UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| | |

| Investment Company Act file number: | | 811-04864 |

| |

| Exact name of registrant as specified in charter: | | JennisonDryden Portfolios |

| |

| Address of principal executive offices: | | Gateway Center 3, 100 Mulberry Street, Newark, New Jersey 07102 |

| |

| Name and address of agent for service: | | Deborah A. Docs Gateway Center 3, 100 Mulberry Street, Newark, New Jersey 07102 |

| |

| Registrant’s telephone number, including area code: | | 800-225-1852 |

| |

| Date of fiscal year end: | | 8/31/2007 |

| | (Registrant changed its fiscal year end from October 31) |

| |

| Date of reporting period: | | 8/31/2007 |

Item 1 – Reports to Stockholders

| | |

| AUGUST 31, 2007 | | ANNUAL REPORT |

Jennison Value Fund

FUND TYPE

Large-capitalization stock

OBJECTIVE

Capital appreciation

This report is not authorized for distribution to prospective investors unless preceded or accompanied by a current prospectus.

The views expressed in this report and information about the Fund’s portfolio holdings are for the period covered by this report and are subject to change thereafter.

JennisonDryden, Jennison, Prudential Financial and the Rock Prudential logo are registered service marks of The Prudential Insurance Company of America, Newark, NJ, and its affiliates.

October 15, 2007

Dear Shareholder:

On the following pages, you’ll find your annual report for the Jennison Value Fund, which includes performance data, an analysis of Fund performance, and a listing of its holdings at period-end. The Fund’s fiscal year has changed from a reporting period that ends October 31 to one that ends August 31. This change should have no impact on the way the Fund is managed. Shareholders will receive future annual and semiannual reports on the new fiscal year-end schedule.

Mutual fund prices and returns will rise or fall over time, and asset managers tend to have periods when they perform better or worse than their long-term average. The best measures of a mutual fund’s quality are its return compared to that of similar investments and the variability of its return over the long term. We recommend that you review your portfolio regularly with your financial adviser.

Sincerely,

Judy A. Rice, President

Jennison Value Fund

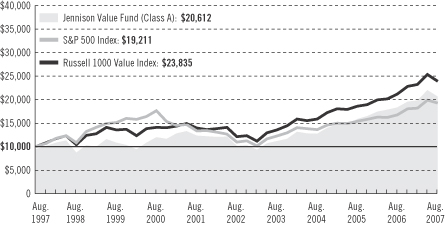

Your Fund’s Performance

Fund objective

The investment objective of the Jennison Value Fund is capital appreciation. There can be no assurance that the Fund will achieve its investment objective.

Performance data quoted represent past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate, so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the past performance data quoted. An investor may obtain performance data as of the most recent month-end by visiting our website at www.jennisondryden.com or by calling (800) 225-1852. Class A and Class L shares have a maximum initial sales charge of 5.50% and 5.75%, respectively. Gross operating expenses: Class A, 1.00%; Class B, 1.70%; Class C, 1.70%; Class L, 1.20%; Class M, 1.70%; Class R, 1.45%; Class X, 1.70%; Class Z, 0.70%. Net operating expenses apply to: Class A, 0.95%; Class B, 1.70%; Class C, 1.70%; Class L, 1.20%; Class M, 1.70%; Class R, 1.20%; Class X, 1.70%; Class Z, 0.70%, after contractual reduction through 2/28/2008.

| | | | | | | | | | | |

| Cumulative Total Returns as of 8/31/07 |

| | | One Year | | | Five Years | | | Ten Years | | | Since Inception1 |

Class A | | 12.88 | % | | 104.03 | % | | 118.11 | % | | — |

Class B | | 12.01 | | | 96.58 | | | 102.34 | | | — |

Class C | | 12.01 | | | 96.57 | | | 102.34 | | | — |

Class L | | N/A | | | N/A | | | N/A | | | 5.28%(3/19/07) |

Class M | | N/A | | | N/A | | | N/A | | | 5.03(3/19/07) |

Class R | | 12.62 | | | N/A | | | N/A | | | 39.37(6/3/05) |

Class X | | N/A | | | N/A | | | N/A | | | 5.03(3/19/07) |

Class Z | | 13.18 | | | 106.55 | | | 123.64 | | | — |

S&P 500 Index2 | | 15.13 | | | 76.18 | | | 92.11 | | | ** |

Russell 1000 Value Index3 | | 12.85 | | | 97.15 | | | 138.35 | | | *** |

Lipper Multi-Cap Value Funds Avg.4 | | 12.83 | | | 87.79 | | | 119.31 | | | **** |

| | |

| 2 | | Visit our website at www.jennisondryden.com |

| | | | | | | | | | | |

| Average Annual Total Returns5 as of 9/30/07 |

| | | One Year | | | Five Years | | | Ten Years | | | Since Inception1 |

Class A | | 9.37 | % | | 17.88 | % | | 7.07 | % | | — |

Class B | | 9.89 | | | 18.23 | | | 6.81 | | | — |

Class C | | 13.89 | | | 18.34 | | | 6.81 | | | — |

Class L | | N/A | | | N/A | | | N/A | | | N/A |

Class M | | N/A | | | N/A | | | N/A | | | N/A |

Class R | | 15.53 | | | N/A | | | N/A | | | 17.16% (6/3/05) |

Class X | | N/A | | | N/A | | | N/A | | | N/A |

Class Z | | 16.03 | | | 19.50 | | | 7.88 | | | — |

S&P 500 Index2 | | 16.42 | | | 15.44 | | | 6.57 | | | ** |

Russell 1000 Value Index3 | | 14.45 | | | 18.07 | | | 8.80 | | | *** |

Lipper Multi-Cap Value Funds Avg.4 | | 13.55 | | | 16.56 | | | 7.78 | | | **** |

The cumulative total returns do not reflect the deduction of applicable sales charges. If reflected, the applicable sales charges would reduce the cumulative total returns performance quoted. The average annual total returns assume the payment of the maximum applicable sales charge. Class A and Class L shares are subject to a maximum front-end sales charge of 5.50% and 5.75%, respectively. Under certain circumstances, Class A shares may be subject to a contingent deferred sales charge (CDSC) of 1%. Class B, Class C, Class L, Class M, and Class X shares are subject to a maximum CDSC of 5%, 1%, 1%, 6%, and 6%, respectively. Class R and Class Z shares are not subject to a sales charge.

Source: Prudential Investments LLC and Lipper Inc. Performance figures may reflect fee waivers and/or expense reimbursements. In the absence of such fee waivers and/or expense reimbursements, total returns would be lower.

1Inception date returns are provided for any share class with less than 10 calendar years.

2The S&P 500 Index is an unmanaged index of 500 stocks of large U.S. public companies. It gives a broad look at how U.S. stock prices have performed.

3The Russell 1000 Value Index is an unmanaged index comprising those securities in the Russell 1000 Index with a less-than-average growth orientation. Companies in this index generally have low price-to-book and price-to-earnings ratios, higher dividend yields, and lower forecasted growth values.

4The Lipper Multi-Cap Value Funds Average (Lipper Average) represents returns based on an average return of all funds in the Lipper Multi-Cap Value Funds category for the periods noted. Funds in the Lipper Average typically have a below-average price-to-earnings ratio, price-to-book ratio, and three-year sales-per-share growth value compared with the S&P SuperComposite 1500 Index.

5The average annual total returns take into account applicable sales charges. Class A, Class B, Class C, Class L, Class M, Class R, and Class X shares are subject to an annual distribution and service (12b-1) fee of up to 0.30%, 1.00%, 1.00%, 0.50%, 1.00%, 0.75%, and 1.00%, respectively. Approximately seven years after purchase, Class B shares will automatically convert to Class A shares on a quarterly basis. Approximately eight years after purchase, Class M shares will automatically convert to Class A shares on a quarterly basis. Approximately 10 years after purchase (eight years in the case of shares purchased prior to August 19, 1998), Class X shares will automatically convert to Class A shares on a quarterly basis. Class Z shares are not subject to a 12b-1 fee. The returns in the tables do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or following the redemption of Fund shares.

Your Fund’s Performance (continued)

**S&P 500 Index Closest Month-End to Inception cumulative total return as of 8/31/07 is 4.52% for Class L, Class M, and Class X; and 29.00% for Class R. S&P 500 Index Closest Month-End to Inception average annual total return as of 9/30/07 is 13.29% for Class R. Class L, Class M, and Class X shares have been in existence for less than one year and have no average annual total return performance information available.

***Russell 1000 Value Index Closest Month-End to Inception cumulative total return as of 8/31/07 is 1.19% for Class L, Class M, and Class X; and 33.19% for Class R. Russell 1000 Value Index Closest Month-End to Inception average annual total return as of 9/30/07 is 14.72% for Class R. Class L, Class M, and Class X shares have been in existence for less than one year and have no average annual total return performance information available.

****Lipper Average Closest Month-End to Inception cumulative total return as of 8/31/07 is 1.36% for Class L, Class M, and Class X; and 29.36% for Class R. Lipper Average Closest Month-End to Inception average annual total return as of 9/30/07 is 12.96% for Class R. Class L, Class M, and Class X shares have been in existence for less than one year and have no average annual total return performance information available.

Investors cannot invest directly in an index. The returns for the S&P 500 Index, the Russell 1000 Value Index, and the Lipper Average would be lower if they included the effects of sales charges, operating expenses of a mutual fund, or taxes. Returns for the Lipper Average reflect the deduction of operating expenses, but not sales charges or taxes.

| | | |

| Five Largest Holdings expressed as a percentage of net assets as of 8/31/07 | | | |

Cadbury Schweppes PLC, Food Products | | 2.5 | % |

Citigroup, Inc., Diversified Financial Services | | 2.4 | |

American International Group, Inc., Insurance | | 2.4 | |

General Electric Co., Industrial Conglomerates | | 2.3 | |

H & R Block, Inc., Diversified Consumer Services | | 2.2 | |

Holdings reflect only long-term investments and are subject to change.

| | | |

| Five Largest Industries expressed as a percentage of net assets as of 8/31/07 | | | |

Oil, Gas & Consumable Fuels | | 14.9 | % |

Insurance | | 6.9 | |

Diversified Financial Services | | 6.6 | |

Media | | 5.4 | |

Food Products | | 4.7 | |

Industry weightings reflect only long-term investments and are subject to change.

| | |

| 4 | | Visit our website at www.jennisondryden.com |

Strategy and Performance Overview

How did the Fund perform during the reporting period?

The Jennison Value Fund’s Class A shares returned 8.66% for the 10-month reporting period from November 1, 2006, through August 31, 2007*, outperforming the 7.14% return of its benchmark, the Russell 1000 Value Index (the Value Index), the 6.96% return of the Lipper Multi-Cap Value Funds Average, and the 7.93% return of the Lipper Large-Cap Value Funds Average.

A diverse group of stocks drove the Fund’s strong performance relative to the Value Index, illustrating the effectiveness of our bottom-up approach to portfolio construction in which we select stocks one at a time based on in-house analysis of individual company fundamentals. The top 10 contributors came from seven different sectors, and all posted double-digit returns. The overarching theme in the current market environment is that there is no theme; it is truly a stock-picker’s market. During the reporting period, every sector, except healthcare, added to the Fund’s returns.

The Fund’s holdings in the poorly performing financials sector were its largest source of relative gain, due to a combination of good stock selection and the Fund’s substantial underweight exposure, especially in commercial banks. We maintained our contrarian stance that banks are fundamentally unattractive because of their understated expenses and their lower earnings. Banks are also prey to a contraction in net interest margin, a percentage that reflects income left over after subtracting interest paid to depositors from interest earned on investments and loans. Stock selection in consumer discretionary, materials, and consumer staples also meaningfully added to the Fund’s relative returns.

In the energy sector, the Fund underperformed the Value Index because it did not own a few large top-performing integrated oil companies, such as Exxon Mobil and Chevron. It did own Trident Resources, which declined in value. (Trident Resources is mentioned in the section below that discusses greatest detractors.) While positions in the telecom services sector added to the Fund’s returns, it trailed its benchmark in this sector primarily because it did not own AT&T, a stock whose fundamentals we continue to dislike even though it rose nearly 20% during the reporting period. The Fund also lagged the Value Index in healthcare and information technology due to individual stock disappointments.

What was the market environment like for value stocks?

In the beginning of the period, U.S. economic growth moderated. Robust foreign economies stepped in to pick up the slack, driving the strongest cumulative growth in global gross domestic product of the decade. The final quarter of 2006 proved to be a

*Fund changed its fiscal year-end to August 31. Refer to the Fund’s previous annual report for performance information prior to November 1, 2006.

Strategy and Performance Overview (continued)

good one for U.S. equities, as well as markets around the globe, thanks to a continued mix of strong corporate profits, low interest rates, and abundant liquidity.

While the market was up the majority of the reporting period, the environment changed in 2007 amid worries that problems in the U.S. market for subprime mortgages (home loans made to borrowers with poor credit histories) might expand into a widespread credit crunch. This, in turn, prompted central banks around the world to inject money into their monetary systems in early August in an effort to ensure liquidity. On August 17, the Federal Open Market Committee (FOMC) cut the discount rate—the rate at which member banks borrow short-term funds directly from a Federal Reserve Bank—to 5.75% from 6.25%. Although recent data suggested the economy would continue to expand at a moderate pace, the FOMC noted that “downside risks to growth have increased appreciably.” It said that it is “prepared to act as needed to mitigate the adverse effects on the economy arising from the disruptions in financial markets.” These actions seem to have had somewhat of a stabilizing effect. While we expect growth to slow over the next two or three quarters, we believe the equity market remains healthy.

Financials shares declined overall, as investors feared the subprime-mortgage contagion would continue to spill into the broader markets. While the Fund did not have holdings that were highly exposed to the mortgage market, its positions were not immune to the negative headlines that chronicled the subprime-mortgage crisis.

What holdings made the largest positive contributions to the Fund’s return?

The Fund’s energy holdings made the strongest contribution to its returns. During the reporting period, the spot price for crude oil climbed steadily and surpassed $78 per barrel, supporting our long-term, bullish outlook for the sector. In our view, supply / demand imbalances will continue, keeping oil prices above historical levels. Hess, Petroleo Brasileiro (Petrobras), and Occidental Petroleum all advanced. Petrobras is a partially government-owned enterprise that operates in all sectors of the oil and gas industry in Brazil and the rest of Latin America, the United States, and offshore-West Africa. Petrobras is rare among its peer group of very large integrated oil companies with estimated production growth roughly 10% per year over the next several years. Production growth is driven by attractive exposure to potential deepwater discoveries located offshore of Brazil and Nigeria. In addition to strong upstream growth prospects, Petrobras implemented refining upgrades, has a growing gas business that should generate cash, and sizeable potential in international markets.

Stock selection in consumer discretionary, materials, consumer staples, industrials, and utilities sectors also meaningfully added to the Fund’s returns. Consumer discretionary stock Liberty Global, materials holding Mosaic, consumer staples

| | |

| 6 | | Visit our website at www.jennisondryden.com |

position Kroger, industrials stock Honeywell International, and utilities position NRG Energy were standout performers. Liberty Global, an international broadband communications provider, gained over 55% during the reporting period. We believe that Liberty Global is poised to benefit from subscriber growth as high definition television, digital cable, and Internet phone become more widespread. We continue to like its attractive valuation, believing it to be one of the cheapest stocks in its peer group.

Mosaic Co. was formed in 2004 through the merger of IMC Global and the fertilizer business of Cargill. It is primarily a producer of fertilizers, including phosphate, potash, and nitrogen. Shares of Mosaic rose dramatically when fertilizer demand and prices surged as U.S. growers prepared for an unprecedented 10 million acre increase in corn plantings to meet the demand from biofuels and export markets. Demand is also increasing in international markets like China and India. We sold the position at a profit because it had become overvalued. Since our initial purchase in June 2003, the stock had appreciated approximately 364%.

Merchant power generation company NRG Energy benefited from the potential acquisition of Texas-based utility company TXU by a private equity firm. The proposed deal demonstrated to the public market that private equity firms are valuing energy generation assets very highly, and NRG rose in price. In our view, NRG is attractively valued and should benefit from declining spare generation capacity as demand growth catches up to supply. Additionally, we believe its portfolio of attractive low-cost power generation plants should help the company increase profit margins in an environment of rising energy and capacity prices.

Although Honeywell International, an aerospace and defense company, lagged its peers, we originally purchased the stock in June 2005 expecting a cyclical upturn due to the high demand for replacement parts following an increase in new airplane sales. We believed this would drive acceleration in revenue growth. Additionally, the company’s aerospace division was undergoing a series of restructuring efforts that, in our view, should result in greater profitability. These assumptions proved correct. In April, Honeywell reported its best quarter since the 1999 Allied Signal merger, beating consensus. The results were strong across aerospace and automation and control units. Honeywell advanced again in July as the company delivered another quarter that exceeded expectations, driven by better-than-expected margin performance. Since our initial purchase, the stock has appreciated significantly. We sold our position at a profit with the view that Honeywell shares had become fairly valued.

The Fund’s holdings in the financials sector delivered a positive total return, while those in the Value Index fell more than 4.0%. Bank of New York Mellon and Loews

Strategy and Performance Overview (continued)

Corporation were among the top contributors. Loews is a holding company with many subsidiaries in several industries. We believe its shares are significantly undervalued, currently trading at approximately an 18% discount based on the total value of its subsidiaries. Impressively, each subsidiary could support itself without financial help from the parent, is strongly capitalized, and generates free cash flow. We also like Loews’ focus on shareholder value via share repurchases and have confidence in management’s capital allocation decisions.

Positions in information technology finished in positive territory; however, performance among individual holdings varied. There were strong gains made by select holdings such as Avaya, a global telecommunications company that was purchased by private equity firms.

What holdings detracted most from the Fund’s return?

Despite the gains made by many of the Fund’s energy holdings, Trident Resources, a Canadian coalbed methane producer, was the weakest position in the Fund. Trident Resources is a privately held company with no publicly traded securities. We originally invested in Trident Resources in March 2005, as we believed it had outstanding reserve potential as well as the potential to benefit from a combination of production growth and favorable natural gas prices. During February, we downwardly revalued the security due to changes in company fundamentals and financials. We are hoping that the company will re-file an initial public offering (IPO) to sell stock within the next couple years. Information related to Trident Resources is confidential. Disclosure and/or use of such information is not permitted without the prior written consent of Jennison Associates.

Healthcare was the only sector that detracted from the Fund’s returns, as Omnicare, Amgen, and Novartis declined. Omnicare is a provider of pharmaceuticals and related pharmacy services to long-term care institutions as well as clinical research to the pharmaceutical and biotechnology industries. Its shares declined as the company failed to meet expectations due to a combination of bed loss (albeit at only 1%), discounting of generics, and higher labor costs. We expect bed growth to resume and continue to believe Omnicare is attractively valued, with its stock trading at a price that is 13 times estimated earnings for the coming year.

Biotech Amgen declined due to warnings issued by a Federal Drug Administration (FDA) cancer panel regarding erythropoiesis-stimulating agents (ESAs), the family of drugs to which Aranesp, the company’s cancer-related anemia treatment, belongs. According to FDA analysis, ESAs reduce survival, which is markedly different from Amgen’s meta-analysis, which suggests no difference in survival. Most recently, the Centers for Medicare and Medicaid Services (CMS) announced its final ESA cancer national coverage determination (NCD), which was not as draconian as the initial

| | |

| 8 | | Visit our website at www.jennisondryden.com |

proposal and mostly in line with Wall Street analysts’ expectations. The final NCD provides coverage with restrictions for the treatment of anemia secondary to myelosuppressive anticancer chemotherapy in certain cancer conditions. The details these restrictions, which include limiting initiation of ESA therapy to when the hemoglobin level is less than 10 grams per deciliter, limiting the ESA treatment duration to a maximum of eight weeks after a chemotherapy session ends, limiting the starting dose to the FDA recommended starting dose, and limiting dose escalation levels. CMS has effectively set a new upper hemoglobin target of 10 grams per deciliter for the use of ESAs in the oncology setting. If duplicated by private payors, this could significantly dent Amgen’s revenue. We continue to hold Amgen, believing its current stock price more than compensates for the declined Aranesp usage.

Within the technology sector, there were declines in Motorola and Spansion. (For Motorola, please see the significant changes section below.)

Shares of Spansion, the world’s number one maker of NOR flash memory chips, performed poorly in the recent market volatility, a victim of major holders with high profile liquidity problems. In our view, Spansion’s fundamentals remain intact and the company stands to benefit from the merger of Intel and STMicro’s NOR flash operations, which should lead to more stable industry pricing. Moreover, we think Spansion’s planned cost cuts and renewed focus on profitability should lead its stock price higher.

Were there significant changes to the portfolio?

Major purchases and sales during the period reflected company-specific fundamentals and developments. Significant new positions were established in Seagate Technology, Best Buy, and XM Satellite Radio.

Seagate Technology is the world’s largest manufacturer of disk drives. We initiated a position in Seagate believing the company stands to benefit from continued consolidation in the hard drive industry. Also, we do not believe that the market is fully pricing in the benefit of Seagate’s technology lead in Perpendicular Magnetic Recording and the cost savings resulting from the closure of the Maxtor facilities. We believe that there are two reasons for the stock’s recent decline: concerns about flash memory replacing the hard disk drive as the primary mode of information storage on personal computers and concerns about lackluster growth in sales of personal computers driven by problems with the Windows Vista operating system. We believe both these concerns are overly discounted in the price of Seagate stock, which currently trades at nine times earnings.

Strategy and Performance Overview (continued)

Best Buy is a specialty retailer of consumer electronics, home-office products, entertainment software, appliances, and related services. Best Buy had generally fallen out of favor with investors due to disappointing earnings in 2006, which was driven, in large part, by rapid declines in large screen TV pricing. However, we believe Best Buy is poised to benefit from a moderation in price declines in 2007 and improvement in other electronics categories. Moreover, Best Buy also offers services such as Geek Squad, home installation, and Best Buy for Business, which we believe have superior revenue growth and comparable margins to that of its core business. Additionally, in our view, the company’s strong balance sheet provides downside protection with high free cash flow, and its business model is stronger than expected.

We purchased shares of XM Satellite Radio as we think its stock price is inexpensive, whether or not the merger with Sirius Satellite Radio occurs. The number of cars where XM will be available on purchase is accelerating 30% per year for the next couple of years. If the merger goes through, the cost cutting and rationalization that result could make the stock price appreciate significantly. We believe the two companies have many synergies that, in the long term, should accommodate Federal Communications Commission conditions aimed at safeguarding the “public interest.” While the Department of Justice (DOJ) has its own specific criteria to satisfy to ensure that the deal is in the “public interest,” we anticipate the DOJ’s antitrust concerns will be assuaged or eliminated.

Holdings in other securities, such as Motorola, Lazard, and Merrill Lynch, were eliminated.

Motorola, the world’s second-largest mobile phone maker, fell primarily due to challenges in the mobile handset business. Although its two other businesses, networks and cable modems, are healthy, a large part of our evaluation was dependent on the state of the mobile handset business. Motorola has had trouble following up the stunning 2004 success of the RAZR with a new product. Margins have fallen, as the company has had to lower prices to sell its units. While we thought the situation at Motorola would be bad, it is even worse than we anticipated; we consequently sold the position.

Lazard operates as an international financial advisory and asset management firm that serves a diverse set of clients, including corporations, partnerships, institutions, government, and high-net worth individuals. We initiated a position in Lazard after its stock price dropped close to 20% below its IPO price and traded at 13 times estimated earnings for the coming year, which was half the multiple of other banks involved in the merger and acquisition (M&A) business. Shares of Lazard gained

| | |

| 10 | | Visit our website at www.jennisondryden.com |

ground as the company reported solid profits amid strong M&A activity, and we sold our position at a profit as the stock became fairly valued.

Merrill Lynch provides broker-dealer, investment banking, financing, wealth management, advisory, asset management, insurance, lending, and related products and services on a global basis. From our initial purchase of Merrill Lynch shares in February 2003 through June 2007, the stock appreciated approximately 140%. We closed our position as the stock had become fairly valued.

Comments on Largest Holdings

| 2.5% | Cadbury Schweppes PLC / Food Products |

We bought shares of Cadbury Schweppes due to its overall business mix of beverages, gum, and chocolate. Moreover, Cadbury is in the process of restructuring. Its cost-cutting program, “Fuel for Growth,” should generate cost savings, simultaneously expand margins and fund the innovation that has led to new gum and mint products, which have been driving revenue growth. We also like the stock’s valuation, both on an absolute (intrinsic) and relative (compared to its peers) basis.

| 2.4% | Citigroup, Inc. / Diversified Financial Services |

Citigroup is a diversified financial services company that, among other things, provides investment banking, retail brokerage, and corporate banking services. In our view, Citigroup represents high growth opportunities due to its international exposure, high return on equity, and cheap valuation at less than 11 times earnings. Citigroup has underperformed what we believe the franchise can achieve.

| 2.4% | American International Group, Inc. / Insurance |

AIG is engaged in a range of insurance and insurance-related activities in the United States and abroad. Its primary activities include general insurance as well as life insurance and retirement services operations. Although AIG shares declined as investors questioned whether the company could grow in the aftermath of management changes stemming from an investigation led by then New York Attorney General Eliot Spitzer, we believe its businesses and competitive position remain intact. As AIG and its management team prove they still can operate efficiently and continue to generate organic growth, the stock’s valuation should continue to recover. We believe AIG is poised to increase revenue and earnings, especially from its international insurance business, particularly in Asia.

| 2.3% | General Electric Co. / Industrial Conglomerates |

General Electric is a diversified conglomerate that recently completed the sale of its plastics business. This sale is part of GE’s strategy of focusing on higher-growth, higher-return technology businesses. The proceeds from this sale will be used to complete its current $27 billion stock buyback program as well as to restructure the company, which we believe will strengthen prospects for future growth. GE’s other divisions also appear healthy, which we think will increase investors’ inclination to pay a higher multiple of earnings for its shares.

| 2.2% | H&R Block, Inc. / Diversified Consumer Services |

H&R Block is primarily a tax preparer with a mortgage business, which the company is selling. We initiated a position in H&R Block, believing the stock was trading at a discount on the basis that selling the company’s parts individually would bring in more money than selling it as a whole. While H&R Block lost market share in its tax preparation business to aggressive competitors over the past several years, it has undertaken efforts to stabilize and grow this business. Additionally, continued

| | |

| 12 | | Visit our website at www.jennisondryden.com |

weakness in the subprime mortgage market has resulted in negative first-quarter results, which in turn caused a sell-off in the stock. Investors feared H&R Block would either get a low price for or cancel the sale of its Option One Mortgage business. We believe it will complete the sale, allowing the company to focus on its steadily improving tax preparation business.

Fees and Expenses (Unaudited)

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments and redemptions, as applicable, and (2) ongoing costs, including management fees, distribution and/or service (12b-1) fees, and other Fund expenses, as applicable. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested on March 1, 2007, at the beginning of the period, and held through the six-month period ended August 31, 2007. The example is for illustrative purposes only; you should consult the Prospectus for information on initial and subsequent minimum investment requirements.

The Fund’s transfer agent may charge additional fees to holders of certain accounts that are not included in the expenses shown in the table on the following page. These fees apply to Individual Retirement Accounts (IRAs) and Section 403(b) accounts. As of the close of the six-month period covered by the table, IRA fees included an annual maintenance fee of $15 per account (subject to a maximum annual maintenance fee of $25 for all accounts held by the same shareholder). Section 403(b) accounts are charged an annual $25 fiduciary maintenance fee. Some of the fees may vary in amount, or may be waived, based on your total account balance or the number of JennisonDryden Funds, including the Fund, that you own. You should consider the additional fees that were charged to your Fund account over the six-month period when you estimate the total ongoing expenses paid over the period and the impact of these fees on your ending account value, as these additional expenses are not reflected in the information provided in the expense table. Additional fees have the effect of reducing investment returns.

Actual Expenses

The first line for each share class in the table on the following page provides information about actual account values and actual expenses. You may use the information on this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value ÷ $1,000 = 8.6), then multiply the result by the number on the first line under the heading “Expenses Paid During the Six-Month Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line for each share class in the table on the following page provides information about hypothetical account values and hypothetical expenses based on

| | |

| 14 | | Visit our website at www.jennisondryden.com |

the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only, and do not reflect any transactional costs such as sales charges (loads). Therefore the second line for each share class in the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | | | | | | | | | | | | |

| Jennison Value Fund | | Beginning Account

Value March 1, 2007 | | Ending Account

Value August 31, 2007 | | Annualized

Expense Ratio

Based on the

Six-Month Period | | | Expenses Paid

During the

Six-Month Period* |

| | | | | | | | | | | | | | |

| Class A | | Actual | | $ | 1,000.00 | | $ | 1,043.50 | | 0.95 | % | | $ | 4.89 |

| | | Hypothetical | | $ | 1,000.00 | | $ | 1,020.42 | | 0.95 | % | | $ | 4.84 |

| | | | | | | | | | | | | | |

| Class B | | Actual | | $ | 1,000.00 | | $ | 1,039.60 | | 1.70 | % | | $ | 8.74 |

| | | Hypothetical | | $ | 1,000.00 | | $ | 1,016.64 | | 1.70 | % | | $ | 8.64 |

| | | | | | | | | | | | | | |

| Class C | | Actual | | $ | 1,000.00 | | $ | 1,039.60 | | 1.70 | % | | $ | 8.74 |

| | | Hypothetical | | $ | 1,000.00 | | $ | 1,016.64 | | 1.70 | % | | $ | 8.64 |

| | | | | | | | | | | | | | |

| Class L | | Actual** | | $ | 1,000.00 | | $ | 1,052.80 | | 1.20 | % | | $ | 5.67 |

| | | Hypothetical | | $ | 1,000.00 | | $ | 1,019.16 | | 1.20 | % | | $ | 6.11 |

| | | | | | | | | | | | | | |

| Class M | | Actual** | | $ | 1,000.00 | | $ | 1,050.30 | | 1.70 | % | | $ | 8.02 |

| | | Hypothetical | | $ | 1,000.00 | | $ | 1,016.64 | | 1.70 | % | | $ | 8.64 |

| | | | | | | | | | | | | | |

| Class R | | Actual | | $ | 1,000.00 | | $ | 1,042.20 | | 1.20 | % | | $ | 6.18 |

| | | Hypothetical | | $ | 1,000.00 | | $ | 1,019.16 | | 1.20 | % | | $ | 6.11 |

| | | | | | | | | | | | | | |

| Class X | | Actual** | | $ | 1,000.00 | | $ | 1,050.30 | | 1.70 | % | | $ | 8.02 |

| | | Hypothetical | | $ | 1,000.00 | | $ | 1,016.64 | | 1.70 | % | | $ | 8.64 |

| | | | | | | | | | | | | | |

| Class Z | | Actual | | $ | 1,000.00 | | $ | 1,044.90 | | 0.70 | % | | $ | 3.61 |

| | | Hypothetical | | $ | 1,000.00 | | $ | 1,021.68 | | 0.70 | % | | $ | 3.57 |

| | | | | | | | | | | | | | |

Fees and Expenses (continued)

* Fund expenses (net of fee waivers or subsidies, if any) for each share class are equal to the annualized expense ratio for each share class (provided in the table), multiplied by the average account value over the period, multiplied by the 184 days in the six-month period ended August 31, 2007, and divided by 365 days (to reflect the six-month period) with the exception of the Class L, Class M and Class X “Actual” information which reflects the 168 day period ended August 31, 2007 due to its inception date of March 16, 2007. Expenses presented in the table include the expenses of any underlying portfolios in which the Fund may invest.

** Class L, M and X shares inception date of March 16, 2007.

| | |

| 16 | | Visit our website at www.jennisondryden.com |

Portfolio of Investments

as of August 31, 2007

| | | | | |

| Shares | | Description | | Value (Note 1) |

| | | | | |

LONG-TERM INVESTMENT 99.8% | | | |

COMMON STOCKS 99.3% | | | |

| |

Auto Components 0.4% | | | |

| 119,800 | | Wabco Holdings Inc. | | $ | 5,422,148 |

| |

Biotechnology 1.4% | | | |

| 365,400 | | Amgen, Inc.(a) | | | 18,310,194 |

| |

Building Products 1.5% | | | |

| 550,300 | | American Standard Cos., Inc. | | | 20,267,549 |

| |

Capital Markets 4.2% | | | |

| 524,362 | | Bank of New York Mellon Corp. (The) | | | 21,199,956 |

| 535,600 | | TD Ameritrade Holding Corp.(a) | | | 9,721,140 |

| 461,700 | | UBS AG | | | 24,119,208 |

| | | | | |

| | | | | 55,040,304 |

| | | | | |

| |

Chemicals 1.0% | | | |

| 268,300 | | E.I. du Pont de Nemours & Co.(b) | | | 13,079,625 |

| |

Commercial Banks 1.5% | | | |

| 1,707,874 | | Royal Bank of Scotland Group PLC (United Kingdom) | | | 19,782,923 |

| |

Commercial Services & Supplies 1.9% | | | |

| 648,760 | | Waste Management, Inc. | | | 24,438,789 |

| |

Communications Equipment 1.2% | | | |

| 385,400 | | QUALCOMM, Inc. | | | 15,373,606 |

| |

Computers & Peripherals 1.9% | | | |

| 968,100 | | Seagate Technology | | | 24,996,342 |

| |

Consumer Finance 2.2% | | | |

| 218,500 | | American Express Co. | | | 12,808,470 |

| 326,400 | | SLM Corp. | | | 16,411,392 |

| | | | | |

| | | | | 29,219,862 |

| | | | | |

| |

Diversified Consumer Services 3.5% | | | |

| 542,700 | | Career Education Corp.(a)(b) | | | 16,118,190 |

| 1,486,600 | | H&R Block, Inc. | | | 29,494,144 |

| | | | | |

| | | | | 45,612,334 |

| | | | | |

See Notes to Financial Statements.

Portfolio of Investments

as of August 31, 2007 continued

| | | | | |

| Shares | | Description | | Value (Note 1) |

| | | | | |

Diversified Financial Services 6.6% | | | |

| 526,403 | | Bank of America Corp. | | $ | 26,678,104 |

| 679,500 | | Citigroup, Inc. | | | 31,854,960 |

| 356,300 | | JPMorgan Chase & Co. | | | 15,862,476 |

| 120,000 | | KKR Private Equity Investors LLP | | | 2,280,000 |

| 536,200 | | KKR Private Equity Investors LLP—RDU, Private Placement, 144A

(cost $13,370,899; purchased 5/3/06 - 5/5/06)(f)(g) | | | 10,187,800 |

| | | | | |

| | | | | 86,863,340 |

| | | | | |

| |

Diversified Telecommunication Services 1.6% | | | |

| 515,150 | | Verizon Communications, Inc. | | | 21,574,482 |

| |

Electric Utilities 2.4% | | | |

| 179,200 | | Entergy Corp. | | | 18,568,704 |

| 270,400 | | Progress Energy, Inc. | | | 12,405,952 |

| | | | | |

| | | | | 30,974,656 |

| | | | | |

| |

Electronic Equipment & Instruments 1.3% | | | |

| 360,200 | | Sony Corp. ADR (Japan) | | | 17,210,356 |

| |

Food & Staples Retailing 3.4% | | | |

| 1,035,000 | | Kroger Co. (The) | | | 27,510,300 |

| 381,600 | | Wal-Mart Stores, Inc. | | | 16,649,208 |

| | | | | |

| | | | | 44,159,508 |

| | | | | |

| |

Food Products 4.7% | | | |

| 700,700 | | Cadbury Schweppes PLC, ADR (United Kingdom) | | | 33,094,062 |

| 1,110,700 | | ConAgra Foods, Inc. | | | 28,556,097 |

| | | | | |

| | | | | 61,650,159 |

| | | | | |

| |

Healthcare Providers & Services 1.8% | | | |

| 721,900 | | Omnicare, Inc. | | | 23,555,597 |

| |

Household Products 1.7% | | | |

| 330,400 | | Kimberly-Clark Corp.(b) | | | 22,695,176 |

| |

Independent Power Producers & Energy Traders 1.5% | | | |

| 521,400 | | NRG Energy, Inc.(a)(b) | | | 19,860,126 |

| |

Industrial Conglomerates 2.3% | | | |

| 770,500 | | General Electric Co. | | | 29,949,335 |

See Notes to Financial Statements.

| | |

| 18 | | Visit our website at www.jennisondryden.com |

| | | | | |

| Shares | | Description | | Value (Note 1) |

| | | | | |

Insurance 6.9% | | | |

| 475,500 | | American International Group, Inc. | | $ | 31,383,000 |

| 428,100 | | Axis Capital Holdings Ltd. | | | 15,454,410 |

| 544,100 | | Loews Corp. | | | 25,578,141 |

| 317,900 | | MBIA, Inc.(b) | | | 19,074,000 |

| | | | | |

| | | | | 91,489,551 |

| | | | | |

| |

Internet & Catalog Retail 1.6% | | | |

| 762,600 | | IAC/InterActiveCorp(a)(b) | | | 21,192,654 |

| |

Media 5.4% | | | |

| 934,800 | | Comcast Corp. (Class A)(a)(b) | | | 24,388,932 |

| 711,512 | | Liberty Global, Inc. (Series C)(a) | | | 28,069,148 |

| 42,400 | | Time Warner, Inc. | | | 804,752 |

| 1,475,400 | | XM Satellite Radio Holdings, Inc. (Class A)(a)(b) | | | 18,398,238 |

| | | | | |

| | | | | 71,661,070 |

| | | | | |

| |

Metals & Mining 1.2% | | | |

| 176,932 | | Freeport-McMoRan Copper & Gold, Inc. | | | 15,467,395 |

| |

Multi-Utilities 1.7% | | | |

| 418,200 | | Sempra Energy | | | 23,013,546 |

| |

Office Electronics 1.4% | | | |

| 1,067,500 | | Xerox Corp.(a) | | | 18,286,275 |

| |

Oil, Gas & Consumable Fuels 14.9% | | | |

| 335,400 | | Anadarko Petroleum Corp.(b) | | | 16,427,892 |

| 143,700 | | Devon Energy Corp. | | | 10,822,047 |

| 440,400 | | Hess Corp. | | | 27,027,348 |

| 400,100 | | Marathon Oil Corp. | | | 21,561,389 |

| 219,000 | | Murphy Oil Corp.(b) | | | 13,345,860 |

| 613,400 | | Nexen, Inc. | | | 17,095,458 |

| 496,000 | | Occidental Petroleum Corp. | | | 28,118,240 |

| 380,700 | | Petroleo Brasileiro SA, ADR (Brazil)(b) | | | 23,542,488 |

| 290,000 | | Suncor Energy, Inc. | | | 25,923,100 |

| 319,000 | | The Williams Cos., Inc. | | | 9,889,000 |

| 236,629 | | Trident Resources Corp., Private (Canada)

(cost $ 9,942,621; purchased 3/11/05 - 1/5/06)(a)(f)(g) | | | 2,240,805 |

| | | | | |

| | | | | 195,993,627 |

| | | | | |

See Notes to Financial Statements.

Portfolio of Investments

as of August 31, 2007 continued

| | | | | |

| Shares | | Description | | Value (Note 1) |

| | | | | |

Pharmaceuticals 4.0% | | | |

| 260,100 | | Abbott Laboratories | | $ | 13,501,791 |

| 380,300 | | Novartis AG, ADR (Switzerland) | | | 20,022,795 |

| 428,200 | | Wyeth | | | 19,825,660 |

| | | | | |

| | | | | 53,350,246 |

| | | | | |

| |

Semiconductors & Semiconductor Equipment 1.7% | | | |

| 2,429,800 | | Spansion, Inc. (Class A)(a)(b) | | | 22,111,180 |

| |

Software 2.9% | | | |

| 456,300 | | Microsoft Corp. | | | 13,109,499 |

| 1,364,400 | | Symantec Corp.(a) | | | 25,664,364 |

| | | | | |

| | | | | 38,773,863 |

| | | | | |

| |

Specialty Retail 1.7% | | | |

| 511,800 | | Best Buy Co., Inc.(b) | | | 22,493,610 |

| |

Textiles, Apparel & Luxury Goods | | | |

| 200 | | NIKE, Inc. (Class B) | | | 11,268 |

| |

Thrifts & Mortgage Finance 2.3% | | | |

| 236,125 | | Fannie Mae | | | 15,492,161 |

| 826,740 | | People’s United Financial, Inc.(b) | | | 14,616,763 |

| | | | | |

| | | | | 30,108,924 |

| |

Tobacco 2.0% | | | |

| 377,840 | | Altria Group, Inc. | | | 26,225,874 |

| |

Wireless Telecommunication Services 3.6% | | | |

| 303,000 | | Alltel Corp. | | | 20,682,780 |

| 1,436,825 | | Sprint Nextel Corp.(b) | | | 27,184,729 |

| | | | | |

| | | | | 47,867,509 |

| | | | | |

| | TOTAL COMMON STOCKS

(cost $1,107,560,023) | | | 1,308,083,003 |

| | | | | |

See Notes to Financial Statements.

| | |

| 20 | | Visit our website at www.jennisondryden.com |

| | | | | | |

Principal

Amount

(000) | | | | Value (Note 1) | |

| | | | | | |

CORPORATE BOND 0.5% | | | | |

| |

Oil, Gas & Consumable Fuels 0.5% | | | | |

| $7,357 | | Trident Resources Corp., Note, Private, 13.04%, 8/12/12(f)(g)

(cost $6,979,462) | |

$ |

6,967,235 |

|

| | | | | | |

| Units | | | | | |

| | | | | | | |

WARRANT | | | | | | |

| |

Oil, Gas & Consumable Fuels | | | | |

| 730,398 | | Trident Resources Corp., Private, expiring 1/01/15(f)(g) (cost $0) | | | 69 | |

| | | | | | |

| | TOTAL LONG-TERM INVESTMENTS

(cost $1,114,539,485) | | | 1,315,050,307 | |

| | | | | | |

| Shares | | | | | |

| | | | | | | |

SHORT-TERM INVESTMENT 16.2% | | | | |

| |

Affiliated Money Market Mutual Fund | | | | |

| 213,758,200 | | Dryden Core Investment Fund - Taxable Money Market Series

(cost $213,758,200; includes $213,758,200 of cash collateral received for securities on loan) (Note 3)(c)(d) | | | 213,758,200 | |

| | | | | | |

| | TOTAL INVESTMENTS(e) 116.0%

(cost $1,328,297,685; Note 5) | | | 1,528,808,507 | |

| | Liabilities in excess of other assets (16.0%) | | | (210,853,093 | ) |

| | | | | | |

| | NET ASSETS 100.0% | | $ | 1,317,955,414 | |

| | | | | | |

The following abbreviations are used in portfolio descriptions:

144A—Securities were purchased pursuant to Rule 144A under the Securities Act of 1933 and may not be resold subject to that rule except to qualified institutional buyers. Unless otherwise noted, 144A securities are deemed to be liquid.

ADR—American Depositary Receipt

RDU—Restricted Depositary Unit

| (a) | Non-income producing security. |

| (b) | All or a portion of security is on loan. The aggregate market value of such securities is $207,592,760; cash collateral of $213,758,200 (included in liabilities) was received with which the Fund purchased highly liquid short-term investments. |

| (c) | Represents security, or portion thereof, purchased with cash collateral received for securities on loan. |

| (d) | Prudential Investments LLC, the Manager of the Fund, also serves as Manager of the Dryden Core Investment Fund—Taxable Money Market Series. |

| (e) | As of August 31, 2007, four securities valued at $19,395,909 and representing 1.5% of the total net assets were fair valued in accordance with the policies adopted by the Board of Trustees. |

| (f) | Indicates an illiquid security. |

| (g) | Indicates a security restricted to resale. The aggregate cost of such a security is $30,292,982. The aggregate value of $19,395,909 is approximately 1.5% of net assets. |

See Notes to Financial Statements.

Portfolio of Investments

as of August 31, 2007 continued

The industry classification of portfolio holdings and liabilities in excess of other assets shown as a percentage of nets assets as of August 31, 2007 were as follows:

| | | |

Affiliated Money Market Mutual Fund (including 16.2% of collateral received for securities on loan) | | 16.2 | % |

Oil, Gas & Consumable Fuels | | 15.4 | |

Insurance | | 6.9 | |

Diversified Financial Services | | 6.6 | |

Media | | 5.4 | |

Food Products | | 4.7 | |

Capital Markets | | 4.2 | |

Pharmaceuticals | | 4.0 | |

Wireless Telecommunication Services | | 3.6 | |

Diversified Consumer Services | | 3.5 | |

Food & Staples Retailing | | 3.4 | |

Software | | 2.9 | |

Electric Utilities | | 2.4 | |

Thrifts & Mortgage Finance | | 2.3 | |

Industrial Conglomerates | | 2.3 | |

Consumer Finance | | 2.2 | |

Tobacco | | 2.0 | |

Computers & Peripherals | | 1.9 | |

Commercial Services & Supplies | | 1.9 | |

Healthcare Products & Services | | 1.8 | |

Speciality Retail | | 1.7 | |

Semiconductors & Semiconductor Equipment | | 1.7 | |

Multi-Utilities | | 1.7 | |

Household Products | | 1.7 | |

Internet & Catalog Retail | | 1.6 | |

Diversified Telecommunication Services | | 1.6 | |

Independent Power Producers & Energy Traders | | 1.5 | |

Commercial Banks | | 1.5 | |

Building Products | | 1.5 | |

Office Electronics | | 1.4 | |

Biotechnology | | 1.4 | |

Electronic Equipment & Instruments | | 1.3 | |

Metals & Mining | | 1.2 | |

Communications Equipment | | 1.2 | |

Chemicals | | 1.0 | |

Auto Components | | 0.4 | |

| | | |

| | 116.0 | |

Liabilities in excess of other assets | | (16.0 | ) |

| | | |

| | 100.0 | % |

| | | |

See Notes to Financial Statements.

| | |

| 22 | | Visit our website at www.jennisondryden.com |

Financial Statements

| | |

| AUGUST 31, 2007 | | ANNUAL REPORT |

Jennison Value Fund

Statement of Assets and Liabilities

as of August 31, 2007

| | | |

Assets | | | |

Investments at value, including securities on loan of $207,592,760: | | | |

Unaffiliated investments (cost $1,114,539,485) | | $ | 1,315,050,307 |

Affiliated investments (cost $213,758,200) | | | 213,758,200 |

Foreign currency, at value (cost $9,935) | | | 10,805 |

Receivable for investments sold | | | 9,274,714 |

Dividends and interest receivable | | | 2,004,476 |

Receivable for Fund shares sold | | | 599,266 |

Foreign tax reclaim receivable | | | 183,774 |

Prepaid expenses | | | 27,413 |

| | | |

Total assets | | | 1,540,908,955 |

| | | |

| |

Liabilities | | | |

Payable to broker for collateral for securities on loan | | | 213,758,200 |

Payable for investments purchased | | | 4,332,678 |

Payable for Fund shares reacquired | | | 2,101,248 |

Loan payable | | | 856,000 |

Management fee payable | | | 593,350 |

Accrued expenses | | | 427,738 |

Distribution fee payable | | | 382,213 |

Payable to custodian | | | 322,136 |

Transfer agent fee payable | | | 170,662 |

Deferred trustees' fees | | | 9,161 |

Loan interest payable | | | 155 |

| | | |

Total liabilities | | | 222,953,541 |

| | | |

| |

Net Assets | | $ | 1,317,955,414 |

| | | |

| | | | |

Net assets were comprised of: | | | |

Shares of beneficial interest, at par | | $ | 605,256 |

Paid-in capital in excess of par | | | 938,069,816 |

| | | |

| | | 938,675,072 |

Undistributed net investment income | | | 7,731,882 |

Accumulated net realized gain on investment and foreign currency transactions | | | 171,029,042 |

Net unrealized appreciation on investments and foreign currencies | | | 200,519,418 |

| | | |

Net assets, August 31, 2007 | | $ | 1,317,955,414 |

| | | |

See Notes to Financial Statements.

| | |

| 24 | | Visit our website at www.jennisondryden.com |

| | | |

Class A | | | |

Net asset value and redemption price per share

($1,010,160,279 ÷ 46,306,779 shares of beneficial interest issued and outstanding) | | $ | 21.81 |

Maximum sales charge (5.50% of offering price) | | | 1.27 |

| | | |

Maximum offering price to public | | $ | 23.08 |

| | | |

| |

Class B | | | |

Net asset value, offering price and redemption price per share

($112,108,415 ÷ 5,209,606 shares of beneficial interest issued and outstanding) | | $ | 21.52 |

| | | |

| |

Class C | | | |

Net asset value, offering price and redemption price per share

($64,730,619 ÷ 3,007,416 shares of beneficial interest issued and outstanding) | | $ | 21.52 |

| | | |

| |

Class L | | | |

Net asset value, offering price and redemption price per share

($5,299,333 ÷ 243,740 shares of beneficial interest issued and outstanding) | | $ | 21.74 |

| | | |

| |

Class M | | | |

Net asset value, offering price and redemption price per share

($15,255,893 ÷ 708,655 shares of beneficial interest issued and outstanding) | | $ | 21.53 |

| | | |

| |

Class R | | | |

Net asset value, offering price and redemption price per share

($1,858,287 ÷ 85,434 shares of beneficial interest issued and outstanding) | | $ | 21.75 |

| | | |

| |

Class X | | | |

Net asset value, offering price and redemption price per share

($3,749,394 ÷ 174,244 shares of beneficial interest issued and outstanding) | | $ | 21.52 |

| | | |

| |

Class Z | | | |

Net asset value, offering price and redemption price per share

($104,793,194 ÷ 4,789,702 shares of beneficial interest issued and outstanding) | | $ | 21.88 |

| | | |

See Notes to Financial Statements.

Statement of Operations

| | | | | | | | |

| | | Ten Months

Ended

August 31, 2007 | | | Year

Ended

October 31, 2006 | |

Net Investment Income | | | | | | | | |

Income | | | | | | | | |

Unaffiliated dividends (net of foreign withholding taxes of $228,658 and $275,596, respectively) | | $ | 18,234,239 | | | $ | 20,418,964 | |

Affiliated dividend income | | | 1,863,807 | | | | 1,285,081 | |

Affiliated income from securities loaned, net | | | 124,167 | | | | 113,339 | |

Unaffiliated interest income | | | 34,457 | | | | — | |

| | | | | | | | |

Total income | | | 20,256,670 | | | | 21,817,384 | |

| | | | | | | | |

| | |

Expenses | | | | | | | | |

Management fee | | | 5,829,409 | | | | 5,854,442 | |

Distribution fee—Class A | | | 2,141,292 | | | | 2,180,195 | |

Distribution fee—Class B | | | 937,619 | | | | 1,120,700 | |

Distribution fee—Class C | | | 437,014 | | | | 248,124 | |

Distribution fee—Class L | | | 13,633 | | | | — | |

Distribution fee—Class M | | | 82,620 | | | | — | |

Distribution fee—Class R | | | 2,854 | | | | 104 | |

Distribution fee—Class X | | | 19,441 | | | | — | |

Transfer agent’s fees and expenses (including affiliated expense of $933,000 and $1,158,000, respectively) (Note 3) | | | 1,487,000 | | | | 1,500,000 | |

Custodian’s fees and expenses | | | 121,000 | | | | 100,000 | |

Registration fees | | | 97,000 | | | | 82,000 | |

Reports to shareholders | | | 50,000 | | | | 140,000 | |

Insurance | | | 26,000 | | | | 27,000 | |

Trustees’ fees | | | 25,000 | | | | 25,000 | |

Audit fee | | | 20,000 | | | | 17,000 | |

Legal fees and expenses | | | 15,000 | | | | 63,000 | |

Loan interest expense (Note 2) | | | 1,432 | | | | — | |

Miscellaneous | | | 21,931 | | | | 22,329 | |

| | | | | | | | |

Total expenses | | | 11,328,245 | | | | 11,379,894 | |

| | | | | | | | |

Net investment income | | | 8,928,425 | | | | 10,437,490 | |

| | | | | | | | |

| | |

Realized And Unrealized Gain (Loss) On Investment And Foreign Currency Transactions | | | | | | | | |

Net realized gain on: | | | | | | | | |

Investment transactions | | | 172,362,563 | | | | 118,758,928 | |

Foreign currency transactions | | | 97,227 | | | | (24,055 | ) |

Short Sales | | | 391,177 | | | | — | |

| | | | | | | | |

| | | 172,850,967 | | | | 118,734,873 | |

| | | | | | | | |

Net change in unrealized appreciation (depreciation) on: | | | | | | | | |

Investments | | | (72,519,336 | ) | | | 61,050,024 | |

Foreign currencies | | | 8,278 | | | | 318 | |

| | | | | | | | |

| | | (72,511,058 | ) | | | 61,050,342 | |

| | | | | | | | |

Net gain on investment and foreign currency transactions | | | 100,339,909 | | | | 179,785,215 | |

| | | | | | | | |

Net Increase In Net Assets Resulting From Operations | | $ | 109,268,334 | | | $ | 190,222,705 | |

| | | | | | | | |

See Notes to Financial Statements.

| | |

| 26 | | Visit our website at www.jennisondryden.com |

Statement of Changes in Net Assets

| | | | | | | | | | | | |

| | | Ten Months

Ended | | | Year Ended October 31, | |

| | August 31, 2007 | | | 2006 | | | 2005 | |

Increase (Decrease) In Net Assets | | | | | | | | | | | | |

Operations | | | | | | | | | | | | |

Net investment income | | $ | 8,928,425 | | | $ | 10,437,490 | | | $ | 5,891,791 | |

Net realized gain on investment and foreign currency transactions | | | 172,850,967 | | | | 118,734,873 | | | | 117,720,036 | |

Net change in unrealized appreciation (depreciation) on investments and foreign currencies | | | (72,511,058 | ) | | | 61,050,342 | | | | 34,179,396 | |

| | | | | | | | | | | | |

Net increase in net assets resulting from operations | | | 109,268,334 | | | | 190,222,705 | | | | 157,791,223 | |

| | | | | | | | | | | | |

Dividends and distributions (Note 1) | | | | | | | | | | | | |

Dividends from net investment income: | | | | | | | | | | | | |

Class A | | | (8,164,199 | ) | | | (5,369,140 | ) | | | (5,295,657 | ) |

Class B | | | (147,136 | ) | | | — | | | | (115,838 | ) |

Class C | | | (45,182 | ) | | | — | | | | (12,108 | ) |

Class R | | | (393 | ) | | | (12 | ) | | | — | |

Class Z | | | (1,038,985 | ) | | | (420,806 | ) | | | (307,762 | ) |

| | | | | | | | | | | | |

| | | (9,395,895 | ) | | | (5,789,958 | ) | | | (5,731,365 | ) |

| | | | | | | | | | | | |

Distributions from net realized gains: | | | | | | | | | | | | |

Class A | | | (95,071,115 | ) | | | (35,966,579 | ) | | | — | |

Class B | | | (10,773,756 | ) | | | (5,595,023 | ) | | | — | |

Class C | | | (3,308,355 | ) | | | (971,592 | ) | | | — | |

Class R | | | (7,650 | ) | | | (128 | ) | | | — | |

Class Z | | | (9,486,716 | ) | | | (2,054,591 | ) | | | — | |

| | | | | | | | | | | | |

| | | (118,647,592 | ) | | | (44,587,913 | ) | | | — | |

| | | | | | | | | | | | |

Fund share transactions (Net of share conversions) (Note 6) | | | | | | | | | | | | |

Net proceeds from shares sold | | | 129,130,638 | | | | 213,569,167 | | | | 115,477,435 | |

Net asset value of shares issued in connection with merger (Note 7) | | | 127,217,340 | | | | — | | | | — | |

Net asset value of shares issued in reinvestment of dividends and distributions | | | 120,759,467 | | | | 47,372,650 | | | | 5,283,291 | |

Cost of shares reacquired | | | (217,035,433 | ) | | | (177,217,214 | ) | | | (170,037,111 | ) |

| | | | | | | | | | | | |

Net increase (decrease) in net assets from Fund share transactions | | | 160,072,012 | | | | 83,724,603 | | | | (49,276,385 | ) |

| | | | | | | | | | | | |

Total increase | | | 141,296,859 | | | | 223,569,437 | | | | 102,783,473 | |

| | | |

Net Assets | | | | | | | | | | | | |

Beginning of period | | | 1,176,658,555 | | | | 953,089,118 | | | | 850,305,645 | |

| | | | | | | | | | | | |

End of period(a) | | $ | 1,317,955,414 | | | $ | 1,176,658,555 | | | $ | 953,089,118 | |

| | | | | | | | | | | | |

(a) Includes undistributed net investment income of: | | $ | 7,731,882 | | | $ | 8,195,035 | | | $ | 3,571,558 | |

| | | | | | | | | | | | |

See Notes to Financial Statements.

Notes to Financial Statements

JennisonDryden Portfolios, Inc.—Jennison Value Fund (the “Fund”) (formerly known as Jennison Value Fund) is registered under the Investment Company Act of 1940 as a diversified, open-end, management investment company. The investment objective of the Fund is capital appreciation. It seeks to achieve this objective by investing primarily in common stocks and convertible securities that provide investment income returns above those of the Standard & Poor’s 500 Composite Stock Price Index or the NYSE Composite Index.

The Fund’s fiscal year has changed from an annual reporting period that ends October 31 to one that ends August 31. This change should have no impact on the way the Fund is managed. Shareholders will receive future annual and semi-annual reports on the new fiscal year-end schedule.

Note 1. Accounting Policies

The following is a summary of significant accounting policies followed by the Fund in the preparation of its financial statements.

Securities Valuation: Securities listed on a securities exchange are valued at the last sale price on such exchange on the day of valuation or, if there was no sale on such day, at the mean between the last reported bid and asked prices, or at the last bid price on such day in the absence of an asked price. Securities traded via Nasdaq are valued at the official closing price provided by Nasdaq. Securities that are actively traded in the over-the-counter market, including listed securities for which the primary market is believed by Prudential Investments LLC (“PI” or “Manager”), in consultation with the subadvisor; to be over-the-counter, are valued at market value using prices provided by an independent pricing agent or principal market maker. Futures contracts and options thereon traded on a commodities exchange or board of trade are valued at the last sale price at the close of trading on such exchange or board of trade or, if there was no sale on the applicable commodities exchange or board of trade on such day, at the mean between the most recently quoted prices on such exchange or board of trade or at the last bid price in the absence of an asked price. Prices may be obtained from independent pricing services which use information provided by market makers or estimates of market values obtained from yield data relating to investments or securities with similar characteristics. Securities for which reliable market quotations are not readily available, or whose values have been affected by events occurring after the close of the security’s foreign market and before the Series’ normal pricing time, are valued at fair value in accordance with the Board of Trustees’ approved fair valuation procedures. When determining the fair

| | |

| 28 | | Visit our website at www.jennisondryden.com |

valuation of securities some of the factors influencing the valuation include, the nature of any restrictions on disposition of the securities; assessment of the general liquidity of the securities; the issuer’s financial condition and the markets in which it does business; the cost of the investment; the size of the holding and the capitalization of issuer; the prices of any recent transactions or bids/offers for such securities or any comparable securities; any available analyst media or other reports or information deemed reliable by the investment adviser regarding the issuer or the markets or industry in which it operates. Using fair value to price securities may result in a value that is different from a security’s most recent closing price and from the price used by other mutual funds to calculate their net asset values. As of August 31, 2007, there were no securities whose values were impacted by events occurring after the close of the security’s foreign market.

Investments in mutual funds are valued at their net asset value as of the close of the New York Stock Exchange on the date of valuation.

Short-term debt securities which mature in 60 days or less are valued at amortized cost, which approximates market-value. The amortized cost method includes valuing a security at its cost on the date of purchase and thereafter assuming a constant amortization to maturity of the difference between the principal amount due at maturity and cost. Short-term debt securities which mature in more than 60 days are valued at current market quotations.

Foreign Currency Translation: The books and records of the Fund are maintained in U.S. dollars. Foreign currency amounts are translated into U.S. dollars on the following basis:

(i) market value of investment securities, other assets and liabilities-at the current rates of exchange;

(ii) purchases and sales of investment securities, income and expenses-at the rates of exchange prevailing on the respective dates of such transactions.

The Fund does not isolate that portion of the results of operations arising as a result of changes in the foreign exchange rates from the fluctuations arising from changes in the market prices of long term securities held at the end of the fiscal year. Similarly, the Fund does not isolate the effect of changes in foreign exchange rates from the fluctuations arising from changes in the market prices of portfolio securities sold during the fiscal year. Accordingly, realized foreign currency gains or losses are included in the reported net realized gains or losses on investment transactions.

Notes to Financial Statements

continued

Net realized gains or losses on foreign currency transactions represent net foreign exchange gains or losses from the holding of foreign currencies, currency gains or losses realized between the trade and settlement dates on security transactions, and the difference between the amounts of dividends, interest and foreign withholding taxes recorded on the Fund’s books and the U.S. dollar equivalent amounts actually received or paid. Net unrealized currency gains or losses from valuing foreign currency denominated assets and liabilities (other than investments) at period end exchange rates are reflected as a component of net unrealized appreciation (depreciation) on foreign currencies.

Foreign security and currency transactions may involve certain considerations and risks not typically associated with those of domestic origin as a result of, among other factors, the possibility of political or economic instability or the level of governmental supervision and regulation of foreign securities markets.

Restricted Securities: The Fund may hold up to 15% of its net assets in illiquid securities, including those which are restricted as to disposition under securities law (“restricted securities”). Restricted securities held by the Fund at the end of the fiscal period may include registration rights under which the Fund may demand registration by the issuers, of which the Fund may bear the cost of such registration. Restricted securities are valued pursuant to the valuation procedures noted above.

Short Sales: The Fund may make short sales of securities as a method of hedging potential price declines in similar securities owned. The Fund may sell a security it does not own in anticipation of a decline in the market value of that security (short sale). When the Fund makes a short sale, it will borrow the security sold short and deliver it to the broker-dealer through which it made the short sale as collateral for its obligation to deliver the security upon conclusion of the sale. The Fund may have to pay a fee to borrow the particular securities and may be obligated to return any interest or dividends received on such borrowed securities. A gain, limited to the price at which the Fund sold the security short, or a loss, unlimited as to dollar amount, will be recognized upon the termination of a short sale if the market price is less or greater than the proceeds originally received, respectively, and is presented in the Statement of Operations as net realized gain or loss on short sales.

Securities Transactions and Net Investment Income: Securities transactions are recorded on the trade date. Realized gains or losses from investment and currency

| | |

| 30 | | Visit our website at www.jennisondryden.com |

transactions are calculated on the identified cost basis. Dividend income is recorded on the ex-dividend date and interest income, including amortization of premium and accretion of discount on debt securities, as required, is recorded on the accrual basis. Expenses are recorded on an accrual basis.

Net investment income or loss, (other than distribution fees, which are charged directly to the respective class) and unrealized and realized gains or losses are allocated daily to each class of shares based upon the relative proportion of net assets of each class at the beginning of the day.

Taxes: For federal income tax purposes, it is the Fund’s policy to continue to meet the requirements under the Internal Revenue Code applicable to regulated investment companies and to distribute all of its taxable net income and capital gains, if any, to shareholders. Therefore, no federal income tax provision is required.

Withholding taxes on foreign dividends are recorded net of reclaimable amounts, at the time the related income is earned.

Dividends and Distributions: The Fund expects to pay dividends of net investment income and distributions of net realized capital and currency gains, if any, annually. Dividends and distributions to shareholders, which are determined in accordance with federal income tax regulations and which may differ from generally accepted accounting principles, are recorded on the ex-dividend date.

Securities Lending: The Fund may lend its portfolio securities to broker-dealers. The loans are secured by collateral at least equal, at all times, to the market value of the securities loaned.

Loans are subject to termination at the option of the borrower or the Fund. Upon termination of the loan, the borrower will return to the lender securities identical to the loaned securities. Should the borrower of the securities fail financially, the Fund has the right to repurchase the securities using the collateral in the open market. The Fund recognizes income, net of any rebate and securities lending agent fees, for lending its securities in the form of fees or interest on the investment of any cash received as collateral. The Fund also continues to receive interest and dividends or amounts equivalent thereto, on the securities loaned and recognizes any unrealized gain or loss in the market price of the securities loaned that may occur during the term of the loan.

Notes to Financial Statements

continued

Estimates: The preparation of the financial statements requires management to make estimates and assumptions that affect the reported amounts and disclosures in the financial statements. Actual results could differ from those estimates.

Note 2. Agreements

The Fund has a management agreement with PI. Pursuant to this agreement, PI has responsibility for all investment advisory services and supervises the subadvisors’ performance of such services. PI has entered into a subadvisory agreement with Jennison Associates LLC (“Jennison”). The subadvisory agreement provides that Jennison furnishes investment advisory services in connection with the management of the Fund. In connection therewith, Jennison assumes the day-to-day management responsibilities of the Fund and is obligated to keep certain books and records of the Fund. PI pays for the services of Jennison, the cost of compensation of officers and employees of the Fund, occupancy and certain clerical and bookkeeping costs of the Fund. The Fund bears all other costs and expenses.

The management fee paid to PI is computed daily and payable monthly at an annual rate of .60 of 1% of the Fund’s average daily net assets up to $500 million, .50 of 1% of the next $500 million, .475 of 1% of the next $500 million and .45 of 1% of the average daily net assets in excess of $1.5 billion. The effective management fee rate was .53 of 1% of the Fund’s average daily net assets for the ten-month period ended August 31, 2007.

The Fund has a distribution agreement with Prudential Investment Management Services LLC (“PIMS”), which acts as the distributor of the Class A, Class B, Class C, Class L, Class M, Class R, Class X and Class Z shares. The Fund compensates PIMS for distributing and servicing the Fund’s Class A, Class B, Class C, Class L, Class M, Class R and Class X shares, pursuant to plans of distribution (the “Class A, B, C, L, M, R and X Plans”), regardless of expenses actually incurred. The distribution fees are accrued daily and payable monthly. No distribution or service fees are paid to PIMS as distributor of the Class Z shares of the Fund. Pursuant to the Class A, B, C, L, M, R and X Plans, the Fund compensates PIMS for distribution related activities at an annual rate of up to .30 of 1%, 1%, 1%, .50 of 1%, 1%, .75 of 1% and 1% of the average daily net assets of the Class A, B, C, L, M, R and X shares, respectively. For the ten-month period ended August 31, 2007, PIMS contractually agreed to limit such fees to .25 of 1% of the average daily net assets of the Class A shares

| | |

| 32 | | Visit our website at www.jennisondryden.com |

through February 28, 2008 and .50% of 1% of the average daily net assets of the Class R shares.

PIMS has advised the Fund that it has received approximately $517,400 in front-end sales charges resulting from sales of Class A shares, during the ten-month period ended August 31, 2007. From these fees, PIMS paid such sales charges to affiliated broker-dealers, which in turn paid commissions to salespersons and incurred other distribution costs.

PIMS has advised the Fund that for the ten-month period ended August 31, 2007, it received approximately $98,500, $3,600, $117,900 and $14,400 in contingent deferred sales charges imposed upon certain redemptions by Class B, Class C, Class M and Class X shareholders, respectively.

PI, PIMS and Jennison are indirect, wholly-owned subsidiaries of Prudential Financial, Inc. (“Prudential”).

The Fund, along with other affiliated registered investment companies (the “Funds”), is a party to a Syndicated Credit Agreement (“SCA”) with two banks. The SCA, which was renewed on October 27, 2006, provides for a commitment of $500 million. Interest on any borrowings under the SCA is incurred at contracted market rates and a commitment fee for the unused amount would be accrued daily and paid quarterly. The Funds pay a commitment fee of .07 of 1% of the unused portion of the renewed SCA. The expiration date of the renewed SCA is October 26, 2007. The SCA is in the process of being renewed through October 24, 2008. For the period from October 29, 2005 through October 26, 2006, the Funds paid a commitment fee of .0725 of 1% of the unused portion of the agreement. The purpose of the SCA is to provide an alternative source of temporary funding for capital share redemptions.

The Fund utilized the line of credit during the ten-month period ended August 31, 2007. The average daily balance for the 5 days the Fund had an outstanding balance was approximately $1,892,400 at a weighted average interest rate of approximately 5.45%. At August 31, 2007, the Fund had an outstanding loan amount of approximately $856,000.

Note 3. Other Transactions with Affiliates

Prudential Mutual Fund Services LLC (“PMFS”), an affiliate of PI and an indirect, wholly-owned subsidiary of Prudential, serves as the Fund’s transfer agent. Transfer agent fees and expenses in the Statement of Operations include certain out-of-pocket expenses paid to non-affiliates, where applicable.

Notes to Financial Statements

continued