UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-4767

EAGLE GROWTH & INCOME FUND

(Exact name of Registrant as Specified in Charter)

880 Carillon Parkway

St. Petersburg, FL 33716

(Address of Principal Executive Office) (Zip Code)

Registrant’s Telephone Number, including Area Code: (727) 567-8143

SUSAN L. WALZER, PRINCIPAL EXECUTIVE OFFICER

880 Carillon Parkway

St. Petersburg, FL 33716

(Name and Address of Agent for Service)

Copy to:

FRANCINE J. ROSENBERGER, ESQ.

K&L Gates, LLP

1601 K Street, NW

Washington, D.C. 20006

Date of fiscal year end: October 31

Date of reporting period: October 31, 2012

Item 1. Reports to Shareholders

| | | | | | |

| | | | Annual Report and Investment Performance Review for the fiscal year ended October 31, 2012 Eagle Capital Appreciation Fund Eagle Growth & Income Fund Eagle International Equity Fund Eagle Investment Grade Bond Fund Eagle Mid Cap Growth Fund Eagle Mid Cap Stock Fund Eagle Small Cap Growth Fund Eagle Smaller Company Fund Privacy Notice Eagle Family of Funds | | |

| | | | | | | | |

| | | | | |

|

| |

| | | | | | |

| | Go Paperless with eDelivery | | visit eagleasset.com/eDelivery | | For more information, see inside. | | |

Table of Contents

Visit eagleasset.com/eDelivery to receive shareholder communications including prospectuses and fund reports with a service that helps protect the environment:

Environmentally friendly. Go green with eDelivery by reducing the number of trees used to produce paper.

Efficient. Stop waiting on regular mail. Your documents will be sent via email as soon as they are available.

Easy. Download and save files using your home computer with a few clicks of a mouse.

President’s Letter

Dear Fellow Shareholders:

I am pleased to present the annual report and investment-performance review of the Eagle Family of Funds for the fiscal year ended October 31, 2012 (the “reporting period”).

This has been a year of ups and downs in the broad equity markets. Most major stock indices climbed steadily higher at the end of 2011 and into the first few months of this year before taking a breather in the spring. They rallied throughout the summer and hit peaks in September. On the fixed-income side, the U.S. Federal Reserve kept its overnight interest rate at near zero percent, suggested it likely would not raise rates until mid-2015 (it previously said 2014) and began its third round of quantitative-easing (often called QE3).

Over-arching news for the year included continued economic malaise in Europe (and the ongoing debt issues of its southern neighbors); a slowing growth rate in China; and the U.S. general elections.

One of the hallmarks of Eagle, over its more than 35 years, has been the fundamental research our managers do in constructing portfolios. Our goal here is to provide superior risk-adjusted returns for our long-term clients. Producing the desired results means avoiding getting caught up in today’s headlines and focusing on individual companies the Portfolio Managers believe have the characteristics necessary to make money for our investors.

I hope you will read the commentaries that follow in which our Portfolio Managers discuss their specific funds.

Here are just a few highlights from this year:

| • | | Many of Eagle’s funds continue to perform well, including the Eagle Growth & Income Fund that finished the ten-year period ended October 31, 2012 with a five-star rating1,2 from Morningstar®. |

| • | | Co-Portfolio Managers Charles Schwartz, CFA®, Betsy Pecor, CFA®, and Matthew McGeary, CFA®, as well as Research Analyst Matthew Spitznagle, CFA®, assumed management of the Eagle Mid Cap Stock Fund on October 1, 2012. They joined Eagle with years of experience managing small- and mid-cap mutual funds. |

| • | | This summer Eagle added David Powers, CFA®, as a Co-Portfolio Manager on the team that manages the Eagle Growth & Income Fund. He brings with him a wealth of experience managing successful portfolios as well as |

| | analyzing companies that are important elements of the value- and dividend-focused benchmarks. He has more than 15 years of investment industry experience as a Portfolio Manager and analyst, including most recently serving as a Portfolio Manager of ING’s highly regarded Large Cap Value and Equity Dividend Focus funds. |

| • | | High-profile media outlets continue to seek Eagle managers for input on current events and investing themes. James Camp, CFA®, who heads the Eagle Investment Grade Bond Fund, and Eric Mintz, CFA®, who is a Co-Portfolio Manager of the Eagle Small Cap Growth and Eagle Mid Cap Growth Funds have been on CNBC many times throughout the past year. The Wall Street Journal and Barron’s have quoted Ed Cowart, CFA®, and John Pandtle, CFA®, who are among the Eagle Growth & Income Fund’s Co-Portfolio Managers. |

| • | | The Board of Trustees changed the name of the Eagle Small Cap Core Value Fund to the Eagle Smaller Company Fund in an effort to better differentiate the Fund and its investments from other Eagle Boston Investment Management accounts and other small cap funds in the industry. |

I would like to remind you that investing in any mutual fund carries certain risks. The principal risk factors for each fund are described at the end of this report. Carefully consider the investment objectives, charges and expenses of any fund before you invest. Contact us at 800.421.4184 or eagleasset.com or your financial advisor for a prospectus, which contains this and other important information about the Eagle Family of Funds.

We are grateful for your continued support of, and confidence in, the Eagle Family of Funds.

Sincerely,

Richard J. Rossi

President

December 20, 2012

1 The Eagle Growth & Income Fund’s Class A shares are rated 5 stars for the 10-year period ended October 31, 2012; 4 stars for the five-year period ended October 31, 2012 and for the overall; and 2 stars for the three-year period ended October 31, 2012 among a total of 585, 926, 1,044 and 1,044 funds respectively, in the large-cap value category. Star ratings may be different for other share classes. Morningstar Rating® is based on risk-adjusted performance adjusted for fees and loads. Past performance is no guarantee of future results. Ratings are subject to change each month.

2 Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at eagleasset.com.

* The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Funds with at least three years of performance history are assigned ratings from the fund’s three-, five- and 10-year average annual returns (when available) and a risk factor that reflects fund performance relative to three-month Treasury bill monthly returns. Fund returns are adjusted for fees and sales loads. Ten percent of the funds in an investment category receive five stars, 22.5% receive four stars, 35% receive three stars, 22.5% receive two stars and the bottom 10% receive one star. Investment return and principal value will vary so that investors have a gain or loss when shares are sold. Funds are rated for up to three time periods (three-, five- and 10-years) and these ratings are combined to produce an overall rating. Ratings may vary among share classes and are based on past performance. Past performance does not guarantee future results.

| | |

| Performance Summary and Commentary |

| Eagle Capital Appreciation Fund | | |

Meet the managers | Steven M. Barry, Joseph B. Hudepohl, CFA®, and Timothy M. Leahy, CFA®, are Portfolio Managers of Goldman Sachs Asset Management, LP’s (“GSAM”) “Growth Team.” Mr. Barry is Chief Investment Officer and has been responsible for the day-to-day management of the Eagle Capital Appreciation Fund (the “Fund”) since 2002. Mr. Hudepohl has been a member of GSAM’s Growth Team since 1999, and assumed day-to-day management of the Fund in December 2011. Mr. Leahy joined GSAM as a Managing Director in 2005, and has been responsible for the day-to-day management of the Fund’s investment portfolio since February 2011.

Investment highlights | The Fund invests primarily in common stocks. The Fund’s portfolio management team believes that wealth is created through the long-term ownership of a growing business. They take a “bottom-up” approach to investing based on in-depth, fundamental research. A bottom-up method of analysis typically emphasizes the outlook at the company and industry level versus reliance on the general economy and/or market trends. The Portfolio Managers use an intensive research process and each company is analyzed as if they were going to own and operate that company indefinitely. Key characteristics of the companies in which the Fund currently seeks to invest may include: dominant market share, established brand name, pricing power, recurring revenue stream, free cash flow, high returns on invested capital, predictable growth, sustainable growth, long product life cycle, enduring competitive advantage, favorable demographic trends and excellent management.

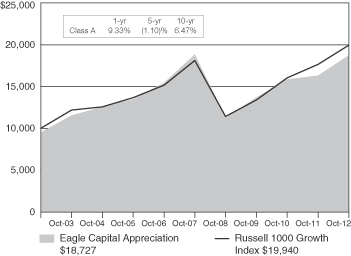

Performance summary | The Fund’s Class A shares returned 14.76% (excluding front-end sales charges) during the fiscal year ended October 31, 2012, outperforming its benchmark index, the Russell 1000® Growth Index (“Russell 1000 Growth”), which returned 13.02%. The Russell 1000 Growth measures performance of those Russell 1000® companies with higher price-to-book ratios and higher forecasted growth values and is representative of U.S. securities exhibiting growth characteristics. Please keep in mind that an index is not available for direct investment; therefore its performance does not reflect the expenses associated with the active management of an actual portfolio.

Growth of a $10,000 investment from 11/1/02 to 10/31/12 (a)

(a) The Fund’s values and returns reflect the maximum front-end sales charge of 4.75%, fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. The value of an investment in other share classes will differ due to each class’s respective sales charges and expenses.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at eagleasset.com.

Performance discussion | The Russell 1000 Growth delivered broad based returns during the one year period ended October 31, 2012, however, the environment was marked by periods of elevated volatility driven by macroeconomic conditions, along with significant fiscal and monetary policy attention. In addition, the annual Russell 1000 Growth reconstitution was completed in late June with significant changes this year, including a more than 500 basis point (bps) decrease in the energy sector’s weight. Other sectors such as materials and industrials lagged, while telecommunication services and health care were the top performing sectors.

The Fund outperformed its benchmark, the Russell 1000 Growth, during the period. On the positive side, stock selection

| | |

| Performance Summary and Commentary |

| Eagle Capital Appreciation Fund (cont’d) | | |

in the telecommunication services and information technology sectors contributed to performance. In contrast, weakness in select health care and energy names detracted from performance.

Top performers | American Tower Corp., a leading owner and operator of wireless and broadcast communication sites, contributed to performance during the reporting period. The Portfolio Managers believe new announcements made in the mobile services industry during the period (including the proposed merger between T-Mobile and Metro PCS and the investment in Sprint by Softbank) bring additional long term stability to the mobile industry, which should ultimately benefit the tower companies. Crown Castle International Corp., a wireless tower owner and operator of shared wireless communications and broadcast infrastructures, also contributed to performance during the period. Its shares rose after the company announced strong first quarter results, driven by better than expected revenues and a significant increase in new leases signed during the quarter compared to last year. The company also raised 2012 guidance due, in large part, to the acquisition of outdoor distributed antennae systems (DAS) company NextG Networks. The Portfolio Managers continue to have conviction in the tower companies over the long term as demand for mobile content grows and wireless carriers are required to add capacity in order to support increased usage, network upgrades and improved coverage. The Fund continues to hold both of these positions.

Shares of Lowe’s Companies, Inc., a home improvement retailer, was a top contributor to performance. Lowe’s recently announced its plan to acquire a Canadian home improvement retailer in the midst of a turnaround strategy of its stores. The Portfolio Managers believe this move challenges the credibility of the management team and makes it increasingly more difficult to believe in the turnaround of its U.S. business. While the Portfolio Managers continue to believe Lowe’s should benefit as the fundamentals of the home improvement industry improve and the housing market recovers, the risk of integrating a sizeable acquisition in the midst of these strategic initiatives raises the risk profile for Lowe’s. As a result, the Fund sold out of its position.

Equinix, Inc., a provider of high performance IT data centers, contributed to performance. The company’s core business remains strong and pricing is up in the three main regions in which it operates, U.S., Europe and Asia. Equinix recently acquired data centers in Frankfurt, Hong Kong, Shanghai and Singapore to further drive growth. In addition, the company

announced that it plans to convert to a real estate investment trust (“REIT”). The Portfolio Managers view this decision favorably and believe it will unlock further shareholder value. The Portfolio Managers continue to have conviction in the company’s ability to drive revenue growth as it benefits from several secular growth drivers, including cloud computing, growth in internet traffic and enterprise outsourcing, and rising demand for optimized network performance. The Fund continues to hold this position.

Apple Inc., a designer and marketer of consumer electronics, computer software, and personal computers, contributed to the Fund during the period. Shares increased significantly as strong demand for the newly released iPad and iPhone continued to validate the value of the Apple franchise and its growth profile. The Portfolio Managers believe there is still a long runway for growth as the company increases penetration of the smartphone and tablet markets, and continues to innovate and enter new markets. In addition, the Portfolio Managers remain positive on Apple and believe the stock’s valuation remains attractive. The Fund continues to hold this position.

Underperformers | Facebook, Inc. (Class A), a social networking service provider, detracted from returns during the period. While the company delivered in line second quarter earnings on a strong increase in ad revenue payments, revenue growth was challenged and a large amount of insider selling, due to the expiration of the lock-up, caused material weakness in the stock. In the Portfolio Managers’ view, Facebook has achieved tremendous scale in the U.S. and has a large market opportunity as its networking effect creates stickiness in its user base. The Portfolio Managers exited the position during the period since they believe the path to growth has been extended and is less certain.

NetApp, Inc., a developer of data storage hardware and software for enterprise clients, detracted from performance as fears surfaced of reduced year end business spending on technology. In the Portfolio Managers’ view, despite the near term headwind, NetApp continues to trade at an attractive valuation, and has a strong competitive position in an industry that has benefited from several secular growth trends, such as virtualization, which should increase demand for the company’s storage products. NetApp specializes in network-attached storage which, in the Portfolio Managers’ view, should continue to take share away from direct-attached products. The Portfolio Managers believe NetApp’s storage devices are easier to buy, install and manage than competing products, which should

| | |

| Performance Summary and Commentary |

| Eagle Capital Appreciation Fund (cont’d) | | |

also drive market share gains. The Fund continues to hold this position.

Shares of Schlumberger Ltd., a large oil services company, pulled back during the period. The stock came under pressure due to macroeconomic concerns and a decline in oil prices. The Portfolio Managers continue to believe the company is well positioned given its extensive and diversified global footprint. In addition, Schlumberger holds dominant market share in most of its product lines and offers a technological advantage over many of its competitors, which the Portfolio Managers view as a significant long term positive. The Fund continues to hold this position.

Halliburton Company, a leading oil services firm, detracted from performance during the period. The lack of a settlement in the Macondo lawsuit, in which BP is seeking to recover all of the costs resulting from the Gulf of Mexico oil spill, weighed on the stock. Additionally, the company has been facing pricing

pressure in its North American pressure pumping business. While the contingent legal liability from the Macondo proceedings could remain a drag on the stock until a settlement is reached, the Portfolio Managers continue to believe the company’s risk/reward profile is attractive at current valuations and the company should continue to be able to generate strong revenue growth and operating margins in North America. The Fund continues to hold this position.

Oracle Corporation, a company that engineers hardware and software, detracted from relative performance during the period. Shares of the stock came under pressure as the broader software/IT sector experienced a difficult spending environment during the period. In the Portfolio Managers’ view, despite the short term weakness in the stock, Oracle is well positioned to benefit from secular growth trends in cloud computing, continued use and adoption of database systems, and a robust pipeline of new products and applications. The Fund continues to hold this position.

| | |

| Performance Summary and Commentary |

| Eagle Growth & Income Fund | | |

Meet the managers | David Blount, CFA®, CPA , Edmund Cowart, CFA®, John Pandtle, CFA®, and David Powers, CFA® are Co-Portfolio Managers of the Eagle Growth & Income Fund (the “Fund”). Messrs. Blount, Cowart, and Pandtle have been jointly responsible for the day-to-day management of the Fund’s investment portfolio since June 2011. Mr. Powers has been Co-Portfolio Manager since June 2012.

Investment highlights | The Fund invests primarily in domestic equity securities (predominantly common stocks) that the Portfolio Managers believe are high-quality, financially strong companies that pay above-market dividends, have cash resources (i.e. free cash flow) and a history of raising dividends. The Fund’s Portfolio Managers select companies based in part upon their belief that those companies have the following characteristics: (1) yield or dividend growth at or above the S&P 500® Index (“S&P 500”); (2) potential for growth; and (3) stock price below its estimated intrinsic value. The Fund can also own a variety of other securities, including fixed income securities, which, in the opinion of the Fund’s Portfolio Managers, offer prospects for meeting the Fund’s investment goals.

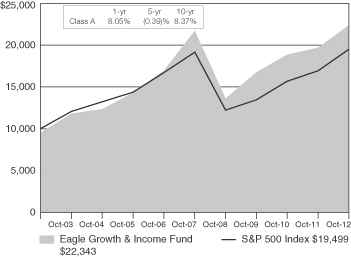

Performance summary | The Fund’s Class A shares returned 13.48% (excluding front-end sales charges) during the fiscal year ended October 31, 2012, underperforming its benchmark index, the S&P 500 which returned 15.21%. The S&P 500 is an unmanaged index of 500 U.S. stocks and gives a broad look at how stock prices have performed. Please keep in mind that an index is not available for direct investment; therefore its performance does not reflect the expenses associated with the active management of an actual portfolio.

Growth of a $10,000 Investment from 11/1/02 to 10/31/12 (a)

(a) The Fund’s values and returns reflect the maximum front-end sales charge of 4.75%, fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. The value of an investment in other share classes will differ due to each class’s respective sales charges and expenses.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at eagleasset.com.

Performance discussion | The equity market as measured by the S&P 500 rallied for the first two quarters of the fiscal year ended October 31, 2012, followed by a period of consolidation during the month of April. The rally was led by the beaten down financial sector, the usually volatile technology sector, and the somewhat unpredictable consumer discretionary sector. Forgotten were those stocks in the utilities, telecommunications, and consumer staples sectors. The equity market began to decline in the second quarter of 2012, reversing a strong rally that began in the fourth quarter of 2011. Continuing sovereign debt and banking crises in Europe, growth challenges in China and softer economic data in the U.S. heightened investor concerns. Federal Reserve Board (the “Fed”) Chairman Ben Bernanke gave a subdued update of the economy in June. The Fed reduced its growth projections for 2012 and 2013 and increased its 2013 unemployment forecast. A recent slowdown in employment growth and household spending may temper the expansion but the Fed still expects the economy to grow at a moderate pace. In the third quarter of 2012, the broad equity market experienced a strong increase in the midst of global economic conditions that remained stressful. Notably, very low transaction volume and a subdued level of volatility accompanied the rally. One factor adding support to the market in the quarter was the anticipation of, and actual start of, the next version of the Fed’s quantitative-easing program (“QE3”). Fed Chairman Ben Bernanke has made it clear he believes in the wealth effect (higher stock prices = higher consumption and economic activity) and he is doing his part to create wealth on behalf of all U.S. stockholders.

For the year, cyclical sectors of the S&P 500 such as energy and materials underperformed during the period as investors preferred the higher yield and stability of telecommunication services, consumer staples and health care. All sectors were positive for the period. Performance was led by the consumer

| | |

| Performance Summary and Commentary |

| Eagle Growth & Income Fund (cont’d) | | |

discretionary and utility sectors, each up over 30% for the year. While the consumer discretionary sector was the top performing sector in the Fund, health care and financials each contributed significantly, both having strong double digit returns and larger exposures within the Fund. The information technology sector had the lowest return in the Fund, but with little exposure in this space, it had very little effect on the total contribution of the Fund. Materials also contributed marginally, as the Fund only had a few holdings within the sector.

The Fund’s performance was below the return of its benchmark index during the period. Relative to benchmark performance, consumer discretionary provided the best attribution as stock selection was strong. Energy and utilities also fared well versus the benchmark with stock selection again being the determining factor. The information technology sector benefited on a relative basis due to the underweight maintained in that sector. Detracting from relative performance were the financial, industrial, and consumer staples sectors. The industrial and consumer staples sectors lagged the benchmark due to stock selection. Within the financials, healing of the banking sector continued, as evidenced by the Fed’s latest round of stress tests. Although there were few exceptions, the Fed’s study showed that banks are back on sound footing. This created a rally in regional banks with weaker balance sheets. The Fund is exposed to higher quality banks and, therefore, underperformed within that segment.

Underperformers | Norfolk Southern Corporation, a rail and intermodal shipping and transportation company, has been the beneficiary of significant productivity, volume, and pricing gains over the last several years. However, coal, which is approximately 25-30% of Norfolk’s revenues, has recently been a cyclical headwind. Over the last few quarters, coal stockpiles have been high and utilities have been switching from coal to natural gas to run their power plants resulting in pricing and margin pressure. The Fund continues to hold this position.

A recent softness in demand for chemical company E.I. du Pont de Nemours and Company’s commodity chemical business led to a reduction in management’s near-term earnings growth outlook. The Portfolio Managers believe the outlook for DuPont’s agriculture and nutrition segment remains robust and, therefore, the Fund continues to hold this position.

Becton, Dickinson and Company is a medical technology company which has suffered from a dearth of volume growth in hospital admissions due to a lackluster economy. As a result, the company has a lack of visibility into improved pricing and

utilization trends making it difficult to drive any sales/profit growth acceleration. As a result, the Fund sold the shares during the period.

Despite a substantial increase in Wells Fargo & Company’s (a diversified financial services company) dividend and solid earnings growth, the market remains concerned about the impact of low interest rates on the company’s near-term growth and profitability. In the view of the Portfolio Managers, Wells Fargo shares remain attractively valued; therefore, the Fund continues to maintain this position.

Despite a substantial increase in the dividend and solid earnings growth for financial services company The PNC Financial Services Group, Inc., the market is concerned about the company’s ability to deliver operating leverage as well as earnings accretion from recent acquisitions. PNC shares remain attractively valued in the Portfolio Managers’ opinion. The Fund continues to hold this position.

Top performers | The Home Depot, Inc., the world’s largest home improvement specialty retailer, has benefitted from strong earnings growth as the housing market has stabilized and internal cost efficiency measures materialize. The Fund continues to hold this position although it has decreased its holdings in order to manage concentration risk in the Fund.

Rapid earnings growth and a 35% increase in their dividend led to outperformance by Mattel, Inc., the world’s largest toy company. The Fund increased its position because the Portfolio Managers are encouraged by the company’s commitment to producing shareholder value.

Abbott Laboratories, a leading global health care company, announced the company would be splitting into two pieces, a medical products business and a pharmaceutical business, thereby unlocking shareholder value. In addition to the perceived increase in value due to the split up, the company’s underlying business performance has remained strong, driven by their rheumatoid arthritis drug, Humira. The Fund continues to hold this position.

Pfizer, Inc., the world’s largest researched-based pharmaceutical company, is completing two major strategic alternatives, the sale of its Nutrition unit and the IPO of its Animal Health business. These moves have allowed Pfizer to increase its dividend and buyback a substantial amount of shares. Additionally, post-Lipitor patent expiration, the company is transforming toward a broad revenue base with development and marketing driven by a more efficient global infrastructure. The Fund continues to hold this position.

| | |

| Performance Summary and Commentary |

| Eagle Growth & Income Fund (cont’d) | | |

Wisconsin Energy Corporation, an electric and natural gas service provider, operates within an attractive regulatory environment and boasts diversified end user sales mix as well as solid demand forecasts that support low volatility EPS growth in the mid-single digits. The company has a major capital investment plan that is winding down following the completion of two large power plants in the last three years. Given reduced capital expenditure needs, management has indicated it plans to increase the dividend payout ratio over the next few years. With the stock having appreciated significantly, the Fund sold its position during the period.

| | |

| Performance Summary and Commentary | | |

| Eagle International Equity Fund | | |

Meet the managers | Richard C. Pell is Chief Investment Officer at Artio Global Management LLC (“Artio Global”). Rudolph-Riad Younes, CFA®, is Head of International Equities at Artio Global. Messrs. Pell and Younes have managed the Eagle International Equity Fund (the “Fund”) since 2002.

Investment highlights | The Fund invests primarily in foreign equity securities. The Fund’s Portfolio Managers seek investment opportunities within the developed and emerging markets. In the developed markets, a “bottom-up” approach is adopted. A bottom-up method of analysis emphasizes the outlook at the company and industry level versus reliance on the general economy and/or market trends. In the emerging markets, a “top-down” assessment consisting of currency/interest rate risks, political environments/leadership assessment, growth rates, structural reforms and risk (liquidity) is applied. A top-down method of analysis emphasizes the significance of economy and market cycles. In Japan, given the highly segmented nature of this market comprised of both strong global competitors and protected domestic industries, a hybrid approach encompassing both bottom-up and top-down analyses is conducted.

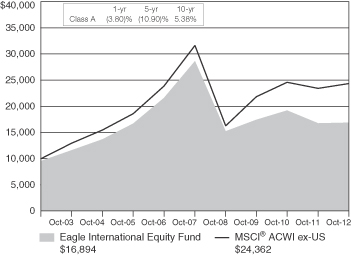

Performance summary | The Fund’s Class A shares returned 0.98% (excluding front-end sales charges) during the fiscal year ended October 31, 2012, underperforming its benchmark index, which returned 3.98%. The Fund’s benchmark index, the Morgan Stanley Capital International® All Country World Index ex-US (“MSCI® ACWI ex-US”), is a free float-adjusted market capitalization index that is designed to measure equity market performance in the the global developed and emerging markets. Please keep in mind that an index is not available for direct investment; therefore its performance does not reflect the expenses associated with the active management of an actual portfolio.

Growth of a $10,000 investment from 11/1/02 to 10/31/12 (a)

(a) The Fund’s values and returns reflect the maximum front-end sales charge of 4.75%, fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. The value of an investment in other share classes will differ due to each class’s respective sales charges and expenses.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at eagleasset.com.

Performance discussion | The market environment over the past year has been highly volatile, with strong positive quarters alternating with equally poor negative ones. Uncertainty with respect to events in Europe (viability of the Euro, Greece, Spain, etc.), Japan (a continuation of stagnant growth), China (whether slowing growth culminates in a hard landing) and the U.S. (election, fiscal cliff) caused markets to ebb and flow over the full period. Over the last year, the benchmark index managed a gain of 3.98%. The best performing sectors included health care, consumer staples and financial while telecommunications, materials, technology and energy sectors lagged the overall market. Returns were not consistent over the full year with the exception of the health care sector which benefited from the industry’s increased exposure to emerging countries and the rising incomes of consumers there, as well as benefiting from historically attractive valuations and high dividend yields. Other sectors rallied and faded based on whether risk was “on” or “off” with cyclical sectors performing best with risk “on” and less sensitive sectors when risk was “off.” From an allocation perspective, the Fund’s underweight to financial stocks in the developed markets was the largest impediment to results. On the positive side, an overweight to health care stocks provided the Fund with a strong tail wind.

For some time, the Portfolio Managers have viewed the financial sector as extremely vulnerable given long-term regulatory issues that are expected to have an impact on potential profits as well as short-term issues relating to deleveraging balance sheets, European sovereign debt exposure and recapitalization. Thus, within financials, the Portfolio Managers look for good bank franchises and market leaders. They remain wary about the sovereign debt problem in the region and its effect on bank balance sheets but are also cognizant of the cheap valuations and central bank pump-priming efforts which provide some level of support and more recently have moved to tactically increase exposure to the European sector. From a stock selection perspective, the

| | |

| Performance Summary and Commentary |

| Eagle International Equity Fund (cont’d) | | |

Fund’s results were weak in the industrials and materials sectors and strongest in health care and technology.

Underperformers | Turquoise Hill Resources Ltd. (formerly Ivanhoe Mines Ltd.) is a Canadian mineral exploration and development company which ran into trouble in the development of the Oyu Tolgoi Project copper and gold mine in southern Mongolia. The company also went through a takeover and management change during the year which led to a drop in price at the end of the first quarter in 2012. The Fund still holds this position, but over the period the position was reduced.

Ctrip.com International Ltd., a leading travel service provider in China, underperformed during the period due to competition from a rival online travel service provider which caused operating margins to fall by 10%. Longer term, the Portfolio Managers believe the company will face consistent deflationary pricing pressures from the Kayak/Priceline equivalent in China. This is not to mention that the Portfolio Managers believe that the company’s biggest strengths will slowly morph into their biggest weakness, namely their large network of call centers amid wage inflation. The Fund no longer holds this position.

Baidu, Inc., a provider of Chinese language internet search services, is facing a similar dilemma to Ctrip.com in that the company is forced to grow out of the old easy money as consumers shift from a non-mobile based web search to a mobile based web search. In addition, Baidu is also seeing its artificial monopoly position given by Google’s exit in China being chipped away from new entrants. The Fund no longer holds this position.

Axis Bank Ltd., the India-based regional bank is highly leveraged to the overall economic health of India. While Axis is a well-run private sector bank, it still has relatively higher exposure to wholesale funding and credit which is more volatile than the retail segment. The company also has greater loan exposure to the agricultural sector of the economy where the expectation of a weak crop yield has led to concerns over non-performing loans in this segment. The greater exposure to both the wholesale and agricultural segments and an economic slowdown in India led to the company being a relative underperformer. The position was sold during a general risk reduction move within the Fund.

Larsen & Toubro Ltd., an India based multinational conglomerate with business interests in engineering, construction, manufacturing, information technology and financial services was sold during the period. Over the course of the last year, a marked deterioration was seen in the current accounts and fiscal deficits for the country which, along with a marked deterioration in the Rupee and political gridlock, caused GDP growth to slip below expectations. The political gridlock was more evident in the infrastructure segment where new projects showed no signs of progress or moving through the bureaucracy. Concerns of a marked slowdown in the order book for Larsen & Toubro, as well as continued declines of the Purchasing Managers Index and a relatively high valuation, caused the company to be a relative underperformer.

Top performers | The global healthcare company Novo Nordisk AS (Class B), which is headquartered in Denmark, is uniquely positioned to capitalize on the proliferation of diabetes and obesity in the developed and emerging markets. The company is an innovation leader at the high end and a cost leader at the low end. It is developing future technologies in oral insulin and stem cell therapy as well as bringing its obesity treatments to market in the middle of the decade.

Sanofi, a diversified global healthcare company located in France, and Roche Holding AG, a research-focused healthcare company located in Switzerland, are pharmaceutical companies with stable growth rates, high dividend yields and increasing exposure to the emerging markets. Health care was the leading sector over the period.

Diageo PLC is a British multinational consumer products company with stable growth and good fundamental dynamics located in Britain. The company is well positioned in emerging markets and will continue to capitalize on this growth via increasing international spirit penetration combined with premiumisation of the overall market.

Samsung Electronics Co., Ltd. is a Korean technology company with a growing exposure to the smart phones segment. Samsung’s dominance in the Android mobile market in both developed and emerging markets has helped drive recent results. It has been a leader in this market by controlling key components (speed and differentiation).

The Fund continues to hold each of the securities noted above as “top performers.”

| | |

| Performance Summary and Commentary | | |

| Eagle Investment Grade Bond Fund | | |

Meet the managers | James C. Camp, CFA®, a Managing Director at Eagle Asset Management (“Eagle”) and Joseph Jackson, CFA®, are Co-Portfolio Managers of the Eagle Investment Grade Bond Fund (the “Fund”) and have been jointly responsible for the day-to-day management of the Fund’s investment portfolio since the Fund’s inception.

Investment highlights | The Fund invests primarily in investment grade fixed income securities. Investment grade is defined as securities rated BBB- or better by Standard & Poor’s Rating Services or an equivalent rating by at least one other nationally recognized statistical rating organization or, for unrated securities, those that are determined to be of equivalent quality by the Fund’s Portfolio Managers. The average portfolio duration of the Fund is expected to vary and may generally range anywhere from two to seven years based upon economic and market conditions. The Fund expects to invest in a variety of fixed income securities including, but not limited to, corporate debt securities of U.S. and non-U.S. issuers, including corporate commercial paper; bank certificates of deposit; debt securities issued by states or local governments and their agencies; obligations of non-U.S. governments and their subdivisions, agencies and government sponsored enterprises; obligations of international agencies or supranational entities (such as the European Union); obligations issued or guaranteed by the U.S. Government and its agencies; mortgage-backed securities and asset-backed securities; commercial real estate securities; and floating rate instruments.

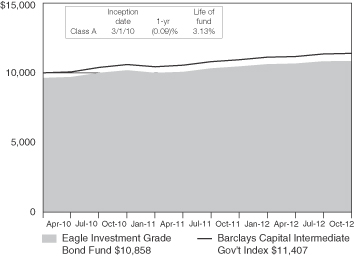

Performance summary | The Fund’s Class A shares returned 3.77% (excluding front-end sales charges) during the fiscal year ended October 31, 2012, underperforming its benchmark index, which returned 4.24%. The Fund’s benchmark index, the Barclays Intermediate Government/Credit Bond Index, includes U.S. government and investment grade credit securities that have a greater than or equal to one year and less than ten years remaining to maturity and have $250 million or more of outstanding face value. Please keep in mind that an index is not available for direct investment; therefore its performance does not reflect the expenses associated with the active management of an actual portfolio.

Growth of a $10,000 investment from 3/1/10 to 10/31/12 (a)

(a) The Fund’s values and returns reflect the maximum front-end sales charge of 3.75%, fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. The value of an investment in other share classes will differ due to each class’s respective sales charges and expenses.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at eagleasset.com.

Performance discussion | Two forces really drove the fixed income markets over the one-year period ended October 31, 2012. The first force was the Eurozone. From the long-term refinancing operations at the end of 2011 and beginning of 2012 convincing markets that all was well to continuing financial problems of peripheral sovereigns, the Eurozone was a focus for investors all year. The Federal Reserve Board (the “Fed”) policy was the second main driver for the period and with the announcement of the Fed quantitative-easing program (“QE3”), the Fed insured another few months of risk-on. Not as large as the prior two issues, but the lead up to the U.S. Presidential elections had some effect on markets as many investors chose to pull back due to the uncertainty of who was going to win and how that outcome would affect the markets. In the Fund’s benchmark index, all sectors posted positive returns for the year. Corporates led the way followed by the financial, industrial and utilities sectors which all posted strong returns. Securitized and government related issues were the next highest sectors and Treasuries were the underperformer of the index, although the sector still posted positive returns.

| | |

| Performance Summary and Commentary |

| Eagle Investment Grade Bond Fund (cont’d) | | |

The Fund underperformed its benchmark index during the period. The chief performance detractor relative to the Fund’s benchmark was attributable to the financials sector as the risk-on mentality of the markets resulted in the highest risk firms in that space (as measured by the option adjustment spread) tightening substantially over the year. Outperformance in industrials and securitized assets in the Fund was not enough to overcome the financial sector drag. The Fund was overweight in corporates and securitized while being underweight Treasuries and government related issues. Overall the allocation decisions were a positive factor in the Fund’s performance, contributing to outperformance in aggregate versus the benchmark.

Underperformers | Anheuser-Busch InBev Worldwide Inc., FRN, 1.10%, 03/26/13, a multinational beverage company and the world’s largest brewer, Georgia Power Company, FRN, 0.71%, 03/15/13, one of the nation’s largest generators of electricity, and Teva Pharmaceutical Finance III BV, FRN, 0.88%, 03/21/14, a global pharmaceutical and drug company, were all affected by the long end of the curve outperforming the short end during the period. In addition, the Fund’s holdings of floating rate notes have very short maturities relative to other issues in the benchmark index.

International Bank for Reconstruction & Development, 2.38%, 05/26/15, an international financial institution, is a high credit quality rated bond with a short maturity duration. During the period, the lower rated credits and the longer duration bonds outperformed these types of bond held by the Fund. The Fund continues to maintain some exposure to this sector despite this individual issue underperforming over the last 12 months.

U.S. Treasury Note, 2.00%, 04/30/16, an intermediate-long Treasury holding, also has the combination of a short maturity

duration and the high credit quality which underperformed in the current market conditions favoring the longer duration, lower rated issues. The Fund continues to maintain some exposure to Treasuries as they are a significant part of the benchmark.

The Fund continues to hold each of the securities noted above as “underperformers.”

Top performers | Mortgage bonds Freddie Mac, REMICs, Series 4098, Class HA, 2.00%, 05/15/41 and Freddie Mac, REMICs, Series 4097, Class BG, 2.00%, 12/15/41, were new additions to the Fund. Late in the period, the Fund rotated out of low beta 5-year corporate positions and into high credit quality rated agency backed CMOs with higher yields and lower volatility.

Gilead Sciences, Inc., 4.50%, 04/01/21, an American biotechnology company that discovers, develops, and commercializes therapeutics, outperformed the industrials sector of the benchmark index by a wide margin during the period. The outperformance was due to a combination of middle-rated credit outperforming high-rated issues, and a scarcity value (there was very little debt outstanding prior to the issuance).

Plum Creek Timberlands, L.P., 4.70%, 03/15/21, the largest and most geographically diverse private landowner in the nation, and Newmont Mining Corporation, 5.13%, 10/01/19, one of the world’s largest gold producers with significant assets or operations on five continents, both outperformed the industrial sector of the benchmark as lower rated credits outperformed higher rated credits.

The Fund continues to hold each of the securities noted above as “top performers.”

| | |

| Performance Summary and Commentary | | |

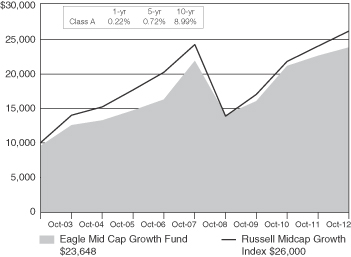

| Eagle Mid Cap Growth Fund | | |

Meet the managers | Bert L. Boksen, CFA®, a Managing Director and Senior Vice President at Eagle Asset Management, Inc. (“Eagle”), is the Portfolio Manager of the Eagle Mid Cap Growth Fund (the “Fund”), and has managed the Fund since its inception. Eric Mintz, CFA®, has been Co-Portfolio Manager since 2011, and Christopher Sassouni, DMD, has served as Assistant Portfolio Manager of the Fund since 2006. Mr. Mintz served as Assistant Portfolio Manager from 2008 through 2011.

Investment highlights | The Fund invests primarily in stocks of mid-capitalization (“mid-cap”) companies. The Fund’s Portfolio Managers seek to capture the significant long-term capital appreciation potential of mid-cap, rapidly growing companies. The Portfolio Managers use a “bottom-up” investment approach through a proprietary research strategy that emphasizes the selection of mid-cap growth stocks that are reasonably priced. A bottom-up method of analysis emphasizes the outlook at the company and industry level versus reliance on the general economy and/or market trends. The Fund’s Portfolio Managers believe that conducting extensive research on mid-cap companies may enable the Fund to capitalize on market inefficiencies and thus outperform the market.

Performance summary | The Fund’s Class A shares returned 5.21% (excluding front-end sales charges) during the fiscal year ended October 31, 2012, underperforming its benchmark index, which returned 9.09%. The Fund’s benchmark index, the Russell Midcap® Growth Index (“Russell Midcap”), measures the performance of those Russell Midcap companies with higher price-to-book ratios and higher forecasted growth values. Please keep in mind that an index is not available for direct investment; therefore its performance does not reflect the expenses associated with the active management of an actual portfolio.

Growth of a $10,000 investment from 11/1/02 to 10/31/12 (a)

(a) The Fund’s values and returns reflect the maximum front-end sales charge of 4.75%, fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. The value of an investment in other share classes will differ due to each class’s respective sales charges and expenses.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at eagleasset.com.

Performance discussion | The Russell Midcap benchmark posted gains during the one year period ended October 31, 2012. All sectors, except energy and information technology, generated positive returns. Telecommunication services, health care and materials posted the strongest returns while energy and information technology somewhat tempered benchmark returns. Within telecommunication services, strong returns in the wireless telecommunication services industry boosted the sector result. Biotechnology contributed most notably to solid performance within the health care sector. In materials, the chemicals industry supported healthy returns. Oil, gas & consumable fuels posted negative returns in the energy sector while weak performance in the software industry tempered returns in the information technology sector.

The Fund underperformed its benchmark index during the period. The information technology, industrials and materials sectors detracted most notably from performance. The information technology sector trailed the benchmark largely due to an overweight in the underperforming software industry. The Fund’s investment in the electrical equipment industry detracted most notably from relative returns within the industrials sector. Weak performance of the Fund’s investments within the metals & mining industry led to underperformance in the materials sector. The Fund outperformed the index in the consumer discretionary, energy and telecommunication services sectors. In consumer discretionary, strong returns generated by the specialty retail and household durables industries led to outperformance in the sector. Within energy, solid performance of the Fund’s investments in the oil, gas & consumable fuels industry boosted relative returns in the sector. Very strong returns generated by the Fund’s investment within the wireless telecommunication services industry also led to meaningful outperformance in the telecommunication services sector.

| | |

| Performance Summary and Commentary |

| Eagle Mid Cap Growth Fund (cont’d) | | |

Underperformers | Rovi Corporation provides digital entertainment technology solutions to the consumer electronics industry as well as service providers. A sharp slowdown in consumer electronics sales led the firm to reduce earnings expectations.

Gentex Corporation is a global, high technology electronics company that specializes in a broad spectrum of automotive, aerospace, and fire protection products. One of the firm’s more prominent growth products, a reverse camera display that is located on a rearview mirror, fell victim to more than one auto manufacturer shifting the primary location for rear camera images from the mirror to the dashboard.

Walter Energy, Inc. is a producer of metallurgical coal for the global steel industry. In the Portfolio Managers’ opinion, the firm saw some after-effect in operational performance due to weather related events as well as a slower than expected export facility upgrade in Canada during the reporting period.

Polypore International, Inc. is a specialty filtration company that makes separation membranes used in lithium ion batteries which have seen significant growth from both consumer electronics and hybrid electric vehicles. The stock underperformed due to concerns about waning sales for the all-electric Chevy Volt, which was the subject of a well-publicized investigation into engine fires that had occurred following crash tests. The investigation has since been resolved; however, there is near term uncertainty resulting from the incident that has clouded growth prospects for the time being.

Informatica Corporation, a top independent provider of data integration software and services, expressed some concern about the trajectory of its growth prospects overseas, which is where the firm generates a substantial portion of its revenues.

The Fund no longer holds any of the securities noted above as “underperformers.”

Top performers | SBA Communications Corporation (Class A) owns and operates wireless communications infrastructure across North and Central America. The firm’s recent acquisition announcement of TowerCo stands to significantly increase operational scale and boost tower leasing opportunities for SBA as soon as late this calendar year. The stock was also boosted by speculation the company could announce a conversion to a real estate investment trust (“REIT”).

Catamaran Corporation, previously named SXC Health Solutions Corp., is a provider of pharmacy benefits management services and healthcare information technology solutions to the healthcare benefits management industry. Positive prospects regarding Catamaran’s recent acquisition of Catalyst Health Solutions boosted the stock during the reporting period. Meaningful synergies created by the acquisition are expected to bolster the firm’s positioning in the pharmacy benefits management space.

Sirius XM Radio, Inc., a satellite radio service provider, saw meaningful traction in the auto production cycle, strong sales through an expanding installed base in lower end cars and continued rapid reduction of debt.

GNC Holdings, Inc. (Class A) is a global specialty retailer of health and wellness products including vitamins, sports nutrition and diet and herbal supplements. The stock continues to benefit from sustained growth trends in the space as the baby boomer generation adopts the daily vitamin philosophy and the general public increases its health awareness.

PulteGroup Inc. is a national residential homebuilding business. Improvements in the North American housing landscape have reflected favorably on PulteGroup. The Portfolio Managers believe that encouraging trends in the space should continue to provide a catalyst for the stock.

The Fund continues to hold each of the securities noted above as “top performers.”

| | |

| Performance Summary and Commentary | | |

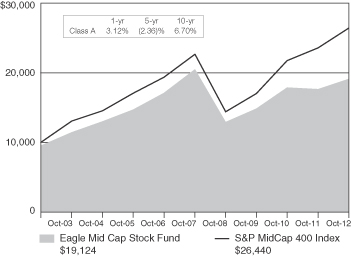

| Eagle Mid Cap Stock Fund | | |

Meet the managers | Charles Schwartz, CFA®, Betsy Pecor, CFA® and Matthew McGeary, CFA® are Co-Portfolio Managers of the Eagle Mid Cap Stock Fund (the “Fund”) and have been jointly responsible for the day-to-day management of the Fund’s investment portfolio since October 2012. Prior to October 2012, the Fund was co-managed by Todd L. McCallister, Ph.D., CFA®, Scott Renner and Stacey Serafini Pittman, CFA®.

Investment highlights | The Fund invests primarily in stocks of mid-capitalization (“mid-cap”) companies. The Portfolio Managers of the Fund employ a “bottom-up” stock-selection process to identify growing, mid-cap companies that are reasonably priced. A bottom-up method of analysis emphasizes the outlook at the company and industry level versus reliance on the general economy and/or market trends. The Portfolio Managers seek to gain a comprehensive understanding of a company’s management, business plan, financials, real rate of growth and competitive threats and advantages.

Performance summary | The Fund’s Class A shares returned 8.26% (excluding front-end sales charges) during the fiscal year ended October 31, 2012, underperforming its benchmark index, the S&P MidCap 400® Index (“S&P MidCap 400”) which returned 12.11%. The S&P MidCap 400 is an unmanaged index that measures the performance of the mid-sized company segment of the U.S. market. Please keep in mind that an index is not available for direct investment; therefore its performance does not reflect the expenses associated with the active management of an actual portfolio.

Growth of a $10,000 investment from 11/1/02 to 10/31/12 (a)

(a) The Fund’s values and returns reflect the maximum front-end sales charge of 4.75%, fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. The value of an investment in other share classes will differ due to each class’s respective sales charges and expenses.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at eagleasset.com.

Performance discussion | The market continued to have mixed growth throughout 2012. The S&P MidCap 400 was up during the reporting year, led by the telecom, healthcare, and consumer discretionary sectors. The energy and technology sectors were the only sectors that were negative in the index. The “risk-on, risk-off” nature of the markets during the past fiscal year was driven by a variety of macro factors and concerns. Continued instability in Europe, concerns about a “hard landing” in China, leadership changes across the globe including the U.S., and intermittent fiscal stimulus have created an environment of unusually high correlation. These high correlations have been seen across asset classes, across sectors and within individual stocks of the benchmark index. Such a situation, with price direction largely driven by factors external to individual companies, has made for a challenging environment for fundamentally oriented stock pickers. These conditions can be challenging in terms of performance relative to a benchmark over the shorter-term, but can also set the stage for future out performance when fundamental factors of individual businesses are again more thoroughly considered by market participants.

On an absolute basis, the Fund’s best performing sectors were financials and consumer discretionary. Total performance for the year lagged the benchmark index but showed strong growth. The telecom and energy sectors were the largest contributors to performance. Both sectors were overweight the benchmark, but much of the performance was due to good stock picking. Detracting sectors were healthcare, technology, and industrials. Each of these sectors was overweight the benchmark as well and poor performance was due to negative selection effect.

| | |

| Performance Summary and Commentary |

| Eagle Mid Cap Stock Fund (cont’d) | | |

Beginning in October 2012, the Fund became modestly overweight in the industrial sector as the new Portfolio Management team focused on pockets of strength over the medium term, such as infrastructure. The Fund also maintains healthy exposure to domestically focused businesses in an effort to limit exposure to weak overseas trends. Similarly, the Fund is focused on infrastructure within the energy sector and, by fiscal year end, held multiple positions within this sector to capitalize on the trend.

The Fund remains overweight in the healthcare and technology sectors. While looming healthcare reforms/legislation and near term election results create uncertainty in the healthcare sector, the Portfolio Managers believe the Fund could stand to benefit from the strong secular tailwinds provided by an aging population. The technology sector has not been a particularly strong relative performer thus far in 2012, however, numerous sector fundamentals, such as solid balance sheets, strong cash flow dynamics and reasonable valuations, remain attractive.

Relative to the Fund’s benchmark, the Fund has an equal weight within the consumer sectors and is maintaining a somewhat defensive posture in this group. While reasonably positive housing statistics bode well for consumer confidence, the Portfolio Managers remain concerned about weak job growth, stagnant personal income trends and looming potential inflation.

Underperformers | QEP Resources, Inc., a leading independent natural gas and oil exploration and production company, underperformed during the past year as the price of natural gas continued to fall. The Fund has sold this holding.

Check Point Software Technologies, Ltd. provides security software to corporations and governments for internet communications and transactions. Lower than expected demand from Europe and the U.S. government has contributed to a price decline. This holding has since been sold by the Fund.

The stock price of Gardner Denver, Inc., a designer, manufacturer, and marketer of engineered industrial machinery and related parts and services, was down as volumes in their natural gas pumps and hydraulic fracturing, or fracking, business were down, even though the company had earnings results that were largely in line with estimates. The stock traded lower again after one of its key pressure pumping customers negatively preannounced earnings due to falling demand in the natural gas fracking business. The Fund sold

out of this position earlier in the year, but purchased it back before fiscal year end because the Portfolio Managers felt that the market was over penalizing the stock for its exposure to the fracking market. Further, since the abrupt departure of their former CEO (Barry Pennypacker), its becoming clear that Gardner Denver is an obvious takeover candidate.

Acacia Research Corporation is a provider of outsourced patent monetization services and an aggregator and licensor of patent assets. Due to the unpredictable nature of their revenue streams, the company has experienced substantial decline in their stock price this year. The Fund’s new portfolio management team sold this holding.

Top performers | Crown Castle International Corporation is a wireless tower owner and operator of shared wireless communications and broadcast infrastructures. The company experienced a significant increase in site leasing and raised 2012 guidance due, in large part, to the acquisition of outdoor distributed antennae systems (DAS) company NextG Networks. This holding has since been sold by the new portfolio management team.

The price of Solutia, Inc., a maker of specialty chemicals and performance materials, was up significantly following the announcement, made in late January, that the company would be acquired by Eastman Chemical Company. The acquisition was completed during the second quarter of 2012. Leading up to the acquisition announcement, Solutia had been experiencing wider profit margins after selling its lower profitability businesses during the downturn. The Fund sold the position prior to the acquisition.

Allied World Assurance Co. Holdings A.G. engages in the provision of property, casualty and specialty insurance, and reinsurance solutions. Allied has experienced strong growth this year due to a steady increase in net written premiums. The Fund has since sold the holding.

Wyndham Worldwide Corporation, the holding company for Wyndham Hotels & Resorts, beat earnings several times this year, but surprised some investors with the strength of its share repurchases. Wyndham’s management has been putting the company’s strong free cash flow directly into the share repurchases. Furthermore, Wyndham’s segments lodging, vacation exchange and vacation ownership units all outperformed expectations this year. The Fund continues to own this security.

| | |

| Performance Summary and Commentary | | |

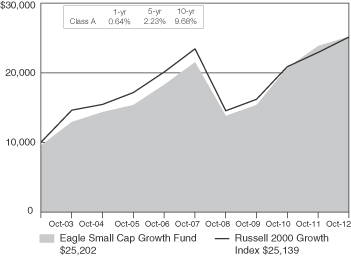

| Eagle Small Cap Growth Fund | | |

Meet the managers | Bert L. Boksen, CFA®, a Managing Director and Senior Vice President at Eagle Asset Management, Inc. (“Eagle”), has been responsible for the management of the Eagle Small Cap Growth Fund (the “Fund”) since 1995. Eric Mintz, CFA®, has been Co-Portfolio Manager since 2011, and previously served as Assistant Portfolio Manager from 2008 through 2011.

Investment highlights | The Fund invests primarily in stocks of small-capitalization (“small-cap”) companies. Using a “bottom-up” approach, the Fund’s Portfolio Managers seek to capture the significant long-term capital appreciation potential of small, rapidly growing companies. A bottom-up method of analysis emphasizes the outlook at the company and industry level versus reliance on the general economy and/or market trends. The Portfolio Managers also look for small-cap growth companies that are reasonably priced. Since small-cap companies often have narrower markets than large-capitalization (“large-cap”) companies, the Portfolio Managers believe that conducting extensive proprietary research on small-cap growth companies may enable the Fund to capitalize on market inefficiencies and thus outperform the market.

Performance summary | The Fund’s Class A shares returned 5.65% (excluding front-end sales charges) during the fiscal year ended October 31, 2012, underperforming its benchmark index, the Russell 2000® Growth Index (“Russell 2000 Growth”), which returned 9.70%. The Russell 2000® Growth is an unmanaged index comprised of Russell 2000® Index (“Russell 2000”) companies with higher price-to-book ratios and higher forecasted growth values. The Russell 2000 is an unmanaged index comprised of the 2,000 smallest companies in the Russell 3000® Index (“Russell 3000”). The Russell 3000 measures the performance of the 3,000 largest U.S. companies based on total market capitalization. Please keep in mind that an index is not available for direct investment; therefore its performance does not reflect the expenses associated with the active management of an actual portfolio.

Growth of a $10,000 investment from 11/1/02 to 10/31/12 (a)

(a) The Fund’s values and returns reflect the maximum front-end sales charge of 4.75%, fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. The value of an investment in other share classes will differ due to each class’s respective sales charges and expenses.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at eagleasset.com.

Performance discussion | The Russell 2000 Growth posted positive returns for the one year period ended October 31, 2012. Health care, telecommunications services and consumer discretionary posted the strongest returns while the energy sector somewhat tempered benchmark returns. In health care, strong returns in the biotechnology and health care equipment & supplies industries boosted the sector result. The diversified telecommunication services industry contributed to solid performance in the telecommunication services sector. In consumer discretionary, the hotels, restaurants & leisure as well as specialty retail industries supported healthy returns. The oil, gas & consumable fuels industry posted negative returns in the energy sector.

The Fund underperformed its benchmark index during the period. The information technology, industrials, and to a lesser extent, financials sectors detracted from the Fund’s performance. The information technology sector trailed the benchmark largely due to an overweight in the underperforming software industry. The Fund’s investments in the professional services and electrical equipment industries

| | |

| Performance Summary and Commentary |

| Eagle Small Cap Growth Fund (cont’d) | | |

detracted most notably from relative returns within the industrials sector. Weak performance of the Fund’s investments within the consumer finance industry led to underperformance in the financial sector. The Fund outperformed the index in the energy and consumer staples sectors. In energy, outperformance was boosted by a modest overweight in the outperforming energy equipment & services industry, in addition to an underweight in the underperforming oil, gas & consumable fuels industry where several benchmark names the Fund did not hold saw material detraction. Strong relative returns within the food and staples retailing industry supported outperformance in the consumer staples sector.

Underperformers | Monster Worldwide, Inc. provides online employment solutions through offerings such as searchable job postings for prospective employees and resume database access for recruiters. The firm engaged investment bankers to do a strategic review that could result in the sale of the company. The stock price declined as investors became concerned over the length of time the review was taking. The Fund continues to hold this position as the Portfolio Managers believe that the company ultimately will be sold at a meaningful premium to its current stock price.

BJ’s Restaurants, Inc. owns and operates casual dining restaurants across the U.S. After having a strong run, BJ’s was hurt by its own success as a high valuation combined with difficult comparables caused a stock price correction. The Portfolio Managers believe that BJ’s remains a well-run concept within the tier of “polished” casual dining restaurants and, therefore, the Fund continues to own this security.

Qlik Technologies, Inc. designs and develops business analytics software solutions. Shares of the stock traded down as significant European exposure negatively affected investor sentiment during the period. The Portfolio Managers continue to favor prospects in the business analytics space and they believe that the secular growth story for Qlik remains intact. The Fund continues to hold this position.

Meritor, Inc. is a supplier of automotive components, including drive trains used in commercial trucking. The firm continues to tighten its operational efficiency through the implementation of restructuring efforts but sustained weakness in several of Meritor’s emerging markets (e.g., Brazil, China and India) has tempered near-term growth prospects. The firm’s strong presence in those regions is expected to generate substantial benefit for Meritor once the environment stabilizes but a comfortable level of earnings visibility has remained elusive; consequently, the Fund sold out of its position in the stock.

Cash America International, Inc. is a specialty financial services provider of pawn loans and unsecured consumer loan

products. The stock has experienced some weakness during the period, which the Portfolio Managers believe reflects an expected hard line on the part of the administration’s new consumer protection agency and associated concerns regarding regulatory reform. The firm has seen some encouraging growth as of late in its e-Commerce lending segment in addition to ongoing restructuring within Cash America’s Mexican component. The Portfolio Managers believe this is expected to benefit the firm’s operations upon completion, so the Fund continues to hold this position.

Top performers | Medidata Solutions, Inc. provides technology that is used to enhance its customers’ efficiency in clinical development and research processes. The firm continues to experience solid demand for its clinical-trial software and is taking market share from competitors at a substantial rate as it leverages its differentiated product offerings. Medidata also has diversified its revenue stream by expanding its customer base and the array of clinical trials to which they provide technological products. The Fund continues to hold this position.

SuccessFactors, Inc. is a provider of cloud-based performance management, succession planning and learning management solutions to organizations. The firm was acquired early in the period by SAP AG at a significant premium. The Fund sold its position prior to the acquisition at a significant premium.

Vitamin Shoppe, Inc. is a specialty retailer of vitamins, sports nutrition, and health and beauty aid products, and GNC Holdings, Inc. (Class A) is a global specialty retailer of health and wellness products including vitamins, sports nutrition and diet and herbal supplements. Both Vitamin Shoppe and GNC have benefitted from favorable U.S. demographics and increased vitamin and supplement utilization amongst the aging baby boomer generation as the general public increases its health awareness. Vitamin Shoppe also continues to grow both earnings and square footage across the country. Since GNC’s market capitalization had moved toward the upper end of the small cap space and the Fund already had exposure to this space through Vitamin Shoppe, the Portfolio Managers opted to retain the Vitamin Shoppe position while moving out of the GNC position.

Onyx Pharmaceuticals, Inc. is a biopharmaceutical company with a focus on the development of drug therapies for kidney, blood based and other forms of cancer. Positive news regarding the Food and Drug Administration advisory panel’s recommendation to approve Onyx’s multiple myeloma drug candidate Kyprolis boosted shares of the firm’s stock during the period. The drug compound has since been approved and initial product launch feedback has been largely positive thus far. The Fund continues to hold this position.

| | |

| Performance Summary and Commentary |

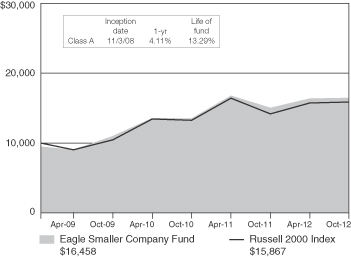

| Eagle Smaller Company Fund | | (formerly known as the Eagle Small Cap Core Value Fund) |

Meet the managers | David M. Adams, CFA®, and John “Jack” McPherson, CFA®, Managing Directors at Eagle Boston Investment Management, Inc. (“EBIM”), are Co-Portfolio Managers of the Eagle Smaller Company Fund (the “Fund”), and have been jointly responsible for the day-to-day management of the Fund’s investment portfolio since its inception.

Investment highlights | The Fund invests primarily in equity securities of small-capitalization (“small-cap”) companies. Using a valuation sensitive approach to investing, the Fund’s Portfolio Managers seek to capture capital growth by selecting securities that the Portfolio Managers believe are selling at a discount relative to their underlying value and then hold them until their market value reflects their intrinsic value. To assess value, a “bottom-up” method of analysis is utilized. A bottom-up method of analysis emphasizes the outlook at the company and industry level versus reliance on the general economy and/or market trends. Other factors that the Portfolio Managers may look for when selecting investments include: management with demonstrated ability and commitment to the company, above-average potential for earnings and revenue growth, low debt levels relative to total capitalization and strong industry fundamentals.

Performance summary | The Fund’s Class A shares returned 9.31% (excluding front-end sales charges) during the fiscal year ended October 31, 2012, underperforming both the primary benchmark index, the Russell 2000® Index (“Russell 2000”), and the secondary benchmark index, the Russell 2500® Index (“Russell 2500”), which returned 12.08% and 13.00%, respectively. The Russell 2000 is an unmanaged index comprised of the 2,000 smallest companies in the Russell 3000® Index (“Russell 3000”), and the Russell 2500 is a market cap weighted index that includes the smallest 2,500 companies in the Russell 3000. The Russell 3000 measures the performance of the 3,000 largest U.S. companies based on total market capitalization. Please keep in mind that an index is not available for direct investment; therefore its performance does not reflect the expenses associated with the active management of an actual portfolio.

Growth of a $10,000 investment from 11/3/08 to 10/31/12 (a)

(a) The Fund’s values and returns reflect the maximum front-end sales charge of 4.75%, fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. The value of an investment in other share classes will differ due to each class’s respective sales charges and expenses.