UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-4108

Oppenheimer Variable Account Funds

(Exact name of registrant as specified in charter)

6803 South Tucson Way, Centennial, Colorado 80112-3924

(Address of principal executive offices) (Zip code)

Arthur S. Gabinet

OFI Global Asset Management, Inc.

Two World Financial Center, New York, New York 10281-1008

(Name and address of agent for service)

Registrant’s telephone number, including area code: (303) 768-3200

Date of fiscal year end: December 31

Date of reporting period: 12/31/2013

Item 1. Reports to Stockholders.

| | | | |

| December 31, 2013 | | |

| | | Oppenheimer Discovery Mid Cap Growth Fund/VA* A Series of Oppenheimer Variable Account Funds | | Annual Report |

| | |

| | ANNUAL REPORT Listing of Top Holdings Fund Performance Discussion Financial Statements *Prior to 4/30/13, the Fund’s name was Oppenheimer Small- & Mid-Cap Growth Fund/VA | | |

Portfolio Manager: Ronald J. Zibelli, Jr., CFA

| | | | | | | | | | | | |

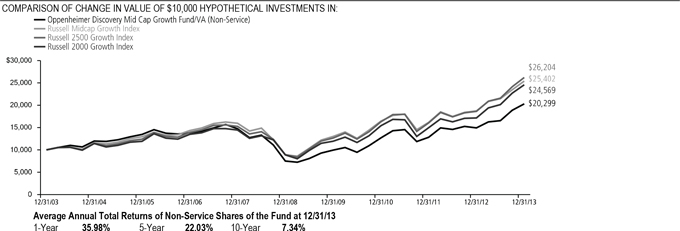

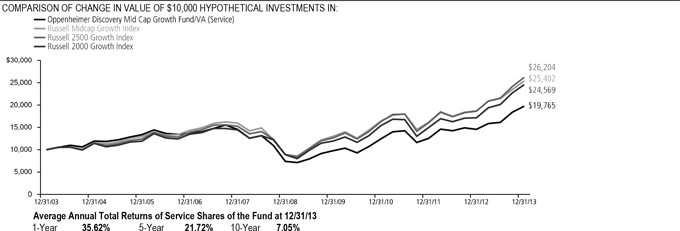

Average Annual Total Returns For the Periods Ended 12/31/13 | |

| | | 1-Year | | | 5-Year | | | 10-Year | |

Non-Service Shares | | | 35.98 | % | | | 22.03% | | | | 7.34% | |

Service Shares | | | 35.62 | % | | | 21.72% | | | | 7.05% | |

Performance data quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. For performance data current to the most recent month end, call us at 1.800.988.8287. The Fund’s total returns should not be expected to be the same as the returns of other funds, whether or not both funds have the same portfolio managers and/or similar names. The Fund’s total returns include changes in share price and reinvested distributions but do not include the charges associated with the separate account products that offer this Fund. Such performance would have been lower if such charges were taken into account.

| | | | |

TOP TEN COMMON STOCK HOLDINGS | | | | |

Tractor Supply Co. | | | 2.2 | % |

Affiliated Managers Group, Inc. | | | 1.9 | |

LinkedIn Corp., Cl. A | | | 1.9 | |

CoStar Group, Inc. | | | 1.7 | |

B/E Aerospace, Inc. | | | 1.6 | |

Wabtec Corp. | | | 1.5 | |

Actavis plc | | | 1.5 | |

Under Armour, Inc., Cl. A | | | 1.5 | |

Hexcel Corp. | | | 1.5 | |

Kansas City Southern | | | 1.5 | |

Portfolio holdings and allocations are subject to change. Percentages are as of December 31, 2013, and are based on net assets. For more current Fund holdings, please visit oppenheimerfunds.com.

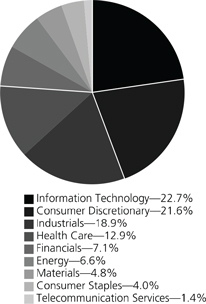

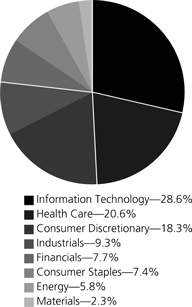

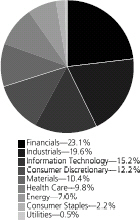

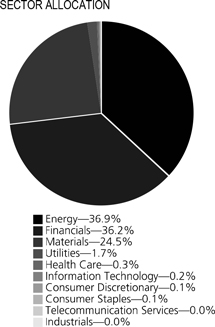

SECTOR ALLOCATION

Portfolio holdings and allocations are subject to change. Percentages are as of December 31, 2013, and are based on the total market value of common stocks.

2 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

| | |

Fund Performance Discussion |

The Fund’s Non-Service shares produced a total return of 35.98% during the one-year reporting period ended December 31, 2013, outperforming the Russell Midcap Growth Index (the “Index”), which returned 35.74%. During the reporting period, the Fund enjoyed good relative performance in the industrials, financials, information technology and energy sectors largely due to positive stock selection. The Fund underperformed the Index in the consumer discretionary sector due to relatively weak stock selection, and in the consumer staples sector, where less favorable stock selection and an underweight position detracted.

For the trailing 3-year period ended December 31, 2013, the Fund’s Non-Service shares produced an annualized return of 16.98% compared to 15.63% for the Russell Midcap Growth Index.

MARKET OVERVIEW

Equities in the U.S. and developed markets throughout the world delivered strong performance in 2013. Accommodative monetary policies on the part of central banks in the U.S., Europe and Japan, combined with supportive equity valuations relative to bonds, were instrumental in this performance. Signs that the U.S. economy was on the mend, demonstrated by rising house prices, also helped sentiment toward stocks. While equities performed well for the year, numerous concerns remained. Namely, in late May, relatively hawkish remarks by Federal Reserve (“Fed”) chairman Ben Bernanke were widely interpreted as a signal that U.S. monetary policymakers would begin to back away from their quantitative easing program sooner than expected, sparking heightened volatility in financial markets throughout the world. Additionally, fears began to creep into the market about a possible slowdown in the world’s emerging economies. However, market conditions generally stabilized over the summer of 2013. While the Fed unexpectedly refrained from reducing its monthly bond purchases in September, in December, the Central Bank announced that it would reduce its monthly bond purchases by $10 billion, from $85 billion to $75 billion, starting in January 2014. The Fed also announced that it would continue to hold short-term interest rates at very low levels until unemployment in the United States subsided below 6.5%. This was lower than its earlier 7% target.

TOP INDIVIDUAL CONTRIBUTORS

During the period, two information technology companies were top performers, LinkedIn Corp. and CoStar Group, Inc. LinkedIn, the largest professional networking website, released strong earnings results throughout the year and all three of the company’s segments grew significantly faster than the overall market. CoStar Group is a leading provider of information services to the commercial real estate industry. As commercial real estate activity accelerated through the year, CoStar reported a series of strong quarterly results. The company also benefited from its 2012 acquisition of LoopNet, as synergies appear to be greater than expected.

Other strong performers during the period included health care company Actavis plc, consumer discretionary stock Tractor Supply Co. and financial services company Affiliated Managers Group, Inc. Actavis has become one of the largest generic drug companies in the world through a series of strategic acquisitions and new generic drug launches. Their most recent acquisition of Warner Chilcott was announced in May 2013 and we believe it will be accretive to earnings. We have owned Actavis for a number of years and it has grown into our largest health care holding. Tractor Supply is the largest domestic operator of retail farm and ranch stores. The company performed positively despite sizable weather challenges.

Our long-term investment in the Affiliated Managers Group, Inc. (“AMG”) made a strong contribution during the period. AMG is an asset management company providing investment management services to mutual funds, institutional clients, and high net worth individuals. Strong relative performance by the company’s affiliate investment managers led to large inflows during the period. AMG remains our largest holding in the financial services sector.

TOP INDIVIDUAL DETRACTORS

The most significant detractors from performance this period were Rackspace Hosting, Inc., Aruba Networks, Inc. and SolarWinds, Inc. Rackspace reported weak results early in 2013 due to unexpected price competition in their core web hosting market. Aruba Networks, a supplier of wireless LAN (WLAN) systems for enterprises, reported disappointing third quarter results and fourth quarter guidance due largely to delayed customer orders. SolarWinds, a provider of infrastructure management tools, reported first quarter revenue below street estimates as growth from new licenses slowed. We sold our position in these three stocks during the period.

STRATEGY & OUTLOOK

At the end of the reporting period relative to the Index, the Fund was overweight in the information technology, industrials and energy sectors while most underweight in consumer discretionary, consumer staples, materials and financials.

Our long-term investment process is unchanged as we focus on outperforming the Index with superior stock selection. We seek dynamic companies with above-average and sustainable revenue and earnings growth potential. We also continue to favor well-established, high-quality growth companies with proven management teams.

3 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

The macroeconomic environment remains characterized by modest economic expansion, slow corporate profit growth and low (albeit more volatile) interest rates. We believe this environment places a bigger premium on companies that can generate organic growth, which is a favorable backdrop for the Fund.

Investors should consider the Fund’s investment objective, risks, charges and expenses carefully before investing. The Fund’s prospectus and summary prospectus contain this and other information about the Fund, and may be obtained by asking your financial advisor or calling us at 1.800.988.8287. Read prospectuses and summary prospectuses carefully before investing.

Total returns include changes in share price and reinvestment of dividends and capital gains distributions in a hypothetical investment for the periods shown.

The Fund’s investment strategy and focus can change over time. The mention of specific fund holdings does not constitute a recommendation by OppenheimerFunds, Inc. or its affiliates.

Shares of Oppenheimer funds are not deposits or obligations of any bank, are not guaranteed by any bank, are not insured by the FDIC or any other agency, and involve investment risks, including the possible loss of the principal amount invested.

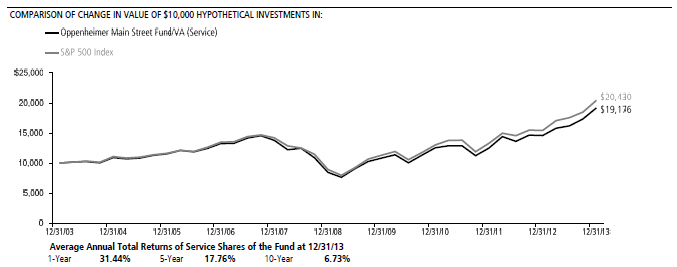

Comparing the Fund’s Performance to the Market. The graphs that follow show the performance of a hypothetical $10,000 investment in each share class of the Fund held until December 31, 2013. Performance is measured over a ten-fiscal-year period for both Classes. Performance information does not reflect charges that apply to separate accounts investing in the Fund. If these charges were taken into account, performance would be lower. The graphs assume that all dividends and capital gains distributions were reinvested in additional shares. Past performance cannot guarantee future results. The Fund’s performance is compared to the performance of the Russell Midcap Growth Index, the Russell 2500 Growth Index and the Russell 2000 Growth Index. The Russell Midcap Growth Index measures the performance of the mid-cap growth segment of the U.S. equity universe. It includes those Russell Midcap Index companies with higher price-to-book ratios and higher forecasted growth values. The Russell 2500 Growth Index measures the performance of the small to mid-cap growth segment of the U.S. equity universe. It includes those Russell 2500 Index companies with higher price-to-book ratios and higher forecasted growth values. The Russell 2000 Growth Index measures the performance of the small-cap growth segment of the U.S. equity universe. It includes those Russell 2000 Index companies with higher price-to-book ratios and higher forecasted growth values. The Fund has changed its benchmarks from the Russell Midcap Growth Index, the Russell 2500 Growth Index and the Russell 2000 Growth Index to the Russell Midcap Growth Index, which it believes is a more appropriate measure of the Fund’s performance. Indices are unmanaged and cannot be purchased directly by investors. Index performance includes reinvestment of income, but does not reflect transaction costs, fees, expenses or taxes. Index performance is shown for illustrative purposes only as a benchmark for the Fund’s performance, and does not predict or depict performance of the Fund. The Fund’s performance reflects the effects of the Fund’s business and operating expenses.

4 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

Performance data quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. For performance data current to the most recent month end, call us at 1.800.988.8287. The Fund’s total returns should not be expected to be the same as the returns of other funds, whether or not both funds have the same portfolio managers and/or similar names. The Fund’s total returns include changes in share price and reinvested distributions but do not include the charges associated with the separate account products that offer this Fund. Such performance would have been lower if such charges were taken into account.

5 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

Fund Expenses. As a shareholder of the Fund, you incur two types of costs: (1) transaction costs and (2) ongoing costs, including management fees; distribution and service fees; and other Fund expenses. These examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The examples are based on an investment of $1,000.00 invested at the beginning of the period and held for the entire 6-month period ended December 31, 2013.

Actual Expenses. The first section of the table provides information about actual account values and actual expenses. You may use the information in this section for the class of shares you hold, together with the amount you invested, to estimate the expense that you paid over the period. Simply divide your account value by $1,000.00 (for example, an $8,600.00 account value divided by $1,000.00 = 8.60), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes.

The second section of the table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio for each class of shares, and an assumed rate of return of 5% per year for each class before expenses, which is not the actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example for the class of shares you hold with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any charges associated with the separate accounts that offer this Fund. Therefore, the “hypothetical” lines of the table are useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these separate account charges were included your costs would have been higher.

| | | | | | | | | | | | | | |

| Actual | | Beginning

Account

Value

July 1, 2013 | | | Ending

Account

Value

December 31, 2013 | | | Expenses

Paid During

6 Months Ended

December 31, 2013 | | | |

Non-Service shares | | $ | 1,000.00 | | | $ | 1,226.90 | | | $ | 4.50 | | | |

Service shares | | | 1,000.00 | | | | 1,225.30 | | | | 5.85 | | | |

| | | | |

Hypothetical | | | | | | | | | | | | | | |

(5% return before expenses) | | | | | | | | | | | | | | |

Non-Service shares | | | 1,000.00 | | | | 1,021.17 | | | | 4.08 | | | |

Service shares | | | 1,000.00 | | | | 1,019.96 | | | | 5.31 | | | |

Expenses are equal to the Fund’s annualized expense ratio for that class, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). Those annualized expense ratios, excluding indirect expenses from affiliated funds, based on the 6-month period ended December 31, 2013 are as follows:

| | | | | | | | | | |

| Class | | Expense Ratios | | |

Non-Service shares | | | | 0.80 | % | | |

Service shares | | | | 1.04 | | | |

The expense ratios reflect contractual waivers and/or reimbursements of expenses by the Fund’s Manager. Some of these undertakings may be modified or terminated at any time, unless approved by the Board of Trustees. The “Financial Highlights” tables in the Fund’s financial statements, included in this report, also show the gross expense ratios, without such waivers or reimbursements and reduction to custodian expenses, if applicable.

6 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

STATEMENT OF INVESTMENTS December 31, 2013

| | | | | | | | | | |

| | | Shares | | | Value | | | |

Common Stocks—99.3% | | | | | | | |

Consumer Discretionary—21.6% | | | | | | | |

Auto Components—1.7% | | | | | | | |

| Delphi Automotive plc | | | 121,850 | | | $ | 7,326,840 | | | |

| TRW Automotive Holdings Corp.1 | | | 69,210 | | | | 5,148,532 | | | |

| | | | | | | | 12,475,372 | | | |

| Distributors—1.4% | | | |

| LKQ Corp.1 | | | 313,780 | | | | 10,323,362 | | | |

| Hotels, Restaurants & Leisure—3.5% | | | |

| Chipotle Mexican Grill, Inc.1 | | | 12,920 | | | | 6,883,518 | | | |

| Domino’s Pizza, Inc. | | | 52,320 | | | | 3,644,088 | | | |

| Dunkin’ Brands Group, Inc. | | | 159,690 | | | | 7,697,058 | | | |

| Hilton Worldwide Holdings, Inc.1 | | | 18,210 | | | | 405,172 | | | |

| Wynn Resorts Ltd. | | | 42,060 | | | | 8,168,473 | | | |

| | | | | | | | 26,798,309 | | | |

| Household Durables—1.3% | | | |

| Harman International Industries, Inc. | | | 124,680 | | | | 10,205,058 | | | |

| Internet & Catalog Retail—2.0% | | | |

| Netflix, Inc.1 | | | 26,290 | | | | 9,679,189 | | | |

| TripAdvisor, Inc.1 | | | 49,350 | | | | 4,087,660 | | | |

| zulily, inc., Cl. A1 | | | 34,230 | | | | 1,418,149 | | | |

| | | | | | | | 15,184,998 | | | |

| Leisure Equipment & Products—1.2% | | | |

| Polaris Industries, Inc. | | | 61,560 | | | | 8,965,598 | | | |

| Media—2.5% | | | |

| AMC Networks, Inc., Cl. A1 | | | 100,860 | | | | 6,869,575 | | | |

| Lions Gate Entertainment Corp. | | | 259,290 | | | | 8,209,121 | | | |

| Sinclair Broadcast Group, Inc., Cl. A | | | 100,950 | | | | 3,606,943 | | | |

| | | | | | | | 18,685,639 | | | |

| Specialty Retail—4.7% | | | |

| Conn’s, Inc.1 | | | 39,918 | | | | 3,145,139 | | | |

| GNC Holdings, Inc., Cl. A | | | 110,740 | | | | 6,472,753 | | | |

| Lumber Liquidators Holdings, Inc.1 | | | 41,120 | | | | 4,230,837 | | | |

| O’Reilly Automotive, Inc.1 | | | 43,430 | | | | 5,589,875 | | | |

| Tractor Supply Co. | | | 216,250 | | | | 16,776,675 | | | |

| | | | | | | | 36,215,279 | | | |

| Textiles, Apparel & Luxury Goods—3.3% | | | |

| Deckers Outdoor Corp.1 | | | 45,370 | | | | 3,831,950 | | | |

| Michael Kors Holdings Ltd.1 | | | 119,280 | | | | 9,684,343 | | | |

| Under Armour, Inc., Cl. A1 | | | 128,290 | | | | 11,199,717 | | | |

| | | | | | | | 24,716,010 | | | |

| Consumer Staples—4.0% | | | | | | | | | | |

| Beverages—0.7% | | | |

| Constellation Brands, Inc., Cl. A1 | | | 79,650 | | | | 5,605,767 | | | |

| Food & Staples Retailing—1.8% | | | |

| Sprouts Farmers Market, Inc.1 | | | 76,080 | | | | 2,923,754 | | | |

| Whole Foods Market, Inc. | | | 190,070 | | | | 10,991,748 | | | |

| | | | | | | | 13,915,502 | | | |

| Food Products—0.4% | | | |

| Hormel Foods Corp. | | | 74,900 | | | | 3,383,233 | | | |

| Personal Products—1.1% | | | |

| Nu Skin Enterprises, Inc., Cl. A | | | 58,208 | | | | 8,045,510 | | | |

| Energy—6.7% | | | | | | | | | | |

| Energy Equipment & Services—3.0% | | | |

| Bristow Group, Inc. | | | 46,400 | | | | 3,482,784 | | | |

| Core Laboratories NV | | | 19,320 | | | | 3,689,154 | | | |

| Dril-Quip, Inc.1 | | | 68,200 | | | | 7,497,226 | | | |

| Oceaneering International, Inc. | | | 92,590 | | | | 7,303,499 | | | |

| | | | | | | | 21,972,663 | | | |

| Oil, Gas & Consumable Fuels—3.7% | | | |

| Antero Resources Corp.1 | | | 67,330 | | | | 4,271,415 | | | |

| Cabot Oil & Gas Corp. | | | 109,060 | | | | 4,227,166 | | | |

| Concho Resources, Inc.1 | | | 36,280 | | | | 3,918,240 | | | |

| Gulfport Energy Corp.1 | | | 106,580 | | | | 6,730,527 | | | |

| Oasis Petroleum, Inc.1 | | | 188,590 | | | | 8,858,072 | | | |

| | | | | | | | 28,005,420 | | | |

| Financials—7.1% | | | | | | | | | | |

| Capital Markets—3.5% | | | |

| Affiliated Managers Group, Inc.1 | | | 66,270 | | | | 14,372,638 | | | |

| Financial Engines, Inc. | | | 123,920 | | | | 8,609,962 | | | |

| | | | | | | | | | |

| | | Shares | | | Value | | | |

| Capital Markets (Continued) | | | |

| Waddell & Reed Financial, Inc., Cl. A | | | 58,830 | | | $ | 3,831,010 | | | |

| | | | | | | | 26,813,610 | | | |

| Commercial Banks—3.1% | | | |

| First Republic Bank | | | 110,540 | | | | 5,786,769 | | | |

| Signature Bank1 | | | 92,080 | | | | 9,891,234 | | | |

| SVB Financial Group1 | | | 73,130 | | | | 7,668,412 | | | |

| | | | | | | | 23,346,415 | | | |

| Diversified Financial Services—0.5% | | | |

| MarketAxess Holdings, Inc. | | | 55,620 | | | | 3,719,309 | | | |

| Health Care—12.8% | | | | | | | | | | |

| Biotechnology—1.6% | | | |

| BioMarin Pharmaceutical, Inc.1 | | | 59,160 | | | | 4,157,173 | | | |

| Incyte Corp.1 | | | 129,490 | | | | 6,556,079 | | | |

| Pharmacyclics, Inc.1 | | | 14,840 | | | | 1,569,775 | | | |

| | | | | | | | 12,283,027 | | | |

| Health Care Equipment & Supplies—1.0% | | | |

| Align Technology, Inc.1 | | | 66,060 | | | | 3,775,329 | | | |

| Cooper Cos., Inc. (The) | | | 29,720 | | | | 3,680,525 | | | |

| | | | | | | | 7,455,854 | | | |

| Health Care Providers & Services—4.4% | | | |

| AmerisourceBergen Corp., Cl. A | | | 108,930 | | | | 7,658,868 | | | |

| Centene Corp.1 | | | 113,430 | | | | 6,686,698 | | | |

| Envision Healthcare Holdings, Inc.1 | | | 172,090 | | | | 6,112,637 | | | |

| Team Health Holdings, Inc.1 | | | 116,960 | | | | 5,327,528 | | | |

| Universal Health Services, Inc., Cl. B | | | 94,440 | | | | 7,674,194 | | | |

| | | | | | | | 33,459,925 | | | |

| Health Care Technology—1.9% | | | |

| athenahealth, Inc.1 | | | 36,470 | | | | 4,905,215 | | | |

| Cerner Corp.1 | | | 179,850 | | | | 10,024,839 | | | |

| | | | | | | | 14,930,054 | | | |

| Life Sciences Tools & Services—1.9% | | | |

| Covance, Inc.1 | | | 63,290 | | | | 5,573,317 | | | |

| Illumina, Inc.1 | | | 81,200 | | | | 8,982,344 | | | |

| | | | | | | | 14,555,661 | | | |

| Pharmaceuticals—2.0% | | | |

| Actavis plc1 | | | 67,430 | | | | 11,328,240 | | | |

| Jazz Pharmaceuticals plc1 | | | 30,160 | | | | 3,817,050 | | | |

| | | | | | | | 15,145,290 | | | |

| Industrials—18.5% | | | | | | | | | | |

| Aerospace & Defense—3.0% | | | |

| B/E Aerospace, Inc.1 | | | 137,056 | | | | 11,927,984 | | | |

| Hexcel Corp.1 | | | 249,140 | | | | 11,134,067 | | | |

| | | | | | | | 23,062,051 | | | |

| Airlines—0.7% | | | |

| Copa Holdings SA, Cl. A | | | 31,330 | | | | 5,016,246 | | | |

| Building Products—2.3% | | | |

| A.O. Smith Corp. | | | 191,720 | | | | 10,341,377 | | | |

| Fortune Brands Home & Security, Inc. | | | 151,270 | | | | 6,913,039 | | | |

| | | | | | | | 17,254,416 | | | |

| Electrical Equipment—2.4% | | | |

| Acuity Brands, Inc. | | | 71,790 | | | | 7,848,083 | | | |

| AMETEK, Inc. | | | 170,302 | | | | 8,969,806 | | | |

| SolarCity Corp.1 | | | 32,530 | | | | 1,848,355 | | | |

| | | | | | | | 18,666,244 | | | |

| Machinery—6.7% | | | |

| Colfax Corp.1 | | | 66,300 | | | | 4,222,647 | | | |

| Flowserve Corp. | | | 50,420 | | | | 3,974,609 | | | |

| Graco, Inc. | | | 56,130 | | | | 4,384,876 | | | |

| Middleby Corp. (The)1 | | | 34,730 | | | | 8,334,158 | | | |

| Pall Corp. | | | 45,590 | | | | 3,891,106 | | | |

| Pentair Ltd. | | | 82,460 | | | | 6,404,668 | | | |

| Proto Labs, Inc.1 | | | 51,090 | | | | 3,636,586 | | | |

| WABCO Holdings, Inc.1 | | | 61,310 | | | | 5,726,967 | | | |

| Wabtec Corp. | | | 153,960 | | | | 11,434,609 | | | |

| | | | | | | | 52,010,226 | | | |

| Professional Services—0.7% | | | |

| Towers Watson & Co., Cl. A | | | 44,420 | | | | 5,668,436 | | | |

| Road & Rail—1.5% | | | |

| Kansas City Southern | | | 89,430 | | | | 11,074,117 | | | |

7 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

STATEMENT OF INVESTMENTS Continued

| | | | | | | | | | |

| | | Shares | | | Value | | | |

| Trading Companies & Distributors—1.2% | | | |

| United Rentals, Inc.1 | | | 120,230 | | | $ | 9,371,928 | | | |

| Information Technology—22.6% | | | |

| Computers & Peripherals—1.3% | | | |

| Stratasys Ltd.1 | | | 71,990 | | | | 9,697,053 | | | |

| Internet Software & Services—6.5% | | | |

| Cornerstone OnDemand, Inc.1 | | | 147,140 | | | | 7,848,448 | | | |

| CoStar Group, Inc.1 | | | 70,470 | | | | 13,007,353 | | | |

| Criteo SA, Sponsored ADR1 | | | 16,810 | | | | 574,902 | | | |

| LinkedIn Corp., Cl. A1 | | | 66,170 | | | | 14,347,641 | | | |

| Pandora Media, Inc.1 | | | 192,940 | | | | 5,132,204 | | | |

| Yelp, Inc., Cl. A1 | | | 64,090 | | | | 4,419,005 | | | |

| Zillow, Inc., Cl. A1 | | | 44,190 | | | | 3,611,649 | | | |

| | | | | | | | 48,941,202 | | | |

| IT Services—2.8% | | | |

| Alliance Data Systems Corp.1 | | | 32,840 | | | | 8,634,621 | | | |

| FleetCor Technologies, Inc.1 | | | 68,170 | | | | 7,987,479 | | | |

| MAXIMUS, Inc. | | | 118,010 | | | | 5,191,260 | | | |

| | | | | | | | 21,813,360 | | | |

| Semiconductors & Semiconductor Equipment—1.7% | | | |

| NXP Semiconductors NV1 | | | 127,090 | | | | 5,837,244 | | | |

| Xilinx, Inc. | | | 143,110 | | | | 6,571,611 | | | |

| | | | | | | | 12,408,855 | | | |

| Software—10.3% | | | |

| Aspen Technology, Inc.1 | | | 215,430 | | | | 9,004,974 | | | |

| Autodesk, Inc.1 | | | 75,950 | | | | 3,822,563 | | | |

| CommVault Systems, Inc.1 | | | 106,110 | | | | 7,945,517 | | | |

| Concur Technologies, Inc.1 | | | 86,498 | | | | 8,924,864 | | | |

| FireEye, Inc.1 | | | 7,070 | | | | 308,323 | | | |

| Guidewire Software, Inc.1 | | | 116,270 | | | | 5,705,369 | | | |

| NetSuite, Inc.1 | | | 100,257 | | | | 10,328,476 | | | |

| ServiceNow, Inc.1 | | | 156,530 | | | | 8,767,245 | | | |

| Splunk, Inc.1 | | | 130,450 | | | | 8,958,001 | | | |

| Tableau Software, Inc., Cl. A1 | | | 71,100 | | | | 4,900,923 | | | |

| Ultimate Software Group, Inc. (The)1 | | | 58,800 | | | | 9,009,336 | | | |

| Workday, Inc., Cl. A1 | | | 14,570 | | | | 1,211,641 | | | |

| | | | | | | 78,887,232 | | | |

| | | | | | | | | | |

| | | Shares | | | Value | | | |

| Materials—4.6% | | | |

| Chemicals—2.5% | | | |

| Methanex Corp. | | | 58,490 | | | $ | 3,464,948 | | | |

| PolyOne Corp. | | | 108,740 | | | | 3,843,959 | | | |

| Sherwin-Williams Co. (The) | | | 21,290 | | | | 3,906,715 | | | |

| Westlake Chemical Corp. | | | 65,910 | | | | 8,045,634 | | | |

| | | | | | | | 19,261,256 | | | |

| Construction Materials—0.8% | | | |

| Eagle Materials, Inc. | | | 74,590 | | | | 5,775,504 | | | |

| Containers & Packaging—0.5% | | | |

| Rock-Tenn Co., Cl. A | | | 39,860 | | | | 4,185,699 | | | |

| Metals & Mining—0.6% | | | |

| Carpenter Technology Corp. | | | 77,790 | | | | 4,838,538 | | | |

| Paper & Forest Products—0.2% | | | |

| KapStone Paper & Packaging Corp.1 | | | 34,010 | | | | 1,899,799 | | | |

| Telecommunication Services—1.4% | | | |

| Wireless Telecommunication Services—1.4% | | | |

| SBA Communications Corp., Cl. A1 | | | 119,840 | | | | 10,766,426 | | | |

Total Common Stocks (Cost $511,038,668) | | | | 756,805,453 | | | |

| | | | | | | | | | |

| Investment Company—0.7% | | | | | | | | | | |

Oppenheimer Institutional Money Market Fund, Cl. E, 0.09%2,3 (Cost $5,136,594) | | | 5,136,594 | | | | 5,136,594 | | | |

Total Investments, at Value (Cost $516,175,262) | | | 100.0 | % | | | 761,942,047 | | | |

| Assets in Excess of Other Liabilities | | | 0.0 | | | | 12,553 | | | |

| Net Assets | | | 100.0 | % | | $ | 761,954,600 | | | |

Footnotes to Statement of Investments

1. Non-income producing security.

2. Is or was an affiliate, as defined in the Investment Company Act of 1940, at or during the period ended December 31, 2013, by virtue of the Fund owning at least 5% of the voting securities of the issuer or as a result of the Fund and the issuer having the same investment adviser. Transactions during the period in which the issuer was an affiliate are as follows:

| | | | | | | | | | | | | | | | |

| | | Shares

December 31, 2012 | | | Gross

Additions | | | Gross

Reductions | | | Shares

December 31, 2013 | |

Oppenheimer Institutional Money Market Fund, Cl. E | | | 11,313,011 | | | | 276,502,708 | | | | 282,679,125 | | | | 5,136,594 | |

| | | | |

| | | | | | | | | Value | | | Income | |

Oppenheimer Institutional Money Market Fund, Cl. E | | | | | | | | | | $ | 5,136,594 | | | $ | 9,846 | |

3. Rate shown is the 7-day yield as of December 31, 2013.

See accompanying Notes to Financial Statements.

8 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

| | |

STATEMENT OF ASSETS AND LIABILITIES December 31, 2013 |

| | | | |

Assets | | | | |

Investments, at value—see accompanying statement of investments: | | | | |

Unaffiliated companies (cost $511,038,668) | | $ | 756,805,453 | |

Affiliated companies (cost $5,136,594) | | | 5,136,594 | |

| | | | 761,942,047 | |

Cash | | | 1,000 | |

Receivables and other assets: | | | | |

Investments sold | | | 1,429,635 | |

Shares of beneficial interest sold | | | 198,255 | |

Dividends | | | 61,668 | |

Expense waivers/reimbursements due from manager | | | 1,890 | |

Other | | | 40,778 | |

Total assets | | | 763,675,273 | |

|

| |

Liabilities | | | | |

Payables and other liabilities: | | | | |

Shares of beneficial interest redeemed | | | 1,567,057 | |

Transfer and shareholder servicing agent fees | | | 63,294 | |

Trustees’ compensation | | | 36,274 | |

Shareholder communications | | | 23,877 | |

Distribution and service plan fees | | | 7,911 | |

Other | | | 22,260 | |

Total liabilities | | | 1,720,673 | |

|

| | |

Net Assets | | $ | 761,954,600 | |

|

| |

Composition of Net Assets | | | | |

Par value of shares of beneficial interest | | $ | 10,242 | |

Additional paid-in capital | | | 568,484,820 | |

Accumulated net investment loss | | | (53,163 | ) |

Accumulated net realized loss on investments | | | (52,254,084 | ) |

Net unrealized appreciation on investments | | | 245,766,785 | |

Net Assets | | $ | 761,954,600 | |

|

| |

Net Asset Value Per Share | | | | |

Non-Service Shares: | | | | |

| Net asset value, redemption price (excludes applicable contingent deferred sales charge) and offering price per share (based on net assets of $725,405,735 and 9,735,984 shares of beneficial interest outstanding) | | | $74.51 | |

| |

Service Shares: | | | | |

| Net asset value, redemption price (excludes applicable contingent deferred sales charge) and offering price per share (based on net assets of $36,548,865 and 506,059 shares of beneficial interest outstanding) | | | $72.22 | |

See accompanying Notes to Financial Statements.

9 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

| | |

STATEMENT OF OPERATIONS For the Year Ended December 31, 2013 |

| | | | |

Investment Income | | | | |

Dividends: | | | | |

Unaffiliated companies (net of foreign withholding taxes of $3,700) | | $ | 3,648,538 | |

Affiliated companies | | | 9,846 | |

Interest | | | 29 | |

Total investment income | | | 3,658,413 | |

|

| | |

Expenses | | | | |

Management fees | | | 4,677,970 | |

Distribution and service plan fees - Service shares | | | 90,237 | |

Transfer and shareholder servicing agent fees: | | | | |

Non-Service shares | | | 618,393 | |

Service shares | | | 35,848 | |

Shareholder communications: | | | | |

Non-Service shares | | | 90,520 | |

Service shares | | | 5,063 | |

Custodian fees and expenses | | | 3,696 | |

Trustees’ compensation | | | 35,577 | |

Other | | | 57,919 | |

Total expenses | | | 5,615,223 | |

Less waivers and reimbursements of expenses | | | (267,471 | ) |

Net expenses | | | 5,347,752 | |

|

| | |

Net Investment Loss | | | (1,689,339 | ) |

|

| | |

Realized and Unrealized Gain | | | | |

Net realized gain on investments from unaffiliated companies | | | 122,245,177 | |

Net change in unrealized appreciation/depreciation on investments | | | 79,850,119 | |

|

| | |

Net Increase in Net Assets Resulting from Operations | | $ | 200,405,957 | |

See accompanying Notes to Financial Statements.

10 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

| | |

STATEMENTS OF CHANGES IN NET ASSETS |

| | | | | | | | | | |

| | | Year Ended

December 31, 2013 | | | | | Year Ended

December 31, 2012 | |

Operations | | | | | | | | | | |

Net investment income (loss) | | $ | (1,689,339) | | | | | $ | 65,784 | |

Net realized gain | | | 122,245,177 | | | | | | 50,857,244 | |

Net change in unrealized appreciation/depreciation | | | 79,850,119 | | | | | | 42,312,507 | |

Net increase in net assets resulting from operations | | | 200,405,957 | | | | | | 93,235,535 | |

|

| |

Dividends and/or Distributions to Shareholders | | | | | | | | | | |

Dividends from net investment income: | | | | | | | | | | |

Non-Service shares | | | (73,101) | | | | | | — | |

Service shares | | | — | | | | | | — | |

| | | (73,101) | | | | | | — | |

|

| |

Beneficial Interest Transactions | | | | | | | | | | |

Net increase (decrease) in net assets resulting from beneficial interest transactions: | | | | | | | | | | |

Non-Service shares | | | (22,913,255) | | | | | | (71,703,483 | ) |

Service shares | | | (10,340,669) | | | | | | (5,448,961 | ) |

| | | (33,253,924) | | | | | | (77,152,444 | ) |

|

| |

Net Assets | | | | | | | | | | |

Total increase | | | 167,078,932 | | | | | | 16,083,091 | |

Beginning of period | | | 594,875,668 | | | | | | 578,792,577 | |

| | | |

End of period (including accumulated net investment income (loss) of $(53,163) and $42,730, respectively) | | $ | 761,954,600 | | | | | $ | 594,875,668 | |

See accompanying Notes to Financial Statements.

11 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

| | | | | | | | | | | | | | | | | | | | |

Non-Service Shares | |

| Year Ended

December

31, 2013 |

| |

| Year Ended

December

31, 2012 |

| |

| Year Ended

December

30, 2011 |

1 | |

| Year Ended

December

31, 2010 |

| |

| Year Ended

December

31, 2009 |

|

Per Share Operating Data | | | | | | | | | | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 54.80 | | | $ | 47.06 | | | $ | 46.55 | | | $ | 36.52 | | | $ | 27.54 | |

Income (loss) from investment operations: | | | | | | | | | | | | | | | | | | | | |

Net investment income (loss)2 | | | (0.16 | ) | | | 0.01 | | | | (0.26 | ) | | | (0.11 | ) | | | (0.05 | ) |

Net realized and unrealized gain | | | 19.88 | | | | 7.73 | | | | 0.77 | | | | 10.14 | | | | 9.03 | |

Total from investment operations | | | 19.72 | | | | 7.74 | | | | 0.51 | | | | 10.03 | | | | 8.98 | |

Dividends and/or distributions to shareholders: | | | | | | | | | | | | | | | | | | | | |

Dividends from net investment income | | | (0.01 | ) | | | 0.00 | | | | 0.00 | | | | 0.00 | | | | 0.00 | |

Net asset value, end of period | | $ | 74.51 | | | $ | 54.80 | | | $ | 47.06 | | | $ | 46.55 | | | $ | 36.52 | |

| | | | | |

| | | | | | | | | | | | | | | | | | | | | |

Total Return, at Net Asset Value3 | | | 35.98% | | | | 16.45% | | | | 1.09% | | | | 27.46% | | | | 32.61% | |

| | | | | | | | | | | | | | | | | | | | | |

Ratios/Supplemental Data | | | | | | | | | | | | | | | | | | | | |

Net assets, end of period (in thousands) | | $ | 725,406 | | | $ | 558,934 | | | $ | 543,020 | | | $ | 611,872 | | | $ | 547,683 | |

Average net assets (in thousands) | | $ | 618,970 | | | $ | 575,072 | | | $ | 605,083 | | | $ | 548,739 | | | $ | 478,968 | |

Ratios to average net assets:4 | | | | | | | | | | | | | | | | | | | | |

Net investment income (loss) | | | (0.24)% | | | | 0.03% | | | | (0.53)% | | | | (0.29)% | | | | (0.17)% | |

Total expenses5 | | | 0.84% | | | | 0.85% | | | | 0.84% | | | | 0.85% | | | | 0.86% | |

| Expenses after payments, waivers and/or reimbursements and reduction to custodian expenses | | | 0.80% | | | | 0.80% | | | | 0.80% | | | | 0.76% | | | | 0.71% | |

Portfolio turnover rate | | | 84% | | | | 66% | | | | 91% | | | | 95% | | | | 102% | |

1. December 30, 2011 represents the last business day of the Fund’s reporting period.

2. Per share amounts calculated based on the average shares outstanding during the period.

3. Assumes an initial investment on the business day before the first day of the fiscal period, with all dividends and distributions reinvested in additional shares on the reinvestment date, and redemption at the net asset value calculated on the last business day of the fiscal period. Total returns are not annualized for periods less than one full year. Total return information does not reflect expenses that apply at the separate account level or to related insurance products. Inclusion of these charges would reduce the total return figures for all periods shown. Returns do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

4. Annualized for periods less than one full year.

5. Total expenses including indirect expenses from affiliated fund were as follows:

| | | | |

Year Ended December 31, 2013 | | | 0.84 | % |

Year Ended December 31, 2012 | | | 0.85 | % |

Year Ended December 30, 2011 | | | 0.84 | % |

Year Ended December 31, 2010 | | | 0.85 | % |

Year Ended December 31, 2009 | | | 0.86 | % |

See accompanying Notes to Financial Statements.

12 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

| | | | | | | | | | | | | | | | | | | | |

Service Shares | |

| Year Ended

December

31, 2013 |

| |

| Year Ended

December

31, 2012 |

| |

| Year Ended

December

30, 2011 |

1 | |

| Year Ended

December

31, 2010 |

| |

| Year Ended

December

31, 2009 |

|

Per Share Operating Data | | | | | | | | | | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 53.25 | | | $ | 45.84 | | | $ | 45.46 | | | $ | 35.75 | | | $ | 27.03 | |

Income (loss) from investment operations: | | | | | | | | | | | | | | | | | | | | |

Net investment loss2 | | | (0.30 | ) | | | (0.12 | ) | | | (0.37 | ) | | | (0.20 | ) | | | (0.13 | ) |

Net realized and unrealized gain | | | 19.27 | | | | 7.53 | | | | 0.75 | | | | 9.91 | | | | 8.85 | |

Total from investment operations | | | 18.97 | | | | 7.41 | | | | 0.38 | | | | 9.71 | | | | 8.72 | |

Dividends and/or distributions to shareholders: | | | | | | | | | | | | | | | | | | | | |

Dividends from net investment income | | | 0.00 | | | | 0.00 | | | | 0.00 | | | | 0.00 | | | | 0.00 | |

Net asset value, end of period | | $ | 72.22 | | | $ | 53.25 | | | $ | 45.84 | | | $ | 45.46 | | | $ | 35.75 | |

| | | | | |

| | | | | | | | | | | | | | | | | | | | | |

Total Return, at Net Asset Value3 | | | 35.62% | | | | 16.17% | | | | 0.83% | | | | 27.16% | | | | 32.26% | |

| | | | | | | | | | | | | | | | | | | | | |

Ratios/Supplemental Data | | | | | | | | | | | | | | | | | | | | |

Net assets, end of period (in thousands) | | $ | 36,549 | | | $ | 35,942 | | | $ | 35,773 | | | $ | 32,669 | | | $ | 26,098 | |

Average net assets (in thousands) | | $ | 35,905 | | | $ | 37,842 | | | $ | 37,775 | | | $ | 27,552 | | | $ | 22,605 | |

Ratios to average net assets:4 | | | | | | | | | | | | | | | | | | | | |

Net investment loss | | | (0.49)% | | | | (0.22)% | | | | (0.78)% | | | | (0.53)% | | | | (0.44)% | |

Total expenses5 | | | 1.09% | | | | 1.10% | | | | 1.09% | | | | 1.10% | | | | 1.12% | |

| Expenses after payments, waivers and/or reimbursements and reduction to custodian expenses | | | 1.05% | | | | 1.05% | | | | 1.05% | | | | 1.01% | | | | 0.97% | |

Portfolio turnover rate | | | 84% | | | | 66% | | | | 91% | | | | 95% | | | | 102% | |

1. December 30, 2011 represents the last business day of the Fund’s reporting period.

2. Per share amounts calculated based on the average shares outstanding during the period.

3. Assumes an initial investment on the business day before the first day of the fiscal period, with all dividends and distributions reinvested in additional shares on the reinvestment date, and redemption at the net asset value calculated on the last business day of the fiscal period. Total returns are not annualized for periods less than one full year. Total return information does not reflect expenses that apply at the separate account level or to related insurance products. Inclusion of these charges would reduce the total return figures for all periods shown. Returns do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

4. Annualized for periods less than one full year.

5. Total expenses including indirect expenses from affiliated fund were as follows:

| | | | |

Year Ended December 31, 2013 | | | 1.09 | % |

Year Ended December 31, 2012 | | | 1.10 | % |

Year Ended December 30, 2011 | | | 1.09 | % |

Year Ended December 31, 2010 | | | 1.10 | % |

Year Ended December 31, 2009 | | | 1.12 | % |

See accompanying Notes to Financial Statements.

13 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

| | |

NOTES TO FINANCIAL STATEMENTS December 31, 2013 |

1. Significant Accounting Policies

Oppenheimer Discovery Mid-Cap Growth Fund/VA (the “Fund”), formerly Oppenheimer Small- & Mid-Cap Growth Fund/VA, is a separate series of Oppenheimer Variable Account Funds, as a diversified open-end management investment company registered under the Investment Company Act of 1940, as amended. The Fund’s investment objective is to seek capital appreciation. The Fund’s investment adviser is OFI Global Asset Management, Inc. (“OFI Global” or the “Manager”), a wholly-owned subsidiary of OppenheimerFunds Inc. (“OFI” or the “Sub-Adviser”). The Manager has entered into a sub-advisory agreement with OFI. Shares of the Fund are sold only to separate accounts of life insurance companies.

The Fund offers two classes of shares. Both classes are sold at their offering price, which is the net asset value per share, to separate investment accounts of participating insurance companies as an underlying investment for variable life insurance policies, variable annuity contracts or other investment products. The class of shares designated as Service shares is subject to a distribution and service plan. Both classes of shares have identical rights and voting privileges with respect to the Fund in general and exclusive voting rights on matters that affect that class alone. Earnings, net assets and net asset value per share may differ due to each class having its own expenses, such as transfer and shareholder servicing agent fees and shareholder communications, directly attributable to that class.

The following is a summary of significant accounting policies consistently followed by the Fund.

Investment in Oppenheimer Institutional Money Market Fund. The Fund is permitted to invest daily available cash balances in an affiliated money market fund. The Fund may invest the available cash in Class E shares of Oppenheimer Institutional Money Market Fund (“IMMF”) to seek current income while preserving liquidity. IMMF is a registered open-end management investment company, regulated as a money market fund under the Investment Company Act of 1940, as amended. The Manager is the investment adviser of IMMF, and the Sub-Adviser provides investment and related advisory services to IMMF. When applicable, the Fund’s investment in IMMF is included in the Statement of Investments. Shares of IMMF are valued at their net asset value per share. As a shareholder, the Fund is subject to its proportional share of IMMF’s Class E expenses, including its management fee. The Manager will waive fees and/or reimburse Fund expenses in an amount equal to the indirect management fees incurred through the Fund’s investment in IMMF.

Allocation of Income, Expenses, Gains and Losses. Income, expenses (other than those attributable to a specific class), gains and losses are allocated on a daily basis to each class of shares based upon the relative proportion of net assets represented by such class. Operating expenses directly attributable to a specific class are charged against the operations of that class.

Federal Taxes. The Fund intends to comply with provisions of the Internal Revenue Code applicable to regulated investment companies and to distribute substantially all of its investment company taxable income, including any net realized gain on investments not offset by capital loss carryforwards, if any, to shareholders. Therefore, no federal income or excise tax provision is required. The Fund files income tax returns in U.S. federal and applicable state jurisdictions. The statute of limitations on the Fund’s tax return filings generally remain open for the three preceding fiscal reporting period ends.

The tax components of capital shown in the following table represent distribution requirements the Fund must satisfy under the income tax regulations, losses the Fund may be able to offset against income and gains realized in future years and unrealized appreciation or depreciation of securities and other investments for federal income tax purposes.

| | | | | | | | | | | | | | |

Undistributed

Net Investment

Income | | | | Undistributed

Long-Term

Gain | | | Accumulated

Loss

Carryforward1,2,3,4 | | | Net Unrealized

Appreciation

Based on cost of

Securities and

Other Investments

for Federal Income

Tax Purposes | |

$— | | | | | $— | | | | $52,017,743 | | | | $245,530,435 | |

1. As of December 31, 2013, the Fund had $50,885,832 of net capital loss carryforwards available to offset future realized capital gains, if any, and thereby reduce future taxable gain distributions. Details of the capital loss carryforwards are included in the table below. Capital loss carryovers with no expiration, if any, must be utilized prior to those with expiration dates.

| | | | |

| Expiring | | | |

2017 | | | $50,885,832 | |

2. As of December 31, 2013, the Fund had $1,131,911 of post-October losses available to offset future realized capital gains, if any.

3. During the fiscal year ended December 31, 2013, the Fund utilized $121,849,981 of capital loss carryforward to offset capital gains realized in that fiscal year.

4. During the fiscal year ended December 31, 2012, the Fund utilized $44,334,654 of capital loss carryforward to offset capital gains realized in that fiscal year.

Net investment income (loss) and net realized gain (loss) may differ for financial statement and tax purposes. The character of dividends and distributions made during the fiscal year from net investment income or net realized gains may differ from their ultimate characterization for federal income tax purposes. Also, due to timing of dividends and distributions, the fiscal year in which amounts are distributed may differ from the fiscal year in which the income or net realized gain was recorded by the Fund.

Accordingly, the following amounts have been reclassified for December 31, 2013. Net assets of the Fund were unaffected by the reclassifications.

14 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

1. Significant Accounting Policies (Continued)

| | | | |

Reduction to Paid-in Capital | | Reduction

to Accumulated

Net Investment

Loss | |

$1,666,547 | | | $1,666,547 | |

The tax character of distributions paid during the years ended December 31, 2013 and December 31, 2012 was as follows:

| | | | | | | | |

| | | Year Ended

December 31, 2013 | | | Year Ended

December 31, 2012 | |

Distributions paid from: | | | | | | | | |

Ordinary income | | $ | 73,101 | | | $ | — | |

The aggregate cost of securities and other investments and the composition of unrealized appreciation and depreciation of securities and other investments for federal income tax purposes as of December 31, 2013 are noted in the following table. The primary difference between book and tax appreciation or depreciation of securities and other investments, if applicable, is attributable to the tax deferral of losses or tax realization of financial statement unrealized gain or loss.

| | | | |

Federal tax cost of securities | | $ | 516,411,612 | |

| | | | |

Gross unrealized appreciation | | $ | 246,805,712 | |

Gross unrealized depreciation | | | (1,275,277) | |

| | | | |

Net unrealized appreciation | | $ | 245,530,435 | |

| | | | |

Trustees’ Compensation. The Board of Trustees has adopted a compensation deferral plan for independent trustees that enables trustees to elect to defer receipt of all or a portion of the annual compensation they are entitled to receive from the Fund. For purposes of determining the amount owed to the Trustee under the plan, deferred amounts are treated as though equal dollar amounts had been invested in shares of the Fund or in other Oppenheimer funds selected by the Trustee. The Fund purchases shares of the funds selected for deferral by the Trustee in amounts equal to his or her deemed investment, resulting in a Fund asset equal to the deferred compensation liability. Such assets are included as a component of “Other” within the asset section of the Statement of Assets and Liabilities. Deferral of trustees’ fees under the plan will not affect the net assets of the Fund, and will not materially affect the Fund’s assets, liabilities or net investment income per share. Amounts will be deferred until distributed in accordance with the compensation deferral plan.

Dividends and Distributions to Shareholders. Dividends and distributions to shareholders, which are determined in accordance with income tax regulations and may differ from U.S. generally accepted accounting principles, are recorded on the ex-dividend date. Income and capital gain distributions, if any, are declared and paid annually or at other times as deemed necessary by the Manager.

Investment Income. Dividend income is recorded on the ex-dividend date or upon ex-dividend notification in the case of certain foreign dividends where the ex-dividend date may have passed. Non-cash dividends included in dividend income, if any, are recorded at the fair market value of the securities received. Interest income is recognized on an accrual basis. Discount and premium, which are included in interest income on the Statement of Operations, are amortized or accreted daily.

Custodian Fees. “Custodian fees and expenses” in the Statement of Operations may include interest expense incurred by the Fund on any cash overdrafts of its custodian account during the period. Such cash overdrafts may result from the effects of failed trades in portfolio securities and from cash outflows resulting from unanticipated shareholder redemption activity. The Fund pays interest to its custodian on such cash overdrafts, to the extent they are not offset by positive cash balances maintained by the Fund, at a rate equal to the Federal Funds Rate plus 0.50%. The “Reduction to custodian expenses” line item, if applicable, represents earnings on cash balances maintained by the Fund during the period. Such interest expense and other custodian fees may be paid with these earnings.

Security Transactions. Security transactions are recorded on the trade date. Realized gains and losses on securities sold are determined on the basis of identified cost.

Indemnifications. The Fund’s organizational documents provide current and former trustees and officers with a limited indemnification against liabilities arising in connection with the performance of their duties to the Fund. In the normal course of business, the Fund may also enter into contracts that provide general indemnifications. The Fund’s maximum exposure under these arrangements is unknown as this would be dependent on future claims that may be made against the Fund. The risk of material loss from such claims is considered remote.

Other. The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and

15 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

| | |

NOTES TO FINANCIAL STATEMENTS Continued |

1. Significant Accounting Policies (Continued)

liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

2. Securities Valuation

The Fund calculates the net asset value of its shares as of the close of the New York Stock Exchange (the “Exchange”), normally 4:00 P.M. Eastern time, on each day the Exchange is open for trading.

The Fund’s Board has adopted procedures for the valuation of the Fund’s securities and has delegated the day-to-day responsibility for valuation determinations under those procedures to the Manager. The Manager has established a Valuation Committee which is responsible for determining a “fair valuation” for any security for which market quotations are not “readily available.” The Valuation Committee’s fair valuation determinations are subject to review, approval and ratification by the Fund’s Board at its next regularly scheduled meeting covering the calendar quarter in which the fair valuation was determined.

Valuation Methods and Inputs

Securities are valued using unadjusted quoted market prices, when available, as supplied primarily by third party pricing services or dealers.

The following methodologies are used to determine the market value or the fair value of the types of securities described below:

Securities traded on a registered U.S. securities exchange (including exchange-traded derivatives other than futures and futures options) are valued based on the last sale price of the security reported on the principal exchange on which it is traded, prior to the time when the Fund’s assets are valued. In the absence of a sale, the security is valued at the last sale price on the prior trading day, if it is within the spread of the current day’s closing “bid” and “asked” prices, and if not, at the current day’s closing bid price. A security of a foreign issuer traded on a foreign exchange, but not listed on a registered U.S. securities exchange, is valued based on the last sale price on the principal exchange on which the security is traded, as identified by the third party pricing service used by the Manager, prior to the time when the Fund’s assets are valued. If the last sale price is unavailable, the security is valued at the most recent official closing price on the principal exchange on which it is traded. If the last sales price or official closing price for a foreign security is not available, the security is valued at the mean between the bid and asked price per the exchange or, if not available from the exchange, obtained from two dealers. If bid and asked prices are not available from either the exchange or two dealers, the security is valued by using one of the following methodologies (listed in order of priority); (1) using a bid from the exchange, (2) the mean between the bid and asked price as provided by a single dealer, or (3) a bid from a single dealer.

Shares of a registered investment company that are not traded on an exchange are valued at that investment company’s net asset value per share.

Corporate and government debt securities (of U.S. or foreign issuers) and municipal debt securities, event-linked bonds, loans, mortgage-backed securities, collateralized mortgage obligations, and asset-backed securities are valued at the mean between the “bid” and “asked” prices utilizing evaluated prices obtained from third party pricing services or broker-dealers who may use matrix pricing methods to determine the evaluated prices.

Short-term money market type debt securities with a remaining maturity of sixty days or less are valued at cost adjusted by the amortization of discount or premium to maturity (amortized cost), which approximates market value. Short-term debt securities with a remaining maturity in excess of sixty days are valued at the mean between the “bid” and “asked” prices utilizing evaluated prices obtained from third party pricing services or broker-dealers.

A description of the standard inputs that may generally be considered by the third party pricing vendors in determining their evaluated prices is provided below.

| | |

| Security Type | | Standard inputs generally considered by third-party pricing vendors |

| Corporate debt, government debt, municipal, mortgage-backed and asset-backed securities | | Reported trade data, broker-dealer price quotations, benchmark yields, issuer spreads on comparable securities, the credit quality, yield, maturity, and other appropriate factors. |

| Loans | | Information obtained from market participants regarding reported trade data and broker-dealer price quotations. |

| Event-linked bonds | | Information obtained from market participants regarding reported trade data and broker-dealer price quotations. |

If a market value or price cannot be determined for a security using the methodologies described above, or if, in the “good faith” opinion of the Manager, the market value or price obtained does not constitute a “readily available market quotation,” or a significant event has occurred that would materially affect the value of the security the security is fair valued either (i) by a standardized fair valuation methodology applicable to the security type or the significant event as previously approved by the Valuation Committee and the Fund’s Board or (ii) as determined in good faith by the Manager’s Valuation Committee. The Valuation Committee considers all relevant facts that are reasonably available, through either public information or information available to the Manager, when determining the fair value of a security. Fair value determinations by the Manager are subject to review, approval and ratification by the Fund’s Board at its next regularly scheduled meeting covering the calendar quarter in which the fair valuation was determined. Those fair valuation standardized methodologies include, but are not limited to, valuing securities at the last sale price or initially at cost and subsequently adjusting the value based on: changes in company specific fundamentals, changes in an appropriate securities index, or changes in the value of similar securities which may be further adjusted for any discounts related to security-specific resale restrictions. When possible, such methodologies use observable market inputs such as unadjusted quoted prices of similar securities, observable interest rates, currency rates and yield

16 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

2. Securities Valuation

curves. The methodologies used for valuing securities are not necessarily an indication of the risks associated with investing in those securities nor can it be assured that the Fund can obtain the fair value assigned to a security if it were to sell the security.

To assess the continuing appropriateness of security valuations, the Manager, or its third party service provider who is subject to oversight by the Manager, regularly compares prior day prices, prices on comparable securities, and sale prices to the current day prices and challenges those prices exceeding certain tolerance levels with the third party pricing service or broker source. For those securities valued by fair valuations, whether through a standardized fair valuation methodology or a fair valuation determination, the Valuation Committee reviews and affirms the reasonableness of the valuations based on such methodologies and fair valuation determinations on a regular basis after considering all relevant information that is reasonably available.

Classifications

Each investment asset or liability of the Fund is assigned a level at measurement date based on the significance and source of the inputs to its valuation. Various data inputs are used in determining the value of each of the Fund’s investments as of the reporting period end. These data inputs are categorized in the following hierarchy under applicable financial accounting standards:

1) Level 1-unadjusted quoted prices in active markets for identical assets or liabilities (including securities actively traded on a securities exchange)

2) Level 2-inputs other than unadjusted quoted prices that are observable for the asset or liability (such as unadjusted quoted prices for similar assets and market corroborated inputs such as interest rates, prepayment speeds, credit risks, etc.)

3) Level 3-significant unobservable inputs (including the Manager’s own judgments about assumptions that market participants would use in pricing asset or liability).

The inputs used for valuing securities are not necessarily an indication of the risks associated with investing in those securities.

The table below categorizes amounts that are included in the Fund’s Statement of Assets and Liabilities as of December 31, 2013 based on valuation input level:

| | | | | | | | | | | | | | | | |

| | | Level 1—

Unadjusted

Quoted Prices | | | Level 2—

Other Significant

Observable Inputs | | | Level 3—

Significant

Unobservable

Inputs | | | Value | |

Assets Table | | | | | | | | | | | | | | | | |

Investments, at Value: | | | | | | | | | | | | | | | | |

Common Stocks | | | | | | | | | | | | | | | | |

Consumer Discretionary | | $ | 163,569,625 | | | $ | — | | | $ | — | | | $ | 163,569,625 | |

Consumer Staples | | | 30,950,012 | | | | — | | | | — | | | | 30,950,012 | |

Energy | | | 49,978,083 | | | | — | | | | — | | | | 49,978,083 | |

Financials | | | 53,879,334 | | | | — | | | | — | | | | 53,879,334 | |

Health Care | | | 97,829,811 | | | | — | | | | — | | | | 97,829,811 | |

Industrials | | | 142,123,664 | | | | — | | | | — | | | | 142,123,664 | |

Information Technology | | | 171,747,702 | | | | — | | | | — | | | | 171,747,702 | |

Materials | | | 35,960,796 | | | | — | | | | — | | | | 35,960,796 | |

Telecommunication Services | | | 10,766,426 | | | | — | | | | — | | | | 10,766,426 | |

Investment Company | | | 5,136,594 | | | | — | | | | — | | | | 5,136,594 | |

| | | | |

Total Assets | | $ | 761,942,047 | | | $ | — | | | $ | — | | | $ | 761,942,047 | |

| | | | |

Currency contracts and forwards, if any, are reported at their unrealized appreciation/ depreciation at measurement date, which represents the change in the contract’s value from trade date. Futures, if any, are reported at their variation margin at measurement date, which represents the amount due to/from the Fund at that date. All additional assets and liabilities included in the above table are reported at their market value at measurement date.

3. Shares of Beneficial Interest

The Fund has authorized an unlimited number of $0.001 par value shares of beneficial interest of each class. Transactions in shares of beneficial interest were as follows:

| | | | | | | | | | | | | | | | | | | | |

| | | Year Ended December 31, 2013 | | | | | Year Ended December 31, 2012 | | | |

| | | Shares | | | Amount | | | | | Shares | | | Amount | | | |

Non-Service Shares | | | | | | | | | | | | | | | | | | | | |

Sold | | | 1,267,875 | | | $ | 87,221,834 | | | | | | 424,674 | | | $ | 22,730,798 | | | |

Dividends and/or distributions reinvested | | | 1,176 | | | | 73,101 | | | | | | — | | | | — | | | |

Redeemed | | | (1,732,026 | ) | | | (110,208,190 | ) | | | | | (1,765,118 | ) | | | (94,434,281) | | | |

| | | |

Net decrease | | | (462,975 | ) | | $ | (22,913,255) | | | | | | (1,340,444) | | | $ | (71,703,483) | | | |

| | | |

| | | | | | | | | | | | | | | | | | | | |

Service Shares | | | | | | | | | | | | | | | | | | | | |

Sold | | | 78,939 | | | $ | 4,862,175 | | | | | | 138,098 | | | $ | 7,173,273 | | | |

Redeemed | | | (247,872 | ) | | | (15,202,844 | ) | | | | | (243,546 | ) | | | (12,622,234 | ) | | |

| | | |

Net decrease | | | (168,933 | ) | | $ | (10,340,669 | ) | | | | | (105,448 | ) | | $ | (5,448,961 | ) | | |

| | | |

17 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

| | |

NOTES TO FINANCIAL STATEMENTS Continued |

4. Purchases and Sales of Securities

The aggregate cost of purchases and proceeds from sales of securities, other than short-term obligations and investments in IMMF, for the year ended December 31, 2013 were as follows:

| | | | | | | | | | |

| | | Purchases | | | | | Sales | |

Investment securities | | | $542,669,332 | | | | | | $566,489,270 | |

5. Fees and Other Transactions with Affiliates

Management Fees. Under the investment advisory agreement, the Fund pays the Manager a management fee based on the daily net assets of the Fund at an annual rate as shown in the following table:

| | | | |

| Fee Schedule | | | |

Up to $200 million | | | 0.75% | |

Next $200 million | | | 0.72 | |

Next $200 million | | | 0.69 | |

Next $200 million | | | 0.66 | |

Next $700 million | | | 0.60 | |

Over $1.5 billion | | | 0.58 | |

Sub-Adviser Fees. The Manager has retained the Sub-Adviser to provide the day-to-day portfolio management of the Fund. Under the Sub-Advisory Agreement, the Manager pays the Sub-Adviser an annual fee in monthly installments, equal to a percentage of the investment management fee collected by the Manager from the Fund, which shall be calculated after any investment management fee waivers. The fee paid to the Sub-Adviser is paid by the Manager, not by the Fund.

Transfer Agent Fees. OFI Global (the “Transfer Agent”) serves as the transfer and shareholder servicing agent for the Fund. Fees incurred by the Fund with respect to these services are detailed in the Statement of Operations.

Sub-Transfer Agent Fees. The Transfer Agent has retained Shareholder Services, Inc., a wholly-owned subsidiary of OFI (the “Sub-Transfer Agent”), to provide the day-to-day transfer agent and shareholder servicing of the Fund. Under the Sub-Transfer Agency Agreement, the Transfer Agent pays the Sub-Transfer Agent an annual fee in monthly installments, equal to a percentage of the transfer agent fee collected by the Transfer Agent from the Fund, which shall be calculated after any applicable fee waivers. The fee paid to the Sub-Transfer Agent is paid by the Transfer Agent, not by the Fund.

Distribution and Service Plan for Service Shares. The Fund has adopted a Distribution and Service Plan (the “Plan”) in accordance with Rule 12b-1 under the Investment Company Act of 1940 for Service shares to pay OppenheimerFunds Distributor, Inc. (the “Distributor”), for distribution related services, personal service and account maintenance for the Fund’s Service shares. Under the Plan, payments are made periodically at an annual rate of 0.25% of the daily net assets of Service shares of the Fund. The Distributor currently uses all of those fees to compensate sponsors of the insurance product that offers Fund shares, for providing personal service and maintenance of accounts of their variable contract owners that hold Service shares. These fees are paid out of the Fund’s assets on an on-going basis and increase operating expenses of the Service shares, which results in lower performance compared to the Fund’s shares that are not subject to a service fee. Fees incurred by the Fund under the Plan are detailed in the Statement of Operations.

Waivers and Reimbursements of Expenses. The Manager has contractually agreed to limit the Fund’s expenses after payments, waivers and/or reimbursements and reduction to custodian expenses, excluding expenses incurred directly or indirectly by the Fund as a result of investments in other investment companies, wholly-owned subsidiaries and pooled investment vehicles; so that those expenses, as percentages of daily net assets, will not exceed the annual rate of 0.80% for Non-Service shares and 1.05% for Service shares. During the year ended December 31, 2013, the Manager waived fees and/or reimbursed the Fund $243,578 and $15,480 for Non-Service and Service shares, respectively.

The Manager will waive fees and/or reimburse Fund expenses in an amount equal to the indirect management fees incurred through the Fund’s investment in IMMF. During the year ended December 31, 2013, the Manager waived fees and/or reimbursed the Fund $8,413 for IMMF management fees.

Some of these undertakings may be modified or terminated at any time; some may not be modified or terminated until after one year from the date of the current prospectus, as indicated therein.

6. Pending Litigation

Since 2009, seven class action lawsuits have been pending in the U.S. District Court for the District of Colorado against OppenheimerFunds, Inc. (“OFI”), OppenheimerFunds Distributor, Inc., the Fund’s principal underwriter and distributor (the “Distributor”), and certain funds (but not including the Fund) advised by OFI Global Asset Management, Inc. and distributed by the Distributor (the “Defendant Funds”). The lawsuits also name as defendants certain officers and current and former trustees of the respective Defendant Funds. The lawsuits raise claims under federal securities law and allege, among other things, that the disclosure documents of the respective Defendant Funds contained misrepresentations and omissions and that the respective Defendant Funds’ investment policies were not followed. The plaintiffs in these actions seek unspecified damages, equitable relief and awards of attorneys’ fees and litigation expenses. The Defendant Funds’ Boards of Trustees have also engaged counsel to represent the Funds and the present and

18 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

6. Pending Litigation (Continued)

former Independent Trustees named in those suits. On August 26, 2013, the parties in six of these lawsuits executed a memorandum of understanding setting forth the terms of proposed settlements of those actions. The proposed settlements are subject to a variety of contingencies, including the execution of settlement agreements, which will require preliminary and final approval by the court. The proposed settlements do not resolve a seventh outstanding lawsuit relating to Oppenheimer California Municipal Fund.

Other class action and individual lawsuits have been filed since 2008 in various state and federal courts against OFI and certain of its affiliates by investors seeking to recover investments they allegedly lost as a result of the “Ponzi” scheme run by Bernard L. Madoff and his firm, Bernard L. Madoff Investment Securities, LLC (“BLMIS”). Plaintiffs in these suits allege that they suffered losses as a result of their investments in several funds managed by an affiliate of OFI and assert a variety of claims, including breach of fiduciary duty, fraud, negligent misrepresentation, unjust enrichment, and violation of federal and state securities laws and regulations, among others. They seek unspecified damages, equitable relief and awards of attorneys’ fees and litigation expenses. Neither the Distributor, nor any of the Oppenheimer mutual funds, their independent trustees or directors are named as defendants in these lawsuits. None of the Oppenheimer mutual funds invested in any funds or accounts managed by Madoff or BLMIS. On February 28, 2011, a stipulation of partial settlement of three groups of consolidated putative class action lawsuits relating to these matters was filed in the U.S. District Court for the Southern District of New York. On August 19, 2011, the court entered an order and final judgment approving the settlement as fair, reasonable and adequate. In September 2011, certain parties filed notices of appeal from the court’s order approving the settlement. The settlement does not resolve other outstanding lawsuits against OFI and its affiliates relating to BLMIS.

On April 16, 2010, a lawsuit was filed in New York state court against (i) OFI, (ii) an affiliate of OFI and (iii) AAArdvark IV Funding Limited (“AAArdvark IV”), an entity advised by OFI’s affiliate, in connection with investments made by the plaintiffs in AAArdvark IV. Plaintiffs allege breach of contract and common law fraud claims against the defendants and seek compensatory damages, costs and disbursements, including attorney fees. On April 11, 2013, the court granted defendants’ motion for summary judgment, dismissing plaintiffs’ fraud claim with prejudice and dismissing their contract claim without prejudice, and granted plaintiffs leave to replead their contract claim to assert a cause of action for specific performance within 30 days. On May 9, 2013, plaintiffs filed a notice of appeal from the court’s dismissal order. On January 7, 2014, the appellate court affirmed the trial court’s dismissal order. On July 15, 2011, a lawsuit was filed in New York state court against OFI, an affiliate of OFI and AAArdvark Funding Limited (“AAArdvark I”), an entity advised by OFI’s affiliate, in connection with investments made by the plaintiffs in AAArdvark I. The complaint alleges breach of contract and common law fraud claims against the defendants and seeks compensatory damages, costs and disbursements, including attorney fees. On November 9, 2011, a lawsuit was filed in New York state court against OFI, an affiliate of OFI and AAArdvark XS Funding Limited (“AAArdvark XS”), an entity advised by OFI’s affiliate, in connection with investments made by the plaintiffs in AAArdvark XS. The complaint alleged breach of contract against the defendants and sought compensatory damages, costs and disbursements, including attorney fees. On November 8, 2013, the parties filed a stipulation of discontinuance dismissing the lawsuit with prejudice.

OFI believes the lawsuits and appeals described above are without legal merit and, with the exception of actions it has settled, is defending against them vigorously. While it is premature to render any opinion as to the outcome in these lawsuits, or whether any costs that the Defendant Funds may bear in defending the suits might not be reimbursed by insurance, OFI believes that these suits should not impair the ability of OFI or the Distributor to perform their respective duties to the Fund, and that the outcome of all of the suits together should not have any material effect on the operations of any of the Oppenheimer mutual funds.

19 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

| | |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM |

The Board of Trustees and Shareholders of Oppenheimer Variable Account Funds:

We have audited the accompanying statement of assets and liabilities of Oppenheimer Discovery Mid Cap Growth Fund/VA, formerly Oppenheimer Small- & Mid-Cap Growth Fund/VA (a separate series of Oppenheimer Variable Account Funds), including the statement of investments, as of December 31, 2013, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years in the five-year period then ended. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.