| | |

| UNITED STATES

SECURITIES AND EXCHANGE COMMISSION |

| | |

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

|

| | |

| Investment Company Act file number: | (811-04345) |

| | |

| Exact name of registrant as specified in charter: | Putnam Tax Free Income Trust |

| | |

| Address of principal executive offices: | One Post Office Square, Boston, Massachusetts 02109 |

| | |

| Name and address of agent for service: | Robert T. Burns, Vice President

One Post Office Square

Boston, Massachusetts 02109 |

| | |

| Copy to: | John W. Gerstmayr, Esq.

Ropes & Gray LLP

800 Boylston Street

Boston, Massachusetts 02199-3600 |

| | |

| Registrant’s telephone number, including area code: | (617) 292-1000 |

| | |

| Date of fiscal year end: | July 31, 2012 |

| | |

| Date of reporting period: | August 1, 2011 — January 31, 2012 |

| | |

|

Item 1. Report to Stockholders: | |

| | |

| The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940: | |

Putnam

AMT-Free

Municipal Fund

Semiannual report

1 | 31 | 12

| | |

| Message from the Trustees | 1 | |

| |

| About the fund | 2 | |

| |

| Performance snapshot | 4 | |

| |

| Interview with your fund’s portfolio manager | 5 | |

| |

| Your fund’s performance | 10 | |

| |

| Your fund’s expenses | 12 | |

| |

| Terms and definitions | 14 | |

| |

| Other information for shareholders | 15 | |

| |

| Financial statements | 16 | |

| |

Message from the Trustees

Dear Fellow Shareholder:

Markets in early 2012 have signaled a more consistently positive direction, supported by strengthening fundamentals. In the United States, where corporate earnings have been strong for more than a year, the employment picture has also brightened in recent months. The Federal Reserve has pledged to leave rates at historic lows at least through the end of 2014, and the beleaguered U.S. housing market has finally shown signs of recovery. The European debt situation and likely recession in that region continue to weigh heavily on markets, of course, alongside high unemployment here at home. However, we are encouraged by the change in investor sentiment.

We believe there are numerous investment opportunities resulting from the many market dislocations in recent years. Putnam’s rigorous bottom-up, fundamental investment approach is well suited to this environment, and the Putnam team is committed to uncovering returns for our shareholders, while seeking to guard against downside risk.

Please join us in welcoming the return of Elizabeth T. Kennan to the Board of Trustees. Dr. Kennan, who served as a Trustee from 1992 until 2010, has rejoined the Board, effective January 1, 2012. Dr. Kennan is a Partner of Cambus-Kenneth Farm (thoroughbred horse breeding and general farming), and is also President Emeritus of Mount Holyoke College.

We would also like to take this opportunity to welcome new shareholders to the fund and to thank all of our investors for your continued confidence in Putnam.

About the fund

Seeking high current income free from federal taxes

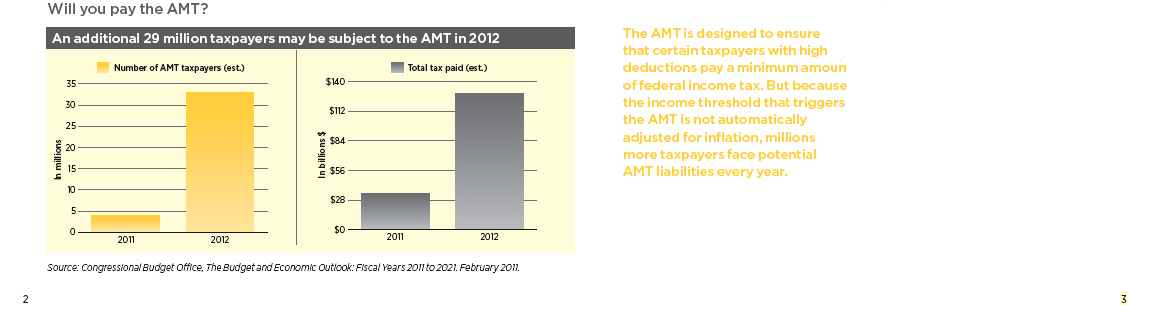

Municipal bonds have long been popular investments because they provide income exempt from federal tax, though capital gains are taxable. Putnam AMT-Free Municipal Fund seeks income exempt from traditional income tax as well as from the federal alternative minimum tax, or AMT.

The AMT is a federal tax that operates in tandem with the regular income tax system. Taxpayers subject to the AMT generally must pay a larger amount in tax determined by AMT rules — and the difference can be thousands of dollars for many with household incomes above $150,000. It is estimated that in 2012, an additional 29 million taxpayers might be paying the AMT, unless the federal government changes the law.

If you are subject to the AMT, investments that could increase your tax liability include private-activity municipal bonds, which back development projects, such as certain housing and resource recovery projects.

Putnam AMT-Free Municipal Fund aims to serve investors subject to the AMT. The fund seeks to avoid bonds whose income would be taxable under AMT rules, though income may be subject to state taxes.

The fund’s portfolio managers research the municipal market to buy bonds that are not subject to the AMT. Pursuing the fund’s mandate, they also keep the fund invested in high-quality bonds, favoring those that have intermediate- to long-term maturities. The managers’ goal is to provide an attractive level of income exempt from all federal taxes.

Consider these risks before investing: Capital gains, if any, are taxable for federal and, in most cases, state purposes. Income from federal tax-exempt funds may be subject to state and local taxes. Funds that invest in bonds are subject to certain risks including interest-rate risk, credit risk, and inflation risk. As interest rates rise, the prices of bonds fall. Long-term bonds are more exposed to interest-rate risk than short-term bonds. Unlike bonds, bond funds have ongoing fees and expenses. The fund may invest significantly in particular segments of the tax-exempt debt market, making it more vulnerable to fluctuations in the values of the securities it holds than a fund that invests more broadly.

Understanding the AMT

The AMT is a separate, parallel federal income tax system, with two marginal tax rates, 26% and 28%, and different exemption amounts.

Under AMT rules, certain exclusions, exemptions, deductions, and credits that would reduce your regular taxable income are not allowed. You must “adjust” your regular taxable income to arrive at your alternative minimum taxable income. Then, after subtracting your AMT exemption amount, if your AMT liability is greater than your regular tax liability, you must pay both your regular tax and the difference. It is important to understand that a higher level of income will not necessarily cause you to owe the AMT. Rather, it is the relationship between your income and various trigger items, such as credits and deductions, that determines your AMT liability.

Managing this relationship can help avoid a costly surprise at tax time. Any number of items may trigger the tax, but large capital gains, personal exemptions, and deductions are the worst culprits.

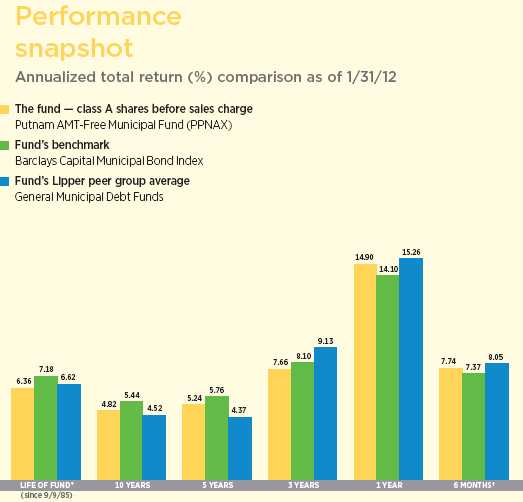

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. Share price, principal value, and return will fluctuate, and you may have a gain or a loss when you sell your shares. Performance of class A shares assumes reinvestment of distributions and does not account for taxes. Fund returns in the bar chart do not reflect a sales charge of 4.00%; had they, returns would have been lower. See pages 5 and 10–12 for additional performance information. For a portion of the periods, the fund had expense limitations, without which returns would have been lower. To obtain the most recent month-end performance, visit putnam.com.

* Performance for class A shares before their inception (9/20/93) is derived from the historical performance of class B shares.

† Returns for the six-month period are not annualized, but cumulative.

4

Interview with your fund’s portfolio manager

How would you describe the environment in the municipal bond market during the six months ended January 31, 2012?

In the second half of the year, the municipal bond market gained back a good deal of what it had lost in the broad sell-off that occurred in the early months of 2011.

Despite last year’s dire predictions for the municipal bond market, widespread defaults never materialized, and the fiscal picture for states in general has been gradually improving. Defaults in 2011 were higher year over year, but generally were contained to the lower-rated sectors of the market. States continued to face challenges in balancing their budgets, but by late in the period all state legislatures that were slated to enact budgets had done so. Income tax receipts also began to modestly improve versus last year. All told, as investors ultimately realized that municipal credit conditions were not nearly as bleak as some had feared, they re-entered the municipal bond market and prices benefited.

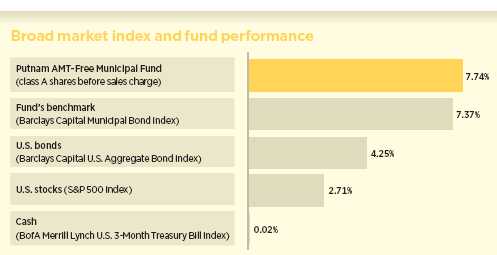

Against this backdrop, tax-exempt bonds posted solid returns and outpaced the broad taxable bond market, as measured by the Barclays Capital U.S. Aggregate Bond Index. Moreover, I am pleased to report that the fund outperformed its benchmark, although it slightly trailed the average return of its Lipper peer group.

This comparison shows your fund’s performance in the context of broad market indexes for the six months ended 1/31/12. See pages 4 and 10–12 for additional fund performance information. Index descriptions can be found on pages 14–15.

5

In August 2011, Standard & Poor’s [S&P] downgraded its credit rating for U.S. Treasuries and a number of municipal bonds. What impact did that have on the market?

On the heels of its August 5 downgrade of U.S. sovereign debt, S&P lowered its ratings from AAA to AA+ for more than 11,000 municipal securities, including taxable and tax-exempt securities. While this number does seem large, it covers less than 1% of the nearly $4 trillion municipal bond market. These securities all had links to the federal government, and according to S&P, the affected issues fall into four broad categories: municipal housing bonds backed by the federal government or invested in U.S. government securities; bonds of certain government-related entities in the housing and public power sectors; bonds backed by federal leases; and defeased bonds secured by U.S. Treasury and government agency securities held in escrow.

The downgrade was not surprising given the interdependence of state and federal finances, and S&P had been suggesting such a move was imminent for some time. That said, the change didn’t necessarily impact the ratings of states, 13 of which maintained their AAA general obligation, or “G.O.,” bond ratings as of January 2012. Rather, we believe S&P’s downgrades underscore the importance of performing intensive fundamental research when investing in the municipal bond market, and at Putnam, we independently research every bond we hold and assess the credit risk it represents before we add it to the portfolio.

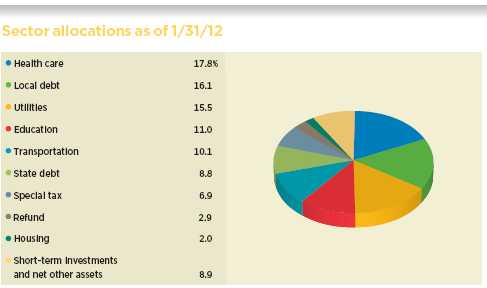

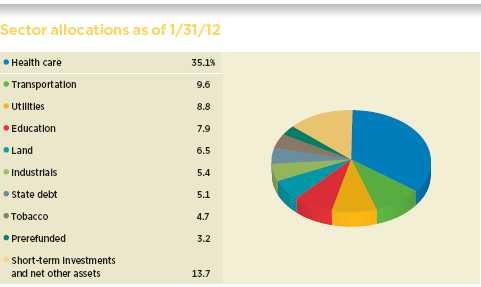

Allocations are represented as a percentage of the fund’s net assets. Summary information may differ from the portfolio schedule included in the financial statements due to the inclusion of derivative securities, the exclusion of as-of trades, if any, and the use of different classifications of securities for presentation purposes. Holdings and allocations may vary over time.

6

What effect did recent policy developments have on the tax-exempt bond market?

Congress’s negotiations over raising the debt ceiling last July created a 12-member bipartisan “super committee” tasked with recommending a plan to reduce the deficit by at least $1.2 trillion over the next 10 years. As their November deadline approached, many in the political press speculated that the committee would be unable to agree on a compromise, and that turned out to be the case. As a result, automatic, across-the-board cuts are slated to be implemented over 10 years, beginning in January 2013, in a process called “sequestration.”

Overall, we believe that this sequestration of funding is not necessarily a negative for municipal bonds, particularly given the recommendations that the super committee might have made. Some speculation arose that the committee, in an effort to raise revenue, would have recommended limiting the amount of municipal-bond interest that top income earners could exclude from their taxable income. In fact, a similar idea resurfaced in President Obama’s fiscal 2013 budget proposal, under which individuals and married couples earning more than $200,000 and $250,000, respectively, would only be able to exclude from federal taxes 28 cents of every dollar of municipal bond income earned. This new taxation of municipal bond interest could have the dual effect of reducing the demand for municipal bonds and increasing the costs to

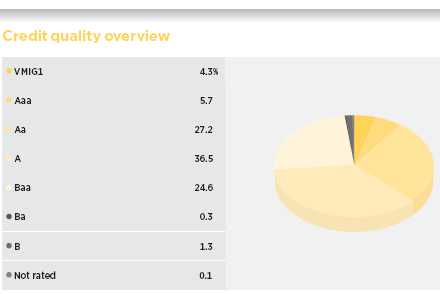

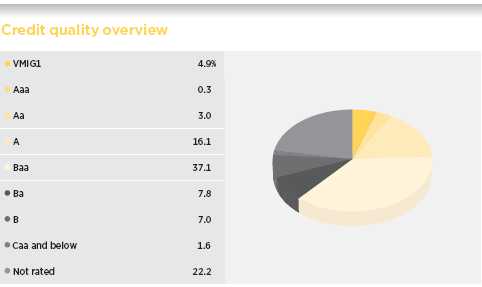

Credit qualities are shown as a percentage of portfolio market value as of 1/31/12. A bond rated Baa or higher (MIG3/VMIG3 or higher, for short-term debt) is considered investment grade. The chart reflects Moody’s ratings; percentages may include bonds or derivatives not rated by Moody’s but rated by Standard & Poor’s (S&P) or, if unrated by S&P, by Fitch, and then included in the closest equivalent Moody’s rating. Ratings will vary over time. Credit qualities are included for portfolio securities and are not included for derivative instruments and cash. The fund itself has not been rated by an independent rating agency.

7

municipal issuers. Although we believe such a change is not imminent, it is likely that a more wide-ranging debate over taxes will continue throughout the 2012 election year.

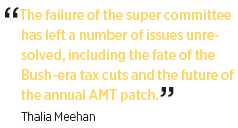

On the subject of taxes, we should also point out that the failure of the super committee to come to an agreement has left a number of other issues unresolved, including the fate of the Bush-era tax cuts and the future of the annual alternative minimum tax [AMT] “patch,” which sets the income threshold associated with the AMT. We believe these issues and others will be debated over the coming months, and we will be closely monitoring developments.

How did you position the portfolio during the past six months?

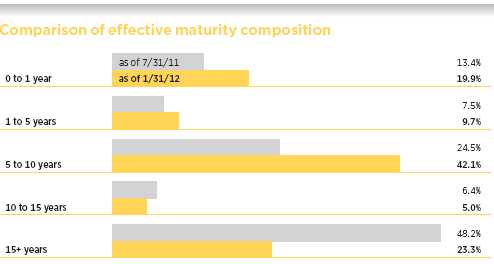

We positioned the portfolio to benefit from improving fundamentals in the municipal bond market. While we felt that the budget challenges faced by many states were significant, we were confident that conditions would improve as long as the broad economy did not stall. Against this backdrop, we believed that essential service revenue bonds remained attractive, while we remained highly selective regarding the fund’s positioning in local G.O.s, which are securities issued at the city or county level. We believe that as the federal government looks to reduce transfer payments to the states — and as states, in turn, seek to close their deficits by reducing spending — these types of bonds are at risk for downgrades or other headline-driven price volatility. And unlike state general obligation bonds, local G.O.s rely more on property tax revenue than on income or sales taxes. With real-estate prices still under pressure in many markets, property taxes have been slower to recover than other tax sources.

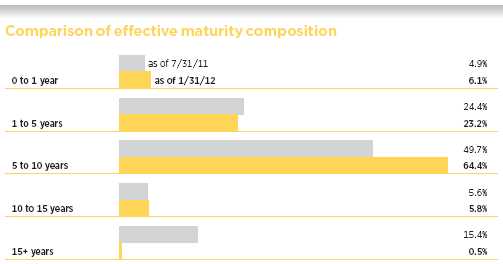

This chart illustrates the fund’s composition by effective maturity, showing the percentage of holdings in different maturity ranges and how the composition has changed over the past six months. Holdings and maturity ranges will vary over time. The effective maturity dates of bonds with call features may change as a result of market conditions.

8

From a credit perspective, we held an overweight position in A- and Baa-rated securities versus the fund’s benchmark. In terms of sectors, we favored higher-education, utility, and health-care bonds, particularly those of hospitals and continuing-care retirement communities. Overall, this positioning generally helped the fund’s relative performance during the past six months.

What is your outlook for the months ahead?

While technical factors in the market have been positive — specifically, lighter supply and stable demand — uncertainty remains. We believe that states will continue to face financial challenges as the economy struggles to find its footing. For the most part, however, we believe that the fiscal conditions of states and municipalities are showing signs of improvement: Tax receipts are beginning to improve, albeit slowly, and we believe defaults will remain relatively low.

We remain focused on the economy and Congress’s plans to reduce the deficit. Higher federal income tax rates, a change in the tax status of municipal bonds, or significant cuts in state funding all would have consequences for the municipal bond market. But for investors with longer time horizons, we believe that our actively managed approach remains a prudent way to diversify holdings and generate tax-exempt income in the municipal bond market.

Thank you, Thalia, for your time and insights today.

The views expressed in this report are exclusively those of Putnam Management and are subject to change. They are not meant as investment advice.

Please note that the holdings discussed in this report may not have been held by the fund for the entire period. Portfolio composition is subject to review in accordance with the fund’s investment strategy and may vary in the future. Current and future portfolio holdings are subject to risk.

Portfolio Manager Thalia Meehan holds a B.A. from Williams College. A CFA charterholder, Thalia joined Putnam in 1989 and has been in the investment industry since 1983.

In addition to Thalia, your fund’s portfolio managers are Paul M. Drury, CFA, and Susan A. McCormack, CFA.

IN THE NEWS

The U.S. unemployment rate fell to 8.3% in January, with the nation’s employers adding 243,000 jobs, according to the Labor Department. This was the fastest pace of job growth since April 2011 and was the fifth straight month of unemployment rate declines. The nation’s jobless rate is still above the 5.2%-to-6% range that Federal Reserve (Fed) officials say is consistent with maximum employment. According to the Labor Department, 12.8 million Americans remain unemployed. In testimony before the Senate Budget Committee in early February, Fed Chairman Ben S. Bernanke said that the U.S. job market is far from “operating normally.” The Fed chairman reiterated that the Fed’s benchmark interest rate will remain near zero at least through late 2014, and again called on U.S. lawmakers to reduce the federal deficit.

9

Your fund’s performance

This section shows your fund’s performance, price, and distribution information for periods ended January 31, 2012, the end of the first half of its current fiscal year. In accordance with regulatory requirements for mutual funds, we also include performance as of the most recent calendar quarter-end and expense information taken from the fund’s current prospectus. Performance should always be considered in light of a fund’s investment strategy. Data represent past performance. Past performance does not guarantee future results. More recent returns may be less or more than those shown. Investment return and principal value will fluctuate, and you may have a gain or a loss when you sell your shares. Performance information does not reflect any deduction for taxes a shareholder may owe on fund distributions or on the redemption of fund shares. For the most recent month-end performance, please visit the Individual Investors section at putnam.com or call Putnam at 1-800-225-1581. Class Y shares are not available to all investors. See the Terms and Definitions section in this report for definitions of the share classes offered by your fund.

Fund performance Total return for periods ended 1/31/12

| | | | | | | | | |

| | Class A | Class B | Class C | Class M | Class Y |

| (inception dates) | (9/20/93) | (9/9/85) | (7/26/99) | (6/1/95) | (1/2/08) |

|

| | Before | After | | | | | Before | After | Net |

| | sales | sales | Before | After | Before | After | sales | sales | asset |

| | charge | charge | CDSC | CDSC | CDSC | CDSC | charge | charge | value |

|

| Annual average | | | | | | | | | |

| (life of fund) | 6.36% | 6.19% | 5.99% | 5.99% | 5.73% | 5.73% | 6.12% | 5.99% | 6.13% |

|

| 10 years | 60.08 | 53.78 | 50.14 | 50.14 | 47.95 | 47.95 | 55.45 | 50.35 | 55.53 |

| Annual average | 4.82 | 4.40 | 4.15 | 4.15 | 3.99 | 3.99 | 4.51 | 4.16 | 4.52 |

|

| 5 years | 29.07 | 24.01 | 24.99 | 22.99 | 24.30 | 24.30 | 27.31 | 23.26 | 29.54 |

| Annual average | 5.24 | 4.40 | 4.56 | 4.23 | 4.45 | 4.45 | 4.95 | 4.27 | 5.31 |

|

| 3 years | 24.78 | 19.68 | 22.37 | 19.37 | 22.02 | 22.02 | 23.76 | 19.78 | 25.71 |

| Annual average | 7.66 | 6.17 | 6.96 | 6.08 | 6.86 | 6.86 | 7.36 | 6.20 | 7.93 |

|

| 1 year | 14.90 | 10.27 | 14.19 | 9.19 | 13.97 | 12.97 | 14.55 | 10.86 | 15.15 |

|

| 6 months | 7.74 | 3.42 | 7.46 | 2.46 | 7.34 | 6.34 | 7.61 | 4.16 | 7.90 |

|

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. After-sales-charge returns for class A and M shares reflect the deduction of the maximum 4.00% and 3.25% sales charge, respectively, levied at the time of purchase. Class B share returns after contingent deferred sales charge (CDSC) reflect the applicable CDSC, which is 5% in the first year, declining over time to 1% in the sixth year, and is eliminated thereafter. Class C share returns after CDSC reflect a 1% CDSC for the first year that is eliminated thereafter. Class Y shares have no initial sales charge or CDSC. Performance for class A, C, M, and Y shares before their inception is derived from the historical performance of class B shares, adjusted for the applicable sales charge (or CDSC) and, for class C shares, the higher operating expenses for such shares.

For a portion of the periods, the fund had expense limitations, without which returns would have been lower.

Class B share performance does not assume conversion to class A shares.

10

Comparative index returns For periods ended 1/31/12

| | |

| | Barclays Capital | Lipper General Municipal Debt Funds |

| | Municipal Bond Index | category average* |

|

| Annual average (life of fund) | 7.18% | 6.62% |

|

| 10 years | 69.79 | 55.89 |

| Annual average | 5.44 | 4.52 |

|

| 5 years | 32.32 | 24.05 |

| Annual average | 5.76 | 4.37 |

|

| 3 years | 26.31 | 30.14 |

| Annual average | 8.10 | 9.13 |

|

| 1 year | 14.10 | 15.26 |

|

| 6 months | 7.37 | 8.05 |

|

Index and Lipper results should be compared with fund performance before sales charge, before CDSC, or at net asset value.

* Over the 6-month, 1-year, 3-year, 5-year, 10-year, and life-of-fund periods ended 1/31/12, there were 258, 246, 223, 194, 161, and 30 funds, respectively, in this Lipper category.

Fund price and distribution information For the six-month period ended 1/31/12

| | | | | | | |

| Distributions | Class A | Class B | Class C | Class M | Class Y |

|

| Number | 6 | 6 | 6 | 6 | 6 |

|

| Income 1 | $0.310229 | $0.263525 | $0.252171 | $0.289944 | $0.327654 |

|

| Capital gains 2 | — | — | — | — | — |

|

| Total | $0.310229 | $0.263525 | $0.252171 | $0.289944 | $0.327654 |

|

| | Before | After | Net | Net | Before | After | Net |

| | sales | sales | asset | asset | sales | sales | asset |

| Share value | charge | charge | value | value | charge | charge | value |

|

| 7/31/11 | $14.66 | $15.27 | $14.67 | $14.69 | $14.69 | $15.18 | $14.66 |

|

| 1/31/12 | 15.47 | 16.11 | 15.49 | 15.51 | 15.51 | 16.03 | 15.48 |

|

| | Before | After | Net | Net | Before | After | Net |

| | sales | sales | asset | asset | sales | sales | asset |

| Current yield (end of period) | charge | charge | value | value | charge | charge | value |

|

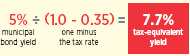

| Current dividend rate 3 | 3.87% | 3.71% | 3.25% | 3.10% | 3.59% | 3.48% | 4.09% |

|

| Taxable equivalent 4 | 5.95 | 5.71 | 5.00 | 4.77 | 5.52 | 5.35 | 6.29 |

|

| Current 30-day SEC yield 5 | N/A | 2.56 | 2.06 | 1.91 | N/A | 2.33 | 2.88 |

|

| Taxable equivalent 4 | N/A | 3.94 | 3.17 | 2.94 | N/A | 3.58 | 4.43 |

|

The classification of distributions, if any, is an estimate. Before-sales-charge share value and current dividend rate for class A and M shares, if applicable, do not take into account any sales charge levied at the time of purchase. After-sales-charge share value, current dividend rate, and current 30-day SEC yield, if applicable, are calculated assuming that the maximum sales charge (4.00% for class A shares and 3.25% for class M shares) was levied at the time of purchase. Final distribution information will appear on your year-end tax forms.

1 For some investors, investment income may be subject to the federal alternative minimum tax.

2 Capital gains, if any, are taxable for federal and, in most cases, state purposes.

3 Most recent distribution, excluding capital gains, annualized and divided by share price before or after sales charge at period-end.

4 Assumes maximum 35.00% federal and state combined tax rate for 2012. Results for investors subject to lower tax rates would not be as advantageous.

5 Based only on investment income and calculated using the maximum offering price for each share class, in accordance with SEC guidelines.

11

Fund performance as of most recent calendar quarter

Total return for periods ended 12/31/11

| | | | | | | | | |

| | Class A | Class B | Class C | Class M | Class Y |

| (inception dates) | (9/20/93) | (9/9/85) | (7/26/99) | (6/1/95) | (1/2/08) |

|

| | Before | After | | | | | Before | After | Net |

| | sales | sales | Before | After | Before | After | sales | sales | asset |

| | charge | charge | CDSC | CDSC | CDSC | CDSC | charge | charge | value |

|

| Annual average | | | | | | | | | |

| (life of fund) | 6.27% | 6.10% | 5.90% | 5.90% | 5.64% | 5.64% | 6.03% | 5.90% | 6.04% |

|

| 10 years | 58.81 | 52.58 | 49.04 | 49.04 | 46.87 | 46.87 | 54.25 | 49.25 | 54.46 |

| Annual average | 4.73 | 4.32 | 4.07 | 4.07 | 3.92 | 3.92 | 4.43 | 4.09 | 4.44 |

|

| 5 years | 25.20 | 20.28 | 21.19 | 19.19 | 20.54 | 20.54 | 23.48 | 19.53 | 25.59 |

| Annual average | 4.60 | 3.76 | 3.92 | 3.57 | 3.81 | 3.81 | 4.31 | 3.63 | 4.66 |

|

| 3 years | 25.36 | 20.36 | 22.88 | 19.88 | 22.42 | 22.42 | 24.22 | 20.29 | 26.26 |

| Annual average | 7.83 | 6.37 | 7.11 | 6.23 | 6.98 | 6.98 | 7.50 | 6.35 | 8.08 |

|

| 1 year | 10.40 | 5.93 | 9.75 | 4.75 | 9.55 | 8.55 | 10.03 | 6.45 | 10.74 |

|

| 6 months | 6.35 | 2.14 | 5.95 | 0.95 | 5.85 | 4.85 | 6.09 | 2.64 | 6.43 |

|

Your fund’s expenses

As a mutual fund investor, you pay ongoing expenses, such as management fees, distribution fees (12b-1 fees), and other expenses. Using the following information, you can estimate how these expenses affect your investment and compare them with the expenses of other funds. You may also pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial representative.

Expense ratios

| | | | | |

| | Class A | Class B | Class C | Class M | Class Y |

|

| Total annual operating expenses for the fiscal year | | | | | |

| ended 7/31/11 | 0.77% | 1.39% | 1.54% | 1.04% | 0.54% |

|

| Annualized expense ratio for the six-month period | | | | | |

| ended 1/31/12 | 0.78% | 1.40% | 1.55% | 1.05% | 0.55% |

|

Fiscal-year expense information in this table is taken from the most recent prospectus, is subject to change, and may differ from that shown for the annualized expense ratio and in the financial highlights of this report. Expenses are shown as a percentage of average net assets.

12

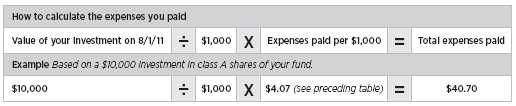

Expenses per $1,000

The following table shows the expenses you would have paid on a $1,000 investment in the fund from August 1, 2011, to January 31, 2012. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

| | | | | |

| | Class A | Class B | Class C | Class M | Class Y |

|

| Expenses paid per $1,000*† | $4.07 | $7.30 | $8.08 | $5.48 | $2.87 |

|

| Ending value (after expenses) | $1,077.40 | $1,074.60 | $1,073.40 | $1,076.10 | $1,079.00 |

|

* Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 1/31/12. The expense ratio may differ for each share class.

† Expenses are calculated by multiplying the expense ratio by the average account value for the period; then multiplying the result by the number of days in the period; and then dividing that result by the number of days in the year.

Estimate the expenses you paid

To estimate the ongoing expenses you paid for the six months ended January 31, 2012, use the following calculation method. To find the value of your investment on August 1, 2011, call Putnam at 1-800-225-1581.

Compare expenses using the SEC’s method

The Securities and Exchange Commission (SEC) has established guidelines to help investors assess fund expenses. Per these guidelines, the following table shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total costs) of investing in the fund with those of other funds. All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

| | | | | |

| | Class A | Class B | Class C | Class M | Class Y |

|

| Expenses paid per $1,000*† | $3.96 | $7.10 | $7.86 | $5.33 | $2.80 |

|

| Ending value (after expenses) | $1,021.22 | $1,018.10 | $1,017.34 | $1,019.86 | $1,022.37 |

|

* Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 1/31/12. The expense ratio may differ for each share class.

† Expenses are calculated by multiplying the expense ratio by the average account value for the period; then multiplying the result by the number of days in the period; and then dividing that result by the number of days in the year.

13

Terms and definitions

Important terms

Total return shows how the value of the fund’s shares changed over time, assuming you held the shares through the entire period and reinvested all distributions in the fund.

Before sales charge, or net asset value, is the price, or value, of one share of a mutual fund, without a sales charge. Before-sales-charge figures fluctuate with market conditions, and are calculated by dividing the net assets of each class of shares by the number of outstanding shares in the class.

After sales charge is the price of a mutual fund share plus the maximum sales charge levied at the time of purchase. After-sales-charge performance figures shown here assume the 4.00% maximum sales charge for class A shares and 3.25% for class M shares.

Contingent deferred sales charge (CDSC) is generally a charge applied at the time of the redemption of class B or C shares and assumes redemption at the end of the period. Your fund’s class B CDSC declines over time from a 5% maximum during the first year to 1% during the sixth year. After the sixth year, the CDSC no longer applies. The CDSC for class C shares is 1% for one year after purchase.

Share classes

Class A shares are generally subject to an initial sales charge and no CDSC (except on certain redemptions of shares bought without an initial sales charge).

Class B shares are not subject to an initial sales charge. They may be subject to a CDSC.

Class C shares are not subject to an initial sales charge and are subject to a CDSC only if the shares are redeemed during the first year.

Class M shares have a lower initial sales charge and a higher 12b-1 fee than class A shares and no CDSC.

Class Y shares are not subject to an initial sales charge or CDSC, and carry no 12b-1 fee. They are generally only available to corporate and institutional clients and clients in other approved programs.

Fixed-income terms

Current yield is the annual rate of return earned from dividends or interest of an investment. Current yield is expressed as a percentage of the price of a security, fund share, or principal investment.

Yield curve is a graph that plots the yields of bonds with equal credit quality against their differing maturity dates, ranging from shortest to longest. It is used as a benchmark for other debt, such as mortgage or bank lending rates.

Comparative indexes

Barclays Capital Municipal Bond Index is an unmanaged index of long-term fixed-rate investment-grade tax-exempt bonds.

Barclays Capital U.S. Aggregate Bond Index is an unmanaged index of U.S. investment-grade fixed-income securities.

BofA (Bank of America) Merrill Lynch U.S. 3-Month Treasury Bill Index is an unmanaged index that seeks to measure the performance of U.S. Treasury bills available in the marketplace.

S&P 500 Index is an unmanaged index of common stock performance.

Indexes assume reinvestment of all distributions and do not account for fees. Securities and performance of a fund and an index will differ. You cannot invest directly in an index.

Lipper is a third-party industry-ranking entity that ranks mutual funds. Its rankings do not reflect sales charges. Lipper rankings are based

14

on total return at net asset value relative to other funds that have similar current investment styles or objectives as determined by Lipper. Lipper may change a fund’s category assignment at its discretion. Lipper category averages reflect performance trends for funds within a category.

Other information for shareholders

Important notice regarding delivery of shareholder documents

In accordance with Securities and Exchange Commission (SEC) regulations, Putnam sends a single copy of annual and semiannual shareholder reports, prospectuses, and proxy statements to Putnam shareholders who share the same address, unless a shareholder requests otherwise. If you prefer to receive your own copy of these documents, please call Putnam at 1-800-225-1581, and Putnam will begin sending individual copies within 30 days.

Proxy voting

Putnam is committed to managing our mutual funds in the best interests of our shareholders. The Putnam funds’ proxy voting guidelines and procedures, as well as information regarding how your fund voted proxies relating to portfolio securities during the 12-month period ended June 30, 2011, are available in the Individual Investors section of putnam.com, and on the SEC’s website, www.sec.gov. If you have questions about finding forms on the SEC’s website, you may call the SEC at 1-800-SEC-0330. You may also obtain the Putnam funds’ proxy voting guidelines and procedures at no charge by calling Putnam’s Shareholder Services at 1-800-225-1581.

Fund portfolio holdings

The fund will file a complete schedule of its portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. Shareholders may obtain the fund’s Forms N-Q on the SEC’s website at www.sec.gov. In addition, the fund’s Forms N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. You may call the SEC at 1-800-SEC-0330 for information about the SEC’s website or the operation of the Public Reference Room.

Trustee and employee fund ownership

Putnam employees and members of the Board of Trustees place their faith, confidence, and, most importantly, investment dollars in Putnam mutual funds. As of January 31, 2012, Putnam employees had approximately $325,000,000 and the Trustees had approximately $75,000,000 invested in Putnam mutual funds. These amounts include investments by the Trustees’ and employees’ immediate family members as well as investments through retirement and deferred compensation plans.

15

Financial statements

A guide to financial statements

These sections of the report, as well as the accompanying Notes, constitute the fund’s financial statements.

The fund’s portfolio lists all the fund’s investments and their values as of the last day of the reporting period. Holdings are organized by asset type and industry sector, country, or state to show areas of concentration and diversification.

Statement of assets and liabilities shows how the fund’s net assets and share price are determined. All investment and non-investment assets are added together. Any unpaid expenses and other liabilities are subtracted from this total. The result is divided by the number of shares to determine the net asset value per share, which is calculated separately for each class of shares. (For funds with preferred shares, the amount subtracted from total assets includes the liquidation preference of preferred shares.)

Statement of operations shows the fund’s net investment gain or loss. This is done by first adding up all the fund’s earnings — from dividends and interest income — and subtracting its operating expenses to determine net investment income (or loss). Then, any net gain or loss the fund realized on the sales of its holdings — as well as any unrealized gains or losses over the period — is added to or subtracted from the net investment result to determine the fund’s net gain or loss for the fiscal period.

Statement of changes in net assets shows how the fund’s net assets were affected by the fund’s net investment gain or loss, by distributions to shareholders, and by changes in the number of the fund’s shares. It lists distributions and their sources (net investment income or realized capital gains) over the current reporting period and the most recent fiscal year-end. The distributions listed here may not match the sources listed in the Statement of operations because the distributions are determined on a tax basis and may be paid in a different period from the one in which they were earned. Dividend sources are estimated at the time of declaration. Actual results may vary. Any non-taxable return of capital cannot be determined until final tax calculations are completed after the end of the fund’s fiscal year.

Financial highlights provide an overview of the fund’s investment results, per-share distributions, expense ratios, net investment income ratios, and portfolio turnover in one summary table, reflecting the five most recent reporting periods. In a semiannual report, the highlights table also includes the current reporting period.

16

The fund’s portfolio 1/31/12 (Unaudited)

| | |

| Key to holding’s abbreviations | | |

| | | |

| ABAG Association Of Bay Area Governments | FRB Floating Rate Bonds: the rate shown is the current | |

| AGM Assured Guaranty Municipal Corporation | interest rate at the close of the reporting period | |

| AMBAC AMBAC Indemnity Corporation | G.O. Bonds General Obligation Bonds | |

| ASC 820 Accounting Standards Codification | GNMA Coll. Government National Mortgage | |

| ASC 820 Fair Value Measurements and Disclosures | Association Collateralized | |

| COP Certificates of Participation | NATL National Public Finance Guarantee Corp. | |

| FGIC Financial Guaranty Insurance Company | PSFG Permanent School Fund Guaranteed | |

| FHA Insd. Federal Housing Administration Insured | SGI Syncora Guarantee, Inc. | |

| FHLMC Coll. Federal Home Loan Mortgage | VRDN Variable Rate Demand Notes, which are | |

| Corporation Collateralized | floating-rate securities with long-term maturities, | |

| FNMA Coll. Federal National Mortgage | that carry coupons that reset every one or seven | |

| Association Collateralized | days. The rate shown is the current interest rate at the | |

| | close of the reporting period. | |

| | |

| | | |

| MUNICIPAL BONDS AND NOTES (99.7%)* | Rating** | Principal amount | Value |

|

| Alabama (2.0%) | | | |

| AL Hsg. Fin. Auth. Rev. Bonds (Single Fam. | | | |

| Mtge.), Ser. G, GNMA Coll., FNMA Coll., FHLMC | | | |

| Coll., 5 1/2s, 10/1/37 | Aaa | $1,350,000 | $1,363,500 |

|

| AL State Port Auth. Docks Fac. Rev. Bonds, | | | |

| 6s, 10/1/40 | BBB+ | 1,000,000 | 1,091,550 |

|

| Cullman Cnty., Hlth. Care Auth. Rev. Bonds | | | |

| (Cullman Regl. Med. Ctr.), Ser. A, 6 3/4s, 2/1/29 | Ba1 | 1,000,000 | 1,012,750 |

|

| Mobile, Special Care Fac. Fin. Auth. VRDN | | | |

| (Infirmary Hlth. Syst.), Ser. A, 0.07s, 2/1/40 | VMIG1 | 2,900,000 | 2,900,000 |

|

| Selma, Indl. Dev. Board Rev. Bonds (Gulf | | | |

| Opportunity Zone Intl. Paper Co.), Ser. A, | | | |

| 6 1/4s, 11/1/33 | BBB | 1,500,000 | 1,662,690 |

|

| | | | 8,030,490 |

| Alaska (0.9%) | | | |

| Anchorage, G.O. Bonds, Ser. D, AMBAC, | | | |

| 5s, 8/1/25 | AA | 3,420,000 | 3,907,316 |

|

| | | | 3,907,316 |

| Arizona (4.3%) | | | |

| Coconino Cnty., Poll. Control Rev. Bonds | | | |

| (Tucson Elec. Pwr. Co. — Navajo), Ser. A, | | | |

| 5 1/8s, 10/1/32 | Baa3 | 1,000,000 | 1,011,610 |

|

| Glendale, Indl. Dev. Auth. Rev. Bonds | | | |

| (Midwestern U.), 5 1/8s, 5/15/40 | A– | 2,125,000 | 2,235,351 |

|

| Glendale, Wtr. & Swr. Rev. Bonds | | | |

| 5s, 7/1/28 ∆ | AA | 1,000,000 | 1,176,700 |

| AMBAC, 5s, 7/1/28 (Prerefunded 7/1/13) | AA | 2,000,000 | 2,132,560 |

|

| Navajo Cnty., Poll. Control Corp. Mandatory | | | |

| Put Bonds (6/1/16), Ser. E, 5 3/4s, 6/1/34 | Baa2 | 3,250,000 | 3,684,883 |

|

| Pinal Cnty., Elec. Rev. Bonds (Dist. No. 3), | | | |

| 5 1/4s, 7/1/36 | A | 1,400,000 | 1,507,604 |

|

| Scottsdale, Indl. Dev. Auth. Hosp. Rev. Bonds | | | |

| (Scottsdale Hlth. Care), Ser. C, AGM, 5s, 9/1/35 | Aa3 | 2,000,000 | 2,168,120 |

|

17

| | | |

| MUNICIPAL BONDS AND NOTES (99.7%)* cont. | Rating** | Principal amount | Value |

|

| Arizona cont. | | | |

| Tempe, Indl. Dev. Auth. Lease Rev. Bonds | | | |

| (ASU Foundation), AMBAC, 5s, 7/1/28 | AA/P | $1,715,000 | $1,724,192 |

|

| U. Med. Ctr. Corp. AZ Hosp. Rev. Bonds, | | | |

| 6 1/2s, 7/1/39 | Baa1 | 1,750,000 | 1,954,400 |

|

| | | | 17,595,420 |

| California (14.8%) | | | |

| ABAG Fin. Auth. for Nonprofit Corps. Rev. Bonds | | | |

| (Episcopal Sr. Cmnty.), 6 1/8s, 7/1/41 | BBB+ | 500,000 | 523,815 |

| (St. Rose Hosp.), Ser. A, 6s, 5/15/29 | A– | 3,000,000 | 3,385,770 |

|

| CA Rev. Bonds | | | |

| (Catholic Hlth. Care West), Ser. A, 6s, 7/1/39 | A2 | 750,000 | 852,045 |

| (Adventist Hlth. Syst.-West), Ser. A, | | | |

| 5 3/4s, 9/1/39 | A | 1,000,000 | 1,104,450 |

|

| CA Muni. Fin. Auth. Rev. Bonds (U. of La Verne), | | | |

| Ser. A, 6 1/4s, 6/1/40 | Baa2 | 1,000,000 | 1,089,900 |

|

| CA Muni. Fin. Auth. Sr. Living Rev. Bonds | | | |

| (Pilgrim Place Claremont), Ser. A, 5 7/8s, 5/15/29 | A– | 1,500,000 | 1,669,065 |

|

| CA State G.O. Bonds, 6 1/2s, 4/1/33 | A1 | 5,000,000 | 6,119,950 |

|

| CA State Econ. Recvy. G.O. Bonds, Ser. A, | | | |

| 5 1/4s, 7/1/21 | Aa3 | 1,000,000 | 1,242,260 |

|

| CA State Pub. Wks. Board Rev. Bonds | | | |

| (Riverside Campus), Ser. B, 6s, 4/1/25 | A2 | 3,000,000 | 3,653,670 |

| Ser. G-1, 5 1/4s, 10/1/23 | A2 | 3,000,000 | 3,449,970 |

|

| CA Statewide Cmnty., Dev. Auth. Rev. Bonds | | | |

| (Sutter Hlth.), Ser. B, 5 1/4s, 11/15/48 | Aa3 | 1,550,000 | 1,628,477 |

| (Sr. Living — Presbyterian Homes), | | | |

| 6 5/8s, 11/15/24 | BBB– | 2,000,000 | 2,227,680 |

| (St. Joseph), NATL, 5 1/8s, 7/1/24 | AA– | 2,000,000 | 2,226,400 |

|

| Golden State Tobacco Securitization Corp. Rev. Bonds | | | |

| (Tobacco Settlement), Ser. B, AMBAC, FHLMC Coll., | | | |

| 5s, 6/1/38 (Prerefunded 6/1/13) | Aaa | 2,475,000 | 2,622,535 |

| Ser. A, AMBAC, zero %, 6/1/24 | A2 | 5,000,000 | 2,816,950 |

|

| Grossmont-Cuyamaca, Cmnty. College Dist. G.O. | | | |

| Bonds (Election of 2002), Ser. B, FGIC, NATL, | | | |

| zero %, 8/1/17 | Aa2 | 2,100,000 | 1,746,780 |

|

| Infrastructure & Econ. Dev. Bank Rev. Rev. Bonds | | | |

| (J. David Gladstone Inst.), Ser. A, 5s, 10/1/31 | A– | 1,000,000 | 1,040,360 |

|

| Los Angeles, Dept. Arpt. Rev. Bonds (Los Angeles | | | |

| Intl. Arpt.), Ser. A, 5s, 5/15/40 | AA | 1,000,000 | 1,097,200 |

|

| M-S-R Energy Auth. Rev. Bonds, Ser. A, | | | |

| 6 1/2s, 11/1/39 | A– | 750,000 | 915,165 |

|

| Merced, City School Dist. G.O. Bonds | | | |

| (Election of 2003), NATL | | | |

| zero %, 8/1/25 | A | 1,190,000 | 608,709 |

| zero %, 8/1/24 | A | 1,125,000 | 609,953 |

| zero %, 8/1/23 | A | 1,065,000 | 614,633 |

| zero %, 8/1/22 | A | 1,010,000 | 619,009 |

|

| Northern CA Pwr. Agcy. Rev. Bonds | | | |

| (Hydroelec. Project No. 1), Ser. A | | | |

| 5s, 7/1/31 | A | 500,000 | 559,395 |

| 5s, 7/1/30 | A | 500,000 | 564,020 |

|

18

| | | |

| MUNICIPAL BONDS AND NOTES (99.7%)* cont. | Rating** | Principal amount | Value |

|

| California cont. | | | |

| Oakland, Unified School Dist. Alameda Cnty., G.O. | | | |

| Bonds (Election 2006), Ser. A, 6 1/2s, 8/1/24 | A2 | $2,500,000 | $2,947,350 |

|

| Sacramento, City Fin. Auth. Tax Alloc. Bonds, | | | |

| Ser. A, FGIC, NATL, zero %, 12/1/21 | A– | 5,500,000 | 3,467,310 |

|

| Sacramento, Muni. Util. Dist. Rev. Bonds, Ser. X, | | | |

| 5s, 8/15/28 | A1 | 650,000 | 764,751 |

|

| San Diego, Unified School Dist. G.O. Bonds | | | |

| (Election of 1998), Ser. E, AGM, 5 1/4s, 7/1/19 | | | |

| (Prerefunded 7/1/13) | Aa2 | 2,000,000 | 2,147,340 |

|

| San Francisco, City & Cnty. Arpt. Comm. Rev. | | | |

| Bonds (Intl. Arpt.), Ser. F, 5s, 5/1/40 | A1 | 1,250,000 | 1,338,788 |

|

| Santa Ana, Fin. Auth. Lease Rev. Bonds | | | |

| (Police Admin. & Hldg. Fac.), Ser. A, NATL, | | | |

| 6 1/4s, 7/1/17 | Baa2 | 3,680,000 | 4,329,446 |

|

| Tuolumne Wind Project Auth. Rev. Bonds | | | |

| (Tuolumne Co.), Ser. A, 5 1/4s, 1/1/24 | A+ | 1,000,000 | 1,144,170 |

|

| Ventura Cnty., COP (Pub. Fin. Auth. III), | | | |

| 5s, 8/15/20 | AA | 1,000,000 | 1,166,200 |

|

| Yucaipa Special Tax Bonds (Cmnty. Fac. Dist. | | | |

| No. 98-1 Chapman Heights), 5 3/8s, 9/1/30 | BBB+ | 375,000 | 389,344 |

|

| | | | 60,682,860 |

| Colorado (1.6%) | | | |

| CO Hlth. Fac. Auth. Rev. Bonds | | | |

| (Evangelical Lutheran), Ser. A, 6 1/8s, 6/1/38 | A3 | 2,545,000 | 2,600,252 |

| (Valley View Assn.), 5 1/4s, 5/15/42 | BBB+ | 2,000,000 | 2,012,660 |

|

| CO Pub. Hwy. Auth. Rev. Bonds (E-470 Pub. Hwy.), | | | |

| Ser. C1, NATL, 5 1/2s, 9/1/24 | Baa2 | 1,000,000 | 1,042,020 |

|

| E-470 Pub. Hwy. Auth. Rev. Bonds, Ser. A, NATL, | | | |

| zero %, 9/1/34 | Baa2 | 3,525,000 | 880,334 |

|

| | | | 6,535,266 |

| Florida (9.6%) | | | |

| Brevard Cnty., Hlth. Care Fac. Auth. Rev. Bonds | | | |

| (Health First, Inc.), 7s, 4/1/39 | A3 | 1,250,000 | 1,453,525 |

|

| Broward Cnty., Arpt. Syst. Rev. Bonds, Ser. O, | | | |

| 5 3/8s, 10/1/29 | A1 | 1,000,000 | 1,127,860 |

|

| FL State Board of Ed. G.O. Bonds (Capital Outlay | | | |

| 2011), Ser. F, 5s, 6/1/30 | AAA | 2,520,000 | 2,988,166 |

|

| Hernando Cnty., Rev. Bonds (Criminal Justice | | | |

| Complex Fin.), FGIC, NATL, 7.65s, 7/1/16 | BBB | 10,000,000 | 12,049,800 |

|

| Lee Cnty., Rev. Bonds, SGI, 5s, 10/1/25 | Aa2 | 2,000,000 | 2,183,620 |

|

| Marco Island, Util. Sys. Rev. Bonds, Ser. A, | | | |

| 5s, 10/1/34 | Aa3 | 1,000,000 | 1,090,120 |

|

| Miami-Dade Cnty., Expressway Auth. Toll Syst. | | | |

| Rev. Bonds, Ser. A, 5s, 7/1/40 | A | 1,000,000 | 1,047,060 |

|

| Miami-Dade Cnty., Wtr. & Swr. Rev. Bonds, AGM, | | | |

| SGI, 5s, 10/1/23 | Aa2 | 1,000,000 | 1,128,920 |

|

| Orlando & Orange Cnty., Expressway Auth. Rev. | | | |

| Bonds, FGIC, NATL, 8 1/4s, 7/1/14 | A2 | 5,000,000 | 5,725,500 |

|

| Orlando Cmnty. Redev. Agcy. Tax Alloc. | | | |

| (Republic Drive/Universal), 5s, 4/1/23 ∆ | A–/F | 1,630,000 | 1,818,281 |

|

19

| | | |

| MUNICIPAL BONDS AND NOTES (99.7%)* cont. | Rating** | Principal amount | Value |

|

| Florida cont. | | | |

| Palm Beach Cnty., Hlth. Fac. Auth. Rev. Bonds | | | |

| (Acts Retirement-Life Cmnty.), 5 1/2s, 11/15/33 | BBB+ | $3,000,000 | $3,088,140 |

|

| South Lake Hosp. Dist. (South Lake Hosp.), | | | |

| Ser. A, 6s, 4/1/29 | Baa2 | 660,000 | 716,206 |

|

| Sumter Cnty., School Dist. Rev. Bonds | | | |

| (Multi-Dist. Loan Program), AGM, 7.15s, 11/1/15 | | | |

| (Escrowed to maturity) | Aa3 | 3,935,000 | 4,853,232 |

|

| | | | 39,270,430 |

| Georgia (1.7%) | | | |

| Atlanta, Arpt. Rev. Bonds, Ser. C, 5 7/8s, 1/1/24 | A1 | 1,500,000 | 1,882,500 |

|

| Atlanta, Wtr. & Waste Wtr. Rev. Bonds, Ser. A, | | | |

| 6 1/4s, 11/1/39 | A1 | 1,500,000 | 1,754,325 |

|

| Fulton Cnty., Dev. Auth. Rev. Bonds (Klaus Pkg. & | | | |

| Fam. Hsg. Project), NATL, 5 1/4s, 11/1/20 | Aa3 | 3,360,000 | 3,556,325 |

|

| | | | 7,193,150 |

| Guam (0.3%) | | | |

| Territory of GU, Rev. Bonds, Ser. A, 5 3/8s, 12/1/24 | BBB– | 1,000,000 | 1,070,750 |

|

| | | | 1,070,750 |

| Illinois (6.5%) | | | |

| Chicago, Board of Ed. G.O. Bonds, Ser. A, NATL, | | | |

| 5 1/4s, 12/1/19 | Aa3 | 1,500,000 | 1,548,720 |

|

| Chicago, O’Hare Intl. Arpt. Rev. Bonds | | | |

| Ser. A, 5 3/4s, 1/1/39 | A1 | 700,000 | 796,103 |

| Ser. F, 5s, 1/1/40 | A1 | 1,045,000 | 1,092,150 |

|

| Cicero, G.O. Bonds, Ser. A, SGI, 5 1/4s, 1/1/21 | A/P | 2,250,000 | 2,301,638 |

|

| Du Page Cnty., Cmnty. High School Dist. | | | |

| G.O. Bonds (Dist. No. 108 — Lake Park), | | | |

| AGM, 5.6s, 1/1/20 | Aa2 | 1,000,000 | 1,042,820 |

|

| IL Fin. Auth. Rev. Bonds | | | |

| (Roosevelt U.), 6 1/4s, 4/1/29 | Baa2 | 1,500,000 | 1,628,925 |

| (Rush U. Med. Ctr.), Ser. B, NATL, 5 3/4s, 11/1/28 | A2 | 2,500,000 | 2,756,225 |

| (Elmhurst Memorial), Ser. A, 5 5/8s, 1/1/37 | Baa1 | 1,000,000 | 1,035,730 |

| (American Wtr. Cap. Corp.), 5 1/4s, 10/1/39 | BBB+ | 1,575,000 | 1,587,726 |

|

| IL State Toll Hwy. Auth. Rev. Bonds, Ser. A-1, | | | |

| AGM, 5s, 1/1/22 | Aa3 | 2,500,000 | 2,819,625 |

|

| Metro. Pier & Exposition Auth. Dedicated State | | | |

| Tax Rev. Bonds (McCormick), Ser. A, NATL, | | | |

| zero %, 12/15/22 | A3 | 5,500,000 | 3,634,070 |

|

| Regl. Trans. Auth. Rev. Bonds, Ser. A, AMBAC, | | | |

| 8s, 6/1/17 | Aa3 | 5,000,000 | 6,349,950 |

|

| | | | 26,593,682 |

| Indiana (1.5%) | | | |

| IN Muni. Pwr. Agcy. Supply Syst. Rev. Bonds, | | | |

| Ser. B, 5 3/4s, 1/1/29 | A1�� | 1,000,000 | 1,159,640 |

|

| IN State Fin. Auth. Rev. Bonds (BHI Sr. Living), | | | |

| 5 3/4s, 11/15/41 | A–/F | 1,000,000 | 1,055,010 |

|

| IN State Hsg. Fin. Auth. Rev. Bonds (Single | | | |

| Family Mtge.), Ser. A-1, GNMA Coll., FNMA Coll., | | | |

| 4.1s, 7/1/15 | Aaa | 55,000 | 57,229 |

|

| Rockport, Poll. Control FRB (IN-MI Pwr. Co.) | | | |

| Ser. A, 6 1/4s, 6/1/25 | Baa2 | 2,000,000 | 2,201,220 |

| Ser. B, 6 1/4s, 6/1/25 | Baa2 | 1,500,000 | 1,651,275 |

|

| | | | 6,124,374 |

20

| | | |

| MUNICIPAL BONDS AND NOTES (99.7%)* cont. | Rating** | Principal amount | Value |

|

| Kansas (0.4%) | | | |

| KS State Dev. Fin. Auth. Rev. Bonds | | | |

| (Lifespace Cmnty’s. Inc.), Ser. S, 5s, 5/15/30 | A/F | $1,455,000 | $1,515,979 |

|

| | | | 1,515,979 |

| Kentucky (0.5%) | | | |

| Owen Cnty., Wtr. Wks. Syst. Rev. Bonds | | | |

| (American Wtr. Co.) | | | |

| Ser. A, 6 1/4s, 6/1/39 | BBB+ | 800,000 | 861,168 |

| Ser. B, 5 5/8s, 9/1/39 | BBB+ | 1,000,000 | 1,039,620 |

|

| | | | 1,900,788 |

| Louisiana (0.8%) | | | |

| LA Pub. Fac. Auth. Rev. Bonds (Entergy LA LLC), | | | |

| 5s, 6/1/30 | A3 | 3,000,000 | 3,184,080 |

|

| | | | 3,184,080 |

| Maryland (0.5%) | | | |

| MD State Hlth. & Higher Edl. Fac. Auth. | | | |

| Rev. Bonds (U. of MD Med. Syst.), AMBAC, | | | |

| 5 1/4s, 7/1/28 | A2 | 2,000,000 | 2,201,780 |

|

| | | | 2,201,780 |

| Massachusetts (3.7%) | | | |

| MA Edl. Fin. Auth. I Ser. A, 5 1/2s, 1/1/22 | AA | 1,000,000 | 1,157,860 |

|

| MA State Dept. Trans. Rev. Bonds (Metro Hwy. | | | |

| Syst.), Ser. B, 5s, 1/1/37 | A | 1,000,000 | 1,072,120 |

|

| MA State Dev. Fin. Agcy. Rev. Bonds | | | |

| (Sabis Intl.), Ser. A, 6.8s, 4/15/22 | BBB | 700,000 | 777,756 |

| (Emerson College), Ser. A, 5 1/2s, 1/1/30 | BBB+ | 2,000,000 | 2,169,200 |

| (Suffolk U.), 5 1/8s, 7/1/40 | Baa2 | 500,000 | 512,505 |

|

| MA State Dev. Fin. Agcy. Solid Waste Disp. | | | |

| Mandatory Put Bonds (5/1/19) (Dominion Energy | | | |

| Brayton 1), Ser. 1, 5 3/4s, 12/1/42 | A– | 1,000,000 | 1,156,670 |

|

| MA State Hlth. & Edl. Fac. Auth. Rev. Bonds | | | |

| (Suffolk U.), Ser. A, 6 1/4s, 7/1/30 | Baa2 | 2,000,000 | 2,223,720 |

| (Baystate Med. Ctr.), Ser. I, 5 3/4s, 7/1/36 | A+ | 500,000 | 537,690 |

| (Harvard U.), Ser. A, 5 1/2s, 11/15/36 | Aaa | 1,815,000 | 2,134,150 |

| (Northeastern U.), Ser. A, 5s, 10/1/35 | A2 | 1,650,000 | 1,782,231 |

|

| Metro. Boston, Trans. Pkg. Corp. Rev. Bonds, | | | |

| 5 1/4s, 7/1/36 | A1 | 1,500,000 | 1,665,675 |

|

| | | | 15,189,577 |

| Michigan (5.0%) | | | |

| Detroit, Swr. Disp. Rev. Bonds, Ser. B, AGM, | | | |

| 7 1/2s, 7/1/33 | AA– | 1,000,000 | 1,264,310 |

|

| Detroit, Wtr. Supply Syst. Rev. Bonds, Ser. B, | | | |

| AGM, 6 1/4s, 7/1/36 | AA– | 1,575,000 | 1,818,842 |

|

| MI State Hosp. Fin. Auth. Rev. Bonds | | | |

| Ser. A, 6 1/8s, 6/1/39 | A1 | 1,000,000 | 1,119,600 |

| (Henry Ford Hlth. Syst.), Ser. A, 5 1/4s, 11/15/46 | A1 | 1,250,000 | 1,282,825 |

| (Henry Ford Hlth.), 5 1/4s, 11/15/24 | A1 | 1,000,000 | 1,114,670 |

|

| MI State Strategic Fund Rev. Bonds | | | |

| (Dow Chemical), Ser. B-2, 6 1/4s, 6/1/14 | BBB | 1,000,000 | 1,108,720 |

|

| MI State Strategic Fund Ltd. Rev. Bonds | | | |

| (Detroit Edison Co.), AMBAC, 7s, 5/1/21 | A2 | 4,000,000 | 5,298,360 |

|

| Midland Cnty., Bldg. Auth. G.O. Bonds, AGM, | | | |

| 5s, 10/1/25 | Aa3 | 1,000,000 | 1,126,980 |

|

21

| | | |

| MUNICIPAL BONDS AND NOTES (99.7%)* cont. | Rating** | Principal amount | Value |

|

| Michigan cont. | | | |

| Northern Michigan U. Rev. Bonds, Ser. A, AGM, | | | |

| 5s, 12/1/27 | Aa3 | $1,775,000 | $1,994,461 |

|

| Wayne Charter Cnty., G.O. Bonds (Bldg. Impt.), | | | |

| Ser. A, 6 3/4s, 11/1/39 | BBB+ | 490,000 | 549,658 |

|

| Western MI U. Rev. Bonds, AGM, 5s, 11/15/28 | Aa3 | 3,500,000 | 3,851,680 |

|

| | | | 20,530,106 |

| Minnesota (1.3%) | | | |

| Minneapolis, Rev. Bonds (National Marrow Donor | | | |

| Program), 4 7/8s, 8/1/25 | BBB | 1,350,000 | 1,369,872 |

|

| Northfield, Hosp. Rev. Bonds, 5 3/8s, 11/1/26 | BBB– | 1,500,000 | 1,571,715 |

|

| St. Paul, Hsg. & Redev. Auth. Hlth. Care Fac. | | | |

| Rev. Bonds (HealthPartners Oblig. Group), | | | |

| 5 1/4s, 5/15/36 | A3 | 1,800,000 | 1,848,816 |

|

| Tobacco Securitization Auth. Rev. Bonds | | | |

| (Tobacco Settlement), Ser. B, 5 1/4s, 3/1/31 | A– | 500,000 | 541,905 |

|

| | | | 5,332,308 |

| Mississippi (0.7%) | | | |

| Bus. Fin. Corp. Gulf Opportunity Zone Rev. Bonds, | | | |

| Ser. A, 5s, 5/1/37 | A3 | 1,750,000 | 1,832,110 |

|

| MS Home Corp. Rev. Bonds (Single Fam. Mtge.), | | | |

| Ser. D-1, GNMA Coll., FNMA Coll., 6.1s, 6/1/38 | Aaa | 1,140,000 | 1,243,751 |

|

| | | | 3,075,861 |

| Missouri (2.5%) | | | |

| Cape Girardeau Cnty., Indl. Dev. Auth. Hlth. Care | | | |

| Fac. Rev. Bonds (St. Francis Med. Ctr.), Ser. A, | | | |

| 5 3/4s, 6/1/39 | A+ | 1,150,000 | 1,252,281 |

|

| MO State Hlth. & Edl. Fac. Auth. Rev. Bonds | | | |

| (Washington U. (The)), Ser. A, 5 3/8s, 3/15/39 | Aaa | 2,000,000 | 2,262,380 |

|

| MO State Hlth. & Edl. Fac. Auth. VRDN | | | |

| (Washington U. (The)), Ser. B, 0.08s, 9/1/30 | VMIG1 | 6,850,000 | 6,850,000 |

|

| | | | 10,364,661 |

| New Hampshire (0.3%) | | | |

| NH State Bus. Fin. Auth. Rev. Bonds (Elliot Hosp. | | | |

| Oblig. Group), Ser. A, 6s, 10/1/27 | Baa1 | 1,300,000 | 1,388,621 |

|

| | | | 1,388,621 |

| New Jersey (1.6%) | | | |

| NJ Hlth. Care Fac. Fin. Auth. Rev. Bonds | | | |

| (St. Peter’s U. Hosp.), 5 3/4s, 7/1/37 | Baa3 | 1,000,000 | 1,030,160 |

|

| NJ State Higher Ed. Assistance Auth. Rev. Bonds | | | |

| (Student Loan), Ser. A, 5 5/8s, 6/1/30 | AA | 1,000,000 | 1,098,280 |

|

| NJ State Tpk. Auth. Rev. Bonds, Ser. A, AMBAC, | | | |

| 5s, 1/1/30 | A+ | 3,000,000 | 3,140,010 |

|

| NJ State Trans. Trust Fund Auth. Rev. Bonds, | | | |

| Ser. B, 5 1/4s, 6/15/36 | A1 | 1,000,000 | 1,120,870 |

|

| | | | 6,389,320 |

| New York (6.9%) | | | |

| Erie Cnty., Indl. Dev. Agcy. School Fac. Rev. | | | |

| Bonds (City School Dist. Buffalo), Ser. A, AGM | | | |

| 5 3/4s, 5/1/28 | Aa3 | 2,275,000 | 2,686,934 |

| 5 3/4s, 5/1/27 | Aa3 | 5,590,000 | 6,637,621 |

|

| Hudson Yards, Infrastructure Corp. Rev. Bonds, | | | |

| Ser. A, 5 3/4s, 2/15/47 | A2 | 1,000,000 | 1,129,950 |

|

22

| | | |

| MUNICIPAL BONDS AND NOTES (99.7%)* cont. | Rating** | Principal amount | Value |

|

| New York cont. | | | |

| Metro. Trans. Auth. Rev. Bonds, Ser. D, | | | |

| 5s, 11/15/36 | A2 | $3,000,000 | $3,240,750 |

|

| NY City, G.O. Bonds, Ser. D-1, 5s, 10/1/36 | Aa2 | 1,400,000 | 1,576,932 |

|

| NY City, Muni. Wtr. & Swr. Fin. Auth. Rev. Bonds, | | | |

| Ser. AA, 5s, 6/15/34 | AA+ | 1,000,000 | 1,144,650 |

|

| NY State Dorm. Auth. Rev. Bonds | | | |

| (Brooklyn Law School), Ser. B, SGI | | | |

| 5 3/8s, 7/1/22 | Baa1 | 2,270,000 | 2,326,773 |

| 5 3/8s, 7/1/20 | Baa1 | 2,215,000 | 2,281,206 |

|

| NY State Dorm. Auth. Personal Income Tax Rev. | | | |

| Bonds (Ed.), Ser. B, 5 3/4s, 3/15/36 | AAA | 2,000,000 | 2,343,040 |

|

| Port Auth. NY & NJ Special Oblig. Rev. Bonds | | | |

| (JFK Intl. Air Term.), 6s, 12/1/42 | Baa3 | 900,000 | 982,998 |

|

| Port Auth. of NY & NJ Rev. Bonds, 5s, 7/15/30 | Aa2 | 2,250,000 | 2,696,714 |

|

| Syracuse, Indl. Dev. Agcy. School Fac. Rev. | | | |

| Bonds (Syracuse City School Dist.), Ser. A, AGM, | | | |

| 5s, 5/1/25 | Aa3 | 1,000,000 | 1,144,910 |

|

| | | | 28,192,478 |

| North Carolina (1.0%) | | | |

| NC Cap. Fin. Agcy. Edl. Fac. Rev. Bonds | | | |

| (Meredith College), 6s, 6/1/31 | BBB | 500,000 | 527,905 |

|

| NC Eastern Muni. Pwr. Agcy. Syst. Rev. Bonds, | | | |

| Ser. A, 5 1/2s, 1/1/26 | A– | 1,500,000 | 1,740,570 |

|

| U. of NC Syst. Pool Rev. Bonds, Ser. C, | | | |

| 5 3/8s, 10/1/29 | A3 | 1,500,000 | 1,697,190 |

|

| | | | 3,965,665 |

| Ohio (5.5%) | | | |

| Allen Cnty., Hosp. Fac. VRDN (Catholic Hlth. | | | |

| Care), Ser. B, 0.06s, 10/1/31 | VMIG1 | 1,170,000 | 1,170,000 |

|

| Buckeye, Tobacco Settlement Fin. Auth. Rev. | | | |

| Bonds, Ser. A-2 | | | |

| 5 3/4s, 6/1/34 | B3 | 500,000 | 373,340 |

| 5 3/8s, 6/1/24 | B3 | 4,195,000 | 3,392,371 |

| 5 1/8s, 6/1/24 | B3 | 1,735,000 | 1,373,790 |

|

| Erie Cnty., Hosp. Fac. Rev. Bonds (Firelands | | | |

| Regl. Med. Ctr.), Ser. A, 5 1/2s, 8/15/22 | A– | 3,150,000 | 3,203,456 |

|

| Hamilton Cnty., Sales Tax Rev. Bonds, Ser. A, | | | |

| 5s, 12/1/32 | A1 | 2,000,000 | 2,164,480 |

|

| Lorain Cnty., Hosp. Rev. Bonds (Catholic), | | | |

| Ser. C-2, AGM, 5s, 4/1/24 | Aa3 | 2,000,000 | 2,194,520 |

|

| Lucas Cnty., Hlth. Care Fac. Rev. Bonds | | | |

| (Sunset Retirement Cmntys.), 5 1/2s, 8/15/30 | A–/F | 650,000 | 678,801 |

|

| OH Hsg. Fin. Agcy. Rev. Bonds | | | |

| (Single Fam. Mtge.), Ser. 1, 5s, 11/1/28 | Aaa | 755,000 | 820,579 |

|

| OH Hsg. Fin. Agcy. Single Fam. Mtge. Rev. Bonds, | | | |

| Ser. 85-A, FGIC, FHA Insd., zero %, 1/15/15 | | | |

| (Escrowed to maturity) | AAA/P | 10,000 | 8,608 |

|

| OH State Air Quality Dev. Auth. Rev. Bonds | | | |

| (First Energy), Ser. A, 5.7s, 2/1/14 | Baa2 | 1,500,000 | 1,610,115 |

| (Valley Elec. Corp.), Ser. E, 5 5/8s, 10/1/19 | Baa3 | 750,000 | 838,088 |

|

23

| | | |

| MUNICIPAL BONDS AND NOTES (99.7%)* cont. | Rating** | Principal amount | Value |

|

| Ohio cont. | | | |

| OH State Higher Edl. Fac. Rev. Bonds | | | |

| (U. of Dayton), Ser. A, 5 5/8s, 12/1/41 | A2 | $1,000,000 | $1,115,860 |

|

| U. of Akron Rev. Bonds, Ser. B, AGM, | | | |

| 5 1/4s, 1/1/26 | Aa3 | 3,375,000 | 3,856,073 |

|

| | | | 22,800,081 |

| Oklahoma (0.3%) | | | |

| Tulsa, Arpt. Impt. Trust Rev. Bonds, Ser. A, | | | |

| 5 3/8s, 6/1/24 | A3 | 1,300,000 | 1,401,738 |

|

| | | | 1,401,738 |

| Oregon (0.2%) | | | |

| OR Hlth. Sciences U. Rev. Bonds, Ser. A, | | | |

| 5 3/4s, 7/1/39 | A1 | 750,000 | 845,730 |

|

| | | | 845,730 |

| Pennsylvania (6.2%) | | | |

| Allegheny Cnty., Hosp. Dev. Auth. Rev. Bonds | | | |

| (U. of Pittsburgh Med.), 5 5/8s, 8/15/39 | Aa3 | 3,000,000 | 3,320,520 |

|

| Berks Cnty., Muni. Auth. Rev. Bonds (Reading | | | |

| Hosp. & Med. Ctr.), Ser. A-3, 5 1/2s, 11/1/31 | AA | 3,000,000 | 3,382,080 |

|

| Dauphin Cnty., Gen. Auth. Hlth. Syst. Rev. Bonds | | | |

| (Pinnacle Hlth. Syst.), Ser. A, 6s, 6/1/29 | A2 | 2,500,000 | 2,764,550 |

|

| Lycoming Cnty., Auth. Hlth. Syst. Rev. Bonds | | | |

| (Susquehanna Hlth. Syst.), Ser. A, 5 3/8s, 7/1/23 | BBB+ | 3,000,000 | 3,266,220 |

|

| Monroe Cnty., Hosp. Auth. Rev. Bonds | | | |

| (Pocono Med. Ctr.), 5s, 1/1/27 | A– | 950,000 | 980,400 |

|

| Montgomery Cnty., Indl. Dev. Auth. Retirement | | | |

| Cmnty. Rev. Bonds (Acts Retirement-Life Cmnty.), | | | |

| Ser. A-1, 5 1/4s, 11/15/16 | BBB+ | 1,100,000 | 1,208,954 |

|

| PA Econ. Dev. Fin. Auth. Wtr. Fac. Rev. Bonds | | | |

| (American Wtr. Co.), 6.2s, 4/1/39 | A2 | 1,900,000 | 2,193,721 |

|

| PA State Higher Edl. Fac. Auth. Rev. Bonds | | | |

| (Edinboro U. Foundation), 6s, 7/1/43 | Baa3 | 500,000 | 531,145 |

|

| PA State Higher Edl. Fac. Auth. Student Hsg. | | | |

| Rev. Bonds (East Stroudsburg U.), 5s, 7/1/31 | Baa3 | 2,760,000 | 2,774,932 |

|

| Philadelphia, Gas Wks. Rev. Bonds, Ser. 9, | | | |

| 5 1/4s, 8/1/40 | BBB+ | 1,400,000 | 1,446,480 |

|

| Pittsburgh G.O. Bonds, Ser. B, 5s, 9/1/25 ∆ | A1 | 1,250,000 | 1,419,550 |

|

| Pittsburgh & Allegheny Cnty., Passports & Exhib. | | | |

| Auth. Hotel Rev. Bonds, AGM, 5s, 2/1/35 | Aa3 | 1,225,000 | 1,286,373 |

|

| Wilkes-Barre, Fin. Auth. Rev. Bonds | | | |

| (U. of Scranton), 5s, 11/1/40 | A | 1,000,000 | 1,076,180 |

|

| | | | 25,651,105 |

| Puerto Rico (3.5%) | | | |

| Cmnwlth. of PR, G.O. Bonds, Ser. C-7, NATL, | | | |

| 6s, 7/1/27 | Baa1 | 1,500,000 | 1,666,320 |

|

| Cmnwlth. of PR, Aqueduct & Swr. Auth. | | | |

| Rev. Bonds, Ser. A, 6s, 7/1/38 | Baa2 | 1,390,000 | 1,509,776 |

|

| Cmnwlth. of PR, Elec. Pwr. Auth. Rev. Bonds, | | | |

| Ser. XX, 5 1/4s, 7/1/40 | A3 | 2,250,000 | 2,379,914 |

|

| Cmnwlth. of PR, Infrastructure Fin. Auth. Special | | | |

| Tax Bonds, Ser. C, FGIC, 5 1/2s, 7/1/19 | Baa1 | 865,000 | 981,879 |

|

| Cmnwlth. of PR, Sales Tax Fin. Corp. Rev. Bonds, | | | |

| Ser. A, 6s, 8/1/42 | A1 | 7,000,000 | 7,894,040 |

|

| | | | 14,431,929 |

24

| | | |

| MUNICIPAL BONDS AND NOTES (99.7%)* cont. | Rating** | Principal amount | Value |

|

| South Dakota (0.3%) | | | |

| SD Hsg. Dev. Auth. Rev. Bonds (Home Ownership | | | |

| Mtge.), Ser. J, 4.6s, 5/1/19 | AAA | $1,250,000 | $1,252,650 |

|

| | | | 1,252,650 |

| Tennessee (0.5%) | | | |

| Johnson City, Hlth. & Edl. Fac. Board Hosp. | | | |

| Rev. Bonds (Mountain States Hlth. Alliance), | | | |

| 6s, 7/1/38 | Baa1 | 1,850,000 | 1,974,357 |

|

| | | | 1,974,357 |

| Texas (8.2%) | | | |

| Dallas Cnty., Util. & Reclamation Dist. G.O. | | | |

| Bonds, Ser. B, AMBAC, 5 3/8s, 2/15/29 | A3 | 2,500,000 | 2,689,475 |

|

| Dallas, Indpt. School Dist. G.O. Bonds | | | |

| (School Bldg.), PSFG, 6s, 2/15/27 | Aaa | 2,500,000 | 3,051,375 |

|

| Harris Cnty., Cultural Ed. Fac. Fin. Corp. VRDN | | | |

| (Texas Med. Ctr.), Ser. B-1, 0.06s, 9/1/31 | VMIG1 | 6,720,000 | 6,720,000 |

|

| Hays Cnty., G.O. Bonds, AGM, 5s, 8/15/24 | Aa2 | 1,190,000 | 1,278,060 |

|

| Houston, Arpt. Syst. Rev. Bonds, AGM, 5s, 7/1/21 | Aa3 | 3,000,000 | 3,038,700 |

|

| La Joya, Indpt. School Dist. G.O. Bonds | | | |

| (School Bldg.), PSFG, 5s, 2/15/30 | Aaa | 2,500,000 | 2,815,174 |

|

| Laredo, I S D Pub. Fac. Corp. Rev. Bonds, Ser. C, | | | |

| AMBAC, 5s, 8/1/29 | A | 1,000,000 | 1,005,970 |

|

| Mansfield, Indpt. School Dist. G.O. Bonds, PSFG, | | | |

| 5s, 2/15/27 | Aaa | 2,000,000 | 2,199,920 |

|

| Matagorda Cnty., Poll. Control Rev. Bonds | | | |

| (Cent Pwr. & Light Co.), Ser. A, 6.3s, 11/1/29 | Baa2 | 600,000 | 683,784 |

|

| North TX Thruway Auth. Rev. Bonds, | | | |

| Ser. A, NATL, 5 1/8s, 1/1/28 | A2 | 1,500,000 | 1,641,660 |

| (First Tier), Ser. A, 6 1/4s, 1/1/24 | A2 | 3,500,000 | 4,159,435 |

|

| Pharr, San Juan — Alamo, Indpt. School Dist. G.O. | | | |

| Bonds (School Bldg.), PSFG, 5s, 2/1/30 | Aaa | 2,000,000 | 2,250,660 |

|

| Texas Tech. U. Rev. Bonds, Ser. A, 5s, 8/15/37 ∆ | AA | 1,000,000 | 1,125,000 |

|

| TX Muni. Gas Acquisition & Supply Corp. I Rev. | | | |

| Bonds, Ser. A, 5 1/4s, 12/15/24 | A– | 1,000,000 | 1,062,540 |

|

| | | | 33,721,753 |

| Virginia (0.4%) | | | |

| Chesterfield Cnty., Econ. Dev. Auth. Poll. | | | |

| Control Rev. Bonds (VA Elec. & Pwr.), Ser. A, | | | |

| 5s, 5/1/23 | A3 | 1,575,000 | 1,792,964 |

|

| | | | 1,792,964 |

| Washington (3.3%) | | | |

| WA State Higher Ed. Fac. Auth. Rev. Bonds | | | |

| (Whitworth U.), 5 1/8s, 10/1/24 | Baa1 | 2,500,000 | 2,626,600 |

|

| WA State Hlth. Care Fac. Auth. Rev. Bonds | | | |

| (WA Hlth. Svcs.), 7s, 7/1/39 | Baa2 | 1,000,000 | 1,081,390 |

| Ser. B, NATL, 5s, 2/15/27 | Baa2 | 2,235,000 | 2,265,127 |

|

| WA State Pub. Pwr. Supply Syst. Rev. Bonds | | | |

| (Nuclear No. 3), Ser. B, NATL, 7 1/8s, 7/1/16 | Aa1 | 6,000,000 | 7,599,720 |

|

| | | | 13,572,837 |

| West Virginia (1.4%) | | | |

| Econ. Dev. Auth. Lease Rev. Bonds (Correctional | | | |

| Juvenile Safety), Ser. A, NATL, 5s, 6/1/29 | Aa2 | 5,000,000 | 5,280,800 |

|

| WV Econ. Dev. Auth. Solid Waste Disp. Fac. FRB | | | |

| (Appalachian Pwr. Co.), Ser. A, 5 3/8s, 12/1/38 | Baa2 | 500,000 | 524,860 |

|

| | | | 5,805,660 |

25

| | | |

| MUNICIPAL BONDS AND NOTES (99.7%)* cont. | Rating** | Principal amount | Value |

|

| Wisconsin (1.0%) | | | |

| WI State Rev. Bonds, Ser. A, 6s, 5/1/27 | Aa3 | $2,000,000 | $2,485,100 |

|

| WI State Hlth. & Edl. Fac. Auth. Rev. Bonds | | | |

| (Prohealth Care, Inc.), 6 5/8s, 2/15/39 | A1 | 1,250,000 | 1,430,463 |

|

| | | | 3,915,563 |

| Wyoming (0.5%) | | | |

| Sweetwater Cnty., Poll. Control Rev. Bonds | | | |

| (Idaho Power Co.), 5 1/4s, 7/15/26 | A2 | 1,800,000 | 2,052,198 |

|

| | | | 2,052,198 |

|

| |

| TOTAL INVESTMENTS | | | |

|

| Total investments (cost $371,707,402) | | | $409,453,527 |

Notes to the fund’s portfolio

Unless noted otherwise, the notes to the fund’s portfolio are for the close of the fund’s reporting period, which ran from August 1, 2011 through January 31, 2012 (the reporting period).

* Percentages indicated are based on net assets of $410,676,048.

** The Moody’s, Standard & Poor’s or Fitch ratings indicated are believed to be the most recent ratings available at the close of the reporting period for the securities listed. Ratings are generally ascribed to securities at the time of issuance. While the agencies may from time to time revise such ratings, they undertake no obligation to do so, and the ratings do not necessarily represent what the agencies would ascribe to these securities at the close of the reporting period. Securities rated by Putnam are indicated by “/P.” Securities rated by Fitch are indicated by “/F.” The rating of an insured security represents what is believed to be the most recent rating of the insurer’s claims-paying ability available at the close of the reporting period and does not reflect any subsequent changes. Security ratings are defined in the Statement of Additional Information.

∆ Forward commitment, in part or in entirety (Note 1).

The rates shown on Mandatory Put Bonds are the current interest rates at the close of the reporting period.

The dates shown parenthetically on Mandatory Put Bonds represent the next mandatory put dates.

The dates shown parenthetically on prerefunded bonds represent the next prerefunding dates.

The dates shown on debt obligations are the original maturity dates.

The fund had the following sector concentrations greater than 10% at the close of the reporting period (as a percentage of net assets):

| |

| Health care | 20.1% |

| Local government | 15.8 |

| Utilities | 15.3 |

| Education | 12.5 |

| Transportation | 10.1 |

The fund had the following insurance concentrations greater than 10% at the close of the reporting period (as a percentage of net assets):

26

ASC 820 establishes a three-level hierarchy for disclosure of fair value measurements. The valuation hierarchy is based upon the transparency of inputs to the valuation of the fund’s investments. The three levels are defined as follows:

Level 1: Valuations based on quoted prices for identical securities in active markets.

Level 2: Valuations based on quoted prices in markets that are not active or for which all significant inputs are observable, either directly or indirectly.

Level 3: Valuations based on inputs that are unobservable and significant to the fair value measurement.

The following is a summary of the inputs used to value the fund’s net assets as of the close of the reporting period:

| | | |

| | | Valuation inputs | |

|

| Investments in securities: | Level 1 | Level 2 | Level 3 |

|

| Municipal bonds and notes | $— | $409,453,527 | $— |

|

| Totals by level | $— | $409,453,527 | $— |

The accompanying notes are an integral part of these financial statements.

27

Statement of assets and liabilities 1/31/12 (Unaudited)

| |

| ASSETS | |

| Investment in securities, at value (Note 1): | |

| Unaffiliated issuers (identified cost $371,707,402) | $409,453,527 |

|

| Cash | 6,467,924 |

|

| Interest and other receivables | 4,260,254 |

|

| Receivable for shares of the fund sold | 1,536,557 |

|

| Receivable for sales of delayed delivery securities (Note 1) | 100,076 |

|

| Receivable for investments sold | 1,625,700 |

|

| Total assets | 423,444,038 |

| |

| LIABILITIES | |

| Distributions payable to shareholders | 281,594 |

|

| Payable for investments purchased | 5,677,958 |

|

| Payable for purchases of delayed delivery securities (Note 1) | 5,484,789 |

|

| Payable for shares of the fund repurchased | 906,636 |

|

| Payable for compensation of Manager (Note 2) | 151,547 |

|

| Payable for investor servicing fees (Note 2) | 16,475 |

|

| Payable for custodian fees (Note 2) | 4,093 |

|

| Payable for Trustee compensation and expenses (Note 2) | 101,921 |

|

| Payable for administrative services (Note 2) | 791 |

|

| Payable for distribution fees (Note 2) | 95,972 |

|

| Other accrued expenses | 46,214 |

|

| Total liabilities | 12,767,990 |

| | |

| Net assets | $410,676,048 |

|

| |

| REPRESENTED BY | |

|

| Paid-in capital (Unlimited shares authorized) (Notes 1 and 4) | $379,303,059 |

|

| Distributions in excess of net investment income (Note 1) | (142,838) |

|

| Accumulated net realized loss on investments (Note 1) | (6,230,298) |

|

| Net unrealized appreciation of investments | 37,746,125 |

|

| Total — Representing net assets applicable to capital shares outstanding | $410,676,048 |

(Continued on next page)

28

| |

| Statement of assets and liabilities (Continued) | |

| | |

| COMPUTATION OF NET ASSET VALUE AND OFFERING PRICE | |

|

| Net asset value and redemption price per class A share | |

| ($355,207,889 divided by 22,954,858 shares) | $15.47 |

|

| Offering price per class A share (100/96.00 of $15.47)* | $16.11 |

|

| Net asset value and offering price per class B share ($3,416,952 divided by 220,623 shares)** | $15.49 |

|

| Net asset value and offering price per class C share ($29,543,668 divided by 1,904,921 shares)** | $15.51 |

|

| Net asset value and redemption price per class M share ($913,661 divided by 58,899 shares) | $15.51 |

|

| Offering price per class M share (100/96.75 of $15.51)† | $16.03 |

|

| Net asset value, offering price and redemption price per class Y share | |

| ($21,593,878 divided by 1,394,754 shares) | $15.48 |

|

* On single retail sales of less than $100,000. On sales of $100,000 or more the offering price is reduced.

** Redemption price per share is equal to net asset value less any applicable contingent deferred sales charge.

† On single retail sales of less than $50,000. On sales of $50,000 or more the offering price is reduced.

The accompanying notes are an integral part of these financial statements.

29

Statement of operations Six months ended 1/31/12 (Unaudited)

| |

| INTEREST INCOME | $9,473,700 |

|

| |

| EXPENSES | |

|

| Compensation of Manager (Note 2) | $857,937 |

|

| Investor servicing fees (Note 2) | 98,339 |

|

| Custodian fees (Note 2) | 4,284 |

|

| Trustee compensation and expenses (Note 2) | 15,964 |

|

| Administrative services (Note 2) | 5,505 |

|

| Distribution fees — Class A (Note 2) | 389,849 |

|

| Distribution fees — Class B (Note 2) | 15,213 |

|

| Distribution fees — Class C (Note 2) | 138,980 |

|

| Distribution fees — Class M (Note 2) | 2,265 |

|

| Other | 75,171 |

|

| Total expenses | 1,603,507 |

| | |

| Expense reduction (Note 2) | (695) |

|

| Net expenses | 1,602,812 |

| | |

| Net investment income | 7,870,888 |

|

| |

| Net realized loss on investments (Notes 1 and 3) | (135,898) |

|

| Net unrealized appreciation of investments during the period | 21,289,068 |

|

| Net gain on investments | 21,153,170 |

| | |

| Net increase in net assets resulting from operations | $29,024,058 |

|

The accompanying notes are an integral part of these financial statements.

30

Statement of changes in net assets

| | |

| INCREASE (DECREASE) IN NET ASSETS | Six months ended 1/31/12* | Year ended 7/31/11 |

|

| Operations: | | |

| Net investment income | $7,870,888 | $17,885,068 |

|

| Net realized loss on investments | (135,898) | (1,363,365) |

|

| Net unrealized appreciation (depreciation) of investments | 21,289,068 | (10,228,708) |

|

| Net increase in net assets resulting from operations | 29,024,058 | 6,292,995 |

|

| Distributions to shareholders (Note 1): | | |

| From ordinary income | | |

| Taxable net investment income | | |

|

| Class A | (169,626) | (2,651) |

|

| Class B | (1,927) | (44) |

|

| Class C | (13,471) | (203) |

|

| Class M | (471) | (8) |

|

| Class Y | (6,916) | (80) |

|

| From tax-exempt net investment income | | |

| Class A | (6,769,753) | (15,897,356) |

|

| Class B | (60,615) | (211,320) |

|

| Class C | (449,362) | (997,972) |

|

| Class M | (16,928) | (45,639) |