UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-04719

The TETON Westwood Funds

(Exact name of registrant as specified in charter)

One Corporate Center

Rye, New York 10580-1422

(Address of principal executive offices) (Zip code)

Bruce N. Alpert

Gabelli Funds, LLC

One Corporate Center

Rye, New York 10580-1422

(Name and address of agent for service)

Registrant's telephone number, including area code: 1-800-422-3554

Date of fiscal year end: September 30

Date of reporting period: September 30, 2018

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The Report to Shareholders is attached herewith.

TETON WESTWOOD FUNDS

|

Mighty MitesSM Fund |

|

| |

SmallCap Equity Fund |

|

| |

Mid-Cap Equity Fund |

|

| |

Convertible Securities Fund |

|

| |

Equity Fund |

|

| |

Balanced Fund |

|

| |

Intermediate Bond Fund |

Annual Report

September 30, 2018

TETON WESTWOOD FUNDS

(Unaudited)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Class AAA Shares | | | | | | Class A Shares | |

| | | Average Annual Returns – September 30, 2018 (a) | | | | | | Average Annual Returns – September 30, 2018 (a)(b)(c) | |

| | | 1 Year | | | 5 Year | | | 10 Year | | | 15 Year | | | Since Inception | | | Gross Expense Ratio | | | Expense Ratio after Adviser Reimburse- ments | | | | | | 1 Year | | | 5 Year | | | 10 Year | | | 15 Year | | | Since Inception | | | Gross Expense Ratio | | | Expense Ratio after Adviser Reimburse- ments | |

Mighty Mites | | | 4.38 | % | | | 8.26 | % | | | 11.37 | % | | | 10.87 | % | | | 11.43 | % | | | 1.41 | % | | | 1.41 | % | | | | | | | (0.03 | )% | | | 7.12 | % | | | 10.66 | % | | | 10.32 | % | | | 10.99 | % | | | 1.66 | % | | | 1.66 | % |

SmallCap Equity | | | 9.68 | | | | 10.55 | | | | 10.86 | | | | 9.97 | | | | 8.13 | | | | 1.74 | | | | 1.25 | | | | | | | | 5.00 | | | | 9.38 | | | | 10.15 | | | | 9.42 | | | | 7.75 | | | | 1.99 | | | | 1.50 | |

Mid-Cap Equity | | | 7.38 | | | | 7.75 | | | | — | | | | — | | | | 8.20 | | | | 3.36 | | | | 1.05 | | | | | | | | 2.86 | | | | 6.62 | | | | — | | | | — | | | | 7.10 | | | | 3.61 | | | | 1.30 | |

Convertible Securities | | | 14.38 | | | | 8.30 | | | | 7.91 | | | | 7.71 | | | | 7.68 | | | | 2.47 | | | | 1.15 | | | | | | | | 9.68 | | | | 7.16 | | | | 7.19 | | | | 7.16 | | | | 7.25 | | | | 2.72 | | | | 1.40 | |

Equity | | | 14.14 | | | | 11.12 | | | | 8.63 | | | | 9.11 | | | | 10.16 | | | | 1.62 | | | | 1.62 | | | | | | | | 9.33 | | | | 9.96 | | | | 7.97 | | | | 8.53 | | | | 9.79 | | | | 1.87 | | | | 1.87 | |

Balanced | | | 9.32 | | | | 7.55 | | | | 6.66 | | | | 6.93 | | | | 8.40 | | | | 1.34 | | | | 1.34 | | | | | | | | 4.72 | | | | 6.42 | | | | 5.97 | | | | 6.38 | | | | 7.98 | | | | 1.59 | | | | 1.59 | |

Intermediate Bond | | | (0.83 | ) | | | 0.76 | | | | 2.31 | | | | 2.46 | | | | 4.32 | | | | 1.52 | | | | 1.00 | | | | | | | | (4.82 | ) | | | (0.15 | ) | | | 1.78 | | | | 2.07 | | | | 4.09 | | | | 1.62 | | | | 1.10 | |

| | | |

| | | Class C Shares | | | | | | Class I Shares | |

| | | Average Annual Returns – September 30, 2018 (a)(c)(d) | | | | | | Average Annual Returns – September 30, 2018 (a)(c) | |

| | | 1 Year | | | 5 Year | | | 10 Year | | | 15 Year | | | Since Inception | | | Gross Expense Ratio | | | Expense Ratio after Adviser Reimburse- ments | | | | | | 1 Year | | | 5 Year | | | 10 Year | | | 15 Year | | | Since Inception | | | Gross Expense Ratio | | | Expense Ratio after Adviser Reimburse- ments | |

Mighty Mites | | | 2.63 | % | | | 7.45 | % | | | 10.55 | % | | | 10.06 | % | | | 10.74 | % | | | 2.16 | % | | | 2.16 | % | | | | | | | 4.67 | % | | | 8.53 | % | | | 11.65 | % | | | 11.07 | % | | | 11.58 | % | | | 1.16 | % | | | 1.16 | % |

SmallCap Equity | | | 7.79 | | | | 9.73 | | | | 10.04 | | | | 9.02 | | | | 7.46 | | | | 2.49 | | | | 2.00 | | | | | | | | 9.90 | | | | 10.83 | | | | 11.15 | | | | 10.16 | | | | 8.26 | | | | 1.49 | | | | 1.00 | |

Mid-Cap Equity | | | 5.59 | | | | 6.96 | | | | — | | | | — | | | | 7.39 | | | | 4.11 | | | | 1.80 | | | | | | | | 7.59 | | | | 8.07 | | | | — | | | | — | | | | 8.50 | | | | 3.11 | | | | 0.80 | |

Convertible Securities | | | 12.55 | | | | 7.49 | | | | 7.11 | | | | 6.92 | | | | 7.10 | | | | 3.22 | | | | 1.90 | | | | | | | | 14.79 | | | | 8.61 | | | | 8.20 | | | | 7.92 | | | | 7.82 | | | | 2.22 | | | | 0.90 | |

Equity | | | 12.32 | | | | 10.31 | | | | 7.83 | | | | 8.29 | | | | 9.64 | | | | 2.37 | | | | 2.37 | | | | | | | | 14.47 | | | | 11.36 | | | | 8.89 | | | | 9.29 | | | | 10.25 | | | | 1.37 | | | | 1.37 | |

Balanced | | | 7.54 | | | | 6.76 | | | | 5.89 | | | | 6.15 | | | | 7.83 | | | | 2.09 | | | | 2.09 | | | | | | | | 9.61 | | | | 7.81 | | | | 6.94 | | | | 7.13 | | | | 8.51 | | | | 1.09 | | | | 1.09 | |

Intermediate Bond | | | (2.50 | ) | | | 0.03 | | | | 1.55 | | | | 1.71 | | | | 3.83 | | | | 2.27 | | | | 1.75 | | | | | | | | (0.49 | ) | | | 1.03 | | | | 2.56 | | | | 2.63 | | | | 4.42 | | | | 1.27 | | | | 0.75 | |

| (a) | Returns represent past performance and do not guarantee future results. Total returns and average annual returns reflect changes in share price, reinvestment of distributions, and are net of expenses. Investment returns and the principal value of an investment will fluctuate. When shares are redeemed, they may be worth more or less than their original cost. Current performance may be lower or higher than the performance data presented. Visit www.tetonadv.com for performance information as of the most recent month end. For the SmallCap Equity, Mid-Cap Equity, Convertible Securities, and Intermediate Bond Funds (and for the Mighty Mites Fund through September 30, 2005), Teton Advisors, Inc. (the Adviser) reimbursed expenses to limit the expense ratio. Had such limitations not been in place, returns would have been lower. The contractual expense limitations are in effect through January 31, 2019 and are renewable annually by the Adviser. The Funds, except for the Equity, Balanced, and Intermediate Bond Funds, impose a 2.00% redemption fee on shares sold or exchanged within seven days after the date of purchase. Investors should carefully consider the investment objectives, risks, charges, and expenses of a Fund before investing. The prospectuses contain information about these and other matters and should be read carefully before investing. To obtain a prospectus, please visit our website at www.tetonadv.com. |

| (b) | Includes the effect of the maximum 4.00% sales charge at the beginning of the period. |

| (c) | The performance of the Class AAA Shares is used to calculate performance for the periods prior to the issuance of Class A Shares, Class C Shares, and Class I Shares, except for Mid-Cap Equity Fund whose performance for all share classes is based on the Fund’s inception date of May 31, 2013. The performance for the Class A Shares and Class C Shares would have been lower due to the additional fees and expenses associated with these classes of shares. The performance for the Class I Shares would have been higher due to the lower expenses associated with this class of shares. The inception dates for the Class AAA Shares and the initial issuance dates for the Class A Shares, Class C Shares, and Class I Shares after which shares remained continuously outstanding are listed below. |

| (d) | Assuming payment of the 1.00% maximum contingent deferred sales charge imposed on redemptions made within one year of purchase. |

| | | | | | | | |

| | | Class AAA Shares | | Class A Shares | | Class C Shares | | Class I Shares |

Mighty Mites | | 05/11/98 | | 11/26/01 | | 08/03/01 | | 01/11/08 |

SmallCap Equity | | 04/15/97 | | 11/26/01 | | 11/26/01 | | 01/11/08 |

Mid-Cap Equity | | 05/31/13 | | 05/31/13 | | 05/31/13 | | 05/31/13 |

Convertible Securities | | 09/30/97 | | 05/09/01 | | 11/26/01 | | 01/11/08 |

Equity | | 01/02/87 | | 01/28/94 | | 02/13/01 | | 01/11/08 |

Balanced | | 10/01/91 | | 04/06/93 | | 09/25/01 | | 01/11/08 |

Intermediate Bond | | 10/01/91 | | 07/26/01 | | 10/22/01 | | 01/11/08 |

The TETON Westwood Funds file complete schedules of portfolio holdings with the Securities and Exchange Commission (the SEC) for the first and third quarters of each fiscal year on Form N-Q. Shareholders may obtain this information at www.tetonadv.com or by calling the Funds at 800-WESTWOOD (800-937-8966). The Funds’ Form N-Q is available on the SEC’s website at www.sec.gov and may also be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling 800-SEC-0330.

Proxy Voting

Each Fund files Form N-PX with its complete proxy voting record for the twelve months ended June 30, no later than August 31 of each year. A description of the Funds’ proxy voting policies, procedures, and how the Funds voted proxies relating to portfolio securities are available without charge, upon request, by (i) calling 800-WESTWOOD (800-937-8966); (ii) writing to The TETON Westwood Funds at One Corporate Center, Rye, NY 10580-1422; and (iii) visiting the SEC’s website at www.sec.gov.

2

Performance Discussion (Unaudited)

Mighty Mites Fund

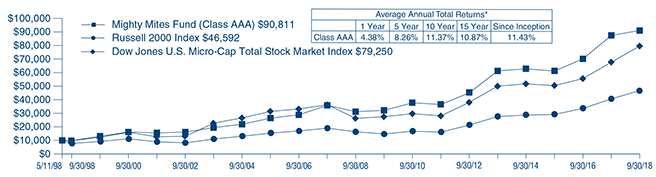

For the fiscal year ended September 30, 2018, the TETON Westwood Mighty Mites Fund net asset value (NAV) per Class AAA Share appreciated 4.4% versus gains of 15.2% for the Russell 2000 Index. See the next page for additional performance information.

The Fund primarily invests in small and micro-cap equity securities that have a market capitalization of $500 million or less at time of initial investment. The portfolio management team focuses on bottom up stock selection, seeking bite sized companies with excellent management teams, strong balance sheets, and superior long term fundamentals. As bottom up, fundamental, research driven investors, the team seeks to purchase the inefficiently priced stocks of excellent companies selling at a discount to their Private Market Value (PMV), and possess a catalyst that can unlock hidden value within the enterprise. As such, (y)our portfolio is diversified across a broad cross section of companies sharing these valuation characteristics.

The first half of the Fund’s fiscal year was mixed, with an essentially flat December for small cap stocks, and the Dow Jones U.S. MicroCap Index down slightly for the month. Micro-cap gains in January and March were nearly offset by declines in February, indicating a more volatile time for stocks, but the U.S. and global economies continued on solid footing as evidenced by strong corporate earnings. U.S. GDP expanded by 2.2% in the March quarter, a seasonally slower growth quarter. The consumer remained healthy as the unemployment rate held steady, while wage increases remained modest.

In the Fund’s third fiscal quarter ended June 30, 2018, earnings reports were broadly positive and economic indicators remained positive. Market optimism was tempered by escalating tensions between the United States and its international trading partners.This dynamic contributed to outperformance by small and micro-cap stocks, which typically have less exposure to global markets. A robust U.S. economy, loosening regulation, and the benefits of tax reform provided an excellent backdrop for strong business performance.

During the Fund’s fourth fiscal quarter the U.S. economy continued to strengthen, as GDP grew at an annual rate of 4.2%, attributable to consumer spending, exports, and business investment. The high rate of growth persisted into the quarter, sustained by steady wage growth of nearly 3% and a 3.7% unemployment rate, the lowest level since 1969. Additionally, household wealth grew to approximately $107 trillion, further supporting consumer spending. Healthy domestic growth coupled with the benefit from the Tax Cut and Jobs Act sustained double digit earnings growth and solid returns for stocks in the quarter.

Among our stronger performing stocks for the year were Casella Waste Systems Inc. (1.3% of net assets as of September 30, 2018), a vertically integrated solid waste and recycling management company based in Vermont and operating in 34 states. Casella reported strong revenues and growth within its industry, including the acquisition of multiple companies as part of a strategic initiative to expand its geographic presence and markets served. Cavco Industries, Inc. (1.0%), a leading designer and builder of systems-built structures including manufactured homes, modular homes, and commercial buildings, benefited from rising construction prices and a decreased labor force (nearly a quarter million open construction jobs in the United States). Prefabricated and modular construction is quickly becoming a preferred method of building due to reduced material and time requirements, increased production flexibility, and sustainable business practices. Marine Products Corp. (1.3%) is a leading manufacturer of fiberglass fishing and sport boats, and profited from growth and increasing participation in the leisure boating industry. Continued advancement in technology and the progressing development of hybrid and electric boat engines drove demand across the U.S. and European markets.

Some of the weaker holdings in the portfolio included Flushing Financial Corp. (1.0%), a holding company for Flushing Bank, which is a community oriented financial institution offering a range of financial services, operating 19 full service offices in the New York Metropolitan area. Flushing was a laggard, as the banking industry struggled to contend with challenges around regulations, disruptive technologies, and increased competition for a more demanding customer base. E.W. Scripps Co. (1.0%), an American broadcaster serving audiences and businesses with a growing portfolio of local and national media brands, struggled early in the year as a restructuring and cost cutting effort took place. In addition, a series of acquisitions failed to produce the profits and benefits expected and the pressure of fewer cable subscribers weighed on the industry. Another portfolio detractor was Astec Industries, Inc. (1.1%), which designs, engineers, manufactures, and markets equipment and components used primarily in road building and related construction activities; oil, gas, and water well drilling; and wood pellet production. In July 2018, Astec announced that it was exiting its contractual obligations regarding its Arkansas wood pellet plant, “driven by unresolved issues, which inhibited the plant’s ability to meet contractual provisions by the date required by the Company’s sales contract.” Astec agreed to pay $68 million in cash in the aggregate and forgive approximately $7 million in receivables. As a result of the disclosure the share price declined more than 20%.

We appreciate your continued confidence and trust.

3

| | | | | | | | | | | | | | | | | | | | |

| Average Annual Returns Through September 30, 2018 (a) (Unaudited) | |

| | | 1 Year | | | 5 Year | | | 10 Year | | | 15 Year | | | Since

Inception

(5/11/98) | |

Mighty Mites Fund Class AAA | | | 4.38% | | | | 8.26% | | | | 11.37% | | | | 10.87% | | | | 11.43% | |

Dow Jones U.S. Micro-Cap Total Stock Market Index | | | 17.37 | | | | 9.69 | | | | 11.71 | | | | 8.68 | | | | 9.07(b) | |

Russell 2000 Index | | | 15.24 | | | | 11.07 | | | | 11.11 | | | | 10.12 | | | | 7.84 | |

Lipper Small Cap Value Fund Average | | | 7.91 | | | | 8.81 | | | | 9.99 | | | | 9.54 | | | | 8.39(b) | |

In the current prospectuses dated January 26, 2018, the expense ratio for Class AAA Shares is 1.41%. See page 44 for the expense ratios for the year ended September 30, 2018. Class AAA Shares do not have a sales charge. | |

(a) Returns represent past performance and do not guarantee future results. Total returns and average annual returns reflect changes in share price, reinvestment of distributions, and are net of expenses. Investment returns and the principal value of an investment will fluctuate. When shares are redeemed, they may be worth more or less than their original cost. Current performance may be lower or higher than the performance data presented. Visit www.tetonadv.com for performance information as of the most recent month end. Teton Advisors, Inc., (the Adviser) reimbursed expenses through September 30, 2005 to limit the expense ratios. Had such limitations not been in place, returns would have been lower. The Fund imposes a 2% redemption fee on shares sold or exchanged within seven days after purchase. Investors should carefully consider the investment objectives, risks, charges, and expenses of the Fund before investing. The prospectuses contain information about these and other matters and should be read carefully before investing. To obtain a prospectus, please visit our website at www.tetonadv.com. Other share classes are available and have different performance characteristics. See page 2 for performance of other classes of shares. The Dow Jones U.S. Micro-Cap Total Stock Market Index is designed to provide a comprehensive measure of the micro-cap segment of the U.S. stock market. The Russell 2000 Index is an unmanaged indicator which measures the performance of the small cap segment of the U.S. equity market. The Lipper Small Cap Value Fund Average reflects the average performance of mutual funds classified in this particular category. Investing in small capitalization securities involves special challenges because these securities may trade less frequently and experience more abrupt price movements than large capitalization securities. Dividends are considered reinvested. You cannot invest directly in an index. (b) Dow Jones U.S. Micro-Cap Total Stock Market Index and Lipper Small Cap Value Fund Average since inception performance is as of April 30, 1998. | |

COMPARISON OF CHANGE IN VALUE OF A $10,000 INVESTMENT IN

THE MIGHTY MITES FUND CLASS AAA, THE RUSSELL 2000 INDEX,

AND THE DOW JONES U.S. MICRO-CAP TOTAL STOCK MARKET INDEX (Unaudited)

*Past performance is not predictive of future results. The performance tables and graph do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

4

SmallCap Equity Fund (Unaudited)

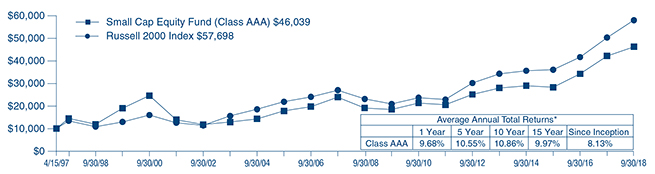

For the fiscal year ended September 30, 2018, the TETON Westwood SmallCap Equity Fund NAV per Class AAA Share appreciated 9.7% compared with a gain of 15.2% for the Russell 2000 Index. See the next page for additional performance information.

The Fund invests primarily in small cap companies that, through bottom-up fundamental research, the portfolio manager believes are attractively priced relative to their earnings growth potential or Private Market Value. The Fund characterizes small capitalization companies as those companies with a market capitalization between $100 million and $2.5 billion at the time of the Fund’s initial investment.

Equity markets rallied to close 2017. While the media coverage was dominated by the drama leading up to the passage of tax reform, a building confidence in improving earnings growth helped to carry the market higher. Corporate profits remained a key focus for investors, as ultimately the profit cycle drives long term returns in the stock market.

Stocks stumbled in the first calendar quarter of 2018 as volatility spiked from historically low levels. While trading was choppy, the market experienced its first real correction in the last several years, lasting from late January through early February. The growing potential for disruptive trade policies, starting with steel and aluminum tariffs enacted by President Trump, moved to the forefront, while corporate profit outlooks remained positive and equity markets, while volatile, remained near all time highs.

The second calendar quarter of 2018 ended on a tumultuous note, with sharp equity market declines driven by fears of a potential trade war with China and Europe. That the market exhibited some indigestion was not surprising, given high asset prices, global monetary tightening, higher interest rates, and relative investor complacency.

Stock indices ended the Fund’s fourth fiscal quarter on the retreat after marking all time highs earlier this summer. The impact was far more pronounced for small capitalization stocks, at nearly two-to-one in the last week of the quarter, as those indices returned to where they began the summer months, generally in line with their 200 day moving averages.

Among the better performing stocks in the year were: Bottomline Technologies Inc. (2.4% of net assets as of September 30, 2018), an innovator in business payment automation technology, whose stock has an impressive record of positive earnings surprises, as it has not missed a consensus earnings estimate in any of the last four quarters; Pandora Media Inc. (2.1%), that provides music streaming and internet radio service, announced in September that SiriusXM agreed to buy Pandora in an all stock deal which would create a $30 billion company that rivals market leader Spotify; and Oxford Industries, Inc. (1.4%), a high end clothing and apparel company which increased its earnings growth over the past year due to increased distribution and retail presence.

Our weaker performing stocks during the year included: Patterson-UTI Energy, Inc. (2.4%), which provides onshore contract drilling services to oil and natural gas operators in the U.S. and Canada. Patterson reported weaker than expected revenues as its pressure pumping business struggled from idled equipment and softening demand; NetScout Systems, Inc. (1.6%), a provider of application and network performance management products, experienced slow revenue growth and high cost growth; and Ethan Allen Interiors, Inc. (1.5%), a manufacturer and retailer of high quality home furnishings, whose stock has fallen in the last few quarters, most notably with fourth quarter results, as revenue rose 5.5% while gross margins compressed sharply. The most concerning aspect of the report was a decrease in retail written orders, which fell 10.8% overall.

We thank you for your continued confidence and trust.

5

| | | | | | | | | | | | | | | | | | | | |

| Average Annual Returns through September 30, 2018 (a) (Unaudited) | |

| | | 1 Year | | | 5 Year | | | 10 Year | | | 15 Year | | | Since

Inception

(4/15/97) | |

SmallCap Equity Fund Class AAA | | | 9.68% | | | | 10.55% | | | | 10.86% | | | | 9.97% | | | | 8.13% | |

Russell 2000 Index | | | 15.24 | | | | 11.07 | | | | 11.11 | | | | 10.12 | | | | 9.20 | |

Russell 2000 Value Index | | | 9.33 | | | | 9.91 | | | | 9.52 | | | | 9.50 | | | | 9.77 | |

In the current prospectuses dated January 26, 2018, the gross expense ratio for Class AAA Shares is 1.74%, and the net expense ratio is 1.25% after contractual reimbursements by Teton Advisors, Inc. (the Adviser) in place through January 31, 2019. See page 45 for the expense ratios for the year ended September 30, 2018. Class AAA Shares do not have a sales charge. | |

(a) Returns represent past performance and do not guarantee future results. Total returns and average annual returns reflect changes in share price, reinvestment of distributions, and are net of expenses. Investment returns and the principal value of an investment will fluctuate. When shares are redeemed, they may be worth more or less than their original cost. Current performance may be lower or higher than the performance data presented. Visit www.tetonadv.com for performance information as of the most recent month end. The Adviser reimbursed expenses to limit the expense ratio. Had such limitation not been in place, returns would have been lower. The Fund imposes a 2% redemption fee on shares sold or exchanged within seven days after purchase. Investors should carefully consider the investment objectives, risks, charges, and expenses of the Fund before investing. The prospectuses contain information about these and other matters and should be read carefully before investing. To obtain a prospectus, please visit our website at www.tetonadv.com. Other share classes are available and have different performance characteristics. See page 2 for performance of other classes of shares. The Russell 2000 Index is an unmanaged indicator which measures the performance of the small cap segment of the U.S. equity market. The Russell 2000 Value Index measure the performance of the small capitalization sector of the U.S. equity market and is a subset of the Russell 2000 Index. Investing in small capitalization securities involves special challenges because these securities may trade less frequently and experience more abrupt price movements than large capitalization securities. Dividends are considered reinvested. You cannot invest directly in an index. | |

COMPARISON OF CHANGE IN VALUE OF A $10,000 INVESTMENT IN THE SMALLCAP EQUITY FUND

CLASS AAA AND THE RUSSELL 2000 INDEX (Unaudited)

| * | Past performance is not predictive of future results. The performance tables and graph do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. |

6

Mid-Cap Equity Fund (Unaudited)

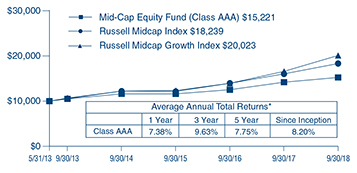

For the fiscal year ended September 30, 2018, the TETON Westwood Mid-Cap Equity Fund NAV per Class AAA Share appreciated 7.4% compared with a gain of 14.0% for the Russell Midcap Index. See the next page for additional performance information.

The Fund invests primarily in mid-cap companies that the portfolio manager believes are undervalued by the market and have above average growth potential. The Fund defines mid-cap companies as those whose market capitalization falls within a range of $1 billion to $20 billion. As bottom up, fundamental, research driven investors, the portfolio manager seeks to invest in attractively valued companies with strong balance sheets, secular growth, experienced management teams, solid earnings prospects, leading market shares, and superior long term fundamentals.

The global stock market ended 2017 on a strong note, surging to either fresh records or multi-year highs as the global economy continued a synchronized recovery, with improving corporate earnings, strengthening economics, and supportive monetary policy from central banks. The market was propelled by corporate tax cuts and a weakening dollar that supported exports. In the Fund’s second fiscal quarter, the market saw volatility caused by threats of trade wars and inflation. Despite seeing a peak in consumer confidence levels and some of the lowest reported unemployment levels in seventeen years, uncertainty over President Trump’s threat of investment restrictions against China caused market gyrations as investors gauged the potential negative impacts.

Investors entered the third fiscal quarter on the defensive, made uneasy by bouts of market volatility and swelling trade rhetoric. Macro data points in April only heightened that concern with job numbers below forecast and inflation data appearing to indicate acceleration. However, by May, the corporate earnings reports remained solid, inflation gains slowed, job growth continued, and wage growth was steady. Incoming Federal Reserve Chairman Jerome Powell also walked back hawkish inflation comments from months prior, showing little desire by officials to end the decade long bull market.

Stock indices ended the Fund’s fourth fiscal quarter on the retreat after marking all time highs earlier this summer. The impact was more pronounced for midcap stocks, at almost two to one in the last week of the quarter, as the Midcap Index moved back towards the level at which it began the summer months, nearly at the 200 day moving average. The economy continued to signal domestic strength, with the unemployment rate at 3.7%. Yet, despite tight employment conditions and many companies citing talent acquisition as a strategic concern, hourly earnings growth and inflation remained at modest levels.

Among the better performing stocks for the fiscal year included Fortinet Inc. (3.4% of net assets as of September 30, 2018), a multinational corporation that develops and markets cybersecurity software, appliances and services, such as firewalls, anti-virus, intrusion prevention, and endpoint security. Fortinet benefited from double digit sales and earnings growth, and a rising number of data breaches driving interest in its core business and cybersecurity stocks in general. Pandora Media, Inc. (2.6%) provides music discovery platform services in the United States and internationally. The company offers streaming radio and on demand music services. Pandora shares surged during the year much in thanks to a growth of over 20% in paying subscribers, enhancements in its advertising technology, and partnerships with companies SNAP and AT&T. In September it was announced that Sirius XM would be acquiring Pandora. CBRE Group Inc. (3.3%) is the world’s largest commercial real estate services and investment company, with the number one global market position in leasing, property sales, outsourcing, property management, and valuation. CBRE experienced particularly strong revenue growth in its combined regional services business, making incremental investments to support future growth, streamline operations, and share some of the benefits of tax reform with its employees. CBRE made acquisitions, highlighted by FacilitySource, a leader in technology based procurement and facility management solutions in the United States.

Some detractors from the portfolio included C&J Energy Services, Inc. (1.5%), a leading provider of well construction, well completions, and well services, which was affected by a sharp decline in the oil services industry and pipeline capacity constraints challenging short term growth. Fortune Brands Home & Security, Inc. (1.9%), a home and security products company built on industry leading brands and innovative cabinetry, plumbing, and door and security products, struggled during the year due to increasing industry competition, high levels of long term debt, and rising costs and expenses. Another poorly performing security was Patterson Companies, Inc. (0.9%), a medical supplies conglomerate primarily in the business of veterinary and dental products. Patterson saw a decrease in consolidated sales as well as a class action lawsuit on behalf of all persons or entities that purchased Patterson securities between June 26, 2015 and February 28, 2018. The complaint alleges that, throughout the period in question, Patterson made false and/or misleading statements, as well as failed to disclose material adverse facts about its business, operations, and prospects.

We appreciate your confidence and trust.

7

| | | | | | | | | | | | | | | | |

| Average Annual Returns through September 30, 2018 (a) (Unaudited) | |

| | | 1 Year | | | 3 Year | | | 5 Year | | | Since

Inception

(5/31/13) | |

Mid-Cap Equity Fund Class AAA | | | 7.38% | | | | 9.63% | | | | 7.75% | | | | 8.20% | |

Russell Midcap Index | | | 13.98 | | | | 14.52 | | | | 11.65 | | | | 11.92(b) | |

Russell Midcap Growth Index | | | 21.10 | | | | 16.65 | | | | 13.00 | | | | 13.51(b) | |

In the current prospectuses dated January 26, 2018, the gross expense ratio for Class AAA Shares is 3.36%, and net expense ratio is 1.05% after contractual reimbursements by Teton Advisors, Inc., (the Adviser) in place through January 31, 2019. See page 46 for the expense ratios for the year ended September 30, 2018. Class AAA Shares do not have a sales charge. | |

(a) Returns represent past performance and do not guarantee future results. Total returns and average annual returns reflect changes in share price, reinvestment of distributions, and are net of expenses. Investment returns and the principal value of an investment will fluctuate. When shares are redeemed, they may be worth more or less than their original cost. Current performance may be lower or higher than the performance data presented. Visit www.tetonadv.com for performance information as of the most recent month end. The Adviser reimbursed expenses to limit the expense ratio. Had such limitation not been in place, returns would have been lower. The Fund imposes a 2% redemption fee on shares sold or exchanged within seven days after purchase. Investors should carefully consider the investment objectives, risks, charges, and expenses of the Fund before investing. The prospectuses contain information about these and other matters and should be read carefully before investing. To obtain a prospectus, please visit our website at www.tetonadv.com. Other share classes are available and have different performance characteristics. See page 2 for performance of other classes of shares. The Russell Midcap Index is an unmanaged indicator which measures the performance of the midcap segment of the U.S. equity market. The Russell Midcap Growth Index is an unmanaged indicator which measures the performance of those Russell Midcap companies with higher price-to-book ratios and higher forecasted growth values. Dividends are considered reinvested. You cannot invest directly in an index. (b) Russell Midcap and Russell Midcap Growth Indices since inception performance is from May 30, 2013. | |

COMPARISON OF CHANGE IN VALUE OF A $10,000 INVESTMENT IN THE MID-CAP EQUITY FUND

CLASS AAA , THE RUSSELL MIDCAP INDEX, AND THE RUSSELL MIDCAP GROWTH INDEX (Unaudited)

| * | Past performance is not predictive of future results. The performance tables and graph do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. |

8

Convertible Securities Fund (Unaudited)

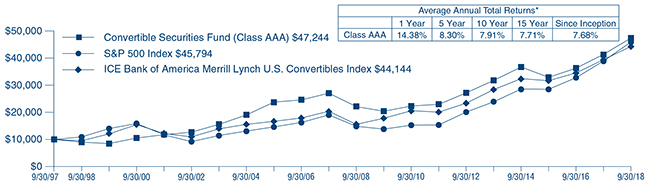

For the fiscal year ended September 30, 2018, the TETON Convertible Securities Fund NAV per Class AAA Share appreciated 14.4% compared with gains of 17.9% and 12.2% for the Standard & Poor’s (S&P) 500 Index and the ICE Bank of America Merrill Lynch U.S. Convertibles Index, respectively. See the next page for additional performance information.

The Fund invests in convertible securities. By investing in convertible securities, the portfolio managers seek the opportunity to participate in the capital appreciation of underlying stocks, while at the same time relying on the fixed income aspect of the convertible securities to provide current income and reduced price volatility, which can limit the risk of loss in a down equity market. The Fund may invest in securities of any market capitalization or credit quality, and may from time to time invest a significant amount of its assets in securities of smaller companies.

We experienced four interest rate hikes and the beginning of the reduction of the Federal Reserve balance sheet during the Fund’s fiscal year, but this did not keep the convertible market from providing strong returns. The Fund’s first fiscal quarter saw convertible securities driven higher by strong equity markets and a stable economic environment. Low volatility was apparent in most asset classes, and convertibles remained competitive with stocks.

Volatility returned in the Fund’s second fiscal quarter. Rising interest rates and uncertainty over global trade policy caused investors and traders to add and remove risk from portfolios in a rather dramatic fashion. Convertibles maintained much greater stability over the course of the quarter which allowed them to outperform other asset classes, as rates remained low and tax code changes limiting deductibility of interest made the structure attractive for issuers.

The bull market continued in the Fund’s third fiscal quarter and convertible securities followed up on their strong beginning to 2018 as they again outperformed U.S. corporate bonds and U.S. government bonds. Among U.S. convertible issues, the Consumer Non-Cyclical, Energy, and Technology sectors added to returns for the year to date. Non-rated issues outperformed investment grade, intermediate grade and junk issues, while mid-capitalization issues outperformed small capitalization and large capitalization issues, in that order.

Convertible securities continued their strong performance in the Fund’s fourth fiscal quarter, outperforming U.S. corporate bonds and U.S. government bonds while lagging the performance of the S&P 500. We continued to see robust issuance with 25 new issues coming to market. The U.S. convertible market ended September with 476 issues and $227 billion in market capitalization. Issuance expanded in 2018 with 118 new issues raising $47 billion, exceeding redemptions for the year, growing the market and giving the portfolio managers a diverse mix of convertibles to choose from for the portfolio.

Among the better performing securities were Teladoc Health Inc., 3.000%, 12/15/22 (2.1% of net assets as of September 30, 2018), a telehealth company that uses telephone and videoconferencing technology to provide on-demand remote medical care via mobile devices. Over the past year Teladoc benefited from segment growth and the growing dependence on virtual care delivery. In addition, expanded capabilities and an announced partnership with Partners Healthcare helped support strong growth. Another security that added to the Fund’s performance was Coupa Software Inc., 0.375%, 01/15/23 (1.6%), a global technology platform for Business Spend Management (BSM) that helps small, medium, and large companies gain visibility into, and control over, the money and resources spent within their organizations. Coupa saw high growth and strong performance in a quickly expanding and highly accessible market, and counts Amazon, Nike, and Coca-Cola Consolidated among its growing customer base. An additional contributor to the portfolio was Neurocrine Biosciences Inc., 2.250%, 05/15/24 (1.4%), a biopharmaceutical company which develops and discovers treatments for neurological and endocrine-related diseases and disorders. Neurocrine saw significant revenue growth from its FDA approved drug Ingrezza, and has clinical stage trials in the pipeline.

Some of the Fund’s weaker holdings included DISH Network Corp., 3.375%, 08/15/26 (2.0%), a network television provider and owner of the direct broadcast satellite provider DISH and Sling TV. DISH’s stock had a downward trajectory for most of the year, mainly due to a steady loss of satellite subscribers and the ongoing trend of “cord cutting.” DISH does not sell broadband service, meaning that users of its Sling TV must get their internet service from alternative providers. Rambus Inc., 1.375%, 02/01/23 (1.6%), provides semiconductor products and focuses on design, development, and manufacturing through partnerships and licensing of technology and solutions related to memory and interfaces. Its solutions provide an interface between analog signals and digital information in systems, such as telecommunications transport systems, enterprise networking equipment, and datacenters. Midway through the year, Rambus’s CEO was unexpectedly terminated due to what the Board determined to be conduct which fell short of the company’s standards. Inphi Corp., 1.125%, 12/01/20 (2.0%), is a provider of analog and mixed signal semiconductor solutions for the communications and datacenter markets. Inphi suffered from a self described down cycle driven by inventory buildups in China long haul and metro markets and lower demand for its linear transimpedance amplifier and linear driver products.

We appreciate your confidence and trust.

9

| | | | | | | | | | | | | | | | | | | | |

| Average Annual Returns Through September 30, 2018 (a) (Unaudited) | |

| | | 1 Year | | | 5 Year | | | 10 Year | | | 15 Year | | | Since

Inception

(9/30/97) | |

Convertible Securities Fund Class AAA | | | 14.38% | | | | 8.30% | | | | 7.91% | | | | 7.71% | | | | 7.68% | |

S&P 500 Index | | | 17.91 | | | | 13.95 | | | | 11.97 | | | | 9.65 | | | | 7.50 | |

ICE Bank of America Merrill Lynch U.S. Convertibles Index | | | 12.22 | | | | 9.32 | | | | 11.01 | | | | 8.01 | | | | 7.32 | |

In the current prospectuses dated January 26, 2018, the gross expense ratio for Class AAA Shares is 2.47%, and the net expense ratio is 1.15%, after contractual reimbursements by Teton Advisors, Inc. (the Adviser) in place through January 31, 2019. See page 47 for the expense ratios for the year ended September 30, 2018. Class AAA Shares do not have a sales charge. | |

(a) Returns represent past performance and do not guarantee future results. Total returns and average annual returns reflect changes in share price, reinvestment of distributions, and are net of expenses. Investment returns and the principal value of an investment will fluctuate. When shares are redeemed, they may be worth more or less than their original cost. Current performance may be lower or higher than the performance data presented. Visit www.tetonadv.com for performance information as of the most recent month end. The Adviser reimbursed expenses to limit the expense ratio. Had such limitation not been in place, returns would have been lower. The Fund imposes a 2% redemption fee on shares sold or exchanged within seven days after purchase. Investors should carefully consider the investment objectives, risks, charges, and expenses of the Fund before investing. The prospectuses contain information about these and other matters and should be read carefully before investing. To obtain a prospectus, please visit our website at www.tetonadv.com. Other share classes are available and have different performance characteristics. See page 2 for performance of other classes of shares. The S&P 500 Index is a market capitalization weighted index of 500 large capitalization stocks commonly used to represent the U.S. equity market. The ICE Bank of America Merrill Lynch U.S. Convertibles Index is a market value weighted index of all dollar denominated convertible securities that are exchangeable into U.S. equities that have a market value of more than $50 million. Dividends are considered reinvested. You cannot invest directly in an index. | |

COMPARISON OF CHANGE IN VALUE OF A $10,000 INVESTMENT IN THE CONVERTIBLE SECURITIES FUND

CLASS AAA, THE S&P 500 INDEX AND

THE ICE BANK OF AMERICA MERRILL LYNCH U.S. CONVERTIBLES INDEX (Unaudited)

| * | Past performance is not predictive of future results. The performance tables and graph do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. |

10

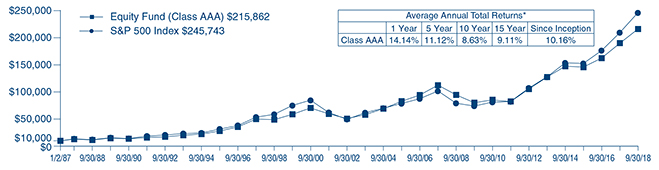

Equity Fund (Unaudited)

The TETON Westwood Equity Fund underperformed the benchmark S&P 500 Index over the fiscal year. For the twelve months ended September 30, 2018, the Equity Fund Class AAA shares posted a gain of 14.1%, net of expenses, versus the S&P 500 Index gain of 17.9%. See the next page for additional performance information.

Equity markets rallied to close 2017. While the media coverage was dominated by the drama leading up to the passage of tax reform, a building confidence in improving earnings growth helped to carry the market higher. Corporate profits remained a key focus for investors, as ultimately the profit cycle drives long term returns in the stock market.

Stocks stumbled in the first calendar quarter of 2018 as volatility spiked from historically low levels. While trading was choppy, the market experienced its first real correction in the last several years, lasting from late January through early February. The growing potential for disruptive trade policies, starting with steel and aluminum tariffs enacted by President Trump, moved to the forefront, while corporate profit outlooks remained positive and equity markets, while volatile, remained near all time highs.

Volatility, which had surfaced earlier in the year, decreased throughout the second calendar quarter, though remained elevated relative to recent historically low levels. The market grappled with continued headlines regarding the potential for trade wars with our international partners on several different fronts.

Stock indices ended the Fund’s fourth fiscal quarter on the retreat after marking all time highs earlier this summer.

Positive drivers of relative Fund performance over the twelve months included: Becton Dickinson & Co. (2.5% of total net assets as of September 30, 2018), a medical technology company that manufactures and sells medical devices, instruments, and systems which benefited from accelerating revenue growth and margin expansions as it continued to successfully acquire and integrate additional products into its lineup and realize meaningful synergies; Abbott Laboratories (3.0%), an American healthcare company with a broad range of branded generic pharmaceuticals, medical devices, diagnostics, and nutrition products, saw solid contribution from its recent acquisitions, as its organic growth exceeded expectations; Motorola Solutions Inc. (2.1%), the data communications and telecommunications equipment provider, gained traction as the leading provider for network and communication solutions for first responders; and Boeing Co. (2.0%), the world’s largest aerospace company, rallied on better earnings and cash flow results seen throughout the year, supported by a backlog for new airplanes that stretches out over the next five years.

Detractors from the Fund’s performance included AT&T Corp. (3.5%), which provides voice, video, and data communications services to businesses, consumers, and governments worldwide, fell as broad concerns on competitive pressures across its business units weighed on shares even though further consolidation in the wireless carrier market could be beneficial to improving industry behavior. General Mills, Inc. (2.0%), which manufactures and markets branded consumer goods worldwide, closed on its acquisition of Blue Buffalo to further expand its product portfolio; however, rising transportation costs particularly hurt margins as did high levels of competitive pressures. Financial services company Morgan Stanley, Inc. (1.6%) shares were pressured as it received a less favorable regulatory ruling on its plan to return additional capital to shareholders. Lam Research Corp. (0.8%), the semiconductor and circuit manufacturer, moved lower over investor fears regarding the semiconductor cycle amid the upcoming lull in activity being indicated by the industry after a strong period of growth.

We appreciate your confidence and trust.

11

| | | | | | | | | | | | | | | | | | | | |

| Average Annual Returns through September 30, 2018 (a) (Unaudited) | |

| | | 1 Year | | | 5 Year | | | 10 Year | | | 15 Year | | | Since

Inception

(1/2/87) | |

Equity Fund Class AAA | | | 14.14% | | | | 11.12% | | | | 8.63% | | | | 9.11% | | | | 10.16% | |

S&P 500 Index | | | 17.91 | | | | 13.95 | | | | 11.97 | | | | 9.65 | | | | 10.61(b) | |

| In the current prospectuses dated January 26, 2018, the expense ratio for Class AAA Shares is 1.62%. See page 48 for the expense ratios for the year ended September 30, 2018. Class AAA Shares do not have a sales charge. | |

(a) Returns represent past performance and do not guarantee future results. Total returns and average annual returns reflect changes in share price, reinvestment of distributions, and are net of expenses. Investment returns and the principal value of an investment will fluctuate. When shares are redeemed, they may be worth more or less than their original cost. Current performance may be lower or higher than the performance data presented. Visit www.tetonadv.com for performance information as of the most recent month end. Investors should carefully consider the investment objectives, risks, charges, and expenses of the Fund before investing. The prospectuses contain information about these and other matters and should be read carefully before investing. To obtain a prospectus, please visit our website at www.tetonadv.com. Other share classes are available and have different performance characteristics. See page 2 for performance of other classes of shares. The S&P 500 Index is a market capitalization weighted index of 500 large capitalization stocks commonly used to represent the U.S. equity market. Dividends are considered reinvested. You cannot invest directly in an index. (b) S&P 500 Index since inception performance is as of December 31, 1986. | |

COMPARISON OF CHANGE IN VALUE OF A $10,000 INVESTMENT IN

THE EQUITY FUND CLASS AAA AND THE S&P 500 INDEX (Unaudited)

| * | Past performance is not predictive of future results. The performance tables and graph do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. |

12

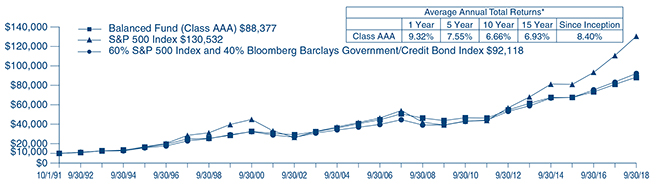

Balanced Fund (Unaudited)

For fiscal year ended September 30, 2018, the TETON Westwood Balanced Fund Class AAA Shares posted a return of 9.3%, net of expenses, versus the Bloomberg Barclays Government/Credit Bond Index return of (1.4%). The Fund’s return was less than a common balanced benchmark comprised of 60% S&P 500 Index and 40% of the Bloomberg Barclays Capital Government/Credit Bond Index which returned 10.2%. See the next page for additional performance information.

Equity markets rallied to close 2017 with even more gains. While the media coverage was dominated by the drama leading up to the passage of tax reform, a building confidence in improving earnings growth helped to carry the market higher. Corporate profits remained a key focus for investors, as ultimately the profit cycle drives long term returns in the stock market.

Stocks stumbled in the first calendar quarter of 2018 as volatility spiked from historically low levels. While trading was choppy, the market experienced its first real correction in the last several years, lasting from late January through early February. The growing potential for disruptive trade policies, starting with steel and aluminum tariffs enacted by President Trump, moved to the forefront, while corporate profit outlooks remained positive and equity markets, while volatile, remained near all time highs.

The second calendar quarter of 2018 ended on a tumultuous note, with sharp equity market declines driven by fears of a potential trade war with China and Europe. That the market exhibited some indigestion was not surprising, given high asset prices, global monetary tightening, higher interest rates, and relative investor complacency.

Volatility, which had surfaced earlier in the year, moderated throughout the second calendar quarter, though remained elevated relative to recent historically low levels. The market grappled with continued headlines regarding the potential for trade wars with our international partners on several different fronts.

The Fund’s fixed income segment outperformed the benchmark in the third calendar quarter. The Fund outperformed in the U.S. Agency and Utility Corporate segments. Key drivers of outperformance were having lower overall portfolio duration, being overweight corporate credit, and being underweight U.S. Treasuries.

Our top contributor for the period was Exxon Mobil 6.5% due 15 Dec 2018 (no longer held as of September 30, 2018). Other top contributors were a floating rate corporate bond and a short maturity corporate bond: Enterprise Products Group Perpetual Floater and Texas Instruments 1.65% due 03 Aug 2019 (no longer held and 0.8%, respectively).

Detracting from performance were intermediate maturity Treasury and U.S. Agency positions; Fannie Mae 2.625% due 06 Sep 2024 (1.7%), U.S. Treasury 2.25% due 15 Nov 2024 (1.5%), and U.S. Treasury 1.625% due 15 Feb 2026 (1.2%).

We appreciate your confidence and trust.

13

| | | | | | | | | | | | | | | | | | | | |

Average Annual Returns through September 30, 2018 (a) (Unaudited) | |

| | | 1 Year | | | 5 Year | | | 10 Year | | | 15 Year | | | Since

Inception

(10/1/91) | |

Balanced Fund Class AAA | | | 9.32% | | | | 7.55% | | | | 6.66% | | | | 6.93% | | | | 8.40% | |

Bloomberg Barclays Government/Credit Bond Index | | | (1.37) | | | | 2.23 | | | | 3.95 | | | | 3.75 | | | | 5.54(b) | |

S&P 500 Index | | | 17.91 | | | | 13.95 | | | | 11.97 | | | | 9.65 | | | | 9.97(b) | |

60% S&P 500 Index and 40% Bloomberg Barclays Government/Credit Bond Index (c) | | | 10.20 | | | | 9.26 | | | | 8.76 | | | | 7.29 | | | | 8.20 | |

In the current prospectuses dated January 26, 2018, the expense ratio for Class AAA Shares is 1.34%. See page 49 for the expense ratios for the year ended September 30, 2018. Class AAA Shares do not have a sales charge. | |

(a) Returns represent past performance and do not guarantee future results. Total returns and average annual returns reflect changes in share price, reinvestment of distributions, and are net of expenses. Investment returns and the principal value of an investment will fluctuate. When shares are redeemed, they may be worth more or less than their original cost. Current performance may be lower or higher than the performance data presented. Visit www.tetonadv.com for performance information as of the most recent month end. Teton Advisors, Inc. (the Adviser) reimbursed expenses in years prior to 1998 to limit the expense ratio. Had such limitation not been in place, returns would have been lower. Investors should carefully consider the investment objectives, risks, charges, and expenses of the Fund before investing. The prospectuses contain information about these and other matters and should be read carefully before investing. To obtain a prospectus, please visit our website at www.tetonadv.com. Other share classes are available and have different performance characteristics. See page 2 for performance of other classes of shares. The Bloomberg Barclays Government/Credit Bond Index is a market value weighted index that tracks the performance of fixed rate, publicly placed, dollar denominated obligations. The S&P 500 Index is a market capitalization weighted index of 500 large capitalization stocks commonly used to represent the U.S. equity market. Dividends are considered reinvested. You cannot invest directly in an index. (b) S&P 500 Index and Bloomberg Barclays Government/Credit Bond Index since inception performances are as of September 30, 1991. (c) The Blended Index consists of a blend of 60% of the S&P 500 Index and 40% of the Bloomberg Barclays Government/Credit Bond Index. | |

COMPARISON OF CHANGE IN VALUE OF A $10,000 INVESTMENT IN THE BALANCED FUND CLASS AAA,

THE S&P 500 INDEX, AND A COMPOSITE OF 60% OF THE S&P 500 INDEX AND 40% OF

THE BLOOMBERG BARCLAYS GOVERNMENT/CREDIT BOND INDEX (Unaudited)

| * | Past performance is not predictive of future results. The performance tables and graph do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. |

14

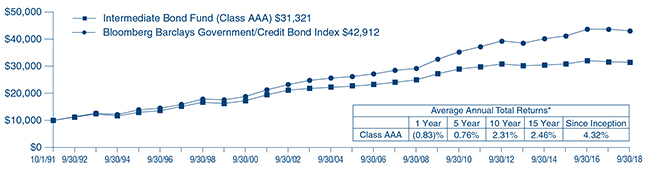

Intermediate Bond Fund (Unaudited)

For the fiscal year ended September 30, 2018, the TETON Westwood Intermediate Bond Fund NAV per Class AAA Share decreased (0.8)% compared with the Bloomberg Barclays Government/Credit Bond Index which was down (1.4)%. See below for additional performance information.

The TETON Westwood Intermediate Bond Fund benefited from its intermediate financial corporate positions during the fourth quarter of 2017. Investment grade credit spreads tightened during the period, with corporates outperforming duration matched Treasury and U.S. Agency positions. Yields on intermediate Treasuries rose, and total returns on investment grade bonds were positive for the period.

The Fund outperformed its benchmark in the first quarter of 2018. Yields on intermediate Treasuries rose, and total returns on investment grade bonds were negative for the period. Yields on the 5 year Treasury note rose 35 basis points from 2.21% to 2.56%, while the 10 year Treasury note rose 33 basis points from 2.41% to 2.74% during the quarter.

Yields on intermediate Treasuries rose, and total returns on investment grade bonds were negative during the Fund’s third fiscal quarter. Yields on the 5 year U.S. Treasury note rose by 18 basis points from 2.56% to 2.74%, while the 10 year Treasury note rose by 12 basis points, from 2.74% to 2.86% during the quarter.

The Fund outperformed the benchmark in the third calendar quarter. Yields on intermediate Treasuries rose, and total returns on investment grade bonds were negative for the period. Yields on the 5 year Treasury note rose by 21 basis points from 2.74% to 2.95%, while the 10 year Treasury note rose by 20 basis points from 2.86% to 3.06% during the quarter. Notwithstanding some inter-period volatility, the trend was clearly up. The U.S. Treasury Yield Curve flattened slightly as the yield differential between 10 year and 2 year Treasuries continued to narrow. Investment grade credit spreads tightened by approximately 15 basis points during the quarter causing U.S. Treasury and Agencies to underperform duration matched corporates.

We thank you for your continued confidence and trust.

| | | | | | | | | | | | | | | | | | | | |

| Average Annual Returns through September 30, 2018 (a) (Unaudited) | |

| | | 1 Year | | | 5 Year | | | 10 Year | | | 15 Year | | | Since

Inception

(10/1/91) | |

Intermediate Bond Fund Class AAA | | | (0.83)% | | | | 0.76% | | | | 2.31% | | | | 2.46% | | | | 4.32% | |

Bloomberg Barclays Government/Credit Bond Index | | | (1.37) | | | | 2.23 | | | | 3.95 | | | | 3.75 | | | | 5.54(b) | |

| In the current prospectuses dated January 26, 2018, the gross expense ratio for AAA Shares is 1.52%, and the net expense ratio is 1.00% after contractual reimbursements by Teton Advisors, Inc., (the Adviser) in place through January 31, 2019. See page 50 for the expense ratios for the year ended September 30, 2018. Class AAA Shares do not have a sales charge. | |

(a) Returns represent past performance and do not guarantee future results. Total returns and average annual returns reflect changes in share price, reinvestment of distributions, and are net of expenses. Investment returns and the principal value of an investment will fluctuate. When shares are redeemed, they may be worth more or less than their original cost. Current performance may be lower or higher than the performance data presented. Visit www.tetonadv.com for performance information as of the most recent month end. The Adviser reimbursed expenses to limit the expense ratio. Had such limitation not been in place, returns would have been lower. Investors should carefully consider the investment objectives, risks, charges, and expenses of the Fund before investing. The prospectuses contain information about these and other matters and should be read carefully before investing. To obtain a prospectus, please visit our website at www.tetonadv.com. Other share classes are available and have different performance characteristics. See page 2 for performance of other classes of shares. The Bloomberg Barclays Government/Credit Bond Index is a market value weighted index that tracks the performance of fixed rate, publicly placed, dollar denominated obligations. Dividends are considered reinvested. You cannot invest directly in an index. (b) The Bloomberg Barclays Government/Credit Bond Index since inception performance is as of September 30, 1991. | |

COMPARISON OF CHANGE IN VALUE OF A $10,000 INVESTMENT IN THE

INTERMEDIATE BOND FUND CLASS AAA AND

THE BLOOMBERG BARCLAYS GOVERNMENT/CREDIT BOND INDEX (Unaudited)

| * | Past performance is not predictive of future results. The performance tables and graph do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. |

15

This page was intentionally left blank.

TETON Westwood Funds

Disclosure of Fund Expenses (Unaudited)

For the Six Month Period from April 1, 2018 through September 30, 2018

We believe it is important for you to understand the impact of fees and expenses regarding your investment. All mutual funds have operating expenses. As a shareholder of a fund, you incur ongoing costs, which include costs for portfolio management, administrative services, and shareholder reports (like this one), among others. Operating expenses, which are deducted from a fund’s gross income, directly reduce the investment return of a fund. When a fund’s expenses are expressed as a percentage of its average net assets, this figure is known as the expense ratio. The following examples are intended to help you understand the ongoing costs (in dollars) of investing in your Fund and to compare these costs with those of other mutual funds. The examples are based on an investment of $1,000 made at the beginning of the period shown and held for the entire period.

The Expense Table on page 18 illustrates your Fund’s costs in two ways:

Actual Fund Return: This section provides information about actual account values and actual expenses. You may use this section to help you to estimate the actual expenses that you paid over the period after any fee waivers and expense reimbursements. The “Ending Account Value” shown is derived from the Fund’s actual return during the past six months, and the Expenses Paid During Period” shows the dollar amount that would have been paid by an investor who started with $1,000 in the Fund. You may use this information, together with the amount you invested, to estimate the expenses that you paid over the period. To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for your Fund under the heading “Expenses Paid During Period” to estimate the expenses you paid during this period.

Hypothetical 5% Return: This section provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio. It assumes a hypothetical annualized return of 5% before expenses during the period shown. In this case – because the hypothetical return used is not the Fund’s actual return – the results do not apply to your investment and you cannot use the hypothetical account value and expense to estimate the actual ending account balance or expenses you paid for the period. This example is useful in making comparisons of the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs such as sales charges (loads), redemption fees, or exchange fees, if any, which are described in the Prospectus. If these costs were applied to your account, your costs would be higher. Therefore, the 5% hypothetical return is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. The “Annualized Expense Ratio” represents the actual expenses for the last six months and may be different from the expense ratio in the Financial Highlights which is for the fiscal year ended September 30, 2018.

17

TETON Westwood Funds

Disclosure of Fund Expenses (Unaudited) (Continued)

For the Six Month Period from April 1, 2018 through September 30, 2018

Expense Table

| | | | | | | | | | | | | | | | |

| | | Actual Fund Return | | Hypothetical 5% Return |

| | | Beginning

Account Value

04/01/18 | | Ending

Account Value

09/30/18 | | Annualized

Expense

Ratio | | Expenses

Paid During

Period* | | Beginning

Account Value

04/01/18 | | Ending

Account Value

09/30/18 | | Annualized

Expense

Ratio | | Expenses

Paid During

Period* |

|

|

TETON Westwood Mighty Mites Fund |

|

Class AAA | | $1,000.00 | | $1,053.70 | | 1.42% | | $ 7.31 | | $1,000.00 | | $1,017.95 | | 1.42% | | $ 7.18 |

Class A | | $1,000.00 | | $1,052.70 | | 1.67% | | $ 8.59 | | $1,000.00 | | $1,016.70 | | 1.67% | | $ 8.44 |

Class C | | $1,000.00 | | $1,050.10 | | 2.17% | | $11.15 | | $1,000.00 | | $1,014.19 | | 2.17% | | $10.96 |

Class I | | $1,000.00 | | $1,055.30 | | 1.16% | | $ 5.98 | | $1,000.00 | | $1,019.25 | | 1.16% | | $ 5.87 |

|

TETON Westwood SmallCap Equity Fund |

|

Class AAA | | $1,000.00 | | $1,058.60 | | 1.25% | | $ 6.45 | | $1,000.00 | | $1,018.80 | | 1.25% | | $ 6.33 |

Class A | | $1,000.00 | | $1,057.30 | | 1.50% | | $ 7.74 | | $1,000.00 | | $1,017.55 | | 1.50% | | $ 7.59 |

Class C | | $1,000.00 | | $1,054.90 | | 2.00% | | $10.30 | | $1,000.00 | | $1,015.04 | | 2.00% | | $10.10 |

Class I | | $1,000.00 | | $1,060.00 | | 1.00% | | $ 5.16 | | $1,000.00 | | $1,020.05 | | 1.00% | | $ 5.06 |

|

TETON Westwood Mid-Cap Equity Fund |

|

Class AAA | | $1,000.00 | | $1,040.30 | | 1.05% | | $ 5.37 | | $1,000.00 | | $1,019.80 | | 1.05% | | $ 5.32 |

Class A | | $1,000.00 | | $1,039.30 | | 1.30% | | $ 6.65 | | $1,000.00 | | $1,018.55 | | 1.30% | | $ 6.58 |

Class C | | $1,000.00 | | $1,036.30 | | 1.80% | | $ 9.19 | | $1,000.00 | | $1,016.04 | | 1.80% | | $ 9.10 |

Class I | | $1,000.00 | | $1,041.20 | | 0.80% | | $ 4.09 | | $1,000.00 | | $1,021.06 | | 0.80% | | $ 4.05 |

|

TETON Convertible Securities Fund |

|

Class AAA | | $1,000.00 | | $1,076.60 | | 1.15% | | $ 5.99 | | $1,000.00 | | $1,019.30 | | 1.15% | | $ 5.82 |

Class A | | $1,000.00 | | $1,075.20 | | 1.40% | | $ 7.28 | | $1,000.00 | | $1,018.05 | | 1.40% | | $ 7.08 |

Class C | | $1,000.00 | | $1,072.20 | | 1.90% | | $ 9.87 | | $1,000.00 | | $1,015.54 | | 1.90% | | $ 9.60 |

Class I | | $1,000.00 | | $1,077.70 | | 0.90% | | $ 4.69 | | $1,000.00 | | $1,020.56 | | 0.90% | | $ 4.56 |

|

TETON Westwood Equity Fund |

|

Class AAA | | $1,000.00 | | $1,078.10 | | 1.59% | | $ 8.28 | | $1,000.00 | | $1,017.10 | | 1.59% | | $ 8.04 |

Class A | | $1,000.00 | | $1,076.70 | | 1.84% | | $ 9.58 | | $1,000.00 | | $1,015.84 | | 1.84% | | $ 9.30 |

Class C | | $1,000.00 | | $1,074.70 | | 2.34% | | $12.17 | | $1,000.00 | | $1,013.34 | | 2.34% | | $11.81 |

Class I | | $1,000.00 | | $1,080.00 | | 1.34% | | $ 6.99 | | $1,000.00 | | $1,018.35 | | 1.34% | | $ 6.78 |

|

TETON Westwood Balanced Fund |

|

Class AAA | | $1,000.00 | | $1,052.20 | | 1.34% | | $ 6.89 | | $1,000.00 | | $1,018.35 | | 1.34% | | $ 6.78 |

Class A | | $1,000.00 | | $1,051.60 | | 1.59% | | $ 8.18 | | $1,000.00 | | $1,017.10 | | 1.59% | | $ 8.04 |

Class C | | $1,000.00 | | $1,048.80 | | 2.09% | | $10.73 | | $1,000.00 | | $1,014.59 | | 2.09% | | $10.56 |

Class I | | $1,000.00 | | $1,054.60 | | 1.09% | | $ 5.61 | | $1,000.00 | | $1,019.60 | | 1.09% | | $ 5.52 |

|

TETON Westwood Intermediate Bond Fund |

|

Class AAA | | $1,000.00 | | $1,001.30 | | 1.00% | | $ 5.02 | | $1,000.00 | | $1,020.05 | | 1.00% | | $ 5.06 |

Class A | | $1,000.00 | | $1,000.80 | | 1.10% | | $ 5.52 | | $1,000.00 | | $1,019.55 | | 1.10% | | $ 5.57 |

Class C | | $1,000.00 | | $ 998.10 | | 1.75% | | $ 8.77 | | $1,000.00 | | $1,016.29 | | 1.75% | | $ 8.85 |

Class I | | $1,000.00 | | $1,003.40 | | 0.75% | | $ 3.77 | | $1,000.00 | | $1,021.31 | | 0.75% | | $ 3.80 |

| * | Expenses are equal to the Funds’ annualized expense ratio for the last six months multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half year (183 days), then divided by 365. |

18

Summary of Portfolio Holdings (Unaudited)

The following tables present portfolio holdings as a percent of net assets as of September 30, 2018:

TETON Westwood Mighty Mites Fund

| | | | |

U.S. Government Obligations | | | 19.8 | % |

Diversified Industrial | | | 9.9 | % |

Health Care | | | 7.6 | % |

Financial Services | | | 6.9 | % |

Equipment and Supplies | | | 5.3 | % |

Hotels and Gaming | | | 3.4 | % |

Electronics | | | 3.3 | % |

Consumer Products | | | 2.9 | % |

Food and Beverage | | | 2.8 | % |

Automotive: Parts and Accessories | | | 2.8 | % |

Machinery | | | 2.7 | % |

Aerospace and Defense | | | 2.7 | % |

Specialty Chemicals | | | 2.5 | % |

Real Estate | | | 2.5 | % |

Telecommunications | | | 2.4 | % |

Business Services | | | 2.0 | % |

Building and Construction | | | 2.0 | % |

Restaurants | | | 1.8 | % |

Manufactured Housing and Recreational Vehicles | | | 1.6 | % |

Computer Software and Services | | | 1.5 | % |

Metals and Mining | | | 1.4 | % |

Aviation: Parts and Services | | | 1.4 | % |

Retail | | | 1.3 | % |

Environmental Control | | | 1.3 | % |

| | | | |

Publishing | | | 1.1 | % |

Broadcasting | | | 1.1 | % |

Entertainment | | | 1.0 | % |

Energy and Utilities: Water | | | 0.9 | % |

Automotive | | | 0.8 | % |

Consumer Services | | | 0.6 | % |

Energy and Utilities: Natural Gas | | | 0.5 | % |

Semiconductors | | | 0.4 | % |

Agriculture | | | 0.3 | % |

Wireless Communications | | | 0.3 | % |

Energy and Utilities: Oil | | | 0.2 | % |

Energy and Utilities: Services | | | 0.2 | % |

Communications Equipment | | | 0.2 | % |

Paper and Forest Products | | | 0.2 | % |

Energy and Utilities: Integrated | | | 0.2 | % |

Airlines | | | 0.2 | % |

Closed-End Funds | | | 0.1 | % |

Educational Services | | | 0.0 | %* |

Transportation | | | 0.0 | %* |

Energy and Utilities | | | 0.0 | %* |

Other Assets and Liabilities (Net) | | | (0.1 | )% |

| | | | |

| | | 100.0 | % |

| | | | |

| * | Amount represents less than 0.05%. |

TETON Westwood SmallCap Equity Fund

| | | | |

Banking | | | 20.3 | % |

Energy and Utilities | | | 12.1 | % |

U.S. Government Obligations | | | 7.9 | % |

Computer Software and Services | | | 6.5 | % |

Health Care | | | 6.0 | % |

Semiconductors | | | 5.9 | % |

Business Services | | | 4.6 | % |

Telecommunications | | | 4.5 | % |

Retail | | | 3.9 | % |

Diversified Industrial | | | 3.9 | % |

Communications | | | 3.8 | % |

Financial Services | | | 3.5 | % |

Electronics | | | 2.3 | % |

| | | | |

Consumer Products | | | 2.3 | % |

Building and Construction | | | 1.9 | % |

Equipment and Supplies | | | 1.8 | % |

Speciality Chemicals | | | 1.7 | % |

Automotive | | | 1.7 | % |

Aerospace | | | 1.4 | % |

Environmental Control | | | 1.2 | % |

Broadcasting | | | 1.2 | % |

Machinery | | | 1.0 | % |

Real Estate | | | 0.9 | % |

Other Assets and Liabilities (Net) | | | (0.3 | )% |

| | | | |

| | | 100.0 | % |

| | | | |

TETON Westwood Mid-Cap Equity Fund

| | | | |

Financials | | | 21.7 | % |

Information Technology | | | 18.2 | % |

Consumer Discretionary | | | 15.7 | % |

Industrials | | | 14.7 | % |

Energy | | | 13.2 | % |

Health Care | | | 8.2 | % |

| | | | |

Materials | | | 3.7 | % |

Consumer Staples | | | 3.1 | % |

Other Assets and Liabilities (Net) | | | 1.5 | % |

| | | | |

| | | 100.0 | % |

| | | | |

19

Summary of Portfolio Holdings (Unaudited) (Continued)

TETON Convertible Securities Fund

| | | | |

Computer Software and Services | | | 19.6 | % |

Health Care | | | 15.0 | % |

Semiconductors | | | 10.5 | % |

U.S. Government Obligations | | | 7.9 | % |

Financial Services | | | 5.7 | % |

Business Services | | | 5.3 | % |

Real Estate Investment Trusts | | | 4.5 | % |

Energy and Utilities: Integrated | | | 4.0 | % |

Communications Equipment | | | 3.5 | % |

Energy and Utilities: Services | | | 3.5 | % |

Telecommunications | | | 2.9 | % |

Consumer Services | | | 2.4 | % |

Industrials | | | 2.1 | % |

| | | | |

Aviation: Parts and Services | | | 2.0 | % |

Cable and Satellite | | | 2.0 | % |

Entertainment | | | 1.8 | % |

Diversified Industrial | | | 1.5 | % |

Food and Beverage | | | 1.3 | % |

Aerospace and Defense | | | 1.2 | % |

Building and Construction | | | 1.1 | % |

Transportation | | | 1.0 | % |

Agriculture | | | 0.4 | % |

Other Assets and Liabilities (Net) | | | 0.8 | % |

| | | | |

| | | 100.0 | % |

| | | | |

TETON Westwood Equity Fund

| | | | |

Health Care | | | 13.5 | % |

Banking | | | 10.4 | % |

Financial Services | | | 9.6 | % |

Computer Software and Services | | | 8.9 | % |

Energy: Integrated | | | 8.0 | % |

Retail | | | 7.2 | % |

Aerospace | | | 6.0 | % |

Food and Beverage | | | 5.8 | % |

Telecommunications | | | 5.6 | % |

Energy and Energy Services | | | 3.7 | % |

Diversified Industrial | | | 3.1 | % |

Business Services | | | 3.0 | % |

| | | | |

Real Estate | | | 2.9 | % |

Transportation | | | 2.5 | % |

Specialty Chemicals | | | 2.0 | % |

Entertainment | | | 2.0 | % |

Consumer Products | | | 2.0 | % |

Energy: Oil | | | 1.9 | % |

Other Investment Companies | | | 1.2 | % |

Semiconductors | | | 0.8 | % |

Other Assets and Liabilities (Net) | | | (0.1 | )% |

| | | | |

| | | 100.0 | % |

| | | | |

TETON Westwood Balanced Fund

| | | | |

Health Care | | | 11.7 | % |

Banking | | | 11.0 | % |

Financial Services | | | 10.6 | % |

Retail | | | 6.5 | % |

U.S. Government Obligations | | | 6.3 | % |

Computer Software and Services | | | 6.0 | % |

Energy: Integrated | | | 5.3 | % |

Telecommunications | | | 4.8 | % |

Aerospace | | | 4.4 | % |

Food and Beverage | | | 4.1 | % |

Consumer Products | | | 3.5 | % |

Diversified Industrial | | | 3.4 | % |

Federal Home Loan Mortgage Corp. | | | 2.7 | % |

Energy and Energy Services | | | 2.4 | % |

| | | | |

Electronics | | | 2.4 | % |

Business Services | | | 2.1 | % |

Energy: Oil | | | 2.1 | % |

Real Estate | | | 1.9 | % |

Federal National Mortgage Association | | | 1.7 | % |

Other Investment Companies | | | 1.5 | % |

Transportation | | | 1.4 | % |

Entertainment | | | 1.4 | % |

Specialty Chemicals | | | 1.3 | % |

Computer Hardware | | | 1.0 | % |

Semiconductors | | | 0.7 | % |

Other Assets and Liabilities (Net) | | | (0.2 | )% |

| | | | |

| | | 100.0 | % |

| | | | |

TETON Westwood Intermediate Bond Fund

| | | | |

Corporate Bonds | | | 50.5 | % |

U.S. Government Obligations | | | 38.2 | % |

U.S. Government Agency Obligations | | | 11.1 | % |

Other Assets and Liabilities (Net) | | | 0.2 | % |

| | | | |

| | | 100.0 | % |

| | | | |

20

TETON Westwood Mighty Mites Fund

Schedule of Investments — September 30, 2018

| | | | | | | | | | | | |

Shares | | | | | Cost | | | Market Value | |

| | | | COMMON STOCKS — 79.5% | | | | | |

| | | | Aerospace and Defense — 2.7% | | | | | |

| | 1,118,900 | | | Aerojet Rocketdyne Holdings Inc.† | | $ | 5,240,670 | | | $ | 38,031,411 | |

| | 2,000 | | | Allied Motion Technologies Inc | | | 77,469 | | | | 108,860 | |

| | 15,000 | | | Chemring Group plc | | | 35,977 | | | | 42,035 | |

| | 123,000 | | | Innovative Solutions & Support Inc.† | | | 472,250 | | | | 312,420 | |

| | 7,000 | | | Kratos Defense & Security Solutions Inc.† | | | 42,963 | | | | 103,460 | |

| | | | | | | | | | | | |

| | | | | | | 5,869,329 | | | | 38,598,186 | |

| | | | | | | | | | | | |

| | |

| | | | Agriculture — 0.3% | | | | | |

| | 500,000 | | | Black Earth Farming Ltd., SDR†(a) | | | 4,345 | | | | 1,744 | |

| | 225 | | | J.G. Boswell Co. | | | 144,676 | | | | 146,587 | |

| | 139,475 | | | Limoneira Co. | | | 2,673,496 | | | | 3,641,692 | |

| | 490,000 | | | S&W Seed Co.† | | | 1,707,556 | | | | 1,200,500 | |

| | | | | | | | | | | | |

| | | | | | | 4,530,073 | | | | 4,990,523 | |

| | | | | | | | | | | | |

| | | |

| | | | Airlines — 0.2% | | | | | | | | |

| | 45,000 | | | American Airlines Group Inc. | | | 18,602 | | | | 1,859,850 | |

| | 225,000 | | | American Airlines Group Inc., Escrow† | | | 3,288 | | | | 331,875 | |

| | | | | | | | | | | | |

| | | | | | | 21,890 | | | | 2,191,725 | |

| | | | | | | | | | | | |

| | | |

| | | | Automotive — 0.8% | | | | | | | | |

| | 27,200 | | | Lithia Motors Inc., Cl. A | | | 517,533 | | | | 2,221,152 | |

| | 20,000 | | | Navistar International Corp.† | | | 152,109 | | | | 770,000 | |

| | 29,605 | | | Rush Enterprises Inc., Cl. A | | | 545,615 | | | | 1,163,773 | |

| | 104,005 | | | Rush Enterprises Inc., Cl. B | | | 1,800,199 | | | | 4,148,759 | |

| | 66,500 | | | Sonic Automotive Inc., Cl. A | | | 849,600 | | | | 1,286,775 | |

| | 70,000 | | | Wabash National Corp. | | | 132,194 | | | | 1,276,100 | |

| | | | | | | | | | | | |

| | | | | | | 3,997,250 | | | | 10,866,559 | |