Term Municipal Investments (continued) | | Amount ($) | | Value ($) |

| |

| |

|

| Texas (continued) | | | | |

| Harris County Health Facilities Development Corp., HR: | | | | |

| (Memorial Hermann Hospital System) | | | | |

| 5.50%, 6/1/2012 (Insured; FSA) | | 8,295,000 | | 9,316,032 |

| (Memorial Hospital System) | | | | |

| 6%, 6/1/2008 (Insured; MBIA) | | 9,080,000 | | 9,822,562 |

| Houston, Utility System Revenue (First Lien) | | | | |

| 5.25%, 5/15/2012 (Insured; MBIA) | | 2,750,000 | | 3,058,770 |

| Port Corpus Christi Industrial Development Corp., | | | | |

| Revenue (Valero): | | | | |

| 5.125%, 4/1/2009 | | 2,250,000 | | 2,384,145 |

| 5.40%, 4/1/2018 | | 1,500,000 | | 1,561,995 |

| San Antonio, Electric & Gas Revenue | | | | |

| 5%, 2/1/2018 | | 5,000,000 | | 5,302,450 |

| Tarrant County Health Facilities Development Corp., | | | | |

| Health Systems Revenue: | | | | |

| (Harris Methodist Health Systems) 6%, 9/1/2010 | | 7,725,000 | | 8,631,606 |

| (Health Resources Systems) | | | | |

| 5.75%, 2/15/2014 (Insured; MBIA) | | 5,000,000 | | 5,766,700 |

| Texas College Student Loan Bonds | | | | |

| 4.75%, 8/1/2008 | | 7,435,000 | | 7,789,426 |

| Texas Municipal Power Agency, Revenue: | | | | |

| Zero Coupon, 9/1/2009 (Insured; AMBAC) | | 170,000 | | 148,028 |

| 4%, 9/1/2012 (Insured; AMBAC) | | 2,690,000 | | 2,710,094 |

| Utah—2.9% | | | | |

| Carbon County, SWDR | | | | |

| (Sunnyside Cogeneration-A) 6.375%, 8/15/2011 | | 8,450,000 | | 8,410,623 |

| Jordanelle Special Service District | | | | |

| (Special Assessment Improvement District) | | | | |

| 8%, 10/1/2011 | | 5,040,000 | | 5,379,394 |

| Orem, Sales Tax Revenue | | | | |

| 5%, 4/15/2018 (Insured; AMBAC) | | 3,325,000 | | 3,590,269 |

| Utah Building Ownership Authority, LR | | | | |

| (State Facilities Master Lease Program) | | | | |

| 5%, 5/15/2017 | | 2,950,000 | | 3,196,738 |

| Utah County, EIR (USX Corporation Project) | | | | |

| 5.05%, 11/1/2011 | | 4,480,000 | | 4,741,139 |

| Virginia—2.5% | | | | |

| Arlington County Industrial Development Authority, RRR | | | | |

| (Ogden Martin System of Alexandria/Arlington | | | | |

| Inc. Project) 5.375%, 1/1/2012 (Insured; FSA) | | 2,530,000 | | 2,689,011 |

| |

| |

| |

| 18 | | | | |

| | | Principal | | | | |

| Long-Term Municipal Investments (continued) | | Amount ($) | | Value ($) |

| |

| |

|

| Virginia (continued) | | | | | | |

| Greater Richmond Convention Center Authority, | | | | | | |

| Hotel Tax Revenue (Convention Center Expansion | | | | | | |

| Project) 6%, 6/15/2011 (Prerefunded 6/15/2010) | | 2,000,000 | | a | | 2,282,940 |

| Peninsula Ports Authority, Revenue | | | | | | |

| (Port Facility—CSX Transportation Project) | | | | | | |

| 6%, 12/15/2012 | | 4,150,000 | | | | 4,652,565 |

| Tobacco Settlement Financing Corp.: | | | | | | |

| 4%, 6/1/2013 | | 5,000,000 | | | | 4,989,850 |

| 5.25%, 6/1/2019 | | 3,000,000 | | | | 3,019,500 |

| Virginia College Building Authority, Educational | | | | | | |

| Facilities Revenue (Hampden—Sydney College | | | | | | |

| Project) 5%, 9/1/2016 | | 1,000,000 | | | | 1,042,350 |

| York County Industrial Development Authority, | | | | | | |

| PCR (Virginia Electric & Power Co.) | | | | | | |

| 5.50%, 7/1/2009 | | 2,750,000 | | | | 2,866,325 |

| Washington—2.4% | | | | | | |

| Energy Northwest | | | | | | |

| Revenue (Wind Project): | | | | | | |

| 4.55%, 7/1/2006 | | 1,600,000 | | | | 1,614,944 |

| 5.60%, 7/1/2015 (Prerefunded 1/1/2007) | | 2,530,000 | | a | | 2,700,244 |

| Goat Hill Properties, LR (Government | | | | | | |

| Office Building Project) | | | | | | |

| 5.25%, 12/1/2020 (Insured; MBIA) | | 2,710,000 | | | | 2,981,190 |

| Seattle Municipal Light & Power, Revenue: | | | | | | |

| 5.25%, 3/1/2010 (Insured; FSA) | | 50,000 | | | | 54,585 |

| 7.446%, 3/1/2010 (Insured; FSA) | | 6,500,000 | | c,e | | 7,692,035 |

| Washington: | | | | | | |

| 5.75%, 10/1/2012 | | 20,000 | | | | 22,621 |

| 5.75%, 10/1/2012 | | 2,305,000 | | | | 2,590,497 |

| Washington Health Care Facilities Authority, | | | | | | |

| Revenue (Sisters of Providence) | | | | | | |

| 5.40%, 10/1/2010 (Insured; AMBAC) | | 3,000,000 | | | | 3,083,250 |

| West Virginia—.4% | | | | | | |

| West Virginia Economic Development Authority, LR | | | | | | |

| (Department of Environmental Protection) | | | | | | |

| 5.50%, 11/1/2022 | | 2,895,000 | | | | 3,233,223 |

| Wisconsin—1.0% | | | | | | |

| Badger Tobacco Asset Securitization Corp., | | | | | | |

| Tobacco Settlement Revenue | | | | | | |

| 5.50%, 6/1/2010 | | 3,500,000 | | | | 3,717,070 |

| | STATEMENT OF INVESTMENTS (continued)

|

| | | Principal | | | | |

| Long-Term Municipal Investments (continued) | | Amount ($) | | Value ($) |

| |

| |

|

| Wisconsin (continued) | | | | | | |

| Racine, SWDR (Republic Services Project) | | | | | | |

| 3.25%, 4/1/2009 | | 1,000,000 | | | | 977,900 |

| Wisconsin Health and Educational Facilities Authority, | | | | | | |

| Revenue (Aurora Medical Group, Inc.) | | | | | | |

| 6%, 11/15/2011 (Insured; FSA) | | 3,500,000 | | | | 4,013,170 |

| U. S. Related—1.4% | | | | | | |

| Childrens Trust Fund, Tobacco Settlement Revenue: | | | | | | |

| 5.75%, 7/1/2010 | | 2,500,000 | | | | 2,799,925 |

| 5.75%, 7/1/2012 (Prerefunded 7/1/2010) | | 5,000,000 | | a | | 5,599,850 |

| 5.75%, 7/1/2013 (Prerefunded 7/1/2010) | | 3,300,000 | | a | | 3,695,901 |

| Total Long-Term Municipal Investments | | | | | | |

| (cost $833,529,740) | | | | | | 864,232,135 |

| |

| |

| |

|

| |

| Short-Term Municipal Investments—1.0% | | | | | | |

| |

| |

| |

|

| Florida—1.0% | | | | | | |

| Collier County Health Facilities Authority, Revenue | | | | | | |

| VRDN (Cleveland Clinic Health) | | | | | | |

| 2.94% (LOC; Bank of America—Idaho N.A.) | | | | | | |

| (cost $9,000,000) | | 9,000,000 | | f | | 9,000,000 |

| |

| |

| |

|

| |

| Total Investments (cost $842,529,740) | | 100.0% | | | | 873,232,135 |

| Liabilities, Less Cash and Receivables | | (.0%) | | (194,018) |

| Net Assets | | 100.0% | | | | 873,038,117 |

| Summary of Abbreviations | | | | |

| |

| AMBAC | | American Municipal Bond | | IDR | | Industrial Development Revenue |

| | | Assurance Corporation | | LOC | | Letter of Credit |

| CIFG | | CDC IxIx Financial Guaranty | | LR | | Lease Revenue |

| COP | | Certificate of Participation | | MBIA | | Municipal Bond Investors Assurance |

| EIR | | Environment Improvement | | | | Insurance Corporation |

| | | Revenue | | MFHR | | Multi Family Housing Revenue |

| FGIC | | Financial Guaranty Insurance | | PCR | | Pollution Control Revenue |

| | | Company | | RRR | | Resources Recovery Revenue |

| FHA | | Federal Housing Administration | | SWDR | | Solid Waste Disposal Revenue |

| FSA | | Financial Security Assurance | | VRDN | | Variable Rate Demand Notes |

| HR | | Hospital Revenue | | XLCA | | XL Capital Assurance |

| |

| |

| |

|

| |

| |

| |

| Summary of Combined Ratings (Unaudited) | | |

| |

| Fitch | | or Moody’s or | | Standard & Poor’s Value (%) † |

| |

| |

|

| AAA | | Aaa | | AAA | | 48.2 |

| AA | | Aa | | AA | | 17.2 |

| A | | A | | A | | 15.1 |

| BBB | | Baa | | BBB | | 14.9 |

| F1 | | MIG1/P1 | | SP1/A1 | | 1.0 |

| Not Rated g | | Not Rated g | | Not Rated g | | 3.6 |

| | | | | | | 100.0 |

| † | | Based on total investments. |

| a | | Bonds which are prerefunded are collateralized by U.S. Government securities which are held in escrow and are used |

| | | to pay principal and interest on the municipal issue and to retire the bonds in full at the earliest refunding date. |

| b | | Zero coupon until a specified date, at which time the stated coupon rate becomes effective until maturity. |

| c | | Securities exempt from registration under Rule 144A of the Securities Act of 1933.These securities may be resold in |

| | | transactions exempt from registration, normally to qualified institutional buyers. At May 31, 2005, these securities |

| | | amounted to $20,276,678 or 2.3% of net assets. |

| d | | Purchased on a delayed delivery basis. |

| e | | Inverse floater security—the interest rate is subject to change periodically. |

| f | | Security payable on demand.Variable interest rate—subject to periodic change. |

| g | | Securities which, while not rated by Fitch, Moody’s and Standard & Poor’s, have been determined by the Manager to |

| | | be of comparable quality to those rated securities in which the fund may invest. |

| See notes to financial statements. |

| | STATEMENT OF ASSETS AND LIABILITIES

May 31, 2005

|

| | | Cost | | Value |

| |

| |

|

| Assets ($): | | | | |

| Investments in securities—See Statement of Investments | | 842,529,740 | | 873,232,135 |

| Cash | | | | 1,217,388 |

| Interest receivable | | | | 14,066,223 |

| Receivable for shares of Common Stock subscribed | | | | 4,828 |

| Prepaid expenses | | | | 29,791 |

| | | | | 888,550,365 |

| |

| |

|

| Liabilities ($): | | | | |

| Due to The Dreyfus Corporation and affiliates | | | | 537,779 |

| Payable for investment securities purchased | | | | 14,237,923 |

| Payable for shares of Common Stock redeemed | | | | 622,811 |

| Accrued expenses | | | | 113,735 |

| | | | | 15,512,248 |

| |

| |

|

| Net Assets ($) | | | | 873,038,117 |

| |

| |

|

| Composition of Net Assets ($): | | | | |

| Paid-in capital | | | | 850,610,254 |

| Accumulated net realized gain (loss) on investments | | | | (8,274,532) |

| Accumulated net unrealized appreciation | | | | |

| (depreciation) on investments | | | | 30,702,395 |

| |

| |

|

| Net Assets ($) | | | | 873,038,117 |

| |

| |

|

| Shares Outstanding | | | | |

| (300 million shares of $.001 par value Common Stock authorized) | | 64,643,715 |

| Net Asset Value, offering and redemption price per share—Note 3(d) ($) | | 13.51 |

| | See notes to financial statements.

|

STATEMENT OF OPERATIONS

Year Ended May 31, 2005

|

| Investment Income ($): | | |

| Interest Income | | 39,672,017 |

| Expenses: | | |

| Management fee—Note 3(a) | | 5,368,719 |

| Shareholder servicing costs—Note 3(b) | | 859,806 |

| Custodian fees | | 76,487 |

| Professional fees | | 68,909 |

| Directors’ fees and expenses—Note 3(c) | | 55,142 |

| Prospectus and shareholders’ reports | | 38,201 |

| Registration fees | | 28,113 |

| Loan commitment fees—Note 2 | | 6,031 |

| Miscellaneous | | 60,068 |

| Total Expenses | | 6,561,476 |

| Less—reduction in management fee | | |

| due to undertaking—Note 3(a) | | (3,869) |

| Less—reduction in custody fee due to | | |

| earnings credits—Note 1(b) | | (7,778) |

| Net Expenses | | 6,549,829 |

| Investment Income—Net | | 33,122,188 |

| |

|

| Realized and Unrealized Gain (Loss) on Investments—Note 4 ($): |

| Net realized gain (loss) on investments | | 6,019,863 |

| Net unrealized appreciation (depreciation) on investments | | 9,115,808 |

| Net Realized and Unrealized Gain (Loss) on Investments | | 15,135,671 |

| Net Increase in Net Assets Resulting from Operations | | 48,257,859 |

See notes to financial statements.

|

STATEMENT OF CHANGES IN NET ASSETS

| | | | | Year Ended May 31, |

| |

| |

|

| | | 2005 | | 2004 |

| |

| |

|

| Operations ($): | | | | |

| Investment income—net | | 33,122,188 | | 37,558,125 |

| Net realized gain (loss) on investments | | 6,019,863 | | 10,267,229 |

| Net unrealized appreciation | | | | |

| (depreciation) on investments | | 9,115,808 | | (55,517,040) |

| Net Increase (Decrease) in Net Assets | | | | |

| Resulting from Operations | | 48,257,859 | | (7,691,686) |

| |

| |

|

| Dividends to Shareholders from ($): | | | | |

| Investment income—net | | (33,363,442) | | (37,207,071) |

| |

| |

|

| Capital Stock Transactions ($): | | | | |

| Net proceeds from shares sold | | 51,829,030 | | 70,360,162 |

| Dividends reinvested | | 24,633,027 | | 27,275,524 |

| Cost of shares redeemed | | (122,535,096) | | (196,272,299) |

| Increase (Decrease) in Net Assets | | | | |

| from Capital Stock Transactions | | (46,073,039) | | (98,636,613) |

| Total Increase (Decrease) in Net Assets | | (31,178,622) | | (143,535,370) |

| |

| |

|

| Net Assets ($): | | | | |

| Beginning of Period | | 904,216,739 | | 1,047,752,109 |

| End of Period | | 873,038,117 | | 904,216,739 |

| Undistributed investment income—net | | — | | 280,714 |

| |

| |

|

| Capital Share Transactions (Shares): | | | | |

| Shares sold | | 3,840,582 | | 5,171,532 |

| Shares issued for dividends reinvested | | 1,826,980 | | 2,014,036 |

| Shares redeemed | | (9,087,026) | | (14,462,858) |

| Net Increase (Decrease) in Shares Outstanding | | (3,419,464) | | (7,277,290) |

| | See notes to financial statements.

|

The following table describes the performance for the fiscal periods indicated. Total return shows how much your investment in the fund would have increased (or decreased) during each period, assuming you had reinvested all dividends and distributions.These figures have been derived from the fund’s financial statements.

| | | | | | | Year Ended May 31, | | |

| |

| |

| |

| |

|

| | | 2005 | | 2004 | | 2003 | | 2002 a | | 2001 |

| |

| |

| |

| |

| |

|

| Per Share Data ($): | | | | | | | | | | |

| Net asset value, | | | | | | | | | | |

| beginning of period | | 13.28 | | 13.91 | | 13.42 | | 13.51 | | 12.94 |

| Investment Operations: | | | | | | | | | | |

| Investment income—net | | .50b | | .52b | | .57b | | .64b | | .65 |

| Net realized and unrealized | | | | | | | | | | |

| gain (loss) on investments | | .23 | | (.63) | | .49 | | (.09) | | .57 |

| Total from Investment Operations | | .73 | | (.11) | | 1.06 | | .55 | | 1.22 |

| Distributions: | | | | | | | | | | |

| Dividends from | | | | | | | | | | |

| investment income—net | | (.50) | | (.52) | | (.57) | | (.64) | | (.65) |

| Net asset value, end of period | | 13.51 | | 13.28 | | 13.91 | | 13.42 | | 13.51 |

| |

| |

| |

| |

| |

|

| Total Return (%) | | 5.59 | | (.81) | | 8.09 | | 4.14 | | 9.54 |

| |

| |

| |

| |

| |

|

| Ratios/Supplemental Data (%): | | | | | | | | | | |

| Ratio of total expenses | | | | | | | | | | |

| to average net assets | | .73 | | .74 | | .74 | | .74 | | .74 |

| Ratio of net expenses | | | | | | | | | | |

| to average net assets | | .73 | | .74 | | .74 | | .74 | | .74 |

| Ratio of net investment income | | | | | | | | | | |

| to average net assets | | 3.70 | | 3.86 | | 4.23 | | 4.74 | | 4.82 |

| Portfolio Turnover Rate | | 37.33 | | 35.07 | | 41.30 | | 27.32 | | 24.32 |

| |

| |

| |

| |

| |

|

| Net Assets, end of period | | | | | | | | | | |

| ($ x 1,000) | | 873,038 | | 904,217 | | 1,047,752 | | 1,057,999 | | 1,065,775 |

| a | | As required, effective June 1, 2001, the fund has adopted the provisions of the AICPA Audit and Accounting Guide |

| | | for Investment Companies and began accreting discount or amortizing premium on a scientific basis for debt securities. |

| | | The effect of this change for the period ended May 31, 2002 was to increase net investment income per share and |

| | | decrease net realized and unrealized gain (loss) on investments by less than $.01 and increase the ratio of net |

| | | investment income to average net assets by less than .01%. Per share data and ratios/supplemental data for periods |

| | | prior to June 1, 2001 have not been restated to reflect this change in presentation. |

| b | | Based on average shares outstanding at each month end. |

| See notes to financial statements. |

NOTES TO FINANCIAL STATEMENTS

NOTE 1—Significant Accounting Policies:

Dreyfus Intermediate Municipal Bond Fund,Inc.(the “fund”) is registered under the Investment Company Act of 1940, as amended (the “Act”), as a diversified open-end management investment company. The fund’s investment objective is to provide the maximum amount of current income exempt from federal income tax as is consistent with the preservation of capital.The Dreyfus Corporation (the “Manager”or “Dreyfus”) serves as the fund’s investment adviser.The Manager is a wholly-owned subsidiary of Mellon Financial Corporation (“Mellon Financial”).Dreyfus Service Corporation (the “Distributor”), a wholly-owned subsidiary of the Manager, is the distributor of the fund’s shares, which are sold to the public without a sales charge.

The fund’s financial statements are prepared in accordance with U.S. generally accepted accounting principles, which may require the use of management estimates and assumptions. Actual results could differ from those estimates.

The fund enters into contracts that contain a variety of indemnifications. The fund’s maximum exposure under these arrangements is unknown.The fund does not anticipate recognizing any loss related to these arrangements.

(a) Portfolio valuation: Investments in securities are valued each business day by an independent pricing service (the “Service”) approved by the Board of Trustees. Investments for which quoted bid prices are readily available and are representative of the bid side of the market in the judgment of the Service are valued at the mean between the quoted bid prices (as obtained by the Service from dealers in such securities) and asked prices (as calculated by the Service based upon its evaluation of the market for such securities). Other investments (which constitute a majority of the portfolio securities) are carried at fair value as determined by the Service, based on methods which include consideration of: yields or prices of municipal securities of comparable quality, coupon, maturity and type; indications as to values from dealers; and general market conditions. Options and financial futures on municipal

and U.S.Treasury securities are valued at the last sales price on the securities exchange on which such securities are primarily traded or at the last sales price on the national securities market on each business day.

(b) Securities transactions and investment income: Securities transactions are recorded on a trade date basis. Realized gain and loss from securities transactions are recorded on the identified cost basis. Interest income, adjusted for accretion of discount and amortization of premium on investments, is earned from settlement date and recognized on the accrual basis. Securities purchased or sold on a when-issued or delayed-delivery basis may be settled a month or more after the trade date.

The fund has an arrangement with the custodian bank whereby the fund receives earnings credits from the custodian when positive cash balances are maintained, which are used to offset custody fees. For financial reporting purposes, the fund includes net earnings credits as an expense offset in the Statement of Operations.

(c) Dividends to shareholders: It is the policy of the fund to declare dividends daily from investment income-net. Such dividends are paid monthly. Dividends from net realized capital gain, if any, are normally declared and paid annually, but the fund may make distributions on a more frequent basis to comply with the distribution requirements of the Internal Revenue Code of 1986, as amended (the “Code”).To the extent that net realized capital gain can be offset by capital loss carryovers, it is the policy of the fund not to distribute such gain. Income and capital gain distributions are determined in accordance with income tax regulations, which may differ from U.S. generally accepted accounting principles.

(d) Federal income taxes: It is the policy of the fund to continue to qualify as a regulated investment company, which can distribute tax exempt dividends, by complying with the applicable provisions of the Code, and to make distributions of income and net realized capital gain sufficient to relieve it from substantially all federal income and excise taxes.

| | NOTES TO FINANCIAL STATEMENTS (continued)

|

At May 31,2005,the components of accumulated earnings on a tax basis were as follows: undistributed tax exempt income $410,130, accumulated capital losses $8,274,532 and unrealized appreciation $30,848,143.

The accumulated capital loss carryover is available to be applied against future net securities profits, if any, realized subsequent to May 31, 2005. If not applied, the carryover expires in fiscal 2011.

The tax character of distributions paid to shareholders during the fiscal periods ended May 31, 2005 and May 31, 2004, were as follows: tax exempt income $33,363,442 and $37,207,071, respectively.

During the period ended May 31, 2005, as a result of permanent book to tax differences, primarily due to the tax treatment for amortization adjustments, the fund decreased accumulated undistributed investment income-net by $39,460, increased accumulated net realized gain (loss) on investments by $25 and increased paid-in capital by $39,435. Net assets were not affected by this reclassification.

NOTE 2—Bank Line of Credit:

|

The fund participates with other Dreyfus-managed funds in a $350 million redemption credit facility (the “Facility”) to be utilized for temporary or emergency purposes, including the financing of redemptions. In connection therewith, the fund has agreed to pay commitment fees on its pro rata portion of the Facility. Interest is charged to the fund based on prevailing market rates in effect at the time of borrowings. During the period ended May 31, 2005, the fund did not borrow under the Facility.

NOTE 3—Management Fee and Other Transactions With Affiliates:

(a) Pursuant to a management agreement (“Agreement”) with the Manager, the management fee is computed at the annual rate of .60 of 1% of the value of the fund’s average daily net assets and is payable monthly. The Manager has undertaken from June 1, 2004 through May 31, 2005 to reduce the management fee paid by the fund, to the extent that the fund’s aggregate annual expenses, exclusive of taxes,

brokerage fees, interest on borrowings, commitment fees and extraordinary expenses, exceed an annual rate of .75 of 1% of the value of the fund’s average daily net assets.The reduction in management fee, pursuant to the undertaking, amounted to $3,869 during the period ended May 31, 2005.

(b) Under the Shareholder Services Plan, the fund reimburses the Distributor an amount not to exceed an annual rate of .25 of 1% of the value of the fund’s average daily net assets for certain allocated expenses of providing personal services and/or maintaining shareholder accounts.The services provided may include personal services relating to shareholder accounts, such as answering shareholder inquires regarding the fund and providing reports and other information, and services related to the maintenance of shareholder accounts. During the period ended May 31, 2005, the fund was charged $436,252 pursuant to the Shareholder Services Plan.

The fund compensates Dreyfus Transfer, Inc., a wholly-owned subsidiary of the Manager, under a transfer agency agreement for providing personnel and facilities to perform transfer agency services for the fund. During the period ended May 31, 2005, the fund was charged $306,448 pursuant to the transfer agency agreement.

During the period ended May 31, 2005, the fund was charged $1,693 for services performed by the Chief Compliance Officer.

The components of Due to The Dreyfus Corporation and affiliates in the Statement of Assets and Liabilities consist of: management fees $444,086, shareholder services plan fees $41,000, chief compliance officer fees $1,693 and transfer agency per account fees $51,000.

(c) Each Board member also serves as a Board member of other funds within the Dreyfus complex. Annual retainer fees and attendance fees are allocated to each fund based on net assets.

(d) A .10% redemption fee is charged and retained by the fund on certain shares redeemed within thirty days following the date of issuance,

| | NOTES TO FINANCIAL STATEMENTS (continued)

|

including redemptions made through the use of the fund’s exchange privilege. During the period ended May 31, 2005, redemption fees charged and retained by the fund amounted to $182.

NOTE 4—Securities Transactions:

|

The aggregate amount of purchases and sales of investment securities, excluding short-term securities, during the period ended May 31, 2005, amounted to $328,024,858 and $360,749,393, respectively.

At May 31,2005,the cost of investments for federal income tax purposes was $842,383,992; accordingly, accumulated net unrealized appreciation on investments was $30,848,143, consisting of $31,656,350 gross unrealized appreciation and $808,207 gross unrealized depreciation.

In early 2004, two purported class and derivative actions were filed against Mellon Financial, Mellon Bank, N.A., Dreyfus, Founders Asset Management LLC, and certain directors of the Dreyfus Funds and the Dreyfus Founders Funds (together, the “Funds”) in the United States District Court for the Western District of Pennsylvania. In September 2004, plaintiffs served a Consolidated Amended Complaint (the “Amended Complaint”) on behalf of a purported class of all persons who acquired interests in any of the Funds between January 30, 1999 and November 17, 2003, and derivatively on behalf of the Funds.The Amended Complaint in the newly styled In re Dreyfus Mutual Funds Fee Litigation also named the Distributor, Premier Mutual Fund Services, Inc. and two additional Fund directors as defendants and alleges violations of the Investment Company Act of 1940, the Investment Advisers Act of 1940, the Pennsylvania Unfair Trade Practices and Consumer Protection Law and common-law claims. Plaintiffs seek to recover allegedly improper and excessive Rule 12b-1 and advisory fees allegedly charged to the Funds for marketing and distribution services. More specifically, plaintiffs claim, among other

things, that 12b-1 fees and directed brokerage were improperly used to pay brokers to recommend the Funds over other funds, and that such payments were not disclosed to investors. In addition, plaintiffs assert that economies of scale and soft-dollar benefits were not passed on to the Funds. Plaintiffs further allege that 12b-1 fees were improperly charged to certain of the Funds that were closed to new investors.The Amended Complaint seeks compensatory and punitive damages, rescission of the advisory contracts, and an accounting and restitution of any unlawful fees, as well as an award of attorneys’ fees and litigation expenses. As noted, some of the claims in this litigation are asserted derivatively on behalf of the Funds that have been named as nominal defendants. With respect to such derivative claims, no relief is sought against the Funds. Dreyfus believes the allegations to be totally without merit and intends to defend the action vigorously. In November 2004, all named defendants moved to dismiss the Amended Complaint in whole or substantial part. Briefing was completed in May 2005.

Additional lawsuits arising out of these circumstances and presenting similar allegations and requests for relief may be filed against the defendants in the future. Neither Dreyfus nor the Funds believe that any of the pending actions will have a material adverse effect on the Funds or Dreyfus’ ability to perform its contract with the Funds.

REPORT OF INDEPENDENT REGISTERED

PUBLIC ACCOUNTING FIRM

|

Shareholders and Board of Directors

Dreyfus Intermediate Municipal Bond Fund, Inc.

|

We have audited the accompanying statement of assets and liabilities of Dreyfus Intermediate Municipal Bond Fund, Inc., including the statement of investments, as of May 31, 2005, and the related statement of operations for the year then ended, the statement of changes in net assets for each of the two years in the period then ended, and financial highlights for each of the years indicated therein.These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. We were not engaged to perform an audit of the Fund’s internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements and financial highlights, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of May 31, 2005 by correspondence with the custodian and others.We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Dreyfus Intermediate Municipal Bond Fund, Inc. at May 31, 2005, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the indicated years, in conformity with U.S. generally accepted accounting principles.

IMPORTANT TAX INFORMATION (Unaudited)

In accordance with federal tax law, the fund hereby designates all the dividends paid from investment income-net during its fiscal year ended May 31, 2005 as “exempt-interest dividends” (not generally subject to regular federal income tax).

As required by federal tax law rules, shareholders will receive notification of their portion of the fund’s taxable ordinary dividends (if any) and capital gains distributions (if any) paid for the 2005 calendar year on Form 1099 DIV which will be mailed by January 31, 2006.

| | INFORMATION ABOUT THE REVIEW AND APPROVAL OF THE

FUND’S INVESTMENT MANAGEMENT AGREEMENT (Unaudited)

|

At a meeting of the Board of Directors held on April 18, 2005, the Board considered the re-approval of the fund’s Management Agreement for another one year term, pursuant to which the Manager provides the fund with investment advisory and administrative ser-vices.The Board members who are not “interested persons” (as defined in the Investment Company Act of 1940, as amended (the “Independent Directors”)) of the fund were assisted in their review by independent legal counsel and met with counsel in executive session separate from representatives of the Manager.

Analysis of Nature, Quality and Extent of Services Provided to the Fund.The Board members received a presentation from representatives of the Manager regarding services provided to the fund and other funds in the Dreyfus complex, and discussed the nature, quality and extent of the services provided to the fund pursuant to its Management Agreement. The presentation included a detailed summary of the services provided to Dreyfus-managed mutual funds by each business unit within the Manager.The Manager’s representatives reviewed the fund’s distribution of accounts and the relationships the Manager has with various intermediaries and the different needs of each.The Manager’s representatives noted the diversity of distribution of the fund as well as among the funds in the Dreyfus complex, and the Manager’s corresponding need for broad, deep, and diverse resources to be able to provide ongoing shareholder services to each of the fund’s distribution channels.The Board also reviewed the number of shareholder accounts in the fund, as well as the fund’s asset size.

The Board members also considered the Manager’s research and portfolio management capabilities and that the Manager also provides oversight of day-to-day fund operations, including fund accounting and administration and assistance in meeting legal and regulatory requirements. The Board members also considered the Manager’s extensive administrative, accounting, and compliance infrastructure.

Comparative Analysis of the Fund’s Performance and Management Fee and Expense Ratio.The Board members reviewed the fund’s performance, management fee and expense ratios and placed significant

emphasis on comparisons to a group of comparable funds and Lipper averages. The Board reviewed the fund’s performance, management fee, and total expense ratio within this comparison group and against the fund’s Lipper category average, and discussed the results of the comparisons.The group of comparable funds was previously approved by the Board for this purpose, and was prepared using a Board-approved selection methodology that was based, in part, on selecting non-affiliated funds reported in the same Lipper category as the fund. The Board members noted that the fund’s income performance was higher than the fund’s respective comparison group averages and Lipper category averages for each reported time period. The Board members also noted that the fund’s total return performance was higher than the fund’s comparison group average and Lipper category average for the reported one-year period, but was below these averages, to varying degrees, for the reported longer-term periods. The Board members also discussed the fund’s management fee and expense ratio, noting the range of management fees in the comparison group and that the fund’s expense ratio was higher than the comparison group average but lower than the Lipper category average.The Board also noted that if the “low cost provider” fund was excluded from the comparison group, the fund’s expense ratio would be lower than the average of the remaining comparison group funds.

The Board also received a presentation from the fund’s portfolio manager during which he discussed the fund’s improved relative total return performance over the past two years and resolution of credit issues that caused total return performance to lag over this time. In this regard, the Board took note of the fund’s reported one-year total return Lipper ranking and competitive two-year total return ranking provided by the portfolio manager.

The Board members also reviewed the fees paid to the Manager or its affiliates by mutual funds managed by the Manager or its affiliates (the “Similar Funds”).These comparison groups compared the management fee and total expense ratios of such funds, and were composed exclusively of investment companies affiliated with the Manager that were

| | INFORMATION ABOUT THE REVIEW AND APPROVAL OF

THE FUND’S INVESTMENT MANAGEMENT AGREEMENT (Unaudited) ( c o n t i n u e d )

|