UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-04409 |

|

Eaton Vance Municipals Trust |

(Exact name of registrant as specified in charter) |

|

The Eaton Vance Building, 255 State Street, Boston, Massachusetts | 02109 |

(Address of principal executive offices) | (Zip code) |

|

Alan R. Dynner

The Eaton Vance Building, 255 State Street, Boston, Massachusetts 02109 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | (617) 482-8260 | |

|

Date of fiscal year end: | September 30 | |

|

Date of reporting period: | March 31, 2005 | |

| | | | | | | |

Item 1. Reports to Stockholders

| | | |

|

Semiannual Report March 31, 2005 | | | |

| | | | |

| | EATON VANCE

NATIONAL

MUNICIPALS

FUND | | |

| | |

IMPORTANT NOTICES REGARDING PRIVACY,

DELIVERY OF SHAREHOLDER DOCUMENTS,

PORTFOLIO HOLDINGS AND PROXY VOTING

Privacy. The Eaton Vance organization is committed to ensuring your financial privacy. Each of the financial institutions identified below has in effect the following policy (“Privacy Policy”) with respect to nonpublic personal information about its customers:

• Only such information received from you, through application forms or otherwise, and information about your Eaton Vance fund transactions will be collected. This may include information such as name, address, social security number, tax status, account balances and transactions.

• None of such information about you (or former customers) will be disclosed to anyone, except as permitted by law (which includes disclosure to employees necessary to service your account). In the normal course of servicing a customer’s account, Eaton Vance may share information with unaffiliated third parties that perform various required services such as transfer agents, custodians and broker/dealers.

• Policies and procedures (including physical, electronic and procedural safeguards) are in place that are designed to protect the confidentiality of such information.

• We reserve the right to change our Privacy Policy at any time upon proper notification to you. Customers may want to review our Policy periodically for changes by accessing the link on our homepage: www.eatonvance.com.

Our pledge of privacy applies to the following entities within the Eaton Vance organization: the Eaton Vance Family of Funds, Eaton Vance Management, Eaton Vance Investment Counsel, Boston Management and Research, and Eaton Vance Distributors, Inc.

In addition, our Privacy Policy only applies to those Eaton Vance customers who are individuals and who have a direct relationship with us. If a customer’s account (i.e. fund shares) is held in the name of a third-party financial adviser/broker-dealer, it is likely that only such adviser’s privacy policies apply to the customer. This notice supersedes all previously issued privacy disclosures.

For more information about Eaton Vance’s Privacy Policy, please call 1-800-262-1122.

Delivery of Shareholder Documents. The Securities and Exchange Commission permits funds to deliver only one copy of shareholder documents, including prospectuses, proxy statements and shareholder reports, to fund investors with multiple accounts at the same residential or post office box address. This practice is often called “householding” and it helps eliminate duplicate mailings to shareholders.

Eaton Vance, or your financial adviser, may household the mailing of your documents indefinitely unless you instruct Eaton Vance, or your financial adviser, otherwise.

If you would prefer that your Eaton Vance documents not be householded, please contact Eaton Vance at 1-800-262-1122, or contact your financial adviser.

Your instructions that householding not apply to delivery of your Eaton Vance documents will be effective within 30 days of receipt by Eaton Vance or your financial adviser.

Portfolio Holdings. Each Eaton Vance Fund and it’s underlying Portfolio will file a schedule of its portfolio holdings on Form N-Q with the SEC for the first and third quarters of each fiscal year. The Form N-Q will be available on the Eaton Vance website www.eatonvance.com, by calling Eaton Vance at 1-800-262-1122 or in the EDGAR database on the SEC’s website at www.sec.gov. Form N-Q may also be reviewed and copied at the SEC’s public reference room in Washington, D.C. (call 1-800-732-0330 for information on the operation of the public reference room).

Proxy Voting. From time to time, funds are required to vote proxies related to the securities held by the funds. The Eaton Vance Funds or their underlying Portfolios (if applicable) vote proxies according to a set of policies and procedures approved by the Funds’ and Portfolios’ Boards. You may obtain a description of these policies and procedures and information on how the Funds or Portfolios voted proxies relating to Portfolio securities during the 12 month period ended June 30, without charge, upon request, by calling

1-800-262-1122. This description is also available on the SEC’s website at www.sec.gov.

Eaton Vance National Municipals Fund as of March 31, 2005

LETTER TO SHAREHOLDERS

Thomas J. Fetter

President

The municipal bond market is a center of capital formation for states, municipalities and, in some cases, private economic initiatives. In this edition of our continuing educational series, we will discuss industrial development revenue (IDR) bonds. IDR bonds have long been used as a financing mechanism by local governments to provide assistance to local employers and encourage job retention and creation within their communities.

IDR bonds finance private activities that benefit the public...

IDR bonds are issued by municipal authorities to finance projects and facilities used by private corporations. Historically, IDR bonds have represented a partnership between the private and public sectors – a source of dedicated funding for companies and a source of job creation in projects beneficial to local communities. The “Private-Activities” provision of the Tax Reform Act of 1986 permits issuance of tax-exempt bonds for specific activities, including pollution control; gas and electric service; water distribution; wastewater systems; solid waste disposal; airports and selected transportation projects; and other industrial projects.

The Act also placed a cap on the dollar amount that may be raised for IDR bonds in each state, limiting the amount to $50 per person/per state/per year, with a $150 million maximum. These limitations provide protection against potential abuse and ensure that tax-exempt IDR bonds will indeed be issued for projects that will benefit the public.

IDR bonds finance utility-related projects and other industrial initiatives...

Typically, IDR bond projects provide financing for manufacturing, processing or utility facilities. Historically, about one-half of these bonds have been issued to finance pollution control facilities for manufacturers and electric utilities. As many utilities and manufacturers have been ordered to comply with stricter environmental and fuel standards, pollution control bonds have helped finance the retrofits of existing plants. Other IDR bonds have served as inducements from state and local issuers to locate plants or build new facilities, in the hope that such construction might generate further economic growth for a community.

IDR bonds are secured by corporate revenues – not those of state or local governments...

IDR bond issues are secured by the credit of the underlying corporation. The municipal issuing authority acts solely as a conduit to permit tax-exempt financing. The corporation pledges to make payments sufficient to meet all debt service obligations. Unlike some revenue issues, IDR bonds are backed by revenues of the entire corporation, not solely by those of the project being financed.

Because IDR bonds are backed by corporate revenues and not by the taxing authority of a state or local jurisdiction, they have historically provided coupon premiums above those of general obligations and other more traditional revenue bonds. Bonds may be either collateralized or unsecured. Collateralized bonds have a lien against the company’s assets, which may provide bond holders enhanced bargaining power in the event of a bankruptcy. Unsecured bonds have no such lien.

While providing new opportunities, IDR bonds require rigorous analysis...

While IDR bonds may provide unusual investment opportunities, they also may entail increased risk and, therefore, demand especially intensive analysis. At Eaton Vance, we have credit analysts and resources dedicated to IDR bond research.

IDR bonds represent a key segment of the municipal bond market and should remain an important source of capital formation. In our view, the experience and resources needed to evaluate these issues further demonstrates the value of professional management. We will continue to look for opportunities in this sector of the municipal market.

| Sincerely, |

| |

| /s/ Thomas J. Fetter | |

| Thomas J. Fetter |

| President |

| May 6, 2005 |

Fund shares are not insured by the FDIC and are not deposits or other obligations of, or guaranteed by, any depository institution. Shares are subject to investment risks, including possible loss of principal invested.

2

MARKET RECAP

The U.S. economy continued to generate moderate growth during the six months ended March 31, 2005. While higher gasoline and energy prices pinched consumers, the weak U.S. dollar raised inflationary concerns and helped push interest rates higher.

After a promising recovery in 2004, slower growth in early 2005...

The nation’s Gross Domestic Product grew by 3.1% in the first quarter of 2005, according to preliminary Commerce Department figures, following a 3.8% rise in the fourth quarter of 2004. Manufacturing activity, which had expanded strongly in the second half of 2004, slackened somewhat in the first quarter of 2005, amid slower industrial production and weakening demand for durable goods.

Consumer spending, which helped fuel the economic recovery over the past year, weakened considerably, as higher fuel costs and rising interest rates on loans and mortgages prompted consumers to tighten their belts. Capital spending also slowed, as businesses curtailed new investments in plants and factories, while reducing the pace of investment in productivity-enhancing equipment and software. Residential construction remained relatively strong, although slightly off the torrid pace set in 2004.

After recovering dramatically in 2004, job creation weakened somewhat in early 2005...

The nation’s labor markets strengthened during the year, although the pace of job creation weakened at the close of the period. Hiring picked up during the year in areas that had suffered large technology sector layoffs. Also, manufacturing, financial services, business services, trucking, shipping, construction, energy, health care, and media also generated new jobs. In the first quarter of 2005, however, employers showed some reticence in hiring practices, as they were forced to cope with unpredictable fuel cost hikes.

Municipal bond yields were 99% of Treasury yields

30-Year AAA-rated | Taxable equivalent yield |

General Obligation (GO) Bonds* | in 35.0% tax bracket |

30-Year Treasury Bond

Principal and interest payments of Treasury securities are guaranteed by the U.S. government.

*GO yields are a compilation of a representative variety of general obligations and are not necessarily representative of the Fund’s yield. Statistics as of March 31, 2005.

Past performance is no guarantee of future results.

Source: Bloomberg, L.P.

The Federal Reserve continued to raise short-term interest rates in 2005...

The Federal Reserve pushed short-term rates higher, suggesting it will continue to raise rates to keep the economy from growing too quickly and, thereby, reviving inflation. Beginning in June 2004, the Fed increased its Federal Funds rate – a key short-term interest rate barometer – on seven occasions, raising that benchmark from 1.00% to 2.75%, including its most recent rate hike in March 2005.

The municipal bond market posted a modest gain for the year, slightly outperforming the Treasury market. For the six months ended March 31, 2005, the Lehman Brothers Municipal Bond Index – an unmanaged index commonly used as a broad measure of municipal bond performance – had a total return of 1.21.%.*

* It is not possible to invest directly in an Index. The Index’s total return does not reflect commissions or expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index.

3

INVESTMENT UPDATE

The Fund

• During the six months ended March 31, 2005, the Fund’s Class A shares had a total return of 4.07%.(1) This return resulted from an increase in net asset value (NAV) per share to $11.06 on March 31, 2005, from $10.92 on September 30, 2004, and the reinvestment of $0.301 per share in tax-free income.(2)

• Class B shares had a total return of 3.89% during the same period.(1) This return resulted from an increase in NAV per share to $10.32 from $10.19 and the reinvestment of $0.264 per share in tax-free income.(2)

• Class C shares had a total return of 3.75% during the same period.(1) This return resulted from an increase in NAV per share to $9.83 from $9.71 and the reinvestment of $0.242 per share in tax-free income.(2)

• Class I shares had a total return of 4.10% during the same period.(1) This return resulted from an increase in NAV per share to $10.24 from $10.12 and the reinvestment of $0.292 per share in tax-free income.(2)

• Based on the most recent dividends and NAVs per share on March 31, 2005, of $11.06 for Class A, $10.32 for Class B, $9.83 for Class C, and $10.24 for Class I, the Fund’s distribution rates were 5.21% for Class A, 4.46% for Class B, 4.46% for Class C, and 5.47% for Class I.(3) The distribution rates are equivalent to taxable rates of 8.02%, 6.86%, 6.86%, and 8.42%, respectively.(4)

• The SEC 30-day yields at March 31, 2005, were 5.34% for Class A, 4.85% for Class B, 4.85% for Class C, and 5.87% for Class I.(5) The SEC 30-day yields are equivalent to taxable yields of 8.22%, 7.46%, 7.46%, and 9.03%, respectively.(4)

• For comparison, the Lehman Brothers Municipal Bond Index had a total return of 1.21% for the six months ended March 31, 2005.(6)

(1) These returns at net asset value do not include the 4.75% maximum sales charge for Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B and Class C shares. If sales charges were deducted, returns would be lower. Class I shares are offered to certain investors at net asset value.

(2) A portion of the Fund’s income may he subject to federal income and/or alternative minimum tax and state income tax.

(3) The Fund’s distribution rate represents actual distributions paid to shareholders and is calculated by dividing the last distribution per share (annualized) by the net asset value.

(4) Taxable-equivalent figures assume a maximum 35.00% federal income tax rate. A lower rate would result in lower tax-equivalent figures.

(5) The Fund’s SEC yield is calculated by dividing the net investment income per share for the 30-day period by the offering price at the end of the period and annualizing the result.

(6) It is not possible to invest directly in an Index. The Index’s total return does not reflect commissions or expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index.

Management Discussion

Thomas M. Metzold

Portfolio Manager

Cynthia J. Clemson

Portfolio Manager

• The Fund outperformed its benchmark for the six months ended March 31, 2005. The Fund adheres to an intensive research process to buy, sell, and monitor municipal bond holdings. Management focuses on the creditworthiness of bond issuers, as well as the fundamental credit characteristics of the various sectors and individual issues. We believe that our emphasis on research and monitoring also helped contribute to the Fund’s performance over the six-month period.

• Municipal bond issuers continued to call bonds at a higher rate than the historical norm because of the low interest-rate environment. As a result, management’s ongoing focus on call protection was beneficial for the Fund’s income and overall performance during the period. As low interest rates continue to prompt refundings, call protection remains an important concern for municipal investors.

• The Fund maintained a significant investment in escrowed and prerefunded bonds, which were the Fund’s largest sector weighting at March 31, 2005. These bonds are either pre-refunded to their approaching call dates or escrowed to maturity. Because they are backed by Treasury bonds, escrowed bonds are considered to be of the highest quality, and generally provide an excellent source of income.

• Effective May 30, 2005, Tom Metzold will resume sole portfolio manager duties for the Fund.

The views expressed throughout this report are those of the portfolio managers and are current only through the end of the period of the report as stated on the cover. These views are subject to change at any time based upon market or other conditions, and the investment adviser disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a fund are based on many factors, may not be relied on as an indication of trading intent on behalf of any Eaton Vance fund.

4

FUND PERFORMANCE

Performance* | | Class A | | Class B | | Class C | | Class I | |

| | | | | | | | | |

Average Annual Total Returns (at net asset value) | | | | | | | | | |

One Year | | 6.36 | % | 5.78 | % | 5.66 | % | 6.57 | % |

Five Years | | 7.87 | | 7.43 | | 7.04 | | 8.08 | |

Ten Years | | 6.92 | | 6.33 | | 6.09 | | N.A. | |

Life of Fund† | | 7.21 | | 6.72 | | 5.28 | | 6.80 | |

| | | | | | | | | |

SEC Average Annual Total Returns (including sales charge or applicable CDSC) | | | | | | | | | |

One Year | | 1.30 | % | 0.78 | % | 4.66 | % | 6.57 | % |

Five Years | | 6.82 | | 7.12 | | 7.04 | | 8.08 | |

Ten Years | | 6.41 | | 6.33 | | 6.09 | | N.A. | |

Life of Fund† | | 6.74 | | 6.72 | | 5.28 | | 6.80 | |

† Inception Dates – Class A: 4/5/94; Class B: 12/19/85; Class C: 12/3/93; Class I: 7/1/99

* Returns at net asset value do not include the 4.75% maximum sales charge for Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B and Class C shares. If sales charges were deducted, returns would be lower. SEC average annual total returns for Class A reflect the maximum 4.75% sales charge. SEC returns for Class B reflect the applicable CDSC based on the following schedule: 5% - 1st and 2nd years; 4% - - 3rd year; 3% - 4th year; 2% - 5th year; 1% - 6th year. SEC 1-Year return for Class C reflects 1% CDSC. Class I shares are offered to certain investors at net asset value.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. For performance as of the most recent month-end, please refer to www.eatonvance.com.

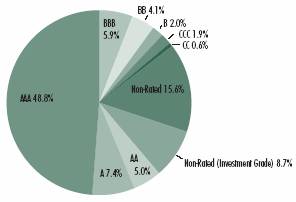

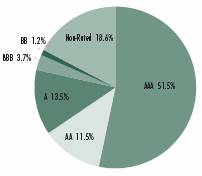

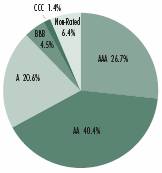

Rating Distribution**

By total investments

Portfolio Statistics**

• Number of Issues: | | 204 | |

• Average Maturity: | | 23.0 years | |

• Average Rating: | | A+ | |

• Average Call: | | 8.9 years | |

• Average Dollar Price: | | $ | 91.03 | |

| | | | |

** Portfolio Statistics and Rating Distribution may not be representative of the Portfolio’s current or future investments due to active management.

5

FUND EXPENSES

Example: As a shareholder of a Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchases and redemption fees (if applicable); and (2) ongoing costs, including management fees; distribution or service fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (October 1, 2004 – March 31, 2005).

Actual Expenses: The first section of each table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes: The second section of each table below provides information about hypothetical account values and hypothetical expenses based on a Fund’s actual expense ratio and an assumed rate of return of 5% per year (before expenses), which is not the actual return of the Fund. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Funds and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) or redemption fees (if applicable). Therefore, the second section of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

Eaton Vance National Municipals Fund

| | Beginning Account Value

(10/1/04) | | Ending Account Value

(3/31/04) | | Expenses Paid During Period*

(10/1/04–3/31/05) | |

| | | | | | | |

Actual | | | | | | | |

Class A | | $ | 1,000.00 | | $ | 1,040.70 | | $ | 3.97 | |

Class B | | $ | 1,000.00 | | $ | 1,038.90 | | $ | 7.78 | |

Class C | | $ | 1,000.00 | | $ | 1,037.50 | | $ | 7.77 | |

Class I | | $ | 1,000.00 | | $ | 1,041.00 | | $ | 2.70 | |

| | | | | | | |

Hypothetical | | | | | | | |

(5% return before expenses) | | | | | | | |

Class A | | $ | 1,000.00 | | $ | 1,021.00 | | $ | 3.93 | |

Class B | | $ | 1,000.00 | | $ | 1,017.40 | | $ | 7.70 | |

Class C | | $ | 1,000.00 | | $ | 1,017.30 | | $ | 7.70 | |

Class I | | $ | 1,000.00 | | $ | 1,022.30 | | $ | 2.67 | |

* Expenses are equal to the Fund’s annualized expense ratio of 0.78% for Class A shares, 1.53% for Class B shares, 1.53% for Class C shares and 0.53% for Class I shares, multiplied by the average account value over the period, multiplied by 182/365 (to reflect the one-half year period). The example assumes that the $1,000 was invested at the net asset value per share determined at the close of business on September 30, 2004.

6

Eaton Vance National Municipals Fund as of March 31, 2005

PORTFOLIO OF INVESTMENTS (Unaudited)

| | Tax-Exempt Investments - 99.0% | | | | | | | | |

Principal Amount

(000's omitted) | | Security | | Value | |

| | Cogeneration - 2.7% | | | | | | | | |

| $ | 22,150 | | | Maryland Energy Cogeneration, (AES Warrior Run),

(AMT), 7.40%, 9/1/19 | | $ | 22,602,746 | | |

| | 6,100 | | | Pennsylvania EDA, (Northampton Generating),

(AMT), 6.50%, 1/1/13 | | | 6,153,802 | | |

| | 21,950 | | | Pennsylvania EDA, (Northampton Generating),

(AMT), 6.60%, 1/1/19 | | | 22,404,365 | | |

| | 5,300 | | | Pennsylvania EDA, (Northampton Generating), Junior Liens,

(AMT), 6.875%, 1/1/11 | | | 5,301,802 | | |

| | 5,000 | | | Pennsylvania EDA, (Northampton Generating), Junior Liens,

(AMT), 6.95%, 1/1/21 | | | 4,985,050 | | |

| | | | | | | $ | 61,447,765 | | |

| | Education - 0.2% | | | | | | | | |

| $ | 4,130 | | | California Educational Facilities Authority, (Stanford

University), Variable Rate, 10.199%, 6/1/27(1) | | $ | 4,803,190 | | |

| | | | | | | $ | 4,803,190 | | |

| | Electric Utilities - 4.3% | | | | | | | | |

| $ | 13,000 | | | Brazos River Authority, TX, (Reliant Energy, Inc.),

7.75%, 12/1/18 | | $ | 14,458,470 | | |

| | 9,000 | | | Connecticut Development Authority, (Connecticut Light

and Power), 5.85%, 9/1/28 | | | 9,549,180 | | |

| | 13,000 | | | Connecticut Development Authority, (Western

Massachusetts Electric), 5.85%, 9/1/28 | | | 13,850,850 | | |

| | 2,000 | | | Matagorda County, TX, Navigation District No.1,

(Reliant Energy), 8.00%, 5/1/29 | | | 2,206,620 | | |

| | 5,000 | | | Matagorda County, TX, Navigation District No.1,

(Reliant Energy), (AMT), 5.95%, 5/1/30 | | | 5,051,700 | | |

| | 8,000 | | | North Carolina Municipal Power Agency, (Catawba),

6.50%, 1/1/20 | | | 8,913,920 | | |

| | 5,500 | | | Pennsylvania EDA, (Reliant Energy, Inc.), (AMT),

6.75%, 12/1/36 | | | 5,894,405 | | |

| | 13,800 | | | Pennsylvania EDA, (Reliant Energy, Inc.), (AMT),

6.75%, 12/1/36 | | | 14,789,598 | | |

| | 20,400 | | | Pennsylvania EDA, (Reliant Energy, Inc.), (AMT),

6.75%, 12/1/36 | | | 21,862,884 | | |

| | | | | | | $ | 96,577,627 | | |

| | Escrowed / Prerefunded - 13.7% | | | | | | | | |

| $ | 2,400 | | | Bexar County, TX, Health Facilities, (St. Luke's Lutheran),

Escrowed to Maturity, 7.00%, 5/1/21 | | $ | 3,083,040 | | |

| | 11,195 | | | Colorado Health Facilities Authority, (Liberty Heights),

Escrowed to Maturity, 0.00%, 7/15/22 | | | 4,782,840 | | |

Principal Amount

(000's omitted) | |

Security | |

Value | |

| | Escrowed / Prerefunded (continued) | | | | | | | | |

| $ | 119,070 | | | Colorado Health Facilities Authority, (Liberty Heights),

Escrowed to Maturity, 0.00%, 7/15/24 | | $ | 45,414,489 | | |

| | 215,825 | | | Dawson Ridge, CO, Metropolitan District #1,

Escrowed to Maturity, 0.00%, 10/1/22(2) | | | 91,252,968 | | |

| | 11,175 | | | Dawson Ridge, CO, Metropolitan District #1,

Escrowed to Maturity, 0.00%, 10/1/22 | | | 4,724,902 | | |

| | 4,960 | | | Delaware County, PA, IDA, (Glen Riddle),

Prerefunded to 9/1/05, (AMT), 8.625%, 9/1/25 | | | 5,226,352 | | |

| | 101,555 | | | Illinois Development Finance Authority, (Regency Park),

Escrowed to Maturity, 0.00%, 7/15/23 | | | 41,084,075 | | |

| | 8,390 | | | Louisiana Public Facilities Authority, (General Health

Systems), Prerefunded to 11/1/06, 6.80%, 11/1/16 | | | 8,827,371 | | |

| | 8,235 | | | Louisiana Public Facilities Authority, (Southern Baptist

Hospitals, Inc.), Escrowed to Maturity, 8.00%, 5/15/12 | | | 9,565,529 | | |

| | 5,675 | | | Maricopa County, AZ, IDA, (Place Five and The Greenery),

Escrowed to Maturity, 6.625%, 1/1/27 | | | 6,222,751 | | |

| | 100,000 | | | Mississippi Housing Finance Corp., Single Family,

Escrowed to Maturity, 0.00%, 6/1/15 | | | 64,052,000 | | |

| | 46,210 | | | San Joaquin Hills Transportation Corridor Agency, CA,

Toll Road Bonds, Escrowed to Maturity, 0.00%, 1/1/20 | | | 23,204,814 | | |

| | | | | | | $ | 307,441,131 | | |

| | General Obligations - 6.8% | | | | | | | | |

| $ | 5,000 | | | California, 5.00%, 6/1/34 | | $ | 5,097,600 | | |

| | 16,000 | | | California, 5.25%, 11/1/29 | | | 16,805,280 | | |

| | 20,000 | | | California, 5.25%, 2/1/30 | | | 20,795,200 | | |

| | 9,875 | | | California, 5.50%, 11/1/33 | | | 10,582,149 | | |

| | 14,000 | | | Georgia, 2.00%, 12/1/23 | | | 9,632,000 | | |

| | 19,510 | | | New York, NY, 5.00%, 3/1/19 | | | 20,290,595 | | |

| | 4,735 | | | New York, NY, Variable Rate, 9.438%, 6/1/28(1)(3) | | | 5,410,969 | | |

| | 28,715 | | | North Carolina, 4.00%, 3/1/24 | | | 26,673,363 | | |

| | 16,175 | | | Puerto Rico, Variable Rate, 7.951%, 7/1/29(3)(4) | | | 19,969,493 | | |

| | 10,900 | | | South Carolina, 3.00%, 8/1/21(5) | | | 8,983,780 | | |

| | 10,000 | | | South Carolina, 3.00%, 8/1/22(5) | | | 8,118,300 | | |

| | | | | | | $ | 152,358,729 | | |

| | Health Care - Miscellaneous - 0.4% | | | | | | | | |

| $ | 1,555 | | | Pittsfield Township, MI, EDC, (Arbor Hospice),

7.875%, 8/15/27 | | $ | 1,499,502 | | |

| | 3,072 | | | Tax Revenue Exempt Securities Trust, Community Health

Provider, (Pooled Loan Program Various States Trust

Certificates), 5.50%, 12/1/36 | | | 2,992,965 | | |

| | 3,295 | | | Tax Revenue Exempt Securities Trust, Community Health

Provider, (Pooled Loan Program Various States Trust

Certificates), 5.875%, 12/1/36 | | | 3,306,250 | | |

| | | | | | | $ | 7,798,717 | | |

See notes to financial statements

7

Eaton Vance National Municipals Fund as of March 31, 2005

PORTFOLIO OF INVESTMENTS (Unaudited) CONT'D

Principal Amount

(000's omitted) | |

Security | |

Value | |

| Hospital - 2.2% | | | | | |

| $ | 12,600 | | | California Health Facilities Authority, (Cedars Sinai

Medical Center), Variable Rate, 9.319%, 12/1/34(3)(4) | | $ | 14,668,164 | | |

| | 4,515 | | | Massachusetts HEFA, (Partners Healthcare System),

5.25%, 7/1/29 | | | 4,651,669 | | |

| | 3,500 | | | New Jersey Health Care Facilities Financing Authority,

(Trinitas Hospital), 7.50%, 7/1/30 | | | 3,909,955 | | |

| | 4,000 | | | Oneida County, NY, Industrial Development Agency,

(Elizabeth Medical Center), 6.00%, 12/1/29 | | | 3,741,440 | | |

| | 3,075 | | | Prince George's County, MD, (Greater Southeast

Healthcare System), 6.375%, 1/1/23(6) | | | 297,967 | | |

| | 7,750 | | | Rhode Island HEFA, (St. Joseph Health Services),

5.50%, 10/1/29 | | | 7,263,455 | | |

| | 12,500 | | | Rochester, MN, Health Care Facilities, (Mayo Clinic),

Variable Rate, 8.40%, 11/15/27(3)(4) | | | 14,029,625 | | |

| | | | | | | $ | 48,562,275 | | |

| Housing - 4.0% | | | | | |

| $ | 3,000 | | | ABAG Finance Authority, CA, (Civic Center Drive

Apartments), (AMT), 6.375%, 9/1/32 | | $ | 2,969,130 | | |

| | 7,345 | | | Arkansas Development Finance Authority, MFMR,

(Park Apartments), (AMT), 5.95%, 12/1/28 | | | 5,516,315 | | |

| | 12,900 | | | California Department of Veterans Affairs, Home

Purchase Revenue, 5.20%, 12/1/28 | | | 12,910,578 | | |

| | 6,360 | | | California Statewide Communities Development

Authority, (Corporate Fund for Housing), (AMT),

Variable Rate, 22.39%, 12/1/29(3)(4)(9) | | | 5,966,252 | | |

| | 600 | | | California Statewide Communities Development

Authority, (Corporate Fund for Housing), (AMT),

Variable Rate, 31.314%, 12/1/34(3)(4)(9) | | | 411,558 | | |

| | 16,000 | | | Charter Mac Equity Trust, TN, (AMT),

6.625%, 6/30/09 | | | 17,532,320 | | |

| | 10,770 | | | Florida Capital Projects Financing Authority, Student

Housing Revenue, (Florida University),

7.85%, 8/15/31 | | | 10,691,379 | | |

| | 9,610 | | | Lake Creek, CO, (Affordable Housing Corp.),

6.25%, 12/1/23 | | | 8,803,625 | | |

| | 1,255 | | | Maricopa County, AZ, IDA, (National Health Facilities II),

6.375%, 1/1/19(6) | | | 970,328 | | |

| | 15,215 | | | New Hampshire Housing Finance Authority, Multifamily

Housing, (AMT), 6.20%, 7/1/36 | | | 15,037,137 | | |

| | 10,590 | | | Texas Student Housing Corp., (University of Northern

Texas), 6.85%, 7/1/31 | | | 9,854,736 | | |

| | | | | | | $ | 90,663,358 | | |

| Industrial Development Revenue - 11.7% | | | | | |

| $ | 8,240 | | | Alliance Airport Authority, TX, (American Airlines, Inc.),

(AMT), 7.50%, 12/1/29 | | $ | 5,820,818 | | |

Principal Amount

(000's omitted) | |

Security | |

Value | |

| Industrial Development Revenue (continued) | | | | | |

| $ | 7,150 | | | Austin, TX, (Cargoport Development LLC), (AMT),

8.30%, 10/1/21 | | $ | 7,523,802 | | |

| | 10,260 | | | Bedford County, VA, IDA, (Nekoosa Packaging),

(AMT), 6.55%, 12/1/25 | | | 10,684,456 | | |

| | 2,250 | | | Calhoun County, AR, Solid Waste Disposal,

(Georgia-Pacific Corp.), (AMT), 6.375%, 11/1/26 | | | 2,336,017 | | |

| | 2,000 | | | Camden County, NJ, (Holt Hauling), (AMT),

9.875%, 1/1/21(6) | | | 255,100 | | |

| | 6,050 | | | Carbon County, UT, (Laidlaw Environmental), (AMT),

7.50%, 2/1/10 | | | 6,215,770 | | |

| | 4,000 | | | Courtland, AL, Solid Waste Disposal, (Champion

International Corp.), (AMT), 6.70%, 11/1/29 | | | 4,332,760 | | |

| | 6,430 | | | Dallas-Fort Worth, TX, International Airport Facility,

(American Airlines), 7.25%, 11/1/30 | | | 4,353,946 | | |

| | 55,500 | | | Denver, CO, City and County Special Facilities,

(United Airlines), (AMT), 6.875%, 10/1/32(6) | | | 47,313,750 | | |

| | 3,500 | | | Effingham County, GA, IDA, PCR, (Georgia Pacific

Corp.), 6.50%, 6/1/31 | | | 3,673,845 | | |

| | 11,190 | | | Effingham County, GA, Solid Waste Disposal,

(Fort James), (AMT), 5.625%, 7/1/18 | | | 11,388,622 | | |

| | 6,645 | | | Hardeman County, TN, (Correctional Facilities Corp.),

7.75%, 8/1/17 | | | 6,930,602 | | |

| | 30,000 | | | Houston, TX, Airport System, (Continental Airlines),

(AMT), 6.75%, 7/1/29 | | | 24,841,800 | | |

| | 10,110 | | | Kenton County, KY, Airport, (Delta Airlines), (AMT),

6.125%, 2/1/22 | | | 7,345,218 | | |

| | 1,530 | | | Kenton County, KY, Airport, (Delta Airlines), (AMT),

7.125%, 2/1/21 | | | 1,275,469 | | |

| | 4,870 | | | Kenton County, KY, Airport, (Delta Airlines), (AMT),

7.50%, 2/1/20 | | | 4,230,910 | | |

| | 5,000 | | | McMinn County, TN, (Calhoun Newsprint - Bowater,

Inc.), (AMT), 7.40%, 12/1/22 | | | 5,025,200 | | |

| | 10,000 | | | Michigan Strategic Fund, (S.D. Warren), (AMT),

7.375%, 1/15/22 | | | 10,554,700 | | |

| | 15,000 | | | Michigan Strategic Fund, (S.D. Warren), (AMT),

7.375%, 1/15/22 | | | 15,832,050 | | |

| | 3,500 | | | Michigan Strategic Fund, (S.D. Warren), (AMT),

7.375%, 1/15/22 | | | 3,694,145 | | |

| | 5,025 | | | New Jersey EDA, (American Airlines), (AMT),

7.10%, 11/1/31 | | | 3,562,524 | | |

| | 18,820 | | | New Jersey EDA, (Continental Airlines), (AMT),

6.25%, 9/15/29 | | | 14,545,978 | | |

| | 4,950 | | | New Jersey EDA, (Continental Airlines), (AMT),

9.00%, 6/1/33 | | | 5,069,938 | | |

| | 17,000 | | | New Jersey EDA, (Holt Hauling), 7.75%, 3/1/27(6) | | | 16,250,470 | | |

| | 1,500 | | | New Jersey EDA, (Holt Hauling), 7.90%, 3/1/27(6) | | | 1,433,895 | | |

| | 12,500 | | | New York City, NY, IDA, (American Airlines, Inc.),

(AMT), 8.50%, 8/1/28 | | | 10,158,875 | | |

See notes to financial statements

8

Eaton Vance National Municipals Fund as of March 31, 2005

PORTFOLIO OF INVESTMENTS (Unaudited) CONT'D

Principal Amount

(000's omitted) | |

Security | |

Value | |

| | Industrial Development Revenue (continued) | | | | | | | | |

| $ | 10,000 | | | New York City, NY, IDA, (American Airlines, Inc.-JFK

International Airport), (AMT), 8.00%, 8/1/12 | | $ | 9,016,300 | | |

| | 12,330 | | | Puerto Rico Port Authority, (American Airlines), (AMT),

6.25%, 6/1/26 | | | 8,672,429 | | |

| | 1,000 | | | Puerto Rico Port Authority, (American Airlines), (AMT),

6.30%, 6/1/23 | | | 703,810 | | |

| | 2,952 | | | Savannah, GA, EDA, (Intercat-Savannah), (AMT),

9.00%, 1/1/15 | | | 2,734,512 | | |

| | 1,589 | | | Savannah, GA, EDA, (Intercat-Savannah), (AMT),

9.75%, 7/1/10 | | | 1,526,517 | | |

| | 5,000 | | | Skowhegan, ME, (S.D. Warren), (AMT),

6.65%, 10/15/15 | | | 5,217,850 | | |

| | | | | | | $ | 262,522,078 | | |

| | Insured-Education - 2.4% | | | | | | | | |

| $ | 165 | | | Puerto Rico Industrial Tourist Educational Medical and

Environmental, DRIVERS, (MBIA), Variable Rate,

250.859%, 7/1/33(3)(4) | | $ | 507,585 | | |

| | 22,675 | | | University of California, (MBIA), 4.75%, 5/15/33 | | | 22,849,371 | | |

| | 31,000 | | | University of California, (MBIA), 4.75%, 5/15/37 | | | 31,212,970 | | |

| | | | | | | $ | 54,569,926 | | |

| | Insured-Electric Utilities - 2.5% | | | | | | | | |

| $ | 7,500 | | | Burlington, KS, PCR, (Kansas Gas & Electric Co.),

(MBIA), 5.30%, 6/1/31 | | $ | 7,937,475 | | |

| | 5,500 | | | Intermountain Power Agency, UT, (MBIA), Variable Rate,

15.223%, 7/1/19(1)(3) | | | 7,102,040 | | |

| | 11,000 | | | Memphis, TN, Electric System, (MBIA), Variable Rate,

15.385%, 12/1/17(1)(3) | | | 13,581,920 | | |

| | 10,000 | | | Puerto Rico Electric Power Authority, (CIFG),

5.00%, 7/1/28(5) | | | 10,485,900 | | |

| | 9,700 | | | Puerto Rico Electric Power Authority, (CIFG),

5.00%, 7/1/29(5) | | | 10,154,930 | | |

| | 6,000 | | | Sacramento, CA, Municipal Electric Utility District, (FSA),

Variable Rate, 9.957%, 8/15/28(1)(3) | | | 6,507,240 | | |

| | | | | | | $ | 55,769,505 | | |

| | Insured-Escrowed / Prerefunded - 1.8% | | | | | | | | |

| $ | 20,505 | | | Massachusetts Turnpike Authority, (FGIC), Escrowed to

Maturity, Variable Rate, 7.316%, 1/1/23(3)(4) | | $ | 23,984,904 | | |

| | 9,500 | | | Massachusetts Turnpike Authority, (FGIC), Escrowed to

Maturity, Variable Rate, 7.391%, 1/1/20(3)(4) | | | 10,877,595 | | |

| | 5,000 | | | Umatilla County, OR, School District No. 008R, (MBIA),

Prerefunded to 6/15/09, Variable Rate,

7.806%, 6/15/19(3)(4) | | | 5,817,450 | | |

| | | | | | | $ | 40,679,949 | | |

Principal Amount

(000's omitted) | |

Security | |

Value | |

| | Insured-General Obligations - 2.9% | | | | | | | | |

| $ | 9,900 | | | California, (AMBAC), Variable Rate,

14.158%, 5/1/26(1)(3) | | $ | 12,542,112 | | |

| | 12,000 | | | California, (MBIA), 4.75%, 3/1/31 | | | 12,040,200 | | |

| | 11,665 | | | California, RITES, (AMBAC), Variable Rate,

9.143%, 2/1/28(1)(3) | | | 14,065,890 | | |

| | 5,310 | | | Chester, NJ, Board of Education, (FSA),

4.50%, 3/1/35 | | | 5,152,612 | | |

| | 12,500 | | | Chicago, IL, Board of Education, (FGIC),

0.00%, 12/1/23 | | | 4,844,500 | | |

| | 16,980 | | | Chicago, IL, Board of Education, (FGIC),

0.00%, 12/1/25 | | | 5,836,026 | | |

| | 14,000 | | | Chicago, IL, Board of Education, (FGIC),

0.00%, 12/1/29 | | | 3,847,900 | | |

| | 5,910 | | | Highland Park, NJ, School District, (FSA),

4.50%, 3/1/30 | | | 5,784,058 | | |

| | | | | | | $ | 64,113,298 | | |

| | Insured-Hospital - 0.9% | | | | | | | | |

| $ | 5,070 | | | Maryland HEFA, (Medlantic), (AMBAC), Variable Rate,

10.665%, 8/15/38(1)(3) | | $ | 6,650,015 | | |

| | 8,320 | | | Tyler, TX, Health Facility Development Corp., (East

Texas Medical Center), (FSA), 5.375%, 11/1/27 | | | 8,724,518 | | |

| | 5,000 | | | Wisconsin HEFA, (Ministry Health Care), (MBIA),

5.125%, 2/15/22 | | | 5,215,050 | | |

| | | | | | | $ | 20,589,583 | | |

| | Insured-Lease Revenue / Certificates of

Participation - 0.3% | | | | | | |

| $ | 34,180 | | | Anaheim, CA, Public Financing Authority, (Public

Improvements), (FSA), 0.00%, 9/1/35 | | $ | 6,911,196 | | |

| | | | | | | $ | 6,911,196 | | |

| | Insured-Miscellaneous - 0.8% | | | | | | | | |

| $ | 25,000 | | | Harris County-Houston, TX, Sports Authority, (MBIA),

0.00%, 11/15/41 | | $ | 3,183,750 | | |

| | 15,250 | | | Harris County-Houston, TX, Sports Authority, (MBIA),

5.25%, 11/15/40 | | | 15,694,690 | | |

| | | | | | | $ | 18,878,440 | | |

| | Insured-Special Tax Revenue - 1.4% | | | | | | | | |

| $ | 13,305 | | | Illinois Sports Facility Authority, (AMBAC),

0.00%, 6/15/23 | | $ | 5,443,342 | | |

| | 31,010 | | | Illinois Sports Facility Authority, (AMBAC),

0.00%, 6/15/24 | | | 11,988,776 | | |

| | 10,000 | | | Illinois Sports Facility Authority, (AMBAC),

0.00%, 6/15/25 | | | 3,643,300 | | |

See notes to financial statements

9

Eaton Vance National Municipals Fund as of March 31, 2005

PORTFOLIO OF INVESTMENTS (Unaudited) CONT'D

Principal Amount

(000's omitted) | |

Security | |

Value | |

| | Insured-Special Tax Revenue (continued) | | | | | | | | |

| $ | 9,185 | | | Regional Transportation Authority, LA, (FGIC),

0.00%, 12/1/15 | | $ | 5,650,612 | | |

| | 9,500 | | | Regional Transportation Authority, LA, (FGIC),

0.00%, 12/1/21 | | | 4,129,745 | | |

| | | | | | | $ | 30,855,775 | | |

| | Insured-Transportation - 13.1% | | | | | | | | |

| $ | 18,220 | | | Alameda, CA, Corridor Transportation Authority, (MBIA),

0.00%, 10/1/35 | | $ | 3,581,870 | | |

| | 34,800 | | | Central, TX, Regional Mobility Authority, (FGIC),

5.00%, 1/1/45 | | | 35,239,524 | | |

| | 10,000 | | | Chicago, IL, O'Hare International Airport, (AMBAC),

(AMT), 5.375%, 1/1/32 | | | 10,370,600 | | |

| | 60,355 | | | Clark County, NV, Airport Authority, (FGIC),

5.00%, 7/1/36 | | | 61,560,289 | | |

| | 5,000 | | | Dallas Fort Worth, TX, International Airport, (FGIC),

(AMT), 5.625%, 11/1/21 | | | 5,374,100 | | |

| | 3,335 | | | Dallas Fort Worth, TX, International Airport, (FSA),

(AMT), Variable Rate, 11.259%, 11/1/17(1)(3) | | | 4,081,039 | | |

| | 4,000 | | | Dallas Fort Worth, TX, International Airport, (MBIA),

(AMT), Variable Rate, 11.259%, 11/1/19(1)(3) | | | 4,859,320 | | |

| | 2,500 | | | Dallas-Fort Worth, TX, International Airport, (FGIC),

(AMT), 5.50%, 11/1/20 | | | 2,657,225 | | |

| | 27,480 | | | Florida Department of Transportation, (Turnpike

Revenue), (FSA), 4.50%, 7/1/34 | | | 26,482,476 | | |

| | 3,305 | | | Kansas Turnpike Authority, (AMBAC), Variable Rate,

6.822%, 9/1/17(1)(3) | | | 3,147,351 | | |

| | 3,330 | | | Kansas Turnpike Authority, (AMBAC), Variable Rate,

6.822%, 9/1/18(1)(3) | | | 3,091,339 | | |

| | 12,000 | | | Massachusetts Turnpike Authority, Metropolitan

Highway System, (AMBAC), 5.00%, 1/1/39 | | | 12,183,960 | | |

| | 17,645 | | | Metropolitan Transportation Authority, NY, (AMBAC),

4.50%, 11/15/34 | | | 17,044,541 | | |

| | 13,600 | | | Metropolitan Transportation Authority, NY, (AMBAC),

5.00%, 11/15/33 | | | 14,081,304 | | |

| | 10,370 | | | Metropolitan Transportation Authority, NY, (MBIA),

4.50%, 11/15/35 | | | 10,010,161 | | |

| | 9,500 | | | Metropolitan Transportation Authority, NY, (MBIA),

4.75%, 11/15/29 | | | 9,590,345 | | |

| | 8,940 | | | Metropolitian Transportation Authority, NY, (AMBAC),

4.75%, 11/15/30 | | | 9,010,090 | | |

| | 10,500 | | | North Texas Tollway Authority, (FSA), 4.50%, 1/1/38 | | | 9,891,105 | | |

| | 9,000 | | | Puerto Rico Highway and Transportation Authority,

(FSA), Variable Rate, 9.955%, 7/1/32(1)(3) | | | 9,918,270 | | |

| | 50,000 | | | San Joaquin Hills, CA, Transportation Corridor Agency

Toll, (MBIA), 0.00%, 1/15/35 | | | 10,449,000 | | |

| | 50,000 | | | Texas Turnpike Authority, (AMBAC), 0.00%, 8/15/22 | | | 20,987,500 | | |

Principal Amount

(000's omitted) | |

Security | |

Value | |

| Insured-Transportation (continued) | | | | | |

| $ | 30,000 | | | Texas Turnpike Authority, (AMBAC), 0.00%, 8/15/26 | | $ | 9,910,800 | | |

| | | | | | | $ | 293,522,209 | | |

| Insured-Utilities - 0.5% | | | | | |

| $ | 10,500 | | | Philadelphia, PA, Gas Works Revenue, (FSA),

5.00%, 7/1/28 | | $ | 10,664,955 | | |

| | | | | | | $ | 10,664,955 | | |

| Insured-Water and Sewer - 3.7% | | | | | |

| $ | 11,915 | | | Atlanta, GA, Water and Sewer, (FGIC),

5.00%, 11/1/38 | | $ | 12,111,240 | | |

| | 10,135 | | | California Water Resources, (Central Valley), (FGIC),

Variable Rate, 12.888%, 12/1/28(1)(3) | | | 11,079,582 | | |

| | 10,445 | | | Castaic Lake, CA, Water Agency Certificates of

Participation, (Water System Improvements), (AMBAC),

0.00%, 8/1/21 | | | 4,643,743 | | |

| | 10,965 | | | Colorado Water Resources and Power Development

Authority, (MBIA), 4.50%, 11/15/35 | | | 10,481,882 | | |

| | 8,375 | | | Houston, TX, Water and Sewer System, (FSA),

0.00%, 12/1/28 | | | 2,445,332 | | |

| | 16,445 | | | Jacksonville Electric Authority, FL, Water and Sewer

System, (MBIA), 4.75%, 10/1/30 | | | 16,501,242 | | |

| | 13,750 | | | King County, WA, Sewer Revenue, (MBIA),

4.50%, 1/1/32(7) | | | 13,117,362 | | |

| | 6,050 | | | Loudoun County, VA, Sanitation Authority, (MBIA),

4.50%, 1/1/35 | | | 5,852,105 | | |

| | 7,325 | | | New York City, NY, Municipal Water Finance Authority,

(Water and Sewer System), (AMBAC),

4.50%, 6/15/29 | | | 7,160,700 | | |

| | | | | | | $ | 83,393,188 | | |

| Lease Revenue / Certificates of Participation - 0.6% | | | | | |

| $ | 6,955 | | | Fairfax County, VA, Economic Development Authority,

(School Board Central Administration Building),

4.50%, 4/1/35 | | $ | 6,690,293 | | |

| | 6,330 | | | New Jersey EDA, (School Facilities), Variable Rate,

9.995%, 6/15/28(1)(3) | | | 6,650,298 | | |

| | | | | | | $ | 13,340,591 | | |

| Nursing Home - 2.8% | | | | | |

| $ | 12,185 | | | Bell County, TX, (Riverside Healthcare, Inc. - Normandy

Terrace), 9.00%, 4/1/23(6) | | $ | 6,917,303 | | |

| | 4,665 | | | Delaware County, PA, (Mainline - Haverford Nursing and

Rehabilitation Centers), 9.00%, 8/1/22(6) | | | 4,446,678 | | |

See notes to financial statements

10

Eaton Vance National Municipals Fund as of March 31, 2005

PORTFOLIO OF INVESTMENTS (Unaudited) CONT'D

Principal Amount

(000's omitted) | |

Security | |

Value | |

| | Nursing Home (continued) | | | | | | | | |

| $ | 9,880 | | | Hillsborough County, FL, IDA, (Tampa Bay Retirement

Center), 7.00%, 6/1/25(8) | | $ | 5,540,605 | | |

| | 2,755 | | | Lackawanna County, PA, IDA, (Edella Street Associates),

8.875%, 9/1/14 | | | 2,754,587 | | |

| | 13,250 | | | Massachusetts IFA, (Age Institute of Massachusetts),

8.05%, 11/1/25 | | | 13,266,695 | | |

| | 11,575 | | | Mississippi Business Finance Corp., (Magnolia

Healthcare), 7.99%, 7/1/25 | | | 9,496,362 | | |

| | 11,265 | | | Montgomery, PA, IDA, (Advancement of Geriatric Health

Care Institute), 8.375%, 7/1/23 | | | 10,532,324 | | |

| | 3,500 | | | Orange County, FL, Health Facilities Authority,

(Westminster Community Care), 6.75%, 4/1/34 | | | 3,023,265 | | |

| | 2,235 | | | Westmoreland, PA, (Highland Health Systems, Inc.),

9.25%, 6/1/22 | | | 2,237,123 | | |

| | 3,890 | | | Wisconsin HEFA, (Wisconsin Illinois Senior Housing),

7.00%, 8/1/29 | | | 3,660,957 | | |

| | | | | | | $ | 61,875,899 | | |

| | Other Revenue - 7.6% | | | | | | | | |

| $ | 22,000 | | | California Statewide Communities Development

Authority, (East Valley Tourist Development Authority),

8.25%, 10/1/14 | | $ | 22,412,280 | | |

| | 10,000 | | | California Statewide Communities Development

Authority, (East Valley Tourist Development Authority),

9.25%, 10/1/20 | | | 10,903,500 | | |

| | 1,500 | | | Capital Trust Agency, FL, (Seminole Tribe Convention),

8.95%, 10/1/33 | | | 1,680,000 | | |

| | 26,400 | | | Capital Trust Agency, FL, (Seminole Tribe Convention),

10.00%, 10/1/33 | | | 29,725,608 | | |

| | 7,695 | | | Golden Tobacco Securitization Corp., CA,

5.00%, 6/1/13 | | | 7,708,466 | | |

| | 10,950 | | | Golden Tobacco Securitization Corp., CA, Variable Rate,

7.697%, 6/1/43(3)(4) | | | 12,193,811 | | |

| | 10,000 | | | Golden Tobacco Securitization Corp., CA, Variable Rate,

7.974%, 6/1/33(3)(4) | | | 11,289,600 | | |

| | 11,300 | | | Golden Tobacco Securitization Corp., CA, Variable Rate,

8.224%, 6/1/38(3)(4) | | | 12,868,666 | | |

| | 10,200 | | | Orange County, NC, (Community Activity Corp.),

8.00%, 3/1/24(6) | | | 3,818,370 | | |

| | 9,000 | | | Sandoval County, NM, (Santa Ana Pueblo),

7.75%, 7/1/15 | | | 9,234,540 | | |

| | 10,885 | | | Tobacco Settlement Financing Corp., NJ,

6.75%, 6/1/39 | | | 11,465,824 | | |

| | 20,700 | | | Tobacco Settlement Financing Corp., NJ, Variable Rate,

10.807%, 6/1/39(3)(4)(9) | | | 22,909,104 | | |

| | 13,000 | | | Tobacco Settlement Management Authority, SC,

6.375%, 5/15/28 | | | 13,266,760 | | |

| | | | | | | $ | 169,476,529 | | |

Principal Amount

(000's omitted) | |

Security | |

Value | |

| Senior Living / Life Care - 4.6% | | | | | |

| $ | 11,650 | | | Albuquerque, NM, Retirement Facilities, (La Vida

Liena Retirement Center), 5.75%, 12/15/28 | | $ | 10,999,348 | | |

| | 9,595 | | | Albuquerque, NM, Retirement Facilities, (La Vida Liena

Retirement Center), 6.60%, 12/15/28 | | | 9,391,394 | | |

| | 6,035 | | | Arizona Health Facilities Authority, (Care Institute,

Inc. - Mesa), 7.625%, 1/1/26(8) | | | 4,793,902 | | |

| | 16,415 | | | Bell County, TX, Health Facilities Authority, (Care

Institute, Inc. - Texas), 9.00%, 11/1/24 | | | 15,540,573 | | |

| | 3,060 | | | Chester, PA, IDA, (Senior Life-Choice of Kimberton),

(AMT), 8.50%, 9/1/25 | | | 3,158,746 | | |

| | 11,570 | | | De Kalb County, GA, Private Hospital Authority, (Atlanta,

Inc.), 8.50%, 3/1/25(8) | | | 4,700,544 | | |

| | 6,680 | | | Glen Cove, NY, IDA, (Regency at Glen Cove),

9.50%, 7/1/12(8) | | | 6,643,794 | | |

| | 14,115 | | | Illinois Development Finance Authority, (Care Institute,

Inc. - Illinois), 7.80%, 6/1/25 | | | 14,472,533 | | |

| | 1,600 | | | Kansas City, MO, IDA, (Kingswood United Methodist

Manor), 5.375%, 11/15/09 | | | 1,567,600 | | |

| | 9,345 | | | New Jersey EDA, (Forsgate), (AMT),

8.625%, 6/1/25(8) | | | 5,076,391 | | |

| | 12,150 | | | North Miami, FL, Health Facilities Authority, (Imperial

Club), 6.75%, 1/1/33 | | | 11,193,674 | | |

| | 800 | | | North Miami, FL, Health Facilities Authority, (Imperial

Club), 9.00%, 1/1/12(6) | | | 42,560 | | |

| | 7,915 | | | Roseville, MN, Elder Care Facility, (Care Institute, Inc. -

Roseville), 7.75%, 11/1/23(8) | | | 6,743,738 | | |

| | 12,140 | | | St. Paul, MN, Housing and Redevelopment, (Care

Institute, Inc. - Highland), 8.75%, 11/1/24(8) | | | 8,422,246 | | |

| | | | | | | $ | 102,747,043 | | |

| Special Tax Revenue - 3.5% | | | | | |

| $ | 22,500 | | | Massachusetts Bay Transportation Authority, Sales Tax,

5.00%, 7/1/29 | | $ | 24,166,125 | | |

| | 25,000 | | | Massachusetts Bay Transportation Authority, Sales Tax,

5.00%, 7/1/31 | | | 26,783,750 | | |

| | 6,000 | | | New Jersey EDA, (Cigarette Tax), 5.50%, 6/15/24 | | | 6,250,980 | | |

| | 10,000 | | | New Jersey EDA, (Cigarette Tax), 5.75%, 6/15/29 | | | 10,513,200 | | |

| | 1,815 | | | New Jersey EDA, (Cigarette Tax), 5.75%, 6/15/34 | | | 1,902,701 | | |

| | 3,000 | | | Tri-County, OR, Metropolitan Transportation District,

Variable Rate, 7.40%, 8/1/19(3)(4) | | | 3,261,960 | | |

| | 4,570 | | | University Square, FL, Community Development

District, 6.75%, 5/1/20 | | | 4,802,704 | | |

| | | | | | | $ | 77,681,420 | | |

| Transportation - 3.3% | | | | | |

| $ | 30,845 | | | Port Authority of New York and New Jersey, (AMT),

4.75%, 12/1/34 | | $ | 30,255,861 | | |

See notes to financial statements

11

Eaton Vance National Municipals Fund as of March 31, 2005

PORTFOLIO OF INVESTMENTS (Unaudited) CONT'D

Principal Amount

(000's omitted) | |

Security | |

Value | |

| Transportation (continued) | | | | | |

| $ | 6,200 | | | Port Authority of New York and New Jersey, (AMT),

5.25%, 7/15/34 | | $ | 6,518,494 | | |

| | 36,950 | | | Puerto Rico Highway and Transportation Authority,

5.125%, 7/1/39 | | | 37,919,199 | | |

| | | | | | | $ | 74,693,554 | | |

| Water and Sewer - 0.3% | | | | | |

| $ | 5,480 | | | California Water Resources, (Central Valley), Variable

Rate, 12.232%, 12/1/24(3)(4) | | $ | 6,374,555 | | |

| | | | | | | $ | 6,374,555 | | |

| | Total Tax-Exempt Investments - 99.0%

(identified cost $2,069,794,275) | | | | | $ | 2,218,312,485 | | |

| | Other Assets, Less Liabilities - 1.0% | | | | | $ | 21,541,325 | | |

| | Net Assets - 100.0% | | | | | $ | 2,239,853,810 | | |

AMT - Interest earned from these securities may be considered a tax preference item for purposes of the Federal Alternative Minimum Tax.

AMBAC - AMBAC Financial Group, Inc.

CIFG - CDC IXIS Financial Guaranty North America, Inc.

FGIC - Financial Guaranty Insurance Company

FSA - Financial Security Assurance, Inc.

MBIA - Municipal Bond Insurance Association

At March 31, 2005, the concentration of the Fund's investments in the various states, determined as a percentage of net assets, is as follows:

California 15.1%

Others, representing less than 10% individually 83.9%

The Fund invests primarily in debt securities issued by municipalities. The ability of the issuers of the debt securities to meet their obligations may be affected by economic developments in a specific industry or municipality. In order to reduce the risk associated with such economic developments, at March 31, 2005, 30.7% of the securities in the portfolio of investments are backed by bond insurance of various financial institutions and financial guaranty assurance agencies. The aggregate percentage insured by an individual financial institution ranged from 0.9% to 9.4% of total investments.

(1) Security has been issued as a leveraged inverse floater bond. The stated interest rate represents the rate in effect at March 31, 2005.

(2) Security (or a portion thereof) has been segregated to cover when-issued securities.

(3) Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be sold in transactions exempt from registration, normally to qualified institutional buyers. At March 31, 2005, the aggregate value of the securities is $273,817,707 or 12.2% of the Fund's net assets.

(4) Security has been issued as an inverse floater bond. The stated interest rate represents the rate in effect at March 31, 2005.

(5) When-issued security.

(6) Defaulted bond.

(7) Security (or a portion thereof) has been segregated to cover margin requirements on open financial futures contracts.

(8) Security is in default and making only partial interest payments.

(9) Security is subject to a shortfall and forbearance agreement.

See notes to financial statements

12

Eaton Vance National Municipals Fund as of March 31, 2005

FINANCIAL STATEMENTS (Unaudited)

Statement of Assets and Liabilities

As of March 31, 2005

| Assets | | | |

| Investments, at value (identified cost, $2,069,794,275) | | $ | 2,218,312,485 | | |

| Cash | | | 159,437 | | |

| Receivable for investments sold | | | 24,523,211 | | |

| Receivable for Fund shares sold | | | 9,216,998 | | |

| Receivable for open swap contracts | | | 94,788 | | |

| Interest receivable | | | 42,695,849 | | |

| Total assets | | $ | 2,295,002,768 | | |

| Liabilities | | | |

| Payable for when-issued securities | | $ | 37,495,569 | | |

| Dividends payable | | | 4,922,999 | | |

| Payable for Fund shares redeemed | | | 4,711,267 | | |

| Payable for daily variation margin on open financial futures contracts | | | 4,382,825 | | |

| Demand note payable | | | 3,200,000 | | |

| Payable to affiliate for distribution and service fees | | | 53,633 | | |

| Accrued expenses | | | 382,665 | | |

| Total liabilities | | $ | 55,148,958 | | |

| Net assets | | $ | 2,239,853,810 | | |

| Sources of Net Assets | | | |

| Paid-in capital | | $ | 2,125,451,223 | | |

Accumulated distributions in excess of net realized gain (computed on

the basis of identified cost) | | | (46,211,892 | ) | |

| Accumulated undistributed net investment income | | | 996,085 | | |

| Net unrealized appreciation (computed on the basis of identified cost) | | | 159,618,394 | | |

| Total | | $ | 2,239,853,810 | | |

| Class A Shares | | | |

| Net Assets | | $ | 1,891,895,556 | | |

| Shares Outstanding | | | 171,129,363 | | |

Net Asset Value and Redemption Price Per Share

(net assets ÷ shares of beneficial interest outstanding) | | $ | 11.06 | | |

Maximum Offering Price Per Share

(100 ÷ 95.25 of $11.06) | | $ | 11.61 | | |

| Class B Shares | | | |

| Net Assets | | $ | 55,832,580 | | |

| Shares Outstanding | | | 5,410,861 | | |

Net Asset Value, Offering Price and Redemption Price Per Share

(net assets ÷ shares of beneficial interest outstanding) | | $ | 10.32 | | |

| Class C Shares | | | |

| Net Assets | | $ | 281,645,548 | | |

| Shares Outstanding | | | 28,651,621 | | |

Net Asset Value, Offering Price and Redemption Price Per Share

(net assets ÷ shares of beneficial interest outstanding) | | $ | 9.83 | | |

| Class I Shares | | | |

| Net Assets | | $ | 10,480,126 | | |

| Shares Outstanding | | | 1,023,096 | | |

Net Asset Value, Offering Price and Redemption Price Per Share

(net assets ÷ shares of beneficial interest outstanding) | | $ | 10.24 | | |

| On sales of $25,000 or more, the offering price of Class A shares is reduced. | | | | | |

Statement of Operations

For the Six Months Ended

March 31, 2005

| Investment Income | | | |

| Interest | | $ | 65,185,212 | | |

| Total investment income | | $ | 65,185,212 | | |

| Expenses | | | |

| Investment adviser fee | | $ | 4,432,774 | | |

| Trustees' fees and expenses | | | 12,064 | | |

Distribution and service fees

Class A | | | 2,281,729 | | |

| Class B | | | 211,391 | | |

| Class C | | | 1,254,325 | | |

| Transfer and dividend disbursing agent fees | | | 530,348 | | |

| Custodian fee | | | 217,236 | | |

| Legal and accounting services | | | 200,308 | | |

| Printing and postage | | | 79,149 | | |

| Registration fees | | | 70,690 | | |

| Miscellaneous | | | 224,290 | | |

| Total expenses | | $ | 9,514,304 | | |

Deduct -

Reduction of custodian fee | | $ | 128,382 | | |

| Total expense reductions | | $ | 128,382 | | |

| Net expenses | | $ | 9,385,922 | | |

| Net investment income | | $ | 55,799,290 | | |

| Realized and Unrealized Gain (Loss) | | | |

Net realized gain (loss) -

Investment transactions (identified cost basis) | | $ | 27,704,306 | | |

| Financial futures contracts | | | (15,766,808 | ) | |

| Swap contracts | | | (5,160,071 | ) | |

| Net realized gain | | $ | 6,777,427 | | |

Change in unrealized appreciation (depreciation) -

Investments (identified cost basis) | | $ | (3,172,086 | ) | |

| Financial futures contracts | | | 16,809,478 | | |

| Swap contracts | | | 5,148,507 | | |

| Net change in unrealized appreciation (depreciation) | | $ | 18,785,899 | | |

| Net realized and unrealized gain | | $ | 25,563,326 | | |

| Net increase in net assets from operations | | $ | 81,362,616 | | |

See notes to financial statements

13

Eaton Vance National Municipals Fund as of March 31, 2005

FINANCIAL STATEMENTS CONT'D

Statements of Changes in Net Assets

Increase (Decrease)

in Net Assets | | Six Months Ended

March 31, 2005

(Unaudited) | | Year Ended

September 30, 2004 | |

From operations -

Net investment income | | $ | 55,799,290 | | | $ | 114,934,782 | | |

Net realized gain (loss) from investment

transactions, financial futures

contracts and swap contracts | | | 6,777,427 | | | | (28,266,585 | ) | |

Net change in unrealized appreciation

(depreciation) from investments,

financial futures contracts and

swap contracts | | | 18,785,899 | | | | 40,846,946 | | |

| Net increase in net assets from operations | | $ | 81,362,616 | | | $ | 127,515,143 | | |

Distributions to shareholders -

From net investment income

Class A | | $ | (49,710,900 | ) | | $ | (56,954,447 | ) | |

| Class B | | | (982,190 | ) | | | (47,956,488 | ) | |

| Class C | | | (5,867,582 | ) | | | (11,224,331 | ) | |

| Class I | | | (205,665 | ) | | | (245,552 | ) | |

| Total distributions to shareholders | | $ | (56,766,337 | ) | | $ | (116,380,818 | ) | |

Transactions in shares of beneficial interest -

Proceeds from sale of shares

Class A | | $ | 188,895,175 | | | $ | 1,733,873,204 | | |

| Class B | | | 28,192,576 | | | | 97,743,866 | | |

| Class C | | | 65,845,671 | | | | 69,517,814 | | |

| Class I | | | 5,686,746 | | | | 3,754,571 | | |

Net asset value of shares issued to

shareholders in payment of

distributions declared

Class A | | | 23,691,959 | | | | 26,195,534 | | |

| Class B | | | 479,318 | | | | 23,491,317 | | |

| Class C | | | 2,929,207 | | | | 5,353,949 | | |

| Class I | | | 61,988 | | | | 76,490 | | |

Cost of shares redeemed

Class A | | | (111,520,916 | ) | | | (223,765,056 | ) | |

| Class B | | | (2,679,517 | ) | | | (1,659,434,034 | ) | |

| Class C | | | (14,754,350 | ) | | | (51,174,017 | ) | |

| Class I | | | (693,242 | ) | | | (876,409 | ) | |

Net asset value of shares exchanged

Class A | | | 67,086 | | | | - | | |

| Class B | | | (67,086 | ) | | | - | | |

Contingent deferred sales charges

Class B | | | - | | | | 325,260 | | |

Net increase in net assets from

Fund share transactions | | $ | 186,134,615 | | | $ | 25,082,489 | | |

| Net increase in net assets | | $ | 210,730,894 | | | $ | 36,216,814 | | |

Increase (Decrease)

in Net Assets | | Six Months Ended

March 31, 2005

(Unaudited) | | Year Ended

September 30, 2004 | |

| Net Assets | | | | | | | | | |

| At beginning of period | | $ | 2,029,122,916 | | | $ | 1,992,906,102 | | |

| At end of period | | $ | 2,239,853,810 | | | $ | 2,029,122,916 | | |

Accumulated undistributed

net investment income

included in net assets | | | | | | | | | |

| At end of period | | $ | 996,085 | | | $ | 1,963,132 | | |

See notes to financial statements

14

Eaton Vance National Municipals Fund as of March 31, 2005

FINANCIAL STATEMENTS CONT'D

Financial Highlights

| | | Class A | |

| | | Six Months Ended

March 31, 2005 | | Year Ended September 30, | |

| | | (Unaudited)(1) | | 2004(1) | | 2003(1) | | 2002(1)(2) | | 2001 | | 2000(1) | |

| Net asset value - Beginning of period | | $ | 10.920 | | | $ | 10.840 | | | $ | 10.920 | | | $ | 10.550 | | | $ | 10.230 | | | $ | 10.440 | | |

| Income (loss) from operations | | | | | | | | | | | | | | | | | | | | | | | | | |

| Net investment income | | $ | 0.295 | | | $ | 0.654 | | | $ | 0.666 | | | $ | 0.656 | | | $ | 0.618 | | | $ | 0.629 | | |

| Net realized and unrealized gain (loss) | | | 0.146 | | | | 0.079 | | | | (0.105 | ) | | | 0.334 | | | | 0.312 | | | | (0.200 | ) | |

| Total income from operations | | $ | 0.441 | | | $ | 0.733 | | | $ | 0.561 | | | $ | 0.990 | | | $ | 0.930 | | | $ | 0.429 | | |

| Less distributions | | | | | | | | | | | | | | | | | | | | | | | | | |

| From net investment income | | $ | (0.301 | ) | | $ | (0.653 | ) | | $ | (0.641 | ) | | $ | (0.620 | ) | | $ | (0.610 | ) | | $ | (0.639 | ) | |

| Total distributions | | $ | (0.301 | ) | | $ | (0.653 | ) | | $ | (0.641 | ) | | $ | (0.620 | ) | | $ | (0.610 | ) | | $ | (0.639 | ) | |

| Net asset value - End of period | | $ | 11.060 | | | $ | 10.920 | | | $ | 10.840 | | | $ | 10.920 | | | $ | 10.550 | | | $ | 10.230 | | |

| Total Return(3) | | | 4.07 | % | | | 6.94 | % | | | 5.46 | % | | | 9.84 | % | | | 9.33 | % | | | 4.39 | % | |

| Ratios/Supplemental Data | | | | | | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of period (000's omitted) | | $ | 1,891,896 | | | $ | 1,769,191 | | | $ | 236,885 | | | $ | 213,456 | | | $ | 181,600 | | | $ | 174,024 | | |

| Ratios (As a percentage of average daily net assets): | | | | | | | | | | | | | | | | | | | | | | | | | |

| Expenses(4) | | | 0.79 | %(5) | | | 0.79 | % | | | 0.78 | % | | | 0.83 | % | | | 0.83 | % | | | 0.66 | % | |

| Expenses after custodian fee reduction(4) | | | 0.78 | %(5) | | | 0.79 | % | | | 0.78 | % | | | 0.82 | % | | | 0.82 | % | | | 0.65 | % | |

| Net investment income | | | 5.35 | %(5) | | | 6.05 | % | | | 6.29 | % | | | 6.31 | % | | | 5.92 | % | | | 6.23 | % | |

| Portfolio Turnover of the Portfolio(6) | | | - | | | | 44 | % | | | 35 | % | | | 32 | % | | | 20 | % | | | 41 | % | |

| Portfolio Turnover of the Fund | | | 27 | % | | | - | | | | - | | | | - | | | | - | | | | - | | |

(1) Net investment income per share was computed using average shares outstanding.

(2) The Fund, through its investment in the Portfolio, has adopted the provisions of the revised AICPA Audit and Accounting Guide for Investment Companies and began using the interest method to amortize premiums on fixed-income securities. The effect of this change for the year ended September 30, 2002 was to increase net investment income per share by $0.003, decrease net realized and unrealized gains per share by $0.003 and increase the ratio of net investment income to average net assets from 6.28% to 6.31%. Per-share data and ratios for t he periods prior to October 1, 2001 have not been restated to reflect this change in presentation.

(3) Returns are historical and are calculated by determining the percentage change in net asset value with all distributions reinvested. Total return is not computed on an annualized basis.

(4) Includes the Fund's share of the Portfolio's allocated expenses while the Fund was making investments directly into the Portfolio.

(5) Annualized.

(6) Portfolio turnover represents the rate of portfolio activity for the period while the Fund was making investments directly into the Portfolio.

See notes to financial statements

15

Eaton Vance National Municipals Fund as of March 31, 2005

FINANCIAL STATEMENTS CONT'D

Financial Highlights

| | | Class B | |

| | | Six Months Ended

March 31, 2005 | | Year Ended September 30, | |

| | | (Unaudited)(1) | | 2004(1) | | 2003(1) | | 2002(1)(2) | | 2001 | | 2000(1) | |

| Net asset value - Beginning of period | | $ | 10.190 | | | $ | 10.130 | | | $ | 10.190 | | | $ | 9.850 | | | $ | 9.550 | | | $ | 9.740 | | |

| Income (loss) from operations | | | | | | | | | | | | | | | | | | | | | | | | | |

| Net investment income | | $ | 0.234 | | | $ | 0.558 | | | $ | 0.581 | | | $ | 0.572 | | | $ | 0.541 | | | $ | 0.532 | | |

| Net realized and unrealized gain (loss) | | | 0.138 | | | | 0.053 | | | | (0.086 | ) | | | 0.303 | | | | 0.300 | | | | (0.188 | ) | |

| Total income from operations | | $ | 0.372 | | | $ | 0.611 | | | $ | 0.495 | | | $ | 0.875 | | | $ | 0.841 | | | $ | 0.344 | | |

| Less distributions | | | | | | | | | | | | | | | | | | | | | | | | | |

| From net investment income | | $ | (0.242 | ) | | $ | (0.555 | ) | | $ | (0.561 | ) | | $ | (0.540 | ) | | $ | (0.545 | ) | | $ | (0.534 | ) | |

| Total distributions | | $ | (0.242 | ) | | $ | (0.555 | ) | | $ | (0.561 | ) | | $ | (0.540 | ) | | $ | (0.545 | ) | | $ | (0.534 | ) | |

| Contingent deferred sales charges | | $ | - | | | $ | 0.004 | | | $ | 0.006 | | | $ | 0.005 | | | $ | 0.004 | | | $ | - | | |

| Net asset value - End of period | | $ | 10.320 | | | $ | 10.190 | | | $ | 10.130 | | | $ | 10.190 | | | $ | 9.850 | | | $ | 9.550 | | |

| Total Return(3) | | | 3.89 | %(4) | | | 6.25 | % | | | 5.17 | % | | | 9.30 | % | | | 9.06 | % | | | 3.72 | % | |

| Ratios/Supplemental Data | | | | | | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of period (000's omitted) | | $ | 55,833 | | | $ | 29,577 | | | $ | 1,553,297 | | | $ | 1,582,772 | | | $ | 1,525,303 | | | $ | 1,483,566 | | |

| Ratios (As a percentage of average daily net assets): | | | | | | | | | | | | | | | | | | | | | | | | | |

| Expenses(5) | | | 1.54 | %(6) | | | 1.17 | % | | | 1.20 | % | | | 1.25 | % | | | 1.26 | % | | | 1.25 | % | |

| Expenses after custodian fee reduction(5) | | | 1.53 | %(6) | | | 1.17 | % | | | 1.20 | % | | | 1.24 | % | | | 1.25 | % | | | 1.24 | % | |

| Net investment income | | | 4.53 | %(6) | | | 5.44 | % | | | 5.88 | % | | | 5.89 | % | | | 5.49 | % | | | 5.63 | % | |

| Portfolio Turnover of the Portfolio(7) | | | - | | | | 44 | % | | | 35 | % | | | 32 | % | | | 20 | % | | | 41 | % | |

| Portfolio Turnover of the Fund | | | 27 | % | | | - | | | | - | | | | - | | | | - | | | | - | | |

(1) Net investment income per share was computed using average shares outstanding.

(2) The Fund, through its investment in the Portfolio, has adopted the provisions of the revised AICPA Audit and Accounting Guide for Investment Companies and began using the interest method to amortize premiums on fixed-income securities. The effect of this change for the year ended September 30, 2002 was to increase net investment income per share by $0.003, decrease net realized and unrealized gains per share by $0.003 and increase the ratio of net investment income to average net assets from 5.86% to 5.89%. Per-share data and ratios for t he periods prior to October 1, 2001 have not been restated to reflect this change in presentation.

(3) Returns are historical and are calculated by determining the percentage change in net asset value with all distributions reinvested. Total return is not computed on an annualized basis.

(4) Total return reflects an increase of 0.17% due to a change in the timing of the payment and reinvestment of distributions.

(5) Includes the Fund's share of the Portfolio's allocated expenses while the Fund was making investments directly into the Portfolio.

(6) Annualized.

(7) Portfolio turnover represents the rate of portfolio activity for the period while the Fund was making investments directly into the Portfolio.

See notes to financial statements

16

Eaton Vance National Municipals Fund as of March 31, 2005

FINANCIAL STATEMENTS CONT'D

Financial Highlights

| | | Class C | |

| | | Six Months Ended

March 31, 2005 | | Year Ended September 30, | |

| | | (Unaudited)(1) | | 2004(1) | | 2003(1) | | 2002(1)(2) | | 2001 | | 2000(1) | |

| Net asset value - Beginning of period | | $ | 9.710 | | | $ | 9.640 | | | $ | 9.710 | | | $ | 9.380 | | | $ | 9.100 | | | $ | 9.280 | | |

| Income (loss) from operations | | | |

| Net investment income | | $ | 0.225 | | | $ | 0.502 | | | $ | 0.522 | | | $ | 0.515 | | | $ | 0.478 | | | $ | 0.477 | | |

| Net realized and unrealized gain (loss) | | | 0.126 | | | | 0.077 | | | | (0.089 | ) | | | 0.297 | | | | 0.274 | | | | (0.175 | ) | |

| Total income from operations | | $ | 0.351 | | | $ | 0.579 | | | $ | 0.433 | | | $ | 0.812 | | | $ | 0.752 | | | $ | 0.302 | | |

| Less distributions | | | |

| From net investment income | | $ | (0.231 | ) | | $ | (0.509 | ) | | $ | (0.503 | ) | | $ | (0.482 | ) | | $ | (0.472 | ) | | $ | (0.482 | ) | |

| Total distributions | | $ | (0.231 | ) | | $ | (0.509 | ) | | $ | (0.503 | ) | | $ | (0.482 | ) | | $ | (0.472 | ) | | $ | (0.482 | ) | |

| Net asset value - End of period | | $ | 9.830 | | | $ | 9.710 | | | $ | 9.640 | | | $ | 9.710 | | | $ | 9.380 | | | $ | 9.100 | | |

| Total Return(3) | | | 3.75 | %(4) | | | 6.15 | % | | | 4.71 | % | | | 9.02 | % | | | 8.47 | % | | | 3.46 | % | |

| Ratios/Supplemental Data | | | |

| Net assets, end of period (000's omitted) | | $ | 281,646 | | | $ | 224,955 | | | $ | 200,310 | | | $ | 185,439 | | | $ | 136,213 | | | $ | 104,455 | | |

| Ratios (As a percentage of average daily net assets): | | | | | | | | | | | | | | | | | | | | | | | | | |

| Expenses(5) | | | 1.54 | %(6) | | | 1.53 | % | | | 1.53 | % | | | 1.57 | % | | | 1.59 | % | | | 1.58 | % | |

| Expenses after custodian fee reduction(5) | | | 1.53 | %(6) | | | 1.53 | % | | | 1.53 | % | | | 1.56 | % | | | 1.58 | % | | | 1.57 | % | |

| Net investment income | | | 4.58 | %(6) | | | 5.19 | % | | | 5.54 | % | | | 5.56 | % | | | 5.16 | % | | | 5.31 | % | |

| Portfolio Turnover of the Portfolio(7) | | | - | | | | 44 | % | | | 35 | % | | | 32 | % | | | 20 | % | | | 41 | % | |

| Portfolio Turnover of the Fund | | | 27 | % | | | - | | | | - | | | | - | | | | - | | | | - | | |

(1) Net investment income per share was computed using average shares outstanding.

(2) The Fund, through its investment in the Portfolio, has adopted the provisions of the revised AICPA Audit and Accounting Guide for Investment Companies and began using the interest method to amortize premiums on fixed-income securities. The effect of this change for the year ended September 30, 2002 was to increase net investment income per share by $0.003, decrease net realized and unrealized gains per share by $0.003 and increase the ratio of net investment income to average net assets from 5.53% to 5.56%. Per-share data and ratios for t he periods prior to October 1, 2001 have not been restated to reflect this change in presentation.

(3) Returns are historical and are calculated by determining the percentage change in net asset value with all distributions reinvested. Total return is not computed on an annualized basis.

(4) Total return reflects an increase of 0.13% due to a change in the timing of the payment and reinvestment of distributions.

(5) Includes the Fund's share of the Portfolio's allocated expenses while the Fund was making investments directly into the Portfolio.

(6) Annualized.

(7) Portfolio turnover represents the rate of portfolio activity for the period while the Fund was making investments directly into the Portfolio.

See notes to financial statements

17

Eaton Vance National Municipals Fund as of March 31, 2005

FINANCIAL STATEMENTS CONT'D

Financial Highlights

| | | Class I | |

| | | Six Months Ended

March 31, 2005 | | Year Ended September 30, | |

| | | (Unaudited)(1) | | 2004(1) | | 2003(1) | | 2002(1)(2) | | 2001 | | 2000(1) | |

| Net asset value - Beginning of period | | $ | 10.120 | | | $ | 10.050 | | | $ | 10.110 | | | $ | 9.770 | | | $ | 9.460 | | | $ | 9.610 | | |

| Income (loss) from operations | | | |

| Net investment income | | $ | 0.281 | | | $ | 0.623 | | | $ | 0.642 | | | $ | 0.637 | | | $ | 0.604 | | | $ | 0.557 | | |

| Net realized and unrealized gain (loss) | | | 0.131 | | | | 0.078 | | | | (0.086 | ) | | | 0.298 | | | | 0.291 | | | | (0.107 | ) | |

| Total income from operations | | $ | 0.412 | | | $ | 0.701 | | | $ | 0.556 | | | $ | 0.935 | | | $ | 0.895 | | | $ | 0.450 | | |

| Less distributions | | | |

| From net investment income | | $ | (0.292 | ) | | $ | (0.631 | ) | | $ | (0.616 | ) | | $ | (0.595 | ) | | $ | (0.585 | ) | | $ | (0.600 | ) | |

| Total distributions | | $ | (0.292 | ) | | $ | (0.631 | ) | | $ | (0.616 | ) | | $ | (0.595 | ) | | $ | (0.585 | ) | | $ | (0.600 | ) | |

| Net asset value - End of period | | $ | 10.240 | | | $ | 10.120 | | | $ | 10.050 | | | $ | 10.110 | | | $ | 9.770 | | | $ | 9.460 | | |

| Total Return(3) | | | 4.10 | % | | | 7.17 | % | | | 5.84 | % | | | 10.05 | % | | | 9.71 | % | | | 4.96 | % | |

| Ratios/Supplemental Data | | | |

| Net assets, end of period (000's omitted) | | $ | 10,480 | | | $ | 5,400 | | | $ | 2,414 | | | $ | 2,193 | | | $ | 389 | | | $ | 598 | | |

| Ratios (As a percentage of average daily net assets): | | | | | | | | | | | | | | | | | | | | | | | | | |

| Expenses(4) | | | 0.54 | %(5) | | | 0.53 | % | | | 0.53 | % | | | 0.57 | % | | | 0.58 | % | | | 0.57 | % | |

| Expenses after custodian fee reduction(4) | | | 0.53 | %(5) | | | 0.53 | % | | | 0.53 | % | | | 0.56 | % | | | 0.57 | % | | | 0.56 | % | |

| Net investment income | | | 5.49 | %(5) | | | 6.18 | % | | | 6.54 | % | | | 6.60 | % | | | 6.22 | % | | | 5.87 | % | |

| Portfolio Turnover of the Portfolio(6) | | | - | | | | 44 | % | | | 35 | % | | | 32 | % | | | 20 | % | | | 41 | % | |

| Portfolio Turnover of the Fund | | | 27 | % | | | - | | | | - | | | | - | | | | - | | | | - | | |