UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-03980

Morgan Stanley Institutional Fund Trust

(Exact name of registrant as specified in charter)

| 522 Fifth Avenue, New York, New York | | 10036 |

| (Address of principal executive offices) | | (Zip code) |

John H. Gernon

522 Fifth Avenue, New York, New York 10036

(Name and address of agent for service)

Registrant's telephone number, including area code: 212-762-1886

Date of fiscal year end: September 30,

Date of reporting period: September 30, 2023

Item 1 - Report to Shareholders

Morgan Stanley Institutional Fund Trust

Core Plus Fixed Income Portfolio

Annual Report

September 30, 2023

Morgan Stanley Institutional Fund Trust

Annual Report — September 30, 2023

Table of Contents (unaudited)

Shareholders' Letter | | | 2 | | |

Expense Example | | | 3 | | |

Investment Overview | | | 4 | | |

Portfolio of Investments | | | 7 | | |

Statement of Assets and Liabilities | | | 16 | | |

Statement of Operations | | | 18 | | |

Statements of Changes in Net Assets | | | 19 | | |

Financial Highlights | | | 21 | | |

Notes to Financial Statements | | | 26 | | |

Report of Independent Registered Public Accounting Firm | | | 38 | | |

Investment Advisory Agreement Approval | | | 39 | | |

Liquidity Risk Management Program | | | 41 | | |

Important Notices | | | 42 | | |

Federal Tax Notice | | | 43 | | |

U.S. Customer Privacy Notice | | | 44 | | |

Trustees and Officers Information | | | 47 | | |

This report is authorized for distribution only when preceded or accompanied by a prospectus or summary prospectus of the applicable Fund of the Morgan Stanley Institutional Fund Trust. To receive a prospectus and/or statement of additional information ("SAI"), which contains more complete information such as investment objectives, charges, expenses, policies for voting proxies, risk considerations and describes in detail each of the Fund's investment policies to the prospective investor, please call toll free 1 (800) 869-6397. Please read the prospectuses carefully before you invest or send money.

Additionally, you can access information about the Fund, including performance, characteristics and investment team commentary through Morgan Stanley Investment Management's website: www.morganstanley.com/im.

Market forecasts provided in this report may not necessarily come to pass. There is no guarantee that any sectors mentioned will continue to perform as discussed herein or that securities in such sectors will be held by the Fund in the future. There is no assurance that a fund will achieve its investment objective. Funds are subject to market risk, which is the possibility that market values of securities owned by the Fund will decline and, therefore, the value of the Fund's shares may be less than what you paid for them. Accordingly, you can lose money investing in this Fund. Please see the prospectus for more complete information on investment risks.

1

Morgan Stanley Institutional Fund Trust

Annual Report — September 30, 2023

Shareholders' Letter (unaudited)

Dear Shareholders,

We are pleased to provide this Annual Report, in which you will learn how your investment in Core Plus Fixed Income Portfolio (the "Fund") performed during the latest twelve-month period.

Morgan Stanley Investment Management is a client-centric, investor-led organization. Our global presence, intellectual capital, and breadth of products and services enable us to partner with investors to meet the evolving challenges of today's financial markets. We aim to deliver superior investment service and to empower our clients to make the informed decisions that help them reach their investment goals.

As always, we thank you for selecting Morgan Stanley Investment Management, and look forward to working with you in the months and years ahead.

Sincerely,

John H. Gernon

President and Principal Executive Officer

October 2023

2

Morgan Stanley Institutional Fund Trust

Annual Report — September 30, 2023

Expense Example (unaudited)

Core Plus Fixed Income Portfolio

As a shareholder of the Fund, you may incur two types of costs: (1) transactional costs, including sales charge (loads) on purchase payments; and (2) ongoing costs, which may include advisory fees, administration fees, distribution and shareholder services fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

This example is based on an investment of $1,000 invested at the beginning of the six-month period ended September 30, 2023 and held for the entire six-month period.

Actual Expenses

The table below provides information about actual account values and actual expenses. You may use the information in this table, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the table under the heading entitled "Actual Expenses Paid During Period" to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The table below provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads, if applicable). Therefore, the information for each class in the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | Beginning

Account

Value

4/1/23 | | Actual Ending

Account

Value

9/30/23 | | Hypothetical

Ending Account

Value | | Actual

Expenses

Paid

During

Period* | | Hypothetical

Expenses Paid

During Period* | | Net

Expense

Ratio

During

Period** | |

Core Plus Fixed Income Portfolio Class I | | $ | 1,000.00 | | | $ | 968.30 | | | $ | 1,023.06 | | | $ | 1.97 | | | $ | 2.03 | | | | 0.40 | % | |

Core Plus Fixed Income Portfolio Class A | | | 1,000.00 | | | | 965.80 | | | | 1,021.36 | | | | 3.65 | | | | 3.75 | | | | 0.74 | | |

Core Plus Fixed Income Portfolio Class L | | | 1,000.00 | | | | 964.40 | | | | 1,020.06 | | | | 4.92 | | | | 5.06 | | | | 1.00 | | |

Core Plus Fixed Income Portfolio Class C | | | 1,000.00 | | | | 962.90 | | | | 1,017.75 | | | | 7.18 | | | | 7.39 | | | | 1.46 | | |

Core Plus Fixed Income Portfolio Class R6 | | | 1,000.00 | | | | 968.50 | | | | 1,023.31 | | | | 1.73 | | | | 1.78 | | | | 0.35 | | |

* Expenses are calculated using each Fund Class' annualized net expense ratio (as disclosed), multiplied by the average account value over the period and multiplied by 183/365 (to reflect the most recent one-half year period).

** Annualized.

3

Morgan Stanley Institutional Fund Trust

Annual Report — September 30, 2023

Investment Overview (unaudited)

Core Plus Fixed Income Portfolio

The Fund seeks above-average total return over a market cycle of three to five years.

Performance

For the fiscal year ended September 30, 2023, the Fund's Class I shares had a total return based on net asset value and reinvestment of distributions per share of 2.03%, net of fees. The Fund's Class I shares outperformed against the Fund's benchmark, the Bloomberg U.S. Aggregate Index(i) (the "Index"), which returned 0.64%.

Factors Affecting Performance

• Government bond yields rose over the period in the U.S. and throughout the world as central banks maintained hawkish positions in their fight against inflation. "Higher for longer" rhetoric was accompanied by recession fears, creating heightened levels of uncertainty in the markets. The portfolio's flat to mildly overweight position in U.S. duration detracted from relative performance, whereas the portfolio's exposure in the euro area, the U.K. and Australia contributed to relative performance. The portfolio's rates positioning in emerging markets (South Africa, Dominican Republic and Indonesia) also contributed to relative performance, as did the portfolio's overweight to emerging markets government-related debt.

• Over the period, the portfolio's investment grade corporate bond positioning contributed to relative performance, as did the convertible bond allocation.

• Overall securitized sector positioning contributed to relative performance during the period amid an increasingly challenging and volatile market. The overweight positioning to asset-backed securities (ABS) was the main contributor. The out-of-Index allocation to non-agency residential mortgage-backed securities (RMBS) and overweight to commercial mortgage-backed securities (CMBS) also contributed to relative performance. The Fund's agency RMBS underweight also helped relative performance as they also underperformed similar-duration Treasuries.

• Currency positioning was mostly flat in terms of relative performance impact, with the long positions in New Zealand dollar and Norwegian krone detracting marginally while the long positions in Mexican peso and Brazilian real contributed on the margin.

Management Strategies

• We believe a reasonable explanation for the market volatility seen in the past few months of the reporting period goes as follows: U.S. economic growth has been accelerating in 2023, which surprised analysts; the U.S. budget situation looks bad, sending more and more U.S. Treasuries into the market at the same time that the Federal Reserve (Fed) is shrinking its balance sheet; and the Fed has been adamant that the inflation game has not been won, so markets should expect the Fed to keep rates unchanged (at the September 2023 Federal Open Market Committee meeting, the Fed eliminated several rate cuts from its 2024 forecasts). In other words, rates would be kept higher for longer; market positioning seems to be skewed toward long interest-rate risk, making bonds vulnerable to disappointing news; and lastly, the coup de grace is that the U.S. yield curve has been highly inverted (meaning that yields on shorter-maturity U.S. Treasury bonds have been higher than yields on longer-maturity U.S. Treasury bonds), making longer-maturity bonds less attractive than shorter-maturity bonds. Add it all up, and you have a good cumulative narrative as to why longer-term yields rose in this period. Importantly, we believe that while the velocity of the Treasury market sell-off looks extreme, the end point — a U.S. Treasury 10-year yield ending September 2023 at 4.57%(ii) — does not.

• One potential casualty of higher yields, wider credit spreads and softer equity prices is the economy, particularly in the U.S. Until September 2023, the probability of a "soft landing" grew as falling inflation, stable unemployment and reasonable growth looked increasingly feasible. However, we believe that the rise in yields on the back of

(i) "Bloomberg®" and the Bloomberg Index/Indices used are service marks of Bloomberg Finance L.P. and its affiliates, and have been licensed for use for certain purposes by Morgan Stanley Investment Management (MSIM). Bloomberg is not affiliated with MSIM, does not approve, endorse, review, or recommend any product, and does not guarantee the timeliness, accurateness, or completeness of any data or information relating to any product.

(ii) Source: Bloomberg L.P. Data as of September 30, 2023.

4

Morgan Stanley Institutional Fund Trust

Annual Report — September 30, 2023

Investment Overview (unaudited) (cont'd)

Core Plus Fixed Income Portfolio

increased confidence the Fed would not lower rates as much and as soon as expected — resulting in a meaningful rise in real interest rates — increases the chances of a harder landing and possibly a recession. While we believe it is far too early to assign this as the most likely scenario given what we currently know about economic activity, credit and equity markets have had to price in this higher probability, resulting in poor performance toward the end of the reporting period. We are also concerned about the ability of higher-risk assets to outperform in an era of inverted yield curves and high cash rates. We believe that the solid fundamentals we have witnessed in the year-to-date through September 2023 (low default rates, more credit rating upgrades than downgrades, etc.) could easily begin to deteriorate over the months ahead. We therefore remain cautious about maintaining anything above a modestly long position in lower-quality fixed income. We believe that selectivity will remain of paramount importance. Avoiding defaults and blow-ups will eventually be key as higher rates and refinancing risks feed into corporate performance and outlooks. The high yields on offer will help blunt underperformance if fundamentals do deteriorate, in our view.

• Within securitized assets, we continue to favor shorter-maturity securitized credit (RMBS, ABS, selected CMBS) as offering the best opportunities in fixed income. That said, the outlook has modestly deteriorated as household balance sheets come under more pressure and excess savings run down. We are trying to take advantage of higher yields on higher quality issuers to achieve our target returns, rather than venturing down the risk/rating spectrum. Our favorite category of securitized credit remains non-agency residential mortgages, despite challenging home affordability. Somewhat surprisingly, U.S. housing looks like it may have bottomed out, with prices rising once again.

• During the period, economic growth outside the U.S. has been much less impressive, with Europe and China flirting with recessionary conditions. However, that did not stop European and emerging markets bond yields from rising over the third quarter of 2023 (China's yields had essentially not moved at all). If growth outside the U.S. had not been so weak, U.S. yields probably would have moved even higher. While non-U.S. bond markets generally outperformed U.S. Treasuries, absolute

yields were driven higher by the surprising strength of the U.S. economy and the doggedness of the Fed in combating inflation with high rates. Therefore, although we believe most central banks are likely finished hiking rates, we expect we are not finished with the era of high rates, the maintenance of which remains critical to win the war against inflation. At period end, although valuations have improved considerably, we are not yet ready to declare they have peaked and remain cautious in interest rate positioning in portfolio. While we believe growth fundamentals are worse outside the U.S. (except ironically perhaps for Japan), we do not think non-U.S. developed market government bonds are much more attractive than U.S. Treasuries. There is a reasonable probability that growth dynamics are in the process of bottoming in Europe and Asia, and could turn up next year at the very time the surge in real yields slows the U.S. economy in our view. As such, at period end, we were fairly neutral on developed market government markets on a relative basis. We did think selective emerging market bond markets look attractive, but that attractiveness has been undermined by the strong U.S. economy, hawkish Fed and rising yields. At period end, we believed that selectivity remains the name of the game and patience is necessary to realize value in many of these markets while the U.S. economy and U.S. dollar outperform.

5

Morgan Stanley Institutional Fund Trust

Annual Report — September 30, 2023

Investment Overview (unaudited) (cont'd)

Core Plus Fixed Income Portfolio

* Minimum Investment

In accordance with SEC regulations, the Fund's performance shown assumes that all recurring fees (including management fees) were deducted and all dividends and distributions were reinvested. The performance of Class A, Class L, Class C and Class R6 shares will vary from the performance of Class I shares based upon their different inception dates and will be negatively impacted by additional fees assessed to those classes (where applicable).

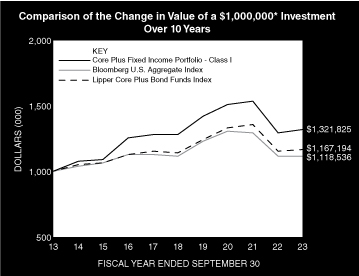

Performance Compared to the Bloomberg U.S. Aggregate Index(1) and the Lipper Core Plus Bond Funds Index(2)

| | | Period Ended September 30, 2023

Total Returns(3) | |

| | | | | Average Annual | |

| | | One

Year | | Five

Years | | Ten

Years | | Since

Inception(9) | |

Fund — Class I Shares

w/o sales charges(4) | | | 2.03 | % | | | 0.61 | % | | | 2.83 | % | | | 6.23 | % | |

Fund — Class A Shares

w/o sales charges(5) | | | 1.59 | | | | 0.26 | | | | 2.47 | | | | 3.83 | | |

Fund — Class A Shares

with maximum 3.25%

sales charges(5) | | | –1.73 | | | | –0.39 | | | | 2.13 | | | | 3.70 | | |

Fund — Class L Shares

w/o sales charges(6) | | | 1.30 | | | | –0.02 | | | | 2.21 | | | | 2.24 | | |

Fund — Class C Shares

w/o sales charges(7) | | | 0.84 | | | | –0.44 | | | | — | | | | 1.07 | | |

Fund — Class C Shares

with maximum 1.00%

deferred sales charges(7) | | | –0.12 | | | | –0.44 | | | | — | | | | 1.07 | | |

Fund — Class R6 Shares

w/o sales charges(8) | | | 1.97 | | | | 0.64 | | | | — | | | | 0.71 | | |

Bloomberg U.S. Aggregate Index | | | 0.64 | | | | 0.10 | | | | 1.13 | | | | 5.91 | | |

Lipper Core Plus Bond Funds Index | | | 1.46 | | | | 0.49 | | | | 1.56 | | | | — | | |

Performance data quoted represents past performance, which is no guarantee of future results, and current performance may be lower or higher than the figures shown. Performance assumes that all dividends and distributions, if any, were reinvested. For the most recent month-end performance figures, please visit www.morganstanley.com/im. Investment returns and principal value will fluctuate so that Fund shares, when redeemed, may be worth more or less than their original cost. Total returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance of share classes will vary due to differences in sales charges and expenses. The Fund returns are calculated based on the net asset value as of the last business day of the period.

(1) The Bloomberg U.S. Aggregate Index tracks the performance of U.S. government agency and Treasury securities, investment-grade corporate debt securities, agency mortgage-backed securities, asset-backed securities and commercial mortgage-backed securities. The Index is unmanaged and its returns do not include any sales charges or fees. Such costs would lower performance. It is not possible to invest directly in an index.

(2) The Lipper Core Plus Bond Funds Index is an equally weighted performance index of the largest qualifying funds (based on net assets) in the Lipper Core Plus Bond Funds classification. The Index, which is adjusted for capital gains distributions and income dividends, is unmanaged and should not be considered an investment. There are currently 30 funds represented in this Index. As of the date of this report, the Fund was in the Lipper Core Plus Bond Funds classification.

(3) Total returns for the Fund reflect expenses waived and/or reimbursed, if applicable, by the Adviser. Without such waivers and/or reimbursements, total returns would have been lower.

(4) Commenced operations on November 14, 1984.

(5) Commenced offering on November 7, 1996.

(6) Commenced offering on April 27, 2012.

(7) Commenced offering on April 30, 2015. Class C shares will generally convert to Class A shares approximately eight years after the end of the calendar month in which the shares were purchased. Performance for periods greater than eight years reflects this conversion (beginning April 2023).

(8) Commenced offering on June 15, 2018.

(9) For comparative purposes, average annual since inception returns listed for the Indexes refer to the inception date of Class I of the Fund, not the inception of the Indexes.

6

Morgan Stanley Institutional Fund Trust

Annual Report — September 30, 2023

Portfolio of Investments

Core Plus Fixed Income Portfolio

| | | Face

Amount

(000) | | Value

(000) | |

Fixed Income Securities (96.9%) | |

Agency Fixed Rate Mortgages (19.7%) | |

Federal Home Loan Mortgage Corporation, | |

Conventional Pools: | |

3.50%, 8/1/49 | | $ | 151 | | | $ | 130 | | |

4.00%, 4/1/49 - 11/1/49 | | | 488 | | | | 438 | | |

4.50%, 2/1/49 | | | 294 | | | | 274 | | |

Gold Pools: | |

3.50%, 1/1/44 - 4/1/49 | | | 742 | | | | 655 | | |

4.00%, 6/1/44 - 1/1/48 | | | 279 | | | | 255 | | |

5.41%, 7/1/37 - 8/1/37 | | | 10 | | | | 9 | | |

5.44%, 1/1/37 - 2/1/38 | | | 40 | | | | 36 | | |

5.46%, 8/1/37 - 1/1/38 | | | 26 | | | | 25 | | |

5.50%, 8/1/37 - 11/1/37 | | | 39 | | | | 37 | | |

5.62%, 12/1/36 - 8/1/37 | | | 43 | | | | 41 | | |

6.00%, 10/1/36 - 8/1/38 | | | 36 | | | | 37 | | |

6.50%, 12/1/25 - 8/1/33 | | | 45 | | | | 46 | | |

7.00%, 6/1/28 - 11/1/31 | | | 13 | | | | 13 | | |

Federal National Mortgage Association, | |

Conventional Pools: | |

3.00%, 9/1/46 - 1/1/50 | | | 2,646 | | | | 2,206 | | |

3.50%, 8/1/45 - 1/1/50 | | | 2,786 | | | | 2,419 | | |

4.00%, 11/1/41 - 9/1/49 | | | 2,427 | | | | 2,211 | | |

4.50%, 3/1/41 - 8/1/49 | | | 946 | | | | 886 | | |

5.00%, 3/1/41 | | | 76 | | | | 75 | | |

5.50%, 6/1/35 - 1/1/37 | | | 27 | | | | 27 | | |

5.62%, 12/1/36 | | | 17 | | | | 16 | | |

6.50%, 4/1/24 - 1/1/34 | | | 356 | | | | 361 | | |

7.00%, 5/1/28 - 12/1/33 | | | 53 | | | | 53 | | |

9.50%, 4/1/30 | | | 8 | | | | 8 | | |

October TBA | |

3.50%, 10/1/53 (a) | | | 24,675 | | | | 21,224 | | |

4.00%, 10/1/53 (a) | | | 7,350 | | | | 6,548 | | |

4.50%, 10/1/52 (a) | | | 24,850 | | | | 22,828 | | |

5.00%, 10/1/53 (a) | | | 9,050 | | | | 8,543 | | |

5.50%, 10/1/53 (a) | | | 32,700 | | | | 31,617 | | |

6.00%, 10/1/53 (a) | | | 5,550 | | | | 5,480 | | |

Government National Mortgage Association, | |

Various Pools: | |

3.50%, 11/20/40 - 7/20/49 | | | 735 | | | | 658 | | |

4.00%, 8/20/41 - 11/20/49 | | | 1,942 | | | | 1,773 | | |

4.50%, 4/20/49 - 7/20/49 | | | 178 | | | | 164 | | |

5.00%, 12/20/48 | | | 23 | | | | 21 | | |

6.50%, 5/15/40 | | | 187 | | | | 191 | | |

| | | | 109,305 | | |

Asset-Backed Securities (9.4%) | |

AASET U.S. Ltd., | |

4.45%, 11/18/38 (b) | | | 1,893 | | | | 1,686 | | |

ACHV ABS Trust, | |

Series 2023-3PL Class B | |

7.17%, 8/19/30 (b) | | | 200 | | | | 201 | | |

| | | Face

Amount

(000) | | Value

(000) | |

Allegro CLO XI Ltd., | |

3 Month Term SOFR + 1.65%,

6.97%, 1/19/33 (b)(c) | | $ | 2,150 | | | $ | 2,151 | | |

American Homes 4 Rent Trust, | |

6.07%, 10/17/52 (b) | | | 1,001 | | | | 981 | | |

Aqua Finance Trust, | |

3.47%, 7/16/40 (b) | | | 734 | | | | 674 | | |

BCMSC Trust, | |

7.51%, 1/15/29 (c) | | | 1,157 | | | | 1,100 | | |

Blackbird Capital Aircraft, | |

2.44%, 7/15/46 (b) | | | 1,229 | | | | 1,051 | | |

Blackbird Capital Aircraft Lease

Securitization Ltd., | |

5.68%, 12/16/41 (b) | | | 694 | | | | 501 | | |

Cascade MH Asset Trust, | |

4.00%, 11/25/44 (b)(c) | | | 1,036 | | | | 986 | | |

Cologix Data Centers US Issuer LLC, | |

3.30%, 12/26/51 (b) | | CAD | 2,125 | | | | 1,875 | | |

4.94%, 1/25/52 (b) | | $ | 3,600 | | | | 2,385 | | |

Conn's Receivables Funding LLC, | |

9.52%, 12/15/26 (b) | | | 2,654 | | | | 2,665 | | |

Series 2023-A Class B | |

10.00%, 1/17/28 (b) | | | 370 | | | | 371 | | |

ContiMortgage Home Equity Loan Trust, | |

8.10%, 8/15/25 | | | 18 | | | | 14 | | |

Diamond Resorts Owner Trust, | |

4.02%, 2/20/32 (b) | | | 266 | | | | 266 | | |

ELFI Graduate Loan Program LLC, | |

4.51%, 8/26/47 (b) | | | 1,402 | | | | 1,315 | | |

Falcon Aerospace Ltd., | |

3.60%, 9/15/39 (b) | | | 1,378 | | | | 1,254 | | |

FortiFi, | |

Series 2023-1A Class A | |

6.23%, 9/20/59 (b) | | | 3,007 | | | | 2,878 | | |

GAIA Aviation Ltd., | |

7.00%, 12/15/44 (b) | | | 1,558 | | | | 836 | | |

GCI Funding I LLC, | |

2.82%, 10/18/45 (b) | | | 653 | | | | 571 | | |

Golub Capital Partners ABS Funding Ltd., | |

2.77%, 4/20/29 (b) | | | 875 | | | | 816 | | |

Class A2 | |

3.21%, 1/22/29 (b) | | | 2,280 | | | | 2,184 | | |

Goodgreen Trust, | |

5.53%, 4/15/55 (b) | | | 1,738 | | | | 1,427 | | |

5.74%, 10/15/56 (b) | | | 2,521 | | | | 2,113 | | |

JOL Air Ltd., | |

4.95%, 4/15/44 (b) | | | 231 | | | | 179 | | |

LUNAR Aircraft Ltd., | |

3.38%, 2/15/45 (b) | | | 347 | | | | 301 | | |

MACH 1 Cayman Ltd., | |

3.47%, 10/15/39 (b) | | | 756 | | | | 647 | | |

The accompanying notes are an integral part of the financial statements.

7

Morgan Stanley Institutional Fund Trust

Annual Report — September 30, 2023

Portfolio of Investments (cont'd)

Core Plus Fixed Income Portfolio

| | | Face

Amount

(000) | | Value

(000) | |

Asset-Backed Securities (cont'd) | |

MAPS Ltd., | |

4.21%, 5/15/43 (b) | | $ | 276 | | | $ | 248 | | |

Marlette Funding Trust, | |

Series 2023-3A Class B | |

6.71%, 9/15/33 (b) | | | 2,300 | | | | 2,297 | | |

METAL LLC, | |

4.58%, 10/15/42 (b) | | | 540 | | | | 333 | | |

Mosaic Solar Loan Trust, | |

2.10%, 4/20/46 (b) | | | 503 | | | | 425 | | |

Newtek Small Business Loan Trust, | |

Daily U.S. Prime Rate - 0.55%,

7.95%, 2/25/44 (b)(c) | | | 204 | | | | 202 | | |

Daily U.S. Prime Rate - 0.50%,

8.00%, 7/25/50 (b)(c) | | | 1,014 | | | | 1,013 | | |

Oxford Finance Funding LLC, | |

5.44%, 2/15/27 (b) | | | 95 | | | | 94 | | |

PMT Issuer Trust — FMSR, | |

1 Month USD LIBOR + 3.00%,

8.43%, 3/25/26 (b)(c) | | | 3,900 | | | | 3,808 | | |

SOFR30A + 4.19%,

9.51%, 6/25/27 (b)(c) | | | 2,700 | | | | 2,707 | | |

PRET 2021-NPL6 LLC, | |

2.49%, 7/25/51 (b) | | | 1,018 | | | | 971 | | |

Progress Residential Trust, | |

2.31%, 5/17/38 (b) | | | 650 | | | | 577 | | |

Raptor Aircraft Finance I LLC, | |

4.21%, 8/23/44 (b) | | | 1,966 | | | | 1,577 | | |

ReadyCap Lending Small Business Loan Trust, | |

Daily U.S. Prime Rate - 0.50%,

8.00%, 12/27/44 (b)(c) | | | 274 | | | | 264 | | |

Republic Finance Issuance Trust, | |

3.54%, 11/20/30 (b) | | | 1,385 | | | | 1,306 | | |

Retained Vantage Data Centers Issuer LLC, | |

Series 2023-1A Class A2A | |

5.00%, 9/15/48 (b) | | | 2,050 | | | | 1,852 | | |

Start II Ltd., | |

4.09%, 3/15/44 (b) | | | 248 | | | | 220 | | |

Start Ltd., | |

4.09%, 5/15/43 (b) | | | 2,351 | | | | 2,056 | | |

Sunbird Engine Finance LLC, | |

3.67%, 2/15/45 (b) | | | 831 | | | | 702 | | |

| | | | 52,080 | | |

Collateralized Mortgage Obligations — Agency Collateral Series (0.4%) | |

Federal Home Loan Mortgage Corp., Multifamily

Structured Pass-Through Certificates, | |

IO | |

4.48%, 11/25/55 (c) | | | 7,625 | | | | 2,098 | | |

Federal Home Loan Mortgage Corporation, | |

IO REMIC | |

5.89% - SOFR30A, 0.57%, 11/15/43 (d) | | | 375 | | | | 22 | | |

Federal National Mortgage Association, | |

IO PAC REMIC | |

8.00%, 9/18/27 | | | 19 | | | | 2 | | |

| | | Face

Amount

(000) | | Value

(000) | |

IO STRIPS | |

6.50%, 9/25/29 - 12/25/29 | | $ | 102 | | | $ | 11 | | |

8.00%, 4/25/24 | | | — | @ | | | — | @ | |

8.50%, 10/25/25 | | | 3 | | | | — | @ | |

REMIC | |

7.00%, 9/25/32 | | | 83 | | | | 85 | | |

Government National Mortgage Association, | |

IO | |

5.00%, 2/16/41 | | | 80 | | | | 16 | | |

| | | | 2,234 | | |

Commercial Mortgage-Backed Securities (14.6%) | |

BANK 2019-BNK21, | |

IO | |

0.96%, 10/17/52 (c) | | | 14,029 | | | | 538 | | |

BANK 2020-BNK30, | |

3.02%, 12/15/53 (c) | | | 4,200 | | | | 2,214 | | |

Benchmark Mortgage Trust, | |

3.76%, 7/15/53 (b) | | | 2,000 | | | | 1,814 | | |

IO | |

0.99%, 9/15/48 (b)(c) | | | 31,000 | | | | 693 | | |

| BF Mortgage Trust, | |

1 Month Term SOFR + 1.75%,

7.08%, 12/15/35 (b)(c) | | | 2,500 | | | | 1,863 | | |

| BPR Trust, | |

1 Month Term SOFR + 3.00%,

8.33%, 5/15/39 (b)(c) | | | 3,170 | | | | 3,168 | | |

BXP Trust, | |

1 Month Term SOFR + 3.05%,

8.38%, 11/15/34 (b)(c) | | | 1,150 | | | | 804 | | |

CG-CCRE Commercial Mortgage Trust, | |

1 Month Term SOFR + 1.97%,

7.30%, 11/15/31 (b)(c) | | | 528 | | | | 513 | | |

Citigroup Commercial Mortgage Trust, | |

3.62%, 12/10/41 (b)(c) | | | 1,100 | | | | 712 | | |

IO | |

0.86%, 11/10/48 (c) | | | 2,288 | | | | 26 | | |

1.02%, 9/10/58 (c) | | | 4,138 | | | | 53 | | |

COMM Mortgage Trust, | |

3.51%, 8/15/57 (b)(c) | | | 1,400 | | | | 1,268 | | |

IO | |

0.81%, 10/10/47 (c) | | | 2,388 | | | | 10 | | |

1.07%, 7/15/47 (c) | | | 2,105 | | | | 6 | | |

CSMC Trust, | |

1 Month Term SOFR + 3.61%,

8.95%, 12/15/35 (b)(c) | | | 5,275 | | | | 5,274 | | |

1 Month Term SOFR + 4.08%,

9.42%, 4/15/26 (b)(c) | | | 2,590 | | | | 2,538 | | |

CSWF Corp., | |

1 Month Term SOFR + 1.68%,

7.01%, 6/15/34 (b)(c) | | | 2,680 | | | | 2,242 | | |

DROP Mortgage Trust, | |

1 Month Term SOFR + 1.26%,

6.60%, 10/15/43 (b)(c) | | | 3,525 | | | | 3,300 | | |

The accompanying notes are an integral part of the financial statements.

8

Morgan Stanley Institutional Fund Trust

Annual Report — September 30, 2023

Portfolio of Investments (cont'd)

Core Plus Fixed Income Portfolio

| | | Face

Amount

(000) | | Value

(000) | |

Commercial Mortgage-Backed Securities (cont'd) | |

Federal Home Loan Mortgage Corp., Multifamily

Structured Pass-Through Certificates, | |

IO | |

0.45%, 11/25/27 (c) | | $ | 23,042 | | | $ | 268 | | |

2.72%, 1/25/49 (c) | | | 21,292 | | | | 3,088 | | |

2.74%, 2/25/49 (c) | | | 9,522 | | | | 1,368 | | |

2.82%, 9/25/48 (c) | | | 16,800 | | | | 2,407 | | |

2.83%, 8/25/48 (c) | | | 5,484 | | | | 760 | | |

2.98%, 1/25/49 (c) | | | 7,514 | | | | 1,259 | | |

3.08%, 1/25/32 (c) | | | 5,775 | | | | 1,014 | | |

3.17%, 11/25/36 (c) | | | 4,400 | | | | 1,129 | | |

3.20%, 4/25/39 (c) | | | 3,200 | | | | 802 | | |

3.32%, 5/25/32 (c) | | | 11,220 | | | | 2,177 | | |

3.58%, 10/25/38 (c) | | | 3,500 | | | | 950 | | |

3.69%, 6/25/54 (c) | | | 6,549 | | | | 1,483 | | |

3.92%, 6/25/50 (c) | | | 8,000 | | | | 1,903 | | |

4.29%, 8/25/54 (c) | | | 5,300 | | | | 1,367 | | |

FREMF 2016-KF21 Mortgage Trust, | |

SOFR30A + 5.36%, 10.68%, 7/25/26 (b)(c) | | | 45 | | | | 43 | | |

FREMF 2017-KF27 Mortgage Trust, | |

SOFR30A + 4.36%, 9.78%, 12/25/26 (b)(c) | | | 61 | | | | 59 | | |

GS Mortgage Securities Trust, | |

4.40%, 8/10/46 (b)(c) | | | 500 | | | | 426 | | |

IO | |

0.83%, 9/10/47 (c) | | | 4,249 | | | | 17 | | |

1.35%, 10/10/48 (c) | | | 4,421 | | | | 83 | | |

Highways 2021 PLC, | |

3 Month GBP SONIA + 1.35%,

6.57%, 12/18/31 (b)(c) | | GBP | 2,775 | | | | 3,294 | | |

Jackson Park Trust, | |

3.35%, 10/14/39 (b)(c) | | $ | 1,700 | | | | 1,233 | | |

JP Morgan Chase Commercial Mortgage

Securities Trust, | |

1 Month Term SOFR + 2.56%,

7.90%, 4/15/38 (b)(c) | | | 2,400 | | | | 2,321 | | |

IO | |

0.61%, 4/15/46 (c) | | | 6,956 | | | | 19 | | |

0.71%, 12/15/49 (c) | | | 3,552 | | | | 49 | | |

0.86%, 7/15/47 (c) | | | 3,618 | | | | 1 | | |

JPMBB Commercial Mortgage Securities Trust, | |

4.78%, 4/15/47 (b)(c) | | | 775 | | | | 713 | | |

IO | |

1.09%, 8/15/47 (c) | | | 2,814 | | | | 8 | | |

Last Mile Logistics Pan Euro Finance DAC, | |

3 Month EURIBOR + 1.90%,

5.69%, 8/17/33 (b)(c) | | EUR | 736 | | | | 729 | | |

Manhattan West Mortgage Trust, | |

2.41%, 9/10/39 (b)(c) | | $ | 1,500 | | | | 1,222 | | |

MF1 2021-W10X, | |

1 Month Term SOFR + 2.82%,

8.15%, 12/15/34 (b)(c) | | | 4,350 | | | | 4,035 | | |

MFT Mortgage Trust, | |

3.39%, 8/10/40 (b)(c) | | | 1,000 | | | | 644 | | |

3.59%, 2/10/42 (b)(c) | | | 800 | | | | 421 | | |

| | | Face

Amount

(000) | | Value

(000) | |

MKT 2020-525M Mortgage Trust, | |

3.04%, 2/12/40 (b)(c) | | $ | 1,000 | | | $ | 271 | | |

Natixis Commercial Mortgage Securities Trust, | |

4.27%, 5/15/39 (b)(c) | | | 2,300 | | | | 1,813 | | |

4.46%, 1/15/43 (b)(c) | | | 800 | | | | 631 | | |

1 Month Term SOFR + 2.28%,

7.61%, 7/15/36 (b)(c) | | | 2,300 | | | | 2,028 | | |

Olympic Tower Mortgage Trust, | |

3.57%, 5/10/39 (b) | | | 2,900 | | | | 2,430 | | |

Real Estate Asset Liquidity Trust, | |

IO | |

1.16%, 2/12/31 (b)(c) | | CAD | 31,560 | | | | 879 | | |

SG Commercial Mortgage Securities Trust, | |

3.85%, 3/15/37 (b)(c) | | $ | 1,900 | | | | 1,648 | | |

SLG Office Trust, | |

IO | |

0.26%, 7/15/41 (b)(c) | | | 34,800 | | | | 495 | | |

Taubman Centers Commercial Mortgage Trust, | |

1 Month Term SOFR + 2.19%,

7.52%, 5/15/37 (b)(c) | | | 3,950 | | | | 3,862 | | |

Vita Scientia 2022-1 DAC, | |

3 Month EURIBOR + 2.49%,

6.27%, 8/27/25 (b)(c) | | EUR | 2,125 | | | | 1,919 | | |

VMC Finance 2021-HT1 LLC, | |

1 Month Term SOFR + 1.76%,

7.10%, 1/18/37 (b)(c) | | $ | 2,387 | | | | 2,335 | | |

WFRBS Commercial Mortgage Trust, | |

4.18%, 5/15/45 (b)(c) | | | 425 | | | | 390 | | |

| | | | 81,029 | | |

Corporate Bonds (25.7%) | |

Finance (9.9%) | |

AIB GROUP PLC, | |

6.61%, 9/13/29 (b) | | | 1,000 | | | | 996 | | |

American International Group, Inc., | |

5.13%, 3/27/33 | | | 183 | | | | 170 | | |

Aviation Capital Group LLC, | |

6.38%, 7/15/30 (b) | | | 1,425 | | | | 1,381 | | |

Banco de Credito e Inversiones SA, | |

2.88%, 10/14/31 (b) | | | 2,275 | | | | 1,824 | | |

Banco Santander SA, | |

4.18%, 3/24/28 | | | 1,400 | | | | 1,293 | | |

Bank Hapoalim BM, | |

3.26%, 1/21/32 | | | 2,075 | | | | 1,777 | | |

Bank of America Corp., | |

2.69%, 4/22/32 | | | 3,675 | | | | 2,890 | | |

4.57%, 4/27/33 | | | 3,225 | | | | 2,865 | | |

Bank of Ireland Group PLC, | |

2.03%, 9/30/27 (b) | | | 1,425 | | | | 1,250 | | |

Bank of Montreal, | |

3.09%, 1/10/37 | | | 1,725 | | | | 1,287 | | |

BNP Paribas SA, | |

4.40%, 8/14/28 (b) | | | 1,525 | | | | 1,419 | | |

| BPCE SA, | |

5.15%, 7/21/24 (b) | | | 2,750 | | | | 2,707 | | |

The accompanying notes are an integral part of the financial statements.

9

Morgan Stanley Institutional Fund Trust

Annual Report — September 30, 2023

Portfolio of Investments (cont'd)

Core Plus Fixed Income Portfolio

| | | Face

Amount

(000) | | Value

(000) | |

Finance (cont'd) | |

CaixaBank SA, | |

6.21%, 1/18/29 (b) | | $ | 1,400 | | | $ | 1,371 | | |

Capital One Financial Corp., | |

5.82%, 2/1/34 | | | 1,575 | | | | 1,421 | | |

Centene Corp., | |

2.50%, 3/1/31 | | | 3,050 | | | | 2,347 | | |

Charles Schwab Corp., | |

5.85%, 5/19/34 | | | 1,370 | | | | 1,304 | | |

Citigroup, Inc., | |

3.79%, 3/17/33 | | | 1,275 | | | | 1,064 | | |

Deutsche Bank AG, | |

7.15%, 7/13/27 | | | 1,800 | | | | 1,813 | | |

Extra Space Storage LP, | |

2.40%, 10/15/31 | | | 1,825 | | | | 1,398 | | |

Fifth Third Bancorp, | |

6.34%, 7/27/29 | | | 400 | | | | 395 | | |

Global Atlantic Fin Co., | |

4.70%, 10/15/51 (b) | | | 1,320 | | | | 958 | | |

Grupo Aval Ltd., | |

4.38%, 2/4/30 (b) | | | 561 | | | | 428 | | |

Jefferies Finance LLC/JFIN Co.-Issuer Corp., | |

5.00%, 8/15/28 (b) | | | 1,490 | | | | 1,256 | | |

Jefferies Financial Group, Inc., | |

5.88%, 7/21/28 | | | 975 | | | | 955 | | |

JPMorgan Chase & Co., | |

5.35%, 6/1/34 | | | 3,275 | | | | 3,108 | | |

Macquarie Group Ltd., | |

2.87%, 1/14/33 (b) | | | 1,350 | | | | 1,022 | | |

Metropolitan Life Global Funding I, | |

5.15%, 3/28/33 (b) | | | 1,050 | | | | 995 | | |

Nationwide Building Society, | |

4.30%, 3/8/29 (b) | | | 1,550 | | | | 1,424 | | |

Nordea Bank Abp, | |

5.38%, 9/22/27 (b) | | | 1,200 | | | | 1,173 | | |

Oversea-Chinese Banking Corp. Ltd., | |

1.83%, 9/10/30 (b) | | | 970 | | | | 893 | | |

Rocket Mortgage LLC/Rocket

Mortgage Co-Issuer, Inc., | |

3.88%, 3/1/31 (b) | | | 1,475 | | | | 1,178 | | |

Societe Generale SA, | |

2.63%, 1/22/25 (b) | | | 1,625 | | | | 1,545 | | |

Toronto-Dominion Bank, | |

8.13%, 10/31/82 | | | 1,625 | | | | 1,621 | | |

Truist Financial Corp., | |

5.87%, 6/8/34 | | | 2,025 | | | | 1,907 | | |

U.S. Bancorp, | |

5.84%, 6/12/34 | | | 1,200 | | | | 1,133 | | |

5.85%, 10/21/33 | | | 175 | | | | 166 | | |

UBS Group AG, | |

6.54%, 8/12/33 (b) | | | 1,550 | | | | 1,533 | | |

United Overseas Bank Ltd., | |

3.86%, 10/7/32 (b) | | | 2,950 | | | | 2,712 | | |

| | | | 54,979 | | |

| | | Face

Amount

(000) | | Value

(000) | |

Industrials (13.7%) | |

Apple, Inc., | |

2.95%, 9/11/49 | | $ | 2,200 | | | $ | 1,454 | | |

Ashtead Capital, Inc., | |

5.95%, 10/15/33 (b) | | | 1,850 | | | | 1,758 | | |

AT&T, Inc., | |

3.55%, 9/15/55 | | | 1,635 | | | | 1,002 | | |

3.65%, 6/1/51 | | | 605 | | | | 390 | | |

BAT Capital Corp., | |

2.26%, 3/25/28 | | | 2,000 | | | | 1,693 | | |

Boeing Co., | |

3.25%, 2/1/35 | | | 1,775 | | | | 1,366 | | |

BP Capital Markets PLC, | |

4.88%, 3/22/30 (e) | | | 700 | | | | 628 | | |

Celanese U.S. Holdings LLC, | |

6.17%, 7/15/27 | | | 2,150 | | | | 2,121 | | |

Charter Communications Operating LLC/

Charter Communications Operating Capital, | |

3.50%, 3/1/42 | | | 3,050 | | | | 1,887 | | |

Concentrix Corp., | |

6.60%, 8/2/28 | | | 1,165 | | | | 1,125 | | |

6.65%, 8/2/26 | | | 1,275 | | | | 1,268 | | |

Dick's Sporting Goods, Inc., | |

4.10%, 1/15/52 | | | 2,225 | | | | 1,353 | | |

Duke University, | |

Series 2020 | |

2.83%, 10/1/55 | | | 1,600 | | | | 982 | | |

Enterprise Products Operating LLC, | |

3.30%, 2/15/53 | | | 300 | | | | 196 | | |

3.70%, 1/31/51 | | | 375 | | | | 266 | | |

5.35%, 1/31/33 | | | 1,450 | | | | 1,419 | | |

Ford Motor Co., | |

3.25%, 2/12/32 | | | 1,875 | | | | 1,447 | | |

Foundry JV Holdco LLC, | |

5.88%, 1/25/34 (b) | | | 1,525 | | | | 1,458 | | |

Garda World Security Corp., | |

9.50%, 11/1/27 (b) | | | 925 | | | | 885 | | |

General Motors Co., | |

6.75%, 4/1/46 | | | 925 | | | | 865 | | |

General Motors Financial Co., Inc., | |

5.80%, 6/23/28 | | | 2,825 | | | | 2,761 | | |

Global Partners LP/GLP Finance Corp., | |

7.00%, 8/1/27 | | | 715 | | | | 697 | | |

Grifols SA, | |

2.25%, 11/15/27 | | EUR | 630 | | | | 588 | | |

HCA, Inc., | |

4.63%, 3/15/52 | | $ | 1,550 | | | | 1,165 | | |

Hyundai Capital America, | |

1.80%, 1/10/28 (b) | | | 2,650 | | | | 2,222 | | |

6.10%, 9/21/28 (b) | | | 1,700 | | | | 1,689 | | |

Imperial Brands Finance PLC, | |

3.13%, 7/26/24 (b) | | | 1,000 | | | | 975 | | |

The accompanying notes are an integral part of the financial statements.

10

Morgan Stanley Institutional Fund Trust

Annual Report — September 30, 2023

Portfolio of Investments (cont'd)

Core Plus Fixed Income Portfolio

| | | Face

Amount

(000) | | Value

(000) | |

Industrials (cont'd) | |

Intel Corp., | |

5.70%, 2/10/53 | | $ | 1,025 | | | $ | 962 | | |

JBS USA LUX SA/JBS USA Food Co./JBS

USA Finance, Inc., | |

2.50%, 1/15/27 | | | 1,575 | | | | 1,393 | | |

Johns Hopkins University, | |

Series A | |

2.81%, 1/1/60 | | | 1,170 | | | | 684 | | |

Lowe's Cos., Inc., | |

5.80%, 9/15/62 | | | 325 | | | | 297 | | |

5.85%, 4/1/63 | | | 200 | | | | 184 | | |

Macy's Retail Holdings LLC, | |

5.88%, 3/15/30 (b)(f) | | | 690 | | | | 586 | | |

McAfee Corp., | |

7.38%, 2/15/30 (b) | | | 1,075 | | | | 901 | | |

McLaren Health Care Corp., | |

Series A | |

4.39%, 5/15/48 (f) | | | 1,175 | | | | 930 | | |

Medline Borrower LP, | |

3.88%, 4/1/29 (b) | | | 1,410 | | | | 1,193 | | |

NBN Co. Ltd., | |

2.63%, 5/5/31 (b) | | | 2,400 | | | | 1,938 | | |

Newcastle Coal Infrastructure Group Pty Ltd., | |

4.40%, 9/29/27 (b) | | | 2,542 | | | | 2,288 | | |

NOVA Chemicals Corp., | |

4.25%, 5/15/29 (b)(f) | | | 1,510 | | | | 1,177 | | |

ONEOK, Inc., | |

6.05%, 9/1/33 | | | 1,450 | | | | 1,425 | | |

Ooredoo International Finance Ltd., | |

2.63%, 4/8/31 (b) | | | 1,268 | | | | 1,059 | | |

Oracle Corp., | |

3.60%, 4/1/50 | | | 2,300 | | | | 1,489 | | |

Peloton Interactive, Inc., | |

0.00%, 2/15/26 | | | 1,215 | | | | 920 | | |

Petrobras Global Finance BV, | |

6.50%, 7/3/33 (f) | | | 1,379 | | | | 1,318 | | |

Resorts World Las Vegas LLC/RWLV

Capital, Inc., | |

4.63%, 4/16/29 (b) | | | 1,400 | | | | 1,119 | | |

Rockies Express Pipeline LLC, | |

3.60%, 5/15/25 (b) | | | 925 | | | | 874 | | |

Rogers Communications, Inc., | |

4.55%, 3/15/52 | | | 2,550 | | | | 1,862 | | |

S&P Global, Inc., | |

5.25%, 9/15/33 (b) | | | 1,800 | | | | 1,756 | | |

Seattle Children's Hospital, | |

Series 2021 | |

2.72%, 10/1/50 | | | 2,750 | | | | 1,621 | | |

Silgan Holdings, Inc., | |

1.40%, 4/1/26 (b) | | | 2,150 | | | | 1,909 | | |

Sirius XM Radio, Inc., | |

3.88%, 9/1/31 (b) | | | 790 | | | | 599 | | |

| | | Face

Amount

(000) | | Value

(000) | |

Splunk, Inc., | |

1.13%, 6/15/27 | | $ | 1,075 | | | $ | 1,020 | | |

Spotify USA, Inc., | |

0.00%, 3/15/26 | | | 1,190 | | | | 1,016 | | |

Standard Industries, Inc., | |

2.25%, 11/21/26 (b) | | EUR | 575 | | | | 538 | | |

Syngenta Finance NV, | |

4.89%, 4/24/25 (b) | | $ | 975 | | | | 951 | | |

Var Energi ASA, | |

7.50%, 1/15/28 (b) | | | 1,025 | | | | 1,054 | | |

Verizon Communications, Inc., | |

1.75%, 1/20/31 | | | 4,100 | | | | 3,091 | | |

VICI Properties LP/VICI Note Co., Inc., | |

5.75%, 2/1/27 (b) | | | 1,025 | | | | 993 | | |

Vontier Corp., | |

2.40%, 4/1/28 | | | 2,700 | | | | 2,256 | | |

Warnermedia Holdings, Inc., | |

5.05%, 3/15/42 | | | 925 | | | | 716 | | |

5.39%, 3/15/62 | | | 1,390 | | | | 1,028 | | |

Williams Cos., Inc., | |

5.30%, 8/15/28 | | | 1,425 | | | | 1,395 | | |

| | | | 76,202 | | |

Utilities (2.1%) | |

Enel Finance America LLC, | |

2.88%, 7/12/41 (b) | | | 2,307 | | | | 1,378 | | |

Eversource Energy, | |

5.13%, 5/15/33 | | | 1,463 | | | | 1,362 | | |

Fells Point Funding Trust, | |

3.05%, 1/31/27 (b) | | | 2,275 | | | | 2,064 | | |

Jersey Central Power & Light Co., | |

2.75%, 3/1/32 (b) | | | 1,400 | | | | 1,098 | | |

Mississippi Power Co., | |

3.95%, 3/30/28 | | | 2,325 | | | | 2,170 | | |

Northern States Power Co., | |

2.90%, 3/1/50 | | | 1,400 | | | | 860 | | |

Pacific Gas & Electric Co., | |

4.95%, 7/1/50 | | | 1,625 | | | | 1,213 | | |

Virginia Electric & Power Co., | |

2.95%, 11/15/51 | | | 2,275 | | | | 1,356 | | |

| | | | 11,501 | | |

| | | | 142,682 | | |

Mortgages — Other (14.4%) | |

510 Asset Backed 2021-NPL1 Trust, | |

2.24%, 6/25/61 (b) | | | 1,417 | | | | 1,327 | | |

Adjustable Rate Mortgage Trust, | |

5.83%, 6/25/35 (c) | | | 32 | | | | 31 | | |

Ajax Mortgage Loan Trust, | |

1.70%, 5/25/59 (b)(c) | | | 1,274 | | | | 1,139 | | |

2.35%, 9/25/65 (b)(c) | | | 725 | | | | 533 | | |

Banc of America Alternative Loan Trust, | |

1 Month Term SOFR + 0.76%,

6.00%, 7/25/46 (c) | | | 92 | | | | 71 | | |

6.36%, 10/25/36 | | | 392 | | | | 110 | | |

The accompanying notes are an integral part of the financial statements.

11

Morgan Stanley Institutional Fund Trust

Annual Report — September 30, 2023

Portfolio of Investments (cont'd)

Core Plus Fixed Income Portfolio

| | | Face

Amount

(000) | | Value

(000) | |

Mortgages — Other (cont'd) | |

Banc of America Funding Trust, | |

5.25%, 7/25/37 | | $ | 11 | | | $ | 10 | | |

BBCMS Mortgage Trust, | |

IO | |

0.64%, 12/15/55 (c) | | | 18,415 | | | | 673 | | |

Bear Stearns ARM Trust, | |

4.02%, 2/25/34 (c) | | | 372 | | | | 340 | | |

BRAVO Residential Funding Trust, | |

2.00%, 5/25/59 (b)(c) | | | 1,486 | | | | 1,314 | | |

Brean Asset Backed Securities Trust, | |

1.40%, 10/25/63 (b)(c) | | | 2,089 | | | | 1,751 | | |

1.75%, 10/25/61 (b)(c) | | | 2,200 | | | | 1,896 | | |

BX Commercial Mortgage Trust, | |

Class A | |

1 Month Term SOFR + 2.28%,

7.61%, 6/15/40 (b)(c) | | | 2,050 | | | | 2,052 | | |

Cascade Funding Mortgage Trust, | |

3.73%, 6/25/36 (b)(c) | | | 3,825 | | | | 3,538 | | |

4.00%, 10/25/68 (b)(c) | | | 2,057 | | | | 1,957 | | |

| CFMT 2022-HB8 LLC, | |

3.75%, 4/25/25 (b)(c) | | | 2,650 | | | | 2,450 | | |

| CFMT LLC, | |

1.94%, 9/25/50 (b)(c) | | | 2,292 | | | | 2,148 | | |

2.91%, 2/25/31 (b)(c) | | | 3,800 | | | | 3,535 | | |

3.25%, 9/25/37 (b)(c) | | | 1,840 | | | | 1,434 | | |

ChaseFlex Trust, | |

6.00%, 2/25/37 | | | 591 | | | | 232 | | |

COLT 2021-RPL1 Trust, | |

1.67%, 9/25/61 (b)(c) | | | 1,260 | | | | 1,083 | | |

Countrywide Alternative Loan Trust, | |

1 Month Term SOFR + 0.47%,

5.79%, 5/25/47 (c) | | | 65 | | | | 58 | | |

E-MAC NL 2004-I BV, | |

3 Month EURIBOR + 0.18%,

5.97%, 7/25/36 (c) | | EUR | 277 | | | | 270 | | |

Eurosail-NL 2007-2 BV, | |

3 Month EURIBOR + 1.80%,

5.46%, 10/17/40 (c) | | | 700 | | | | 730 | | |

Federal Home Loan Mortgage Corp.

Whole Loan Securities Trust, | |

3.00%, 7/25/46 - 5/25/47 | | $ | 935 | | | | 786 | | |

3.50%, 5/25/45 - 5/25/47 | | | 349 | | | | 295 | | |

4.00%, 5/25/45 | | | 8 | | | | 6 | | |

FMC GMSR Issuer Trust, | |

7.90%, 7/25/27 (b) | | | 2,675 | | | | 2,640 | | |

GCAT 2022-NQM3 Trust, | |

4.35%, 4/25/67 (b)(c) | | | 4,343 | | | | 4,044 | | |

Headlands Residential 2021-RPL1 LLC, | |

2.49%, 9/25/26 (b)(c) | | | 3,320 | | | | 3,190 | | |

IM Pastor 3 FTH, | |

3 Month EURIBOR + 0.14%,

4.07%, 3/22/43 (c) | | EUR | 271 | | | | 251 | | |

| | | Face

Amount

(000) | | Value

(000) | |

Imperial Fund Mortgage Trust, | |

2.49%, 2/25/67 (b)(c) | | $ | 2,403 | | | $ | 2,062 | | |

JP Morgan Mortgage Trust, | |

4.40%, 6/25/37 (c) | | | 50 | | | | 39 | | |

Legacy Mortgage Asset Trust, | |

6.25%, 2/25/60 (b)(c) | | | 1,819 | | | | 1,798 | | |

Lehman Mortgage Trust, | |

6.50%, 9/25/37 | | | 623 | | | | 197 | | |

LHOME Mortgage Trust, | |

Series 2023-RTL2 Class A1 | |

8.00%, 6/25/28 (b)(c) | | | 425 | | | | 425 | | |

NYMT Loan Trust, | |

2.94%, 10/25/60 (b)(c) | | | 2,260 | | | | 2,220 | | |

OBX Trust, | |

3.50%, 2/25/60 (b)(c) | | | 356 | | | | 299 | | |

Pepper Residential Securities Trust, | |

1 Month Term SOFR + 1.04%,

6.37%, 3/12/61 (b)(c) | | | 111 | | | | 111 | | |

PMC PLS ESR Issuer LLC, | |

5.11%, 2/25/27 (b) | | | 1,798 | | | | 1,719 | | |

Preston Ridge Partners Mortgage LLC, | |

1.74%, 9/25/26 (b)(c) | | | 1,766 | | | | 1,627 | | |

2.36%, 10/25/26 (b)(c) | | | 1,935 | | | | 1,812 | | |

PRPM LLC, | |

5.56%, 6/25/27 (b) | | | 2,155 | | | | 2,115 | | |

Sage AR Funding Holdings Ltd., | |

3 Month GBP SONIA + 1.85%,

7.07%, 11/17/51 (b)(c) | | GBP | 3,625 | | | | 4,155 | | |

Seasoned Credit Risk Transfer Trust, | |

3.00%, 9/25/55 - 10/25/58 | | $ | 5,123 | | | | 4,276 | | |

4.00%, 8/25/56 - 2/25/59 (b)(c) | | | 2,187 | | | | 1,955 | | |

4.25%, 8/25/59 - 11/25/60 (b)(c) | | | 6,550 | | | | 5,640 | | |

4.50%, 6/25/57 | | | — | @ | | | — | @ | |

4.75%, 7/25/56 - 10/25/58 (b)(c)(c) | | | 2,682 | | | | 2,461 | | |

Stanwich Mortgage Loan Co. LLC, | |

2.74%, 10/16/26 (b) | | | 1,932 | | | | 1,770 | | |

TDA 27 FTA, | |

3 Month EURIBOR + 0.19%,

4.13%, 12/28/50 (c) | | EUR | 1,114 | | | | 998 | | |

VOLT CV LLC, | |

2.49%, 11/27/51 (b) | | $ | 1,468 | | | | 1,377 | | |

VOLT XCIII LLC, | |

1.89%, 2/27/51 (b) | | | 1,549 | | | | 1,465 | | |

VOLT XCIV LLC, | |

2.24%, 2/27/51 (b) | | | 1,885 | | | | 1,785 | | |

| | | | 80,200 | | |

Municipal Bonds (0.7%) | |

Chicago O'Hare International Airport, IL,

O'Hare International Airport Revenue, | |

Series 2010B | |

6.40%, 1/1/40 | | | 255 | | | | 272 | | |

City of New York, NY, | |

Series G-1 | |

5.97%, 3/1/36 | | | 270 | | | | 279 | | |

The accompanying notes are an integral part of the financial statements.

12

Morgan Stanley Institutional Fund Trust

Annual Report — September 30, 2023

Portfolio of Investments (cont'd)

Core Plus Fixed Income Portfolio

| | | Face

Amount

(000) | | Value

(000) | |

Municipal Bonds (cont'd) | |

Illinois State Toll Highway Authority, IL,

Highway Revenue, Build America Bonds, | |

Series A | |

6.18%, 1/1/34 | | $ | 477 | | | $ | 492 | | |

Onondaga Civic Development Corp., NY, | |

3.07%, 12/1/55 | | | 2,925 | | | | 1,758 | | |

University of Michigan, MI, | |

Series A | |

4.45%, 4/1/2122 | | | 1,645 | | | | 1,260 | | |

| | | | 4,061 | | |

Sovereign (2.8%) | |

Dominican Republic International Bond, | |

5.88%, 1/30/60 (b) | | | 700 | | | | 504 | | |

11.25%, 9/15/35 (b) | | DOP | 109,900 | | | | 2,001 | | |

13.63%, 2/3/33 (b) | | | 117,700 | | | | 2,446 | | |

Export-Import Bank of India, | |

3.25%, 1/15/30 (b) | | $ | 670 | | | | 572 | | |

3.88%, 2/1/28 (b) | | | 505 | | | | 468 | | |

Ivory Coast Government International Bond, | |

4.88%, 1/30/32 (b) | | EUR | 1,360 | | | | 1,098 | | |

Mexico Government International Bond, | |

3.25%, 4/16/30 | | $ | 750 | | | | 640 | | |

3.75%, 4/19/71 | | | 850 | | | | 487 | | |

Petroleos Mexicanos, | |

6.70%, 2/16/32 | | | 2,727 | | | | 2,027 | | |

Philippine Government International Bond, | |

4.20%, 3/29/47 | | | 420 | | | | 327 | | |

Republic of South Africa Government Bond, | |

8.00%, 1/31/30 | | ZAR | 22,750 | | | | 1,049 | | |

8.25%, 3/31/32 | | | 34,230 | | | | 1,476 | | |

Uruguay Government International Bond, | |

9.75%, 7/20/33 | | UYU | 89,340 | | | | 2,344 | | |

| | | | 15,439 | | |

Supranational (0.2%) | |

Banque Ouest Africaine de Developpement, | |

2.75%, 1/22/33 (b) | | EUR | 270 | | | | 204 | | |

4.70%, 10/22/31 (b) | | $ | 1,240 | | | | 989 | | |

| | | | 1,193 | | |

U.S. Treasury Securities (9.0%) | |

U.S. Treasury Note, | |

3.50%, 4/30/28 | | | 29,125 | | | | 27,763 | | |

4.25%, 5/31/25 (f) | | | 22,900 | | | | 22,562 | | |

| | | | 50,325 | | |

Total Fixed Income Securities (Cost $591,157) | | | 538,548 | | |

| | | Shares | | | |

Short-Term Investments (18.5%) | |

Investment Company (9.8%) | |

Morgan Stanley Institutional Liquidity

Funds — Government Portfolio —

Institutional Class (See Note G)

(Cost $54,421) | | | 54,421,134 | | | | 54,421 | | |

| | | Shares | | Value

(000) | |

Securities held as Collateral on Loaned Securities (0.4%) | |

Investment Company (0.4%) | |

Morgan Stanley Institutional Liquidity

Funds — Government Portfolio —

Institutional Class (See Note G)

(Cost $2,451) | | | 2,450,510 | | | $ | 2,451 | | |

| | | Face

Amount

(000) | | | |

U.S. Treasury Securities (8.3%) | |

U.S. Treasury Bill, | |

5.01%, 11/30/23 (g) | | $ | 2,300 | | | | 2,280 | | |

5.32%, 12/14/23 (g) | | | 23,000 | | | | 22,753 | | |

5.40%, 11/30/23 (g) | | | 300 | | | | 297 | | |

U.S. Treasury Note, | |

0.25%, 11/15/23 | | | 20,850 | | | | 20,740 | | |

Total U.S. Treasury Securities (Cost $46,077) | | | 46,070 | | |

Total Short-Term Investments (Cost $102,949) | | | 102,942 | | |

Total Investments (115.4%) (Cost $694,106)

Including $25,307 of Securities Loaned (h)(i) | | | 641,490 | | |

Liabilities in Excess of Other Assets (–15.4%) | | | (85,370 | ) | |

Net Assets (100.0%) | | $ | 556,120 | | |

@ Face Amount/Value is less than $500.

(a) Security is subject to delayed delivery.

(b) 144A security — Certain conditions for public sale may exist. Unless otherwise noted, these securities are deemed to be liquid.

(c) Floating or variable rate securities: The rates disclosed are as of September 30, 2023. For securities based on a published reference rate and spread, the reference rate and spread are indicated in the description in the Portfolio of Investments. Certain variable rate securities may not be based on a published reference rate and spread but are determined by the issuer or agent and are based on current market conditions. These securities do not indicate a reference rate and spread in their description in the Portfolio of Investments.

(d) Inverse Floating Rate Security — Interest rate fluctuates with an inverse relationship to an associated interest rate. Indicated rate is the effective rate at September 30, 2023.

(e) Perpetual — One or more securities do not have a predetermined maturity date. Rates for these securities are fixed for a period of time after which they revert to a floating rate. Interest rates in effect are as of September 30, 2023.

(f) All or a portion of this security was on loan at September 30, 2023.

(g) Rate shown is the yield to maturity at September 30, 2023.

(h) Securities are available for collateral in connection with securities purchased on a forward commitment basis, open foreign currency exchange contracts, futures contracts and swap agreements.

(i) At September 30, 2023, the aggregate cost for federal income tax purposes is approximately $691,085,000. The aggregate gross unrealized appreciation is approximately $5,954,000 and the aggregate gross unrealized depreciation is approximately $58,745,000, resulting in net unrealized depreciation of approximately $52,791,000.

CLO Collateralized Loan Obligation.

DAC Designated Activity Company.

The accompanying notes are an integral part of the financial statements.

13

Morgan Stanley Institutional Fund Trust

Annual Report — September 30, 2023

Portfolio of Investments (cont'd)

Core Plus Fixed Income Portfolio

EURIBOR Euro Interbank Offered Rate.

IO Interest Only Security.

LIBOR London Interbank Offered Rate.

PAC Planned Amortization Class.

REMIC Real Estate Mortgage Investment Conduit.

SOFR Secured Overnight Financing Rate.

SOFR30A 30-Day Average SOFR.

SONIA Sterling Overnight Index Average.

STRIPS Separate Trading of Registered Interest and Principal of Securities.

TBA To Be Announced.

USD United States Dollar.

Foreign Currency Forward Exchange Contracts:

The Fund had the following foreign currency forward exchange contracts open at September 30, 2023:

Counterparty | | Contracts to

Deliver

(000) | | In Exchange

For

(000) | | Delivery

Date | | Unrealized

Appreciation

(Depreciation)

(000) | |

Australia & New Zealand Banking Group Ltd. | | $ | 45 | | | CAD | 60 | | | 11/10/23 | | $ | (— | @) | |

Bank of America NA | | NZD | 4,459 | | | $ | 2,623 | | | 11/10/23 | | | (49 | ) | |

Barclays Bank PLC | | $ | 77 | | | GBP | 60 | | | 11/10/23 | | | (3 | ) | |

BNP Paribas SA | | CNH | 20,105 | | | $ | 2,825 | | | 11/10/23 | | | 67 | | |

BNP Paribas SA | | EUR | 7,014 | | | $ | 7,768 | | | 11/10/23 | | | 341 | | |

BNP Paribas SA | | IDR | 48,716,250 | | | $ | 3,206 | | | 11/10/23 | | | 55 | | |

Citibank NA | | DOP | 31,709 | | | $ | 550 | | | 11/10/23 | | | (3 | ) | |

Citibank NA | | $ | 23 | | | CAD | 31 | | | 11/10/23 | | | (— | @) | |

JPMorgan Chase Bank NA | | CAD | 6,333 | | | $ | 4,744 | | | 11/10/23 | | | 79 | | |

JPMorgan Chase Bank NA | | MXN | 79,486 | | | $ | 4,557 | | | 11/10/23 | | | 25 | | |

JPMorgan Chase Bank NA | | NOK | 28,805 | | | $ | 2,693 | | | 11/10/23 | | | (3 | ) | |

JPMorgan Chase Bank NA | | $ | 2,778 | | | INR | 230,813 | | | 11/10/23 | | | (4 | ) | |

JPMorgan Chase Bank NA | | $ | 4,272 | | | MXN | 76,008 | | | 11/10/23 | | | 62 | | |

JPMorgan Chase Bank NA | | $ | 2,836 | | | NOK | 28,805 | | | 11/10/23 | | | (141 | ) | |

JPMorgan Chase Bank NA | | $ | 2,733 | | | NZD | 4,459 | | | 11/10/23 | | | (60 | ) | |

JPMorgan Chase Bank NA | | ZAR | 51,837 | | | $ | 2,782 | | | 11/10/23 | | | 53 | | |

UBS AG | | GBP | 5,902 | | | $ | 7,530 | | | 11/10/23 | | | 328 | | |

| | | | | | | | | $ | 747 | | |

Futures Contracts:

The Fund had the following futures contracts open at September 30, 2023:

| | | Number

of

Contracts | | Expiration

Date | | Notional

Amount

(000) | | Value

(000) | | Unrealized

Appreciation

(Depreciation)

(000) | |

Long: | |

U.S. Treasury Long Bond (United States) | | | 358 | | | Dec-23 | | $ | 35,800 | | | $ | 40,734 | | | $ | (2,347 | ) | |

U.S. Treasury Ultra Bond (United States) | | | 200 | | | Dec-23 | | | 20,000 | | | | 23,738 | | | | (1,286 | ) | |

U.S. Treasury 2 yr. Note (United States) | | | 281 | | | Dec-23 | | | 56,200 | | | | 56,962 | | | | (29 | ) | |

U.S. Treasury 5 yr. Note (United States) | | | 95 | | | Dec-23 | | | 9,500 | | | | 10,009 | | | | 15 | | |

U.S. Treasury 10 yr. Note (United States) | | | 170 | | | Dec-23 | | | 17,000 | | | | 18,371 | | | | (281 | ) | |

Short: | |

EURO OAT Index (Germany) | | | 11 | | | Dec-23 | | EUR | (1,100 | ) | | | (1,433 | ) | | | 37 | | |

Euro-Buxl 30 yr. Bond (Germany) | | | 3 | | | Dec-23 | | | (300 | ) | | | (388 | ) | | | 33 | | |

U.S. Treasury 10 yr. Ultra Note (United States) | | | 21 | | | Dec-23 | | $ | (2,100 | ) | | | (2,343 | ) | | | (8 | ) | |

| | | | | | | | | | | $ | (3,866 | ) | |

Credit Default Swap Agreement:

The Fund had the following credit default swap agreement open at September 30, 2023:

Swap Counterparty

and Reference Obligation | | Credit

Rating of

Reference

Obligation† | | Buy/Sell

Protection | | Pay/Received

Fixed Rate | | Payment

Frequency | | Maturity

Date | | Notional

Amount

(000) | | Value

(000) | | Upfront

Payment

Received

(000) | | Unrealized

Depreciation

(000) | |

Morgan Stanley & Co. LLC*

CDX.NA.HY.S41 | | NR | | Buy | | | 5.00 | % | | Quarterly | | 12/20/28 | | $ | 11,900 | | | $ | (112 | ) | | $ | (78 | ) | | $ | (34 | ) | |

The accompanying notes are an integral part of the financial statements.

14

Morgan Stanley Institutional Fund Trust

Annual Report — September 30, 2023

Portfolio of Investments (cont'd)

Core Plus Fixed Income Portfolio

† Credit rating as issued by Standard & Poor's.

* Cleared swap agreement, the broker is Morgan Stanley & Co. LLC.

CAD — Canadian Dollar

CNH — Chinese Yuan Renminbi Offshore

DOP — Dominican Peso

EUR — Euro

GBP — British Pound

IDR — Indonesian Rupiah

INR — Indian Rupee

MXN — Mexican Peso

NOK — Norwegian Krone

NZD — New Zealand Dollar

USD — United States Dollar

UYU — Uruguayan Peso

ZAR — South African Rand

Portfolio Composition*

Classification | | Percentage of

Total Investments | |

Agency Fixed Rate Mortgages | | | 17.1 | % | |

Short-Term Investments | | | 15.7 | | |

Commercial Mortgage-Backed Securities | | | 12.7 | | |

Mortgages — Other | | | 12.6 | | |

Industrials | | | 11.9 | | |

Finance | | | 8.6 | | |

Asset-Backed Securities | | | 8.2 | | |

U.S. Treasury Securities | | | 7.9 | | |

Other** | | | 5.3 | | |

Total Investments | | | 100.0 | %*** | |

* Percentages indicated are based upon total investments (excluding Securities held as Collateral on Loaned Securities) as of September 30, 2023.

** Industries and/or investment types representing less than 5% of total investments.

*** Does not include open long/short futures contracts with a value of approximately $153,978,000 and net unrealized depreciation of approximately $3,866,000. Does not include open foreign currency forward exchange contracts with net unrealized appreciation of approximately $747,000. Also does not include an open swap agreement with total unrealized depreciation of approximately $34,000.

The accompanying notes are an integral part of the financial statements.

15

Morgan Stanley Institutional Fund Trust

Annual Report — September 30, 2023

Core Plus Fixed Income Portfolio

Statement of Assets and Liabilities | | September 30, 2023

(000) | |

Assets: | |

Investments in Securities of Unaffiliated Issuers, at Value(1) (Cost $637,234) | | $ | 584,618 | | |

Investment in Security of Affiliated Issuer, at Value (Cost $56,872) | | | 56,872 | | |

Total Investments in Securities, at Value (Cost $694,106) | | | 641,490 | | |

Foreign Currency, at Value (Cost $3,332) | | | 3,296 | | |

Cash | | | 1,999 | | |

Receivable for Variation Margin on Futures Contracts | | | 3,985 | | |

Interest Receivable | | | 3,896 | | |

Receivable for Investments Sold | | | 1,525 | | |

Unrealized Appreciation on Foreign Currency Forward Exchange Contracts | | | 1,010 | | |

Due from Broker | | | 371 | | |

Receivable for Fund Shares Sold | | | 315 | | |

Receivable from Affiliate | | | 280 | | |

Tax Reclaim Receivable | | | 10 | | |

Receivable from Securities Lending Income | | | 4 | | |

Other Assets | | | 79 | | |

Total Assets | | | 658,260 | | |

Liabilities: | |

Payable for Investments Purchased | | | 98,247 | | |

Collateral on Securities Loaned, at Value | | | 2,451 | | |

Payable for Variation Margin on Swap Agreements | | | 341 | | |

Unrealized Depreciation on Foreign Currency Forward Exchange Contracts | | | 263 | | |

Payable for Fund Shares Redeemed | | | 220 | | |

Payable for Advisory Fees | | | 210 | | |

Payable for Professional Fees | | | 84 | | |

Payable for Sub Transfer Agency Fees — Class I | | | 62 | | |

Payable for Sub Transfer Agency Fees — Class A | | | 8 | | |

Payable for Sub Transfer Agency Fees — Class L | | | — | @ | |

Payable for Sub Transfer Agency Fees — Class C | | | 2 | | |

Payable for Administration Fees | | | 37 | | |

Deferred Capital Gain Country Tax | | | 25 | | |

Payable for Custodian Fees | | | 20 | | |

Payable for Shareholder Services Fees — Class A | | | 11 | | |

Payable for Distribution and Shareholder Services Fees — Class L | | | — | @ | |

Payable for Distribution and Shareholder Services Fees — Class C | | | 9 | | |

Payable for Transfer Agency Fees — Class I | | | 3 | | |

Payable for Transfer Agency Fees — Class A | | | 1 | | |

Payable for Transfer Agency Fees — Class L | | | — | @ | |

Payable for Transfer Agency Fees — Class C | | | 1 | | |

Payable for Transfer Agency Fees — Class R6 | | | 1 | | |

Other Liabilities | | | 144 | | |

Total Liabilities | | | 102,140 | | |

Net Assets | | $ | 556,120 | | |

Net Assets Consist of: | |

Paid-in-Capital | | $ | 719,659 | | |

Total Accumulated Loss | | | (163,539 | ) | |

Net Assets | | $ | 556,120 | | |

The accompanying notes are an integral part of the financial statements.

16

Morgan Stanley Institutional Fund Trust

Annual Report — September 30, 2023

Core Plus Fixed Income Portfolio

Statement of Assets and Liabilities (cont'd) | | September 30, 2023

(000) | |

CLASS I: | |

Net Assets | | $ | 423,920 | | |

| Shares Outstanding (unlimited number of shares authorized, no par value) (not in 000's) | | | 46,345,129 | | |

Net Asset Value, Offering and Redemption Price Per Share | | $ | 9.15 | | |

CLASS A: | |

Net Assets | | $ | 54,277 | | |

| Shares Outstanding (unlimited number of shares authorized, no par value) (not in 000's) | | | 5,922,982 | | |

Net Asset Value, Redemption Price Per Share | | $ | 9.16 | | |

Maximum Sales Load | | | 3.25 | % | |

Maximum Sales Charge | | $ | 0.31 | | |

Maximum Offering Price Per Share | | $ | 9.47 | | |

CLASS L: | |

Net Assets | | $ | 704 | | |

| Shares Outstanding (unlimited number of shares authorized, no par value) (not in 000's) | | | 76,712 | | |

Net Asset Value, Offering and Redemption Price Per Share | | $ | 9.17 | | |

CLASS C: | |

Net Assets | | $ | 11,044 | | |

| Shares Outstanding (unlimited number of shares authorized, no par value) (not in 000's) | | | 1,214,845 | | |

Net Asset Value, Offering and Redemption Price Per Share | | $ | 9.09 | | |

CLASS R6: | |

Net Assets | | $ | 66,175 | | |

| Shares Outstanding (unlimited number of shares authorized, no par value) (not in 000's) | | | 7,238,137 | | |

Net Asset Value, Offering and Redemption Price Per Share | | $ | 9.14 | | |

(1) Including:

Securities on Loan, at Value: | | $ | 25,307 | | |

@ Amount is less than $500.

The accompanying notes are an integral part of the financial statements.

17

Morgan Stanley Institutional Fund Trust

Annual Report — September 30, 2023

Core Plus Fixed Income Portfolio

Statement of Operations | | Year Ended

September 30, 2023

(000) | |

Investment Income: | |

Interest from Securities of Unaffiliated Issuers (Net of $4 of Foreign Taxes Withheld) | | $ | 26,893 | | |

Dividends from Security of Affiliated Issuer (Note G) | | | 3,290 | | |

Income from Securities Loaned — Net | | | 88 | | |

Total Investment Income | | | 30,271 | | |

Expenses: | |

Advisory Fees (Note B) | | | 2,181 | | |

Administration Fees (Note C) | | | 465 | | |

Sub Transfer Agency Fees — Class I | | | 361 | | |

Sub Transfer Agency Fees — Class A | | | 66 | | |

Sub Transfer Agency Fees — Class L | | | 1 | | |

Sub Transfer Agency Fees — Class C | | | 8 | | |

Shareholder Services Fees — Class A (Note D) | | | 148 | | |

Distribution and Shareholder Services Fees — Class L (Note D) | | | 4 | | |

Distribution and Shareholder Services Fees — Class C (Note D) | | | 129 | | |

Professional Fees | | | 202 | | |

Registration Fees | | | 90 | | |

Custodian Fees (Note F) | | | 70 | | |

Pricing Fees | | | 61 | | |

Shareholder Reporting Fees | | | 47 | | |

Transfer Agency Fees — Class I (Note E) | | | 20 | | |

Transfer Agency Fees — Class A (Note E) | | | 6 | | |

Transfer Agency Fees — Class L (Note E) | | | 2 | | |

Transfer Agency Fees — Class C (Note E) | | | 6 | | |

Transfer Agency Fees — Class R6 (Note E) | | | 4 | | |

Trustees' Fees and Expenses | | | 15 | | |

Other Expenses | | | 40 | | |

Total Expenses | | | 3,926 | | |

Waiver of Advisory Fees (Note B) | | | (1,019 | ) | |

Reimbursement of Class Specific Expenses — Class I (Note B) | | | (164 | ) | |

Reimbursement of Class Specific Expenses — Class L (Note B) | | | (2 | ) | |

Reimbursement of Class Specific Expenses — Class R6 (Note B) | | | (4 | ) | |

Rebate from Morgan Stanley Affiliate (Note G) | | | (112 | ) | |

Net Expenses | | | 2,625 | | |

Net Investment Income | | | 27,646 | | |

Realized Loss: | |

Investments Sold (Net of $5 of Capital Gain Country Tax) | | | (39,035 | ) | |

Foreign Currency Forward Exchange Contracts | | | (236 | ) | |

Foreign Currency Translation | | | (5 | ) | |

Futures Contracts | | | (15,470 | ) | |

Swap Agreements | | | (1,470 | ) | |

Net Realized Loss | | | (56,216 | ) | |

Change in Unrealized Appreciation (Depreciation): | |

Investments | | | 39,467 | | |

Foreign Currency Forward Exchange Contracts | | | (1,792 | ) | |

Foreign Currency Translation | | | (24 | ) | |

Futures Contracts | | | 3,370 | | |

Swap Agreements | | | 61 | | |

Net Change in Unrealized Appreciation (Depreciation) | | | 41,082 | | |

Net Realized Loss and Change in Unrealized Appreciation (Depreciation) | | | (15,134 | ) | |

Net Increase in Net Assets Resulting from Operations | | $ | 12,512 | | |

The accompanying notes are an integral part of the financial statements.

18

Morgan Stanley Institutional Fund Trust

Annual Report — September 30, 2023

Core Plus Fixed Income Portfolio

Statements of Changes in Net Assets | | Year Ended

September 30, 2023

(000) | | Year Ended

September 30, 2022

(000) | |

Increase (Decrease) in Net Assets: | |

Operations: | |

Net Investment Income | | $ | 27,646 | | | $ | 22,264 | | |

Net Realized Loss | | | (56,216 | ) | | | (52,539 | ) | |

Net Change in Unrealized Appreciation (Depreciation) | | | 41,082 | | | | (103,962 | ) | |

Net Increase (Decrease) in Net Assets Resulting from Operations | | | 12,512 | | | | (134,237 | ) | |

Dividends and Distributions to Shareholders: | |

Class I | | | (22,827 | ) | | | (18,106 | ) | |

Class A | | | (2,906 | ) | | | (2,149 | ) | |

Class L | | | (41 | ) | | | (23 | ) | |

Class C | | | (551 | ) | | | (407 | ) | |

Class R6* | | | (3,945 | ) | | | (3,666 | ) | |

Total Dividends and Distributions to Shareholders | | | (30,270 | ) | | | (24,351 | ) | |

Capital Share Transactions:(1) | |

Class I: | |

Subscribed | | | 160,654 | | | | 196,934 | | |

Distributions Reinvested | | | 22,491 | | | | 17,880 | | |

Redeemed | | | (216,246 | ) | | | (356,596 | ) | |

Class A: | |

Subscribed | | | 7,658 | | | | 11,728 | | |

Distributions Reinvested | | | 2,905 | | | | 2,149 | | |

Redeemed | | | (15,882 | ) | | | (35,681 | ) | |

Class L: | |

Exchanged | | | 100 | | | | 41 | | |

Distributions Reinvested | | | 41 | | | | 23 | | |

Redeemed | | | (270 | ) | | | (99 | ) | |

Class C: | |

Subscribed | | | 1,929 | | | | 1,327 | | |

Distributions Reinvested | | | 547 | | | | 404 | | |

Redeemed | | | (6,012 | ) | | | (8,945 | ) | |

Class R6:* | |

Subscribed | | | 7,701 | | | | 16,068 | | |

Distributions Reinvested | | | 3,621 | | | | 3,243 | | |

Redeemed | | | (46,653 | ) | | | (18,923 | ) | |

Net Decrease in Net Assets Resulting from Capital Share Transactions | | | (77,416 | ) | | | (170,447 | ) | |

Total Decrease in Net Assets | | | (95,174 | ) | | | (329,035 | ) | |

Net Assets: | |

Beginning of Period | | | 651,294 | | | | 980,329 | | |

End of Period | | $ | 556,120 | | | $ | 651,294 | | |

The accompanying notes are an integral part of the financial statements.

19

Morgan Stanley Institutional Fund Trust

Annual Report — September 30, 2023

Core Plus Fixed Income Portfolio

Statements of Changes in Net Assets (cont'd) | | Year Ended

September 30, 2023

(000) | | Year Ended

September 30, 2022

(000) | |

(1) Capital Share Transactions: | |

Class I: | |

Shares Subscribed | | | 16,899 | | | | 18,315 | | |

Shares Issued on Distributions Reinvested | | | 2,365 | | | | 1,657 | | |

Shares Redeemed | | | (22,718 | ) | | | (33,337 | ) | |

Net Decrease in Class I Shares Outstanding | | | (3,454 | ) | | | (13,365 | ) | |

Class A: | |

Shares Subscribed | | | 805 | | | | 1,069 | | |

Shares Issued on Distributions Reinvested | | | 305 | | | | 198 | | |

Shares Redeemed | | | (1,674 | ) | | | (3,299 | ) | |

Net Decrease in Class A Shares Outstanding | | | (564 | ) | | | (2,032 | ) | |

Class L: | |

Shares Exchanged | | | 11 | | | | 4 | | |

Shares Issued on Distributions Reinvested | | | 4 | | | | 2 | | |

Shares Redeemed | | | (29 | ) | | | (9 | ) | |

Net Decrease in Class L Shares Outstanding | | | (14 | ) | | | (3 | ) | |

Class C: | |

Shares Subscribed | | | 203 | | | | 120 | | |

Shares Issued on Distributions Reinvested | | | 58 | | | | 38 | | |

Shares Redeemed | | | (637 | ) | | | (842 | ) | |

Net Decrease in Class C Shares Outstanding | | | (376 | ) | | | (684 | ) | |

Class R6:* | |

Shares Subscribed | | | 819 | | | | 1,486 | | |

Shares Issued on Distributions Reinvested | | | 381 | | | | 302 | | |

Shares Redeemed | | | (4,900 | ) | | | (1,863 | ) | |

Net Decrease in Class R6 Shares Outstanding | | | (3,700 | ) | | | (75 | ) | |

* Effective April 29, 2022, Class IS shares were renamed Class R6 shares.

The accompanying notes are an integral part of the financial statements.

20

Morgan Stanley Institutional Fund Trust

Annual Report — September 30, 2023

Financial Highlights

Core Plus Fixed Income Portfolio

| | | Class I | |

| | | Year Ended September 30, | |

Selected Per Share Data and Ratios | | 2023 | | 2022 | | 2021 | | 2020 | | 2019 | |

Net Asset Value, Beginning of Period | | $ | 9.45 | | | $ | 11.53 | | | $ | 11.91 | | | $ | 11.58 | | | $ | 10.84 | | |

Income (Loss) from Investment Operations: | |

Net Investment Income(1) | | | 0.46 | | | | 0.29 | | | | 0.26 | | | | 0.31 | | | | 0.37 | | |

Net Realized and Unrealized Gain (Loss) | | | (0.26 | ) | | | (2.06 | ) | | | (0.07 | ) | | | 0.40 | | | | 0.78 | | |

Total from Investment Operations | | | 0.20 | | | | (1.77 | ) | | | 0.19 | | | | 0.71 | | | | 1.15 | | |

Distributions from and/or in Excess of: | |

Net Investment Income | | | (0.50 | ) | | | (0.28 | ) | | | (0.26 | ) | | | (0.30 | ) | | | (0.41 | ) | |

Net Realized Gain | | | — | | | | (0.03 | ) | | | (0.31 | ) | | | (0.08 | ) | | | — | | |

Total Distributions | | | (0.50 | ) | | | (0.31 | ) | | | (0.57 | ) | | | (0.38 | ) | | | (0.41 | ) | |

Net Asset Value, End of Period | | $ | 9.15 | | | $ | 9.45 | | | $ | 11.53 | | | $ | 11.91 | | | $ | 11.58 | | |

Total Return(2) | | | 2.03 | % | | | (15.58 | )% | | | 1.61 | % | | | 6.27 | % | | | 10.83 | %(3) | |

Ratios to Average Net Assets and Supplemental Data: | |

Net Assets, End of Period (Thousands) | | $ | 423,920 | | | $ | 470,728 | | | $ | 727,989 | | | $ | 662,724 | | | $ | 457,610 | | |

Ratio of Expenses Before Expense Limitation | | | 0.63 | % | | | 0.63 | % | | | 0.62 | % | | | 0.64 | % | | | 0.67 | % | |

Ratio of Expenses After Expense Limitation | | | 0.40 | %(4) | | | 0.41 | %(4) | | | 0.41 | %(4) | | | 0.40 | %(4) | | | 0.41 | %(4) | |

Ratio of Expenses After Expense Limitation Excluding Interest Expenses | | | N/A | | | | N/A | | | | N/A | | | | 0.40 | %(4) | | | N/A | | |

Ratio of Net Investment Income | | | 4.81 | %(4) | | | 2.74 | %(4) | | | 2.26 | %(4) | | | 2.63 | %(4) | | | 3.29 | %(4) | |

Ratio of Rebate from Morgan Stanley Affiliates | | | 0.02 | % | | | 0.01 | % | | | 0.01 | % | | | 0.02 | % | | | 0.01 | % | |

Portfolio Turnover Rate | | | 431 | % | | | 266 | % | | | 434 | % | | | 287 | % | | | 217 | % | |

(1) Per share amount is based on average shares outstanding.

(2) Calculated based on the net asset value as of the last business day of the period.