UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORMN-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number:811-03752

AMG FUNDS III

(Exact name of registrant as specified in charter)

600 Steamboat Road, Suite 300, Greenwich, Connecticut 06830

(Address of principal executive offices) (Zip code)

AMG Funds LLC

600 Steamboat Road, Suite 300, Greenwich, Connecticut 06830

(Name and address of agent for service)

Registrant’s telephone number, including area code: (203)299-3500

Date of fiscal year end: DECEMBER 31

Date of reporting period: JANUARY 1, 2019 – DECEMBER 31, 2019

(Annual Shareholder Report)

| Item 1. | Reports to Shareholders |

| | |

| | ANNUAL REPORT |

| | | | | | | | |

| | | AMG Funds | | | | |

| | | | |

| | | December 31, 2019 | | | | |

| | |

| | | AMG Managers Loomis Sayles Bond Fund |

| | | Class N: MGFIX | | Class I: MGBIX | | | | |

| | |

| | | AMG Managers Global Income Opportunity Fund |

| | | Class N:MGGBX |

| | |

| | | AMG Managers Special Equity Fund |

| | | Class N: MGSEX | | Class I: MSEIX | | | | |

| | | | | | | | | |

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Funds’ shareholder reports like this one will no longer be sent by mail, unless you specifically request paper copies of the reports from the Funds or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on the Funds’ website (https://www.amgfunds.com/resources/order_literature.html), and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Funds electronically at any time by contacting your financial intermediary or, if you invest directly with the Funds, by logging into your account at www.amgfunds.com.

You may elect to receive all future reports in paper free of charge. If you invest through a financial intermediary, you can contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. If you invest directly with the Funds, you can call 1.800.548.4539 to inform the Funds that you wish to continue receiving paper copies of your shareholder reports. Your election to receive reports in paper will apply to all funds in the AMG Funds Family of Funds held in your account if you invest through your financial intermediary or all funds in the AMG Funds Family of Funds held with the fund complex if you invest directly with the Funds.

| | | | | | |

amgfunds.com | | | | 123119 | | AR078 |

|

AMG Funds Annual Report – December 31, 2019 |

| | | | | | |

| | | TABLE OF CONTENTS | | PAGE | |

| | | |

| | | LETTER TO SHAREHOLDERS | | | 2 | |

| | | |

| | | ABOUT YOUR FUND’S EXPENSES | | | 3 | |

| | | |

| | | PORTFOLIO MANAGER’S COMMENTS, FUND SNAPSHOTS AND SCHEDULES OF PORTFOLIO INVESTMENTS | | | | |

| | | |

| | | AMG Managers Loomis Sayles Bond Fund | | | 4 | |

| | | |

| | | AMG Managers Global Income Opportunity Fund | | | 14 | |

| | | |

| | | AMG Managers Special Equity Fund | | | 23 | |

| | | |

| | | FINANCIAL STATEMENTS | | | | |

| | | |

| | | Statement of Assets and Liabilities | | | 35 | |

| | | |

| | | Balance sheets, net asset value (NAV) per share computations and cumulative distributable earnings (loss) | | | | |

| | | |

| | | Statement of Operations | | | 37 | |

| | | |

| | | Detail of sources of income, expenses, and realized and unrealized gains (losses) during the fiscal year | | | | |

| | | |

| | | Statements of Changes in Net Assets | | | 38 | |

| | | |

| | | Detail of changes in assets for the past two fiscal years | | | | |

| | | |

| | | Financial Highlights | | | 39 | |

| | | |

| | | Historical net asset values per share, distributions, total returns, income and expense ratios, turnover ratios and net assets | | | | |

| | | |

| | | Notes to Financial Statements | | | 44 | |

| | | |

| | | Accounting and distribution policies, details of agreements and transactions with Fund management and affiliates, and descriptions of certain investment risks | | | | |

| | | |

| | | REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM | | | 53 | |

| | | |

| | | OTHER INFORMATION | | | 54 | |

| | | |

| | | TRUSTEES AND OFFICERS | | | 55 | |

Nothing contained herein is to be considered an offer, sale or solicitation of an offer to buy shares of any series of the AMG Funds Family of Funds. Such offering is made only by prospectus, which includes details as to offering price and other material information.

| | | | |

| | Letter to Shareholders | | |

Dear Shareholder:

The U.S. bull market celebrated its10-year anniversary during the fiscal year ended December 31, 2019, as stocks proved resilient in the face of global economic weakness, rising geopolitical tensions, and the ongoing trade war. After a painful selloff in late 2018, a dovish pivot from global central banks rescued investors and fueled a strong rebound early in 2019. The rally picked up steam in the final months of the year, as trade tensions eased when the U.S. and China agreed to a limited “phase one” deal in December following months of tenseback-and-forth negotiations. The yield curve, which had inverted earlier in the year and raised investor anxiety given its track record for predicting an impending recession, was no longer inverted byyear-end as the U.S. Federal Reserve (the Fed) cut short-term rates. Worries over a near-term recession lifted while the yield curve steepened and trade developments improved, leading to a wave of investor confidence and strong equity returns, with the S&P 500® Index returning 31.49%. International equities were also resistant to pressures facing the global economy and generated a 21.51% return as measured by the MSCI All Country World ex USA Index.

In total, all eleven sectors of the S&P 500® Index were strongly positive during the prior twelve months, each producing double-digit returns. The higher growth information technology sector led the way with a 50.31% return while the communication services and financial sectors followed closely behind. Energy was the worst performing sector during the fiscal year, yet still produced a very respectable 11.81% return. Growth stocks outperformed Value stocks for the full fiscal year with returns of 36.39% and 26.54% for the Russell 1000® Growth and Russell 1000® Value Indexes, respectively. The cycle of U.S. outperformance over international equities continued but international developed and emerging markets still produced solid positive returns, with the MSCI EAFE and MSCI Emerging Markets Index returning 22.01% and 18.42%, respectively.

Interest rates fell dramatically over the fiscal year and led to strong returns for bond investors as the Fed shifted to a more dovish policy stance early in 2019 and eventually cut short-term rates three times during the year. The10-year Treasury yield fell from its recent high of 3.24% last November to a low of 1.47% in early September and then edged slightly higher to finish the year at 1.92%. The plunge in long-term interest rates caused the yield curve to briefly invert with2-year yields rising higher than the10-year yields. The Bloomberg Barclays U.S. Aggregate Bond Index, a broad measure of U.S. bond market performance, ended the fiscal year with an 8.72% return. High yield bonds outperformed the broader bond market and returned 14.32% as measured by the return of the Bloomberg Barclays U.S. Corporate High Yield Bond Index. Municipal bonds also performed strongly with a 7.54% return for the Bloomberg Barclays Municipal Bond Index.

AMG Funds appreciates the privilege of providing investment tools to you and your clients. Our foremost goal is to provide investment solutions that help our shareholders successfully reach their long-term investment goals. AMG Funds provides access to a distinctive array of actively managed return-oriented investment strategies. We thank you for your continued confidence and investment in AMG Funds. You can rest assured that under all market conditions our team is focused on delivering excellent investment management services for your benefit.

Respectfully,

Keitha Kinne

President

AMG Funds

| | | | | | | | | | | | | | |

Average Annual Total Returns | | Periods ended December 31, 2019* | |

| | | | |

| Stocks: | | | | 1 Year | | | 3 Years | | | 5 Years | |

| | | | |

Large Cap | | (S&P 500® Index) | | | 31.49% | | | | 15.27% | | | | 11.70% | |

| | | | |

Small Cap | | (Russell 2000® Index) | | | 25.52% | | | | 8.59% | | | | 8.23% | |

| | | | |

International | | (MSCI All Country World ex USA Index) | | | 21.51% | | | | 9.87% | | | | 5.51% | |

Bonds: | | | | | | | | | | | | | | |

| | | | |

Investment Grade | | (Bloomberg Barclays U.S. Aggregate Bond Index) | | | 8.72% | | | | 4.03% | | | | 3.05% | |

| | | | |

High Yield | | (Bloomberg Barclays U.S. Corporate High Yield Bond Index) | | | 14.32% | | | | 6.37% | | | | 6.13% | |

| | | | |

Tax-exempt | | (Bloomberg Barclays Municipal Bond Index) | | | 7.54% | | | | 4.72% | | | | 3.53% | |

| | | | |

Treasury Bills | | (ICE BofAML U.S. 6-Month Treasury Bill Index) | | | 2.57% | | | | 1.81% | | | | 1.26% | |

*Source: FactSet. Past performance is no guarantee of future results.

2

|

About Your Fund’s Expenses |

| | | | | | | | | | | | |

As a shareholder of a Fund, you may incur two types of costs: (1) transaction costs, which may include sales charges (loads) on purchase payments; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution(12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on $1,000 invested at the beginning of the period and held for the entire period as indicated below. ACTUAL EXPENSES The first line of the following table provides information about the actual account values and | | | | | | actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period. HYPOTHETICAL EXAMPLE FOR COMPARISON PURPOSES The second line of the following table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed annual rate of return of 5% before expenses, which is not the Fund’s | | | | | | actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds by comparing this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds. Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. |

| | | | | | | | | | | | | | | | |

Six Months Ended December 31, 2019 | | Expense

Ratio for the Period | | | Beginning

Account

Value

07/01/19 | | | Ending

Account

Value

12/31/19 | | | Expenses

Paid

During

the Period* |

AMG Managers Loomis Sayles Bond Fund | |

|

Based on Actual Fund Return | |

| | | | |

Class N | | | 0.72% | | | | $1,000 | | | | $1,034 | | | | $3.69 | |

| | | | |

Class I | | | 0.53% | | | | $1,000 | | | | $1,035 | | | | $2.72 | |

|

Based on Hypothetical 5% Annual Return | |

| | | | |

Class N | | | 0.72% | | | | $1,000 | | | | $1,022 | | | | $3.67 | |

| | | | |

Class I | | | 0.53% | | | | $1,000 | | | | $1,023 | | | | $2.70 | |

| | | | | | | | | | | | | | | | |

AMG Managers Global Income Opportunity Fund | |

|

Based on Actual Fund Return | |

| | | | |

Class N | | | 0.89% | | | | $1,000 | | | | $1,010 | | | | $4.51 | |

|

Based on Hypothetical 5% Annual Return | |

| | | | |

Class N | | | 0.89% | | | | $1,000 | | | | $1,021 | | | | $4.53 | |

| | | | | | | | | | | | | | | | |

Six Months Ended December 31, 2019 | | Expense

Ratio for the Period | | | Beginning

Account

Value

07/01/19 | | | Ending

Account

Value

12/31/19 | | | Expenses

Paid

During

the Period* |

AMG Managers Special Equity Fund | |

|

Based on Actual Fund Return | |

| | | | |

Class N | | | 1.36% | | | | $1,000 | | | | $1,016 | | | | $6.91 | |

| | | | |

Class I | | | 1.11% | | | | $1,000 | | | | $1,017 | | | | $5.64 | |

|

Based on Hypothetical 5% Annual Return | |

| | | | |

Class N | | | 1.36% | | | | $1,000 | | | | $1,018 | | | | $6.92 | |

| | | | |

Class I | | | 1.11% | | | | $1,000 | | | | $1,020 | | | | $5.65 | |

| * | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (184), then divided by 365. |

3

| | |

| | AMG Managers Loomis Sayles Bond Fund Portfolio Manager’s Comments(unaudited) |

| | | | | | | | | | | | |

THE YEAR IN REVIEW AMG Managers Loomis Sayles Bond Fund (Class N shares) (the Fund) returned 11.10% for the year ended December 31, 2019, outperforming the Bloomberg Barclays U.S. Government/Credit Bond Index, which returned 9.71%. The Fund posted absolute positive returns for the year. The relative outperformance can be largely attributed to strong security selection in high yield and investment grade corporates, as well as positive sector allocation. Our slightly longer-than-benchmark duration detracted from returns. Investment grade corporates boosted returns, as credit spreads tightened throughout the year. Strong security selection within the sector contributed nicely, with credits in banking, communications, and consumer cyclicals leading the charge. Strong security selection within the high yield sector outweighed the slightly negative allocation effects and also contributed to returns. Relative to the benchmark, the strategy maintained a meaningful underweight to U.S. Treasurys. The underweight contributed to the Fund’s outperformance as risk assets rallied throughout the year. The U.S. Treasury position was also longer duration than the benchmark, which contributed to performance as interest rates fell.Net-net, the Treasury/duration impact was the largest contributor to excess returns for the year. Our allocation tonon-U.S. dollar denominated issues produced positive returns during the year. Holdings denominated in the Mexican peso were the largest drivers to excess performance. A small allocation to equities and convertibles contributed to performance, with the S&P 500® Index ending 2019 with the highest return since 2013 of 31.49%. An allocation to and weak security selection within the emerging market credit sector detracted from relative returns. Positioning within securitized credit also limited returns. The Fund’s large cash & equivalents positioning was the largest drag on performance for the year. | | | | | | LOOKING FORWARD We continue to believe we are late in the credit cycle1 rather than at the end of it. Probabilities of a shift to a downturn in the cycle declined over the fourth quarter as the U.S. Federal Reserve (the “Fed”) provided additional rate cuts, a phase one deal with China became increasingly likely, and odds of ano-deal Brexit declined. We do not see the U.S. economy sliding into recession in 2020. These developments fueled further support for corporate bonds and risk assets, driving valuations up and delivering a strong year for fixed income assets in 2019. Our macro outlook remains benign and the market backdrop has largely remained supportive. We believe that Fed rate cuts and relatively good news on trade and Brexit will allow the U.S. to emerge from a third “mini cycle” slowdown within this long-running late cycle phase without a recession. We expect global manufacturing to continue to improve into 2020 as uncertainty regarding global trade declines. We anticipate that slow but positive global growth will continue and that this will help supportmid-single digit corporate profit growth and allow for reasonably strong corporate credit metrics in 2020. We expect the Fed to remain on hold for most, if not all, of 2020. Inflation remains well contained. Overall yield levels in the U.S. should remain within current established ranges, although there could be some modest upward pressure on yields should the global macro environment firm more quickly on better-than-expected news on the trade front. From a duration perspective, the Fund remains modestly short relative to the broad market. Nonetheless, global developed market yields will likely remain low and relatively high U.S. yields should be a supportive technical factor for U.S. bonds. The double-barreled market rally of lower yields and tighter spreads has pushed valuations on corporate bonds higher. High yield and investment grade corporate bond risk premiums declined over the course of 2019. While we believe that the global demand for yield and a continued late cycle environment can support spreads at current levels, we expect returns to be based more on carry in 2020. We believe corporate credit quality will | | | | | | continue to marginally decline but not enough to cause a dramatic move wider in spreads or a large uptick in corporate defaults. That said, we retain a cautious and “up in quality” bias. By historic standards we have less exposure to high yield bonds than usual, while retaining relatively high liquidity which can be deployed should opportunities develop within the sector. We continue to strive for positive issue selection through our credit research efforts. The Fund is by credits we believe are attractively priced relative to the credit quality we assign them. Communications and cable and media issues account for the bulk of this exposure, along with select areas within consumer cyclical. We believe that opportunities for positive carry in emerging market corporate bonds could expand should global growth strengthen. While we have pulled back some of our energy exposure, we believe sentiment regarding the sector has become too negative relative to the actual fundamentals. Accordingly, we believe there is upside potential for some of our best picks in this sector. We also remain comfortable with the securitized sector, which largely lagged the bigger moves in other fixed income sectors in 2019. We still like the defensive nature of the sector based on good carry for higher quality. Overall, we believe that the large rally seen in 2019 presents a challenge to fixed income return potential in 2020. However, some of those same market drivers could provide support as we enter a new year. These include global demand for yield, reduced uncertainty on global trade and Brexit, and positive global growth. The late cycle environment is likely to continue. We remain focused on maintaining favorable carry/yield, seeking to identify attractively priced bonds, and retaining the liquidity and flexibility to adapt should the benign market conditions deteriorate. 1A credit cycle is a cyclical pattern that follows credit availability and corporate health. This commentary reflects the viewpoints of Loomis, Sayles & Company, L.P. and is not intended as a forecast or guarantee of future results. |

4

| | |

| | AMG Managers Loomis Sayles Bond Fund Portfolio Manager’s Comments(continued) |

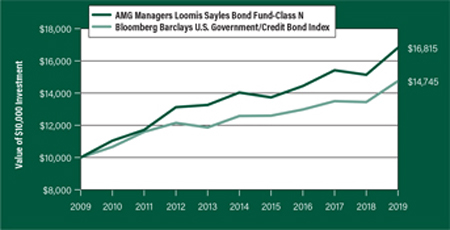

CUMULATIVE TOTAL RETURN PERFORMANCE

AMG Managers Loomis Sayles Bond Fund’s cumulative total return is based on the daily change in net asset value (NAV), and assumes that all dividends and distributions were reinvested. The graph compares a hypothetical $10,000 investment made in the AMG Managers Loomis Sayles Bond Fund’s Class N Shares on December 31, 2009, to a $10,000 investment made in the Bloomberg Barclays U.S. Government/Credit Bond Index for the same time period. The graph and table do not reflect the deduction of taxes that a shareholder would pay on a Fund distribution or redemption of shares. The listed returns for the Fund are net expenses and the returns for the index exclude expenses. Total returns would have been lower had certain expenses not been reduced.

The table below shows the average annual total returns for the AMG Managers Loomis Sayles Bond Fund and the Bloomberg Barclays U.S. Government/Credit Bond Index for the same time periods ended December 31, 2019.

| | | | | | | | | | | | | | | | | | | | |

| Average Annual Total Returns1 | | One Year | | | Five

Years | | | Ten Years | | | Since

Inception | | | Inception

Date | |

| |

AMG Managers Loomis Sayles Bond Fund2, 3, 4, 5, 6, 7, 8 | | | | | |

| | | | | |

Class N | | | 11.10% | | | | 3.68 | % | | | 5.34% | | | | 7.99% | | | | 06/01/84 | |

| | | | | |

Class I | | | 11.32% | | | | 3.81 | % | | | — | | | | 3.61% | | | | 04/01/13 | |

Bloomberg Barclays U.S. Government/ Credit Bond Index9 | | | 9.71% | | | | 3.23 | % | | | 3.96% | | | | 7.19% | | | | 06/01/84 | † |

The performance data shown represents past performance. Past performance is not a guarantee of future results. Current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

Investors should carefully consider the Fund’s investment objectives, risks, charges and expenses before investing. For performance information through the most recent month end, current net asset values per share for the Fund and other information, please call 800.548.4539 or visit our website at amgfunds.com for a free prospectus. Read it carefully before investing or sending money.

Distributed by AMG Distributors, Inc., member FINRA/SIPC.

| † | Date reflects inception date of the Fund, not the index. |

| 1 | Total return equals income yield plus share price change and assumes reinvestment of all dividends and capital gain distributions. Returns are net of fees and may reflect offsets of Fund expenses as described in the prospectus. No adjustment has been made for taxes payable by shareholders on their reinvested dividends and |

|

capital gain distributions. Returns for periods greater than one year are annualized. The listed returns on the Fund are net of expenses and based on the published NAV as of December 31, 2019. All returns are in U.S. dollars($). 2 From time to time, the Fund’s advisor has waived fees and/or absorbed Fund expenses, which has resulted in higher returns. 3 The Fund is subject to the risks associated with investments in debt securities, such as default risk and fluctuations in the perception of the debtor’s ability to pay its creditors. Changing interest rates may adversely affect the value of an investment. An increase in interest rates typically causes the value of bonds and other fixed income securities to fall. 4 To the extent that the Fund invests in asset-backed or mortgage-backed securities, its exposure to prepayment and extension risks may be greater than investments in other fixed income securities. 5 The Fund may invest in derivatives such as options and futures; the complexity and rapidly changing structure of derivatives markets may increase the possibility of market losses. 6 High-yield bonds (also known as “junk bonds”) may be subject to greater levels of interest rate, credit, and liquidity risk than investments in higher rated securities. These securities are considered predominantly speculative with respect to the issuer’s continuing ability to make principal and interest payments. The issuers of the Fund’s holdings may be involved in bankruptcy proceedings, reorganizations, or financial restructurings, and are not as strong financially as higher-rated issuers. 7 Investments in international securities are subject to certain risks of overseas investing including currency fluctuations and changes in political and economic conditions, which could result in significant market fluctuations. These risks are magnified in emerging markets. |

8 The Fund is subject to currency risk resulting from fluctuations in exchange rates that may affect the total loss or gain on anon-U.S. Dollar investment when converted back to U.S. Dollars. 9 The Bloomberg Barclays U.S. Government/Credit Bond Index is an index of investment grade government and corporate bonds with a maturity date of more than one year. Unlike the Fund, the Bloomberg Barclays U.S. Government/Credit Bond Index is unmanaged, is not available for investment and does not incur expenses. Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). BARCLAYS® is a trademark and service mark of Barclays Bank Plc (collectively with its affiliates, |

5

| | |

| | AMG Managers Loomis Sayles Bond Fund Portfolio Manager’s Comments(continued) |

| | | | | | | | | | | | |

“Barclays”), used under license. Bloomberg or Bloomberg’s licensors, including Barclays, own all proprietary rights in the Bloomberg Barclays Indices. Neither Bloomberg nor Barclays approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes | | | | | | any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith. | | | | | | Not FDIC insured, nor bank guaranteed. May lose value. |

6

| | |

| | AMG Managers Loomis Sayles Bond Fund Fund Snapshots(unaudited) December 31, 2019 |

PORTFOLIO BREAKDOWN

| | | | | |

| Category | | % of Net Assets |

| | |

Corporate Bonds and Notes | | | | 60.3 | |

| | |

U.S. Government and Agency Obligations | | | | 17.4 | |

| | |

Foreign Government Obligations | | | | 4.7 | |

| | |

Common Stocks | | | | 2.2 | |

| | |

Municipal Bonds | | | | 1.2 | |

| | |

Preferred Stocks | | | | 1.0 | |

| | |

Asset-Backed Securities | | | | 0.7 | |

| | |

Mortgage-Backed Securities | | | | 0.0 | 1 |

| | |

Short-Term Investments | | | | 13.3 | |

| | |

Other Assets Less Liabilities | | | | (0.8 | ) |

1 Less than 0.05%

| | | | | |

| |

| Rating | | % of Market Value1 |

| | |

U.S. Government and Agency Obligations | | | | 20.4 | |

| | |

Aaa/AAA | | | | 1.6 | |

| | |

Aa/AA | | | | 2.9 | |

| | |

A | | | | 31.9 | |

| | |

Baa/BBB | | | | 33.8 | |

| | |

Ba/BB | | | | 7.7 | |

| | |

B | | | | 1.4 | |

| | |

Caa/CCC & lower | | | | 0.3 | |

1 Includes market value of long-term fixed-income securities only.

TOP TEN HOLDINGS

| | | | |

| Security Name | | % of Net Assets |

| | |

U.S. Treasury Bonds, 1.500%, 10/31/21 | | | 8.0 | |

| | |

U.S. Treasury Bonds, 1.500%, 09/30/21 | | | 6.1 | |

| | |

Verizon Communications, Inc., 3.500%, 11/01/24 | | | 2.4 | |

| | |

Ford Motor Credit Co. LLC, 4.389%, 01/08/26 | | | 2.3 | |

| | |

Mexican Bonos Bonds, Series M 20, 10.000%, 12/05/24 (Mexico) | | | 2.3 | |

| | |

U.S. Treasury Bonds, 3.000%, 08/15/48 | | | 2.0 | |

| | |

Lloyds Banking Group PLC, 4.582%, 12/10/25 (United Kingdom) | | | 1.8 | |

| | |

Banco Santander, S.A., 5.179%, 11/19/25 (Spain) | | | 1.6 | |

| | |

Transcontinental Gas Pipe Line Co. LLC, 7.850%, 02/01/26 | | | 1.6 | |

| | |

American Airlines2016-2 Class B Pass Through Trust, 4.375%, 06/15/24 | | | 1.5 | |

| | | | | |

Top Ten as a Group | | | 29.6 | |

| | | | | |

| | | | | |

Credit quality ratings shown above reflect the highest rating assigned by either Standard & Poor’s (“S&P”), Moody’s Investors Service, Inc. (“Moody’s”) or Fitch. These rating agencies are independent, nationally recognized statistical rating organizations and are widely used. Investment grade ratings are credit ratings of BBB/Baa or higher. Below investment grade ratings are credit ratings of BB/Ba or lower. Investments designated N/R are not rated by either rating agency. Unrated investments do not necessarily indicate low credit quality. Credit quality ratings are subject to change.

Because a fund’s strategy may result in multiple investments in particular sectors of the economy, its performance may depend on the performance of those sectors and may fluctuate more widely than investments diversified across more sectors. For additional information on these and other risk considerations, please see the Fund’s prospectus.

Any sectors, industries, or securities discussed should not be perceived as investment recommendations. Mention of a specific security should not be considered a recommendation to buy or solicitation to sell that security. Specific securities mentioned in this report may have been sold from the Fund’s portfolio of investments by the time you receive this report.

7

| | |

| | AMG Managers Loomis Sayles Bond Fund Schedule of Portfolio Investments December 31, 2019 |

| | | | | | | | |

| | | Principal

Amount† | | | Value | |

| |

Corporate Bonds and Notes - 60.3% | | | | | |

| | |

Financials - 21.3% | | | | | | | | |

| | |

Ally Financial, Inc. | | | | | | | | |

4.125%, 02/13/22 | | | $7,915,000 | | | | $8,172,237 | |

8.000%, 11/01/31 | | | 1,267,000 | | | | 1,758,723 | |

| | |

Alta Wind Holdings LLC | | | | | | | | |

7.000%, 06/30/351 | | | 4,642,717 | | | | 5,178,646 | |

| | |

American International Group, Inc. | | | | | | | | |

4.875%, 06/01/22 | | | 560,000 | | | | 597,869 | |

| | |

Banco Santander, S.A. (Spain) | | | | | | | | |

5.179%, 11/19/252 | | | 17,200,000 | | | | 19,272,322 | |

| | |

Bank of America Corp. | | | | | | | | |

(3 month LIBOR + 1.040%) | | | | | | | | |

3.419%, 12/20/283 | | | 12,410,000 | | | | 13,032,284 | |

| | |

Brighthouse Financial Inc. | | | | | | | | |

4.700%, 06/22/472 | | | 890,000 | | | | 824,683 | |

| | |

Cooperatieve Centrale | | | | | | | | |

Raiffeisen-Boerenleenbank (Netherlands) | | | | | | | | |

3.875%, 02/08/22 | | | 9,090,000 | | | | 9,467,139 | |

3.950%, 11/09/22 | | | 2,190,000 | | | | 2,289,878 | |

| | |

Equifax, Inc. | | | | | | | | |

7.000%, 07/01/37 | | | 4,421,000 | | | | 5,687,654 | |

| | |

The Goldman Sachs Group, Inc. | | | | | | | | |

6.750%, 10/01/37 | | | 9,880,000 | | | | 13,724,592 | |

| | |

iStar, Inc. | | | | | | | | |

3.125%, 09/15/224 | | | 2,055,000 | | | | 2,304,325 | |

| | |

Jefferies Group LLC | | | | | | | | |

5.125%, 01/20/23 | | | 8,800,000 | | | | 9,503,812 | |

| | |

JPMorgan Chase & Co. | | | | | | | | |

4.125%, 12/15/26 | | | 11,005,000 | | | | 12,056,448 | |

| | |

Lloyds Banking Group PLC (United Kingdom) | | | | | | | | |

4.582%, 12/10/25 | | | 20,972,000 | | | | 22,714,838 | |

| | |

Marsh & McLennan Cos., Inc. | | | | | | | | |

5.875%, 08/01/33 | | | 8,295,000 | | | | 10,816,551 | |

| | |

MBIA Insurance Corp. | | | | | | | | |

13.261%, 01/15/331,3 | | | 525,000 | | | | 359,260 | |

| | |

Morgan Stanley | | | | | | | | |

3.950%, 04/23/27 | | | 17,265,000 | | | | 18,523,729 | |

GMTN, 4.350%, 09/08/26 | | | 5,000,000 | | | | 5,469,419 | |

MTN, 6.250%, 08/09/26 | | | 11,000,000 | | | | 13,398,361 | |

| | |

National Life Insurance Co. | | | | | | | | |

10.500%, 09/15/391 | | | 5,000,000 | | | | 8,252,107 | |

| | |

Navient Corp. | | | | | | | | |

5.500%, 01/25/23 | | | 14,070,000 | | | | 15,019,725 | |

| | |

Old Republic International Corp. | | | | | | | | |

4.875%, 10/01/24 | | | 4,915,000 | | | | 5,390,185 | |

| | |

Quicken Loans, Inc. | | | | | | | | |

5.250%, 01/15/281 | | | 2,080,000 | | | | 2,152,800 | |

5.750%, 05/01/251 | | | 1,815,000 | | | | 1,876,256 | |

| | |

Realty Income Corp. | | | | | | | | |

5.750%, 01/15/212 | | | 2,125,000 | | | | 2,186,070 | |

| | | | | | | | |

| | | Principal

Amount† | | | Value | |

| | |

Royal Bank of Scotland Group PLC (United Kingdom) | | | | | | | | |

6.125%, 12/15/22 | | | $4,650,000 | | | | $5,089,945 | |

| | |

Societe Generale, S.A. (France) | | | | | | | | |

4.750%, 11/24/251 | | | 11,000,000 | | | | 11,923,268 | |

5.200%, 04/15/211 | | | 7,000,000 | | | | 7,280,431 | |

| | |

Springleaf Finance Corp. | | | | | | | | |

8.250%, 10/01/23 | | | 8,015,000 | | | | 9,337,475 | |

| | |

Weyerhaeuser Co. | | | | | | | | |

6.875%, 12/15/33 | | | 12,890,000 | | | | 17,069,268 | |

| | |

Total Financials | | | | | | | 260,730,300 | |

| | |

Industrials - 36.7% | | | | | | | | |

| | |

America Movil SAB de CV (Mexico) | | | | | | | | |

6.450%, 12/05/22 | | | 169,300,000 | MXN | | | 8,674,302 | |

| | |

American Airlines2016-2 Class B Pass Through Trust | | | | | | | | |

4.375%, 06/15/241 | | | 18,250,000 | | | | 18,710,104 | |

| | |

American Airlines2016-3 Class B Pass Through Trust | | | | | | | | |

3.750%, 10/15/25 | | | 6,631,142 | | | | 6,705,870 | |

| | |

American Airlines2017-1B Class B Pass Through Trust | | | | | | | | |

Series B | | | | | | | | |

4.950%, 02/15/25 | | | 3,191,285 | | | | 3,369,576 | |

| | |

American Airlines2017-2 Class B Pass Through Trust | | | | | | | | |

Series B | | | | | | | | |

3.700%, 10/15/25 | | | 2,455,946 | | | | 2,482,679 | |

| | |

APL, Ltd. | | | | | | | | |

8.000%, 01/15/24 | | | 250,000 | | | | 222,525 | |

| | |

Apple, Inc. | | | | | | | | |

1.800%, 05/11/20 | | | 18,480,000 | | | | 18,463,415 | |

| | |

ArcelorMittal, S.A. (Luxembourg) | | | | | | | | |

6.750%, 03/01/41 | | | 11,065,000 | | | | 13,180,100 | |

7.000%, 10/15/39 | | | 6,604,000 | | | | 8,049,795 | |

| | |

AT&T, Inc. | | | | | | | | |

3.400%, 05/15/25 | | | 13,530,000 | | | | 14,169,596 | |

4.300%, 02/15/30 | | | 14,685,000 | | | | 16,317,840 | |

| | |

Booking Holdings, Inc. | | | | | | | | |

0.900%, 09/15/212,4 | | | 10,970,000 | | | | 12,641,548 | |

| | |

CenturyLink, Inc. | | | | | | | | |

Series S | | | | | | | | |

6.450%, 06/15/21 | | | 5,900,000 | | | | 6,175,825 | |

| | |

Chesapeake Energy Corp. | | | | | | | | |

5.500%, 09/15/264 | | | 3,580,000 | | | | 1,705,455 | |

8.000%, 06/15/272 | | | 965,000 | | | | 598,300 | |

| | |

Continental Airlines, Inc.2000-1Class A-1 | | | | | | | | |

Pass Through Trust | | | | | | | | |

Series 00A1 | | | | | | | | |

8.048%, 11/01/20 | | | 14,509 | | | | 14,785 | |

The accompanying notes are an integral part of these financial statements.

8

| | |

| | AMG Managers Loomis Sayles Bond Fund Schedule of Portfolio Investments(continued) |

| | | | | | | | |

| | | Principal

Amount† | | | Value | |

| |

Industrials - 36.7%(continued) | | | | | |

| | |

Continental Airlines, Inc.2007-1 Class A | | | | | | | | |

Pass Through Trust | | | | | | | | |

Series 071A | | | | | | | | |

5.983%, 04/19/22 | | | $11,737,143 | | | | $12,347,118 | |

| | |

Continental Airlines, Inc.2007-1 Class B | | | | | | | | |

Pass Through Trust | | | | | | | | |

Series 071B | | | | | | | | |

6.903%, 04/19/22 | | | 738,367 | | | | 777,217 | |

| | |

Continental Resources, Inc. | | | | | | | | |

3.800%, 06/01/24 | | | 2,025,000 | | | | 2,094,432 | |

4.500%, 04/15/23 | | | 385,000 | | | | 402,265 | |

| | |

Corning, Inc. | | | | | | | | |

6.850%, 03/01/29 | | | 9,142,000 | | | | 11,393,618 | |

| | |

Cox Communications, Inc. | | | | | | | | |

4.800%, 02/01/351 | | | 3,369,000 | | | | 3,732,021 | |

| | |

Cummins, Inc. | | | | | | | | |

5.650%, 03/01/98 | | | 6,460,000 | | | | 8,183,572 | |

| | |

Dell International LLC / EMC Corp. | | | | | | | | |

6.020%, 06/15/261 | | | 3,270,000 | | | | 3,764,424 | |

8.100%, 07/15/361 | | | 3,110,000 | | | | 4,089,457 | |

8.350%, 07/15/461 | | | 2,990,000 | | | | 4,120,032 | |

| | |

Delta Air Lines, Inc. | | | | | | | | |

Series 071B | | | | | | | | |

8.021%, 08/10/22 | | | 2,481,495 | | | | 2,714,409 | |

| | |

Dillard’s, Inc. | | | | | | | | |

7.000%, 12/01/28 | | | 225,000 | | | | 250,119 | |

| | |

Embraer Netherlands Finance BV (Netherlands) | | | | | | | | |

5.400%, 02/01/27 | | | 2,325,000 | | | | 2,616,811 | |

| | |

Enable Midstream Partners, LP | | | | | | | | |

5.000%, 05/15/44 | | | 2,725,000 | | | | 2,501,370 | |

| | |

Enbridge Energy Partners, LP | | | | | | | | |

7.375%, 10/15/45 | | | 1,870,000 | | | | 2,793,723 | |

| | |

Energy Transfer Partners, LP/Regency | | | | | | | | |

Energy Finance Corp. | | | | | | | | |

4.500%, 11/01/23 | | | 700,000 | | | | 741,688 | |

| | |

EnLink Midstream Partners, LP | | | | | | | | |

4.150%, 06/01/25 | | | 6,145,000 | | | | 5,776,300 | |

| | |

Enterprise Products Operating LLC | | | | | | | | |

4.050%, 02/15/22 | | | 2,219,000 | | | | 2,311,280 | |

| | |

ERAC USA Finance LLC | | | | | | | | |

7.000%, 10/15/371 | | | 12,000,000 | | | | 16,975,457 | |

| | |

Ford Motor Co. | | | | | | | | |

6.375%, 02/01/29 | | | 1,990,000 | | | | 2,145,072 | |

| | |

Ford Motor Credit Co. LLC, GMTN | | | | | | | | |

4.389%, 01/08/26 | | | 28,075,000 | | | | 28,535,065 | |

| | |

General Motors Co. | | | | | | | | |

5.200%, 04/01/45 | | | 2,760,000 | | | | 2,787,606 | |

| | |

General Motors Financial Co., Inc. | | | | | | | | |

5.250%, 03/01/26 | | | 9,680,000 | | | | 10,735,321 | |

| | | | | | | | |

| | | Principal

Amount† | | | Value | |

| | |

Georgia-Pacific LLC | | | | | | | | |

5.400%, 11/01/201 | | | $5,175,000 | | | | $5,318,650 | |

| | |

HCA, Inc. | | | | | | | | |

4.500%, 02/15/27 | | | 3,040,000 | | | | 3,278,612 | |

7.500%, 11/06/33 | | | 75,000 | | | | 94,500 | |

| | |

Hewlett Packard Enterprise Co. | | | | | | | | |

6.350%, 10/15/45 | | | 2,243,000 | | | | 2,700,870 | |

| | |

International Business Machines Corp. | | | | | | | | |

1.625%, 05/15/20 | | | 5,980,000 | | | | 5,978,069 | |

| | |

Kinder Morgan Energy Partners, LP | | | | | | | | |

3.500%, 09/01/23 | | | 6,685,000 | | | | 6,928,306 | |

4.150%, 03/01/22 | | | 5,620,000 | | | | 5,829,370 | |

5.800%, 03/01/21 | | | 4,320,000 | | | | 4,497,224 | |

| | |

KLA Corp. | | | | | | | | |

5.650%, 11/01/34 | | | 4,590,000 | | | | 5,501,721 | |

| | |

Marks & Spencer PLC (United Kingdom) | | | | | | | | |

7.125%, 12/01/371 | | | 4,725,000 | | | | 5,337,284 | |

| | |

Masco Corp. | | | | | | | | |

6.500%, 08/15/32 | | | 254,000 | | | | 311,838 | |

7.750%, 08/01/29 | | | 499,000 | | | | 647,624 | |

| | |

Noble Energy, Inc. | | | | | | | | |

3.900%, 11/15/24 | | | 3,670,000 | | | | 3,879,707 | |

| | |

Nuance Communications, Inc. | | | | | | | | |

1.000%, 12/15/354 | | | 2,140,000 | | | | 2,152,035 | |

1.250%, 04/01/254 | | | 1,585,000 | | | | 1,760,622 | |

1.500%, 11/01/354 | | | 50,000 | | | | 52,697 | |

| | |

ONEOK Partners, LP | | | | | | | | |

4.900%, 03/15/25 | | | 13,736,000 | | | | 15,129,173 | |

6.200%, 09/15/43 | | | 245,000 | | | | 310,275 | |

| | |

Owens Corning | | | | | | | | |

7.000%, 12/01/36 | | | 2,715,000 | | | | 3,382,514 | |

| | |

PulteGroup, Inc. | | | | | | | | |

6.000%, 02/15/35 | | | 8,860,000 | | | | 9,878,900 | |

6.375%, 05/15/33 | | | 5,135,000 | | | | 5,995,112 | |

| | |

Qwest Corp. | | | | | | | | |

7.250%, 09/15/252 | | | 990,000 | | | | 1,139,046 | |

| | |

Reliance Holding USA, Inc. | | | | | | | | |

5.400%, 02/14/221 | | | 3,250,000 | | | | 3,439,410 | |

| | |

Samsung Electronics Co., Ltd. (South Korea) | | | | | | | | |

7.700%, 10/01/271 | | | 1,760,000 | | | | 2,020,026 | |

| | |

Sealed Air Corp. | | | | | | | | |

5.500%, 09/15/251 | | | 1,580,000 | | | | 1,738,000 | |

| | |

SM Energy Co. | | | | | | | | |

6.625%, 01/15/272 | | | 2,155,000 | | | | 2,118,052 | |

| | |

Telecom Italia Capital, S.A. (Luxembourg) | | | | | | | | |

6.000%, 09/30/34 | | | 4,665,000 | | | | 5,003,212 | |

6.375%, 11/15/33 | | | 3,530,000 | | | | 3,918,300 | |

| | |

Telefonica Emisiones SAU (Spain) | | | | | | | | |

4.570%, 04/27/23 | | | 900,000 | | | | 968,529 | |

| | |

Time Warner Cable LLC | | | | | | | | |

5.500%, 09/01/412 | | | 805,000 | | | | 899,271 | |

The accompanying notes are an integral part of these financial statements.

9

| | |

| | AMG Managers Loomis Sayles Bond Fund Schedule of Portfolio Investments(continued) |

| | | | | | | | |

| | | Principal

Amount† | | | Value | |

| |

Industrials - 36.7%(continued) | | | | | |

| | |

The Toro Co. | | | | | | | | |

6.625%, 05/01/37 | | | $6,810,000 | | | | $8,741,348 | |

| | |

Transcontinental Gas Pipe Line Co. LLC | | | | | | | | |

7.850%, 02/01/26 | | | 15,140,000 | | | | 19,242,318 | |

| | |

UAL2007-1 Pass Through Trust | | | | | | | | |

Series 071A | | | | | | | | |

6.636%, 07/02/22 | | | 7,845,901 | | | | 8,330,935 | |

| | |

United Airlines2016-2 Class B | | | | | | | | |

Pass Through Trust | | | | | | | | |

Series16-2 | | | | | | | | |

3.650%, 10/07/25 | | | 1,949,111 | | | | 1,967,818 | |

| | |

United States Steel Corp. | | | | | | | | |

6.650%, 06/01/372 | | | 3,120,000 | | | | 2,527,200 | |

| | |

US Airways2011-1 Class A Pass Through | | | | | | | | |

Series A | | | | | | | | |

7.125%, 10/22/23 | | | 1,893,105 | | | | 2,126,166 | |

| | |

Vale Overseas, Ltd. (Brazil) | | | | | | | | |

6.875%, 11/21/36 | | | 1,759,000 | | | | 2,286,700 | |

| | |

Verizon Communications, Inc. | | | | | | | | |

3.500%, 11/01/24 | | | 27,900,000 | | | | 29,587,163 | |

| | |

WestRock MWV LLC | | | | | | | | |

7.550%, 03/01/47 | | | 970,000 | | | | 1,334,639 | |

| | |

Total Industrials | | | | | | | 449,623,328 | |

| | |

Utilities - 2.3% | | | | | | | | |

| | |

DCP Midstream Operating, LP | | | | | | | | |

6.450%, 11/03/361 | | | 870,000 | | | | 913,500 | |

| | |

Empresa Nacional de Electricidad S.A. | | | | | | | | |

(Cayman Islands) | | | | | | | | |

7.875%, 02/01/27 | | | 2,900,000 | | | | 3,369,324 | |

| | |

Enel Finance International, N.V. (Netherlands) | | | | | | | | |

6.000%, 10/07/391 | | | 11,152,000 | | | | 14,051,783 | |

| | |

Enterprise Products Operating LLC | | | | | | | | |

3.900%, 02/15/24 | | | 6,400,000 | | | | 6,791,527 | |

| | |

Tenaga Nasional Bhd (Malaysia) | | | | | | | | |

7.500%, 11/01/251 | | | 2,000,000 | | | | 2,465,612 | |

| | |

Total Utilities | | | | | | | 27,591,746 | |

| |

Total Corporate Bonds and Notes

(Cost $648,747,456) | | | | 737,945,374 | |

| |

Asset-Backed Security - 0.7% | | | | | |

| | |

FAN Engine Securitization, Ltd. (Ireland) | | | | | | | | |

Series2013-1A, Class 1A | | | | | | | | |

4.625%, 10/15/431 | | | 8,351,435 | | | | 8,351,200 | |

| |

Total Asset-Backed Security

(Cost $8,261,888) | | | | 8,351,200 | |

| |

Mortgage-Backed Securities - 0.0%# | | | | | |

| | |

Commercial Mortgage Trust | | | | | | | | |

Series 2014-UBS4, Class A2 | | | | | | | | |

2.963%, 08/10/47 | | | 91,095 | | | | 91,395 | |

| | | | | | | | |

| | | Principal

Amount† | | | Value | |

| | |

WFRBS Commercial Mortgage Trust | | | | | | | | |

Series2011-C3, Class D | | | | | | | | |

5.683%, 03/15/441,3 | | | $435,000 | | | | $332,460 | |

| |

Total Mortgage-Backed Securities

(Cost $491,696) | | | | 423,855 | |

| |

Municipal Bonds - 1.2% | | | | | |

| | |

Illinois State | | | | | | | | |

5.100%, 06/01/33 | | | 1,070,000 | | | | 1,153,492 | |

| | |

Michigan Tobacco Settlement Finance Authority | | | | | | | | |

7.309%, 06/01/46 | | | 1,950,000 | | | | 2,018,270 | |

| | |

Virginia Tobacco Settlement Financing Corp. | | | | | | | | |

6.706%, 06/01/46 | | | 11,510,000 | | | | 11,085,856 | |

| |

Total Municipal Bonds

(Cost $13,925,387) | | | | 14,257,618 | |

| |

U.S. Government and Agency

Obligations - 17.4% | | | | | |

| |

Fannie Mae - 0.1% | | | | | |

| | |

FNMA, | | | | | | | | |

3.000%, 07/01/27 | | | 1,111,176 | | | | 1,140,349 | |

6.000%, 07/01/29 | | | 782 | | | | 876 | |

| | |

Total Fannie Mae | | | | | | | 1,141,225 | |

| |

Freddie Mac - 0.0%# | | | | | |

| | |

FHLMC Gold, | | | | | | | | |

5.000%, 12/01/31 | | | 14,760 | | | | 15,887 | |

| |

U.S. Treasury Obligations - 17.3% | | | | | |

| | |

U.S. Treasury Bonds, | | | | | | | | |

1.500%, 09/30/21 to 11/30/212 | | | 187,710,000 | | | | 187,442,232 | |

3.000%, 08/15/482 | | | 21,295,000 | | | | 24,044,218 | |

| |

Total U.S. Treasury Obligations | | | | 211,486,450 | |

| |

Total U.S. Government and Agency Obligations

(Cost $208,136,317) | | | | 212,643,562 | |

| |

Foreign Government Obligations - 4.7% | | | | | |

| | |

Brazilian Government International Bonds | | | | | | | | |

8.500%, 01/05/24 | | | 6,650,000 | BRL | | | 1,768,837 | |

10.250%, 01/10/28 | | | 5,750,000 | BRL | | | 1,681,032 | |

| | |

Canadian When Issued Government Bond | | | | | | | | |

Series 0001 | | | | | | | | |

0.750%, 09/01/20 | | | 15,225,000 | CAD | | | 11,646,296 | |

| | |

European Investment Bank Bonds | | | | | | | | |

0.000%, 03/10/215 | | | 5,000,000 | AUD | | | 3,452,441 | |

| | |

Mexican Bonos | | | | | | | | |

Series M | | | | | | | | |

8.000%, 12/07/23 | | | 122,500,000 | MXN | | | 6,748,368 | |

| | |

Mexican Bonos Bonds | | | | | | | | |

Series M 7.750%, 05/29/31 | | | 49,000,000 | MXN | | | 2,764,551 | |

Series M 20 10.000%, 12/05/24 | | | 461,500,000 | MXN | | | 27,703,181 | |

| | |

Norway Government Bonds | | | | | | | | |

Series 474 | | | | | | | | |

3.750%, 05/25/211 | | | 13,210,000 | NOK | | | 1,554,780 | |

| |

Total Foreign Government Obligations

(Cost $79,185,683) | | | | 57,319,486 | |

The accompanying notes are an integral part of these financial statements.

10

| | |

| | AMG Managers Loomis Sayles Bond Fund Schedule of Portfolio Investments(continued) |

| | | | | | | | |

| | |

Shares | | | Value | |

Common Stocks - 2.2% | | | | | | | | |

| |

Communication Services - 1.0% | | | | | |

| | |

AT&T, Inc. | | | 314,704 | | | | $12,298,633 | |

| | |

Health Care - 0.5% | | | | | | | | |

| | |

Bristol-Myers Squibb Co. | | | 91,569 | | | | 5,877,814 | |

| |

Information Technology - 0.7% | | | | | |

| | |

Corning, Inc.2 | | | 281,220 | | | | 8,186,314 | |

| |

Total Common Stocks

(Cost $21,594,608) | | | | 26,362,761 | |

| | |

Preferred Stocks - 1.0% | | | | | | | | |

| | |

Financials - 1.0% | | | | | | | | |

| | |

Bank of America Corp., 7.25% 2,4 | | | 7,808 | | | | 11,313,792 | |

| | |

Navient Corp., 6.00% | | | 41,250 | | | | 990,412 | |

| | |

Total Financials | | | | | | | 12,304,204 | |

| | |

Utilities - 0.0%# | | | | | | | | |

| | |

Wisconsin Electric Power Co., 3.60% | | | 3,946 | | | | 355,140 | |

| |

Total Preferred Stocks

(Cost $8,303,212) | | | | 12,659,344 | |

| | |

| | | Principal

Amount | | | | |

Short-Term Investments - 13.3% | | | | | |

| |

Joint Repurchase Agreements - 1.4%6 | | | | | |

| | |

Cantor Fitzgerald Securities, Inc., dated 12/31/19, due 01/02/20, 1.580% total to be received $4,035,140 (collateralized by various U.S. Government Agency Obligations and U.S. Treasuries, 0.000% - 8.500%, 01/25/20 - 10/15/60, totaling $4,115,482) | | | $4,034,786 | | | | 4,034,786 | |

| | |

Citadel Securities LLC, dated 12/31/19, due 01/02/20, 1.600% total to be received $2,688,592 (collateralized by various U.S. Treasuries, 0.000% - 8.500%, 01/15/20 - 11/15/48, totaling $2,742,364) | | | 2,688,353 | | | | 2,688,353 | |

| | |

Citigroup Global Markets, Inc., dated 12/31/19, due 01/02/20, 1.570% total to be received $4,035,138 (collateralized by various U.S. Government Agency Obligations and U.S. Treasuries, 0.000% - 9.000%, 02/13/20 - 09/20/69, totaling $4,115,482) | | | 4,034,786 | | | | 4,034,786 | |

| | | | | | | | |

| | | Principal

Amount | | | Value | |

| | |

RBC Dominion Securities, Inc., dated 12/31/19, due 01/02/20, 1.570% total to be received $4,035,138 (collateralized by various U.S. Government Agency Obligations and U.S. Treasuries, 0.000% - 6.500%, 06/30/21 - 12/01/49, totaling $4,115,482) | | | $4,034,786 | | | | $4,034,786 | |

| | |

State of Wisconsin Investment Board, dated 12/31/19, due 01/02/20, 1.750% total to be received $2,195,331 (collateralized by various U.S. Treasuries, 0.125% - 3.875%, 04/15/21 - 02/15/47, totaling $2,239,081) | | | 2,195,118 | | | | 2,195,118 | |

| |

Total Joint Repurchase Agreements | | | | 16,987,829 | |

| |

U.S. Government Obligations - 10.4% | | | | | |

| | |

U.S. Treasury Bills, 0.257%, 01/23/202,7 | | | 24,915,000 | | | | 24,883,909 | |

| | |

U.S. Treasury Bills, 0.448%, 01/30/207 | | | 5,000,000 | | | | 4,993,632 | |

| | |

U.S. Treasury Bills, 0.584%, 02/27/207 | | | 59,265,000 | | | | 59,093,092 | |

| | |

U.S. Treasury Bills, 0.796%, 04/02/202,7 | | | 18,670,000 | | | | 18,598,030 | |

| | |

U.S. Treasury Bills, 0.867%, 04/09/202,7 | | | 20,000,000 | | | | 19,916,958 | |

| |

Total U.S. Government Obligations | | | | 127,485,621 | |

| | |

| | | Shares | | | | |

Other Investment Companies - 1.5% | | | | | |

| | |

Dreyfus Government Cash Management Fund, Institutional Shares, 1.51%8 | | | 6,104,693 | | | | 6,104,693 | |

| | |

Dreyfus Institutional Preferred Government Money Market Fund, Institutional Shares, 1.55%8 | | | 6,104,693 | | | | 6,104,693 | |

| | |

JPMorgan U.S. Government Money Market Fund, IM Shares, 1.53%8 | | | 6,289,685 | | | | 6,289,685 | |

| |

Total Other Investment Companies | | | | 18,499,071 | |

| |

Total Short-Term Investments

(Cost $162,962,129) | | | | 162,972,521 | |

| | |

Total Investments - 100.8%

(Cost $1,151,608,376) | | | | | | | 1,232,935,721 | |

| |

Other Assets, less Liabilities - (0.8)% | | | | (9,202,459 | ) |

| | |

Net Assets - 100.0% | | | | | | | $1,223,733,262 | |

| † | Principal amount stated in U.S. dollars unless otherwise stated. |

| 1 | Security exempt from registration under Rule 144A of the Securities Act of 1933. This security may be resold in transactions exempt from registration, normally to qualified buyers. At December 31, 2019, the value of these securities amounted to $133,936,968 or 10.9% of net assets. |

| 2 | Some of these securities, amounting to $180,616,082 or 14.8% of net assets, were out on loan to various borrowers and are collateralized by cash and various U.S. Treasury Obligations and U.S. Government Agency Obligations. See Note 4 of Notes to Financial Statements. |

| 3 | Variable rate security. The rate shown is based on the latest available information as of December 31, 2019. Certain variable rate securities are not based on a published reference rate and spread but are determined by the issuer or agent and are based on current market conditions. These securities do not indicate a reference rate and spread in their description above. |

| 4 | Convertible Security. A corporate bond or preferred stock, usually a junior debenture, that can be converted, at the option of the holder, for a specific number of shares of the company’s preferred stock or common stock. The market value of convertible bonds and convertible preferred stocks at December 31, 2019, amounted to $31,930,474 or 2.6% of net assets. |

The accompanying notes are an integral part of these financial statements.

11

| | |

| | AMG Managers Loomis Sayles Bond Fund Schedule of Portfolio Investments(continued) |

| 6 | Cash collateral received for securities lending activity was invested in these joint repurchase agreements. |

| 7 | Represents yield to maturity at December 31, 2019. |

| 8 | Yield shown represents the December 31, 2019, seven day average yield, which refers to the sum of the previous seven days’ dividends paid, expressed as an annual percentage. |

| GMTN | Global Medium-Term Notes |

| LIBOR | London Interbank Offered Rate |

CURRENCY ABBREVIATIONS:

The following table summarizes the inputs used to value the Fund’s investments by the fair value hierarchy levels as of December 31, 2019:

| | | | | | | | | | | | | | | | |

| | | Level 1 | | | Level 21 | | | Level 3 | | | Total | |

Investments in Securities | | | | | | | | | | | | | | | | |

| | | | |

Corporate Bonds and Notes† | | | — | | | | $737,945,374 | | | | — | | | | $737,945,374 | |

| | | | |

Asset-Backed Security | | | — | | | | 8,351,200 | | | | — | | | | 8,351,200 | |

| | | | |

Mortgage-Backed Securities | | | — | | | | 423,855 | | | | — | | | | 423,855 | |

| | | | |

Municipal Bonds | | | — | | | | 14,257,618 | | | | — | | | | 14,257,618 | |

| | | | |

U.S. Government and Agency Obligations† | | | — | | | | 212,643,562 | | | | — | | | | 212,643,562 | |

| | | | |

Foreign Government Obligations | | | — | | | | 57,319,486 | | | | — | | | | 57,319,486 | |

| | | | |

Common Stocks†† | | | $26,362,761 | | | | — | | | | — | | | | 26,362,761 | |

| | | | |

Preferred Stocks†† | | | 12,659,344 | | | | — | | | | — | | | | 12,659,344 | |

| | | | |

Short-Term Investments | | | | | | | | | | | | | | | | |

| | | | |

Joint Repurchase Agreements | | | — | | | | 16,987,829 | | | | — | | | | 16,987,829 | |

| | | | |

U.S. Government Obligations | | | — | | | | 127,485,621 | | | | — | | | | 127,485,621 | |

| | | | |

Other Investment Companies | | | 18,499,071 | | | | — | | | | — | | | | 18,499,071 | |

| | | | | | | | | | | | | | | | |

Total Investments in Securities | | | $57,521,176 | | | | $1,175,414,545 | | | | — | | | | $1,232,935,721 | |

| | | | | | | | | | | | | | | | |

| † | All corporate bonds and notes and U.S. government and agency obligations held in the Fund are Level 2 securities. For a detailed breakout of corporate bonds and notes and U.S. government and agency obligations by major industry or agency classification, please refer to the Fund’s Schedule of Portfolio Investments. |

| †† | All common stocks and preferred stocks held in the Fund are Level 1 securities. For a detailed breakout of common stocks and preferred stocks by major industry classification, please refer to the Fund’s Schedule of Portfolio Investments. |

| 1 | An external pricing service is used to reflect any impact on security value due to market movements between the time the Fund valued such foreign securities and the earlier closing of foreign markets. |

For the fiscal year ended December 31, 2019, there were no transfers in or out of Level 3.

The accompanying notes are an integral part of these financial statements.

12

| | |

| | AMG Managers Loomis Sayles Bond Fund Schedule of Portfolio Investments(continued) |

The following table below is a reconciliation of investments in which significant unobservable inputs (Level 3) were used in determining fair value at December 31, 2019:

| | | | |

| | | Asset-Backed Securities |

| |

Balance as of December 31, 2018 | | | $11,579,866 | |

| |

Accrued discounts (premiums) | | | (953 | ) |

| |

Realized gain (loss) | | | (65,955 | ) |

| |

Change in unrealized appreciation/depreciation | | | 425,049 | |

| |

Purchases | | | — | |

| |

Sales | | | — | |

| |

Paydowns | | | (11,938,007 | ) |

| |

Transfers in to Level 3 | | | — | |

| |

Transfers out of Level 3 | | | — | |

| |

Balance as of December 31, 2019 | | | — | |

| | | — | |

Net change in unrealized appreciation/depreciation on investments still held at December 31, 2019 | | | — | |

The country allocation in the Schedule of Portfolio Investments at December 31, 2019, was as follows:

| | | | |

| Country | | % of Long-Term

Investments |

| |

Brazil | | | 0.5 | |

| |

Canada | | | 1.1 | |

| |

Cayman Islands | | | 0.3 | |

| |

France | | | 1.8 | |

| |

Ireland | | | 0.8 | |

| |

Luxembourg | | | 3.1 | |

| |

Malaysia | | | 0.2 | |

| |

Mexico | | | 4.3 | |

| |

Netherlands | | | 2.7 | |

| |

Norway | | | 0.2 | |

| |

South Korea | | | 0.2 | |

| |

Spain | | | 1.9 | |

| |

United Kingdom | | | 3.1 | |

| |

United States | | | 79.8 | |

| | | | |

| | | 100.0 | |

| | | | |

The accompanying notes are an integral part of these financial statements.

13

| | |

| |

AMG Managers Global Income Opportunity Fund Portfolio Manager’s Comments(unaudited) |

| | | | | | | | | | | | |

THE YEAR IN REVIEW AMG Managers Global Income Opportunity Fund (Class N shares) (the “Fund”) returned 7.67% during the year ended December 31, 2019, compared with the 6.84% return for the Bloomberg Barclays Global Aggregate Bond Index. Allocation to select corporate credit sectors and issuers, including high yield bonds, were the main contributor to performance over the past 12 months. Despite the slowdown in global growth and weaker corporate profits, investment grade credit spreads tightened and significantly outperformed duration-matched global treasuries. In response to the weaker economic growth backdrop, major central banks adopted more accommodative monetary policies. Choices in the banking sector positively contributed to overall performance. Favored U.K. and European banks were among the top credit picks. We remain focused on well-diversified institutions with excellent liquidity, high quality assets, and healthy balance sheets. Issuer selections in the electric utility space added value, particularly in European names. Underweight positioning in Eurozone treasuries and Agency MBS sectors did hold back performance somewhat. Duration and yield curve positioning was a source of positive excess returns. Curve positioning in the5-and10-year part of the U.S.dollar-pay curves proved most beneficial. The allocation of duration into select emerging markets such as Mexico and Colombia also proved beneficial. Although a small exposure to duration, our small overweight to South African rand contributed positively to overall yield curve performance. Overall currency allocation was a drag on results. Overweight positions in the Japanese yen and euro and an underweight position in the Chilean peso | | | | | | represent the main detractors. On the other hand, overweight allocations in the Canadian dollar and Australian dollar were moderate contributors to relative performance. The Fund uses currency forwards in order to gain exposure to select currencies without investing in the underlying bond market or to hedge certain currency positions based on our strategic view during a certain period. The portfolio’s currency forward positions detracted from relative performance by roughly 165 bps over the past 12 months, largely due to layering in FX forwards to gain exposure to the euro in order to risk control the portfolio’s EUR relative position versus benchmark. The hedging costs to hedge Mexican peso exposure detracted as well, as we were comfortable with the local Mexican bond market although we were cautious on the currency volatility due to ongoing slowing global growth and geopolitical uncertainties. Although the Mexican Peso rallied into year end to finish the year as the best performing Latin America EM currency, risks remain elevated due to erratic policy decisions by President Lopez Obrador . In addition, FX forwards used to hedge the portfolio’s underweight to JPY hurt relative performance as the risk sentiment improved. LOOKING FORWARD We believe the U.S. will exit the manufacturing slowdown without dipping into recession. The three FOMC (Federal Open Market Committee) rate cuts will provide support to an economy that has been hampered by trade conflict, slumping exports, and abuild-up in inventories. Global Purchasing Manager Indicies (PMIs) have been improving and we are seeing green shoots in other survey-based economic indicators, but we need to see more evidence for stabilization in hard data. | | | | | | Credit spreads are tight, but should continue to receive support. Improvement in economic data and the U.S. Federal Reserve (the Fed) remaining relaxed and accommodative in a low growth, low inflation environment should enable credit spreads to stay well contained. Higher wages and employment costs are pressuring profit margins, buttop-line revenue growth has been respectable. We expect the U.S. dollar to stay in a relatively tight band in the near term, which should help emerging market currencies and risk assets in general. While there has been some recent weakness in the dollar, there hasn’t been a substantial breakout in either direction. We are watching for more convincing evidence that economic activity is accelerating at a faster pace outside the U.S., which would apply greater downward pressure on the dollar. Stability in economic growth should lead to better profit growth in 2020, albeit in the low single-digit range. We expect S&P 500® Index profits to grow around 5% in 2020, up from low single digits in 2019. A profits recession—with profits down 10% or more—would substantially increase recession risks, but that is not our base case. We do not expect further escalation in the trade conflict between the U.S. and China. The phase one trade agreement is an important step in the right direction and a key support to risk appetite. The deal could deliver upside surprise if it is more comprehensive than expected, but the general truce has been enough to keep risk assets moving in a positive direction. This commentary reflects the viewpoints of Loomis, Sayles & Company and is not intended as a forecast or guarantee of future results. |

14

| | |

| | AMG Managers Global Income Opportunity Fund Portfolio Manager’s Comments(continued) |

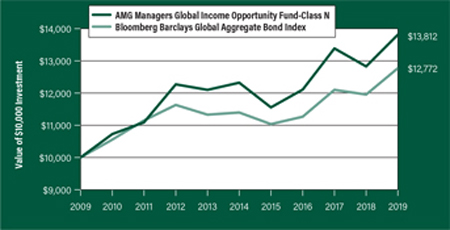

CUMULATIVE TOTAL RETURN PERFORMANCE

AMG Managers Global Income Opportunity Fund’s cumulative total return is based on the daily change in net asset value (NAV), and assumes that all dividends and distributions were reinvested. The graph compares a hypothetical $10,000 investment made in the AMG Managers Global Income Opportunity Fund’s Class N shares on December 31, 2009, to a $10,000 investment made in the Bloomberg Barclays Global Aggregate Bond Index for the same time period. The graph and table do not reflect the deduction of taxes that a shareholder would pay on a Fund distribution or redemption of shares. The listed returns for the Fund are net expenses and the returns for the index exclude expenses. Total returns would have been lower had certain expenses not been reduced.

The table below shows the average annual total returns for the AMG Managers Global Income Opportunity Fund and the Bloomberg Barclays Global Aggregate Bond Index for the same time periods ended December 31, 2019.

| | | | | | | | | | | | |

| Average Annual Total Returns1 | | One Year | | | Five

Years | | | Ten Years | |

| |

AMG Managers Global Income Opportunity Fund2, 3, 4, 5, 6,7 | | | | | |

Class N | | | 7.67% | | | | 2.31% | | | | 3.28% | |

Bloomberg Barclays Global Aggregate Bond Index8 | | | 6.84% | | | | 2.31% | | | | 2.48% | |

The performance data shown represents past performance. Past performance is not a guarantee of future results. Current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

Investors should carefully consider the Fund’s investment objectives, risks, charges and expenses before investing. For performance information through the most recent month end, current net asset values per share for the Fund and other information, please call 800.548.4539 or visit our website at amgfunds.com for a free prospectus. Read it carefully before investing or sending money.

Distributed by AMG Distributors, Inc., member FINRA/SIPC.

| 1 | Total return equals income yield plus share price change and assumes reinvestment of all dividends and capital gain distributions. Returns are net of fees and may reflect offsets of Fund expenses as described in the prospectus. No adjustment has been made for taxes payable by shareholders on their reinvested dividends and capital gain distributions. Returns for periods greater than one year are annualized. The listed returns on the Fund are net of expenses and based on the published NAV as of December 31, 2019. All returns are in U.S. dollars($). |

| 2 | From time to time the Fund’s advisor has waived it’s fees and/or absorbed Fund expenses, which has resulted in higher returns. |

|

3 The Fund is subject to currency risk resulting from fluctuations in exchange rates that may affect the total loss or gain on anon-U.S. Dollar investment when converted back to U.S. Dollars. 4 The Fund is subject to the risks associated with investments in debt securities, such as default risk and fluctuations in the perception of the debtor’s ability to pay its creditors. Changing interest rates may adversely affect the value of an investment. An increase in interest rates typically causes the value of bonds and other fixed income securities to fall. 5 High-yield bonds (also known as “junk bonds”) may be subject to greater levels of interest rate, credit, and liquidity risk than investments in higher rated securities. These securities are considered predominantly speculative with respect to the issuer’s continuing ability to make principal and interest payments. The issuers of the Fund’s holdings may be involved in bankruptcy proceedings, reorganizations, or financial restructurings, and are not as strong financially as higher-rated issuers. 6 Investments in international securities are subject to certain risks of overseas investing including currency fluctuations and changes in political and economic conditions, which could result in significant market fluctuations. These risks are magnified in emerging markets. 7 The Fund is subject to the risks associated with investments in emerging markets, such as erratic earnings patterns, economic and political instability, changing exchange controls, limitations on repatriation of foreign capital and changes in local government attitudes toward private investment, possibly leading to nationalization or confiscation of investor assets. |

8 The Bloomberg Barclays Global Aggregate Bond Index provides a broad-based measure of the global investment-grade fixed income markets. The three major components of this index are the U.S. Aggregate, thePan-European Aggregate, and the Asian-Pacific Aggregate Indices. The Index also includes Eurodollar andEuro-Yen corporate bonds, Canadian government, agency and corporate securities, and USD investment grade 144A securities. Unlike the Fund, the Bloomberg Barclays Global Aggregate Bond Index is unmanaged, is not available for investment and does not incur expenses. |

| |

Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). BARCLAYS® is a trademark and service mark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Bloomberg or Bloomberg’s licensors, including Barclays, own all proprietary rights in the Bloomberg Barclays Indices. |

15

| | |

| | AMG Managers Global Income Opportunity Fund Portfolio Manager’s Comments(continued) |

| | | | | | | | | | | | |

| Neither Bloomberg nor Barclays approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to | | | | | | be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith. | | | | | | Not FDIC insured, nor bank guaranteed. May lose value |

16

| | |

| | AMG Managers Global Income Opportunity Fund Fund Snapshots(unaudited) December 31, 2019 |

PORTFOLIO BREAKDOWN

| | | | | |

| Category | | % of Net Assets |

| | |

Corporate Bonds and Notes | | | | 44.2 | |

| | |

Foreign Government Obligations | | | | 34.0 | |

| | |

U.S. Government and Agency Obligations | | | | 19.0 | |

| | |

Short-Term Investments | | | | 2.5 | |

| | |

Other Assets Less Liabilities | | | | 0.3 | |

| | | | | |

| Rating | | % of Market Value1 |

| | |

U.S. Government and Agency Obligations | | | | 19.6 | |

| | |

Aaa/AAA | | | | 7.0 | |

| | |

Aa/AA | | | | 8.4 | |

| | |

A | | | | 30.8 | |

| | |

Baa/BBB | | | | 29.0 | |

| | |

Ba/BB | | | | 4.7 | |

| | |

B | | | | 0.3 | |

| | |

Caa/CCC & lower | | | | 0.2 | |

| 1 | Includes market value of long-term fixed-income securities only. |

TOP TEN HOLDINGS

| | | | |

| Security Name | | % of

Net Assets |

| | |

U.S. Treasury Notes, 1.625%, 08/15/29 | | | 6.2 | |

| | |

U.S. Treasury Notes, 3.125%, 11/15/28 | | | 4.0 | |

| | |

FNMA, 3.500%, 07/01/49 | | | 3.8 | |

| | |

French Republic Government Bond OAT, 4.250%, 10/25/23 (France) | | | 2.8 | |

| | |

Indonesia Government International Bonds, 4.750%, 01/08/26 (Indonesia) | | | 2.3 | |

| | |

Energy Transfer Partners, LP, 4.050%, 03/15/25 | | | 2.3 | |

| | |

Enel Finance International NV, 4.625%, 09/14/25 (Netherlands) | | | 2.3 | |

| | |

Alfa, SAB de CV, 5.250%, 03/25/24 (Mexico) | | | 2.2 | |

| | |

Lloyds Banking Group PLC, 4.500%, 11/04/24 (United Kingdom) | | | 2.2 | |

| | |

Barclays PLC, 3.650%, 03/16/25 (United Kingdom) | | | 2.2 | |

| | | | | |

Top Ten as a Group | | | 30.3 | |

| | | | | |

| | | | | |

Credit quality ratings shown above reflect the highest rating assigned by either Standard & Poor’s (“S&P”), Moody’s Investors Service, Inc. (“Moody’s”) or Fitch. These rating agencies are independent, nationally recognized statistical rating organizations and are widely used. Investment grade ratings are credit ratings of BBB/Baa or higher. Below investment grade ratings are credit ratings of BB/Ba or lower. Investments designated N/R are not rated by either rating agency. Unrated investments do not necessarily indicate low credit quality. Credit quality ratings are subject to change.

Because a fund’s strategy may result in multiple investments in particular sectors of the economy, its performance may depend on the performance of those sectors and may fluctuate more widely than investments diversified across more sectors. For additional information on these and other risk considerations, please see the Fund’s prospectus.

Any sectors, industries, or securities discussed should not be perceived as investment recommendations. Mention of a specific security should not be considered a recommendation to buy or solicitation to sell that security. Specific securities mentioned in this report may have been sold from the Fund’s portfolio of investments by the time you receive this report.

17

| | |

| | AMG Managers Global Income Opportunity Fund Schedule of Portfolio Investments December 31, 2019 |

| | | | | | | | |

| | | Principal

Amount†

| | | Value | |

| | |

Corporate Bonds and Notes - 44.2% | | | | | | | | |

| | |

Financials - 15.0% | | | | | | | | |

| | |

American Homes 4 Rent LP | | | | | | | | |

4.900%, 02/15/29 | | | $25,000 | | | | $28,002 | |

| | |

Bank of America Corp. | | | | | | | | |

Series MTN | | | | | | | | |

4.200%, 08/26/24 | | | 130,000 | | | | 139,596 | |

| | |

Barclays PLC (United Kingdom) | | | | | | | | |

3.650%, 03/16/25 | | | 200,000 | | | | 208,175 | |

| | |

Brookfield Finance, Inc. (Canada) | | | | | | | | |

4.850%, 03/29/29 | | | 25,000 | | | | 28,628 | |

| | |

Citigroup, Inc. | | | | | | | | |

4.400%, 06/10/25 | | | 75,000 | | | | 81,532 | |

| | |

Goodman Australia Industrial Fund Bond Issuer Pty, Ltd. (Australia) | | | | | | | | |

3.400%, 09/30/261 | | | 60,000 | | | | 60,842 | |

| | |

HSBC Holdings PLC (United Kingdom) | | | | | | | | |

Series EMTN | | | | | | | | |

5.750%, 12/20/27 | | | 55,000 | GBP | | | 89,221 | |

| | |

JPMorgan Chase & Co. | | | | | | | | |

3.875%, 02/01/24 | | | 25,000 | | | | 26,685 | |

3.900%, 07/15/25 | | | 50,000 | | | | 54,004 | |

Series X, (3 month LIBOR + 3.330%), 6.100%, 04/01/682,3 | | | 65,000 | | | | 70,934 | |

| | |

Lloyds Banking Group PLC (United Kingdom) | | | | | | | | |

4.500%, 11/04/24 | | | 200,000 | | | | 213,913 | |

| | |

Mid-America Apartments, LP | | | | | | | | |

4.200%, 06/15/28 | | | 95,000 | | | | 104,825 | |

| | |

Old Republic International Corp. | | | | | | | | |

4.875%, 10/01/24 | | | 100,000 | | | | 109,668 | |

| | |

Royal Bank of Canada, GMTN (Canada) | | | | | | | | |

2.250%, 11/01/24 | | | 50,000 | | | | 50,212 | |

| | |

Santander Holdings USA, Inc. | | | | | | | | |

2.650%, 04/17/20 | | | 110,000 | | | | 110,125 | |

| | |

Ventas Realty, LP | | | | | | | | |

3.100%, 01/15/23 | | | 70,000 | | | | 71,652 | |

| | |

Total Financials | | | | | | | 1,448,014 | |

| | |

Industrials - 22.9% | | | | | | | | |

| | |

Air Canada2017-1 Class AA Pass Through Trust (Canada) | | | | | | | | |

3.300%, 01/15/301 | | | 47,440 | | | | 48,359 | |

| | |

Alfa, SAB de CV (Mexico) | | | | | | | | |

5.250%, 03/25/241 | | | 200,000 | | | | 216,002 | |

| | |

Anheuser-Busch InBev Worldwide, Inc. | | | | | | | | |

4.750%, 01/23/29 | | | 45,000 | | | | 52,163 | |

| | |

BMW US Capital LLC | | | | | | | | |

3.150%, 04/18/241 | | | 25,000 | | | | 25,862 | |

| | |

Broadcom Inc. | | | | | | | | |

4.250%, 04/15/261 | | | 25,000 | | | | 26,554 | |

| | | | | | | | |

| | | Principal

Amount†

| | | Value | |

| | |

Burlington Northern Santa Fe LLC | | | | | | | | |

4.050%, 06/15/48 | | | $65,000 | | | | $73,719 | |

| | |

Covanta Holding Corp. | | | | | | | | |

5.875%, 07/01/25 | | | 30,000 | | | | 31,650 | |

| | |

CSX Corp. | | | | | | | | |

3.800%, 03/01/28 | | | 70,000 | | | | 76,396 | |

| | |

CVS Health Corp. | | | | | | | | |

4.100%, 03/25/25 | | | 50,000 | | | | 53,683 | |

4.300%, 03/25/28 | | | 25,000 | | | | 27,311 | |

| | |