UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORMN-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number:811-03752

AMG Funds III

(Exact name of registrant as specified in charter)

600 Steamboat Road, Suite 300, Greenwich, Connecticut 06830

(Address of principal executive offices) (Zip code)

AMG Funds LLC

600 Steamboat Road, Suite 300, Greenwich, Connecticut 06830

(Name and address of agent for service)

Registrant’s telephone number, including area code: (203)299-3500

Date of fiscal year end: May 31

Date of reporting period: June 1, 2018 – May 31, 2019

(Annual Shareholder Report)

| Item 1. | Reports to Shareholders |

| | |

| | ANNUAL REPORT |

| | | | | | |

| | | AMG Funds | | |

| | | | |

| | | May 31, 2019 | | | | |

| | |

| | | AMG Managers Cadence Mid Cap Fund |

| | | Class N: MCMAX | | | Class I: MCMYX | | | Class Z: MCMFX |

| | |

| | | AMG Managers Cadence Emerging Companies Fund |

| | | Class N: MECAX | | | Class I: MECIX | | | Class Z:MECZX |

| | |

| | | |

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Funds’ shareholder reports like this one will no longer be sent by mail, unless you specifically request paper copies of the reports from the Funds or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on the Funds’ website (https://www.amgfunds.com/resources/order_literature.html), and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Funds electronically at any time by contacting your financial intermediary or, if you invest directly with the Funds, by logging into your account at www.amgfunds.com.

You may elect to receive all future reports in paper free of charge. If you invest through a financial intermediary, you can contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. If you invest directly with the Funds, you can call 1.800.548.4539 to inform the Funds that you wish to continue receiving paper copies of your shareholder reports. Your election to receive reports in paper will apply to all funds in the AMG Funds Family of Funds held in your account if you invest through your financial intermediary or all funds in the AMG Funds Family of Funds held with the fund complex if you invest directly with the Funds.

| | |

| | |

| | | |

amgfunds.com | | 053119 AR065 |

| | |

|

| |

AMG Funds |

| Annual Report — May 31, 2019 |

| | | | | | | | |

| | TABLE OF CONTENTS | | | PAGE | | | |

| | | LETTER TO SHAREHOLDERS | | | 2 | | | |

| | | | |

| | | ABOUT YOUR FUND’S EXPENSES | | | 3 | | | |

| | | | |

| | | PORTFOLIO MANAGER’S COMMENTS, FUND SNAPSHOTS AND SCHEDULES OF PORTFOLIO INVESTMENTS | | | | | | |

| | | | |

| | | AMG Managers Cadence Mid Cap Fund | | | 4 | | | |

| | | | |

| | | AMG Managers Cadence Emerging Companies Fund | | | 9 | | | |

| | | | |

| | | FINANCIAL STATEMENTS | | | | | | |

| | | | |

| | | Statement of Assets and Liabilities | | | 15 | | | |

| | | Balance sheets, net asset value (NAV) per share computations and cumulative distributable earnings (loss) | | | | | | |

| | | | |

| | | Statement of Operations | | | 17 | | | |

| | | Detail of sources of income, expenses, and realized and unrealized gains (losses) during the fiscal year | | | | | | |

| | | | |

| | | Statements of Changes in Net Assets | | | 18 | | | |

| | | Detail of changes in assets for the past two fiscal years | | | | | | |

| | | | |

| | | Financial Highlights | | | 19 | | | |

| | | Historical net asset values per share, distributions, total returns, income and expense ratios, turnover ratios and net assets | | | | | | |

| | | | |

| | | Notes to Financial Statements | | | 25 | | | |

| | | Accounting and distribution policies, details of agreements and transactions with Fund management and affiliates, and descriptions of certain investment risks | | | | | | |

| | | | |

| | | REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM | | | 31 | | | |

| | | | |

| | | OTHER INFORMATION | | | 32 | | | |

| | | | |

| | | TRUSTEES AND OFFICERS | | | 33 | | | |

Nothing contained herein is to be considered an offer, sale or solicitation of an offer to buy shares of any series of the AMG Funds family of mutual funds. Such offering is made only by prospectus, which includes details as to offering price and other material information.

| | | | |

| | | | |

| | Letter to Shareholders | | |

| | | | |

Dear Shareholder:

The fiscal year ended May 31, 2019, was a volatile period for financial markets and led to mixed returns for investors. U.S. stock markets climbed to new record highs through the summer of 2018 as a strong domestic economy enabled investors to shrug off rising interest rates and mounting global macro risks. Resiliency gave way to volatility as hawkish U.S. Federal Reserve (“Fed”) policy and an escalation of the U.S./China trade war triggered a global selloff late in 2018. A dovish pivot from global central banks fueled a strong rebound in 2019 as the U.S. bull market celebrated its10-year anniversary. However, trade tensions resurfaced in May and remained a key risk for global investors. The S&P 500® Index returned a modestly positive 3.78% during the fiscal year period. International equities were less resistant to pressures facing the global economy and returned-6.26% as measured by the MSCI All Country World ex USA Index.

In total, only seven out of eleven sectors of the S&P 500® Index were positive during the prior 12 months. There was significant dispersion in the Index as defensive stocks significantly outperformed more cyclical stocks. The real estate and utilities sectors led the Index with returns of 19.88% and 18.17%, respectively. Companies within the energy and materials sectors lagged other sectors with returns of-20.00% and-6.94%, respectively. Growth stocks outperformed value with returns of 5.39% and 1.45%, respectively, for the Russell 1000® Growth and Russell 1000® Value Indexes. International developed and emerging markets demonstrated significantly weaker returns, with the MSCI EAFE and MSCI Emerging Markets Index returning-5.75% and-8.70%, respectively, in the 12 months ending May 31, 2019.

The Fed raised short-term interest rates four times over the course of the year to end at a target rate of 2.25%–2.50%. The yield on the10-year U.S. Treasury note crossed above 3% at the end of September but fell dramatically as investors sought to insulate themselves from market volatility. As the Fed shifted to a more dovish stance in 2019, the10-year Treasury yield fell more than 1% to a yield of 2.14% as of May 31, 2019. The plunge in long-term interest rates caused the yield curve to partially invert with3-month yields rising higher than the10-year yield. By the end of the fiscal year, federal funds futures probabilities were signaling a strong likelihood the Fed would cut their target interest rate at the July meeting1.The Bloomberg Barclays U.S. Aggregate Bond Index, a broad measure of U.S. bond market performance, ended the fiscal year with a 6.40% return. High yield bonds lagged the broader bond market and returned 5.51% as measured by the return of the Bloomberg Barclays U.S. Corporate High Yield Bond Index. Municipal bonds performed strongly with a 6.40% return for the Bloomberg Barclays Municipal Bond Index.

AMG Funds appreciates the privilege of providing investment tools to you and your clients. Our foremost goal is to provide investment solutions that help our

shareholders successfully reach their long-term investment goals. AMG Funds provides access to a distinctive array of actively managed capital appreciation investment strategies. We thank you for your continued confidence and investment in AMG Funds. You can rest assured that under all market conditions our team is focused on delivering excellent investment management services for your benefit.

Respectfully,

Keitha Kinne

President

AMG Funds

| | | | | | | | |

| Average Annual Total Returns | | Periods ended

May 31, 2019* |

| | | | |

Stocks: | | | | 1 Year | | 3 Years | | 5 Years |

| | | | |

| Large Caps | | (S&P 500® Index) | | 3.78% | | 11.72% | | 9.66% |

| | | | |

Small Caps | | (Russell 2000® Index) | | -9.04% | | 9.75% | | 6.71% |

| | | | |

International | | (MSCI All Country World Ex USA Index) | | -6.26% | | 6.72% | | 1.31% |

Bonds: | | | | | | | | |

| Investment Grade | | (Bloomberg Barclays U.S. Aggregate Bond Index) | | 6.40% | | 2.50% | | 2.70% |

| | | | |

| High Yield | | (Bloomberg Barclays U.S. Corporate High Yield Bond Index) | | 5.51% | | 7.04% | | 4.40% |

| | | | |

| Tax-exempt | | (Bloomberg Barclays Municipal Bond Index) | | 6.40% | | 2.96% | | 3.58% |

| | | | |

| Treasury Bills | | (ICE BofAML U.S.6-Month Treasury Bill Index) | | 2.40% | | 1.46% | | 0.99% |

1 CME FedWatch tool

*Source: FactSet. Past performance is no guarantee of future results.

| | | | |

| | | | | |

| | | About Your Fund’s Expenses | | |

| | | | |

| | | | |

As a shareholder of a Fund, you may incur two types of costs: (1) transaction costs, which may include sales charges (loads) on purchase payments; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution(12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on $1,000 invested at the beginning of the period and held for the entire period as indicated below. ACTUAL EXPENSES The first line of the following table provides information about the actual account values and | | actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period. HYPOTHETICAL EXAMPLE FOR COMPARISON PURPOSES The second line of the following table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed annual rate of return of 5% before expenses, which is not the Fund’s | | actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds by comparing this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds. Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. |

| | | | | |

| | | | | | | | | | |

Six Months Ended May 31, 2019 | | Expense

Ratio for

the Period | | Beginning

Account

Value 12/01/18 | | Ending

Account

Value

05/31/19 | | Expenses Paid

During

the Period* | |

AMG Managers Cadence Mid Cap Fund | |

| |

| Based on Actual Fund Return | | | | |

| | | | |

| Class N | | 1.06% | | $1,000 | | $985 | | | $5.25 | |

| | | | |

| Class I | | 0.87% | | $1,000 | | $986 | | | $4.31 | |

| | | | |

| Class Z | | 0.72% | | $1,000 | | $987 | | | $3.57 | |

| |

| Based on Hypothetical 5% Annual Return | | | | |

| | | | |

| Class N | | 1.06% | | $1,000 | | $1,020 | | | $5.34 | |

| | | | |

| Class I | | 0.87% | | $1,000 | | $1,021 | | | $4.38 | |

| | | | |

Class Z | | 0.72% | | $1,000 | | $1,021 | | | $3.63 | |

|

| AMG Managers Cadence Emerging Companies Fund | |

| |

| Based on Actual Fund Return | | | | |

| | | | |

| Class N | | 1.15% | | $1,000 | | $925 | | | $5.52 | |

| | | | |

| Class I | | 1.00% | | $1,000 | | $925 | | | $4.80 | |

| | | | |

| Class Z | | 0.89% | | $1,000 | | $926 | | | $4.27 | |

| |

| Based on Hypothetical 5% Annual Return | | | | |

| | | | |

| Class N | | 1.15% | | $1,000 | | $1,019 | | | $5.79 | |

| | | | |

| Class I | | 1.10% | | $1,000 | | $1,020 | | | $5.04 | |

| | | | |

| Class Z | | 0.89% | | $1,000 | | $1,020 | | | $4.48 | |

| * | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (182), then divided by 365. | |

| | | | |

| | | | | |

| | | AMG Managers Cadence Mid Cap Fund | | |

| | | Portfolio Manager’s Comments(unaudited) | | |

| | | | | | | | |

For the fiscal year ended May 31, 2019, the AMG Managers Cadence Mid Cap Fund (Class Z) (the “Fund” or “Portfolio”) returned (3.73%), lagging its benchmark, the Russell Midcap® Growth Index, which returned 6.87%. PERFORMANCE SUMMARY The fiscal year ending May 31, 2019, was a volatile time in U.S. markets. Early strength was followed by near bear market conditions for the broad market in the fourth quarter of 2018, driven by fears of a Chinese trade war and indications of prolonged interest rate hikes from the U.S. Federal Reserve (the “Fed”). Trade deal optimism and a dovish pivot by the Fed spawned a strong recovery in Q1, leading the broad market (Russell 3000® Index) to almost hit new highs by early May 2019, before a breakdown in trade talks sent the market south bymonth-end. Smaller companies did not recover as strongly as larger-caps and remain well below their 2018 highs. As mentioned, the fiscal year ended May 31, 2019, was a very volatile time in U.S. markets with a great deal of performance dispersion across styles and capitalization. Within themid-cap space growth trounced value with the Russell Midcap Growth Index up 6.87%, outperforming value by nearly 9%. The Fund’s disciplined growth strategy invests in stocks that exhibit a combination of growth, quality, and valuation. For the second year in a row, these attributes in our process served as a drag on results. Valuation underperformed as investors placed a strong premium on growth at any price. For example, our analysis shows the grouping ofmid-cap growth stocks with a price-earnings ratio less than 24x (bottom two quintiles) strongly lagged the overall benchmark. When viewed from a price to cashflow perspective, results were even more revealing, with stocks with a P/CF of under 14x (again the bottom two quintiles) falling for the period while those with a P/CF over 18x (the top two quintiles) rose over 14% in the benchmark. In keeping with our approach, the Fund was overweight the more attractively valued stocks (lower valuation ratios) and underweight the more expensive ones (higher ratios). This pattern of | | | | reasonably valued stocks underperforming more expensive ones was pervasive across sectors, broadly hurting stock selection. Thus, our more conservative growth approach faced strong headwinds, whereas aggressive growth strategies once again had a strong tailwind. While the valuation component of our process has not been rewarded during this period, we believe consistent inclusion of valuation in our strategy is an important underpinning of sound investing over longer investment horizons. At the sector level, technology was the dominant sector over this period and accounted for 65% of the Russell Midcap Growth’s performance. This sector detracted over-2% from relative performance, due to both allocation (underweighting a strong sector) and stock selection. Almost all of the strong returns in the benchmark were derived from the software and services industry group, which at approximately 21% of the benchmark was by far the largest weighting of all 24 industry groups. The Portfolio’s software and services holdings rose 22%, better than the benchmark’s 21%. Nevertheless, the Portfolio’s underallocation (11% vs. 21%) detracted from relative performance. Many of this fiscal year’s top performing software and services stocks have elevated valuations and thus are beyond the reach of our disciplined growth process, accounting for much of the underweight. Stock selection in the semiconductor space also contributed to underperformance as this group was hurt most by sentiment around trade tensions, global growth worries, and supply chain concerns. The consumer discretionary sector was also a large detractor with overweights in the auto industry and stock selection in retailing hurting performance. Stock performance in auto and auto parts was also a detractor, with all four of our holdings falling more than-25% for the year. At the other end of the spectrum, healthcare and energy were top contributors to performance. While we held a market weight in healthcare, stock selection helped us outperform the benchmark by over 15% in the sector. Energy (the poorest | | | | performing sector in the index) was a different story in that we outperformed by avoiding the group altogether. MARKET OUTLOOK Looking ahead, economic statistics from employment to consumer spending continue to be healthy, although some, like industrial production, have retreated from recent highs. We wrote last year that trade policy has now taken center stage, and there it remains. The recent failure to strike a deal with China and the subsequenttit-for-tat tariff volleys have the market on edge. An escalation of tensions could negatively impact corporate earnings, and business confidence could suffer. The combination of cooling economic statistics and tariff uncertainty has not only paused the Fed’s pattern of rate increases over the last several years but has led to rising expectations for a Fed rate cut. Despite recent machinations, we are optimistic about a trade resolution byyear-end (as it is in the best interest of all parties) and continue to anticipate a generally favorable economic backdrop of modest growth. We remain optimistic regarding the potential impact of other fiscal or regulatory actions which would be beneficial for prospective earnings growth. Tax cuts have been favorable for corporate earnings and M&A activity. While gridlock rules Washington, bipartisan infrastructure-related initiatives may be still to come. While overall market valuations have risen broadly with 2019’s sharp market bounce, they continue to look reasonable given the low interest rate environment. Going forward, we remain focused on the implementation of our disciplined investment process, centered aroundbottom-up investment decision making, which over the long term has generated alpha from stock selection. Thank you for your continued support. This commentary reflects the viewpoints of the Cadence Capital Management, LLC. as of May 31, 2019, and is not intended as a forecast or guarantee of future results. |

| | | | |

| | | | | |

| | | AMG Managers Cadence Mid Cap Fund | | |

| | | Portfolio Manager’s Comments(continued) | | |

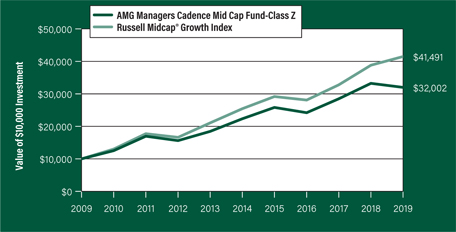

CUMULATIVE TOTAL RETURN PERFORMANCE

AMG Managers Cadence Mid Cap Fund’s cumulative total return is based on the daily change in net asset value (NAV), and assumes that all dividends and distributions were reinvested. This graph compares a hypothetical $10,000 investment made in the AMG Managers Cadence Mid Cap Fund’s Class Z shares on May 31, 2009, to a $10,000 investment made in the Russell Midcap® Growth Index for the same time period. The graph and table do not reflect the deduction of taxes that a shareholder would pay on a Fund distribution or redemption of shares. The listed returns for the Fund are net of expenses and the returns for the index exclude expenses. Total returns would have been lower had certain expenses not been reduced.

The table below shows the average annual total returns for the AMG Managers Cadence Mid Cap Fund and the Russell Midcap® Growth Index for the same time periods ended May 31, 2019.

| | | | | | | | | | | | |

| Average Annual Total Returns1 | | One Year | | | Five

Years | | | Ten Years | |

AMG Managers Cadence Mid Cap Fund2,3, 4, 5, 6, 7 | |

Class N | | | (4.06% | ) | | | 7.05% | | | | 11.90% | |

| | | |

Class I | | | (3.90% | ) | | | 7.24% | | | | 12.07% | |

| | | |

Class Z | | | (3.73% | ) | | | 7.46% | | | | 12.34% | |

| | | | |

Russell Midcap® Growth Index8 | | | 6.87% | | | | 10.28% | | | | 15.29% | |

The performance data shown represents past performance. Past performance is not a guarantee of future results. Current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

Investors should carefully consider the Fund’s investment objectives, risks, charges and expenses before investing. For performance information through the most recent month end, current net asset values per share for the Fund and other information, please call 800.548.4539 or visit our website at amgfunds.com for a free prospectus. Read it carefully before investing or sending money.

Distributed by AMG Distributors, Inc., member FINRA/SIPC.

| 1 | Total return equals income yield plus share price change and assumes reinvestment of all dividends and capital gain distributions. Returns are net of fees and may reflect offsets of Fund expenses as described in the prospectus. No adjustment has been made for taxes payable by shareholders on their reinvested dividends and capital gain distributions. Returns for periods greater than one year are annualized. The listed returns on the Fund are net of expenses and based on the published NAV as of May 31, 2019. All returns are in U.S. dollars ($). |

| | |

| | | 2 From time to time, the Fund’s advisor has waived its fees and/or absorbed Fund expenses, which has resulted in higher returns. |

| | | 3 The Fund is subject to risks associated with investments inmid-capitalization companies such as greater price volatility, lower trading volume, and less liquidity than the stocks of larger, more established companies. |

| | | 4 Active and frequent trading of a fund may result in higher transaction costs and increased tax liability. |

| | | 5 The Fund is subject to special risk considerations similar to those associated with the direct ownership of real estate. Real estate valuations may be subject to factors such as changing general and local economic, financial, competitive, and environmental conditions. |

| | | 6 The Fund invests in growth stocks, which may be more sensitive to market movements because their prices tend to reflect future investor expectations rather than just current profits. Growth stocks may underperform value stocks during given periods. |

| | | 7 Companies that are in similar businesses may be similarly affected by particular economic or market events; to the extent the Fund has substantial holdings within a particular sector, the risks associated with that sector increase. |

| | | 8 The Russell Midcap® Growth Index measures the performance of those Russell Midcap® companies with higher price/book ratios and higher forecasted growth values. The stocks are also members of the Russell 1000® Growth Index. Unlike the Fund, the Russell Midcap® Growth Index is unmanaged, is not available for investment, and does not incur expenses. |

| | | The Russell Indices are trademarks of the London Stock Exchange Group companies. |

| | | Not FDIC insured, nor bank guaranteed. May lose value. |

| | |

| | | |

| | |

| | | |

| | |

| | | |

| | |

| | | |

| | | | |

| | | | | |

| | | AMG Managers Cadence Mid Cap Fund | | |

| | | Fund Snapshots(unaudited) May 31, 2019 | | |

PORTFOLIO BREAKDOWN

| | | | | | |

| Sector | | %of

Net Assets | | | |

| | | |

Information Technology | | 29.3 | | | | |

| | | |

Consumer Discretionary | | 20.2 | | | | |

| | | |

Health Care | | 15.3 | | | | |

| | | |

Industrials | | 11.6 | | | | |

| | | |

Financials | | 10.2 | | | | |

| | | |

Consumer Staples | | 4.7 | | | | |

| | | |

Communication Services | | 3.4 | | | | |

| | | |

Real Estate | | 1.4 | | | | |

| | | |

Utilities | | 1.4 | | | | |

| | | |

Materials | | 0.9 | | | | |

| | | |

Short-Term Investments | | 1.6 | | | | |

| | | |

Other Assets Less Liabilities | | 0.01 | | | | |

TOP TEN HOLDINGS

| | |

| Security Name | | %of

Net Assets |

| | |

VeriSign, Inc. | | 2.1 |

| | |

Veeva Systems, Inc., Class A | | 1.9 |

| | |

Aspen Technology, Inc. | | 1.8 |

| | |

Cadence Design Systems, Inc. | | 1.8 |

| | |

Motorola Solutions, Inc. | | 1.8 |

| | |

Credit Acceptance Corp. | | 1.6 |

| | |

Broadridge Financial Solutions, Inc. | | 1.6 |

| | |

KLA-Tencor Corp. | | 1.6 |

| | |

Paychex, Inc. | | 1.5 |

| | |

Fortinet, Inc. | | 1.5 |

| | | |

| | |

Top Ten as a Group | | 17.2 |

| | |

Because a fund’s strategy may result in multiple investments in particular sectors of the economy, its performance may depend on the performance of those sectors and may fluctuate more widely than investments diversified across more sectors. For additional information on these and other risk considerations, please see the Fund’s prospectus.

Any sectors, industries, or securities discussed should not be perceived as investment recommendations. Mention of a specific security should not be considered a recommendation to buy or solicitation to sell that security. Specific securities mentioned in this report may have been sold from the Fund’s portfolio of investments by the time you receive this report.

| | | | |

| | | | |

| | | AMG Managers Cadence Mid Cap Fund Schedule of Portfolio Investments | | |

| | | May 31, 2019 | | |

| | | | | | | | |

| | | | Shares | | | | Value | |

| | |

Common Stocks - 98.4% | | | | | | | | |

| | |

Communication Services - 3.4% | | | | | | | | |

| | |

AMC Networks, Inc., Class A*,1 | | | 22,292 | | | | $1,176,349 | |

| | |

Lions Gate Entertainment Corp., Class B | | | 73,920 | | | | 1,017,139 | |

| | |

Omnicom Group, Inc. | | | 15,493 | | | | 1,198,539 | |

| | |

Total Communication Services | | | | | | | 3,392,027 | |

| | |

Consumer Discretionary - 20.2% | | | | | | | | |

| | |

AutoZone, Inc.* | | | 1,353 | | | | 1,389,680 | |

| | |

Best Buy Co., Inc. | | | 16,438 | | | | 1,030,169 | |

| | |

BorgWarner, Inc. | | | 23,946 | | | | 849,604 | |

| | |

Burlington Stores, Inc.* | | | 8,043 | | | | 1,259,373 | |

| | |

Choice Hotels International, Inc.1 | | | 15,928 | | | | 1,310,715 | |

| | |

Columbia Sportswear Co. | | | 14,375 | | | | 1,348,087 | |

| | |

Darden Restaurants, Inc. | | | 12,814 | | | | 1,490,524 | |

| | |

Foot Locker, Inc.1 | | | 20,110 | | | | 791,329 | |

| | |

Kontoor Brands, Inc.* | | | 1,919 | | | | 56,227 | |

| | |

Lear Corp. | | | 8,294 | | | | 987,235 | |

| | |

Lennar Corp., Class A | | | 18,326 | | | | 910,069 | |

| | |

Lululemon Athletica, Inc. (Canada)* | | | 9,227 | | | | 1,527,899 | |

| | |

Nordstrom, Inc. | | | 30,865 | | | | 966,074 | |

| | |

PulteGroup, Inc. | | | 41,051 | | | | 1,272,581 | |

| | |

Ross Stores, Inc. | | | 15,913 | | | | 1,479,750 | |

| | |

Thor Industries, Inc.1 | | | 11,909 | | | | 614,981 | |

| | |

Under Armour, Inc., Class C*,1 | | | 57,899 | | | | 1,171,297 | |

| | |

Urban Outfitters, Inc.* | | | 27,280 | | | | 612,982 | |

| | |

VF Corp. | | | 13,436 | | | | 1,100,140 | |

| | |

Total Consumer Discretionary | | | | | | | 20,168,716 | |

| | |

Consumer Staples - 4.7% | | | | | | | | |

| | |

Church & Dwight Co., Inc. | | | 18,190 | | | | 1,353,518 | |

| | |

Herbalife Nutrition, Ltd.*,1 | | | 22,551 | | | | 942,181 | |

| | |

Nu Skin Enterprises, Inc., Class A | | | 19,523 | | | | 911,529 | |

| | |

Sysco Corp. | | | 20,965 | | | | 1,442,811 | |

| | |

Total Consumer Staples | | | | | | | 4,650,039 | |

| | |

Financials - 10.2% | | | | | | | | |

| | |

Ameriprise Financial, Inc. | | | 8,863 | | | | 1,225,132 | |

| | |

Arch Capital Group, Ltd. (Bermuda)* | | | 38,600 | | | | 1,328,998 | |

| | |

Credit Acceptance Corp.* | | | 3,536 | | | | 1,613,795 | |

| | |

E*TRADE Financial Corp. | | | 20,292 | | | | 909,082 | |

| | |

Evercore, Inc., Class A | | | 10,959 | | | | 846,364 | |

| | |

OneMain Holdings, Inc. | | | 35,796 | | | | 1,069,226 | |

| | |

SVB Financial Group* | | | 4,608 | | | | 928,051 | |

| | |

Synchrony Financial | | | 39,144 | | | | 1,316,413 | |

| | | | | | | | |

| | | | Shares | | | | Value | |

| | |

Western Alliance Bancorp.* | | | 23,589 | | | | $970,687 | |

| | |

Total Financials | | | | | | | 10,207,748 | |

| | |

Health Care - 15.3% | | | | | | | | |

| | |

Agilent Technologies, Inc. | | | 17,757 | | | | 1,190,607 | |

| | |

Bruker Corp. | | | 30,741 | | | | 1,284,052 | |

| | |

Centene Corp.* | | | 21,030 | | | | 1,214,483 | |

| | |

Charles River Laboratories International, Inc.* | | | 8,812 | | | | 1,105,465 | |

| | |

Encompass Health Corp. | | | 16,098 | | | | 948,494 | |

| | |

Jazz Pharmaceuticals PLC (Ireland)* | | | 8,220 | | | | 1,032,021 | |

| | |

Molina Healthcare, Inc.* | | | 7,830 | | | | 1,113,896 | |

| | |

PerkinElmer, Inc.1 | | | 12,804 | | | | 1,105,497 | |

| | |

PRA Health Sciences, Inc.* | | | 11,397 | | | | 988,462 | |

| | |

Premier, Inc., Class A* | | | 29,936 | | | | 1,100,148 | |

| | |

Veeva Systems, Inc., Class A* | | | 12,235 | | | | 1,887,738 | |

| | |

Waters Corp.* | | | 5,528 | | | | 1,109,525 | |

| | |

Zoetis, Inc. | | | 11,963 | | | | 1,208,861 | |

| | |

Total Health Care | | | | | | | 15,289,249 | |

| | |

Industrials - 11.6% | | | | | | | | |

| | |

Allison Transmission Holdings, Inc. | | | 30,148 | | | | 1,247,826 | |

| | |

CH Robinson Worldwide, Inc. | | | 14,619 | | | | 1,164,111 | |

| | |

Cummins, Inc. | | | 6,770 | | | | 1,020,645 | |

| | |

Expeditors International of Washington, Inc. | | | 16,760 | | | | 1,166,328 | |

| | |

HD Supply Holdings, Inc.* | | | 25,175 | | | | 1,044,511 | |

| | |

Landstar System, Inc. | | | 10,280 | | | | 989,450 | |

| | |

Masco Corp. | | | 27,535 | | | | 961,522 | |

| | |

Parker-Hannifin Corp. | | | 6,365 | | | | 969,517 | |

| | |

Robert Half International, Inc. | | | 18,007 | | | | 966,256 | |

| | |

Rockwell Automation, Inc. | | | 7,514 | | | | 1,118,459 | |

| | |

WW Grainger, Inc. | | | 3,540 | | | | 926,382 | |

| | |

Total Industrials | | | | | | | 11,575,007 | |

| | |

Information Technology - 29.3% | | | | | | | | |

| | |

Arista Networks, Inc.* | | | 6,111 | | | | 1,494,689 | |

| | |

Aspen Technology, Inc.* | | | 15,757 | | | | 1,790,153 | |

| | |

Booz Allen Hamilton Holding Corp. | | | 23,514 | | | | 1,485,379 | |

| | |

Broadridge Financial Solutions, Inc. | | | 12,762 | | | | 1,593,591 | |

| | |

Cadence Design Systems, Inc.* | | | 28,137 | | | | 1,788,669 | |

| | |

Citrix Systems, Inc. | | | 14,198 | | | | 1,336,316 | |

| | |

Dell Technologies, Inc., Class C* | | | 20,630 | | | | 1,228,517 | |

| | |

F5 Networks, Inc.* | | | 7,254 | | | | 958,108 | |

| | |

Fortinet, Inc.* | | | 21,367 | | | | 1,548,680 | |

| | |

KLA-Tencor Corp. | | | 15,241 | | | | 1,570,890 | |

| | |

Motorola Solutions, Inc. | | | 11,801 | | | | 1,769,560 | |

| | |

NetApp, Inc. | | | 23,377 | | | | 1,383,918 | |

|

|

The accompanying notes are an integral part of these financial statements. 7 |

| | | | |

| | | | | |

| | | AMG Managers Cadence Mid Cap Fund | | |

| | | Schedule of Portfolio Investments(continued) | | |

| | | | | | | | |

| | | Shares | | | Value | |

| |

Information Technology - 29.3%

(continued) | | | | | |

| | |

ON Semiconductor Corp.* | | | 24,117 | | | | $428,318 | |

| | |

Palo Alto Networks, Inc.* | | | 5,420 | | | | 1,084,759 | |

| | |

Paychex, Inc. | | | 18,271 | | | | 1,567,469 | |

| | |

Skyworks Solutions, Inc. | | | 13,109 | | | | 873,453 | |

| | |

Teradyne, Inc. | | | 27,937 | | | | 1,177,265 | |

| | |

Ubiquiti Networks, Inc. | | | 11,659 | | | | 1,402,694 | |

| | |

VeriSign, Inc.* | | | 10,642 | | | | 2,074,977 | |

| | |

Xilinx, Inc. | | | 13,003 | | | | 1,330,337 | |

| | |

Zebra Technologies Corp., Class A* | | | 7,990 | | | | 1,369,806 | |

| | |

Total Information Technology | | | | | | | 29,257,548 | |

| |

Materials - 0.9% | | | | | |

| | |

Element Solutions, Inc.*,1 | | | 100,650 | | | | 952,149 | |

| | |

Real Estate - 1.4% | | | | | | | | |

| | |

CBRE Group, Inc., Class A* | | | 30,979 | | | | 1,415,740 | |

| | |

Utilities - 1.4% | | | | | | | | |

| | |

NRG Energy, Inc. | | | 40,883 | | | | 1,391,657 | |

| | |

Total Common Stocks

(Cost $89,598,320) | | | | | | | 98,299,880 | |

| | | | | | | | |

| | | Shares | | | Value | |

| |

Short-Term Investments - 1.6% | | | | | |

| |

Other Investment Companies - 1.6% | | | | | |

| | |

Dreyfus Government Cash Management Fund, Institutional Shares, 2.28%2 | | | 524,826 | | | | $524,826 | |

| | |

Dreyfus Institutional Preferred Government Money Market Fund, Institutional Shares, 2.34%2 | | | 524,827 | | | | 524,827 | |

| | |

JPMorgan U.S. Government Money Market Fund, IM Shares, 2.34%2 | | | 540,731 | | | | 540,731 | |

| |

Total Short-Term Investments

(Cost $1,590,384) | | | | 1,590,384 | |

| |

Total Investments - 100.0%

(Cost $91,188,704) | | | | 99,890,264 | |

| |

Other Assets, less Liabilities - (0.0)%# | | | | (30,003 | ) |

| | |

Net Assets - 100.0% | | | | | | | $99,860,261 | |

| * | Non-income producing security. |

| 1 | Some or all of these securities, amounting to $6,025,915 or 6.0% of net assets, were out on loan to various borrowers and are collateralized by various U.S. Treasury Obligations. See Note 4 of Notes to Financial Statements. |

| 2 | Yield shown represents the May 31, 2019, seven day average yield, which refers to the sum of the previous seven days’ dividends paid, expressed as an annual percentage. |

The following table summarizes the inputs used to value the Fund’s investments by the fair value hierarchy levels as of May 31, 2019:

| | | | | | | | | | | | | | | | |

| | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| | | |

| Investments in Securities | | | | | | | | | | |

| | | | |

Common Stocks† | | $ | 98,299,880 | | | | — | | | | — | | | $ | 98,299,880 | |

| | | | |

Short-Term Investments | | | | | | | | | | | | | | | | |

| | | | |

Other Investment Companies | | | 1,590,384 | | | | — | | | | — | | | | 1,590,384 | |

| | | | | | | | | | | | | | | | |

| | | | |

Total Investments in Securities | | $ | 99,890,264 | | | | — | | | | — | | | $ | 99,890,264 | |

| | | | | | | | | | | | | | | | |

| † | All common stocks held in the Fund are Level 1 securities. For a detailed breakout of common stocks by major industry classification, please refer to the Fund’s Schedule of Portfolio Investments. |

For the fiscal year ended May 31, 2019, there were no transfers in or out of Level 3.

|

|

The accompanying notes are an integral part of these financial statements. 8 |

| | | | |

| | | | | |

| | | AMG Managers Cadence Emerging Companies Fund | | |

| | | Portfolio Manager’s Comments(unaudited) | | |

| | | | | | | | |

For the fiscal year ended May 31, 2019, the AMG Managers Cadence Emerging Companies Fund (Class I) (the “Fund” or “Portfolio”) returned (10.82%), outperforming its benchmark, the Russell Microcap® Growth Index, which returned (14.25%). PERFORMANCE SUMMARY The fiscal year ending May 31, 2019, was a volatile time in U.S. markets. Early strength was followed by near bear market conditions for the broad market in the fourth quarter of 2018, driven by fears of a Chinese trade war and indications of prolonged interest rate hikes from the U.S. Federal Reserve (the “Fed”).Smaller-cap names did indeed enter bear market territory, falling over 25% from their highs in early September. Trade deal optimism and a dovish pivot by the Fed spawned a strong recovery in Q1, leading the broad market (Russell 3000® Index) to almost hit new highs by early May 2019, before a breakdown in trade talks sent the market south bymonth-end.Small-cap companies did not recover as strongly as larger-caps and remain well below their 2018 highs. As mentioned, the fiscal year ended May 31, 2019, was a very volatile time in U.S. markets with a great deal of performance dispersion across styles and capitalization. The Fund’s primary benchmark, the Russell Microcap Growth Index, fell-14.25% for the period. This loss trailed well behind the Fund’s secondary benchmark, the Russell 2000® Growth Index, which fell-6.88%. Small cap indices underperformed larger cap indices for the year. The Russell 1000® Growth Index and Russell Midcap® Growth Index rose 5.39% and 6.87%, respectively, as growth indices continued to trounce value benchmarks across the broad market. The Fund’s focus on smaller small cap stocks (from the bottom half of the Russell 2000®) worked against Portfolio returns given the notable underperformance of microcap stocks. The Fund’s outperformance vs. its primary benchmark was driven by positive stock selection. At the sector level, healthcare, industrials, and information technology accounted for much of the Fund’s outperformance. Consumer discretionary detracted from relative performance. Healthcare had the strongest contribution to relative outperformance. The Portfolio’s holdings in the pharmaceuticals, biotechnology, and life sciences industry group outpaced the benchmark’s-20.3% decline due to strong stock selection and an | | | | underweight position. We remind Fund investors that the Portfolio is historically underweight this industry group, as it is comprised of many companies which lose money, are not self-financing, and have business models predicated on scientific breakthroughs and regulatory approvals. This Portfolio positioning has added value over the long run, as it did this year. Nevertheless, there are periods, such as fiscal year 2018’s strong up market, when the underweight hurts results. It is gratifying that this year’s +385 basis point relative contribution in the sector more than offset last year’s-331 basis point hit. Industrials were also a notable contributor to outperformance. Fund holdings in the capital goods industry group rose 5.5% compared to the benchmark’s capital goods position which fell-14.0%. Portfolio holdings ranged from industrial distributors to engineering & construction. There were no significant losers among the Fund’s holdings in this sector. Information technology was another contributor to outperformance. Hardware stocks were top contributors, paced by manufacturers of optical components and wireless equipment. The Portfolio’s allocation to this sector rose during the year from approximately 15% to 20%, with attractive investments viewed across each of the three industry groups. Fund holdings in defensive sectors contributed modestly to outperformance. The market peaked roughly around the beginning of the Fund’s fiscal year and closed the fiscal year with a negative return. The benchmark’s three top performing sectors were utilities, real estate, and consumer staples, with gains of 16% to 26%. These buoyant sectors also likely benefited from falling interest rates during the period. The Portfolio’s allocation to these three sectors represented only 7.5% of the Portfolio, yet it was overweight the benchmark’s 4.7%, and this over-allocation contributed modestly to outperformance. Consumer discretionary was a notable detractor from relative performance, primarily due to poor stock selection in consumer durables and apparel. Several holdings, ranging from housing-related to electronics accessories, declined during the period and were sold from the Fund. These sales contributed to the decline in the Portfolio’s sector allocation during the year from approximately 11% to 8%. Cyclicality weighed on performance, as many | | | | stocks of economically sensitive companies were weak during the fiscal year as investors grappled with a potential peak in growth rates. This year’s performance in consumer discretionary is a bit of a give-back of 2018 performance, during which the sector was the top contributor. The sector has been strong contributor over the recent three- and five-year period, and longer. MARKET OUTLOOK Looking ahead, we intend to maintain the Portfolio’spro-cyclical positioning. Economic statistics from employment to consumer spending continue to be healthy though some, like industrial production, have retreated from recent highs. We wrote last year that trade policy has now taken center stage, and there it remains. The recent failure to strike a deal with China and the subsequenttit-for-tat tariff volleys have the market on edge. An escalation of tensions could negatively impact corporate earnings and business confidence could suffer. The combination of cooling economic statistics and tariff uncertainty has not only paused the Fed’s pattern of rate increases over the last several years but has led to rising expectations for a Fed rate cut. Despite recent machinations, we are optimistic about a trade resolution byyear-end (as it is in the best interest of all parties) and continue to anticipate a generally favorable economic backdrop of modest growth. We remain optimistic regarding the potential impact of other fiscal or regulatory actions which would be beneficial for prospective earnings growth. Tax cuts have been favorable for corporate earnings and M&A activity. While gridlock rules in Washington, bipartisan infrastructure-related initiatives may be still to come. While valuations have risen broadly with 2019’s sharp market bounce, they continue to look reasonable given the low interest rate environment, and small caps trade at a discount to large cap stocks. Going forward, we remain focused on the implementation of our disciplined investment process, centered aroundbottom-up investment decision making, which over the long term and short term has generated alpha from strong stock selection. Thank you for your continued support. This commentary reflects the viewpoints of the Cadence Capital Management, LLC as of May 31, 2019, and is not intended as a forecast or guarantee of future results. |

| | | | |

| | | | | |

| | | AMG Managers Cadence Emerging Companies Fund | | |

| | | Portfolio Manager’s Comments(continued) | | |

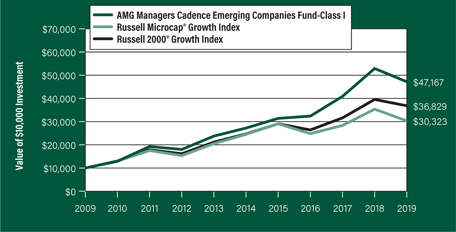

CUMULATIVE TOTAL RETURN PERFORMANCE

AMG Managers Cadence Emerging Companies Fund’s cumulative total return is based on the daily change in net asset value (NAV), and assumes that all dividends and distributions were reinvested. This graph compares a hypothetical $10,000 investment made in the AMG Managers Cadence Emerging Companies Fund’s Class I shares on May 31, 2009, to a $10,000 investment made in the Russell Microcap® Growth Index and the Russell 2000® Growth Index for the same time period. The graph and table do not reflect the deduction of taxes that a shareholder would pay on a Fund distribution or redemption of shares. The listed returns for the Fund are net of expenses and the returns for the index exclude expenses. Total returns would have been lower had certain expenses not been reduced.

The table below shows the average annual total returns for the AMG Managers Cadence Emerging Companies Fund and the Russell Microcap® Growth Index and the Russell 2000® Growth Index for the same time periods ended May 31, 2019.

| | | | | | | | | | | | | | | | | | | | | | |

Average Annual Total Returns1 | | One

Year | | | Five

Years | | | Ten

Years | | | Since

Inception | | | Inception

Date | |

AMG Managers Cadence Emerging Companies Fund2, 3, 4, 5, 6, 7 | |

| | | | | | |

| | Class N | | | (10.92% | ) | | | 11.41% | | | | 16.52% | | | | 10.37% | | | | 04/01/96 | |

| | | | | | |

| | Class I | | | (10.82% | ) | | | 11.62% | | | | 16.78% | | | | 11.74% | | | | 06/25/93 | |

| | | | | | |

| | Class Z | | | (10.73% | ) | | | — | | | | — | | | | 7.53% | | | | 05/31/17 | |

| | | | | | | |

| | Russell Microcap® Growth Index8,10 | | | (14.25% | ) | | | 4.34% | | | | 11.73% | | | | — | | | | — | |

| | | | | | |

| | | Russell 2000® Growth Index9,10 | | | (6.88% | ) | | | 8.32% | | | | 13.93% | | | | 7.71% | | | | 06/25/93 | † |

The performance data shown represents past performance. Past performance is not a guarantee of future results. Current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

Investors should carefully consider the Fund’s investment objectives, risks, charges and expenses before investing. For performance information through the most recent month end, current net asset values per share for the Fund and other information, please call 800.548.4539 or visit our website at amgfunds.com for a free prospectus. Read it carefully before investing or sending money.

Distributed by AMG Distributors, Inc., member FINRA/SIPC.

| † | Date reflects the inception date of the Fund, not the index. |

| 1 | Total return equals income yield plus share price change and assumes reinvestment of all dividends and capital gain distributions. Returns are net of fees and may reflect offsets of Fund expenses as described in the prospectus. No adjustment has been made for taxes payable by shareholders on their reinvested dividends and capital gain distributions. Returns for periods greater than one year are annualized. The listed returns on the Fund are net of expenses and based on the published NAV as of May 31, 2019. All returns are in U.S. dollars ($). |

| | |

| | | 2 From time to time, the Fund’s advisor has waived its fees and/or absorbed Fund expenses, which has resulted in higher returns. |

| | | 3 The Fund is subject to the special risks associated with investments inmicro-cap companies, such as relatively short earnings history, competitive conditions, less publicly available corporate information, and reliance on a limited number of products. |

| | | 4 The Fund is subject to risks associated with investments in small-capitalization companies, such as erratic earnings patterns, competitive conditions, limited earnings history and a reliance on one or a limited number of products. |

| | | 5 The Fund is subject to special risk considerations similar to those associated with the direct ownership of real estate. Real estate valuations may be subject to factors such as changing general and local economic, financial, competitive, and environmental conditions. |

| | | 6 The Fund invests in growth stocks, which may be more sensitive to market movements because their prices tend to reflect future investor expectations rather than just current profits. Growth stocks may underperform value stocks during given periods. |

| | | 7 Companies that are in similar businesses may be similarly affected by particular economic or market events; to the extent the Fund has substantial holdings within a particular sector, the risks associated with that sector increase. |

| | | 8 The Russell Microcap® Growth Index measures the performance of the microcap growth segment of the U.S. Equity market. It includes those Russell Microcap® Index companies with higherprice-to-book ratios and higher forecasted growth values. |

| | | 9 The Russell 2000® Growth Index measures the performance of the Russell 2000® companies with higherprice-to-book ratios and higher forecasted growth values. |

| | | 10 Unlike the Fund, the indices are unmanaged, are not available for investment, and do not incur expenses. |

| | | The Russell Indices are trademarks of the London Stock Exchange Group companies. Not FDIC insured, nor bank guaranteed. May lose value. |

| | | | |

| | | | |

| | | AMG Managers Cadence Emerging Companies Fund | | |

| | | Fund Snapshots(unaudited) May 31, 2019 | | |

PORTFOLIO BREAKDOWN

| | | | | | |

| Sector | | % of

Net Assets | | | |

| | | |

Health Care | | 30.3 | | | | |

| | | |

Information Technology | | 23.0 | | | | |

| | | |

Industrials | | 14.8 | | | | |

| | | |

Financials | | 10.7 | | | | |

| | | |

Consumer Discretionary | | 6.6 | | | | |

| | | |

Real Estate | | 3.8 | | | | |

| | | |

Consumer Staples | | 3.5 | | | | |

| | | |

Communication Services | | 2.7 | | | | |

| | | |

Energy | | 2.6 | | | | |

| | | |

Utilities | | 1.9 | | | | |

| | | |

Short-Term Investments | | 3.5 | | | | |

| | | |

Other Assets Less Liabilities | | (3.4) | | | | |

TOP TEN HOLDINGS

| | |

| Security Name | | % of

Net Assets |

| | |

NMI Holdings, Inc., Class A | | 1.9 |

| | |

Blue Bird Corp. | | 1.7 |

| | |

Addus HomeCare Corp. | | 1.6 |

| | |

Fluidigm Corp. | | 1.6 |

| | |

American Software, Inc., Class A | | 1.6 |

| | |

UMH Properties, Inc. | | 1.6 |

| | |

Zix Corp. | | 1.6 |

| | |

Simulations Plus, Inc. | | 1.6 |

| | |

Energy Recovery, Inc. | | 1.6 |

| | |

BioLife Solutions, Inc. | | 1.5 |

| | | |

| | |

Top Ten as a Group | | 16.3 |

| | |

Because a fund’s strategy may result in multiple investments in particular sectors of the economy, its performance may depend on the performance of those sectors and may fluctuate more widely than investments diversified across more sectors. For additional information on these and other risk considerations, please see the Fund’s prospectus.

Any sectors, industries, or securities discussed should not be perceived as investment recommendations. Mention of a specific security should not be considered a recommendation to buy or solicitation to sell that security. Specific securities mentioned in this report may have been sold from the Fund’s portfolio of investments by the time you receive this report.

| | | | |

| | | | |

| | | AMG Managers Cadence Emerging Companies Fund | | |

| | | Schedule of Portfolio Investments May 31, 2019 | | |

| | | | | | | | |

| | | | Shares | | | | Value | |

| | |

Common Stocks - 99.9% | | | | | | | | |

| | |

Communication Services - 2.7% | | | | | | | | |

| | |

QuinStreet, Inc.*,1 | | | 163,284 | | | | $2,503,144 | |

| | |

TechTarget, Inc.* | | | 122,027 | | | | 2,306,310 | |

| | |

Total Communication Services | | | | | | | 4,809,454 | |

| | |

Consumer Discretionary - 6.6% | | | | | | | | |

| | |

Century Communities, Inc.* | | | 34,359 | | | | 917,385 | |

| | |

Crocs, Inc.*,1 | | | 112,229 | | | | 2,168,264 | |

| | |

Denny’s Corp.* | | | 90,203 | | | | 1,775,195 | |

| | |

Lindblad Expeditions Holdings, Inc.* | | | 145,369 | | | | 2,372,422 | |

| | |

Malibu Boats, Inc., Class A* | | | 38,572 | | | | 1,384,735 | |

| | |

RTW RetailWinds, Inc.* | | | 561,587 | | | | 1,072,631 | |

| | |

Ruth’s Hospitality Group, Inc. | | | 78,373 | | | | 1,792,391 | |

| | |

Total Consumer Discretionary | | | | | | | 11,483,023 | |

| | |

Consumer Staples - 3.5% | | | | | | | | |

| | |

Calavo Growers, Inc.1 | | | 26,462 | | | | 2,314,102 | |

| | |

The Chefs’ Warehouse, Inc.* | | | 59,131 | | | | 1,872,679 | |

| | |

Turning Point Brands, Inc. | | | 40,572 | | | | 1,997,359 | |

| | |

Total Consumer Staples | | | | | | | 6,184,140 | |

| | |

Energy - 2.6% | | | | | | | | |

| | |

Profire Energy, Inc.* | | | 560,084 | | | | 840,126 | |

| | |

Renewable Energy Group, Inc.*,1 | | | 69,204 | | | | 1,082,351 | |

| | |

Solaris Oilfield Infrastructure, Inc., Class A1 | | | 116,370 | | | | 1,655,945 | |

| | |

Vertex Energy, Inc.* | | | 810,971 | | | | 1,054,262 | |

| | |

Total Energy | | | | | | | 4,632,684 | |

| | |

Financials - 10.7% | | | | | | | | |

| | |

Bryn Mawr Bank Corp. | | | 54,605 | | | | 1,996,359 | |

| | |

Enova International, Inc.* | | | 95,300 | | | | 2,034,655 | |

| | |

Kinsale Capital Group, Inc. | | | 26,675 | | | | 2,235,098 | |

| | |

NMI Holdings, Inc., Class A* | | | 121,459 | | | | 3,310,972 | |

| | |

On Deck Capital, Inc.* | | | 261,326 | | | | 1,050,531 | |

| | |

Pacific City Financial Corp. | | | 58,495 | | | | 998,510 | |

| | |

Preferred Bank | | | 38,678 | | | | 1,692,936 | |

| | |

Pzena Investment Management, Inc., Class A | | | 132,593 | | | | 1,172,122 | |

| | |

Silvercrest Asset Management Group, Inc., Class A | | | 122,309 | | | | 1,632,825 | |

| | |

Veritex Holdings, Inc. | | | 100,131 | | | | 2,546,331 | |

| | |

Total Financials | | | | | | | 18,670,339 | |

| | |

Health Care - 30.3% | | | | | | | | |

| | |

Addus HomeCare Corp.*,1 | | | 42,240 | | | | 2,888,371 | |

| | |

ANI Pharmaceuticals, Inc.*,1 | | | 32,417 | | | | 2,258,168 | |

| | |

BioDelivery Sciences International, Inc.* | | | 412,548 | | | | 1,790,458 | |

| | |

BioLife Solutions, Inc.* | | | 152,173 | | | | 2,698,027 | |

| | | | | | | | |

| | | | Shares | | | | Value | |

| | |

BioSpecifics Technologies Corp.* | | | 28,801 | | | | $1,703,579 | |

| | |

CareDx, Inc.*,1 | | | 54,300 | | | | 1,716,966 | |

| | |

Champions Oncology, Inc.* | | | 213,370 | | | | 1,997,143 | |

| | |

Fluidigm Corp.* | | | 213,503 | | | | 2,794,754 | |

| | |

Harvard Bioscience, Inc.* | | | 406,101 | | | | 921,849 | |

| | |

HealthStream, Inc.* | | | 103,343 | | | | 2,583,575 | |

| | |

iRadimed Corp.*,1 | | | 101,533 | | | | 2,118,994 | |

| | |

Lantheus Holdings, Inc.* | | | 80,791 | | | | 1,938,176 | |

| | |

MTBC, Inc.*,1 | | | 175,458 | | | | 842,199 | |

| | |

Orthofix Medical, Inc.* | | | 45,116 | | | | 2,225,572 | |

| | |

The Providence Service Corp.* | | | 37,489 | | | | 2,424,789 | |

| | |

R1 RCM, Inc.* | | | 187,901 | | | | 2,205,958 | |

| | |

RadNet, Inc.*,1 | | | 196,286 | | | | 2,371,135 | |

| | |

Recro Pharma, Inc.* | | | 107,254 | | | | 1,025,348 | |

| | |

Simulations Plus, Inc. | | | 108,953 | | | | 2,731,452 | |

| | |

STAAR Surgical Co.*,1 | | | 88,278 | | | | 2,045,401 | |

| | |

Tabula Rasa HealthCare, Inc.*,1 | | | 39,509 | | | | 1,784,622 | |

| | |

US Physical Therapy, Inc. | | | 21,279 | | | | 2,377,077 | |

| | |

Vanda Pharmaceuticals, Inc.* | | | 145,044 | | | | 2,129,246 | |

| | |

Veracyte, Inc.* | | | 94,134 | | | | 2,133,077 | |

| | |

Vericel Corp.*,1 | | | 96,462 | | | | 1,509,630 | |

| | |

Vocera Communications, Inc.* | | | 59,978 | | | | 1,940,888 | |

| | |

Total Health Care | | | | | | | 53,156,454 | |

| | |

Industrials - 14.8% | | | | | | | | |

| | |

BG Staffing, Inc. | | | 58,332 | | | | 992,811 | |

| | |

Blue Bird Corp.* | | | 160,635 | | | | 3,023,151 | |

| | |

CRA International, Inc. | | | 53,397 | | | | 1,999,184 | |

| | |

Douglas Dynamics, Inc. | | | 59,334 | | | | 2,201,291 | |

| | |

Energy Recovery, Inc.*,1 | | | 288,055 | | | | 2,722,120 | |

| | |

Heritage-Crystal Clean, Inc.* | | | 97,090 | | | | 2,427,250 | |

| | |

Kadant, Inc. | | | 22,002 | | | | 1,786,122 | |

| | |

Kforce, Inc. | | | 52,122 | | | | 1,811,240 | |

| | |

Lawson Products, Inc.* | | | 57,555 | | | | 2,111,117 | |

| | |

NV5 Global, Inc.*,1 | | | 23,105 | | | | 1,796,414 | |

| | |

PGT Innovations, Inc.* | | | 121,570 | | | | 1,818,687 | |

| | |

Rush Enterprises, Inc., Class A | | | 48,990 | | | | 1,727,877 | |

| | |

Willdan Group, Inc.*,1 | | | 48,426 | | | | 1,507,017 | |

| | |

Total Industrials | | | | | | | 25,924,281 | |

| | |

Information Technology - 23.0% | | | | | | | | |

| | |

Adesto Technologies Corp.* | | | 224,764 | | | | 1,692,473 | |

| | |

Airgain, Inc.* | | | 147,392 | | | | 1,889,565 | |

| | |

American Software, Inc., Class A | | | 218,380 | | | | 2,766,875 | |

| | |

Blucora, Inc.* | | | 83,473 | | | | 2,585,159 | |

|

|

The accompanying notes are an integral part of these financial statements. 12 |

| | | | |

| | | | | |

| | | AMG Managers Cadence Emerging Companies Fund Schedule of Portfolio Investments(continued) | | |

| | | | | | | | |

| | | Shares | | | Value | |

| |

Information Technology - 23.0%

(continued) | | | | | |

| | |

CalAmp Corp.* | | | 120,938 | | | | $1,228,730 | |

| | |

Carbonite, Inc.*,1 | | | 89,500 | | | | 2,118,465 | |

| | |

Clearfield, Inc.*,1 | | | 65,397 | | | | 869,126 | |

| | |

CyberOptics Corp.* | | | 89,444 | | | | 1,372,965 | |

| | |

eGain Corp.* | | | 177,629 | | | | 1,399,717 | |

| | |

Everi Holdings, Inc.* | | | 177,440 | | | | 1,976,682 | |

| | |

The Hackett Group, Inc. | | | 120,639 | | | | 1,941,082 | |

| | |

inTEST Corp.* | | | 186,379 | | | | 935,623 | |

| | |

Lantronix, Inc.* | | | 372,903 | | | | 1,312,619 | |

| | |

PAR Technology Corp.*,1 | | | 78,490 | | | | 2,206,354 | |

| | |

PCM, Inc.* | | | 94,957 | | | | 2,426,151 | |

| | |

PRGX Global, Inc.*,1 | | | 207,375 | | | | 1,354,159 | |

| | |

Rudolph Technologies, Inc.* | | | 86,799 | | | | 2,002,453 | |

| | |

Silicom, Ltd. (Israel)* | | | 64,430 | | | | 1,942,564 | |

| | |

TTEC Holdings, Inc. | | | 50,880 | | | | 2,018,918 | |

| | |

Unisys Corp.* | | | 142,523 | | | | 1,382,473 | |

| | |

Upland Software, Inc.* | | | 47,675 | | | | 2,230,713 | |

| | |

Zix Corp.* | | | 304,967 | | | | 2,732,504 | |

| | |

Total Information Technology | | | | | | | 40,385,370 | |

| |

Real Estate - 3.8% | | | | | |

| | |

Clipper Realty, Inc., REIT | | | 147,532 | | | | 1,883,984 | |

| | |

NexPoint Residential Trust, Inc., REIT | | | 47,966 | | | | 1,922,477 | |

| | |

UMH Properties, Inc., REIT | | | 207,463 | | | | 2,761,333 | |

| | |

Total Real Estate | | | | | | | 6,567,794 | |

| |

Utilities - 1.9% | | | | | |

| | |

Pure Cycle Corp.* | | | 192,380 | | | | 1,812,219 | |

| | |

The York Water Co. | | | 41,268 | | | | 1,422,921 | |

| | |

Total Utilities | | | | | | | 3,235,140 | |

| | |

Total Common Stocks

(Cost $179,802,660) | | | | | | | 175,048,679 | |

| | |

| | | Principal

Amount | | | | |

| |

Short-Term Investments - 3.5% | | | | | |

| |

Joint Repurchase Agreements - 3.0%2 | | | | | |

| | |

BNP Paribas S.A., dated 05/31/19, due 06/03/19, 2.480% total to be received $259,909 (collateralized by various U.S. Treasuries, 0.000% - 7.250%,

06/04/19 -09/09/49, totaling $265,052) | | | $259,855 | | | | 259,855 | |

| | | | | | | | |

| | | Principal

Amount | | | Value | |

| | |

Citigroup Global Markets, Inc., dated 05/31/19, due 06/03/19, 2.500% total to be received $1,236,267 (collateralized by various U.S. Government Agency Obligations and U.S. Treasuries, 0.000% - 10.000%, 06/11/19 -04/20/69, totaling $1,260,729) | | | $1,236,009 | | | | $1,236,009 | |

| | |

Daiwa Capital Markets America, dated 05/31/19, due 06/03/19, 2.500% total to be received $1,236,267 (collateralized by various U.S. Government Agency Obligations and U.S. Treasuries, 0.000% - 6.500%, 06/13/19 -05/20/49, totaling $1,260,729) | | | 1,236,009 | | | | 1,236,009 | |

| | |

HSBC Securities USA, Inc., dated 05/31/19, due 06/03/19, 2.500% total to be received $1,236,267 (collateralized by various U.S. Government Agency Obligations, 3.000% -5.500%, 07/01/26 - 05/01/49, totaling $1,260,729) | | | 1,236,009 | | | | 1,236,009 | |

| | |

Morgan, Stanley & Co. LLC, dated 05/31/19, due 06/03/19, 2.510% total to be received $1,236,268 (collateralized by various U.S. Government Agency Obligations and U.S. Treasuries, 0.000% - 9.000%, 06/04/19 -05/20/49, totaling $1,260,729) | | | 1,236,009 | | | | 1,236,009 | |

| |

Total Joint Repurchase Agreements | | | | 5,203,891 | |

| | |

| | | Shares | | | | | |

| |

Other Investment Companies - 0.5% | | | | | |

| | |

Dreyfus Government Cash Management Fund, Institutional Shares, 2.28%3 | | | 325,698 | | | | 325,698 | |

| | |

Dreyfus Institutional Preferred Government Money Market Fund, Institutional Shares, 2.34%3 | | | 325,698 | | | | 325,698 | |

| | |

JPMorgan U.S. Government Money Market Fund, IM Shares, 2.34%3 | | | 335,567 | | | | 335,567 | |

| |

Total Other Investment Companies | | | | 986,963 | |

| |

Total Short-Term Investments

(Cost $6,190,854) | | | | 6,190,854 | |

| |

Total Investments - 103.4%

(Cost $185,993,514) | | | | 181,239,533 | |

| |

Other Assets, less Liabilities - (3.4)% | | | | (5,974,424 | ) |

| |

Net Assets - 100.0% | | | | $175,265,109 | |

|

|

| The accompanying notes are an integral part of these financial statements. |

13 |

| | | | |

| | | | | |

| | | AMG Managers Cadence Emerging Companies Fund | | |

| | | Schedule of Portfolio Investments(continued) | | |

| * | Non-income producing security. |

| 1 | Some or all of these securities, amounting to $24,078,486 or 13.7% of net assets, were out on loan to various borrowers and are collateralized by cash and various U.S. Treasury Obligations. See Note 4 of Notes to Financial Statements. |

| 2 | Cash collateral received for securities lending activity was invested in these joint repurchase agreements. |

| 3 | Yield shown represents the May 31, 2019, seven day average yield, which refers to the sum of the previous seven days’ dividends paid, expressed as an annual percentage. |

| REIT | Real Estate Investment Trust |

The following table summarizes the inputs used to value the Fund’s investments by the fair value hierarchy levels as of May 31, 2019:

| | | | | | | | | | | | | | | | |

| | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| | | |

| Investments in Securities | | | | | | | | | | |

| | | | |

Common Stocks† | | | $175,048,679 | | | | — | | | | — | | | | $175,048,679 | |

| | | | |

Short-Term Investments | | | | | | | | | | | | | | | | |

| | | | |

Joint Repurchase Agreements | | | — | | | | $5,203,891 | | | | — | | | | 5,203,891 | |

| | | | |

Other Investment Companies | | | 986,963 | | | | — | | | | — | | | | 986,963 | |

| | | | | | | | | | | | | | | | |

| | | | |

Total Investments in Securities | | | $176,035,642 | | | | $5,203,891 | | | | — | | | | $181,239,533 | |

| | | | | | | | | | | | | | | | |

| † | All common stocks held in the Fund are Level 1 securities. For a detailed breakout of common stocks by major industry classification, please refer to the Fund’s Schedule of Portfolio Investments. |

For the fiscal year ended May 31, 2019, there were no transfers in or out of Level 3.

|

|

The accompanying notes are an integral part of these financial statements. |

14 |

| | | | |

| | | | | |

| | | Statement of Assets and Liabilities | | |

| | | May 31, 2019 | | |

| | | | | | | | |

| | | AMG

Managers

Cadence Mid

Cap Fund | | | AMG

Managers Cadence

Emerging

Companies Fund | |

| | |

Assets: | | | | | | | | |

| | |

Investments at value1(including securities on loan valued at $6,025,915, and $24,078,486, respectively) | | | $99,890,264 | | | | $181,239,533 | |

| | |

Receivable for investments sold | | | — | | | | 551,362 | |

| | |

Dividend, interest and other receivables | | | 113,367 | | | | 101,792 | |

| | |

Receivable for Fund shares sold | | | 13,127 | | | | 44,510 | |

| | |

Receivable from affiliate | | | 4,477 | | | | 23,476 | |

| | |

Prepaid expenses and other assets | | | 24,720 | | | | 32,215 | |

| | |

Total assets | | | 100,045,955 | | | | 181,992,888 | |

| | |

Liabilities: | | | | | | | | |

| | |

Payable upon return of securities loaned | | | — | | | | 5,203,891 | |

| | |

Payable for investments purchased | | | — | | | | 1,108,207 | |

| | |

Payable for Fund shares repurchased | | | 46,777 | | | | 178,348 | |

| | |

Accrued expenses: | | | | | | | | |

| | |

Investment advisory and management fees | | | 40,463 | | | | 109,351 | |

| | |

Administrative fees | | | 13,488 | | | | 23,772 | |

| | |

Distribution fees | | | 14,504 | | | | — | |

| | |

Shareholder service fees | | | 5,021 | | | | 30,797 | |

| | |

Other | | | 65,441 | | | | 73,413 | |

| | |

Total liabilities | | | 185,694 | | | | 6,727,779 | |

| | | | | | | | |

| | |

Net Assets | | | $99,860,261 | | | | $175,265,109 | |

| | |

1Investments at cost | | | $91,188,704 | | | | $185,993,514 | |

|

|

| The accompanying notes are an integral part of these financial statements. |

| 15 |

| | | | |

| | | | | |

| | | Statement of Assets and Liabilities(continued) | | |

| | | | | |

| | | | | | | | |

| | | AMG

Managers

Cadence Mid

Cap Fund | | | AMG

Managers Cadence

Emerging

Companies Fund | |

| | |

Net Assets Represent: | | | | | | | | |

| | |

Paid-in capital | | | $90,079,953 | | | | $188,140,919 | |

| | |

Total distributable earnings (loss) | | | 9,780,308 | | | | (12,875,810) | |

| | |

Net Assets | | | $99,860,261 | | | | $175,265,109 | |

| | |

Class N: | | | | | | | | |

| | |

Net Assets | | | $64,332,965 | | | | $32,440,224 | |

| | |

Shares outstanding | | | 2,658,558 | | | | 678,053 | |

| | |

Net asset value, offering and redemption price per share | | | $24.20 | | | | $47.84 | |

| | |

Class I: | | | | | | | | |

| | |

Net Assets | | | $14,737,685 | | | | $116,100,591 | |

| | |

Shares outstanding | | | 584,963 | | | | 2,219,104 | |

| | |

Net asset value, offering and redemption price per share | | | $25.19 | | | | $52.32 | |

| | |

Class Z: | | | | | | | | |

| | |

Net Assets | | | $20,789,611 | | | | $26,724,294 | |

| | |

Shares outstanding | | | 780,145 | | | | 509,704 | |

| | |

Net asset value, offering and redemption price per share | | | $26.65 | | | | $52.43 | |

|

|

| The accompanying notes are an integral part of these financial statements. |

| 16 |

| | | | |

| | | | | |

| | | Statement of Operations | | |

| | | For the fiscal year ended May 31, 2019 | | |

| | | | | | | | |

| | | AMG

Managers

Cadence Mid

Cap Fund | | | AMG

Managers Cadence

Emerging

Companies Fund | |

Investment Income: | | | | | | | | |

| | |

Dividend income | | | $1,335,825 | | | | $983,953 | |

| | |

Interest income | | | — | | | | 715 | |

| | |

Securities lending income | | | 26,023 | | | | 41,700 | |

| | |

Total investment income | | | 1,361,848 | | | | 1,026,368 | |

Expenses: | | | | | | | | |

| | |

Investment advisory and management fees | | | 520,926 | | | | 1,246,974 | |

| | |

Administrative fees | | | 173,642 | | | | 271,081 | |

| | |

Distribution fees - Class N | | | 188,474 | | | | — | |

| | |

Shareholder servicing fees - Class N | | | 74,706 | | | | 83,585 | |

| | |

Shareholder servicing fees - Class I | | | 24,204 | | | | 115,307 | |

| | |

Registration fees | | | 52,675 | | | | 60,601 | |

| | |

Professional fees | | | 35,218 | | | | 38,595 | |

| | |

Reports to shareholders | | | 28,533 | | | | 40,047 | |

| | |

Custodian fees | | | 23,010 | | | | 42,529 | |

| | |

Transfer agent fees | | | 20,894 | | | | 6,943 | |

| | |

Trustee fees and expenses | | | 8,378 | | | | 11,569 | |

| | |

Miscellaneous | |

| 5,182

|

| |

| 5,982

|

|

| | |

Total expenses before offsets | | | 1,155,842 | | | | 1,923,213 | |

| | |

Expense reimbursements | | | (34,975) | | | | (115,905) | |

| | |

Net expenses | | | 1,120,867 | | | | 1,807,308 | |

| | | | | | | | |

Net investment income (loss) | | | 240,981 | | | | (780,940) | |

Net Realized and Unrealized Loss: | | | | | | | | |

| | |

Net realized gain (loss) on investments | | | 8,978,011 | | | | (734,635) | |

| | |

Net change in unrealized appreciation/depreciation on investments | | | (13,958,181) | | | | (22,994,817) | |

| | |

Net realized and unrealized loss | | | (4,980,170) | | | | (23,729,452)�� | |

| | | | | | | | |

Net decrease in net assets resulting from operations | | | $(4,739,189) | | | | $(24,510,392) | |

|

|

| The accompanying notes are an integral part of these financial statements. |

| 17 |

| | | | |

| | | | | |

| | | Statements of Changes in Net Assets | | |

| | | For the fiscal years ended May 31, | | |

| | | | | | | | | | | | | | | | |

| | | AMG | | | AMG | |

| | | Managers | | | Managers Cadence | |

| | | Cadence Mid Cap Fund | | | Emerging Companies Fund | |

| | | | |

| | | 2019 | | | 2018 | | | 2019 | | | 2018 | |

| | | |

Increase (Decrease) in Net Assets Resulting From Operations: | | | | | | | | | | | | | |

| | | | |

Net investment income (loss) | | | $240,981 | | | | $147,767 | | | | $(780,940 | ) | | | $(372,051 | ) |

| | | | |

Net realized gain (loss) on investments | | | 8,978,011 | | | | 13,993,660 | | | | (734,635 | ) | | | 14,455,489 | |

| | | | |

Net change in unrealized appreciation/depreciation on investments | | | (13,958,181 | ) | | | 5,322,340 | | | | (22,994,817 | ) | | | 10,412,277 | |

| | | | |

Net increase (decrease) in net assets resulting from operations | | | (4,739,189 | ) | | | 19,463,767 | | | | (24,510,392 | ) | | | 24,495,715 | |

| | | |

Distributions to Shareholders:1 | | | | | | | | | | | | | |

| | | | |

Class N | | | (11,671,054 | ) | | | (9,470,697 | ) | | | (3,105,279 | ) | | | — | |

| | | | |

Class I | | | (2,512,248 | ) | | | (1,635,519 | ) | | | (8,893,635 | ) | | | — | |

| | | | |

Class Z | | | (3,599,803 | ) | | | (2,690,280 | ) | | | (2,214,428 | ) | | | — | |

| | | | |

Total distributions to shareholders | | | (17,783,105 | ) | | | (13,796,496 | ) | | | (14,213,342 | ) | | | — | |

| | | |

Capital Share Transactions:2 | | | | | | | | | | | | | |

| | | | |

Net increase (decrease) from capital share transactions | | | (6,080,790 | ) | | | (2,318,922 | ) | | | 81,488,589 | | | | 37,608,483 | |

| | | | | | | | | | | | | | | | |

Total increase (decrease) in net assets | | | (28,603,084 | ) | | | 3,348,349 | | | | 42,764,855 | | | | 62,104,198 | |

| | | |

Net Assets:3 | | | | | | | | | | | | | |

| | | | |

Beginning of year | | | 128,463,345 | | | | 125,114,996 | | | | 132,500,254 | | | | 70,396,056 | |

| | | | |

End of year | | | $99,860,261 | | | | $128,463,345 | | | | $175,265,109 | | | | $132,500,254 | |

| | | | |

| | | | | | | | | | | | | | | | |

| 1 | See Note 1(d) of the Notes to Financial Statements. |

| 2 | See Note 1(g) of the Notes to Financial Statements. |

| 3 | Net assets - End of year includes undistributed (distributions in excess of) net investment income of $159,559 and $(188,620) for AMG Managers Cadence Mid Cap Fund and AMG Managers Cadence Emerging Companies Fund, respectively, in 2018. During the fiscal year ended May 31, 2019, the requirement to disclose undistributed (distribution in excess of) net investment income was eliminated. |

|

|

| The accompanying notes are an integral part of these financial statements. |

| 18 |

| | | | |

| | | | |

| | | AMG Managers Cadence Mid Cap Fund | | |

| | | Financial Highlights | | |

| | | For a share outstanding throughout each fiscal year | | |

| | | | | | | | | | | | | | | | | | | | |

| | | For the fiscal years ended May 31, | |

| | | | | |

| Class N | | 2019 | | | 2018 | | | 20171 | | | 2016 | | | 2015 | |

| | | | | |

Net Asset Value, Beginning of Year | | | $30.86 | | | | $29.66 | | | | $26.87 | | | | $32.15 | | | | $34.15 | |

| | | | | |

Income (loss) from Investment Operations: | | | | | | | | | | | | | | | | | | | | |

| | | | | |

Net investment income (loss)2,3 | | | 0.03 | | | | 0.01 | | | | (0.09) | | | | 0.19 | 4 | | | (0.06) | |

| | | | | |

Net realized and unrealized gain (loss) on investments | | | (1.78) | | | | 4.75 | | | | 4.58 | | | | (2.32) | | | | 4.88 | |

| | | | | |

Total income (loss) from investment operations | | | (1.75) | | | | 4.76 | | | | 4.49 | | | | (2.13) | | | | 4.82 | |

| | | | | |

| Less Distributions to Shareholders from: | | | | | | | | | | | | | | | |

| | | | | |

Net investment income | | | (0.03) | | | | — | | | | (0.16) | | | | — | | | | — | |

| | | | | |

Net realized gain on investments | | | (4.88) | | | | (3.56) | | | | (1.54) | | | | (3.15) | | | | (6.82) | |

| | | | | |

Total distributions to shareholders | | | (4.91) | | | | (3.56) | | | | (1.70) | | | | (3.15) | | | | (6.82) | |

| | | | | |

Net Asset Value, End of Year | | | $24.20 | | | | $30.86 | | | | $29.66 | | | | $26.87 | | | | $32.15 | |

| | | | | |

Total Return3,5 | | | (4.06) | % | | | 16.25 | % | | | 17.23 | % | | | (6.64) | % | | | 15.14 | % |

| | | | | |

Ratio of net expenses to average net assets6 | | | 1.07 | % | | | 1.08 | % | | | 1.10 | % | | | 1.11 | % | | | 1.12 | % |

| | | | | |

Ratio of gross expenses to average net assets7 | | | 1.10 | % | | | 1.09 | % | | | 1.14 | % | | | 1.21 | % | | | 1.19 | % |

| | | | | |

Ratio of net investment income (loss) to average net assets3 | | | 0.11 | % | | | 0.02 | % | | | (0.31) | % | | | 0.67 | % | | | (0.16) | % |

| | | | | |

Portfolio turnover | | | 46 | % | | | 72 | % | | | 141 | % | | | 149 | % | | | 130 | % |

| | | | | |

Net assets end of year (000’s) omitted | | | $64,333 | | | | $86,096 | | | | $84,873 | | | | $89,179 | | | | $116,666 | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | |

| | | AMG Managers Cadence Mid Cap Fund | | |

| | | Financial Highlights | | |

| | | For a share outstanding throughout each fiscal year | | |

| | | | | | | | | | | | | | | | | | | | |

| | | For the fiscal years ended May 31, | |

| | | | | |

Class I | | 2019 | | | 2018 | | | 20171 | | | 2016 | | | 2015 | |