UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number | 811-03940 |

| |

| Strategic Funds, Inc. | |

| (Exact name of Registrant as specified in charter) | |

| | |

| c/o The Dreyfus Corporation 200 Park Avenue New York, New York 10166 | |

| (Address of principal executive offices) (Zip code) | |

| | |

| Bennett A. MacDougall, Esq. 200 Park Avenue New York, New York 10166 | |

| (Name and address of agent for service) | |

|

Registrant's telephone number, including area code: | (212) 922-6400 |

| |

Date of fiscal year end: | 12/31 | |

Date of reporting period: | 12/31/18 | |

| | | | | | | |

The following N-CSR relates only to the Registrant's series listed below and does not relate to any series of the Registrant with a different fiscal year end and, therefore, different N-CSR reporting requirements. A separate N-CSR will be filed for any series with a different fiscal year end, as appropriate.

Dreyfus Active MidCap Fund

FORM N-CSR

Item 1. Reports to Stockholders.

Dreyfus Active MidCap Fund

| | | |

| | ANNUAL REPORT December 31, 2018 |

| |

Save time. Save paper. View your next shareholder report online as soon as it’s available. Log into www.dreyfus.com and sign up for Dreyfus eCommunications. It’s simple and only takes a few minutes. |

| |

The views expressed in this report reflect those of the portfolio manager(s) only through the end of the period covered and do not necessarily represent the views of Dreyfus or any other person in the Dreyfus organization. Any such views are subject to change at any time based upon market or other conditions and Dreyfus disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Dreyfus fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Dreyfus fund. |

| |

Not FDIC-Insured • Not Bank-Guaranteed • May Lose Value |

Contents

THE FUND

FOR MORE INFORMATION

Back Cover

| | | | |

| |

Dreyfus Active MidCap Fund

| | The Fund |

A LETTER FROM THE PRESIDENT OF DREYFUS

Dear Shareholder:

We are pleased to present this annual report for Dreyfus Active MidCap Fund, covering the 12-month period from January 1, 2018 through December 31, 2018. For information about how the fund performed during the reporting period, as well as general market perspectives, we provide a Discussion of Fund Performance on the pages that follow.

The reporting period began with major global economies achieving above-trend growth. In the United States, a robust economy and strong labor market encouraged the Federal Reserve to continue moving away from its accommodative monetary policy while other major central banks began to consider monetary tightening. Both U.S. and non-U.S. equity markets remained on an uptrend. Interest rates rose across the yield curve, putting pressure on bond prices.

A few months into the reporting period, global growth trends began to diverge and market volatility returned. While the U.S. economy continued to grow at a healthy rate, other developed markets began to weaken. However, robust growth and strong corporate earnings continued to support U.S. stock returns while other developed markets declined throughout the summer. In the fall, a broad sell-off occurred, partially offsetting earlier U.S. gains. Emerging markets remained under pressure as weakness in their currencies relative to the U.S. dollar added to investors’ uneasiness. Global equities continued their general decline through the end of the period.

Fixed income markets struggled during the first half of the period as interest rates rose and favorable U.S. equity markets fed investor risk appetites. However, in autumn volatility crept in, the yield curve began a flattening trend that continued through the end of December. As long-term debt yields fell, prices rose for many bonds, leading to moderately positive returns for several fixed income market sectors.

Despite continuing political variables, U.S. inflationary pressures and flagging growth rates, we are optimistic that the U.S. economy will remain strong in the near term. However, we remain attentive to signs that point to potential changes on the horizon. As always, we encourage you to discuss the risks and opportunities in today’s investment environment with your financial advisor.

Thank you for your continued confidence and support.

Sincerely,

Renee Laroche-Morris

President

The Dreyfus Corporation

January 15, 2019

2

DISCUSSION OF FUND PERFORMANCE(Unaudited)

For the period from January 1, 2018 through December 31, 2018, as provided by C. Wesley Boggs, William S. Cazalet, CAIA, Peter D. Goslin, CFA, and Syed A. Zamil, CFA, Portfolio Managers

Market and Fund Performance Overview

For the 12-month period ended December 31, 2018, Dreyfus Active MidCap Fund’s Class A shares achieved a total return of -14.31%, Class C shares returned -15.04%, Class I shares returned -14.12%, and Class Y shares returned -14.11%.1 In comparison, the fund’s benchmark, the Russell Midcap® Index (the “Index”), achieved a total return of -9.06% for the same period.2

Mid-cap stocks lost value in a volatile market over the reporting period amid escalating trade tensions and slowing global economic growth rates. The fund lagged the Index primarily due to security selection shortfalls in the financials, consumer staples, materials and information technology sectors.

The Fund’s Investment Approach

The fund seeks to maximize capital appreciation. To pursue its goal, the fund normally invests at least 80% of its net assets, plus any borrowings for investment purposes, in the stocks of midsized companies. The fund currently defines “midsized companies” as companies included in the Index. We apply a systematic, quantitative investment approach designed to identify and exploit relative misvaluations primarily within mid-cap stocks in the U.S. stock market.

We use a proprietary valuation model that identifies and ranks stocks to construct the fund’s portfolio. We construct the fund’s portfolio through a systematic structured approach, focusing on stock selection as opposed to making proactive decisions as to industry or sector exposure. Within each sector and style subset, the fund overweights the most attractive stocks and underweights or zero weights the stocks that have been ranked least attractive. The fund typically will hold between 100 and 250 securities.

Positive U.S. Economic Indicators Amid Volatility

A positive economic backdrop supported U.S. equity markets at the start of 2018, including sustained GDP growth, a robust labor market and higher growth forecasts from the Federal Reserve Board (the “Fed”). Enactment of corporate tax cuts as part of major tax-reform legislation in late December 2017 sparked additional market gains, driving the Index to new all-time highs in January.

In the first few months of 2018, volatility entered the picture as concerns over inflation and the potential for trade disputes roiled markets. However, U.S. markets were able to stabilize, and the upward trend continued on the back of continued positive economic data, corporate balance sheet strength and robust consumer spending. However, non-U.S. markets retreated as the rate of economic improvement in areas including the Eurozone stalled. In late summer, continued political rhetoric in the U.S. regarding trade and midterm elections, along with concerns over issues abroad in areas such as Italy, Turkey, Argentina and the United Kingdom weighed on sentiment. Despite strong underlying fundamentals, volatility crept back into the picture in U.S. markets. Firm labor markets, tightening monetary policy and the possibility of slowing growth provoked a defensive posture among investors. In October, markets reversed course and started to move lower. Continued worries over rising interest rates, trade disputes and falling commodity prices pressured equity markets throughout the rest of the period.

In this environment, large-cap stocks generally outperformed their mid- and small-cap counterparts.

3

DISCUSSION OF FUND PERFORMANCE(Unaudited) (continued)

Security Selection Constrained Fund Performance

The fund’s performance compared to the Index was undermined by stock selection shortfalls across several market sectors. In the financials sector, insurance companies generally weighed on relative results: Unum Group reported disappointing quarterly earnings, increased its reserve requirement and experienced pressure from its exposure to the long-term care insurance market. Synchrony Financial was also a main individual detractor. The price of the financial service company fell when it lost a high-revenue client and the client later filed suit against the company. Among consumer staples companies, a position in Conagra Brands dampened relative performance as the price slid during the fourth quarter after the company reduced future guidance due to a recent acquisition. Stock selection throughout the rest of the food products industry also weighed on returns, as did stock holdings within the materials and information technology sectors.

The fund achieved better results in other market sectors. We identified several positive contributors in the energy sector, as the fund avoided many of the sector’s weaker stocks. In addition, the fund had an emphasis on refining companies, which fared better than energy reserves and equipment stocks, helping relative returns. Selection within electric utilities also boosted results. Within the health care sector, stock selection within the health care providers industry was also beneficial. A position inWellCare Health Plans was a significant contributor to overall performance. The provider beat estimates and raised guidance several times during the year. The stock was eliminated during the fourth quarter. Elsewhere in the markets, a position in consumer discretionary company Deckers Outdoor was among the top individual contributors to performance. The outdoor shoe and apparel retailer beat earnings every quarter of the year and raised guidance several times. Information technology company Red Hat, whose price increased during the fourth quarter due to an acquisition by IBM, was another top contributor.

A Disciplined Approach to Stock Picking

As of the reporting period’s end, our quantitative models have continued to identify what we believe are attractive investment opportunities across a broad spectrum of mid-cap companies and industry groups. Stock market volatility experienced in 2018 has provided opportunities to purchase the stocks of companies ranked highly by our process. When the fund’s holdings reach what we perceive to be fuller valuations, we expect to replace them with high-quality companies that display then-currently attractive valuations in our model. In addition, we continue to maintain a broadly diversified portfolio.

January 15, 2019

¹ Total return includes reinvestment of dividends and any capital gains paid, and does not take into consideration the maximum initial sales charge in the case of Class A shares or the applicable contingent deferred sales charge imposed on redemptions in the case of Class C shares. Had these charges been reflected, returns would have been lower. Past performance is no guarantee of future results. Share price and investment return fluctuate such that upon redemption, fund shares may be worth more or less than their original cost.

² Source: Lipper Inc. — The Russell Midcap®Index measures the performance of the mid-cap segment of the U.S. equity universe. The Index is a subset of the Russell 1000® Index. It includes approximately 800 of the smallest securities based on a combination of their market cap and current index membership. The Index represents approximately 31% of the total market capitalization of the Russell 1000 companies. The Index is constructed to provide a comprehensive and unbiased barometer for the mid-cap segment. The Index is completely reconstituted annually to ensure larger stocks do not distort the performance and characteristics of the true mid-cap opportunity set. Investors cannot invest directly in any index.

Please note: the position in any security highlighted with italicized typeface was sold during the reporting period.

Equities are subject generally to market, market sector, market liquidity, issuer, and investment style risks, among other factors, to varying degrees, all of which are more fully described in the fund’s prospectus.

Stocks of mid-cap companies often experience sharper price fluctuations than stocks of large-cap companies.

4

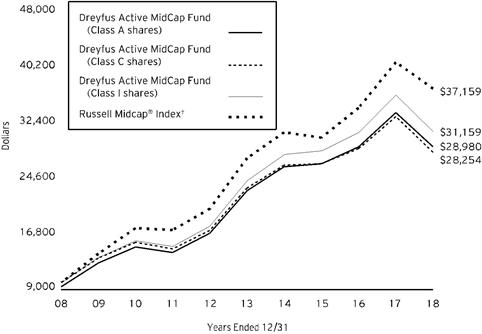

FUND PERFORMANCE(Unaudited)

Comparison of change in value of a $10,000 investment in Class A shares, Class C shares and Class I shares of Dreyfus Active MidCap Fund with a hypothetical investment of $10,000 in the Russell Midcap® Index (the “Index”).

† Source: Lipper Inc.

Past performance is not predictive of future performance.

The above graph compares a hypothetical $10,000 investment made in each of the Class A, Class C, and Class I shares of Dreyfus Active MidCap Fund on 12/31/08 to a hypothetical investment of $10,000 made in the Index on that date. All dividends and capital gain distributions are reinvested.

The fund’s performance shown in the line graph above takes into account the maximum initial sales charge on Class A shares and all other applicable fees and expenses of the applicable classes. The Index measures the performance of the mid-cap segment of the U.S. equity universe. The Index is a subset of the Russell 1000® Index. It includes approximately 800 of the smallest securities based on a combination of their market cap and current index membership. The Index represents approximately 31% of the total market capitalization of the Russell 1000 companies. The Index is constructed to provide a comprehensive and unbiased barometer for the mid-cap segment. The Index is completely reconstituted annually to ensure larger stocks do not distort the performance and characteristics of the true mid-cap opportunity set. Unlike a mutual fund, the Index is not subject to charges, fees and other expenses. Investors cannot invest directly in any index. Further information relating to fund performance, including expense reimbursements, if applicable, is contained in the Financial Highlights section of the prospectus and elsewhere in this report.

5

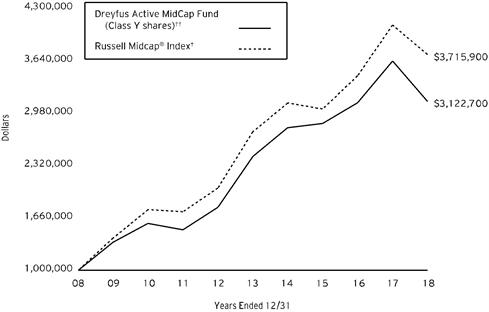

FUND PERFORMANCE(Unaudited) (continued)

Comparison of change in value of a $1,000,000 investment in Class Y shares of Dreyfus Active MidCap Fund with a hypothetical investment of $1,000,000 in the Russell Midcap® Index (the “Index”).

† Source: Lipper Inc.

†† The total return figures presented for Class Y shares of the fund reflect the performance of the fund’s Class I shares for the period prior to 9/1/15 (the inception date for Class Y shares).

Past performance is not predictive of future performance.

The above graph compares a hypothetical $1,000,000 investment in Class Y shares of Dreyfus Active MidCap Fund on 12/31/08 to a hypothetical investment of $1,000,000 made in the Index on that date. All dividends and capital gain distributions are reinvested.

The fund’s performance shown in the line graph above takes into account all applicable fees and expenses of the fund’s Class Y shares.The Index measures the performance of the mid-cap segment of the U.S. equity universe. The Index is a subset of the Russell 1000® Index. It includes approximately 800 of the smallest securities based on a combination of their market cap and current index membership. The Index represents approximately 31% of the total market capitalization of the Russell 1000 companies. The Index is constructed to provide a comprehensive and unbiased barometer for the mid-cap segment. The Index is completely reconstituted annually to ensure larger stocks do not distort the performance and characteristics of the true mid-cap opportunity set. Unlike a mutual fund, the Index is not subject to charges, fees and other expenses. Investors cannot invest directly in any index. Further information relating to fund performance, including expense reimbursements, if applicable, is contained in the Financial Highlights section of the prospectus and elsewhere in this report.

6

| | | | | |

Average Annual Total Returns as of12/31/18 |

| Inception Date | 1 Year | 5 Years | 10 Years |

Class A shares | | | | |

with maximum sales charge (5.75%) | 1/29/85 | -19.23% | 3.62% | 11.23% |

without sales charge | 1/29/85 | -14.31% | 4.85% | 11.89% |

Class C shares | | | | |

with applicable redemption charge† | 11/27/02 | -15.80% | 3.97% | 10.95% |

without redemption | 11/27/02 | -15.04% | 3.97% | 10.95% |

Class I shares | 11/27/02 | -14.12% | 5.07% | 12.04% |

Class Y shares | 9/1/15 | -14.11% | 5.12%†† | 12.06%†† |

Russell Midcap® Index | | -9.06% | 6.26% | 14.03% |

† The maximum contingent deferred sales charge for Class C shares is 1% for shares redeemed within one year of the date of purchase.

†† The total return figures presented for Class Y shares of the fund reflect the performance of the fund’s Class I shares for the period prior to 9/1/15 (the inception date for Class Y shares).

The performance data quoted represents past performance, which is no guarantee of future results. Share price and investment return fluctuate and an investor’s shares may be worth more or less than original cost upon redemption. Current performance may be lower or higher than the performance quoted. Go to Dreyfus.com for the fund’s most recent month-end returns.

The fund’s performance shown in the graphs and table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. In addition to the performance of Class A shares shown with and without a maximum sales charge, the fund’s performance shown in the table takes into account all other applicable fees and expenses on all classes.

7

UNDERSTANDING YOUR FUND’S EXPENSES(Unaudited)

As a mutual fund investor, you pay ongoing expenses, such as management fees and other expenses. Using the information below, you can estimate how these expenses affect your investment and compare them with the expenses of other funds. You also may pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial adviser.

Review your fund’s expenses

The table below shows the expenses you would have paid on a $1,000 investment in Dreyfus Active MidCap Fund from July 1, 2018 to December 31, 2018. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

| | | | | | | | | |

Expenses and Value of a $1,000 Investment |

assuming actual returns for the six months ended December 31, 2018 |

| | Class A | Class C | Class I | Class Y |

Expenses paid per $1,000† | | $5.29 | | $9.38 | | $4.30 | | $4.21 |

Ending value (after expenses) | | $873.80 | | $869.70 | | $874.60 | | $874.80 |

COMPARING YOUR FUND’S EXPENSES

WITH THOSE OF OTHER FUNDS(Unaudited)

Using the SEC’s method to compare expenses

The Securities and Exchange Commission (“SEC”) has established guidelines to help investors assess fund expenses. Per these guidelines, the table below shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total cost) of investing in the fund with those of other funds. All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

| | | | | | | | | | | |

Expenses and Value of a $1,000 Investment |

assuming a hypothetical 5% annualized return for the six months ended December 31, 2018 |

| | | Class A | Class C | Class I | Class Y |

Expenses paid per $1,000† | | $5.70 | | $10.11 | | $4.63 | | $4.53 |

Ending value (after expenses) | | $1,019.56 | | $1,015.17 | | $1,020.62 | | $1,020.72 |

† Expenses are equal to the fund’s annualized expense ratio of 1.12% for Class A, 1.99% for Class C, .91% for Class I and .89% Class Y, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period).

8

STATEMENT OF INVESTMENTS

December 31, 2018

| | | | | | | | |

| |

Description | | | | Shares | | Value ($) | |

Common Stocks - 99.6% | | | | | |

Automobiles & Components - 1.7% | | | | | |

Gentex | | | | 122,625 | | 2,478,251 | |

Lear | | | | 41,995 | | 5,159,506 | |

| | | | | 7,637,757 | |

Banks - 3.9% | | | | | |

Cathay General Bancorp | | | | 33,575 | | 1,125,770 | |

Citizens Financial Group | | | | 24,940 | | 741,466 | |

Comerica | | | | 95,460 | | 6,557,147 | |

Popular | | | | 129,880 | | 6,132,934 | |

Regions Financial | | | | 202,365 | | 2,707,644 | |

| | | | | 17,264,961 | |

Capital Goods - 7.1% | | | | | |

Allison Transmission Holdings | | | | 159,105 | | 6,986,301 | |

Curtiss-Wright | | | | 60,300 | | 6,157,836 | |

Harris | | | | 3,475 | | 467,909 | |

Huntington Ingalls Industries | | | | 25,045 | | 4,766,314 | |

Ingersoll-Rand | | | | 49,970 | | 4,558,763 | |

Pentair | | | | 46,940 | | 1,773,393 | |

Spirit AeroSystems Holdings, Cl. A | | | | 93,910 | | 6,769,972 | |

| | | | | 31,480,488 | |

Commercial & Professional Services - 1.5% | | | | | |

Copart | | | | 139,605 | a | 6,670,327 | |

Consumer Durables & Apparel - 4.3% | | | | | |

Deckers Outdoor | | | | 52,200 | a | 6,678,990 | |

KB Home | | | | 33,940 | | 648,254 | |

NVR | | | | 2,000 | a | 4,873,980 | |

PulteGroup | | | | 270,060 | b | 7,018,859 | |

| | | | | 19,220,083 | |

Consumer Services - .5% | | | | | |

Hilton Worldwide Holdings | | | | 23,740 | | 1,704,532 | |

Hyatt Hotels, Cl. A | | | | 8,465 | | 572,234 | |

| | | | | 2,276,766 | |

Diversified Financials - 6.2% | | | | | |

Discover Financial Services | | | | 126,610 | | 7,467,458 | |

Evercore, Cl. A | | | | 20,290 | | 1,451,952 | |

FactSet Research Systems | | | | 8,600 | b | 1,721,118 | |

LPL Financial Holdings | | | | 115,105 | | 7,030,614 | |

Moody's | | | | 9,940 | | 1,391,998 | |

SEI Investments | | | | 39,145 | | 1,808,499 | |

Synchrony Financial | | | | 288,840 | | 6,776,186 | |

| | | | | 27,647,825 | |

9

STATEMENT OF INVESTMENTS (continued)

| | | | | | | | |

| |

Description | | | | Shares | | Value ($) | |

Common Stocks - 99.6% (continued) | | | | | |

Energy - 4.4% | | | | | |

Continental Resources | | | | 61,015 | a | 2,452,193 | |

HollyFrontier | | | | 121,945 | | 6,233,828 | |

Marathon Petroleum | | | | 93,735 | | 5,531,302 | |

PBF Energy, Cl. A | | | | 166,645 | b | 5,444,292 | |

| | | | | 19,661,615 | |

Food, Beverage & Tobacco - 1.4% | | | | | |

ConAgra Brands | | | | 210,390 | | 4,493,930 | |

Ingredion | | | | 18,940 | | 1,731,116 | |

| | | | | 6,225,046 | |

Health Care Equipment & Services - 4.6% | | | | | |

Cerner | | | | 21,685 | a | 1,137,161 | |

Edwards Lifesciences | | | | 5,620 | a | 860,815 | |

Haemonetics | | | | 65,990 | a | 6,602,300 | |

ICU Medical | | | | 9,330 | a | 2,142,448 | |

IDEXX Laboratories | | | | 2,570 | a | 478,071 | |

ResMed | | | | 16,955 | | 1,930,666 | |

Varian Medical Systems | | | | 63,280 | a | 7,170,257 | |

| | | | | 20,321,718 | |

Household & Personal Products - 1.6% | | | | | |

Herbalife | | | | 116,730 | a,b | 6,881,234 | |

Insurance - 5.6% | | | | | |

First American Financial | | | | 86,250 | | 3,850,200 | |

Kemper | | | | 38,370 | | 2,547,001 | |

Lincoln National | | | | 105,345 | | 5,405,252 | |

Torchmark | | | | 92,795 | | 6,916,011 | |

Unum | | | | 210,730 | | 6,191,247 | |

| | | | | 24,909,711 | |

Materials - 5.5% | | | | | |

Celanese, Ser. A | | | | 43,375 | b | 3,902,449 | |

CF Industries Holdings | | | | 166,530 | | 7,245,720 | |

Chemours | | | | 14,550 | | 410,601 | |

Huntsman | | | | 255,140 | | 4,921,651 | |

Louisiana-Pacific | | | | 140,785 | | 3,128,243 | |

Westlake Chemical | | | | 71,025 | b | 4,699,724 | |

| | | | | 24,308,388 | |

Media & Entertainment - 1.0% | | | | | |

AMC Networks, Cl. A | | | | 18,180 | a,b | 997,718 | |

Sirius XM Holdings | | | | 99,060 | b | 565,633 | |

Tribune Media | | | | 18,390 | | 834,538 | |

TripAdvisor | | | | 34,430 | a | 1,857,154 | |

| | | | | 4,255,043 | |

Pharmaceuticals Biotechnology & Life Sciences - 7.8% | | | | | |

Agilent Technologies | | | | 114,050 | | 7,693,813 | |

10

| | | | | | | | |

| |

Description | | | | Shares | | Value ($) | |

Common Stocks - 99.6% (continued) | | | | | |

Pharmaceuticals Biotechnology & Life Sciences - 7.8% (continued) | | | | | |

Bruker | | | | 29,270 | | 871,368 | |

Illumina | | | | 3,210 | a | 962,775 | |

Jazz Pharmaceuticals | | | | 47,770 | a | 5,921,569 | |

Mettler-Toledo International | | | | 8,875 | a,b | 5,019,523 | |

Waters | | | | 41,145 | a | 7,762,004 | |

Zoetis | | | | 75,505 | | 6,458,698 | |

| | | | | 34,689,750 | |

Real Estate - 6.0% | | | | | |

First Industrial Realty Trust | | | | 216,610 | c | 6,251,365 | |

Host Hotels & Resorts | | | | 339,630 | c | 5,661,632 | |

Kilroy Realty | | | | 8,655 | b,c | 544,226 | |

Lamar Advertising, Cl. A | | | | 62,040 | c | 4,291,927 | |

Medical Properties Trust | | | | 127,550 | c | 2,051,004 | |

Piedmont Office Realty Trust, Cl. A | | | | 19,180 | b,c | 326,827 | |

Prologis | | | | 46,215 | c | 2,713,745 | |

Weingarten Realty Investors | | | | 189,340 | c | 4,697,525 | |

| | | | | 26,538,251 | |

Retailing - 7.7% | | | | | |

American Eagle Outfitters | | | | 179,860 | b | 3,476,694 | |

Best Buy | | | | 121,655 | | 6,442,849 | |

Dick's Sporting Goods | | | | 169,795 | b | 5,297,604 | |

Foot Locker | | | | 75,080 | | 3,994,256 | |

Kohl's | | | | 101,250 | | 6,716,925 | |

Ross Stores | | | | 100,570 | | 8,367,424 | |

| | | | | 34,295,752 | |

Semiconductors & Semiconductor Equipment - 1.6% | | | | | |

KLA-Tencor | | | | 49,490 | | 4,428,860 | |

Skyworks Solutions | | | | 38,460 | | 2,577,589 | |

| | | | | 7,006,449 | |

Software & Services - 13.8% | | | | | |

Broadridge Financial Solutions | | | | 70,580 | | 6,793,325 | |

Cadence Design Systems | | | | 13,760 | a | 598,285 | |

CDK Global | | | | 124,165 | | 5,945,020 | |

Citrix Systems | | | | 70,910 | | 7,265,439 | |

DXC Technology | | | | 70,010 | | 3,722,432 | |

Fair Isaac | | | | 14,940 | a | 2,793,780 | |

Fiserv | | | | 115,590 | a | 8,494,709 | |

MAXIMUS | | | | 96,955 | | 6,310,801 | |

Paychex | | | | 120,695 | | 7,863,279 | |

Red Hat | | | | 35,895 | a | 6,304,598 | |

VeriSign | | | | 33,020 | a | 4,896,536 | |

| | | | | 60,988,204 | |

11

STATEMENT OF INVESTMENTS (continued)

| | | | | | | | |

| |

Description | | | | Shares | | Value ($) | |

Common Stocks - 99.6% (continued) | | | | | |

Technology Hardware & Equipment - 5.1% | | | | | |

CDW | | | | 45,175 | | 3,661,434 | |

F5 Networks | | | | 44,905 | a | 7,275,957 | |

NetApp | | | | 104,285 | | 6,222,686 | |

Zebra Technologies, Cl. A | | | | 32,645 | a | 5,198,063 | |

| | | | | 22,358,140 | |

Transportation - 1.9% | | | | | |

Old Dominion Freight Line | | | | 19,930 | | 2,461,156 | |

United Continental Holdings | | | | 68,590 | a | 5,743,041 | |

| | | | | 8,204,197 | |

Utilities - 6.4% | | | | | |

Avangrid | | | | 93,160 | b | 4,666,384 | |

IDACORP | | | | 34,235 | | 3,185,909 | |

MDU Resources Group | | | | 273,470 | | 6,519,525 | |

NRG Energy | | | | 183,220 | | 7,255,512 | |

OGE Energy | | | | 174,780 | b | 6,849,628 | |

| | | | | 28,476,958 | |

Total Common Stocks(cost $432,578,983) | | | | 441,318,663 | |

| | | 1-Day

Yield (%) | | | | | |

Investment of Cash Collateral for Securities Loaned - 2.0% | | | | | |

Registered Investment Companies - 2.0% | | | | | |

Dreyfus Institutional Preferred Government Money Market Fund, Institutional Shares

(cost $8,850,252) | | 2.69 | | 8,850,252 | d | 8,850,252 | |

Total Investments(cost $441,429,235) | | 101.6% | | 450,168,915 | |

Liabilities, Less Cash and Receivables | | (1.6%) | | (7,145,388) | |

Net Assets | | 100.0% | | 443,023,527 | |

a Non-income producing security.

b Security, or portion thereof, on loan. At December 31, 2018, the value of the fund’s securities on loan was $54,266,376 and the value of the collateral held by the fund was $54,988,285, consisting of cash collateral of $8,850,252 and U.S. Government & Agency securities valued at $46,138,033.

c Investment in real estate investment trust.

d Investment in affiliated issuer. The investment objective of this investment company is publicly available and can be found within the investment company’s prospectus.

12

| | |

Portfolio Summary (Unaudited)† | Value (%) |

Information Technology | 20.4 |

Financials | 15.8 |

Consumer Discretionary | 14.3 |

Health Care | 12.4 |

Industrials | 10.5 |

Utilities | 6.4 |

Real Estate | 6.0 |

Materials | 5.5 |

Energy | 4.4 |

Consumer Staples | 2.9 |

Investment Companies | 2.0 |

Communication Services | 1.0 |

| | 101.6 |

† Based on net assets.

See notes to financial statements.

13

STATEMENT OF INVESTMENTS IN AFFILIATED ISSUERS

| | | | | | | |

Registered Investment Company | Value

12/31/17($) | Purchases($) | Sales($) | Value

12/31/18($) | Net

Assets(%) | Dividends/

Distributions($) |

Dreyfus Institutional Preferred Government Plus Money Market Fund | 3,000,588 | 63,868,444 | 66,869,032 | - | - | 20,281 |

Dreyfus Institutional Preferred Government Money Market Fund, Institutional Shares | 14,165,799 | 97,657,078 | 102,972,625 | 8,850,252 | 2.0 | - |

Total | 17,166,387 | 161,525,522 | 169,841,657 | 8,850,252 | 2.0 | 20,281 |

See notes to financial statements.

14

STATEMENT OF ASSETS AND LIABILITIES

December 31, 2018

| | | | | | | |

| | | | | | |

| | | Cost | | Value | |

Assets ($): | | | | |

Investments in securities—See Statement of Investments

(including securities on loan, valued at $54,266,376)—Note 1(b): | | | |

Unaffiliated issuers | 432,578,983 | | 441,318,663 | |

Affiliated issuers | | 8,850,252 | | 8,850,252 | |

Receivable for investment securities sold | | 5,340,504 | |

Dividends, interest and securities lending income receivable | | 539,038 | |

Receivable for shares of Common Stock subscribed | | 55,375 | |

Prepaid expenses | | | | | 33,697 | |

| | | | | 456,137,529 | |

Liabilities ($): | | | | |

Due to The Dreyfus Corporation and affiliates—Note 3(c) | | | | 431,624 | |

Cash overdraft due to Custodian | | | | | 2,435,250 | |

Liability for securities on loan—Note 1(b) | | 8,850,252 | |

Payable for shares of Common Stock redeemed | | 1,256,990 | |

Directors fees and expenses payable | | 10,000 | |

Interest payable—Note 2 | | 2,335 | |

Accrued expenses | | | | | 127,551 | |

| | | | | 13,114,002 | |

Net Assets ($) | | | 443,023,527 | |

Composition of Net Assets ($): | | | | |

Paid-in capital | | | | | 433,720,232 | |

Total distributable earnings (loss) | | | | | 9,303,295 | |

Net Assets ($) | | | 443,023,527 | |

| | | | | | |

Net Asset Value Per Share | Class A | Class C | Class I | Class Y | |

Net Assets ($) | 403,112,678 | 3,338,429 | 36,322,544 | 249,876 | |

Shares Outstanding | 8,379,613 | 76,333 | 748,568 | 5,233 | |

Net Asset Value Per Share ($) | 48.11 | 43.74 | 48.52 | 47.75 | |

| | | | | | |

See notes to financial statements. | | | | | |

15

STATEMENT OF OPERATIONS

Year Ended December 31, 2018

| | | | | | | |

| | | | | | |

| | | | | | |

Investment Income ($): | | | | |

Income: | | | | |

Cash dividends (net of $3,308 foreign taxes withheld at source): | |

Unaffiliated issuers | | | 8,557,502 | |

Affiliated issuers | | | 20,281 | |

Income from securities lending—Note 1(b) | | | 94,599 | |

Total Income | | | 8,672,382 | |

Expenses: | | | | |

Management fee—Note 3(a) | | | 4,392,359 | |

Shareholder servicing costs—Note 3(c) | | | 1,681,680 | |

Professional fees | | | 88,803 | |

Directors’ fees and expenses—Note 3(d) | | | 61,498 | |

Registration fees | | | 60,706 | |

Distribution fees—Note 3(b) | | | 39,080 | |

Prospectus and shareholders’ reports | | | 37,232 | |

Loan commitment fees—Note 2 | | | 13,924 | |

Custodian fees—Note 3(c) | | | 4,820 | |

Interest expense—Note 2 | | | 3,491 | |

Miscellaneous | | | 45,696 | |

Total Expenses | | | 6,429,289 | |

Less—reduction in fees due to earnings credits—Note 3(c) | | | (310) | |

Net Expenses | | | 6,428,979 | |

Investment Income—Net | | | 2,243,403 | |

Realized and Unrealized Gain (Loss) on Investments—Note 4 ($): | | |

Net realized gain (loss) on investments | 37,116,597 | |

Net unrealized appreciation (depreciation) on investments | | | (118,004,288) | |

Net Realized and Unrealized Gain (Loss) on Investments | | | (80,887,691) | |

Net (Decrease) in Net Assets Resulting from Operations | | (78,644,288) | |

| | | | | | | |

See notes to financial statements. | | | | | |

16

STATEMENT OF CHANGES IN NET ASSETS

| | | | | | | | | | |

| | | | Year Ended December 31, |

| | | | 2018 | | 2017a | |

Operations ($): | | | | | | | | |

Investment income—net | | | 2,243,403 | | | | 1,927,480 | |

Net realized gain (loss) on investments | | 37,116,597 | | | | 68,623,757 | |

Net unrealized appreciation (depreciation)

on investments | | (118,004,288) | | | | 26,611,817 | |

Net Increase (Decrease) in Net Assets

Resulting from Operations | (78,644,288) | | | | 97,163,054 | |

Distributions ($): | |

Distributions to shareholders: | | | | | | | | |

Class A | | | (42,133,548) | | | | (55,541,786) | |

Class C | | | (419,306) | | | | (772,033) | |

Class I | | | (5,265,139) | | | | (12,143,058) | |

Class Y | | | (23,498) | | | | (137) | |

Total Distributions | | | (47,841,491) | | | | (68,457,014) | |

Capital Stock Transactions ($): | |

Net proceeds from shares sold: | | | | | | | | |

Class A | | | 11,899,593 | | | | 20,785,000 | |

Class C | | | 205,340 | | | | 886,253 | |

Class I | | | 18,587,593 | | | | 47,322,190 | |

Class Y | | | 596,408 | | | | - | |

Distributions reinvested: | | | | | | | | |

Class A | | | 39,540,454 | | | | 51,552,754 | |

Class C | | | 374,310 | | | | 690,943 | |

Class I | | | 5,003,542 | | | | 10,860,666 | |

Class Y | | | 23,387 | | | | - | |

Cost of shares redeemed: | | | | | | | | |

Class A | | | (71,694,692) | | | | (81,598,204) | |

Class C | | | (2,928,054) | | | | (6,192,712) | |

Class I | | | (86,263,850) | | | | (29,903,356) | |

Class Y | | | (302,206) | | | | - | |

Increase (Decrease) in Net Assets

from Capital Stock Transactions | (84,958,175) | | | | 14,403,534 | |

Total Increase (Decrease) in Net Assets | (211,443,954) | | | | 43,109,574 | |

Net Assets ($): | |

Beginning of Period | | | 654,467,481 | | | | 611,357,907 | |

End of Period | | | 443,023,527 | | | | 654,467,481 | |

17

STATEMENT OF CHANGES IN NET ASSETS (continued)

| | | | | | | | | | |

| | | | Year Ended December 31, |

| | | | 2018 | | 2017a | |

Capital Share Transactions (Shares): | |

Class Ab | | | | | | | | |

Shares sold | | | 200,012 | | | | 328,444 | |

Shares issued for distributions reinvested | | | 807,613 | | | | 828,048 | |

Shares redeemed | | | (1,198,702) | | | | (1,306,872) | |

Net Increase (Decrease) in Shares Outstanding | (191,077) | | | | (150,380) | |

Class Cb | | | | | | | | |

Shares sold | | | 3,713 | | | | 15,215 | |

Shares issued for distributions reinvested | | | 8,322 | | | | 12,038 | |

Shares redeemed | | | (54,312) | | | | (102,900) | |

Net Increase (Decrease) in Shares Outstanding | (42,277) | | | | (75,647) | |

Class Ib | | | | | | | | |

Shares sold | | | 300,113 | | | | 754,930 | |

Shares issued for distributions reinvested | | | 97,961 | | | | 173,754 | |

Shares redeemed | | | (1,454,882) | | | | (470,536) | |

Net Increase (Decrease) in Shares Outstanding | (1,056,808) | | | | 458,148 | |

Class Yb | | | | | | | | |

Shares sold | | | 9,530 | | | | - | |

Shares issued for distributions reinvested | | | 500 | | | | - | |

Shares redeemed | | | (4,815) | | | | - | |

Net Increase (Decrease) in Shares Outstanding | 5,215 | | | | - | |

| | | | | | | | | | |

a Distributions to shareholders include $1,926,247 Class A, $884,044 Class I and $12 Class Y of distributions from net investment income and $53,615,539 Class A, $772,033 Class C, $11,259,014 Class I and $125 Class Y distributions from net realized gains. Undistributed investment income—net was $686,269 in 2017 and is no longer presented as a result of the adoption of SEC’s Disclosure Update and Simplification Rule. | |

b During the period ended December 31, 2018, 917 Class C shares representing $50,857 were automatically converted to 841 Class A shares 4,804 Class A shares representing $303,409 were exchanged for 4,786 Class Y shares, 4,786 Class Y shares representing $300,537 were exchanged for 4,781 Class I shares, 624 Class A shares representing $39,700 were exchanged for 622 Class I shares and during the period ended December 31, 2017, 6,684 Class C shares representing $422,962 were automatically converted to 6,195 Class A shares and 1,201 Class A shares representing $74,977 were exchanged for 1,195 Class I shares. | |

See notes to financial statements.

| | | | | | | | |

18

FINANCIAL HIGHLIGHTS

The following tables describe the performance for each share class for the fiscal periods indicated. All information (except portfolio turnover rate) reflects financial results for a single fund share. Total return shows how much your investment in the fund would have increased (or decreased) during each period, assuming you had reinvested all dividends and distributions. These figures have been derived from the fund’s financial statements.

| | | | | | | |

| | | |

| | | |

| | | Year Ended December 31, |

Class A Shares | | 2018 | 2017 | 2016 | 2015 | 2014 |

Per Share Data ($): | | | | | | |

Net asset value, beginning of period | | 62.37 | 59.60 | 55.36 | 56.12 | 49.11 |

Investment Operations: | �� | | | | | |

Investment income—neta | | .22 | .18 | .33 | .33 | .15 |

Net realized and unrealized

gain (loss) on investments | | (9.12) | 9.65 | 4.51 | .64 | 7.01 |

Total from Investment Operations | | (8.90) | 9.83 | 4.84 | .97 | 7.16 |

Distributions: | | | | | | |

Dividends from

investment income—net | | (.26) | (.24) | (.18) | (.33) | (.15) |

Dividends from

net realized gain on investments | | (5.10) | (6.82) | (.42) | (1.40) | - |

Total Distributions | | (5.36) | (7.06) | (.60) | (1.73) | (.15) |

Net asset value, end of period | | 48.11 | 62.37 | 59.60 | 55.36 | 56.12 |

Total Return (%)b | | (14.31) | 16.64 | 8.81 | 1.69 | 14.58 |

Ratios/Supplemental Data (%): | | | | | | |

Ratio of total expenses to

average net assets | | 1.12 | 1.13 | 1.14 | 1.13 | 1.15 |

Ratio of net expenses to

average net assets | | 1.12 | 1.13 | 1.14 | 1.13 | 1.14 |

Ratio of net investment income

to average net assets | | .36 | .28 | .59 | .57 | .28 |

Portfolio Turnover Rate | | 68.30 | 63.75 | 60.22 | 60.96 | 73.99 |

Net Assets, end of period ($ x 1,000) | | 403,113 | 534,563 | 519,763 | 488,571 | 491,786 |

a Based on average shares outstanding.

b Exclusive of sales charge.

See notes to financial statements.

19

FINANCIAL HIGHLIGHTS (continued)

| | | | | | | |

| | | |

| | | |

| | | Year Ended December 31, |

Class C Shares | | 2018 | 2017 | 2016 | 2015 | 2014 |

Per Share Data ($): | | | | | | |

Net asset value, beginning of period | | 57.44 | 55.61 | 51.97 | 52.92 | 46.57 |

Investment Operations: | | | | | | |

Investment (loss)—neta | | (.26) | (.33) | (.12) | (.14) | (.28) |

Net realized and unrealized

gain (loss) on investments | | (8.34) | 8.98 | 4.18 | .59 | 6.63 |

Total from Investment Operations | | (8.60) | 8.65 | 4.06 | .45 | 6.35 |

Distributions: | | | | | | |

Dividends from

net realized gain on investments | | (5.10) | (6.82) | (.42) | (1.40) | - |

Net asset value, end of period | | 43.74 | 57.44 | 55.61 | 51.97 | 52.92 |

Total Return (%)b | | (15.04) | 15.64 | 7.90 | .82 | 13.64 |

Ratios/Supplemental Data (%): | | | | | | |

Ratio of total expenses to

average net assets | | 1.96 | 1.97 | 1.99 | 1.98 | 2.01 |

Ratio of net expenses to

average net assets | | 1.96 | 1.97 | 1.99 | 1.98 | 2.00 |

Ratio of net investment (loss) to

average net assets | | (.48) | (.57) | (.24) | (.26) | (.57) |

Portfolio Turnover Rate | | 68.30 | 63.75 | 60.22 | 60.96 | 73.99 |

Net Assets, end of period ($ x 1,000) | | 3,338 | 6,813 | 10,803 | 7,405 | 5,380 |

a Based on average shares outstanding.

b Exclusive of sales charge.

See notes to financial statements.

20

| | | | | | | |

| | | |

| | | |

| | | Year Ended December 31, |

Class I Shares | | 2018 | 2017 | 2016 | 2015 | 2014 |

Per Share Data ($): | | | | | | |

Net asset value, beginning of period | | 62.64 | 59.97 | 55.74 | 56.67 | 49.65 |

Investment Operations: | | | | | | |

Investment income—neta | | .38 | .33 | .49 | .52 | .26 |

Net realized and unrealized

gain (loss) on investments | | (9.18) | 9.70 | 4.50 | .57 | 7.10 |

Total from Investment Operations | | (8.80) | 10.03 | 4.99 | 1.09 | 7.36 |

Distributions: | | | | | | |

Dividends from

investment income—net | | (.22) | (.54) | (.34) | (.62) | (.34) |

Dividends from

net realized gain on investments | | (5.10) | (6.82) | (.42) | (1.40) | - |

Total Distributions | | (5.32) | (7.36) | (.76) | (2.02) | (.34) |

Net asset value, end of period | | 48.52 | 62.64 | 59.97 | 55.74 | 56.67 |

Total Return (%) | | (14.12) | 16.91 | 9.02 | 1.88 | 14.84 |

Ratios/Supplemental Data (%): | | | | | | |

Ratio of total expenses to

average net assets | | .89 | .90 | .94 | .93 | .94 |

Ratio of net expenses to

average net assets | | .89 | .90 | .94 | .93 | .94 |

Ratio of net investment income

to average net assets | | .60 | .53 | .85 | .92 | .50 |

Portfolio Turnover Rate | | 68.30 | 63.75 | 60.22 | 60.96 | 73.99 |

Net Assets, end of period ($ x 1,000) | | 36,323 | 113,090 | 80,790 | 35,359 | 7,617 |

a Based on average shares outstanding.

See notes to financial statements.

21

FINANCIAL HIGHLIGHTS (continued)

| | | | | | |

| | | |

| | | |

| | | Year Ended December 31, |

Class Y Shares | | 2018 | 2017 | 2016 | 2015a |

Per Share Data ($): | | | | | |

Net asset value, beginning of period | | 62.58 | 60.00 | 55.74 | 54.64 |

Investment Operations: | | | | | |

Investment income—netb | | .43 | .34 | .53 | .24 |

Net realized and unrealized gain

(loss) on investments | | (9.23) | 9.70 | 4.56 | 2.76 |

Total from Investment Operations | | (8.80) | 10.04 | 5.09 | 3.00 |

Distributions: | | | | | |

Dividends from investment income—net | | (.93) | (.64) | (.41) | (.50) |

Dividends from

net realized gain on investments | | (5.10) | (6.82) | (.42) | (1.40) |

Total Distributions | | (6.03) | (7.46) | (.83) | (1.90) |

Net asset value, end of period | | 47.75 | 62.58 | 60.00 | 55.74 |

Total Return (%) | | (14.11) | 16.93 | 9.18 | 5.46c |

Ratios/Supplemental Data (%): | | | | | |

Ratio of total expenses to average net assets | | .88 | .87 | .78 | .79d |

Ratio of net expenses to average net assets | | .88 | .87 | .78 | .79d |

Ratio of net investment

income to average net assets | | .71 | .54 | .98 | 1.25d |

Portfolio Turnover Rate | | 68.30 | 63.75 | 60.22 | 60.96 |

Net Assets, end of period ($ x 1,000) | | 250 | 1 | 1 | 1 |

a From September 1, 2015 (commencement of initial offering) to December 31, 2015.

b Based on average shares outstanding.

c Not annualized.

d Annualized.

See notes to financial statements.

22

NOTES TO FINANCIAL STATEMENTS

NOTE 1—Significant Accounting Policies:

Dreyfus Active MidCap Fund (the “fund”) is a separate diversified series of Strategic Funds, Inc. (the “Company”), which is registered under the Investment Company Act of 1940, as amended (the “Act”), as an open-end management investment company and operates as a series company currently offering six series, including the fund. The fund’s investment objective is to seek to maximize capital appreciation. The Dreyfus Corporation (the “Manager” or “Dreyfus”), a wholly-owned subsidiary of The Bank of New York Mellon Corporation (“BNY Mellon”), serves as the fund’s investment adviser.

MBSC Securities Corporation (the “Distributor”), a wholly-owned subsidiary of Dreyfus, is the distributor of the fund’s shares. The fund is authorized to issue 270 million shares of $.001 par value Common Stock. The fund currently has authorized four classes of shares: Class A (40 million shares authorized), Class C (15 million shares authorized), Class I (15 million shares authorized), Class T (100 million shares authorized) and Class Y (100 million shares authorized). Class A and Class T shares generally are subject to a sales charge imposed at the time of purchase. Class C shares are subject to a contingent deferred sales charge (“CDSC”) imposed on Class C shares redeemed within one year of purchase. Class C shares automatically convert to Class A shares ten years after the date of purchase, without the imposition of a sales charge. Class I and Class Y shares are sold at net asset value per share generally to institutional investors. As of the date of this report, the fund did not offer Class T shares for purchase. Other differences between the classes include the services offered to and the expenses borne by each class, the allocation of certain transfer agency costs, and certain voting rights. Income, expenses (other than expenses attributable to a specific class), and realized and unrealized gains or losses on investments are allocated to each class of shares based on its relative net assets.

The Company accounts separately for the assets, liabilities and operations of each series. Expenses directly attributable to each series are charged to that series’ operations; expenses which are applicable to all series are allocated among them on a pro rata basis.

The Financial Accounting Standards Board (“FASB”) Accounting Standards Codification is the exclusive reference of authoritative U.S. generally accepted accounting principles (“GAAP”) recognized by the FASB to be applied by nongovernmental entities. Rules and interpretive releases of the Securities and Exchange Commission (“SEC”) under authority of federal laws are also sources of authoritative GAAP for SEC

23

NOTES TO FINANCIAL STATEMENTS(continued)

registrants. The fund’s financial statements are prepared in accordance with GAAP, which may require the use of management estimates and assumptions. Actual results could differ from those estimates.

The Companyenters into contracts that contain a variety of indemnifications. The fund’s maximum exposure under these arrangements is unknown. The fund does not anticipate recognizing any loss related to these arrangements.

(a) Portfolio valuation: The fair value of a financial instrument is the amount that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date (i.e., the exit price). GAAP establishes a fair value hierarchy that prioritizes the inputs of valuation techniques used to measure fair value. This hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements).

Additionally, GAAP provides guidance on determining whether the volume and activity in a market has decreased significantly and whether such a decrease in activity results in transactions that are not orderly. GAAP requires enhanced disclosures around valuation inputs and techniques used during annual and interim periods.

Various inputs are used in determining the value of the fund’s investments relating to fair value measurements. These inputs are summarized in the three broad levels listed below:

Level 1—unadjusted quoted prices in active markets for identical investments.

Level 2—other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.).

Level 3—significant unobservable inputs (including the fund’s own assumptions in determining the fair value of investments).

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

Changes in valuation techniques may result in transfers in or out of an assigned level within the disclosure hierarchy. Valuation techniques used to value the fund’s investments are as follows:

Investments in securities are valued at the last sales price on the securities exchange or national securities market on which such securities are primarily traded. Securities listed on the National Market System for which

24

market quotations are available are valued at the official closing price or, if there is no official closing price that day, at the last sales price. For open short positions, asked prices are used for valuation purposes. Bid price is used when no asked price is available. Registered investment companies that are not traded on an exchange are valued at their net asset value. All of the preceding securities are generally categorized within Level 1 of the fair value hierarchy.

Securities not listed on an exchange or the national securities market, or securities for which there were no transactions, are valued at the average of the most recent bid and asked prices. These securities are generally categorized within Level 2 of the fair value hierarchy.

Fair valuing of securities may be determined with the assistance of a pricing service using calculations based on indices of domestic securities and other appropriate indicators, such as prices of relevant American Depository Receipts and futures. Utilizing these techniques may result in transfers between Level 1 and Level 2 of the fair value hierarchy.

When market quotations or official closing prices are not readily available, or are determined not to accurately reflect fair value, such as when the value of a security has been significantly affected by events after the close of the exchange or market on which the security is principally traded (for example, a foreign exchange or market), but before the fund calculates its net asset value, the fund may value these investments at fair value as determined in accordance with the procedures approved by the Company’s Board of Directors (the “Board”). Certain factors may be considered when fair valuing investments such as: fundamental analytical data, the nature and duration of restrictions on disposition, an evaluation of the forces that influence the market in which the securities are purchased and sold, and public trading in similar securities of the issuer or comparable issuers. These securities are either categorized within Level 2 or 3 of the fair value hierarchy depending on the relevant inputs used.

For restricted securities where observable inputs are limited, assumptions about market activity and risk are used and such securities are generally categorized within Level 3 of the fair value hierarchy.

The following is a summary of the inputs used as of December 31, 2018in valuing the fund’s investments:

25

NOTES TO FINANCIAL STATEMENTS(continued)

| | | | | |

| | Level 1 -

Unadjusted

Quoted Prices | Level 2 – Other

Significant

Observable

Inputs | Level 3 -

Significant

Unobservable

Inputs | Total |

Assets ($) | | | | |

Investments in Securities: | | | |

Equity Securities - Common Stocks† | 441,318,663 | - | - | 441,318,663 |

Investment Companies | 8,850,252 | - | - | 8,850,252 |

† See Statement of Investments for additional detailed categorizations.

At December 31, 2018, there were no transfers between levels of the fair value hierarchy. It is the fund’s policy to recognize transfers between levels at the end of the reporting period.

(b)Securities transactions and investment income: Securities transactions are recorded on a trade date basis. Realized gains and losses from securities transactions are recorded on the identified cost basis. Dividend income is recognized on the ex-dividend date and interest income, including, where applicable, accretion of discount and amortization of premium on investments, is recognized on the accrual basis.

Pursuant to a securities lending agreement with The Bank of New York Mellon, a subsidiary of BNY Mellon and an affiliate of Dreyfus, the fund may lend securities to qualified institutions. It is the fund’s policy that, at origination, all loans are secured by collateral of at least 102% of the value of U.S. securities loaned and 105% of the value of foreign securities loaned. Collateral equivalent to at least 100% of the market value of securities on loan is maintained at all times. Collateral is either in the form of cash, which can be invested in certain money market mutual funds managed by Dreyfus, or U.S. Government and Agency securities. The fund is entitled to receive all dividends, interest and distributions on securities loaned, in addition to income earned as a result of the lending transaction. Should a borrower fail to return the securities in a timely manner, The Bank of New York Mellon is required to replace the securities for the benefit of the fund or credit the fund with the market value of the unreturned securities and is subrogated to the fund’s rights against the borrower and the collateral. Additionally, the contractual maturity of security lending transactions are on an overnight and continuous basis. During the period ended December 31, 2018, The Bank of New York Mellon earned $19,613 from lending portfolio securities, pursuant to the securities lending agreement.

(c) Affiliated issuers: Investments in other investment companies advised by Dreyfus are considered “affiliated” under the Act.

26

(d) Dividends and distributions to shareholders: Dividends and distributions are recorded on the ex-dividend date. Dividends from investment income-net and dividends from net realized capital gains, if any, are normally declared and paid annually, but the fund may make distributions on a more frequent basis to comply with the distribution requirements of the Internal Revenue Code of 1986, as amended (the “Code”). To the extent that net realized capital gains can be offset by capital loss carryovers, it is the policy of the fund not to distribute such gains. Income and capital gain distributions are determined in accordance with income tax regulations, which may differ from GAAP.

(e) Federal income taxes: It is the policy of the fund to continue to qualify as a regulated investment company, if such qualification is in the best interests of its shareholders, by complying with the applicable provisions of the Code, and to make distributions of taxable income and net realized capital gain sufficient to relieve it from substantially all federal income and excise taxes.

As of and during the period ended December 31, 2018, the fund did not have any liabilities for any uncertain tax positions. The fund recognizes interest and penalties, if any, related to uncertain tax positions as income tax expense in the Statement of Operations. During the period ended December 31, 2018, the fund did not incur any interest or penalties.

Each tax year in the four-year period ended December 31, 2018 remains subject to examination by the Internal Revenue Service and state taxing authorities.

At December 31, 2018, the components of accumulated earnings on a tax basis were as follows: undistributed ordinary income $499,069, undistributed capital gains $173,477 and unrealized appreciation $8,591,150.

The tax character of distributions paid to shareholders during the fiscal periods ended December 31, 2018 and December 31, 2017 were as follows: ordinary income $4,655,716 and $5,861,876 , and long-term capital gains $43,185,775 and $62,595,138, respectively.

(f) New Accounting Pronouncements: In August 2018, the FASB issued Accounting Standards Update 2018-13, Fair Value Measurement (Topic 820): Disclosure Framework—Changes to the Disclosure Requirements for Fair Value Measurement (“ASU 2018-13”). The update provides guidance that eliminates, adds and modifies certain disclosure requirements for fair value measurements. ASU 2018-13 will be effective for annual periods beginning after December 15, 2019. Management is

27

NOTES TO FINANCIAL STATEMENTS(continued)

currently assessing the potential impact of these changes to future financial statements.

NOTE 2—Bank Lines of Credit:

The fund participates with other Dreyfus-managed long-term open-end funds in a $1.030 billion unsecured credit facility led by Citibank, N.A. (the “Citibank Credit Facility”) and a $300 million unsecured credit facility provided by The Bank of New York Mellon (the “BNYM Credit Facility”), each to be utilized primarily for temporary or emergency purposes, including the financing of redemptions (each, a “Facility”). The Citibank Credit Facility is available in two tranches: (i) Tranche A is in an amount equal to $830 million and is available to all long-term open-ended funds, including the fund, and (ii) Tranche B is in amount equal to $200 million and is available only to the Dreyfus Floating Rate Income Fund, a series of The Dreyfus/Laurel Funds, Inc. Prior to October 3, 2018, the unsecured credit facility with Citibank, N.A. was $830 million. In connection therewith, the fund has agreed to pay its pro rata portion of commitment fees for Tranche A of the Citibank Credit Facility and the BNYM Credit Facility. Interest is charged to the fund based on rates determined pursuant to the terms of the respective Facility at the time of borrowing.

The average amount of borrowings outstanding under the Facilities during the period ended December 31, 2018, was approximately $117,300 with a related weighted average annualized interest rate of 2.98%.

NOTE 3—Management Fee and Other Transactions with Affiliates:

(a)Pursuant to a management agreement with Dreyfus, the management fee is computed at the annual rate of .75% of the value of the fund’s average daily net assets and is payable monthly.

During the period ended December 31, 2018, the Distributor retained $3,814 from commissions earned on sales of the fund’s Class A shares and $612 from CDSC fees on redemptions of the fund’s Class C shares.

(b) Under the Distribution Plan adopted pursuant to Rule 12b-1 under the Act, Class C shares pay the Distributor for distributing its shares at an annual rate of .75% of the value of its average daily net assets. During the period ended December 31, 2018, Class C shares were charged $39,080 pursuant to the Distribution Plan.

(c)Under the Shareholder Services Plan, Class A and Class C shares pay the Distributor at an annual rate of .25% of the value of their average daily net assets for the provision of certain services. The services provided may include personal services relating to shareholder accounts, such as

28

answering shareholder inquiries regarding the fund and providing reports and other information, and services related to the maintenance of shareholder accounts. The Distributor may make payments to Service Agents (securities dealers, financial institutions or other industry professionals) with respect to these services. The Distributor determines the amounts to be paid to Service Agents. During the period ended December 31, 2018, Class A and Class C shares were charged $1,244,729and $13,027, respectively, pursuant to the Shareholder Services Plan.

The fund has arrangements with the transfer agent and the custodian whereby the fund may receive earnings credits when positive cash balances are maintained, which are used to offset transfer agency and custody fees. For financial reporting purposes, the fund includes net earnings credits, if any, as an expense offset in the Statement of Operations.

The fund compensates Dreyfus Transfer, Inc., a wholly-owned subsidiary of Dreyfus, under a transfer agency agreement for providing transfer agency and cash management services for the fund. The majority of transfer agency fees are comprised of amounts paid on a per account basis, while cash management fees are related to fund subscriptions and redemptions. During the period ended December 31, 2018, the fund was charged $188,347 for transfer agency services. These fees are included in Shareholder servicing costs in the Statement of Operations.

The fund compensates The Bank of New York Mellon under a custody agreement for providing custodial services for the fund. These fees are determined based on net assets, geographic region and transaction activity. During the period ended December 31, 2018, the fund was charged $4,820 pursuant to the custody agreement. These fees were offset by earnings credits of $310.

During the period ended December 31, 2018, the fund was charged $12,774 for services performed by the Chief Compliance Officer and his staff. These fees are included in Miscellaneous in the Statement of Operations.

The components of “Due to The Dreyfus Corporation and affiliates” in the Statement of Assets and Liabilities consist of: management fees $296,025, Distribution Plan fees $2,382, Shareholder Services Plan fees $89,086, custodian fees $6,000, Chief Compliance Officer fees $6,289 and transfer agency fees $31,842.

(d) Each Board member also serves as a Board member of other funds within the Dreyfus complex. Annual retainer fees and attendance fees are allocated to each fund based on net assets.

29

NOTES TO FINANCIAL STATEMENTS(continued)

NOTE 4—Securities Transactions:

The aggregate amount of purchases and sales of investment securities, excluding short-term securities, during the period ended December 31, 2018, amounted to $397,780,502 and $526,363,772, respectively.

At December 31, 2018, the cost of investments for federal income tax purposes was $441,577,765; accordingly, accumulated net unrealized appreciation on investments was $8,591,150, consisting of $55,470,486 gross unrealized appreciation and $46,879,336 gross unrealized depreciation.

NOTE 5—Pending Legal Matters:

The fund and many other entities have been named as defendants in numerous pending litigations as a result of their participation in the leveraged buyout transaction (“LBO”) of the Tribune Company (“Tribune”).

The State Law Cases: The Tribune LBO was executed in two-steps - a voluntary tender offer in June 2007, and a mandatory go-private merger in December 2007. In 2008, approximately one year after the LBO was concluded, Tribune filed for bankruptcy protection under Chapter 11 of the Bankruptcy Code (the “Code”). Beginning in June 2011, Tribune creditors filed complaints in various courts throughout the country, which alleged that the payments made to shareholders in the LBO were “fraudulent conveyances” under state and/or federal law, and that the shareholders must return the payments they received for their shares to satisfy the plaintiffs’ unpaid claims (collectively, “the state law cases”). The state law cases were consolidated for pre-trial proceedings in the United States District Court for the Southern District of New York, in a case styledIn re Tribune Company Fraudulent Conveyance Litigation(S.D.N.Y. Nos. 11-md-2296 and 12-mc-2296 (RJS) (“Tribune MDL”)). On November 6, 2012, the defendants filed a motion to dismiss most of the cases in the Tribune MDL. On September 23, 2013, the Court dismissed 50 cases, including at least one case in which the fund was a defendant. On September 30, 2013, plaintiffs appealed the District Court’s decision to the U.S. Court of Appeals for the Second Circuit. On March 29, 2016, the Second Circuit affirmed the dismissal on the ground that the plaintiffs’ claims were preempted by section 546(e) of the Code, which exempts qualified transfers that were made “… by or to (or for the benefit of),” among other specified entities, “a financial institution …” On September 9, 2016, Plaintiffs filed a petition forcertiorarito the U.S. Supreme Court.

During the pendency of the plaintiffs’cert. petition, the Supreme Court agreed to hear the appeal ofMerit Management Group, LP v. FTIConsulting,

30

Inc. (“Merit Mgmt.”), a Seventh Circuit case that concerned the scope of Section 546(e) of the Code. In contrast to the Second Circuit, the Seventh Circuit had held that Section 546(e) does not exempt qualified transfers from avoidance that passed through “financial institutions.”

On February 27, 2018, the Supreme Court affirmed the Seventh Circuit’s decision. Noting that “the parties … d[id] not contend that either the debtor or petitioner … qualified as a ‘financial institution,’” the Court declined to address the effect that such an assertion would have had on the application Section 546(e). While theMerit Mgmt. decision likely will make it more difficult for some defendants to assert a defense under Section 546(e), the decision appears to be less consequential for registered investment company defendants, such as the Dreyfus Fund defendants, which are specifically defined as “financial institutions” under Section 101(22)(B) of the Code.

On April 3, 2018, Justices Kennedy and Thomas issued a Statement stating that “consideration of [the petition for certiorari filed by the Tribune plaintiffs] will be deferred for an additional period of time” to allow the Second Circuit or the District Court to consider whether to vacate the earlier judgment or provide other relief in light ofMeritMgmt. On April 10, 2018, the plaintiffs/appellants moved the Second Circuit to recall its mandate, vacate its decision, and remand the case to the district court for further proceedings. The defendants’ filed an opposition brief on April 20, 2018; plaintiffs/appellants filed their reply on April 27, 2018. On May 15, 2018, the Second Circuit issued an Order stating that “the mandate in this case is recalled in anticipation of further panel review.” As of February 14, 2019, there has been no subsequent activity in the state law cases.

TheFitzSimonsLitigation: On November 1, 2010, a case styledThe Official Committee of Unsecured Creditors of Tribune Co. v. FitzSimons,et al., Adv. Pro. No-10-54010(KJC) was filed in the United States Bankruptcy Court for the District of Delaware. (“theFitzSimons Litigation”). The case was subsequently transferred to the Tribune MDL. Count One of the multi-count Complaint sought recovery of alleged “fraudulent conveyances” from more than 5,000 Tribune shareholders (“Shareholder Defendants”), including the fund, that participated in the Tribune LBO. On January 10, 2013, Mark S. Kirchner, as Litigation Trustee for the Tribune Litigation Trust, became the successor plaintiff to the Creditors Committee. The case is now proceeding as:Mark S. Kirchner, as Litigation Trustee for the Tribune Litigation Trust v. FitzSimons, et al., S.D.N.Y. No. 12-cv-2652 (RJS). On August 1, 2013, the plaintiff filed a Fifth Amended Complaint, which did not change the legal basis of the claims against the Shareholder Defendants. On May 23, 2014, the defendants filed a motion to dismiss

31

NOTES TO FINANCIAL STATEMENTS(continued)

Count One against the Shareholder Defendants, which the Court granted on January 9, 2017. The plaintiff then sought leave to file an interlocutory appeal. On February 23, 2017, the Court entered an order stating that it would permit the plaintiff to file an interlocutory appeal after the Court decided other pending motions.

On March 8, 2018, following the U.S. Supreme Court’s decision inMerit Management, the Plaintiff in the FitzSimons Litigation submitted a letter to the Court seeking permission to file another amended complaint or a motion for leave to amend in order to add a claim of constructive fraudulent transfer. On June 18, 2018, the Court issued an order staying the Trustee’s request pending further action by the Second Circuit in the state law cases. The Court also ordered counsel for all of the parties to file a joint letter “indicating how they wish to proceed with respect to a potential global resolution of this multi-district litigation.” On July 9, 2018, the parties submitted the joint letter requested by the Court expressing their views regarding a potential mediation. On November 30, 2018, the Court issued an Opinion and Order resolving the remaining motions by dismissing most, but not all, of the claims asserted against the individual defendants. After Judge Richard J. Sullivan issued the Opinion and Order, the U.S. Judicial Panel on Multidistrict Litigation reassigned the entire litigation to Judge Denise Cote. As of February 14, 2019, there has been no subsequent activity in FitzSimons Litigation.

At this stage in the proceedings, management does not believe that a loss is probable and, in any event, is unable to reasonably estimate the possible loss that may result.

32

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Shareholders and the Board of Directors of Dreyfus Active MidCap Fund

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities of Dreyfus Active MidCap Fund (the “Fund”) (one of the funds constituting Strategic Funds, Inc.), including the statements of investments and investments in affiliated issuers, as of December 31, 2018, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, the financial highlights for each of the five years in the period then ended and the related notes (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund (one of the funds constituting Strategic Funds, Inc.) at December 31, 2018, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended and its financial highlights for each of the five years in the period then ended, in conformity with U.S. generally accepted accounting principles.

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Fund is not required to have, nor were we engaged to perform, an audit of the Fund’s internal control over financial reporting. As part of our audits, we are required to obtain an understanding of internal control over financial reporting, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of December 31, 2018, by correspondence with the custodian and others or by other appropriate auditing procedures where replies from others were not received. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

We have served as the auditor of one or more Dreyfus investment companies since at least 1957, but we are unable to determine the specific year.

New York, New York

February 27, 2019

33

IMPORTANT TAX INFORMATION(Unaudited)

In accordance with federal tax law, the fund hereby reports 100% of the ordinary dividends paid during the fiscal year ended December 31, 2018 as qualifying for the corporate dividends received deduction. For the fiscal year ended December 31, 2018, certain dividends paid by the fund may be subject to a maximum tax rate of 15%, as provided for by the Jobs and Growth Tax Relief Reconciliation Act of 2003. Of the distributions paid during the fiscal year, $4,655,716 represents the maximum amount that may be considered qualified dividend income. Shareholders will receive notification in early 2019 of the percentage applicable to the preparation of their 2018 income tax returns. Also, the fund hereby reports $.2207 per share as a short-term capital gain distribution and $.5958 per share as a long-term capital gain distribution paid on March 22, 2018 and the fund also reports $4.2820 per share as a long-term capital gain distribution paid on December 20, 2018.

34

INFORMATION ABOUT THE RENEWAL OF THE FUND’S MANAGEMENT AGREEMENT (Unaudited)

At a meeting of the fund’s Board of Directors held on November 5-6, 2018, the Board considered the renewalof the fund’s Management Agreement pursuant to which Dreyfus provides the fund with investment advisory and administrative services (the “Agreement”). The Board members, a majority of whom are not “interested persons” (as defined in the Investment Company Act of 1940, as amended) of the fund, were assisted in their review by independent legal counsel and met with counsel in executive session separate from Dreyfus representatives. In considering the renewal of the Agreement, the Board considered all factors that it believed to be relevant, including those discussed below. The Board did not identify any one factor as dispositive, and each Board member may have attributed different weights to the factors considered.

Analysis of Nature, Extent, and Quality of Services Provided to the Fund. The Board considered information provided to it at the meeting and in previous presentations from Dreyfus representatives regarding the nature, extent, and quality of the services provided to funds in the Dreyfus fund complex. Dreyfus provided the number of open accounts in the fund, the fund’s asset size and the allocation of fund assets among distribution channels. Dreyfus also had previously provided information regarding the diverse intermediary relationships and distribution channels of funds in the Dreyfus fund complex (such as retail direct or intermediary, in which intermediaries typically are paid by the fund and/or Dreyfus) and Dreyfus’ corresponding need for broad, deep, and diverse resources to be able to provide ongoing shareholder services to each intermediary or distribution channel, as applicable to the fund.

The Board also considered research support available to, and portfolio management capabilities of, the fund’s portfolio management personnel and that Dreyfus also provides oversight of day-to-day fund operations, including fund accounting and administration and assistance in meeting legal and regulatory requirements. The Board also considered Dreyfus’ extensive administrative, accounting and compliance infrastructures. The Board also considered portfolio management’s brokerage policies and practices (including policies and practices regarding soft dollars) and the standards applied in seeking best execution.