UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORMN-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number:811-03752

AMG FUNDS III

(Exact name of registrant as specified in charter)

600 Steamboat Road, Suite 300, Greenwich, Connecticut 06830

(Address of principal executive offices) (Zip code)

AMG Funds LLC

600 Steamboat Road, Suite 300, Greenwich, Connecticut 06830

(Name and address of agent for service)

Registrant’s telephone number, including area code: (203)299-3500

Date of fiscal year end: DECEMBER 31

Date of reporting period: JANUARY 1, 2018 – DECEMBER 31, 2018

(Annual Shareholder Report)

| Item 1. | Reports to Shareholders |

| | |

| | ANNUAL REPORT |

| | | | | | | | |

| | | AMG Funds | | | | |

| | | | |

| | | December 31, 2018 | | | | |

| | |

| | | AMG Managers Loomis Sayles Bond Fund |

| | | Class N: MGFIX | | Class I: MGBIX | | | | |

| | |

| | | AMG Managers Global Income Opportunity Fund |

| | | Class N:MGGBX |

| | |

| | | AMG Managers Special Equity Fund |

| | | Class N: MGSEX | | Class I: MSEIX | | | | |

| | | | | | | | | |

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Funds’ shareholder reports like this one will no longer be sent by mail, unless you specifically request paper copies of the reports from the Funds or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on the Funds’ website (https://www.amgfunds.com/resources/order_literature.html), and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Funds electronically at any time by contacting your financial intermediary or, if you invest directly with the Funds, by logging into your account at www.amgfunds.com.

You may elect to receive all future reports in paper free of charge. If you invest through a financial intermediary, you can contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. If you invest directly with the Funds, you can call 1-800-548-4539 to inform the Funds that you wish to continue receiving paper copies of your shareholder reports. Your election to receive reports in paper will apply to all funds in the AMG Funds Family of Funds held in your account if you invest through your financial intermediary or all funds in the AMG Funds Family of Funds held with the fund complex if you invest directly with the Funds.

| | | | | | |

amgfunds.com | | | | 123118 | | AR078 |

|

AMG Funds Annual Report — December 31, 2018 |

| | | | | | |

| | | TABLE OF CONTENTS | | PAGE | |

| | | LETTER TO SHAREHOLDERS | | | 2 | |

| | | |

| | | ABOUT YOUR FUND’S EXPENSES | | | 3 | |

| | | |

| | | PORTFOLIO MANAGER’S COMMENTS, FUND SNAPSHOTS AND SCHEDULES OF PORTFOLIO INVESTMENTS | | | | |

| | | |

| | | AMG Managers Loomis Sayles Bond Fund | | | 4 | |

| | | |

| | | AMG Managers Global Income Opportunity Fund | | | 15 | |

| | | |

| | | AMG Managers Special Equity Fund | | | 23 | |

| | | |

| | | FINANCIAL STATEMENTS | | | | |

| | | |

| | | Statement of Assets and Liabilities | | | 34 | |

| | | |

| | | Balance sheets, net asset value (NAV) per share computations and cumulative distributable earnings (loss) | | | | |

| | | |

| | | Statement of Operations | | | 36 | |

| | | |

| | | Detail of sources of income, expenses, and realized and unrealized gains (losses) during the fiscal year | | | | |

| | | |

| | | Statements of Changes in Net Assets | | | 37 | |

| | | |

| | | Detail of changes in assets for the past two fiscal years | | | | |

| | | |

| | | Financial Highlights | | | 38 | |

| | | |

| | | Historical net asset values per share, distributions, total returns, income and expense ratios, turnover ratios and net assets | | | | |

| | | |

| | | Notes to Financial Statements | | | 43 | |

| | | |

| | | Accounting and distribution policies, details of agreements and transactions with Fund management and affiliates, and descriptions of certain investment risks | | | | |

| | | |

| | | REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM | | | 52 | |

| | | |

| | | OTHER INFORMATION | | | 53 | |

| | | |

| | | TRUSTEES AND OFFICERS | | | 54 | |

Nothing contained herein is to be considered an offer, sale or solicitation of an offer to buy shares of any series of the AMG Funds family of mutual funds. Such offering is made only by prospectus, which includes details as to offering price and other material information.

| | | | |

| | Letter to Shareholders | | |

Dear Shareholder:

It was a difficult year for financial markets in 2018. Strong domestic economic growth fueled equity returns for the majority of the year, but a pullback in the fourth quarter reversed returns, leaving indices across market caps firmly in negative territory. Investors were driven by signs of deceleration in growth across the globe combined with political uncertainty and tighter monetary policy. The S&P 500® Index, a widely followed barometer of the U.S. equity market, returned +9.9% in the first three quarters of the year before a period of heightened volatility resulted in a fourth quarter return of -13.5% and a -4.4% return for the full fiscal year.

In 2018, there was wide performance dispersion across the eleven economic sectors of the S&P 500® Index. Despite a weak fourth quarter, health care, utilities, information technology, and consumer discretionary sectors ended the year on a positive note with returns of +6.4%, +4.1%, +3.4% and +1.9%, respectively. Corporate earnings are expected to continue growing at double digits for the fifth consecutive quarter. According to FactSet, fourth quarter earnings growth for S&P 500® companies is +10.9% (as of January 25, 2019). Growth stocks outperformed value for the first three quarters of the year until the fourth quarter’s risk off environment reversed the trend. Full year returns for the Russell 1000® Growth and Russell 1000® Value Indexes were -1.5% and -8.3%, respectively.

Despite skittish investor sentiment, the U.S. economy continued to show signs of growth, albeit at a slower pace with third quarter GDP growth ringing in at 3.4%. The Federal Reserve raised short-term interest rates four times over the course of the year to end the year at a target rate of 2.25%–2.50%. Higher interest rates eroded the performance of bonds in the first three quarters of the year and a risk off fourth quarter resulted in mixed results. The Bloomberg Barclays U.S. Aggregate Bond Index, a broad measure of U.S. bond market performance, ended the year where it began with a 0.0% return for 2018. The yield on the 10-year U.S. Treasury note crossed above 3% at the end of September but fell dramatically as investors sought to insulate themselves from market volatility. During the past year, the short end of the yield curve has risen faster than the longer end, resulting in the 2–10 year Treasury spread of 0.21%. As expected, high yield bonds held up in the rising interest rate environment but struggled in the fourth quarter as investors removed risk from their portfolios. As a result, spreads between investment grade and high yield corporate debt climbed past 300 bps. In 2018, the Bloomberg Barclays U.S. Aggregate Credit Index and Bloomberg Barclays U.S. Corporate High Yield Bond Index returned -2.1% and -2.1%, respectively.

Economic conditions outside the U.S. started the year with strong growth indicators but finished with signs of deceleration. At the European Central Bank’s most recent monetary policy meeting, the governing council issued guidance that quantitative easing measures would continue and interest rates would remain at their present levels through summer of 2019. This is a departure from guidance earlier in the year which indicated the asset repurchase program would come to an end in December 2018 and rates would rise in 2019. The Bank of England increased its target rate in August for the first time since 2009, but deceleration in growth and increased downside risks, including a disorderly Brexit, have halted discussion of additional hikes in the near future.

International equities and emerging markets demonstrated significantly weaker returns, with the MSCI EAFE and MSCI Emerging Markets Index returning -13.8% and -14.6%, respectively, in the 12 months ending December 31, 2018. In a recent speech at the Hudson Institute, Vice President Mike Pence acknowledged China’s

aggressive actions toward the United States and highlighted a dramatic shift in U.S foreign policy with China: “We seek a relationship grounded in fairness, reciprocity and respect for sovereignty, and we have taken strong and swift action to achieve that goal.” This new tone combined with two rounds of new U.S. tariffs for Chinese imports and signs of a slowing economy acted as a drag on the largest economy within the MSCI Emerging Markets Index. Concurrently, the U.S. Dollar strengthened against most major global currencies, particularly in emerging markets, where those with large current account deficits faced significant pressure, adding to the drag on performance for emerging markets.

AMG Funds appreciates the privilege of providing investment tools to you and your clients. Our foremost goal is to provide investment solutions that help our shareholders successfully reach their long-term investment goals. AMG Funds provides access to a distinctive array of actively managed return-oriented investment strategies. We thank you for your continued confidence and investment in AMG Funds. You can rest assured that under all market conditions our team is focused on delivering excellent investment management services for your benefit.

Respectfully,

Keitha Kinne

President

AMG Funds

| | | | | | | | | | | | | | |

| Average Annual Total Returns | | Periods ended December 31, 2018* | |

| | | | |

| Stocks: | | | | 1 Year | | | 3 Years | | | 5 Years | |

| | | | |

Large Caps | | (S&P 500® Index) | | | (4.38)% | | | | 9.26% | | | | 8.49% | |

| | | | |

Small Caps | | (Russell 2000® Index) | | | (11.01)% | | | | 7.36% | | | | 4.41% | |

| | | | |

International | | (MSCI All Country World Index ex USA) | | | (14.20)% | | | | 4.48% | | | | 0.68% | |

Bonds: | | | | | | | | | | | | | | |

| | | | |

Investment Grade | | (Bloomberg Barclays U.S. Aggregate Bond Index) | | | 0.01% | | | | 2.06% | | | | 2.52% | |

| | | | |

High Yield | | (Bloomberg Barclays U.S. Corporate High Yield Bond Index) | | | (2.08)% | | | | 7.23% | | | | 3.83% | |

| | | | |

Tax-exempt | | (Bloomberg Barclays Municipal Bond Index) | | | 1.28% | | | | 2.30% | | | | 3.82% | |

| | | | |

Treasury Bills | | (ICE BofAML U.S. 6-Month Treasury Bill Index) | | | 1.92% | | | | 1.18% | | | | 0.78% | |

*Source: FactSet. Past performance is no guarantee of future results.

2

|

About Your Fund’s Expenses |

| | | | | | | | | | | | |

As a shareholder of a Fund, you may incur two types of costs: (1) transaction costs, which may include sales charges (loads) on purchase payments; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on $1,000 invested at the beginning of the period and held for the entire period as indicated below. ACTUAL EXPENSES The first line of the following table provides information about the actual account values and | | | | | | actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period. HYPOTHETICAL EXAMPLE FOR COMPARISON PURPOSES The second line of the following table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed annual rate of return of 5% before expenses, which is not the Fund’s | | | | | | actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds by comparing this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds. Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. |

| | | | | | | | | | | | | | | | |

Six Months Ended December 31, 2018 | | Expense

Ratio for the Period | | | Beginning

Account

Value

07/01/18 | | | Ending

Account

Value

12/31/18 | | | Expenses

Paid

During

the Period* |

AMG Managers Loomis Sayles Bond Fund | |

Based on Actual Fund Return | |

Class N | | | 0.97% | | | | $1,000 | | | | $1,001 | | | | $4.89 | |

Class I | | | 0.87% | | | | $1,000 | | | | $1,001 | | | | $4.39 | |

Based on Hypothetical 5% Annual Return | |

Class N | | | 0.97% | | | | $1,000 | | | | $1,020 | | | | $4.94 | |

Class I | | | 0.87% | | | | $1,000 | | | | $1,021 | | | | $4.43 | |

| | | | | | | | | | | | | | | | |

AMG Managers Global Income Opportunity Fund | |

Based on Actual Fund Return | |

Class N | | | 0.89% | | | | $1,000 | | | | $991 | | | | $4.47 | |

Based on Hypothetical 5% Annual Return | |

Class N | | | 0.89% | | | | $1,000 | | | | $1,021 | | | | $4.53 | |

| | | | | | | | | | | | | | | | |

Six Months Ended December 31, 2018 | | Expense

Ratio for the Period | | | Beginning

Account

Value

07/01/18 | | | Ending

Account

Value

12/31/18 | | | Expenses

Paid

During

the Period* |

AMG Managers Special Equity Fund | |

Based on Actual Fund Return | |

Class N | | | 1.36% | | | | $1,000 | | | | $844 | | | | $6.32 | |

Class I | | | 1.11% | | | | $1,000 | | | | $845 | | | | $5.16 | |

Based on Hypothetical 5% Annual Return | |

Class N | | | 1.36% | | | | $1,000 | | | | $1,018 | | | | $6.92 | |

Class I | | | 1.11% | | | | $1,000 | | | | $1,020 | | | | $5.65 | |

| * | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (184), then divided by 365. |

3

|

AMG Managers Loomis Sayles Bond Fund Portfolio Manager’s Comments(unaudited) |

| | | | | | | | | | | | |

THE YEAR IN REVIEW The AMG Managers Loomis Sayles Bond Fund (Class N) (the Fund) returned -1.82% for the year ended December 31, 2018, underperforming the Bloomberg Barclays U.S. Government/Credit Bond Index, which returned -0.42%. The Fund posted negative absolute returns for the year. The underperformance can be largely attributed to sector allocation followed by weak security selection in investment grade corporate bonds. Investment grade credit spreads widened throughout the year. Weak security selection within the sector due to a BBB quality bias hurt relative return. Credits in banking, automotive, and metals and mining were the largest contributors to underperformance. The allocation to high yield corporates had a minimal negative impact on returns as credit spreads widened significantly in the fourth quarter. Relative to the benchmark, the strategy maintained a meaningful underweight to U.S. Treasuries with the bulk of our Treasury holdings in short-duration cash equivalents. While the underweight contributed to underperformance as Treasury bond returns were greater than corporate bond returns last year, the short duration of both the fund and our Treasury holdings benefited performance for the year. The treasury/duration impact combined to have a small negative effect on relative return. Our allocation to non-U.S. Dollar-denominated issues produced slight negative returns during the period. Holdings denominated in the Canadian and New Zealand Dollars were the largest detractors to relative performance. A small exposure to equities and convertible bonds detracted from performance as equity markets were volatile and had negative returns in 2018. An allocation to Securitized proved beneficial, with strong security selection boosting return. A small allocation and positive issue election within | | | | | | emerging markets also aided performance as emerging market bonds were one of the few markets to generate a positive return for the year. LOOKING FORWARD Driven by market volatility, Federal Reserve (“Fed”) policy, and a fragile geopolitical environment, our outlook is evolving. While the U.S. economy has experienced positive growth and strong employment, business uncertainty is rising and the pace of growth is slowing at the periphery. The recent growth and strong employment has generated some wage pressures but inflation still appears contained and the dramatic move in oil should remove some inflationary pressures. Fed policy has been under pressure and rates have moved dramatically lower with markets appearing to price with no more hikes and possibly a rate cut. The market volatility and lowering growth expectations, we believe, may cause the Fed to pause with at most one more rate hike in 2019. Despite the volatility, we do believe the U.S. economy is strong and we are not in the camp of those who say “the cycle is turning.” We believe a fair amount of slowing growth is due to the inventory cycle and do see the potential for some pickup in growth after a slow first quarter. Given the move down in U.S. interest rates we remain cautious about taking on more interest rate risk at present levels; however, our forward looking view is that rates will be lower for this cycle. Geopolitical and political risks are rising and outcomes from trade negotiations, actual Fed policy, and developments abroad could have meaningful impacts on forward yield curve moves. As we enter 2019, our strategy is to maintain a higher quality bias within credit markets as a whole given the aging of the credit cycle. We continue to favor sectors that are exhibiting credit improvement, such as banking, and those with defensive characteristics, such as telecommunications and cable. We see more opportunity with the recent selloff in oil and have been selectively adding. We are limiting our | | | | | | exposure to industries with more challenging business trends, such as retail and home construction. In both investment grade and high yield markets, liquidity has been choppy. We remain very focused on liquidity conditions and strive to exploit opportunities. We reduced our exposure to convertible debt earlier this year following strong performance and elevated valuations, particularly in the biotechnology and pharmaceutical areas. Given the decline in the equity market, we have seen opportunities increase and have become a selective buyer. We have focused on higher quality issues in technology, industrials, and energy. Interest rates and the expected path for U.S. rates have adjusted down relative to the rest of the world. Most developed market central banks were becoming less accommodative but U.S. rate differentials were quite high. This is beginning to change. For the moment we remain cautious on non-U.S. Dollar exposure, but the backdrop favoring a stronger U.S. Dollar has diminished. A key risk to our outlook is the health of the global economy and markets outside of the United States, particularly Europe and parts of Asia, which have already experienced slowing growth. China is likely the most important economy to watch, given its large contribution to global growth. A negative outcome from trade policy discussions has the potential to significantly weaken risk appetite and accelerate an economic slowdown. Conversely, an agreement on trade could lead to a meaningful market recovery. As we enter the new year, we continue to favor an allocation to selected higher quality U.S. investment grade and below investment-grade bonds with an emphasis on solid fundamentals, attractive yield, and liquidity. This commentary reflects the viewpoints of the portfolio manager, Loomis, Sayles & Company, as of December 31, 2018 and is not intended as a forecast or guarantee of future results. |

4

| | |

| | AMG Managers Loomis Sayles Bond Fund Portfolio Manager’s Comments(continued) |

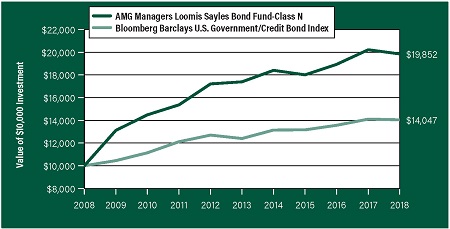

CUMULATIVE TOTAL RETURN PERFORMANCE

AMG Managers Loomis Sayles Bond Fund’s cumulative total return is based on the daily change in net asset value (NAV), and assumes that all dividends and distributions were reinvested. The graph compares a hypothetical $10,000 investment made in the AMG Managers Loomis Sayles Bond Fund’s Class N Shares on December 31, 2008, to a $10,000 investment made in the Bloomberg Barclays U.S. Government/Credit Bond Index for the same time period. The graph and table do not reflect the deduction of taxes that a shareholder would pay on a Fund distribution or redemption of shares. The listed returns for the Fund are net expenses and the returns for the index exclude expenses. Total returns would have been lower had certain expenses not been reduced.

The table below shows the average annual total returns for the AMG Managers Loomis Sayles Bond Fund and the Bloomberg Barclays U.S. Government/Credit Bond Index for the same time periods ended December 31, 2018.

| | | | | | | | | | | | | | | | | | |

| Average Annual Total Returns1 | | One Year | | | Five

Years | | | Ten Years | | | Since

Inception | | | Inception

Date |

AMG Managers Loomis Sayles Bond Fund2, 3, 4, 5, 6, 7 | | | |

| | | | | |

Class N | | | (1.82%) | | | | 2.68 | % | | | 7.10% | | | | 7.90% | | | 06/01/84 |

| | | | | |

Class I | | | (1.72%) | | | | 2.78 | % | | | — | | | | 2.33% | | | 04/01/13 |

Bloomberg Barclays U.S. Government/ Credit Bond Index8 | | | (0.42%) | | | | 2.53 | % | | | 3.46% | | | | 7.12% | | | 06/01/84† |

The performance data shown represents past performance. Past performance is not a guarantee of future results. Current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

Investors should carefully consider the Fund’s investment objectives, risks, charges and expenses before investing. For performance information through the most recent month end, current net asset values per share for the Fund and other information, please call 800.835.3879 or visit our website at amgfunds.com for a free prospectus. Read it carefully before investing or sending money.

Distributed by AMG Distributors, Inc., member FINRA/SIPC.

| † | Date reflects inception date of the Fund, not the index. |

| 1 | Total return equals income yield plus share price change and assumes reinvestment of all dividends and capital gain distributions. Returns are net of fees and may reflect offsets of Fund expenses as described in the prospectus. No adjustment has been made for taxes payable by shareholders on their reinvested dividends and |

|

capital gain distributions. Returns for periods greater than one year are annualized. The listed returns on the Fund are net of expenses and based on the published NAV as of December 31, 2018. All returns are in U.S. dollars($). 2 From time to time, the Fund’s advisor has waived fees and/or absorbed Fund expenses, which has resulted in higher returns. 3 The Fund is subject to the risks associated with investments in debt securities, such as default risk and fluctuations in the perception of the debtor’s ability to pay its creditors. Changing interest rates may adversely affect the value of an investment. An increase in interest rates typically causes the value of bonds and other fixed income securities to fall. 4 To the extent that the Fund invests in asset-backed or mortgage-backed securities, its exposure to prepayment and extension risks may be greater than investments in other fixed income securities. 5 The Fund may invest in derivatives such as options and futures; the complexity and rapidly changing structure of derivatives markets may increase the possibility of market losses. 6 High-yield bonds (also known as “junk bonds”) may be subject to greater levels of interest rate, credit, and liquidity risk than investments in higher rated securities. These securities are considered predominantly speculative with respect to the issuer’s continuing ability to make principal and interest payments. The issuers of the Fund’s holdings may be involved in bankruptcy proceedings, reorganizations, or financial restructurings, and are not as strong financially as higher-rated issuers. |

7 Investments in international securities are subject to certain risks of overseas investing including currency fluctuations and changes in political and economic conditions, which could result in significant market fluctuations. 8 The Bloomberg Barclays U.S. Government/Credit Bond Index is an index of investment grade government and corporate bonds with a maturity date of more than one year. Unlike the Fund, the Bloomberg Barclays U.S. Government/Credit Bond Index is unmanaged, is not available for investment and does not incur expenses. Not FDIC insured, nor bank guaranteed. May lose value. |

5

| | |

| | | AMG Managers Loomis Sayles Bond Fund Fund Snapshots(unaudited) December 31, 2018 |

PORTFOLIO BREAKDOWN

| | | | | |

| Category | | % of Net Assets |

| | |

Corporate Bonds and Notes | | | | 59.8 | |

| | |

Foreign Government Obligations | | | | 5.1 | |

| | |

Asset-Backed Securities | | | | 2.2 | |

| | |

U.S. Government and Agency Obligations | | | | 1.8 | |

| | |

Common Stocks | | | | 1.4 | |

| | |

Municipal Bonds | | | | 0.8 | |

| | |

Preferred Stocks | | | | 0.6 | |

| | |

Mortgage-Backed Securities | | | | 0.5 | |

| | |

Short-Term Investments | | | | 28.1 | |

| | |

Other Assets Less Liabilities | | | | (0.3 | ) |

| | | | | |

| |

| Rating | | % of Market Value1 |

| | |

U.S. Government and Agency Obligations | | | | 2.6 | |

| | |

Aaa | | | | 3.0 | |

| | |

Aa | | | | 3.4 | |

| | |

A | | | | 23.4 | |

| | |

Baa | | | | 56.8 | |

| | |

Ba | | | | 5.0 | |

| | |

B | | | | 3.9 | |

| | |

N/R | | | | 1.9 | |

1 Includes market value of fixed-income securities only.

TOP TEN HOLDINGS

| | | | |

| Security Name | | % of Net Assets |

| | |

U.S. Treasury Bill, 0.992%, 02/07/19 | | | 11.0 | |

| | |

U.S. Treasury Bill, 1.129%, 02/14/19 | | | 5.5 | |

| | |

U.S. Treasury Bill, 1.984%, 05/30/19 | | | 5.5 | |

| | |

Ford Motor Credit Co. LLC, 4.389%, 01/08/26 | | | 3.4 | |

| | |

U.S. Treasury Bill, 0.059%, 01/03/19 | | | 2.6 | |

| | |

Bank of America Corp., 6.110%, 01/29/37 | | | 2.3 | |

| | |

Mexican Bonos Bonds, Series M 20, 10.000%, 12/05/24 (Mexico) | | | 2.3 | |

| | |

AT&T, Inc., 4.300%, 02/15/30 | | | 1.9 | |

| | |

U.S. Treasury Bonds, 3.000%, 08/15/48 | | | 1.7 | |

| | |

ONEOK Partners, LP, 4.900%, 03/15/25 | | | 1.6 | |

| | | | | |

Top Ten as a Group | | | 37.8 | |

| | | | | |

| | | | | |

Credit quality ratings shown above reflect the highest rating assigned by either Standard & Poor’s (“S&P”) or Moody’s Investors Service, Inc. (“Moody’s”). These rating agencies are independent, nationally recognized statistical rating organizations and are widely used. Investment grade ratings are credit ratings of BBB/Baa or higher. Below investment grade ratings are credit ratings of BB/Ba or lower. Investments designated N/R are not rated by either rating agency. Unrated investments do not necessarily indicate low credit quality. Credit quality ratings are subject to change.

Because a fund’s strategy may result in multiple investments in particular sectors of the economy, its performance may depend on the performance of those sectors and may fluctuate more widely than investments diversified across more sectors. For additional information on these and other risk considerations, please see the Fund’s prospectus.

Any sectors, industries, or securities discussed should not be perceived as investment recommendations. Mention of a specific security should not be considered a recommendation to buy or solicitation to sell that security. Specific securities mentioned in this report may have been sold from the Fund’s portfolio of investments by the time you receive this report.

6

|

AMG Managers Loomis Sayles Bond Fund |

Schedule of Portfolio Investments |

December 31, 2018 |

| | | | | | | | |

| | | Principal

Amount† | | | Value | |

| |

Corporate Bonds and Notes - 59.8% | | | | | |

| | |

Financials - 22.9% | | | | | | | | |

| | |

Ally Financial, Inc. | | | | | | | | |

4.125%, 02/13/22 | | | $7,915,000 | | | | $7,687,444 | |

8.000%, 11/01/311 | | | 1,267,000 | | | | 1,406,370 | |

| | |

Alta Wind Holdings LLC | | | | | | | | |

7.000%, 06/30/352 | | | 5,179,895 | | | | 5,622,818 | |

| | |

American International Group, Inc. | | | | | | | | |

4.875%, 06/01/22 | | | 560,000 | | | | 581,015 | |

| | |

Banco Santander, S.A. (Spain) | | | | | | | | |

5.179%, 11/19/251 | | | 27,800,000 | | | | 27,662,393 | |

| | |

Bank of America Corp. | | | | | | | | |

(3 month LIBOR + 1.040%), 3.419%, 12/20/283 | | | 27,155,000 | | | | 25,366,830 | |

6.110%, 01/29/37 | | | 38,050,000 | | | | 41,818,349 | |

MTN, 4.250%, 10/22/26 | | | 2,610,000 | | | | 2,538,482 | |

| | |

Canadian Imperial Bank of Commerce (Canada) | | | | | | | | |

1.600%, 09/06/19 | | | 2,120,000 | | | | 2,100,875 | |

| | |

Citigroup, Inc. | | | | | | | | |

5.130%, 11/12/19 | | | 5,835,000 | NZD | | | 3,993,211 | |

| | |

Cooperatieve Centrale | | | | | | | | |

Raiffeisen-Boerenleenbank (Netherlands) | | | | | | | | |

3.875%, 02/08/22 | | | 9,090,000 | | | | 9,190,443 | |

3.950%, 11/09/22 | | | 2,190,000 | | | | 2,182,856 | |

| | |

Equifax, Inc. | | | | | | | | |

7.000%, 07/01/37 | | | 4,421,000 | | | | 5,059,384 | |

| | |

The Goldman Sachs Group, Inc. | | | | | | | | |

6.750%, 10/01/37 | | | 14,590,000 | | | | 16,476,251 | |

| | |

iStar, Inc. | | | | | | | | |

3.125%, 09/15/22 | | | 2,055,000 | | | | 1,851,637 | |

| | |

Jefferies Group LLC | | | | | | | | |

5.125%, 01/20/23 | | | 8,800,000 | | | | 8,997,728 | |

| | |

JPMorgan Chase & Co. | | | | | | | | |

4.125%, 12/15/26 | | | 14,350,000 | | | | 14,001,017 | |

| | |

JPMorgan Chase Bank, N.A. | | | | | | | | |

BKNT | | | | | | | | |

1.650%, 09/23/19 | | | 8,457,000 | | | | 8,379,178 | |

| | |

Lloyds Banking Group PLC (United Kingdom) | | | | | | | | |

4.500%, 11/04/24 | | | 18,500,000 | | | | 17,864,071 | |

4.582%, 12/10/25 | | | 20,972,000 | | | | 19,854,249 | |

| | |

Marsh & McLennan Cos., Inc. | | | | | | | | |

5.875%, 08/01/33 | | | 8,295,000 | | | | 9,691,756 | |

| | |

MBIA Insurance Corp. | | | | | | | | |

(3 month LIBOR + 11.260%) | | | | | | | | |

13.696%, 01/15/332,3 | | | 525,000 | | | | 320,250 | |

| | |

Morgan Stanley | | | | | | | | |

3.950%, 04/23/27 | | | 17,265,000 | | | | 16,277,345 | |

GMTN, 4.350%, 09/08/26 | | | 5,000,000 | | | | 4,859,022 | |

MTN, 4.100%, 05/22/23 | | | 12,910,000 | | | | 12,928,646 | |

MTN, 6.250%, 08/09/26 | | | 11,000,000 | | | | 12,180,517 | |

| | |

Mutual of Omaha Insurance Co. | | | | | | | | |

6.800%, 06/15/362 | | | 13,925,000 | | | | 17,334,265 | |

| | | | | | | | |

| | | Principal

Amount† | | | Value | |

| | |

National City Corp. | | | | | | | | |

6.875%, 05/15/19 | | | $1,905,000 | | | | $1,931,143 | |

| | |

National Life Insurance Co. | | | | | | | | |

10.500%, 09/15/392 | | | 5,000,000 | | | | 7,940,601 | |

| | |

Navient Corp. | | | | | | | | |

5.500%, 01/25/23 | | | 18,070,000 | | | | 15,811,250 | |

| | |

Old Republic International Corp. | | | | | | | | |

4.875%, 10/01/24 | | | 4,915,000 | | | | 5,108,881 | |

| | |

The Penn Mutual Life Insurance Co. | | | | | | | | |

7.625%, 06/15/402 | | | 8,885,000 | | | | 11,684,523 | |

| | |

Quicken Loans, Inc. | | | | | | | | |

5.250%, 01/15/282 | | | 2,080,000 | | | | 1,840,800 | |

5.750%, 05/01/252 | | | 1,815,000 | | | | 1,697,025 | |

| | |

Realty Income Corp. | | | | | | | | |

5.750%, 01/15/21 | | | 2,125,000 | | | | 2,210,945 | |

| | |

Royal Bank of Canada (Canada) | | | | | | | | |

Series GMTN | | | | | | | | |

1.625%, 04/15/19 | | | 1,348,000 | | | | 1,343,404 | |

| | |

Royal Bank of Scotland Group PLC (United Kingdom) | | | | | | | | |

6.125%, 12/15/22 | | | 4,650,000 | | | | 4,712,587 | |

| | |

Societe Generale, S.A. (France) | | | | | | | | |

4.750%, 11/24/252 | | | 11,000,000 | | | | 10,866,017 | |

5.200%, 04/15/212 | | | 7,000,000 | | | | 7,290,674 | |

| | |

Springleaf Finance Corp. | | | | | | | | |

5.250%, 12/15/19 | | | 12,890,000 | | | | 12,920,678 | |

8.250%, 10/01/23 | | | 10,865,000 | | | | 11,163,787 | |

| | |

Weyerhaeuser Co. | | | | | | | | |

6.875%, 12/15/33 | | | 12,890,000 | | | | 15,350,194 | |

7.375%, 10/01/19 | | | 3,915,000 | | | | 4,022,765 | |

7.375%, 03/15/32 | | | 1,930,000 | | | | 2,360,075 | |

| | |

Total Financials | | | | | | | 414,481,751 | |

| | |

Industrials - 35.1% | | | | | | | | |

| | |

America Movil SAB de CV (Mexico) | | | | | | | | |

6.450%, 12/05/22 | | | 169,300,000 | MXN | | | 7,602,745 | |

| | |

American Airlines 2013-1 Class A Pass | | | | | | | | |

Through Trust | | | | | | | | |

4.000%, 07/15/25 | | | 1,799,460 | | | | 1,785,694 | |

| | |

American Airlines 2016-1 Class B Pass | | | | | | | | |

Through Trust, Series B | | | | | | | | |

5.250%, 01/15/24 | | | 19,236,043 | | | | 19,801,465 | |

| | |

American Airlines 2016-2 Class B Pass | | | | | | | | |

Through Trust | | | | | | | | |

4.375%, 06/15/242 | | | 20,500,000 | | | | 20,104,350 | |

| | |

American Airlines 2016-3 Class B Pass | | | | | | | | |

Through Trust | | | | | | | | |

3.750%, 10/15/25 | | | 7,343,071 | | | | 7,048,504 | |

| | |

American Airlines 2017-1B Class B Pass | | | | | | | | |

Through Trust | | | | | | | | |

Series B | | | | | | | | |

4.950%, 02/15/25 | | | 3,558,262 | | | | 3,567,887 | |

The accompanying notes are an integral part of these financial statements.

7

| | |

| | AMG Managers Loomis Sayles Bond Fund Schedule of Portfolio Investments(continued) |

| | | | | | | | |

| | | Principal

Amount† | | Value | |

| |

Industrials - 35.1%(continued) | | | | | |

| | |

American Airlines 2017-2 Class B Pass | | | | | | | | |

Through Trust | | | | | | | | |

Series B | | | | | | | | |

3.700%, 10/15/25 | | | $2,748,649 | | | | $2,658,588 | |

| | |

APL, Ltd. | | | | | | | | |

8.000%, 01/15/24 | | | 250,000 | | | | 240,000 | |

| | |

Apple, Inc. | | | | | | | | |

1.100%, 08/02/19 | | | 485,000 | | | | 480,178 | |

1.550%, 02/07/20 | | | 2,180,000 | | | | 2,153,604 | |

1.800%, 05/11/20 | | | 18,480,000 | | | | 18,247,207 | |

| | |

ArcelorMittal (Luxembourg) | | | | | | | | |

6.750%, 03/01/414 | | | 11,065,000 | | | | 11,684,883 | |

7.000%, 10/15/394 | | | 6,604,000 | | | | 6,957,976 | |

| | |

AT&T Inc. | | | | | | | | |

4.500%, 03/09/48 | | | 2,935,000 | | | | 2,511,500 | |

4.550%, 03/09/49 | | | 3,230,000 | | | | 2,780,369 | |

| | |

AT&T, Inc. | | | | | | | | |

3.400%, 05/15/25 | | | 13,530,000 | | | | 12,740,563 | |

3.950%, 01/15/25 | | | 4,345,000 | | | | 4,248,782 | |

4.300%, 02/15/30 | | | 35,605,000 | | | | 33,646,216 | |

| | |

Booking Holdings, Inc. | | | | | | | | |

0.900%, 09/15/211,5 | | | 11,970,000 | | | | 13,209,338 | |

| | |

CenturyLink, Inc. | | | | | | | | |

Series S | | | | | | | | |

6.450%, 06/15/21 | | | 5,900,000 | | | | 5,885,250 | |

| | |

Chesapeake Energy Corp. | | | | | | | | |

6.625%, 08/15/20 | | | 55,000 | | | | 53,213 | |

6.875%, 11/15/20 | | | 85,000 | | | | 82,450 | |

| | |

Choice Hotels International, Inc. | | | | | | | | |

5.700%, 08/28/201 | | | 11,900,000 | | | | 12,108,250 | |

| | |

Continental Airlines, Inc. 2000-1 Class A-1 Pass Through Trust | | | | | | | | |

Series 00A1 | | | | | | | | |

8.048%, 11/01/20 | | | 27,698 | | | | 28,620 | |

| | |

Continental Airlines, Inc. 2007-1 Class A Pass Through Trust | | | | | | | | |

Series 071A | | | | | | | | |

5.983%, 04/19/22 | | | 12,402,012 | | | | 12,950,181 | |

| | |

Continental Airlines, Inc. 2007-1 Class B Pass Through Trust | | | | | | | | |

Series 071B | | | | | | | | |

6.903%, 04/19/22 | | | 1,210,076 | | | | 1,243,474 | |

| | |

Continental Resources, Inc. | | | | | | | | |

3.800%, 06/01/24 | | | 2,025,000 | | | | 1,917,005 | |

4.500%, 04/15/23 | | | 385,000 | | | | 378,908 | |

| | |

Corning, Inc. | | | | | | | | |

6.850%, 03/01/29 | | | 9,142,000 | | | | 10,843,223 | |

| | |

Cox Communications, Inc. | | | | | | | | |

4.800%, 02/01/352 | | | 3,369,000 | | | | 3,071,584 | |

| | |

Cummins, Inc. | | | | | | | | |

5.650%, 03/01/98 | | | 6,460,000 | | | | 7,043,164 | |

| | | | | | | | |

| | | Principal

Amount† | | Value | |

| | |

Dell International LLC / EMC Corp. | | | | | | | | |

6.020%, 06/15/262 | | | $3,270,000 | | | | $3,284,786 | |

8.100%, 07/15/362 | | | 5,470,000 | | | | 5,945,064 | |

8.350%, 07/15/462 | | | 2,990,000 | | | | 3,237,543 | |

| | |

Delta Air Lines, Inc. | | | | | | | | |

2007-1 Class B Pass Through Trust | | | | | | | | |

Series 071B | | | | | | | | |

8.021%, 08/10/22 | | | 4,767,669 | | | | 5,187,701 | |

| | |

Devon Energy Corp. | | | | | | | | |

3.250%, 05/15/22 | | | 5,256,000 | | | | 5,121,710 | |

| | |

Dillard’s, Inc. | | | | | | | | |

7.000%, 12/01/28 | | | 225,000 | | | | 231,582 | |

| | |

Embarq Corp. | | | | | | | | |

7.995%, 06/01/36 | | | 3,335,000 | | | | 3,018,175 | |

| | |

Embraer Netherlands Finance BV (Netherlands) | | | | | | | | |

5.400%, 02/01/27 | | | 2,325,000 | | | | 2,400,586 | |

| | |

Enable Midstream Partners, LP | | | | | | | | |

5.000%, 05/15/441,4 | | | 2,725,000 | | | | 2,239,674 | |

| | |

Enbridge Energy Partners, LP | | | | | | | | |

7.375%, 10/15/45 | | | 1,870,000 | | | | 2,316,165 | |

| | |

Energy Transfer Partners, LP / Regency Energy | | | | | | | | |

Finance Corp. | | | | | | | | |

4.500%, 11/01/23 | | | 700,000 | | | | 700,227 | |

| | |

EnLink Midstream Partners, LP | | | | | | | | |

4.150%, 06/01/251 | | | 6,145,000 | | | | 5,539,946 | |

| | |

Enterprise Products Operating LLC | | | | | | | | |

4.050%, 02/15/22 | | | 2,219,000 | | | | 2,253,149 | |

| | |

ERAC USA Finance LLC | | | | | | | | |

6.700%, 06/01/342 | | | 1,250,000 | | | | 1,484,745 | |

7.000%, 10/15/372 | | | 19,033,000 | | | | 23,663,202 | |

| | |

Foot Locker, Inc. | | | | | | | | |

8.500%, 01/15/22 | | | 220,000 | | | | 243,925 | |

| | |

Ford Motor Co. | | | | | | | | |

6.375%, 02/01/29 | | | 1,990,000 | | | | 1,988,569 | |

| | |

Ford Motor Credit Co. LLC, GMTN | | | | | | | | |

4.389%, 01/08/26 | | | 68,075,000 | | | | 61,370,009 | |

| | |

General Motors Co. | | | | | | | | |

5.200%, 04/01/45 | | | 2,760,000 | | | | 2,287,364 | |

| | |

General Motors Financial Co., Inc. | | | | | | | | |

5.250%, 03/01/26 | | | 9,680,000 | | | | 9,471,909 | |

| | |

Georgia-Pacific LLC | | | | | | | | |

5.400%, 11/01/202 | | | 5,175,000 | | | | 5,362,202 | |

| | |

HCA, Inc. | | | | | | | | |

4.500%, 02/15/27 | | | 3,040,000 | | | | 2,872,800 | |

7.500%, 11/06/33 | | | 75,000 | | | | 78,750 | |

| | |

Hewlett Packard Enterprise Co. | | | | | | | | |

6.350%, 10/15/454 | | | 2,243,000 | | | | 2,093,693 | |

| | |

International Business Machines Corp. | | | | | | | | |

1.625%, 05/15/20 | | | 5,980,000 | | | | 5,861,884 | |

| | |

INVISTA Finance LLC | | | | | | | | |

4.250%, 10/15/192 | | | 14,000,000 | | | | 13,896,314 | |

The accompanying notes are an integral part of these financial statements.

8

| | |

| | AMG Managers Loomis Sayles Bond Fund Schedule of Portfolio Investments(continued) |

| | | | | | | | |

| | | Principal Amount† | | Value | |

Industrials - 35.1%(continued) | | | | | |

| | |

Kinder Morgan Energy Partners, LP | | | | | | | | |

3.500%, 09/01/23 | | | $6,685,000 | | | | $6,493,617 | |

4.150%, 03/01/22 | | | 5,620,000 | | | | 5,661,439 | |

4.150%, 02/01/241 | | | 14,000,000 | | | | 13,874,955 | |

5.300%, 09/15/20 | | | 1,415,000 | | | | 1,453,257 | |

5.800%, 03/01/21 | | | 4,320,000 | | | | 4,508,941 | |

| | |

KLA-Tencor Corp. | | | | | | | | |

5.650%, 11/01/34 | | | 4,590,000 | | | | 4,679,099 | |

| | |

Macy’s Retail Holdings, Inc. | | | | | | | | |

4.500%, 12/15/34 | | | 21,000 | | | | 16,803 | |

| | |

Marks & Spencer PLC (United Kingdom) | | | | | | | | |

7.125%, 12/01/372 | | | 4,725,000 | | | | 5,004,000 | |

| | |

Masco Corp. | | | | | | | | |

6.500%, 08/15/32 | | | 254,000 | | | | 280,784 | |

7.125%, 03/15/20 | | | 357,000 | | | | 372,931 | |

7.750%, 08/01/291 | | | 499,000 | | | | 594,658 | |

| | |

Methanex Corp. (Canada) | | | | | | | | |

5.250%, 03/01/22 | | | 350,000 | | | | 352,949 | |

| | |

Microsoft Corp. | | | | | | | | |

1.100%, 08/08/19 | | | 3,819,000 | | | | 3,780,982 | |

| | |

New Albertson’s, Inc. | | | | | | | | |

7.450%, 08/01/29 | | | 3,165,000 | | | | 2,532,000 | |

7.750%, 06/15/26 | | | 915,000 | | | | 777,750 | |

MTN, Series C, 6.625%, 06/01/28 | | | 1,045,000 | | | | 773,300 | |

| | |

Newell Brands, Inc. | | | | | | | | |

4.000%, 12/01/24 | | | 3,085,000 | | | | 3,039,212 | |

| | |

Noble Energy, Inc. | | | | | | | | |

3.900%, 11/15/24 | | | 3,670,000 | | | | 3,555,051 | |

| | |

Nuance Communications, Inc. | | | | | | | | |

1.000%, 12/15/355 | | | 2,140,000 | | | | 1,853,548 | |

1.250%, 04/01/255 | | | 1,585,000 | | | | 1,396,087 | |

1.500%, 11/01/355 | | | 50,000 | | | | 46,805 | |

| | |

ONEOK Partners, LP | | | | | | | | |

4.900%, 03/15/25 | | | 28,736,000 | | | | 29,114,061 | |

6.200%, 09/15/43 | | | 245,000 | | | | 262,608 | |

| | |

Owens Corning | | | | | | | | |

7.000%, 12/01/36 | | | 2,715,000 | | | | 3,002,686 | |

| | |

Petrobras Global Finance BV (Netherlands) | | | | | | | | |

5.625%, 05/20/43 | | | 580,000 | | | | 486,046 | |

| | |

PulteGroup, Inc. | | | | | | | | |

6.000%, 02/15/35 | | | 8,860,000 | | | | 7,663,900 | |

6.375%, 05/15/331 | | | 5,135,000 | | | | 4,685,687 | |

| | |

Qwest Capital Funding, Inc. | | | | | | | | |

6.875%, 07/15/28 | | | 1,055,000 | | | | 884,755 | |

| | |

Qwest Corp. | | | | | | | | |

6.875%, 09/15/33 | | | 5,857,000 | | | | 5,232,310 | |

7.250%, 09/15/25 | | | 1,185,000 | | | | 1,220,055 | |

| | |

Reliance Holding USA, Inc. | | | | | | | | |

5.400%, 02/14/222 | | | 3,250,000 | | | | 3,365,622 | |

| | |

Samsung Electronics Co., Ltd. (South Korea) | | | | | | | | |

7.700%, 10/01/272 | | | 1,980,000 | | | | 2,197,523 | |

| | | | | | | | |

| | | Principal Amount† | | Value | |

| | |

Sealed Air Corp. | | | | | | | | |

5.500%, 09/15/251,2 | | | $1,580,000 | | | | $1,560,250 | |

| | |

Telecom Italia Capital, S.A. (Luxembourg) | | | | | | | | |

6.000%, 09/30/34 | | | 4,665,000 | | | | 4,035,225 | |

6.375%, 11/15/33 | | | 3,530,000 | | | | 3,186,284 | |

| | |

Telefonica Emisiones SAU (Spain) | | | | | | | | |

4.570%, 04/27/23 | | | 900,000 | | | | 924,449 | |

| | |

Telekom Malaysia Bhd (Malaysia) | | | | | | | | |

7.875%, 08/01/252 | | | 250,000 | | | | 304,050 | |

| | |

Time Warner Cable LLC | | | | | | | | |

5.500%, 09/01/41 | | | 805,000 | | | | 733,583 | |

| | |

The Toro Co. | | | | | | | | |

6.625%, 05/01/37 | | | 6,810,000 | | | | 7,925,787 | |

| | |

Transcontinental Gas Pipe Line Co. LLC | | | | | | | | |

7.850%, 02/01/26 | | | 15,140,000 | | | | 18,302,542 | |

| | |

UAL 2007-1 Pass Through Trust | | | | | | | | |

Series 071A | | | | | | | | |

6.636%, 07/02/22 | | | 8,814,166 | | | | 9,165,851 | |

| | |

United Airlines 2014-1 Class A Pass Through Trust | | | | | | | | |

Series A | | | | | | | | |

4.000%, 04/11/26 | | | 7,443,333 | | | | 7,416,686 | |

| | |

United Airlines 2016-2 Class B Pass Through Trust | | | | | | | | |

Series 16-2 | | | | | | | | |

3.650%, 10/07/25 | | | 2,150,556 | | | | 2,037,866 | |

| | |

United States Steel Corp. | | | | | | | | |

6.650%, 06/01/371 | | | 3,595,000 | | | | 2,705,238 | |

| | |

US Airways 2011-1 Class A Pass Through Trust | | | | | | | | |

Series A | | | | | | | | |

7.125%, 10/22/23 | | | 2,140,267 | | | | 2,335,673 | |

| | |

Vale Overseas, Ltd. (Brazil) | | | | | | | | |

6.875%, 11/21/36 | | | 1,759,000 | | | | 2,011,417 | |

| | |

Verizon Communications, Inc. | | | | | | | | |

3.500%, 11/01/24 | | | 27,900,000 | | | | 27,517,134 | |

4.862%, 08/21/46 | | | 25,890,000 | | | | 25,443,920 | |

| | |

Virgin Australia 2013-1A Trust (Australia) | | | | | | | | |

5.000%, 10/23/232 | | | 399,207 | | | | 404,317 | |

| | |

WestRock MWV LLC | | | | | | | | |

7.550%, 03/01/47 | | | 970,000 | | | | 1,184,662 | |

Total Industrials | | | | | | | 635,585,200 | |

Utilities - 1.8% | | | | | | | | |

| | |

DCP Midstream Operating, LP | | | | | | | | |

6.450%, 11/03/362 | | | 870,000 | | | | 843,900 | |

| | |

EDP Finance, B.V. (Netherlands) | | | | | | | | |

4.900%, 10/01/192 | | | 600,000 | | | | 604,554 | |

| | |

Empresa Nacional de Electricidad S.A. (Cayman Islands) | | | | | | | | |

7.875%, 02/01/27 | | | 2,900,000 | | | | 3,495,844 | |

The accompanying notes are an integral part of these financial statements.

9

| | |

| | AMG Managers Loomis Sayles Bond Fund Schedule of Portfolio Investments(continued) |

| | | | | | | | |

| | | Principal Amount† | | Value | |

| | |

Utilities - 1.8%(continued) | | | | | | | | |

| | |

Enel Finance International N.V., EMTN (Netherlands) | | | | | | | | |

5.750%, 09/14/40 | | | 210,000 | GBP | | | $315,859 | |

6.000%, 10/07/392 | | | $18,382,000 | | | | 18,222,646 | |

| | |

Enterprise Products Operating LLC | | | | | | | | |

3.900%, 02/15/24 | | | 6,400,000 | | | | 6,454,235 | |

| | |

Tenaga Nasional Bhd (Malaysia) | | | | | | | | |

7.500%, 11/01/252 | | | 2,000,000 | | | | 2,382,573 | |

| | |

Total Utilities | | | | | | | 32,319,611 | |

| | |

Total Corporate Bonds and Notes

(Cost $1,044,188,329) | | | | | | | 1,082,386,562 | |

| | |

Asset-Backed Securities - 2.2% | | | | | | | | |

| | |

FAN Engine Securitization, Ltd. | | | | | | | | |

Series 2013-1A, Class 1A | | | | | | | | |

4.625%, 10/15/432 | | | 10,459,044 | | | | 10,338,765 | |

| | |

Rise, Ltd. (Bermuda) | | | | | | | | |

Series 2014-1, Class A | | | | | | | | |

4.750%, 02/15/396,7 | | | 11,938,007 | | | | 11,579,866 | |

| | |

Shenton Aircraft Investment I, Ltd. | | | | | | | | |

Series 2015-1A, Class A | | | | | | | | |

4.750%, 10/15/422 | | | 17,277,072 | | | | 17,492,051 | |

| | |

Total Asset-Backed Securities

(Cost $39,482,225) | | | | | | | 39,410,682 | |

| | |

Mortgage-Backed Securities - 0.5% | | | | | | | | |

| | |

Commercial Mortgage Trust | | | | | | | | |

Series 2014-LC15, Class A2

2.840%, 04/10/47 | | | 3,614,394 | | | | 3,610,302 | |

Series 2014-UBS4, Class A2

2.963%, 08/10/47 | | | 2,275,531 | | | | 2,271,768 | |

| | |

JPMorgan Chase Commercial Mortgage Securities Trust | | | | | | | | |

Series 2014-C20, Class A2 | | | | | | | | |

2.872%, 07/15/47 | | | 1,550,707 | | | | 1,546,320 | |

| | |

Morgan Stanley Bank of America Merrill Lynch Trust | | | | | | | | |

Series 2014-C14, Class A2 | | | | | | | | |

2.916%, 02/15/47 | | | 264,843 | | | | 264,441 | |

| | |

WFRBS Commercial Mortgage Trust | | | | | | | | |

Series 2011-C3, Class D | | | | | | | | |

5.683%, 03/15/442,7 | | | 435,000 | | | | 395,196 | |

| | |

Total Mortgage-Backed Securities

(Cost $8,105,610) | | | | | | | 8,088,027 | |

| | |

Municipal Bonds - 0.8% | | | | | | | | |

| | |

Illinois State | | | | | | | | |

5.100%, 06/01/33 | | | 1,070,000 | | | | 1,020,170 | |

| | |

Michigan Tobacco Settlement Finance Authority | | | | | | | | |

7.309%, 06/01/34 | | | 2,055,000 | | | | 2,005,762 | |

| | |

Virginia Tobacco Settlement Financing Corp. | | | | | | | | |

6.706%, 06/01/46 | | | 11,675,000 | | | | 11,017,348 | |

| | |

Total Municipal Bonds

(Cost $14,182,183) | | | | | | | 14,043,280 | |

| | | | | | | | |

| | | Principal Amount† | | Value | |

| | |

U.S. Government and Agency Obligations - 1.8% | | | | | | | | |

| | |

Fannie Mae - 0.1% | | | | | | | | |

| | |

FNMA, | | | | | | | | |

3.000%, 07/01/27 | | | $1,437,986 | | | | $1,442,487 | |

6.000%, 07/01/29 | | | 997 | | | | 1,087 | |

| | |

Total Fannie Mae | | | | | | | 1,443,574 | |

| | |

Freddie Mac - 0.0%# | | | | | | | | |

| | |

FHLMC Gold, | | | | | | | | |

5.000%, 12/01/31 | | | 15,870 | | | | 16,656 | |

| | |

U.S. Treasury Obligations - 1.7% | | | | | | | | |

| | |

U.S. Treasury Bonds, | | | | | | | | |

3.000%, 08/15/481 | | | 31,825,000 | | | | 31,674,577 | |

| | |

Total U.S. Government and Agency Obligations

(Cost $31,014,519) | | | | | | | 33,134,807 | |

| | |

Foreign Government Obligations - 5.1% | | | | | | | | |

| | |

Brazilian Government International Bonds | | | | | | | | |

8.500%, 01/05/24 | | | 6,650,000 | BRL | | | 1,724,376 | |

10.250%, 01/10/28 | | | 5,750,000 | BRL | | | 1,645,769 | |

| | |

Canadian Government Bond | | | | | | | | |

Series 0001 | | | | | | | | |

0.750%, 09/01/20 | | | 15,225,000 | CAD | | | 10,951,919 | |

| | |

European Investment Bank Bonds | | | | | | | | |

0.000%, 03/10/218 | | | 5,000,000 | AUD | | | 3,326,790 | |

| | |

Mexican Bonos | | | | | | | | |

Series M | | | | | | | | |

8.000%, 12/07/23 | | | 122,500,000 | MXN | | | 6,083,687 | |

| | |

Mexican Bonos Bonds | | | | | | | | |

Series M 7.750%, 05/29/31 | | | 49,000,000 | MXN | | | 2,300,925 | |

Series M 20 7.500%, 06/03/27 | | | 111,000,000 | MXN | | | 5,246,020 | |

Series M 20 8.500%, 05/31/29 | | | 36,000,000 | MXN | | | 1,800,976 | |

Series M 20 10.000%, 12/05/24 | | | 761,500,000 | MXN | | | 41,156,475 | |

| | |

New Zealand Government Notes | | | | | | | | |

Series 319 | | | | | | | | |

5.000%, 03/15/19 | | | 14,845,000 | NZD | | | 10,029,280 | |

| | |

Norway Government Bonds | | | | | | | | |

Series 473 4.500%, 05/22/192 | | | 18,955,000 | NOK | | | 2,222,603 | |

Series 474 3.750%, 05/25/212 | | | 13,210,000 | NOK | | | 1,621,438 | |

| | |

Saudi Government International Bond | | | | | | | | |

3.250%, 10/26/262 | | | 5,170,000 | | | | 4,833,619 | |

| | |

Total Foreign Government Obligations

(Cost $140,277,196) | | | | | | | 92,943,877 | |

| | |

| | | Shares | | | |

Common Stocks - 1.4% | | | | | | | | |

| | |

Communication Services - 1.0% | | | | | | | | |

| | |

AT&T, Inc. | | | 614,704 | | | | 17,543,652 | |

| | |

Health Care - 0.2% | | | | | | | | |

| | |

Bristol-Myers Squibb Co. | | | 64,144 | | | | 3,334,205 | |

| | |

Industrials - 0.1% | | | | | | | | |

| | |

Arconic, Inc. | | | 154,805 | | | | 2,610,012 | |

The accompanying notes are an integral part of these financial statements.

10

| | |

| | AMG Managers Loomis Sayles Bond Fund Schedule of Portfolio Investments(continued) |

| | | | | | | | |

| | | Shares | | Value | |

| | |

Information Technology - 0.1% | | | | | | | | |

| | |

Corning, Inc. | | | 49,999 | | | | $1,510,470 | |

Total Common Stocks

(Cost $27,097,430) | | | | | | | 24,998,339 | |

| | |

Preferred Stocks - 0.6% | | | | | | | | |

| | |

Financials - 0.6% | | | | | | | | |

| | |

Bank of America Corp., 7.25%5 | | | 7,808 | | | | 9,779,520 | |

| | |

Navient Corp., 6.00%1 | | | 41,250 | | | | 680,625 | |

| | |

Total Financials | | | | | | | 10,460,145 | |

| | |

Utilities - 0.0%# | | | | | | | | |

| | |

Wisconsin Electric Power Co., 3.60% | | | 3,946 | | | | 342,907 | |

| | |

Total Preferred Stocks

(Cost $8,303,212) | | | | | | | 10,803,052 | |

| | |

| | | Principal

Amount | | | |

Short-Term Investments - 28.1% | | | | | | | | |

| | |

Joint Repurchase Agreements - 0.8%9 | | | | | | | | |

| | |

Bank of Nova Scotia, dated 12/31/18, due 01/02/19, 2.950% total to be received $746,294 (collateralized by various U.S. Treasuries, 0.000% - 8.750%, 01/08/19 - 09/09/49, totaling $761,220) | | | $746,172 | | | | 746,172 | |

| | |

Cantor Fitzgerald Securities, Inc., dated 12/31/18, due 01/02/19, 3.350% total to be received $3,560,015 (collateralized by various U.S. Government Agency Obligations and U.S. Treasuries, 0.000% - 10.000%, 01/25/19 - 10/20/68, totaling $3,630,540) | | | 3,559,353 | | | | 3,559,353 | |

| | |

Daiwa Capital Markets America, dated 12/31/18, due 01/02/19, 3.050% total to be received $3,559,956 (collateralized by various U.S. Government Agency Obligations, 2.000% - 6.500%, 01/25/19 - 02/01/49, totaling $3,630,540) | | | 3,559,353 | | | | 3,559,353 | |

| | |

RBC Dominion Securities, Inc., dated 12/31/18, due 01/02/19, 3.020% total to be received $3,559,950 (collateralized by various U.S. Government Agency Obligations, 3.000% - 7.000%, 10/01/25 - 10/20/48, totaling $3,630,540) | | | 3,559,353 | | | | 3,559,353 | |

| | | | | | | | |

| | | Principal Amount | | Value | |

| | |

State of Wisconsin Investment Board, dated 12/31/18, due 01/02/19, 3.370% total to be received $3,560,019 (collateralized by various U.S. Treasuries, 0.125% - 3.875%, 07/15/20 - 02/15/47, totaling $3,630,597) | | | $3,559,353 | | | | $3,559,353 | |

| | |

Total Joint Repurchase Agreements | | | | | | | 14,983,584 | |

| | |

U.S. Government Obligations - 25.7% | | | | | | | | |

| | |

U.S. Treasury Bill, 0.059%, 01/03/191,10 | | | 47,270,000 | | | | 47,264,329 | |

| | |

U.S. Treasury Bill, 0.764%, 04/25/191,10 | | | 20,000,000 | | | | 19,848,941 | |

| | |

U.S. Treasury Bill, 0.992%, 02/07/191,10 | | | 200,000,000 | | | | 199,526,194 | |

| | |

U.S. Treasury Bill, 1.129%, 02/14/191,10 | | | 100,000,000 | | | | 99,717,667 | |

| | |

U.S. Treasury Bill, 1.984%, 05/30/191,10 | | | 100,000,000 | | | | 99,002,542 | |

| | |

Total U.S. Government Obligations | | | | | | | 465,359,673 | |

| | |

| | | Shares | | | |

Other Investment Companies - 1.6% | | | | | | | | |

| | |

Dreyfus Government Cash Management Fund, Institutional Shares, 2.29%11 | | | 9,538,257 | | | | 9,538,257 | |

| | |

Dreyfus Institutional Preferred Government Money Market Fund, Institutional Shares, 2.40%11 | | | 9,538,257 | | | | 9,538,257 | |

| | |

JPMorgan U.S. Government Money Market Fund, IM Shares, 2.36%11 | | | 9,827,296 | | | | 9,827,296 | |

| | |

Total Other Investment Companies | | | | | | | 28,903,810 | |

| | |

Total Short-Term Investments

(Cost $509,238,717) | | | | | | | 509,247,067 | |

| | |

Total Investments - 100.3%

(Cost $1,821,889,421) | | | | | | | 1,815,055,693 | |

| | |

Other Assets, less Liabilities - (0.3)% | | | | | | | (4,767,322 | ) |

| | |

Net Assets - 100.0% | | | | | | | $1,810,288,371 | |

| † | Principal amount stated in U.S. dollars unless otherwise stated. |

| 1 | Some or all of these securities, amounting to $486,940,260 or 26.9% of net assets, were out on loan to various brokers and are collateralized by cash and various U.S. Treasury Obligations. See Note 4 of Notes to Financial Statements. |

| 2 | Security exempt from registration under Rule 144A of the Securities Act of 1933. This security may be resold in transactions exempt from registration, normally to qualified buyers. At December 31, 2018, the value of these securities amounted to $216,439,870 or 12.0% of net assets. |

| 3 | Variable rate security. The rate shown is based on the latest available information as of December 31, 2018. |

| 4 | Step Bond: A debt instrument with either deferred interest payments or an interest rate that resets at specific times during its term. |

| 5 | Convertible Security. A corporate bond or preferred stock, usually a junior debenture, that can be converted, at the option of the holder, for a specific number of shares of the company’s preferred stock or common stock. The market value of convertible bonds and convertible preferred stocks at December 31, 2018, amounted to $26,285,298 or 1.5% of net assets. |

| 6 | Security’s value was determined by using significant unobservable inputs. |

The accompanying notes are an integral part of these financial statements.

11

| | |

| | AMG Managers Loomis Sayles Bond Fund Schedule of Portfolio Investments(continued) |

| 7 | Certain variable rate securities are not based on a published reference rate and spread but are determined by the issuer or agent and are based on current market conditions. These securities do not indicate a reference rate and spread in their description above. |

| 9 | Cash collateral received from brokers for securities lending was invested in these joint repurchase agreements. |

| 10 | Represents yield to maturity at December 31, 2018. |

| 11 | Yield shown represents the December 31, 2018, seven day average yield, which refers to the sum of the previous seven days’ dividends paid, expressed as an annual percentage. |

| EMTN | European Medium Term Note |

| GMTN | Global Medium-Term Notes |

| LIBOR | London Interbank Offered Rate |

CURRENCY ABBREVIATIONS:

The accompanying notes are an integral part of these financial statements.

12

| | |

| | AMG Managers Loomis Sayles Bond Fund Schedule of Portfolio Investments(continued) |

The following table summarizes the inputs used to value the Fund’s investments by the fair value hierarchy levels as of December 31, 2018:

| | | | | | | | | | | | | | | | |

| | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

Investments in Securities | | | | | | | | | | | | | | | | |

| | | | |

Corporate Bonds and Notes† | | | — | | | | $1,082,386,562 | | | | — | | | | $1,082,386,562 | |

| | | | |

Asset-Backed Securities | | | — | | | | 27,830,816 | | | | $11,579,866 | | | | 39,410,682 | |

| | | | |

Mortgage-Backed Securities | | | — | | | | 8,088,027 | | | | — | | | | 8,088,027 | |

| | | | |

Municipal Bonds | | | — | | | | 14,043,280 | | | | — | | | | 14,043,280 | |

| | | | |

U.S. Government and Agency Obligations† | | | — | | | | 33,134,807 | | | | — | | | | 33,134,807 | |

| | | | |

Foreign Government Obligations | | | — | | | | 92,943,877 | | | | — | | | | 92,943,877 | |

| | | | |

Common Stocks†† | | | $24,998,339 | | | | — | | | | — | | | | 24,998,339 | |

| | | | |

Preferred Stocks | | | | | | | | | | | | | | | | |

| | | | |

Financials | | | 10,460,145 | | | | — | | | | — | | | | 10,460,145 | |

| | | | |

Utilities | | | — | | | | 342,907 | | | | — | | | | 342,907 | |

| | | | |

Short-Term Investments | | | | | | | | | | | | | | | | |

| | | | |

Joint Repurchase Agreements | | | — | | | | 14,983,584 | | | | — | | | | 14,983,584 | |

| | | | |

U.S. Government Obligations | | | — | | | | 465,359,673 | | | | — | | | | 465,359,673 | |

| | | | |

Other Investment Companies | | | 28,903,810 | | | | — | | | | — | | | | 28,903,810 | |

| | | | | | | | | | | | | | | | |

Total Investments in Securities | | | $64,362,294 | | | | $1,739,113,533 | | | | $11,579,866 | | | | $1,815,055,693 | |

| | | | | | | | | | | | | | | | |

| † | All corporate bonds and notes and U.S. government and agency obligations held in the Fund are Level 2 securities. For a detailed breakout of corporate bonds and notes and U.S. government and agency obligations by major industry or agency classification, please refer to the Fund’s Schedule of Portfolio Investments. |

| †† | All common stocks held in the Fund are Level 1 securities. For a detailed breakout of common stocks by major industry classification, please refer to the Fund’s Schedule of Portfolio Investments. |

For the fiscal year ended December 31, 2018, there were no transfers in or out of Level 3.

The following table below is a reconciliation of investments in which significant unobservable inputs (Level 3) were used in determining fair value at December 31, 2018:

| | | | |

| | | Asset-Backed Securities |

Balance as of December 31, 2017 | | | $13,986,585 | |

| |

Accrued discounts (premiums) | | | (5,164 | ) |

| |

Realized gain (loss) | | | (12,266 | ) |

| |

Change in unrealized appreciation/depreciation | | | (270,426 | ) |

| |

Purchases | | | — | |

| |

Sales | | | (2,118,863 | ) |

| |

Transfers in to Level 3 | | | — | |

| |

Transfers out of Level 3 | | | — | |

| |

Balance as of December 31, 2018 | | | $11,579,866 | |

| | | — | |

Net change in unrealized appreciation/depreciation on investments still held at December 31, 2018 | | | $(297,033 | ) |

The Fund’s investment that is categorized as Level 3 is valued utilizing third party pricing information without adjustment (broker quote). Such valuations are based on unobservable inputs. A significant change in third party information inputs could result in a significantly lower or higher value of such Level 3 investment.

The accompanying notes are an integral part of these financial statements.

13

| | |

| | AMG Managers Loomis Sayles Bond Fund Schedule of Portfolio Investments(continued) |

| | | | |

Country | | % of Long-Term

Investments |

Australia | | | 0.0 | # |

| | |

Bermuda | | | 0.9 | |

| |

Brazil | | | 0.4 | |

| |

Canada | | | 1.1 | |

| |

Cayman Islands | | | 1.6 | |

| |

France | | | 1.4 | |

| |

Ireland | | | 0.8 | |

| |

Luxembourg | | | 2.2 | |

| |

Malaysia | | | 0.2 | |

| |

Mexico | | | 4.9 | |

| |

Netherlands | | | 2.6 | |

| |

New Zealand | | | 0.8 | |

| |

Norway | | | 0.3 | |

| |

Saudi Arabia | | | 0.4 | |

| |

South Korea | | | 0.2 | |

| |

Spain | | | 2.2 | |

| |

United Kingdom | | | 3.6 | |

| |

United States | | | 76.4 | |

| | | | |

| | | 100.0 | |

| | | | |

The accompanying notes are an integral part of these financial statements.

14

|

AMG Managers Global Income Opportunity Fund Portfolio Manager’s Comments(unaudited) |

| | | | | | | | | | | | |

THE YEAR IN REVIEW AMG Managers Global Income Opportunity Fund (Class N) (the Fund) returned -4.18% during the year ended December 31, 2018, compared with the -1.20% return for the Bloomberg Barclays Global Aggregate Bond Index. Allocation to select corporate credit sectors and issuers, including high yield bonds, were the main detractors from performance over the past 12 months. Volatile equities stemming mostly from trade dispute concerns, slowing global growth, and Federal Reserve (“Fed”) rate hikes have been mostly to blame for the increased investor uneasiness and underperformance across credit markets. Positioning among high yield credit was also negative during the “risk-off” environment. Overweight allocation to the Banking sector was a main source of negative performance during the year. In particular, U.S., U.K., and Eurozone banking issuers weighed on performance given weakness in the sector on regional and global growth concerns. Also, selections in subordinated banks and insurance detracted value as these securities underperformed seniors amid damped risk sentiment. Security selection among Emerging Markets (“EM”) hard currency issuers from Latin America also weighed on results. Geopolitical uncertainties in several key Latin American countries—Argentina, Brazil, and Mexico—led to reduced investor risk appetite. Duration and yield curve positioning was a source of positive excess returns. Curve positioning in the 5-and 10-year part of the U.S. Dollar-pay curves proved | | | | | | most beneficial. The allocation of duration into select emerging markets such as Mexico, Indonesia, Colombia, and Brazil proved beneficial. Currency and hedging also weighed on relative returns during the year. Allocation to select EM currencies such as Brazilian Real, Indonesian Rupiah, and South African Rand proved a negative source of performance as country-specific factors and global growth concerns saw most currencies depreciate against the U.S. Dollar. Overweight to the Colombian Peso was also negative as the Peso was hampered by the drop in crude oil prices. An underweight to the strong performing Japanese Yen also weighed on performance. On the other hand, underweights to the Euro, Sterling, and overweight to the Mexican Peso were moderate contributors to relative performance. LOOKING FORWARD Consensus 2019 forecasts have been revised down throughout most of the world as downside risks appear to outweigh upside supports. Our view is that we are late in the cycle—not at the end of the cycle—and while growth and profit momentum should slow, there is still opportunity for risk sentiment to recover Growth in China is still set to slow moderately. Policy statements have called for the greater use of monetary and fiscal stimulus to stabilize growth. We don’t see a broad policy easing bias, but expect increased use of targeted policy measures to offset growing downside risks from a U.S.-China tariff war. These may be insufficient to provide a meaningful knock-on boost to global growth. | | | | | | Our inflation forecasts for the world’s major economies are slightly below consensus estimates. Given the sharp decline in oil prices over the past quarter, the risk of an oil shock severely inflating prices is less likely in the near term. At the same time, growth is seemingly converging toward levels which could have more limited upward pressure on resource and wage price levels. In a November speech, Fed Chairman Powell remarked that a major risk in the U.S. economy stems from high debt levels for businesses. We agree with this assessment at this point in the credit cycle, although corporate credit fundamentals across both Europe and the U.S. remain largely stable for now and need not deteriorate soon. We do not see a catalyst for a return to the significantly tighter global credit spread levels that prevailed a year ago, but we also do not agree with the significantly above average recession risk increasingly reflected across many asset class valuations. Persistent global trade tensions and protectionist actions would provide support for the U.S. Dollar. However, the U.S. Dollar already appears expensive under many valuation models. Therefore, we believe the Dollar is likely to remain range bound over the coming months while macro risks continue to dominate headlines and global growth stabilizes. This commentary reflects the viewpoints of the portfolio manager, Loomis, Sayles & Company, as of December 31, 2018 and is not intended as a forecast or guarantee of future results. |

15

| | |

| | AMG Managers Global Income Opportunity Fund Portfolio Manager’s Comments(continued) |

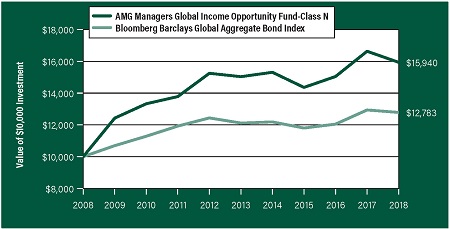

CUMULATIVE TOTAL RETURN PERFORMANCE

AMG Managers Global Income Opportunity Fund’s cumulative total return is based on the daily change in net asset value (NAV), and assumes that all dividends and distributions were reinvested. The graph compares a hypothetical $10,000 investment made in the AMG Managers Global Income Opportunity Fund’s Class N shares on December 31, 2008, to a $10,000 investment made in the Bloomberg Barclays Global Aggregate Bond Index for the same time period. The graph and table do not reflect the deduction of taxes that a shareholder would pay on a Fund distribution or redemption of shares. The listed returns for the Fund are net expenses and the returns for the index exclude expenses. Total returns would have been lower had certain expenses not been reduced.

The table below shows the average annual total returns for the AMG Managers Global Income Opportunity Fund and the Bloomberg Barclays Global Aggregate Bond Index for the same time periods ended December 31, 2018.

| | | | | | | | | | | | |

Average Annual Total Returns1 | | One Year | | | Five

Years | | | Ten Years | |

AMG Managers Global Income Opportunity Fund2, 3, 4, 5, 6,7, 8, 9 | | | | | |

Class N | | | (4.18% | ) | | | 1.18% | | | | 4.77% | |

Bloomberg Barclays Global Aggregate Bond Index10 | | | (1.20% | ) | | | 1.08% | | | | 2.49% | |

The performance data shown represents past performance. Past performance is not a guarantee of future results. Current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

Investors should carefully consider the Fund’s investment objectives, risks, charges and expenses before investing. For performance information through the most recent month end, current net asset values per share for the Fund and other information, please call 800.835.3879 or visit our website at amgfunds.com for a free prospectus. Read it carefully before investing or sending money.

Distributed by AMG Distributors, Inc., member FINRA/SIPC.

| 1 | Total return equals income yield plus share price change and assumes reinvestment of all dividends and capital gain distributions. Returns are net of fees and may reflect offsets of Fund expenses as described in the prospectus. No adjustment has been made for taxes payable by shareholders on their reinvested dividends and capital gain distributions. Returns for periods greater than one year are annualized. The listed returns on the Fund are net of expenses and based on the published NAV as of December 31, 2018. All returns are in U.S. dollars($). |

| 2 | From time to time the Fund’s advisor has waived it’s fees and/or absorbed Fund expenses, which has resulted in higher returns. |

|

3 A short-term redemption fee of 1% will be charged on shares held for less than 60 days. Effective March 1, 2019, the Fund will eliminate this redemption fee. 4 The Fund is subject to currency risk resulting from fluctuations in exchange rates that may affect the total loss or gain on a non-U.S. Dollar investment when converted back to U.S. Dollars. 5 The Fund is subject to the risks associated with investments in debt securities, such as default risk and fluctuations in the perception of the debtor’s ability to pay its creditors. Changing interest rates may adversely affect the value of an investment. An increase in interest rates typically causes the value of bonds and other fixed income securities to fall. 6 To the extent that the Fund invests in asset-backed or mortgage-backed securities, its exposure to prepayment and extension risks may be greater than investments in other fixed income securities. 7 The Fund may invest in derivatives such as foreign currency contracts, options and futures; the complexity and rapidly changing structure of derivatives markets may increase the possibility of market losses. 8 High-yield bonds (also known as “junk bonds”) may be subject to greater levels of interest rate, credit, and liquidity risk than investments in higher rated securities. These securities are considered predominantly speculative with respect to the issuer’s continuing ability to make principal and interest payments. The issuers of the Fund’s holdings may be involved in bankruptcy proceedings, reorganizations, or financial restructurings, and are not as strong financially as higher-rated issuers. |

9 Investments in international securities are subject to certain risks of overseas investing including currency fluctuations and changes in political and economic conditions, which could result in significant market fluctuations. 10 The Bloomberg Barclays Global Aggregate Bond Index provides a broad-based measure of the global investment-grade fixed income markets. The three major components of this index are the U.S. Aggregate, the Pan-European Aggregate, and the Asian-Pacific Aggregate Indices. The Index also includes Eurodollar and Euro-Yen corporate bonds, Canadian government, agency and corporate securities, and USD investment grade 144A securities. Unlike the Fund, the Bloomberg Barclays Global Aggregate Bond Index is unmanaged, is not available for investment and does not incur expenses. |

| |

Not FDIC insured, nor bank guaranteed. May lose value |

16

|

AMG Managers Global Income Opportunity Fund Fund Snapshots(unaudited) December 31, 2018 |

|

PORTFOLIO BREAKDOWN

| | | | | |

Category | | % of Net Assets |

Corporate Bonds and Notes | | | | 53.9 | |

| | |

Foreign Government Obligations | | | | 42.4 | |

| | |

U.S. Government and Agency Obligations | | | | 6.1 | |

| | |

Asset-Backed Securities | | | | 0.7 | |

| | |

Short-Term Investments | | | | 0.8 | |

| | |

Other Assets Less Liabilities | | | | (3.9 | ) |

| | | | | |

Rating | | % of Market Value1 |

U.S. Government and Agency Obligations | | | | 6.0 | |

| | |

Aaa | | | | 7.5 | |

| | |

Aa | | | | 11.1 | |

| | |

A | | | | 17.5 | |

| | |

Baa | | | | 45.6 | |

| | |

Ba | | | | 8.0 | |

| | |

B | | | | 3.1 | |

| | |

N/R | | | | 1.2 | |

| 1 | Includes market value of fixed-income securities only. |

TOP TEN HOLDINGS

| | | | |

Security Name | | % of

Net Assets |

French Republic Government Bond OAT, 4.250%, 10/25/23 (France) | | | 5.9 | |

| | |

Indonesia Treasury Bonds, Series FR53, 8.250%, 07/15/21 (Indonesia) | | | 3.4 | |

| | |

South Africa Government Bond, Series R213, 7.000%, 02/28/31 (South Africa) | | | 2.9 | |

| | |

U.S. Treasury Notes, 2.875%, 08/15/28 | | | 2.8 | |

| | |

Corp. Nacional del Cobre de Chile, 4.500%, 09/16/25 (Chile) | | | 2.4 | |

| | |

New South Wales Treasury Corp., Bonds, Series 22, 6.000%, 03/01/22 (Australia) | | | 2.3 | |

| | |

Kinder Morgan Energy Partners, LP, 4.250%, 09/01/24 | | | 2.1 | |

| | |