UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-04367

Columbia Funds Series Trust I

(Exact name of registrant as specified in charter)

225 Franklin Street

Boston, Massachusetts 02110

(Address of principal executive offices) (Zip code)

Ryan Larrenaga

c/o Columbia Management Investment Advisers, LLC

225 Franklin Street

Boston, MA 02110

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800) 345-6611

Date of fiscal year end: August 31

Date of reporting period: August 31, 2017

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

Annual Report

August 31, 2017

Columbia Contrarian Core Fund

Not FDIC Insured • No bank guarantee • May lose value

Dear Shareholders,

The current outlook for financial markets is clouded by two primary concerns: the high valuation of equities and the direction of interest rates. Following the U.S. presidential election, U.S. equities rallied based on the assumption that the new administration’s policies would stimulate growth quickly. Unfortunately it’s unclear whether those measures will get passed, much less passed quickly. In fixed income, uncertainty stems from the possibility that interest rates won’t rise as rapidly as expected if the administration’s proposed growth policies are not implemented.

Given this uncertainty, investors value a consistent approach more than ever. Investors want strong, repeatable risk-adjusted returns. Consistency — not surprises. As a leading global asset manager, we believe our consistent, collaborative investment approach enables us to deliver the dependable experience your portfolio demands. So, how do we strive to deliver a consistent investment experience?

Better insights

Your portfolio benefits from the investment insights uncovered by our talented investment teams around the world.

Better decisions

Our collaborative, interactive environment enables our investment teams to construct portfolios that take advantage of the best investment ideas.

Better outcomes

We aim to deliver a consistent experience, which means fewer surprises, dependable insights, and products designed to do the thing you want.

Whether you’re trying to save money to help your children go to college or for your own retirement, it’s the consistency of the return that is most essential. People who chase higher returns are usually also the first to sell when that investment goes through a bad patch. We try to combat this behavioral tendency by offering strategies that aim for a more consistent return. Our goal is for investors to panic less during periods of volatility, which can have a significant effect on their long-term results.

Nothing is more important to us than making sure those who have entrusted us to protect and grow their assets can do what matters most to them: build a nest egg, leave a legacy, and live confidently — now and throughout retirement. It’s why our talented professionals around the world work together to uncover uncommon opportunities and why our process encourages challenge and debate around our most compelling ideas to ensure better informed investment decisions, which hopefully lead to better outcomes for you.

Your success is our priority. Talk to your financial advisor about how working with Columbia Threadneedle Investments may help you position your portfolio for consistent, sustainable outcomes, no matter the market conditions.

Sincerely,

Christopher O. Petersen

President, Columbia Funds

Investors should consider the investment objectives, risks, charges and expenses of a mutual fund carefully before investing. For a free prospectus and summary prospectus, which contains this and other important information about a fund, visit investor.columbiathreadneedleus.com. The prospectus should be read carefully before investing.

Columbia Funds are distributed by Columbia Management Investment Distributors, Inc., member FINRA, and managed by Columbia Management Investment Advisers, LLC.

© 2017 Columbia Management Investment Advisers, LLC. All rights reserved.

Columbia Contrarian Core Fund | Annual Report 2017

Columbia Contrarian Core Fund | Annual Report 2017

Investment objective

Columbia Contrarian Core Fund (the Fund) seeks total return, consisting of long-term capital appreciation and current income.

Portfolio management

Guy Pope, CFA

Manager

Managed Fund since 2005

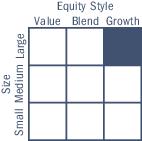

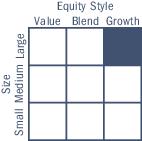

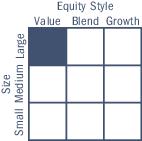

Morningstar style boxTM

The Morningstar Style Box is based on a fund’s portfolio holdings. For equity funds, the vertical axis shows the market capitalization of the stocks owned, and the horizontal axis shows investment style (value, blend, or growth). Information shown is based on the most recent data provided by Morningstar.

© 2017 Morningstar, Inc. All rights reserved. The Morningstar information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information.

| Average annual total returns (%) (for the period ended August 31, 2017) |

| | | Inception | 1 Year | 5 Years | 10 Years |

| Class A | Excluding sales charges | 11/01/98 | 15.61 | 14.85 | 9.35 |

| | Including sales charges | | 8.96 | 13.50 | 8.70 |

| Class C | Excluding sales charges | 12/09/02 | 14.80 | 14.00 | 8.53 |

| | Including sales charges | | 13.80 | 14.00 | 8.53 |

| Class K* | 03/07/11 | 15.78 | 15.00 | 9.48 |

| Class R* | 09/27/10 | 15.34 | 14.58 | 9.09 |

| Class R4* | 11/08/12 | 15.91 | 15.15 | 9.62 |

| Class R5* | 11/08/12 | 16.05 | 15.28 | 9.69 |

| Class T* | Excluding sales charges | 09/27/10 | 15.62 | 14.84 | 9.35 |

| | Including sales charges | | 12.73 | 14.27 | 9.07 |

| Class V | Excluding sales charges | 02/12/93 | 15.61 | 14.83 | 9.31 |

| | Including sales charges | | 8.95 | 13.47 | 8.66 |

| Class Y* | 11/08/12 | 16.14 | 15.35 | 9.72 |

| Class Z | 12/14/92 | 15.95 | 15.14 | 9.62 |

| Russell 1000 Index | | 16.16 | 14.37 | 7.73 |

Returns for Class A and Class V shares are shown with and without the maximum initial sales charge of 5.75%. Returns for Class C shares are shown with and without the 1.00% contingent deferred sales charge for the first year only. Returns for Class T shares are shown with and without the maximum initial sales charge of 2.50% per transaction. Prior to March 27, 2017, Class T shares were known as Class W shares and were not subject to sales charges. The Fund’s other share classes are not subject to sales charges and have limited eligibility. Please see the Fund’s prospectus for details. Performance for different share classes will vary based on differences in sales charges and fees associated with each share class. All results shown assume reinvestment of distributions during the period. Returns do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or on the redemption of Fund shares. Performance results reflect the effect of any fee waivers or reimbursements of Fund expenses by Columbia Management Investment Advisers, LLC and/or any of its affiliates. Absent these fee waivers or expense reimbursement arrangements, performance results would have been lower.

The performance information shown represents past performance and is not a guarantee of future results. The investment return and principal value of your investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance information shown. You may obtain performance information current to the most recent month-end by contacting your financial intermediary, visiting investor.columbiathreadneedleus.com or calling 800.345.6611.

| * | The returns shown for periods prior to the share class inception date (including returns for the Life of the Fund, if shown, which are since Fund inception) include the returns of the Fund’s oldest share class. These returns are adjusted to reflect any higher class-related operating expenses of the newer share classes, as applicable. Please visit investor.columbiathreadneedleus.com/investment-products/mutual-funds/appended-performance for more information. |

The Russell 1000 Index tracks the performance of 1,000 of the largest U.S. companies, based on market capitalization.

Indices are not available for investment, are not professionally managed and do not reflect sales charges, fees, brokerage commissions, taxes or other expenses of investing. Securities in the Fund may not match those in an index.

| 2 | Columbia Contrarian Core Fund | Annual Report 2017 |

Fund at a Glance (continued)

Performance of a hypothetical $10,000 investment (August 31, 2007 — August 31, 2017)

The chart above shows the change in value of a hypothetical $10,000 investment in Class A shares of Columbia Contrarian Core Fund during the stated time period, and does not reflect the deduction of taxes that a shareholder may pay on Fund distributions or on the redemption of Fund shares.

| Top 10 holdings (%) (at August 31, 2017) |

| Apple, Inc. | 4.8 |

| Berkshire Hathaway, Inc., Class B | 3.3 |

| JPMorgan Chase & Co. | 3.2 |

| Microsoft Corp. | 3.2 |

| Citigroup, Inc. | 3.2 |

| Philip Morris International, Inc. | 3.0 |

| Facebook, Inc., Class A | 2.8 |

| Johnson & Johnson | 2.7 |

| Comcast Corp., Class A | 2.6 |

| Honeywell International, Inc. | 2.4 |

Percentages indicated are based upon total investments (excluding Money Market Funds).

For further detail about these holdings, please refer to the section entitled “Portfolio of Investments.”

Fund holdings are as of the date given, are subject to change at any time, and are not recommendations to buy or sell any security.

| Portfolio breakdown (%) (at August 31, 2017) |

| Common Stocks | 96.1 |

| Money Market Funds | 3.9 |

| Total | 100.0 |

Percentages indicated are based upon total investments. The Fund’s portfolio composition is subject to change.

| Equity sector breakdown (%) (at August 31, 2017) |

| Consumer Discretionary | 11.7 |

| Consumer Staples | 6.9 |

| Energy | 6.8 |

| Financials | 17.8 |

| Health Care | 17.8 |

| Industrials | 7.8 |

| Information Technology | 23.9 |

| Materials | 1.8 |

| Real Estate | 1.6 |

| Telecommunication Services | 2.6 |

| Utilities | 1.3 |

| Total | 100.0 |

Percentages indicated are based upon total equity investments. The Fund’s portfolio composition is subject to change.

Columbia Contrarian Core Fund | Annual Report 2017

| 3 |

Manager Discussion of Fund Performance

For the 12-month period that ended August 31, 2017, the Fund’s Class A shares returned 15.61% excluding sales charges. The Fund’s benchmark, the Russell 1000 Index, returned 16.16% for the same time period. In a sharply rising market, cash had a negative impact on performance. Cash, which the benchmark does not hold, and management fees, which the benchmark does not incur, generally accounted for the Fund’s modest shortfall relative to the benchmark.

U.S. equity markets delivered solid gains

Global events, political uncertainty and mixed economic data were enough to keep investors off balance early in the 12-month period, as financial markets moved sharply in reaction to each significant change on the world stage. However, the end of a contentious U.S. presidential contest in November 2016 eliminated a key element of uncertainty, and the U.S. equity markets moved solidly higher through the end of the period. Global growth picked up early in 2017. Positive U.S. economic data, steady job growth, rising corporate earnings and accelerated manufacturing activity further bolstered investor confidence.

The Federal Reserve (the Fed) raised the target range of its benchmark short-term interest rate three times during the period, bringing it to between 1.00% and 1.25% in June 2017. The Fed signaled that it was prepared to raise rates more aggressively on the heels of strong job gains and progress towards its 2.0% inflation target, creating expectations that the June rate hike may not be the last during the calendar year.

Against this backdrop, the U.S. equity markets moved solidly higher during the period. The S&P 500 Index rose 16.23%, with dividends reinvested. Small cap stocks outperformed large and mid-cap stocks.

Contributors and detractors

During the period, stock selection was particularly strong in the information technology, financials and materials sectors. Within information technology, Activision, a leading electronic gaming company, and Apple were top performers for the Fund. Activision continued to benefit from the migration to digital, and Apple rose on expectations for the iPhone 8 and 10 (or X). Within financials, Morgan Stanley, Citigroup and JPMorgan all benefited from expectations of a slightly more lenient regulatory environment under the new administration and the impact of rising interest rates, which are helpful to financial companies. After years of building capital on their balance sheets, these companies increased the amount of capital returned to shareholders, and the acceleration of capital return was met with investor approval. In the materials sector, Sherwin Williams was a big winner for the Fund. The company’s core paint business did well in a favorable environment for housing. The acquisition of competitor Valspar proved to be accretive to the overall company and helped give earnings an extra boost.

Elsewhere in the portfolio, the consumer discretionary sector yielded many stocks with returns in excess of 20% for the period, including Royal Caribbean, McDonalds, Marriott, Comcast and Expedia. Royal Caribbean rebounded after a challenging 2016, during which concerns about the Zika virus and about excess capacity in China weighed on industry prospects. However, the outlook got stronger going into the winter months of 2016-2017, pricing firmed up and Royal Caribbean was the beneficiary of this turnaround. Investors responded favorably to good execution by McDonalds management. Marriott benefited as the merger with Starwood has gone smoothly so far. Comcast and Expedia were two other solid holdings during the period. Health care was another area where the Fund found opportunities -- Vertex and Anthem, in particular. Vertex outperformed based on favorable data showing the potential for expanded market opportunity for its cystic fibrosis treatment. Anthem benefited as health maintenance organizations got a boost as uncertainty created by merger and acquisition activity receded and from a perception that the new administration’s policies would be good for the industry.

Industrials, telecommunication services and health care were the biggest sector detractors from relative Fund results for the period. In the industrials sector, Dun & Bradstreet and Nielsen Holdings were major laggards. With Dun & Bradstreet, we were anticipating an organic growth turnaround, which failed to materialize. Nielsen’s revenues were hurt as big consumer staples customers pulled back on their spending. In the telecommunication services sector, fundamental trends hurt Verizon and AT&T, making it difficult to increase top line growth. Elsewhere in the portfolio, Michael’s lost ground on weaker same-store sales as retailers continued to struggle against online competition and a tough retail environment. Kroger was hurt by increased competition in food retailing and concerns about the impact of Amazon’s purchase of Whole Foods. We eliminated both Michael’s and Kroger from the portfolio.

| 4 | Columbia Contrarian Core Fund | Annual Report 2017 |

Manager Discussion of Fund Performance (continued)

Managing through a challenging year

The Fund’s solid results for the 12-month period had two different phases. The first four months were dominated by the U.S. presidential election. It was a period of underperformance for the Fund, as investors rapidly rotated into and out of stocks that they viewed as beneficiaries of the new administration and its policies. However, we did not get carried away with these trends, many of which turned out to be transitory, at least in the short term. In fact, we took advantage of selloffs to add to names such as Phillip Morris International, where our conviction was strong, and added new positions based on our contrarian approach. As a result, the Fund enjoyed a significant comeback in 2017 and ended the period with performance in line with its benchmark. We stayed with our core contrarian philosophy in constructing the portfolio and managing it from day to day, and we believe this discipline served our shareholders well.

Market risk may affect a single issuer, sector of the economy, industry or the market as a whole. Foreign investments subject the Fund to risks, including political, economic, market, social and others within a particular country, as well as to currency instabilities and less stringent financial and accounting standards generally applicable to U.S. issuers. Growth securities, at times, may not perform as well as value securities or the stock market in general and may be out of favor with investors. Value securities may be unprofitable if the market fails to recognize their intrinsic worth or the portfolio manager misgauged that worth. The Fund may invest significantly in issuers within a particular sector, which may be negatively affected by market, economic or other conditions, making the Fund more vulnerable to unfavorable developments in the sector. See the Fund’s prospectus for more information on these and other risks.

The views expressed in this report reflect the current views of the respective parties. These views are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict, so actual outcomes and results may differ significantly from the views expressed. These views are subject to change at any time based upon economic, market or other conditions and the respective parties disclaim any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Columbia fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any particular Columbia fund. References to specific securities should not be construed as a recommendation or investment advice.

Columbia Contrarian Core Fund | Annual Report 2017

| 5 |

Understanding Your Fund’s Expenses

(Unaudited)

As an investor, you incur two types of costs. There are transaction costs, which generally include sales charges on purchases and may include redemption fees. There are also ongoing costs, which generally include management fees, distribution and/or service fees, and other fund expenses. The following information is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to help you compare these costs with the ongoing costs of investing in other mutual funds.

Analyzing your Fund’s expenses

To illustrate these ongoing costs, we have provided examples and calculated the expenses paid by investors in each share class of the Fund during the period. The actual and hypothetical information in the table is based on an initial investment of $1,000 at the beginning of the period indicated and held for the entire period. Expense information is calculated two ways and each method provides you with different information. The amount listed in the “Actual” column is calculated using the Fund’s actual operating expenses and total return for the period. You may use the Actual information, together with the amount invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the results by the expenses paid during the period under the “Actual” column. The amount listed in the “Hypothetical” column assumes a 5% annual rate of return before expenses (which is not the Fund’s actual return) and then applies the Fund’s actual expense ratio for the period to the hypothetical return. You should not use the hypothetical account values and expenses to estimate either your actual account balance at the end of the period or the expenses you paid during the period. See “Compare with other funds” below for details on how to use the hypothetical data.

Compare with other funds

Since all mutual funds are required to include the same hypothetical calculations about expenses in shareholder reports, you can use this information to compare the ongoing cost of investing in the Fund with other funds. To do so, compare the hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds. As you compare hypothetical examples of other funds, it is important to note that hypothetical examples are meant to highlight the ongoing costs of investing in a fund only and do not reflect any transaction costs, such as sales charges, or redemption or exchange fees. Therefore, the hypothetical calculations are useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. If transaction costs were included in these calculations, your costs would be higher.

| March 1, 2017 — August 31, 2017 |

| | Account value at the

beginning of the

period ($) | Account value at the

end of the

period ($) | Expenses paid during

the period ($) | Fund’s annualized

expense ratio (%) |

| | Actual | Hypothetical | Actual | Hypothetical | Actual | Hypothetical | Actual |

| Class A | 1,000.00 | 1,000.00 | 1,073.10 | 1,019.96 | 5.43 | 5.30 | 1.04 |

| Class C | 1,000.00 | 1,000.00 | 1,069.00 | 1,016.18 | 9.33 | 9.10 | 1.79 |

| Class K | 1,000.00 | 1,000.00 | 1,073.40 | 1,020.47 | 4.91 | 4.79 | 0.94 |

| Class R | 1,000.00 | 1,000.00 | 1,071.70 | 1,018.70 | 6.74 | 6.56 | 1.29 |

| Class R4 | 1,000.00 | 1,000.00 | 1,074.30 | 1,021.22 | 4.13 | 4.02 | 0.79 |

| Class R5 | 1,000.00 | 1,000.00 | 1,074.80 | 1,021.73 | 3.61 | 3.52 | 0.69 |

| Class T (formerly Class W) | 1,000.00 | 1,000.00 | 1,072.60 | 1,020.06 | 5.33 | 5.19 | 1.02 |

| Class V (formerly Class T) | 1,000.00 | 1,000.00 | 1,072.90 | 1,019.96 | 5.43 | 5.30 | 1.04 |

| Class Y | 1,000.00 | 1,000.00 | 1,075.20 | 1,021.93 | 3.40 | 3.31 | 0.65 |

| Class Z | 1,000.00 | 1,000.00 | 1,074.20 | 1,021.22 | 4.13 | 4.02 | 0.79 |

Expenses paid during the period are equal to the annualized expense ratio for each class as indicated above, multiplied by the average account value over the period and then multiplied by the number of days in the Fund’s most recent fiscal half year and divided by 365.

Expenses do not include fees and expenses incurred indirectly by the Fund from its investment in underlying funds, including affiliated and non-affiliated pooled investment vehicles, such as mutual funds and exchange-traded funds.

| 6 | Columbia Contrarian Core Fund | Annual Report 2017 |

Portfolio of Investments

August 31, 2017

(Percentages represent value of investments compared to net assets)

| Common Stocks 96.2% |

| Issuer | Shares | Value ($) |

| Consumer Discretionary 11.3% |

| Hotels, Restaurants & Leisure 2.6% |

| Marriott International, Inc., Class A | 252,663 | 26,170,834 |

| McDonald’s Corp. | 775,400 | 124,040,738 |

| Royal Caribbean Cruises Ltd. | 238,855 | 29,727,893 |

| Starbucks Corp. | 1,848,350 | 101,400,481 |

| Total | | 281,339,946 |

| Household Durables 0.4% |

| Newell Brands, Inc. | 1,027,705 | 49,617,597 |

| Internet & Direct Marketing Retail 0.6% |

| Expedia, Inc. | 148,140 | 21,978,050 |

| Liberty Interactive Corp., Class A(a) | 1,971,945 | 43,619,424 |

| Total | | 65,597,474 |

| Media 2.9% |

| Comcast Corp., Class A | 6,631,916 | 269,322,109 |

| Walt Disney Co. (The) | 419,230 | 42,426,076 |

| Total | | 311,748,185 |

| Multiline Retail 0.7% |

| Dollar General Corp. | 1,024,045 | 74,304,705 |

| Specialty Retail 2.1% |

| AutoZone, Inc.(a) | 55,221 | 29,180,985 |

| Lowe’s Companies, Inc. | 2,672,269 | 197,453,957 |

| Total | | 226,634,942 |

| Textiles, Apparel & Luxury Goods 2.0% |

| Coach, Inc. | 2,477,920 | 103,329,264 |

| PVH Corp. | 926,953 | 116,694,113 |

| Total | | 220,023,377 |

| Total Consumer Discretionary | 1,229,266,226 |

| Consumer Staples 6.6% |

| Beverages 1.5% |

| PepsiCo, Inc. | 1,436,875 | 166,289,544 |

| Food & Staples Retailing 1.3% |

| CVS Health Corp. | 527,081 | 40,764,444 |

| SYSCO Corp. | 1,993,565 | 105,001,069 |

| Total | | 145,765,513 |

| Food Products 0.9% |

| Kellogg Co. | 1,484,275 | 97,160,642 |

| Common Stocks (continued) |

| Issuer | Shares | Value ($) |

| Tobacco 2.9% |

| Philip Morris International, Inc. | 2,693,225 | 314,918,799 |

| Total Consumer Staples | 724,134,498 |

| Energy 6.5% |

| Energy Equipment & Services 0.9% |

| Halliburton Co. | 2,638,154 | 102,808,861 |

| Oil, Gas & Consumable Fuels 5.6% |

| Canadian Natural Resources Ltd. | 4,356,664 | 134,272,384 |

| Chevron Corp. | 1,567,713 | 168,717,273 |

| EOG Resources, Inc. | 1,167,828 | 99,253,702 |

| Exxon Mobil Corp. | 2,717,235 | 207,406,548 |

| Total | | 609,649,907 |

| Total Energy | 712,458,768 |

| Financials 17.1% |

| Banks 8.3% |

| Citigroup, Inc. | 4,866,786 | 331,087,452 |

| JPMorgan Chase & Co. | 3,677,188 | 334,219,617 |

| Wells Fargo & Co. | 4,599,458 | 234,894,320 |

| Total | | 900,201,389 |

| Capital Markets 4.4% |

| Bank of New York Mellon Corp. (The) | 4,426,431 | 231,413,813 |

| BlackRock, Inc. | 64,267 | 26,928,516 |

| Invesco Ltd. | 724,859 | 23,760,878 |

| Morgan Stanley | 3,500,285 | 159,262,967 |

| S&P Global, Inc. | 283,050 | 43,683,106 |

| Total | | 485,049,280 |

| Diversified Financial Services 3.2% |

| Berkshire Hathaway, Inc., Class B(a) | 1,911,413 | 346,271,579 |

| Insurance 1.2% |

| Aon PLC | 945,650 | 131,596,654 |

| Total Financials | 1,863,118,902 |

The accompanying Notes to Financial Statements are an integral part of this statement.

Columbia Contrarian Core Fund | Annual Report 2017

| 7 |

Portfolio of Investments (continued)

August 31, 2017

| Common Stocks (continued) |

| Issuer | Shares | Value ($) |

| Health Care 17.1% |

| Biotechnology 4.0% |

| Alexion Pharmaceuticals, Inc.(a) | 375,310 | 53,447,897 |

| Biogen, Inc.(a) | 557,285 | 176,414,140 |

| Celgene Corp.(a) | 1,282,541 | 178,183,421 |

| Vertex Pharmaceuticals, Inc.(a) | 206,221 | 33,106,719 |

| Total | | 441,152,177 |

| Health Care Equipment & Supplies 2.7% |

| Abbott Laboratories | 2,448,709 | 124,737,237 |

| Medtronic PLC | 1,357,392 | 109,432,943 |

| Zimmer Biomet Holdings, Inc. | 507,310 | 57,970,314 |

| Total | | 292,140,494 |

| Health Care Providers & Services 4.0% |

| Anthem, Inc. | 664,445 | 130,257,798 |

| Cardinal Health, Inc. | 1,947,483 | 131,377,203 |

| CIGNA Corp. | 944,720 | 171,995,723 |

| Total | | 433,630,724 |

| Pharmaceuticals 6.4% |

| Allergan PLC | 579,640 | 133,015,787 |

| Bristol-Myers Squibb Co. | 1,358,115 | 82,138,795 |

| Johnson & Johnson | 2,170,111 | 287,257,593 |

| Pfizer, Inc. | 5,846,200 | 198,303,104 |

| Total | | 700,715,279 |

| Total Health Care | 1,867,638,674 |

| Industrials 7.5% |

| Air Freight & Logistics 2.2% |

| FedEx Corp. | 1,138,931 | 244,164,028 |

| Building Products 0.8% |

| Johnson Controls International PLC | 2,095,718 | 82,969,475 |

| Electrical Equipment 0.7% |

| Eaton Corp. PLC | 1,087,251 | 78,021,132 |

| Industrial Conglomerates 3.3% |

| General Electric Co. | 4,113,055 | 100,975,500 |

| Honeywell International, Inc. | 1,823,624 | 252,152,491 |

| Total | | 353,127,991 |

| Common Stocks (continued) |

| Issuer | Shares | Value ($) |

| Professional Services 0.5% |

| Nielsen Holdings PLC | 1,500,535 | 58,295,785 |

| Total Industrials | 816,578,411 |

| Information Technology 23.0% |

| Communications Equipment 1.5% |

| Cisco Systems, Inc. | 4,401,440 | 141,770,383 |

| Palo Alto Networks, Inc.(a) | 123,935 | 16,444,935 |

| Total | | 158,215,318 |

| Internet Software & Services 6.3% |

| Alphabet, Inc., Class A(a) | 156,518 | 149,512,254 |

| Alphabet, Inc., Class C(a) | 258,077 | 242,419,468 |

| Facebook, Inc., Class A(a) | 1,733,375 | 298,088,499 |

| Total | | 690,020,221 |

| IT Services 3.9% |

| Fidelity National Information Services, Inc. | 1,377,510 | 127,998,229 |

| FleetCor Technologies, Inc.(a) | 101,974 | 14,660,802 |

| MasterCard, Inc., Class A | 1,558,114 | 207,696,596 |

| Total System Services, Inc. | 1,011,000 | 69,880,320 |

| Total | | 420,235,947 |

| Semiconductors & Semiconductor Equipment 2.1% |

| Broadcom Ltd. | 846,955 | 213,491,947 |

| MACOM Technology Solutions Holdings, Inc.(a) | 383,742 | 17,475,611 |

| Total | | 230,967,558 |

| Software 4.6% |

| Activision Blizzard, Inc. | 2,150,885 | 141,012,021 |

| Electronic Arts, Inc.(a) | 230,211 | 27,970,636 |

| Microsoft Corp. | 4,453,597 | 332,995,448 |

| Total | | 501,978,105 |

| Technology Hardware, Storage & Peripherals 4.6% |

| Apple, Inc. | 3,041,051 | 498,732,364 |

| Total Information Technology | 2,500,149,513 |

| Materials 1.8% |

| Chemicals 1.0% |

| Sherwin-Williams Co. (The) | 323,854 | 109,873,946 |

The accompanying Notes to Financial Statements are an integral part of this statement.

| 8 | Columbia Contrarian Core Fund | Annual Report 2017 |

Portfolio of Investments (continued)

August 31, 2017

| Common Stocks (continued) |

| Issuer | Shares | Value ($) |

| Containers & Packaging 0.8% |

| Ball Corp. | 717,450 | 28,690,826 |

| Sealed Air Corp. | 1,174,540 | 52,126,085 |

| Total | | 80,816,911 |

| Total Materials | 190,690,857 |

| Real Estate 1.5% |

| Equity Real Estate Investment Trusts (REITS) 1.5% |

| American Tower Corp. | 1,140,022 | 168,780,257 |

| Total Real Estate | 168,780,257 |

| Telecommunication Services 2.5% |

| Diversified Telecommunication Services 2.5% |

| AT&T, Inc. | 4,870,100 | 182,433,946 |

| Verizon Communications, Inc. | 1,764,608 | 84,648,246 |

| Total | | 267,082,192 |

| Total Telecommunication Services | 267,082,192 |

| Utilities 1.3% |

| Electric Utilities 1.3% |

| Edison International | 452,117 | 36,250,741 |

| Southern Co. (The) | 2,161,365 | 104,307,475 |

| Total | | 140,558,216 |

| Total Utilities | 140,558,216 |

Total Common Stocks

(Cost $7,538,845,241) | 10,480,456,514 |

|

| Money Market Funds 3.9% |

| | Shares | Value ($) |

| Columbia Short-Term Cash Fund, 1.146%(b),(c) | 424,293,769 | 424,293,769 |

Total Money Market Funds

(Cost $424,274,369) | 424,293,769 |

Total Investments

(Cost: $7,963,119,610) | 10,904,750,283 |

| Other Assets & Liabilities, Net | | (12,487,795) |

| Net Assets | 10,892,262,488 |

Notes to Portfolio of Investments

| (a) | Non-income producing investment. |

| (b) | The rate shown is the seven-day current annualized yield at August 31, 2017. |

| (c) | As defined in the Investment Company Act of 1940, an affiliated company is one in which the Fund owns 5% or more of the company’s outstanding voting securities, or a company which is under common ownership or control with the Fund. Holdings and transactions in these affiliated companies during the year ended August 31, 2017 are as follows: |

| Issuer | Beginning

shares | Shares

purchased | Shares

sold | Ending

shares | Realized gain

(loss) ($) | Net change in

unrealized

appreciation

(depreciation) ($) | Dividends —

affiliated

issuers($) | Value ($) |

| Columbia Short-Term Cash Fund, 1.146% | 305,769,244 | 2,154,536,319 | (2,036,011,794) | 424,293,769 | (26,117) | 19,400 | 2,120,968 | 424,293,769 |

Fair value measurements

The Fund categorizes its fair value measurements according to a three-level hierarchy that maximizes the use of observable inputs and minimizes the use of unobservable inputs by prioritizing that the most observable input be used when available. Observable inputs are those that market participants would use in pricing an investment based on market data obtained from sources independent of the reporting entity. Unobservable inputs are those that reflect the Fund’s assumptions about the information market participants would use in

The accompanying Notes to Financial Statements are an integral part of this statement.

Columbia Contrarian Core Fund | Annual Report 2017

| 9 |

Portfolio of Investments (continued)

August 31, 2017

Fair value measurements (continued)

pricing an investment. An investment’s level within the fair value hierarchy is based on the lowest level of any input that is deemed significant to the asset’s or liability’s fair value measurement. The input levels are not necessarily an indication of the risk or liquidity associated with investments at that level. For example, certain U.S. government securities are generally high quality and liquid, however, they are reflected as Level 2 because the inputs used to determine fair value may not always be quoted prices in an active market.

Fair value inputs are summarized in the three broad levels listed below:

| • | Level 1 – Valuations based on quoted prices for investments in active markets that the Fund has the ability to access at the measurement date. Valuation adjustments are not applied to Level 1 investments. |

| • | Level 2 – Valuations based on other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risks, etc.). |

| • | Level 3 – Valuations based on significant unobservable inputs (including the Fund’s own assumptions and judgment in determining the fair value of investments). |

Inputs that are used in determining fair value of an investment may include price information, credit data, volatility statistics, and other factors. These inputs can be either observable or unobservable. The availability of observable inputs can vary between investments, and is affected by various factors such as the type of investment, and the volume and level of activity for that investment or similar investments in the marketplace. The inputs will be considered by the Investment Manager, along with any other relevant factors in the calculation of an investment’s fair value. The Fund uses prices and inputs that are current as of the measurement date, which may include periods of market dislocations. During these periods, the availability of prices and inputs may be reduced for many investments. This condition could cause an investment to be reclassified between the various levels within the hierarchy.

Certain investments that have been measured at fair value using the net asset value (NAV) per share (or its equivalent) are not categorized in the fair value hierarchy. The fair value amounts presented in the table are intended to reconcile the fair value hierarchy to the amounts presented in the Portfolio of Investments. The Columbia Short-Term Cash Fund seeks to provide shareholders with maximum current income consistent with liquidity and stability of principal. Columbia Short-Term Cash Fund prices its shares with a floating NAV and no longer seeks to maintain a stable NAV.

Investments falling into the Level 3 category are primarily supported by quoted prices from brokers and dealers participating in the market for those investments. However, these may be classified as Level 3 investments due to lack of market transparency and corroboration to support these quoted prices. Additionally, valuation models may be used as the pricing source for any remaining investments classified as Level 3. These models may rely on one or more significant unobservable inputs and/or significant assumptions by the Investment Manager. Inputs used in valuations may include, but are not limited to, financial statement analysis, capital account balances, discount rates and estimated cash flows, and comparable company data.

Under the direction of the Fund’s Board of Trustees (the Board), the Investment Manager’s Valuation Committee (the Committee) is responsible for overseeing the valuation procedures approved by the Board. The Committee consists of voting and non-voting members from various groups within the Investment Manager’s organization, including operations and accounting, trading and investments, compliance, risk management and legal.

The Committee meets at least monthly to review and approve valuation matters, which may include a description of specific valuation determinations, data regarding pricing information received from approved pricing vendors and brokers and the results of Board-approved valuation control policies and procedures (the Policies). The Policies address, among other things, instances when market quotations are or are not readily available, including recommendations of third party pricing vendors and a determination of appropriate pricing methodologies; events that require specific valuation determinations and assessment of fair value techniques; securities with a potential for stale pricing, including those that are illiquid, restricted, or in default; and the effectiveness of third party pricing vendors, including periodic reviews of vendors. The Committee meets more frequently, as needed, to discuss additional valuation matters, which may include the need to review back-testing results, review time-sensitive information or approve related valuation actions. The Committee reports to the Board, with members of the Committee meeting with the Board at each of its regularly scheduled meetings to discuss valuation matters and actions during the period, similar to those described earlier.

For investments categorized as Level 3, the Committee monitors information similar to that described above, which may include: (i) data specific to the issuer or comparable issuers, (ii) general market or specific sector news and (iii) quoted prices and specific or similar security transactions. The Committee considers this data and any changes from prior periods in order to assess the reasonableness of observable and unobservable inputs, any assumptions or internal models used to value those securities and changes in fair value. This data is also used to corroborate, when available, information received from approved pricing vendors and brokers. Various factors impact the frequency of monitoring this information (which may occur as often as daily). However, the Committee may determine that changes to inputs, assumptions and models are not required as a result of the monitoring procedures performed.

The following table is a summary of the inputs used to value the Fund’s investments at August 31, 2017:

| | Level 1

quoted prices

in active

markets for

identical

assets ($) | Level 2

other

significant

observable

inputs ($) | Level 3

significant

unobservable

inputs ($) | Investments

measured at

net asset

value ($) | Total ($) |

| Investments | | | | | |

| Common Stocks | | | | | |

| Consumer Discretionary | 1,229,266,226 | — | — | — | 1,229,266,226 |

| Consumer Staples | 724,134,498 | — | — | — | 724,134,498 |

| Energy | 712,458,768 | — | — | — | 712,458,768 |

| Financials | 1,863,118,902 | — | — | — | 1,863,118,902 |

| Health Care | 1,867,638,674 | — | — | — | 1,867,638,674 |

| Industrials | 816,578,411 | — | — | — | 816,578,411 |

| Information Technology | 2,500,149,513 | — | — | — | 2,500,149,513 |

| Materials | 190,690,857 | — | — | — | 190,690,857 |

| Real Estate | 168,780,257 | — | — | — | 168,780,257 |

The accompanying Notes to Financial Statements are an integral part of this statement.

| 10 | Columbia Contrarian Core Fund | Annual Report 2017 |

Portfolio of Investments (continued)

August 31, 2017

Fair value measurements (continued)

| | Level 1

quoted prices

in active

markets for

identical

assets ($) | Level 2

other

significant

observable

inputs ($) | Level 3

significant

unobservable

inputs ($) | Investments

measured at

net asset

value ($) | Total ($) |

| Telecommunication Services | 267,082,192 | — | — | — | 267,082,192 |

| Utilities | 140,558,216 | — | — | — | 140,558,216 |

| Total Common Stocks | 10,480,456,514 | — | — | — | 10,480,456,514 |

| Money Market Funds | — | — | — | 424,293,769 | 424,293,769 |

| Total Investments | 10,480,456,514 | — | — | 424,293,769 | 10,904,750,283 |

See the Portfolio of Investments for all investment classifications not indicated in the table.

There were no transfers of financial assets between levels during the period.

The accompanying Notes to Financial Statements are an integral part of this statement.

Columbia Contrarian Core Fund | Annual Report 2017

| 11 |

Statement of Assets and Liabilities

August 31, 2017

| Assets | |

| Investments in unaffiliated issuers, at cost | $7,538,845,241 |

| Investments in affiliated issuers, at cost | 424,274,369 |

| Investments in unaffiliated issuers, at value | 10,480,456,514 |

| Investments in affiliated issuers, at value | 424,293,769 |

| Receivable for: | |

| Investments sold | 30,694,547 |

| Capital shares sold | 11,082,672 |

| Dividends | 18,674,608 |

| Foreign tax reclaims | 81,149 |

| Prepaid expenses | 72,942 |

| Trustees’ deferred compensation plan | 406,825 |

| Total assets | 10,965,763,026 |

| Liabilities | |

| Payable for: | |

| Investments purchased | 62,541,659 |

| Capital shares purchased | 8,487,147 |

| Management services fees | 181,085 |

| Distribution and/or service fees | 36,460 |

| Transfer agent fees | 1,539,163 |

| Plan administration fees | 1,441 |

| Compensation of board members | 2,880 |

| Compensation of chief compliance officer | 732 |

| Other expenses | 303,146 |

| Trustees’ deferred compensation plan | 406,825 |

| Total liabilities | 73,500,538 |

| Net assets applicable to outstanding capital stock | $10,892,262,488 |

| Represented by | |

| Paid in capital | 7,503,609,394 |

| Undistributed net investment income | 64,041,928 |

| Accumulated net realized gain | 382,980,493 |

| Unrealized appreciation (depreciation) on: | |

| Investments - unaffiliated issuers | 2,941,611,273 |

| Investments - affiliated issuers | 19,400 |

| Total - representing net assets applicable to outstanding capital stock | $10,892,262,488 |

The accompanying Notes to Financial Statements are an integral part of this statement.

| 12 | Columbia Contrarian Core Fund | Annual Report 2017 |

Statement of Assets and Liabilities (continued)

August 31, 2017

| Class A | |

| Net assets | $1,941,061,841 |

| Shares outstanding | 76,378,059 |

| Net asset value per share | $25.41 |

| Maximum offering price per share(a) | $26.96 |

| Class C | |

| Net assets | $748,147,943 |

| Shares outstanding | 32,406,315 |

| Net asset value per share | $23.09 |

| Class K | |

| Net assets | $6,282,641 |

| Shares outstanding | 245,584 |

| Net asset value per share | $25.58 |

| Class R | |

| Net assets | $132,392,329 |

| Shares outstanding | 5,210,921 |

| Net asset value per share | $25.41 |

| Class R4 | |

| Net assets | $596,703,706 |

| Shares outstanding | 22,932,510 |

| Net asset value per share | $26.02 |

| Class R5 | |

| Net assets | $779,002,230 |

| Shares outstanding | 29,947,267 |

| Net asset value per share | $26.01 |

| Class T(b) | |

| Net assets | $1,356,520 |

| Shares outstanding | 53,383 |

| Net asset value per share | $25.41 |

| Maximum offering price per share(c) | $26.06 |

| Class V(d) | |

| Net assets | $154,392,300 |

| Shares outstanding | 6,131,216 |

| Net asset value per share | $25.18 |

| Maximum offering price per share(e) | $26.72 |

| Class Y | |

| Net assets | $1,574,824,274 |

| Shares outstanding | 60,510,665 |

| Net asset value per share | $26.03 |

| Class Z | |

| Net assets | $4,958,098,704 |

| Shares outstanding | 193,592,317 |

| Net asset value per share | $25.61 |

| (a) | The maximum offering price per share is calculated by dividing the net asset value per share by 1.0 minus the maximum sales charge of 5.75% for Class A. |

| (b) | Prior to March 27, 2017, Class T shares were known as Class W shares. |

| (c) | The maximum offering price per share is calculated by dividing the net asset value per share by 1.0 minus the maximum sales charge of 2.50% for Class T. |

| (d) | Prior to January 24, 2017, Class V shares were known as Class T shares. |

| (e) | The maximum offering price per share is calculated by dividing the net asset value per share by 1.0 minus the maximum sales charge of 5.75% for Class V. |

The accompanying Notes to Financial Statements are an integral part of this statement.

Columbia Contrarian Core Fund | Annual Report 2017

| 13 |

Statement of Operations

Year Ended August 31, 2017

| Net investment income | |

| Income: | |

| Dividends — unaffiliated issuers | $188,454,539 |

| Dividends — affiliated issuers | 2,120,968 |

| Foreign taxes withheld | (363,863) |

| Total income | 190,211,644 |

| Expenses: | |

| Management services fees | 62,449,221 |

| Distribution and/or service fees | |

| Class A | 6,061,118 |

| Class B(a) | 38,763 |

| Class C | 7,086,541 |

| Class R | 569,474 |

| Class T(b) | 165,466 |

| Class V(c) | 371,584 |

| Transfer agent fees | |

| Class A | 3,967,584 |

| Class B(a) | 6,356 |

| Class C | 1,157,567 |

| Class I(d) | 7,946 |

| Class K | 3,168 |

| Class R | 185,891 |

| Class R4 | 757,184 |

| Class R5 | 376,866 |

| Class T(b) | 109,790 |

| Class V(c) | 242,878 |

| Class Y | 47,788 |

| Class Z | 7,884,001 |

| Plan administration fees | |

| Class K | 13,931 |

| Compensation of board members | 202,340 |

| Custodian fees | 63,445 |

| Printing and postage fees | 595,248 |

| Registration fees | 621,673 |

| Audit fees | 38,115 |

| Legal fees | 296,879 |

| Compensation of chief compliance officer | 4,444 |

| Other | 238,288 |

| Total expenses | 93,563,549 |

| Expense reduction | (14,065) |

| Total net expenses | 93,549,484 |

| Net investment income | 96,662,160 |

| Realized and unrealized gain (loss) — net | |

| Net realized gain (loss) on: | |

| Investments — unaffiliated issuers | 476,663,247 |

| Investments — affiliated issuers | (26,117) |

| Foreign currency translations | 8,644 |

| Net realized gain | 476,645,774 |

| Net change in unrealized appreciation (depreciation) on: | |

| Investments — unaffiliated issuers | 930,021,745 |

| Investments — affiliated issuers | 19,400 |

| Foreign currency translations | 2 |

| Net change in unrealized appreciation (depreciation) | 930,041,147 |

| Net realized and unrealized gain | 1,406,686,921 |

| Net increase in net assets resulting from operations | $1,503,349,081 |

The accompanying Notes to Financial Statements are an integral part of this statement.

| 14 | Columbia Contrarian Core Fund | Annual Report 2017 |

Statement of Operations (continued)

Year Ended August 31, 2017

| (a) | Effective July 17, 2017, Class B shares were automatically converted to Class A shares. |

| (b) | Prior to March 27, 2017, Class T shares were known as Class W shares. |

| (c) | Prior to January 24, 2017, Class V shares were known as Class T shares. |

| (d) | Effective March 27, 2017, Class I shares were redeemed or exchanged for Class Y shares. |

The accompanying Notes to Financial Statements are an integral part of this statement.

Columbia Contrarian Core Fund | Annual Report 2017

| 15 |

Statement of Changes in Net Assets

| | Year Ended

August 31, 2017 | Year Ended

August 31, 2016 |

| Operations | | |

| Net investment income | $96,662,160 | $62,122,462 |

| Net realized gain | 476,645,774 | 8,905,471 |

| Net change in unrealized appreciation (depreciation) | 930,041,147 | 815,597,430 |

| Net increase in net assets resulting from operations | 1,503,349,081 | 886,625,363 |

| Distributions to shareholders | | |

| Net investment income | | |

| Class A | (19,193,883) | (61,603,501) |

| Class B(a) | — | (169,643) |

| Class C | (1) | (9,230,922) |

| Class I(b) | (3,453,777) | (11,959,112) |

| Class K | (40,230) | (3,093) |

| Class R | (451,640) | (1,343,578) |

| Class R4 | (3,562,542) | (7,021,383) |

| Class R5 | (5,967,141) | (11,778,388) |

| Class T(c) | (843,456) | (1,414,819) |

| Class V(d) | (968,097) | (3,614,625) |

| Class Y | (3,854,161) | (1,957,696) |

| Class Z | (38,846,630) | (65,021,880) |

| Net realized gains | | |

| Class A | (21,919,791) | (71,377,749) |

| Class B(a) | (42,890) | (281,084) |

| Class C | (5,729,742) | (15,383,736) |

| Class I(b) | (2,474,135) | (11,792,193) |

| Class K | (39,271) | (3,406) |

| Class R | (797,594) | (1,730,183) |

| Class R4 | (3,005,305) | (7,412,136) |

| Class R5 | (4,473,015) | (11,842,976) |

| Class T(c) | (958,481) | (1,639,301) |

| Class V(d) | (1,115,823) | (4,210,566) |

| Class Y | (2,760,953) | (1,934,742) |

| Class Z | (32,770,414) | (68,474,886) |

| Total distributions to shareholders | (153,268,972) | (371,201,598) |

| Increase (decrease) in net assets from capital stock activity | (392,465,869) | 3,228,540,706 |

| Total increase in net assets | 957,614,240 | 3,743,964,471 |

| Net assets at beginning of year | 9,934,648,248 | 6,190,683,777 |

| Net assets at end of year | $10,892,262,488 | $9,934,648,248 |

| Undistributed net investment income | $64,041,928 | $45,532,775 |

| (a) | Effective July 17, 2017, Class B shares were automatically converted to Class A shares. |

| (b) | Effective March 27, 2017, Class I shares were redeemed or exchanged for Class Y shares. |

| (c) | Prior to March 27, 2017, Class T shares were known as Class W shares. |

| (d) | Prior to January 24, 2017, Class V shares were known as Class T shares. |

The accompanying Notes to Financial Statements are an integral part of this statement.

| 16 | Columbia Contrarian Core Fund | Annual Report 2017 |

Statement of Changes in Net Assets (continued)

| | Year Ended | Year Ended |

| | August 31, 2017 | August 31, 2016 |

| | Shares | Dollars ($) | Shares | Dollars ($) |

| Capital stock activity |

| Class A(a) | | | | |

| Subscriptions (b) | 24,532,402 | 567,339,209 | 48,128,391 | 1,017,079,358 |

| Fund reorganization | — | — | 2,911,441 | 60,325,156 |

| Distributions reinvested | 1,703,138 | 38,796,444 | 6,161,108 | 126,980,438 |

| Redemptions | (78,222,523) | (1,845,678,165) | (36,847,943) | (778,168,494) |

| Net increase (decrease) | (51,986,983) | (1,239,542,512) | 20,352,997 | 426,216,458 |

| Class B(a) | | | | |

| Subscriptions | 10,229 | 211,772 | 45,719 | 884,791 |

| Distributions reinvested | 2,033 | 42,206 | 23,557 | 443,344 |

| Redemptions (b) | (309,670) | (6,756,778) | (264,258) | (5,049,400) |

| Net decrease | (297,408) | (6,502,800) | (194,982) | (3,721,265) |

| Class C | | | | |

| Subscriptions | 8,279,732 | 176,276,614 | 14,095,386 | 272,495,550 |

| Fund reorganization | — | — | 1,127,343 | 21,281,992 |

| Distributions reinvested | 237,660 | 4,945,710 | 1,091,134 | 20,578,795 |

| Redemptions | (9,109,741) | (195,062,192) | (4,401,923) | (85,094,434) |

| Net increase (decrease) | (592,349) | (13,839,868) | 11,911,940 | 229,261,903 |

| Class I(c) | | | | |

| Subscriptions | 619,606 | 13,527,383 | 4,361,594 | 90,879,128 |

| Fund reorganization | — | — | 94 | 1,955 |

| Distributions reinvested | 258,970 | 5,927,821 | 1,147,398 | 23,751,142 |

| Redemptions | (16,890,162) | (398,885,486) | (9,376,151) | (201,335,473) |

| Net decrease | (16,011,586) | (379,430,282) | (3,867,065) | (86,703,248) |

| Class K | | | | |

| Subscriptions | 18,689 | 455,856 | 248,597 | 5,280,131 |

| Distributions reinvested | 3,468 | 79,454 | 306 | 6,336 |

| Redemptions | (13,564) | (307,763) | (17,292) | (383,527) |

| Net increase | 8,593 | 227,547 | 231,611 | 4,902,940 |

| Class R | | | | |

| Subscriptions | 2,442,785 | 57,295,465 | 2,493,106 | 52,783,290 |

| Fund reorganization | — | — | 348,131 | 7,216,396 |

| Distributions reinvested | 40,077 | 914,165 | 102,297 | 2,112,434 |

| Redemptions | (1,605,994) | (37,805,368) | (963,209) | (20,257,607) |

| Net increase | 876,868 | 20,404,262 | 1,980,325 | 41,854,513 |

| Class R4 | | | | |

| Subscriptions | 10,776,230 | 260,548,555 | 8,232,471 | 177,759,473 |

| Fund reorganization | — | — | 364,058 | 7,717,423 |

| Distributions reinvested | 279,486 | 6,506,429 | 682,566 | 14,368,022 |

| Redemptions | (4,694,624) | (112,458,762) | (3,193,911) | (69,241,659) |

| Net increase | 6,361,092 | 154,596,222 | 6,085,184 | 130,603,259 |

| Class R5 | | | | |

| Subscriptions | 11,090,361 | 270,140,698 | 19,032,190 | 414,631,025 |

| Fund reorganization | — | — | 926,239 | 19,625,841 |

| Distributions reinvested | 448,671 | 10,436,073 | 1,117,699 | 23,505,208 |

| Redemptions | (9,119,270) | (216,839,757) | (9,009,812) | (190,228,689) |

| Net increase | 2,419,762 | 63,737,014 | 12,066,316 | 267,533,385 |

| Class T(d) | | | | |

| Subscriptions | 1,447,862 | 32,641,606 | 9,044,630 | 190,637,528 |

| Fund reorganization | — | — | 95 | 1,963 |

| Distributions reinvested | 79,099 | 1,801,867 | 148,179 | 3,053,977 |

| Redemptions | (11,365,827) | (257,363,851) | (4,860,868) | (105,635,402) |

| Net increase (decrease) | (9,838,866) | (222,920,378) | 4,332,036 | 88,058,066 |

The accompanying Notes to Financial Statements are an integral part of this statement.

Columbia Contrarian Core Fund | Annual Report 2017

| 17 |

Statement of Changes in Net Assets (continued)

| | Year Ended | Year Ended |

| | August 31, 2017 | August 31, 2016 |

| | Shares | Dollars ($) | Shares | Dollars ($) |

| Class V(e) | | | | |

| Subscriptions | 49,241 | 1,134,243 | 110,941 | 2,272,788 |

| Distributions reinvested | 64,778 | 1,462,036 | 266,648 | 5,444,949 |

| Redemptions | (633,299) | (14,654,904) | (524,066) | (11,080,577) |

| Net decrease | (519,280) | (12,058,625) | (146,477) | (3,362,840) |

| Class Y(c) | | | | |

| Subscriptions | 49,850,577 | 1,240,699,466 | 12,749,816 | 268,717,492 |

| Fund reorganization | — | — | 65,725 | 1,392,855 |

| Distributions reinvested | 271,473 | 6,314,467 | 132,077 | 2,777,583 |

| Redemptions | (4,056,941) | (98,611,716) | (950,699) | (20,822,683) |

| Net increase | 46,065,109 | 1,148,402,217 | 11,996,919 | 252,065,247 |

| Class Z | | | | |

| Subscriptions | 85,852,060 | 2,044,682,517 | 56,743,145 | 1,206,996,663 |

| Fund reorganization | — | — | 59,654,609 | 1,245,149,414 |

| Distributions reinvested | 2,284,114 | 52,351,890 | 4,076,451 | 84,504,832 |

| Redemptions | (83,135,098) | (2,002,573,073) | (30,828,122) | (654,818,621) |

| Net increase | 5,001,076 | 94,461,334 | 89,646,083 | 1,881,832,288 |

| Total net increase (decrease) | (18,513,972) | (392,465,869) | 154,394,887 | 3,228,540,706 |

| (a) | Effective July 17, 2017, Class B shares were automatically converted to Class A shares. |

| (b) | Includes conversions of Class B shares to Class A shares, if any. |

| (c) | Effective March 27, 2017, Class I shares were redeemed or exchanged for Class Y shares. |

| (d) | Prior to March 27, 2017, Class T shares were known as Class W shares. |

| (e) | Prior to January 24, 2017, Class V shares were known as Class T shares. |

The accompanying Notes to Financial Statements are an integral part of this statement.

| 18 | Columbia Contrarian Core Fund | Annual Report 2017 |

[THIS PAGE INTENTIONALLY LEFT BLANK]

Columbia Contrarian Core Fund | Annual Report 2017

| 19 |

The following table is intended to help you understand the Fund’s financial performance. Certain information reflects financial results for a single share of a class held for the periods shown. Per share net investment income (loss) amounts are calculated based on average shares outstanding during the period. Total return assumes reinvestment of all dividends and distributions, if any. Total return does not reflect payment of sales charges, if any. Total return and portfolio turnover are not annualized for periods of less than one year. The portfolio turnover rate is calculated without regard to purchase and sales transactions of short-term instruments and certain derivatives, if any. If such transactions were included, the Fund’s portfolio turnover rate may be higher.

| Year ended | Net asset value,

beginning of

period | Net

investment

income

(loss) | Net

realized

and

unrealized

gain (loss) | Total from

investment

operations | Distributions

from net

investment

income | Distributions

from net

realized

gains |

| Class A |

| 8/31/2017 | $22.29 | 0.19 | 3.25 | 3.44 | (0.15) | (0.17) |

| 8/31/2016 | $21.27 | 0.15 | 2.05 | 2.20 | (0.55) | (0.63) |

| 8/31/2015 | $22.37 | 0.65 (d) | (0.23) | 0.42 | (0.10) | (1.42) |

| 8/31/2014 | $19.15 | 0.14 | 4.32 | 4.46 | (0.11) | (1.13) |

| 8/31/2013 | $15.68 | 0.13 | 3.48 | 3.61 | (0.12) | (0.02) |

| Class C |

| 8/31/2017 | $20.28 | 0.01 | 2.97 | 2.98 | (0.00) (e) | (0.17) |

| 8/31/2016 | $19.43 | (0.00) (e) | 1.86 | 1.86 | (0.38) | (0.63) |

| 8/31/2015 | $20.62 | 0.50 (d) | (0.27) | 0.23 | — | (1.42) |

| 8/31/2014 | $17.77 | (0.01) | 3.99 | 3.98 | — | (1.13) |

| 8/31/2013 | $14.55 | (0.00) (e) | 3.25 | 3.25 | (0.01) | (0.02) |

| Class K |

| 8/31/2017 | $22.43 | 0.22 | 3.28 | 3.50 | (0.18) | (0.17) |

| 8/31/2016 | $21.40 | 0.23 | 2.01 | 2.24 | (0.58) | (0.63) |

| 8/31/2015 | $22.50 | 0.61 (d) | (0.16) | 0.45 | (0.13) | (1.42) |

| 8/31/2014 | $19.26 | 0.17 | 4.33 | 4.50 | (0.13) | (1.13) |

| 8/31/2013 | $15.77 | 0.15 | 3.51 | 3.66 | (0.15) | (0.02) |

| Class R |

| 8/31/2017 | $22.29 | 0.14 | 3.25 | 3.39 | (0.10) | (0.17) |

| 8/31/2016 | $21.26 | 0.10 | 2.05 | 2.15 | (0.49) | (0.63) |

| 8/31/2015 | $22.37 | 0.65 (d) | (0.29) | 0.36 | (0.05) | (1.42) |

| 8/31/2014 | $19.15 | 0.09 | 4.32 | 4.41 | (0.06) | (1.13) |

| 8/31/2013 | $15.68 | 0.08 | 3.49 | 3.57 | (0.08) | (0.02) |

| Class R4 |

| 8/31/2017 | $22.81 | 0.26 | 3.33 | 3.59 | (0.21) | (0.17) |

| 8/31/2016 | $21.74 | 0.21 | 2.09 | 2.30 | (0.60) | (0.63) |

| 8/31/2015 | $22.83 | 0.80 (d) | (0.32) | 0.48 | (0.15) | (1.42) |

| 8/31/2014 | $19.52 | 0.20 | 4.40 | 4.60 | (0.16) | (1.13) |

| 8/31/2013 (f) | $15.84 | 0.16 | 3.70 | 3.86 | (0.16) | (0.02) |

The accompanying Notes to Financial Statements are an integral part of this statement.

| 20 | Columbia Contrarian Core Fund | Annual Report 2017 |

Total

distributions to

shareholders | Net

asset

value,

end of

period | Total

return | Total gross

expense

ratio to

average

net assets(a) | Total net

expense

ratio to

average

net assets(a),(b) | Net investment

income (loss)

ratio to

average

net assets | Portfolio

turnover | Net

assets,

end of

period

(000’s) |

| |

| (0.32) | $25.41 | 15.61% | 1.04% | 1.04% (c) | 0.82% | 52% | $1,941,062 |

| (1.18) | $22.29 | 10.79% | 1.07% | 1.07% (c) | 0.72% | 47% | $2,860,806 |

| (1.52) | $21.27 | 1.99% | 1.09% | 1.09% (c) | 2.93% | 60% | $2,297,176 |

| (1.24) | $22.37 | 24.15% | 1.11% | 1.11% (c) | 0.69% | 65% | $1,659,841 |

| (0.14) | $19.15 | 23.23% | 1.15% | 1.14% (c) | 0.73% | 47% | $913,212 |

| |

| (0.17) | $23.09 | 14.80% | 1.79% | 1.79% (c) | 0.07% | 52% | $748,148 |

| (1.01) | $20.28 | 9.98% | 1.83% | 1.83% (c) | (0.02%) | 47% | $669,226 |

| (1.42) | $19.43 | 1.17% | 1.85% | 1.85% (c) | 2.46% | 60% | $409,798 |

| (1.13) | $20.62 | 23.22% | 1.86% | 1.86% (c) | (0.06%) | 65% | $222,834 |

| (0.03) | $17.77 | 22.36% | 1.90% | 1.89% (c) | (0.02%) | 47% | $115,940 |

| |

| (0.35) | $25.58 | 15.78% | 0.94% | 0.94% | 0.92% | 52% | $6,283 |

| (1.21) | $22.43 | 10.92% | 0.95% | 0.95% | 1.08% | 47% | $5,317 |

| (1.55) | $21.40 | 2.12% | 0.96% | 0.96% | 2.73% | 60% | $115 |

| (1.26) | $22.50 | 24.27% | 0.97% | 0.97% | 0.81% | 65% | $113 |

| (0.17) | $19.26 | 23.40% | 1.00% | 1.00% | 0.87% | 47% | $144 |

| |

| (0.27) | $25.41 | 15.34% | 1.29% | 1.29% (c) | 0.57% | 52% | $132,392 |

| (1.12) | $22.29 | 10.55% | 1.32% | 1.32% (c) | 0.49% | 47% | $96,586 |

| (1.47) | $21.26 | 1.69% | 1.34% | 1.34% (c) | 2.93% | 60% | $50,048 |

| (1.19) | $22.37 | 23.86% | 1.36% | 1.36% (c) | 0.44% | 65% | $30,291 |

| (0.10) | $19.15 | 22.93% | 1.39% | 1.39% (c) | 0.46% | 47% | $13,102 |

| |

| (0.38) | $26.02 | 15.91% | 0.80% | 0.80% (c) | 1.07% | 52% | $596,704 |

| (1.23) | $22.81 | 11.07% | 0.82% | 0.82% (c) | 0.99% | 47% | $377,946 |

| (1.57) | $21.74 | 2.25% | 0.85% | 0.85% (c) | 3.53% | 60% | $227,941 |

| (1.29) | $22.83 | 24.44% | 0.86% | 0.86% (c) | 0.94% | 65% | $105,458 |

| (0.18) | $19.52 | 24.61% | 0.89% (g) | 0.89% (c),(g) | 1.04% (g) | 47% | $46,212 |

Columbia Contrarian Core Fund | Annual Report 2017

| 21 |

Financial Highlights (continued)

| Year ended | Net asset value,

beginning of

period | Net

investment

income

(loss) | Net

realized

and

unrealized

gain (loss) | Total from

investment

operations | Distributions

from net

investment

income | Distributions

from net

realized

gains |

| Class R5 |

| 8/31/2017 | $22.80 | 0.28 | 3.33 | 3.61 | (0.23) | (0.17) |

| 8/31/2016 | $21.73 | 0.24 | 2.09 | 2.33 | (0.63) | (0.63) |

| 8/31/2015 | $22.83 | 0.78 (d) | (0.28) | 0.50 | (0.18) | (1.42) |

| 8/31/2014 | $19.52 | 0.23 | 4.39 | 4.62 | (0.18) | (1.13) |

| 8/31/2013 (h) | $15.84 | 0.15 | 3.73 | 3.88 | (0.18) | (0.02) |

| Class T(i) |

| 8/31/2017 | $22.29 | 0.17 | 3.27 | 3.44 | (0.15) | (0.17) |

| 8/31/2016 | $21.27 | 0.15 | 2.05 | 2.20 | (0.55) | (0.63) |

| 8/31/2015 | $22.38 | 0.50 (d) | (0.09) | 0.41 | (0.10) | (1.42) |

| 8/31/2014 | $19.16 | 0.14 | 4.32 | 4.46 | (0.11) | (1.13) |

| 8/31/2013 | $15.69 | 0.13 | 3.48 | 3.61 | (0.12) | (0.02) |

| Class V(j) |

| 8/31/2017 | $22.09 | 0.19 | 3.22 | 3.41 | (0.15) | (0.17) |

| 8/31/2016 | $21.08 | 0.15 | 2.04 | 2.19 | (0.55) | (0.63) |

| 8/31/2015 | $22.19 | 0.55 (d) | (0.15) | 0.40 | (0.09) | (1.42) |

| 8/31/2014 | $19.01 | 0.13 | 4.28 | 4.41 | (0.10) | (1.13) |

| 8/31/2013 | $15.56 | 0.12 | 3.47 | 3.59 | (0.12) | (0.02) |

| Class Y |

| 8/31/2017 | $22.81 | 0.30 | 3.33 | 3.63 | (0.24) | (0.17) |

| 8/31/2016 | $21.75 | 0.27 | 2.06 | 2.33 | (0.64) | (0.63) |

| 8/31/2015 | $22.84 | 1.19 (d) | (0.67) | 0.52 | (0.19) | (1.42) |

| 8/31/2014 | $19.52 | 0.24 | 4.40 | 4.64 | (0.19) | (1.13) |

| 8/31/2013 (k) | $15.84 | 0.24 | 3.64 | 3.88 | (0.18) | (0.02) |

| Class Z |

| 8/31/2017 | $22.45 | 0.25 | 3.29 | 3.54 | (0.21) | (0.17) |

| 8/31/2016 | $21.42 | 0.21 | 2.05 | 2.26 | (0.60) | (0.63) |

| 8/31/2015 | $22.52 | 0.66 (d) | (0.18) | 0.48 | (0.16) | (1.42) |

| 8/31/2014 | $19.27 | 0.19 | 4.35 | 4.54 | (0.16) | (1.13) |

| 8/31/2013 | $15.78 | 0.17 | 3.50 | 3.67 | (0.16) | (0.02) |

| Notes to Financial Highlights |

| (a) | In addition to the fees and expenses that the Fund bears directly, the Fund indirectly bears a pro rata share of the fees and expenses of any other funds in which it invests. Such indirect expenses are not included in the Fund’s reported expense ratios. |

| (b) | Total net expenses include the impact of certain fee waivers/expense reimbursements made by the Investment Manager and certain of its affiliates, if applicable. |

| (c) | The benefits derived from expense reductions had an impact of less than 0.01%. |

| (d) | Net investment income per share includes special dividends. The per share effect of these dividends amounted to: |

| Year ended | Class A | Class C | Class K | Class R | Class R4 | Class R5 | Class T | Class V | Class Y | Class Z |

| 08/31/2015 | $ 0.54 | $ 0.55 | $ 0.47 | $ 0.60 | $ 0.63 | $ 0.58 | $ 0.40 | $ 0.45 | $ 0.96 | $ 0.50 |

| (e) | Rounds to zero. |

| (f) | Class R4 shares commenced operations on November 8, 2012. Per share data and total return reflect activity from that date. |

| (g) | Annualized. |

| (h) | Class R5 shares commenced operations on November 8, 2012. Per share data and total return reflect activity from that date. |

| (i) | Prior to March 27, 2017, Class T shares were known as Class W shares. |

| (j) | Prior to January 24, 2017, Class V shares were known as Class T shares. |

| (k) | Class Y shares commenced operations on November 8, 2012. Per share data and total return reflect activity from that date. |

The accompanying Notes to Financial Statements are an integral part of this statement.

| 22 | Columbia Contrarian Core Fund | Annual Report 2017 |

Total

distributions to

shareholders | Net

asset

value,

end of

period | Total

return | Total gross

expense

ratio to

average

net assets(a) | Total net

expense

ratio to

average

net assets(a),(b) | Net investment

income (loss)

ratio to

average

net assets | Portfolio

turnover | Net

assets,

end of

period

(000’s) |

| |

| (0.40) | $26.01 | 16.05% | 0.69% | 0.69% | 1.17% | 52% | $779,002 |

| (1.26) | $22.80 | 11.22% | 0.70% | 0.70% | 1.12% | 47% | $627,659 |

| (1.60) | $21.73 | 2.34% | 0.71% | 0.71% | 3.45% | 60% | $336,043 |

| (1.31) | $22.83 | 24.60% | 0.73% | 0.73% | 1.08% | 65% | $209,498 |

| (0.20) | $19.52 | 24.75% | 0.75% (g) | 0.75% (g) | 1.01% (g) | 47% | $68,709 |

| |

| (0.32) | $25.41 | 15.62% | 1.04% | 1.04% (c) | 0.74% | 52% | $1,357 |

| (1.18) | $22.29 | 10.79% | 1.07% | 1.07% (c) | 0.71% | 47% | $220,502 |

| (1.52) | $21.27 | 1.95% | 1.09% | 1.09% (c) | 2.26% | 60% | $118,262 |

| (1.24) | $22.38 | 24.15% | 1.10% | 1.10% (c) | 0.67% | 65% | $124,021 |

| (0.14) | $19.16 | 23.21% | 1.14% | 1.14% (c) | 0.73% | 47% | $254,377 |

| |

| (0.32) | $25.18 | 15.61% | 1.04% | 1.04% (c) | 0.82% | 52% | $154,392 |

| (1.18) | $22.09 | 10.83% | 1.08% | 1.08% (c) | 0.71% | 47% | $146,879 |

| (1.51) | $21.08 | 1.92% | 1.11% | 1.11% (c) | 2.49% | 60% | $143,304 |

| (1.23) | $22.19 | 24.06% | 1.16% | 1.16% (c) | 0.63% | 65% | $151,430 |

| (0.14) | $19.01 | 23.22% | 1.20% | 1.19% (c) | 0.68% | 47% | $131,732 |

| |

| (0.41) | $26.03 | 16.14% | 0.65% | 0.65% | 1.23% | 52% | $1,574,824 |

| (1.27) | $22.81 | 11.22% | 0.65% | 0.65% | 1.23% | 47% | $329,514 |

| (1.61) | $21.75 | 2.44% | 0.66% | 0.66% | 5.26% | 60% | $53,246 |

| (1.32) | $22.84 | 24.71% | 0.68% | 0.68% | 1.12% | 65% | $2,514 |

| (0.20) | $19.52 | 24.79% | 0.72% (g) | 0.72% (g) | 1.60% (g) | 47% | $79 |

| |

| (0.38) | $25.61 | 15.95% | 0.80% | 0.80% (c) | 1.07% | 52% | $4,958,099 |

| (1.23) | $22.45 | 11.05% | 0.82% | 0.82% (c) | 0.99% | 47% | $4,234,639 |

| (1.58) | $21.42 | 2.24% | 0.84% | 0.84% (c) | 2.97% | 60% | $2,119,278 |

| (1.29) | $22.52 | 24.45% | 0.86% | 0.86% (c) | 0.93% | 65% | $1,831,114 |

| (0.18) | $19.27 | 23.50% | 0.90% | 0.89% (c) | 0.98% | 47% | $1,315,874 |

Columbia Contrarian Core Fund | Annual Report 2017

| 23 |

Notes to Financial Statements

August 31, 2017

Note 1. Organization

Columbia Contrarian Core Fund (the Fund), a series of Columbia Funds Series Trust I (the Trust), is a diversified fund. The Trust is registered under the Investment Company Act of 1940, as amended (the 1940 Act), as an open-end management investment company organized as a Massachusetts business trust.

Fund shares

The Trust may issue an unlimited number of shares (without par value). Although all share classes generally have identical voting, dividend and liquidation rights, each share class votes separately when required by the Trust’s organizational documents or by law. Different share classes pay different distribution amounts to the extent the expenses of such share classes differ, and distributions in liquidation will be proportional to the net asset value of each share class. Each share class has its own expense and sales charge structure. The Fund offers each of the share classes identified below.

Class A shares are subject to a maximum front-end sales charge of 5.75% based on the initial investment amount. Class A shares purchased without an initial sales charge in accounts aggregating $1 million to $50 million at the time of purchase are subject to a contingent deferred sales charge (CDSC) if the shares are sold within 18 months after purchase, charged as follows: 1.00% CDSC if redeemed within 12 months after purchase, and 0.50% CDSC if redeemed more than 12, but less than 18, months after purchase.

Class B shares of the Fund are no longer offered for sale. When available, Class B shares were subject to a maximum CDSC of 5.00% based upon the holding period after purchase. Effective July 17, 2017, Class B shares were automatically converted to Class A shares without a CDSC. On August 4, 2017, the capital owned by Columbia Management Investment Advisers, LLC in Class B shares was redeemed without a CDSC.

Class C shares are subject to a 1.00% CDSC on shares redeemed within 12 months after purchase.

The Fund no longer accepts investments by new or existing investors in Class I shares. Class I shares, when available, were not subject to sales charges, and were made available only to the Columbia Family of Funds. On March 27, 2017, Class I shares were redeemed or exchanged for Class Y shares of the Fund in a tax free transaction that had no impact on the fees and expenses paid by shareholders.

Class K shares are not subject to sales charges; however, this share class is closed to new investors.

Class R shares are not subject to sales charges and are generally available only to certain retirement plans and other investors as described in the Fund’s prospectus.

Class R4 shares are not subject to sales charges and are generally available only to omnibus retirement plans and certain investors as described in the Fund’s prospectus. Effective November 1, 2017, Class R4 shares will be renamed Advisor Class shares.

Class R5 shares are not subject to sales charges and are generally available only to investors purchasing through authorized investment professionals and omnibus retirement plans as described in the Fund’s prospectus. Effective November 1, 2017, Class R5 shares will be renamed Institutional 2 Class shares.

Class T shares are subject to a maximum front-end sales charge of 2.50% per transaction and must be purchased through financial intermediaries that, by written agreement with Columbia Management Investment Distributors, Inc., are specifically authorized to sell Class T shares. Prior to March 27, 2017, Class T shares were known as Class W shares, were not subject to sales charges, and were generally available only to investors purchasing through authorized investment programs managed by investment professionals, including discretionary managed accounts.

Class V shares are subject to a maximum front-end sales charge of 5.75% based on the investment amount. Class V shares purchased without an initial sales charge in accounts aggregating $1 million to $50 million at the time of purchase are subject to a CDSC if the shares are sold within 18 months after purchase, charged as follows: 1.00% CDSC if redeemed within 12 months after purchase, and 0.50% CDSC if redeemed more than 12, but less than 18, months after purchase.

| 24 | Columbia Contrarian Core Fund | Annual Report 2017 |

Notes to Financial Statements (continued)

August 31, 2017

Class V shares are available only to investors who received (and who have continuously held) Class V shares in connection with previous fund reorganizations. Prior to January 24, 2017, Class V shares were known as Class T shares. Class V shares have no relation to, or connection with, the Fund’s current Class T shares.

Class Y shares are not subject to sales charges and are available to institutional and certain other investors as described in the Fund’s prospectus. Effective November 1, 2017, Class Y shares will be renamed Institutional 3 Class shares.

Class Z shares are not subject to sales charges and are generally available only to eligible investors, which are subject to different investment minimums as described in the Fund’s prospectus. Effective November 1, 2017, Class Z shares will be renamed Institutional Class shares.

Note 2. Summary of significant accounting policies

Basis of preparation

The Fund is an investment company that applies the accounting and reporting guidance in the Financial Accounting Standards Board (FASB) Accounting Standards Codification Topic 946, Financial Services - Investment Companies (ASC 946). The financial statements are prepared in accordance with U.S. generally accepted accounting principles (GAAP), which requires management to make certain estimates and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of income and expenses during the reporting period. Actual results could differ from those estimates.

The following is a summary of significant accounting policies followed by the Fund in the preparation of its financial statements.

Security valuation

All equity securities are valued at the close of business of the New York Stock Exchange. Equity securities are valued at the last quoted sales price on the principal exchange or market on which they trade, except for securities traded on the NASDAQ Stock Market, which are valued at the NASDAQ official close price. Unlisted securities or listed securities for which there were no sales during the day are valued at the mean of the latest quoted bid and ask prices on such exchanges or markets.