UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

| | |

| Investment Company Act file number: | 811-4627 | |

|

| Name of Registrant: | Vanguard Convertible Securities Fund |

| |

| Address of Registrant: | P.O. Box 2600 |

| | Valley Forge, PA 19482 |

| |

| Name and address of agent for service: | Heidi Stam, Esquire |

| | P.O. Box 876 |

| | Valley Forge, PA 19482 |

| | |

| Registrant’s telephone number, including area code: (610) 669-1000 |

|

| Date of fiscal year end: November 30 | |

| |

| Date of reporting period: December 1, 2010 – May 31, 2011 |

|

| Item 1: Reports to Shareholders | |

| Vanguard Convertible Securities Fund |

| Semiannual Report |

|

| May 31, 2011 |

> For the fiscal half-year ended May 31, 2011, Vanguard Convertible Securities Fund returned 11.21%, ahead of its benchmark index and the average return of its peer group.

> Consistent with their hybrid investment characteristics, convertible securities produced returns between those of the broad U.S. stock and bond markets—after an extended period of outperforming both.

> The fund benefited from merger and acquisition activity and from its exposure to mid- and small-capitalization convertible securities.

| Contents | |

| |

| Your Fund’s Total Returns. | 1 |

| Chairman’s Letter. | 2 |

| Advisor’s Report. | 7 |

| Fund Profile. | 11 |

| Performance Summary. | 13 |

| Financial Statements. | 14 |

| About Your Fund’s Expenses. | 27 |

| Trustees Approve Advisory Arrangement. | 29 |

| Glossary. | 30 |

Please note: The opinions expressed in this report are just that—informed opinions. They should not be considered promises or advice.

Also, please keep in mind that the information and opinions cover the period through the date on the front of this report. Of course, the

risks of investing in your fund are spelled out in the prospectus.

See the Glossary for definitions of investment terms used in this report.

Cover photograph: Jean Maher.

Your Fund’s Total Returns

| |

| Six Months Ended May 31, 2011 | |

| | Total |

| | Returns |

| Vanguard Convertible Securities Fund | 11.21% |

| Spliced Convertibles Composite Index | 9.00 |

| Convertible Securities Funds Average | 10.88 |

Spliced Convertibles Composite Index: CS First Boston Convertible Securities Index through November 30, 2004; Bank of America Merrill

Lynch All US Convertibles Index (formerly Bank of America Merrill Lynch All Convertibles-All Qualities Index) through December 31, 2010; and

70% Bank of America Merrill Lynch All US Convertibles Index and 30% Bank of America Merrill Lynch Global 300 Convertibles ex-US Index

(hedged) thereafter.

Convertible Securities Funds Average: Derived from data provided by Lipper Inc.

Your Fund’s Performance at a Glance

November 30, 2010 , Through May 31, 2011

| | | | |

| | | | Distributions Per Share |

| | Starting | Ending | Income | Capital |

| | Share Price | Share Price | Dividends | Gains |

| Vanguard Convertible Securities Fund | $13.85 | $14.12 | $0.257 | $0.955 |

1

Chairman’s Letter

Dear Shareholder,

For the six months ended May 31, 2011, investors continued to endorse convertible securities in general and the holdings of Vanguard Convertible Securities Fund in particular. The fund returned 11.21% for the period, better than the 9.00% return of its convertibles market benchmark index and the 10.88% average return of its peer group.

Consistent with our expectations for these hybrid securities, the convertibles market produced six-month returns between those of the broader U.S. stock and bond markets. While the fund had outperformed these two asset classes for more than two years, those were atypical times. The price of convertibles rose on increased demand, as investors sought alternatives to the generally lower yields available in the broader bond market without taking on the potentially greater risk of equities.

Please note that on May 11, we lowered the minimum investment requirement to open and maintain an account for several Vanguard funds, including Convertible Securities, to $3,000. This was done as part of our ongoing efforts to increase the accessibility of our funds.

2

Stock prices followed corporate profits higher

During the past six months, global stock markets powered past a series of unnerving developments—financial drama in Europe, natural and nuclear disaster in Japan, and geopolitical upheaval in commodity markets. The broad U.S. stock market returned more than 15% for the period, buoyed by surprising strength in corporate profits. Toward the end of the fiscal half-year, however, a pullback in the manufacturing sector and unexpected weakness in the labor market sounded notes of caution.

International stocks followed a similar trajectory, returning almost 14% for the period. In emerging markets and in most developed markets, strength in local currencies boosted returns for U.S.-based investors.

In the broad U.S. bond market, a late-stage change of direction

Through much of the fiscal half-year, bond market returns hovered near—or below—0%. With the economy seeming to find its footing, interest rates rose slowly but steadily. Investors were concerned that accelerating growth might eventually lead to higher inflation, perhaps sooner rather than later. Rising rates put pressure on bond prices.

| | | |

| Market Barometer | | | |

| |

| | Total Returns |

| | Periods Ended May 31, 2011 |

| | Six | One | Five Years |

| | Months | Year | (Annualized) |

| Stocks | | | |

| Russell 1000 Index (Large-caps) | 15.49% | 26.81% | 3.69% |

| Russell 2000 Index (Small-caps) | 17.34 | 29.75 | 4.70 |

| Dow Jones U.S. Total Stock Market Index | 15.20 | 27.10 | 4.07 |

| MSCI All Country World Index ex USA (International) | 13.58 | 29.95 | 3.95 |

| |

| Bonds | | | |

| Barclays Capital U.S. Aggregate Bond Index (Broad | | | |

| taxable market) | 1.91% | 5.84% | 6.63% |

| Barclays Capital Municipal Bond Index (Broad | | | |

| tax-exempt market) | 2.04 | 3.18 | 4.78 |

| Citigroup Three-Month U.S. Treasury Bill Index | 0.06 | 0.15 | 1.94 |

| |

| CPI | | | |

| Consumer Price Index | 3.27% | 3.57% | 2.22% |

3

Later in the period, however, disappointing economic news—including in the housing and labor markets—doused worries about inflation. Perhaps counterintuitively, bad news for the economy spells good news for bonds: As yields retreated, bond prices rallied.

The returns of money market instruments, such as 3-month Treasury bills, remained near 0%, consistent with the Federal Reserve Board’s target for short-term interest rates.

Convertible securities climb as stock market continues to rise

Vanguard Convertible Securities Fund provides diversified exposure to a relatively small asset class that includes attractive

features of both stocks and bonds. While the performance of convertibles is tied to the price of their underlying common stocks, convertibles feature more downside protection than their equity counterparts. The more that the relevant stock rises in price, the more a convertible security’s price will rally, simply because the security gives the investor the right to convert into stock at a specified price (the conversion price). Because the instrument is a bond (or bond-like, in the case of convertible preferred stock), however, there’s a limit to how much its price can fall––unless the issuer defaults. Such occurrences have been rare under the watch of the experienced credit research department of Oaktree Capital

Management, L.P., the fund’s advisor.

| | |

| Expense Ratios | | |

| Your Fund Compared With Its Peer Group | | |

| | | Peer Group |

| | Fund | Average |

| Convertible Securities Fund | 0.68% | 1.40% |

The fund expense ratio shown is from the prospectus dated March 23, 2011, and represents estimated costs for the current fiscal year. For

the six months ended May 31, 2011, the fund’s annualized expense ratio was 0.68%. The peer-group expense ratio is derived from data

provided by Lipper Inc. and captures information through year-end 2010.

Peer group: Convertible Securities Funds.

4

The stock market’s advance over the past six months is, of course, reflected in the Convertible Securities Fund’s performance for this period, as its holdings appreciated in value, especially over the first three months. Demand for convertible securities was strong, especially for the limited supply of new issues as some companies replaced convertibles with nonconvertible bonds. (With interest rates low, some companies retired their convertible debt, which has the potential to dilute equity, and replaced it with straight debt at prevailing low rates.)

Compared with its benchmark, the fund benefited from heavier exposure to secur-ities issued by medium- and small-sized companies, which outperformed those issued by large companies. Selected holdings in the health care and information technology sectors boosted the fund’s performance. Merger and acquisition activity in these two sectors also helped the fund, as the completed acquisitions validated the advisor’s assessments of company valuations. The advisor’s decision to sidestep some of the weaker segments of the financial sector also helped the fund.

On December 20, 2010, the trustees expanded the fund’s investment strategy. The fund, which previously was limited to investing up to 20% of its assets in foreign securities, now has no global restrictions. This mandate increases the fund’s range of investment opportunities, particularly at

the higher-quality end of the convertibles spectrum, as international companies that issue convertible debt typically have higher credit ratings than their domestic counterparts. As a result of the fund’s expanded mandate, effective January 1, 2011, the fund uses a composite bench-mark of U.S. and global securities.

Oaktree portfolio managers Jean-Paul

Nedelec and Abe Ofer direct the fund’s international holdings separately from long-time portfolio manager Larry Keele, whose team continues to direct the fund’s domestic assets. Messrs. Nedelec and Ofer have boosted the fund’s international allocation to about 15% of assets, on its way to the trustees’ target allocation of 30% of assets.

Oaktree’s expertise, talent have served fund well

Given their unusual hybrid nature, convert-ible securities occupy a unique place in the investment landscape. Because of the idiosyncrasies of this relatively obscure corner of the capital markets, a talented advisor can also uncover opportunities that are not available in other asset classes.

This year Vanguard Convertible Securities Fund marks the 15th anniversary of its relationship with advisor Oaktree. Since assuming responsibility for the portfolio, Oaktree has distinguished itself as an uncommonly skilled arbiter of opportunity in the complex convertibles market.

5

On June 17, just after the close of the

fiscal period, the Convertible Securities

Fund celebrated another milestone—its

25th anniversary. Much has changed in

the financial markets in the ensuing years,

but the principles on which the fund was

based still hold true.

Of course, no one can ever know what the

future holds for the financial markets or

convertible securities. At Vanguard, we

encourage you to create a diversified and

well-balanced portfolio that is appropriate

for your long-term goals, risk tolerance, and

time horizon. With its expert management

and low costs, the Convertible Securities

Fund can play a useful role in such a

diversified portfolio.

Thank you for entrusting your assets

to Vanguard.

Sincerely,

F. William McNabb III

Chairman and Chief Executive Officer

June 13, 2011

Advisor’s Report

We are pleased to report that during the first half of its 2011 fiscal year Vanguard Convertible Securities Fund continued to meet its long-term objective of producing positive equity-type returns. The fund’s attractive absolute return for the six months ended May 31, 2011, was ahead of the return of its convertibles benchmark index. The fund also participated in a reasonably high percentage of the return of the strong stock market, capturing 75% of the return of the S&P 500 stock index for the period.

The six months were a positive time for investing in financial assets, though at times negative macroeconomic events took a toll on the investing environment.

The fund invests in a highly diversified global portfolio of convertible bonds and convertible preferred shares, with an emphasis on investments in convertible bonds that have a relatively near-term maturity or put date. We concentrate on what we call “balanced” convertibles,

| |

| Major Portfolio Changes | |

| Six Months Ended May 31, 2011 | |

| |

| Additions | Comments |

| |

| Illumina Inc. | Short-dated convertible on high-growth, high-credit-quality life |

| (0.25% convertible note due 3/15/16) | sciences company. |

| |

| James River Coal Company | Attractive long-term investment in the coal industry. |

| (3.125% convertible note due 3/15/18) | |

| Mentor Graphics Corp. | New-issue convertible with attractive yield and reasonable |

| (4.00% convertible note due 4/1/31) | upside potential. |

| |

| Omnicare Inc. | Cheap convertible preferred with improving equity story. |

| (4.00% convertible preferred) | |

| San Miguel Corporation | San Miguel operates in the brewing, food, power generation, and |

| (2.00% convertible note due 5/5/14) | infrastructure industries in the Philippines. The convertible provides |

| | a balanced exposure to the performance of the underlying share. |

| |

| YTL Corporation | YTL is a prominent Malaysian company that controls companies in |

| (1.875% convertible note due 3/18/15) | utilities, construction, and property development. The convertible |

| | has very good downside protection and should capture a |

| | reasonable portion of the equity’s advance. |

| |

| Reductions | Comments |

| Cephalon Inc. | Sold after company agreed to be acquired by Teva Pharmaceutical. |

| (2.50% convertible note due 5/1/14) | |

| Ciena Corp. | Sold out of both issues because of rapid appreciation. |

| (3.75% convertible note due 10/15/18 and | |

| 4.00% convertible note due 3/15/15) | |

| Dana Holding Corp. | Sold all after substantial appreciation. |

| (4.00% convertible preferred) | |

| Lincare Holdings Inc. | Sold all after the convertible became statistically unattractive. |

| (2.75% convertible note due 11/1/37) | |

7

securities that in our opinion have a reasonable yield and stable credit quality as well as good call protection and low-to-moderate conversion premiums. We believe these securities have a favorable balance of upside potential to downside risk. In addition, while the fund underweights riskier, yet potentially higher return, convertible preferred shares, we do consider them part of our investable universe and we make some use of them. The fund does not invest in common stocks or nonconvertible debt. We do not attempt market timing and therefore keep the fund fully invested, holding only a small percentage in cash reserves for potential investments. We believe that with careful security selection, a portfolio of attractive convertible securities can produce equity-type returns with lower volatility and lower structural risk over the long term.

The investment environment

Convertible securities performed very well during the period, on both an absolute and a relative basis. They captured a significant amount of the return of their underlying stocks—in a period when most stocks performed well. Most important, convertibles provided a strong measure of downside protection during the times of market weakness. Convertibles tend to be highly correlated with the Russell 2000 Index, which tracks small- and mid-capitalization stocks; thus, the fund’s performance reflects the large advance made by that index during the period. It is also interesting to note that the largest-capitalization equities (e.g., the Dow Jones stocks) were moving sharply higher at the

same time. Continuing the trend of recent reporting periods, we saw strong and steady demand for convertibles from a wide variety of investors.

New convertible issuance in the United States remained at a relatively low level, with only $18.4 billion of new paper coming to market during the six months ended

May 31. Some of the largest convertible deals were issued by Clearwire, Illumina, MetLife, and PPL Corp. Given the overall strong demand for convertibles, all of the new issues were well oversubscribed—but, unfortunately, this led to some issues being repriced to richer terms. Not surpris-ingly, some of these repriced deals ended up cheapening after issuance, as some of the indicated strong demand quickly faded. We remain highly selective in our purchases of new deals and believe that the cheapening of deals right after issuance will engender more realistic prices for deals down the road. We expect to see vastly increased issuance only after a rise in interest rates makes straight debt financing less attractive to issuers.

Given the combination of equity strength and volatility, we were reasonably busy throughout the period, with a wide variety of names affecting our portfolio and its performance. We took profits on several names that had posted large gains during late 2010 and early 2011, while we reduced or exited our positions in others as they became unattractive from a convertible valuation perspective or because of weakening company fundamentals.

8

Our successes

Our positive performance compared to the benchmark index in the six-month period occurred because many of our investments advanced at an above-average rate and because of an absence of serious detractors from performance. Our best contributors during the period were convertibles from Cubist Pharmaceuticals, MGM Resorts International, Micron Technology, and SandRidge Energy. The portfolio benefited from an increase in mergers and acquisitions, as a couple of the companies we held were acquired.

Given the high absolute return, we were reasonably active in profit-taking as several convertibles appreciated to pure-equity levels. We sold these positions and invested the proceeds into more balanced securities sourced from the primary or secondary markets. Our scaled profit-taking has the desirable effect of reducing the overall equity sensitivity of the portfolio (and the resulting downside risk) as prices rise. Despite the overall positive investing sentiment and the strong demand for convertible paper, we had no trouble finding attractive, balanced convertibles in which to reinvest the sale proceeds.

Our shortfalls

Unsurprisingly, given the market’s overall strong advance during the period, the fund had very few absolute negative performers. Of course, any well-diversified portfolio will have its share of relative underperformers, and our positions in AMR, Eastman Kodak, Paladin Energy, and ShengdaTech did not perform as well as expected. On balance, we had very few negative fundamental surprises during the period, and we were able to outperform the fund’s convertibles index through careful security selection and our normal discipline of scaled selling.

The fund’s positioning

Toward the end of 2010, the fund adopted a more global mandate, which meant that the previous limit (up to 20% of assets) on foreign holdings was eliminated. As a result of this shift in mandate, we enlisted the expertise of our non-U.S. convertibles management team. The team led by Abe Ofer and Jean-Paul Nedelec, who have managed Oaktree’s non-U.S. convertible portfolios since 1994, follows the same investment strategy as the U.S. convertibles team. The non-U.S. strategy focuses on non-U.S. company convertibles around the globe, a market which is about the same size as the U.S. convertibles market. Thus this expansion of the mandate gives the fund a more global approach and increases its possibilities and its diversification.

9

Both the fund’s U.S. and non-U.S. managers will continue to invest in “balanced” convertibles and take profits in highly appreciated securities, redeploying the proceeds into securities with a more attractive upside/downside profile, via both new issues and secondary market purchases. The portfolio remains fully invested, and we continue to find purchase opportunities across many parts of the market. However, given the advances in prices, it is now much more difficult to find attractive convertibles than it was a year ago. The fund’s current yield is relatively attractive, and our average conversion premium is about 30.0%, affording the portfolio reasonable upside participation if the equity market advances. Overall, both the fundamental underpinnings and the technical picture of the convertible market appear favorable at present.

Larry W. Keele, CFA

Principal and Founder

Jean-Paul Nedelec, Managing Director

Abe Ofer, Managing Director

Oaktree Capital Management, L.P.

June 20, 2011

10

Convertible Securities Fund

Fund Profile

As of May 31, 2011

| |

| Portfolio Characteristics | |

| Ticker Symbol | VCVSX |

| Number of Securities | 205 |

| 30-Day SEC yield | 3.09% |

| Conversion Premium | 31.7% |

| Average Weighted Maturity | 5.0 years |

| Average Coupon | 2.9% |

| Average Duration | 4.4 years |

| Foreign Holdings | 15.1% |

| Turnover Rate (Annualized) | 103% |

| Expense Ratio1 | 0.68% |

| Short-Term Reserves | 3.3% |

| |

| Distribution by Maturity (% of fixed income |

| portfolio) | |

| Under 1 Year | 0.9% |

| 1 - 5 Years | 74.4 |

| 5 - 10 Years | 21.0 |

| 20 - 30 Years | 3.7 |

| |

| Distribution by Credit Quality (% of fixed | |

| income portfolio) | |

| AAA | 0.1% |

| AA | 0.3 |

| A | 4.6 |

| BBB | 3.3 |

| BB | 18.5 |

| B | 16.7 |

| Below B | 7.3 |

| Not Rated | 49.2 |

| For information about these ratings, see the Glossary entry for Credit Quality. |

| | |

| Total Fund Volatility Measures | |

| | Spliced | DJ |

| | Conv. | U.S. Total |

| | Comp. | Market |

| | Index | Index |

| R-Squared | 0.97 | 0.79 |

| Beta | 0.94 | 0.72 |

| These measures show the degree and timing of the fund’s fluctuations compared with the indexes over 36 months. |

| | |

| Ten Largest Holdings (% of total net assets) |

| Micron Technology Inc. | Semiconductors | 3.0% |

| Gilead Sciences Inc. | Biotechnology | 2.6 |

| SBA Communications | Wireless | |

| Corp. | Telecommunication | |

| | Services | 2.5 |

| Illumina Inc. | Biotechnology | 2.2 |

| MGM Resorts | | |

| International | Casinos & Gaming | 2.2 |

| James River Coal Co. | Industrial Metals & | |

| | Minerals | 1.9 |

| General Motors Co. | Automobile | |

| | Manufacturers | 1.9 |

| Owens-Brockway Glass | Packaging & | |

| Container Inc. | Containers | 1.7 |

| SunPower Corp. | Semiconductors | 1.7 |

| Lennar Corp. | Residential | |

| | Construction | 1.6 |

| Top Ten | | 21.3% |

| The holdings listed exclude any temporary cash investments and equity index products. |

1 The expense ratio shown is from the prospectus dated March 23, 2011, and represents estimated costs for the current fiscal year. For the

six months ended May 31, 2011, the annualized expense ratio was 0.68%.

11

Convertible Securities Fund

| |

| Sector Diversification (% of market | |

| exposure) | |

| |

| Consumer | |

| Discretionary | 12.0% |

| Consumer Staples | 1.4 |

| Energy | 10.6 |

| Financials | 10.8 |

| Health Care | 16.3 |

| Industrials | 9.9 |

| Information | |

| Technology | 26.1 |

| Materials | 7.8 |

| Telecommunication | |

| Services | 4.6 |

| Utilities | 0.5 |

12

Convertible Securities Fund

Performance Summary

All of the returns in this report represent past performance, which is not a guarantee of future results that may be achieved by the fund. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at vanguard.com/performance.) Note, too, that both investment returns and principal value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost. The returns shown do not reflect taxes that a shareholder would pay on fund distributions or on the sale of fund shares.

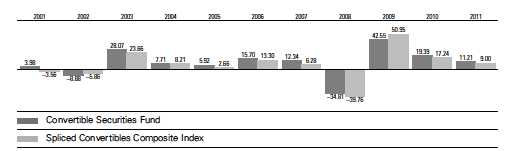

Fiscal-Year Total Returns (%): November 30, 2000, Through May 31, 2011

Spliced Convertibles Composite Index: CS First Boston Convertible Securities Index through November 30, 2004; Bank of America Merrill

Lynch All US Convertibles Index (formerly Bank of America Merrill Lynch All Convertibles-All Qualities Index) through December 31, 2010; and

70% Bank of America Merrill Lynch All US Convertibles Index and 30% Bank of America Merrill Lynch Global 300 Convertibles ex-US Index

(hedged) thereafter.

Note: For 2011, performance data reflect the six months ended May 31, 2011.

Average Annual Total Returns: Periods Ended March 31, 2011

This table presents returns through the latest calendar quarter—rather than through the end of the fiscal period.

Securities and Exchange Commission rules require that we provide this information.

| | | | | | |

| | | | | Ten Years |

| | Inception Date | One Year | Five Years | Income | Capital | Total |

| Convertible Securities | | | | | | |

| Fund | 6/17/1986 | 18.94% | 7.44% | 3.84% | 4.18% | 8.02% |

Vanguard fund returns do not reflect the 1% fee on redemptions of shares held for less than one year.

See Financial Highlights for dividend and capital gains information.

13

Convertible Securities Fund

Financial Statements (unaudited)

Statement of Net Assets

As of May 31, 2011

The fund reports a complete list of its holdings in regulatory filings four times in each fiscal year, at the quarter-ends. For the second and fourth fiscal quarters, the lists appear in the fund’s semiannual and annual reports to shareholders. For the first and third fiscal quarters, the fund files the lists with the Securities and Exchange Commission on Form N-Q. Shareholders can look up the fund’s Forms N-Q on the SEC’s website at sec.gov. Forms N-Q may also be reviewed and copied at the SEC’s Public Reference Room (see the back cover of this report for further information).

| | | | |

| | | | Face | Market |

| | | Maturity | Amount‡ | Value |

| | Coupon | Date | (000) | ($000) |

| Convertible Bonds (84.2%) | | | | |

| Consumer Discretionary (7.8%) | | | | |

| 1 Aegis Group Capital Cvt. | 2.500% | 4/20/15 | 2,400 | 4,565 |

| 2 Aeon Co. Ltd. Cvt. | 0.300% | 11/22/13 | 107,000 | 1,474 |

| Central European Media Enterprises Ltd. Cvt. | 5.000% | 11/15/15 | 780 | 727 |

| 3 Gaylord Entertainment Co. Cvt. | 3.750% | 10/1/14 | 9,285 | 12,500 |

| 4 GOME Electrical Appliances Holding Ltd. Cvt. | 3.000% | 9/25/14 | 14,500 | 2,793 |

| 3 Iconix Brand Group Inc. Cvt. | 2.500% | 6/1/16 | 5,930 | 6,278 |

| Interpublic Group of Cos. Inc. Cvt. | 4.750% | 3/15/23 | 7,440 | 9,207 |

| 5 Intime Department Store Group Co. Ltd. Cvt. | 1.750% | 10/27/13 | 19,000 | 2,993 |

| 3 Lennar Corp. Cvt. | 2.750% | 12/15/20 | 33,075 | 36,217 |

| Liberty Media LLC Cvt. | 3.125% | 3/30/23 | 22,835 | 27,545 |

| MGM Resorts International Cvt. | 4.250% | 4/15/15 | 40,795 | 47,475 |

| Newford Capital Ltd. Cvt. | 0.000% | 5/12/16 | 4,700 | 4,658 |

| 6 Nokian Renkaat OYJ Cvt. | 0.000% | 6/27/14 | 3,000 | 5,035 |

| 5 Power Regal Group Ltd. Cvt. | 2.250% | 6/2/14 | 15,810 | 2,331 |

| 6 Steinhoff Finance Holding GmbH Cvt. | 5.000% | 5/22/16 | 3,150 | 4,946 |

| 1 TUI Travel PLC Cvt. | 4.900% | 4/27/17 | 1,900 | 3,058 |

| | | | | 171,802 |

| Consumer Staples (1.3%) | | | | |

| 5 Glory River Holdings Ltd. Cvt. | 1.000% | 7/29/15 | 26,600 | 3,638 |

| Nash Finch Co. Cvt. | 1.631% | 3/15/35 | 12,230 | 5,794 |

| Olam International Ltd. Cvt. | 6.000% | 10/15/16 | 1,800 | 2,429 |

| 6 Pescanova SA Cvt. | 5.125% | 4/20/17 | 1,250 | 1,775 |

| 6 Pescanova SA Cvt. | 6.750% | 3/5/15 | 2,050 | 3,483 |

| San Miguel Corp. Cvt. | 2.000% | 5/5/14 | 5,400 | 5,792 |

| Smithfield Foods Inc. Cvt. | 4.000% | 6/30/13 | 3,315 | 3,870 |

| Wilmar International Ltd. Cvt. | 0.000% | 12/18/12 | 2,000 | 2,542 |

| | | | | 29,323 |

| Energy (6.7%) | | | | |

| 6 Aabar Investments PJSC Cvt. | 4.000% | 5/27/16 | 1,300 | 1,878 |

| BPZ Resources Inc. Cvt. | 6.500% | 3/1/15 | 7,010 | 7,255 |

| ChesapeakeEnergy Corp. Cvt. | 2.750% | 11/15/35 | 15,520 | 17,790 |

| 6 Cie Generale de Geophysique - Veritas Cvt. | 1.750% | 1/1/16 | 2,060 | 3,377 |

| Goodrich Petroleum Corp. Cvt. | 5.000% | 10/1/29 | 585 | 587 |

| 3 James River Coal Co. Cvt. | 3.125% | 3/15/18 | 24,305 | 24,700 |

| 3 James River Coal Co. Cvt. | 4.500% | 12/1/15 | 15,440 | 17,949 |

| Lukoil International Finance BV Cvt. | 2.625% | 6/16/15 | 4,700 | 5,457 |

| Massey Energy Co. Cvt. | 3.250% | 8/1/15 | 14,510 | 16,142 |

14

| | | | |

| Convertible Securities Fund | | | | |

| |

| |

| |

| | | | Face | Market |

| | | Maturity | Amount‡ | Value |

| | Coupon | Date | (000) | ($000) |

| Newpark Resources Inc. Cvt. | 4.000% | 10/1/17 | 2,880 | 3,528 |

| Paladin Energy Ltd. Cvt. | 3.625% | 11/4/15 | 4,757 | 4,555 |

| Peabody Energy Corp. Cvt. | 4.750% | 12/15/41 | 9,470 | 11,932 |

| PetroBakken Energy Ltd. Cvt. | 3.125% | 2/8/16 | 3,600 | 3,411 |

| 3 Petroleum Development Corp. Cvt. | 3.250% | 5/15/16 | 8,245 | 8,925 |

| Petrominerales Ltd. Cvt. | 2.625% | 8/25/16 | 2,400 | 2,946 |

| 7 Progress Energy Resources Corp. Cvt. | 5.250% | 10/31/14 | 3,467 | 3,651 |

| 6 Renewable Energy Corp. ASA Cvt. | 6.500% | 6/4/14 | 1,850 | 2,509 |

| Seadrill Ltd. Cvt. | 3.375% | 10/27/17 | 2,700 | 3,275 |

| Subsea 7 SA Cvt. | 2.250% | 10/11/13 | 1,500 | 1,864 |

| 6 Technip SA Cvt. | 0.500% | 1/1/16 | 831 | 1,349 |

| TMK Bonds SA Cvt. | 5.250% | 2/11/15 | 3,800 | 4,195 |

| | | | | 147,275 |

| Financials (7.3%) | | | | |

| 3 American Equity Investment Life Holding Co. Cvt. | 3.500% | 9/15/15 | 14,045 | 16,854 |

| 3 American Equity Investment Life Holding Co. Cvt. | 5.250% | 12/6/29 | 5,755 | 8,726 |

| BES Finance Ltd. Cvt. | 1.625% | 4/15/13 | 5,600 | 5,337 |

| Billion Express Investments Ltd. Cvt. | 0.750% | 10/18/15 | 3,700 | 4,565 |

| 3 BioMed Realty LP Cvt. | 3.750% | 1/15/30 | 6,785 | 8,320 |

| 8 CapitaLand Ltd. Cvt. | 2.875% | 9/3/16 | 5,500 | 4,448 |

| Dollar Financial Corp. Cvt. | 3.000% | 4/1/28 | 13,780 | 18,345 |

| 6 Fonciere Des Regions Cvt. | 3.340% | 1/1/17 | 2,569 | 3,765 |

| Forest City Enterprises Inc. Cvt. | 3.625% | 10/15/14 | 2,085 | 2,924 |

| 3 Goldman Sachs Group Inc. Cvt. | 0.250% | 2/28/17 | 27,190 | 25,615 |

| 9 Graubuendner Kantonalbank Cvt. | 2.000% | 5/8/14 | 4,540 | 5,569 |

| 3 Host Hotels & Resorts LP Cvt. | 2.500% | 10/15/29 | 14,445 | 20,133 |

| 6 Industrivarden AB Cvt. | 1.875% | 2/27/17 | 1,350 | 1,946 |

| 6 Kreditanstalt fuer Wiederaufbau Cvt. | 1.500% | 7/30/14 | 1,200 | 1,960 |

| 3 NorthStar Realty Finance LP Cvt. | 7.500% | 3/15/31 | 9,105 | 8,855 |

| Old Republic International Corp. Cvt. | 3.750% | 3/15/18 | 2,425 | 2,416 |

| PHH Corp. Cvt. | 4.000% | 9/1/14 | 12,305 | 13,566 |

| 4 ShuiOn Land Ltd. Cvt. | 4.500% | 9/29/15 | 17,100 | 2,708 |

| 6 Wereldhave NV Cvt. | 2.875% | 11/18/15 | 2,000 | 2,821 |

| 8 Yanlord Land Group Ltd. Cvt. | 5.850% | 7/13/14 | 3,000 | 2,492 |

| | | | | 161,365 |

| Health Care (14.4%) | | | | |

| Alere Inc. Cvt. | 3.000% | 5/15/16 | 17,605 | 20,356 |

| BioMarin Pharmaceutical Inc. Cvt. | 1.875% | 4/23/17 | 6,145 | 9,171 |

| 6 Celesio Finance B.V. Cvt. | 3.750% | 10/29/14 | 600 | 915 |

| CharlesRiver Laboratories International Inc. Cvt. | 2.250% | 6/15/13 | 15,802 | 16,474 |

| ChemedCorp. Cvt. | 1.875% | 5/15/14 | 17,417 | 18,070 |

| ChinaMedical Technologies Inc. Cvt. | 4.000% | 8/15/13 | 1,274 | 1,077 |

| 3 ChinaMedical Technologies Inc. Cvt. | 6.250% | 12/15/16 | 10,651 | 10,132 |

| Cubist Pharmaceuticals Inc. Cvt. | 2.500% | 11/1/17 | 11,250 | 16,425 |

| Gilead Sciences Inc. Cvt. | 0.625% | 5/1/13 | 3,420 | 4,113 |

| 3 Gilead Sciences Inc. Cvt. | 1.625% | 5/1/16 | 46,220 | 53,789 |

| Hologic Inc. Cvt. | 2.000% | 12/15/37 | 19,665 | 23,254 |

| 3 Illumina Inc. Cvt. | 0.250% | 3/15/16 | 46,035 | 48,509 |

| LifePoint Hospitals Inc. Cvt. | 3.500% | 5/15/14 | 17,037 | 18,826 |

| Molina Healthcare Inc. Cvt. | 3.750% | 10/1/14 | 11,085 | 12,886 |

| 6 Orpea Cvt. | 3.875% | 1/1/16 | 1,559 | 2,346 |

| Qiagen Euro Finance SA Cvt. | 3.250% | 5/16/26 | 2,300 | 2,789 |

| Salix Pharmaceuticals Ltd. Cvt. | 2.750% | 5/15/15 | 13,113 | 14,998 |

| Teleflex Inc. Cvt. | 3.875% | 8/1/17 | 7,755 | 9,005 |

| 2 Unicharm Corp. Cvt. | 0.000% | 9/24/15 | 260,000 | 3,466 |

15

| | | | |

| Convertible Securities Fund | | | | |

| |

| |

| |

| | | | Face | Market |

| | | Maturity | Amount‡ | Value |

| | Coupon | Date | (000) | ($000) |

| Vertex Pharmaceuticals Inc. Cvt. | 3.350% | 10/1/15 | 10,760 | 13,692 |

| Viropharma Inc. Cvt. | 2.000% | 3/15/17 | 12,853 | 15,970 |

| | | | | 316,263 |

| Industrials (9.3%) | | | | |

| 3 AAR Corp. Cvt. | 1.625% | 3/1/14 | 2,505 | 2,511 |

| 6 Abengoa SA Cvt. | 4.500% | 2/3/17 | 3,250 | 4,733 |

| Alliant Techsystems Inc. Cvt. | 3.000% | 8/15/24 | 15,298 | 17,229 |

| AMR Corp. Cvt. | 6.250% | 10/15/14 | 29,252 | 30,130 |

| 2 Asahi Glass Co. Ltd. Cvt. | 0.000% | 11/14/14 | 415,000 | 5,538 |

| Avis Budget Group Inc. Cvt. | 3.500% | 10/1/14 | 680 | 881 |

| Barnes Group Inc. Cvt. | 3.375% | 3/15/27 | 8,215 | 8,862 |

| 3 Barnes Group Inc. Cvt. | 3.375% | 3/15/27 | 5,240 | 5,653 |

| 4 Bright North Ltd. Cvt. | 1.250% | 4/13/16 | 17,000 | 2,676 |

| 3 CBIZInc. Cvt. | 4.875% | 10/1/15 | 2,565 | 3,209 |

| Covanta Holding Corp. Cvt. | 3.250% | 6/1/14 | 17,570 | 20,293 |

| General Cable Corp. Cvt. | 0.875% | 11/15/13 | 16,209 | 17,323 |

| 3 Greenbrier Cos. Inc. Cvt. | 3.500% | 4/1/18 | 15,755 | 16,149 |

| 6 Iliad SA Cvt. | 2.200% | 1/1/12 | 400 | 612 |

| 3 Kaman Corp. Cvt. | 3.250% | 11/15/17 | 5,305 | 6,625 |

| 6 Kloeckner & Co. Financial Services SA Cvt. | 2.500% | 12/22/17 | 2,950 | 4,823 |

| Larsen & Toubro Ltd. Cvt. | 3.500% | 10/22/14 | 2,600 | 3,061 |

| Meritor Inc. Cvt. | 4.000% | 2/15/27 | 4,125 | 4,012 |

| Meritor Inc. Cvt. | 4.625% | 3/1/26 | 11,410 | 12,637 |

| 6 Misarte Cvt. | 3.250% | 1/1/16 | 2,842 | 4,624 |

| Navistar International Corp. Cvt. | 3.000% | 10/15/14 | 4,815 | 7,006 |

| 6 Nexans SA Cvt. | 1.500% | 1/1/13 | 2,182 | 3,666 |

| 2 Nidec Corp. Cvt. | 0.000% | 9/18/15 | 270,000 | 3,437 |

| PB Issuer No 2 Ltd. Cvt. | 1.750% | 4/12/16 | 2,810 | 2,735 |

| 7 Russel Metals Inc. Cvt. | 7.750% | 9/30/16 | 3,015 | 3,603 |

| 6 SGL Carbon SE Cvt. | 0.750% | 5/16/13 | 1,750 | 2,714 |

| 6 SGL Carbon SE Cvt. | 3.500% | 6/30/16 | 1,000 | 1,973 |

| 6 Societa Iniziative Autostradali e Servizi SPA Cvt. | 2.625% | 6/30/17 | 2,993 | 4,329 |

| 6 TEM Cvt. | 4.250% | 1/1/15 | 1,758 | 2,761 |

| | | | | 203,805 |

| Information Technology (25.0%) | | | | |

| 6 Alcatel-Lucent Cvt. | 5.000% | 1/1/15 | 748 | 1,510 |

| Alliance Data Systems Corp. Cvt. | 1.750% | 8/1/13 | 15,660 | 20,006 |

| 6 Atos Origin SA Cvt. | 2.500% | 1/1/16 | 2,466 | 4,113 |

| 1 Autonomy Corp. PLC Cvt. | 3.250% | 3/4/15 | 1,900 | 3,604 |

| CACIInternational Inc. Cvt. | 2.125% | 5/1/14 | 9,215 | 11,807 |

| 3 CACIInternational Inc. Cvt. | 2.125% | 5/1/14 | 1,575 | 2,018 |

| 3 Cadence Design Systems Inc. Cvt. | 2.625% | 6/1/15 | 3,825 | 5,852 |

| Ciena Corp. Cvt. | 0.875% | 6/15/17 | 23,375 | 22,528 |

| Comtech Telecommunications Corp. Cvt. | 3.000% | 5/1/29 | 8,830 | 9,183 |

| 3 Concur Technologies Inc. Cvt. | 2.500% | 4/15/15 | 3,555 | 4,115 |

| 3 CSG Systems International Inc. Cvt. | 3.000% | 3/1/17 | 2,795 | 2,886 |

| 3 Digital River Inc. Cvt. | 2.000% | 11/1/30 | 23,080 | 23,195 |

| 6 Econocom Group Cvt. | 4.000% | 6/1/16 | 1,946 | 2,784 |

| 2 Elpida Memory Inc. Cvt. | 0.500% | 10/26/15 | 143,000 | 1,997 |

| Epistar Corp. Cvt. | 0.000% | 1/27/16 | 1,700 | 1,766 |

| EquinixInc. Cvt. | 2.500% | 4/15/12 | 11,275 | 11,951 |

| EquinixInc. Cvt. | 3.000% | 10/15/14 | 3,850 | 4,379 |

| EquinixInc. Cvt. | 4.750% | 6/15/16 | 10,350 | 14,710 |

| Hon Hai Precision Industry Co. Ltd. Cvt. | 0.000% | 10/12/13 | 200 | 206 |

| 6 Ingenico Cvt. | 2.750% | 1/1/17 | 1,256 | 2,168 |

| Intel Corp. Cvt. | 3.250% | 8/1/39 | 26,641 | 33,035 |

16

| | | | | |

| Convertible Securities Fund | | | | |

| |

| |

| |

| | | | | Face | Market |

| | | | Maturity | Amount‡ | Value |

| | | Coupon | Date | (000) | ($000) |

| 3 | Ixia Cvt. | 3.000% | 12/15/15 | 3,520 | 3,977 |

| 3 | Lam Research Corp. Cvt. | 0.500% | 5/15/16 | 11,705 | 12,027 |

| 3 | Lam Research Corp. Cvt. | 1.250% | 5/15/18 | 14,725 | 15,130 |

| 3 | Mentor Graphics Corp. Cvt. | 4.000% | 4/1/31 | 22,140 | 22,361 |

| | Micron Technology Inc. Cvt. | 1.875% | 6/1/14 | 30,575 | 32,295 |

| | Micron Technology Inc. Cvt. | 1.875% | 6/1/27 | 28,950 | 32,931 |

| 1 | Misys PLC Cvt. | 2.500% | 11/22/15 | 1,500 | 2,902 |

| 6 | Neopost SA Cvt. | 3.750% | 2/1/15 | 2,845 | 4,293 |

| 3 | Novellus Systems Inc. Cvt. | 2.625% | 5/15/41 | 10,725 | 11,556 |

| | Nuance Communications Inc. Cvt. | 2.750% | 8/15/27 | 10,635 | 14,118 |

| | ONSemiconductor Corp. Cvt. | 2.625% | 12/15/26 | 28,353 | 36,115 |

| 3 | Photronics Inc. Cvt. | 3.250% | 4/1/16 | 3,550 | 4,384 |

| 3 | Quantum Corp. Cvt. | 3.500% | 11/15/15 | 5,950 | 6,255 |

| 3 | Renesola Ltd. Cvt. | 4.125% | 3/15/18 | 1,895 | 1,728 |

| | RF Micro Devices Inc. Cvt. | 1.000% | 4/15/14 | 6,900 | 7,443 |

| 3 | RightNow Technologies Inc. Cvt. | 2.500% | 11/15/30 | 11,215 | 14,005 |

| | Rovi Corp. Cvt. | 2.625% | 2/15/40 | 7,480 | 10,276 |

| | SanDisk Corp. Cvt. | 1.500% | 8/15/17 | 27,905 | 31,881 |

| | SunPower Corp. Cvt. | 4.500% | 3/15/15 | 33,960 | 37,780 |

| | Suntech Power Holdings Co. Ltd. Cvt. | 3.000% | 3/15/13 | 4,360 | 3,962 |

| 3 | Telvent GIT SA Cvt. | 5.500% | 4/15/15 | 1,965 | 2,424 |

| | TPK Holding Co. Ltd. Cvt. | 0.000% | 4/20/14 | 2,300 | 2,513 |

| | TTM Technologies Inc. Cvt. | 3.250% | 5/15/15 | 4,537 | 5,870 |

| | VeriSign Inc. Cvt. | 3.250% | 8/15/37 | 6,339 | 7,520 |

| 3 | Vishay Intertechnology Inc. Cvt. | 2.250% | 5/15/41 | 4,770 | 4,669 |

| 3 | WebMD Health Corp. Cvt. | 2.250% | 3/31/16 | 13,820 | 13,319 |

| 3 | WebMD Health Corp. Cvt. | 2.500% | 1/31/18 | 17,185 | 17,035 |

| 3 | Xilinx Inc. Cvt. | 2.625% | 6/15/17 | 6,065 | 8,013 |

| | | | | | 550,595 |

| Materials (7.5%) | | | | |

| | AngloGold Ashanti Holdings Finance PLC Cvt. | 3.500% | 5/22/14 | 1,400 | 1,676 |

| | Aquarius Platinum Ltd. Cvt. | 4.000% | 12/18/15 | 2,400 | 2,685 |

| 3 | Cemex SAB de CV Cvt. | 3.750% | 3/15/18 | 8,470 | 8,470 |

| | Cemex SAB de CV Cvt. | 4.875% | 3/15/15 | 20,065 | 20,065 |

| | Goldcorp Inc. Cvt. | 2.000% | 8/1/14 | 1,085 | 1,396 |

| 3 | Kaiser Aluminum Corp. Cvt. | 4.500% | 4/1/15 | 8,285 | 10,498 |

| 3 | Owens-BrockwayGlass Container Inc. Cvt. | 3.000% | 6/1/15 | 36,415 | 37,781 |

| | Petropavlovsk 2010 Ltd. Cvt. | 4.000% | 2/18/15 | 3,100 | 3,140 |

| | RTIInternational Metals Inc. Cvt. | 3.000% | 12/1/15 | 10,820 | 13,971 |

| 6 | Salzgitter Finance BV Cvt. | 1.125% | 10/6/16 | 1,300 | 1,836 |

| 6 | Salzgitter Finance BV Cvt. | 2.000% | 11/8/17 | 2,650 | 4,262 |

| 3 | ShengdaTechInc. Cvt. | 6.500% | 12/15/15 | 460 | 230 |

| 3 | Sino-Forest Corp. Cvt. | 4.250% | 12/15/16 | 10,894 | 12,705 |

| | Steel Dynamics Inc. Cvt. | 5.125% | 6/15/14 | 23,205 | 28,397 |

| | Stillwater Mining Co. Cvt. | 1.875% | 3/15/28 | 9,605 | 10,926 |

| | Tata Steel Ltd. Cvt. | 4.500% | 11/21/14 | 3,431 | 3,983 |

| | Welspun Corp. Ltd. Cvt. | 4.500% | 10/17/14 | 2,700 | 2,710 |

| 10 | Western Areas NL Cvt. | 6.375% | 7/2/14 | 1,185 | 1,392 |

| | | | | | 166,123 |

| Telecommunication Services (4.4%) | | | | |

| 3 | InterDigital Inc. Cvt. | 2.500% | 3/15/16 | 9,805 | 10,577 |

| | SBACommunications Corp. Cvt. | 1.875% | 5/1/13 | 50,169 | 55,876 |

| | SKTelecom Co. Ltd. Cvt. | 1.750% | 4/7/14 | 2,961 | 3,553 |

| | twtelecom inc Cvt. | 2.375% | 4/1/26 | 21,865 | 27,769 |

| | | | | | 97,775 |

17

| | | | |

| Convertible Securities Fund | | | | |

| |

| |

| |

| | | | Face | Market |

| | | Maturity | Amount‡ | Value |

| | Coupon | Date | (000) | ($000) |

| Utilities (0.5%) | | | | |

| 6 International Power Finance Jersey III Ltd. Cvt. | 4.750% | 6/5/15 | 1,500 | 2,332 |

| Tata Power Co. Ltd. Cvt. | 1.750% | 11/21/14 | 1,700 | 1,868 |

| YTL Corp. Finance Labuan Ltd. Cvt. | 1.875% | 3/18/15 | 5,800 | 6,344 |

| | | | | 10,544 |

| Total Convertible Bonds (Cost $1,686,281) | | | | 1,854,870 |

| |

| | | | Shares | |

| Convertible Preferred Stocks (12.1%) | | | | |

| Consumer Discretionary (3.7%) | | | | |

| General Motors Co. Pfd. | 4.750% | | 826,600 | 41,433 |

| Interpublic Group of Cos. Inc. Pfd. | 5.250% | | 20,050 | 22,030 |

| Stanley Black & Decker Inc. Pfd. | 4.750% | | 152,120 | 18,331 |

| | | | | 81,794 |

| Energy (3.5%) | | | | |

| Apache Corp. Pfd. | 6.000% | | 334,700 | 22,237 |

| ATP Oil & Gas Corp. Pfd. | 8.000% | | 57,660 | 6,198 |

| 3 ChesapeakeEnergy Corp. Pfd. | 5.750% | | 8,590 | 11,371 |

| Energy XXI Bermuda Ltd. Pfd. | 5.625% | | 57,610 | 21,460 |

| Goodrich Petroleum Corp. Pfd. | 5.375% | | 349,900 | 15,920 |

| | | | | 77,186 |

| Financials (3.1%) | | | | |

| Citigroup Inc. Pfd. | 7.500% | | 129,100 | 15,460 |

| Entertainment Properties Trust Pfd. | 5.750% | | 206,200 | 4,319 |

| Fifth Third Bancorp Pfd. | 8.500% | | 138,440 | 19,883 |

| MetLife Inc. Pfd. | 5.000% | | 338,700 | 28,014 |

| | | | | 67,676 |

| Health Care (1.3%) | | | | |

| Healthsouth Corp. Pfd. | 6.500% | | 12,050 | 14,219 |

| Omnicare Capital Trust II Pfd. | 4.000% | | 305,500 | 15,084 |

| | | | | 29,303 |

| Industrials (0.3%) | | | | |

| Continental Airlines Finance Trust II Pfd. | 6.000% | | 160,200 | 6,148 |

| |

| Information Technology (0.2%) | | | | |

| Unisys Corp. Pfd. | 6.250% | | 59,700 | 4,888 |

| Total Convertible Preferred Stocks (Cost $227,919) | | | | 266,995 |

| Temporary Cash Investment (3.3%) | | | | |

| Money Market Fund (3.3%) | | | | |

| 11 Vanguard Market Liquidity Fund (Cost $72,449) | 0.155% | | 72,449,022 | 72,449 |

| Total Investments (99.6%) (Cost $1,986,649) | | | | 2,194,314 |

| Other Assets and Liabilities (0.4%) | | | | |

| Other Assets | | | | 30,840 |

| Liabilities | | | | (21,043) |

| | | | | 9,797 |

| Net Assets (100%) | | | | |

| Applicable to 156,083,881 outstanding $.001 par value shares of | | | |

| beneficial interest (unlimited authorization) | | | | 2,204,111 |

| Net Asset Value Per Share | | | | $14.12 |

18

Convertible Securities Fund

| |

| At May 31, 2011, net assets consisted of: | |

| | Amount |

| | ($000) |

| Paid-in Capital | 1,877,100 |

| Undistributed Net Investment Income | 19,404 |

| Accumulated Net Realized Gains | 101,440 |

| Unrealized Appreciation (Depreciation) | |

| Investment Securities | 207,665 |

| Forward Currency Contracts | (1,639) |

| Foreign Currencies | 141 |

| Net Assets | 2,204,111 |

See Note A in Notes to Financial Statements.

‡ Face amount is stated in U.S. dollars unless otherwise indicated.

1 Face amount denominated in British pounds.

2 Face amount denominated in Japanese yen.

3 Security exempt from registration under Rule 144A of the Securities Act of 1933. Such securities may be sold in transactions exempt from

registration, normally to qualified institutional buyers. At May 31, 2011, the aggregate value of these securities was $608,230,000,

representing 27.6% of net assets.

4 Face amount denominated in Chinese yuan.

5 Face amount denominated in Hong Kong dollars.

6 Face amount denominated in euro.

7 Face amount denominated in Canadian dollars.

8 Face amount denominated in Singapore dollars.

9 Face amount denominated in Swiss francs.

10 Face amount denominated in Australian dollars.

11 Affiliated money market fund available only to Vanguard funds and certain trusts and accounts managed by Vanguard. Rate shown is the

7-day yield.

See accompanying Notes, which are an integral part of the Financial Statements.

19

Convertible Securities Fund

Statement of Operations

| |

| | SixMonths Ended |

| | May 31, 2011 |

| | ($000) |

| Investment Income | |

| Income | |

| Dividends | 6,828 |

| Interest1,2 | 33,948 |

| Total Income | 40,776 |

| Expenses | |

| Investment Advisory Fees—Note B | |

| Basic Fee | 3,472 |

| Performance Adjustment | 1,252 |

| The Vanguard Group—Note C | |

| Management and Administrative | 1,952 |

| Marketing and Distribution | 263 |

| Custodian Fees | 30 |

| Shareholders’ Reports | 12 |

| Trustees’ Fees and Expenses | 2 |

| Total Expenses | 6,983 |

| Net Investment Income | 33,793 |

| Realized Net Gain (Loss) | |

| Investment Securities Sold | 116,198 |

| Foreign Currencies and Forward Currency Contracts | (3,880) |

| Realized Net Gain (Loss) | 112,318 |

| Change in Unrealized Appreciation (Depreciation) | |

| Investment Securities | 58,571 |

| Foreign Currencies and Forward Currency Contracts | (1,498) |

| Change in Unrealized Appreciation (Depreciation) | 57,073 |

| Net Increase (Decrease) in Net Assets Resulting from Operations | 203,184 |

| 1 Interest income is net of foreign withholding taxes of $21,000. |

| 2 Interest income from an affiliated company of the fund was $77,000. |

See accompanying Notes, which are an integral part of the Financial Statements.

20

Convertible Securities Fund

Statement of Changes in Net Assets

| | |

| | Six Months Ended | Year Ended |

| | May 31, | November 30, |

| | 2011 | 2010 |

| | ($000) | ($000) |

| Increase (Decrease) in Net Assets | | |

| Operations | | |

| Net Investment Income | 33,793 | 68,729 |

| Realized Net Gain (Loss) | 112,318 | 188,469 |

| Change in Unrealized Appreciation (Depreciation) | 57,073 | 40,819 |

| Net Increase (Decrease) in Net Assets Resulting from Operations | 203,184 | 298,017 |

| Distributions | | |

| Net Investment Income | (35,562) | (73,612) |

| Realized Capital Gain† | (121,860) | — |

| Total Distributions | (157,422) | (73,612) |

| Capital Share Transactions | | |

| Issued | 451,637 | 212,318 |

| Issued in Lieu of Cash Distributions | 138,979 | 62,394 |

| Redeemed1 | (164,858) | (481,368) |

| Net Increase (Decrease) from Capital Share Transactions | 425,758 | (206,656) |

| Total Increase (Decrease) | 471,520 | 17,749 |

| Net Assets | | |

| Beginning of Period | 1,732,591 | 1,714,842 |

| End of Period2 | 2,204,111 | 1,732,591 |

| † Includes fiscal 2011 short-term gain distributions totaling $71,840,000. Short-term gain distributions are treated as ordinary income dividends for tax purposes. |

| 1 Net of redemption fees for fiscal 2011 and 2010 of $234,000 and $318,000, respectively. |

| 2 Net Assets—End of Period includes undistributed net investment income of $19,404,000 and $10,647,000. |

See accompanying Notes, which are an integral part of the Financial Statements.

21

Convertible Securities Fund

Financial Highlights

| | | | | | |

| Six Months | | | | | |

| | Ended | | | | | |

| For a Share Outstanding | May 31, | Year Ended November 30, |

| Throughout Each Period | 2011 | 2010 | 2009 | 2008 | 2007 | 2006 |

| Net Asset Value, Beginning of Period | $13.85 | $12.12 | $8.86 | $14.95 | $14.81 | $13.57 |

| Investment Operations | | | | | | |

| Net Investment Income | .229 | .555 | .475 | .401 | .420 | .430 |

| Net Realized and Unrealized Gain (Loss) | | | | | | |

| on Investments | 1.253 | 1.742 | 3.211 | (5.170) | 1.250 | 1.620 |

| Total from Investment Operations | 1.482 | 2.297 | 3.686 | (4.769) | 1.670 | 2.050 |

| Distributions | | | | | | |

| Dividends from Net Investment Income | (.257) | (.567) | (.426) | (.501) | (.510) | (.380) |

| Distributions from Realized Capital Gains | (.955) | — | — | (.820) | (1.020) | (.430) |

| Total Distributions | (1.212) | (.567) | (.426) | (1.321) | (1.530) | (.810) |

| Net Asset Value, End of Period | $14.12 | $13.85 | $12.12 | $8.86 | $14.95 | $14.81 |

| |

| Total Return1 | 11.21% | 19.39% | 42.55% | -34.81% | 12.34% | 15.70% |

| |

| Ratios/Supplemental Data | | | | | | |

| Net Assets, End of Period (Millions) | $2,204 | $1,733 | $1,715 | $716 | $872 | $727 |

| Ratio of Total Expenses to | | | | | | |

| Average Net Assets2 | 0.68% | 0.68% | 0.72% | 0.71% | 0.77% | 0.87% |

| Ratio of Net Investment Income to | | | | | | |

| Average Net Assets | 3.29% | 4.08% | 4.65% | 3.28% | 2.83% | 3.14% |

| Portfolio Turnover Rate | 103% | 103% | 103% | 77% | 116% | 138% |

The expense ratio, net income ratio, and turnover rate for the current period have been annualized.

1 Total returns do not include transaction or account service fees that may have applied in the periods shown. Fund prospectuses provide

information about any applicable transaction and account service fees.

2 Includes performance-based investment advisory fee increases (decreases) of 0.12%, 0.12%, 0.12%, 0.15%, 0.16%, and 0.22%.

See accompanying Notes, which are an integral part of the Financial Statements.

22

Convertible Securities Fund

Notes to Financial Statements

Vanguard Convertible Securities Fund is registered under the Investment Company Act of 1940 as an open-end investment company, or mutual fund. The fund invests in securities of foreign issuers, which may subject it to investment risks not normally associated with investing in securities of United States corporations.

A. The following significant accounting policies conform to generally accepted accounting principles for U.S. mutual funds. The fund consistently follows such policies in preparing its financial statements.

1. Security Valuation: Securities are valued as of the close of trading on the New York Stock Exchange (generally 4 p.m., Eastern time) on the valuation date. Equity securities are valued at the latest quoted sales prices or official closing prices taken from the primary market in which each security trades; such securities not traded on the valuation date are valued at the mean of the latest quoted bid and asked prices. Bonds, and temporary cash investments acquired over 60 days to maturity, are valued using the latest bid prices or using valuations based on a matrix system (which considers such factors as security prices, yields, maturities, and ratings), both as furnished by independent pricing services. Investments in Vanguard Market Liquidity Fund are valued at that fund’s net asset value. Other temporary cash investments are valued at amortized cost, which approximates market value. Securities for which market quotations are not readily available, or whose values have been materially affected by events occurring before the fund’s pricing time but after the close of the securities’ primary markets, are valued by methods deemed by the board of trustees to represent fair value.

2. Foreign Currency: Securities and other assets and liabilities denominated in foreign currencies are translated into U.S. dollars using exchange rates obtained from an independent third party as of the fund’s pricing time on the valuation date. Realized gains (losses) and unrealized appreciation (depreciation) on investment securities include the effects of changes in exchange rates since the securities were purchased, combined with the effects of changes in security prices. Fluctuations in the value of other assets and liabilities resulting from changes in exchange rates are recorded as unrealized foreign currency gains (losses) until the assets or liabilities are settled in cash, at which time they are recorded as realized foreign currency gains (losses).

3. Forward Currency Contracts: The fund enters into forward currency contracts to protect the value of securities and related receivables and payables against changes in future foreign exchange rates. The fund’s risks in using these contracts include movement in the values of the foreign currencies relative to the U.S. dollar and the ability of the counterparties to fulfill their obligations under the contracts. Counterparty risk is mitigated by entering into forward currency contracts only with highly rated counterparties, by a master netting arrangement between the fund and the counterparty, and by the posting of collateral by the counterparty. The forward currency contracts contain provisions whereby a counterparty may terminate open contracts if the fund’s net assets decline below a certain level, triggering a payment by the fund if the fund is in a net liability position at the time of the termination. The payment amount would be reduced by any collateral the fund has posted.

Any securities posted as collateral for open contracts are noted in the Statement of Net Assets.

Forward currency contracts are valued at their quoted daily prices obtained from an independent third party, adjusted for currency risk based on the expiration date of each contract. The aggregate principal amounts of the contracts are not recorded in the Statement of Net Assets. Fluctuations in the value of the contracts are recorded in the Statement of Net Assets as an asset (liability) and in the Statement of Operations as unrealized appreciation (depreciation) until the contracts are closed, when they are recorded as realized forward currency contract gains (losses).

23

Convertible Securities Fund

4. Federal Income Taxes: The fund intends to continue to qualify as a regulated investment company and distribute all of its taxable income. Management has analyzed the fund’s tax positions taken for all open federal income tax years (November 30, 2007–2010), and for the period ended May 31, 2011, and has concluded that no provision for federal income tax is required in the fund’s financial statements.

5. Distributions: Distributions to shareholders are recorded on the ex-dividend date.

6. Other: Dividend income is recorded on the ex-dividend date. Interest income includes income distributions received from Vanguard Market Liquidity Fund and is accrued daily. Premiums and discounts on debt securities purchased are amortized and accreted, respectively, to interest income over the lives of the respective securities. Security transactions are accounted for on the date securities are bought or sold. Costs used to determine realized gains (losses) on the sale of investment securities are those of the specific securities sold. Fees assessed on redemptions of capital shares are credited to paid-in-capital.

B. Oaktree Capital Management, L.P., provides investment advisory services to the fund for a fee calculated at an annual percentage rate of average net assets. Effective March 1, 2011 the basic fee is subject to quarterly adjustments based on the fund’s performance for the preceding three years relative to the Bank of America Merrill Lynch All US Convertibles Index (previously Merrill Lynch All Convertibles-All Qualities Index) for periods prior to March 1, 2011, and a composite index weighted 70% Bank of America Merrill Lynch All US Convertibles Index and 30% Bank of America Merrill Lynch Global 300 Convertibles ex-US Index (hedged) thereafter. The benchmark change will be fully phased in by February 2014. For the six months ended May 31, 2011, the investment advisory fee represented an effective annual basic rate of 0.34% of the fund’s average net assets before an increase of $1,252,000 (0.12%) based on performance.

C. The Vanguard Group furnishes at cost corporate management, administrative, marketing, and distribution services. The costs of such services are allocated to the fund under methods approved by the board of trustees. The fund has committed to provide up to 0.40% of its net assets in capital contributions to Vanguard. At May 31, 2011, the fund had contributed capital of $346,000 to Vanguard (included in Other Assets), representing 0.02% of the fund’s net assets and 0.14% of Vanguard’s capitalization. The fund’s trustees and officers are also directors and officers of Vanguard.

D. Various inputs may be used to determine the value of the fund’s investments. These inputs are summarized in three broad levels for financial statement purposes. The inputs or methodologies used to value securities are not necessarily an indication of the risk associated with investing in those securities.

Level 1—Quoted prices in active markets for identical securities.

Level 2—Other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.).

Level 3—Significant unobservable inputs (including the fund’s own assumptions used to determine the fair value of investments).

24

Convertible Securities Fund

The following table summarizes the fund’s investments as of May 31, 2011, based on the inputs used to value them:

| | | |

| | Level 1 | Level 2 | Level 3 |

| Investments | ($000) | ($000) | ($000) |

| Convertible Bonds | — | 1,854,870 | — |

| Convertible Preferred Stocks | 266,995 | — | — |

| Temporary Cash Investments | 72,449 | — | — |

| Forward Currency Contracts—Assets | — | 150 | — |

| Forward Currency Contracts—Liabilities | — | (1,789) | — |

| Total | 339,444 | 1,853,231 | — |

E. At May 31, 2011, the fund had open forward currency contracts to receive and deliver currencies as follows. Unrealized appreciation (depreciation) on open forward currency contracts is treated as realized gain (loss) for tax purposes.

| | | | | | |

| | | | | | | Unrealized |

| | Contract | | | | | Appreciation |

| | Settlement | Contract Amount (000) | (Depreciation) |

| Counterparty | Date | | Receive | | Deliver | ($000) |

| UBS AG | 7/21/11 | USD | 91,603 | EUR | 63,800 | (1,095) |

| UBS AG | 7/21/11 | USD | 15,118 | JPY | 1,227,915 | (183) |

| UBS AG | 7/21/11 | USD | 12,616 | GBP | 7,670 | (174) |

| UBS AG | 7/21/11 | USD | 9,110 | HKD | 70,835 | 4 |

| UBS AG | 7/21/11 | USD | 7,406 | CAD | 7,185 | (10) |

| UBS AG | 7/21/11 | USD | 7,179 | EUR | 5,000 | 117 |

| UBS AG | 7/21/11 | USD | 7,161 | SGD | 8,840 | (83) |

| UBS AG | 7/21/11 | USD | 5,646 | CHF | 4,814 | (214) |

| UBS AG | 7/21/11 | USD | 1,487 | AUD | 1,405 | (30) |

| UBS AG | 7/21/11 | USD | 1,165 | GBP | 708 | 18 |

| UBS AG | 7/21/11 | USD | 938 | JPY | 76,200 | 11 |

AUD—Australian dollar.

CAD—Canadian dollar.

CHF—Swiss franc.

EUR—euro.

GBP—British pound.

HKD—Hong Kong dollar.

JPY—Japanese yen.

SGD—Singapore dollar.

USD—U.S. dollar.

F. Distributions are determined on a tax basis and may differ from net investment income and realized capital gains for financial reporting purposes. Differences may be permanent or temporary. Permanent differences are reclassified among capital accounts in the financial statements to reflect their tax character. Temporary differences arise when certain items of income, expense, gain, or loss are

25

Convertible Securities Fund

recognized in different periods for financial statement and tax purposes; these differences will reverse at some time in the future. Differences in classification may also result from the treatment of short-term gains as ordinary income for tax purposes. The fund’s tax-basis capital gains and losses are determined only at the end of each fiscal year.

During the six months ended May 31, 2011, the fund realized net foreign currency gains of $52,000, (including the foreign currency component on sales of foreign currency denominated bonds) which increased distributable net income for tax purposes; accordingly, such gains have been reclassified from accumulated net realized gains to undistributed net investment income.

Certain of the fund’s convertible preferred stock investments are treated as debt securities for tax purposes. During the six months ended May 31, 2011, the fund realized losses of $105,000 from the sale of these securities, which are included in distributable net investment income for tax purposes; accordingly, such losses have been reclassified from accumulated net realized gains to undistributed net investment income.

Certain of the fund’s convertible bond investments are in securities considered to be “contingent payment debt instruments,” for which any realized gains increase (and all or part of any realized losses decrease) income for tax purposes. During the six months ended May 31, 2011, the fund realized net gains of $10,579,000 from the sale of these securities, which increased distributable net income for tax purposes; accordingly, such gains have been reclassified from accumulated net realized gains to undistributed net investment income.

At May 31, 2011, the cost of investment securities for tax purposes was $1,986,965,000. Net unrealized appreciation of investment securities for tax purposes was $207,349,000, consisting of unrealized gains of $221,375,000 on securities that had risen in value since their purchase and $14,026,000 in unrealized losses on securities that had fallen in value since their purchase.

G. During the six months ended May 31, 2011, the fund purchased $1,278,008,000 of investment securities and sold $1,012,177,000 of investment securities, other than temporary cash investments.

H. Capital shares issued and redeemed were:

| | |

| | Six Months Ended | Year Ended |

| | May 31, | November 30, |

| | 2011 | 2010 |

| | Shares | Shares |

| | (000) | (000) |

| Issued | 32,439 | 16,162 |

| Issued in Lieu of Cash Distributions | 10,335 | 4,846 |

| Redeemed | (11,820) | (37,355) |

| Net Increase (Decrease) in Shares Outstanding | 30,954 | (16,347) |

I. In preparing the financial statements as of May 31, 2011, management considered the impact of subsequent events for potential recognition or disclosure in these financial statements.

26

About Your Fund’s Expenses

As a shareholder of the fund, you incur ongoing costs, which include costs for portfolio management, administrative services, and shareholder reports (like this one), among others. Operating expenses, which are deducted from a fund’s gross income, directly reduce the investment return of the fund.

A fund’s expenses are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The following examples are intended to help you understand the ongoing costs (in dollars) of investing in your fund and to compare these costs with those of other mutual funds. The examples are based on an investment of $1,000 made at the beginning of the period shown and held for the entire period.

The accompanying table illustrates your fund’s costs in two ways:

• Based on actual fund return. This section helps you to estimate the actual expenses that you paid over the period. The ”Ending Account Value“ shown is derived from the fund‘s actual return, and the third column shows the dollar amount that would have been paid by an investor who started with $1,000 in the fund. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period.

To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for your fund under the heading ”Expenses Paid During Period.“

• Based on hypothetical 5% yearly return. This section is intended to help you compare your fund‘s costs with those of other mutual funds. It assumes that the fund had a yearly return of 5% before expenses, but that the expense ratio is unchanged. In this case—because the return used is not the fund’s actual return—the results do not apply to your investment. The example is useful in making comparisons because the Securities and Exchange Commission requires all mutual funds to calculate expenses based on a 5% return. You can assess your fund’s costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

Note that the expenses shown in the table are meant to highlight and help you compare ongoing costs only and do not reflect transaction costs incurred by the fund for buying and selling securities. Further, the expenses do not include any purchase, redemption, or account service fees described in the fund prospectus. If such fees were applied to your account, your costs would be higher. Your fund does not carry a “sales load.”

The calculations assume no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

You can find more information about the fund’s expenses, including annual expense ratios, in the Financial Statements section of this report. For additional information on operating expenses and other shareholder costs, please refer to your fund’s current prospectus.

27

| | | |

| Six Months Ended May 31, 2011 | | | |

| | Beginning | Ending | Expenses |

| | Account Value | Account Value | Paid During |

| Convertible Securities Fund | 11/30/2010 | 5/31/2011 | Period |

| Based on Actual Fund Return | $1,000.00 | $1,112.09 | $3.58 |

| Based on Hypothetical 5% Yearly Return | 1,000.00 | 1,021.54 | 3.43 |

The calculations are based on expenses incurred in the most recent six-month period. The fund’s annualized six-month expense ratio for that

period is 0.68%. The dollar amounts shown as “Expenses Paid” are equal to the annualized expense ratio multiplied by the average account

value over the period, multiplied by the number of days in the most recent six-month period, then divided by the number of days in the most

recent 12-month period.

28

Trustees Approve Advisory Agreement

The board of trustees of Vanguard Convertible Securities Fund has approved an amended investment advisory agreement with Oaktree Capital Management, L.P. Effective March 1, 2011, the compensation benchmark for Oaktree Capital Management, L.P., the Bank of America Merrill Lynch All US Convertibles Index, was replaced with a composite benchmark made up of 70% Bank of America Merrill Lynch All US Convertibles Index/30% Bank of America Merrill Lynch Global 300 Convertibles ex-US Index (hedged). The board concluded that changing the benchmark to a composite benchmark better reflects the fund’s recently adopted global mandate. The board determined that retaining Oaktree and amending the agreement was in the best interests of the fund and its shareholders.

The board based its decision upon an evaluation of the advisor’s investment staff, portfolio management process, and performance. The trustees considered the factors discussed below, among others. However, no single factor determined whether the board approved the agreement. Rather, it was the totality of the circumstances that drove the board’s decision.

Nature, extent, and quality of services

The board considered the quality of the fund’s investment management over both the short and long term, and took into account the organizational depth and stability of the advisor. The board noted that Oaktree, founded in 1995, specializes in managing convertible securities. The advisor uses a bottom-up investment approach to select convertible securities with the best balance of upside potential and downside protection. Discipline is key to the fund’s management; Oaktree invests predominantly in convertibles possessing an attractive combination of conversion and income features—true hybrid securities—and sells the issues when their characteristics become too similar to those of conventional bonds or common stocks. Oaktree has advised the fund since 1996.

The board concluded that the advisor’s experience, stability, and performance, among other factors, warranted both amendment and continuation of the advisory agreement.

Investment performance

The board considered the short- and long-term performance of the fund, including any periods of outperformance or underperformance of a relevant benchmark and peer group. The board concluded that the advisor has carried out the fund’s investment strategy in disciplined fashion, and that performance results have allowed the fund to remain competitive versus its benchmark and its peer group. Information about the fund’s most recent performance can be found in the Performance Summary section of this report.

Cost

The board concluded that the fund’s expense ratio was well below the average expense ratio charged by funds in its peer group and that the fund’s advisory fee rate was also well below the peer-group average. Information about the fund’s expenses appears in the About Your Fund’s Expenses section of this report as well as in the Financial Statements section, which also includes information about the advisory fee rate.

The board did not consider profitability of Oaktree in determining whether to approve the advisory fee, because Oaktree is independent of Vanguard and the advisory fee is the result of arm’s-length negotiations.

The benefit of economies of scale

The board concluded that the fund’s shareholders benefit from economies of scale because of breakpoints in the fund’s advisory fee schedule. The breakpoints reduce the effective rate of the fee as the fund’s assets increase.

The board will consider whether to renew the advisory agreement again after a one-year period.

29

Glossary

30-Day SEC Yield. A fund’s 30-day SEC yield is derived using a formula specified by the U.S. Securities and Exchange Commission. Under the formula, data related to the fund’s security holdings in the previous 30 days are used to calculate the fund’s hypothetical net income for that period, which is then annualized and divided by the fund’s estimated average net assets over the calculation period. For the purposes of this calculation, a security’s income is based on its current market yield to maturity (in the case of bonds) or its projected dividend yield (for stocks). Because the SEC yield represents hypothetical annualized income, it will differ—at times significantly—from the fund’s actual experience. As a result, the fund’s income distributions may be higher or lower than implied by the SEC yield.

Average Coupon. The average interest rate paid on the fixed income securities held by a fund. It is expressed as a percentage of face value.

Average Duration. An estimate of how much the value of the bonds held by a fund will fluctuate in response to a change in interest rates. To see how the value could change, multiply the average duration by the change in rates. If interest rates rise by 1 percentage point, the value of the bonds in a fund with an average duration of five years would decline by about 5%. If rates decrease by a percentage point, the value would rise by 5%.

Average Weighted Maturity. The average length of time until fixed income securities held by a fund reach maturity and are repaid. The figure reflects the proportion of fund assets represented by each security.

Beta. A measure of the magnitude of a fund’s past share-price fluctuations in relation to the ups and downs of a given market index. The index is assigned a beta of 1.00. Compared with a given index, a fund with a beta of 1.20 typically would have seen its share price rise or fall by 12% when the index rose or fell by 10%. For this report, beta is based on returns over the past 36 months for both the fund and the index. Note that a fund’s beta should be reviewed in conjunction with its R-squared (see definition). The lower the R-squared, the less correlation there is between the fund and the index, and the less reliable beta is as an indicator of volatility.

Conversion Premium. The average percentage by which the weighted average market price of the convertible securities held by a fund exceeds the weighted average market price of their underlying common stocks. For example, if a stock is trading at $25 per share and a bond that is convertible into the stock is trading at a price equivalent to $30 per share of stock, the conversion premium is 20% ($5 ÷ $25 = 20%).

Credit Quality. For this report, credit-quality ratings are measured on a scale that generally ranges from AAA (highest) to D (lowest). “Not Rated” is used to classify securities for which a rating is not available. Credit-quality ratings are obtained from S&P.

Expense Ratio. The percentage of a fund’s average net assets used to pay its annual administrative and advisory expenses. These expenses directly reduce returns to investors.

Foreign Holdings. The percentage of a fund represented by securities or depositary receipts of companies based outside the United States.

30

Inception Date. The date on which the assets of a fund (or one of its share classes) are first invested in accordance with the fund’s investment objective. For funds with a subscription period, the inception date is the day after that period ends. Investment performance is measured from the inception date.

Market Exposure. A measure that reflects a fund’s security investments excluding any holdings in short-term reserves.

R-Squared. A measure of how much of a fund’s past returns can be explained by the returns from the market in general, as measured by a given index. If a fund’s total returns were precisely synchronized with an index’s returns, its R-squared would be 1.00. If the fund’s returns bore no relationship to the index’s returns, its R-squared would be 0. For this report, R-squared is based on returns over the past 36 months for both the fund and the index.

Short-Term Reserves. The percentage of a fund invested in highly liquid, short-term securities that can be readily converted to cash.

Turnover Rate. An indication of the fund’s trading activity. Funds with high turnover rates incur higher transaction costs and may be more likely to distribute capital gains (which may be taxable to investors). The turnover rate excludes in-kind transactions, which have minimal impact on costs.

31

The People Who Govern Your Fund

The trustees of your mutual fund are there to see that the fund is operated and managed in your best interests since, as a shareholder, you are a part owner of the fund. Your fund’s trustees also serve on the board of directors of The Vanguard Group, Inc., which is owned by the Vanguard funds and provides services to them on an at-cost basis.

A majority of Vanguard’s board members are independent, meaning that they have no affiliation with Vanguard or the funds they oversee, apart from the sizable personal investments they have made as private individuals. The independent board members have distinguished backgrounds in business, academia, and public service. Each of the trustees and executive officers oversees 177 Vanguard funds.

The following table provides information for each trustee and executive officer of the fund. More information about the trustees is in the Statement of Additional Information, which can be obtained, without charge, by contacting Vanguard at 800-662-7447, or online at vanguard.com.

| |

| Interested Trustee1 | and President (2006–2008) of Rohm and Haas Co. |

| | (chemicals); Director of Tyco International, Ltd. |

| F. William McNabb III | (diversified manufacturing and services) and Hewlett- |

| Born 1957. Trustee Since July 2009. Chairman of the | Packard Co. (electronic computer manufacturing); |

| Board. Principal Occupation(s) During the Past Five | Senior Advisor at New Mountain Capital; Trustee |

| Years: Chairman of the Board of The Vanguard Group, | of The Conference Board; Member of the Board of |