UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number811-04367

Columbia Funds Series Trust I

(Exact name of registrant as specified in charter)

290 Congress Street

Boston, MA 02210

(Address of principal executive offices) (Zip code)

Daniel J. Beckman

c/o Columbia Management Investment Advisers, LLC

290 Congress Street

Boston, MA 02210

Ryan C. Larrenaga, Esq.

c/o Columbia Management Investment Advisers, LLC

290 Congress Street

Boston, MA 02210

(Name and address of agent for service)

Registrant's telephone number, including area code: (800) 345-6611

Date of fiscal year end: July 31

Date of reporting period: July 31, 2022

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

Annual Report

July 31, 2022

Columbia Large Cap Growth Fund

Not FDIC or NCUA Insured • No Financial Institution Guarantee • May Lose Value

If you elect to receive the shareholder report for Columbia Large Cap Growth Fund (the Fund) in paper, mailed to you, the Fund mails one shareholder report to each shareholder address, unless such shareholder elects to receive shareholder reports from the Fund electronically via e-mail or by having a paper notice mailed to you (Postcard Notice) that your Fund’s shareholder report is available at the Columbia funds’ website (columbiathreadneedleus.com/investor/). If you would like more than one report in paper to be mailed to you, or would like to elect to receive reports via e-mail or access them through Postcard Notice, please call shareholder services at 800.345.6611 and additional reports will be sent to you.

Proxy voting policies and procedures

The policy of the Board of Trustees is to vote the proxies of the companies in which the Fund holds investments consistent with the procedures as stated in the Statement of Additional Information (SAI). You may obtain a copy of the SAI without charge by calling 800.345.6611; contacting your financial intermediary; visiting columbiathreadneedleus.com/investor/; or searching the website of the Securities and Exchange Commission (SEC) at sec.gov. Information regarding how the Fund voted proxies relating to portfolio securities is filed with the SEC by August 31st for the most recent 12-month period ending June 30th of that year, and is available without charge by visiting columbiathreadneedleus.com/investor/, or searching the website of the SEC at sec.gov.

Quarterly schedule of investments

The Fund files a complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-PORT. The Fund’s Form N-PORT filings are available on the SEC’s website at sec.gov. The Fund’s complete schedule of portfolio holdings, as filed on Form N-PORT, is available on columbiathreadneedleus.com/investor/ or can also be obtained without charge, upon request, by calling 800.345.6611.

Additional Fund information

For more information about the Fund, please visit columbiathreadneedleus.com/investor/ or call 800.345.6611. Customer Service Representatives are available to answer your questions Monday through Friday from 8 a.m. to 7 p.m. Eastern time.

Fund investment manager

Columbia Management Investment Advisers, LLC (the Investment Manager)

290 Congress Street

Boston, MA 02210

Fund distributor

Columbia Management Investment Distributors, Inc.

290 Congress Street

Boston, MA 02210

Fund transfer agent

Columbia Management Investment Services Corp.

P.O. Box 219104

Kansas City, MO 64121-9104

Columbia Large Cap Growth Fund | Annual Report 2022

Fund at a Glance

(Unaudited)

Investment objective

The Fund seeks long-term capital appreciation.

Portfolio management

Melda Mergen, CFA, CAIA

Co-Portfolio Manager

Managed Fund since 2019

Tiffany Wade

Co-Portfolio Manager

Managed Fund since 2021

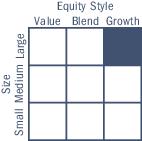

Morningstar style boxTM

The Morningstar Style Box is based on a fund’s portfolio holdings. For equity funds, the vertical axis shows the market capitalization of the stocks owned, and the horizontal axis shows investment style (value, blend, or growth). Information shown is based on the most recent data provided by Morningstar.

© 2022 Morningstar, Inc. All rights reserved. The Morningstar information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information.

| Average annual total returns (%) (for the period ended July 31, 2022) |

| | | Inception | 1 Year | 5 Years | 10 Years |

| Class A | Excluding sales charges | 11/01/98 | -17.35 | 13.15 | 14.35 |

| | Including sales charges | | -22.10 | 11.82 | 13.67 |

| Advisor Class* | 11/08/12 | -17.15 | 13.43 | 14.63 |

| Class C | Excluding sales charges | 11/18/02 | -17.96 | 12.31 | 13.49 |

| | Including sales charges | | -18.70 | 12.31 | 13.49 |

| Class E | Excluding sales charges | 09/22/06 | -17.61 | 12.95 | 14.18 |

| | Including sales charges | | -21.32 | 11.92 | 13.66 |

| Institutional Class | 12/14/90 | -17.15 | 13.44 | 14.63 |

| Institutional 2 Class | 03/07/11 | -17.13 | 13.48 | 14.72 |

| Institutional 3 Class | 07/15/09 | -17.09 | 13.54 | 14.79 |

| Class R | 09/27/10 | -17.56 | 12.87 | 14.06 |

| Class V | Excluding sales charges | 12/14/90 | -17.36 | 13.16 | 14.33 |

| | Including sales charges | | -22.12 | 11.82 | 13.65 |

| Russell 1000 Growth Index | | -11.93 | 16.30 | 15.95 |

Returns for Class A and Class V shares are shown with and without the maximum initial sales charge of 5.75%. Returns for Class C shares are shown with and without the 1.00% contingent deferred sales charge for the first year only. Returns for Class E shares are shown with and without the maximum sales charge of 4.50%. The Fund’s other share classes are not subject to sales charges and have limited eligibility. Please see the Fund’s prospectus for details. Performance for different share classes will vary based on differences in sales charges and fees associated with each share class. All results shown assume reinvestment of distributions during the period. Returns do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or on the redemption of Fund shares. Performance results reflect the effect of any fee waivers or reimbursements of Fund expenses by Columbia Management Investment Advisers, LLC and/or any of its affiliates. Absent these fee waivers or expense reimbursement arrangements, performance results would have been lower.

The performance information shown represents past performance and is not a guarantee of future results. The investment return and principal value of your investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance information shown. You may obtain performance information current to the most recent month-end by contacting your financial intermediary, visiting columbiathreadneedleus.com/investor/ or calling 800.345.6611.

| * | The returns shown for periods prior to the share class inception date (including returns for the Life of the Fund, if shown, which are since Fund inception) include the returns of the Fund’s oldest share class. Since the Fund launched more than one share class at its inception, Institutional Class shares were used. These returns are adjusted to reflect any higher class-related operating expenses of the newer share classes, as applicable. Please visit columbiathreadneedleus.com/investor/investment-products/mutual-funds/appended-performance for more information. |

The Russell 1000 Growth Index, an unmanaged index, measures the performance of those Russell 1000 Index companies with higher price-to-book ratios and higher forecasted growth values.

Indices are not available for investment, are not professionally managed and do not reflect sales charges, fees, brokerage commissions, taxes or other expenses of investing. Securities in the Fund may not match those in an index.

Columbia Large Cap Growth Fund | Annual Report 2022

| 3 |

Fund at a Glance (continued)

(Unaudited)

Performance of a hypothetical $10,000 investment (July 31, 2012 — July 31, 2022)

The chart above shows the change in value of a hypothetical $10,000 investment in Class A shares of Columbia Large Cap Growth Fund during the stated time period, and does not reflect the deduction of taxes that a shareholder may pay on Fund distributions or on the redemption of Fund shares.

| Portfolio breakdown (%) (at July 31, 2022) |

| Common Stocks | 96.8 |

| Money Market Funds | 3.2 |

| Total | 100.0 |

Percentages indicated are based upon total investments excluding investments in derivatives, if any. The Fund’s portfolio composition is subject to change.

| Equity sector breakdown (%) (at July 31, 2022) |

| Communication Services | 10.1 |

| Consumer Discretionary | 17.1 |

| Consumer Staples | 4.0 |

| Energy | 1.3 |

| Financials | 1.7 |

| Health Care | 13.1 |

| Industrials | 8.4 |

| Information Technology | 43.0 |

| Real Estate | 1.3 |

| Total | 100.0 |

Percentages indicated are based upon total equity investments. The Fund’s portfolio composition is subject to change.

| Equity sub-industry breakdown (%) (at July 31, 2022) |

| Information Technology | |

| Application Software | 4.4 |

| Data Processing & Outsourced Services | 3.5 |

| Electronic Equipment & Instruments | 1.4 |

| Electronic Manufacturing Services | 1.3 |

| Semiconductor Equipment | 1.6 |

| Semiconductors | 5.6 |

| Systems Software | 14.3 |

| Technology Hardware, Storage & Peripherals | 10.9 |

| Total | 43.0 |

Percentages indicated are based upon total equity investments. The Fund’s portfolio composition is subject to change.

| 4 | Columbia Large Cap Growth Fund | Annual Report 2022 |

Manager Discussion of Fund Performance

(Unaudited)

For the 12-month period that ended July 31, 2022, Class A shares of Columbia Large Cap Growth Fund returned -17.35% excluding sales charges. The Fund underperformed its benchmark, the Russell 1000 Growth Index, which returned -11.93% for the same time period.

Market overview

U.S. equities fell in 2022 from record highs, ending three consecutive years of robust gains. Lingering Omicron-related worries were a headwind, as were fears around inflation, durability of growth and the end of more than a decade of easy monetary policy coming from the U.S. Federal Reserve (Fed) and other global central banks. Volatility and risk-off sentiment spiked as investor concerns expanded to include ramifications of a prolonged Russia-Ukraine conflict. Commodity prices surged, particularly for oil and wheat, as the conflict in eastern Europe escalated into war and further complicated global supply chains. Oil prices, which were already elevated on supply-demand imbalances, shot through a decade-high of more than $120 per barrel before retreating somewhat.

Despite mostly resilient corporate earnings reports, equities continued a choppy decline. The Fed raised interest rates by 25 basis points (bps) at its March 2022 meeting, 50 bps in May 2022, 75 bps in June 2022 and 75 bps in July 2022, ending at a target rate of 2.25-2.50% by July 31, 2022. (A basis point is 1/100 of a percent.) Investor sentiment was dominated by an increasing focus on persistent inflation, the ongoing war in Ukraine, slowing economic growth leading to a possible recession and continued supply-chain snarls.

The energy sector was the strongest-performing sector in the benchmark during the period, delivering gains in excess of 68%. Consumer staples and utilities also ended the period with positive gains, though far smaller than that of the energy sector. The communication services sector was the bottom-performing sector during the period, down more than 33%. The materials, consumer discretionary, health care, financials, information technology and industrials sectors also ended the period in negative territory.

The Fund’s notable detractors during the period

| · | The Fund’s underperformance relative to the benchmark during the period was driven by stock selection as well as sector allocation. |

| · | The largest area of relative outperformance came from the Fund’s selections within information technology. Notable individual detractors included PayPal Holdings, Inc., Apple, Inc. and Fidelity National Information Services, Inc. |

| ○ | Payments firm PayPal sold off in the first quarter of 2022, along with other high-growth names, as interest rates rose higher. Management provided more than one disappointing earnings outlook as the company struggled with execution issues and slowing e-commerce demand. We sold the shares during the year. |

| ○ | The Fund maintained a sizable weighting in technology giant Apple during the period, which delivered a strong gain for the Fund. The Fund’s position, however, was less than that of the benchmark, which maintained more than a 10% weighting in the stock, detracting from the Fund’s results relative to the benchmark. |

| ○ | An out-of-benchmark position in Fidelity National Information Services, detracted from relative results as the global payments provider reported disappointing results and increasing competition from new payments companies has led to a sentiment overhang on incumbent payment merchant acquiring companies. |

| · | The consumer discretionary space was another area in which stock selection drove relative underperformance. An underweighting in the strong performing stock of electric vehicle manufacturer Tesla Motors, Inc. hurt from a relative perspective. Tesla has managed supply chain constraints better than most auto manufacturers and reported gross margins that were well above expectations. |

| ○ | Target Corp. also detracted from results. After several years of impressive execution the company is now dealing with changing consumer spending preferences and an excess of inventory which led the company to significantly reduce its margin and earnings outlook for the year. |

Columbia Large Cap Growth Fund | Annual Report 2022

| 5 |

Manager Discussion of Fund Performance (continued)

(Unaudited)

| · | Within the communication services sector, online dating services company Match Group, Inc. was among the Fund’s top relative detractors during the period. Match suffered along with other high-growth stocks in the face of rising rates. The company also struggled with delayed reopening activity globally dampening demand for dating services and lower-than-expected revenue from its acquisition of Korea-based Hyperconnect due to product launch delays. |

| · | The Fund’s underweighted allocation to the consumer staples sector, which delivered positively for the benchmark during the period also hindered relative results. |

The Fund’s notable contributors during the period

| · | Stock selection within the health care and financials sector contributed to Fund performance versus the benchmark during the period. |

| · | Within health care, the Fund generated strong gains from its holdings in Eli Lily & Co., Vertex Pharmaceuticals, Inc. and Johnson & Johnson. |

| ○ | Pharmaceutical company Eli Lily was a leading contributor as the company’s diabetes drug Tirzepatide has shown positive indications as a weight loss drug. |

| ○ | Biotechnology company Vertex Pharmaceuticals outperformed. The company’s core cystic fibrosis drug continued to perform well and the company reported positive data points for several promising drugs in its pipeline. |

| ○ | An out-of-benchmark position in pharmaceutical company Johnson & Johnson fared well in the first quarter of 2022 as the market largely sold-off. The company is viewed as a relatively defensive name. |

| · | Within the financials sector, information technology industry-focused lender SVB Financial Group was a stand-out performer early in the reporting period for the Fund. The company benefited from the tailwind of rising interest rates. We sold the Fund’s position in the first half of the period. |

| · | Semiconductor manufacturer Broadcom Inc. within the information technology sector was a top contributor to Fund performance versus the benchmark, though most of its gains were early in the period. Shares of the chip maker have performed well on the strength of its networking and server storage segments. The company has also benefited from its announcement of its planned acquisition of VMware in one of the biggest tech deals on record. |

| · | Though overall the communications sector detracted slightly from relative results, within the sector, Electronic Arts Inc was a positive contributor. The company is viewed as relatively more defensive in negative economic environments. Further, the company continued to make good progress growing its live services offerings. |

| · | Not owning shares in streaming giant Netflix also benefited relative results. The company saw its stock plummet following its announcement of a sizable decrease in subscribers in the first quarter of 2022 to be followed by another decline in the second quarter of 2022. |

Market risk may affect a single issuer, sector of the economy, industry or the market as a whole. Growth securities, at times, may not perform as well as value securities or the stock market in general and may be out of favor with investors. Foreign investments subject the Fund to risks, including political, economic, market, social and others within a particular country, as well as to currency instabilities and less stringent financial and accounting standards generally applicable to U.S. issuers. The Fund may invest significantly in issuers within a particular sector, which may be negatively affected by market, economic or other conditions, making the Fund more vulnerable to unfavorable developments in the sector. See the Fund’s prospectus for more information on these and other risks.

The views expressed in this report reflect the current views of the respective parties who contributed to this report. These views are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict, so actual outcomes and results may differ significantly from the views expressed. These views are subject to change at any time based upon economic, market or other conditions and the respective parties disclaim any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Columbia fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any particular Columbia fund. References to specific securities should not be construed as a recommendation or investment advice.

| 6 | Columbia Large Cap Growth Fund | Annual Report 2022 |

Understanding Your Fund’s Expenses

(Unaudited)

As an investor, you incur two types of costs. There are shareholder transaction costs, which generally include sales charges on purchases and may include redemption fees. There are also ongoing fund costs, which generally include management fees, distribution and/or service fees, and other fund expenses. The following information is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to help you compare these costs with the ongoing costs of investing in other mutual funds.

Analyzing your Fund’s expenses

To illustrate these ongoing costs, we have provided examples and calculated the expenses paid by investors in each share class of the Fund during the period. The actual and hypothetical information in the table is based on an initial investment of $1,000 at the beginning of the period indicated and held for the entire period. Expense information is calculated two ways and each method provides you with different information. The amount listed in the “Actual” column is calculated using the Fund’s actual operating expenses and total return for the period. You may use the Actual information, together with the amount invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the results by the expenses paid during the period under the “Actual” column. The amount listed in the “Hypothetical” column assumes a 5% annual rate of return before expenses (which is not the Fund’s actual return) and then applies the Fund’s actual expense ratio for the period to the hypothetical return. You should not use the hypothetical account values and expenses to estimate either your actual account balance at the end of the period or the expenses you paid during the period. See “Compare with other funds” below for details on how to use the hypothetical data.

Compare with other funds

Since all mutual funds are required to include the same hypothetical calculations about expenses in shareholder reports, you can use this information to compare the ongoing cost of investing in the Fund with other funds. To do so, compare the hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds. As you compare hypothetical examples of other funds, it is important to note that hypothetical examples are meant to highlight the ongoing costs of investing in a fund only and do not reflect any transaction costs, such as sales charges, or redemption or exchange fees. Therefore, the hypothetical calculations are useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. If transaction costs were included in these calculations, your costs would be higher.

| February 1, 2022 — July 31, 2022 |

| | Account value at the

beginning of the

period ($) | Account value at the

end of the

period ($) | Expenses paid during

the period ($) | Fund’s annualized

expense ratio (%) |

| | Actual | Hypothetical | Actual | Hypothetical | Actual | Hypothetical | Actual |

| Class A | 1,000.00 | 1,000.00 | 847.40 | 1,019.67 | 4.48 | 4.90 | 0.99 |

| Advisor Class | 1,000.00 | 1,000.00 | 848.50 | 1,020.89 | 3.35 | 3.67 | 0.74 |

| Class C | 1,000.00 | 1,000.00 | 844.60 | 1,015.99 | 7.87 | 8.60 | 1.74 |

| Class E | 1,000.00 | 1,000.00 | 846.10 | 1,018.00 | 6.02 | 6.58 | 1.33 |

| Institutional Class | 1,000.00 | 1,000.00 | 848.50 | 1,020.89 | 3.35 | 3.67 | 0.74 |

| Institutional 2 Class | 1,000.00 | 1,000.00 | 848.70 | 1,021.04 | 3.22 | 3.52 | 0.71 |

| Institutional 3 Class | 1,000.00 | 1,000.00 | 848.90 | 1,021.23 | 3.04 | 3.32 | 0.67 |

| Class R | 1,000.00 | 1,000.00 | 846.40 | 1,018.44 | 5.61 | 6.14 | 1.24 |

| Class V | 1,000.00 | 1,000.00 | 847.40 | 1,019.67 | 4.48 | 4.90 | 0.99 |

Expenses paid during the period are equal to the annualized expense ratio for each class as indicated above, multiplied by the average account value over the period and then multiplied by the number of days in the Fund’s most recent fiscal half year and divided by 365.

Expenses do not include fees and expenses incurred indirectly by the Fund from its investment in underlying funds, including affiliated and non-affiliated pooled investment vehicles, such as mutual funds and exchange-traded funds.

Columbia Large Cap Growth Fund | Annual Report 2022

| 7 |

Portfolio of Investments

July 31, 2022

(Percentages represent value of investments compared to net assets)

Investments in securities

| Common Stocks 96.8% |

| Issuer | Shares | Value ($) |

| Communication Services 9.7% |

| Entertainment 1.2% |

| Electronic Arts, Inc. | 401,451 | 52,682,415 |

| Interactive Media & Services 8.5% |

| Alphabet, Inc., Class A(a) | 1,189,800 | 138,397,536 |

| Alphabet, Inc., Class C(a) | 1,685,440 | 196,589,722 |

| ZoomInfo Technologies, Inc., Class A(a) | 999,204 | 37,859,839 |

| Total | | 372,847,097 |

| Total Communication Services | 425,529,512 |

| Consumer Discretionary 16.6% |

| Automobiles 3.4% |

| Tesla Motors, Inc.(a) | 168,910 | 150,574,819 |

| Hotels, Restaurants & Leisure 1.2% |

| Hilton Worldwide Holdings, Inc. | 396,182 | 50,739,029 |

| Internet & Direct Marketing Retail 7.1% |

| Amazon.com, Inc.(a) | 2,298,960 | 310,244,652 |

| Multiline Retail 1.2% |

| Target Corp. | 317,789 | 51,920,367 |

| Specialty Retail 2.0% |

| Home Depot, Inc. (The) | 288,719 | 86,887,096 |

| Textiles, Apparel & Luxury Goods 1.7% |

| NIKE, Inc., Class B | 662,446 | 76,128,294 |

| Total Consumer Discretionary | 726,494,257 |

| Consumer Staples 3.9% |

| Beverages 2.1% |

| Coca-Cola Co. (The) | 1,425,480 | 91,473,052 |

| Household Products 1.8% |

| Procter & Gamble Co. (The) | 563,107 | 78,221,193 |

| Total Consumer Staples | 169,694,245 |

| Energy 1.3% |

| Oil, Gas & Consumable Fuels 1.3% |

| Pioneer Natural Resources Co. | 235,648 | 55,836,794 |

| Total Energy | 55,836,794 |

| Common Stocks (continued) |

| Issuer | Shares | Value ($) |

| Financials 1.7% |

| Capital Markets 1.7% |

| S&P Global, Inc. | 194,691 | 73,384,879 |

| Total Financials | 73,384,879 |

| Health Care 12.6% |

| Biotechnology 2.6% |

| BioMarin Pharmaceutical, Inc.(a) | 242,326 | 20,852,152 |

| Exact Sciences Corp.(a) | 449,487 | 20,271,864 |

| Horizon Therapeutics PLC(a) | 269,204 | 22,335,856 |

| Vertex Pharmaceuticals, Inc.(a) | 178,734 | 50,118,801 |

| Total | | 113,578,673 |

| Health Care Equipment & Supplies 2.2% |

| Boston Scientific Corp.(a) | 1,143,464 | 46,939,197 |

| Stryker Corp. | 243,232 | 52,234,072 |

| Total | | 99,173,269 |

| Health Care Providers & Services 3.4% |

| UnitedHealth Group, Inc. | 272,172 | 147,609,762 |

| Life Sciences Tools & Services 1.3% |

| IQVIA Holdings, Inc.(a) | 239,771 | 57,609,778 |

| Pharmaceuticals 3.1% |

| Eli Lilly & Co. | 282,701 | 93,203,693 |

| Johnson & Johnson | 243,521 | 42,499,285 |

| Total | | 135,702,978 |

| Total Health Care | 553,674,460 |

| Industrials 8.2% |

| Aerospace & Defense 1.1% |

| Raytheon Technologies Corp. | 508,678 | 47,413,876 |

| Building Products 1.4% |

| Trane Technologies PLC | 409,647 | 60,214,013 |

| Commercial Services & Supplies 1.5% |

| Cintas Corp. | 153,138 | 65,158,688 |

| Construction & Engineering 1.2% |

| MasTec, Inc.(a) | 636,969 | 50,275,963 |

| Electrical Equipment 1.2% |

| AMETEK, Inc. | 434,741 | 53,690,513 |

The accompanying Notes to Financial Statements are an integral part of this statement.

| 8 | Columbia Large Cap Growth Fund | Annual Report 2022 |

Portfolio of Investments (continued)

July 31, 2022

| Common Stocks (continued) |

| Issuer | Shares | Value ($) |

| Road & Rail 1.8% |

| Union Pacific Corp. | 355,176 | 80,731,505 |

| Total Industrials | 357,484,558 |

| Information Technology 41.6% |

| Electronic Equipment, Instruments & Components 2.5% |

| TE Connectivity Ltd. | 411,853 | 55,077,102 |

| Zebra Technologies Corp., Class A(a) | 160,650 | 57,462,898 |

| Total | | 112,540,000 |

| IT Services 3.4% |

| Visa, Inc., Class A | 702,205 | 148,944,703 |

| Semiconductors & Semiconductor Equipment 7.0% |

| Applied Materials, Inc. | 661,294 | 70,083,938 |

| Broadcom, Inc. | 164,936 | 88,319,929 |

| NVIDIA Corp. | 813,611 | 147,776,166 |

| Total | | 306,180,033 |

| Software 18.1% |

| Adobe, Inc.(a) | 236,534 | 97,007,324 |

| Fortinet, Inc.(a) | 1,020,556 | 60,876,165 |

| Intuit, Inc. | 195,722 | 89,282,505 |

| Microsoft Corp.(b) | 1,467,536 | 411,996,057 |

| Common Stocks (continued) |

| Issuer | Shares | Value ($) |

| Palo Alto Networks, Inc.(a) | 122,166 | 60,973,050 |

| ServiceNow, Inc.(a) | 163,836 | 73,178,988 |

| Total | | 793,314,089 |

| Technology Hardware, Storage & Peripherals 10.6% |

| Apple, Inc. | 2,854,510 | 463,886,420 |

| Total Information Technology | 1,824,865,245 |

| Real Estate 1.2% |

| Equity Real Estate Investment Trusts (REITS) 1.2% |

| Prologis, Inc. | 410,669 | 54,438,283 |

| Total Real Estate | 54,438,283 |

Total Common Stocks

(Cost $2,147,695,563) | 4,241,402,233 |

|

| Money Market Funds 3.2% |

| | Shares | Value ($) |

| Columbia Short-Term Cash Fund, 1.712%(c),(d) | 142,313,694 | 142,242,537 |

Total Money Market Funds

(Cost $142,239,058) | 142,242,537 |

Total Investments in Securities

(Cost: $2,289,934,621) | 4,383,644,770 |

| Other Assets & Liabilities, Net | | (259,087) |

| Net Assets | 4,383,385,683 |

At July 31, 2022, securities and/or cash totaling $814,146 were pledged as collateral.

| Long futures contracts |

| Description | Number of

contracts | Expiration

date | Trading

currency | Notional

amount | Value/Unrealized

appreciation ($) | Value/Unrealized

depreciation ($) |

| S&P 500 Index E-mini | 41 | 09/2022 | USD | 8,473,675 | 477,343 | — |

Notes to Portfolio of Investments

| (a) | Non-income producing investment. |

| (b) | This security or a portion of this security has been pledged as collateral in connection with derivative contracts. |

| (c) | The rate shown is the seven-day current annualized yield at July 31, 2022. |

| (d) | As defined in the Investment Company Act of 1940, as amended, an affiliated company is one in which the Fund owns 5% or more of the company’s outstanding voting securities, or a company which is under common ownership or control with the Fund. The value of the holdings and transactions in these affiliated companies during the year ended July 31, 2022 are as follows: |

| Affiliated issuers | Beginning

of period($) | Purchases($) | Sales($) | Net change in

unrealized

appreciation

(depreciation)($) | End of

period($) | Realized gain

(loss)($) | Dividends($) | End of

period shares |

| Columbia Short-Term Cash Fund, 1.712% |

| | 53,826,343 | 668,405,189 | (579,993,438) | 4,443 | 142,242,537 | (19,265) | 256,676 | 142,313,694 |

The accompanying Notes to Financial Statements are an integral part of this statement.

Columbia Large Cap Growth Fund | Annual Report 2022

| 9 |

Portfolio of Investments (continued)

July 31, 2022

Currency Legend

Fair value measurements

The Fund categorizes its fair value measurements according to a three-level hierarchy that maximizes the use of observable inputs and minimizes the use of unobservable inputs by prioritizing that the most observable input be used when available. Observable inputs are those that market participants would use in pricing an investment based on market data obtained from sources independent of the reporting entity. Unobservable inputs are those that reflect the Fund’s assumptions about the information market participants would use in pricing an investment. An investment’s level within the fair value hierarchy is based on the lowest level of any input that is deemed significant to the asset’s or liability’s fair value measurement. The input levels are not necessarily an indication of the risk or liquidity associated with investments at that level. For example, certain U.S. government securities are generally high quality and liquid, however, they are reflected as Level 2 because the inputs used to determine fair value may not always be quoted prices in an active market.

Fair value inputs are summarized in the three broad levels listed below:

| ■ | Level 1 — Valuations based on quoted prices for investments in active markets that the Fund has the ability to access at the measurement date. Valuation adjustments are not applied to Level 1 investments. |

| ■ | Level 2 — Valuations based on other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risks, etc.). |

| ■ | Level 3 — Valuations based on significant unobservable inputs (including the Fund’s own assumptions and judgment in determining the fair value of investments). |

Inputs that are used in determining fair value of an investment may include price information, credit data, volatility statistics, and other factors. These inputs can be either observable or unobservable. The availability of observable inputs can vary between investments, and is affected by various factors such as the type of investment, and the volume and level of activity for that investment or similar investments in the marketplace. The inputs will be considered by the Investment Manager, along with any other relevant factors in the calculation of an investment’s fair value. The Fund uses prices and inputs that are current as of the measurement date, which may include periods of market dislocations. During these periods, the availability of prices and inputs may be reduced for many investments. This condition could cause an investment to be reclassified between the various levels within the hierarchy.

Investments falling into the Level 3 category are primarily supported by quoted prices from brokers and dealers participating in the market for those investments. However, these may be classified as Level 3 investments due to lack of market transparency and corroboration to support these quoted prices. Additionally, valuation models may be used as the pricing source for any remaining investments classified as Level 3. These models may rely on one or more significant unobservable inputs and/or significant assumptions by the Investment Manager. Inputs used in valuations may include, but are not limited to, financial statement analysis, capital account balances, discount rates and estimated cash flows, and comparable company data.

Under the direction of the Fund’s Board of Trustees (the Board), the Investment Manager’s Valuation Committee (the Committee) is responsible for overseeing the valuation procedures approved by the Board. The Committee consists of voting and non-voting members from various groups within the Investment Manager’s organization, including operations and accounting, trading and investments, compliance, risk management and legal.

The Committee meets at least monthly to review and approve valuation matters, which may include a description of specific valuation determinations, data regarding pricing information received from approved pricing vendors and brokers and the results of Board-approved valuation control policies and procedures (the Policies). The Policies address, among other things, instances when market quotations are or are not readily available, including recommendations of third party pricing vendors and a determination of appropriate pricing methodologies; events that require specific valuation determinations and assessment of fair value techniques; securities with a potential for stale pricing, including those that are illiquid, restricted, or in default; and the effectiveness of third party pricing vendors, including periodic reviews of vendors. The Committee meets more frequently, as needed, to discuss additional valuation matters, which may include the need to review back-testing results, review time-sensitive information or approve related valuation actions. The Committee reports to the Board, with members of the Committee meeting with the Board at each of its regularly scheduled meetings to discuss valuation matters and actions during the period, similar to those described earlier.

The following table is a summary of the inputs used to value the Fund’s investments at July 31, 2022:

| | Level 1 ($) | Level 2 ($) | Level 3 ($) | Total ($) |

| Investments in Securities | | | | |

| Common Stocks | | | | |

| Communication Services | 425,529,512 | — | — | 425,529,512 |

| Consumer Discretionary | 726,494,257 | — | — | 726,494,257 |

| Consumer Staples | 169,694,245 | — | — | 169,694,245 |

| Energy | 55,836,794 | — | — | 55,836,794 |

| Financials | 73,384,879 | — | — | 73,384,879 |

| Health Care | 553,674,460 | — | — | 553,674,460 |

| Industrials | 357,484,558 | — | — | 357,484,558 |

| Information Technology | 1,824,865,245 | — | — | 1,824,865,245 |

| Real Estate | 54,438,283 | — | — | 54,438,283 |

| Total Common Stocks | 4,241,402,233 | — | — | 4,241,402,233 |

| Money Market Funds | 142,242,537 | — | — | 142,242,537 |

| Total Investments in Securities | 4,383,644,770 | — | — | 4,383,644,770 |

| Investments in Derivatives | | | | |

| Asset | | | | |

| Futures Contracts | 477,343 | — | — | 477,343 |

| Total | 4,384,122,113 | — | — | 4,384,122,113 |

The accompanying Notes to Financial Statements are an integral part of this statement.

| 10 | Columbia Large Cap Growth Fund | Annual Report 2022 |

Portfolio of Investments (continued)

July 31, 2022

Fair value measurements (continued)

See the Portfolio of Investments for all investment classifications not indicated in the table.

Derivative instruments are valued at unrealized appreciation (depreciation).

The accompanying Notes to Financial Statements are an integral part of this statement.

Columbia Large Cap Growth Fund | Annual Report 2022

| 11 |

Statement of Assets and Liabilities

July 31, 2022

| Assets | |

| Investments in securities, at value | |

| Unaffiliated issuers (cost $2,147,695,563) | $4,241,402,233 |

| Affiliated issuers (cost $142,239,058) | 142,242,537 |

| Receivable for: | |

| Capital shares sold | 1,179,409 |

| Dividends | 629,048 |

| Interfund lending | 900,000 |

| Variation margin for futures contracts | 123,000 |

| Prepaid expenses | 50,222 |

| Trustees’ deferred compensation plan | 382,321 |

| Total assets | 4,386,908,770 |

| Liabilities | |

| Payable for: | |

| Capital shares purchased | 2,708,584 |

| Management services fees | 76,544 |

| Distribution and/or service fees | 17,923 |

| Transfer agent fees | 203,740 |

| Compensation of board members | 41,787 |

| Other expenses | 92,188 |

| Trustees’ deferred compensation plan | 382,321 |

| Total liabilities | 3,523,087 |

| Net assets applicable to outstanding capital stock | $4,383,385,683 |

| Represented by | |

| Paid in capital | 2,351,628,543 |

| Total distributable earnings (loss) | 2,031,757,140 |

| Total - representing net assets applicable to outstanding capital stock | $4,383,385,683 |

The accompanying Notes to Financial Statements are an integral part of this statement.

| 12 | Columbia Large Cap Growth Fund | Annual Report 2022 |

Statement of Assets and Liabilities (continued)

July 31, 2022

| Class A | |

| Net assets | $2,203,136,691 |

| Shares outstanding | 46,292,390 |

| Net asset value per share | $47.59 |

| Maximum sales charge | 5.75% |

| Maximum offering price per share (calculated by dividing the net asset value per share by 1.0 minus the maximum sales charge for Class A shares) | $50.49 |

| Advisor Class | |

| Net assets | $17,602,579 |

| Shares outstanding | 337,228 |

| Net asset value per share | $52.20 |

| Class C | |

| Net assets | $44,314,468 |

| Shares outstanding | 1,254,463 |

| Net asset value per share | $35.33 |

| Class E | |

| Net assets | $15,022,236 |

| Shares outstanding | 319,555 |

| Net asset value per share | $47.01 |

| Maximum sales charge | 4.50% |

| Maximum offering price per share (calculated by dividing the net asset value per share by 1.0 minus the maximum sales charge for Class E shares) | $49.23 |

| Institutional Class | |

| Net assets | $1,066,893,655 |

| Shares outstanding | 21,068,281 |

| Net asset value per share | $50.64 |

| Institutional 2 Class | |

| Net assets | $83,838,022 |

| Shares outstanding | 1,651,958 |

| Net asset value per share | $50.75 |

| Institutional 3 Class | |

| Net assets | $704,376,824 |

| Shares outstanding | 13,808,889 |

| Net asset value per share | $51.01 |

| Class R | |

| Net assets | $8,043,074 |

| Shares outstanding | 172,534 |

| Net asset value per share | $46.62 |

| Class V | |

| Net assets | $240,158,134 |

| Shares outstanding | 5,111,825 |

| Net asset value per share | $46.98 |

| Maximum sales charge | 5.75% |

| Maximum offering price per share (calculated by dividing the net asset value per share by 1.0 minus the maximum sales charge for Class V shares) | $49.85 |

The accompanying Notes to Financial Statements are an integral part of this statement.

Columbia Large Cap Growth Fund | Annual Report 2022

| 13 |

Statement of Operations

Year Ended July 31, 2022

| Net investment income | |

| Income: | |

| Dividends — unaffiliated issuers | $38,332,261 |

| Dividends — affiliated issuers | 256,676 |

| Interfund lending | 519 |

| Foreign taxes withheld | (26,240) |

| Total income | 38,563,216 |

| Expenses: | |

| Management services fees | 32,952,655 |

| Distribution and/or service fees | |

| Class A | 6,534,287 |

| Class C | 658,348 |

| Class E | 63,370 |

| Class R | 46,578 |

| Class V | 700,906 |

| Transfer agent fees | |

| Class A | 2,029,055 |

| Advisor Class | 20,030 |

| Class C | 50,765 |

| Class E | 50,812 |

| Institutional Class | 968,541 |

| Institutional 2 Class | 54,883 |

| Institutional 3 Class | 42,334 |

| Class R | 7,232 |

| Class V | 217,761 |

| Compensation of board members | 73,653 |

| Custodian fees | 28,923 |

| Printing and postage fees | 170,799 |

| Registration fees | 189,668 |

| Audit fees | 32,760 |

| Legal fees | 63,192 |

| Interest on collateral | 1,061 |

| Compensation of chief compliance officer | 1,482 |

| Other | 79,939 |

| Total expenses | 45,039,034 |

| Expense reduction | (9,062) |

| Total net expenses | 45,029,972 |

| Net investment loss | (6,466,756) |

| Realized and unrealized gain (loss) — net | |

| Net realized gain (loss) on: | |

| Investments — unaffiliated issuers | 114,779,920 |

| Investments — affiliated issuers | (19,265) |

| Foreign currency translations | (61) |

| Futures contracts | (7,044,891) |

| Net realized gain | 107,715,703 |

| Net change in unrealized appreciation (depreciation) on: | |

| Investments — unaffiliated issuers | (1,031,455,213) |

| Investments — affiliated issuers | 4,443 |

| Futures contracts | (620,161) |

| Net change in unrealized appreciation (depreciation) | (1,032,070,931) |

| Net realized and unrealized loss | (924,355,228) |

| Net decrease in net assets resulting from operations | $(930,821,984) |

The accompanying Notes to Financial Statements are an integral part of this statement.

| 14 | Columbia Large Cap Growth Fund | Annual Report 2022 |

Statement of Changes in Net Assets

| | Year Ended

July 31, 2022 | Year Ended

July 31, 2021 |

| Operations | | |

| Net investment loss | $(6,466,756) | $(5,476,420) |

| Net realized gain | 107,715,703 | 566,809,565 |

| Net change in unrealized appreciation (depreciation) | (1,032,070,931) | 1,069,452,837 |

| Net increase (decrease) in net assets resulting from operations | (930,821,984) | 1,630,785,982 |

| Distributions to shareholders | | |

| Net investment income and net realized gains | | |

| Class A | (244,133,175) | (286,697,027) |

| Advisor Class | (2,720,087) | (1,594,971) |

| Class C | (7,868,155) | (13,498,493) |

| Class E | (1,646,962) | (2,128,937) |

| Institutional Class | (112,671,169) | (131,489,967) |

| Institutional 2 Class | (8,905,905) | (2,328,003) |

| Institutional 3 Class | (69,227,245) | (63,006,305) |

| Class R | (875,965) | (1,425,169) |

| Class V | (26,358,603) | (30,981,331) |

| Total distributions to shareholders | (474,407,266) | (533,150,203) |

| Increase in net assets from capital stock activity | 99,431,405 | 365,711,826 |

| Total increase (decrease) in net assets | (1,305,797,845) | 1,463,347,605 |

| Net assets at beginning of year | 5,689,183,528 | 4,225,835,923 |

| Net assets at end of year | $4,383,385,683 | $5,689,183,528 |

The accompanying Notes to Financial Statements are an integral part of this statement.

Columbia Large Cap Growth Fund | Annual Report 2022

| 15 |

Statement of Changes in Net Assets (continued)

| | Year Ended | Year Ended |

| | July 31, 2022 | July 31, 2021 |

| | Shares | Dollars ($) | Shares | Dollars ($) |

| Capital stock activity |

| Class A | | | | |

| Subscriptions | 1,281,703 | 71,064,106 | 1,692,261 | 92,180,209 |

| Distributions reinvested | 3,855,701 | 235,930,336 | 5,459,391 | 276,791,144 |

| Redemptions | (5,133,783) | (283,380,156) | (5,058,719) | (274,713,720) |

| Net increase | 3,621 | 23,614,286 | 2,092,933 | 94,257,633 |

| Advisor Class | | | | |

| Subscriptions | 275,762 | 18,054,519 | 119,324 | 7,179,335 |

| Distributions reinvested | 37,295 | 2,498,765 | 24,561 | 1,353,575 |

| Redemptions | (280,142) | (16,225,069) | (57,075) | (3,289,468) |

| Net increase | 32,915 | 4,328,215 | 86,810 | 5,243,442 |

| Class C | | | | |

| Subscriptions | 183,635 | 7,860,947 | 232,886 | 9,800,732 |

| Distributions reinvested | 168,255 | 7,677,476 | 339,260 | 13,163,270 |

| Redemptions | (805,442) | (33,037,725) | (1,003,644) | (42,194,435) |

| Net decrease | (453,552) | (17,499,302) | (431,498) | (19,230,433) |

| Class E | | | | |

| Subscriptions | 2,538 | 138,782 | 230 | 10,962 |

| Distributions reinvested | 27,191 | 1,646,962 | 42,367 | 2,128,937 |

| Redemptions | (38,887) | (2,152,800) | (54,829) | (2,953,716) |

| Net decrease | (9,158) | (367,056) | (12,232) | (813,817) |

| Institutional Class | | | | |

| Subscriptions | 1,424,087 | 84,807,393 | 1,241,974 | 71,615,653 |

| Distributions reinvested | 1,613,140 | 104,854,093 | 2,277,626 | 122,057,961 |

| Redemptions | (2,479,529) | (144,313,236) | (2,869,901) | (163,390,306) |

| Net increase | 557,698 | 45,348,250 | 649,699 | 30,283,308 |

| Institutional 2 Class | | | | |

| Subscriptions | 248,736 | 15,191,996 | 1,359,264 | 87,695,216 |

| Distributions reinvested | 136,672 | 8,901,412 | 43,360 | 2,328,003 |

| Redemptions | (359,667) | (21,334,730) | (110,786) | (6,394,925) |

| Net increase | 25,741 | 2,758,678 | 1,291,838 | 83,628,294 |

| Institutional 3 Class | | | | |

| Subscriptions | 1,793,471 | 99,804,051 | 6,124,493 | 331,787,174 |

| Distributions reinvested | 754,572 | 49,379,219 | 679,477 | 36,637,408 |

| Redemptions | (1,880,381) | (116,684,279) | (3,441,935) | (200,663,745) |

| Net increase | 667,662 | 32,498,991 | 3,362,035 | 167,760,837 |

| Class R | | | | |

| Subscriptions | 36,034 | 2,024,734 | 71,838 | 3,791,386 |

| Distributions reinvested | 13,640 | 818,807 | 21,288 | 1,060,751 |

| Redemptions | (43,786) | (2,446,653) | (163,052) | (8,872,547) |

| Net increase (decrease) | 5,888 | 396,888 | (69,926) | (4,020,410) |

| Class V | | | | |

| Subscriptions | 112,136 | 6,547,297 | 144,581 | 7,309,544 |

| Distributions reinvested | 325,429 | 19,655,902 | 457,788 | 22,935,181 |

| Redemptions | (320,901) | (17,850,744) | (404,125) | (21,641,753) |

| Net increase | 116,664 | 8,352,455 | 198,244 | 8,602,972 |

| Total net increase | 947,479 | 99,431,405 | 7,167,903 | 365,711,826 |

The accompanying Notes to Financial Statements are an integral part of this statement.

| 16 | Columbia Large Cap Growth Fund | Annual Report 2022 |

[THIS PAGE INTENTIONALLY LEFT BLANK]

Columbia Large Cap Growth Fund | Annual Report 2022

| 17 |

The following table is intended to help you understand the Fund’s financial performance. Certain information reflects financial results for a single share of a class held for the periods shown. Per share net investment income (loss) amounts are calculated based on average shares outstanding during the period. Total return assumes reinvestment of all dividends and distributions, if any. Total return does not reflect payment of sales charges, if any. Total return and portfolio turnover are not annualized for periods of less than one year. The portfolio turnover rate is calculated without regard to purchase and sales transactions of short-term instruments and certain derivatives, if any. If such transactions were included, the Fund’s portfolio turnover rate may be higher.

| | Net asset value,

beginning of

period | Net

investment

income

(loss) | Net

realized

and

unrealized

gain (loss) | Total from

investment

operations | Distributions

from net

investment

income | Distributions

from net

realized

gains | Total

distributions to

shareholders |

| Class A |

| Year Ended 7/31/2022 | $62.66 | (0.13) | (9.54) | (9.67) | — | (5.40) | (5.40) |

| Year Ended 7/31/2021 | $50.90 | (0.11) | 18.52 | 18.41 | (0.07) | (6.58) | (6.65) |

| Year Ended 7/31/2020 | $43.43 | (0.01) | 11.15 | 11.14 | — | (3.67) | (3.67) |

| Year Ended 7/31/2019 | $43.86 | (0.04) | 2.98 | 2.94 | — | (3.37) | (3.37) |

| Year Ended 7/31/2018 | $39.81 | (0.05) | 6.62 | 6.57 | — | (2.52) | (2.52) |

| Advisor Class |

| Year Ended 7/31/2022 | $68.22 | 0.03 | (10.50) | (10.47) | — | (5.55) | (5.55) |

| Year Ended 7/31/2021 | $54.87 | 0.02 | 20.10 | 20.12 | (0.19) | (6.58) | (6.77) |

| Year Ended 7/31/2020 | $46.43 | 0.10 | 12.01 | 12.11 | — | (3.67) | (3.67) |

| Year Ended 7/31/2019 | $46.53 | 0.07 | 3.20 | 3.27 | — | (3.37) | (3.37) |

| Year Ended 7/31/2018 | $42.06 | 0.05 | 7.00 | 7.05 | (0.06) | (2.52) | (2.58) |

| Class C |

| Year Ended 7/31/2022 | $47.73 | (0.41) | (7.05) | (7.46) | — | (4.94) | (4.94) |

| Year Ended 7/31/2021 | $40.39 | (0.39) | 14.31 | 13.92 | — | (6.58) | (6.58) |

| Year Ended 7/31/2020 | $35.43 | (0.27) | 8.90 | 8.63 | — | (3.67) | (3.67) |

| Year Ended 7/31/2019 | $36.70 | (0.29) | 2.39 | 2.10 | — | (3.37) | (3.37) |

| Year Ended 7/31/2018 | $33.95 | (0.30) | 5.57 | 5.27 | — | (2.52) | (2.52) |

| Class E |

| Year Ended 7/31/2022 | $61.99 | (0.29) | (9.46) | (9.75) | — | (5.23) | (5.23) |

| Year Ended 7/31/2021 | $50.50 | (0.26) | 18.35 | 18.09 | (0.02) | (6.58) | (6.60) |

| Year Ended 7/31/2020 | $43.15 | (0.06) | 11.08 | 11.02 | — | (3.67) | (3.67) |

| Year Ended 7/31/2019 | $43.65 | (0.08) | 2.95 | 2.87 | — | (3.37) | (3.37) |

| Year Ended 7/31/2018 | $39.67 | (0.10) | 6.60 | 6.50 | — | (2.52) | (2.52) |

| Institutional Class |

| Year Ended 7/31/2022 | $66.34 | 0.01 | (10.16) | (10.15) | — | (5.55) | (5.55) |

| Year Ended 7/31/2021 | $53.52 | 0.03 | 19.56 | 19.59 | (0.19) | (6.58) | (6.77) |

| Year Ended 7/31/2020 | $45.38 | 0.10 | 11.71 | 11.81 | — | (3.67) | (3.67) |

| Year Ended 7/31/2019 | $45.56 | 0.06 | 3.13 | 3.19 | — | (3.37) | (3.37) |

| Year Ended 7/31/2018 | $41.23 | 0.06 | 6.86 | 6.92 | (0.07) | (2.52) | (2.59) |

| Institutional 2 Class |

| Year Ended 7/31/2022 | $66.47 | 0.02 | (10.18) | (10.16) | — | (5.56) | (5.56) |

| Year Ended 7/31/2021 | $53.62 | (0.00)(e) | 19.64 | 19.64 | (0.21) | (6.58) | (6.79) |

| Year Ended 7/31/2020 | $45.44 | 0.12 | 11.73 | 11.85 | — | (3.67) | (3.67) |

| Year Ended 7/31/2019 | $45.59 | 0.09 | 3.13 | 3.22 | — | (3.37) | (3.37) |

| Year Ended 7/31/2018 | $41.25 | 0.08 | 6.87 | 6.95 | (0.09) | (2.52) | (2.61) |

The accompanying Notes to Financial Statements are an integral part of this statement.

| 18 | Columbia Large Cap Growth Fund | Annual Report 2022 |

Financial Highlights (continued)

| | Net

asset

value,

end of

period | Total

return | Total gross

expense

ratio to

average

net assets(a) | Total net

expense

ratio to

average

net assets(a),(b) | Net investment

income (loss)

ratio to

average

net assets | Portfolio

turnover | Net

assets,

end of

period

(000’s) |

| Class A |

| Year Ended 7/31/2022 | $47.59 | (17.35%) | 0.98%(c) | 0.98%(c) | (0.23%) | 46% | $2,203,137 |

| Year Ended 7/31/2021 | $62.66 | 39.24% | 0.99%(c) | 0.99%(c),(d) | (0.21%) | 52% | $2,900,684 |

| Year Ended 7/31/2020 | $50.90 | 27.48% | 1.02% | 1.02%(d) | (0.03%) | 46% | $2,249,478 |

| Year Ended 7/31/2019 | $43.43 | 7.84% | 1.04% | 1.04% | (0.10%) | 35% | $1,932,367 |

| Year Ended 7/31/2018 | $43.86 | 17.26% | 1.05% | 1.05%(d) | (0.13%) | 32% | $1,976,097 |

| Advisor Class |

| Year Ended 7/31/2022 | $52.20 | (17.15%) | 0.73%(c) | 0.73%(c) | 0.05% | 46% | $17,603 |

| Year Ended 7/31/2021 | $68.22 | 39.60% | 0.74%(c) | 0.74%(c),(d) | 0.03% | 52% | $20,760 |

| Year Ended 7/31/2020 | $54.87 | 27.81% | 0.77% | 0.77%(d) | 0.21% | 46% | $11,934 |

| Year Ended 7/31/2019 | $46.43 | 8.11% | 0.79% | 0.79% | 0.15% | 35% | $12,088 |

| Year Ended 7/31/2018 | $46.53 | 17.52% | 0.80% | 0.80%(d) | 0.12% | 32% | $14,629 |

| Class C |

| Year Ended 7/31/2022 | $35.33 | (17.96%) | 1.73%(c) | 1.73%(c) | (0.96%) | 46% | $44,314 |

| Year Ended 7/31/2021 | $47.73 | 38.22% | 1.74%(c) | 1.74%(c),(d) | (0.93%) | 52% | $81,519 |

| Year Ended 7/31/2020 | $40.39 | 26.54% | 1.77% | 1.77%(d) | (0.78%) | 46% | $86,411 |

| Year Ended 7/31/2019 | $35.43 | 7.03% | 1.79% | 1.79% | (0.86%) | 35% | $78,293 |

| Year Ended 7/31/2018 | $36.70 | 16.37% | 1.80% | 1.80%(d) | (0.87%) | 32% | $75,872 |

| Class E |

| Year Ended 7/31/2022 | $47.01 | (17.61%) | 1.28%(c) | 1.28%(c) | (0.53%) | 46% | $15,022 |

| Year Ended 7/31/2021 | $61.99 | 38.87% | 1.27%(c) | 1.26%(c),(d) | (0.48%) | 52% | $20,376 |

| Year Ended 7/31/2020 | $50.50 | 27.37% | 1.12% | 1.12%(d) | (0.13%) | 46% | $17,216 |

| Year Ended 7/31/2019 | $43.15 | 7.71% | 1.14% | 1.14% | (0.20%) | 35% | $15,875 |

| Year Ended 7/31/2018 | $43.65 | 17.14% | 1.15% | 1.15%(d) | (0.23%) | 32% | $16,877 |

| Institutional Class |

| Year Ended 7/31/2022 | $50.64 | (17.15%) | 0.73%(c) | 0.73%(c) | 0.02% | 46% | $1,066,894 |

| Year Ended 7/31/2021 | $66.34 | 39.61% | 0.74%(c) | 0.74%(c),(d) | 0.04% | 52% | $1,360,640 |

| Year Ended 7/31/2020 | $53.52 | 27.79% | 0.77% | 0.77%(d) | 0.22% | 46% | $1,062,936 |

| Year Ended 7/31/2019 | $45.38 | 8.11% | 0.79% | 0.79% | 0.15% | 35% | $975,664 |

| Year Ended 7/31/2018 | $45.56 | 17.54% | 0.80% | 0.80%(d) | 0.13% | 32% | $996,845 |

| Institutional 2 Class |

| Year Ended 7/31/2022 | $50.75 | (17.13%) | 0.71%(c) | 0.71%(c) | 0.04% | 46% | $83,838 |

| Year Ended 7/31/2021 | $66.47 | 39.63% | 0.72%(c) | 0.72%(c) | (0.00%)(e) | 52% | $108,093 |

| Year Ended 7/31/2020 | $53.62 | 27.84% | 0.73% | 0.73% | 0.26% | 46% | $17,929 |

| Year Ended 7/31/2019 | $45.44 | 8.17% | 0.74% | 0.74% | 0.20% | 35% | $13,783 |

| Year Ended 7/31/2018 | $45.59 | 17.63% | 0.73% | 0.73% | 0.19% | 32% | $12,715 |

The accompanying Notes to Financial Statements are an integral part of this statement.

Columbia Large Cap Growth Fund | Annual Report 2022

| 19 |

Financial Highlights (continued)

| | Net asset value,

beginning of

period | Net

investment

income

(loss) | Net

realized

and

unrealized

gain (loss) | Total from

investment

operations | Distributions

from net

investment

income | Distributions

from net

realized

gains | Total

distributions to

shareholders |

| Institutional 3 Class |

| Year Ended 7/31/2022 | $66.78 | 0.05 | (10.23) | (10.18) | — | (5.59) | (5.59) |

| Year Ended 7/31/2021 | $53.84 | 0.05 | 19.70 | 19.75 | (0.23) | (6.58) | (6.81) |

| Year Ended 7/31/2020 | $45.59 | 0.14 | 11.78 | 11.92 | — | (3.67) | (3.67) |

| Year Ended 7/31/2019 | $45.70 | 0.11 | 3.15 | 3.26 | — | (3.37) | (3.37) |

| Year Ended 7/31/2018 | $41.35 | 0.09 | 6.88 | 6.97 | (0.10) | (2.52) | (2.62) |

| Class R |

| Year Ended 7/31/2022 | $61.49 | (0.26) | (9.36) | (9.62) | — | (5.25) | (5.25) |

| Year Ended 7/31/2021 | $50.11 | (0.23) | 18.19 | 17.96 | — | (6.58) | (6.58) |

| Year Ended 7/31/2020 | $42.92 | (0.12) | 10.98 | 10.86 | — | (3.67) | (3.67) |

| Year Ended 7/31/2019 | $43.49 | (0.14) | 2.94 | 2.80 | — | (3.37) | (3.37) |

| Year Ended 7/31/2018 | $39.59 | (0.14) | 6.56 | 6.42 | — | (2.52) | (2.52) |

| Class V |

| Year Ended 7/31/2022 | $61.93 | (0.13) | (9.42) | (9.55) | — | (5.40) | (5.40) |

| Year Ended 7/31/2021 | $50.37 | (0.11) | 18.32 | 18.21 | (0.07) | (6.58) | (6.65) |

| Year Ended 7/31/2020 | $43.01 | (0.01) | 11.04 | 11.03 | — | (3.67) | (3.67) |

| Year Ended 7/31/2019 | $43.47 | (0.04) | 2.95 | 2.91 | — | (3.37) | (3.37) |

| Year Ended 7/31/2018 | $39.48 | (0.05) | 6.56 | 6.51 | — | (2.52) | (2.52) |

| Notes to Financial Highlights |

| (a) | In addition to the fees and expenses that the Fund bears directly, the Fund indirectly bears a pro rata share of the fees and expenses of any other funds in which it invests. Such indirect expenses are not included in the Fund’s reported expense ratios. |

| (b) | Total net expenses include the impact of certain fee waivers/expense reimbursements made by the Investment Manager and certain of its affiliates, if applicable. |

| (c) | Ratios include interest on collateral expense which is less than 0.01%. |

| (d) | The benefits derived from expense reductions had an impact of less than 0.01%. |

| (e) | Rounds to zero. |

The accompanying Notes to Financial Statements are an integral part of this statement.

| 20 | Columbia Large Cap Growth Fund | Annual Report 2022 |

Financial Highlights (continued)

| | Net

asset

value,

end of

period | Total

return | Total gross

expense

ratio to

average

net assets(a) | Total net

expense

ratio to

average

net assets(a),(b) | Net investment

income (loss)

ratio to

average

net assets | Portfolio

turnover | Net

assets,

end of

period

(000’s) |

| Institutional 3 Class |

| Year Ended 7/31/2022 | $51.01 | (17.09%) | 0.66%(c) | 0.66%(c) | 0.09% | 46% | $704,377 |

| Year Ended 7/31/2021 | $66.78 | 39.70% | 0.66%(c) | 0.66%(c) | 0.09% | 52% | $877,535 |

| Year Ended 7/31/2020 | $53.84 | 27.91% | 0.68% | 0.68% | 0.31% | 46% | $526,471 |

| Year Ended 7/31/2019 | $45.59 | 8.24% | 0.69% | 0.69% | 0.26% | 35% | $394,049 |

| Year Ended 7/31/2018 | $45.70 | 17.65% | 0.69% | 0.69% | 0.20% | 32% | $428,819 |

| Class R |

| Year Ended 7/31/2022 | $46.62 | (17.56%) | 1.23%(c) | 1.23%(c) | (0.48%) | 46% | $8,043 |

| Year Ended 7/31/2021 | $61.49 | 38.92% | 1.24%(c) | 1.24%(c),(d) | (0.44%) | 52% | $10,247 |

| Year Ended 7/31/2020 | $50.11 | 27.14% | 1.27% | 1.27%(d) | (0.28%) | 46% | $11,856 |

| Year Ended 7/31/2019 | $42.92 | 7.57% | 1.29% | 1.29% | (0.35%) | 35% | $13,233 |

| Year Ended 7/31/2018 | $43.49 | 16.96% | 1.30% | 1.30%(d) | (0.35%) | 32% | $15,911 |

| Class V |

| Year Ended 7/31/2022 | $46.98 | (17.36%) | 0.98%(c) | 0.98%(c) | (0.23%) | 46% | $240,158 |

| Year Ended 7/31/2021 | $61.93 | 39.26% | 0.99%(c) | 0.99%(c),(d) | (0.21%) | 52% | $309,330 |

| Year Ended 7/31/2020 | $50.37 | 27.49% | 1.02% | 1.02%(d) | (0.03%) | 46% | $241,606 |

| Year Ended 7/31/2019 | $43.01 | 7.84% | 1.04% | 1.04% | (0.11%) | 35% | $205,528 |

| Year Ended 7/31/2018 | $43.47 | 17.25% | 1.05% | 1.05%(d) | (0.13%) | 32% | $208,329 |

The accompanying Notes to Financial Statements are an integral part of this statement.

Columbia Large Cap Growth Fund | Annual Report 2022

| 21 |

Notes to Financial Statements

July 31, 2022

Note 1. Organization

Columbia Large Cap Growth Fund (the Fund), a series of Columbia Funds Series Trust I (the Trust), is a diversified fund. The Trust is registered under the Investment Company Act of 1940, as amended (the 1940 Act), as an open-end management investment company organized as a Massachusetts business trust.

Fund shares

The Trust may issue an unlimited number of shares (without par value). The Fund offers each of the share classes listed in the Statement of Assets and Liabilities. Although all share classes generally have identical voting, dividend and liquidation rights, each share class votes separately when required by the Trust’s organizational documents or by law. Each share class has its own expense and sales charge structure. Different share classes may have different minimum initial investment amounts and pay different net investment income distribution amounts to the extent the expenses of distributing such share classes vary. Distributions to shareholders in a liquidation will be proportional to the net asset value of each share class.

As described in the Fund’s prospectus, Class A and Class C shares are offered to the general public for investment. Class C shares automatically convert to Class A shares after 8 years. Advisor Class, Institutional Class, Institutional 2 Class, Institutional 3 Class and Class R shares are available for purchase through authorized investment professionals to omnibus retirement plans or to institutional investors and to certain other investors as also described in the Fund’s prospectus. Class E shares are trust shares which are held in an irrevocable trust until the specified trust termination date and are closed to new investors and new accounts. Class V shares are available only to investors who received (and who continuously held) Class V shares in connection with previous fund reorganizations.

Note 2. Summary of significant accounting policies

Basis of preparation

The Fund is an investment company that applies the accounting and reporting guidance in the Financial Accounting Standards Board (FASB) Accounting Standards Codification Topic 946, Financial Services - Investment Companies (ASC 946). The financial statements are prepared in accordance with U.S. generally accepted accounting principles (GAAP), which requires management to make certain estimates and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of income and expenses during the reporting period. Actual results could differ from those estimates.

The following is a summary of significant accounting policies followed by the Fund in the preparation of its financial statements.

Security valuation

Equity securities listed on an exchange are valued at the closing price or last trade price on their primary exchange at the close of business of the New York Stock Exchange. Securities with a closing price not readily available or not listed on any exchange are valued at the mean between the closing bid and ask prices. Listed preferred stocks convertible into common stocks are valued using an evaluated price from a pricing service.

Foreign equity securities are valued based on the closing price or last trade price on their primary exchange at the close of business of the New York Stock Exchange. If any foreign equity security closing prices are not readily available, the securities are valued at the mean of the latest quoted bid and ask prices on such exchanges or markets. Foreign currency exchange rates are determined at the scheduled closing time of the New York Stock Exchange. Many securities markets and exchanges outside the U.S. close prior to the close of the New York Stock Exchange; therefore, the closing prices for securities in such markets or on such exchanges may not fully reflect events that occur after such close but before the close of the New York Stock Exchange. In those situations, foreign securities will be fair valued pursuant to a policy adopted by the Board of Trustees. Under the policy, the Fund may utilize a third-party pricing service to determine these fair values. The third-party pricing service takes into account multiple factors, including, but not limited to, movements in the U.S. securities markets, certain depositary receipts, futures contracts and foreign exchange rates that have occurred subsequent to the

| 22 | Columbia Large Cap Growth Fund | Annual Report 2022 |

Notes to Financial Statements (continued)

July 31, 2022

close of the foreign exchange or market, to determine a good faith estimate that reasonably reflects the current market conditions as of the close of the New York Stock Exchange. The fair value of a security is likely to be different from the quoted or published price, if available.

Investments in open-end investment companies (other than exchange-traded funds (ETFs)), are valued at the latest net asset value reported by those companies as of the valuation time.

Futures and options on futures contracts are valued based upon the settlement price at the close of regular trading on their principal exchanges or, in the absence of a settlement price, at the mean of the latest quoted bid and ask prices.

Investments for which market quotations are not readily available, or that have quotations which management believes are not reflective of market value or reliable, are valued at fair value as determined in good faith under procedures approved by and under the general supervision of the Board of Trustees. If a security or class of securities (such as foreign securities) is valued at fair value, such value is likely to be different from the quoted or published price for the security, if available.

The determination of fair value often requires significant judgment. To determine fair value, management may use assumptions including but not limited to future cash flows and estimated risk premiums. Multiple inputs from various sources may be used to determine fair value.

GAAP requires disclosure regarding the inputs and valuation techniques used to measure fair value and any changes in valuation inputs or techniques. In addition, investments shall be disclosed by major category. This information is disclosed following the Fund’s Portfolio of Investments.

Foreign currency transactions and translations

The values of all assets and liabilities denominated in foreign currencies are generally translated into U.S. dollars at exchange rates determined at the close of regular trading on the New York Stock Exchange. Net realized and unrealized gains (losses) on foreign currency transactions and translations include gains (losses) arising from the fluctuation in exchange rates between trade and settlement dates on securities transactions, gains (losses) arising from the disposition of foreign currency and currency gains (losses) between the accrual and payment dates on dividends, interest income and foreign withholding taxes.

For financial statement purposes, the Fund does not distinguish that portion of gains (losses) on investments which is due to changes in foreign exchange rates from that which is due to changes in market prices of the investments. Such fluctuations are included with the net realized and unrealized gains (losses) on investments in the Statement of Operations.

Derivative instruments

The Fund invests in certain derivative instruments, as detailed below, in seeking to meet its investment objectives. Derivatives are instruments whose values depend on, or are derived from, in whole or in part, the value of one or more securities, currencies, commodities, indices, or other assets or instruments. Derivatives may be used to increase investment flexibility (including to maintain cash reserves while maintaining desired exposure to certain assets), for risk management (hedging) purposes, to facilitate trading, to reduce transaction costs and to pursue higher investment returns. The Fund may also use derivative instruments to mitigate certain investment risks, such as foreign currency exchange rate risk, interest rate risk and credit risk. Derivatives may involve various risks, including the potential inability of the counterparty to fulfill its obligations under the terms of the contract, the potential for an illiquid secondary market (making it difficult for the Fund to sell or terminate, including at favorable prices) and the potential for market movements which may expose the Fund to gains or losses in excess of the amount shown in the Statement of Assets and Liabilities. The notional amounts of derivative instruments, if applicable, are not recorded in the financial statements.

A derivative instrument may suffer a marked-to-market loss if the value of the contract decreases due to an unfavorable change in the market rates or values of the underlying instrument. Losses can also occur if the counterparty does not perform its obligations under the contract. The Fund’s risk of loss from counterparty credit risk on over-the-counter derivatives is generally limited to the aggregate unrealized gain netted against any collateral held by the Fund and the amount of any variation margin held by the counterparty, plus any replacement costs or related amounts. With exchange-traded or centrally cleared derivatives, there is reduced counterparty credit risk to the Fund since the clearinghouse or central counterparty

Columbia Large Cap Growth Fund | Annual Report 2022

| 23 |

Notes to Financial Statements (continued)

July 31, 2022

(CCP) provides some protection in the case of clearing member default. The clearinghouse or CCP stands between the buyer and the seller of the contract; therefore, failure of the clearinghouse or CCP may pose additional counterparty credit risk. However, credit risk still exists in exchange-traded or centrally cleared derivatives with respect to initial and variation margin that is held in a broker’s customer account. While clearing brokers are required to segregate customer margin from their own assets, in the event that a clearing broker becomes insolvent or goes into bankruptcy and at that time there is a shortfall in the aggregate amount of margin held by the clearing broker for all its clients and such shortfall is remedied by the CCP or otherwise, U.S. bankruptcy laws will typically allocate that shortfall on a pro-rata basis across all the clearing broker’s customers (including the Fund), potentially resulting in losses to the Fund.

In order to better define its contractual rights and to secure rights that will help the Fund mitigate its counterparty risk, the Fund may enter into an International Swaps and Derivatives Association, Inc. Master Agreement (ISDA Master Agreement) or similar agreement with its derivatives counterparties. An ISDA Master Agreement is an agreement between the Fund and a counterparty that governs over-the-counter derivatives and foreign exchange forward contracts and contains, among other things, collateral posting terms and netting provisions in the event of a default and/or termination event. Under an ISDA Master Agreement, the Fund may, under certain circumstances, offset with the counterparty certain derivative instruments’ payables and/or receivables with collateral held and/or posted and create one single net payment. The provisions of the ISDA Master Agreement typically permit a single net payment in the event of default (close-out netting), including the bankruptcy or insolvency of the counterparty. Note, however, that bankruptcy or insolvency laws of a particular jurisdiction may impose restrictions on or prohibitions against the right of offset or netting in bankruptcy, insolvency or other events.

Collateral (margin) requirements differ by type of derivative. Margin requirements are established by the clearinghouse or CCP for exchange-traded and centrally cleared derivatives. Brokers can ask for margin in excess of the minimum in certain circumstances. Collateral terms for most over-the-counter derivatives are subject to regulatory requirements to exchange variation margin with trading counterparties and may have contract specific margin terms as well. For over-the-counter derivatives traded under an ISDA Master Agreement, the collateral requirements are typically calculated by netting the marked-to-market amount for each transaction under such agreement and comparing that amount to the value of any variation margin currently pledged by the Fund and/or the counterparty. Generally, the amount of collateral due from or to a party has to exceed a minimum transfer amount threshold (e.g., $250,000) before a transfer has to be made. To the extent amounts due to the Fund from its counterparties are not fully collateralized, contractually or otherwise, the Fund bears the risk of loss from counterparty nonperformance. The Fund may also pay interest expense on cash collateral received from the broker. Any interest expense paid by the Fund is shown in the Statement of Operations. The Fund attempts to mitigate counterparty risk by only entering into agreements with counterparties that it believes have the financial resources to honor their obligations and by monitoring the financial stability of those counterparties.

Certain ISDA Master Agreements allow counterparties of over-the-counter derivatives transactions to terminate derivatives contracts prior to maturity in the event the Fund’s net asset value declines by a stated percentage over a specified time period or if the Fund fails to meet certain terms of the ISDA Master Agreement, which would cause the Fund to accelerate payment of any net liability owed to the counterparty. The Fund also has termination rights if the counterparty fails to meet certain terms of the ISDA Master Agreement. In determining whether to exercise such termination rights, the Fund would consider, in addition to counterparty credit risk, whether termination would result in a net liability owed from the counterparty.

For financial reporting purposes, the Fund does not offset derivative assets and derivative liabilities that are subject to netting arrangements in the Statement of Assets and Liabilities.

Futures contracts

Futures contracts are exchange-traded and represent commitments for the future purchase or sale of an asset at a specified price on a specified date. The Fund bought and sold futures contracts to maintain appropriate equity market exposure while keeping sufficient cash to accommodate daily redemptions. These instruments may be used for other purposes in future periods. Upon entering into futures contracts, the Fund bears risks that it may not achieve the anticipated benefits of the futures contracts and may realize a loss. Additional risks include counterparty credit risk, the possibility of an illiquid market, and that a change in the value of the contract or option may not correlate with changes in the value of the underlying asset.

| 24 | Columbia Large Cap Growth Fund | Annual Report 2022 |

Notes to Financial Statements (continued)

July 31, 2022

Upon entering into a futures contract, the Fund deposits cash or securities with the broker, known as a futures commission merchant (FCM), in an amount sufficient to meet the initial margin requirement. The initial margin deposit must be maintained at an established level over the life of the contract. Cash deposited as initial margin is recorded in the Statement of Assets and Liabilities as margin deposits. Securities deposited as initial margin are designated in the Portfolio of Investments. Subsequent payments (variation margin) are made or received by the Fund each day. The variation margin payments are equal to the daily change in the contract value and are recorded as variation margin receivable or payable and are offset in unrealized gains or losses. The Fund generally expects to earn interest income on its margin deposits. The Fund recognizes a realized gain or loss when the contract is closed or expires. Futures contracts involve, to varying degrees, risk of loss in excess of the variation margin disclosed in the Statement of Assets and Liabilities.

Effects of derivative transactions in the financial statements