UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-3990

Northwestern Mutual Series Fund, Inc.

(Exact name of registrant as specified in charter)

720 East Wisconsin Avenue,

Milwaukee Wisconsin 53202

(Address of principal executive offices) (Zip code)

Barbara E. Courtney, Controller and Chief Accounting Officer Northwestern Mutual Series Fund, Inc.

(Name and address of agent for service)

Registrant’s telephone number, including area code: 414-271-1444

Date of fiscal year end: December 31

Date of reporting period: December 31, 2014

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

| Item 1. | Reports to Stockholders |

[Attached EDGARIZED ANNUAL REPORT]

Annual Report December 31, 2014

Northwestern Mutual Series Fund, Inc.

A Series Fund Offering 27 Portfolios

| | · | | Focused Appreciation Portfolio |

| | · | | Large Cap Core Stock Portfolio |

| | · | | Large Cap Blend Portfolio |

| | · | | Index 500 Stock Portfolio |

| | · | | Large Company Value Portfolio |

| | · | | Domestic Equity Portfolio |

| | · | | Equity Income Portfolio |

| | · | | Mid Cap Growth Stock Portfolio |

| | · | | Index 400 Stock Portfolio |

| | · | | Mid Cap Value Portfolio |

| | · | | Small Cap Growth Stock Portfolio |

| | · | | Index 600 Stock Portfolio |

| | · | | Small Cap Value Portfolio |

| | · | | International Growth Portfolio |

| | · | | Research International Core Portfolio |

| | · | | International Equity Portfolio |

| | · | | Emerging Markets Equity Portfolio |

| | · | | Short-Term Bond Portfolio |

| | · | | Long-Term U.S. Government Bond Portfolio |

| | · | | Inflation Protection Portfolio |

| | · | | High Yield Bond Portfolio |

| | · | | Multi-Sector Bond Portfolio |

| | · | | Asset Allocation Portfolio |

Letter to Contract Holders

December 31, 2014

In last year’s letter to contract holders, we discussed how investment markets for the past several years had been driven by broad economic themes, as opposed to individual, company specific factors. Economic themes continued to influence market performance during 2014, but investors demonstrated a greater appreciation for the fundamental drivers of different asset classes, countries and types of securities. For example, U.S. stocks and the U.S. dollar posted strong gains, as investors rewarded the U.S. economy’s strength relative to most major nations. With unsteady growth and political uncertainty throughout the world in 2014, investors embraced the U.S. economy’s improving growth and steady reduction in monetary stimulus.

Despite the overall strength of the U.S. market in 2014, the path for the market was uneven, as stocks fell sharply at the beginning of the year when global growth concerns dampened the outlook. Stocks rebounded thereafter, as improving economic growth in the U.S. led to optimism. The Federal Reserve (the “Fed”) steadily decreased its unprecedented stimulus program during the year, finishing its final bond purchasing program in October 2014. In September, the stock market dropped sharply again, as investors reduced risk in light of the Fed’s impending policy shift. Investors quickly returned to the U.S., as the Fed reaffirmed its commitment to a zero interest rate policy and the U.S. economy delivered solid growth, propelling the S&P 500® Index to an all-time high.

The U.S. stock market outperformed most foreign markets, while most major stock indices outperformed bonds. In general, emerging markets lagged during China’s economic slowdown, while the European Union continued to experience stagnant economic growth, sparking deflationary fears. A relatively new global theme emerged during the final months of the year when the U.S. dollar rallied relative to other major currencies due to rising economic prospects in the U.S. and the Fed’s termination of bond purchases. Subsequently, the rising dollar and record U.S. oil and gas production helped drive oil prices to a five-year low.

In that environment, investors were somewhat more discerning than in years past, as they developed a nuanced taste for risk assets. At the highest level, investors continued to embrace risk in stocks over the relative safety of bonds, although some clear risk-reduction themes emerged within both asset classes.

In the U.S., investors preferred the stability of larger-capitalization stocks, as the S&P 500® Index delivered a double-digit gain. Mid- and small-sized companies, on the other hand, produced more modest returns. Investors’ clear preference for large, liquid stocks was a notable divergence from the risk preference of prior years.

Similarly, within fixed income markets, bonds that offered more stability and lower yields—Treasurys and mortgage-backed securities—posted solid performance, while the higher yielding and higher risk corporate bond market

delivered mediocre returns. Here again, markets expressed a subtle shift toward risk reduction.

The U.S. economy grew at a moderate pace with contained inflation in 2014. An unseasonably cold winter led to a sharp economic contraction at the beginning of the year. Nevertheless, economic growth improved in each subsequent quarter with a strong finish in the latter half of the year. As a result, the U.S. unemployment rate dipped to 5.6% in December 2014. The improving job market and rising home prices led to relatively steady consumer spending, while solid profit growth and healthy balance sheets continued to propel Corporate America.

Despite the many strong and improving stories of 2014, we still find reasons to proceed with caution. Europe is struggling with stagnant economic growth and the risk of deflation, Japanese economic growth remains sluggish despite large amounts of economic stimulus, and declining oil prices could be a harbinger of weak demand. The Fed’s policy trajectory is tilting toward less economic stimulus, but the Fed’s interest rate policy remains uncertain, which may contribute to market volatility.

Although myriad economic, political and business events during 2015 may cause the investment markets to be volatile, this can serve as a reminder for investors to assess whether their portfolios remain adequately diversified in accordance with their long-term investment goals and risk tolerance. Portfolios tend to become unbalanced over time, as the outperformance of a certain asset class can lead to a higher concentration of that asset class in an investor’s portfolio. In light of this, an investor might consider whether it would be appropriate to return to his or her previously established asset class allocation levels by reallocating the gains of higher performing classes.1

Similar to all financial decisions, an investor should approach rebalancing with the guidance of a financial professional to pinpoint the appropriate allocation for his or her individual portfolio, current financial situation and overall financial plan. As always, we encourage you to work closely with your financial professional through the ups and downs of the financial markets in 2015, as they can help you develop and adhere to a plan that will be guided by your long-term goals, rather than the short-term fluctuations of the market.

Kate M. Fleming

President of Northwestern Mutual Series Fund, Inc.

1 A strategy involving portfolio rebalancing cannot assure a profit or protect against loss in a declining market. Not intended to be investment advice.

Northwestern Mutual Series Fund, Inc.

Table of Contents

| | | | |

Expense Examples | | | i | |

Series Fund Overviews and Schedules of Investments: | | | | |

Growth Stock Portfolio | | | 1 | |

Focused Appreciation Portfolio | | | 4 | |

Large Cap Core Stock Portfolio | | | 8 | |

Large Cap Blend Portfolio | | | 11 | |

Index 500 Stock Portfolio | | | 14 | |

Large Company Value Portfolio | | | 21 | |

Domestic Equity Portfolio | | | 25 | |

Equity Income Portfolio | | | 28 | |

Mid Cap Growth Stock Portfolio | | | 33 | |

Index 400 Stock Portfolio | | | 36 | |

Mid Cap Value Portfolio | | | 42 | |

Small Cap Growth Stock Portfolio | | | 47 | |

Index 600 Stock Portfolio | | | 51 | |

Small Cap Value Portfolio | | | 59 | |

International Growth Portfolio | | | 63 | |

Research International Core Portfolio | | | 67 | |

International Equity Portfolio | | | 72 | |

Emerging Markets Equity Portfolio | | | 77 | |

Money Market Portfolio | | | 82 | |

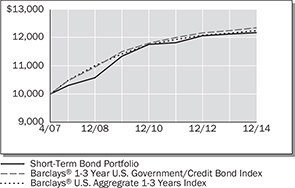

Short-Term Bond Portfolio | | | 86 | |

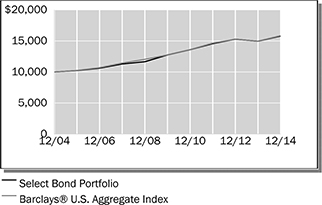

Select Bond Portfolio | | | 98 | |

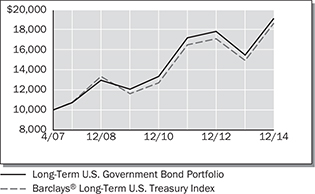

Long-Term U.S. Government Bond Portfolio | | | 110 | |

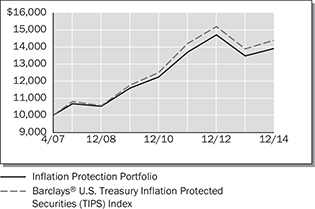

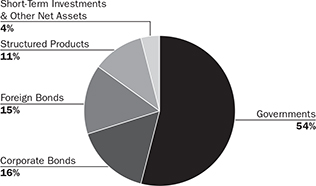

Inflation Protection Portfolio | | | 116 | |

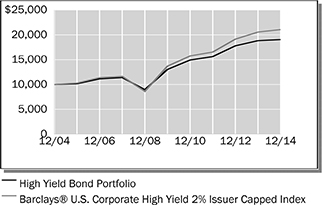

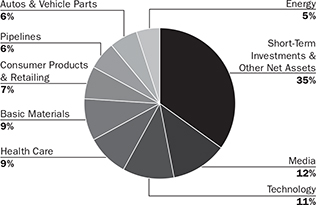

High Yield Bond Portfolio | | | 128 | |

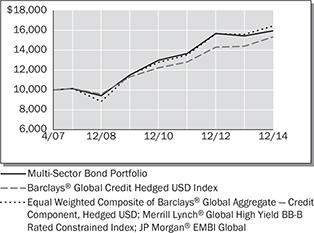

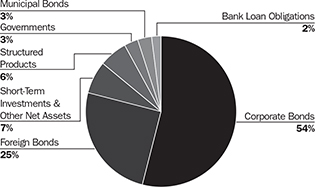

Multi-Sector Bond Portfolio | | | 138 | |

Balanced Portfolio | | | 158 | |

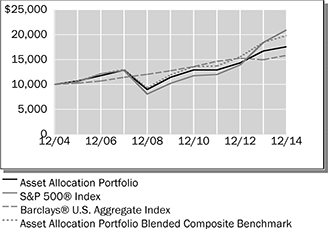

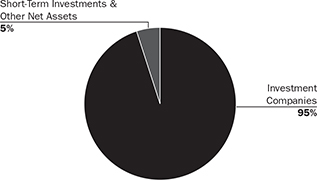

Asset Allocation Portfolio | | | 163 | |

Benchmark Definitions | | | 168 | |

Statements of Assets and Liabilities | | | 170 | |

Statements of Operations | | | 174 | |

Statements of Changes in Net Assets | | | 178 | |

Statement of Cash Flows | | | 186 | |

Financial Highlights | | | 188 | |

Notes to Financial Statements | | | 196 | |

Report of Independent Registered Public Accounting Firm | | | 218 | |

Proxy Voting and Portfolio Holdings | | | 219 | |

Director and Officer Information | | | 220 | |

Approval and Continuance of Investment Sub-Advisory Agreements | | | 223 | |

Mason Street Advisors, LLC (“Mason Street Advisors”), adviser to the Northwestern Mutual Series Fund, Inc., is a wholly owned subsidiary of The Northwestern Mutual Life Insurance Company. Mason Street Advisors is the principal investment adviser for all the Portfolios of the Northwestern Mutual Series Fund, Inc., and has engaged and oversees sub-advisers who provide day-to-day management for certain of the Portfolios. Each sub-adviser may be replaced without the approval of shareholders. Please see the Series Fund prospectus for more information.

The views expressed in the portfolio manager commentaries set forth in the following pages reflect those of the portfolio managers only through the end of the period covered by this report and do not necessarily represent the views of any affiliated organization. The views expressed are not guarantees of future performance or economic results and involve certain risks, uncertainties and assumptions that could cause actual outcomes and results to differ materially from the views expressed herein. These views are subject to change at any time based upon market conditions or other events and should not be relied upon as investment advice. Mason Street Advisors disclaims any responsibility to update these views.

Expense Examples (unaudited)

Example

As a shareholder of each Portfolio, you incur two types of costs: (1) transaction costs and (2) ongoing costs, including management fees and other Portfolio expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Portfolios and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (July 1, 2014 to December 31, 2014).

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below for each Portfolio provides information about hypothetical account values and hypothetical expenses based on each Portfolio’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Portfolio’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in a Portfolio and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs or separate account charges. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs or separate account charges were included, your costs would have been higher.

| | | | | | | | | | | | | | | | |

| | | Beginning Account Value

July 1, 2014 | | | Ending Account Value

December 31, 2014 | | | Expenses Paid During

Period July 1, 2014 to

December 31, 2014* | | | Annualized

Expense Ratio | |

| | | | |

Growth Stock Portfolio | | | | | | | | | | | | | | | | |

Actual | | | $1,000.00 | | | | $1,045.13 | | | | $2.11 | | | | 0.41 | % |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | | 1,023.14 | | | | 2.09 | | | | 0.41 | |

| | | | |

Focused Appreciation Portfolio | | | | | | | | | | | | | | | | |

Actual | | | 1,000.00 | | | | 1,085.46 | | | | 3.36 | | | | 0.64 | |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | | 1,021.98 | | | | 3.26 | | | | 0.64 | |

| | | | |

Large Cap Core Stock Portfolio | | | | | | | | | | | | | | | | |

Actual | | | 1,000.00 | | | | 1,010.77 | | | | 2.23 | | | | 0.44 | |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | | 1,022.99 | | | | 2.24 | | | | 0.44 | |

| | | | |

Large Cap Blend Portfolio | | | | | | | | | | | | | | | | |

Actual | | | 1,000.00 | | | | 1,038.71 | | | | 4.16 | | | | 0.81 | |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | | 1,021.12 | | | | 4.13 | | | | 0.81 | |

| | | | |

Index 500 Stock Portfolio | | | | | | | | | | | | | | | | |

Actual | | | 1,000.00 | | | | 1,060.23 | | | | 1.09 | | | | 0.21 | |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | | 1,024.15 | | | | 1.07 | | | | 0.21 | |

Expense Examples (unaudited)

| | | | | | | | | | | | | | | | |

| | | Beginning Account Value

July 1, 2014 | | | Ending Account Value

December 31, 2014 | | | Expenses Paid During

Period July 1, 2014 to

December 31, 2014* | | | Annualized

Expense Ratio | |

| | | | |

Large Company Value Portfolio | | | | | | | | | | | | | | | | |

Actual | | | 1,000.00 | | | | 1,047.05 | | | | 3.66 | | | | 0.71 | |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | | 1,021.63 | | | | 3.62 | | | | 0.71 | |

| | | | |

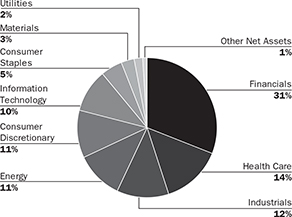

Domestic Equity Portfolio | | | | | | | | | | | | | | | | |

Actual | | | 1,000.00 | | | | 1,049.13 | | | | 2.84 | | | | 0.55 | |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | | 1,022.43 | | | | 2.80 | | | | 0.55 | |

| | | | |

Equity Income Portfolio | | | | | | | | | | | | | | | | |

Actual | | | 1,000.00 | | | | 1,012.57 | | | | 3.35 | | | | 0.66 | |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | | 1,021.88 | | | | 3.36 | | | | 0.66 | |

| | | | |

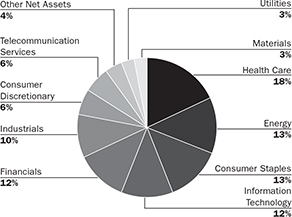

Mid Cap Growth Stock Portfolio | | | | | | | | | | | | | | | | |

Actual | | | 1,000.00 | | | | 1,057.44 | | | | 2.64 | | | | 0.51 | |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | | 1,022.63 | | | | 2.60 | | | | 0.51 | |

| | | | |

Index 400 Stock Portfolio | | | | | | | | | | | | | | | | |

Actual | | | 1,000.00 | | | | 1,019.61 | | | | 1.37 | | | | 0.27 | |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | | 1,023.84 | | | | 1.38 | | | | 0.27 | |

| | | | |

Mid Cap Value Portfolio | | | | | | | | | | | | | | | | |

Actual | | | 1,000.00 | | | | 1,059.22 | | | | 4.05 | | | | 0.78 | |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | | 1,021.27 | | | | 3.97 | | | | 0.78 | |

| | | | |

Small Cap Growth Stock Portfolio | | | | | | | | | | | | | | | | |

Actual | | | 1,000.00 | | | | 1,038.16 | | | | 2.93 | | | | 0.57 | |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | | 1,022.33 | | | | 2.91 | | | | 0.57 | |

| | | | |

Index 600 Stock Portfolio | | | | | | | | | | | | | | | | |

Actual | | | 1,000.00 | | | | 1,022.68 | | | | 1.89 | | | | 0.35 | |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | | 1,023.34 | | | | 1.89 | | | | 0.35 | |

| | | | |

Small Cap Value Portfolio | | | | | | | | | | | | | | | | |

Actual | | | 1,000.00 | | | | 972.84 | | | | 4.38 | | | | 0.88 | |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | | 1,020.77 | | | | 4.48 | | | | 0.88 | |

| | | | |

International Growth Portfolio | | | | | | | | | | | | | | | | |

Actual | | | 1,000.00 | | | | 913.19 | | | | 3.62 | | | | 0.75 | |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | | 1,021.42 | | | | 3.82 | | | | 0.75 | |

| | | | |

Research International Core Portfolio | | | | | | | | | | | | | | | | |

Actual | | | 1,000.00 | | | | 905.35 | | | | 4.51 | | | | 0.94 | |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | | 1,020.47 | | | | 4.79 | | | | 0.94 | |

| | | | |

International Equity Portfolio | | | | | | | | | | | | | | | | |

Actual | | | 1,000.00 | | | | 887.78 | | | | 3.14 | | | | 0.66 | |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | | 1,021.88 | | | | 3.36 | | | | 0.66 | |

Expense Examples (unaudited)

| | | | | | | | | | | | | | | | |

| | | Beginning Account Value

July 1, 2014 | | | Ending Account Value

December 31, 2014 | | | Expenses Paid During

Period July 1, 2014 to

December 31, 2014* | | | Annualized

Expense Ratio | |

| | | | |

Emerging Markets Equity Portfolio | | | | | | | | | | | | | | | | |

Actual | | | 1,000.00 | | | | 894.31 | | | | 6.45 | | | | 1.35 | |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | | 1,018.40 | | | | 6.87 | | | | 1.35 | |

| | | | |

Money Market Portfolio | | | | | | | | | | | | | | | | |

Actual | | | 1,000.00 | | | | 1,000.17 | | | | 0.55 | | | | 0.11 | |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | | 1,024.65 | | | | 0.56 | | | | 0.11 | |

| | | | |

Short-Term Bond Portfolio | | | | | | | | | | | | | | | | |

Actual | | | 1,000.00 | | | | 997.98 | | | | 2.06 | | | | 0.41 | |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | | 1,023.14 | | | | 2.09 | | | | 0.41 | |

| | | | |

Select Bond Portfolio | | | | | | | | | | | | | | | | |

Actual | | | 1,000.00 | | | | 1,016.63 | | | | 1.63 | | | | 0.32 | |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | | 1,023.59 | | | | 1.63 | | | | 0.32 | |

| | | | |

Long-Term U.S. Government Bond Portfolio | | | | | | | | | | | | | | | | |

Actual | | | 1,000.00 | | | | 1,104.62 | | | | 3.40 | | | | 0.65 | |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | | 1,021.98 | | | | 3.26 | | | | 0.65 | |

| | | | |

Inflation Protection Portfolio | | | | | | | | | | | | | | | | |

Actual | | | 1,000.00 | | | | 978.94 | | | | 2.94 | | | | 0.59 | |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | | 1,022.23 | | | | 3.01 | | | | 0.59 | |

| | | | |

High Yield Bond Portfolio | | | | | | | | | | | | | | | | |

Actual | | | 1,000.00 | | | | 965.41 | | | | 2.33 | | | | 0.47 | |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | | 1,022.84 | | | | 2.40 | | | | 0.47 | |

| | | | |

Multi-Sector Bond Portfolio | | | | | | | | | | | | | | | | |

Actual | | | 1,000.00 | | | | 971.28 | | | | 3.97 | | | | 0.80 | |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | | 1,021.17 | | | | 4.08 | | | | 0.80 | |

| | | | |

Balanced Portfolio | | | | | | | | | | | | | | | | |

Actual | | | 1,000.00 | | | | 1,012.88 | | | | 0.56 | | | | 0.11 | |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | | 1,024.65 | | | | 0.56 | | | | 0.11 | |

| | | | |

Asset Allocation Portfolio | | | | | | | | | | | | | | | | |

Actual | | | 1,000.00 | | | | 1,006.57 | | | | 0.81 | | | | 0.16 | |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | | 1,024.40 | | | | 0.82 | | | | 0.16 | |

| * | Expenses are equal to the Portfolio’s annualized expense ratio, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). |

Growth Stock Portfolio (unaudited)

| | | | |

| Objective: | | Portfolio Strategy: | | Net Assets: |

| Long-term growth of capital. Current income is a secondary objective. | | Invest in the equity securities of medium and large capitalization companies exhibiting the potential for earnings growth or share price appreciation. | | $886 million |

Portfolio Overview

Mason Street Advisors, LLC (“Mason Street Advisors”), the investment adviser for the Growth Stock Portfolio (the “Portfolio”), has engaged The Boston Company Asset Management, LLC (“The Boston Company”) to act as sub-adviser for the Portfolio. The Portfolio invests in the equity securities of medium and large capitalization companies. The Portfolio invests in stocks selected by a team of core research analysts, with each analyst responsible for investments in his or her area of expertise. These analysts use a fundamental, bottom-up research process to identify investments for the Portfolio. The Portfolio invests in those companies in which the analysts have the highest degree of conviction or have identified the potential for a strong near-term catalyst for earnings growth or share price appreciation.

Market Overview

Global equities produced mixed returns for 2014, according to various global indexes, as investors digested a medley of encouraging U.S. data, increasing volatility and rising geopolitical risk. Positive economic data helped U.S. stocks, as measured by the Russell 3000® Index, during the first quarter despite an unseasonably harsh winter that threatened consumer sentiment. By the second quarter, U.S. investors largely shrugged off reports that the economy shrank during the first three months of the year, while the U.S. Federal Reserve (the “Fed”) underlined an improving economy by announcing it would wind down its monthly bond purchases. U.S. stocks logged third-quarter gains, as investors cheered better-than-expected growth indicators, which included improvements in consumer spending, tourism and manufacturing. In the final quarter of 2014, U.S. stocks tallied another solid quarterly gain, as the Fed offered a mostly upbeat assessment of the country’s economic prospects.

Portfolio Results

The Portfolio returned 9.02% for the twelve months ended December 31, 2014. By comparison, the Portfolio’s benchmark, the Russell 1000® Growth Index (the “Index”), returned 13.05%. (This Index is unmanaged, cannot be invested in directly and does not include administrative expenses or sales charges.) According to Lipper® Analytical Services, Inc., an independent mutual fund ranking agency, the average return of the Large Cap Growth Funds peer group was 10.04% for 2014.

The Portfolio delivered solid performance in January and February, but in March, the markets began a correction, rotating away from the momentum stocks that had been 2013’s market leaders. This caused significant relative underperformance in March and April. From May through December, the Portfolio trailed the Index, but much less so relative to March/April. For the year, Industrials, Consumer Staples, Information Technology and Consumer Discretionary were the worst relative performers by sector, partially offset by outperformance in Health Care and a lack of exposure to Telecommunication Services.

The Healthcare sector delivered the best performance in both the Portfolio and the Index. The Portfolio’s outperformance was driven primarily by holdings in the biotechnology and life sciences tools & services segments. Within biotechnology, a position in Alexion Pharmaceuticals, Inc. moved higher, as the company’s Soliris treatment continued to generate improving earnings.

The Portfolio’s relative performance in the Industrials sector was hurt primarily by holdings in the construction & engineering and aerospace & defense segments. Shares of global construction & engineering firm Fluor Corp. fell despite several strong earnings reports, largely on concerns that lower oil prices may impact its backlog due to postponed projects.

The Portfolio’s relative underperformance in the Consumer Staples sector was mostly due to holdings in food & staples retailing and food products. Shares of specialty food retailer Whole Foods Market, Inc. dropped after disappointing earnings reports, demonstrating decelerating sales and margin compression.

Underperformance in the Consumer Discretionary sector was attributable to holdings in Internet & catalog retail and media. A position in television and media streaming service Netflix, Inc. fell amid weak subscriber growth with lackluster reviews for recent original content. As a result, the portfolio managers sold the position.

Portfolio Manager Outlook

The following forward looking comments are the opinion of The Boston Company, the Portfolio’s sub-adviser.

The U.S. economy continues to improve in key areas such as employment and manufacturing, and overall, we believe the economy remains well positioned for continued expansion in 2015. Lower oil prices could serve as a tailwind for the broader economy, as businesses realize lower input costs and consumers benefit from a boost to disposable income, which may drive retail spending in 2015. Coupled with early signs of rising wages and multi-year highs in consumer confidence, the consumer could be a particular source of economic strength.

Growth Stock Portfolio (unaudited)

Inflation remains subdued, and a strong dollar is likely to weigh on commodity prices for some time. The direction of interest rates and a potential rate hike by the Fed remain notable market uncertainties. While rates are widely expected to rise, we have yet to see that materialize. Market volatility could be further influenced by concerns about the new political mix in Washington, slow growth in Europe and Asia and extended weakness in oil, which could emerge as a source of instability. Overall, we continue to believe a healthier U.S. economy, strong corporate underpinnings and secular tailwinds will remain supportive of U.S. equities.

Relative Performance

| | | | | | | | | | | | |

Average Annual Total Returns

For Periods Ended December 31, 2014 | |

| | | 1 Year | | | 5 Years | | | 10 Years | |

Growth Stock Portfolio | | | 9.02 | % | | | 13.16 | % | | | 7.21 | % |

Russell 1000® Growth Index | | | 13.05 | % | | | 15.81 | % | | | 8.49 | % |

Lipper® Variable Insurance Products (VIP) Large Cap Growth Funds Average | | | 10.04 | % | | | 14.09 | % | | | 7.73 | % |

The performance data quoted represents past performance. Past performance is historical and does not guarantee future performance. Investment return and principal value will fluctuate, so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end performance information visit www.northwesternmutual.com.

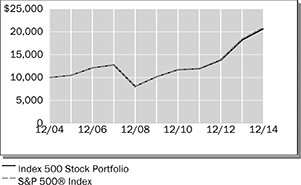

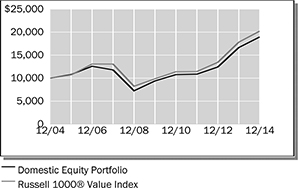

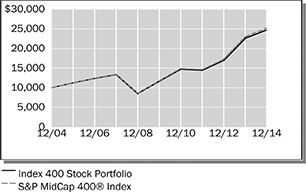

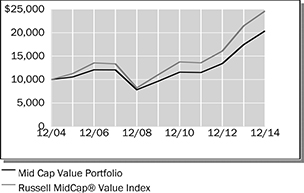

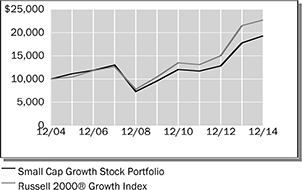

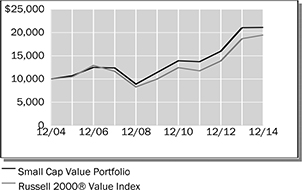

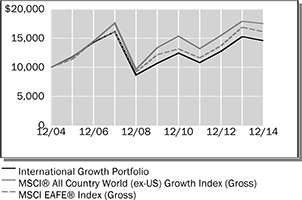

This chart assumes an initial investment of $10,000 made on 12/31/04. Returns shown include deductions for management and other portfolio expenses, and reinvestment of all dividends. Returns exclude deductions for separate account sale loads and account fees. Please refer to the Benchmark Definitions section of this report for information about the indices cited in the above chart and graph.

Top 10 Equity Holdings 12/31/14

| | | | |

Security Description | | | % of Net Assets | |

Apple, Inc. | | | 6.9 | % |

Microsoft Corp. | | | 2.8 | % |

PepsiCo, Inc. | | | 2.8 | % |

Facebook, Inc. - Class A | | | 2.8 | % |

Visa, Inc. - Class A | | | 2.7 | % |

The Home Depot, Inc. | | | 2.4 | % |

Gilead Sciences, Inc. | | | 2.1 | % |

Honeywell International, Inc. | | | 2.1 | % |

Comcast Corp. - Class A | | | 2.0 | % |

Schlumberger, Ltd. | | | 2.0 | % |

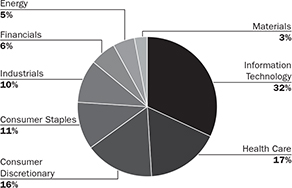

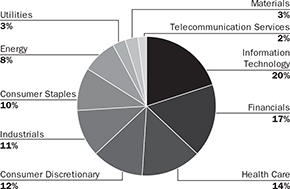

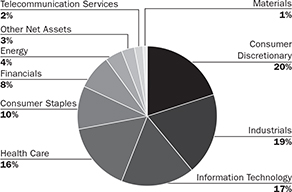

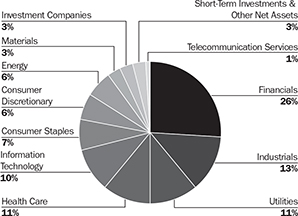

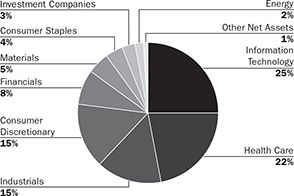

Sector Allocation 12/31/14

Sector Allocation is based on Net Assets.

Sector Allocation and Top 10 Holdings are subject to change.

Growth Stock Portfolio

Schedule of Investments

December 31, 2014

| | | | | | | | | | |

| | | Common Stocks (99.5%) | | Shares/

$ Par | | | Value

$ (000’s) | |

| |

| | Consumer Discretionary (16.3%) | |

| * | | AMC Networks, Inc. - Class A | | | 100,486 | | | | 6,408 | |

| | Comcast Corp. - Class A | | | 312,294 | | | | 18,116 | |

| | Delphi Automotive PLC | | | 97,960 | | | | 7,124 | |

| * | | Dollar General Corp. | | | 113,400 | | | | 8,017 | |

| | The Home Depot, Inc. | | | 202,260 | | | | 21,231 | |

| | The Interpublic Group of Cos., Inc. | | | 429,810 | | | | 8,927 | |

| * | | Michael Kors Holdings, Ltd. | | | 137,645 | | | | 10,337 | |

| | NIKE, Inc. - Class B | | | 146,070 | | | | 14,045 | |

| * | | Priceline.com, Inc. | | | 13,111 | | | | 14,949 | |

| | PVH Corp. | | | 89,830 | | | | 11,514 | |

| * | | Ulta Salon, Cosmetics & Fragrance, Inc. | | | 69,980 | | | | 8,946 | |

| * | | Under Armour, Inc. | | | 71,510 | | | | 4,856 | |

| | Viacom, Inc. - Class B | | | 127,530 | | | | 9,597 | |

| | | | | | | | | | |

| | Total | | | | | | | 144,067 | |

| | | | | | | | | | |

| |

| | Consumer Staples (10.8%) | |

| | Coca-Cola Enterprises, Inc. | | | 253,410 | | | | 11,206 | |

| | Colgate-Palmolive Co. | | | 207,980 | | | | 14,390 | |

| | Costco Wholesale Corp. | | | 79,456 | | | | 11,263 | |

| | CVS Caremark Corp. | | | 124,790 | | | | 12,018 | |

| | The Estee Lauder Cos., Inc. - Class A | | | 163,800 | | | | 12,482 | |

| | Mondelez International, Inc. | | | 281,670 | | | | 10,232 | |

| | PepsiCo, Inc. | | | 258,560 | | | | 24,449 | |

| | | | | | | | | | |

| | Total | | | | | | | 96,040 | |

| | | | | | | | | | |

| |

| | Energy (4.5%) | |

| | EOG Resources, Inc. | | | 142,900 | | | | 13,157 | |

| | Kinder Morgan, Inc. | | | 213,291 | | | | 9,024 | |

| | Schlumberger, Ltd. | | | 209,360 | | | | 17,882 | |

| | | | | | | | | | |

| | Total | | | | | | | 40,063 | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | Common Stocks (99.5%) | | Shares/

$ Par | | | Value

$ (000’s) | |

| |

| | Financials (6.0%) | |

| | Ameriprise Financial, Inc. | | | 86,660 | | | | 11,461 | |

| | BlackRock, Inc. | | | 30,910 | | | | 11,052 | |

| | Discover Financial Services | | | 115,530 | | | | 7,566 | |

| | Intercontinental Exchange, Inc. | | | 52,540 | | | | 11,521 | |

| | Marsh & McLennan Cos., Inc. | | | 204,835 | | | | 11,725 | |

| | | | | | | | | | |

| | Total | | | | | | | 53,325 | |

| | | | | | | | | | |

| |

| | Health Care (16.7%) | |

| * | | Actavis PLC | | | 57,783 | | | | 14,874 | |

| * | | Alexion Pharmaceuticals, Inc. | | | 62,990 | | | | 11,655 | |

| * | | Biogen Idec, Inc. | | | 38,440 | | | | 13,049 | |

| | Bristol-Myers Squibb Co. | | | 144,090 | | | | 8,506 | |

| * | | Celgene Corp. | | | 144,040 | | | | 16,112 | |

| * | | Gilead Sciences, Inc. | | | 198,590 | | | | 18,719 | |

| * | | Illumina, Inc. | | | 49,638 | | | | 9,162 | |

| | McKesson Corp. | | | 68,710 | | | | 14,263 | |

| | Perrigo Co. PLC | | | 61,101 | | | | 10,214 | |

| * | | Regeneron Pharmaceuticals, Inc. | | | 20,780 | | | | 8,525 | |

| | UnitedHealth Group, Inc. | | | 104,960 | | | | 10,610 | |

| * | | Vertex Pharmaceuticals, Inc. | | | 102,520 | | | | 12,179 | |

| | | | | | | | | | |

| | Total | | | | | | | 147,868 | |

| | | | | | | | | | |

| |

| | Industrials (10.4%) | |

| | Cummins, Inc. | | | 76,890 | | | | 11,085 | |

| | Danaher Corp. | | | 129,240 | | | | 11,077 | |

| | FedEx Corp. | | | 58,430 | | | | 10,147 | |

| | Fluor Corp. | | | 142,268 | | | | 8,626 | |

| | Honeywell International, Inc. | | | 181,930 | | | | 18,178 | |

| | Precision Castparts Corp. | | | 54,720 | | | | 13,181 | |

| | Raytheon Co. | | | 86,320 | | | | 9,337 | |

| | Tyco Interntional PLC | | | 234,990 | | | | 10,307 | |

| | | | | | | | | | |

| | Total | | | | | | | 91,938 | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | Common Stocks (99.5%) | | Shares/

$ Par | | | Value

$ (000’s) | |

| |

| | Information Technology (31.9%) | |

| | Accenture PLC - Class A | | | 93,590 | | | | 8,359 | |

| * | | Adobe Systems, Inc. | | | 130,390 | | | | 9,479 | |

| * | | Akamai Technologies, Inc. | | | 117,250 | | | | 7,382 | |

| | Apple, Inc. | | | 554,980 | | | | 61,259 | |

| * | | Cognizant Technology Solutions Corp. - Class A | | | 175,590 | | | | 9,247 | |

| | EMC Corp. | | | 390,970 | | | | 11,627 | |

| * | | Facebook, Inc. - Class A | | | 313,271 | | | | 24,441 | |

| * | | Fortinet, Inc. | | | 230,984 | | | | 7,082 | |

| * | | Google, Inc. - Class A | | | 31,610 | | | | 16,774 | |

| * | | Google, Inc. - Class C | | | 31,610 | | | | 16,640 | |

| | Intuit, Inc. | | | 160,490 | | | | 14,796 | |

| * | | LinkedIn Corp. - Class A | | | 39,950 | | | | 9,177 | |

| | Microsoft Corp. | | | 533,082 | | | | 24,762 | |

| | Oracle Corp. | | | 293,248 | | | | 13,187 | |

| * | | Salesforce.com, Inc. | | | 215,550 | | | | 12,784 | |

| | SanDisk Corp. | | | 115,130 | | | | 11,280 | |

| | Visa, Inc. - Class A | | | 92,830 | | | | 24,340 | |

| | | | | | | | | | |

| | Total | | | | | | | 282,616 | |

| | | | | | | | | | |

| |

| | Materials (2.9%) | |

| | The Dow Chemical Co. | | | 188,630 | | | | 8,603 | |

| | Martin Marietta Materials, Inc. | | | 66,060 | | | | 7,288 | |

| | Praxair, Inc. | | | 74,670 | | | | 9,674 | |

| | | | | | | | | | |

| | Total | | | | | | | 25,565 | |

| | | | | | | | | | |

| | Total Common Stocks | | | | | | | | |

| | (Cost: $683,284) | | | | | | | 881,482 | |

| | | | | | | | | | |

| | Total Investments (99.5%) | | | | | | | | |

| | (Cost: $683,284)(a) | | | | | | | 881,482 | |

| | | | | | | | | | |

| | Other Assets, Less | | | | | | | | |

| | Liabilities (0.5%) | | | | | | | 4,398 | |

| | | | | | | | | | |

| | Net Assets (100.0%) | | | | | | | 885,880 | |

| | | | | | | | | | |

| (a) | At December 31, 2014, the aggregate cost of securities for federal tax purposes (in thousands) was $684,921 and the net unrealized appreciation of investments based on that cost was $196,561 which is comprised of $199,956 aggregate gross unrealized appreciation and $3,395 aggregate gross unrealized depreciation. |

The following is a summary of the inputs used in valuing the Portfolio’s assets and liabilities at December 31, 2014. See Note 3 for additional information on portfolio valuation.

| | | | | | | | | | | | | | |

| | | Valuation Inputs | | | |

| Description | | Level 1 –

Quoted Prices | | | Level 2 –

Other Significant

Observable Inputs | | | Level 3 – Significant

Unobservable Inputs | | | |

| | | (Amounts in thousands) | | | |

Assets: | | | | | | | | | | | | | | |

Domestic Common Stocks | | $ | 881,482 | | | $ | - | | | $ | - | | | |

Total | | $ | 881,482 | | | $ | - | | | $ | - | | | |

The Accompanying Notes are an Integral Part of the Financial Statements.

Focused Appreciation Portfolio (unaudited)

| | | | |

| Objective: | | Portfolio Strategy: | | Net Assets: |

| Long-term growth of capital. | | Invest in equity securities selected for their growth potential. | | $722 million |

Portfolio Overview

Mason Street Advisors, LLC (“Mason Street Advisors”), the investment adviser for the Focused Appreciation Portfolio (the “Portfolio”), has engaged Janus Capital Management LLC (“Janus”) to act as sub-adviser for the Portfolio. In seeking to implement its growth strategy, the Portfolio employs a “bottom up” approach in choosing investments for the Portfolio. That is, the Portfolio looks at companies one at a time to determine if a company is an attractive investment opportunity and is consistent with the Portfolio’s investment policies. The Portfolio may invest in companies of any size, from larger, well established companies to smaller, emerging growth companies. As a non-diversified fund, the Portfolio may hold larger positions in a smaller number of companies and, in anticipation of such investments, may hold a correspondingly larger position in cash pending investment. The Portfolio invests primarily in a core group of 20-40 common stocks.

Market Overview

U.S. large-cap equities, as measured by the Russell 1000® Index, enjoyed another year of strong gains. Generally positive corporate earnings reports, a declining unemployment rate and a pickup in economic growth later in the year provided evidence the U.S. economy was strengthening. Low interest rates in most developed regions also provided a supportive backdrop for equities. While the U.S. equity market, measured by the Russell 3000® Index, enjoyed strong gains, volatility increased considerably in the final months of the year.

Portfolio Results

The Portfolio returned 9.43% for the twelve months ended December 31, 2014. By comparison, the Portfolio’s benchmark, the Russell 1000® Growth Index (the “Index”), returned 13.05%. (This Index is unmanaged, cannot be invested in directly and does not include administrative expenses or sales charges.) According to Lipper® Analytical Services, Inc., an independent mutual fund ranking agency, the average return of the Large Cap Growth Funds peer group was 10.04% for 2014.

As part of the Portfolio’s investment strategy, the portfolio managers seek companies that have clear, sustainable competitive moats around their businesses based on their view that sustainable competitive advantages should help grow market share within their respective industries over time. Important competitive advantages could include a strong brand, network effects from a product or service that would be hard for a competitor to replicate, a lower cost structure than competitors in the industry, a distribution advantage or patent protection over valuable intellectual property.

For the majority of companies in the Portfolio, the portfolio managers continued to see confirmation of their views on the strength of their competitive advantages, and the portfolio managers’ view of the long-term growth potential of these companies remained unchanged. However, the Portfolio did hold some stocks that produced disappointing results, and played a large role in the Portfolio’s underperformance relative to the Index.

Stock selection in the Technology and Financial sectors were the largest detractors from performance relative to the Index. The Portfolio’s relative underperformance in both sectors was stock specific, rather than the result of a broad underlying trend. Within the Information Technology sector, the Portfolio’s decision to not own Apple, Inc. was a significant detractor. The Portfolio’s position in Citigroup, Inc. held back results in the Financials sector.

The Portfolio’s underweight to the Energy sector and overweight to the Healthcare sector were the largest contributors to relative results. Within the Healthcare sector, the Portfolio held several biotechnology companies that announced encouraging results about innovative therapies under development, which was a large driver of performance. The Portfolio had a longstanding underweight to the Energy sector due to the sensitivity many businesses in the sector have to commodity prices. The decision to be underweight the sector was beneficial in the fourth quarter, when energy stocks generally declined as oil prices sank.

Portfolio Manager Outlook

The following forward looking comments are the opinion of Janus, the Portfolio’s sub-adviser.

Heading into 2015, we have a positive outlook for both the U.S. economy and domestic equities. In our view, the U.S. is clearly showing economic strength relative to the rest of the world. While declining commodity prices may create some short-term uncertainty, lower oil prices ultimately represent a tax cut for most consumers around the world. In a country such as the U.S., where such a large portion of the economy is driven by consumer spending, the tailwind from a sharp drop in oil prices can be considerable.

Looking at equity markets, we believe valuations are reasonable. However, after rising valuations in 2013 and the first half of 2014, we believe further stock price appreciation will need to be accompanied by earnings growth. If earnings growth again becomes the primary driver of stock returns next year, we believe such an environment could be favorable for our investment process.

| | | | |

| 4 | | Focused Appreciation Portfolio | | |

Focused Appreciation Portfolio (unaudited)

Relative Performance

| | | | | | | | | | | | |

Average Annual Total Returns

For Periods Ended December 31, 2014 | |

| | | 1 Year | | | 5 Years | | | 10 Years | |

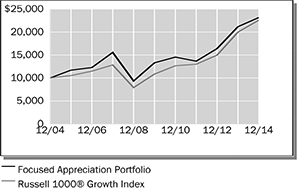

Focused Appreciation Portfolio | | | 9.43 | % | | | 11.73 | % | | | 8.76 | % |

Russell 1000® Growth Index | | | 13.05 | % | | | 15.81 | % | | | 8.49 | % |

Lipper® Variable Insurance Products (VIP) Large Cap Growth Funds Average | | | 10.04 | % | | | 14.09 | % | | | 7.73 | % |

The performance data quoted represents past performance. Past performance is historical and does not guarantee future performance. Investment return and principal value will fluctuate, so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end performance information visit www.northwesternmutual.com.

This chart assumes an initial investment of $10,000 made on 12/31/04. Returns shown include deductions for management and other portfolio expenses, and reinvestment of all dividends. Returns exclude deductions for separate account sale loads and account fees. Please refer to the Benchmark Definitions section of this report for information about the indices cited in the above chart and graph.

As a non-diversified portfolio, the Portfolio may hold fewer securities because of its focused investment strategy. Holding fewer securities increases the risk that the value of the Portfolio could go down because of the poor performance of a single investment.

Top 10 Equity Holdings 12/31/14

| | | | |

Security Description | | | % of Net Assets | |

Precision Castparts Corp. | | | 4.5 | % |

Lowe’s Cos., Inc. | | | 4.4 | % |

Celgene Corp. | | | 4.1 | % |

Google, Inc. - Class C | | | 3.9 | % |

Endo International PLC | | | 3.9 | % |

Valeant Pharmaceuticals International, Inc. | | | 3.6 | % |

Salesforce.com, Inc. | | | 3.4 | % |

Delphi Automotive PLC | | | 3.4 | % |

Zoetis, Inc. | | | 3.3 | % |

Canadian Pacific Railway, Ltd. | | | 3.3 | % |

Sector Allocation 12/31/14

Sector Allocation is based on Net Assets.

Sector Allocation and Top 10 Holdings are subject to change.

| | | | | | |

| | Focused Appreciation Portfolio | | | 5 | |

Focused Appreciation Portfolio

Schedule of Investments

December 31, 2014

| | | | | | | | | | |

| | | Common Stocks (94.5%) | | Shares/

$ Par | | | Value

$ (000’s) | |

| | | |

| | Consumer Discretionary (23.5%) | | | | | | | | |

| * | | Amazon.com, Inc. | | | 65,404 | | | | 20,298 | |

| | Comcast Corp. - Class A | | | 310,420 | | | | 18,007 | |

| | Delphi Automotive PLC | | | 336,260 | | | | 24,453 | |

| | Las Vegas Sands Corp. | | | 137,682 | | | | 8,008 | |

| | Lowe’s Cos., Inc. | | | 465,229 | | | | 32,008 | |

| | Marriott International, Inc. - Class A | | | 193,305 | | | | 15,084 | |

| * | | Priceline.com, Inc. | | | 16,236 | | | | 18,512 | |

| | Starbucks Corp. | | | 215,092 | | | | 17,648 | |

| | The TJX Cos., Inc. | | | 230,328 | | | | 15,796 | |

| | | | | | | | | | |

| | Total | | | | | | | 169,814 | |

| | | | | | | | | | |

| | | |

| | Energy (0.5%) | | | | | | | | |

| | Baker Hughes, Inc. | | | 64,164 | | | | 3,598 | |

| | | | | | | | | | |

| | Total | | | | | | | 3,598 | |

| | | | | | | | | | |

| | | |

| | Financials (10.8%) | | | | | | | | |

| | Aon PLC | | | 194,316 | | | | 18,427 | |

| | Crown Castle International Corp. | | | 213,534 | | | | 16,805 | |

| * | | E*TRADE Financial Corp. | | | 462,625 | | | | 11,221 | |

| | Intercontinental Exchange, Inc. | | | 63,477 | | | | 13,920 | |

| | U.S. Bancorp | | | 395,744 | | | | 17,789 | |

| | | | | | | | | | |

| | Total | | | | | | | 78,162 | |

| | | | | | | | | | |

| | | |

| | Health Care (21.0%) | | | | | | | | |

| * | | athenahealth, Inc. | | | 32,461 | | | | 4,729 | |

| * | | Biogen Idec, Inc. | | | 48,369 | | | | 16,419 | |

| * | | Boston Scientific Corp. | | | 552,602 | | | | 7,322 | |

| * | | Celgene Corp. | | | 262,388 | | | | 29,351 | |

| * | | Endo International PLC | | | 390,387 | | | | 28,155 | |

| * | | Pharmacyclics, Inc. | | | 91,561 | | | | 11,194 | |

| * | | Salix Pharmaceuticals, Ltd. | | | 43,782 | | | | 5,032 | |

| * | | Valeant Pharmaceuticals International, Inc. | | | 179,421 | | | | 25,677 | |

| | Zoetis, Inc. | | | 551,482 | | | | 23,730 | |

| | | | | | | | | | |

| | Total | | | | | | | 151,609 | |

| | | | | | | | | | |

| | | |

| | Industrials (12.0%) | | | | | | | | |

| | Canadian Pacific Railway, Ltd. | | | 122,793 | | | | 23,661 | |

| | Kansas City Southern | | | 81,989 | | | | 10,005 | |

| | Nielsen NV | | | 447,052 | | | | 19,997 | |

| | Precision Castparts Corp. | | | 136,144 | | | | 32,794 | |

| | | | | | | | | | |

| | Total | | | | | | | 86,457 | |

| | | | | | | | | | |

| | | |

| | Information Technology (23.7%) | | | | | | | | |

| * | | Adobe Systems, Inc. | | | 198,691 | | | | 14,445 | |

| * | | Alibaba Group Holding, Ltd., ADR | | | 166,832 | | | | 17,340 | |

| | Amphenol Corp. - Class A | | | 166,915 | | | | 8,982 | |

| | ARM Holdings PLC, ADR | | | 313,413 | | | | 14,511 | |

| * | | CoStar Group, Inc. | | | 75,290 | | | | 13,825 | |

| * | | Google, Inc. - Class C | | | 53,499 | | | | 28,162 | |

| * | | LinkedIn Corp. - Class A | | | 43,979 | | | | 10,102 | |

| | | | | | | | | | | | |

| | | Common Stocks (94.5%) | | | | Shares/

$ Par | | | Value

$ (000’s) | |

| | |

| | Information Technology continued | | | | | |

| | MasterCard, Inc. - Class A | | | | | 274,266 | | | | 23,631 | |

| * | | NetSuite, Inc. | | | | | 58,318 | | | | 6,367 | |

| * | | Salesforce.com, Inc. | | | | | 413,357 | | | | 24,516 | |

| * | | Yahoo!, Inc. | | | | | 179,111 | | | | 9,047 | |

| | | | | | | | | | | | |

| | Total | | | | | | | | | 170,928 | |

| | | | | | | | | | | | |

| | | | |

| | Materials (2.0%) | | | | | | | | | | |

| | Monsanto Co. | | | | | 119,970 | | | | 14,333 | |

| | | | | | | | | | | | |

| | Total | | | | | | | | | 14,333 | |

| | | | | | | | | | | | |

| | | |

| | Telecommunication Services (1.0%) | | | | | | | | |

| * | | T-Mobile US, Inc. | | | | | 271,298 | | | | 7,309 | |

| | | | | | | | | | | | |

| | Total | | | | | | | | | 7,309 | |

| | | | | | | | | | | | |

| | | |

| | Total Common Stocks | | | | | | | | |

| | (Cost: $549,916) | | | | | | | | | 682,210 | |

| | | | | | | | | | | | |

| | | | |

| | | Foreign Common Stocks (3.3%) | | Country | | | | | | | | |

| | | |

| | Information Technology (1.4%) | | | | | | | | |

| | Tencent Holdings, Ltd. | | Cayman Islands | | | 717,000 | | | | 10,288 | |

| | | | | | | | | | | | |

| | Total | | | | | | | | | 10,288 | |

| | | | | | | | | | | | |

| | | | |

| | Telecommunication Services (1.9%) | | | | | | | | | | |

| | Iliad SA | | France | | | 57,416 | | | | 13,771 | |

| | | | | | | | | | | | |

| | Total | | | | | | | | | 13,771 | |

| | | | | | | | | | | | |

| | | |

| | Total Foreign Common Stocks | | | | | | | | |

| | (Cost: $23,485) | | | | | | | 24,059 | |

| | | | | | | | | | | | |

| | | |

| | Total Investments (97.8%) | | | | | | | | |

| | (Cost: $573,401)(a) | | | | | | | 706,269 | |

| | | | | | | | | | | | |

| | Other Assets, Less | | | | | | | | | | |

| | Liabilities (2.2%) | | | | | | | | | 16,110 | |

| | | | | | | | | | | | |

| | Net Assets (100.0%) | | | | | | | | | 722,379 | |

| | | | | | | | | | | | |

The Accompanying Notes are an Integral Part of the Financial Statements.

| | | | |

| 6 | | Focused Appreciation Portfolio | | |

Focused Appreciation Portfolio

ADR after the name of a security represents—American Depositary Receipt.

| (a) | At December 31, 2014, the aggregate cost of securities for federal tax purposes (in thousands) was $573,986 and the net unrealized appreciation of investments based on that cost was $132,283 which is comprised of $133,202 aggregate gross unrealized appreciation and $919 aggregate gross unrealized depreciation. |

The following is a summary of the inputs used in valuing the Portfolio’s assets and liabilities at December 31, 2014. See Note 3 for additional information on portfolio valuation.

| | | | | | | | | | | | | | |

| | | Valuation Inputs | | | |

| Description | | Level 1 – Quoted Prices | | | Level 2 –

Other Significant

Observable Inputs | | | Level 3 –

Significant

Unobservable Inputs | | | |

| | | (Amounts in thousands) | | | |

Assets: | | | | | | | | | | | | | | |

Domestic Common Stocks | | $ | 682,210 | | | $ | - | | | $ | - | | | |

Foreign Common Stocks | | | - | | | | 24,059 | | | | - | | | |

Total | | $ | 682,210 | | | $ | 24,059 | | | $ | - | | | |

For the period ended December 31, 2014, there were transfers from a Level 1 to a Level 2 in the amount of $24,059 thousand. These transfers were the result of the use of fair value procedures on certain foreign securities in the portfolio on December 31, 2014. These securities did not require the use of fair value procedures on December 31, 2013.

The Accompanying Notes are an Integral Part of the Financial Statements.

| | | | | | |

| | Focused Appreciation Portfolio | | | 7 | |

Large Cap Core Stock Portfolio (unaudited)

| | | | |

| Objective: | | Portfolio Strategy: | | Net Assets: |

| Long-term growth of capital and income. | | Invest primarily in common stocks of large capitalization U.S. and foreign based companies listed on U.S. exchanges. | | $556 million |

Portfolio Overview

Mason Street Advisors, LLC (“Mason Street Advisors”), the investment adviser for the Large Cap Core Stock Portfolio (the “Portfolio”), has engaged Fayez Sarofim & Co. (“Sarofim & Co.”) to act as sub-adviser for the Portfolio. In choosing securities, the Portfolio’s portfolio managers first identify structurally attractive economic sectors they believe can support longer term profit growth. Using fundamental analysis, the Portfolio’s portfolio managers then seek companies within these sectors that have dominant positions and sustainable competitive advantages in their industries, superior management that productively redeploys cash flow, sustained patterns of profitability, strong balance sheets, expanding global presence and the potential to achieve predictable, above-average earnings and dividend growth over the next three to five years or longer. The Portfolio may also invest in companies which the portfolio managers consider undervalued in terms of earnings, assets or growth prospects.

Market Overview

The S&P 500® Index recorded a series of successive new highs in 2014, despite five short-lived sell-offs, and has now more than tripled from its March 2009 low. The S&P 500® Index outpaced other developed market indices, as domestic economic growth gained traction and the U.S. Federal Reserve (the “Fed”) ended quantitative easing. In contrast, economic weakness and financial strains resurfaced abroad, and foreign central banks generally stepped up stimulative efforts. The U.S. dollar strengthened against nearly every major currency in 2014, while oil prices plunged 50%. Concerns about global growth intensified in the second half prompting increased market volatility. The relative performance of large cap stocks (S&P 500® Index) versus small caps (S&P SmallCap 600® Index) began to strengthen over the last six months, reversing the trend that has persisted through most of this liquidity-driven recovery. Utilities, Health Care, and Information Technology were the leading sectors in the S&P 500® Index for the year, while Energy was the only sector with a negative return.

Portfolio Results

The Portfolio returned 8.56% for the twelve months ended December 31, 2014. By comparison, the S&P 500® Index (the “Index”) returned 13.69%. (This Index is unmanaged, cannot be invested in directly and does not include administrative expenses or sales charges.) According to Lipper® Analytical Services, Inc., an independent mutual fund ranking agency, the average return of the Large Cap Core Funds peer group was 11.51% for 2014.

The Portfolio’s overweight allocation to the weak Energy sector was a primary factor weighing on results relative to Index. This impact, however, was mitigated by advantageous stock selection within the sector, reflecting the emphasis on the major integrated oil companies and the avoidance of the more volatile oilfield service and equipment stocks. The portfolio managers believed that the Portfolio’s Energy sector holdings offered compelling valuations, strong balance sheets, established records of returning capital to shareholders and disciplined cost controls.

Another factor impeding relative performance was stock selection in the Consumer Staples sector. Weakening demand in international markets, particularly in Europe, and the strength of the U.S. dollar detracted from the Portfolio’s holdings in the Consumer Staples sector, which included several global companies. Stock selection ultimately weighed on performance relative to the Index, although an overweight in the rallying sector limited the negative impact.

Stock selection in the Financials and Health Care sectors also detracted from relative performance.

On the upside, factors that supported results relative to the Index included the limited and selectively focused representations in the Consumer Discretionary and Materials sectors, two lagging sectors. The underweighted allocation to the Industrials sector and the lack of exposure to the Telecommunication Services sector also added value relative to the Index.

Turning to the performance of individual holdings, Portfolio holdings that delivered the largest contributions to absolute return were Apple, Inc., Altria Group, Inc., Walgreen Boots Alliance, Inc., Johnson & Johnson, AbbVie, Inc., Texas Instruments, Inc., Intel Corp. and The Walt Disney Co. Holdings that detracted from absolute performance were International Business Machines Corp., Exxon Mobil Corp., Chevron Corp., Occidental Petroleum Corp., Total Sponsored ADR, General Electric Co., Diageo PLC Sponsored ADR and Philip Morris International, Inc.

Portfolio Manager Outlook

The following forward looking comments are the opinion of Sarofim & Co., the Portfolio’s sub-adviser.

Although the U.S. economy seems to be gaining self-sustaining momentum, the global backdrop has grown less supportive. We expect the relative performance of the larger cap issues in the Portfolio to strengthen in the year ahead as equity markets adjust to desynchronized global trends and the potential shift in Fed policy. We believe the industry leaders that are the focus of the Portfolio’s investment strategy have the financial resources, operational discipline and competitive advantages to sustain

| | | | |

| 8 | | Large Cap Core Stock Portfolio | | |

Large Cap Core Stock Portfolio (unaudited)

longer-term earnings growth if interest rates begin to rise. Our strategic stock selection emphasizes structurally attractive industries with less cyclical attributes where pricing power is stronger and margins are more stable. We also continue to focus on companies with established records of returning capital to shareholders in the form of dividends and share repurchases, providing investors a degree of downside protection if market conditions continue to shift and volatility increases.

Relative Performance

| | | | | | | | | | | | |

Average Annual Total Returns

For Periods Ended December 31, 2014 | |

| | | 1 Year | | | 5 Years | | | 10 Years | |

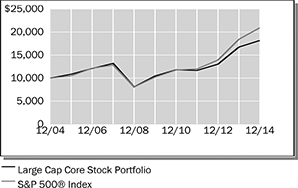

Large Cap Core Stock Portfolio | | | 8.56 | % | | | 11.69 | % | | | 6.15 | % |

S&P 500® Index | | | 13.69 | % | | | 15.45 | % | | | 7.67 | % |

Lipper® Variable Insurance Products (VIP) Large Cap Core Funds Average | | | 11.51 | % | | | 13.87 | % | | | 7.21 | % |

The performance data quoted represents past performance. Past performance is historical and does not guarantee future performance. Investment return and principal value will fluctuate, so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end performance information visit www.northwesternmutual.com.

This chart assumes an initial investment of $10,000 made on 12/31/04. Returns shown include deductions for management and other portfolio expenses, and reinvestment of all dividends. Returns exclude deductions for separate account sale loads and account fees. Please refer to the Benchmark Definitions section of this report for information about the indices cited in the above chart and graph.

Top 10 Equity Holdings 12/31/14

| | | | |

Security Description | | | % of Net Assets | |

Apple, Inc. | | | 4.9 | % |

Exxon Mobil Corp. | | | 4.5 | % |

Philip Morris International, Inc. | | | 4.2 | % |

The Coca-Cola Co. | | | 4.0 | % |

Chevron Corp. | | | 3.5 | % |

Nestle SA, ADR | | | 2.9 | % |

JPMorgan Chase & Co. | | | 2.5 | % |

Altria Group, Inc. | | | 2.5 | % |

Johnson & Johnson | | | 2.5 | % |

The Procter & Gamble Co. | | | 2.4 | % |

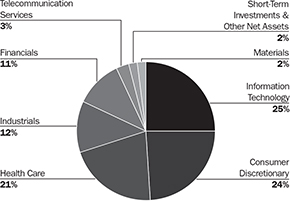

Sector Allocation 12/31/14

Sector Allocation is based on Net Assets.

Sector Allocation and Top 10 Holdings are subject to change.

| | | | | | |

| | Large Cap Core Stock Portfolio | | | 9 | |

Large Cap Core Stock Portfolio

Schedule of Investments

December 31, 2014

| | | | | | | | | | |

| | | Common Stocks (99.8%) | | Shares/

$ Par | | | Value

$ (000’s) | |

| |

| | Consumer Discretionary (8.0%) | |

| | Comcast Corp. - Class A | | | 119,152 | | | | 6,912 | |

| | McDonald’s Corp. | | | 89,278 | | | | 8,365 | |

| | Target Corp. | | | 92,553 | | | | 7,026 | |

| | Time Warner Cable, Inc. | | | 22,288 | | | | 3,389 | |

| | Twenty-First Century Fox, Inc. | | | 238,510 | | | | 9,160 | |

| | Twenty-First Century Fox, Inc. - Class B | | | 20,000 | | | | 738 | |

| | The Walt Disney Co. | | | 94,133 | | | | 8,866 | |

| | | | | | | | | | |

| | Total | | | | | | | 44,456 | |

| | | | | | | | | | |

| |

| | Consumer Staples (26.2%) | |

| | Altria Group, Inc. | | | 286,708 | | | | 14,126 | |

| | Anheuser-Busch InBev NV, ADR | | | 50,000 | | | | 5,616 | |

| | The Coca-Cola Co. | | | 529,535 | | | | 22,357 | |

| | Diageo PLC | | | 41,833 | | | | 4,773 | |

| | The Estee Lauder Cos., Inc. - Class A | | | 115,311 | | | | 8,787 | |

| | Mondelez International, Inc. | | | 74,689 | | | | 2,713 | |

| | Nestle SA, ADR | | | 221,932 | | | | 16,190 | |

| | PepsiCo, Inc. | | | 103,025 | | | | 9,742 | |

| | Philip Morris International, Inc. | | | 286,328 | | | | 23,321 | |

| | The Procter & Gamble Co. | | | 148,522 | | | | 13,529 | |

| | SABMiller PLC, ADR | | | 107,053 | | | | 5,519 | |

| | Walgreens Boots Alliance, Inc. | | | 142,358 | | | | 10,848 | |

| | Wal-Mart Stores, Inc. | | | 90,647 | | | | 7,785 | |

| | | | | | | | | | |

| | Total | | | | | | | 145,306 | |

| | | | | | | | | | |

| |

| | Energy (16.9%) | |

| * | | California Resources Corp. | | | 59,116 | | | | 326 | |

| | Chevron Corp. | | | 174,747 | | | | 19,603 | |

| | ConocoPhillips | | | 154,170 | | | | 10,647 | |

| | | | | | | | | | |

| | | Common Stocks (99.8%) | | Shares/

$ Par | | | Value

$ (000’s) | |

| |

| | Energy continued | |

| | EOG Resources, Inc. | | | 36,822 | | | | 3,390 | |

| | Exxon Mobil Corp. | | | 269,581 | | | | 24,923 | |

| | Imperial Oil, Ltd. | | | 125,732 | | | | 5,410 | |

| | Occidental Petroleum Corp. | | | 147,790 | | | | 11,913 | |

| | Phillips 66 | | | 43,579 | | | | 3,125 | |

| | Royal Dutch Shell PLC - Class A, ADR | | | 115,227 | | | | 7,714 | |

| | Total SA, ADR | | | 138,507 | | | | 7,092 | |

| | | | | | | | | | |

| | Total | | | | | | | 94,143 | |

| | | | | | | | | | |

| |

| | Financials (11.3%) | |

| | ACE, Ltd. | | | 56,944 | | | | 6,541 | |

| | American Express Co. | | | 109,017 | | | | 10,143 | |

| | BlackRock, Inc. | | | 28,303 | | | | 10,120 | |

| | Franklin Resources, Inc. | | | 158,502 | | | | 8,776 | |

| | JPMorgan Chase & Co. | | | 225,755 | | | | 14,128 | |

| | State Street Corp. | | | 85,500 | | | | 6,712 | |

| | Wells Fargo & Co. | | | 120,523 | | | | 6,607 | |

| | | | | | | | | | |

| | Total | | | | | | | 63,027 | |

| | | | | | | | | | |

| |

| | Health Care (13.2%) | |

| | Abbott Laboratories | | | 210,638 | | | | 9,483 | |

| | AbbVie, Inc. | | | 171,972 | | | | 11,254 | |

| * | | Celgene Corp. | | | 50,000 | | | | 5,593 | |

| * | | Gilead Sciences, Inc. | | | 64,000 | | | | 6,033 | |

| | Johnson & Johnson | | | 132,101 | | | | 13,814 | |

| | Novartis AG, ADR | | | 88,303 | | | | 8,182 | |

| | Novo Nordisk A/S, ADR | | | 233,235 | | | | 9,870 | |

| | Roche Holding AG, ADR | | | 262,964 | | | | 8,938 | |

| | | | | | | | | | |

| | Total | | | | | | | 73,167 | |

| | | | | | | | | | |

| |

| | Industrials (5.6%) | |

| | Canadian Pacific Railway, Ltd. | | | 39,854 | | | | 7,679 | |

| | Caterpillar, Inc. | | | 58,273 | | | | 5,334 | |

| | | | | | | | | | |

| | | Common Stocks (99.8%) | | Shares/

$ Par | | | Value

$ (000’s) | |

| |

| | Industrials continued | |

| | General Electric Co. | | | 110,792 | | | | 2,800 | |

| | Union Pacific Corp. | | | 30,000 | | | | 3,574 | |

| | United Technologies Corp. | | | 102,676 | | | | 11,808 | |

| | | | | | | | | | |

| | Total | | | | | | | 31,195 | |

| | | | | | | | | | |

| |

| | Information Technology (15.6%) | |

| | Apple, Inc. | | | 248,089 | | | | 27,384 | |

| | ASML Holding N.V. | | | 30,000 | | | | 3,235 | |

| | Automatic Data Processing, Inc. | | | 86,475 | | | | 7,209 | |

| | Intel Corp. | | | 160,564 | | | | 5,827 | |

| | International Business Machines Corp. | | | 73,519 | | | | 11,795 | |

| | Oracle Corp. | | | 162,624 | | | | 7,313 | |

| | Qualcomm, Inc. | | | 122,918 | | | | 9,137 | |

| | Texas Instruments, Inc. | | | 206,633 | | | | 11,048 | |

| | Xilinx, Inc. | | | 83,444 | | | | 3,612 | |

| | | | | | | | | | |

| | Total | | | | | | | 86,560 | |

| | | | | | | | | | |

| |

| | Materials (3.0%) | |

| | Air Products and Chemicals, Inc. | | | 35,897 | | | | 5,177 | |

| | Praxair, Inc. | | | 88,526 | | | | 11,470 | |

| | | | | | | | | | |

| | Total | | | | | | | 16,647 | |

| | | | | | | | | | |

| | | |

| | Total Common Stocks | | | | | | | | |

| | (Cost: $443,372) | | | | | | | 554,501 | |

| | | | | | | | | | |

| | | |

| | Total Investments (99.8%) | | | | | | | | |

| | (Cost: $443,372)(a) | | | | | | | 554,501 | |

| | | | | | | | | | |

| | Other Assets, Less | | | | | | | | |

| | Liabilities (0.2%) | | | | | | | 1,138 | |

| | | | | | | | | | |

| | Net Assets (100.0%) | | | | | | | 555,639 | |

| | | | | | | | | | |

ADR after the name of a security represents—American Depositary Receipt.

| (a) | At December 31, 2014, the aggregate cost of securities for federal tax purposes (in thousands) was $443,396 and the net unrealized appreciation of investments based on that cost was $111,105 which is comprised of $114,229 aggregate gross unrealized appreciation and $3,124 aggregate gross unrealized depreciation. |

The following is a summary of the inputs used in valuing the Portfolio’s assets and liabilities at December 31, 2014. See Note 3 for additional information on portfolio valuation.

| | | | | | | | | | | | | | |

| | | Valuation Inputs | | | |

| Description | | Level 1 – Quoted Prices | | | Level 2 – Other Significant

Observable Inputs | | | Level 3 – Significant

Unobservable Inputs | | | |

| | | (Amounts in thousands) | | | |

Assets: | | | | | | | | | | | | | | |

Domestic Common Stocks | | $ | 554,501 | | | $ | - | | | $ | - | | | |

Total | | $ | 554,501 | | | $ | - | | | $ | - | | | |

The Accompanying Notes are an Integral Part of the Financial Statements.

| | | | |

| 10 | | Large Cap Core Stock Portfolio | | |

Large Cap Blend Portfolio (unaudited)

| | | | |

| Objective: | | Portfolio Strategy: | | Net Assets: |

| Long-term growth of capital and income. | | Invest primarily in equity securities of U.S. large capitalization companies listed or traded on U.S. securities exchanges. | | $167 million |

Portfolio Overview

Mason Street Advisors, LLC (“Mason Street Advisors”), the investment adviser for the Large Cap Blend Portfolio (the “Portfolio”), has engaged Fiduciary Management, Inc. (“FMI”) to act as sub-adviser for the Portfolio. Normally, the Portfolio invests in equity securities of large capitalization companies listed or traded on U.S. securities exchanges or U.S. securities associations. In selecting investments, greater consideration is given to potential appreciation and future dividends than to current income. The Portfolio uses fundamental analysis to look for stocks of good businesses that are selling at value prices. The Portfolio employs a focused investment strategy, typically investing in a core group of 20-30 large capitalization stocks and ADRs.

Market Overview

The U.S. stock market rally completed its 69th month since the market bottomed on March 9, 2009. Since then, large cap stocks, as measured by the S&P 500® Index, gained 244%, while small cap stocks, measured by the Russell 2000® Index, appreciated 280%. Improving economic growth with mild inflation prompted the U.S. Federal Reserve (the “Fed”) to gradually complete its bond purchasing program and maintain its zero interest rate policy during 2014, though Fed policy contributed to uncertainty during the second half of the year. Throughout the year, the Fed decreased its bond purchasing at a measured $10 billion monthly pace. Market volatility preceded the Fed’s last bond purchase in October, as investors became concerned that the Fed’s zero interest rate policy might be the next tightening of monetary stimulus. The Fed reaffirmed its commitment to zero interest rate policy for a considerable period, which reassured investors. Markets rallied on the news, while improving economic growth late in the year also increased investors’ optimism.

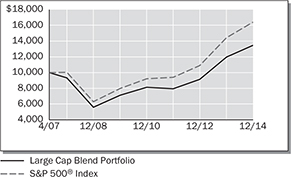

Portfolio Results

The Portfolio returned 12.58% for the twelve months ended December 31, 2014. By comparison, the S&P 500® Index (the “Index”) returned 13.69%. (This Index is unmanaged, cannot be invested in directly and does not include administrative expenses or sales charges.) According to Lipper® Analytical Services, Inc., an independent mutual fund ranking agency, the average return of the Large Cap Core Funds peer group was 11.51% for 2014.

Overall, stock selection was solid, particularly in Healthcare. UnitedHealth Group, Inc., AmerisourceBergen Corp. and Covidien PLC (sold in June after the buyout announcement by Medtronic) were among the top contributors relative to the Index in Healthcare. Other stock picks that helped performance relative to the Index were Ross Stores, Inc., Cintas Corp. and Berkshire Hathaway, Inc.

The Energy sector of the Portfolio delivered solid relative performance. The Portfolio’s positions in Devon Energy Corp. and Schlumberger, Ltd. both declined in the fourth quarter during the energy selloff, but still performed much better relative to the Index’s energy holdings.

The detractors in 2014 were the Portfolio’s elevated cash level (approximately 9%) and American Depository Receipts (ADR) exposure, including Danone SA, Nestle SA, and Unilever PLC. In those three investments, the depreciation in the Euro, Swiss Franc, and British Pound also detracted from the Portfolio’s return. The portfolio managers believed all three companies had strong franchises with above average growth prospects, relative to their U.S. counterparts. The portfolio managers added to positions in Danone SA and Unilever PLC during the year.

Portfolio Manager Outlook

The following forward looking comments are the opinion of FMI, the Portfolio’s sub-adviser.

Given the stock market’s significant appreciation in recent years, we would be surprised if returns over the next five years are anywhere close to returns of the past five years. The increased volatility in the fourth quarter may be a harbinger of future volatility. We believe volatile markets could give us more opportunities to maneuver in 2015. A recent investment letter that was discussing the rapid and steep drop in oil prices, quoted the renowned German economist, Rudiger Dornbusch; “In economics, things take longer to happen than you think they will, and then happen much quicker than you thought they could.” We believe this observation also applies to stock markets. Until good businesses are offered again at relatively inexpensive prices, we will focus on owning good businesses at somewhat elevated prices. The Portfolio trades at a significant discount to the Index, which we believe has the potential to help the Portfolio’s performance relative to the Index in 2015.

| | | | | | |

| | Large Cap Blend Portfolio | | | 11 | |

Large Cap Blend Portfolio (unaudited)

Relative Performance

| | | | | | | | | | | | |

Average Annual Total Returns

For Periods Ended December 31, 2014 | |

| | | 1 Year | | | 5 Years | | | Since Inception* | |

Large Cap Blend Portfolio | | | 12.58 | % | | | 13.64 | % | | | 3.98 | % |

S&P 500® Index | | | 13.69 | % | | | 15.45 | % | | | 6.66 | % |

Lipper® Variable Insurance Products (VIP) Large Cap Core Funds Average | | | 11.51 | % | | | 13.87 | % | | | - | |

| * | Inception date of 4/30/07 |

The performance data quoted represents past performance. Past performance is historical and does not guarantee future performance. Investment return and principal value will fluctuate, so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end performance information visit www.northwesternmutual.com.

This chart assumes an initial investment of $10,000 made on 4/30/07 (commencement of the Portfolio’s operations). Returns shown reflect fee waivers, deductions for management and other portfolio expenses, and reinvestment of all dividends. In the absence of fee waivers, total return would be reduced. Returns exclude deductions for separate account sale loads and account fees. Please refer to the Benchmark Definitions section of this report for information about the indices cited in the above chart and graph.

The Portfolio may hold fewer securities than other diversified portfolios because of its more focused investment strategy. Holding fewer securities increases the risk that the value of the Portfolio could go down because of the poor performance of a single investment.

Top 10 Equity Holdings 12/31/14

| | | | |

Security Description | | | % of Net Assets | |

Potash Corp. of Saskatchewan, Inc. | | | 5.7 | % |

UnitedHealth Group, Inc. | | | 5.6 | % |

Accenture PLC - Class A | | | 5.4 | % |

Berkshire Hathaway, Inc. - Class B | | | 5.2 | % |

The Bank of New York Mellon Corp. | | | 5.0 | % |

AmerisourceBergen Corp. | | | 4.5 | % |

Devon Energy Corp. | | | 3.7 | % |

American Express Co. | | | 3.7 | % |

DANONE SA, ADR | | | 3.7 | % |

The Progressive Corp. | | | 3.6 | % |

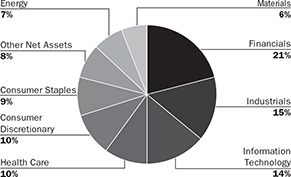

Sector Allocation 12/31/14

Sector Allocation is based on Net Assets.

Sector Allocation and Top 10 Holdings are subject to change.

| | | | |

| 12 | | Large Cap Blend Portfolio | | |

Large Cap Blend Portfolio

Schedule of Investments

December 31, 2014

| | | | | | | | | | |

| | | Common Stocks (92.2%) | | Shares/

$ Par | | | Value

$ (000’s) | |

| |

| | Consumer Discretionary (9.7%) | |

| | Comcast Corp. - Class A | | | 90,350 | | | | 5,241 | |

| | Omnicom Group, Inc. | | | 70,125 | | | | 5,432 | |

| | Ross Stores, Inc. | | | 58,950 | | | | 5,557 | |

| | | | | | | | | | |

| | Total | | | | | | | 16,230 | |

| | | | | | | | | | |

| |

| | Consumer Staples (9.0%) | |

| | DANONE SA, ADR | | | 471,250 | | | | 6,134 | |

| | Nestle SA, ADR | | | 70,925 | | | | 5,174 | |

| | Unilever PLC, ADR | | | 91,025 | | | | 3,685 | |

| | | | | | | | | | |

| | Total | | | | | | | 14,993 | |

| | | | | | | | | | |

| |

| | Energy (7.2%) | |

| | Devon Energy Corp. | | | 102,200 | | | | 6,255 | |

| | Schlumberger, Ltd. | | | 68,350 | | | | 5,838 | |

| | | | | | | | | | |

| | Total | | | | | | | 12,093 | |

| | | | | | | | | | |

| |

| | Financials (20.8%) | |

| | American Express Co. | | | 67,025 | | | | 6,236 | |

| | The Bank of New York Mellon Corp. | | | 205,100 | | | | 8,321 | |

| | | | | | | | | | |

| | | Common Stocks (92.2%) | | Shares/

$ Par | | | Value

$ (000’s) | |

| |

| | Financials continued | |

| * | | Berkshire Hathaway, Inc. - Class B | | | 57,625 | | | | 8,652 | |

| | Comerica, Inc. | | | 119,050 | | | | 5,576 | |

| | The Progressive Corp. | | | 220,175 | | | | 5,943 | |

| | | | | | | | | | |

| | Total | | | | | | | 34,728 | |

| | | | | | | | | | |

| |

| | Health Care (10.1%) | |

| | AmerisourceBergen Corp. | | | 82,475 | | | | 7,436 | |

| | UnitedHealth Group, Inc. | | | 92,775 | | | | 9,379 | |

| | | | | | | | | | |

| | Total | | | | | | | 16,815 | |

| | | | | | | | | | |

| |

| | Industrials (15.0%) | |

| | 3M Co. | | | 31,775 | | | | 5,221 | |

| | Cintas Corp. | | | 44,700 | | | | 3,506 | |

| | Expeditors International of Washington, Inc. | | | 104,550 | | | | 4,664 | |

| | Honeywell International, Inc. | | | 58,800 | | | | 5,875 | |

| | PACCAR, Inc. | | | 85,125 | | | | 5,790 | |

| | | | | | | | | | |

| | Total | | | | | | | 25,056 | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | Common Stocks (92.2%) | | Shares/

$ Par | | | Value

$ (000’s) | |

| |

| | Information Technology (14.7%) | |