Pamela M. Krill

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. s 3507.

Table of Contents

| | Page |

| Management’s Discussion of Fund Performance | |

| Economic Overview | 2 |

| Outlook | 2 |

| Conservative Allocation Fund | 3 |

| Moderate Allocation Fund | 4 |

| Aggressive Allocation Fund | 6 |

| Bond Fund | 7 |

| High Income Fund | 9 |

| Diversified Income Fund | 11 |

| Large Cap Value Fund | 13 |

| Large Cap Growth Fund | 14 |

| Mid Cap Value Fund | 16 |

| Mid Cap Growth Fund | 17 |

| Small Cap Value Fund | 19 |

| Small Cap Growth Fund | 21 |

| Global Securities Fund | 22 |

| International Stock Fund | 24 |

| Target Retirement 2020 Fund | 26 |

| Target Retirement 2030 Fund | 28 |

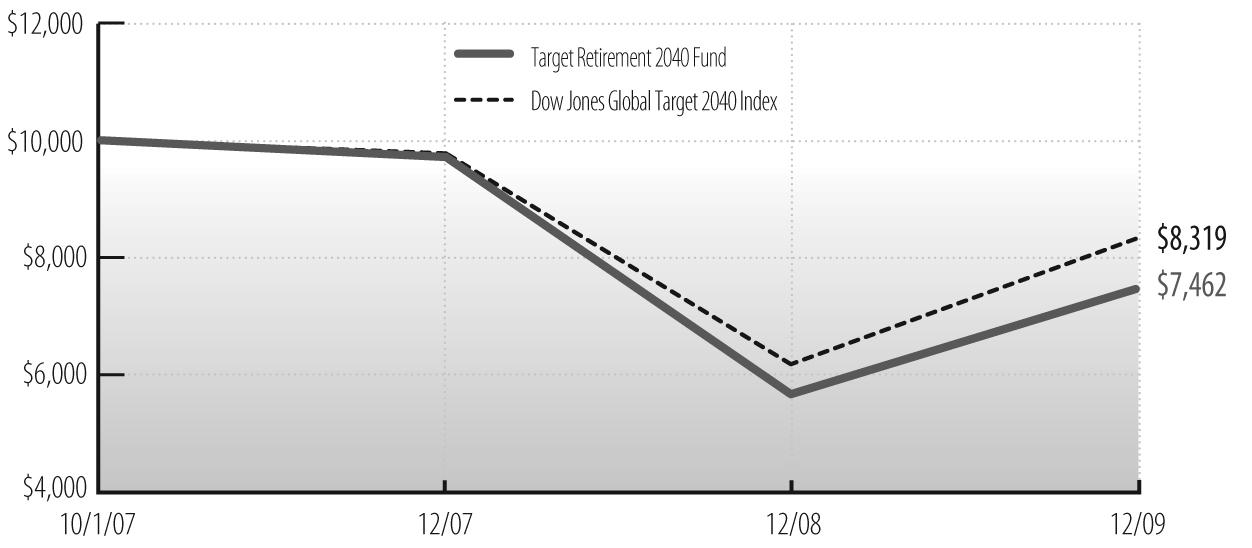

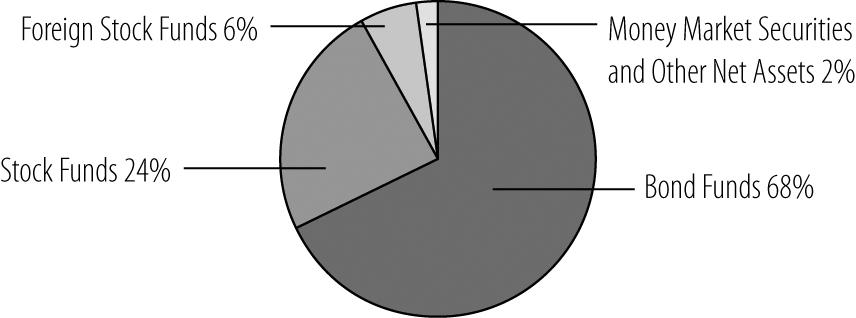

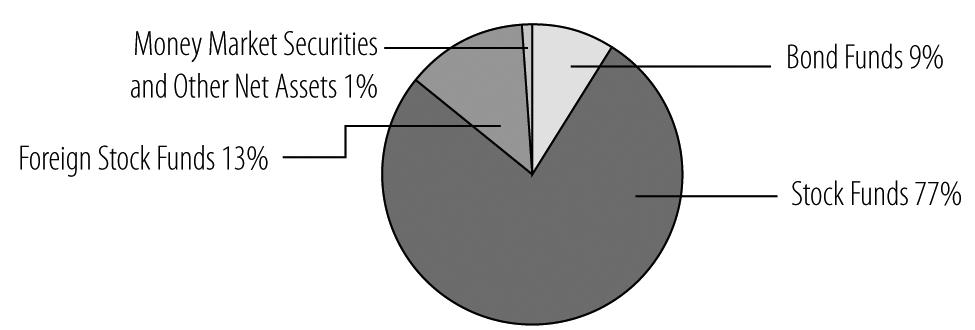

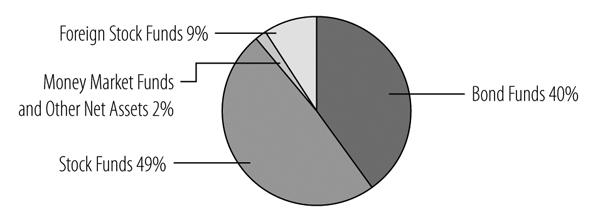

| Target Retirement 2040 Fund | 29 |

| Notes to Management’s Discussion of Fund Performance | 32 |

| Portfolios of Investments | |

| Conservative Allocation Fund | 34 |

| Moderate Allocation Fund | 35 |

| Aggressive Allocation Fund | 36 |

| Money Market Fund | 37 |

| Bond Fund | 38 |

| High Income Fund | 42 |

| Diversified Income Fund | 47 |

| Large Cap Value Fund | 51 |

| Large Cap Growth Fund | 53 |

| Mid Cap Value Fund | 55 |

| Mid Cap Growth Fund | 57 |

| Small Cap Value Fund | 59 |

| Small Cap Growth Fund | 61 |

| Global Securities Fund | 63 |

| International Stock Fund | 65 |

| Target Retirement 2020 Fund | 67 |

| Target Retirement 2030 Fund | 68 |

| Target Retirement 2040 Fund | 69 |

| Financial Statements | |

| Statements of Assets and Liabilities | 70 |

| Statements of Operations | 74 |

| Statements of Changes in Net Assets | 78 |

| Financial Highlights | 84 |

| Notes to Financial Statements | 102 |

| Report of Independent Registered Public Accounting Firm | 119 |

| Other Information | 120 |

| Trustees and Officers | 122 |

Nondeposit investment products are not federally insured, involve investment risk, may lose value and are not obligations of or guaranteed by any financial institution. For more complete information about Ultra Series Fund, including charges and expenses, request a prospectus from your financial advisor or from CUNA Mutual Insurance Society, 2000 Heritage Way, Waverly, IA 50677. Consider the investment objectives, risks, and charges and expenses of any fund carefully before investing. The prospectus contains this and other information about the investment company. For more current Ultra Series Fund performance information, please call 1-800-670-3600. Current performance may be lower or higher than the performance data quoted within. Past performance does not guarantee future results. Nothing in this report represents a recommendation of a security by the investment adviser. Portfolio holdings may have changed since the date of this report.

Management’s Discussion of Fund Performance

REVIEW OF PERIOD

With a sense of relief, U.S. equity markets ended the year in much better form than they began. Following the deep market losses of 2008, the first months of 2009 saw further market decline as we endured a severe recession, which some were characterizing as the start of a new depression. Housing was in disarray, the auto market had serious problems, unemployment was rising and the credit markets were deteriorating. There was widespread fear that the major banks would be nationalized and by early March, these factors had driven the market down by some 25% on top of the severe drop of 2008. In response, the government and Federal Reserve instituted an unprecedented stimulus campaign. The Fed lowered rates to close to zero and in February, a $787 billion stimulus package was signed into law. Over the course of the year, the government continued to introduce incentives to boost the economy, including the highly publicized car trade-in program, "Cash for Clunkers," and an $8,000 tax incentive for first-time home buyers.

The global economic crisis seen in early 2009 sparked governments and central banks around the world to follow the U.S.’s lead in producing unprecedented monetary and fiscal action to ease liquidity, unclog credit markets, ensure financial stability and stimulate domestic demand. As we progressed through 2009, global economic data indicated continued improvement in the underlying fundamentals of the worldwide economy.

The global stimulus and upticks in leading economic indicators powered a sizable recovery in stock markets around the world, producing a record rally in a very short time. The massive government stimuli helped unfreeze the credit markets and produced a consensus that economic recovery was underway. In early March, market psychology shifted from fear to optimism, and as the markets rallied, some would say hyper-optimism. Even though domestic unemployment remained stubborn, peaking at 10.2% in October, the highest level in 26 years, the S&P 500 managed a very strong 26.5% return in 2009 with a 6.0% boost coming in the fourth quarter.

Sector leadership in the domestic stock markets was led by cyclical, economically sensitive sectors, such as Technology, Consumer Discretionary and Materials. The exception was strong performance from the traditionally defensive Health Care Sector which rebounded as health care reform initiatives appeared less onerous than expected. Telecommunications was the lagging sector, followed by Utilities and Energy. The appetite for risk was clearly apparent in the outperformance of lower-quality stocks over higher-quality and emerging markets over developed. In terms of company size, the rally was broad across capitalization ranges, with mid-cap stocks leading both small and large stock.

Despite the tremendous rally in the stock market, investors still seemed leery of the stock market losses of 2008 and early 2009 and based on mutual fund flows, sent most of their money into bond funds. In a reversal of 2008, when a flight to safety rewarded investors in the most conservative bonds, 2009 produced a strong disparity of returns favoring lower-quality and riskier bonds. While Treasuries were the top-performing bond class in fear-filled 2008, they were the laggards in 2009, with the Barclay’s Treasury Index falling -3.6% in 2009 after a 13.7% rise in 2008. Low quality bonds rallied along with stocks beginning in March, with high-yield or "junk bonds" having a banner year.

OUTLOOK

With 2009 providing a turning point in the stock market and economy, our outlook for 2010 is optimistic, although tempered by the fact that the market has already enjoyed such a strong recovery. We expect the economy to improve in 2010, especially internationally. Corporate profitability should continue to expand behind solid margins, productivity gains and improving revenue growth. Even though interest rates may move upward, they should remain at a relatively low level, which is positive for valuations. We also see substantial assets still in cash and lower yielding bonds which could come back into the stock market and provide support. Although deep recessions, such as the one we have recently experienced, are historically followed by steep recoveries, we believe the current recovery will likely be slower than history might suggest due to some lingering headwinds.

Management’s Discussion of Fund Performance

High unemployment, stagnant wage growth and the prospect of higher taxes are causing consumers to save more and spend less, crimping a key economic driver. Additionally, the financial system, while recovering, remains wounded as does the housing market. In general, we expect economic growth to be moderately positive but below the long-term trend line of 3-4%.

The explosive stock market rally from the March 2009 lows was focused on lower quality and economically sensitive areas with the expectation that the economy would bounce back. This is characteristic of the first leg of a recovery. As we move to the next leg, the market should take its direction from actual signs of improving economic and company fundamentals.

In terms of bonds, our bigger concern looking forward is with the seemingly endless growth of government deficit spending, and with it the rapid increase in Treasury debt issuance. With foreign investors pulling back on their dollar-denominated investments, where will the capital come from to finance this debt? It seems that interest rates must eventually rise to continue attracting capital. There seems to be three ways out: responsible fiscal policy, inflation and/or dollar-devaluation. In any case, we would caution bond investors to have modest total return expectations over the next annual period.

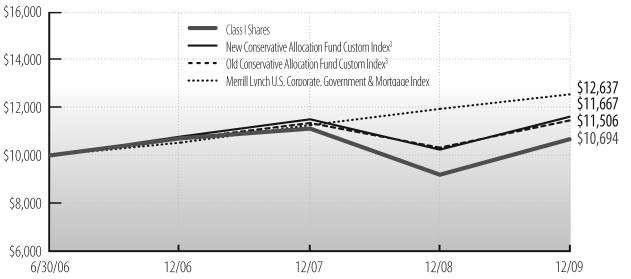

CONSERVATIVE ALLOCATION FUND

How did the fund perform for the period January 1, 2009 – December 31, 2009?

For the trailing year ended December 31, 2009, the Ultra Series Conservative Allocation Fund returned 16.76% (Class I shares), outperforming the New Conservative Allocation Custom Fund Index return of 13.86% and the Old Conservative Allocation Custom Index return of 11.37%. Exceptional returns in a number of the fund’s equity holdings as well as an equity-like return from our high yield bond allocation accounted for the outperformance versus the index.

What significant changes did you make to the portfolio since January 1, 2009?

When we assessed potential market opportunities in early 2009, we were drawn to the corporate bond market. During the height of the financial crisis, yield spreads, the difference in yield between corporate bonds and US Treasuries, reached historical levels. By the start of 2009, it was increasingly clear to us that these elevated yield spreads had created a unique opportunity in both investment grade and high yield bonds. To capitalize on this attractive circumstance, we added Dodge & Cox Income Fund to the portfolio during the first quarter. At the time, Dodge & Cox held one of the largest allocations to corporate bonds among active core bond managers. We also slightly increased our allocation to our high yield bond fund. For the calendar year, Dodge & Cox Income Fund returned 16.1%, far exceeding the return of 5.9% on the Barclays U.S. Aggregate Bond Index. High yield bonds proved even more rewarding, and the MEMBERS High Income Fund Class Y returned 31.5% for the year.

We also wound down and then eliminated the fund’s mid cap holding during the fourth quarter. Mid cap stocks led the equity markets off the March lows and we took the opportunity to pare back our exposure, as small to mid size stocks appeared overvalued. The proceeds from the mid cap sale were used to increase the fund’s fixed income holdings. Additionally, the fund’s international equity position was reduced in favor of U.S. large cap equities. Among equities, high quality U.S. mega caps, which derive a large amount of their revenue from multinational and overseas operations, potentially offer an attractive and relatively lower risk alternative to international stocks in the near term.

What were the strongest contributors to fund performance?

In addition to the strong returns from investment grade and high yield bonds, the fund was boosted by solid performance from a pair of the fund’s large cap equity holdings. The Fairholme Fund returned 39.0% for the year and MEMBERS Large Cap Growth Fund Class Y returned 38.0%. The fund’s relative overweight allocation to growth and position in the MEMBERS Large Cap Growth Fund Class Y also contributed significantly as growth outperformed value by a wide margin for the year. In comparison, the fund’s value holding, MEMBERS Large Cap Value Fund Class Y, returned 16.3% for the year.

Management’s Discussion of Fund Performance

CONSERVATIVE ALLOCATION FUND (continued)

What were the largest constraints on performance?

The fund was held back by underperformance from our largest holding, MEMBERS Bond Fund Class Y. The high quality positioning of MEMBERS Bond Fund Class Y that served investors so well in 2008 was out of favor in 2009 and the Bond Fund finished the year with a return of 3.1%. The other noteworthy constraint was our modest position in Nakoma Absolute Return Fund, which returned -9.1% for the year.

Cumulative Performance of $10,000 Investment Since Inception1,2

Average Annual Total Return through December 31, 20091 |

| | | | | |

| Class I Shares | 16.76% | -0.12% | 1.93% | — |

| Class II Shares | — | — | — | 14.91% |

New Conservative Allocation Fund Custom Index3 | 13.86 | 2.57 | 4.49 | 13.88 |

Old Conservative Allocation Fund Custom Index3 | 11.37 | 2.45 | 4.08 | 11.29 |

| Merrill Lynch U.S. Corporate, Government & Mortgage Index | 5.24 | 6.20 | 6.90 | 4.96 |

See accompanying Notes to Management’s Discussion of Fund Performance.

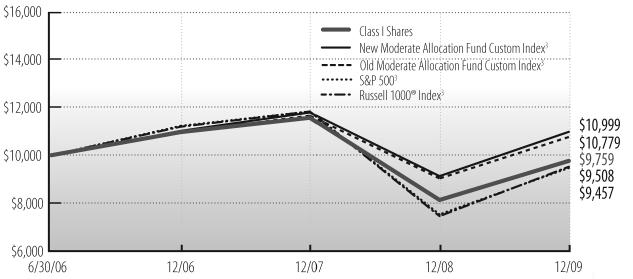

MODERATE ALLOCATION FUND

How did the fund perform for the period January 1, 2009 – December 31, 2009?

For the trailing year ended December 31, 2009, the Ultra Series Moderate Allocation Fund returned 20.61% (Class I shares), in line with the New Moderate Allocation Custom Fund Index return of 20.74% and outperforming the Old Moderate Allocation Custom Fund Index return of 19.63%. Strong returns from a number of our holdings were modestly offset by disappointing returns in both our core bond and large cap value funds and accounted for the slight underperformance. In addition, the fund’s focus on risk management and striving for more consistent returns through higher-quality investments constrained performance in general as low-quality investments led the market.

What significant changes did you make to the portfolio since January 1, 2009?

When we assessed potential market opportunities in early 2009, we were drawn to the corporate bond market. During the height of the financial crisis, yield spreads, the difference in yield between corporate bonds and U.S. Treasuries, reached historical levels. By the start of 2009, it was increasingly clear to us that these elevated yield spreads had created a unique opportunity in both

Management’s Discussion of Fund Performance

MODERATE ALLOCATION FUND (continued)

investment grade and high yield bonds. To capitalize on this attractive circumstance, we added the Dodge & Cox Income Fund to the portfolio during the first quarter. At the time, Dodge & Cox Income Fund held one of the largest allocations to corporate bonds among active core bond managers. We also slightly increased our allocation to our high yield bond fund. For the calendar year, Dodge & Cox Income Fund returned 16.1%, far exceeding the return of 5.9% on the Barclays U.S. Aggregate Bond Index. High yield bonds proved even more rewarding and the MEMBERS High Income Fund Class Y returned 31.5% for the year.

We also reduced the fund’s U.S. small and mid cap holdings during the fourth quarter. Smaller cap stocks led the equity markets off the March lows and we took the opportunity to pare back our exposure, as small to mid size stocks appeared overvalued. The reduction in small and mid caps was used to slightly increase the fund’s fixed income positions. Additionally, the fund’s international equity position was reduced in favor of U.S. large cap equities. Among equities, high quality U.S. mega caps, which derive a large amount of their revenue from multinational and overseas operations, potentially offer an attractive and relatively lower risk alternative to international stocks in the near term.

What were the strongest contributors to fund performance?

Solid performance from a pair of the fund’s large cap equity holdings were the strongest contributors to performance. The Fairholme Fund returned 39.0% for the year and MEMBERS Large Cap Growth Fund Class Y returned 38.0%. The fund’s relative overweight allocation to growth and position in the MEMBERS Large Cap Growth Fund Class Y also contributed significantly, as growth outperformed value by a wide margin for the year. In comparison, the fund’s value holding, MEMBERS Large Cap Value Fund Class Y, returned 16.3% for the year.

What were the largest constraints on performance?

The fund was held back by underperformance from our core bond position, MEMBERS Bond Fund Class Y, and our large cap value fund, MEMBERS Large Cap Value Fund Class Y. The high quality positioning of MEMBERS Bond Fund Class Y that served investors so well in 2008 was out of favor in 2009, and the Bond Fund finished the year with a return of 3.1%. Additionally, even though the decision to underweight our position in the MEMBERS Large Cap Value Fund Class Y proved correct, its 16.3% return was a detriment to 2009 performance.

Cumulative Performance of $10,000 Investment Since Inception1,2

Management’s Discussion of Fund Performance

MODERATE ALLOCATION FUND (continued)

Average Annual Total Return through December 31, 20091 |

| | | | | |

| Class I Shares | 20.61% | -3.87% | -0.69% | — |

| Class II Shares | — | — | — | 18.82% |

New Moderate Allocation Fund Custom Index3 | 20.74 | -0.12 | 2.75 | 21.39 |

Old Moderate Allocation Fund Custom Index3 | 19.63 | -0.60 | 2.16 | 20.21 |

S&P 500 Index3 | 26.46 | -5.63 | -1.58 | 29.70 |

Russell 1000¨ Index3 | 28.43 | -5.36 | -1.43 | 30.25 |

See accompanying Notes to Management’s Discussion of Fund Performance.

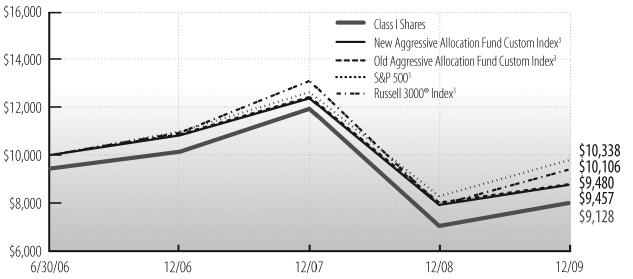

AGGRESSIVE ALLOCATION FUND

How did the fund perform for the period January 1, 2009 – December 31, 2009?

For the trailing year ended December 31, 2009, the Ultra Series Aggressive Allocation Fund returned 27.91% (Class I shares), nicely ahead of the S&P 500 Index return of 26.46% and slightly underperforming the New Aggressive Allocation Fund Custom Index return of 28.21% and the Old Aggressive Allocation Fund Custom Index return of 34.30%. Disappointing returns from the fund’s large value and international stock fund allocations accounted for the underperformance. In addition, the fund’s focus on risk management and striving for more consistent returns through higher-quality investments constrained performance in general as low-quality investments led the market.

What significant changes did you make to the portfolio since January 1, 2009?

During the fourth quarter, we reduced the fund’s U.S. small and mid cap holdings. Smaller cap stocks led the equity markets off the March lows and we took the opportunity to pare back our exposure, as small to mid size stocks appeared overvalued. The reduction in small and mid caps was used to slightly increase the fund’s fixed income and alternative asset class positions. Additionally, the fund’s international equity position was reduced in favor of U.S. large cap equities. Among equities, high quality U.S. mega caps, which derive a large amount of their revenue from multinational and overseas operations, potentially offer an attractive and relatively lower risk alternative to international stocks in the near term.

Finally, in late December, we initiated a position in T. Rowe Price New Era Fund, an active energy and natural resources fund. While we believe that emerging markets offer the greatest growth potential in the global economy, we feel emerging market stocks have become overbought with the MSCI Emerging Markets Index gaining over 100% since the market rally began in early March. Our research shows that the correlation between emerging markets and energy/natural resources has risen dramatically over the past ten years. As China, India, Brazil, and the rest of the emerging world has grown, so has their demand for energy and natural resources, and we believe this trend will continue to put upward pressure on commodity based stocks. Energy and natural resources equities appear to offer similar returns with lower volatility. Thus we view the addition of the T. Rowe Price New Era Fund as a way to participate in the growth of the emerging markets with less downside risk than owning emerging markets stocks directly at current market levels.

What were the strongest contributors to fund performance?

Solid performance from a pair of the fund’s large cap equity holdings were the strongest contributors to performance. The Fairholme Fund was up 39.0% for the year and MEMBERS Large Cap Growth Fund Class Y returned 38.0%. The fund’s relative overweight allocation to growth and position in the MEMBERS Large Cap Growth Fund Class Y also contributed significantly as growth outperformed value by a wide margin for the year. In comparison, the fund’s value holding, MEMBERS Large Cap Value

Management’s Discussion of Fund Performance

AGGRESSIVE ALLOCATION FUND (continued)

Fund Class Y, returned 16.3% for the year. Finally, MEMBERS Mid Cap Growth Fund Class Y’s 46.7% return contributed positively to the fund’s return.

What were the largest constraints on performance?

The fund was held back by underperformance from two of the fund’s largest holdings, MEMBERS Large Cap Value Fund Class Y and MEMBERS International Stock Fund Class Y. As mentioned above, value stocks underperformed growth in 2009 and the MEMBERS Large Cap Value Fund Class Y’s 16.3% return, while quite good in absolute terms, detracted from relative performance in a year where the S&P 500 Index was up 26.5%. MEMBERS International Stock Fund Class Y also had a challenging year in relation to the MSCI EAFE Index, as that fund returned 26.2% in comparison to the 31.8% return of the index. Finally, Gateway Fund was a significant laggard finishing 2009 with a 6.8% return.

Cumulative Performance of $10,000 Investment Since Inception1,2

Average Annual Total Return through December 31, 20091 |

| | | | | |

| Class I Shares | 27.91% | -6.73% | -2.57% | — |

| Class II Shares | — | — | — | 25.09% |

New Aggressive Allocation Fund Custom Index3 | 28.21 | -2.95 | 0.95 | 29.93 |

Old Aggressive Allocation Fund Custom Index3 | 34.30 | -4.12 | 0.30 | 34.66 |

S&P 500 Index3 | 26.46 | -5.63 | -1.58 | 29.70 |

Russell 3000¨ Index3 | 28.34 | -5.42 | -1.51 | 30.19 |

See accompanying Notes to Management’s Discussion of Fund Performance.

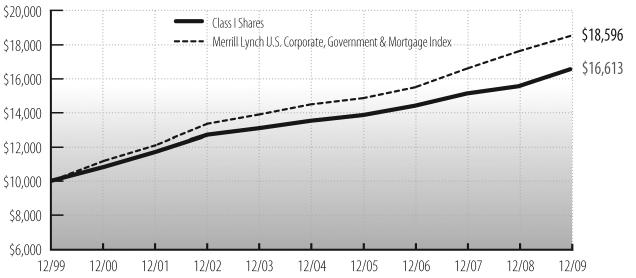

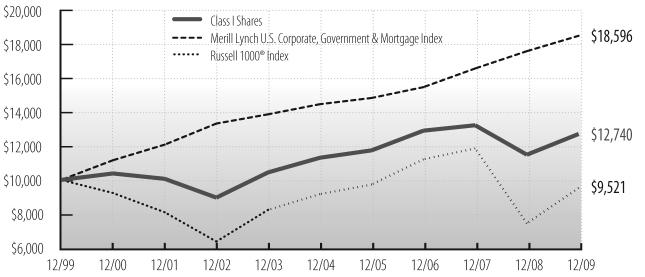

BOND FUND

How did the fund perform for the period January 1, 2009 – December 31, 2009?

For the trailing year ended December 31, 2009, the Ultra Series Bond Fund returned 6.50% (Class I shares), while the Merrill Lynch U.S. Corporate, Government & Mortgage Index returned 5.24%.

Management’s Discussion of Fund Performance

BOND FUND (continued)

What were the strongest contributors to fund performance?

The fund benefited from a modest overweight in corporate bonds with securities rated below A posting the largest gains following the sharp declines in 2008. The fund also benefited from a slightly lower duration (interest rate exposure) in a generally rising rate environment. Finally, the fund benefited from good security selection and a modest exposure to asset backed securities.

What were the largest constraints on performance?

Performance was hurt to a modest degree by less exposure to the financial sector of corporate bonds versus the index and an underexposure to residential mortgage backed securities during a period when the Federal Reserve was a massive purchaser of these securities.

How is the fund positioned going forward?

The fund is positioned for a volatile environment in 2010 given the numerous policy issues that are open to question. We expect interest rates to rise during the course of the year. The combination of very large Treasury issuance by the government and the possibility the Fed will commence raising short rates later in the year suggests a defensive posture is prudent. Given the Fed plans to curtail its purchases of mortgage securities by March 31, we expect to maintain an underweight position in this sector at least in the near term as it seems artificially rich due to the Fed’s current support. Also in the near term we expect to be somewhat neutral in the corporate sector until we have a clearer view of the trend in economic activity.

Cumulative Performance of $10,000 Investment Since Inception1

Average Annual Total Return through December 31, 20091 |

| | | | | | |

| Class I Shares | 6.50% | 4.79% | 4.18% | 5.21% | — |

| Class II Shares | — | — | — | — | 5.55% |

| Merrill Lynch U.S. Corporate, Government & Mortgage Index | 5.24 | 6.20 | 5.09 | 6.40 | 4.96 |

See accompanying Notes to Management’s Discussion of Fund Performance.

Management’s Discussion of Fund Performance

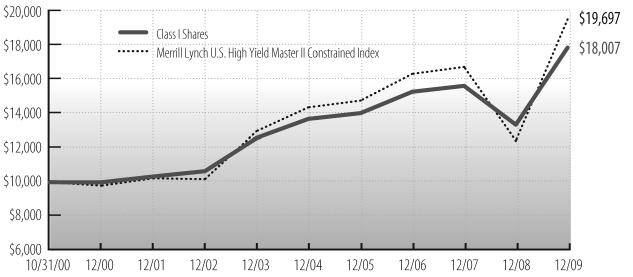

HIGH INCOME FUND

Shenkman Capital Management, Inc. - Subadviser

What a difference a year makes. In December 2008, the high yield market had just experienced its worst performance year on record with a decline of 26%. At that time, investors were feeling the hangover effects of a risk taking party that had endured for several years; there was severe apprehension with respect to the U.S. economic outlook, and risk premiums for investing in high yield were at unprecedented high levels. As we fast forward twelve months to December 2009, the high yield market has just completed its best performance year on record with an annual performance of 58.10% and risk premiums are rapidly approaching historical average levels. Indeed, never has the saying "what a difference a year makes" been so apt.

One of the most significant factors impacting all U.S. financial markets in 2009 was the dramatic turnaround in the ability for companies to access the credit markets. At the beginning of the year, some pundits questioned not only when, but also if the U.S. credit markets would ever attain the previous levels of normal activity. This concern was especially acute for high yield companies as their lower credit quality and the investor’s risk aversion appeared to be problematic. Yet, by year end 2009, the final tally showed that high yield companies issued the most securities on record as $160 billion of paper cleared the market. The preponderance of this new issuance was strictly for refinancing, much of it came with very attractive yield premiums, and the overall structure of the issuance was significantly superior to the vintages of 2006-2008. More importantly, the ability for companies to access capital, waive covenants, and extend maturities steadily diminished the universe of prospective defaulting issuers. With this prospect of lower default expectations, high yield spreads continued to ratchet down and the high yield market posted gains. These gains led to further inflows into high yield which allowed for further capital to be extended to high yield issuers. This virtuous cycle was in effect consistent for every month from March through December 2009. This dynamic of factors (i.e., attractive yields, favorable structures, and rapidly declining default expectations), combined to create an extremely favorable environment for high yield investors and spurred the record performance for the sector.

A key driver for high yield was the near record inflows into high yield mutual funds, as approximately $31 billion flowed into the market. Equally impressive was how steady this demand was throughout the balance of the year. Even after the significant market rally in the second and third quarters, inflows continued to be steady in the fourth quarter.

In fact, the dynamics for high yield during the fourth quarter were generally similar to trends that persisted for much of the year. That is, high yield outperformed most other asset sectors, lower quality securities outperformed demand for high yield (as measured by mutual fund inflows), new issue supply was robust, yield premiums (spreads) tightened, and the volume of high yield defaults continued to grind lower.

During the fourth quarter of 2009, the high yield market, as measured by the Merrill Lynch High Yield Master II Constrained Index, was one of the best performing sectors compared to both fixed income and equity markets as the average high yield index gained 6.0% in the fourth quarter. This strong performance bested other fixed income sectors such as 10-year Treasuries, investment grade debt, and emerging market debt which posted fourth quarter returns of negative 3.5%, 1.2% and 1.5%, respectively. High yield’s fourth quarter returns also beat many equity sectors as the S&P and Russell 2000 generated returns of 6.0% and 3.9% for the quarter, respectively.

How did the fund perform for the period January 1, 2009 – December 31, 2009?

For the trailing year ended December 31, 2009, the Ultra Series High Income Fund returned 34.29% (Class I shares), underperforming the Merrill Lynch U.S. High Yield Master II Constrained Index return of 58.10%. Consistent with fund’s performance for every quarter during the year, the 2009 return was solid on an absolute basis, but lagged on a relative basis. Since our goal is to preserve capital in down markets, achieve solid returns in up markets, and limit risk as measured by security price

Management’s Discussion of Fund Performance

HIGH INCOME FUND (continued)

volatility and defaults, we believe the fund has performed well. For example, for the combined period 2008 and 2009, the fund generated a return of 16.39% as compared to a return of 6.38% for the Lipper High Yield Index (30 Largest Mutual Funds). An alternative way of looking at this two year performance for the fund is to analyze the fund’s capture ratio for down and up markets. Our goal is to minimize our participation in down markets and maximize participation in up markets. As measured by Lipper, the average high yield mutual fund captured 101% of the market’s downside in 2008’s worst yearly performance on record, and the average high yield mutual fund captured only 78% of the market’s record up year in 2009; resulting in a combined cumulative 6.6% performance for the two year period. By comparison, the Ultra Series High Income Fund participated in only 50% of the market’s record downdraft in 2008 and captured 61% of the market’s record upside in 2009, resulting in a combined two-year cumulative performance of 16.39%.

What were the strongest contributors and largest constraints to fund performance?

Discounted bonds (i.e., bonds priced below $70) were the best performing sector for the overall high yield market during the year, returning more than 194%. The fund’s underweight position in these securities detracted from relative returns for the period. CCC rated bonds were the best performing rating sector for the year, and the fund’s underweight position in these securities also hurt relative returns in 2009. Additionally, the Financial Sector was the top performing sector for the year, and the fund’s strategic underweighting in this sector negatively contributed to relative performance for the reporting period. Lastly, although the fund’s out-of-index positions in convertible bonds positively contributed to returns, this did not offset the underperformance described above.

How is the fund positioned going forward?

Given that the high yield sector’s 2009 performance was so strong, it is only natural to question if there is any gas in the tank for 2010. The initial reaction may be that a near 60% return for any fixed income sector is a sign of a bubble and that danger awaits the greedy. However, we believe it is more important to evaluate current valuations as opposed to how far the market has run over the past 12 months. Specifically, yield spreads as of December 31, 2009 are at 634 basis points which is slightly above historical averages and well above the spread levels typically experienced in a positive credit cycle. Moreover, trailing twelve month default rates are forecast to drop precipitously over the next twelve months and end 2010 below historical averages. For pessimists who argue that high yield cannot post a good year following a great year of performance, history would suggest otherwise. For example, the high yield market followed its previous record year 39.2% return in 1991 with an impressive 17.4% return in 1992; similarly, the high yield market posted a 10.9% return in 2004 following the 28.1% return of 2003. We clearly recognize that 2009’s 58% return is in unchartered territory, but the 26.1% decline in 2008 was also unprecedented. We believe high yield can still post above average returns over the next twelve months as long as the U.S. economy continues to gradually heal. Also supporting our positive outlook is our belief that overall interest rates should remain muted over the balance of 2010 as the Federal Reserve is more focused on achieving sustainable recovery rather than being overly concerned with the prospect of an over stimulated economy. In effect, we expect a gradual increase in interest rates as opposed to a sharp rise over the balance of 2010. Given this relatively low yield environment, we believe demand will remain strong for the incremental yield that high yield offers.

Management’s Discussion of Fund Performance

HIGH INCOME FUND (continued)

Cumulative Performance of $10,000 Investment Since Inception1

Average Annual Total Return through December 31, 20091 |

| | | | | | |

| Class I Shares | 34.29% | 5.41% | 5.54% | 6.62% | — |

| Class II Shares | — | — | — | — | 17.49% |

| Merrill Lynch U.S. High Yield Master II Constrained Index | 58.10 | 6.20 | 6.40 | 7.67 | 34.61 |

See accompanying Notes to Management’s Discussion of Fund Performance.

DIVERSIFIED INCOME FUND

How did the fund perform for the period January 1, 2009-December 31, 2009?

For the trailing year ended December 31, 2009, the Ultra Series Diversified Income Fund returned 10.74% (Class I shares) compared to the Russell 1000¨ Index return of 28.43% and the Merrill Lynch U.S. Corporate, Government & Mortgage Index return of 5.24%.

For the equity portion of the fund, good stock selection in the Consumer Staples Sector, along with positive allocation in the Industrials Sector partially offset poor stock selection across the Financials, Information Technology, and Consumer Discretionary Sectors. In addition, underweight positions in the Financials and Information Technology Sectors hurt returns relative to the Russell 1000¨ Index.

What significant changes did you make to the portfolio since January 1, 2009?

Throughout the year we reduced the number of stock holdings in the fund from 61 to 52, reflecting our desire to hold larger positions in stocks of companies in which we have higher conviction. During 2009 we reduced our position in Financials from 19% to 12% of the equity portion of the portfolio, and Health Care from 20% to 15%. We also increased sector weights in Industrials from 11% to 17%, Consumer Staples from 12% to 15%, and Information Technology from 4% to 7%. The fund continues to have a bias towards higher quality, higher dividend-paying companies. The bond portion of the fund modestly reduced duration and thus interest rate exposure during the course of the year. Sector allocations remained relatively constant with minor variations due to maturing securities.

Management’s Discussion of Fund Performance

DIVERSIFIED INCOME FUND (continued)

What were the strongest contributors to fund performance?

Within the equity segment of the fund, we found many good values within the Consumer Staples and Industrials Sectors and held overweight positions relative to the Russell 1000¨ Index in these sectors. In addition, stock selection within the Consumer Staples Sector was quite positive. On an individual holdings basis, the fund’s strongest stock contributors for the twelve month period included Wyeth, Procter & Gamble Company, Intel Corp, and Tyco International Ltd. In addition, not owning index-holding Exxon Mobil Corp as its shares fell over 12% aided relative performance.

The bond portion of the fund is oriented toward the generation of income. Consequently, it held a significant overweight position in corporate credit, particularly industrial and utility securities. Within that context, it was also significantly overweighted ‘BBB’ rated securities. Overall corporate securities earned 19.8% in 2009 while those rated ‘BBB’ earned 31.4%. This compares to a - -3.2% return for Treasury securities.

What were the largest constraints on performance?

For the equity segment of the fund, our conservative stock selection helped early in 2009, but was a detractor from relative performance for the entire year. During the period, U.S. stocks experienced a cascade of dividend reductions, unlike anything seen since the depression of the 1930s. For the equity portion of the fund, we chose to protect the fund’s income stream in a move that turned out to be more costly relative to Russell 1000¨ Index returns than we anticipated. We replaced many of our financial stocks that reduced their dividend payouts with higher yielding stocks. The financial stocks we sold subsequently rebounded sharply in price. Detracting from performance within the equity segment of the fund on an individual basis included holdings of JPMorgan Chase & Co., Bank of America Corp, US Bancorp, and General Electric Co.

The bond portion of the fund was very modestly hurt by an underexposure to mortgage backed securities at a time when the Fed was purchasing them and a 2% relative underweight position in Banks.

How is the fund positioned going forward?

We think the outlook for companies with strong balance sheets, stable cash flow, and attractive dividend yield is very positive. These stocks have lagged the recent market surge and are likely to move higher over the next few years. Additionally, we expect the fund should continue to be positioned to have a higher yield than the overall market in order to meet the objective of earning income while not taking undue risks.

Cumulative Performance of $10,000 Investment Since Inception1

Management’s Discussion of Fund Performance

DIVERSIFIED INCOME FUND (continued)

Average Annual Total Return through December 31, 20091 |

| | | | | | |

| Class I Shares | 10.74% | -0.51% | 2.39% | 2.45% | — |

| Class II Shares | — | — | — | — | 14.43% |

| Russell 1000¨ Index | 28.43 | -5.36 | 0.79 | -0.49 | 30.25 |

| Merrill Lynch U.S. Corporate, Government & Mortgage Index | 5.24 | 6.20 | 5.09 | 6.40 | 4.96 |

See accompanying Notes to Management’s Discussion of Fund Performance.

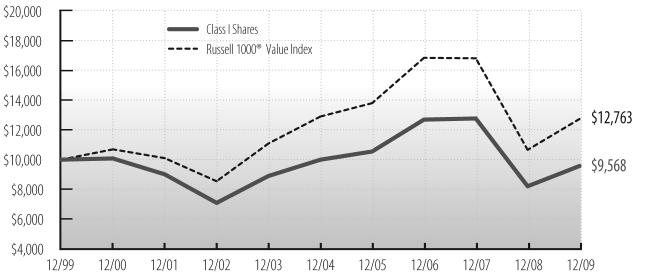

LARGE CAP VALUE FUND

How did the fund perform for the period January 1, 2009 – December 31, 2009?

For the trailing year ended December 31, 2009, the Ultra Series Large Cap Value Fund returned 16.79% (Class I shares), lagging the Russell¨ 1000 Value Index return of 19.69%. Good stock selection in the Health Care Sector, along with positive allocation in the Information Technology Sector partially offset poor stock selection in the Consumer Discretionary, Telecommunication Services, and Consumer Staples Sectors. In addition, our underweight position in the Consumer Discretionary Sector hurt returns relative to the index.

What significant changes did you make to the portfolio since January 1, 2009?

The focus of the fund was narrowed to our favorite holdings where we had the highest conviction for longer-term outperformance which resulted in fewer stocks, dropping the portfolio holdings to approximately 60 stocks from approximately 135 held as of January 1, 2009. Overall portfolio diversification was taken into account, though we did find better value in Energy and Health Care, so our weighting rose in those sectors.

What were the strongest contributors to fund performance?

The fund’s overweight position in Information Technology contributed to relative performance. Technology valuations were attractive given companies’ strong balance sheets, low inventories, and replacement cycles combined with improving global demand. Also contributing was the fund’s overweight position in Health Care along with good stock selection within the sector. Attractive valuations drove us to an overweight position in this sector. Securities in the Health Care industries were very inexpensive and, in our opinion, had great long term demand. On an individual holdings basis, the strongest contributors included Freeport-McMoran Copper, Life Technologies Corporation, Deere & Co., IBM Corp, and Goldman Sachs Group Inc.

What were the largest constraints on performance?

Our weakest portfolio sector was Consumer Discretionary, where our stock selection was too conservative and we were underweight in a sector which returned over +47% for the period. In Telecommunication Services, our conservative stock selection also worked against the fund as some benchmark stocks rose over 100% for the period. On an individual holdings basis, the largest detractors from performance included Weatherford International, Dow Chemical Company, and Bank of New York Mellon Corp. Also, not owning index-holding Ford Motor Co. hurt performance as it shot up over 300% for the period.

How is the fund positioned going forward?

We believe the outlook for undervalued stocks is attractive. Many stocks with strong balance sheets and stable cash flow have lagged the market advance and we believe these companies offer attractive risk/return profiles. Versus the benchmark, the fund has overweight positions in industries in the Health Care, Energy, and Information Technology sectors of the economy, while underweight positions in Consumer Discretionary, Finance, and Utilities.

Management’s Discussion of Fund Performance

LARGE CAP VALUE FUND (continued)

Cumulative Performance of $10,000 Investment Since Inception1

Average Annual Total Return through December 31, 20091 |

| | | | | | |

| Class I Shares | 16.79% | -9.06% | -0.87% | -0.44% | — |

| Class II Shares | — | — | — | — | 26.09% |

| Russell 1000¨ Value Index | 19.69 | -8.96 | -0.25 | 2.47 | 29.88 |

See accompanying Notes to Management’s Discussion of Fund Performance.

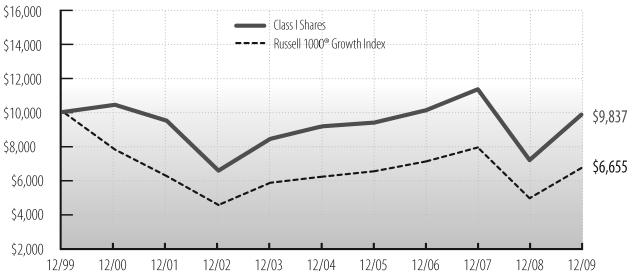

LARGE CAP GROWTH FUND

How did the fund perform for the period January 1, 2009 – December 31, 2009?

The Ultra Series Large Cap Growth Fund had strong absolute as well as relative results for the trailing year ended December 31, 2009. On an absolute basis, positive gains of 37.98% (Class I shares) were achieved. The fund beat the 37.21% return for the Russell 1000¨ Growth Index. The fund had a very solid year of performance despite very unstable market conditions. Our philosophy and process kept us open-minded during the periods of high market volatility experienced this year. It helped us continue to refresh the fund with attractive stocks as stock prices moved in response to recessionary forces and attempts to avert financial collapse. We sought companies with strong balance sheets, that generate excess cash flow, and that have intrinsic factors leading to growth in earnings or cash flow, as higher quality companies tend to have more resources to weather a financial calamity. These stocks were ultimately recognized by the market during the period and are reflected in the fund’s relative outperformance.

What significant changes did you make to the portfolio since January 1, 2009?

Over time, we have reduced the number of holdings in the fund to approximately 65 from approximately 100, as we gained more conviction on our best ideas due to more clarity in the stability of economic conditions. The fund continues to have a bias towards quality growth companies and remains well diversified.

What were the strongest contributors to fund performance?

The largest contributors to performance included the fund’s holdings within the Health Care and Energy Sectors. Health Care was an area of focus since incipient policy reform created heightened uncertainty about future operating conditions, causing other investors to step back from the sector and creating what we thought were attractive stock price entry points. On an individual

Management’s Discussion of Fund Performance

LARGE CAP GROWTH FUND (continued)

basis, the fund’s significant holding in Genentech within the Health Care Sector materially added to performance. The fund’s emphasis in the Energy Sector, due to our anticipation of a rise in oil prices as a result of decreased drilling productivity and potential supply disruption, aided results throughout the period. Within this sector, Petrohawk Energy Corp., a high growth natural gas producer, was a strong contributor to performance.

What were the largest constraints on performance?

Specific holdings in consumer related industries and the Materials Sector detracted from fund performance for the reporting period. Yum! Brands Inc, the quick-service restaurant company which operates Pizza Hut, Taco Bell, and KFC, disappointed for the period. However, we believe its strong growth in China will separate it from competitors.

How is the fund positioned going forward?

We expect overall market volatility to increase as questions develop about the sustainability of the recovery. Also, we believe it is likely the market will narrow rather than broaden and stock selection will become increasingly important. The recovery will be questioned because the economic problems are structural rather than merely cyclical. While we do not think "it is different this time," we do believe the recent past and current environment is foreign to most individuals and policy makers. Since there is no playbook for answers, we believe there will be more false steps along the path to prosperity.

Notwithstanding, some companies will thrive in the "new normal" economy. Our bias is that investors will gravitate towards those companies which continue to demonstrate superiority. We envision bouts of broad speculative moves such as last quarter, to be followed by sharp sell offs in companies which do not meet expectations. Investors will likely gravitate towards those that don’t disappoint. Our portfolio is positioned to take advantage of this market environment.

Cumulative Performance of $10,000 Investment Since Inception1

Average Annual Total Return through December 31, 20091 |

| | | | | | |

| Class I Shares | 37.98% | -0.89% | 1.47% | -0.16% | — |

| Class II Shares | — | — | — | — | 26.21% |

| Russell 1000¨ Growth Index | 37.21 | -1.89 | 1.63 | -3.99 | 30.57 |

See accompanying Notes to Management’s Discussion of Fund Performance.

Management’s Discussion of Fund Performance

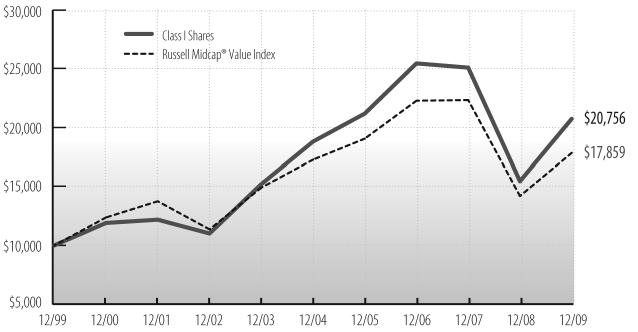

MID CAP VALUE FUND

Wellington Management Company, LLP - Subadviser; Smaller cap portion of the fund January 1, 2009 - June 30, 2009

How did the fund perform for the period January 1, 2009 – December 31, 2009?

For the trailing year ended December 31, 2009, the Ultra Series Mid Cap Value Fund returned 25.67% (Class I Shares), while the Russell¨ Midcap Value Index returned 34.21%. The year was particularly difficult with the fund outperforming early in the year, given its defensive stance that included underweight positions in consumer discretionary and financial stocks, but then underperforming for the remainder of the year. Following the market’s bottoming in March, high-beta and low quality stocks began what turned out to be a sustained rally that continued through the remainder of the year. The fund was instead positioned somewhat more defensively, concentrated in higher quality stocks that participated in the rally but at a reduced rate.

What significant changes did you make to the portfolio since January 1, 2009?

Wellington Management’s small/mid cap value investment team was removed from managing approximately 20% of the fund’s assets on July 1, 2009. Livia Asher of Madison Asset Management remains the lead portfolio manager of the fund. Subsequently, the number of individual stock holdings was reduced and concentrated during the latter half of the year into a "best ideas" portfolio comprised of roughly 70 stocks, down from roughly 230, where we have the highest conviction for longer-term outperformance. Stock valuation dispersion has narrowed allowing the portfolio to upgrade quality at a reasonable price. We also favored stocks where we saw sustainable cash dividends as a means to add to relative returns.

What were the strongest contributors to fund performance?

Greatest relative outperformance during the year came from stock selection within the Health Care Sector as our holdings of Life Technology Corporation and CIGNA Corporation, each returning more than 100%, were positioned with an overweight in the fund. Additional areas of relative positive performance were more broad-based. For example, the overweight position in semiconductor stocks, including Micron Technology, Inc. and Maxim Integrated Products, Inc. as they returned over 80% and almost 300% respectively, offset losses elsewhere in the Information Technology Sector. While the fund was generally underweight in the Financial Sector, the fund did own several out-of-benchmark names that generated positive alpha, including BlackRock, Inc. and JPMorgan Chase & Co. At the same time, not owning several poorly performing commercial banks, like Huntington Bancshares Incorporated and Synovus Financial Corp. were also additive. Another area that the fund avoided was airlines which were poor performers as a group. Within the media industry, owning The Interpublic Group of Companies, Inc. and Scripps Networks Interactive were good choices, though not owning several others in that sector: Liberty Media Corp. – Interactive, Liberty Media Corp. - Capital, Discovery Communications, Inc. and others that returned as much as 400%, offset that gain. The fund also owned copper and gold producer Freeport-McMoRan Copper & Gold Inc., an out of benchmark name that returned over 200% for the year; but we trimmed the position a little prematurely. Finally, The TJX Companies, Inc., the discount retailer, returned almost 82% and was an out-of-benchmark name which contributed to performance.

What were the largest constraints on performance?

The greatest relative underperformance came from both sector allocation and security selection within the Consumer Discretionary Sector. Stocks within the sector returned 69% on average and the fund was both underweight the index here and avoided the "junk" trade—which happened to be the greatest area of above-average stock performance. For example, the fund did not own stocks within the auto and auto components industries where individual stocks returned as much as 500%; similarly, hotels, restaurants & leisure stocks were avoided, however these gained 50-100% or more. Several media names, noted above, had outsized gains and were not owned. Within the other industries, the same pattern was evident: poor quality insurance names, Genworth Financial Inc. and XL Capital Ltd soared 300-400%; paper stocks returned over 150%+; bottlers returned over 80%--none of which were held in the portfolio. Finally, in a market that rose 34%, any cash position results in negative relative performance—in 2009, that cost us 100 basis points.

Management’s Discussion of Fund Performance

MID CAP VALUE FUND (continued)

Additional Comments

Economic improvement appears to be gaining traction, however we believe stock price moves may be more subdued in 2010 as much of that improvement is already largely reflected in valuations. We anticipate top-line improvement and decisive earnings "beats" will be valued over expense-driven margin improvement, and late cycle industries and quality will take over leadership from early cycle and low-quality names. Additionally, we expect, as is typically the case in post-recessionary periods, that earnings estimates are too high and will ultimately be cut, also putting a damper on valuation expansion.

Cumulative Performance of $10,000 Investment Since Inception1

Average Annual Total Return through December 31, 20091 |

| | | | | | |

| Class I Shares | 25.67% | -7.14% | 0.65% | 5.97% | — |

| Class II Shares | — | — | — | — | 24.36% |

| Russell Midcap¨ Value Index | 34.21 | -6.62 | 1.98 | 7.58 | 34.78 |

See accompanying Notes to Management’s Discussion of Fund Performance.

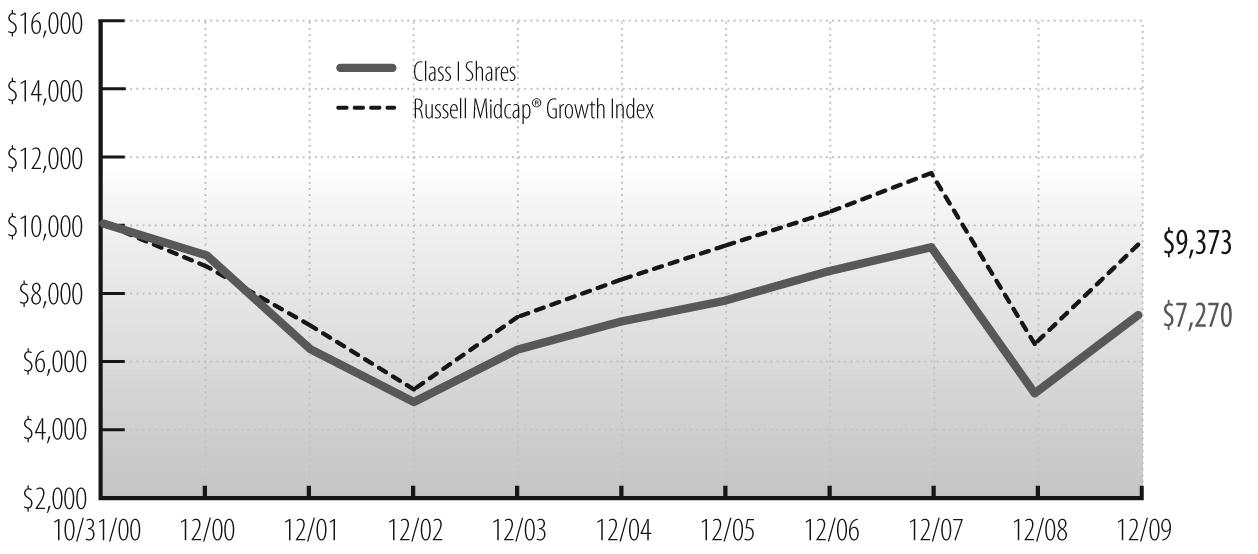

MID CAP GROWTH FUND

Wellington Management Company, LLP - Subadviser; January 1, 2009 - June 30, 2009

How did the fund perform for the period January 1, 2009 – December 31, 2009?

For the trailing year ended December 31, 2009, the Ultra Series Mid Cap Growth Fund returned 47.28% (Class I shares), slightly outperforming the Russell Midcap¨ Growth Index return of 46.29%.

Stock selection in the Consumer Discretionary, Financial, and Information Technology Sectors contributed the most to relative outperformance versus the Russell Midcap¨ Growth Index. In addition, an overweight position in the Energy Sector along with an underweight to Utilities, Consumer Staples, Telecommunication Services and Industrials Sectors were positive contributors to relative returns. These favorable results were partially offset by weak stock selection in the Industrials, Health Care, and Telecommunication Services Sectors, along with negative allocation in the Consumer Discretionary, Financial and Technology

Management’s Discussion of Fund Performance

MID CAP GROWTH FUND (continued)

Sectors. Overall, both stock selection and asset allocation were positive which resulted in outperformance compared to the Russell Midcap¨ Growth Index.

What significant changes did you make to the portfolio since January 1, 2009?

Rich Eisinger, head of Madison’s mid-cap equity team, became the portfolio manager of the fund mid-year. Rich and his team replaced Wellington Management’s mid-cap growth investment team on July 1, 2009.

Subsequently, as the year progressed, we increased our exposure to the Financial Sector, particularly in the insurance industry, and now maintain an overweight position. New insurance purchases in the year included Odyssey Re, specialty insurer Markel and property & casualty insurer RLI. Top active positions include Brookfield Asset Management and diversified holding company Leucadia. We expect to maintain an overweight position relative to the index in the insurance and asset management industries in the Financials Sector as we believe long-term prospects are excellent and valuations are attractive.

After maintaining an overweight position relative to the index in the Technology Sector for most of the year, we reduced our Technology exposure and now have an underweight position. Our Technology holdings generated very strong returns in the first eight months of the year. With valuations less attractive, we felt it prudent to reduce exposure and rotate into other sectors with better return prospects.

What were the strongest contributors to fund performance?

Key individual contributors to relative performance in the Consumer Discretionary Sector were apparel companies True Religion, Aeropostale, the Buckle, and Guess. Luxury jeweler Tiffany and specialty retailer of automotive aftermarket parts O’Reilly Automotive were also strong contributors. In Financials, supplemental health and life insurer Aflac, along with re-insurer Odyssey Re were top performers. In Information Technology, networking solutions supplier Brocade Communication Systems, communications solutions provider Polycom, and Akamai Technologies, a provider of services for accelerating the delivery of content and application over the Internet, were strong relative performers. Atwood Oceanics (energy) was also a top performer.

What were the largest constraints on performance?

Detractors from relative performance in Industrials included asset-light freight transportation management company Hub Group, and Terex, a global manufacturer of construction machinery. Hercules Offshore (energy), Psychiatric Solutions and Amedisys (health care), and Huntington Bancshares (financials) were also relatively weak.

Additional Comments

As we enter 2010, we remain cautiously optimistic about further market gains. Many leading economic indicators are signaling the end of the recession and problematic areas such as home prices appear to be stabilizing. Although the mood is more upbeat, economic support has come mainly from inventory destocking and government stimulus. The sustainability of the economic recovery will be largely dependent on a resurgence in consumer demand beyond short term fixes such as "Cash for Clunkers." High unemployment rates, stagnant personal income growth and a growing savings rate leave us questioning the strength of a consumer rebound. While we remain optimistic about the prospect for a sustained economic recovery, we believe it may unfold at a slower pace than many currently expect.

Management’s Discussion of Fund Performance

MID CAP GROWTH FUND (continued)

Cumulative Performance of $10,000 Investment Since Inception1

Average Annual Total Return through December 31, 20091 |

| | | | | | |

| Class I Shares | 47.28% | -5.34% | 0.54% | -3.42% | — |

| Class II Shares | — | — | — | — | 26.13% |

| Russell Midcap¨ Growth Index | 46.29 | -3.18 | 2.40 | -0.70 | 32.55 |

See accompanying Notes to Management’s Discussion of Fund Performance.

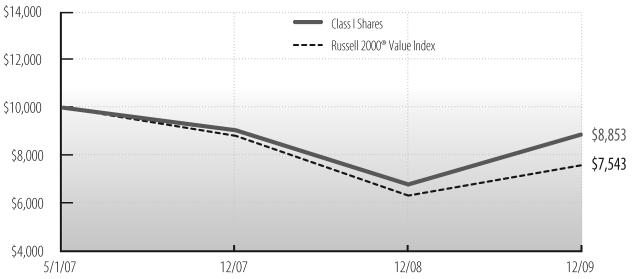

SMALL CAP VALUE FUND

Wellington Management Company, LLP - Subadviser

How did the fund perform for the period January 1, 2009-December 31, 2009?

For the trailing year ended December 31, 2009, the Ultra Series Small Cap Value Fund returned 31.56% (Class I shares), outperforming the Russell¨ 2000 Value Index return of 20.58%.

Consistent with our bottom-up portfolio construction process, stock selection was a large contributor to relative results. Allocation among sectors, a residual of the stock selection process, was also significantly additive during the year. Stock selection was particularly strong within industries in the Financials, Industrials, and Consumer Staples Sectors of the economy. Selection in Consumer Discretionary, Materials, and Information Technology detracted from relative returns. The fund’s underweight position to the Financials Sector contributed to positive relative performance while our underweight position to the Information Technology Sector was a negative relative contributor.

What significant changes did you make to the portfolio since January 1, 2009?

The fund’s investment approach emphasizes individual stock selection; sector weights are a residual of the process. We do, however, carefully consider diversification across economic sectors to limit risk. Based on these bottom-up decisions, the portfolio’s underweight position in the Financials Sector narrowed and Materials moved from a modest overweight to an underweight, while overweight positions within the Consumer Discretionary and Industrials Sectors decreased.

Management’s Discussion of Fund Performance

SMALL CAP VALUE FUND (continued)

What were the strongest contributors to fund performance?

Key individual contributors to relative performance were Carlisle (Industrials), Xyratex (Information Technology), and Herbalife (Consumer Staples). Shares of diversified global manufacturing company Carlisle gained on strong earnings results. We continue to hold Carlisle as the shares are inexpensive and the company’s operational improvements position it to benefit from an improving economy. Disk drive test equipment and data storage company Xyratex posted profits that beat estimates, helped partly by design wins at major customers, sending its shares higher. We continue to hold the security. Herbalife, the leading worldwide direct marketer of health and nutrition products, rose as earnings results exceeded expectations and the company raised full-year guidance. We maintain our position as the stock remains attractively valued and the shares should benefit from improving operational and international trends.

What were the largest constraints on performance?

Detractors from relative performance during the period included Modine Manufacturing (Consumer Discretionary), Penn Virginia (Energy), and Sonic (Consumer Discretionary). Modine, a manufacturer of vehicle heating-and-cooling parts, faced a challenging automotive environment early in the year, sending its shares lower. U.S. drive-in restaurant chain Sonic saw its shares decline on reduced earnings guidance. Independent oil and gas exploration company Penn Virginia also hurt results. The company had disappointing drilling results and lowered its production growth target. We eliminated our position in Modine but continued to hold Penn Virginia and Sonic at year-end.

How is the fund positioned going forward?

Based on our two- to three-year time horizon, we continue to find what we believe are attractively valued investment opportunities in a volatile environment.

Cumulative Performance of $10,000 Investment Since Inception1

Average Annual Total Return through December 31, 20091 |

| | | | |

| Class I Shares | 31.56% | -4.46% | — |

| Class II Shares | — | — | 31.57% |

| Russell 2000¨ Value Index | 20.58 | -10.01 | 29.49 |

See accompanying Notes to Management’s Discussion of Fund Performance.

Management’s Discussion of Fund Performance

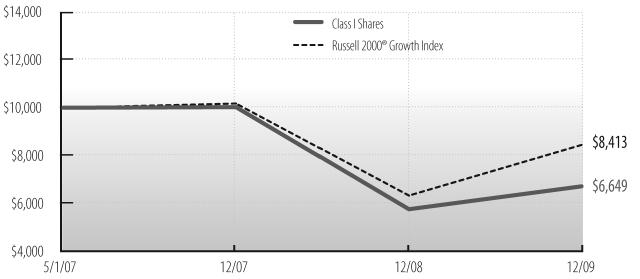

SMALL CAP GROWTH FUND

Paradigm Asset Management Company, LLC - Subadviser; January 1, 2009 - November 30, 2009

How did the fund perform for the period January 1, 2009 – December 31, 2009?

For the twelve month period ended December 31, 2009, the Ultra Series Small Cap Growth Fund returned 17.18% (Class I shares) which lagged the Russell¨ 2000 Growth Index return of 34.47%. The period included a recession and some of the most volatile markets witnessed in the last 20 years. These markets caused tremendous disruptions to quantitative processes and risk models alike. Effective November 30, 2009, subadviser Paradigm Asset Management Company, LLC, was replaced with Madison Asset Management as manager of the fund.

What significant changes have you made to the portfolio since January 1, 2009?

Effective November 30, 2009, Paradigm no longer sub-advises the fund and instead, Madison Asset Management has retained full management responsibilities over the fund. Neither the fund’s investment objective nor its principal investment strategies have changed as a result of this change in management. As the overall stock market continued to surge late in the year, the fund has taken a somewhat more defensive posture with proceeds from profit taking moving cash holdings higher.

What were the strongest contributors to fund performance?

The strongest contributing sectors to overall fund performance for the period were Materials, Telecommunication Services, and Utilities. The top five contributors from a security standpoint were Allscripts-Misys Healthcare Solutions Inc., MPS Group Inc., SPSS Inc, American Medical Systems Holdings Inc., and Rovi Corp.

What were the largest constraints on performance?

The first quarter of 2009 contained the inflection point of March 9, and the fund did not keep pace following this rapid shift in market drivers. The portfolio was further disadvantaged during the second quarter of 2009 by a rally in poorer quality securities. Although the returns for second quarter were impressive, the underlying fundamentals were not; consequently, the rally was labeled as a ‘dash to trash’ in which the fund did not participate. Also detracting from performance in early third quarter of 2009 was the relatively larger weighted average market cap versus the index in the quarter. The third quarter of 2009 did provide strong double digit returns in the face of a concerning economic backdrop. Unemployment breeched 10%, foreclosure rates had reached all time highs and government economic interaction continued at unprecedented levels.

More specifically from a sector stand point, the fund lost ground primarily from stock selection within industries in the Information Technology, Consumer Discretionary, and Health Care Sectors. Asset allocation was a detractor as well in each. Information Technology was a strong performing sector for the Russell¨ 2000 Growth Index, and the fund was slightly underweight in the sector which detracted from performance. The larger shortfall came from poor stock selection within the sector. Names such as Polycom Inc., ValueClick Inc., and IXYS Corp accounted for performance shortfall within information technology.

In Consumer Discretionary, benchmark names which were not held in the fund cost the portfolio relative performance. Tupperware Brands Corp., J Crew and Bally Technologies were a few of the names that were costly by omission. The sector was the best performer for the period and an underweight position relative to the benchmark was a detractor from an asset allocation standpoint and cost the fund performance. Health Care saw similar results of performance shortfall due to benchmark names which performed well and were not held in the fund. Human Genome, CV Therapeutics and Medarex Inc were a few such names.

The majority of performance shortfall for the fund was due to stock selection. The fund struggled through this period as a combination of extreme volatility coupled with poor quality securities driving performance left high quality portfolios out of favor. From a security standpoint the five largest detractors were Forrester Research Inc., Penn Virginia Corp., Wabtec, Immucor Inc, and Martek Biosciences Corp.

Management’s Discussion of Fund Performance

SMALL CAP GROWTH FUND (continued)

Cumulative Performance of $10,000 Investment Since Inception1

Average Annual Total Return through December 31, 20091 |

| | | | |

| Class I Shares | 17.18% | -14.17% | — |

| Class II Shares | — | — | 18.13% |

| Russell 2000¨ Growth Index | 34.47 | -6.26 | 29.49 |

See accompanying Notes to Management’s Discussion of Fund Performance.

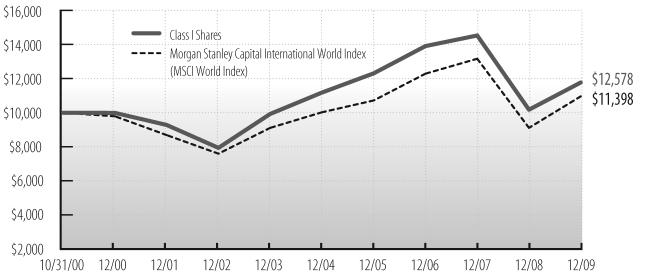

GLOBAL SECURITIES FUND

Mondrian Investment Partners Limited - Subadviser

How did the fund perform for the period January 1, 2009-December 31, 2009?

For the trailing year ended December 31, 2009, the Ultra Series Global Securities Fund returned 22.59% (Class I shares), compared with the MSCI World Index which returned 30.79%.

The year 2009 was very difficult for the global economy. Full data is not yet available, but it seems likely that the decline in economic activity was the sharpest in at least half a century. Particularly damaging for output was the swinging cuts to inventory levels, driven by retailers and wholesalers seeking to preserve cash. In part, this was the result of tight constraints on credit imposed by capital-short banks in the US, Europe and elsewhere. Early on in the year, markets reflected the weakening economic climate, with the MSCI World Index declining by a quarter over the first 10 weeks of the year. However, more positive sentiment emerged as government involvement in the financial sector suggested that the financial crisis would pass its lowest point early on in 2009. Over the rest of the year, the Index recovered by over 70%, leaving it 30% up for the year overall.

What were the strongest contributors and largest constraints to fund performance?

In 2009, our analysis found value in economic sectors such as Consumer Staples, Health Care and Telecommunications. These are sectors which traditionally are seen as having a defensive earnings profile. For instance, in terms of new stocks, we added General Mills, the US food producer, and Vodafone, the UK mobile phone operator to the portfolio. Over the year, our full allocation to these areas, although delivering strong, positive returns, did not allow the portfolio to match the benchmark when market’s switched to a more optimistic tack. However, with our defensive stance and our cautious economic outlook, as discussed below, we continue

Management’s Discussion of Fund Performance

GLOBAL SECURITIES FUND (continued)

to see this allocation as prudent. Among industries in the Financials Sector, we found Zurich Financial Services attractively valued, in part, because of its global spread of operations affording diverse revenue streams.

Although it delivered strong absolute returns, the fund underperformed the index in 2009. On a geographic basis, this underperformance was mainly due to stock selection rather than market allocation. In particular, stock performance in the UK, Spain, the USA, Japan and France held back performance. These adverse influences were only partly offset by positive selection effects in Italy and Canada. More supportive was market selection. For this, the allocation to the strong Singaporean, Taiwanese, Spanish and Australian markets helped returns. But, this was partly offset by low allocations to the strong US and Canadian markets, and nil weighting in Sweden and Hong Kong.

Analyzing performance with reference to a sector breakdown, stock selection was a positive for performance. Good returns relative to their sectors from Financial, Consumer Staple, Utility and Materials stocks buoyed up performance. This was partly offset by weak stock performance among Energy, Health Care, Consumer Discretionary and Industrial holdings.

Our investment approach has a value-oriented defensive style. We assess value by analysis of the potential for company earnings and dividends to grow over time. By relating these to current share prices, we seek to find companies that are under-valued. Our process emphasizes in-depth business analysis and a long time horizon for researching a company’s potential going forward. One aim of this is to include in the portfolio businesses with more resilient cash flows, which should reduce the volatility of returns. This process has led us to find attractive valuations among stocks associated with a defensive earnings’ profile, such as the Telecommunications, Health Care and Consumer Staples Sectors. From the spring on, investor sentiment was focused on recovery, which led these sectors to deliver strong, but sub-benchmark returns. As such, the allocation to them hindered performance. In the same vein, below-average allocations to growth-oriented sectors, such as, Materials and Information Technology also held back performance. However, we expect muted growth among developed markets overall for some time, with households emphasizing debt reduction and necessary over discretionary spending, and a similar picture in the public sector. With this in mind, we remain comfortable with the fund’s positions.

Additional Comments

Some indicators suggest a sharp recovery in output is likely over the coming year or so. Indeed, a boost from re-stocking is likely. But, it is not clear that this will be a full-fledged recovery as enjoyed in earlier periods. Household debt in many areas, for instance in the US and the UK, is at near-record highs and low interest rates will not persist indefinitely. Government indebtedness is high and rising as spending is used to pump-prime broader economic growth. Taxes are already increasing in the UK and fiscal tightening is likely elsewhere too. As yet, emerging markets have fared better, with huge monetary expansion in China supporting growth there, albeit at the risk of an inflationary bubble at some stage. Indeed, domestic demand in these markets may provide some support for export-oriented businesses among developed countries, especially those with weaker currencies, which helps to improve international competitiveness. Overall, we expect muted growth ahead, with households emphasizing debt reduction and necessary over discretionary spending, and a similar picture in the public sector.

Management’s Discussion of Fund Performance

GLOBAL SECURITIES FUND (continued)

Cumulative Performance of $10,000 Investment Since Inception1

Average Annual Total Return through December 31, 20091 |

| | | | | | |

| Class I Shares | 22.59% | -7.09% | 1.42% | 2.53% | — |

| Class II Shares | — | — | — | — | 33.79% |

| MSCI World Index | 30.79 | -5.09 | 2.57 | 1.44 | 33.18 |

See accompanying Notes to Management’s Discussion of Fund Performance.

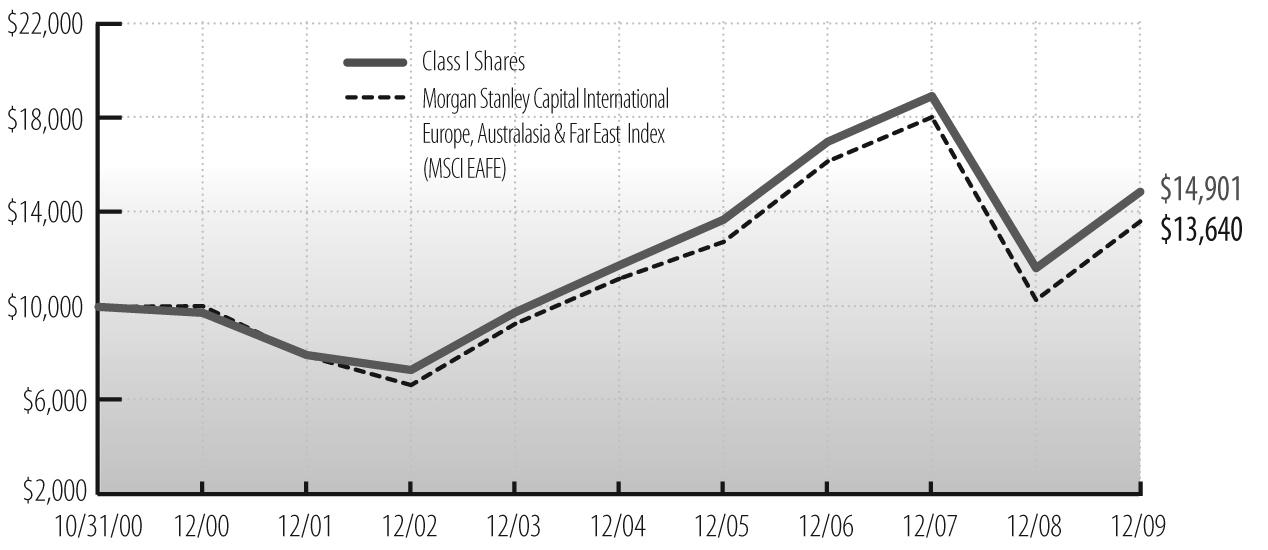

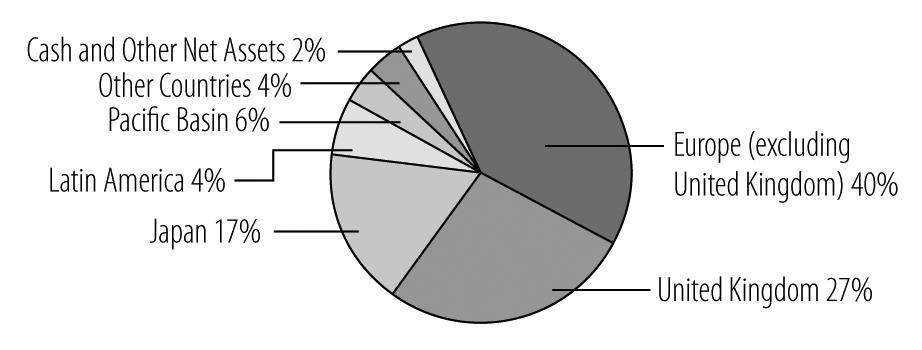

INTERNATIONAL STOCK FUND

Lazard Asset Management, LLC - Subadviser

International stocks experienced a tremendous rally since the lows reached in March 2009, as the world continued to recover from one of the worst economic and financial crises in decades. Risks to the global financial system subsided over the past year due to the unprecedented monetary and fiscal actions taken by major central banks and governments. The recent flow of positive economic data indicated continued improvement in the underlying fundamentals of the global economy. This stabilization, coupled with policymakers’ signaling the likelihood of prolonged accommodative monetary policy, encouraged investors to buy into riskier assets. International small-cap equities performed particularly well throughout 2009, outperforming large-cap stocks for the year.

In Europe, Norway performed the best, as the oil-rich country benefited from a strong recovery in crude oil prices. However, the overall performance of stocks was mixed amid increasing divergences within the European Union, and the downgrade of Greece’s credit rating rekindled fears over sovereign debt risks. In Asia, Hong Kong and Singapore performed well on the expected benefits stemming from strong growth in China. Japan continued to underperform its regional peers, although it appeared to regain some positive momentum in December amid easing concerns over the strong yen. Emerging markets performed strongly on investors’ belief that emerging market economic growth would significantly outpace developed world growth. For the year as a whole, the MSCI Emerging Markets Index increased by almost 79%, with Latin American equities significantly outperforming shares in Eastern Europe, the Middle East, Africa and in Asia.

In currency markets, the U.S. dollar weakened following the March trough, as investors were attracted to higher-yielding currencies, such as the Australian dollar. However, the U.S. dollar rebounded in recent months, appreciating against major

Management’s Discussion of Fund Performance

INTERNATIONAL STOCK FUND (continued)

currencies. This appreciation coincided with an apparent change in investors’ sentiment toward the U.S. dollar amid improving U.S. economic data, which led to some speculation that the U.S. Federal Reserve might raise interest rates sooner than expected. Additionally, the euro was hurt by the downgrade of Greece’s (one of its member countries) sovereign debt.

After a period in which the MSCI EAFE Index reached an all-time high driven by euphoria (October 2007), it declined more than 50% due to indiscriminate selling (March 2009), and subsequently rallied over 70% due to a dash toward risk (December 2009). Financial markets were, once again, driven by fundamentals by the end of the year.

How did the fund perform for the period January 1, 2009-December 31, 2009?

For the trailing year ended December 31, 2009, the Ultra Series International Stock Fund returned 27.90% (Class I shares), compared to the MSCI EAFE Index return of 32.46%.

What significant changes did you make to the portfolio since January 1, 2009?

During 2009, driven by its bottom-up approach, the fund continued to move toward a less defensive stance, adding overall exposure to cyclically exposed companies that were trading at attractive multiples, while many defensive stocks reached fair value. The Consumer Discretionary Sector figured prominently, as the fund invested in automobile companies BMW and Honda, as did the Materials Sector, where the fund increased exposure. We also invested in several high-quality companies at historically low valuations, including Novo Nordisk, Fanuc, and Esprit. We increased our exposure to industries in the Financial Sector during the period – primarily in higher-quality investment banks, insurance companies, and surviving banks. Reductions across defensive sectors included the sales of Japan Tobacco, BT Group, and E.ON AG. Going forward, we believe there will be a marked differentiation between winning and losing business models.

What were the strongest contributors to fund performance?

The fund benefited from strong stock selection in the Information Technology Sector, as Ericsson, Hoya, and Canon each contributed to returns. A low exposure relative to the index to the Utilities Sector also helped performance, as the sector was hurt by concerns about overcapacity in the power generation market. Exposure to emerging markets contributed significantly to returns over the year, as shares of Banco do Brasil, Lukoil, and the Industrial & Commercial Bank of China performed well.

What were largest constraints on performance?

The biggest drag on performance was a low exposure relative to the index to the Materials Sector, which benefited from the improving economic environment and emerging market demand. The high exposure to, and stock selection in, Telecommunication Services also detracted from returns, as investors rotated into more cyclical sectors. Within the Telecommunication Services Sector, positions in KDDI, Telus, and Vodafone Group hurt performance.

Management’s Discussion of Fund Performance

INTERNATIONAL STOCK FUND (continued)

Cumulative Performance of $10,000 Investment Since Inception1

Average Annual Total Return through December 31, 20091 |

| | | | | | |

| Class I Shares | 27.90% | -4.36% | 4.83% | 4.45% | — |

| Class II Shares | — | — | — | — | 32.30% |

| MSCI EAFE Index | 32.46 | -5.57 | 4.02 | 3.44 | 36.11 |

See accompanying Notes to Management’s Discussion of Fund Performance.

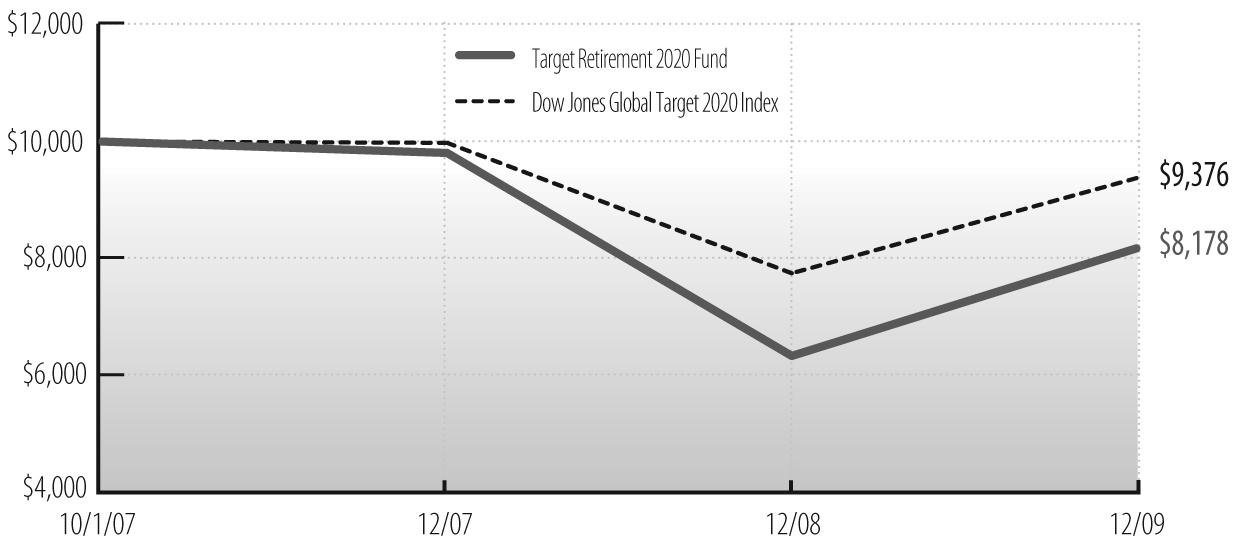

TARGET RETIREMENT 2020 FUND

How did the fund perform for the period January 1, 2009 – December 31, 2009?