UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-04861

Fidelity Garrison Street Trust

(Exact name of registrant as specified in charter)

245 Summer St., Boston, MA 02210

(Address of principal executive offices) (Zip code)

Margaret Carey, Secretary

245 Summer St.

Boston, Massachusetts 02210

(Name and address of agent for service)

Registrant's telephone number, including area code:

617-563-7000

| |

Date of fiscal year end: | December 31 |

|

|

Date of reporting period: | June 30, 2023 |

Item 1.

Reports to Stockholders

Fidelity® VIP Investment Grade Central Fund

Semi-Annual Report

June 30, 2023

Contents

To view a fund's proxy voting guidelines and proxy voting record for the 12-month period ended June 30, visit http://www.fidelity.com/proxyvotingresults or visit the Securities and Exchange Commission's (SEC) web site at http://www.sec.gov.

You may also call 1-800-544-8544 to request a free copy of the proxy voting guidelines.

Standard & Poor's, S&P and S&P 500 are registered service marks of The McGraw-Hill Companies, Inc. and have been licensed for use by Fidelity Distributors Corporation.

Other third-party marks appearing herein are the property of their respective owners.

All other marks appearing herein are registered or unregistered trademarks or service marks of FMR LLC or an affiliated company. © 2023 FMR LLC. All rights reserved.

A fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-PORT. Forms N-PORT are available on the SEC's web site at http://www.sec.gov. A fund's Forms N-PORT may be reviewed and copied at the SEC's Public Reference Room in Washington, DC. Information regarding the operation of the SEC's Public Reference Room may be obtained by calling 1-800-SEC-0330.

A fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-PORT. Forms N-PORT are available on the SEC's web site at http://www.sec.gov. A fund's Forms N-PORT may be reviewed and copied at the SEC's Public Reference Room in Washington, DC. Information regarding the operation of the SEC's Public Reference Room may be obtained by calling 1-800-SEC-0330.

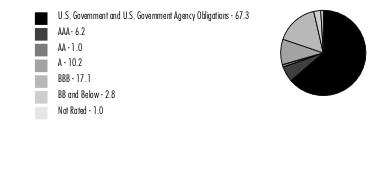

Quality Diversification (% of Fund's net assets) |

|

Short-Term Investments and Net Other Assets (Liabilities) - (5.6)%* |

|

| |

| We have used ratings from Moody's Investors Service, Inc. Where Moody's® ratings are not available, we have used S&P® ratings. All ratings are as of the date indicated and do not reflect subsequent changes. |

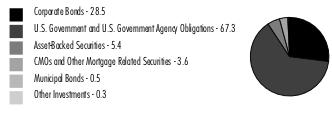

Asset Allocation (% of Fund's net assets) |

|

Short-Term Investments and Net Other Assets (Liabilities) - (5.6)% |

Percentages in the above tables are adjusted for the effect of TBA Sale Commitments. |

|

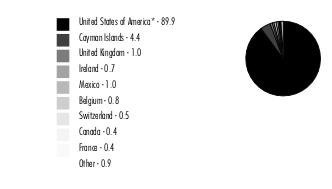

Geographic Diversification (% of Fund's net assets) |

|

* Includes Short-Term investments and Net Other Assets (Liabilities). Percentages are adjusted for the effect of derivatives, if applicable. |

| |

Showing Percentage of Net Assets

| Nonconvertible Bonds - 28.5% |

| | | Principal Amount (a) | Value ($) |

| COMMUNICATION SERVICES - 2.5% | | | |

| Diversified Telecommunication Services - 0.7% | | | |

| AT&T, Inc.: | | | |

| 2.55% 12/1/33 | | 4,584,000 | 3,600,622 |

| 3.8% 12/1/57 | | 4,678,000 | 3,386,860 |

| 4.3% 2/15/30 | | 859,000 | 815,384 |

| 4.75% 5/15/46 | | 4,816,000 | 4,251,018 |

| Verizon Communications, Inc.: | | | |

| 2.1% 3/22/28 | | 1,835,000 | 1,611,997 |

| 2.55% 3/21/31 | | 1,698,000 | 1,417,716 |

| 3% 3/22/27 | | 397,000 | 370,445 |

| 4.862% 8/21/46 | | 2,282,000 | 2,092,142 |

| 5.012% 4/15/49 | | 89,000 | 83,569 |

| | | | 17,629,753 |

| Entertainment - 0.3% | | | |

| The Walt Disney Co.: | | | |

| 3.8% 3/22/30 | | 7,061,000 | 6,672,822 |

| 4.7% 3/23/50 | | 2,229,000 | 2,130,740 |

| | | | 8,803,562 |

| Media - 1.2% | | | |

| Charter Communications Operating LLC/Charter Communications Operating Capital Corp.: | | | |

| 2.25% 1/15/29 | | 1,100,000 | 915,948 |

| 4.4% 4/1/33 | | 1,073,000 | 941,832 |

| 4.908% 7/23/25 | | 1,184,000 | 1,161,086 |

| 5.25% 4/1/53 | | 1,073,000 | 866,643 |

| 5.375% 5/1/47 | | 5,574,000 | 4,607,218 |

| 5.5% 4/1/63 | | 1,073,000 | 863,909 |

| 6.484% 10/23/45 | | 842,000 | 791,579 |

| Comcast Corp.: | | | |

| 2.937% 11/1/56 | | 2,100,000 | 1,367,568 |

| 3.9% 3/1/38 | | 329,000 | 285,850 |

| 4.65% 7/15/42 | | 779,000 | 718,370 |

| Discovery Communications LLC: | | | |

| 3.625% 5/15/30 | | 1,066,000 | 935,071 |

| 4.65% 5/15/50 | | 2,883,000 | 2,196,136 |

| Fox Corp.: | | | |

| 4.03% 1/25/24 | | 389,000 | 385,103 |

| 4.709% 1/25/29 | | 563,000 | 547,100 |

| 5.476% 1/25/39 | | 555,000 | 518,434 |

| 5.576% 1/25/49 | | 368,000 | 344,548 |

| Magallanes, Inc.: | | | |

| 3.428% 3/15/24 | | 1,267,000 | 1,243,962 |

| 3.638% 3/15/25 | | 694,000 | 669,380 |

| 3.755% 3/15/27 | | 1,357,000 | 1,265,764 |

| 4.054% 3/15/29 | | 470,000 | 429,636 |

| 4.279% 3/15/32 | | 1,970,000 | 1,747,145 |

| 5.05% 3/15/42 | | 996,000 | 839,496 |

| 5.141% 3/15/52 | | 1,583,000 | 1,288,955 |

| Time Warner Cable LLC: | | | |

| 4.5% 9/15/42 | | 283,000 | 211,682 |

| 5.5% 9/1/41 | | 521,000 | 433,438 |

| 5.875% 11/15/40 | | 460,000 | 405,789 |

| 6.55% 5/1/37 | | 6,199,000 | 5,942,821 |

| 7.3% 7/1/38 | | 1,160,000 | 1,182,121 |

| | | | 33,106,584 |

| Wireless Telecommunication Services - 0.3% | | | |

| Rogers Communications, Inc.: | | | |

| 3.2% 3/15/27 (b) | | 1,461,000 | 1,358,284 |

| 3.8% 3/15/32 (b) | | 1,275,000 | 1,114,505 |

| T-Mobile U.S.A., Inc.: | | | |

| 3.75% 4/15/27 | | 1,871,000 | 1,771,099 |

| 3.875% 4/15/30 | | 2,705,000 | 2,492,032 |

| 4.375% 4/15/40 | | 404,000 | 356,770 |

| 4.5% 4/15/50 | | 793,000 | 680,430 |

| | | | 7,773,120 |

TOTAL COMMUNICATION SERVICES | | | 67,313,019 |

| CONSUMER DISCRETIONARY - 0.5% | | | |

| Automobiles - 0.0% | | | |

| General Motors Financial Co., Inc. 5.85% 4/6/30 | | 953,000 | 944,674 |

| Hotels, Restaurants & Leisure - 0.0% | | | |

| McDonald's Corp.: | | | |

| 3.5% 7/1/27 | | 517,000 | 492,176 |

| 3.6% 7/1/30 | | 615,000 | 572,159 |

| | | | 1,064,335 |

| Household Durables - 0.1% | | | |

| Toll Brothers Finance Corp. 4.875% 3/15/27 | | 1,135,000 | 1,098,983 |

| Leisure Products - 0.1% | | | |

| Hasbro, Inc. 3% 11/19/24 | | 1,348,000 | 1,295,184 |

| Specialty Retail - 0.3% | | | |

| AutoNation, Inc. 4.75% 6/1/30 | | 234,000 | 218,791 |

| AutoZone, Inc.: | | | |

| 3.625% 4/15/25 | | 350,000 | 337,765 |

| 4% 4/15/30 | | 1,629,000 | 1,512,613 |

| Lowe's Companies, Inc.: | | | |

| 3.35% 4/1/27 | | 211,000 | 199,268 |

| 3.75% 4/1/32 | | 649,000 | 587,393 |

| 4.25% 4/1/52 | | 2,647,000 | 2,159,634 |

| 4.45% 4/1/62 | | 2,720,000 | 2,183,905 |

| 4.5% 4/15/30 | | 1,170,000 | 1,137,395 |

| O'Reilly Automotive, Inc. 4.2% 4/1/30 | | 361,000 | 340,844 |

| | | | 8,677,608 |

TOTAL CONSUMER DISCRETIONARY | | | 13,080,784 |

| CONSUMER STAPLES - 2.0% | | | |

| Beverages - 1.1% | | | |

| Anheuser-Busch InBev Finance, Inc.: | | | |

| 4.7% 2/1/36 | | 2,842,000 | 2,764,171 |

| 4.9% 2/1/46 | | 3,531,000 | 3,374,897 |

| Anheuser-Busch InBev Worldwide, Inc.: | | | |

| 3.5% 6/1/30 | | 1,135,000 | 1,055,421 |

| 4.35% 6/1/40 | | 1,082,000 | 994,942 |

| 4.5% 6/1/50 | | 1,534,000 | 1,414,571 |

| 4.6% 6/1/60 | | 1,135,000 | 1,022,943 |

| 4.75% 4/15/58 | | 1,764,000 | 1,635,357 |

| 5.45% 1/23/39 | | 1,439,000 | 1,489,004 |

| 5.55% 1/23/49 | | 3,287,000 | 3,464,477 |

| 5.8% 1/23/59 (Reg. S) | | 3,472,000 | 3,783,395 |

| Molson Coors Beverage Co.: | | | |

| 3% 7/15/26 | | 2,300,000 | 2,148,423 |

| 5% 5/1/42 | | 4,016,000 | 3,718,904 |

| The Coca-Cola Co.: | | | |

| 3.375% 3/25/27 | | 1,742,000 | 1,679,398 |

| 3.45% 3/25/30 | | 1,064,000 | 1,003,889 |

| | | | 29,549,792 |

| Food Products - 0.4% | | | |

| General Mills, Inc. 2.875% 4/15/30 | | 220,000 | 195,371 |

| JBS U.S.A. Lux SA / JBS Food Co.: | | | |

| 2.5% 1/15/27 (b) | | 4,189,000 | 3,669,983 |

| 3% 5/15/32 (b) | | 3,400,000 | 2,609,331 |

| 3.625% 1/15/32 (b) | | 320,000 | 259,661 |

| 5.125% 2/1/28 (b) | | 1,340,000 | 1,286,759 |

| 5.5% 1/15/30 (b) | | 380,000 | 364,534 |

| 5.75% 4/1/33 (b) | | 2,700,000 | 2,537,873 |

| | | | 10,923,512 |

| Tobacco - 0.5% | | | |

| Altria Group, Inc.: | | | |

| 4.25% 8/9/42 | | 1,696,000 | 1,322,911 |

| 4.5% 5/2/43 | | 1,137,000 | 904,199 |

| 4.8% 2/14/29 | | 311,000 | 302,464 |

| 5.375% 1/31/44 | | 1,030,000 | 968,430 |

| 5.95% 2/14/49 | | 407,000 | 386,385 |

| Imperial Tobacco Finance PLC: | | | |

| 4.25% 7/21/25 (b) | | 4,751,000 | 4,556,583 |

| 6.125% 7/27/27 (b) | | 1,136,000 | 1,137,979 |

| Reynolds American, Inc.: | | | |

| 4.45% 6/12/25 | | 718,000 | 697,709 |

| 5.7% 8/15/35 | | 373,000 | 350,559 |

| 6.15% 9/15/43 | | 1,227,000 | 1,180,353 |

| 7.25% 6/15/37 | | 909,000 | 951,326 |

| | | | 12,758,898 |

TOTAL CONSUMER STAPLES | | | 53,232,202 |

| ENERGY - 3.2% | | | |

| Energy Equipment & Services - 0.0% | | | |

| Halliburton Co.: | | | |

| 3.8% 11/15/25 | | 18,000 | 17,385 |

| 4.85% 11/15/35 | | 661,000 | 622,429 |

| | | | 639,814 |

| Oil, Gas & Consumable Fuels - 3.2% | | | |

| Canadian Natural Resources Ltd.: | | | |

| 3.8% 4/15/24 | | 2,081,000 | 2,046,997 |

| 5.85% 2/1/35 | | 766,000 | 743,863 |

| Cenovus Energy, Inc.: | | | |

| 3.75% 2/15/52 | | 2,600,000 | 1,840,017 |

| 5.25% 6/15/37 | | 2,691,000 | 2,476,810 |

| Columbia Pipeline Group, Inc. 4.5% 6/1/25 | | 410,000 | 400,083 |

| DCP Midstream Operating LP: | | | |

| 5.6% 4/1/44 | | 376,000 | 356,389 |

| 6.45% 11/3/36 (b) | | 760,000 | 780,404 |

| 6.75% 9/15/37 (b) | | 1,037,000 | 1,100,547 |

| Enbridge, Inc.: | | | |

| 4% 10/1/23 | | 863,000 | 859,561 |

| 4.25% 12/1/26 | | 544,000 | 524,649 |

| Energy Transfer LP: | | | |

| 3.75% 5/15/30 | | 710,000 | 640,639 |

| 3.9% 5/15/24 (c) | | 405,000 | 398,145 |

| 4.2% 9/15/23 | | 364,000 | 362,645 |

| 4.5% 4/15/24 | | 387,000 | 382,552 |

| 4.95% 6/15/28 | | 1,242,000 | 1,204,704 |

| 5% 5/15/50 | | 2,045,000 | 1,727,131 |

| 5.25% 4/15/29 | | 629,000 | 614,056 |

| 5.4% 10/1/47 | | 414,000 | 364,888 |

| 5.8% 6/15/38 | | 692,000 | 663,002 |

| 6% 6/15/48 | | 451,000 | 427,685 |

| 6.25% 4/15/49 | | 432,000 | 421,925 |

| Enterprise Products Operating LP 3.7% 2/15/26 | | 1,472,000 | 1,419,213 |

| Exxon Mobil Corp. 3.482% 3/19/30 | | 4,122,000 | 3,866,111 |

| Hess Corp.: | | | |

| 4.3% 4/1/27 | | 1,500,000 | 1,438,643 |

| 5.6% 2/15/41 | | 4,059,000 | 3,883,547 |

| 7.125% 3/15/33 | | 308,000 | 335,965 |

| 7.3% 8/15/31 | | 411,000 | 450,686 |

| 7.875% 10/1/29 | | 1,346,000 | 1,483,458 |

| Kinder Morgan Energy Partners LP 6.55% 9/15/40 | | 141,000 | 143,155 |

| Kinder Morgan, Inc. 5.55% 6/1/45 | | 747,000 | 688,189 |

| MPLX LP: | | | |

| 4.8% 2/15/29 | | 345,000 | 332,706 |

| 4.875% 12/1/24 | | 839,000 | 826,883 |

| 4.95% 9/1/32 | | 2,116,000 | 2,021,228 |

| 5.5% 2/15/49 | | 1,036,000 | 938,819 |

| Occidental Petroleum Corp.: | | | |

| 5.55% 3/15/26 | | 1,587,000 | 1,566,766 |

| 6.2% 3/15/40 | | 521,000 | 513,492 |

| 6.45% 9/15/36 | | 1,412,000 | 1,449,135 |

| 6.6% 3/15/46 | | 1,751,000 | 1,802,742 |

| 7.5% 5/1/31 | | 2,356,000 | 2,572,375 |

| Petroleos Mexicanos: | | | |

| 4.5% 1/23/26 | | 1,632,000 | 1,451,460 |

| 5.95% 1/28/31 | | 1,097,000 | 799,307 |

| 6.35% 2/12/48 | | 4,049,000 | 2,440,170 |

| 6.49% 1/23/27 | | 1,175,000 | 1,042,225 |

| 6.5% 3/13/27 | | 1,481,000 | 1,314,388 |

| 6.5% 1/23/29 | | 1,705,000 | 1,411,058 |

| 6.7% 2/16/32 | | 1,810,000 | 1,373,700 |

| 6.75% 9/21/47 | | 3,713,000 | 2,320,217 |

| 6.84% 1/23/30 | | 5,684,000 | 4,503,149 |

| 6.95% 1/28/60 | | 2,417,000 | 1,494,915 |

| 7.69% 1/23/50 | | 4,972,000 | 3,351,029 |

| Phillips 66 Co. 3.85% 4/9/25 | | 188,000 | 182,772 |

| Plains All American Pipeline LP/PAA Finance Corp.: | | | |

| 3.55% 12/15/29 | | 405,000 | 356,881 |

| 3.6% 11/1/24 | | 426,000 | 412,165 |

| Sabine Pass Liquefaction LLC 4.5% 5/15/30 | | 2,447,000 | 2,326,026 |

| The Williams Companies, Inc.: | | | |

| 3.5% 11/15/30 | | 2,609,000 | 2,332,322 |

| 3.9% 1/15/25 | | 373,000 | 362,011 |

| 4.3% 3/4/24 | | 1,671,000 | 1,652,107 |

| 4.5% 11/15/23 | | 537,000 | 534,703 |

| 4.55% 6/24/24 | | 4,091,000 | 4,035,608 |

| 4.65% 8/15/32 | | 2,206,000 | 2,089,109 |

| 5.3% 8/15/52 | | 500,000 | 461,000 |

| Transcontinental Gas Pipe Line Co. LLC: | | | |

| 3.25% 5/15/30 | | 312,000 | 277,294 |

| 3.95% 5/15/50 | | 1,007,000 | 776,526 |

| Western Gas Partners LP: | | | |

| 3.95% 6/1/25 | | 266,000 | 255,510 |

| 4.5% 3/1/28 | | 613,000 | 578,371 |

| 4.65% 7/1/26 | | 2,778,000 | 2,672,439 |

| 4.75% 8/15/28 | | 354,000 | 335,984 |

| | | | 85,212,251 |

TOTAL ENERGY | | | 85,852,065 |

| FINANCIALS - 13.7% | | | |

| Banks - 6.3% | | | |

| Bank of America Corp.: | | | |

| 2.299% 7/21/32 (c) | | 4,656,000 | 3,723,714 |

| 3.419% 12/20/28 (c) | | 5,817,000 | 5,334,326 |

| 3.5% 4/19/26 | | 1,541,000 | 1,478,207 |

| 3.864% 7/23/24 (c) | | 1,340,000 | 1,338,358 |

| 3.95% 4/21/25 | | 1,265,000 | 1,225,018 |

| 4.2% 8/26/24 | | 6,127,000 | 6,012,105 |

| 4.25% 10/22/26 | | 1,307,000 | 1,261,510 |

| 4.45% 3/3/26 | | 465,000 | 451,946 |

| 5.015% 7/22/33 (c) | | 17,054,000 | 16,682,968 |

| Barclays PLC: | | | |

| 2.852% 5/7/26 (c) | | 2,482,000 | 2,324,602 |

| 4.375% 1/12/26 | | 1,908,000 | 1,832,792 |

| 5.088% 6/20/30 (c) | | 2,253,000 | 2,048,762 |

| 5.2% 5/12/26 | | 1,908,000 | 1,840,739 |

| 5.829% 5/9/27 (c) | | 2,670,000 | 2,633,698 |

| 6.224% 5/9/34 (c) | | 2,277,000 | 2,267,972 |

| BNP Paribas SA 2.219% 6/9/26 (b)(c) | | 2,313,000 | 2,139,091 |

| Citigroup, Inc.: | | | |

| 3.352% 4/24/25 (c) | | 1,521,000 | 1,486,881 |

| 3.875% 3/26/25 | | 2,914,000 | 2,814,066 |

| 4.3% 11/20/26 | | 532,000 | 509,159 |

| 4.412% 3/31/31 (c) | | 3,258,000 | 3,063,372 |

| 4.45% 9/29/27 | | 5,245,000 | 5,008,075 |

| 4.6% 3/9/26 | | 673,000 | 651,564 |

| 4.91% 5/24/33 (c) | | 3,492,000 | 3,379,052 |

| 5.5% 9/13/25 | | 1,694,000 | 1,684,197 |

| 6.174% 5/25/34 (c) | | 1,574,000 | 1,587,713 |

| 6.27% 11/17/33 (c) | | 7,000,000 | 7,429,920 |

| Citizens Financial Group, Inc. 2.638% 9/30/32 | | 1,490,000 | 1,053,149 |

| Commonwealth Bank of Australia 3.61% 9/12/34 (b)(c) | | 802,000 | 674,067 |

| Discover Bank 4.2% 8/8/23 | | 874,000 | 872,289 |

| HSBC Holdings PLC: | | | |

| 4.25% 3/14/24 | | 675,000 | 666,381 |

| 4.95% 3/31/30 | | 437,000 | 430,211 |

| Intesa Sanpaolo SpA: | | | |

| 5.017% 6/26/24 (b) | | 1,330,000 | 1,288,232 |

| 5.71% 1/15/26 (b) | | 3,922,000 | 3,732,895 |

| JPMorgan Chase & Co.: | | | |

| 2.956% 5/13/31 (c) | | 1,324,000 | 1,135,264 |

| 3.797% 7/23/24 (c) | | 1,754,000 | 1,751,903 |

| 3.875% 9/10/24 | | 13,419,000 | 13,100,870 |

| 4.125% 12/15/26 | | 4,319,000 | 4,157,992 |

| 4.493% 3/24/31 (c) | | 3,926,000 | 3,773,940 |

| 4.586% 4/26/33 (c) | | 12,887,000 | 12,285,080 |

| 4.912% 7/25/33 (c) | | 5,229,000 | 5,109,640 |

| 5.717% 9/14/33 (c) | | 2,500,000 | 2,536,233 |

| NatWest Group PLC 3.073% 5/22/28 (c) | | 1,427,000 | 1,283,398 |

| Rabobank Nederland 4.375% 8/4/25 | | 2,285,000 | 2,205,342 |

| Santander Holdings U.S.A., Inc.: | | | |

| 2.49% 1/6/28 (c) | | 1,754,000 | 1,514,895 |

| 6.499% 3/9/29 (c) | | 2,600,000 | 2,571,747 |

| Societe Generale: | | | |

| 1.038% 6/18/25 (b)(c) | | 4,852,000 | 4,566,589 |

| 1.488% 12/14/26 (b)(c) | | 2,986,000 | 2,627,570 |

| Wells Fargo & Co.: | | | |

| 2.406% 10/30/25 (c) | | 1,400,000 | 1,333,090 |

| 3.526% 3/24/28 (c) | | 2,893,000 | 2,700,180 |

| 4.478% 4/4/31 (c) | | 4,386,000 | 4,170,199 |

| 4.897% 7/25/33 (c) | | 5,000,000 | 4,796,061 |

| 5.013% 4/4/51 (c) | | 6,470,000 | 6,026,197 |

| Westpac Banking Corp. 4.11% 7/24/34 (c) | | 1,139,000 | 990,466 |

| | | | 167,563,687 |

| Capital Markets - 3.2% | | | |

| Affiliated Managers Group, Inc.: | | | |

| 3.5% 8/1/25 | | 1,700,000 | 1,607,044 |

| 4.25% 2/15/24 | | 1,315,000 | 1,297,653 |

| Ares Capital Corp.: | | | |

| 3.875% 1/15/26 | | 3,822,000 | 3,543,432 |

| 4.2% 6/10/24 | | 2,732,000 | 2,666,590 |

| Deutsche Bank AG 4.5% 4/1/25 | | 3,669,000 | 3,483,930 |

| Deutsche Bank AG New York Branch 6.72% 1/18/29 (c) | | 1,600,000 | 1,602,281 |

| Goldman Sachs Group, Inc.: | | | |

| 2.383% 7/21/32 (c) | | 2,893,000 | 2,317,290 |

| 3.102% 2/24/33 (c) | | 1,545,000 | 1,305,144 |

| 3.691% 6/5/28 (c) | | 12,774,000 | 12,001,723 |

| 3.8% 3/15/30 | | 4,751,000 | 4,393,525 |

| 4.25% 10/21/25 | | 696,000 | 670,714 |

| 6.75% 10/1/37 | | 689,000 | 741,050 |

| Moody's Corp.: | | | |

| 3.25% 1/15/28 | | 732,000 | 681,643 |

| 3.75% 3/24/25 | | 1,557,000 | 1,513,352 |

| 4.875% 2/15/24 | | 413,000 | 410,762 |

| Morgan Stanley: | | | |

| 3.125% 7/27/26 | | 6,737,000 | 6,308,822 |

| 3.622% 4/1/31 (c) | | 3,078,000 | 2,773,557 |

| 3.625% 1/20/27 | | 3,374,000 | 3,203,645 |

| 4.431% 1/23/30 (c) | | 1,348,000 | 1,282,535 |

| 4.889% 7/20/33 (c) | | 6,522,000 | 6,277,093 |

| 5% 11/24/25 | | 4,489,000 | 4,412,992 |

| 6.296% 10/18/28 (c) | | 2,500,000 | 2,568,876 |

| 6.342% 10/18/33 (c) | | 5,000,000 | 5,319,016 |

| Peachtree Corners Funding Trust 3.976% 2/15/25 (b) | | 1,534,000 | 1,476,690 |

| UBS Group AG: | | | |

| 1.494% 8/10/27 (b)(c) | | 1,788,000 | 1,535,590 |

| 2.593% 9/11/25 (b)(c) | | 3,245,000 | 3,093,040 |

| 3.75% 3/26/25 | | 1,429,000 | 1,367,409 |

| 3.869% 1/12/29 (b)(c) | | 1,233,000 | 1,114,629 |

| 4.125% 9/24/25 (b) | | 1,614,000 | 1,542,210 |

| 4.194% 4/1/31 (b)(c) | | 2,950,000 | 2,625,675 |

| 4.55% 4/17/26 | | 790,000 | 759,321 |

| | | | 83,897,233 |

| Consumer Finance - 2.4% | | | |

| AerCap Ireland Capital Ltd./AerCap Global Aviation Trust: | | | |

| 1.65% 10/29/24 | | 3,388,000 | 3,183,735 |

| 2.45% 10/29/26 | | 1,236,000 | 1,103,934 |

| 2.875% 8/14/24 | | 1,839,000 | 1,767,264 |

| 3% 10/29/28 | | 1,295,000 | 1,119,725 |

| 3.3% 1/30/32 | | 1,385,000 | 1,133,067 |

| 3.5% 1/15/25 | | 2,546,000 | 2,437,561 |

| 4.45% 4/3/26 | | 959,000 | 915,627 |

| 4.875% 1/16/24 | | 1,538,000 | 1,527,193 |

| 6.5% 7/15/25 | | 1,112,000 | 1,117,499 |

| Ally Financial, Inc.: | | | |

| 1.45% 10/2/23 | | 678,000 | 668,895 |

| 5.125% 9/30/24 | | 656,000 | 643,581 |

| 5.8% 5/1/25 | | 1,606,000 | 1,578,676 |

| 6.7% 2/14/33 | | 5,000,000 | 4,423,940 |

| 7.1% 11/15/27 | | 2,560,000 | 2,581,975 |

| 8% 11/1/31 | | 829,000 | 860,602 |

| Capital One Financial Corp.: | | | |

| 2.636% 3/3/26 (c) | | 1,495,000 | 1,395,992 |

| 3.273% 3/1/30 (c) | | 1,912,000 | 1,623,439 |

| 3.65% 5/11/27 | | 4,134,000 | 3,839,722 |

| 3.8% 1/31/28 | | 2,165,000 | 1,989,478 |

| 4.927% 5/10/28 (c) | | 2,300,000 | 2,182,285 |

| 4.985% 7/24/26 (c) | | 2,151,000 | 2,084,858 |

| 5.247% 7/26/30 (c) | | 2,770,000 | 2,611,304 |

| 5.468% 2/1/29 (c) | | 1,952,000 | 1,869,943 |

| 5.817% 2/1/34 (c) | | 2,680,000 | 2,556,921 |

| Discover Financial Services: | | | |

| 3.95% 11/6/24 | | 873,000 | 841,267 |

| 4.1% 2/9/27 | | 875,000 | 811,773 |

| 4.5% 1/30/26 | | 1,437,000 | 1,376,062 |

| 6.7% 11/29/32 | | 537,000 | 553,235 |

| Ford Motor Credit Co. LLC: | | | |

| 4.063% 11/1/24 | | 5,400,000 | 5,225,464 |

| 5.584% 3/18/24 | | 1,916,000 | 1,902,400 |

| Synchrony Financial: | | | |

| 3.95% 12/1/27 | | 2,356,000 | 2,052,544 |

| 4.25% 8/15/24 | | 2,051,000 | 1,977,433 |

| 4.375% 3/19/24 | | 1,677,000 | 1,644,236 |

| 5.15% 3/19/29 | | 2,576,000 | 2,337,162 |

| | | | 63,938,792 |

| Financial Services - 0.9% | | | |

| Blackstone Private Credit Fund: | | | |

| 4.7% 3/24/25 | | 5,035,000 | 4,849,360 |

| 7.05% 9/29/25 | | 2,656,000 | 2,649,113 |

| Brixmor Operating Partnership LP: | | | |

| 4.05% 7/1/30 | | 1,554,000 | 1,400,723 |

| 4.125% 6/15/26 | | 1,425,000 | 1,330,992 |

| 4.125% 5/15/29 | | 1,549,000 | 1,381,701 |

| Corebridge Financial, Inc.: | | | |

| 3.5% 4/4/25 | | 646,000 | 615,431 |

| 3.65% 4/5/27 | | 2,280,000 | 2,128,550 |

| 3.85% 4/5/29 | | 904,000 | 812,982 |

| 3.9% 4/5/32 | | 1,076,000 | 934,933 |

| 4.35% 4/5/42 | | 245,000 | 197,693 |

| 4.4% 4/5/52 | | 724,000 | 569,191 |

| Equitable Holdings, Inc. 4.35% 4/20/28 | | 1,304,000 | 1,220,343 |

| Jackson Financial, Inc.: | | | |

| 5.17% 6/8/27 | | 1,014,000 | 965,646 |

| 5.67% 6/8/32 | | 1,281,000 | 1,215,300 |

| Park Aerospace Holdings Ltd. 5.5% 2/15/24 (b) | | 1,871,000 | 1,849,689 |

| Pine Street Trust I 4.572% 2/15/29 (b) | | 1,750,000 | 1,603,194 |

| Pine Street Trust II 5.568% 2/15/49 (b) | | 1,748,000 | 1,571,083 |

| | | | 25,295,924 |

| Insurance - 0.9% | | | |

| AIA Group Ltd.: | | | |

| 3.2% 9/16/40 (b) | | 1,070,000 | 820,502 |

| 3.375% 4/7/30 (b) | | 2,257,000 | 2,063,250 |

| American International Group, Inc. 2.5% 6/30/25 | | 2,432,000 | 2,290,478 |

| Five Corners Funding Trust II 2.85% 5/15/30 (b) | | 3,419,000 | 2,904,266 |

| Liberty Mutual Group, Inc. 4.569% 2/1/29 (b) | | 1,255,000 | 1,183,549 |

| Marsh & McLennan Companies, Inc.: | | | |

| 4.375% 3/15/29 | | 1,220,000 | 1,185,063 |

| 4.75% 3/15/39 | | 560,000 | 527,728 |

| Massachusetts Mutual Life Insurance Co. 3.729% 10/15/70 (b) | | 1,782,000 | 1,211,606 |

| MetLife, Inc. 4.55% 3/23/30 | | 3,527,000 | 3,446,481 |

| Pacific LifeCorp 5.125% 1/30/43 (b) | | 1,611,000 | 1,491,088 |

| Swiss Re Finance Luxembourg SA 5% 4/2/49 (b)(c) | | 600,000 | 573,000 |

| Teachers Insurance & Annuity Association of America 4.9% 9/15/44 (b) | | 1,640,000 | 1,484,937 |

| TIAA Asset Management Finance LLC 4.125% 11/1/24 (b) | | 543,000 | 527,253 |

| Unum Group: | | | |

| 3.875% 11/5/25 | | 1,491,000 | 1,409,804 |

| 4% 6/15/29 | | 1,353,000 | 1,244,574 |

| 5.75% 8/15/42 | | 2,232,000 | 2,053,691 |

| | | | 24,417,270 |

TOTAL FINANCIALS | | | 365,112,906 |

| HEALTH CARE - 1.5% | | | |

| Biotechnology - 0.3% | | | |

| Amgen, Inc.: | | | |

| 5.15% 3/2/28 | | 1,463,000 | 1,461,683 |

| 5.25% 3/2/30 | | 1,336,000 | 1,338,666 |

| 5.25% 3/2/33 | | 1,508,000 | 1,509,923 |

| 5.6% 3/2/43 | | 1,433,000 | 1,437,336 |

| 5.65% 3/2/53 | | 712,000 | 721,046 |

| 5.75% 3/2/63 | | 1,298,000 | 1,316,740 |

| | | | 7,785,394 |

| Health Care Providers & Services - 1.0% | | | |

| Centene Corp.: | | | |

| 2.45% 7/15/28 | | 3,009,000 | 2,571,654 |

| 2.625% 8/1/31 | | 1,403,000 | 1,118,023 |

| 3.375% 2/15/30 | | 1,564,000 | 1,344,164 |

| 4.25% 12/15/27 | | 1,762,000 | 1,647,391 |

| 4.625% 12/15/29 | | 2,738,000 | 2,520,156 |

| Cigna Group: | | | |

| 3.05% 10/15/27 | | 982,000 | 905,474 |

| 4.375% 10/15/28 | | 1,860,000 | 1,798,530 |

| 4.8% 8/15/38 | | 1,158,000 | 1,093,167 |

| 4.9% 12/15/48 | | 1,157,000 | 1,076,783 |

| CVS Health Corp.: | | | |

| 3% 8/15/26 | | 192,000 | 179,986 |

| 3.625% 4/1/27 | | 551,000 | 523,055 |

| 4.78% 3/25/38 | | 1,830,000 | 1,688,855 |

| 5% 1/30/29 | | 1,114,000 | 1,103,263 |

| 5.25% 1/30/31 | | 457,000 | 455,566 |

| HCA Holdings, Inc.: | | | |

| 3.5% 9/1/30 | | 1,260,000 | 1,104,452 |

| 3.625% 3/15/32 (b) | | 287,000 | 249,118 |

| 5.625% 9/1/28 | | 1,311,000 | 1,311,824 |

| 5.875% 2/1/29 | | 1,446,000 | 1,455,385 |

| Humana, Inc. 3.7% 3/23/29 | | 827,000 | 757,429 |

| Sabra Health Care LP 3.2% 12/1/31 | | 2,870,000 | 2,140,916 |

| Toledo Hospital 5.325% 11/15/28 | | 647,000 | 524,070 |

| | | | 25,569,261 |

| Pharmaceuticals - 0.2% | | | |

| Bayer U.S. Finance II LLC 4.25% 12/15/25 (b) | | 1,338,000 | 1,291,034 |

| Elanco Animal Health, Inc. 6.65% 8/28/28 (c) | | 409,000 | 396,840 |

| Mylan NV 4.55% 4/15/28 | | 1,227,000 | 1,155,984 |

| Utah Acquisition Sub, Inc. 3.95% 6/15/26 | | 782,000 | 742,733 |

| Viatris, Inc.: | | | |

| 1.65% 6/22/25 | | 302,000 | 277,849 |

| 2.7% 6/22/30 | | 1,533,000 | 1,240,551 |

| 3.85% 6/22/40 | | 668,000 | 461,619 |

| 4% 6/22/50 | | 1,153,000 | 762,524 |

| | | | 6,329,134 |

TOTAL HEALTH CARE | | | 39,683,789 |

| INDUSTRIALS - 0.7% | | | |

| Aerospace & Defense - 0.2% | | | |

| BAE Systems PLC 3.4% 4/15/30 (b) | | 696,000 | 629,374 |

| The Boeing Co.: | | | |

| 5.04% 5/1/27 | | 909,000 | 897,881 |

| 5.15% 5/1/30 | | 909,000 | 900,228 |

| 5.705% 5/1/40 | | 920,000 | 917,706 |

| 5.805% 5/1/50 | | 920,000 | 916,643 |

| 5.93% 5/1/60 | | 908,000 | 899,272 |

| | | | 5,161,104 |

| Professional Services - 0.0% | | | |

| Thomson Reuters Corp. 3.85% 9/29/24 | | 317,000 | 307,327 |

| Trading Companies & Distributors - 0.3% | | | |

| Air Lease Corp.: | | | |

| 3% 9/15/23 | | 269,000 | 267,373 |

| 3.375% 7/1/25 | | 1,977,000 | 1,873,747 |

| 3.875% 7/3/23 | | 1,712,000 | 1,712,000 |

| 4.25% 2/1/24 | | 1,761,000 | 1,742,380 |

| 4.25% 9/15/24 | | 1,093,000 | 1,066,783 |

| | | | 6,662,283 |

| Transportation Infrastructure - 0.2% | | | |

| Avolon Holdings Funding Ltd.: | | | |

| 3.95% 7/1/24 (b) | | 640,000 | 620,832 |

| 4.25% 4/15/26 (b) | | 485,000 | 451,833 |

| 4.375% 5/1/26 (b) | | 1,433,000 | 1,338,956 |

| 5.25% 5/15/24 (b) | | 1,170,000 | 1,149,494 |

| 6.375% 5/4/28 (b) | | 2,451,000 | 2,424,681 |

| | | | 5,985,796 |

TOTAL INDUSTRIALS | | | 18,116,510 |

| INFORMATION TECHNOLOGY - 0.9% | | | |

| Electronic Equipment, Instruments & Components - 0.1% | | | |

| Dell International LLC/EMC Corp.: | | | |

| 5.85% 7/15/25 | | 397,000 | 398,450 |

| 6.02% 6/15/26 | | 480,000 | 487,876 |

| 6.1% 7/15/27 | | 729,000 | 751,023 |

| 6.2% 7/15/30 | | 631,000 | 655,605 |

| | | | 2,292,954 |

| Semiconductors & Semiconductor Equipment - 0.4% | | | |

| Broadcom, Inc.: | | | |

| 1.95% 2/15/28 (b) | | 510,000 | 441,049 |

| 2.45% 2/15/31 (b) | | 4,340,000 | 3,529,728 |

| 2.6% 2/15/33 (b) | | 4,340,000 | 3,391,681 |

| 3.5% 2/15/41 (b) | | 3,505,000 | 2,621,833 |

| 3.75% 2/15/51 (b) | | 1,645,000 | 1,209,707 |

| | | | 11,193,998 |

| Software - 0.4% | | | |

| Oracle Corp.: | | | |

| 1.65% 3/25/26 | | 1,992,000 | 1,807,842 |

| 2.3% 3/25/28 | | 3,147,000 | 2,777,102 |

| 2.8% 4/1/27 | | 1,797,000 | 1,651,675 |

| 2.875% 3/25/31 | | 3,303,000 | 2,819,812 |

| 3.6% 4/1/40 | | 1,797,000 | 1,390,172 |

| | | | 10,446,603 |

TOTAL INFORMATION TECHNOLOGY | | | 23,933,555 |

| REAL ESTATE - 2.4% | | | |

| Equity Real Estate Investment Trusts (REITs) - 2.0% | | | |

| Alexandria Real Estate Equities, Inc. 4.9% 12/15/30 | | 1,278,000 | 1,236,921 |

| American Homes 4 Rent LP: | | | |

| 2.375% 7/15/31 | | 231,000 | 183,420 |

| 3.625% 4/15/32 | | 989,000 | 854,687 |

| Boston Properties, Inc.: | | | |

| 3.25% 1/30/31 | | 1,190,000 | 969,549 |

| 4.5% 12/1/28 | | 1,193,000 | 1,095,212 |

| 6.75% 12/1/27 | | 1,655,000 | 1,673,715 |

| Corporate Office Properties LP: | | | |

| 2% 1/15/29 | | 199,000 | 151,658 |

| 2.25% 3/15/26 | | 510,000 | 451,683 |

| 2.75% 4/15/31 | | 509,000 | 386,763 |

| Healthcare Trust of America Holdings LP: | | | |

| 3.1% 2/15/30 | | 402,000 | 344,346 |

| 3.5% 8/1/26 | | 419,000 | 385,489 |

| Healthpeak OP, LLC: | | | |

| 3.25% 7/15/26 | | 176,000 | 163,908 |

| 3.5% 7/15/29 | | 201,000 | 180,238 |

| Hudson Pacific Properties LP 4.65% 4/1/29 | | 2,374,000 | 1,675,308 |

| Invitation Homes Operating Partnership LP 4.15% 4/15/32 | | 1,453,000 | 1,301,207 |

| Kite Realty Group Trust: | | | |

| 4% 3/15/25 | | 1,912,000 | 1,816,174 |

| 4.75% 9/15/30 | | 2,980,000 | 2,678,531 |

| LXP Industrial Trust (REIT): | | | |

| 2.7% 9/15/30 | | 560,000 | 447,220 |

| 4.4% 6/15/24 | | 442,000 | 431,459 |

| Omega Healthcare Investors, Inc.: | | | |

| 3.25% 4/15/33 | | 1,945,000 | 1,444,436 |

| 3.375% 2/1/31 | | 1,027,000 | 814,603 |

| 3.625% 10/1/29 | | 1,814,000 | 1,486,615 |

| 4.375% 8/1/23 | | 381,000 | 380,178 |

| 4.5% 1/15/25 | | 821,000 | 786,742 |

| 4.5% 4/1/27 | | 4,967,000 | 4,612,761 |

| 4.75% 1/15/28 | | 1,958,000 | 1,787,319 |

| 4.95% 4/1/24 | | 415,000 | 409,160 |

| 5.25% 1/15/26 | | 1,744,000 | 1,679,156 |

| Piedmont Operating Partnership LP 2.75% 4/1/32 | | 451,000 | 303,664 |

| Realty Income Corp.: | | | |

| 2.2% 6/15/28 | | 244,000 | 211,264 |

| 2.85% 12/15/32 | | 301,000 | 244,796 |

| 3.25% 1/15/31 | | 313,000 | 273,574 |

| 3.4% 1/15/28 | | 489,000 | 450,845 |

| Retail Opportunity Investments Partnership LP: | | | |

| 4% 12/15/24 | | 300,000 | 287,378 |

| 5% 12/15/23 | | 226,000 | 222,684 |

| Simon Property Group LP 2.45% 9/13/29 | | 499,000 | 420,080 |

| SITE Centers Corp.: | | | |

| 3.625% 2/1/25 | | 694,000 | 653,085 |

| 4.25% 2/1/26 | | 906,000 | 848,575 |

| Store Capital Corp.: | | | |

| 2.75% 11/18/30 | | 2,676,000 | 1,933,449 |

| 4.625% 3/15/29 | | 550,000 | 463,000 |

| Sun Communities Operating LP: | | | |

| 2.3% 11/1/28 | | 512,000 | 430,363 |

| 2.7% 7/15/31 | | 1,323,000 | 1,045,385 |

| Ventas Realty LP: | | | |

| 3% 1/15/30 | | 2,340,000 | 2,001,473 |

| 3.5% 2/1/25 | | 1,976,000 | 1,892,277 |

| 4% 3/1/28 | | 688,000 | 636,430 |

| 4.125% 1/15/26 | | 478,000 | 457,188 |

| 4.375% 2/1/45 | | 234,000 | 187,656 |

| 4.75% 11/15/30 | | 3,072,000 | 2,907,716 |

| VICI Properties LP: | | | |

| 4.375% 5/15/25 | | 256,000 | 247,412 |

| 4.75% 2/15/28 | | 2,029,000 | 1,921,126 |

| 4.95% 2/15/30 | | 2,648,000 | 2,484,036 |

| 5.125% 5/15/32 | | 720,000 | 673,664 |

| Vornado Realty LP 2.15% 6/1/26 | | 578,000 | 489,642 |

| WP Carey, Inc.: | | | |

| 2.4% 2/1/31 | | 1,166,000 | 937,270 |

| 3.85% 7/15/29 | | 391,000 | 354,729 |

| 4% 2/1/25 | | 1,644,000 | 1,591,848 |

| | | | 54,399,067 |

| Real Estate Management & Development - 0.4% | | | |

| Brandywine Operating Partnership LP: | | | |

| 3.95% 11/15/27 | | 1,415,000 | 1,122,185 |

| 4.1% 10/1/24 | | 1,555,000 | 1,492,091 |

| 4.55% 10/1/29 | | 1,792,000 | 1,295,930 |

| 7.55% 3/15/28 | | 2,334,000 | 2,099,969 |

| CBRE Group, Inc. 2.5% 4/1/31 | | 1,708,000 | 1,373,776 |

| Tanger Properties LP: | | | |

| 2.75% 9/1/31 | | 1,346,000 | 976,775 |

| 3.125% 9/1/26 | | 1,874,000 | 1,661,587 |

| | | | 10,022,313 |

TOTAL REAL ESTATE | | | 64,421,380 |

| UTILITIES - 1.1% | | | |

| Electric Utilities - 0.5% | | | |

| Alabama Power Co. 3.05% 3/15/32 | | 2,030,000 | 1,763,689 |

| Cleco Corporate Holdings LLC: | | | |

| 3.375% 9/15/29 | | 1,057,000 | 896,511 |

| 3.743% 5/1/26 | | 4,043,000 | 3,784,071 |

| Duke Energy Corp. 2.45% 6/1/30 | | 854,000 | 717,139 |

| Duquesne Light Holdings, Inc.: | | | |

| 2.532% 10/1/30 (b) | | 405,000 | 323,649 |

| 2.775% 1/7/32 (b) | | 1,402,000 | 1,093,248 |

| Entergy Corp. 2.8% 6/15/30 | | 876,000 | 742,511 |

| Exelon Corp.: | | | |

| 2.75% 3/15/27 | | 449,000 | 410,857 |

| 3.35% 3/15/32 | | 546,000 | 474,417 |

| 4.05% 4/15/30 | | 534,000 | 499,011 |

| 4.1% 3/15/52 | | 404,000 | 325,675 |

| 4.7% 4/15/50 | | 238,000 | 210,332 |

| IPALCO Enterprises, Inc. 3.7% 9/1/24 | | 662,000 | 640,032 |

| | | | 11,881,142 |

| Gas Utilities - 0.0% | | | |

| Nakilat, Inc. 6.067% 12/31/33 (b) | | 494,955 | 516,629 |

| Independent Power and Renewable Electricity Producers - 0.2% | | | |

| Emera U.S. Finance LP 3.55% 6/15/26 | | 580,000 | 548,425 |

| The AES Corp.: | | | |

| 2.45% 1/15/31 | | 673,000 | 543,976 |

| 3.3% 7/15/25 (b) | | 2,635,000 | 2,488,331 |

| 3.95% 7/15/30 (b) | | 2,298,000 | 2,060,198 |

| | | | 5,640,930 |

| Multi-Utilities - 0.4% | | | |

| Berkshire Hathaway Energy Co. 4.05% 4/15/25 | | 3,813,000 | 3,721,632 |

| Consolidated Edison Co. of New York, Inc. 3.35% 4/1/30 | | 242,000 | 219,845 |

| NiSource, Inc.: | | | |

| 2.95% 9/1/29 | | 2,624,000 | 2,297,654 |

| 3.6% 5/1/30 | | 1,602,000 | 1,442,728 |

| Puget Energy, Inc.: | | | |

| 4.1% 6/15/30 | | 1,032,000 | 939,630 |

| 4.224% 3/15/32 | | 1,875,000 | 1,684,812 |

| WEC Energy Group, Inc. 3 month U.S. LIBOR + 2.610% 7.4332% 5/15/67 (c)(d) | | 437,000 | 367,543 |

| | | | 10,673,844 |

TOTAL UTILITIES | | | 28,712,545 |

| TOTAL NONCONVERTIBLE BONDS (Cost $833,867,887) | | | 759,458,755 |

| | | | |

| U.S. Treasury Obligations - 44.2% |

| | | Principal Amount (a) | Value ($) |

| U.S. Treasury Bonds: | | | |

| 1.125% 5/15/40 | | 12,353,900 | 8,008,319 |

| 1.75% 8/15/41 | | 43,542,800 | 30,590,518 |

| 1.875% 11/15/51 | | 13,856,800 | 9,146,570 |

| 2% 11/15/41 | | 16,500,000 | 12,077,871 |

| 2% 8/15/51 | | 108,411,200 | 73,901,713 |

| 2.25% 2/15/52 | | 36,300,000 | 26,232,422 |

| 2.875% 5/15/52 | | 23,300,000 | 19,308,965 |

| 3% 2/15/47 | | 25,251,500 | 21,260,579 |

| 3.375% 8/15/42 | | 34,200,000 | 31,043,180 |

| 3.625% 5/15/53 | | 3,100,000 | 2,979,391 |

| U.S. Treasury Notes: | | | |

| 0.25% 7/31/25 | | 68,520,600 | 62,351,070 |

| 0.375% 12/31/25 | | 17,431,400 | 15,712,092 |

| 0.75% 3/31/26 | | 52,072,200 | 47,064,319 |

| 0.75% 4/30/26 | | 41,407,700 | 37,286,340 |

| 0.75% 8/31/26 | | 15,336,200 | 13,677,973 |

| 1.25% 5/31/28 | | 63,257,700 | 55,177,517 |

| 1.75% 1/31/29 | | 24,900,000 | 22,011,211 |

| 1.875% 2/28/27 | | 6,800,000 | 6,233,156 |

| 2.375% 3/31/29 | | 20,000,000 | 18,259,375 |

| 2.5% 3/31/27 | | 25,000,000 | 23,428,711 |

| 2.75% 8/15/32 | | 36,698,000 | 33,643,178 |

| 2.875% 5/15/32 | | 38,075,000 | 35,302,664 |

| 3.375% 5/15/33 | | 45,400,000 | 43,782,625 |

| 3.5% 2/15/33 | | 63,000,000 | 61,365,938 |

| 3.75% 5/31/30 | | 49,700,000 | 49,008,859 |

| 3.875% 11/30/27 | | 55,000,000 | 54,220,117 |

| 3.875% 12/31/27 | | 75,000,000 | 73,932,908 |

| 3.875% 11/30/29 | | 123,000,000 | 121,885,313 |

| 3.875% 12/31/29 | | 85,000,000 | 84,259,570 |

| 4.125% 10/31/27 | | 10,000,000 | 9,947,656 |

| 4.125% 11/15/32 | | 71,600,000 | 73,166,250 |

| TOTAL U.S. TREASURY OBLIGATIONS (Cost $1,313,788,642) | | | 1,176,266,370 |

| | | | |

| U.S. Government Agency - Mortgage Securities - 23.1% |

| | | Principal Amount (a) | Value ($) |

| Fannie Mae - 5.7% | | | |

| 12 month U.S. LIBOR + 1.480% 3.73% 7/1/34 (c)(d) | | 830 | 835 |

| 12 month U.S. LIBOR + 1.550% 3.803% 6/1/36 (c)(d) | | 2,098 | 2,121 |

| 12 month U.S. LIBOR + 1.630% 4.24% 11/1/36 (c)(d) | | 23,124 | 23,304 |

| 12 month U.S. LIBOR + 1.700% 5.188% 6/1/42 (c)(d) | | 16,896 | 17,109 |

| 12 month U.S. LIBOR + 1.730% 5.105% 5/1/36 (c)(d) | | 16,591 | 16,770 |

| 12 month U.S. LIBOR + 1.750% 4.306% 7/1/35 (c)(d) | | 1,591 | 1,601 |

| 12 month U.S. LIBOR + 1.780% 4.163% 2/1/36 (c)(d) | | 6,623 | 6,669 |

| 12 month U.S. LIBOR + 1.800% 4.05% 7/1/41 (c)(d) | | 6,610 | 6,710 |

| 12 month U.S. LIBOR + 1.810% 4.068% 9/1/41 (c)(d) | | 5,505 | 5,623 |

| 12 month U.S. LIBOR + 1.810% 4.119% 7/1/41 (c)(d) | | 10,735 | 10,983 |

| 12 month U.S. LIBOR + 1.820% 4.195% 12/1/35 (c)(d) | | 6,704 | 6,781 |

| 12 month U.S. LIBOR + 1.830% 4.08% 10/1/41 (c)(d) | | 4,552 | 4,480 |

| 12 month U.S. LIBOR + 1.950% 4.4% 9/1/36 (c)(d) | | 12,441 | 12,565 |

| 12 month U.S. LIBOR + 1.950% 5.496% 7/1/37 (c)(d) | | 4,702 | 4,788 |

| 6 month U.S. LIBOR + 1.310% 4.438% 5/1/34 (c)(d) | | 9,852 | 9,821 |

| 6 month U.S. LIBOR + 1.420% 3.572% 9/1/33 (c)(d) | | 17,442 | 17,351 |

| 6 month U.S. LIBOR + 1.550% 5.984% 10/1/33 (c)(d) | | 1,155 | 1,171 |

| 6 month U.S. LIBOR + 1.560% 5.603% 7/1/35 (c)(d) | | 1,122 | 1,140 |

| U.S. TREASURY 1 YEAR INDEX + 1.940% 3.87% 10/1/33 (c)(d) | | 17,856 | 18,200 |

| U.S. TREASURY 1 YEAR INDEX + 2.200% 4.583% 3/1/35 (c)(d) | | 1,606 | 1,627 |

| U.S. TREASURY 1 YEAR INDEX + 2.220% 4.405% 8/1/36 (c)(d) | | 20,503 | 20,888 |

| U.S. TREASURY 1 YEAR INDEX + 2.280% 4.405% 10/1/33 (c)(d) | | 2,808 | 2,872 |

| U.S. TREASURY 1 YEAR INDEX + 2.420% 4.778% 5/1/35 (c)(d) | | 3,482 | 3,546 |

| 1.5% 11/1/35 to 6/1/51 (e) | | 10,946,398 | 9,270,048 |

| 2% 10/1/35 to 3/1/52 (e) | | 50,539,481 | 42,358,425 |

| 2.5% 7/1/31 to 1/1/52 | | 41,983,870 | 36,119,802 |

| 3% 8/1/32 to 2/1/52 | | 18,663,303 | 16,886,193 |

| 3.5% 8/1/37 to 3/1/52 | | 9,883,511 | 9,128,214 |

| 4% 7/1/39 to 4/1/52 | | 10,371,748 | 9,912,165 |

| 4.5% to 4.5% 5/1/25 to 12/1/52 | | 8,411,634 | 8,190,988 |

| 5% 9/1/25 to 12/1/52 | | 4,793,351 | 4,738,012 |

| 5.5% 10/1/52 to 6/1/53 | | 8,861,972 | 8,858,209 |

| 6% 10/1/34 to 6/1/53 | | 6,635,684 | 6,789,802 |

| 6.5% 12/1/23 to 8/1/36 | | 159,888 | 164,518 |

| 7% to 7% 11/1/23 to 2/1/29 | | 20,302 | 20,944 |

| 7.5% to 7.5% 9/1/25 to 11/1/31 | | 26,481 | 27,246 |

| 8.5% 6/1/25 | | 73 | 74 |

TOTAL FANNIE MAE | | | 152,661,595 |

| Freddie Mac - 5.0% | | | |

| 12 month U.S. LIBOR + 1.370% 3.634% 3/1/36 (c)(d) | | 13,644 | 13,602 |

| 12 month U.S. LIBOR + 1.880% 4.13% 9/1/41 (c)(d) | | 8,197 | 8,315 |

| 12 month U.S. LIBOR + 1.880% 5.255% 4/1/41 (c)(d) | | 2,123 | 2,137 |

| 12 month U.S. LIBOR + 1.910% 4.16% 6/1/41 (c)(d) | | 5,379 | 5,514 |

| 12 month U.S. LIBOR + 1.910% 5.22% 5/1/41 (c)(d) | | 17,110 | 17,271 |

| 12 month U.S. LIBOR + 1.910% 5.364% 6/1/41 (c)(d) | | 16,565 | 16,762 |

| 12 month U.S. LIBOR + 1.910% 5.568% 5/1/41 (c)(d) | | 17,862 | 18,037 |

| 12 month U.S. LIBOR + 2.030% 4.158% 3/1/33 (c)(d) | | 170 | 171 |

| 12 month U.S. LIBOR + 2.160% 4.41% 11/1/35 (c)(d) | | 2,758 | 2,791 |

| 6 month U.S. LIBOR + 1.650% 6.179% 4/1/35 (c)(d) | | 11,221 | 11,346 |

| 6 month U.S. LIBOR + 2.680% 6.988% 10/1/35 (c)(d) | | 1,906 | 1,958 |

| U.S. TREASURY 1 YEAR INDEX + 2.240% 4.372% 1/1/35 (c)(d) | | 1,734 | 1,755 |

| 1.5% 8/1/35 to 4/1/51 | | 31,924,573 | 26,546,465 |

| 2% 6/1/35 to 3/1/52 | | 28,838,681 | 24,632,161 |

| 2.5% 8/1/32 to 3/1/52 | | 19,763,475 | 17,030,050 |

| 3% 6/1/31 to 3/1/52 | | 9,415,960 | 8,455,281 |

| 3.5% 3/1/32 to 4/1/52 | | 28,220,417 | 26,132,061 |

| 4% 5/1/37 to 10/1/52 | | 8,021,122 | 7,687,355 |

| 4.5% 7/1/25 to 10/1/52 (e) | | 6,793,951 | 6,613,243 |

| 5% 1/1/40 to 12/1/52 | | 4,718,946 | 4,673,046 |

| 5.5% 10/1/52 to 5/1/53 (e) | | 7,458,554 | 7,494,744 |

| 6% 4/1/32 to 6/1/53 | | 1,994,914 | 2,036,793 |

| 6.5% 1/1/53 | | 1,048,557 | 1,072,656 |

| 7.5% 8/1/26 to 11/1/31 | | 3,120 | 3,250 |

| 8% 4/1/27 to 5/1/27 | | 253 | 258 |

| 8.5% 5/1/27 to 1/1/28 | | 479 | 490 |

TOTAL FREDDIE MAC | | | 132,477,512 |

| Ginnie Mae - 5.3% | | | |

| 3% 12/20/42 to 4/20/47 | | 2,035,892 | 1,840,835 |

| 3.5% 12/20/40 to 1/20/50 | | 1,442,315 | 1,343,338 |

| 4% 3/15/40 to 4/20/48 | | 5,708,738 | 5,482,636 |

| 4.5% 5/15/39 to 5/20/41 | | 1,231,046 | 1,205,568 |

| 5% 3/15/39 to 4/20/48 | | 690,485 | 692,385 |

| 6.5% 4/15/35 to 11/15/35 | | 14,809 | 15,315 |

| 7% 1/15/28 to 7/15/32 | | 82,530 | 84,539 |

| 7.5% to 7.5% 1/15/24 to 10/15/28 | | 14,077 | 14,331 |

| 8% 3/15/30 to 9/15/30 | | 2,056 | 2,143 |

| 2% 11/20/50 to 2/20/51 | | 8,936,147 | 7,526,204 |

| 2% 7/1/53 (f) | | 7,100,000 | 5,961,445 |

| 2% 7/1/53 (f) | | 9,450,000 | 7,934,599 |

| 2% 7/1/53 (f) | | 2,350,000 | 1,973,154 |

| 2% 7/1/53 (f) | | 2,975,000 | 2,497,929 |

| 2% 7/1/53 (f) | | 4,725,000 | 3,967,299 |

| 2% 8/1/53 (f) | | 4,700,000 | 3,951,082 |

| 2% 8/1/53 (f) | | 2,350,000 | 1,975,541 |

| 2% 8/1/53 (f) | | 950,000 | 798,623 |

| 2.5% 6/20/51 to 12/20/51 | | 5,836,224 | 5,059,513 |

| 2.5% 7/1/53 (f) | | 7,800,000 | 6,750,277 |

| 2.5% 7/1/53 (f) | | 5,150,000 | 4,456,914 |

| 2.5% 7/1/53 (f) | | 7,250,000 | 6,274,296 |

| 2.5% 7/1/53 (f) | | 2,300,000 | 1,990,466 |

| 2.5% 7/1/53 (f) | | 5,100,000 | 4,413,643 |

| 2.5% 7/1/53 (f) | | 5,800,000 | 5,019,437 |

| 2.5% 7/1/53 (f) | | 4,450,000 | 3,851,119 |

| 2.5% 8/1/53 (f) | | 5,100,000 | 4,420,266 |

| 2.5% 8/1/53 (f) | | 10,250,000 | 8,880,264 |

| 3% 7/1/53 (f) | | 5,900,000 | 5,270,787 |

| 3% 7/1/53 (f) | | 4,675,000 | 4,176,429 |

| 3% 7/1/53 (f) | | 650,000 | 580,680 |

| 3% 7/1/53 (f) | | 1,700,000 | 1,518,701 |

| 3% 7/1/53 (f) | | 2,400,000 | 2,144,049 |

| 3.5% 7/1/53 (f) | | 5,150,000 | 4,752,053 |

| 3.5% 7/1/53 (f) | | 2,400,000 | 2,214,549 |

| 3.5% 7/1/53 (f) | | 2,450,000 | 2,260,685 |

| 3.5% 7/1/53 (f) | | 500,000 | 461,364 |

| 3.5% 8/1/53 (f) | | 5,550,000 | 5,122,445 |

| 4% 7/1/53 (f) | | 3,650,000 | 3,451,176 |

| 4.5% 7/1/53 (f) | | 2,400,000 | 2,315,675 |

| 4.5% 7/1/53 (f) | | 2,400,000 | 2,315,675 |

| 5.5% 7/1/53 (f) | | 5,200,000 | 5,177,121 |

TOTAL GINNIE MAE | | | 140,144,550 |

| Uniform Mortgage Backed Securities - 7.1% | | | |

| 1.5% 7/1/38 (f) | | 500,000 | 431,261 |

| 1.5% 7/1/38 (f) | | 1,200,000 | 1,035,026 |

| 1.5% 7/1/38 (f) | | 1,350,000 | 1,164,404 |

| 2% 7/1/38 (f) | | 2,050,000 | 1,816,541 |

| 2% 7/1/53 (f) | | 13,500,000 | 11,000,966 |

| 2% 7/1/53 (f) | | 13,450,000 | 10,960,222 |

| 2% 7/1/53 (f) | | 8,850,000 | 7,211,745 |

| 2% 7/1/53 (f) | | 10,050,000 | 8,189,608 |

| 2% 7/1/53 (f) | | 16,150,000 | 13,160,415 |

| 2% 7/1/53 (f) | | 7,875,000 | 6,417,230 |

| 2% 7/1/53 (f) | | 7,875,000 | 6,417,230 |

| 2% 8/1/53 (f) | | 9,500,000 | 7,753,296 |

| 2.5% 7/1/38 (f) | | 300,000 | 273,000 |

| 2.5% 7/1/53 (f) | | 14,600,000 | 12,372,928 |

| 2.5% 7/1/53 (f) | | 21,350,000 | 18,093,288 |

| 2.5% 7/1/53 (f) | | 2,100,000 | 1,779,668 |

| 2.5% 7/1/53 (f) | | 750,000 | 635,596 |

| 3% 7/1/53 (f) | | 20,200,000 | 17,772,841 |

| 3% 7/1/53 (f) | | 17,725,000 | 15,595,228 |

| 3.5% 7/1/53 (f) | | 4,900,000 | 4,463,210 |

| 3.5% 7/1/53 (f) | | 1,800,000 | 1,639,547 |

| 4% 7/1/53 (f) | | 5,100,000 | 4,784,835 |

| 4% 7/1/53 (f) | | 7,750,000 | 7,271,072 |

| 4% 7/1/53 (f) | | 2,875,000 | 2,697,333 |

| 4.5% 7/1/53 (f) | | 2,800,000 | 2,690,626 |

| 4.5% 7/1/53 (f) | | 2,650,000 | 2,546,485 |

| 5% 7/1/53 (f) | | 750,000 | 734,795 |

| 5% 7/1/53 (f) | | 700,000 | 685,809 |

| 5.5% 7/1/53 (f) | | 19,650,000 | 19,555,572 |

TOTAL UNIFORM MORTGAGE BACKED SECURITIES | | | 189,149,777 |

| TOTAL U.S. GOVERNMENT AGENCY - MORTGAGE SECURITIES (Cost $639,118,834) | | | 614,433,434 |

| | | | |

| Asset-Backed Securities - 5.4% |

| | | Principal Amount (a) | Value ($) |

| AASET Trust: | | | |

| Series 2018-1A Class A, 3.844% 1/16/38 (b) | | 727,810 | 454,158 |

| Series 2019-1 Class A, 3.844% 5/15/39 (b) | | 539,852 | 388,104 |

| Series 2019-2: | | | |

Class A, 3.376% 10/16/39 (b) | | 1,349,026 | 1,131,870 |

Class B, 4.458% 10/16/39 (b) | | 315,410 | 110,813 |

| Series 2021-1A Class A, 2.95% 11/16/41 (b) | | 1,600,200 | 1,378,589 |

| Series 2021-2A Class A, 2.798% 1/15/47 (b) | | 3,030,599 | 2,571,463 |

| Aimco Series 2021-BA Class AR, 3 month U.S. LIBOR + 1.100% 6.3603% 1/15/32 (b)(c)(d) | | 529,405 | 523,911 |

| AIMCO CLO Ltd. Series 2021-11A Class AR, 3 month U.S. LIBOR + 1.130% 6.3903% 10/17/34 (b)(c)(d) | | 1,280,878 | 1,257,424 |

| AIMCO CLO Ltd. / AIMCO CLO LLC Series 2021-14A Class A, 3 month U.S. LIBOR + 0.990% 6.2404% 4/20/34 (b)(c)(d) | | 3,132,569 | 3,068,809 |

| Allegro CLO XV, Ltd. / Allegro CLO VX LLC Series 2022-1A Class A, CME Term SOFR 3 Month Index + 1.500% 6.5485% 7/20/35 (b)(c)(d) | | 1,736,000 | 1,707,743 |

| Allegro CLO, Ltd. Series 2021-1A Class A, 3 month U.S. LIBOR + 1.140% 6.3904% 7/20/34 (b)(c)(d) | | 1,532,085 | 1,497,504 |

| Apollo Aviation Securitization Equity Trust Series 2020-1A Class A, 3.351% 1/16/40 (b) | | 461,173 | 387,089 |

| Ares CLO Series 2019-54A Class A, 3 month U.S. LIBOR + 1.320% 6.5803% 10/15/32 (b)(c)(d) | | 1,676,859 | 1,660,600 |

| Ares LIX CLO Ltd. Series 2021-59A Class A, 3 month U.S. LIBOR + 1.030% 6.2851% 4/25/34 (b)(c)(d) | | 1,039,487 | 1,014,955 |

| Ares LV CLO Ltd. Series 2021-55A Class A1R, 3 month U.S. LIBOR + 1.130% 6.3903% 7/15/34 (b)(c)(d) | | 1,931,133 | 1,901,274 |

| Ares LVIII CLO LLC Series 2022-58A Class AR, CME Term SOFR 3 Month Index + 1.330% 6.3163% 1/15/35 (b)(c)(d) | | 2,545,000 | 2,472,829 |

| Ares XLI CLO Ltd. / Ares XLI CLO LLC Series 2021-41A Class AR2, 3 month U.S. LIBOR + 1.070% 6.3303% 4/15/34 (b)(c)(d) | | 2,173,138 | 2,127,222 |

| Ares XXXIV CLO Ltd. Series 2020-2A Class AR2, 3 month U.S. LIBOR + 1.250% 6.5103% 4/17/33 (b)(c)(d) | | 665,897 | 654,892 |

| Babson CLO Ltd. Series 2021-1A Class AR, 3 month U.S. LIBOR + 1.150% 6.4103% 10/15/36 (b)(c)(d) | | 1,292,534 | 1,264,856 |

| Barings CLO Ltd.: | | | |

| Series 2021-1A Class A, 3 month U.S. LIBOR + 1.020% 6.2751% 4/25/34 (b)(c)(d) | | 2,282,638 | 2,239,373 |

| Series 2021-4A Class A, 3 month U.S. LIBOR + 1.220% 6.4704% 1/20/32 (b)(c)(d) | | 2,070,385 | 2,049,754 |

| Beechwood Park CLO Ltd. Series 2022-1A Class A1R, CME Term SOFR 3 Month Index + 1.300% 6.2863% 1/17/35 (b)(c)(d) | | 2,560,000 | 2,508,582 |

| BETHP Series 2021-1A Class A, 3 month U.S. LIBOR + 1.130% 6.3903% 1/15/35 (b)(c)(d) | | 1,953,217 | 1,912,266 |

| Blackbird Capital Aircraft: | | | |

| Series 2016-1A: | | | |

Class A, 4.213% 12/16/41 (b) | | 1,909,119 | 1,755,760 |

Class AA, 2.487% 12/16/41 (b)(c) | | 140,895 | 134,772 |

| Series 2021-1A Class A, 2.443% 7/15/46 (b) | | 2,251,941 | 1,938,970 |

| Bristol Park CLO, Ltd. Series 2020-1A Class AR, 3 month U.S. LIBOR + 0.990% 6.2503% 4/15/29 (b)(c)(d) | | 1,837,162 | 1,819,509 |

| Castlelake Aircraft Securitization Trust Series 2019-1A: | | | |

| Class A, 3.967% 4/15/39 (b) | | 1,188,542 | 1,055,130 |

| Class B, 5.095% 4/15/39 (b) | | 666,261 | 481,527 |

| Castlelake Aircraft Structured Trust: | | | |

| Series 2018-1 Class A, 4.125% 6/15/43 (b) | | 666,398 | 601,310 |

| Series 2021-1A Class A, 3.474% 1/15/46 (b) | | 447,935 | 409,412 |

| Cedar Funding Ltd.: | | | |

| Series 2021-10A Class AR, 3 month U.S. LIBOR + 1.100% 6.3504% 10/20/32 (b)(c)(d) | | 1,561,530 | 1,537,033 |

| Series 2022-15A Class A, CME Term SOFR 3 Month Index + 1.320% 6.3685% 4/20/35 (b)(c)(d) | | 2,429,000 | 2,366,327 |

| Cedar Funding XII CLO Ltd. / Cedar Funding XII CLO LLC Series 2021-12A Class A1R, 3 month U.S. LIBOR + 1.130% 6.3851% 10/25/34 (b)(c)(d) | | 1,198,676 | 1,175,249 |

| Cedar Funding Xvii Clo Ltd. Series 2023-17A Class A, CME Term SOFR 3 Month Index + 1.850% 1.85% 7/20/36 (b)(c)(d) | | 1,848,000 | 1,848,000 |

| CEDF Series 2021-6A Class ARR, 3 month U.S. LIBOR + 1.050% 6.3004% 4/20/34 (b)(c)(d) | | 1,887,884 | 1,838,489 |

| Cent CLO Ltd. / Cent CLO Series 2021-29A Class AR, 3 month U.S. LIBOR + 1.170% 6.4204% 10/20/34 (b)(c)(d) | | 1,944,015 | 1,889,705 |

| Columbia Cent CLO 31 Ltd. Series 2021-31A Class A1, 3 month U.S. LIBOR + 1.200% 6.4504% 4/20/34 (b)(c)(d) | | 2,085,721 | 2,032,085 |

| Columbia Cent Clo 32 Ltd. / Coliseum Series 2022-32A Class A1, CME Term SOFR 3 Month Index + 1.700% 6.7706% 7/24/34 (b)(c)(d) | | 2,607,000 | 2,567,853 |

| Columbia Cent CLO Ltd. / Columbia Cent CLO Corp. Series 2021-30A Class A1, 3 month U.S. LIBOR + 1.310% 6.5604% 1/20/34 (b)(c)(d) | | 2,729,841 | 2,686,000 |

| DB Master Finance LLC Series 2017-1A Class A2II, 4.03% 11/20/47 (b) | | 1,751,928 | 1,601,214 |

| Dryden 98 CLO Ltd. Series 2022-98A Class A, CME Term SOFR 3 Month Index + 1.300% 6.3485% 4/20/35 (b)(c)(d) | | 1,361,000 | 1,321,106 |

| Dryden CLO, Ltd.: | | | |

| Series 2021-76A Class A1R, 3 month U.S. LIBOR + 1.150% 6.4004% 10/20/34 (b)(c)(d) | | 1,290,693 | 1,269,446 |

| Series 2021-83A Class A, 3 month U.S. LIBOR + 1.220% 6.4817% 1/18/32 (b)(c)(d) | | 1,582,694 | 1,562,782 |

| Dryden Senior Loan Fund: | | | |

| Series 2020-78A Class A, 3 month U.S. LIBOR + 1.180% 6.4403% 4/17/33 (b)(c)(d) | | 1,318,912 | 1,302,387 |

| Series 2021-85A Class AR, 3 month U.S. LIBOR + 1.150% 6.4103% 10/15/35 (b)(c)(d) | | 1,717,039 | 1,680,988 |

| Series 2021-90A Class A1A, 3 month U.S. LIBOR + 1.130% 6.5091% 2/20/35 (b)(c)(d) | | 1,021,083 | 999,619 |

| Eaton Vance CLO, Ltd.: | | | |

| Series 2021-1A Class AR, 3 month U.S. LIBOR + 1.100% 6.3603% 4/15/31 (b)(c)(d) | | 885,205 | 875,040 |

| Series 2021-2A Class AR, 3 month U.S. LIBOR + 1.150% 6.4103% 1/15/35 (b)(c)(d) | | 2,283,000 | 2,245,579 |

| Eaton Vance CLO, Ltd. / Eaton Vance CLO LLC Series 2021-1A Class A13R, 3 month U.S. LIBOR + 1.250% 6.5103% 1/15/34 (b)(c)(d) | | 444,749 | 438,152 |

| Flatiron CLO Ltd. Series 2021-1A: | | | |

| Class A1, 3 month U.S. LIBOR + 1.110% 6.375% 7/19/34 (b)(c)(d) | | 1,392,832 | 1,370,912 |

| Class AR, 3 month U.S. LIBOR + 1.080% 6.3983% 11/16/34 (b)(c)(d) | | 1,993,704 | 1,963,968 |

| Flatiron CLO Ltd. / Flatiron CLO LLC Series 2020-1A Class A, 3 month U.S. LIBOR + 1.300% 6.6791% 11/20/33 (b)(c)(d) | | 2,529,561 | 2,504,050 |

| Horizon Aircraft Finance I Ltd. Series 2018-1 Class A, 4.458% 12/15/38 (b) | | 720,889 | 621,766 |

| Horizon Aircraft Finance Ltd. Series 2019-1 Class A, 3.721% 7/15/39 (b) | | 2,525,319 | 2,156,587 |

| Invesco CLO Ltd. Series 2021-3A Class A, 3 month U.S. LIBOR + 1.130% 6.4027% 10/22/34 (b)(c)(d) | | 1,367,988 | 1,342,195 |

| KKR CLO Ltd. Series 2022-41A Class A1, CME Term SOFR 3 Month Index + 1.330% 6.3163% 4/15/35 (b)(c)(d) | | 3,167,000 | 3,070,324 |

| Lucali CLO Ltd. Series 2021-1A Class A, 3 month U.S. LIBOR + 1.210% 6.4703% 1/15/33 (b)(c)(d) | | 981,516 | 972,357 |

| Madison Park Funding Series 2020-19A Class A1R2, 3 month U.S. LIBOR + 0.920% 6.1927% 1/22/28 (b)(c)(d) | | 1,135,732 | 1,129,032 |

| Madison Park Funding L Ltd. / Madison Park Funding L LLC Series 2021-50A Class A, CME Term SOFR 3 Month Index + 1.400% 6.4295% 4/19/34 (b)(c)(d) | | 2,186,940 | 2,152,743 |

| Madison Park Funding LII Ltd. / Madison Park Funding LII LLC Series 2021-52A Class A, 3 month U.S. LIBOR + 1.100% 6.3727% 1/22/35 (b)(c)(d) | | 2,223,747 | 2,174,969 |

| Madison Park Funding XLV Ltd./Madison Park Funding XLV LLC Series 2021-45A Class AR, 3 month U.S. LIBOR + 1.120% 6.3803% 7/15/34 (b)(c)(d) | | 1,390,072 | 1,367,920 |

| Madison Park Funding XXXII, Ltd. / Madison Park Funding XXXII LLC Series 2021-32A Class A2R, 3 month U.S. LIBOR + 1.200% 6.4727% 1/22/31 (b)(c)(d) | | 573,573 | 563,385 |

| Magnetite CLO LTD Series 2023-36A Class A, CME Term SOFR 3 Month Index + 1.800% 6.9585% 4/22/36 (b)(c)(d) | | 1,275,000 | 1,274,355 |

| Magnetite CLO Ltd. Series 2021-27A Class AR, 3 month U.S. LIBOR + 1.140% 6.3904% 10/20/34 (b)(c)(d) | | 461,006 | 452,700 |

| Magnetite IX, Ltd. / Magnetite IX LLC Series 2021-30A Class A, 3 month U.S. LIBOR + 1.130% 6.3851% 10/25/34 (b)(c)(d) | | 2,357,478 | 2,313,733 |

| Magnetite XXI Ltd. Series 2021-21A Class AR, 3 month U.S. LIBOR + 1.020% 6.2704% 4/20/34 (b)(c)(d) | | 1,823,166 | 1,791,045 |

| Magnetite XXIII, Ltd. Series 2021-23A Class AR, 3 month U.S. LIBOR + 1.130% 6.3851% 1/25/35 (b)(c)(d) | | 5,340,000 | 5,236,682 |

| Magnetite XXIX, Ltd. / Magnetite XXIX LLC Series 2021-29A Class A, 3 month U.S. LIBOR + 0.990% 6.2503% 1/15/34 (b)(c)(d) | | 1,904,754 | 1,884,966 |

| Milos CLO, Ltd. Series 2020-1A Class AR, 3 month U.S. LIBOR + 1.070% 6.3204% 10/20/30 (b)(c)(d) | | 1,918,098 | 1,902,191 |

| Park Place Securities, Inc. Series 2005-WCH1 Class M4, 1 month U.S. LIBOR + 1.240% 6.3954% 1/25/36 (c)(d) | | 41,427 | 40,554 |

| Peace Park CLO, Ltd. Series 2021-1A Class A, 3 month U.S. LIBOR + 1.130% 6.3804% 10/20/34 (b)(c)(d) | | 760,982 | 747,404 |

| Planet Fitness Master Issuer LLC: | | | |

| Series 2019-1A Class A2, 3.858% 12/5/49 (b) | | 1,433,990 | 1,214,958 |

| Series 2022-1A: | | | |

Class A2I, 3.251% 12/5/51 (b) | | 1,554,325 | 1,381,420 |

Class A2II, 4.008% 12/5/51 (b) | | 1,388,425 | 1,140,545 |

| Project Silver Series 2019-1 Class A, 3.967% 7/15/44 (b) | | 1,265,349 | 1,074,421 |

| Rockland Park CLO Ltd. Series 2021-1A Class A, 3 month U.S. LIBOR + 1.120% 6.3704% 4/20/34 (b)(c)(d) | | 2,604,698 | 2,568,472 |

| RR 7 Ltd. Series 2022-7A Class A1AB, CME Term SOFR 3 Month Index + 1.340% 6.3263% 1/15/37 (b)(c)(d) | | 2,626,000 | 2,567,270 |

| Sapphire Aviation Finance Series 2020-1A Class A, 3.228% 3/15/40 (b) | | 1,324,949 | 1,113,858 |

| SBA Tower Trust: | | | |

| Series 2019, 2.836% 1/15/50 (b) | | 1,902,000 | 1,805,813 |

| 1.884% 7/15/50 (b) | | 733,000 | 658,247 |

| 2.328% 7/15/52 (b) | | 560,000 | 479,020 |

| Stratus CLO, Ltd. Series 2022-1A Class A, CME Term SOFR 3 Month Index + 1.750% 6.7985% 7/20/30 (b)(c)(d) | | 391,104 | 389,595 |

| SYMP Series 2022-32A Class A1, CME Term SOFR 3 Month Index + 1.320% 6.3906% 4/23/35 (b)(c)(d) | | 2,727,000 | 2,666,357 |

| Symphony CLO XXI, Ltd. Series 2021-21A Class AR, 3 month U.S. LIBOR + 1.060% 6.3203% 7/15/32 (b)(c)(d) | | 256,728 | 253,160 |

| Symphony CLO XXV Ltd. / Symphony CLO XXV LLC Series 2021-25A Class A, 3 month U.S. LIBOR + 0.980% 6.245% 4/19/34 (b)(c)(d) | | 2,313,924 | 2,262,768 |

| Symphony CLO XXVI Ltd. / Symphony CLO XXVI LLC Series 2021-26A Class AR, 3 month U.S. LIBOR + 1.080% 6.3304% 4/20/33 (b)(c)(d) | | 2,177,375 | 2,140,662 |

| Terwin Mortgage Trust Series 2003-4HE Class A1, 1 month U.S. LIBOR + 0.860% 6.0104% 9/25/34 (c)(d) | | 2,132 | 2,045 |

| Thunderbolt Aircraft Lease Ltd. Series 2018-A Class A, 4.147% 9/15/38 (b)(c) | | 1,464,128 | 1,250,482 |

| Thunderbolt III Aircraft Lease Ltd. Series 2019-1 Class A, 3.671% 11/15/39 (b) | | 1,949,387 | 1,625,905 |

| Voya CLO Ltd. Series 2019-2A Class A, 3 month U.S. LIBOR + 1.270% 6.5204% 7/20/32 (b)(c)(d) | | 2,009,654 | 1,988,561 |

| Voya CLO Ltd./Voya CLO LLC: | | | |

| Series 2021-2A Class A1R, 3 month U.S. LIBOR + 1.160% 6.425% 7/19/34 (b)(c)(d) | | 1,277,198 | 1,253,765 |

| Series 2021-3A Class AR, 3 month U.S. LIBOR + 1.150% 6.4004% 10/20/34 (b)(c)(d) | | 2,613,900 | 2,565,065 |

| Voya CLO, Ltd. Series 2021-1A Class AR, 3 month U.S. LIBOR + 1.150% 6.4103% 7/16/34 (b)(c)(d) | | 1,289,773 | 1,267,853 |

| TOTAL ASSET-BACKED SECURITIES (Cost $149,103,303) | | | 142,421,604 |

| | | | |

| Collateralized Mortgage Obligations - 0.0% |

| | | Principal Amount (a) | Value ($) |

| Private Sponsor - 0.0% | | | |

| Cascade Funding Mortgage Trust Series 2021-HB6 Class A, 0.8983% 6/25/36 (b) | | 878,361 | 828,884 |

| Sequoia Mortgage Trust floater Series 2004-6 Class A3B, 6 month U.S. LIBOR + 0.880% 6.546% 7/20/34 (c)(d) | | 435 | 379 |

TOTAL PRIVATE SPONSOR | | | 829,263 |

| U.S. Government Agency - 0.0% | | | |

| Fannie Mae planned amortization class: | | | |

| Series 1999-54 Class PH, 6.5% 11/18/29 | | 3,876 | 3,872 |

| Series 1999-57 Class PH, 6.5% 12/25/29 | | 19,077 | 19,122 |

TOTAL U.S. GOVERNMENT AGENCY | | | 22,994 |

| TOTAL COLLATERALIZED MORTGAGE OBLIGATIONS (Cost $900,720) | | | 852,257 |

| | | | |

| Commercial Mortgage Securities - 3.6% |

| | | Principal Amount (a) | Value ($) |

| BAMLL Commercial Mortgage Securities Trust: | | | |

| floater Series 2022-DKLX: | | | |

Class A, CME Term SOFR 1 Month Index + 1.150% 6.297% 1/15/39 (b)(c)(d) | | 1,415,000 | 1,375,329 |

Class B, CME Term SOFR 1 Month Index + 1.550% 6.697% 1/15/39 (b)(c)(d) | | 267,000 | 257,934 |

Class C, CME Term SOFR 1 Month Index + 2.150% 7.297% 1/15/39 (b)(c)(d) | | 191,000 | 183,384 |

| sequential payer Series 2019-BPR Class ANM, 3.112% 11/5/32 (b) | | 1,183,000 | 1,076,080 |

| Series 2019-BPR: | | | |

Class BNM, 3.465% 11/5/32 (b) | | 265,000 | 223,364 |

Class CNM, 3.8425% 11/5/32 (b)(c) | | 110,000 | 87,428 |

| BANK sequential payer: | | | |

| Series 2018-BN10 Class A5, 3.688% 2/15/61 | | 118,089 | 108,856 |

| Series 2019-BN21 Class A5, 2.851% 10/17/52 | | 201,824 | 172,088 |

| Benchmark Mortgage Trust: | | | |

| sequential payer: | | | |

Series 2018-B4 Class A5, 4.121% 7/15/51 | | 420,518 | 391,294 |

Series 2019-B10 Class A4, 3.717% 3/15/62 | | 389,846 | 352,277 |

| Series 2018-B8 Class A5, 4.2317% 1/15/52 | | 2,882,896 | 2,645,224 |

| BFLD Trust floater sequential payer Series 2020-OBRK Class A, CME Term SOFR 1 Month Index + 2.160% 7.3115% 11/15/28 (b)(c)(d) | | 1,079,000 | 1,073,211 |

| BPR Trust floater Series 2022-OANA: | | | |

| Class A, CME Term SOFR 1 Month Index + 1.890% 7.045% 4/15/37 (b)(c)(d) | | 5,047,000 | 4,895,603 |

| Class B, CME Term SOFR 1 Month Index + 2.440% 7.594% 4/15/37 (b)(c)(d) | | 1,341,000 | 1,305,383 |

| BX Commercial Mortgage Trust floater: | | | |

| Series 2021-PAC: | | | |

Class A, 1 month U.S. LIBOR + 0.680% 5.8831% 10/15/36 (b)(c)(d) | | 2,648,253 | 2,568,511 |

Class B, 1 month U.S. LIBOR + 0.890% 6.0928% 10/15/36 (b)(c)(d) | | 396,287 | 381,620 |

Class C, 1 month U.S. LIBOR + 1.090% 6.2926% 10/15/36 (b)(c)(d) | | 530,325 | 507,039 |

Class D, 1 month U.S. LIBOR + 1.290% 6.4923% 10/15/36 (b)(c)(d) | | 514,682 | 487,725 |

Class E, 1 month U.S. LIBOR + 1.940% 7.1415% 10/15/36 (b)(c)(d) | | 1,789,733 | 1,704,416 |

| Series 2022-LP2: | | | |

Class A, CME Term SOFR 1 Month Index + 1.010% 6.1599% 2/15/39 (b)(c)(d) | | 3,336,634 | 3,234,429 |

Class B, CME Term SOFR 1 Month Index + 1.310% 6.4593% 2/15/39 (b)(c)(d) | | 1,005,446 | 964,104 |

Class C, CME Term SOFR 1 Month Index + 1.560% 6.7087% 2/15/39 (b)(c)(d) | | 1,005,446 | 951,760 |

Class D, CME Term SOFR 1 Month Index + 1.960% 7.1078% 2/15/39 (b)(c)(d) | | 1,005,446 | 955,776 |

| Bx Commercial Mortgage Trust 2: | | | |

| floater Series 2019-IMC: | | | |

Class B, 1 month U.S. LIBOR + 1.300% 6.493% 4/15/34 (b)(c)(d) | | 1,007,281 | 987,433 |

Class C, 1 month U.S. LIBOR + 1.600% 6.793% 4/15/34 (b)(c)(d) | | 665,897 | 651,507 |

Class D, 1 month U.S. LIBOR + 1.900% 7.093% 4/15/34 (b)(c)(d) | | 699,023 | 683,029 |

| floater sequential payer Series 2019-IMC Class A, 1 month U.S. LIBOR + 1.000% 6.193% 4/15/34 (b)(c)(d) | | 1,656,308 | 1,638,408 |

| BX Trust: | | | |

| floater: | | | |

Series 2019-XL: | | | |

| Class B, CME Term SOFR 1 Month Index + 1.190% 6.3415% 10/15/36 (b)(c)(d) | | 806,653 | 799,267 |

| Class C, CME Term SOFR 1 Month Index + 1.360% 6.5115% 10/15/36 (b)(c)(d) | | 1,014,182 | 1,003,295 |

| Class D, CME Term SOFR 1 Month Index + 1.560% 6.7115% 10/15/36 (b)(c)(d) | | 1,436,280 | 1,419,049 |

| Class E, CME Term SOFR 1 Month Index + 1.910% 7.0615% 10/15/36 (b)(c)(d) | | 2,018,196 | 1,990,162 |

Series 2022-GPA Class A, CME Term SOFR 1 Month Index + 2.160% 7.312% 10/15/39 (b)(c)(d) | | 1,404,000 | 1,401,799 |

Series 2022-IND: | | | |

| Class A, CME Term SOFR 1 Month Index + 1.490% 6.638% 4/15/37 (b)(c)(d) | | 2,489,606 | 2,451,486 |

| Class B, CME Term SOFR 1 Month Index + 1.940% 7.087% 4/15/37 (b)(c)(d) | | 1,269,067 | 1,246,140 |

| Class C, CME Term SOFR 1 Month Index + 2.290% 7.437% 4/15/37 (b)(c)(d) | | 286,593 | 279,452 |

| Class D, CME Term SOFR 1 Month Index + 2.830% 7.986% 4/15/37 (b)(c)(d) | | 239,896 | 229,977 |

| floater sequential payer Series 2019-XL Class A, CME Term SOFR 1 Month Index + 1.030% 6.1815% 10/15/36 (b)(c)(d) | | 482,314 | 479,314 |

| CF Hippolyta Issuer LLC sequential payer Series 2021-1A Class A1, 1.53% 3/15/61 (b) | | 2,918,461 | 2,527,719 |

| CHC Commercial Mortgage Trust floater Series 2019-CHC Class C, 1 month U.S. LIBOR + 1.750% 6.943% 6/15/34 (b)(c)(d) | | 234,074 | 228,148 |

| COMM Mortgage Trust sequential payer Series 2014-CR18 Class A5, 3.828% 7/15/47 | | 387,699 | 378,290 |

| Credit Suisse Mortgage Trust: | | | |

| floater Series 2019-ICE4: | | | |

Class B, 1 month U.S. LIBOR + 1.230% 6.423% 5/15/36 (b)(c)(d) | | 1,286,799 | 1,277,961 |

Class C, 1 month U.S. LIBOR + 1.430% 6.623% 5/15/36 (b)(c)(d) | | 242,397 | 239,782 |

| sequential payer Series 2020-NET Class A, 2.2569% 8/15/37 (b) | | 591,140 | 528,710 |

| Series 2018-SITE: | | | |

Class A, 4.284% 4/15/36 (b) | | 1,129,357 | 1,089,157 |

Class B, 4.5349% 4/15/36 (b) | | 347,211 | 331,831 |

Class C, 4.9414% 4/15/36 (b)(c) | | 233,110 | 222,275 |

Class D, 4.9414% 4/15/36 (b)(c) | | 465,913 | 439,509 |

| ELP Commercial Mortgage Trust floater Series 2021-ELP Class A, 1 month U.S. LIBOR + 0.700% 5.895% 11/15/38 (b)(c)(d) | | 3,658,294 | 3,550,445 |

| Extended Stay America Trust floater Series 2021-ESH: | | | |

| Class A, 1 month U.S. LIBOR + 1.080% 6.274% 7/15/38 (b)(c)(d) | | 1,168,050 | 1,144,961 |

| Class B, 1 month U.S. LIBOR + 1.380% 6.574% 7/15/38 (b)(c)(d) | | 664,979 | 648,705 |

| Class C, 1 month U.S. LIBOR + 1.700% 6.894% 7/15/38 (b)(c)(d) | | 2,406,454 | 2,341,521 |

| Class D, 1 month U.S. LIBOR + 2.250% 7.444% 7/15/38 (b)(c)(d) | | 988,795 | 960,875 |

| GS Mortgage Securities Trust floater Series 2021-IP: | | | |

| Class A, 1 month U.S. LIBOR + 0.950% 6.143% 10/15/36 (b)(c)(d) | | 1,559,690 | 1,466,817 |

| Class B, 1 month U.S. LIBOR + 1.150% 6.343% 10/15/36 (b)(c)(d) | | 241,085 | 222,877 |

| Class C, 1 month U.S. LIBOR + 1.550% 6.743% 10/15/36 (b)(c)(d) | | 2,497,757 | 2,275,854 |

| Intown Mortgage Trust floater sequential payer Series 2022-STAY Class A, CME Term SOFR 1 Month Index + 2.480% 7.6356% 8/15/39 (b)(c)(d) | | 2,328,000 | 2,327,997 |

| JPMorgan Chase Commercial Mortgage Securities Trust Series 2018-WPT: | | | |

| Class CFX, 4.9498% 7/5/33 (b) | | 223,602 | 191,620 |

| Class DFX, 5.3503% 7/5/33 (b) | | 386,779 | 323,725 |

| Class EFX, 5.3635% 7/5/33 (b)(c) | | 470,207 | 386,497 |

| Life Financial Services Trust floater Series 2022-BMR2: | | | |

| Class A1, CME Term SOFR 1 Month Index + 1.290% 6.4422% 5/15/39 (b)(c)(d) | | 3,430,000 | 3,356,054 |

| Class B, CME Term SOFR 1 Month Index + 1.790% 6.9409% 5/15/39 (b)(c)(d) | | 2,383,000 | 2,327,726 |

| Class C, CME Term SOFR 1 Month Index + 2.090% 7.2401% 5/15/39 (b)(c)(d) | | 1,335,000 | 1,297,340 |

| Class D, CME Term SOFR 1 Month Index + 2.540% 7.6889% 5/15/39 (b)(c)(d) | | 1,187,000 | 1,129,371 |

| LIFE Mortgage Trust floater Series 2021-BMR: | | | |

| Class A, CME Term SOFR 1 Month Index + 0.810% 5.9615% 3/15/38 (b)(c)(d) | | 2,199,143 | 2,142,530 |

| Class B, CME Term SOFR 1 Month Index + 0.990% 6.1415% 3/15/38 (b)(c)(d) | | 530,641 | 514,648 |

| Class C, CME Term SOFR 1 Month Index + 1.210% 6.3615% 3/15/38 (b)(c)(d) | | 333,761 | 321,292 |

| Class D, CME Term SOFR 1 Month Index + 1.510% 6.6615% 3/15/38 (b)(c)(d) | | 464,311 | 446,237 |

| Class E, CME Term SOFR 1 Month Index + 1.860% 7.0115% 3/15/38 (b)(c)(d) | | 405,819 | 387,730 |

| Morgan Stanley Capital I Trust: | | | |

| floater Series 2018-BOP: | | | |

Class B, 1 month U.S. LIBOR + 1.250% 6.443% 8/15/33 (b)(c)(d) | | 1,059,546 | 845,794 |

Class C, 1 month U.S. LIBOR + 1.500% 6.693% 8/15/33 (b)(c)(d)(g) | | 2,551,942 | 1,832,918 |

| sequential payer Series 2019-MEAD Class A, 3.17% 11/10/36 (b) | | 2,570,651 | 2,386,610 |

| Series 2018-H4 Class A4, 4.31% 12/15/51 | | 1,895,246 | 1,763,412 |

| Series 2019-MEAD: | | | |

Class B, 3.283% 11/10/36 (b)(c) | | 371,442 | 340,792 |

Class C, 3.283% 11/10/36 (b)(c) | | 356,413 | 320,247 |

| Prima Capital Ltd. floater sequential payer Series 2021-9A Class A, 1 month U.S. LIBOR + 1.450% 6.6066% 12/15/37 (b)(c)(d)(g) | | 139,306 | 138,872 |

| Providence Place Group Ltd. Partnership Series 2000-C1 Class A2, 7.75% 7/20/28 (b) | | 870,943 | 876,720 |

| SPGN Mortgage Trust floater Series 2022-TFLM: | | | |

| Class B, CME Term SOFR 1 Month Index + 2.000% 7.147% 2/15/39 (b)(c)(d) | | 642,000 | 607,759 |

| Class C, CME Term SOFR 1 Month Index + 2.650% 7.797% 2/15/39 (b)(c)(d) | | 334,000 | 315,093 |

| SREIT Trust floater Series 2021-MFP: | | | |

| Class A, 1 month U.S. LIBOR + 0.730% 5.9241% 11/15/38 (b)(c)(d) | | 2,470,353 | 2,399,514 |

| Class B, 1 month U.S. LIBOR + 1.070% 6.2731% 11/15/38 (b)(c)(d) | | 1,414,917 | 1,372,318 |

| Class C, 1 month U.S. LIBOR + 1.320% 6.5223% 11/15/38 (b)(c)(d) | | 878,763 | 846,519 |

| Class D, 1 month U.S. LIBOR + 1.570% 6.7715% 11/15/38 (b)(c)(d) | | 577,561 | 554,739 |

| VLS Commercial Mortgage Trust: | | | |

| sequential payer Series 2020-LAB Class A, 2.13% 10/10/42 (b) | | 1,766,729 | 1,378,071 |

| Series 2020-LAB Class B, 2.453% 10/10/42 (b) | | 113,488 | 87,556 |

| Wells Fargo Commercial Mortgage Trust: | | | |

| floater Series 2021-FCMT Class A, 1 month U.S. LIBOR + 1.200% 6.393% 5/15/31 (b)(c)(d) | | 1,349,000 | 1,286,192 |

| sequential payer Series 2015-C26 Class A4, 3.166% 2/15/48 | | 1,026,911 | 976,077 |

| Series 2018-C48 Class A5, 4.302% 1/15/52 | | 850,545 | 798,560 |

| TOTAL COMMERCIAL MORTGAGE SECURITIES (Cost $101,344,810) | | | 95,319,120 |

| | | | |

| Municipal Securities - 0.5% |

| | | Principal Amount (a) | Value ($) |

| Illinois Gen. Oblig.: | | | |

| Series 2003, 5.1% 6/1/33 | | 1,475,000 | 1,449,493 |

| Series 2010-1, 6.63% 2/1/35 | | 3,480,000 | 3,631,677 |

| Series 2010-3: | | | |

6.725% 4/1/35 | | 2,686,154 | 2,820,238 |

7.35% 7/1/35 | | 1,578,571 | 1,701,274 |

| New Jersey Econ. Dev. Auth. State Pension Fdg. Rev. Series 1997, 7.425% 2/15/29 (Nat'l. Pub. Fin. Guarantee Corp. Insured) | | 2,221,000 | 2,385,529 |

| TOTAL MUNICIPAL SECURITIES (Cost $12,551,269) | | | 11,988,211 |

| | | | |

| Foreign Government and Government Agency Obligations - 0.2% |

| | | Principal Amount (a) | Value ($) |

| Emirate of Abu Dhabi 3.875% 4/16/50 (b) | | 1,748,000 | 1,466,992 |

| Kingdom of Saudi Arabia: | | | |

| 3.25% 10/22/30 (b) | | 966,000 | 874,578 |

| 4.5% 4/22/60 (b) | | 736,000 | 635,845 |

| State of Qatar 4.4% 4/16/50 (b) | | 2,181,000 | 1,979,803 |

| TOTAL FOREIGN GOVERNMENT AND GOVERNMENT AGENCY OBLIGATIONS (Cost $5,810,461) | | | 4,957,218 |

| | | | |

| Bank Notes - 0.1% |

| | | Principal Amount (a) | Value ($) |

| Discover Bank 4.682% 8/9/28 (c) | | 847,000 | 774,418 |

| Regions Bank 6.45% 6/26/37 | | 2,368,000 | 2,329,884 |

| TOTAL BANK NOTES (Cost $3,285,406) | | | 3,104,302 |

| | | | |

| Money Market Funds - 5.2% |

| | | Shares | Value ($) |

Fidelity Cash Central Fund 5.14% (h) (Cost $139,340,417) | | 139,312,949 | 139,340,811 |

| | | | |

| TOTAL INVESTMENT IN SECURITIES - 110.8% (Cost $3,199,111,749) | 2,948,142,082 |

NET OTHER ASSETS (LIABILITIES) - (10.8)% | (287,971,114) |

| NET ASSETS - 100.0% | 2,660,170,968 |

| | |

| TBA Sale Commitments |

| | Principal Amount (a) | Value ($) |

| Ginnie Mae | | |

| 2% 7/1/53 | (4,700,000) | (3,946,308) |

| 2% 7/1/53 | (950,000) | (797,658) |

| 2% 7/1/53 | (2,350,000) | (1,973,154) |

| 2.5% 7/1/53 | (5,100,000) | (4,413,643) |

| 2.5% 7/1/53 | (10,250,000) | (8,870,556) |

| 2.5% 7/1/53 | (5,100,000) | (4,413,643) |

| 2.5% 7/1/53 | (5,800,000) | (5,019,437) |

| 2.5% 7/1/53 | (4,450,000) | (3,851,119) |

| 3.5% 7/1/53 | (5,550,000) | (5,121,144) |

| | | |

| TOTAL GINNIE MAE | | (38,406,662) |

| | | |

| Uniform Mortgage Backed Securities | | |

| 1.5% 7/1/38 | (2,500,000) | (2,156,304) |

| 2% 7/1/38 | (1,800,000) | (1,595,011) |

| 2% 7/1/38 | (250,000) | (221,529) |

| 2% 7/1/53 | (9,500,000) | (7,741,421) |

| 2% 7/1/53 | (7,600,000) | (6,193,137) |

| 2.5% 7/1/53 | (150,000) | (127,119) |

| 4.5% 7/1/53 | (1,900,000) | (1,825,782) |

| 5% 7/1/53 | (1,100,000) | (1,077,699) |

| 5.5% 7/1/53 | (2,600,000) | (2,587,506) |

| | | |

| TOTAL UNIFORM MORTGAGE BACKED SECURITIES | | (23,525,508) |

| | | |

TOTAL TBA SALE COMMITMENTS (Proceeds $62,133,076) | | (61,932,170) |

Legend

| (a) | Amount is stated in United States dollars unless otherwise noted. |

| (b) | Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers. At the end of the period, the value of these securities amounted to $326,205,662 or 12.3% of net assets. |

| (c) | Coupon rates for floating and adjustable rate securities reflect the rates in effect at period end. |

| (d) | Coupon is indexed to a floating interest rate which may be multiplied by a specified factor and/or subject to caps or floors. |

| (e) | Security or a portion of the security has been segregated as collateral for mortgage-backed or asset-backed securities purchased on a delayed delivery or when-issued basis. At period end, the value of securities pledged amounted to $2,080,937. |

| (f) | Security or a portion of the security purchased on a delayed delivery or when-issued basis. |

| (h) | Affiliated fund that is generally available only to investment companies and other accounts managed by Fidelity Investments. The rate quoted is the annualized seven-day yield of the fund at period end. A complete unaudited listing of the fund's holdings as of its most recent quarter end is available upon request. In addition, each Fidelity Central Fund's financial statements are available on the SEC's website or upon request. |

Affiliated Central Funds

Fiscal year to date information regarding the Fund's investments in Fidelity Central Funds, including the ownership percentage, is presented below.

| Affiliate | Value, beginning of period ($) | Purchases ($) | Sales Proceeds ($) | Dividend Income ($) | Realized Gain (loss) ($) | Change in Unrealized appreciation (depreciation) ($) | Value, end of period ($) | % ownership, end of period |

| Fidelity Cash Central Fund 5.14% | 167,330,367 | 252,441,466 | 280,431,022 | 4,399,060 | - | - | 139,340,811 | 0.4% |

| Fidelity Securities Lending Cash Central Fund 5.14% | 53,359,291 | 513,649,132 | 567,008,423 | 34,082 | - | - | - | 0.0% |

| Total | 220,689,658 | 766,090,598 | 847,439,445 | 4,433,142 | - | - | 139,340,811 | |

| | | | | | | | | |

Amounts in the dividend income column in the above table include any capital gain distributions from underlying funds, which are presented in the corresponding line item in the Statement of Operations, if applicable.

Amounts in the dividend income column for Fidelity Securities Lending Cash Central Fund represents the income earned on investing cash collateral, less rebates paid to borrowers and any lending agent fees associated with the loan, plus any premium payments received for lending certain types of securities.

Amounts included in the purchases and sales proceeds columns may include in-kind transactions, if applicable.

Investment Valuation

The following is a summary of the inputs used, as of June 30, 2023, involving the Fund's assets and liabilities carried at fair value. The inputs or methodology used for valuing securities may not be an indication of the risk associated with investing in those securities. For more information on valuation inputs, and their aggregation into the levels used below, please refer to the Investment Valuation section in the accompanying Notes to Financial Statements.

| Valuation Inputs at Reporting Date: |

| Description | Total ($) | Level 1 ($) | Level 2 ($) | Level 3 ($) |

Investments in Securities: | | | | |

|

| Corporate Bonds | 759,458,755 | - | 759,458,755 | - |

|

| U.S. Government and Government Agency Obligations | 1,176,266,370 | - | 1,176,266,370 | - |

|

| U.S. Government Agency - Mortgage Securities | 614,433,434 | - | 614,433,434 | - |

|

| Asset-Backed Securities | 142,421,604 | - | 142,421,604 | - |

|

| Collateralized Mortgage Obligations | 852,257 | - | 852,257 | - |

|

| Commercial Mortgage Securities | 95,319,120 | - | 93,347,330 | 1,971,790 |

|

| Municipal Securities | 11,988,211 | - | 11,988,211 | - |

|

| Foreign Government and Government Agency Obligations | 4,957,218 | - | 4,957,218 | - |

|

| Bank Notes | 3,104,302 | - | 3,104,302 | - |

|

| Money Market Funds | 139,340,811 | 139,340,811 | - | - |

| Total Investments in Securities: | 2,948,142,082 | 139,340,811 | 2,806,829,481 | 1,971,790 |

Other Financial Instruments: | | | | |

|

| TBA Sale Commitments | (61,932,170) | - | (61,932,170) | - |

| Total Other Financial Instruments: | (61,932,170) | - | (61,932,170) | - |

| Statement of Assets and Liabilities |

| | | | June 30, 2023 (Unaudited) |

| | | | | |

| Assets | | | | |

| Investment in securities, at value - See accompanying schedule: | | | | |

Unaffiliated issuers (cost $3,059,771,332) | $ | 2,808,801,271 | | |

Fidelity Central Funds (cost $139,340,417) | | 139,340,811 | | |

| | | | | |

| | | | | |

| Total Investment in Securities (cost $3,199,111,749) | | | $ | 2,948,142,082 |

| Receivable for investments sold | | | | 6,819,621 |

| Receivable for TBA sale commitments | | | | 62,133,076 |

| Receivable for fund shares sold | | | | 559 |

| Interest receivable | | | | 18,831,138 |

| Distributions receivable from Fidelity Central Funds | | | | 674,571 |

Total assets | | | | 3,036,601,047 |

| Liabilities | | | | |

| Payable for investments purchased | | | | |

Regular delivery | $ | 6,283,174 | | |

Delayed delivery | | 307,745,808 | | |

| TBA sale commitments, at value | | 61,932,170 | | |

| Payable for fund shares redeemed | | 466,788 | | |

| Other payables and accrued expenses | | 2,139 | | |

| Total Liabilities | | | | 376,430,079 |

| Net Assets | | | $ | 2,660,170,968 |

| Net Assets consist of: | | | | |

| Paid in capital | | | $ | 2,973,694,695 |

| Total accumulated earnings (loss) | | | | (313,523,727) |

| Net Assets | | | $ | 2,660,170,968 |

Net Asset Value , offering price and redemption price per share ($2,660,170,968 ÷ 28,770,358 shares) | | | $ | 92.46 |

| Statement of Operations |

| | | | Six months ended June 30, 2023 (Unaudited) |

| Investment Income | | | | |

| Interest | | | $ | 44,847,325 |

| Income from Fidelity Central Funds (including $34,082 from security lending) | | | | 4,433,142 |

| Total Income | | | | 49,280,467 |

| Expenses | | | | |

| Custodian fees and expenses | $ | 4,597 | | |

| Independent trustees' fees and expenses | | 4,454 | | |

| Total expenses before reductions | | 9,051 | | |

| Expense reductions | | (5,420) | | |

| Total expenses after reductions | | | | 3,631 |

| Net Investment income (loss) | | | | 49,276,836 |

| Realized and Unrealized Gain (Loss) | | | | |

| Net realized gain (loss) on: | | | | |

| Investment Securities: | | | | |

| Unaffiliated issuers | | (12,780,378) | | |

| Total net realized gain (loss) | | | | (12,780,378) |

| Change in net unrealized appreciation (depreciation) on: | | | | |

| Investment Securities: | | | | |

| Unaffiliated issuers | | 30,118,114 | | |

| TBA Sale commitments | | (2,126,509) | | |

| Total change in net unrealized appreciation (depreciation) | | | | 27,991,605 |

| Net gain (loss) | | | | 15,211,227 |

| Net increase (decrease) in net assets resulting from operations | | | $ | 64,488,063 |