UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-04015 |

|

Eaton Vance Mutual Funds Trust |

(Exact name of registrant as specified in charter) |

|

The Eaton Vance Building, 255 State Street, Boston, Massachusetts | | 02109 |

(Address of principal executive offices) | | (Zip code) |

|

Alan R. Dynner The Eaton Vance Building, 255 State Street, Boston, Massachusetts 02109 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | (617) 482-8260 | |

|

Date of fiscal year end: | October 31 | |

|

Date of reporting period: | October 31, 2006 | |

| | | | | | | | |

Item 1. Reports to Stockholders

Annual Report October 31, 2006

EATON VANCE

TAX-MANAGED

DIVIDEND

INCOME

FUND

IMPORTANT NOTICES REGARDING PRIVACY,

DELIVERY OF SHAREHOLDER DOCUMENTS,

PORTFOLIO HOLDINGS AND PROXY VOTING

Privacy. The Eaton Vance organization is committed to ensuring your financial privacy. Each of the financial institutions identified below has in effect the following policy ("Privacy Policy") with respect to nonpublic personal information about its customers:

• Only such information received from you, through application forms or otherwise, and information about your Eaton Vance fund transactions will be collected. This may include information such as name, address, social security number, tax status, account balances and transactions.

• None of such information about you (or former customers) will be disclosed to anyone, except as permitted by law (which includes disclosure to employees necessary to service your account). In the normal course of servicing a customer's account, Eaton Vance may share information with unaffiliated third parties that perform various required services such as transfer agents, custodians and broker/dealers.

• Policies and procedures (including physical, electronic and procedural safeguards) are in place that are designed to protect the confidentiality of such information.

• We reserve the right to change our Privacy Policy at any time upon proper notification to you. Customers may want to review our Policy periodically for changes by accessing the link on our homepage: www.eatonvance.com.

Our pledge of privacy applies to the following entities within the Eaton Vance organization: the Eaton Vance Family of Funds, Eaton Vance Management, Eaton Vance Investment Counsel, Boston Management and Research, and Eaton Vance Distributors, Inc.

In addition, our Privacy Policy only applies to those Eaton Vance customers who are individuals and who have a direct relationship with us. If a customer's account (i.e., fund shares) is held in the name of a third-party financial adviser/ broker-dealer, it is likely that only such adviser's privacy policies apply to the customer. This notice supersedes all previously issued privacy disclosures.

For more information about Eaton Vance's Privacy Policy, please call 1-800-262-1122.

Delivery of Shareholder Documents. The Securities and Exchange Commission (the "SEC") permits funds to deliver only one copy of shareholder documents, including prospectuses, proxy statements and shareholder reports, to fund investors with multiple accounts at the same residential or post office box address. This practice is often called "householding" and it helps eliminate duplicate mailings to shareholders.

Eaton Vance, or your financial adviser, may household the mailing of your documents indefinitely unless you instruct Eaton Vance, or your financial adviser, otherwise.

If you would prefer that your Eaton Vance documents not be householded, please contact Eaton Vance at 1-800-262-1122, or contact your financial adviser.

Your instructions that householding not apply to delivery of your Eaton Vance documents will be effective within 30 days of receipt by Eaton Vance or your financial adviser.

Portfolio Holdings. Each Eaton Vance Fund and its underlying Portfolio (if applicable) will file a schedule of its portfolio holdings on Form N-Q with the SEC for the first and third quarters of each fiscal year. The Form N-Q will be available on the Eaton Vance website www.eatonvance.com, by calling Eaton Vance at 1-800-262-1122 or in the EDGAR database on the SEC's website at www.sec.gov. Form N-Q may also be reviewed and copied at the SEC's public reference room in Washington, D.C. (call 1-800-732-0330 for information on the operation of the public reference room).

Proxy Voting. From time to time, funds are required to vote proxies related to the securities held by the funds. The Eaton Vance Funds or their underlying Portfolios (if applicable) vote proxies according to a set of policies and procedures approved by the Funds' and Portfolios' Boards. You may obtain a description of these policies and procedures and information on how the Funds or Portfolios voted proxies relating to portfolio securities during the most recent 12 month period ended June 30, without charge, upon request, by calling 1-800-262-1122. This description is also available on the SEC's website at www.sec.gov.

Eaton Vance Tax-Managed Dividend Income Fund as of October 31, 2006

MANAGEMENT'S DISCUSSION OF FUND PERFORMANCE

Aamer Khan, CFA

Co-Portfolio Manager

Thomas H. Luster, CFA

Co-Portfolio Manager

Michael R. Mach, CFA

Co-Portfolio Manager

Judith A. Saryan, CFA

Co-Portfolio Manager

The Fund

Performance for the Period Ended October 31, 2006

· The fiscal year end for Eaton Vance Tax-Managed Dividend Income Fund (the Fund) has been changed from April 30 to October 31. For the period from April 30, 2006, through October 31, 2006, the Fund’s Class A shares had a total return of 6.14%. This return was the result of an increase in net asset value (NAV) per share to $13.40 on October 31, 2006, from $12.99 on April 30, 2006, and the reinvestment of $0.363 per share in dividend income.(1)

· The Fund’s Class B shares had a total return of 5.76% during the same period, the result of an increase in NAV per share to $13.37 from $12.96, and the reinvestment of $0.316 per share in dividend income.(1)

· The Fund’s Class C shares had a total return of 5.76% during the same period, the result of an increase in NAV per share to $13.37 from $12.96, and the reinvestment of $0.316 per share in dividend income.(1)

· For comparison, the Fund’s benchmark, the Russell 1000 Value Index – a broad-based, unmanaged market index of 1000 U.S. value stocks – had a total return of 7.61% during the same period. The Fund’s peer group, the Lipper Equity Income Funds Classification, had an average return at NAV of 6.13% for the same period.(2)

Management Discussion

· U.S. equity markets were volatile, but moved upward at a moderate pace during the period from April 30, 2006 to October 31, 2006. Equities generally rallied after a correction early in the period. Stock prices declined in early May 2006 on fears that global interest rates could continue to rise and concerns about record-high energy prices. In the latter months of the period, however, stocks again rallied, driven by a sharp decline in energy prices, fewer geopolitical worries, and moderate U.S. inflation numbers that eased concerns about future interest-rate increases by the U.S. Federal Reserve Board (the “Fed”). International stocks outperformed U.S. stocks in this late-period rally and for the period.

· Based on the Fund’s objective of providing after-tax total return consisting primarily of tax-favored dividend income and capital appreciation, the Fund was primarily invested in securities that generated a relatively high level of qualified dividend income (QDI) during the period ended October 31, 2006. At the end of the period, the Fund had approximately 90% of total investments in common stocks, approximately 9% of total investments in preferred stocks and 1% of total investments in cash equivalents. Within the common stock portfolio, the Fund had a significant exposure to the higher-yielding utility and financial sectors. In addition, the Fund maintained a diversified exposure to the consumer, industrial, energy, health care and materials sectors.(3)

· During the period, the Fund underperformed its benchmark index, and the Fund’s Class A shares slightly outperformed its Lipper Classification average (although Class B and Class C shares underperformed the Lipper Classification average). The Fund underperformed the Russell 1000 Value Index primarily because of lagging performance of Fund holdings in the energy, materials, and telecommunications sectors.(2) In the energy sector, the Fund’s holdings in the equipment and services industries were disappointing. Despite strong long-term performance, energy stocks underperformed the broader market during the six month period due to a sharp decline in the price of oil during the fall of 2006. In the materials sector, Fund

(1) These returns do not include the 5.75% maximum sales charge for Class A shares or the applicable contingent deferred sales charge (CDSC) for Class B and Class C shares. If sales charges were deducted, the returns would be lower.

(2) It is not possible to invest directly in an Index or Lipper Classification. The Index’s total return does not reflect commissions or expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index. The Lipper Average is the average total return, at net asset value, of the funds that are in the same Lipper Classification as the Fund.

(3) Sector weightings are subject to change due to active management.

See pages 3 and 4 for more performance information, including after-tax returns.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. For performance as of the most recent month end, please refer to www.eatonvance.com.

Fund shares are not insured by the FDIC and are not deposits or other obligations of, or guaranteed by, any depository institution. Shares are subject to investment risks, including possible loss of principal invested.

1

holdings in metals and mining stocks underperformed, also as a result of falling commodity prices among key metals. The Fund's telecommunications stocks detracted from performance primarily because of one holding in the wireless industry.

· On the other hand, the Fund saw positive contributions to performance in the financials and utilities sectors. In the financial sector, the Fund was underweighted relative to the Russell 1000 Value Index, and this allocation decision contributed positively. Within the sector, the Fund’s financial holdings — especially in the insurance industry — outperformed those in the Index, so selection also contributed positively to the Fund’s performance.(1) In the utilities sector, management continued to diversify and seek high-quality companies, with independent power producers and electric utilities showing particularly strong results.(2)

· The Fund’s preferred stock holdings continued to be influenced by interest rates in the market place. During the period, the Fed appeared to bring an end to its two-year tightening cycle in June 2006, which sparked a bond market rally that pushed longer rates down. Falling interest rates drove preferred stock prices higher during the period, while credit quality remained solid.

· During the period, a portion of Fund assets was invested in non-U.S. common and preferred stocks. These investments provided the Fund with international diversification and dividend yields often more attractive than the yields available on stocks issued by similar domestic corporations. As of October 31, 2006, approximately 17% of the Fund’s total investments was invested in non-U.S. dollar-denominated common stocks. In addition, approximately 4% of the Fund’s total investments was invested in “Yankee” preferreds. Yankee preferreds are preferred stocks generally issued by large, highly-rated, European financial institutions but denominated in U.S. dollars.

· We are pleased to report that since inception through October 31, 2006, the Fund has increased its monthly dividend 5 times for all share classes. Since its inception, all of the income generated by the Fund has come from dividends paid by the Fund’s common and preferred stock holdings. The Fund expects that all of the dividends paid by the Fund in fiscal 2006 will be qualified dividends subject to federal income tax at long-term capital gain rates (up to 15%, as long ascertain holding periods and other requirements have been met by receiving Fund shareholders).

· The increases in the Fund’s monthly dividend reflected both the effective implementation of the Fund’s dividend capture strategy and the significant number of dividend increases announced by companies represented in the Fund’s common stock portfolio.

· Effective July 1, 2006, Thomas Luster joined the portfolio management team of the Fund. Mr. Luster has been a Vice President of Eaton Vance and its subsidiary, Boston Management and Research (“BMR”) for more than five years, and he manages or co-manages other Eaton Vance portfolios.

· In closing, we would like to thank the shareholders for their continued confidence and participation in the Fund.

(1) It is not possible to invest directly in an Index. The Index’s total return does not reflect commissions or expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index.

(2) Sector weightings are subject to change due to active management.

The views expressed throughout this report are those of the portfolio managers and are current only through the end of the period of the report as stated on the cover. These views are subject to change at any time based upon market or other conditions, and the investment adviser disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a fund are based on many factors, may not be relied on as an indication of trading intent on behalf of any Eaton Vance fund.

Top Ten Holdings* | | | |

By net assets | | | |

Altria Group | | 3.2 | % |

Exxon | | 2.8 | % |

UBS | | 2.8 | % |

Bank of America | | 2.7 | % |

Bellsouth Corporation | | 2.6 | % |

Citigroup | | 2.5 | % |

TXU Corporation | | 2.4 | % |

Wachovia Corp | | 2.4 | % |

First Energy Corp | | 2.3 | % |

Verizon Communications | | 2.2 | % |

* Top Ten Holdings represented 25.9% of Fund net assets as of October 31, 2006. Holdings are subject to change due to active management.

2

Eaton Vance Tax-Managed Dividend Income Fund as of October 31, 2006

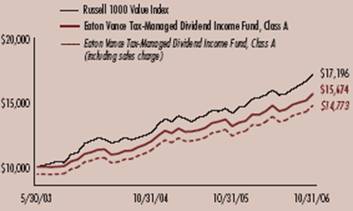

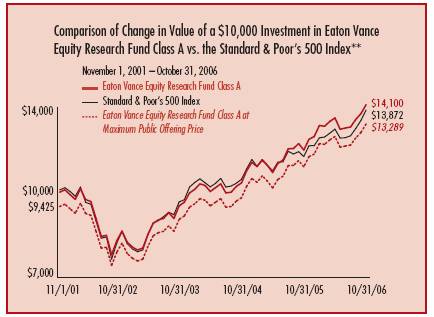

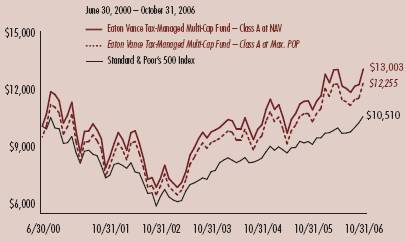

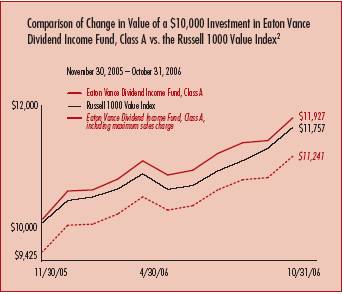

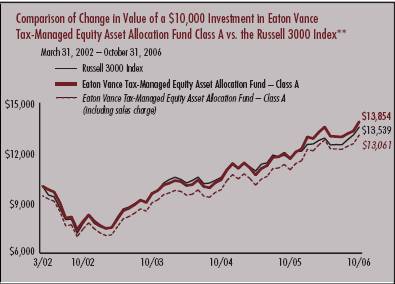

FUND PERFORMANCE

The line graphs and table set forth below provide information about the Fund's performance. The line graphs compare the performance of Class A, Class B and Class C of the Fund with that of the Russell 1000 Value Index, a broad-based, unmanaged market index of 1000 U.S. value stocks. The lines on the graph represent the total returns of a hypothetical investment of $10,000 in each of Class A, Class B and Class C of the Fund and the Russell 1000 Value Index. Class A total returns are presented at net asset value and maximum public offering price. The table includes the total returns of each class of the Fund at net asset value and public offering price. The performance presented below does not reflect the deduction of taxes, if any, that a shareholder would pay on distributions or redemptions of Fund shares.

Performance* | | Class A | | Class B | | Class C | |

Average Annual Total Returns (at net asset value) | | | | | | | |

One Year | | 19.14 | % | 18.22 | % | 18.22 | % |

Life of Fund† | | 14.00 | % | 13.17 | % | 13.17 | % |

SEC Average Annual Total Returns (including sales charge or applicable CDSC) | | | | | | | |

One Year | | 12.25 | % | 13.22 | % | 17.22 | % |

Life of Fund† | | 12.05 | % | 12.52 | % | 13.17 | % |

† Inception Dates – Class A: 5/30/03; Class B: 5/30/03; Class C: 5/30/03

* Average Annual Total Returns do not include the 5.75% maximum sales charge for Class A shares or the applicable contingent deferred sales charge (CDSC) for Class B and Class C shares. If sales charges were deducted, the returns would be lower. SEC average annual total returns for Class A reflect the maximum 5.75% sales charge. SEC returns for Class B shares reflect the applicable CDSC based on the following schedule: 5% - 1st and 2nd years; 4% - 3rd year; 3% - 4th year; 2% - 5th year; 1% - 6th year. SEC returns for Class C reflect a 1% CDSC for the first year. Absent an allocation of certain expenses to the administrator, the returns would be lower.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. For performance as of the most recent month end, please refer to www.eatonvance.com.

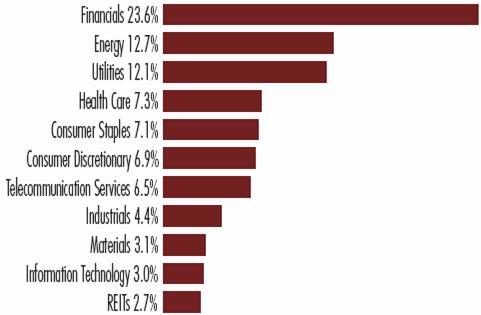

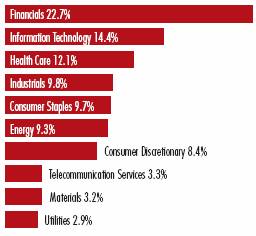

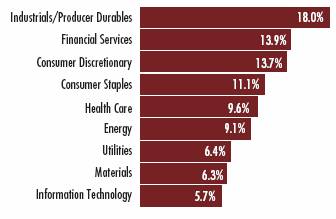

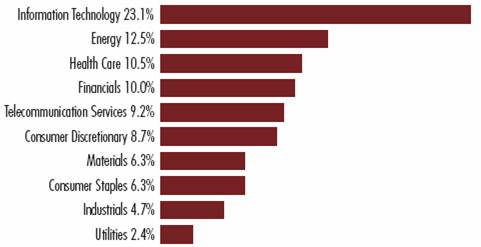

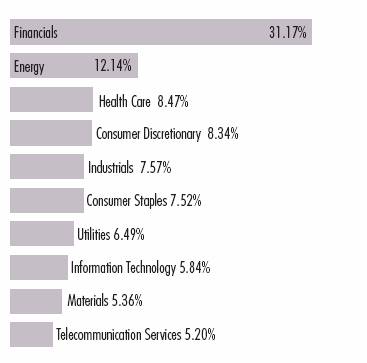

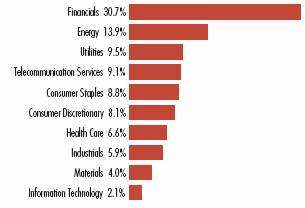

Fund Common Stock Investment by Sector††

By net assets

†† Fund information may not be representative of the Fund's current or future investments and may change due to active management.

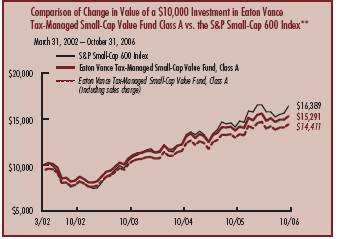

Comparison of Change in value of a $10,000 Investment in Eaton Vance Tax-Managed Dividend Income Fund Class A vs. the Russell 1000 Value Index**

May 30, 2003 – October 31, 2006

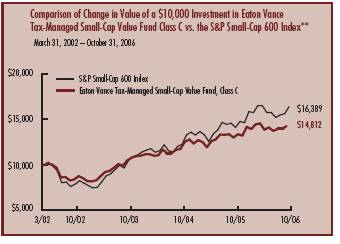

Comparison of Change in value of a $10,000 Investment in Eaton Vance Tax-Managed Dividend Income Fund Class B vs. the Russell 1000 Value Index**

May 30, 2003 – October 31, 2006

Comparison of Change in value of a $10,000 Investment in Eaton Vance Tax-Managed Dividend Income Fund Class C vs. the Russell 1000 Value Index**

May 30, 2003 – October 31, 2006

** Source: Thomson Financial. Investment operations commenced 5/30/03. It is not possible to invest directly in an Index. The Index’s total returns do not reflect any commissions or expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index.

3

“Return Before Taxes” does not take into consideration shareholder taxes. It is most relevant to tax-free or tax-deferred shareholder accounts. “Return After Taxes on Distributions” reflects the impact of federal income taxes due on Fund distributions of dividends and capital gains. It is most relevant to taxpaying shareholders who continue to hold their shares.

“Return After Taxes on Distributions and Sale of Fund Shares” also reflects the impact of taxes on capital gain or loss realized upon a sale of shares. It is most relevant to taxpaying shareholders who sell their shares.

Average Annual Total Returns

(For the periods ended October 31, 2006)

Returns at Net Asset Value (NAV) (Class A)

| | One Year | | Life of Fund | |

Return Before Taxes | | 19.14 | % | 14.00 | % |

Return After Taxes on Distributions | | 18.15 | % | 13.22 | % |

Return After Taxes on Distributions and Sale of Fund Shares | | 13.61 | % | 12.02 | % |

Returns at Public Offering Price (POP) (Class A)

| | One Year | | Life of Fund | |

Return Before Taxes | | 12.25 | % | 12.05 | % |

Return After Taxes on Distributions | | 11.31 | % | 11.29 | % |

Return After Taxes on Distributions and Sale of Fund Shares | | 9.06 | % | 10.30 | % |

Average Annual Total Returns

(For the periods ended October 31, 2006)

Returns at Net Asset Value (NAV) (Class B)

| | One Year | | Life of Fund | |

Return Before Taxes | | 18.22 | % | 13.17 | % |

Return After Taxes on Distributions | | 17.35 | % | 12.51 | % |

Return After Taxes on Distributions and Sale of Fund Shares | | 12.86 | % | 11.31 | % |

Returns at Public Offering Price (POP) (Class B)

| | One Year | | Life of Fund | |

Return Before Taxes | | 13.22 | % | 12.52 | % |

Return After Taxes on Distributions | | 12.35 | % | 11.85 | % |

Return After Taxes on Distributions and Sale of Fund Shares | | 9.61 | % | 10.73 | % |

Average Annual Total Returns

(For the periods ended October 31, 2006)

Returns at Net Asset Value (NAV) (Class C)

| | One Year | | Life of Fund | |

Return Before Taxes | | 18.22 | % | 13.17 | % |

Return After Taxes on Distributions | | 17.35 | % | 12.51 | % |

Return After Taxes on Distributions and Sale of Fund Shares | | 12.86 | % | 11.31 | % |

Returns at Public Offering Price (POP) (Class C)

| | One Year | | Life of Fund | |

Return Before Taxes | | 17.22 | % | 13.17 | % |

Return After Taxes on Distributions | | 16.35 | % | 12.51 | % |

Return After Taxes on Distributions and Sale of Fund Shares | | 12.21 | % | 11.31 | % |

Class A, Class B and Class C commenced operations on 5/30/03. Returns at Public Offering Price (POP) reflect the deduction of the maximum initial sales charge and applicable CDSC, while Returns at Net Asset Value (NAV) do not.

After-tax returns are calculated using the highest historical individual federal income tax rate and do not reflect the impact of state and local taxes. Actual after-tax returns depend on a shareholder’s tax situation and may differ from those shown. After-tax returns are not relevant for shareholders who hold Fund shares in tax-deferred accounts or to shares held by non-taxable entities. Return After Taxes on Distributions for a period may be the same as Return Before Taxes for that period because no distributions were paid during that period, or because the taxable portion of distributions made during the period was insignificant. Also, Return After Taxes on Distributions and Sale of Fund Shares for a period may be greater than Return After Taxes on Distributions for the same period because of realized losses on the sale of Fund shares. Absent an allocation of certain expenses to the administrator, the returns would be lower.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. For performance as of the most recent month end, please refer to www.eatonvance.com.

4

Eaton Vance Tax-Managed Dividend Income Fund as of October 31, 2006

FUND EXPENSES

Example: As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchases and redemption fees (if applicable); and (2) ongoing costs, including management fees; distribution or service fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (May 1, 2006 – October 31, 2006).

Actual Expenses: The first section of the table below provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled "Expenses Paid During Period" to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes: The second section of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratio and an assumed rate of return of 5% per year (before expenses), which is not the actual return of the Fund. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) or redemption fees (if applicable). Therefore, the second section of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

Eaton Vance Tax-Managed Dividend Income Fund

| | | Beginning Account Value

(5/1/06) | | Ending Account Value

(10/31/06) | | Expenses Paid During Period*

(5/1/06 – 10/31/06) | |

| Actual | |

| Class A | | $ | 1,000.00 | | | $ | 1,061.40 | | | $ | 6.18 | | |

| Class B | | $ | 1,000.00 | | | $ | 1,057.60 | | | $ | 10.06 | | |

| Class C | | $ | 1,000.00 | | | $ | 1,057.60 | | | $ | 10.06 | | |

| Hypothetical | |

| (5% return per year before expenses) | |

| Class A | | $ | 1,000.00 | | | $ | 1,019.20 | | | $ | 6.06 | | |

| Class B | | $ | 1,000.00 | | | $ | 1,015.40 | | | $ | 9.86 | | |

| Class C | | $ | 1,000.00 | | | $ | 1,015.40 | | | $ | 9.86 | | |

* Expenses are equal to the Fund's annualized expense ratio of 1.19% for Class A shares, 1.94% for Class B shares and 1.94% for Class C shares, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). The Example assumes that the $1,000 was invested at the net asset value per share determined at the close of business on April 30, 2006.

5

Eaton Vance Tax-Managed Dividend Income Fund as of October 31, 2006

PORTFOLIO OF INVESTMENTS

Common Stocks — 89.3%

| Security | | Shares | | Value | |

| Capital Markets — 4.2% | |

| Goldman Sachs Group, Inc. (The) | | | 100,000 | | | $ | 18,979,000 | | |

| UBS AG(1) | | | 600,000 | | | | 35,904,000 | | |

| | | $ | 54,883,000 | | |

| Commercial Banks — 8.0% | |

| National City Corp. | | | 350,000 | | | $ | 13,037,500 | | |

| Toronto-Dominion Bank, (The)(1) | | | 450,000 | | | | 26,068,500 | | |

| U.S. Bancorp | | | 250,000 | | | | 8,460,000 | | |

| Wachovia Corp. | | | 550,000 | | | | 30,525,000 | | |

| Wells Fargo & Co. | | | 700,000 | | | | 25,403,000 | | |

| | | $ | 103,494,000 | | |

| Communications Equipment — 1.5% | |

| Nokia Oyj ADR | | | 1,000,000 | | | $ | 19,880,000 | | |

| | | $ | 19,880,000 | | |

| Computer Peripherals — 1.4% | |

| International Business Machines Corp. | | | 200,000 | | | $ | 18,466,000 | | |

| | | $ | 18,466,000 | | |

| Diversified Financial Services — 7.2% | |

| Bank of America Corp. | | | 650,000 | | | $ | 35,015,500 | | |

| Citigroup, Inc. | | | 650,000 | | | | 32,604,000 | | |

| JPMorgan Chase & Co. | | | 550,000 | | | | 26,092,000 | | |

| | | $ | 93,711,500 | | |

| Diversified Telecommunication Services — 6.5% | |

| BellSouth Corp. | | | 750,000 | | | $ | 33,825,000 | | |

| Citizens Communications Co. | | | 1,500,000 | | | | 21,990,000 | | |

| Verizon Communications, Inc. | | | 750,000 | | | | 27,750,000 | | |

| | | $ | 83,565,000 | | |

| Electric Utilities — 7.9% | |

| CEZ AS(1) | | | 225,000 | | | $ | 8,894,132 | | |

| E.ON AG(1) | | | 100,000 | | | | 12,041,660 | | |

| Edison International | | | 550,000 | | | | 24,442,000 | | |

| FirstEnergy Corp. | | | 500,000 | | | | 29,425,000 | | |

| Fortum Oyj(1) | | | 600,000 | | | | 16,565,097 | | |

| Iberdrola SA(1) | | | 222,000 | | | | 10,174,899 | | |

| | | $ | 101,542,788 | | |

| Security | | Shares | | Value | |

| Electrical Equipment — 1.0% | |

| Emerson Electric Co. | | | 150,000 | | | $ | 12,660,000 | | |

| | | $ | 12,660,000 | | |

| Energy Equipment & Services — 0.7% | |

| GlobalSantaFe Corp.(1) | | | 175,000 | | | $ | 9,082,500 | | |

| | | $ | 9,082,500 | | |

| Food & Staples Retailing — 1.1% | |

| Wal-Mart Stores, Inc. | | | 300,000 | | | $ | 14,784,000 | | |

| | | $ | 14,784,000 | | |

| Food Products — 1.3% | |

| Nestle SA(1) | | | 50,000 | | | $ | 17,088,506 | | |

| | | $ | 17,088,506 | | |

| Hotels, Restaurants & Leisure — 2.0% | |

| McDonald's Corp. | | | 600,000 | | | $ | 25,152,000 | | |

| | | $ | 25,152,000 | | |

| Household Durables — 0.7% | |

| Stanley Works (The) | | | 200,000 | | | $ | 9,530,000 | | |

| | | $ | 9,530,000 | | |

| Household Products — 1.5% | |

| Kimberly-Clark Corp. | | | 150,000 | | | $ | 9,978,000 | | |

| Kimberly-Clark de Mexico SA de CV(1) | | | 2,250,000 | | | | 9,406,536 | | |

| | | $ | 19,384,536 | | |

Independent Power Producers &

Energy Traders — 2.4% | |

| TXU Corp. | | | 500,000 | | | $ | 31,565,000 | | |

| | | $ | 31,565,000 | | |

| Industrial Conglomerates — 1.9% | |

| General Electric Co. | | | 700,000 | | | $ | 24,577,000 | | |

| | | $ | 24,577,000 | | |

| Insurance — 4.1% | |

| Lincoln National Corp. | | | 250,000 | | | $ | 15,827,500 | | |

| St. Paul Travelers Cos., Inc. (The) | | | 500,000 | | | | 25,565,000 | | |

| Willis Group Holdings Ltd.(1) | | | 300,000 | | | | 11,409,000 | | |

| | | $ | 52,801,500 | | |

See notes to financial statements

6

Eaton Vance Tax-Managed Dividend Income Fund as of October 31, 2006

PORTFOLIO OF INVESTMENTS CONT'D

| Security | | Shares | | Value | |

| Metals & Mining — 3.1% | |

| Freeport-McMoRan Copper & Gold, Inc., Class B | | | 300,000 | | | $ | 18,144,000 | | |

| Nucor Corp. | | | 200,000 | | | | 11,682,000 | | |

| Southern Copper Corp. | | | 200,000 | | | | 10,276,000 | | |

| | | $ | 40,102,000 | | |

| Multiline Retail — 1.8% | |

| J.C. Penney Company, Inc. | | | 300,000 | | | $ | 22,569,000 | | |

| | | $ | 22,569,000 | | |

| Multi-Utilities — 1.9% | |

| RWE AG(1) | | | 150,000 | | | $ | 14,857,043 | | |

| Veolia Environnement(1) | | | 150,000 | | | | 9,179,706 | | |

| | | $ | 24,036,749 | | |

| Oil, Gas & Consumable Fuels — 12.0% | |

| BP PLC ADR | | | 250,000 | | | $ | 16,775,000 | | |

| ChevronTexaco Corp. | | | 400,000 | | | | 26,880,000 | | |

| ENI SpA ADR | | | 300,000 | | | | 18,213,000 | | |

| Exxon Mobil Corp. | | | 500,000 | | | | 35,710,000 | | |

| Marathon Oil Corp. | | | 300,000 | | | | 25,920,000 | | |

| Statoil ASA ADR | | | 450,000 | | | | 11,412,000 | | |

| Total SA ADR | | | 300,000 | | | | 20,442,000 | | |

| | | $ | 155,352,000 | | |

| Pharmaceuticals — 7.3% | |

| Eli Lilly & Co. | | | 400,000 | | | $ | 22,404,000 | | |

| GlaxoSmithKline PLC ADR | | | 300,000 | | | | 15,975,000 | | |

| Johnson & Johnson | | | 400,000 | | | | 26,960,000 | | |

| Pfizer, Inc. | | | 250,000 | | | | 6,662,500 | | |

| Wyeth | | | 450,000 | | | | 22,963,500 | | |

| | | $ | 94,965,000 | | |

| Real Estate Investment Trusts (REITs) — 2.7% | |

| Boston Properties, Inc. | | | 50,000 | | | $ | 5,341,500 | | |

| Equity Residential | | | 200,000 | | | | 10,922,000 | | |

| Host Hotels & Resorts, Inc. | | | 400,000 | | | | 9,224,000 | | |

| Simon Property Group, Inc. | | | 100,000 | | | | 9,710,000 | | |

| | | $ | 35,197,500 | | |

| Road & Rail — 1.5% | |

| Canadian National Railway Co.(1) | | | 400,000 | | | $ | 19,056,000 | | |

| | | $ | 19,056,000 | | |

| Security | | Shares | | Value | |

| Specialty Retail — 1.0% | |

| Kingfisher PLC(1) | | | 2,500,000 | | | $ | 12,538,700 | | |

| | | $ | 12,538,700 | | |

| Textiles, Apparel & Luxury Goods — 1.5% | |

| VF Corp. | | | 250,000 | | | $ | 19,002,500 | | |

| | | $ | 19,002,500 | | |

| Tobacco — 3.1% | |

| Altria Group, Inc. | | | 500,000 | | | $ | 40,665,000 | | |

| | | $ | 40,665,000 | | |

Total Common Stocks

(identified cost $983,238,153) | | $ | 1,155,651,779 | | |

| Preferred Stocks — 8.8% | |

| Security | | Shares | | Value | |

| Automobiles — 0.4% | |

| Porsche International Finance PLC, 7.20%(1)(2) | | | 55,000 | | | $ | 5,598,725 | | |

| | | $ | 5,598,725 | | |

| Commercial Banks — 2.5% | |

| Abbey National Capital Trust I, 8.963%(2)(4) | | | 47,500 | | | $ | 6,469,049 | | |

| Auction Pass-Through Trust 2006-5B - USB H, 9.81%(3)(4) | | | 40 | | | | 1,225,010 | | |

| Auction Pass-Through Trust 2006-6B - USB H, 9.45%(3)(4) | | | 40 | | | | 1,225,010 | | |

| DB Capital Funding VIII, 6.375% | | | 150,000 | | | | 3,825,000 | | |

| First Republic Bank, 6.25% | | | 95,000 | | | | 2,356,000 | | |

| First Republic Bank, 6.70% | | | 162,000 | | | | 4,064,580 | | |

| First Tennessee Bank, 6.22%(3)(4) | | | 2,250 | | | | 2,317,359 | | |

| HSBC Capital Funding LP., 10.176%(1)(2)(4) | | | 32,500 | | | | 4,939,938 | | |

| Royal Bank of Scotland Group PLC, 5.75%(1) | | | 71,000 | | | | 1,706,130 | | |

| Royal Bank of Scotland Group PLC, 6.40%(1) | | | 145,000 | | | | 3,706,200 | | |

| | | $ | 31,834,276 | | |

| Consumer Finance — 0.1% | |

| Ford Motor Credit Co., 7.375% | | | 40,000 | | | $ | 840,800 | | |

| | | $ | 840,800 | | |

| Diversified Financial Services — 1.0% | |

| Bank of America Corp., Series D, 6.204% | | | 200,000 | | | $ | 5,178,000 | | |

| ING Groep NV, 6.125%(1) | | | 242,000 | | | | 6,045,160 | | |

See notes to financial statements

7

Eaton Vance Tax-Managed Dividend Income Fund as of October 31, 2006

PORTFOLIO OF INVESTMENTS CONT'D

| Security | | Shares | | Value | |

| Diversified Financial Services (continued) | |

Structured Auction Rate Securities/Stock

Custodial-Receipts Merrill H, 6.15%(3)(4) | | | 2,100 | | | $ | 2,228,025 | | |

| | | $ | 13,451,185 | | |

| Food Products — 0.1% | |

| Ocean Spray Cranberries, Inc., 6.25%(3) | | | 13,250 | | | $ | 1,093,125 | | |

| | | $ | 1,093,125 | | |

| Gas Utilities — 0.2% | |

| Southern Union Co., 7.55% | | | 118,300 | | | $ | 3,089,996 | | |

| | | $ | 3,089,996 | | |

| Insurance — 2.6% | |

| Ace Ltd., 7.80%(1) | | | 45,500 | | | $ | 1,197,560 | | |

| Aegon NV, 6.50%(1) | | | 205,000 | | | | 5,241,850 | | |

| Arch Capital Group, Ltd., 7.875%(1) | | | 26,500 | | | | 679,990 | | |

| Arch Capital Group, Ltd., 8.00%(1) | | | 185,500 | | | | 4,869,375 | | |

| Endurance Specialty Holdings, Ltd., 7.75%(1) | | | 231,550 | | | | 5,927,680 | | |

| MetLife, Inc., 6.39% | | | 146,000 | | | | 3,796,000 | | |

| MetLife, Inc., 6.50% | | | 70,000 | | | | 1,820,000 | | |

| PartnerRe, Ltd., 6.50%(1) | | | 137,000 | | | | 3,411,300 | | |

| PartnerRe, Ltd., 6.75%(1) | | | 139,700 | | | | 3,555,365 | | |

| RenaissanceRe Holdings, Ltd., 6.08%(1) | | | 107,000 | | | | 2,493,100 | | |

| | | $ | 32,992,220 | | |

| Real Estate Investment Trusts (REITs) — 1.4% | |

| AMB Property Corp., 6.75% | | | 79,900 | | | $ | 2,010,284 | | |

| BRE Properties, Series D, 6.75% | | | 40,000 | | | | 996,000 | | |

| Duke Realty Corp., 6.95% | | | 120,000 | | | | 3,067,200 | | |

| Health Care Property, 7.10% | | | 150,000 | | | | 3,807,000 | | |

| Prologis Trust, 6.75% | | | 65,000 | | | | 1,638,000 | | |

| PS Business Parks, Inc., 7.00% | | | 50,000 | | | | 1,262,500 | | |

| PS Business Parks, Inc., 7.95% | | | 110,000 | | | | 2,883,100 | | |

| Vornado Realty Trust, 6.75% | | | 75,000 | | | | 1,875,000 | | |

| | | $ | 17,539,084 | | |

| Thrifts & Mortgage Finance — 0.5% | |

| Federal National Mortgage Association, Series K, 5.396% | | | 140,000 | | | $ | 7,035,000 | | |

| | | $ | 7,035,000 | | |

Total Preferred Stocks

(identified cost $110,473,783) | | $ | 113,474,411 | | |

| Short-Term Investments — 1.3% | |

| Security | | Principal

Amount

(000's omitted) | | Value | |

| Societe Generale Time Deposit, 5.31%, 11/1/06 | | $ | 16,408 | | | $ | 16,408,000 | | |

Total Short-Term Investments

(at amortized cost, $16,408,000) | | $ | 16,408,000 | | |

Total Investments — 99.4%

(identified cost $1,110,119,936) | | $ | 1,285,534,190 | | |

| Other Assets, Less Liabilities — 0.6% | | $ | 8,203,084 | | |

| Net Assets — 100.0% | | $ | 1,293,737,274 | | |

ADR - American Depository Receipt

(1) Foreign security.

(2) Security valued at fair value using methods determined in good faith by or at the direction of the Trustees.

(3) Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be sold in transactions exempt from registration, normally to qualified institutional buyers. At October 31, 2006, the aggregate value of the securities is $8,088,529 or 0.6% of the Fund's net assets.

(4) Variable rate security. The stated interest rate represents the rate in effect at October 31, 2006.

See notes to financial statements

8

Eaton Vance Tax-Managed Dividend Income Fund as of October 31, 2006

PORTFOLIO OF INVESTMENTS CONT'D

Country Concentration of Portfolio

| Country | | Percentage of

Total Investments | | Value | |

| United States | | | 79.7 | % | | $ | 1,023,895,538 | | |

| Switzerland | | | 4.1 | | | | 52,992,506 | | |

| Canada | | | 3.5 | | | | 45,124,500 | | |

| Bermuda | | | 2.5 | | | | 32,345,810 | | |

| Germany | | | 2.1 | | | | 26,898,703 | | |

| United Kingdom | | | 1.8 | | | | 22,890,968 | | |

| Finland | | | 1.3 | | | | 16,565,097 | | |

| Netherlands | | | 0.9 | | | | 11,287,010 | | |

| Cayman Islands | | | 0.8 | | | | 10,280,060 | | |

| Spain | | | 0.8 | | | | 10,174,899 | | |

| Mexico | | | 0.7 | | | | 9,406,536 | | |

| France | | | 0.7 | | | | 9,179,706 | | |

| Czech Republic | | | 0.7 | | | | 8,894,132 | | |

| Ireland | | | 0.4 | | | | 5,598,725 | | |

| Total | | | 100.0 | % | | $ | 1,285,534,190 | | |

See notes to financial statements

9

Eaton Vance Tax-Managed Dividend Income Fund as of October 31, 2006

FINANCIAL STATEMENTS

Statement of Assets and Liabilities

As of October 31, 2006

| Assets | |

| Investments, at value (identified cost, $1,110,119,936) | | $ | 1,285,534,190 | | |

| Cash | | | 954 | | |

| Receivable for investments sold | | | 12,708,089 | | |

| Receivable for Fund shares sold | | | 10,898,228 | | |

| Dividends and interest receivable | | | 2,846,507 | | |

| Tax reclaim receivable | | | 113,432 | | |

| Total assets | | $ | 1,312,101,400 | | |

| Liabilities | |

| Payable for investments purchased | | $ | 14,887,860 | | |

| Payable for Fund shares redeemed | | | 1,706,181 | | |

| Payable to affiliate for distribution and service fees | | | 650,045 | | |

| Payable to affiliate for investment advisory fees | | | 620,725 | | |

| Payable to affiliate for administration fees | | | 157,549 | | |

| Payable to affiliate for Trustees' fees | | | 1,133 | | |

| Accrued expenses | | | 340,633 | | |

| Total liabilities | | $ | 18,364,126 | | |

| Net Assets | | $ | 1,293,737,274 | | |

| Sources of Net Assets | |

| Paid-in capital | | $ | 1,149,995,479 | | |

| Accumulated net realized loss (computed on the basis of identified cost) | | | (38,955,634 | ) | |

| Accumulated undistributed net investment income | | | 7,267,903 | | |

| Net unrealized appreciation (computed on the basis of identified cost) | | | 175,429,526 | | |

| Total | | $ | 1,293,737,274 | | |

| Class A Shares | |

| Net Assets | | $ | 659,949,547 | | |

| Shares Outstanding | | | 49,250,699 | | |

Net Asset Value and Redemption Price Per Share

(net assets ÷ shares of beneficial interest outstanding) | | $ | 13.40 | | |

Maximum Offering Price Per Share

(100 ÷ 94.25 of $13.40) | | $ | 14.22 | | |

| Class B Shares | |

| Net Assets | | $ | 143,731,310 | | |

| Shares Outstanding | | | 10,750,714 | | |

Net Asset Value, Offering Price and Redemption Price Per Share

(net assets ÷ shares of beneficial interest outstanding) | | $ | 13.37 | | |

| Class C Shares | |

| Net Assets | | $ | 490,056,417 | | |

| Shares Outstanding | | | 36,647,620 | | |

Net Asset Value, Offering Price and Redemption Price Per Share

(net assets ÷ shares of beneficial interest outstanding) | | $ | 13.37 | | |

| On sales of $50,000 or more, the offering price of Class A shares is reduced. | |

Statement of Operations

| Investment Income | | Period Ended

October 31, 2006(1) | | Year Ended

April 30, 2006 | |

Dividends (net of foreign taxes, $761,373

and $1,839,086, respectively) | | $ | 25,459,389 | | | $ | 57,850,384 | | |

| Interest | | | 449,562 | | | | 408,310 | | |

| Total investment income | | $ | 25,908,951 | | | $ | 58,258,694 | | |

| Expenses | |

| Investment adviser fee | | $ | 3,346,304 | | | $ | 4,380,016 | | |

| Administration fee | | | 790,226 | | | | 1,010,657 | | |

| Trustees' fees and expenses | | | 11,386 | | | | 22,566 | | |

| Distribution and service fees | |

| Class A | | | 658,646 | | | | 791,449 | | |

| Class B | | | 635,212 | | | | 981,272 | | |

| Class C | | | 1,998,375 | | | | 2,590,647 | | |

| Transfer and dividend disbursing agent fees | | | 381,817 | | | | 506,323 | | |

| Custodian fee | | | 161,990 | | | | 353,449 | | |

| Legal and accounting services | | | 67,060 | | | | 49,090 | | |

| Registration fees | | | 61,353 | | | | 120,053 | | |

| Printing and postage | | | 56,279 | | | | 66,440 | | |

| Miscellaneous | | | 72,488 | | | | 42,966 | | |

| Total expenses | | $ | 8,241,136 | | | $ | 10,914,928 | | |

Deduct —

Reduction of custodian fee | | $ | 6,347 | | | $ | 11,462 | | |

| Reduction of investment advisory fee | | | — | | | | 67,418 | | |

| Total expense reductions | | $ | 6,347 | | | $ | 78,880 | | |

| Net expenses | | $ | 8,234,789 | | | $ | 10,836,048 | | |

| Net investment income | | $ | 17,674,162 | | | $ | 47,422,646 | | |

| Realized and Unrealized Gain (Loss) | |

Net realized gain (loss) —

Investment transactions (identified cost basis) | | $ | (32,073,633 | ) | | $ | (5,869,280 | ) | |

| Foreign currency transactions | | | (86,078 | ) | | | (426,079 | ) | |

| Net realized loss | | $ | (32,159,711 | ) | | $ | (6,295,359 | ) | |

Change in unrealized appreciation (depreciation) —

Investments (identified cost basis) | | $ | 85,267,150 | | | $ | 60,865,840 | | |

| Foreign currency | | | (117,718 | ) | | | 126,025 | | |

Net change in unrealized appreciation

(depreciation) | | $ | 85,149,432 | | | $ | 60,991,865 | | |

| Net realized and unrealized gain | | $ | 52,989,721 | | | $ | 54,696,506 | | |

| Net increase in net assets from operations | | $ | 70,663,883 | | | $ | 102,119,152 | | |

(1) For the six months ended October 31, 2006.

See notes to financial statements

10

Eaton Vance Tax-Managed Dividend Income Fund as of October 31, 2006

FINANCIAL STATEMENTS CONT'D

Statements of Changes in Net Assets

| Increase (Decrease) in Net Assets | | Period Ended

October 31, 2006(1) | | Year Ended

April 30, 2006 | | Year Ended

April 30, 2005 | |

From operations —

Net investment income | | $ | 17,674,162 | | | $ | 47,422,646 | | | $ | 20,653,197 | | |

| Net realized loss from investment transactions and foreign currency | | | (32,159,711 | ) | | | (6,295,359 | ) | | | (2,129,197 | ) | |

| Net change in unrealized appreciation (depreciation) of investments and foreign currency | | | 85,149,432 | | | | 60,991,865 | | | | 27,134,694 | | |

| Net increase in net assets from operations | | $ | 70,663,883 | | | $ | 102,119,152 | | | $ | 45,658,694 | | |

Distributions to shareholders —

From net investment income

Class A | | $ | (14,892,374 | ) | | $ | (16,854,194 | ) | | $ | (7,435,167 | ) | |

| Class B | | | (3,116,092 | ) | | | (4,458,473 | ) | | | (2,537,028 | ) | |

| Class C | | | (9,831,898 | ) | | | (11,849,664 | ) | | | (5,638,474 | ) | |

| Total distributions to shareholders | | $ | (27,840,364 | ) | | $ | (33,162,331 | ) | | $ | (15,610,669 | ) | |

Transactions in shares of beneficial interest —

Proceeds from sale of shares

Class A | | $ | 211,021,600 | | | $ | 251,392,106 | | | $ | 125,098,185 | | |

| Class B | | | 26,571,508 | | | | 42,104,047 | | | | 38,656,600 | | |

| Class C | | | 139,299,888 | | | | 162,588,198 | | | | 89,783,302 | | |

| Net asset value of shares issued to shareholders in payment of distributions declared | |

| Class A | | | 9,886,452 | | | | 11,286,235 | | | | 4,995,133 | | |

| Class B | | | 1,971,057 | | | | 2,821,775 | | | | 1,573,826 | | |

| Class C | | | 5,144,929 | | | | 6,109,408 | | | | 2,801,624 | | |

| Cost of shares redeemed | |

| Class A | | | (37,791,536 | ) | | | (60,580,545 | ) | | | (31,957,287 | ) | |

| Class B | | | (7,675,616 | ) | | | (12,211,050 | ) | | | (6,044,426 | ) | |

| Class C | | | (21,329,327 | ) | | | (29,585,505 | ) | | | (11,250,437 | ) | |

| Net asset value of shares exchanged | |

| Class A | | | 1,952,983 | | | | 2,017,596 | | | | 412,800 | | |

| Class B | | | (1,952,983 | ) | | | (2,017,596 | ) | | | (412,800 | ) | |

| Net increase in net assets from Fund share transactions | | $ | 327,098,955 | | | $ | 373,924,669 | | | $ | 213,656,520 | | |

| Net increase in net assets | | $ | 369,922,474 | | | $ | 442,881,490 | | | $ | 243,704,545 | | |

| Net Assets | |

| At beginning of period | | $ | 923,814,800 | | | $ | 480,933,310 | | | $ | 237,228,765 | | |

| At end of period | | $ | 1,293,737,274 | | | $ | 923,814,800 | | | $ | 480,933,310 | | |

Accumulated undistributed net investment

income included in net assets | |

| At end of period | | $ | 7,267,903 | | | $ | 17,520,182 | | | $ | 5,284,430 | | |

(1) For the six months ended October 31, 2006.

See notes to financial statements

11

Eaton Vance Tax-Managed Dividend Income Fund as of October 31, 2006

FINANCIAL STATEMENTS CONT'D

Financial Highlights

| | | Class A | |

| | | Period Ended | | Year Ended April 30, | | Period Ended | |

| | | October 31, 2006(1) | | 2006 | | 2005 | | April 30, 2004(2) | |

| Net asset value — Beginning of period | | $ | 12.990 | | | $ | 11.820 | | | $ | 10.640 | | | $ | 10.000 | | |

| Income (loss) from operations | |

| Net investment income(3) | | $ | 0.239 | | | $ | 0.922 | | | $ | 0.743 | | | $ | 0.500 | | |

| Net realized and unrealized gain | | | 0.534 | | | | 0.889 | | | | 0.989 | | | | 0.437 | | |

| Total income from operations | | $ | 0.773 | | | $ | 1.811 | | | $ | 1.732 | | | $ | 0.937 | | |

| Less distributions | |

| From net investment income | | $ | (0.363 | ) | | $ | (0.641 | ) | | $ | (0.552 | ) | | $ | (0.297 | ) | |

| Total distributions | | $ | (0.363 | ) | | $ | (0.641 | ) | | $ | (0.552 | ) | | $ | (0.297 | ) | |

| Net asset value — End of period | | $ | 13.400 | | | $ | 12.990 | | | $ | 11.820 | | | $ | 10.640 | | |

| Total Return(4) | | | 6.14 | % | | | 15.78 | % | | | 16.54 | % | | | 9.44 | % | |

| Ratios/Supplemental Data | |

| Net assets, end of period (000's omitted) | | $ | 659,950 | | | $ | 452,785 | | | $ | 215,759 | | | $ | 104,169 | | |

| Ratios (As a percentage of average daily net assets): | |

| Expenses before custodian fee reduction(5) | | | 1.19 | %(6) | | | 1.21 | % | | | 1.25 | % | | | 1.40 | %(6) | |

| Expenses after custodian fee reduction(5) | | | 1.19 | %(6) | | | 1.21 | % | | | 1.25 | % | | | 1.40 | %(6) | |

| Net investment income | | | 3.69 | %(6) | | | 7.49 | % | | | 6.46 | % | | | 5.05 | %(6) | |

| Portfolio Turnover | | | 46 | % | | | 247 | % | | | 162 | % | | | 117 | % | |

(1) For the six month period ended October 31, 2006. During the current period, Fund changed its fiscal year end from April 30 to October 31.

(2) For the period from the start of business, May 30, 2003 to April 30, 2004.

(3) Net investment income per share was computed using average shares outstanding.

(4) Returns are historical and are calculated by determining the percentage change in net asset value with all distributions reinvested. Total return is not computed on an annualized basis.

(5) The investment adviser waived a portion of its advisory fee and/or the administrator subsized certain operating expenses (equal to 0.01%, 0.01% and 0.07% of average daily net assets for the fiscal years ended April 30, 2006, 2005 and 2004, respectively).

(6) Annualized.

See notes to financial statements

12

Eaton Vance Tax-Managed Dividend Income Fund as of October 31, 2006

FINANCIAL STATEMENTS CONT'D

Financial Highlights

| | | Class B | |

| | | Period Ended | | Year Ended April 30, | | Period Ended | |

| | | October 31, 2006(1) | | 2006 | | 2005 | | April 30, 2004(2) | |

| Net asset value — Beginning of period | | $ | 12.960 | | | $ | 11.790 | | | $ | 10.630 | | | $ | 10.000 | | |

| Income (loss) from operations | |

| Net investment income(3) | | $ | 0.200 | | | $ | 0.801 | | | $ | 0.648 | | | $ | 0.427 | | |

| Net realized and unrealized gain | | | 0.526 | | | | 0.919 | | | | 0.986 | | | | 0.446 | | |

| Total income from operations | | $ | 0.726 | | | $ | 1.720 | | | $ | 1.634 | | | $ | 0.873 | | |

| Less distributions | |

| From net investment income | | $ | (0.316 | ) | | $ | (0.550 | ) | | $ | (0.474 | ) | | $ | (0.243 | ) | |

| Total distributions | | $ | (0.316 | ) | | $ | (0.550 | ) | | $ | (0.474 | ) | | $ | (0.243 | ) | |

| Net asset value — End of period | | $ | 13.370 | | | $ | 12.960 | | | $ | 11.790 | | | $ | 10.630 | | |

| Total Return(4) | | | 5.76 | % | | | 14.97 | % | | | 15.57 | % | | | 8.79 | % | |

| Ratios/Supplemental Data | |

| Net assets, end of period (000's omitted) | | $ | 143,731 | | | $ | 120,272 | | | $ | 79,871 | | | $ | 40,731 | | |

| Ratios (As a percentage of average daily net assets): | |

| Expenses before custodian fee reduction(5) | | | 1.94 | %(6) | | | 1.96 | % | | | 2.00 | % | | | 2.15 | %(6) | |

| Expenses after custodian fee reduction(5) | | | 1.94 | %(6) | | | 1.96 | % | | | 2.00 | % | | | 2.15 | %(6) | |

| Net investment income | | | 3.11 | %(6) | | | 6.53 | % | | | 5.65 | % | | | 4.31 | %(6) | |

| Portfolio Turnover | | | 46 | % | | | 247 | % | | | 162 | % | | | 117 | % | |

(1) For the six month period ended October 31, 2006. During the current period, the Fund changed its fiscal year end from April 30 to October 31.

(2) For the period from the start of business, May 30, 2003, to April 30, 2004.

(3) Net investment income per share was computed using average shares outstanding.

(4) Returns are historical and are calculated by determining the percentage change in net asset value with all distributions reinvested. Total return is not computed on an annualized basis.

(5) The investment adviser waived a portion of its advisory fee and/or the administrator subsized certain operating expenses (equal to 0.01%, 0.01% and 0.07% of average daily net assets for the fiscal years ended April 30, 2006, 2005 and 2004, respectively).

(6) Annualized.

See notes to financial statements

13

Eaton Vance Tax-Managed Dividend Income Fund as of October 31, 2006

FINANCIAL STATEMENTS CONT'D

Financial Highlights

| | | Class C | |

| | | Period Ended | | Year Ended April 30, | | Period Ended | |

| | | October 31, 2006(1) | | 2006 | | 2005 | | April 30, 2004(2) | |

| Net asset value — Beginning of period | | $ | 12.960 | | | $ | 11.800 | | | $ | 10.630 | | | $ | 10.000 | | |

| Income (loss) from operations | |

| Net investment income(3) | | $ | 0.192 | | | $ | 0.817 | | | $ | 0.653 | | | $ | 0.432 | | |

| Net realized and unrealized gain | | | 0.534 | | | | 0.893 | | | | 0.991 | | | | 0.441 | | |

| Total income from operations | | $ | 0.726 | | | $ | 1.710 | | | $ | 1.644 | | | $ | 0.873 | | |

| Less distributions | |

| From net investment income | | $ | (0.316 | ) | | $ | (0.550 | ) | | $ | (0.474 | ) | | $ | (0.243 | ) | |

| Total distributions | | $ | (0.316 | ) | | $ | (0.550 | ) | | $ | (0.474 | ) | | $ | (0.243 | ) | |

| Net asset value — End of period | | $ | 13.370 | | | $ | 12.960 | | | $ | 11.800 | | | $ | 10.630 | | |

| Total Return(4) | | | 5.76 | % | | | 14.87 | % | | | 15.66 | % | | | 8.79 | % | |

| Ratios/Supplemental Data | |

| Net assets, end of period (000's omitted) | | $ | 490,056 | | | $ | 350,758 | | | $ | 185,303 | | | $ | 92,329 | | |

| Ratios (As a percentage of average daily net assets): | |

| Expenses before custodian fee reduction(5) | | | 1.94 | %(6) | | | 1.96 | % | | | 2.00 | % | | | 2.15 | %(6) | |

| Expenses after custodian fee reduction(5) | | | 1.94 | %(6) | | | 1.96 | % | | | 2.00 | % | | | 2.15 | %(6) | |

| Net investment income | | | 2.98 | %(6) | | | 6.65 | % | | | 5.69 | % | | | 4.34 | %(6) | |

| Portfolio Turnover | | | 46 | % | | | 247 | % | | | 162 | % | | | 117 | % | |

(1) For the six month period ended October 31, 2006. During the current period, the Fund changed its fiscal year end from April 30 to October 31.

(2) For the period from the start of business, May 30, 2003 to April 30, 2004.

(3) Net investment income per share was computed using average shares outstanding.

(4) Returns are historical and are calculated by determining the percentage change in net asset value with all distributions reinvested. Total return is not computed on an annualized basis.

(5) The investment adviser waived a portion of its advisory fee and/or the administrator subsized certain operating expenses (equal to 0.01%, 0.01% and 0.07% of average daily net assets for the fiscal fiscal years ended April 30, 2006, 2005 and 2004, respectively).

(6) Annualized.

See notes to financial statements

14

Eaton Vance Tax-Managed Dividend Income Fund as of October 31, 2006

NOTES TO FINANCIAL STATEMENTS

1 Significant Accounting Policies

Eaton Vance Tax-Managed Dividend Income Fund (the Fund) is a diversified series of Eaton Vance Mutual Funds Trust (the Trust). The Trust is an entity of the type commonly known as a Massachusetts business trust and is registered under the Investment Company Act of 1940, as amended, as an open-end management investment company. The Fund seeks to achieve after-tax total return by investing primarily in a diversified portfolio of common and preferred stocks that pay dividends that qualify for federal income taxation at long–term capital gains rates ("tax-favored dividends"). The Fund offers three classes of shares. Class A shares are generally sold subject to a sales charge imposed at time of purchase. Class B and Class C shares are sold at net asset value and are subject to a contingent deferred sales charge (see Note 6). Class B shares held for eight years will automatically convert to Class A shares. Each class represents a pro rata interest in the Fund, but votes separately on class-specific matters and (as noted below) is subject to different expenses. Realized and unrealized gains and losses and net investment income and losses, other than class specific expenses, are allocated daily to each class of shares based on the relative net assets of each class to the total net assets of the Fund. Each class of shares differs in its distribution plan and certain other class specific expenses.

The following is a summary of significant accounting policies consistently followed by the Fund in the preparation of its financial statements. The policies are in conformity with accounting principles generally accepted in the United States of America.

A Investment Valuation — Securities listed on a U.S. securities exchange generally are valued at the last sale price on the day of valuation or, if no sales took place on such date, at the mean between the closing bid and asked prices therefore on the exchange where such securities are principally traded. Equity securities listed on the NASDAQ National Market System generally are valued at the official NASDAQ closing price. Unlisted or listed securities for which closing sales prices or closing quotations are not available are valued at the mean between the latest available bid and asked prices or, in the case of preferred equity securities that are not listed or traded in the over-the-counter market, by an independent pricing service. The value of preferred equity securi ties that are valued by a pricing service on a bond basis will be adjusted by an income factor, to be determined by the investment adviser, to reflect the next anticipated regular dividend. Exchange-traded options are valued at the last sale price for the day of valuation as quoted on the principal exchange or board of trade on which the options are traded or, in the absence of sales on such date, at the mean between the latest bid and asked prices therefore. Futures positions on securities and currencies generally are valued at closing settlement prices. Short-term debt securities with a remaining maturity of 60 days or less are valued at amortized cost. If short-term debt securities are acquired with a remaining maturity of more than 60 days, they will be valued by a pricing service. Other fixed income and debt securities, including listed securities and securities for which price quotations are available, will normally be valued on th e basis of valuations furnished by a pricing service. Foreign securities and currencies are valued in U.S. dollars, based on foreign currency exchange rate quotations supplied by an independent quotation service. The daily valuation of exchange-traded foreign securities generally is determined as of the close of trading on the principal exchange on which such securities trade. Events occurring after the close of trading on foreign exchanges may result in adjustments to the valuation of foreign securities to more accurately reflect their fair value as of the close of regular trading on the New York Stock Exchange. When valuing foreign equity securities that meet certain criteria, the Trustees have approved the use of a fair value service that values such securities to reflect market trading that occurs after the close of the applicable foreign markets of comparable securities or other instruments that have a strong correlation to the fair-valued securities. Investments held by the Fund for which valuations or market quotations are unavailable are valued at fair value using methods determined in good faith by or at the direction of the Trustees of the Fund considering relevant factors, data and information including the market value of freely tradable securities of the same class in the principal market on which such securities are normally traded.

B Income — Dividend income is recorded on the ex-dividend date for dividends received in cash and/or securities. However, if the ex-dividend date has passed, certain dividends from foreign securities are recorded as the Fund is informed of the ex-dividend date. Withholding taxes on foreign dividends and capital gains have been provided for in accordance with the Fund's understanding of the applicable countries' tax rules and rates. Interest income is recorded on the accrual basis.

C Expenses — The majority of expenses of the Trust are directly identifiable to an individual fund. Expenses which are not readily identifiable to a specific fund are allocated taking into consideration, among other things,

Eaton Vance Tax-Managed Dividend Income Fund as of October 31, 2006

NOTES TO FINANCIAL STATEMENTS CONT'D

the nature and type of expense and the relative size of the funds.

D Federal Taxes — The Fund's policy is to comply with the provisions of the Internal Revenue Code applicable to regulated investment companies and to distribute to shareholders each year all of its taxable income, including any net realized capital gain on investments. Accordingly, no provision for federal income or excise tax is necessary. At October 31, 2006, the Fund, for federal income tax purposes, had a capital loss carryover of $38,835,761 which will reduce the taxable income arising from future net realized gain in investments, if any, to the extent permitted by the Internal Revenue Code and thus will reduce the amount of distributions to shareholders which would otherwise be necessary to relieve the Fund of any liability for federal income or excise tax. Such cap ital loss carryover will expire on: October 31, 2011 ($252,492), October 31, 2012 ($2,039,433), October 31, 2013 ($4,586,180) and October 31, 2014 ($31,957,656).

E Expense Reduction — Investors Bank & Trust Company (IBT) serves as custodian of the Fund. Pursuant to the custodian agreement, IBT receives a fee reduced by credits which are determined based on the average daily cash balance the Fund maintains with IBT. All credit balances used to reduce the Fund's custodian fees are reported as a reduction of expenses in the Statements of Operations.

F Financial Futures Contracts — Upon entering a financial futures contract, the Fund is required to deposit (initial margin) either in cash or securities an amount equal to a certain percentage of the purchase price indicated in the financial futures contract. Subsequent payments are made or received by the Fund (margin maintenance) each day, dependent on the daily fluctuations in the value of the underlying security, and are recorded for book purposes as unrealized gains or losses by the Fund. The Fund's investment in financial futures contracts is designed to hedge against anticipated future changes in price of current or anticipated Fund positions. Should prices move unexpectedly, the Fund may not achieve the anticipated benefits of the financial futures contracts and may realize a loss.

G Foreign Currency Translation — Investment valuations, other assets, and liabilities initially expressed in foreign currencies are converted each business day into U.S. dollars based upon current exchange rates. Purchases and sales of foreign investment securities and income and expenses are converted into U.S. dollars based upon currency exchange rates prevailing on the respective dates of such transactions. Recognized gains or losses on investment transactions attributable to changes in foreign currency exchange rates are recorded for financial statement purposes as net realized gains and losses on investments. That portion of unrealized gains and losses on investments that results from fluctuation s in foreign currency exchange rates is not separately disclosed.

H Purchased Options — Upon the purchase of a put option by the Fund, the premium paid is recorded as an investment, the value of which is marked-to-market daily. When a purchased option expires, the Fund will realize a loss in the amount of the cost of the option. When the Fund enters into a closing sale transaction, the Fund will realize a gain or loss depending on whether the sales proceeds from the closing sale transaction are greater or less than the cost of the option. When the Fund exercises a put option, settlement is made in cash. The risk associated with purchasing options is limited to the premium originally paid.

I Securities Sold Short — The Fund may sell individual securities short if it owns at least an equal amount of the security sold short or has at the time of sale a right to obtain securities equivalent in kind and amount to the securities sold and provided that, if such right is conditional, the sale is made upon the same conditions (a covered short sale). The Fund may sell short securities representing an index or basket of securities whose constituents the Fund holds in whole or in part. A short sale of an index or basket security will be a covered short sale if the underlying index or basket of securities is the same or substantially identical to securities held by the Fund.

The seller of a short position generally realizes a profit on the transaction if the price it receives on the short sale exceeds the cost of closing out the position by purchasing securities in the market, but generally realizes a loss if the cost of closing out the short position exceeds the proceeds of the short sale. The exposure to loss on covered short sales (to the extent the value of the security sold short rises instead of falls) is offset by the increase in the value of the underlying security or securities retained. The profit or loss on a covered short sale is also affected by the borrowing cost of any securities borrowed in connection with the short sale (which will vary with market conditions) and use of the proceeds of the short sale. The Fund expects normally to close its covered short sales by delivering newly-acquired stock.

Eaton Vance Tax-Managed Dividend Income Fund as of October 31, 2006

NOTES TO FINANCIAL STATEMENTS CONT'D

Exposure to loss on an index or basket security sold short will not be offset by gains on other securities holdings to the extent that the constituent securities of the index or basket security sold short are not held by the Fund. Such losses may be substantial.

J Use of Estimates — The preparation of the financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of income and expense during the reporting period. Actual results could differ from those estimates.

K Indemnifications — Under the Trust's organizational documents, its officers and Trustees may be indemnified against certain liabilities and expenses arising out of the performance of their duties to the Fund, and shareholders are indemnified against personal liability for the obligations of the Trust. Additionally, in the normal course of business, the Fund enters into agreements with service providers that may contain indemnification clauses. The Fund's maximum exposure under these arrangements is unknown as this would involve future claims that may be made against the Fund that have not yet occurred.

L Other — Investment transactions are accounted for on the date the securities are purchased or sold. Realized gains and losses on securities sold are determined on the basis of identified cost.

2 Distribution to Shareholders

It is the present policy of the Fund to make monthly dividend distributions to shareholders and at least one distribution annually of all or substantially all of its net realized capital gains, if any (reduced by available capital loss carryforwards from prior years, if any). Distributions are declared separately for each class of shares. Distributions are paid in the form of additional shares of the same class of the Fund or, at the election of the shareholder, in cash. Shareholders may reinvest all distributions in additional shares of the same class of the Fund at the net asset value as of the close of business on the ex-dividend date. The Fund distinguishes between distributions on a tax basis and a financial reporting basis. Accounting principles generally accepted in the United States of America require that only distributions in excess of tax basis ea rnings and profits be reported in the financial statements as a return of capital. Permanent differences between book and tax accounting relating to distributions are reclassified to paid-in capital.

The tax character of distributions paid for the period from May 1, 2006 to October 31, 2006 and the years ended April 30, 2006 and April 30, 2005 was as follows:

| | | Year Ended | |

| | | October 31, 2006 | | April 30, 2006 | | April 30, 2005 | |

| Distributions declared from: | | | | | | | |

|

| Ordinary income | | $ | 27,840,364 | | | $ | 33,162,331 | | | $ | 15,610,669 | | |

|

During the period from May 1, 2006 to October 31, 2006, accumulated undistributed net investment income was decreased by $86,077 and accumulated net realized loss was decreased by $86,077 primarily due to differing treatment of certain dividends received from the Fund's investment in Real Estate Investment Trusts (REITs). This change had no effect on the net assets or the net asset value per share.

As of October 31, 2006, the components of distributable earnings (accumulated losses) on a tax basis were as follows:

| Undistributed income | | $ | 7,140,643 | | |

| Capital loss carryforwards | | $ | (38,835,761 | ) | |

| Unrealized gain | | $ | 175,436,913 | | |

3 Shares of Beneficial Interest

The Agreement and Declaration of Trust permits the Trustees to issue an unlimited number of full and fractional shares of beneficial interest (without par value). Transactions in shares were as follows:

| Class A | | Period Ended

October 31,

2006(1) | | Year Ended

April 30,

2006 | | Year Ended

April 30,

2005 | |

| Sales | | | 16,412,434 | | | | 20,439,240 | | | | 10,852,656 | | |

Issued to shareholders electing

to receive payments of

distributions in Fund shares | | | 776,077 | | | | 918,038 | | | | 431,760 | | |

| Redemptions | | | (2,959,859 | ) | | | (4,913,417 | ) | | | (2,847,599 | ) | |

| Exchanges from Class B shares | | | 154,366 | | | | 163,619 | | | | 35,461 | | |

| Net increase | | | 14,383,018 | | | | 16,607,480 | | | | 8,472,278 | | |

Eaton Vance Tax-Managed Dividend Income Fund as of October 31, 2006

NOTES TO FINANCIAL STATEMENTS CONT'D

| Class B | | Period Ended

October 31,

2006(1) | | Year Ended

April 30,

2006 | | Year Ended

April 30,

2005 | |

| Sales | | | 2,071,311 | | | | 3,436,193 | | | | 3,368,539 | | |

Issued to shareholders electing

to receive payments of

distributions in Fund shares | | | 155,293 | | | | 230,280 | | | | 136,088 | | |

| Redemptions | | | (602,906 | ) | | | (993,777 | ) | | | (528,003 | ) | |

| Exchanges to Class A shares | | | (154,674 | ) | | | (163,946 | ) | | | (35,527 | ) | |

| Net increase | | | 1,469,024 | | | | 2,508,750 | | | | 2,941,097 | | |

| Class C | | Period Ended

October 31,

2006(1) | | Year Ended

April 30,

2006 | | Year Ended

April 30,

2005 | |

| Sales | | | 10,852,246 | | | | 13,261,839 | | | | 7,760,896 | | |

Issued to shareholders electing

to receive payments of

distributions in Fund shares | | | 404,714 | | | | 497,886 | | | | 242,047 | | |

| Redemptions | | | (1,671,681 | ) | | | (2,407,104 | ) | | | (978,209 | ) | |

| Net increase | | | 9,585,279 | | | | 11,352,621 | | | | 7,024,734 | | |

(1) For the period from May 1, 2006 to October 31, 2006.

4 Investment Adviser Fee and Other Transactions with Affiliates

The investment adviser fee is earned by Eaton Vance Management (EVM), as compensation for management and investment advisory services rendered to the Fund. Under the advisory agreement, EVM receives a monthly advisory fee equal to 0.650% annually of average daily net assets of the Fund up to $500 million, and at reduced rates as daily net assets exceed that level. The Fund's advisory fee was 0.61% of the Fund's average daily net assets for the period ended October 31, 2006 and the year ended Apri 30, 2006. For the period from May 1, 2006 to October 31, 2006, the advisory fee amounted to $3,346,304. For the year ended April 30, 2006, the advisory fee amounted to $4,380,016. EVM has agreed to reduce the investment adviser fee by an amount equal to that portion of commissions paid to broker dealers in execution of Fund portfolio transactions that is consideration for third-party research services. For the period from May 1, 2006 to October 31, 2006, EVM did not waive any of its advisory fee. For the year ended April 30, 2006, EVM waived $67,418 of its advisory fee. An administration fee is earned by EVM for managing and administering the business affairs of the Fund. Under the administration agreement, EVM earns a fee in the amount of 0.15% per annum of the average daily net assets of the Fund. For the period from May 1, 2006 to October 31, 2006, the administration fee amounted to $790,226. For the year ended April 30, 2006, the administration fee amounted to $1,010,657.

Except for Trustees of the Fund who are not members of EVM's organization, officers and Trustees receive remuneration for their services to the Fund out of the investment adviser fee earned by EVM. Trustees of the Fund who are not affiliated with EVM may elect to defer receipt of all or a percentage of their annual fees in accordance with the terms of the Trustees Deferred Compensation Plan. For the period from May 1, 2006 to October 31, 2006 and the year ended April 30, 2006, no significant amounts have been deferred.

EVM serves as the sub-transfer agent of the Fund and receives from the transfer agent an aggregate fee based upon the actual expenses incurred by EVM in the performance of those activities. For the period from May 1, 2006 to October 31, 2006 and the year ended April 30, 2006, EVM received $36,216 and $30,576 in sub-transfer agent fees, respectively.

Eaton Vance Distributors, Inc. (EVD), a subsidiary of EVM and the Fund's principal underwriter, received $569,929 and $666,228 as its portion of the sales charge on sales of Class A shares for the period from May 1, 2006 to October 31, 2006 and the year ended April 30, 2006, respectively.

Certain officers and Trustees of the Fund are officers of the above organizations.

5 Distribution Plans

Class A has in effect a distribution plan pursuant to Rule 12b-1 under the Investment Company Act of 1940 (Class A Plan). The Class A Plan provides that the Fund will pay EVD a distribution and service fee of 0.25% of the Fund's average daily net assets attributable to Class A shares for each fiscal year for distribution services and facilities provided to the Fund by EVD, as well as for personal services and/or the maintenance of shareholder accounts. Distribution and service fees paid or accrued for the period from May 1, 2006 to October 31, 2006 amounted to $658,646 for Class A shares. Distribution and service fees paid or accrued for the year ended April 30, 2006 amounted to $791,449. The Fund also has in effect distribution plans for Class B shares (Class B Plan) and Class C shares (Class C Plan) pursuant to Rule 12b-1 under the Investment Company Act of 1940 (collectively, "the Plans"). The Class B and Class C Plans requir e the Fund to pay EVD amounts equal to 1/365 of

Eaton Vance Tax-Managed Dividend Income Fund as of October 31, 2006

NOTES TO FINANCIAL STATEMENTS CONT'D