UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-4108

Oppenheimer Variable Account Funds

(Exact name of registrant as specified in charter)

6803 South Tucson Way, Centennial, Colorado 80112-3924

(Address of principal executive offices) (Zip code)

Cynthia Lo Bessette

OFI Global Asset Management, Inc.

225 Liberty Street, New York, New York 10281-1008

(Name and address of agent for service)

Registrant’s telephone number, including area code: (303) 768-3200

Date of fiscal year end: December 31

Date of reporting period: 6/30/2017

Item 1. Reports to Stockholders.

| | | | |

| |

| | |

| | | June 30, 2017 | | |

| | Oppenheimer | | |

| | Discovery Mid Cap Growth Fund/VA | | Semiannual Report |

| | A Series of Oppenheimer Variable Account Funds | | |

| | | SEMIANNUAL REPORT | | |

| | Listing of Top Holdings | | |

| | Fund Performance Discussion | | |

| | Financial Statements | | |

PORTFOLIO MANAGERS: Ronald J. Zibelli, Jr., CFA and Justin Livengood, CFA

AVERAGE ANNUAL TOTAL RETURNS FOR THE PERIODS ENDED 6/30/17

| | | | | | | | | | | | | | | | | | | | |

| | | Inception

Date | | | 6-Months | | | 1-Year | | | 5-Year | | | 10-Year | |

Non-Service Shares | | | 8/15/86 | | | | 14.58% | | | | 15.38% | | | | 12.98% | | | | 6.04% | |

Service Shares | | | 10/16/00 | | | | 14.45 | | | | 15.09 | | | | 12.70 | | | | 5.77 | |

Russell MidCap Growth Index | | | | | | | 11.40 | | | | 17.05 | | | | 14.19 | | | | 7.87 | |

Performance data quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. For performance data current to the most recent month end, call us at 1.800.988.8287. The Fund’s total returns should not be expected to be the same as the returns of other funds, whether or not both funds have the same portfolio managers and/or similar names. The Fund’s total returns include changes in share price and reinvested distributions but do not include the charges associated with the separate account products that offer this Fund. Such performance would have been lower if such charges were taken into account. Returns for periods of less than one year are cumulative and not annualized. See Fund prospectuses and summary prospectuses for more information on share classes and sales charges.

The Fund’s performance is compared to the performance of the Russell MidCap Growth Index. The Russell MidCap Growth Index measures the performance of the mid-cap growth segment of the U.S. equity universe. It includes those Russell MidCap companies with higher price-to-book ratios and higher forecasted growth values. The Index is unmanaged and cannot be purchased directly by investors. While index comparisons may be useful to provide a benchmark for the Fund’s performance, it must be noted that the Fund’s investments are not limited to the investments comprising the Index. Index performance includes reinvestment of income, but does not reflect transaction costs, fees, expenses or taxes. Index performance is shown for illustrative purposes only as a benchmark for the Fund’s performance, and does not predict or depict performance of the Fund. The Fund’s performance reflects the effects of the Fund’s business and operating expenses.

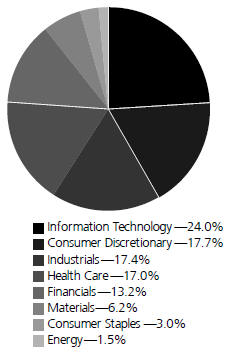

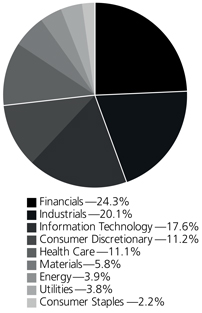

TOP HOLDINGS AND ALLOCATIONS

TOP TEN COMMON STOCK HOLDINGS

| | | | | | | | |

Restaurant Brands International, Inc. | | | 2.1 | % | | | | |

Domino’s Pizza, Inc. | | | 2.0 | | | | | |

Waste Connections, Inc. | | | 1.9 | | | | | |

Vail Resorts, Inc. | | | 1.9 | | | | | |

First Republic Bank | | | 1.9 | | | | | |

Pool Corp. | | | 1.8 | | | | | |

Microchip Technology, Inc. | | | 1.7 | | | | | |

Rockwell Automation, Inc. | | | 1.7 | | | | | |

SBA Communications Corp., Cl. A | | | 1.7 | | | | | |

Electronic Arts, Inc. | | | 1.6 | | | | | |

Portfolio holdings and allocations are subject to change. Percentages are as of June 30, 2017, and are based on net assets. For more current Fund holdings, please visit oppenheimerfunds.com.

SECTOR ALLOCATION

Portfolio holdings and allocations are subject to change. Percentages are as of June 30, 2017, and are based on the total market value of common stocks.

2 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

Fund Performance Discussion

The Fund’s Non-Service shares produced a return of 14.58% during the reporting period, outperforming the Russell Midcap Growth Index (the “Index”) return of 11.40%. The Morningstar U.S. Insurance Fund Mid-Cap Growth peer group produced a return of 13.77%.

The Fund outperformed the Index in nine out of eleven sectors of the Index, led by Consumer Discretionary, Consumer Staples and Information Technology. Stock selection and underweight positions in these sectors contributed positively to performance. The Fund underperformed the Index mainly in the Energy sector, where an overweight position detracted from performance.

MARKET OVERVIEW

Bullish sentiment from Trump’s election victory last year continued into the new year, resulting in U.S. equity markets realizing one of the best first quarter performances in several years. Investors anticipated an administration friendly to both the economy and financial markets. Less regulation, tax reform and other policies favorable to domestic economic growth were on the new administration’s agenda. Consumer and business confidence remained high, corporate earnings strengthened, and other macro factors (employment, capital expenditures) were favorable, while inflationary pressures (wage growth, commodity prices, interest rates) seemed contained.

Domestic equities performed well across all capitalization segments, but there was a distinct performance reversal from 2016. Large caps led the way this reporting period, followed by mid-caps. Small caps trailed after many years of relative outperformance. The performance reversal also held true stylistically.

Growth indices, across all cap ranges, outperformed their Value counterparts. Specifically, for midcap equities, Growth outperformed Value during the reporting period.

TOP INDIVIDUAL CONTRIBUTORS

Top performing stocks for the Fund this reporting period included Veeva Systems, Inc., Domino’s Pizza, Inc. and Autodesk, Inc.

Veeva Systems is a SaaS (software-as-a-service) company focused on providing customer relationship management software to the biotechnology and pharmaceutical industries. The company has experienced strong growth in recent years, as their technology allows pharmaceutical companies to more efficiently develop, market and sell their products to health care providers.

Domino’s Pizza, the leading pizza delivery company in the U.S., has continued to experience strong revenue growth due to its unique competitive positioning in the industry. We believe they are one of the most innovative restaurant companies in the mid-cap space, with particular leadership in online ordering. Continued robust capital expenditure spending on new technology and advertising may help stimulate further growth going forward.

Autodesk is a top provider of computer-aided design (CAD) software. The company reported healthy subscriber growth and recurring revenues grew significantly year-over year. Autodesk operates using a SaaS delivery model, which provides many advantages over traditional software delivery, including visibility and stability of revenues, increased efficiency and lower costs.

TOP INDIVIDUAL DETRACTORS

Detractors from performance this reporting period included Diamondback Energy, Nabors Industries Ltd. and Acuity Brands, Inc.

Diamondback Energy is an oil and gas company focused in the Permian Basin in west Texas. The company reported solid results during the period, but the stock underperformed due to the decline in oil prices. While we are not optimistic about the outlook for oil prices, Diamondback Energy has one of the lowest cost structures in the industry, which allows it to earn strong returns even at current oil prices. The company has also done some acquisitions in the Permian Basin that we believe can support growth.

Nabors Industries is one of the largest operators of land drilling rigs in the U.S. The company reported somewhat disappointing fourth-quarter results related to higher-than-expected operating costs, which seem likely to persist. In addition, there are growing concerns that oil prices are unlikely to surpass current levels for a variety of reasons, which would limit the growth opportunity for land rig operators such as Nabors. We have exited our position.

3 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

Acuity Brands is a producer of lighting solutions for commercial, institutional, industrial, infrastructure and residential applications. The company’s fiscal first quarter results disappointed, with earnings per share below consensus, and the stock traded down. Weakness in small projects and lingering production inefficiencies led to the lowest organic growth since 2013 and a drop in gross margin. We have since exited our position in Acuity Brands.

STRATEGY & OUTLOOK

Our long-term investment process remains the same. We seek dynamic companies with above-average and sustainable revenue and earnings growth that we believe are positioned to outperform. This includes leading firms in structurally attractive industries with committed management teams that have proven records of performance. At the end of the period, the Fund was overweight in the Industrial and Healthcare sectors while underweight the Consumer Discretionary, Consumer Staples, and Information Technology sectors relative to the benchmark.

Looking forward, we expect the U.S. economy to continue on the 2% growth trajectory that it has been on for the last several years. Although interest rates remain very low in a historical context, monetary stimulus has peaked. We believe the Federal Reserve will gradually raise short term rates while buying fewer bonds. Meanwhile, corporate profits are growing at a healthy pace and cash flows are being directed to dividends, buybacks and acquisitions. Equity valuations remain high but the bull market may persist given the favorable macro conditions. While the initial market enthusiasm about the Trump agenda of corporate tax reform, infrastructure spending and deregulation has waned, future progress on these topics could provide upside to our outlook. Technology driven disruption remains abundant across the economy and is at the forefront of our fundamental research. We are cautiously optimistic about the prospects for small and mid-cap growth stocks. We believe our opportunity set remains compelling and we think stock selection can continue to drive our relative performance.

The Fund’s investment strategy and focus can change over time. The mention of specific fund holdings does not constitute a recommendation by OppenheimerFunds, Inc. or its affiliates.

Shares of Oppenheimer funds are not deposits or obligations of any bank, are not guaranteed by any bank, are not insured by the FDIC or any other agency, and involve investment risks, including the possible loss of the principal amount invested.

The Morningstar U.S. Insurance Fund Mid-Cap Growth Funds Category Average is the average return of the mutual funds within the investment category as defined by Morningstar. Returns include the reinvestment of distributions but do not consider sales charges. Morningstar U.S. Insurance Fund Mid-Cap Growth Funds Category Average performance is shown for illustrative purposes only and does not predict or depict the performance of the Fund.

4 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

Fund Expenses

Fund Expenses. As a shareholder of the Fund, you incur two types of costs: (1) transaction costs and (2) ongoing costs, including management fees; distribution and service fees; and other Fund expenses. These examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The examples are based on an investment of $1,000.00 invested at the beginning of the period and held for the entire 6-month period ended June 30, 2017.

Actual Expenses. The first section of the table provides information about actual account values and actual expenses. You may use the information in this section for the class of shares you hold, together with the amount you invested, to estimate the expense that you paid over the period. Simply divide your account value by $1,000.00 (for example, an $8,600.00 account value divided by $1,000.00 = 8.60), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During 6 Months Ended June 30, 2017” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes.

The second section of the table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio for each class of shares, and an assumed rate of return of 5% per year for each class before expenses, which is not the actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example for the class of shares you hold with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any charges associated with the separate accounts that offer this Fund. Therefore, the “hypothetical” lines of the table are useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these separate account charges were included your costs would have been higher.

| | | | | | | | | | | | | | | | | | |

| Actual | | Beginning

Account Value

January 1, 2017 | | | | | Ending

Account Value

June 30, 2017 | | | | | Expenses

Paid During

6 Months Ended

June 30, 2017 | | | |

Non-Service shares | | $ | 1,000.00 | | | | | $ | 1,145.80 | | | | | $ | 4.26 | | | |

Service shares | | | 1,000.00 | | | | | | 1,144.50 | | | | | | 5.60 | | | |

| | | | | | |

Hypothetical (5% return before expenses) | | | | | | | | | | | | | | | |

Non-Service shares | | | 1,000.00 | | | | | | 1,020.83 | | | | | | 4.02 | | | |

Service shares | | | 1,000.00 | | | | | | 1,019.59 | | | | | | 5.27 | | | |

Expenses are equal to the Fund’s annualized expense ratio for that class, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period). Those annualized expense ratios, excluding indirect expenses from affiliated funds, based on the 6-month period ended June 30, 2017 are as follows:

| | | | | | |

| Class | | Expense Ratios | | | |

Non-Service shares | | | 0.80% | | | |

Service shares | | | 1.05 | | | |

The expense ratios reflect voluntary and/or contractual waivers and/or reimbursements of expenses by the Fund’s Manager. Some of these undertakings may be modified or terminated at any time, as indicated in the Fund’s prospectus. The “Financial Highlights” tables in the Fund’s financial statements, included in this report, also show the gross expense ratios, without such waivers or reimbursements and reduction to custodian expenses, if applicable.

5 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

STATEMENT OF INVESTMENTS June 30, 2017 Unaudited

| | | | | | | | |

| | | Shares | | | Value | |

Common Stocks—97.4% | | | | | | | | |

Consumer Discretionary—17.3% | | | | | | | | |

Distributors—1.8% | | | | | | | | |

Pool Corp. | | | 105,420 | | | $ | 12,394,229 | |

Hotels, Restaurants & Leisure—9.6% | |

Domino’s Pizza, Inc. | | | 65,570 | | | | 13,870,022 | |

Hilton Worldwide Holdings, Inc. | | | 168,493 | | | | 10,421,292 | |

MGM Resorts International | | | 233,280 | | | | 7,299,331 | |

Restaurant Brands International, Inc. | | | 232,140 | | | | 14,518,036 | |

Royal Caribbean Cruises Ltd. | | | 65,180 | | | | 7,119,612 | |

Vail Resorts, Inc. | | | 64,510 | | | | 13,084,563 | |

| | | | | | | 66,312,856 | |

Household Durables—1.3% | |

Mohawk Industries, Inc.1 | | | 36,650 | | | | 8,857,939 | |

Internet & Catalog Retail—1.2% | |

Expedia, Inc. | | | 54,680 | | | | 8,144,586 | |

Media—1.3% | |

CBS Corp., Cl. B | | | 89,840 | | | | 5,729,995 | |

Live Nation Entertainment, Inc.1 | | | 99,870 | | | | 3,480,470 | |

| | | | | | | | 9,210,465 | |

Specialty Retail—2.1% | |

Burlington Stores, Inc.1 | | | 42,380 | | | | 3,898,536 | |

Ulta Beauty, Inc.1 | | | 36,430 | | | | 10,467,796 | |

| | | | | | | | 14,366,332 | |

Consumer Staples—2.9% | |

Beverages—1.3% | | | | | | | | |

Constellation Brands, Inc., Cl. A | | | 44,870 | | | | 8,692,665 | |

Food Products—1.6% | |

Lamb Weston Holdings, Inc. | | | 127,610 | | | | 5,619,944 | |

Pinnacle Foods, Inc. | | | 94,030 | | | | 5,585,382 | |

| | | | | | | 11,205,326 | |

Energy—1.4% | | | | | | | | |

Energy Equipment & Services—0.6% | |

RPC, Inc. | | | 204,270 | | | | 4,128,297 | |

Oil, Gas & Consumable Fuels—0.8% | |

Diamondback Energy, Inc.1 | | | 66,886 | | | | 5,940,145 | |

Financials—12.8% | | | | | | | | |

Capital Markets—3.8% | |

CBOE Holdings, Inc. | | | 72,000 | | | | 6,580,800 | |

MarketAxess Holdings, Inc. | | | 50,570 | | | | 10,169,627 | |

MSCI, Inc., Cl. A | | | 34,350 | | | | 3,537,707 | |

Raymond James Financial, Inc. | | | 72,320 | | | | 5,801,510 | |

| | | | | | | 26,089,644 | |

Commercial Banks—2.8% | |

First Republic Bank | | | 128,800 | | | | 12,892,880 | |

SVB Financial Group1 | | | 35,330 | | | | 6,210,661 | |

| | | | | | | 19,103,541 | |

Consumer Finance—0.6% | |

SLM Corp.1 | | | 386,230 | | | | 4,441,645 | |

Diversified Financial Services—1.2% | |

IHS Markit Ltd.1 | | | 186,220 | | | | 8,201,129 | |

Insurance—1.3% | |

Athene Holding Ltd., Cl. A1 | | | 72,690 | | | | 3,606,151 | |

Progressive Corp. (The) | | | 126,890 | | | | 5,594,580 | |

| | | | | | | | 9,200,731 | |

Real Estate Investment Trusts (REITs)—3.1% | |

Equinix, Inc. | | | 23,510 | | | | 10,089,551 | |

SBA Communications Corp., Cl. A1 | | | 85,530 | | | | 11,537,997 | |

| | | | | | | 21,627,548 | |

Health Care—16.6% | | | | | | | | |

Biotechnology—2.2% | | | | | | | | |

BioMarin Pharmaceutical, Inc.1 | | | 68,280 | | | | 6,201,190 | |

| | | | | | | | |

| | | Shares | | | Value | |

Biotechnology (Continued) | | | | | | | | |

Exelixis, Inc.1 | | | 78,010 | | | $ | 1,921,386 | |

Incyte Corp.1 | | | 55,130 | | | | 6,941,418 | |

| | | | | | | | 15,063,994 | |

Health Care Equipment & Supplies—7.7% | |

ABIOMED, Inc.1 | | | 14,650 | | | | 2,099,345 | |

Align Technology, Inc.1 | | | 49,660 | | | | 7,454,959 | |

Cooper Cos., Inc. (The) | | | 39,350 | | | | 9,421,177 | |

DexCom, Inc.1 | | | 21,760 | | | | 1,591,744 | |

Hologic, Inc.1 | | | 131,850 | | | | 5,983,353 | |

IDEXX Laboratories, Inc.1 | | | 67,190 | | | | 10,845,810 | |

Intuitive Surgical, Inc.1 | | | 10,890 | | | | 10,186,179 | |

West Pharmaceutical Services, Inc. | | | 58,090 | | | | 5,490,667 | |

| | | | | | | 53,073,234 | |

Health Care Providers & Services—0.9% | |

WellCare Health Plans, Inc.1 | | | 32,790 | | | | 5,887,773 | |

Health Care Technology—1.3% | |

Veeva Systems, Inc., Cl. A1 | | | 147,420 | | | | 9,038,320 | |

Life Sciences Tools & Services—3.4% | |

Agilent Technologies, Inc. | | | 152,050 | | | | 9,018,085 | |

Bio-Rad Laboratories, Inc., Cl. A1 | | | 18,370 | | | | 4,157,315 | |

Mettler-Toledo International, Inc.1 | | | 18,090 | | | | 10,646,689 | |

| | | | | | | | 23,822,089 | |

Pharmaceuticals—1.1% | |

Jazz Pharmaceuticals plc1 | | | 23,310 | | | | 3,624,705 | |

Zoetis, Inc., Cl. A | | | 65,340 | | | | 4,075,909 | |

| | | | | | | | 7,700,614 | |

Industrials—16.9% | |

Aerospace & Defense—1.5% | |

BWX Technologies, Inc. | | | 72,170 | | | | 3,518,288 | |

L3 Technologies, Inc. | | | 42,840 | | | | 7,157,707 | |

| | | | | | | | 10,675,995 | |

Air Freight & Couriers—1.4% | |

XPO Logistics, Inc.1 | | | 153,240 | | | | 9,903,901 | |

Airlines—0.6% | | | | | | | | |

Alaska Air Group, Inc. | | | 43,850 | | | | 3,935,976 | |

Building Products—3.2% | | | | |

A.O. Smith Corp. | | | 169,390 | | | | 9,541,739 | |

Lennox International, Inc. | | | 47,220 | | | | 8,671,481 | |

Owens Corning | | | 60,460 | | | | 4,045,983 | |

| | | | | | | | 22,259,203 | |

Commercial Services & Supplies—3.1% | |

Copart, Inc.1 | | | 253,650 | | | | 8,063,534 | |

Waste Connections, Inc. | | | 203,815 | | | | 13,129,762 | |

| | | | | | | | 21,193,296 | |

Construction & Engineering—1.1% | | | | | | | | |

Quanta Services, Inc.1 | | | 221,710 | | | | 7,298,693 | |

Electrical Equipment—1.7% | | | | | | | | |

Rockwell Automation, Inc. | | | 71,810 | | | | 11,630,347 | |

Machinery—2.1% | | | | | | | | |

Nordson Corp. | | | 82,420 | | | | 9,999,194 | |

Xylem, Inc. | | | 79,960 | | | | 4,432,183 | |

| | | | | | | | 14,431,377 | |

Professional Services—1.4% | | | | | | | | |

TransUnion1 | | | 231,180 | | | | 10,012,406 | |

Road & Rail—0.8% | | | | | | | | |

Norfolk Southern Corp. | | | 44,660 | | | | 5,435,122 | |

Information Technology—23.4% | | | | | | | | |

| Electronic Equipment, Instruments, & Components—2.6% | | | | | |

CDW Corp. | | | 104,220 | | | | 6,516,877 | |

Cognex Corp. | | | 55,090 | | | | 4,677,141 | |

6 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

| | | | | | | | |

| | | Shares | | | Value | |

Electronic Equipment, Instruments, & Components (Continued) | |

Trimble, Inc.1 | | | 192,600 | | | $ | 6,870,042 | |

| | | | | | | | 18,064,060 | |

Internet Software & Services—1.5% | | | | | |

CoStar Group, Inc.1 | | | 13,290 | | | | 3,503,244 | |

MercadoLibre, Inc. | | | 27,320 | | | | 6,854,042 | |

| | | | | | | | 10,357,286 | |

IT Services—5.2% | | | | | | | | |

Booz Allen Hamilton Holding Corp., Cl. A | | | 134,250 | | | | 4,368,495 | |

Fiserv, Inc.1 | | | 84,580 | | | | 10,347,517 | |

Gartner, Inc.1 | | | 58,280 | | | | 7,198,163 | |

Global Payments, Inc. | | | 77,930 | | | | 7,038,638 | |

Total System Services, Inc. | | | 120,830 | | | | 7,038,347 | |

| | | | | | | | 35,991,160 | |

Semiconductors & Semiconductor Equipment—6.7% | |

Analog Devices, Inc. | | | 91,570 | | | | 7,124,146 | |

KLA-Tencor Corp. | | | 76,670 | | | | 7,016,071 | |

Lam Research Corp. | | | 35,530 | | | | 5,025,008 | |

Marvell Technology Group Ltd. | | | 349,340 | | | | 5,771,097 | |

Microchip Technology, Inc. | | | 155,680 | | | | 12,015,382 | |

Skyworks Solutions, Inc. | | | 64,660 | | | | 6,204,127 | |

Teradyne, Inc. | | | 106,360 | | | | 3,193,991 | |

| | | | | | | | 46,349,822 | |

Software—7.4% | | | | | | | | |

Autodesk, Inc.1 | | | 101,890 | | | | 10,272,550 | |

Electronic Arts, Inc.1 | | | 106,070 | | | | 11,213,720 | |

PTC, Inc.1 | | | 176,000 | | | | 9,701,120 | |

| | | | | | | | |

| | | Shares | | | Value | |

Software (Continued) | | | | | | | | |

Red Hat, Inc.1 | | | 96,210 | | | $ | 9,212,108 | |

ServiceNow, Inc.1 | | | 66,170 | | | | 7,014,020 | |

Workday, Inc., Cl. A1 | | | 34,630 | | | | 3,359,110 | |

| | | | | | | | 50,772,628 | |

Materials—6.1% | | | | | | | | |

Chemicals—3.3% | | | | | | | | |

Albemarle Corp. | | | 96,940 | | | | 10,231,047 | |

Celanese Corp., Cl. A | | | 79,940 | | | | 7,589,504 | |

FMC Corp. | | | 65,860 | | | | 4,811,073 | |

| | | | | | | | 22,631,624 | |

Construction Materials—0.7% | | | | | | | | |

Vulcan Materials Co. | | | 35,060 | | | | 4,441,401 | |

Containers & Packaging—1.6% | | | | | | | | |

Berry Global Group, Inc.1 | | | 72,410 | | | | 4,128,094 | |

Packaging Corp. of America | | | 63,400 | | | | 7,062,126 | |

| | | | | | | | 11,190,220 | |

Metals & Mining—0.5% | | | | | | | | |

Steel Dynamics, Inc. | | | 102,900 | | | | 3,684,849 | |

Total Common Stocks (Cost $544,422,953) | | | | | |

| 672,762,468

|

|

Investment Company—1.9% | | | | | | | | |

| Oppenheimer Institutional Government Money Market Fund, Cl. E, 0.86%2,3 (Cost $12,785,087) | | | 12,785,087 | | | | 12,785,087 | |

| Total Investments, at Value (Cost $557,208,040) | | | 99.3 | % | | | 685,547,555 | |

Net Other Assets (Liabilities) | | | 0.7 | | | | 4,654,903 | |

Net Assets | | | 100.0 | % | | $ | 690,202,458 | |

| | | | | | | | |

Footnotes to Statement of Investments

1. Non-income producing security.

2. Rate shown is the 7-day yield at period end.

3. Is or was an affiliate, as defined in the Investment Company Act of 1940, as amended, at or during the reporting period, by virtue of the Fund owning at least 5% of the voting securities of the issuer or as a result of the Fund and the issuer having the same investment adviser. Transactions during the reporting period in which the issuer was an affiliate are as follows:

| | | | | | | | |

| | | Shares

December 31, 2016 | | Gross Additions | | Gross Reductions | | Shares June 30, 2017 |

Oppenheimer Institutional Government Money Market Fund, Cl. E | | 21,498,967 | | 163,864,082 | | 172,577,962 | | 12,785,087 |

| | | | |

| | | | | | | Value | | Income |

Oppenheimer Institutional Government Money Market Fund, Cl. E | | | | | | $ 12,785,087 | | $ 44,126 |

See accompanying Notes to Financial Statements.

7 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

STATEMENT OF ASSETS AND LIABILITIES June 30, 2017 Unaudited

| | | | |

| | |

Assets | | | | |

Investments, at value—see accompanying statement of investments: | | | | |

Unaffiliated companies (cost $544,422,953) | | $ | 672,762,468 | |

Affiliated companies (cost $12,785,087) | | | 12,785,087 | |

| | | 685,547,555 | |

Cash | | | 500,000 | |

Receivables and other assets: | | | | |

Investments sold | | | 6,222,989 | |

Dividends | | | 385,890 | |

Shares of beneficial interest sold | | | 17,766 | |

Other | | | 59,579 | |

Total assets | | | 692,733,779 | |

| | |

Liabilities | | | | |

Payables and other liabilities: | | | | |

Shares of beneficial interest redeemed | | | 2,435,726 | |

Trustees’ compensation | | | 53,322 | |

Shareholder communications | | | 18,101 | |

Distribution and service plan fees | | | 7,259 | |

Other | | | 16,913 | |

Total liabilities | | | 2,531,321 | |

Net Assets | | $ | 690,202,458 | |

| | | | |

| | | | |

| | |

Composition of Net Assets | | | | |

Par value of shares of beneficial interest | | $ | 9,237 | |

Additional paid-in capital | | | 500,199,760 | |

Accumulated net investment loss | | | (296,397) | |

Accumulated net realized gain on investments | | | 61,950,343 | |

Net unrealized appreciation on investments | | | 128,339,515 | |

Net Assets | | $ | 690,202,458 | |

| | | | |

| | | | |

| | |

Net Asset Value Per Share | | | | |

Non-Service Shares: | | | | |

| Net asset value, redemption price per share and offering price per share (based on net assets of $655,266,817 and 8,745,676 shares of beneficial interest outstanding) | | $ | 74.92 | |

Service Shares: | | | | |

| Net asset value, redemption price per share and offering price per share (based on net assets of $34,935,641 and 490,950 shares of beneficial interest outstanding) | | $ | 71.16 | |

See accompanying Notes to Financial Statements.

8 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

STATEMENT OF OPERATIONS For the Six Months Ended June 30, 2017 Unaudited

| | | | |

Investment Income | | | | |

Dividends: | | | | |

Unaffiliated companies (net of foreign withholding taxes of $18,272) | | $ | 2,446,895 | |

Affiliated companies | | | 44,126 | |

Total investment income | | | 2,491,021 | |

Expenses | | | | |

Management fees | | | 2,398,518 | |

Distribution and service plan fees - Service shares | | | 42,046 | |

Transfer and shareholder servicing agent fees: | | | | |

Non-Service shares | | | 319,543 | |

Service shares | | | 16,821 | |

Shareholder communications: | | | | |

Non-Service shares | | | 25,322 | |

Service shares | | | 1,333 | |

Trustees’ compensation | | | 12,679 | |

Borrowing fees | | | 6,068 | |

Custodian fees and expenses | | | 2,491 | |

Other | | | 39,309 | |

Total expenses | | | 2,864,130 | |

Less reduction to custodian expenses | | | (212) | |

Less waivers and reimbursements of expenses | | | (124,897) | |

Net expenses | | | 2,739,021 | |

Net Investment Loss | | | (248,000) | |

Realized and Unrealized Gain | | | | |

Net realized gain on investment transactions in unaffiliated companies | | | 64,161,458 | |

Net change in unrealized appreciation/depreciation | | | 27,462,502 | |

Net Increase in Net Assets Resulting from Operations | | $ | 91,375,960 | |

| | | | |

See accompanying Notes to Financial Statements.

9 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

STATEMENTS OF CHANGES IN NET ASSETS

| | | | | | | | |

| | | Six Months Ended | | | | |

| | | June 30, 2017 | | | Year Ended | |

| | | (Unaudited) | | | December 31, 2016 | |

| | | |

Operations | | | | | | | | |

Net investment income (loss) | | $ | (248,000) | | | $ | 192,842 | |

Net realized gain | | | 64,161,458 | | | | 74,319,102 | |

Net change in unrealized appreciation/depreciation | | | 27,462,502 | | | | (60,542,760) | |

Net increase in net assets resulting from operations | | | 91,375,960 | | | | 13,969,184 | |

| | | |

Dividends and/or Distributions to Shareholders | | | | | | | | |

Dividends from net investment income: | | | | | | | | |

Non-Service shares | | | (202,565) | | | | — | |

Service shares | | | — | | | | — | |

| | | | (202,565) | | | | — | |

Distributions from net realized gain: | | | | | | | | |

Non-Service shares | | | (66,541,431) | | | | (48,415,668) | |

Service shares | | | (3,695,269) | | | | (2,737,189) | |

| | | (70,236,700) | | | | (51,152,857) | |

| | | |

Beneficial Interest Transactions | | | | | | | | |

Net increase (decrease) in net assets resulting from beneficial interest transactions: | | | | | | | | |

Non-Service shares | | | 31,452,503 | | | | (21,717,260) | |

Service shares | | | 1,853,068 | | | | (2,617,902) | |

| | | 33,305,571 | | | | (24,335,162) | |

| | | |

Net Assets | | | | | | | | |

Total increase (decrease) | | | 54,242,266 | | | | (61,518,835) | |

Beginning of period | | | 635,960,192 | | | | 697,479,027 | |

End of period (including accumulated net investment income (loss) of $(296,397) and $154,168, respectively) | | $ | 690,202,458 | | | $ | 635,960,192 | |

| | | | | | | | |

See accompanying Notes to Financial Statements.

10 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

FINANCIAL HIGHLIGHTS

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Six Months Ended June 30, 2017 (Unaudited) | | | Year Ended December 31, 2016 | | | Year Ended December 31, 2015 | | | Year Ended December 31, 2014 | | | Year Ended December 31, 2013 | | | Year Ended December 31, 2012 | |

| | | | | | | |

| | | | | | | |

| Non-Service Shares | | | | | | |

| | | | | | | |

Per Share Operating Data | | | | | | | | | | | | | | | | | | | | | | | | |

Net asset value, beginning of period | | | $72.65 | | | | $76.85 | | | | $78.82 | | | | $74.51 | | | | $54.80 | | | | $47.06 | |

| Income (loss) from investment operations: | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income (loss)1 | | | (0.02) | | | | 0.03 | | | | (0.19) | | | | (0.29) | | | | (0.16) | | | | 0.01 | |

Net realized and unrealized gain | | | 10.71 | | | | 1.69 | | | | 5.67 | | | | 4.60 | | | | 19.88 | | | | 7.73 | |

Total from investment operations | | | 10.69 | | | | 1.72 | | | | 5.48 | | | | 4.31 | | | | 19.72 | | | | 7.74 | |

Dividends and/or distributions to shareholders: | | | | | | | | | | | | | | | | | | | | | | | | |

Dividends from net investment income | | | (0.03) | | | | 0.00 | | | | 0.00 | | | | 0.00 | | | | (0.01) | | | | 0.00 | |

Distributions from net realized gain | | | (8.39) | | | | (5.92) | | | | (7.45) | | | | 0.00 | | | | 0.00 | | | | 0.00 | |

| Total dividends and/or distributions to shareholders | | | (8.42) | | | | (5.92) | | | | (7.45) | | | | 0.00 | | | | (0.01) | | | | 0.00 | |

Net asset value, end of period | | | $74.92 | | | | $72.65 | | | | $76.85 | | | | $78.82 | | | | $74.51 | | | | $54.80 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

Total Return, at Net Asset Value2 | | | 14.58% | | | | 2.34% | | | | 6.61% | | | | 5.78% | | | | 35.98% | | | | 16.45% | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

Ratios/Supplemental Data | | | | | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of period (in thousands) | | | $655,267 | | | | $603,708 | | | | $660,450 | | | | $682,515 | | | | $725,406 | | | | $558,934 | |

Average net assets (in thousands) | | | $644,955 | | | | $621,110 | | | | $695,736 | | | | $688,259 | | | | $618,970 | | | | $575,072 | |

Ratios to average net assets:3 | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income (loss) | | | (0.06)% | | | | 0.04% | | | | (0.24)% | | | | (0.39)% | | | | (0.24)% | | | | 0.03% | |

| Expenses excluding specific expenses listed below | | | 0.84% | | | | 0.84% | | | | 0.83% | | | | 0.83% | | | | 0.84% | | | | 0.85% | |

Interest and fees from borrowings | | | 0.00%4 | | | | 0.00%4 | | | | 0.00%4 | | | | 0.00% | | | | 0.00% | | | | 0.00% | |

Total expenses5 | | | 0.84% | | | | 0.84% | | | | 0.83% | | | | 0.83% | | | | 0.84% | | | | 0.85% | |

| Expenses after payments, waivers and/or reimbursements and reduction to custodian expenses | | | 0.80% | | | | 0.80% | | | | 0.80% | | | | 0.80% | | | | 0.80% | | | | 0.80% | |

Portfolio turnover rate | | | 65% | | | | 141% | | | | 81% | | | | 113% | | | | 84% | | | | 66% | |

1. Per share amounts calculated based on the average shares outstanding during the period.

2. Assumes an initial investment on the business day before the first day of the fiscal period, with all dividends and distributions reinvested in additional shares on the reinvestment date, and redemption at the net asset value calculated on the last business day of the fiscal period. Total returns are not annualized for periods less than one full year. Total return information does not reflect expenses that apply at the separate account level or to related insurance products. Inclusion of these charges would reduce the total return figures for all periods shown. Returns do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

3. Annualized for periods less than one full year.

4. Less than 0.005%.

5. Total expenses including indirect expenses from affiliated fund fees and expenses were as follows:

| | | | |

| | | | |

| | Six Months Ended June 30, 2017 | | 0.84% |

| | Year Ended December 31, 2016 | | 0.84% |

| | Year Ended December 31, 2015 | | 0.83% |

| | Year Ended December 31, 2014 | | 0.83% |

| | Year Ended December 31, 2013 | | 0.84% |

| | Year Ended December 31, 2012 | | 0.85% |

See accompanying Notes to Financial Statements.

11 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

FINANCIAL HIGHLIGHTS Continued

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Six Months Ended June 30, 2017 (Unaudited) | | | Year Ended December 31, 2016 | | | Year Ended December 31, 2015 | | | Year Ended December 31, 2014 | | | Year Ended December 31, 2013 | | | Year Ended December 31, 2012 | |

| | | | | | | |

| | | | | | | |

| Service Shares | | | | | | |

| | | | | | | |

Per Share Operating Data | | | | | | | | | | | | | | | | | | | | | | | | |

Net asset value, beginning of period | | | $69.43 | | | | $73.88 | | | | $76.21 | | | | $72.22 | | | | $53.25 | | | | $45.84 | |

Income (loss) from investment operations: | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment loss1 | | | (0.12) | | | | (0.15) | | | | (0.38) | | | | (0.46) | | | | (0.30) | | | | (0.12) | |

Net realized and unrealized gain | | | 10.24 | | | | 1.62 | | | | 5.50 | | | | 4.45 | | | | 19.27 | | | | 7.53 | |

Total from investment operations | | | 10.12 | | | | 1.47 | | | | 5.12 | | | | 3.99 | | | | 18.97 | | | | 7.41 | |

| Dividends and/or distributions to shareholders: | | | | | | | | | | | | | | | | | | | | | | | | |

Dividends from net investment income | | | 0.00 | | | | 0.00 | | | | 0.00 | | | | 0.00 | | | | 0.00 | | | | 0.00 | |

Distributions from net realized gain | | | (8.39) | | | | (5.92) | | | | (7.45) | | | | 0.00 | | | | 0.00 | | | | 0.00 | |

| Total dividends and/or distributions to shareholders | | | (8.39) | | | | (5.92) | | | | (7.45) | | | | 0.00 | | | | 0.00 | | | | 0.00 | |

Net asset value, end of period | | | $71.16 | | | | $69.43 | | | | $73.88 | | | | $76.21 | | | | $72.22 | | | | $53.25 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

Total Return, at Net Asset Value2 | | | 14.45% | | | | 2.08% | | | | 6.35% | | | | 5.53% | | | | 35.62% | | | | 16.17% | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

Ratios/Supplemental Data | | | | | | | | | | | | | | | | | | | | | | | | |

Net assets, end of period (in thousands) | | | $34,935 | | | | $32,252 | | | | $37,029 | | | | $30,964 | | | | $36,549 | | | | $35,942 | |

Average net assets (in thousands) | | | $33,949 | | | | $33,797 | | | | $32,812 | | | | $32,927 | | | | $35,905 | | | | $37,842 | |

Ratios to average net assets:3 | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment loss | | | (0.31)% | | | | (0.21)% | | | | (0.49)% | | | | (0.64)% | | | | (0.49)% | | | | (0.22)% | |

| Expenses excluding specific expenses listed below | | | 1.09% | | | | 1.09% | | | | 1.08% | | | | 1.08% | | | | 1.09% | | | | 1.10% | |

Interest and fees from borrowings | |

| 0.00%4

|

| |

| 0.00%4

|

| |

| 0.00%4

|

| | | 0.00% | | | | 0.00% | | | | 0.00% | |

Total expenses5 | | | 1.09% | | | | 1.09% | | | | 1.08% | | | | 1.08% | | | | 1.09% | | | | 1.10% | |

| Expenses after payments, waivers and/or reimbursements and reduction to custodian expenses | | | 1.05% | | | | 1.05% | | | | 1.05% | | | | 1.05% | | | | 1.05% | | | | 1.05% | |

Portfolio turnover rate | | | 65% | | | | 141% | | | | 81% | | | | 113% | | | | 84% | | | | 66% | |

| 1. | Per share amounts calculated based on the average shares outstanding during the period. |

| 2. | Assumes an initial investment on the business day before the first day of the fiscal period, with all dividends and distributions reinvested in additional shares on the reinvestment date, and redemption at the net asset value calculated on the last business day of the fiscal period. Total returns are not annualized for periods less than one full year. Total return information does not reflect expenses that apply at the separate account level or to related insurance products. Inclusion of these charges would reduce the total return figures for all periods shown. Returns do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. |

| 3. | Annualized for periods less than one full year. |

| 5. | Total expenses including indirect expenses from affiliated fund fees and expenses were as follows: |

| | | | | | |

| | | | | | |

| | Six Months Ended June 30, 2017 | | | 1.09 | % |

| | Year Ended December 31, 2016 | | | 1.09 | % |

| | Year Ended December 31, 2015 | | | 1.08 | % |

| | Year Ended December 31, 2014 | | | 1.08 | % |

| | Year Ended December 31, 2013 | | | 1.09 | % |

| | Year Ended December 31, 2012 | | | 1.10 | % |

See accompanying Notes to Financial Statements.

12 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

NOTES TO FINANCIAL STATEMENTS June 30, 2017 Unaudited

1. Organization

Oppenheimer Discovery Mid Cap Growth Fund/VA (the “Fund”), a separate series of Oppenheimer Variable Account Funds, is a diversified open-end management investment company registered under the Investment Company Act of 1940 (“1940 Act”), as amended. The Fund’s investment objective is to seek capital appreciation. The Fund’s investment adviser is OFI Global Asset Management, Inc. (“OFI Global” or the “Manager”), a wholly-owned subsidiary of OppenheimerFunds, Inc. (“OFI” or the “Sub-Adviser”). The Manager has entered into a sub-advisory agreement with OFI.

Shares of the Fund are sold only to separate accounts of life insurance companies.

The Fund offers two classes of shares. Both classes are sold at their offering price, which is the net asset value per share, to separate investment accounts of participating insurance companies as an underlying investment for variable life insurance policies, variable annuity contracts or other investment products. The class of shares designated as Service shares is subject to a distribution and service plan. Both classes of shares have identical rights and voting privileges with respect to the Fund in general and exclusive voting rights on matters that affect that class alone. Earnings, net assets and net asset value per share may differ due to each class having its own expenses, such as transfer and shareholder servicing agent fees and shareholder communications, directly attributable to that class.

The following is a summary of significant accounting policies followed in the Fund’s preparation of financial statements in accordance with accounting principles generally accepted in the United States (“U.S. GAAP”).

2. Significant Accounting Policies

Security Valuation. All investments in securities are recorded at their estimated fair value, as described in Note 3.

Foreign Currency Translation. The books and records of the Fund are maintained in U.S. dollars. Any foreign currency amounts are translated into U.S. dollars on the following basis:

(1) Value of investment securities, other assets and liabilities — at the exchange rates prevailing at Market Close as described in Note 3.

(2) Purchases and sales of investment securities, income and expenses — at the rates of exchange prevailing on the respective dates of such transactions.

Although the net assets and the values are presented at the foreign exchange rates at Market Close, the Fund does not isolate the portion of the results of operations resulting from changes in foreign exchange rates on investments from the fluctuations arising from changes in prices of securities held. Such fluctuations are included with the net realized and unrealized gains or losses from investments shown in the Statement of Operations.

For securities, which are subject to foreign withholding tax upon disposition, realized gains or losses on such securities are recorded net of foreign withholding tax.

Reported net realized foreign exchange gains or losses arise from sales of foreign currencies, currency gains or losses realized between the trade and settlement dates on securities transactions, the difference between the amounts of dividends, interest, and foreign withholding tax reclaims recorded on Fund’s books, and the U.S. dollar equivalent of the amounts actually received or paid. Net unrealized foreign exchange gains and losses arise from changes in the value of assets and liabilities other than investments in securities, resulting from changes in the exchange rate.

Allocation of Income, Expenses, Gains and Losses. Income, expenses (other than those attributable to a specific class), gains and losses are allocated on a daily basis to each class of shares based upon the relative proportion of net assets represented by such class. Operating expenses directly attributable to a specific class are charged against the operations of that class.

Dividends and Distributions to Shareholders. Dividends and distributions to shareholders, which are determined in accordance with income tax regulations and may differ from U.S. GAAP, are recorded on the ex-dividend date. Income and capital gain distributions, if any, are declared and paid annually or at other times as deemed necessary by the Manager.

The tax character of distributions is determined as of the Fund’s fiscal year end. Therefore, a portion of the Fund’s distributions made to shareholders prior to the Fund’s fiscal year end may ultimately be categorized as a tax return of capital.

Investment Income. Dividend income is recorded on the ex-dividend date or upon ex-dividend notification in the case of certain foreign dividends where the ex-dividend date may have passed. Non-cash dividends included in dividend income, if any, are recorded at the fair value of the securities received. Withholding taxes on foreign dividends, if any, and capital gains taxes on foreign investments, if any, have been provided for in accordance with the Fund’s understanding of the applicable tax rules and regulations. Interest income is recognized on an accrual basis. Discount and premium, which are included in interest income on the Statement of Operations, are amortized or accreted daily.

Return of Capital Estimates. Distributions received from the Fund’s investments in Real Estate Investments Trusts (REITs), generally are comprised of income and return of capital. The Fund records investment income and return of capital based on estimates. Such estimates are based on historical information available from each REIT and other industry sources. These estimates may subsequently be revised based on information received from REITs after their tax reporting periods are concluded.

Custodian Fees. “Custodian fees and expenses” in the Statement of Operations may include interest expense incurred by the Fund on any cash overdrafts of its custodian account during the period. Such cash overdrafts may result from the effects of failed trades in portfolio securities and from cash outflows resulting from unanticipated shareholder redemption activity. The Fund pays interest to its custodian on such cash overdrafts, to the extent they are not offset by positive cash balances maintained by the Fund, at a rate equal to the Federal Funds Rate plus 2.00%. The “Reduction to custodian

13 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

NOTES TO FINANCIAL STATEMENTS Unaudited / Continued

2. Significant Accounting Policies (Continued)

expenses” line item, if applicable, represents earnings on cash balances maintained by the Fund during the period. Such interest expense and other custodian fees may be paid with these earnings.

Security Transactions. Security transactions are recorded on the trade date. Realized gains and losses on securities sold are determined on the basis of identified cost.

Indemnifications. The Fund’s organizational documents provide current and former Trustees and officers with a limited indemnification against liabilities arising in connection with the performance of their duties to the Fund. In the normal course of business, the Fund may also enter into contracts that provide general indemnifications. The Fund’s maximum exposure under these arrangements is unknown as this would be dependent on future claims that may be made against the Fund. The risk of material loss from such claims is considered remote.

Federal Taxes. The Fund intends to comply with provisions of the Internal Revenue Code applicable to regulated investment companies and to distribute substantially all of its investment company taxable income to shareholders. Therefore, no federal income or excise tax provision is required. The Fund files income tax returns in U.S. federal and applicable state jurisdictions. The statute of limitations on the Fund’s tax return filings generally remains open for the three preceding fiscal reporting period ends. The Fund has analyzed its tax positions for the fiscal year ended December 31, 2016, including open tax years, and does not believe there are any uncertain tax positions requiring recognition in the Fund’s financial statements.

During the fiscal year ended December 31, 2016, the Fund did not utilize any capital loss carryforward to offset capital gains realized in that fiscal year. Capital loss carryforwards with no expiration, if any, must be utilized prior to those with expiration dates. Capital losses with no expiration will be carried forward to future years if not offset by gains.

At period end, it is estimated that there would be no capital loss carryforwards. The estimated capital loss carryforward represents the carryforward as of the end of the last fiscal year, increased or decreased by capital losses or gains realized in the first six months of the current fiscal year. During the reporting period, it is estimated that the Fund will not utilize any capital loss carryforward to offset realized capital gains.

Net investment income (loss) and net realized gain (loss) may differ for financial statement and tax purposes. The character of dividends and distributions made during the fiscal year from net investment income or net realized gains are determined in accordance with federal income tax requirements, which may differ from the character of net investment income or net realized gains presented in those financial statements in accordance with U.S. GAAP. Also, due to timing of dividends and distributions, the fiscal year in which amounts are distributed may differ from the fiscal year in which the income or net realized gain was recorded by the Fund.

The aggregate cost of securities and other investments and the composition of unrealized appreciation and depreciation of securities and other investments for federal income tax purposes at period end are noted in the following table. The primary difference between book and tax appreciation or depreciation of securities and other investments, if applicable, is attributable to the tax deferral of losses or tax realization of financial statement unrealized gain or loss.

| | | | |

Federal tax cost of securities | | $ | 558,338,039 | |

| | | | |

Gross unrealized appreciation | | $ | 131,109,201 | |

Gross unrealized depreciation | | | (3,899,685) | |

Net unrealized appreciation | | $ | 127,209,516 | |

| | | | |

Use of Estimates. The preparation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

Recent Accounting Pronouncement. In October 2016, the Securities and Exchange Commission (“SEC”) adopted amendments to rules under the Investment Company Act of 1940 (“final rules”) intended to modernize the reporting and disclosure of information by registered investment companies. The final rules amend Regulation S-X and require funds to provide standardized, enhanced derivative disclosure in fund financial statements in a format designed for individual investors. The amendments to Regulation S-X also update the disclosures for other investments and investments in, and advances to affiliates and amend the rules regarding the general form and content of fund financial statements. The compliance date for the amendments to

Regulation S-X is for reporting periods after August 1, 2017. OFI Global is currently evaluating the amendments and their impact, if any, on the Fund’s financial statements.

3. Securities Valuation

The Fund calculates the net asset value of its shares as of 4:00 P.M. Eastern time, on each day the New York Stock Exchange (the “Exchange”) is open for trading, except in the case of a scheduled early closing of the Exchange, in which case the Fund will calculate net asset value of the shares as of the scheduled early closing time of the Exchange.

The Fund’s Board has adopted procedures for the valuation of the Fund’s securities and has delegated the day-to-day responsibility for valuation determinations under those procedures to the Manager. The Manager has established a Valuation Committee which is responsible for determining a fair valuation for any security for which market quotations are not readily available. The Valuation Committee’s fair valuation determinations are subject to review, approval and ratification by the Fund’s Board at its next regularly scheduled meeting covering the calendar quarter in which the fair valuation

14 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

3. Securities Valuation (Continued)

was determined.

Valuation Methods and Inputs

Securities are valued primarily using unadjusted quoted market prices, when available, as supplied by third party pricing services or broker-dealers.

The following methodologies are used to determine the market value or the fair value of the types of securities described below:

Equity securities traded on a securities exchange (including exchange-traded derivatives other than futures and futures options) are valued based on the official closing price on the principal exchange on which the security is traded, as identified by the Manager, prior to the time when the Fund’s assets are valued. If the official closing price is unavailable, the security is valued at the last sale price on the principal exchange on which it is traded, or if no sales occurred, the security is valued at the mean between the quoted bid and asked prices. Over-the-counter equity securities are valued at the last published sale price, or if no sales occurred, at the mean between the quoted bid and asked prices. Events occurring after the close of trading on foreign exchanges may result in adjustments to the valuation of foreign securities to more accurately reflect their fair value as of the time when the Fund’s assets are valued.

Shares of a registered investment company that are not traded on an exchange are valued at that investment company’s net asset value per share.

Securities for which market quotations are not readily available or a significant event has occurred that would materially affect the value of the security, the security is fair valued either (i) by a standardized fair valuation methodology applicable to the security type or the significant event as previously approved by the Valuation Committee and the Fund’s Board or (ii) as determined in good faith by the Manager’s Valuation Committee. The Valuation Committee considers all relevant facts that are reasonably available, through either public information or information available to the Manager, when determining the fair value of a security. Those standardized fair valuation methodologies include, but are not limited to, valuing securities at the last sale price or initially at cost and subsequently adjusting the value based on: changes in company specific fundamentals, changes in an appropriate securities index, or changes in the value of similar securities which may be further adjusted for any discounts related to security-specific resale restrictions. When possible, such methodologies use observable market inputs such as unadjusted quoted prices of similar securities, observable interest rates, currency rates and yield curves. The methodologies used for valuing securities are not necessarily an indication of the risks associated with investing in those securities nor can it be assured that the Fund can obtain the fair value assigned to a security if it were to sell the security.

Classifications

Each investment asset or liability of the Fund is assigned a level at measurement date based on the significance and source of the inputs to its valuation. Various data inputs may be used in determining the value of each of the Fund’s investments as of the reporting period end. These data inputs are categorized in the following hierarchy under applicable financial accounting standards:

1) Level 1-unadjusted quoted prices in active markets for identical assets or liabilities (including securities actively traded on a securities exchange)

2) Level 2-inputs other than unadjusted quoted prices that are observable for the asset or liability (such as unadjusted quoted prices for similar assets and market corroborated inputs such as interest rates, prepayment speeds, credit risks, etc.)

3) Level 3-significant unobservable inputs (including the Manager’s own judgments about assumptions that market participants would use in pricing the asset or liability).

The inputs used for valuing securities are not necessarily an indication of the risks associated with investing in those securities.

The Fund classifies each of its investments in investment companies which are publicly offered as Level 1. Investment companies that are not publicly offered, if any, are classified as Level 2 in the fair value hierarchy.

The table below categorizes amounts that are included in the Fund’s Statement of Assets and Liabilities at period end based on valuation input level:

| | | | | | | | | | | | | | | | |

| | | Level 1— Unadjusted Quoted Prices | | | Level 2— Other Significant

Observable Inputs | | | Level 3— Significant

Unobservable Inputs | | | Value | |

Assets Table | | | | | | | | | | | | | | | | |

Investments, at Value: | | | | | | | | | | | | | | | | |

Common Stocks | | | | | | | | | | | | | | | | |

Consumer Discretionary | | $ | 119,286,407 | | | $ | — | | | $ | — | | | $ | 119,286,407 | |

Consumer Staples | | | 19,897,991 | | | | — | | | | — | | | | 19,897,991 | |

Energy | | | 10,068,442 | | | | — | | | | — | | | | 10,068,442 | |

Financials | | | 88,664,238 | | | | — | | | | — | | | | 88,664,238 | |

Health Care | | | 114,586,024 | | | | — | | | | — | | | | 114,586,024 | |

Industrials | | | 116,776,316 | | | | — | | | | — | | | | 116,776,316 | |

Information Technology | | | 161,534,956 | | | | — | | | | — | | | | 161,534,956 | |

Materials | | | 41,948,094 | | | | — | | | | — | | | | 41,948,094 | |

Investment Company | | | 12,785,087 | | | | — | | | | — | | | | 12,785,087 | |

Total Assets | | $ | 685,547,555 | | | $ | — | | | $ | — | | | $ | 685,547,555 | |

Forward currency exchange contracts and futures contracts, if any, are reported at their unrealized appreciation/depreciation at measurement date, which represents the change in the contract’s value from trade date. All additional assets and liabilities included in the above table are reported at their market value at measurement date.

15 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

NOTES TO FINANCIAL STATEMENTS Unaudited / Continued

4. Investments and Risks

Investments in Affiliated Funds. The Fund is permitted to invest in other mutual funds advised by the Manager (“Affiliated Funds”). Affiliated Funds are open-end management investment companies registered under the 1940 Act, as amended. The Manager is the investment adviser of, and the Sub-Adviser provides investment and related advisory services to, the Affiliated Funds. When applicable, the Fund’s investments in Affiliated Funds are included in the Statement of Investments. Shares of Affiliated Funds are valued at their net asset value per share. As a shareholder, the Fund is subject to its proportional share of the Affiliated Funds’ expenses, including their management fee. The Manager will waive fees and/or reimburse Fund expenses in an amount equal to the indirect management fees incurred through the Fund’s investment in the Affiliated Funds.

Each of the Affiliated Funds in which the Fund invests has its own investment risks, and those risks can affect the value of the Fund’s investments and therefore the value of the Fund’s shares. To the extent that the Fund invests more of its assets in one Affiliated Fund than in another, the Fund will have greater exposure to the risks of that Affiliated Fund.

Investments in Money Market Instruments. The Fund is permitted to invest its free cash balances in money market instruments to provide liquidity or for defensive purposes. The Fund may invest in money market instruments by investing in Class E shares of Oppenheimer Institutional Government Money Market Fund (“IGMMF”), which is an Affiliated Fund. IGMMF is regulated as a money market fund under the 1940 Act, as amended. The Fund may also invest in money market instruments directly or in other affiliated or unaffiliated money market funds.

Equity Security Risk. Stocks and other equity securities fluctuate in price. The value of the Fund’s portfolio may be affected by changes in the equity markets generally. Equity markets may experience significant short-term volatility and may fall sharply at times. Different markets may behave differently from each other and U.S. equity markets may move in the opposite direction from one or more foreign stock markets. Adverse events in any part of the equity or fixed-income markets may have unexpected negative effects on other market segments.

The prices of individual equity securities generally do not all move in the same direction at the same time and a variety of factors can affect the price of a particular company’s securities. These factors may include, but are not limited to, poor earnings reports, a loss of customers, litigation against the company, general unfavorable performance of the company’s sector or industry, or changes in government regulations affecting the company or its industry.

Shareholder Concentration. At period end, one shareholder owned 20% or more of the Fund’s total outstanding shares.

The shareholder is a related party of the Fund. Related parties may include, but are not limited to, the investment manager and its affiliates, affiliated broker dealers, fund of funds, and directors or employees. The related party owned 67% of the Fund’s total outstanding shares at period end.

5. Market Risk Factors

The Fund’s investments in securities and/or financial derivatives may expose the Fund to various market risk factors:

Commodity Risk. Commodity risk relates to the change in value of commodities or commodity indexes as they relate to increases or decreases in the commodities market. Commodities are physical assets that have tangible properties. Examples of these types of assets are crude oil, heating oil, metals, livestock, and agricultural products.

Credit Risk. Credit risk relates to the ability of the issuer of debt to meet interest and principal payments, or both, as they come due. In general, lower-grade, higher-yield debt securities are subject to credit risk to a greater extent than lower-yield, higher-quality securities.

Equity Risk. Equity risk relates to the change in value of equity securities as they relate to increases or decreases in the general market.

Foreign Exchange Rate Risk. Foreign exchange rate risk relates to the change in the U.S. dollar value of a security held that is denominated in a foreign currency. The U.S. dollar value of a foreign currency denominated security will decrease as the dollar appreciates against the currency, while the U.S. dollar value will increase as the dollar depreciates against the currency.

Interest Rate Risk. Interest rate risk refers to the fluctuations in value of fixed-income securities resulting from the inverse relationship between price and yield. For example, an increase in general interest rates will tend to reduce the market value of already issued fixed-income investments, and a decline in general interest rates will tend to increase their value. In addition, debt securities with longer maturities, which tend to have higher yields, are subject to potentially greater fluctuations in value from changes in interest rates than obligations with shorter maturities.

Volatility Risk. Volatility risk refers to the magnitude of the movement, but not the direction of the movement, in a financial instrument’s price over a defined time period. Large increases or decreases in a financial instrument’s price over a relative time period typically indicate greater volatility risk, while small increases or decreases in its price typically indicate lower volatility risk.

6. Shares of Beneficial Interest

The Fund has authorized an unlimited number of $0.001 par value shares of beneficial interest of each class. Transactions in shares of beneficial interest were as follows:

16 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

6. Shares of Beneficial Interest (Continued)

| | | | | | | | | | | | | | | | | | | | |

| | | Six Months Ended June 30, 2017 | | | | | | Year Ended December 31, 2016 | |

| | | Shares | | | Amount | | | | | | Shares | | | Amount | |

Non-Service Shares | | | | | | | | | | | | | | | | | | | | |

Sold | | | 147,480 | | | $ | 11,251,319 | | | | | | | | 260,318 | | | $ | 19,152,890 | |

Dividends and/or distributions reinvested | | | 881,557 | | | | 66,743,996 | | | | | | | | 674,971 | | | | 48,415,668 | |

Redeemed | | | (593,088) | | | | (46,542,812) | | | | | | | | (1,219,400) | | | | (89,285,818) | |

Net increase (decrease) | | | 435,949 | | | $ | 31,452,503 | | | | | | | | (284,111) | | | $ | (21,717,260) | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | | | | | |

Service Shares | | | | | | | | | | | | | | | | | | | | |

Sold | | | 23,924 | | | $ | 1,807,373 | | | | | | | | 50,885 | | | $ | 3,568,573 | |

Dividends and/or distributions reinvested | | | 51,387 | | | | 3,695,269 | | | | | | | | 39,878 | | | | 2,737,189 | |

Redeemed | | | (48,900) | | | | (3,649,574) | | | | | | | | (127,436) | | | | (8,923,664) | |

Net increase (decrease) | | | 26,411 | | | $ | 1,853,068 | | | | | | | | (36,673) | | | $ | (2,617,902) | |

| | | | | | | | | | | | | | | | | | | | |

7. Purchases and Sales of Securities

The aggregate cost of purchases and proceeds from sales of securities, other than short-term obligations and investments in IGMMF, for the reporting period were as follows:

| | | | | | | | | | | | |

| | | Purchases | | | | | | Sales | |

Investment securities | | $ | 426,986,726 | | | | | | | $ | 467,440,092 | |

8. Fees and Other Transactions with Affiliates

Management Fees. Under the investment advisory agreement, the Fund pays the Manager a management fee based on the daily net assets of the Fund at an annual rate as shown in the following table:

| | | | |

| Fee Schedule | | | |

Up to $200 million | | | 0.75% | |

Next $200 million | | | 0.72 | |

Next $200 million | | | 0.69 | |

Next $200 million | | | 0.66 | |

Next $700 million | | | 0.60 | |

Over $1.5 billion | | | 0.58 | |

The Fund’s effective management fee for the reporting period was 0.71% of average annual net assets before any applicable waivers.

Sub-Adviser Fees. The Manager has retained the Sub-Adviser to provide the day-to-day portfolio management of the Fund. Under the Sub-Advisory Agreement, the Manager pays the Sub-Adviser an annual fee in monthly installments, equal to a percentage of the investment management fee collected by the Manager from the Fund, which shall be calculated after any investment management fee waivers. The fee paid to the Sub-Adviser is paid by the Manager, not by the Fund.

Transfer Agent Fees. OFI Global (the “Transfer Agent”) serves as the transfer and shareholder servicing agent for the Fund. The Fund pays the Transfer Agent a fee based on annual net assets. Fees incurred and average net assets for each class with respect to these services are detailed in the Statement of Operations and Financial Highlights, respectively.

Sub-Transfer Agent Fees. The Transfer Agent has retained Shareholder Services, Inc., a wholly-owned subsidiary of OFI (the “Sub-Transfer Agent”), to provide the day-to-day transfer agent and shareholder servicing of the Fund. Under the Sub-Transfer Agency Agreement, the Transfer Agent pays the Sub-Transfer Agent an annual fee in monthly installments, equal to a percentage of the transfer agent fee collected by the Transfer Agent from the Fund, which shall be calculated after any applicable fee waivers. The fee paid to the Sub-Transfer Agent is paid by the Transfer Agent, not by the Fund.

Trustees’ Compensation. The Fund’s Board of Trustees (“Board”) has adopted a compensation deferral plan for Independent Trustees that enables Trustees to elect to defer receipt of all or a portion of the annual compensation they are entitled to receive from the Fund. For purposes of determining the amount owed to the Trustees under the plan, deferred amounts are treated as though equal dollar amounts had been invested in shares of the Fund or in other Oppenheimer funds selected by the Trustees. The Fund purchases shares of the funds selected for deferral by the Trustees in amounts equal to his or her deemed investment, resulting in a Fund asset equal to the deferred compensation liability. Such assets are included as a component of “Other” within the asset section of the Statement of Assets and Liabilities. Deferral of Trustees’ fees under the plan will not affect the net assets of the Fund and will not materially affect the Fund’s assets, liabilities or net investment income per share. Amounts will be deferred until distributed in accordance with the compensation deferral plan.

Distribution and Service Plan for Service Shares. The Fund has adopted a Distribution and Service Plan (the “Plan”) pursuant to Rule 12b-1 under the 1940 Act for Service shares to pay OppenheimerFunds Distributor, Inc. (the “Distributor”), for distribution related services, personal service and

17 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

NOTES TO FINANCIAL STATEMENTS Unaudited / Continued

8. Fees and Other Transactions with Affiliates (Continued)

account maintenance for the Fund’s Service shares. Under the Plan, payments are made periodically at an annual rate of 0.25% of the daily net assets of Service shares of the Fund. The Distributor currently uses all of those fees to compensate sponsors of the insurance product that offers Fund shares, for providing personal service and maintenance of accounts of their variable contract owners that hold Service shares. These fees are paid out of the Fund’s assets on an on-going basis and increase operating expenses of the Service shares, which results in lower performance compared to the Fund’s shares that are not subject to a service fee. Fees incurred by the Fund under the Plan are detailed in the Statement of Operations.

Waivers and Reimbursements of Expenses. The Manager has contractually agreed to limit the Fund’s expenses after payments, waivers and/or reimbursements and reduction to custodian expenses, excluding any applicable dividend expense, taxes, interest and fees from borrowing, any subsidiary expenses, Acquired Fund Fees and Expenses, brokerage commissions, unusual and infrequent expenses and certain other Fund expenses; so that those expenses, as percentages of daily net assets, will not exceed the annual rate of 0.80% for Non-Service shares and 1.05% for Service shares.

During the reporting period, the Manager waived fees and/or reimbursed the Fund as follows:

| | | | |

Non-Service shares | | $ | 111,600 | |

Service shares | | | 5,893 | |

This fee waiver and/or expense reimbursement may not be amended or withdrawn for one year from the date of the Fund’s prospectus, unless approved by the Board.

The Manager will waive fees and/or reimburse Fund expenses in an amount equal to the indirect management fees incurred through the Fund’s investment in IGMMF. During the reporting period, the Manager waived fees and/or

reimbursed the Fund $7,404 for IGMMF management fees. This fee waiver and/or expense reimbursement may not be amended or withdrawn for one year from the date of the Fund’s prospectus, unless approved by the Board.

9. Borrowings and Other Financing

Joint Credit Facility. A number of mutual funds managed by the Manager participate in a $1.3 billion revolving credit facility (the “Facility”) intended to provide short-term financing, if necessary, subject to certain restrictions in connection with atypical redemption activity. Expenses and fees related to the Facility are paid by the participating funds and are disclosed separately or as other expenses on the Statement of Operations. The Fund did not utilize the Facility during the reporting period.

18 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

PORTFOLIO PROXY VOTING POLICIES AND GUIDELINES; UPDATES TO STATEMENTS OF INVESTMENTS Unaudited

The Fund has adopted Portfolio Proxy Voting Policies and Guidelines under which the Fund votes proxies relating to securities (“portfolio proxies”) held by the Fund. A description of the Fund’s Portfolio Proxy Voting Policies and Guidelines is available (i) without charge, upon request, by calling the Fund toll-free at 1.800.CALL OPP (225.5677), (ii) on the Fund’s website at www.oppenheimerfunds.com, and (iii) on the SEC’s website at www.sec.gov. In addition, the Fund is required to file Form N-PX, with its complete proxy voting record for the 12 months ended June 30th, no later than August 31st of each year. The Fund’s voting record is available (i) without charge, upon request, by calling the Fund toll-free at 1.800.CALL OPP (225.5677), and (ii) in the Form N-PX filing on the SEC’s website at www.sec.gov.

The Fund files its complete schedule of portfolio holdings with the SEC for the first quarter and the third quarter of each fiscal year on Form N-Q. The Fund’s Form N-Q filings are available on the SEC’s website at www.sec.gov. Those forms may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

19 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

DISTRIBUTION SOURCES Unaudited

For any distribution that took place over the last six months of the Fund’s reporting period, the table below details on a per-share basis the percentage of the Fund’s total distribution payment amount that was derived from the following sources: net income, net profit from the sale of securities, and other capital sources. Other capital sources represent a return of capital. A return of capital may occur, for example, when some or all of the money that you invested in the Fund is paid back to you. A return of capital distribution does not necessarily reflect the Fund’s investment performance and should not be confused with “yield” or “income.” You should not draw any conclusions about each Fund’s investment performance from the amounts of these distributions. This information is based upon income and capital gains using generally accepted accounting principles as of the date of each distribution. Because the Fund is actively managed, the relative amount of the Fund’s total distributions derived from various sources over the calendar year may change. Please note that this information should not be used for tax reporting purposes as the tax character of distributable income may differ from the amounts used for this notification. You will receive communication in the first quarter of each calendar year detailing the actual amount of the taxable and non-taxable portion of distributions paid to you during the tax year.

For the most current information, please go to oppenheimerfunds.com. Select your Fund, then the ’Detailed’ tab; where ‘Dividends’ are shown, the Fund’s latest pay date will be followed by the sources of any distribution, updated daily.

| | | | | | | | | | | | | | | | |

Fund Name | | Pay

Date | | | Net Income | | | Net Profit

from Sale | | | Other

Capital

Sources | |

Oppenheimer Discovery Mid Cap Growth Fund/VA | | | 6/20/17 | | | | 0.0% | | | | 50.5% | | | | 49.5% | |

20 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

THIS PAGE INTENTIONALLY LEFT BLANK.

21 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

THIS PAGE INTENTIONALLY LEFT BLANK.

22 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

THIS PAGE INTENTIONALLY LEFT BLANK.

23 OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

OPPENHEIMER DISCOVERY MID CAP GROWTH FUND/VA

A Series of Oppenheimer Variable Account Funds

| | |

Trustees and Officers | | Robert J. Malone, Chairman of the Board of Trustees and Trustee |

| | Andrew J. Donohue, Trustee |

| | Jon S. Fossel, Trustee |

| | Richard F. Grabish, Trustee |