Item 1. Reports to Stockholders

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-04409 |

|

Eaton Vance Municipals Trust |

(Exact name of registrant as specified in charter) |

|

The Eaton Vance Building, 255 State Street, Boston, Massachusetts | | 02109 |

(Address of principal executive offices) | | (Zip code) |

|

Alan R. Dynner

The Eaton Vance Building, 255 State Street, Boston, Massachusetts 02109 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | (617) 482-8260 | |

|

Date of fiscal year end: | August 31 | |

|

Date of reporting period: | February 28, 2005 | |

| | | | | | | | |

[EV LOGO] | | | | [GRAPHIC IMAGE] |

| | | | |

| | | | |

| | | | |

Semiannual Report February 28, 2005 | | |

| | | | Alabama |

| | EATON VANCE | | |

[GRAPHIC IMAGE] | | MUNICIPALS | | Arkansas |

| | TRUST | | |

| | | | Georgia |

| | | | |

[GRAPHIC IMAGE] | | | | Kentucky |

| | | | |

| | | | Louisiana |

| | | | |

| | | | Maryland |

| | | | |

| | | | Missouri |

| | | | |

| | | | North Carolina |

| | | | |

| | | | Oregon |

| | | | |

| | | | South Carolina |

| | | | |

| | | | Tennessee |

| | | | |

| | | | Virginia |

IMPORTANT NOTICES REGARDING PRIVACY,

DELIVERY OF SHAREHOLDER DOCUMENTS,

PORTFOLIO HOLDINGS AND PROXY VOTING

Privacy. The Eaton Vance organization is committed to ensuring your financial privacy. Each of the financial institutions identified below has in effect the following policy (“Privacy Policy”) with respect to nonpublic personal information about its customers:

• Only such information received from you, through application forms or otherwise, and information about your Eaton Vance fund transactions will be collected. This may include information such as name, address, social security number, tax status, account balances and transactions.

• None of such information about you (or former customers) will be disclosed to anyone, except as permitted by law (which includes disclosure to employees necessary to service your account). In the normal course of servicing a customer’s account, Eaton Vance may share information with unaffiliated third parties that perform various required services such as transfer agents, custodians and broker/dealers.

• Policies and procedures (including physical, electronic and procedural safeguards) are in place that are designed to protect the confidentiality of such information.

• We reserve the right to change our Privacy Policy at any time upon proper notification to you. Customers may want to review our Policy periodically for changes by accessing the link on our homepage: www.eatonvance.com.

Our pledge of privacy applies to the following entities within the Eaton Vance organization: the Eaton Vance Family of Funds, Eaton Vance Management, Eaton Vance Investment Counsel, Boston Management and Research, and Eaton Vance Distributors, Inc.

In addition, our Privacy Policy only applies to those Eaton Vance customers who are individuals and who have a direct relationship with us. If a customer’s account (i.e. fund shares) is held in the name of a third-party financial adviser/ broker-dealer, it is likely that only such adviser’s privacy policies apply to the customer. This notice supersedes all previously issued privacy disclosures.

For more information about Eaton Vance’s Privacy Policy, please call 1-800-262-1122.

Delivery of Shareholder Documents. The Securities and Exchange Commission permits funds to deliver only one copy of shareholder documents, including prospectuses, proxy statements and shareholder reports, to fund investors with multiple accounts at the same residential or post office box address. This practice is often called “householding” and it helps eliminate duplicate mailings to shareholders.

Eaton Vance, or your financial adviser, may household the mailing of your documents indefinitely unless you instruct Eaton Vance, or your financial adviser, otherwise.

If you would prefer that your Eaton Vance documents not be householded, please contact Eaton Vance at 1-800-262-1122, or contact your financial adviser.

Your instructions that householding not apply to delivery of your Eaton Vance documents will be effective within 30 days of receipt by Eaton Vance or your financial adviser.

Portfolio Holdings. Each Eaton Vance Fund and it’s underlying Portfolio will file a schedule of its portfolio holdings on Form N-Q with the SEC for the first and third quarters of each fiscal year. The Form N-Q will be available on the Eaton Vance website www.eatonvance.com, by calling Eaton Vance at 1-800-262-1122 or in the EDGAR database on the SEC’s website at www.sec.gov. Form N-Q may also be reviewed and copied at the SEC’s public reference room in Washington, D.C. (call 1-800-732-0330 for information on the operation of the public reference room).

Proxy Voting. From time to time, funds are required to vote proxies related to the securities held by the funds. The Eaton Vance Funds or their underlying Portfolios (if applicable) vote proxies according to a set of policies and procedures approved by the Funds’ and Portfolios’ Boards. You may obtain a description of these policies and procedures and information on how the Funds or Portfolios voted proxies relating to Portfolio securities during the 12 month period ended June 30, without charge, upon request, by calling

1-800-262-1122. This description is also available on the SEC’s website at www.sec.gov.

Eaton Vance Municipals Funds as of February 28, 2005

TABLE OF CONTENTS

President’s Letter to Shareholders | 2 |

| |

Market Recap | 3 |

| |

Fund Investment Updates | |

| |

Alabama | 4 |

Arkansas | 6 |

Georgia | 8 |

Kentucky | 10 |

Louisiana | 12 |

Maryland | 14 |

Missouri | 16 |

North Carolina | 18 |

Oregon | 20 |

South Carolina | 22 |

Tennessee | 24 |

Virginia | 26 |

| |

Disclosure of Fund Expenses | 28 |

| |

Financial Statements | 33 |

| |

Investment Management | 112 |

1

LETTER TO SHAREHOLDERS

Thomas J. Fetter

President

The municipal bond market is a center of capital formation for states, municipalities and, in some cases, private economic initiatives. In this edition of our continuing educational series, we will discuss industrial development revenue (IDR) bonds. IDR bonds have long been used as a financing mechanism by local governments to provide assistance to local employers and encourage job retention and creation within their communities.

IDR bonds finance private activities that benefit the public...

IDR bonds are issued by municipal authorities to finance projects and facilities used by private corporations. Historically, IDR bonds have represented a partnership between the private and public sectors – a source of dedicated funding for companies and a source of job creation in projects beneficial to local communities. The “Private-Activities” provision of the Tax Reform Act of 1986 permits issuance of tax-exempt bonds for specific activities, including pollution control; gas and electric service; water distribution; wastewater systems; solid waste disposal; airports and selected transportation projects; and other industrial projects.

The Act also placed a cap on the dollar amount that may be raised for IDR bonds in each state, limiting the amount to $50 per person/per state/per year, with a $150 million maximum. These limitations provide protection against potential abuse and ensure that tax-exempt IDR bonds will indeed be issued for projects that will benefit the public.

IDR bonds finance utility-related projects and other industrial initiatives...

Typically, IDR bond projects provide financing for manufacturing, processing or utility facilities. Historically, about one-half of these bonds have been issued to finance pollution control facilities for manufacturers and electric utilities. As many utilities and manufacturers have been ordered to comply with stricter environmental and fuel standards, pollution control bonds have helped finance the retrofits of existing plants. Other IDR bonds have served as inducements from state and local issuers to locate plants or build new facilities, in the hope that such construction might generate further economic growth for a community.

IDR bonds are secured by corporate revenues – not those of state or local governments...

IDR bond issues are secured by the credit of the underlying corporation. The municipal issuing authority acts solely as a conduit to permit tax-exempt financing. The corporation pledges to make payments sufficient to meet all debt service obligations. Unlike some revenue issues, IDR bonds are backed by revenues of the entire corporation, not solely by those of the project being financed.

Because IDR bonds are backed by corporate revenues and not by the taxing authority of a state or local jurisdiction, they have historically provided coupon premiums above those of general obligations and other more traditional revenue bonds. Bonds may be either collateralized or unsecured. Collateralized bonds have a lien against the company’s assets, which may provide bond holders enhanced bargaining power in the event of a bankruptcy. Unsecured bonds have no such lien.

While providing new opportunities, IDR bonds require rigorous analysis...

While IDR bonds may provide unusual investment opportunities, they also may entail increased risk and, therefore, demand especially intensive analysis. At Eaton Vance, we have credit analysts and resources dedicated to IDR bond research.

IDR bonds represent a key segment of the municipal bond market and should remain an important source of capital formation. In our view, the experience and resources needed to evaluate these issues further demonstrates the value of professional management. We will continue to look for opportunities in this sector of the municipal market.

Fund shares are not insured by the FDIC and are not deposits or other obligations of, or guaranteed by, any depository institution. Shares are subject to investment risks, including possible loss of principal invested.

| Sincerely, |

| |

|

|

| |

| Thomas J. Fetter |

| President |

| April 6, 2005 |

2

MARKET RECAP

The U.S. economy continued to generate moderate growth during the six months ended February 28, 2005. However, the relentless hikes in gasoline and energy prices were increasingly felt by consumers. Meanwhile, the weak U.S. dollar kept U.S. exports competitive, but raised inflationary concerns and helped push interest rates higher.

The long-depressed manufacturing sector showed signs of life during the period...

The nation’s Gross Domestic Product grew by 3.8% in the fourth quarter of 2004, according to Commerce Department figures, following a 4.0% rise in the third quarter. Manufacturing activity expanded strongly, especially durable goods manufacturing, driven by the production of machine tools, trucks, defense-related products and selected technology products.

Despite higher gas and fuel prices, consumers remained active, although the pace of auto sales weakened somewhat. Travel and tourism activity was strong, benefiting the service and hospitality industries. Housing and residential construction remained robust, while commercial building gained new momentum in selected markets.

The economy enjoyed impressive job growth in late 2004 and early 2005...

The nation’s labor markets strengthened during the period. The pace of hiring picked up in areas that had suffered large technology sector layoffs in recent years. Manufacturing, financial services, business services, trucking, shipping, construction, energy, health care, and media also generated impressive new job creation, while temporary employment agencies witnessed strong demand. As a result of increased job growth, the nation’s unemployment rate fell to 5.2% in February 2005, down from 5.7% a year earlier.

Municipal bond yields equal 95% of Treasury yields

4.48% | | 6.89% |

| | |

30-Year AAA-rated | | Taxable equivalent yield |

General Obligation (GO) Bonds* | | in 35.0% tax bracket |

4.72% | | |

| | |

30-Year Treasury bond | | |

Pricipal and interest payments of Treasury securities are guaranteed by the U.S. government.

*GO yields are a compilation of a representative variety of general obligations and are not necessary representative of the Funds’ yield. Statistics as of February 28, 2005

Past performance is no guarantee of future results.

Source: Bloomberg, LP.

The Federal Reserve continued to raise short-term interest rates in 2005...

The Federal Reserve pushed short-term rates higher, suggesting it will continue to raise rates to keep the economy from growing too quickly and, thereby, reviving inflation. Beginning in June 2004, the Fed increased its Federal Funds rate – a key short-term interest rate barometer – on seven occasions, raising that benchmark from 1.00% to 2.75%, including its most recent rate hike in March 2005.

The municipal bond market managed a respectable gain for the six months, outperforming the Treasury market. For the six months ended February 28, 2005, the Lehman Brothers Municipal Bond Index had a total return of 2.40%.*

* It is not possible to invest directly in an Index. The Index’s total return does not reflect expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index.

The views expressed throughout this report are those of the portfolio managers and are current only through the end of the period of the report as stated on the cover. These views are subject to change at any time based upon market or other conditions, and the investment adviser disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a fund are based on many factors, may not be relied on as an indication of trading intent on behalf of any Eaton Vance fund.

3

Eaton Vance Alabama Municipals fund as of february 28, 2005

INVESTMENT UPDATE

The Fund

Performance for the Past Six Months

• The Fund’s Class A shares had a total return of 2.79% during the six months ended February 28, 2005.(1) This return was the result of an increase in net asset value (NAV) to $9.85 per share on February 28, 2005 from $9.80 on August 31, 2004, and the reinvestment of $0.221 in dividends.(2)

• The Fund’s Class B shares had a total return of 2.61% during the six months ended February 28, 2005.(1) This return was the result of an increase in NAV to $10.83 per share on February 28, 2005 from $10.77 on August 31, 2004, and the reinvestment of $0.219 in dividends.(2)

• For comparison, the Lehman Municipal Bond Index had a total return of 2.40% for the six months ended February 28, 2005.(3)

• Based on the Fund’s most recent dividends and NAVs on February 28, 2005 of $9.85 per share for Class A and $10.83 for Class B, the Fund’s distribution rates were 4.30% and 3.55%, respectively.(4) The distribution rates of Class A and Class B are equivalent to taxable rates of 6.96% and 5.75%, respectively.(5)

• The SEC 30-day yields for Class A and Class B shares at February 28, 2005 were 3.45% and 2.87%, respectively.(6) The SEC 30-day yields of Class A and Class B are equivalent to taxable yields of 5.59% and 4.65%, respectively.(5)

William H. Ahern

Portfolio Manager

Management Discussion

• Alabama experienced moderate economic growth in late 2004, although job growth remained sluggish. The exodus of apparel, textile, and paper production continued, although auto production benefited from direct investment by foreign manufacturers. The state’s jobless rate was 5.2% in February 2005, down from 5.6% a year ago.

• Insured* water and sewer bonds remained the Fund’s largest sector weighting at February 28, 2005. Alabama communities have increased the level of capital investment in recent years. Having suffered from drought in recent years, some communities have initiated programs aimed at watershed protection and drought-resistant facilities.

• In the Alabama hospital sector, the Fund remained very selective. Management focused on insured* bonds of hospitals it believes have a sound financial profile, as well as a competitive advantage due to in-demand health care services, such as rehabilitation, cancer care and children’s health services.

• Insured* general obligations (GOs) remained a significant investment. The Fund’s investments focused on cities and towns with a relatively strong tax base and sound economic underpinning, two key determinants for investors in general obligations.

• Management adjusted the Fund’s coupon mix to reflect changing market conditions. Management also continued its efforts to upgrade the Fund’s call protection. The Fund sold bonds with approaching call dates in favor of high quality, non-callable bonds and bonds with more attractive call characteristics.

* Private insurance does not decrease the risk of loss of principal associated with this investment.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. For performance as of the most recent month end, please refer to www.eatonvance.com.

(1) These returns do not include the 4.75% maximum sales charge for the Fund’s Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B shares. If the sales charge were deducted, returns would be lower.

(2) A portion of the Fund’s income may be subject to federal income and/or alternative minimum tax and state and local taxes.

(3) It is not possible to invest directly in an Index. The Index’s total return does not reflect the expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index.

(4) The Fund’s distribution rate represents actual distributions paid to shareholders and is calculated by dividing the last distribution per share (annualized) by the net asset value.

(5) Taxable-equivalent figures assume a maximum 38.25% combined federal and state income tax rate. A lower rate would result in lower tax-equivalent figures.

(6) The Fund’s SEC yield is calculated by dividing the net investment income per share for the 30-day period by the offering price at the end of the period and annualizing the result.

4

FUND PERFORMANCE

Performance(1) | | Class A | | Class B | |

| | | | | |

Average Annual Total Returns (at net asset value) | | | | | |

One Year | | 1.99 | % | 1.41 | % |

Five Years | | 6.85 | | 6.09 | |

Ten Years | | 5.53 | | 4.87 | |

Life of Fund† | | 4.86 | | 5.24 | |

| | | | | |

SEC Average Annual Total Returns (including sales charge or applicable CDSC) | | | | | |

One Year | | -2.81 | % | -3.47 | % |

Five Years | | 5.82 | | 5.78 | |

Ten Years | | 5.02 | | 4.87 | |

Life of Fund† | | 4.41 | | 5.24 | |

†Inception date: Class A: 12/7/93; Class B: 5/1/92

(1) Average annual total returns do not include the 4.75% maximum sales charge for Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B shares. If sales charges were deducted, returns would be lower. SEC average annual total returns for Class A reflect the maximum 4.75% sales charge. SEC returns for Class B reflect applicable CDSC based on the following schedule: 5% - 1st and 2nd years; 4% - 3rd year; 3% - 4th year; 2% - 5th year; 1% - 6th year.

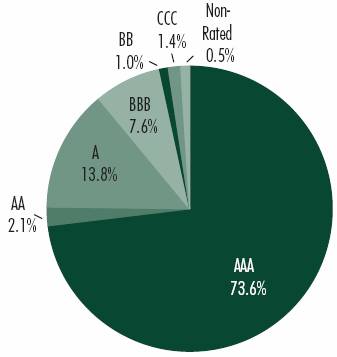

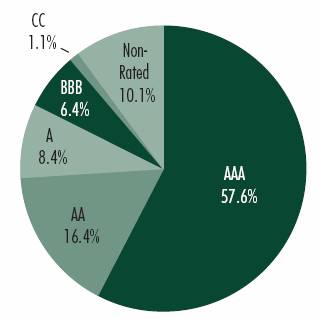

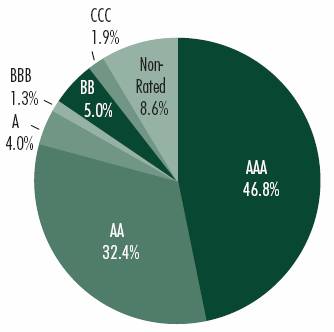

Diversification by Credit Quality(2)

(2) As a percentage of total investments, as of February 28, 2005. Holdings subject to change due to active management.

5

Eaton Vance Arkansas Municipals Fund as of February 28, 2005

INVESTMENT UPDATE

The Fund

Performance for the Past Six Months

• The Fund’s Class A shares had a total return of 2.62% during the six months ended February 28, 2005.(1) This return was the result of an increase in net asset value (NAV) to $9.90 per share on February 28, 2005 from $9.88 on August 31, 2004, and the reinvestment of $0.236 in dividends.(2)

• The Fund’s Class B shares had a total return of 2.48% during the six months ended February 28, 2005.(1) This return was the result of an increase in NAV to $10.64 per share on February 28, 2005 from $10.61 on August 31, 2004, and the reinvestment of $0.231 in dividends.(2)

• For comparison, the Lehman Municipal Bond Index had a total return of 2.40% for the six months ended February 28, 2005.(3)

• Based on the Fund’s most recent dividends and NAVs on February 28, 2005 of $9.90 per share for Class A and $10.64 for Class B, the Fund’s distribution rates were 4.74% and 3.98%, respectively.(4) The distribution rates of Class A and Class B are equivalent to taxable rates of 7.84% and 6.58%, respectively.(5)

• The SEC 30-day yields for Class A and Class B shares at February 28, 2005 were 3.76% and 3.20%, respectively.(6) The SEC 30-day yields of Class A and Class B are equivalent to taxable yields of 6.22% and 5.29%, respectively.(5)

* Private insurance does not decrease the risk of loss of principal associated with this investment.

Thomas M. Metzold

Co-Portfolio Manager

William H. Ahern

Co-Portfolio Manager

Management Discussion

• Arkansas’ economic condition improved in 2004, as the state registered its fastest job growth since 2000. With the exception of the manufacturing sector, all major state employment sectors posted positive year-over-year growth. Leisure, education and health care paced new job creation. The state jobless rate was 5.5% in February 2005, down from 5.7% a year ago.

• Hospital bonds were the Fund’s largest sector weighting at February 28, 2005. The Fund’s investments included uninsured and insured* issues for geographically diverse facilities throughout the state. The Fund’s investments emphasized competitive hospitals with attractive health care specialties and strong underlying finances.

• Industrial development revenue bonds played a prominent role in the Fund, although management remained selective within the sector. The Fund’s investments included paper and airline bonds – areas that, in management’s view, are likely to enjoy stronger demand in sustained economic recovery.

• The Fund maintained a significant exposure to essential services bonds, including insured* water and sewer issues. Because the revenues for these issues are based on fees and water payments, they are considered less subject to economic fluctuations.

• The Fund continued to pursue broad diversification by sector, issuer and coupon distribution. In addition, management extended its efforts to update call protection, a key strategic consideration in a period of relatively low rates.

• Effective May 2, 2005, Thomas M. Metzold will be the Fund’s sole portfolio manager.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. For performance as of the most recent month end, please refer to www.eatonvance.com.

(1) These returns do not include the 4.75% maximum sales charge for the Fund’s Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B shares. If the sales charge were deducted, returns would be lower.

(2) A portion of the Fund’s income may be subject to federal income and/or alternative minimum tax and state and local taxes.

(3) It is not possible to invest directly in an Index. The Index’s total return does not reflect the expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index.

(4) The Fund’s distribution rate represents actual distributions paid to shareholders and is calculated by dividing the last distribution per share (annualized) by the net asset value.

(5) Taxable-equivalent figures assume a maximum 39.55% combined federal and state income tax rate. A lower rate would result in lower tax-equivalent figures.

(6) The Fund’s SEC yield is calculated by dividing the net investment income per share for the 30-day period by the offering price at the end of the period and annualizing the result.

6

FUND PERFORMANCE

Performance(1) | | Class A | | Class B | |

| | | | | |

Average Annual Total Returns (at net asset value) | | | | | |

One Year | | 1.94 | % | 1.32 | % |

Five Years | | 6.68 | | 5.94 | |

Ten Years | | 5.64 | | 4.95 | |

Life of Fund† | | 5.01 | | 5.11 | |

| | | | | |

SEC Average Annual Total Returns (including sales charge or applicable CDSC) | | | | | |

One Year | | -2.91 | % | -3.54 | % |

Five Years | | 5.64 | | 5.62 | |

Ten Years | | 5.12 | | 4.95 | |

Life of Fund† | | 4.55 | | 5.11 | |

†Inception date: Class A: 2/9/94; Class B: 10/2/92

(1) Average annual total returns do not include the 4.75% maximum sales charge for Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B shares. If sales charges were deducted, returns would be lower. SEC average annual total returns for Class A reflect the maximum 4.75% sales charge. SEC returns for Class B reflect applicable CDSC based on the following schedule: 5% - 1st and 2nd years; 4% - 3rd year; 3% - 4th year; 2% - 5th year; 1% - 6th year.

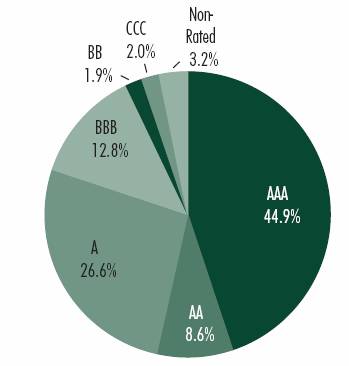

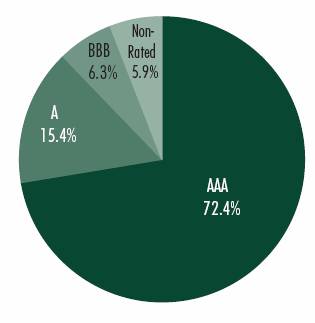

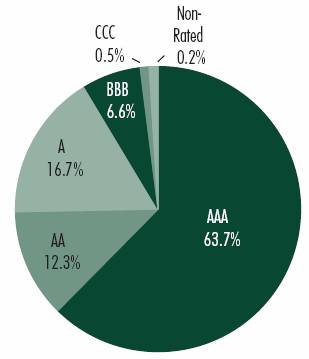

Diversification by Credit Quality(2)

(2) As a percentage of total investments, as of February 28, 2005. Holdings subject to change due to active management.

7

Eaton Vance Georgia Municipals Fund as of February 28, 2005

INVESTMENT UPDATE

The Fund

Performance for the Past Six Months

• The Fund’s Class A shares had a total return of 2.65% during the six months ended February 28, 2005.(1) This return was the result of an increase in net asset value (NAV) to $9.50 per share on February 28, 2005 from $9.48 on August 31, 2004, and the reinvestment of $0.229 in dividends.(2)

• The Fund’s Class B shares had a total return of 2.34% during the six months ended February 28, 2005.(1) This return was the result of an increase in NAV to $10.14 per share on February 28, 2005 from $10.13 on August 31, 2004, and the reinvestment of $0.225 in dividends.(2)

• For comparison, the Lehman Municipal Bond Index had a total return of 2.40% for the six months ended February 28, 2005.(3)

• Based on the Fund’s most recent dividends and NAVs on February 28, 2005 of $9.50 per share for Class A and $10.14 for Class B, the Fund’s distribution rates were 4.80% and 4.04%, respectively.(4) The distribution rates of Class A and Class B are equivalent to taxable rates of 7.86% and 6.61%, respectively.(5)

• The SEC 30-day yields for Class A and Class B shares at February 28, 2005 were 4.02% and 3.47%, respectively.(6) The SEC 30-day yields of Class A and Class B are equivalent to taxable yields of 6.58% and 5.68%, respectively.(5)

Cynthia J. Clemson

Portfolio Manager

Management Discussion

• Georgia’s economy continued to expand during the fiscal year, although lagging the national pace, as the state’s manufacturing industries have seen continuing layoffs. Georgia’s Atlanta-based technology sector generated some gains, although it has not yet recovered to pre-recession levels of 2000. The state’s jobless rate was 5.1% in February 2005, up from 4.3% a year ago.

• Insured* water and sewer bonds were the Fund’s largest sector weighting at February 28, 2005. Revenues for essential services, including water utilities, have historically been less impacted by changes in the overall economy. Georgia’s population growth and surging residential and commercial development have necessitated major improvements in the state’s water infrastructure.

• Industrial development revenue bonds constituted large investments. The Fund’s investments represented economically sensitive companies, as well as defensive industries. Investments included paper manufacturers, consumer products, beverages, airlines and a maker of chemical catalysts used in oil refining.

• Insured* transportation bonds were a major commitment for the Fund. Investments focused predominantly on Atlanta’s rapid transit system. The bonds have helped finance the system’s expansion needed to accommodate the city’s urban sprawl.

• Management continued to update the Fund’s coupon distribution to reflect a changing interest rate outlook. In addition, management continued to upgrade call protection, where possible, to protect against untimely calls and improve the Fund’s appreciation potential.

* Private insurance does not decrease the risk of loss of principal associated with this investment.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. For performance as of the most recent month end, please refer to www.eatonvance.com.

(1) These returns do not include the 4.75% maximum sales charge for the Fund’s Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B shares. If the sales charge were deducted, returns would be lower.

(2) A portion of the Fund’s income may be subject to federal income and/or alternative minimum tax and state and local taxes.

(3) It is not possible to invest directly in an Index. The Index’s total return does not reflect the expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index.

(4) The Fund’s distribution rate represents actual distributions paid to shareholders and is calculated by dividing the last distribution per share (annualized) by the net asset value.

(5) Taxable-equivalent figures assume a maximum 38.90% combined federal and state income tax rate. A lower rate would result in lower tax-equivalent figures.

(6) The Fund’s SEC yield is calculated by dividing the net investment income per share for the 30-day period by the offering price at the end of the period and annualizing the result.

8

FUND PERFORMANCE

Performance(1) | | Class A | | Class B | |

| | | | | |

Average Annual Total Returns (at net asset value) | | | | | |

One Year | | 2.32 | % | 1.58 | % |

Five Years | | 7.32 | | 6.53 | |

Ten Years | | 5.63 | | 4.97 | |

Life of Fund† | | 4.69 | | 4.93 | |

| | | | | |

SEC Average Annual Total Returns (including sales charge or applicable CDSC) | | | | | |

One Year | | -2.57 | % | -3.29 | % |

Five Years | | 6.28 | | 6.22 | |

Ten Years | | 5.13 | | 4.97 | |

Life of Fund† | | 4.24 | | 4.93 | |

†Inception date: Class A: 12/7/93; Class B: 12/23/91

(1) Average annual total returns do not include the 4.75% maximum sales charge for Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B shares. If sales charges were deducted, returns would be lower. SEC average annual total returns for Class A reflect the maximum 4.75% sales charge. SEC returns for Class B reflect applicable CDSC based on the following schedule: 5% - 1st and 2nd years; 4% - 3rd year; 3% - 4th year; 2% - 5th year; 1% - 6th year.

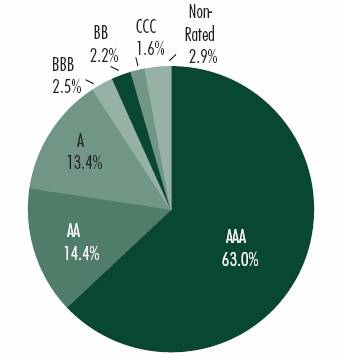

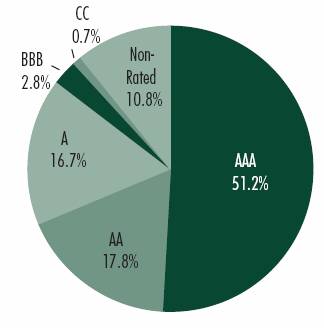

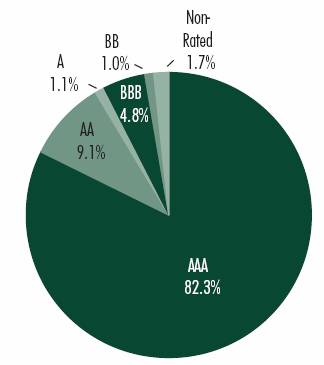

Diversification by Credit Quality(2)

(2) As a percentage of total investments, as of February 28, 2005. Holdings subject to change due to active management.

9

Eaton Vance Kentucky Municipals Fund as of February 28, 2005

INVESTMENT UPDATE

The Fund

Performance for the Past Six Months

• The Fund’s Class A shares had a total return of 2.11% during the six months ended February 28, 2005.(1) This return was the result of a decrease in net asset value (NAV) to $9.30 per share on February 28, 2005 from $9.32 on August 31, 2004, and the reinvestment of $0.215 in dividends.(2)

• The Fund’s Class B shares had a total return of 1.91% during the six months ended February 28, 2005.(1) This return was the result of a decrease in NAV to $10.04 per share on February 28, 2005 from $10.06 on August 31, 2004, and the reinvestment of $0.210 in dividends.(2)

• For comparison, the Lehman Municipal Bond Index had a total return of 2.40% for the six months ended February 28, 2005.(3)

• Based on the Fund’s most recent dividends and NAVs on February 28, 2005 of $9.30 per share for Class A and $10.04 for Class B, the Fund’s distribution rates were 4.59% and 3.83%, respectively.(4) The distribution rates of Class A and Class B are equivalent to taxable rates of 7.51% and 6.27%, respectively.(5)

• The SEC 30-day yields for Class A and Class B shares at February 28, 2005 were 3.23% and 2.64%, respectively.(6) The SEC 30-day yields of Class A and Class B are equivalent to taxable yields of 5.29% and 4.32%, respectively.(5)

William H. Ahern

Portfolio Manager

Management Discussion

• Kentucky’s economy improved significantly in 2004 and early 2005, with employment gains at the fastest pace since the 2001 recession. Most major sectors saw impressive gains during the year. While manufacturing continued to shed jobs, the rate of job loss was markedly lower than that seen during the recession. The state’s jobless rate was 5.2% in February 2005, down from 5.7% a year ago.

• Insured* transportation bonds bonds were the Fund’s largest sector weighting at February 28, 2005. The Fund’s investments included issues for highway, turn-pike and regional airport authorities. With the region’s air passenger and freight traffic doubling in the past decade, these bonds have helped finance a much-needed expansion.

• Industrial development revenue bonds were significant holdings for the Fund. Amid signs of a stronger economy, the Fund’s investments included issues in economically sensitive areas such as the airline, chemical, retailing, energy and metals industries.

• Insured* lease revenue/certificates of participation (COPs) constituted prominent investments. COPs are an alternative financing tool employed by some communities to finance educational facilities and assorted public improvements.

• Management sought to diversify the Fund’s investments according to issuer, sector and insurer and coupon allocation. In addition, management continued to monitor call characteristics. Call features can have a significant influence on the Fund’s ability to respond to changes in interest rates.

* Private insurance does not decrease the risk of loss of principal associated with this investment.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. For performance as of the most recent month end, please refer to www.eatonvance.com.

(1) These returns do not include the 4.75% maximum sales charge for the Fund’s Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B shares. If the sales charge were deducted, returns would be lower.

(2) A portion of the Fund’s income may be subject to federal income and/or alternative minimum tax and state and local taxes.

(3) It is not possible to invest directly in an Index. The Index’s total return does not reflect the expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index.

(4) The Fund’s distribution rate represents actual distributions paid to shareholders and is calculated by dividing the last distribution per share (annualized) by the net asset value.

(5) Taxable-equivalent figures assume a maximum 38.90% combined federal and state income tax rate. A lower rate would result in lower tax-equivalent figures.

(6) The Fund’s SEC yield is calculated by dividing the net investment income per share for the 30-day period by the offering price at the end of the period and annualizing the result.

10

FUND PERFORMANCE

Performance(1) | | Class A | | Class B | |

| | | | | |

Average Annual Total Returns (at net asset value) | | | | | |

One Year | | 1.93 | % | 1.30 | % |

Five Years | | 5.72 | | 4.99 | |

Ten Years | | 5.30 | | 4.64 | |

Life of Fund† | | 4.47 | | 4.78 | |

| | | | | |

SEC Average Annual Total Returns (including sales charge or applicable CDSC) | | | | | |

One Year | | -2.94 | % | -3.57 | % |

Five Years | | 4.69 | | 4.66 | |

Ten Years | | 4.79 | | 4.64 | |

Life of Fund† | | 4.02 | | 4.78 | |

†Inception date: Class A: 12/7/93; Class B: 12/23/91

(1) Average annual total returns do not include the 4.75% maximum sales charge for Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B shares. If sales charges were deducted, returns would be lower. SEC average annual total returns for Class A reflect the maximum 4.75% sales charge. SEC returns for Class B reflect applicable CDSC based on the following schedule: 5% - 1st and 2nd years; 4% - 3rd year; 3% - 4th year; 2% - 5th year; 1% - 6th year.

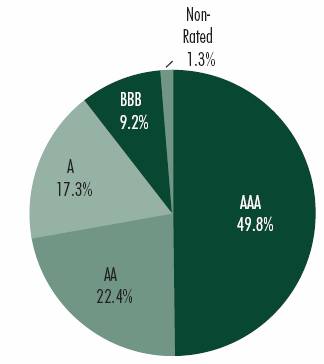

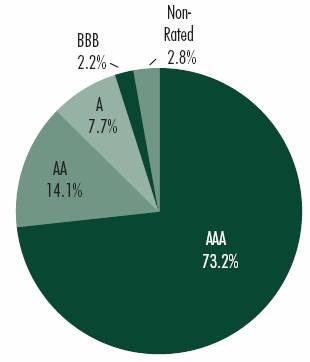

Diversification by Credit Quality(2)

(2) As a percentage of total investments, as of February 28, 2005. Holdings subject to change due to active management.

11

Eaton Vance Louisiana Municipals Fund as of February 28, 2005

INVESTMENT UPDATE

The Fund

Performance for the Past Six Months

• The Fund’s Class A shares had a total return of 3.72% during the six months ended February 28, 2005.(1) This return was the result of an increase in net asset value (NAV) to $9.97 per share on February 28, 2005 from $9.84 on August 31, 2004, and the reinvestment of $0.233 in dividends.(2)

• The Fund’s Class B shares had a total return of 3.54% during the six months ended February 28, 2005.(1) This return was the result of an increase in NAV to $10.54 per share on February 28, 2005 from $10.40 on August 31, 2004, and the reinvestment of $0.225 in dividends.(2)

• For comparison, the Lehman Municipal Bond Index had a total return of 2.40% for the six months ended February 28, 2005.(3) As quality spreads tightened during the period, the Fund’s lower-investment-grade investments fared especially well, which accounted for its outperformance of the Index.

• Based on the Fund’s most recent dividends and NAVs on February 28, 2005 of $9.97 per share for Class A and $10.54 for Class B, the Fund’s distribution rates were 4.65% and 3.91%, respectively.(4) The distribution rates of Class A and Class B are equivalent to taxable rates of 7.61% and 6.40%, respectively.(5)

• The SEC 30-day yields for Class A and Class B shares at February 28, 2005 were 3.97% and 3.41%, respectively.(6) The SEC 30-day yields of Class A and Class B are equivalent to taxable yields of 6.50% and 5.58%, respectively.(5)

Robert B. MacIntosh

Portfolio Manager

Management Discussion

• Louisiana has seen uneven job growth in the past year. The state’s key chemical sector lost ground, as the industry was hurt by high natural gas prices. Education, health care, retail and telecommunications generated meaningful growth. Manufacturing was generally flat, although there was a pick-up in auto and ship building. The state’s jobless rate was 6.0% in February 2005, up from 5.7% a year ago.

• Insured* education bonds were the Fund’s largest sector weighting at February 28, 2005. The education sector has historically tended to be less sensitive to the vagaries of the economy. The Fund’s investments included state and local finance authority bonds that provided financing for the construction of student housing, classroom and lab facilities.

• Insured* general obligations (GOs) represented a large investment for the Fund. With the state’s key energy industry hurt by weather-related shutdowns and the chemical industry hurt by high natural gas prices, insured* state, parish and local GOs provided an attractive measure of revenue stability.

• Insured* special tax revenue bonds constituted a major commitment for the Fund. These issues gave Louisiana communities an alternative financing source for public facilities, with revenue streams generated by gas and fuel taxes and local district sales taxes.

• Management continued to update the Fund’s call protection, when possible, trading bonds with near-term calls for non-callable bonds or issues with longer-dated call provisions.

• From a coupon standpoint, management maintained a well-diversified allocation, balancing defensive, higher-coupon issues with interest-rate-sensitive, low- and zero-coupon issues for appreciation potential.

* Private insurance does not decrease the risk of loss of principal associated with this investment.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. For performance as of the most recent month end, please refer to www.eatonvance.com.

(1) These returns do not include the 4.75% maximum sales charge for the Fund’s Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B shares. If the sales charge were deducted, returns would be lower.

(2) A portion of the Fund’s income may be subject to federal income and/or alternative minimum tax and state and local taxes.

(3) It is not possible to invest directly in an Index. The Index’s total return does not reflect the expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index.

(4) The Fund’s distribution rate represents actual distributions paid to shareholders and is calculated by dividing the last distribution per share (annualized) by the net asset value.

(5) Taxable-equivalent figures assume a maximum 38.90% combined federal and state income tax rate. A lower rate would result in lower tax-equivalent figures.

(6) The Fund’s SEC yield is calculated by dividing the net investment income per share for the 30-day period by the offering price at the end of the period and annualizing the result.

12

FUND PERFORMANCE

Performance(1) | | Class A | | Class B | |

| | | | | |

Average Annual Total Returns (at net asset value) | | | | | |

One Year | | 4.48 | % | 3.87 | % |

Five Years | | 7.65 | | 6.88 | |

Ten Years | | 5.75 | | 5.07 | |

Life of Fund† | | 5.17 | | 5.21 | |

| | | | | |

SEC Average Annual Total Returns (including sales charge or applicable CDSC) | | | | | |

One Year | | -0.49 | % | -1.11 | % |

Five Years | | 6.60 | | 6.57 | |

Ten Years | | 5.24 | | 5.07 | |

Life of Fund† | | 4.70 | | 5.21 | |

†Inception date: Class A: 2/14/94; Class B: 10/2/92

(1) Average annual total returns do not include the 4.75% maximum sales charge for Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B shares. If sales charges were deducted, returns would be lower. SEC average annual total returns for Class A reflect the maximum 4.75% sales charge. SEC returns for Class B reflect applicable CDSC based on the following schedule: 5% - 1st and 2nd years; 4% - 3rd year; 3% - 4th year; 2% - 5th year; 1% - 6th year.

Diversification by Credit Quality(2)

(2) As a percentage of total investments, as of February 28, 2005. Holdings subject to change due to active management.

13

Eaton Vance Maryland Municipals Fund as of February 28, 2005

INVESTMENT UPDATE

The Fund

Performance for the Past Six Months

• The Fund’s Class A shares had a total return of 3.19% during the six months ended February 28, 2005.(1) This return was the result of an increase in net asset value (NAV) to $9.57 per share on February 28, 2005 from $9.49 on August 31, 2004, and the reinvestment of $0.220 in dividends.(2)

• The Fund’s Class B shares had a total return of 3.00% during the six months ended February 28, 2005.(1) This return was the result of an increase in NAV to $10.44 per share on February 28, 2005 from $10.35 on August 31, 2004, and the reinvestment of $0.218 in dividends.(2)

• For comparison, the Lehman Municipal Bond Index had a total return of 2.40% for the six months ended February 28, 2005.(3) As quality spreads tightened during the period, the Fund’s lower-investment-grade investments fared especially well, which accounted for its outperformance of the Index.

• Based on the Fund’s most recent dividends and NAVs on February 28, 2005 of $9.57 per share for Class A and $10.44 for Class B, the Fund’s distribution rates were 4.48% and 3.75%, respectively.(4) The distribution rates of Class A and Class B are equivalent to taxable rates of 7.24% and 6.06%, respectively.(5)

• The SEC 30-day yields for Class A and Class B shares at February 28, 2005 were 4.06% and 3.51%, respectively.(6) The SEC 30-day yields of Class A and Class B are equivalent to taxable yields of 6.56% and 5.67%, respectively.(5)

Craig Brandon

Portfolio Manager

Management Discussion

• Maryland’s job growth outpaced that of the nation during the past year, helped, in part, by increased spending for homeland security. In addition, the region’s key tourism industry has recovered significantly since 2001, boosting the leisure, lodging and services sectors. Maryland’s jobless rate was 4.2% in February 2005, unchanged from a year ago.

• Education bonds were the Fund’s largest sector weighting at February 28, 2005. The education sector has generally been less sensitive to the vagaries of the economy. The Fund’s investments included public and private institutions that have relatively strong applicant demand and stable-to-rising tuition and fee income.

• Insured* and uninsured hospital issues played a major role in the Fund. Management remained very selective, focusing on the more competitive institutions that have sound management, favorable cost structures, good market share and low bed-vacancy rates.

• Insured* water and sewer bonds were large investments. Essential service revenues of water utilities tend to be relatively stable, generally unaffected by changes in the overall economy. The Fund’s investments included bonds for Baltimore’s water and wastewater systems, which include the city’s reservoir watersheds, wastewater treatment facilities and water filtration plants.

• The Fund had significant investments in insured* transportation bonds. Among the Fund’s investments were bonds that helped finance an ongoing $1.8 billion improvement project for Baltimore-Washington airport. Improvements included a terminal expansion, new parking lots, rental car facilities and widened access roads.

* Private insurance does not decrease the risk of loss of principal associated with this investment.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. For performance as of the most recent month end, please refer to www.eatonvance.com.

(1) These returns do not include the 4.75% maximum sales charge for the Fund’s Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B shares. If the sales charge were deducted, returns would be lower.

(2) A portion of the Fund’s income may be subject to federal income and/or alternative minimum tax and state and local taxes.

(3) It is not possible to invest directly in an Index. The Index’s total return does not reflect the expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index.

(4) The Fund’s distribution rate represents actual distributions paid to shareholders and is calculated by dividing the last distribution per share (annualized) by the net asset value.

(5) Taxable-equivalent figures assume a maximum 38.09% combined federal and state income tax rate. A lower rate would result in lower tax-equivalent figures.

(6) The Fund’s SEC yield is calculated by dividing the net investment income per share for the 30-day period by the offering price at the end of the period and annualizing the result.

14

FUND PERFORMANCE

Performance(1) | | Class A | | Class B | |

| | | | | |

Average Annual Total Returns (at net asset value) | | | | | |

One Year | | 2.34 | % | 1.71 | % |

Five Years | | 6.60 | | 5.79 | |

Ten Years | | 5.35 | | 4.67 | |

Life of Fund† | | 4.59 | | 4.93 | |

| | | | | |

SEC Average Annual Total Returns (including sales charge or applicable CDSC) | | | | | |

One Year | | -2.54 | % | -3.17 | % |

Five Years | | 5.57 | | 5.47 | |

Ten Years | | 4.84 | | 4.67 | |

Life of Fund† | | 4.14 | | 4.93 | |

†Inception date: Class A: 12/10/93; Class B: 2/3/92

(1) Average annual total returns do not include the 4.75% maximum sales charge for Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B shares. If sales charges were deducted, returns would be lower. SEC average annual total returns for Class A reflect the maximum 4.75% sales charge. SEC returns for Class B reflect applicable CDSC based on the following schedule: 5% - 1st and 2nd years; 4% - 3rd year; 3% - 4th year; 2% - 5th year; 1% - 6th year.

Diversification by Credit Quality(2)

(2) As a percentage of total investments, as of February 28, 2005. Holdings subject to change due to active management.

15

Eaton Vance Missouri Municipals Fund as of February 28, 2005

INVESTMENT UPDATE

The Fund

Performance for the Past Six Months

• The Fund’s Class A shares had a total return of 2.65% during the six months ended February 28, 2005.(1) This return was the result of an increase in net asset value (NAV) to $10.10 per share on February 28, 2005 from $10.08 on August 31, 2004, and the reinvestment of $0.244 in dividends.(2)

• The Fund’s Class B shares had a total return of 2.43% during the six months ended February 28, 2005.(1) This return was the result of an increase in NAV to $11.16 per share on February 28, 2005 from $11.14 on August 31, 2004, and the reinvestment of $0.248 in dividends.(2)

• For comparison, the Lehman Municipal Bond Index had a total return of 2.40% for the six months ended February 28, 2005.(3)

• Based on the Fund’s most recent dividends and NAVs on February 28, 2005 of $10.10 per share for Class A and $11.16 for Class B, the Fund’s distribution rates were 4.70% and 3.96%, respectively.(4) The distribution rates of Class A and Class B are equivalent to taxable rates of 7.69% and 6.48%, respectively.(5)

• The SEC 30-day yields for Class A and Class B shares at February 28, 2005 were 3.43% and 2.84%, respectively.(6) The SEC 30-day yields of Class A and Class B are equivalent to taxable yields of 5.61% and 4.65%, respectively.(5)

Cynthia J. Clemson

Portfolio Manager

Management Discussion

• Missouri’s economy grew unevenly in the past year. Around 5,000 manufacturing jobs were generated, a modest recouping of the 57,000 such jobs lost in the past five years in the metals, machinery, and electronic equipment areas. Construction saw impressive growth, amid a stronger housing and commercial climate. The state’s jobless rate was 5.8% in February 2005, up from 5.5% a year ago.

• Insured* lease revenue/certificates of participation (COPs) were the Fund’s largest sector weightings at February 28, 2005. These bonds represented a financing alternative that gave Missouri issuers increased financial flexibility. The bonds financed a variety of public projects, including convention center and hotel construction, sports facilities and other capital improvement programs.

• Insured* and uninsured hospital issues were significant investments for the Fund. Amid rising costs and more stringent reimbursement rules, management emphasized hospitals with sound underlying fundamentals, and a reputation for quality care and marketable health care specialties.

• The Fund had investments in selected industrial development revenue bonds (IDRs). IDRs tend to be more sensitive to the economy and may be helped by a recovery in industrial activity. The Fund’s investments included retailing, consumer products, chemicals, air freight and beverages.

• The Fund continued its efforts at diversification. In addition to diversifying according to issuer, sector and insurer, management had a balanced coupon allocation. Management also emphasized good call protection, which remains a strategic priority.

* Private insurance does not decrease the risk of loss of principal associated with this investment.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. For performance as of the most recent month end, please refer to www.eatonvance.com.

(1) These returns do not include the 4.75% maximum sales charge for the Fund’s Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B shares. If the sales charge were deducted, returns would be lower.

(2) A portion of the Fund’s income may be subject to federal income and/or alternative minimum tax and state and local taxes.

(3) It is not possible to invest directly in an Index. The Index’s total return does not reflect the expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index.

(4) The Fund’s distribution rate represents actual distributions paid to shareholders and is calculated by dividing the last distribution per share (annualized) by the net asset value.

(5) Taxable-equivalent figures assume a maximum 38.90% combined federal and state income tax rate. A lower rate would result in lower tax-equivalent figures.

(6) The Fund’s SEC yield is calculated by dividing the net investment income per share for the 30-day period by the offering price at the end of the period and annualizing the result.

16

FUND PERFORMANCE

Performance(1) | | Class A | | Class B | |

| | | | | |

Average Annual Total Returns (at net asset value) | | | | | |

One Year | | 3.71 | % | 3.11 | % |

Five Years | | 7.42 | | 6.61 | |

Ten Years | | 6.09 | | 5.37 | |

Life of Fund† | | 5.28 | | 5.66 | |

| | | | | |

SEC Average Annual Total Returns (including sales charge or applicable CDSC) | | | | | |

One Year | | -1.20 | % | -1.81 | % |

Five Years | | 6.37 | | 6.30 | |

Ten Years | | 5.58 | | 5.37 | |

Life of Fund† | | 4.82 | | 5.66 | |

†Inception date: Class A: 12/7/93; Class B: 5/1/92

(1) Average annual total returns do not include the 4.75% maximum sales charge for Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B shares. If sales charges were deducted, returns would be lower. SEC average annual total returns for Class A reflect the maximum 4.75% sales charge. SEC returns for Class B reflect applicable CDSC based on the following schedule: 5% - 1st and 2nd years; 4% - 3rd year; 3% - 4th year; 2% - 5th year; 1% - 6th year.

Diversification by Credit Quality(2)

(2) As a percentage of total investments, as of February 28, 2005. Holdings subject to change due to active management.

17

Eaton Vance North Carolina Municipals Fund as of February 28, 2005

INVESTMENT UPDATE

The Fund

Performance for the Past Six Months

• The Fund’s Class A shares had a total return of 2.39% during the six months ended February 28, 2005.(1) This return was the result of an increase in net asset value (NAV) to $9.40 per share on February 28, 2005 from $9.39 on August 31, 2004, and the reinvestment of $0.212 in dividends.(2)

• The Fund’s Class B shares had a total return of 2.07% during the six months ended February 28, 2005.(1) This return was the result of no change in NAV from $10.10 on August 31, 2004, and the reinvestment of $0.207 in dividends.(2)

• For comparison, the Lehman Municipal Bond Index had a total return of 2.40% for the six months ended February 28, 2005.(3)

• Based on the Fund’s most recent dividends and NAVs on February 28, 2005 of $9.40 per share for Class A and $10.10 for Class B, the Fund’s distribution rates were 4.36% and 3.62%, respectively.(4) The distribution rates of Class A and Class B are equivalent to taxable rates of 7.27% and 6.04%, respectively.(5)

• The SEC 30-day yields for Class A and Class B shares at February 28, 2005 were 3.57% and 2.99%, respectively.(6) The SEC 30-day yields of Class A and Class B are equivalent to taxable yields of 5.95% and 4.99%, respectively.(5)

* Private insurance does not decrease the risk of loss of principal associated with this investment.

Thomas M. Metzold

Co-Portfolio Manager

William H. Ahern

Co-Portfolio Manager

Management Discussion

• North Carolina’s economic recovery gained ground in the past year. The state’s technology sector was boosted by planned expansions and new facilities by computer manufacturers and suppliers. In contrast, the textile and furniture industries have been challenged by the removal of import quotas. The state jobless rate was 5.4% in February 2005, down from 5.8% a year ago.

• Electric utilities bonds were the Fund’s largest sector weighting at February 28, 2005. These essential services bonds are prized by investors for their stable revenues independent of the overall economy. The Fund’s investments included county and state issuers, as well as selected Puerto Rico zero coupon issues.

• Escrowed/prerefunded bonds were prominent investments for the Fund. Pre-refunded to maturity and backed by Treasury bonds, escrowed bonds are considered very high credit quality, have relatively stable trading characteristics and may have above-average coupons.

• The Fund maintained a significant exposure to education bonds. Investments included some of the state’s premier universities, which enjoy excellent academic reputations, strong applicant demand and very stable tuition-based revenues.

• Diversification has been a major emphasis of the Fund. Management has sought a broad representation within the Fund on an issue, sector, coupon and structural basis. Given the relatively low level of interest rates, call protection has remained another key consideration.

• Effective May 2, 2005, Thomas M. Metzold will be the Fund’s sole portfolio manager.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. For performance as of the most recent month end, please refer to www.eatonvance.com.

(1) These returns do not include the 4.75% maximum sales charge for the Fund’s Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B shares. If the sales charge were deducted, returns would be lower

(2) A portion of the Fund’s income may be subject to federal income and/or alternative minimum tax and state intangibles tax.

(3) It is not possible to invest directly in an Index. The Index’s total return does not reflect the expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index.

(4) The Fund’s distribution rate represents actual distributions paid to shareholders and is calculated by dividing the last distribution per share (annualized) by the net asset value.

(5) Taxable-equivalent figures assume a maximum 40.04% combined federal and state income tax rate. A lower rate would result in lower tax-equivalent figures.

(6) The Fund’s SEC yield is calculated by dividing the net investment income per share for the 30-day period by the offering price at the end of the period and annualizing the result.

18

FUND PERFORMANCE

Performance(1) | | Class A | | Class B | |

| | | | | |

Average Annual Total Returns (at net asset value) | | | | | |

One Year | | 1.46 | % | 0.75 | % |

Five Years | | 6.13 | | 5.36 | |

Ten Years | | 5.26 | | 4.56 | |

Life of Fund† | | 4.51 | | 4.80 | |

| | | | | |

SEC Average Annual Total Returns (including sales charge or applicable CDSC) | | | | | |

One Year | | -3.33 | % | -4.09 | % |

Five Years | | 5.11 | | 5.03 | |

Ten Years | | 4.75 | | 4.56 | |

Life of Fund† | | 4.06 | | 4.80 | |

†Inception date: Class A: 12/7/93; Class B: 10/23/91

(1) Average annual total returns do not include the 4.75% maximum sales charge for Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B shares. If sales charges were deducted, returns would be lower. SEC average annual total returns for Class A reflect the maximum 4.75% sales charge. SEC returns for Class B reflect applicable CDSC based on the following schedule: 5% - 1st and 2nd years; 4% - 3rd year; 3% - 4th year; 2% - 5th year; 1% - 6th year.

Diversification by Credit Quality(2)

(2) As a percentage of total investments, as of February 28, 2005. Holdings subject to change due to active management.

19

Eaton Vance Oregon Municipals Fund as of February 28, 2005

INVESTMENT UPDATE

The Fund

Performance for the Past Six Months

• The Fund’s Class A shares had a total return of 2.69% during the six months ended February 28, 2005.(1) This return was the result of an increase in net asset value (NAV) to $9.49 per share on February 28, 2005 from $9.48 on August 31, 2004, and the reinvestment of $0.242 in dividends.(2)

• The Fund’s Class B shares had a total return of 2.39% during the six months ended February 28, 2005.(1) This return was the result of no change in NAV from $10.37 on August 31, 2004, and the reinvestment of $0.245 in dividends.(2)

• For comparison, the Lehman Municipal Bond Index had a total return of 2.40% for the six months ended February 28, 2005.(3)

• Based on the Fund’s most recent dividends and NAVs on February 28, 2005 of $9.49 per share for Class A and $10.37 for Class B, the Fund’s distribution rates were 5.01% and 4.26%, respectively.(4) The distribution rates of Class A and Class B are equivalent to taxable rates of 8.47% and 7.20%, respectively.(5)

• The SEC 30-day yields for Class A and Class B shares at February 28, 2005 were 4.26% and 3.72%, respectively.(6) The SEC 30-day yields of Class A and Class B are equivalent to taxable yields of 7.20% and 6.29%, respectively.(5)

* Private insurance does not decrease the risk of loss of principal associated with this investment.

Thomas M. Metzold

Co-Portfolio Manager

William H. Ahern

Co-Portfolio Manager

Management Discussion

• After a three-year downtrend, Oregon’s job growth outpaced the nation in 2004. Most sectors in the state generated job increases during this period, especially business services and manufacturing. The manufacturing sector received a boost from a rebound in semiconductor production. The state jobless rate was 6.6% in February 2005, down from 7.7% a year ago.

• Housing bonds were the Fund’s largest sector weighting at February 28, 2005. Housing bonds typically constitute a large portion of Oregon’s municipal issuance. The Fund’s investments were represented by city, county and state issuers, and included single- and multi-family housing projects.

• General obligations (GOs) played a prominent role in the Fund. The Fund’s GO investments included issues for the state’s board of education, local school districts, elderly and disabled housing and veterans’ welfare services.

• Industrial development revenue bonds (IDRs) provided the Fund an exposure to the economic cycle. The Fund’s IDR investments focused primarily on the state’s key paper industry and on airline bonds, each potential beneficiaries of a sustained economic recovery.

• The Fund had selected investments in Puerto Rico issues, providing diversification by issuer and coupon. The Fund’s Puerto Rico investments included GOs, electric utilities, education, IDRs, lease revenue and special tax revenue bonds.

• Effective May 2, 2005, Thomas M. Metzold will be the Fund’s sole portfolio manager.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. For performance as of the most recent month end, please refer to www.eatonvance.com.

(1) These returns do not include the 4.75% maximum sales charge for the Fund’s Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B shares. If the sales charge were deducted, returns would be lower.

(2) A portion of the Fund’s income may be subject to federal income and/or alternative minimum tax and state and local taxes.

(3) It is not possible to invest directly in an Index. The Index’s total return does not reflect the expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index.

(4) The Fund’s distribution rate represents actual distributions paid to shareholders and is calculated by dividing the last distribution per share (annualized) by the net asset value.

(5) Taxable-equivalent figures assume a maximum 40.85% combined federal and state income tax rate. A lower rate would result in lower tax-equivalent figures.

(6) The Fund’s SEC yield is calculated by dividing the net investment income per share for the 30-day period by the offering price at the end of the period and annualizing the result.

20

FUND PERFORMANCE

Performance(1) | | Class A | | Class B | |

| | | | | |

Average Annual Total Returns (at net asset value) | | | | | |

One Year | | 1.50 | % | 0.83 | % |

Five Years | | 6.45 | | 5.64 | |

Ten Years | | 5.43 | | 4.72 | |

Life of Fund† | | 4.69 | | 5.07 | |

| | | | | |

SEC Average Annual Total Returns (including sales charge or applicable CDSC) | | | | | |

One Year | | -3.31 | % | -3.98 | % |

Five Years | | 5.41 | | 5.32 | |

Ten Years | | 4.92 | | 4.72 | |

Life of Fund† | | 4.23 | | 5.07 | |

†Inception date: Class A: 12/28/93; Class B: 12/24/91

(1) Average annual total returns do not include the 4.75% maximum sales charge for Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B shares. If sales charges were deducted, returns would be lower. SEC average annual total returns for Class A reflect the maximum 4.75% sales charge. SEC returns for Class B reflect applicable CDSC based on the following schedule: 5% - 1st and 2nd years; 4% - 3rd year; 3% - 4th year; 2% - 5th year; 1% - 6th year.

Diversification by Credit Quality(2)

(2) As a percentage of total investments, as of February 28, 2005. Holdings subject to change due to active management.

21

Eaton Vance South Carolina Municipals Fund as of February 28, 2005

INVESTMENT UPDATE

The Fund

Performance for the Past Six Months

• The Fund’s Class A shares had a total return of 4.87% during the six months ended February 28, 2005.(1) This return was the result of an increase in net asset value (NAV) to $9.93 per share on February 28, 2005 from $9.71 on August 31, 2004, and the reinvestment of $0.248 in dividends.(2)

• The Fund’s Class B shares had a total return of 4.65% during the six months ended February 28, 2005.(1) This return was the result of an increase in NAV to $10.53 per share on February 28, 2005 from $10.30 on August 31, 2004, and the reinvestment of $0.244 in dividends.(2)

• For comparison, the Lehman Municipal Bond Index had a total return of 2.40% for the six months ended February 28, 2005.(3) As quality spreads tightened during the period, the Fund’s lower-investment-grade investments fared especially well, which accounted for its outperformance of the Index.

• Based on the Fund’s most recent dividends and NAVs on February 28, 2005 of $9.93 per share for Class A and $10.53 for Class B, the Fund’s distribution rates were 4.79% and 4.05%, respectively.(4) The distribution rates of Class A and Class B are equivalent to taxable rates of 7.92% and 6.70%, respectively.(5)

• The SEC 30-day yields for Class A and Class B shares at February 28, 2005 were 4.01% and 3.45%, respectively.(6) The SEC 30-day yields of Class A and Class B are equivalent to taxable yields of 6.63% and 5.71%, respectively.(5)

Thomas J. Fetter

Portfolio Manager

Management Discussion

• South Carolina continued its economic recovery, despite a downturn in non-durable manufacturing, as the apparel and textile industries remained vulnerable to global outsourcing. However, the state’s auto sector remained a notable success story. Meanwhile, coastal regions were strong beneficiaries of growth in the tourism and leisure industries. The state’s jobless rate was 7.1% in February 2005, up from 6.7% a year ago.

• Insured* education bonds were the Fund’s largest sector weighting at February 28, 2005. Unlike more cyclical areas of the economy, demand within the education sector has tended to be less impacted by shifts in the overall economy. The Fund’s investments included some of South Carolina’s finest state-supported institutions.

• Insured* water and sewer bonds were significant investments. The demands imposed by widespread residential construction and large economic developments and manufacturing facilities have necessitated major new water infrastructure projects. Those initiatives have been supported in part by these insured* issues.

• Insured* utility bonds were prominent holdings in the Fund. As essential service bonds, these issues enjoy relatively stable revenues. The Fund’s investments included high quality issuers such as the state public service authority and a regional municipal power agency.

• Management adjusted the Fund’s coupon structure, where possible, to reflect the shift in interest rates. Management also continued to update call protection, eliminating issues with unfavorable call features in favor of bonds with longer-dated call provisions.

* Private insurance does not decrease the risk of loss of principal associated with this investment.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. For performance as of the most recent month end, please refer to www.eatonvance.com.

(1) These returns do not include the 4.75% maximum sales charge for the Fund’s Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B shares. If the sales charge were deducted, returns would be lower.

(2) A portion of the Fund’s income may be subject to federal income and/alternative minimum tax and state and local taxes.

(3) It is not possible to invest directly in an Index. The Index’s total return does not reflect the expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index.

(4) The Fund’s distribution rate represents actual distributions paid to shareholders and is calculated by dividing the last distribution per share (annualized) by the net asset value.

(5) Taxable-equivalent figures assume a maximum 39.55% combined federal and state income tax rate. A lower rate would result in lower tax-equivalent figures.

(6) The Fund’s SEC yield is calculated by dividing the net investment income per share for the 30-day period by the offering price at the end of the period and annualizing the result.

22

FUND PERFORMANCE

Performance(1) | | Class A | | Class B | |

| | | | | |

Average Annual Total Returns (at net asset value) | | | | | |

One Year | | 4.74 | % | 4.26 | % |

Five Years | | 7.67 | | 6.88 | |

Ten Years | | 5.89 | | 5.26 | |

Life of Fund† | | 5.12 | | 5.15 | |

| | | | | |

SEC Average Annual Total Returns (including sales charge or applicable CDSC) | | | | | |

One Year | | -0.25 | % | -0.72 | % |

Five Years | | 6.63 | | 6.57 | |

Ten Years | | 5.38 | | 5.26 | |

Life of Fund† | | 4.65 | | 5.15 | |

†Inception date: Class A: 2/14/94; Class B: 10/2/92

(1) Average annual total returns do not include the 4.75% maximum sales charge for Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B shares. If sales charges were deducted, returns would be lower. SEC average annual total returns for Class A reflect the maximum 4.75% sales charge. SEC returns for Class B reflect applicable CDSC based on the following schedule: 5% - 1st and 2nd years; 4% - 3rd year; 3% - 4th year; 2% - 5th year; 1% - 6th year.

Diversification by Credit Quality(2)

(2) As a percentage of total investments, as of February 28, 2005. Holdings subject to change due to active management.

23

Eaton Vance Tennessee Municipals Fund as of February 28, 2005

INVESTMENT UPDATE

The Fund

Performance for the Past Six Months

• The Fund’s Class A shares had a total return of 2.25% during the six months ended February 28, 2005.(1) This return was the result of a decrease in net asset value (NAV) to $9.89 per share on February 28, 2005 from $9.90 on August 31, 2004, and the reinvestment of $0.230 in dividends.(2)

• The Fund’s Class B shares had a total return of 2.04% during the six months ended February 28, 2005.(1) This return was the result of a decrease in NAV to $10.77 per share on February 28, 2005 from $10.78 on August 31, 2004, and the reinvestment of $0.229 in dividends.(2)

• For comparison, the Lehman Municipal Bond Index had a total return of 2.40% for the six months ended February 28, 2005.(3)

• Based on the Fund’s most recent dividends and NAVs on February 28, 2005 of $9.89 per share for Class A and $10.77 for Class B, the Fund’s distribution rates were 4.51% and 3.76%, respectively.(4) The distribution rates of Class A and Class B are equivalent to taxable rates of 7.38% and 6.15%, respectively.(5)

• The SEC 30-day yields for Class A and Class B shares at February 28, 2005 were 3.26% and 2.67%, respectively.(6) The SEC 30-day yields of Class A and Class B are equivalent to taxable yields of 5.34% and 4.37%, respectively.(5)

Cynthia J. Clemson

Portfolio Manager

Management Discussion

• Tennessee’s economy generated job growth during the past year in selected sectors, including construction, education, health care and tourism. Manufacturing also gained momentum, led by the state’s growing auto sector and the plans announced by Japanese manufacturers for future plant locations. Nonetheless, the state’s jobless rate was 5.9% in February 2005, up from 5.4% a year ago.