UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-04409 |

|

Eaton Vance Municipals Trust |

(Exact name of registrant as specified in charter) |

|

The Eaton Vance Building, 255 State Street, Boston, Massachusetts | | 02109 |

(Address of principal executive offices) | | (Zip code) |

|

Maureen A. Gemma

The Eaton Vance Building, 255 State Street, Boston, Massachusetts 02109 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | (617) 482-8260 | |

|

Date of fiscal year end: | August 31, 2008 | |

|

Date of reporting period: | February 29, 2008 | |

| | | | | | | |

Item 1. Reports to Stockholders

Semiannual Report February 29, 2008

EATON VANCE

MUNICIPALS

TRUST

Alabama

Arkansas

Georgia

Kentucky

Louisiana

Maryland

Missouri

North Carolina

Oregon

South Carolina

Tennessee

Virginia

IMPORTANT NOTICES REGARDING PRIVACY,

DELIVERY OF SHAREHOLDER DOCUMENTS,

PORTFOLIO HOLDINGS AND PROXY VOTING

Privacy. The Eaton Vance organization is committed to ensuring your financial privacy. Each of the financial institutions identified below has in effect the following policy ("Privacy Policy") with respect to nonpublic personal information about its customers:

• Only such information received from you, through application forms or otherwise, and information about your Eaton Vance fund transactions will be collected. This may include information such as name, address, social security number, tax status, account balances and transactions.

• None of such information about you (or former customers) will be disclosed to anyone, except as permitted by law (which includes disclosure to employees necessary to service your account). In the normal course of servicing a customer's account, Eaton Vance may share information with unaffiliated third parties that perform various required services such as transfer agents, custodians and broker/dealers.

• Policies and procedures (including physical, electronic and procedural safeguards) are in place that are designed to protect the confidentiality of such information.

• We reserve the right to change our Privacy Policy at any time upon proper notification to you. Customers may want to review our Policy periodically for changes by accessing the link on our homepage: www.eatonvance.com.

Our pledge of privacy applies to the following entities within the Eaton Vance organization: the Eaton Vance Family of Funds, Eaton Vance Management, Eaton Vance Investment Counsel, Boston Management and Research, and Eaton Vance Distributors, Inc.

In addition, our Privacy Policy only applies to those Eaton Vance customers who are individuals and who have a direct relationship with us. If a customer's account (i.e., fund shares) is held in the name of a third-party financial adviser/ broker-dealer, it is likely that only such adviser's privacy policies apply to the customer. This notice supersedes all previously issued privacy disclosures.

For more information about Eaton Vance's Privacy Policy, please call 1-800-262-1122.

Delivery of Shareholder Documents. The Securities and Exchange Commission (the "SEC") permits funds to deliver only one copy of shareholder documents, including prospectuses, proxy statements and shareholder reports, to fund investors with multiple accounts at the same residential or post office box address. This practice is often called "householding" and it helps eliminate duplicate mailings to shareholders.

Eaton Vance, or your financial adviser, may household the mailing of your documents indefinitely unless you instruct Eaton Vance, or your financial adviser, otherwise.

If you would prefer that your Eaton Vance documents not be householded, please contact Eaton Vance at 1-800-262-1122, or contact your financial adviser.

Your instructions that householding not apply to delivery of your Eaton Vance documents will be effective within 30 days of receipt by Eaton Vance or your financial adviser.

Portfolio Holdings. Each Eaton Vance Fund and its underlying Portfolio (if applicable) will file a schedule of its portfolio holdings on Form N-Q with the SEC for the first and third quarters of each fiscal year. The Form N-Q will be available on the Eaton Vance website www.eatonvance.com, by calling Eaton Vance at 1-800-262-1122 or in the EDGAR database on the SEC's website at www.sec.gov. Form N-Q may also be reviewed and copied at the SEC's public reference room in Washington, D.C. (call 1-800-732-0330 for information on the operation of the public reference room).

Proxy Voting. From time to time, funds are required to vote proxies related to the securities held by the funds. The Eaton Vance Funds or their underlying Portfolios (if applicable) vote proxies according to a set of policies and procedures approved by the Funds' and Portfolios' Boards. You may obtain a description of these policies and procedures and information on how the Funds or Portfolios voted proxies relating to portfolio securities during the most recent 12 month period ended June 30, without charge, upon request, by calling 1-800-262-1122. This description is also available on the SEC's website at www.sec.gov.

Eaton Vance Municipals Funds as of February 29, 2008

TABLE OF CONTENTS

Investment Update | | 2 |

| | |

Morningstar RatingsTM | | 3 |

| | |

Fund Investment Updates | | |

Alabama | | 4 |

Arkansas | | 5 |

Georgia | | 6 |

Kentucky | | 7 |

Louisiana | | 8 |

Maryland | | 9 |

Missouri | | 10 |

North Carolina | | 11 |

Oregon | | 12 |

South Carolina | | 13 |

Tennessee | | 14 |

Virginia | | 15 |

| | |

Fund Expenses | | 16 |

| | |

Financial Statements | | 23 |

| | |

Board of Trustees’ Annual Approval of the Investment Advisory Agreements | | 123 |

| | |

Investment Management | | 126 |

1

Eaton Vance Municipals Funds as of February 29, 2008

INVESTMENT UPDATE

The investment objective of each Eaton Vance Municipals Fund (the “Funds”) is to provide current income exempt from regular federal income tax and from particular state or local income or other taxes. The Funds primarily invest in investment-grade municipal obligations but may also invest in lower rated obligations.

Economic and Market Conditions

Economic growth in the fourth quarter of 2007 measured 0.6%, following the 4.9% growth rate achieved in the third quarter, according to preliminary Commerce Department data reported in January 2008. The housing sector continued to struggle due to market concerns related to subprime mortgages. While the weaker dollar was having a beneficial effect on export-related industries, tourism, and U.S.-based multinational companies, there were signs that consumers were starting to curtail spending by February 29, 2008.

The Federal Reserve (the Fed) lowered its target for the Federal Funds Rate by 0.75% to 3.50% in an unscheduled meeting on January 22, 2008. In its statement, the Fed pointed to a weakening economic outlook, continued deterioration in broader financial market conditions and tighter credit for some businesses and households. The Fed further lowered the Federal Funds Rate to 3.00% in a scheduled meeting on January 30, 2008 noting considerable financial market stress and continued credit tightening. After the period, on March 18, 2008, the Fed again lowered the Federal Funds Rate to 2.25%, down from 5.25% since September 18, 2007, and it also lowered the Discount Rate – the rate charged to banks borrowing directly from the Fed to 2.50%, down from 6.25% since August 17, 2007. Management believes these moves were aimed at providing liquidity during this period of increased uncertainty and tighter credit conditions that first surfaced in August 2007.

Management Discussion

The Funds invest primarily in bonds with stated maturities of 10 years or longer, as longer-maturity bonds historically have provided greater tax-exempt income for investors than shorter-maturity bonds.

The Funds underperformed their benchmark, the Lehman Brothers Municipal Bond Index – a broad-based, unmanaged index of municipal bonds – during the six months ended February 29, 2008.(1) Management believes that much of the underperformance can be attributed to the broader-based credit scare that has shaken the fixed-income markets since August 2007, and led to a flight-to-quality bid in the Treasury market, particularly in shorter-maturity bonds. This move was originally driven by uncertainty surrounding financial companies’ exposure to mortgage-backed collateralized debt obligations (CDOs). More recently, the municipal bond market has been impacted by the downgrade of major municipal bond insurers due to their exposure to mortgage-related CDO debt. As a result of an active management style that focuses on income and longer call protection, the Funds generally hold longer-duration bonds. Accordingly, management believes that investor flight to shorter-maturity uninsured bonds from longer-maturity insured bonds resulted in the Funds’ relative underperformance for the period.

The ratio of yields on current coupon AAA-rated insured bonds to the yield on 30-year Treasury bonds was 119% as of February 29, 2008, with many individual bonds trading higher than 119%.(2) Management believes that this was the result of dislocation in the fixed-income marketplace caused by the subprime contagion fears, insurance companies’ mark-to-market risks and the decentralized nature of the municipal marketplace Historically, this is a rare occurrence in the municipal bond market and is generally considered a signal that municipal bonds are significantly undervalued compared to Treasuries.

With this backdrop, Eaton Vance continues to manage all of its municipal funds with the same relative value approach that it has traditionally employed – maintaining a long-term perspective when markets exhibit extreme short-term volatility. We believe this approach has provided excellent long-term benefits to our investors over time.

(1) It is not possible to invest directly in an Index. The Index’s total return does not reflect expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index.

(2) Source: Bloomberg L.P. Yields are a compilation of a representative variety of general obligations and are not necessarily representative of a Fund’s yield.

Past performance is no guarantee of future results.

Fund shares are not insured by the FDIC and are not deposits or other obligations of, or guaranteed by, any depository institution. Shares are subject to investment risks, including possible loss of principal invested.

The views expressed throughout this report are those of the portfolio managers and are current only through the end of the period of the report as stated on the cover. These views are subject to change at any time based upon market or other conditions, and the investment adviser disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a fund are based on many factors, may not be relied on as an indication of trading intent on behalf of any Eaton Vance fund. Portfolio information provided in the report may not be representative of the Fund’s current or future investments and may change due to active management.

2

Eaton Vance Municipals Funds as of February 29, 2008

MORNING STAR RATINGSTM

As of February 29, 2008

FUND | | OVERALL | | 3-YEAR | | 5-YEAR | | 10-YEAR | |

| | | | | | | | | |

ALABAMA MUNICIPALS FUND – CLASS A | | *** | | ** | | *** | | *** | |

Load waived | | **** | | **** | | **** | | *** | |

MUNI SINGLE STATE LONG CATEGORY | | 339 FUNDS | | 339 FUNDS | | 339 FUNDS | | 297 FUNDS | |

| | | | | | | | | |

ARKANSAS MUNICIPALS FUND – CLASS A | | ** | | * | | *** | | *** | |

Load waived | | **** | | *** | | ***** | | **** | |

MUNI SINGLE ESTATE INTERMEDIATE CATEGORY | | 284 FUNDS | | 284 FUNDS | | 281 FUNDS | | 221 FUNDS | |

| | | | | | | | | |

GEORGIA MUNICIPALS FUND – CLASS A | | ** | | * | | ** | | *** | |

Load waived | | *** | | *** | | **** | | *** | |

MUNI SINGLE STATE LONG CATEGORY | | 339 FUNDS | | 339 FUNDS | | 339 FUNDS | | 297 FUNDS | |

| | | | | | | | | |

KENTUCKY MUNICIPALS FUND – CLASS A | | ** | | ** | | ** | | ** | |

Load waived | | *** | | *** | | *** | | **** | |

MUNI SINGLE STATE LONG CATEGORY | | 339 FUNDS | | 339 FUNDS | | 339 FUNDS | | 297 FUNDS | |

| | | | | | | | | |

LOUISIANA MUNICIPALS FUND – CLASS A | | *** | | ** | | *** | | *** | |

Load waived | | **** | | *** | | **** | | **** | |

MUNI SINGLE STATE LONG CATEGORY | | 339 FUNDS | | 339 FUNDS | | 339 FUNDS | | 297 FUNDS | |

| | | | | | | | | |

MARYLAND MUNICIPALS FUND – CLASS A | | ** | | ** | | ** | | ** | |

Load waived | | *** | | *** | | *** | | **** | |

MUNI SINGLE STATE LONG CATEGORY | | 339 FUNDS | | 339 FUNDS | | 339 FUNDS | | 297 FUNDS | |

| | | | | | | | | |

MISSOURI MUNICIPALS FUND – CLASS A | | *** | | * | | *** | | *** | |

Load waived | | **** | | *** | | **** | | **** | |

MUNI SINGLE STATE LONG CATEGORY | | 339 FUNDS | | 339 FUNDS | | 339 FUNDS | | 297 FUNDS | |

| | | | | | | | | |

NORTH CAROLINA MUNICIPALS FUND – CLASS A | | *** | | ** | | *** | | *** | |

Load waived | | **** | | **** | | **** | | **** | |

MUNI SINGLE STATE LONG CATEGORY | | 339 FUNDS | | 339 FUNDS | | 339 FUNDS | | 297 FUNDS | |

| | | | | | | | | |

OREGON MUNICIPALS FUND – CLASS A | | *** | | ** | | *** | | *** | |

Load waived | | **** | | *** | | **** | | **** | |

MUNI SINGLE STATE LONG CATEGORY | | 339 FUNDS | | 339 FUNDS | | 339 FUNDS | | 297 FUNDS | |

| | | | | | | | | |

SOUTH CAROLINA MUNICIPALS FUND – CLASS A | | *** | | * | | *** | | *** | |

Load waived | | *** | | ** | | **** | | *** | |

MUNI SINGLE STATE LONG CATEGORY | | 339 FUNDS | | 339 FUNDS | | 339 FUNDS | | 297 FUNDS | |

| | | | | | | | | |

TENNESSEE MUNICIPALS FUND – CLASS A | | ** | | * | | ** | | *** | |

Load waived | | **** | | *** | | *** | | *** | |

MUNI SINGLE STATE LONG CATEGORY | | 339 FUNDS | | 339 FUNDS | | 339 FUNDS | | 297 FUNDS | |

| | | | | | | | | |

VIRGINIA MUNICIPALS FUND – CLASS A | | ** | | * | | * | | ** | |

Load waived | | *** | | ** | | *** | | *** | |

MUNI SINGLE STATE LONG CATEGORY | | 339 FUNDS | | 339 FUNDS | | 339 FUNDS | | 297 FUNDS | |

Based on risk-adjusted returns. Eaton Vance offers other mutual funds that are not listed here and that do not have similar performance records.

The Overall Morningstar Rating™ for a fund is derived from a weighted average of the performance figures associated with its 3-, 5- and 10-year (if applicable) Morningstar Rating™ metrics.

©2008 Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers is responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results. For each fund with at least a three-year history, Morningstar calculates a Morningstar Rating™ based on how a fund ranks on a Morningstar Risk-Adjusted Return measure against other funds in the same category. This measure takes into account variations in a fund’s monthly performance after adjusting for sales loads (except for load-waived A shares), redemption fees, and the risk-free rate, placing more emphasis on downward variations and rewarding consistent performance. The top 10% of funds in each category receive 5 stars; the next 22.5% receive 4 stars; the next 35% receive 3 stars; the next 22.5% receive 2 stars, and the bottom 10% receive 1 star.

Load-waived A share star ratings do not include any front-end sales load and are intended for those investors who have access to such purchase terms (e.g., plan participants of a defined contribution plan). Not all A share mutual funds for which Morningstar calculates a load-waived A share star rating may actually waive their front-end sales load. Therefore, Morningstar strongly encourages investors to contact their investment professional to determine whether they are eligible to purchase the A share without paying the front-end sales load. The Morningstar Rating may differ among share classes of a mutual fund as a result of different sales loads and/or expense structure.

As interest rates rise, the value of fixed-income securities is likely to decrease. Fluctuations in the value of securities may not affect interest income on existing securities, but will be reflected in the Funds’ net asset values. For state municipal funds, a portion of income may be subject to federal, state and local tax; a portion may be subject to federal alternative minimum tax. Please see the Funds’ prospectus for more information. Consult your tax/legal advisor before making any tax-related investment decisions.

For information regarding each Fund’s performance, please refer to pages titled “Performance Information and Portfolio Composition” contained in this report.

3

Eaton Vance Alabama Municipals Fund as of February 29, 2008

PERFORMANCE INFORMATION AND PORTFOLIO COMPOSITION

Fund Performance(1) | | Class A | | Class B | | Class C | |

Share Class Symbol | | ETALX | | EVALX | | ECALX | |

| | | | | | | |

Average Annual Total Returns (at net asset value) | | | | | | | |

Six Months | | -3.48 | % | -3.83 | % | -3.73 | % |

One Year | | -5.28 | | -6.01 | | -5.91 | |

Five Years | | 2.76 | | 2.02 | | N.A. | |

Ten Years | | 3.73 | | 2.97 | | N.A. | |

Life of Fund† | | 4.16 | | 4.38 | | -0.61 | |

| | | | | | | |

SEC Average Annual Total Returns (including sales charge or applicable CDSC) | | | | | | | |

Six Months | | -8.07 | % | -8.54 | % | -4.68 | % |

One Year | | -9.80 | | -10.54 | | -6.82 | |

Five Years | | 1.77 | | 1.68 | | N.A. | |

Ten Years | | 3.23 | | 2.97 | | N.A. | |

Life of Fund† | | 3.80 | | 4.38 | | -0.61 | |

†Inception date: Class A: 12/7/93; Class B: 5/01/92; Class C: 3/21/06

Total Annual | | | | | | | |

Operating Expenses (2),* | | Class A | | Class B | | Class C | |

Expense Ratio | | 0.91 | % | 1.66 | % | 1.66 | % |

*Source: Prospectus dated 12/1/07.

Distribution Rates/Yields | | Class A | | Class B | | Class C | |

| | | | | | | |

Distribution Rate(3) | | 4.38 | % | 3.57 | % | 3.57 | % |

Taxable-Equivalent Distribution Rate(3),(4) | | 7.09 | | 5.78 | | 5.78 | |

SEC 30-day Yield(5) | | 3.75 | | 3.13 | | 3.16 | |

Taxable-Equivalent SEC 30-day Yield(4),(5) | | 6.07 | | 5.07 | | 5.12 | |

Index Performance(6)

Lehman Brothers Municipal Bond Index (Average Annual Total Returns) | | | |

Six Months | | -0.60 | % |

One Year | | -1.17 | |

Five Years | | 3.35 | |

Ten Years | | 4.71 | |

Lipper Averages(7)

Lipper Alabama Municipal Debt Funds Classification (Average Annual Total Returns) | | | |

Six Months | | -2.11 | % |

One Year | | -3.54 | |

Five Years | | 2.50 | |

Ten Years | | 3.60 | |

Portfolio Manager: William H. Ahern, CFA

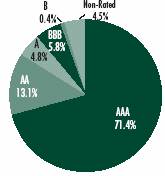

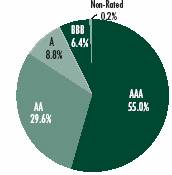

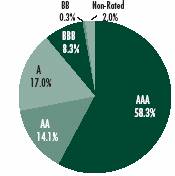

Rating Distribution**,(8)

By total investments

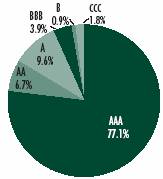

** The rating distribution presented above includes the ratings of securities held by special purpose vehicles in which the Fund holds a residual interest. See Note 1I to the Fund’s financial statements. Absent such securities, the Fund’s rating distribution at 2/29/08, is as follows, and the average rating is AA+.

AAA | | 78.3 | % |

AA | | 4.9 | % |

A | | 9.9 | % |

BBB | | 4.0 | % |

B | | 0.9 | % |

CCC | | 1.8 | % |

Not Rated | | 0.2 | % |

Fund Statistics(9)

· Number of Issues: | | 54 | |

· Average Maturity: | | 20.8 years | |

· Average Effective Maturity: | | 16.4 years | |

· Average Call Protection: | | 7.2 years | |

· Average Dollar Price: | | $ | 93.31 | |

| | | | |

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. For performance as of the most recent month end, please refer to www.eatonvance.com.

(1) Average Annual Total Returns do not include the 4.75% maximum sales charge for Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B and Class C shares. If sales charges were deducted, the returns would be lower. SEC Average Annual Total Returns for Class A reflect the maximum 4.75% sales charge. SEC Average Annual Total Returns for Class B reflect the applicable CDSC based on the following schedule: 5% - 1st and 2nd years; 4% - 3rd year; 3% - - 4th year; 2% - 5th year; 1% - 6th year. SEC Average Annual Total Returns for Class C reflect a 1% CDSC for the first year.

(2) Includes interest expense of 0.16% relating to the Fund’s liability with respect to floating rate notes held by third parties in conjunction with inverse floater securities transactions by the Fund. The Fund also records offsetting interest income relating to the municipal obligation underlying such transactions, and as a result net asset value and performance have not been affected by this expense.

(3) The Fund’s distribution rate represents actual distributions paid to shareholders and is calculated by dividing the last distribution per share (annualized) by the net asset value.

(4) Taxable-equivalent figure assumes a maximum 38.25% combined federal and state income tax rate. A lower tax rate would result in lower tax-equivalent figures.

(5) The Fund’s SEC yield is calculated by dividing the net investment income per share for the 30-day period by the offering price at the end of the period and annualizing the result.

(6) It is not possible to invest directly in an Index. The Index’s total return does not reflect the expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index. Index performance is available as of month end only.

(7) The Lipper Averages are the average annual total returns, at net asset value, of the funds that are in the same Lipper Classification as the Fund. It is not possible to invest in a Lipper Classification. Lipper Classifications may include insured and uninsured funds, as well as leveraged and unleveraged funds. The Lipper Alabama Municipal Debt Funds Classification contained 13, 13, 9 and 7 funds for the 6-month, 1-year, 5-year and 10-year time periods, respectively. Lipper Averages are available as of month end only.

(8) Rating Distribution is determined by dividing the total market value of the issues by the total investments of the Fund

(9) Excludes securities held by special purpose vehicles in which the Fund holds a residual interest. See Note 1I to the Fund’s financial statements.

4

Eaton Vance Arkansas Municipals Fund as of February y 29, 2008

PERFORMANCE INFORMATION AND PORTFOLIO COMPOSITION

Fund Performance(1) | | Class A | | Class B | | Class C | |

Share Class Symbol | | ETARX | | EVARX | | ECARX | |

| | | | | | | |

Average Annual Total Returns (at net asset value) | | | | | | | |

Six Months | | -6.23 | % | -6.59 | % | -6.60 | % |

One Year | | -8.28 | | -8.97 | | -8.98 | |

Five Years | | 2.53 | | 1.76 | | N.A. | |

Ten Years | | 3.72 | | 2.94 | | N.A. | |

Life of Fund† | | 4.12 | | 4.11 | | -1.80 | |

| | | | | | | |

SEC Average Annual Total Returns (including sales charge or applicable CDSC) | | | | | | | |

Six Months | | -10.64 | % | -11.18 | % | -7.52 | % |

One Year | | -12.67 | | -13.36 | | -9.86 | |

Five Years | | 1.54 | | 1.43 | | N.A. | |

Ten Years | | 3.21 | | 2.94 | | N.A. | |

Life of Fund† | | 3.76 | | 4.11 | | -1.80 | |

†Inception date: Class A: 2/9/94; Class B: 10/2/92; Class C: 4/28/06

Total Annual | | | | | | | |

Operating Expenses(2),* | | Class A | | Class B | | Class C | |

| | | | | | | |

Expense Ratio | | 0.95 | % | 1.70 | % | 1.70 | % |

*Source: Prospectus dated 12/1/07.

Distribution Rates/Yields | | Class A | | Class B | | Class C | |

| | | | | | | |

Distribution Rate(3) | | 4.84 | % | 4.02 | % | 4.02 | % |

Taxable-Equivalent Distribution Rate(3),(4) | | 8.01 | | 6.65 | | 6.65 | |

SEC 30-day Yield(5) | | 4.20 | | 3.61 | | 3.62 | |

Taxable-Equivalent SEC 30-day Yield(4),(5) | | 6.95 | | 5.97 | | 5.99 | |

Index Performance(6)

Lehman Brothers Municipal Bond Index (Average Annual Total Returns) | | | |

Six Months | | -0.60 | % |

One Year | | -1.17 | |

Five Years | | 3.35 | |

Ten Years | | 4.71 | |

Lipper Averages(7)

Lipper Other States Municipal Debt Funds Classification (Average Annual Total Returns) | | | |

Six Months | | -2.06 | % |

One Year | | -3.06 | |

Five Years | | 2.31 | |

Ten Years | | 3.46 | |

Portfolio Manager: Adam Weigold, CFA

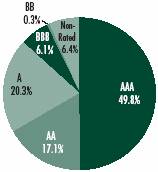

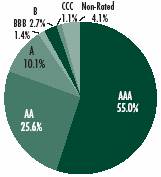

Rating Distribution**,(8)

By total investments

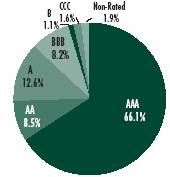

**The rating distribution presented above includes the ratings of securities held by special purpose vehicles in which the Fund holds a residual interest. See Note 1I to the Fund’s financial statements. Absent such securities, the Fund’s rating distribution at 2/29/08, is as follows, and the average rating is AA.

AAA | | 64.8 | % |

AA | | 8.9 | % |

A | | 13.0 | % |

BBB | | 8.5 | % |

B | | 1.2 | % |

CCC | | 1.7 | % |

Not Rated | | 1.9 | % |

Fund Statistics(9)

· Number of Issues: | | 77 | |

· Average Maturity: | | 20.8 years | |

· Average Effective Maturity: | | 18.8 years | |

· Average Call Protection: | | 8.7 years | |

· Average Dollar Price: | | $ | 91.93 | |

| | | | |

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. For performance as of the most recent month end, please refer to www.eatonvance.com.

(1) Average Annual Total Returns do not include the 4.75% maximum sales charge for Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B and Class C shares. If sales charges were deducted, the returns would be lower. SEC Average Annual Total Returns for Class A reflect the maximum 4.75% sales charge. SEC Average Annual Total Returns for Class B reflect the applicable CDSC based on the following schedule: 5% - 1st and 2nd years; 4% - 3rd year; 3% - - 4th year; 2% - 5th year; 1% - 6th year. SEC Average Annual Total Returns for Class C reflect a 1% CDSC for the first year.

(2) Includes interest expense of 0.20% relating to the Fund’s liability with respect to floating rate notes held by third parties in conjunction with inverse floater securities transactions by the Fund. The Fund also records offsetting interest income relating to the municipal obligation underlying such transactions, and as a result net asset value and performance have not been affected by this expense.

(3) The Fund’s distribution rate represents actual distributions paid to shareholders and is calculated by dividing the last distribution per share (annualized) by the net asset value.

(4) Taxable-equivalent figure assumes a maximum 39.55% combined federal and state income tax rate. A lower tax rate would result in lower tax-equivalent figures.

(5) The Fund’s SEC yield is calculated by dividing the net investment income per share for the 30-day period by the offering price at the end of the period and annualizing the result.

(6) It is not possible to invest directly in an Index. The Index’s total return does not reflect the expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index. Index performance is available as of month end only.

(7) The Lipper Averages are the average annual total returns, at net asset value, of the funds that are in the same Lipper Classification as the Fund. It is not possible to invest in a Lipper Classification. Lipper Classifications may include insured and uninsured funds, as well as leveraged and unleveraged funds. The Lipper Other States Municipal Debt Funds Classification contained 74, 74, 71 and 52 funds for the 6-month, 1-year, 5-year and 10-year time periods, respectively. Lipper Averages are available as of month end only.

(8) Rating Distribution is determined by dividing the total market value of the issues by the total investments of the Fund.

(9) Excludes securities held by special purpose vehicles in which the Fund holds a residual interest. See Note 11 to the Fund’s financial statements.

5

Eaton Vance Georgia Municipals Fund as of February 29, 2008

PERFORMANCE INFORMATION AND PORTFOLIO COMPOSITION

Fund Performance(1) | | Class A | | Class B | | Class C | |

Share Class Symbol | | ETGAX | | EVGAX | | ECGAX | |

| | | | | | | |

Average Annual Total Returns (at net asset value) | | | | | | | |

Six Months | | -6.00 | % | -6.36 | % | -6.46 | % |

One Year | | -8.23 | | -8.95 | | -9.04 | |

Five Years | | 2.38 | | 1.62 | | N.A. | |

Ten Years | | 3.49 | | 2.72 | | N.A. | |

Life of Fund† | | 3.76 | | 3.92 | | -2.20 | |

| | | | | | | |

SEC Average Annual Total Returns (including sales charge or applicable CDSC) | | | | | | | |

Six Months | | -10.51 | % | -10.96 | % | -7.38 | % |

One Year | | -12.62 | | -13.35 | | -9.92 | |

Five Years | | 1.39 | | 1.28 | | N.A. | |

Ten Years | | 2.99 | | 2.72 | | N.A. | |

Life of Fund† | | 3.40 | | 3.92 | | -2.20 | |

†Inception date: Class A: 12/7/93; Class B: 12/23/91; Class C: 4/25/06

Total Annual | | | | | | | |

Operating Expenses(2),* | | Class A | | Class B | | Class C | |

| | | | | | | |

Expense Ratio | | 1.05 | % | 1.80 | % | 1.80 | % |

*Source: Prospectus dated 12/1/07.

Distribution Rates/Yields | | Class A | | Class B | | Class C | |

| | | | | | | |

Distribution Rate(3) | | 4.71 | % | 3.88 | % | 3.88 | % |

Taxable-Equivalent Distribution Rate(3),(4) | | 7.71 | | 6.35 | | 6.35 | |

SEC 30-day Yield(5) | | 3.94 | | 3.33 | | 3.51 | |

Taxable-Equivalent SEC 30-day Yield(4),(5) | | 6.45 | | 5.45 | | 5.74 | |

Index Performance(6)

Lehman Brothers Municipal Bond Index (Average Annual Total Returns) | | | | | | | |

Six Months | | | | | | -0.60 | % |

One Year | | | | | | -1.17 | |

Five Years | | | | | | 3.35 | |

Ten Years | | | | | | 4.71 | |

Lipper Averages(7)

Lipper Georgia Municipal Debt Funds Classification (Average Annual Total Returns) | | | | | | | |

Six Months | | | | | | -2.19 | % |

One Year | | | | | | -3.52 | |

Five Years | | | | | | 2.13 | |

Ten Years | | | | | | 3.55 | |

Portfolio Manager: Adam Weigold, CFA

Rating Distribution**,(8)

By total investments

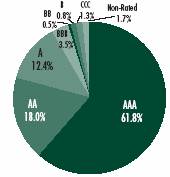

**The rating distribution presented above includes the ratings of securities held by special purpose vehicles in which the Fund holds a residual interest. See Note 1I to the Fund’s financial statements. Absent such securities, the Fund’s rating distribution at 2/29/08, is as follows, and the average rating is AA+.

AAA | | 60.7 | % |

AA | | 18.5 | % |

A | | 12.8 | % |

BBB | | 3.6 | % |

BB | | 0.6 | % |

B | | 0.8 | % |

CCC | | 1.3 | % |

Not Rated | | 1.7 | % |

Fund Statistics(9)

· Number of Issues: | | 81 | |

· Average Maturity: | | 22.0 years | |

· Average Effective Maturity: | | 20.6 years | |

· Average Call Protection: | | 10.0 years | |

· Average Dollar Price: | | $ | 94.68 | |

| | | | |

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. For performance as of the most recent month end, please refer to www.eatonvance.com.

(1) Average Annual Total Returns do not include the 4.75% maximum sales charge for Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B and Class C shares. If sales charges were deducted, the returns would be lower. SEC Average Annual Total Returns for Class A reflect the maximum 4.75% sales charge. SEC Average Annual Total Returns for Class B reflect the applicable CDSC based on the following schedule: 5% - 1st and 2nd years; 4% - 3rd year; 3% - - 4th year; 2% - 5th year; 1% - 6th year. SEC Average Annual Total Returns for Class C reflect a 1% CDSC for the first year.

(2) Includes interest expense of 0.29% relating to the Fund’s liability with respect to floating rate notes held by third parties in conjunction with inverse floater securities transactions by the Fund. The Fund also records offsetting interest income relating to the municipal obligation underlying such transactions, and as a result net asset value and performance have not been affected by this expense.

(3) The Fund’s distribution rate represents actual distributions paid to shareholders and is calculated by dividing the last distribution per share (annualized) by the net asset value.

(4) Taxable-equivalent figure assumes a maximum 38.90% combined federal and state income tax rate. A lower tax rate would result in lower tax-equivalent figures.

(5) The Fund’s SEC yield is calculated by dividing the net investment income per share for the 30-day period by the offering price at the end of the period and annualizing the result.

(6) It is not possible to invest directly in an Index. The Index’s total return does not reflect the expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index. Index performance is available as of month end only.

(7) The Lipper Averages are the average annual total returns, at net asset value, of the funds that are in the same Lipper Classification as the Fund. It is not possible to invest in a Lipper Classification. Lipper Classifications may include insured and uninsured funds, as well as leveraged and unleveraged funds. The Lipper Georgia Municipal Debt Funds Classification contained 27, 27, 26 and 22 funds for the 6-month, 1-year, 5-year and 10-year time periods, respectively. Lipper Averages are available as of month end only.

(8) Rating Distribution is determined by dividing the total market value of the issues by the total investments of the Fund.

(9) Excludes securities held by special purpose vehicles in which the Fund holds a residual interest. See Note 1I to the Fund’s financial statements.

6

Eaton Vance Kentucky Municipals Fund as of February 29, 2008

PERFORMANCE INFORMATION AND PORTFOLIO COMPOSITION

Fund Performance(1) | | Class A | | Class B | | Class C | |

Share Class Symbol | | ETKYX | | EVKYX | | ECKYX | |

| | | | | | | |

Average Annual Total Returns (at net asset value) | | | | | | | |

Six Months | | -4.09 | % | -4.43 | % | -4.43 | % |

One Year | | -5.29 | | -5.94 | | -5.94 | |

Five Years | | 2.11 | | 1.39 | | N.A. | |

Ten Years | | 3.27 | | 2.53 | | N.A. | |

Life of Fund† | | 3.74 | | 3.93 | | -1.08 | |

| | | | | | | |

SEC Average Annual Total Returns (including sales charge or applicable CDSC) | | | | | | | |

Six Months | | -8.67 | % | -9.12 | % | -5.37 | % |

One Year | | -9.77 | | -10.48 | | -6.85 | |

Five Years | | 1.13 | | 1.06 | | N.A. | |

Ten Years | | 2.77 | | 2.53 | | N.A. | |

Life of Fund† | | 3.39 | | 3.93 | | -1.08 | |

†Inception date: Class A: 12/7/93; Class B: 12/23/91; Class C: 3/23/06

Total Annual | | | | | | | |

Operating Expenses(2),* | | Class A | | Class B | | Class C | |

| | | | | | | |

Expense Ratio | | 0.84 | % | 1.59 | % | 1.59 | % |

*Source: Prospectus dated 12/1/07.

Distribution Rates/Yields | | Class A | | Class B | | Class C | |

| | | | | | | |

Distribution Rate(3) | | 4.60 | % | 3.76 | % | 3.76 | % |

Taxable-Equivalent Distribution Rate(3),(4) | | 7.53 | | 6.15 | | 6.15 | |

SEC 30-day Yield(5) | | 3.98 | | 3.38 | | 3.39 | |

Taxable-Equivalent SEC 30-day Yield(4),(5) | | 6.51 | | 5.53 | | 5.55 | |

Index Performance(6)

Lehman Brothers Municipal Bond Index (Average Annual Total Returns) | | | |

Six Months | | -0.60 | % |

One Year | | -1.17 | |

Five Years | | 3.35 | |

Ten Years | | 4.71 | |

Lipper Averages(7)

Lipper Kentucky Municipal Debt Funds Classification (Average Annual Total Returns) | | | |

Six Months | | -2.17 | % |

One Year | | -3.44 | |

Five Years | | 2.24 | |

Ten Years | | 3.48 | |

Portfolio Manager: Adam Weigold, CFA

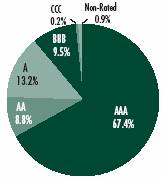

Rating Distribution**,(8)

By total investments

**The rating distribution presented above includes the ratings of securities held by special purpose vehicles in which the Fund holds a residual interest. See Note 1I to the Fund’s financial statements. Absent such securities, the Fund’s rating distribution at 2/29/08, is as follows, and the average rating is AA+.

AAA | | 69.4 | % |

AA | | 14.0 | % |

A | | 5.2 | % |

BBB | | 6.2 | % |

BB | | 0.4 | % |

Not Rated | | 4.8 | % |

Fund Statistics(9)

· Number of Issues: | | 47 | |

· Average Maturity: | | 18.5 years | |

· Average Effective Maturity: | | 15.0 years | |

· Average Call Protection: | | 6.8 years | |

· Average Dollar Price: | | $ | 87.49 | |

| | | | |

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. For performance as of the most recent month end, please refer to www.eatonvance.com.

(1) Average Annual Total Returns do not include the 4.75% maximum sales charge for Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B and Class C shares. If sales charges were deducted, the returns would be lower. SEC Average Annual Total Returns for Class A reflect the maximum 4.75% sales charge. SEC Average Annual Total Returns for Class B reflect the applicable CDSC based on the following schedule: 5% - 1st and 2nd years; 4% - 3rd year; 3% - 4th year; 2% - 5th year; 1% - 6th year. SEC Average Annual Total Returns for Class C reflect a 1% CDSC for the first year.

(2) Includes interest expense of 0.06% relating to the Fund’s liability with respect to floating rate notes held by third parties in conjunction with inverse floater securities transactions by the Fund. The Fund also records offsetting interest income relating to the municipal obligation underlying such transactions, and as a result net asset value and performance have not been affected by this expense.

(3) The Fund’s distribution rate represents actual distributions paid to shareholders and is calculated by dividing the last distribution per share (annualized) by the net asset value.

(4) Taxable-equivalent figure assumes a maximum 38.90% combined federal and state income tax rate. A lower tax rate would result in lower tax-equivalent figures.

(5) The Fund’s SEC yield is calculated by dividing the net investment income per share for the 30-day period by the offering price at the end of the period and annualizing the result.

(6) It is not possible to invest directly in an Index. The Index’s total return does not reflect the expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index. Index performance is available as of month end only.

(7) The Lipper Averages are the average annual total returns, at net asset value, of the funds that are in the same Lipper Classification as the Fund. It is not possible to invest in a Lipper Classification. Lipper Classifications may include insured and uninsured funds, as well as leveraged and unleveraged funds. The Lipper Kentucky Municipal Debt Funds Classification contained 18, 18, 17 and 11 funds for the 6-month, 1-year, 5-year and 10-year time periods, respectively. Lipper Averages are available as of month end only.

(8) Rating Distribution is determined by dividing the total market value of the issues by the total investments of the Fund.

(9) Excludes securities held by special purpose vehicles in which the Fund holds a residual interest. See Note 1I to the Fund’s financial statements.

7

Eaton Vance Louisiana Municipals Fund as of February 29, 2008

PERFORMANCE INFORMATION AND PORTFOLIO COMPOSITION

Fund Performance(1) | | Class A | | Class B | | Class C | |

Share Class Symbol | | ETLAX | | EVLAX | | ELACX | |

| | | | | | | |

Average Annual Total Returns (at net asset value) | | | | | | | |

Six Months | | -5.58 | % | -5.93 | % | N.A. | |

One Year | | -7.50 | | -8.16 | | N.A. | |

Five Years | | 2.70 | | 1.95 | | N.A. | |

Ten Years | | 3.80 | | 3.03 | | N.A. | |

Life of Fund† | | 4.21 | | 4.18 | | -6.98 | % |

| | | | | | | |

SEC Average Annual Total Returns (including sales charge or applicable CDSC) | | | | | | | |

Six Months | | -10.05 | % | -10.55 | % | N.A. | |

One Year | | -11.87 | | -12.58 | | N.A. | |

Five Years | | 1.70 | | 1.61 | | N.A. | |

Ten Years | | 3.29 | | 3.03 | | N.A. | |

Life of Fund† | | 3.85 | | 4.18 | | -7.90 | % |

†Inception date: Class A: 2/14/94; Class B: 10/2/92; Class C: 12/4/07

Total Annual | | | | | | | |

Operating Expenses(2),* | | Class A | | Class B | | Class C | |

| | | | | | | |

Expense Ratio | | 0.98 | % | 1.73 | % | 1.73 | % |

*Source: Prospectus dated 12/1/07.

Distribution Rates/Yields | | Class A | | Class B | | Class C | |

| | | | | | | |

Distribution Rate(3) | | 4.81 | % | 3.97 | % | 3.97 | % |

Taxable-Equivalent Distribution Rate(3),(4) | | 7.87 | | 6.50 | | 6.50 | |

SEC 30-day Yield(5) | | 4.35 | | 3.76 | | 3.75 | |

Taxable-Equivalent SEC 30-day Yield(4),(5) | | 7.12 | | 6.15 | | 6.14 | |

Index Performance(6)

Lehman Brothers Municipal Bond Index (Average Annual Total Returns) | | | |

Six Months | | -0.60 | % |

One Year | | -1.17 | |

Five Years | | 3.35 | |

Ten Years | | 4.71 | |

Lipper Averages(7)

Lipper Louisiana Municipal Debt Funds Classification (Average Annual Total Returns) | | | |

Six Months | | -2.60 | % |

One Year | | -3.07 | |

Five Years | | 2.32 | |

Ten Years | | 3.61 | |

Portfolio Manager: Robert B. MacIntosh, CFA

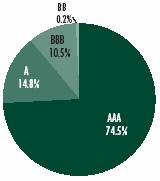

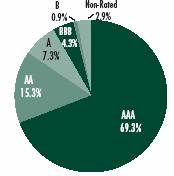

Rating Distribution**,(8)

By total investments

**The rating distribution presented above includes the ratings of securities held by special purpose vehicles in which the Fund holds a residual interest. See Note 1I to the Fund’s financial statements. Absent such securities, the Fund’s rating distribution at 2/29/08, is as follows, and the average rating is AA+.

AAA | | 71.5 | % |

A | | 15.6 | % |

BBB | | 11.0 | % |

BB | | 0.2 | % |

Non-Rated | | 1.7 | % |

Fund Statistics(9)

· Number of Issues: | | 54 | |

· Average Maturity: | | 23.1 years | |

· Average Effective Maturity: | | 20.5 years | |

· Average Call Protection: | | 7.4 years | |

· Average Dollar Price: | | $ | 89.17 | |

| | | | |

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. For performance as of the most recent month end, please refer to www.eatonvance.com.

(1) Average Annual Total Returns do not include the 4.75% maximum sales charge for Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B and Class C shares. If sales charges were deducted, the returns would be lower. SEC Average Annual Total Returns for Class A reflect the maximum 4.75% sales charge. SEC Average Annual Total Returns for Class B reflect the applicable CDSC based on the following schedule: 5% - 1st and 2nd years; 4% - 3rd year; 3% - 4th year; 2% - 5th year; 1% - 6th year. SEC Average Annual Total Returns for Class C reflect a 1% CDSC for the first year.

(2) Includes interest expense of 0.26% relating to the Fund’s liability with respect to floating rate notes held by third parties in conjunction with inverse floater securities transactions by the Fund. The Fund also records offsetting interest income relating to the municipal obligation underlying such transactions, and as a result net asset value and performance have not been affected by this expense.

(3) The Fund’s distribution rate represents actual distributions paid to shareholders and is calculated by dividing the last distribution per share (annualized) by the net asset value.

(4) Taxable-equivalent figure assumes a maximum 38.90% combined federal and state income tax rate. A lower tax rate would result in lower tax-equivalent figures.

(5) The Fund’s SEC yield is calculated by dividing the net investment income per share for the 30-day period by the offering price at the end of the period and annualizing the result.

(6) It is not possible to invest directly in an Index. The Index’s total return does not reflect the expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index. Index performance is available as of month end only.

(7) The Lipper Averages are the average annual total returns, at net asset value, of the funds that are in the same Lipper Classification as the Fund. It is not possible to invest in a Lipper Classification. Lipper Classifications may include insured and uninsured funds, as well as leveraged and unleveraged funds. The Lipper Louisiana Municipal Debt Funds Classification contained 13, 13, 13 and 11 funds for the 6-month, 1-year, 5-year and 10-year time periods, respectively. Lipper Averages are available as of month end only.

(8) Rating Distribution is determined by dividing the total market value of the issues by the total investments of the Fund.

(9) Excludes securities held by special purpose vehicles in which the Fund holds a residual interest. See Note 1I to the Fund’s financial statements.

8

Eaton Vance Maryland Municipals Fund as of February 29, 2008

PERFORMANCE INFORMATION AND PORTFOLIO COMPOSITION

Fund Performance(1) | | Class A | | Class B | | Class C | |

Share Class Symbol | | ETMDX | | EVMYX | | ECMDX | |

| | | | | | | |

Average Annual Total Returns (at net asset value) | | | | | | | |

Six Months | | -5.03 | % | -5.30 | % | -5.30 | % |

One Year | | -7.88 | | -8.54 | | -8.45 | |

Five Years | | 2.08 | | 1.35 | | N.A. | |

Ten Years | | 3.24 | | 2.47 | | N.A. | |

Life of Fund† | | 3.80 | | 4.02 | | -1.61 | |

| | | | | | | |

SEC Average Annual Total Returns (including sales charge or applicable CDSC) | | | | | | | |

Six Months | | -9.53 | % | -9.95 | % | -6.23 | % |

One Year | | -12.29 | | -12.94 | | -9.33 | |

Five Years | | 1.09 | | 1.01 | | N.A. | |

Ten Years | | 2.74 | | 2.47 | | N.A. | |

Life of Fund† | | 3.45 | | 4.02 | | -1.61 | |

†Inception date: Class A: 12/10/93; Class B: 2/3/92; Class C: 5/2/06

Total Annual | | | | | | | |

Operating Expenses(2),* | | Class A | | Class B | | Class C | |

| | | | | | | |

Expense Ratio | | 1.19 | % | 1.94 | % | 1.94 | % |

*Source: Prospectus dated 12/1/07.

Distribution Rates/Yields | | Class A | | Class B | | Class C | |

| | | | | | | |

Distribution Rate(3) | | 4.86 | % | 4.03 | % | 4.03 | % |

Taxable-Equivalent Distribution Rate(3),(4) | | 7.91 | | 6.56 | | 6.56 | |

SEC 30-day Yield(5) | | 4.10 | | 3.52 | | 3.50 | |

Taxable-Equivalent SEC 30-day Yield(4),(5) | | 6.68 | | 5.73 | | 5.70 | |

Index Performance(6)

Lehman Brothers Municipal Bond Index (Average Annual Total Returns) | | | |

Six Months | | -0.60 | % |

One Year | | -1.17 | |

Five Years | | 3.35 | |

Ten Years | | 4.71 | |

Lipper Averages(7)

Lipper Maryland Municipal Debt Funds Classification (Average Annual Total Returns) | | | |

Six Months | | -1.97 | % |

One Year | | -3.61 | |

Five Years | | 2.21 | |

Ten Years | | 3.55 | |

Portfolio Manager: Craig R. Brandon, CFA

Rating Distribution**,(8)

By total investments

**The rating distribution presented above includes the ratings of securities held by special purpose vehicles in which the Fund holds a residual interest. See Note 1I to the Fund’s financial statements. Absent such securities, the Fund’s rating distribution at 2/29/08, is as follows, and the average rating is AA.

AAA | | 47.1 | % |

AA | | 18.0 | % |

A | | 21.4 | % |

BBB | | 6.4 | % |

BB | | 0.3 | % |

Non-Rated | | 6.8 | % |

Fund Statistics(9)

· Number of Issues: | | 73 | |

· Average Maturity: | | 24.3 years | |

· Average Effective Maturity: | | 19.6 years | |

· Average Call Protection: | | 9.1 years | |

· Average Dollar Price: | | $ | 95.33 | |

| | | | |

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. For performance as of the most recent month end, please refer to www.eatonvance.com.

(1) Average Annual Total Returns do not include the 4.75% maximum sales charge for Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B and Class C shares. If sales charges were deducted, the returns would be lower. SEC Average Annual Total Returns for Class A reflect the maximum 4.75% sales charge. SEC Average Annual Total Returns for Class B reflect the applicable CDSC based on the following schedule: 5% - 1st and 2nd years; 4% - 3rd year; 3% - 4th year; 2% - 5th year; 1% - 6th year. SEC Average Annual Total Returns for Class C reflect a 1% CDSC for the first year.

(2) Includes interest expense of 0.41% relating to the Fund’s liability with respect to floating rate notes held by third parties in conjunction with inverse floater securities transactions by the Fund. The Fund also records offsetting interest income relating to the municipal obligation underlying such transactions, and as a result net asset value and performance have not been affected by this expense.

(3) The Fund’s distribution rate represents actual distributions paid to shareholders and is calculated by dividing the last distribution per share (annualized) by the net asset value.

(4) Taxable-equivalent figure assumes a maximum 38.58% combined federal and state income tax rate. A lower tax rate would result in lower tax-equivalent figures.

(5) The Fund’s SEC yield is calculated by dividing the net investment income per share for the 30-day period by the offering price at the end of the period and annualizing the result.

(6) It is not possible to invest directly in an Index. The Index’s total return does not reflect the expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index. Index performance is available as of month end only.

(7) The Lipper Averages are the average annual total returns, at net asset value, of the funds that are in the same Lipper Classification as the Fund. It is not possible to invest in a Lipper Classification. Lipper Classifications may include insured and uninsured funds, as well as leveraged and unleveraged funds. The Lipper Maryland Municipal Debt Funds Classification contained 40, 40, 35 and 26 funds for the 6-month, 1-year, 5-year and 10-year time periods, respectively. Lipper Averages are available as of month end only.

(8) Rating Distribution is determined by dividing the total market value of the issues by the total investments of the Fund.

(9) Excludes securities held by special purpose vehicles in which the Fund holds a residual interest. See Note 1I to the Fund’s financial statements.

9

Eaton Vance Missouri Municipals Fund as of February 29, 2008

PERFORMANCE INFORMATION AND PORTFOLIO COMPOSITION

Fund Performance(1) | | Class A | | Class B | | Class C | |

Share Class Symbol | | ETMOX | | EVMOX | | ECMOX | |

| | | | | | | |

Average Annual Total Returns (at net asset value) | | | | | | | |

Six Months | | -5.46 | % | -5.77 | % | -5.86 | % |

One Year | | -7.97 | | -8.63 | | -8.64 | |

Five Years | | 2.40 | | 1.66 | | N.A. | |

Ten Years | | 3.72 | | 2.93 | | N.A. | |

Life of Fund† | | 4.26 | | 4.53 | | -2.00 | |

| | | | | | | |

SEC Average Annual Total Returns (including sales charge or applicable CDSC) | | | | | | | |

Six Months | | -9.99 | % | -10.40 | % | -6.79 | % |

One Year | | -12.35 | | -13.05 | | -9.52 | |

Five Years | | 1.42 | | 1.33 | | N.A. | |

Ten Years | | 3.21 | | 2.93 | | N.A. | |

Life of Fund† | | 3.91 | | 4.53 | | -2.00 | |

†Inception date: Class A: 12/7/93; Class B: 5/1/92; Class C: 2/16/06

Total Annual | | | | | | | |

Operating Expenses(2),* | | Class A | | Class B | | Class C | |

| | | | | | | |

Expense Ratio | | 0.92 | % | 1.67 | % | 1.67 | % |

*Source: Prospectus dated 12/1/07.

Distribution Rates/Yields | | Class A | | Class B | | Class C | |

| | | | | | | |

Distribution Rate(3) | | 4.61 | % | 3.79 | % | 3.79 | % |

Taxable-Equivalent Distribution Rate(3),(4) | | 7.55 | | 6.20 | | 6.20 | |

SEC 30-day Yield(5) | | 4.16 | | 3.56 | | 3.56 | |

Taxable-Equivalent SEC 30-day Yield(4),(5) | | 6.81 | | 5.83 | | 5.83 | |

Index Performance(6)

Lehman Brothers Municipal Bond Index (Average Annual Total Returns) | | | |

Six Months | | -0.60 | % |

One Year | | -1.17 | |

Five Years | | 3.35 | |

Ten Years | | 4.71 | |

Lipper Averages(7)

Lipper Missouri Municipal Debt Funds Classification (Average Annual Total Returns) | | | |

Six Months | | -2.48 | % |

One Year | | -4.07 | |

Five Years | | 2.34 | |

Ten Years | | 3.71 | |

Portfolio Manager: Cynthia J. Clemson

Rating Distribution**,(8)

By total investments

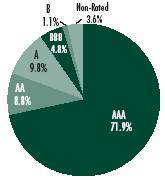

**The rating distribution presented above includes the ratings of securities held by special purpose vehicles in which the Fund holds a residual interest. See Note 1I to the Fund’s financial statements. Absent such securities, the Fund’s rating distribution at 2/29/08, is as follows, and the average rating is AA+.

AAA | | 71.1 | % |

AA | | 9.1 | % |

A | | 10.1 | % |

BBB | | 4.9 | % |

B | | 1.1 | % |

Not Rated | | 3.7 | % |

Fund Statistics(9)

· Number of Issues: | | 93 | |

· Average Maturity: | | 20.3 years | |

· Average Effective Maturity: | | 18.2 years | |

· Average Call Protection: | | 9.1 years | |

· Average Dollar Price: | | $ | 91.20 | |

| | | | |

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. For performance as of the most recent month end, please refer to www.eatonvance.com.

(1) Average Annual Total Returns do not include the 4.75% maximum sales charge for Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B and Class C shares. If sales charges were deducted, the returns would be lower. SEC Average Annual Total Returns for Class A reflect the maximum 4.75% sales charge. SEC Average Annual Total Returns for Class B reflect the applicable CDSC based on the following schedule: 5% - 1st and 2nd years; 4% - 3rd year; 3% - 4th year; 2% - 5th year; 1% - 6th year. SEC Average Annual Total Returns for Class C reflect a 1% CDSC for the first year.

(2) Includes interest expense of 0.17% relating to the Fund’s liability with respect to floating rate notes held by third parties in conjunction with inverse floater securities transactions by the Fund. The Fund also records offsetting interest income relating to the municipal obligation underlying such transactions, and as a result net asset value and performance have not been affected by this expense.

(3) The Fund’s distribution rate represents actual distributions paid to shareholders and is calculated by dividing the last distribution per share (annualized) by the net asset value.

(4) Taxable-equivalent figure assumes a maximum 38.90% combined federal and state income tax rate. A lower tax rate would result in lower tax-equivalent figures.

(5) The Fund’s SEC yield is calculated by dividing the net investment income per share for the 30-day period by the offering price at the end of the period and annualizing the result.

(6) It is not possible to invest directly in an Index. The Index’s total return does not reflect the expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index. Index performance is available as of month end only.

(7) The Lipper Averages are the average annual total returns, at net asset value, of the funds that are in the same Lipper Classification as the Fund. It is not possible to invest in a Lipper Classification. Lipper Classifications may include insured and uninsured funds, as well as leveraged and unleveraged funds. The Lipper Missouri Municipal Debt Funds Classification contained 18, 18, 17 and 15 funds for the 6-month, 1-year, 5-year and 10-year time periods, respectively. Lipper Averages are available as of month end only.

(8) Rating Distribution is determined by dividing the total market value of the issues by the total investments of the Fund.

(9) Excludes securities held by special purpose vehicles in which the Fund holds a residual interest. See Note 1I to the Fund’s financial statements.

10

Eaton Vance North Carolina Municipals Fund as of February 29, 2008

PERFORMANCE INFORMATION AND PORTFOLIO COMPOSITION

Fund Performance(1) | | Class A | | Class B | | Class C | |

Share Class Symbol | | ETNCX | | EVNCX | | ECNCX | |

| | | | | | | |

Average Annual Total Returns (at net asset value) | | | | | | | |

Six Months | | -4.62 | % | -5.03 | % | -5.03 | % |

One Year | | -5.83 | | -6.64 | | -6.55 | |

Five Years | | 2.31 | | 1.57 | | N.A. | |

Ten Years | | 3.40 | | 2.64 | | N.A. | |

Life of Fund† | | 3.80 | | 3.99 | | -0.56 | |

| | | | | | | |

SEC Average Annual Total Returns (including sales charge or applicable CDSC) | | | | | | | |

Six Months | | -9.18 | % | -9.70 | % | -5.96 | % |

One Year | | -10.28 | | -11.15 | | -7.45 | |

Five Years | | 1.31 | | 1.23 | | N.A. | |

Ten Years | | 2.90 | | 2.64 | | N.A. | |

Life of Fund† | | 3.44 | | 3.99 | | -0.56 | |

†Inception date: Class A: 12/7/93; Class B: 10/23/91; Class C: 5/2/06

Total Annual | | | | | | | |

Operating Expenses(2),* | | Class A | | Class B | | Class C | |

| | | | | | | |

Expense Ratio | | 1.35 | % | 2.10 | % | 2.09 | % |

*Source: Prospectus dated 12/1/07.

Distribution Rates/Yields | | Class A | | Class B | | Class C | |

| | | | | | | |

Distribution Rate(3) | | 4.62 | % | 3.80 | % | 3.80 | % |

Taxable-Equivalent Distribution Rate(3),(4) | | 7.73 | | 6.35 | | 6.35 | |

SEC 30-day Yield(5) | | 3.84 | | 3.25 | | 3.26 | |

Taxable-Equivalent SEC 30-day Yield(4),(5) | | 6.42 | | 5.43 | | 5.45 | |

Index Performance(6)

Lehman Brothers Municipal Bond Index (Average Annual Total Returns) | | | |

Six Months | | -0.60 | % |

One Year | | -1.17 | |

Five Years | | 3.35 | |

Ten Years | | 4.71 | |

Lipper Averages(7)

Lipper North Carolina Municipal Debt Funds Classification (Average Annual Total Returns) | | | |

Six Months | | -2.50 | % |

One Year | | -4.09 | |

Five Years | | 2.19 | |

Ten Years | | 3.53 | |

Portfolio Manager: Thomas M. Metzold, CFA

Rating Distribution**,(8)

By total investments

**The rating distribution presented above includes the ratings of securities held by special purpose vehicles in which the Fund holds a residual interest. See Note 1I to the Fund’s financial statements. Absent such securities, the Fund’s rating distribution at 2/29/08, is as follows, and the average rating is AA+.

AAA | | 54.4 | % |

AA | | 28.6 | % |

A | | 9.5 | % |

BBB | | 6.9 | % |

Not Rated | | 0.6 | % |

Fund Statistics(9)

· Number of Issues: | | 72 | |

· Average Maturity: | | 19.5 years | |

· Average Effective Maturity: | | 15.5 years | |

· Average Call Protection: | | 7.2 years | |

· Average Dollar Price: | | $ | 94.03 | |

| | | | |

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. For performance as of the most recent month end, please refer to www.eatonvance.com.

(1) Average Annual Total Returns do not include the 4.75% maximum sales charge for Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B and Class C shares. If sales charges were deducted, the returns would be lower. SEC Average Annual Total Returns for Class A reflect the maximum 4.75% sales charge. SEC Average Annual Total Returns for Class B reflect the applicable CDSC based on the following schedule: 5% - 1st and 2nd years; 4% - 3rd year; 3% - 4th year; 2% - 5th year; 1% - 6th year. SEC Average Annual Total Returns for Class C reflect a 1% CDSC for the first year.

(2) Includes interest expense of 0.58% relating to the Fund’s liability with respect to floating rate notes held by third parties in conjunction with inverse floater securities transactions by the Fund. The Fund also records offsetting interest income relating to the municipal obligation underlying such transactions, and as a result net asset value and performance have not been affected by this expense.

(3) The Fund’s distribution rate represents actual distributions paid to shareholders and is calculated by dividing the last distribution per share (annualized) by the net asset value.

(4) Taxable-equivalent figure assumes a maximum 40.20% combined federal and state income tax rate. A lower tax rate would result in lower tax-equivalent figures.

(5) The Fund’s SEC yield is calculated by dividing the net investment income per share for the 30-day period by the offering price at the end of the period and annualizing the result.

(6) It is not possible to invest directly in an Index. The Index’s total return does not reflect the expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index. Index performance is available as of month end only.

(7) The Lipper Averages are the average annual total returns, at net asset value, of the funds that are in the same Lipper Classification as the Fund. It is not possible to invest in a Lipper Classification. Lipper Classifications may include insured and uninsured funds, as well as leveraged and unleveraged funds. The Lipper North Carolina Municipal Debt Funds Classification contained 31, 31, 25 and 23 funds for the 6-month, 1-year, 5-year and 10-year time periods, respectively. Lipper Averages are available as of month end only.

(8) Rating Distribution is determined by dividing the total market value of the issues by the total investments of the Fund.

(9) Excludes securities held by special purpose vehicles in which the Fund holds a residual interest. See Note 1I to the Fund’s financial statements.

11

Eaton Vance Oregon Municipals Fund as of February 29, 2008

PERFORMANCE INFORMATION AND PORTFOLIO COMPOSITION

Fund Performance(1) | | Class A | | Class B | | Class C | |

Share Class Symbol | | ETORX | | EVORX | | ECORX | |

| | | | | | | |

Average Annual Total Returns (at net asset value) | | | | | | | |

Six Months | | -7.01 | % | -7.38 | % | -7.37 | % |

One Year | | -9.33 | | -10.11 | | -10.10 | |

Five Years | | 2.37 | | 1.61 | | N.A. | |

Ten Years | | 3.52 | | 2.73 | | N.A. | |

Life of Fund† | | 3.81 | | 4.08 | | -2.35 | |

| | | | | | | |

SEC Average Annual Total Returns (including sales charge or applicable CDSC) | | | | | | | |

Six Months | | -11.41 | % | -11.93 | % | -8.28 | % |

One Year | | -13.60 | | -14.44 | | -10.97 | |

Five Years | | 1.37 | | 1.28 | | N.A. | |

Ten Years | | 3.02 | | 2.73 | | N.A. | |

Life of Fund† | | 3.45 | | 4.08 | | -2.35 | |

†Inception date: Class A: 12/28/93; Class B: 12/24/91; Class C: 3/2/06

Total Annual | | | | | | | |

Operating Expenses(2),* | | Class A | | Class B | | Class C | |

| | | | | | | |

Expense Ratio | | 1.25 | % | 2.00 | % | 2.00 | % |

*Source: Prospectus dated 12/1/07.

Distribution Rates/Yields | | Class A | | Class B | | Class C | |

| | | | | | | |

Distribution Rate(3) | | 4.99 | % | 4.14 | % | 4.14 | % |

Taxable-Equivalent Distribution Rate(3),(4) | | 8.44 | | 7.00 | | 7.00 | |

SEC 30-day Yield(5) | | 4.35 | | 3.76 | | 3.75 | |

Taxable-Equivalent SEC 30-day Yield(4),(5) | | 7.35 | | 6.36 | | 6.34 | |

Index Performance(6)

Lehman Brothers Municipal Bond Index (Average Annual Total Returns) | | | |

Six Months | | -0.60 | % |

One Year | | -1.17 | |

Five Years | | 3.35 | |

Ten Years | | 4.71 | |

Lipper Averages(7)

Lipper Oregon Municipal Debt Funds Classification (Average Annual Total Returns) | | | |

Six Months | | -2.11 | % |

One Year | | -3.11 | |

Five Years | | 2.56 | |

Ten Years | | 3.69 | |

Portfolio Manager: Thomas M. Metzold, CFA

Rating Distribution**,(8)

By total investments

**The rating distribution presented above includes the ratings of securities held by special purpose vehicles in which the Fund holds a residual interest. See Note 1I to the Fund’s financial statements. Absent such securities, the Fund’s rating distribution at 2/29/08, is as follows, and the average rating is AA.

AAA | | 54.0 | % |

AA | | 27.5 | % |

A | | 8.6 | % |

BBB | | 1.5 | % |

B | | 2.9 | % |

CCC | | 1.1 | % |

Not Rated | | 4.4 | % |

Fund Statistics(9)

· Number of Issues: | | 98 | |

· Average Maturity: | | 21.8 years | |

· Average Effective Maturity: | | 17.4 years | |

· Average Call Protection: | | 8.9 years | |

· Average Dollar Price: | | $ | 88.57 | |

| | | | |

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. For performance as of the most recent month end, please refer to www.eatonvance.com.

(1) Average Annual Total Returns do not include the 4.75% maximum sales charge for Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B and Class C shares. If sales charges were deducted, the returns would be lower. SEC Average Annual Total Returns for Class A reflect the maximum 4.75% sales charge. SEC Average Annual Total Returns for Class B reflect the applicable CDSC based on the following schedule: 5% - 1st and 2nd years; 4% - 3rd year; 3% - 4th year; 2% - 5th year; 1% - 6th year. SEC Average Annual Total Returns for Class C reflect a 1% CDSC for the first year.

(2) Includes interest expense of 0.47% relating to the Fund’s liability with respect to floating rate notes held by third parties in conjunction with inverse floater securities transactions by the Fund. The Fund also records offsetting interest income relating to the municipal obligation underlying such transactions, and as a result net asset value and performance have not been affected by this expense.

(3) The Fund’s distribution rate represents actual distributions paid to shareholders and is calculated by dividing the last distribution per share (annualized) by the net asset value.

(4) Taxable-equivalent figure assumes a maximum 40.85% combined federal and state income tax rate. A lower tax rate would result in lower tax-equivalent figures.

(5) The Fund’s SEC yield is calculated by dividing the net investment income per share for the 30-day period by the offering price at the end of the period and annualizing the result.

(6) It is not possible to invest directly in an Index. The Index’s total return does not reflect the expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index. Index performance is available as of month end only.

(7) The Lipper Averages are the average annual total returns, at net asset value, of the funds that are in the same Lipper Classification as the Fund. It is not possible to invest in a Lipper Classification. Lipper Classifications may include insured and uninsured funds, as well as leveraged and unleveraged funds. The Lipper Oregon Municipal Debt Funds Classification contained 16, 16, 15 and 14 funds for the 6-month, 1-year, 5-year and 10-year time periods, respectively. Lipper Averages are available as of month end only.

(8) Rating Distribution is determined by dividing the total market value of the issues by the total investments of the Fund.

(9) Excludes securities held by special purpose vehicles in which the Fund holds a residual interest. See Note 1I to the Fund’s financial statements.

12

Eaton Vance South Carolina Municipals Fund as of February 29, 2008

PERFORMANCE INFORMATION AND PORTFOLIO COMPOSITION

Fund Performance(1) | | Class A | | Class B | | Class C | |

Share Class Symbol | | EASCX | | EVSCX | | ECSCX | |

| | | | | | | |

Average Annual Total Returns (at net asset value) | | | | | | | |

Six Months | | -9.18 | % | -9.49 | % | -9.39 | % |

One Year | | -12.43 | | -13.02 | | -12.93 | |

Five Years | | 2.47 | | 1.74 | | N.A. | |

Ten Years | | 3.49 | | 2.71 | | N.A. | |

Life of Fund† | | 3.91 | | 3.89 | | -2.86 | |

| | | | | | | |

SEC Average Annual Total Returns (including sales charge or applicable CDSC) | | | | | | | |

Six Months | | -13.46 | % | -13.93 | % | -10.28 | % |

One Year | | -16.57 | | -17.22 | | -13.77 | |

Five Years | | 1.48 | | 1.40 | | N.A. | |

Ten Years | | 2.98 | | 2.71 | | N.A. | |

Life of Fund† | | 3.55 | | 3.89 | | -2.86 | |

†Inception date: Class A: 2/14/94; Class B: 10/2/92; Class C: 1/12/06

Total Annual | | | | | | | |

Operating Expenses(2),* | | Class A | | Class B | | Class C | |

| | | | | | | |

Expense Ratio | | 1.21 | % | 1.96 | % | 1.96 | % |

*Source: Prospectus dated 12/1/07.

Distribution Rates/Yields | | Class A | | Class B | | Class C | |

| | | | | | | |

Distribution Rate(3) | | 4.95 | % | 4.11 | % | 4.11 | % |

Taxable-Equivalent Distribution Rate(3),(4) | | 8.19 | | 6.80 | | 6.80 | |

SEC 30-day Yield(5) | | 5.03 | | 4.43 | | 4.43 | |

Taxable-Equivalent SEC 30-day Yield(4),(5) | | 8.32 | | 7.33 | | 7.33 | |

Index Performance(6)

Lehman Brothers Municipal Bond Index (Average Annual Total Returns) | | | |

Six Months | | -0.60 | % |

One Year | | -1.17 | |

Five Years | | 3.35 | |

Ten Years | | 4.71 | |

Lipper Averages(7)

Lipper Other States Municipal Debt Funds Classification (Average Annual Total Returns) | | | |

Six Months | | -2.06 | % |

One Year | | -3.06 | |

Five Years | | 2.31 | |

Ten Years | | 3.46 | |

Portfolio Manager: Thomas M. Metzold, CFA

Rating Distribution**,(8)

By total investments

** The rating distribution presented above includes the ratings of securities held by special purpose vehicles in which the Fund holds a residual interest. See Note 1I to the Fund’s financial statements. Absent such securities, the Fund’s rating distribution at 2/29/08, is as follows, and the average rating is AA+.

AAA | | 65.6 | % |

AA | | 8.0 | % |

A | | 14.3 | % |

BBB | | 10.3 | % |

CCC | | 0.3 | % |

Not Rated | | 1.5 | % |

Fund Statistics(9)

· Number of Issues: | | 89 | |

· Average Maturity: | | 23.2 years | |

· Average Effective Maturity: | | 20.2 years | |

· Average Call Protection: | | 8.7 years | |

· Average Dollar Price: | | $ | 91.13 | |

| | | | |

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. For performance as of the most recent month end, please refer to www.eatonvance.com.

(1) Average Annual Total Returns do not include the 4.75% maximum sales charge for Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B and Class C shares. If sales charges were deducted, the returns would be lower. SEC Average Annual Total Returns for Class A reflect the maximum 4.75% sales charge. SEC Average Annual Total Returns for Class B reflect the applicable CDSC based on the following schedule: 5% - 1st and 2nd years; 4% - 3rd year; 3% - 4th year; 2% - 5th year; 1% - 6th year. SEC Average Annual Total Returns for Class C reflect a 1% CDSC for the first year.

(2) Includes interest expense of 0.45% relating to the Fund’s liability with respect to floating rate notes held by third parties in conjunction with inverse floater securities transactions by the Fund. The Fund also records offsetting interest income relating to the municipal obligation underlying such transactions, and as a result net asset value and performance have not been affected by this expense.

(3) The Fund’s distribution rate represents actual distributions paid to shareholders and is calculated by dividing the last distribution per share (annualized) by the net asset value.

(4) Taxable-equivalent figure assumes a maximum 39.55% combined federal and state income tax rate. A lower tax rate would result in lower tax-equivalent figures.

(5) The Fund’s SEC yield is calculated by dividing the net investment income per share for the 30-day period by the offering price at the end of the period and annualizing the result.

(6) It is not possible to invest directly in an Index. The Index’s total return does not reflect the expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index. Index performance is available as of month end only.