UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-04000

CaLvert Variable Products, Inc.

(Exact name of registrant as specified in charter)

4550 Montgomery Avenue

Suite 1000N

Bethesda, Maryland 20814

(Address of Principal Executive Offices)

William M. Tartikoff, Esq.

4550 Montgomery Avenue

Suite 1000N

Bethesda, Maryland 20814

(Name and Address of Agent for Service)

Registrant's telephone number, including area code: (301) 951-4800

Date of fiscal year end: December 31

Date of reporting period: Year ended December 31, 2012

Item 1. Report to Stockholders.

[Calvert VP SRI Large Cap Value Portfolio Annual Report to Shareholders]

[Calvert VP S&P 500 Index Portfolio Annual Report to Shareholders]

[Calvert VP S&P MidCap 400 Index Portfolio Annual Report to Shareholders]

[Calvert VP Nasdaq-100 Index Portfolio Annual Report to Shareholders]

[Calvert VP Russell 2000 Small Cap Index Portfolio Annual Report to Shareholders]

[Calvert VP EAFE International Index Portfolio Annual Report to Shareholders]

[Calvert VP Barclays Capital Aggregate Bond Index Portfolio Annual Report to Shareholders]

[Calvert VP Inflation Protected Plus Portfolio Annual Report to Shareholders]

[Calvert VP Natural Resources Portfolio Annual Report to Shareholders]

CALVERT VP SRI LARGE CAP VALUE PORTFOLIO

Portfolio within Calvert Variable Products, Inc.

Managed by Calvert Investment Management, Inc.

PERFORMANCE

For the 12-month period ended December 31, 2012, Calvert VP SRI Large Cap Value Portfolio returned 17.03% versus the 17.51% return of the Russell 1000 Value Index. Holdings in the Materials, Telecommunication Services, and Health Care sectors contributed to the relative underperformance.

INVESTMENT CLIMATE

The most overused phrase dominating year-end headlines was “fiscal cliff,” as inaction in Washington dominated after President Obama’s re-election. The gridlock cast a pall over the financial markets and incited fear in investors’ hearts. The uncertainty tempted investors to sell securities to avoid inevitable higher tax rates. We expect the debt ceiling to dominate in the first quarter of 2013.

Meanwhile, high unemployment continued to be the number-one economic problem for the country. The rate is slowly dropping--although it remained relatively high at 7.8% as of December 2012--and would benefit from higher economic growth. The Federal Reserve (Fed) continued a highly stimulative monetary policy in an attempt to boost economic growth out of the doldrums. The economy did grow 3.1% in the third quarter and housing starts reached a four-year high. Automobile sales also began to rebound thanks to a loosening of lending standards and the aging auto fleet.

Globally, nearly all central banks were employing stimulative monetary policies by year end. Most established democracies were confronting the reality of spending more than they tax. So far, the easiest route for the politicians and voters has been to nibble away at some of the programs

| | AVERAGE ANNUAL TOTAL RETURN | |

| | (period ended 12.31.12) | |

| |

| One year | 17.03 | % |

| Five year | -0.51 | % |

| Ten year | 7.31 | % |

The performance data shown represents past performance, does not guarantee future results and assumes reinvestment of all dividends and distributions. All performance data reflects fee waivers and/or expense limitations, if any are in effect; in their absence performance would be lower. See Note B in Notes to Financial Statements. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Visit www.calvert.com/ institutional-VP-performance.html for current performance data. The gross expense ratio from the current prospectus for the Portfolio is 0.85%. This number may vary from the expense ratio shown elsewhere in this report because it is based on a different time period and, if applicable, does not include fee or expense waivers. The performance data and expense ratio reflect deduction of Portfolio operating expenses, but do not reflect charges and expenses imposed under the variable annuity or life insurance contract.

www.calvert.com CALVERT VP SRI LARGE CAP VALUE PORTFOLIO ANNUAL REPORT 4

and raise taxes on the “rich.” But that has not been enough to balance the budget.

PORTFOLIO STRATEGY

Although economic growth has been anemic, the underpinnings of a recovery finally seem to be set in place. To take advantage of the consumer-led recovery, we added Target, DirecTV, and DuPont. Occidental Petroleum was also added given the potential rise in energy prices from the Fed’s policies. We believe new holding Norfolk Southern should benefit from a rise in coal prices. We added Southern Company for its stable dividend yield.

Two more defensive holdings were initiated with a common theme of corporate restructuring. Abbot will be spinning off a division that we believe should realize greater value on a stand-alone basis, and PepsiCo management has been put on notice to focus more on shareholder returns than on other stakeholders. We also purchased American International Group and Citigroup, two companies we believe are experiencing a rebirth and sell at substantial discounts to book value.

To fund these new holdings, we eliminated Spectra Energy, News Corp, CME Group, Pentair, Cisco, Diamond Offshore, Wal-Mart Stores, 3M, and Travelers as they reached their expected full value. We also sold Frontier Communications, Hewlett-Packard, Alliance Bernstein, Legg Mason, Exelon, and Gannett either because their fundamentals had weakened or we deemed other holdings more attractive.

| | % OF TOTAL | |

| ECONOMIC SECTORS | INVESTMENTS | |

| |

| Consumer Discretionary | 12.3 | % |

| Consumer Staples | 6.8 | % |

| Energy | 15.9 | % |

| Financials | 22.6 | % |

| Health Care | 11.5 | % |

| Industrials | 6.1 | % |

| Information Technology | 9.5 | % |

| Materials | 6.0 | % |

| Short-Term Investments | 2.5 | % |

| Telecommunication Services | 2.9 | % |

| Utilities | 3.9 | % |

| Total | 100 | % |

Detractors from Performance

The fund’s top three detractors from performance were the Materials, Telecommunication Services, and Health Care sectors. Materials underperformed due to overweights in mining company Newmont and chemical company DuPont. Both companies, along with many high dividend payers, lost ground in the fourth quarter of 2012.

In Telecommunication Services, Frontier Communications lagged the market before we sold it. WellPoint was the main detractor in Health Care, as it struggled following the acquisition of 1-800-Contacts and Amerigroup. The CEO was also dismissed mid-year.

Contributors to Performance

The top three contributors to relative performance were the Energy, Information Technology, and Financials sectors. Energy enjoyed strong stock selection as ConocoPhillips and Marathon Petroleum outpaced competitors, particularly Chevron, which we do not hold. eBay drove performance in Information Technology. We also exited Hewlett-Packard to reduce potential losses as the stock continued to slide.

The Financials sector benefited from both stock and industry selection. We took advantage of undervalued names, particularly in the capital markets, diversified financial services, and insurers industries. Insurer Hartford Financial Services was the largest driver of positive performance. Bank of America bounced back from a dismal 2011 to

www.calvert.com CALVERT VP SRI LARGE CAP VALUE PORTFOLIO ANNUAL REPORT 5

become one of the best performers within the Financials sector.

OUTLOOK

The economy has been growing for more than two years. With the unemployment rate at 7.8% as of December and housing just beginning to recover, the Fed remains in stimulus mode and has set a major goal to reduce unemployment (they have mentioned a goal of 6.5%). It is ostensibly not worried about inflation.

Reduced unemployment would also be a positive for deficit reduction, providing increased revenues and decreased unemployment expenditures. Congress agrees that fiscal policy should be stimulative, even if that might be construed as inflationary. The increase in taxes on dividends and interest that Congress passed were also much less onerous than they could have been if the previous rates had merely expired.

Overall, equities are in a much more favorable position than fixed-income securities. That being said, continued shocks to investors over the years prompted them to walk away from equities. However, many companies have excellent dividends--greater than their corporate bond yields--and many have significantly reduced their outstanding shares. High dividend yields for equities are due to investors’ lack of interest. Furthermore, their extreme desire for non-volatile fixed income has driven bond yields to very low levels--again creating a favorable position for equities.

As equity investors, we plan to remain diversified among sectors, investing with the expectations of returning cost inflation and rising interest rates. We will also remain fully invested to benefit from an economic rebound, which most investors don’t seem to believe will arrive.

January 2013

As of December 31, 2012, the following companies represented the following percentages of Portfolio net assets: Target 2.49%, DirecTV 2.45%, DuPont 2.28%, Occidental Petroleum 2.30%, Norfolk Southern 0.80%, Southern Company 1.99%, Abbott 0.47%, PepsiCo 1.97%, American International Group 1.50%, Citigroup 0.59%, Spectra Energy 0%, News Corp 0%, CME Group 0%, Pentair 0%, Cisco 0%, Diamond Offshore 0%, Wal-Mart Stores 0%, 3M 0%, Travelers 0%, Frontier Communications 0%, Hewlett-Packard 0%, Alliance Bernstein 0%, Legg Mason 0%, Exelon 0%, Gannett 0%, Newmont 1.36%, WellPoint 2.08%, 1-800-Contacts 0%, Amerigroup 0%, ConocoPhillips 2.17%, Marathon Petroleum 1.52%, Chevron 0%, eBay 1.81%, Hartford Financial Services 2.00%, and Bank of America 2.06%. Holdings are subject to change.

www.calvert.com CALVERT VP SRI LARGE CAP VALUE PORTFOLIO ANNUAL REPORT 6

SHAREHOLDER EXPENSE EXAMPLE

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, and (2) ongoing costs, including management fees and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

This Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (July 1, 2012 to December 31, 2012).

Note: Expenses do not reflect charges and expenses of the variable annuity or variable universal life contract.

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare the 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | BEGINNING | ENDING | EXPENSES PAID |

| | ACCOUNT VALUE | ACCOUNT VALUE | DURING PERIOD* |

| | 7/1/12 | 12/31/12 | 7/1/12 - 12/31/12 |

| |

| Actual | $1,000.00 | $1,093.85 | $4.03 |

| |

| Hypothetical (5% return per year before expenses) | $1,000.00 | $1,021.28 | $3.89 |

* Expenses are equal to the Fund’s annualized expense ratio of 0.77%, multiplied by the average account value over the period, multiplied by 184/366 (to reflect the one-half year period).

www.calvert.com CALVERT VP SRI LARGE CAP VALUE PORTFOLIO ANNUAL REPORT 7

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

The Board of Directors of Calvert Variable Products, Inc. and Shareholders of Calvert VP SRI Large Cap Value Portfolio:

We have audited the accompanying statement of net assets of the Calvert VP SRI Large Cap Value Portfolio (the Portfolio), a series of Calvert Variable Products, Inc., as of December 31, 2012, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years in the five-year period then ended. These financial statements and financial highlights are the responsibility of the Portfolio’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of December 31, 2012, by correspondence with the custodian and brokers or by other appropriate auditing procedures. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of the Calvert VP SRI Large Cap Value Portfolio as of December 31, 2012, the results of its operations for the year then ended, the changes in its net assets for each of the years in the two-year period then ended and the financial highlights for each of the years in the five-year period then ended, in conformity with accounting principles generally accepted in the United States of America.

Philadelphia, Pennsylvania

February 25, 2013

www.calvert.com CALVERT VP SRI LARGE CAP VALUE PORTFOLIO ANNUAL REPORT 8

| | | |

| STATEMENT OF NET ASSETS |

| DECEMBER 31, 2012 |

| |

| |

| |

| EQUITY SECURITIES - 98.1% | SHARES | | VALUE |

| Beverages - 2.0% | | | |

| PepsiCo, Inc | 37,900 | $ | 2,593,497 |

| |

| Capital Markets - 4.1% | | | |

| Goldman Sachs Group, Inc | 20,800 | | 2,653,248 |

| Morgan Stanley | 139,400 | | 2,665,328 |

| | | | 5,318,576 |

| |

| Chemicals - 4.7% | | | |

| Dow Chemical Co. | 97,700 | | 3,157,664 |

| E. I. du Pont de Nemours & Co | 66,700 | | 2,999,499 |

| | | | 6,157,163 |

| |

| Commercial Banks - 6.2% | | | |

| PNC Financial Services Group, Inc. | 56,100 | | 3,271,191 |

| US Bancorp | 58,200 | | 1,858,908 |

| Wells Fargo & Co | 85,800 | | 2,932,644 |

| | | | 8,062,743 |

| |

| Commercial Services & Supplies - 3.0% | | | |

| The ADT Corp | 27,412 | | 1,274,384 |

| Tyco International Ltd | 91,025 | | 2,662,481 |

| | | | 3,936,865 |

| |

| Diversified Financial Services - 4.8% | | | |

| Bank of America Corp. | 234,184 | | 2,716,534 |

| Citigroup, Inc. | 20,000 | | 791,200 |

| JPMorgan Chase & Co. | 62,204 | | 2,735,110 |

| | | | 6,242,844 |

| |

| Diversified Telecommunication Services - 2.9% | | | |

| AT&T, Inc. | 77,300 | | 2,605,783 |

| Verizon Communications, Inc. | 28,400 | | 1,228,868 |

| | | | 3,834,651 |

| |

| Electric Utilities - 3.9% | | | |

| Duke Energy Corp | 39,581 | | 2,525,268 |

| The Southern Co. | 61,100 | | 2,615,691 |

| | | | 5,140,959 |

| |

| Electrical Equipment - 0.5% | | | |

| Emerson Electric Co. | 12,400 | | 656,704 |

| |

| Electronic Equipment & Instruments - 1.5% | | | |

| TE Connectivity Ltd | 54,925 | | 2,038,816 |

| |

| Food & Staples Retailing - 1.8% | | | |

| CVS Caremark Corp. | 49,700 | | 2,402,995 |

www.calvert.com CALVERT VP SRI LARGE CAP VALUE PORTFOLIO ANNUAL REPORT 9

| | | |

| EQUITY SECURITIES - CONT’D | SHARES | | VALUE |

| Food Products - 1.3% | | | |

| Unilever NV, NY Shares | 44,600 | $ | 1,708,180 |

| |

| Health Care Equipment & Supplies - 1.0% | | | |

| Abbott Laboratories | 9,400 | | 615,700 |

| Covidien plc | 11,125 | | 642,357 |

| | | | 1,258,057 |

| |

| Health Care Providers & Services - 2.1% | | | |

| WellPoint, Inc. | 45,000 | | 2,741,400 |

| |

| Household Durables - 0.6% | | | |

| Sony Corp. (ADR) | 66,500 | | 744,800 |

| |

| Household Products - 1.8% | | | |

| Procter & Gamble Co | 34,000 | | 2,308,260 |

| |

| Industrial Conglomerates - 1.8% | | | |

| General Electric Co | 110,800 | | 2,325,692 |

| |

| Insurance - 7.7% | | | |

| American International Group, Inc.* | 56,100 | | 1,980,330 |

| Berkshire Hathaway, Inc., Class B* | 26,950 | | 2,417,415 |

| Hartford Financial Services Group, Inc | 117,400 | | 2,634,456 |

| MetLife, Inc. | 92,100 | | 3,033,774 |

| | | | 10,065,975 |

| |

| Internet Software & Services - 4.4% | | | |

| eBay, Inc.* | 46,700 | | 2,382,634 |

| Google, Inc.* | 4,800 | | 3,404,976 |

| | | | 5,787,610 |

| |

| IT Services - 1.4% | | | |

| International Business Machines Corp. | 9,600 | | 1,838,880 |

| |

| Media - 7.0% | | | |

| CBS Corp., Class B | 51,974 | | 1,977,611 |

| Comcast Corp | 32,300 | | 1,207,374 |

| DIRECTV* | 64,400 | | 3,230,304 |

| Time Warner, Inc. | 56,766 | | 2,715,118 |

| | | | 9,130,407 |

| |

| Metals & Mining - 1.4% | | | |

| Newmont Mining Corp | 38,400 | | 1,783,296 |

| |

| Multiline Retail - 2.5% | | | |

| Target Corp. | 55,300 | | 3,272,101 |

| |

| Oil, Gas & Consumable Fuels - 16.0% | | | |

| ConocoPhillips | 49,142 | | 2,849,745 |

| Devon Energy Corp. | 43,800 | | 2,279,352 |

| Exxon Mobil Corp | 37,300 | | 3,228,315 |

| Marathon Oil Corp | 78,400 | | 2,403,744 |

| Marathon Petroleum Corp | 31,650 | | 1,993,950 |

www.calvert.com CALVERT VP SRI LARGE CAP VALUE PORTFOLIO ANNUAL REPORT 10

| | | | | |

| EQUITY SECURITIES - CONT’D | | SHARES | | VALUE | |

| Oil, Gas & Consumable Fuels - Cont’d | | | | | |

| Occidental Petroleum Corp. | | 39,500 | $ | 3,026,095 | |

| Phillips 66 Co. | | 37,621 | | 1,997,675 | |

| Royal Dutch Shell plc (ADR) | | 44,900 | | 3,095,855 | |

| | | | | 20,874,731 | |

| |

| Pharmaceuticals - 8.5% | | | | | |

| GlaxoSmithKline plc (ADR) | | 75,500 | | 3,281,985 | |

| Johnson & Johnson | | 28,200 | | 1,976,820 | |

| Merck & Co., Inc. | | 63,700 | | 2,607,878 | |

| Pfizer, Inc | | 131,200 | | 3,290,496 | |

| | | | | 11,157,179 | |

| |

| Road & Rail - 0.8% | | | | | |

| Norfolk Southern Corp | | 17,100 | | 1,057,464 | |

| |

| Software - 2.1% | | | | | |

| Microsoft Corp. | | 105,200 | | 2,811,996 | |

| |

| Specialty Retail - 2.3% | | | | | |

| Lowe’s Co.’s, Inc | | 86,800 | | 3,083,136 | |

| |

| |

| Total Equity Securities (Cost $114,547,824) | | | | 128,334,977 | |

| |

| |

| | | PRINCIPAL | | | |

| TIME DEPOSIT - 2.5% | | AMOUNT | | | |

| State Street Bank Time Deposit, 0.12%, 1/2/13 | | $3,288,443 | | 3,288,443 | |

| |

| Total Time Deposit (Cost $3,288,443) | | | | 3,288,443 | |

| |

| |

| |

| TOTAL INVESTMENTS (Cost $117,836,267) - 100.6% | | | | 131,623,420 | |

| Other assets and liabilities, net - (0.6%) | | | | (790,591 | ) |

| NET ASSETS - 100% | | | $ | 130,832,829 | |

See notes to financial statements.

www.calvert.com CALVERT VP SRI LARGE CAP VALUE PORTFOLIO ANNUAL REPORT 11

| | | |

| NET ASSETS CONSIST OF: | | | |

| Paid-in capital applicable to 1,772,730 shares of common stock outstanding; | | | |

| $0.10 par value, 40,000,000 shares authorized | $ | 160,929,005 | |

| Undistributed net investment income | | 561,838 | |

| Accumulated net realized gain (loss) | | (44,445,167 | ) |

| Net unrealized appreciation (depreciation) | | 13,787,153 | |

| |

| |

| NET ASSETS | $ | 130,832,829 | |

| |

| NET ASSET VALUE PER SHARE | $ | 73.80 | |

*Non-income producing security.

Abbreviations:

ADR: American Depositary Receipts

plc: Public Limited Company

See notes to financial statements.

www.calvert.com CALVERT VP SRI LARGE CAP VALUE PORTFOLIO ANNUAL REPORT 12

| | | |

| STATEMENT OF OPERATIONS |

| YEAR ENDED DECEMBER 31, 2012 |

| |

| |

| NET INVESTMENT INCOME | | | |

| Investment Income: | | | |

| Dividend income (net of foreign taxes withheld of $31,693) | $ | 3,312,683 | |

| Interest income | | 3,763 | |

| Total investment income | | 3,316,446 | |

| |

| |

| Expenses: | | | |

| Investment advisory fee | | 801,897 | |

| Transfer agency fees and expenses | | 1,742 | |

| Directors’ fees and expenses | | 22,920 | |

| Administrative fees | | 125,296 | |

| Accounting fees | | 20,171 | |

| Custodian fees | | 10,562 | |

| Reports to shareholders | | 44,241 | |

| Professional fees | | 26,764 | |

| Miscellaneous | | 7,285 | |

| Total expenses | | 1,060,878 | |

| Reimbursement from Advisor | | (92,256 | ) |

| Fees paid indirectly | | (80 | ) |

| Net expenses | | 968,542 | |

| |

| |

| NET INVESTMENT INCOME | | 2,347,904 | |

| |

| |

| REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS | | | |

| Net realized gain (loss) | | (7,024,450 | ) |

| Change in unrealized appreciation (depreciation) | | 24,420,581 | |

| |

| |

| NET REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS | | 17,396,131 | |

| |

| INCREASE (DECREASE) IN NET ASSETS | | | |

| RESULTING FROM OPERATIONS | $ | 19,744,035 | |

See notes to financial statements.

www.calvert.com CALVERT VP SRI LARGE CAP VALUE PORTFOLIO ANNUAL REPORT 13

| | | | |

STATEMENTS OF CHANGES IN NET ASSETS |

| |

| |

| | YEAR ENDED | | YEAR ENDED | |

| | DECEMBER 31, | | DECEMBER 31, | |

| INCREASE (DECREASE) IN NET ASSETS | 2012 | | 2011 | |

| Operations: | | | | |

| Net investment income | $2,347,904 | | $2,616,979 | |

| Net realized gain (loss) | (7,024,450 | ) | 1,946,416 | |

| Change in unrealized appreciation (depreciation) | 24,420,581 | | (5,314,602 | ) |

| |

| |

| INCREASE (DECREASE) IN NET ASSETS | | | | |

| RESULTING FROM OPERATIONS | 19,744,035 | | (751,207 | ) |

| |

| Distributions to shareholders from: | | | | |

| Net investment income | (2,332,014 | ) | (2,640,184 | ) |

| Total distributions | (2,332,014 | ) | (2,640,184 | ) |

| |

| |

| |

| Capital share transactions: | | | | |

| Shares sold | 5,545,985 | | 4,082,008 | |

| Reinvestment of distributions | 2,332,014 | | 2,640,184 | |

| Shares redeemed | (11,582,336 | ) | (51,068,355 | ) |

| Total capital share transactions | (3,704,337 | ) | (44,346,163 | ) |

| |

| |

| |

| TOTAL INCREASE (DECREASE) IN NET ASSETS | 13,707,684 | | (47,737,554 | ) |

| |

| |

| NET ASSETS | | | | |

| Beginning of year | 117,125,145 | | 164,862,699 | |

End of year (including undistributed net investment income of $561,838 and $672,504, respectively) | $130,832,829 | | $117,125,145 | |

| |

| |

| CAPITAL SHARE ACTIVITY | | | | |

| Shares sold | 80,826 | | 62,020 | |

| Reinvestment of distributions | 32,090 | | 40,965 | |

| Shares redeemed | (164,029 | ) | (746,338 | ) |

| Total capital share activity | (51,113 | ) | (643,353 | ) |

See notes to financial statements.

www.calvert.com CALVERT VP SRI LARGE CAP VALUE PORTFOLIO ANNUAL REPORT 14

NOTES TO FINANCIAL STATEMENTS

NOTE A –- SIGNIFICANT ACCOUNTING POLICIES

General: Calvert VP SRI Large Cap Value Portfolio (the “Portfolio”), a series of Calvert Variable Products, Inc. (the “Fund”), is registered under the Investment Company Act of 1940 as a diversified, open-end management investment company. The Fund is comprised of nine separate portfolios. The operations of each series of the Fund are accounted for separately. Shares of the Portfolio are sold without sales charge to affiliated and unaffiliated insurance companies for allocation to certain of their variable separate accounts.

Security Valuation: Net asset value per share is determined every business day as of the close of the regular session of the New York Stock Exchange (generally 4:00 p.m. Eastern time). The Portfolio uses independent pricing services approved by the Board of Directors (“the Board”) to value its investments wherever possible. Investments for which market quotations are not available or deemed not reliable are fair valued in good faith under the direction of the Board.

The Board has adopted Valuation Procedures (the “Procedures”) to determine the fair value of securities and other financial instruments for which market prices are not readily available or which may not be reliably priced. The Board has delegated the day-to-day responsibility for determining the fair value of assets of the Portfolio to Calvert Investment Management, Inc. (the “Advisor” or “Calvert”) and has provided these Procedures to govern Calvert in its valuation duties.

Calvert has chartered an internal Valuation Committee to oversee the implementation of these Procedures and to assist it in carrying out the valuation responsibilities that the Board has delegated.

The Valuation Committee meets on a regular basis to review illiquid securities and other investments which may not have readily available market prices. The Valuation Committee’s fair valuation determinations are subject to review, approval and ratification by the Board at its next regularly scheduled meeting covering the calendar quarter in which the fair valuation was determined.

The Valuation Committee utilizes various methods to measure the fair value of the Portfolio’s investments. Generally Accepted Accounting Principles (GAAP) establishes a disclosure hierarchy that categorizes the inputs to valuation techniques used to value assets and liabilities at measurement date. These inputs are summarized in the three broad levels listed below:

Level 1 – quoted prices in active markets for identical securities

Level 2 – other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.)

Level 3 – significant unobservable inputs (including the Portfolio’s own assumptions in determining the fair value of investments)

The inputs or methodologies used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

Changes in valuation techniques may result in transfers in or out of an investment’s assigned level within the hierarchy during the period. Valuation techniques used to value the Portfolio’s investments by major category are as follows:

www.calvert.com CALVERT VP SRI LARGE CAP VALUE PORTFOLIO ANNUAL REPORT 15

Equity securities, including restricted securities, for which market quotations are readily available, are valued at the last reported sale price or official closing price as reported by an independent pricing service on the primary market or exchange on which they are traded and are categorized as Level 1 in the hierarchy. In the event there were no sales during the day or closing prices are not available, securities are valued at the last quoted bid price or may be valued using the last available price and are categorized as Level 2 in the hierarchy. Foreign securities are valued based on quotations from the principal market in which such securities are normally traded. If events occur after the close of the principal market in which foreign securities are traded, and before the close of business of the Portfolio, that are expected to materially affect the value of those securities, then they are valued at their fair value taking these events into account. For restricted securities and private placements where observable inputs are limited, assumptions about market activity and risk are used and such securities are categorized as Level 3 in the hierarchy.

Short-term securities of sufficient credit quality with remaining maturities of sixty days or less for which quotations are not readily available are valued at amortized cost, which approximates fair value, and are categorized as Level 2 in the hierarchy.

If a market value cannot be determined for a security using the methodologies described above, or if, in the good faith opinion of the Advisor, the market value does not constitute a readily available market quotation, or if a significant event has occurred that would materially affect the value of the security, the security will be fair valued as determined in good faith by the Valuation Committee.

The Valuation Committee considers a number of factors, including significant unobservable valuation inputs when arriving at fair value. It considers all significant facts that are reasonably available and relevant to the determination of fair value.

The Valuation Committee primarily employs a market-based approach which may use related or comparable assets or liabilities, recent transactions, market multiples, book values, and other relevant information for the investment to determine the fair value of the investment. When more appropriate, the fund may employ an income-based or cost approach. An income-based valuation approach discounts anticipated future cash flows of the investment to calculate a present amount (discounted). The measurement is based on the value indicated by current market expectations about those future amounts. Discounts may also be applied due to the nature or duration of any restrictions on the disposition of the investments. A cost based approach is based on the amount that currently would be required to replace the service capacity of an asset (current replacement cost). From the seller’s perspective, the price that would be received for the asset is determined based on the cost to a buyer to acquire or construct a substitute asset of comparable utility, adjusted for obsolescence.

The values assigned to fair value investments are based on available information and do not necessarily represent amounts that might ultimately be realized. Further, due to the inherent uncertainty of valuations of such investments, the fair values may differ significantly from the values that would have been used had an active market existed, and the differences could be material. The Valuation Committee employs various methods for calibrating these valuation approaches including a regular review of key inputs and assumptions, transactional back-testing or disposition analysis and reviews of any related market activity.

www.calvert.com CALVERT VP SRI LARGE CAP VALUE PORTFOLIO ANNUAL REPORT 16

At December 31, 2012, no securities were fair valued in good faith under the direction of the Board.

The following is a summary of the inputs used to value the Portfolio’s net assets as of December 31, 2012:

| | | VALUATION INPUTS | |

| INVESTMENTS IN SECURITIES | LEVEL 1 | LEVEL 2 | LEVEL 3 | TOTAL |

| Equity securities* | $128,334,977 | — | — | $128,334,977 |

| Other debt obligations | — | $3,288,443 | — | 3,288,443 |

| TOTAL | $128,334,977 | $3,288,443 | — | $131,623,420 |

*For further breakdown of Equity Securities by industry type, please refer to the Statement of Net Assets.

Security Transactions and Investment Income: Security transactions are accounted for on trade date. Realized gains and losses are recorded on an identified cost basis and may include proceeds from litigation. Dividend income is recorded on the ex-dividend date or, in the case of dividends on certain foreign securities, as soon as the Portfolio is informed of the ex-dividend date. Withholding taxes on foreign dividends have been provided for in accordance with the Portfolio’s understanding of the applicable country’s tax rules and rates. Distributions received on securities that represent a return of capital or capital gain are recorded as a reduction of cost of investments and/or as a realized gain. Interest income, which includes amortization of premium and accretion of discount on debt securities, is accrued as earned.

Foreign Currency Transactions: The Portfolio’s accounting records are maintained in U.S. dollars. For valuation of assets and liabilities on each date of net asset value determination, foreign denominations are converted into U.S. dollars using the current exchange rate. Security transactions, income and expenses are translated at the prevailing rate of exchange on the date of the event. The effect of changes in foreign exchange rates on securities is included with the net realized and unrealized gain or loss on investments.

Distributions to Shareholders: Distributions to shareholders are recorded by the Portfolio on ex-dividend date. Dividends from net investment income and distributions from net realized capital gains, if any, are paid at least annually. Distributions are determined in accordance with income tax regulations which may differ from generally accepted accounting principles; accordingly, periodic reclassifications are made within the Portfolio’s capital accounts to reflect income and gains available for distribution under income tax regulations.

Estimates: The preparation of financial statements in conformity with accounting principles generally accepted in the United States requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of income and expenses during the reporting period. Actual results could differ from those estimates.

Expense Offset Arrangements: During the year ended December 31, 2012, the Portfolio had an arrangement with its custodian bank whereby the custodian’s fees may have been paid indirectly by credits earned on the Portfolio’s cash on deposit with the bank. These credits were used to reduce the Portfolio’s expenses. However, this arrangement was suspended effective January 1, 2013, until further notice, due to low interest rates. Such a deposit arrangement was an alternative to overnight investments.

www.calvert.com CALVERT VP SRI LARGE CAP VALUE PORTFOLIO ANNUAL REPORT 17

Federal Income Taxes: No provision for federal income or excise tax is required since the Portfolio intends to continue to qualify as a regulated investment company under the Internal Revenue Code and to distribute substantially all of its taxable earnings.

Management has analyzed the Portfolio’s tax positions taken for all open federal income tax years and has concluded that no provision for federal income tax is required in the Portfolio’s financial statements. A Portfolio’s federal tax return is subject to examination by the Internal Revenue Service for a period of three years.

NOTE B — RELATED PARTY TRANSACTIONS

Calvert Investment Management, Inc. (the “Advisor”) is wholly-owned by Calvert Investments, Inc., which is indirectly wholly owned by Ameritas Mutual Holding Company (formerly known as UNIFI Mutual Holding Company). The Advisor provides investment advisory services and pays the salaries and fees of officers and Directors of the Fund who are employees of the Advisor or its affiliates. For its services, the Advisor receives an annual fee, payable monthly, of .64% of the Portfolio’s average daily net assets. Under the terms of the agreement, $70,432 was payable at year end. In addition, $11,323 was payable at year end for operating expenses paid by the Advisor during December 2012.

The Advisor has contractually agreed to limit net annual portfolio operating expenses through April 30, 2013. The contractual expense cap is .78% (.76% prior to May 1, 2012). For the purpose of this expense limit, operating expenses do not include interest expense, brokerage commissions, taxes, and extraordinary expenses. To the extent any expense credits are earned, the Advisor’s obligation under the contractual limitation may be reduced and the Advisor may benefit from the expense offset arrangement.

Calvert Investment Administrative Services, Inc., an affiliate of the Advisor, provides administrative services to the Portfolio for an annual fee, payable monthly, of .10% of the average daily net assets of the Portfolio. Under the terms of the agreement, $11,020 was payable at year end.

Calvert Investment Services, Inc. (“CIS”), an affiliate of the Advisor, acts as shareholder servicing agent for the Portfolio. For its services, CIS received a fee of $64 for the year ended December 31, 2012. Under the terms of the agreement, $5 was payable at year end. Boston Financial Data Services, Inc. is the transfer and dividend disbursing agent.

Each Director of the Fund who is not an employee of the Advisor or its affiliates receives a fee of $1,500 for each Board and Committee meeting attended plus an annual fee of $30,000 ($40,000 effective January 1, 2013). Committee chairs receive an additional $5,000 annual retainer. Directors’ fees are allocated to each of the portfolios served.

NOTE C — INVESTMENT ACTIVITY AND TAX INFORMATION

During the year, the cost of purchases and proceeds from sales of investments, other than short-term securities, were $62,001,721 and $66,032,356, respectively.

www.calvert.com CALVERT VP SRI LARGE CAP VALUE PORTFOLIO ANNUAL REPORT 18

| | |

| CAPITAL LOSS CARRYFORWARD | | |

| |

| EXPIRATION DATE | | |

| 31-Dec-15 | ($953,081 | ) |

| 31-Dec-17 | (28,385,593 | ) |

| 31-Dec-18 | (8,033,097 | ) |

| |

| NO EXPIRATION DATE | | |

| Long-term | ($6,297,289 | ) |

Capital losses may be utilized to offset future capital gains until expiration; however, the Portfolio’s use of capital loss carryforwards acquired from CVS Ameritas Income & Growth Portfolio may be limited under certain tax provisions. Under the Regulated Investment Company Modernization Act of 2010, capital losses incurred in taxable years beginning after December 22, 2010 can be carried forward for an unlimited period. These losses are required to be utilized prior to the losses incurred in pre-enactment taxable years and retain their character as either short-term or long-term capital losses.

The tax character of dividends and distributions paid during the years ended December 31, 2012 and December 31, 2011 was as follows:

| Distributions paid from: | 2012 | 2011 |

| Ordinary income | $2,332,014 | $2,640,184 |

| Total | $2,332,014 | $2,640,184 |

As of December 31, 2012, the tax basis components of distributable earnings/ (accumulated losses) and the federal tax cost were as follows:

| Unrealized appreciation | $18,399,219 | |

| Unrealized (depreciation) | (5,388,173 | ) |

| Net unrealized appreciation/(depreciation) | $13,011,046 | |

| Undistributed ordinary income | $561,838 | |

| Capital loss carryforward | ($43,669,060 | ) |

| |

| Federal income tax cost of investments | $118,612,374 | |

www.calvert.com CALVERT VP SRI LARGE CAP VALUE PORTFOLIO ANNUAL REPORT 19

The differences between the components of distributable earnings on a tax basis and the amounts reflected in the statement of net assets are primarily due to temporary book-tax differences that will reverse in a subsequent period. These differences are due to wash sales and partnerships.

Reclassifications, as shown in the table below, have been made to the Portfolio’s components of net assets to reflect income and gains available for distribution (or available capital loss carryovers, as applicable) under income tax law and regulations. These reclassifications are due to permanent book-tax differences and have no impact on net assets. The primary permanent differences causing such reclassifications for the Portfolio are due to partnerships.

| Undistributed net investment income | ($126,556 | ) |

| Accumulated net realized gain (loss) | 155,179 | |

| Paid-in capital | (28,623 | ) |

NOTE D — LINE OF CREDIT

A financing agreement is in place with the Calvert Funds and State Street Corporation (“SSC”). Under the agreement, SSC provides an unsecured line of credit facility, in the aggregate amount of $50 million ($25 million committed and $25 million uncommitted), accessible by the Funds for temporary or emergency purposes only. Borrowings under the committed facility bear interest at the higher of the London Interbank Offered Rate (LIBOR) or the overnight Federal Funds Rate plus 1.25% per annum. A commitment fee of .11% per annum is incurred on the unused portion of the committed facility, which is allocated to all participating funds. The Portfolio had no borrowings under the agreement during the year ended December 31, 2012.

NOTE E — SUBSEQUENT EVENTS

In preparing the financial statements as of December 31, 2012, no subsequent events or transactions occurred that would have required recognition or disclosure in these financial statements.

www.calvert.com CALVERT VP SRI LARGE CAP VALUE PORTFOLIO ANNUAL REPORT 20

| | | | | | |

| FINANCIAL HIGHLIGHTS |

| |

| | | | YEARS ENDED | | | |

| | DECEMBER 31, | | DECEMBER 31, | | DECEMBER 31, | |

| | 2012 | | 2011 | (z) | 2010 | (z) |

| Net asset value, beginning | $64.22 | | $66.82 | | $60.76 | |

| Income from investment operations: | | | | | | |

| Net investment income | 1.36 | | 1.24 | | 1.05 | |

| Net realized and unrealized gain (loss) | 9.56 | | (2.36 | ) | 6.00 | |

| Total from investment operations | 10.92 | | (1.12 | ) | 7.05 | |

| Distributions from: | | | | | | |

| Net investment income | (1.34 | ) | (1.48 | ) | (.99 | ) |

| Total distributions | (1.34 | ) | (1.48 | ) | (.99 | ) |

| Total increase (decrease) in net asset value | 9.58 | | (2.60 | ) | 6.06 | |

| Net asset value, ending | $73.80 | | $64.22 | | $66.82 | |

| |

| Total return* | 17.03 | % | (1.68 | %) | 11.60 | % |

| Ratios to average net assets: A | | | | | | |

| Net investment income | 1.87 | % | 1.85 | % | 1.70 | % |

| Total expenses | .85 | % | .85 | % | .84 | % |

| Expenses before offsets | .77 | % | .75 | % | .74 | % |

| Net expenses | .77 | % | .75 | % | .74 | % |

| Portfolio turnover | 51 | % | 16 | % | 27 | % |

| Net assets, ending (in thousands) | $130,833 | | $117,125 | | $164,863 | |

| |

| |

| | | | YEARS ENDED | |

| | | | DECEMBER 31, | | DECEMBER 31, | |

| | | | 2009 | | 2008 | |

| Net asset value, beginning | | | $49.45 | | $92.96 | |

| Income from investment operations: | | | | | | |

| Net investment income | | | 1.16 | | .61 | |

| Net realized and unrealized gain (loss) | | | 11.41 | | (34.05 | ) |

| Total from investment operations | | | 12.57 | | (33.44 | ) |

| Distributions from: | | | | | | |

| Net investment income | | | (1.14 | ) | (1.95 | ) |

| Net realized gain | | | (.12 | ) | (8.12 | ) |

| Total distributions | | | (1.26 | ) | (10.07 | ) |

| Total increase (decrease) in net asset value | | | 11.31 | | (43.51 | ) |

| Net asset value, ending | | | $60.76 | | $49.45 | |

| |

| Total return* | | | 25.40 | % | (39.49 | %) |

| Ratios to average net assets: A | | | | | | |

| Net investment income | | | 2.19 | % | 2.14 | % |

| Total expenses | | | .85 | % | .90 | % |

| Expenses before offsets | | | .74 | % | .90 | % |

| Net expenses | | | .74 | % | .90 | % |

| Portfolio turnover | | | 29 | % | 34 | % |

| Net assets, ending (in thousands) | | | $178,063 | | $144,425 | |

See notes to financial highlights.

www.calvert.com CALVERT VP SRI LARGE CAP VALUE PORTFOLIO ANNUAL REPORT 21

A Total expenses do not reflect amounts reimbursed and/or waived by the Advisor or reductions from expense offset arrangements. Expenses before offsets reflect expenses after reimbursement and/or waiver by the Advisor but prior to reductions from expense offset arrangements. Net expenses are net of all reductions and represent the net expenses paid by the portfolio.

(z) Per share figures calculated using the Average Shares Method.

* Total return is not annualized for periods of less than one year and does not reflect charges and expenses of the variable annuity or variable universal life contract.

See notes to financial statements.

www.calvert.com CALVERT VP SRI LARGE CAP VALUE PORTFOLIO ANNUAL REPORT 22

EXPLANATION OF FINANCIAL TABLES

SCHEDULE OF INVESTMENTS

The Schedule of Investments is a snapshot of all securities held in the fund at their market value, on the last day of the reporting period. Securities are listed by asset type (e.g., common stock, corporate bonds, U.S. government obligations) and may be further broken down into sub-groups and by industry classification.

STATEMENT OF ASSETS AND LIABILITIES

The Statement of Assets and Liabilities is often referred to as the fund’s balance sheet. It lists the value of what the fund owns, is due and owes on the last day of the reporting period. The fund’s assets include the market value of securities owned, cash, receivables for securities sold and shareholder subscriptions, and receivables for dividends and interest payments that have been earned, but not yet received. The fund’s liabilities typically include payables for securities purchased and shareholder redemptions, and expenses owed but not yet paid. The statement also reports the fund’s net asset value (NAV) per share on the last day of the reporting period. The NAV is calculated by dividing the fund’s net assets (assets minus liabilities) by the number of shares outstanding. This statement is accompanied by a Schedule of Investments. Alternatively, if certain conditions are met, a Statement of Net Assets may be presented in lieu of this statement and the Schedule of Investments.

STATEMENT OF NET ASSETS

The Statement of Net Assets provides a detailed list of the fund’s holdings, including each security’s market value on the last day of the reporting period. The Statement of Net Assets includes a Schedule of Investments. Other assets are added and other liabilities subtracted from the investments total to calculate the fund’s net assets. Finally, net assets are divided by the outstanding shares of the fund to arrive at its share price, or Net Asset Value (NAV) per share.

At the end of the Statement of Net Assets is a table displaying the composition of the fund’s net assets. Paid in Capital is the money invested by shareholders and represents the bulk of net assets. Undistributed Net Investment Income and Accumulated Net Realized Gains usually approximate the amounts the fund had available to distribute to shareholders as of the statement date. Accumulated Realized Losses will appear as negative balances. Unrealized Appreciation (Depreciation) is the difference between the market value of the fund’s investments and their cost, and reflects the gains (losses) that would be realized if the fund were to sell all of its investments at their statement-date values.

STATEMENT OF OPERATIONS

The Statement of Operations summarizes the fund’s investment income earned and expenses incurred in operating the fund. Investment income includes dividends earned from stocks and interest earned from interest-bearing securities in the fund. Expenses incurred in operating the fund include the advisory fee paid to the investment advisor, administrative services fees, distribution plan expenses (if applicable), transfer agent fees, shareholder servicing expenses, custodial, legal, and audit fees, and the printing and postage expenses related to shareholder reports. Expense offsets (fees paid indirectly) are also shown. Credits earned from offset arrangements are used to reduce the fund’s expenses. This statement also shows net gains (losses) realized on the sale of investments and the increase or decrease in the unrealized appreciation (depreciation) on investments held during the period.

STATEMENT OF CHANGES IN NET ASSETS

The Statement of Changes in Net Assets shows how the fund’s total net assets changed during the two most recent reporting periods. Changes in the fund’s net assets are attributable to investment operations, distributions and capital share transactions.

www.calvert.com CALVERT VP SRI LARGE CAP VALUE PORTFOLIO ANNUAL REPORT (UNAUDITED) 23

The Operations section of the report summarizes information detailed in the Statement of Operations. The Distribution section shows the dividend and capital gain distributions made to shareholders. The amounts shown as distributions in this section may not match the net investment income and realized gains amounts shown in the Operations section because distributions are determined on a tax basis and certain investments or transactions may be treated differently for financial statement and tax purposes. The Capital Share Transactions section shows the amount shareholders invested in the fund, either by purchasing shares or by reinvesting distributions, and the amounts redeemed. The corresponding numbers of shares issued, reinvested and redeemed are shown at the end of the report.

FINANCIAL HIGHLIGHTS

The Financial Highlights table provides a per-share breakdown by class of the components that affect the fund’s net asset value for current and past reporting periods. The table provides total return, total distributions, expense ratios, portfolio turnover and net assets for the applicable period. Total return is a measure of a fund’s performance that encompasses all elements of return: dividends, capital gain distributions and changes in net asset value. Total return is the change in value of an investment over a given period, assuming reinvestment of any dividends and capital gain distributions, expressed as a percentage of the initial investment. Total distributions include distributions from net investment income and net realized gains. Long-term gains are earned on securities held in the fund more than one year. Short-term gains, on the sale of securities held less than one year, are treated as ordinary dividend income for tax purposes. The expense ratio is a fund’s cost of doing business, expressed as a percentage of net assets. These expenses directly reduce returns to shareholders. Portfolio turnover measures the trading activity in a fund’s investment portfolio – how often securities are bought and sold by a fund. Portfolio turnover is affected by market conditions, changes in the size of the fund, the nature of the fund’s investments and the investment style of the portfolio manager.

PROXY VOTING

The Proxy Voting Guidelines that the Portfolio uses to determine how to vote proxies relating to portfolio securities is provided as an Appendix to the Fund’s Statement of Additional Information. The Statement of Additional Information can be obtained free of charge by calling the Fund at 1-800-368-2745, by visiting the Calvert website at www.calvert.com or by visiting the SEC’s website at www.sec.gov.

Information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30 is available by calling the Fund, by visiting the Calvert website at www.calvert.com or visiting the SEC’s website at www.sec.gov.

AVAILABILITY OF QUARTERLY PORTFOLIO HOLDINGS

The Fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. The Fund’s Form N-Q is available on the SEC’s website at www.sec.gov. The Fund’s Form N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC; information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

www.calvert.com CALVERT VP SRI LARGE CAP VALUE PORTFOLIO ANNUAL REPORT (UNAUDITED) 24

BASIS FOR BOARD’S APPROVAL OF INVESTMENT ADVISORY CONTRACT

At a meeting held on December 12, 2012, the Board of Directors, and by a separate vote, the disinterested Directors, approved the continuance of the Investment Advisory Agreement between the Fund and the Advisor with respect to the Portfolio.

In evaluating the Investment Advisory Agreement, the Board considered a variety of information relating to the Portfolio and the Advisor. The disinterested Directors reviewed a report prepared by the Advisor regarding various services provided to the Portfolio by the Advisor and its affiliates. Such report included, among other data, information regarding the Advisor’s personnel and the Advisor’s revenue and cost of providing services to the Portfolio, and a separate report prepared by an independent third party, which provided a statistical analysis comparing the Portfolio’s investment performance, expenses, and fees to comparable mutual funds.

The disinterested Directors were separately represented by independent legal counsel with respect to their consideration of the reapproval of the Investment Advisory Agreement. Prior to voting, the disinterested Directors reviewed the proposed continuance of the Investment Advisory Agreement with management and also met in private sessions with their counsel at which no representatives of management were present.

In the course of its deliberations regarding the Investment Advisory Agreement, the Board considered the following factors, among others: the nature, extent and quality of the services provided by the Advisor, including the personnel providing such services; the Advisor’s financial condition; the level and method of computing the Portfolio’s advisory fee; comparative performance, fee and expense information for the Portfolio; the profitability of the Calvert Family of Funds to the Advisor and its affiliates; the allocation of the Portfolio’s brokerage, including the Advisor’s process for monitoring “best execution”; the direct and indirect benefits, if any, derived by the Advisor and its affiliates from their relationship with the Portfolio; the effect of the Portfolio’s growth and size on the Portfolio’s performance and expenses; the Advisor’s compliance programs and policies; the Advisor’s performance of substantially similar duties for other funds; and any possible conflicts of interest.

In considering the nature, extent and quality of the services provided by the Advisor under the Investment Advisory Agreement, the Board reviewed information provided by the Advisor relating to its operations and personnel, including, among other information, biographical information on the Advisor’s investment, supervisory and professional staff and descriptions of its organizational and management structure. The Board also took into account similar information provided periodically throughout the previous year by the Advisor as well as the Board’s familiarity with the Advisor’s management through Board of Directors’ meetings, discussions and other reports. The Board considered the Advisor’s management style and its performance in employing its investment strategies, as well as its current level of staffing and overall resources. The Board also noted that it reviewed on a quarterly basis information regarding the Advisor’s compliance with applicable policies and procedures, including those related to personal investing. The Advisor’s administrative capabilities, including its ability to supervise the other service providers for the Portfolio, were also considered. The Board also took into account the environmental, social, sustainability and governance research and analysis provided by the Advisor to the Portfolio. The Board observed that the scope of services provided by the Advisor generally had expanded over time as a result of regulatory, market and other changes. The Board concluded that it was satisfied with the nature, extent and quality of services provided to the Portfolio by the Advisor under the Investment Advisory Agreement.

www.calvert.com CALVERT VP SRI LARGE CAP VALUE PORTFOLIO ANNUAL REPORT (UNAUDITED) 25

In considering the Portfolio’s performance, the Board noted that it reviewed on a quarterly basis detailed information about the Portfolio’s performance results, portfolio composition and investment strategies. In addition, the Board took into account overall financial market conditions. The Board also reviewed various comparative data provided to it in connection with its consideration of the renewal of the Investment Advisory Agreement, including, among other information, a comparison of the Portfolio’s total return with its Lipper index and with that of other mutual funds deemed to be in its peer group by an independent third party in its report. This comparison indicated that the Portfolio performed above the median of its peer group for the one-year period ended June 30, 2012 and below the median of its peer group for the three- and five-year periods ended June 30, 2012. The data also indicated that the Portfolio outperformed its Lipper index for the one-year period ended June 30, 2012, and underperformed its Lipper index for the three- and five-year periods ended June 30, 2012. The Board took into account management’s discussion of the Portfolio’s performance, including the recent improvement in performance, and management’s continued monitoring of the Portfolio’s performance. Based upon its review, the Board concluded that appropriate action was being taken with respect to the Portfolio’s performance.

In considering the Portfolio’s fees and expenses, the Board compared the Portfolio’s fees and total expense ratio with various comparative data for the funds in its peer group. Among other findings, the data indicated that the Portfolio’s advisory fee (after taking into account expense reimbursements) was below the median of its peer group and that total expenses (net of expense reimbursements) were also below the median of its peer group. The Board noted that the allocation of advisory and administrative fees may vary among the Portfolio’s peer group. In addition, the Board took into account the fees the Advisor charged to its other clients and considered these fee comparisons in light of the differences in managing these other accounts. The Board noted that the Advisor had reimbursed a portion of the Portfolio’s expenses. The Board also took into account the Advisor’s current undertaking to maintain expense limitations for the Portfolio and management’s discussion of the Portfolio’s expenses and certain factors that affected the level of such expenses, including the current size of the Portfolio and the cost of providing the environmental, social, sustainability and governance research and analysis provided by the Advisor. The Board noted that in 2011, the transfer agency fees paid by the Calvert Family of Funds had been renegotiated, resulting in an overall reduction in the transfer agency fees across the Calvert Family of Funds complex. Based upon its review, the Board determined that the advisory fee was reasonable in view of the quality of services received by the Portfolio from the Advisor and the other factors considered.

The Board reviewed the Advisor’s profitability on a portfolio-by-portfolio basis. In reviewing the overall profit-ability of the advisory fee to the Portfolio’s Advisor, the Board also considered the fact that affiliates of the Advisor provided shareholder servicing and administrative services to the Portfolio for which they received compensation. The information considered by the Board included Calvert’s operating profit margin information both before and after tax expenses with respect to the services that the Advisor and its affiliates provided to the Calvert Family of Funds complex. The Board reviewed the profitability of the Advisor’s relationship with the Portfolio in terms of the total amount of annual advisory fees it received with respect to the Portfolio and whether the Advisor had the financial wherewithal to continue to provide a high level of services to the Portfolio. The Board also considered that the Advisor derived benefits to its reputation and other indirect benefits from its relationship with the Portfolio. In addition, the Board took into account that affiliates of the Advisor may benefit from certain indirect tax benefits relating to dividend received deductions and foreign tax credits. The Board noted that the Advisor had reimbursed a portion of the expenses of the Portfolio. Based upon its review, the Board concluded that the Advisor’s and its affiliates’ level of profitability from their relationship with the Portfolio was reasonable.

www.calvert.com CALVERT VP SRI LARGE CAP VALUE PORTFOLIO ANNUAL REPORT (UNAUDITED) 26

The Board considered the effect of the Portfolio’s growth and size on its performance and fees. Although the Portfolio’s advisory fee did not contain breakpoints that would reduce the advisory fee rate on assets above speci-fied asset levels, the Board noted that if the Portfolio’s assets increased over time, the Portfolio might realize other economies of scale if assets increased proportionally more than certain other expenses. The Board also noted that given the Portfolio’s current level of assets, the Portfolio would be unlikely to recognize economies of scale by implementing a breakpoint in the advisory fee at this time.

In reapproving the Investment Advisory Agreement, the Board, including the disinterested Directors, did not identify any single factor as controlling, and each Director may have attributed different weight to various factors.

CONCLUSIONS

The Board reached the following conclusions regarding the Investment Advisory Agreement, among others: (a) the Advisor has demonstrated that it possesses the capability and resources to perform the duties required of it under the Investment Advisory Agreement; (b) the Advisor maintains appropriate compliance programs; (c) appropriate action is being taken with respect to the Portfolio’s performance; (d) the Advisor is likely to execute its investment strategies consistently over time; and (e) the Portfolio’s advisory fee is reasonable relative to those of similar funds and to the services to be provided by the Advisor. Based on its conclusions, the Board determined that reapproval of the Investment Advisory Agreement would be in the best interests of the Portfolio and its shareholders.

This report is intended to provide fund information to shareholders. It is not authorized for distribution to prospective investors unless preceded or accompanied by a prospectus.

Note: The information on our website is not incorporated by reference into this report; our website address is included as an inactive textual reference only.

Investors should carefully consider the investment objectives, risks, charges and expenses of the Calvert Funds. This and other important information is contained in the fund’s summary prospectus and prospectus, which can be obtained from your financial professional and should be read carefully before investing. You may also call Calvert at 800/368-2745.

www.calvert.com CALVERT VP SRI LARGE CAP VALUE PORTFOLIO ANNUAL REPORT (UNAUDITED) 27

www.calvert.com CALVERT VP SRI LARGE CAP VALUE PORTFOLIO ANNUAL REPORT (UNAUDITED) 28

www.calvert.com CALVERT VP SRI LARGE CAP VALUE PORTFOLIO ANNUAL REPORT (UNAUDITED) 29

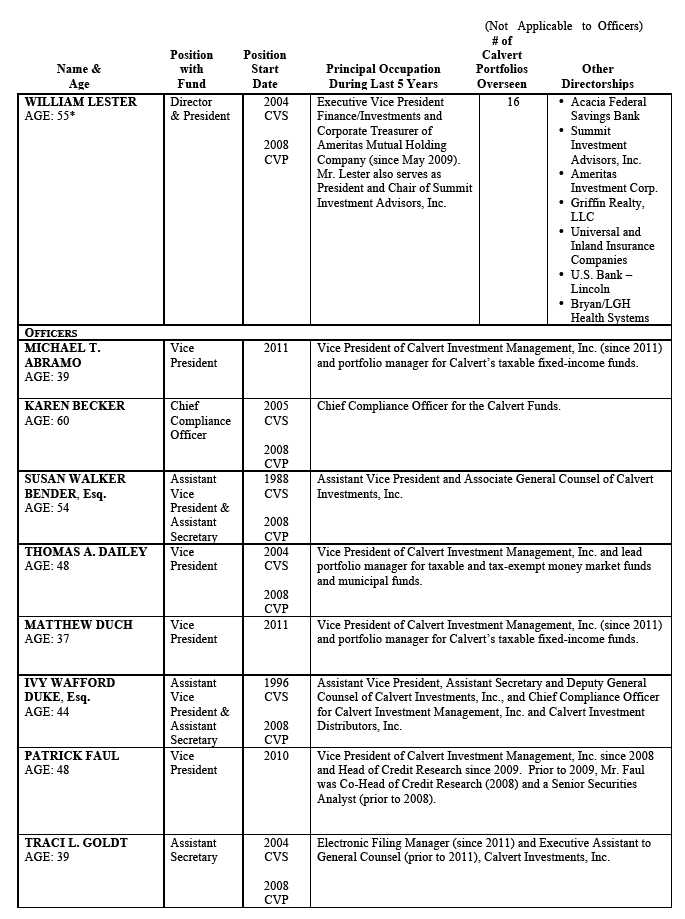

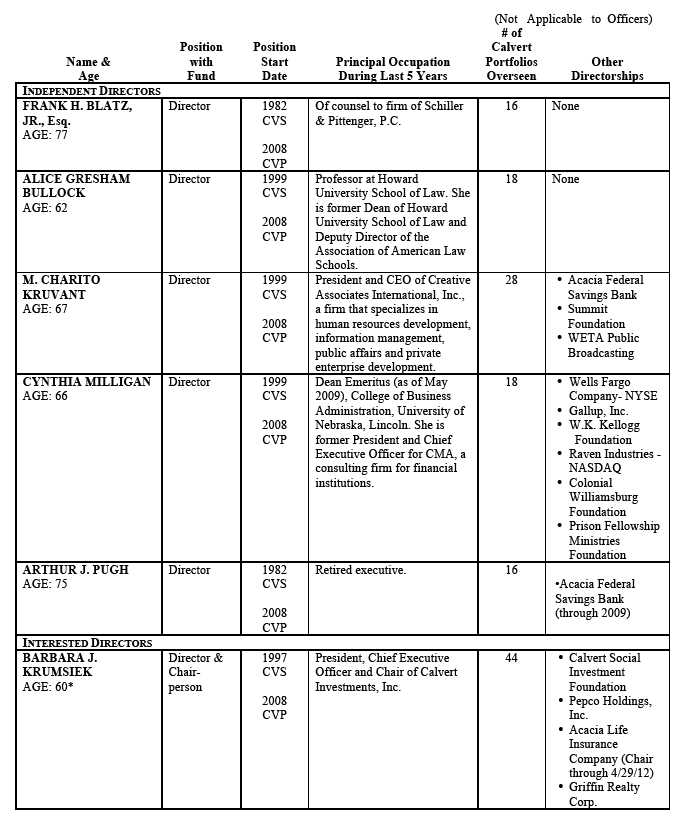

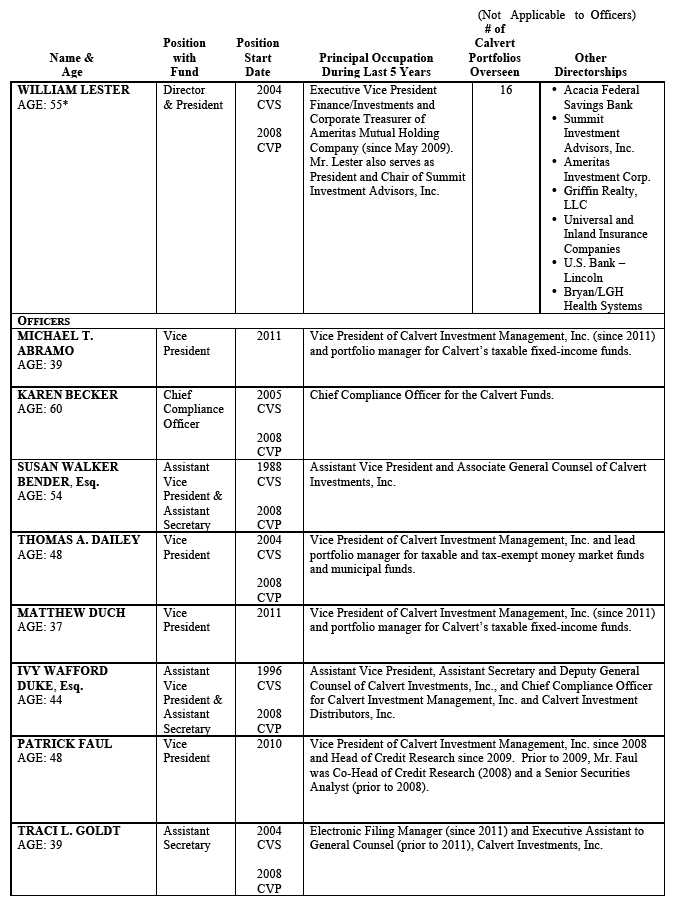

*The address of Directors and Officers is 4550 Montgomery Avenue, Suite 1000N, Bethesda, Maryland 20814. Ms. Krumsiek is an interested person of the Fund since she is an officer and director of the Fund’s Advisor and its affiliates. Mr. Lester is an interested person of the Fund since he is an officer and director of the parent company of the Fund’s Advisor.

Additional information about the Fund’s Directors can be found in the Statement of Additional Information (SAI). You can get a free copy of the SAI by contacting your broker, or the Fund at 1-800-368-2745.

www.calvert.com CALVERT VP SRI LARGE CAP VALUE PORTFOLIO ANNUAL REPORT (UNAUDITED) 30

CALVERT VP S&P 500 INDEX PORTFOLIO

Portfolio within Calvert Variable Products, Inc.

Managed by Summit Investment Advisors, Inc., Subadvisor

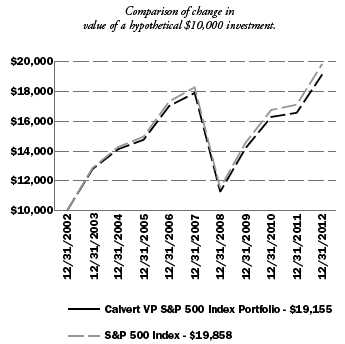

PERFORMANCE

For the year ended December 31, 2012, Calvert VP S&P 500 Index Portfolio returned 15.55% compared with 16.00% for the Standard & Poor’s (S&P) 500 Index. The underperformance relative to the Index was largely attributable to fees and operating expenses, which the Index does not have.

INVESTMENT CLIMATE

Equity markets earned positive returns in 2012, with large-cap, mid-cap, and small-cap stocks all providing similar returns. Aside from the month of May and the week after the presidential election, equity markets generally performed well throughout the year.

Optimism for a global economic recovery, continued strong corporate earnings, and continued strong Federal Reserve bond purchasing helped propel stocks higher. Domestic GDP continued at a moderate pace and interest rates gave no sign of inflation fears in the market. Overall, a combination of factors made 2012 a good environment for the equity markets.

| | AVERAGE ANNUAL TOTAL RETURN | |

| | (period ended 12.31.12) | |

| One year | 15.55 | % |

| Five year | 1.36 | % |

| Ten year | 6.72 | % |

The performance data shown represents past performance, does not guarantee future results and assumes reinvestment of all dividends and distributions. All performance data reflects fee waivers and/or expense limitations, if any are in effect; in their absence performance would be lower. See Note B in Notes to Financial Statements. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Visit www.calvert.com/ institutional-VP-performance.html for current performance data. The gross expense ratio from the current prospectus for the Portfolio is 0.46%. This number may vary from the expense ratio shown elsewhere in this report because it is based on a different time period and, if applicable, does not include fee or expense waivers. The performance data and expense ratio reflect deduction of Portfolio operating expenses, but do not reflect charges and expenses imposed under the variable annuity or life insurance contract.

PORTFOLIO STRATEGY

As an index fund, the Portfolio seeks, as closely as possible, to replicate the holdings and match the performance of the S&P 500 Index. In pursuit of this objective, the fund employs a passive management approach to replicate the Index.

At year end,the Index’s largest exposures were to the Information Technology and Financials sectors at 19.0% and 15.6%, respectively. Other significant weightings included Health Care, Consumer Discretionary, and Energy, which ranged from 11.0% to 12.0%. The smallest exposures were to Telecommunication Services and Utilities.

www.calvert.com CALVERT VP S&P 500 INDEX PORTFOLIO ANNUAL REPORT 4

The top performers were Financials, up 28.9%, Consumer Discretionary, up 24.1%, and Telecommunication Services, which rose 18.3%. The weakest-performing sectors were Utilities and Energy.

During 2012, the Portfolio continued to meet its investment objective of closely tracking the total return of the Index. Market fluctuation, cash flows, and corporate actions may cause the Portfolio to hold a slightly different weighting than the Index. Since the S&P 500 Index is not an actual mutual fund, it is not possible to invest directly in it. Unlike the Index, the Portfolio incurs operating expenses.

| | % OF TOTAL | |

| ECONOMIC SECTORS | INVESTMENTS | |

| |

| Consumer Discretionary | 11.3 | % |

| Consumer Staples | 10.4 | % |

| Energy | 10.6 | % |

| Exchange Traded Funds | 0.8 | % |

| Financials | 15.1 | % |

| Government | 0.2 | % |

| Health Care | 11.6 | % |

| Industrials | 9.9 | % |

| Information Technology | 18.6 | % |

| Materials | 3.5 | % |

| Short-Term Investments | 1.6 | % |

| Telecommunication Services | 3.0 | % |

| Utilities | 3.4 | % |

| Total | 100 | % |

OUTLOOK

In 2013, the primary caveats that temper the equities outlook are chronic U.S. government deficits, the government’s inability to function properly, and slow worldwide economic growth. Tax increases implemented on January 1 will shave small amount from GDP growth. However, a failure in Washington to deal with the long-term issues relating to entitlements, government spending, and revenue generation could worsen the forecast materially this year and beyond.

While China appears to have engineered a soft landing, Europe still has considerable issues to deal with, which could negatively impact the United States. Sluggish growth could also hurt companies with a large amount of European exposure.

January 2013

www.calvert.com CALVERT VP S&P 500 INDEX PORTFOLIO ANNUAL REPORT 5

SHAREHOLDER EXPENSE EXAMPLE

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, and (2) ongoing costs, including management fees and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

This Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (July 1, 2012 to December 31, 2012).

Note: Expenses do not reflect charges and expenses of the variable annuity or variable universal life contract.

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare the 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | BEGINNING | ENDING | EXPENSES PAID |

| | ACCOUNT VALUE | ACCOUNT VALUE | DURING PERIOD* |

| | 7/1/12 | 12/31/12 | 7/1/12 - 12/31/12 |

| |

| Actual | $1,000.00 | $1,057.26 | $2.10 |

| |

| Hypothetical (5% return per year before expenses) | $1,000.00 | $1,023.09 | $2.07 |

* Expenses are equal to the Fund’s annualized expense ratio of 0.41%, multiplied by the average account value over the period, multiplied by 184/366 (to reflect the one-half year period).

www.calvert.com CALVERT VP S&P 500 INDEX PORTFOLIO ANNUAL REPORT 6

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

The Board of Directors of Calvert Variable Products, Inc. and Shareholders of Calvert VP S&P 500 Index Portfolio:

We have audited the accompanying statement of net assets of the Calvert VP S&P 500 Index Portfolio (the Portfolio), a series of Calvert Variable Products, Inc., as of December 31, 2012, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years in the five-year period then ended. These financial statements and financial highlights are the responsibility of the Portfolio’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of December 31, 2012, by correspondence with the custodian and brokers or by other appropriate auditing procedures. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of the Calvert VP S&P 500 Index Portfolio as of December 31, 2012, the results of its operations for the year then ended, the changes in its net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years in the five-year period then ended, in conformity with accounting principles generally accepted in the United States of America.

Philadelphia, Pennsylvania

February 25, 2013

www.calvert.com CALVERT VP S&P 500 INDEX PORTFOLIO ANNUAL REPORT 7

| | | |

| STATEMENT OF NET ASSETS |

| DECEMBER 31, 2012 |

| |

| |

| EQUITY SECURITIES - 96.8% | SHARES | | VALUE |

| Aerospace & Defense - 2.3% | | | |

| General Dynamics Corp. | 7,236 | $ | 501,238 |

| Honeywell International, Inc. | 17,031 | | 1,080,958 |

| L-3 Communications Holdings, Inc. | 2,098 | | 160,749 |

| Lockheed Martin Corp. | 5,875 | | 542,204 |

| Northrop Grumman Corp. | 5,394 | | 364,526 |

| Precision Castparts Corp | 3,129 | | 592,695 |

| Raytheon Co | 7,179 | | 413,223 |

| Rockwell Collins, Inc. | 3,124 | | 181,723 |

| Textron, Inc | 6,111 | | 151,492 |

| The Boeing Co. | 14,764 | | 1,112,615 |

| United Technologies Corp | 18,304 | | 1,501,111 |

| | | | 6,602,534 |

| |

| Air Freight & Logistics - 0.7% | | | |

| C.H. Robinson Worldwide, Inc | 3,583 | | 226,517 |

| Expeditors International of Washington, Inc. | 4,629 | | 183,077 |

| FedEx Corp | 6,372 | | 584,440 |

| United Parcel Service, Inc., Class B | 15,490 | | 1,142,078 |

| | | | 2,136,112 |

| |

| Airlines - 0.1% | | | |

| Southwest Airlines Co | 16,533 | | 169,298 |

| |

| Auto Components - 0.3% | | | |

| BorgWarner, Inc.* | 2,502 | | 179,193 |

| Delphi Automotive plc* | 6,393 | | 244,532 |

| Goodyear Tire & Rubber Co.* | 5,316 | | 73,414 |

| Johnson Controls, Inc | 14,769 | | 453,409 |

| | | | 950,548 |

| |

| Automobiles - 0.5% | | | |

| Ford Motor Co. | 82,560 | | 1,069,152 |

| Harley-Davidson, Inc | 4,956 | | 242,051 |

| | | | 1,311,203 |

| |

| Beverages - 2.3% | | | |

| Beam, Inc | 3,356 | | 205,018 |

| Brown-Forman Corp., Class B | 3,306 | | 209,105 |

| Coca-Cola Enterprises, Inc | 6,041 | | 191,681 |

| Constellation Brands, Inc.* | 3,287 | | 116,327 |

| Dr Pepper Snapple Group, Inc. | 4,505 | | 199,031 |

| Molson Coors Brewing Co., Class B | 3,374 | | 144,373 |

| Monster Beverage Corp.* | 3,300 | | 174,504 |

| PepsiCo, Inc | 33,487 | | 2,291,515 |

| The Coca-Cola Co | 83,503 | | 3,026,984 |

| | | | 6,558,538 |