UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number | 811-04813 |

| |

| BNY Mellon Investment Funds I | |

| (Exact name of Registrant as specified in charter) | |

| | |

| c/o BNY Mellon Investment Adviser, Inc. 240 Greenwich Street New York, New York 10286 | |

| (Address of principal executive offices) (Zip code) | |

| | |

| Bennett A. MacDougall, Esq. 240 Greenwich Street New York, New York 10286 | |

| (Name and address of agent for service) | |

|

Registrant's telephone number, including area code: | (212) 922-6400 |

| |

Date of fiscal year end: | 12/31 | |

Date of reporting period: | 12/31/19 | |

| | | | | | | |

The following N-CSR relates only to the Registrant's series listed below and does not relate to any series of the Registrant with a different fiscal year end and, therefore, different N-CSR reporting requirements. A separate N-CSR will be filed for any series with a different fiscal year end, as appropriate.

BNY Mellon Global Fixed Income Fund

FORM N-CSR

Item 1. Reports to Stockholders.

BNY Mellon Global Fixed Income Fund

| |

ANNUAL REPORT December 31, 2019 |

| |

Save time. Save paper. View your next shareholder report online as soon as it’s available. Log into www.bnymellonim.com/us and sign up for eCommunications. It’s simple and only takes a few minutes. |

| |

The views expressed in this report reflect those of the portfolio manager(s) only through the end of the period covered and do not necessarily represent the views of BNY Mellon Investment Adviser, Inc. or any other person in the BNY Mellon Investment Adviser, Inc. organization. Any such views are subject to change at any time based upon market or other conditions and BNY Mellon Investment Adviser, Inc. disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a fund in the BNY Mellon Family of Funds are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any fund in the BNY Mellon Family of Funds. |

| |

Not FDIC-Insured • Not Bank-Guaranteed • May Lose Value |

Contents

THE FUND

FOR MORE INFORMATION

Back Cover

| | | | |

| |

BNY Mellon Global Fixed Income Fund

| | The Fund |

A LETTER FROM THE PRESIDENT OF BNY MELLON INVESTMENT ADVISER, INC.

Dear Shareholder:

We are pleased to present this annual report for BNY Mellon Global Fixed Income Fund (formerly, Dreyfus/Standish Global Fixed Income Fund), covering the 12-month period from January 1, 2019 through December 31, 2019. For information about how the fund performed during the reporting period, as well as general market perspectives, we provide a Discussion of Fund Performance on the pages that follow.

In January 2019, a pivot in stance from the U.S. Federal Reserve (the “Fed”) helped stimulate a rebound across equity markets that continued into the second quarter of the year. However, escalating trade tensions disrupted equity markets in May. The dip was short-lived, as markets rose once again in June and July of 2019, when a trade deal appeared more likely and the pace of U.S. economic growth remained steady. Nevertheless, concerns continued to emerge over slowing global growth, resulting in bouts of market volatility in August 2019. Stocks rebounded in September and continued an upward path through most of October 2019, bolstered by central bank policy and consistent consumer spending. The rally generally continued through the end of the period, supported in part by an announcement from President Trump that the first phase of a trade deal with China was in process. U.S. equity markets reached new highs during the final months of the period.

In fixed-income markets, the year began with a recovery from the prior months’ volatility. After the Fed’s supportive statements in January 2019, other developed-market central banks followed suit and reiterated their abilities to buttress flagging growth rates by continuing accommodative policies. The Fed cut rates in July, September and October 2019, for a total 75 basis point reduction in the federal funds rate during the 12 months. Rates across much of the Treasury curve saw a slight increase during the month of November, and the long end of the curve rose in December. The yield curve steepened during the latter portion of the period. However, demand for fixed-income instruments during the year was strong, which helped to support positive bond market returns.

We believe that over the near term, the outlook for the U.S. remains positive, but we will monitor relevant data for any signs of a change. As always, we encourage you to discuss the risks and opportunities in today’s investment environment with your financial advisor.

Thank you for your continued confidence and support.

Sincerely,

Renee LaRoche-Morris

President

BNY Mellon Investment Adviser, Inc.

January 15, 2020

2

DISCUSSION OF FUND PERFORMANCE(Unaudited)

For the period from January 1, 2019 through December 31, 2019, as provided by portfolio managers David Leduc, CFA, Brendan Murphy, CFA and Scott Zaleski, CFA, of Mellon Investments Corporation (formerly, BNY Mellon Asset Management North America Corporation), Sub-Investment Adviser

Market and Fund Performance Overview

For the 12-month period ended December 31, 2019, BNY Mellon Global Fixed Income Fund (formerly, Dreyfus/Standish Global Fixed Income Fund) Class A shares achieved a total return of 8.06%, Class C shares returned 7.25%, Class I shares returned 8.33% and Class Y shares returned 8.39%.1 In comparison, the Bloomberg Barclays Global Aggregate Index (Hedged) (the “Index”), the fund’s benchmark, produced a total return of 8.22% for the same period.2

Global bond markets posted positive returns during the period, amid low interest rates and accommodative central bank policies. The fund’s relative performance versus the Index was mainly due to successful security selection and asset allocation decisions.

The Fund’s Investment Approach

The fund seeks to maximize total return, while realizing a market level of income consistent with preserving principal and liquidity. To pursue its goal, the fund normally invests at least 80% of its net assets, plus any borrowings for investment purposes, in U.S. dollar- and non-U.S. dollar-denominated, fixed-income securities of governments and companies located in various countries, including emerging markets. The fund invests principally in bonds, notes, mortgage-related securities, asset-backed securities, floating rate loans (limited to up to 20% of the fund’s net assets) and other floating rate securities and Eurodollar and Yankee dollar instruments. The fund generally invests in eight or more countries, but always invests in at least three countries, one of which may be the United States. The fund may invest up to 25% of its assets in emerging markets generally and up to 7% of its net assets in any single, emerging-market country.

We focus on identifying undervalued government bond markets, currencies, sectors and securities and de-emphasize the use of interest-rate forecasting. We look for fixed-income securities with the potential for credit upgrades, unique structural characteristics or innovative features. We select securities by using fundamental economic research and quantitative analysis to allocate assets among countries and currencies, by focusing on sectors and individual securities that appear to be relatively undervalued, and by actively trading among sectors.

Supportive Central Bank Policies Bolster Returns

Bonds produced strong returns over the 12-month period, in an environment of moderate economic growth and supportive policies from the U.S. Federal Reserve (the “Fed”), and other central banks around the world. Prior to the start of 2019, concerns over tightening in the face of unsupportive data by the Fed, and the conclusion of quantitative easing programs by the European Central Bank (ECB) and Bank of Japan (BOJ) roiled fixed-income markets. In January 2019, the environment turned a corner when Chairman Powell made comments that the Fed would be patient and flexible with the pace of future interest-rate increases. Soon after, the ECB and the BOJ made statements indicating they would continue to

3

DISCUSSION OF FUND PERFORMANCE(Unaudited) (continued)

support growth if needed, and that rates would likely stay lower for longer. This reassured investors, as did progress toward a trade resolution between the U.S. and China. Rates generally fell during the period, supporting Treasury returns. After significant widening of spreads at the end of 2018, tightening occurred across many asset classes during the period, allowing risk assets to perform well, with corporate debt leading the broader market. In May, equity markets sputtered due to resurfacing trade issues, causing investors to seek safe-haven assets, depressing yields and providing an additional boost to fixed-income market values. The Fed reiterated its patient stance regarding future rate hikes and its willingness to take action to support economic growth rates during its May meeting.

However, concerns over slowing economic growth continued, and inflation floundered. The Fed decided to provide additional stimulus by cutting the fed funds rate. It did so three times during the period, each time by 25 basis points. These cuts occurred in July, September and October. Rates across the Treasury curve fell, and the curve continued its flattening trend with portions of the yield curve inverting during the middle of the period. After the cuts, the Fed signaled it would pause, and expectations for better growth prospects in 2020 emerged due to progress in U.S./China trade negotiations and stronger forward-looking economic data. Rates at the long end of the curve began to rise, and the yield curve steepened during the last months of the year.

Successful Security Selection and Allocation Bolstered Fund Performance

The fund’s performance relative to the Index was helped by security selection and asset allocation decisions. A position in General Electric performed well. Investors have reacted favorably to recent governance changes at the organization, leading to spread tightening. The CEO made comments which caused investors to believe the bonds might be called, and they continued to rally. High-quality, European corporate, agency and covered bonds also worked to boost relative performance. Prices of these bonds fell early in January 2019 when it looked as though the ECB would not maintain its accommodative stance. During this time, we increased the portfolio’s allocation to these bonds. After the ECB pivoted, valuations on these bonds rose, contributing to strong performance. Selections within emerging-markets sovereign debt were also favorable. Frontier markets such as Kenya and Ghana provided a tailwind to performance, as did euro-denominated bonds from Senegal. Among bonds denominated in local currencies, Russia was a standout performer. In addition, allocations to and yield curve positioning among European-periphery countries, such as Greece, Spain, Italy and Cyprus, also contributed positively to results.

Conversely, a position in inflation-linked notes underperformed in the low-inflation environment. An overweight allocation to securitized products such as asset- and mortgage-backed securities also provided a headwind to results. These sectors produced positive absolute returns and excess return over Treasuries during the 12 months, but underperformed corporate debt, and thus the broader market, during the period. Lastly, the underweight allocation to the U.S. dollar, which rallied during the period, also constrained results.

Constructively Positioned and Cautiously Optimistic

We are cautiously optimistic regarding a continued rate of moderate economic growth. Stabilization of trade rhetoric may help stoke growth rates outside of the U.S. We believe this may be favorable for risk assets. However, as of the end of the period, we were reducing

4

corporate credit exposure in the portfolio, as we thought spreads were tight and left little room for continued price appreciation. We have overweight exposure to structured products, asset-backed securities, mortgage-backed securities and commercial mortgage-backed securities, as we believe the valuations on these instruments look relatively cheap when compared to corporate debt. We have an overweight allocation to emerging-market credit, but in a highly selective fashion. The goal is to select countries that are poised to maintain an accommodative monetary stance, and that have stable growth rates. Examples of this currently include China, South Korea and Russia. We have an underweight allocation to developed-market sovereign debt, as we expect that growth may pick up as trade tensions ease. This may lead to rising interest rates. In addition, we think it’s possible that labor cost pressures may continue to mount, given the low U.S. unemployment rate. This could stoke inflation, which may increase the value of inflation-linked notes.

January 15, 2020

1 Total return includes reinvestment of dividends and any capital gains paid and does not take into consideration the maximum initial sales charge in the case of Class A shares or the applicable contingent deferred sales charge imposed on redemptions in the case of Class C shares. Had these charges been reflected, returns would have been lower. Class I and Class Y are not subject to any initial or deferred sales charge. Past performance is no guarantee of future results. Share price and investment return fluctuate such that upon redemption, fund shares may be worth more or less than their original cost.

2 Source: FactSet. — The Bloomberg Barclays Global Aggregate Index (Hedged) is a flagship measure of global, investment-grade debt from 24 local currency markets. This multi-currency benchmark includes treasury, government-related, corporate and securitized, fixed-rate bonds from both developed- and emerging-market issuers. Currency exposure is hedged to the U.S. dollar. Investors cannot invest directly in any index.

Bonds are subject generally to interest-rate, credit, liquidity and market risks, to varying degrees, all of which are more fully described in the fund’s prospectus. Generally, all other factors being equal, bond prices are inversely related to interest-rate changes, and rate increases can cause price declines.

Foreign bonds are subject to special risks, including exposure to currency fluctuations, changing political and economic conditions and potentially less liquidity. The fixed-income securities of issuers located in emerging markets can be more volatile and less liquid than those of issuers in more mature economies.

Investments in foreign currencies are subject to the risk that those currencies will decline in value relative to the U.S. dollar, or, in the case of hedged positions, that the U.S. dollar will decline relative to the currency being hedged. Currency rates in foreign countries may fluctuate significantly over short periods of time. A decline in the value of foreign currencies relative to the U.S. dollar will reduce the value of securities held by the fund and denominated in those currencies.

High-yield bonds are subject to increased credit risk and are considered speculative in terms of the issuer’s perceived ability to continue making interest payments on a timely basis and to repay principal upon maturity.

The fund may, but is not required to, use derivative instruments. A small investment in derivatives could have a potentially large impact on the fund’s performance. The use of derivatives involves risks different from, or possibly greater than, the risks associated with investing directly in the underlying assets.

5

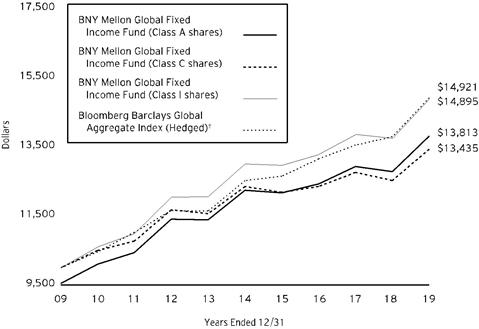

FUND PERFORMANCE(Unaudited)

Comparison of change in value of a $10,000 investment in Class A shares, Class C shares and Class I shares of BNY Mellon Global Fixed Income Fund with a hypothetical investment of $10,000 in the Bloomberg Barclays Global Aggregate Index (Hedged) (the “Index”).

† Source: FactSet

Past performance is not predictive of future performance.

The above graph compares a hypothetical $10,000 investment made in each of the Class A, Class C and Class I shares of BNY Mellon Global Fixed Income Fund on 12/31/09 to a hypothetical investment of $10,000 made in the Index on that date. All dividends and capital gain distributions are reinvested.

The fund’s performance shown in the line graph above takes into account the maximum initial sales charge on Class A shares and all other applicable fees and expenses of the applicable classes. The Index is a flagship measure of global investment-grade debt from 24 local currency markets. This multi-currency benchmark includes treasury, government-related, corporate and securitized fixed-rate bonds from both developed and emerging markets issuers. Currency exposure is hedged to the U.S. dollar. Unlike a mutual fund, the Index is not subject to charges, fees and other expenses. Investors cannot invest directly in any index. Further information relating to fund performance, including expense reimbursements, if applicable, is contained in the Financial Highlights section of the prospectus and elsewhere in this report.

6

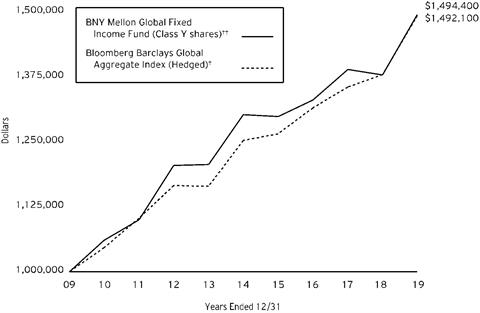

Comparison of change in value of a $1,000,000 investment in Class Y shares of BNY Mellon Global Fixed Income Fund with a hypothetical investment of $1,000,000 in the Bloomberg Barclays Global Aggregate Index (Hedged) (the “Index”).

† Source: FactSet

†† The total return figures presented for Class Y shares of the fund reflect the performance of the fund’s Class I shares for the period prior to 7/1/13 (the inception date for Class Y shares).

Past performance is not predictive of future performance.

The above graph compares a hypothetical $1,000,000 investment made in Class Y shares of BNY Mellon Global Fixed Income Fund on 12/31/09 to a hypothetical investment of $1,000,000 made in the Index on that date. All dividends and capital gain distributions are reinvested.

The fund’s performance shown in the line graph above takes into account all applicable fees and expenses of the fund’s Class Y shares. The Index is a flagship measure of global investment-grade debt from 24 local currency markets. This multi-currency benchmark includes treasury, government-related, corporate and securitized fixed-rate bonds from both developed and emerging markets issuers. Currency exposure is hedged to the U.S. dollar. Unlike a mutual fund, the Index is not subject to charges, fees and other expenses. Investors cannot invest directly in any index. Further information relating to fund performance, including expense reimbursements, if applicable, is contained in the Financial Highlights section of the prospectus and elsewhere in this report.

7

FUND PERFORMANCE(Unaudited) (continued)

| | | | | | | |

Average Annual Total Returns as of 12/31/19 |

| Inception

Date | 1 Year | 5 Years | | 10 Years | |

Class A shares | | | | | | |

with maximum sales charge (4.5%) | 12/2/09 | 3.19% | 1.50% | | 3.28% | |

without sales charge | 12/2/09 | 8.06% | 2.44% | | 3.76% | |

Class C shares | | | | | | |

with applicable redemption charge† | 12/2/09 | 6.25% | 1.70% | | 3.00% | |

without redemption | 12/2/09 | 7.25% | 1.70% | | 3.00% | |

Class I shares | 1/1/94 | 8.33% | 2.75% | | 4.06% | |

Class Y shares | 7/1/13 | 8.39% | 2.79% | | 4.10% | †† |

Bloomberg Barclays Global

Aggregate Index ( Hedged ) | | 8.22% | 3.57% | | 4.08% | |

† The maximum contingent deferred sales charge for Class C shares is 1% for shares redeemed within one year of the date of purchase.

†† The total return performance figures presented for Class Y shares of the fund reflect the performance of the fund’s Class I shares for the period prior to 7/1/13 (the inception date for Class Y shares).

The performance data quoted represents past performance, which is no guarantee of future results. Share price and investment return fluctuate and an investor’s shares may be worth more or less than original cost upon redemption. Current performance may be lower or higher than the performance quoted. Go to www.bnymellonim.com/us for the fund’s most recent month-end returns.

The fund’s performance shown in the graphs and table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. In addition to the performance of Class A shares shown with and without a maximum sales charge, the fund’s performance shown in the table takes into account all other applicable fees and expenses on all classes.

8

UNDERSTANDING YOUR FUND’S EXPENSES(Unaudited)

As a mutual fund investor, you pay ongoing expenses, such as management fees and other expenses. Using the information below, you can estimate how these expenses affect your investment and compare them with the expenses of other funds. You also may pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial adviser.

Review your fund’s expenses

The table below shows the expenses you would have paid on a $1,000 investment in BNY Mellon Global Fixed Income Fund from July 1, 2019 to December 31, 2019. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

| | | | | | | |

Expenses and Value of a $1,000 Investment | |

Assume actual returns for the six months ended December 31, 2019 | |

| | | | | | |

| | Class A | Class C | Class I | Class Y | |

Expense paid per $1,000† | $3.96 | $7.76 | $2.54 | $2.29 | |

Ending value (after expenses) | $1,016.60 | $1,013.20 | $1,018.30 | $1,018.50 | |

COMPARING YOUR FUND’S EXPENSES

WITH THOSE OF OTHER FUNDS(Unaudited)

Using the SEC’s method to compare expenses

The Securities and Exchange Commission (“SEC”) has established guidelines to help investors assess fund expenses. Per these guidelines, the table below shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total cost) of investing in the fund with those of other funds. All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

| | | | | | | |

Expenses and Value of a $1,000 Investment | |

Assuming a hypothetical 5% annualized return for the six months ended December 31, 2019 | |

| | | | | | |

| | Class A | Class C | Class I | Class Y | |

Expense paid per $1,000† | $3.97 | $7.78 | $2.55 | $2.29 | |

Ending value (after expenses) | $1,021.27 | $1,017.49 | $1,022.68 | $1,022.94 | |

†Expenses are equal to the fund’s annualized expense ratio of .78% for Class A, 1.53% for Class C, .50% for Class I and .45% for Class Y, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). |

9

STATEMENT OF INVESTMENTS

December 31, 2019

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity

Date | | Principal

Amount ($) | a | Value ($) | |

Bonds and Notes - 96.0% | | | | | |

Australia - 1.2% | | | | | |

Australia, Sr. Unscd. Bonds, Ser. 150 | AUD | 3.00 | | 3/21/2047 | | 37,050,000 | | 31,527,493 | |

Driver Australia Four Trust, Ser. 4, Cl. A, 1 Month BBSW +.95% | AUD | 1.81 | | 8/21/2025 | | 424,594 | b | 298,088 | |

Driver Australia Six Trust, Ser. 6, Cl. A, 1 Month BBSW +.90% | AUD | 1.76 | | 12/21/2027 | | 11,003,870 | b | 7,711,618 | |

Driver Australia Three Trust, Ser. 3, Cl. A, 1 Month BBSW +1.70% | AUD | 2.56 | | 5/21/2024 | | 837,008 | b | 588,152 | |

| | 40,125,351 | |

Belgium - 2.2% | | | | | |

Kingdom of Belgium, Unscd. Bonds, Ser. 74 | EUR | 0.80 | | 6/22/2025 | | 22,900,000 | c | 27,199,808 | |

Kingdom of Belgium, Unscd. Bonds, Ser. 78 | EUR | 1.60 | | 6/22/2047 | | 32,880,000 | c | 43,774,094 | |

| | 70,973,902 | |

British Virgin - .4% | | | | | |

Sinopec Group Overseas Development, Gtd. Notes | | 2.50 | | 8/8/2024 | | 12,840,000 | c | 12,897,670 | |

Canada - 2.9% | | | | | |

Canadian Pacer Auto Receivables Trust, Ser. 2017-1A, Cl. A4 | | 2.29 | | 1/19/2022 | | 6,275,000 | c | 6,281,712 | |

CNH Capital Canada Receivables Trust, Ser. 2017-1A, Cl. A2 | CAD | 1.71 | | 5/15/2023 | | 3,840,257 | c | 2,946,193 | |

Enbridge, Gtd. Notes | | 4.00 | | 11/15/2049 | | 7,900,000 | d | 8,238,457 | |

Ford Auto Securitization Trust, Ser. 2017-R2, Cl. A2 | CAD | 1.42 | | 4/15/2021 | | 310,818 | | 239,303 | |

Ford Auto Securitization Trust, Ser. 2017-R5A, Cl. A3 | CAD | 2.38 | | 3/15/2023 | | 4,550,000 | c | 3,509,585 | |

Ford Auto Securitization Trust, Ser. 2018-AA, Cl. A3 | CAD | 2.71 | | 9/15/2023 | | 8,175,000 | c | 6,340,811 | |

Ford Auto Securitization Trust, Ser. 2018-BA, Cl. A3 | CAD | 2.84 | | 1/15/2024 | | 10,425,000 | c | 8,112,642 | |

Ford Auto Securitization Trust, Ser. 2019-BA, Cl. A2 | CAD | 2.32 | | 10/15/2023 | | 11,150,000 | c | 8,592,253 | |

GMF Canada Leasing Trust, Ser. 2017-1A, Cl. A3 | CAD | 2.47 | | 9/20/2022 | | 2,663,664 | c | 2,052,204 | |

Golden Credit Card Trust, Ser. 2018-4A, Cl. A | | 3.44 | | 10/15/2025 | | 8,500,000 | c | 8,868,220 | |

MBarc Credit Canada, Ser. 2019-AA, Cl. A3 | CAD | 2.72 | | 10/16/2023 | | 8,405,000 | c | 6,516,488 | |

Province of Ontario Canada, Sr. Unscd. Notes | CAD | 2.65 | | 2/5/2025 | | 10,500,000 | | 8,318,089 | |

Royal Bank of Canada, Sr. Unscd. Notes | | 2.55 | | 7/16/2024 | | 8,700,000 | | 8,831,700 | |

10

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity

Date | | Principal

Amount ($) | a | Value ($) | |

Bonds and Notes - 96.0% (continued) | | | | | |

Canada - 2.9% (continued) | | | | | |

Silver Arrow Canada, Ser. 2018-1A, Cl. A3 | CAD | 3.17 | | 8/15/2025 | | 14,450,000 | c | 11,285,811 | |

Teck Resources, Sr. Unscd. Notes | | 6.25 | | 7/15/2041 | | 1,870,000 | | 2,142,716 | |

| | 92,276,184 | |

Cayman Islands - .8% | | | | | |

Allegro CLO III, Ser. 2015-1A, Cl. AR, 3 Month LIBOR +.84% | | 2.78 | | 7/25/2027 | | 7,990,524 | b,c | 7,992,072 | |

Barings CLO, Ser. 2013-IA, Cl. AR, 3 Month LIBOR +.80% | | 2.77 | | 1/20/2028 | | 5,530,000 | b,c | 5,527,257 | |

CK Hutchison Europe Finance 18, Gtd. Bonds | EUR | 1.25 | | 4/13/2025 | | 2,045,000 | | 2,365,450 | |

CK Hutchison Finance 16 II, Gtd. Bonds | EUR | 0.88 | | 10/3/2024 | | 5,185,000 | | 5,914,154 | |

DP World Crescent, Sr. Unscd. Notes | | 3.75 | | 1/30/2030 | | 2,575,000 | | 2,609,907 | |

| | 24,408,840 | |

Chile - .4% | | | | | |

Bonos de la Tesoreria de la Republica en pesos, Bonds | CLP | 4.50 | | 3/1/2021 | | 8,890,000,000 | | 12,186,668 | |

China - 3.5% | | | | | |

China, Unscd. Bonds, Ser. 1827 | CNY | 3.25 | | 11/22/2028 | | 610,600,000 | | 88,551,939 | |

China Development Bank, Unscd. Bonds, Ser. 1905 | CNY | 3.48 | | 1/8/2029 | | 178,000,000 | | 25,148,246 | |

| | 113,700,185 | |

Colombia - .2% | | | | | |

Colombia, Sr. Unscd. Bonds | | 4.00 | | 2/26/2024 | | 7,600,000 | | 8,015,644 | |

Ecuador - .8% | | | | | |

Ecuador, Sr. Unscd. Bonds | | 10.75 | | 3/28/2022 | | 18,035,000 | | 18,401,327 | |

Ecuador, Sr. Unscd. Notes | | 10.75 | | 1/31/2029 | | 7,195,000 | d | 7,035,613 | |

| | 25,436,940 | |

Egypt - .4% | | | | | |

Egypt, Sr. Unscd. Bonds | EUR | 4.75 | | 4/16/2026 | | 3,000,000 | | 3,550,180 | |

Egypt, Sr. Unscd. Notes | | 6.13 | | 1/31/2022 | | 2,800,000 | | 2,920,403 | |

Egypt, Sr. Unscd. Notes | | 6.20 | | 3/1/2024 | | 1,550,000 | c | 1,679,008 | |

Egypt, Sr. Unscd. Notes | | 7.05 | | 1/15/2032 | | 3,390,000 | d | 3,559,737 | |

| | 11,709,328 | |

France - 1.3% | | | | | |

AXA, Sub. Notes | EUR | 5.25 | | 4/16/2040 | | 3,500,000 | | 3,983,449 | |

BNP Paribas, Sr. Unscd. Notes | EUR | 1.13 | | 10/10/2023 | | 6,915,000 | | 8,017,633 | |

Credit Agricole Home Loan SFH, Covered Notes | EUR | 1.25 | | 3/24/2031 | | 6,700,000 | | 8,312,618 | |

Engie, Jr. Sub. Bonds | EUR | 1.38 | | 1/16/2023 | | 7,300,000 | | 8,284,542 | |

Orange, Sr. Unscd. Notes | EUR | 0.00 | | 9/4/2026 | | 12,100,000 | | 13,207,020 | |

| | 41,805,262 | |

11

STATEMENT OF INVESTMENTS (continued)

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity

Date | | Principal

Amount ($) | a | Value ($) | |

Bonds and Notes - 96.0% (continued) | | | | | |

Germany - .3% | | | | | |

Allianz, Jr. Sub. Bonds | EUR | 3.38 | | 9/18/2024 | | 3,100,000 | | 3,879,219 | |

Allianz, Sub. Notes | EUR | 5.63 | | 10/17/2042 | | 4,300,000 | | 5,538,197 | |

| | 9,417,416 | |

Ghana - .2% | | | | | |

Ghana, Sr. Unscd. Bonds | | 7.88 | | 3/26/2027 | | 3,500,000 | c | 3,687,446 | |

Ghana, Sr. Unscd. Bonds | | 8.13 | | 1/18/2026 | | 1,325,000 | | 1,431,574 | |

Ghana, Sr. Unscd. Notes | | 7.88 | | 8/7/2023 | | 2,625,000 | | 2,889,443 | |

| | 8,008,463 | |

Hungary - .2% | | | | | |

Hungary, Sr. Unscd. Bonds | EUR | 1.25 | | 10/22/2025 | | 4,530,000 | | 5,406,067 | |

Indonesia - .6% | | | | | |

Indonesia, Sr. Unscd. Notes | EUR | 1.40 | | 10/30/2031 | | 3,870,000 | | 4,325,134 | |

Indonesia, Sr. Unscd. Notes | EUR | 3.75 | | 6/14/2028 | | 3,130,000 | | 4,239,700 | |

Indonesia Asahan Aluminium, Sr. Unscd. Notes | | 5.23 | | 11/15/2021 | | 3,650,000 | c | 3,832,500 | |

Perusahaan Listrik Negara, Sr. Unscd. Notes | EUR | 1.88 | | 11/5/2031 | | 5,100,000 | | 5,703,508 | |

| | 18,100,842 | |

Ireland - .2% | | | | | |

AerCap Global Aviation Trust, Gtd. Notes | | 4.50 | | 5/15/2021 | | 4,550,000 | | 4,696,414 | |

Ireland, Bonds | EUR | 2.00 | | 2/18/2045 | | 2,150,000 | | 3,085,110 | |

| | 7,781,524 | |

Israel - .1% | | | | | |

Israel, Bonds, Ser. 327 | ILS | 2.00 | | 3/31/2027 | | 12,975,000 | | 4,095,719 | |

Italy - 2.1% | | | | | |

Intesa Sanpaolo, Covered Notes | EUR | 1.38 | | 12/18/2025 | | 6,500,000 | | 7,884,720 | |

Italy, Sr. Unscd. Notes | | 2.88 | | 10/17/2029 | | 15,400,000 | | 14,665,361 | |

Italy Buoni Poliennali Del Tesoro, Bonds | EUR | 0.95 | | 3/15/2023 | | 16,295,000 | | 18,697,639 | |

Italy Buoni Poliennali Del Tesoro, Unscd. Bonds | EUR | 4.00 | | 2/1/2037 | | 18,300,000 | c | 26,426,211 | |

| | 67,673,931 | |

Ivory Coast - .3% | | | | | |

Ivory Coast, Sr. Unscd. Notes | EUR | 5.88 | | 10/17/2031 | | 7,125,000 | | 8,337,372 | |

Japan - 12.3% | | | | | |

Japan, Sr. Unscd. Bonds, Ser. 19 | JPY | 0.10 | | 9/10/2024 | | 6,214,887,000 | e | 58,170,725 | |

Japan, Sr. Unscd. Bonds, Ser. 20 | JPY | 0.10 | | 3/10/2025 | | 6,300,171,300 | e | 59,055,952 | |

Japan, Sr. Unscd. Bonds, Ser. 21 | JPY | 0.10 | | 3/10/2026 | | 3,632,956,480 | e | 34,171,290 | |

Japan, Sr. Unscd. Bonds, Ser. 22 | JPY | 0.10 | | 3/10/2027 | | 6,764,657,144 | e | 63,907,971 | |

Japan, Sr. Unscd. Bonds, Ser. 23 | JPY | 0.10 | | 3/10/2028 | | 8,882,425,200 | e | 84,119,604 | |

Japan (20 Year Issue), Sr. Unscd. Bonds, Ser. 156 | JPY | 0.40 | | 3/20/2036 | | 3,425,650,000 | | 32,627,523 | |

12

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity

Date | | Principal

Amount ($) | a | Value ($) | |

Bonds and Notes - 96.0% (continued) | | | | | |

Japan - 12.3% (continued) | | | | | |

Japan (30 Year Issue), Sr. Unscd. Bonds, Ser. 44 | JPY | 1.70 | | 9/20/2044 | | 1,013,000,000 | | 12,314,877 | |

Japan (30 Year Issue), Sr. Unscd. Bonds, Ser. 61 | JPY | 0.70 | | 12/20/2048 | | 453,900,000 | | 4,516,202 | |

Oscar US Funding Trust VI, Ser. 2017-1A, Cl. A4 | | 3.30 | | 5/10/2024 | | 3,560,000 | c | 3,605,331 | |

Oscar US Funding Trust VII, Ser. 2017-2A, Cl. A3 | | 2.45 | | 12/10/2021 | | 1,846,339 | c | 1,848,826 | |

Oscar US Funding Trust VII, Ser. 2017-2A, Cl. A4 | | 2.76 | | 12/10/2024 | | 8,430,000 | c | 8,515,617 | |

Oscar US Funding Trust VIII, Ser. 2018-1A, Cl. A4 | | 3.50 | | 5/12/2025 | | 7,750,000 | c | 7,967,236 | |

Oscar US Funding X, Ser. 2019-1A, Cl. A4 | | 3.27 | | 5/11/2026 | | 6,750,000 | c | 6,948,756 | |

Oscar US Funding XI, Ser. 2019-2A, Cl. A4 | | 2.68 | | 9/10/2026 | | 9,520,000 | c | 9,599,394 | |

Takeda Pharmaceutical, Sr. Unscd. Bonds | EUR | 3.00 | | 11/21/2030 | | 6,500,000 | | 8,686,032 | |

| | 396,055,336 | |

Kazakhstan - .6% | | | | | |

Development Bank of Kazakhstan, Sr. Unscd. Notes | | 4.13 | | 12/10/2022 | | 2,025,000 | | 2,110,536 | |

Kazakhstan, Sr. Unscd. Notes | EUR | 0.60 | | 9/30/2026 | | 11,265,000 | | 12,624,212 | |

KazMunayGas National, Sr. Unscd. Notes | | 6.38 | | 10/24/2048 | | 4,290,000 | | 5,535,130 | |

| | 20,269,878 | |

Kenya - .2% | | | | | |

Kenya, Sr. Unscd. Notes | | 7.25 | | 2/28/2028 | | 4,650,000 | c | 5,067,314 | |

Luxembourg - 1.1% | | | | | |

Becton Dickinson Euro Finance, Gtd. Bonds | EUR | 0.63 | | 6/4/2023 | | 2,980,000 | | 3,379,391 | |

CK Hutchison Group Telecom Finance, Gtd. Notes | EUR | 1.13 | | 10/17/2028 | | 8,670,000 | | 9,699,649 | |

DH Europe Finance II, Gtd. Bonds | EUR | 0.20 | | 3/18/2026 | | 6,120,000 | | 6,789,737 | |

DH Europe Finance II, Gtd. Notes | | 2.60 | | 11/15/2029 | | 6,525,000 | | 6,505,371 | |

E-Carat, Ser. 2016-1, Cl. A, 1 Month EURIBOR +.45% @ Floor | EUR | 0.45 | | 10/18/2024 | | 207,892 | b | 233,288 | |

Gazprom OAO Via Gaz Capital, Sr. Unscd. Bonds | EUR | 2.50 | | 3/21/2026 | | 4,150,000 | | 5,028,065 | |

Medtronic Global Holdings, Gtd. Notes | EUR | 1.63 | | 3/7/2031 | | 2,000,000 | | 2,464,430 | |

| | 34,099,931 | |

Malaysia - 1.3% | | | | | |

Malaysia, Sr. Unscd. Bonds, Ser. 219 | MYR | 3.89 | | 8/15/2029 | | 161,250,000 | | 41,257,194 | |

13

STATEMENT OF INVESTMENTS (continued)

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity

Date | | Principal

Amount ($) | a | Value ($) | |

Bonds and Notes - 96.0% (continued) | | | | | |

Mexico - .3% | | | | | |

Infraestructura Energetica Nova, Sr. Unscd. Notes | | 4.88 | | 1/14/2048 | | 3,950,000 | | 3,775,943 | |

Petroleos Mexicanos, Gtd. Notes | EUR | 5.13 | | 3/15/2023 | | 4,560,000 | | 5,724,066 | |

| | 9,500,009 | |

Netherlands - 3.6% | | | | | |

ABN AMRO Bank, Covered Bonds | EUR | 0.88 | | 1/14/2026 | | 9,200,000 | | 10,936,148 | |

ABN AMRO Bank, Sub. Notes | EUR | 2.88 | | 1/18/2028 | | 3,700,000 | | 4,443,284 | |

ABN AMRO Bank, Sub. Notes | | 4.75 | | 7/28/2025 | | 5,100,000 | c | 5,567,722 | |

Cooperatieve Rabobank, Sub. Bonds | EUR | 2.50 | | 5/26/2026 | | 6,180,000 | | 7,156,096 | |

EDP Finance, Sr. Unscd. Notes | EUR | 0.38 | | 9/16/2026 | | 5,815,000 | | 6,448,559 | |

Enel Finance International, Gtd. Notes | EUR | 0.38 | | 6/17/2027 | | 7,275,000 | | 8,088,091 | |

Equate Petrochemical, Gtd. Notes | | 3.00 | | 3/3/2022 | | 5,295,000 | d | 5,329,232 | |

Iberdrola International, Gtd. Notes | EUR | 1.13 | | 1/27/2023 | | 1,400,000 | | 1,623,007 | |

Iberdrola International, Gtd. Notes | EUR | 2.63 | | 3/26/2024 | | 5,600,000 | | 6,721,792 | |

ING Groep, Sub. Bonds | EUR | 2.00 | | 3/22/2030 | | 4,600,000 | | 5,457,281 | |

ING Groep, Sub. Notes | EUR | 3.00 | | 4/11/2028 | | 5,200,000 | | 6,289,627 | |

MDGH - GMTN, Gtd. Notes | | 2.50 | | 11/7/2024 | | 3,550,000 | | 3,565,840 | |

Petrobras Global Finance, Gtd. Notes | | 5.09 | | 1/15/2030 | | 2,185,000 | c | 2,343,981 | |

SABIC Capital II, Gtd. Bonds | | 4.00 | | 10/10/2023 | | 10,200,000 | c | 10,759,419 | |

VEON Holdings, Sr. Unscd. Notes | | 3.95 | | 6/16/2021 | | 8,050,000 | | 8,195,705 | |

VEON Holdings, Sr. Unscd. Notes | | 4.00 | | 4/9/2025 | | 8,535,000 | | 8,904,651 | |

Volkswagen International Finance, Gtd. Bonds, Ser. 10Y | EUR | 1.88 | | 3/30/2027 | | 6,800,000 | | 8,083,772 | |

WPC Eurobond, Gtd. Bonds | EUR | 2.25 | | 7/19/2024 | | 2,975,000 | | 3,595,917 | |

WPC Eurobond, Gtd. Notes | EUR | 1.35 | | 4/15/2028 | | 2,200,000 | | 2,444,507 | |

WPC Eurobond, Gtd. Notes | EUR | 2.13 | | 4/15/2027 | | 685,000 | | 813,708 | |

| | 116,768,339 | |

Nigeria - .2% | | | | | |

Nigeria, Sr. Unscd. Notes | | 5.63 | | 6/27/2022 | | 3,550,000 | | 3,701,202 | |

Nigeria, Sr. Unscd. Notes | | 6.50 | | 11/28/2027 | | 4,100,000 | c | 4,197,855 | |

| | 7,899,057 | |

Norway - .2% | | | | | |

Equinor, Gtd. Notes | | 3.25 | | 11/18/2049 | | 7,350,000 | | 7,405,775 | |

Panama - .2% | | | | | |

Panama, Sr. Unscd. Notes | | 3.16 | | 1/23/2030 | | 6,000,000 | | 6,189,000 | |

Philippines - .1% | | | | | |

Philippine, Sr. Unscd. Notes | EUR | 0.88 | | 5/17/2027 | | 3,000,000 | | 3,436,608 | |

Romania - .2% | | | | | |

Romania, Sr. Unscd. Notes | EUR | 2.50 | | 2/8/2030 | | 5,745,000 | c | 6,979,677 | |

Russia - 2.6% | | | | | |

Russia, Bonds, Ser. 6212 | RUB | 7.05 | | 1/19/2028 | | 4,906,990,000 | | 83,507,674 | |

14

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity

Date | | Principal

Amount ($) | a | Value ($) | |

Bonds and Notes - 96.0% (continued) | | | | | |

Saudi Arabia - .1% | | | | | |

Saudi Arabian Oil, Sr. Unscd. Notes | | 2.75 | | 4/16/2022 | | 3,150,000 | c | 3,186,585 | |

Senegal - .2% | | | | | |

Senegal, Sr. Unscd. Bonds | EUR | 4.75 | | 3/13/2028 | | 6,750,000 | | 8,005,957 | |

Singapore - 1.2% | | | | | |

Singapore, Sr. Unscd. Bonds | SGD | 2.63 | | 5/1/2028 | | 31,000,000 | | 24,707,130 | |

Temasek Financial I, Gtd. Notes | EUR | 1.25 | | 11/20/2049 | | 11,125,000 | | 12,743,178 | |

| | 37,450,308 | |

South Korea - 1.8% | | | | | |

Korea Treasury Bond, Sr. Unscd. Bonds, Ser. 2812 | KRW | 2.38 | | 12/10/2028 | | 55,462,300,000 | | 50,657,117 | |

Korea Treasury Bond, Sr. Unscd. Bonds, Ser. 4903 | KRW | 2.00 | | 3/10/2049 | | 8,000,000,000 | | 7,425,057 | |

| | 58,082,174 | |

Spain - 3.0% | | | | | |

Banco Santander, Covered Notes | EUR | 0.88 | | 5/9/2031 | | 6,800,000 | | 8,043,651 | |

Spain, Notes | EUR | 0.60 | | 10/31/2029 | | 29,600,000 | c | 33,656,420 | |

Spain, Sr. Unscd. Bonds | EUR | 2.90 | | 10/31/2046 | | 32,070,000 | c | 49,254,696 | |

Telefonica Emisiones, Gtd. Notes | EUR | 1.53 | | 1/17/2025 | | 5,300,000 | d | 6,324,407 | |

| | 97,279,174 | |

Sri Lanka - .2% | | | | | |

Sri Lanka, Sr. Unscd. Notes | | 6.25 | | 10/4/2020 | | 3,025,000 | d | 3,073,385 | |

Sri Lanka, Sr. Unscd. Notes | | 6.85 | | 3/14/2024 | | 2,825,000 | c | 2,864,392 | |

| | 5,937,777 | |

Supranational - 1.8% | | | | | |

Arab Petroleum Investments, Sr. Unscd. Notes | | 4.13 | | 9/18/2023 | | 9,760,000 | c,d | 10,381,528 | |

Asian Development Bank, Sr. Unscd. Notes | NZD | 3.50 | | 5/30/2024 | | 12,575,000 | | 9,102,386 | |

Banque Ouest Africaine de Developpement, Sr. Unscd. Notes | | 5.00 | | 7/27/2027 | | 7,720,000 | | 8,202,500 | |

Corp. Andina de Fomento, Sr. Unscd. Notes | | 3.25 | | 2/11/2022 | | 8,250,000 | | 8,397,015 | |

International Finance, Sr. Unscd. Notes | INR | 6.30 | | 11/25/2024 | | 951,180,000 | | 13,476,177 | |

The African Export-Import Bank, Sr. Unscd. Notes | | 5.25 | | 10/11/2023 | | 7,500,000 | | 8,137,680 | |

| | 57,697,286 | |

Sweden - .3% | | | | | |

Sweden, Bonds, Ser. 1061 | SEK | 0.75 | | 11/12/2029 | | 84,375,000 | c | 9,538,316 | |

Switzerland - .2% | | | | | |

Credit Suisse Group, Sr. Unscd. Notes | | 4.28 | | 1/9/2028 | | 5,725,000 | c | 6,227,384 | |

Thailand - 1.8% | | | | | |

Thailand, Sr. Unscd. Bonds | THB | 2.13 | | 12/17/2026 | | 492,750,000 | | 17,293,758 | |

15

STATEMENT OF INVESTMENTS (continued)

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity

Date | | Principal

Amount ($) | a | Value ($) | |

Bonds and Notes - 96.0% (continued) | | | | | |

Thailand - 1.8% (continued) | | | | | |

Thailand, Sr. Unscd. Bonds | THB | 2.88 | | 12/17/2028 | | 1,100,000,000 | | 41,102,715 | |

| | 58,396,473 | |

Turkey - .3% | | | | | |

Turkey, Sr. Unscd. Notes | | 5.60 | | 11/14/2024 | | 8,150,000 | | 8,307,417 | |

Ukraine - .4% | | | | | |

Ukraine, Sr. Unscd. Notes | | 7.75 | | 9/1/2020 | | 6,150,000 | | 6,339,506 | |

Ukraine, Sr. Unscd. Notes | | 7.75 | | 9/1/2022 | | 7,400,000 | | 8,001,250 | |

| | 14,340,756 | |

United Arab Emirates - .9% | | | | | |

Abu Dhabi, Sr. Unscd. Bonds | | 2.50 | | 9/30/2029 | | 18,025,000 | | 17,991,203 | |

Abu Dhabi Crude Oil Pipeline, Sr. Scd. Bonds | | 4.60 | | 11/2/2047 | | 4,650,000 | c | 5,385,281 | |

DP World, Sr. Unscd. Notes | | 6.85 | | 7/2/2037 | | 4,040,000 | | 5,329,980 | |

| | 28,706,464 | |

United Kingdom - 5.0% | | | | | |

Anglo American Capital, Gtd. Notes | EUR | 1.63 | | 3/11/2026 | | 2,760,000 | | 3,224,257 | |

Anglo American Capital, Gtd. Notes | EUR | 1.63 | | 9/18/2025 | | 1,950,000 | | 2,283,395 | |

Barclays, Jr. Sub. Bonds | | 7.88 | | 3/15/2022 | | 2,675,000 | | 2,890,083 | |

Barclays, Sr. Unscd. Notes | | 4.97 | | 5/16/2029 | | 8,125,000 | | 9,157,503 | |

BAT International Finance, Gtd. Notes | EUR | 2.25 | | 1/16/2030 | | 6,900,000 | | 8,092,000 | |

Lanark Master Issuer, Ser. 2019-1A, Cl. 1A1, 3 Month LIBOR +.77% | | 2.67 | | 12/22/2069 | | 6,066,667 | b,c | 6,076,744 | |

Lloyds Banking Group, Sr. Unscd. Notes | | 3.75 | | 1/11/2027 | | 6,305,000 | | 6,627,234 | |

Penarth Master Issuer, Ser. 2018-2A, Cl. A1, 1 Month LIBOR +.45% | | 2.19 | | 9/18/2022 | | 7,800,000 | b,c | 7,798,280 | |

Permanent Master Issuer, Ser. 2019-1A, Cl. 1A1, 3 Month LIBOR +.55% | | 2.54 | | 7/15/2058 | | 7,420,000 | b,c | 7,425,246 | |

Royal Bank of Scotland Group, Sr. Unscd. Notes | | 3.88 | | 9/12/2023 | | 12,625,000 | | 13,230,156 | |

Santander UK Group Holdings, Sr. Unscd. Notes | | 3.57 | | 1/10/2023 | | 3,525,000 | | 3,609,074 | |

Silverstone Master Issuer, Ser. 2019-1A, Cl. 2A, 3 Month SONIO +.75% | GBP | 1.46 | | 1/21/2070 | | 7,440,000 | b,c | 9,896,750 | |

United Kingdom, Bonds | GBP | 1.50 | | 7/22/2047 | | 10,355,000 | | 14,218,110 | |

United Kingdom, Bonds | GBP | 3.25 | | 1/22/2044 | | 35,550,000 | | 65,512,838 | |

| | 160,041,670 | |

United States - 37.8% | | | | | |

Abbott Laboratories, Sr. Unscd. Notes | | 3.75 | | 11/30/2026 | | 1,616,000 | | 1,765,926 | |

AbbVie, Sr. Unscd. Bonds | EUR | 1.38 | | 5/17/2024 | | 1,230,000 | | 1,453,362 | |

AbbVie, Sr. Unscd. Notes | | 2.95 | | 11/21/2026 | | 2,115,000 | c | 2,149,886 | |

AbbVie, Sr. Unscd. Notes | | 4.25 | | 11/21/2049 | | 2,600,000 | c | 2,748,042 | |

16

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity

Date | | Principal

Amount ($) | a | Value ($) | |

Bonds and Notes - 96.0% (continued) | | | | | |

United States - 37.8% (continued) | | | | | |

AEP Transmission, Sr. Unscd. Notes | | 3.10 | | 12/1/2026 | | 3,680,000 | | 3,812,753 | |

Amazon.com, Sr. Unscd. Notes | | 3.15 | | 8/22/2027 | | 11,875,000 | | 12,566,407 | |

American Express, Sr. Unscd. Notes | | 2.50 | | 7/30/2024 | | 7,700,000 | | 7,788,605 | |

American Homes 4 Rent Trust, Ser. 2014-SFR3, Cl. A | | 3.68 | | 12/17/2036 | | 4,118,702 | c | 4,278,388 | |

American International Group, Sr. Unscd. Notes | | 4.20 | | 4/1/2028 | | 2,790,000 | | 3,069,796 | |

AmeriCredit Automobile Receivables Trust, Ser. 2016-4, Cl. D | | 2.74 | | 12/8/2022 | | 3,300,000 | | 3,321,568 | |

Anheuser-Busch Inbev Worldwide, Gtd. Notes | | 4.00 | | 4/13/2028 | | 3,810,000 | | 4,191,276 | |

Apple, Sr. Unscd. Notes | | 3.25 | | 2/23/2026 | | 8,895,000 | | 9,418,545 | |

AT&T, Sr. Unscd. Notes | EUR | 0.25 | | 3/4/2026 | | 4,725,000 | | 5,195,950 | |

AT&T, Sr. Unscd. Notes | EUR | 1.80 | | 9/14/2039 | | 3,680,000 | | 3,947,622 | |

AT&T, Sr. Unscd. Notes | EUR | 2.35 | | 9/5/2029 | | 300,000 | | 376,608 | |

Bank, Ser. 2018-BN13, Cl. A5 | | 4.22 | | 8/15/2061 | | 3,300,000 | | 3,698,640 | |

Bank, Ser. 2019-BN19, Cl. A2 | | 2.93 | | 8/15/2061 | | 7,850,000 | | 8,059,736 | |

Bank, Ser. 2019-BN24, Cl. AS | | 3.28 | | 11/15/2062 | | 7,400,000 | | 7,600,322 | |

Bank of America, Sr. Unscd. Notes | | 3.37 | | 1/23/2026 | | 3,375,000 | | 3,530,870 | |

Bank of America, Sr. Unscd. Notes | | 3.97 | | 3/5/2029 | | 5,895,000 | | 6,421,175 | |

BBCMS Mortgage Trust, Ser. 2019-BWAY, Cl. A, 1 Month LIBOR +.96% | | 2.70 | | 11/25/2034 | | 6,400,000 | b,c | 6,375,983 | |

BBCMS Trust, Ser. 2013-TYSN, Cl. A2 | | 3.76 | | 9/5/2032 | | 1,245,000 | c | 1,251,913 | |

Bear Stearns Commercial Mortgage Securities Trust, Ser. 2005-PW10, Cl. AJ | | 5.78 | | 12/11/2040 | | 190,193 | | 192,845 | |

Benchmark Mortgage Trust, Ser. 2019-B15, Cl. A5 | | 2.93 | | 12/15/2072 | | 8,075,000 | | 8,271,432 | |

CAMB Commercial Mortgage Trust, Ser. 2019-LIFE, Cl. A, 1 Month LIBOR +1.07% | | 2.81 | | 12/15/2037 | | 6,350,000 | b,c | 6,368,519 | |

Cameron LNG, Sr. Scd. Notes | | 2.90 | | 7/15/2031 | | 8,575,000 | c | 8,592,939 | |

CarMax Auto Owner Trust, Ser. 2018-1, Cl. D | | 3.37 | | 7/15/2024 | | 1,360,000 | | 1,382,216 | |

CarMax Auto Owner Trust, Ser. 2019-3, Cl. B | | 2.50 | | 4/15/2025 | | 3,445,000 | | 3,457,726 | |

CarMax Auto Owner Trust, Ser. 2019-3, Cl. C | | 2.60 | | 6/16/2025 | | 3,065,000 | | 3,073,759 | |

CCO Holdings, Sr. Unscd. Notes | | 5.88 | | 4/1/2024 | | 1,710,000 | c | 1,771,278 | |

CCUBS Commercial Mortgage Trust, Ser. 2017-C1, Cl. A4 | | 3.54 | | 11/15/2050 | | 7,326,000 | | 7,807,972 | |

CGDB Commercial Mortgage Trust, Ser. 2019-MOB, Cl. A, 1 Month LIBOR +.95% | | 2.69 | | 11/15/2036 | | 5,750,000 | b,c | 5,748,174 | |

17

STATEMENT OF INVESTMENTS (continued)

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity

Date | | Principal

Amount ($) | a | Value ($) | |

Bonds and Notes - 96.0% (continued) | | | | | |

United States - 37.8% (continued) | | | | | |

CHC Commercial Mortgage Trust, Ser. 2019-CHC, Cl. A, 1 Month LIBOR +1.12% | | 2.86 | | 6/15/2034 | | 9,000,000 | b,c | 8,999,145 | |

CHC Commercial Mortgage Trust, Ser. 2019-CHC, Cl. B, 1 Month LIBOR +1.50% | | 3.24 | | 6/15/2034 | | 3,400,000 | b,c | 3,395,477 | |

Cheniere Corpus Christi Holdings, Sr. Scd. Notes | | 3.70 | | 11/15/2029 | | 9,515,000 | c | 9,714,716 | |

Cheniere Energy Partners, Gtd. Notes | | 4.50 | | 10/1/2029 | | 5,150,000 | c | 5,301,667 | |

Cheniere Energy Partners, Sr. Scd. Notes | | 5.25 | | 10/1/2025 | | 3,935,000 | | 4,110,422 | |

Comcast, Gtd. Notes | | 2.65 | | 2/1/2030 | | 5,575,000 | | 5,597,524 | |

Commercial Mortgage Trust, Ser. 2014-CR16, Cl. A3 | | 3.78 | | 4/10/2047 | | 8,988,822 | | 9,440,715 | |

Conagra Brands, Sr. Unscd. Notes | | 3.80 | | 10/22/2021 | | 3,200,000 | | 3,302,206 | |

Concho Resources, Gtd. Notes | | 3.75 | | 10/1/2027 | | 3,750,000 | | 3,942,595 | |

Consumer Loan Underlying Bond CLUB Credit Trust, Ser. 2019-P2, Cl. A | | 2.47 | | 10/15/2026 | | 4,279,258 | c | 4,282,051 | |

Crown Castle International, Sr. Unscd. Notes | | 3.15 | | 7/15/2023 | | 3,150,000 | | 3,250,658 | |

CVS Health, Sr. Unscd. Notes | | 2.63 | | 8/15/2024 | | 2,500,000 | d | 2,521,936 | |

CVS Health, Sr. Unscd. Notes | | 4.30 | | 3/25/2028 | | 7,170,000 | | 7,830,540 | |

CyrusOne, Gtd. Notes | | 2.90 | | 11/15/2024 | | 1,280,000 | | 1,287,584 | |

CyrusOne, Gtd. Notes | | 3.45 | | 11/15/2029 | | 3,400,000 | | 3,415,606 | |

Dell Equipment Finance Trust, Ser. 2018-1, Cl. B | | 3.34 | | 6/22/2023 | | 2,090,000 | c | 2,116,746 | |

Dell Equipment Finance Trust, Ser. 2018-2, Cl. C | | 3.72 | | 10/22/2023 | | 4,200,000 | c | 4,310,061 | |

Dell International, Sr. Scd. Notes | | 6.02 | | 6/15/2026 | | 4,650,000 | c | 5,352,005 | |

Diamondback Energy, Gtd. Notes | | 2.88 | | 12/1/2024 | | 7,000,000 | | 7,079,903 | |

Diamondback Energy, Gtd. Notes | | 5.38 | | 5/31/2025 | | 3,325,000 | | 3,491,055 | |

Digital Euro Finco, Gtd. Bonds | EUR | 2.63 | | 4/15/2024 | | 5,814,000 | | 7,069,321 | |

Dollar Tree, Sr. Unscd. Notes | | 4.20 | | 5/15/2028 | | 2,050,000 | | 2,198,242 | |

DPL | | 4.35 | | 4/15/2029 | | 1,025,000 | | 988,882 | |

DPL, Sr. Unscd. Notes | | 4.35 | | 4/15/2029 | | 7,110,000 | c | 6,859,467 | |

Drive Auto Receivables Trust, Ser. 2016-CA, Cl. D | | 4.18 | | 3/15/2024 | | 7,575,126 | c | 7,667,576 | |

Drive Auto Receivables Trust, Ser. 2019-4, Cl. B | | 2.23 | | 1/16/2024 | | 4,390,000 | | 4,392,422 | |

DT Auto Owner Trust, Ser. 2018-2A, Cl. C | | 3.67 | | 3/15/2024 | | 8,925,000 | c | 9,010,190 | |

DT Auto Owner Trust, Ser. 2019-4A, Cl. B | | 2.36 | | 1/16/2024 | | 4,950,000 | c | 4,952,139 | |

Duke Energy, Sr. Unscd. Notes | | 2.65 | | 9/1/2026 | | 2,800,000 | | 2,812,921 | |

18

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity

Date | | Principal

Amount ($) | a | Value ($) | |

Bonds and Notes - 96.0% (continued) | | | | | |

United States - 37.8% (continued) | | | | | |

Edison International, Sr. Unscd. Notes | | 4.13 | | 3/15/2028 | | 2,745,000 | | 2,815,784 | |

Edison International, Sr. Unscd. Notes | | 5.75 | | 6/15/2027 | | 1,565,000 | | 1,757,946 | |

Energy Transfer Operating, Gtd. Notes | | 4.20 | | 4/15/2027 | | 2,050,000 | | 2,146,364 | |

Energy Transfer Operating, Gtd. Notes | | 4.50 | | 4/15/2024 | | 2,000,000 | | 2,128,855 | |

Energy Transfer Operating, Gtd. Notes | | 5.25 | | 4/15/2029 | | 2,700,000 | | 3,032,509 | |

Energy Transfer Operating, Jr. Sub. Debs., Ser. A | | 6.25 | | 2/15/2023 | | 2,365,000 | | 2,226,695 | |

Enterprise Fleet Financing, Ser. 2017-3, Cl. A2 | | 2.13 | | 5/22/2023 | | 2,726,120 | c | 2,725,529 | |

Enterprise Fleet Financing, Ser. 2019-3, Cl. A3 | | 2.19 | | 5/20/2025 | | 7,200,000 | c | 7,184,002 | |

Exeter Automobile Receivables Trust, Ser. 2019-3A, Cl. B | | 2.58 | | 8/15/2023 | | 7,600,000 | c | 7,631,815 | |

Federal Home Loan Mortgage Corp. Multifamily Structured Pass Through Certificates, Ser. K087, Cl. A2 | | 3.77 | | 12/25/2028 | | 2,400,000 | f | 2,640,246 | |

Federal Home Loan Mortgage Corp. Multifamily Structured Pass Through Certificates, Ser. K088, Cl. A2 | | 3.69 | | 1/25/2029 | | 7,800,000 | f | 8,542,293 | |

Federal Home Loan Mortgage Corp. Multifamily Structured Pass Through Certificates, Ser. K159, Cl. A2 | | 3.95 | | 11/25/2030 | | 5,140,000 | f | 5,764,383 | |

Federal Home Loan Mortgage Corp. Multifamily Structured Pass Through Certificates, Ser. KC02, Cl. A2 | | 3.37 | | 7/25/2025 | | 6,365,000 | f | 6,636,486 | |

Federal Home Loan Mortgage Corp. Multifamily Structured Pass Through Certificates, Ser. KL3W, Cl. AFLW, 1 Month LIBOR +.45% | | 2.15 | | 8/25/2025 | | 4,000,000 | b,f | 4,009,396 | |

Federal National Mortgage Association, Ser. 2017-T1, Cl. A | | 2.90 | | 6/25/2027 | | 7,685,005 | | 7,895,702 | |

Fidelity National Information Services, Sr. Unscd. Notes | EUR | 1.50 | | 5/21/2027 | | 4,280,000 | | 5,080,172 | |

General Electric, Jr. Sub. Debs., Ser. D | | 5.00 | | 1/21/2021 | | 1,060,000 | | 1,039,839 | |

General Electric, Sr. Unscd. Bonds | EUR | 0.38 | | 5/17/2022 | | 2,935,000 | | 3,297,255 | |

GM Financial Automobile Leasing Trust, Ser. 2018-2, Cl. C | | 3.50 | | 4/20/2022 | | 5,710,000 | | 5,765,659 | |

19

STATEMENT OF INVESTMENTS (continued)

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity

Date | | Principal

Amount ($) | a | Value ($) | |

Bonds and Notes - 96.0% (continued) | | | | | |

United States - 37.8% (continued) | | | | | |

GM Financial Automobile Leasing Trust, Ser. 2018-3, Cl. B | | 3.48 | | 7/20/2022 | | 4,715,000 | | 4,775,399 | |

GM Financial Automobile Leasing Trust, Ser. 2018-3, Cl. C | | 3.70 | | 7/20/2022 | | 7,960,000 | | 8,075,024 | |

GS Mortgage Securities Trust, Ser. 2016-GS2, Cl. A2 | | 2.64 | | 5/10/2049 | | 4,200,000 | | 4,214,060 | |

HCA, Gtd. Notes | | 5.88 | | 2/1/2029 | | 1,625,000 | d | 1,880,938 | |

Healthcare Trust of America Holdings, Gtd. Notes | | 3.10 | | 2/15/2030 | | 3,485,000 | | 3,460,291 | |

Healthcare Trust of America Holdings, Gtd. Notes | | 3.50 | | 8/1/2026 | | 3,055,000 | | 3,188,376 | |

Hewlett Packard Enterprise, Sr. Unscd. Notes | | 2.25 | | 4/1/2023 | | 8,090,000 | | 8,082,931 | |

HPLY Trust, Ser. 2019-HIT, Cl. A, 1 Month LIBOR +1.00% | | 2.74 | | 11/15/2036 | | 7,996,585 | b,c | 7,984,263 | |

Intown Hotel Portfolio Trust, Ser. 2018-STAY, Cl. A, 1 Month LIBOR +.70% | | 2.44 | | 1/15/2033 | | 3,750,000 | b,c | 3,740,938 | |

Intown Hotel Portfolio Trust, Ser. 2018-STAY, Cl. B, 1 Month LIBOR +1.05% | | 2.79 | | 1/15/2033 | | 2,750,000 | b,c | 2,742,967 | |

Invitation Homes Trust, Ser. 2018-SFR3, Cl. A, 1 Month LIBOR +1.00% | | 2.74 | | 7/17/2037 | | 6,623,278 | b,c | 6,634,849 | |

JP Morgan Chase Commercial Mortgage Securities Trust, Ser. 2013-C16, Cl. A3 | | 3.88 | | 12/15/2046 | | 4,000,000 | | 4,226,594 | |

JPMorgan Chase & Co., Sr. Unscd. Notes | | 3.30 | | 4/1/2026 | | 6,525,000 | | 6,867,116 | |

Keurig Dr Pepper, Gtd. Notes | | 4.06 | | 5/25/2023 | | 2,500,000 | | 2,636,608 | |

KeyCorp Student Loan Trust, Ser. 1999-B, Cl. CTFS, 3 Month LIBOR +.90% | | 2.81 | | 11/25/2036 | | 4,014 | b | 4,009 | |

Kinder Morgan, Gtd. Notes | | 4.30 | | 6/1/2025 | | 1,950,000 | | 2,115,416 | |

Marsh & McLennan, Sr. Unscd. Bonds | EUR | 1.98 | | 3/21/2030 | | 6,970,000 | | 8,555,824 | |

Metropolitan Life Global Funding I, Sr. Scd. Notes | | 3.00 | | 9/19/2027 | | 5,475,000 | c | 5,678,096 | |

MGM Growth Properties Operating Partnership, Gtd. Notes | | 5.75 | | 2/1/2027 | | 3,070,000 | c | 3,434,563 | |

Morgan Stanley, Sr. Unscd. Notes | | 4.00 | | 7/23/2025 | | 3,450,000 | | 3,733,186 | |

Morgan Stanley Capital I Trust, Ser. 2019-H7, Cl. A3 | | 3.01 | | 7/15/2052 | | 6,825,000 | | 6,998,448 | |

Morgan Stanley Capital I Trust, Ser. 2019-L2, Cl. A3 | | 3.81 | | 3/15/2052 | | 9,750,000 | | 10,648,543 | |

MPLX, Sr. Unscd. Notes | | 3.50 | | 12/1/2022 | | 2,175,000 | c | 2,239,546 | |

20

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity

Date | | Principal

Amount ($) | a | Value ($) | |

Bonds and Notes - 96.0% (continued) | | | | | |

United States - 37.8% (continued) | | | | | |

Navient Private Education Refi Loan Trust, Ser. 2019-A, Cl. A1 | | 3.03 | | 1/15/2043 | | 1,703,618 | c | 1,711,486 | |

NYT Mortgage Trust, Ser. 2019-NYT, Cl. A, 1 Month LIBOR +1.20% | | 2.94 | | 11/15/2035 | | 7,500,000 | b,c | 7,531,674 | |

Occidental Petroleum, Sr. Unscd. Notes | | 3.00 | | 2/15/2027 | | 3,480,000 | | 3,488,178 | |

PayPal Holdings, Sr. Unscd. Notes | | 2.40 | | 10/1/2024 | | 6,410,000 | | 6,476,708 | |

Pfizer, Sr. Unscd. Notes | | 3.45 | | 3/15/2029 | | 1,400,000 | d | 1,507,899 | |

Plains All American Pipeline, Sr. Unscd. Notes | | 3.55 | | 12/15/2029 | | 8,200,000 | | 8,087,676 | |

Pricoa Global Funding I, Scd. Notes | | 2.40 | | 9/23/2024 | | 5,575,000 | c | 5,609,888 | |

Prime Security Services Borrower, Scd. Notes | | 9.25 | | 5/15/2023 | | 433,000 | c | 454,921 | |

Prosper Marketplace Issuance Trust, Ser. 2018-2A, Cl. A | | 3.35 | | 10/15/2024 | | 1,690,684 | c | 1,694,077 | |

Republic Services, Sr. Unscd. Notes | | 2.50 | | 8/15/2024 | | 3,400,000 | | 3,439,556 | |

Reynolds Group Issuer, Gtd. Notes | | 7.00 | | 7/15/2024 | | 1,610,000 | c | 1,667,356 | |

RMF Buyout Issuance Trust, Ser. 2018-1, Cl. A | | 3.44 | | 11/25/2028 | | 1,266,798 | c | 1,268,848 | |

Santander Drive Auto Receivables Trust, Ser. 2015-5, Cl. D | | 3.65 | | 12/15/2021 | | 475,666 | | 476,792 | |

Santander Retail Auto Lease Trust, Ser. 2019-B, Cl. C | | 2.77 | | 8/21/2023 | | 3,600,000 | c | 3,617,060 | |

SBA Tower Trust, Scd. Notes | | 2.84 | | 1/15/2025 | | 8,030,000 | c | 8,118,650 | |

SCF Equipment Leasing, Ser. 2019-1A, Cl. A2 | | 3.23 | | 10/20/2024 | | 2,800,000 | c | 2,819,843 | |

Seasoned Credit Risk Transfer Trust, Ser. 2017-4, Cl. M45T | | 4.50 | | 6/25/2057 | | 5,590,354 | | 5,976,976 | |

Seasoned Credit Risk Transfer Trust, Ser. 2018-4, Cl. M55D | | 4.00 | | 3/25/2058 | | 7,092,994 | | 7,499,858 | |

Seasoned Credit Risk Transfer Trust, Ser. 2019-1, Cl. MA | | 3.50 | | 7/25/2058 | | 10,093,631 | | 10,419,017 | |

Seasoned Credit Risk Transfer Trust, Ser. 2019-3, Cl. M55D | | 4.00 | | 10/25/2058 | | 5,110,508 | | 5,400,476 | |

Seasoned Loans Structured Transaction, Ser. 2018-2, Cl. A1 | | 3.50 | | 11/25/2028 | | 9,464,768 | | 9,801,017 | |

Seasoned Loans Structured Transaction, Ser. 2019-1, Cl. A2 | | 3.50 | | 5/25/2029 | | 5,000,000 | | 5,201,607 | |

Seasoned Loans Structured Transaction Trust, Ser. 2019-2, Cl. A1C | | 2.75 | | 9/25/2029 | | 8,191,289 | | 8,247,889 | |

Seasoned Loans Structured Transaction Trust, Ser. 2019-3, Cl. A2C | | 2.75 | | 11/25/2029 | | 6,425,000 | | 6,499,094 | |

SoFi Consumer Loan Program, Ser. 2016-3, Cl. A | | 3.05 | | 12/26/2025 | | 109,088 | c | 109,281 | |

21

STATEMENT OF INVESTMENTS (continued)

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity

Date | | Principal

Amount ($) | a | Value ($) | |

Bonds and Notes - 96.0% (continued) | | | | | |

United States - 37.8% (continued) | | | | | |

Southern California Edison, First Mortgage Bonds | | 2.85 | | 8/1/2029 | | 8,100,000 | d | 8,097,481 | |

Southern Copper, Sr. Unscd. Notes | | 5.88 | | 4/23/2045 | | 2,510,000 | | 3,146,679 | |

Springleaf Funding Trust, Ser. 2016-AA, Cl. A | | 2.90 | | 11/15/2029 | | 2,557,337 | c | 2,558,437 | |

Sprint Communications, Sr. Unscd. Notes | | 7.00 | | 8/15/2020 | | 1,455,000 | | 1,487,592 | |

Sprint Spectrum, Sr. Scd. Notes | | 4.74 | | 3/20/2025 | | 8,375,000 | c | 8,893,371 | |

Starwood Waypoint Homes Trust, Ser. 2017-1, Cl. A, 1 Month LIBOR +.95% | | 2.69 | | 1/17/2035 | | 17,538,475 | b,c | 17,521,245 | |

Steel Dynamics, Sr. Unscd. Notes | | 3.45 | | 4/15/2030 | | 2,550,000 | | 2,581,855 | |

Sunoco Logistics Partners Operations, Gtd. Notes | | 4.00 | | 10/1/2027 | | 4,575,000 | | 4,731,832 | |

Targa Resources Partners, Gtd. Bonds | | 5.13 | | 2/1/2025 | | 1,705,000 | | 1,773,183 | |

Tesla Auto Lease Trust, Ser. 2019-A, Cl. B | | 2.41 | | 12/20/2022 | | 13,400,000 | c | 13,360,751 | |

The Boeing Company, Sr. Unscd. Notes | | 3.20 | | 3/1/2029 | | 1,280,000 | | 1,334,233 | |

The Estee Lauder Companies, Sr. Unscd. Notes | | 2.00 | | 12/1/2024 | | 425,000 | | 426,574 | |

The Estee Lauder Companies, Sr. Unscd. Notes | | 2.38 | | 12/1/2029 | | 3,025,000 | | 3,023,326 | |

The Goldman Sachs Group, Sr. Unscd. Notes | | 3.69 | | 6/5/2028 | | 4,200,000 | | 4,461,944 | |

The Southern Company, Sr. Unscd. Notes | | 3.25 | | 7/1/2026 | | 7,725,000 | | 8,045,739 | |

The Walt Disney Company, Gtd. Notes | | 3.70 | | 10/15/2025 | | 2,600,000 | | 2,813,607 | |

Tricon American Homes Trust, Ser. 2016-SFR1, Cl. A | | 2.59 | | 11/17/2033 | | 12,780,629 | c | 12,758,999 | |

Tricon American Homes Trust, Ser. 2017-SFR2, Cl. A | | 2.93 | | 1/17/2036 | | 8,276,520 | c | 8,338,693 | |

Tricon American Homes Trust, Ser. 2019-SFR1, Cl. A | | 2.75 | | 3/17/2038 | | 7,520,000 | c | 7,543,612 | |

Truist Bank, Sub. Notes | | 3.63 | | 9/16/2025 | | 4,750,000 | | 5,061,493 | |

Truist Financial, Sr. Unscd. Notes | | 2.50 | | 8/1/2024 | | 5,000,000 | | 5,063,140 | |

U.S. Bancorp, Sr. Unscd. Notes | | 2.40 | | 7/30/2024 | | 7,575,000 | | 7,676,406 | |

United Technologies, Sr. Unscd. Bonds | EUR | 2.15 | | 5/18/2030 | | 2,775,000 | | 3,534,437 | |

United Technologies, Sr. Unscd. Notes | | 4.13 | | 11/16/2028 | | 3,925,000 | | 4,421,396 | |

UnitedHealth Group, Sr. Unscd. Notes | | 2.38 | | 8/15/2024 | | 4,310,000 | | 4,366,088 | |

22

| | | | | | | | | | |

| |

Description | Coupon

Rate (%) | | Maturity

Date | | Principal

Amount ($) | a | Value ($) | |

Bonds and Notes - 96.0% (continued) | | | | | |

United States - 37.8% (continued) | | | | | |

UnitedHealth Group, Sr. Unscd. Notes | | 2.88 | | 8/15/2029 | | 2,155,000 | | 2,217,594 | |

VNDO Mortgage Trust, Ser. 2013-PENN, Cl. A | | 3.81 | | 12/13/2029 | | 10,400,000 | c | 10,504,579 | |

Wells Fargo & Co., Sr. Unscd. Notes | | 3.00 | | 4/22/2026 | | 6,125,000 | | 6,296,827 | |

Wells Fargo Commercial Mortgage Trust, Ser. 2019-C51, Cl. A4 | | 3.31 | | 6/15/2052 | | 8,200,000 | | 8,639,714 | |

Western Midstream Operating, Sr. Unscd. Notes | | 4.50 | | 3/1/2028 | | 2,450,000 | | 2,417,976 | |

Western Midstream Operating, Sr. Unscd. Notes | | 4.65 | | 7/1/2026 | | 1,810,000 | d | 1,853,126 | |

Westlake Automobile Receivables Trust, Ser. 2018-2A, Cl. C | | 3.50 | | 1/16/2024 | | 8,575,000 | c | 8,660,018 | |

Westlake Automobile Receivables Trust, Ser. 2018-1A, Cl. C | | 2.92 | | 5/15/2023 | | 5,150,000 | c | 5,163,894 | |

Xcel Energy, Sr. Unscd. Notes | | 3.50 | | 12/1/2049 | | 5,050,000 | | 5,140,204 | |

Federal Home Loan Mortgage Corp.: | | | |

2.50%, 1/1/2029-10/1/2031 | | | 22,110,848 | f | 22,438,467 | |

3.00%, 2/1/2047-9/1/2049 | | | 38,755,685 | f | 39,467,784 | |

4.50%, 7/1/2049 | | | 11,945,263 | f | 12,627,429 | |

Federal National Mortgage Association: | | | |

2.50% | | | 32,095,000 | f,g | 32,368,674 | |

2.50%, 11/1/2034 | | | 4,586,329 | f | 4,626,665 | |

3.00% | | | 23,950,000 | f,g | 24,276,443 | |

3.00%, 11/1/2031-1/1/2059 | | | 96,398,907 | f | 98,738,822 | |

3.50%, 8/1/2056 | | | 7,185,201 | f | 7,558,618 | |

4.00%, 9/1/2042-1/1/2057 | | | 64,055,507 | f | 67,313,804 | |

4.50%, 7/1/2040-6/1/2051 | | | 40,829,485 | f | 43,855,538 | |

5.00%, 1/1/2049 | | | 6,978,206 | f | 7,652,336 | |

Government National Mortgage Association: | | | |

3.50%, 9/20/2063 | | | 3,380,969 | | 3,407,646 | |

Government National Mortgage Association II: | | | |

3.00% | | | 46,800,000 | g | 48,044,728 | |

3.97%, 7/20/2062 | | | 227,553 | | 228,835 | |

4.23%, 1/20/2063 | | | 2,602,845 | | 2,622,633 | |

| | 1,214,893,214 | |

TotalBonds and Notes

(cost $2,992,472,359) | | 3,088,884,055 | |

Description /Number of Contracts/Counterparty | Exercise

Price | | Expiration Date | | Notional Amount ($) | | Value ($) | |

Options Purchased - .0% | | | | | |

Call Options - .0% | | | | | |

Japanese Yen, Contracts 32,175,000 UBS Securities | | 109.10 | | 1/21/2020 | | 32,175,000 | | 87,784 | |

23

STATEMENT OF INVESTMENTS (continued)

| | | | | | | | | | |

| |

Description /Number of Contracts/Counterparty | Exercise

Price | | Expiration Date | | Notional Amount ($) | | Value ($) | |

Options Purchased - .0%(continued) | | | | | |

Call Options - .0% (continued) | | | | | |

U.S Treasury 10 Year March Future, Contracts 2,008 | | 129.50 | | 1/24/2020 | | 200,800,000 | | 282,375 | |

| | 370,159 | |

Put Options - .0% | | | | | |

Japanese Yen, Contracts 32,175,000 UBS Securities | | 109.10 | | 1/21/2020 | | 32,175,000 | | 253,336 | |

South African Rand, Contracts 16,160,000 Morgan Stanley | | 14.60 | | 1/30/2020 | | 16,160,000 | | 666,954 | |

| | 920,290 | |

TotalOptions Purchased

(cost $853,816) | | 1,290,449 | |

Description | Annualized

Yield (%) | | Maturity Date | | Principal Amount ($) | | | |

Short-Term Investments - 3.9% | | | | | |

U.S. Government Securities | | | | | |

U.S. Treasury Bills | | 1.55 | | 1/14/2020 | | 105,300,000 | h | 105,248,666 | |

U.S. Treasury Bills | | 1.58 | | 4/16/2020 | | 21,260,000 | h,i | 21,166,202 | |

TotalShort-Term Investments

(cost $126,404,707) | | 126,414,868 | |

Description | 1-Day

Yield (%) | | | | Shares | | | |

Investment Companies - 2.7% | | | | | |

Registered Investment Companies - 2.7% | | | | | |

Dreyfus Institutional Preferred Government Plus Money Market Fund

(cost $86,672,157) | | 1.60 | | | | 86,672,157 | j | 86,672,157 | |

24

| | | | | | | | | | |

| |

Description | 1-Day

Yield (%) | | | | Shares | | Value ($) | |

Investment of Cash Collateral for Securities Loaned - .5% | | | | | |

Registered Investment Companies - .5% | | | | | |

Dreyfus Institutional Preferred Government Plus Money Market Fund

(cost $14,976,500) | | 1.60 | | | | 14,976,500 | j | 14,976,500 | |

Total Investments(cost $3,221,379,539) | | 103.1% | 3,318,238,029 | |

Liabilities, Less Cash and Receivables | | (3.1%) | (99,933,486) | |

Net Assets | | 100.0% | 3,218,304,543 | |

BBSW—Bank Bill Swap Rate

EURIBOR—Euro Interbank Offered Rate

LIBOR—London Interbank Offered Rate

SONIO—Sterling Overnight Index Average

AUD—Australian Dollar

CAD—Canadian Dollar

CLP—Chilean Peso

CNY—Chinese Yuan Renminbi

EUR—Euro

GBP—British Pound

ILS—Israeli Shekel

INR—Indian Rupee

JPY—Japanese Yen

KRW—South Korean Won

MYR—Malaysian Ringgit

NZD—New Zealand Dollar

RUB—Russian Ruble

SEK—Swedish Krona

SGD—Singapore Dollar

THB—Thai Baht

a Amount stated in U.S. Dollars unless otherwise noted above.

b Variable rate security—rate shown is the interest rate in effect at period end.

c Security exempt from registration pursuant to Rule 144A under the Securities Act of 1933. These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers. At December 31, 2019, these securities were valued at $713,764,348 or 22.18% of net assets.

d Security, or portion thereof, on loan. At December 31, 2019, the value of the fund’s securities on loan was $23,567,268 and the value of the collateral was $24,565,019, consisting of cash collateral of $14,976,500 and U.S. Government & Agency securities valued at $9,588,519.

e Principal amount for accrual purposes is periodically adjusted based on changes in the Consumer Price Index.

f The Federal Housing Finance Agency (“FHFA”) placed the Federal Home Loan Mortgage Corporation and Federal National Mortgage Association into conservatorship with FHFA as the conservator. As such, the FHFA oversees the continuing affairs of these companies.

g Purchased on a forward commitment basis.

h Security is a discount security. Income is recognized through the accretion of discount.

i Held by a counterparty for open exchange traded derivative contracts.

j Investment in affiliated issuer. The investment objective of this investment company is publicly available and can be found within the investment company’s prospectus.

25

STATEMENT OF INVESTMENTS (continued)

| | |

Portfolio Summary (Unaudited)† | Value (%) |

Foreign Governmental | 38.5 |

U.S. Government Agencies Mortgage-Backed | 13.1 |

Commercial Mortgage Pass-Through Ctfs. | 8.8 |

Asset-Backed Ctfs./Auto Receivables | 6.4 |

Banks | 5.9 |

Energy | 4.2 |

U.S. Treasury Securities | 3.9 |

Investment Companies | 3.2 |

Utilities | 2.5 |

Telecommunication Services | 2.1 |

Supranational Bank | 1.8 |

Health Care | 1.7 |

Real Estate | 1.2 |

Diversified Financials | 1.2 |

Insurance | 1.1 |

Collateralized Municipal-Backed Securities | .9 |

Technology Hardware & Equipment | .7 |

Asset-Backed Certificates | .7 |

Metals & Mining | .5 |

Asset-Backed Ctfs./Credit Cards | .5 |

Chemicals | .5 |

Commercial & Professional Services | .5 |

Collateralized Loan Obligations Debt | .4 |

Internet Software & Services | .4 |

Retailing | .3 |

Media | .3 |

Aerospace & Defense | .3 |

Agriculture | .3 |

Automobiles & Components | .2 |

Beverage Products | .2 |

Information Technology | .2 |

Industrial | .1 |

Consumer Staples | .1 |

Environmental Control | .1 |

Food Products | .1 |

Asset-Backed Ctfs./Student Loans | .1 |

Materials | .1 |

Options Purchased | .0 |

| | 103.1 |

† Based on net assets.

See notes to financial statements.

26

STATEMENT OF INVESTMENTS IN AFFILIATED ISSUERS

| | | | | | | |

Investment Companies | Value

12/31/18($) | Purchases($) | Sales ($) | Value

12/31/19($) | Net

Assets(%) | Dividends/

Distributions($) |

Registered Investment

Companies; | | | | |

Dreyfus Institutional Preferred Government Plus Money Market Fund | 50,195,156 | 1,646,488,277 | 1,610,011,276 | 86,672,157 | 2.7 | 1,357,637 |

Investment

of Cash

Collateral

for Securities

Loaned; | | |

Dreyfus Institutional Preferred Government Plus Money Market Fund | 28,724,069 | 311,623,456 | 325,371,025 | 14,976,500 | .5 | - |

Total | 78,919,225 | 1,958,111,733 | 1,935,382,301 | 101,648,657 | 3.2 | 1,357,637 |

See notes to financial statements.

27

STATEMENT OF FUTURES

December 31, 2019

| | | | | | | |

Description | Number of

Contracts | Expiration | Notional

Value ($) | Value ($) | Unrealized Appreciation (Depreciation) ($) | |

Futures Long | | |

Australian 10 Year Bond | 103 | 3/16/2020 | 10,558,431a | 10,333,050 | (225,381) | |

Australian 3 Year Bond | 767 | 3/16/2020 | 62,340,564a | 61,905,217 | (435,347) | |

Canadian 10 Year Bond | 563 | 3/20/2020 | 60,699,601a | 59,605,899 | (1,093,702) | |

Euro BTP Italian Government Bond | 243 | 3/6/2020 | 38,711,976a | 38,830,764 | 118,788 | |

Euro-Bobl | 601 | 3/6/2020 | 90,319,805a | 90,085,555 | (234,250) | |

Japanese 10 Year Bond | 176 | 3/13/2020 | 246,628,213a | 246,502,048 | (126,165) | |

Long Gilt | 95 | 3/27/2020 | 16,703,691a | 16,532,465 | (171,226) | |

Long Term French Government Future | 757 | 3/6/2020 | 139,737,091a | 138,212,386 | (1,524,705) | |

U.S. Treasury 2 Year Notes | 511 | 3/31/2020 | 110,194,535 | 110,120,500 | (74,035) | |

U.S. Treasury Long Bond | 281 | 3/20/2020 | 44,196,455 | 43,809,656 | (386,799) | |

U.S. Treasury Ultra Long Bond | 9 | 3/20/2020 | 1,684,138 | 1,634,906 | (49,232) | |

Futures Short | | |

Euro 30 Year Bond | 97 | 3/6/2020 | 22,089,490a | 21,584,716 | 504,774 | |

Euro-Bond | 516 | 3/6/2020 | 99,492,736a | 98,679,135 | 813,601 | |

Euro-Schatz | 7 | 3/6/2020 | 879,172a | 878,667 | 505 | |

U.S. Treasury 10 Year Notes | 1,174 | 3/20/2020 | 152,042,004 | 150,767,287 | 1,274,717 | |

U.S. Treasury 5 Year Notes | 1,462 | 3/31/2020 | 173,969,318 | 173,406,914 | 562,404 | |

Ultra 10 Year U.S. Treasury Notes | 200 | 3/20/2020 | 28,415,800 | 28,140,626 | 275,174 | |

Gross Unrealized Appreciation | | 3,549,963 | |

Gross Unrealized Depreciation | | (4,320,842) | |

a Notional amounts in foreign currency have been converted to USD using relevant foreign exchange rates.

See notes to financial statements.

28

STATEMENT OF OPTIONS WRITTEN

December 31, 2019

| | | | | | | |

Description/ Contracts/ Counterparties | Exercise Price | Expiration Date | Notional Amount | a | Value ($) | |

Call Options: | | | | | | |

Brazilian Real,

Contracts 32,800,000, Citigroup | 4.18 | 1/16/2020 | 32,800,000 | | (24,370) | |

South African Rand,

Contracts 16,160,000, Morgan Stanley | 16 | 1/30/2020 | 16,160,000 | | (2,273) | |

Swiss Franc,

Contracts 32,060,000, Goldman Sachs | 0.991 | 1/2/2020 | 32,060,000 | | - | |

Turkish Lira,

Contracts 32,850,000, Citigroup | 5.93 | 1/15/2020 | 32,850,000 | | (415,062) | |

Put Options: | | | | | | |

Pound Sterling,

Contracts 24,650,000, Morgan Stanley | 1.285 | 1/9/2020 | 24,650,000 | GBP | (4,892) | |

U.S Treasury 10 Year March Future,

Contracts 2,008 | 126.5 | 1/24/2020 | 200,800,000 | | (94,125) | |

U.S Treasury Bond March Future,

Contracts 620 | 153 | 1/24/2020 | 62,000,000 | | (184,062) | |

Total Options Written (premiums received $1,203,697) | | | | (724,784) | |

a Notional amount stated in U.S. Dollars unless otherwise indicated.

GBP—British Pound

See notes to financial statements.

29

STATEMENT OF FORWARD FOREIGN CURRENCY EXCHANGE CONTRACTSDecember 31, 2019

| | | | | | |

Counterparty/ Purchased

Currency | Purchased Currency

Amounts | Currency

Sold | Sold

Currency

Amounts | Settlement Date | Unrealized Appreciation (Depreciation)($) |

Barclays Capital | | | |

United States Dollar | 13,091,344 | Chilean Peso | 9,414,640,000 | 1/14/2020 | 568,323 |

Euro | 51,580,000 | United States Dollar | 57,519,391 | 1/31/2020 | 449,308 |

South Korean Won | 17,173,420,000 | United States Dollar | 14,619,409 | 1/14/2020 | 235,618 |

United States Dollar | 6,946,050 | Malaysian Ringgit | 28,840,000 | 3/13/2020 | (92,984) |

United States Dollar | 2,627,852 | Thai Baht | 79,600,000 | 1/14/2020 | (30,506) |

United States Dollar | 42,898,705 | Swedish Krona | 400,470,000 | 1/31/2020 | 78,222 |

Citigroup | | | |

Hong Kong Dollar | 265,100,000 | United States Dollar | 33,927,589 | 4/14/2020 | 68,475 |

Chilean Peso | 6,500,000,000 | United States Dollar | 8,477,339 | 1/14/2020 | 168,731 |

South Korean Won | 16,764,880,000 | United States Dollar | 14,261,914 | 1/14/2020 | 239,725 |

United States Dollar | 94,512,142 | South Korean Won | 111,226,615,000 | 1/14/2020 | (1,699,000) |

Brazilian Real | 32,700,000 | United States Dollar | 7,774,700 | 2/4/2020 | 345,558 |

Goldman Sachs | | | |

United States Dollar | 132,813,985 | Euro | 119,105,000 | 1/31/2020 | (1,043,360) |

HSBC | | | |

Norwegian Krone | 177,610,000 | United States Dollar | 19,758,891 | 1/31/2020 | 474,486 |

United States Dollar | 145,350,943 | British Pound | 110,405,000 | 1/31/2020 | (1,021,798) |

United States Dollar | 24,568,503 | Russian Ruble | 1,580,250,000 | 1/14/2020 | (848,210) |

United States Dollar | 22,718,609 | New Zealand Dollar | 34,505,000 | 1/31/2020 | (520,853) |

United States Dollar | 115,195,961 | Chinese Yuan Renminbi | 816,820,000 | 1/14/2020 | (2,114,566) |

United States Dollar | 17,211,666 | Swiss Franc | 16,850,000 | 1/31/2020 | (237,540) |

South Korean Won | 13,221,970,000 | United States Dollar | 11,142,735 | 1/14/2020 | 294,283 |

J.P. Morgan Securities | | | |

United States Dollar | 34,039,548 | Hong Kong Dollar | 265,100,000 | 4/14/2020 | 43,484 |

30

| | | | | | |

Counterparty/ Purchased

Currency | Purchased Currency

Amounts | Currency

Sold | Sold

Currency

Amounts | Settlement Date | Unrealized Appreciation (Depreciation)($) |

J.P. Morgan Securities (continued) |

United States Dollar | 186,760,848 | Euro | 167,485,000 | 1/31/2020 | (1,468,844) |

Egyptian Pound | 135,000,000 | United States Dollar | 8,196,721 | 2/27/2020 | 135,633 |

United States Dollar | 44,545,377 | Russian Ruble | 2,868,700,000 | 1/14/2020 | (1,594,744) |

United States Dollar | 24,117,483 | Singapore Dollar | 32,780,000 | 1/14/2020 | (257,194) |

United States Dollar | 55,121,105 | Thai Baht | 1,669,260,000 | 1/14/2020 | (626,273) |

Nigerian Naira | 2,900,000,000 | United States Dollar | 7,869,742 | 2/14/2020 | 19,865 |

Merrill Lynch, Pierce, Fenner & Smith | | | |

Polish Zloty | 30,750,000 | United States Dollar | 7,995,632 | 1/14/2020 | 109,770 |

Euro | 16,760,000 | United States Dollar | 18,700,832 | 1/31/2020 | 135,062 |

United States Dollar | 83,008,044 | Euro | 74,440,000 | 1/31/2020 | (652,094) |

Norwegian Krone | 149,590,000 | United States Dollar | 16,641,753 | 1/31/2020 | 399,578 |

Morgan Stanley | | | |

Chilean Peso | 5,890,000,000 | United States Dollar | 8,134,235 | 1/14/2020 | (299,566) |

United States Dollar | 7,676,767 | Malaysian Ringgit | 31,920,000 | 1/14/2020 | (122,890) |

Mexican Peso | 157,150,000 | United States Dollar | 8,053,142 | 1/14/2020 | 241,359 |

Euro | 17,010,000 | United States Dollar | 18,895,422 | 1/31/2020 | 221,437 |

United States Dollar | 2,292,821 | Euro | 2,050,000 | 1/31/2020 | (11,092) |

Swiss Franc | 9,500,000 | United States Dollar | 9,705,324 | 1/31/2020 | 132,507 |

United States Dollar | 55,519,636 | Australian Dollar | 80,580,000 | 1/31/2020 | (1,071,698) |

United States Dollar | 5,218,408 | Indian Rupee | 375,000,000 | 1/14/2020 | (28,134) |

United States Dollar | 26,136,443 | Malaysian Ringgit | 108,710,000 | 3/13/2020 | (396,614) |

Japanese Yen | 1,100,000,000 | United States Dollar | 10,096,378 | 1/31/2020 | 44,595 |

United States Dollar | 301,350,261 | Japanese Yen | 32,928,543,000 | 1/31/2020 | (2,220,173) |

UBS Securities | | | |

United States Dollar | 61,366,392 | Canadian Dollar | 80,490,000 | 1/31/2020 | (628,155) |

31